Embed Size (px)

Citation preview

4September 2015 www.textilevaluechain.com

��������

Ms. Jigna ShahEditor & Publisher

All rights reserved Worldwide; Reproduction of any of the content from this issue is prohibitedwithout explicit written permission of the��������� ��� ���� ���� ��� ���� ��� ���and present factual and accurate information.The views expressed in the articles published in this magazine are that of the respective authorsand not necessarily that of the publisher. TextileValue chain is not responsible for any unlikelyerrors that might occur or any steps takenbased in the information provided herewith.

����������� �Innovative Media and Information Co.189/5263, Sanmati, Pantnagar,Ghatkopar (East), Mumbai 400075.Maharashtra, INDIA.Tel : +91-22-21026386Cell: +91-9769442239 Email: [email protected]

[email protected] Web: www.textilevaluechain.com

Owner, Publisher, Printer & EditorMs. Jigna ShahPrinted & Processed by her at, Impression Graphics, Gala no.13, Shivai Industrial Estate,Andheri Kurla Road,Sakinaka, Andheri (East), Mumbai 400072,Maharashtra, India.

Technical textile or Unconventional textiles or Function-al textiles whichever name you say, this textiles are highly technical& non- technical ie. Non Wovens. Both segments developing slowly in India not only for domestic use but alsofor international consumption too.

We always here in textile conference / seminar, techni-cal textile on growth stage in India. But industry is confusedabout where is the market in India?? Industry experts havedivided segment by 12 ways depending on the Usage and Ap-plication. There are 2 extremely opposite segments are con-sidered in technical textile, still we consider as one textile.

One, Non woven is now becoming alternative to dispos-able paper, its “use and throw fabric”. This concept is quite new in India, with the traditional mindset, religious belief,diverse culture makes hindrance of use & throw fabric. Nonwoven currently widely use in FMCG, Medical, packaging, fashion accessories, hotel, many more. Manufacturing of Nonwoven is simple, fast, quantity oriented. Generally Cot-�����������������������������������������������������absorbency, air permeable quality. This segments manufac-turing done by top international brand ( Kimberly-Clark, etc)who brand their products internationally. Other segment areIndian company who have non brand / local brand which sells and marketed only in India. This segment in India have-fairly done good in last decades, but now due to globalisa-����������������������������������������������������-����������������������������������

Other technical textile area are highly technical, spec���������������������������������������������for Aircraft, automobiles, construction, Geology many other

area where strength and longitivity of fabric is the most es-sential. Manufacturing of this fabrics are complex, spec/ de-tail oriented, quality oriented. Manufacturer are mostly pre-sent in developed country where there is a good researchfacility available. Indian manufacture are making and supply-ing to developed country. Generally polyester, nylon, other ������������������������!������������������

Though government appointed COE (Center of Excel-���"�����������������������������������������!������������������������������������������������same. No research report given to media.

Skill labour for this technical fabric knowledge is rare inIndia. No course is developed for this segment as yet, so senior position in the industry only knows the technology of highly technical fabric. So there is lot of gap, in skill area.

Technical textile market in India is peanuts, as compareto international market. In developed country in world theyalready using this fabrics from decades, they understand theimportance of this fabric as compare to conventional fabrics. Consumers in developed country have awareness and usethe fabrics in their daily life. Geo textiles which is used for construction, road levelling, many more functional areas. Indeveloped country like EU its mandatory to use Geo textilein road building.

Technical textile, be it any application / use, if consumer awareness will increase, market of this segment will increase automatically in India. We as industry need to unite together and make a awareness campaign for this segment…!!!

Wish you happy reading & happy business..!!!

�� ��� ������������������������������

6September 2015 www.textilevaluechain.com

Back Page: RaymondBack Inside : RieterFront Inside : QMAX Page 3: Narain SyntheticsPage 5: Bajaj FabPage 7 : SGS InnovationPage 8 :Machinary ExpoPage 9 :RabatexPage 10 :Techtexil

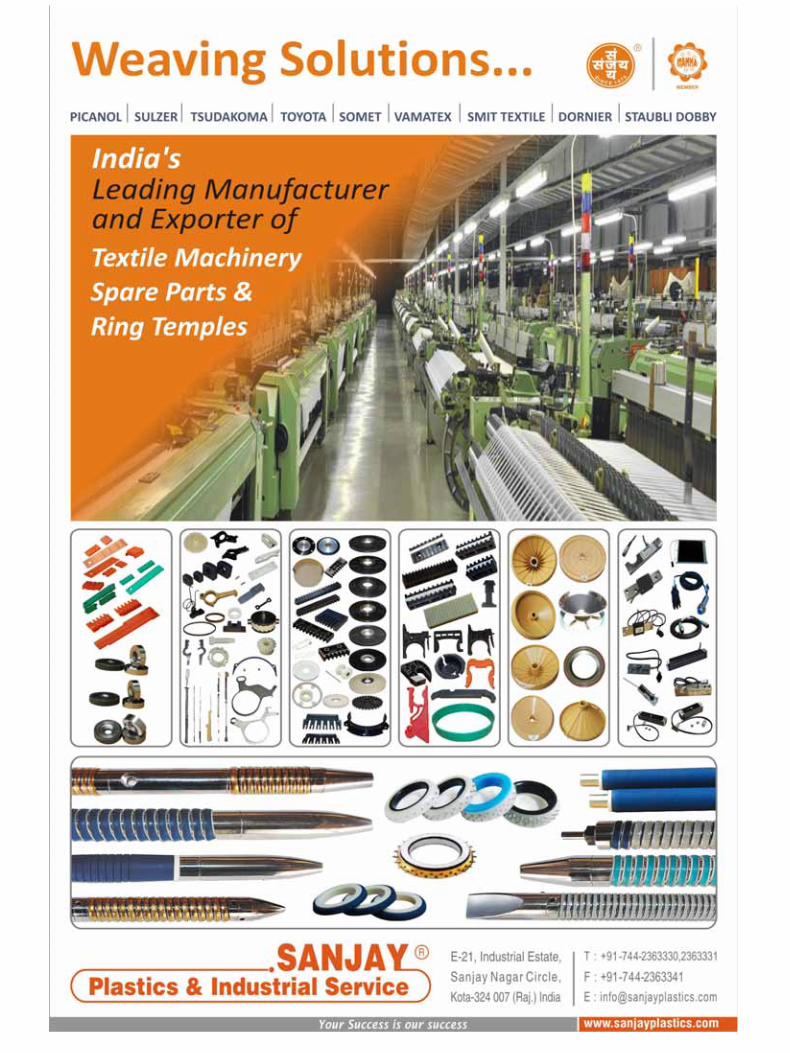

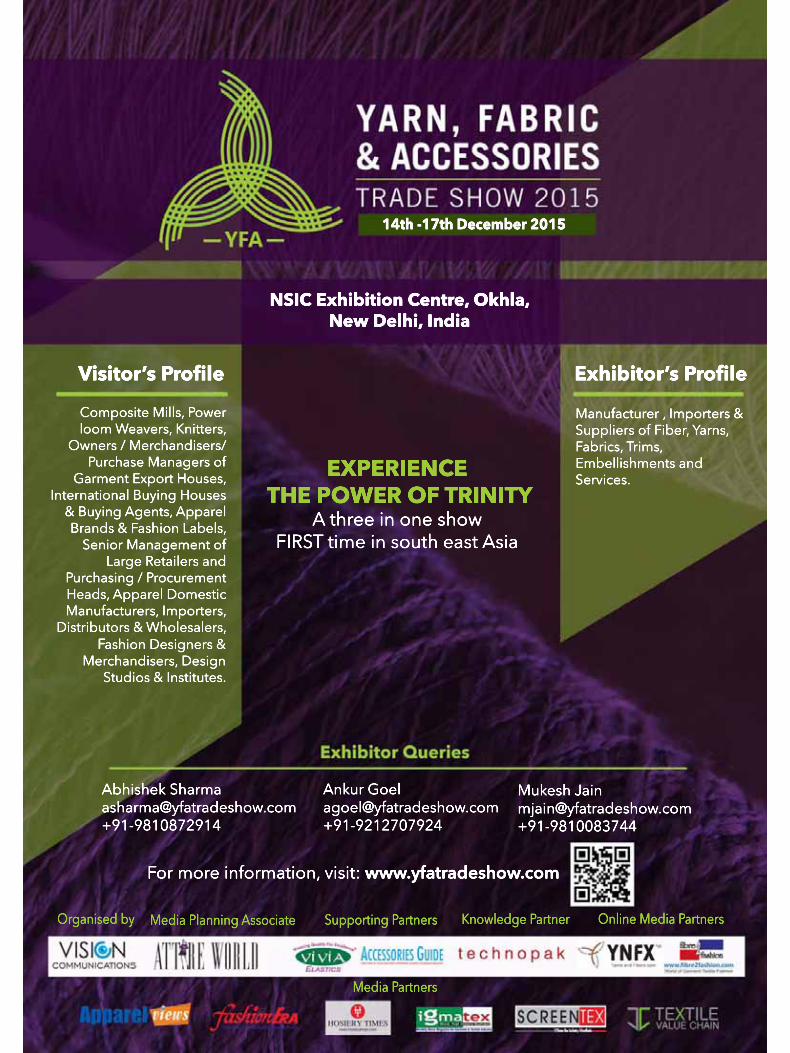

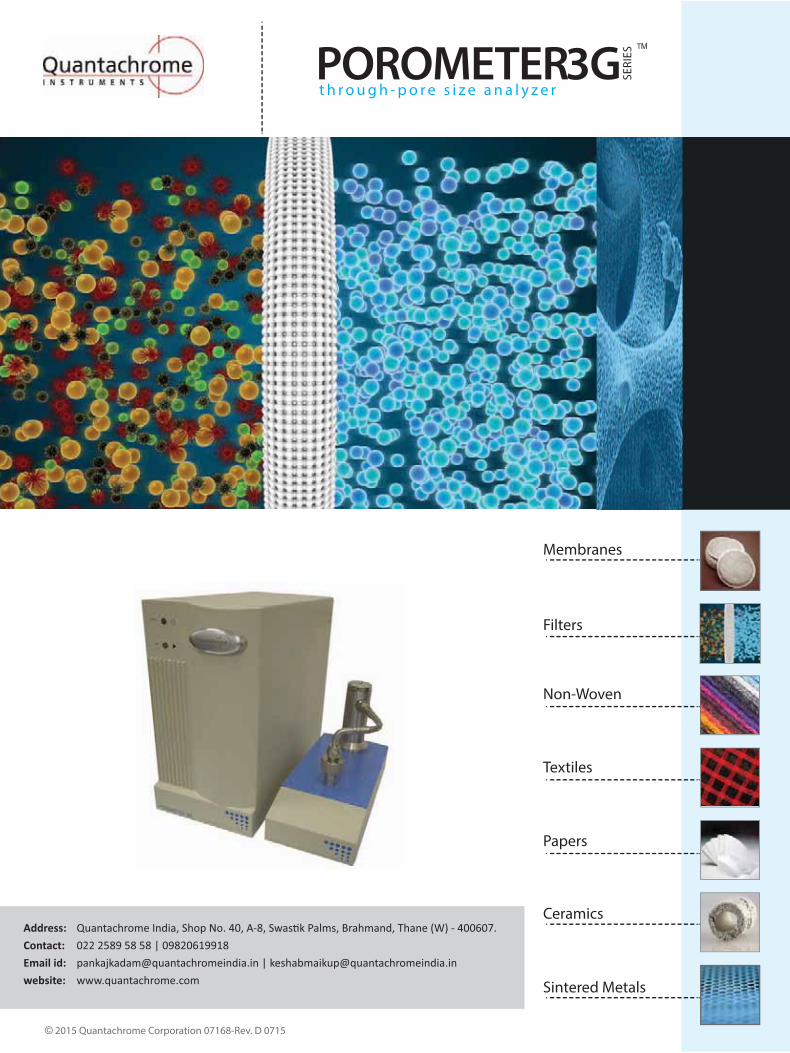

Page 43 :Sanjay PlasticPage 44 : ITMACHPage 45 : Shree ram TextilePage 46 : PRD cottonPage : 47: BSL SuitingPage 48 : YFAPage 49 : ITF- DubaiPage 50 : Quantachrome

EDITORIAL TEAMEditor & PublisherMs. Jigna ShahEditorial AdvisorShri V.Y. TamhaneConsulting EditorMr. Avinash MayekarGraphic DesignerMr. Anant A. Jogale

INDUSTRYMr. Devchand ChhedaCity Editor - Vyapar ( Janmabhumi Group)Mr. Manohar SamuelPresident, Birla Cellulose, Grasim IndustriesDr. M. K. TalukdarVP, Kusumgar CorporatesMr. Shailendra PandeyVP (Head – Sales and Marketing), Indian RayonMr. Ajay Sharma GM RSWM (LNJ Bhilwara Group)

EDUCATION / RESEARCHMr. B.V. DoctorHOD knitting, SASMIRADr. Ela DedhiaAssociate Professor, Nirmala Niketan CollegeDr. Mangesh D. TeliProfessor, Dean ICTDr. S.K. ChattopadhyayPrincipal Scientist & Head MPD Dr. Rajan NachaneRetired Scientist, CIRCOT

CONSULTANT / ASSOCIATIONMr. Shivram KrishnanSenior Textile AdvisorMr. G. BenerjeeManagement & Industrial ConsultantMr. Uttam JainDirector PDEXCIL; VP of Hindustan Chamber of CommerceMr. Shiv KanodiaSec General, Bharat Merchant ChamberMr. N.D. MhatreDy. Director, ITAMMA

September 2015 ISSUE

CONTENT

����������� ���

Cover Story Technical Textile for Generation Next...

11 Future of Technical textileby Mr.Avinash Mayekar

13 $�������������%�'����������������������technology

News 16 - Association

17 - Corporate

19 -MOU

30 -TEXPROCIL

ARTICLES 18- A Stitch in time by Mr. Vishnu Govind

20 -Technical : ���������������������������resistance properties by DKTE Professors

23- Scenario in BRICS region & textile potential byMr. Arvind Sinha

25- Achhe din kab ayenge by Mr. Sanjay Jain

SHOW/ EVENT REPORT

22- ITAMMA Madurai Catalog show

28- AGM Speech : TMMA

31- HGH India

32- Career Opportunities in Nirmala Niketan college

34- Intex South Asia 2015

34- ITMA 2019

40- Birla Cellulose

REPORT

35 - Yarn

37- Cotton

41- Show Calendar

5

8June 2015www.textilevaluechain.com

VISIT US: Hall No. 1Stall No. G116

Your Centre of Innovation24 – 26 September 2015Hall 6, Bombay Convention & Exhibition Centre, Mumbai

International Trade Fair for

Technical Textiles and Nonwovens

India’s leading trade platform that enables

you to Interact and Network with Industry

heads from Global Markets

For more information please contact:Anisha Britto+91 22 6757 5969 | [email protected]

www. techtextil-india.co.in

Register Now!

11September 2015 www.textilevaluechain.com

Introduction“Make in India” is one of the most appreciable initiatives taken

by our respected PM “NarendraModi” to fuel growth of Indian manufacturing sector. Textile Industry is one of the core segments of Indian Manufacturing Industry contributing 14% of total industrial output & employing about 45 Million populations directly.Though Textile Industry has its huge contribution in terms of export earn-ings, industrial output & employment generation when it comes to investment initiatives, Indian entrepreneurs are turning back to the sector. So let’s analyze why most of Indian entrepreneurs are turn-ing back towards the sector which has presence in country since ancient times.

If we look at the mindsets of most of the investors while in-��������������������������������������������������������period, sustainability, faster returns & easy returns of investments. Unlike all above, most of conventional textile businesses give lower ������������!���������������������������������������������most of the existing Textile players are looking for opportunities to diversify into other businesses. The questions to all these investors may be

� <� =����������������������������������������������in your own industry?

� <� >�����������������������������������������upcoming market trends in Textile sector globally?

� <� =���������������������Z������[����������!�������are prospective Textile growth sectors?

� <� [����������\]�^�India has a strong history of Convectional Textiles. It is tradi-

tional industry where generations to generations are involved into ���� ������������ �������� ���� �����_�� ������� ��� ������� Z��spite of growing demands of domestic & international markets, convectional textile sector is highly saturated. It is facing challeng-���������������������������������������`���������������������������������������������!�����������������������������-els. So Textile entrepreneurs have no other alternative than diver-sifying into other business. But why can’t they think of “Technical Textiles” as potential investment sector which goes parallel to the conventional textile industry.

Technical Textiles - Opportunity for IndiaUnlike conventional textiles, Technical textile has huge poten-

tial in India, as the sector is in introductory phase. Indian Technical [�����Z���������������������������������������{|}�����~��{�%�~����~���%{��!�����������������������������~�}�����������������������������|������������~�{|%{���

The income of Indian consumer is also growing very fast. This rise will enable them to make more discretionary spent on techni-cal textile products viz. Hometech, Clothtech, Mobiltech, Sportech ����'�������Z����_�������������������������������������{��������������������~�����~�{�%{������������������������{������-lion economy( Source: Economics times)

[�������������������������������������������������������-�����������������������������������~���������������������[��middle class is well educated and receptive to the many technical textile products particularly the disposable products which have huge market in western countries. This combined with the growth of organized retail in the country is a key growth driver for techni-cal textiles used in consumer products.

�������������������}��������������������������~�����������vibrant segment for any market. Also India leads the world with �������������������������������������������Z��������������straight quarter) – showing optimism of consumers in economy. �������]���������������������������Z�����������������~�{{"�

Their wide range of applications, lack of competition and grow-ing consumer and industrial demands make it a big opportunity area and an attractive option to invest in. Add to this, the factors conducive for the growth of manufacturing and consumption of technical textiles are also available within the country. Though In-����������~���������������������������������������������������������������������������������������������������������}�������total consumption.

Currently, we have very few market players in Technical Textile segment. Technical Textiles itself is a vast sector. Depending on the product characteristics, functional requirements and end-user ap-�����������������������������������������������������������������������������{~���������

As Technical Textile products are highly engineered products ����������� ����� ��� ���� ����������� ������� ��� ������� ����they are higher value products, so they fetch higher returns to man-���������������������������������[��Z�������������������-ing paradigm shift towards westernization, so the new generation entrepreneurs should think of untapped market segments. As we are moving towards globalization, our needs and market demands are changing and I am sure the products like wet wipes, disposable home textiles, travel kits, air bags, high end sports textiles and dis-posable products like medical textiles will be products of daily con-sumption in near future.

Z�������{�%~����������������������������������������������diapers or wipes, were hardly used by mass population. But today,

Technical Textile – Future of Indian Textile Industry!

����������

Shri Avinash Mayekar MD Suvin Advisor Pvt. Ltd.

12September 2015 www.textilevaluechain.com

these products are reached to rural parts of India. So time has come to change our mindset from “Conventional Textiles” to high value “Technical Textiles” as investment options. Investors need to direct themselves from basics to high engineered niche products.

Major chunk of Technical Textiles are manufactured by Non-wo-ven technologies. These are compact technologies and give much higher production and are emerging technologies to produce com-plex products as well. As the process is very short, the utility con-sumption is much lower and due to huge production, the operating costs are minimal.

Moreover, there is hardly any involvement of human beings and hence quality is determined by technology and very less chance for ��������������Z��Z����������{~}����[��������[������������������������������]�����������������������������~�}����usage in the world. So India still has long way to go to meet global requirements of nonwovens.

Positioning India Time has come to position India as manufacturing hub for Tech-

������ [������ �[["�� Z�� ��� ��� ��������� ��� ��� ������� ������ ����we need to understand Technical Textiles thoroughly. We need to create awareness amongst each verticals of Textiles industry. Gov-ernment is been taking initiatives to promote TT among the value ������� ���� ����� ����� ��� �������� �� ���� ������� ���� ����step into positioning India as TT hub is to carve out clear vision, strategy & action plan for TT. We need to map out existing TT de-�����!����������������������������{~�[[���������������-tic as well as global market. Once demand assessment is done; we need to analyze our current potentials in terms of raw materials, infrastructure, technology level & human resource. The demand-supply analysis will give us clear picture of enormous opportuni-ties available in the TT segment & we can frame out our vision for Technical Textile segment. The assessment of additional raw mate-rial, infrastructure, technology level & skill development required to match the global & domestic demand & make India as leading global player.

Each & every state of India can be mapped out for type, quality !������������������������!������������}�����������������directly exported. Based on this data, we can work out how much ��������������������������������������������������������-ing it as raw material. This value addition into TT will not only give ���������������������������������������������������

���� �� ���� ���� ��� ��������� �� �� ���� ��� ���� ����additional investments required & level of infrastructure to be de-velopment. Hereafter role of government will be to introduce vari-ous schemes & policies favorable for the investment in TT sector. This will create conducive environment amongst the investors.e.g. Capital subsidies & interest subsidies to the investors into Technical Textile sector.

As Technical Textile is high engineered product, it requires high skilled labor trained with international skills and standards. It is nec-essary to check whether existing educational programs are capable to create such high skilled human resource. Educational seminars & training programs can help to create good human resources. In ������ ��� �� ������������ ����������� ���� ���� �� �����������and have experience in training to textile experts as well as labors. Such kind of training programs can develop a good skilled work-force. Government can support such skill development programs & training centers for growth of TT segment.

Technology advancement plays crucial role for growth TT seg-ment e.g. if our vision is to double market share in next 5 years, but we do not have state-of-the art technology to produce inter-national standard goods, then we can never achieve our vision. In [�������� [������� ������� ��������������� ��� ��������� =����the obsolete machineries, we cannot achieve desired norms & standards of products competitive to international standards. We have to update ourselves with the latest state-of-the are technol-ogy. Government has launched TUFS scheme to support technol-ogy development which is an appreciable initiative. However, it ���� ������ ������������� ���� ��������� ������ ��� �����chain. More such Government schemes are needed to bring about technology advancement.

Last but not the least is government policy framework. Govern-ment policies should be in tune with our vision. Various central & state government schemes can help to boost investment in TT sec-�����������������������������������������������������!�������subsidies should be given to promote TT sector. Subsidies on ma-chineries of Technical Textiles will be helpful. Similar to Textile Park concept, Technical Textile Park can stimulate positive environment for the growth of TT sector.

[���� �� ���� �������� ��������� Z����� ��� ��������� ���� ���Technical Textile provided, we develop world class infrastructure, technology level, skill development program & Government policy framework which will support our vision…

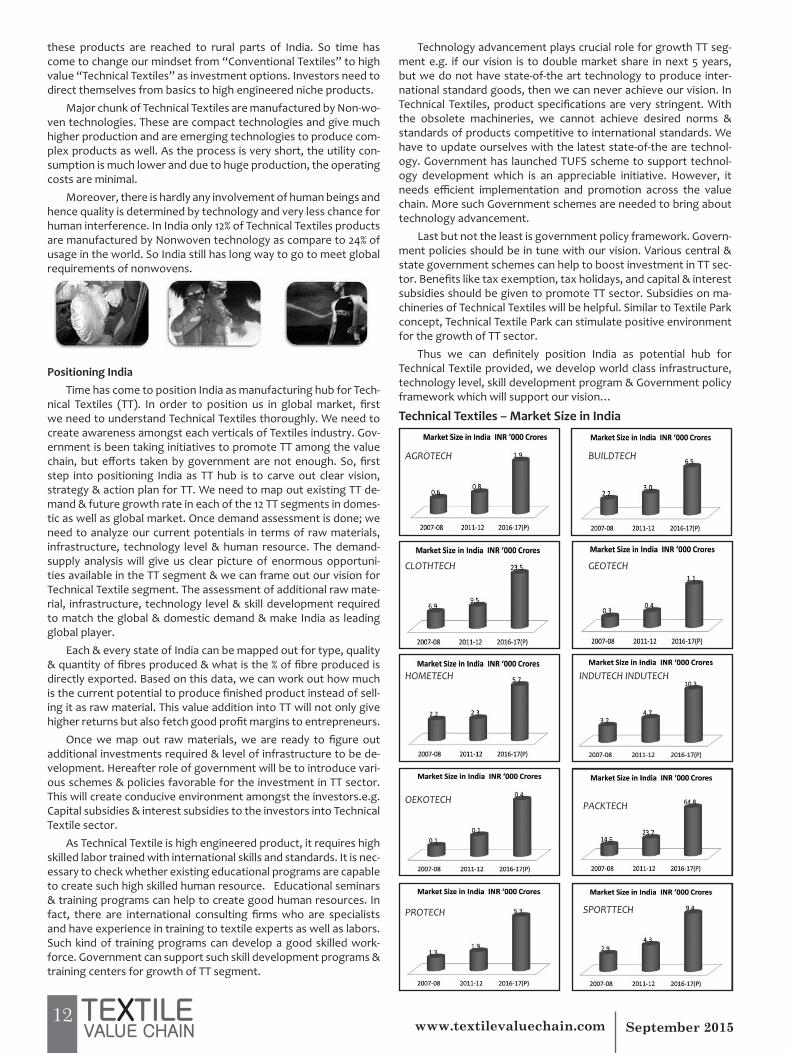

Technical Textiles – Market Size in India

AGROTECH

CLOTHTECH

HOMETECH

OEKOTECH

PROTECH

BUILDTECH

GEOTECH

INDUTECH INDUTECH

PACKTECH

SPORTTECH

13September 2015 www.textilevaluechain.com

ABSTRACT Laser cutting is meanwhile being used for a wide range of materials across all sectors of industry. This cutting meth-�����������������������������������������������������������������������������������������������������[�����������-�������� ��������� ������ �� ������� ������� ��� ��� ���������������$���������������������������������������������-����������������������������������������������������

$����������������������������������������������%����� ������� �� ��� ����� ��������� ������� ���� ���� ������� ������� ������ ������ ������ �� �������� ������� >����� ��� ����� ������������������������������������������������������small or medium-sized quantities soon become necessary and it ��� �� ����� ���������� �������� ����� ���� ������� ��� `��������������������[�������������� ����������� ��������������������������� ����� ��� ���� ��� ��� �������� ������������� ��� ��� ������������������������������������������������������������-��������������������������������������������������������-����������������������������%������������������������������������������������������������������������������������

=���������������������������������~��������������������������%�������������������������������������>�����������-��������� ������ ��� ��� ����� ������ [������ ������������ ��� �����������������������������������������������������������[������������������ ������������������� �������������������������������������������������������������������������-ting directly from the roll and routed after laser cutting directly to ����������������=����������������������������������������������������������������������������������������������������������������������[������������������������������������������������$������������������������������������-���������� ��� ��� �������� ������ ��� ��� ��� ��� ������� ��� ���������������������������������������[���� ������������������������ ��� ��������� ������� ������� ���� ����� ����������� -��������������������������������������������

KEYWORDSLaser cutting, Finishing, Process Optimisation, Fabric Finish-

������ ��� �

������� ���������������������������"���#��� ����$���%�����

Laser cutting is meanwhile being used for a wide range of ma-����������������������������������[��������������������������������������������������������������������������������������������������������������������[���������������������-����������������������������������������� ���������$�������������������������������������������������������������������������������������������������

[������������������������������������������������������-���`����������`���������������������������������%���������������������������������������������������������� ��-������� ��� ����������� ��������� ���������� ���� �����������therewith related non-deforming cutting are crucial arguments for �����������������������������������������������������������

'��'�(��)�*���+�3���6*����(7)�WITH LASER TECHNOLOGY

������ �������������>�����������{����~{�������������������

{�{���������������������������������[���������������_����������������������������������������������������������������������������������������������������������-����������������������������������������������������������-����������������������%���������������������������������������������������$�����������������������������������������������������������������

89���������#����� ��������#�� ������=���������������������������������~�����������������������

���%�������������������������������������>�����������-������������������������������������������>���������{������������ ���� ����� ������������ {��� �������� ��� ��� ��� ������������������~��������������������������%��������������

������������������������ ������������������������������������������������������������������������������������$�������������������������������������������������[��������-���������������������������������������������������������������%������������������������$����������������������������������������������� ����������� �������� ��������[�������� ����� ��� ��������� ������������ ��������� [���� �������������������������������������������������������������������������������[����~�������������������������������������������������������������������������������

[��������������������� �������������������������������������� ������ ���������� $���� ��� ��� ������ �� ���������������� ��� �� ������� �������� ��� ���� ���� �� ������� ��-�������������������������������������������������������=������������������ ���������������������������������������������������������������������������������������������`����������������������������������������������������������%�������������� ���� ����������������$������������������������� ��������������Z����������������������������������������������-������������������������������������������[�������������������������������������������������������������������������-ing methods in just one single machine.;���<������� ���������� ��� ����������

[�� ���� ������ ���������� ������ ���>�� ������� ����������������"����������������������������������������

����������

14September 2015 www.textilevaluechain.com

������������=��������]���������_��¡�%�~��������������-��������������������~{������������������������

Today, automations for the textile processing are indispensa-ble for an economical production. In this case, eurolaser applies the Conveyor System for roll material. By using this automatic material feed, textiles can be fed for laser cutting directly from the roll and routed after laser cutting directly to a table extension. With a high degree of connecting accuracy after a material feed cycle, sections, which for all practical purposes are endless, can be produced. The bale material is fed via an automatic feeding unit. A feeding system edge controller ensures precise positioning of the material. Fur-ther, there is even an option to add a winding unit to the Conveyor System. This is used for the even winding of previously processed textiles and this accordingly results in a completely automated cut-ting process.

A special table concept is used for textile machining. This com-prises a stainless steel wire mesh and is particularly suitable for thin ����`���������������������������������� ����������������-rial support for the machining process and, on the other hand, the transport element for the Conveyor System.

��������������������Z���'�����������������������������%���������������������������������[�����������simple, economical and contact-free marking methods is growing continuously, particularly for sewing markings (clippings) in the textile manufacturing branch. The universal jet system operates �������������������� ��� ������������������� ������� ������-tridge. Materials such as polyester, polypropylene and acrylic plus almost all natural textiles, can be marked with the adjustable jet �~%��������������"��

The eurolaser laser system works based on a variety of software ��������������������������{���}����������������������������_�data can be easily transferred – including CDR, EPS, HPGL and AI. =�������������������� ����������_���������������������������������`����������������������������������������-ing module for the automatic nesting of blanks to save material or the camera recognition of optical registration marks. ' ���� ��<"����=���� ��%������

[�� ����� �� ������� ��������������������� ��� ��������� ��� ����������� ������ �� ���������� ���� ����� ������� �� ������ ������_�are indispensible for mechanic separation. Wherever products are manufactured, their quality positively improved or

a simple selection carried out, �� ���� ��� ��� ����� ��� ��� ����Filters have proved simple but ������ ��� ������� ��� ����and played an important role in �����������������{��������~����centuries. There was a continu-ous revolution in progress with �������������������������this time. This was due to knowledge gained about new materials on the one hand and change driven by increasingly higher dissolu-tions in analytics that led simultaneously to higher demands on the ��������������������������Filter materials

[�����������������������%�������������������������������������������������������$��������������������������������-��������������������������]����������������������������well-read and aware his rights where quality and health are con-�����'�������������������������������������������by-products. However, frequently, the separated material is also the desired product.

[�����������������������������������������`������������������������������Z�����������������`��������������������%��������������������� ��� ������ ���������� ����������������������������<>�?����%�� ����=�����

��������������������`��������������������������������������������������������������%���������������������������������� ������������������������������� �������������������������technology. Whether for underground ventilation for mines or for the air supply in the interior of cars -nowadays separating pollut-���������������������������������������������%¢������������������������������£������������������������������-rial but also to processing methods. In many applications, the mate-�������������������������������������������������������������are in continuous operation. The capacity for individual fabrication ��� ����� ���� ���� ����� ��� ���� ��� ��� �������� ������������� ���the materials to the operators are strong arguments for the use of laser technology.

Laser processing – contactless and clean – makes it possible. A ���������������������������������������������%�����fabrics are in fact technical textiles and can generally be formed �����������������������������������>����������������������-cesses are integrated in changing operational processes, small or medium-sized quantities soon become necessary and it is here that �������������������������������������`�������������������

[�����������������������������������������������������-ically by machine within a few minutes. The focussed light of the laser can cut a multitude of non¬woven fabrics with consistently high precision, without any preparatory measures. Application of the laser cut is as clean as it is simple. There is no need to create a tool and no tool changeover. Thus, there is no wear on the cutting

15September 2015 www.textilevaluechain.com

blade. Beside, you do not even have to clamp the material.

This New Generation is necessary if the high demands of indus-��������������������������������������������������������������������������������������������������������even with low quantities and dimensions of up to 3,210 x 3,200 mm with no problem at all. In order to ensure that serial production can ������������������������������������������������������Laser is the tool. Thanks to a sophisticated system technology, al single processing steps, such as material transport, recognition, positioning and material cutting are carried out fully automatically for the most part. Material handling has such a wide range that light to heavy materials can be transported to the laser with equal accuracy. The CO2 laser beam – a laser that emits in the infrared range – is focussed above the material to be processed and hits the surface of the material at a point of 2/100 mm2 and with a power of 100 to 400 watt. Exposed to such a concentration of energy, most materials sublime within fractions of a second. A process gas is in-troduced – usually simple compressed air of approx. 2-3 bar – in order to accelerate the cutting process and ensure clean cut edges. The cutting emissions in the form of smoke are evacuated to 100%, ����� ���� ��������� ��� ��� ������ ]�� ����� �������� ����-�������̀ ���������������������������������������$��������the ‘lasered’ product is ready for further processing without the need of any post processing.

Z�� ����� ����������� ��� �������� ��� ��� ����� ����� �� ���� ���������������������������������

� Automatic welding of the cutting edges prevents fraying � No tool wear -no reduction in quality � �>����`�����������������������������������������������-

ous additional options � High precision and repetition accuracy � Virtually dust-free cutting � Optimal material utilisation � No application of force through stretching or punching � Large format cutting, by considering a roll width of up to 3,200

mm � Optional automatic material feed and removal

Z����������������������������������������������%�������-ter industry began investing in laser technology. Today, a sophisti-cated system technology is available at a comparatively low invest-ment cost. In its own application lab, eurolaser demonstrates how ��������������������������������������Z�����������������and a pending new generation of non-woven fabric processing are leading to higher productivity. On all accounts, it is certainly worth-while making a comparison and ordering a trial sampling. �

The International Textile Fair is pleased to announce a partner-ship with the Ethical Fashion Forum’s sustainable fashion business platform, SOURCE, to bring a dedicated sustainability seminar to the October tradeshow.

Held over two days, the International Textile Fair welcomes over 6000 visitors to the UAE, which is now the fourth largest trad-ing centre for fashion and apparel.

Mallory Giardino, SOURCE Membership Director, will present a seminar on both days of the tradeshow looking at the business case for sustainability in today’s fashion industry. With over 50% of global online consumers now willing to pay more for products and services from companies that are committed to positive social and environmental impact*, sustainability is no longer about phi-lanthropy; it is a huge business opportunity for fashion businesses to tap into.

Giardino will cover an introduction to the issues around sustain-

able fashion, some facts on the global market, and some of the key sustainability trends in the industry.

The International Textile Fair Dubai is now onto its third event and has already grown immensely. It is estimated that by 2016, the UAE will become the world’s leading high-end textile and garment re-export centre. With this massive growth in fashion businesses in the UAE, the opportunity really is now to integrate sustainability and gain a competitive advantage as they make their mark on the global fashion stage.

For more details about how to attend ITF Dubai and the SOURCE Seminar on Sustainability in Fashion and Textiles, visit their web-����������������������������������������

��� ��� ������� ������ ��� ��¦�� � ��������� ������ �������source.ethicalfashionforum.com

*Neilson 2014 Global Survey on Corporate Social Responsibility

SOURCE Partners with the International Textile FairDubai for Sustainable Fashion Business Seminar

���������������

16September 2015 www.textilevaluechain.com

���������� � ���

The predominantly cotton based tex-tile industry has been facing severe chal-lenges in the processing sector mainly dueto the treatment and disposal of textile ef-`����� ��� �� ����� ������ ����� �������compromising the environmental stand-ards and remain globally competitive.During the last decade, several hundredsof dyeing units were closed across the Na-����� ��� ��� ������ �������� ��� §����without proper treatment. Later, an unvi-able zero liquid discharge technology wascommitted by one of the dyeing clusters,which is commercially unviable. Againstthis background, the Government of Indiaproposed implementing marine dischargetechnology which is practiced all over the��������������������}������������Scheme for Integrated Textile Parks (SITP)���� ��}� ����� ���� Z������� £����-ing Development Scheme (IPDS) to install�����������%���������������������technology.

The State governments also give�}����������Z[£�����~�}���������Z£¨�������� ������� ��� ��� ������� ����� ���Ministry of Environment and Forest, Mari-time Board, State Pollution Control Board, Central Pollution Control Board, etc. Sever-al parks have been promoted across the Na-tion taking advantage of the schemes. The survival of the textile industry which em-����� ������� ���� ��������� ��� {���� ���people predominantly women and rural areas depend upon the growth of the tex-tile processing sector. China has a global share of 38% in textiles while India has only 5% of the share though it has all resources and raw material mainly due to the tech-

nological constraints in the processing sec-tor. The Southern India Mills’ Association (SIMA) which has spearheaded many Cen-tral Government schemes and also took the responsibility of promoting a model park with latest technology at Cuddalore in Ta-mil Nadu. SIMA would ink MoU during the �������Z�������'������{���������������group companies in the State are going to establish their processing units in the park.

In a Press Release issued here to-day, Mr.T.Rajkumar, Chairman, SIMA has stated that the said park and the technol-������������������������������§�����has been approved by the Tamil Nadu Pol-lution Control Board, Maritime Board, Cen-tral Pollution Control Board, Ministry of En-vironment and Forest and the technology support and guidance is given by Anna Uni-versity and various other competent insti-tutions and agencies. SIMA Chairman has stated that the proposed park would gener-����������������������������������������� ����� ��� ~������ ����� ������� ����years. He has added that several meetings were organized by the District Collector, Cuddalore and all the village people and the general public have been clearly educated about the project and the technology and their fear have been allayed.

In the meanwhile, the argu-ments raised against the park by few peo-ple against the project is baseless said, Mr.Rajkumar, as the project is closely moni-tored by SIMA, TNPCB, Maritime Board and Ministry of Environment and Forest. He has added that such projects are already in operation in Andhra Pradesh, Gujarat, Ma-harashtra and in almost all the developed

countries across the world. Mr.Rajkumar has stated that the processing units pre-dominantly use common salt for dyeing cotton fabrics which is harmless when dis-������ ����� ���� ���� ������ ����� ��� ���same is left on the surface. He has added that the textile processing does not involve any toxic chemicals which are hazardous to the marine life and fool proof technology with on-line monitoring system would be implemented and monitored by a compe-tent third party agency under the supervi-sion of Pollution Control Board. He has stressed that the park is being developed by the Central Government and the State Government and closely monitored by the Project Apprisal Committee of Central Government and the State Government is facilitating the project implementation apart from giving necessary grant. He has ������������������������§����������marine standards would be discharged un-��������������|������������������implementation of the project, the samples will be tested frequently and monitored by the government authorities.

SIMA chief has stated that regard-ing the ground water, it would be taken�����{����������������������������taken only after conducting a study by SIP-COT by engaging Geological Department. Therefore, the fear of depleting groundwater does not arise. He has further stated���������������}���� ��� ��������������in favour of the project while only very fewpeople predominantly from outside the vil-lage of the project and having vested inter-est are making hue and cry against the pro-ject.

SIMA promotes world-class eco standard textile processing park at Cuddalore jointly with State and Central Governments

�����%���� $������ ����� '����� ��� �[�$� ���� ���� ��� ���������~�{��

In this meeting, Mr. M.L. Jhunjhunwala, President, RSWM Ltd.,was elected as Chairman of BTRA Governing Council and Mr. Nar-endra Dalmia, Managing Director, Strata India Ltd., was elected asDeputy Chairman of BTRA Governing Council. Mr. C.K. Thackersey,Executive Director, Hindoostan Spinning & Weaving Mills and Mr.Anil Gupta, Managing Director, Wellknown Polyester Ltd., wereelected as members of BTRA Governing Council.

Mr. M.L. Jhunjhunwala Mr. Narendra Dalmia

BTRA NEWS

�

�

17September 2015 www.textilevaluechain.com

� $���������������������Z������operations of SEPHORA with a currentpresence of 3 stores in Delhi and 1 in Pune

� £�����������������������������next 5 years

� � £>��$���������������~��world-class brands, exclusive brands and its own private-label brands ¨����� ������ {{���� ~�{��� $�����

Limited, India’s largest integrated textileand Apparels Company with a strong retail presence and a pioneer of denim in India, has announced its entry into the beauty and cosmetics segment today through a partnership with SEPHORA, owned by LVMH Moet Hennessy Louis Vuitton, A French Luxury Conglomerate. With this partnership, Arvind will now manage SE-PHORA’s portfolio of 3 stores in Delhi and 1 in Pune. SEPHORA is the world’s largestand leading beauty retailer with a presencein 31 countries.

“We are looking forward to partner-ing with Arvind Lifestyle Brands who have demonstrated excellent skills in building brands in India and who have been very supportive of our expansion plans. We have met with great teams that are fully en-gaged and committed to making our Indianoperations a success. Sephora and Arvind will build our brand in a promising market

��� ��� ������ ���� ������������ ���-cept has a strong power of attraction and will make premium beauty more accessible to the Indian consumer. On top of the phys-ical stores, we are thrilled to announce this partnership will also extend to the internet sphere which growth has been and is ex-pected to be, phenomenal in India.” said ���?���( ���@���(�#�������%��7��Q

“We are proud to welcome India as the 8th country in the Sephora Asia organiza-tion” added Anne-Véronique Bruel, Sepho-ra Asia President.

“The addition of SEPHORA to Arvind’s bouquet of fashion brands further strength-ens our position in the fashion and lifestyle segment. We are excited to operate Se-phora store operations in India. Overall, the Beauty & Personal Care market is around����{������������������£�����������������~������������������������$������~�}�Given this large opportunity, we expect Se-������������������������������������������������������������������^������J. Suresh, Managing Director & CEO, Arvind Lifestyle Brands Ltd.

In the fast growing, look good and feel good wave, Arvind looks to establish itself as a brand that builds consumer connects directly. Arvind will lead the geographical retail expansion of SEPHORA with a focuson urban centres through the key beauty

categories of makeup, fragrances, skincare and haircare.

About SephoraSephora has transformed the customer

experience into an exclusive opportunity to indulge in beauty, fostering strong relation-ships with its brand and products. Sephora ethos remains unchanged: to present a leading beauty selection and always be on ��� �������� ��� ����_�� ���� ������ ��������� ������ ��� ����� ~��� ������� ���exclusive brands plus its own private label, the enterprising retailer is never short of surprising new ideas. Its unexpected con-cepts and non-conformist attitude are also evident both in its boutiques around the world and on its website, which together make Sephora an unparalleled internation-al beauty leader.

ARVIND MARKS IT ENTRY INTO THE BEAUTY ANDCOSMETICS SEGMENT: PARTNERSHIP WITH WORLD’SLEADING BEAUTY RETAILER “SEPHORA”

���������� ���

'�����'��������������������������-dustrial company in the world. The group �������������{�������'��©��������������-la. Company have mastered the craft of ���������������������������������� ������that are at par with international standard. Today Mukut Mani is one of the leading manufacturers in the textile industry. The Company’s market value worth 10 Million USD.Values of Brand: Innovation, Reliability, Commitment, Passion, Focus, Speed Infrastructure & FABLAB

Company expertise has been brought forth by our in-house research & develop-ment team. Innovation have become mile-

stones in the especially in the fabrication (shirting & suiting) industry. Company has a strong analytical capability with state-of-the-art equipment and multi disciplinary technical experts who can assist clients with testing, consultancy and research projects. Production Capability� Plant : ���������������������� Ready Stock : 3 million meter � Goods packed : 15 million meter

(p.a)� WEAVING MACHINE Quality : English,

Rapier, Sulzer, Airjet, Waterjet� =Z¨[>�'���������������|����������

inch, 58 inchZ��� ��@�����[

{�� ������� ��� ��_��� ��_��� |�_��� ��_��� {���~�~����������~�����������|����!����������������£����������������|����������������~�������� ¦������ ������ ��� ��������� ����%��� ����������������£���������|����������������~�����|�� £������ ª������ ��� |������ ������ ������ �ª�� ��� ��� ����� ��}� ������� �������{��}�£�����\Z��� � ]��������[ Plain, Stripe, Checks, Dobby, Twill, Oxford, Satin, chambray, Fila-Fil, Cross Designs, Panel Designs, Self – Dob-by & Lining, Program basis (according to cli-ent’s designs or cads and color)\+��^���[ USA, South (Latin) America, Thailand, Africa, UAE, Vietnam, Bangladesh, Indonesia, Srilanka, India ��

Mukut Mani Creation Pvt. Ltd.

�

18September 2015 www.textilevaluechain.com

Impatience is seen as avirtue; willingness to wait is interpret-ed as lack of aggression. We are in the era of instant food, homedelivery of groceries and internet on the go. Readymade clothingdoesn’t seem fresh enough a phenomenon to rub shoulders with some of the path-breaking consumer trends we see around. If we����������������������������������������������������������-talgia, think of a time when we would take a piece of shirting tothe neighborhood tailor and wait for him to stitch it for us. Closer ���������������������������������=��������������������it those days.

Fabric to ReadymadeWith time things changed; yesterday’s luxury is today’s want

and tomorrow’s necessity. Today if we like a garment on a retailwindow at a mall, or on your mobile screen, you just can’t wait to`���������������������������������������������������=need everythingreadymade! There are businesses that are basedon a core competency in fabric retailing; they have been facing theheat of a declining market trend in recent times. It is the readymadeapparel brands that are riding the wave now, the ones that comewith a fashion competency. The apparel brands need fabrics as rawmaterials, which they source from the fabric players and this drives�~��������������������������������������������������������������������������������������~�������������������������a look at how established players with rich fabric legacy, could sus-tain their connect with customers.

[�� ������ �� ������ ��������� ��� ���� �� ������ ����could react to a market shift. The solution often does not lie in asingle step, the issue is something that would need to be counteredthroughmultiple approaches. While we could always talk with thewisdom of hindsight after a certain period of time, the key here isto act in time and take pre-emptive measures. Let us look at someof the challenges that a traditional business encounters whenfaced with a shifting market trend.

�����������������������������������������������������this is easier said than done. Past performance is not a guarantee�����������������������������������������������=����������-sumed in our own strengths that we forget that the customer willbuy only what he wants, and not exactly what we would like him tobuy. We have even seen people who blame the customer for notappreciating the unique features they put into the product. Let’snot forget that if the customer does not understand our features,the loss is ours, not his, for he has lot many options. In recent times,�������������������������������������������������_�����consumer marketing. The problem, however, in many cases, is thefact that the focus takes quite a while to manifest itself as actions.

The more successful we are in a certain context, the more dif-������ ���������������������������������������������������changes. The same attributes, which have helped build your busi-ness, like culture, history, skills and other such aspects,could be-

come impediments to change. A readymade business cannot berun the way a fabric business is run. Therefore, structural changesalso often come into play when there is a strategic shift. There arefully integrated textile business conglomerates that have success-fully bound togetherthe businesses of fabrics, fashion, retail andgarment manufacturing. This is something that comes with years of�����������������������������������������������������all with an eye on the ever-evolving customer tastes.

Pros and ConsWhile we are in the context of fashion, let me refer to OTC fab-

rics as textile and readymade garments as apparel, as has becomesome kind of an industry-accepted practice. Why did the marketswing the apparel way? A few reasons for this could be resting in������������������������������������ ��� ������������ ��������������������=� ���������� ������ ���� �� ��� ��� ��� ��� ���-diately. Readymade clothing comes with brand-approved styling;in fact the whole brand play becomes a potent force in the ready-made space- it becomes a stamp of approval and a representationof who you are. Readymade businesses lend well to post-garment-����������������������������������������������������� ��in unique hand feel, stylized featureslike puckered looks in casual�����������������������������������������������������������������������������������

On the contrary, the textile supporters also have their argu-ments. The biggest among them, of course, is the scope of getting ��������������������������������=���������������������������exactly the same measurements that we are comfortable with; this is an advantage over readymade garments that come in standard ����%������������������������������������������������������������[���������������������������������������������������sleeve length, waist size, collar type etc. exactly as per your needs. Therefore, every custom-tailored garment is unique!

Flowing with the trendWell, let us accept that there is no major debate on the issue

������������������������������������������������������sales at desired levels. How do some of the business conglomer-ates that come with a fabric legacy, counter the declining market trend? There are two aspects to this. First is the possibility of ex-tending the fabric brand into the readymade space. It is a logical thing to do and makes sense from the point of view of marketingtheories. The challenges that the organization could face will be at�����������

i) The brand imagery in the consumer’s mind will be in linewith that of a fabric brand. This could normally mean a few things;���� �� ������ ��� �� ��� ��� ������� ��������� ������������� ��well with planned purchases, like a wedding in the family, for in-�������Z�����������������������������������������������������������-pulse buying. The other aspect here is the fact that the brand maynot score well on contemporariness as an attribute because of theabsence of stylized garments as would be available in a readymade

A STITCH IN TIME

������ ������

Shri Vishnu GovindIndependent Brand ConsultantBusiness Director - Thinkkloud

19September 2015 www.textilevaluechain.com

collection. ii) The second issue that I would highlight here is less

about the consumer psyche and more about matters intrinsic to the organization. The core competencies, business practices, cost structures and other cultural aspects do not go well with the re-quirements of a readymade business. This transition is as much a challenge as the issues concerning market perception of the prod-ucts.

Fighting the trendWhile the extension to readymade space is something business-

�������������������������������������������������������������the decline in fabric sales. This business will normally be the bread ��������������������������������������������������������keep working on the category and prolong the inevitable decline. Attempts ought to be made to see how OTC fabrics can cater to the evolving consumer preferences of today. Let us take a look at what are some of the steps that could be taken in this regard.

Play to your strengths; as much as it sounds like a cliché, it is a statement that you got to agree with. Fabric brands should tap into ������������������������������������������������������������������]����������������������������������������������������������������������������������������[������������today could see advantages of fabrics that have special features, like if they are stretchable, or has heat management properties, or can absorb moisture, just to name a few characteristics for illustra-tive purposes.

With the advent of readymade clothing, consumers now are ha-bituated to seeing how they look in the clothes before they make ��� ������� ��������� [���� ��� ��� ������ ����� �~�� ������ ������need to overcome. Use of catalogues help these brands in show-ing how a tailored garment could look on a consumer; then again, for practical reasons, cataloguing and photography can showcase

only a small fraction of the collection. Having said that, let’s make no mistake about realizing the fact that catalogues serve a big pur-pose here. They help to showcase the latest from the brand, both in terms of new fabrics as well as new styles that can be tailored, as sort of a recommendation from the brand.

Can technology be used to showcase fabric collections? For sure the catalogue can be shown using a tablet or other electronic �����������������=��������������������������������������fabrics will drape on a body form? Possible, but not yet scaled up in �������������������`���������������������Z������

Tailoring is integral to OTC fabric businesses. It must be said that even in evolved fashion markets, there is still a huge premium ��� ��� ���������� [���� ��� ��� ��� ��������� �������� ���� ������������������������������������������������������~�����-ric businesses could be supported by improvements in tailoring as �� ������ '��� ��� '���� ��� �� ����� ���� ��� ����� �������while the exact nature of service might vary slightly from one brand to the other, what is interesting here is the fact that you could get ���������������������������������Z�������������������������-ments in a store and a fabric is cut in a factory in some other city so that work is underway to get a suit stitched for you! Yes, you will have to wait a bit to wear it. Thistime delay is a factor that is ������������������������~���������������������������������second visit to the store to collect it. How about giving your meas-urements in a store in a mall, watching a movie, and then coming �����������������������������������������������������������«�¦��������������������������������������������������������

Change is the only thing constant; market evolution is a contin-uous process. If you are a category leader in a space where growths are stagnating because of changing market trends, then it is your job to take up the cause of your category, for there is a lot at stake for you! �

The Haryana Skill Development Mission, Govt. of Haryana signed an MOU with the Apparel Made-Ups & Home Furnishing �������������������������������~�{���������������

The MOU was signed by Shri Subhash Goel, IAS and Dr. Roopak Vasishtha, CEO and Director General, AMH SSC. Under the MOU, all the Training Providers of HSDM, across Haryana shall get aligned to the AMH SSC for the Skilling trainings in the Apparel, Made-ups and Home Furnishing Sector by aligning their course curricula to the National Occupational Standards (NOSs) of the AMH SSC and �������������������������������$'>������[��������������of the AMH SSC, which has been formed by the NSDC would have National /International Recognition and would help the youth of Haryana State to not only get a decent employment in India but would also become eligible for International Openings. This step ����������������������������������������� Z����_������'������India’ Missions of the Govt. of India and of Govt. of Haryana.

The Haryana Skill development Mission plans to getmany youth ����������������������$'>�������������~�{�%~�{|�������$�-parel, Made-ups and Home Furnishing Sector. This MOU would be �����������������������������~�{���

A pic of the event is enclosed for reference. Dr. Roopak VasishthaCEO and Director General

Mr Subhash Goel, IAS and Dr. Roopak Vasishtha, CEO and Director General, Apparel, Made-ups & Home Furnishing Sector Skill Council exchanging MOU signed between both the organisations on 9th Sept, 2015 at Chandigarh. Also seen in the pic are Ms Dheera Khandelwal, IAS: Principal Secretary – Technical Education & Vice President – HSDM and ShriK.K.Kataria, Director ����������� ��������������������������������

���� ���

20September 2015 www.textilevaluechain.com

AbstractThis paper represents the new research on various comfort

aspects of woven cotton fabric.This paper aims to investigate the ����������� ����� ������ ������ ���� ������� �����"������������������������Z���������������������������������weaves as well as derivatives of basic weave structure were stud-ied. Comfort properties of fabric in terms of air permeability and thermal resistance were determined. It was found that the fabric with plain weave structure showed the highest thermal resistance ������� ��� �������� ��� ����� ��������� ������������ [�� ��� ���� ~�~�matt weave depicted the lowest thermal resistance which makes it appropriate for hot climatic conditions.Keywords: Fabric Structure, comfort, weaves, thermal resistance, air permeability, etc.

IntroductionClothing is an integral part of human life. The primary role

of clothing is to form a layer/s of barriers that protects the body against unsuitable physical environments. This protection of body ����������������������������������������������������������-ronment to the body, which is essential for its survival and prevent-ing the body from being injured by abrasion, radiation, wind, elec-tricity, chemical and microbiological substances. These traditionally ������������������������������������� ������������� ��������������important role at the interface between human body and its sur-rounding environment in determining the subjective perception of comfort status of wearer.[1]

Clothing has a number of functions like adornment, status, modesty & protection. To be competitive, modern clothing besides having good mechanical and technological properties and being of easy care, must possess good comfort characteristics. Comfort has totally replaced the durability as far as the selection of garment is concerned [1]._Q6� ����*�$��� ���7�"����Z��#����������������

The comfort is considered as a fundamental property when a textile product is valued. The comfort characteristics of fabrics mainly depend on the structure, type of row material used, weight, moisture absorption, heat transmission and skin perception.[11]

The clothing system which is suitable for one climate may not be suitable for another climate. For example, good thermal insula-tion properties are needed for clothing which is to be worn in cold climates. The thermal insulation of textiles depends on number of ������� ������ ���������� ����� ��� ������ ����� ��� ��������`���������������������������������������°{±��[�����������������������������������������������������������

� Fabric Structure � Yarn structure � Fiber

From the comfort point of view, the suitable fabric must be

developed by textile technologist through the proper selection of ��������������������������������������������������������������������[���������������������������������������������������������������������������������������������-ing given to fabric.1.2 Thermal comfort

Thermal comfort of a clothing system is associated with the thermal balance of the body and its thermoregulatory responses to the dynamic interactions with the clothing and the environment. It is necessary to design fabrics with necessary thermal properties for ����������������Z��������������������������������������������moisture and heat through the clothing system take place in steady state, but is continuously exposed to transients in physical activity and environmental conditions [11].Need of thermal comfort

Human body tries to maintain a constant core temperature ����������������[����������������������������������������������from person to person but it is always in a narrow range. The com-fortable surrounding environment temperature for human body in Z��������~{����=������������������������������������������discomfort as a result human body needs some external agency to maintain this temperature and clothing is one of the most common devices to provide comfort in this regard. The body must be kept in thermal balance in order to maintain the required comfort lev-el; the metabolic heat generated together with the heat received from external sources must be matched by the loss from the body of an equivalent amount of heat. If the heat gain and the heat loss are not in balance then the body temperature will either rise or fall, leading to a serious threat to life [3].

6� ���'@� �����������"��Z�����"�� ���6�%�� �[��������������������������������������������

of fabric among which thermal insulation plays vital role in prevent-ing heat loss from body. A. Gericke and J. van der Pol [4] stated �����������������������`��������������������������������as thermal resistance. Research carried out by H. N. Yoon and A. Buckley [5] with series of polyester, cotton, and polyester/cotton blend fabrics concluded that both the fabric construction and the ��������������������������������������������������stated that thermal insulation, air permeability, and water vapor transmission rate are dependent mainly on the fabric geometrical ������� ����������������������������������������������°|±�found that the thermal protective performance increases with the entrapped air inside the fabric in both convective and radiant ex-��������������Z�������°�±�����������������������������������������������������������������������������������������������������������������������������������������`�����������������������������������[����������������������������������������������������������������������������`�-ence their comfort and comfort properties of woven fabrics can be achieved not only by the choice of thickness or the fabric cover fac-

EFFECT OF DIFFERENT WEAVES ON THERMAL RESISTANCE PROPERTIES SHRTING COTTON FABRIC

R. G. Shrivas Department of Textiles

D.K.T.E. Society’s Textile and Engineering Institute, “Rajwada”, Z����������%�{|{{��'����������Z���� ����²���������������³���������

L.G. PatilDepartment of Textiles

���� �����������

21September 2015 www.textilevaluechain.com

���������������������������������������������������������processes and raw materials.

Fabric properties like cover factor and thickness also have an impact on the thermal comfort of the fabric. Bilskaet al. [8] studied�������������������������������������������������fabric and found that plain fabrics have the highest value of ther-mal resistance following their compact structure. The compactness of the structure of plain weave reduces the porosity of the fabric, which results in lower thermal conductivity; canvas weave has a better thermal conductivity due to a comparatively open structure;and twill weave has the lowest value of thermal resistance and the highest value of thermal conductivity due toits open structure��������������̀ ���������������������������������������������porosity of the fabric.2. Material and Method

~����]�����������������������������������������������-facturing of fabric. Before manufacturing of fabric all yarn testedfor tensile properties, evenness, hairiness and twist level. Seven dif-ferent basic weaves as well as derivatives of basic weave structure�����£������~�~�����������������{�[������>�������������������������and crepe were manufactured on rapier weaving machine. The de-���������������������������������[���~�{�������������������-lowed after fabric manufacturing, with normal process sequence as followed in the shirting industry. Finished fabric specimens were evaluated for fabric thickness, areal density, air permeability and thermal resistance under standard atmospheric condition.

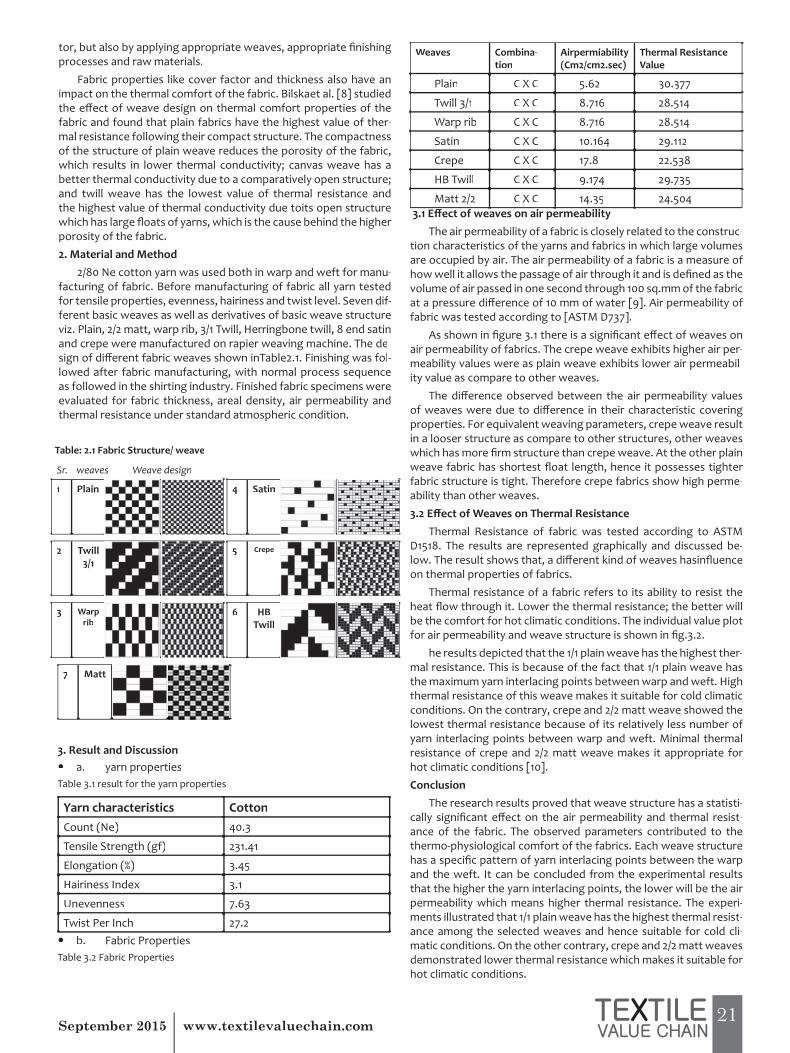

Table: 2.1 Fabric Structure/ weave

1 Plain

2 Twill 3/1

3 Warp rib

4 Satin

5 Crepe

6 HBTwill

Sr. weaves Weave design

3. Result and Discussion � a. yarn propertiesTable 3.1 result for the yarn properties

Yarn characteristics CottonCount (Ne) ����

Tensile Strength (gf) ~�{��{

Elongation (%) 3.45

Hairiness Index 3.1

Unevenness ��|�

Twist Per Inch ~��~� b. Fabric Properties[������~�������£������

7 Matt

Weaves Combina-tion

Airpermiability (Cm2/cm2.sec)

Thermal ResistanceValue

Plain C X C ��|~ ������

Twill 3/1 C X C ���{| ~���{�

Warp rib C X C ���{| ~���{�

Satin C X C {��{|� ~��{{~

Crepe C X C {��� ~~����

HB Twill C X C ��{�� ~�����

'����~�~ C X C 14.35 ~������Q_�@� ���>��?�������#��"��%�����

The air permeability of a fabric is closely related to the construc-tion characteristics of the yarns and fabrics in which large volumesare occupied by air. The air permeability of a fabric is a measure of ��������������������������������������������������������������������������������������������������{����������������������������������������{������������°�±��$������������������������������������������°$�['�¨���±�

$�����������������{����������������������������������air permeability of fabrics. The crepe weave exhibits higher air per-meability values were as plain weave exhibits lower air permeabil-ity value as compare to other weaves.

[�� ������ ������ ����� ��� ��� ���������� ��������������� ��� ��������� ��� ����������������������properties. For equivalent weaving parameters, crepe weave resultin a looser structure as compare to other structures, other weaves������������������������������������$�����������������������������������`��������������������������������fabric structure is tight. Therefore crepe fabrics show high perme-ability than other weaves.�Q8�@� ������?��������"���������� �

Thermal Resistance of fabric was tested according to ASTMD1518. The results are represented graphically and discussed be-�����[���������������������������������������������`���on thermal properties of fabrics.

Thermal resistance of a fabric refers to its ability to resist the����`�����������������������������������������������be the comfort for hot climatic conditions. The individual value plot������������������������������������������������~�

he results depicted that the 1/1 plain weave has the highest ther-mal resistance. This is because of the fact that 1/1 plain weave hasthe maximum yarn interlacing points between warp and weft. Highthermal resistance of this weave makes it suitable for cold climatic���������������������������������~�~������������������lowest thermal resistance because of its relatively less number ofyarn interlacing points between warp and weft. Minimal thermal�������� ��� ��� ���� ~�~� ����� ���� ����� ��� ��������� ���������������������������°{�±�Conclusion

The research results proved that weave structure has a statisti-������ ����������� ���� ��� ��� ��� ���������� ���� ������ ����-ance of the fabric. The observed parameters contributed to thethermo-physiological comfort of the fabrics. Each weave structure�������������������������������������������������������and the weft. It can be concluded from the experimental resultsthat the higher the yarn interlacing points, the lower will be the air permeability which means higher thermal resistance. The experi-ments illustrated that 1/1 plain weave has the highest thermal resist-ance among the selected weaves and hence suitable for cold cli-�������������������������������������������~�~�����������demonstrated lower thermal resistance which makes it suitable for hot climatic conditions.

22September 2015 www.textilevaluechain.com

ITAMMA successfully organized its 14th Product - Cum -Cata-�����������������©�����~�{��������>����������£��������'������The show was inaugurated by Mr. TRS Karthikeyan, Managing Di-rector, Aruppukottai Sri Jayavilas Mills Ltd.

The trade show received an overwhelming response with 45 ������������������������������|����������������������������Why at Madurai?

“Madurai” a hub of the textile industry in Tamil Nadu����������������������������������������~�������������

���[�����]���_����������������������������'����������������Z�-dia. But Tamil Nadu’s mills are of smaller size and give compara-tively less production. Other important centres are Rajapalayam, Madurai, Tirunelveli, Arrupukottai, Salem, Tuticorin, etc.

Loyal Textile Mills Ltd., has four spinning mills located at ´���������� ��� ��������� ������� ����� ��� �|�|��� �������� ���� {|������%������������������$������������������"���������|��{~����������������������{������������������'���������£���'��������������������������|��[������������ {|��������Z[ ����-����� �������� ���� �~�� ����� ��� �������� �������"�� $�������{{�|����������������������������������������������������-����������|���������������������{��������"�

Over the years, Madurai has grown as a leading hub for Textile Manufacturing, and occupies a vital position in the industrial sce-nario of Tamil Nadu. There are various kinds of Mills located around Madurai producing Spindles and drums of winding machines. Keep-ing this mind, ITAMMA decided to conduct the Product- Cum- Cata-logue Show in Madurai, which also attracted visitors from neigh-bouring cities like ,Tirunelveli, Dindigul, Arrupukottai, Thirunelvel and Rajapalayam.

Thus it conveys that the potential for spinning sector was re-markable which was followed by weaving industry.

Details of the Show � The 14th Product –Cum- Catalogue Show conducted by Indian

Textile Accessories & Machinery Manufacturers’ Association (ITAMMA), provided an ideal platform to the textile user in-dustry of Madurai to interact with the suppliers (Manufactur-ers, Dealers and Traders) of textile machines and accessories. During the show the visitors of the Textile Industry of Madurai got an opportunity to get the information of the quality �����������'�������!�$��������������������������������Weaving & Wet Processing.

� Also the show has recorded the same trend of response from our member exhibitors where out of total 45 Exhibitors about |�}����������������������������������������������������Z�����������������������������~��}�����=������Z�������

� �[������������������������������������|�����������������|�}��������������Z��������~�}�����=������Z��������{�}�����=��£������������{�}�����������Z����������������%��}���������������������}�����������������������person and about 5% were from research associations & col-leges like SITRA, Kumarguru, PSG etc. Key Take Away

� ITAMMA member exhibitors expressed their satisfaction �������������������������������������%��}���������their remarks as “excellent” for this show.

� �[��`����������������������������������������~%��������thus conveying the message of their interest in knowing the products of our members and spending their valuable time in fruitful business interaction with our member exhibitors.

� �[���������������������������������������������������of our members like Basant Wire Industries Pvt .Ltd (Jaipur), Super Tex Industries (Mumbai), Simta Machinery Pvt. Ltd (Coimbatore), Caretex Engineers (Coimbatore) has helped us to present the show at the world class standard within the budgetary expenses. �

INDIAN TEXTILE ACCESSORIES & MACHINERY MANUFACTURERS’ ASSOCIATION

������� ��������

REFERENCES1. N. GokarneshanFabric Structure and Design, New Age International (p)

��������£��������~���������%���

~�� $�� '������������� Z�� ��� ������ ���� '�� ������ ���������� ��� �������properties of polyester-viscose suiting fabrics. Indian Journal of Fiber& [������������~���'����~��~�������~%�|�

��� ������'��!�]�������� ������������������������������������on thermal properties of fabric. Journal of Textile Association, March-$����~�{�������~%����

4. A. Gericke& J. van der Pol,A Comparative Study of Regenerated Bam-boo, Cotton and Viscose RayonFabrics. Part 1: Selected ComfortProper-����©���������������� �����������������������������~�{������|�%���

��� >�]����������$����������Z������������������������~��������-����������������������[�����������©�����������©���{������������%�|��

|�� ��� ���������� ��� '���� ���� ��� ���������[����� �������� £���������~%�������´������������������![������ ��� ����� �����{���~���"��$�����©���~���������|%���

��� Z�������������¨������������©��������������!�[������ ��� ����� �-�����������¨����~��~�

8. Frydrych, I., Dziworska, G. and Bilska, J. Comparative analysis of the ther-mal insulation properties of fabrics made of natural and man-made cellu-�����������������[��������� ����� ���������"��~��~��������%���

��� ���£����������£��������[���������[������=����>���£�������������[���������������� ��������[~����~�������{���

{������ $������ ��� $������ $�� $������ $�� ������� '�� '������ ���� ]�� $������ �������������������������%���������������������������������������$����������©�������{����{"��'����~�{��������%���

11. http://www.slideshare.net/kotharivr/comfort-properties-of-fab-���%�~|~��|���

23September 2015 www.textilevaluechain.com

����������

Information on BRICS CountriesIn the past few decades, some large economies such as Brazil,

Russia, India, China and South Africa (BRICS) have acquired a vitalrole in the world economy as producers of goods and services, re-ceivers of capital, and as potential consumer markets. The BRICS�������� ���� ��� �������� ��� ���� ��� ��� ������� ������countries and the engines of the global recovery process, which�������������������������������������� ����������%~�countries forum, BRICS are playing a formidable role in shaping�����������������������������������������������$�����������������������������������������������������������¨£in terms of PPP. If one compares the GDP in PPP terms, four econo-�������������������������������������Z������������������������������$��������~���������|�������~|���������������������Z�����of contribution to growth of PPP-adjusted global GDP of the world,������������������������������������������~���%������their contribution is expected to rise in the coming years.

The BRICS comprise a huge land share of the world and, as aresult, own vast natural resources. China, which has a land area�����������|���������������������������%�������������������������������������������������������������������������������~���-��������������_����������������������������������������{~percent of the world’s mineral resources. In terms of agricultural�����������������{~{������������������������������������������������������������$�������������������%������������������world (8.5 million sq.km), surpassed only by Russia, Canada, China,and the United States of America.

Economic GrowthIt is widely perceived that over the next few decades the

growth generated by the largest developing countries, particular-��� ��� ��Z���� ������ ����� �� ����� ��� ����������� ���� ��� ��world economy. Among the BRICS, India and Brazil are relativelymore domestic demand-driven economies. As a group, they wit-������������������������������~�����������������������advanced and other emerging market economies. Although theyhave strong external linkages, they have nonetheless undergone������������������������������������������������������sectors in the post-crisis

period. The four original BRIC countries are expected to repre-������������������������¨£����~����������������������������������������������������_��{������������������$����������change that we may expect over the medium to long term is that�������{���������������������¨£�����������������������{���������� ��������������������¨£��[�����������������the BRICS emanates from strong domestic demand-based econo-���� ��� ��� ���� ��� Z����� ���� ������ ���� ��� ����������� ����������������������������������� �������$����������������������resource base proximity to untapped growth potential of the Afri-can continent.

The BRICS ReportThe salient features of the BRICS economies are their large geo-

graphical dimensions and size of population. It is widely perceivedthat all the BRICS markets have great potential for establishing themost stabilizing of forces, that is, a prosperous middle class. Thismiddle-income group in each country is growing at varying ratesbut the future direction is clear, that is, the middle class will bothbroaden and deepen, providing a solid base for the growth and de-velopment of the economies. Textile Industry in BRICS Countries

We can comfortably say that BRICS Countries is providing tex-�������������������������������������������������� ���������-ever they are, using some textiles products manufactured by BRICSCountries.

������ ���� Z����� �� ��� ����� � [��� ��������� ������� ��}� ���������[���������������������������������������

China ~����������

India ����������

Global �����������

Hence talking about India and China will take days and I am sure everybody present here knows about textile volumes and scales in India and China hence, I will discuss textile business in Brazil, Russia and South Africa.

BRAZIL Textile Figures� In terms of international Commerce, the participation is very

������Z�������������������������~|������������������������textiles).

� Last three years, the excessive valorization of the national coincaused new outbreak of growth of the imports and stagnationof the Brazilian exports of textile products and apparel.

� Z����������{|��������������¦�¨�{��������������������only in textile machines.

� [�������������������������������}���������������������������������������������������������������{��}�if we consider only the clothing, and the growth was even�����~~�}�������������������¦��������������$����Commerce Department Figures).

� Brazil ranking among the eight largest world producers ofyarns, fabric and knitwear, and ranks seven in the productionof apparel, behind only China, India, USA, Mexico, Turkey andSouth Korea.[�����������������%��������������������������� ���

their neighbours in the Americas. Socio economic groups A and �����������}��������������������������������������{}����}�������������������������������{�������������������������������������������������������������������������������������-������������}"�����������������������~�}"����������% �����

Scenario in BRICS Region and Textile Potential

Shri Arvind SinhaCEO, Business Advisors Group

National President , TAI

24September 2015 www.textilevaluechain.com

������~��}"��|�}��������������������������������������������������_�����������_��������������������ª��������������{}����������������������������������}�������������������������������������������}����������������}��������������made in cash & 34% of credit sales are made with store cards. (US Commerce Service)South Africa’s textile industry

�����{��������¦��{%������������������������������������modernizing South Africa’s textile, clothing and footwear industry, ������� ��� ������ ���� ���� ��� ������ ��������������� � ������$����������������������������`�������������������������developed markets, and the local textile and clothing industry has ���������������������������������������������������������������������������������������%���������������������������������������������������������������

With technological developments, local textile production has ��������������������%��������������������������������������in increasing proportions.Achievements

Although the industry is still relatively small, it boasts some impressive results in world markets: Local yarn manufacturer Sans ����� �������� ��}� ��� ��� ������ ����� ���� ��� ��� ����_�� ��-parel sewing operations. Local fabric mill Gelvenor Textiles supplies ����������}�����������_���������������������������������suit manufacturer House of Monatic has delivered its one millionth suit to the UK market.Market access