Embed Size (px)

Citation preview

Self-Managed Super Funds

Take Control of Your Future

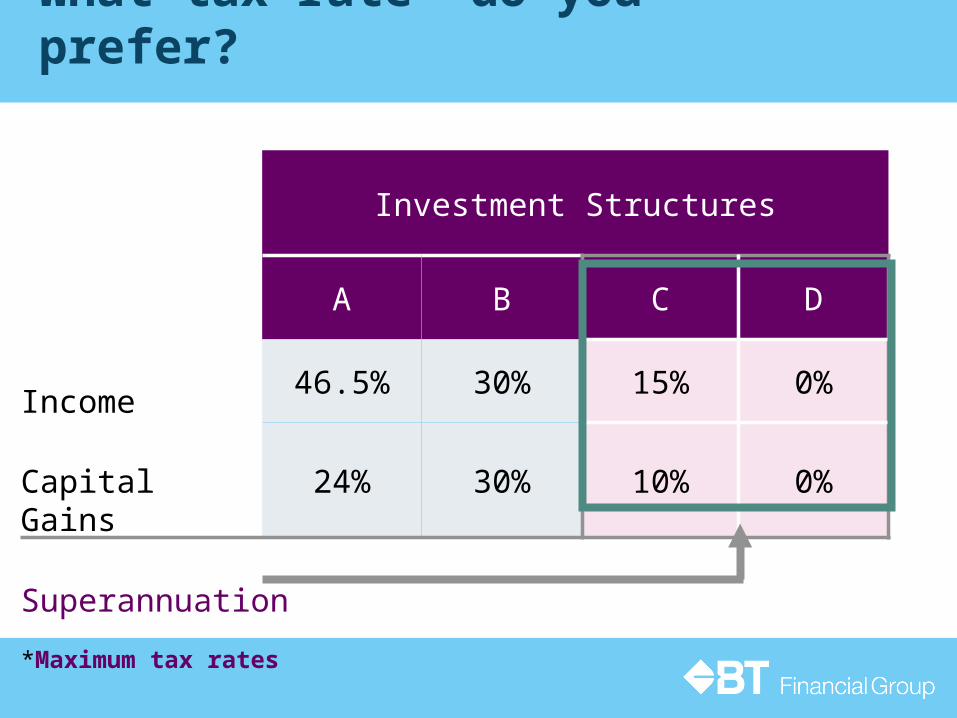

What tax rate* do you prefer?

Investment Structures

A B C D

Income 46.5% 30% 15% 0%

Capital Gains 24% 30% 10% 0%

Superannuation

*Maximum tax rates

3

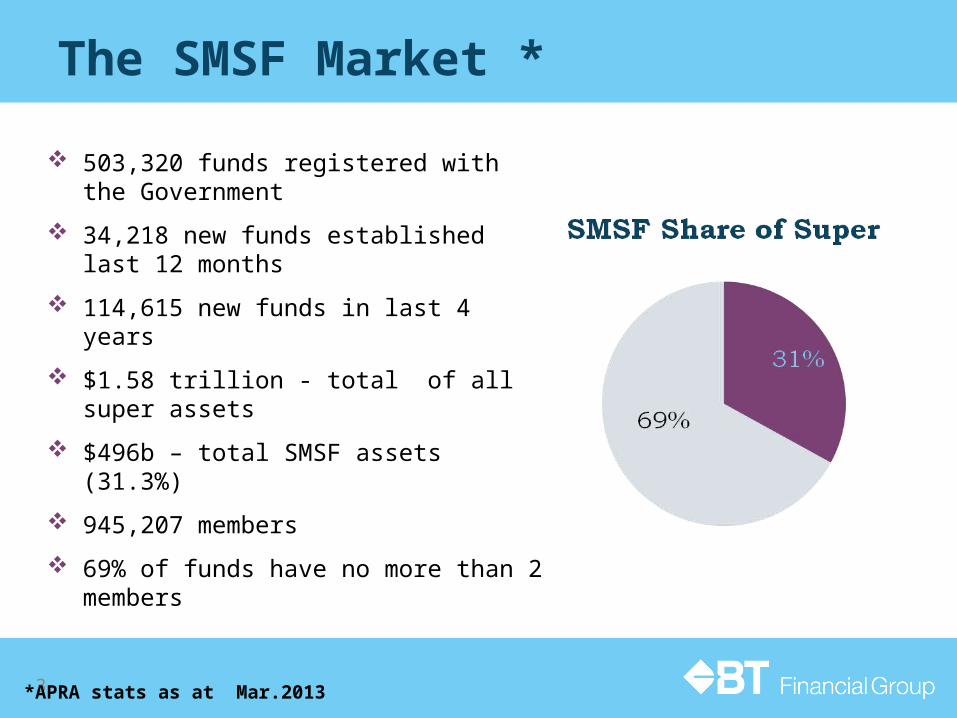

The SMSF Market * 503,320 funds registered with the

Government 34,218 new funds established last 12

months 114,615 new funds in last 4 years $1.58 trillion - total of all super assets $496b – total SMSF assets (31.3%) 945,207 members 69% of funds have no more than 2

members

*APRA stats as at Mar.2013

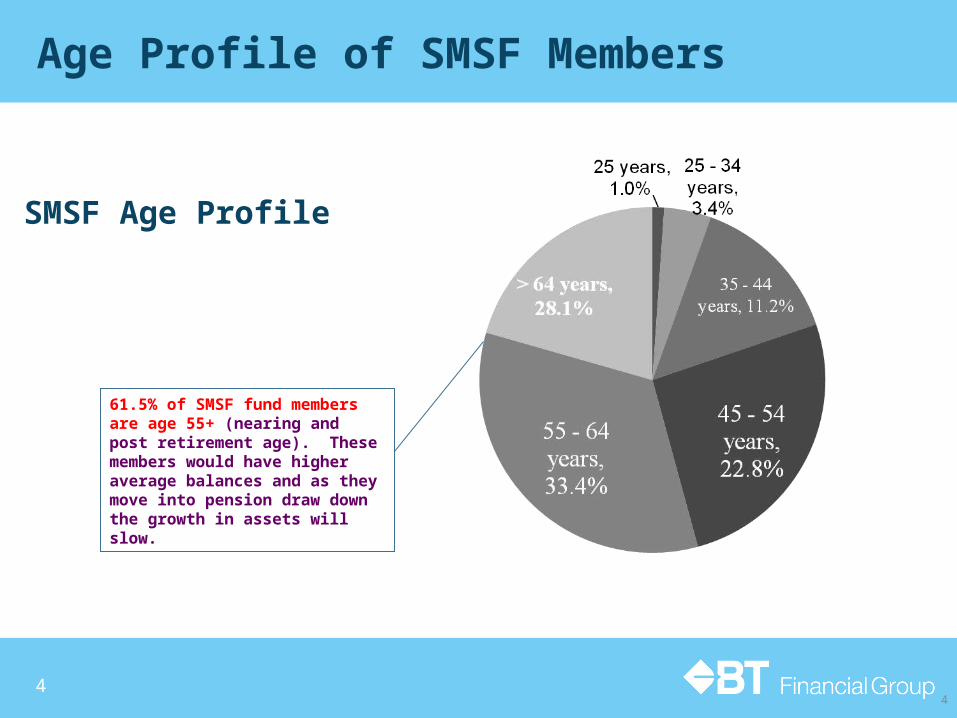

Age Profile of SMSF Members

4

SMSF Age Profile

61.5% of SMSF fund members are age 55+ (nearing and post retirement age). These members would have higher average balances and as they move into pension draw down the growth in assets will slow.

4

5

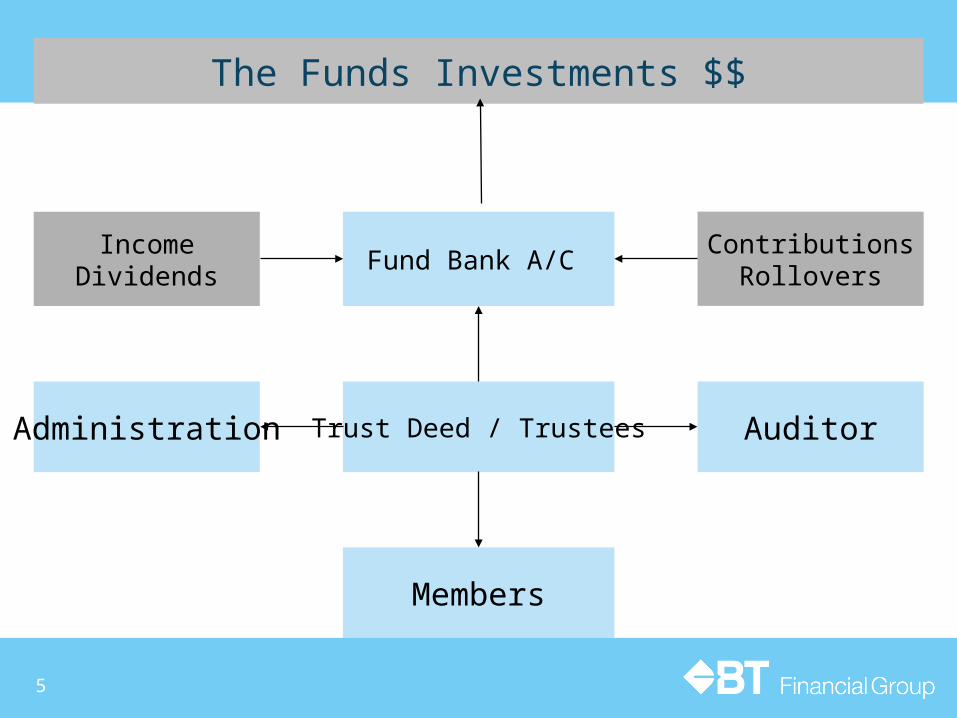

IncomeDividends

ContributionsRolloversFund Bank A/C

Trust Deed / TrusteesAdministration Auditor

Members

The Funds Investments $$

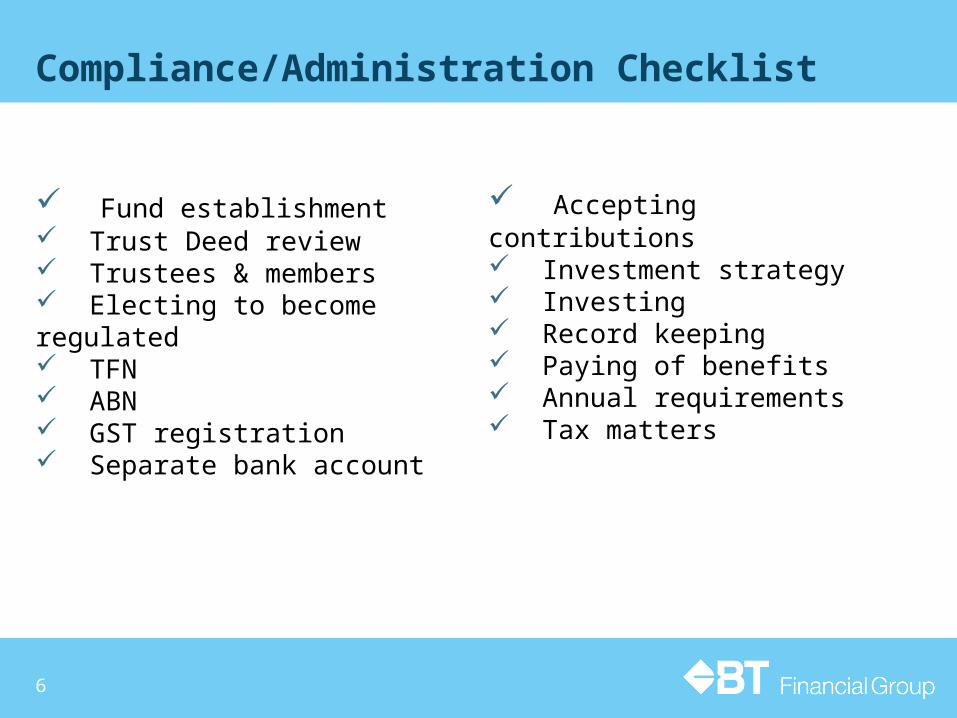

Compliance/Administration Checklist

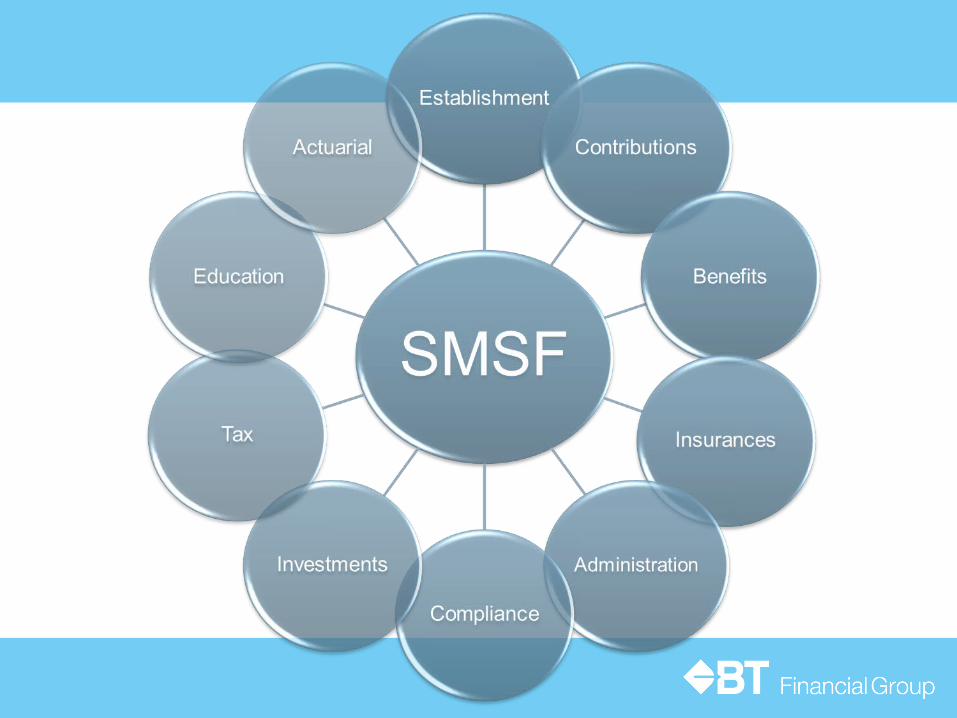

Fund establishment Trust Deed review Trustees & members Electing to become regulated TFN ABN GST registration Separate bank account

Accepting contributions Investment strategy Investing Record keeping Paying of benefits Annual requirements Tax matters

6

7

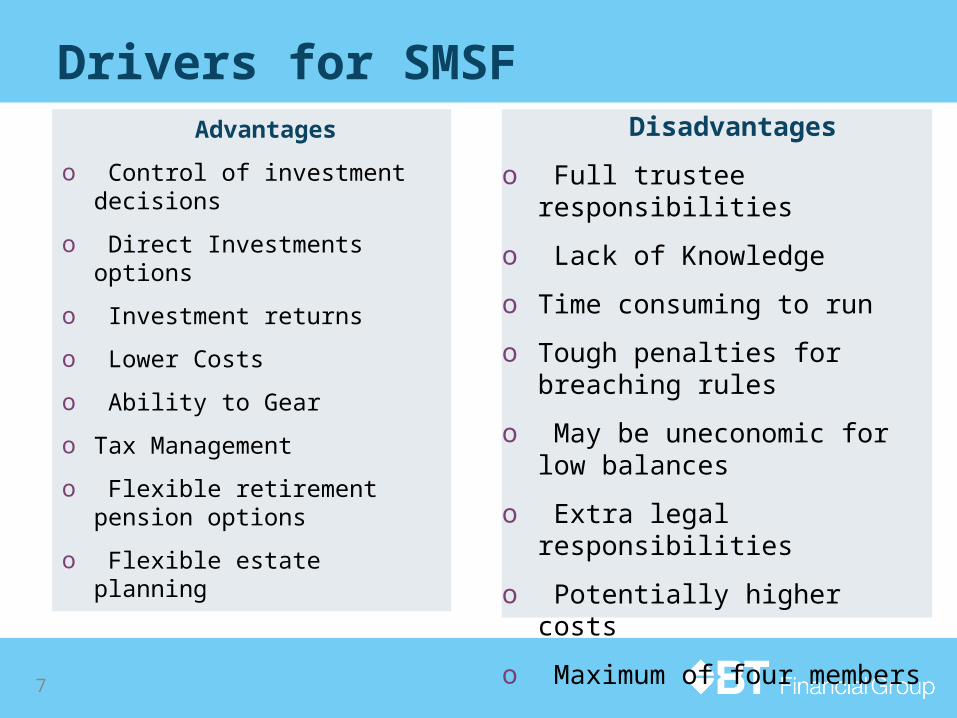

Drivers for SMSF Advantages

o Control of investment decisions

o Direct Investments options

o Investment returns

o Lower Costs

o Ability to Gear

o Tax Management

o Flexible retirement pension options

o Flexible estate planning

Disadvantages

o Full trustee responsibilities

o Lack of Knowledge

o Time consuming to run

o Tough penalties for breaching rules

o May be uneconomic for low balances

o Extra legal responsibilities

o Potentially higher costs

o Maximum of four members

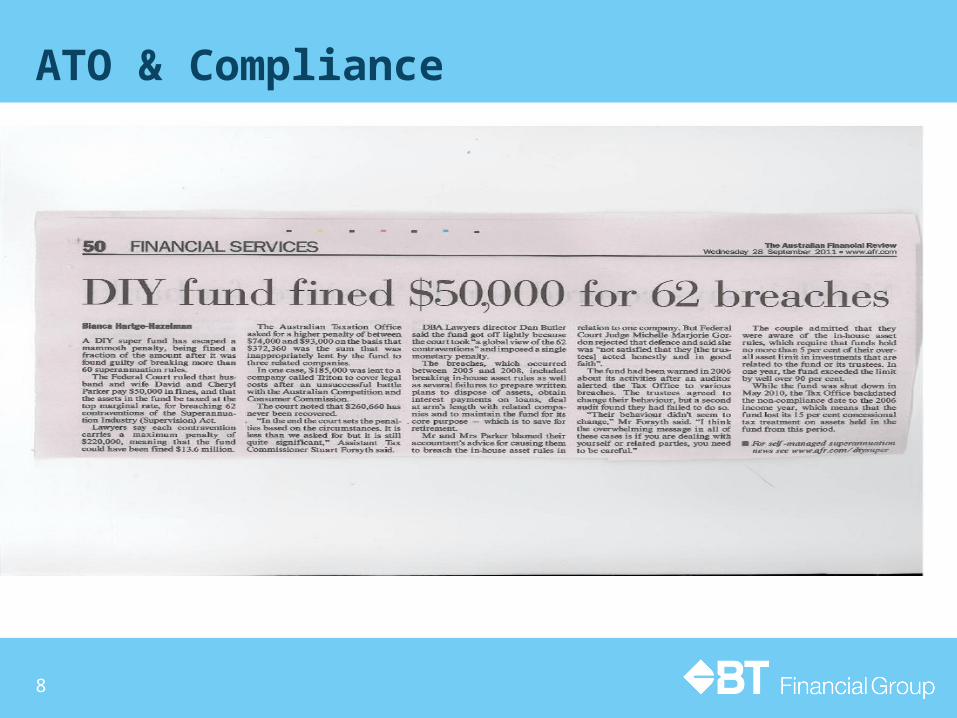

ATO & Compliance

8

How Should Trustees Be Investing ?

9

10

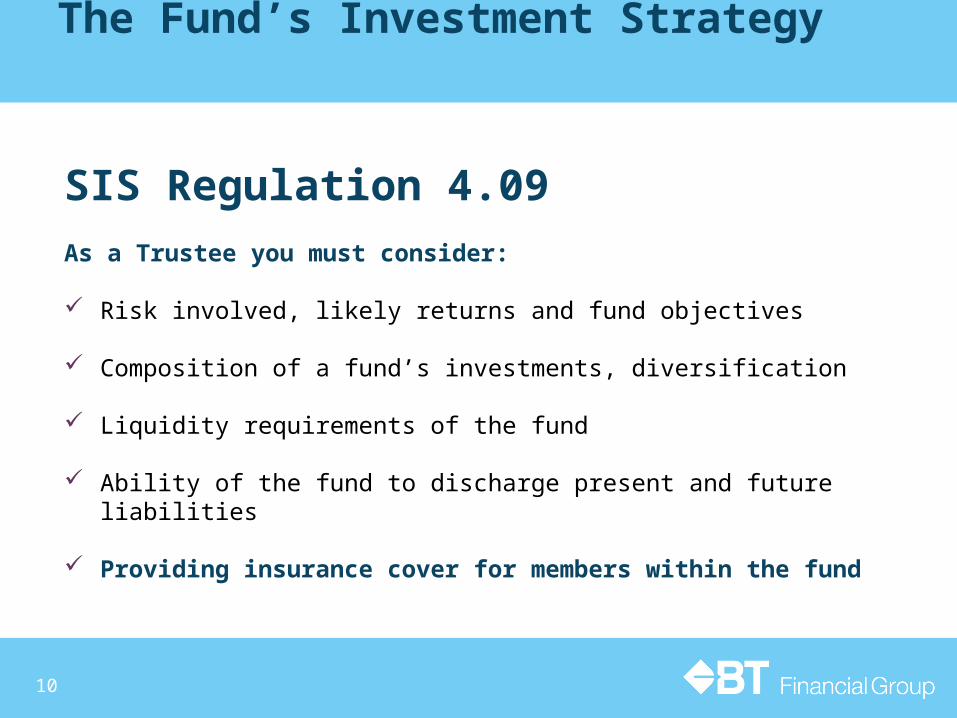

The Fund’s Investment Strategy

SIS Regulation 4.09 As a Trustee you must consider:

Risk involved, likely returns and fund objectives

Composition of a fund’s investments, diversification

Liquidity requirements of the fund

Ability of the fund to discharge present and future liabilities

Providing insurance cover for members within the fund

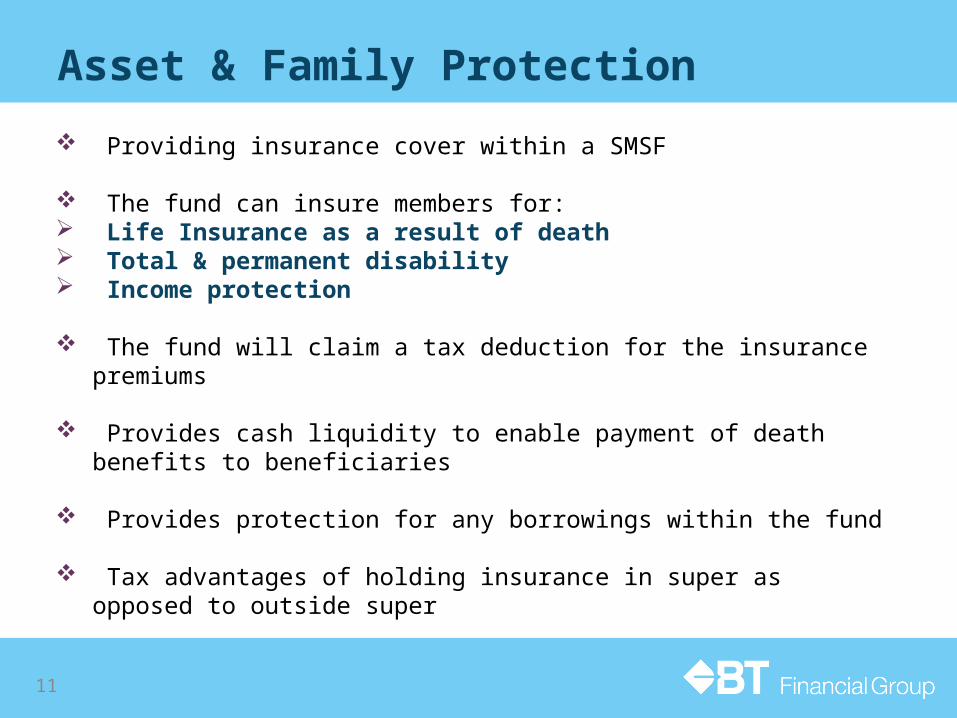

Asset & Family Protection

Providing insurance cover within a SMSF

The fund can insure members for: Life Insurance as a result of death Total & permanent disability Income protection

The fund will claim a tax deduction for the insurance premiums

Provides cash liquidity to enable payment of death benefits to beneficiaries

Provides protection for any borrowings within the fund

Tax advantages of holding insurance in super as opposed to outside super

11

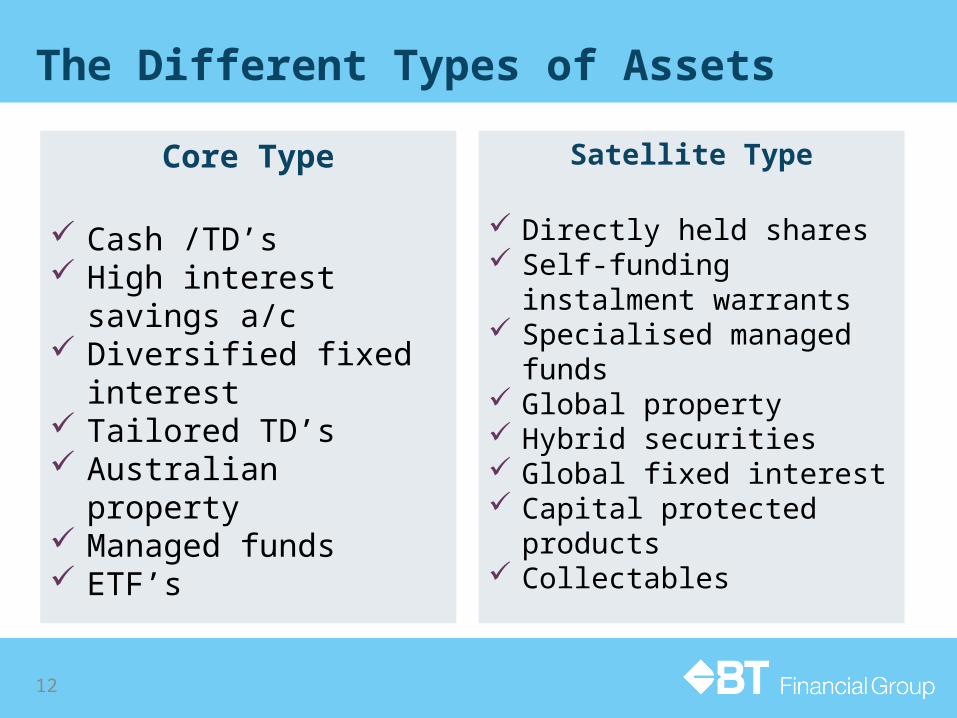

The Different Types of Assets

Core Type

Cash /TD’s High interest savings a/c Diversified fixed interest Tailored TD’s Australian property Managed funds ETF’s

Satellite Type

Directly held shares Self-funding instalment

warrants Specialised managed funds Global property Hybrid securities Global fixed interest Capital protected products Collectables

12

Concessional Caps Increased

* Estimate only indexation expected from 1 July 2014 **Those aged 59 on 30 June 2013 also eligible for $35,000 (2013/14) Those aged 49 on 30 June 2014 also eligible for $35,000 (2014/15)

Concessional Cap 2012-13 2013-14 2014-15

Under age 50 $25,000 $25,000 $30,000*

Aged 50 - 59 $25,000 $25,000 $35,000**

Aged 60 + $25,000 $35,000** $35,000**

14

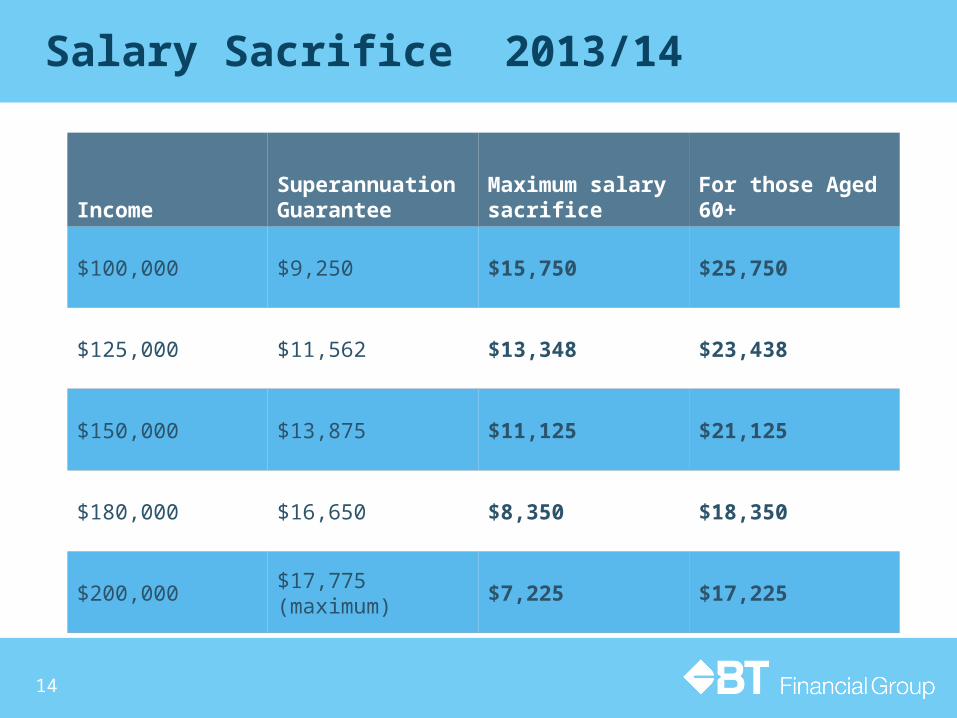

Salary Sacrifice 2013/14

IncomeSuperannuation Guarantee

Maximum salary sacrifice

For those Aged 60+

$100,000 $9,250 $15,750 $25,750

$125,000 $11,562 $13,348 $23,438

$150,000 $13,875 $11,125 $21,125

$180,000 $16,650 $8,350 $18,350

$200,000 $17,775 (maximum) $7,225 $17,225

15

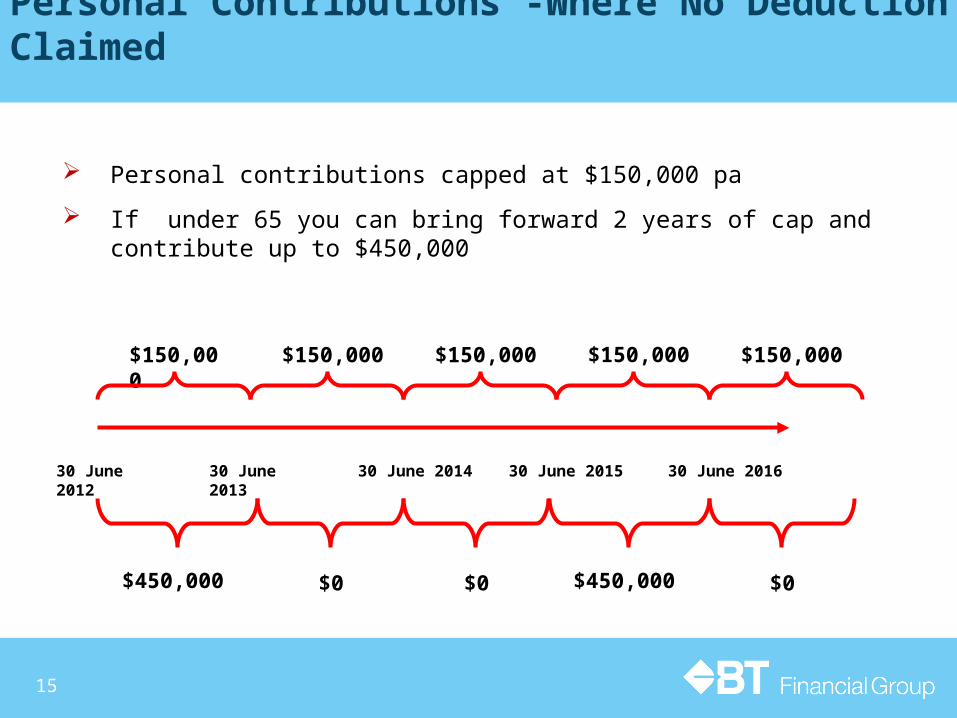

Personal Contributions -Where No Deduction Claimed

Personal contributions capped at $150,000 pa

If under 65 you can bring forward 2 years of cap and contribute up to $450,000

$150,000 $150,000 $150,000 $150,000

30 June 2012 30 June 2013 30 June 2014 30 June 2015

$450,000 $0 $0 $450,000 $0

30 June 2016

$150,000

SMSF Borrowing To Invest

16

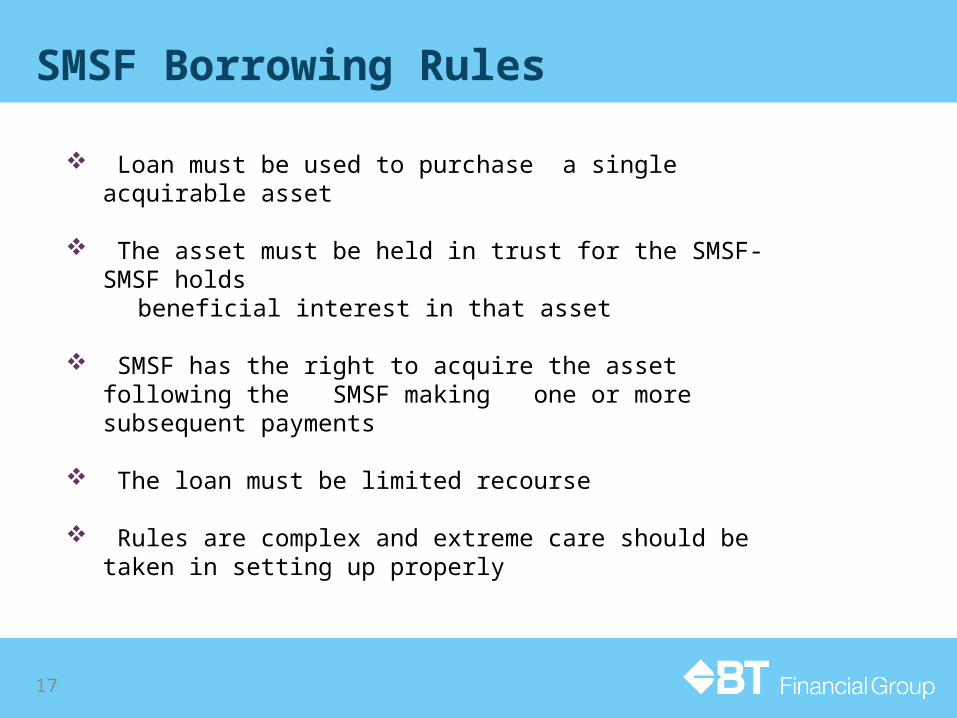

SMSF Borrowing Rules

Loan must be used to purchase a single acquirable asset

The asset must be held in trust for the SMSF- SMSF holds beneficial interest in that asset

SMSF has the right to acquire the asset following the SMSF making one or more subsequent payments

The loan must be limited recourse

Rules are complex and extreme care should be taken in setting up properly

17

18

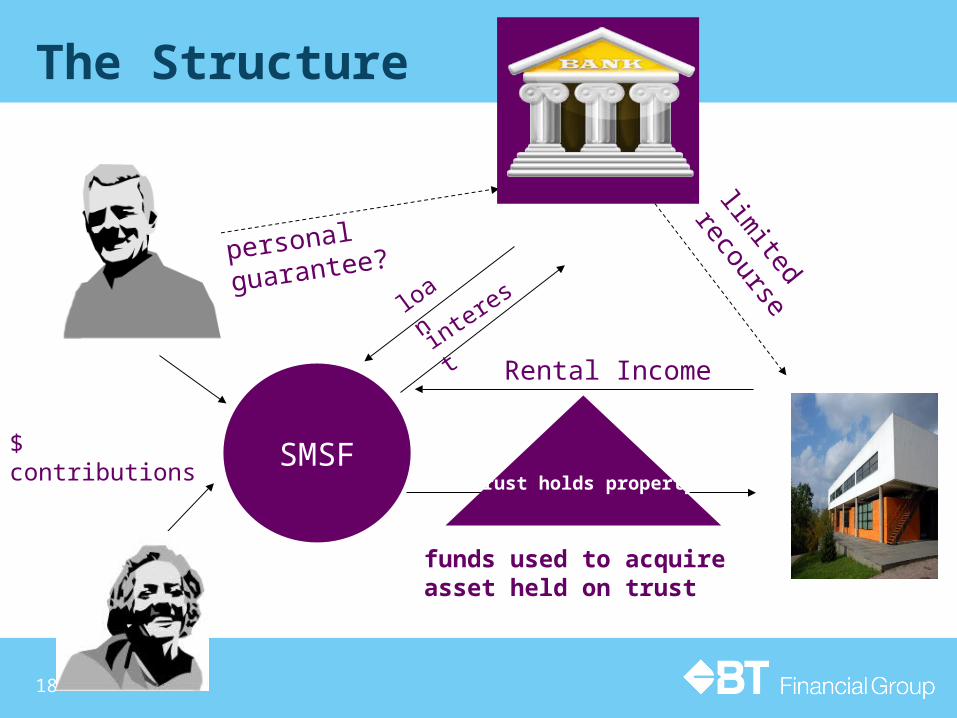

The Structure

SMSF$ contributions

loan

funds used to acquire asset held on trust

Rental Income

Trust holds property

interestpersonal guarantee? limited

recourse

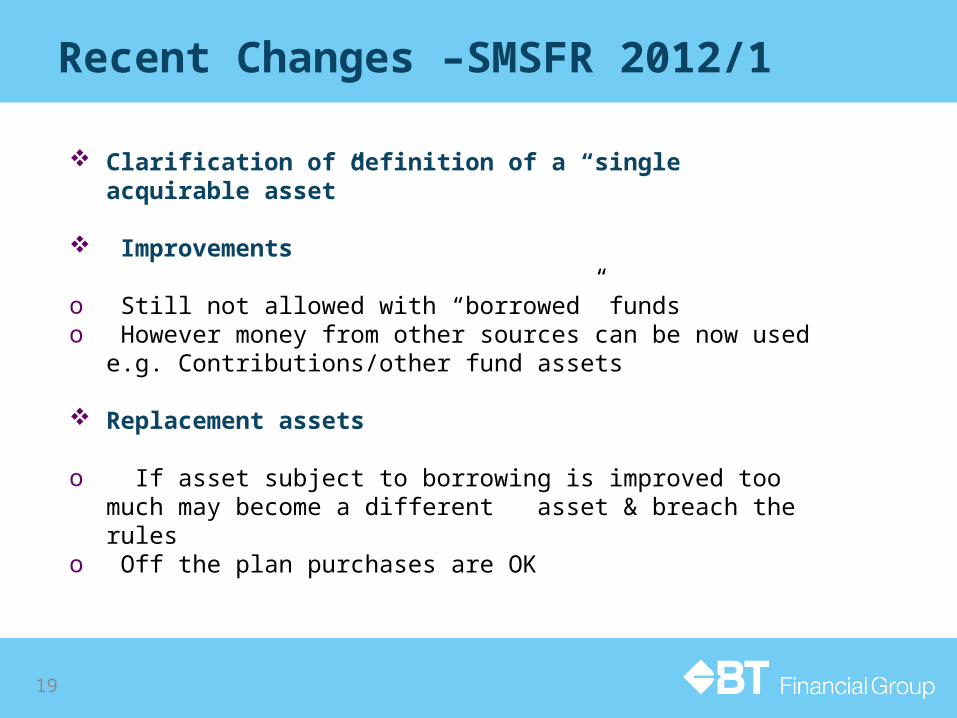

Recent Changes –SMSFR 2012/1

Clarification of definition of a “single acquirable asset”

Improvements

o Still not allowed with “borrowed” fundso However money from other sources can be now used e.g.

Contributions/other fund assets

Replacement assets

o If asset subject to borrowing is improved too much may become a different asset & breach the rules

o Off the plan purchases are OK

19

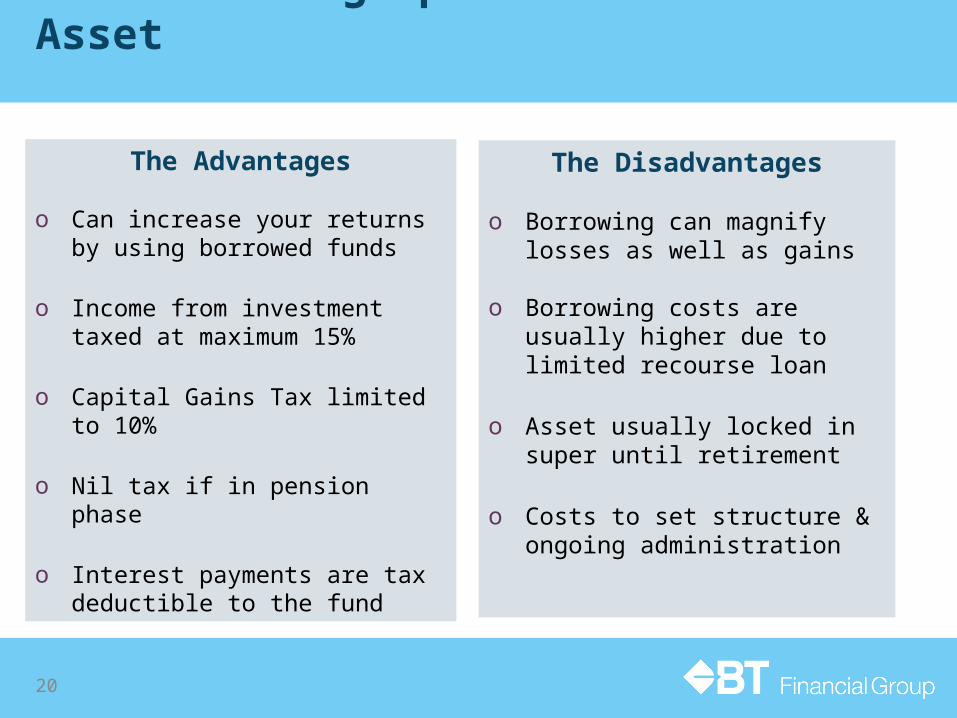

The Borrowing Option to Purchase Asset

The Advantages

o Can increase your returns by using borrowed funds

o Income from investment taxed at maximum 15%

o Capital Gains Tax limited to 10%

o Nil tax if in pension phase

o Interest payments are tax deductible to the fund

The Disadvantages

o Borrowing can magnify losses as well as gains

o Borrowing costs are usually higher

due to limited recourse loan

o Asset usually locked in super until retirement

o Costs to set structure & ongoing administration

20

The Transition to Retirement Option (TTR)

“How to get a free kick-start for your retirement”

22

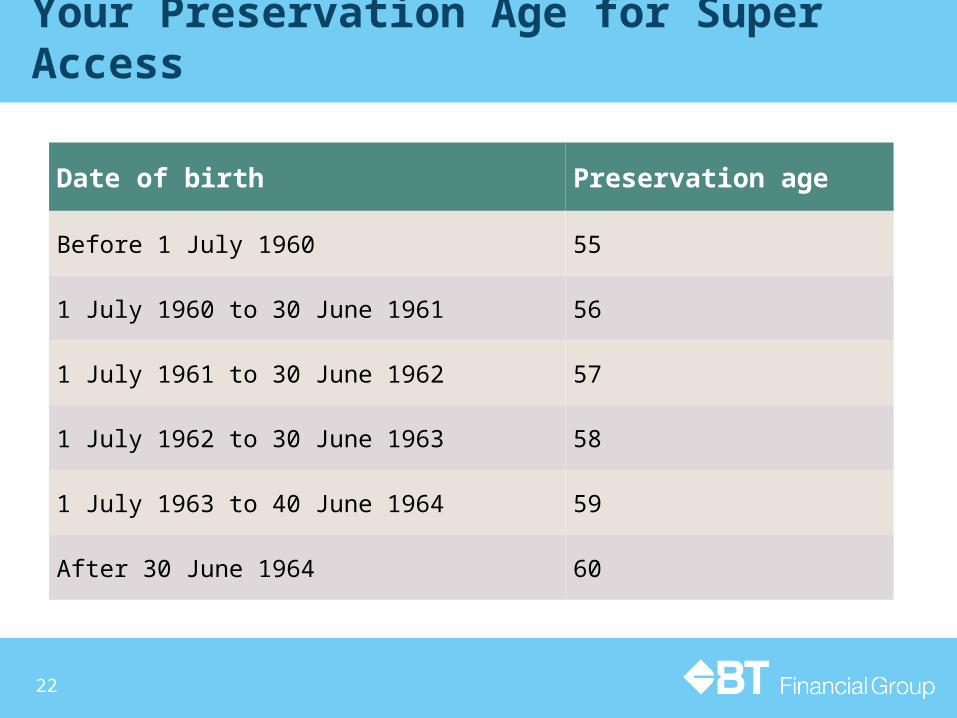

Your Preservation Age for Super Access

Date of birth Preservation age

Before 1 July 1960 55

1 July 1960 to 30 June 1961 56

1 July 1961 to 30 June 1962 57

1 July 1962 to 30 June 1963 58

1 July 1963 to 40 June 1964 59

After 30 June 1964 60

23

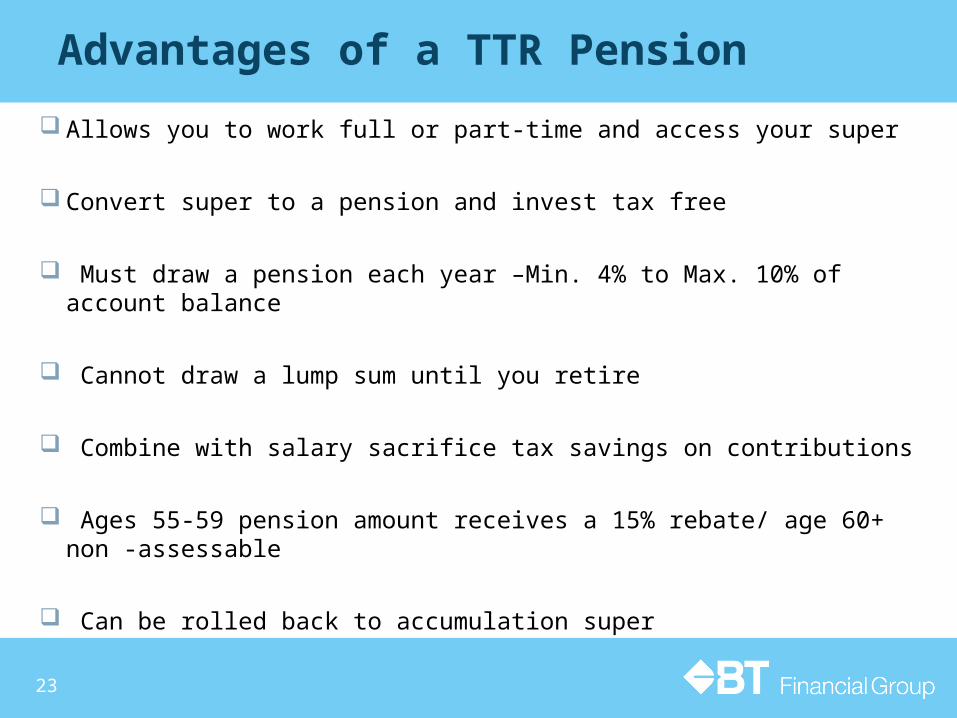

Advantages of a TTR Pension Allows you to work full or part-time and access your super

Convert super to a pension and invest tax free

Must draw a pension each year –Min. 4% to Max. 10% of account balance

Cannot draw a lump sum until you retire

Combine with salary sacrifice tax savings on contributions Ages 55-59 pension amount receives a 15% rebate/ age 60+ non -assessable

Can be rolled back to accumulation super

24

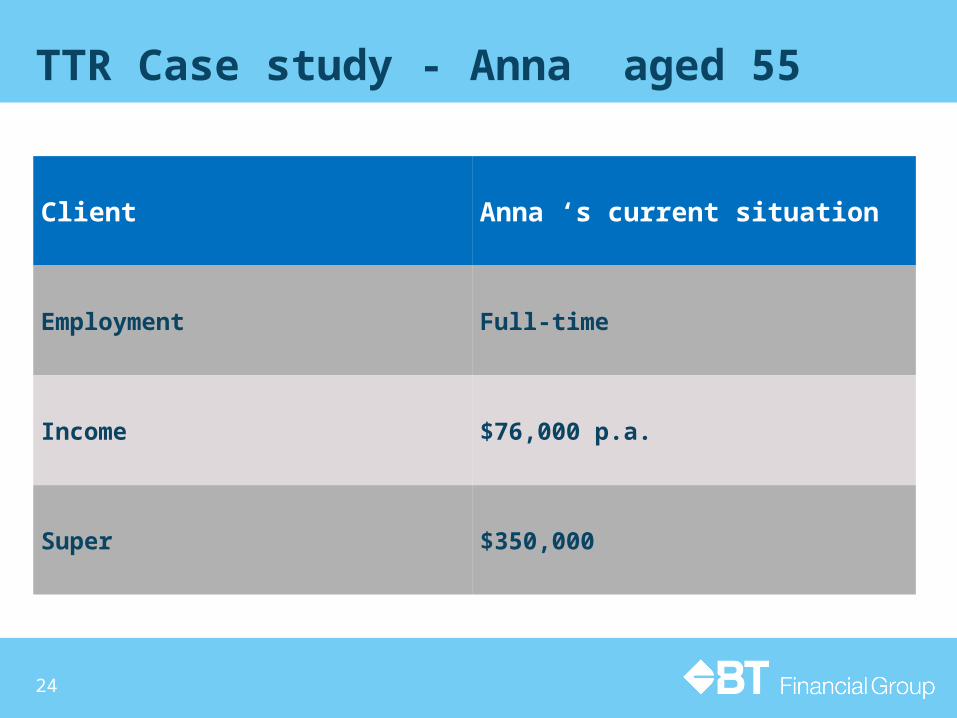

TTR Case study - Anna aged 55

Client Anna ‘s current situation

Employment Full-time

Income $76,000 p.a.

Super $350,000

25

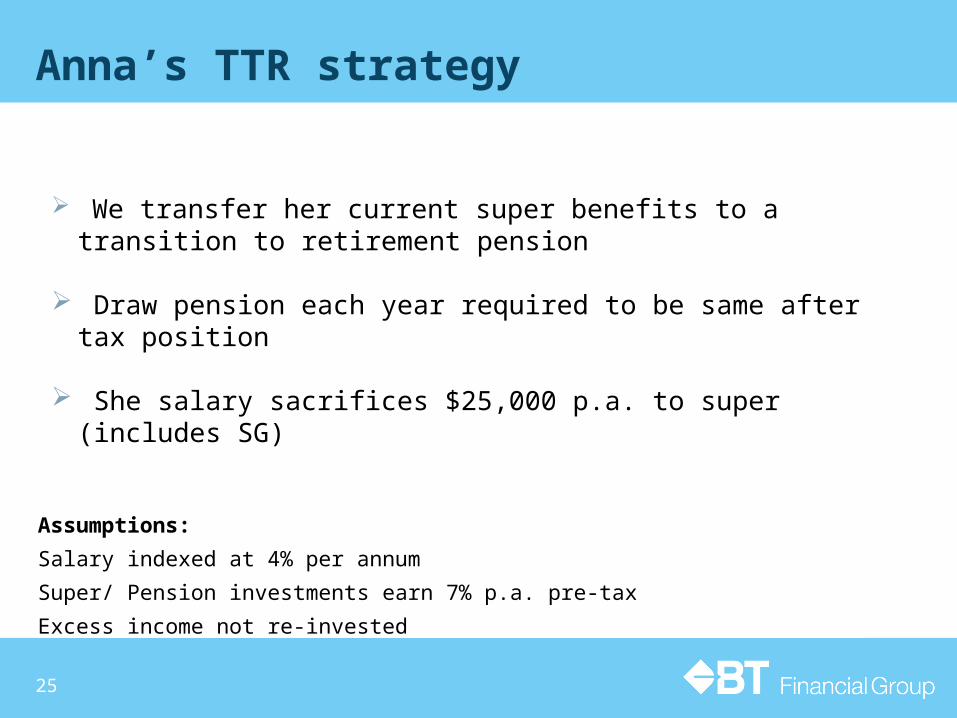

Anna’s TTR strategy

We transfer her current super benefits to a transition to retirement pension

Draw pension each year required to be same after tax position

She salary sacrifices $25,000 p.a. to super (includes SG)

Assumptions:Salary indexed at 4% per annumSuper/ Pension investments earn 7% p.a. pre-taxExcess income not re-invested

26

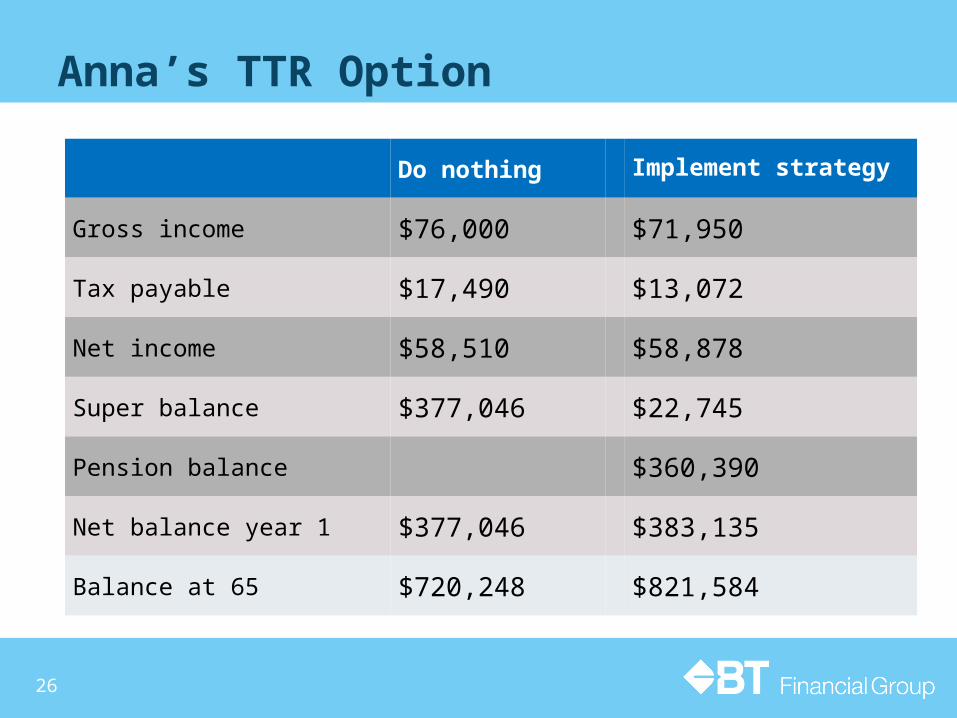

Anna’s TTR Option

Do nothing Implement strategy

Gross income $76,000 $71,950

Tax payable $17,490 $13,072

Net income $58,510 $58,878

Super balance $377,046 $22,745

Pension balance $360,390

Net balance year 1 $377,046 $383,135

Balance at 65 $720,248 $821,584

27

$300,000.00

$400,000.00

$500,000.00

$600,000.00

$700,000.00

$800,000.00

$900,000.00

56 57 58 59 60 61 62 63 64 65

Super balances

Current

Transition to retirement

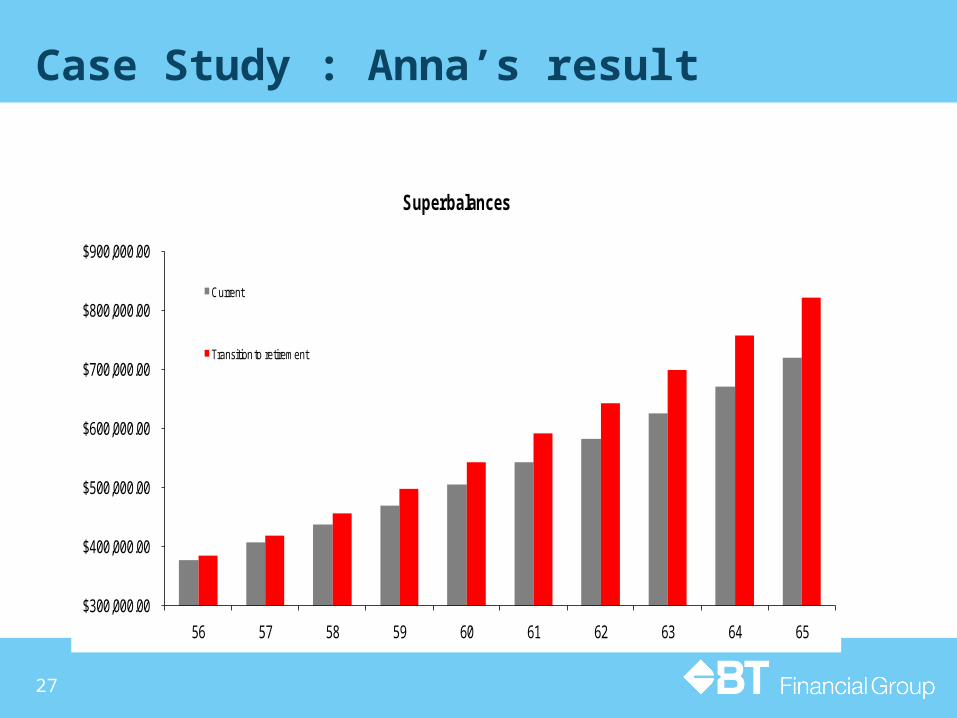

Case Study : Anna’s result

SMSF & Estate Planning

28

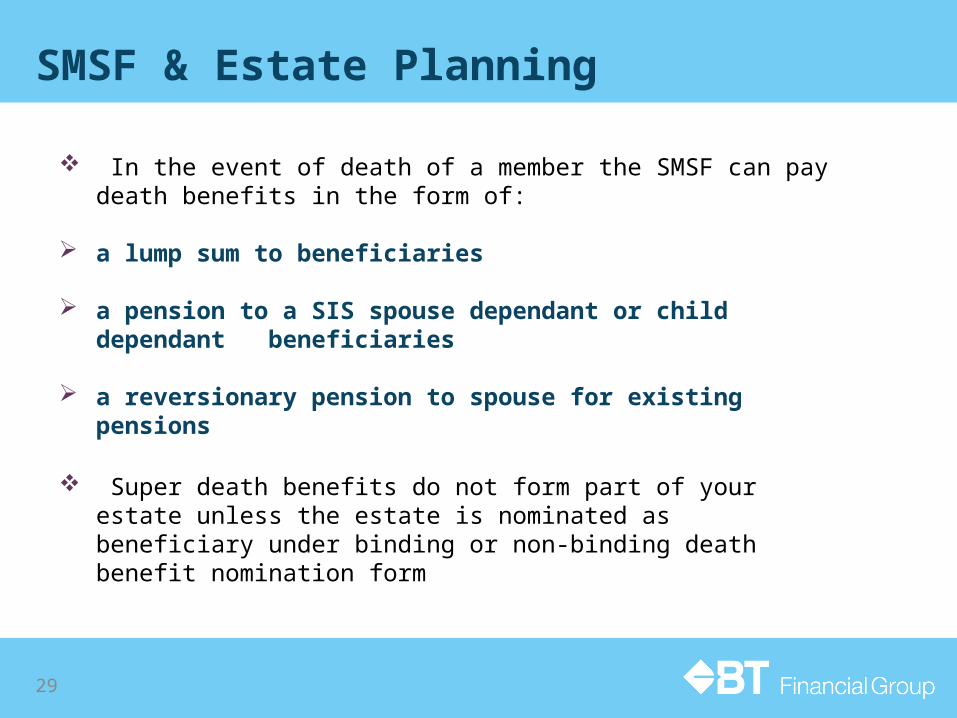

SMSF & Estate Planning

In the event of death of a member the SMSF can pay death benefits in the form of:

a lump sum to beneficiaries

a pension to a SIS spouse dependant or child dependant beneficiaries

a reversionary pension to spouse for existing pensions

Super death benefits do not form part of your estate unless the estate is nominated as beneficiary under binding or non-binding death benefit nomination form

29

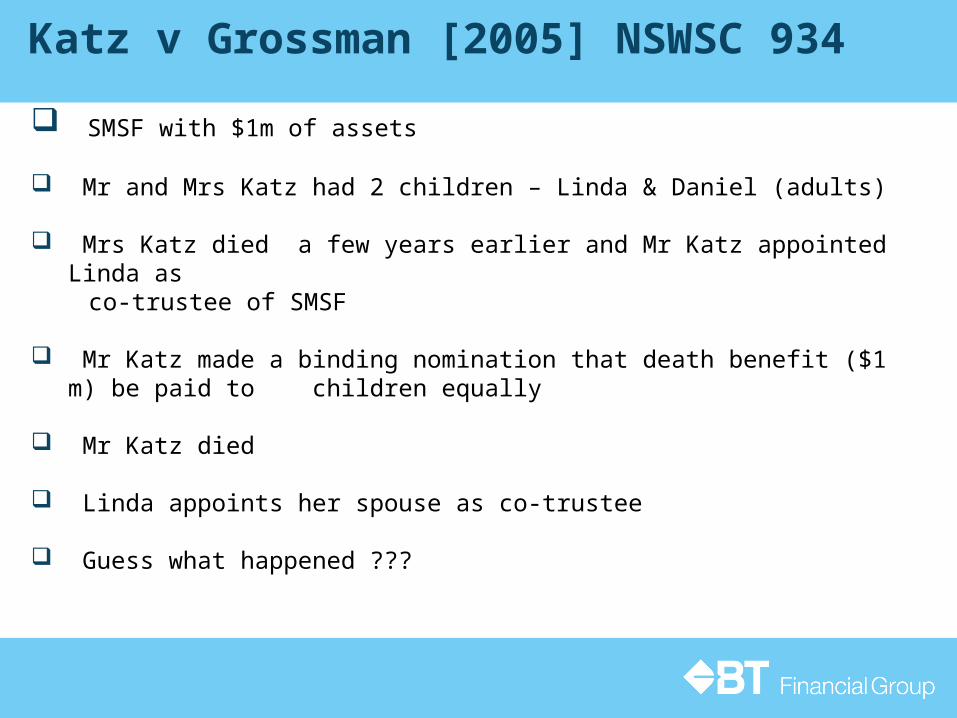

Katz v Grossman [2005] NSWSC 934

SMSF with $1m of assets

Mr and Mrs Katz had 2 children – Linda & Daniel (adults)

Mrs Katz died a few years earlier and Mr Katz appointed Linda as co-trustee of SMSF

Mr Katz made a binding nomination that death benefit ($1 m) be paid to children equally

Mr Katz died

Linda appoints her spouse as co-trustee

Guess what happened ???

3232

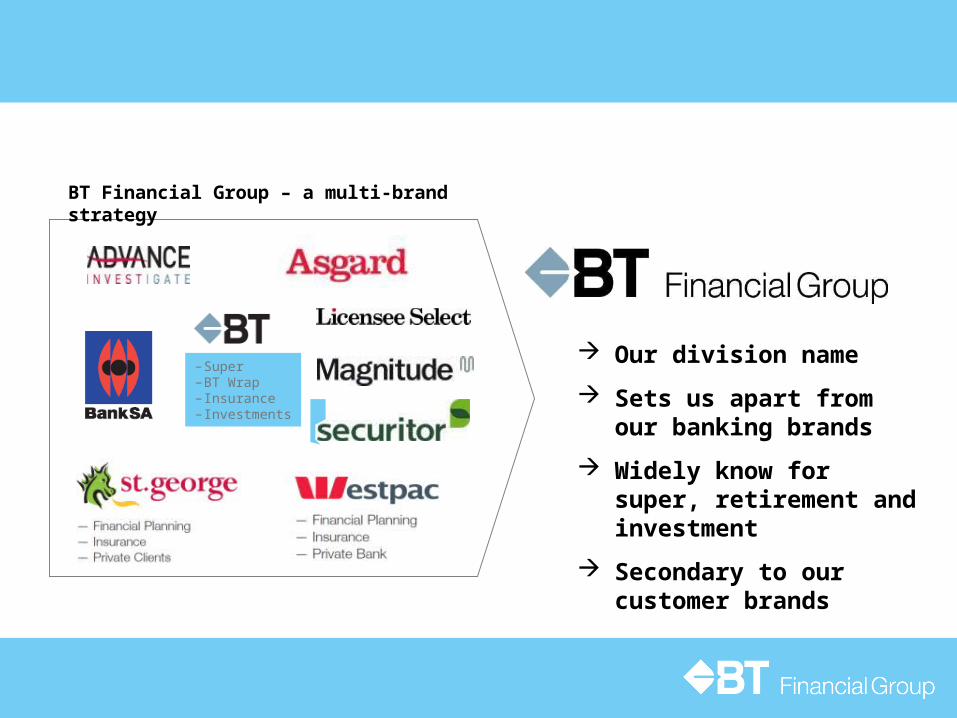

Our division name Sets us apart from our

banking brands Widely know for super,

retirement and investment Secondary to our

customer brands

–Super–BT Wrap– Insurance– Investments

BT Financial Group – a multi-brand strategy

33

This presentation has been prepared by BT Financial Group Limited (ABN 63 002 916 458) ‘BT’ and is for general information only. Every effort has been made to ensure that it is accurate, however it is not intended to be a complete description of the matters described. The presentation has been prepared without taking into account any personal objectives, financial situation or needs. It does not contain and is not to be taken as containing any securities advice or securities recommendation. Furthermore, it is not intended that it be relied on by recipients for the purpose of making investment decisions and is not a replacement of the requirement for individual research or professional tax advice. BT does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this presentation. Except insofar as liability under any statute cannot be excluded, BT and its directors, employees and consultants do not accept any liability for any error or omission in this presentation or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise noted, BT is the source of all charts; and all performance figures are calculated using exit to exit prices and assume reinvestment of income, take into account all fees and charges but exclude the entry fee. It is important to note that past performance is not a reliable indicator of future performance.

This document was accompanied by an oral presentation, and is not a complete record of the discussion held.

No part of this presentation should be used elsewhere without prior consent from the author.

For more information, please call BT Customer Relations on 132 135 8:00am to 6:30pm (Sydney time)

![SMSF Borrowing Rules[1]](https://img.pdfslide.net/doc/110x75/577d20e71a28ab4e1e93feca/smsf-borrowing-rules1.jpg)