Embed Size (px)

Citation preview

Retained Earnings

Mrs. Paz Castro

Overview

A 2-for-2 share split gives shareholders one additional share of ordinary shares for each share they own.

Share dividends also give shareholders additional shares based on the value of their holdings, but have a different effect on the shareholders’ equity section of the statement of financial position.

A cash dividend is a distribution of cash based on the number of shares owned.

Retained earnings represent the component of the shareholders’ equity arising from the retention of assets generated from the profit-directed activities of the corporation.

At the end of the accounting period, the Income Summary account of a corporation is closed to the Retained Earnings account.

The Retained Earnings account is credited with the corporation’s profit or debited with the loss.

Distributions to shareholders of cash, property or stocks from unrestricted retained earnings on the basis of all issued and fully paid shares, and all subscribed par value shares except treasury shares are called dividends.

Dividend declarations reduce retained earnings. Other less common situations that cause

increases and decreases in retained earnings: debits resulting from reissuance of treasury stocks below cost and loss on retirement of treasury stocks and debits or credits for prior period errors.

Prior period errors are errors discovered in the current period that are of such significance that the financial statements of one or more prior periods can no longer be considered to have been reliable at the date of their issue. Credit entries increase the retained earnings balance and debits decrease it.

A debit balance in the Retained Earnings account resulting from accumulated losses is called a deficit.

Retained earnings may be restricted or appropriated, and unrestricted or unappropriated.

Unrestricted retained earnings are free and can be declares as dividends.

Retained earnings restrictions may be legal, contractual or voluntary.

Dividends in General

An owners’ equity account representing claim on all assets in general and not on any asset in particular.

Shareholders are not guaranteed dividends and dividends do not become a liability of the company until the board of directors has formally declared a dividend distribution.

Section 43 of the Corporation Code states that dividends should only be declared out of the unrestricted retained earnings.

Dividends may take the form of cash, property or additional shares of stock of the corporation.

Any form of dividend declaration should be based on the total subscription of a shareholder and not merely on the shares already paid.

Subscribers are considered shareholders from the time their subscriptions are accepted by the corporation and not from the time they are issued stock certificates.

DATE OF DECLARATION The board of directors will adopt a

resolution declaring that a dividend is to be paid.

The resolution will specify the amount, type and date of payment of this dividend. It will also set a date of record.

Cash dividends are declared solely by the board of directors while share dividends will necessitate the concurrence of at least two-thirds of the outstanding shareholders.

Legally, declared dividends are obligations of the firm. Dividends to be paid in cash or property became a liability on this date. Shares distributable is also recognized.

An entry is made debiting Retained Earnings and crediting a dividend liability of Shares Distributable account. Some companies debit a Dividends Declared account instead of the Retained Earnings account. This account is nevertheless closed to the Retained Earnings account at the end of the year.

Paragraph 10 of IFRIC 17 provides that the liability to pay a dividend shall be recognized when the dividend is appropriately authorized and is no longer at the discretion of the entity, which is the date: When declaration of the dividend, e.g. by

management or the board of directors, is approved by the relevant authority, e.g. the shareholders, if the jurisdiction requires such approval, or

When the dividend is declared, e.g. by management or the board of directors, if the jurisdiction does not require further approval.

IFRIC 17 Distributions of Non-cash Assets to Owners was developed by the International Financial Reporting Interpretation Committee and issued by the Internal Accounting Standards Board in Nov. 2008. Its effectivity date is July 1 2009.

DATE OF RECORD A list of shareholders entitled to the declared

dividends is prepared at the date of record. If an investor buys a share of stock after this date,

he will not receive the dividends. This share is said to be traded ex-dividend.

No entry is required on this date. DATE OF PAYMENT

The corporation settles its liability on this date.

An entry is made debiting the dividend liability or shares distributable account and crediting cash, property distributed or share capital.

Cash Dividends

Majority of dividends distributed by corporations is paid in cash.

A company must have both an appropriate amount of retained earnings and the necessary amount of cash.

A corporation, however, may successfully accumulate earnings and at the same time not be sufficiently liquid to pay large dividends.

Dividends on par value shares are stated as a certain percentage of the par value.

As to no-par value shares, the dividends are stated at a certain amount per share.

When the board of directors declares a cash dividend, an entry is made debiting Retained Earnings and crediting Cash Dividends Payable. Ex.: A nationally-known business books distribution

company declared a cash dividend of P12 per share of ordinary shares of July 1. the dividends are payable on August 1 to shareholders of record on July 21. The company

has 100,000 ordinary shares issued of which 7,000 shares are held in treasury. The entries to record the dividend declaration and payment are as follows:

Retained Earning 1,116,000Cash Dividends 1,116,000

To record declaration of dividend. The account, Cash Dividend, may be used

in place of the debit to Retained Earnings. At the end of the accounting period, this temporary shareholders’ equity account will be closed by debiting Retained Earnings and crediting Cash Dividends Declared.

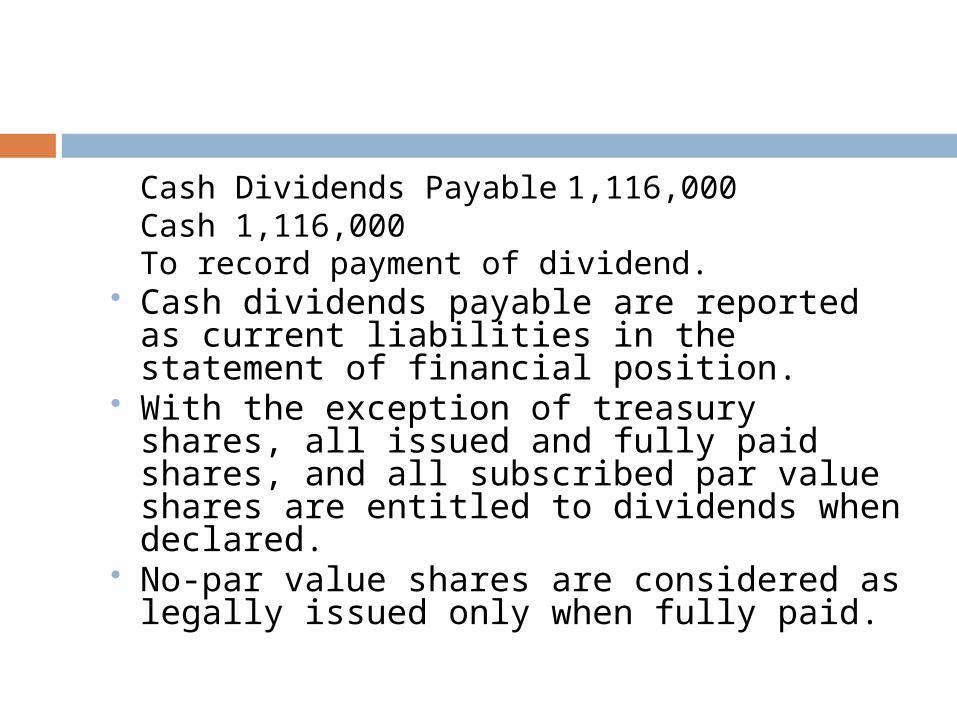

Cash Dividends Payable 1,116,000Cash 1,116,000

To record payment of dividend. Cash dividends payable are reported as

current liabilities in the statement of financial position.

With the exception of treasury shares, all issued and fully paid shares, and all subscribed par value shares are entitled to dividends when declared.

No-par value shares are considered as legally issued only when fully paid.

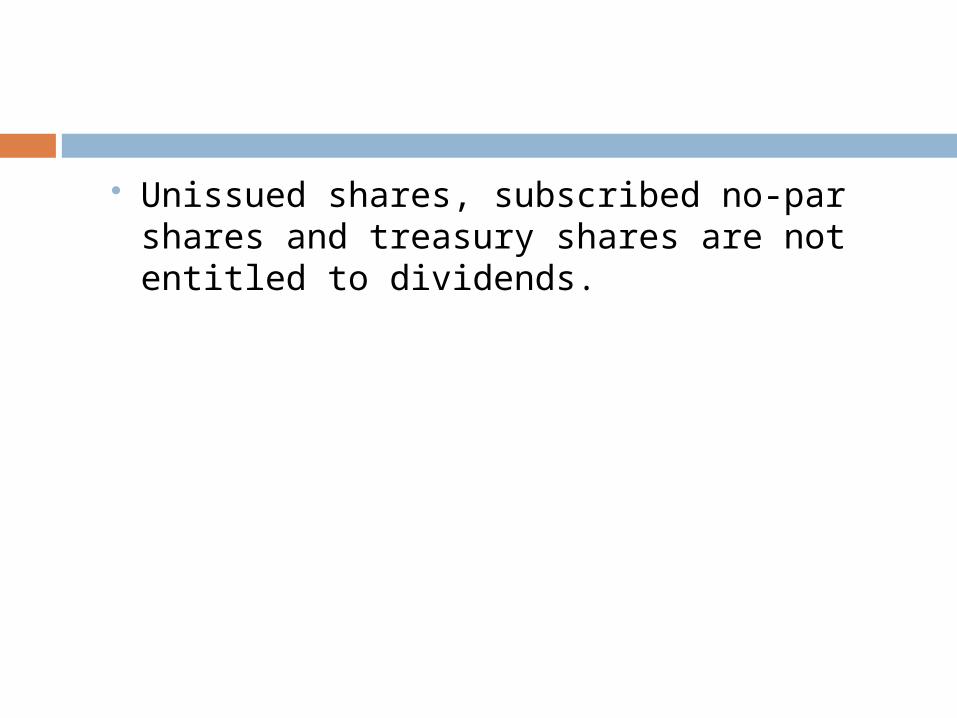

Unissued shares, subscribed no-par shares and treasury shares are not entitled to dividends.

Property Dividends

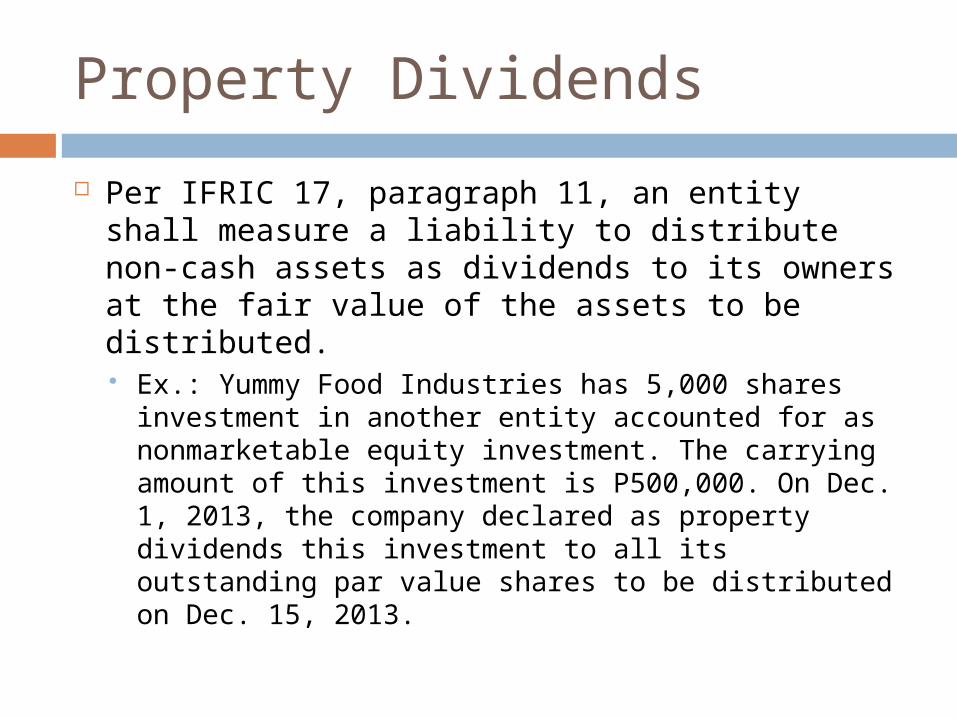

Per IFRIC 17, paragraph 11, an entity shall measure a liability to distribute non-cash assets as dividends to its owners at the fair value of the assets to be distributed. Ex.: Yummy Food Industries has 5,000 shares

investment in another entity accounted for as nonmarketable equity investment. The carrying amount of this investment is P500,000. On Dec. 1, 2013, the company declared as property dividends this investment to all its outstanding par value shares to be distributed on Dec. 15, 2013.

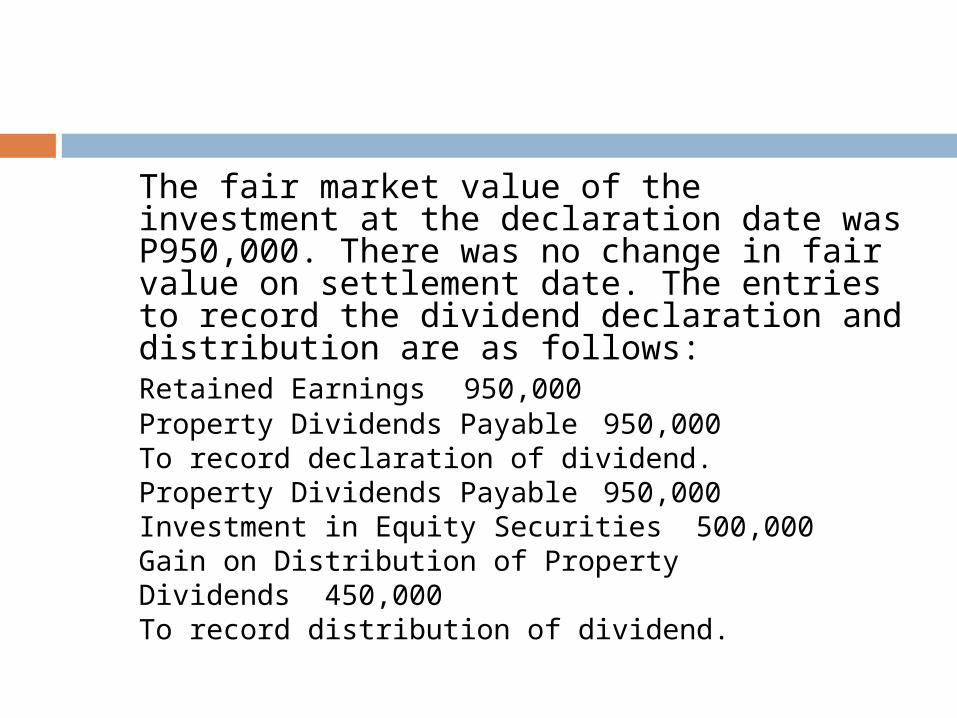

The fair market value of the investment at the declaration date was P950,000. There was no change in fair value on settlement date. The entries to record the dividend declaration and distribution are as follows:

Retained Earnings 950,000Property Dividends Payable 950,000

To record declaration of dividend.Property Dividends Payable 950,000

Investment in Equity Securities 500,000Gain on Distribution of Property

Dividends 450,000To record distribution of dividend.

Because of the use of fair value, a problem will arise at settlement date if the fair value of the assets to be distributed has changed. The following offers the pertinent guidance: Per IFRIC 17, paragraph 13, at the end of each reporting

period and at the date of settlement, the entity shall review and adjust the carrying amount of the dividend payable, with any changes in the carrying amount of the dividends payable recognized in equity as adjustments to the amount of the distribution.

Paragraph 14, when an entity settles the dividends payable, it shall recognize the difference, if any, between the carrying amount of the assets distributed and the carrying amount of the dividend payable in profit or loss.

IFRS 5, paragraph 5A, states that the classification, presentation and measurement requirements in this IFRS is applicable to a non-current asset (or disposal group) that is classified as held for distribution to owners.

Paragraph 15A provides that an entity shall measure a non-current asset (or disposal group) classified as held for distribution to owners at the lower of its carrying amount and fair value less costs to distribute.

Share Dividends

A corporation may distribute to shareholders additional shares of the company’s own share as share dividends.

This type of dividend affects only the accounts within the shareholders’ equity.

Share dividends increase the total share capital and decrease the retained earnings account.

Because both of these are components of shareholders’ equity, total shareholders’ equity is unchanged.

From the shareholders’ point of view, a share dividend does not change their percentage interests in the corporation although total outstanding shares have increased.

SMALL SHARE DIVIDENDS Additional shares issued are less than 20% of the

previously outstanding shares. Recorded by transferring from retained earnings to

share capital (ordinary shares and share premium accounts) the fair market value of the additional shares to be issued.

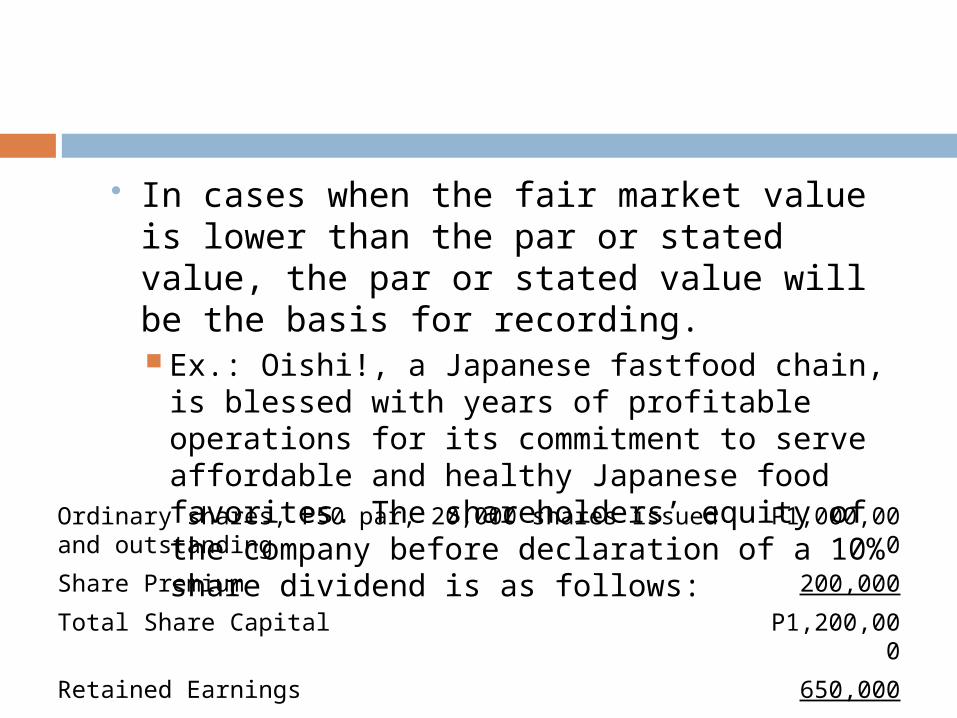

In cases when the fair market value is lower than the par or stated value, the par or stated value will be the basis for recording. Ex.: Oishi!, a Japanese fastfood chain, is

blessed with years of profitable operations for its commitment to serve affordable and healthy Japanese food favorites. The shareholders’ equity of the company before declaration of a 10% share dividend is as follows:Ordinary shares, P50 par, 20,000 shares issued and

outstandingP1,000,00

0

Share Premium 200,000

Total Share Capital P1,200,000

Retained Earnings 650,000

Total Shareholders’ Equity P1,850,000

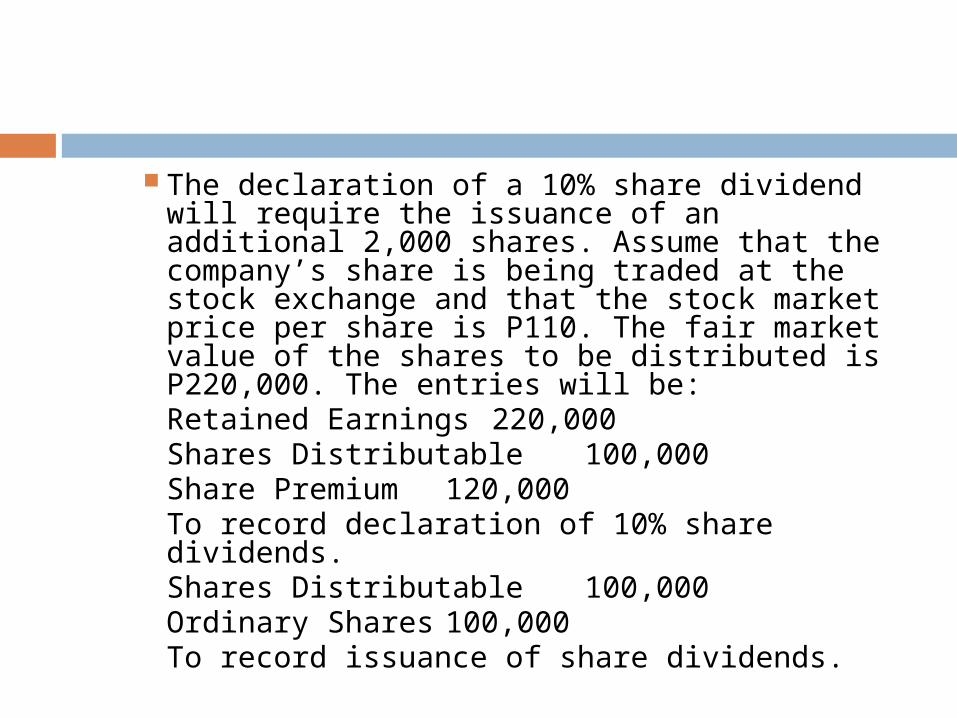

The declaration of a 10% share dividend will require the issuance of an additional 2,000 shares. Assume that the company’s share is being traded at the stock exchange and that the stock market price per share is P110. The fair market value of the shares to be distributed is P220,000. The entries will be:Retained Earnings 220,000

Shares Distributable 100,000Share Premium 120,000

To record declaration of 10% share dividends.Shares Distributable 100,000

Ordinary Shares 100,000To record issuance of share dividends.

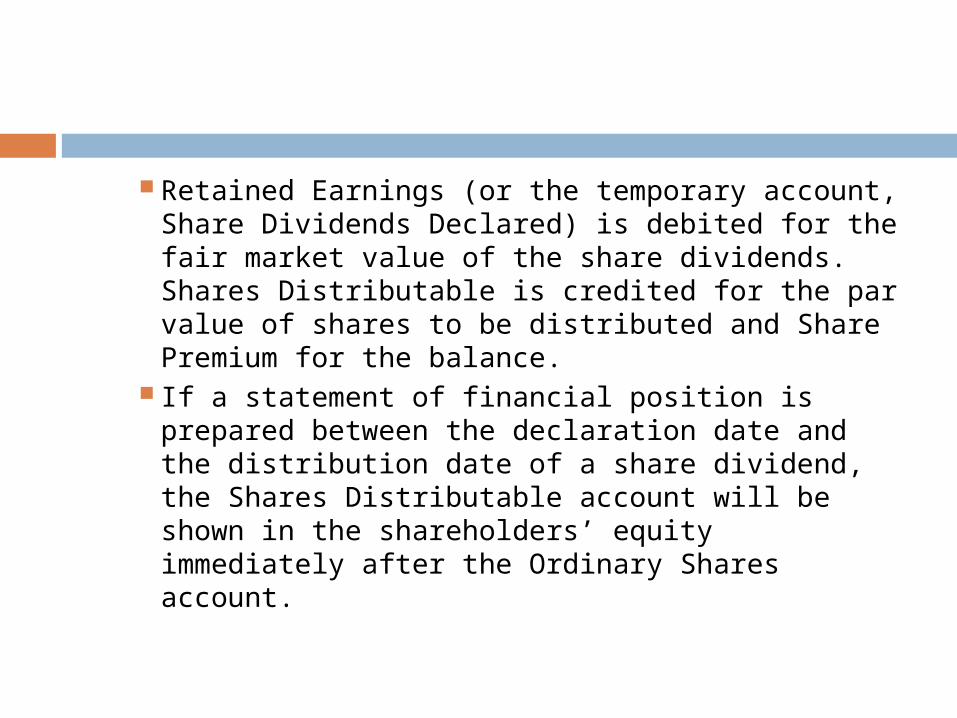

Retained Earnings (or the temporary account, Share Dividends Declared) is debited for the fair market value of the share dividends. Shares Distributable is credited for the par value of shares to be distributed and Share Premium for the balance.

If a statement of financial position is prepared between the declaration date and the distribution date of a share dividend, the Shares Distributable account will be shown in the shareholders’ equity immediately after the Ordinary Shares account.

When the share is distributed, only the components of the shareholders’ equity changes; retained earnings decreased by P220,000 and total share capital increased by P220,000. The total shareholders’ equity did not change. Before

DividendsAfter

DividendsIncrease

(Decrease)

Ordinary Shares, P50 par, 20,000 shares issued and outstanding

P1,000,000

P1,100,000

P100,000

Share Premium 200,000 320,000 120,000

Total Share Capital P1,200,000

P1,420,000

P220,000

Retained Earnings 650,000 430,000 (220,000)

Total Shareholders’ Equity P1,850,000

P1,850,000

-

Shares Issued and Outstanding 20,000 22,000 2,000

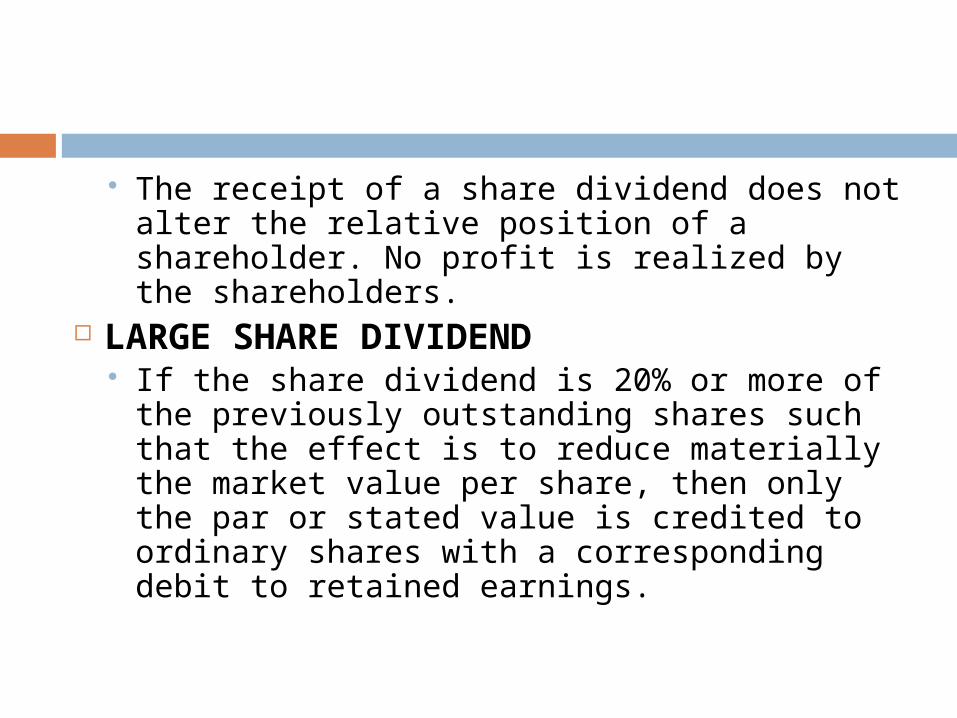

The receipt of a share dividend does not alter the relative position of a shareholder. No profit is realized by the shareholders.

LARGE SHARE DIVIDEND If the share dividend is 20% or more of the

previously outstanding shares such that the effect is to reduce materially the market value per share, then only the par or stated value is credited to ordinary shares with a corresponding debit to retained earnings.

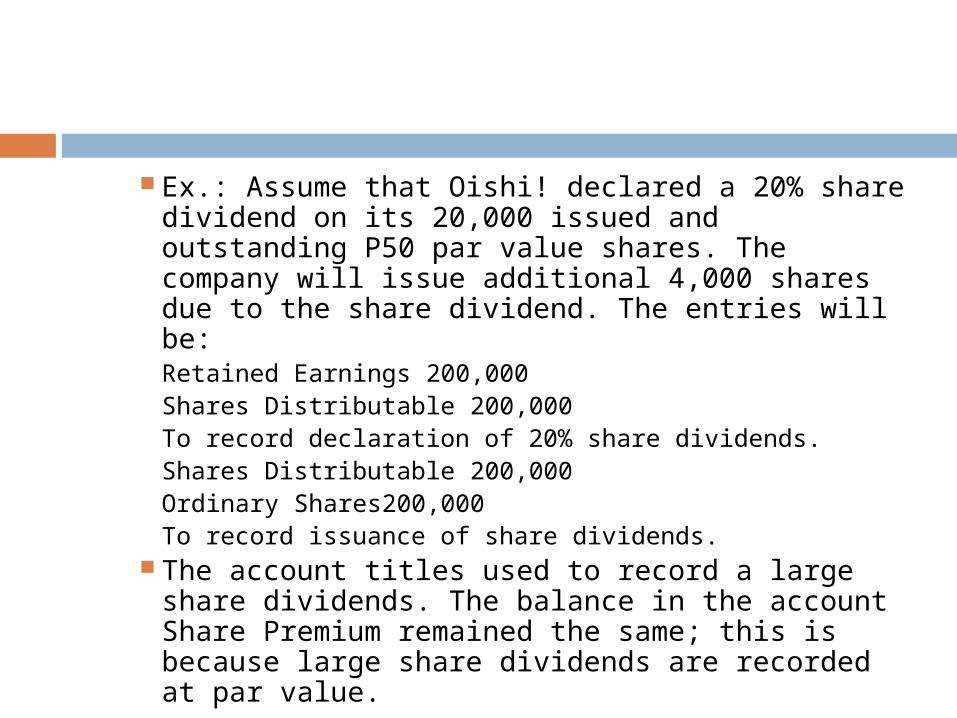

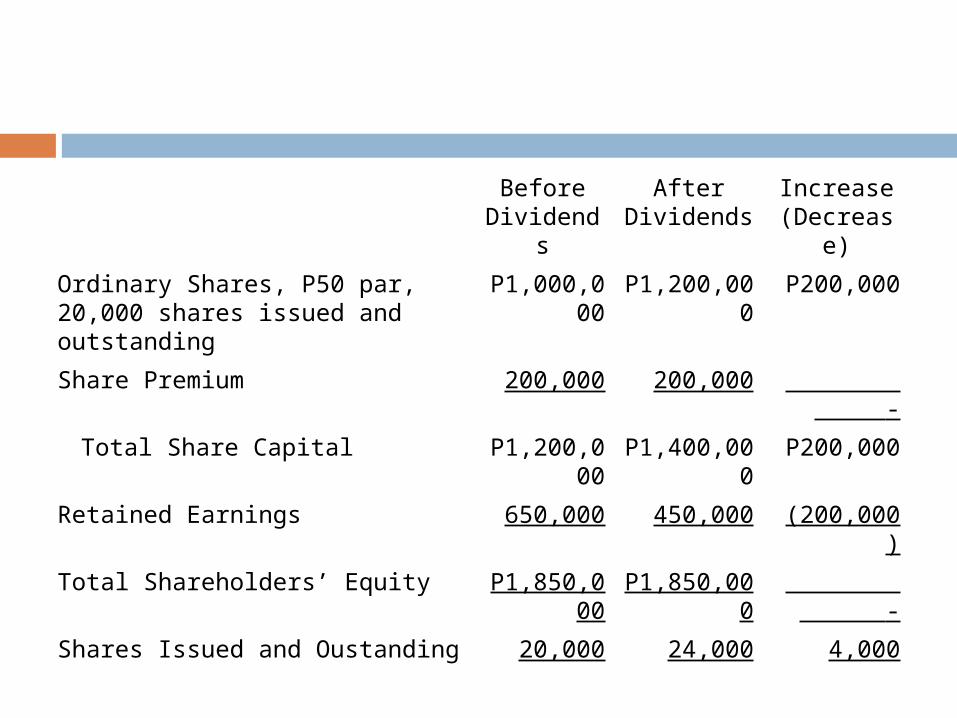

Ex.: Assume that Oishi! declared a 20% share dividend on its 20,000 issued and outstanding P50 par value shares. The company will issue additional 4,000 shares due to the share dividend. The entries will be:Retained Earnings 200,000

Shares Distributable 200,000To record declaration of 20% share dividends.Shares Distributable 200,000

Ordinary Shares 200,000To record issuance of share dividends.

The account titles used to record a large share dividends. The balance in the account Share Premium remained the same; this is because large share dividends are recorded at par value.

Before Dividends

After Dividends

Increase (Decrease

)

Ordinary Shares, P50 par, 20,000 shares issued and outstanding

P1,000,000

P1,200,000

P200,000

Share Premium 200,000 200,000 -

Total Share Capital P1,200,000

P1,400,000

P200,000

Retained Earnings 650,000 450,000 (200,000)

Total Shareholders’ Equity P1,850,000

P1,850,000

-

Shares Issued and Oustanding 20,000 24,000 4,000

Liquidating Dividends

Returns of capital to the investing shareholders.

This type of dividend can be legally paid only under either of the following circumstances: When the corporation is under dissolution

and liquidation, or When the corporation is engaged in the

exploration of natural resources.

Share Splits

Corporations reduce the par or stated value of its share capital and issues additional shares to its shareholders through the practice referred to as share splits.

The par or stated value per share will decrease with a corresponding increase in the number of authorized, issued and outstanding shares. In effect, there is not change in the balances of the shareholders’ equity accounts.

The following are some reasons behind a share split: To adjust the market price of the

company’s shares to a level where more individuals can afford to invest in the stock.

To spread the shareholder base by increasing the number of outstanding shares.

To benefit existing shareholders by allowing them to take advantage of an imperfect adjustment following the split.

When shares are selling below a desired price or when management wishes to take control of the company, the corporation may consider a reverse split that can be accomplished by increasing the par or stated value of its share and reducing the shares outstanding. There will be no entry required; a memo entry is sufficient.

Ex.: The International School of Business and Sciences, Inc. has 10,000 P10 par value ordinary shares issued and outstanding when the board of directors decided to split the share 5-for-1. this means that a shareholder would receive 5 shares with a new par value of P20 for each share held. Ordinary shares will remain unchanged at P1,000,000. the issued and outstanding shares will now be 50,000 and the par value reduced to P20 per share.

Summary of the Effects of Dividends and Share Splits

Effect on: Declaration of Cash Dividends

Payment of

Cash Dividen

ds

Declaration and Distribution of

Small Share

Dividends

Large Share

Dividends

Share Split

Retained Earnings

Decrease - Decrease Decrease -

Ordinary Shares - - Increase Increase -

Share Premium - - Increase - -

Total Shareholders’ Equity

Decrease - - - -

Total Liabilities Increase Decrease - - -

Total Assets - Decrease - - -

Shares Outstanding

- - Increase Increase Increase

Dividends on Preference and Ordinary Shares A corporation may issue both preference

and ordinary shares. When the board of directors declares

cash dividends, preference shareholders are entitled to dividends before ordinary shareholders receive any distribution.

The dividend is stated as a percentage of the par value preference shares.

The corporation is not obliged to declare dividends annually.

When the board does not declare dividends, the dividends for cumulative preference shares accumulate; these are called dividends in arrears.

Preference shares may contain one of the following combinations of features: Non-cumulative and non-participating Non-cumulative and participating Cumulative and non-participating Cumulative and participating

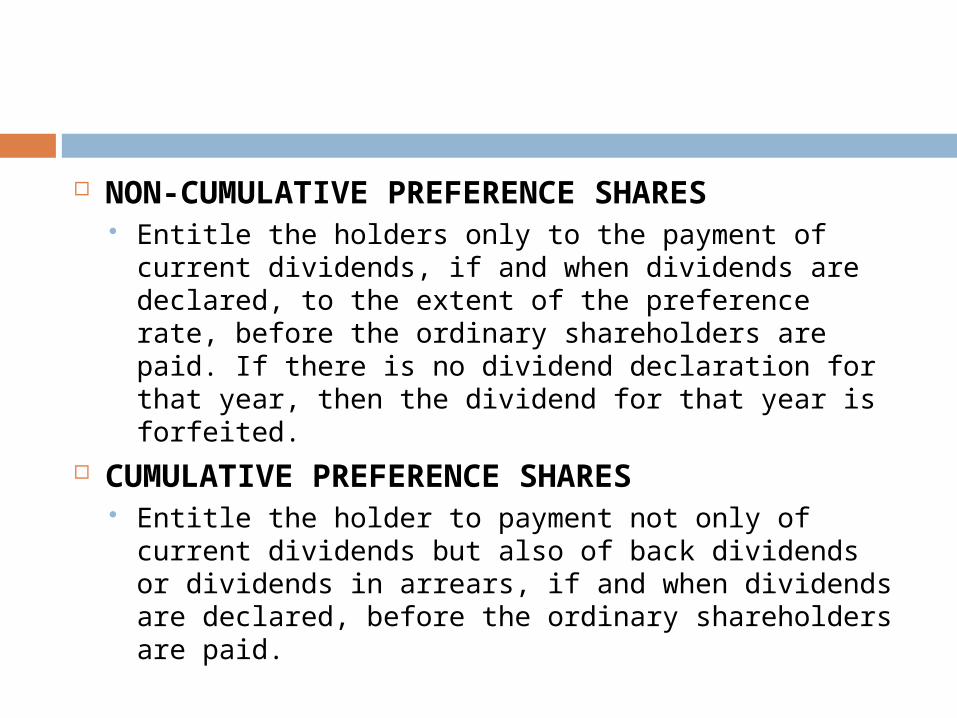

NON-CUMULATIVE PREFERENCE SHARES Entitle the holders only to the payment of current

dividends, if and when dividends are declared, to the extent of the preference rate, before the ordinary shareholders are paid. If there is no dividend declaration for that year, then the dividend for that year is forfeited.

CUMULATIVE PREFERENCE SHARES Entitle the holder to payment not only of current

dividends but also of back dividends or dividends in arrears, if and when dividends are declared, before the ordinary shareholders are paid.

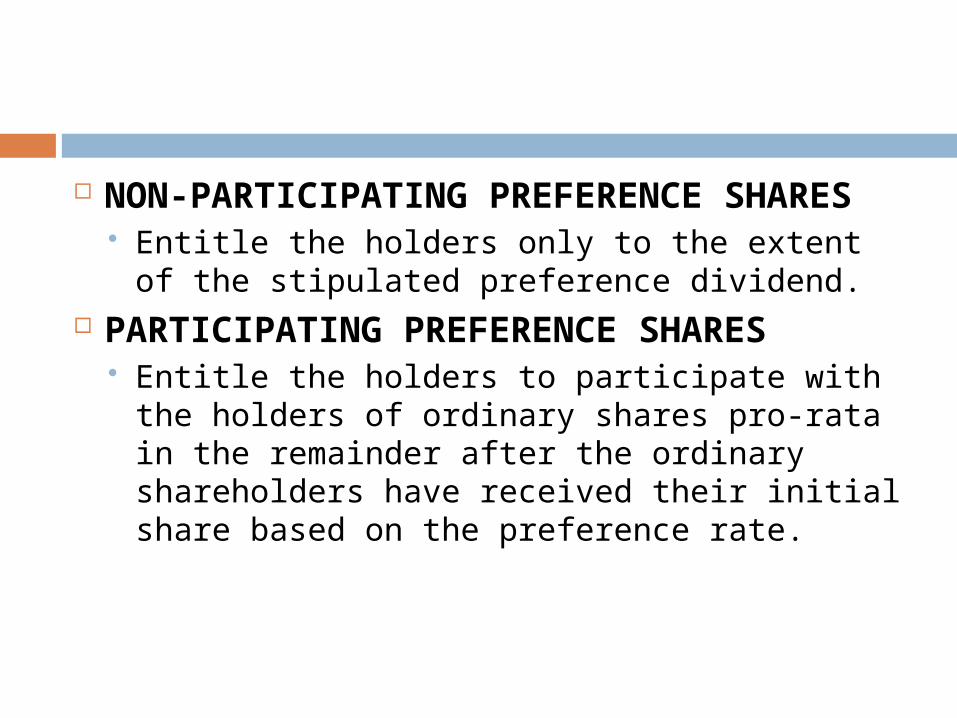

NON-PARTICIPATING PREFERENCE SHARES Entitle the holders only to the extent of the

stipulated preference dividend. PARTICIPATING PREFERENCE SHARES

Entitle the holders to participate with the holders of ordinary shares pro-rata in the remainder after the ordinary shareholders have received their initial share based on the preference rate.

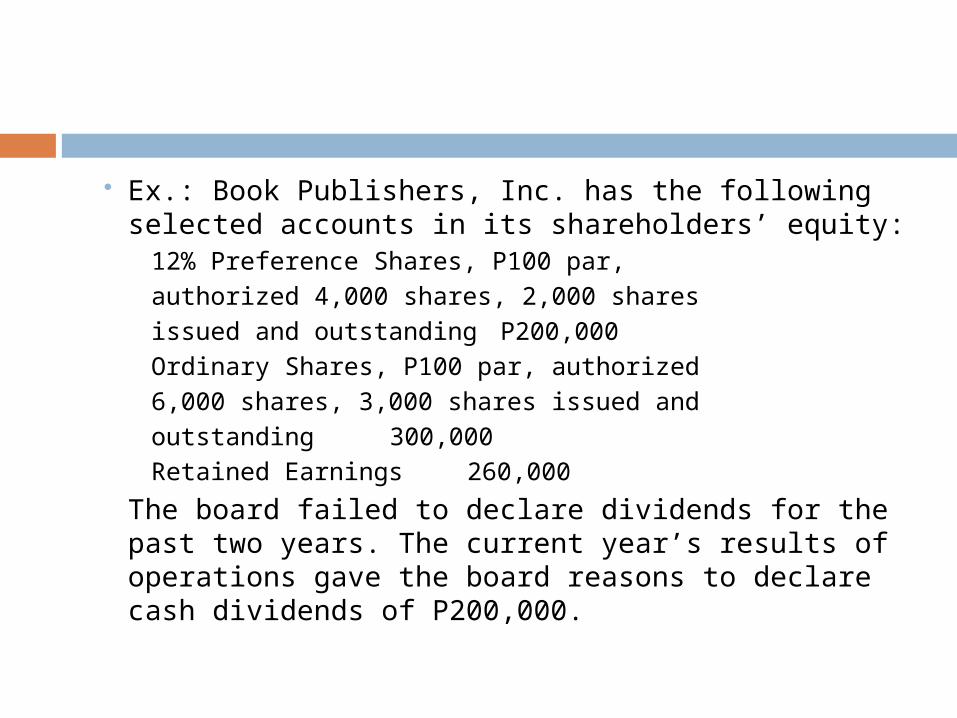

Ex.: Book Publishers, Inc. has the following selected accounts in its shareholders’ equity:

12% Preference Shares, P100 par,authorized 4,000 shares, 2,000 sharesissued and outstanding P200,000Ordinary Shares, P100 par, authorized6,000 shares, 3,000 shares issued andoutstanding 300,000Retained Earnings 260,000

The board failed to declare dividends for the past two years. The current year’s results of operations gave the board reasons to declare cash dividends of P200,000.

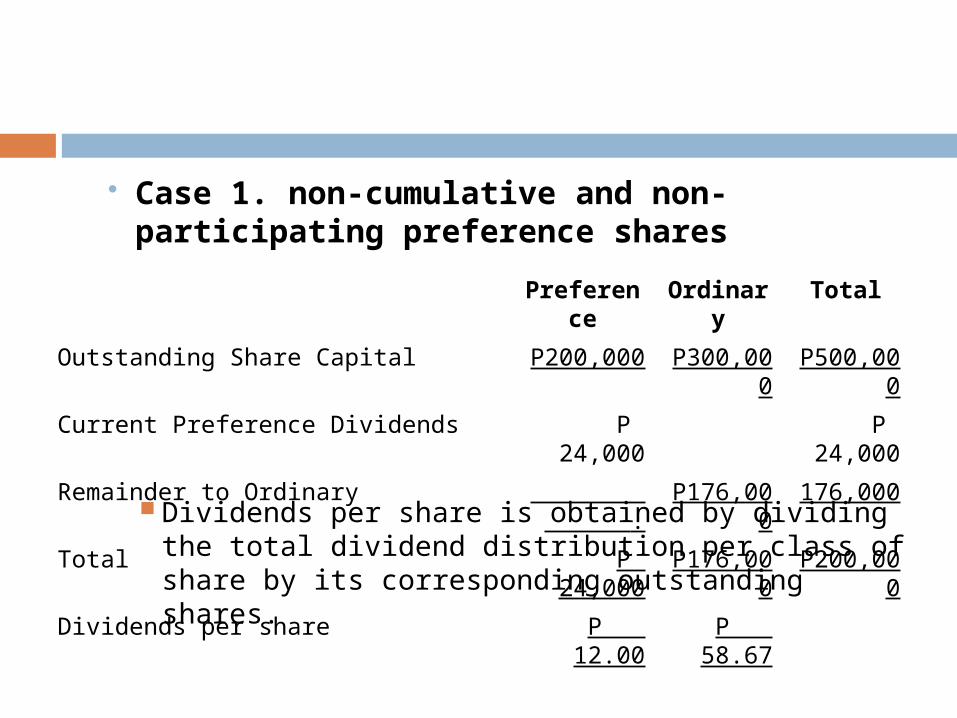

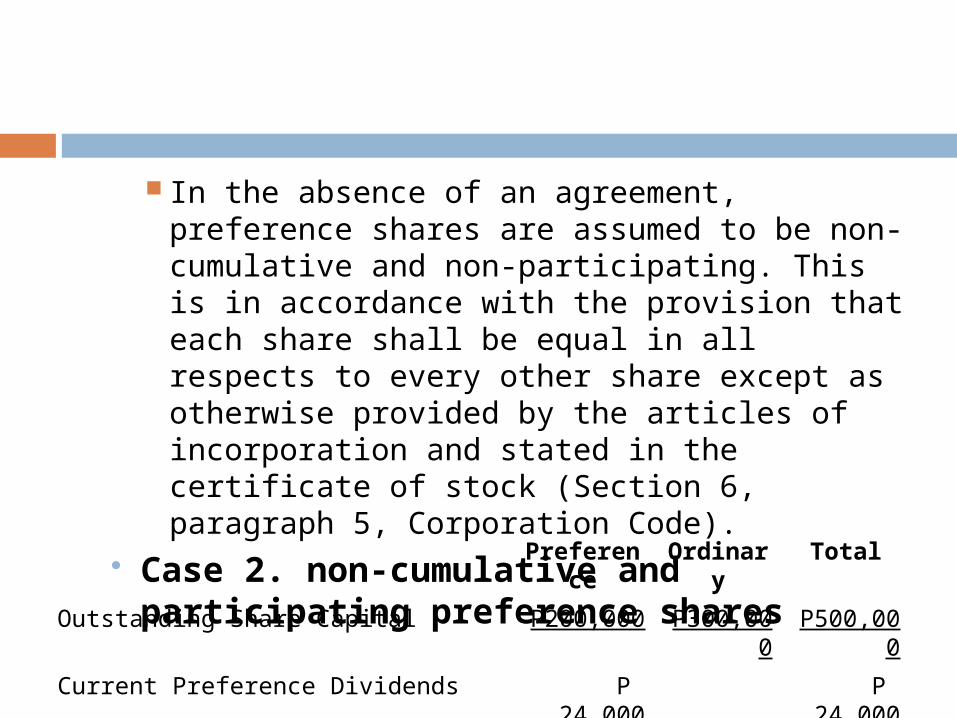

Case 1. non-cumulative and non-participating preference shares

Dividends per share is obtained by dividing the total dividend distribution per class of share by its corresponding outstanding shares.

Preference

Ordinary

Total

Outstanding Share Capital P200,000 P300,000

P500,000

Current Preference Dividends P 24,000 P 24,000

Remainder to Ordinary . P176,000

176,000

Total P 24,000 P176,000

P200,000

Dividends per share P 12.00 P 58.67

In the absence of an agreement, preference shares are assumed to be non-cumulative and non-participating. This is in accordance with the provision that each share shall be equal in all respects to every other share except as otherwise provided by the articles of incorporation and stated in the certificate of stock (Section 6, paragraph 5, Corporation Code).

Case 2. non-cumulative and participating preference shares

Preference

Ordinary

Total

Outstanding Share Capital P200,000 P300,000

P500,000

Current Preference Dividends P 24,000 P 24,000

Current Ordinary Dividends P 36,000

36,000

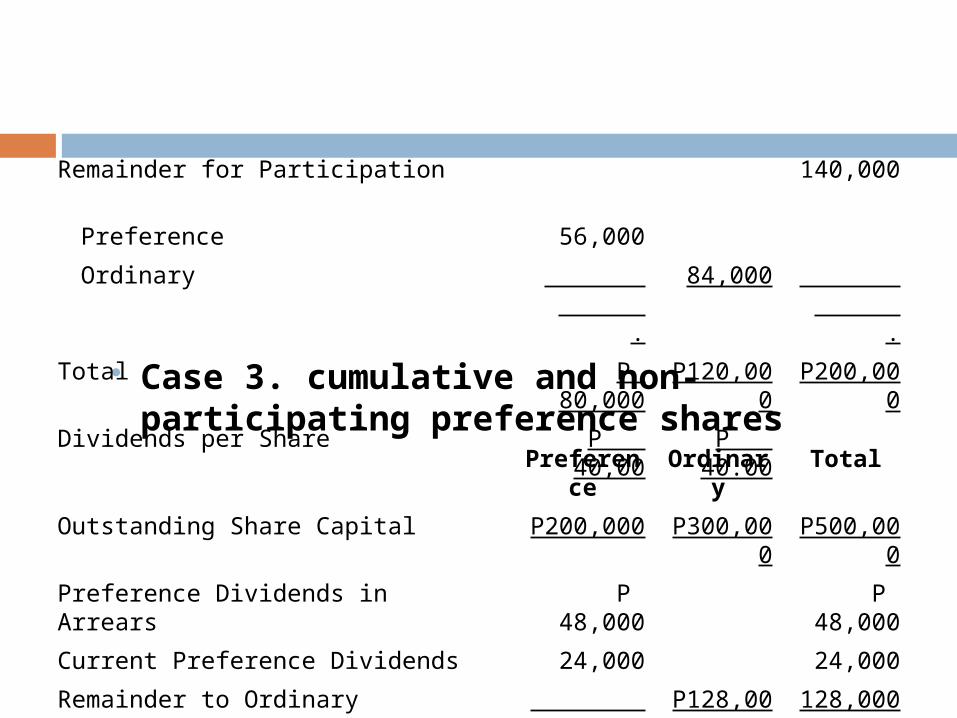

Case 3. cumulative and non-participating preference shares

Remainder for Participation 140,000

Preference 56,000

Ordinary .

84,000 .

Total P 80,000

P120,000

P200,000

Dividends per Share P 40,00

P 40.00

Preference

Ordinary

Total

Outstanding Share Capital P200,000 P300,000

P500,000

Preference Dividends in Arrears P 48,000 P 48,000

Current Preference Dividends 24,000 24,000

Remainder to Ordinary . P128,000

128,000

Total P 72,000 P128,000

P200,000

Dividends per Share P 36.00 P 42.67

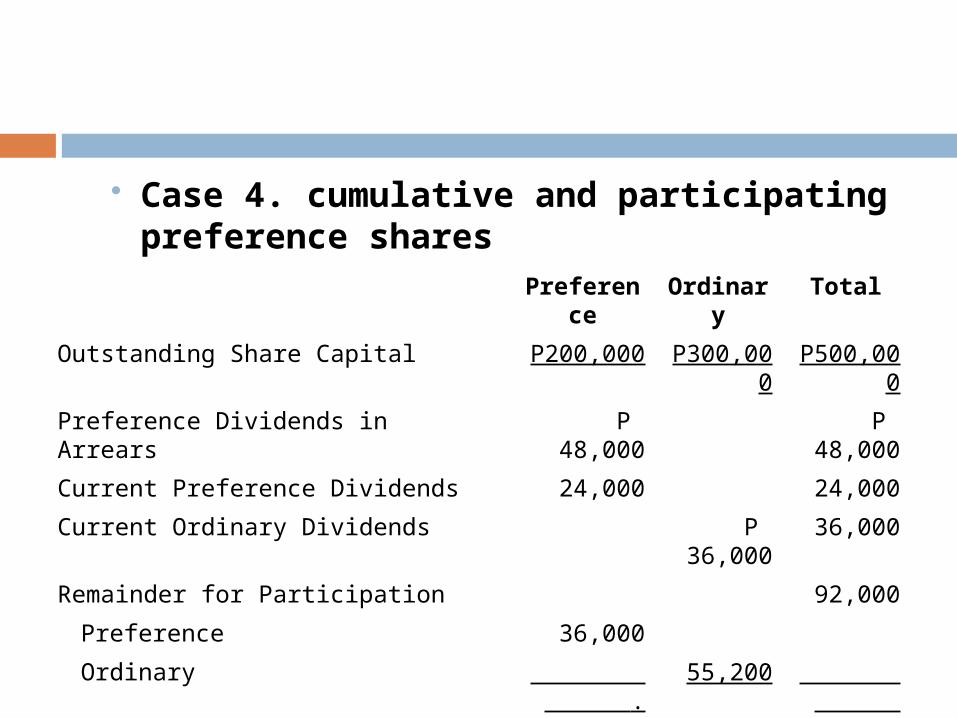

Case 4. cumulative and participating preference shares

Preference

Ordinary

Total

Outstanding Share Capital P200,000 P300,000

P500,000

Preference Dividends in Arrears P 48,000 P 48,000

Current Preference Dividends 24,000 24,000

Current Ordinary Dividends P 36,000

36,000

Remainder for Participation 92,000

Preference 36,000

Ordinary . 55,200 .

Total P108,000 P 91,200

P200,000

Dividends per Share P 54.40 P 30.40

Prior Period Errors

Per IAS No. 8, Accounting Policies, Changes in Accounting Estimates and Errors, prior period errors are omissions from and other misstatements of the entity’s financial statements for one more prior periods that are discovered in the current period.

Errors may occur as a result of mathematical mistakes, mistakes in applying accounting policies, misinterpretations of facts, fraud or oversights.

Material prior periods must be restated to report financial position and results of operations as they would have been presented had the error never taken place.

Reported by adjusting the opening balances of retained earnings and affected assets and liabilities.

The correction of a prior period error is excluded from profit or loss for the period in which the error is discovered.

If an error resulted in an understatement of profit in previous periods, a correcting entry would be needed to increase retained earnings.

If an error overstated profit in prior periods, then retained earnings would have to be decreased. Ex.: In 2012, the bookkeeper of Castro

Realty, Inc. debited Advertising Expense and credited Cash to record the purchase of a small parcel of land to be used as the company’s sale training

venue. The entry should have been a debit to Land and a credit to Cash of P250,000. The effect of this prior period error is to overstate 2012 advertising expense and ultimately, understate 2012 profit by the same amount. Land is also understated by P250,000. The external auditors discovered the prior period error in 2013. The correcting entry will be:

Land 250,000Retained Earnings 250,000

This entry increased assets and shareholders’ equity by P250,000. Advertising expense, a temporary account, is closed to income summary and income summary is in turn closed to retained earnings; therefore, any corrections to income or expense of the prior periods should be made directly to the retained earnings account. The preceding analysis purposely did not include the income tax effects of the error.

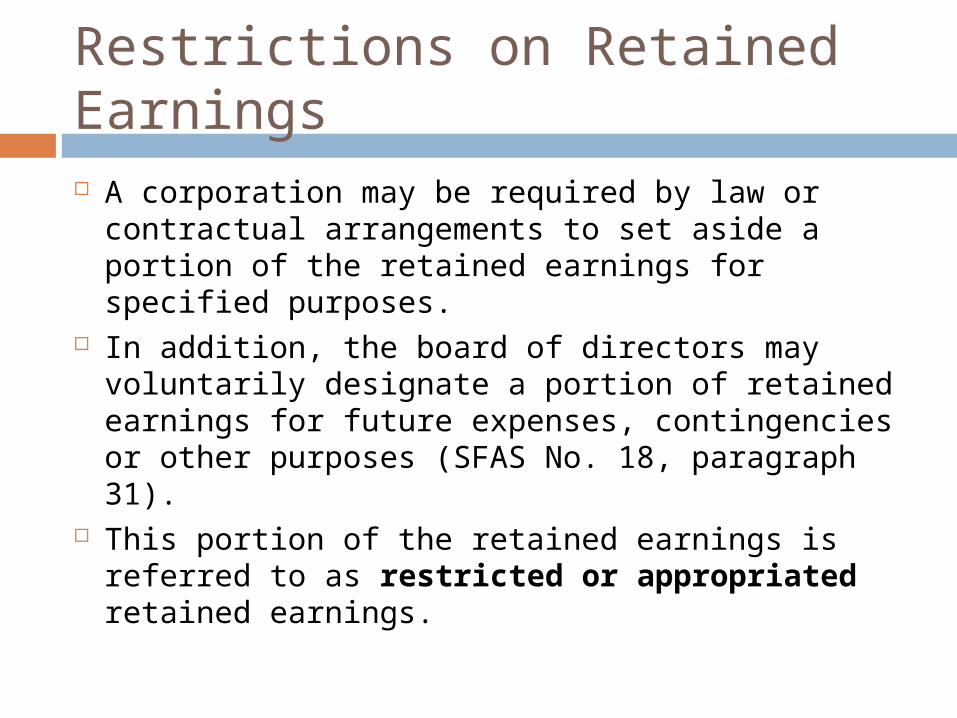

Restrictions on Retained Earnings A corporation may be required by law or

contractual arrangements to set aside a portion of the retained earnings for specified purposes.

In addition, the board of directors may voluntarily designate a portion of retained earnings for future expenses, contingencies or other purposes (SFAS No. 18, paragraph 31).

This portion of the retained earnings is referred to as restricted or appropriated retained earnings.

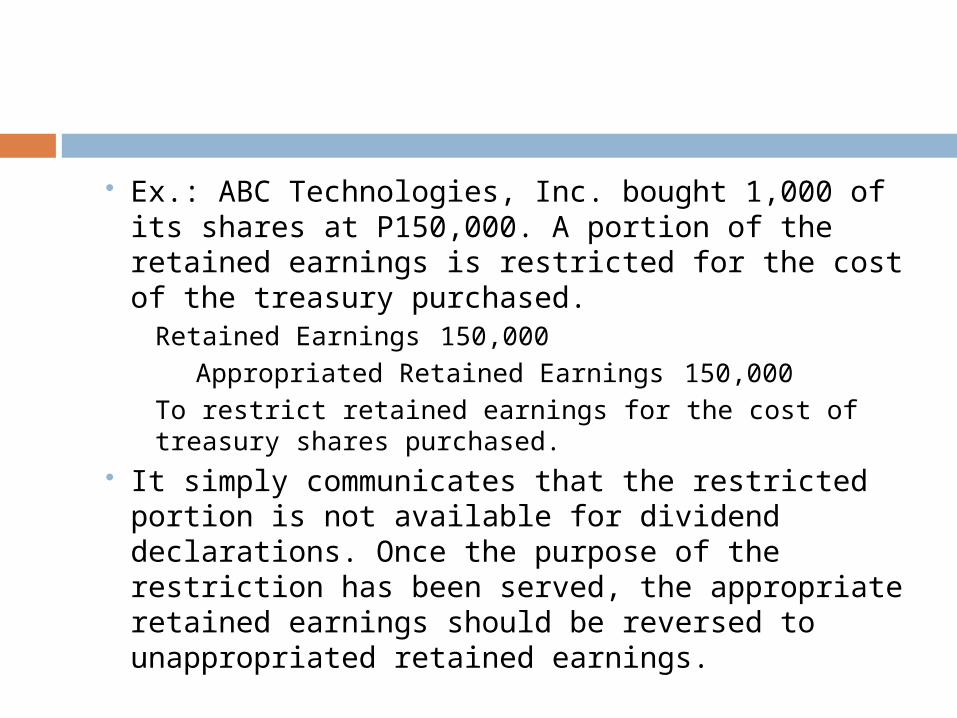

Ex.: ABC Technologies, Inc. bought 1,000 of its shares at P150,000. A portion of the retained earnings is restricted for the cost of the treasury purchased.

Retained Earnings 150,000Appropriated Retained Earnings 150,000

To restrict retained earnings for the cost of treasury shares purchased.

It simply communicates that the restricted portion is not available for dividend declarations. Once the purpose of the restriction has been served, the appropriate retained earnings should be reversed to unappropriated retained earnings.

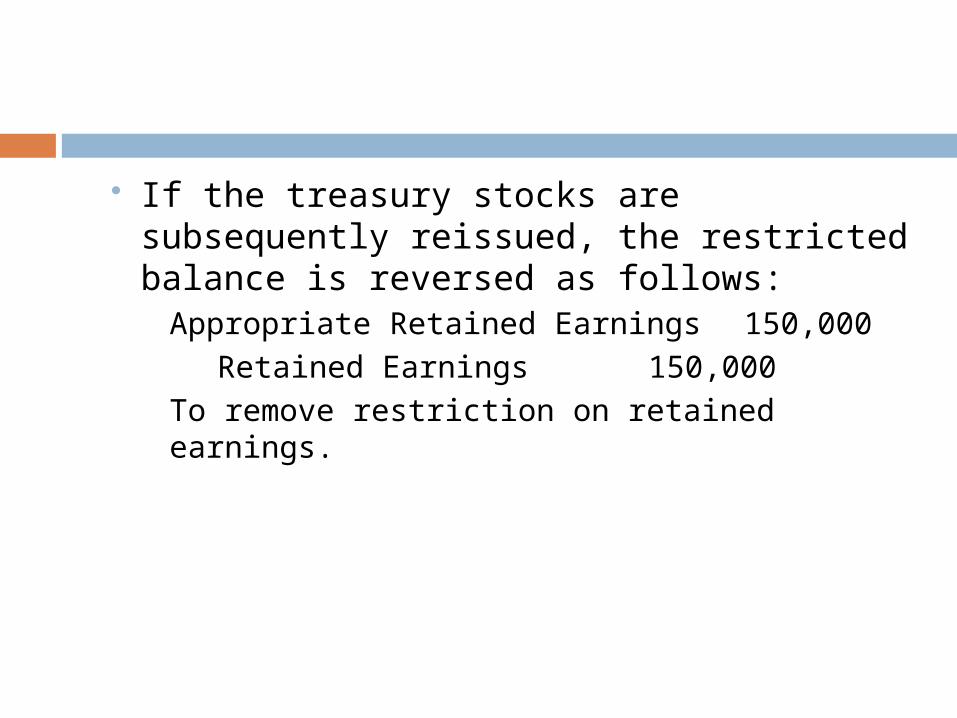

If the treasury stocks are subsequently reissued, the restricted balance is reversed as follows:

Appropriate Retained Earnings 150,000Retained Earnings 150,000

To remove restriction on retained earnings.

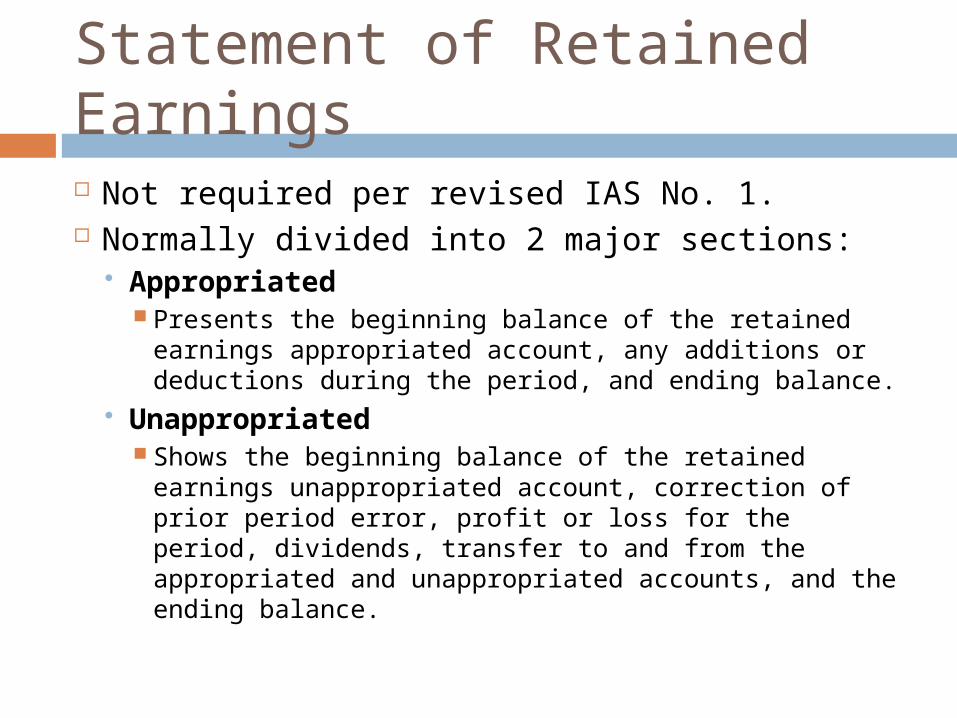

Statement of Retained Earnings Not required per revised IAS No. 1. Normally divided into 2 major sections:

Appropriated Presents the beginning balance of the retained

earnings appropriated account, any additions or deductions during the period, and ending balance.

Unappropriated Shows the beginning balance of the retained

earnings unappropriated account, correction of prior period error, profit or loss for the period, dividends, transfer to and from the appropriated and unappropriated accounts, and the ending balance.

Bookstore CorporationStatement of Retained Earnings

For the Year Ended Dec. 31, 2013

Appropriated:

Balance, 1/1/13 as reported P 180,000

For Treasury Stocks, 4/8/13 100,000

Retained Earnings Appropriated, 12/31/13

P 280,000

Unappropriated:

Balance, 1/1/13, as previously reported P1,414,500

Correction of Prior period error 100,000

Balance, 1/1/13, as restated P1,514,000

Add: Profit 480,000

Total P1,994,500

Less: Cash Dividends Declared P 65,000

Share Dividends Declared 60,000

Transfer Dividends Declared 100,000 225,000

Retained Earnings Unappropriated, 12/31/13

1,769,500

Total Retained P2,049,500

Statement of Changes in Shareholders’ Equity Significant changes in shareholders’ equity

should be reported in the period in which they occur.

May be prepared in columnar format, where each column represents a major shareholders’ equity classification.

The ending balances of the accounts are presented at the bottom of the statement. These accounts and their related balances compose the shareholders’ equity section of the statement of financial position.

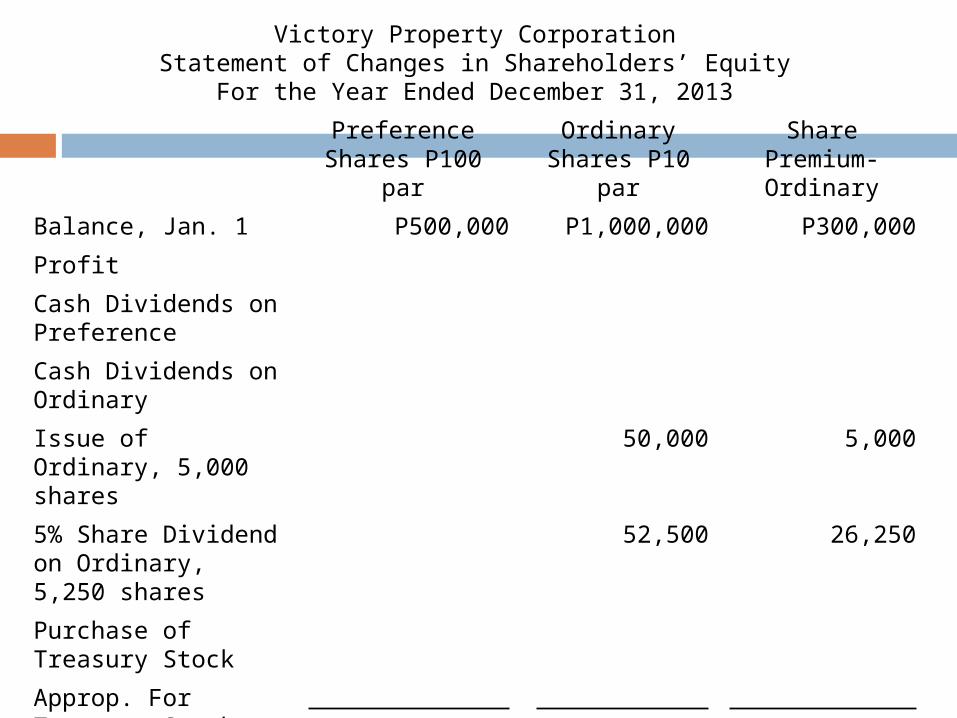

Victory Property CorporationStatement of Changes in Shareholders’ Equity

For the Year Ended December 31, 2013

Preference Shares P100 par

Ordinary Shares P10

par

Share Premium- Ordinary

Balance, Jan. 1 P500,000 P1,000,000 P300,000

Profit

Cash Dividends on Preference

Cash Dividends on Ordinary

Issue of Ordinary, 5,000 shares

50,000 5,000

5% Share Dividend on Ordinary, 5,250 shares

52,500 26,250

Purchase of Treasury Stock

Approp. For Treasury Stock

. . .

Balance, Dec. 31 P500,000 P1,102,500 P331,250

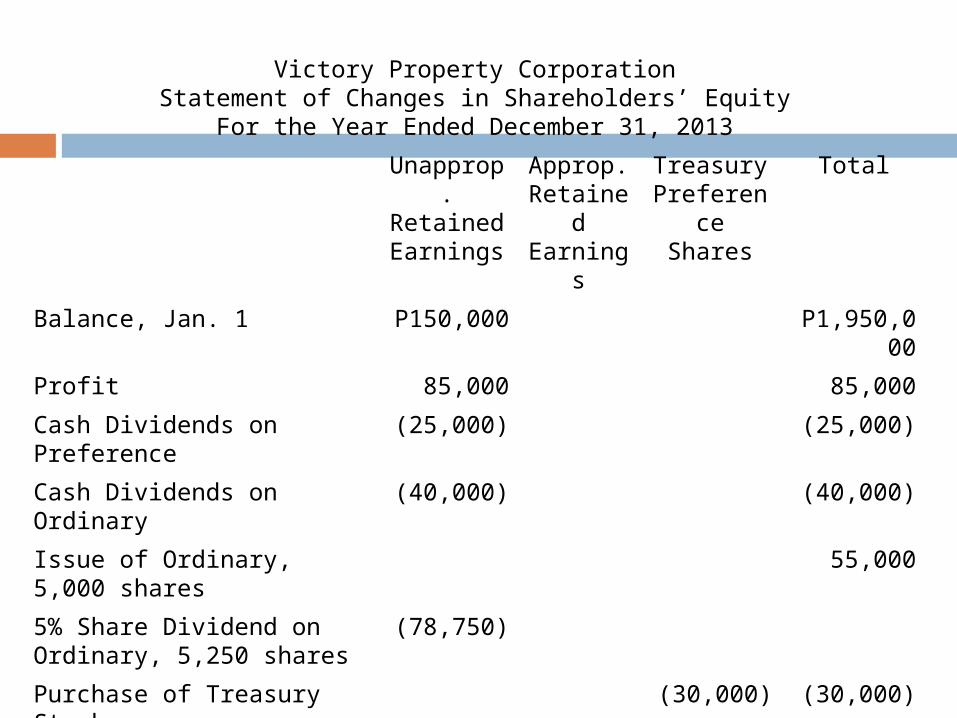

Victory Property CorporationStatement of Changes in Shareholders’ Equity

For the Year Ended December 31, 2013

Unapprop. Retained Earnings

Approp. Retaine

d Earning

s

Treasury Preference Shares

Total

Balance, Jan. 1 P150,000 P1,950,000

Profit 85,000 85,000

Cash Dividends on Preference

(25,000) (25,000)

Cash Dividends on Ordinary

(40,000) (40,000)

Issue of Ordinary, 5,000 shares

55,000

5% Share Dividend on Ordinary, 5,250 shares

(78,750)

Purchase of Treasury Stock (30,000) (30,000)

Approp. For Treasury Stock (30,000) 30,000 . .

Balance, Dec. 31 P 61,250 P30,000 P(30,000) P1,995,000

Shareholders’ Equity

Share Capital

Preference Shares-P100 par, 10,000 shares authorized, 5,000 shares issued and 4,750 shares outstanding

P 500,000

Ordinary Shares-P10 par, 150,000 shares authorized, 110,250 shares issued and outstanding

P1,102,500

Share Premium-Ordinary 331,250 1,433,750

Total Share Capital P1,933,750

Retained Earnings

Unappropriated P61,250

Appropriated for Treasury Stock 30,000 91,250

Total Share Capital and Retained Earnings P2,025,000

Less: Treasury-Preference, 250 shares at cost 30,000

Total Shareholders’ Equity P1,995,000

Book Value per Share

The amount that would be paid on each share if the corporation is liquidated.

The amount available to shareholders is exactly the amount reported as shareholders’ equity.

When only a single class of share is outstanding, the book value per share is computed by dividing the total shareholders’ equity by the number of shares outstanding.

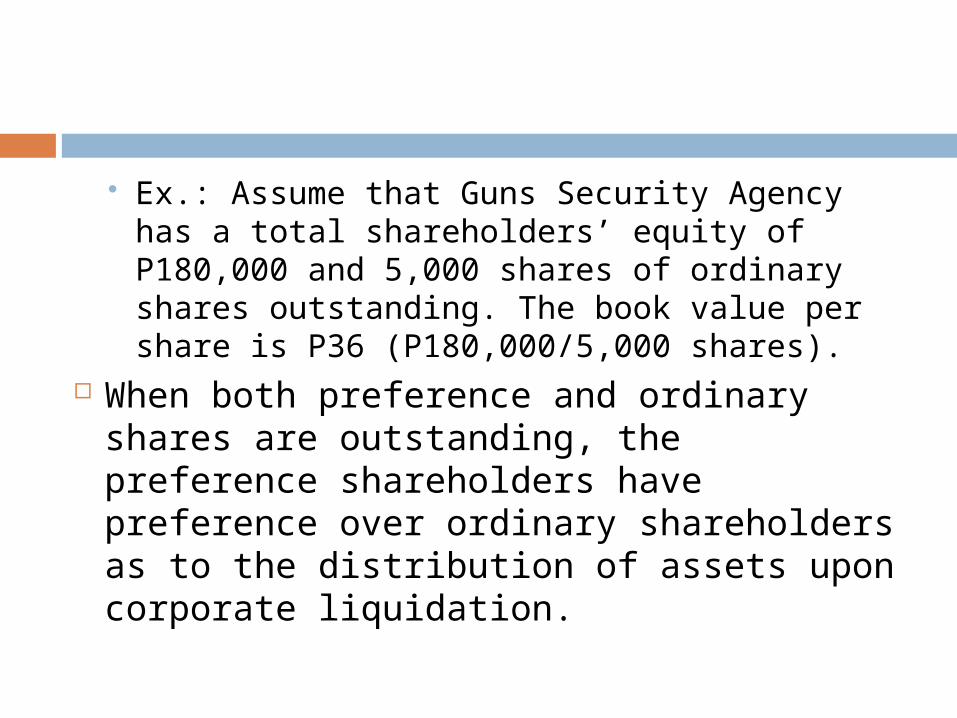

Ex.: Assume that Guns Security Agency has a total shareholders’ equity of P180,000 and 5,000 shares of ordinary shares outstanding. The book value per share is P36 (P180,000/5,000 shares).

When both preference and ordinary shares are outstanding, the preference shareholders have preference over ordinary shareholders as to the distribution of assets upon corporate liquidation.

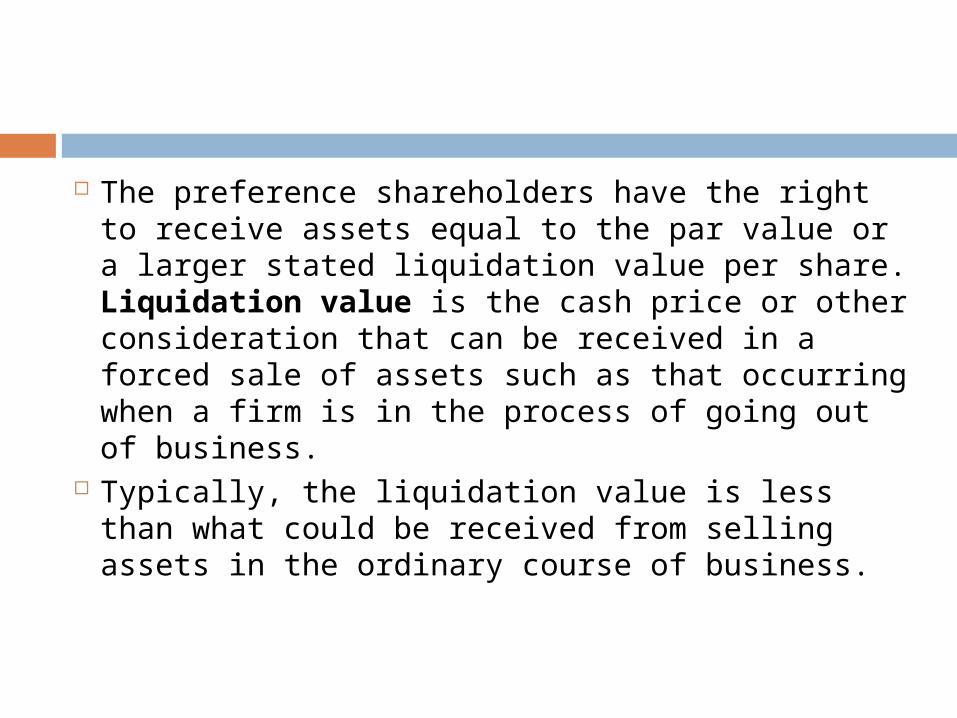

The preference shareholders have the right to receive assets equal to the par value or a larger stated liquidation value per share. Liquidation value is the cash price or other consideration that can be received in a forced sale of assets such as that occurring when a firm is in the process of going out of business.

Typically, the liquidation value is less than what could be received from selling assets in the ordinary course of business.

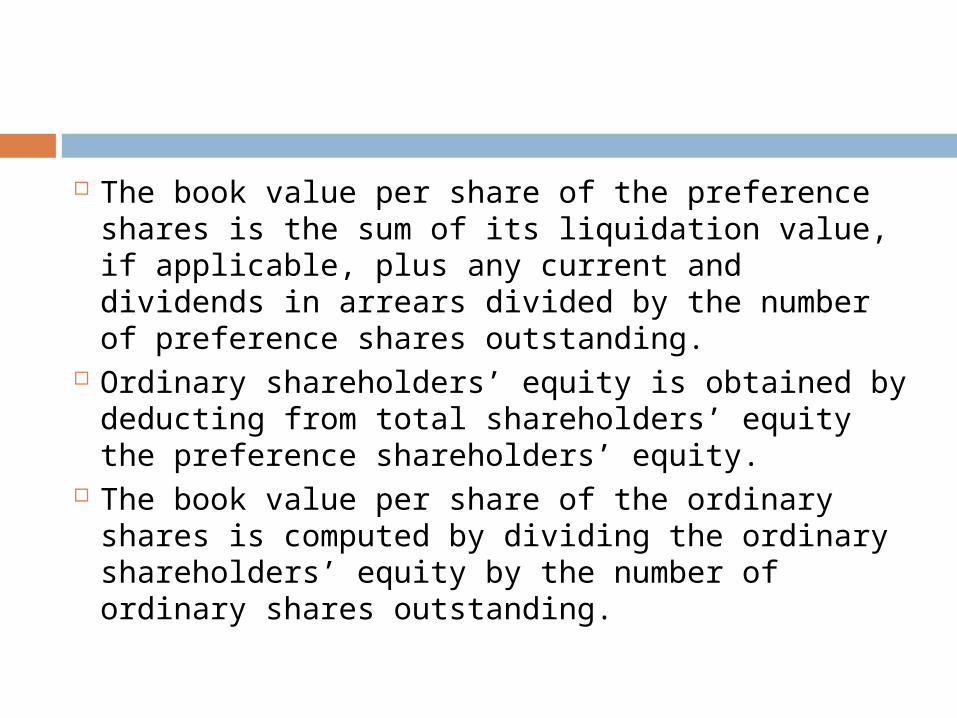

The book value per share of the preference shares is the sum of its liquidation value, if applicable, plus any current and dividends in arrears divided by the number of preference shares outstanding.

Ordinary shareholders’ equity is obtained by deducting from total shareholders’ equity the preference shareholders’ equity.

The book value per share of the ordinary shares is computed by dividing the ordinary shareholders’ equity by the number of ordinary shares outstanding.

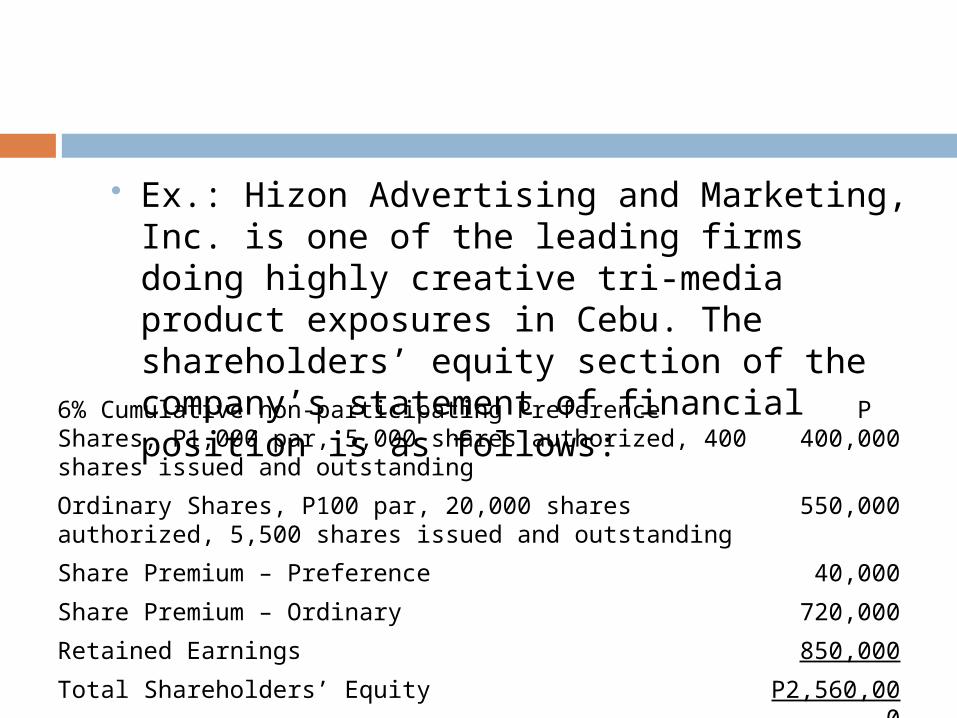

Ex.: Hizon Advertising and Marketing, Inc. is one of the leading firms doing highly creative tri-media product exposures in Cebu. The shareholders’ equity section of the company’s statement of financial position is as follows:6% Cumulative non-participating Preference Shares,

P1,000 par, 5,000 shares authorized, 400 shares issued and outstanding

P 400,000

Ordinary Shares, P100 par, 20,000 shares authorized, 5,500 shares issued and outstanding

550,000

Share Premium – Preference 40,000

Share Premium – Ordinary 720,000

Retained Earnings 850,000

Total Shareholders’ Equity P2,560,000

Suppose that the preference shares has a liquidation value of P1,300 and dividends are in arrears for 3 years. The computation of the preference book value per share follows:Preference Shares:

Liquidation Value, P1,300 x 400 shares P520,000

Dividends in Arrears, 6% x P400,000 x 3 yrs.

72,000

Current Dividends, 6% x P400,000 24,000

Preference Shareholders’ Equity P616,000

Book Value per Share, P616,000/400 shares

P 1,540

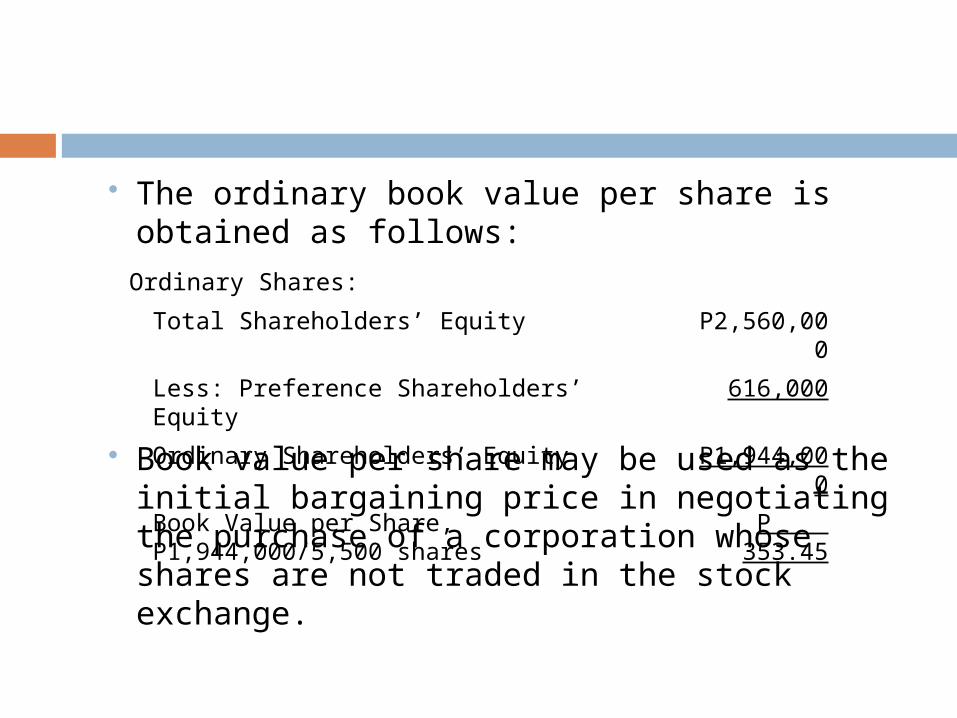

The ordinary book value per share is obtained as follows:

Book value per share may be used as the initial bargaining price in negotiating the purchase of a corporation whose shares are not traded in the stock exchange.

Ordinary Shares:

Total Shareholders’ Equity P2,560,000

Less: Preference Shareholders’ Equity 616,000

Ordinary Shareholders’ Equity P1,944,000

Book Value per Share, P1,944,000/5,500 shares

P 353.45

On the other hand, investors in the stock market may utilize book value as one of the basis for evaluating whether a stock is undervalued or not.

It is also significant in many contracts and in court cases where the rights of the individual parties are based on cost information.

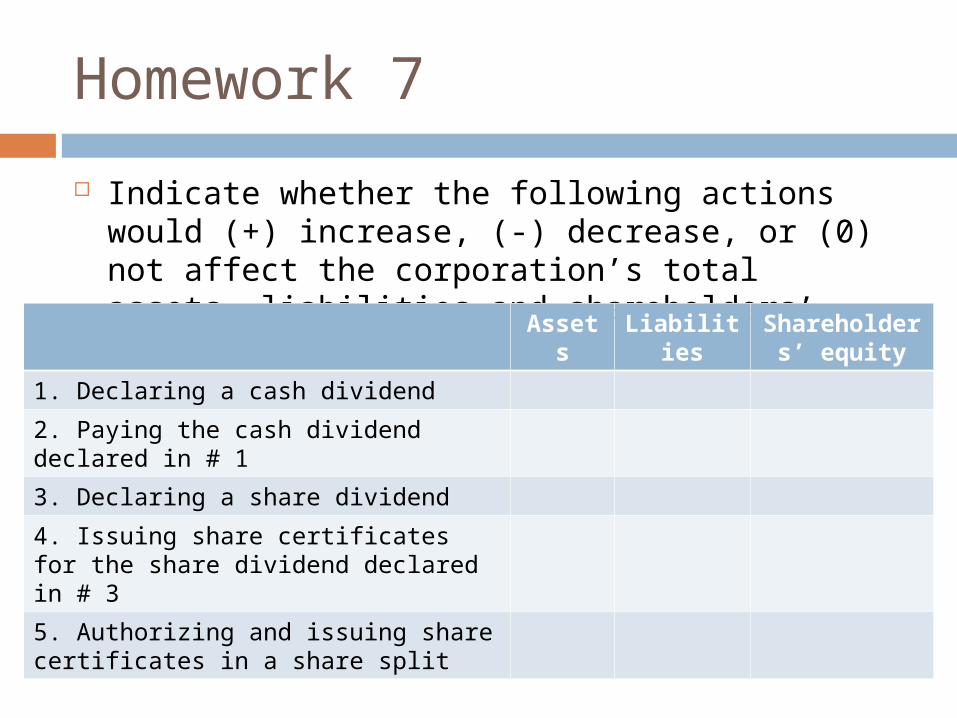

Homework 7

Indicate whether the following actions would (+) increase, (-) decrease, or (0) not affect the corporation’s total assets, liabilities and shareholders’ equity. Asset

sLiabiliti

esShareholders’ equity

1. Declaring a cash dividend

2. Paying the cash dividend declared in # 1

3. Declaring a share dividend

4. Issuing share certificates for the share dividend declared in # 3

5. Authorizing and issuing share certificates in a share split

Ysmael Corporation’s board of directors declared a P750,000 cash dividend on Sept. 1, 2011, payable on Oct. 1, to shareholders of record on Sept. 15. Prepare all appropriate entries needed on the declaration, record and payment dates.

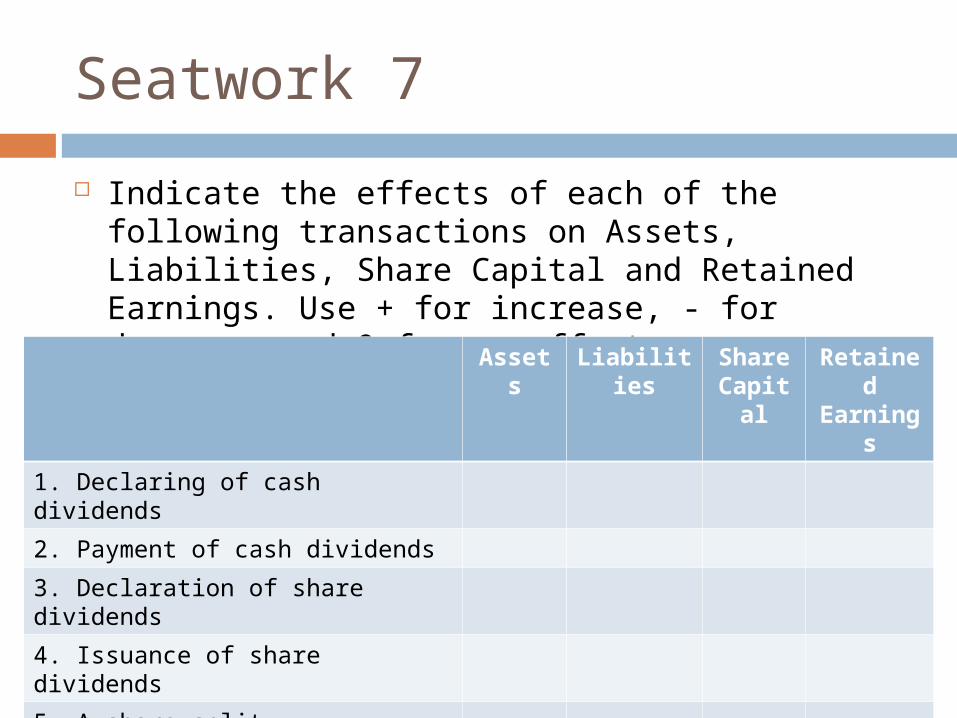

Seatwork 7

Indicate the effects of each of the following transactions on Assets, Liabilities, Share Capital and Retained Earnings. Use + for increase, - for decrease and 0 for no effect.

Assets

Liabilities

Share Capit

al

Retained

Earnings

1. Declaring of cash dividends

2. Payment of cash dividends

3. Declaration of share dividends

4. Issuance of share dividends

5. A share split

6. Cash purchase of treasury stock

7. Sale of treasury stock below cost

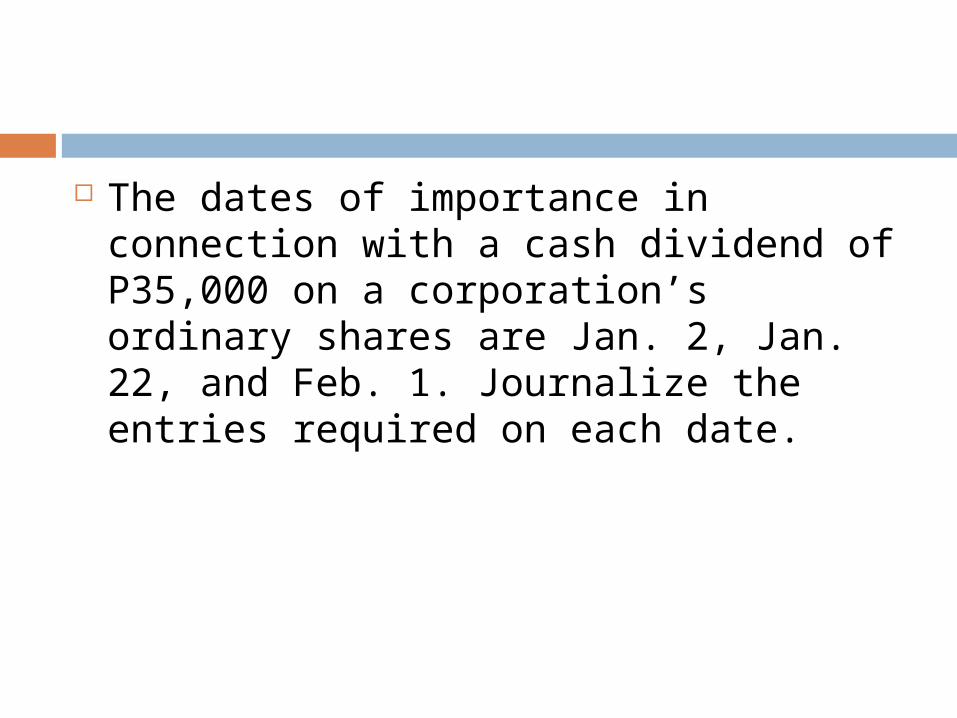

The dates of importance in connection with a cash dividend of P35,000 on a corporation’s ordinary shares are Jan. 2, Jan. 22, and Feb. 1. Journalize the entries required on each date.

![The Effect of Retained Earnings on Dividend Policy from the ...Retained earnings positively related to dividend payments [6]. Retained earnings have a greater impact on the likelihood](https://img.pdfslide.net/doc/110x75/612f81ca1ecc515869437da3/the-effect-of-retained-earnings-on-dividend-policy-from-the-retained-earnings.jpg)