Embed Size (px)

Citation preview

Phoenix Lamps

- A Quality business under a smart Owner- Operator at cheap Valuations

Content Index

• Phoenix Lamps– Investment Snapshot :- Slide #3

• Phoenix – Elevator Investment Pitch :- Slide #4

• Phoenix Lamps – 10 Key Investment Highlights :- Slide #8

• Our Research Head’s Investment Note on the Stock :- Slide #11

• Auto components – Industry Overview :- Slide #20

• Phoenix Lamps – Company Overview:- Slide #30

• Phoenix Lamps – Business Overview:- Slide #36

• Actis management issues:- Slide #42

• Suprajit Engineering Ltd.-A value creator:- Slide #44

• Peer Comparison:- Slide #48

• Phoenix Lamps – Financial Overview:- Slide #52

• Risks & Concerns :- Slide #60

• Conclusion :- Slide #62

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps – Investment Snapshot (as on May 28, 2015)

Recommendation :- BUY

Maximum Portfolio Allocation :- 5%

Investment Phases & Buying Strategy

1st Phase (Now) of Accumulation :- 100%

Current Accumulation Range :- 110 – 130 Rs.

We believe that Investors can accumulate the shares at the current price which we believe is attractive for Investors. Core Investment Thesis :

A Quality business (Cost competitive moat enablingsustainable ROCE’s of 35%+) under a smart Owner-Operator (Mr. Ajith Rai of Suprajit Engineering) isavailable at cheap valuations (~ 6X EV/ EBIDTA & ~10%+ OCF Yield)

“ Specialists in discovering Multibagger stocks “

Stock Information :-

Current Market Price Rs.112

Current Dividend Yield

14%

Bloomberg/Reuters Code

PHLL IN/ HALONIX

BSE / NSE Code 517296 / PHOENIXLL

Market Cap (INR Cr.) 313

Total Equity Shares 28.7mn.

Face Value Rs.10

52 Week High / Low Rs.178 / Rs.85.8

Promoter’s Holding 61.88%

Institutional Holding 2.27%

Elevator Investment Pitch

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps Ltd

Attractive Valuations

EV / EBITDA - 5x/7x

P/E – 8x/12x(FY14/FY15)

Dominant Market Share

-50%-60% of total installed

capacity in India.

- 50% in PV, 70% in LCV,

85% in two & three wheelers

Cost Competitiveness- Low cost manufacturing

- Low marginal costs

- High operating leverage

Strong Financials

- 47%/28% ROCE

- 18%/14% EBITDA Margin(FY15 Stand alone/Consolidated)

Attractive Cash Flows- 40 cr. of EBITDA avg.

- 30cr.Free cash flow avg.

ManagementChange of management

from PE firm to reputed

and proven ancillary

business leader

A Few Key points to be noted

“ Specialists in discovering Multibagger stocks “

A Few Key points to be noted

“ Specialists in discovering Multibagger stocks “

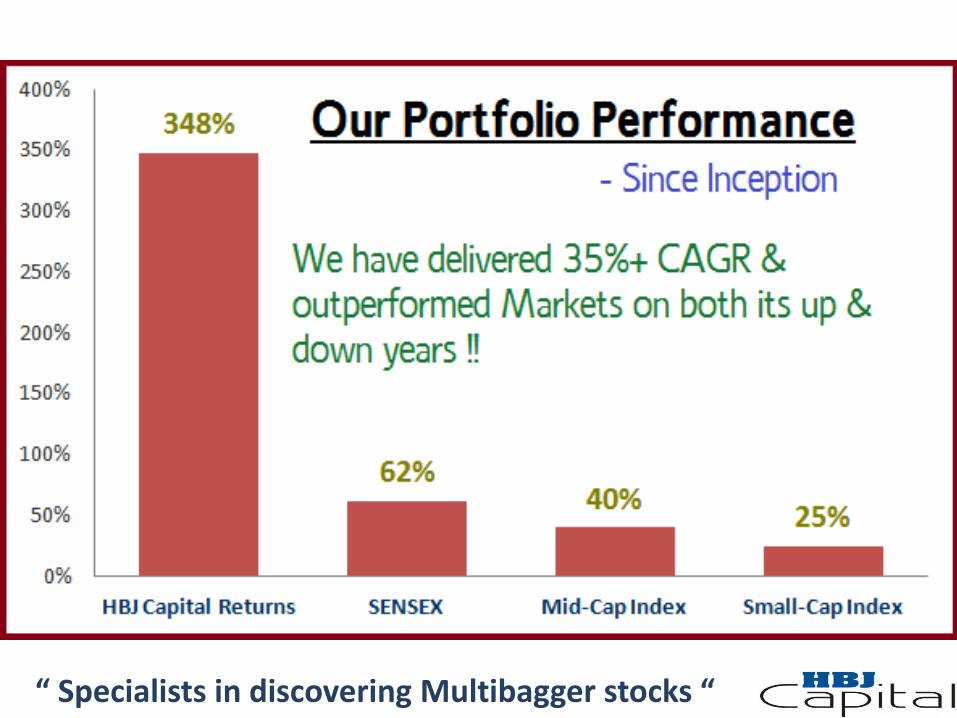

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps – 10 Key Investment Highlights

1.) Phoenix Lamps is the dominant market leader in the Halogen lighting segment

with market shares of 85% in two & three wheelers, 73% in LCV, 50-53% in MC-

HCV and 50% market share in Passenger vehicle segment.

2.) With the management is being transferred from Actis to Suprajit Engineering

which is a proven leader in the same ancillary business will add to the Phoenix’s

brand strength.

3.) Suprajit and Phoenix has a lot of common ground in terms of customers,

geographies, distribution etc. that will enable Phoenix to grow better under the

new Management team.

4.) Company’s biggest competitor - Philips imports bulbs to supply to OEM’s

(Philips per bulb cost is 30%-40% higher than Phoenix bulbs in India) and

hence Phoenix with a strong manufacturing network across India has huge cost

advantage. It’s well entrenched relationships with big OEM’s also works as an

entry barrier to newer players.

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps – 10 Key Investment Highlights

5.) Company has a strong brand “Halonix” and a robust distribution network

across various countries that has enabled it to create a robust After-Sales market.

This is essentially a B2C business with healthy Moats.

6.) The erstwhile management sold off general lighting business in August 2013

and has used the 160 Cr proceeds to retire debt and it currently has a robust

balance sheet which it leverage to invest and capitalize on growth opportunities in

the Auto lighting space. The company has showed good growth since demerger.

7.) Company’s domestic Auto-Lighting business is a high quality business that has

been able to generate ROCE’s of >35% even during the years of slowdown. We

believe that incremental ROCE’s will continue to be very attractive considering

Industry dynamics.

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps – 10 Key Investment Highlights

8.) Company has been able to build a strong International aftermarket business

segment which is currently contributing around 50% of total revenues. It exports

to over 50 countries and has built a distribution network based on “Value for

Money” proposition for the product.

9.) Company’s international Margins are 1/4th compared to its domestic business

as 75% of its International sales is in Un-Branded form. There has been strong

focus on increasing the branded sales component and this will help in improving

the overall consolidated margins.

10.) Phoenix Lamps is currently trading at attractive valuations which we believe

is reasonable for a quality business which has Margin levers as well as a trigger

for Value unlocking.

“ Specialists in discovering Multibagger stocks “

Our Research Head’s investment note on the Stock

“ Specialists in discovering Multibagger stocks “

HBJ Capital - Phoenix Lamps Limited. – May, 2015

Dear Members of Multibagger,

We have been tracking Phoenix Lamps for a long time now. Our analysis pointed to a dominant Auto ancillary business with

superior financial metrics whose quality got sub-merged under a bad general lighting business. The bad business was eventually de-merged

and sold last year (One of our favorite themes in hunting for Market Inefficiency is to look for mis-pricing of quality businesses due to

capital mis-allocation issues in other segments with a clarity on possible value unlocking in the Quality segment). With the sale of General

lighting business, we were happy recommending the stock as part of our Quality Auto ancillary bucket with a low allocation in the month

of January.

While we felt extremely comfortable with the business quality, we were concerned about Management quality as the then-

controlling shareholder was a private equity firm - Actis Capital which came with a baggage of Capital Misallocation mistakes and poor

managing track record (highlighted in slides 42-43). Since, there were clear indications of the promoters wanting to sell their controlling

stake - we were happy to take a small allocation. Now that the business has been bought by Suprajit Engineering (well known firm among

the Value Investing Crowd), a lot of our Management concerns, growth issues etc. goes away and long term stability, appropriate capital

allocation comes into the picture. Thus, we are happy to increase our allocation to this business around current price levels.

The one line investment thesis in Phoenix Lamps is “A Quality business (Cost competitive moat enabling sustainable ROCE’s of 35%+)

under a smart Owner- Operator (Mr. Ajith Rai of Suprajit Engineering) is available at cheap valuations (~ 6X EV/ EBIDTA & ~ 10%+ OCF

Yield)”. Let’s understand the detailed Investment rationale by elaborating on each of the point given below:

- Moat/ Competitive Advantage for Phoenix Lamps.

- Inherent Operational Leverage/ Margin Triggers.

- Management Delta (Actis to Suprajit).

HBJ Capital - Phoenix Lamps Limited. – May, 2015

- Robust Cash Flows and Return Metrics.

- Attractive Valuations & Huge P/E Arbitrage.

We would interpret and analyze details under these heads, while the raw data itself is presented in the later stages of this research

report. Before getting into the details of the Investment rationale, let me brief about the main risk in the thesis. Company’s export business

still continues to be dominated (~ 73% of Exports) by Non-Branded (Private Labelling) business which gets affected severely by cross-

currency movements. While the company has a healthy cost advantage, the cross currency impact will fluctuate the overall earnings. The

recent 20% depreciation of the Euro and the weak European economy acts as headwinds as can be seen from the latest results. These

temporary issues can result in longer than expected waiting period for valuation re-rating. Over the long term, company’s cost advantage

and the stable after-market sales will enable it to grow profitably despite these temporary issues.

1.) Moat/ Competitive Advantage for Phoenix Lamps:

The quality of Phoenix’s auto business comes from the Product characteristics and Scale/ Cost advantages of mass manufacturing.

Phoenix manufacturers “Halogen Bulbs” for the automobile headlight segment. This is a very niche segment in which Phoenix holds an

extremely dominant 60% Market share in India. Halogen Bulbs have the following product characteristics that makes it suitable for mass

manufacturing:

- Standardized Products (doesn’t change from one OEM to another and is same for the entire Industry).

- Low Value, High Critical product (Usually costs approximately 1-2 $’s which is insignificant in terms of overall costing, but it is critical

enough that quality of the product matters).

HBJ Capital - Phoenix Lamps Limited. – May, 2015

- Light Weight product, easy to be transported (Single Location manufacturing plant, catering to various locations enables

manufacturers to build plants with huge economies of scale).

- Capital Intensive for Greenfield manufacturing (Gross Fixed Asset turnovers for Greenfield manufacturing of halogen bulbs is less

than 0.7X and hence ROCE returns aren’t healthy for new players to come-in).

- Extremely Long Replacement Cycle (Halogen bulbs usually lasts for over 2200 hours (or) 6-7 years, denting the probability of

customers trying new products on the shelf when established brands are present).

- Stringent norms and Longer Vendor verification cycles (tough for new players to penetrate OEM buyers as product differentiation is

nothing and low cost & high quality is crucial).

As we have written above - the criticality of a 1 $ to 1.5$ Halogen Bulb is far higher than what its price point suggests, enabling

quality manufacturers such as Phoenix Lamps to sustainably generate healthy Gross Margins of around 55%. The costs in between Gross

Margins and EBIDTA Margins of (20%) are based upon the scale of manufacturing and hence we believe that there is enough savings a

scale manufacturer achieves from higher volumes of production.

Phoenix Lamps has a manufacturing capacity of 87 Million bulbs/ Year which is almost 50% of the total installed capacity for

Halogen bulbs in India. The manufacturing scale of Phoenix is unparalleled in India and its foreign competitors who primarily import bulbs

can’t even think of competing on cost with Phoenix. We believe that this is an important differentiating factor that will enable Phoenix to

continue demonstrating superior economics. Phoenix has domestic and export focused plants (within a SEZ), both in Noida. There is

enough land for adding more manufacturing lines and increase capacity in this factory which will be a very cost-effective brown-field

expansion.

HBJ Capital - Phoenix Lamps Limited. – May, 2015

We believe that the current per unit economics of Phoenix Lamps are attractive with realizations of around 1$ and cost of

production around 0.75$/ 0.80$ (if freight costs are included). We believe that EBIDTA margins can easily average around the historical

17% number with a few good years of 20%+ margins. There are also multiple triggers for Margin expansion as can be seen later.

One of the biggest advantages of Phoenix Lamps is its depreciated large scale manufacturing plant that has scope for

brownfield expansion with light incremental CAPEX. The company’s current Fixed Assets on its balance sheet is just around 30 Cr while

the Gross Assets is around 140 Cr (110 Cr of depreciated assets). We are pretty much sure that manufacturers who would like to put up a

similar manufacturing capacity at current land/ construction prices will find the CAPEX to replicate Phoenix Lamps capacity to be much

much higher.

Our scuttle butt with Industry players and analysis of companies such as Jagan Lamps (a very tiny manufacturer of Halogen

bulbs which is listed in BSE) shows that the fixed asset turnover for a greenfield plant is just around 0.5X to 1X at current levels. Hence a

large scale plant which is almost fully depreciated provides tremendous cost advantages for Phoenix Lamps. The company’s domestic sales

is almost fully branded under its “Halonix” brand. With good quality of products, an established brand and strong distribution network

- the company’s domestic business is literally a cash cow with healthy free cash flows.

On the export side, the branded sales are increasing but still constitutes only 25% of the exports pie. The company’s biggest

USP in the exports markets is its “Value for Money” proposition of bulbs which are similar in quality with Philips/ Osram but priced at a

healthy discount to these brands. They have very strong “Private Labelling” clients such as Bosch in Germany. While there are low cost

Chinese products, quality is an issue. Company’s entire exports business is catered towards the After-Market sales business. Company

has acquired distributors and is setting up its own distribution channels. With Low Cost manufacturing + Growing Distribution network,

company certainly can grow profitably in the exports market.

HBJ Capital - Phoenix Lamps Limited. – May, 2015

We have not been able to get the exact break-up of the Margins between its domestic and exports business as the accounting

policies on intercompany sales aren’t clear. Hence, we have been using consolidated EBIDTA margins and Consolidated ROCE’s in all

calculations. Exports business introduces volatility into the numbers and hasn’t shown any growth, while the domestic revenues have

grown at 10%+. Despite this the consolidated Margins and Return Ratios have been extremely healthy for Phoenix as shown in Slide - 39.

The quality of Phoenix’s business is extremely attractive to any Investor as it has durable Moats, strong free cash flows, healthy returns

on incremental investments etc.

2.) Inherent Operational Leverage/ Margin Triggers:

We believe that the business has several near term triggers for improved Margin performance. The economics of the business

is such that the marginal cost for production is low and profitability improves as capacity utilization increases. The current capacity

utilization is just around 75%. As the domestic auto cycle picks up, we believe that utilization levels will improve. The volumes can grow

around the 8 to 10% range as per historical numbers. The company has also been increasing its branded product sales. This will provide

another lever to Margins. There has also been foreign currency losses on the back of Euro Depreciation. Adjusting for all these, it is pretty

clear that the probability of Margins moving up is higher over the next 2-3 years. There can also be an added bonus from the synergies

that Suprajit can derive out of Phoenix Lamps.

3.) Management Delta: (Actis Private Equity to Suprajit Engineering)

The biggest reason for us to increase our allocation to Phoenix Lamps is the entry of Suprajit Engineering. We believe that

Suprajit’s management runs a business which has totally similar economic characteristics as Phoenix’s and hence will be able to derive

best value out of this business. Similar to Halogen bulb business, Suprajit’s business has the following characteristics: Low Value, Tier-2

Suppliers, High Volume, Standardized product, Critical in use, Mass Manufacturing etc. But unlike Phoenix Lamps, Suprajit follows a

multi-geography manufacturing plant as logistics makes it non-economical to run a single plant operation.

HBJ Capital - Phoenix Lamps Limited. – May, 2015

Suprajit’s CEO - Mr. Ajit Rai is one of the best owner-operator in Auto Ancillary business with a stupendous track record of

wealth creation for shareholders. We have shown several numbers to prove this point in slides 44-46. We believe that they understand

this business extremely well and will be able to drive the business better operationally. The customer profiles are similar and there are

enough distributional synergies (Slide - 47) to improve operations. We can expect them to execute strongly on both the OEM & After-

Market business to gain market share and grow the business. While we are not modelling anything as of now, we believe that this is a

bonus in the offing.

Even in a dull business such as auto cable manufacturing, Suprajit has shown that you can continue to grow - if you are pushing

hard enough. The company has consistently created new avenues for growth from domestic expansion, Export markets, after-sales

markets etc. It has always been able to grow 5 to 10% above Industry average and has been delivering Margins that are in the top 5

percentile of Auto Component manufacturers. We believe that though Phoenix Lamps over the next 2-3 years (lot of approvals/ regulatory

burdens will ensure a long time line) will be a standalone entity, there is a very high probability of it merging with Suprajit later.

We believe that Actis has been mis-managing Phoenix for a long time. While the cost structure doesn’t appear too bloated,

we believe there are enough low hanging fruits to improve margins. The bigger improvement will be on Capital Allocation and Long Term

focus that Suprajit will bring in to Phoenix. The capital allocation track record of Suprajit is stellar while that of Actis is poor. We understand

from our scuttlebutt that growth has not been pushed strongly because of lax in top Management. Our understanding is that every

stakeholder from distributors, employees to OEM partners would be happy dealing with a long term owner.

There can be long term investments in to the business that can drive growth in the future by improving Market Share, gaining

new Customers etc. We have shown details about the frequent Management changes, Audit issues etc. under the previous promoters in

slides 42 & 43. The previous discount on Intrinsic Value for the stock was justified to an extent by the bad track record of Management

and little growth prospects. This gets corrected under Suprajit Engineering and hence we believe that Valuation should get re-rated.

HBJ Capital - Phoenix Lamps Limited. – May, 2015

4.) Robust Cash Flows and Return Metrics:

We believe that the quality of business is reflected in its Financials. The company’s consolidated ROCE’s calculated have

been healthy at over 30% for the last several years. In case, you are eliminating the Goodwill on Consolidation and calculating the returns

on tangible capital employed (roughly around 100 Cr Rs)- it is even more. We believe that such return metrics will not only sustain but

can improve significantly from here on. The company has been making a few bolt-on CAPEX investments over the last 5 years which have

resulted in very healthy returns on incremental capital invested. The operating cash generation has been strong and with very minimal

incremental CAPEX (1-2 Cr/ Year), the business has been generating strong Free Cash Flows. We believe that Suprajit Engineering might

increase the overall CAPEX levels (bolt-on + fresh capacities) to improve efficiencies and grow the business over the long term. All the

financial details with respect to Return Ratios and Incremental returns are captured in Slides 39.

5.) Attractive Valuations & Huge P/E arbitrage:

Finally, at the end of the day - what makes the deal sweet is the price which we are paying for a quality business with

moderate growth. Let’s understand the valuations from the prism of past earnings of Phoenix Lamps in a period which had a rough auto

cycle, operated under a not-so efficient Management, currency price fluctuations etc. Even on the average trailing numbers, the stock is

quoting at around 10%+ Operating Cash Flow yield. With minimal CAPEX and Finance costs, the stock has a similar Free Cash Flow yield.

Even on an average EV/ EBIDTA basis - the current trailing valuations of 7X looks attractive for a business with healthy return metrics.

So while the absolute valuations look attractive, what looks even more interesting is relative valuations. I am not able to

understand reason behind the huge P/E arbitrage between Suprajit Engineering and Phoenix Lamps. Surely, I am making apple to apple

comparison with both companies having similar product level characteristics, same Management, competitive positioning, Market shares,

quality of business and similar financial Return metrics. Yes, Suprajit’s track record is strong and its inherent growth potential is slightly

higher than Phoenix Lamps. It also doesn’t have the International distribution issues that Phoenix is facing, but the valuation differential

HBJ Capital - Phoenix Lamps Limited. – May, 2015

is just too huge to ignore. Suprajit Engineering is quoting at around 15X EV/ EBIDTA and > 30X Price/ Earnings. We also have a bonus

speculative element in this bet that there is a high possibility that in the next 2-3 years, Phoenix and Suprajit might eventually be merged.

While at the current valuations, it would mean swapping a cheap stock with a costly stock - I believe that the probability of the Market re-

rating Phoenix lamps as performance improves over the next 2-3 years is higher and also there is always a high chance that Market re-

rates Phoenix as it senses the eventual merger happening. This will ensure that some amount of P/E arbitrage is captured by Phoenix

Investors. All said and done, this is just a speculative bonus element in the Investment thesis and we believe that there is enough Margin

of Safety in the idea even without such bonuses.

Conclusion:

Two of the other reasons which Investors give for low valuation to Phoenix is the inherent Technology risk (Markets might move

away from Halogen bulbs) and a huge write-off (because of earlier Capital allocation mistakes). We believe that these are extremely low

probability tail risks. The company’s auditors have been changed to the reputed E&Y group around 2 years back and the Goodwill which

is left on the balance sheet is not meaningful. The technology risk is overstated. In a low value product such as Halogen bulbs, the pace of

change to new technology is very slow and the company will have enough time to adapt itself. The current market for Halogen bulbs is

still growing and there is a huge Market that Phoenix can go and attack. Hence, we believe that Phoenix Lamps does quality to us a good

Investment bet with asymmetric risk-reward characteristics, in favor of the Investor.

Regards,

Gokul Raj. P - Director & Head: Investments.

Auto Components-Industry Overview

“ Specialists in discovering Multibagger stocks “

Strong Growth potential across segments

“ Specialists in discovering Multibagger stocks “

Source: www.tankrich.com

Indian Auto Ancillary Industry-2015

“ Specialists in discovering Multibagger stocks “

Source: www.tankrich.com

Strong Growth potential across segments

“ Specialists in discovering Multibagger stocks “

Long Runway for growth

“ Specialists in discovering Multibagger stocks “

Auto Components Overview

“ Specialists in discovering Multibagger stocks “

Huge Export Growth Opportunity

“ Specialists in discovering Multibagger stocks “

Healthy growth over the next several years

“ Specialists in discovering Multibagger stocks “

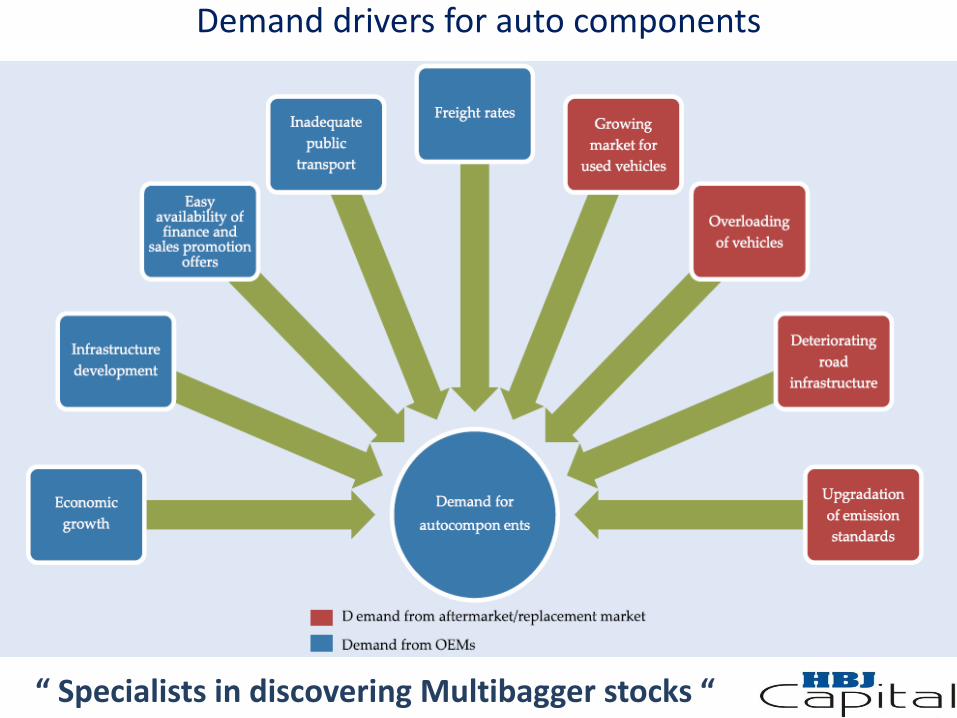

Demand drivers for auto components

“ Specialists in discovering Multibagger stocks “

Sub segments of Auto Ancillaries

“ Specialists in discovering Multibagger stocks “

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps - Company Overview

Company Overview

“ Specialists in discovering Multibagger stocks “

• Sale of general lighting business completed end August 2013. Company is now a fullyfocused automotive lighting player

• Comprehensive product portfolio of halogen bulbs for the automotive industry with existingcapacity of around 87mn units p.a. in auto halogen bulbs

• Largest manufacturer in India controlling ~50 - 60% of the total manufacturing capacity inthe country and among the top 5 globally with 20+ years of manufacturing excellence andinstitutionalized knowledge

• Well entrenched relationships with the leading Japanese, Korean, European and IndianOEMs who have approved the manufacturing facilities

• Strong International presence with exports to more than 50 countries. Overseas operationsin Europe through international subsidiaries, Luxlite and Trifa with significant market share inthe aftermarket segment

• Nearly half of sales (~45%) are under own brands including India’s oldest domesticaftermarket brand and 90 year old European brand for international markets (~86% of salesin India is branded and ~24% of export sales is branded)

Large Automated Manufacturing Facilities

“ Specialists in discovering Multibagger stocks “

Unit LocationManufacturing facilities in both domestic tariff area and special economic

zone in Noida enables meeting diverse customer requirements

Accreditations

Compliance with international standards ECE37R, MVSS108, ISO

9001:2008, OHSAS 1881:2007, ISO/IES 17025:2005 and AIS-037 (ICAT)

and E1 homologation certificates

Key Products H4, HS1, H1, H7, H3, H8, M5, 9000 series and long life variants

Current Annual

CapacityAround 87 mn lamps across 14 production lines

Workforce 1,041 employees

Manufacturing Capabilities and Advantages

“ Specialists in discovering Multibagger stocks “

• Adequate controls in place to meet OEM quality

requirements

• Stable operations resulting from over 20 years of

experience in running large scale cost-competitive

capacities for halogen bulbs

• Low lead time in terms of approval for products by

OEMs

• Operating Cost advantage vis-à-vis competition

• Ability to procure standard operational lines and

customize /automate them at low costs

• Technology & skilled man power base which is

critical for bulb manufacturing with high precision

Tube Cutting Length Checking

Bridge Making Process Mount Making Process

Bulb Forming Process Sealing Process

Products Overview

“ Specialists in discovering Multibagger stocks “

Bulb Type

H4/ H4 LL H1 H7 9000 series

Description • Dual filament• Single filament

with high beam• Single filament

with low beam

• Base designed to prevent corrosion

• Single/ double filaments

Vehicle type 4 wheelers 4 wheelers 4 wheelers 4 wheelers

Application Headlamp Headlamp Headlamp Headlamp

Volts 12 and 24 V 12 and 24 V 12 V and 24 V 12 V

Products Overview

“ Specialists in discovering Multibagger stocks “

Bulb Type

H3 H8 / H9 / H11 HS1 M5

Description

• Single horizontal filament

• Visibility during fog by bright yellow lights

• Single filament lamps

• Special corrosionpreventive base

• Dual filament • Dual Filament

Vehicle type 4 wheelers 4 / 2 Wheelers 2 / 3 wheelers 2 wheelers

Application Fog Lamp Head / Fog Lamp Headlamp Headlamp

Volts 12 V and 24 V 12 V 12 V 12 V

Phoenix Lamps - Business Overview

“ Specialists in discovering Multibagger stocks “

Key Information

“ Specialists in discovering Multibagger stocks “

Stable Margin Trend

“ Specialists in discovering Multibagger stocks “

Quality Automotive Business

“ Specialists in discovering Multibagger stocks “

*-Approximate Numbers

High Quality Domestic Business

“ Specialists in discovering Multibagger stocks “

Subsidiaries Business

“ Specialists in discovering Multibagger stocks “

Actis – Management Issues

“ Specialists in discovering Multibagger stocks “

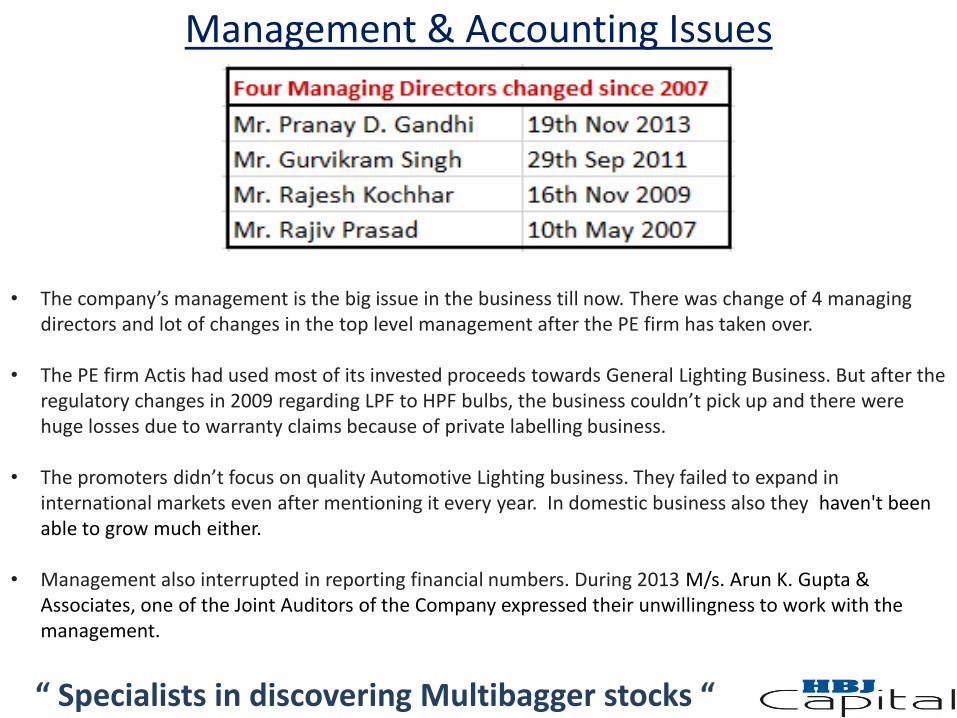

Management & Accounting Issues

“ Specialists in discovering Multibagger stocks “

• The company’s management is the big issue in the business till now. There was change of 4 managing directors and lot of changes in the top level management after the PE firm has taken over.

• The PE firm Actis had used most of its invested proceeds towards General Lighting Business. But after the regulatory changes in 2009 regarding LPF to HPF bulbs, the business couldn’t pick up and there were huge losses due to warranty claims because of private labelling business.

• The promoters didn’t focus on quality Automotive Lighting business. They failed to expand in international markets even after mentioning it every year. In domestic business also they haven't been able to grow much either.

• Management also interrupted in reporting financial numbers. During 2013 M/s. Arun K. Gupta & Associates, one of the Joint Auditors of the Company expressed their unwillingness to work with the management.

Suprajit Engineering Ltd.- A Value Creator

“ Specialists in discovering Multibagger stocks “

Suprajit Engineering Financial Overview

“ Specialists in discovering Multibagger stocks “

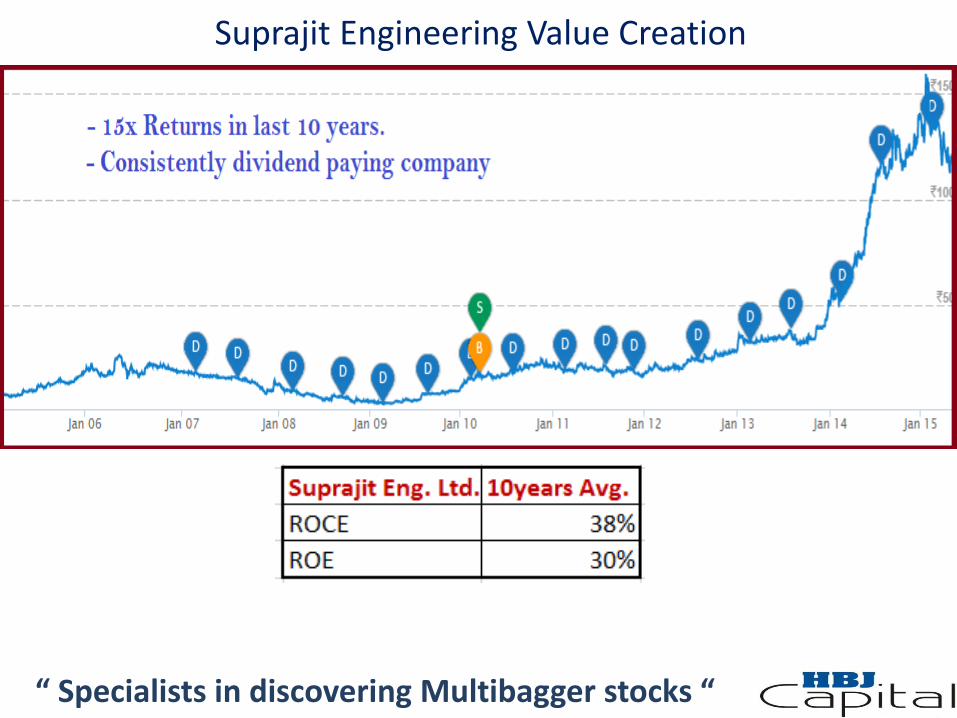

Suprajit Engineering Value Creation

“ Specialists in discovering Multibagger stocks “

Possible synergies going forward

“ Specialists in discovering Multibagger stocks “

• Phoenix and Suprajit are mass manufacturers of Halogen bulbs and Automotive cablesrespectively and both enjoy competitive cost advantage.

• After market distribution can be increased substantially in both domestic and internationalmarkets using their strength of distribution network.

• Suprajit is already having marketing team in USA for its products which is an advantage forPhoenix to step into North American region. Suprajit is also having strong team in Europeand can help in improving Phoenix subsidiaries sales.

• Present capacity utilization of phoenix is around 75%, even if demand grows there is enoughland available for expansion at current manufacturing plant.

• Suprajit has a demonstrated track record of above-market growth rate and can expect thesame thing for Phoenix Lamps in coming future.

• The stock might eventually get merged into Suprajit Engineering (at least a few years away).Suprajit is currently trading at a huge P/E premium compared to Phoenix as on today'svaluations. The valuation gap will narrow meaningfully going forward and with the expectedMerger, Phoenix lamps can be a cheaper way to play Suprajit story.

Peer Comparison

Peer Comparison

“ Specialists in discovering Multibagger stocks “

Source: www.tankrich.com

Peer Comparison

“ Specialists in discovering Multibagger stocks “

Courtesy: Arun Gopalan

Peer Comparison

• Phoenix lamps is having better position among the auto component manufacturers.

• Larger players like Phoenix will have huge competitive advantage over small players in terms of cost structure and capital efficiency.

• Margin numbers and Capital efficient numbers are on par with Suprajit Engineering even during moderate performance years.

“ Specialists in discovering Multibagger stocks “

Phoenix Lamps - Financial Overview

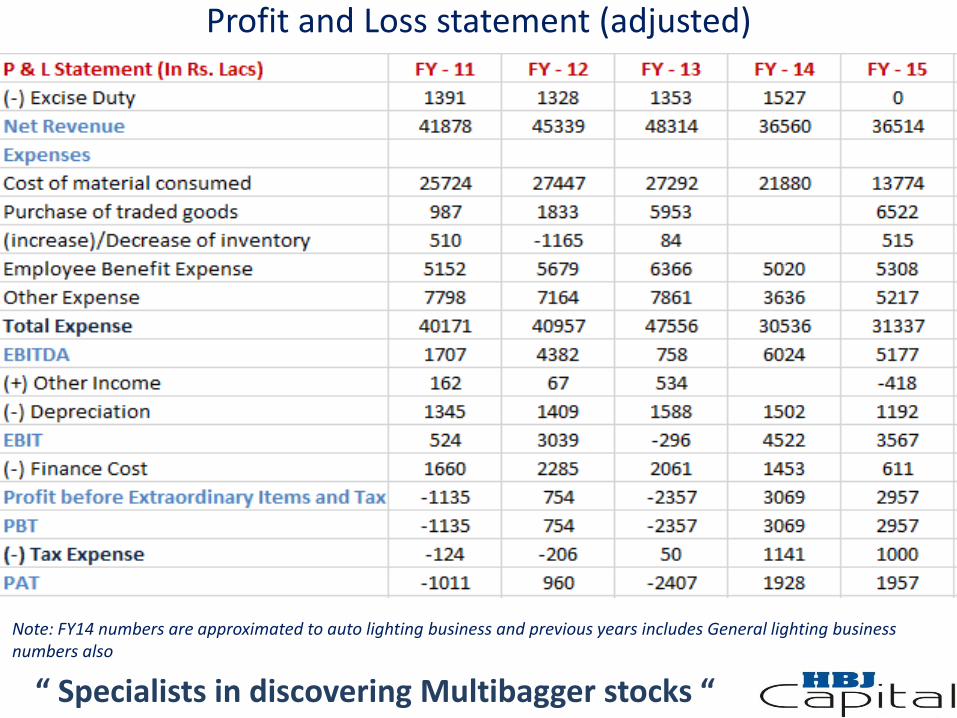

Profit and Loss statement (adjusted)

“ Specialists in discovering Multibagger stocks “

Note: FY14 numbers are approximated to auto lighting business and previous years includes General lighting business numbers also

Balance Sheet(Liabilities)

“ Specialists in discovering Multibagger stocks “Note: FY13 and previous years includes General lighting business numbers also

Balance Sheet (Assets)

“ Specialists in discovering Multibagger stocks “Note: FY13 and previous years includes General lighting business numbers also

Common size profit and loss statement

“ Specialists in discovering Multibagger stocks “

Note: FY14 numbers are approximated to auto lighting business and previous years includes General lighting business numbers also

Common size Balance Sheet(Liabilities)

“ Specialists in discovering Multibagger stocks “Note: FY13 and previous years includes General lighting business numbers also

Common size Balance Sheet (Assets)

“ Specialists in discovering Multibagger stocks “Note: FY13 and previous years includes General lighting business numbers also

Euro impact on P&L

“ Specialists in discovering Multibagger stocks “

• Company derives most of its export revenue from Europe region. During the year the Euro currency had depreciated by around 20% against rupee.

• Due to depreciation company has experienced a loss of Rs.5cr on profit and loss statement for the financial year 2015.

• The ongoing economic turbulence in the Europe region has also effected the sales of International subsidiaries.

Risks & Concerns – Phoenix Lamps

“ Specialists in discovering Multibagger stocks “

• Worse Macro Economic situation in Europe leads to continuous loss in its Subsidiary.

• Decreased usage of Halogen lamps as technology progresses to newer forms.

• Failure of the Management to shift sales from Un-Branded to Branded products.

• There is Rs.53cr. of Contingent liabilities demands from the Indian Tax authorities on account of addition in sales, disallowance of purchases and other expenses for the years of 2009-10 and 2010-2011.

• Entry of foreign players into India to manufacture bulbs due to cost advantage.

• Excessive volatility in company’s key raw materials and Currency rates.

• Regulatory changes in usage of certain halogen lamps.

Price Chart – Phoenix Lamps

• Phoenix Lamps has got re-rated after the demerger and sale of its Non-Auto business.

• Stock price has came down in the last one year due to distress selling by PE firm in open market.

• Institutional holding is extremely low and most of the holdings is with retail investors who have been accumulating the shares off late.

“ Specialists in discovering Multibagger stocks “

Share Holding Pattern (%)

Mar2015

Dec2014

Sep2014

Jun2014

Promoters 61.88 67.4 70.1 70.9

FII 2.20 2 2 2.36

DII 0.07 0.02 0.01 0.01

Conclusion

We are happy that Actis has exited in favor of Suprajit Engineering. We have been trackingSuprajit for many years and have huge confidence in Mr. Ajit Kumar Rai's execution leadershipand capital allocation skills. We believe that the asset is far more valuable in the hands ofSuprajit than it was with Actis Private equity.

We have already given Phoenix Lamps as one of our Multibagger Ideas during the month ofJanuary as part of our basket buying in quality Auto Ancillary ideas available at attractivevaluations. With the corporate acquisition of Phoenix Lamps by Suprajit Engineering, we arehappy to increase the allocation to Phoenix and upgrade it from being a Tail Bet to a CorePortfolio Idea.

We have been investing in ancillary stocks and high operational leverage businesses for quitesome time now. Phoenix also belongs to the same category with high operational leverage andhuge competitive advantage. It is difficult for small players to operate in this kind of businessand we expect that the market will consolidate under larger players going forward due to theiroperating efficiency. The stock is also available at substantial Margin of Safety. This gives us theopportunity to take position in the stock which we believe that can deliver strong returns incoming 2-3 years.

“ Specialists in discovering Multibagger stocks “

“ Specialists in discovering Multibagger stocks “

THANK YOU

“ Specialists in discovering Multibagger stocks “