Embed Size (px)

Citation preview

The EMIX Europe Low Volatility Index

“Since we acquired our index business in autumn 2013 we have been carefully assessing the benchmarking needs of the financial industry. We have identified a pressing need among investors for access to cost effective, robust indices which are suited to today’s investment environment. The inclusion of smaller companies in our indices offers a more complete representation of the European market through an investable, liquid index.”

Sui Chung, Managing Director, Euromoney Indices.

The EMIX Europe Low Volatility Index at a glance

Introducing EMIX Europe Low Volatility

The EMIX Europe Low Volatility Index offers a lower volatility alternative to the benchmark EMIX Europe Index, a broad capitalisation index comprising Europe’s largest companies and its most liquid smaller companies.

By selecting the stocks with the lowest volatilities, whilst excluding those with poor liquidity and allowing for a broad industry coverage, the EMIX Europe Low Volatility Index brings the additional benefits of:

• Lower risk

• High correlation with EMIX Europe

• Access to the Low Volatility Premium

Companies in the index

128

644

EMIX Europe Low Volatility EMIX Europe

Weighting methodology

Inverse volatility

Free float market capAnnualised volatility

11.6%

15.6%Correlation vs EMIX Europe

93.6%

100.0%Values as at 23 March 2015

Building EMIX Europe Low VolatilityLiquidity screening Although EMIX Europe has been designed with liquidity in mind, it is a free float market capitalisation weighted index. As such, a smaller company with lower volatility might be considered liquid at its free float market capitalisation weighting, but it will be less liquid at its inverse volatility weighting, which is the method used for the EMIX Europe Low Volatility Index. Consequently, all potential constituents of the EMIX Europe Low Volatility Index are expected to demonstrate an average daily traded value (ADTV) of EUR 5 million or more.

Companies represented in EMIX Europe by more than one constituent have only their most liquid constituent considered for the EMIX Europe Low Volatility Index.

Distribution of constituents by volatility and liquidity, showing EUR 5m requirement

Volatility ranking Each constituent of EMIX Europe has its volatility calculated as its 252-day standard deviation of its daily returns in Euros. Constituents with fewer than 252 days of trading are excluded. Constituents are then ranked first by whether or not they pass the Liquidity Screening and second by ascending volatility within their EMICS Industry Group. Finally an overall ranking is calculated using the relative ranking across industry groups of each of the constituents.

Quarterly rebalancing Each quarter, the EMIX Europe Index is rebalanced. Following that rebalancing, the EMIX Europe Low Volatility Index is rebalanced using the Volatility Ranking as the quantity which determines a constituent’s inclusion or exclusion.

Any existing EMIX Europe Low Volatility Index constituent which ranks in the first 40% by number remains in the index. Existing constituents ranking outside the first 40%, or which are no longer constituents of the EMIX Europe Index, are removed. Non-constituents are then added, starting with the stock with the lowest Volatility Ranking, to make the number of constituents of the EMIX Europe Low Volatility Index equal to 20% of the number of companies represented in EMIX Europe, and which have 252 days of trading.

Constituents are weighted by Inverse Volatility, with a limit placed on the lowest volatility constituents to avoid disproportionately high weightings.

Volatility (%)

ADTV

(EUR

)

100k

1m

1007550250

10m

100m

1000m

EMIX Europe Low Volatility EMIX Europe

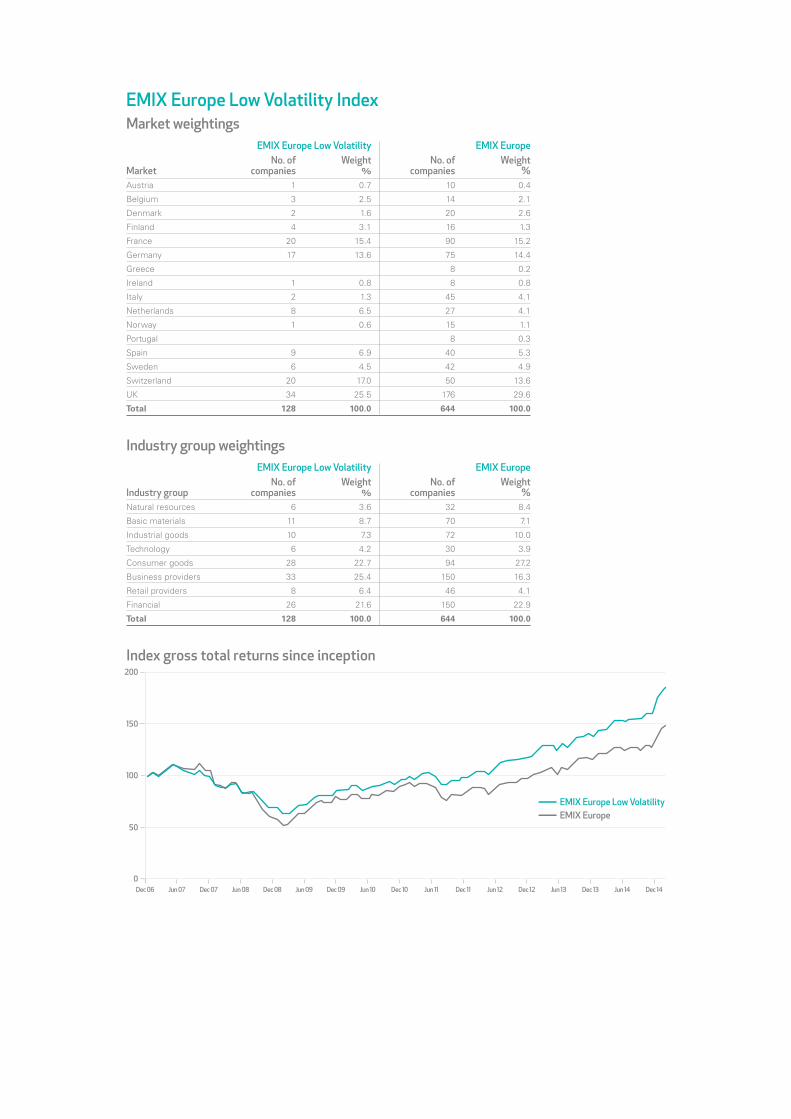

EMIX Europe Low Volatility IndexMarket weightings EMIX Europe Low Volatility EMIX Europe No. of Weight No. of Weight Market companies % companies %Austria 1 0.7 10 0.4

Belgium 3 2.5 14 2.1

Denmark 2 1.6 20 2.6

Finland 4 3.1 16 1.3

France 20 15.4 90 15.2

Germany 17 13.6 75 14.4

Greece 8 0.2

Ireland 1 0.8 8 0.8

Italy 2 1.3 45 4.1

Netherlands 8 6.5 27 4.1

Norway 1 0.6 15 1.1

Portugal 8 0.3

Spain 9 6.9 40 5.3

Sweden 6 4.5 42 4.9

Switzerland 20 17.0 50 13.6

UK 34 25.5 176 29.6

Total 128 100.0 644 100.0

Industry group weightings EMIX Europe Low Volatility EMIX Europe No. of Weight No. of Weight Industry group companies % companies %Natural resources 6 3.6 32 8.4

Basic materials 11 8.7 70 7.1

Industrial goods 10 7.3 72 10.0

Technology 6 4.2 30 3.9

Consumer goods 28 22.7 94 27.2

Business providers 33 25.4 150 16.3

Retail providers 8 6.4 46 4.1

Financial 26 21.6 150 22.9

Total 128 100.0 644 100.0

Index gross total returns since inception

Dec 06 Jun 08 Jun 09 Jun 10 Jun 11 Jun 12 Jun 13Jun 07 Dec 14Jun 14Dec 08 Dec 09 Dec 10 Dec 11 Dec 12 Dec 13Dec 07

50

0

100

150

200

– EMIX Europe Low Volatility – EMIX Europe

Committing to valueEuromoney Indices provides a range of fully comprehensive data services, including daily constituent files, daily divisor and trader files and a five day forward looking corporate actions calendar.

EMIX Europe’s fully transparent licences permit the use of the index name and data in all marketing materials, anywhere in the world, both in print and online. The EMIX Europe licences • Index Values only • Intra Day Index Values • Monthly Constituents • Daily Constituents • Daily Corporate Actions Licences include • All region, country, currency and return indices • Use of indices for in-house blended indices • Use of indices for fund publications • Performance licence included • Custodian licence included • EMICS classification licence included • Index values since inception • Multi-platform delivery For more information: Scott Thomson Phone: 0131 220 9090 Email: [email protected]

Sui Chung Phone: 020 7779 8647 Email: [email protected]

Euromoney Indices Hobart House, 80 Hanover Street, Edinburgh EH2 1EL, UK

To view the full list of indices within the EMIX Europe Index Series see Bloomberg, Thomson Reuters or visit euromoneyindices.com

Euromoney Indices is an independent team of analysts providing an index service dedicated exclusively to the needs of today’s investment professionals.

We focus on devising the comprehensive index tools that underpin and validate successful asset management strategies.

With over twenty five years’ experience, we combine intellectual rigour with operational flexibility. We deliver a service to our customers that has a personal dimension and transparent pricing structure that’s unique in the industry.

Issued by Euromoney Trading Limited. Registered office: 8 Bouverie Street, London EC4Y 8AX. Registration Number: 5935420 – England. Part of the Euromoney Institutional Investor PLC group.