Embed Size (px)

Citation preview

Transformation of media- Digital technology and new business models

Johan Winbladh March 2016

[email protected]: 21915612www.medieinnovation.dk

Grphic: Erik Johansson – Go Your Own Way

• Movie Production

• Musician

• Marketing Strategist

• Market Researcher

• Digital Commissioning Editor

• Project Manager

• Media Innovation Consultant

• Startup mentor

• Business Change Manager

About me (2)The ’about me’ slide

THE CHANGING MEDIA MARKET

- Basics for strategies and product development

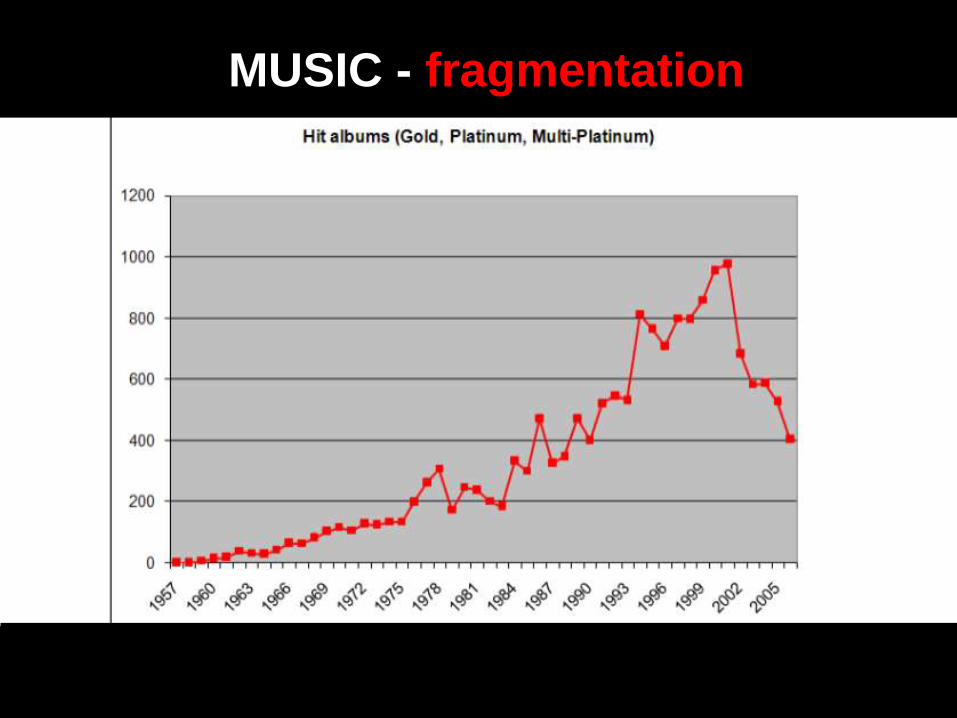

MUSIC - fragmentation

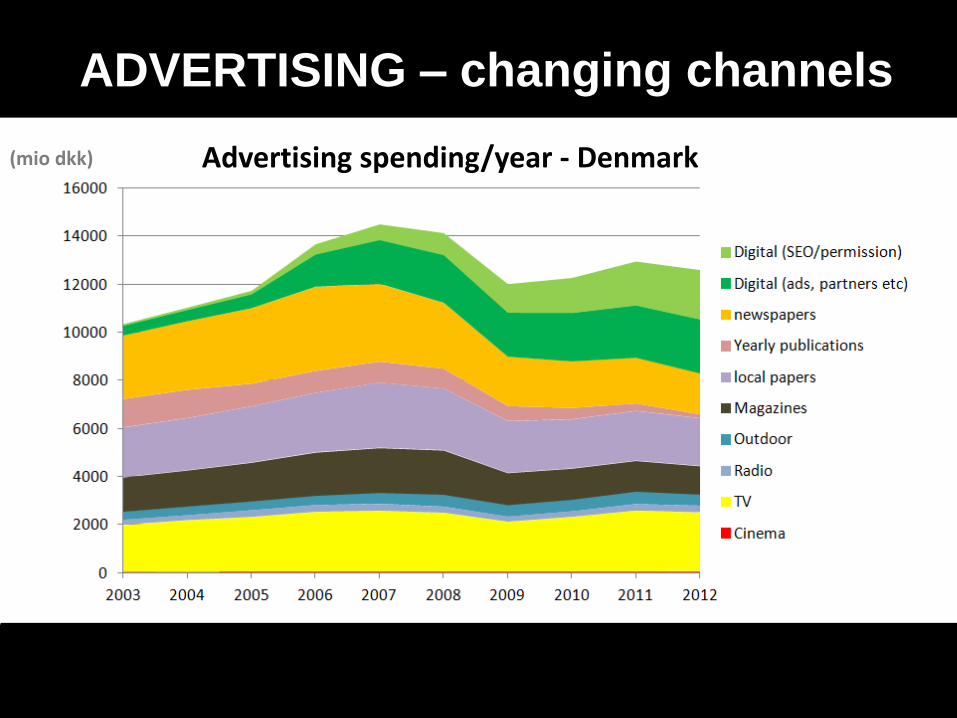

The money flow changes channels

(mio dkk) Advertising spending/year - Denmark

ADVERTISING – changing channels

Own figure, data provided through Mediawatch/FDIM

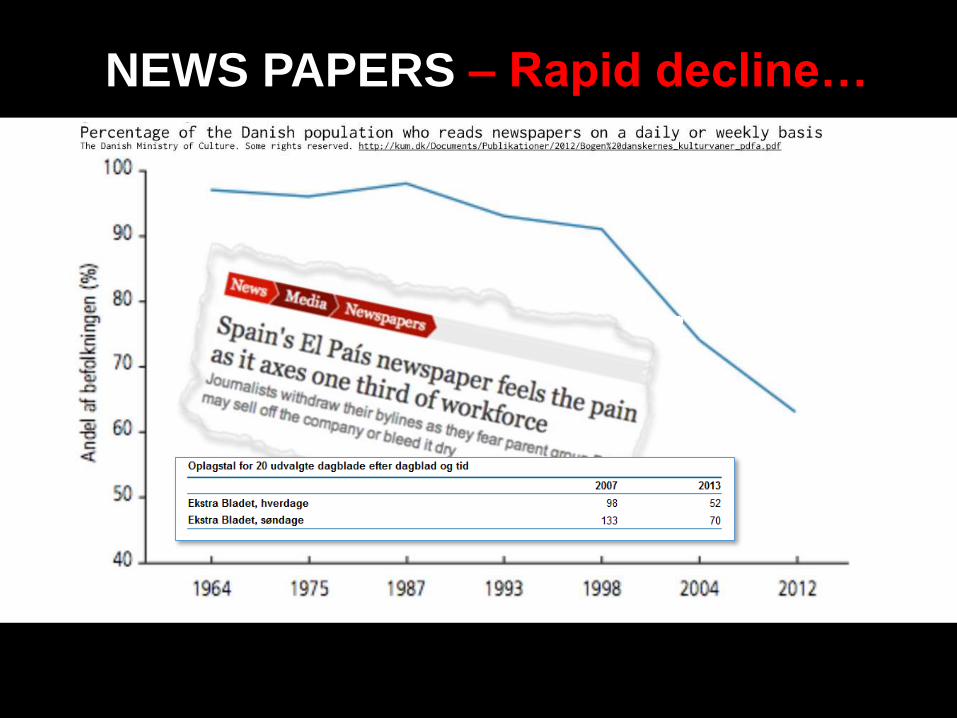

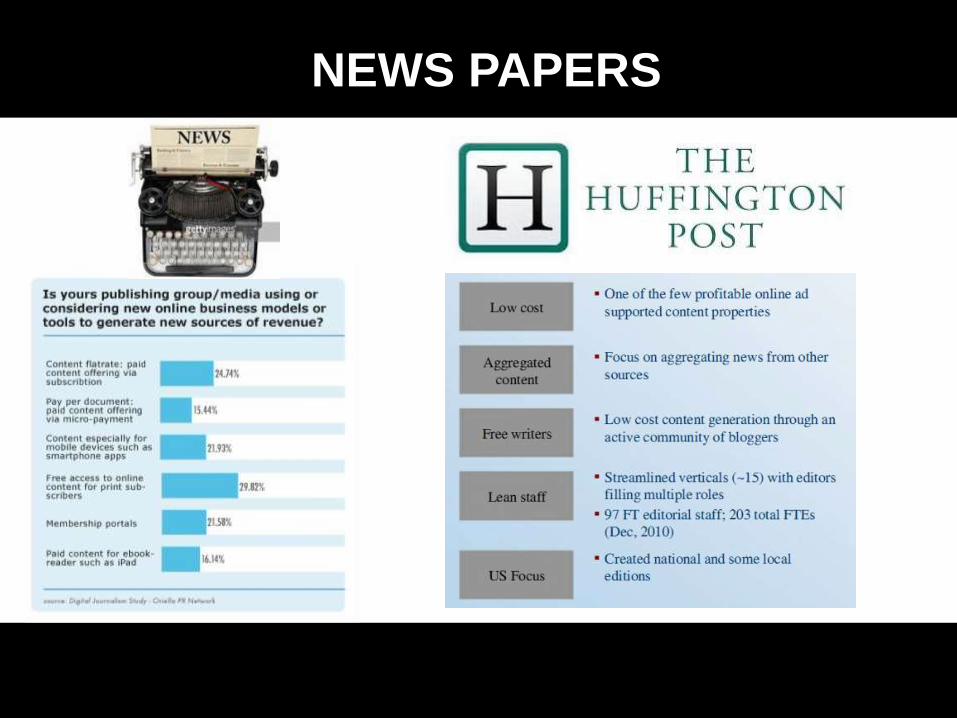

NEWS PAPERS – Rapid decline…

Borrowed from Jon Lund

NEWS PAPERS

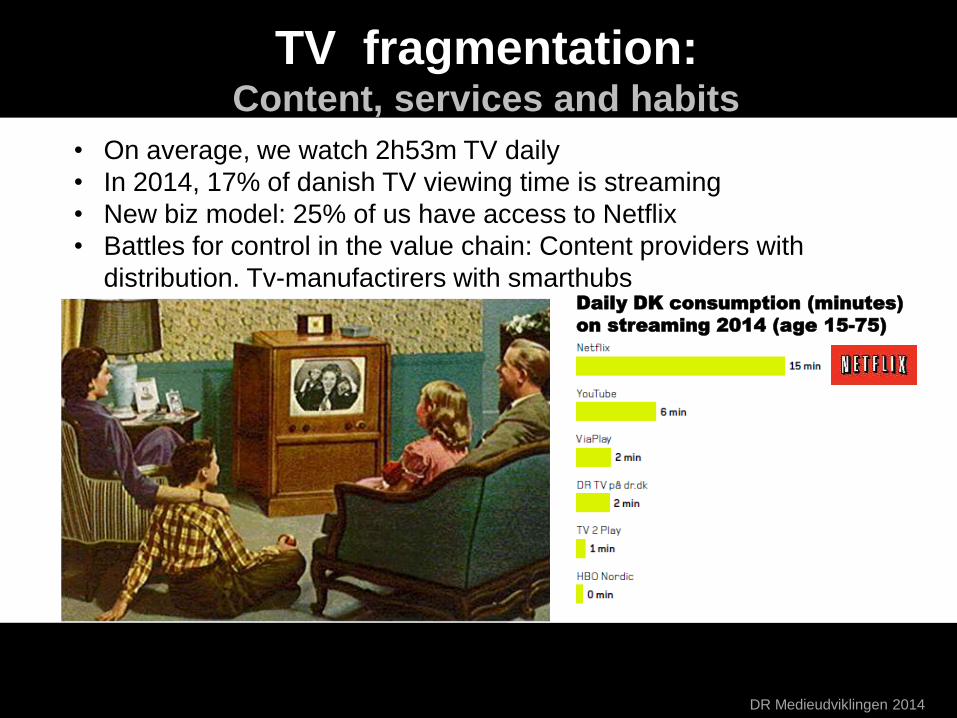

The money flow changes channelsTV fragmentation:

Content, services and habits

DR Medieudviklingen 2014

• On average, we watch 2h53m TV daily

• In 2014, 17% of danish TV viewing time is streaming

• New biz model: 25% of us have access to Netflix

• Battles for control in the value chain: Content providers with

distribution. Tv-manufactirers with smarthubsDaily DK consumption (minutes)

on streaming 2014 (age 15-75)

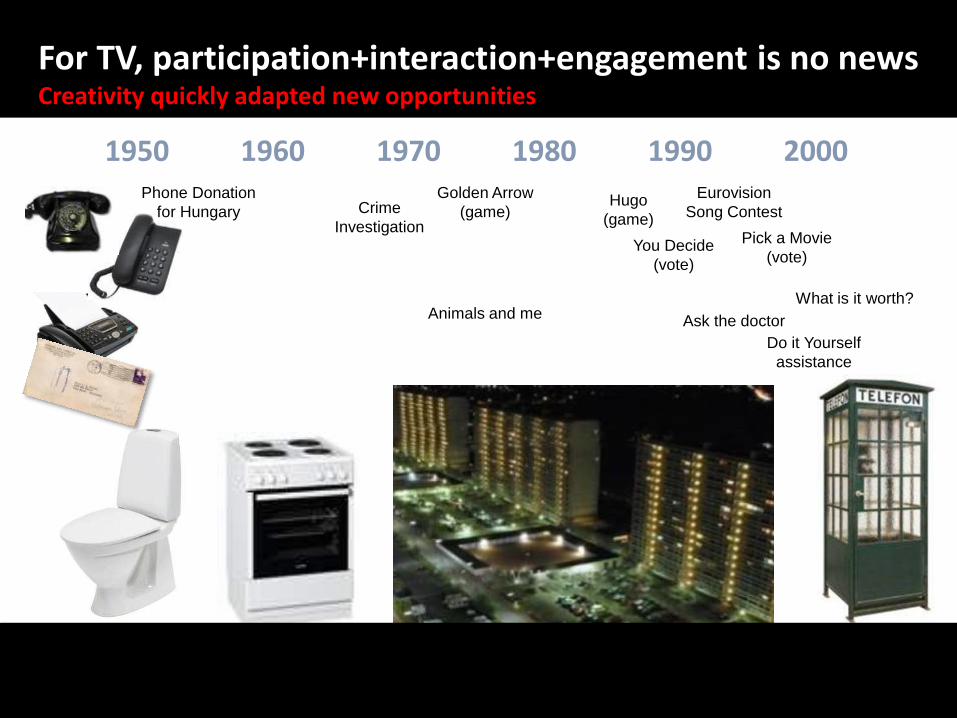

1950 1970 19901980 20001960Phone Donation

for Hungary Crime

Investigation

Ask the doctor

You Decide

(vote)

Golden Arrow

(game)Hugo

(game)Pick a Movie

(vote)

Eurovision

Song Contest

Animals and me

Do it Yourself

assistance

What is it worth?

For TV, participation+interaction+engagement is no newsCreativity quickly adapted new opportunities

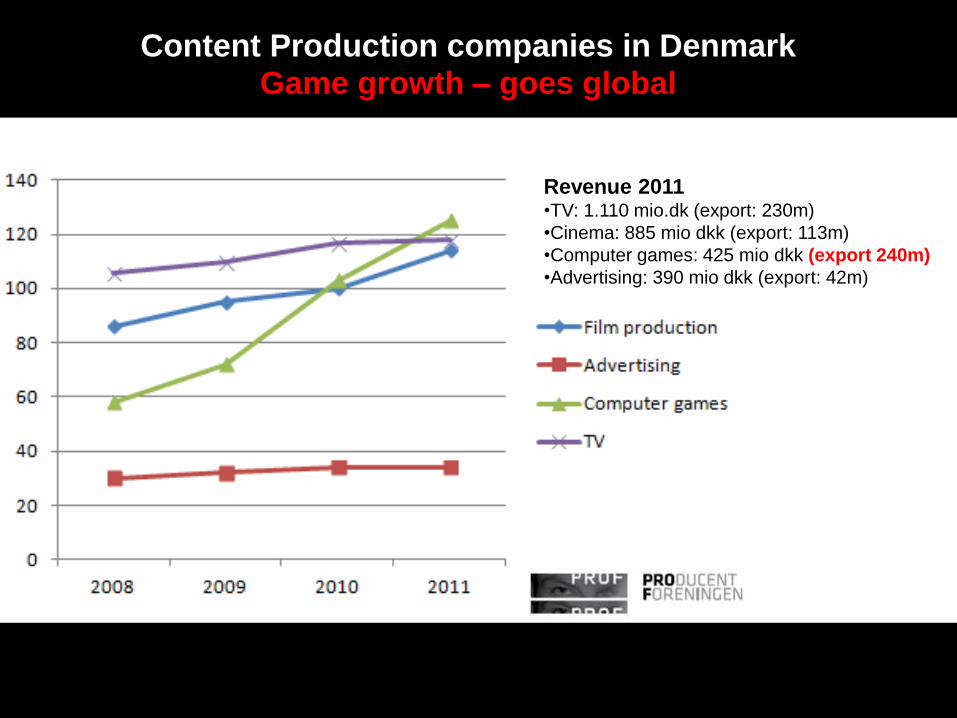

Revenue 2011•TV: 1.110 mio.dk (export: 230m)

•Cinema: 885 mio dkk (export: 113m)

•Computer games: 425 mio dkk (export 240m)

•Advertising: 390 mio dkk (export: 42m)

Content Production companies in DenmarkGame growth – goes global

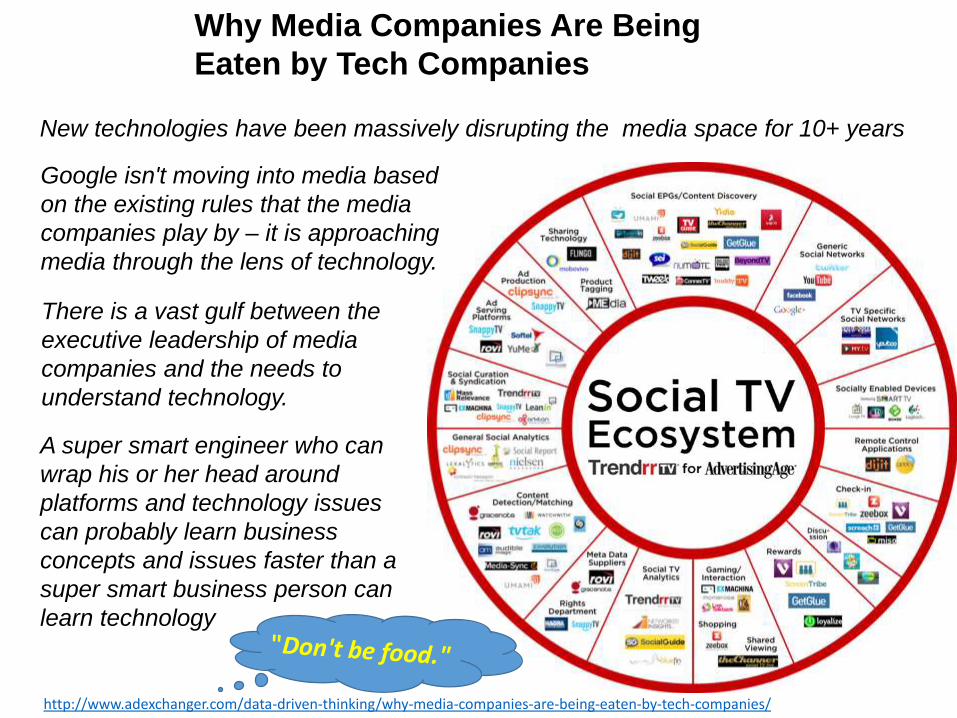

http://www.adexchanger.com/data-driven-thinking/why-media-companies-are-being-eaten-by-tech-companies/

Why Media Companies Are Being

Eaten by Tech Companies

Google isn't moving into media based

on the existing rules that the media

companies play by – it is approaching

media through the lens of technology.

New technologies have been massively disrupting the media space for 10+ years

There is a vast gulf between the

executive leadership of media

companies and the needs to

understand technology.

A super smart engineer who can

wrap his or her head around

platforms and technology issues

can probably learn business

concepts and issues faster than a

super smart business person can

learn technology

Mikkel Rasmussen (ReD Associates)*

* http://cko.dk/gruppeindlaeg/status-mediebranchen-i-danmark

”Media sector has a shared understanding that 80% of revenue must come from radical innovation.

The rest comes from continousimprovements in existing business

Reality is completely the opposite”

N E W B U S I N E S S M O D E L S

G E N E R AT I N G N E W

R E V E N U E S T R E A M S

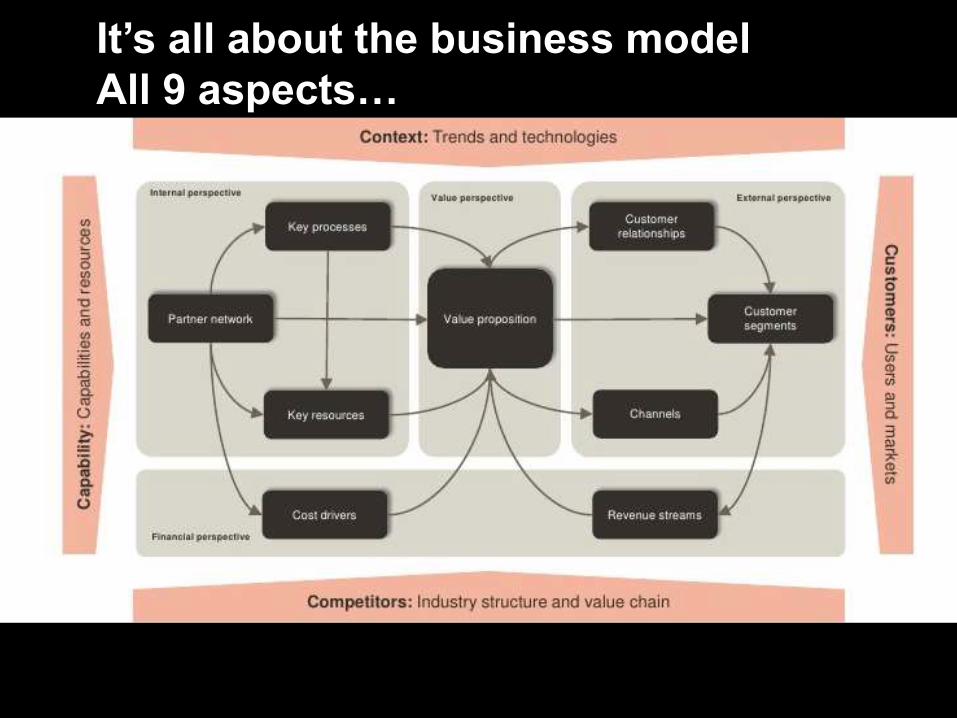

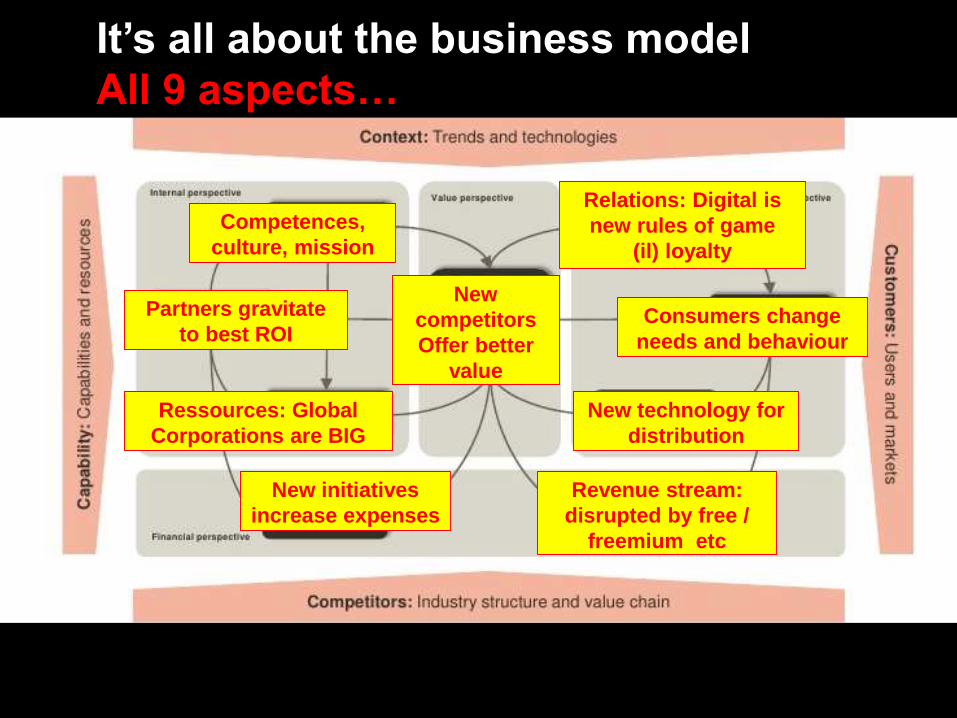

It’s all about the business model

All 9 aspects…

New

competitors

Offer better

value

Consumers change

needs and behaviour

Relations: Digital is

new rules of game

(il) loyalty

New technology for

distribution

New initiatives

increase expenses

Revenue stream:

disrupted by free /

freemium etc

Ressources: Global

Corporations are BIG

Competences,

culture, mission

Partners gravitate

to best ROI

It’s all about the business model

All 9 aspects…

• Create new revenue streams (business development)

• Find new + maintain partners (increase brand position,)

• Improve customer service (ARPU, Cable-co open channels etc)

• Establish content paywalls (subscribe, micro, freemium)

• Reduce cost: Downsizing, outsourcing, processing

• Play politics (governmental support/funding)

• Improve products (Behav.target., BigData, 2nd Screen etc)

• Establish culture of innovation (departments, initiatives, Incubation)

• Re organize to meet demands (structure, roles, tasks)

BUILDNING NEW BUSINESS MODELS

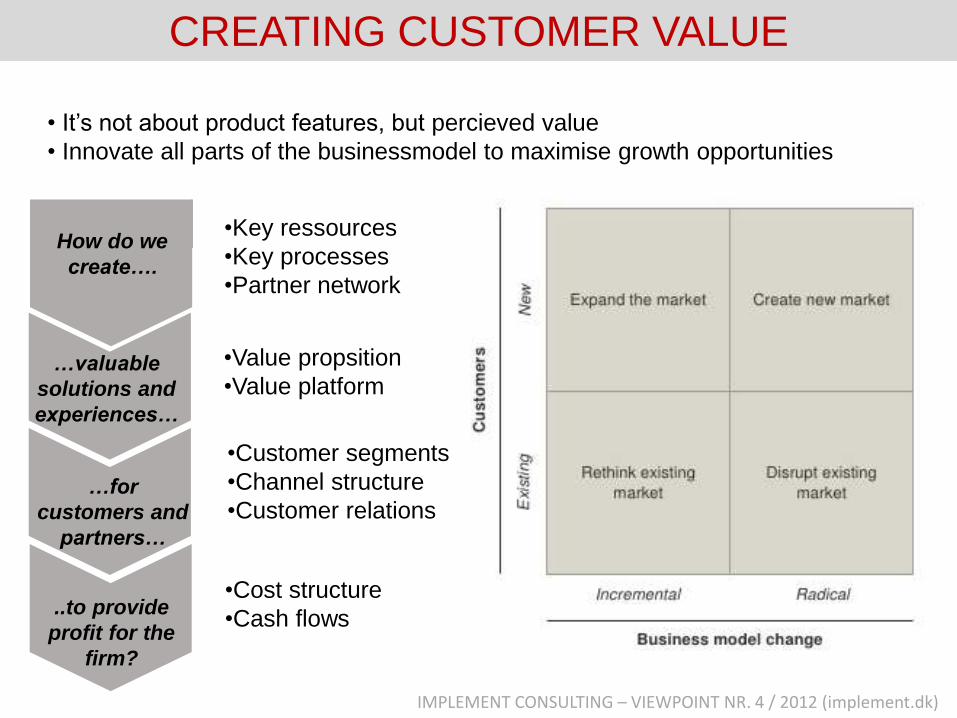

• It’s not about product features, but percieved value

• Innovate all parts of the businessmodel to maximise growth opportunities

CREATING CUSTOMER VALUE

IMPLEMENT CONSULTING – VIEWPOINT NR. 4 / 2012 (implement.dk)

•Key ressources

•Key processes

•Partner network

•Value propsition

•Value platform

•Customer segments

•Channel structure

•Customer relations

•Cost structure

•Cash flows

How do we

create….

…valuable

solutions and

experiences…

…for

customers and

partners…

..to provide

profit for the

firm?

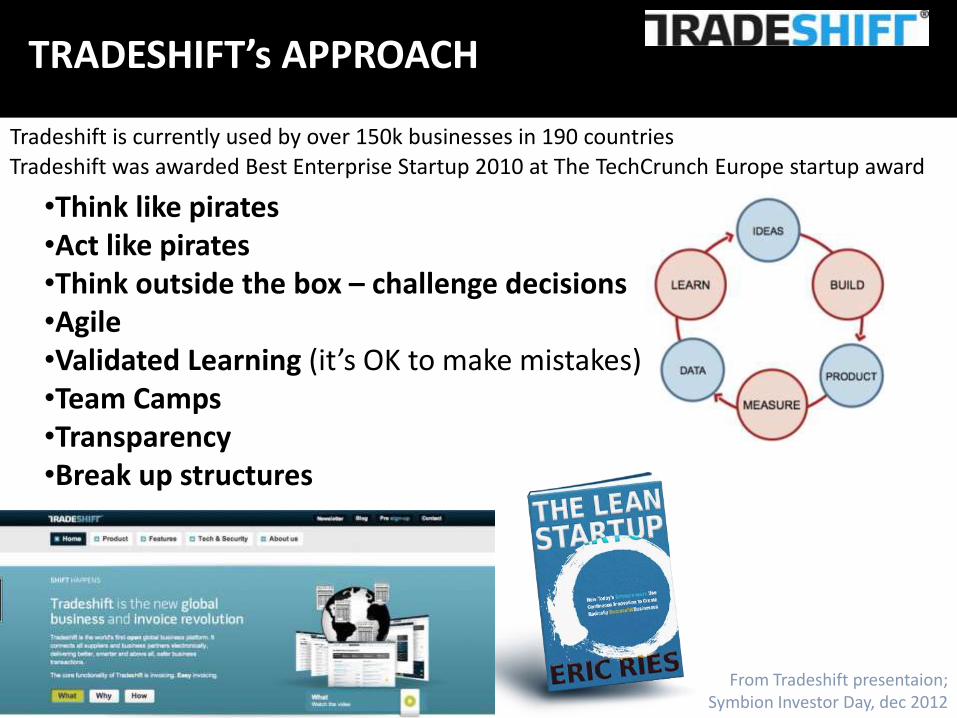

Tradeshift was awarded Best Enterprise Startup 2010 at The TechCrunch Europe startup awardTradeshift is currently used by over 150k businesses in 190 countries

•Think like pirates•Act like pirates•Think outside the box – challenge decisions•Agile •Validated Learning (it’s OK to make mistakes)•Team Camps•Transparency•Break up structures

TRADESHIFT’s APPROACH

From Tradeshift presentaion; Symbion Investor Day, dec 2012

Disruption from the inside: Media companies seek hope as incubators

“If you continue to disrupt our industry, we want to work with you.”

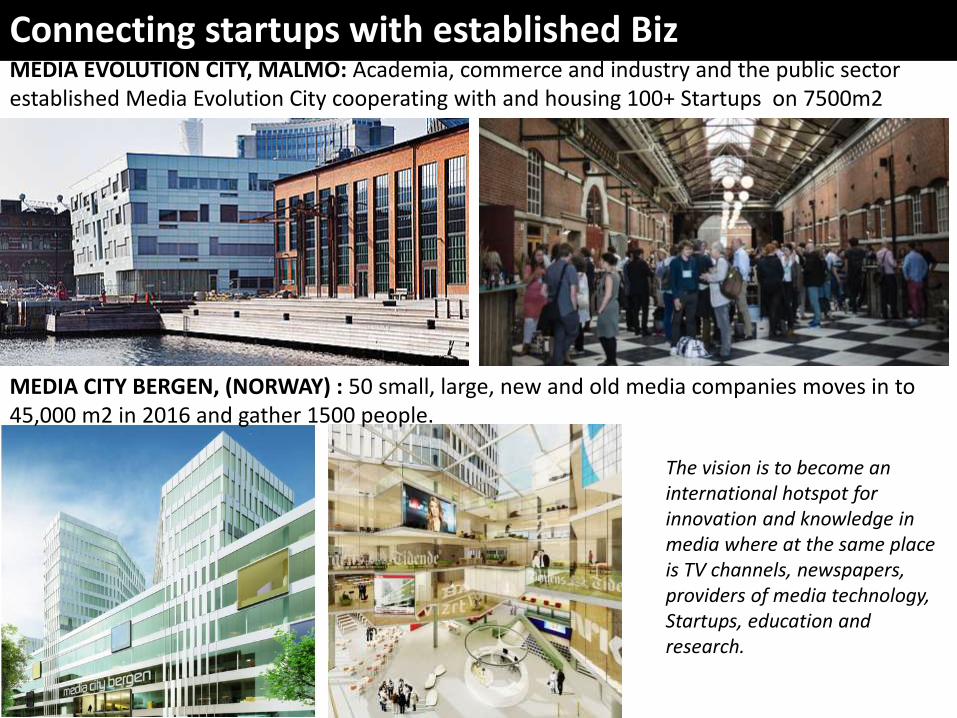

MEDIA EVOLUTION CITY, MALMÖ: Academia, commerce and industry and the public sector established Media Evolution City cooperating with and housing 100+ Startups on 7500m2

MEDIA CITY BERGEN, (NORWAY) : 50 small, large, new and old media companies moves in to 45,000 m2 in 2016 and gather 1500 people.

The vision is to become an international hotspot for innovation and knowledge in media where at the same place is TV channels, newspapers, providers of media technology, Startups, education and research.

Connecting startups with established Biz

NEW STRATEGIES > new jobs

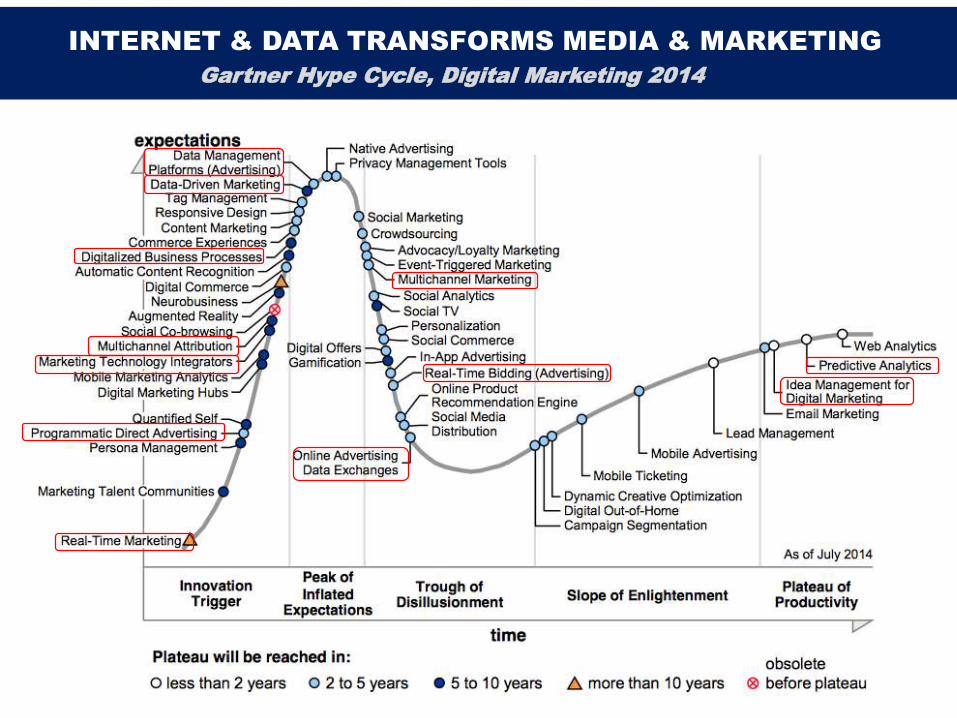

Gartner Hype Cycle, Digital Marketing 2014

INTERNET & DATA TRANSFORMS MEDIA & MARKETING

Data driven

approach

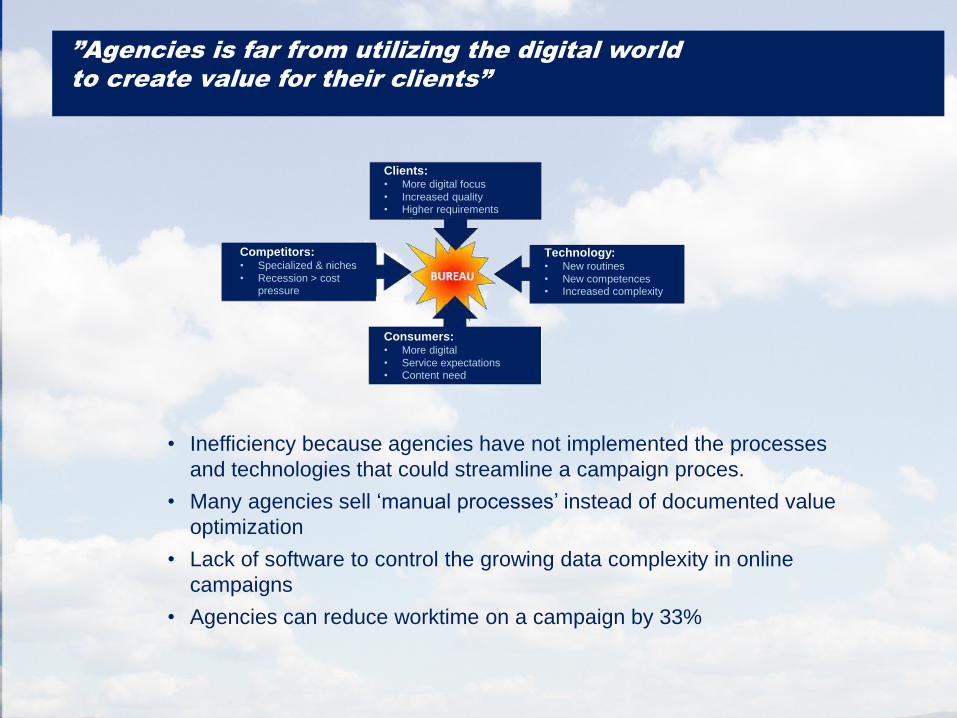

• Inefficiency because agencies have not implemented the processes

and technologies that could streamline a campaign proces.

• Many agencies sell ‘manual processes’ instead of documented value

optimization

• Lack of software to control the growing data complexity in online

campaigns

• Agencies can reduce worktime on a campaign by 33%

”Agencies is far from utilizing the digital world

to create value for their clients”

Consumers:• More digital

• Service expectations• Content need

Technology:• New routines

• New competences• Increased complexity

Competitors:• Specialized & niches

• Recession > costpressure

Clients:• More digital focus

• Increased quality• Higher requirements

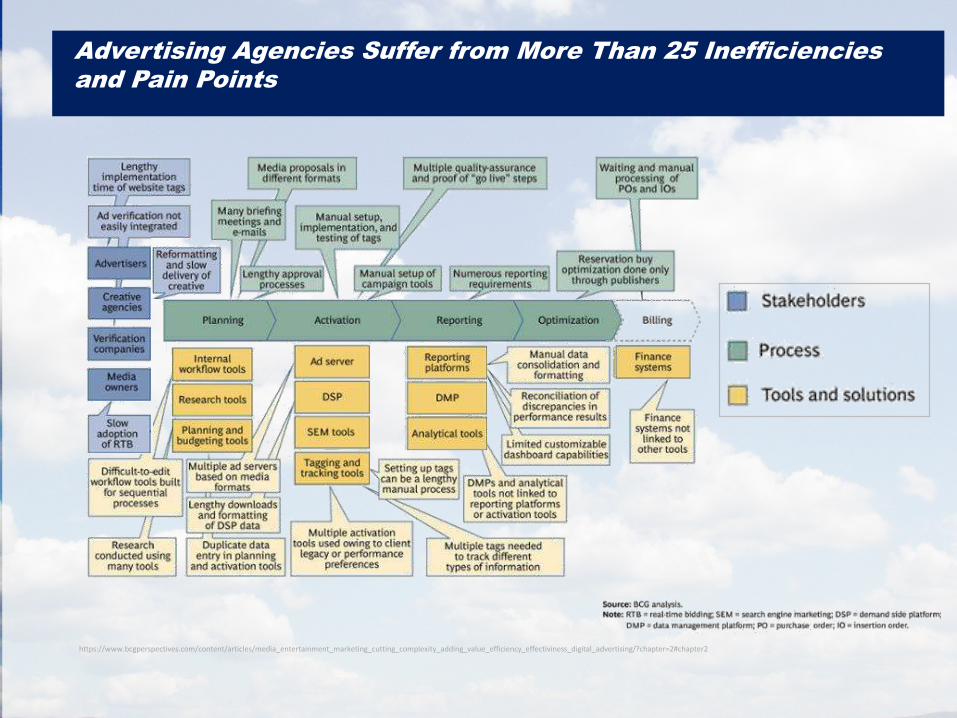

https://www.bcgperspectives.com/content/articles/media_entertainment_marketing_cutting_complexity_adding_value_efficiency_effectiviness_digital_advertising/?chapter=2#chapter2

Advertising Agencies Suffer from More Than 25 Inefficiencies

and Pain Points

B u s i n e s s C h a n g e

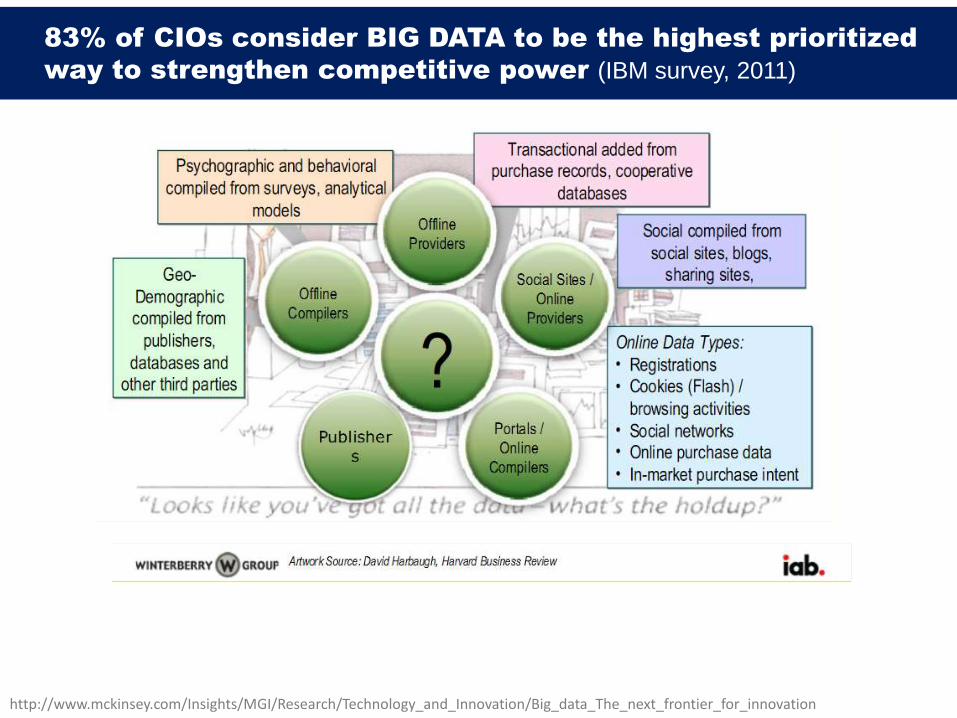

http://www.mckinsey.com/Insights/MGI/Research/Technology_and_Innovation/Big_data_The_next_frontier_for_innovation

83% of CIOs consider BIG DATA to be the highest prioritized

way to strengthen competitive power (IBM survey, 2011)

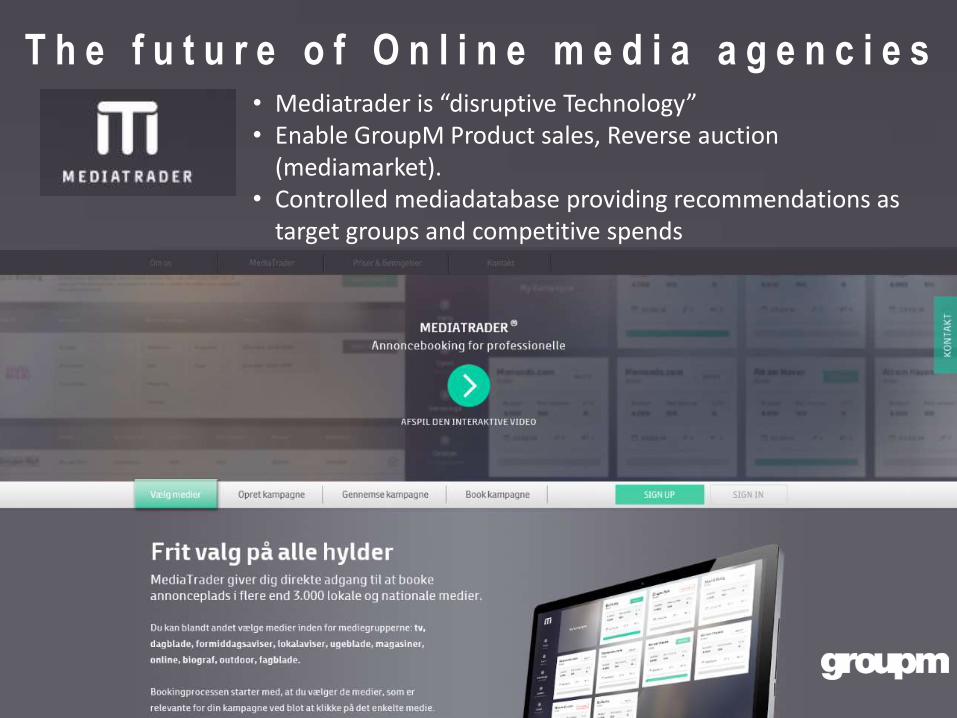

T h e f u t u r e o f O n l i n e m e d i a a g e n c i e s• Mediatrader is “disruptive Technology”• Enable GroupM Product sales, Reverse auction

(mediamarket). • Controlled mediadatabase providing recommendations as

target groups and competitive spends

PROGRESS CHALLENGES

Cooperation, culture and innovation clashes

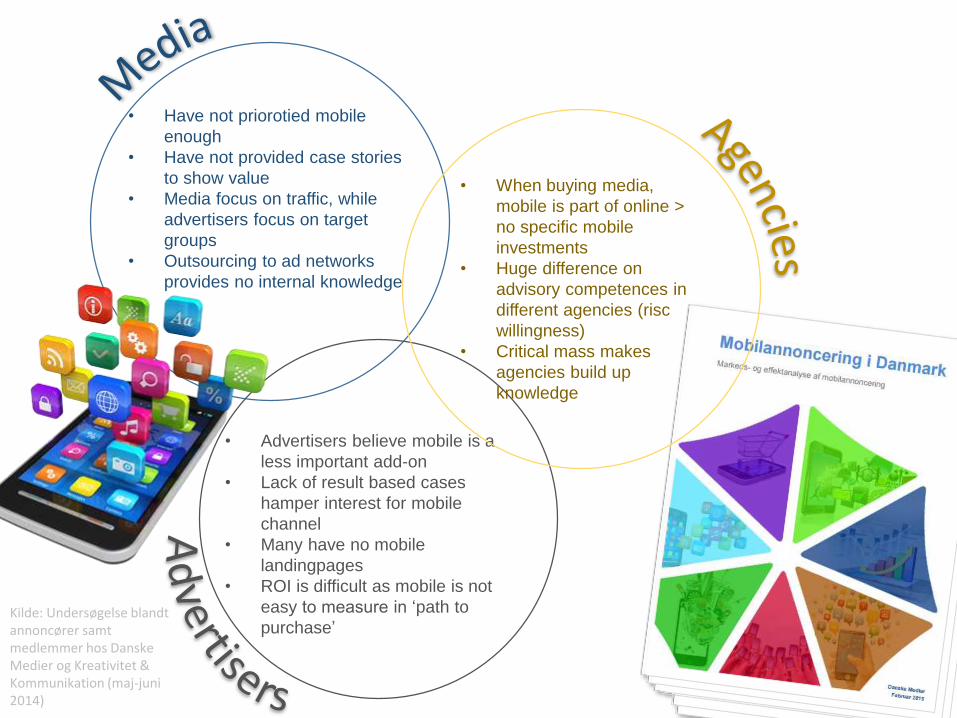

Kilde: Undersøgelse blandt annoncører samt medlemmer hos Danske Medier og Kreativitet & Kommunikation (maj-juni 2014)

• Have not priorotied mobile

enough

• Have not provided case stories

to show value

• Media focus on traffic, while

advertisers focus on target

groups

• Outsourcing to ad networks

provides no internal knowledge

• Advertisers believe mobile is a

less important add-on

• Lack of result based cases

hamper interest for mobile

channel

• Many have no mobile

landingpages

• ROI is difficult as mobile is not

easy to measure in ‘path to

purchase’

• When buying media,

mobile is part of online >

no specific mobile

investments

• Huge difference on

advisory competences in

different agencies (risc

willingness)

• Critical mass makes

agencies build up

knowledge

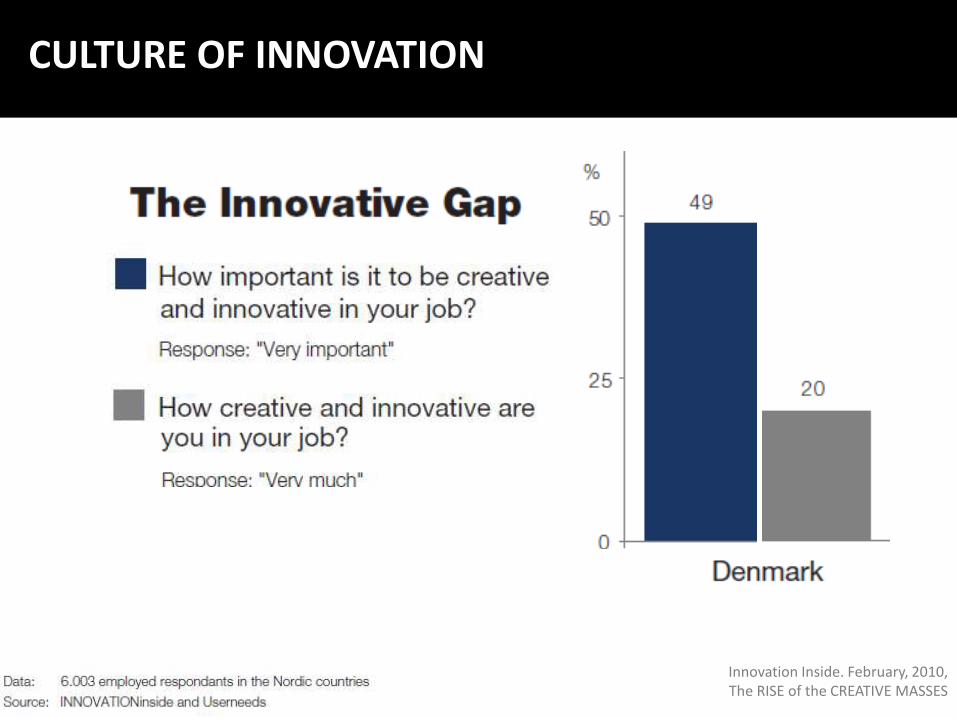

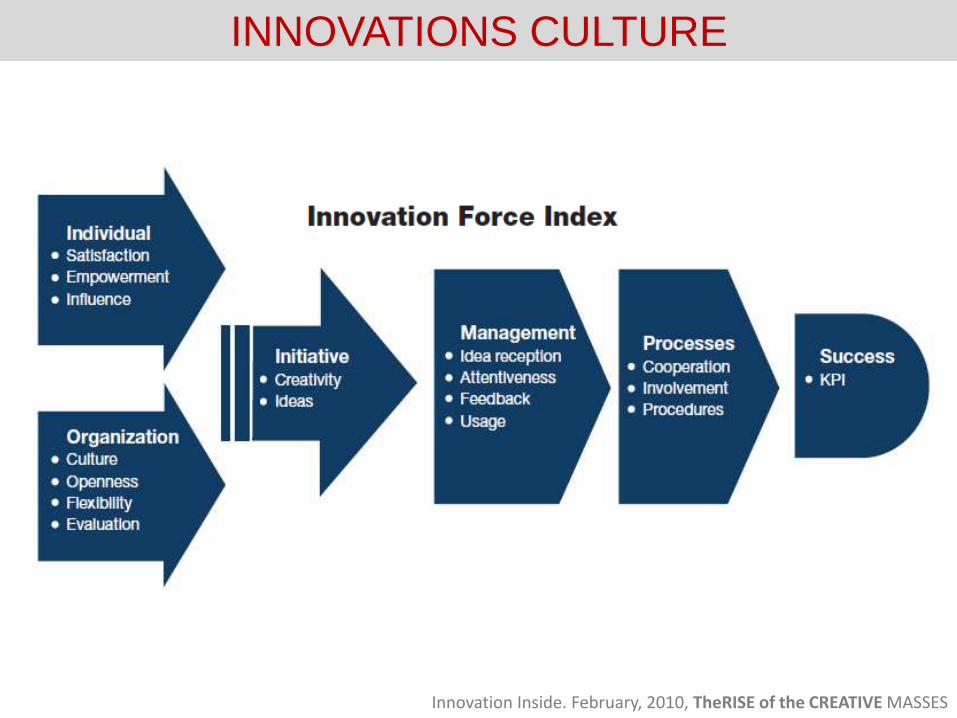

Innovation Inside. February, 2010, The RISE of the CREATIVE MASSES

CULTURE OF INNOVATION

Innovation Inside. February, 2010, TheRISE of the CREATIVE MASSES

INNOVATIONS CULTURE

http://www.15inno.com/wp-content/uploads/2012/06/Screen-Shot-2012-06-06-at-08.43.21.png

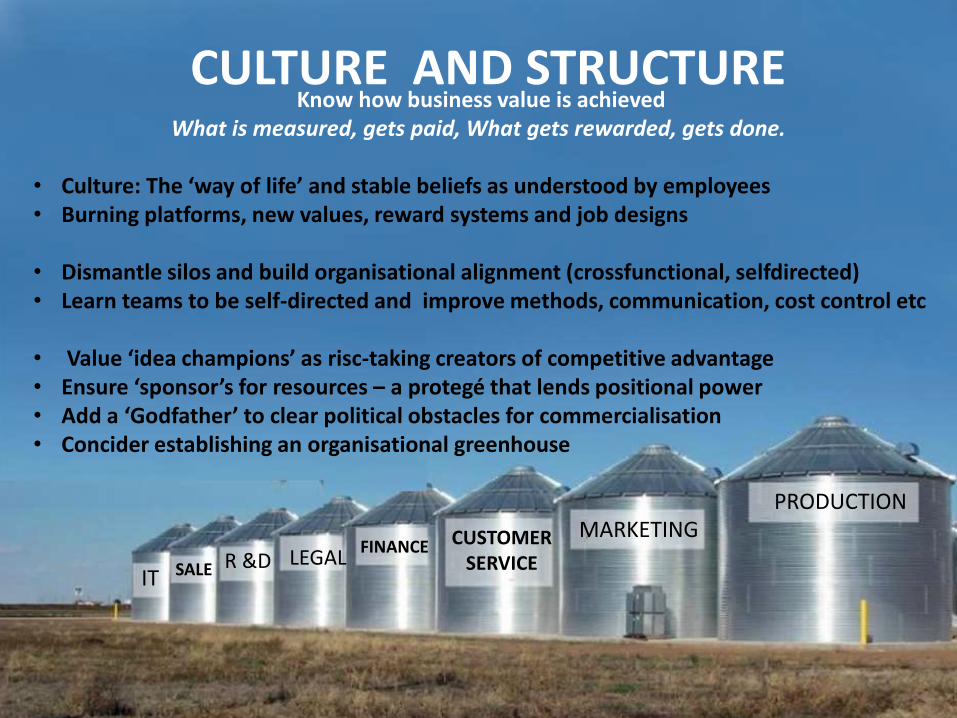

READY FOR OPEN INNOVATION ?

MARKETING

SALEIT

PRODUCTION

R &DCUSTOMER

SERVICELEGALFINANCE

CULTURE AND STRUCTUREKnow how business value is achieved

What is measured, gets paid, What gets rewarded, gets done.

• Culture: The ‘way of life’ and stable beliefs as understood by employees• Burning platforms, new values, reward systems and job designs

• Dismantle silos and build organisational alignment (crossfunctional, selfdirected)• Learn teams to be self-directed and improve methods, communication, cost control etc

• Value ‘idea champions’ as risc-taking creators of competitive advantage• Ensure ‘sponsor’s for resources – a protegé that lends positional power• Add a ‘Godfather’ to clear political obstacles for commercialisation• Concider establishing an organisational greenhouse