Embed Size (px)

Citation preview

Multimedia Communications

0

October 2013

Multimedia Communications

José Salas PiresPortugal Telecom

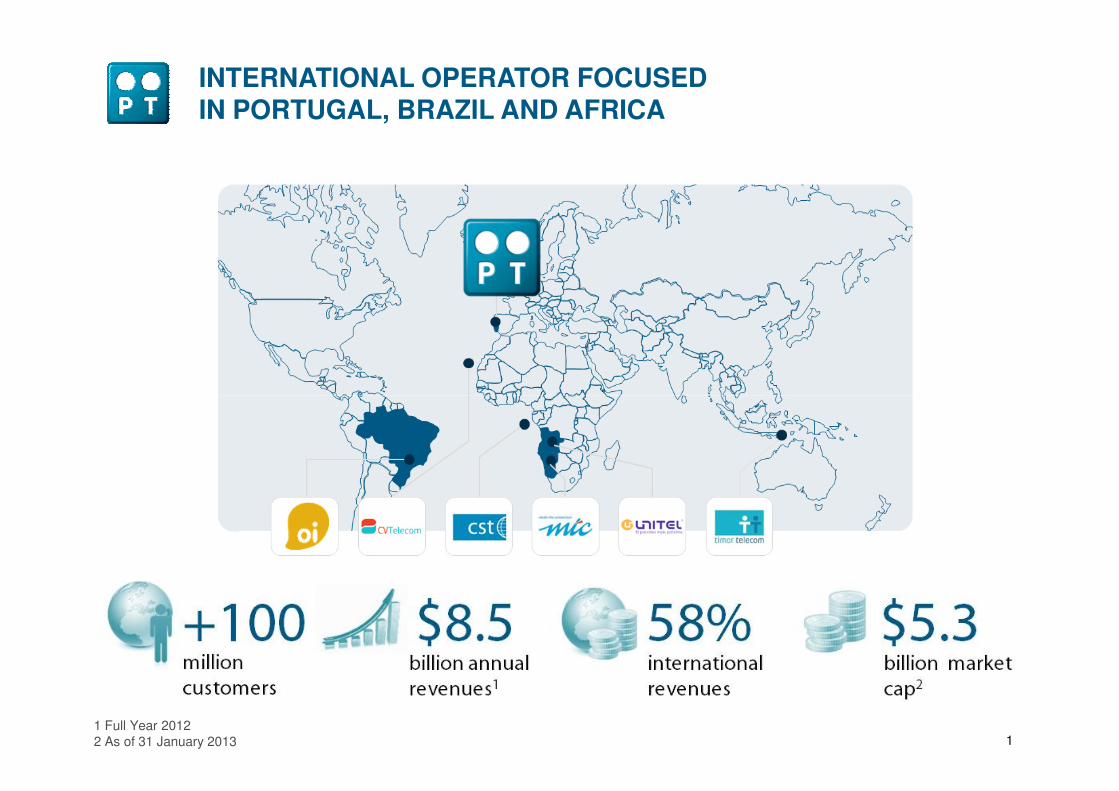

INTERNATIONAL OPERATOR FOCUSED IN PORTUGAL, BRAZIL AND AFRICA

11 Full Year 20122 As of 31 January 2013

$5.3

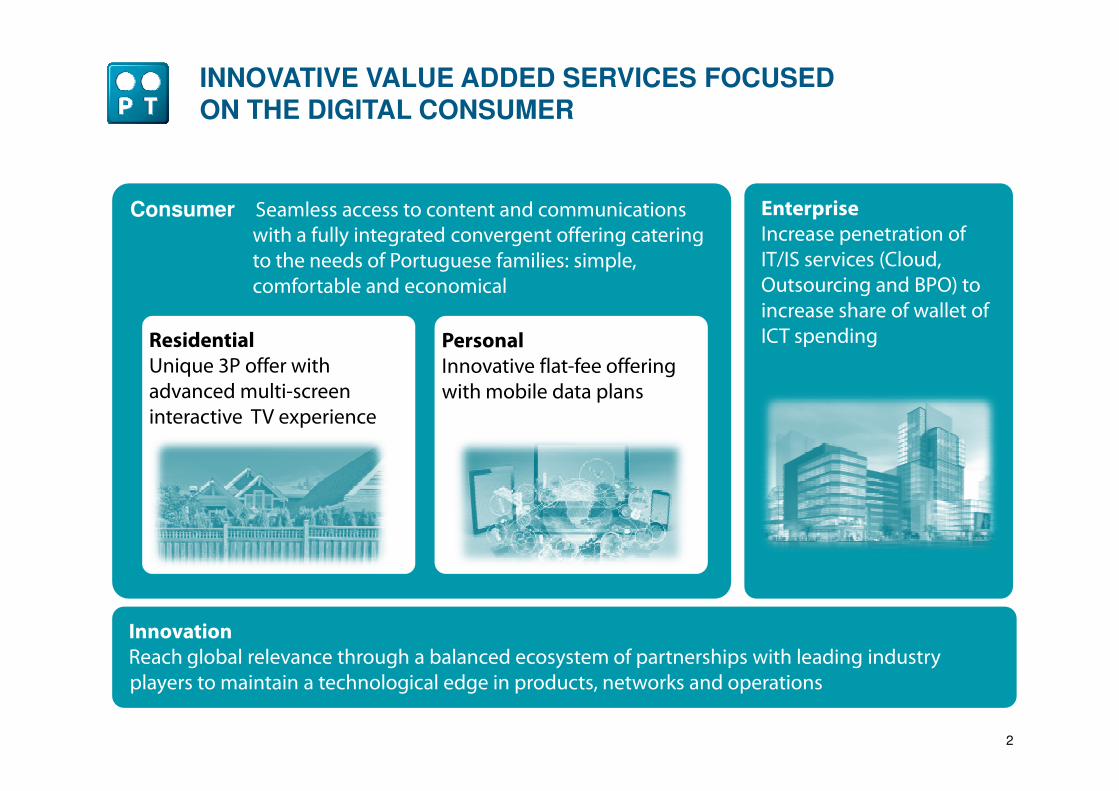

INNOVATIVE VALUE ADDED SERVICES FOCUSED ON THE DIGITAL CONSUMER

Consumer Seamless access to content and communications

with a fully integrated convergent offering catering

to the needs of Portuguese families: simple,

comfortable and economical

Personal

Innovative flat-fee offering

with mobile data plans

Enterprise

Increase penetration of

IT/IS services (Cloud,

Outsourcing and BPO) to

increase share of wallet of

ICT spendingResidential

Unique 3P offer with

advanced multi-screen

2

with mobile data plansadvanced multi-screen

interactive TV experience

Innovation

Reach global relevance through a balanced ecosystem of partnerships with leading industry

players to maintain a technological edge in products, networks and operations

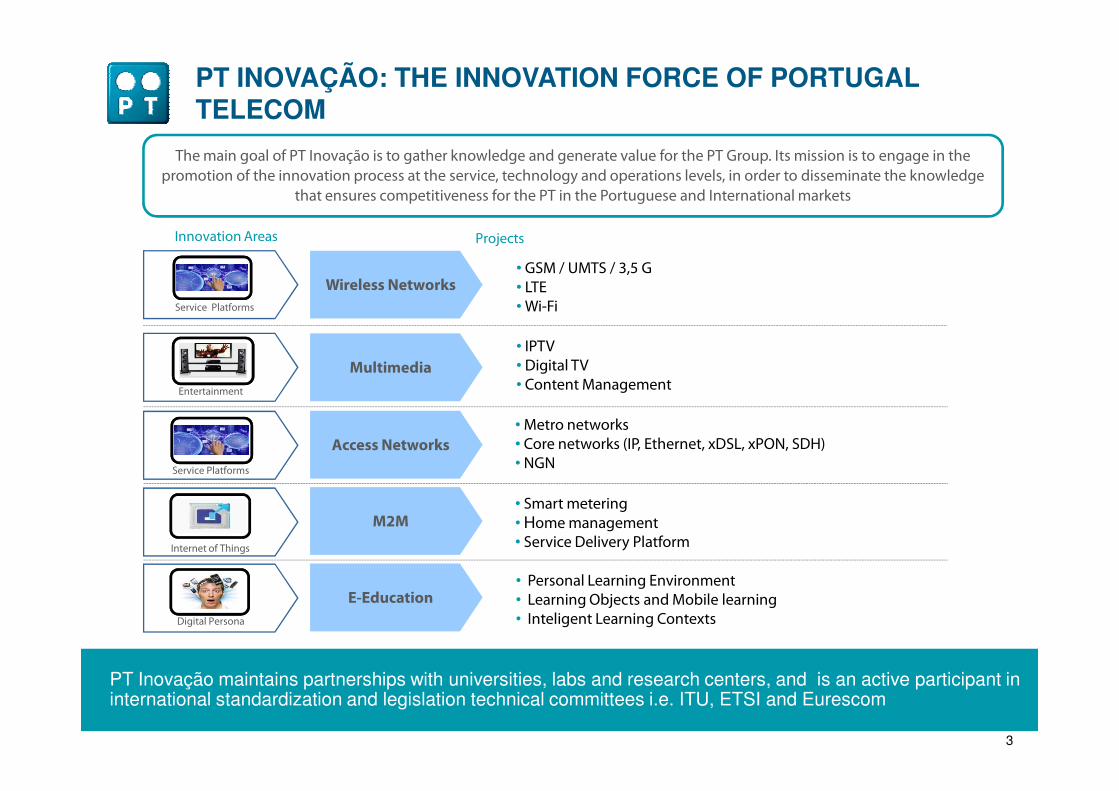

Multimedia

The main goal of PT Inovação is to gather knowledge and generate value for the PT Group. Its mission is to engage in the

promotion of the innovation process at the service, technology and operations levels, in order to disseminate the knowledge

that ensures competitiveness for the PT in the Portuguese and International markets

Wireless Networks• GSM / UMTS / 3,5 G• LTE•Wi-Fi

• IPTV• Digital TV• Content Management

Service Platforms

Innovation Areas Projects

Entertainment

PT INOVAÇÃO: THE INNOVATION FORCE OF PORTUGAL TELECOM

3

E-Education

M2M

Access Networks

•Metro networks• Core networks (IP, Ethernet, xDSL, xPON, SDH)• NGN

• Smart metering• Home management• Service Delivery Platform

• Personal Learning Environment• Learning Objects and Mobile learning• Inteligent Learning Contexts

Entertainment

Service Platforms

Internet of Things

Digital Persona

• PT Inovação maintains partnerships with universities, labs and research centers, and is an active participant in international standardization and legislation technical committees i.e. ITU, ETSI and Eurescom

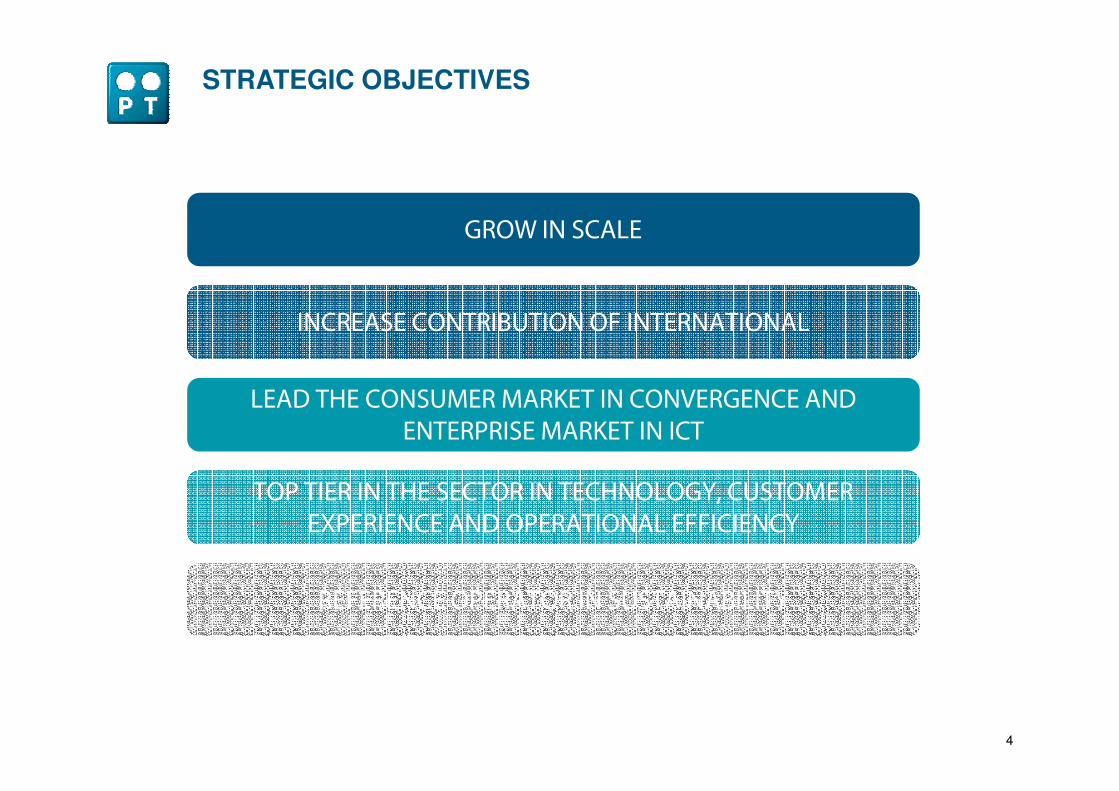

STRATEGIC OBJECTIVES

GROW IN SCALE

INCREASE CONTRIBUTION OF INTERNATIONAL

LEAD THE CONSUMER MARKET IN CONVERGENCE AND

4

LEAD THE CONSUMER MARKET IN CONVERGENCE AND

ENTERPRISE MARKET IN ICT

TOP TIER IN THE SECTOR IN TECHNOLOGY, CUSTOMER

EXPERIENCE AND OPERATIONAL EFFICIENCY

REFERENCE OPERATOR IN SUSTAINABILITY

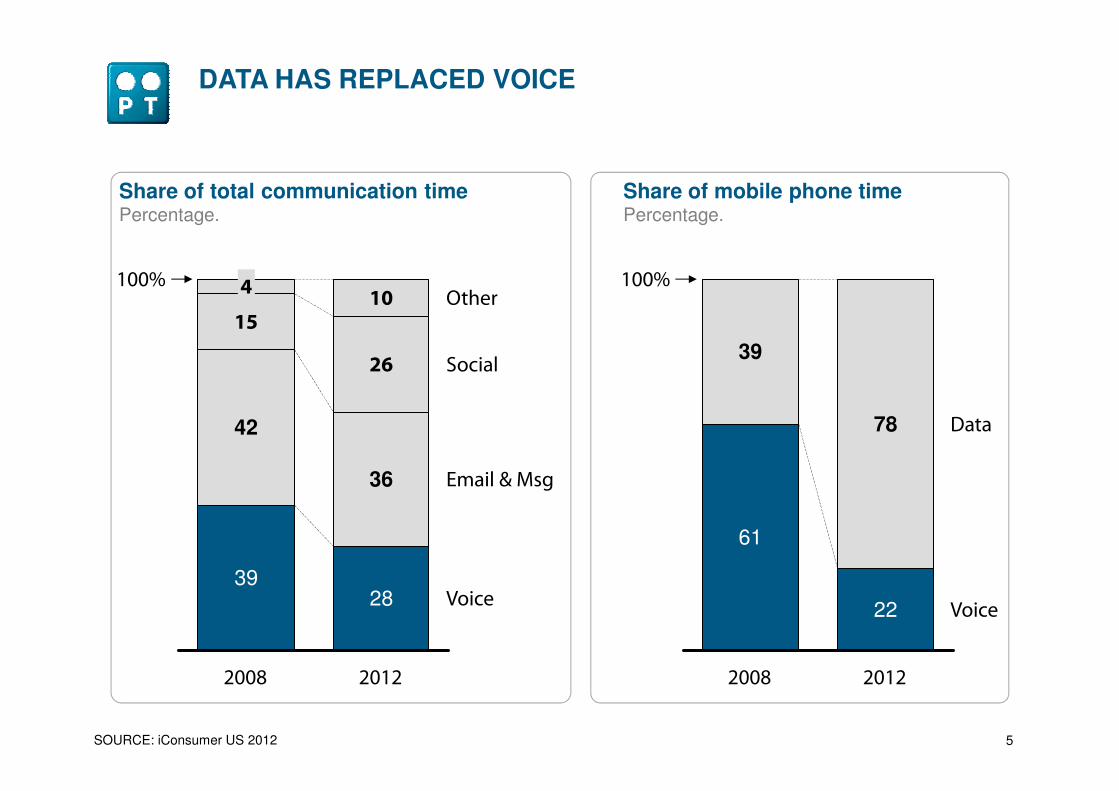

DATA HAS REPLACED VOICE

Social

Other

26

1015

100% 4

Share of total communication timePercentage.

100%

39

Share of mobile phone timePercentage.

5SOURCE: iConsumer US 2012

Voice

Email & Msg

2012

28

36

2008

39

42

Voice22

Data

2012

78

2008

61

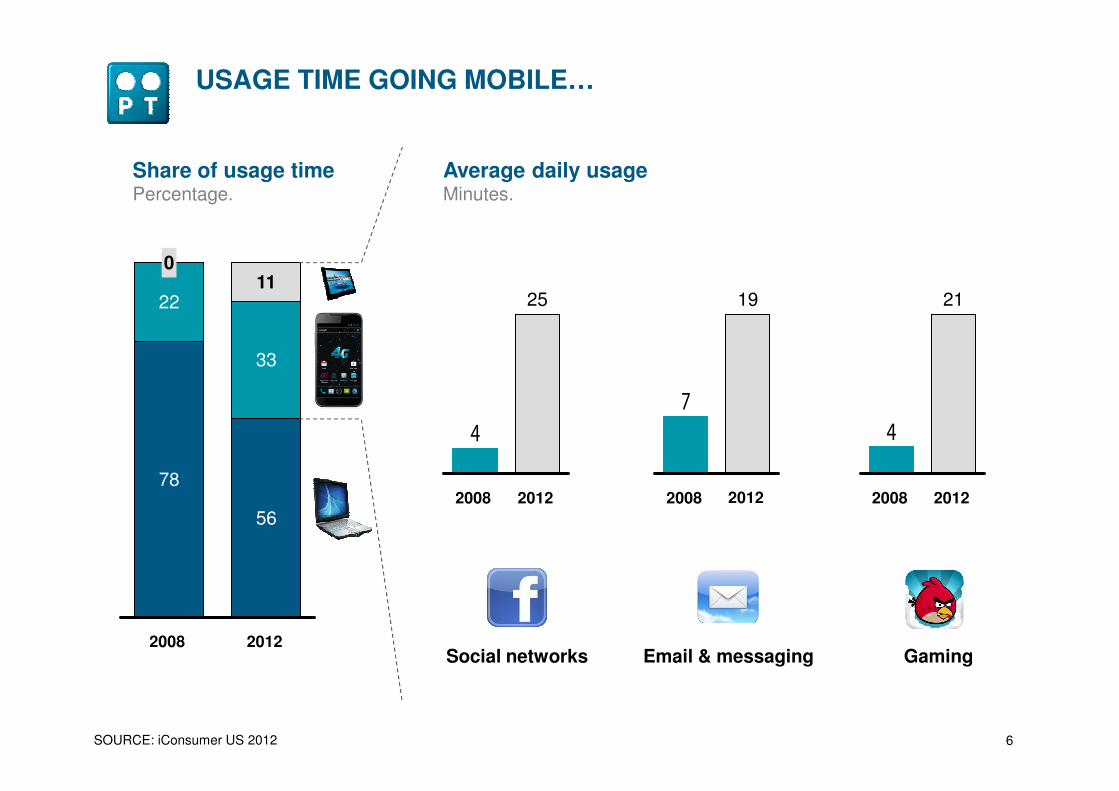

USAGE TIME GOING MOBILE…

25

7

19 21

011

22

33

Share of usage timePercentage.

Average daily usageMinutes.

6

Social networks Email & messaging Gaming

4

2008 2012

7

20122008

4

2008 2012

SOURCE: iConsumer US 2012

2012

56

2008

78

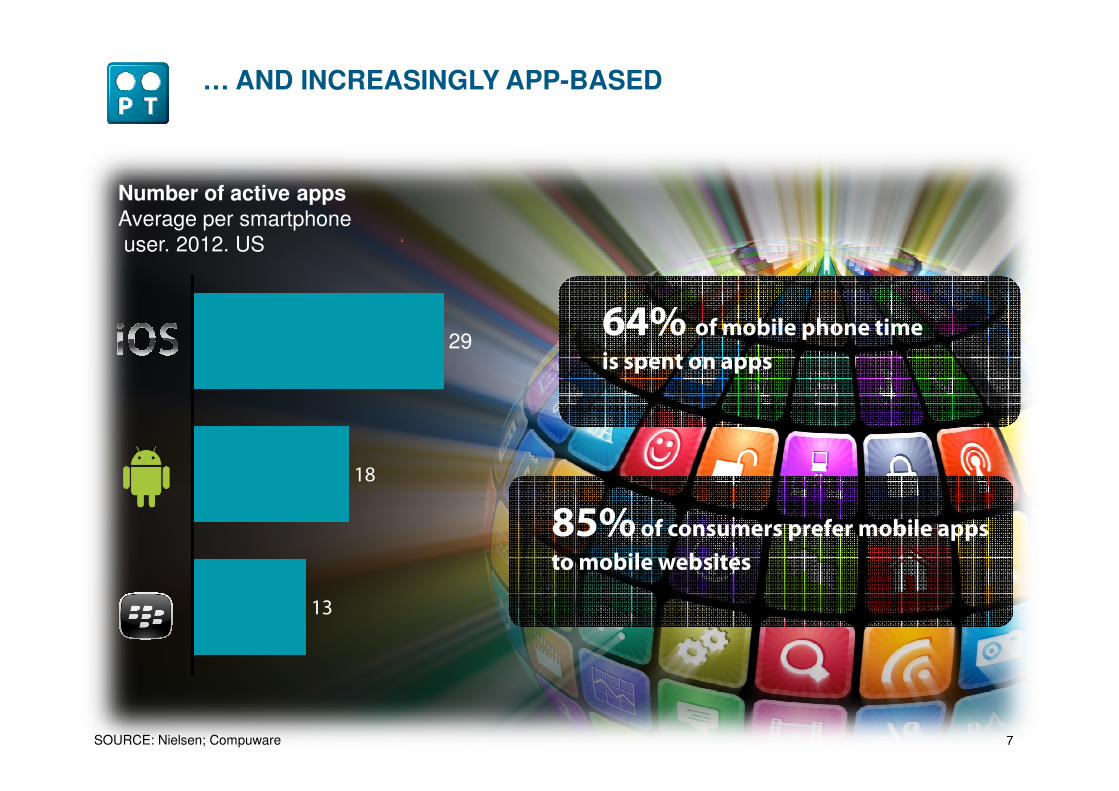

… AND INCREASINGLY APP-BASED

29

Number of active appsAverage per smartphoneuser. 2012. US

64% of mobile phone time

is spent on apps

7SOURCE: Nielsen; Compuware

18

13

85% of consumers prefer mobile apps

to mobile websites

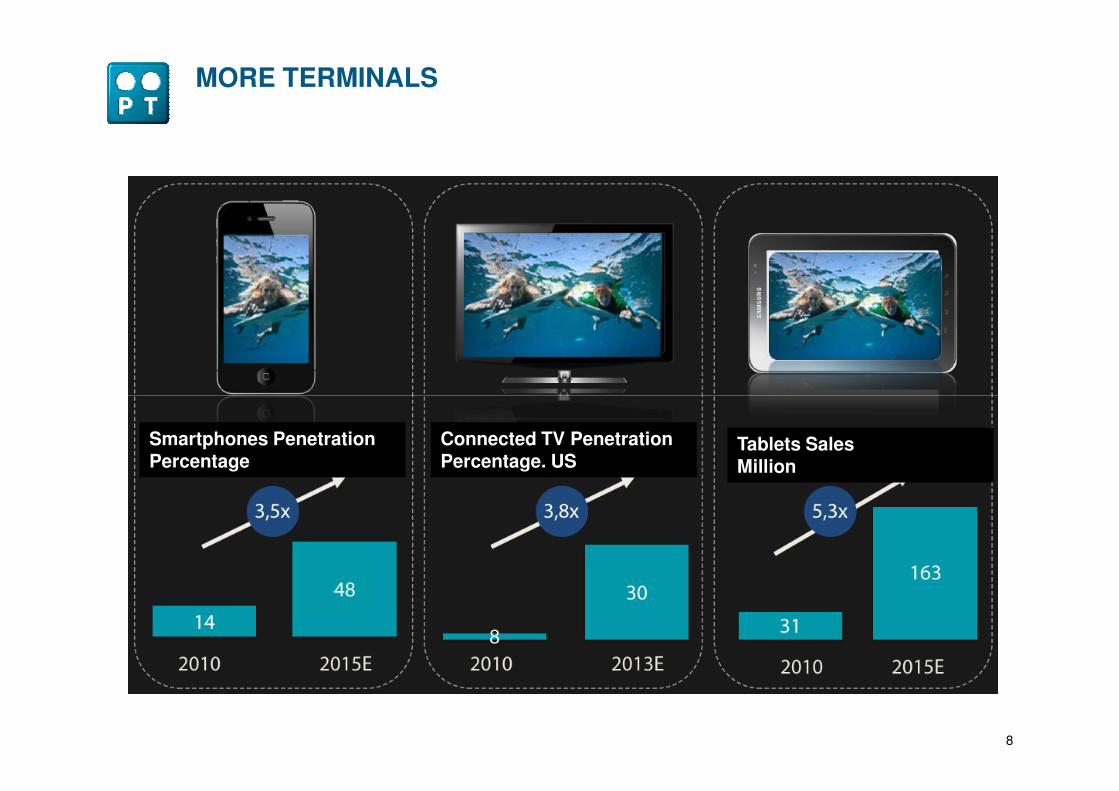

MORE TERMINALS

8

Smartphones PenetrationPercentage

Connected TV PenetrationPercentage. US

Tablets SalesMillion

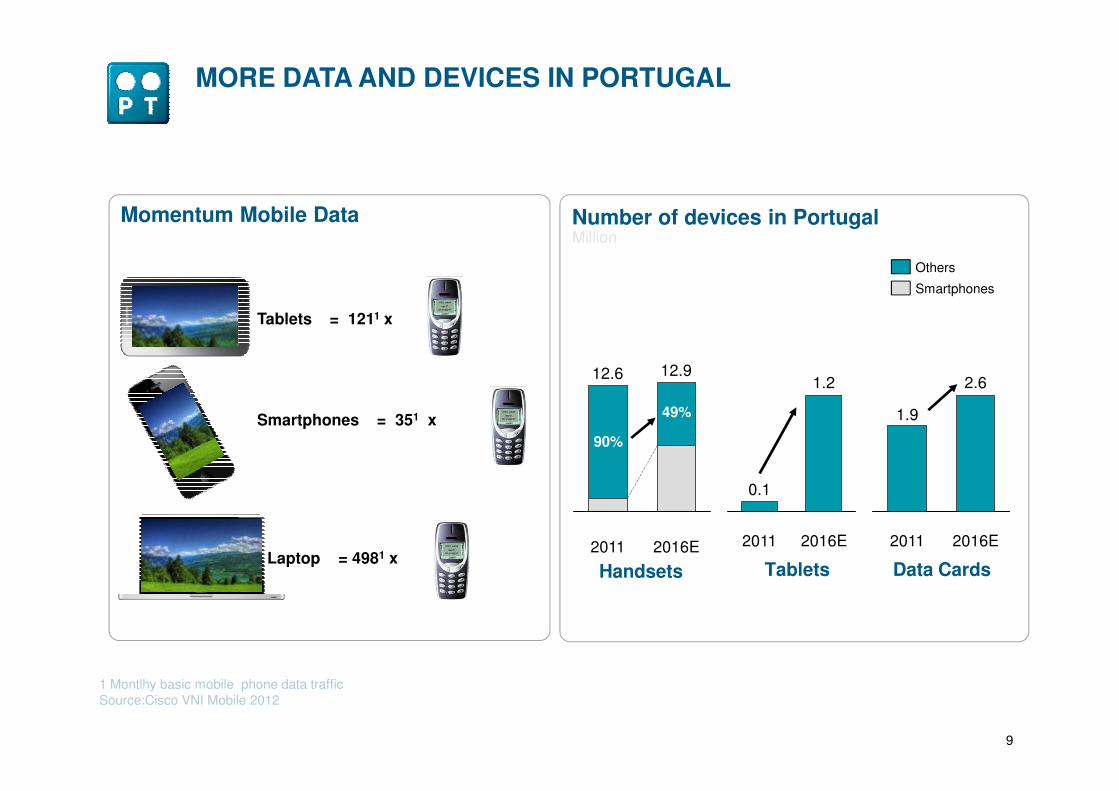

Number of devices in PortugalMillion

Momentum Mobile Data

Tablets = 1211 x

12.912.61.2 2.6

Smartphones

Others

MORE DATA AND DEVICES IN PORTUGAL

9

Laptop = 4981 x

Smartphones = 351 x

2016E

49%

2011

90%

Handsets

2016E2011

0.1

Tablets

2016E2011

1.9

Data Cards

1 Montlhy basic mobile phone data trafficSource:Cisco VNI Mobile 2012

TV

• INTERACTIVITY

• NON LINEAR SERVICES

INTERNET

• MOBILITY

• DATA CONSUMPTION

Fixed Mobile

Convergence

• TV

• VOICE

•

TRENDS IN CUSTOMER BEHAVIOUR

10

• INTERNET

Anytime

Anywhere

Any Service

Any Equipment

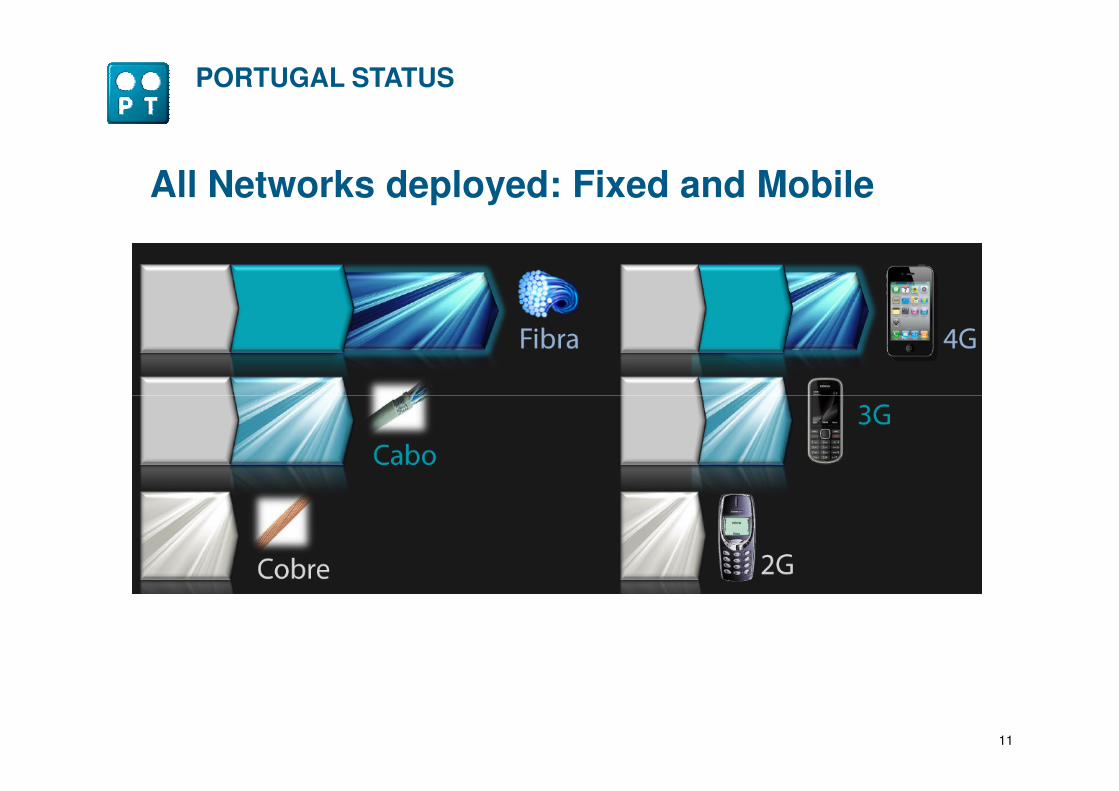

PORTUGAL STATUS

All Networks deployed: Fixed and Mobile

11

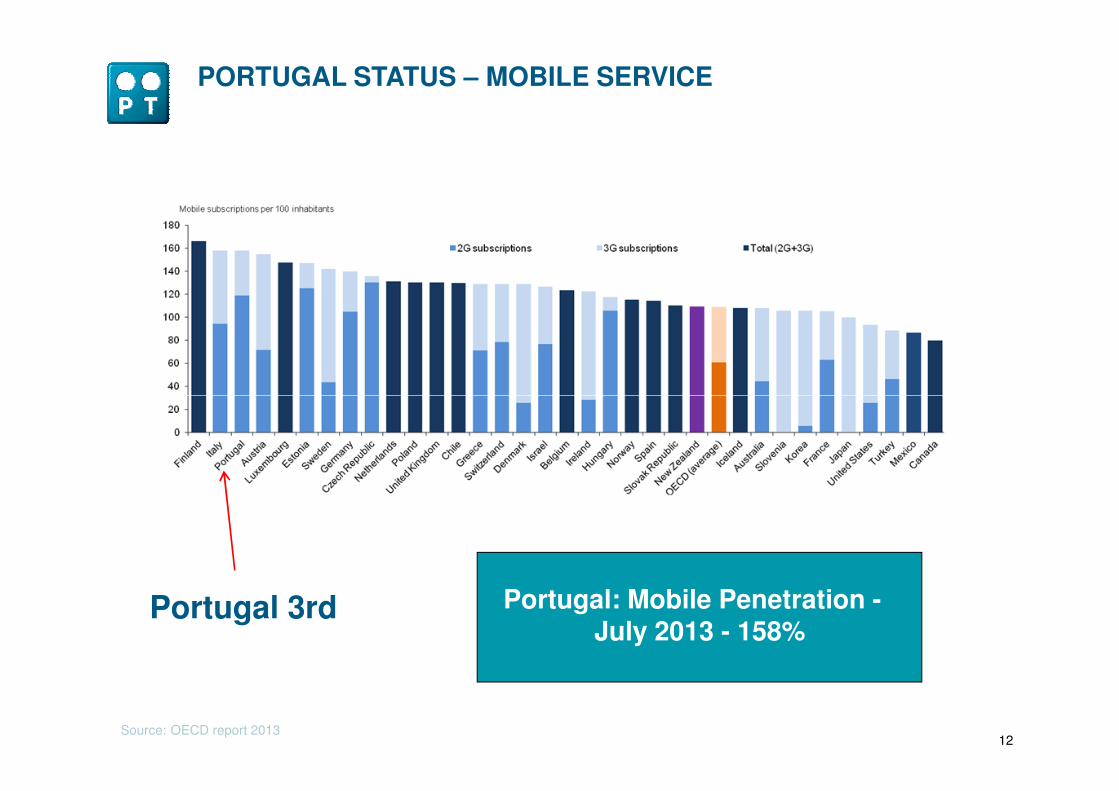

PORTUGAL STATUS – MOBILE SERVICE

12Source: OECD report 2013

Portugal: Mobile Penetration -July 2013 - 158%

Portugal 3rd

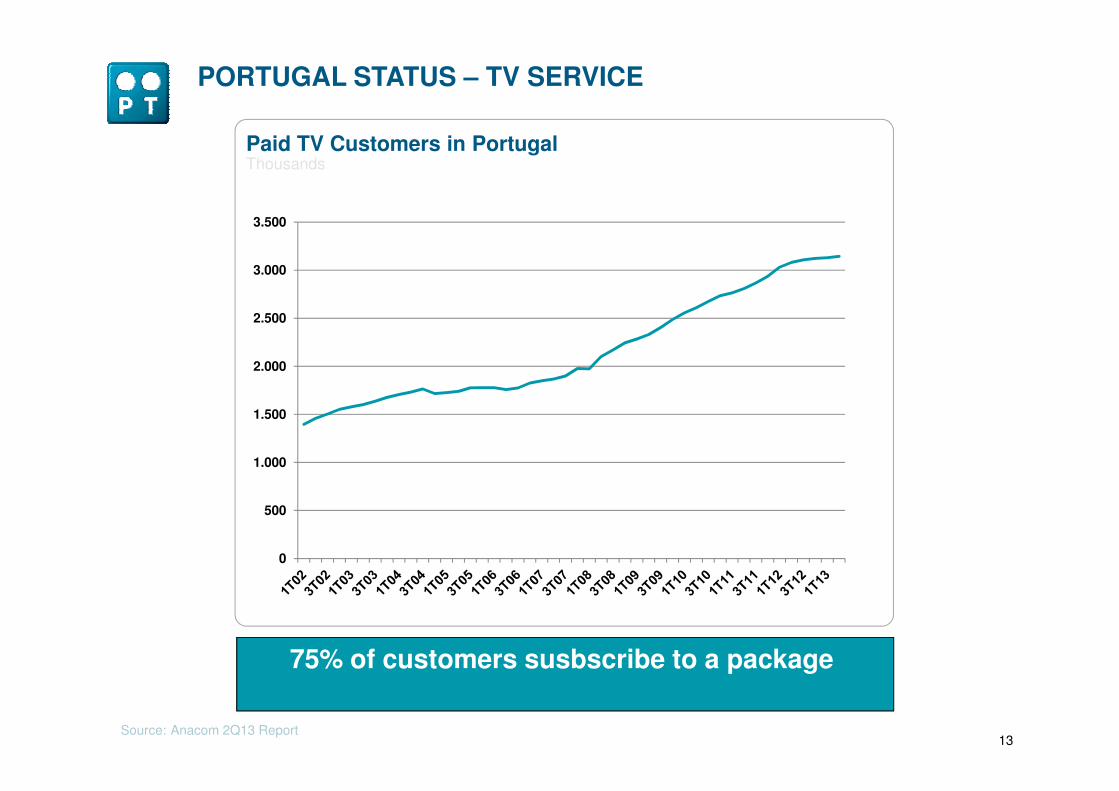

PORTUGAL STATUS – TV SERVICE

2.000

2.500

3.000

3.500

Paid TV Customers in PortugalThousands

13Source: Anacom 2Q13 Report

0

500

1.000

1.500

75% of customers susbscribe to a package

MEO IS INNOVATION WORLDWIDE

14

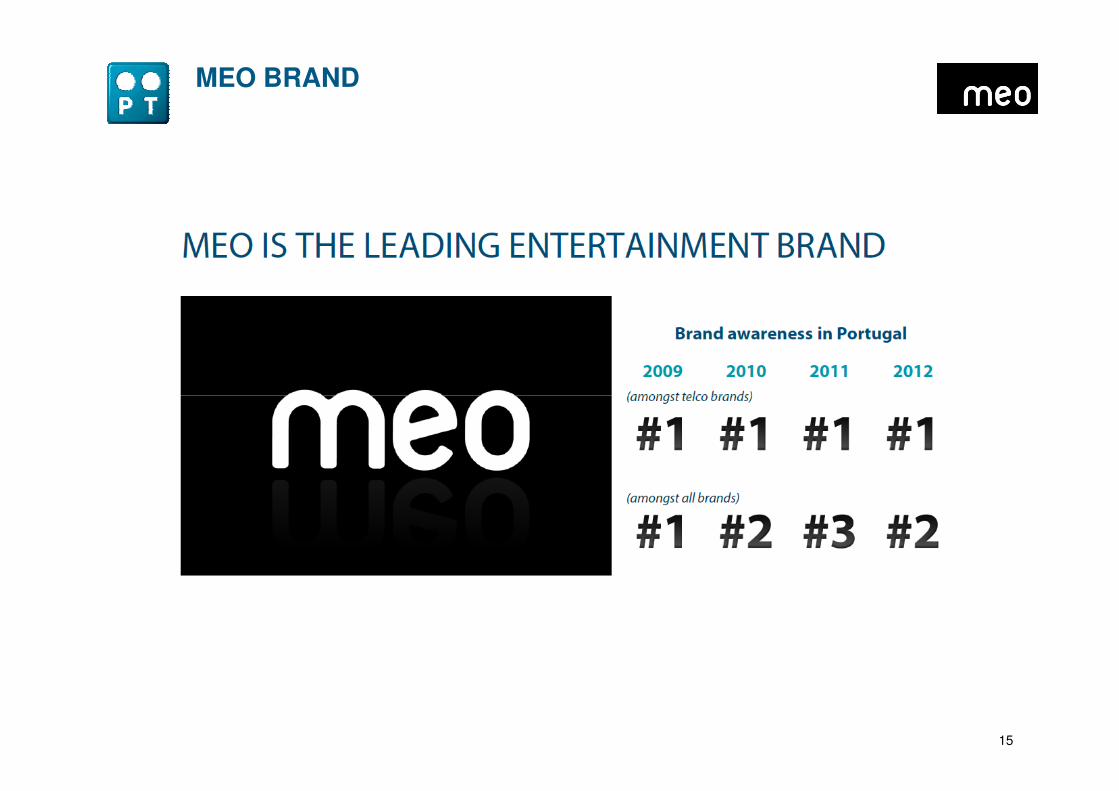

MEO BRAND

15

MEO IS INNOVATION WORLWIDE

16

MEO INNOVATIVE SERVICES

INTERATIVITY

•Social Networks, Sport, Kids / Kiddy, News

BENFICA TVMEO KIDDYSAPO NOTÍCIAS

17

• 170 channels (HD and 3D channels)

• Video On Demand

• Fast zapping with PIP

• MEO Kanal – MEO Community

• Cloud TV and MEO Cloud

MEO INNOVATIVE SERVICES

18Este documento é propriedade intelectual da PT e fica proibida a sua utilização ou propagação sem expressa autorização escrita

• Cloud TV and MEO Cloud

• Meo Go: Multi screen

• Music Box

• MEO Games

• Restart TV / Catch-up

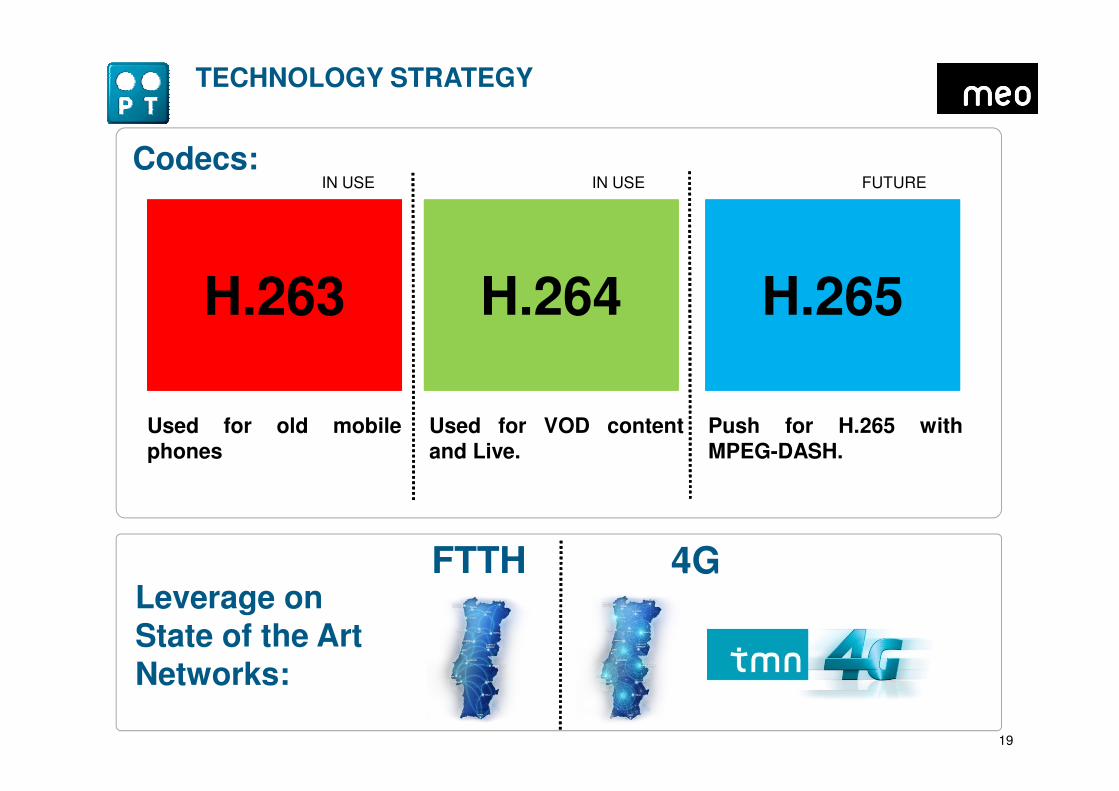

H.264H.264 H.265H.265H.263H.263

IN USE IN USE FUTURE

TECHNOLOGY STRATEGY

Codecs:

19

Used for old mobilephones

Used for VOD contentand Live.

Push for H.265 withMPEG-DASH.

Leverage on State of the Art Networks:

FTTH 4G

20

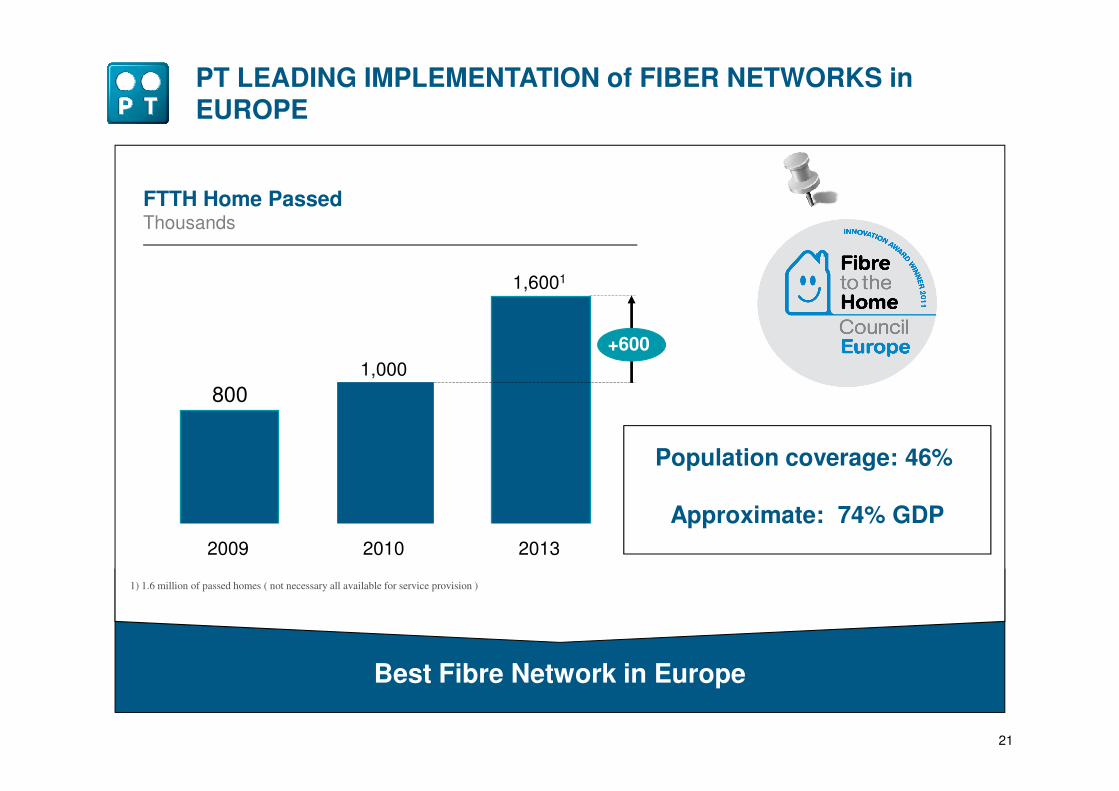

FTTH Network

8001,000

1,6001

+600

FTTH Home Passed Thousands

PT LEADING IMPLEMENTATION of FIBER NETWORKS in EUROPE

21

Best Fibre Network in Europe

800

2009 20132010

Population coverage: 46%

Approximate: 74% GDP

1) 1.6 million of passed homes ( not necessary all available for service provision )

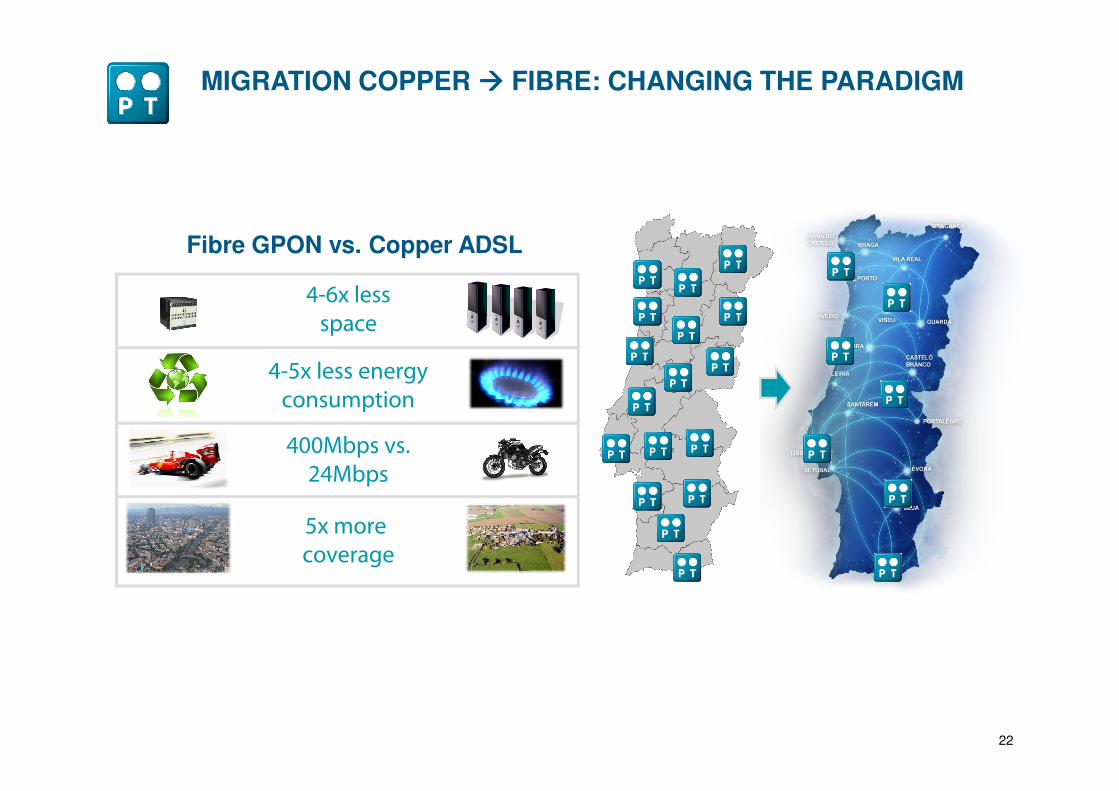

Fibre GPON vs. Copper ADSL

MIGRATION COPPER ���� FIBRE: CHANGING THE PARADIGM

4-6x less

space

4-5x less energy

consumption

22

consumption

400Mbps vs.

24Mbps

5x more

coverage

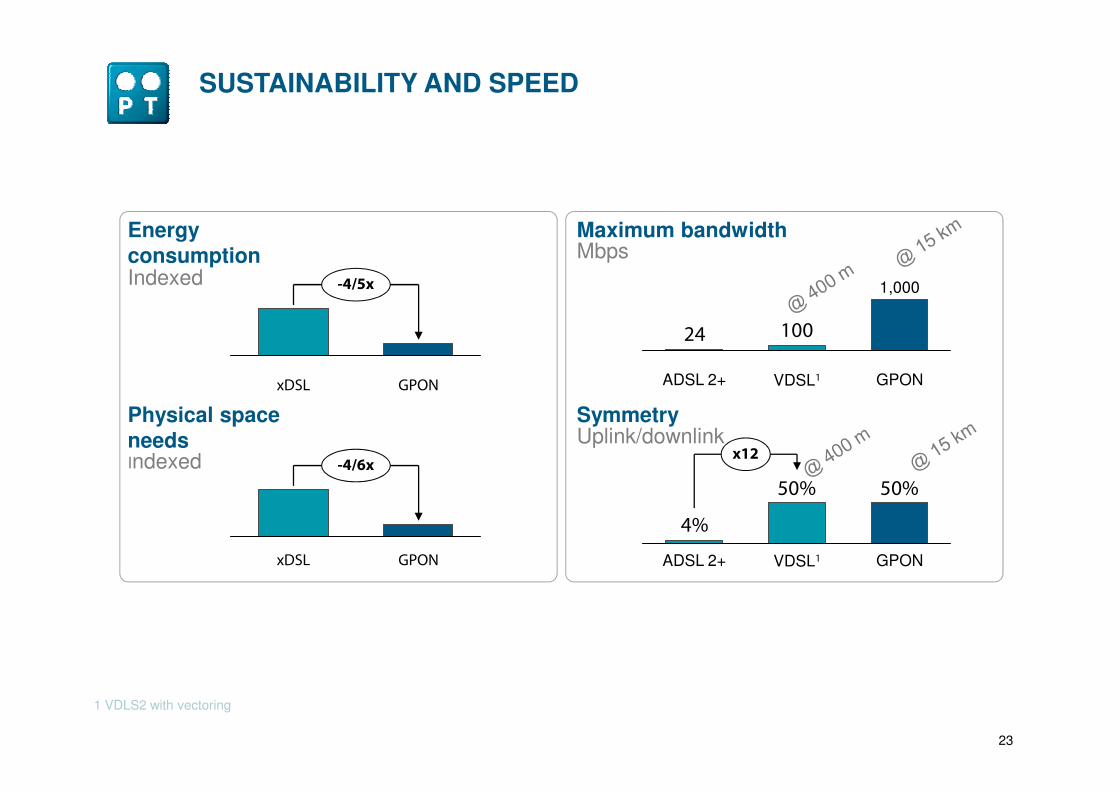

SUSTAINABILITY AND SPEED

Energy consumptionIndexed

Maximum bandwidthMbps

xDSL

-4/5x

GPON

10024

GPON

1,000

VDSL1ADSL 2+

23

1 VDLS2 with vectoring

GPON

-4/6x

xDSL

50%50%

4%

x12

GPONVDSL1ADSL 2+

Physical space needsIndexed

SymmetryUplink/downlink

FIBRE ADVANTAGES

Almost no civil work is needed:widely spread duct infrastructure

RF-Overlay:Not possible with copper

24

Street cabinets require municipal licenses in Portugal

Not possible with copper

Fibre has attractive cost structure (Capex and Opex)

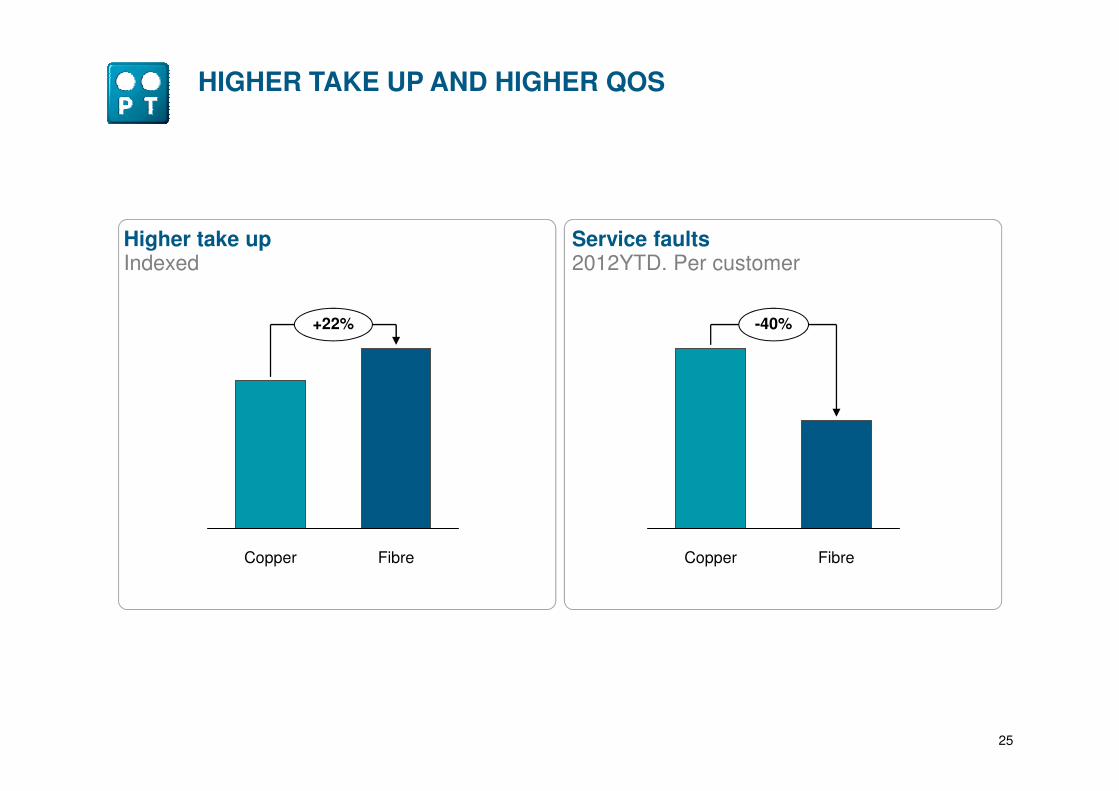

HIGHER TAKE UP AND HIGHER QOS

Indexed

+22%

Service faults2012YTD. Per customer

Higher take up

-40%

25

FibreCopper FibreCopper

PT BUILT A FUTURE PROOF ACCESS NETWORK

GPON today allows for 2.5Gbps per PON

26

NGPON2 will allow in the future for 40Gbps per PON

LIS-151138090911

Speed

Quality

Simultaneity

27

Mobile Networks

Simultaneity

QoE: QUALITY OF EXPERIENCE

Real Time Interaction: Games and Browsing

Bandwidth

28

MEO GAMES also available “FIBER IN THE AIR”

Bandwidth

4x less

latency

CAPACITY

29

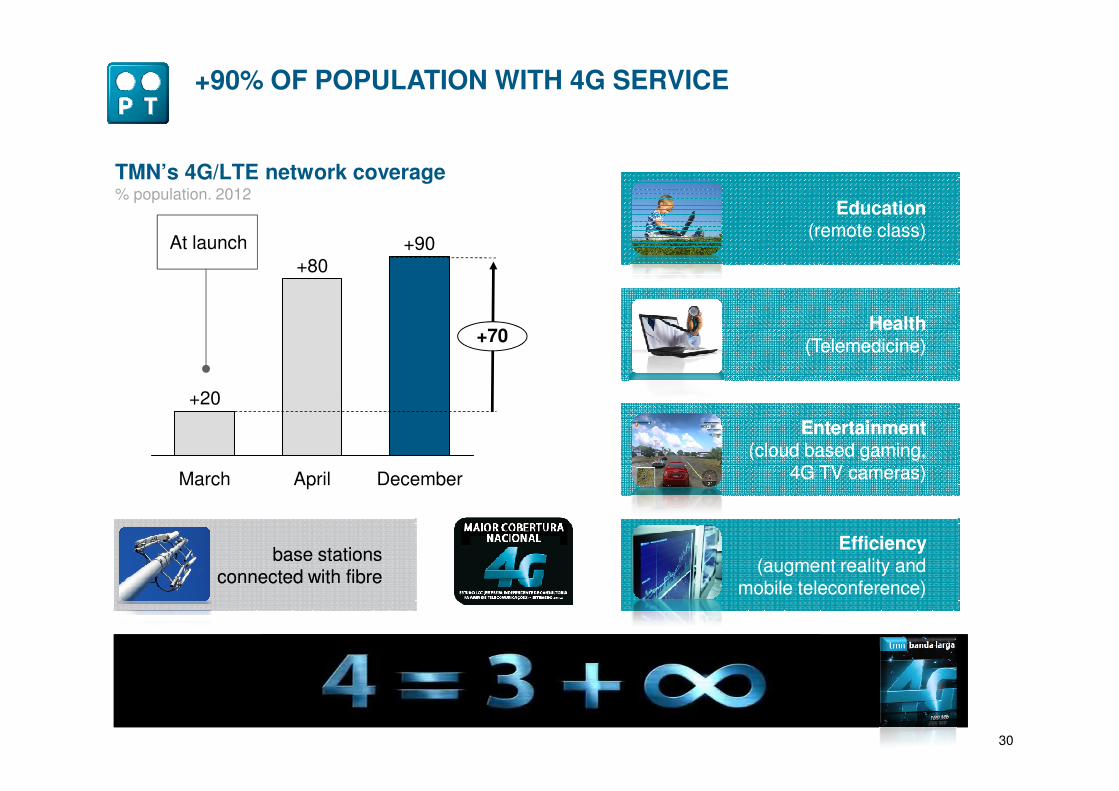

+90% OF POPULATION WITH 4G SERVICE

TMN’s 4G/LTE network coverage% population. 2012

Education(remote class)

Education(remote class)

Health(Telemedicine)

Health(Telemedicine)

At launch

+70

+90+80

+20

30

Efficiency (augment reality and

mobile teleconference)

Efficiency (augment reality and

mobile teleconference)

Entertainment (cloud based gaming,

4G TV cameras)

Entertainment (cloud based gaming,

4G TV cameras)

base stations connected with fibre

base stations connected with fibre

DecemberAprilMarch

+20

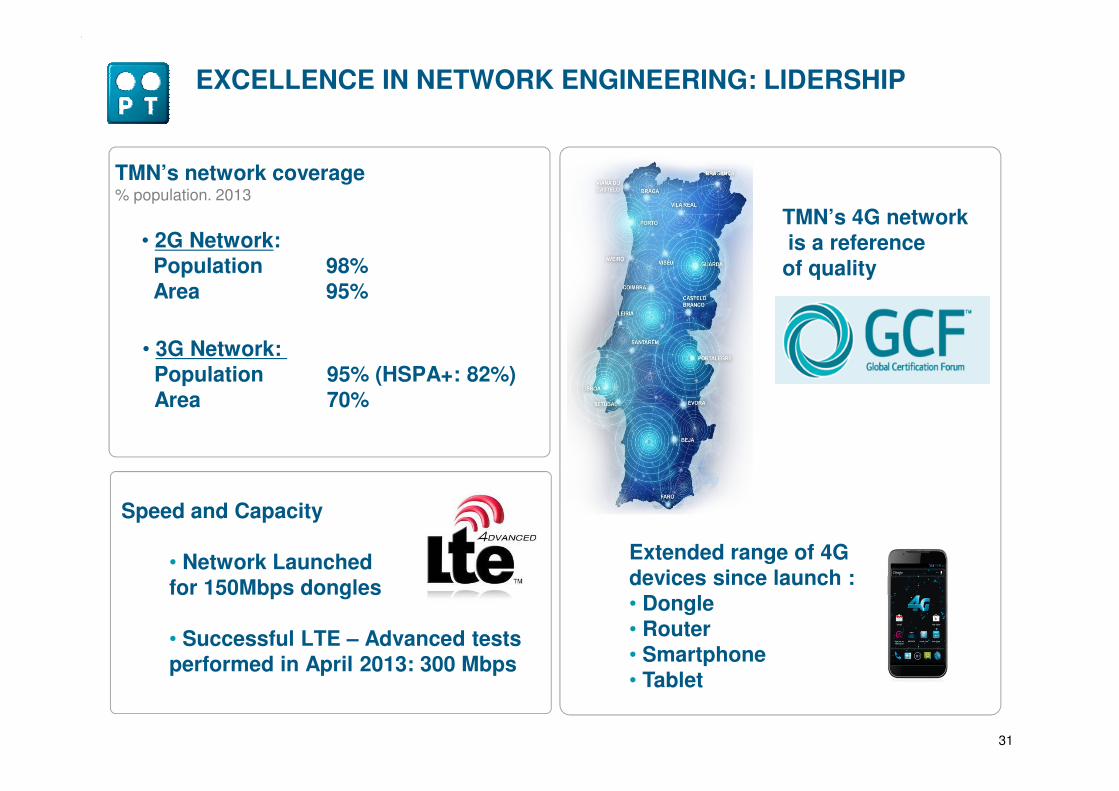

EXCELLENCE IN NETWORK ENGINEERING: LIDERSHIP

TMN’s network coverage% population. 2013

TMN’s 4G networkis a reference of quality

• 2G Network: Population 98%Area 95%

• 3G Network:Population 95% (HSPA+: 82%) Area 70%

31

Extended range of 4G devices since launch :• Dongle• Router• Smartphone• Tablet

Speed and Capacity

• Network Launched for 150Mbps dongles

• Successful LTE – Advanced tests performed in April 2013: 300 Mbps

Area 70%

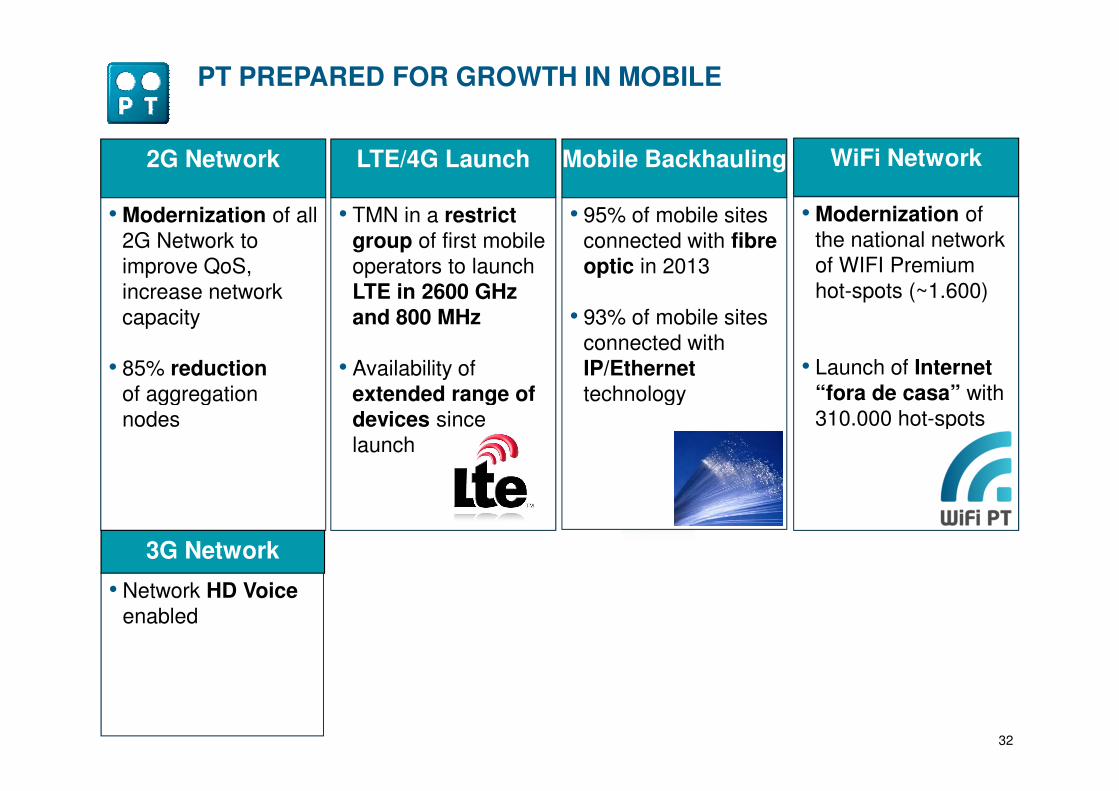

WiFi Network

• Modernization of the national network of WIFI Premium hot-spots (~1.600)

• Launch of Internet “fora de casa” with

2G Network

• Modernization of all 2G Network to improve QoS, increase network capacity

• 85% reductionof aggregation

PT PREPARED FOR GROWTH IN MOBILE

Mobile Backhauling

• 95% of mobile sites connected with fibre optic in 2013

• 93% of mobile sites connected with IP/Ethernet technology

LTE/4G Launch

• TMN in a restrict group of first mobile operators to launch LTE in 2600 GHz and 800 MHz

• Availability of extended range of

32

“fora de casa” with310.000 hot-spots

of aggregation nodes

3G Network

• Network HD Voice enabled

technologyextended range of devices since launch

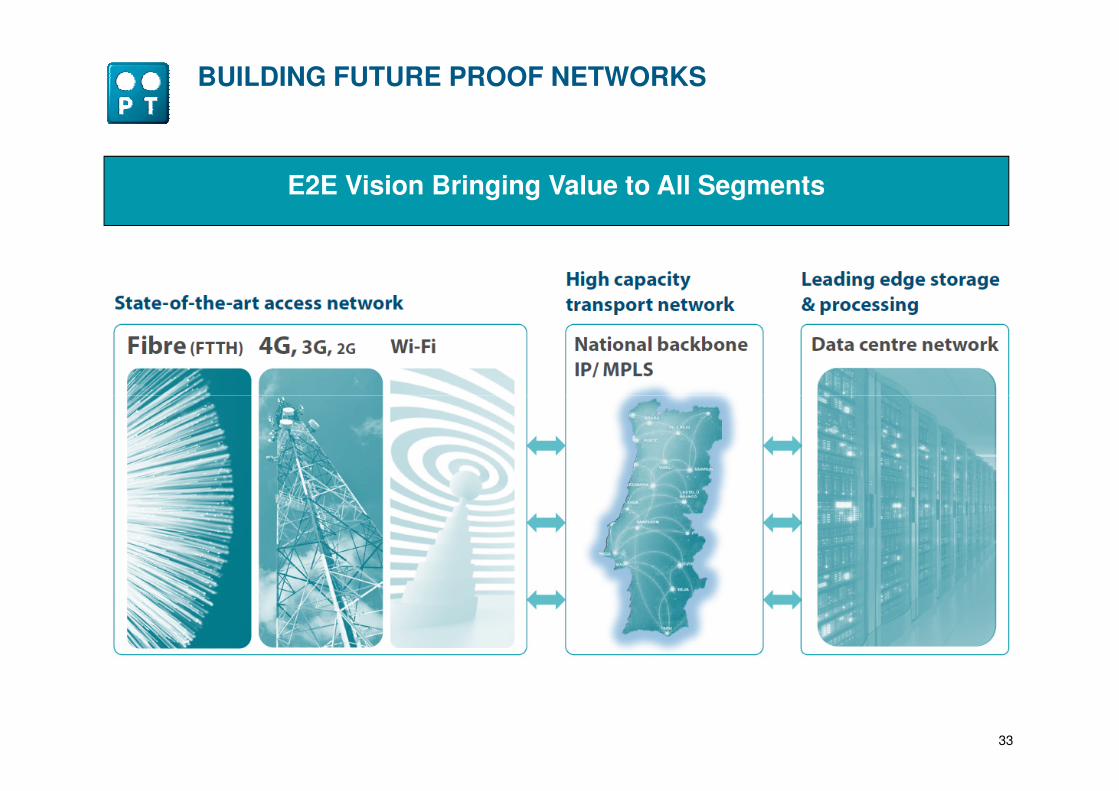

BUILDING FUTURE PROOF NETWORKS

E2E Vision Bringing Value to All Segments

33

34

Thank you

![[Type text] - Telecom Asia · PDF fileVoLTE implementation can take different paths based on factors such as each operator’s spectrum ... IP Multimedia Subsystem ... all-IP multimedia](https://img.pdfslide.net/doc/110x75/5a9f71427f8b9a84178cd515/type-text-telecom-asia-implementation-can-take-different-paths-based-on-factors.jpg)