Embed Size (px)

Citation preview

Three Rules

THREE SIMPLE RULES THEO A. BOERS

Financial Counselorand

Workshop Leader

Theo A. Boers is an entrepreneur and a businessman whoset up a Financial Counseling Ministry at his church inthe early nineties. After counseling hundreds of familiesand training many counselors he decided to summarizewhat he had learned in this book. He wrote it especiallyfor young people and young couples,

Second Edition

reading this book they would avoid financial difficulties.

Free copies of this book may be downloaded atwww.ThreeRules.org

Training Manualcomments regarding this book and any relatedfinancial questions to the author at:

Simple

]|xHISBN 0-9749105-0-3

Copyright 2003

Theo A. Boers

All rights reserved. No part of this book may be reproduced in any form, except for the inclusionof brief quotations in a review, without permission in writing from the author.

Scriptures marked as NIV are taken from the Holy Bible New International Version Copyright© 1973, 1978, 1984 by the International Bible Society.

Scriptures marked as The Message are taken from The Message. Copyright © 1993, 1994, 1995,1996, 2000, 2001, 2002. Used by permission of NavPress Publishing Group.

Scriptures marked as CEV are taken from the Contemporary English Version Copyright © 1995by American Bible Society.

Scriptures marked as The Living Bible are taken from the Life Application Bible for Students:the Living Bible, Copyright © 1992 by Tyndale House Publishers, Inc.

Free copies of Three Simple Rules Guaranteed to Improve Your Finances! may be downloadedat www.ThreeRules.org

Printed copies of this manual and the Three Simple Rules book are available at cost of printingand shipping. Check our web site for details.

Second Edition, printed September 2004

INDEX

FIRST BANK of TABS

Financial Counseling

Pre-Marriage Mentoring

Financial Workshop

Case Studies

SECOND BANK of TABS

Case Study Answers

Forms

Financial Workshop Tools

Appendix

Introduction

The Financial Counselor and Workshop Leader Training Manual is a self-teaching course on:

(a) How to become a Financial Counselor.

(b) How to do Pre-Marriage Financial Mentoring.

(c) How to conduct small group Financial Workshops.

It consists of this manual and the book written by the same author entitled Three Simple RulesGuaranteed to Improve Your Finances. If you haven’t already done so you should read ThreeSimple Rules before proceeding with this manual.

This manual is based on material that the author, who has been involved in financial counselingfor over ten years, has used in a classroom environment to teach financial counseling for overseven years.

The Financial Counselor section of this manual prepares the reader to offer Financial Budget andDebt Counseling from a Christian Perspective to individuals and/or families. It providesappropriate Bible verses, simple tools for setting up counseling sessions and concreteinformation on counseling dos and don’ts.

The Pre-Marriage Mentoring section of this manual will prepare the reader to offer a pre-marriage mentoring session focused on the couple’s compatibility in the area of finance-relatedvalues.

The Financial Workshop section of this manual will prepare the reader to conduct a structuredfour week financial workshop for small groups.

The Three Simple Rules book is an integral part of all three aspects of this manual.

Three Rules

THREE SIMPLE RULES THEO A. BOERS

Section One:

Financial

Theo A. Boers is an entrepreneur and a businessman whoset up a Financial Counseling Ministry at his church inthe early nineties. After counseling hundreds of familiesand training many counselors he decided to summarizewhat he had learned in this book. He wrote it especiallyfor young people and young couples, in the hope that byreading this book they would avoid financial difficulties.

Free copies of this book may be downloaded atwww.ThreeRules.org

Counselingcomments regarding this book and any relatedfinancial questions to the author at:

Simple

]|xHISBN 0-9749105-0-3

Financial Counseling

Introduction………………………………………………………pg. 1

Why is Financial Counseling NecessaryWhy People Have Financial ProblemsThree Simple RulesTypes of Counseling SituationsCounseling ObjectivesWhat People Think Causes Financial ProblemsThe Client’s CommitmentThe Client’s GoalsNo Magic WandsRecognize Your LimitsCounseling from a Christian Perspective

Dos and Don’ts……………………………………………pg. 11

Where to CounselWhen to CounselSession LengthCautionsConfidentialityCounseling TechniqueSet Healthy Limits

The Counseling Process……….………………………………pg. 15

Meeting Number OneMeeting Number TwoMeeting Number ThreeMeeting Number Four and beyond

Conclusion………………………………………………...pg. 32

1

Why is Financial Counseling Necessary?

Personal bankruptcies hit an all time high of 1.6 million in 2003. On a per capita basis this rateof bankruptcy is 10 times greater than it was during the Great Depression.

Last year over 9 million people, who averaged $16,000 in unsecured debt, sought help from debtcounseling agencies. Experts estimate that for every person who seeks council there are 4 whoare still in denial.

Why are record numbers of Americans filing bankruptcy and seeking debt relief?

The primary cause of the rampant rise in personal financial problems in the last 20 years hasbeen the ever increasing easy availability of credit. Financial institutions have been “selling”money in ways we have never before experienced.

Houses can now be financed for 125% of value.

Cars can be bought and financed at 0% interest.

Everything from carpets to carports can be purchased with no down payment, no interest and nopayments for 6 – 36 months.

Credit cards companies now aggressively pursue non-traditional markets such as collegestudents, senior citizens, the working poor and even the recently bankrupt.

Almost anyone can borrow money to buy almost anything.

Credit card balances of “revolvers”, people who do not pay off their balance every month, is nowover $12,000.

We now live in a world where we are no longer reminded that if we buy now we have to paylater. Instead we are repeatedly told to:

“Master the possibilities with Master Card.”

“Visa. It’s everywhere you want to be.”

The message is subtle but it sinks in. Master Card and Visa can help you live a better life, dowhat you want to do and go where you want to go. The message is totally directed at personalself-gratification. There is no hint of personal responsibility, no reference to interest rates, fees,penalties and payback time except for in the fine print.

As a result of all this easy credit an unprecedented number of families are now struggling withserious financial problems and the consequent tension it creates in marriages.

This manual is designed to help you help these families.

2

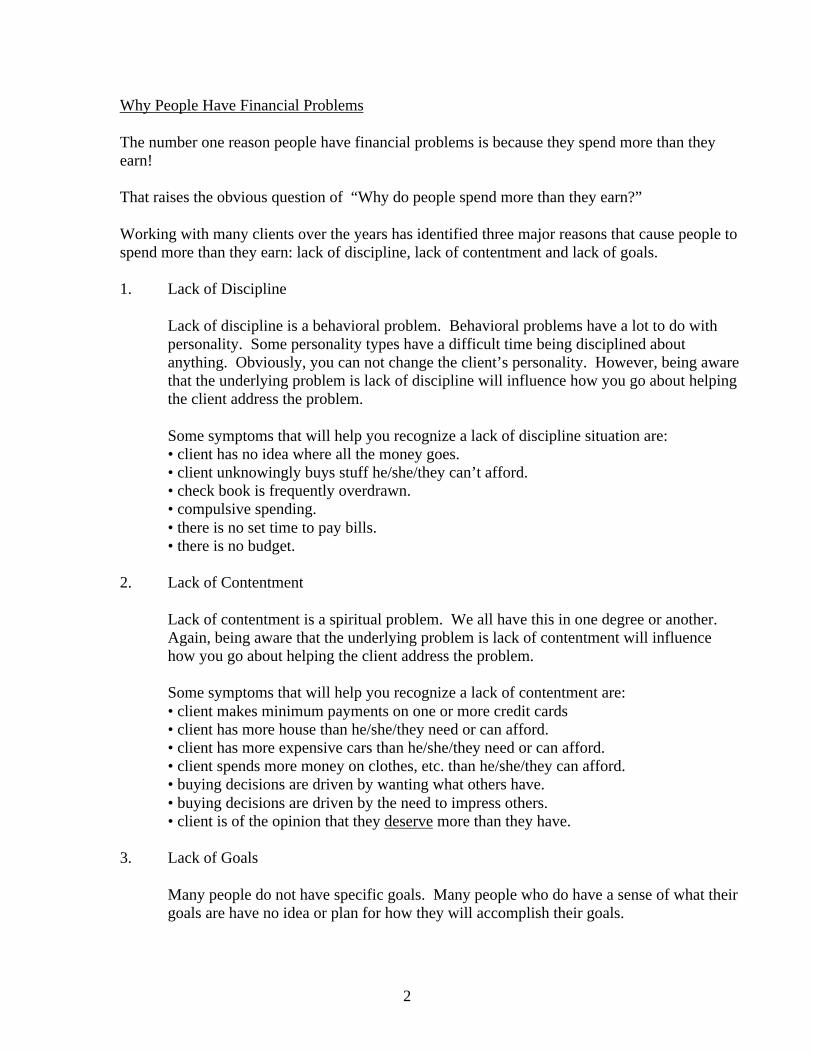

Why People Have Financial Problems

The number one reason people have financial problems is because they spend more than theyearn!

That raises the obvious question of “Why do people spend more than they earn?”

Working with many clients over the years has identified three major reasons that cause people tospend more than they earn: lack of discipline, lack of contentment and lack of goals.

1. Lack of Discipline

Lack of discipline is a behavioral problem. Behavioral problems have a lot to do withpersonality. Some personality types have a difficult time being disciplined aboutanything. Obviously, you can not change the client’s personality. However, being awarethat the underlying problem is lack of discipline will influence how you go about helpingthe client address the problem.

Some symptoms that will help you recognize a lack of discipline situation are:• client has no idea where all the money goes.• client unknowingly buys stuff he/she/they can’t afford.• check book is frequently overdrawn.• compulsive spending.• there is no set time to pay bills.• there is no budget.

2. Lack of Contentment

Lack of contentment is a spiritual problem. We all have this in one degree or another.Again, being aware that the underlying problem is lack of contentment will influencehow you go about helping the client address the problem.

Some symptoms that will help you recognize a lack of contentment are:• client makes minimum payments on one or more credit cards• client has more house than he/she/they need or can afford.• client has more expensive cars than he/she/they need or can afford.• client spends more money on clothes, etc. than he/she/they can afford.• buying decisions are driven by wanting what others have.• buying decisions are driven by the need to impress others.• client is of the opinion that they deserve more than they have.

3. Lack of Goals

Many people do not have specific goals. Many people who do have a sense of what theirgoals are have no idea or plan for how they will accomplish their goals.

3

This is especially true in the financial area. That is why many people reach theirretirement years basically broke.

When you ask people if they would like to be financially free almost all of them will say yes.When you tell them that step one toward that goal is to become totally debt free they look at youwith a blank stare because they don’t even believe that to be possible.

That is part of the counselor’s challenge. As a counselor you have to reverse what people havebeen hearing all of their lives and that is that debt is normal.

You have to reverse that perception and help your clients to understand that they will never befinancially free until they owe no man anything!

Sometimes you will need to get your clients’ attention by whacking them over the head with theproverbial two by four. I sometimes do that by projecting where they will be, based on theircurrent spending habits, in five, ten or fifteen years. Generally, the projection is so scary that Iget their attention so that we can begin to set some goals and lay out plans for how to accomplishthem.

Lack of discipline, lack of contentment and lack of goals are not the only reasons that peoplespend more than they earn. Budgeting is another contributing factor. Budgeting isn’t easy - it’scomplicated. The reason budgeting is complicated is because:

• Some bills are monthly, some are quarterly, some may be semi-annual or annual andsome, like doctor or dentist bills, are just unpredictable.

• Some people are paid weekly, some bi-weekly, some monthly and some are oncommission.

As a result, matching up money coming in and money going out is difficult. This manual and theThree Simple Rules book will provide detailed information on how to teach your clients how toaddress these complicated variables.

Other reasons why budgeting is difficult are:

• Many people have simply never been trained to budget their money.

• Budgeting takes time.

• Balancing a budget means making choices - a lot of people don’t like making choices.

• People assume that their lifestyle, whatever it is, is the minimum acceptable lifestyle.We all become accustomed to our standard of living whatever it is. Financial advisor

4

Andrew Tobias states, “A luxury once sampled becomes a necessity.” Therefore, whenour budget tells us we have to cut back in certain areas it’s a difficult thing to do.

Three Simple Rules

As Christian Financial Counselors, our goal is to help people who are experiencing financialdifficulties to understand how to apply three of the Bible’s basic money management principles.

The three principles are:

1. Spend less than you earn.

Don’t fall in love with money. Be satisfied with what you have. The Lord has promisedthat he will not leave us or desert us. Hebrews 13:5, CEV

2. Save now! Buy later.

The wise man saves for the future, but the foolish man spends whatever he gets.Proverbs 21:20, The Living Bible

3. Know the consequences of debt.

The poor are always ruled over by the rich, so don’t borrow and put yourself under theirpower. Proverbs 22:7, The Message

As you get involved in financial counseling you will discover that much of the financial hardshipand heartache that you will see is a result of people violating these three God-given principles.

Types of Counseling Situations

In financial counseling it is our objective to help the individual or the family work through aparticular financial problem.

There are at least six common types of counseling situations. They are:

1. Young couples, perhaps newly married, who need some help setting up a budget.

2. People who need help thinking through a “major” financial decision. For example,perhaps they found a house they would really like to buy, but they are not sure they canafford it.

3. People who tell you that things are always tight and would like some help just thinkingthings through. Perhaps all they really want to know is if they are doing anything wrong.

5

4. People whose circumstances have changed and cash flow went from positive to negative.Perhaps this was the result of a loss of job, a particularly severe illness, or a divorce.

5. Probably the most frequent situation that you will see will be people who have had amonthly negative cash flow for quite some time and it’s beginning to catch up with them.

6. One more type of counseling situation that you may experience is an individual or afamily that is so significantly behind on loan payments that they are being threatenedwith foreclosure and/or repossession.

Situations 1 - 3 are people who are looking for advice. It is frequently possible to give them thatadvice in one or two meetings. In many situations you may want to ask them to read some or allof Three Simple Rules and then meet to discuss their particular issues.

Situations 4 - 6 will take longer. They will require analysis, review of options, making ofdecisions and then helping the client to develop the discipline necessary to carry out thosedecisions.

Counseling Objectives

What do we hope to accomplish as a result of agreeing to provide financial counsel?

Obviously, the primary objective of financial counseling is to help clients eliminate currentfinancial problems and to help them prevent future financial problems. However, there are somesub-objectives of which you should be aware:

The first one is to simply give them hope – to help them understand that there is a way out of thismess. I’ve had many clients walk into my office convinced that they had no choice but to filebankruptcy only to learn that they did have options. That gave them hope.

A second objective is to help the clients define their goals. Many people have never done thatbefore. Helping them define their goals and then focusing on accomplishing those goals willhelp them stay on the right financial track.

A third objective is to teach them some basic money management skills. Many people havenever even been taught the basics.

Another objective is to teach them that the Bible has a lot of very practical advice when it comesto money. Advice, which if not followed, causes financial problems.

I say all this because you may not be successful in accomplishing the primary goal. We’ll talkmore about that later. However, that does not mean that the time you invested was wasted.

6

What People Think Causes Their Financial Problems

If you were to ask first-time clients, “So, what’s the problem?” many of them will tell you thatthey just don’t make enough money. In a sense they are right. They don’t make enough moneyto pay for their excessive spending habits. But inevitably, not making enough money is not thereal problem. It isn’t that they don’t make enough money. The real problem is that they spendtoo much money.

I know that’s true because I’ve counseled people who made $30,000 per year and people whomade $130,000 per year and they all say the same thing: they don’t make enough money. Mostpeople think that more money will solve all of their financial problems. Perhaps that’s whylottery tickets are so popular. Unfortunately, we know that even with lottery winners moremoney is not the answer.

For this reason, whenever we begin to look for solutions to a financial problem we always firstlook at where we can reduce expenses. (More about that later.)

The Client’s Commitment

When I first meet with a counseling client I always ask them what to them seems like a strangequestion. The question is this, “Will you do whatever it takes to fix this problem?” The answeris generally, “Of course we will.” Unfortunately, I know from experience that many of them willnot. Old habits are just too hard to break.

I ask them the question anyway, “Will you do whatever it takes to fix this problem?” This allowsme to help them understand that I can’t fix their problem. I can only give them advice. Theyhave to fix the problem. I can show them the “how to,” but they are responsible for the “will to”and the “will do.”

I then share with them something I learned from Pastor Henry Wildeboer. He frequentlyincorporates the Four D’s into his messages.

The Four D’s

He suggests that having the Desire to change something in your life is not unusual and not hardto do. Everyone desires something: to lose weight, to stop smoking, to spend quiet time withGod every day, etc. Having desire is normal and not difficult.

Then comes Decision: the Decision to do something that will get you where you want to be.Decision is a little bit harder than Desire, but still not terribly difficult. We all make manyDecisions every day.

But then comes Discipline. Discipline is tough. Discipline means actually doing what it is wemade a Decision to do. Not only once, but over and over and over again. Discipline is where the

7

rubber hits the road. Unless we have the Discipline we will never accomplish what we want toaccomplish. It’s that simple.

But if we do, if we do have the Discipline to do what we have to do to get what we want to go,we will experience DELIGHT! That’s the fourth “D” of Pastor Henry’s little talk and it appliesin almost all areas of our life, including attaining financial freedom.

The Client’s Goals

Another area I cover in the early part of the counseling process is encouraging the client toidentify specific goals. Obviously they want the pain of financial problems to go away but I tryto get them to be much more specific. As a result they will often identify goals like:

• stopping the creditor calls.• having some savings.• buying a better car so they won’t have unreliable transportation.• being able to help send their kids to college.• saving some money for retirement.• etc.

The reason I believe it is so important to encourage them to identify their goals up front is so youcan remind them of those goals later on in the counseling process. As you work with them overa period of weeks or perhaps months there are going to be times when they want to give up.

Changing old spending habits is tough.

They may have to make some very difficult choices like:• seriously cutting back on their spending habits in certain categories.• selling a car, boat or motorcycle.• moving to a smaller house.• working more hours.

That’s when I remind them of their goals. Would they rather keep the boat or would they ratherget that nasty collection agency off their back? That frequently brings them back to reality.

No Magic Wands

People you counsel also need to understand that you do not have a magic wand. They also needto understand that it is their problem, not your problem and they have to do the heavy lifting tosolve the problem. Don’t let them make their problem your problem.

You are there to help them analyze their situation, to make recommendations and, to the extentthat they will let you, hold them accountable, but you can not fix their problem.

8

Counseling from a Christian Perspective

For many people, money is considered to be a secular commodity. After all, money has to dowith buying and selling, business and the marketplace. However, what they forget is thatChristianity also has to do with the things of everyday life. Jesus talked a lot about money andcertainly used everyday life examples in most of his parables.

If we were to counsel from a purely secular perspective we would focus on doing whatever isnecessary to solve the financial problem. However, when we counsel from a Christianperspective we are going to recognize that violating God’s money management principles mayhave caused the problem and that applying these principles and asking for his help is a key tosolving the problem.

From a practical standpoint the following will differentiate Christian financial counseling fromsecular financial counseling:

1. We will open the counseling session with prayer asking for God’s guidance and wisdomas we work through this problem.

2. We will apply Scriptural principles to financial decisions. For example:

• We will encourage the client to be absolutely honest in all their financial dealings.

Who may stay in God’s temple or live on the holy mountain of the LORD? Onlythose who obey God and do as they should. They speak the truth and don’t spreadgossip; they treat others fairly and don’t say cruel things. They hate worthlesspeople, but show respect for all who worship the LORD. And they keep theirpromises, no matter what the cost. They lend their money without charginginterest, and they don’t take bribes to hurt the innocent. Those who do thesethings will always stand firm. Psalm 15:1-5, CEV

• We will deal with the concepts of needs vs. wants. God has promised to supply all ourneeds, not necessarily all of our wants, if we live within his will.

You can be sure that God will take care of everything you need, his generosityexceeding even yours in the glory that pours from Jesus. Philippians 4:19, TheMessage

• In the process of dealing with needs vs. wants we will refer to the Scriptural concept ofcontentment.

Do not want anything that belongs to someone else. Don’t want anyone’s house,wife or husband, slaves, oxen, donkeys or anything else. Exodus 20:17, CEV

•We will recognize a need to give back to God irrespective of whether we can “afford it.”

9

You have been treated generously, so live generously. Matthew 10:8b, TheMessage

•We will not consider bankruptcy an easy out.

An evil person borrows and never pays back; a good person is generous and neverstops giving. Psalm 37:21, CEV

3. We will close the counseling session with prayer asking for God’s guidance and wisdomas we work through this problem. In some cases it may be appropriate to encourage theclients to repent of their mistakes and to ask for God’s forgiveness.

One Caution - There is obviously much opportunity to refer to God’s Word in the process offinancial counseling. The caution is that you need to earn the right to share God’s Word withyour clients. This means you need to build rapport and create a trust and respect level. Youshould never “preach” at your clients. Your clients came to you because of a financial problem.A better understanding of God’s Word will inevitably be a part of the solution, but you have notearned the right to start talking about the solution until they agree that you understand theproblem.

10

11

Dos and Don’ts

Recognize Your Limits

If you are not an attorney, do not give any legal advice.

If you are not an accountant, do not give any accounting or tax advice.

If you are not a marriage counselor, do not deal with marriage issues that may be intertwinedwith the financial issues. Financial problems and marriage problems are frequently interrelated,one causing or contributing to the other. If you are a marriage counselor by profession you canuse your own judgment to what extent you want to do marriage counseling. If you are not amarriage counselor but detect some tension in the marriage you should suggest that your clientsmake an appointment with a marriage counselor or a pastor.

If you detect some tension resulting from differences of opinion between husband and wife youmay want to ask them to complete the Values Questionnaire (located in the Forms section). Thisprocess may help to point out some areas the couple needs to work through with a pastor ormarriage counselor.

If you are not an investment advisor, do not give investment advice. However, if you are aninvestment advisor I would urge you to stay far away from any advice that could in any way beperceived as a conflict of interest. If you can somehow gain from any advice that you might givea counseling client, no matter how good that advice might be, you have crossed the line. Thiswill come back to hurt you or the organization (church, etc.) that you represent. The financialcounseling business is not a good place to be prospecting for investment clients.

Where to Counsel

Setting a safe and appropriate environment for your counseling sessions is important. I wouldstrongly advise that you not meet in your home or your client’s home. If you meet in your homethe client may be uncomfortable because your home may be much nicer than his or her home. Ifyou meet in the client’s home you may lose control by having to compete with kids, dogs andtelevision sets.

I do most of my counseling at my business office. Other places that are appropriate are a quiet,private room at your local library or a quiet, private room at your church. I almost alwayscounsel at my church if I am counseling someone who is not a Christian. This just helps me tounderscore that I am counseling from a Christian point of view.

There are some times that it is appropriate for you to meet at a restaurant. However, I only usethat option for “get acquainted” sessions or situations where we are just going to talk over arelatively simple situation. Obviously, if we are going to get into the nitty gritty of a financial

12

analysis a restaurant is not private enough and doesn’t have the room to lay out the necessarypaperwork.

When to Counsel

You are the counselor. Chances are that you are volunteering your time to help others.Therefore the short answer is that you should counsel based on your availability. Within reason Iwould encourage you to offer to meet based on when it is convenient for you.

I typically meet with counseling clients once per week in the early stages. Sometimes I meetthem during the day, sometimes in the evening and sometimes before or after a church service.In all situations I recognize my responsibilities to my family and to my day job before agreeingto meet with a client.

Session Length

Typically a counseling session will last one to one-and-a-half hours. If they run any longer thanthat you are probably not being very productive.

Cautions

1. Do not counsel family members or friends.

Rightly or wrongly, finances in our culture are a very private matter. As a result, friendsand relatives may not tell you what you need to know. It is also possible that they willtell you stuff that you really didn’t want to know.

2. Do not counsel the opposite sex alone.

This one should be self-explanatory.

3. Do not counsel half of a couple.

Finances are a family matter. If there are financial problems significant decisions willneed to be made to correct the problem. Both spouses should be part of that decisionmaking process.

4. Do not solve the client’s problem by giving them money.

If you are like me you will feel sorry for some of the people you counsel. That in turnmay tempt you to give them money. Don’t do it. You are an advisor and you do notwant to create a dependency. If there is a critical cash need refer them to the deacons oftheir church.

13

Confidentiality

You will want to keep some records, notes and copies of budgets as you work through thefinancial situation. You will need them as you develop your recommendations. However, youneed to have a place where you can keep this information under lock and key so as to protect theconfidentiality of your clients.

Counseling Technique

1. Ask questions and listen. This is especially true in the first several meetings. You needto figure out what created the problems before you can begin to address them.

2. DON’T LET THEM MAKE THEIR PROBLEM YOUR PROBLEM. They would likethat. They would like to just leave their problem with you for you to fix, but that won’twork. All you can do is show them what they have to do if they want the problem to goaway.

3. Keep it simple. Many people who are drawn to becoming financial counselors are theanalytical type. Most are quite comfortable with numbers and may know a lot of stuffabout money and money management that not everyone needs to know. Therefore, keepit simple. Don’t overwhelm your client with everything you know. Address what theyneed to know.

Healthy Counseling Relationships

You are probably reading this manual because you want to become a volunteer financialcounselor. As a financial counselor you will deal with people who are experiencing seriousfinancial difficulties. You are offering to help, but you need to be careful that you do notbecome consumed.

Both you and your client need to understand that you may have the “how to” but they have tohave the “will to” and they have to commit to the “will do.” You may be able to walk alongsidethem but you can’t solve their problem for them. That is something that only the client can do.

The following is an excerpt from an article written by Mike Taylor in a 1998 edition of“Counselor’s Corner,” a publication of Christian Financial Concepts, Inc. In this article Mr.Taylor outlines six steps that will help you to keep your counseling relationships healthy.

1. Pray for God to grant you a wise and discerning spirit. Call to me and I will answeryou and tell you great and unsearchable things you do not know. (Jeremiah 33:3) He willhelp you to distinguish between the person being crushed by life’s circumstances and theone avoiding personal responsibility in life. Paul writes, “Let your speech always be withgrace, season, as it were, with salt, so that you may know how you should respond toeach person.” (Colossians 4:6)

14

2. Clearly communicate that you are volunteering your time to help, but you are not a“rescuer.” Your role as a volunteer counselor is to help people apply biblical principlesto everyday problems. You are trained to show “how,” but the the counselee must takeresponsibility for applying your objective insights.

3. Make homework assignments and hold the person(s) accountable for completing thestudy work. The goal of Christian counseling is not only seeing financial freedomactualized but long-term life changes under the lordship of Jesus Christ. Such behaviorchange is unlikely in a person who is unwilling to study.

4. Prepare yourself that many – perhaps the majority – of the counselees will beunwilling to do the hard work that long-term solutions require. Some may show upfor a session or two and never come back. That is discouraging. Jesus faced a similarsituation: “As a result of this many of his disciples withdrew, and were not walking withHim anymore” (John 6:66). Be careful not to measure the success of your counselingministry in numbers.

5. Stay focused on your area of expertise – biblical financial counseling. If you’re not aprofessionally trained marriage counselor, don’t get involved in marital conflicts. Ifyou’re not a trained CFP, don’t pretend to know everything about investing and estateplanning. If you’re not trained as a tax specialist, don’t give advice that could get yourcounselee’s in trouble with the IRS. When you step outside the boundaries of yourtraining, you are flirting with trouble.

6. Watch your time investment. When you begin spending more time on a case than thecounselees themselves, you may be heading for trouble. You counsel; allow thecounselees to do the legwork.

Remember that volunteer financial counseling is a marathon – don’t try to run it at a sprintspeed. May God grant you wisdom and insight as you faithfully serve those He sends your way.

15

The Counseling Process

The counseling process will generally consist of a series of meetings. The number of meetingswill vary depending on the complexity of the situation and the clients’ ability and willingness todo what needs to be done. The following is an outline of what is likely to happen at thesemeetings.

Meeting Number One

Prior to the first meeting give or send your client(s) a copy of Three Simple Rules and ask yourclient(s) to read the Introduction and Part One.

Also give or send your client(s) a copy of the Personal Financial Habit Assessment (located inthe Forms section) and ask them to complete it and bring it to the first meeting.

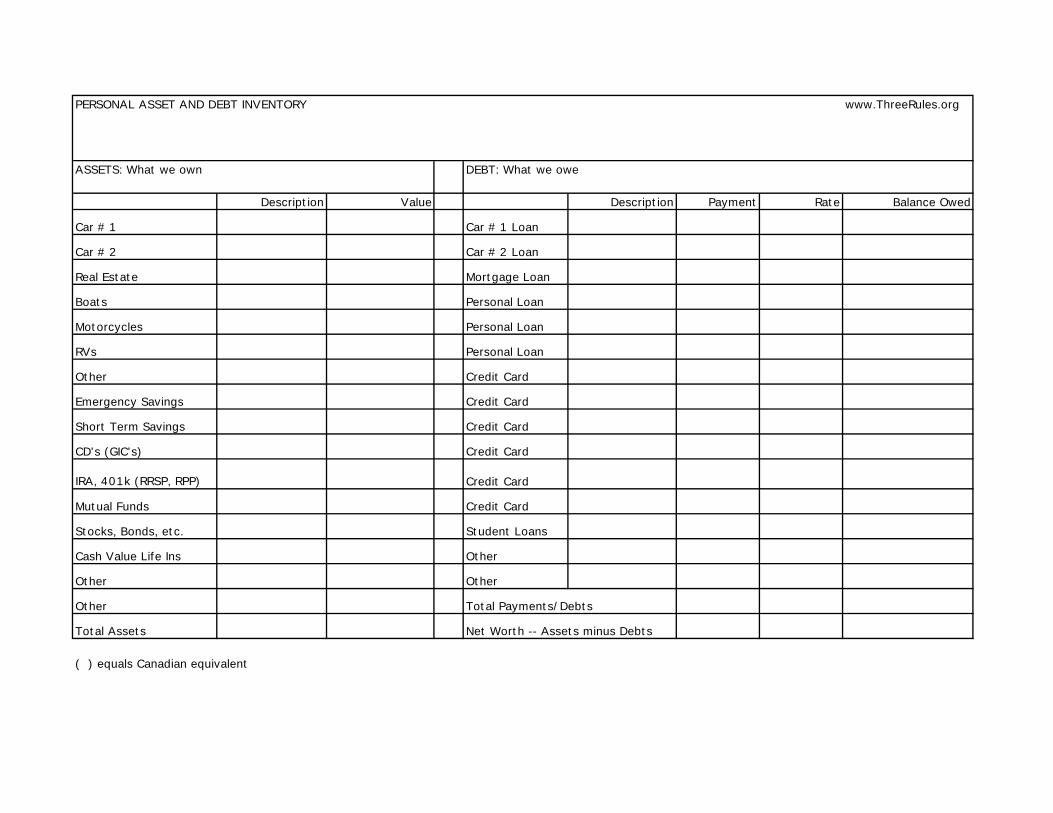

The purpose of the first meeting is:• for the counselor and the client to get to know each other.• for the client to understand the counseling process.• for the client to understand the two primary forms, the Personal Asset and Debt Inventory and

the Personal Cash Flow Plan.• for the client to understand that there will be homework between sessions and that they will be

expected to do it.

At the first meeting:

1. I like to start with 5 - 10 minutes of small talk just to make the clients comfortable.

2. Open with prayer. (Ask God’s blessing on your time together.)

3. Give them an overview of the counseling process. Explain that this will probably take atleast 3-4 meetings and that they will have to do some homework between meetings.

4. Ask them if they did the homework and what they thought of what they read.

Some questions to ask:

• “What did you think of Steve and Jessica’s story? Can you tell me some of the mistakesthey made?”

• “Have you made any of the mistakes Steve and Jessica made?”• “What did you learn from reading Part One of Three Simple Rules?”• “How do you plan to apply what you learned?”

Ask them for the completed copy of the Personal Financial Habit Assessment. Youmight scan it but I would suggest not commenting too much on it at this time. Reviewingthe Personal Financial Habit Assessment will give you a quick and early read on the

16

habits that may be causing their financial problems. If they answered “No” to any of thequestions 1-8, this may be a suspect area. If they answered “Yes” to any of questions 9-16, this may also be a suspect area.

If they did not do the homework, that is a big red light. If they did not do the homeworkbefore the first meeting, chances are they are not going to work very hard betweensubsequent meetings. You may need to point out that unless they do what you ask themto do, you may not be able to help them.

5. Ask them if you can take some notes so that you will be able to help them better.

6. Complete the top part of the Client Profile. (Located in the Forms section.) Follow theClient Profile as you ask questions and gather information about their financial situation.

7. Ask some general questions to determine their assessment of their financial situation:

“Why are you here and how can I help?”

“When did the problems start?”

“What do you think caused the problem?”

8. Ask some questions to assess their expectations and commitment:

“What do you hope to achieve as a result of this process?”

“If your financial situation was perfect, what would be different?”

“What are your three primary financial goals?”

“How badly do you want to accomplish these goals? Are you willing to do whatever ittakes?” (If you don’t we’re wasting our time!)

Explain that for things to get better some behavior and habits will have to change.

9. Explain the 4D’s of changing a condition from what it is to what you want it to be. Thisapplies whether we are trying to stop smoking, lose weight or eliminate a financialproblem.

• Desire (Having a desire for change is easy.)• Decision (Making a decision to do what is necessary to change is not difficult.)• Discipline (Having the discipline to do what needs to be done is where the rubber hitsthe road.)• Delight (If we hang in there with the discipline we will have the delight ofaccomplishing our goal.)

17

10. Ask some specific questions to get an overview of how they manage their money:

“How often do you get paid?”

“What happens to the paychecks?”

“How many checking accounts and savings accounts do you have?”

“Who pays the bills? When? How often?”

“How much cash do you go through per week?”

“Did you have to pay additional taxes or did you get money back as a result of last year’stax return?”

“How is your credit record?”

“Are there bills that are past due?” (Helps determine the urgency of the situation.)

“Is there anything that is close to repossession or foreclosure?”

“Are you current on your taxes?”

11. Explain the Financial Physical Concept.

Explain that before we can make recommendations on how to correct their financialsituation we need to totally understand their financial situation. We call that the financialphysical.

Explain the two forms that we use to help us understand the financial situation.

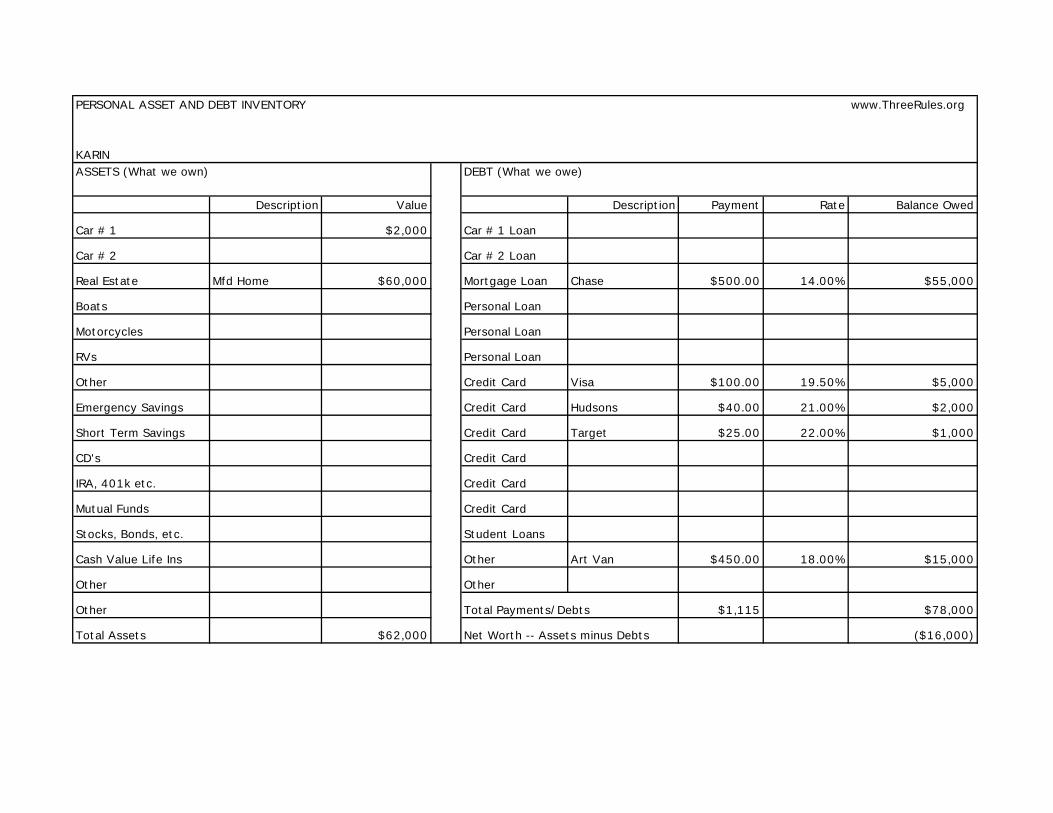

•Personal Asset and Debt Inventory (X-ray) - The Personal Asset and Debt Inventory islike an x-ray. It gives a picture at a point in time.

• Personal Cash Flow Plan (Stress Test) - The Personal Cash Flow Plan is like a StressTest. It tells us what’s happening over time.

Complete parts of each form starting with the Personal Asset and Debt Inventory.Complete the parts that they know, primarily for the purpose of getting them comfortablewith the forms. (Forms are available in the Forms section.)

Part Two of Three Simple Rules has more information on how to complete these twoforms.

If in the process of explaining and completing the Personal Cash Flow Plan it becomesobvious that the client has no idea how much they are spending in some or all of the

18

categories, suggest to them that they refresh their memory by going through theircheckbook and their credit card statements for the last three months.

Prior to reading the following section, pull a copy of the Personal Asset and DebtInventory and the Personal Cash Flow Plan out of the Forms section and refer to them asyou review these instructions.

PERSONAL ASSET & DEBT INVENTORY

Assets

Try to establish value for assets but don’t be too concerned about exact value. If theclient does want to get a good estimate on the value of their car, you can refer them towww.nadaguides.com.

Do not include furniture, clothing, etc.

The primary purpose of analyzing assets is to get an idea of approximate value andwhether any assets could be turned into cash.

Debts

Try to get as accurate a picture of the client’s debt as possible.

Have the client look up the last statement or call the company if necessary to get anaccurate balance.

Make sure the list is complete. People have a tendency to “forget” about some loans theymay have.

Probe for money owed to parents, other relatives, doctors/hospitals, student loans, loanson 401K (Replacement Pension Plan in Canada), loans on life insurance, etc.

PERSONAL CASH FLOW PLAN

Income

Don’t be shy about asking them about their income.Probe for all income sources.Income needs to be defined on a monthly basis.

19

Expenses

Explain why we use three categories of expenses. (See Three Simple Rules for arefresher if necessary.)All expenses need to be defined on a monthly basis.

CATEGORY ONE EXPENSES

Giving

Explain why giving is listed first.Honor the Lord by giving him the first part of all your income, and he will fill your barnswith wheat and barley and overflow your wine vats with the finest wines. Proverbs 3: 9-10, The Living Bible

Do not focus on their giving amount at this time. This is something you can come back tolater in the prescription phase.

Taxes

The easiest way to compute tax liability is to start with information from the clients’paycheck(s). Assuming that they were not significantly over- or under-withheld in theprior year and assuming that nothing has changed in their status, the current withholdingsshould be pretty accurate.

If this is not the case, there are a number of internet sites that can be used to helpcalculate tax liability. One of these is www.quiken.com/taxes/tools

Certain low-income families are eligible for Earned Income Tax Credits (US only).Check the latest IRS rules on the internet or check with an accountant.

Debt Retirement

The information necessary to complete this section should be on the debt side of thePersonal Asset and Debt Inventory.

Savings

Most of your counseling clients will not be saving on a regular basis.

This section is an opportunity to reinforce the need to save on a regular basis.

Emergency Savings Account ––• For emergencies like a broken refrigerator, major car repairs, unexpected dental bill,etc.

20

• Build up an emergency account until it equals 5% of annual income.• If some of the money is used it needs to be replenished.

Short-Term Savings Account ––• For big ticket items that will be needed in the next three to five years like cars,furniture, appliances, major home repairs, etc.• Amount needed in this account will be based on short-term goals.

Long-Term Savings Account ––• For children’s education, retirement, etc.• Amount needed will be based on long-term goals.• Any regular contributions to a 401K (Replacement Pension Plan in Canada) or IRA(Registered Retirement Savings Plan in Canada) should be listed here.

Focus on the savings accounts in the order listed. Fund the emergency account beforebeing concerned about the other two.

Use the Savings Comparison Chart (located in the Financial Workshop Tools section) todemonstrate the importance of starting a savings plan early. The number one ruleregarding saving and investing is to get started.

CATEGORY TWO EXPENSES

Housing

Taxes and insurance may already be included in the mortgage payment under the debtretirement section of Category One if they are included in the mortgage payment. If thatis the case, do not list them again.

Food

Do not include bought lunches or eating out. These are found in the miscellaneous andentertainment sections below. Typically, this category will include everything purchasedat the grocery store including toiletries and cleaning supplies.

Car

Car loans are listed in the debt retirement section of Category One Expenses.

Insurance

If medical insurance is provided by an employer, only show the portion of the premiumfor which the client is responsible.

21

Entertainment

This is an area where clients frequently do not know how much money they spend. Anestimate is acceptable for now.

Tuition/Childcare

Christian School tuition is a possible area of conflict between husband and wife. Referthem to a pastor or a marriage counselor if you detect conflict over this issue.

Miscellaneous

Probe for “other” expense categories that may be unique to this particular client.

CATEGORY THREE EXPENSES

Any expenses that do not occur on a regular weekly or monthly basis should beaccounted for here.

For many of these expenses, you will need to estimate the annual cost and then divide bytwelve to estimate what the monthly budget should be.

12. Assign Homework

Read Part Two and The Addendum of Three Simple Rules.

Complete both forms as much as possible.

What they should bring to the second counseling session:

Recent typical pay stub(s)Personal Asset and Debt Inventory (Completed as much as possible)Personal Cash Flow Plan (Completed as much as possible)

13. Schedule the next counseling session. The second counseling session should bescheduled for one or two weeks later. I like to stay with the same day, time and place soas to minimize confusion.

14. Close with prayer.

22

23

Meeting Number Two

Prior to the second meeting you will want to review your notes from the first meeting and yourclient’s Personal Financial Habit Assessment. This review will refresh your memory of yourclient’s situation and give you some insight into how your client tends to make money decisions.

The purpose of the second meeting with your counseling client is to understand their financialsituation as accurately as possible.

By the end of the second meeting it is your goal to understand:• what they have in the way of assets.• what their liabilities are.• how much income they have and where it is coming from.• how they are spending their money.

In the process of finalizing the financial forms, be sure that the numbers remain their numbers,not your numbers. You can question their numbers if you believe they are high or low, but theyhave to remain their numbers.

To accomplish that you will do the following at the second meeting:

1. Some small talk.

2. Open with prayer.

3. Review that they did the homework.

Some questions to ask:• “What did you learn from reading Part Two or the addendum pages of Three SimpleRules?”

• “How do you plan to apply what you learned?”

The counselor should be familiar with the addendum forms in case questions arise.(Many of the forms are available in the Financial Workshop Tools section.)

Depending on what you think their problem is, ask them specific questions aboutaddendum exhibits that relate to their problem.

4. Review forms.

Start with the Personal Asset and Debt Inventory.

Go through all the numbers making sure that you understand their numbers, that they arecomplete, and that they make sense.

24

Review the Personal Cash Flow Plan.

Go through all the numbers making sure that you understand their numbers, that they arecomplete, and that they make sense.

5. ID missing numbers. If there are missing numbers and they do not know them ask themto look them up at home and call you as soon as they have them.

6. Review their goals again (see Client Profile) to see if you understand them correctly andto remind them of what this is all about.

7. Assign Homework

Clients:Read Part Three of Three Simple Rules and prepare your own diagnosis and prescriptionof your situation.

Counselor:Prepare your diagnosis of your client’s situation and your recommended prescription.You will share this with your clients at Meeting Number Three.

8. Schedule the next session.

9. Close in prayer.

25

Meeting Number Three

The purpose of the third meeting (assuming you are ready to do this) is to help your clients tounderstand their financial situation and for you to share recommendations for corrective action.

Before the meeting you will want to rewrite or reprint (if you used computer forms) the budgetforms based on the numbers they gave you because at this point they will probably be somewhatmessy.

Before the meeting, you will also prepare your diagnosis and prescription.

At the meeting:

1. Open with prayer.

2. Review that they did their homework.• “What according to them is the diagnosis of their financial situation?”• “What should be the prescription?”

3. Give them your diagnosis and prescription of their financial situation. Put it in writing.Be very specific and frank. You can use the Diagnosis and Prescription form (located inthe Forms section) as a guide. Some examples of a Diagnosis and Prescription areprovided in the Case Study Answers section.

Tell them what you think is the cause of the problem in simple, direct, frank, no beating-around-the-bush terms.

Help them understand their current financial situation.

Start by focusing on the bottom line of the Personal Cash Flow Plan.

If it is negative, that is obviously a problem that needs to be corrected.

Then focus on line items where they are not accomplishing their goals (Savings, Giving,Debt Retirement, etc.).

Next, focus on the Personal Asset and Debt Inventory.

Compare their total assets and their total debts. Help them understand the concept ofequity.

Break their debt down into credit card, auto, mortgage and other.

4. Review their goals again. (Located in the Client Profile.)

Talk about what has to happen if they are to accomplish their goals.

26

5. Offer optional solutions that will help them correct the problem that is preventing themfrom accomplishing their goals.

In most cases the obvious problem is that they spent or are spending more than they earn.

Help them develop a balanced budget using the following approach:

(a) Test each expense category to see if it can be reduced. (This is the mostimportant and the most difficult part of the process. Most clients will tell you thatthey can’t possibly reduce expenses. This is where you have to remind them oftheir goals. Hopefully, accomplishing their goals will become the incentive forthem to do what they have to do.) Start at Category Two because it is unlikelythat Category One expenses can be reduced. Refer to the Expense Guidelinesaddendum in the Three Simple Rules book for some recommended categorypercentages.

(b) Evaluate whether there are assets that could be sold so that the proceeds can beused to pay off debt.

(c) Can income be increased?• change jobs• more overtime• additional part-time job• offer day-care• children get part-time jobs• rent out a room• etc.

Do not explore whether income can be increased until all options in (a) and (b)have been exhausted. Typically, increasing income without tackling expensereduction will result in future expenses catching up to the new income level.

If part of the solution is to increase income by working additional hours it shouldtypically be structured as a short-term solution to earn additional money for theprimary purpose of reducing or eliminating debt.

(d) Many clients will suggest debt restructuring (refinancing their home, home equityloans or a debt consolidation loan) as the solution to their debt problem. In mostcases this should be strongly discouraged. This solution may offer a short termfix but it generally does not serve as a long-term solution. The result willtypically be temporary because unless the client(s) change their spending habits,chances are that one year from now they will again have the same credit cardbalances that got them into trouble in the first place. Plus, if they use a homeequity loan to restructure or consolidate their debt, their home may be subject toforeclosure.

27

These four steps are deliberately in this order. Do not make the mistake of reversing thisorder, which many of your clients will be inclined to do. Unless the bad habits thatcaused the problem in the first place are corrected, there will not be any long-termsolutions.

In the process of going through this exercise it is important that you let the clients makethe decisions. You can attempt to lead them to the correct decisions but they have tomake the decisions because they are the ones who are going to have to execute the plan.They may execute their plan but they won’t execute your plan because they won’t believeit can be done.

In many cases the decisions that need to be made will be too complicated for the clientsto make at this meeting. If that is the case, focus on helping them understand what theoptions are and suggest that they think about what they want to do so that they can tellyou what they decided at the next meeting.

Again, the client will not like most of the options that you give them and they mayexpress that. When that happens keep reminding them that implementing these options isthe only way they will accomplish their goals.

There is an old saying that applies in this situation:

“If you always do what you’ve always done you will always get what youalways got. If you want something different you have to do somethingdifferent.”

You may need to remind your clients several times that if their behavior doesn’t change,neither will their circumstances!!!

If they do not change their behavior they will in all likelihood never achieve their goals!

In fact, for emphasis you may want to calculate what their financial situation will looklike in five, ten or fifteen years if they do not take the appropriate action now.

Once the tough decisions have been made and you have updated the Personal Cash FlowPlan to show the impact of these decisions, you should have a balanced budget. Abalanced budget allows adequate funds for the necessary expenses while stillaccomplishing your client’s goals in the area of saving, giving and debt retirement.

However, just having a balanced budget is only half the battle. All we’ve done so far ismake the “Decision” to have a balanced budget. We still have to execute the“Discipline” to actually change the habits that created the financial problems in the firstplace.

We will address that in Meeting Number Four.

28

6. Assign HomeworkRead Part Four and Five of Three Simple Rules.

7. Schedule the next session.

8. Close in prayer.

29

Meeting Number Four and subsequent meetings as necessary

We will assume that you now have a balanced budget that your clients agree will accomplishtheir goals.

What we mean by a balanced budget is that the Personal Cash Flow Plan no longer has a deficitand that the client’s goals of debt retirement, saving and giving are being met.

The purpose of the fourth meeting is to help your client learn how to exercise the “Discipline”that will change the habits that will help them live according to their balanced budget.

This is also where the Personal Financial Habit Assessment comes in again. By now you shouldhave highlighted the “bad habits” that need to be corrected. Again, if they answered “No” to anyof questions 1-8, this may be a suspect area. “Yes” answers to questions 9-16 may also besuspect areas.

1. Review the Personal Financial Habit Assessment with your client to help themunderstand the habits that are contributing to the problem and therefore the habits thatneed to be changed.

Explain that the Three Rules were designed to help them change those habits.

2. Review that they did their homework:• “What did you learn about the Paycheck Management System?”• “What did you learn about the Spending Management System?”• “Which one of the Three Rules will it be hardest for you to follow? Why?”• “What did you think about Part Five - Living by God’s Rules?”(Use this question to reinforce the fact that when we violate God’s rules for our livesthere will be a consequence.)

3. Help your client think through how to follow Rule One – Spend Less than You Earn.

The Paycheck Management System is a critical component to helping your clients spendless than they earn. Unless your clients immediately deposit or direct-deposit paychecksinto the appropriate accounts, the chances of accomplishing their goals is greatlydiminished.

Talk about how to:• set up special accounts. (Savings, Reserve, General)• calculate the appropriate amounts for each account.• distribute every paycheck into the appropriate bank account. (Direct deposit is best.)

Once the Paycheck Management System is in place you can focus on helping your clientsimplement the Spending Management System. When you are focusing on the SpendingManagement System do not overwhelm your clients. They may have poor spendinghabits in a lot of different areas.

30

I like to start by focusing on the Budget Busters. For most families the Budget bustersare:

• Food• Clothing• Eating Out• Entertainment• Vacation• Gifts• Cash

See Part Four of Three Simple Rules for ideas on how to help your clients get certainspending areas under control.

You will probably be most successful by focusing on a maximum of three spending areasat a time. In some cases you may want to focus on only one spending area until it isunder control. Remember, you are trying to change engrained habits and changing habitsis hard to do. Once you have worked on and been successful in a few of the spendingareas you can move on to others.

4. Help your client think through how to follow Rule Two – Save Now! Buy Later.

There are two keys to having a successful savings plan.

The first key is DECIDING how much to save. That step should have been accomplishedduring the process of completing the Personal Spending Plan for this client.

The second key is DISCIPLINE. Your client has to have the discipline to execute theplan. The Paycheck Management System we talked about earlier is the best way to helpyour client accomplish their savings goals.

5. Help your client think through how to follow Rule Three – Know Debt.

The reason it is important to Know Debt (understand debt) is so that wise decisions canbe made about debt. There are five keys to really understanding debt.

The first step is to Know how much debt you have. This step should have beenaccomplished in the process of completing the Personal Asset and Debt Inventory.

The second step is to Know the consequences of debt. The consequences of debt are:

(a) Debt reduces your future standard of living.(b) Debt reduces your ability to save.(c) Debt reduces your ability to give.(d) Debt creates personal frustration and stress.(e) Debt results in relational problems between husband and wife.

31

The third step is to Know the different types of debt:

• Credit Card• Consumer Debt• Real Estate Debt• Student Debt

The fourth step is to Know the borrowing test. If and when you do decide to borrowmoney there are a few questions that you should ask yourself. Any question to whichyou answer “yes” is a warning light that should cause you to reconsider your borrowingdecision.

Am I seeking contentment with this purchase?

Am I borrowing money to pay for an impulsive purchase?

Am I borrowing money to pay for a purchase driven by pride/ego?

Am I justifying my buying decision on the basis that everyone is doing it?

Is the item I am about to buy likely to depreciate?

Is my loan for this item longer than absolutely necessary?

Is there a possibility that I may not be able to make the payments on this loan?

Will repayment of this loan threaten my ability to save?

Will repayment of this loan threaten my ability to give?

Will repayment of this loan threaten my ability to take care of my family?

Am I questioning whether taking out this loan is a good decision?

Does my spouse have any concern about borrowing money for this purchase?

The last key is to Know how to Get out of Debt! That should be everyone’s goal. Thesteps for getting out of debt are listed on the “How to Get Out of Debt” page of theFinancial Workshop Tools section.

Once you are satisfied that your client understands the basics of how to implement the ThreeRules, subsequent meetings may be scheduled as much as three months later, primarily to seehow things are going and for the purpose of accountability. In the interim, you may want to stayin touch with your client by phone to see how it’s going and for encouragement.

32

Conclusion

Now that you are familiar with the entire cycle of Financial Counseling it’s time to get your feetwet. However, before meeting with real clients we are going to start by looking at some casestudies of typical counseling situations.

There are five case studies located in the Case Studies section. Read the story, answer thequestions and then compare your answers to those in the Case Study Answers section.

Once you have completed the Case Studies you are ready to work with actual counseling clients.To learn more about where to get actual counseling clients see the section entitled “How to Starta Financial Counseling Ministry in Your Church” located in the Appendix section of thismanual.

For additional support, we’ve also provided you with some Counseling Session Agendas. Go tothe “Getting Started” section of the Appendix and you will find brief outlines of each meetingthat will help you to prepare and keep yourself on track during the meeting itself.

And one final reminder. You are not alone. If at any time you get confused or have a questionabout how to handle a unique situation you can always contact us through our website atwww.ThreeRules.org.

Three Rules

THREE SIMPLE RULES THEO A. BOERS

Section Two:

Pre-Marriage

Theo A. Boers is an entrepreneur and a businessman whoset up a Financial Counseling Ministry at his church inthe early nineties. After counseling hundreds of familiesand training many counselors he decided to summarizewhat he had learned in this book. He wrote it especiallyfor young people and young couples, in the hope that byreading this book they would avoid financial difficulties.

Free copies of this book may be downloaded atwww.ThreeRules.org

Mentoringcomments regarding this book and any relatedfinancial questions to the author at:

Simple

]|xHISBN 0-9749105-0-3

1

Pre-Marriage Financial Mentoring

Researchers have told us for years that family financial problems are the number one cause ofmarriage failure. The good news is that there is something we can do about it. The two primarycontributing factors to these financial problems can be addressed. As a result, many of thesefamily financial problems can be prevented provided they are addressed prior to or early in themarriage.

The two primary contributing factors to family financial problems that need to be addressed are:

1) Different Values

The two people who are about to be married may have significantly differentvalues when it comes to money. This may be a result of personality or it may be aresult of upbringing or both. One may be a spender, the other may be a saver.One may believe in giving, the other may not. One may have a problem withdebt, the other may think it is normal. Frequently young couples are not awarethat this is the case prior to the marriage. In their pre-marital bliss they are eitherin denial or they figure they will deal with it later.

2) Lack of a Financial Plan

The lack of a financial plan is the second contributing factor to family financialproblems. In the absence of a financial plan we tend to spend based on perceivedneeds rather than based on what we can afford. The best time to get into thehabit of living within our means, building savings and minimizing debt is beforewe get into financial difficulty.

The Pre-Marriage Financial Mentoring process outlined in this manual is designed to addressboth of these issues. It attempts to ferret out these value differences and give the couple anopportunity to talk about them before they tie the knot. It also walks them through the stepstoward creating a Personal Cash Flow Plan that can be used to determine what they can affordand what they need to postpone.

This section assumes that you (the mentor) have read the Three Simple Rules book as well as theFinancial Counseling section of this manual.

In our church it is our policy that our pastors will not marry a couple unless they do a number ofthings. One of those “things” is to meet with a financial mentor. That is why this Pre-MarriageFinancial Mentoring material was developed.

The Pre-Marriage Financial Mentoring sessions typically occur three to twelve months before thewedding. They generally consist of three sessions lasting one to one-and-a-half hours each. Itwould be ideal if the mentoring program extended well into the marriage but from a practicalstandpoint, once the couple is married, the leverage to motivate them to participate in this

2

process is gone. I typically offer to meet with them at any time in the future and some takeadvantage of that offer.

Process:

Since this program is a normal part of the marriage process at our church, the couple is told tocontact the financial counseling ministry for an appointment. When the bride-to-be calls (yes,it’s usually the bride-to-be) the couple is assigned to one of our mentors. The mentor calls thecouple and arranges a mutually convenient time to meet.

The mentor will then mail a letter to the couple confirming the date and time as well as directionsto the agreed-upon meeting place. (See sample letter in this section.)

The mentor will also include two copies of the Values Questionnaire (located in the Formssection) along with the letter. The couple is asked to complete the Values Questionnaireindependent from each other and to bring the forms to the meeting.

Typically there will be three meetings over a period of three weeks. I like to set the meetings forthe same day of the week and at the same time and place.

Meeting Number One

At the first meeting the mentor will:

1. Spend 5 – 10 minutes in informal talk for the purpose of making everyone comfortablewith each other.

2. Open with prayer.

3. Use the Values Questionnaire as the agenda for the main part of the first meeting.

I typically start by asking the bride-to-be what her answer was to the first question. ThenI will ask the groom-to-be the same question.

If they do not have the same answer we talk about whether that will become a problemand suggest that they spend some more time with that issue. That could happen on thespot or later.

If they agree on the answer I make a judgment as to whether their answer is appropriate.

In the case of Question 1 it doesn’t really matter how they answer, just as long as theyagree. However, in the case of many of the other questions there is definitely a right anda wrong answer.

3

For example, if they agreed that they needed zero credit cards or one credit card I wouldconclude that that is an appropriate answer. If they agreed that they should have sevencredit cards I would not agree that that is an appropriate answer and I would discuss thedanger of credit cards.

Once we are finished with the first question I would address the next question to thegroom-to-be and then to the bride-to-be. I continue alternating until we are done with allof the questions. This typically takes about one hour.

In the process you will likely discover some areas where there is disagreement and orareas where both of them could be agreeing to make decisions that could result infinancial disaster. That is where I typically focus my time. If the problems are seriousenough I make a note to visit the area again in future sessions or suggest that they seekother counsel for the sake of their marriage.

4. An Early Wedding Gift

Once we have gone through the Values Questionnaire I give them an early wedding gift -a copy of Three Simple Rules - Guaranteed to Improve your Finances. I explain theThree Rules and refer them to the Scripture verses in Part Five of the book that supportthe Three Rules.

5. Assign Homework:Read the Introduction and Parts One and Two of Three Simple Rules.

Meeting Number Two

At the second meeting the mentor will:

1. Open in prayer.

2. Ask them if they have any questions about the homework assignment.• “What did you learn from reading Parts One and Two of Three Simple Rules.”• “How do you plan to apply what you learned?”

3. Introduce the two primary Family Financial Planning Forms:

• Personal Asset and Debt Inventory

• Personal Cash Flow Plan

The objective of this meeting is to familiarize the couple with these two forms so thatthey can complete them as a homework assignment. The forms can be partiallycompleted based on the numbers that the couple knows. The rest they may have toresearch as part of the homework assignment.

4

See the Counseling Section of this manual for more information about how to explainthese two forms.

4. Discuss GoalsAny additional time can be used to talk about goals the couple may have regarding:• Saving.• Giving.• Debt Management and Debt Retirement.

5. Assign Homework:• Complete the Personal Asset and Debt Inventory.• Complete the Personal Cash Flow Plan.• Read Parts Three, Four, Five and the Addendum of Three Simple Rules.

Meeting Number Three

The objective of the third meeting is to:

• Make sure that the two primary Family Financial Planning Forms are fully completed,• That the numbers on these forms are realistic, and• That the Personal Cash Flow Plan is balanced while accomplishing the couple’s saving goals,

giving goals and debt retirement goals.

At the third meeting, the mentor will:

1. Open in prayer.

2. Ask them if they have any questions about the homework assignment.• “What did you learn from reading Parts Four and Five of Three Simple Rules.”• “Do you have any questions about completing the two forms?”• “How do you plan to apply what you learned?”

3. Review the Family Planning Forms.• Touch on each number in the two forms, first in the Asset and Debt Inventory and thenin the Cash Flow Plan.• Anything that does not look complete or realistic should be addressed.

4. Future Planning.• Teach the couple the importance of reviewing The Financial Plan periodically aschanges occur in income or expense. For example, when they decide to start a family,this may increase expenses and reduce income and preparations would need to be made.

After asking if they have any questions about anything we covered, I ask if I can pray fortheir future together and then we end our session in prayer.

Dear John and Kelley,

I’m looking forward to meeting with you at 7:30 PM on Monday September 30.

I have enclosed two surveys, one for each of you.

Please complete the enclosed surveys independently prior to that time and bring them with youto our get together. You are certainly welcome to talk about your answers prior to our meeting.

We will meet at my office which is located at 3215 Memory Lane.

Directions:

_________________________________________________________________

_________________________________________________________________

_________________________________________________________________

_________________________________________________________________

Looking forward to meeting you.

Tom Counselor

Three Rules

THREE SIMPLE RULES THEO A. BOERS

Section Three:

Financial

Theo A. Boers is an entrepreneur and a businessman whoset up a Financial Counseling Ministry at his church inthe early nineties. After counseling hundreds of familiesand training many counselors he decided to summarizewhat he had learned in this book. He wrote it especiallyfor young people and young couples, in the hope that byreading this book they would avoid financial difficulties.

Free copies of this book may be downloaded atwww.ThreeRules.org

Workshopcomments regarding this book and any relatedfinancial questions to the author at:

Simple

]|xHISBN 0-9749105-0-3

12nd Edition

Revised 10/04/04www.ThreeRules.org

Three Simple Rules Financial Workshop

The Three Simple Rules Financial Workshop is designed to be offered once per week for fourweeks.

The objective of the workshop is to:

(a) help participants understand the importance of the Three Simple Rules.

(b) give an overview of basic budgeting principles.

(c) teach participants how to create a budget unique to their circumstances.

(d) introduce several simple systems that will assist participants in living according to theirbudget.

(e) share the Biblical perspective of handling money.

The four week workshop could be offered as part of an Adult Sunday School Curriculum or as astand alone weekday evening education series.

The material is sufficiently flexible that class time can range from 45 minutes to 1 1/2 hours andclass size can range from as little as six to as many as thirty.

The following pages describe how to conduct the four-session financial workshop. The ThreeSimple Rules book is an integral part of this workshop. The instruction pages assume that theworkshop leader has read the book and the Financial Counseling section of this manual. It is alsoassumed that each workshop participant will receive a copy of Three Simple Rules at the end ofthe first session.

The following announcement was designed to recruit people to attend the financial workshop.

Need a little help getting your financial house in order? You are invited toattend the Three Simple Rules Financial Workshop. This four-sessionworkshop is being offered on (day of week) at (starting and ending time)starting on (date) at (location). At this workshop you will learn about the threesimple rules that are guaranteed to improve your financial situation. You willalso learn how to give yourself a financial physical and how to identify andchange the financial habits that are preventing you from accomplishing yourfinancial goals. Call (person) at (phone number) for more information.

The following pages outline the Objective and the Talking Points for each session.

A PowerPoint Presentation for the Financial Workshops is available free of charge. Just [email protected] and ask for the Workshop PowerPoint Presentation. We would also behappy to give you a digital version of this section so that you can customize it to your situation.

22nd Edition

Revised 10/04/04www.ThreeRules.org

Session One – The Three Rules

(Note: The symbol (PPt) is a reminder to go to the next Power Point page. If you are using anoverhead projector you may want to make transparencies of the pages in the Financial WorkshopTools Section and the Forms Section.)

Objective – To help the group understand the three simple rules and how to apply them.

Preparation –• read or reread the Introduction and Part One of Three Simple Rules.

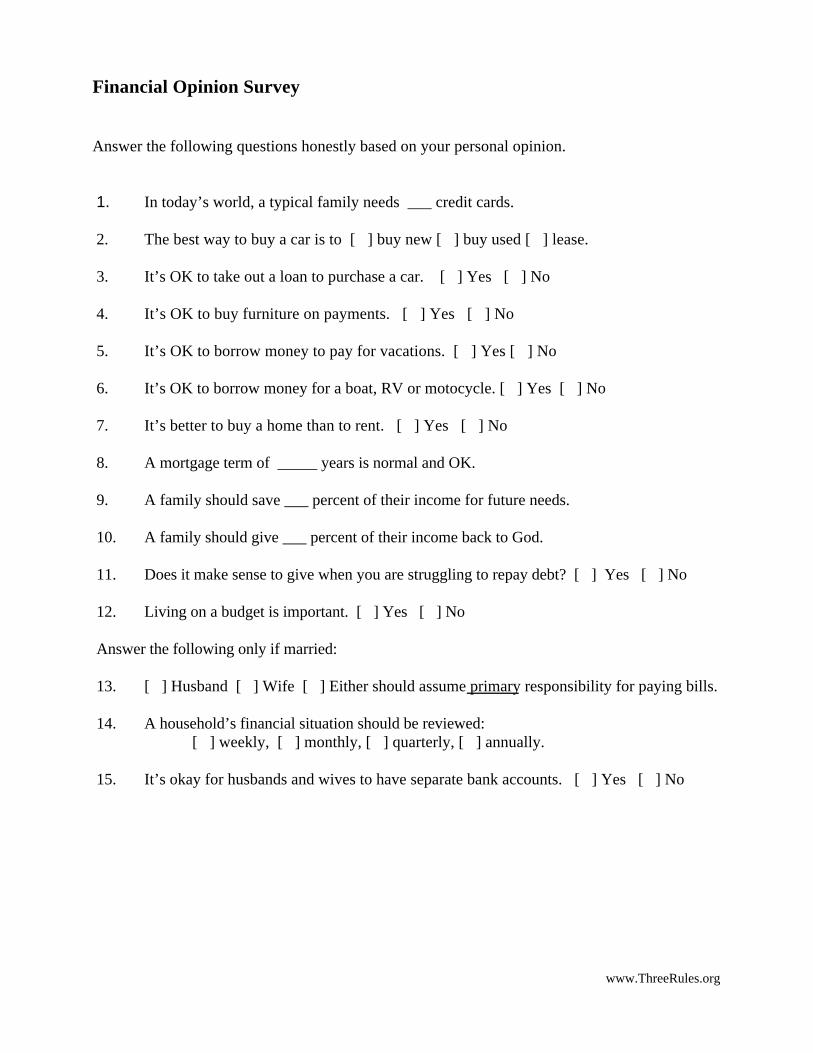

Handout Materials Needed – Bring along a copy of the following for each participant:• Three Simple Rules book• Student Notes Cover Page for Session One (See the back of this section.)• Financial Opinion Survey (Forms Section)• Personal Financial Habit Assessment (Forms Section)

Talking Points:

1. Welcome to Week One of the Three Simple Rules Financial Workshop. (PPt)

• The workshop is based on the book - Three Simple Rules - Guaranteed to Improve YourFinances.

• You will all receive a copy of the book tonight.

• We will cover Part One of the book tonight.

• The rest of the book will be covered over the next three sessions.

• Since each part of the book builds on the previous parts you will benefit the most if youcan attend all four sessions.

2. Give each participant a copy of the Financial Opinion Survey.

Let them know that this is simply a chance to start thinking through some of the questionsthat will be discussed in the next few sessions. Ask participants to individually answerthe questions. Collect the answers and tell them you will summarize the answers andshare the results with them next week.

3. How the Three Simple Rules Book Came into Existence.

The author is an entrepreneur and a businessman who set up a Financial CounselingMinistry at his church in the early nineties. After counseling hundreds of families and

32nd Edition

Revised 10/04/04www.ThreeRules.org

training many counselors he decided to summarize what he had learned in this book. Hewrote it especially for young people and young couples, in the hope that by reading thisbook they would avoid financial difficulties.

4. Some Questions (PPt)

Q. Should a Christian’s Spending Habits be different than a non-Christian? (PPt)

A. Giving (firstfruits)A. Contentment (want what you have)A. Christian Education may be part of the budgetA. Christians need to question their buying motives

Q. What is your favorite Bible verse about money? (PPt)

A. See Part Five of the Three Simple Rules book for some Bible verses about money.

Q. Would Jesus drive a BMW? (PPt)

A. This is an opportunity to talk about testing our decisions from the perspective ofWWJD – What Would Jesus Do?

5. Steve and Jessica’s Story (PPt)

• Read the Steve and Jessica story from the Introduction of Three Simple Rules to thegroup. (Read through to the end of the paragraph on the third page that starts with “Earlylast year…”)• Ask audience to write down Steve and Jessica’s financial mistakes, as you tell the story.• After telling the story ask the audience to ID Steve and Jessica’s financial mistakes.• Review the mistakes list. (PPt)• For some startling information regarding Steve and Jessica’s credit card debt situation,see “Steve and Jessica’s Credit Card Debt” located in the Financial Workshop Toolssection. Share this information with the class.

Encourage further group discussion regarding Steve and Jessica’s financial mistakes byasking:

Q. Do you think these financial mistakes are typical? (PPt)

Q. Which mistake do you think is most dangerous? (PPt)

Q. What caused Steve and Jessica to make these mistakes? (PPt)

42nd Edition

Revised 10/04/04www.ThreeRules.org

6. Talk about the Personal Financial Habits Assessment. (PPt)

• Introduce by explaining that many financial problems are simply a result of bad habits.• In order to fix the problem we have to change the habits (just like a diet).• Hand out blank forms. Have audience take the test.• Tell them how to score the test. (PPt)(Questions 1 – 8 are good habits, therefore the correct answer is Yes; 9 – 16 are badhabits, therefore the correct answer is No.)

Group discussion regarding habits:

Q. What is the most difficult Good Habit to maintain?

A. For many people it is Savings and/or knowing how much cash they spend.

Q. What is the most difficult Bad Habit to break?

A. Anything dealing with debt. (7 of the 8 bad habits deal with borrowing money.)

7. Introduction to The Three Rules (PPt)

1) Spend Less than You Earn. (PPt)2) Save Now! Buy Later. (PPt)3) Know Debt. (PPt)

Explain that we will now look at each of the three rules in detail.

8. Rule One –– Spend Less Than You Earn. (PPt)

This is the key rule because it makes complying with the other rules possible.

Most financial problems are a result of people spending too much money.

Q. What happens when you spend more than you earn?