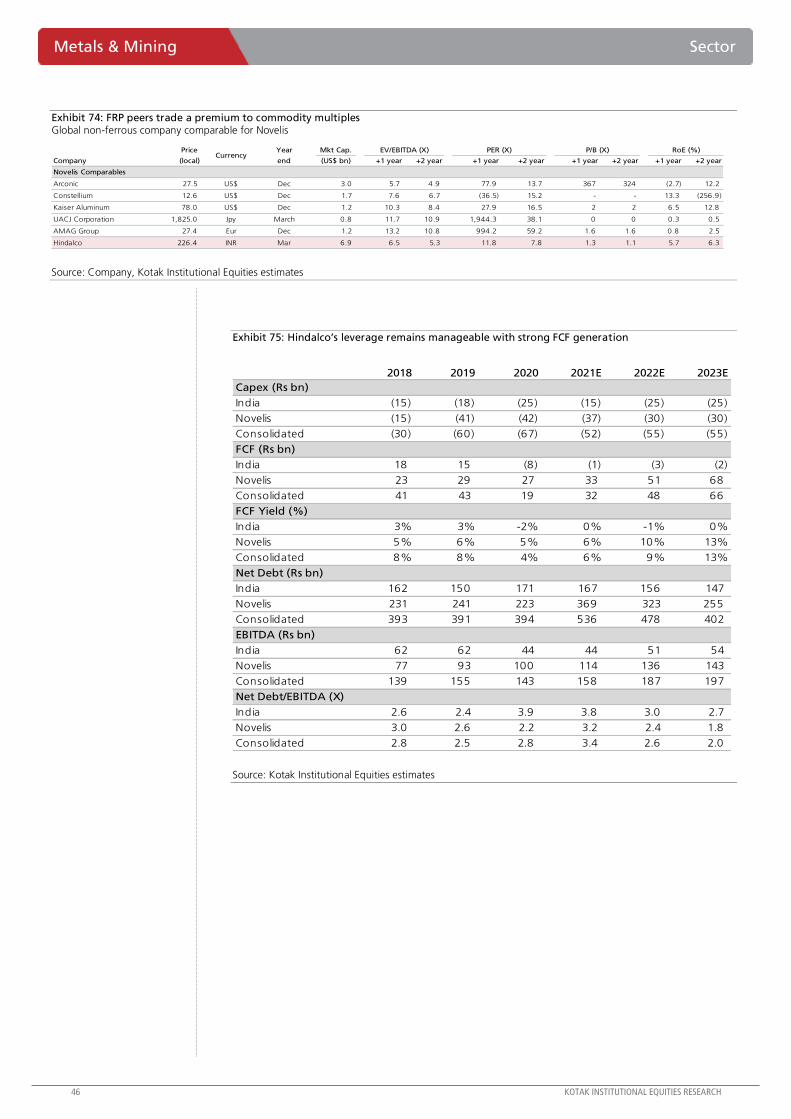

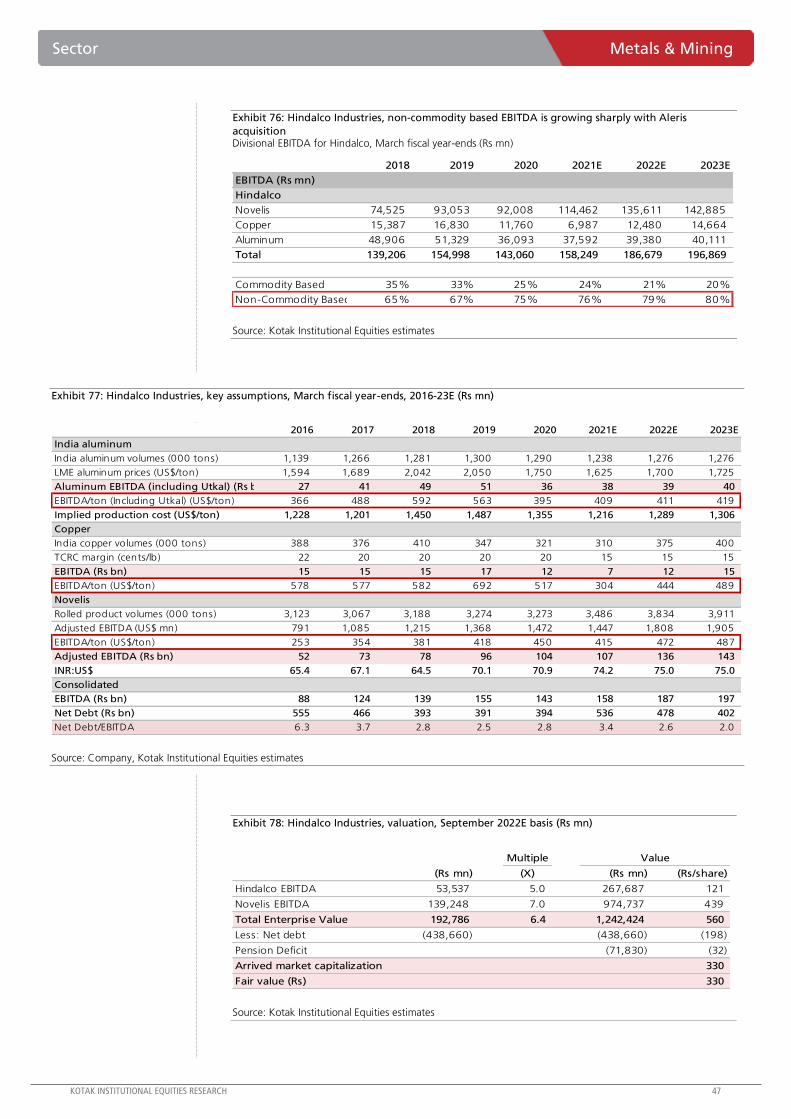

Embed Size (px)

Citation preview

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

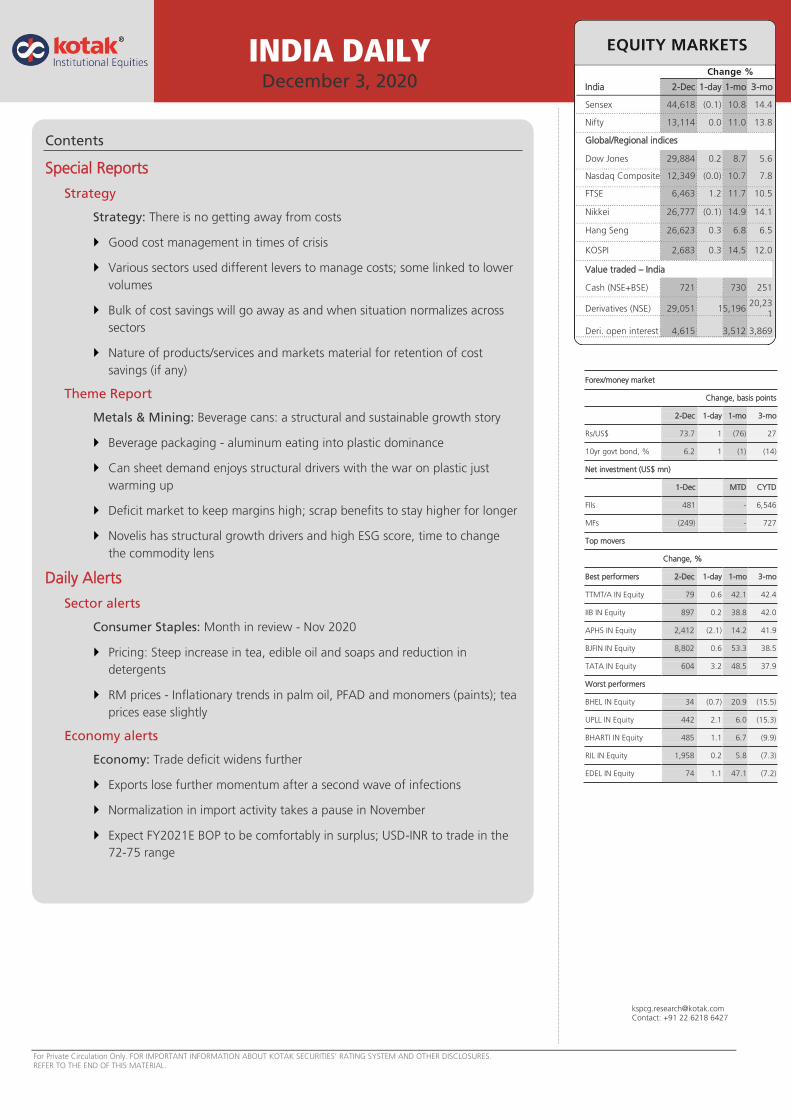

Contents

Special Reports

Strategy

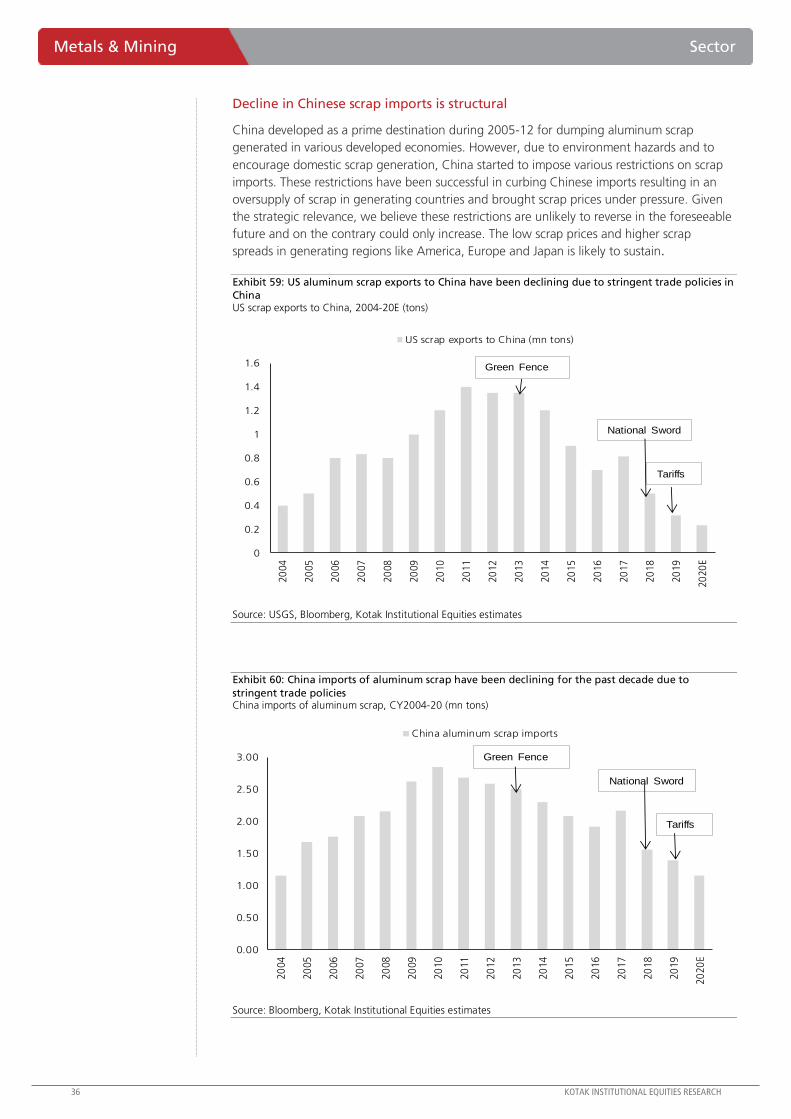

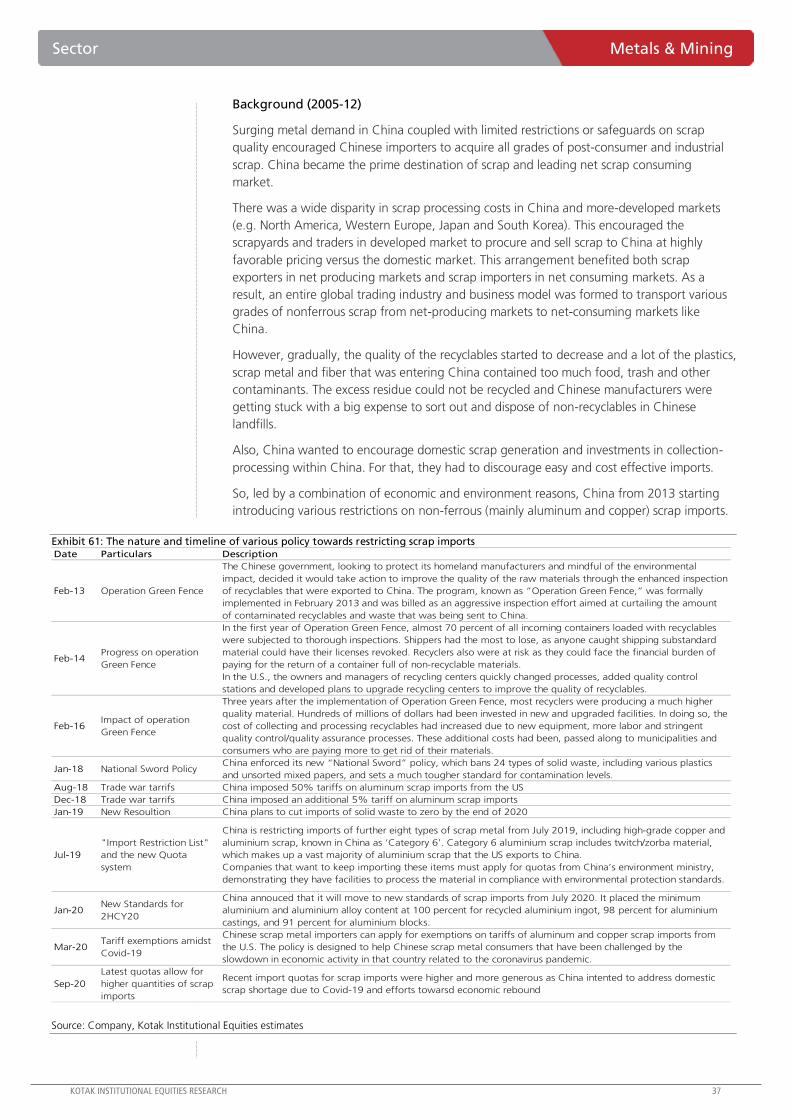

Strategy: There is no getting away from costs

Good cost management in times of crisis

Various sectors used different levers to manage costs; some linked to lower

volumes

Bulk of cost savings will go away as and when situation normalizes across

sectors

Nature of products/services and markets material for retention of cost

savings (if any)

Theme Report

Metals & Mining: Beverage cans: a structural and sustainable growth story

Beverage packaging - aluminum eating into plastic dominance

Can sheet demand enjoys structural drivers with the war on plastic just

warming up

Deficit market to keep margins high; scrap benefits to stay higher for longer

Novelis has structural growth drivers and high ESG score, time to change

the commodity lens

Daily Alerts

Sector alerts

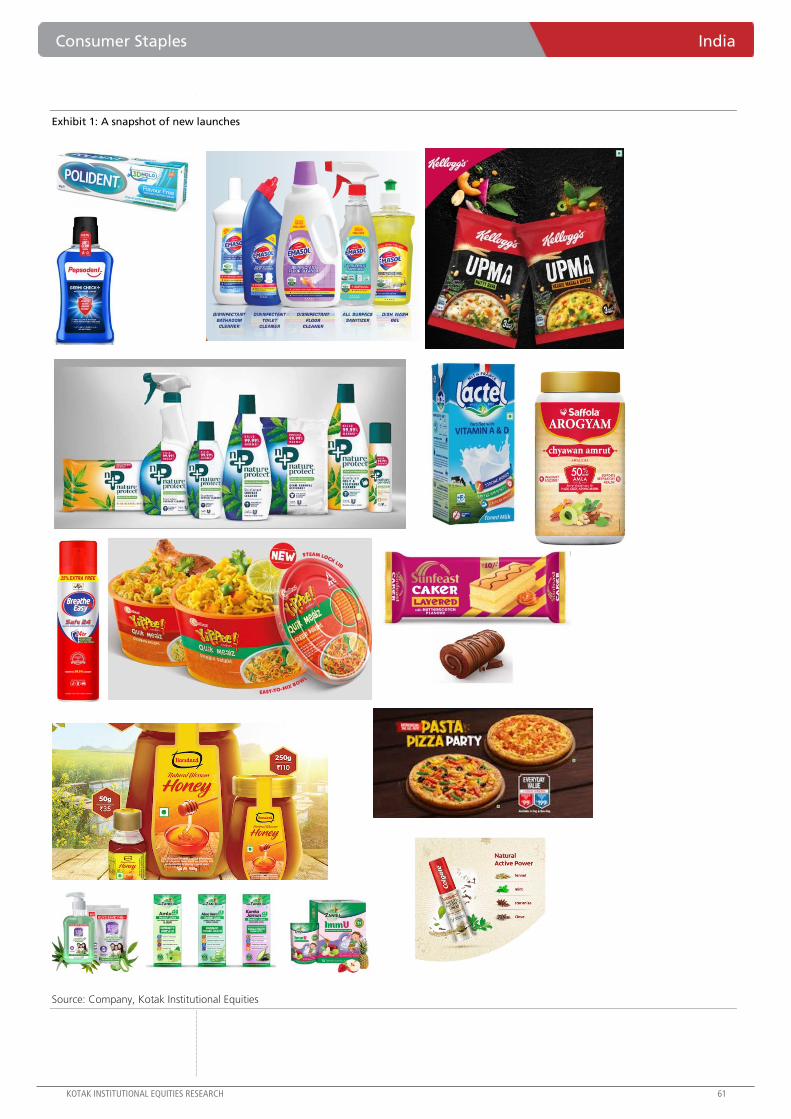

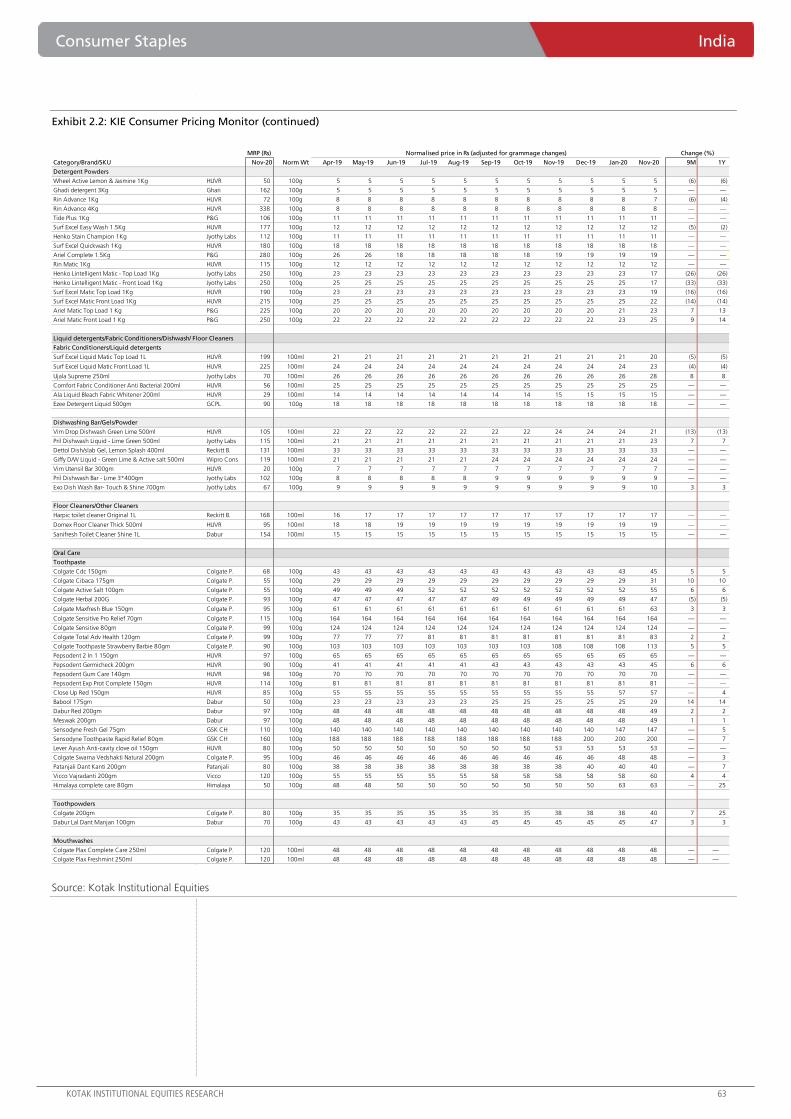

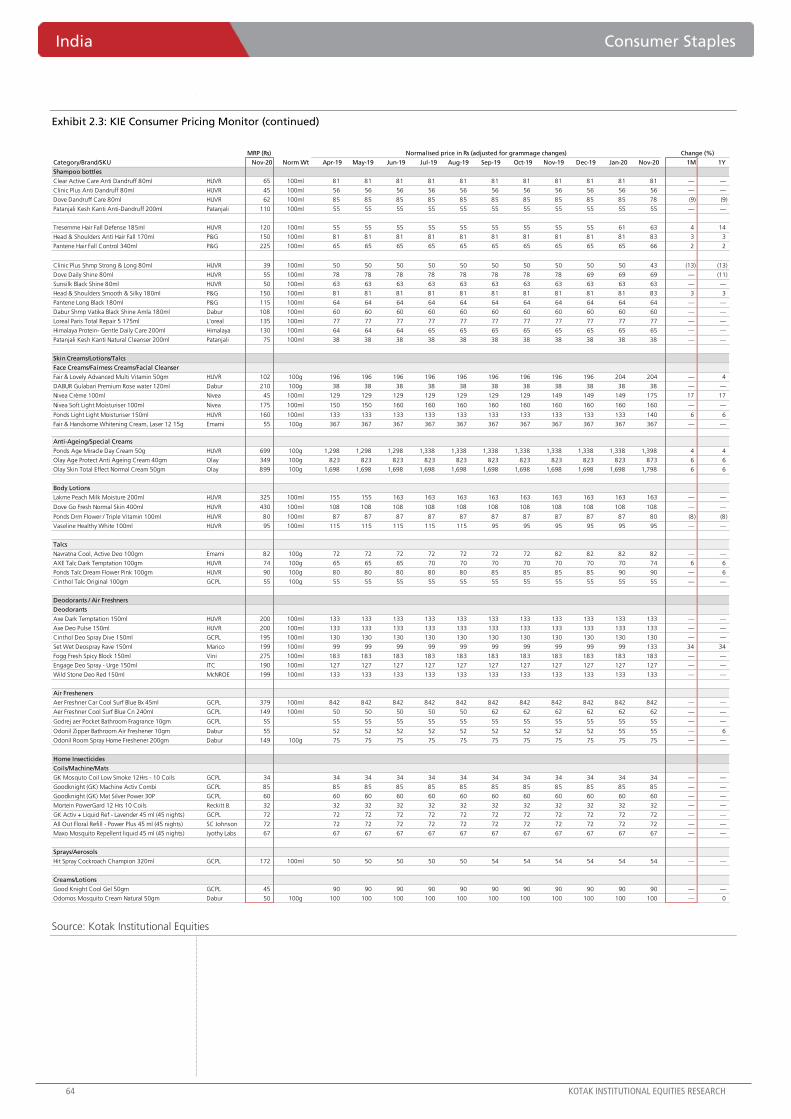

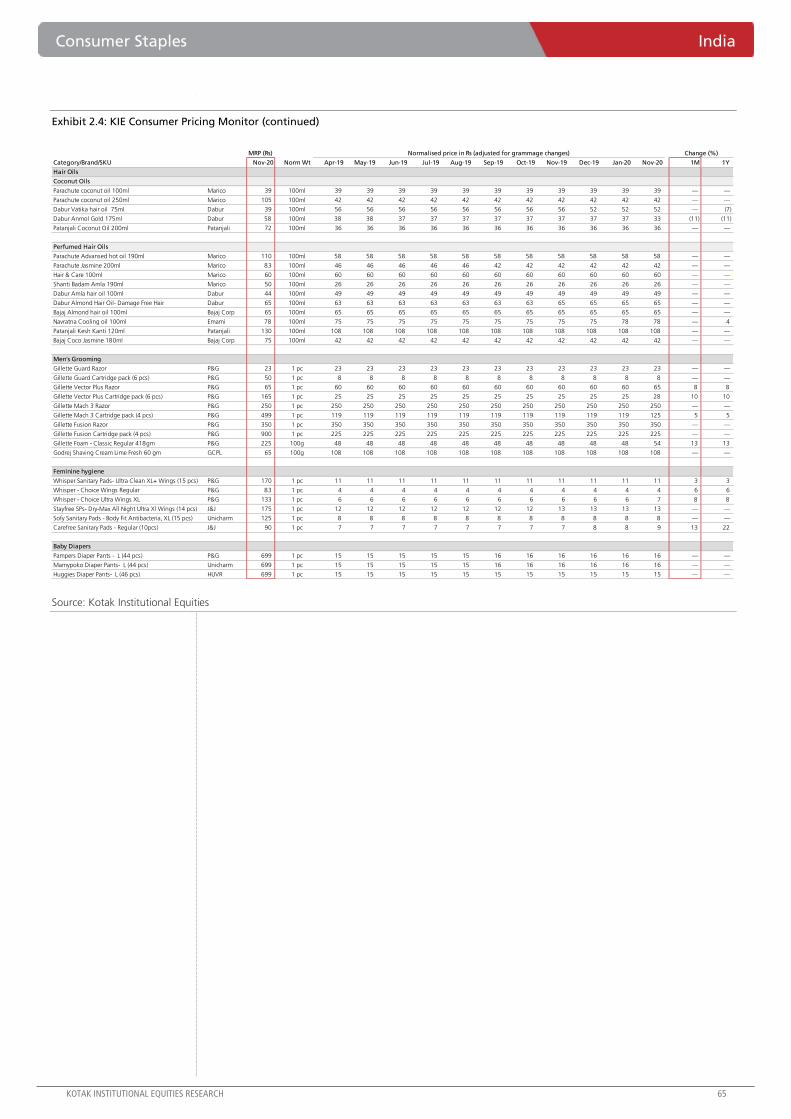

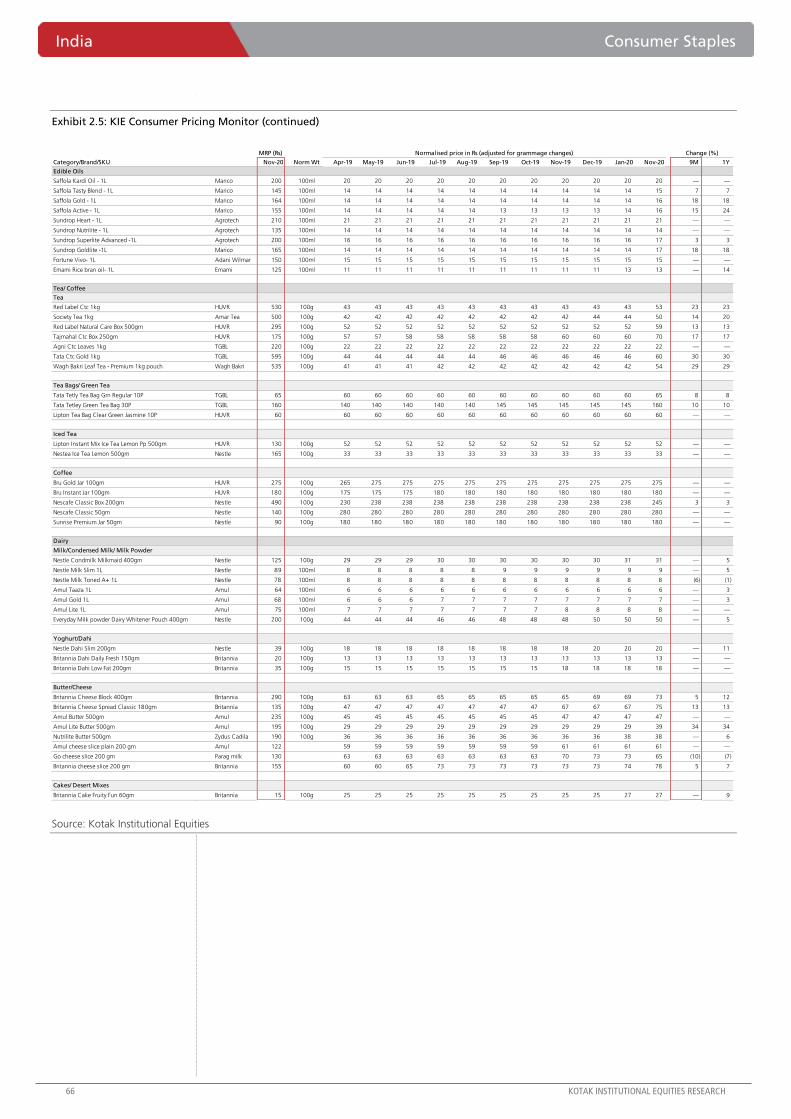

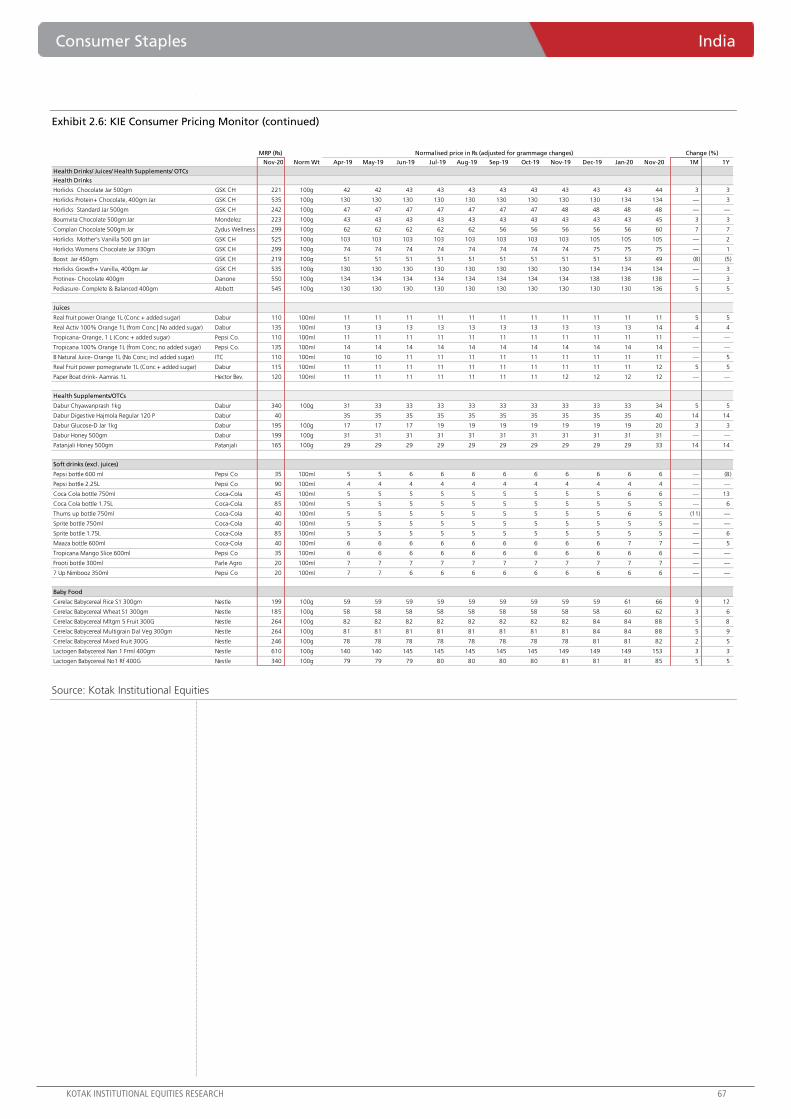

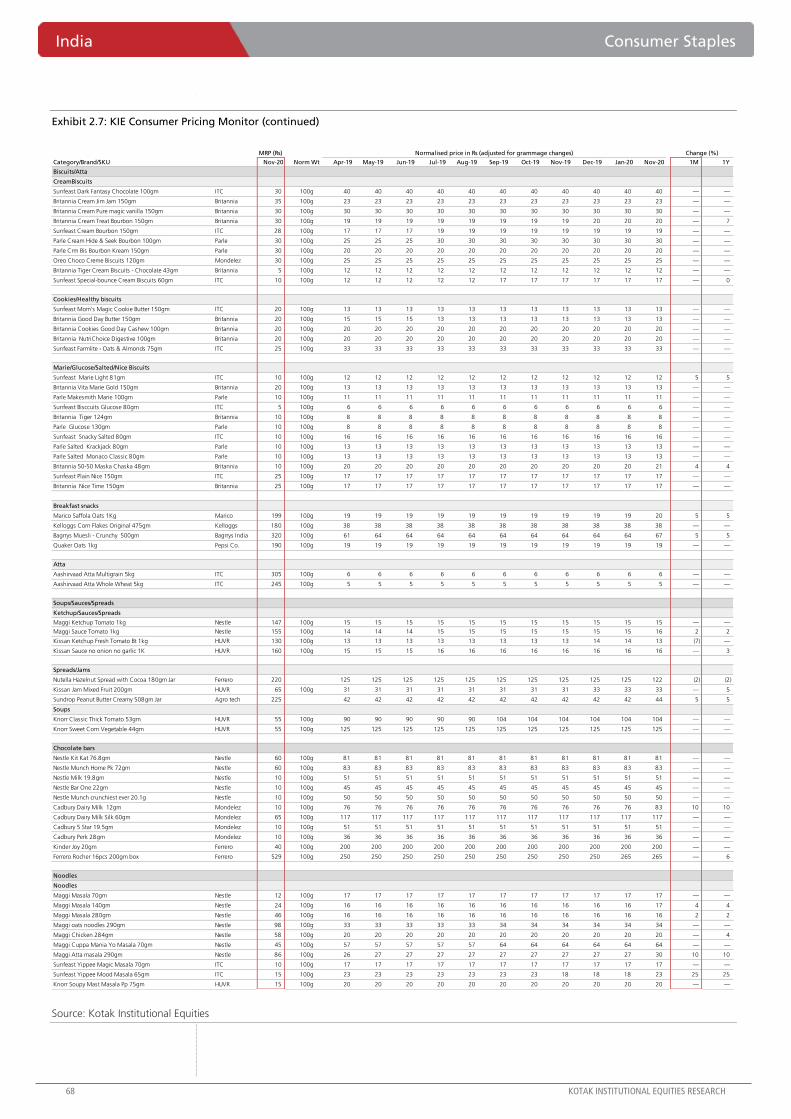

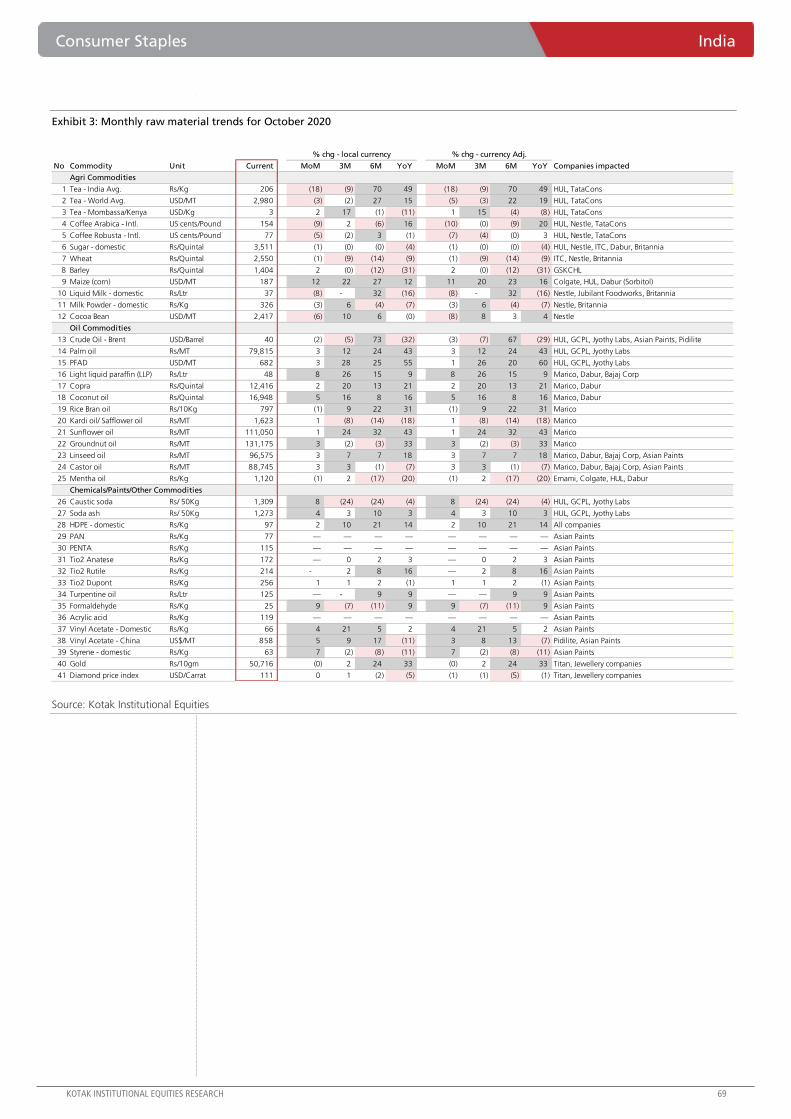

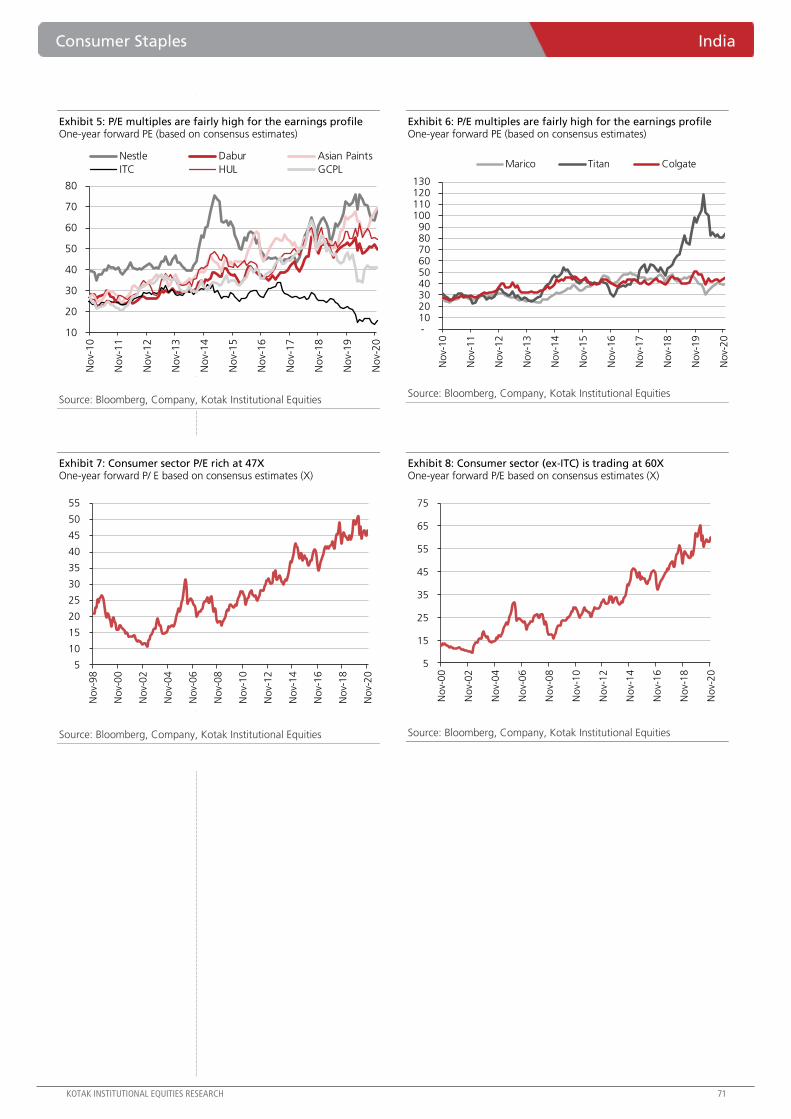

Consumer Staples: Month in review - Nov 2020

Pricing: Steep increase in tea, edible oil and soaps and reduction in

detergents

RM prices - Inflationary trends in palm oil, PFAD and monomers (paints); tea

prices ease slightly

Economy alerts

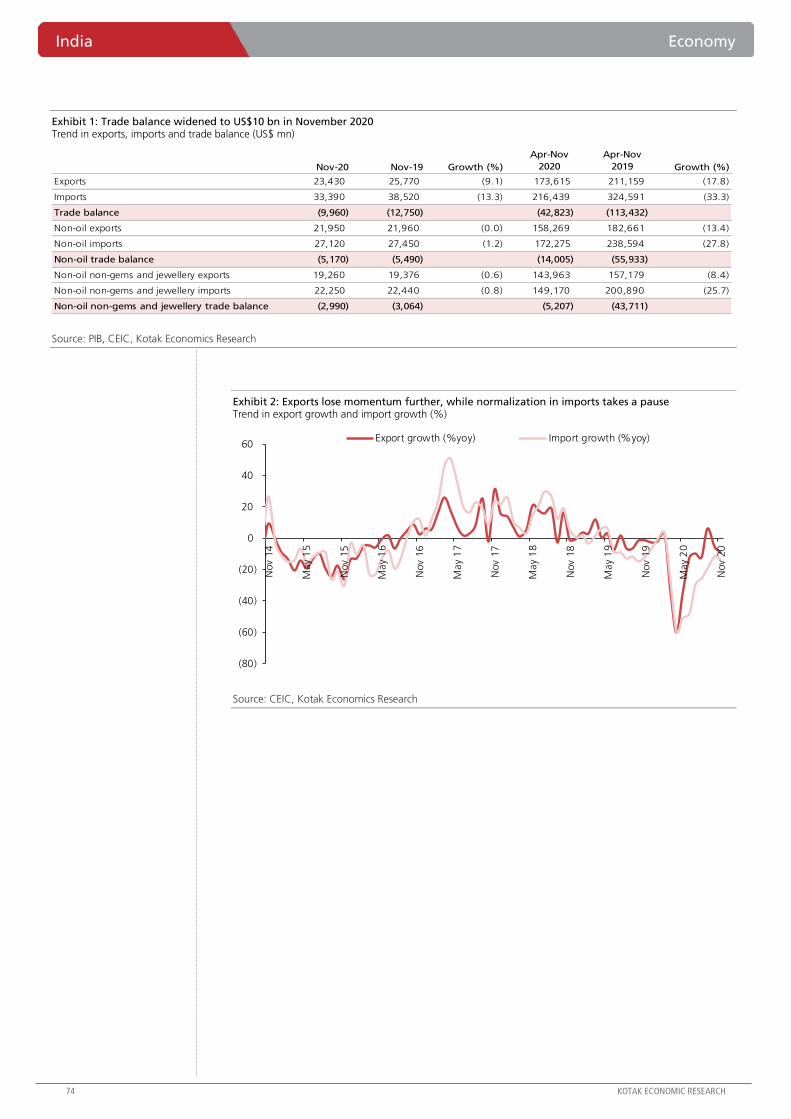

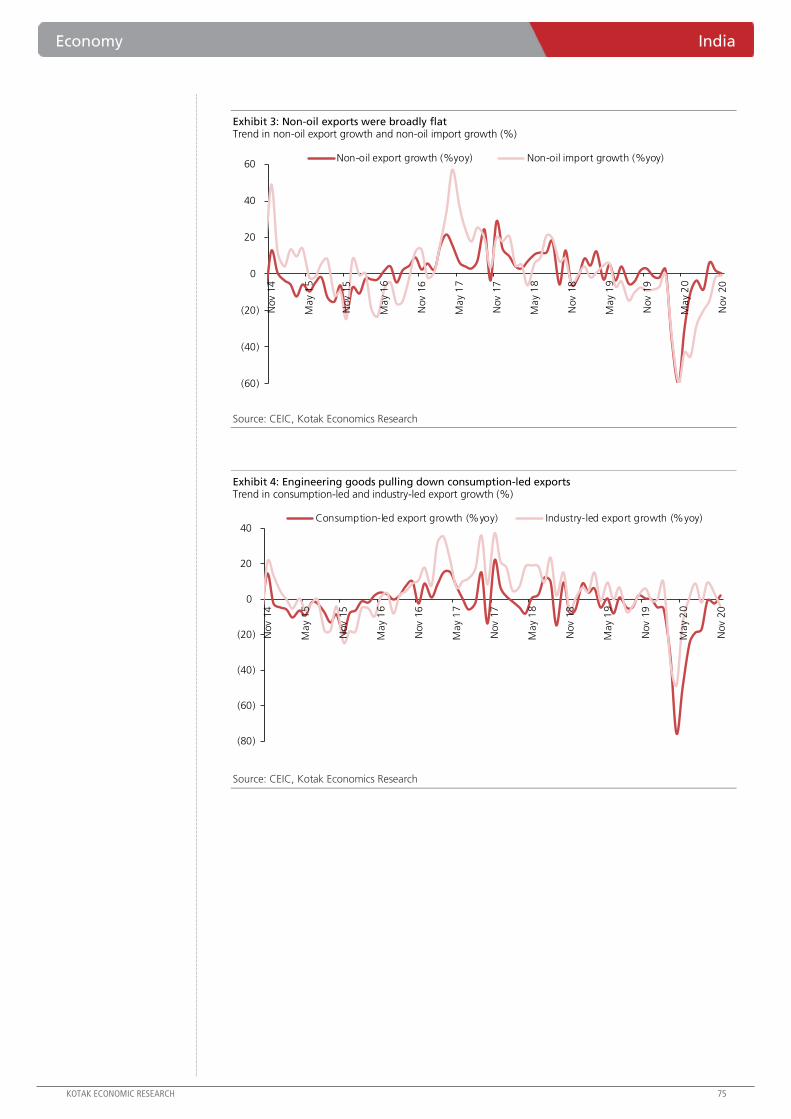

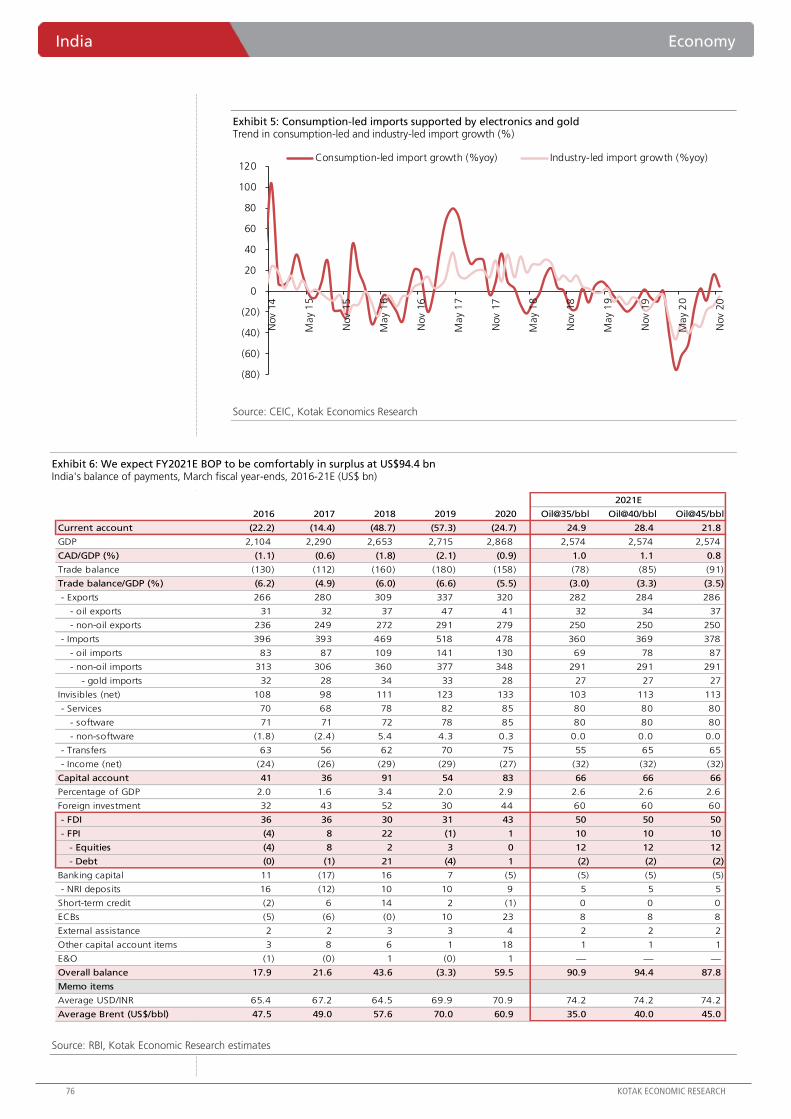

Economy: Trade deficit widens further

Exports lose further momentum after a second wave of infections

Normalization in import activity takes a pause in November

Expect FY2021E BOP to be comfortably in surplus; USD-INR to trade in the

72-75 range

INDIA DAILY December 3, 2020 India 2-Dec 1-day 1-mo 3-mo

Sensex 44,618 (0.1) 10.8 14.4

Nifty 13,114 0.0 11.0 13.8

Global/Regional indices

Dow Jones 29,884 0.2 8.7 5.6

Nasdaq Composite 12,349 (0.0) 10.7 7.8

FTSE 6,463 1.2 11.7 10.5

Nikkei 26,777 (0.1) 14.9 14.1

Hang Seng 26,623 0.3 6.8 6.5

KOSPI 2,683 0.3 14.5 12.0

Value traded – India

Cash (NSE+BSE) 721 730 251

Derivatives (NSE) 29,051 15,196 20,23

1

Deri. open interest 4,615 3,512 3,869

Forex/money market

Change, basis points

2-Dec 1-day 1-mo 3-mo

Rs/US$ 73.7 1 (76) 27

10yr govt bond, % 6.2 1 (1) (14)

Net investment (US$ mn)

1-Dec MTD CYTD

FIIs 481 - 6,546

MFs (249) - 727

Top movers

Change, %

Best performers 2-Dec 1-day 1-mo 3-mo

TTMT/A IN Equity 79 0.6 42.1 42.4

IIB IN Equity 897 0.2 38.8 42.0

APHS IN Equity 2,412 (2.1) 14.2 41.9

BJFIN IN Equity 8,802 0.6 53.3 38.5

TATA IN Equity 604 3.2 48.5 37.9

Worst performers

BHEL IN Equity 34 (0.7) 20.9 (15.5)

UPLL IN Equity 442 2.1 6.0 (15.3)

BHARTI IN Equity 485 1.1 6.7 (9.9)

RIL IN Equity 1,958 0.2 5.8 (7.3)

EDEL IN Equity 74 1.1 47.1 (7.2)

[email protected]: +91 22 6218 6427

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

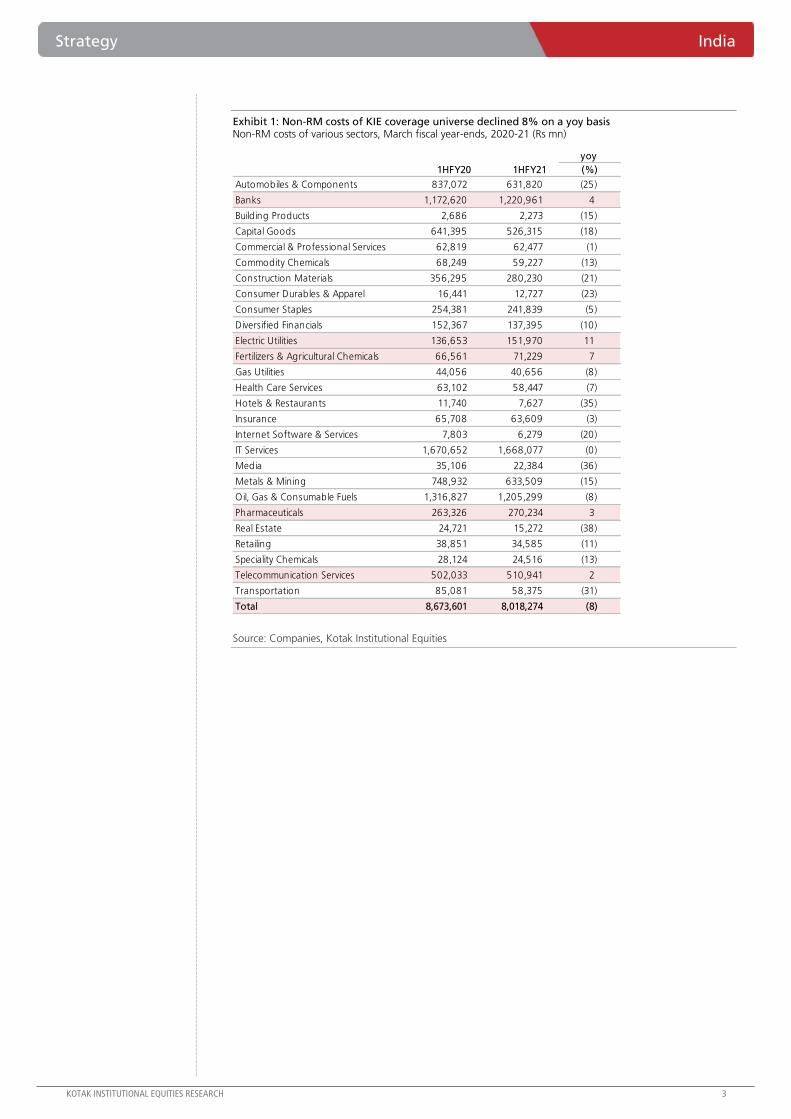

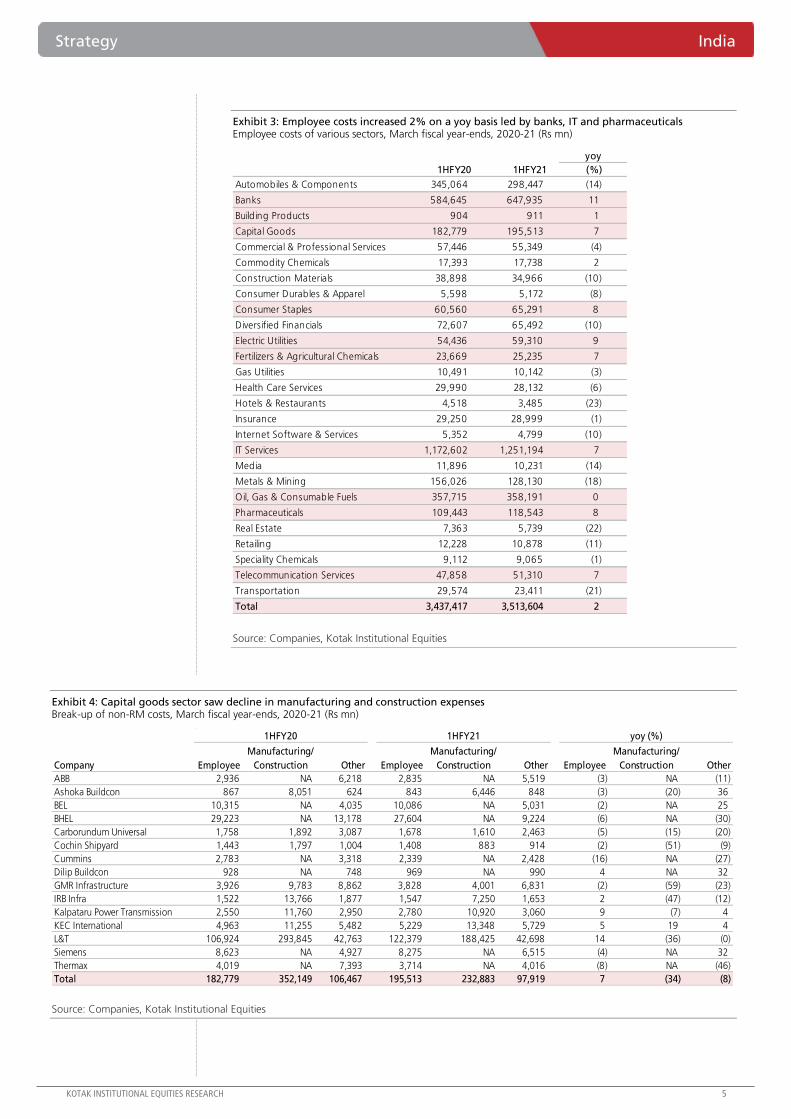

Good cost management in times of crisis

Non-RM costs of KIE coverage universe declined 7.6% on a yoy basis (see Exhibit 1) with many

sectors reporting a double-digit decline. The decline was entirely led by non-employee costs as

overall employee costs increased modestly despite sharp decline in employee costs in several

stressed sectors (see Exhibits 2-3). We would note that part of the non-RM and non-employee

costs are variable in nature (for example, freight and power & fuel costs in the case of

construction materials companies). Thus, we would be careful about reading too much or

extrapolating the cost reductions seen in 1HFY21.

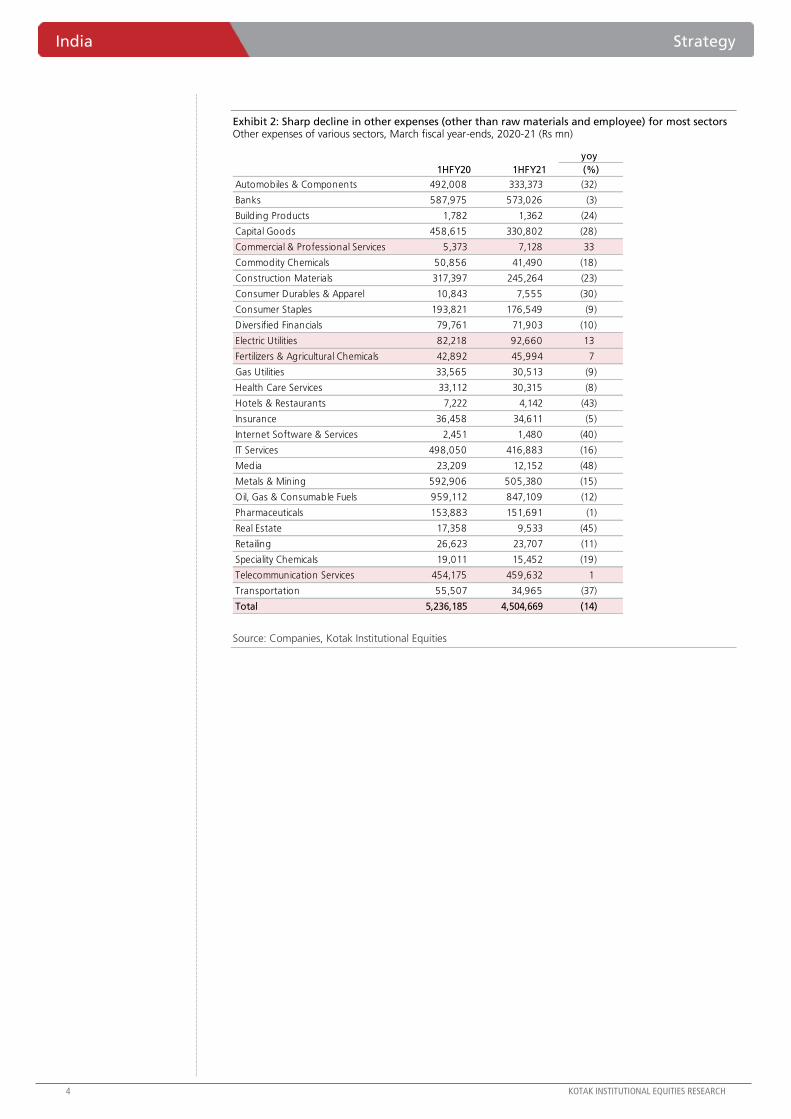

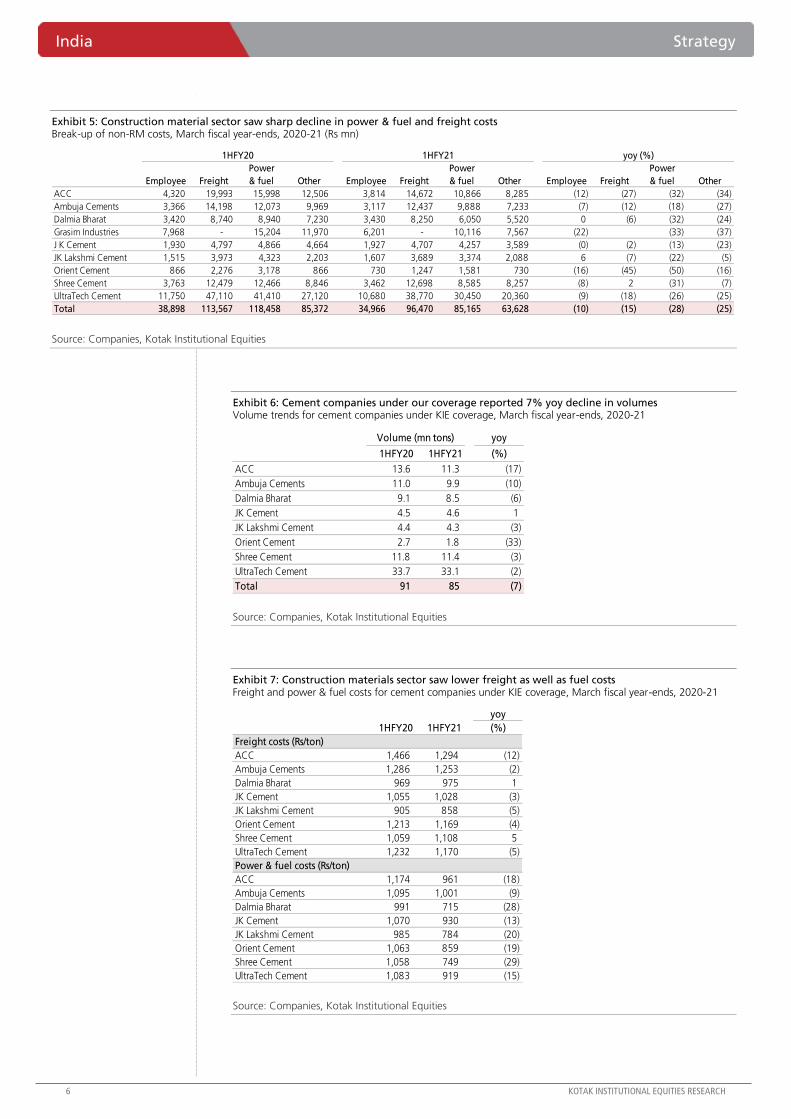

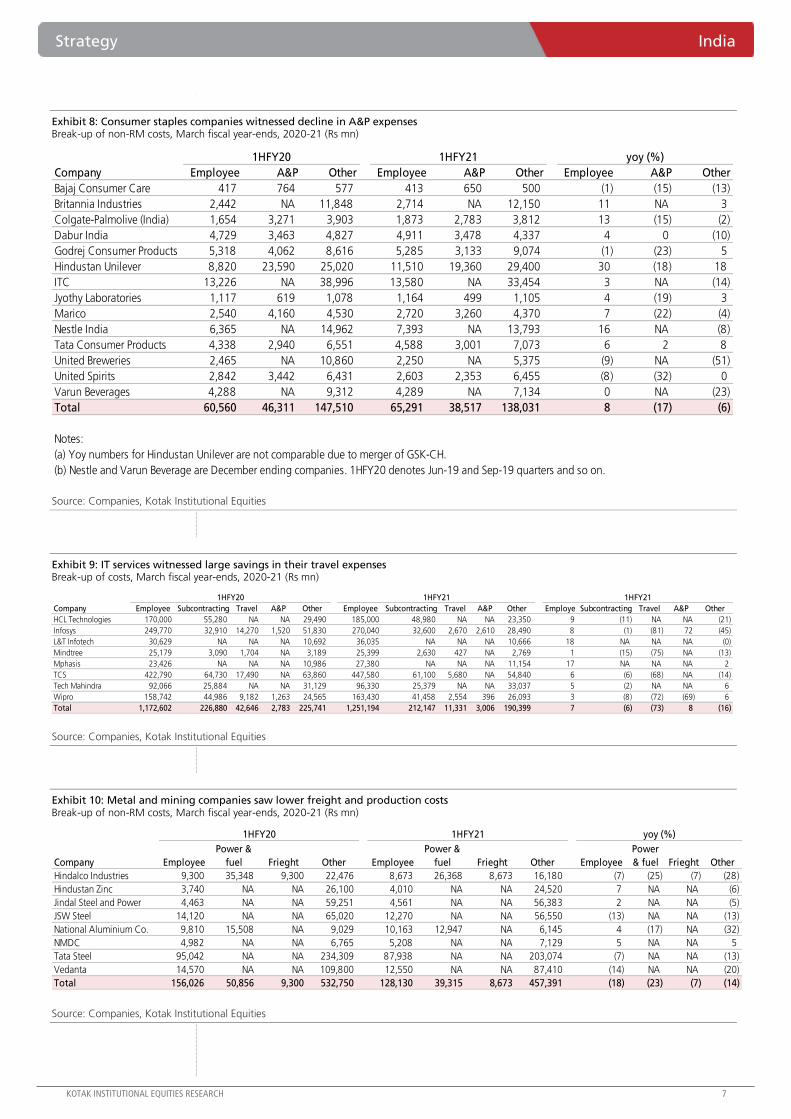

Various sectors used different levers to manage costs; some linked to lower volumes

A few sectors saw sharp decline in 1HFY21 costs. Capital goods saw lower manufacturing costs

(see Exhibit 4) but this reflects lower volumes too, construction materials saw lower freight as

well as fuel costs linked to lower volumes and per unit costs (see Exhibits 5-7), consumer staples

cut their A&P expenses (see Exhibit 8), IT services companies saved large amounts in travel

expenses (see Exhibit 9) while metal and mining companies also saw lower freight and

production costs (see Exhibit 10) on lower volumes.

Bulk of cost savings will go away as and when situation normalizes across sectors

In our view, the large ‘cuts’ seen in 1HFY21 may not sustain over FY2022-23 as operations

normalize across sectors. In some cases (capital goods, construction materials, metals & mining),

higher volumes would automatically result in higher non-RM costs. In others, employee costs

will increase sharply as companies restore employee levels to pre-Covid levels; this is true for

hotels & restaurants, real estate and retailing sectors, which saw job losses and wage cuts. Even

in the consumer staples sector, we would expect A&P expenses to increase unless companies

want to risk underinvesting in their brands; this seems unlikely.

Nature of products/services and markets material for retention of cost savings (if any)

The extent of benefit to companies in the form of higher profitability (from cost ‘savings’) will

depend on the nature of their products and markets even assuming they can retain a portion of

the cost savings. Based on a simple 2X2 matrix of product (nature of product: commodity, non-

commodity) and market (structure of market: low, high competition), we would expect (1) any

cost savings to be passed on to consumers in B2C businesses with high competition and in B2B

businesses in general (commodities, IT services sector where clients have deep knowledge of

vendor costs) and (2) some cost savings to be retained in B2C businesses with low competition

due to strong business moats (staples, alcohol, tobacco) or in B2C businesses with low

competition due to artificial factors (unregulated monopolies, cartelization).

Strategy Market

There is no getting away from costs. We believe the bulk of cost ‘savings’ seen in

1HFY21 will likely disappear over the next few quarters. 1HFY21 employee costs for

companies under our coverage increased 2% yoy despite sharp job and salary cuts in a

few stressed sectors; these jobs will return as and when capacity utilizations improve.

Also, we doubt even consumer companies can get away with lower A&P expenses as

continued investment in brands is important for long-term volume growth.

INDIA

DECEMBER 02, 2020

NEW RELEASE

BSE-30: 44,618

QUICK NUMBERS

1HFY21 non-RM

costs of KIE

coverage universe

declined 8% yoy

1HFY21 employee

costs of KIE

coverage universe

increased 2% yoy

1HFY21 other costs

of KIE coverage

universe declined

14% yoy

Sanjeev Prasad

Anindya Bhowmik

Sunita Baldawa

[email protected]: +91 22 6218 6427

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Exhibit 1: Non-RM costs of KIE coverage universe declined 8% on a yoy basis Non-RM costs of various sectors, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

1HFY20 1HFY21

Automobiles & Components 837,072 631,820 (25)

Banks 1,172,620 1,220,961 4

Building Products 2,686 2,273 (15)

Capital Goods 641,395 526,315 (18)

Commercial & Professional Services 62,819 62,477 (1)

Commodity Chemicals 68,249 59,227 (13)

Construction Materials 356,295 280,230 (21)

Consumer Durables & Apparel 16,441 12,727 (23)

Consumer Staples 254,381 241,839 (5)

Diversified Financials 152,367 137,395 (10)

Electric Utilities 136,653 151,970 11

Fertilizers & Agricultural Chemicals 66,561 71,229 7

Gas Utilities 44,056 40,656 (8)

Health Care Services 63,102 58,447 (7)

Hotels & Restaurants 11,740 7,627 (35)

Insurance 65,708 63,609 (3)

Internet Software & Services 7,803 6,279 (20)

IT Services 1,670,652 1,668,077 (0)

Media 35,106 22,384 (36)

Metals & Mining 748,932 633,509 (15)

Oil, Gas & Consumable Fuels 1,316,827 1,205,299 (8)

Pharmaceuticals 263,326 270,234 3

Real Estate 24,721 15,272 (38)

Retailing 38,851 34,585 (11)

Speciality Chemicals 28,124 24,516 (13)

Telecommunication Services 502,033 510,941 2

Transportation 85,081 58,375 (31)

Total 8,673,601 8,018,274 (8)

yoy

(%)

India Strategy

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2: Sharp decline in other expenses (other than raw materials and employee) for most sectors Other expenses of various sectors, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

1HFY20 1HFY21

Automobiles & Components 492,008 333,373 (32)

Banks 587,975 573,026 (3)

Building Products 1,782 1,362 (24)

Capital Goods 458,615 330,802 (28)

Commercial & Professional Services 5,373 7,128 33

Commodity Chemicals 50,856 41,490 (18)

Construction Materials 317,397 245,264 (23)

Consumer Durables & Apparel 10,843 7,555 (30)

Consumer Staples 193,821 176,549 (9)

Diversified Financials 79,761 71,903 (10)

Electric Utilities 82,218 92,660 13

Fertilizers & Agricultural Chemicals 42,892 45,994 7

Gas Utilities 33,565 30,513 (9)

Health Care Services 33,112 30,315 (8)

Hotels & Restaurants 7,222 4,142 (43)

Insurance 36,458 34,611 (5)

Internet Software & Services 2,451 1,480 (40)

IT Services 498,050 416,883 (16)

Media 23,209 12,152 (48)

Metals & Mining 592,906 505,380 (15)

Oil, Gas & Consumable Fuels 959,112 847,109 (12)

Pharmaceuticals 153,883 151,691 (1)

Real Estate 17,358 9,533 (45)

Retailing 26,623 23,707 (11)

Speciality Chemicals 19,011 15,452 (19)

Telecommunication Services 454,175 459,632 1

Transportation 55,507 34,965 (37)

Total 5,236,185 4,504,669 (14)

yoy

(%)

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Exhibit 3: Employee costs increased 2% on a yoy basis led by banks, IT and pharmaceuticals Employee costs of various sectors, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

Exhibit 4: Capital goods sector saw decline in manufacturing and construction expenses Break-up of non-RM costs, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

1HFY20 1HFY21

Automobiles & Components 345,064 298,447 (14)

Banks 584,645 647,935 11

Building Products 904 911 1

Capital Goods 182,779 195,513 7

Commercial & Professional Services 57,446 55,349 (4)

Commodity Chemicals 17,393 17,738 2

Construction Materials 38,898 34,966 (10)

Consumer Durables & Apparel 5,598 5,172 (8)

Consumer Staples 60,560 65,291 8

Diversified Financials 72,607 65,492 (10)

Electric Utilities 54,436 59,310 9

Fertilizers & Agricultural Chemicals 23,669 25,235 7

Gas Utilities 10,491 10,142 (3)

Health Care Services 29,990 28,132 (6)

Hotels & Restaurants 4,518 3,485 (23)

Insurance 29,250 28,999 (1)

Internet Software & Services 5,352 4,799 (10)

IT Services 1,172,602 1,251,194 7

Media 11,896 10,231 (14)

Metals & Mining 156,026 128,130 (18)

Oil, Gas & Consumable Fuels 357,715 358,191 0

Pharmaceuticals 109,443 118,543 8

Real Estate 7,363 5,739 (22)

Retailing 12,228 10,878 (11)

Speciality Chemicals 9,112 9,065 (1)

Telecommunication Services 47,858 51,310 7

Transportation 29,574 23,411 (21)

Total 3,437,417 3,513,604 2

yoy

(%)

Manufacturing/ Manufacturing/ Manufacturing/

Company Employee Construction Other Employee Construction Other Employee Construction Other

ABB 2,936 NA 6,218 2,835 NA 5,519 (3) NA (11)

Ashoka Buildcon 867 8,051 624 843 6,446 848 (3) (20) 36

BEL 10,315 NA 4,035 10,086 NA 5,031 (2) NA 25

BHEL 29,223 NA 13,178 27,604 NA 9,224 (6) NA (30)

Carborundum Universal 1,758 1,892 3,087 1,678 1,610 2,463 (5) (15) (20)

Cochin Shipyard 1,443 1,797 1,004 1,408 883 914 (2) (51) (9)

Cummins 2,783 NA 3,318 2,339 NA 2,428 (16) NA (27)

Dilip Buildcon 928 NA 748 969 NA 990 4 NA 32

GMR Infrastructure 3,926 9,783 8,862 3,828 4,001 6,831 (2) (59) (23)

IRB Infra 1,522 13,766 1,877 1,547 7,250 1,653 2 (47) (12)

Kalpataru Power Transmission 2,550 11,760 2,950 2,780 10,920 3,060 9 (7) 4

KEC International 4,963 11,255 5,482 5,229 13,348 5,729 5 19 4

L&T 106,924 293,845 42,763 122,379 188,425 42,698 14 (36) (0)

Siemens 8,623 NA 4,927 8,275 NA 6,515 (4) NA 32

Thermax 4,019 NA 7,393 3,714 NA 4,016 (8) NA (46)

Total 182,779 352,149 106,467 195,513 232,883 97,919 7 (34) (8)

1HFY20 1HFY21 yoy (%)

India Strategy

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 5: Construction material sector saw sharp decline in power & fuel and freight costs Break-up of non-RM costs, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

Exhibit 6: Cement companies under our coverage reported 7% yoy decline in volumes Volume trends for cement companies under KIE coverage, March fiscal year-ends, 2020-21

Source: Companies, Kotak Institutional Equities

Exhibit 7: Construction materials sector saw lower freight as well as fuel costs Freight and power & fuel costs for cement companies under KIE coverage, March fiscal year-ends, 2020-21

Source: Companies, Kotak Institutional Equities

Power Power Power

Employee Freight & fuel Other Employee Freight & fuel Other Employee Freight & fuel Other

ACC 4,320 19,993 15,998 12,506 3,814 14,672 10,866 8,285 (12) (27) (32) (34)

Ambuja Cements 3,366 14,198 12,073 9,969 3,117 12,437 9,888 7,233 (7) (12) (18) (27)

Dalmia Bharat 3,420 8,740 8,940 7,230 3,430 8,250 6,050 5,520 0 (6) (32) (24)

Grasim Industries 7,968 - 15,204 11,970 6,201 - 10,116 7,567 (22) (33) (37)

J K Cement 1,930 4,797 4,866 4,664 1,927 4,707 4,257 3,589 (0) (2) (13) (23)

JK Lakshmi Cement 1,515 3,973 4,323 2,203 1,607 3,689 3,374 2,088 6 (7) (22) (5)

Orient Cement 866 2,276 3,178 866 730 1,247 1,581 730 (16) (45) (50) (16)

Shree Cement 3,763 12,479 12,466 8,846 3,462 12,698 8,585 8,257 (8) 2 (31) (7)

UltraTech Cement 11,750 47,110 41,410 27,120 10,680 38,770 30,450 20,360 (9) (18) (26) (25)

Total 38,898 113,567 118,458 85,372 34,966 96,470 85,165 63,628 (10) (15) (28) (25)

1HFY20 1HFY21 yoy (%)

yoy

1HFY20 1HFY21 (%)

ACC 13.6 11.3 (17)

Ambuja Cements 11.0 9.9 (10)

Dalmia Bharat 9.1 8.5 (6)

JK Cement 4.5 4.6 1

JK Lakshmi Cement 4.4 4.3 (3)

Orient Cement 2.7 1.8 (33)

Shree Cement 11.8 11.4 (3)

UltraTech Cement 33.7 33.1 (2)

Total 91 85 (7)

Volume (mn tons)

yoy

1HFY20 1HFY21 (%)

Freight costs (Rs/ton)

ACC 1,466 1,294 (12)

Ambuja Cements 1,286 1,253 (2)

Dalmia Bharat 969 975 1

JK Cement 1,055 1,028 (3)

JK Lakshmi Cement 905 858 (5)

Orient Cement 1,213 1,169 (4)

Shree Cement 1,059 1,108 5

UltraTech Cement 1,232 1,170 (5)

Power & fuel costs (Rs/ton)

ACC 1,174 961 (18)

Ambuja Cements 1,095 1,001 (9)

Dalmia Bharat 991 715 (28)

JK Cement 1,070 930 (13)

JK Lakshmi Cement 985 784 (20)

Orient Cement 1,063 859 (19)

Shree Cement 1,058 749 (29)

UltraTech Cement 1,083 919 (15)

Strategy India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Exhibit 8: Consumer staples companies witnessed decline in A&P expenses Break-up of non-RM costs, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

Exhibit 9: IT services witnessed large savings in their travel expenses Break-up of costs, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

Exhibit 10: Metal and mining companies saw lower freight and production costs Break-up of non-RM costs, March fiscal year-ends, 2020-21 (Rs mn)

Source: Companies, Kotak Institutional Equities

Company Employee A&P Other Employee A&P Other Employee A&P Other

Bajaj Consumer Care 417 764 577 413 650 500 (1) (15) (13)

Britannia Industries 2,442 NA 11,848 2,714 NA 12,150 11 NA 3

Colgate-Palmolive (India) 1,654 3,271 3,903 1,873 2,783 3,812 13 (15) (2)

Dabur India 4,729 3,463 4,827 4,911 3,478 4,337 4 0 (10)

Godrej Consumer Products 5,318 4,062 8,616 5,285 3,133 9,074 (1) (23) 5

Hindustan Unilever 8,820 23,590 25,020 11,510 19,360 29,400 30 (18) 18

ITC 13,226 NA 38,996 13,580 NA 33,454 3 NA (14)

Jyothy Laboratories 1,117 619 1,078 1,164 499 1,105 4 (19) 3

Marico 2,540 4,160 4,530 2,720 3,260 4,370 7 (22) (4)

Nestle India 6,365 NA 14,962 7,393 NA 13,793 16 NA (8)

Tata Consumer Products 4,338 2,940 6,551 4,588 3,001 7,073 6 2 8

United Breweries 2,465 NA 10,860 2,250 NA 5,375 (9) NA (51)

United Spirits 2,842 3,442 6,431 2,603 2,353 6,455 (8) (32) 0

Varun Beverages 4,288 NA 9,312 4,289 NA 7,134 0 NA (23)

Total 60,560 46,311 147,510 65,291 38,517 138,031 8 (17) (6)

Notes:

(a) Yoy numbers for Hindustan Unilever are not comparable due to merger of GSK-CH.

(b) Nestle and Varun Beverage are December ending companies. 1HFY20 denotes Jun-19 and Sep-19 quarters and so on.

1HFY20 1HFY21 yoy (%)

Company Employee Subcontracting Travel A&P Other Employee Subcontracting Travel A&P Other Employe Subcontracting Travel A&P Other

HCL Technologies 170,000 55,280 NA NA 29,490 185,000 48,980 NA NA 23,350 9 (11) NA NA (21)

Infosys 249,770 32,910 14,270 1,520 51,830 270,040 32,600 2,670 2,610 28,490 8 (1) (81) 72 (45)

L&T Infotech 30,629 NA NA NA 10,692 36,035 NA NA NA 10,666 18 NA NA NA (0)

Mindtree 25,179 3,090 1,704 NA 3,189 25,399 2,630 427 NA 2,769 1 (15) (75) NA (13)

Mphasis 23,426 NA NA NA 10,986 27,380 NA NA NA 11,154 17 NA NA NA 2

TCS 422,790 64,730 17,490 NA 63,860 447,580 61,100 5,680 NA 54,840 6 (6) (68) NA (14)

Tech Mahindra 92,066 25,884 NA NA 31,129 96,330 25,379 NA NA 33,037 5 (2) NA NA 6

Wipro 158,742 44,986 9,182 1,263 24,565 163,430 41,458 2,554 396 26,093 3 (8) (72) (69) 6

Total 1,172,602 226,880 42,646 2,783 225,741 1,251,194 212,147 11,331 3,006 190,399 7 (6) (73) 8 (16)

1HFY20 1HFY21 1HFY21

Company Employee

Power &

fuel Frieght Other Employee

Power &

fuel Frieght Other Employee

Power

& fuel Frieght Other

Hindalco Industries 9,300 35,348 9,300 22,476 8,673 26,368 8,673 16,180 (7) (25) (7) (28)

Hindustan Zinc 3,740 NA NA 26,100 4,010 NA NA 24,520 7 NA NA (6)

Jindal Steel and Power 4,463 NA NA 59,251 4,561 NA NA 56,383 2 NA NA (5)

JSW Steel 14,120 NA NA 65,020 12,270 NA NA 56,550 (13) NA NA (13)

National Aluminium Co. 9,810 15,508 NA 9,029 10,163 12,947 NA 6,145 4 (17) NA (32)

NMDC 4,982 NA NA 6,765 5,208 NA NA 7,129 5 NA NA 5

Tata Steel 95,042 NA NA 234,309 87,938 NA NA 203,074 (7) NA NA (13)

Vedanta 14,570 NA NA 109,800 12,550 NA NA 87,410 (14) NA NA (20)

Total 156,026 50,856 9,300 532,750 128,130 39,315 8,673 457,391 (18) (23) (7) (14)

1HFY20 1HFY21 yoy (%)

Company Report

For Private Circulation Only. In the US, this document may only be distributed to QIBs (qualified institutional buyers) as defined under rule 144A of the Securities Act of 1933. This document is not for public distribution

and has been furnished to you solely for your information and may not be reproduced or redistributed to any other person. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

Metals & Mining

Sector

Beverage cans: a structural and sustainable growth story. Aluminum beverage

cans have shown demand resilience during Covid-19 as in past crises. Aluminum’s

infinite recyclability makes it the most sustainable alternative to plastic – the shift

from plastics and a growing market offer a structural impetus to can demand. Supply

remains constrained and should keep margins of can sheet producers elevated.

Secular growth drivers and a high ESG score accord market leader Novelis a deserving

premium multiple. We raise our Fair Value for Hindalco to Rs330 (from Rs300).

Beverage packaging – aluminum eating into plastic dominance

The packaging material landscape is changing. Cans are beginning to threaten plastic’s

dominance, with ~70% share in new brand/product launches in 2019 versus 32% five years

ago. Plastics (or PET – polyethylene terephthalate) dominate the global beverage packaging

industry with a 38% market share led by its cost effectiveness and flexibility. Cans (aluminum)

with 28% share take up the second spot followed by glass and cartons.

Can sheet demand enjoys structural drivers with the war on plastic just warming up

The market share shift from plastics to cans in the past few years should continue in the

current decade. The war on plastic is just in its initial phase given the growing backlash against

plastic-led pollution. Aluminum, being infinitely recyclable, is the most sustainable alternative.

ESG focus is increasing among all stakeholders and is unlikely to remain discretionary for long.

Cans should see 4-6% demand CAGR over CY2019-29E versus industry CAGR of 2-3%.

Deficit market to keep margins high; scrap benefits to stay higher for longer

Hot mill capacity is the key bottleneck in the can supply chain. Hot mill is the most capital

intensive in the entire supply chain and growth pipeline is lean. North American markets have

been facing a deficit since (1) can sheet major Arconic exited the market and (2) hot mill

supply began to be diverted from can sheets to higher-margin auto sheets. A persistent deficit

in such major markets is likely to keep conversion margins strong. The scrap market is likely to

remain oversupplied in western economies as China’s restrictive scrap import policy is unlikely

to reverse. A surplus scrap market would keep scrap spreads elevated.

Novelis has structural growth drivers and high ESG score, time to change the commodity lens

Novelis is a market leader in can sheets with a 35% global market share in an oligopoly

market. Can sheets form 58% of Novelis shipments and ~40% HNDL FY2022E EBITDA. ESG

metrics are increasingly dominating investment discussions and high scores warrant a premium

multiple. With 21% EPS CAGR over FY2022-23E, 12-15% FCF yield along with strong ESG

positioning, Hindalco (HNDL) offers a strong re-rating case. We increase our Fair Value to

Rs330/share (from Rs300) on SoTP (adjusted for pension) September 2022E at 7X EV/EBITDA

(6.5X earlier) to Novelis division factoring the structural growth drivers.

ATTRACTIVE

December 02, 2020

THEME

BSE-30: 44,618

Sumangal Nevatia

Prayatn Mahajan

[email protected]: +91 22 6218 6427

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

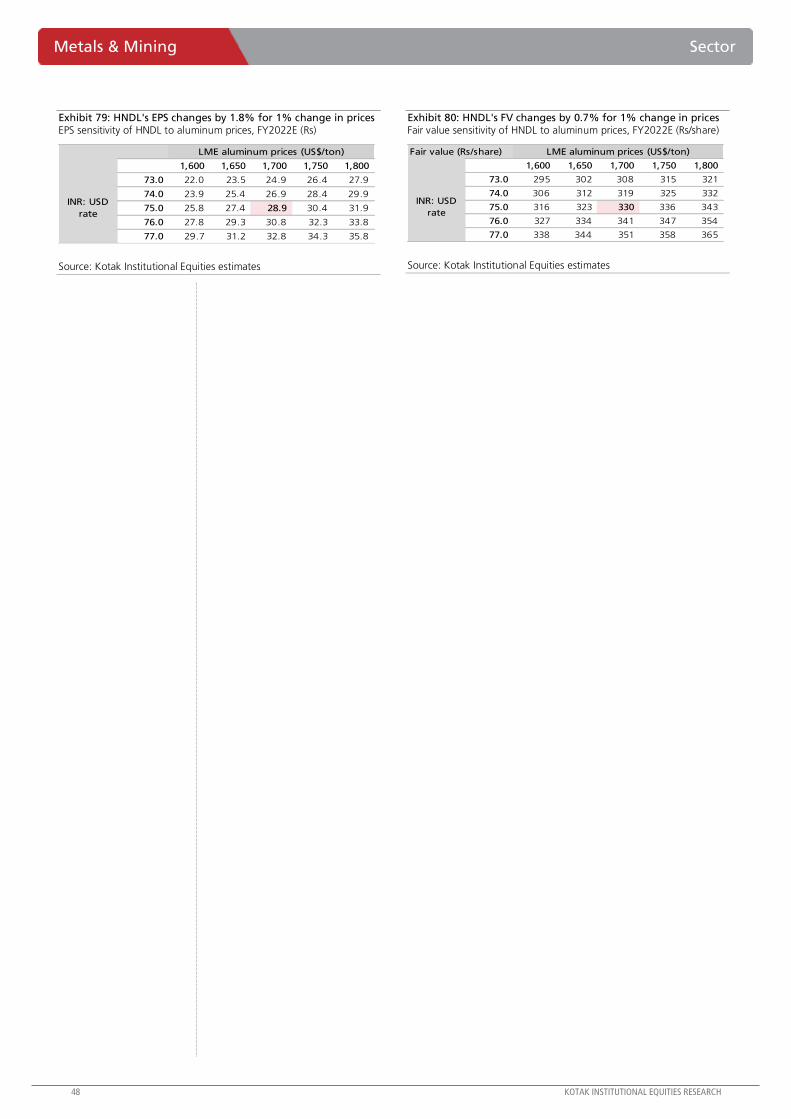

Sector Metals & Mining

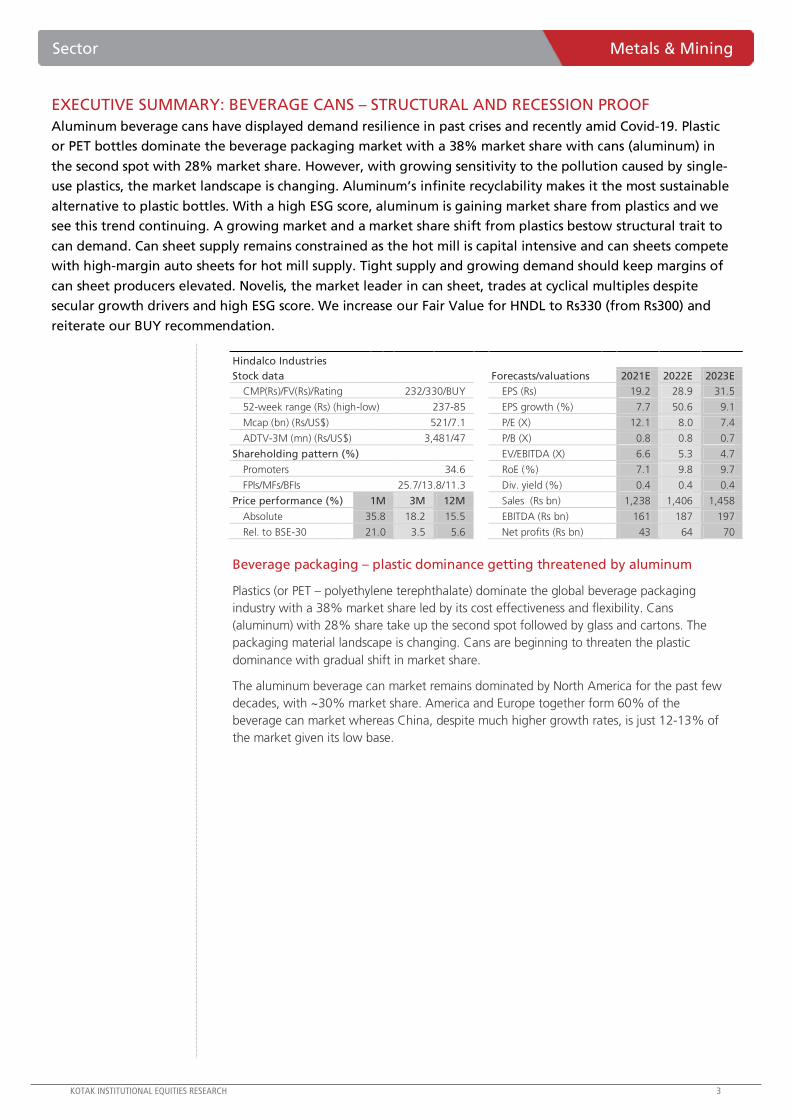

EXECUTIVE SUMMARY: BEVERAGE CANS – STRUCTURAL AND RECESSION PROOF

Aluminum beverage cans have displayed demand resilience in past crises and recently amid Covid-19. Plastic

or PET bottles dominate the beverage packaging market with a 38% market share with cans (aluminum) in

the second spot with 28% market share. However, with growing sensitivity to the pollution caused by single-

use plastics, the market landscape is changing. Aluminum’s infinite recyclability makes it the most sustainable

alternative to plastic bottles. With a high ESG score, aluminum is gaining market share from plastics and we

see this trend continuing. A growing market and a market share shift from plastics bestow structural trait to

can demand. Can sheet supply remains constrained as the hot mill is capital intensive and can sheets compete

with high-margin auto sheets for hot mill supply. Tight supply and growing demand should keep margins of

can sheet producers elevated. Novelis, the market leader in can sheet, trades at cyclical multiples despite

secular growth drivers and high ESG score. We increase our Fair Value for HNDL to Rs330 (from Rs300) and

reiterate our BUY recommendation.

Hindalco Industries

Stock data

Forecasts/valuations

2021E 2022E 2023E

CMP(Rs)/FV(Rs)/Rating 232/330/BUY

EPS (Rs) 19.2 28.9 31.5

52-week range (Rs) (high-low) 237-85

EPS growth (%) 7.7 50.6 9.1

Mcap (bn) (Rs/US$) 521/7.1

P/E (X) 12.1 8.0 7.4

ADTV-3M (mn) (Rs/US$) 3,481/47

P/B (X) 0.8 0.8 0.7

Shareholding pattern (%)

EV/EBITDA (X) 6.6 5.3 4.7

Promoters 34.6

RoE (%) 7.1 9.8 9.7

FPIs/MFs/BFIs 25.7/13.8/11.3

Div. yield (%) 0.4 0.4 0.4

Price performance (%) 1M 3M 12M

Sales (Rs bn) 1,238 1,406 1,458

Absolute 35.8 18.2 15.5

EBITDA (Rs bn) 161 187 197

Rel. to BSE-30 21.0 3.5 5.6

Net profits (Rs bn) 43 64 70

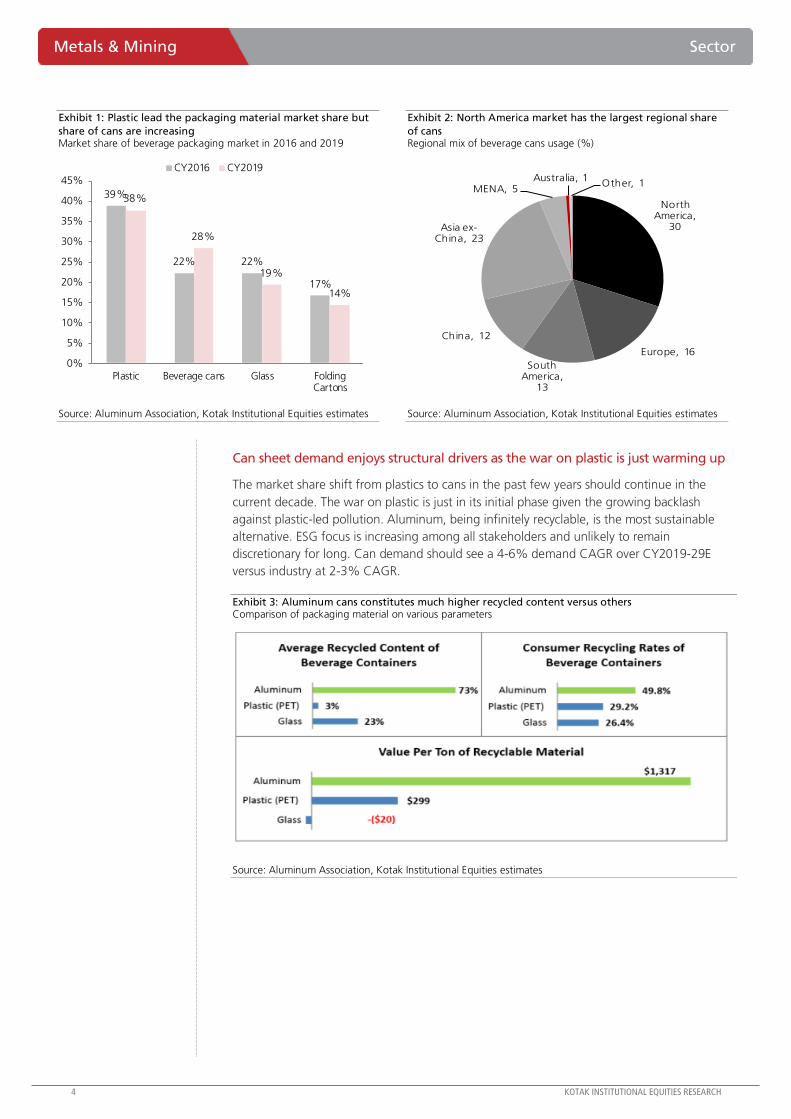

Beverage packaging – plastic dominance getting threatened by aluminum

Plastics (or PET – polyethylene terephthalate) dominate the global beverage packaging

industry with a 38% market share led by its cost effectiveness and flexibility. Cans

(aluminum) with 28% share take up the second spot followed by glass and cartons. The

packaging material landscape is changing. Cans are beginning to threaten the plastic

dominance with gradual shift in market share.

The aluminum beverage can market remains dominated by North America for the past few

decades, with ~30% market share. America and Europe together form 60% of the

beverage can market whereas China, despite much higher growth rates, is just 12-13% of

the market given its low base.

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

Exhibit 1: Plastic lead the packaging material market share but

share of cans are increasing Market share of beverage packaging market in 2016 and 2019

39%

22% 22%

17%

38%

28%

19%

14%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Plastic Beverage cans Glass FoldingCartons

CY2016 CY2019

Source: Aluminum Association, Kotak Institutional Equities estimates

Exhibit 2: North America market has the largest regional share

of cans Regional mix of beverage cans usage (%)

North America,

30

Europe, 16

South America,

13

China, 12

Asia ex-China, 23

MENA, 5 Australia, 1

Other, 1

Source: Aluminum Association, Kotak Institutional Equities estimates

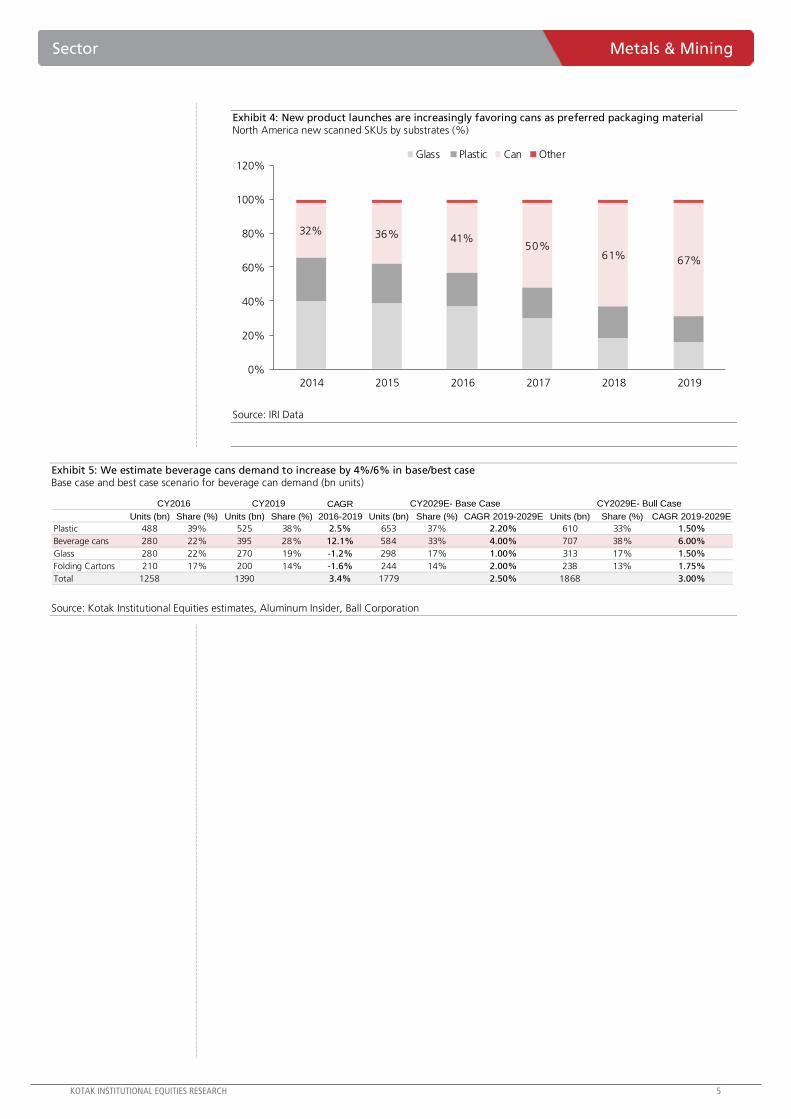

Can sheet demand enjoys structural drivers as the war on plastic is just warming up

The market share shift from plastics to cans in the past few years should continue in the

current decade. The war on plastic is just in its initial phase given the growing backlash

against plastic-led pollution. Aluminum, being infinitely recyclable, is the most sustainable

alternative. ESG focus is increasing among all stakeholders and unlikely to remain

discretionary for long. Can demand should see a 4-6% demand CAGR over CY2019-29E

versus industry at 2-3% CAGR.

Exhibit 3: Aluminum cans constitutes much higher recycled content versus others Comparison of packaging material on various parameters

Source: Aluminum Association, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Sector Metals & Mining

Exhibit 4: New product launches are increasingly favoring cans as preferred packaging material North America new scanned SKUs by substrates (%)

32% 36% 41%50%

61% 67%

0%

20%

40%

60%

80%

100%

120%

2014 2015 2016 2017 2018 2019

Glass Plastic Can Other

Source: IRI Data

Exhibit 5: We estimate beverage cans demand to increase by 4%/6% in base/best case Base case and best case scenario for beverage can demand (bn units)

CAGR

Units (bn) Share (%) Units (bn) Share (%) 2016-2019 Units (bn) Share (%) CAGR 2019-2029E Units (bn) Share (%) CAGR 2019-2029E

Plastic 488 39% 525 38% 2.5% 653 37% 2.20% 610 33% 1.50%

Beverage cans 280 22% 395 28% 12.1% 584 33% 4.00% 707 38% 6.00%

Glass 280 22% 270 19% -1.2% 298 17% 1.00% 313 17% 1.50%

Folding Cartons 210 17% 200 14% -1.6% 244 14% 2.00% 238 13% 1.75%

Total 1258 1390 3.4% 1779 2.50% 1868 3.00%

CY2029E- Base Case CY2029E- Bull CaseCY2019CY2016

Source: Kotak Institutional Equities estimates, Aluminum Insider, Ball Corporation

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

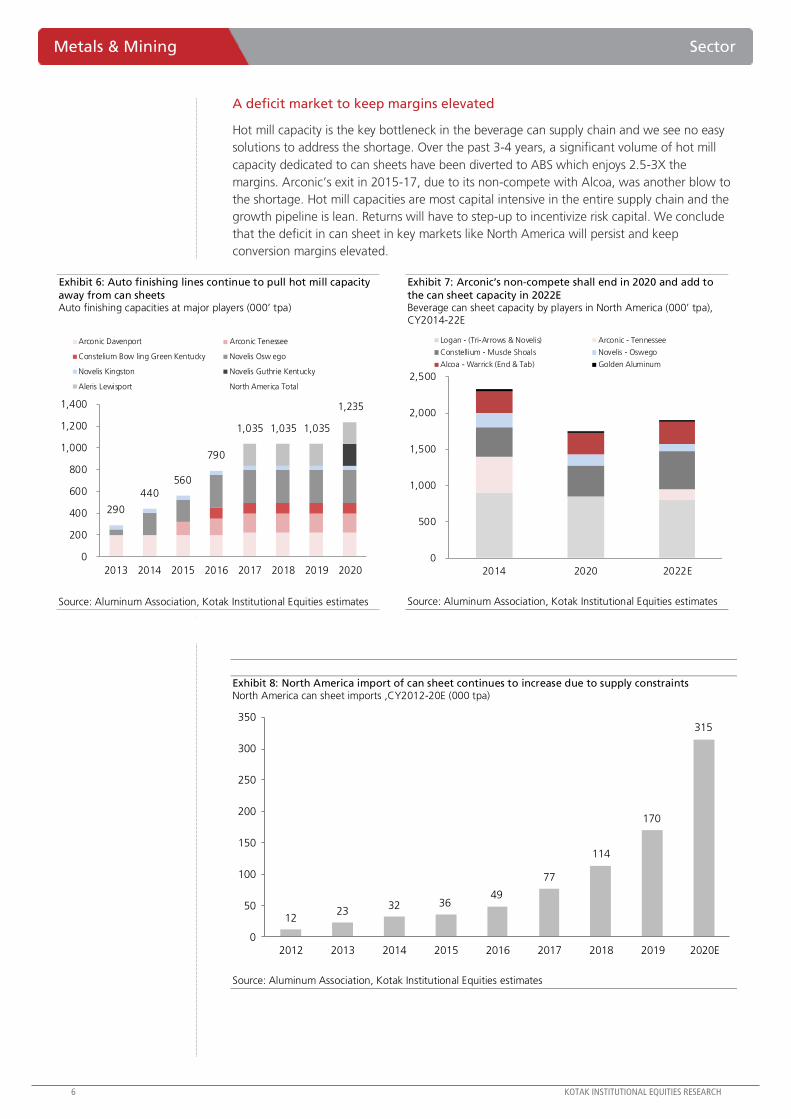

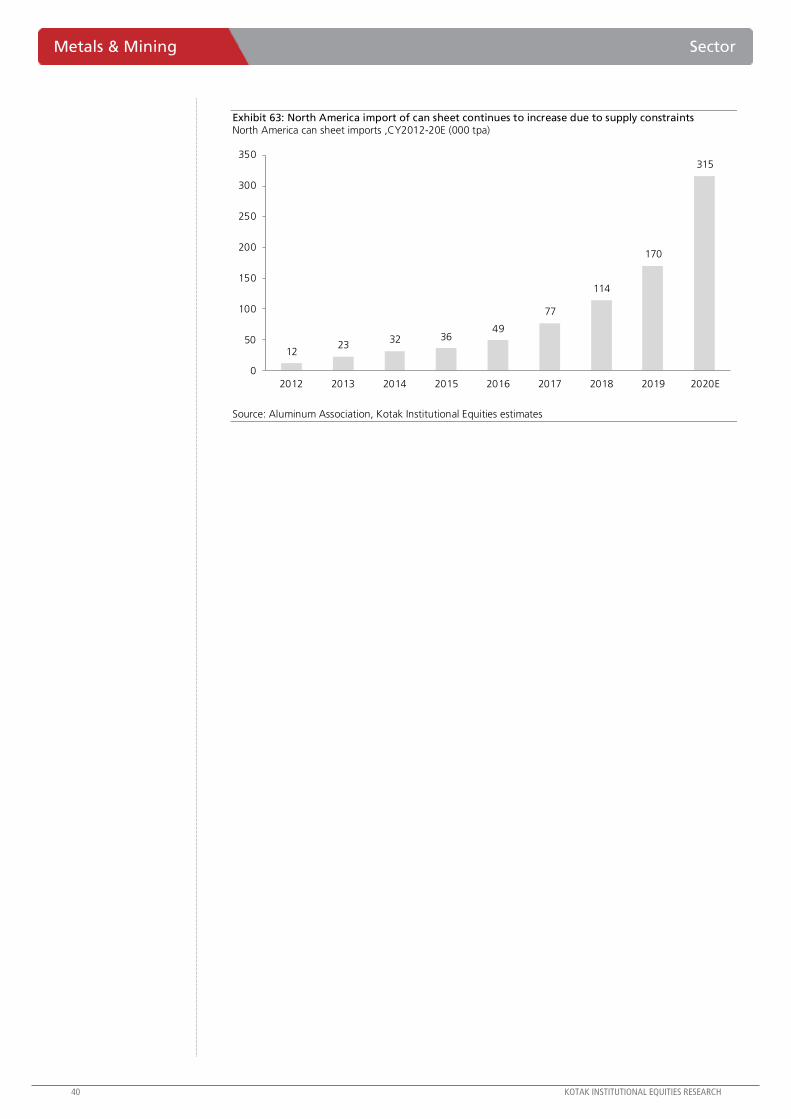

A deficit market to keep margins elevated

Hot mill capacity is the key bottleneck in the beverage can supply chain and we see no easy

solutions to address the shortage. Over the past 3-4 years, a significant volume of hot mill

capacity dedicated to can sheets have been diverted to ABS which enjoys 2.5-3X the

margins. Arconic’s exit in 2015-17, due to its non-compete with Alcoa, was another blow to

the shortage. Hot mill capacities are most capital intensive in the entire supply chain and the

growth pipeline is lean. Returns will have to step-up to incentivize risk capital. We conclude

that the deficit in can sheet in key markets like North America will persist and keep

conversion margins elevated.

Exhibit 6: Auto finishing lines continue to pull hot mill capacity

away from can sheets Auto finishing capacities at major players (000’ tpa)

290

440

560

790

1,035 1,035 1,035

1,235

0

200

400

600

800

1,000

1,200

1,400

2013 2014 2015 2016 2017 2018 2019 2020

Arconic Davenport Arconic Tenessee

Constelium Bow ling Green Kentucky Novelis Osw ego

Novelis Kingston Novelis Guthrie Kentucky

Aleris Lewisport North America Total

Source: Aluminum Association, Kotak Institutional Equities estimates

Exhibit 7: Arconic’s non-compete shall end in 2020 and add to

the can sheet capacity in 2022E Beverage can sheet capacity by players in North America (000’ tpa), CY2014-22E

0

500

1,000

1,500

2,000

2,500

2014 2020 2022E

Logan - (Tri-Arrows & Novelis) Arconic - Tennessee

Constellium - Muscle Shoals Novelis - Oswego

Alcoa - Warrick (End & Tab) Golden Aluminum

Source: Aluminum Association, Kotak Institutional Equities estimates

Exhibit 8: North America import of can sheet continues to increase due to supply constraints North America can sheet imports ,CY2012-20E (000 tpa)

1223

32 3649

77

114

170

315

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016 2017 2018 2019 2020E

Source: Aluminum Association, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Sector Metals & Mining

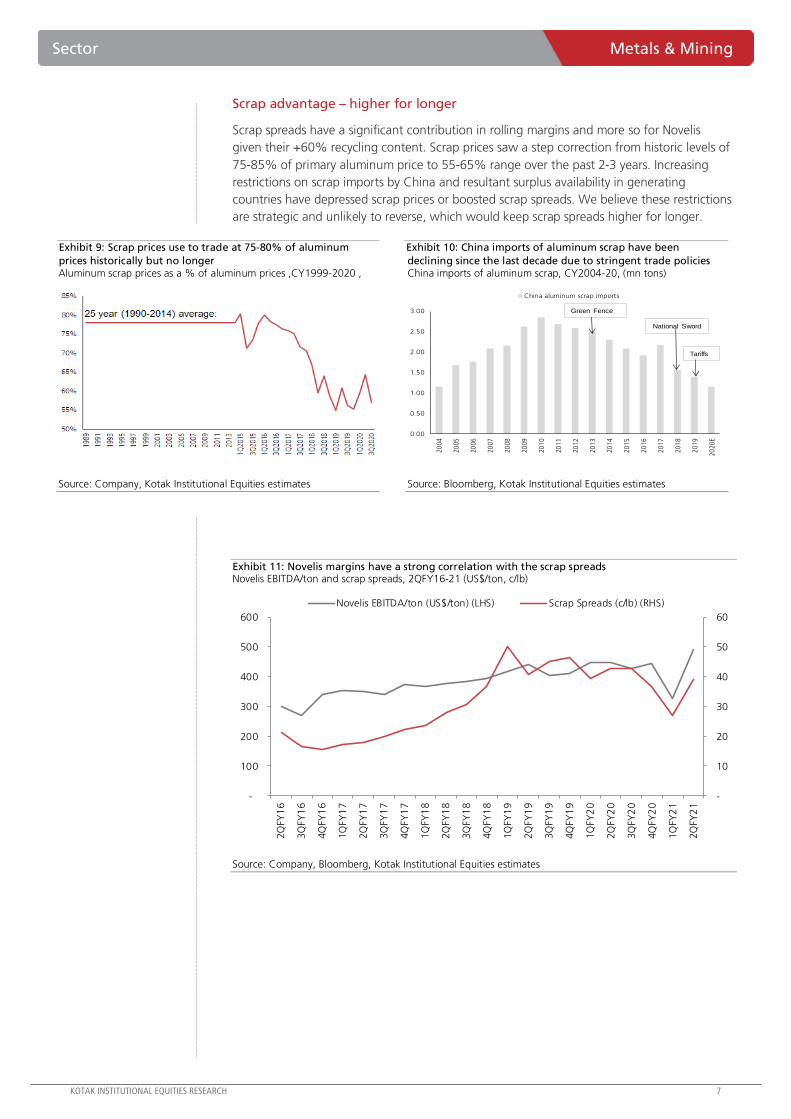

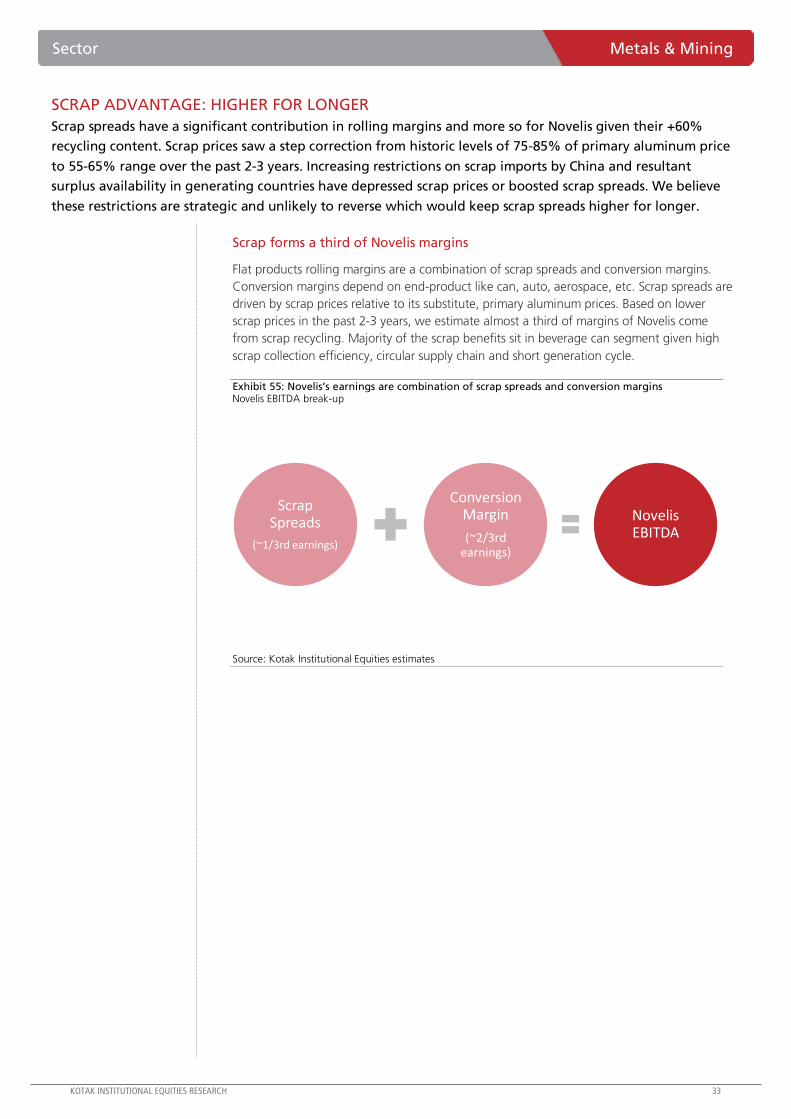

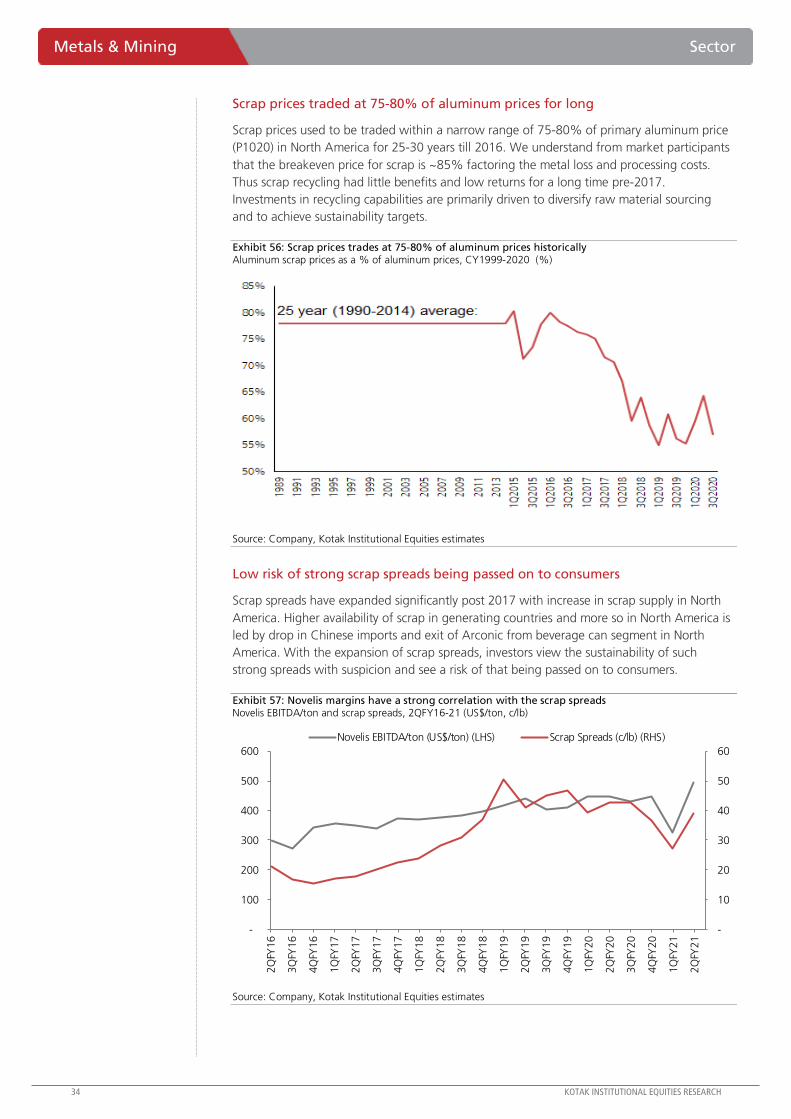

Scrap advantage – higher for longer

Scrap spreads have a significant contribution in rolling margins and more so for Novelis

given their +60% recycling content. Scrap prices saw a step correction from historic levels of

75-85% of primary aluminum price to 55-65% range over the past 2-3 years. Increasing

restrictions on scrap imports by China and resultant surplus availability in generating

countries have depressed scrap prices or boosted scrap spreads. We believe these restrictions

are strategic and unlikely to reverse, which would keep scrap spreads higher for longer.

Exhibit 9: Scrap prices use to trade at 75-80% of aluminum

prices historically but no longer Aluminum scrap prices as a % of aluminum prices ,CY1999-2020 ,

Source: Company, Kotak Institutional Equities estimates

Exhibit 10: China imports of aluminum scrap have been

declining since the last decade due to stringent trade policies China imports of aluminum scrap, CY2004-20, (mn tons)

Source: Bloomberg, Kotak Institutional Equities estimates

Exhibit 11: Novelis margins have a strong correlation with the scrap spreads Novelis EBITDA/ton and scrap spreads, 2QFY16-21 (US$/ton, c/lb)

-

10

20

30

40

50

60

-

100

200

300

400

500

600

2Q

FY1

6

3Q

FY1

6

4Q

FY1

6

1Q

FY1

7

2Q

FY1

7

3Q

FY1

7

4Q

FY1

7

1Q

FY1

8

2Q

FY1

8

3Q

FY1

8

4Q

FY1

8

1Q

FY1

9

2Q

FY1

9

3Q

FY1

9

4Q

FY1

9

1Q

FY2

0

2Q

FY2

0

3Q

FY2

0

4Q

FY2

0

1Q

FY2

1

2Q

FY2

1

Novelis EBITDA/ton (US$/ton) (LHS) Scrap Spreads (c/lb) (RHS)

Source: Company, Bloomberg, Kotak Institutional Equities estimates

0.00

0.50

1.00

1.50

2.00

2.50

3.00

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

E

China aluminum scrap imports

Green Fence

National Sword

Tariffs

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

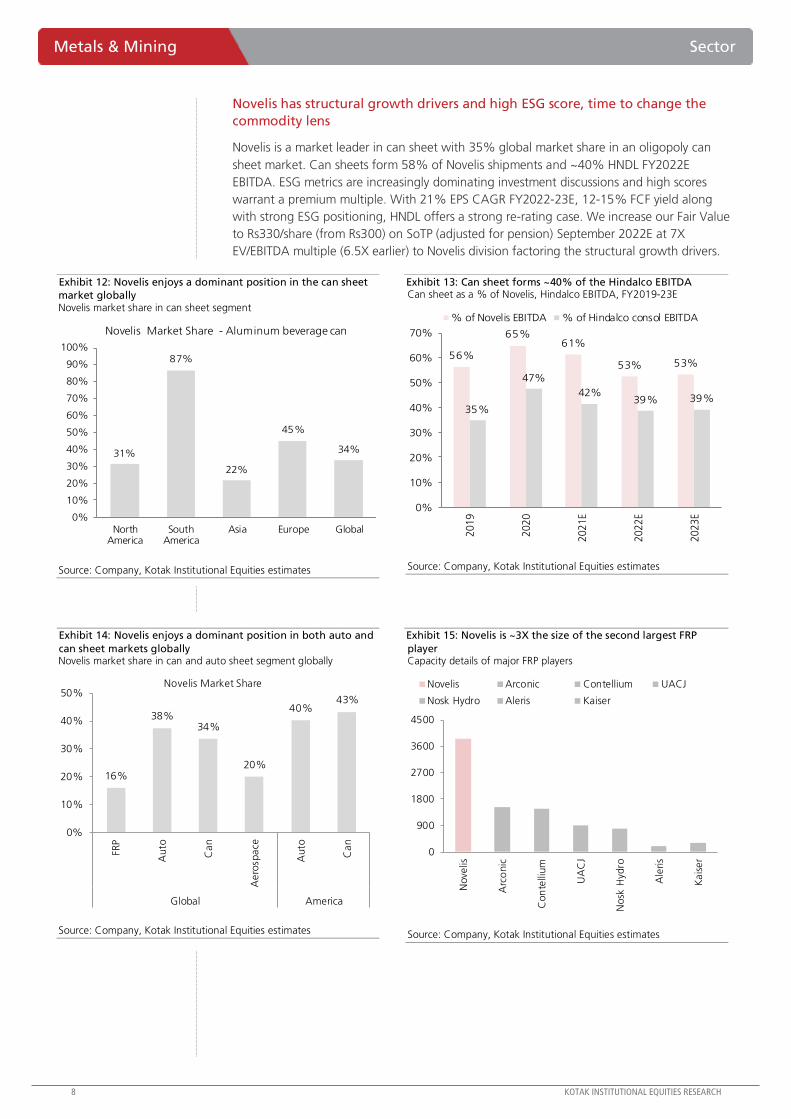

Novelis has structural growth drivers and high ESG score, time to change the

commodity lens

Novelis is a market leader in can sheet with 35% global market share in an oligopoly can

sheet market. Can sheets form 58% of Novelis shipments and ~40% HNDL FY2022E

EBITDA. ESG metrics are increasingly dominating investment discussions and high scores

warrant a premium multiple. With 21% EPS CAGR FY2022-23E, 12-15% FCF yield along

with strong ESG positioning, HNDL offers a strong re-rating case. We increase our Fair Value

to Rs330/share (from Rs300) on SoTP (adjusted for pension) September 2022E at 7X

EV/EBITDA multiple (6.5X earlier) to Novelis division factoring the structural growth drivers.

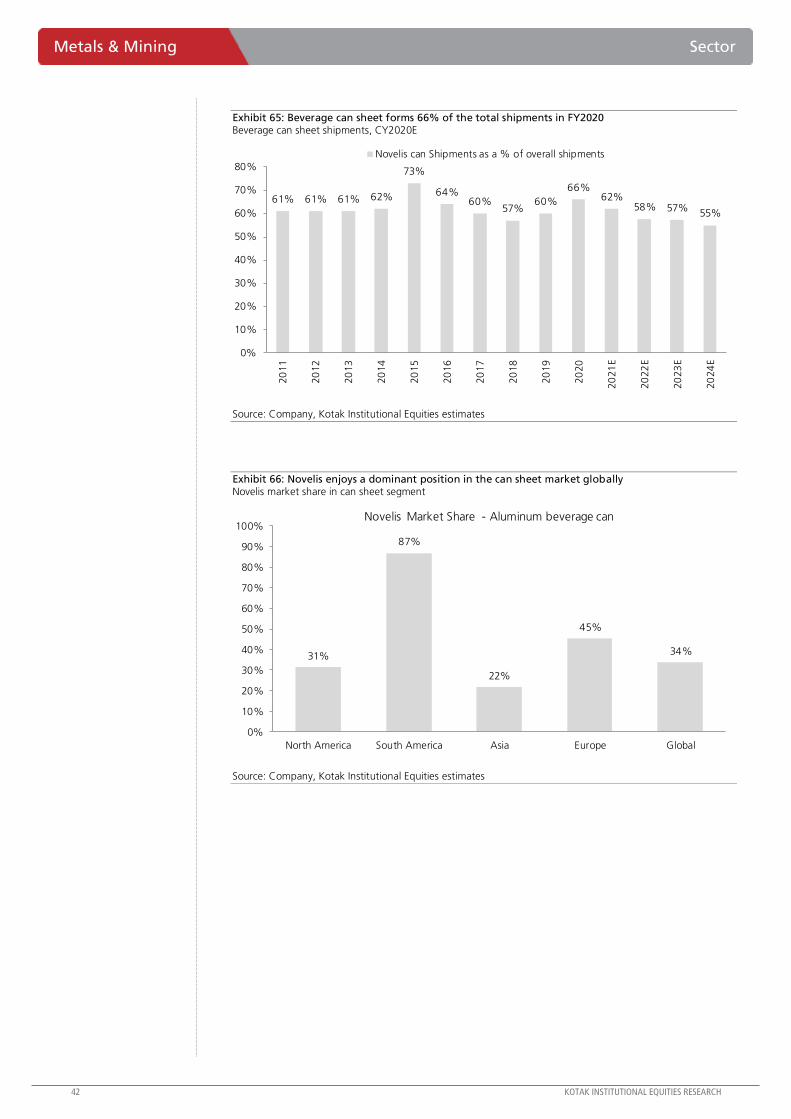

Exhibit 12: Novelis enjoys a dominant position in the can sheet

market globally Novelis market share in can sheet segment

31%

87%

22%

45%

34%

NorthAmerica

SouthAmerica

Asia Europe Global0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Novelis Market Share - Aluminum beverage can

Source: Company, Kotak Institutional Equities estimates

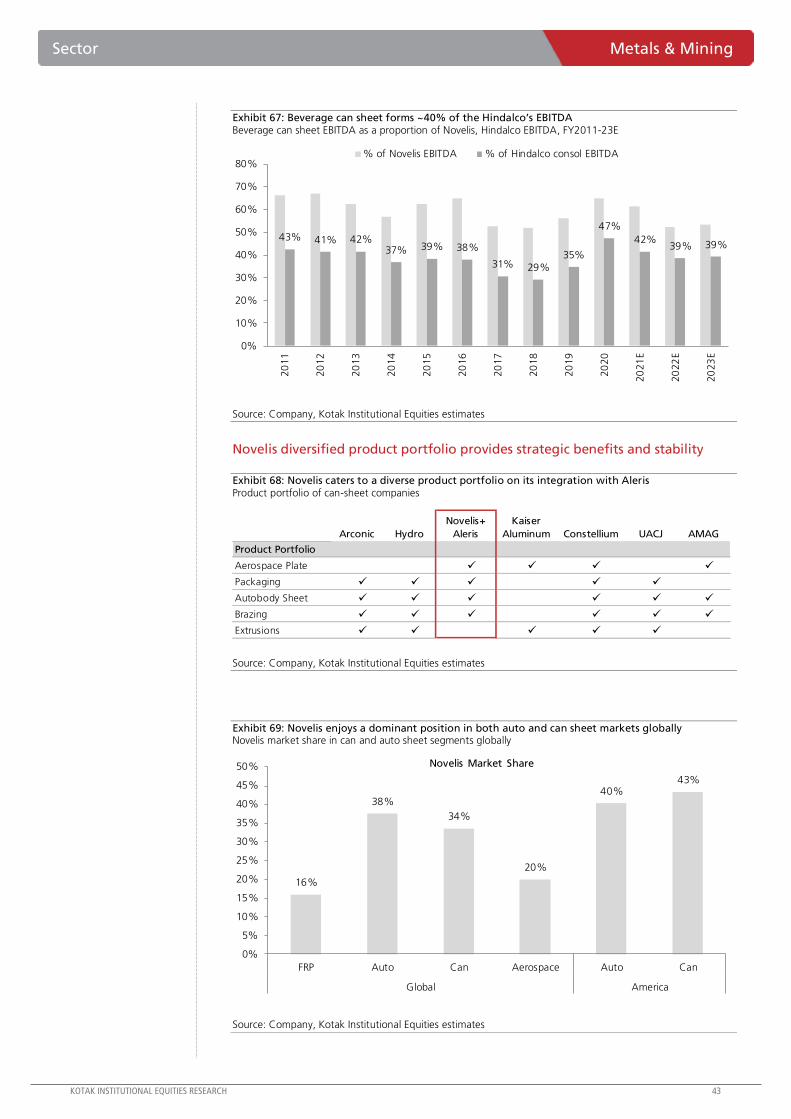

Exhibit 13: Can sheet forms ~40% of the Hindalco EBITDA Can sheet as a % of Novelis, Hindalco EBITDA, FY2019-23E

56%

65%61%

53% 53%

35%

47%

42%39% 39%

0%

10%

20%

30%

40%

50%

60%

70%

2019

2020

2021E

2022E

2023E

% of Novelis EBITDA % of Hindalco consol EBITDA

Source: Company, Kotak Institutional Equities estimates

Exhibit 14: Novelis enjoys a dominant position in both auto and

can sheet markets globally Novelis market share in can and auto sheet segment globally

16%

38%34%

20%

40%43%

0%

10%

20%

30%

40%

50%

FRP

Auto

Can

Aero

space

Auto

Can

Global America

Novelis Market Share

Source: Company, Kotak Institutional Equities estimates

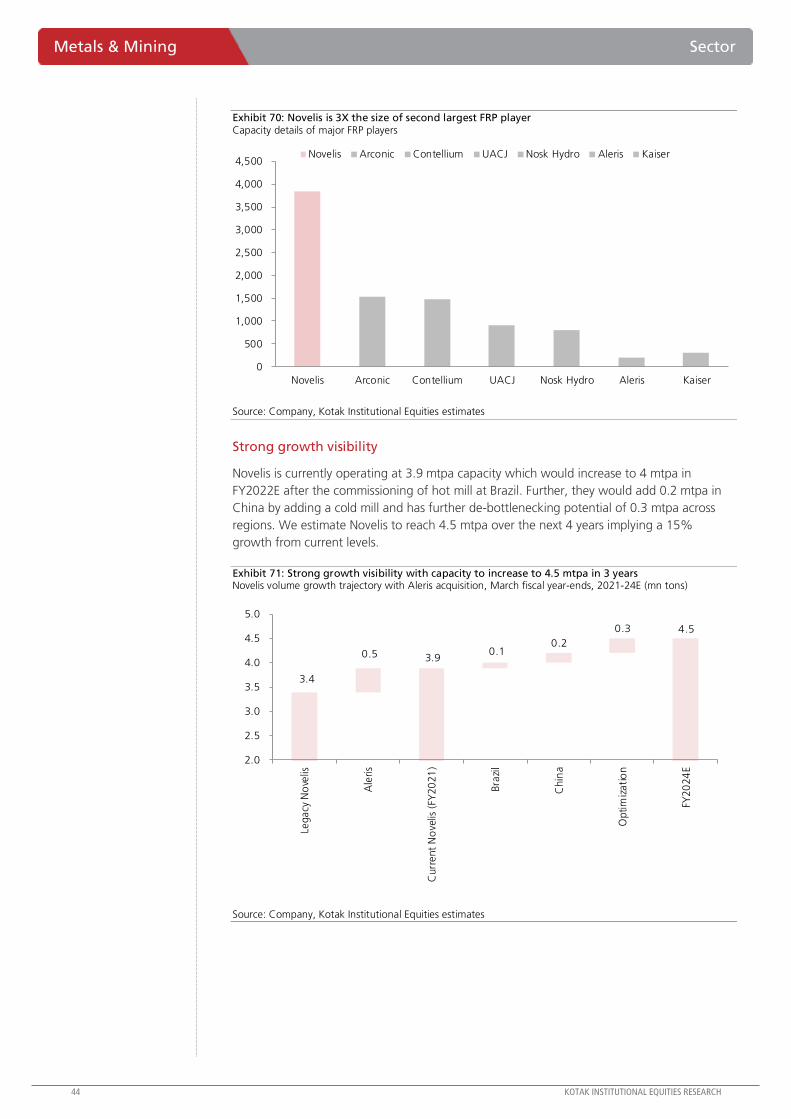

Exhibit 15: Novelis is ~3X the size of the second largest FRP

player Capacity details of major FRP players

0

900

1800

2700

3600

4500

Nove

lis

Arc

onic

Con

telli

um

UA

CJ

Nosk

Hyd

ro

Ale

ris

Kais

er

Novelis Arconic Contellium UACJ

Nosk Hydro Aleris Kaiser

Source: Company, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

Sector Metals & Mining

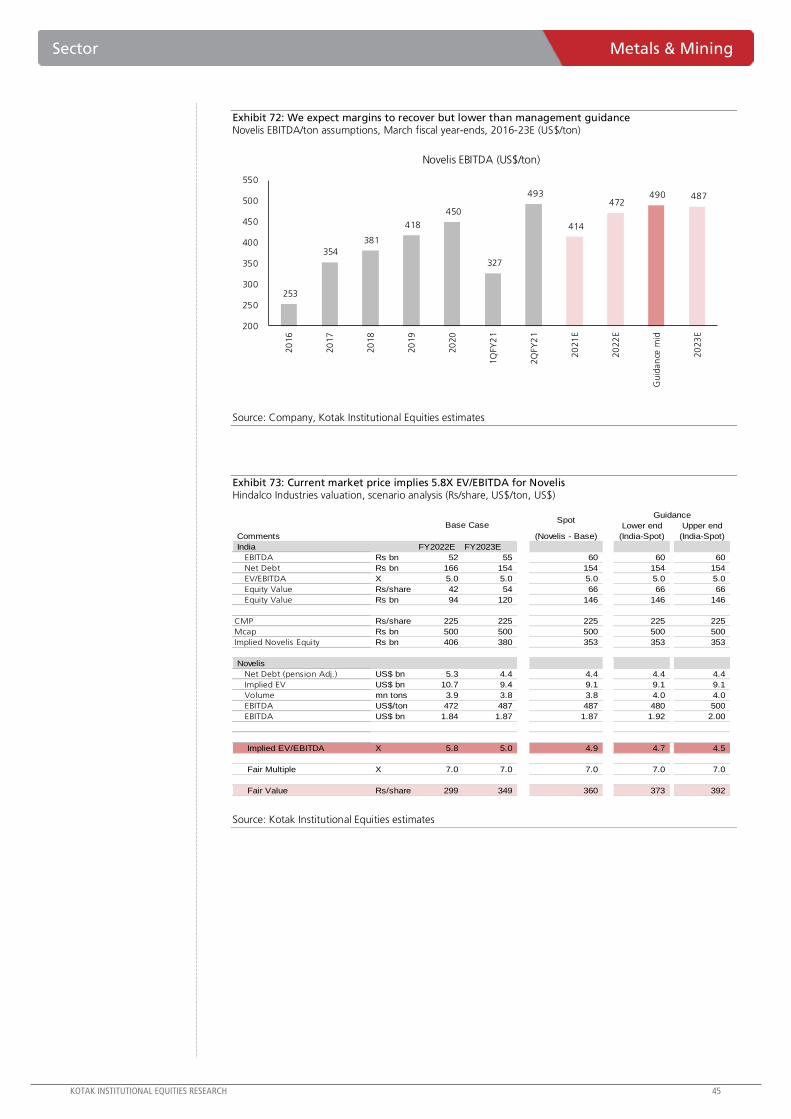

Exhibit 16: Spot commodity prices implies 5X EV/EBITDA for Novelis Hindalco Industries valuation, scenario analysis (Rs/share, US$/ton, US$)

Lower end Upper end

Comments (Novelis - Base) (India-Spot) (India-Spot)

India FY2022E FY2023E

EBITDA Rs bn 52 55 60 60 60

Net Debt Rs bn 166 154 154 154 154

EV/EBITDA X 5.0 5.0 5.0 5.0 5.0

Equity Value Rs/share 42 54 66 66 66

Equity Value Rs bn 94 120 146 146 146

CMP Rs/share 225 225 225 225 225

Mcap Rs bn 500 500 500 500 500

Implied Novelis Equity Rs bn 406 380 353 353 353

Novelis

Net Debt (pension Adj.) US$ bn 5.3 4.4 4.4 4.4 4.4

Implied EV US$ bn 10.7 9.4 9.1 9.1 9.1

Volume mn tons 3.9 3.8 3.8 4.0 4.0

EBITDA US$/ton 472 487 487 480 500

EBITDA US$ bn 1.84 1.87 1.87 1.92 2.00

Implied EV/EBITDA X 5.8 5.0 4.9 4.7 4.5

Fair Multiple X 7.0 7.0 7.0 7.0 7.0

Fair Value Rs/share 299 349 360 373 392

GuidanceSpot

Base Case

Source: Kotak Institutional Equities estimates

Exhibit 17: Hindalco Industries, valuation, September, 2022E basis (Rs mn)

Multiple

(Rs mn) (X) (Rs mn) (Rs/share)

Hindalco EBITDA 53,537 5.0 267,687 121

Novelis EBITDA 139,248 7.0 974,737 439

Total Enterprise Value 192,786 6.4 1,242,424 560

Less: Net debt (438,660) (438,660) (198)

Pension Deficit (71,830) (32)

Arrived market capitalization 330

Fair value (Rs) 330

Value

Source: Kotak Institutional Equities estimates

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

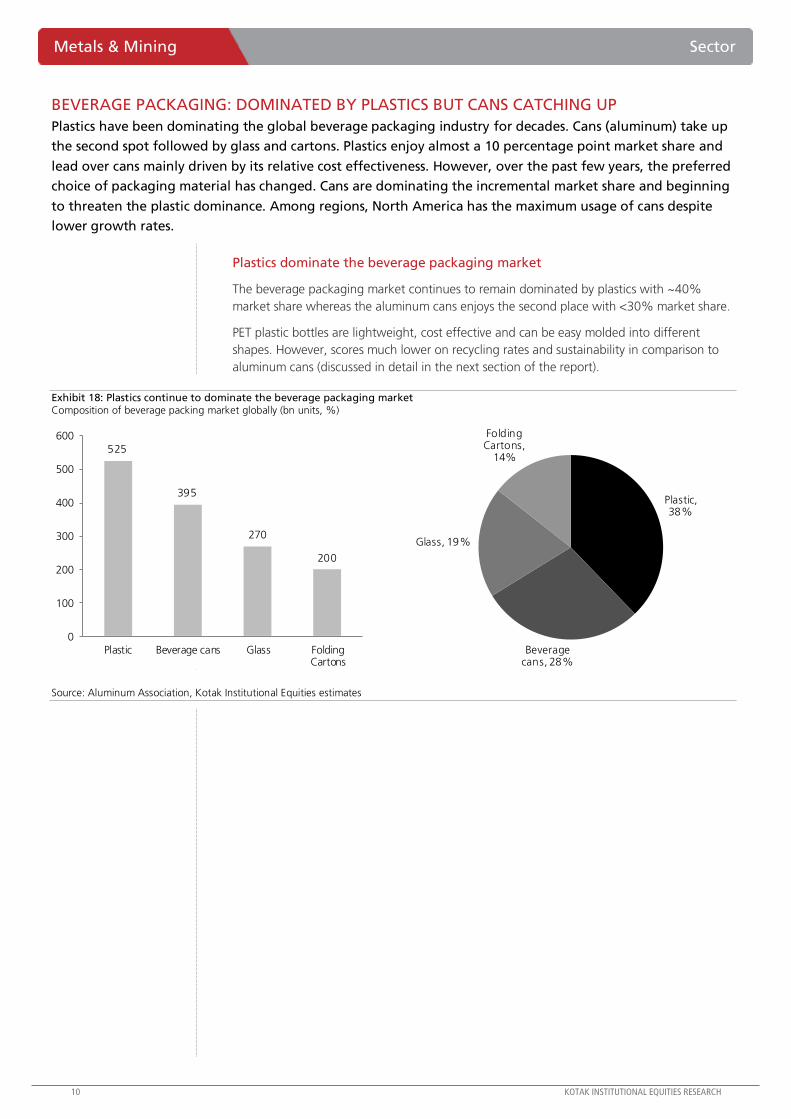

BEVERAGE PACKAGING: DOMINATED BY PLASTICS BUT CANS CATCHING UP

Plastics have been dominating the global beverage packaging industry for decades. Cans (aluminum) take up

the second spot followed by glass and cartons. Plastics enjoy almost a 10 percentage point market share and

lead over cans mainly driven by its relative cost effectiveness. However, over the past few years, the preferred

choice of packaging material has changed. Cans are dominating the incremental market share and beginning

to threaten the plastic dominance. Among regions, North America has the maximum usage of cans despite

lower growth rates.

Plastics dominate the beverage packaging market

The beverage packaging market continues to remain dominated by plastics with ~40%

market share whereas the aluminum cans enjoys the second place with <30% market share.

PET plastic bottles are lightweight, cost effective and can be easy molded into different

shapes. However, scores much lower on recycling rates and sustainability in comparison to

aluminum cans (discussed in detail in the next section of the report).

Exhibit 18: Plastics continue to dominate the beverage packaging market Composition of beverage packing market globally (bn units, %)

525

395

270

200

0

100

200

300

400

500

600

Plastic Beverage cans Glass FoldingCartons

Plastic, 38%

Beverage cans, 28%

Glass, 19%

Folding Cartons,

14%

Source: Aluminum Association, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Sector Metals & Mining

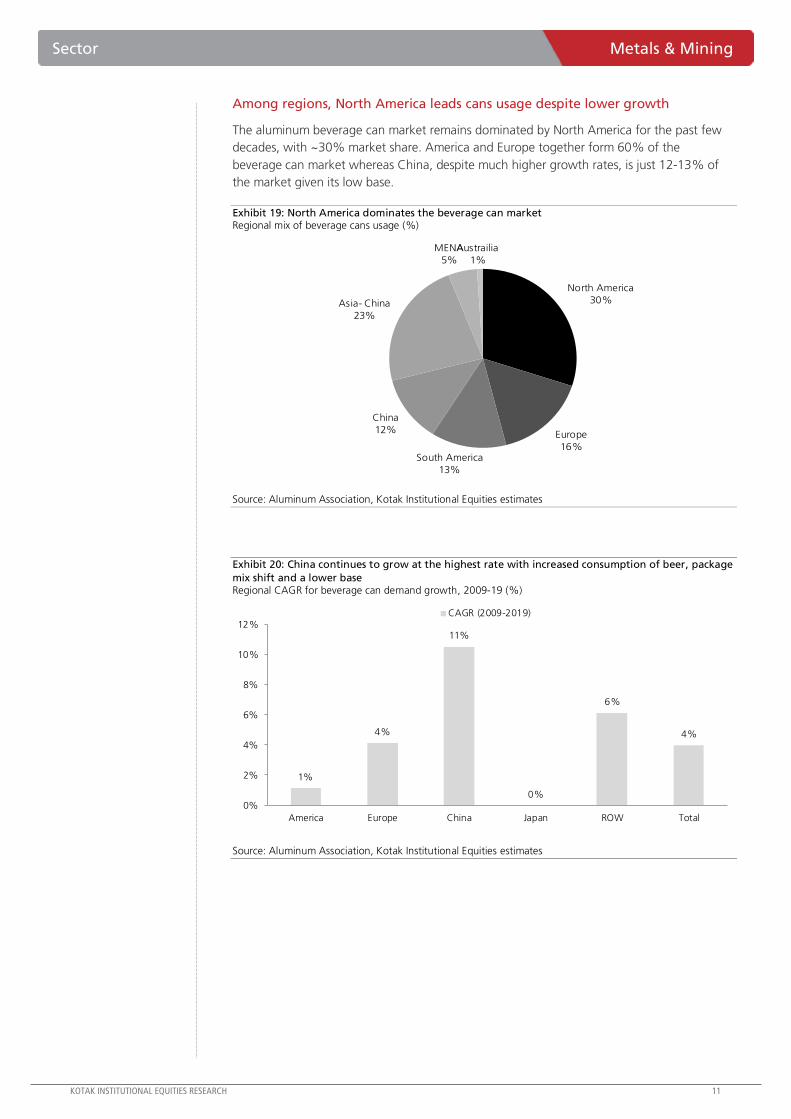

Among regions, North America leads cans usage despite lower growth

The aluminum beverage can market remains dominated by North America for the past few

decades, with ~30% market share. America and Europe together form 60% of the

beverage can market whereas China, despite much higher growth rates, is just 12-13% of

the market given its low base.

Exhibit 19: North America dominates the beverage can market Regional mix of beverage cans usage (%)

North America

30%

Europe

16%South America

13%

China

12%

Asia- China

23%

MENA

5%

Austrailia

1%

Source: Aluminum Association, Kotak Institutional Equities estimates

Exhibit 20: China continues to grow at the highest rate with increased consumption of beer, package

mix shift and a lower base Regional CAGR for beverage can demand growth, 2009-19 (%)

1%

4%

11%

0%

6%

4%

0%

2%

4%

6%

8%

10%

12%

America Europe China Japan ROW Total

CAGR (2009-2019)

Source: Aluminum Association, Kotak Institutional Equities estimates

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

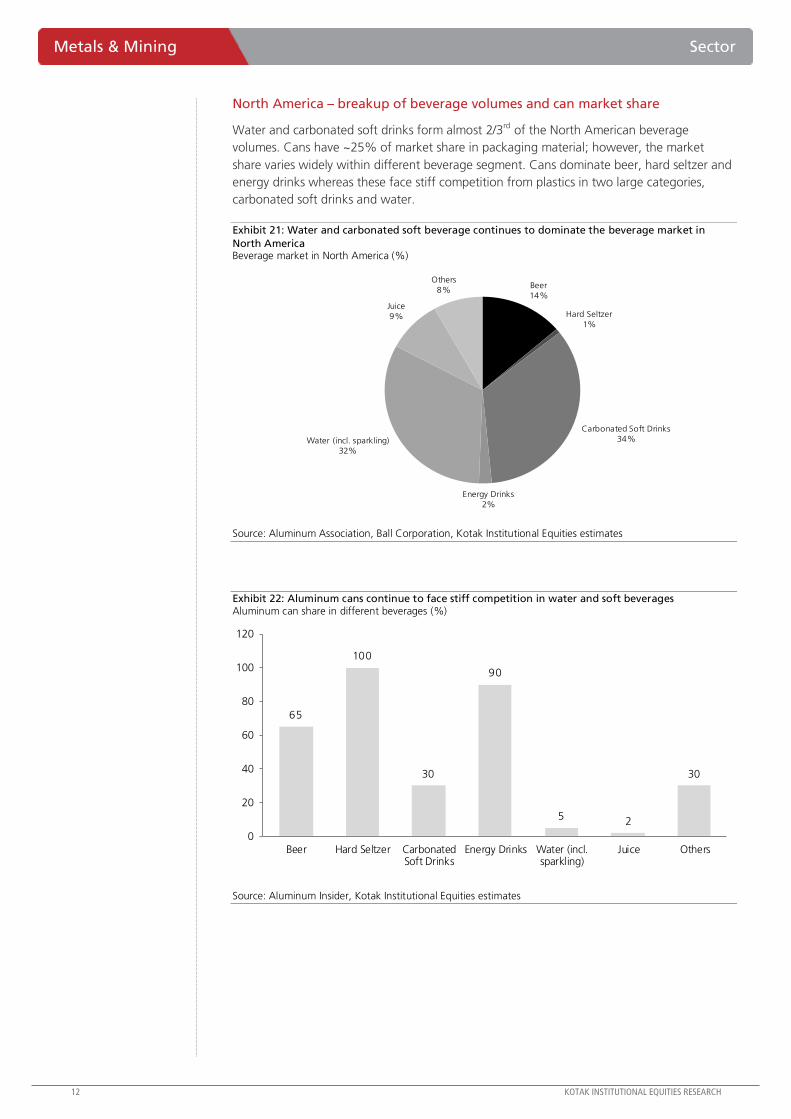

North America – breakup of beverage volumes and can market share

Water and carbonated soft drinks form almost 2/3rd of the North American beverage

volumes. Cans have ~25% of market share in packaging material; however, the market

share varies widely within different beverage segment. Cans dominate beer, hard seltzer and

energy drinks whereas these face stiff competition from plastics in two large categories,

carbonated soft drinks and water.

Exhibit 21: Water and carbonated soft beverage continues to dominate the beverage market in

North America Beverage market in North America (%)

Beer

14%

Hard Seltzer

1%

Carbonated Soft Drinks

34%

Energy Drinks

2%

Water (incl. sparkling)

32%

Juice

9%

Others

8%

Source: Aluminum Association, Ball Corporation, Kotak Institutional Equities estimates

Exhibit 22: Aluminum cans continue to face stiff competition in water and soft beverages Aluminum can share in different beverages (%)

65

100

30

90

5 2

30

Beer Hard Seltzer CarbonatedSoft Drinks

Energy Drinks Water (incl.sparkling)

Juice Others0

20

40

60

80

100

120

Source: Aluminum Insider, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Sector Metals & Mining

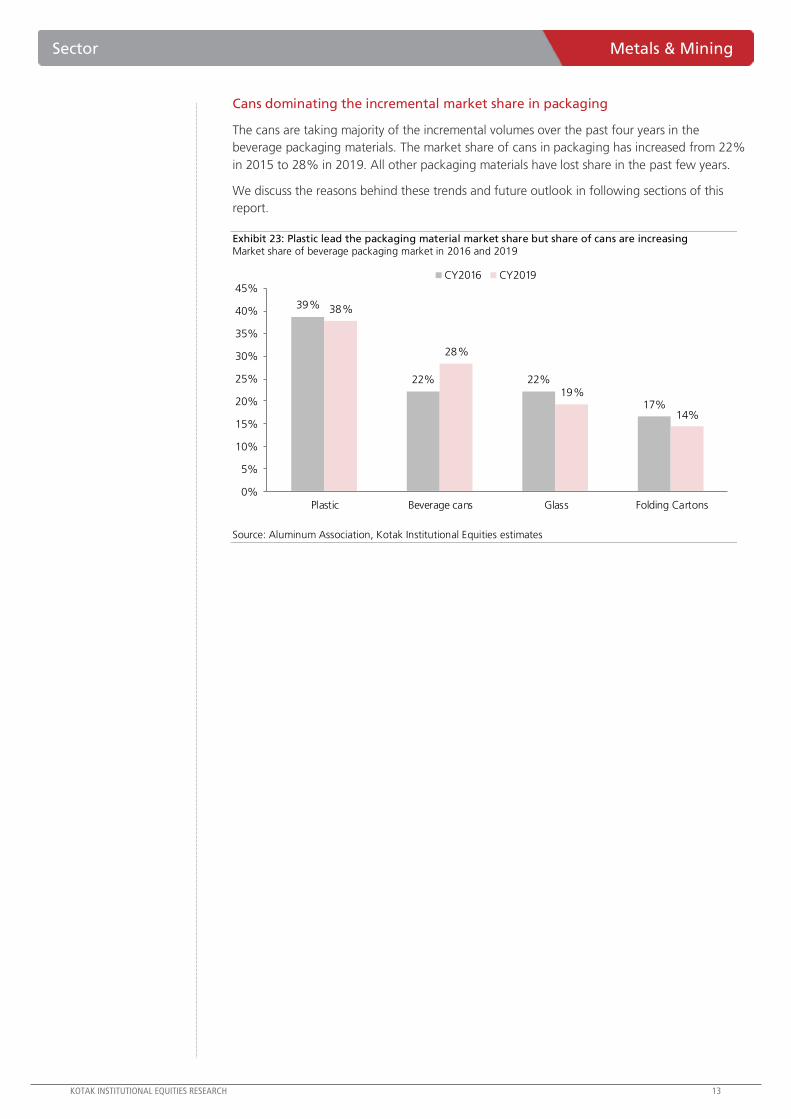

Cans dominating the incremental market share in packaging

The cans are taking majority of the incremental volumes over the past four years in the

beverage packaging materials. The market share of cans in packaging has increased from 22%

in 2015 to 28% in 2019. All other packaging materials have lost share in the past few years.

We discuss the reasons behind these trends and future outlook in following sections of this

report.

Exhibit 23: Plastic lead the packaging material market share but share of cans are increasing Market share of beverage packaging market in 2016 and 2019

39%

22% 22%

17%

38%

28%

19%

14%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Plastic Beverage cans Glass Folding Cartons

CY2016 CY2019

Source: Aluminum Association, Kotak Institutional Equities estimates

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

THE CAN ADVANTAGE AND GROWING GLOBAL PARTICIPATION

Aluminum cans are by far the most suitable beverage container. It scores significantly above its substitutes –

glass and plastic on convenience and sustainability. Aluminum cans protect the flavors of beverages, chills

quickly and most importantly, it is infinitely recyclable thus more sustainable. With growing backlash against

polluting plastics, aluminum can offers the most sustainable alternative. Almost 75% of aluminum ever

produced is still in use and it offers a truly circular supply chain with a 60-day turnaround.

Aluminum cans – multiple benefits

The aluminum cans sheets are extensively used in beverage packaging. Aluminum cans are

the most sustainable beverage package and are infinitely recyclable. They chill quickly,

provide a superior metal canvas to print on and, perhaps most importantly, protect the

flavor and integrity of beverages. It is lightweight, has a high recycling rate with easy

fabrication process as it can be molded in innovative shapes and sizes.

Key advantages of beverage can are below:

The most sustainable beverage container. As the most valuable package in the bin,

aluminum cans are, by far, the most recycled beverage container. The average can

contain 70% recycled metal.

Shipping efficiency: the weight advantage. Aluminum cans are lightweight and easily

stacked. This provides storage and shipping efficiencies and limits overall transportation

carbon emissions through logistics and supply chain.

True closed loop recycling. Aluminum cans are recycled over and over again in a true

‘closed loop‘ recycling process. Glass and plastic are typically ‘down-cycled‘ into products

like carpet fiber or landfill liner.

Maintains product quality. Nearly 500 craft beer brewers use aluminum to can more

than 1,700 different beers. Protection from light and oxygen are two key benefits of

aluminum packaging, which help preserve the product life.

Enhanced marketing. Aluminum provides a much superior metal canvas to print on,

which allows more efficient marketing from the producer.

The virtuous cycle

Aluminum can scrap is a vital input for the industry and allows can manufacturers to make

beverage containers in the most environment friendly and economical way possible.

Recycling aluminum saves more than 90% of the energy needed to produce new, or primary,

aluminum.

In addition, aluminum’s recycling profile and the high value of the material means that,

unlike competing packages like glass and plastic bottles, the aluminum used beverage

container (UBC) is most often recycled directly back into itself. This process occurs repeatedly

without degradation in product quality. This closed-loop process drives a virtuous cycle of

high recycling rates, a large percentage of recycled content in the average aluminum can

and an economically sustainable process that effectively subsidizes municipal recycling

programs nationwide.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Sector Metals & Mining

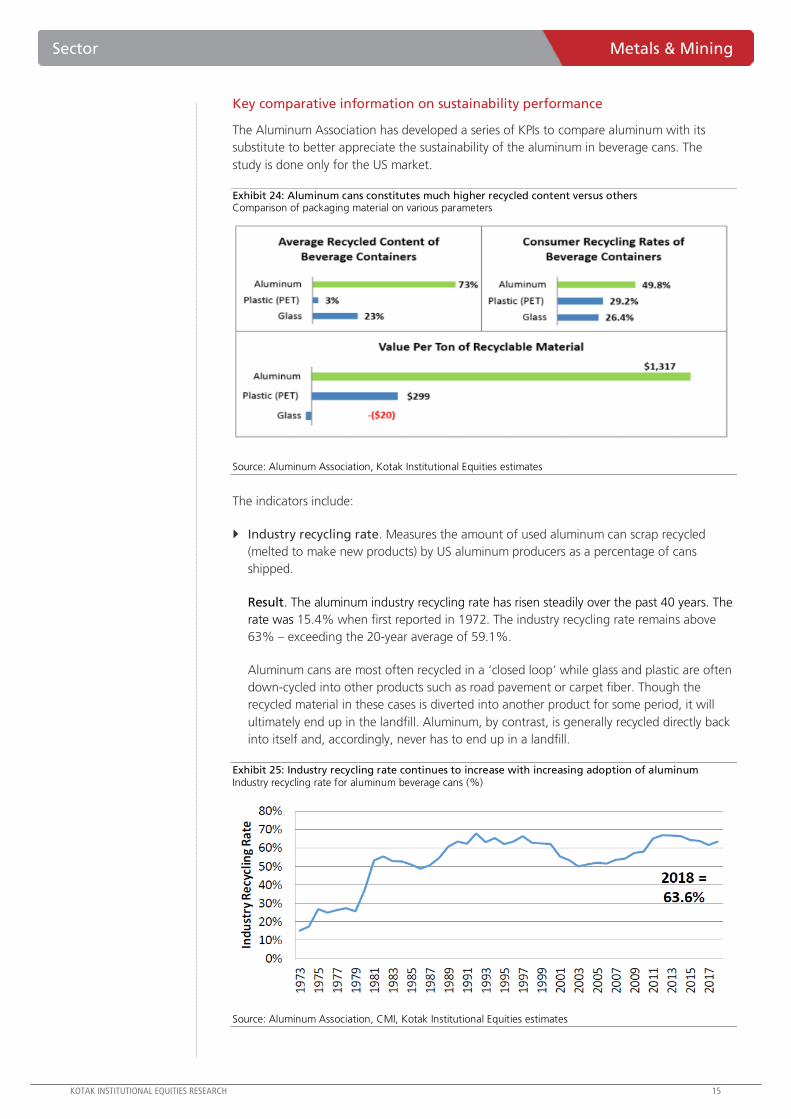

Key comparative information on sustainability performance

The Aluminum Association has developed a series of KPIs to compare aluminum with its

substitute to better appreciate the sustainability of the aluminum in beverage cans. The

study is done only for the US market.

Exhibit 24: Aluminum cans constitutes much higher recycled content versus others Comparison of packaging material on various parameters

Source: Aluminum Association, Kotak Institutional Equities estimates

The indicators include:

Industry recycling rate. Measures the amount of used aluminum can scrap recycled

(melted to make new products) by US aluminum producers as a percentage of cans

shipped.

Result. The aluminum industry recycling rate has risen steadily over the past 40 years. The

rate was 15.4% when first reported in 1972. The industry recycling rate remains above

63% – exceeding the 20-year average of 59.1%.

Aluminum cans are most often recycled in a ‘closed loop‘ while glass and plastic are often

down-cycled into other products such as road pavement or carpet fiber. Though the

recycled material in these cases is diverted into another product for some period, it will

ultimately end up in the landfill. Aluminum, by contrast, is generally recycled directly back

into itself and, accordingly, never has to end up in a landfill.

Exhibit 25: Industry recycling rate continues to increase with increasing adoption of aluminum Industry recycling rate for aluminum beverage cans (%)

Source: Aluminum Association, CMI, Kotak Institutional Equities estimates

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

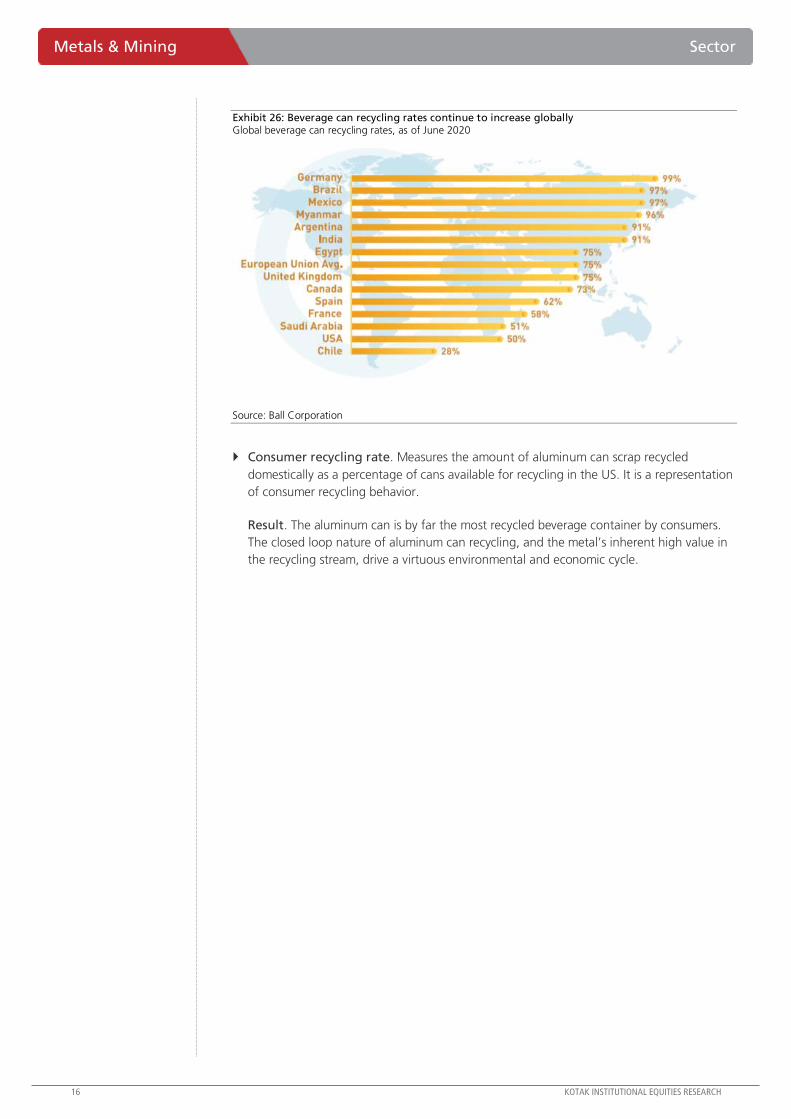

Exhibit 26: Beverage can recycling rates continue to increase globally Global beverage can recycling rates, as of June 2020

Source: Ball Corporation

Consumer recycling rate. Measures the amount of aluminum can scrap recycled

domestically as a percentage of cans available for recycling in the US. It is a representation

of consumer recycling behavior.

Result. The aluminum can is by far the most recycled beverage container by consumers.

The closed loop nature of aluminum can recycling, and the metal’s inherent high value in

the recycling stream, drive a virtuous environmental and economic cycle.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

Sector Metals & Mining

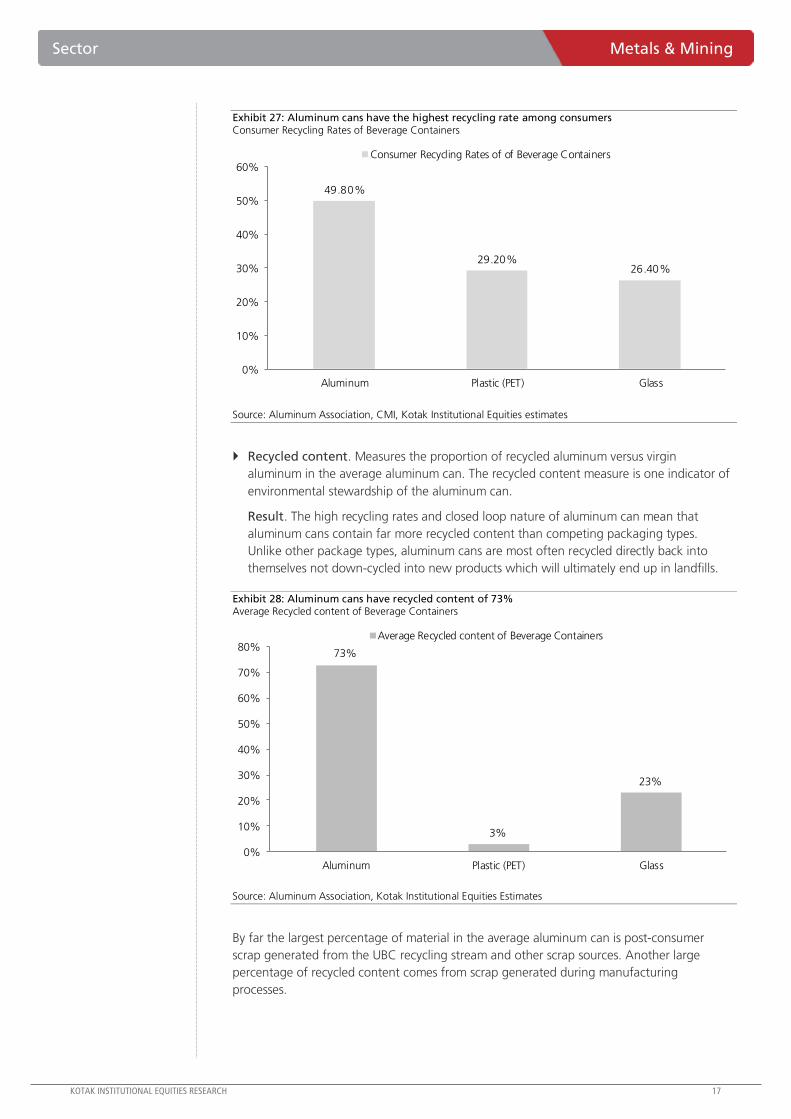

Exhibit 27: Aluminum cans have the highest recycling rate among consumers Consumer Recycling Rates of Beverage Containers

49.80%

29.20%26.40%

0%

10%

20%

30%

40%

50%

60%

Aluminum Plastic (PET) Glass

Consumer Recycling Rates of of Beverage Containers

Source: Aluminum Association, CMI, Kotak Institutional Equities estimates

Recycled content. Measures the proportion of recycled aluminum versus virgin

aluminum in the average aluminum can. The recycled content measure is one indicator of

environmental stewardship of the aluminum can.

Result. The high recycling rates and closed loop nature of aluminum can mean that

aluminum cans contain far more recycled content than competing packaging types.

Unlike other package types, aluminum cans are most often recycled directly back into

themselves not down-cycled into new products which will ultimately end up in landfills.

Exhibit 28: Aluminum cans have recycled content of 73% Average Recycled content of Beverage Containers

73%

3%

23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Aluminum Plastic (PET) Glass

Average Recycled content of Beverage Containers

Source: Aluminum Association, Kotak Institutional Equities Estimates

By far the largest percentage of material in the average aluminum can is post-consumer

scrap generated from the UBC recycling stream and other scrap sources. Another large

percentage of recycled content comes from scrap generated during manufacturing

processes.

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

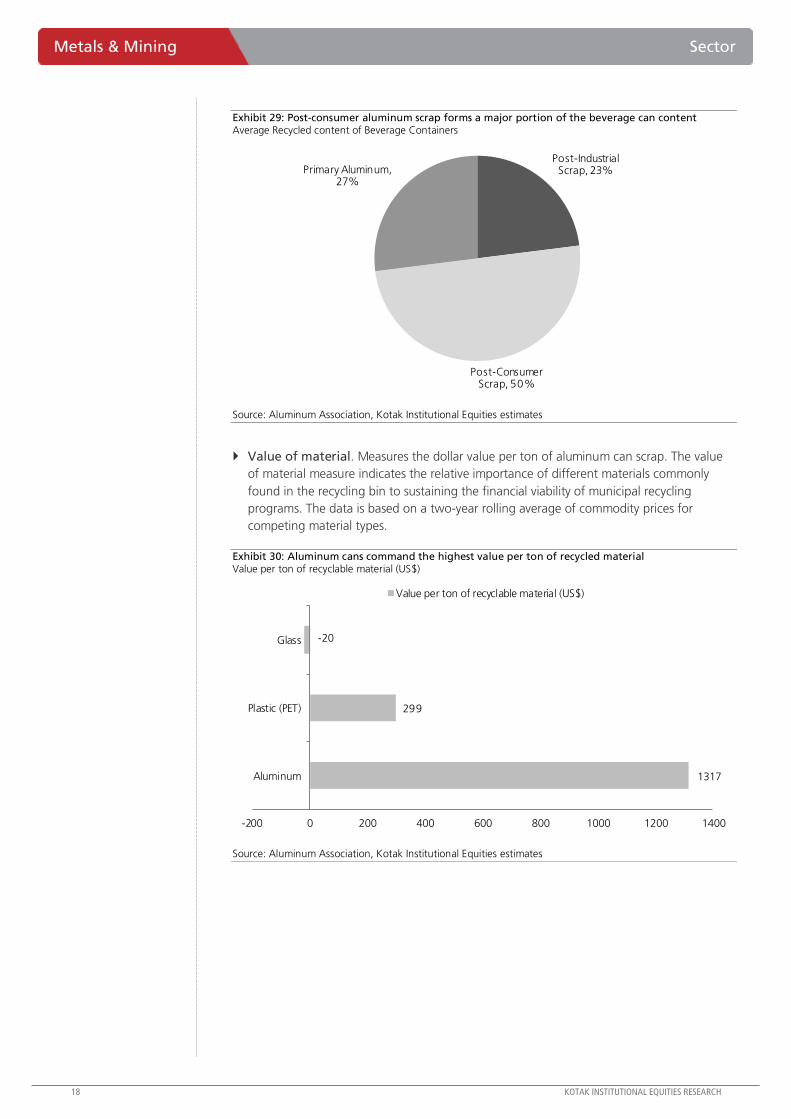

Exhibit 29: Post-consumer aluminum scrap forms a major portion of the beverage can content Average Recycled content of Beverage Containers

Post-Industrial Scrap, 23%

Post-Consumer Scrap, 50%

Primary Aluminum, 27%

Source: Aluminum Association, Kotak Institutional Equities estimates

Value of material. Measures the dollar value per ton of aluminum can scrap. The value

of material measure indicates the relative importance of different materials commonly

found in the recycling bin to sustaining the financial viability of municipal recycling

programs. The data is based on a two-year rolling average of commodity prices for

competing material types.

Exhibit 30: Aluminum cans command the highest value per ton of recycled material Value per ton of recyclable material (US$)

1317

299

-20

-200 0 200 400 600 800 1000 1200 1400

Aluminum

Plastic (PET)

Glass

Value per ton of recyclable material (US$)

Source: Aluminum Association, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

Sector Metals & Mining

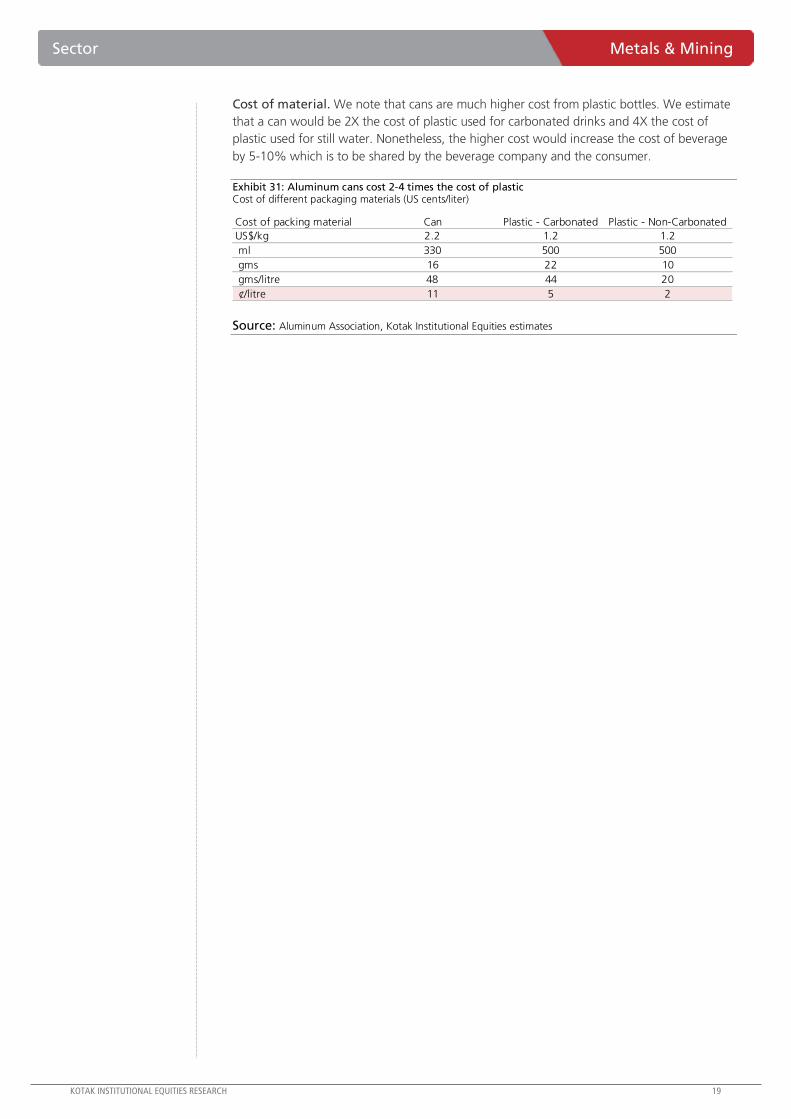

Cost of material. We note that cans are much higher cost from plastic bottles. We estimate

that a can would be 2X the cost of plastic used for carbonated drinks and 4X the cost of

plastic used for still water. Nonetheless, the higher cost would increase the cost of beverage

by 5-10% which is to be shared by the beverage company and the consumer.

Exhibit 31: Aluminum cans cost 2-4 times the cost of plastic Cost of different packaging materials (US cents/liter)

Cost of packing material Can Plastic - Carbonated Plastic - Non-Carbonated

US$/kg 2.2 1.2 1.2

ml 330 500 500

gms 16 22 10

gms/litre 48 44 20

¢/litre 11 5 2

Source: Aluminum Association, Kotak Institutional Equities estimates

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

Plastic – bleak future

In recent years, a groundswell of negative publicity and consumer backlash has emerged

against disposable plastic products, particularly bottles. Images of bottles overflowing

landfills and adversely impacting ecosystems have soured consumers and drawn the ire of

environmental organizations and activists worldwide. As a result, many are calling for

increased government and industry intervention to address the growing problem.

According to the Ocean Conservancy, a nonprofit environmental advocacy group, plastic

drink bottles are the third most common type of waste item found on shorelines – behind

cigarette butts and food wrappers.

Exhibit 32: Plastic beverage bottles were the topmost polluting items in US and Europe Top 10 items collected at shore lines in Europe and America

Source: Ocean Conservancy

Exhibit 33: China and US continue to be the top contributors to plastic waste Plastic waste generated by select countries as of 2019 (mn tons)

Source: Statista

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

Sector Metals & Mining

Exhibit 34: EU imposed a ban on single-use plastics Plastic ban imposed by EU government

Source: Europe Parliament

In May 2018, a new EU packaging waste directive was adopted which set much more

ambitious recycling targets including a 50% recycling rate for all aluminum packaging by

2025. The new legislation requires that all member states adopt legally binding targets for

waste recycling and the reduction of landfilling. The municipal waste recycling target is set

to 55% by 2025, 60% by 2030, and 65% by 2035.

Although beverage companies are trying to substitute the use of plastic by investing in new

PET packaging recycling technologies (r PET), the adoption remains limited due to limited

supply, higher processing costs and higher costs with respect to virgin PET.

The industry shift towards aluminum cans is evident in the bottled water and the carbonated

soft drinks (CSD) markets where single-use PET plastic bottles represent the predominant

form of packaging.

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

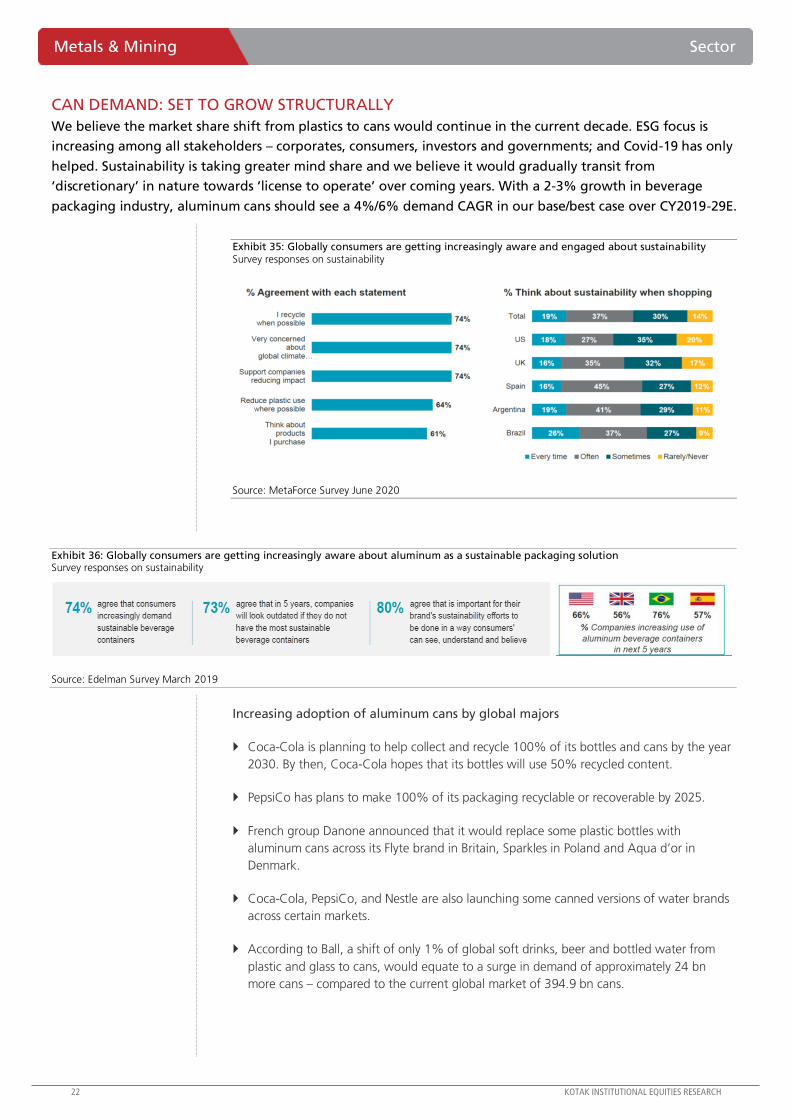

CAN DEMAND: SET TO GROW STRUCTURALLY

We believe the market share shift from plastics to cans would continue in the current decade. ESG focus is

increasing among all stakeholders – corporates, consumers, investors and governments; and Covid-19 has only

helped. Sustainability is taking greater mind share and we believe it would gradually transit from

‘discretionary’ in nature towards ‘license to operate’ over coming years. With a 2-3% growth in beverage

packaging industry, aluminum cans should see a 4%/6% demand CAGR in our base/best case over CY2019-29E.

Exhibit 35: Globally consumers are getting increasingly aware and engaged about sustainability Survey responses on sustainability

Source: MetaForce Survey June 2020

Exhibit 36: Globally consumers are getting increasingly aware about aluminum as a sustainable packaging solution Survey responses on sustainability

Source: Edelman Survey March 2019

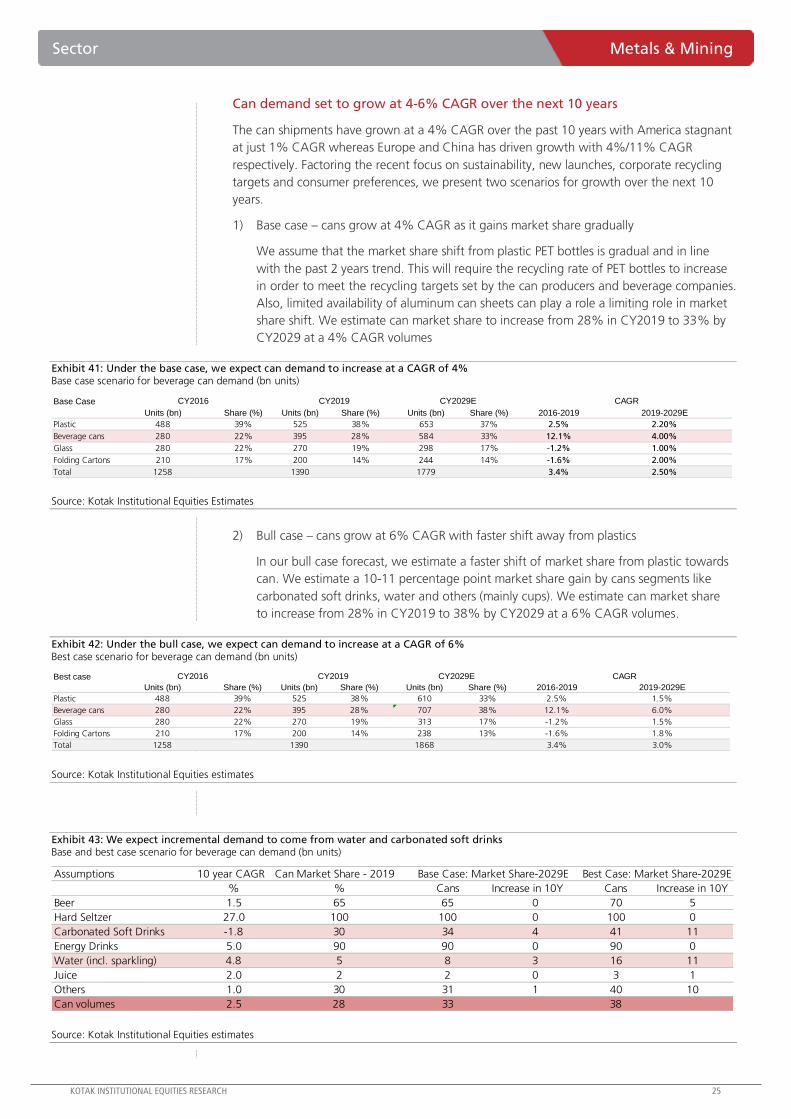

Increasing adoption of aluminum cans by global majors

Coca-Cola is planning to help collect and recycle 100% of its bottles and cans by the year

2030. By then, Coca-Cola hopes that its bottles will use 50% recycled content.

PepsiCo has plans to make 100% of its packaging recyclable or recoverable by 2025.

French group Danone announced that it would replace some plastic bottles with

aluminum cans across its Flyte brand in Britain, Sparkles in Poland and Aqua d’or in

Denmark.

Coca-Cola, PepsiCo, and Nestle are also launching some canned versions of water brands

across certain markets.

According to Ball, a shift of only 1% of global soft drinks, beer and bottled water from

plastic and glass to cans, would equate to a surge in demand of approximately 24 bn

more cans – compared to the current global market of 394.9 bn cans.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

Sector Metals & Mining

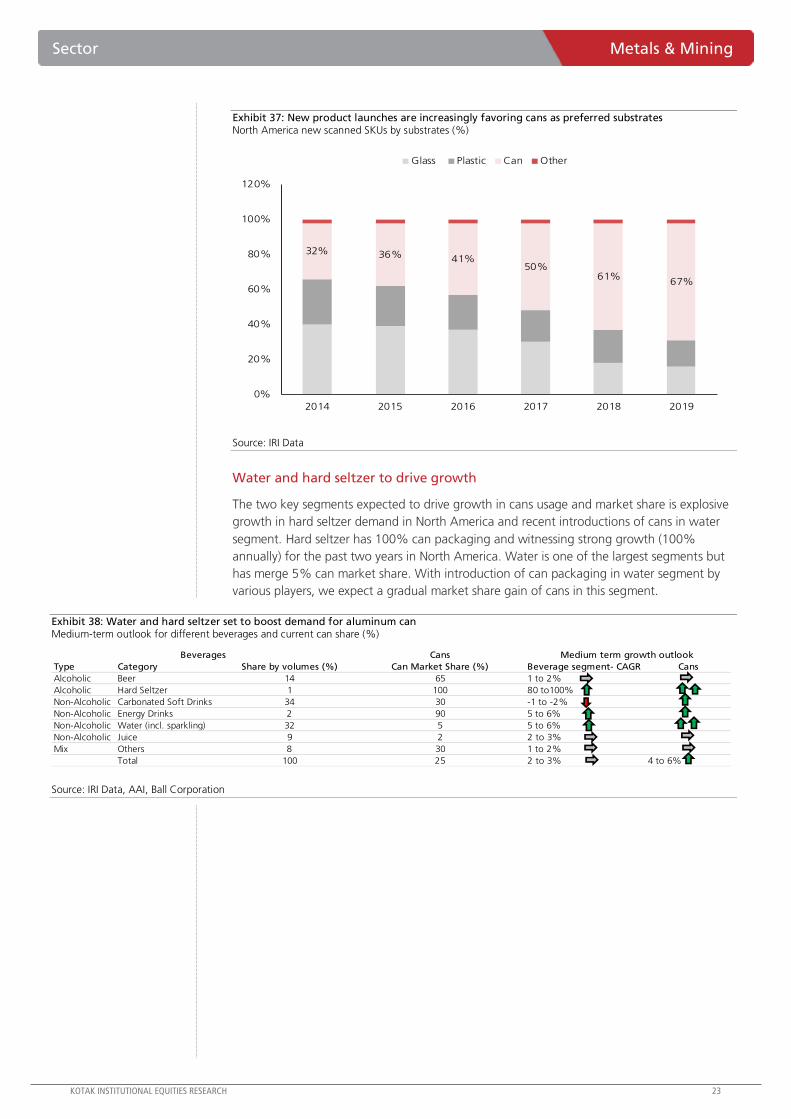

Exhibit 37: New product launches are increasingly favoring cans as preferred substrates North America new scanned SKUs by substrates (%)

32% 36% 41%50%

61%67%

0%

20%

40%

60%

80%

100%

120%

2014 2015 2016 2017 2018 2019

Glass Plastic Can Other

Source: IRI Data

Water and hard seltzer to drive growth

The two key segments expected to drive growth in cans usage and market share is explosive

growth in hard seltzer demand in North America and recent introductions of cans in water

segment. Hard seltzer has 100% can packaging and witnessing strong growth (100%

annually) for the past two years in North America. Water is one of the largest segments but

has merge 5% can market share. With introduction of can packaging in water segment by

various players, we expect a gradual market share gain of cans in this segment.

Exhibit 38: Water and hard seltzer set to boost demand for aluminum can Medium-term outlook for different beverages and current can share (%)

Cans

Type Category Share by volumes (%) Can Market Share (%) Beverage segment- CAGR Cans

Alcoholic Beer 14 65 1 to 2%

Alcoholic Hard Seltzer 1 100 80 to100%

Non-Alcoholic Carbonated Soft Drinks 34 30 -1 to -2%

Non-Alcoholic Energy Drinks 2 90 5 to 6%

Non-Alcoholic Water (incl. sparkling) 32 5 5 to 6%

Non-Alcoholic Juice 9 2 2 to 3%

Mix Others 8 30 1 to 2%

Total 100 25 2 to 3% 4 to 6%

Medium term growth outlook Beverages

Source: IRI Data, AAI, Ball Corporation

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

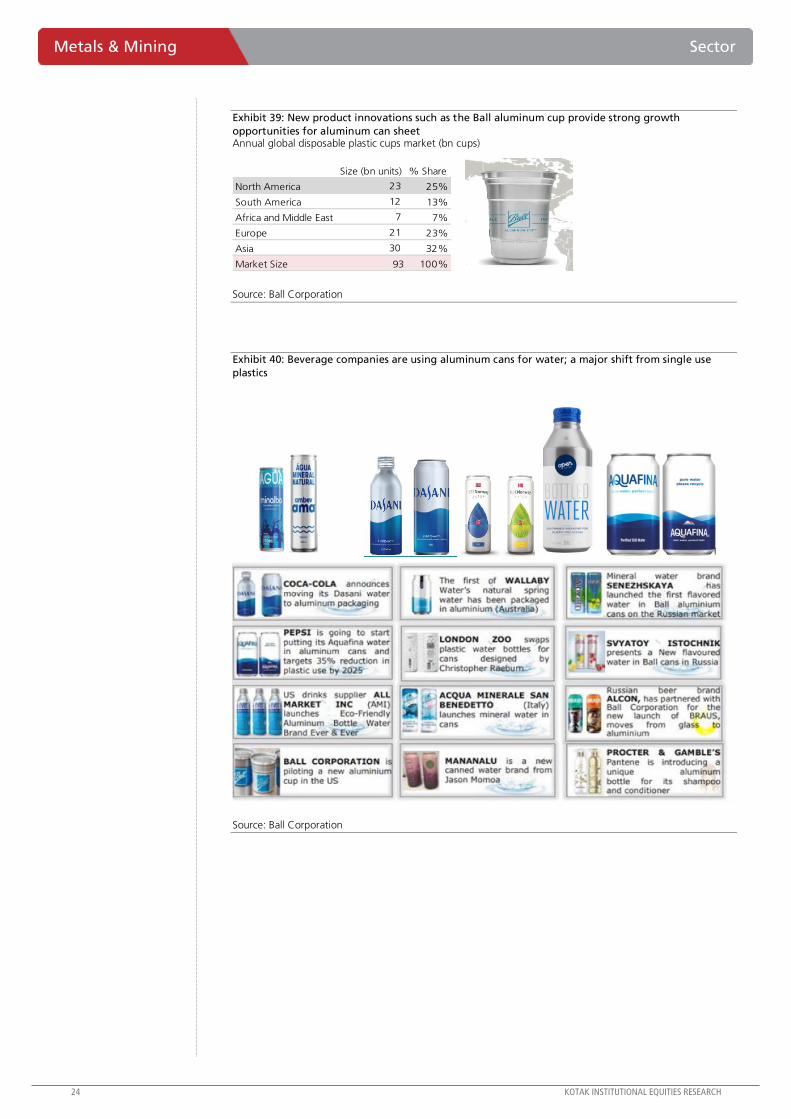

Exhibit 39: New product innovations such as the Ball aluminum cup provide strong growth

opportunities for aluminum can sheet Annual global disposable plastic cups market (bn cups)

Size (bn units) % Share

North America 23 25%

South America 12 13%

Africa and Middle East 7 7%

Europe 21 23%

Asia 30 32%

Market Size 93 100%

Source: Ball Corporation

Exhibit 40: Beverage companies are using aluminum cans for water; a major shift from single use

plastics

Source: Ball Corporation

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

Sector Metals & Mining

Can demand set to grow at 4-6% CAGR over the next 10 years

The can shipments have grown at a 4% CAGR over the past 10 years with America stagnant

at just 1% CAGR whereas Europe and China has driven growth with 4%/11% CAGR

respectively. Factoring the recent focus on sustainability, new launches, corporate recycling

targets and consumer preferences, we present two scenarios for growth over the next 10

years.

1) Base case – cans grow at 4% CAGR as it gains market share gradually

We assume that the market share shift from plastic PET bottles is gradual and in line

with the past 2 years trend. This will require the recycling rate of PET bottles to increase

in order to meet the recycling targets set by the can producers and beverage companies.

Also, limited availability of aluminum can sheets can play a role a limiting role in market

share shift. We estimate can market share to increase from 28% in CY2019 to 33% by

CY2029 at a 4% CAGR volumes

Exhibit 41: Under the base case, we expect can demand to increase at a CAGR of 4% Base case scenario for beverage can demand (bn units)

Base Case

Units (bn) Share (%) Units (bn) Share (%) Units (bn) Share (%) 2016-2019 2019-2029E

Plastic 488 39% 525 38% 653 37% 2.5% 2.20%

Beverage cans 280 22% 395 28% 584 33% 12.1% 4.00%

Glass 280 22% 270 19% 298 17% -1.2% 1.00%

Folding Cartons 210 17% 200 14% 244 14% -1.6% 2.00%

Total 1258 1390 1779 3.4% 2.50%

CAGRCY2016 CY2019 CY2029E

Source: Kotak Institutional Equities Estimates

2) Bull case – cans grow at 6% CAGR with faster shift away from plastics

In our bull case forecast, we estimate a faster shift of market share from plastic towards

can. We estimate a 10-11 percentage point market share gain by cans segments like

carbonated soft drinks, water and others (mainly cups). We estimate can market share

to increase from 28% in CY2019 to 38% by CY2029 at a 6% CAGR volumes.

Exhibit 42: Under the bull case, we expect can demand to increase at a CAGR of 6% Best case scenario for beverage can demand (bn units)

Best case

Units (bn) Share (%) Units (bn) Share (%) Units (bn) Share (%) 2016-2019 2019-2029E

Plastic 488 39% 525 38% 610 33% 2.5% 1.5%

Beverage cans 280 22% 395 28% 707 38% 12.1% 6.0%

Glass 280 22% 270 19% 313 17% -1.2% 1.5%

Folding Cartons 210 17% 200 14% 238 13% -1.6% 1.8%

Total 1258 1390 1868 3.4% 3.0%

CAGRCY2016 CY2019 CY2029E

Source: Kotak Institutional Equities estimates

Exhibit 43: We expect incremental demand to come from water and carbonated soft drinks Base and best case scenario for beverage can demand (bn units)

Assumptions 10 year CAGR Can Market Share - 2019

% % Cans Increase in 10Y Cans Increase in 10Y

Beer 1.5 65 65 0 70 5

Hard Seltzer 27.0 100 100 0 100 0

Carbonated Soft Drinks -1.8 30 34 4 41 11

Energy Drinks 5.0 90 90 0 90 0

Water (incl. sparkling) 4.8 5 8 3 16 11

Juice 2.0 2 2 0 3 1

Others 1.0 30 31 1 40 10

Can volumes 2.5 28 33 38

Base Case: Market Share-2029E Best Case: Market Share-2029E

Source: Kotak Institutional Equities estimates

26 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

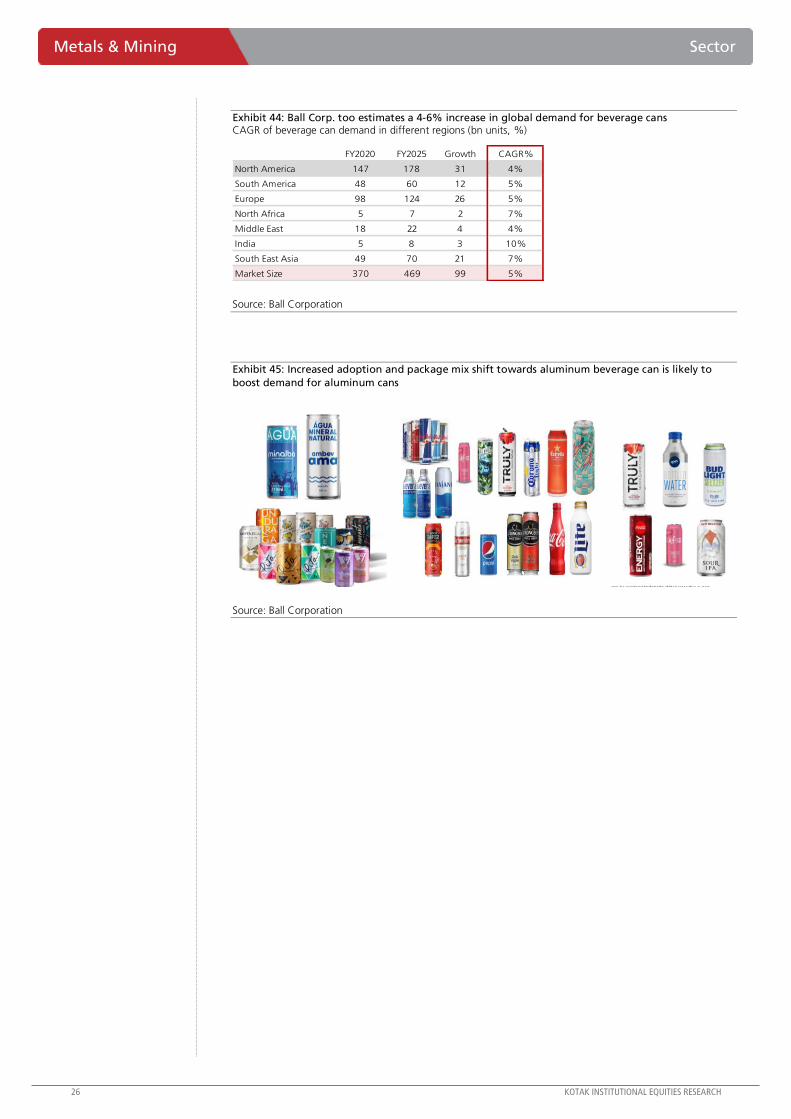

Exhibit 44: Ball Corp. too estimates a 4-6% increase in global demand for beverage cans CAGR of beverage can demand in different regions (bn units, %)

FY2020 FY2025 Growth CAGR%

North America 147 178 31 4%

South America 48 60 12 5%

Europe 98 124 26 5%

North Africa 5 7 2 7%

Middle East 18 22 4 4%

India 5 8 3 10%

South East Asia 49 70 21 7%

Market Size 370 469 99 5%

Source: Ball Corporation

Exhibit 45: Increased adoption and package mix shift towards aluminum beverage can is likely to

boost demand for aluminum cans

Source: Ball Corporation

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

Sector Metals & Mining

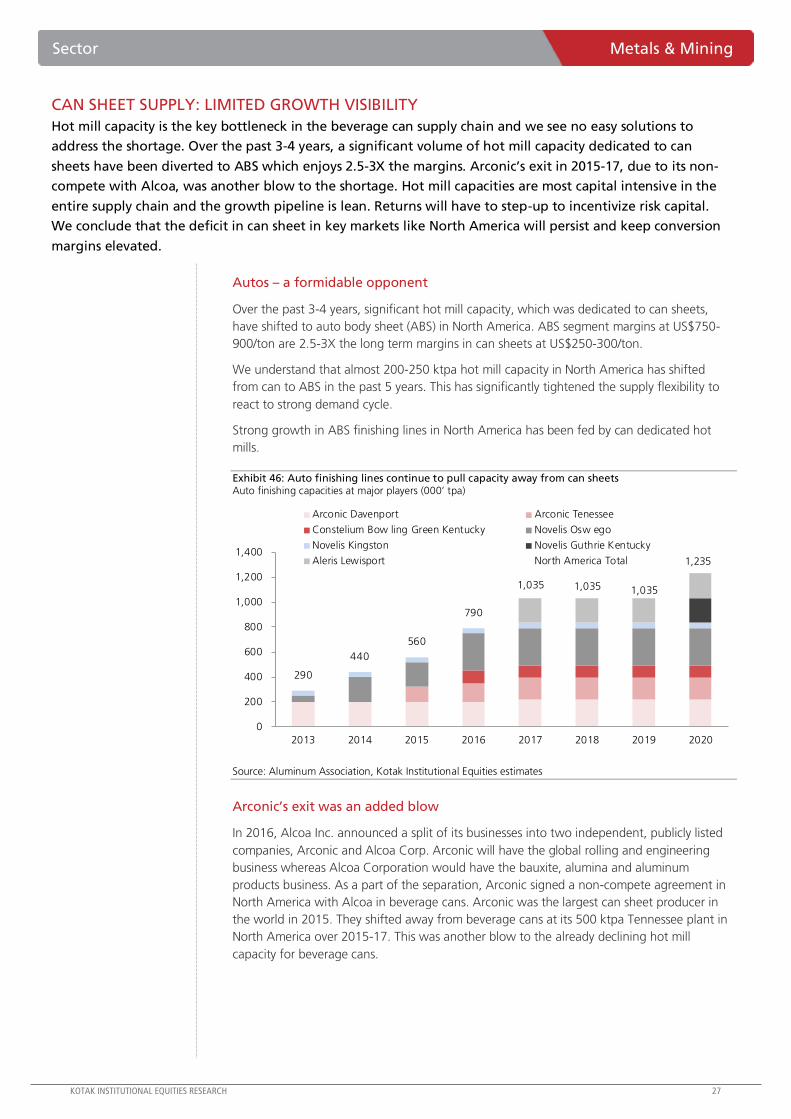

CAN SHEET SUPPLY: LIMITED GROWTH VISIBILITY

Hot mill capacity is the key bottleneck in the beverage can supply chain and we see no easy solutions to

address the shortage. Over the past 3-4 years, a significant volume of hot mill capacity dedicated to can

sheets have been diverted to ABS which enjoys 2.5-3X the margins. Arconic’s exit in 2015-17, due to its non-

compete with Alcoa, was another blow to the shortage. Hot mill capacities are most capital intensive in the

entire supply chain and the growth pipeline is lean. Returns will have to step-up to incentivize risk capital.

We conclude that the deficit in can sheet in key markets like North America will persist and keep conversion

margins elevated.

Autos – a formidable opponent

Over the past 3-4 years, significant hot mill capacity, which was dedicated to can sheets,

have shifted to auto body sheet (ABS) in North America. ABS segment margins at US$750-

900/ton are 2.5-3X the long term margins in can sheets at US$250-300/ton.

We understand that almost 200-250 ktpa hot mill capacity in North America has shifted

from can to ABS in the past 5 years. This has significantly tightened the supply flexibility to

react to strong demand cycle.

Strong growth in ABS finishing lines in North America has been fed by can dedicated hot

mills.

Exhibit 46: Auto finishing lines continue to pull capacity away from can sheets Auto finishing capacities at major players (000’ tpa)

290

440

560

790

1,035 1,035 1,035

1,235

0

200

400

600

800

1,000

1,200

1,400

2013 2014 2015 2016 2017 2018 2019 2020

Arconic Davenport Arconic Tenessee

Constelium Bow ling Green Kentucky Novelis Osw ego

Novelis Kingston Novelis Guthrie Kentucky

Aleris Lewisport North America Total

Source: Aluminum Association, Kotak Institutional Equities estimates

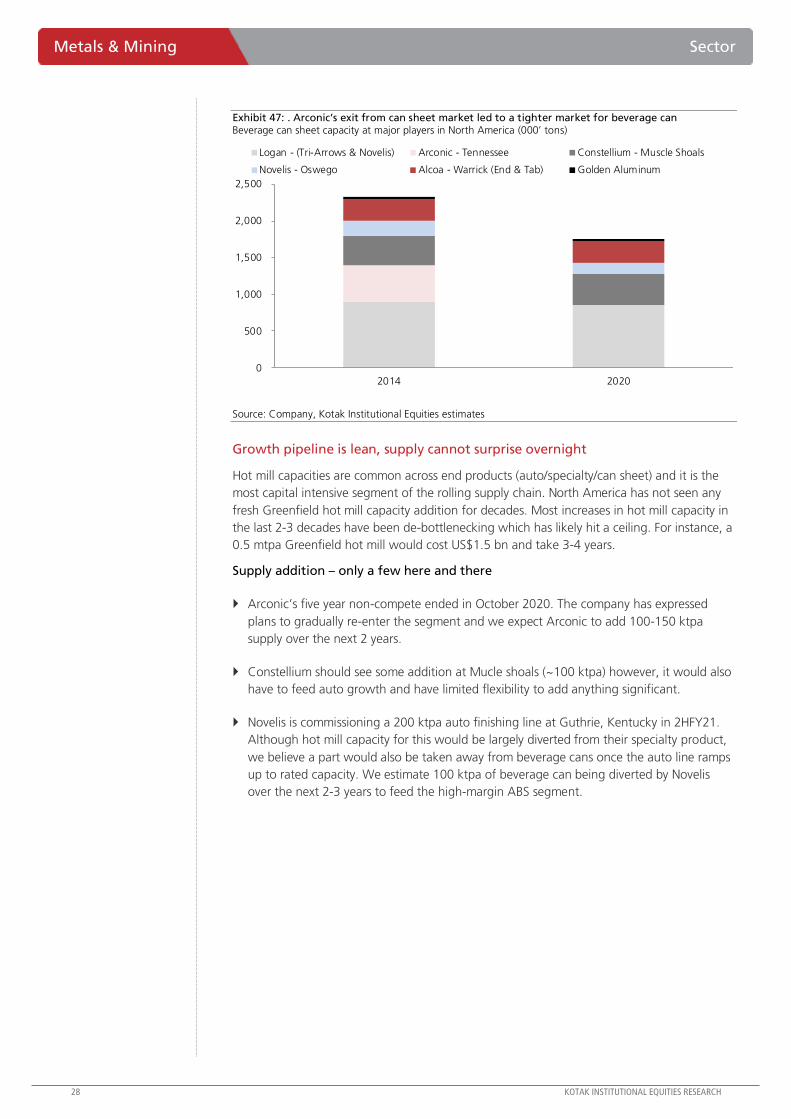

Arconic’s exit was an added blow

In 2016, Alcoa Inc. announced a split of its businesses into two independent, publicly listed

companies, Arconic and Alcoa Corp. Arconic will have the global rolling and engineering

business whereas Alcoa Corporation would have the bauxite, alumina and aluminum

products business. As a part of the separation, Arconic signed a non-compete agreement in

North America with Alcoa in beverage cans. Arconic was the largest can sheet producer in

the world in 2015. They shifted away from beverage cans at its 500 ktpa Tennessee plant in

North America over 2015-17. This was another blow to the already declining hot mill

capacity for beverage cans.

28 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

Exhibit 47: . Arconic’s exit from can sheet market led to a tighter market for beverage can Beverage can sheet capacity at major players in North America (000’ tons)

0

500

1,000

1,500

2,000

2,500

2014 2020

Logan - (Tri-Arrows & Novelis) Arconic - Tennessee Constellium - Muscle Shoals

Novelis - Oswego Alcoa - Warrick (End & Tab) Golden Aluminum

Source: Company, Kotak Institutional Equities estimates

Growth pipeline is lean, supply cannot surprise overnight

Hot mill capacities are common across end products (auto/specialty/can sheet) and it is the

most capital intensive segment of the rolling supply chain. North America has not seen any

fresh Greenfield hot mill capacity addition for decades. Most increases in hot mill capacity in

the last 2-3 decades have been de-bottlenecking which has likely hit a ceiling. For instance, a

0.5 mtpa Greenfield hot mill would cost US$1.5 bn and take 3-4 years.

Supply addition – only a few here and there

Arconic’s five year non-compete ended in October 2020. The company has expressed

plans to gradually re-enter the segment and we expect Arconic to add 100-150 ktpa

supply over the next 2 years.

Constellium should see some addition at Mucle shoals (~100 ktpa) however, it would also

have to feed auto growth and have limited flexibility to add anything significant.

Novelis is commissioning a 200 ktpa auto finishing line at Guthrie, Kentucky in 2HFY21.

Although hot mill capacity for this would be largely diverted from their specialty product,

we believe a part would also be taken away from beverage cans once the auto line ramps

up to rated capacity. We estimate 100 ktpa of beverage can being diverted by Novelis

over the next 2-3 years to feed the high-margin ABS segment.

KOTAK INSTITUTIONAL EQUITIES RESEARCH 29

Sector Metals & Mining

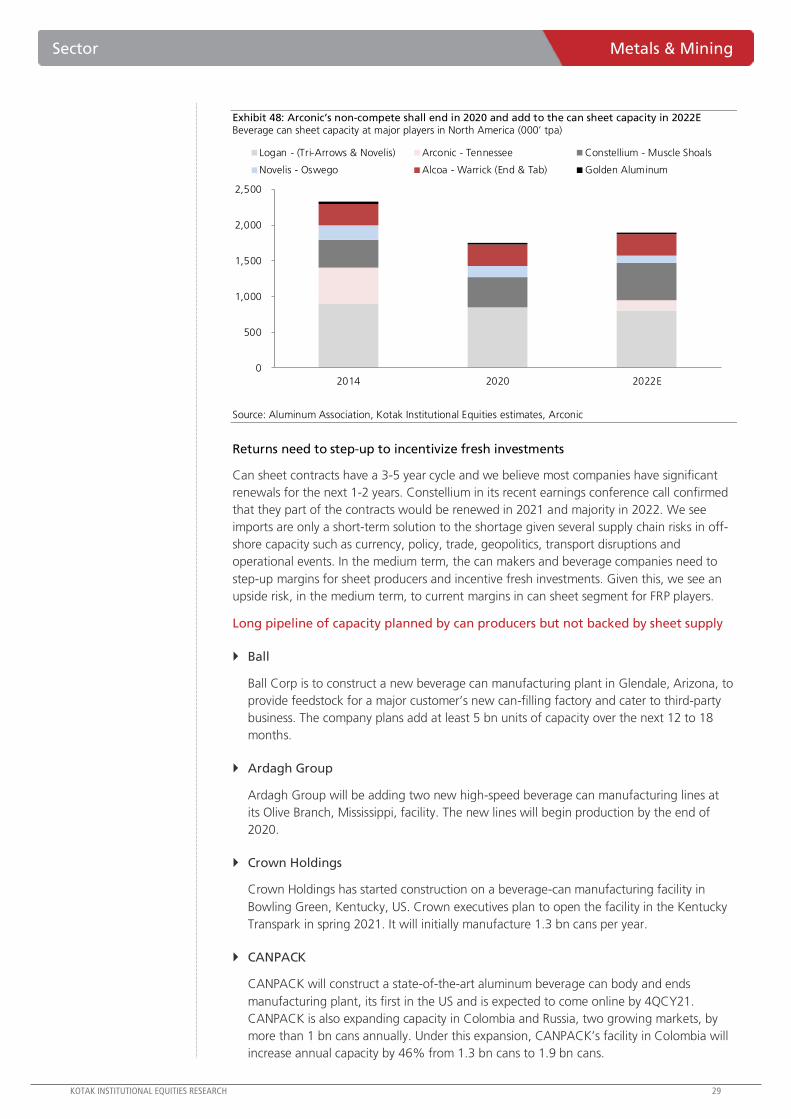

Exhibit 48: Arconic’s non-compete shall end in 2020 and add to the can sheet capacity in 2022E Beverage can sheet capacity at major players in North America (000’ tpa)

0

500

1,000

1,500

2,000

2,500

2014 2020 2022E

Logan - (Tri-Arrows & Novelis) Arconic - Tennessee Constellium - Muscle Shoals

Novelis - Oswego Alcoa - Warrick (End & Tab) Golden Aluminum

Source: Aluminum Association, Kotak Institutional Equities estimates, Arconic

Returns need to step-up to incentivize fresh investments

Can sheet contracts have a 3-5 year cycle and we believe most companies have significant

renewals for the next 1-2 years. Constellium in its recent earnings conference call confirmed

that they part of the contracts would be renewed in 2021 and majority in 2022. We see

imports are only a short-term solution to the shortage given several supply chain risks in off-

shore capacity such as currency, policy, trade, geopolitics, transport disruptions and

operational events. In the medium term, the can makers and beverage companies need to

step-up margins for sheet producers and incentive fresh investments. Given this, we see an

upside risk, in the medium term, to current margins in can sheet segment for FRP players.

Long pipeline of capacity planned by can producers but not backed by sheet supply

Ball

Ball Corp is to construct a new beverage can manufacturing plant in Glendale, Arizona, to

provide feedstock for a major customer’s new can-filling factory and cater to third-party

business. The company plans add at least 5 bn units of capacity over the next 12 to 18

months.

Ardagh Group

Ardagh Group will be adding two new high-speed beverage can manufacturing lines at

its Olive Branch, Mississippi, facility. The new lines will begin production by the end of

2020.

Crown Holdings

Crown Holdings has started construction on a beverage-can manufacturing facility in

Bowling Green, Kentucky, US. Crown executives plan to open the facility in the Kentucky

Transpark in spring 2021. It will initially manufacture 1.3 bn cans per year.

CANPACK

CANPACK will construct a state-of-the-art aluminum beverage can body and ends

manufacturing plant, its first in the US and is expected to come online by 4QCY21.

CANPACK is also expanding capacity in Colombia and Russia, two growing markets, by

more than 1 bn cans annually. Under this expansion, CANPACK’s facility in Colombia will

increase annual capacity by 46% from 1.3 bn cans to 1.9 bn cans.

30 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

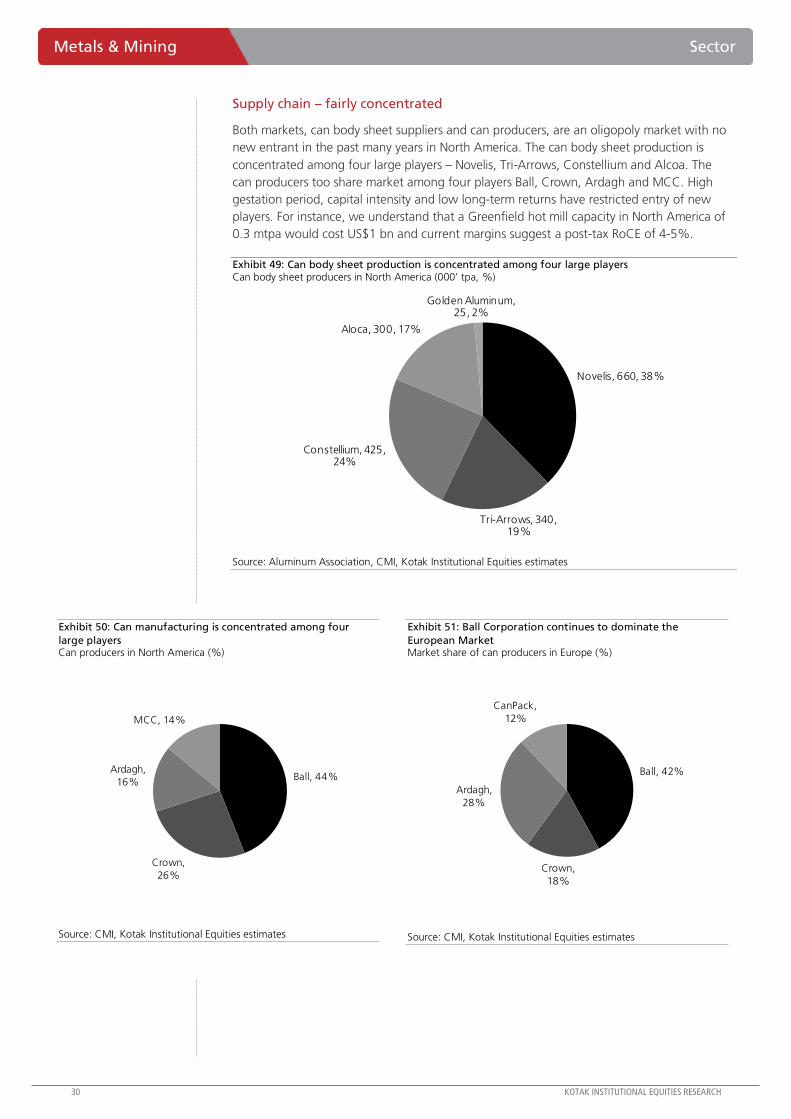

Supply chain – fairly concentrated

Both markets, can body sheet suppliers and can producers, are an oligopoly market with no

new entrant in the past many years in North America. The can body sheet production is

concentrated among four large players – Novelis, Tri-Arrows, Constellium and Alcoa. The

can producers too share market among four players Ball, Crown, Ardagh and MCC. High

gestation period, capital intensity and low long-term returns have restricted entry of new

players. For instance, we understand that a Greenfield hot mill capacity in North America of

0.3 mtpa would cost US$1 bn and current margins suggest a post-tax RoCE of 4-5%.

Exhibit 49: Can body sheet production is concentrated among four large players Can body sheet producers in North America (000’ tpa, %)

Novelis, 660, 38%

Tri-Arrows, 340, 19%

Constellium, 425, 24%

Aloca, 300, 17%

Golden Aluminum, 25, 2%

Source: Aluminum Association, CMI, Kotak Institutional Equities estimates

Exhibit 50: Can manufacturing is concentrated among four

large players Can producers in North America (%)

Ball, 44%

Crown,

26%

Ardagh,

16%

MCC, 14%

Source: CMI, Kotak Institutional Equities estimates

Exhibit 51: Ball Corporation continues to dominate the

European Market Market share of can producers in Europe (%)

Ball, 42%

Crown,

18%

Ardagh,

28%

CanPack,

12%

Source: CMI, Kotak Institutional Equities estimates

KOTAK INSTITUTIONAL EQUITIES RESEARCH 31

Sector Metals & Mining

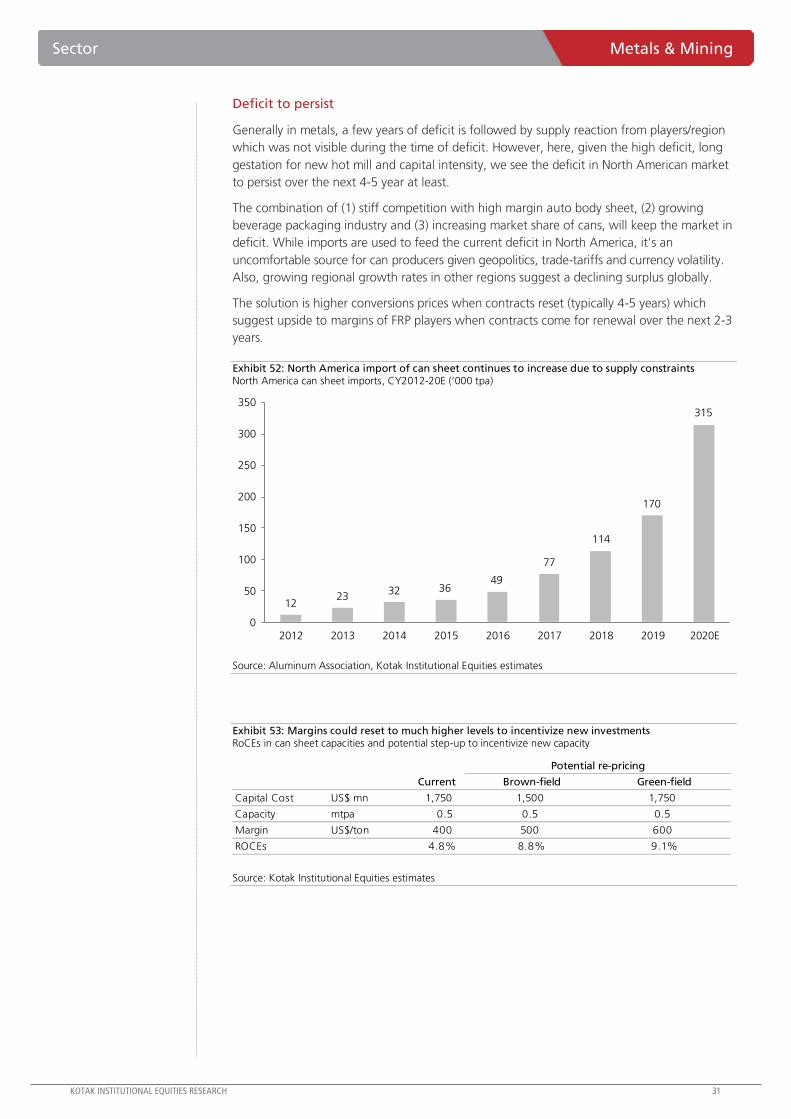

Deficit to persist

Generally in metals, a few years of deficit is followed by supply reaction from players/region

which was not visible during the time of deficit. However, here, given the high deficit, long

gestation for new hot mill and capital intensity, we see the deficit in North American market

to persist over the next 4-5 year at least.

The combination of (1) stiff competition with high margin auto body sheet, (2) growing

beverage packaging industry and (3) increasing market share of cans, will keep the market in

deficit. While imports are used to feed the current deficit in North America, it’s an

uncomfortable source for can producers given geopolitics, trade-tariffs and currency volatility.

Also, growing regional growth rates in other regions suggest a declining surplus globally.

The solution is higher conversions prices when contracts reset (typically 4-5 years) which

suggest upside to margins of FRP players when contracts come for renewal over the next 2-3

years.

Exhibit 52: North America import of can sheet continues to increase due to supply constraints North America can sheet imports, CY2012-20E (‘000 tpa)

1223

32 3649

77

114

170

315

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016 2017 2018 2019 2020E

Source: Aluminum Association, Kotak Institutional Equities estimates

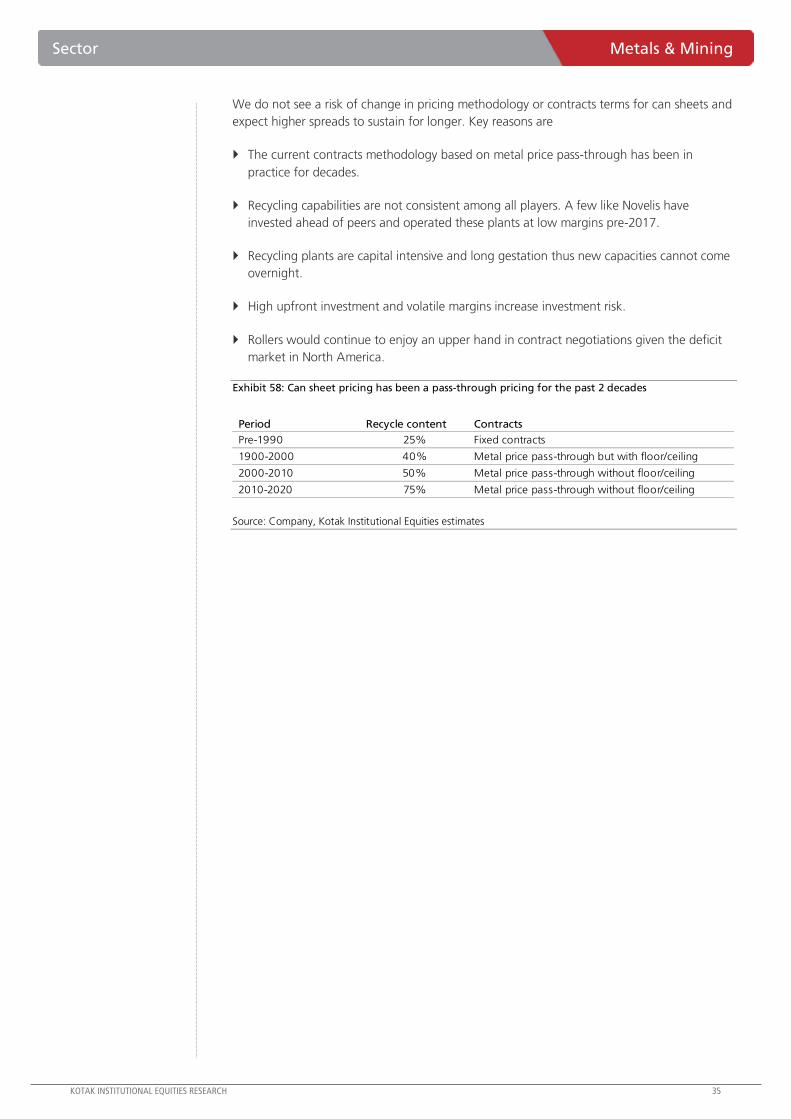

Exhibit 53: Margins could reset to much higher levels to incentivize new investments RoCEs in can sheet capacities and potential step-up to incentivize new capacity

Current Brown-field Green-field

Capital Cost US$ mn 1,750 1,500 1,750

Capacity mtpa 0.5 0.5 0.5

Margin US$/ton 400 500 600

ROCEs 4.8% 8.8% 9.1%

Potential re-pricing

Source: Kotak Institutional Equities estimates

32 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Metals & Mining Sector

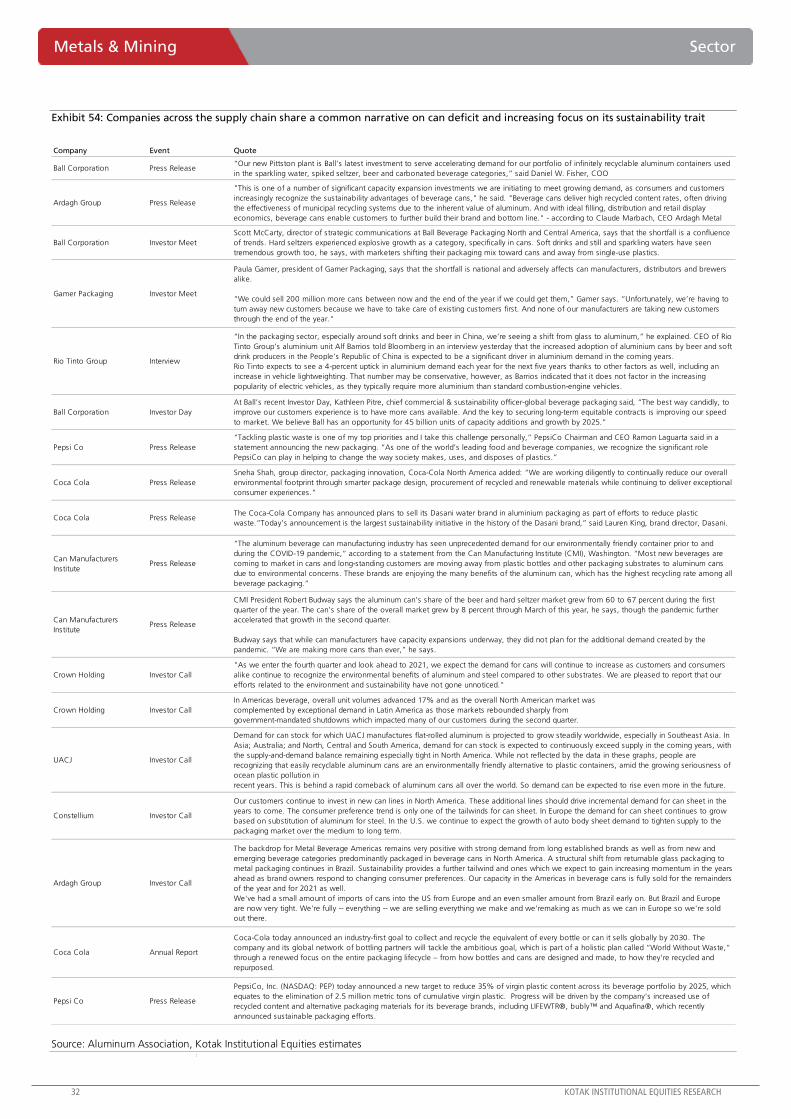

Exhibit 54: Companies across the supply chain share a common narrative on can deficit and increasing focus on its sustainability trait

Company Event Quote

Ball Corporation Press Release“Our new Pittston plant is Ball’s latest investment to serve accelerating demand for our portfolio of infinitely recyclable aluminum containers used

in the sparkling water, spiked seltzer, beer and carbonated beverage categories,” said Daniel W. Fisher, COO

Ardagh Group Press Release

"This is one of a number of significant capacity expansion investments we are initiating to meet growing demand, as consumers and customers

increasingly recognize the sustainability advantages of beverage cans," he said. "Beverage cans deliver high recycled content rates, often driving

the effectiveness of municipal recycling systems due to the inherent value of aluminum. And with ideal filling, distribution and retail display

economics, beverage cans enable customers to further build their brand and bottom line." - according to Claude Marbach, CEO Ardagh Metal

Ball Corporation Investor Meet

Scott McCarty, director of strategic communications at Ball Beverage Packaging North and Central America, says that the shortfall is a confluence

of trends. Hard seltzers experienced explosive growth as a category, specifically in cans. Soft drinks and still and sparkling waters have seen

tremendous growth too, he says, with marketers shifting their packaging mix toward cans and away from single-use plastics.

Gamer Packaging Investor Meet

Paula Gamer, president of Gamer Packaging, says that the shortfall is national and adversely affects can manufacturers, distributors and brewers

alike.

“We could sell 200 million more cans between now and the end of the year if we could get them,” Gamer says. “Unfortunately, we’re having to

turn away new customers because we have to take care of existing customers first. And none of our manufacturers are taking new customers

through the end of the year."

Rio Tinto Group Interview

“In the packaging sector, especially around soft drinks and beer in China, we’re seeing a shift from glass to aluminum,” he explained. CEO of Rio

Tinto Group’s aluminium unit Alf Barrios told Bloomberg in an interview yesterday that the increased adoption of aluminium cans by beer and soft

drink producers in the People’s Republic of China is expected to be a significant driver in aluminium demand in the coming years.

Rio Tinto expects to see a 4-percent uptick in aluminium demand each year for the next five years thanks to other factors as well, including an

increase in vehicle lightweighting. That number may be conservative, however, as Barrios indicated that it does not factor in the increasing

popularity of electric vehicles, as they typically require more aluminium than standard combustion-engine vehicles.

Ball Corporation Investor Day

At Ball’s recent Investor Day, Kathleen Pitre, chief commercial & sustainability officer-global beverage packaging said, “The best way candidly, to

improve our customers experience is to have more cans available. And the key to securing long-term equitable contracts is improving our speed

to market. We believe Ball has an opportunity for 45 billion units of capacity additions and growth by 2025.”

Pepsi Co Press Release

“Tackling plastic waste is one of my top priorities and I take this challenge personally,” PepsiCo Chairman and CEO Ramon Laguarta said in a

statement announcing the new packaging. “As one of the world’s leading food and beverage companies, we recognize the significant role