Embed Size (px)

Citation preview

General Accounting & Financial

System

of

Dekko Accessories Limited

Internship Report

On

General Accounting & Financial system

of

Dekko Accessories Limited

Submitted To

Ms. Rubina Afroze

Senior Lecturer,

Department of Business Administration

ASA University Bangladesh.

Submitted By

Md. Shumon Iftikher ID: 103-12-0030.

BBA, 11th

Batch (Major in Finance)

Course Code: BUS-499

Department of Business Administration

ASA University Bangladesh.

Date of Submission 25th August, 2014

25th

August, 2014

Ms. Rubina Afroze

Senior Lecturer,

Department of Business Administration

ASA University Bangladesh.

Subject: Submission of the Internship Report.

Dear Madam,

I am very happy to submit my internship report on “General Accounting & Financial system of Dekko

Accessories Limited” which is an essential requirement for the completion of BBA Program. This report

is the result of the Internship Program that I have conducted in Dekko Accessories Limited at Dhanmondi

Branch from 15th May, 2014 to 15

th August, 2014. I truly believe that this report will satisfy your

requirements and expectations.

Working in Dekko Accessories Limited was an inspiring experience for me. I believe that the knowledge

and the experience I gathered will facilitate me a lot in my future career life. With my limited knowledge,

I have tried my best to prepare the report worthwhile.

May I, therefore, wish and hope that you would be gracious enough to accept my effort and oblige

thereby.

Yours Sincerely,

Md. Shumon Iftikher

ID: 103-12-0030.

BBA, 11th

Batch (Major in Finance)

Course Code: BUS-499

Department of Business Administration

ASA University Bangladesh.

Student’s Declaration

I am Md. Shumon Iftikher hereby declare that the work presented in this report titled “General

Accounting & Financial system of Dekko Accessories Limited” has been carried out by me and has

not been previously submitted to any other University or organization for an academic

qualification, certificate, diploma, or degree.

-----------------------------------

Md. Shumon Iftikher

ID: 103-12-0030.

BBA, 11th

Batch (Major in Finance)

Course Code: BUS-499

Department of Business Administration

ASA University Bangladesh.

Supervisor’s Certification

This is to certify that the Thesis Report titled “General Accounting & Financial system of Dekko

Accessories Limited” for the award of Bachelor degree in business administration from ASA

University Bangladesh, Dhaka, has been carried out by Md. Shumon Iftikher bearing ID: 103-12-

0030 under my supervision and guidance. The report embodies result of original work and

studies carried out by the student himself and the contents of the report do not form the basis for

award of any other degree to the candidate or to anybody else.

----------------------------------

Ms. Rubina Afroze

Senior Lecturer

Department of Business Administration

ASA University Bangladesh.

Page No Acknowledgement VIII Executive Summary IX

Chapter 1: Introduction 1.1 Origin of the Report

1.2 Objective of the Report

1.3 Scope of the Report

1.4 Limitation

2

2

3

3

Chapter 2: Overview of the Company 2.1 Historical Background of Dekko Accessories Ltd

2.2 Objective of the Company

2.3 Factory Size

2.4 Corporate Office

2.5 Products & Services

2.6 The Bank of transaction

2.7 Major Customers

2.8 Strengths

2.9 Weaknesses

2.10 Opportunities

2.11Threats

2.12 Organizational Structure

6

7

7

9

9

10

10

10

10

11

11

12

Chapter 3: Methodology 3.1 Study Design

3.2 Study Place

3.3 Time period of making the report

3.4 Data collection Technique

3.5 Data processing and Analysis Techniques

15

15

16

16

16

Chapter 4: Project Findings 4.1 Accounting Principles & Policies Dekko Accessories Ltd

4.1.1 Basis of Accounting

4.1.2 Significant Accounting Policies

4.2 Category of Financial Transaction Dekko Accessories Ltd

4.2.1 Category of Financial Transaction

4.2.2 Receipts

4.2.3 Payments

4.2.4 Contra

4.2.5 Journal Voucher

4.3 Financial Management & Control Dekko Accessories Ltd

4.3.1 General

4.3.2 Custody of the Fund

18

18

18

22

22

22

23

24

24

25

25

25

Table of Contents

4.3.3 Opening & Closing of Bank Account

4.3.4 Certification and Approval of Payment

4.3.5 Petty Cash

4.3.6 Petty cash Advances

4.4 Maintenance of Accounts on Dekko Accessories Ltd

4.4.1 General

4.4.2 Responsibility

4.4.3 Presentation of Financial Statements

4.4.4 Contents of Financial Statements

4.4.5 Books & Chart of Accounts

4.5 Letter of Credit

4.5.1 Features

4.5.2 Operations supported on LC

4.5.3 Processing Commissions and Charges

4.6 Financial Ratio Analysis of DAL

4.6.1 Liquidity Ratio

4.6.2 Activity Ratio

4.6.3 Profitability Ratios

25

27

27

28

28

28

28

28

29

29

30

30

31

31

32

32

35

36

Chapter 5: Discussion on findings 5.1 Discussion on findings 42

Chapter 6: Conclusion Conclusion 44

Chapter 7: Recommendations 7.1 Recommendations 46

Bibliography & Appendix Bibliography 48

Appendix 49

Acknowledgement

The report titled as “General Accounting & Financial system of Dekko Accessories Limited” has

been prepared to fulfill the requirements of BBA degree. I am very much fortunate that I have received

sincere guidance, supervision and co-operation from various respected people while preparing this report.

Many people helped me to prepare this report. First of all I would like to thank my academic supervisor of

the Internship Program Rubina Afroze, Senior Lecture, ASA University Bangladesh for giving

me the opportunity to prepare this report. Without his guidance, advice and assistance, this report would

not be a comprehensive one.

Then I would profusely like to express my gratitude to all the people from Dekko Accessories Limited of

Dhanmondi Branch who has always been kind enough to answer my queries despite their extremely

demanding work. I would like to express my gratitude to Md. Arifur Rahaman, Sr. Manager (Accounts &

Finance) of Dekko Accessories Limited for giving me the opportunity to complete my internship in such

a reputed organization.

My peers and colleagues at the organization had also been very helpful; and they made my internship a

more enjoyable and eventful one. I would like to specially thank Syed Akhtar Jamal, Director, Dekko

Accessories Ltd. for giving me the internship opportunity.

Executive Summary

As a student of business administration, analyzing today‟s business world is very crucial to observe in this

complex situation. It is necessary to go through all fields of knowledge, both theoretical and practical.

After passing four years BBA program, I was sent out to have practical knowledge in business life as a

part of my academic program. An internship program is organized to give me an opportunity for

enhancing my capabilities. My internship topic is “General Accounting & Financial system of Dekko

Accessories Limited”. I have tried to highlight the accounting and budgetary control system of Dekko

Accessories Limited. The report investigates the accounting and budgetary control system of Dekko

Accessories Ltd. It also identifies general financial operation of DAl, at Dhanmondi Branch. Dekko

Accessories Limited is a successful reputed organization of our country. DAL follows all the rules and

regulation of Bangladesh Govt. scheduled for a privet business organization. The function of the company

is to manufacture and export RMG accessories internationally. RMG is one of the major sectors that have

highest contribution in foreign earnings in our country. To get succeed, they need to be able to process

data and use information effectively. So in my report I describe all the information‟s that how they are

keeping their accounting information‟s, the budgetary system of them. Strategies they are following to

implement production, distribution, management, marketing, and HR management operations are also

discussed in the report. SWOT analysis of DAL and their competitors are described in the report which

shows that DAL has greater opportunity to expand their market globally. Some financial analysis of

data‟s also representing the financial condition of the organization in this report. I have tried to follow the

right methodology for preparing this report. In the case study of Dekko Accessories Ltd. effort has been

given to disclose about organization‟s system and procedure step by step. Finally, conclusion and findings

are also included in the report.

1.1 ORIGIN OF THE REPORT

Internship Program of ASA University Bangladesh is a Post-Graduation requirement for the BBA

students. This study is a partial requirement of the Internship program of BBA curriculum at the ASA

University Bangladesh. The main purpose of internship is to get the student exposed to the job world.

Being an intern the main challenge was to translate the theoretical concepts into real life experience.

The internship program and the study have following purposes:

To get and organize detail knowledge on the job responsibility.

To experience the real business world.

To compare the real scenario with the lessons learned in ASA University Bangladesh.

To fulfill the requirement of BBA Program.

This report is the result of three months long internship program conducted in Dekko Accessories

Limited and is prepared as a requirement for the completion of the BBA program of ASA University

Bangladesh. As a result I need to submit this report based on the “General Accounting & Financial

system of Dekko Accessories Limited”. This report also includes information on the products and

services of Dekko Accessories Limited, the overview of the organization and also facilities they offer to

satisfy their employees.

1.2 Objective of the report

The objective of the report can be viewed in two forms:

General Objective

Specific Objective

General Objective:

This internship report is prepared primarily to fulfill the Bachelor of Business Administration (B.B.A)

degree requirement under the Faculty of ASA Business School, ASA University.

Specific Objective:

To have an overview of Dekko Accessories ltd.

To analyze the strength and weakness of the organization.

To know about the financial management of Dekko.

To prepare this report the operation of Dekko Accessories ltd. and its global policy for keeping

accounting records. This report fully focused to prepare a guideline to keep record accounting

data to smoothen the overall operation.

Despite this topic there are many sectors for working and analysis, like:

Financial performance of Dekko

Analysis the annual report of 2011-12 & 2012-13

An overview of Dekko Accessories Limited.

1.3 Scope of the Report

The main intention of the study is see the accounting & financial system of the company. Find

out what is their strengths, weaknesses, opportunities, threats & what should they have to do to reduce

their weaknesses & threats.

As I was assigned to the Dekko Accessories Limited, Dhanmondi Branch, there is enough scope of the

study as it is the head office. The report covers the topic “General Accounting & Financial system of

Dekko Accessories Limited”. To prepare this report the operation of Dekko Accessories ltd. and its

global policy for keeping accounting records. This report fully focused to prepare a guideline to keep

record accounting data to smoothen the overall operation.

Despite this topic there are many sectors for working and analysis, like:

An overview of Dekko Accessories Limited

Financial performance of Dekko

1.4 Limitation

Although I have obtained whole hearted co-operation from all levels of personnel of Dekko Accessories

Limited, but on the way of my study I have faced the following obstacles that may be termed as the

limitations.

Lack of sufficient hard copy documents provided by the company.

The confidential nature of information because of the company‟s policy.

Sufficient publications, facts, figure regarding accessories industries in Bangladesh is not

available.

Very little research has been undertaken on Dekko Accessories Limited.

Restriction of higher management to disclose any financial activities related internal data.

Due to time constraints a good portion of the study remains may un noticed.

All employees are busy in their respective job.

Three months is not enough for study in the field of total systematic

accounting, budgeting and costing policy and procedure.

Dekko Accessories Ltd. is belongs to Dekko Group having businesses concentration in garments,

accessories, food, distribution, publication, paint and real estate sector. The Group has 2 sister

concern in accessories sector. All the concern produced world class accessories product.

Garment accessories units performed as backward linkage of RMG units of the group. These two

accessories concern supports other different RMG concerns of the group. Rests of the concerns

of the Group are engaging in other different sector of business.

2.1 Historical Background of Dekko Accessories Ltd

Dekko Accessories Limited is actually a success story of a sole-person that Mr. M. Shahadat

Hossain Kiron has proved himself as a successful entrepreneur of independent Bangladesh. He

started his business in the garments sector in 1983 and in 1995 when he was the owner of six

garments factories then he found that there is no reliable garments backward linkage industry in

Bangladesh. Then he established Dekko Accessories Ltd. with a small capacity. He also realizes

that 30% of total production capacity of Dekko Accessories may be consumed by his own

garments factories. Those also inspire him to establish Dekko Accessories.

Dekko has all the attributes that made her one of leading manufacturer, which stretches up to 16

years. Dekko, which entered into business with a small capacity of production in 1995, today,

has become one of the leading garments accessories manufacturers in Bangladesh. In 1995, it

started with 3 label machines, one polybag making machine and 8 button manufacturing

machines. In the next decades, the company made major growths and expansions in production

and marketing.

Label Unit

2.2 OBJECTIVE OF THE COMPANY

To get acquaintance with quality product, competitive price and in time delivery.

Vision:

Influence the market and focus as a leader in garments accessories sector in Bangladesh.

Mission:

Dekko Accessories Ltd. aims to achieve its vision through being number „one‟ not only in terms

of sale but also in quality garments accessories production and supply.

2.3 Factory Size

Total factory area is about 1,10,835 square ft.( 3.950 Acres) . About 750 employees are employed

by the company including factory workers, sales representatives and company personnel's.

Factory Location: Hemayetpur, Savar, Dhaka.

Building structure:

One 6 storied building: I. Grand Floor – Store, CD- 74 machine

room, Button ( Polish )

II. 1st Floor – PPI, Design room,

III. 2nd

Floor – Poly

IV. 3rd

Floor – Belt

V. 4th

Floor – Belt

VI. 5th

Floor – Screen Print

VII. Top – Open roof Top, reserve Fire water

One 3 storied building

1. Grand Floor – Button ( Turning, Polish, Casting, office )

2. 1st Floor – Button ( Turning & Packing ), PPI, Office & conference room,

PVC (paper cutting), QA Lab, QA office

3. 2nd

Floor – PL & HTL

4. Top –PVC, Female Prayer room, Open roof Top

One 2 storied building

1. Grand Floor – Woven Label, yarn store, general store, Audit office

2. 1st Floor – Woven Label, woven label maintenance room, Design room, Label

Office room.

CD 74

One 3 storied building

1. Grand Floor – Maintenance room, Generator, Workshop

2. 1st Floor – Female Dining, Male Prayer room, Officer‟s Dining, Ansar Dormitory

3. 2nd Floor – Male Dining, HR-Admin & Compliance room, Sample room, kitchen

4. Top – Canteen & Open roof Top

Medical building

1. Grand Floor – Free / Chemical

2. 1st Floor – Medical room, Childcare room

3. Top – Open roof Top

Shades 3

1. Shade one – General store

2. Shade two – Finishing Goods room, cut

3. Shade three – Injection molding room

4. Shade four – Wastage area

Power station: 815 KVA

Generator: 02 (1125 KVA & 800 KVA) with canopy.

Gas generator – 1125 KVA

Diesel generator – 800KVA

The said generator installed as per Bangladesh Power Development Board-PDB and Fire

Service Civil Defense Authority guide line.

Power distribution board:

MDB= 22 ,

SDB=61 with fully automated switch gear.

Emergency Power off switch : installed each floor with SDB & MD

Water preserver: 60,000 Gallon / 218400 Liter reserve tank in top floor (Roof Top).

Earth Conductor :30

Fire Safety team strength:

Total manpower in (Dekko) : 907

DAL Officer : 112

DAL Worker : 795

Medical officer: 01 (Registered Doctor-Full Time)

Paper Print Label Button

Medical Assistant: 01 (Registered Nurse-Full time)

Care taker-Day care center:01(Trained)

Fire safety officer: 01

Fire Fighter: 143 (Trained by Bangladesh Fire

Service & Civil Defense)

Rescuer : 95

First Aider: 50

2.4 Corporate Office

Suvastu Zenim Plaza.

H# 37, R# 16 (Old-27) Dhanmondi, Dhaka-1209, Bangladesh.

Phone: 9130904, 9130974 & 9130955 Fax: 880-2-8128055.

2.5 PRODUCTS AND SERVICES

Button, Poly Propylene, Poly Ethylene, BOPP, Polyester Resin, Cotton & Polyester Yarn, Paper

Boards, PVC Sheets, Belt.

2.6 The Bank of transaction

Sonali Bank,

City Bank,

Markentile Bank,

HSBC

2.7 Major Customers

Wall-Mart,

Tesco,

Peacocks UK,

Van-Husen,

OBSL etc.

2.8 Strengths

1. Wider product mix.

2. Initial move advantage.

3. Above average quality level.

4. Immense reserve of fund.

5. Good competitive skills.

6. An acknowledged market leader.

7. Cost advantage.

8. Better advertising campaigns.

9. Better manufacturing capability.

2.9 Weaknesses

1. Relatively expensive.

2. Inconsistent delivery.

3. Interrupted material flow and healthy supply chain.

4. Lack of sense of belongingness and motivation among employees.

5. Average collection period is around 90 days.

6. Absence of system for measurement & control.

7. Absence of scale of economy.

8. Large centralized organization structure.

9. Tendency to shift responsibilities to others.

10. Inability to react quickly in accordance to the market.

11. Deals with price sensitive products.

2.10 Opportunities

1. Huge unpenetrated market.

2. New product/ technology development.

3. Scope of more nomination.

4. Establishment of high quality image.

5. ISO certification.

6. Establishment of proper supply chain plan.

7. Alternate sources for raw materials can be explored.

8. Possibility of any other backward linkage or acquisition can be explored.

9. Strong scopes to become global.

10. Utilizing deal outlets efficiently by diversifying into related products like Composite

Knit Project, Textile Project etc.

2.11 Threats

1. Legal issue with customs.

2. Renewal of bond license uncertain.

3. Bank guarantee and indemnity blocked.

4. Uncertainty linked with Neo- Global scenario after 2005.

5. New entrants with strong political support and with third generation. Technologies are

coming with diversified product range.

6. Entry of low-cost foreign products.

7. Growing bargaining power of customers or suppliers.

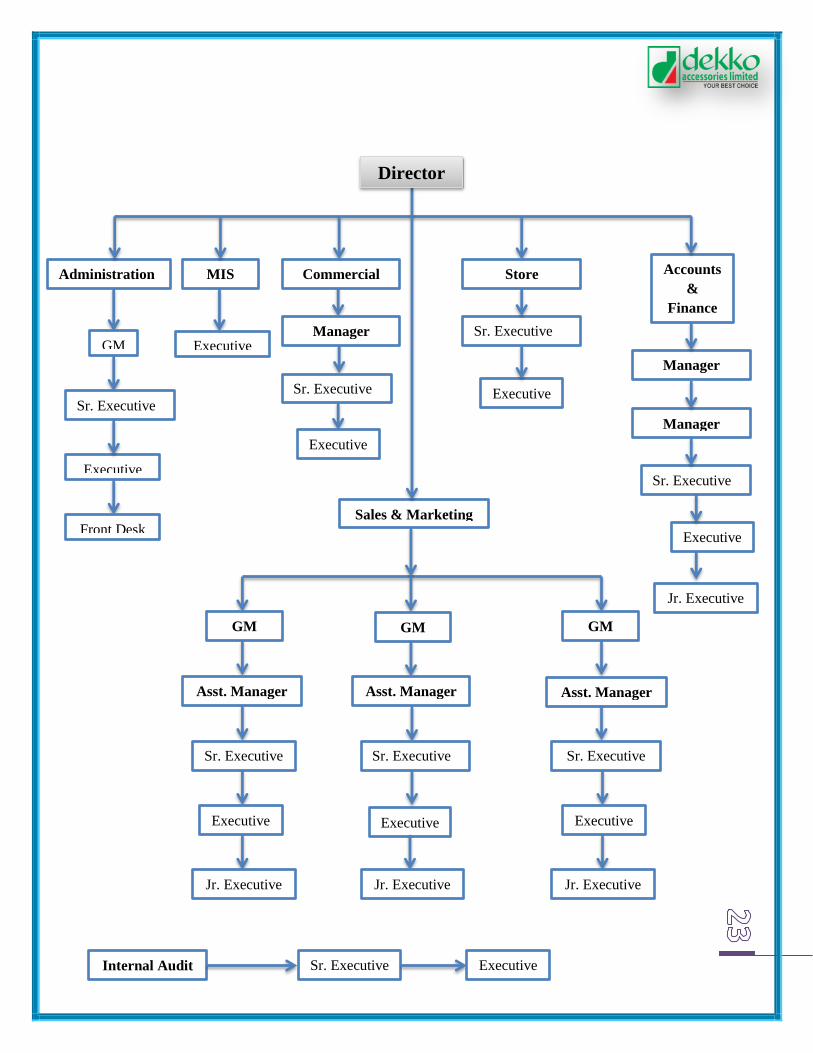

2.12 Organizational Structure

The Organizational Structure is headed by Managing Director and the lowest level Occupied by

distributors sales representatives.

Administration Accounts

&

Finance

MIS

GM

Executive

Front Desk

Executive

Sales & Marketing

GM GM GM

Asst. Manager Asst. Manager Asst. Manager

Sr. Executive Sr. Executive Sr. Executive

Executive Executive Executive

Jr. Executive Jr. Executive Jr. Executive

Commercial

Manager

Sr. Executive

Executive

Store

Sr. Executive

Internal Audit Sr. Executive Executive

Executive

Manager

Manager

Sr. Executive

Executive

Jr. Executive

Director

Sr. Executive

3.1 Study Design

This is an explanatory research. The data and the information are summarized according to the

concepts of corporate strategy, ethics and business policy, tables, charts and statistical analysis

graphs are used make the analyses clean and more understandable. Critical assessment in draw

from the data and information are:

Primary Source of Information

Observation during the total internship period.

Involvement with the operational process.

Official records of Dekko Accessories.

Face to face interview with different personal of the Dekko Accessories ltd. to get in

depth information.

Secondary Sources of Information

Annual report, quarterly revenue mobilization report, other various monthly reports were

used as the secondary sources.

Theoretical portion is summarized from my text materials etc.

For primary data direct conversation with senior executives and other officials took place

several times.

Secondary data are taken from different manual.

Internet.

3.2 Study Place

Suvastu Zenim Plaza.

H# 37, R# 16 (Old-27) Dhanmondi, Dhaka-1209, Bangladesh.

3.3 Time period of making the report

3.4 Data collection Technique

Data are collect form the annual report of DAL, from their employees, from the website

http://www.dekkogroup.com/dekko_accessories, Report on “Execution of Accounting & Budgetary

Control System – A Closure Observation” Made by Fahima Fatima (UIU) about Dekko Group. etc.

3.5 Data processing and Analysis Techniques

Data processing & analysis made by the Microsoft word & Excel.

Department Time Period

Accounts & Finance From 15 May to 15 August.

4.1 Accounting Principles & Policies Dekko Accessories Ltd

In the below try to discuses about the Accounting Principles & Policies Dekko Accessories Ltd.:

4.1.1 Basis of Accounting

Dekko Accessories Ltd. maintains its accounts in accordance with the International Accounting

Standards, as applicable. All incomes or expenditure received or paid and/or accrued during any

particular year is accounted for in the year to which it relates.

Accounting Period:

The accounting year of the company is from 1st July to 30

th June in year.

4.1.2 Significant Accounting Policies

Income Recognition:

Any income or receipt due / accrued against sales or service provided to any company or

otherwise by any of the Dekko Accessories Ltd. outlets is recorded on the date of sale and,

accordingly, accounted for in the year of origin.

Journal:

Cash/Bank/Accounts Receivable/LC Dr.

Sale of goods Cr.

Expenses:

Any payment or obligation for payment for a particular year is recognized as expenditure

in the year to which it relates. Expenditure accrued or incurred but not paid shall also be

considered as expenditure in the year it was actually committed.

Journal:

Particular Expense A/C Dr.

Particular Expense Payable Cr.

When the expense paid:

Particular Expense Payable Dr.

Cash/Bank Cr.

Any expenditure are booked / accounted for in the respective account and in the

respective cost center / department in pursuance to the chart of accounts.

Journal:

Marketing Department Dr.

Finance Department Dr.

General Department Dr.

Particulars Expense A/C Cr.

Any bank charge / commission paid or deducted by bank for usual banking transaction or

on the bank overdraft are considered as expense.

Journal:

Bank Charge / Bank interest Dr.

Cash / Bank Cr.

Any bank charge, commission, interest or fee paid or deducted by bank for import of

stock or capital asset is debited to the respective material or asset account.

Journal:

Particulars Assets A/C Dr.

Cash / Bank Cr.

Any bank interest charged against loans received for contraction building facilities and

major renovation of the company is capitalized instead of charging as expenditure.

Journal:

Capital work in progress A/C Dr.

Cash / Bank Cr.

Allocation of Expenditure:

Common cost incurred by the company incurred or accrued must be allocated among the related

cost centers / departments in proportion of their usage / share.

Journal:

Marketing Department Dr.

Finance Department Dr.

General Department Dr.

Particulars Expense A/C Cr.

Capitalization of asset:

Fixed Assets are recorded at actual cost. The ownership of all fixed assets purchased by Dekko

Accessories Ltd. is in the name of the organization. Any asset purchased by them is capitalized

when it satisfies following three conditions:

Minimum value for capitalization of an asset is taka 1000. Any asset whose purchase value is

less than taka 1000 shall not be considered as an asset and, accordingly charged as expenditure.

Expected useful life of the asset must be at least for 4 years.

In the case where cost of an asset is less than 1000 but expected usedful life is more than 4 years

that item shall be considered as expenses. However, records for non-capital items are maintained

separately for control purposes.

Depreciation Policy:

Full month depreciation is charged on fixed assets in the month of acquisition.

Journal:

Depreciation Expense – Asset Name Dr.

Accumulated Depreciation – Asset Name Cr.

Depreciation is not charge in the month of disposal or in the month of writing off any asset.

Dekko Accessories Ltd. follows the Diminishing Balance method in calculating on its fixed

assets.

In the terminal year of depreciation, the depreciation charge should by reduce by

taka 5.00 for identification of the assets. That means the value of an asset shall never

be depreciated fully. Such book should remain unchanged until the asset is disposed of or written

off from the books.

Rate of Depreciation:

Depreciation is charged in each financial year on every capital assets at the rates approved in

Third Schedule of Income Tax Ordinance of 1984.

Investment of Fund:

Dekko Accessories Ltd., for time to time, invest its fund in such form and in such a manner as

laid down for tax holiday companies under income tax ordinance 1984.

Journal:

Investment account Dr.

Bank A/C Cr.

Reserve & Surpluses:

General Reserve Fund

A general reserve fund @ 15% of the net profit of the company earn during the year is

transferred to the General Reserve Fund to meet future capital commitments and necessity under

the directives of the board.

Provident Fund

Dekko Accessories Ltd. makes provision for its liability on account of contribution to

employee‟s provident fund on monthly basis, at the time of disbursing the monthly salary. This

provision has being done in pursuance to the approved employee‟s provident funds rule.

After disbursement of salary, employee‟s contribution so deducted from the salary of the

employees and Dekko Accessories Ltd.‟s contribution to the PF a/c is transferred to the

nominated Employees Provident Fund Account. Amount so deducted and / or Dekko

Accessories Ltd. contribution not transferred to the Employee provident Fund Account must be

reflected in the financial statement of the Company as liability.

Journal:

Salary & Allowance (both contribution) Dr.

Liability for Provident Fund Cr.

When PF deposit in to Bank:

Liability for Provident Fund Dr.

Bank / Cash Cr.

4.2 Category of Financial Transaction Dekko Accessories Ltd

In the below try to discuses about the Category of Financial Transaction Dekko Accessories Ltd:

4.2.1 Category of Financial Transaction

Dekko Accessories Ltd. uses 6 types of voucher to record its financial transactions depending

upon the nature and type of transactions. These are:

4.2.2 Receipts

There are two types of receipts, they are:

Cash Receipts &

Bank Receipts.

Cash Receipts

Any amount received in cash by way of sale, loan, share capital, interest, or repayment of loans /

advances, collection against dues, etc. are treated as cash receipt transaction. All cash receipt

transactions are accounted for through cash receipt voucher.

Journal:

Cash Account Dr.

Sale/Loan/Capital/Interest etc. Cr.

Bank Receipts

Any amount received in the form of cheque / pay order / demand draft or in any form other than

cash by way of sale, share capital loans, or repayment of loans / advances, collection against

dues are treated as bank receipt transaction through bank receipt voucher.

All bank receipt transactions are recorded through bank receipt voucher.

Journal:

Received Bank Account Dr.

Sale/Loan/Capital/interest etc. Cr.

4.2.3 Payments

There are two types of payments, they are:

Cash Payments &

Bank Payments.

Cash Payments

Any amount paid in cash on account of expenditure, purchase of assets, purchase of stocks, and

settlement of accounts or any other payment made by Dekko Accessories Ltd. are considered as

cash payment transaction.

All cash payment transactions are accounted for through cash payment vouchers.

Journal:

Particular Expense / Assets Accounts Dr.

Cash Cr.

Bank Payments

Any amount paid by cheque, draft, pay order or account transfer on account of expenditure,

purchase of assets, purchase of stocks, settlement of accounts or any other payment other than

cash made by Dekko Accessories Ltd. are considered as bank payment transactions.

All bank payment transactions are accounted for through bank payment voucher.

Journal:

Particular Expense / Assets Accounts Dr.

Bank Cr.

4.2.4 Contra

Any transfer of fund by way of cash deposit to bank, withdrawal of cash from bank, transfer of

fund from one bank account to another bank account of the same or another bank are treated as

contra transaction and accordingly accounted for through contra voucher.

Journal:

Received Bank / Cash Accounts Dr.

Paid Bank / Cash Accounts Cr.

4.2.5 Journal Voucher

Journal voucher is recognized as voucher for paper transactions, where receipt or payment of

fund is not involved. Journal voucher are used for transfer or adjustment of ledger account

balances from one account to another account.

All account adjustments or transfer of general ledger account balances are recorded though

journal voucher. For example salary expense are booked in the end of the month, but not paid.

Journal:

Salary & Wages Accounts Dr.

Salary & wages Payable Cr.

4.3 Financial Management & Control Dekko Accessories Ltd

In the below try to discuses about the Financial Management & Control Dekko Accessories Ltd:

4.3.1 General

Financial Management is one of the most important tasks in as organization. Due consideration

has been given to all activities involving fund to ensure overall economy, efficiency and best

value for money for the greater interest of the organization.

4.3.2 Custody of the Fund

The Finance Director act as custodian of Dekko Accessories Ltd. Fund and ensure proper

utilization of fund in consultation with Manager of Cost Centre & Members of budget committee

of the Company.

The Director Finance may delegate such authority with respect to financial control and custody

of funds to Manager of Cost Centre & Members of budget committee of the Company to

facilitate the efficient and effective management of Dekko Accessories Ltd.funds, if felt

necessary to the circumstances.

4.3.3 Opening & Closing of Bank Account

The Financial Director is only empowered to authorize opening and closing of any bank account

of whatever nature in the name of Dekko Accessories Ltd. For its transactions subject has to

approval of the board. Such authority of opening / closing of bank account shall not be delegated

to any other official.

The board designates the signatories to operate the banks accounts with such limit as may be

expedient to the circumstances.

Reconciliation of Bank Account

The bank account must be reconciled on daily and monthly basis, before closing the monthly

accounts, with the bank statement provided by bank by some designated finance official

independent of the person preparing check or approving payments.

Fund Management

a) On the basis of amounts expected to be available and after taking into consideration-

anticipated utilization in a particular period, the Director Finance may designate those

funds in a away beneficial to the Company to avoid accumulation of excessive

balances.

b) Fund in excess of requirements of its operations may be placed in term-deposit, short-

term deposits or otherwise by the Director Finance. All such deposits or investments

must be made in the name of Dekko Accessories Ltd.

c) The authorized Officers of Dekko Accessories Ltd. Should preferably receive all

payment against sales or services, interest, miscellaneous incomes and/ or any other

income in cash or pay order.

d) Payments from vendor may be received through account L/C, Endorsements, payee in

favor of Dekko Accessories Ltd. Nopostdated cheque is allowed to receive by the

Officers or any authorized personnel from the finance department.

e) Officers must issue the money receipt at the time of receipt of the money (L/C,

Endorsements, cash / cheque / pay order / demand draft) from whatever source. Sales

Officers provides system-generated invoice with paid seal and signature an

acknowledgement of receipt of money.

f) Every single collection by the Officers must be deposited with the finance &

Accounts department on the same day of receipt. Finance & Accounts department

deposit all collected fund to the nominated bank account on the following day.

g) The Finance & Accounts department immediately prepares credit voucher or update

the system for all such funds received and enters in the book of account.

All idle funds should be kept in interest-bearing term deposit accounts or fixed deposit accounts.

Finance Director has to explore the investment opportunities and closely monitor the fund

position to ensure maximum benefit out of the idle fund, and also advice the Director Finance on

investment issues.

Internal Control

a) The Finance Director, with the approval of MD or Chairman, may from time to time

establish financial rules and regulations in order to ensure effective financial

administration, good governance and accountability. Such rules and procedures must be

communicated in writing under the signature of the Director Finance. If any such rules

and regulation affect the Managers of the Company, the decision is also be

communicated to all-department head of the Company.

b) The Finance Director may approve credit limit to three party‟s to enjoy

credit facilities in the company. Before sanctioning such credit limit, the

Finance Director analyzes the individual party past payment mode, general behaviors,

etc. Then Finance Director enables departmental manager to allow credit.

c) All payments are to be made only after approval for payment from the competent

authority and on the basis of supporting vouchers and other documents to ensure that:

1. Approved purchase orders have been place upon against supply of good or

services.

2. Goods or services have been received as per specification / requirement.

3. Invoice, memo, bill and other necessary supporting vouchers and documents are

enclosed.

4. Fulfilled the terms and conditions of the contract.

5. Payments are for the benefit of the company.

d) Establish Segregation of Duties (SOD) in such a way that ensures checking of one

employee‟s work by another employee, as a matter of routine work.

e) All documents used for financial transactions, i.e. Money Receipt, Purchase order, etc., of

Dekko Accessories Ltd. must be pre-numbered or system generated.

f) Designate officials in writing, who may receive money, incur obligations or

commitments, make payments, and sign correspondences on behalf of the Company.

g) Job Description of each staff / officer been proved by Dekko Accessories Ltd. at the time

of joining the organization and also at the time of transfer from one area to another area

in case of creation of new position.

4.3.4 Certification and Approval of Payment

The Account Controller is the designated Certifying Officer.

The Finance Director acts as the Approving Officer

The function performed by an Approving Officer is distinct from, and subsequent to,

those performed by a Certifying Officer.

Approving and Certifying Officer should not sign payments made to them unless it is

recorded that there is no substitute at the time of payment.

4.3.5 Petty Cash

Petty cash up to taka 10000 are maintained at the office to meet daily petty expenses.

Replenishment of petty cash should be processed when the balance reduced more than

taka 5000

Officers working in the others departments keeps an impress fund up to taka 25000 for

changes.

Summary of petty cash should be prepared according to format.

4.3.6 Petty cash Advances

All temporary advances should be made through the request for advance as per.

Temporary petty cash advances may be made to officials for the purpose of petty

purchase or meeting urgent requirements through I.O.U slip.

Proper track of all temporary advances made through I.O.U shall be kept by the cashier.

Director Finance shall approve the temporary advance before the disbursement is made.

Previous temporary advance must be adjusted before taking further advance. If the

advance are not adjust within one month, that should deduct from the advance taker.

Expense vouchers, as against of temporary voucher, must be submitted to the officer by

the end of next working day or refund the cash.

The officer must prepare payment and receipt vouchers on the day of payment or receipt

and prepare a summary of petty cash statement at the end of the day.

The officer is personally responsible for safekeeping of the cash. The accounts controller,

internal auditor or some designated official will conduct spot-checking from time to time.

4.4 Maintenance of Accounts on Dekko Accessories Ltd

In the below try to discuses about the Maintenance of Accounts on Dekko Accessories Ltd:

4.4.1 General

The accounting of financial transaction is managed with a properly designed computerized

Accounting System in accordance with international accounting standards to the extent

applicable to Dekko Accessories Ltd.

4.4.2 Responsibility

Under the overall supervision of Finance Director, the accounts controllers are responsible for

maintenance of financial accounts, generation of periodic reports and providing information to

the management.

4.4.3 Presentation of Financial Statements

The accounts controller is responsible for preparation and presentation of monthly financial

statement within 30 days of closing the month and annual financial statement within 30 days of

closing the year after all adjustments provisions.

4.4.4 Contents of Financial Statements

The financial statement includes:

Balance Sheet

Income Statement

Receipt and Payment Account

Comparative Statement: Budget VS Actual

Daily Cash Projection (DCP)

All supporting schedules with regard to:

o Fixed Assets.

o Accounts Receivable.

o Advance, Deposit and Prepayments.

o Accounts Payable.

o Liabilities and all unpaid obligations.

o Sources and Application of Fund.

o Others, as may be required.

4.4.5 Books & Chart of Accounts

The books of account are maintained strictly as per the Chart of Accounts and other codes to

facilitate generating any financial information on demand with every detail.

The designed system ensures the facility of coding and decoding financial figures with following

component such as:

Accounting Year

The accounting year of Dekko Accessories Ltd. is from 1st July to 30

th June.

Document Control

All payment vouchers, receipt vouchers, journal vouchers, money receipts, debit notes, credit

notes, invoices must be printed and sequentially numbered or programmed. All these printed

vouchers / Documents must be used chronologically in order to keep track of any missing

vouchers / documents.

Any printed vouchers / documents becoming unusable for any reason are crossed out and marked

as VOID and shall be kept with the voucher book for subsequent verification.

Record Keeping

All vouchers are kept chronologically according to its number in a file. Separate file for different

series of vouchers / documents (payment voucher, receipt voucher, journal voucher, etc.) shall be

maintained. All voucher / documents files are kept under safe custody and only authorized

persons are given access to those vouchers / documents.

Book Keeping

Dekko Accessories Ltd. maintains its Primary Books of Accounts in electronic form (Accounting

Software- TALLY). The account is maintained in accordance with the Chart of Accounts

illustrated in this manual.

Accounts Controller has the authority to add new account code according to its need in

accordance with the basic structure of the Chart of Accounts.

4.5 Letter of Credit

A Letter of Credit is an undertaking by the bank issuing it to pay the beneficiary of the credit provided

stipulated documents are presented and other terms and conditions of the LC are complied with. It is the

preferred mode of settlement between a buyer and a seller under the following circumstances:

They are not well-known to each other.

They are located in different countries and the seller is not sure of the credit worthiness of the

buyer.

In such cases, the seller would like a bank to provide assurance of payment. As an instrument of

international trade, it is one of the most secure methods for a seller to be paid. Besides credit risk

considerations, LCs is the customary business practice for long distance trade and a particularly important

commission earning service for any bank.

4.5.1 Features

The Letters of Credit module supports the processing of all types of clean and documentary LCs. These

include:

Import LCs

Export LCs

Guarantees

Shipping Guarantees

Clean LCs

Standby Guarantees

Reimbursement

4.5.2 Operations supported on LC

The following are the operations supported on an LC:

Open an import LC or guarantee

Open and confirm an import LC

Pre-advice an export LC

Advice an export LC

Advice and confirm an export LC

Confirm an export LC

Advice a guarantee

Import LC with pre-advice

In addition to amendment of the terms of an LC such as the expiry date, the amount, the latest shipment

date, etc. the operation on an LC as follows:

Open to open and confirm of an import LC

Pre-advice to advice of an export LC

Pre-advice to advice and confirm an export LC

Advice to advice and confirm an export LC

4.5.3 Processing Commissions and Charges

The method of collecting commissions and levying charges is flexible. Commissions can be collected for

the initiation and amendment events of an LC. The definition of commission rules facilitate the uniform

and efficient application of commission across all LCs processed under a product. Commissions can be

collected in advance or in arrears, periodically or non-periodically Various charges such as handling

charges, SWIFT charges, etc. can be processed.

1.50

1.60

1.70

1.80

1.90

2012-13 2013-14

4.6 Financial Ratio Analysis of DAL

Ratio analysis involves methods of calculating and interpreting financial ratios to assess the

Companies/firm‟s performance. Ratio analysis of a firm‟s financial statements is of interest to

shareholders, creditors and firm‟s own management. Ratio analysis is the starting point in developing the

information desired by the analyst. Ratio analysis provides only a single snapshot, the analysis being for

one given point or period in time. In ratio analysis it is possible to compare the company ratio with a

standard one.

4.6.1 Liquidity Ratio

The liquidity ratios measure the ability of an enterprise to meet its short-term obligations and reflect the

short-term financial strength of an enterprise. Analysis of liquidity is very important in knowing the

liquidity status, movement of funds, idle fund (if any) which will not only help financial management to

keep the liquidity position of the company in order but also make sure of payment to short-term creditors,

interested in short-term solvency of the company. Current ratio, quick ratio and working capital to total

asset ratio can be used to measure the liquidity position of the enterprise.

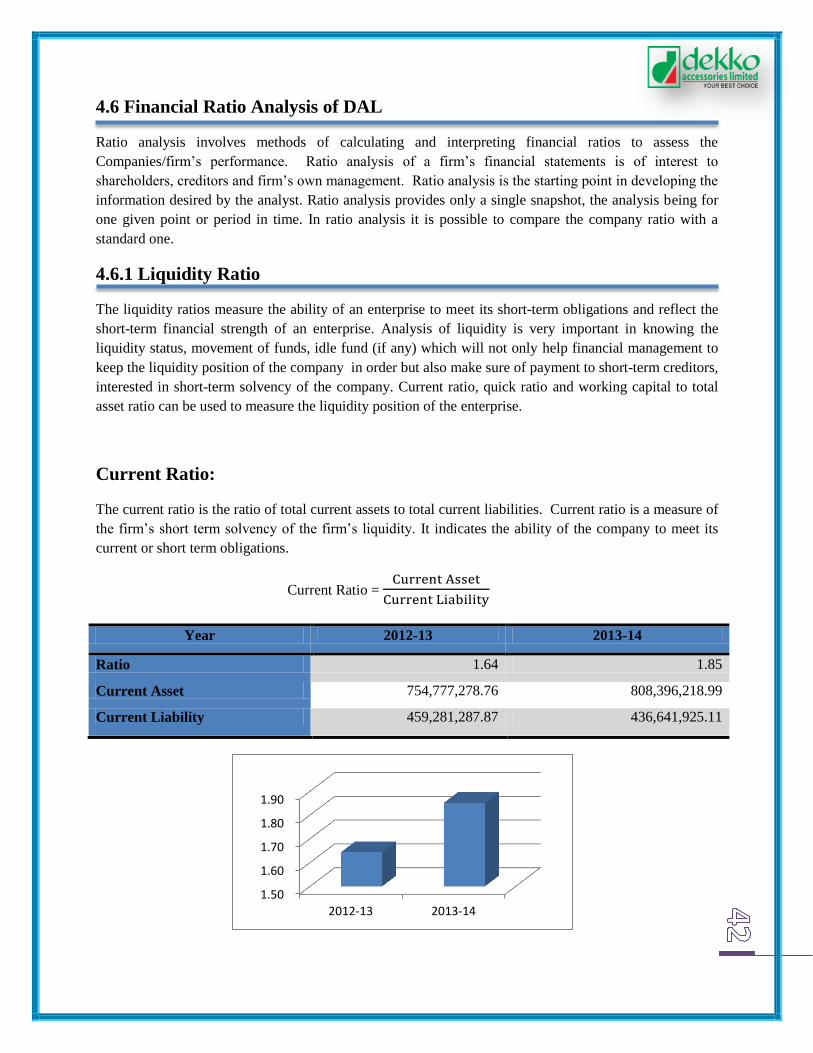

Current Ratio:

The current ratio is the ratio of total current assets to total current liabilities. Current ratio is a measure of

the firm‟s short term solvency of the firm‟s liquidity. It indicates the ability of the company to meet its

current or short term obligations.

Current Ratio =

Year 2012-13 2013-14

Ratio 1.64 1.85

Current Asset 754,777,278.76 808,396,218.99

Current Liability 459,281,287.87 436,641,925.11

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

2012-13 2013-14

Interpretation

The graph shows that the ratio of DAL is lower in 2012-13 than in 2013-14 because of an increase in total

current liabilities more than increase in total current assets.

Reasons

From our balance sheet I see that in 2012-13 current assets are increases specially Cash and Inventory

rather than 2013-14.

Comment

Here we can see that year by year the ratio is going up which is good for the company. Because

sometimes the assets has been going up and sometimes down. It means the company‟s asset management

quality is not good.

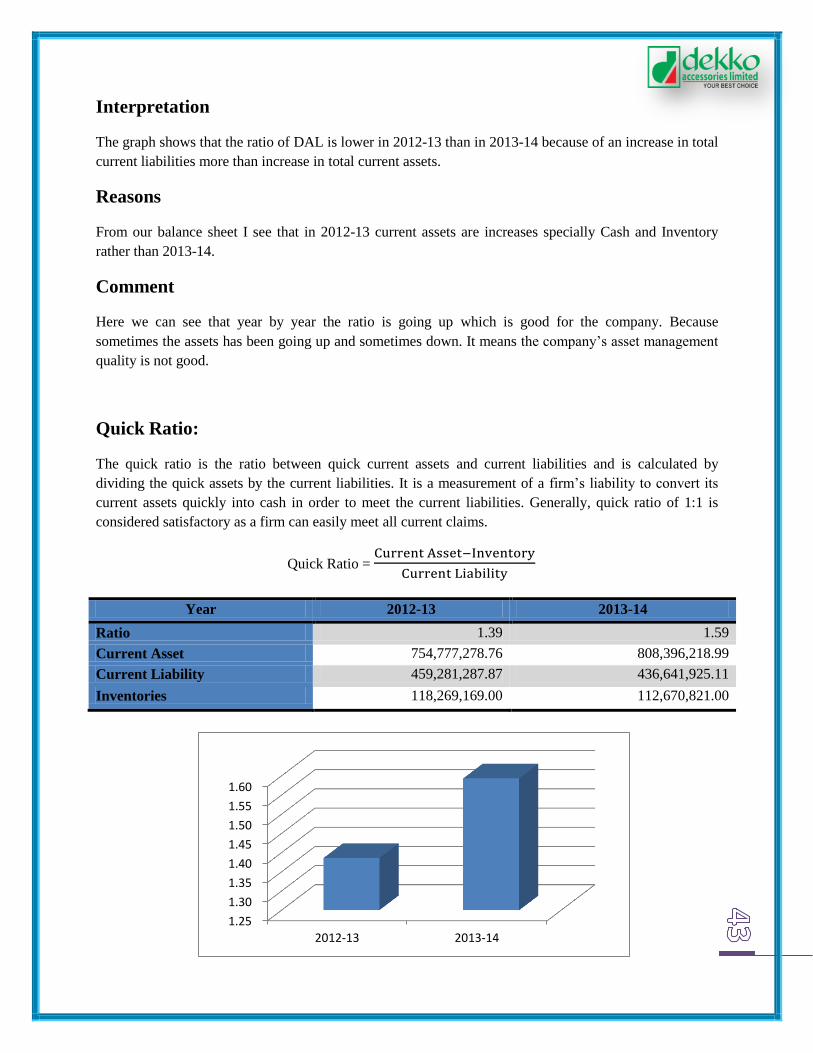

Quick Ratio:

The quick ratio is the ratio between quick current assets and current liabilities and is calculated by

dividing the quick assets by the current liabilities. It is a measurement of a firm‟s liability to convert its

current assets quickly into cash in order to meet the current liabilities. Generally, quick ratio of 1:1 is

considered satisfactory as a firm can easily meet all current claims.

Quick Ratio =

Year 2012-13 2013-14

Ratio 1.39 1.59

Current Asset 754,777,278.76 808,396,218.99

Current Liability 459,281,287.87 436,641,925.11

Inventories 118,269,169.00 112,670,821.00

-

0.01

0.02

0.03

0.04

0.05

0.06

0.07

2012-13 2013-14

Interpretation

The graph exhibits that the ratio of DAL is higher in 2013-14 than in 2012-13 because of a decrease in

total current liabilities, inventory and prepaid expenses as well.

Reason

For the reason of inventory up and down the quick ratio also change every year. The quick ratio is

increasing year by year because of increasing current assets and decreasing inventory, prepaid expenses

and liabilities which is the sign of good condition for the Company.

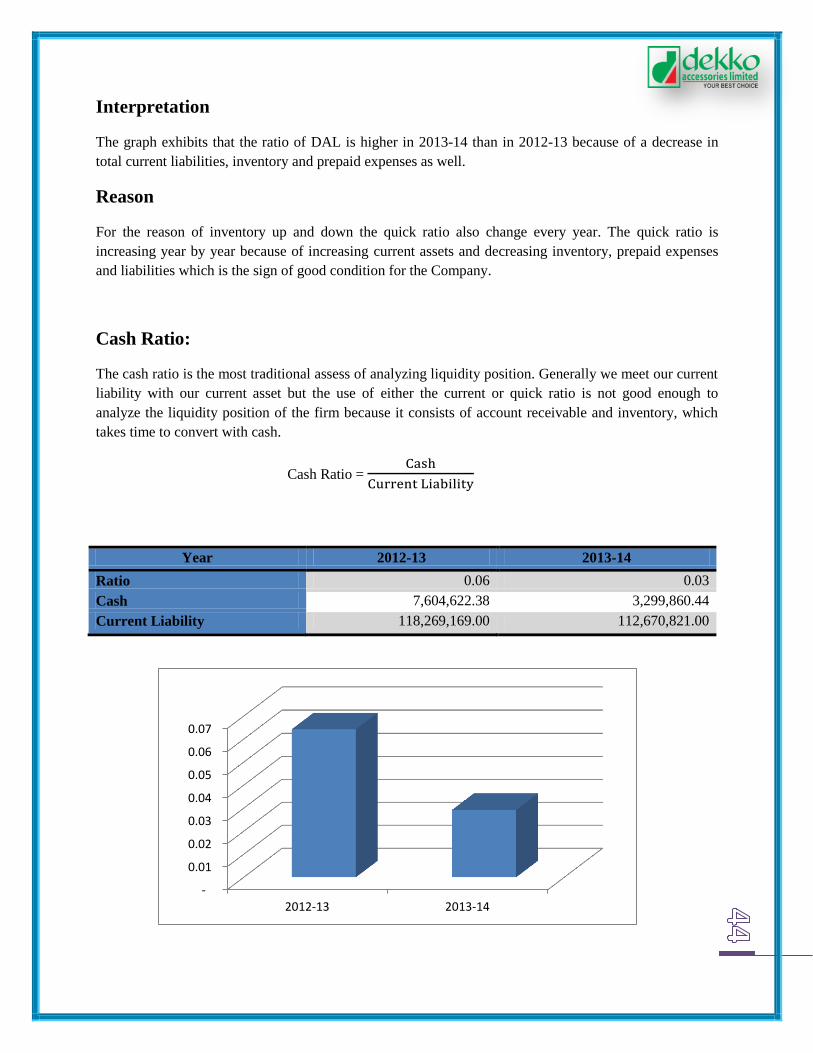

Cash Ratio:

The cash ratio is the most traditional assess of analyzing liquidity position. Generally we meet our current

liability with our current asset but the use of either the current or quick ratio is not good enough to

analyze the liquidity position of the firm because it consists of account receivable and inventory, which

takes time to convert with cash.

Cash Ratio =

Year 2012-13 2013-14

Ratio 0.06 0.03

Cash 7,604,622.38 3,299,860.44

Current Liability 118,269,169.00 112,670,821.00

Interpretation

From the graph it is evident that through all the 2 years the cash ratio of DAL is continuously decreasing

because of decreasing amount of cash.

Reason

To the year 2012-13 and 2013-14 cash are decreases because the costs of production are increase.

Comment

By analyzing the graph, it can be said that the company is not making good amount of cash year by year

and it is less than standard. So it is not very good sign for the company.

4.6.2 Activity Ratio

Activity ratio is concerned with measuring the efficiency in asset management. The efficiency with which

the assets are used would be reflected in the speed and rapidity with which assets converted into sales.

The greater is the rate of return over or conversion, the more efficient is the utilization of assets, other

things being equal.

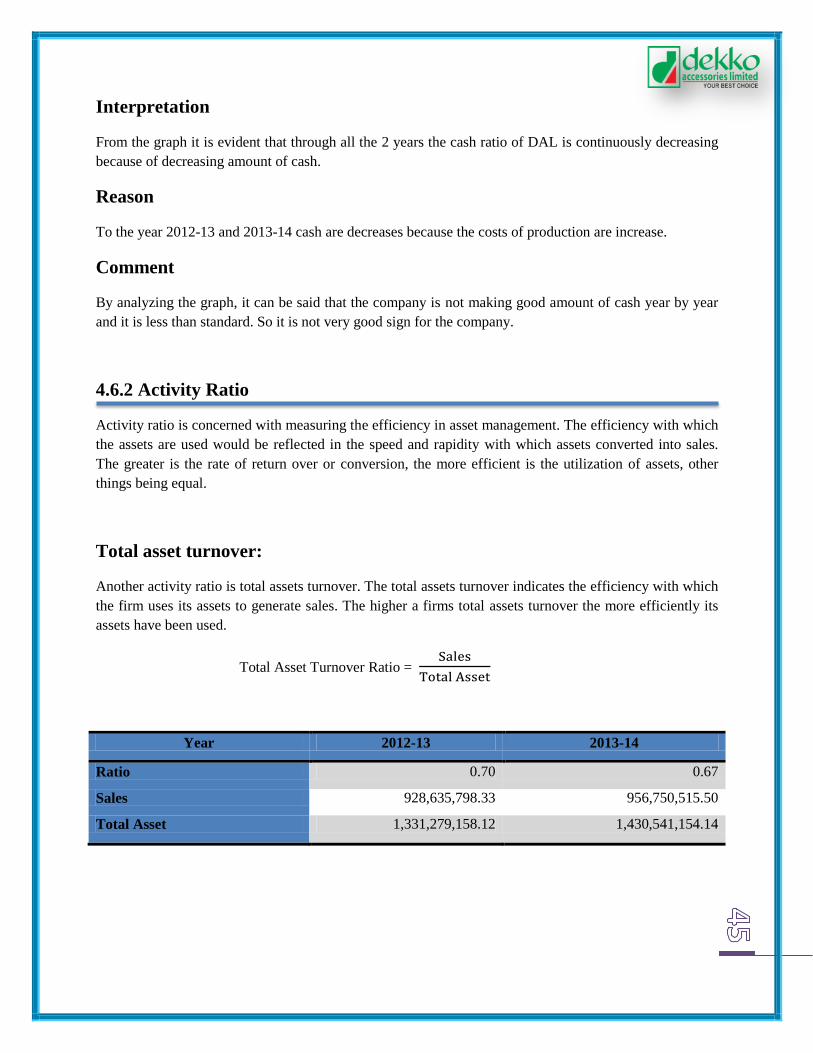

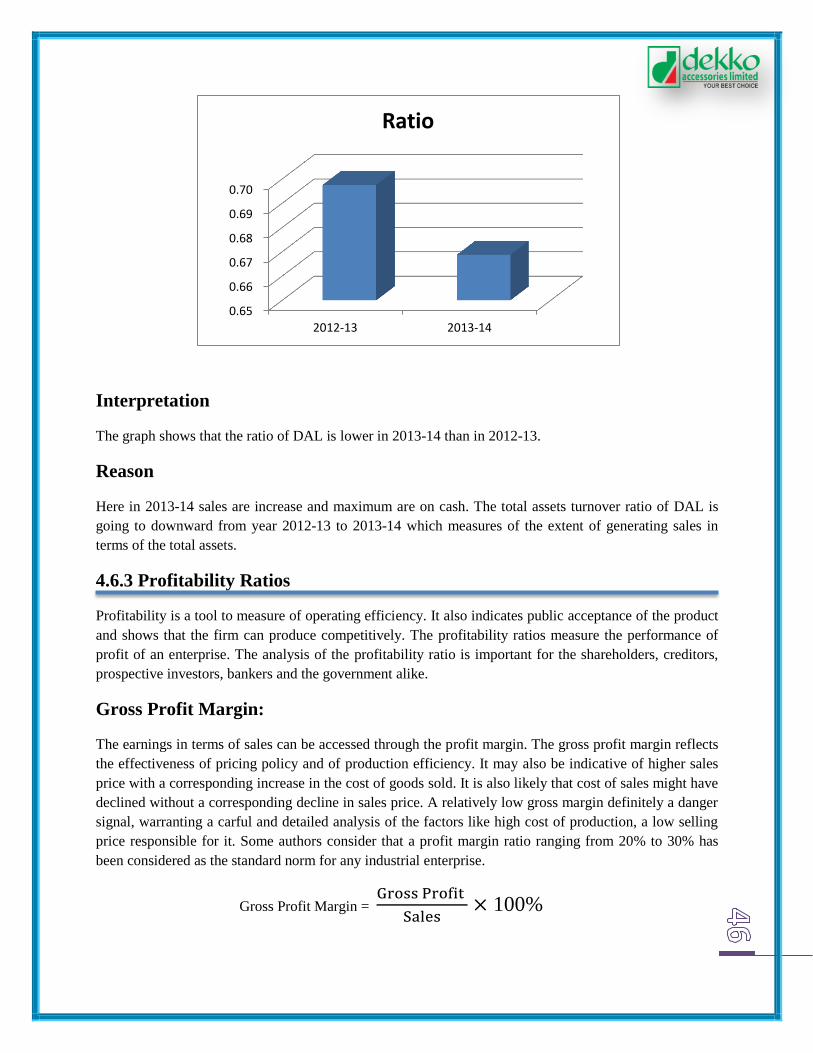

Total asset turnover:

Another activity ratio is total assets turnover. The total assets turnover indicates the efficiency with which

the firm uses its assets to generate sales. The higher a firms total assets turnover the more efficiently its

assets have been used.

Total Asset Turnover Ratio =

Year 2012-13 2013-14

Ratio 0.70 0.67

Sales 928,635,798.33 956,750,515.50

Total Asset 1,331,279,158.12 1,430,541,154.14

0.65

0.66

0.67

0.68

0.69

0.70

2012-13 2013-14

Ratio

Interpretation

The graph shows that the ratio of DAL is lower in 2013-14 than in 2012-13.

Reason

Here in 2013-14 sales are increase and maximum are on cash. The total assets turnover ratio of DAL is

going to downward from year 2012-13 to 2013-14 which measures of the extent of generating sales in

terms of the total assets.

4.6.3 Profitability Ratios

Profitability is a tool to measure of operating efficiency. It also indicates public acceptance of the product

and shows that the firm can produce competitively. The profitability ratios measure the performance of

profit of an enterprise. The analysis of the profitability ratio is important for the shareholders, creditors,

prospective investors, bankers and the government alike.

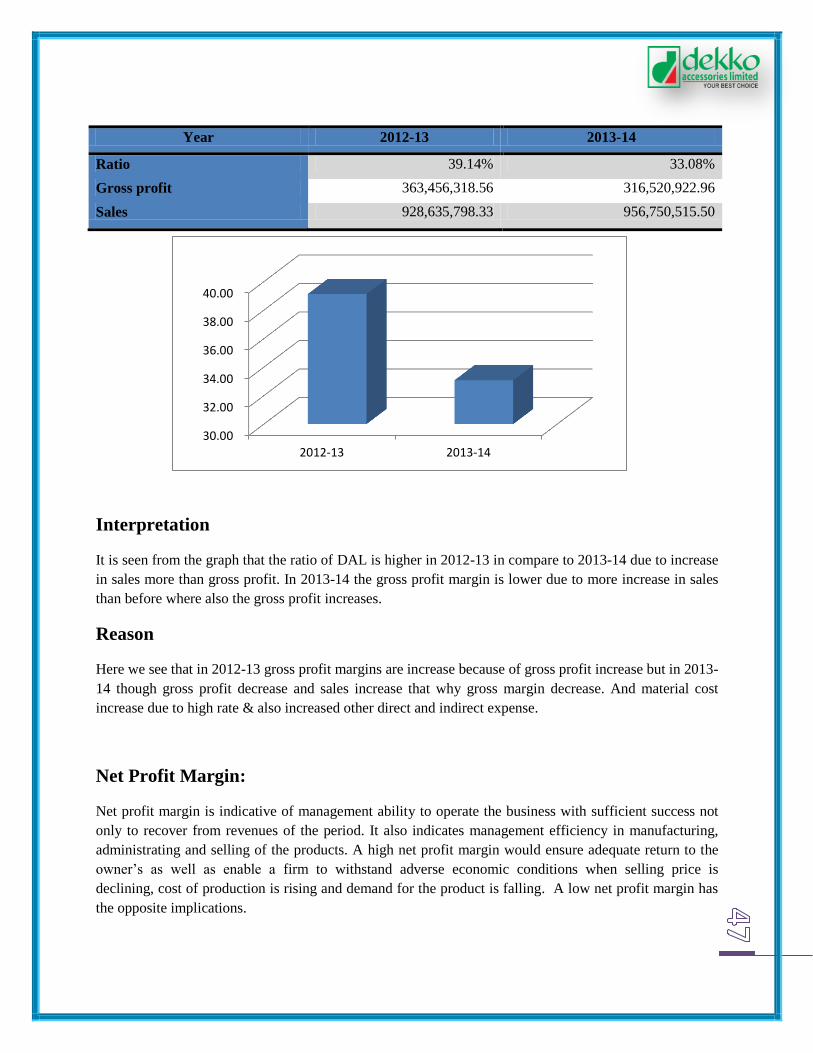

Gross Profit Margin:

The earnings in terms of sales can be accessed through the profit margin. The gross profit margin reflects

the effectiveness of pricing policy and of production efficiency. It may also be indicative of higher sales

price with a corresponding increase in the cost of goods sold. It is also likely that cost of sales might have

declined without a corresponding decline in sales price. A relatively low gross margin definitely a danger

signal, warranting a carful and detailed analysis of the factors like high cost of production, a low selling

price responsible for it. Some authors consider that a profit margin ratio ranging from 20% to 30% has

been considered as the standard norm for any industrial enterprise.

Gross Profit Margin =

100%

30.00

32.00

34.00

36.00

38.00

40.00

2012-13 2013-14

Year 2012-13 2013-14

Ratio 39.14% 33.08%

Gross profit 363,456,318.56 316,520,922.96

Sales 928,635,798.33 956,750,515.50

Interpretation

It is seen from the graph that the ratio of DAL is higher in 2012-13 in compare to 2013-14 due to increase

in sales more than gross profit. In 2013-14 the gross profit margin is lower due to more increase in sales

than before where also the gross profit increases.

Reason

Here we see that in 2012-13 gross profit margins are increase because of gross profit increase but in 2013-

14 though gross profit decrease and sales increase that why gross margin decrease. And material cost

increase due to high rate & also increased other direct and indirect expense.

Net Profit Margin:

Net profit margin is indicative of management ability to operate the business with sufficient success not

only to recover from revenues of the period. It also indicates management efficiency in manufacturing,

administrating and selling of the products. A high net profit margin would ensure adequate return to the

owner‟s as well as enable a firm to withstand adverse economic conditions when selling price is

declining, cost of production is rising and demand for the product is falling. A low net profit margin has

the opposite implications.

-

5.00

10.00

15.00

20.00

2012-13 2013-14

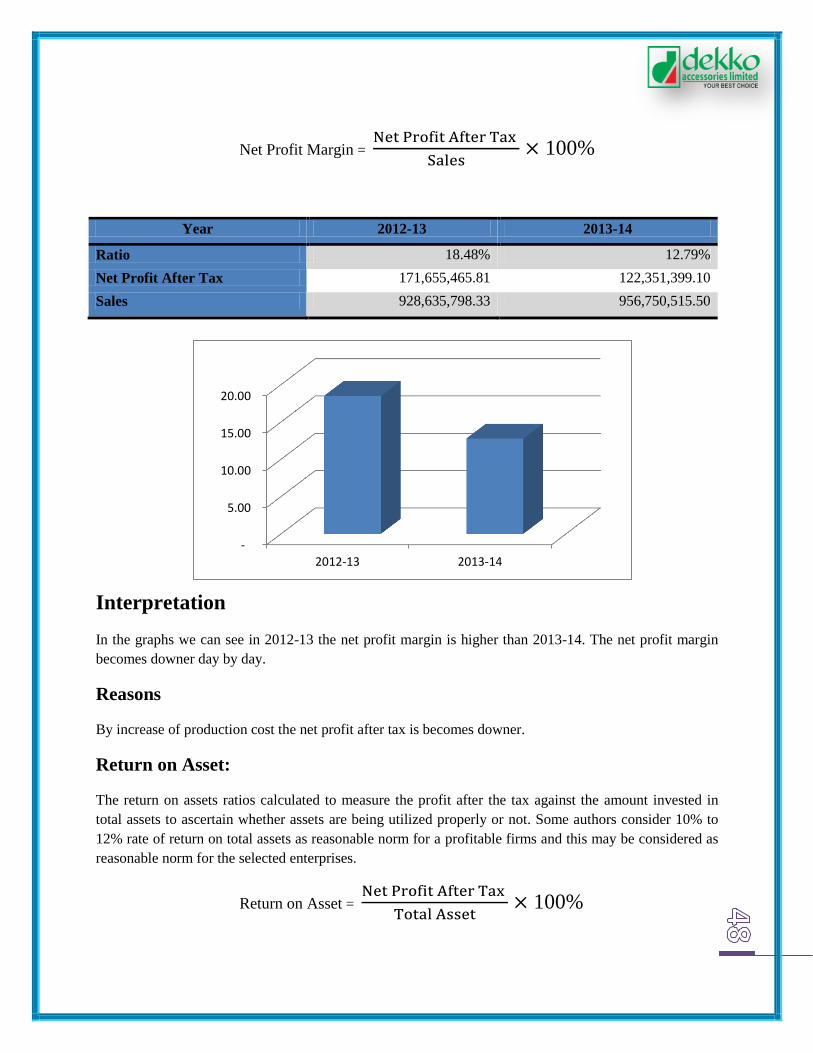

Net Profit Margin =

100%

Year 2012-13 2013-14

Ratio 18.48% 12.79%

Net Profit After Tax 171,655,465.81 122,351,399.10

Sales 928,635,798.33 956,750,515.50

Interpretation

In the graphs we can see in 2012-13 the net profit margin is higher than 2013-14. The net profit margin

becomes downer day by day.

Reasons

By increase of production cost the net profit after tax is becomes downer.

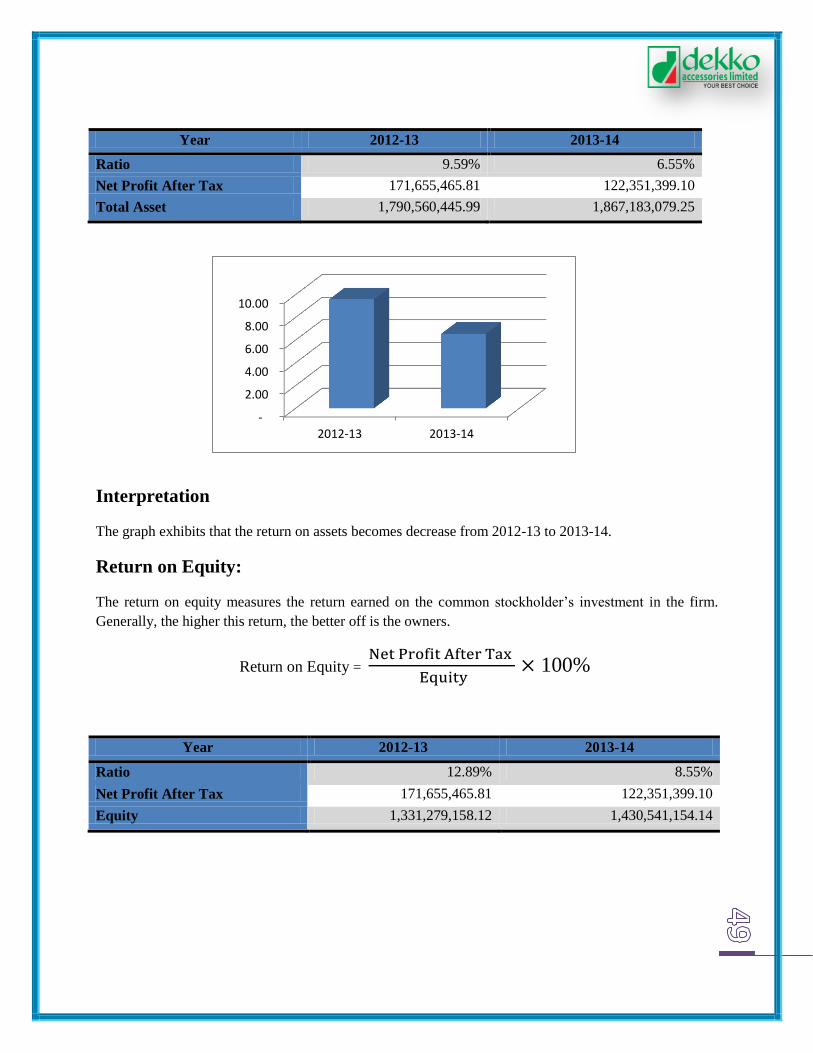

Return on Asset:

The return on assets ratios calculated to measure the profit after the tax against the amount invested in

total assets to ascertain whether assets are being utilized properly or not. Some authors consider 10% to

12% rate of return on total assets as reasonable norm for a profitable firms and this may be considered as

reasonable norm for the selected enterprises.

Return on Asset =

100%

-

2.00

4.00

6.00

8.00

10.00

2012-13 2013-14

Year 2012-13 2013-14

Ratio 9.59% 6.55%

Net Profit After Tax 171,655,465.81 122,351,399.10

Total Asset 1,790,560,445.99 1,867,183,079.25

Interpretation

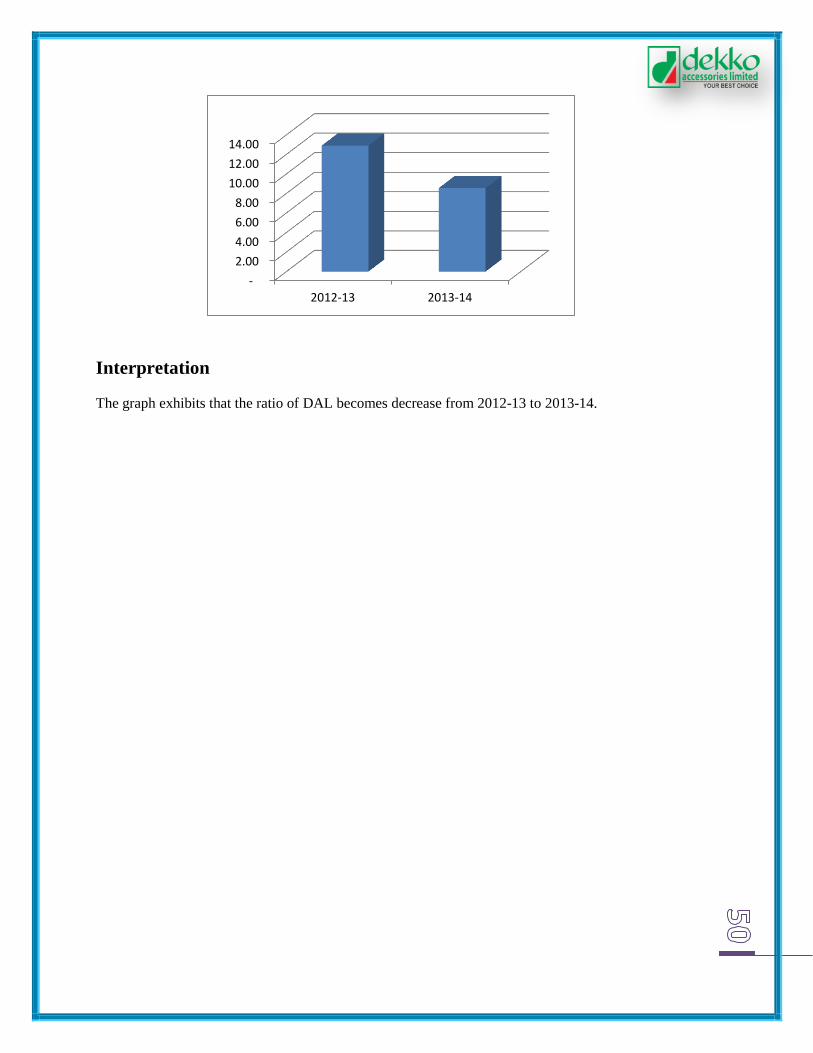

The graph exhibits that the return on assets becomes decrease from 2012-13 to 2013-14.

Return on Equity:

The return on equity measures the return earned on the common stockholder‟s investment in the firm.

Generally, the higher this return, the better off is the owners.

Return on Equity =

100%

Year 2012-13 2013-14

Ratio 12.89% 8.55%

Net Profit After Tax 171,655,465.81 122,351,399.10

Equity 1,331,279,158.12 1,430,541,154.14

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2012-13 2013-14

Interpretation

The graph exhibits that the ratio of DAL becomes decrease from 2012-13 to 2013-14.

5.1 Discussion on findings

From my practical experience and in depth analysis of different personnel of Dekko Accessories

Limited the following findings can be pointed out:

Dekko Accessories Limited is pioneer in starting its business but the company was not

pioneer in setting effective organizational strategies.

Internal cost control system is moderate and need to improve for growing profit.

Quality of garments accessories is the strength of dekko accessories ltd. which is

maintaining strictly.

Market demand of garments accessories is so high due to quality of the production.

The company was not very much concern about their competitors and they also could not

read the marketing strategies of its competitors properly.

The company was very slow to react in the changing business environment.

The company was not prompt to take and implement any decision.

As it follows a diversified business strategy, this business unit (Dekko Accessories

Limited) is the largest contributing company in this group.

The company doesn't follow a well-established recruiting policy.

Diversified business strategy does not work well if all the business units cannot be

nourished properly.

To get competitive advantage and to sustain it for long run it needs to be prepared for

future changes in business environment and must outperform competitors.

Most of the employees are not happy about their salary, for that key employees are gone

when they get better opportunity.

Management has some problem with the internal auditors.

Bangladesh is an over populated country of South Asia. It is a full of natural resources. But the economic

condition is very poor and unemployed rate of population is another burden for developing our country.

Creating new employment opportunity in our country by investing large capital must be needed. DAL is

playing a vital role for our country economy.

Accounts Department of Dekko Accessories Ltd. is working all the time to sustain and satisfy its

employees. According to my own experience the working environment of the organization is very

inspiring. However, the organization needs to work a lot to satisfy its experienced and old employees. The

organization is always keen to implement new rules and actions for improvement.

To become a pioneer in an industry is easy than to be market leader for long time. To be a market

leader a company needs to provide superior customer value to consumers, to build and sustain

competitive advantage for long time, and to outperform competitors in every aspect. To outperform

competitors, the company must have clear idea about its own SWOT analysis and also try to study

competitors SWOT analysis.

So at last, from the analysis and discussion, I may conclude that DAL is being grown up industry because

of its Byers areas, Fractural development, Production capacity, Human resources and Bank activities

which are quite satisfactory.

7.1 Recommendations

The following suggestions can be taken into consideration by the Dekko Accessories Limited for

ensuring smooth running of the company & to take over major market share in the future market.

To get advantage from the superior marketing strategies the company needs to build and

sustain competitive advantage for long time.

The company needs to conduct extensive marketing research to get a clear picture of its

present condition and also about the activities of the competitors.

All of the products of Dekko Accessories Limited are to be well finished and accurate so

that lucrative appearance can be possible. Because well finished and accuracy play a

pivotal role particularly in the garments sector.

Every business unit should have equal importance and need to nourish properly.

Dekko Accessories Limited must have separate guideline and marketing strategies for

changing business environment of near future.

Top management's support is vital for the success of the company so they should take

any decision as soon as possible and allocate sufficient resources to support the decision

if necessary.

The company must follow a well establish recruiting policy. It should try to include

experienced and skilled employees as well as potential young employees.

The company should conduct both on the job and off the job training facilities for their

employees.

The company should prepare effective promotional strategy and allocate sufficient fund

for advertisement.

The Managing Director along with all employees should work sincerely and seriously to

revive the company position.

Dekko Group needs a FCA for their internal audit.

Bibliography

1. Dekko Accessories Ltd. Annual Report 2012-2013. Dhaka: Dekko Group.

2. Dekko Accessories Ltd. Annual Report 2013-2014. Dhaka: Dekko Group.

3. Fatima Fahima, 2012, Report on “Execution of Accounting & Budgetary Control System – A

Closure Observation”(UIU) about Dekko Group.

4. Gerald I. White; Ashwinpaul C. Sondhi; Dov Fried “The Analysis and use of Financial

Statement” (3rd

Edition) by Jhon Wiley & Sons, Inc.

5. Weygandt, J.J. Kimmel, D.P. and Kieso, E.D., 2011. Accounting Principles. 9th ed. USA:

John Wiley & Sons, Inc.

6. Dekko Accessories Ltd. Overview, Pruducts, Unit info, Available at:

http://www.dekkogroup.com/dekko_accessories (Accessed 8 February 2014)

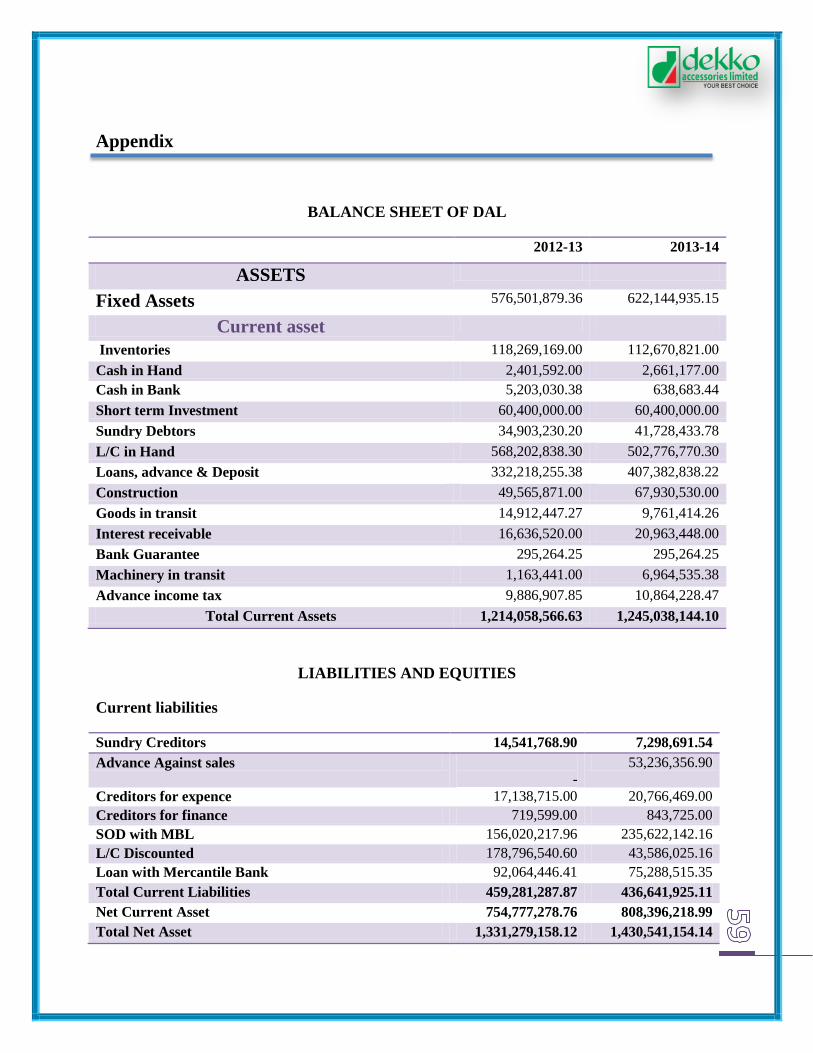

Appendix

BALANCE SHEET OF DAL

2012-13 2013-14

ASSETS

Fixed Assets 576,501,879.36 622,144,935.15

Current asset

Inventories 118,269,169.00 112,670,821.00

Cash in Hand 2,401,592.00 2,661,177.00

Cash in Bank 5,203,030.38 638,683.44

Short term Investment 60,400,000.00 60,400,000.00

Sundry Debtors 34,903,230.20 41,728,433.78

L/C in Hand 568,202,838.30 502,776,770.30

Loans, advance & Deposit 332,218,255.38 407,382,838.22

Construction 49,565,871.00 67,930,530.00

Goods in transit 14,912,447.27 9,761,414.26

Interest receivable 16,636,520.00 20,963,448.00

Bank Guarantee 295,264.25 295,264.25

Machinery in transit 1,163,441.00 6,964,535.38

Advance income tax 9,886,907.85 10,864,228.47

Total Current Assets 1,214,058,566.63 1,245,038,144.10

LIABILITIES AND EQUITIES

Current liabilities

Sundry Creditors 14,541,768.90 7,298,691.54

Advance Against sales

-

53,236,356.90

Creditors for expence 17,138,715.00 20,766,469.00

Creditors for finance 719,599.00 843,725.00

SOD with MBL 156,020,217.96 235,622,142.16

L/C Discounted 178,796,540.60 43,586,025.16

Loan with Mercantile Bank 92,064,446.41 75,288,515.35

Total Current Liabilities 459,281,287.87 436,641,925.11

Net Current Asset 754,777,278.76 808,396,218.99

Total Net Asset 1,331,279,158.12 1,430,541,154.14

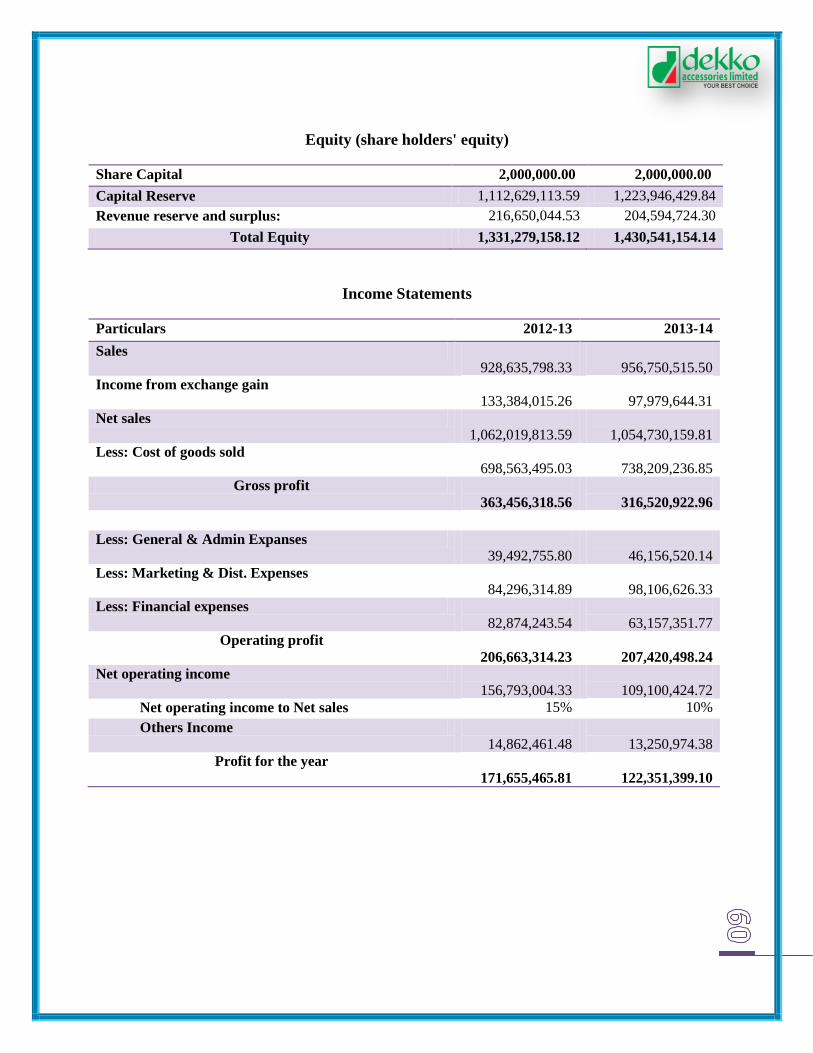

Equity (share holders' equity)

Share Capital 2,000,000.00 2,000,000.00

Capital Reserve 1,112,629,113.59 1,223,946,429.84

Revenue reserve and surplus: 216,650,044.53 204,594,724.30

Total Equity 1,331,279,158.12 1,430,541,154.14

Income Statements

Particulars 2012-13 2013-14

Sales

928,635,798.33

956,750,515.50

Income from exchange gain

133,384,015.26

97,979,644.31

Net sales

1,062,019,813.59

1,054,730,159.81

Less: Cost of goods sold

698,563,495.03

738,209,236.85

Gross profit

363,456,318.56

316,520,922.96

Less: General & Admin Expanses

39,492,755.80

46,156,520.14

Less: Marketing & Dist. Expenses

84,296,314.89

98,106,626.33

Less: Financial expenses

82,874,243.54

63,157,351.77

Operating profit

206,663,314.23

207,420,498.24

Net operating income

156,793,004.33

109,100,424.72

Net operating income to Net sales 15% 10%

Others Income

14,862,461.48

13,250,974.38

Profit for the year

171,655,465.81

122,351,399.10