Embed Size (px)

Citation preview

AN OPEN LETTER TO THE CHAIRMAN & CEO OF MACANDREWS & FORBES

Dear Mr. Perelman,

After conducting an in-depth valuation analysis of Revlon, we believe the shares are deeply undervalued and not reflective of the overall company ’s equity value. This distorted “minority class” share price not only affects non -controll ing shareholders, but also depresses the value of MacAndrew’s & Forbes’ (M&F) controll ing stake.

In the fol lowing presentation, we propose strategies with which to address the public f loat in order to maximize Revlon’s long term enterprise value. A couple of these options require a proactive stance by M&F, while one is a defensive strategy minority investors can employ. M&F and minority investors should each be aware of the other ’s options. One strategy available to you is particularly attractive with respect to its potential profitabil ity.

Similar to the tender offer M&F made in 1987 for the 63% of Revlon it did not own, we believe a tender today for the remaining 22% public f loat of Revlon that M&F does not own could increase f irm value by $2.2B, and allow your holding company to capture $1.7 bil l ion in profits, net of the tender cost. This equates to $1.3B of net marginal profits above and beyond potential value realization through a sale of the company to a strategic acquirer with no preceding M&F tender offer .

While we know you take pride in building and adding value to companies rather than capturing arbitrage, we hope you wil l embrace the logic of our proposal and the embedded opportunity within Revlon. Please feel free to contact our off ice with any questions.

Happy Holidays,

Bradd Kern Managing Director Armored Wolf, LLC [email protected]

REVLON:

VALUE IS ON

A PROPOSAL TO MAXIMIZE FIRM

VALUE FOR ALL STAKEHOLDERS

REVLON (REV) IS AN 80-YEAR OLD BEAUTY

& PERSONAL CARE PRODUCT COMPANY

Consumer Professional

REV operates in two segments with multiple brands

PF LTM 9/30/14 Consumer % Total Professional % Total Total

Sales ($ millions) $1,429.2 74.0% $501.8 26.0% $1,931.0

Segment EBITDA $338.9 78.0% $95.4 22.0% $434.3

% margin 23.7% 19.0% 22.5%

1

REVLON SELLS INTO THE MASS MARKET

AND PROFESSIONAL CHANNELS GLOBALLY

United States

International

Consumer Professional

52% of sales

48% of sales

2

RECENT DEVELOPMENTS

October 2013: Revlon simplifies capital structure when Perelman converts

all 3.125M of M&F’s Class B shares (entitling him to ten votes per share) to

egalitarian Class A shares.

October 2013: Completes $660M acquisition of The Colomer Group (TCG)

from CVC Partners for 9.2x EBITDA, a business Revlon had sold to CVC 13

years ago.

TCG’s CEO Lorenzo Delpani named president and CEO

Professional products adds a new distribution channel

$30M to $35M of annualized cost reductions identified for

implementation by end of 2015.

August 2014: Armored Wolf sends confidential letter to Ron Perelman to

recommend options for Revlon value creation. Receipt is acknowledged but

no other response is provided

November 2014: Following Delpani’s stated product strategy mantra of

“fewer, bigger, better”, Revlon unveils a “global brand re -launch” featuring

the “Love Is On” advertising campaign

3

HIGH, STABLE FREE CASH FLOW SUPPORTS

A LEVERED CAPITAL STRUCTURE

4

Cash and Equivalents 178.4

Acquisition Term Loan due 2019 693.3

2011 Term Loan due 2017 671.3

5.75% Senior Notes due 2021 500.0

Other 8.6

Total Debt 1,873.2

Market Capitalization @ $34.57/share 1,810.0

Enterprise Value 3,504.8

Net Debt 1,694.8

2014E Adj. EBITDA 365.4

EV / EBITDA (2014E) 9.6x

Net Leverage '14E 4.6x

Interest Coverage '14E 3.8x

Capitalization as of 9/30/14

EBITDA 365.4

Capex* -95.0

Cash Interest -96.9

Cash Taxes -20.0

Changes in W/C 0.0

Pension Contribution -25.0

Free Cash Flow 128.5

REV Market Cap 1,810.0

FCF Yield 7.1%

*includes purchase of permanent wall displays

Levered Beta (2-year) 0.98

Unlevered Beta 0.57

Free Cash Flow (2014E)

THROUGH WHOLLY OWNED HOLDING COMPANY

MACANDREWS & FORBES, RON PERELMAN OWNS

78% OF REVLON CLASS A SHARES

Minority Shareholders Own 22% of Class A Shares

100%

78%

5

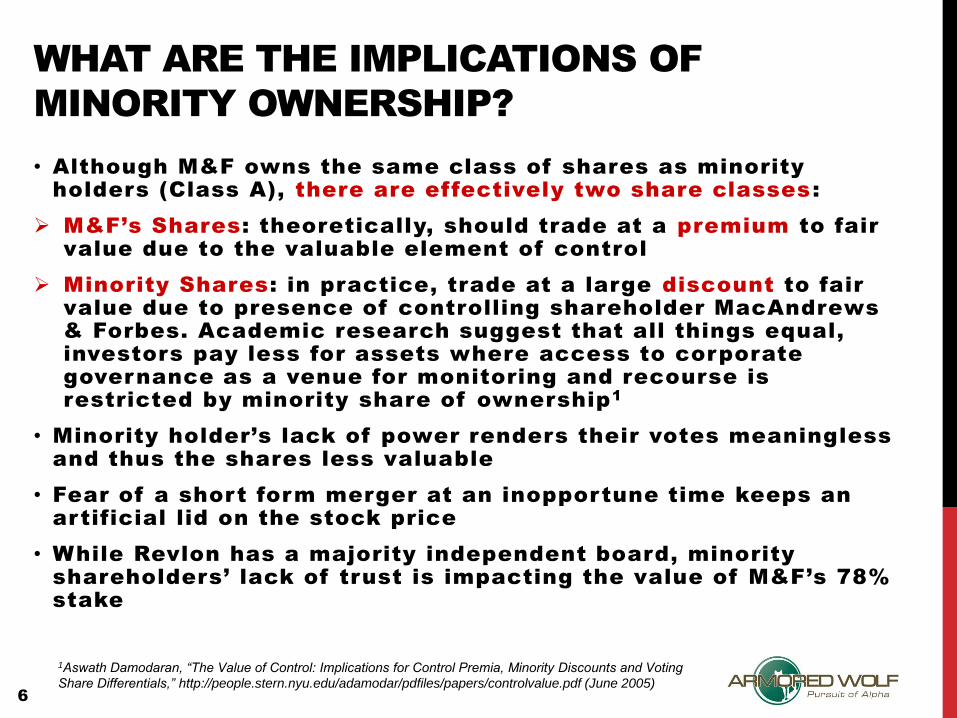

WHAT ARE THE IMPLICATIONS OF

MINORITY OWNERSHIP?

• Although M&F owns the same class of shares as minority

holders (Class A), there are effectively two share classes:

M&F’s Shares: theoretically, should trade at a premium to fair

value due to the valuable element of control

Minority Shares: in practice, trade at a large discount to fair

value due to presence of controlling shareholder MacAndrews

& Forbes. Academic research suggest that all things equal,

investors pay less for assets where access to corporate

governance as a venue for monitoring and recourse is

restricted by minority share of ownership1

• Minority holder’s lack of power renders their votes meaningless

and thus the shares less valuable

• Fear of a short form merger at an inopportune time keeps an

artificial lid on the stock price

• While Revlon has a majority independent board, minority

shareholders’ lack of trust is impacting the value of M&F’s 78%

stake

6

1Aswath Damodaran, “The Value of Control: Implications for Control Premia, Minority Discounts and Voting

Share Differentials,” http://people.stern.nyu.edu/adamodar/pdfiles/papers/controlvalue.pdf (June 2005)

CONTROLLED OWNERSHIP RESULTS IN A

MASSIVE DISCOUNT TO GLOBAL PEERS

• Comps imply REV is worth $61/share, 76% upside from

$34.57/share. An adjusted present value-style DCF to

accommodate REV’s rapid de -leveraging yields a similar value

• Despite above average EBITDA margins of over 19%, REV trades

at an astounding 4x EBITDA discount to global peers

• The comps with the most similar EV/EBITDA ratio to REV are

Natura, which is a Brazilian cosmetics manufacturer that sells

through multi-level marketing, and Shiseido, a Japanese

consumer product company with only 10% EBITDA margins.

These are clearly not the closest comps of the group

7

Company Share Price

Unlevered

beta (2Y)

Market

Cap ($M) EV ($M)

Sales

(TTM, $M)

EV/ EBITDA

(FY1)

P/E

(FY 15)

P/S

(TTM)

GPM

(TTM, %)

EBITDA

Margin

(TTM, %)

Net

Leverage

(TTM)

REVLON INC-A* 34.57 0.57 1,810 3,505 1,938 9.6 16.9 0.9 65.6 18.9 4.8x

ESTEE LAUDER 75.78 0.80 28,767 28,719 10,925 13.8 22.1 2.7 80.3 19.4 0.0x

L'OREAL 137.45 0.47 94,578 93,455 27,537 16.1 22.9 3.7 71.3 20.9 -0.2x

L'OCCITANE INTL 19.04 0.47 3,626 3,424 1,345 12.9 21.5 2.7 80.7 18.0 -0.9x

PROCTER & GAMBLE 92.00 0.36 248,595 272,857 83,788 14.0 19.6 3.0 48.8 20.7 1.3x

SHISEIDO CO LTD 1682 0.49 5,660 5,853 6,456 9.9 28.4 0.9 75.5 10.2 0.0x

NATURA 30.92 0.22 5,007 5,931 2,776 9.5 14.1 1.8 69.5 21.7 1.5x

COTY INC-CL A* 20.04 0.67 7,128 9,464 4,556 12.0 20.8 1.6 58.8 17.5 3.0x

AMOREPACIFIC COR 2259000 0.86 11,981 11,598 3,266 18.4 27.6 3.7 72.8 18.3 -0.7x

Average (ex-Revlon) 0.54 13.3 22.1 2.5 69.7 18.3 0.5x

Median (ex-Revlon) 0.48 13.4 21.8 2.7 72.0 18.9 0.0x

Implied REV price based on average $60.5

Implied REV price based on median $61.0

Weighting: 50% average and 50% median $60.7

*For REV, using LTM 12/31/14E rather than trailing twelve months (TTM); Coty EBITDA margin and net leverage based on FYE 6/30/15E

Source: Bloomberg, Armored Wolf

Upside / (Downside)

75.7%

WHY IS THE DISCOUNT A PROBLEM?

• The 22% outstanding minority shares distort 100% of the enterprise

value. It will be difficult for M&F to maximize Revlon's value as long

as the shares remain outstanding because studies show (Daniel

Kahneman) potential acquirer’s will be “anchored” to the “minority

class” share price

This anchor dynamic affects Perelman's controlling 78% stake as

much (and much more on a $ basis) as the 22% minority class

• 76% upside to fair value of $61/share would merely normalize REV’s

value by reversing the effects of the minority discount. $61 is before

any control premium. Assuming a 25% control premium, when is the

last time an acquirer of a public, multi -billion consumer company paid

a 120% premium ([1.76*1.25]-1 = 120%)?

Any potential takeover price will be depressed until the issue is fixed

• The company’s “weak currency” in the form of a depressed share

price is a long-term disadvantage for M&A

• When MacAndrews & Forbes pledges Revlon shares in order to borrow

(which they do), M&F’s borrowing base is depressed by the low price

of the 22% public float

In summary, the value of Revlon is not being maximized

due to the distortionary effects of REV’s share price

8

HOW TO ELIMINATE THE DISCOUNT?

THERE ARE TWO VIABLE OPTIONS

• Perelman could tender for the remaining 22% of shares

• Under Delaware law, if just 12% of REV shares tender,

increasing M&F ownership to 90%, M&F can effect a

“freeze-out” merger and pay the remaining 10% of holdouts

the final price paid that raised M&F ownership to 90%

• By eradicating the minority “share class” along with its

distorted share price, potential acquirers will no longer be

anchored to an inappropriately low value

• Valuations thereafter can only focus on comps and

intrinsic value, both of which imply >$60/share

1) M&F can tender for shares and effect a short form merger

At a 25% premium, a REV tender would cost $498M but

yield a future value benefit to M&F of $1.3B on margin (in

excess of a sale at 35% control premium with no tender),

net of the tender cost, assuming a sale at fair value

($61/share) plus a 25% control premium ($76/share)

9

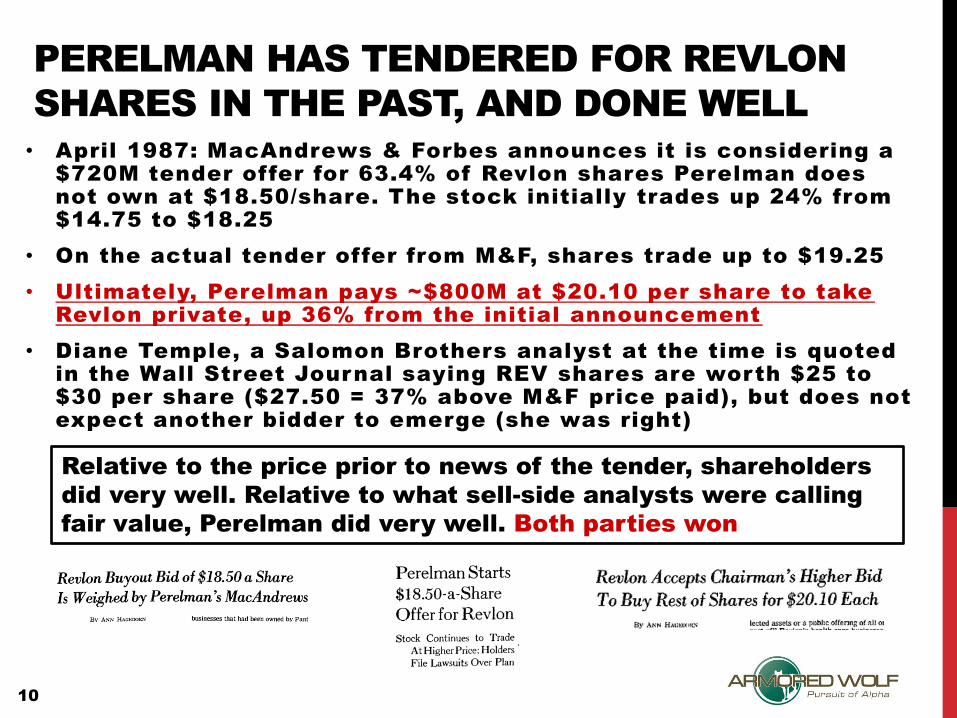

PERELMAN HAS TENDERED FOR REVLON

SHARES IN THE PAST, AND DONE WELL

• April 1987: MacAndrews & Forbes announces it is considering a

$720M tender offer for 63.4% of Revlon shares Perelman does

not own at $18.50/share. The stock initially trades up 24% from

$14.75 to $18.25

• On the actual tender offer from M&F, shares trade up to $19.25

• Ultimately, Perelman pays ~$800M at $20.10 per share to take

Revlon private, up 36% from the initial announcement

• Diane Temple, a Salomon Brothers analyst at the time is quoted

in the Wall Street Journal saying REV shares are worth $25 to

$30 per share ($27.50 = 37% above M&F price paid), but does not

expect another bidder to emerge (she was right)

Relative to the price prior to news of the tender, shareholders

did very well. Relative to what sell-side analysts were calling

fair value, Perelman did very well. Both parties won

10

HOW TO ELIMINATE THE DISCOUNT?

THE SECOND OPTION

• Revlon is one of the most recognizable and historically

significant brands in beauty products

• Revlon should appeal to both U.S. and international buyers

due to its balanced mix of global revenues and assets

• However, integration with The Colomer Group is still

underway and it would be unusual for a company to sell

itself before attempting to realize its target synergies on a

significant deal

• In the past, various strategic buyers have expressed

interest in a Revlon acquisition

2) M&F can seek a strategic buyer for the entire company

We estimate Revlon would fetch a 35% or higher premium

in a takeover, equating to at least $47 per share.

11

COMPARISON OF TWO M&F STRATEGIES

Net of the $498M tender cost, Perelman could

generate $1.7B in net profits by tendering today

for Revlon minority shares at a 25% premium

Tendering at a 25% premium, followed by a sale to a strategic

acquirer with a 25% control premium would yield $1,299 million

($1,684.5 – $385.4) more in profits for M&F than a sale with a

35% control premium not preceded by an M&F tender offer

12

#2: Sale to Strategic Only #1: Tender + Sale to Strategic

Current

Fair

Value

+25% Control

Premium

Gross $

Gain

Per Share Value $34.57 $61.00 $76.25 $41.68

% change 76.5% 120.6%

Equity Value $1,810.0 $3,193.8 $3,992.2 $2,182.2

Existing M&F

Ownership

Tendered

Shares Total

78.0% 22.0% 100.0%

$1,702.1 $480.1 $2,182.2

40.838 11.518 52.357

- $43.2 $43.2

- -$497.7 -$497.7

$1,702.1 -$17.7 $1,684.5

Attribution Analysis

% split

$ Attribution, gross

# shares

Tender Cost

Tender Price/Share (25% Premium)

$ Attribution, net

Current

Fair

Value

+35% Control

Premium

Gross REV

$ Gain

Per Share Value $34.57 Not $46.67 $12.10

% change Achievable 35.0%

Equity Value $1,810.0 $2,443.5 $494.1

Note: 78% Ownership

M&F

Ownership

Public

Float Total

78.0% 22.0% 100.0%

$385.4 $108.7 $494.1

40.838 11.518 52.357

$385.4 $108.7 $494.1$ Attribution, net

Attribution Analysis

% split

$ Attribution, gross

# shares

RANGE OF PROFITABILITY, NET OF TENDER COST

TENDER + SALE STRATEGY

Profits, net of tender:

13

Control Premium Paid By Strategic Acquirer

Te

nd

er P

re

miu

m

Pa

id

B

y M

&F

$1,684.5 20.0% 22.5% 25.0% 27.5% 30.0%

17.5% $1,555 $1,635 $1,714 $1,794 $1,874

20.0% $1,545 $1,625 $1,704 $1,784 $1,864

22.5% $1,535 $1,615 $1,694 $1,774 $1,854

25.0% $1,525 $1,605 $1,684 $1,764 $1,844

27.5% $1,515 $1,595 $1,675 $1,754 $1,834

30.0% $1,505 $1,585 $1,665 $1,744 $1,824

32.5% $1,495 $1,575 $1,655 $1,734 $1,814

Marginal net profits in

excess of sale only:

Control Premium Paid By Strategic Acquirer

Te

nd

er P

re

miu

m

Pa

id

B

y M

&F

Sale only scenario

(option # 2) assumes

35% control premium

Net profit of $1.68B

million corresponds

with gross profit of

$2.18B (tender cost

of $498 million)

$1,299.1 20.0% 22.5% 25.0% 27.5% 30.0%

17.5% $1,169 $1,249 $1,329 $1,409 $1,489

20.0% $1,159 $1,239 $1,319 $1,399 $1,479

22.5% $1,149 $1,229 $1,309 $1,389 $1,469

25.0% $1,139 $1,219 $1,299 $1,379 $1,459

27.5% $1,129 $1,209 $1,289 $1,369 $1,449

30.0% $1,119 $1,199 $1,279 $1,359 $1,439

32.5% $1,110 $1,189 $1,269 $1,349 $1,429

REVLON SHARE VALUE SCHEMATIC

$34.57 $47 $61 $67 $76+

Minority

Share Value =

Market Value

of REV Shares

REV + 35%

Control

Premium

M&F Share

Value = FV +

10% control

premium

REV Fair

Value (FV)

Value to

Strategic = FV

+ 25% Control

Premium

+35% +76% +94% +120%

M&F should pursue option #1 and tender for 22% of shares at

~$43/share to capture upside to $76/share on 100% of shares

Multiple of EBITDA:

9.6x 11.4x 13.4x 14.2x 15.5x

14

RISKS TO M&F WAITING

1. REV shares will appreciate over time due to a combination

of i) the stock’s deeply undervalued nature, ii) rapid de -

leveraging that accrues to equity, and iii) new management

initiatives to boost sales and improve financial results,

making M&F’s cost to take Revlon private more expensive

2. Through open market and block purchases, one or multiple

minority shareholders could build a combined 10% position

and either independently or in partnership with another

one or two large holders make a short form merger either

impossible or much more expensive. With more dispersed

ownership, success at blocking a squeeze-out, or even an

attempt to do so, is less likely

3. Even in the absence of significant improvement at Revlon,

the minority discount that makes REV shares such a

bargain may close over time if investors were simply to

announce that they had formed a 10% consortium to block

the possibility of a short form merger

We each own 4%, Bill has

another 2%. Let’s block a

REV squeeze-out merger.

I like the way you

think. Love Is On!

15

FINAL THOUGHTS

• Based on valuation and gradually improving company

fundamentals, REV shares are attractive whether M&F

tenders or not. The possibility of a tender is a free call

option

• Tendering for the remaining 22% of shares adds

demonstrable value to the entire M&F stake, plus provides

M&F with 100% of the future upside versus only 78%.

• Leaving $1.3B of marginal value on the table would be

antithetical to capitalist values

• While Perelman considers his options, new and existing

minority investors should consider what actions they can

take to reduce the minority discount in the absence of a

tender, such as forming a blocking position against

Perelman’s ability to effect a short form merger

• M&F will never achieve the highest price for its stake while

the minority shares remain outstanding. The sooner the

tender, the less relevant the current, distorted minority

class share price will be to the value of the overall firm

16

![Revlon Media Kit Final[1] - The Future of Women's …swhr.org/wp-content/uploads/2016/09/Revlon-Media-Kit_Final_2016.pdf · Revlon’“LoveIs’On”’Campaign’Social’Media’Kit](https://img.pdfslide.net/doc/110x75/5b94da7409d3f2d7438b59d4/revlon-media-kit-final1-the-future-of-womens-swhrorgwp-contentuploads201609revlon-media-kitfinal2016pdf.jpg)