Embed Size (px)

Citation preview

0 IdentityMind Global™ ©2016 All Rights Reserved

Risk Beyond Acquiring The Importance of Merchant Risk Across FinTech

1

About IdentityMind

IdentityMind Global’s core technology, Electronic DNA™ (eDNA™), builds digital identities for both consumers and business and evaluates their reputation. Two fundamental aspects make this technology a superior solution to prevent account origination fraud:

1. It describes and recognizes an identity based on its digital attributes, which are dynamically validated and constantly updated in real-time as more transactions are evaluated, making sure the information is always relevant.

2. It associates the identity's digital attributes with an aggregated reputation value based on financial transactions behavior.

© IdentityMind Global 2016

2

AGENDA

• Quick Overview of IDM’s view on Merchant Risk

• Merchant Risk in FinTech: 3 Use Cases

Use Case #1 Merchant Sentinel: An alternative strategy to De-Risk.

Use Case #2 Payment Service Provider managing risk portfolio.

Use Case #3 An alternative currency goes into payments.

• Conclusions

© IdentityMind Global 2016

3

IDM Takes on Merchant Risk• Take Control: Underwriting and Monitoring

o Lots of effort before opening an account and lots of effort while

account is operational

• Merchant Sentinel: Collaborative

o Compliance collaboration framework for high-risk merchants and

Processing Banks/Payment Service Providers

• OnBoard for Businesses

o The intersection between BSA compliance and account origination

protection for immediate decisioning© IdentityMind Global 2016

4

Use Case #1:Merchant SentinelAn Alternative Strategy to “De-Risk”

CLICK HERE TO LEARN MORE

© IdentityMind Global 2016

5

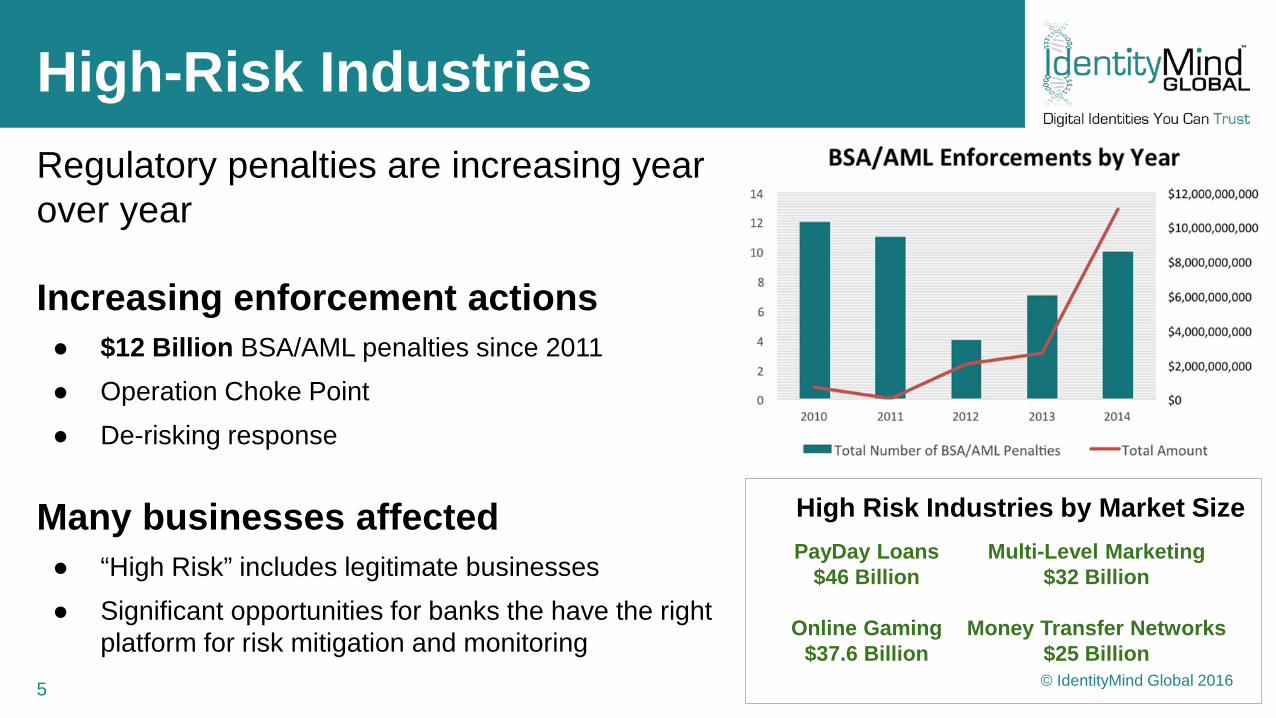

High-Risk IndustriesRegulatory penalties are increasing year over year

Increasing enforcement actions● $12 Billion BSA/AML penalties since 2011● Operation Choke Point● De-risking response

Many businesses affected ● “High Risk” includes legitimate businesses● Significant opportunities for banks the have the right

platform for risk mitigation and monitoring

High Risk Industries by Market SizeMulti-Level Marketing

$32 Billion

Money Transfer Networks$25 Billion

PayDay Loans$46 Billion

Online Gaming$37.6 Billion

© IdentityMind Global 2016

6

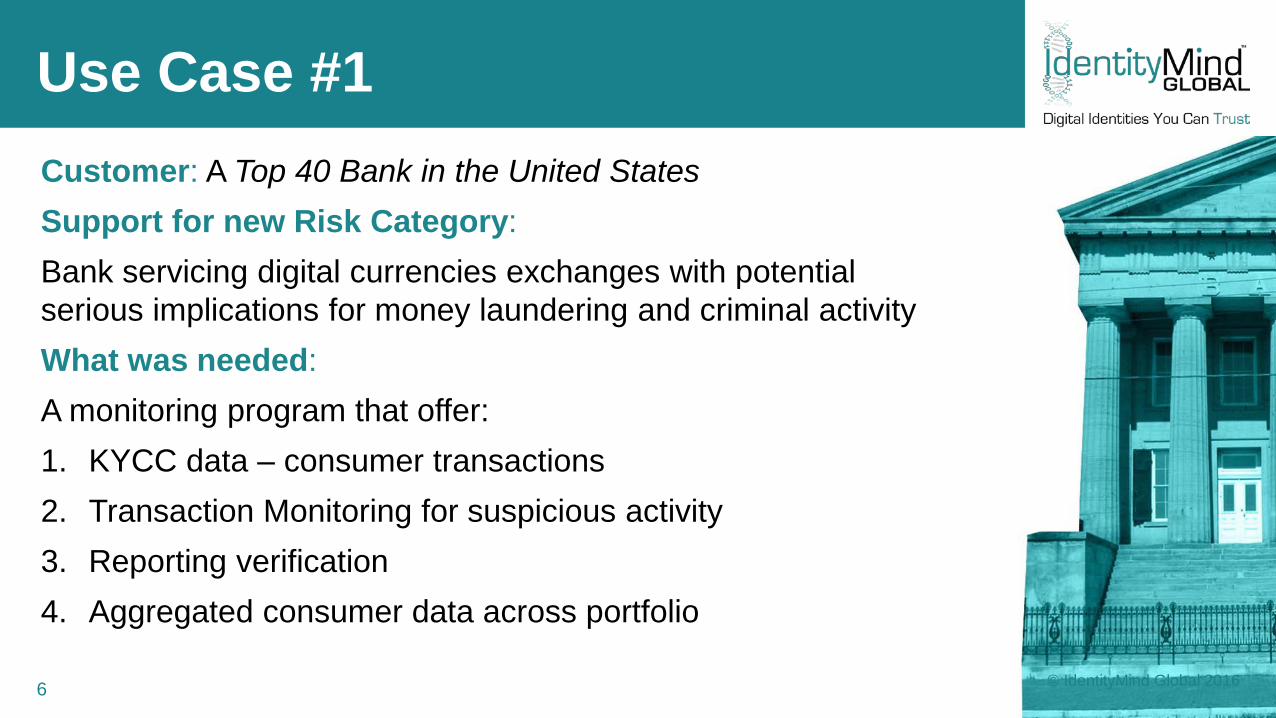

Use Case #1Customer: A Top 40 Bank in the United StatesSupport for new Risk Category:Bank servicing digital currencies exchanges with potential serious implications for money laundering and criminal activity What was needed:A monitoring program that offer:1. KYCC data – consumer transactions2. Transaction Monitoring for suspicious activity3. Reporting verification4. Aggregated consumer data across portfolio

© IdentityMind Global 2016

7

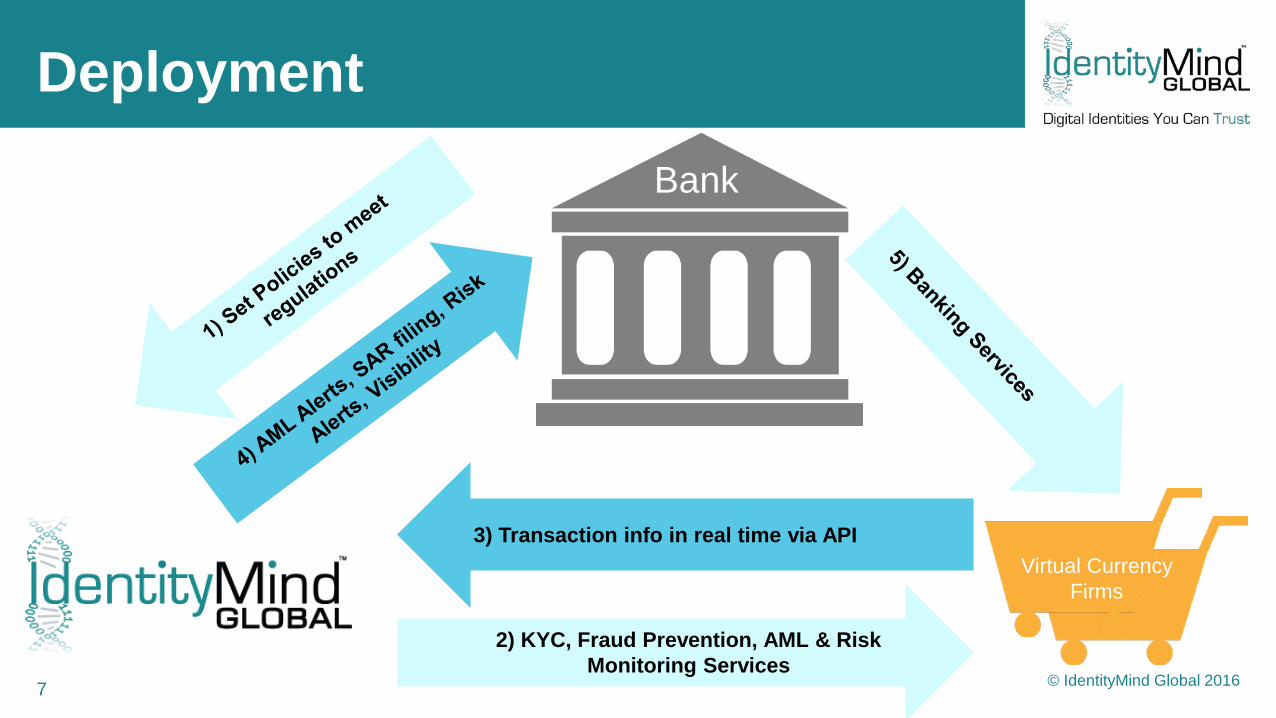

Deployment

Virtual CurrencyFirms

3) Transaction info in real time via API

2) KYC, Fraud Prevention, AML & Risk Monitoring Services

Bank

© IdentityMind Global 2016

8

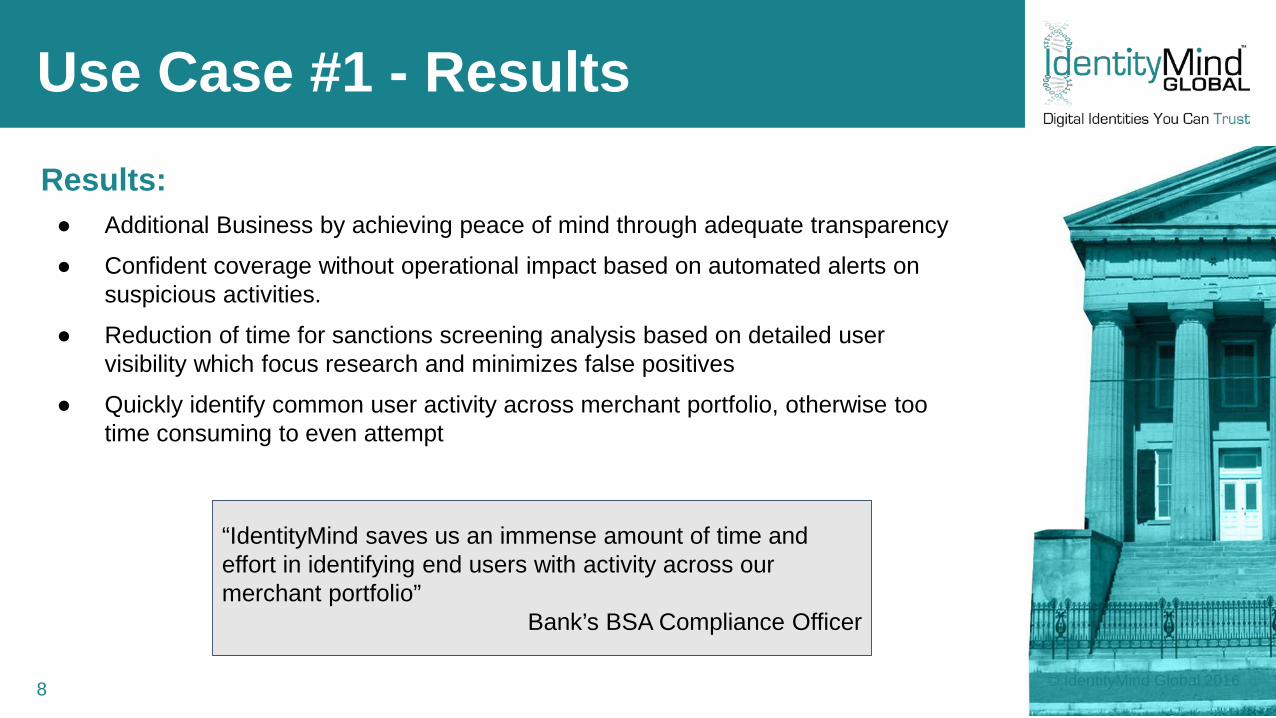

Use Case #1 - ResultsResults:● Additional Business by achieving peace of mind through adequate transparency ● Confident coverage without operational impact based on automated alerts on

suspicious activities.● Reduction of time for sanctions screening analysis based on detailed user

visibility which focus research and minimizes false positives ● Quickly identify common user activity across merchant portfolio, otherwise too

time consuming to even attempt

“IdentityMind saves us an immense amount of time and effort in identifying end users with activity across our merchant portfolio”

Bank’s BSA Compliance Officer

© IdentityMind Global 2016

9

Use Case #2:PSP ManagingRisk PortfolioAggregated and centralized fraud prevention

© IdentityMind Global 2016

10

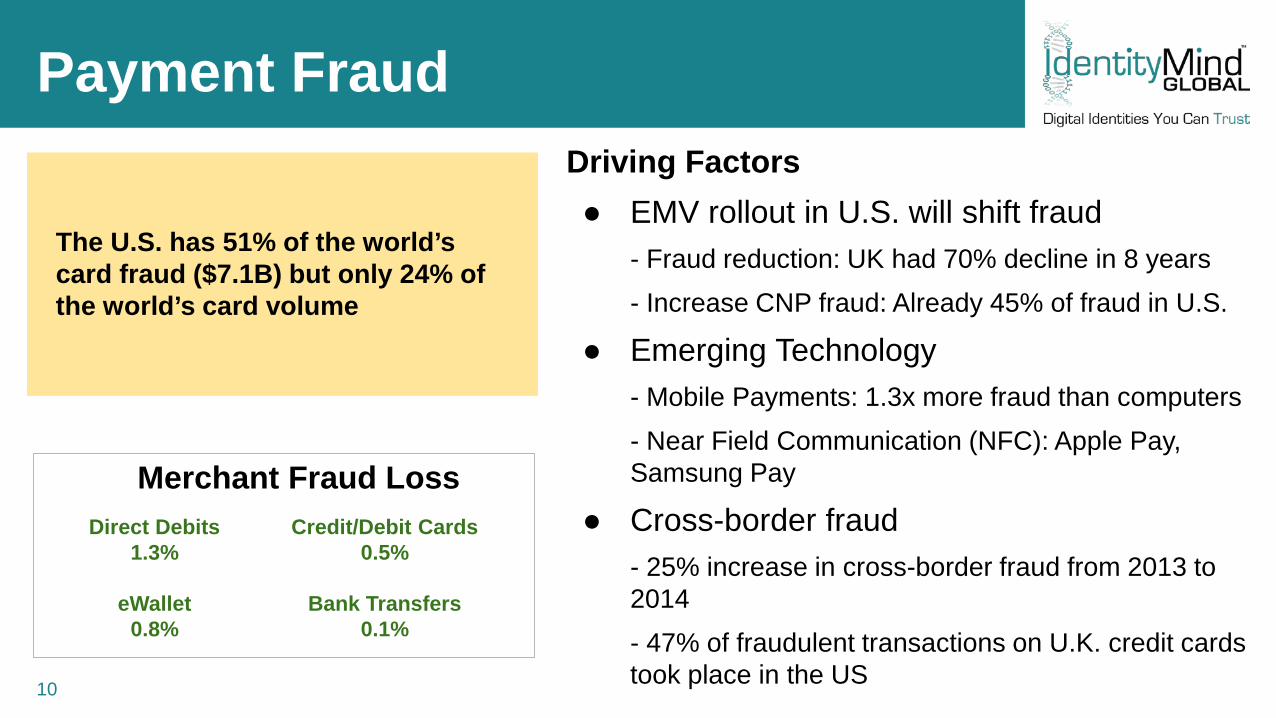

Payment FraudDriving Factors● EMV rollout in U.S. will shift fraud

- Fraud reduction: UK had 70% decline in 8 years- Increase CNP fraud: Already 45% of fraud in U.S.

● Emerging Technology- Mobile Payments: 1.3x more fraud than computers- Near Field Communication (NFC): Apple Pay, Samsung Pay

● Cross-border fraud- 25% increase in cross-border fraud from 2013 to 2014- 47% of fraudulent transactions on U.K. credit cards took place in the US

The U.S. has 51% of the world’s card fraud ($7.1B) but only 24% of the world’s card volume

Direct Debits1.3%

eWallet0.8%

Merchant Fraud LossCredit/Debit Cards

0.5%

Bank Transfers0.1%

11

Use Case #2Customer: European Payment Service ProviderTake Fraud Prevention OperationsPSP operates with clients in Europe but most consumers from the US. • Growing fraud rates across portfolio.• Clients going international with lack of cross border

payments risk expertise• Fraud tools cobbled togetherWhat was needed:A platform that could offer centralized fraud prevention for diverse set of requirements.Leverage similarities across merchant base

© IdentityMind Global 2016

12

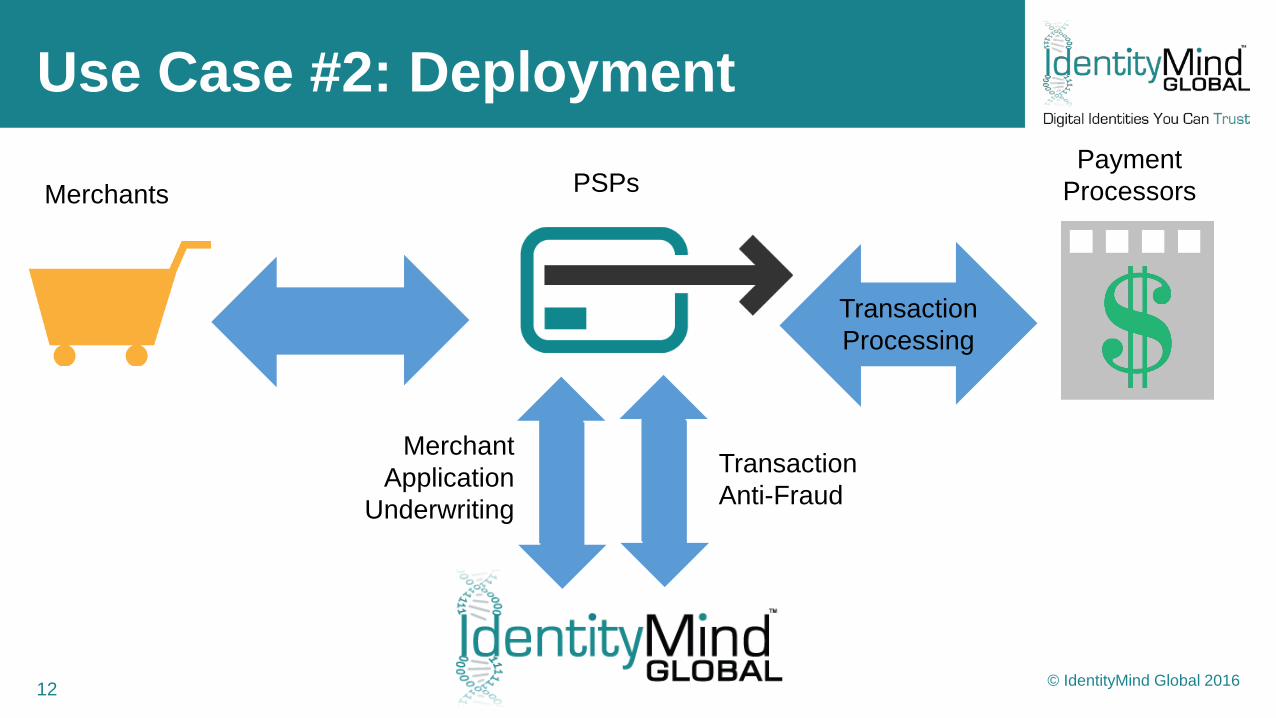

Use Case #2: Deployment

Merchants PSPsPayment

Processors

TransactionProcessing

TransactionAnti-Fraud

Merchant Application

Underwriting

© IdentityMind Global 2016

13

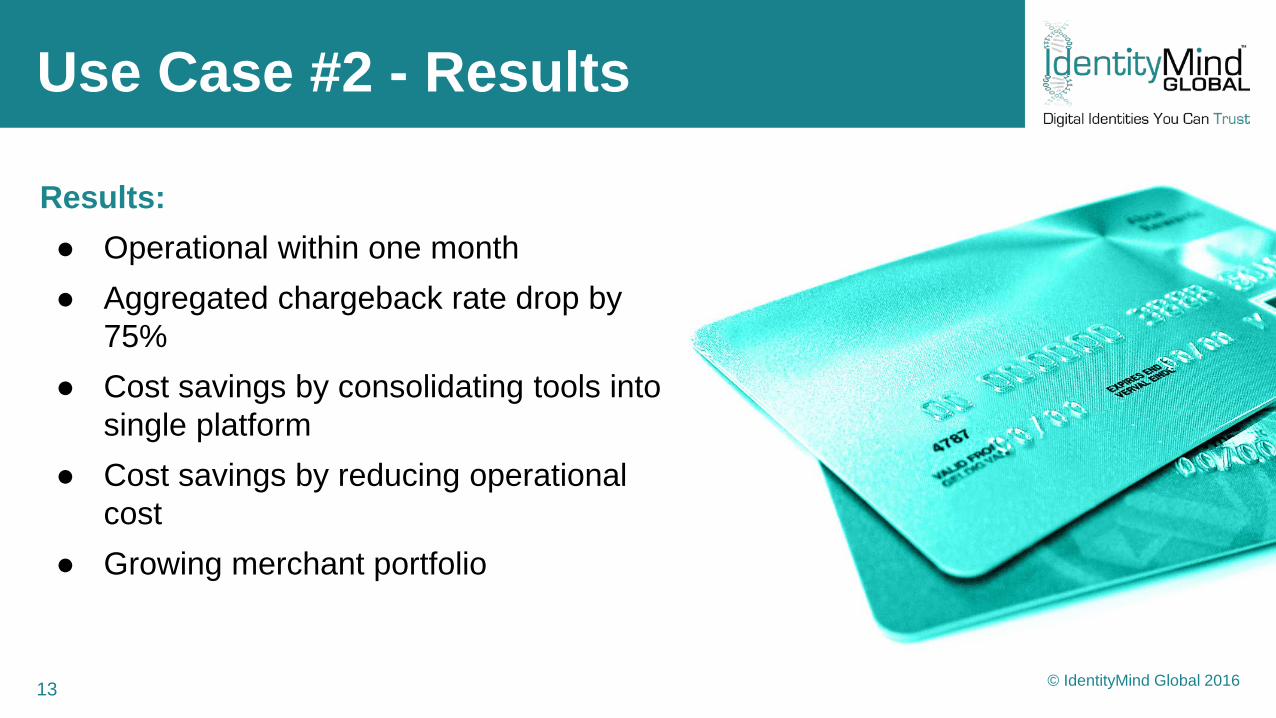

Use Case #2 - Results

Results:● Operational within one month● Aggregated chargeback rate drop by

75%● Cost savings by consolidating tools into

single platform● Cost savings by reducing operational

cost● Growing merchant portfolio

© IdentityMind Global 2016

14

Use Case #3:Alternative Currencygoes intoPayments

Aggregated and centralized fraud prevention

© IdentityMind Global 2016

15

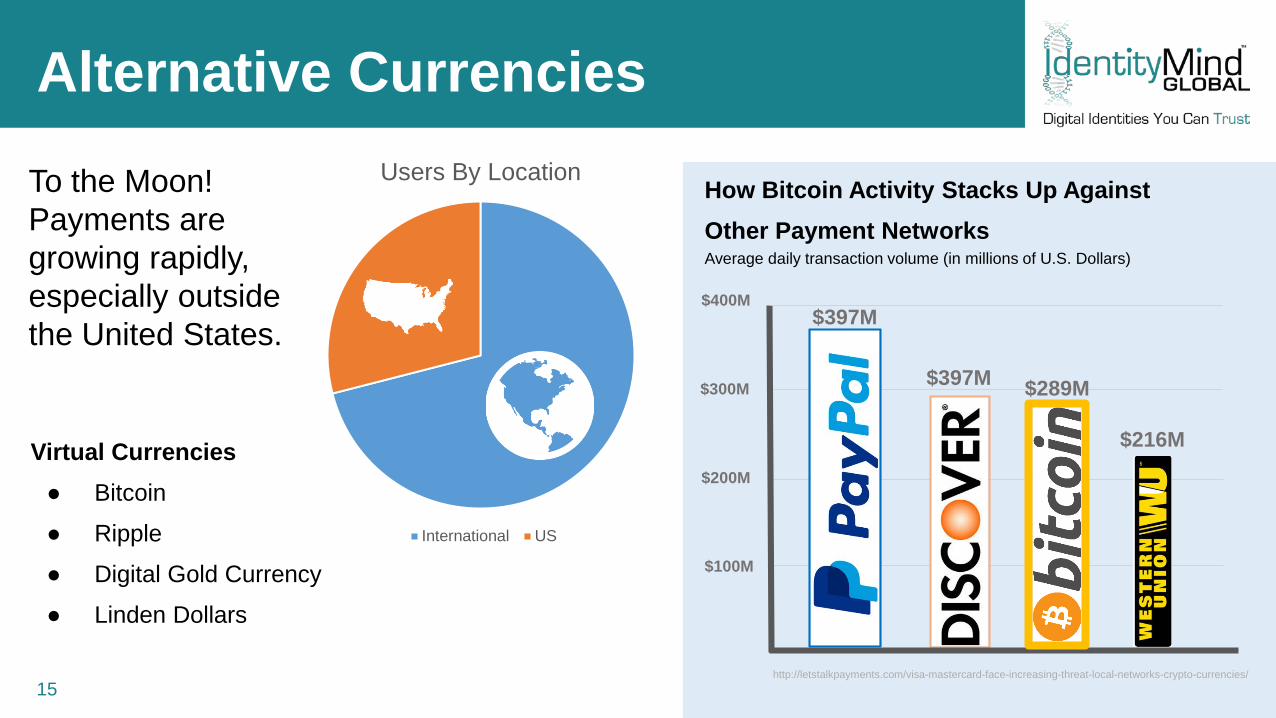

Alternative CurrenciesTo the Moon! Payments are growing rapidly, especially outside the United States.

How Bitcoin Activity Stacks Up Against Other Payment NetworksAverage daily transaction volume (in millions of U.S. Dollars)

$400M

$200M

$300M

$100M

$397M

$397M $289M

$216M

http://letstalkpayments.com/visa-mastercard-face-increasing-threat-local-networks-crypto-currencies/

Users By Location

International US

Virtual Currencies● Bitcoin● Ripple● Digital Gold Currency ● Linden Dollars

16

Use Case #3Customer: Canadian provider of alternative currency backed by GoldTurning Currency into Payment Options at MerchantsStarts onboarding merchants to accept their currency as a form of payment• Translate acquiring practices however not as strict.

Liability is quite different.• Heavy scrutiny for Money Laundering• Small merchants – Fraud preventionWhat was needed:A platform that can offer business onboarding with heavy focus on money laundering.

© IdentityMind Global 2016

17

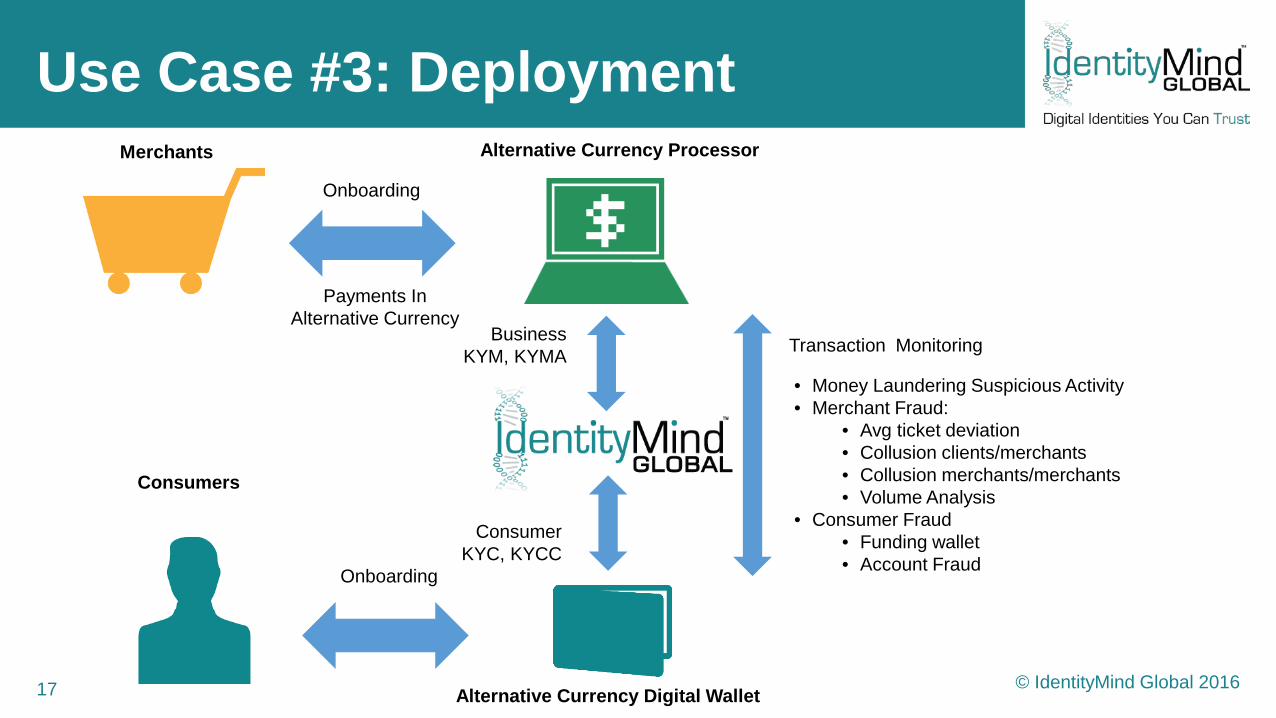

Use Case #3: DeploymentMerchants

Onboarding

Payments InAlternative Currency

Alternative Currency Processor

Alternative Currency Digital Wallet

Transaction Monitoring

• Money Laundering Suspicious Activity• Merchant Fraud:

• Avg ticket deviation• Collusion clients/merchants• Collusion merchants/merchants• Volume Analysis

• Consumer Fraud• Funding wallet• Account Fraud

BusinessKYM, KYMA

ConsumerKYC, KYCC

Onboarding

Consumers

© IdentityMind Global 2016

18

Use Case #3 - ResultsResults:● Integrated staged onboarding for

merchants in real-time● Merchant’s adoption of alternative

currency is slow

© IdentityMind Global 2016

19

Conclusions

• FinTech is moving fast. Merchant Risk practices common on the acquiring world are being selectively adopted.

• Self inflicted “De-Risking” is leaving a very profitable opportunity for acquirers with deep monitoring practices.

• Online onboarding is real time and less concerned about Financial Risk

• KYCC is being pushed from the banks downstream given AML regulations

• Financial terrorism will continue to drive extended visibility across portfolio actions.

© IdentityMind Global 2016

20

Learn More

For more case studies and in-depth content related to onboarding and acquiring risk,

CLICK HERE

© IdentityMind Global 2016