Embed Size (px)

Citation preview

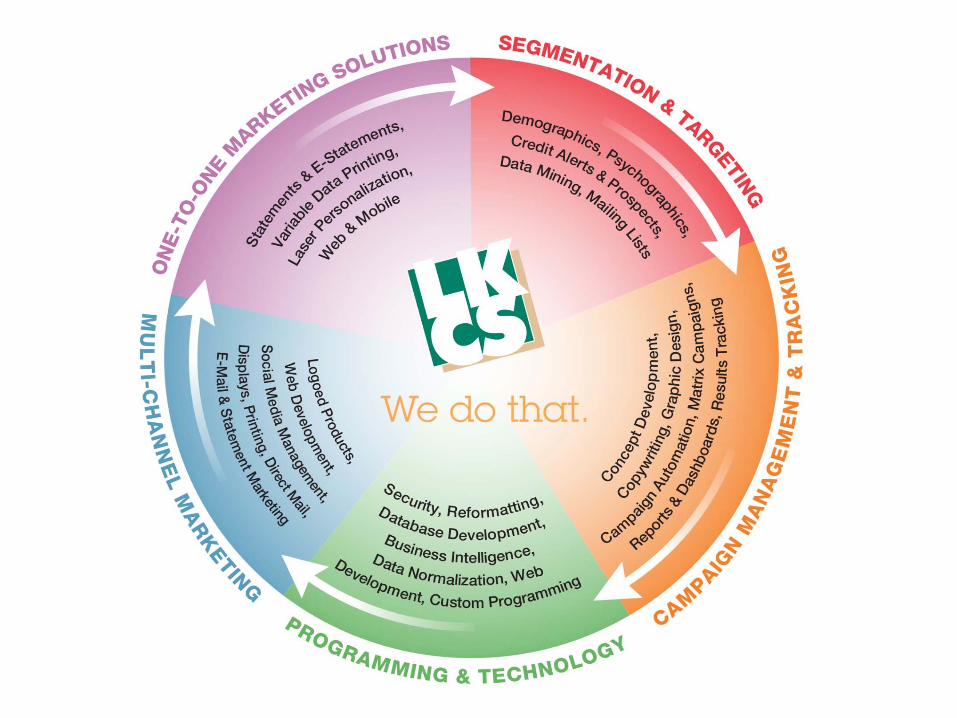

Credit Alerting & ProspectingLeverage Credit Inquiry Data to Improve

Acquisition, Retention and Lifetime Value

Are You Losing Good Loans?

• Be Aware, Over Half of your Account Holders will be Looking for an Auto, Mortgage, HELOC, or Credit Card Loan in the Next Year!

• Competition is More Fierce than Ever Before. Are you Prepared?

• Gain the Ability to Monitor and Close Loans from Accounts When they are Looking to Close.

• Be able to Make the Right Offer at Just the Right Time!

Are You Losing Good Loans?

• Gain Loans from Prospects that Meet and Exceed your Qualifications.

• Stop Spending Time Reviewing Loan Requests that don’t meet you Loan Criteria.

• You can set the Parameters for New Loan Leads!

• LKCS can Assist you in Winning the Qualified Loans Management is Looking for!

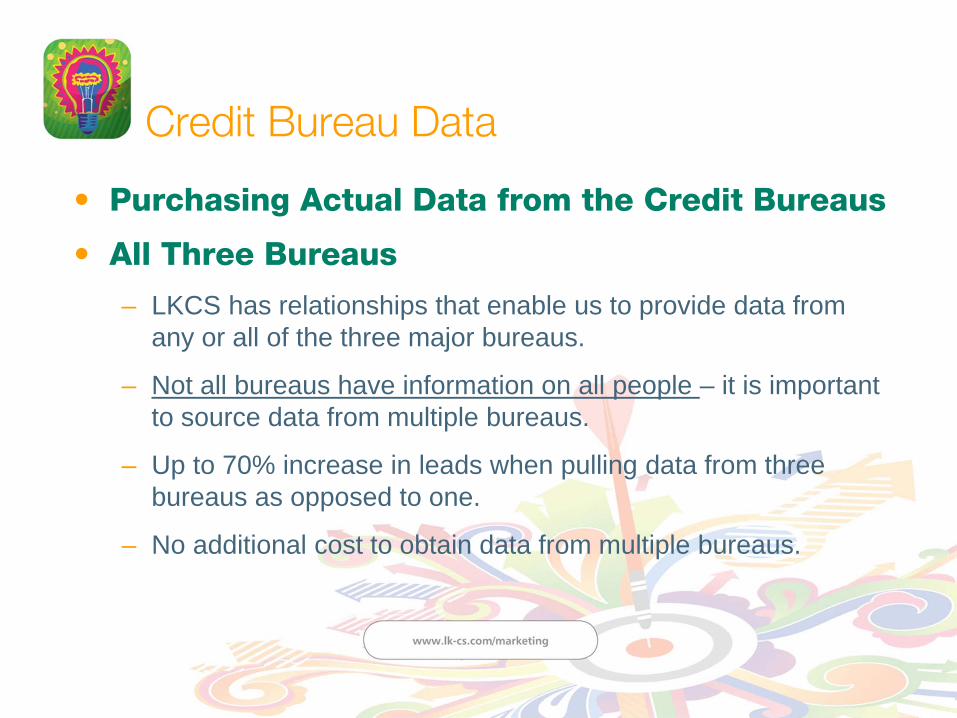

Credit Bureau Data

• Purchasing Actual Data from the Credit Bureaus

• All Three Bureaus

– LKCS has relationships that enable us to provide data from any or all of the three major bureaus.

– Not all bureaus have information on all people – it is important to source data from multiple bureaus.

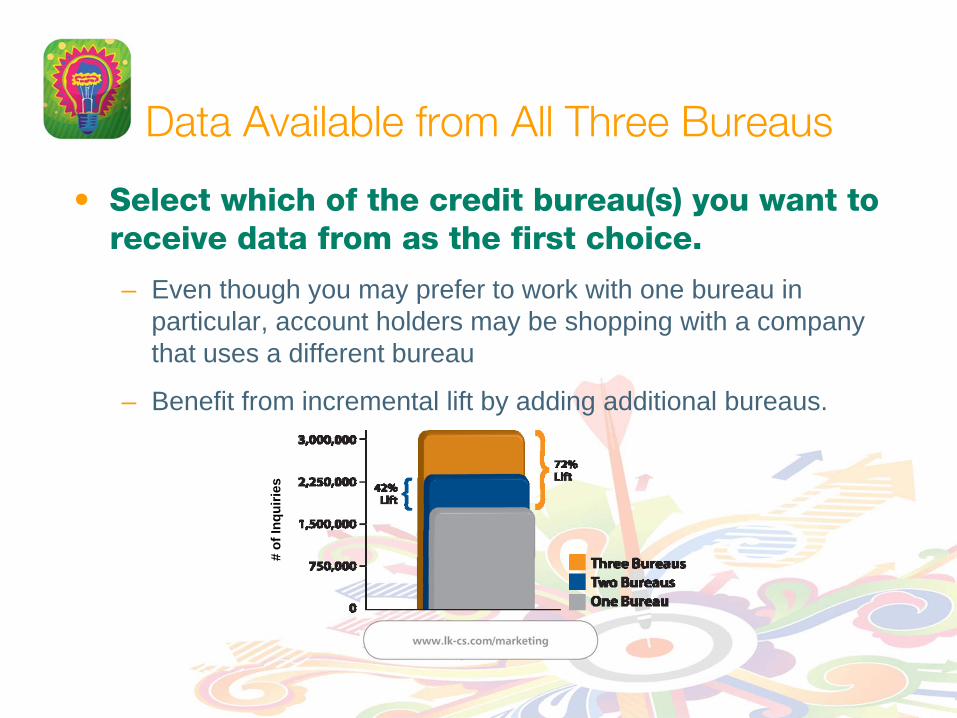

– Up to 70% increase in leads when pulling data from three bureaus as opposed to one.

– No additional cost to obtain data from multiple bureaus.

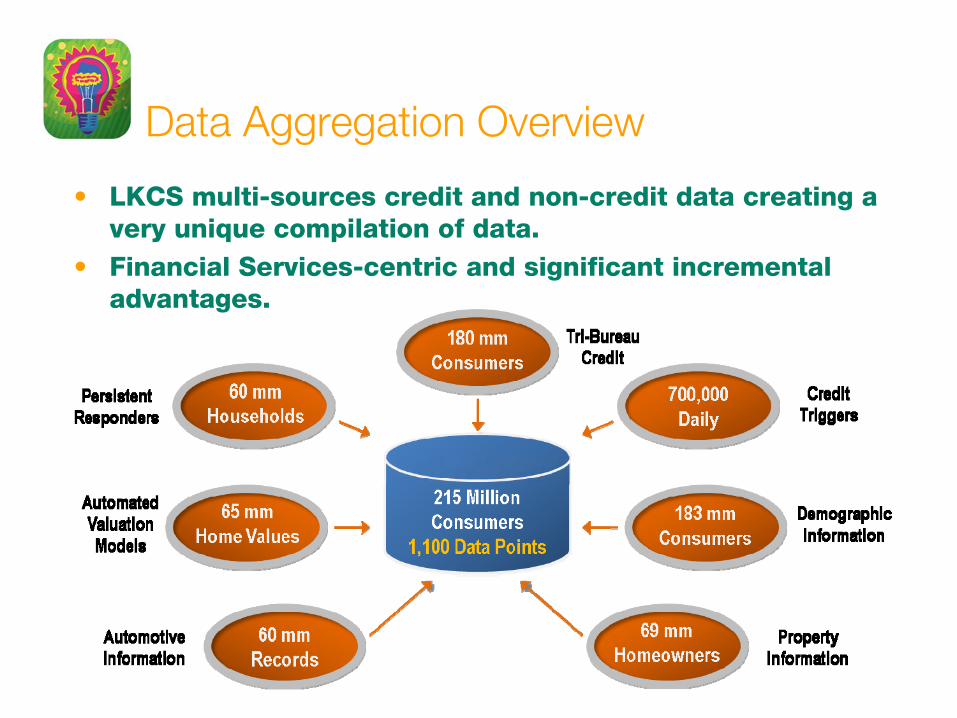

Data Aggregation Overview

• LKCS multi-sources credit and non-credit data creating a very unique compilation of data.

• Financial Services-centric and significant incremental advantages.

Data Available from All Three Bureaus

• Select which of the credit bureau(s) you want to receive data from as the first choice.

– Even though you may prefer to work with one bureau in particular, account holders may be shopping with a company that uses a different bureau

– Benefit from incremental lift by adding additional bureaus.

# of

Inqu

iries

Credit Prospecting vs. Credit Alerting

• Credit Prospecting– Use credit data PROACTIVELY. – Market to prospects or existing account holders with specific

demographic and/or credit-based traits.

• Credit Alerting– Use credit data REACTIVELY.– Market to prospects or existing account holders actively

seeking a loan elsewhere.

Using Credit Data

• Specify Your Lending Guidelines– Only market to prospects and account holders meeting your

specific credit criteria (ie – FICO Score, LTV, Credit History, etc.).

• Firm Offers of Credit– Credit data can only be used when you are extending credit

offers. More on this later…– Must be compliant with the Fair Credit Reporting Act.– LKCS helps with this!

Firm Offers of Credit

• When using Credit Bureau data, marketing materials must include:

– Indications that the recipient is pre-selected, pre-screened, or pre-approved .

– Terms and conditions; eligibility requirements.• Including why credit may not be extended after all.

– Minimum dollar amount for which the recipient has been qualified.

– Opt-out notice and disclosure.

DataFlex Credit Alerting

Member Retention and Cross-SellCredit Alerting

Credit-Based Loyalty Programs

• React with the RIGHT offer at the RIGHT time.

• Gain the ability to reach account holders who may be defecting to your competition in near real time.

• Based on actual credit bureau data.

• Deliver a firm offer of credit to cross-sell additional products at the moment a need has been identified.

Credit-Based Alerts

• Here’s What Happens:

– When your account holder applies for credit ANYWHERE, an inquiry is posted to his or her credit file.

– These inquiries are categorized according to the type of financial product the account holder is seeking: mortgage, auto loan, installment loan, credit card or insurance.

– Your account holder database is cross-referenced DAILY with these inquiries and a “lead” is generated each time there is a match with the credit file.

• Respond with a firm offer of credit or insurance immediately after receiving the lead.

Credit-Based Alerts (cont.)

• Select which category(ies) of inquiry(ies) you wish to target

• Leads are then pre-screened using your qualification criteria

– Criteria can be based on numerous attributes including credit score, debt load, etc.

• Daily alerts from Equifax, TransUnion and Experian!

– LKCS provides you with a list of all leads and fulfills any direct mail and/or e-mail offers on the same day.

Credit Alerting

• We provide credit-based activity alerts from ALL THREE major credit bureaus.

– Close loans that would have gone to other lenders by comparing credit bureau activity each day!

– Monitor and identify your account holders DAILY for auto loan, mortgage, consumer loan and/or credit card inquiries.

– Set criteria to identify prospects that will qualify for a loan offer based on your specific pre-screen requirements.

– Send direct mail, e-mail and/or statement onserts to contacts whose credit has been checked and meet your pre-screen criteria.

– Provide outbound call lists for your call center to contact these account holders.

Credit Prospecting

Member AcquisitionCredit Prospecting

Credit Prospecting

• Available for any pre-screen marketing campaigns:– Auto Loans– Mortgages– HELOCs– Auto and Mortgage Refinancing– Credit Cards

• Pre-screen your existing account holders or reach out to credit-qualified prospects in your area(s).

Credit Prospecting Campaigns

• Extend pre-approved offers of credit to account holders and non-account holders based on actual credit score information.

– Set criteria to identify recipients that will qualify for a loan offer based on your specific pre-screen requirements.

– Send direct mail loan offers, e-mail offers, statement-based campaigns and make outbound phone calls to qualified account holder and non-account holder prospects.

– And you can utilize our DataFlex reporting engine to measure the results of these campaigns!

Potential Credit Prospecting Campaigns

• Leverage credit data to generate loans.• We have a few EXAMPLES of how you can

utilize the data.– Be creative – brainstorm campaigns that make sense for your

institution.

• ADJUST as needed.– Adjust the credit parameters, etc. as needed to fit your lending

guidelines and goals.

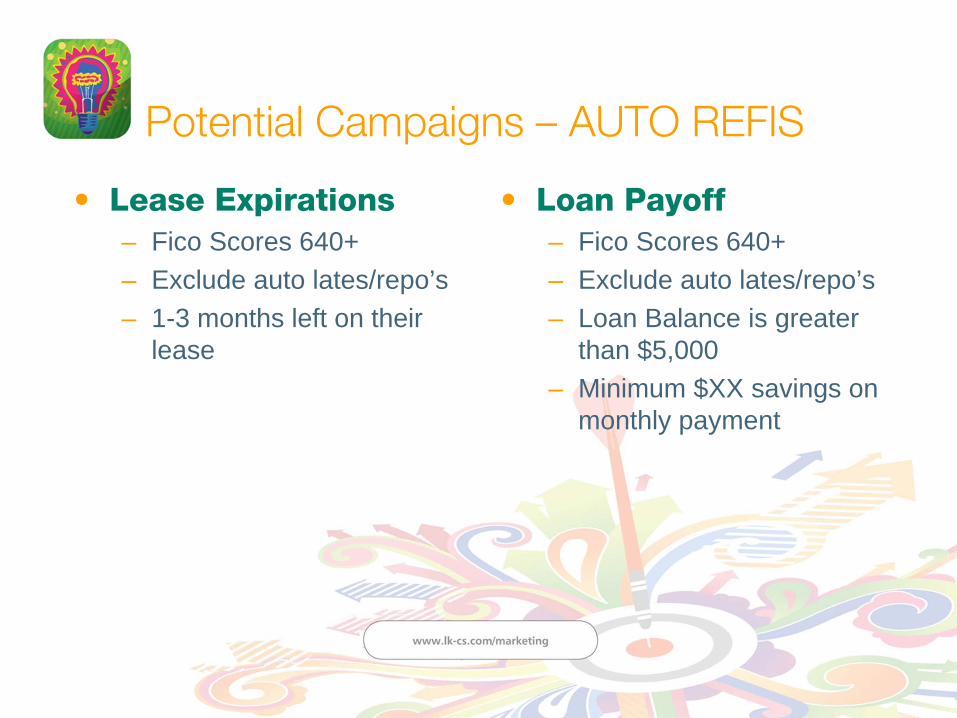

Potential Campaigns – AUTO REFIS

• Lease Expirations– Fico Scores 640+ – Exclude auto lates/repo’s– 1-3 months left on their

lease

• Loan Payoff– Fico Scores 640+– Exclude auto lates/repo’s– Loan Balance is greater

than $5,000– Minimum $XX savings on

monthly payment

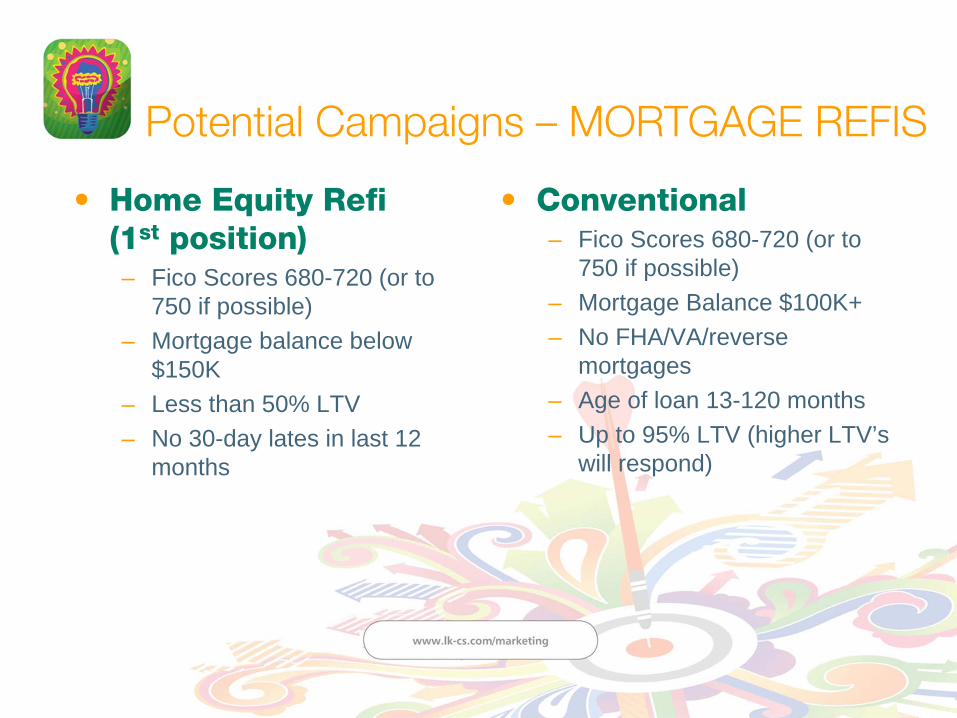

Potential Campaigns – MORTGAGE REFIS

• Home Equity Refi(1st position)– Fico Scores 680-720 (or to

750 if possible)– Mortgage balance below

$150K– Less than 50% LTV– No 30-day lates in last 12

months

• Conventional– Fico Scores 680-720 (or to

750 if possible)– Mortgage Balance $100K+ – No FHA/VA/reverse

mortgages– Age of loan 13-120 months– Up to 95% LTV (higher LTV’s

will respond)

Sample Campaigns

• Direct Mailer

First-Time Home Buyers Offer

Sample Campaigns

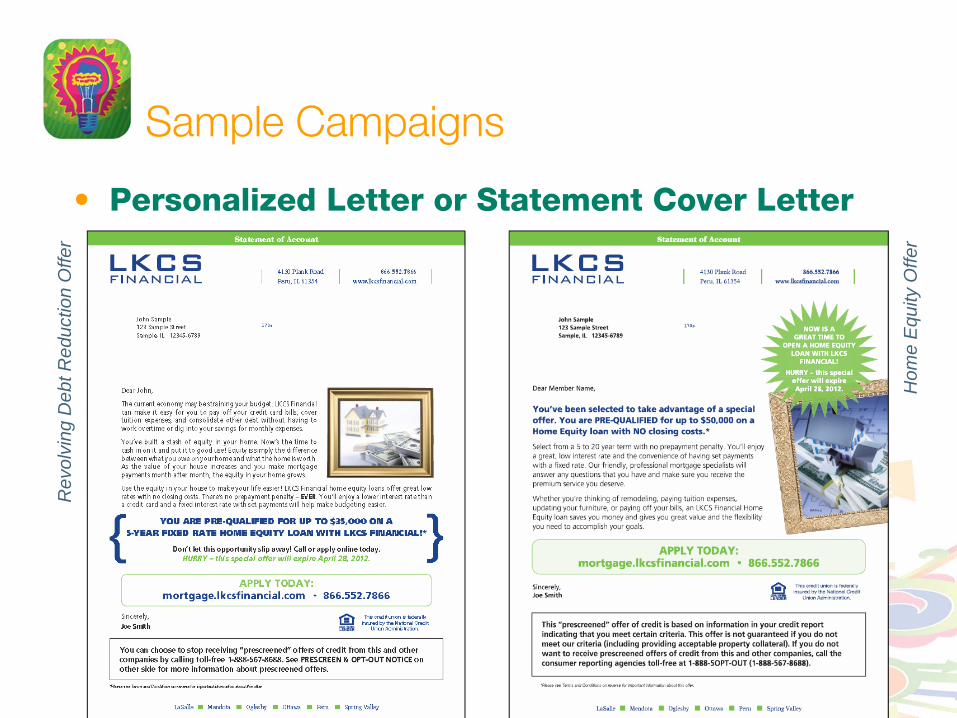

• Personalized Letter or Statement Cover Letter

Rev

olvi

ng D

ebt R

educ

tion

Offe

r

Hom

e E

quity

Offe

r

Sample Campaigns

• E-Mail Marketing

Firs

t Tim

e H

ome

Buy

ers

Offe

r

Home Equity Offer

Pricing Factors

• Credit Prospecting– Pricing depends on several factors including:

• Number of records purchased

• Demographic selects purchased

• Credit bureau minimum charges

– FREE List Counts and Estimates• LKCS will run counts at no charge to determine feasibility and cost

of your next pre-screen marketing campaign.

Pricing Factors

• Credit Alerting– Based on number of account holders and/or prospects

screened each month

– FREE Opportunity Analysis

• We will review your account holder credit activity over the past 30 days and provide you with the following data: credit activity by inquiry type, state and credit bureau, as well as qualification rates using your specific qualification criteria!

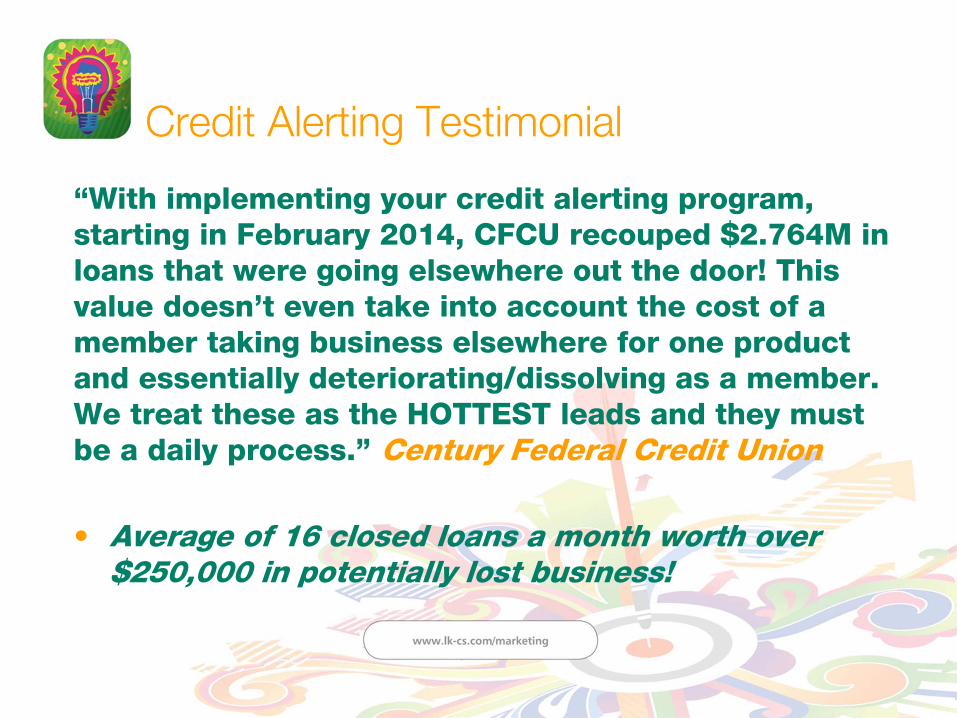

Credit Alerting Testimonial

“With implementing your credit alerting program, starting in February 2014, CFCU recouped $2.764M in loans that were going elsewhere out the door! This value doesn’t even take into account the cost of a member taking business elsewhere for one product and essentially deteriorating/dissolving as a member. We treat these as the HOTTEST leads and they must be a daily process.” Century Federal Credit Union

• Average of 16 closed loans a month worth over $250,000 in potentially lost business!

Thank You!

John DudekVP of Sales

Direct: 815-228-7075 E-Mail: [email protected]

www.lk-cs.comwww.facebook.com/lkcsperu

http://www.linkedin.com/company/lkcshttps://twitter.com/lkcsperu

http://www.youtube.com/lkcsperuhttp://www.slideshare.net/lkcsperu