Embed Size (px)

Citation preview

JOHN MCCONNELL GROUP CFO

Joined

Inchcape in

1999

Appointed

Group CFO

October 2009

Supply Chain Management and Working Capital

• World class supply chain management

processes seamlessly integrated with

market understanding and forecasting

models

• Minimise investment and working capital

– Meet market demand

– Low Capital Employed

– Ensure fast inventory turn

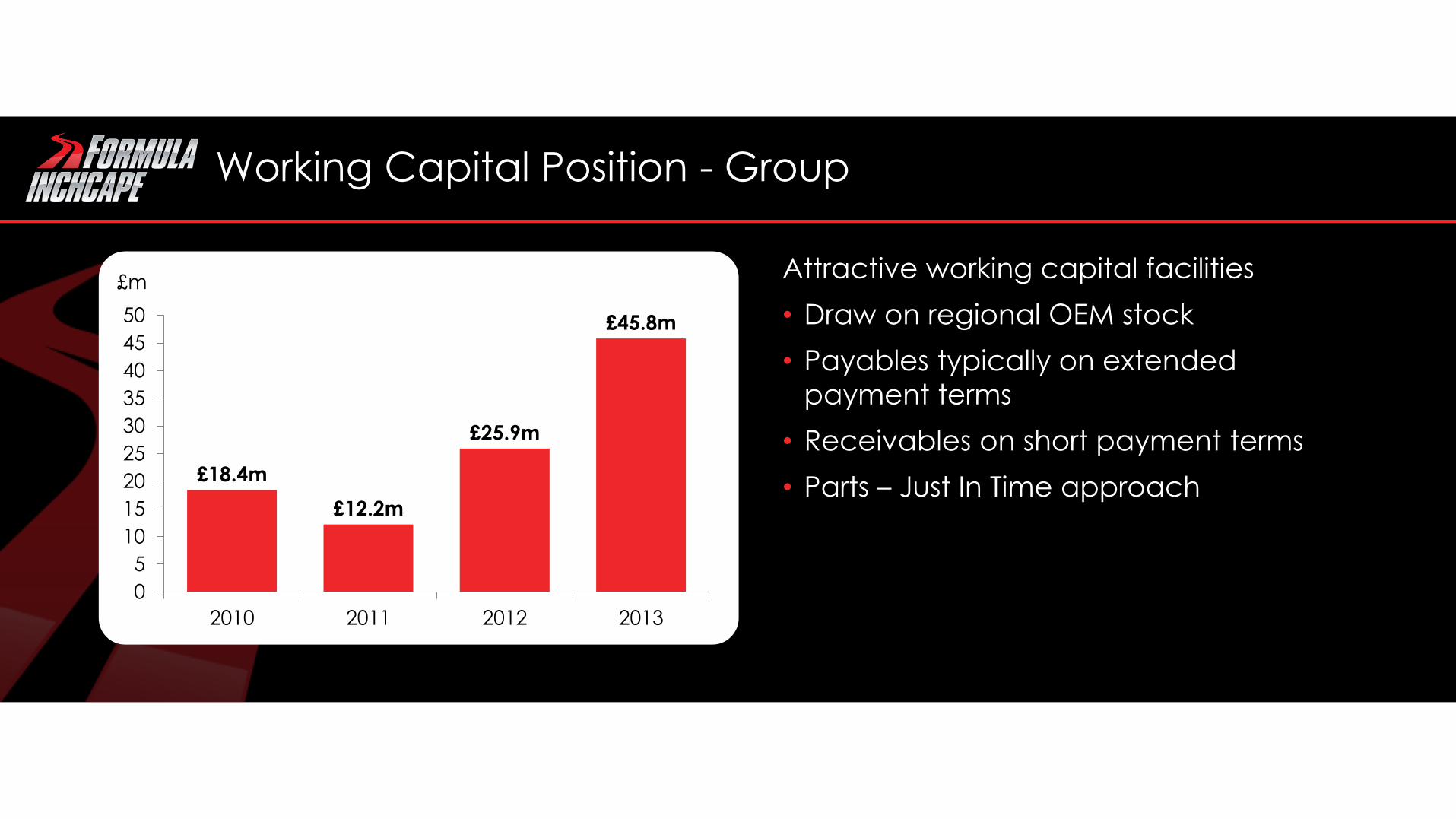

Working Capital Position - Group

Attractive working capital facilities

• Draw on regional OEM stock

• Payables typically on extended

payment terms

• Receivables on short payment terms

• Parts – Just In Time approach

£18.4m

£12.2m

£25.9m

£45.8m

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013

£m

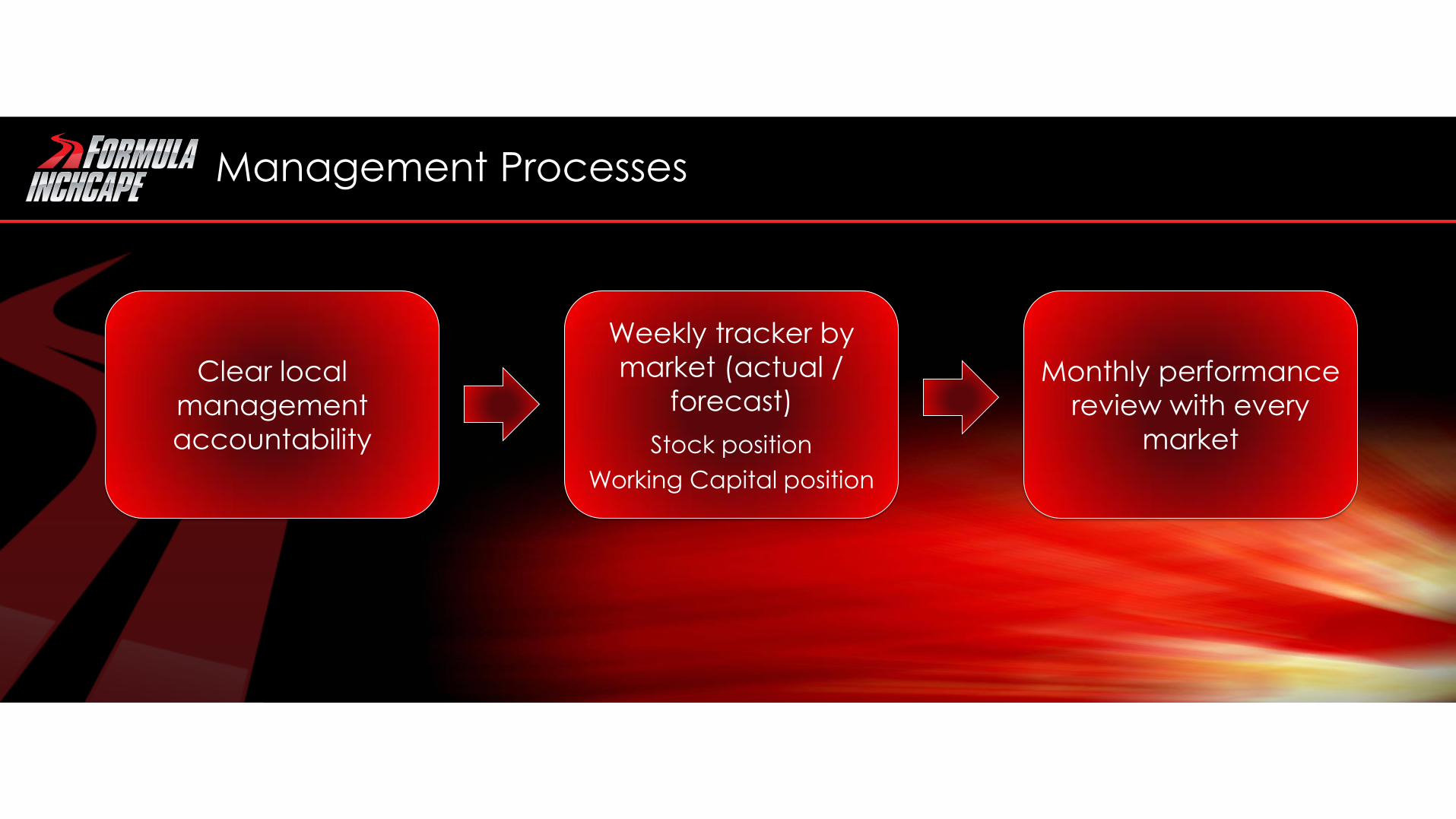

Management Processes

Clear local

management

accountability

Weekly tracker by

market (actual /

forecast)

Stock position

Working Capital position

Monthly performance

review with every

market

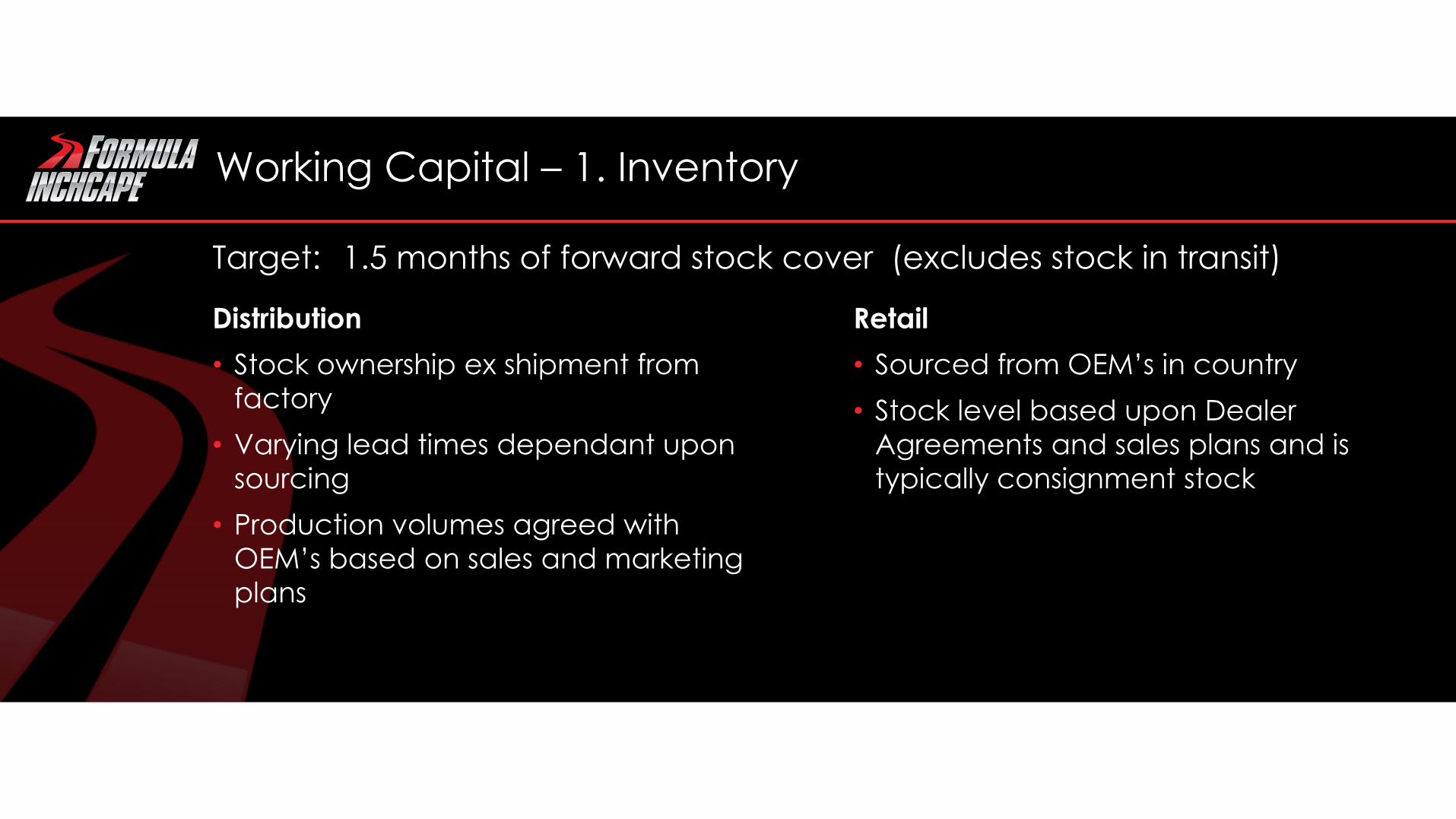

Working Capital – 1. Inventory

Retail

• Sourced from OEM’s in country

• Stock level based upon Dealer

Agreements and sales plans and is

typically consignment stock

Target: 1.5 months of forward stock cover (excludes stock in transit)

Distribution

• Stock ownership ex shipment from

factory

• Varying lead times dependant upon

sourcing

• Production volumes agreed with

OEM’s based on sales and marketing

plans

Working Capital – 2. Trade and Other Receivables

Retail

• Minimal credit exposure as require

cleared funds for retail customers

At December 2013 - £337m (16 days)

Distribution

• Vehicles – minimal exposure as require

cleared funds to release cars to

dealers

– managed credit risk to fleets

• Parts – managed credit risk to dealers

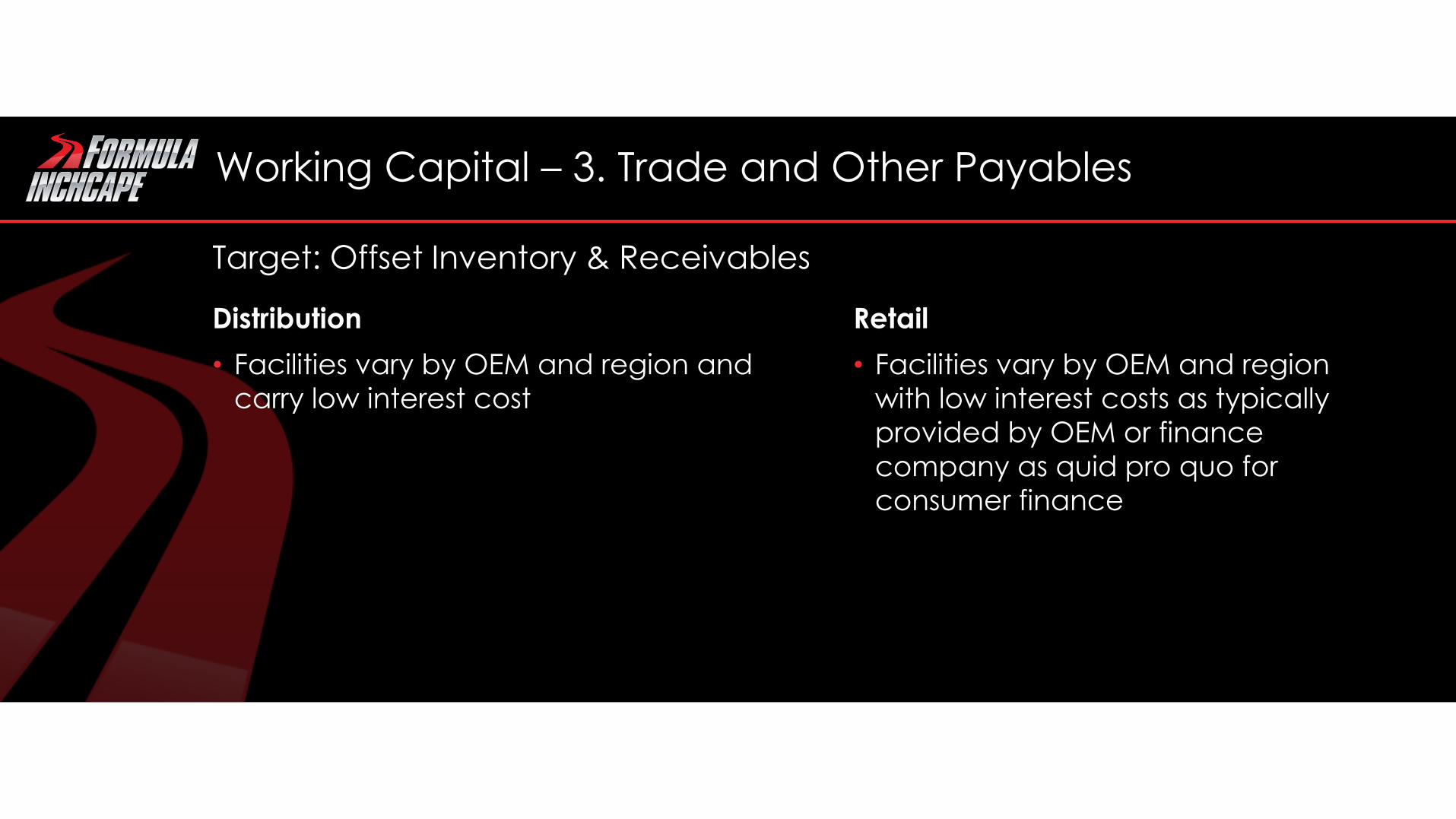

Working Capital – 3. Trade and Other Payables

Retail

• Facilities vary by OEM and region

with low interest costs as typically

provided by OEM or finance

company as quid pro quo for

consumer finance

Target: Offset Inventory & Receivables

Distribution

• Facilities vary by OEM and region and

carry low interest cost

LOUIS FALLENSTEIN CEO EMERGING MARKETS

30 years Motor

Retail

Experience

Joined

Inchcape in

2006 as part of

EMH acquisition

• Stock profiling and ordering from the OEM to meet market targets

• Receipt and storage in centralised bonded compound

• Transportation to dealers just in time for delivery to user

• Supply chain benefits from just one vehicle movement

– Efficiency of operation

– Clear payment path

– Reduces distribution costs

Distribution and VIR

New

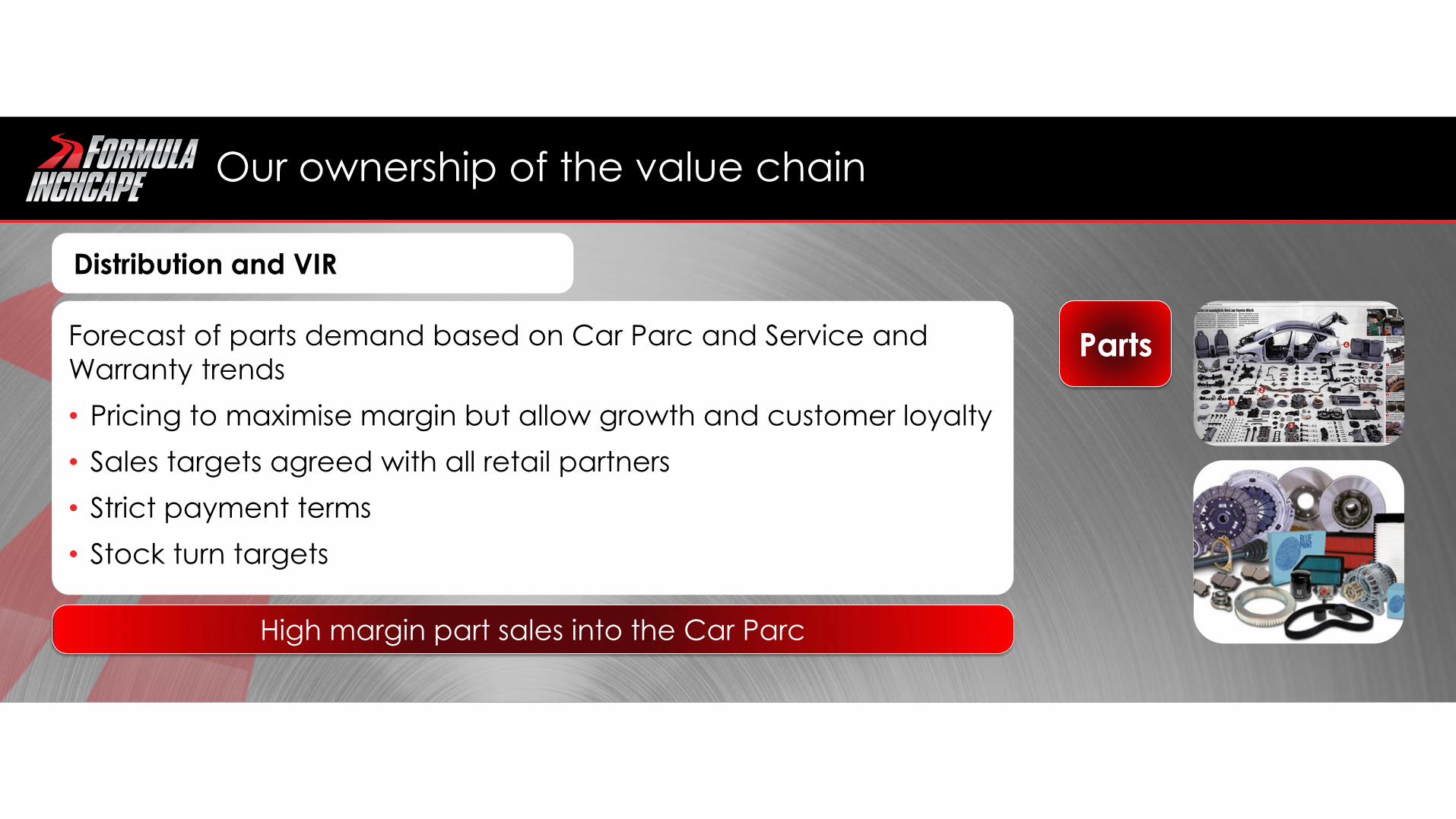

Our ownership of the value chain

Inchcape controls the volume into market

Our ownership of the value chain

Forecast of parts demand based on Car Parc and Service and

Warranty trends

• Pricing to maximise margin but allow growth and customer loyalty

• Sales targets agreed with all retail partners

• Strict payment terms

• Stock turn targets

Distribution and VIR

High margin part sales into the Car Parc

Parts

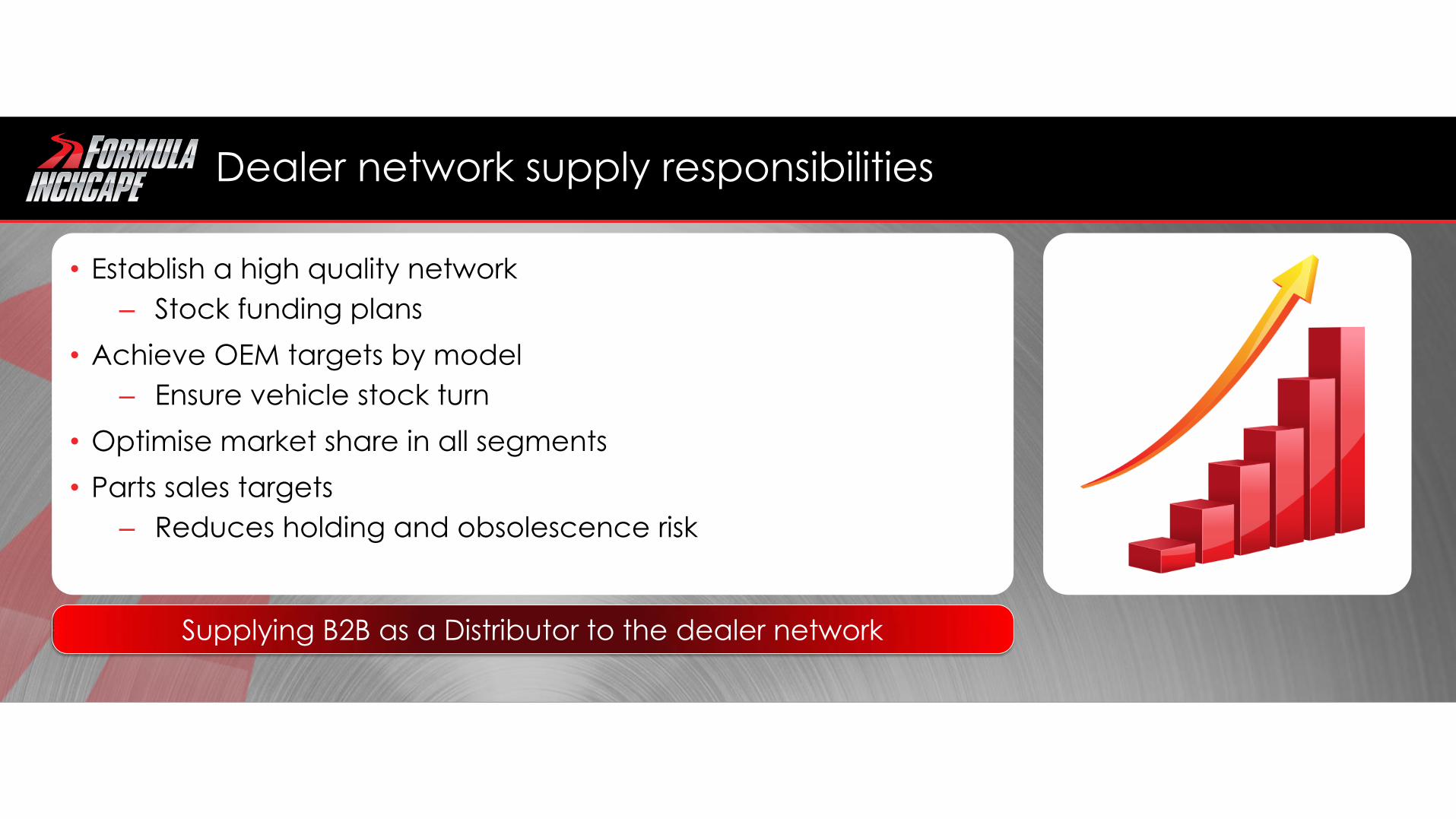

Dealer network supply responsibilities

• Establish a high quality network

– Stock funding plans

• Achieve OEM targets by model

– Ensure vehicle stock turn

• Optimise market share in all segments

• Parts sales targets

– Reduces holding and obsolescence risk

Supplying B2B as a Distributor to the dealer network

Supply strategy to deliver growth across value drivers

New Vehicles

• Right stock at the right time

• Management of stock funding

Used Cars

• Managing stock risk

Aftersales

• Parts logistics, depth of cover and pricing

• Developing volume through independent networks

1.5x months

fwd stock cover

New vehicle supply – South America

• New models in 2014 – 2 Series, X4, X6

• Establishing the correct

supply

– BMW aspirations

– Segment size

– Competitor products

– Conquest opportunities

– Establishing the marketing to create

early demand

Production Order Planning - Chile

• Current demand

• Seasonality

• Manufacturing capacity

• Sales Plan

• Competitor actions

• Model introductions

• Historic demand

• Current stock and pipeline

Production schedule based on:

Financial processes and controls

• Key stock KPI’s exist in every market and across Group Stock cover in months

• Effective stock control is key to margin protection and minimising interest costs

• Rigorous review of stock to minimise exposure on a weekly basis

Strong Local and Group discipline on stock ageing

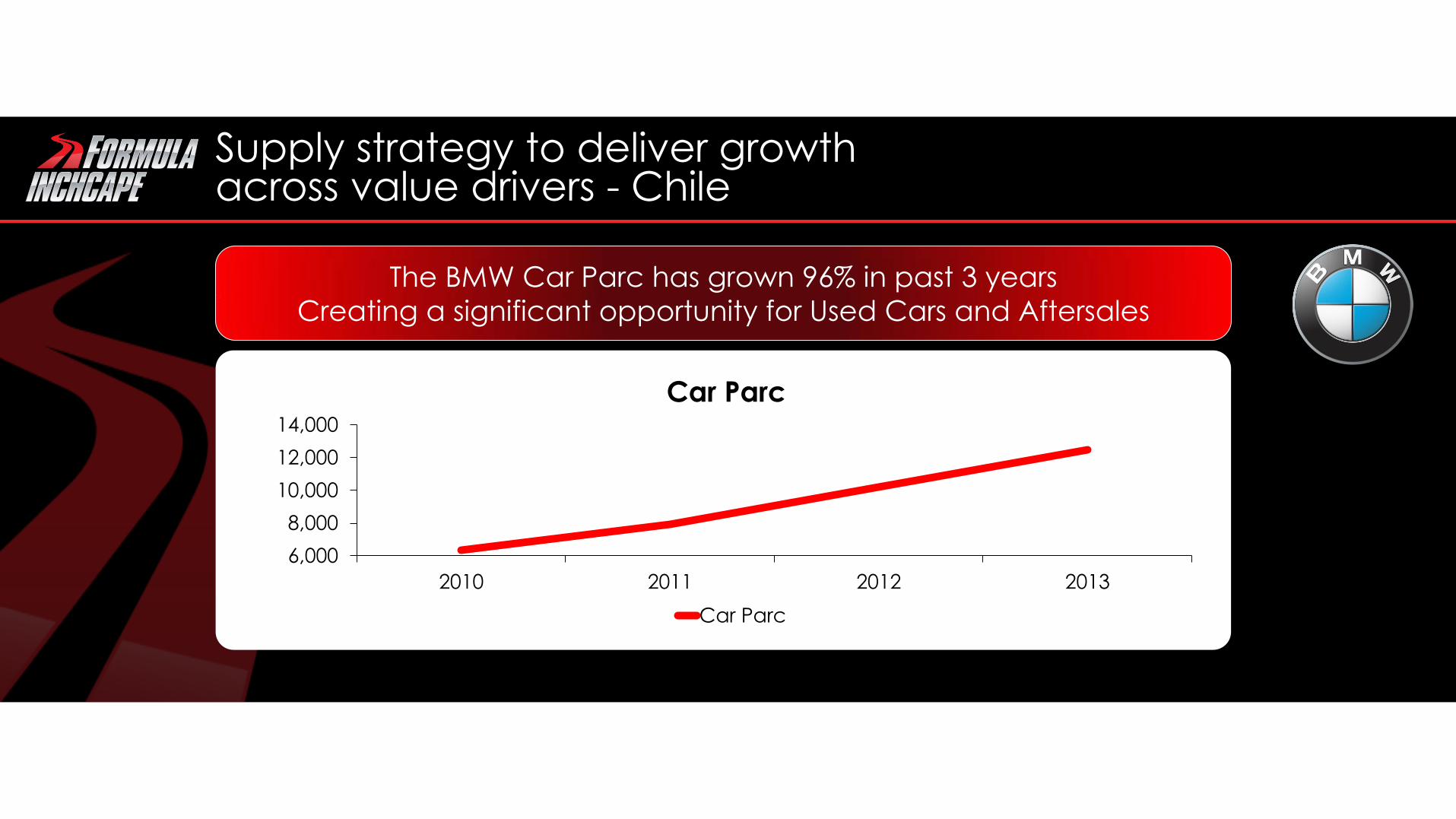

Supply strategy to deliver growth across value drivers - Chile

The BMW Car Parc has grown 96% in past 3 years

Creating a significant opportunity for Used Cars and Aftersales

6,000

8,000

10,000

12,000

14,000

2010 2011 2012 2013

Car Parc

Car Parc

BMW Used Car volume

growth in Chile 37.2%

over the past 3 years

Used vehicle supply - Chile

Sourcing used car stock

• Focus on new car customer retention

• Active purchasing from private

individuals

• Own daily rental company supplies

high quality used cars

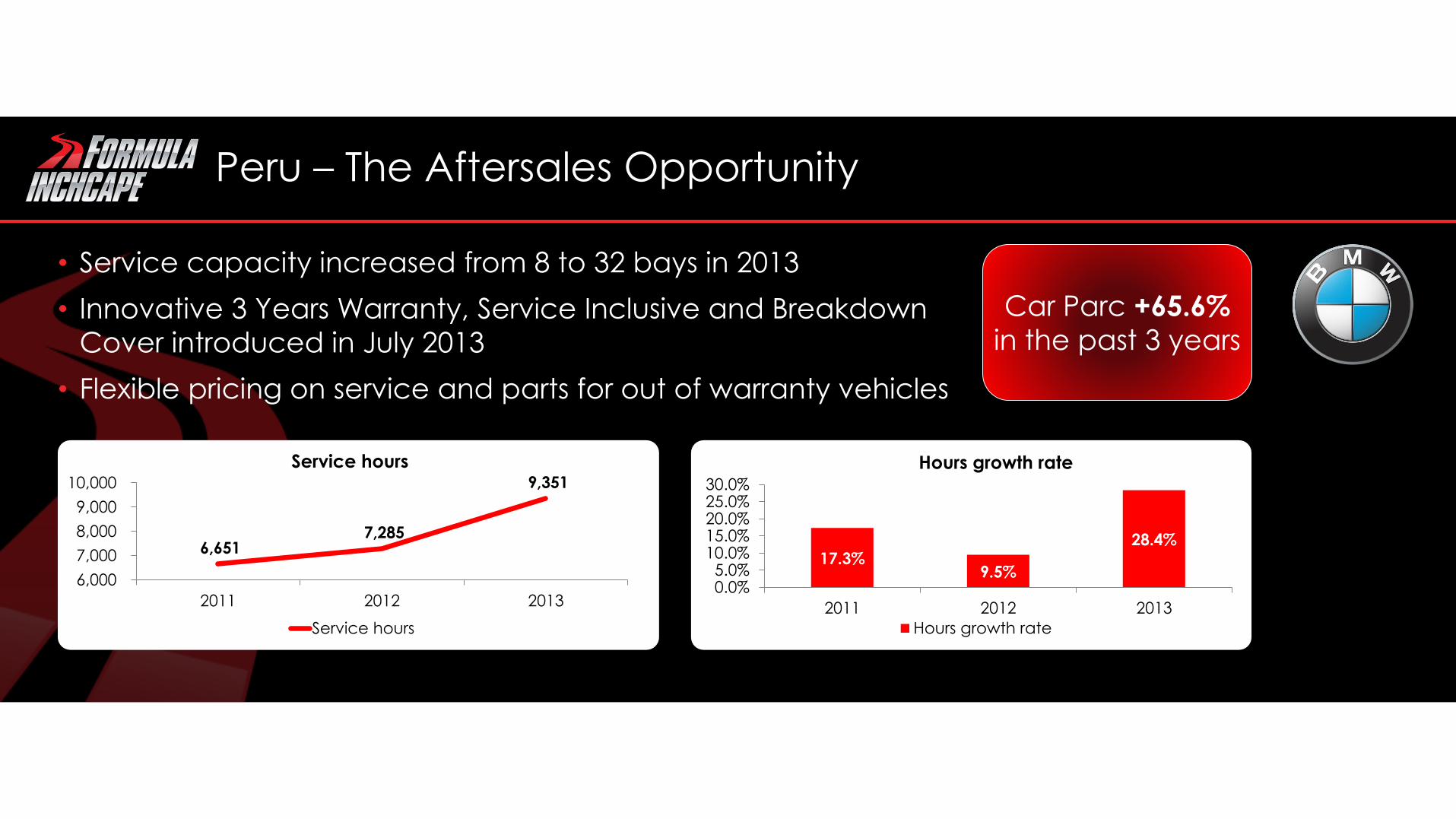

Peru – The Aftersales Opportunity

• Service capacity increased from 8 to 32 bays in 2013

• Innovative 3 Years Warranty, Service Inclusive and Breakdown

Cover introduced in July 2013

• Flexible pricing on service and parts for out of warranty vehicles

17.3% 9.5%

28.4%

0.0%5.0%

10.0%15.0%20.0%25.0%30.0%

2011 2012 2013

Hours growth rate

Hours growth rate

6,651 7,285

9,351

6,000

7,000

8,000

9,000

10,000

2011 2012 2013

Service hours

Service hours

Car Parc +65.6%

in the past 3 years

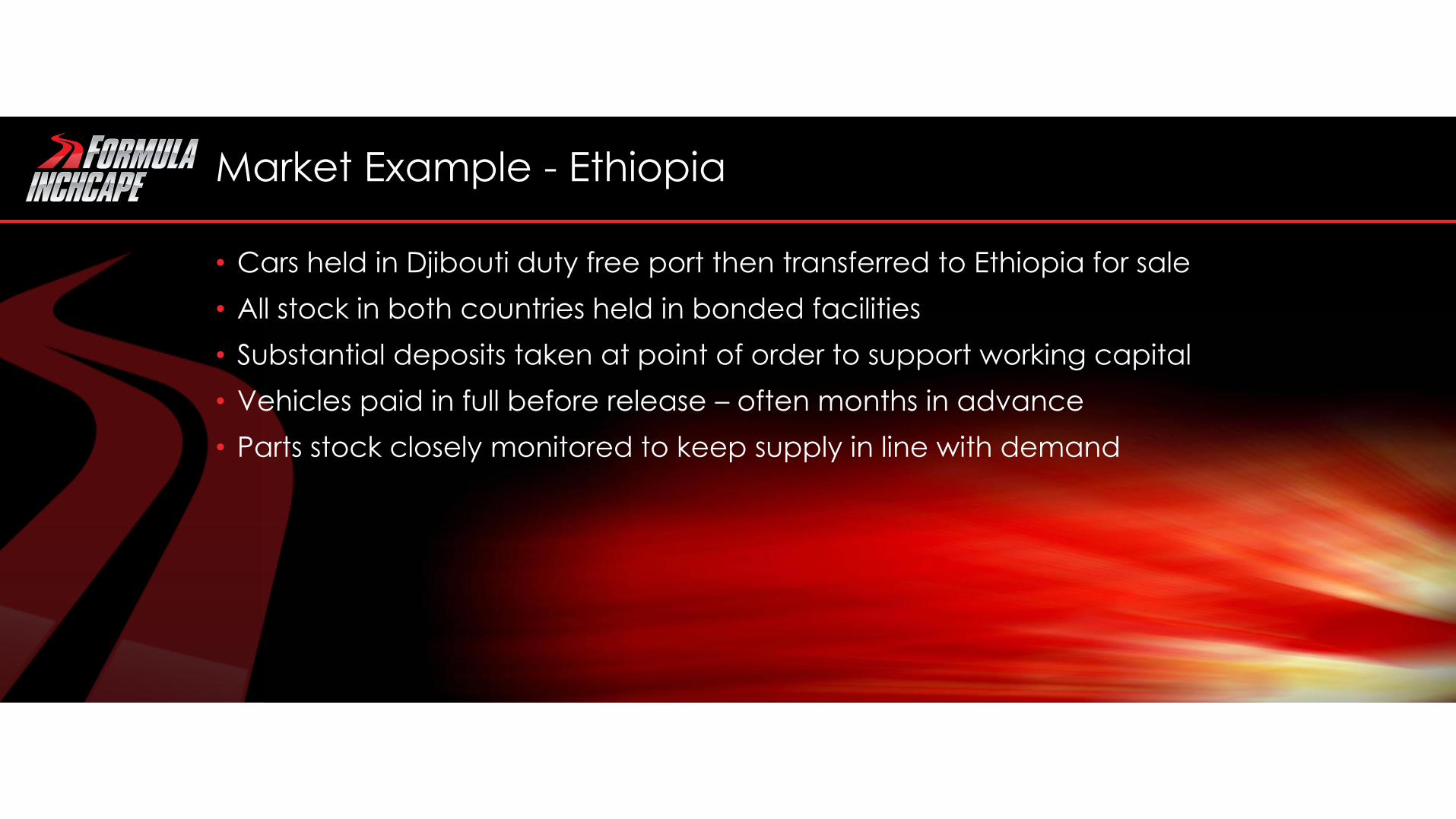

Market Example - Ethiopia

• Cars held in Djibouti duty free port then transferred to Ethiopia for sale

• All stock in both countries held in bonded facilities

• Substantial deposits taken at point of order to support working capital

• Vehicles paid in full before release – often months in advance

• Parts stock closely monitored to keep supply in line with demand

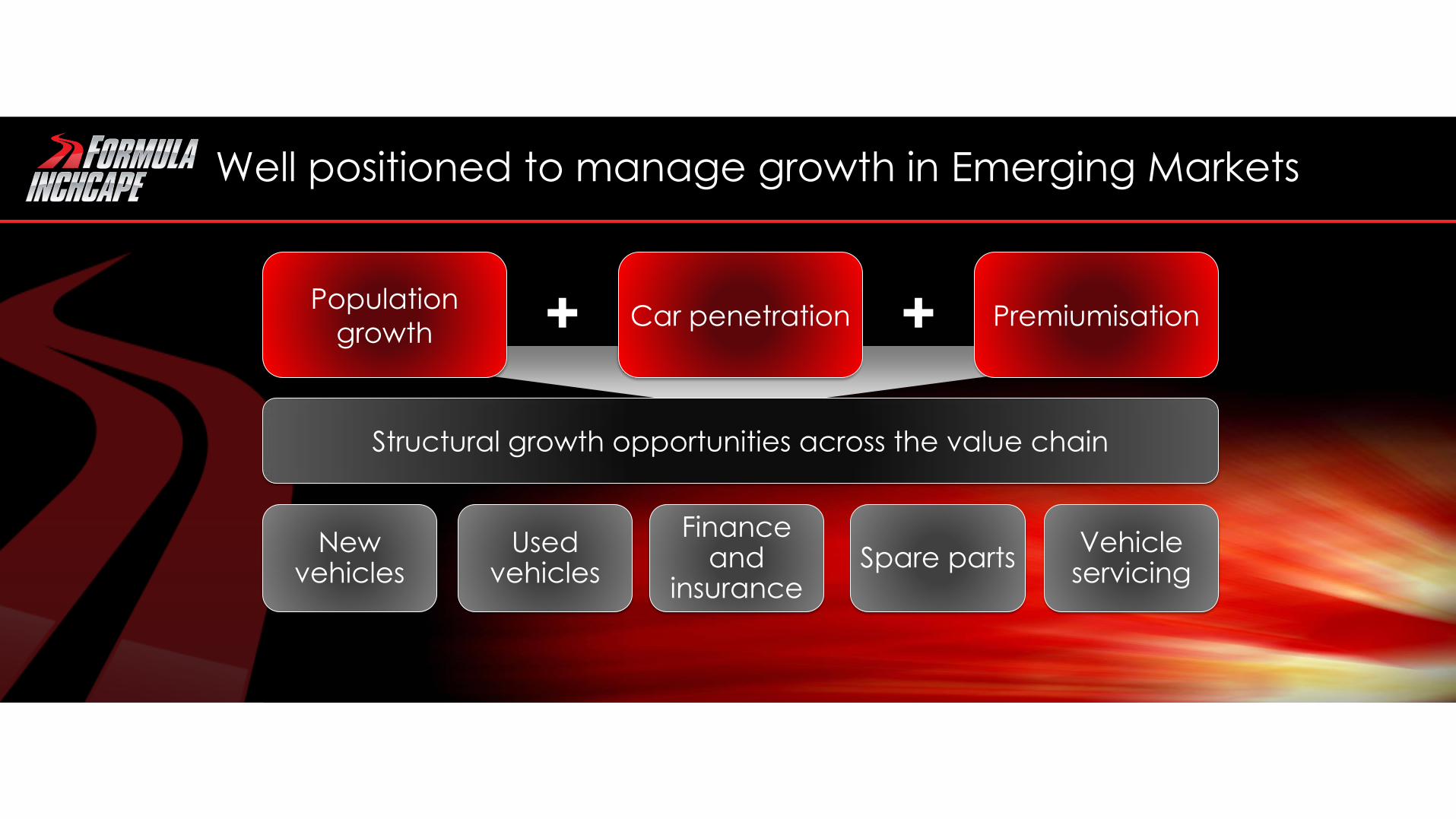

Well positioned to manage growth in Emerging Markets

Population

growth Car penetration Premiumisation

Structural growth opportunities across the value chain

New vehicles

Used vehicles

Finance and

insurance Spare parts

Vehicle servicing

+ +