Embed Size (px)

Citation preview

AL

MT41410,

I� i1CP11d�

t i

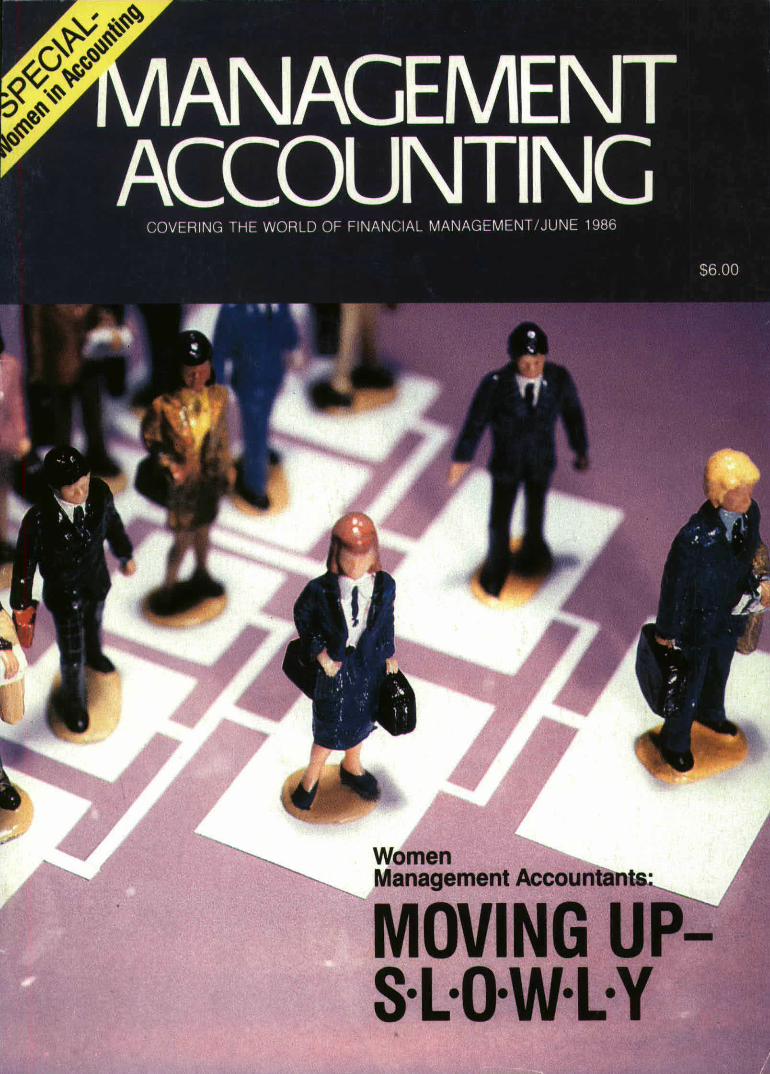

WomenManagement Accountants:

OVING U

SuperCalc

CA " thesoftwareto ha when

ha one,It's unfair.No matter how many copies of a top

micro software program you buy foryour corporation, you're forced to paya price.

Ahigh price. For every copy.Well, now you don't have to.take it any-

more. Introduc-ingthe ComputerAssociates Cor-porate LicensingProgram.

Now you canprovide yourcompany withthe strongestline of micro soft-ware in the world.From a single

Themoreeopies vendoryou buy, Programs like

the more you save. SuperCalcO3

Release 2 integrated spreadsheet, data-base, and graphics package,SuperProject® Plus, thepowerful resource man-agement software pack - ,age. EasyBusinessSystemsTM integratedaccounting software. AndEasyWriter II® for wordprocessing.

� c

So you can standardize yourcom-pany's micro software. From 25 copiesto an unlimited license.

And along with each CorporateLicense, we also offer the most com-prehensive support and maintenance

N . program in the industry. Andour reproducible masterdiskgives you total control oversoftware distribution in your

The Corporate LicensingProgram includes free prod-

uct upgrades and enhance -ments. Expert technical support.

Optional seminars, product training,

The way /as CANCircle number 9 on reply card.

Computer Associates produc tivity softw are: SuperCakg3 Release Y: SuperCq03al Superi'mlec ts: Ea'yWnter II , System ; EasyPlannar '`. F.asyFilPm:' Easy Bus iness Systems " accottmmg soltware: EasyPlus " : EasyPlus" Network Manager, General Ledger and Fimnnal Reprmer : ActV Wms IRecewa6le: Inventory Control and Analysis: Order Emry: Payroll: Retail Inmiang: Time. Billing, and Client Receivables: job Costing.

C 1986 Computer Assaiates International, Inc.

and application development. Evencomplete docu-mentation and f" ,

We also include the strongestsupport program in the industry.

reference materials.Corporate Licensing. Anotherbusiness solution from ComputerAssociates. The world's mostexperienced independent busi-ness software maker. With a clientfist alone that includes over 80% of

the Fortune 1000.For more information on our

Corporate Licensing program, callPat Williams at 1-800. 227 -0112(in CA, call 1 -800- 228 - 1090).

Because our Corporate Licensingprogram is an idea that makes morethan dollars for your company.

It makes sense.

R OMPUTERSSMIATES

Softwaresuperior by design.

ON HIRING,FIRING

For your free booklet contact one of100 Accountemps offices on three continents, or write:

Accountemps, Administrative Services Dept.,522 Fifth Avenue, New York, NY 10036

accounImps. _ yWorld's largest temporary service

specializing in accounting, bookkeeping, and data processing.Circle number 3 on reply card

P 1986 Robert Hall International Inc Offices independently owned and operated.

MANAGEMENTACCOUNTING

Profession Women in Management Accounting: Moving Up... Slowly 20By Susan Jayson and Kathy Williams

More women than ever are carving out careers in accounting and finance. To find out howwell they are doing in business and industry, MANAGEMENT ACCOUNTING surveyed 500 ofNAA's women managers, controllers, chief financial officers, and company presidents —and here are the results.

Women Accountants —Do They Earn as Much as Men? 27By Josephine Olson and Irene Frieze

Contrary to popular belief, not all women with MBAs in accounting believe their careerchoice offers a lucrative salary and an executive title.

Surviving Your First Job 32By Patricia Douglas, Teresa Beed, Karen Clark, and Sylvia Weisenburger

Technical proficiency is the first step, but it doesn't guarantee success. You also need tomaster office politics, behavior, and attire appropriate to your company, and social skills.

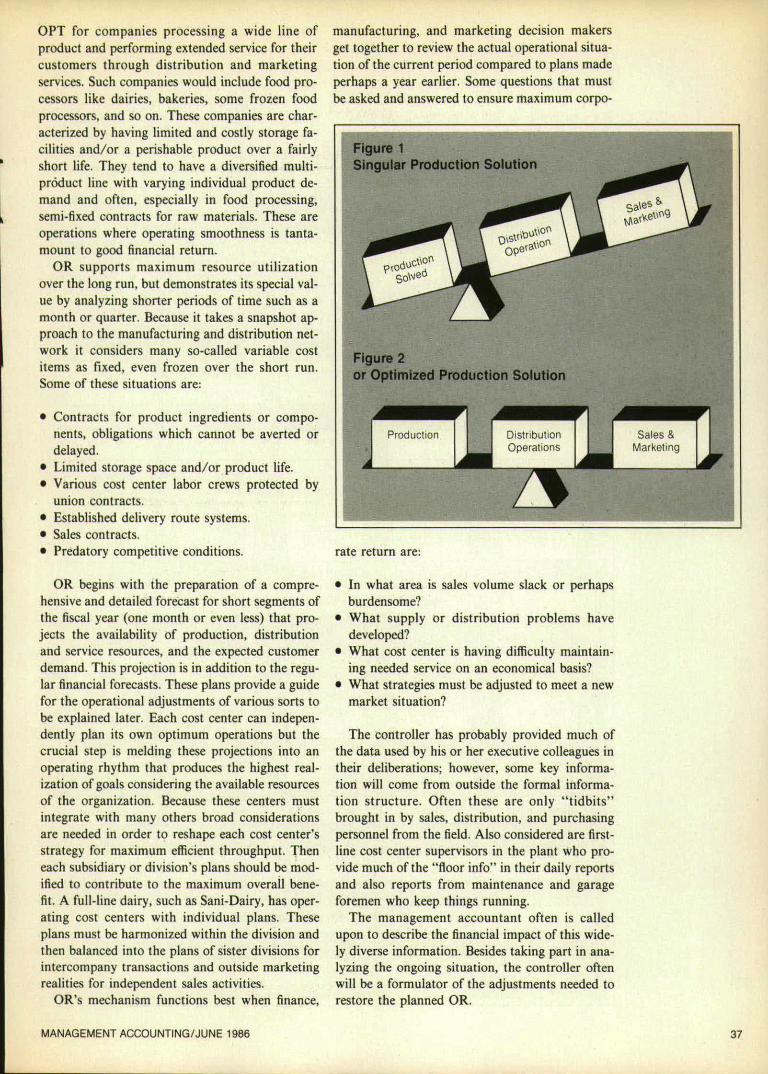

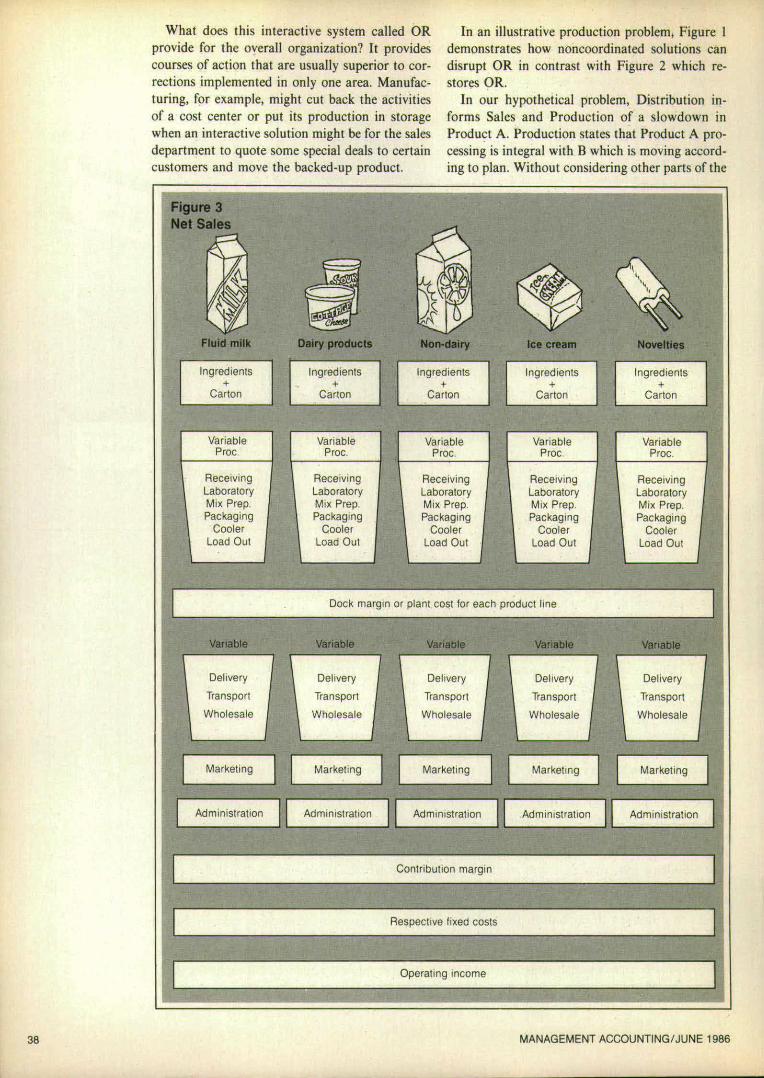

Manufacturing Operating Rhythm 36By James Wagner

The introduction of production and inventory management techniques such as MRP, JIT,and OPT have made factories more efficient. Operating rhythm (OR) goes one step fur-ther— building on OPT to ensure that a company's operations harmonize for a greatercorporate return.

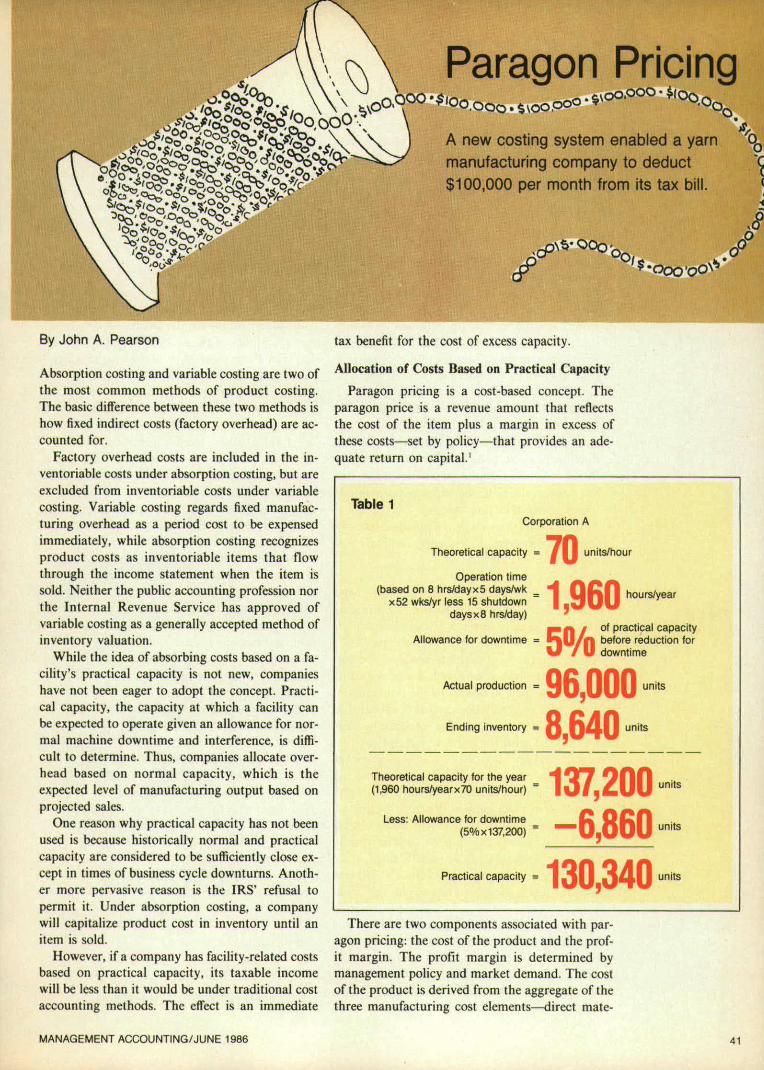

Cost Paragon Pricing 41Control By John A. Pearson

Manufacturers using a costing system based on practical capacity receive immediate taxbenefits when they go through periods of economic downturn-

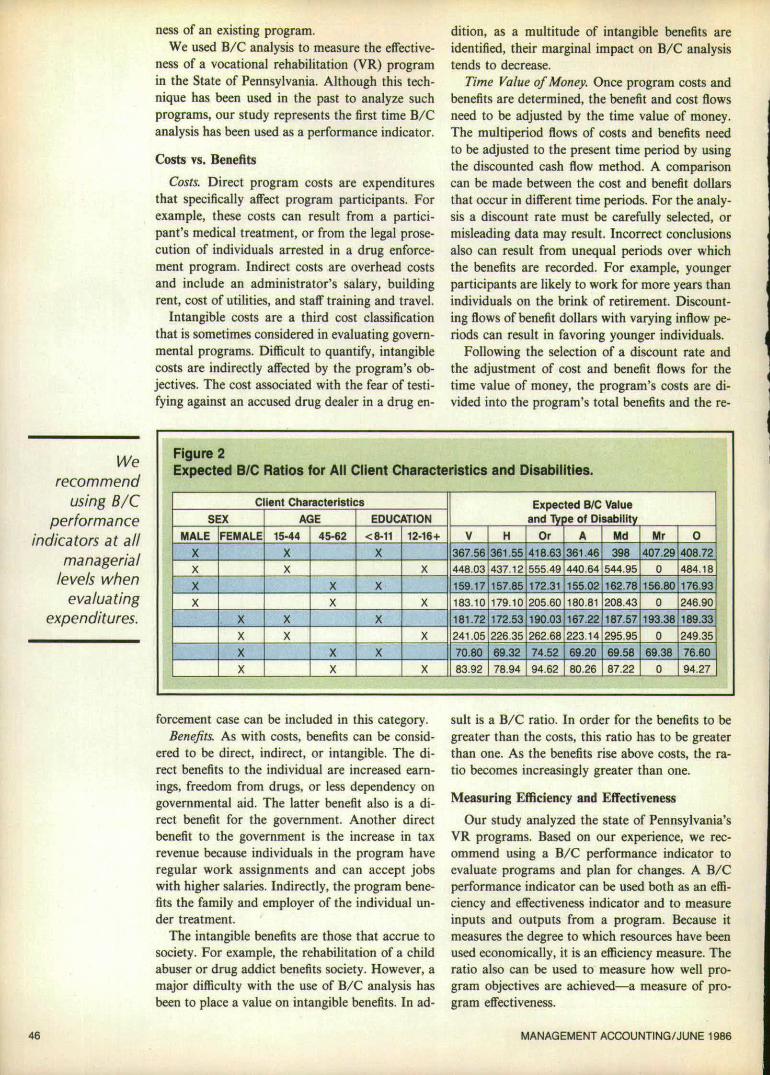

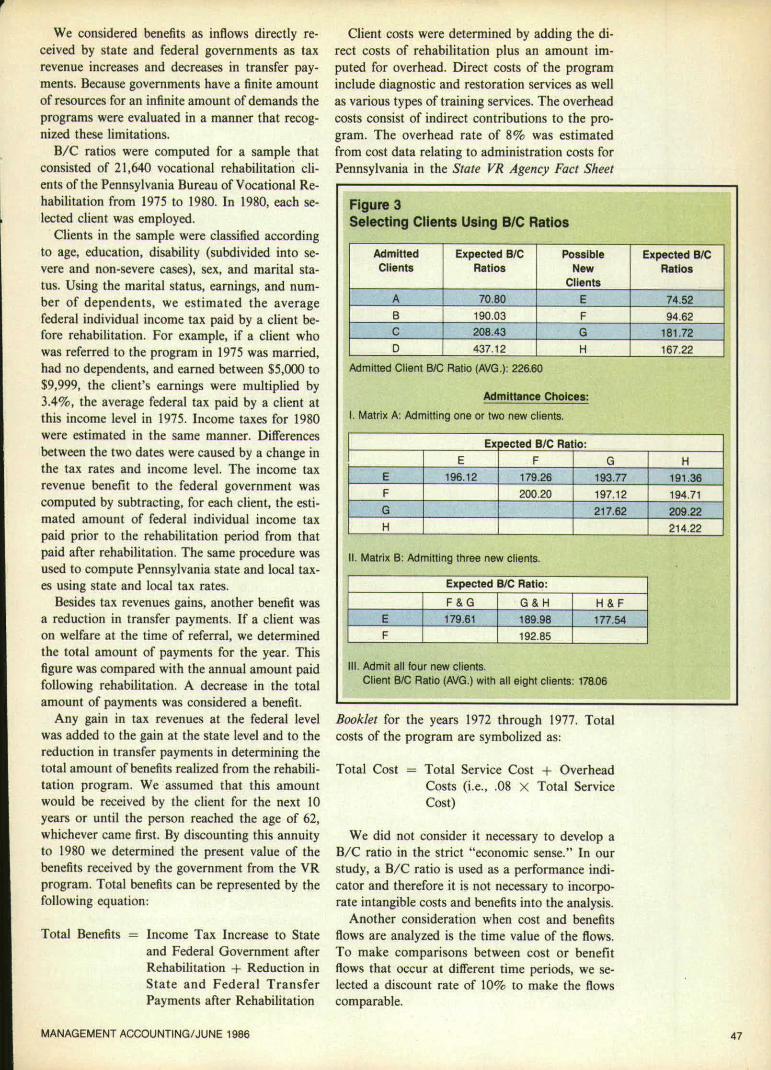

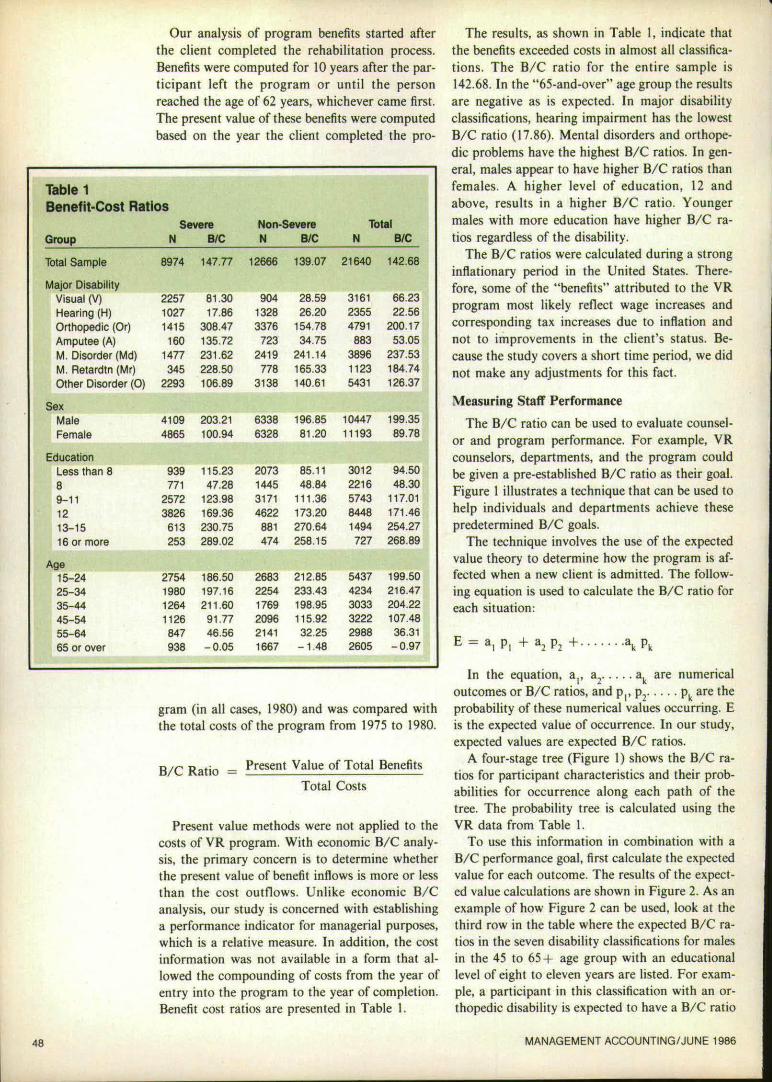

Benefit-Cost Analysis as a Performance Indicator 44By G. Stevenson Smith and M.S. Tseng

This management accounting technique can evaluate the efficiency and effectiveness ofan organization's programs and personnel.

Contracting Restoring Public Confidence in Government Contractors 51By Fred J. Newton

When taxpayers learn that the Pentagon has been buying three -cent screws for $91 theybecome highly irate and lose faith in government contracting. A government auditor de-scribes how faith can be restored in government contracting and still allow contractors tomake a decent return.

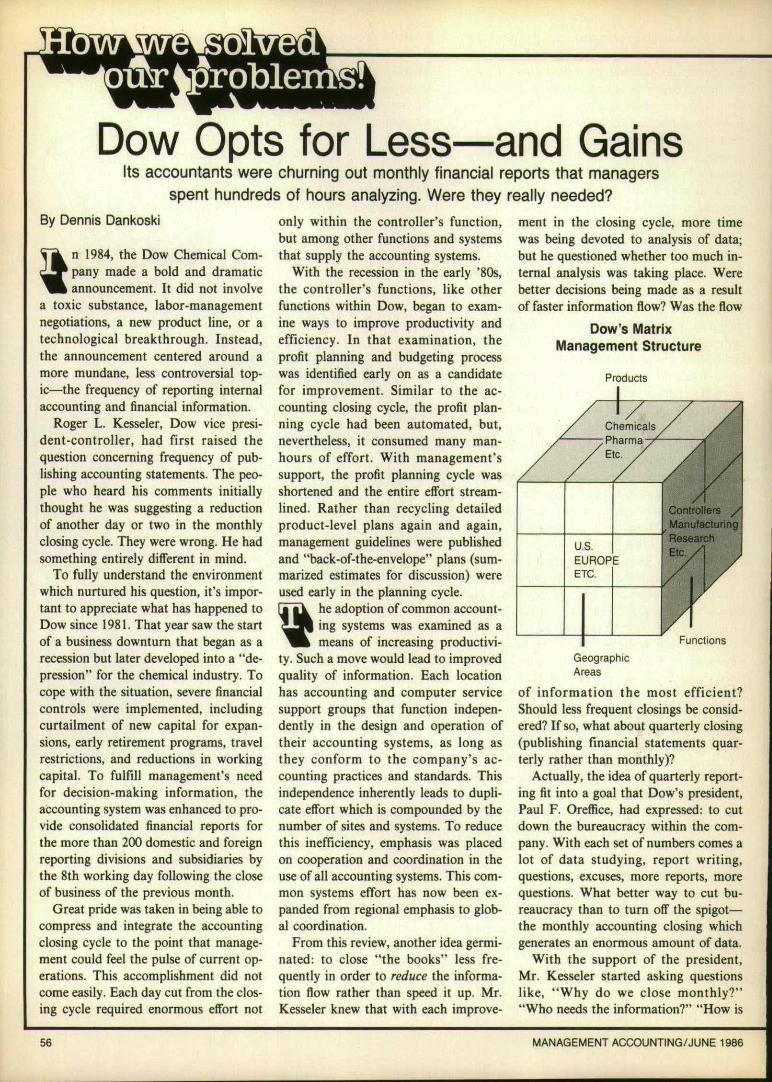

Brainstorming Dow Opts for Less —and Gains 56By Dennis Dankowski

In the first of a series on how members solved critical accounting and financial problems, aDow manager tells how the company decided to reduce its reporting —not increase it.

MANAGEMENT ACCOUNTING /JUNE 1986

MAP MAP Statement of Purpose and Operation 58This new Statement on Management Accounting explains the purpose and operation ofthe series.

NAA NAA Topical Index Vol. LXVII 65By Staff

Departments Perspectives economic service 4

Opinion the entrepreneurial instinct is sti ll wi th us 6

Taxes cash boo t received treated as capital gain 8

Computers and Accounting a super IBM XT compatible 10

Management Accounting Practices MAP committee actions 12

Research advising small businesses on microcomputer so ftware 14

Letters to the Editor accounting education: the Ph.D. `problem' 15

Data Sheet more U.S. f i rms borrow abroad 17

Managing Your Career how to tell the boss the bad news 18

Institute of Certified Management Accountants Beyer medal winners 40

Accounting Education more NAA student chapters needed 50

In the Library 61

People in the News 70

New Products /Services 72

Advertisers' Index 72

Cover: By Mandel & Wagreich, Inc.

Views expressed herein are authors' and do not represent Association policy unless so stated. Publi-cation of paid advertising and new product and service information does not constitute an endorse-ment by the Association of the advertiser or the product or service. Quantity reprints of any article inMANAGEMENT ACCOUNTING or back issues (subject to availability) may be obtained from Special OrderDepartment, NAA, P.O. Box 433, Montvale, NJ 07645 -0433.

Authorization to photocopy items for internal or personal use, or the internal or personal use of specif-ic clients, is granted by the National Association of Accountants to libraries and other users registeredwith the Copyright Clearance Center (CCC) Transactional Reporting Service, provided that the basefee of $1.00 per copy, plus 10c per page, is paid directly to CCC, 21 Congress St., Salem, MA 01970.0025- 1690/86 $1.00 + 10c.

MANAGEMENT ACCOUNTING /JUNE 1986 3

PERSPECTIVES

Economic Service

The National Association of Accountants is a recognized education-al organization. It concentrates its interests within the fields of finan-cial management and professional accounting. In those areas ithopes to render a broad economic service to its membership and tothe financial community. Maximizing this service is the challengethat faces each administration.

The Association effort stands firm on three legs. First, it dependson the paid staff at Montvale. This group provides the organizationalexpertise and the operating continuity that sustains the effective ca-pacity of the total effort.

The second element of organizational capacity is represented bythe national commit t ees and their ad hoc counterparts. Thesegroups are expected to provide the innovative thrusts that discoverand organize new programs and carry them forward to their goals. Itusually happens that only a few of the committees receive specialattention in any given year. In part this is due to the energy of partic-ular chairpersons or committee members; more probably the spe-cial notoriety occurs because of the timeliness of the subject mat-ter. Undeniably, however, the professional reputation of theAssociation becomes enhanced as new activities are started andthe Association is led into new arenas of economic service.

The third element of strength —and probably the most essential —lies in the chapter and council activity. It is at this level of operationthat contact is made with the full 90,000 members. The NAA existsprimarily to be of service to that membership and its interests. Onlyif tasks are competently and enthusiastically done at the chapterlevel will the membership be serviced and the needed resourcesmade available for the work of the national committees and staff.

During the past year I have heard at various times that "nationalis not interested in what the field wants" and I have heard it saidthat "the field is not interested in professional matters; it only wantsto have pleasant little dinner sessions." These are isolated com-ments and obviously they do not represent the majority view. How-ever, they are an evidence of dissatisfaction and a fragmenting ofour unified thrust. It is appropriate, therefore, to ask what service anindividual member is looking to get. I am led to believe that the indi-vidual members of NAA want: camaraderie, technical information,training opportunities, assistance for the needy, professional reputa-tion, career contacts, and an improved profession.

It is this set of interests which must be organized and financedyear after year. It is no small task. If you, as a member, found itimpossible to be an active part of last year's Association program,be concerned now with what you can do in the next year to supple-ment field or headquarters efforts. If you, as a chapter officer ordirector, came up a little short in your achievements, take steps nowto regain the lost ground.

It is incumbent upon all of us to identify what we expect the Asso-ciation to do and what we are prepared to contribute to the effort.We need talent, we need ideas, we need enthusiasm! Let us moveforward toward common goals —let us have a unity of purpose —letus be cohesive in optimizing our economic service to the member-ship and to the community.

HERBERT C. KNORTZNAA President, 1985 -86

MANAGEMENTACCOUNTING

(ISSN 0025 -1690)

VOL. LXVII NO. 12 JUNE 1986

official publication of theNational Association of Accountants

Executive DirectorRobert L. Shultis

PUBLISHERJames D. Collier

EDITORErwin S. Koval

MANAGING EDITORRobert F. Randall

TECHNICAL EDITORSusan Jayson

FEATURE EDITORKathy Williams

ASSISTANT EDITORElizabeth Warren

CONTRIBUTING EDITORRobert Half

EDITORIAL ASSISTANTEllen Rose

ADVERTISINGDoryne Gerstein, Manager

Deborah R. Moore, Assistant

CIRCULATIONJoseph Loren, Manager

PRODUCTIONStephen McCrea, ManagerHelen G. Caso, Assistant

ADVERTISING REPRESENTATIVESMontvale, NJ 07645— Doryne Gerstein, NAA,10 Paragon Dr., (201) 573 -6275.

San Jose, CA 95120 —Neal Manning, 6628Tam O'Shanter Or., (408) 997.2929.

Pasadena, CA 91105 —Karin Altonaga.JJH &S, 119 W. Bellevue Dr., (818) 796 -9200.

Montgomery, AL 36104 — Charlotte Bass, theLongshore Group, Inc., 603 Martha Street.(205) 263 -6050.

BPA membership applied forDecember 1985

MANAGEMENT ACCOUNTING (ISSN 0025 -1690) is pub-lished monthly by the National Association of Accountants.10 Paragon Dr., Montvale, N.J., 07645, (201) 573 -9000. Price$6.00 per copy. Subscription rates, per year. $27 (non -de-ductible from dues). nonmembers. $54.00. Second classpostage paid at Montvale. N.J., and additional mailing of-fices. To ensure uninterrupted mail service, send present ad-dress label and new address including ZIP number to Mem-bership Records Dept., NAA, Montvale, N.J.. 07645. Allowsix weeks for change. NAA's telex number is 181 -162: fac-simile number is 201573 -8185. POSTMASTER, Send ad-dress changes to MANAGEMeNT ACCOUNTING, Montvale, N.J..07645 -0433

Copyright 1986 by theNational Association of Accountants

MANAGEMENT ACCOUNTING /JUNE 1986

Rates: $2.00 per word, 15 wordminimum. Abbreviat ions, ZIPcodes, and phone numbers countas one word each. All classif iedadvert ising must be prepaid.Non- commissionable.

Closing Date: Deadline for copy isthe first day of the month precedingpublication date.

Classified

WANTED: Adverti sers who wantto reach tho usa nds Of MANAGE-MENT ACCOUNTING decis ion -mak ers for only $2.00 a word.Whether you are buying, sell ing,looking, or hiring, you will be moreeffective On the MANAGEMENT AC-COUNTING Classified page, startingin Augus t .

Copy: All advertising must be sub-mitted in typewritten, double -spaced form. No telephone ordersaccepted.

Box Number: Inquire ClassifiedDept.

Display Classif ied: One- twelfthpage (one column x 2% ") is avail-able at $395.

Payment: Payment in U.S. fundsmust accompany each order. Mailcopy to Doryne Gerstein, MANAGE-MENT ACCOUNTING, 10 ParagonDrive, POB 433, Montvale, NJ07645.

Acceptance: Publisher reservesthe right to accept or reject adver-tisements for MANAGEMENT AC-COUNTING Classified.

Up to 50 words FREE ' to compan-ies that are looking for employeeswho hold CMA certificates and sospecify in advertisement.

' Up to six insertions

OpinionRobert L. Shultis, Executive Director

The Entrepreneurial Instinct IsStill With Us

Receipt recently of some material from theCommission on the Bicentennial of the UnitedStates Constitution sent me back, as a long-time history buff, to one of the nation's first andbest efforts at public relations, The FederalistPapers. These, you will recall, were a series ofsome 85 essays by Alexander Hamilton, JamesMadison, and John Jay, published in newspa-pers in New York City in 1787 and 1788 to con-vince New Yorkers and others to support thesoon -to -be -voted -upon Constitution of the Unit-ed States.

What has this to do with entrepreneurs, ac-countants, and such? Plenty! Whether we re-member or not, the basis for our whole societyand our whole economy rests on a principlepromulgated in the Constitution and reiteratedby the authors of The Federalist. In The Feder-alist No. 12, Hamilton offered the following:"The prosperity of commerce is now percei-ved... to be the most useful as well as themost productive source of national wealth, andhas accordingly become a primary object oftheir political cares." In other words, foster apolitical climate where people can enjoy thefruits of their labors (their property) and theeconomy will grow and the country prosper.

That's been happening to a greater or lesserdegree for the past 200 years. Our founding fa-thers were right. The entrepreneurial instinctwas there then; it is still with us. According to arecent Dun & Bradstreet survey, U.S. business-es plan to create nearly three million new jobsin 1986, two - thirds of which will be with compa-nies employing fewer than 100 workers.

Accountants can certainly participate in thisgrowth. Recently Jack Fox (Washington, D.C.Chapter) paid us a visit. Jack has been anNAAer since the '70s, but one recent claim tofame was his article published in the April 1983issue of MANAGEMENT ACCOUNTING, titled "HowI Started My Own Accounting Business," whichelicited more comment and inquiries from read-ers than any other single article in recent mem-

ory. This article was the genesis for his book,Starting and Building Your Own AccountingBusiness, published by John Wiley. Accoun-tants can join the ranks of entrepreneurs, too.

In addition, they can be a big help to otherentrepreneurs, offering advice and designingan information system adequate to the needsof the owners. That occasion arose recentlywhen two young people opened a new restau-rant in the area. Neither had had any experi-ence with restaurants nor any formal collegeeducation or business training. What they didhave in large measure was ambition, enthusi-asm, and —most importantly —a concept, anidea.

Once the concept was developed — "fondueis fun" —and the location decided upon, thework really began: interior design, review andapprovals, redesign, construction, furniture andappliances, and as opening day approached,menus, pricing, buying, and organizing the sys-tem. Lots of professional skills contributed —lawyers, carpenters, electricians, and, ofcourse, accountants.

How can we as accountants contribute tostart -up businesses? Much depends on the lev-el of sophistication and business expertise ofthe entrepreneurs. In the case referred toabove, the owners were probably typical offirst - timers —long on ideas and short on busi-ness skills and money. The most importantarea where accountants contributed was inplanning and budgeting: nothing very sophisti-cated, but at least a rough breakeven point tosee if the business could be successful andwhen such success might be expected.

Then, there was an accounting and informa-tion system to be developed, with particularemphasis on revenue and cash control. Origi-nally, it was too easy to pay for deliveries out ofthe cash drawer, without keeping an adequaterecord. That made it pretty tough to reconciledaily the cash with the sales checks. After afew weeks, it became important to know whatwas selling best and when it was selling. (Thechocolate fondue, based on a secret recipe,was drawing raves and going great guns withthe after -8:00 p.m. crowd.) Using a PC was anatural here.

All this, of course, is nothing new for an ac-countant. That's what we do and why we exist.It is new for many of our budding business peo-ple as they struggle to succeed in this competi-tive society. What was true 200 years ago whenthe Constitution was in process of developmentis still true today. Thanks partly to the businessclimate it engendered, there is still opportunityfor those who have an idea and the courage

$#69

6 MANAGEMENT ACCOUNTING /JUNE 1986

( r■� .� C i cy:

a

In mainframe financial software, as in anythingelse, you get what you pay for Remember that

when you read about rampant discountingandprice slashing. At Data Design, we don't cut ourprices to make a sale. That's becauseafterthe salewe don't plan to cut service and support, either. So,while getting a "bargain" may make your day, wedprefer to make your next ten years.

We have a hard -eamed reputation to uphold. Areputation built on 13 years of providing the high-est quality systems and support in the mainframeindustry. And nationally recognized independentsoftware surveys confirm Data Design's unsurpass-ed record of user satisfaction —year after year.

We believe that the fast, trouble -free installationand responsive, knowledgeable support bymanage-ment levelpeople is worth what we charge for it. Sodo companies like Alcoa, Gerber, Pillsbury, Sherwin-

7

Gi

Q1 no A , . - - -

Williams, Merrill Lynch, Bankers' Trust, Bristol -Myers, Federal Express, Litton, Lloyd's Bank, TheNew York Times Company, Owens- Corning, RoyalBusiness Machines, Warner-Lambert and hundredsof other FORTUNE 1000 companies who chooseData Design over other major vendors.

Our customers know that it's important to keepthe purchase pricein perspective, The cost of amainframe system is comprised of three elements:1) The purchase price of the package; 2) The cost ofinstallation andconversion and 3) The cost of dailysystem operation and maintenance. Of these threecost elements, the first isbyfar the smallest. What'sthe point of savingeven S50,000 on the purchaseprice if implementation and operations costs even-tually add several hundred thousand dollars to thetotal? The trouble with cheap financial software isthat you may never stop paying for it.

Circle number 6 on reply card.

Financial software by Data Design. When youcan't afford anything but the best.

GENERAL LEDGERACCOUNTS PAYABLE

PURCHASE ORDER CONTROLFIXED ASSETS

CAPITAL PROJECT MANAGEMENTLearn more about the best financial software

available. Call Betty Fulton toll -free at 800 -556 -5511.

DATAS� JATES

F ,.xcellenceinfinancialsoJtware. By design.1279 Oakmead Parkway, Sunnyvale, CA 94086

Taxes

Israel Blumenfrucht, Editor

Cash Boot ReceivedTreated as Capital Gain

A recent decision of the Tax Court in Clark (86TC No. 10), makes it easier for a taxpayer whoreceives cash "boot" as part of a tax -free reor-ganization to treat the cash received as capitalgain and not as an ordinary dividend.

In the case at hand, NL Corporation acquiredall of the outstanding shares of Basin Surveys,Inc., in a tax -free reorganization from Donald E.Clark, the sole shareholder of Basin. NL offeredClark a choice between 425,000 shares of NLcommon stock and no cash or, a combinationof 300,000 shares of NL common stock and$3,250,000. Clark accepted NL's combinedstock and cash offer in exchange for all the out-standing shares of Basin.

In general, no gain or loss is recognized in anexchange of stock of one corporation solely forstock of another corporation if the exchangeoccurs pursuant to a plan of reorganization.However, there are instances where, in addi-tion to the new securities issued, the Code al-lows for cash or other property ( "boot ") to beissued without affecting the general nature ofthe reorganization. When such boot is re-ceived, gain is recognized up to the value of theboot received. Generally, the gain is consid-ered a cap ital gain, but under Sect ion356(a)(2), an exchange which has the effect ofa dividend is taxable as ordinary income. TheCode provides certain tests for determiningwhether a distribution is considered a dividendor not.

One of these tests, referred to as a "safeharbor" test, can be applied to tax -free reorga-nizations involving cash boot, if the cash re-ceived is considered a redemption of the newsecurities the taxpayer could have received ifhe had not received any cash. The "safe har-bor" test automatically allows a taxpayer re-ceiving a cash distribution in redemption of hisstock to treat any gain as capital gain if: (1) theshareholder's interest in the stock of the corpo-ration after the redemption is less than 80% ofhis interest before the redemption, and (2) after

the redemption the shareholder owns less than50% of the voting stock.

Clark argued that he qualified under this safeharbor test because had he accepted onlystock from NL he would have owned 1.3% ofits outstanding common stock; by acceptingpart cash, his holdings were 0.92% of the totalcommon outstanding. Thus, by accepting thecash instead of the stock and treating the cashdistribution as a redemption of the NL stock,Clark's interest in NL was reduced to only 71 %(from 1.3% to 0.92 %) of what it would havebeen had he received only stock. Coupled withthe fact that he owned less than 50% of NLCorporation's outstanding stock, he satisfiedboth aspects of the safe harbor test and thecash he received must qualify for capital gaintreatment.

The IRS did not disagree that the exchangequalified as a tax -free reorganization. However,it contended that the cash received by Clarkmust be treated as a dividend. In support of itsargument, the IRS pointed to a case decided bythe Fifth Circuit in 1978 in Shimberg (577 F.21D283 (CA -5 1978)) where the court held that theIRS may treat a cash boot distribution in a tax -free reorganization as if it were made by the ac-quired, and not the acquiring, corporation to itsshareholder and thereby negate the ability ofthe taxpayer to use the safe harbor test. TheIRS argued that if this were not done, then in allcases involving factual circumstances similar tothe instant case, in which the "whale" swallowsthe "minnow," the safe harbor test would resultin an automatic capital gain rule. If a sharehold-er in a smal l closely held corporation ex-changes his interest in that corporation forwhat must be, almost by definit ion, a muchsmaller percent of ownership in a large publiclyheld corporation, a comparison of these per-centage ownership figures will always be sodisparate as to qualify as a redemption of stockby the acquiring corporation and will not resultin an ordinary dividend.

The Tax Court, however, rejected the IRS'sargument and supported its conclusion by cit-ing a similar case decided by the Eighth Circuitin 1973 in Wright (482 F.2d 600 (CA -8, 1973))where the court treated boot as a distributionby the acquiring corporation in a hypotheticalredemption of stock that would have been re-ceived if the target shareholder had receivedadditional stock in lieu of cash. Furthermore,the Tax Court stated, "... we think that, on bal-ance, the Wright test is the more suitable vehi-cle for decision principally because its applica-tion produces a result more within the scope ofthe type of reorganization Congress had in

111# 43

8 MANAGEMENT ACCOUNTING /JUNE 1986

The Tandy®R6000 brings itall t affordably.

0p I

` L

y.>•..n.t� tilatadl� l�rigid�tati� iY

1 r. r r rr r r rr

j

Increase productivitywith a complete multiuseraccounting system

Here's the efficient way to putyour entire office "on line" with apowerful accounting system. TheTandy 6000 computer provides si-multaneous job handling withoutthe expense of multiple computers.Up to six employees can access theTandy 6000 simultaneously, usinglow -cost data terminals.

Plus, we offer the powerful mul-tiuser accounting software youneed. Since several people have ac-cess to the 'Dandy 6000's software,your sales department can checkinventory levels while someone inaccounting updates your generalledger�—at�the�same�time�someoneelse is working on the payroll.

i i i 1 i i i i j '1 ' 1 ' 1 " 1 ' 1 ' 1 I i l c ' I ' I

And since many of our programsinteract with one another, yourTandy 6000 forms the heart of atruly unified accounting system.The Tandy 6000 General Ledgerprogram interacts with our Payroll,Accounts Payable and AccountsReceivable programs. Wheneveraccounts are updated within theseprograms, the General Ledger isautomatically updated.

We also offer many other power-ful multiuser business programs forapplications like database manage-ment and word processing.

The 512K Tandy 6000 HD(26 -6022) comes with the XENIX®multiuser operating system, a high -resolution 12" monitor, plus a built -in�15-�megabyte�hard�disk�drive�—allfor�just�$3499�►.�Add�up�to�five�termi-nals as your business requires.

.ter

— , d a l i f i eA � � h icali f —

Available at over 1200Radio Shack Computer Centers and at

participating Radio Shack stores and dealers.

Radio J'haekCOMPUTER CENTERS

A DIVISION OF TANDY CORPORATION

rm m m m m m m i

Send me a Tandy 6000 brochure.Radio Shack, Dept. 86 -A-720 1

300 One Tandy Center, Fort Worth, TX 76102

Name

Company ,

Address

City

State ZIP ,

Phone

Prices app ly at Rad io Shack Computer Centers and particip ating stores and dealers . XENIX/Registered TM Micros oft Corp.

Circle number 5 on reply card

ComputersandAccountingAlfred M. King, Editor

A Super IBM XT Compatible

Product tested: ITT Xtra XP, with 1024K memo-ry, 10 megabyte hard disk, one 360K diskettedrive, color monitor, color card, standard serialand parallel ports. Price as tested, $5,185. Forfurther information, contact: ITT InformationSystems, 2350 Qume Drive, San Jose, Calif.95131, 1 -800- 321 -7661 (in California 1 -800-368- 7300).

When IBM introduced its family of PC com-puters, many other manufacturers jumped onthe bandwagon with similar machines. Most ofthe early compatibles, however, had a fatalflaw. They could not run many of the IBM PCsoftware packages available unless the soft-ware was modified. The marketplace yawned,and no one bought.

ITT profited by being a latecomer to the PCmarket. Using advanced technology, ITT hascreated an IBM PC XT compatible that is fasterthan an IBM AT and that can run virtually all thesoftware available for the XT. I believe the ap-parent ITT strategy is sound because the XT isstill the microcomputer chosen most often forbusiness use.

What distinguishes the ITT Xtra XP from therest of the compatibles? Our firm owns a com-patible advertised as a "clone" of the IBM XT.After testing it, we believe the ITT XP is morecompatible with the XT than our so- called"clone" despite all the technical advances in-corporated into the XP. We tested softwaresuch as Lotus 1 -2 -3, dBase II /III, WordStar,Multimate, the Norton utilities, and DacEasy,TCS client writeup, and Open Systems ac-counting packages. All ran without problem.We did have problems running SideKick andCopy II PC on the XP, but we believe the overallcompatibility with an IBM PC XT is good.

The ITT XP has several advantages. ITT de-signed the XP for performance by using a fasterprocessor (CPU), faster memory, disk caching,

and a print buffer. The CPU can be set to twospeeds, normal and fast, but normal speedwould be used only to run software that is de-pendent on the processor operating at stan-dard speed.

Disk caching is a process whereby part ofmemory is set aside as a disk work area. Then,large blocks of records are read into the diskwork area at one time from the disk drive.When the next record is required by a program,it is read from the disk work area, not the diskdrive. The processing cycle takes less time be-cause accessing the record in the disk workarea is much faster than actually reading it fromthe disk drive.

The documentation provided is outstandingand includes reference cards for commonlyused commands. After no activity for 15 min-utes, the computer will blank the screen, pre-venting screen burnout. Extensive diagnosticroutines are built into the computer, minimizingrepair time.

The computer has been reliable throughoutseveral months of testing. If service is required,one may call the dealer or ITT Servcom, a na-tionwide service network.

We also are aware of one company that usesITT computers as a base for a multiuser, PC-DOS compatible systems.

The keyboard is not suitable for heavy elec-tronic spreadsheet use because the numerickeypad and cursor keys are combined. A Key -tronics 5151 keyboard with these functionsseparated can be purchased as a replacement.

A typical purchaser would buy this machinewith a 20 megabyte hard disk. Backing up thishard disk to 360K floppy disks would take onehour and 55 floppies. I would recommend thatITT use a dual density (360K / 1.2 meg) dis-kette drive as the IBM AT does to alleviate thisbottleneck.

Clarity of text displayed with the standardcolor card was only fair.

The ITT Xtra XP certainly will run ringsaround the IBM XT, but it seems the enhance-ments stop a little short of making it the leaderin its class. I would use the XP when an XTcompatible is needed, and it would be used fre-quently. Then the performance of the XP willpay for the purchase premium.

One note: a Qume 11 /90 letter quality printerwas provided with the computer for review. Wecannot express an opinion on the printer be-cause it was defective. However, there was noattempt by Qume to fix the printer despite notifi-cation. Draw your own conclusion as to Qumeservice and attitude. ElAlvin Dziurzynski, CPA, CDPAccess Systems, Inc., Knoxville, Tenn.

10 MANAGEMENT ACCOUNTING /JUNE 1986

l „ I l e ' f d h t IWe started out looking fora new General Ledgersystem. We came up witha system that's somuchmore: Consco's AIS Ac-counting Information Sys-tem. Only AIS gives us ourdata the way we need it.It lets us tell the systemwhat we look like and whatwe want. It has no limits onfields or field sizes ... whichallows us to put a lot moredata into AIS, and get a lotmore useful informationout. Using its active datadictionary, we have beenable to add informationabout Firestone's cus-tomers and products, thenanalyze this data to findout what is selling, and towhom.

"Integrated intoConsco's AIS is theirCONSOL Consolidationsystem, the only system

4mmanage todayyou have to takeinto account yourwhole competitiveenvironment andyou have to ask alot more questions.Consco's account-

ing software divesus the answers.17

LarryBurdenMIS VPFIRESTONE

N

Circle number 12 on reply card.

weve oun + a com-pletely automates our inter-company eliminations,allows fast restatementsand reorganizations, plusfully handles our foreigncurrency requirements.

"Best of all, theseConsco systems areready to use. We found wedidn't have to tell themeverything... the basicstructure is all in there.What Consco's done isgive us the ability to modifythem to our needs asrequired ... on line, realtime, no problems!"

To find out how AISand CONSOL can giveyou the answers you'relooking for, write or callConsco Enterprises Inc.,400 Corporate Court,South Plainfield, NJ07080. Telephone (201)561 -2111.

I .

ConscoSystems...for the way youdo business.

C

ManagementAccountingPracticesLouis Bisgay, Editor

MAP Committee Actions Taken

On March 25, NAA's Management AccountingPractices Committee met at the offices of theFinancial Accounting Standards Board in Stam-ford. Before attending to items on the agenda,MAP Committee members heard a report fromMartin Ives, vice chairman of the GovernmentalAccounting Standards Board, on the evolutionand status of the GASB's agenda. In addition,FASB representatives briefed the Committeeon the status of certain FASB projects, includ-ing Accounting for Income Taxes, Accountingfor Stock Compensation Plans, and The Re-porting Entity.

Among other actions, the MAP Committee:

• Approved in principle the proposed State-ment on Management Accounting, "Defini-tion and Measurement of Direct MaterialCost" (MAP, May '86). The Subcommittee onMAP Statement Promulgation will decidewhether input received from external com-mentators warrants change sufficiently sub-stan tive to retu rn the draft to the MAPCommittee.

• Approved a proposed SMA, "Statements onManagement Accounting: Statement of Pur-pose and Operation,,, which explains therole, authority, and developmental processrelat ive to S tatements on ManagementAccounting.

• Agreed to submit letters of comment toGASB on Objectives of Financial Reporting;to AICPA on Reports on the Application ofAccounting Principles; and to IFAC on theImplementation and Enforcement of EthicalRequirements,

Emerging Issues

The FASB's Emerging Issues Task Force wasformed in 1984 to identify and define emergingaccounting issues. From meetings of the Task

Force, the FASB learns whether there is a di-vergence of views on how a particular transac-tion should be reported and obtains insight asto whether (a) additional guidance may beneeded on a timely basis, (b) guidance canawait consideration in an existing FASB pro-ject, or (c) guidance does not appear to beneeded. EITF meetings are open to public ob-servation, and minutes of the meetings, alongwith issue summary packages, are available tothe public.

As of March 1986, the EITF has discussed104 issues. For readers who may be interestedto learn the types of issues that have been cov-ered, here is a summary:

Subject No. of Issues

Income taxes 13Financial institutions 19Financial instruments 23Off- balance sheet financing 10Pensions /employee benefits 5Business combinations 10Inventory/fixed assets /leases 8Real estate 5Other 11

Total 104

Cash Flow Reporting Conclusions

One of the FASB's major agenda projects is"Cash Flow Statements." The Board intends toissue standards that would amend, or replace,APB Opinion 19, "Reporting Changes in Finan-cial Position." At a recent meeting, the Boardreached certain tentative conclusions:

• Investing and financing transactions that donot directly affect cash, currently included instatements of changes in financial position,should be disclosed in a full set of financialstatements, but flexibility may be neededabout whether such disclosures are separatefrom or included within the body of the cashflow statement.

• Guidelines should be established for classify-ing information in cash flow statements intooperating, financing, and investing activities.Interest and taxes would fall under operatingactivities.

• Either the direct or the indirect method of re-porting cash flows would be acceptable.

News Notes

The investigation of the accounting profes-sion by the House Energy and Commerce

0# 43

12 MANAGEMENT ACCOUNTING /JUNE 1986

,A

Standards set so high, they soar.In the world of the professional business

calculator, the name the others are judged by isCanon. And that's the way it's been for over .4%20 years —as long as we've been makingcalculators.

Our Professional Calculatorsare sleek, trim —with weightedand contoured keys for hours ofcomfortable operation. A

And before they ever deliver thefirst in a long life of totals, we make sure thatin design, quality and performance, they meet our

goal of making your office work better, and youroffice a better place to work.

Call 1- 800 - 323 -1000 to find out moreabout Canon Professional Calculators.They're the better answer for years to come.

Because first, they have to answer to us,

CPl218D

Olher CP mooels mcluu..

CP12080 CP1208!CP10180. CP1008D. CP1008

Circle number 2 on reply card.

Where qualify is the constant factor.

CamonELECTRONIC CALCULATORSCanon U.S.A., Inc., One Canon Plaza. Lake Success. NY 11002

case s Gnaw S 1..

NAAResearchPatrick L. Romano, Editor

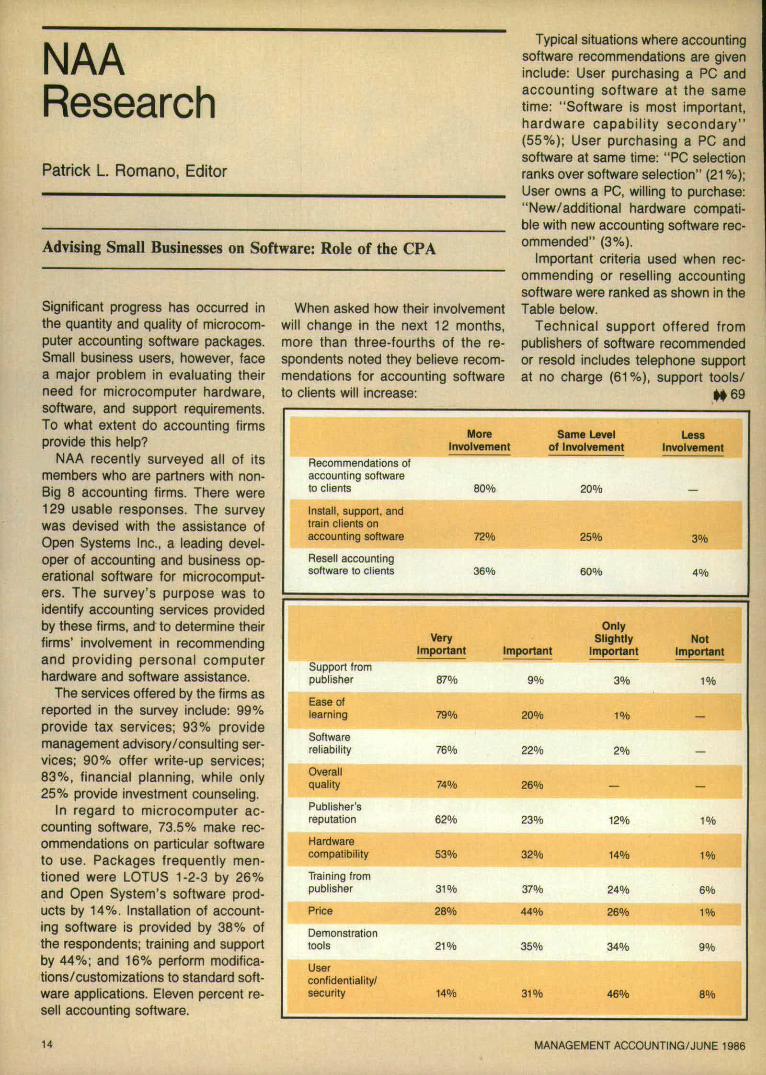

Advising Small Businesses on Software: Role of the CPA

Significant progress has occurred inthe quantity and quality of microcom-puter accounting software packages.Small business users, however, facea major problem in evaluating theirneed for microcomputer hardware,software, and support requirements.To what extent do accounting firmsprovide this help?

NAA recently surveyed all of itsmembers who are partners with non -Big 8 accounting firms. There were129 usable responses. The surveywas devised with the assistance ofOpen Systems Inc., a leading devel-oper of accounting and business op-erational software for microcomput-ers. The survey's purpose was toidentify accounting services providedby these firms, and to determine theirfirms' involvement in recommendingand providing personal computerhardware and software assistance.

The services offered by the firms asreported in the survey include: 99%provide tax services; 93% providemanagement advisory/consulting ser-vices; 90% offer write -up services;83 %, financial planning, while only25% provide investment counseling.

In regard to microcomputer ac-counting software, 73.5% make rec-ommendations on particular softwareto use. Packages frequently men-tioned were LOTUS 1 -2 -3 by 26%and Open System's software prod-ucts by 14 %. Installation of account-ing software is provided by 38% ofthe respondents; training and supportby 44 %; and 16% perform modifica-tions /customizations to standard soft-ware applications. Eleven percent re-sell accounting software.

When asked how their involvementwill change in the next 12 months,more than three - fourths of the re-spondents noted they believe recom-mendations for accounting softwareto clients will increase:

Typical situations where accountingsoftware recommendations are giveninclude: User purchasing a PC andaccount ing software at the sametime: "Software is most important,hardware capability secondary"(55 %); User purchasing a PC andsoftware at same time: "PC selectionranks over software selection" (21 %);User owns a PC, willing to purchase:"New /additional hardware compati-ble with new accounting software rec-ommended" (3 %).

Important criteria used when rec-ommending or reselling accountingsoftware were ranked as shown in theTable below.

Technical support offered frompublishers of software recommendedor resold includes telephone supportat no charge (61 %), support tools/

$# 69

More Same Level LessInvolvement of Involvement Involvement

Recommendations ofaccounting softwareto clients 800/0 20%

—

Install, support, andtrain clients onaccounting software 72% 25% 30/6

Resell accountingsoftware to clients 3640 60 4%

OnlyVery Slightly Not

Important Important Important ImportantSupport frompublisher 8740 9% 311

c

Ease oflearning 79% 20'0 1 + -o —Softwarereliability 76% 22% 24.0

—

Overallquality 74% 26%

—

—

Publisher'sreputation 62% 2340 12°:e 1

Hardwarecompatibility 53% 32% 144.0 1 010

Training frompublisher 31 PO 37/0 24 % 6qo

Price 28% 44% 26% 140

Demonstrationtools 21% 35% 340 o 94 -b

Userconfidentiality!security 14% 31% 46% 8%

14 MANAGEMENT ACCOUNTING /JUNE 1986

LettersTO T HE EDITOR

Erwin S. Koval, Editor

This department welcomes comments on any topic

of interest affecting the accounting community ingeneral and NAA in particular. Correspondence isnot limited to comments about material previouslypublished in this magazine. Letters cannot be ac-knowledged individually, and the Editor reservesthe right to edit for .space or for other reasons. Allcorrespondence must be signed, but your identitywill be protected tf requested. Address all letters toTire Editor. Management Accounting. Montvale,NJ 07645.0433.

Accounting Education:The Ph.D. `Problem'

I was discouraged by the commentsmade by Dr. McGee in the April issue.Apparently Dr. McGee does not havean appreciation of the advantages to abroad education in developing an ac-counting educator's skills. For example,when teaching accounting, are educa-tors supposed to focus narrowly on thedebits and credits while ignoring therole of accounting in society as a whole?Should our students become numbercrunchers or are we training them to bedecision makers? If debits and creditsare the sole raison d'etre of accounting,I would leave the profession in aminute.

Furthermore, are FASB, NAA,AICPA, and the SEC wrong in con-ducting and sponsoring research? Theconceptual framework clearly states theobjective of accounting is to provide in-formation that is decision useful. Unlessresearchers have taken so- called "irrele-vent" courses in economics, statistics,psychology, and the like, how can theybe competent to determine what infor-mat ion is useful and what issuperfluous?

Finally, as a doctoral candidate, Iwould be offended if my Ph.D. studiesconsisted of glorified trade - school -typecourses. The wide gamut of disciplines Ihave studied has enabled me to gain a

0#19

NNW

HIGHEST AND BEST USE OFREAL ESTATE APPRAISAL TALENT

SRA to contact the real estateSenior Residential Appraiser professionals,

call 1 -800- 331 -SREASRPA for a free, national directory

Senior Real Property Appraiser of designated members(In Illinois: 312 -346 -7422)

SREA the people who made realSenior Real Estate Analyst estate appraisal a profession

QTHE SOCIETY OF REAL ESTATE APPRAISERS

645 North Michigan AvenueChicago, Illinois 60611

(In Illinois call: 312 -346 -7422)

Circle number 8 on reply card.

MANAGEMENT ACCOUNTING /JUNE 1986 15

How to,

control the M70rIf you've always found foreign affairs less than intrig-

uing, get ready. Now there's an international p4yment systemthat gives you what you've always wanted — ' orld control.

Because it's part paper, there's an au fit trail for quicktraceability and a tangible record of every payffnent made.

Because it's electronically supported ,+ transactions,status inquiries and stop payments can occur at;the speed of light.

The system is WorldLink. And it lets you do thingsyou never imagined possible.

You can issue checks in the world's major trading

currencies without leaving your office. You caft easily payoverseas vendors in their own currencies and r "duce your FXexposure. You can even use the WorldLink PC software tosignificantly reduce transaction errors and the -kissuance time.

And that's just part of the story.If all this makes you wonder how

you ever lived without the WorldLink system,stop wondering. Call Gerald Gualano at CiticorpServices Inc., at 1(312) 380 -5215.

Tell him you want the world on a string.

A better way to move money around the world.CITICORP WORLDLIN(Citicorp Services Inc. ICSI) provides remittance and other services to and on behalf of Citicorp entities. e 1986 CSI. All nghts reserved . World Link is a service mark of Citicorp.

Circle number 1 on reply card.

Data Sheet

Robert F. Randall, Editor

More U.S. Firms Borrow Abroad

More and more U.S. companies are using for-eign financial outlets for their external financingneeds, according to a Conference Board study.Reasons: interest rates in international marketsare sometimes significantly lower for U.S. com-panies and foreign sources provide additonalfund - raising alternatives. More than 48% of adiversified group of 108 companies already aretapping foreign financial sources, and manyamong those not currently using foreignsources say they plan to do so in the near fu-ture. Foreign sources now account for 20 %, onthe average, of all the borrowings of 32 compa-nies analyzed in depth. The rapid growth of theEuromarket has been one of the critical factorscontributing to the trend. The report, "Corpo-rate Financing in International Markets," isavailable from the Conference Board, 845 ThirdAve., New York, N.Y. 10022.

Have Software Industry Leaders Failed?

A financial planning expert has accused thesoftware industry of betraying the revolution infinancial planning begun by the developers ofVisiCalc. W.R. Purcell, Jr., founder and presi-dent of X -Y-See Software, Evergreen, Colo.,said: "Today's software gives us easy accessto computer power for crunching and printingfloods of numbers, which is fine clerical help forfinancial people, to use by themselves. But tohelp the 20 million nonfinancial people whomanage most business, what everybody needsmuch more is new ways to set up and deliverfinancial analysis so managers can get and useits real value —so managers can see the finan-cial priorities and the best opportunities andplans and decisions, instead of just floods ofnumbers." Of the small fraction of nonfinancialusers who do use spreadsheets, most do notrealize the real financial planning power —theyuse their spreadsheets only for trivial clericaltasks, such as printing a budget neatly. Mr. Pur-cell spoke at the AICPA Annual IndustryConference.

Wages Replace Energy as Concern

American manufacturers now are more con-cerned with wages and unionization than ener-gy costs, according to the latest survey byGrant Thornton (formerly Alexander Grant &Co.) of general manufacturing climates. Energycosts, which ranked No. 1 every year since1981, have moved to the third position, re-placed by wages, and unionization concernsmoved from No. 3 to No. 2. The complete"Seventh Annual Study of General Manufactur-ing Climates of the 48 Contiguous States ofAmerica" will be released by the Chicago firmthis month.

Business /Accounting Briefs

The widespread shutdown of plants and otherfacilities are causing companies to set up newprograms to ease the pain for dislocated em-ployees, according to a Conference Board sur-vey of 512 companies. Some 59% had to shutdown at least one of their facilities or make sig-nificant cutbacks in their workforces between1982 and the beginning of 1985, and 44% hadto close at least one of their facilities perma-nently. To help displaced employees, compa-nies are offering advance notice, severancepay, extended health -care benefits, and outpla-cement help. More than half the companiesgave three months or more notice; 28% gavesix months or more. Of 79% extending health-care benefits, 49% offered such benefits forfive months or less; 16% offered them for six to11 months; another 12% offered them for oneyear or more. The Conference Board Report(No. 878), "Company Programs to Ease the Im-pact of Shutdowns," is available from theBoard, 845 Th ird Ave. , New York, N.Y.10022.... Paul G. Simpson, a partner of Ernst& Whinney, has been appointed executive di-rector of the Financial Accounting StandardsAdvisory Council. He succeeds Clyde W.Moonie.... For mid - sized, private companieswith annual revenues from $1 million to $50million, a merger or acquisition can take fromnine to 15 months from the time the businessowner has made the emotional decision to selluntil the check is in his hands at the closing.Most of the time is spent in negotiating thestructure, says Geneva Marketing Services, amerger and acquisition services firm in CostaMesa, Calif, .. , Stock options are the mostprevalent type of capital accumulation andlong -term incentive plans among the 500 larg-est industrials, according to a Peat Marwick re-port. Some 446 companies (89 %) used this in-centive in 1985.

MANAGEMENT ACCOUNTING /JUNE 1986 17

Managing Your CareerRobert Half, Contributing Editor

How to Tell the Boss the Bad News

I was burned in my last job as aninternal auditor because I was toofree in expressing myself to myboss. I never hesitated to bring himbad news, and it backfired. Insteadof thanking me, he viewed me notonly as the carrier of the bad news,but as the cause of it. I eventuallyresigned and have now started anew job. My new boss seems to beopen to a free exchange of ideasand information, but after my lastexperience I'm definitely gunshy.Any guidelines on what to tell aboss, and what to hold back?

The question of how best to keep asuperior informed is a universal one.Any answers must take into account avariety of intangibles that only theperson on the scene can make judg-ments about.

Of course, an effective managerencourages employees to bring in thebad news, and to do it fast before thesituation gets worse. It sounds asthough your previous employer want-ed only to hear happy, upbeat news.

Like so many things in life, timing iscrucial in this situation. I certainlywouldn't decide to break bad news tomy employer at quitting time on Fri-day, or first thing in the morning, andprobably not just before lunch. If a sit-uation is critical and demands imme-diate action, any time will do, but mostproblems aren't so acute that somejudicious thinking about when to bringthem up isn't in order.

A decision also has to be made asto how important the news really is,and whether it's the sort of problemthat your particular employer wouldwant to be consulted on. Your newsuperior might be the sort of personwho expects his people to solve prob-

lems, rather than air them. On theother hand, there are executives whoenjoy getting involved with every de-tail. This really gets to the heart of thematter. It isn't so much limning strate-gies for passing on bad news as it isdeveloping an overall strategy forkeeping a superior informed on alllevels. That depends, to a great ex-tent, on coming up with a reasonedevaluation of your superior's person-ality and managerial style, as well asestablishing a more formal system ofcommunication to satisfy his or herneeds, as well as the needs of the de-partment, and company.

Before going to your boss with aproblem (or any piece of information),subject it to some evaluation. Is itsomething that might have a direct ef-fect on your boss's job or reputation?If so, don't delay. Is it potential badnews that will negatively impact uponyou? Again, if the answer is "yes,"don't hesitate to provide your bosswith some advance warning. Is itsomething that would benefit fromyour boss's expertise? That's worthbringing up, provided you've exhaust-ed your own areas of knowledge andexperience. No boss wants to becalled upon to solve problems forwhich he or she is paying you goodmoney to handle.

Too many younger managers, inse-cure in their positions, have a needconstantly to touch base with theboss which, after awhile, can be an-noying. I'm a believer in using writtennotes to pass along items of interest,nothing long and formal, just a line ortwo for the boss to glance at. It takesfar less time than a conversation, andleaves the busy executive free to dealwith the subject of the note at his orher convenience.

I'd suggest that you pick an oppor-tune moment to sit down with yourboss to discuss general guidelines forcommunication between you two. It'simportant, especially in light of yourprevious experience, that you set upparameters with which you are com-forable, and unless you establish, inyour own mind, a clear -cut set ofrules, you might find yourself in thesame predicament as in your previousjob.

It would also benefit you, I think, totry and take a long, hard look at yourprevious communication difficulties.Sometimes, this sort of problem isonly symptomatic of an underlying dif-ficulty in the relationship betweenmanager and superior. If that's thecase (and it will take honesty withyourself to determine it), your discus-sions with your boss might have to beexpanded to include a broader rangeof issues, including your responsibil-ities, performance, and other aspectsof your job in which communicationplays only a part.

In the meantime, don't hesitate tocome forward with bad news that yourboss should be aware of. There arefew successful executives aroundwho deal only with happy news, andI'd be surprised if you have ended upwith two in a row. El

Robert Half is the author of RobertHalf on Hiring. He heads Robert HalfInternational, Inc., which specializesin financial and EDP jobs.

17A,VA, ; Ekrl

"Yes, R. Y, there is a reason why Isent you a book with chapter eleven

torn out!"

18 MANAGEMENT ACCOUNTING /JUNE 1986

Letters

1 5 0finer appreciation of the important roleof the accounting profession.

It is exciting to realize that we areproviding a means of more efficiently al-locating our society's resources. Cer-tain ly, at times, the doctoral levelcourses seem impossible, but as RobertBrowning once wrote, "A man's reachshould exceed his grasp." If we heedDr. McGee's advice, the return of themyth of the "green eyeshade accoun-tant" is inevitable!

Jeffrey R. Cohen, CMA, MBAInstructor, Boston College

Granby, Mass.

We Support Our Software

We take exception to the review pub-lished (Jan. '86) about BPI Systems ac-counting software. The quality of thisreview was not consistent with other re-views of accounting software publishedin your special supplement.

We are, however, amendable to con-structive criticism. We have been awareof difficulties that our customers havehad in reaching us during peak hours ofthe business day, and are in the processof increasing access by providing addi-tional telephone lines and implementingan electronic access system.

In response to the reviewer's com-ment regarding the warranty providedon the out side of our packages , heshould be aware that the wording of thiswarranty is standard throughout ac-counting software packages.

This warranty does not mean that wedo not support our software. Upon re-ceipt of registration, each user is enti-tled to 90 days of free, toll -free tele-phone support. We have an experiencedstaff of technical support analysts, and aproduct support staff whose sole pur-pose is to maintain our software.

Gerald M. BaldwinVice President Sales /Marketing

BPI SystemsAustin, Texas

Simplified Income Tax

One day after House Republicans$# 43

BUSINESS INIERRUPTION INSURINCEby Robert M. Morrison, J.D., CPCU;

Alan G. Miller, J.D., CPCU;Stephen J. Paris, J.D., CPCU, CLU

What are the P's and E's? Twelve words — Parties, Property, Perils, Productiv-ity, Period, Profit and Extent, Experience, Exclusions, Efforts, Extras, Enough— offering you an easy way to understand the complex business interruptioncontract. You'll find this unique approach only in BUSINESS INTERRUP-TION INSURANCE: ITS THEORY AND PRACTICE.

This new book from The National Underwriter Company includes ananalysis of the Insurance Services Office's new Business Income Coverageforms which are slated for introduction in 1986, and mandatory for use inJanuary 1987.

New forms are just one reason why BUSINESS INTERRUPTION INSUR-ANCE should be part of your professional library. You'll also appreciate the factthat it's ...

• written by three authors who are well- respected throughout the insurancecommunity for their extensive experience with this form of insurance;

• thorough ... with approximately 400 pages;• easy to understand ... for it assumes no prior knowledge. And the glos-

sary clearly defines important words;• well- documented ... with endnotes for each chapter ... and a special

section of cases and citations.What's more, it's well organized. Part I ...

• introduces you to the 1986 Business Income Coverage forms ... andexplains the unique 6 P's and 6 E's method for analyzing businessinterruption contracts;

• explores the theoryand historybehind these forms.Part H shows you business interruption insurance in practice. You'll meet

the various people who have a stake in this coverage ... and their involvementat each step:

• Process of Insuring the RiskThe owner ... the intermediary (agent) ... the underwriter

• First Steps When Loss OccursThe loss manager ... the adjuster ... the accountant

• Process ofSettling the Claim ... Determination of Insured's Liability• Process of Litigation

The attorneyTo order your copies of the first new book on this subject in over a decade —

BUSINESS INTERRUPTION INSURANCE — use the order coupon below... or call TOLIrFREE 1- 800 -543 -0874. Single copy: $35.00

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -THE NATIONAL UNDERWRITER CO. 2 -35420 E. FOURTH ST.

I CINCINNATI, OH 45202 II II Please send me copies of BUSINESS INTERRUPTION INSURANCEl and bill me (Shipping & handling charges are additional)

I II I

Name

I II Compa"r

I II ""dmw II I

city state zip II

------------------------------

- - - - - ICircle number 11 on reply card.

MANAGEMENT ACCOUNTING /JUNE 1986 19

Womenin Management Accounting:

'IMoving Up...S�•1•o•w•1•y

l i e 'women c-0 e su CG.esSfUl

, ro grave thatfallen psi;� t is a c Man it' B

rTagers' Mas

rna Assistant

F P - ' '!fiffi,

By Susan Jayson and Kathy Williams

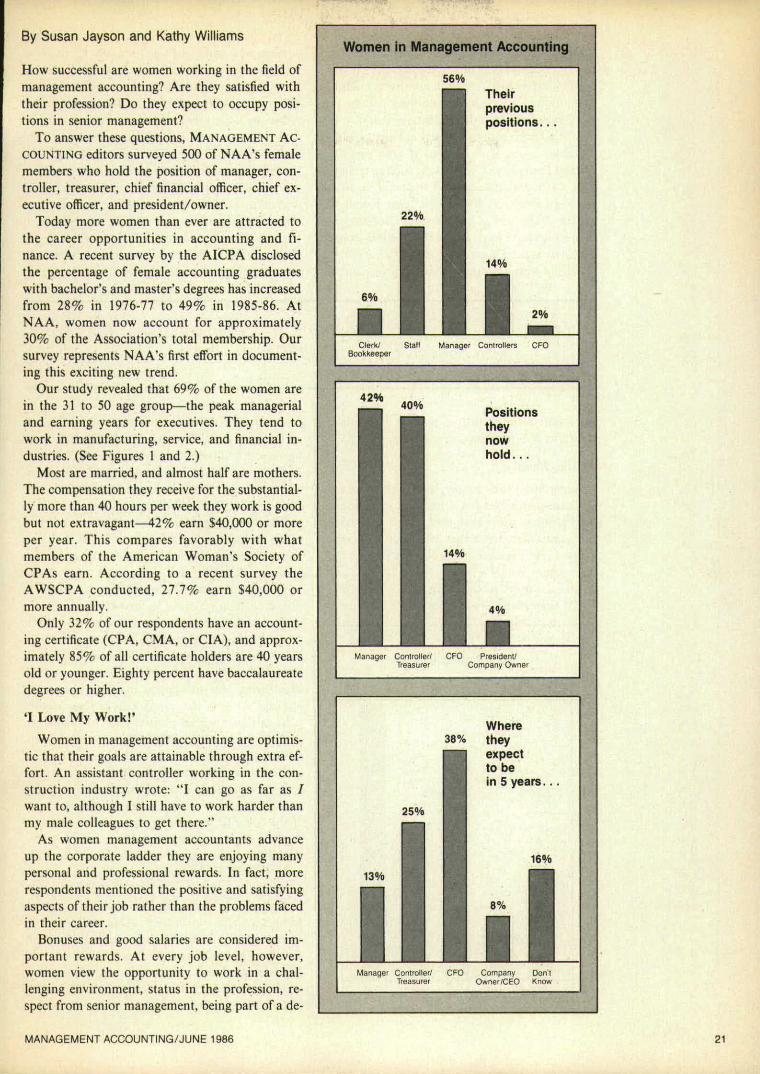

How successful are women working in the field ofmanagement accounting? Are they satisfied withtheir profession? Do they expect to occupy posi-tions in senior management?

To answer these questions, MANAGEMENT AC-COUNTING editors surveyed 500 of NAA's femalemembers who hold the position of manager, con-troller, treasurer, chief financial officer, chief ex-ecutive officer, and president /owner.

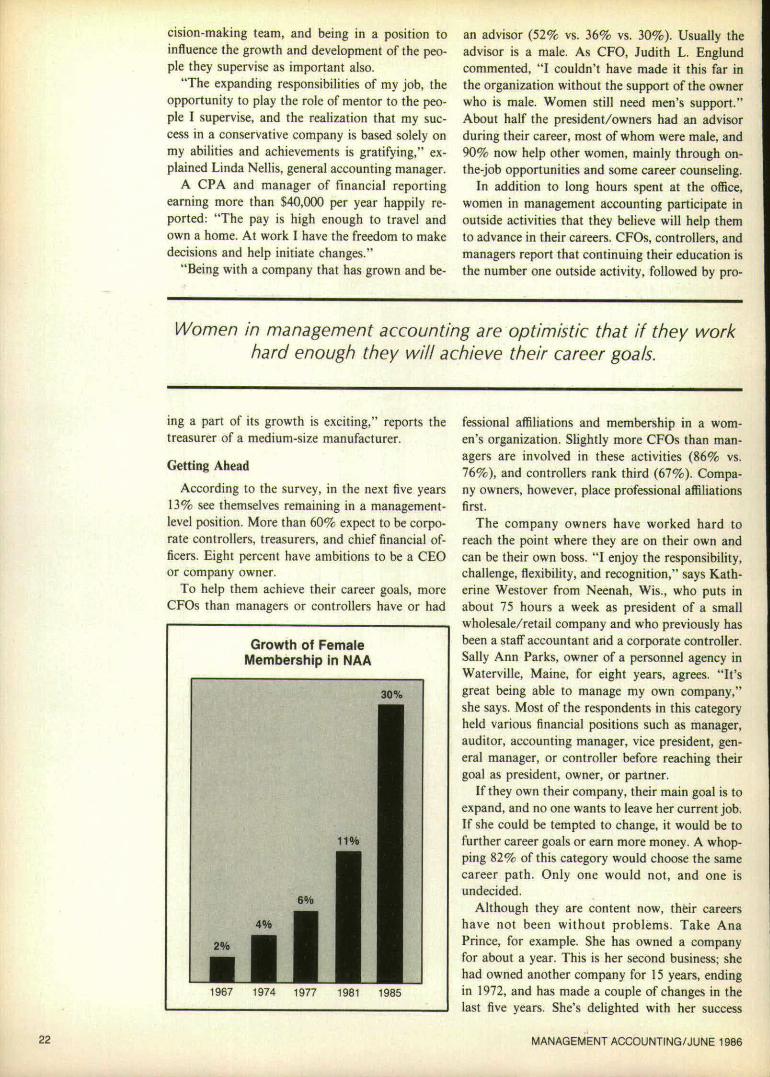

Today more women than ever are attracted tothe career opportunities in accounting and fi-nance. A recent survey by the AICPA disclosedthe percentage of female accounting graduateswith bachelor's and master's degrees has increasedfrom 28% in 1976 -77 to 49% in 1985 -86. AtNAA, women now account for approximately30% of the Association's total membership. Oursurvey represents NAA's first effort in document-ing this exciting new trend.

Our study revealed that 69% of the women arein the 31 to 50 age group —the peak managerialand earning years for executives. They tend towork in manufacturing, service, and financial in-dustries. (See Figures 1 and 2.)

Most are married, and almost half are mothers.The compensation they receive for the substantial-ly more than 40 hours per week they work is goodbut not extravagant -42% earn $40,000 or moreper year. This compares favorably with whatmembers of the American Woman's Society ofCPAs earn. According to a recent survey theAWSCPA conducted, 27.7% earn $40,000 ormore annually.

Only 32% of our respondents have an account-ing certificate (CPA, CMA, or CIA), and approx-imately 85% of all certificate holders are 40 yearsold or younger. Eighty percent have baccalaureatedegrees or higher.

`I Love My Work!'

Women in management accounting are optimis-tic that their goals are attainable through extra ef-fort. An assistant controller working in the con-struction industry wrote: "I can go as far as Iwant to, although I still have to work harder thanmy male colleagues to get there."

As women management accountants advanceup the corporate ladder they are enjoying manypersonal and professional rewards. In fact, morerespondents mentioned the positive and satisfyingaspects of their job rather than the problems facedin their career.

Bonuses and good salaries are considered im-portant rewards. At every job level, however,women view the opportunity to work in a chal-lenging environment, status in the profession, re-spect from senior management, being part of a de-

Women in Management Accounting

56%Theirpreviouspositions...

22%.

14%

6%

2%

Clerk/ Stall Manager Controllers CFOBookkeeper

4 2 0/o4000

Positionstheynowhold. . .

14%

4%

Manager Controller/ CFO Presitlenl!Treasurer Company Owner

Where38% they

expectto bein 5 years...

25%

16%

13%

8%

Manager Controller/ CFO Company Don'tTreasurer OwneNCEC) Knnv,

MANAGEMENT ACCOUNTING /JUNE 1986 21

vision- making team, and being in a position toinfluence the growth and development of the peo-ple they supervise as important also.

"The expanding responsibilities of my job, theopportunity to play the role of mentor to the peo-ple I supervise, and the realization that my suc-cess in a conservative company is based solely onmy abilities and achievements is gratifying," ex-plained Linda Nellis, general accounting manager.

A CPA and manager of financial reportingearning more than $40,000 per year happily re-ported: "The pay is high enough to travel andown a home. At work I have the freedom to makedecisions and help initiate changes."

"Being with a company that has grown and be-

an advisor (52% vs. 36% vs. 30 %). Usually theadvisor is a male. As CFO, Judith L. Englundcommented, "I couldn't have made it this far inthe organization without the support of the ownerwho is male. Women still need men's support."About half the president /owners had an advisorduring their career, most of whom were male, and90% now help other women, mainly through on-the-job opportunities and some career counseling.

In addition to long hours spent at the office,women in management accounting participate inoutside activities that they believe will help themto advance in their careers. CFOs, controllers, andmanagers report that continuing their education isthe number one outside activity, followed by pro-

Women in management accounting are optimistic that if they workhard enough they will achieve their career goals.

ing a part of its growth is exciting," reports thetreasurer of a medium -size manufacturer.

Getting Ahead

According to the survey, in the next five years13% see themselves remaining in a management -level position. More than 60% expect to be corpo-rate controllers, treasurers, and chief financial of-ficers. Eight percent have ambitions to be a CEOor company owner.

To help them achieve their career goals, moreCFOs than managers or controllers have or had

Growth of FemaleMembership in NAA

30%

11%

6%

4%

2%

1967 1974 1977 1981 1985

fessional affiliations and membership in a wom-en's organization. Slightly more CFOs than man-agers are involved in these activities (86% vs.76 %), and controllers rank third (67 %). Compa-ny owners, however, place professional affiliationsfirst.

The company owners have worked hard toreach the point where they are on their own andcan be their own boss. "I enjoy the responsibility,challenge, flexibility, and recognition," says Kath-erine Westover from Neenah, Wis., who puts inabout 75 hours a week as president of a smallwholesale /retail company and who previously hasbeen a staff accountant and a corporate controller.Sally Ann Parks, owner of a personnel agency inWaterville, Maine, for eight years, agrees. "It 'sgreat being able to manage my own company,"she says. Most of the respondents in this categoryheld various financial positions such as manager,auditor, accounting manager, vice president, gen-eral manager, or controller before reaching theirgoal as president, owner, or partner.

If they own their company, their main goal is toexpand, and no one wants to leave her current job.If she could be tempted to change, it would be tofurther career goals or earn more money. A whop-ping 82% of this category would choose the samecareer path. Only one would not, and one isundecided.

Although they are content now, their careershave not been without problems. Take AnaPrince, for example. She has owned a companyfor about a year. This is her second business; shehad owned another company for 15 years, endingin 1972, and has made a couple of changes in thelast five years. She's delighted with her success

MANAGEMENT ACCOUNTING /JUNE 1986

now, but recalls she "was asked to type and takeshorthand with her master's degree and men werenot, even with an associate degree." Mrs. Prince,incidentally, holds three college degrees in addi-tion to her master's in accounting.

Kate Farley Moynahan, owner of a financialservices business for the past seven years, and whohas been in accounting for 14 years, notes: "Iworked for an insurance company and was openlydiscriminated against. I left the job because thesituation was intolerable." She also says that, inhindsight, "I would have been stronger and moreassertive during my first five to ten years in busi-ness." Now she serves as a mentor to o therwomen.

Jean Barnett, a 30 -year veteran of the businessworld, has been president of a small computer in-stallation /sales /support company for the past fiveyears that she considers "a progressive group"that accepted her on merit. Previously she "wasnot always accepted as part of the team when oth-

er women managers were not present."One management consultant and owner of her

own firm who has been in accounting more than20 years and self - employed for eight remarked,"There was no work in my small southern townfor women in management eight years ago so Ihad to open my own business. I still have to out-perform men to be accepted."

On the other side, Judy Thompson, president ofan executive search firm in San Diego for nineyears, says she has experienced no career prob-lems: "I've never accepted sex as being a reasonfor discrimination against me."

Anne C. Ransdell, controller of a printing com-pany and nominee for NAA vice president, notes:"If I as a woman had been given the opportunitieswomen are today when I began working forNASA in 1945, I would be at the top of the corpo-rate ladder in a Fortune 500 now. I worked veryhard to be where I am today."

Fair and Equal Treatment

How do women view the work performed bytheir male colleagues, and do they believe theyhave the same chances as their male counterpartsfor advancement within the company they workfor? Their opinions depend on what job they nowhold in the corporate hierarchy.

When asked whether they spent the sameamount of time as their male counterpart did inpreparing for his career, the CFOs overwhelming-ly (86 %) reported that they spent the sameamount of time as the men. More than half theother groups agree, but a significant percentagebelieve that they have devoted more effort to pre-paring for their career.

When asked if they put the same amount of ef-fort into their work as their male colleagues do,

MANAGEMENT ACCOUNTING /JUNE 1986

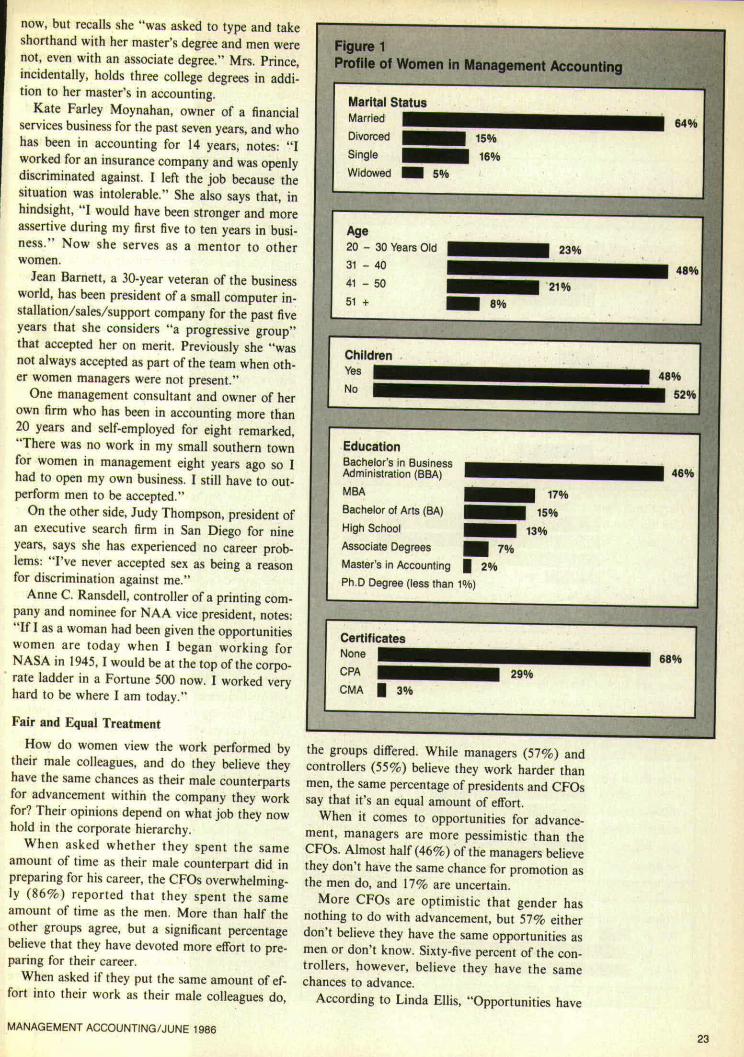

Figure 1Profile of Women in Management Account ing

Marital StatusMarried 640/6Divorced 15%

Single 16%

Widowed = 5%

Age20 - 30 Years Old 23%

31 - 40 48 ° -b41 - 50 21%

51 + _ 8%

ChildrenYes 48%

No 52%

EducationBachelor's in BusinessAdministration (BBA) 46%

MBA 17%

Bachelor of Arts (BA) 15%

High School 13%Associate Degrees - 7%

Master's in Accounting , 2%

Ph.D Degree (less than 1%)

Certi f icates

None 68%CPA 29%

CMA , 3%

the groups differed. While managers (57 %) andcontrollers (55 %) believe they work harder thanmen, the same percentage of presidents and CFOssay that it's an equal amount of effort.

When it comes to opportunities for advance-ment, managers are more pessimistic than theCFOs. Almost half (46 %) of the managers believethey don't have the same chance for promotion asthe men do, and 17% are uncertain.

More CFOs are optimistic that gender hasnothing to do with advancement, but 57% eitherdon't believe they have the same opportunities asmen or don't know. Sixty -five percent of the con-trollers, however, beli eve they have the samechances to advance.

According to Linda Ellis, "Opportunities have

23

increased at the middle management level, but ac-cess to upper management seems to be almost asrestricted as ever."

I Quit!

Instances of discrimination or sexual harrass-ment were noted. A concern for many respon-

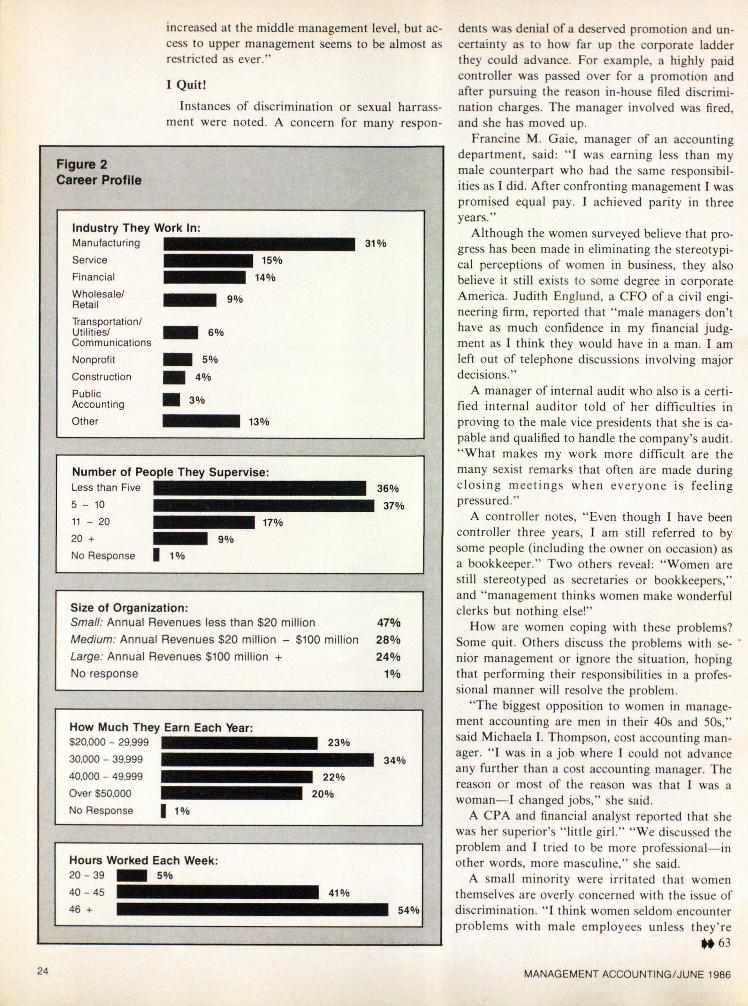

Figure 2Career Profil e

Industry They Work In:

Manufacturing 31 q%Service - , 15%

Financial 14 0/0

Wholesale/Retail 9%

Transportation/Utilities/ 6 0/b

CommunicationsNonprofit 59.0

Construction 41/o

Public ■ 300AccountingOther

-

13%

Number of People They Supervise:Less than Five 36%

5-

10 37 0/o11

-

20 17%

20 + 9 %

No Response 1 1%

Size of Organization:Small: Annual Revenues less than $20 million 47%

Medium: Annual Revenues $20 mill ion-

$100 million 28%

Large: Annual Revenues $100 million + 24%

No response 1%

How Much They Earn Each Year:$20,000

-

29,999 23%

30,000-

39,999 34"o

40,000-

49,999 2 2 Q o

Over $50,000 20 0/0

No Response ' 1 0/ 0

Hours Worked Each Week:20

-

39 _ 5%

40 - 4 5 41%

46 + 54%

dents was denial of a deserved promotion and un-cer ta in ty as to how far up the corporate ladderthey could advance. For example, a highly paidcontroller was passed over for a promotion andafter pursuing the reason in -house filed discrimi-nation charges. The manager involved was fired,and she has moved up.

Francine M. Gaie , manager of an accountingdepartment, said: " I was earning less than mymale counterpart who had the same responsibil-ities as I did. After confronting management I waspromised equal pay. I achieved parity in threeyears."

Although the women surveyed believe that pro-gress has been made in eliminating the stereotypi-cal perceptions of women in business, they alsobelieve it sti ll exists to some degree in corporateAmerica. Judith Englund, a CFO of a civil engi-neering firm, reported that "male managers don'thave as much confidence in my financial judg-ment as I think they would have in a man. I amleft out of telephone discussions involving majordecisions."

A manager of internal audit who also is a certi-fied internal auditor told of her di fficult ies inproving to the male vice presidents that she is ca-pable and qualified to handle the company's audit."Wha t makes my work more d i ffi cul t a t e themany sexist remarks that often are made duringclos ing meet ings when eve r yon e is feel ingpressured."

A controller notes, "Even though I have beencontroller three years, I am still referred to bysome people (including the owner on occasion) asa bookkeeper." Two others reveal: "Women arestill stereotyped as secretaries or bookkeepers,"and "management thinks women make wonderfulclerks but nothing else!"

How are women coping with these problems?Some quit . Others discuss the problems with se-nior management or ignore the situation, hopingthat performing their responsibilities in a profes-sional manner will resolve the problem.

"The biggest opposit ion to women in manage-ment accounting are men in their 40s and 50s,"said Michaela I. Thompson, cost accounting man-ager. "I was in a job where I could not advanceany further than a cost accounting manager. Thereason or most of the reason was that I was awoman —I changed jobs," she said.

A CPA and financial analyst reported that shewas her superior 's "litt le girl." "We discussed theproblem and I tried to be more professional —inother words, more masculine," she said.

A small minority were irritated that womenthemselves are overly concerned with the issue ofdiscrimination. "I think women seldom encounterproblems with male employees unless they're

0 6 3

MANAGEMENT ACCOUNTING /JUNE 1986

,Jo5� Eir • , R r

20774

I L

I r y K l e i n ._.E.DsqFMw+

42516Ew , 0 6 ~

..

36274Ea04rw tbAFFr

—03273

74898EmpugF Nmpi

24048

D s . . l F F w . r o r -�

85681EAOngF NneFr

Le e B o V l a a

138•i(1E A D F g A N F A e .

Vivian Riley . _EADAgA w1°F Ago-

36160Effoor.e~.a.

--39389

E f f O b g e f t ~

35045

15196EAObwF Nn s w - - -

52690:ADFq.N.e.

41389 ;

40404 !-I19502 r ,

Phil Sklar � f AEAOSSNF Mwr

1 _ —� -27147 FA A ,

Enown *A"—W -

17251EA aF ) F FNF � 4 r __

24003

32815E r o b r . . A y r i p y - -- -

Fir,31700

21838_ E npbgF ICd.

19649E� a..N..e.

V— t — . ,

62540

►lattr� .aw f � w . . . . � _ . .

25030-- ti,,,,,,,� .� .— -

12055E " O f t " % ~

Ma t t B u dEAOetFFM..F

—_ EAOSOn�MnOF�

21177

49203

-- -U 3� cs � Arato_ (•

00038

.._ . . . 15218E , � W " — � N . A e « - -

283"1EADAr»N.ea _

13818Ew OMMA � � J y

25027EAoM'•.N.e. A

� . . . . . - - x• -87036 orE.DgwMFwew

Larry Aarons

NOMER PiYROLL SOFTWMETREW IMFi E NUMBERS11KE PEOPLE.

Tnat's because these numbers are relations functions as well. existing or new software. Sotheycan talkpeople. And not only does our system pay, it to one another. In English.

And finally there's a payroll system pays accurately. It allows you to prepare That's why MSA system is used to pro -that recognizes that fact. Ours. reports on time, anytime. Plus it automatic- cess over $100 billion in payroll each year A

We're Management Science America, ally offers salary history, FICA wages, Social total none of our competitors can add up to.Inc. Our system is Payroll /Personnel. And it Security projections, and benefits on a For more information call Robertdoes more than just provide all the informa- plan year basis, too. Carpenter at this number: 404 - 239 -2000.tion for your human resource functions. It Along with all this you get the added He'll treat you like a person, too,helps improve your organization's human dividend of INFORMATION

EXPERT. T" The fourth gener- WELLGENCE Of A NIGHER ORDER:1985 Ma k ge eat 5ce-Ce A& ee cd, irc ation technology that alintegrates a ourg y Circle number 14 on reply card.

0

Many businesses, fearful of computerizingtheir accounting, still use pencils to keep theirbooks.

But what those businesses really should fearare pencils.

Pencils, for example, can't track receivableson a daily basis-a feature that can pay for account-ing software just in receivables collected alone.

And with accounting software like OpenSystems, you can receive immediate financialand business operations advice that alerts you toproblem areas. Our easy -to -useOpen for Business' package is sofull - featured it'll do just that; obvi-ously, a pencil won't.

In addition, only integratedbusiness and accounting soft-ware like our Harmony lets youcombine information fromaccounting and business opera-tions with word processing, spreadsheets anddata bases. Actually, pencils aren't the only thingsthat can't do all that; most, quote, "integrated"software packages can't do all that, either.

Obviously, a pencil can generate only lim-ited information. But OSAST"gives you unlimitedchoices. You can customize the system toprovide the exact, comprehensive accountingand business operations information your man-agement needs.

In fact, all three Open Systems solutionsprovide the management information you need,when you need it, in the form you want it.

So don't settle for any old number twosolution.

0

more than any company in America.We offer the security of backing from UCCEL

corporation, With annual revenues exceeding$200million, UCCEL is one of the world's largestsoftware companies.

We also offer you more to choose from.A selection so broad that you can find the systemthat meets your distinctive needs.

And then we offer a unique promise. Wepromise you can't go wrong.

In a warranty without precedent in our

Insist, instead, on number one.Open Systems offers you the comfort of our

10 years of experience installing over370,000 accounting and businesspackages in American businesses-

1986 ptmn Systems Inc lI

industry, we promise that if you're not completelysatisfied with any Open Systems software, we'll re-place it with one better matched to your business.

Will you need our guarantee? Not likely.A remarkable 89/0 of our customers report com-plete satisfaction with our software.In fact,theyreport no individual area of dissatisfaction.

So we stand by number one.And there's more of us standing behind it

than behind any other accounting software inthe country.

So we suggest you get off the pencil and geton the phone, and see what number one can do.Just call or write Open Systems, 6477 CityWest Parkway, Minneapolis, MN 55344,1- 800 - 328 -2276.

After all, we guarantee you can't go wrong— with number one. Which is a lot

OPENSYSTEMS-Accouwm &&JSINESSSOETWARE

1-800-328 -2276 A UCCEL COMPANYCircle number 13 on reply card.

Women Accountants—Do They Earn asMuch as Men?

A woman in the account ing profess ion earns a lmost $4,000less each yea r than her ma le counterpar t .She a lso makes more persona l sacr ifices .

By J oseph i ne E . O l son

an d I r en e H ans on Fr ieze

The number of women in the accounting profes-sion and the number of women with MBA degreeshave both increased dramatically in the last 13years. But are these career women reaching thesame level in the corporate hierarchy, earning thesame income, and enjoying the same job satisfac-tion as their male counterparts?