Embed Size (px)

Citation preview

Emil Chan

Unleashing the O2O Business when the Local Mobile Payment Services are Taking off

9 Oct 2015

Alibaba’s 11.11 Carnival in 2014

57B

500M

600M

217

24B

How about the performance of other Platforms?

O D 14

10 2

O 20 C

P O 487%

The Big 4 of eCommerce in China

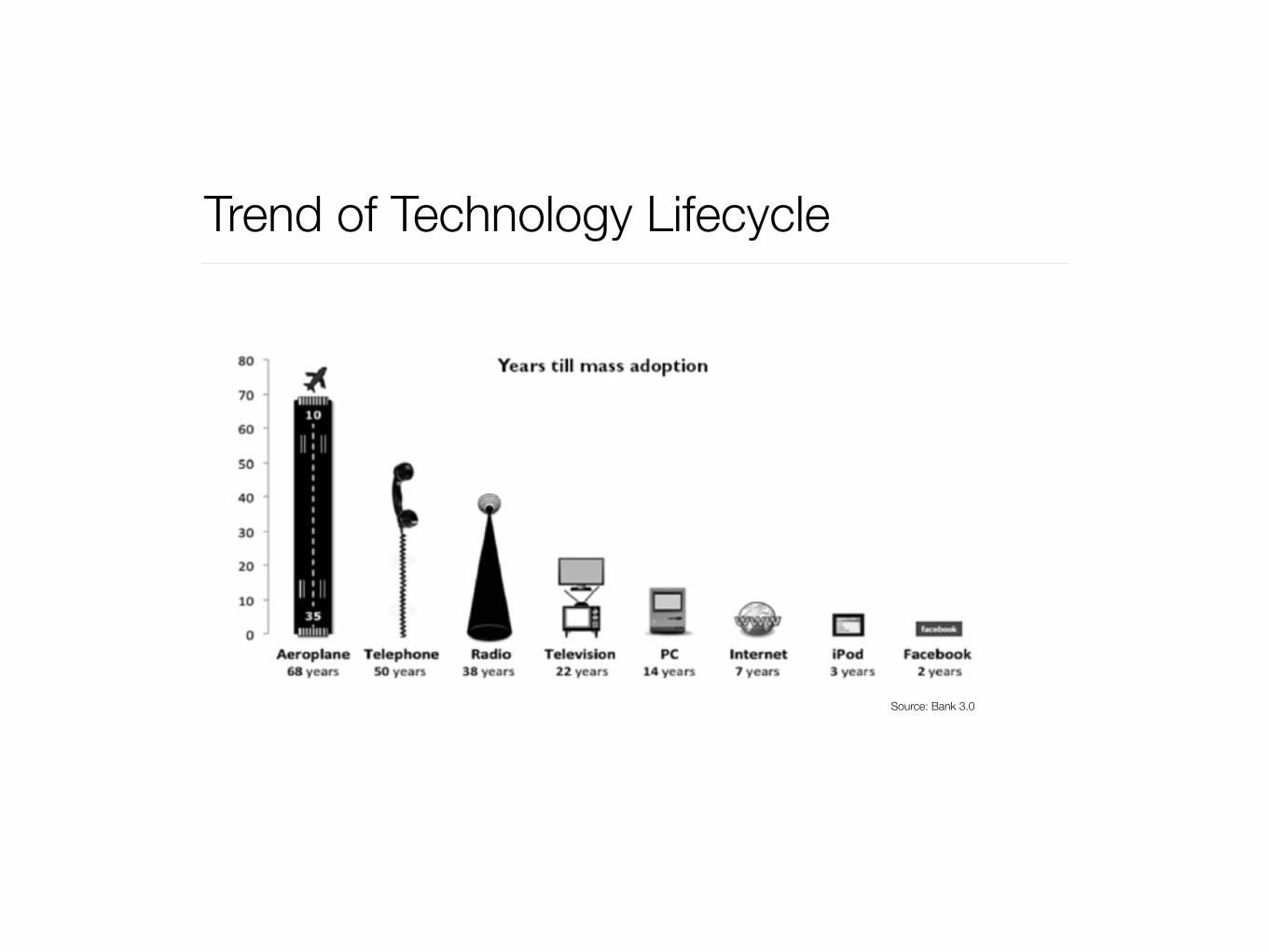

Trend of Technology Lifecycle

Source: Bank 3.0

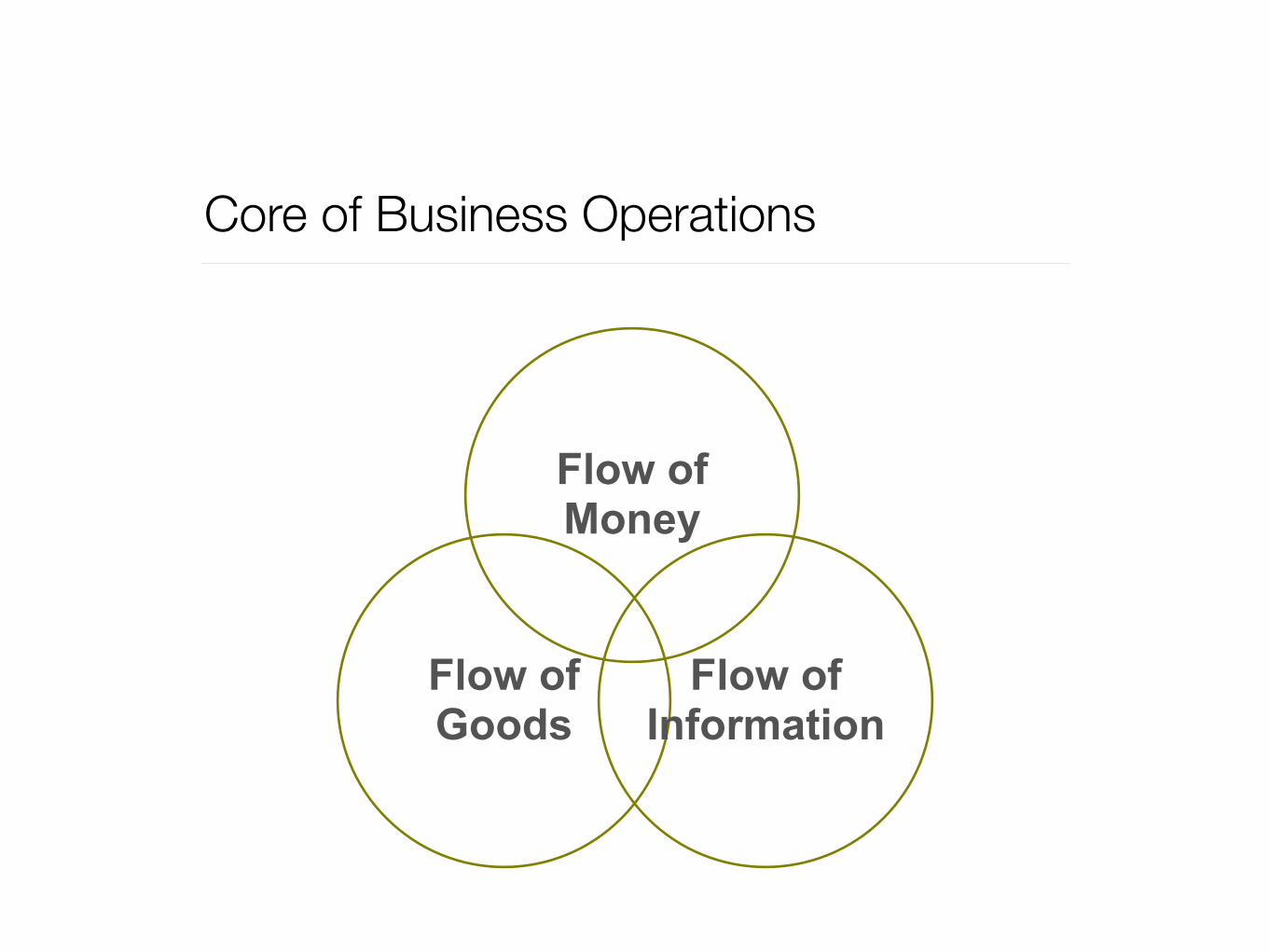

Core of Business Operations

Flow of Goods

Flow of Money

Flow of Information

Are they 3rd Party Payment Agents?

Major 3rd Party Retail Payment Agents inChina and Hong Kong

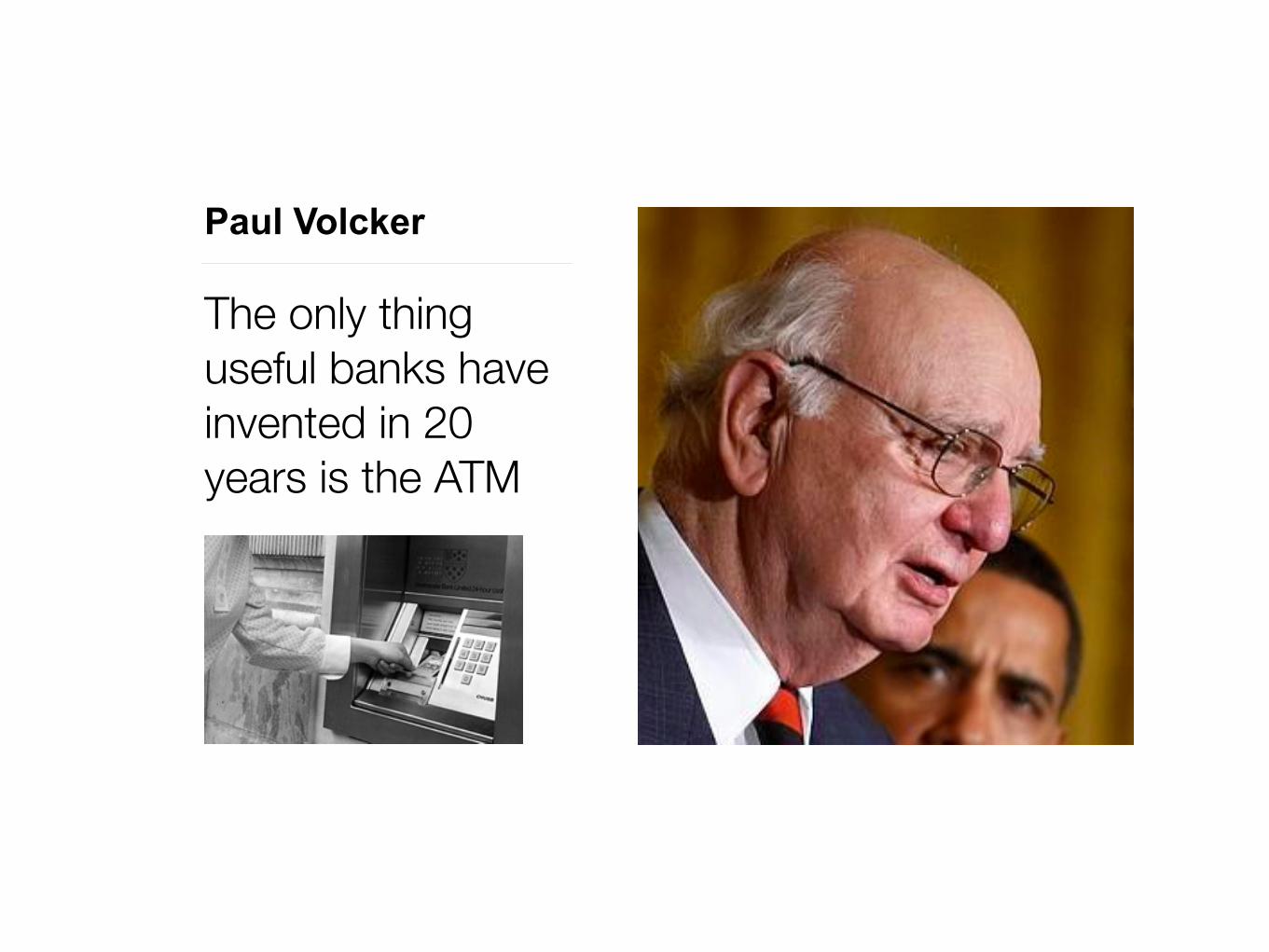

Paul Volcker

The only thing useful banks have invented in 20 years is the ATM

Internet Thinking

Wool comes from the pig's back One gets the benefit for free and the price is paid by someone else

Bigs can fly if they find where wind blows

Uber Everyone’s own Private Driver

Airbnb Welcome Home

Segway the leader in personal, green transportation

AliPay KFC

The Salt Merchant

Rent-Seeking• Textile Quota

• Utility companies

• Taxi

• Tunnels

• Financial Services

FinTech

Banks move into the digital world

Digital World taking over banks

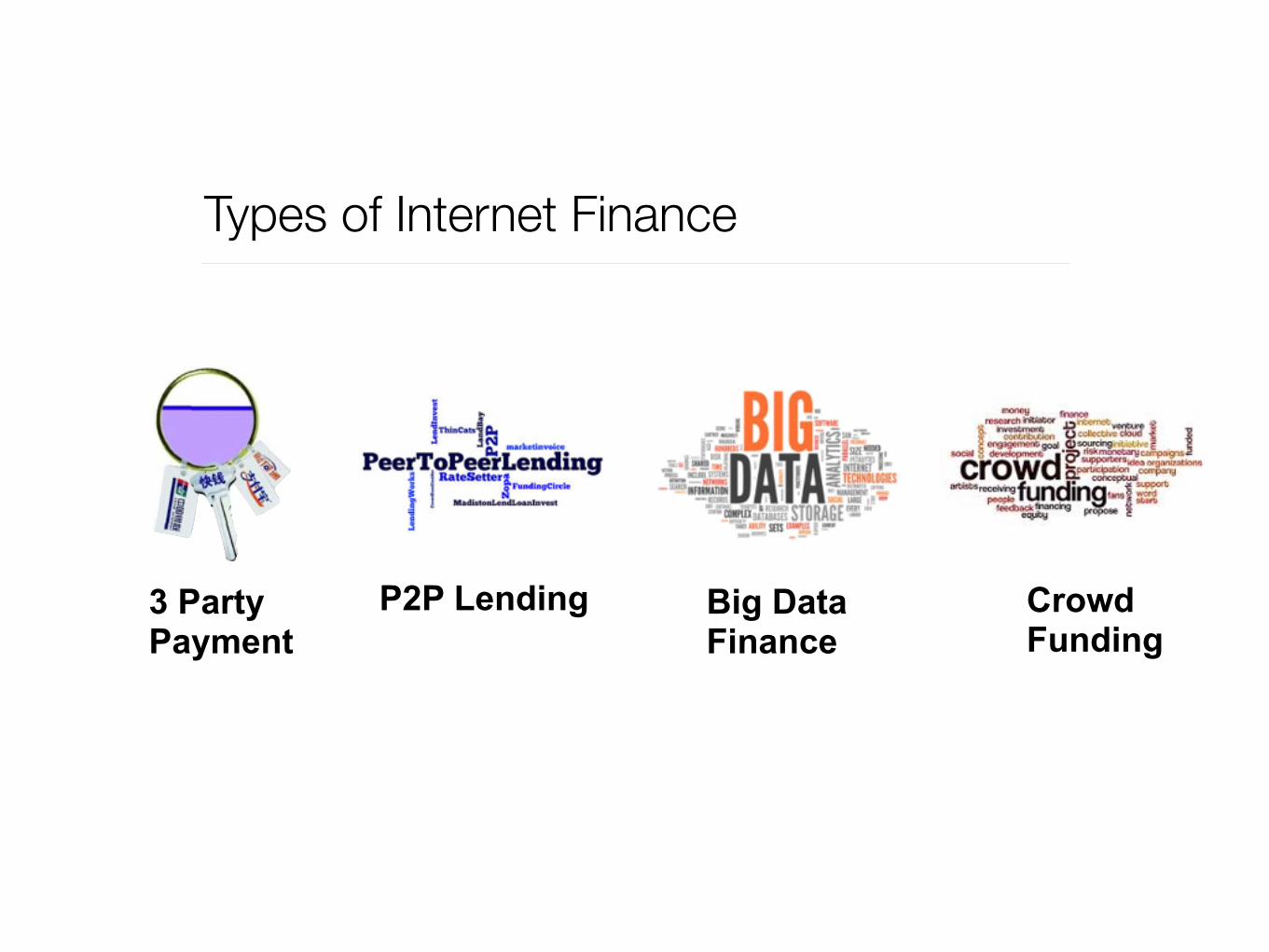

Types of Internet Finance

3 Party Payment

P2P Lending Big Data Finance

CrowdFunding

FinTech Payment Innovation

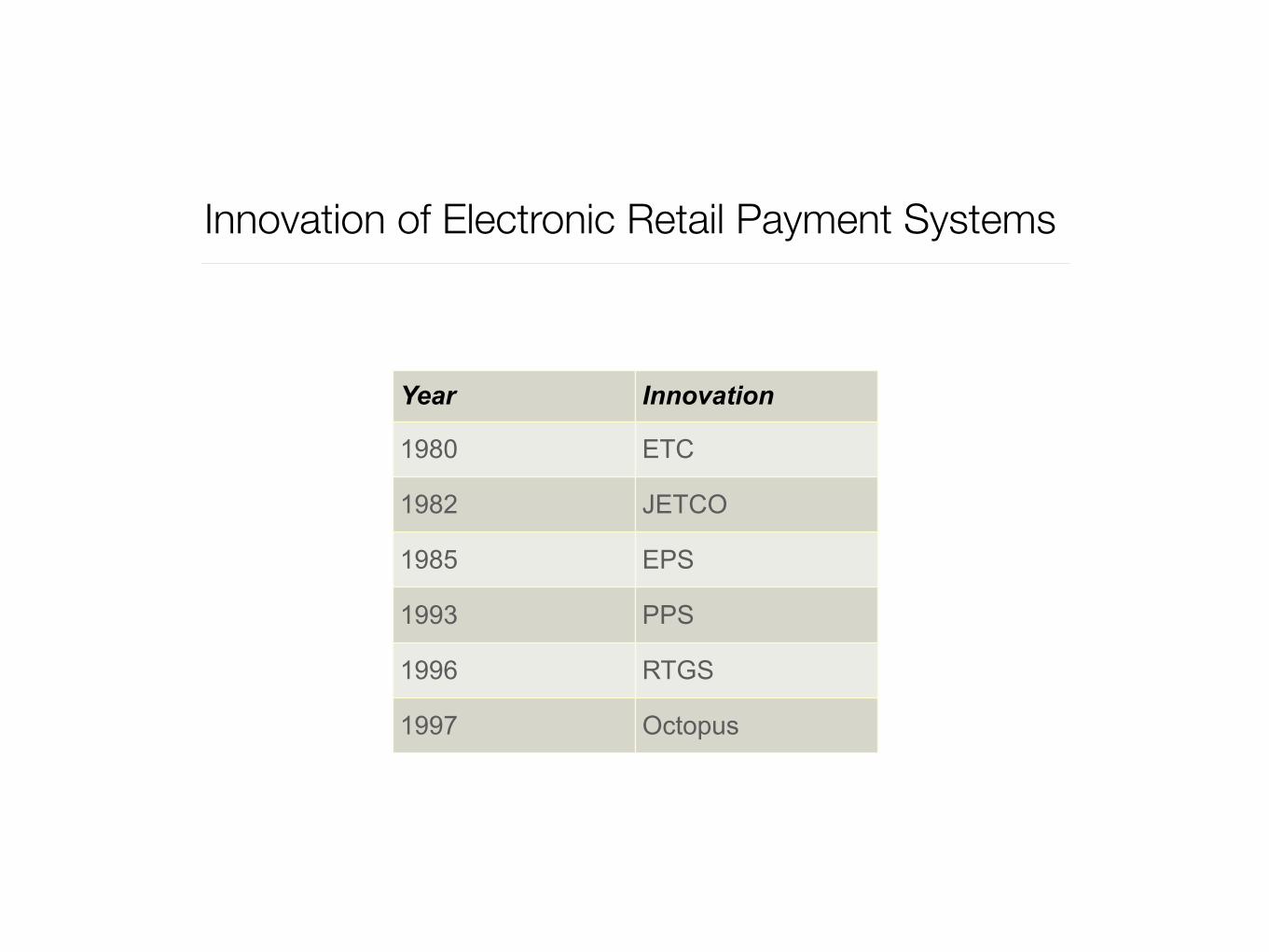

Innovation of Electronic Retail Payment Systems

Year Innovation

1980 ETC

1982 JETCO

1985 EPS

1993 PPS

1996 RTGS

1997 Octopus

EPS Refill cancelled in 2007

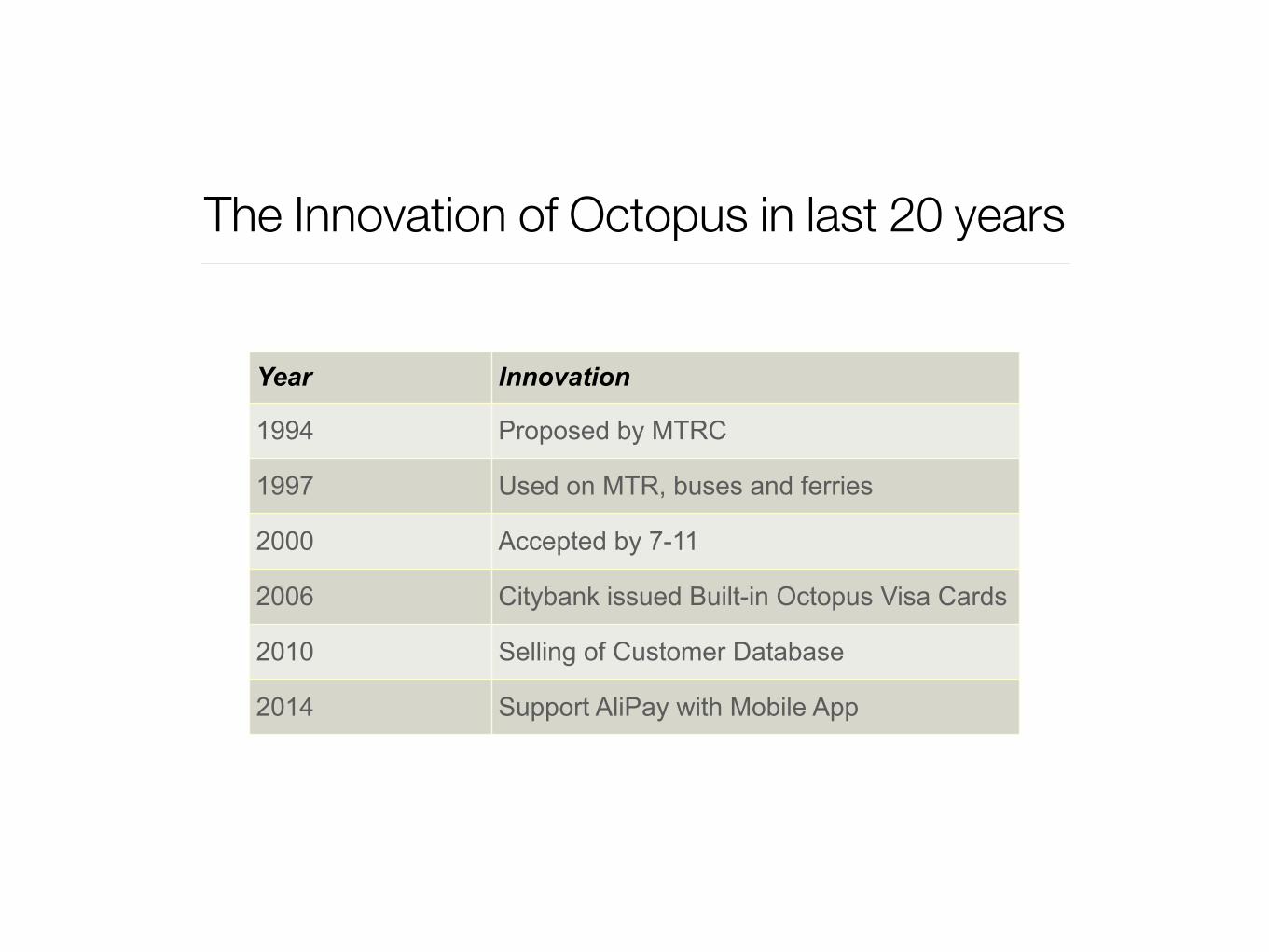

The Innovation of Octopus in last 20 years

Year Innovation

1994 Proposed by MTRC

1997 Used on MTR, buses and ferries

2000 Accepted by 7-11

2006 Citybank issued Built-in Octopus Visa Cards

2010 Selling of Customer Database

2014 Support AliPay with Mobile App

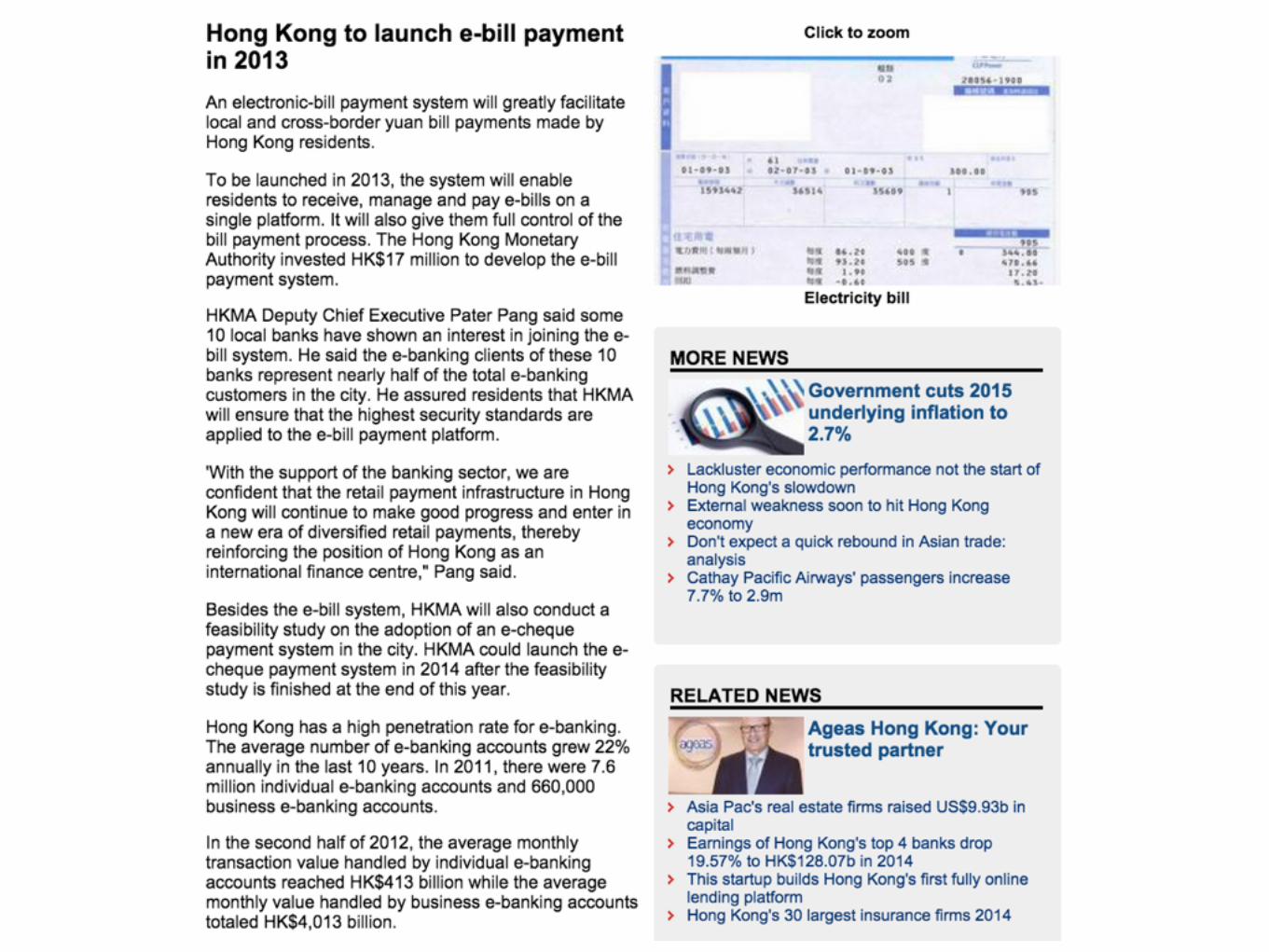

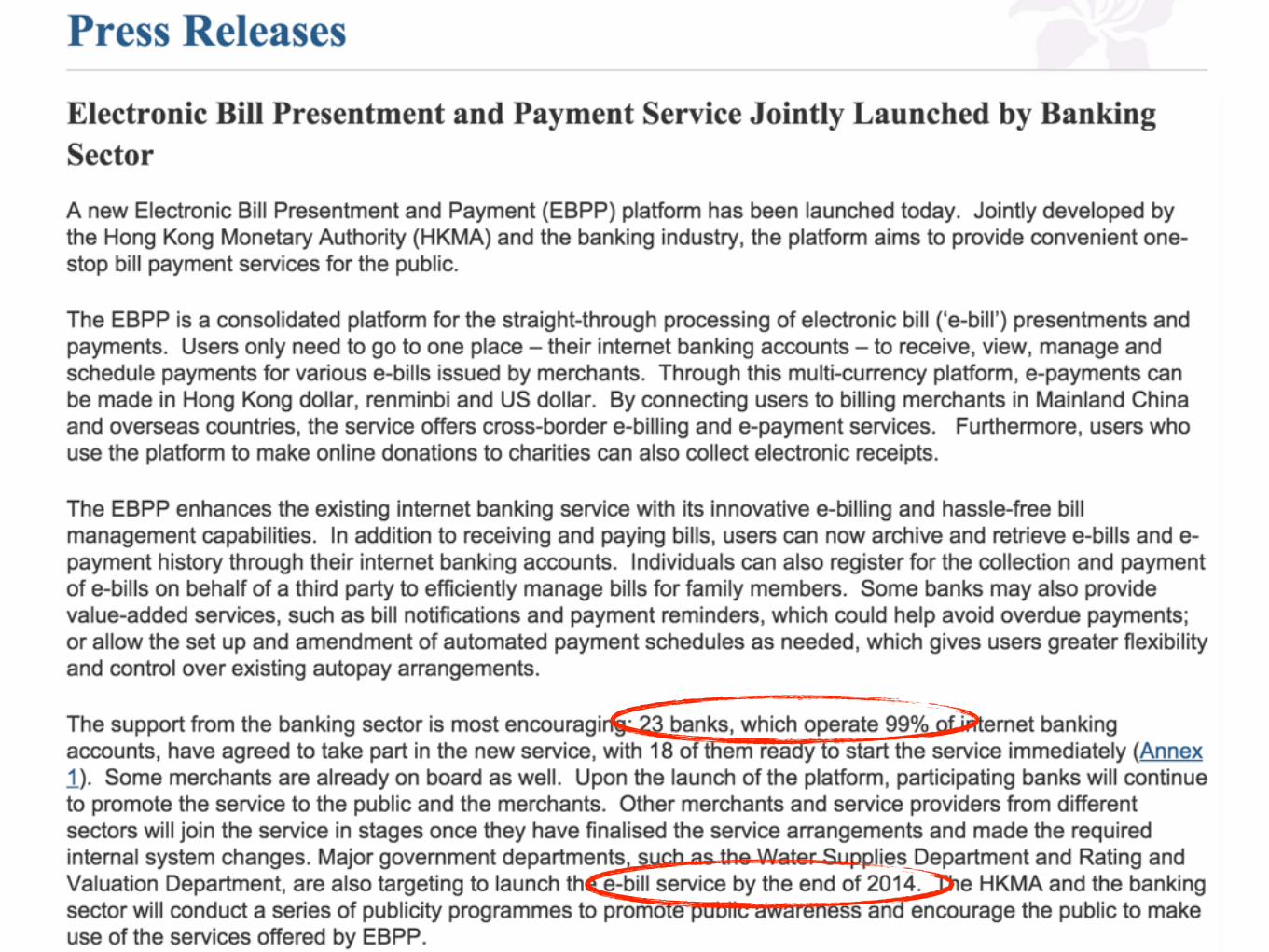

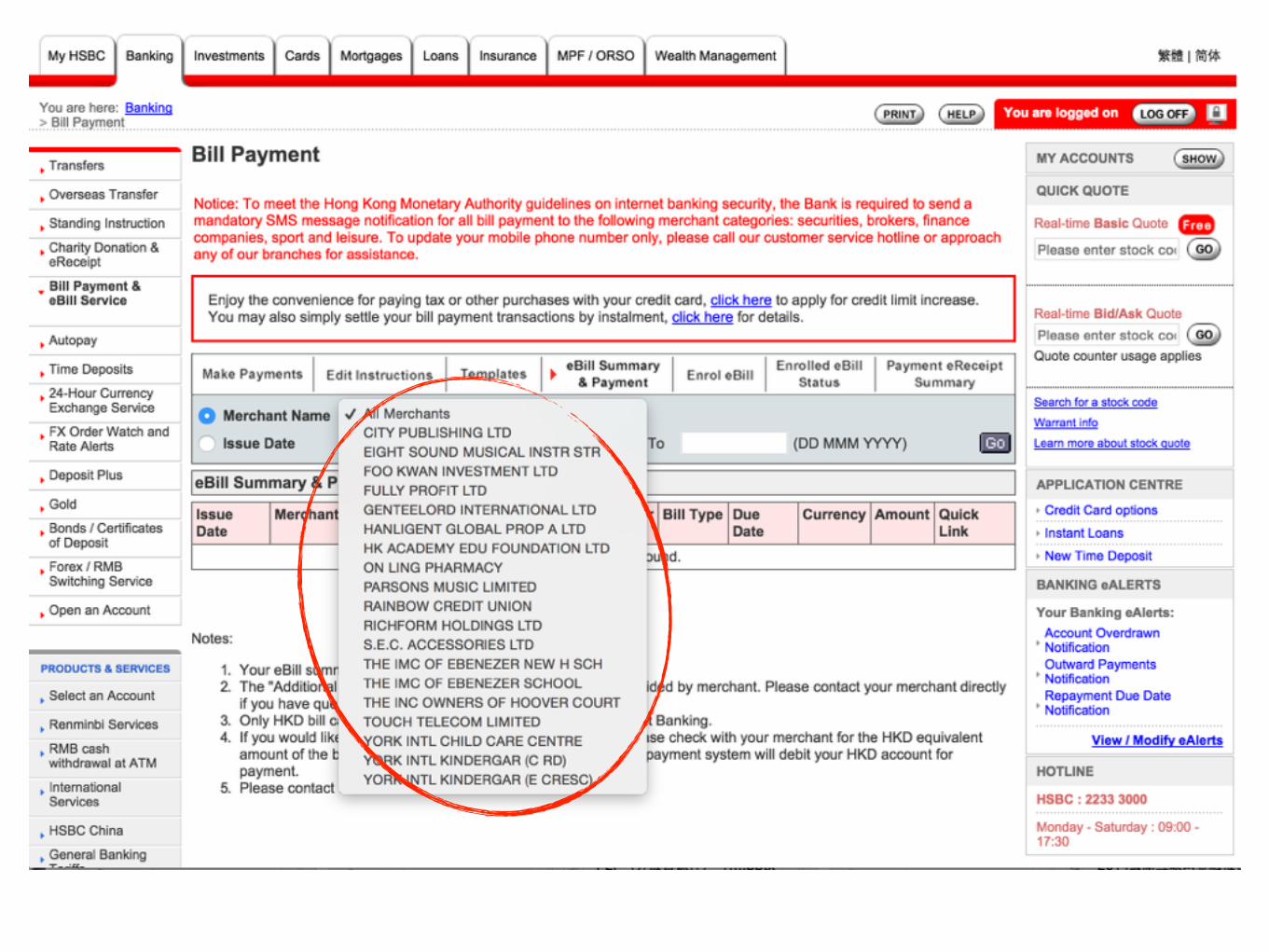

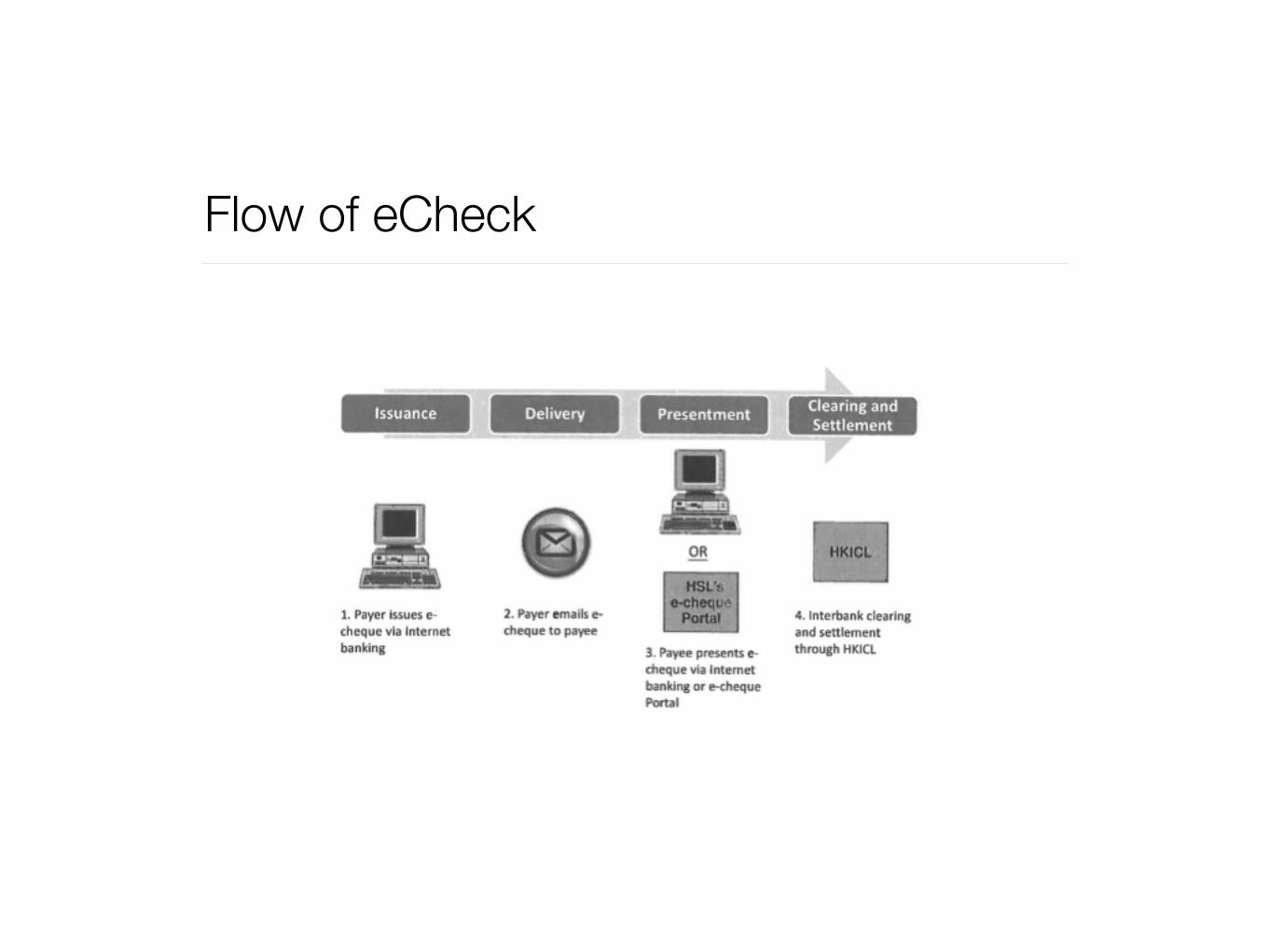

HKMA’s roles on FinTech

As a facilitator

• E-bill presentment and payment platform

• E-cheque

• NFC Mobile payment

Flow of eCheck

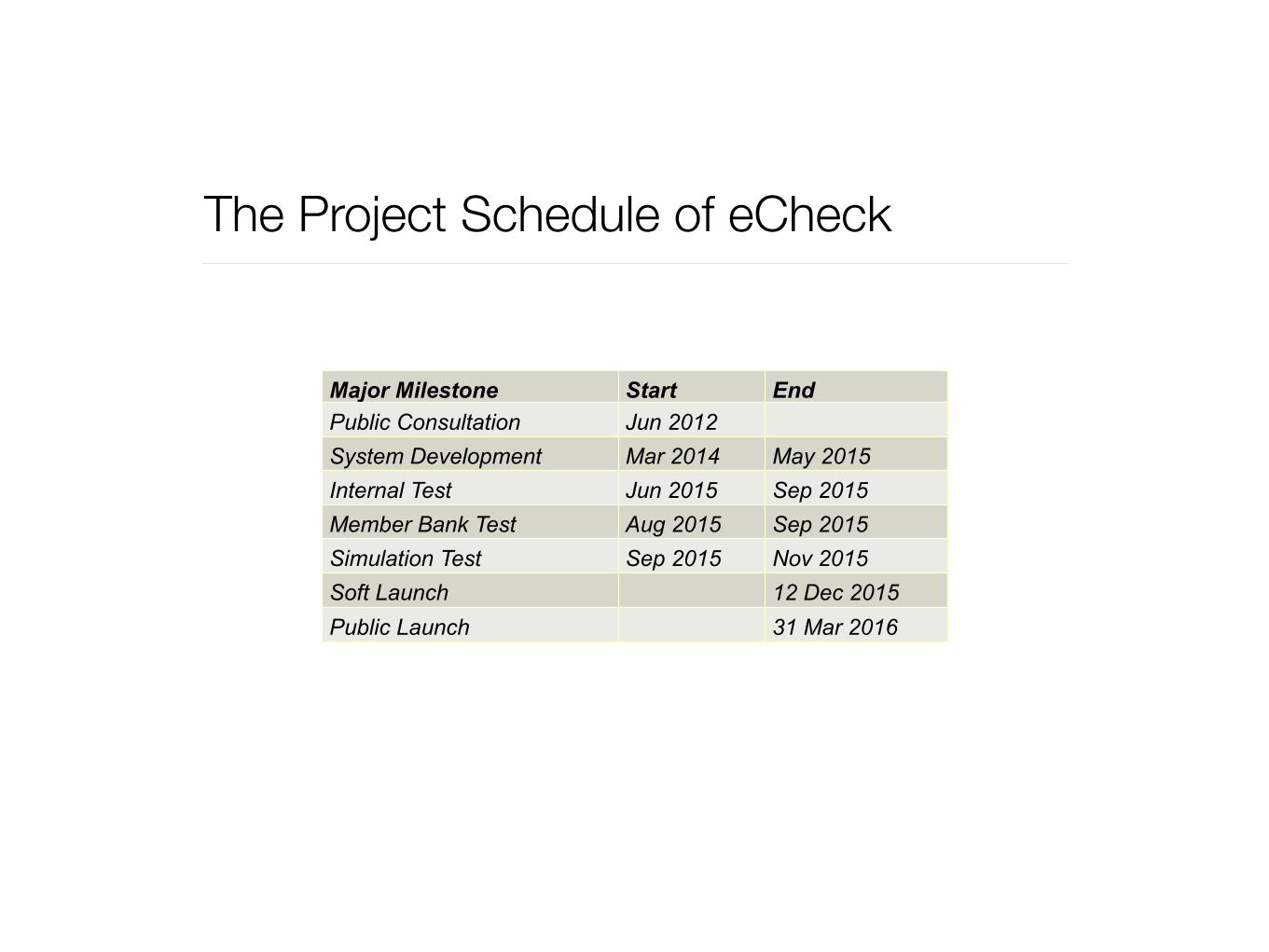

The Project Schedule of eCheck

Major Milestone Start EndPublic Consultation Jun 2012System Development Mar 2014 May 2015Internal Test Jun 2015 Sep 2015Member Bank Test Aug 2015 Sep 2015Simulation Test Sep 2015 Nov 2015Soft Launch 12 Dec 2015Public Launch 31 Mar 2016

HKMA’s roles on FinTech

As a regulator

• Proposed a regulatory regime for Stored Value Facilities (SVFs) and Retail Payment Systems (RPSs)

Licensing regime for SVF • Propose to implement a licensing regime, covering device‐based (e.g. stored value

cards) and non‐device based (e.g. online stored value account) multipurpose SVF, to ensure the safety and soundness of issuers, and protection of users’ float

• Issuing SVF without a licence will be a criminal offence

• No licence is required for single‐purpose SVF

• The Hong Kong Monetary Authority (“HKMA”) may exempt the following SVF from applying for a licence - SVF for use within, or within close proximity to, the issuer’s premises; or- SVF for purchasing limited range of goods or services from a limited group of goods and services providers

• As licensed banks are already subject to regulation under BO, they are deemed to be licensed to issue SVF

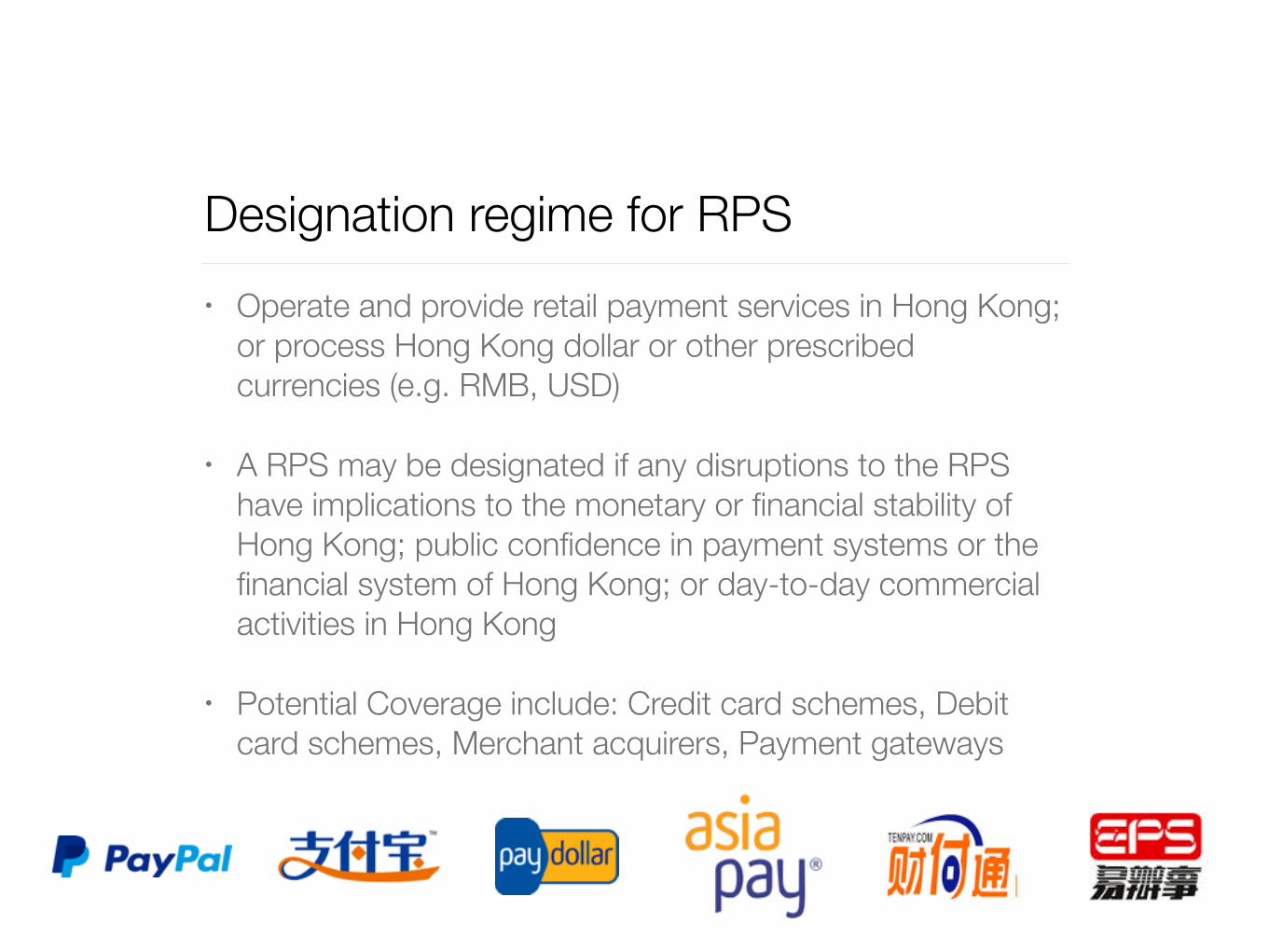

Designation regime for RPS • Operate and provide retail payment services in Hong Kong;

or process Hong Kong dollar or other prescribed currencies (e.g. RMB, USD)

• A RPS may be designated if any disruptions to the RPS have implications to the monetary or financial stability of Hong Kong; public confidence in payment systems or the financial system of Hong Kong; or day-to-day commercial activities in Hong Kong

• Potential Coverage include: Credit card schemes, Debit card schemes, Merchant acquirers, Payment gateways

Objectives of the regulatory regime • ensure the safety and soundness of the operation of SVF and

RPS in Hong Kong;

• ensure adequate protection and no misappropriation of float of SVF;

• foster innovation in retail payment products and services in Hong Kong by providing clarity in the legislation and a level playing field for market participants; and

• maintain Hong Kong’s status as an international financial centre, by putting the retail payment legislation on par with what other major financial centres are pursuing.

Status of Legislation • The Clearing and Settlement Systems (Amendment)

Bill 2015 gazetted on 23 January 2015

• The Bill was introduced into the Legislative Council for first reading on February 4, 2015

• Bills Committee on Clearing and Settlement Systems (Amendment) Bill 2015 – First meeting on Monday, 2 March 2015

• Target completion of legislation: end of 2015

Benefits to FinTech development By introducing the regulation, we can

• provide clarity in the legislation;

• provide a level playing field for market participants; andmaintain Hong Kong’s status as an international financial centre;

Benefits to FinTech development

• foster innovation in retail payment products and services in Hong Kong

• attract more e-money issuers to establish business in HKcreate more opportunities for IT support and security services companies in HK

When the coach is also the referee

9 Banks With iPhone Remote Check Deposit Apps - APPS MOBILE 06/13/2011

• According to a recent Federal study, the use of paper checks have declined 7.1% since 2006 thanks to a 45% growth in electronic payments; but that doesn’t mean we are done with good old-fashioned paper checks that account for 24.5 billion in annual payments

• Odds are no matter how digital you make your life you’ll still receive a few paper checks each year. With this in mind, we found 9 banks that will let you use your iPhone camera to remotely deposit your check, no matter where you are

A�W#A�cV& ��d

A�G�+�cV& ��d

@(/%:

,^��! 8S���49��"B_2-OQ_1I�Q

�X)FKD

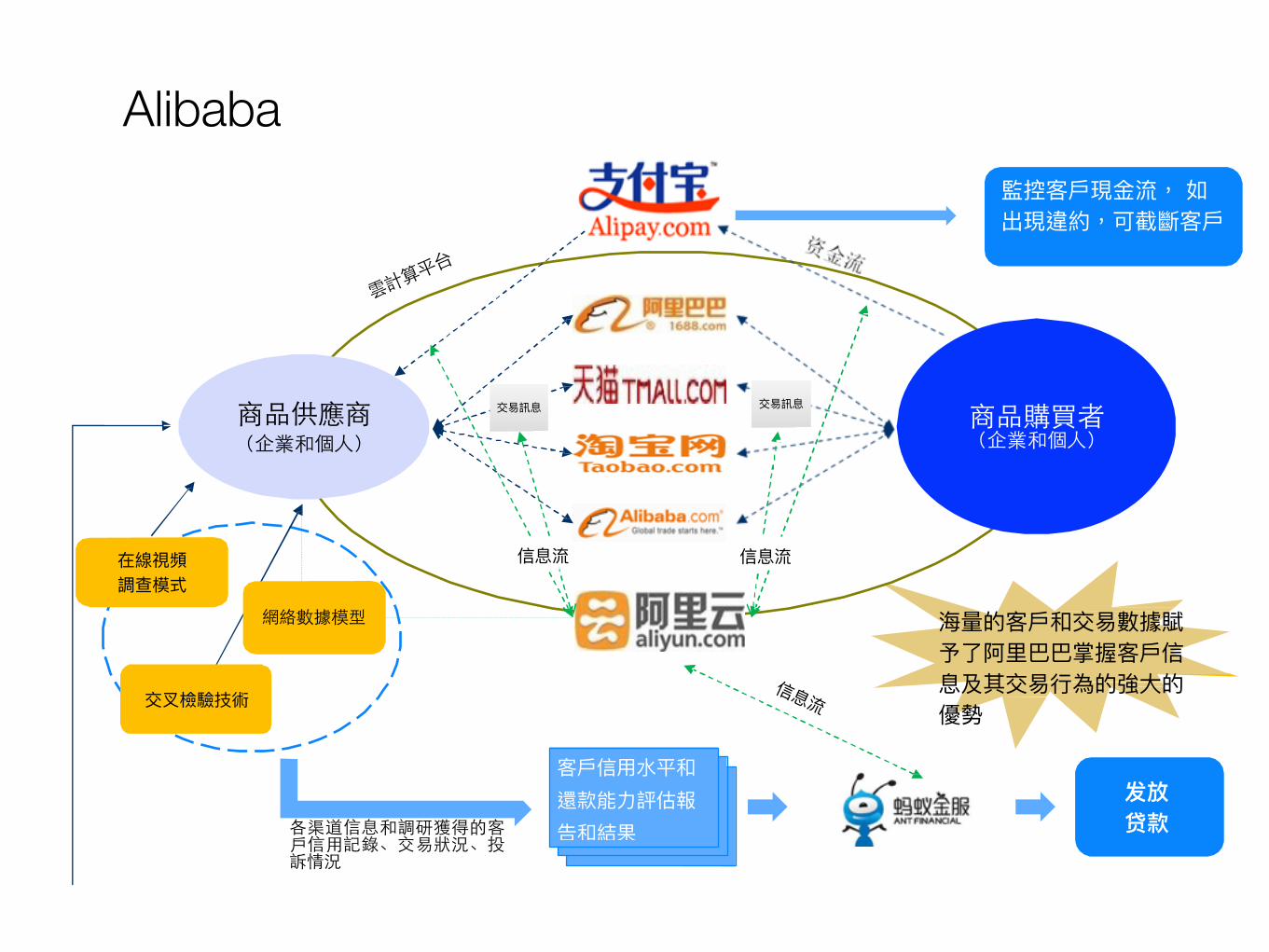

Alibaba

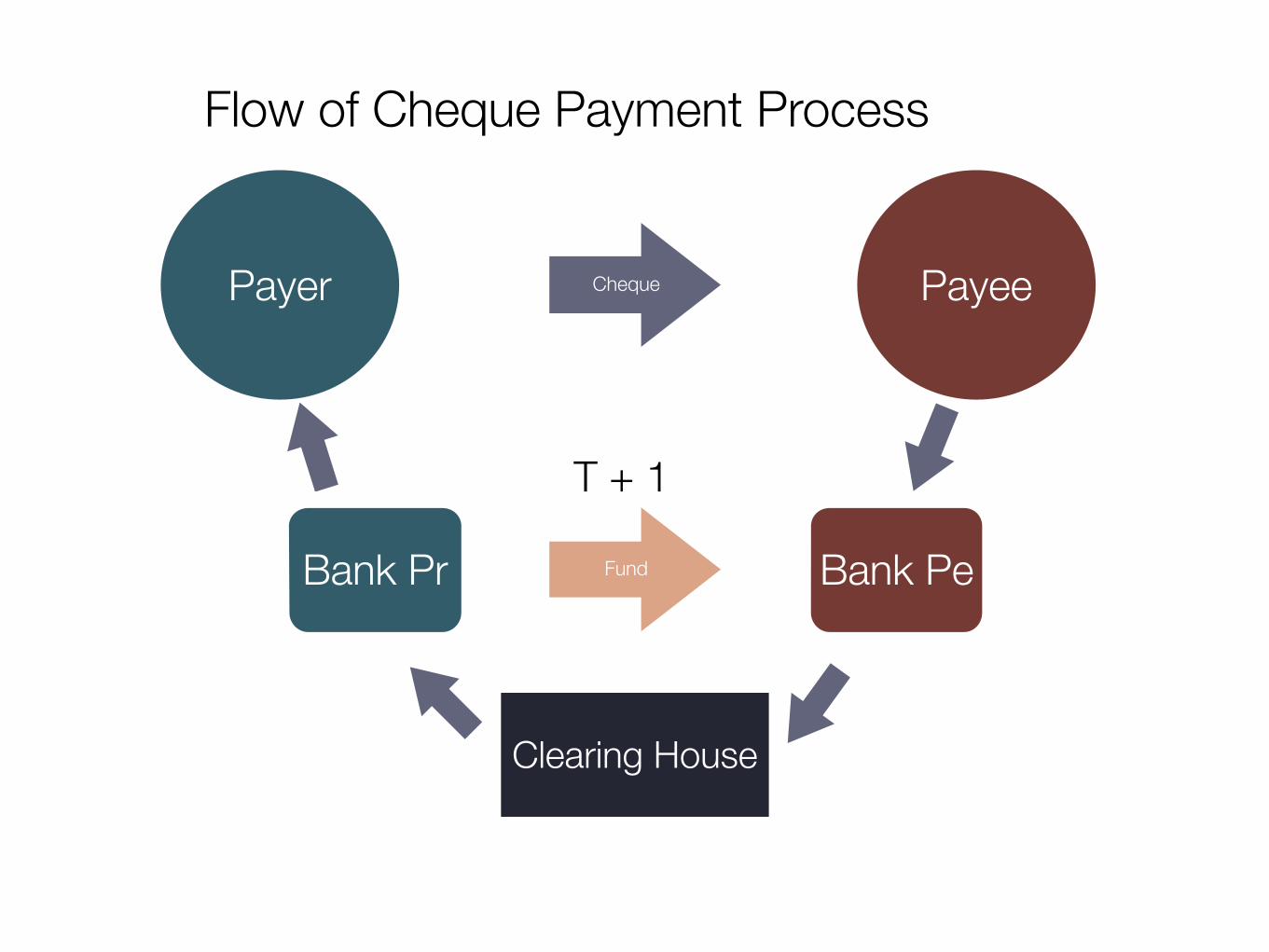

Payer Payee

Clearing House

Bank Pr Bank Pe

Cheque

Fund

Flow of Cheque Payment Process

T + 1

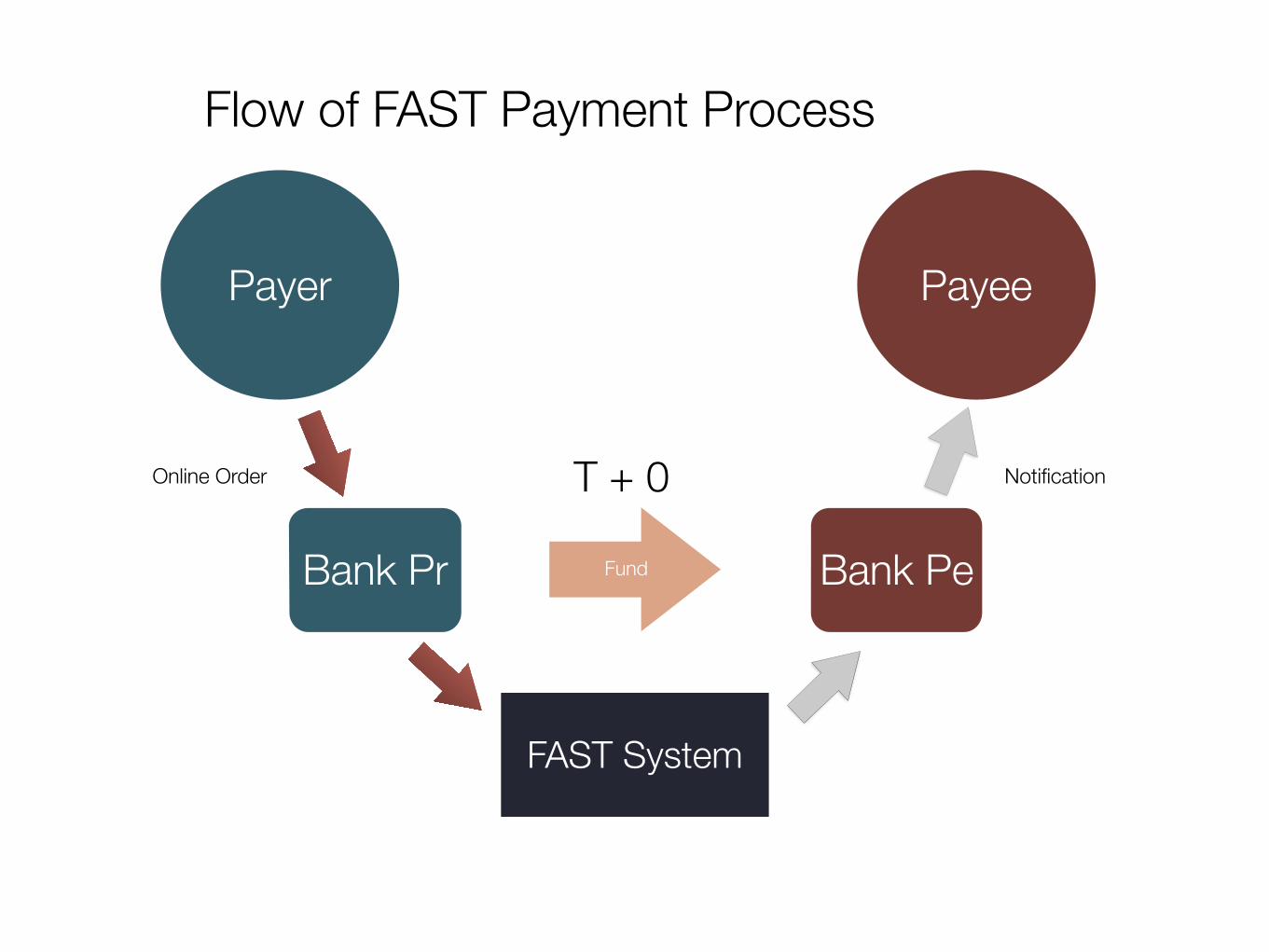

Payer Payee

FAST System

Bank Pr Bank PeFund

Flow of FAST Payment Process

Online Order NotificationT + 0

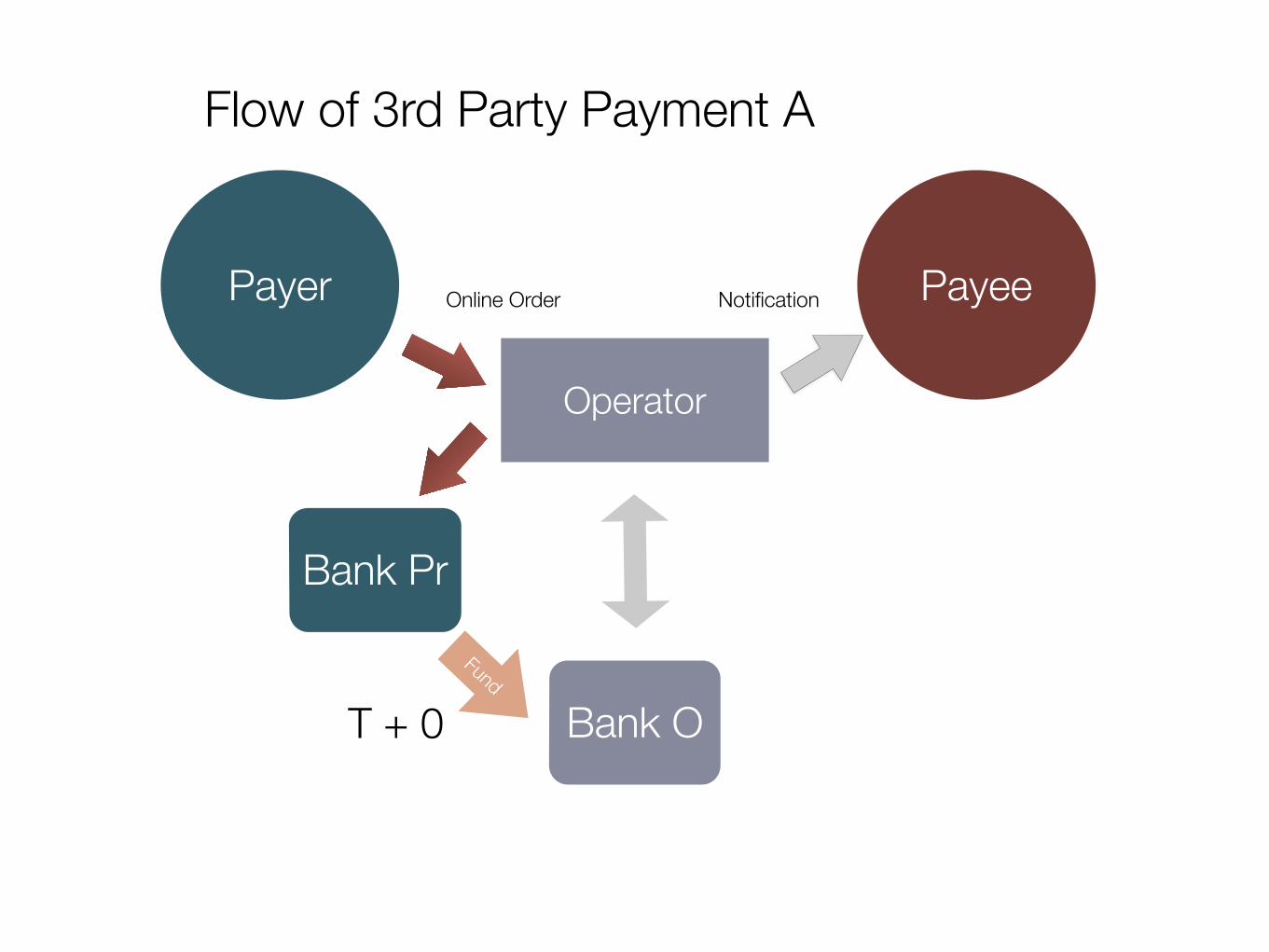

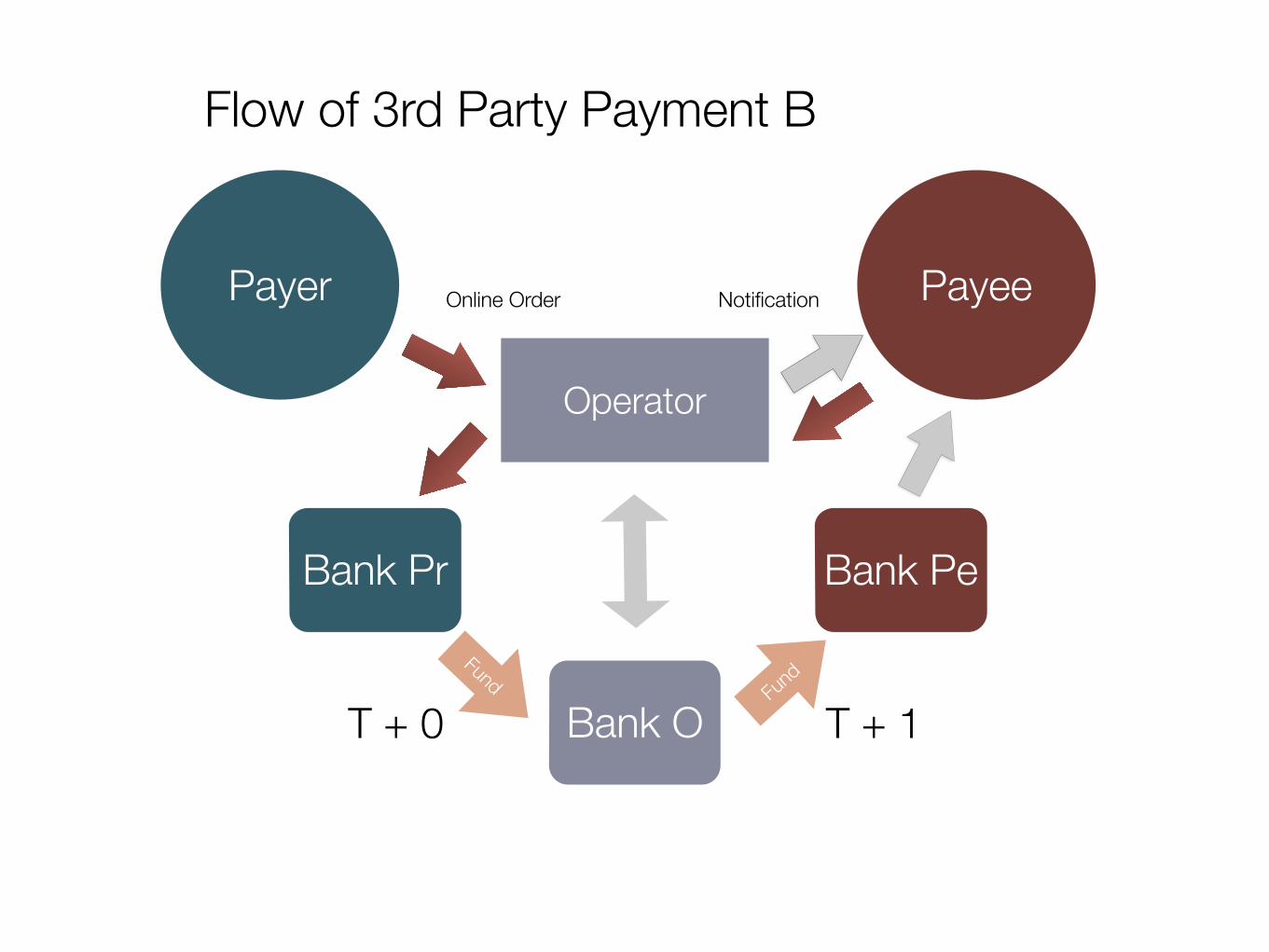

Payer Payee

Operator

Bank Pr

Fund

Flow of 3rd Party Payment A

Online Order Notification

Bank OT + 0

Payer Payee

Operator

Bank Pr

Flow of 3rd Party Payment B

Online Order Notification

Bank Pe

FundFund

Bank O T + 1T + 0

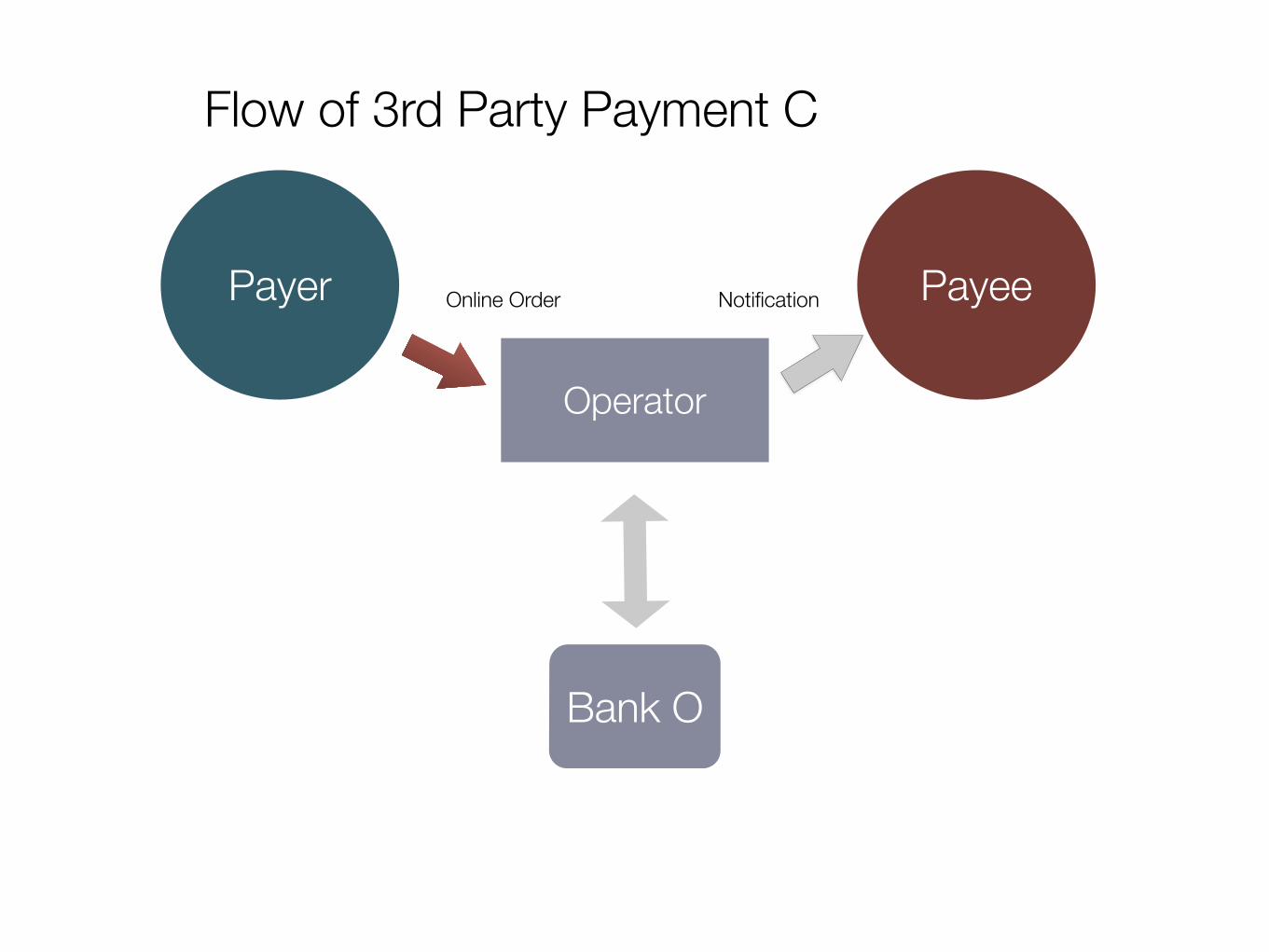

Payer Payee

Operator

Flow of 3rd Party Payment C

Online Order Notification

Bank O

App vs Wechat

WeChat Payment

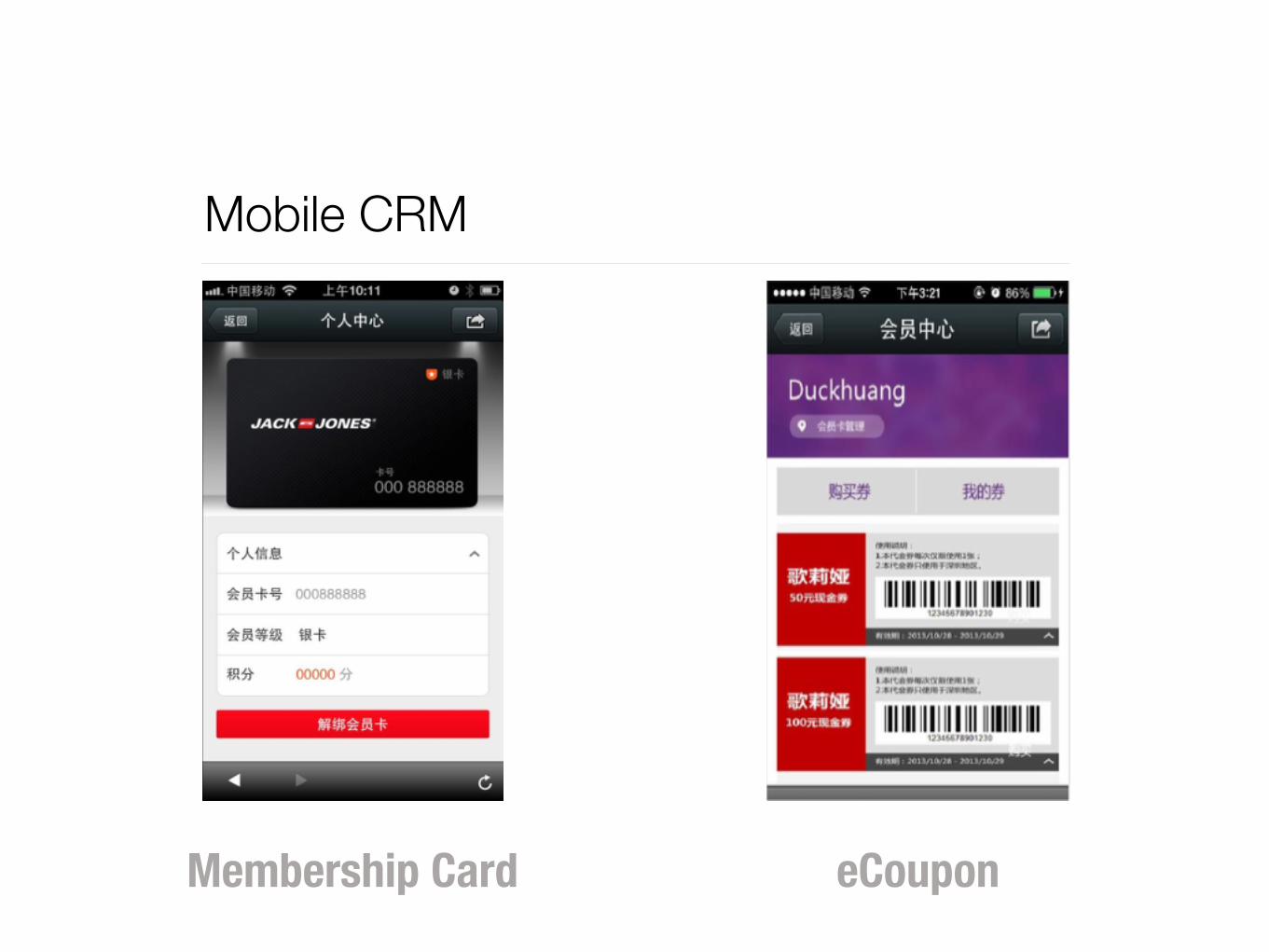

Mobile CRM

Membership Card eCoupon

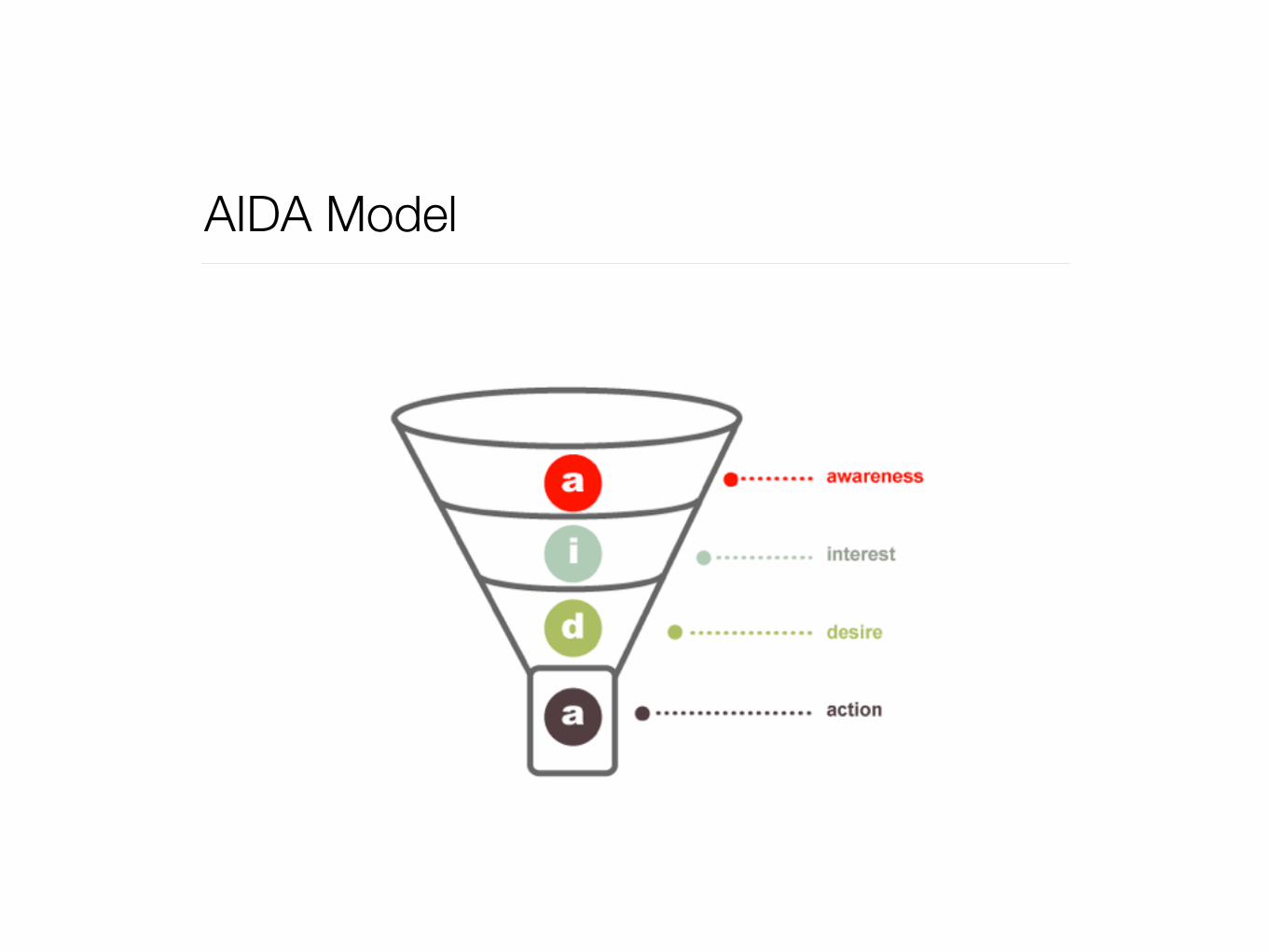

AIDA Model

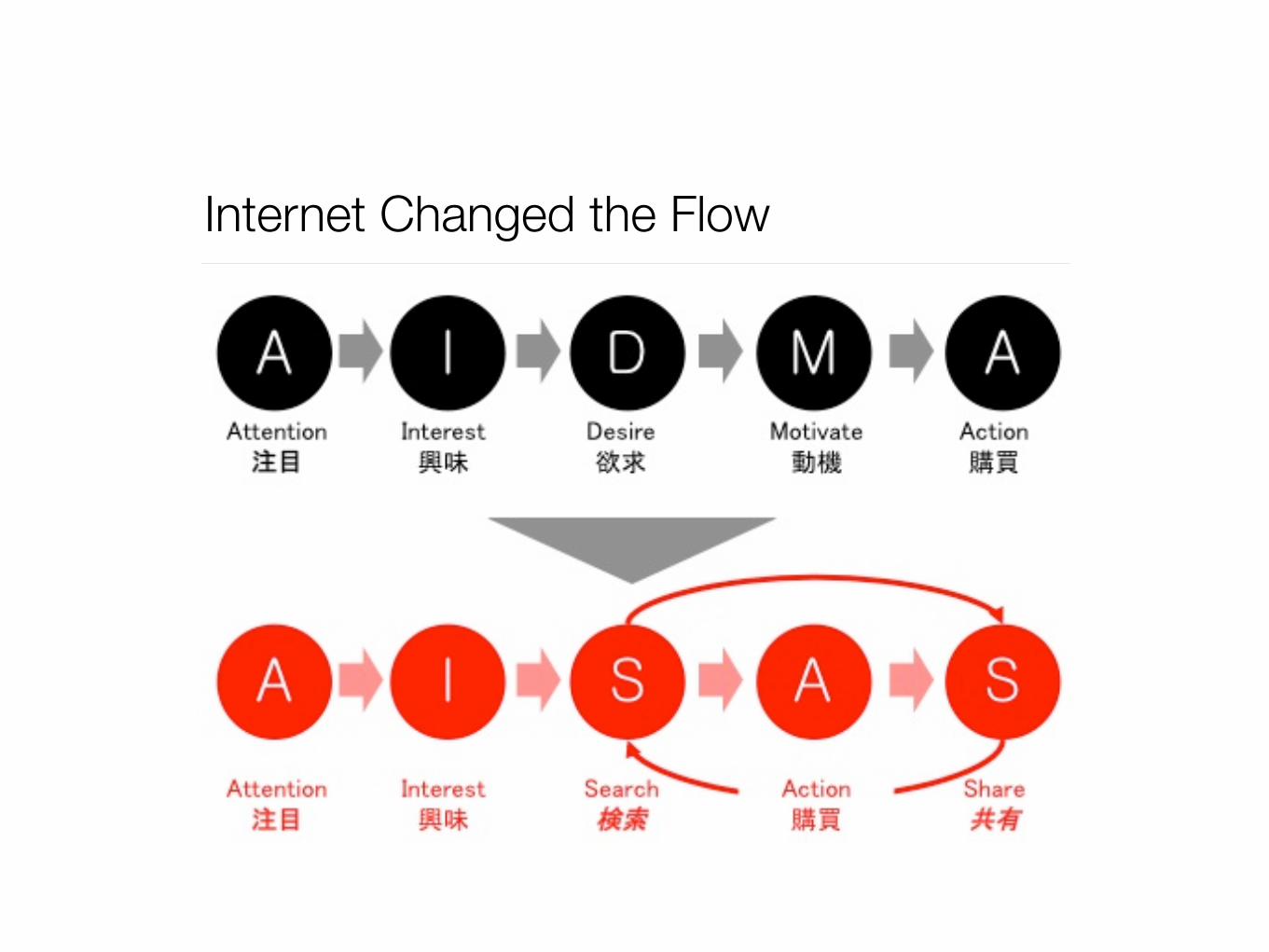

Internet Changed the Flow

The New Model

AIDA AISAS

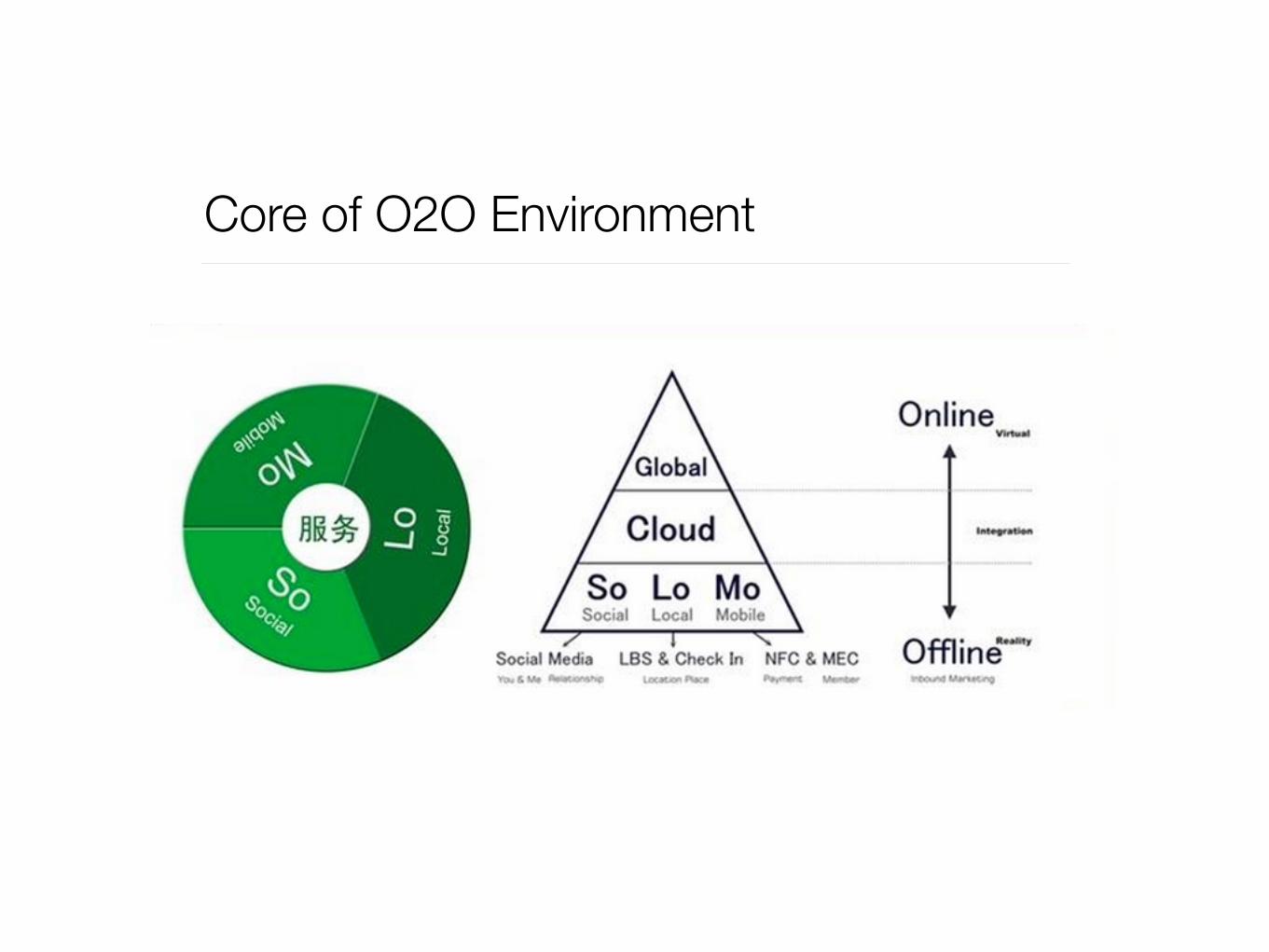

Core of O2O Environment

Cross-border ePayment

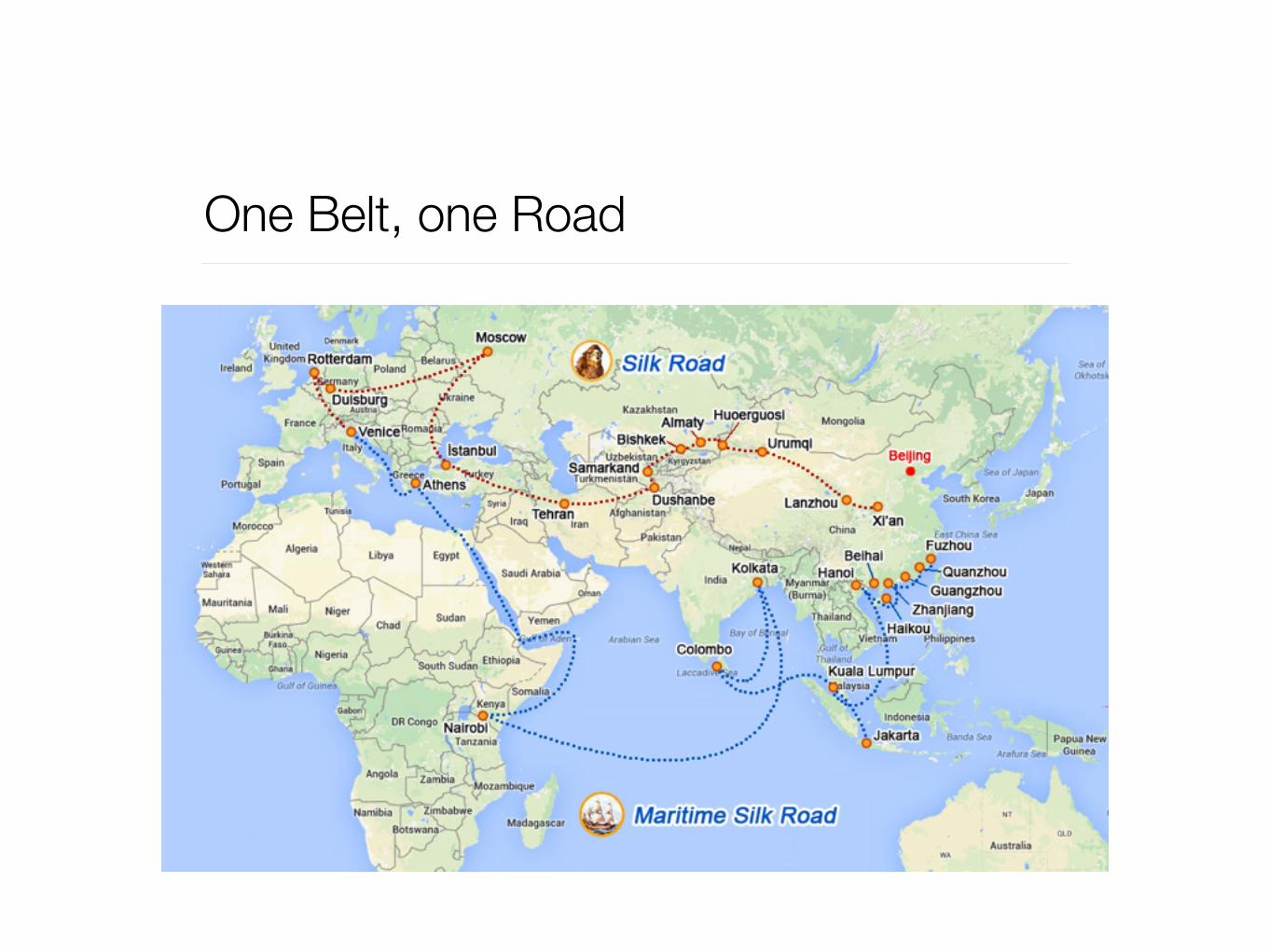

One Belt, one Road

10 Aug 2015 - \]>$��5H Z�7e�E�U_3L0e'=JTNa;���b`6RNM��<e���a����b.P[?a�*CY�b

Leung mulls SME support in ‘One Belt, One Road’ pursuit

Crossborder Trading

Free Trade Zones

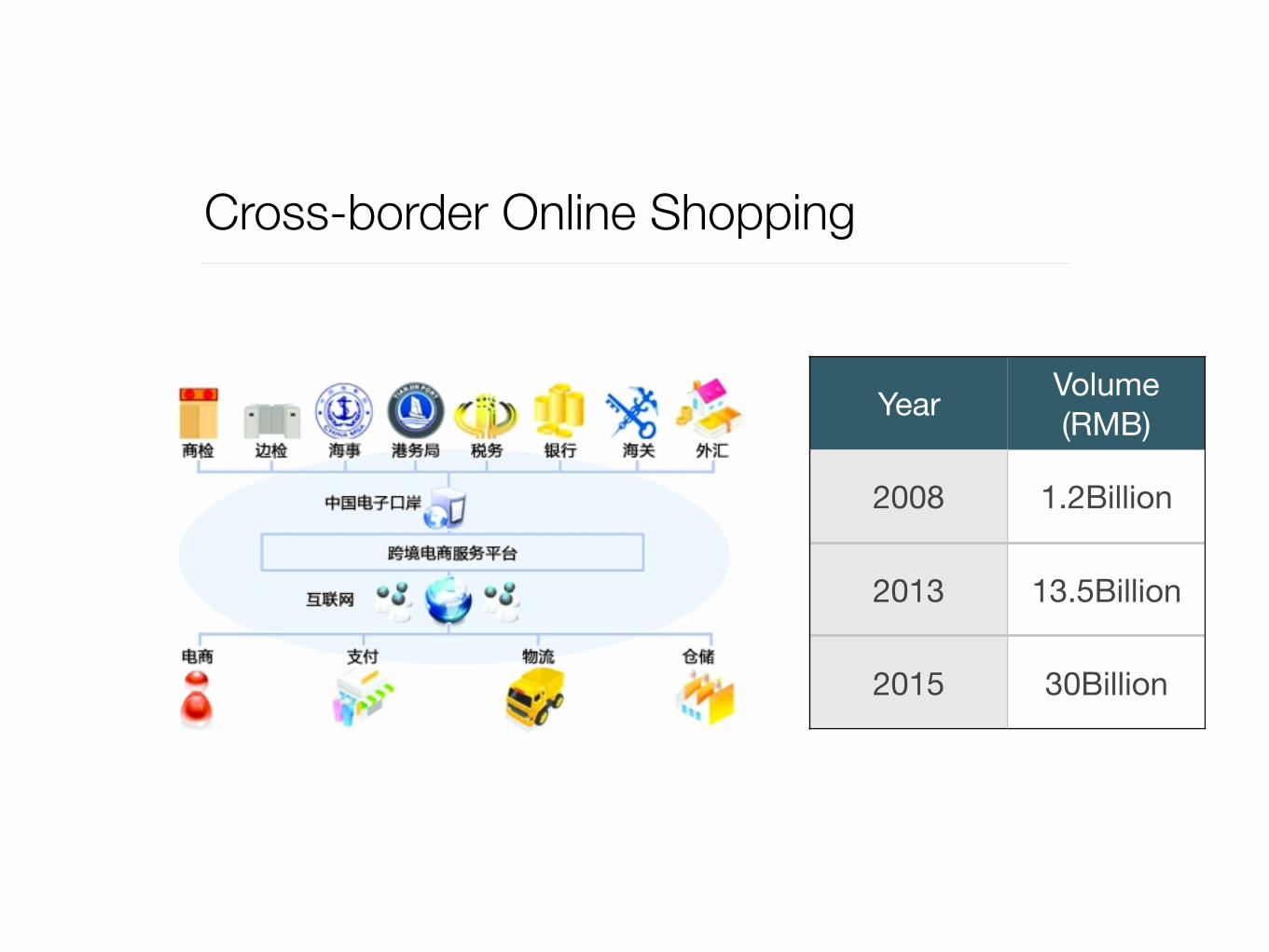

Cross-border Online Shopping

Year Volume (RMB)

2008 1.2Billion

2013 13.5Billion

2015 30Billion