Embed Size (px)

Citation preview

TSI Coking Coal Indices

Carbon Forum

November 19th, 2015 Tim Hard, Director TSI

- TSI (The Steel Index) Introduction

- Index methodology

- Valuing coal properties, not relativities

- Key Considerations

Agenda

Dedicated pricing service, solely for international ferrous markets. Founded in 2006, we were the pioneers, and currently industry leaders in data-driven, volume weighted

index production, as evidenced through methodology adoption by our various peers.

Proponents of a methodology designed to maximise participation, minimise

opportunities for manipulation and remove subjectivity from the process.

Non-Disclosure Agreements signed with index participants, enabling price data to be

reported confidentially with no fear of disclosure to the wider market.

Acquired in 2011, TSI continues to operate as an independent unit within Platts.

No access to any aspect of each other’s data.

What is The Steel Index (TSI)?

What we do:

• TSI’s coking coal benchmark: Offered by suppliers and traders for physical index-

linking, now the most widely referenced index for FOB Australia.

• TSI’s iron ore benchmark: used to settle over 99% of all cash-settled iron ore futures/ derivatives trading. Over 1 billion tonnes has traded to date, and listed on

5 exchanges

• TSI’s HRC regional benchmarks: North & South European steel for physical users and ‘paper’ (hedging), as well as the regional ASEAN market.

• TSI’s Turkish scrap benchmark: The pre-eminent benchmark for physical users and derivatives in the most-watched scrap market. Now used as the basis for the new

LME scrap contract

What we don’t do:

• Journalism/Forecasting

TSI exists solely to provide robust, accurate pricing benchmarks and indices to the

ferrous industry, nothing more.

Who are the Steel Index (TSI)?

TSI uses physical market transactions to produce

“daily spot value” reflective prices.

Mathematical methodology, devised to increase participation

and limit opportunity for manipulation.

TSI indices suitable for settling “floating” physical deals as well as

the underlier for derivatives.

Using the same index for physical and financial contracts minimises basis

risk.

TSI: Interacting with the Ferrous Markets

TSI Indices

Physical e-trading platforms

Derivatives

Companies involved in

physical spot trade

Long-term physical

contracts

TSI has over 650 companies participating as data providers

Floating deals basis TSI available on platforms.

TSI used in non-spot (long-term) floating deals.

SPOT DATA

SPOT DATA

- TSI (The Steel Index) Introduction

- Index methodology

- Valuing coal properties, not relativities

- Key Considerations

Agenda

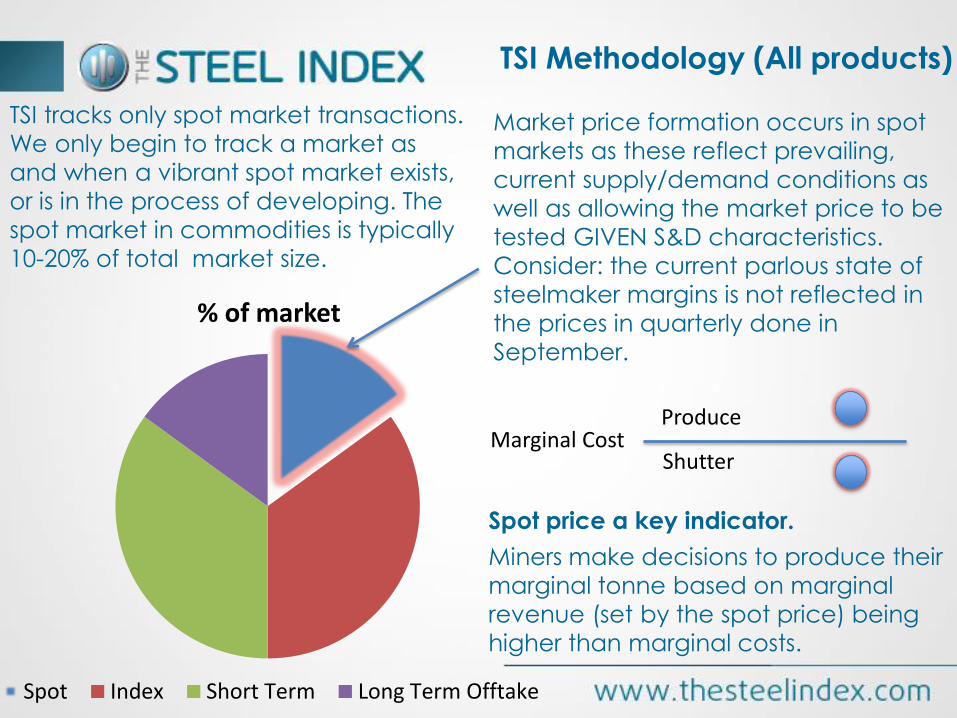

TSI tracks only spot market transactions.

We only begin to track a market as

and when a vibrant spot market exists,

or is in the process of developing. The

spot market in commodities is typically

10-20% of total market size.

TSI Methodology (All products)

% of market

Spot Index Short Term Long Term Offtake

Market price formation occurs in spot

markets as these reflect prevailing,

current supply/demand conditions as

well as allowing the market price to be

tested GIVEN S&D characteristics.

Consider: the current parlous state of

steelmaker margins is not reflected in

the prices in quarterly done in

September.

Miners make decisions to produce their

marginal tonne based on marginal

revenue (set by the spot price) being

higher than marginal costs.

Marginal Cost Produce

Shutter

Spot price a key indicator.

Normalisation

• Translating all relevant data submitted to a common basis (TSI’s reference product specification).

Statistical

Analysis

• Running TSI’s algorithm to remove outliers and inconsistent data points.

Checks &

Balances

• Minimising opportunities for manipulation/data bias.

Spot Market Transaction Data Collection and Screening

Volume-weighted Average Daily Price Calculation

TSI employs one approach to all ferrous markets covered.

TSI Methodology (All products)

Trades normalising

to LESS than one

standard deviation

from the mean and

the lowest price are

excluded

Data set included

in index

calculation

proceeds to

volume-weighting

stage.

Trades normalising to

MORE than one

standard deviation

from the mean and

the highest price are

excluded

NB: Data submissions

exhibiting inexplicable

trends or inconsistencies

are also excluded, as are

those falling outside of

TSI’s published spec (i.e.

outside loading windows,

too low a volume, etc.)

- 1 Standard Dev. + 1 Standard Dev.

Statistical Analysis

A volume-weighted average is calculated from

screened, normalised data conforming to TSI’s

stated conditions:

• Data points include transactions and only if

required, firm bids and offers

• Bid/Offer data is given a reduced 10% weighting

(i,.e. a 75kt Handymax bid would see its volume

automatically reduced to 7,500 tonnes). The

rationale for weight reduction is our belief in the

primacy of transaction data.

• Transaction data gets full weighting (a 75kt spot

trade gets 75kt weighting in the sheet.

• Checks and balances employed: no single data

provider can comprise more than 40% of the

volume. We endeavor to achieve a buy/sell

balance

• Volume-weighted average produced.

Screened, normalised transactions

TSI published price

TSI statistical and

checks and balances

filter

Checks and Balances

Coal brands sold into both markets achieve different prices. Hence TSI produces

independent FOB & CFR indices. There is NO CROSS-OVER of spot transactions. Each

transaction ONLY applies to its RELEVANT pricing point

FOB

CFR

TSI Premium Coking Coal Benchmarks

- TSI (The Steel Index) Introduction

- Index methodology

- Valuing coal properties, not relativities

- Key Considerations

Agenda

TSI’s approach to coking coal markets is to value the coal based on it’s properties. For

each factor (ash, volatile matter, CSR etc.) we assign a value-in-use figure, based on

isolating that variable and performing regressions on spot data history.

The relative value of one brand of coal versus another is immaterial in the calculation

process: market participants attribute their own value during the spot-buying process.

Premium FOB Australia Premium CFR China (JM25)

You will note the differences in CFR China and FOB Australia indices, where

feedback and regressions showed a necessity to use differing variables.

Valuing coals, from the bottom up

Buyers continue targeting select properties – continued disruption of the normal

‘hierarchy’. Some low-vol coals are failing to hit theoretical prices due to relative

abundance in an FOB marketplace emphasizing fluidity found in some mid-vols.

Compression of prices between grades is greater than normal (the wide spreads

relatively recently seen between coals has tightened further).

Accounting for those valuations through VIU remains explicable and predictable….

Low-vol/

mid-vol

spread

highly

variable. 70

80

90

100

110

120

130

Low Vol Mid Vol

VIU Remains the way to value coals

- TSI (The Steel Index) Introduction

- Index methodology

- Valuing coal properties, not relativities

- Key Considerations

Agenda

1. Index Liquidity

2. Structure and Pricing

3. Long Term vision for TSI

Index Robustness

Key Considerations

Index Credibility

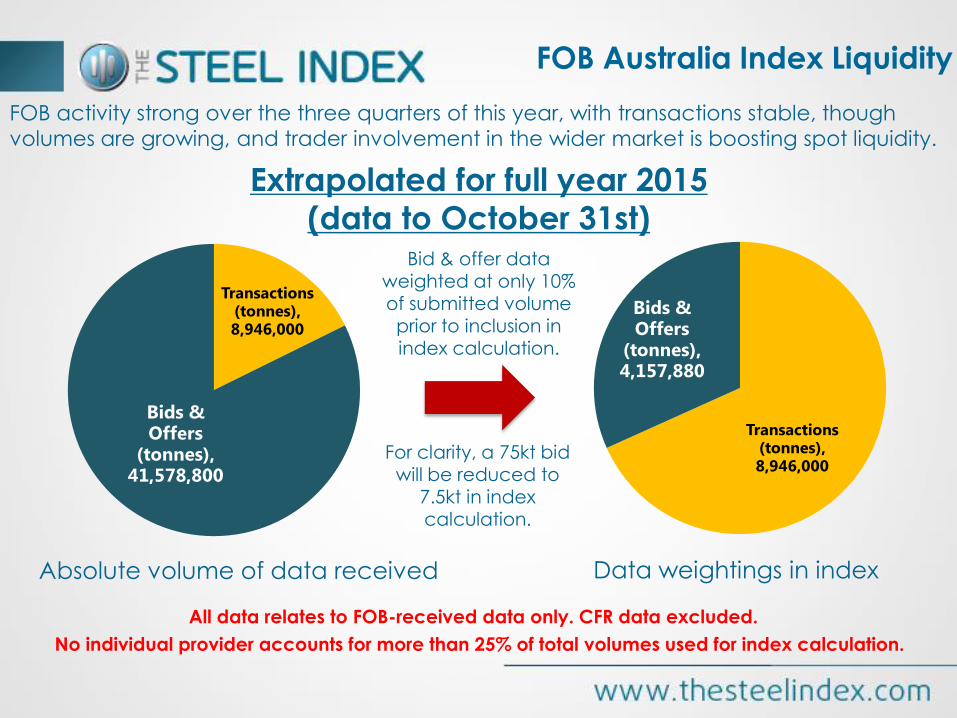

All following data refers only to TSI’s FOB Australia PHCC index. It is:

- Our index against which most physical deals are linked or referred to.

- The settlement index used by SGX for derivatives trade.

- The pricing point which TSI believes to be the long-term global

benchmark/anchor-point.

FOB activity strong over the three quarters of this year, with transactions stable, though

volumes are growing, and trader involvement in the wider market is boosting spot liquidity.

Transactions (tonnes), 8,946,000

Bids & Offers

(tonnes), 41,578,800

Extrapolated for full year 2015

(data to October 31st)

Transactions (tonnes), 8,946,000

Bids & Offers

(tonnes), 4,157,880

Absolute volume of data received

Bid & offer data weighted at only 10%

of submitted volume prior to inclusion in index calculation.

Data weightings in index

All data relates to FOB-received data only. CFR data excluded.

No individual provider accounts for more than 25% of total volumes used for index calculation.

FOB Australia Index Liquidity

For clarity, a 75kt bid will be reduced to

7.5kt in index calculation.

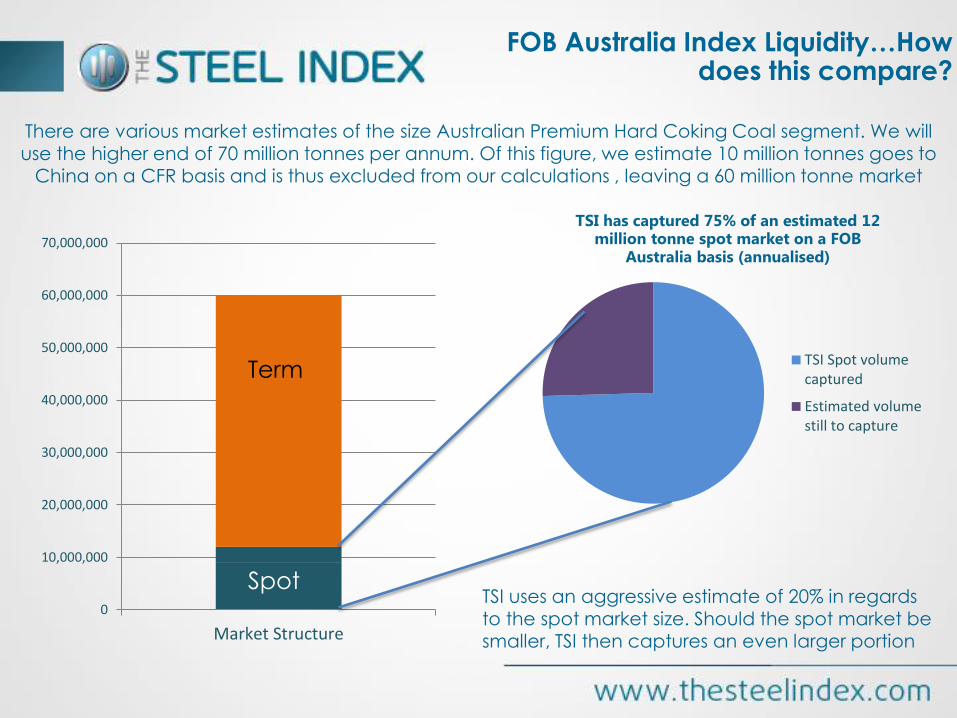

There are various market estimates of the size Australian Premium Hard Coking Coal segment. We will

use the higher end of 70 million tonnes per annum. Of this figure, we estimate 10 million tonnes goes to China on a CFR basis and is thus excluded from our calculations , leaving a 60 million tonne market

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

Market Structure

TSI has captured 75% of an estimated 12 million tonne spot market on a FOB

Australia basis (annualised)

TSI Spot volumecaptured

Estimated volumestill to capture

Term

Spot TSI uses an aggressive estimate of 20% in regards to the spot market size. Should the spot market be smaller, TSI then captures an even larger portion

FOB Australia Index Liquidity…How does this compare?

Pre-normalised data points

FOB Australia Index Liquidity…How this looks in practise

$70

$90

$110

$130

$150

$170

$190

20

13

-01

-14

20

13

-02

-14

20

13

-03

-14

20

13

-04

-14

20

13

-05

-14

20

13

-06

-14

20

13

-07

-14

20

13

-08

-14

20

13

-09

-14

20

13

-10

-14

20

13

-11

-14

20

13

-12

-14

20

14

-01

-14

20

14

-02

-14

20

14

-03

-14

20

14

-04

-14

20

14

-05

-14

20

14

-06

-14

20

14

-07

-14

20

14

-08

-14

20

14

-09

-14

20

14

-10

-14

20

14

-11

-14

20

14

-12

-14

20

15

-01

-14

20

15

-02

-14

20

15

-03

-14

20

15

-04

-14

20

15

-05

-14

20

15

-06

-14

20

15

-07

-14

20

15

-08

-14

20

15

-09

-14

20

15

-10

-14

FOB Australia

Bid

Offer

Transaction

2015 data-to-date132 Transactions452 Bids/Offers

• The TSI index is 70% driven by transaction data. 30% is firm bid/offer volumes. Bid offer

data is extremely useful to see transactions developing through narrowing spreads and

adds additional data.

• Annualised, TSI will receive around 8,946,000 tonnes of spot FOB Australia data in 2015.

We received 7.445mmt by October 31st. Transaction volumes get full (100%) weighting.

• In supplementary data, TSI will also receive 41,578,800 tonnes of bid/offer data. Bid/offer

volumes only get a 10% weighting.

• Using aggressively high estimates of the total spot market, TSI will capture 75% of trades

• Annualised, TSI will receive around 694 data points for FOB Australia coking coal (156

transactions). By Oct 31st, we received 130 transactions and 448 bids and offers.

• If there is no transaction on a given day, the prior transaction is rolled-over at a reduced

weighting. Though a day old, it remains relevant and sets buyer and seller expectations.

• Any spot market actor can take part in the index, after signing our legal agreement. Miner/trader/coke maker/mill. TSI is a neutral, industry-impartial organisation.

FOB Australia Index Liquidity…Key takeaways

Index Development

• The Steel Index was founded in order to develop long-term ferrous benchmarks, through

direct industry participation.

• Any spot market actor can take part in the index, after signing our legal agreement.

Miner/trader/coke maker/mill. TSI is a neutral, industry-impartial organisation.

• TSI seeks to get 100% participation in our indices. There is no commercial disincentive to

participation: TSI offers legal guarantees of the confidentiality of data provided to us.

The data is ring-fenced for use in indices only.

• Direct participation in the indices engenders greater confidence in the process – you

can see how your reported spot trades effect the index directly.

• The Steel Index will continue to solicit industry feedback in all of our products in order to

produce, develop and maintain robust and accurate ferrous indices.

• We are happy to present one-to-one so that buyers and sellers are able to drill down

directly into the index methodology. Contact us to arrange a discussion about physical

index use, liquidity-growth for price risk management, or direct index participation.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

0

50000

100000

150000

200000

250000

300000

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

CME

SGX share of total volumes

%

Vo

lum

e

SGX

TSI-linked FOB Australian swaps and futures volumes picking up at SGX.

TSI aims to produce indices which are accurate not only for the physical industry

embedding them, but also for the financial instruments doing the same: so that companies

who manage risk find their hedge to be highly effective in practice.

Derivatives

TD

Steel: since 2006

Iron Ore: since 2008

Scrap: since 2010

Coking Coal: since 2012

Regional Virtual Steel Mill: since 2014

Thank you for your attention!