Embed Size (px)

Citation preview

Pension freedoms Opportunities and compliance challenges for Wealth

firms

Neil Walkling – May 2015

2

Agenda – pension freedoms

1. Background and context

2. Overview of the pension freedoms

3. Implications for professional advice market

4. Suitability considerations

5. Controls over advice quality and reducing risks

of poor outcomes

6. Key messages

1. Background & context

4

Government pension reform agenda

Flat rate state

pension

Auto

enrolment

Rising

state

pension

age

Charge caps

and

governance

Freedom

and

choice

2. Overview of the pension freedoms

6

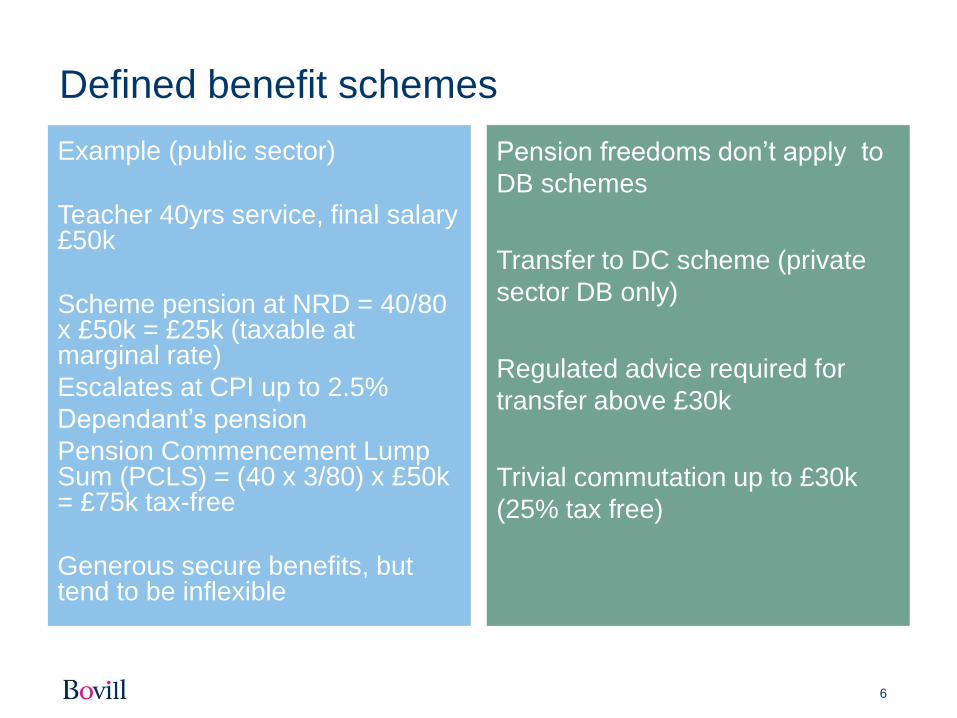

Defined benefit schemes

Example (public sector)

Teacher 40yrs service, final salary £50k

Scheme pension at NRD = 40/80 x £50k = £25k (taxable at marginal rate)

Escalates at CPI up to 2.5%

Dependant’s pension

Pension Commencement Lump Sum (PCLS) = (40 x 3/80) x £50k = £75k tax-free

Generous secure benefits, but tend to be inflexible

Pension freedoms don’t apply to

DB schemes

Transfer to DC scheme (private

sector DB only)

Regulated advice required for

transfer above £30k

Trivial commutation up to £30k

(25% tax free)

7

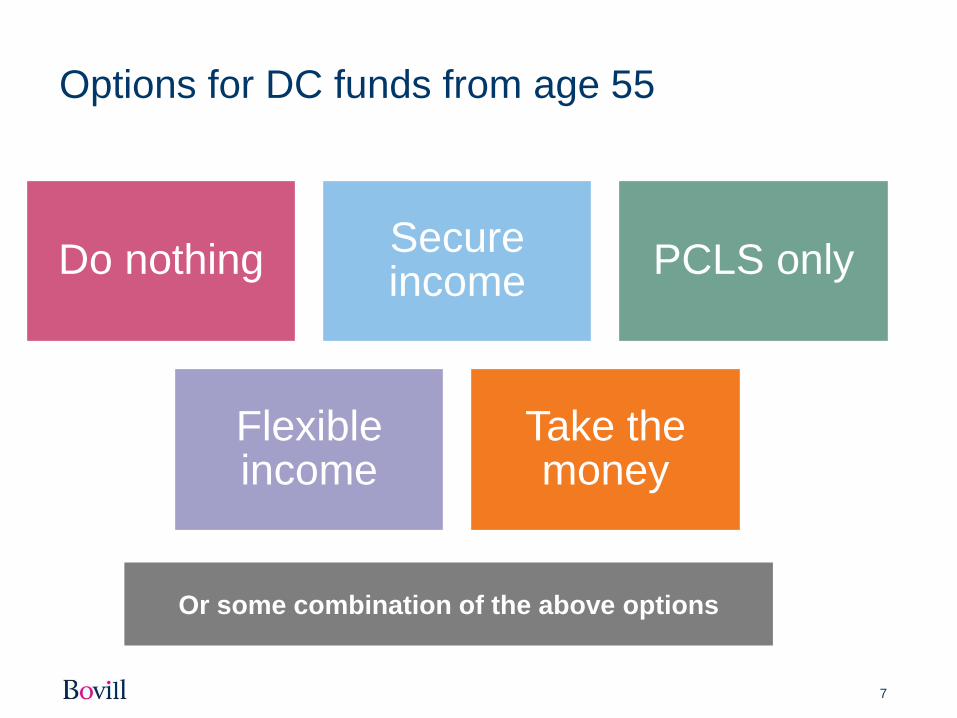

Options for DC funds from age 55

Do nothing Secure income

PCLS only

Flexible income

Take the money

Or some combination of the above options

8

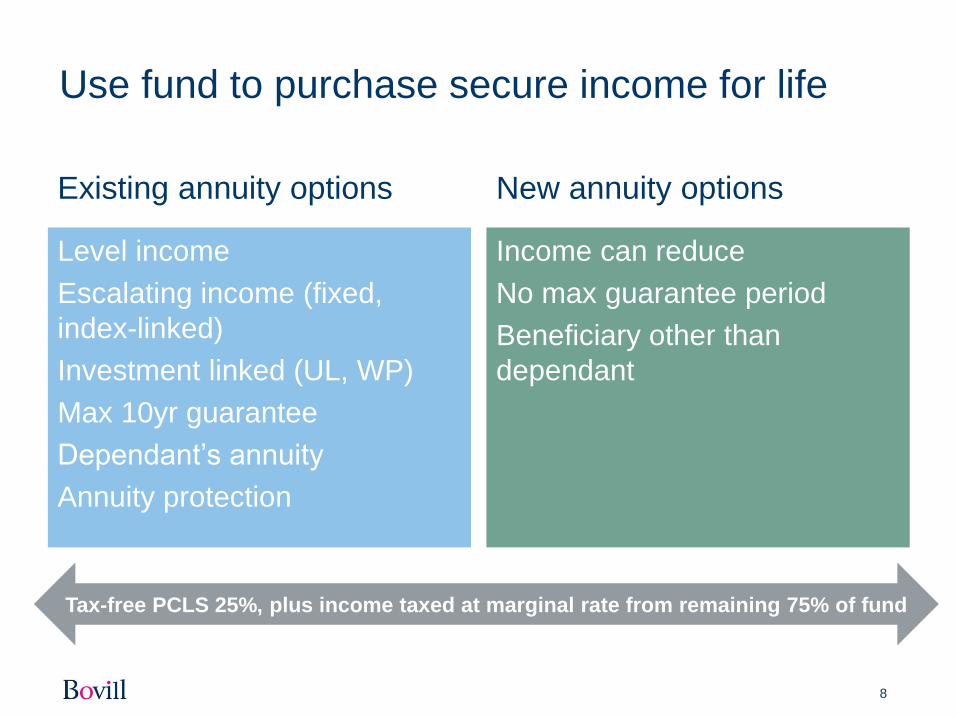

Use fund to purchase secure income for life

Existing annuity options

Level income

Escalating income (fixed,

index-linked)

Investment linked (UL, WP)

Max 10yr guarantee

Dependant’s annuity

Annuity protection

New annuity options

Income can reduce

No max guarantee period

Beneficiary other than

dependant

Tax-free PCLS 25%, plus income taxed at marginal rate from remaining 75% of fund

9

Annuities – value for money?

Scenario

Age 65, good health

£500K fund

£125k PCLS leaves £375k for annuity

Single life – no dependant’s pension

No guarantee period

Male 65

83

Quote 2

Inflation

linked

A: £23,323

B: £18,468

C: £20,198

A: £15,218

B: £11,933

C: £13,625

Quote 1

Level

annuity

Female 65

86

Expected age of death (England)

Level annuity

£363564

Level annuity

£424158

RPI @ 3%

£279404

RPI @ 3%

£342158

If client lives 7yrs longer than average

Level annuity

£504875

1.2% pa gross

Level annuity

£565544

2.0% pa gross

RPI @ 3%

£435068

0.6% pa gross

RPI @ 3%

£512295

1.1% pa gross

Gross: before income tax at marginal rate

10

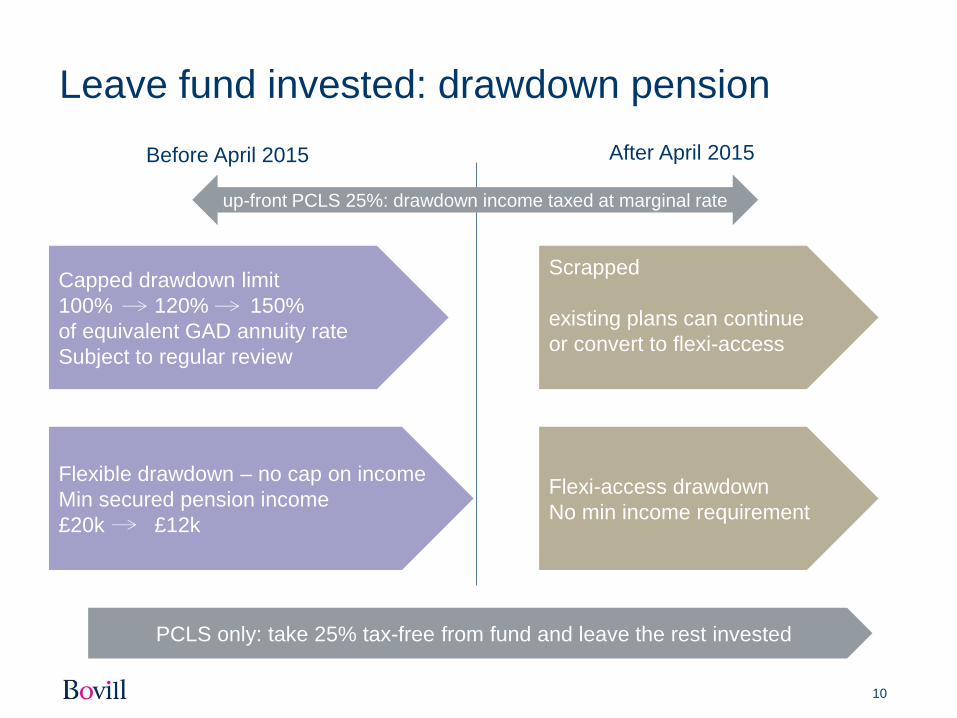

Leave fund invested: drawdown pension

Capped drawdown limit

100% 120% 150%

of equivalent GAD annuity rate

Subject to regular review

Before April 2015 After April 2015

Scrapped

existing plans can continue

or convert to flexi-access

Flexible drawdown – no cap on income

Min secured pension income

£20k £12k

Flexi-access drawdown

No min income requirement

PCLS only: take 25% tax-free from fund and leave the rest invested

up-front PCLS 25%: drawdown income taxed at marginal rate

11

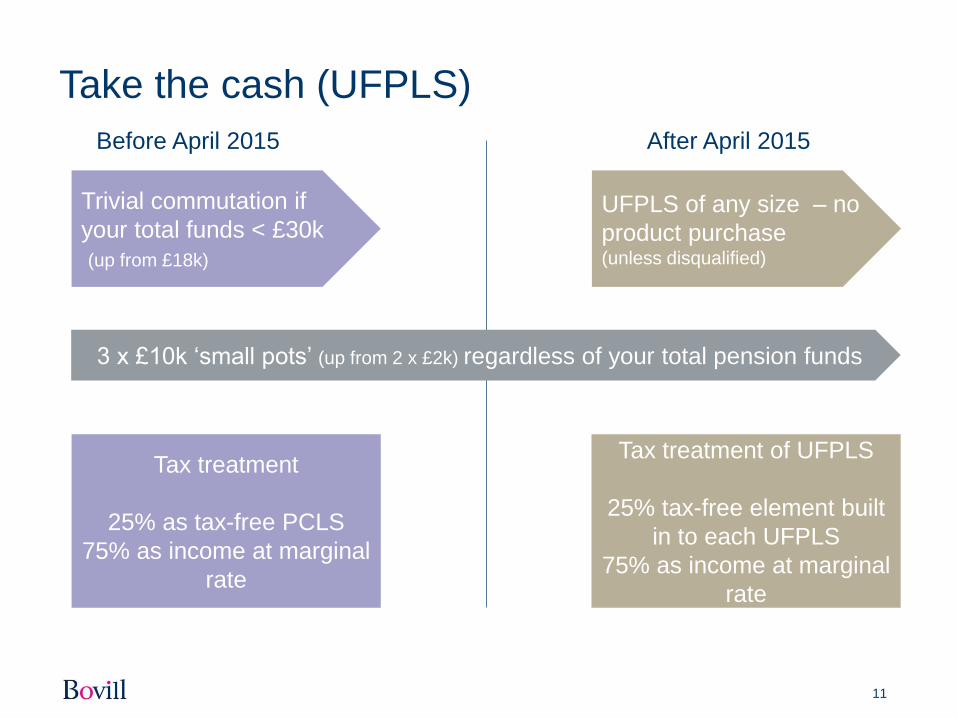

Take the cash (UFPLS)

Before April 2015 After April 2015

Trivial commutation if

your total funds < £30k

(up from £18k)

UFPLS of any size – no

product purchase (unless disqualified)

3 x £10k ‘small pots’ (up from 2 x £2k) regardless of your total pension funds

Tax treatment

25% as tax-free PCLS

75% as income at marginal

rate

Tax treatment of UFPLS

25% tax-free element built

in to each UFPLS

75% as income at marginal

rate

12

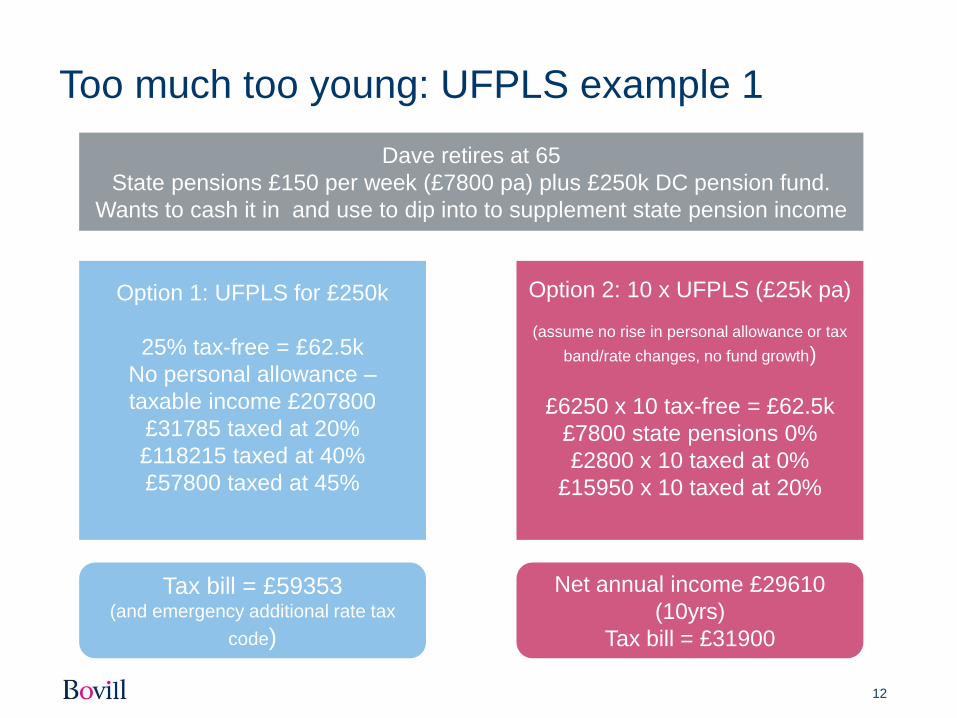

Too much too young: UFPLS example 1

Dave retires at 65

State pensions £150 per week (£7800 pa) plus £250k DC pension fund.

Wants to cash it in and use to dip into to supplement state pension income

Option 1: UFPLS for £250k

25% tax-free = £62.5k

No personal allowance –

taxable income £207800

£31785 taxed at 20%

£118215 taxed at 40%

£57800 taxed at 45%

Option 2: 10 x UFPLS (£25k pa)

(assume no rise in personal allowance or tax

band/rate changes, no fund growth)

£6250 x 10 tax-free = £62.5k

£7800 state pensions 0%

£2800 x 10 taxed at 0%

£15950 x 10 taxed at 20%

Tax bill = £59353 (and emergency additional rate tax

code)

Net annual income £29610

(10yrs)

Tax bill = £31900

13

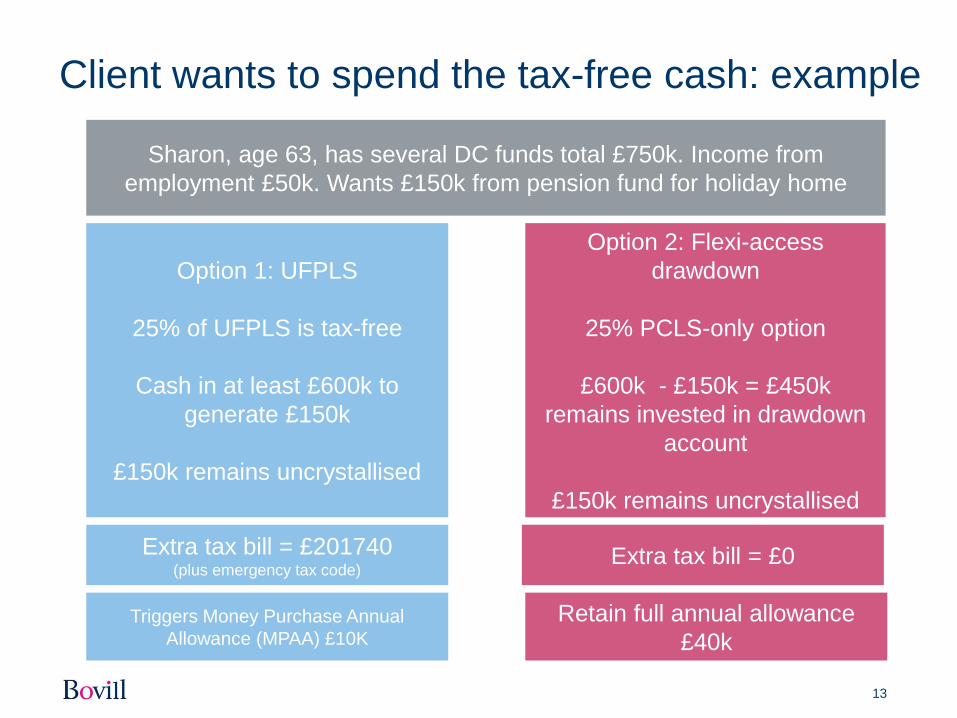

Client wants to spend the tax-free cash: example

Sharon, age 63, has several DC funds total £750k. Income from

employment £50k. Wants £150k from pension fund for holiday home

Option 1: UFPLS

25% of UFPLS is tax-free

Cash in at least £600k to

generate £150k

£150k remains uncrystallised

Option 2: Flexi-access

drawdown

25% PCLS-only option

£600k - £150k = £450k

remains invested in drawdown

account

£150k remains uncrystallised

Extra tax bill = £201740 (plus emergency tax code)

Extra tax bill = £0

Triggers Money Purchase Annual

Allowance (MPAA) £10K

Retain full annual allowance

£40k

14

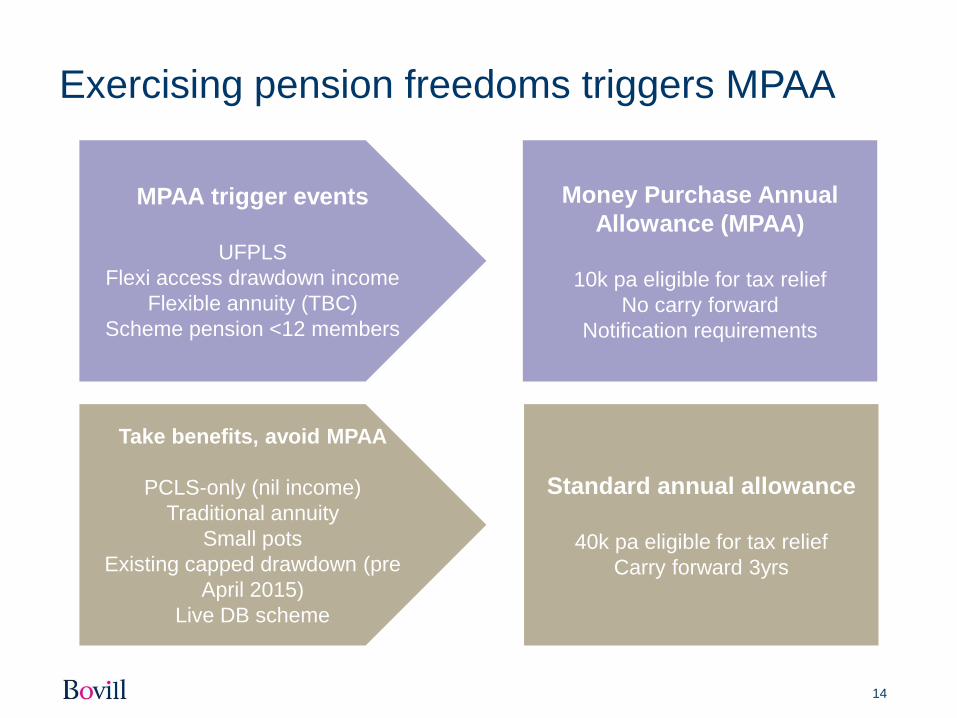

Exercising pension freedoms triggers MPAA

MPAA trigger events

UFPLS

Flexi access drawdown income

Flexible annuity (TBC)

Scheme pension <12 members

Money Purchase Annual

Allowance (MPAA)

10k pa eligible for tax relief

No carry forward

Notification requirements

Standard annual allowance

40k pa eligible for tax relief

Carry forward 3yrs

Take benefits, avoid MPAA

PCLS-only (nil income)

Traditional annuity

Small pots

Existing capped drawdown (pre

April 2015)

Live DB scheme

15

Tax charges on death reduced

Death before age 75 Death on or after age 75

Tax position Lifetime

Allowance test

applies?

Tax position

(income)

Tax position (lump

sum) *

Uncrystallised

pension fund

Tax free Yes Marginal rate

(of beneficiary)

45%

Funds in

drawdown

Tax free No Marginal rate

(of beneficiary)

45%

Annuity

protection

Tax free No Marginal rate

(of beneficiary)

45%

Unspent

UFPLS

proceeds

IHT No N/A IHT

* For 2015/16. Govt intends to change to marginal rate from 2016/17

3. Implications for professional

advice market

17

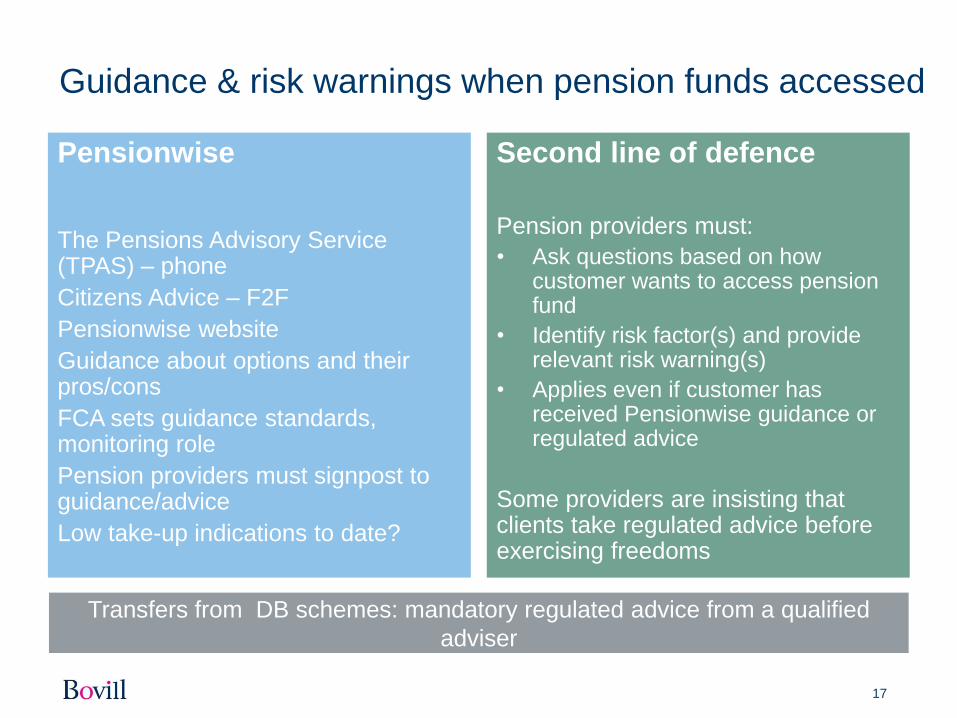

Guidance & risk warnings when pension funds accessed

Pensionwise

The Pensions Advisory Service (TPAS) – phone

Citizens Advice – F2F

Pensionwise website

Guidance about options and their pros/cons

FCA sets guidance standards, monitoring role

Pension providers must signpost to guidance/advice

Low take-up indications to date?

Second line of defence

Pension providers must:

• Ask questions based on how customer wants to access pension fund

• Identify risk factor(s) and provide relevant risk warning(s)

• Applies even if customer has received Pensionwise guidance or regulated advice

Some providers are insisting that clients take regulated advice before exercising freedoms

Transfers from DB schemes: mandatory regulated advice from a qualified

adviser

18

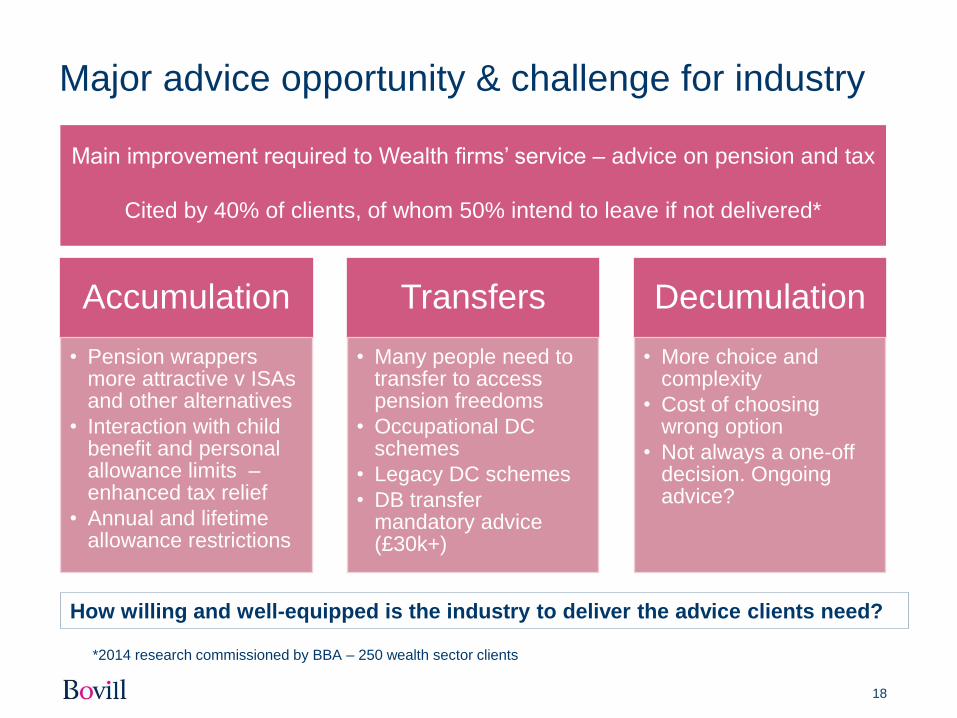

Major advice opportunity & challenge for industry

Accumulation

• Pension wrappers more attractive v ISAs and other alternatives

• Interaction with child benefit and personal allowance limits – enhanced tax relief

• Annual and lifetime allowance restrictions

Transfers

• Many people need to transfer to access pension freedoms

• Occupational DC schemes

• Legacy DC schemes

• DB transfer mandatory advice (£30k+)

Decumulation

• More choice and complexity

• Cost of choosing wrong option

• Not always a one-off decision. Ongoing advice?

Main improvement required to Wealth firms’ service – advice on pension and tax

Cited by 40% of clients, of whom 50% intend to leave if not delivered*

How willing and well-equipped is the industry to deliver the advice clients need?

*2014 research commissioned by BBA – 250 wealth sector clients

19

Do keep up…post A-day changes

Pot follows

member

Accelerated

rise in state

pension age

from 65 to

66

Min pension

age up from

50 to 55

Fixed

protection

2012

Min income

for flexible

drawdown

cut from

£20k to £12k

Capped

drawdown

income up

from 100%

to 120% of

GAD

Flat rate

state

pension

from 2016

Annual

allowance

cut from

£50k to £40k

Cut in yrs

needed for

full state

pension

Fixed

protection

2014

No longer

need to

annuitize by

age 75

Annual

allowance

cut from

£250k to

£50k

USP and

ASP

replaced by

drawdown

pension

Small pots

limit

increases

from £2k to

£10k

Contracting

out of S2P

abolished for

DC schemes

Individual

protection

2014

Lifetime

allowance

cut from

£1.5m to

£1.25m

Default

retirement

age

scrapped

Carry

forward 3yrs

unused

annual

allowance

Trivial

commutation

limit up from

£18k to £30k

Capped

drawdown

income up

from 100%

to 150% of

GAD

Gradual rise

in female

state

pension age

to 65

State

pension age

to rise to

age 67 and

beyond

Lifetime

allowance

cut from

£1.8m to

£1.5m

Max number

of small pots

up from 2 to

3

Onset of

auto

enrolment

into

workplace

pensions

Public sector

pension

accrual

reforms

Contracting

out of S2P

abolished for

DB schemes

from2016

Age

discrimination

outlawed

Pension

Freedoms

20

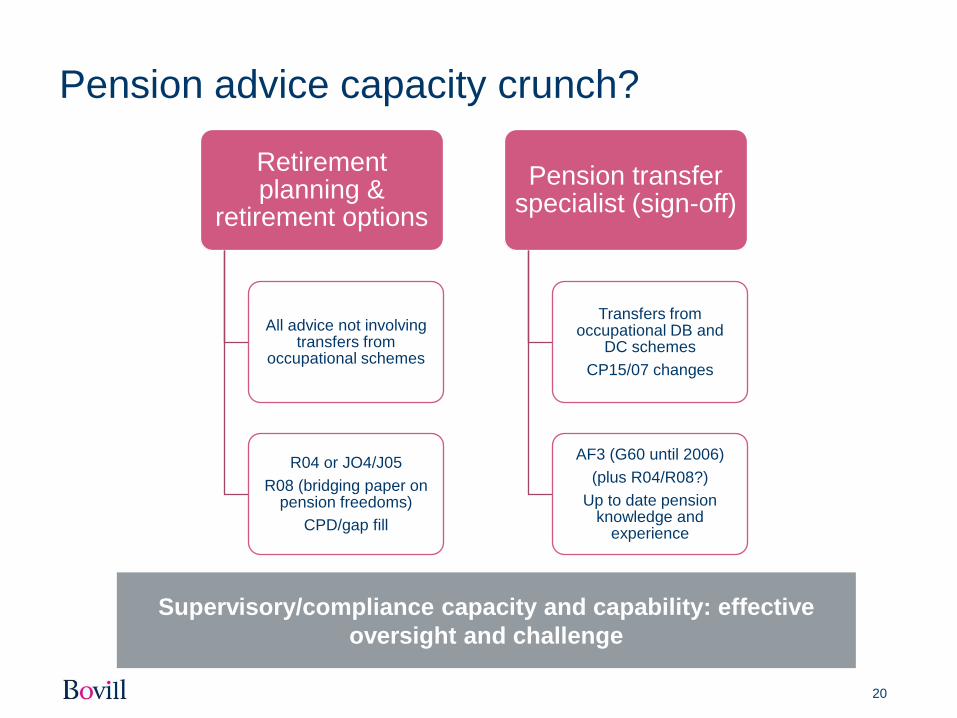

Pension advice capacity crunch?

Retirement planning &

retirement options

All advice not involving transfers from

occupational schemes

R04 or JO4/J05

R08 (bridging paper on pension freedoms)

CPD/gap fill

Pension transfer specialist (sign-off)

Transfers from occupational DB and

DC schemes

CP15/07 changes

AF3 (G60 until 2006)

(plus R04/R08?)

Up to date pension knowledge and

experience

Supervisory/compliance capacity and capability: effective

oversight and challenge

21

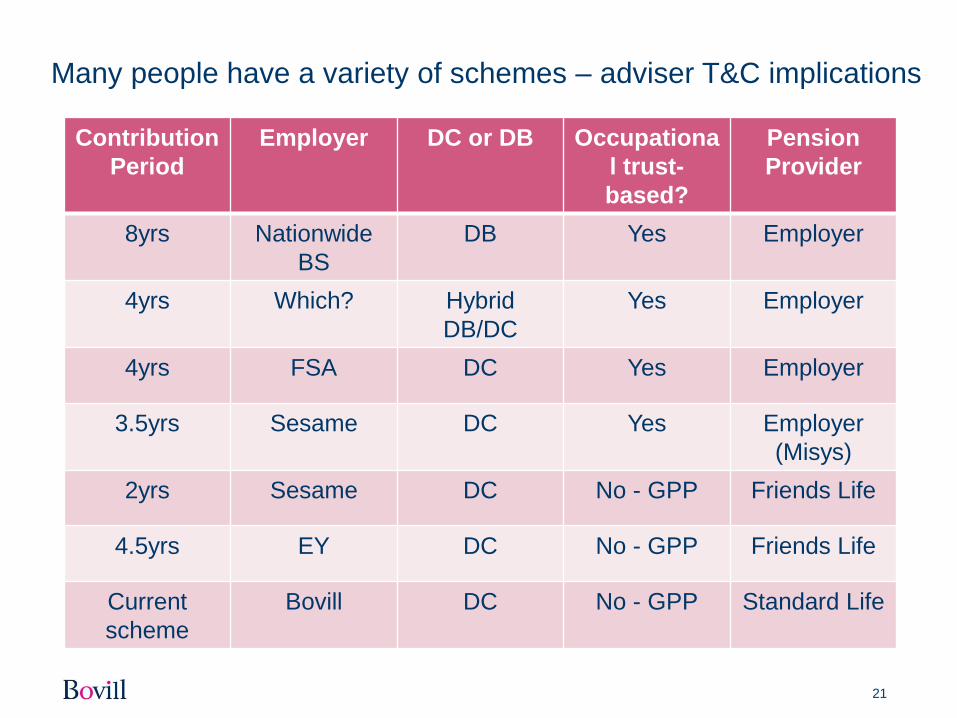

Many people have a variety of schemes – adviser T&C implications

Contribution

Period

Employer DC or DB Occupationa

l trust-

based?

Pension

Provider

8yrs Nationwide

BS

DB Yes Employer

4yrs Which? Hybrid

DB/DC

Yes Employer

4yrs FSA DC Yes Employer

3.5yrs Sesame DC Yes Employer

(Misys)

2yrs Sesame DC No - GPP Friends Life

4.5yrs EY DC No - GPP Friends Life

Current

scheme

Bovill DC No - GPP Standard Life

4. Some retirement planning

suitability considerations

23

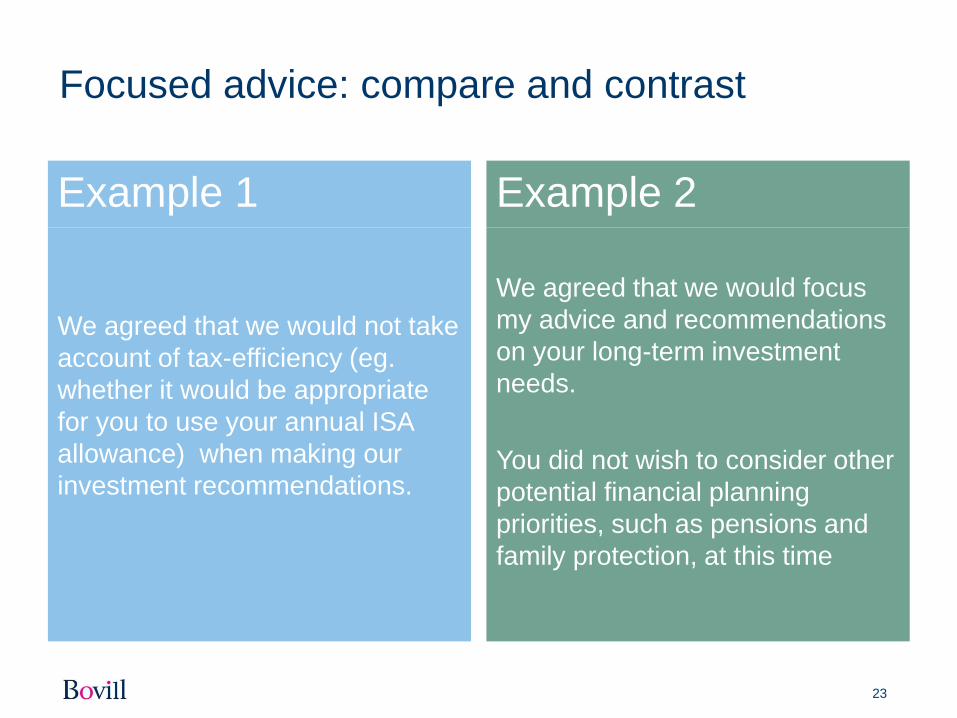

Focused advice: compare and contrast

Example 1

We agreed that we would not take

account of tax-efficiency (eg.

whether it would be appropriate

for you to use your annual ISA

allowance) when making our

investment recommendations.

Example 2

We agreed that we would focus

my advice and recommendations

on your long-term investment

needs.

You did not wish to consider other

potential financial planning

priorities, such as pensions and

family protection, at this time

24

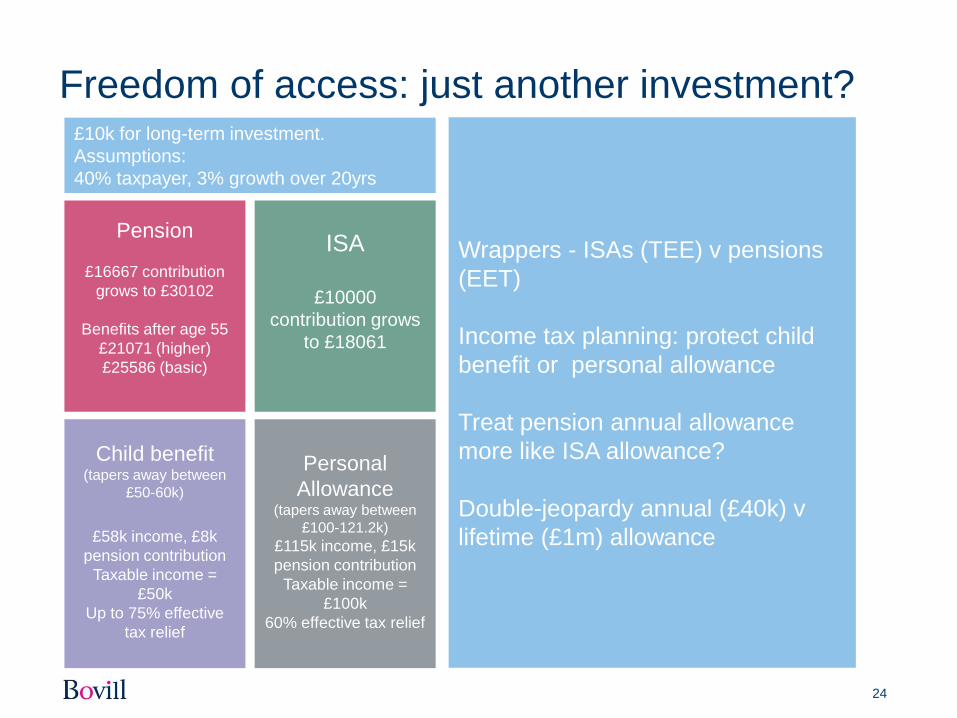

Freedom of access: just another investment?

Pension

£16667 contribution

grows to £30102

Benefits after age 55

£21071 (higher)

£25586 (basic)

ISA

£10000

contribution grows

to £18061

£10k for long-term investment.

Assumptions:

40% taxpayer, 3% growth over 20yrs

Child benefit (tapers away between

£50-60k)

£58k income, £8k

pension contribution

Taxable income =

£50k

Up to 75% effective

tax relief

Personal

Allowance (tapers away between

£100-121.2k)

£115k income, £15k

pension contribution

Taxable income =

£100k

60% effective tax relief

Wrappers - ISAs (TEE) v pensions

(EET)

Income tax planning: protect child

benefit or personal allowance

Treat pension annual allowance

more like ISA allowance?

Double-jeopardy annual (£40k) v

lifetime (£1m) allowance

25

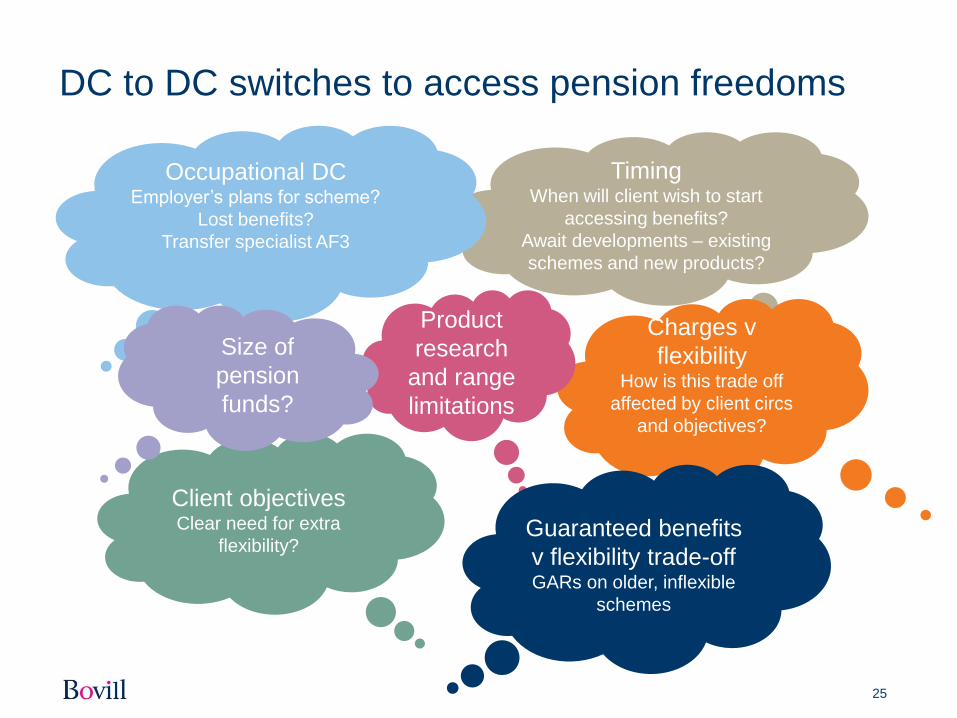

DC to DC switches to access pension freedoms

Timing When will client wish to start

accessing benefits?

Await developments – existing

schemes and new products?

Charges v

flexibility How is this trade off

affected by client circs

and objectives?

Client objectives Clear need for extra

flexibility?

Occupational DC Employer’s plans for scheme?

Lost benefits?

Transfer specialist AF3

Product

research

and range

limitations

Size of

pension

funds?

Guaranteed benefits

v flexibility trade-off GARs on older, inflexible

schemes

26

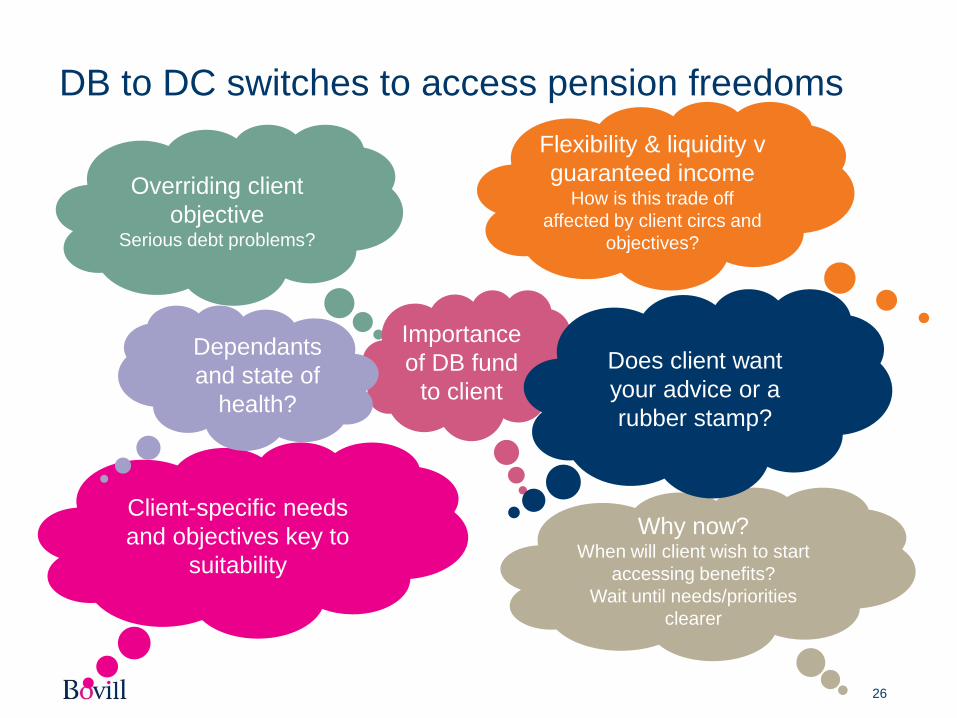

DB to DC switches to access pension freedoms

Why now? When will client wish to start

accessing benefits?

Wait until needs/priorities

clearer

Overriding client

objective Serious debt problems?

Client-specific needs

and objectives key to

suitability

Importance

of DB fund

to client

Dependants

and state of

health?

Does client want

your advice or a

rubber stamp?

Flexibility & liquidity v

guaranteed income How is this trade off

affected by client circs and

objectives?

27

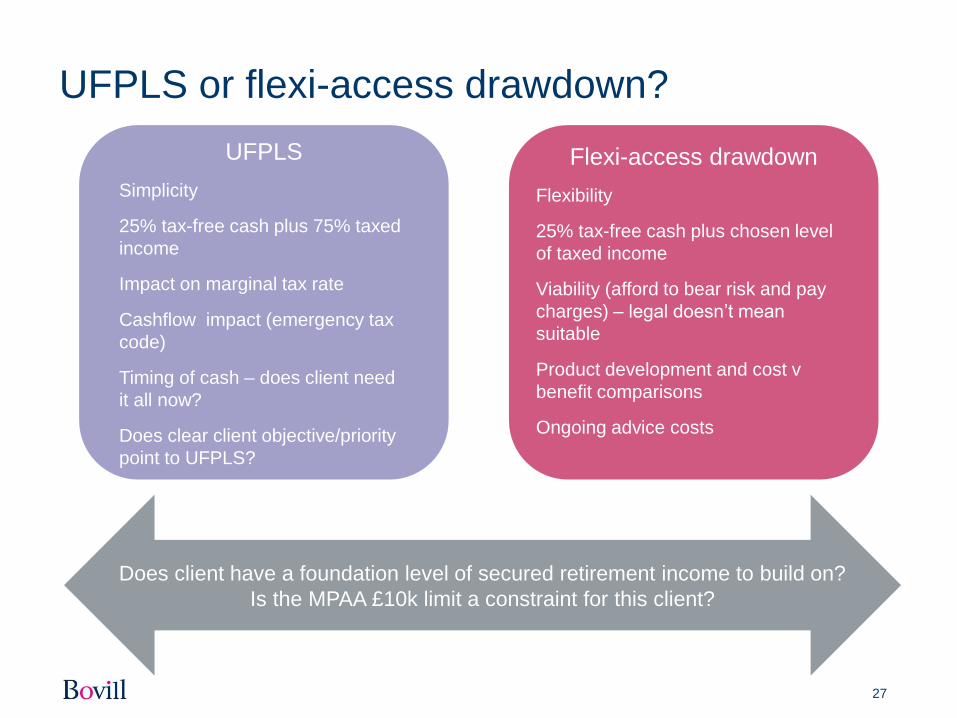

UFPLS or flexi-access drawdown?

UFPLS

Simplicity

25% tax-free cash plus 75% taxed

income

Impact on marginal tax rate

Cashflow impact (emergency tax

code)

Timing of cash – does client need

it all now?

Does clear client objective/priority

point to UFPLS?

Flexi-access drawdown

Flexibility

25% tax-free cash plus chosen level

of taxed income

Viability (afford to bear risk and pay

charges) – legal doesn’t mean

suitable

Product development and cost v

benefit comparisons

Ongoing advice costs

Does client have a foundation level of secured retirement income to build on?

Is the MPAA £10k limit a constraint for this client?

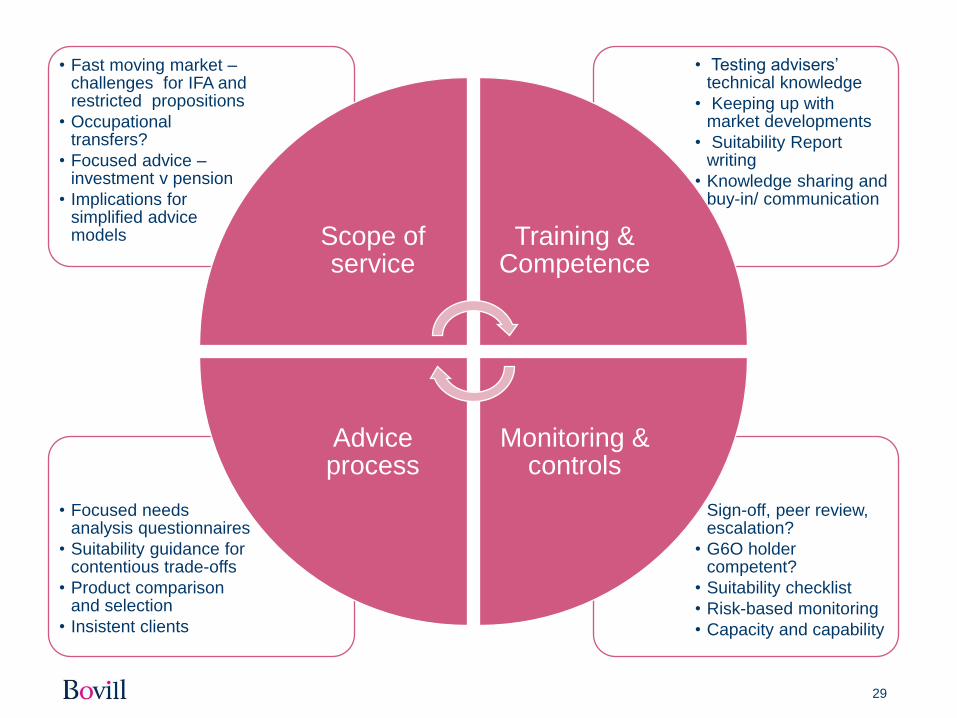

5. Controls over advice quality –

reducing risk of poor outcomes

29

• Sign-off, peer review, escalation?

• G6O holder competent?

• Suitability checklist

• Risk-based monitoring

• Capacity and capability

• Focused needs analysis questionnaires

• Suitability guidance for contentious trade-offs

• Product comparison and selection

• Insistent clients

• Testing advisers’ technical knowledge

• Keeping up with market developments

• Suitability Report writing

• Knowledge sharing and buy-in/ communication

• Fast moving market – challenges for IFA and restricted propositions

• Occupational transfers?

• Focused advice – investment v pension

• Implications for simplified advice models

Scope of service

Training & Competence

Monitoring & controls

Advice process

30

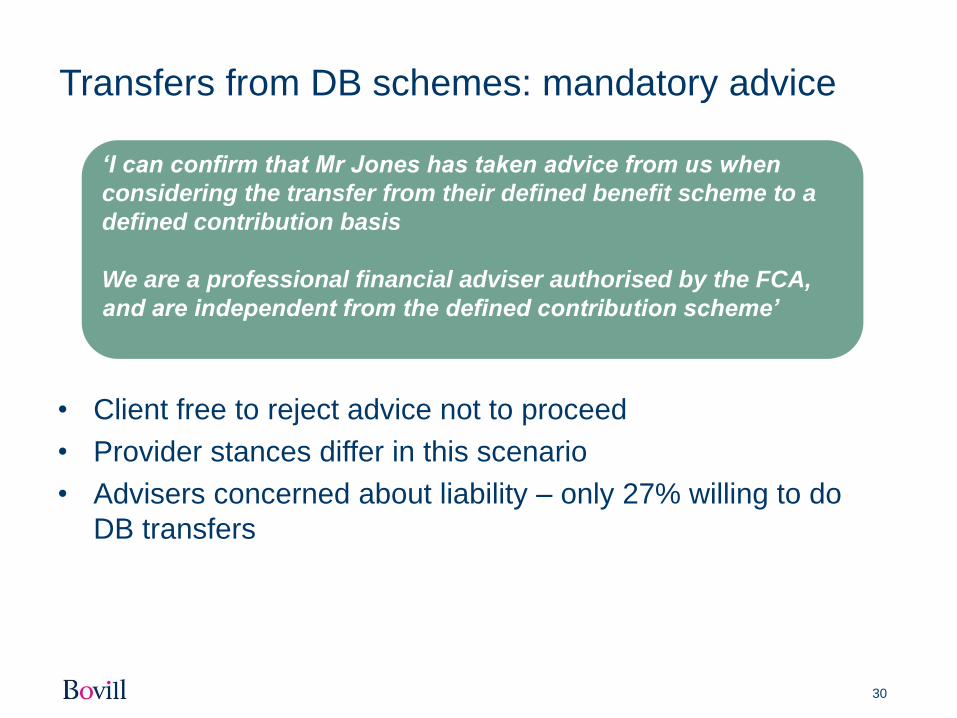

Transfers from DB schemes: mandatory advice

• Client free to reject advice not to proceed

• Provider stances differ in this scenario

• Advisers concerned about liability – only 27% willing to do

DB transfers

‘I can confirm that Mr Jones has taken advice from us when

considering the transfer from their defined benefit scheme to a

defined contribution basis

We are a professional financial adviser authorised by the FCA,

and are independent from the defined contribution scheme’

31

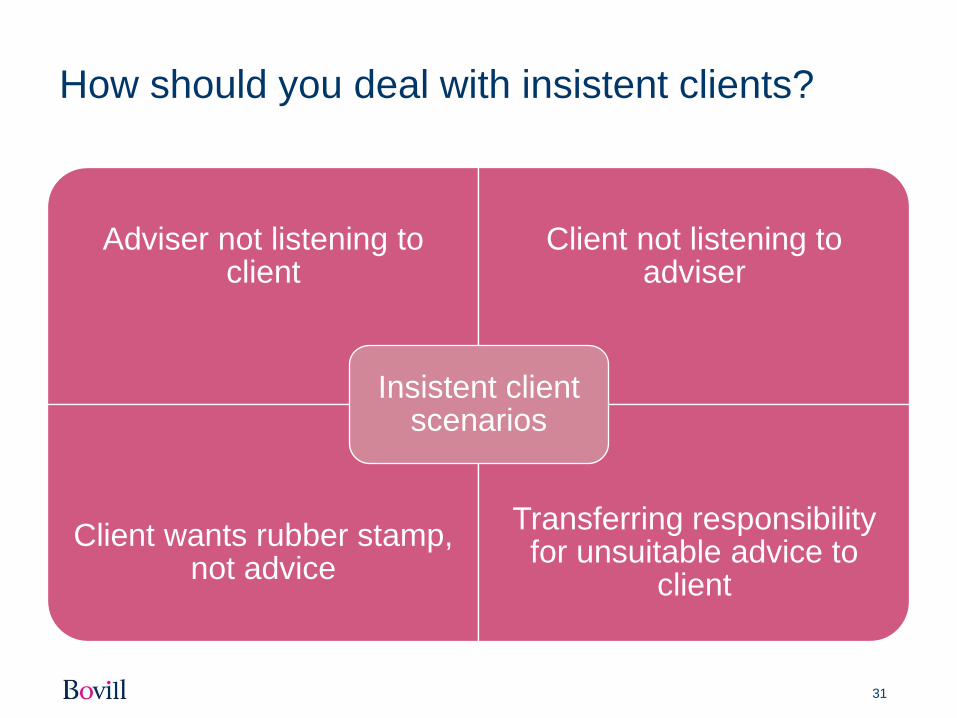

How should you deal with insistent clients?

Adviser not listening to client

Client not listening to adviser

Client wants rubber stamp, not advice

Transferring responsibility for unsuitable advice to

client

Insistent client scenarios

32

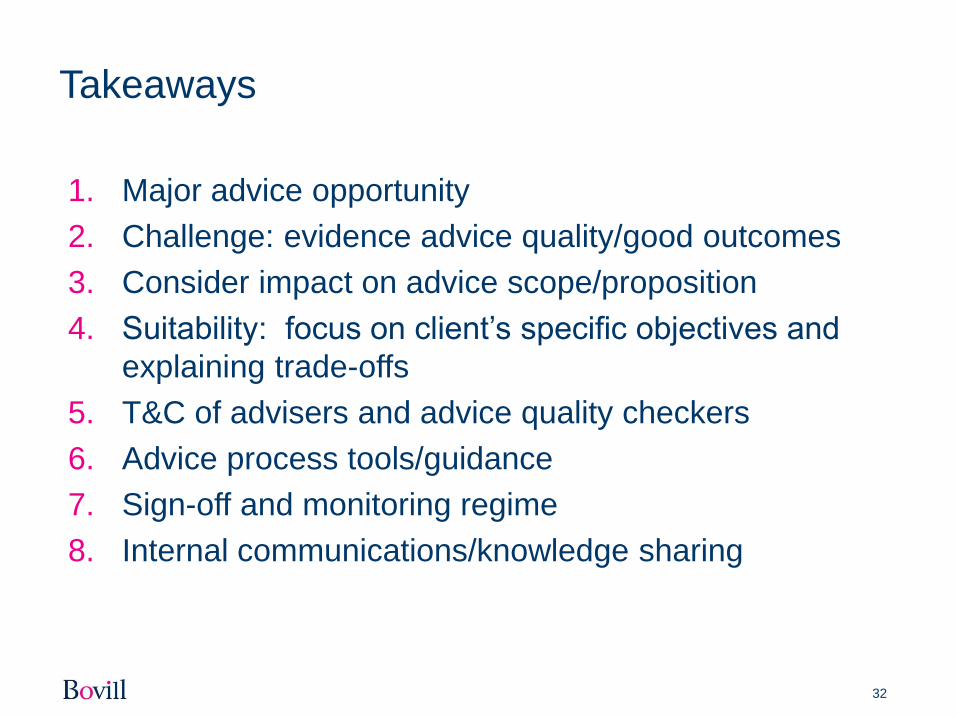

Takeaways

1. Major advice opportunity

2. Challenge: evidence advice quality/good outcomes

3. Consider impact on advice scope/proposition

4. Suitability: focus on client’s specific objectives and

explaining trade-offs

5. T&C of advisers and advice quality checkers

6. Advice process tools/guidance

7. Sign-off and monitoring regime

8. Internal communications/knowledge sharing

Questions?

33