Embed Size (px)

Citation preview

© OECD/IEA 2017

Power, renewables and energy efficiency

7 December 2017

© OECD/IEA 2017

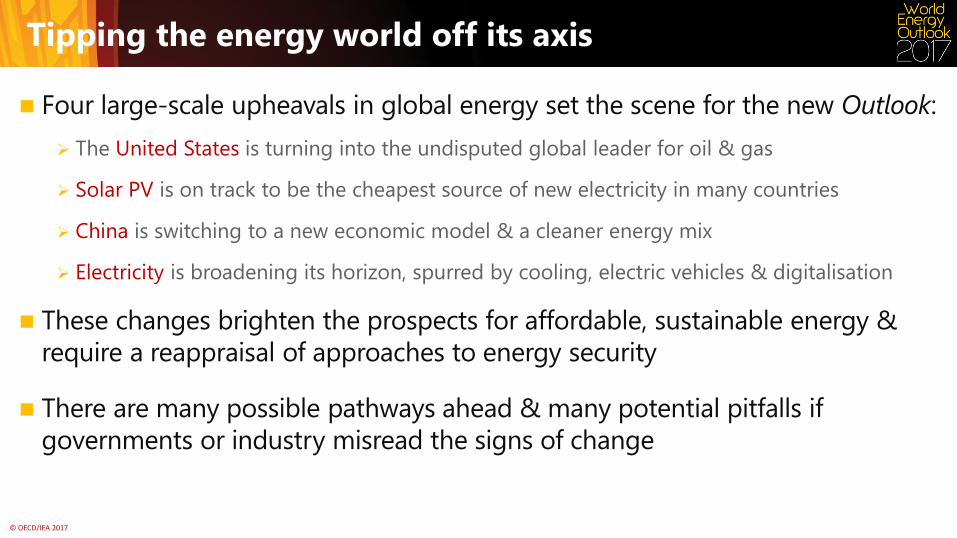

Tipping the energy world off its axis

Four large-scale upheavals in global energy set the scene for the new Outlook:

The United States is turning into the undisputed global leader for oil & gas

Solar PV is on track to be the cheapest source of new electricity in many countries

China is switching to a new economic model & a cleaner energy mix

Electricity is broadening its horizon, spurred by cooling, electric vehicles & digitalisation

These changes brighten the prospects for affordable, sustainable energy &

require a reappraisal of approaches to energy security

There are many possible pathways ahead & many potential pitfalls if

governments or industry misread the signs of change

© OECD/IEA 2017

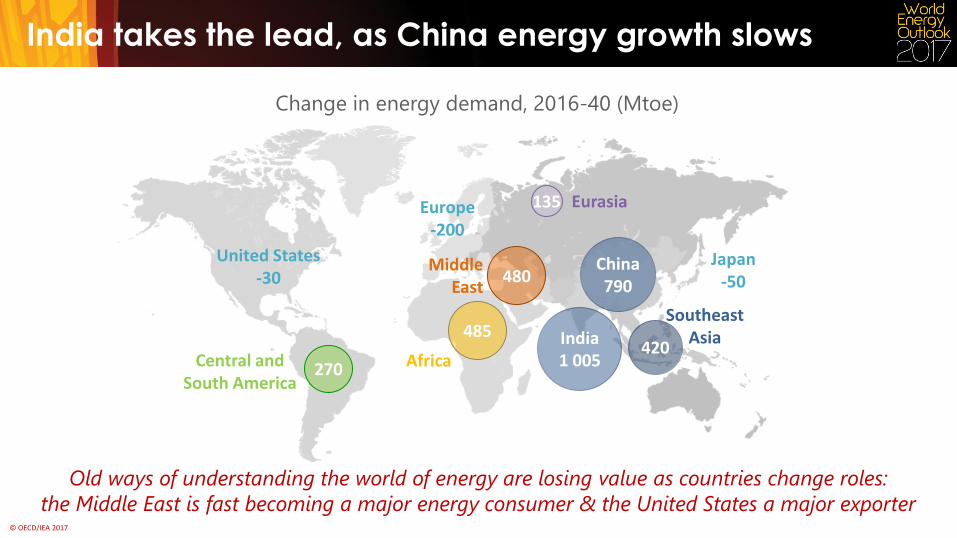

India takes the lead, as China energy growth slows

Change in energy demand, 2016-40 (Mtoe)

Old ways of understanding the world of energy are losing value as countries change roles:

the Middle East is fast becoming a major energy consumer & the United States a major exporter

India 1 005

420

Southeast Asia

China 790

United States -30

Japan -50

Europe -200

270 Central and South America

485

Africa

135 Eurasia

480 Middle

East

© OECD/IEA 2017

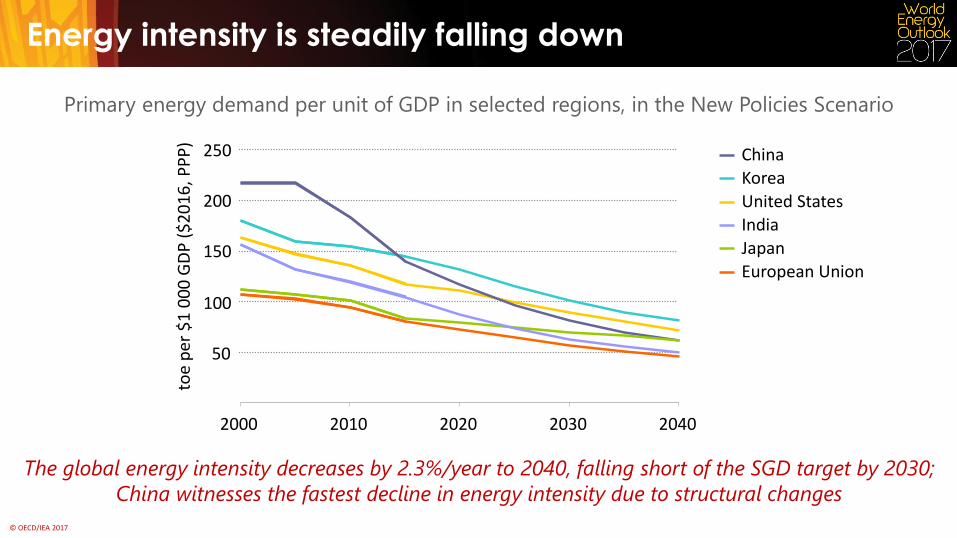

Energy intensity is steadily falling down

The global energy intensity decreases by 2.3%/year to 2040, falling short of the SGD target by 2030;

China witnesses the fastest decline in energy intensity due to structural changes

50

100

150

200

250

2000 2010 2020 2030 2040

Korea

United States

China

Japan

India

European Union

toe

per

$1

00

0 G

DP

($

20

16

, PP

P)

Primary energy demand per unit of GDP in selected regions, in the New Policies Scenario

© OECD/IEA 2017

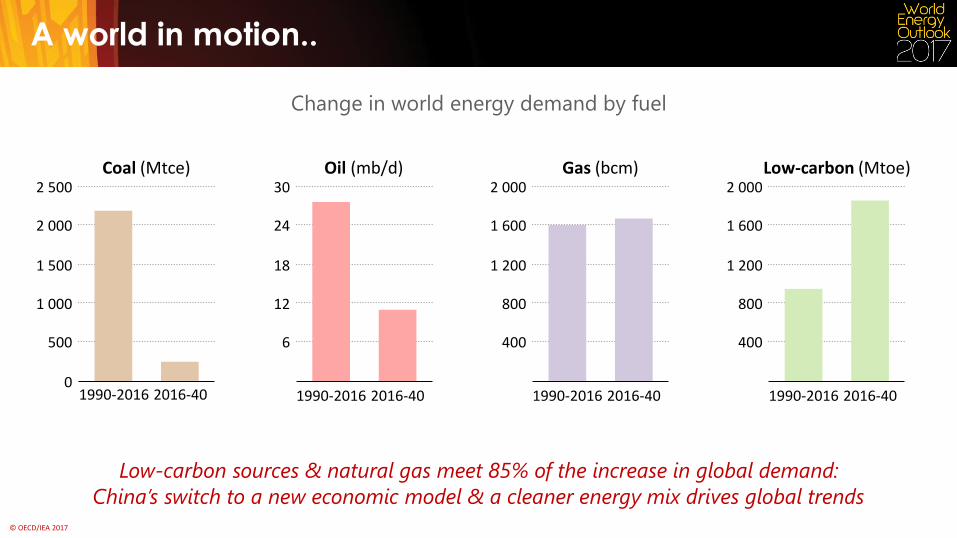

Change in world energy demand by fuel

Low-carbon sources & natural gas meet 85% of the increase in global demand:

Coal (Mtce)

0

500

1 000

1 500

2 000

2 500 Oil (mb/d)

6

12

18

24

30

1990-2016 2016-40

Gas (bcm)

400

800

1 200

1 600

2 000

1990-2016 2016-40

Low-carbon (Mtoe)

400

800

1 200

1 600

2 000

1990-2016 2016-40 1990-2016 2016-40

A world in motion..

China’s switch to a new economic model & a cleaner energy mix drives global trends

© OECD/IEA 2017

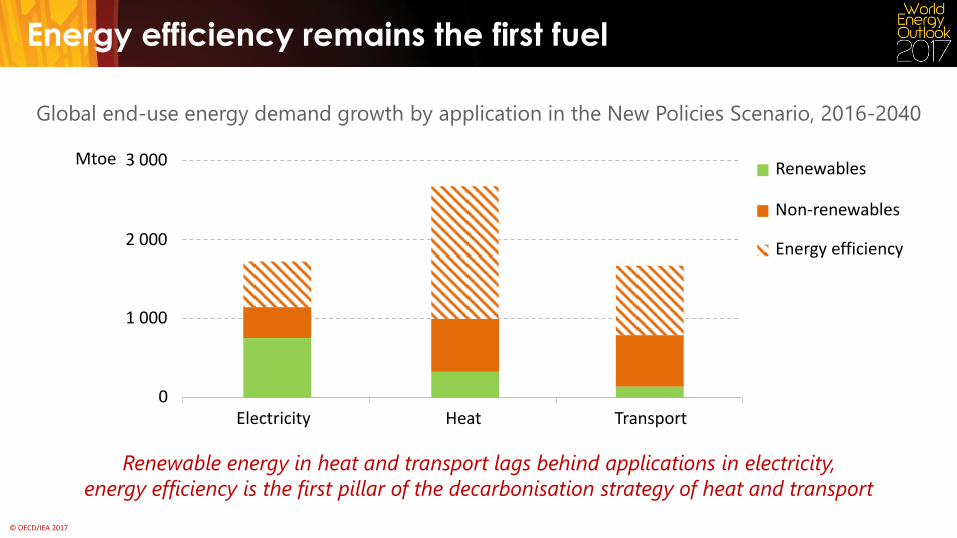

Energy efficiency remains the first fuel

Renewable energy in heat and transport lags behind applications in electricity,

energy efficiency is the first pillar of the decarbonisation strategy of heat and transport

Global end-use energy demand growth by application in the New Policies Scenario, 2016-2040

Renewables

Energy efficiency

Electricity Heat Transport

Non-renewables

1 000

2 000

3 000 Mtoe

0

© OECD/IEA 2017

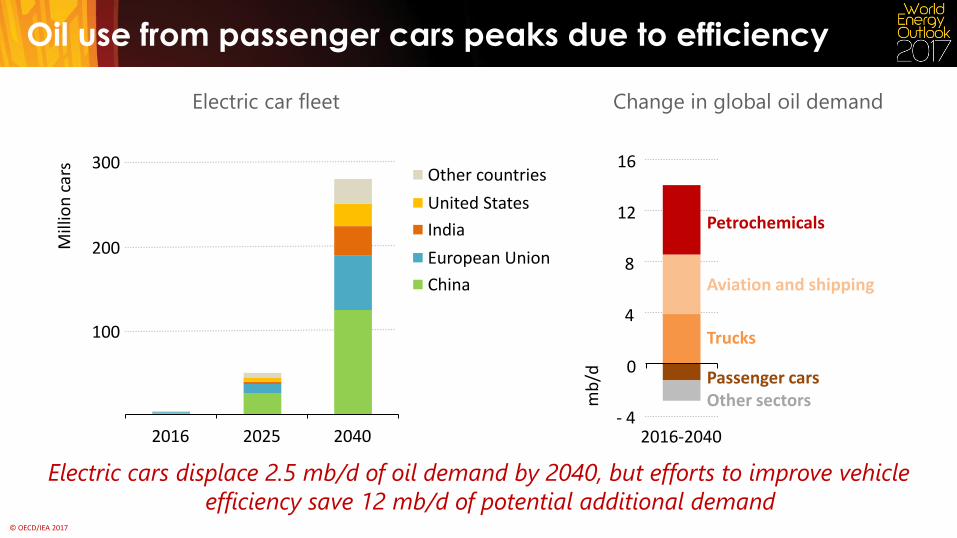

Oil use from passenger cars peaks due to efficiency

Electric car fleet

100

200

300

2016 2025 2040

Mill

ion

car

s

Other countries

United States

India

European Union

China

Passenger cars Other sectors

Change in global oil demand

4

8

12

16

Petrochemicals

Aviation and shipping

Trucks

mb

/d

- 4 2016-2040

0

Electric cars displace 2.5 mb/d of oil demand by 2040, but efforts to improve vehicle

efficiency save 12 mb/d of potential additional demand

© OECD/IEA 2017

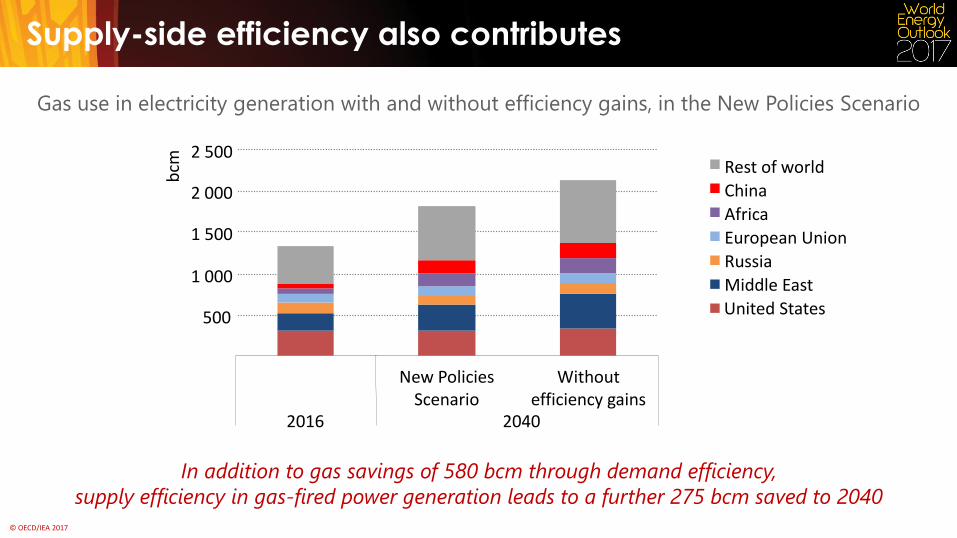

Supply-side efficiency also contributes

Gas use in electricity generation with and without efficiency gains, in the New Policies Scenario

In addition to gas savings of 580 bcm through demand efficiency,

supply efficiency in gas-fired power generation leads to a further 275 bcm saved to 2040

500

1 000

1 500

2 000

2 500

New Policies Scenario

Without efficiency gains

2040

bcm

Rest of world

China

Africa

European Union

Russia

Middle East

United States

2016

© OECD/IEA 2017

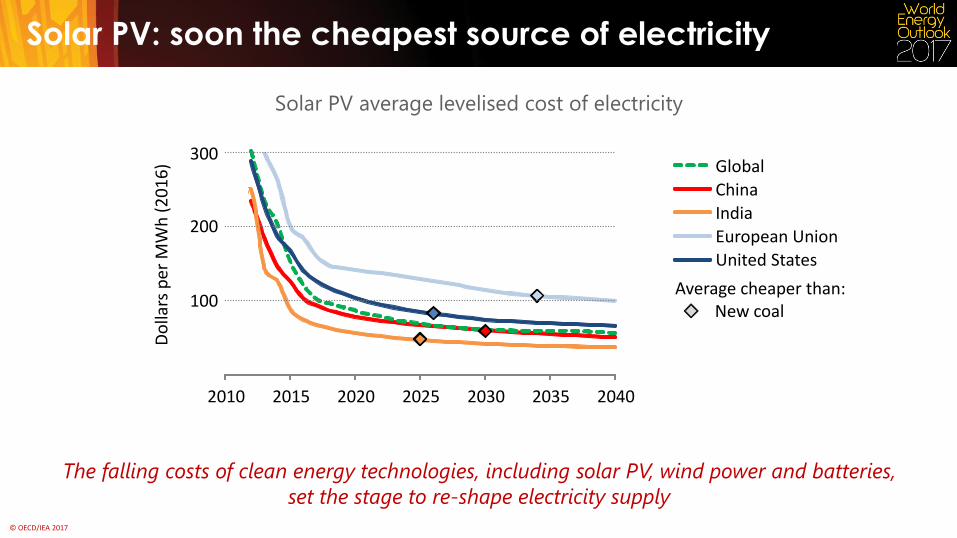

Solar PV: soon the cheapest source of electricity

Solar PV average levelised cost of electricity

The falling costs of clean energy technologies, including solar PV, wind power and batteries,

set the stage to re-shape electricity supply

100

200

300

2010 2015 2020 2025 2030 2035 2040

Do

llars

per

MW

h (

20

16

) Global

China

India

European Union

United States

New coal Average cheaper than:

© OECD/IEA 2017

GW

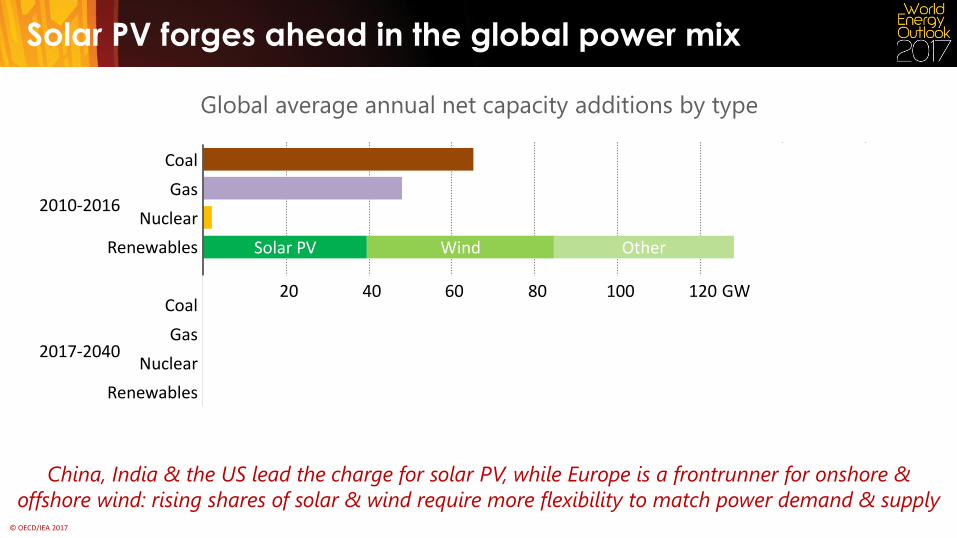

Solar PV forges ahead in the global power mix

Global average annual net capacity additions by type

China, India & the US lead the charge for solar PV, while Europe is a frontrunner for onshore &

offshore wind: rising shares of solar & wind require more flexibility to match power demand & supply

Renewables

Nuclear

Gas

Coal

Renewables

Nuclear

Gas

Coal

20 40 60 80 100 120 140 160 GW

2010-2016

2017-2040

Solar PV Wind

Solar PV Wind Other

Other

20 40 60 80 100 120 GW

© OECD/IEA 2017

10

20

30

40

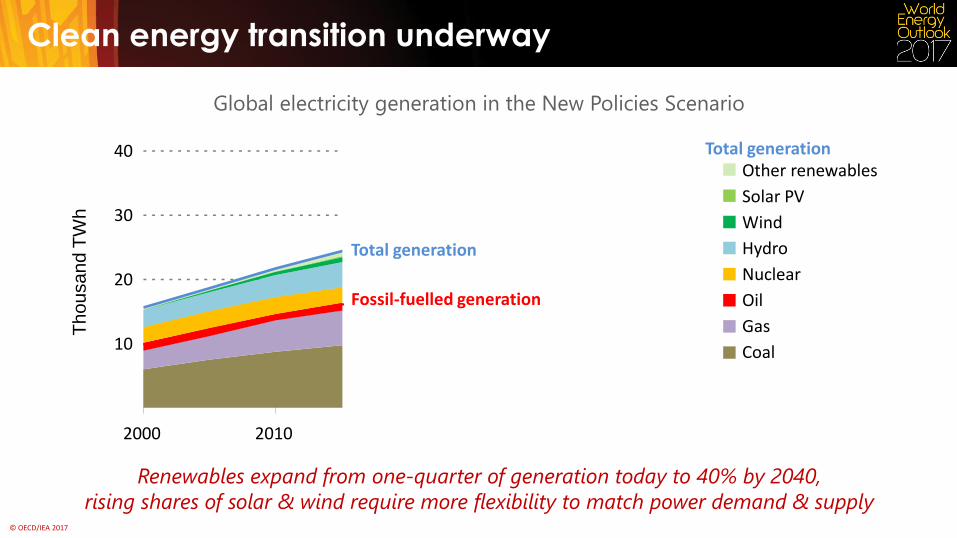

Clean energy transition underway

Renewables expand from one-quarter of generation today to 40% by 2040,

rising shares of solar & wind require more flexibility to match power demand & supply

Global electricity generation in the New Policies Scenario

2000 2010 2020 2030 2040

Th

ou

sa

nd

TW

h

Other renewables

Solar PV

Wind

Hydro

Nuclear

Oil

Gas

Coal

Total generation

Fossil-fuelled generation

Total generation

© OECD/IEA 2017

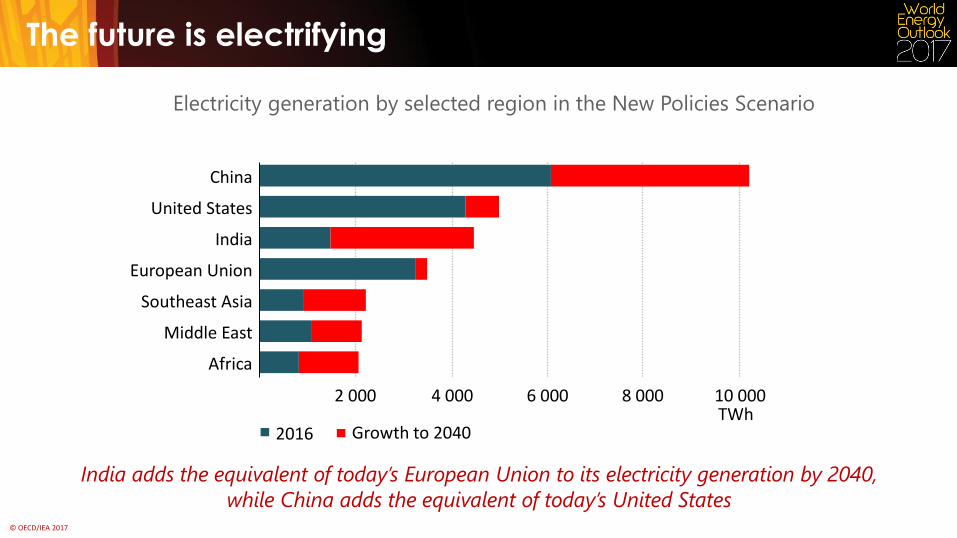

The future is electrifying

Electricity generation by selected region in the New Policies Scenario

India adds the equivalent of today’s European Union to its electricity generation by 2040,

Middle East

2 000 4 000 6 000 8 000 10 000

Africa

Southeast Asia

European Union

India

United States

China

TWh 2016 Growth to 2040

while China adds the equivalent of today’s United States

© OECD/IEA 2017

2040

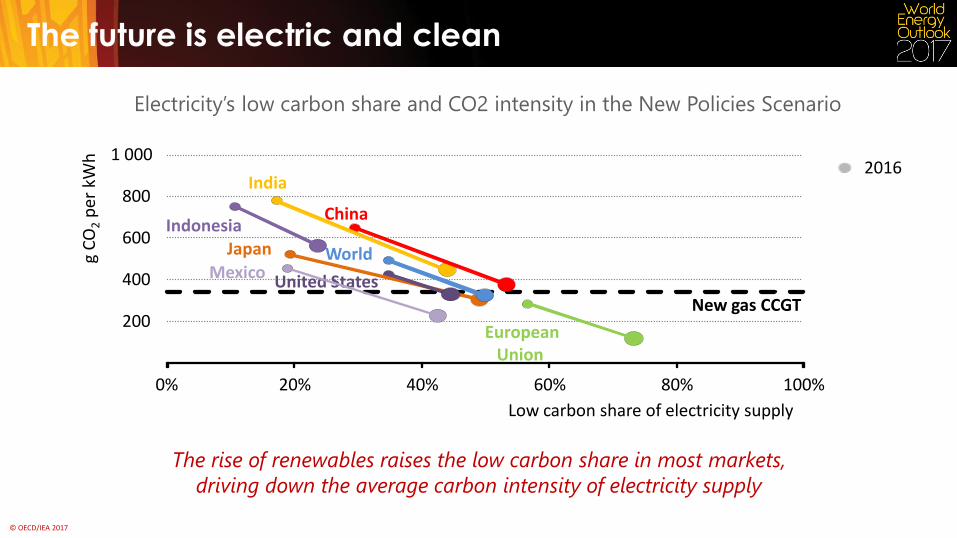

The future is electric and clean

The rise of renewables raises the low carbon share in most markets,

driving down the average carbon intensity of electricity supply

Electricity’s low carbon share and CO2 intensity in the New Policies Scenario

200

400

600

800

1 000

0% 20% 40% 60% 80% 100%

g C

O2 p

er k

Wh

Low carbon share of electricity supply

Japan

India

Indonesia China

European Union

United States Mexico

New gas CCGT

World

2016

© OECD/IEA 2017

10

20

30

40

2000 2010 2020 2030 2040 G

t

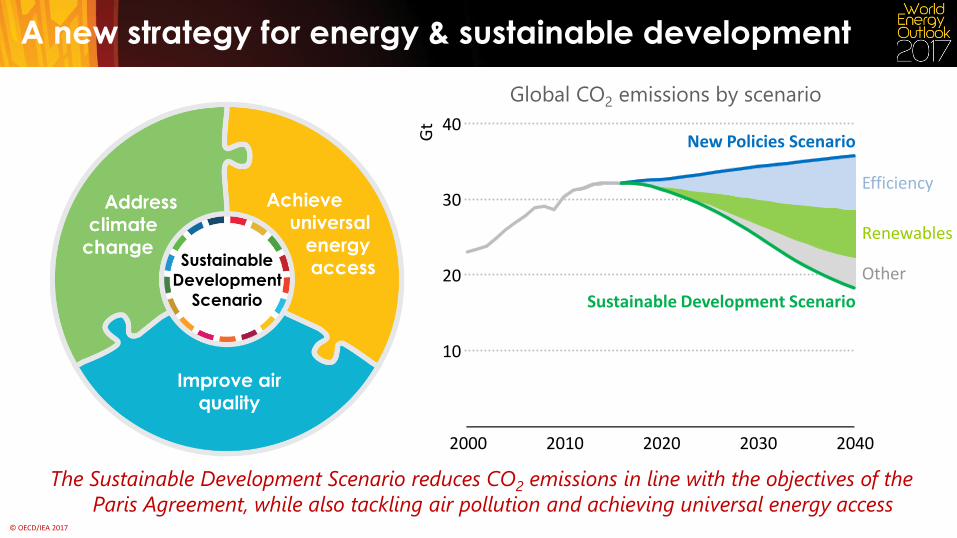

A new strategy for energy & sustainable development

Sustainable

Development

Scenario

The Sustainable Development Scenario reduces CO2 emissions in line with the objectives of the

Paris Agreement, while also tackling air pollution and achieving universal energy access

New Policies Scenario

Sustainable Development Scenario

Global CO2 emissions by scenario

Efficiency

Renewables

Other

© OECD/IEA 2017

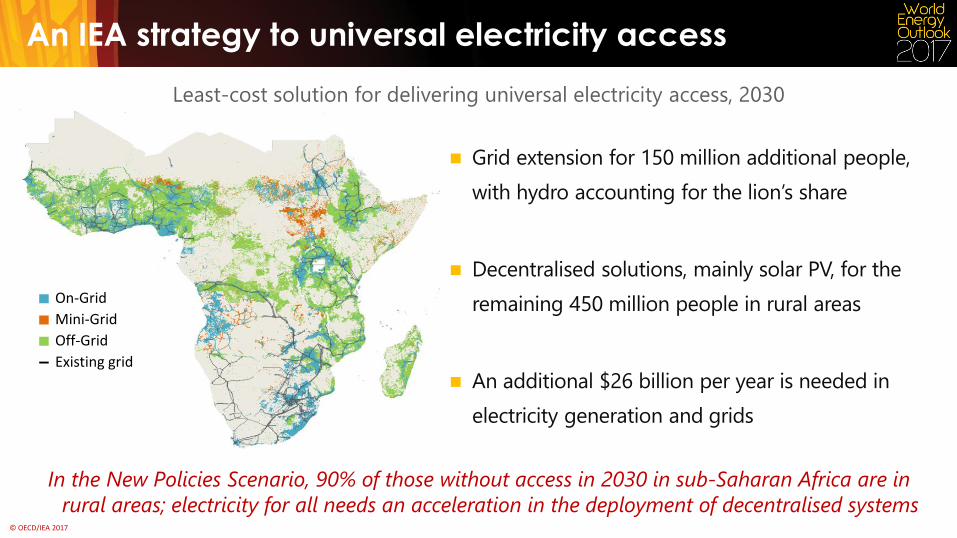

An IEA strategy to universal electricity access

On-Grid

Mini-Grid

Off-Grid

Existing grid

Grid extension for 150 million additional people,

with hydro accounting for the lion’s share

Decentralised solutions, mainly solar PV, for the

remaining 450 million people in rural areas

An additional $26 billion per year is needed in

electricity generation and grids

In the New Policies Scenario, 90% of those without access in 2030 in sub-Saharan Africa are in

rural areas; electricity for all needs an acceleration in the deployment of decentralised systems

Least-cost solution for delivering universal electricity access, 2030

© OECD/IEA 2017

200

400

600

NPS

TWh

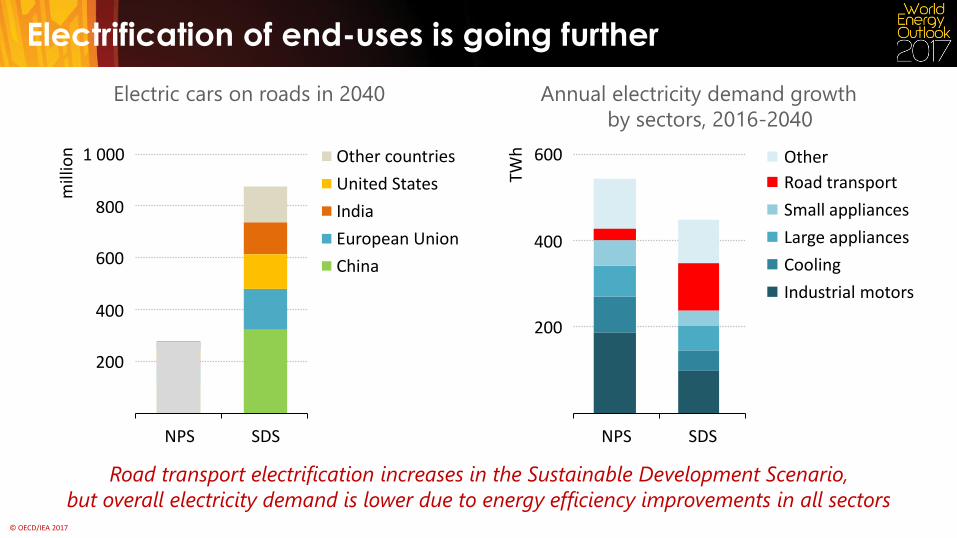

Electrification of end-uses is going further

Electric cars on roads in 2040

Road transport electrification increases in the Sustainable Development Scenario,

but overall electricity demand is lower due to energy efficiency improvements in all sectors

200

400

600

800

1 000

NPS SDS

mill

ion

SDS

Other

Road transport

Small appliances

Large appliances

Cooling

Industrial motors

Other countries

United States

India

European Union

China

Annual electricity demand growth

by sectors, 2016-2040

© OECD/IEA 2017

Industry

Transport Buildings

NPS

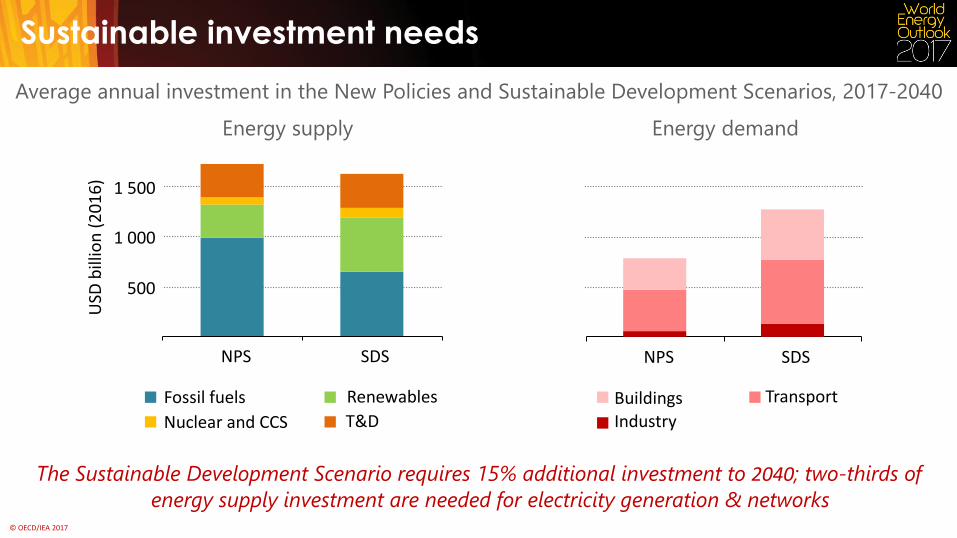

Average annual investment in the New Policies and Sustainable Development Scenarios, 2017-2040

Sustainable investment needs

The Sustainable Development Scenario requires 15% additional investment to 2040; two-thirds of

energy supply investment are needed for electricity generation & networks

T&D Nuclear and CCS

Renewables Fossil fuels

Energy supply

500

1 000

1 500

NPS SDS

USD

bill

ion

(2

01

6)

SDS

Energy demand

© OECD/IEA 2017

Conclusions

Progress is being made towards the SDGs, but under current trends the goals on

climate change, air pollution and universal access will not be met

There are strong synergies between renewable energy and energy efficiency that can

be harnessed to accelerate the clean energy transition

Our strategy for sustainable energy shows that concerted action to address climate

change is fully compatible with global goals on universal access & air quality

The Sustainable Development Scenario requires an additional 15% of investment and

profound changes in energy production & use

Electrification & digitalisation are the future for many parts of the global energy system,

creating new opportunities but also risks that policy makers have to address

© OECD/IEA 2017

iea.org/weo

![[Webinar Slides] Advanced distribution management system integration of renewables and storage](https://img.pdfslide.net/doc/110x75/554a07c5b4c905e56c8b5840/webinar-slides-advanced-distribution-management-system-integration-of-renewables-and-storage.jpg)