Embed Size (px)

Citation preview

Financing opportunities Pontus Engström, PhD, MSc

Session 3

Financing of a firm is usually done through either DEBT or EQUITY

2

Difference between Debt and Equity

3

ASSETS

EQUITY

DEBT Business sales

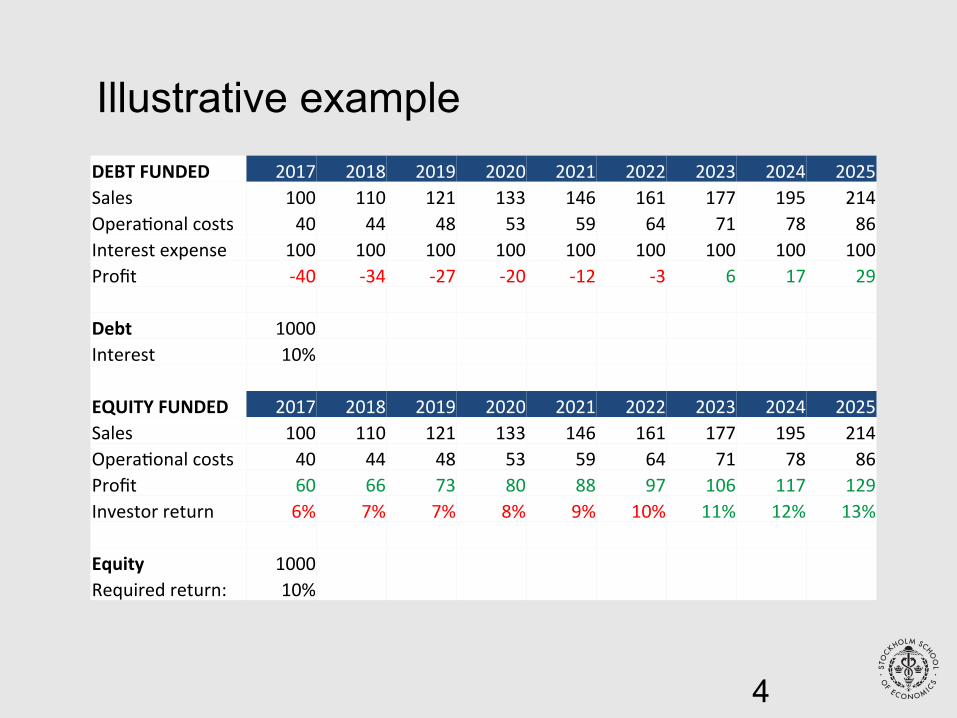

DEBTFUNDED 2017 2018 2019 2020 2021 2022 2023 2024 2025Sales 100 110 121 133 146 161 177 195 214Opera4onalcosts 40 44 48 53 59 64 71 78 86Interestexpense 100 100 100 100 100 100 100 100 100Profit -40 -34 -27 -20 -12 -3 6 17 29 Debt 1000 Interest 10% EQUITYFUNDED 2017 2018 2019 2020 2021 2022 2023 2024 2025Sales 100 110 121 133 146 161 177 195 214Opera4onalcosts 40 44 48 53 59 64 71 78 86Profit 60 66 73 80 88 97 106 117 129Investorreturn 6% 7% 7% 8% 9% 10% 11% 12% 13% Equity 1000 Requiredreturn: 10%

4

Illustrative example

Pecking-order (Myers and Majluf, 1984) Capital structure emerges as a result of the various financing options available to the firm, where internal is preferred if available. Trade-off choice (Myers and Majluf, 1984) The firm weighs the costs and benefits of additional and different forms of financing, for instance tax benefits.

Theories of financing

5

Cap

ital S

truct

ure

Deb

t vs

Equ

ity (

%)

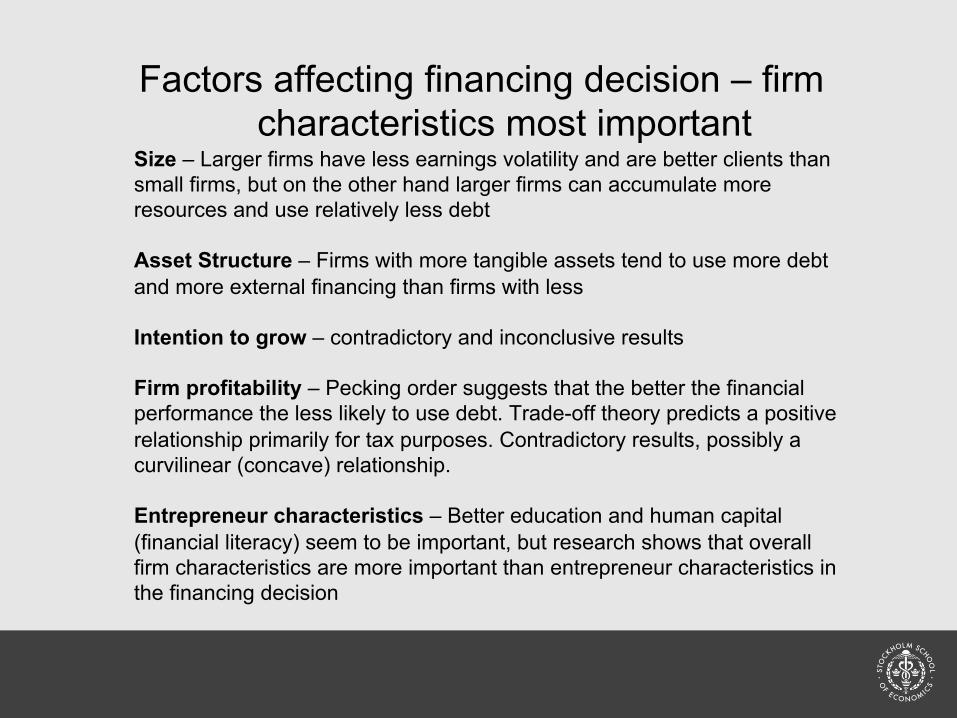

Size

Size – Larger firms have less earnings volatility and are better clients than small firms, but on the other hand larger firms can accumulate more resources and use relatively less debt Asset Structure – Firms with more tangible assets tend to use more debt and more external financing than firms with less Intention to grow – contradictory and inconclusive results Firm profitability – Pecking order suggests that the better the financial performance the less likely to use debt. Trade-off theory predicts a positive relationship primarily for tax purposes. Contradictory results, possibly a curvilinear (concave) relationship. Entrepreneur characteristics – Better education and human capital (financial literacy) seem to be important, but research shows that overall firm characteristics are more important than entrepreneur characteristics in the financing decision

Factors affecting financing decision – firm characteristics most important

Fred Wilson: Union Square Ventures: “The amount of money that start-ups raise in their Seed and Series A rounds is inversely correlated with success.”

Let’s Face an Uncomfortable Fact

7

Talk with your neighbor • 1 minute • 2 top reasons, please

Why Might This Be So?

8

My take on it: • Too much money makes you sloppy, stupid • Plan A rarely works. But your funder wants you to

(flawlessly) implement it anyway!

Question: Might it be wiser to wait and seek to fund customer traction, instead of a plan?

Why Might This Be So?

9

• Fact: the vast majority of fast-growing businesses never raise venture capital (nor write business plans, either)

• Nor should they, at the outset, I argue: why?

• Raising capital too early – whether from angels or VCs – is a dangerous practice, on both sides of the table

Let’s Be Candid…

10

• Distraction: takes the entrepreneur’s eye off the ball, now, and later, too

• Higher risk = lower stake for the founder

• And the baggage that comes with it in the shareholders’ agreement

• Is this good news for the investor in such a deal?

The Killer Drawbacks of Raising Capital Too Early

11

Let’s Consider Some Evidence: US Venture Fund Returns

12

Returns from inception to 12/31/11. Source: Josh Lerner analysis of Thomson/Reuters data.

So, Is There an Alternative? The Customer-Funded Business

13

Your Customer

Pay-in Advance Models

Matchmaker Models

Subscription Models

Scarcity-Based Models

Service-to-Product Models

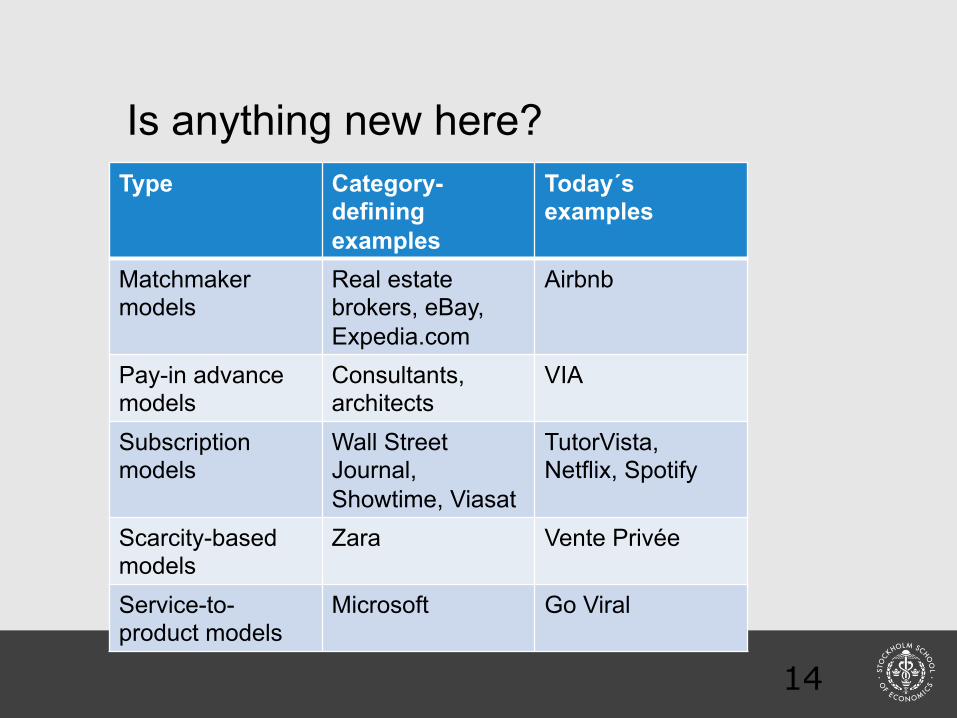

Is anything new here?

14

Type Category-defining examples

Today´s examples

Matchmaker models

Real estate brokers, eBay, Expedia.com

Airbnb

Pay-in advance models

Consultants, architects

VIA

Subscription models

Wall Street Journal, Showtime, Viasat

TutorVista, Netflix, Spotify

Scarcity-based models

Zara Vente Privée

Service-to-product models

Microsoft Go Viral

Vinay Gupta 2006: A Pay-in-Advance Model

15

Brian Chesky & Joe Gebbia 2007: A Matchmaker Model

16

Krishnan Ganesh 2005: A Subscription Model

17

Krishnan Ganesh 2005: A Subscription Model

18

Jacques-Antoine Granjon 2001: A Scarcity Model

19

Balder Olrik, Claus Moseholm 2003: A Service-to-Product Model

20

1. Negative working capital – love thy float!

2. They required essentially no external capital to get started

3. When they did raise capital to grow once the concept was proven, there was an eager queue of angels or VCs lined up at their doors

These Examples Share Three Attributes in Common

21

First, what NOT to do Prepare • Pages of prose • Reams of spreadsheets • All in support of the perfect Plan A (that probably

won’t get you where you’d like to go!)

OK, “So What?” As an Entrepreneur, What Should You Do?

22

Mark Suster, Upfront Ventures

“I say ring the freaking cash register. I have said so for years!”

In other words, get some customers, now!

OK, “So What?” As an Entrepreneur, What Should You Do?

23

• Not necessarily. It’s the timing that concerns me.

• And it concerns Venture Capitalist´s too!

• If you’ve got a venture that’s firing on all cylinders, perhaps yours, that’s when to add fuel!

So, Is Venture Capital – from Angels or VCs – Bad for You?

24

Consider the rejection rates

• YCombinator 97.1%• Angel List 98.9%• Andreessen Horowitz 99.3%• And it’s even worse in Europe!

Is pursuing customer funding a better way to spend your precious time? And it’s cheaper, too!

But Can You Get Funded by a Good Angel or VC?

25

“The customer is not just king.He can be your VC, too!”Bernie Auyang, Angel Investor, Shanghai

And it is hard work, “there are no shortcuts to success”Olav Nils Sunde, Investor and Businessman, Oslo

In a Nutshell…

26

On the growth of small and medium enterprises in

developing economies. The role of private equity.

Financing opportunities in

developing countries

27

• According to the World Bank, all low and middle income countries with a GDP per capita less than USD 4,036 dollars.

• Higher income countries start at USD 12,476. • Sweden has a GDP per capita of USD 55186, or 14 times

higher than a developing country. Source: World Economic Outlook, April 2015.

What is a developing economy?

28

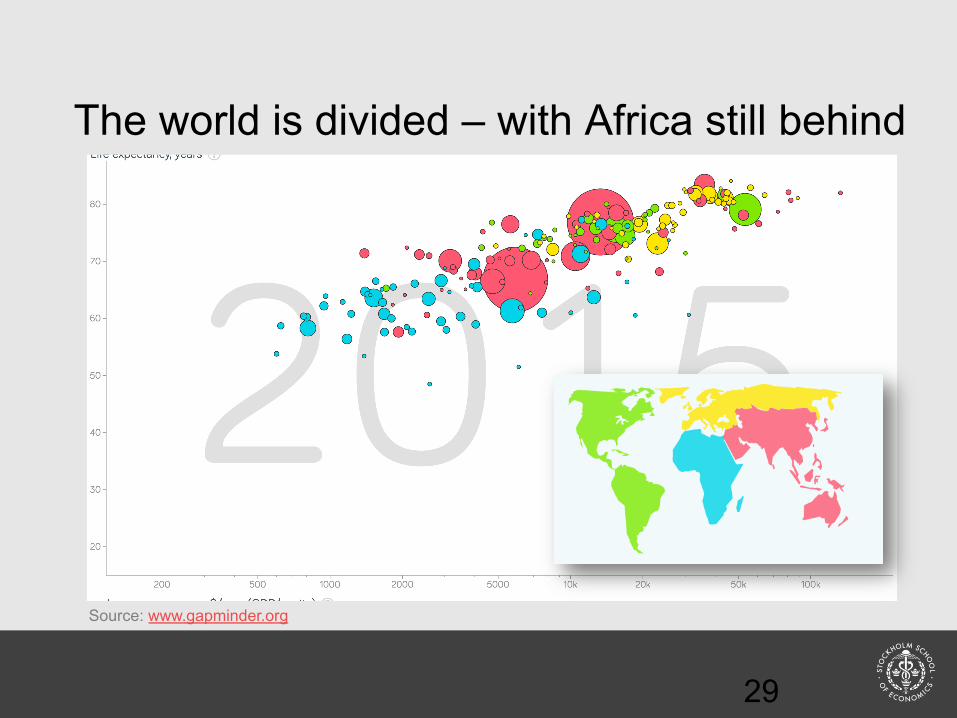

The world is divided – with Africa still behind

29

Source: www.gapminder.org

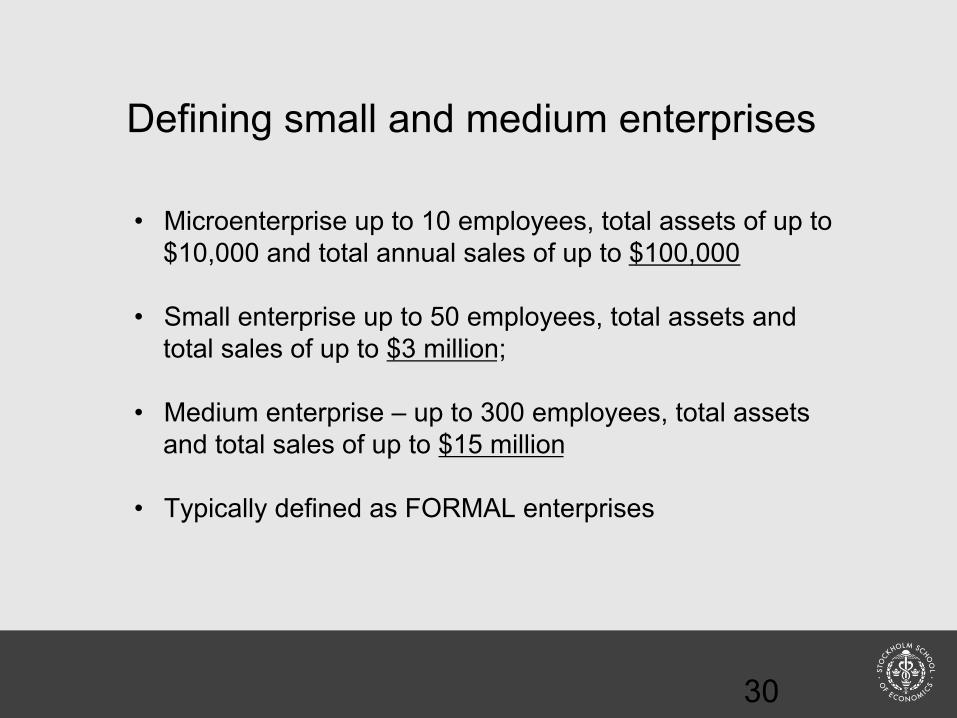

• Microenterprise up to 10 employees, total assets of up to $10,000 and total annual sales of up to $100,000

• Small enterprise up to 50 employees, total assets and

total sales of up to $3 million;

• Medium enterprise – up to 300 employees, total assets and total sales of up to $15 million

• Typically defined as FORMAL enterprises

Defining small and medium enterprises

30

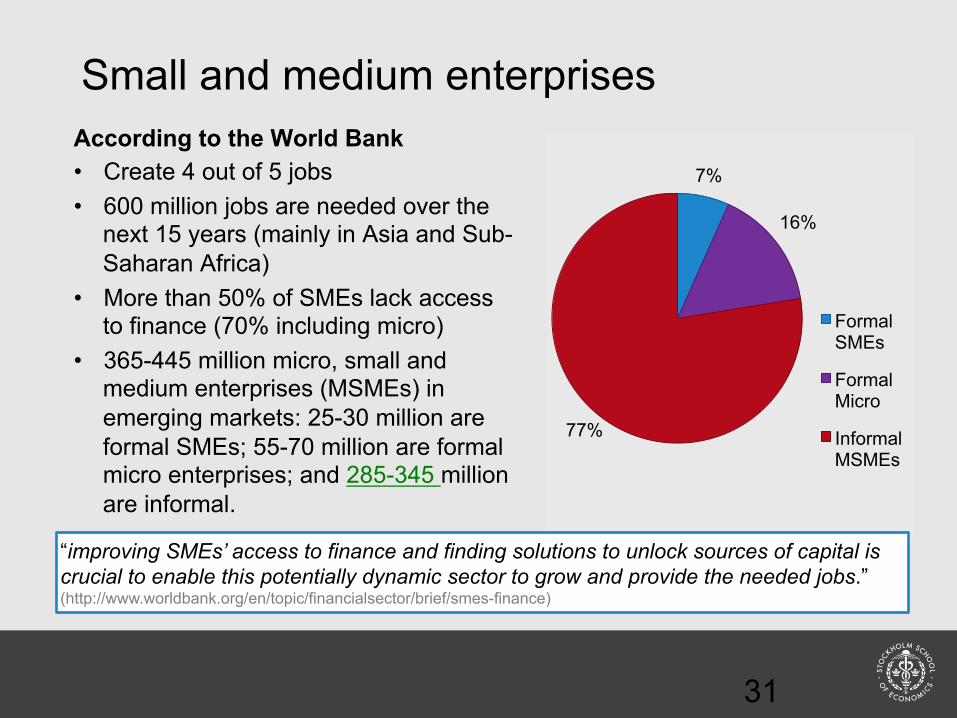

According to the World Bank • Create 4 out of 5 jobs • 600 million jobs are needed over the

next 15 years (mainly in Asia and Sub-Saharan Africa)

• More than 50% of SMEs lack access to finance (70% including micro)

• 365-445 million micro, small and medium enterprises (MSMEs) in emerging markets: 25-30 million are formal SMEs; 55-70 million are formal micro enterprises; and 285-345 million are informal.

Small and medium enterprises

7%

16%

77%

Formal SMEs

Formal Micro

Informal MSMEs

31

“improving SMEs’ access to finance and finding solutions to unlock sources of capital is crucial to enable this potentially dynamic sector to grow and provide the needed jobs.” (http://www.worldbank.org/en/topic/financialsector/brief/smes-finance)

Higher income per capita has more MSMEs per 1,000 people

32

Source: MSME Indicators, World Development Indicators Note Statistically significant at the 5% level

Regional distribution – more MSMEs in

MSMES are key to economic growth

• Private equity is a source of investment capital from high net worth individuals and institutions for the purpose of investing and acquiring equity ownership in companies.

• Partners at private-equity firms raise funds and manage these monies to yield favorable returns for their shareholder clients, typically with an investment horizon between four and seven years.

• These funds can be used in purchasing shares of private companies, or in public companies that eventually become delisted from public stock exchanges under go-private deals.

• The minimum amount of capital required for investors can vary depending on the firm and fund raised. Some funds have a $250,000 minimum investment requirement; others can require millions of dollars.

• Typically a management fee of 2% and 20% upon gross profit from sale of assets

What is Private Equity?

33

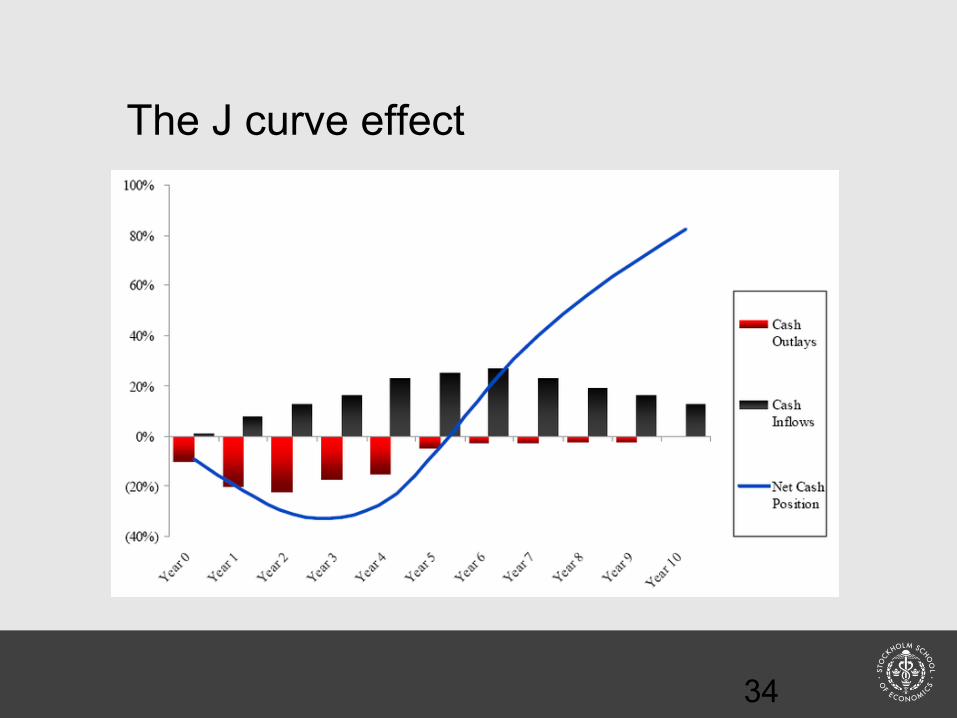

Private Equity often attracts top talent, consultants, and lawyers and often require large transactions in order to be economically viable

The J curve effect

34

Interest in Africa has never been higher and it continues to see strong interest from investors – Ernst & Young 2015

Current status

35

Private Equity (PE) Exits in Africa hit record levels in 2015, but is still only half of Europe

36

Source: AVCA

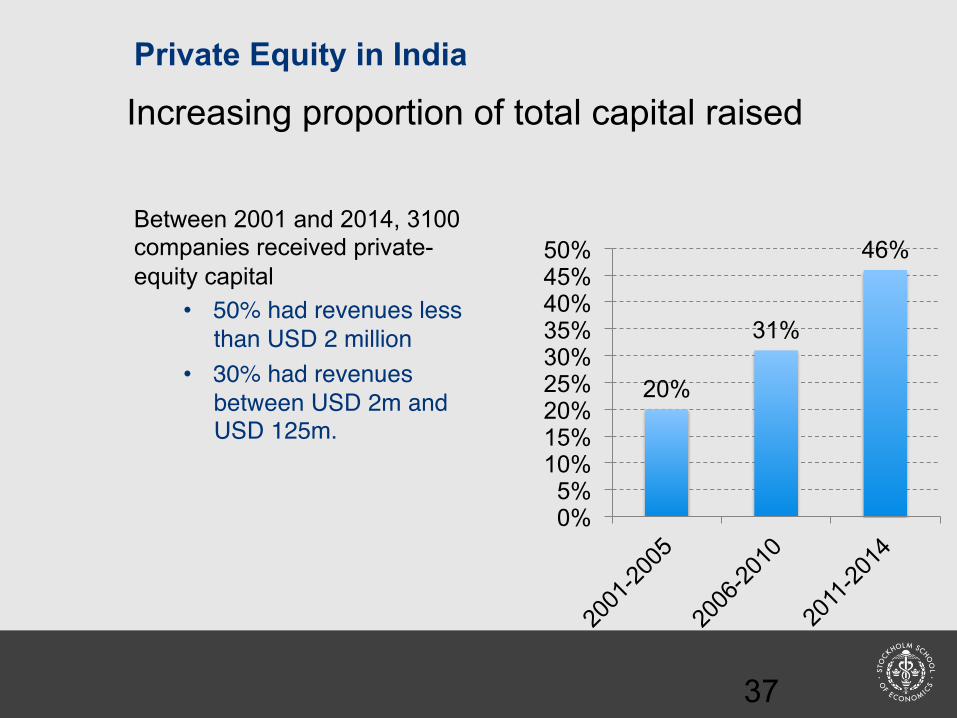

Between 2001 and 2014, 3100 companies received private-equity capital

• 50% had revenues less than USD 2 million

• 30% had revenues between USD 2m and USD 125m.

Increasing proportion of total capital raised Private Equity in India

20%

31%

46%

0% 5%

10% 15% 20% 25% 30% 35% 40% 45% 50%

37

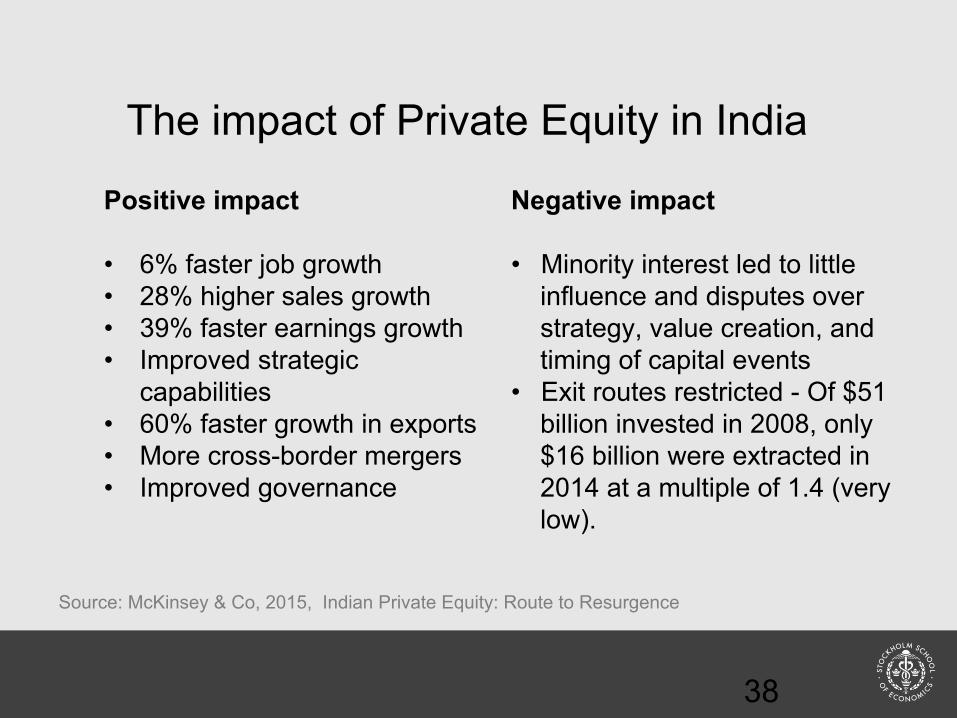

The impact of Private Equity in India

Positive impact • 6% faster job growth • 28% higher sales growth • 39% faster earnings growth • Improved strategic

capabilities • 60% faster growth in exports • More cross-border mergers • Improved governance

Negative impact • Minority interest led to little

influence and disputes over strategy, value creation, and timing of capital events

• Exit routes restricted - Of $51 billion invested in 2008, only $16 billion were extracted in 2014 at a multiple of 1.4 (very low).

38

Source: McKinsey & Co, 2015, Indian Private Equity: Route to Resurgence

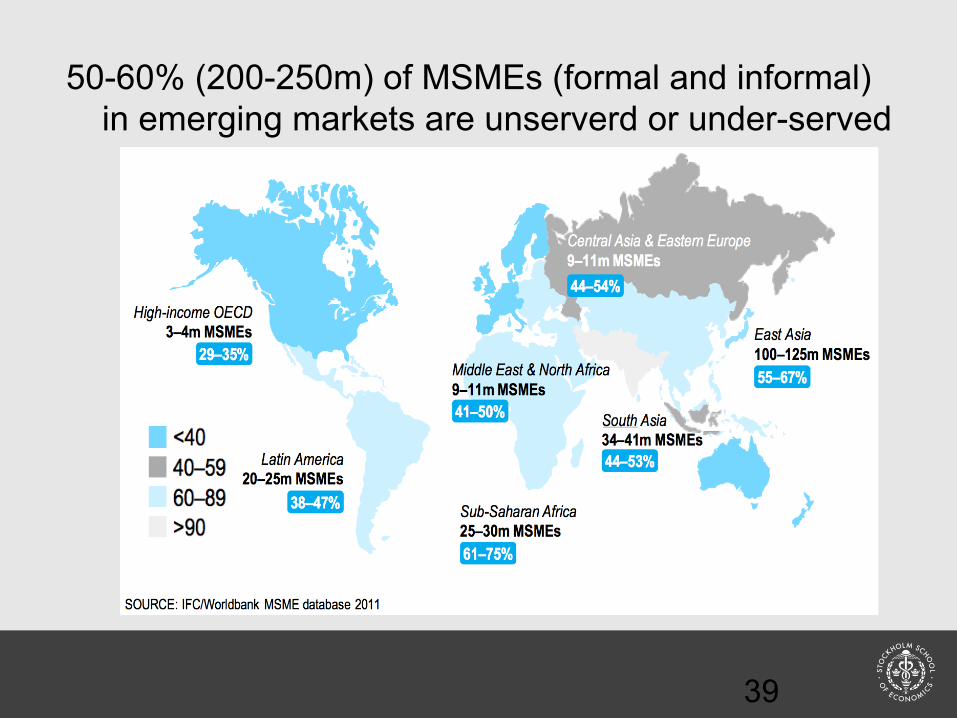

50-60% (200-250m) of MSMEs (formal and informal) in emerging markets are unserverd or under-served

39

• Developing countries have a large number of microenterprises and some large firms, but far fewer small and medium enterprises.

• In high-income countries, small and medium enterprises (SMEs) are responsible for over 50% of GDP and over 60% of employment, but in low-income countries they are less than half of that: 30% of employment and 17% of GDP.

• This SME gap is called the 'missing middle’ – but note that also large companies in reality are missing to a large extent

The Missing Middle

40

Source: Center for International Development at Harvard University

Evidence of the Missing Middle

41

LOCAL PRESENCE IS KEY “I think that private equity very well has a place in Africa. I think the private equity firm must be local. It must have a strong local presence, because otherwise it is difficult to bridge and communicate about the challenges that you have locally. Thus, being in the same market, it is easier to obtain mutual confidence between the private equity firm, and those who receive money, the management of that company.”

42 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

EQUITY IS NEEDED BUT AFRICA IS NOT FAMILIAR WITH PE “Africa needs much equity. That's the challenge, and there Private Equity has a role. It is difficult to borrow money, and if want you to speed up a project, yes then you need to strengthen the balance sheet with other people's money. However, knowledge is generally low in Africa if you take the help of private equity companies.”

43 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

EXTENDED HOLDING PERIOD & CONSOLIDATE CROSS BORDER “I think that you should be prepared to extend the time period and I think that as a private equity player one may be also find companies in other parts of Africa to create consolidation and speed up Pan African solutions faster.”

44 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

TRUST IS KEY “Trust in Africa is generally low. People deceive and cheat more. People do not dare to invite others in to own, or to be transparent. There is often double or triple book-keeping. Some books for the employees, some for the tax-authorities and some for investors. This is of course not ok.

45 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

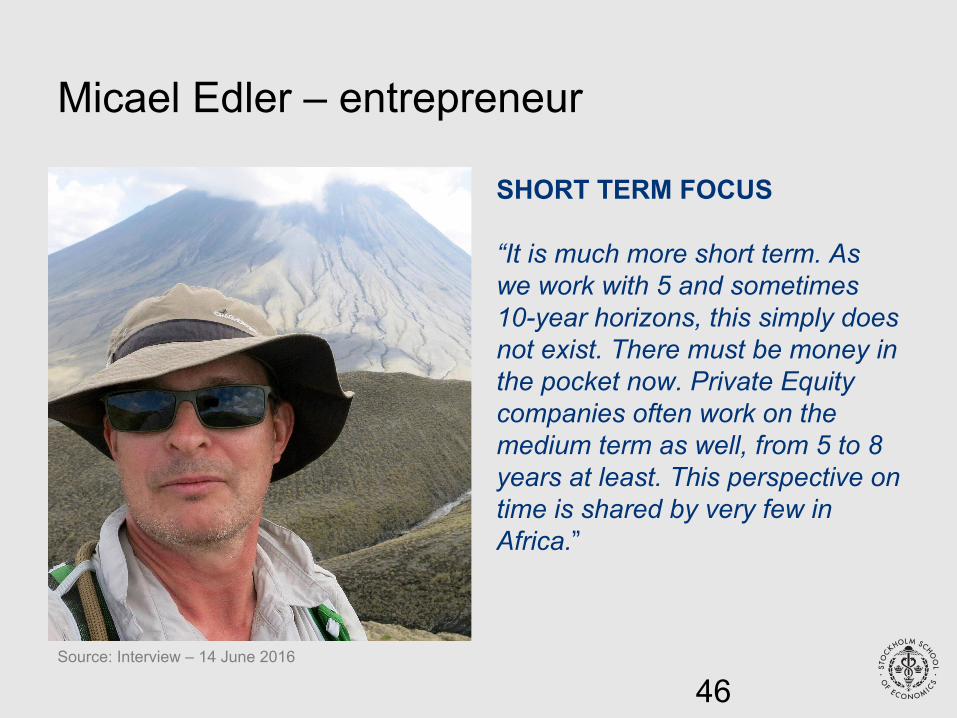

SHORT TERM FOCUS “It is much more short term. As we work with 5 and sometimes 10-year horizons, this simply does not exist. There must be money in the pocket now. Private Equity companies often work on the medium term as well, from 5 to 8 years at least. This perspective on time is shared by very few in Africa.”

46 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

CREATING A WALLET, NOT VALUE “If you are an entrepreneur in northern Europe, you know that you have to follow the rules to create value, whereas entrepreneurs in Africa often see this as a way of creating a wallet where one early can extract money. It is not value creation, but a cash flow creation for own consumption which preferably is grey or black in order to avoid taxation.”

47 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

FEW WELL MANAGED COMPANIES “It is also difficult for PE companies to find well managed firms. Again, it is a matter of trust, and of course they say they are well managed, but then you see quite soon that they are not, break rules and misbehave.”

48 Source: Interview – 14 June 2016

Micael Edler – entrepreneur

Thank you for the attention!

Pontus Engström, PhD, MSc. Stockholm School of Economics E-mail: [email protected]