Embed Size (px)

Citation preview

THE SWOT’S FACED BY FOREIGN BANKS WORKING IN PAKISTAN; A COMPARITIVE

STUDY OF CITI BANK AND FAYSAL BANK LTD

A dissertation submitted in partial fulfillment of the requirements for the Degree of Master of Business Administration

by

Malka Khan Thebo

Department Of Management Science Faculty of Computer & Management Sciences

Isra University, Hyderabad

October 2009

THE SWOT’S FACED BY FOREIGN BANKS WORKING IN PAKISTAN; A COMPARITIVE

STUDY OF CITI BANK AND FAYSAL BANK LTD

by

Malka Khan Thebo

Examination Committee

Asst. Professor Najeeb Hassan Brohi (Supervisor) Assistant Professor

Prof.Dr. Muhammad Ayoob Shaikh(Co-Supervisor)

Professor of Management Sciences

Asst. Professor Qamaruddin Mahar (Co-Supervisor) Assistant Professor of Management Sciences

ACKNOWLEDGEMENTS

First of all, I reverently thank Almighty Allah who made me skillful

enough so that I can make some contributions to the huge understanding of

the world and who also awarded me the capability to complete the MBA

dissertation fruitfully which otherwise would have been unfeasible for me to

complete.

I am tremendously thankful to my supervisor Assistant Professor Mr.

Najeeb Brohi, Department of Management Sciences, Isra University

Hyderabad for his faithful attention, continuous suggestions, and

encouragement in compiling my research work. His creativity and logical

judgment were of large help during the whole writing of this dissertation.

I would like to convey the extraordinary and great thankfulness to

Assistant Professor Dr. Muhammad Ayoob Shaikh, Department of

Management Sciences, Isra University, for his wholehearted effort and

concern. With his precious advice, help and encouragement, I was able to

comply with this dissertation.

I would like to expand my gratitude to Assistant Professor Mr. Qamar-

udin-Mahar for his great support during the dissertation work.

I am grateful to Professor Dr. Gulham Hussain Siddiqui Director

Research, Extension and Advisory Services, as well as Professor Iqbal Bhatti

Dean Faculty of Computer and Management Sciences Isra University for

providing me their supervision and support and helping me in carrying out the

dissertation on time.

ABSTRACT

Banking is one of the most thin-skinned businesses all over the world.

Banks play very important role in the financial system / economy of a country

and Pakistan is no exception to this condition. Banks are guardian to the

assets of the general lots. The banking sector plays a significant role in a

modern world of money and economy and Banks also play a very positive

and vital role in the overall economic improvement of the country. With each

passing year various foreign banks enter in Pakistan and establish their

branches here showing the world a positive image of the Pakistani banking

sector growth and prosperity. I thoroughly examined the S.W.O.Ts faced by

foreign banks in Pakistan by conducting a comparative analysis of the two

selected banks i.e. Citi bank and Faysal bank limited. Since that time the

banking sector is affected by the global liquidity crisis going around the world.

Since from last 2 to 3 year, Pakistani banking sector is not performing well

many fluctuation and variation have been observed in the performance of

foreign banks and during this period various S.W.O.Ts are faced by them I

have tried to clarify that situation through my comparative analysis of the

sample banks i.e. Citi Bank and Faysal Bank Limited. Despite of all these

facts one of the worlds largest banking network i.e. Barclays bank came to

Pakistan in 2008 showing the world the strength of the Pakistani banking

sector to combat with any challenge.

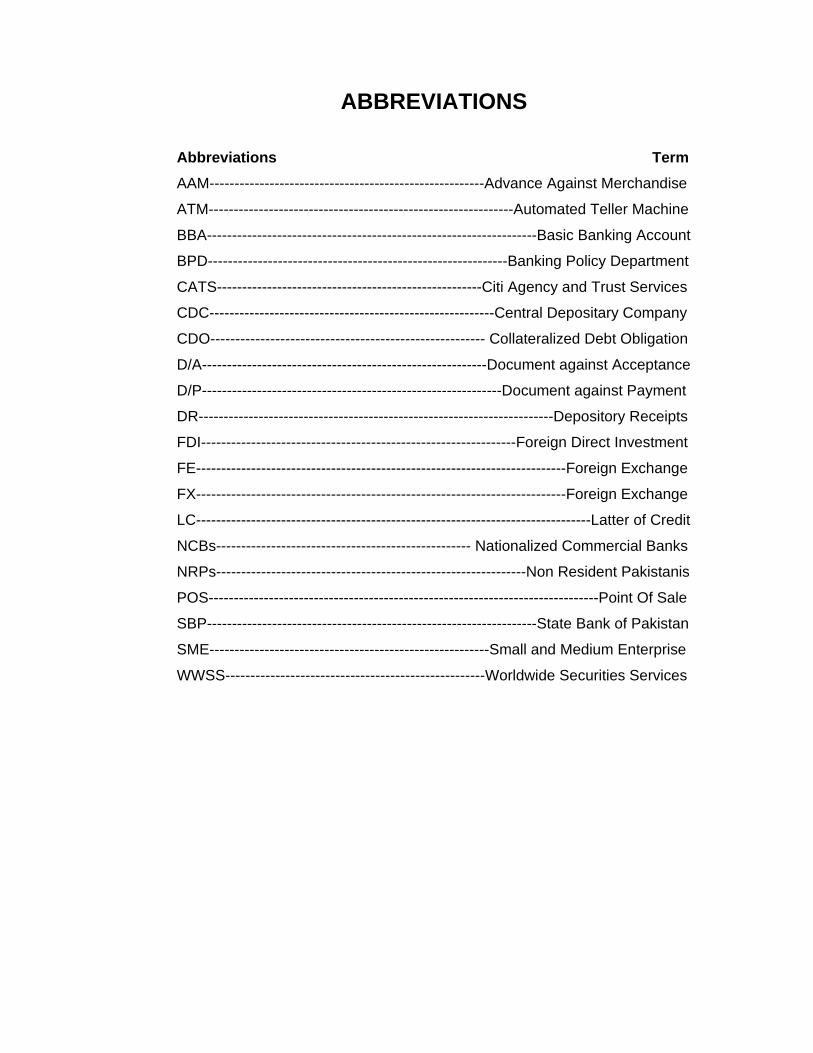

ABBREVIATIONS

Abbreviations Term

AAM-------------------------------------------------------Advance Against Merchandise

ATM-------------------------------------------------------------Automated Teller Machine

BBA------------------------------------------------------------------Basic Banking Account

BPD------------------------------------------------------------Banking Policy Department

CATS-----------------------------------------------------Citi Agency and Trust Services

CDC---------------------------------------------------------Central Depositary Company

CDO------------------------------------------------------- Collateralized Debt Obligation

D/A---------------------------------------------------------Document against Acceptance

D/P------------------------------------------------------------Document against Payment

DR-----------------------------------------------------------------------Depository Receipts

FDI---------------------------------------------------------------Foreign Direct Investment

FE--------------------------------------------------------------------------Foreign Exchange

FX--------------------------------------------------------------------------Foreign Exchange

LC-------------------------------------------------------------------------------Latter of Credit

NCBs--------------------------------------------------- Nationalized Commercial Banks

NRPs--------------------------------------------------------------Non Resident Pakistanis

POS------------------------------------------------------------------------------Point Of Sale

SBP------------------------------------------------------------------State Bank of Pakistan

SME--------------------------------------------------------Small and Medium Enterprise

WWSS----------------------------------------------------Worldwide Securities Services

TABLE OF CONTENTS PageACKNOWLEDGEMENTS---------------------------------------------------------- iii ABSTRACT----------------------------------------------------------------------------- iv ABBREVIATIONS-------------------------------------------------------------------- V TABLE OF CONTENTS------------------------------------------------------------- Vi LIST OF TABLES--------------------------------------------------------------------- X LIST OF FIGURES------------------------------------------------------------------- Xi CHAPTER I - INTRODUCTION--------------------------------------------------- 1 1. General------------------------------------------------------------------------------- 1 1.1. Impact of Global Liquidity Crisis on Pakistani Banking Sector---- 2 2. Problem Definition----------------------------------------------------------------- 4 3. Objectives of the Study ---------------------------------------------------------- 5 4. Hypothesis -------------------------------------------------------------------------- 5 5. Research Methodology ---------------------------------------------------------- 6 6. Scope of the Study --------------------------------------------------------------- 6 CHAPTER II – LITERATURE REVIEW----------------------------------------- 7 1. Financial Sector Review: Pakistan’s banking sector remarkably resilient despite challenging environment------------------------------------ 7 2. Foreign Banks in Poor Countries: theory and evidence----------------- 8 3. Role of Foreign banks in Developing Countries--------------------------- 9 4. How does Foreign Entry affects the Domestic Banking Market------- 11 5. Foreign, Private Domestic and Government Banks: New evidence from Emerging Markets------------------------------------------------------------- 12 6.Impact of Financial Reforms on Efficiency of State-owned, Private and Foreign Banks in Pakistan---------------------------------------------------- 14 7. Foreign Banks in Pakistan------------------------------------------------------ 16 8. What Drives Bank Competition? Some International Evidence-------- 17 9. Transforming Banking in Pakistan-------------------------------------------- 18 10. Corporate Governance of Banks in Pakistan----------------------------- 19 11. Pakistan’s Banking Sector Remains Strong------------------------------ 21 CHAPTER III – STRENGTHS AND WEAKNESSES: A COMPARATIVE ANALYSIS BETWEEN CITI BANK AND FAYSAL BANK LIMITED------------------------------------------------------------------------ 23 1.Introduction-------------------------------------------------------------------------- 23 2. Citi Bank Limited ------------------------------------------------------------------ 23 2.1Products and Services Offered by Citi Bank Limited----------------- 25 2.1.1 Deposit Accounts------------------------------------------------------- 25 2.1.1.1 Citi bank Rupee Current Account ------------------------ 25 2.1.1.2 Citibank Rupee Savings Account ------------------------ 25

2.1.1.3 Rupee Citi Ultimate Savings Account ------------------- 26 2.1.1.4 Current Account Premium --------------------------------- 26 2.1.1.5 Citibank Premium Profit------------------------------------- 27 2.1.1.6 Citi One --------------------------------------------------------- 27 2.1.1.7 Premium FCY Savings Account -------------------------- 28 2.1.2 Citi Bank Cards --------------------------------------------------------- 28 2.1.2.1 Citi Bank Gold Credit Card -------------------------------- 28 2.1.2.2 Citi Bank Silver Credit Card ------------------------------- 28 2.1.2.3 Citi Bank Mobilink Credit Card ---------------------------- 29 2.1.2.4 Citi Bank Caltex Credit Card ------------------------------ 29 2.1.2.5 Citi Bank E-Card --------------------------------------------- 30 2.1.2.6 Citibank Shaheen Affinity Credit Card ------------------ 31 2.1.2.7 Citi Bank Debit Card ---------------------------------------- 31 2.1.3 Corporate Banking Products ---------------------------------------- 32 2 1.3.1 Cash Management------------------------------------------- 32 2.1.3.2 Treasury ------------------------------------------------------- 33 2.1.3.3 Loan Products ------------------------------------------------ 33 2.1.3.4 Citi Service ---------------------------------------------------- 34 2.1.4 Securities Services ---------------------------------------------------- 34 2.1.4.1 Agency and Trust Services (CATS)---------------------- 35 2.1.4.2 Securities Lending-------------------------------------------- 35 2.1.4.3 Depository Receipts------------------------------------------ 35 2.1.4.4 Local Settlement Services---------------------------------- 36 2.1.4.5 Local Safekeeping Services------------------------------- 36 2.1.5 Trade----------------------------------------------------------------------- 37 2.1.5.1 Exports--------------------------------------------------------- 37 2.1.5.2 Imports---------------------------------------------------------- 37 2.1.5.3 Guarantees---------------------------------------------------- 38 2.1.6 Merger & Acquisition Advisory-------------------------------------- 39 2.2 Credit Rating-------------------------------------------------------------------- 40 2.3 Branch Network---------------------------------------------------------------- 40 2.4 HR Practices-------------------------------------------------------------------- 41 2.5 Recognized Innovations----------------------------------------------------- 42 2.5.1 Advisory Projects------------------------------------------------------ 43 3. Faysal Bank Limited-------------------------------------------------------------- 44 3.1 Products and Services Offered By Faysal Bank Limited----------- 44 3.1.1 Deposit Accounts----------------------------------------------------- 45 3.1.1.1 Faysal Savings---------------------------------------------- 45 3.1.1.2 Faysal Sahulat----------------------------------------------- 45 3.1.1.3 Rozana Munafa Plus--------------------------------------- 46 3.1.1.4 Basic Banking Account------------------------------------ 47 3.1.1.5 Faysal Moavin Savings Account------------------------ 48 3.1.1.6 Faysal Premium--------------------------------------------- 49 3.1.1.7 Faysal Izafa--------------------------------------------------- 50

3.1.1.8 Faysal Mahfooz Sarmaya---------------------------------- 51 3.1.1.9 FCY Saving Plus---------------------------------------------- 52 3.1.2 Consumer Loans-------------------------------------------------------- 52 3.1.2.1 Faysal Car Finance------------------------------------------ 53 3.1.2.2 House Finance------------------------------------------------ 53 3.1.2.3 Faysal Finance------------------------------------------------ 54 3.1.3 Corporate and Investment Products------------------------------- 55 3.1.3.1 Corporate Financing----------------------------------------- 55 3.1.3.2 SME Financing------------------------------------------------ 55 3.1.3.3 Trade Financing----------------------------------------------- 55 3.1.3.4 Treasury and Capital Markets----------------------------- 56 3.1.3.5 Investment Banking------------------------------------------ 56 3.1.3.6 Agriculture Financing---------------------------------------- 56 3.1.3.7 Cash Management------------------------------------------- 58 3.1.4 Services------------------------------------------------------------------- 59 3.1.4.1 PocketMate Visa Debit Card------------------------------- 59 3.1.4.2 Transfer of Funds-------------------------------------------- 60 3.2 Credit Rating-------------------------------------------------------------------- 60 3.3 Branch Network---------------------------------------------------------------- 61 3.4 HR Practices-------------------------------------------------------------------- 62 4. Comparative Study between Citi Bank Limited and Faysal Bank Limited------------------------------------------------------------------------------------ 63 4.1 Citi Bank Limited-------------------------------------------------------------- 63 4.1.1 Strengths---------------------------------------------------------------- 63 4.1.2 Weaknesses------------------------------------------------------------ 66 4.2 Faysal Bank Limited--------------------------------------------------------- 66 4.2.1 Strengths---------------------------------------------------------------- 66

4.2.2 Weaknesses------------------------------------------------------------ 67 CHAPTER IV- OPPORTUNITIES AND THREATS EXPERIENCED BY CITI BANK AND FAYSAL BANK LIMITED WHILE WORKING IN PAKISTAN------------------------------------------------------------------------------ 68 1. Opportunities----------------------------------------------------------------------- 68 1.1 International Economic Conditions--------------------------------------- 69 1.2 Bank Reforms----------------------------------------------------------------- 70 2. Threats------------------------------------------------------------------------------- 71 2.1.International Economic Conditions--------------------------------------- 71 2.2. Political Conditions---------------------------------------------------------- 72 CHAPTER V- DISCUSSION------------------------------------------------------- 73 1. General------------------------------------------------------------------------------- 73 2. Survey Forms----------------------------------------------------------------------- 73 2.1 Critical Analysis--------------------------------------------------------------- 73 2.2 Purpose of the Survey------------------------------------------------------- 73

2.3 Scope of the Survey--------------------------------------------------------- 74

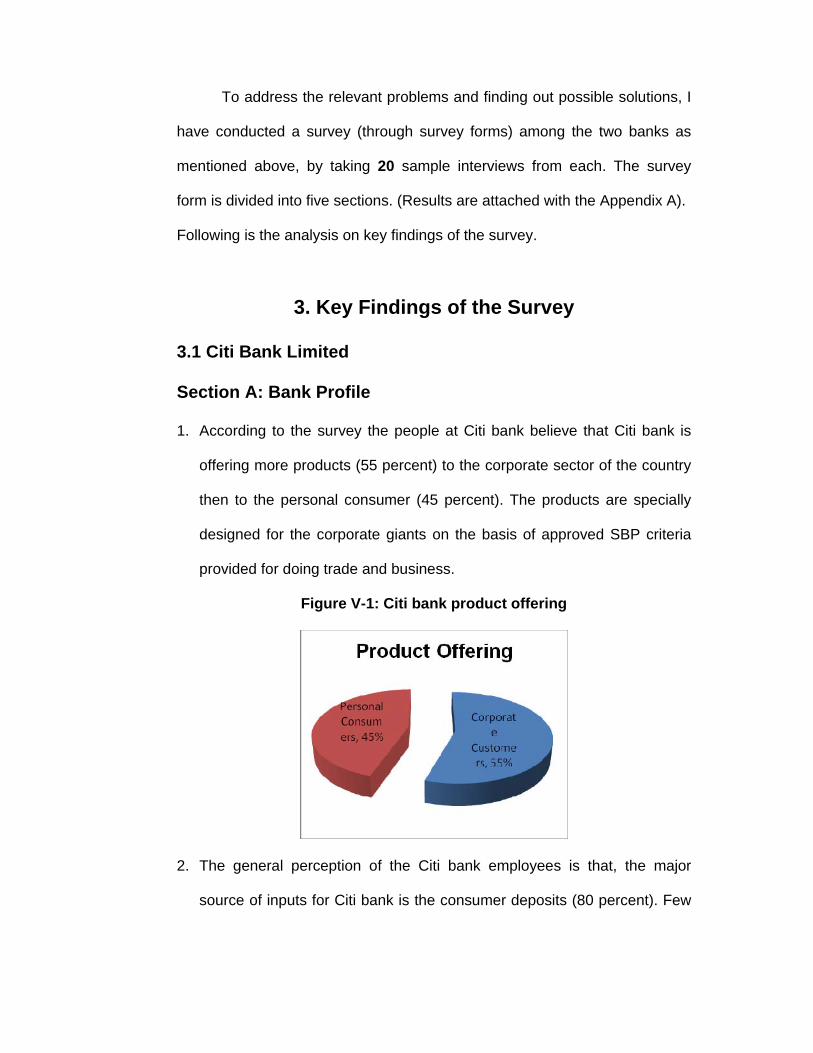

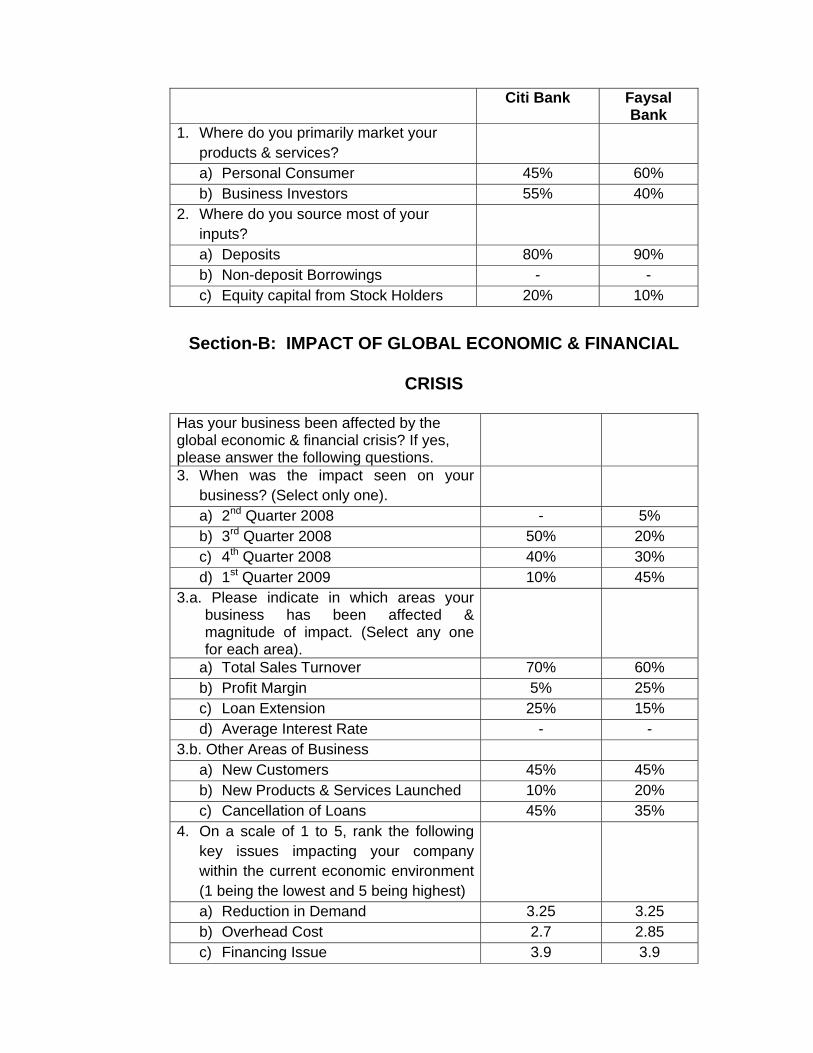

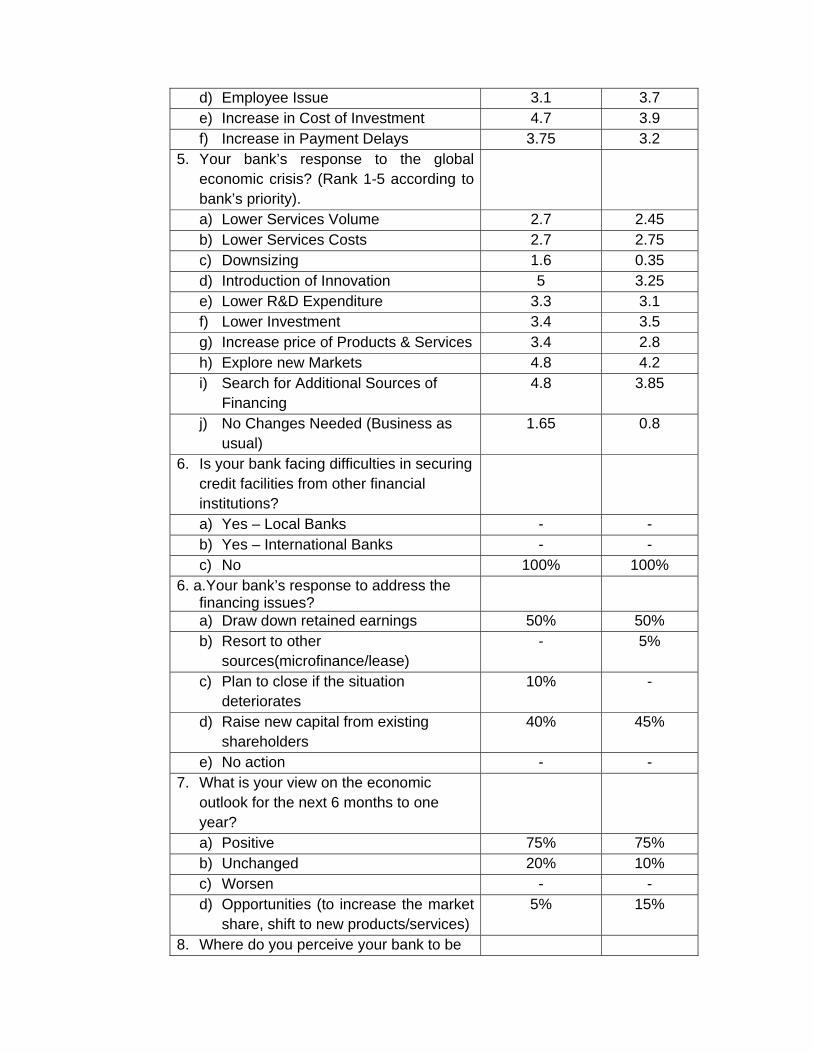

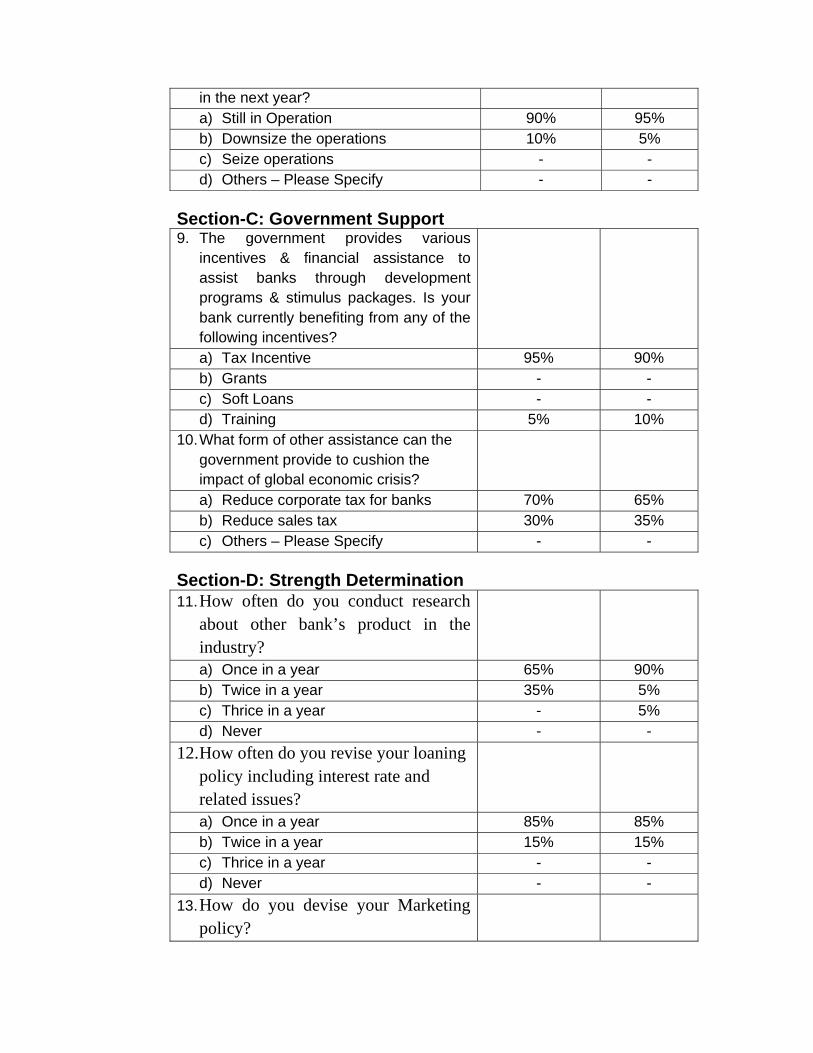

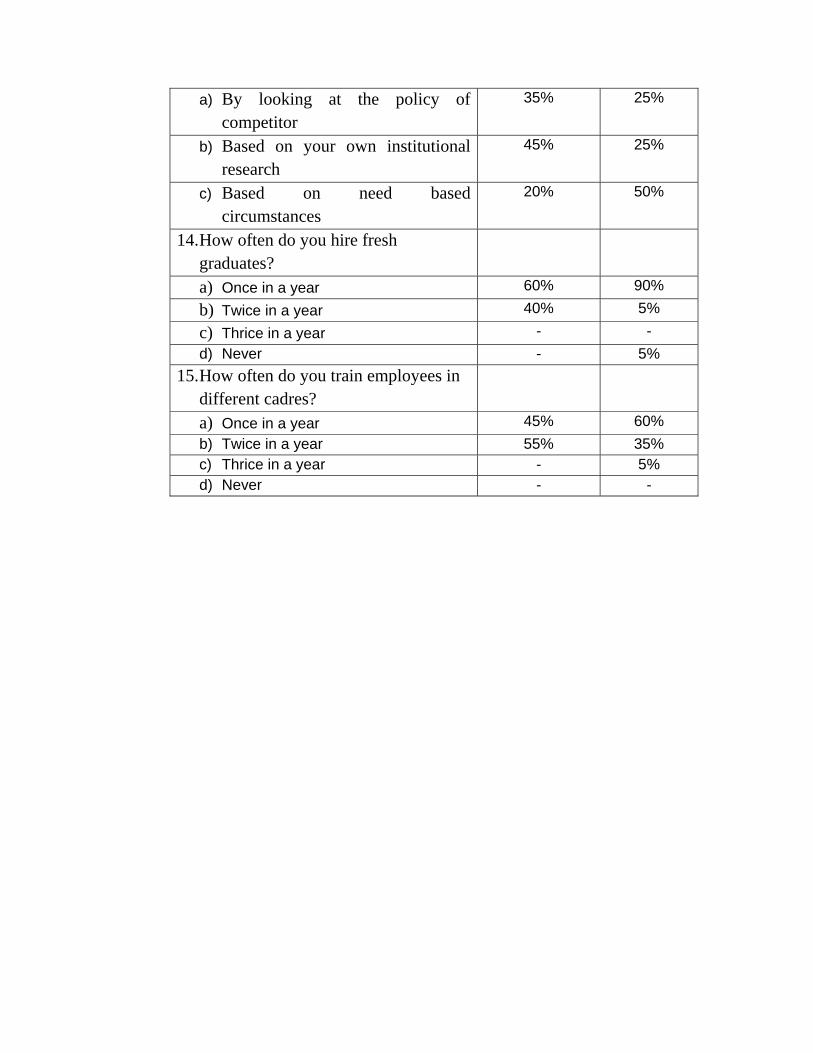

3. Key Findings of the Survey----------------------------------------------------- 74 3.1 Citi Bank Limited-------------------------------------------------------------- 74 3.2 Faysal Bank Limited--------------------------------------------------------- 80 CHAPTER VI- CONCLUSIONS--------------------------------------------------- 86 CHAPTER VII- RECOMMANDATION------------------------------------------- 89

REFRENCES-------------------------------------------------------------------------- 90

APPENDIX- A-------------------------------------------------------------------------- 92

LIST OF TABLES

Table Page

Table III- 1: Amount Spent through Caltex Credit Card and Free Fuel

Obtained on it-------------------------------------------------------------------------- 30

Table III-2: Credit Rating of Citi Bank Limited--------------------------------- 40

Table III-3: Citi Bank’s Branch and ATM Network---------------------------- 41

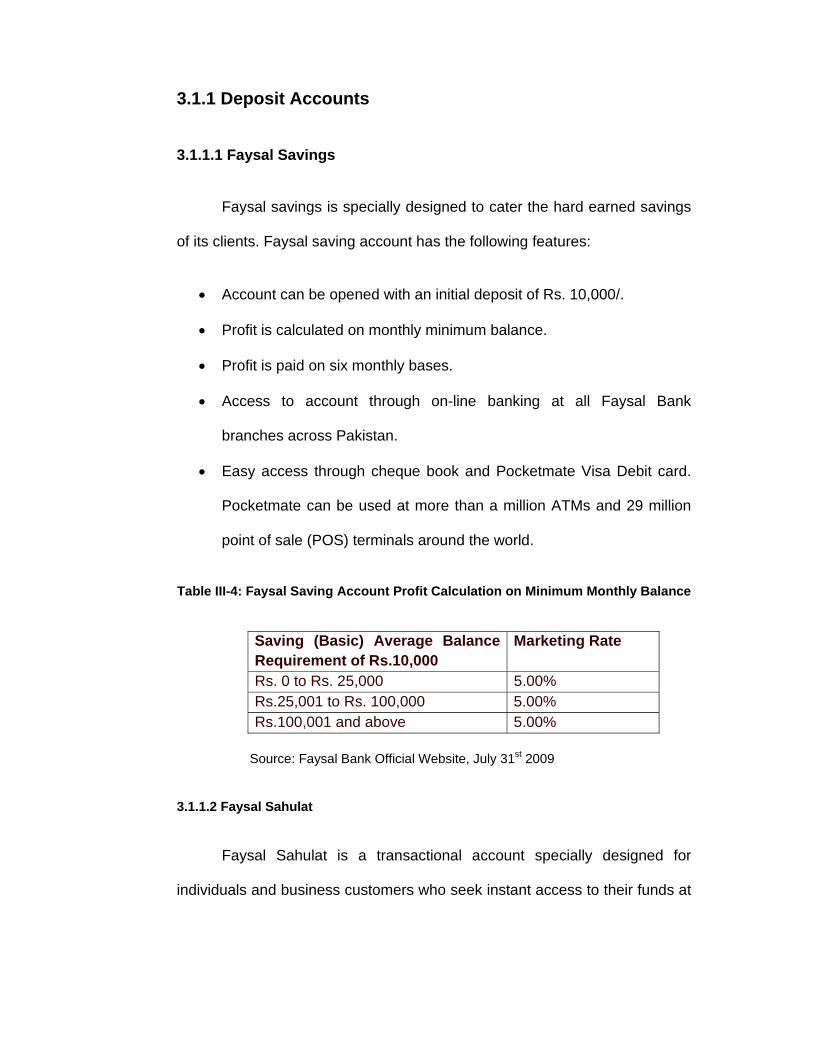

Table III-4: Faysal Saving Account Profit Calculation on Minimum

Monthly Balance---------------------------------------------------------------------- 45

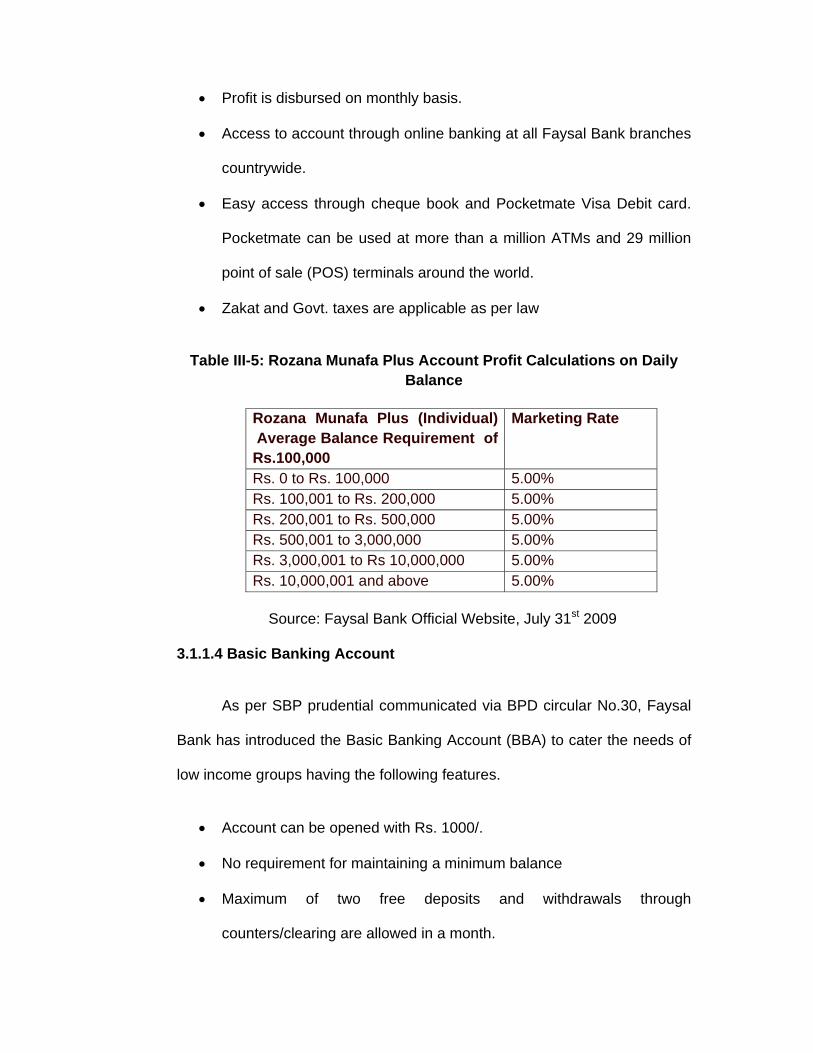

Table III-5: Rozana Munafa Plus Account Profit Calculations on Daily

Balance---------------------------------------------------------------------------------- 47

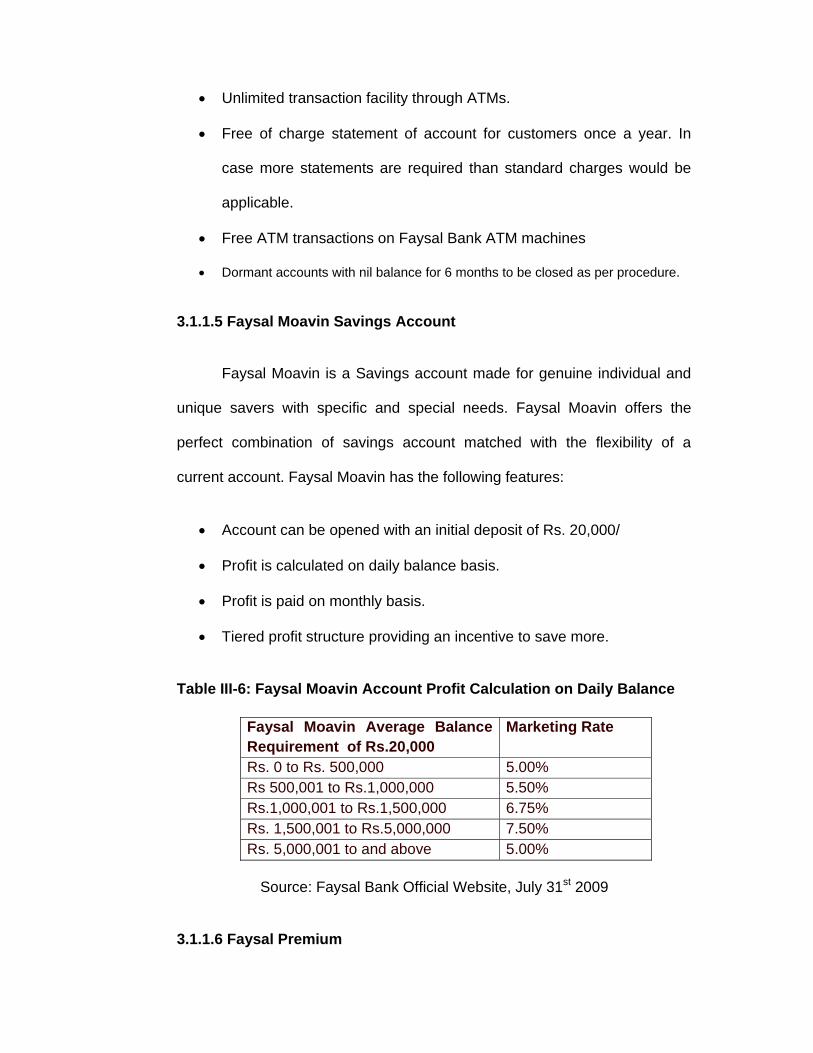

Table III-6: Faysal Moavin Account Profit Calculation on Daily Balance---- 48

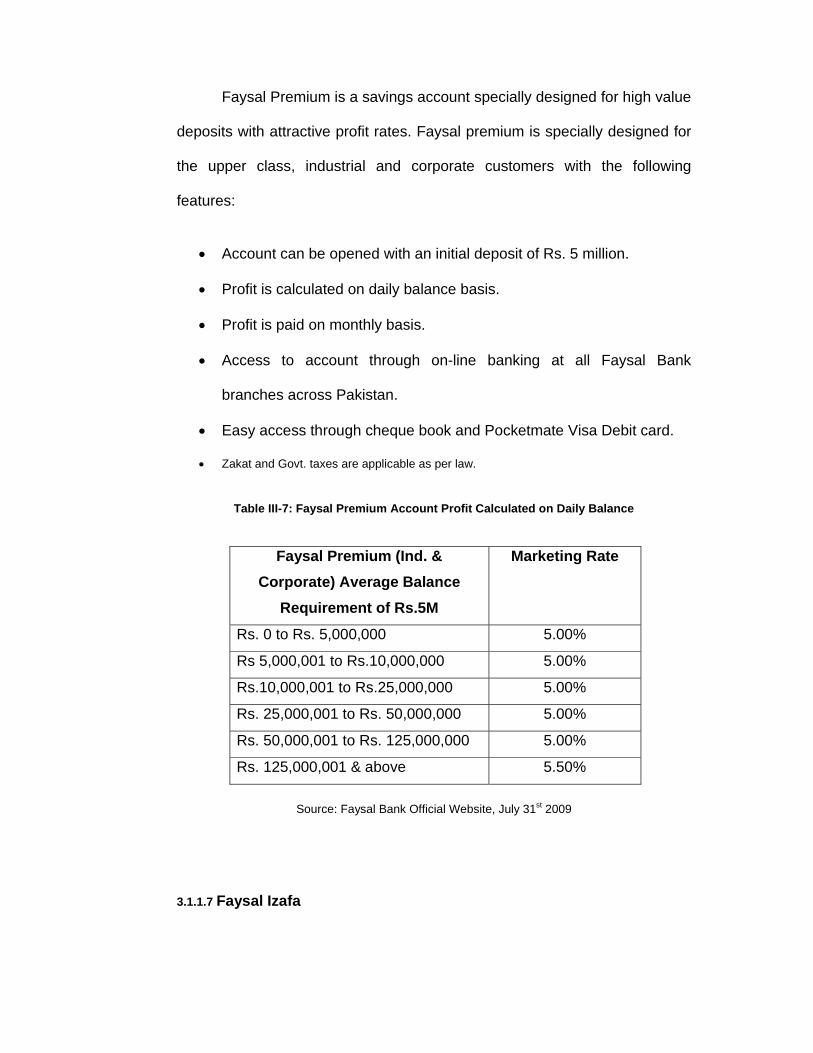

Table III-7: Faysal Premium Account Profit Calculated on Daily Balance-- 49

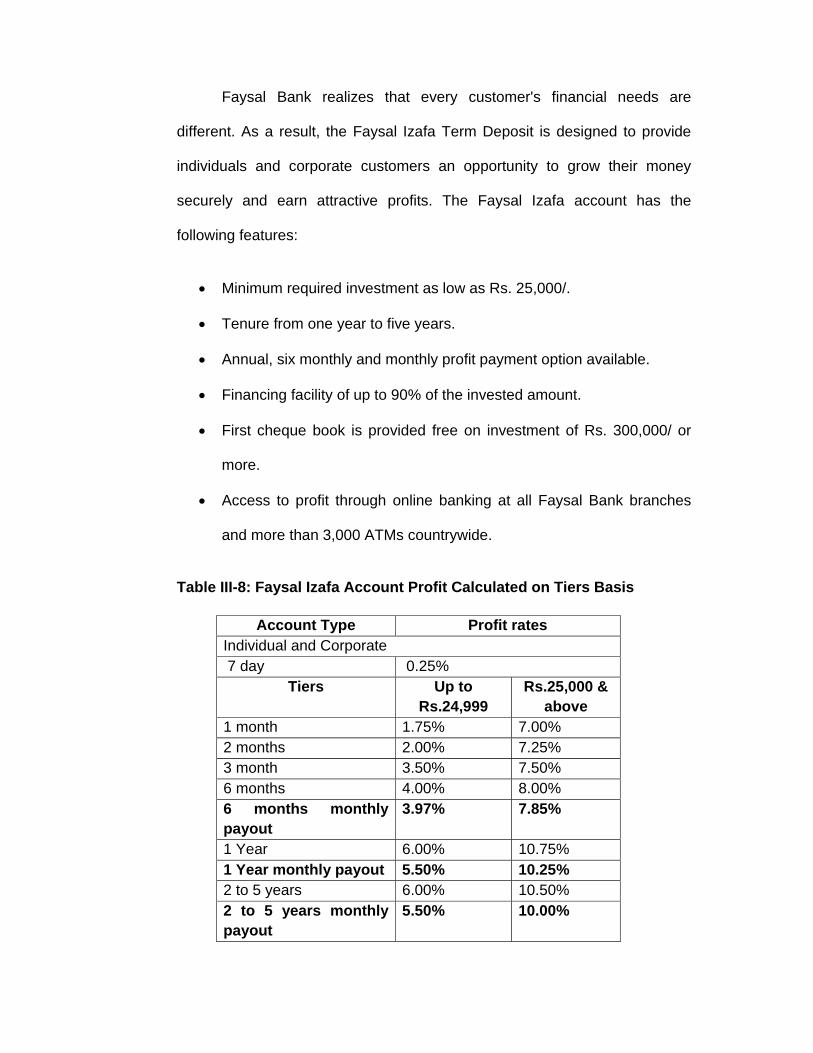

Table III-8: Faysal Izafa Account Profit Calculated on Tiers Basis------- 50

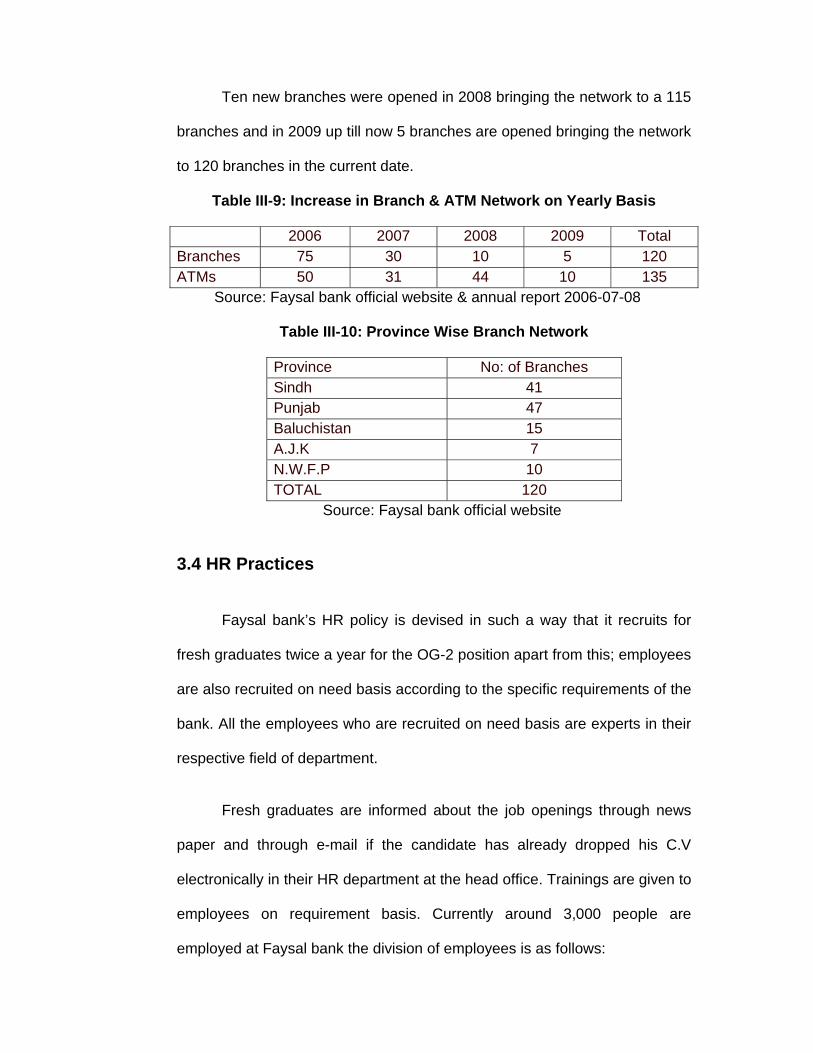

Table III-9: Increase in Branch & ATM Network on Yearly Basis--------- 62

Table III-10: Province Wise Branch Network---------------------------------- 62

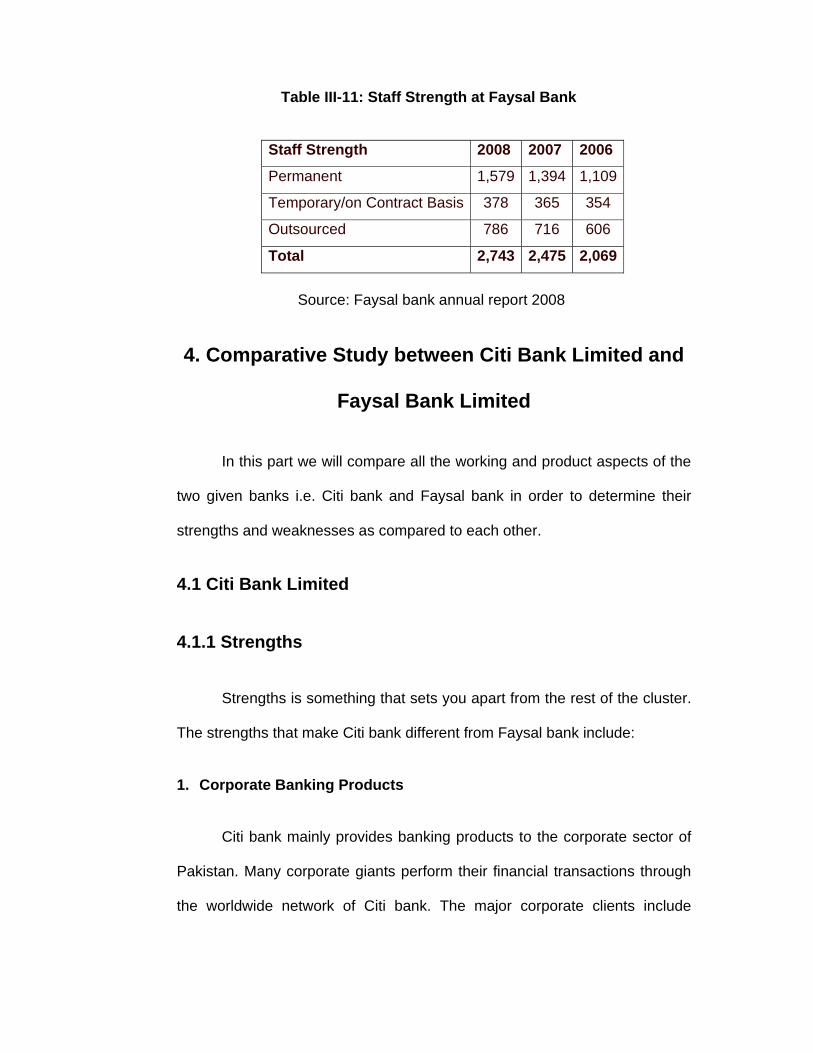

Table III-11: Staff Strength at Faysal Bank------------------------------------- 63

LIST OF FIGURES

Figure Page

Figure III-1: Ownership of Citi Bank----------------------------------------- 24

Figure V-1: Citi bank product offering--------------------------------------- 74

Figure V-2: Key Issues Impacting Citi bank------------------------------- 76

Figure V-3: Citi bank Response to Global Economic Crisis----------- 77

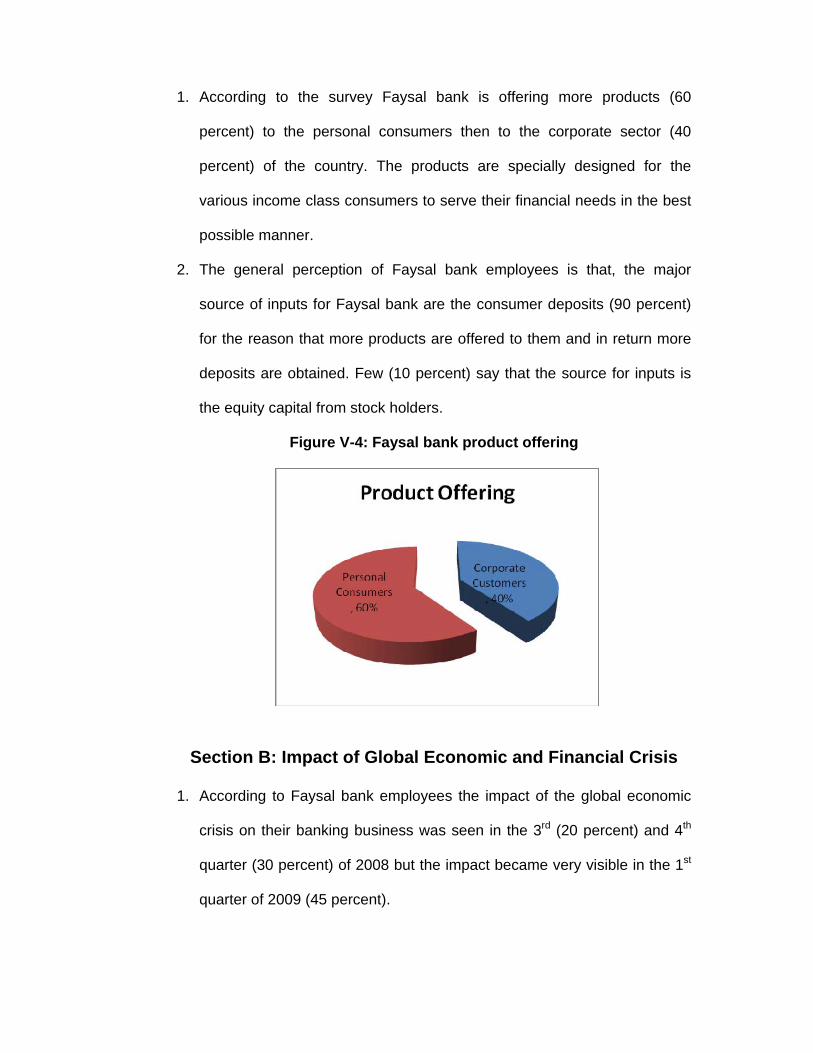

Figure V-4: Faysal bank product offering---------------------------------- 80

Figure V-5: Key Issues Impacting Faysal bank--------------------------- 82

Figure V-6: Faysal bank Response to Global Economic Crisis------ 83

CHAPTER I INTRODUCTION

1. General

The banking industry has traditionally been the engine of development

for many countries across the world, and the banking industry has dominated

the economies of many countries. It has always been one of the crucial

elements for the well-being of the economic structure of a country but from

the past three years i.e. 2007-09 the banking industry across the globe is

facing extreme financial turmoil.

Year 2008 will be remembered as one of the most turbulent years in

world’s economic history, the worst of its kind since Great Depression.

Impact of the sequence of global events, ranging from global financial turmoil

to surge in global commodity prices, has impacted regions differently and

unevenly. United States being the epicenter of the Tsunami of financial

market upheaval, has witnessed deeper and steeper reverberations whose

tremors have impacted all of Europe.

From what started as turmoil in one segment of financial markets i.e.

Subprime mortgage markets and CDOs etc., which constituted a very small

part of the global financial assets, the ravaging fire has spread across all

segments of financial sector, and across continents. The liquidity crisis

became prominently visible in September, 2008 with the failure of several

large United States based financial firms. Global stock markets fell and high-

yielding currencies have lost value.

USA, Britain, France, Italy, Japan, China, Germany and many

countries of Latin America are worried about the global economic meltdown

due to persistence global liquidity crisis. They are all trying to seek a common

strategy to combat with this economic and financial situation. Emerging

market countries are turning to the International Monetary Fund (IMF) to help

shore up confidence in their financial systems strained by a global credit

crunch. The crisis is ongoing and continues to change, evolving at the close

of October 2008 into a currency crisis with investors transferring vast capital

resources into stronger currencies such as Yen, the Dollar and the Swiss

Franc.

1.1 Impact of Global Liquidity Crisis on Pakistani Banking Sector

Wracked by political instability and hard hit by the global economic

crisis, Pakistan is teetering on the brink of default. Pakistan Finance Ministry

has said that it is left with overall foreign reserves of $7.3 billion as of October

17, 2008, of which the SBP possesses $3.98 billion and the commercial

banks $3.32 billion. Out of $3.98 billion, $1.5 billion have been consumed in

the wake of forward booking liabilities, leaving the central bank with only $

2.48 billion of net foreign exchange reserves, which were barely enough to

cater to the needs of one-and-half month of imports.

The rupee has fallen sharply. The international credit rating agency,

Standard & Poor’s, has downgraded Pakistan to a position superior only to

the Seychelles, which has already defaulted. SBP has decided to take the

following actions to ease the immediate liquidity situation.

Cash Reserve Requirement (CRR) for all deposits up to 1 year

maturity is being reduced by 200bps to 6.00%. This will release an

additional liquidity of about Rs 60 billion into the system.

It has been decided to fully exempt the time deposit of 1 year tenor

and above from Statutory Liquidity Requirements (SLR). This will

inject about Rs 120 billion in the market.

Another Rs 30 billion will be released on 15th November.

Cumulatively SBP from 17th October to 15th November, 2008 will

have released liquidity of Rs 210 billion.

However banking system of Pakistan has escaped the major ravaging

effects of recent financial market turmoil. Dr: Shamshad Akhtar, President

SBP said;

“The financial markets in Pakistan have not been hit by the

subprime markets or the associated contagion directly as Pakistan’s banking

system from July 2007 to September 2008 did not face any liquidity

problems”.

While speaking at The Asian Banker Dialogue on “The Banks We Like

and the Impact of the Global Financial Crisis on Pakistan’s Banks. The

capital adequacy ratio of the banking system is strong at 12.1%, well above

the internationally acceptable minimum requirement of 8%. Pakistan’s

banking sector is quite resilient and fully capable of withstanding market

shocks and adverse macro economic conditions. State Bank of Pakistan

launched financial sector reforms in July 2008 to lay foundations for further

enhancing the robustness of the financial system to cope with the emerging

challenges.

According to assessment of State Bank of Pakistan Financial Stability

Review 2007-2008, the stability of the financial system is derived essentially

from the banking sector. An assessment of the performance of the banking

sector from January 2007, to June 2008 shows that Pakistan’s banking

sector has over the years nurtured itself such that it is able to withstand some

of the shocks it has faced in the last 18 months or so.

The Pak-rupee regained its strength against the dollar in the open

market, on 30th December 2008, which shows the ability of the Pakistani

Banking Sector to pull back it self from critical financial crisis affecting all the

currencies globally. The greenback started the day’s trading at Rs 78.70 for

buying and after losing strength closed at Rs 78.50 for buying and Rs 79.50

for selling. Therefore, the rupee incurred a gain of 20 paisa.

The European single currency was also down against the rupee as it

started the day’s trading at Rs: 110.15 for buying, posted losses and was

changing hands at Rs 109.06 for buying and Rs: 112.59 for selling at the end

of the day’s trading. Therefore, the rupee was up by Rs: 1.09. Similarly, the

British currency depreciated against the rupee as it commenced the day’s

trading at Rs: 112.58 for buying and after shedding grounds closed at Rs:

111.35 for buying and Rs: 114.95 for selling at the end of the day’s trading.

Thus, the rupee incurred a gain of Rs: 1.23.

2. Problem Definition

The study analyses some conceptual and empirical issues of the

Pakistani banking sector. Despite of the liquidity turmoil going around the

world where banks are going bankrupt in various developed countries of the

world foreign banks are entering in Pakistan. The major emphasis of the

study is to answer the following questions: What are the strengths and

weaknesses of the Pakistani banking sector? What are the opportunities and

challenges faced by Pakistani banking sector with the arrival of foreign banks

in the country? What are the strengths and weaknesses of foreign banks

working in Pakistan? What are the opportunities and challenges faced by

foreign banks while working in Pakistan?

3. Objectives of the Study

Specific objectives of the study are:

1. To investigate and conduct an analysis to determine the strengths and

weaknesses of foreign banks working in Pakistan by picking the model of

Citi Bank and Faysal Bank Limited.

2. To investigate and conduct an analysis to determine the opportunities and

threats faced by foreign banks working in Pakistan.

3. To investigate the impact of entry of foreign banks on the Pakistani

banking sector.

4. Hypotheses

1. Citi bank in the capacity of foreign bank failed to perform under severe

liquidity crisis.

2. Faysal bank in the capacity of a domestic financial institution has

performed well under severe liquidity crunch.

5. Research Methodology

The main method of determining and collecting the data is based on

studying reviewed literature. For comparative study structured interviews and

questionnaire is constructed and analyzed. Comparative study of Citi bank

and Faysal bank was conducted to authenticate the hypotheses. My research

is based on secondary and tertiary data which includes:

Structured Interviews

State bank of Pakistan – Library

Semiannual Periodicals in Economics

Internet

Books

Newspapers - Articles

6. Scope of the Study

This piece of research will investigate the SWOT’s faced by foreign banks

working in Pakistan and the threats imposed on Pakistani banks with the arrival

of foreign banks. A comparative study of Citi Bank and Faysal bank limited from

2007-08 is considered. Data is collected from above said bank and analyzed

respectively to determine the SWOT’s faced by both the banks during the

financial crisis of 2007-08.

CHAPTER II

REVIEW OF LITERATURE

1. Financial Stability Review: Pakistan’s banking sector remarkably resilient despite challenging

environment

DAILY TIMES (2008) says that Pakistan’s banking sector has

remained remarkably strong and resilient, despite facing pressures arising

from weakening macroeconomic environment since late 2007. According to

the assessment of the State Bank of Pakistan Financial Stability Review

2007-08 the banking system is on strong footing and has long term potential

– a feature which has served to attract a substantial amount of FDI in the

sector. Performance of the banking sector from January 2007 to June 2008

shows that Pakistan’s banking system has over the years nurtured itself such

that it is able to withstand some of the shocks it has faced in the last 18

months or so.

Aggregate financial soundness indicators have improved since early

2000, and continue to exhibit strong performance. Tighter provisioning

requirements may have reduced profits, but have positioned banks well.

The way forward for the financial sector is to maintain both the

simplicity and transparency of product structures. Effective regulation is the

preferred route for central banks responsible for safeguarding both monetary

and financial stability.

Profitability of the banking system continues to be impressive, largely

emanating from the persistent growth in high-yield earning assets and

expanded business volumes. Before-tax Return on Assets of the banking

system remains strong at 2.3 percent in June 2008. The strengths built up

over the years are now coming in handy in managing the recent financial

strains. [DAILY TIMES, December 31, 2008]

2. Foreign Banks in Poor Countries: Theory and

Evidence

Enrica Detragiache, Thierry Tressel and Poonam Gupta (2006) have

mentioned that the proponents of foreign bank entry claim that these banks

can achieve better economies of scale and risk diversification than domestic

banks, introduce more advanced technology (especially risk management),

and increase competition. Opponents point out that an important part of

bank’s business, namely lending, to informationally opaque firms, such as

small firms, is inherently local in nature and is not easily carried out by large

organizations managed from far away. We have found that foreign banks in

lower-income countries (LICs) such as South and East Asian countries and

Latin American countries lend predominantly to the safer and more

informationally transparent customers, such as multinational corporations,

large domestic firms, or the government.

Foreign banks are better than domestic banks at monitoring

“hard” information, such as accounting information or collateral values, but

not at monitoring “soft” information, such as the borrower’s entrepreneurial

ability or trustworthiness.

Based on cross-country studies, foreign-owned banks have been

found to have lower operating costs and higher profitability than private

domestic banks. Foreign bank entry in developing countries also appears to

lower interest margins and profitability, suggesting an increase in

competition.

Drawing on an exceptionally rich dataset of 80,000 business loans in

Pakistan we found that the private domestic banks lend more to

informationally opaque businesses than foreign banks, and that they are

more successful at recovering defaulted debt. [IMF WORKING PAPER

(WP/06/18), January, 2006].

3. The Role of Foreign Banks in Developing Countries: A Survey of the Evidence

Joydeep Bhattacharya (2000) has analyzed that there are four broad

reasons as to why banks establish branches and subsidiaries in foreign

countries.

1. Home-Country Customer Relations: The most cited explanation is

to “follow-the-customer” hypothesis. Banks go multinational to better

serve the foreign operations of the domestic corporate entities.

Foreign banks have a comparative advantage over local banks in that

over the years, through investment in information and relationship

capital, they have reduced the cost of monitoring the financial

conditions of the MNC in question.

2. Business Opportunities: Banks in some countries may be inefficient

(outdated technology) or uncompetitive. Such conditions may attract

foreign entrants to operate and to penetrate these markets by

employing newer technology or better marketing tools.

3. Regulatory Arbitrage: Banks, in general face strict regulatory

practices wherever they are based. However, some nations may

choose to open up and allow foreign banks to enter in a relatively relax

regulatory regime if the perceived gains are high and thus attract

foreign banks.

4. Diversification and Interest Rate Differentials: The optimal policy

for a multinational bank is to maximize profit for a given level of risk or

to minimize risk given a desired level of profit. The total portfolio risk of

both the domestic and foreign portfolio assets has been lower then the

risk of purely domestic portfolio.

When a foreign bank enters a host country there are certain common

concerns that the country has in allowing a foreign bank entry.

1. Fear of Foreign Domination: A stated fear in the minds of central

bankers and government is that unrestricted entry of foreign banks

may result in their assuming dominant positions in the domestic

market, by driving out less efficient or less resourceful domestic

banks.

2. Cream-Skimming Behavior: Foreign banks carve out a niche for

themselves in the upper/richer end of the market. Thus they cream-

skim the market, by taking a disproportionate share of the best of local

business away from domestic banks.

3. Lack of Local Commitment: Under times of local distress, it is

believed that foreign banks will be the first once to “leave the ship”. In

times of distress (eg. a bad recession) in the foreign banks’ home

country; foreign banks may wind-up foreign operations in order to

stabilize earnings at home.

Countries allowing foreign banks to enter broadly expect two types of

benefits to flow in to the domestic economy.

1. A Boost to Domestic Banking Sector: Countries expect foreign

banks to enter and shock the domestic banking sector by bringing in

“healthy competition”. Domestic banks, are expected to react to the

foreign presence and compete fiercely to retain their previous market

shares, thereby lifting domestic banking sector to international levels

of efficiency.

2. Greater Access to International Markets: Countries, expect from

foreign banks to aid in the development of trade and foreign direct

investment. First, their domestic operations will benefit local producers

and, in particular export/import companies and MNCs. Secondly;

foreign banks are expected to increase foreign currency inflows into

the country. [www.econ.iastate]

4. How Does Foreign Entry Affects the Domestic Banking Market

Sting Claessens, Aali Demirguc-Kunt, Harry Huizinga (1998) has

explored that the potential benefits of foreign bank entry for the domestic

economy are in terms of better resource allocation and higher efficiency. It

has been found that foreign banks may

Improve the quality and availability of financial services in domestic

market by increasing bank competition.

Serve to stimulate the development of the underlying bank supervisory

and legal framework.

Enhance a country’s access to international capital.

Bhattacharaya (1993) reports specific cases in Pakistan, Turkey, and

Korea, where foreign banks helped to make foreign capital accessible to fund

domestic projects.

We estimate empirically how foreign bank entry affects the operations

of domestic banks. We found that entry of foreign banks reduces the

profitability of domestic banks, while there is some evidence that the non-

interest income and the overall expenses of domestic banks are also

negatively affected by foreign bank entry.

In developing countries, foreign banks may be able to realize high

interest margins, because they are frequently exempt from credit allocation

regulations and other such restrictions, especially in countries where

domestic banking markets are dominated by State banks.

[www.worldbank.org, WPS 1900 (WPS 1918) 1998]

5. Foreign, Private Domestic and Government Banks: New Evidence from Emerging Markets

Atif Mian (2003) has pointed out that, banks as financial

intermediaries are considered an important element for growth in emerging

economies by most. Yet less is known about the strengths and weaknesses

of different types of bank organization and their design. The three dominant

types of banks in emerging markets are government, private domestic and

foreign banks.

The differences are important to document and analyze because the

three types of banks differ in important ways, in the structure of their

incentives, organization, and regulation. For eg: government banks suffer

from the moral hazard problem of being both the owner and the regulator,

private domestic banks have higher cash-flows incentives, and greater

distance between the regulator and the ownership. Foreign banks on the

other hand being relatively similar to private domestic banks in terms of

incentives and regulation, but they differ in their organizational structure.

Our analysis reveals that private domestic banks appear to be more

“aggressive” in their lending than foreign banks. They hold significantly less

liquid assets than foreign banks, and correspondingly hold more assets in the

form of loans. Moreover, of the loans that each type of bank gives out, private

domestic banks earn 2.6% higher return than foreign banks. The higher

return on loans despite similar default rates implies that private domestic

banks are more profitable than foreign banks on the loan side.

However, the picture reverses on the deposit and banking services

side. Private domestic banks have higher interest expense on deposits, and

lower revenue from the sale of banking services. Consequently there is no

significant difference in the average profitability of private domestic and

foreign banks in emerging economies. Foreign banks are comparatively less

likely to lend to “soft information” firms, and more likely to lend to “hard

information” firms. “Soft information” refers to information that cannot be

easily publicly verified by a third party. Stein (2002) argues that organizations

with more hierarchical structures are more likely to rely on “hard information”

as opposed to organizations with flatter structures. The reason is that flatter

organizations have better control and information on their managers, and

thus can afford to give them more freedom to decide what should be done.

We measure the relative sensitivity (correlation) of banks to different

types of macro shocks. These correlations show two effects: the response of

bank to the shock, and the exposure of the bank to the shock. There is an

interesting separation in the type of shocks that private domestic and foreign

banks are sensitive to. In particular, private domestic banks respond more to

macro shocks affecting the local (private) corporate sector, whereas foreign

banks respond more to macro shocks affecting the foreign corporate and

government sectors. Foreign banks are more sensitive to changes in the

aggregate foreign currency deposits, whereas private domestic banks are

more sensitive to changes in the aggregate domestic currency deposits.

With respect to government banks, we find that government banks

perform significantly worse than both private domestic and foreign banks in

terms of overall profitability. [JOURNAL OF BANKING AND FINANCE, 2003]

6. Impact of Financial Reforms on Efficiency of State-owned, Private and Foreign Banks in

Pakistan

Abid .A. Burki, G.S.K. Niazi (2006) has found that government

ownership of banks is very common in emerging markets where, after

decades of excessive government regulatory controls and dominance of

state-owned banks, foreign and private banks have recently been allowed to

compete freely. Financial reforms in Pakistan have transformed the banking

industry during the 1990s. These reforms included licensing of several new

private and foreign banks, higher supervision and strengthening of prudential

regulations aimed at improving financial systems and monetary

management.

To study the relationship, we divide the sample into pre-reform (1991-

92), first-reform (1993-96) and second reform (1997-00) periods. The results

obtained indicate strong evidence that the first-phase of reforms failed to

convert cost inefficient banks into efficient banks.

With nationalization of the entire banking and insurance sector in

1972, five nationalized commercial banks (NCBs) were set up after merger of

some nationalized banks. These five public sector banks dominated the

scene with their holding of 92% share in total banking assets while the rest of

the share was in the hands of foreign commercial banks. Since the

nationalization of commercial banks in 1972, private ownership of banks was

not allowed until this ban was lifted as part of financial sector reforms in

1991.

The first-reform period was characterized by liberalization and

institutional strengthening of the banking sector. Liberalization started when

ten new private banks were granted permission to operate in 1991.

A temporary ban was introduced on new banks in 1995, private and

foreign banks were allowed to grow and extend operations by easing of

branch policy in 1995 whereby controls on opening of new bank branches

were removed. The first set of reforms became effective from 1993-96 while

a second set of further reforms were initiated between 1997 and 2000.

The minimum paid up capital requirement was set at Rs.500 million in

December 1997. Due to the embryonic role of foreign and private banks, the

share of state-owned banks in bank deposits gradually declined from 93% in

1990 to only 56% in 2000 while the share of private banks increased from

zero to about 30% in the same period. [LAHORE UNIVERSITY OF MGT

SICENCES, CMER WORKING PAPER (06-49) 2006]

7. Foreign Banks in Pakistan

Shabbir H. Kazmi (1999) has mentioned that the foreign banks,

operating in the country, have posted very poor results for the period ending

December 31, 1998 after a long time. Foreign exchange deposits, a strong

base for these banks in the past, are no longer available. Declining yield on

T-Bills is another reason for reduction in the profit. None of these banks is

expected to take an exit from Pakistan but further expansion in branch

network may not take place in near future.

A closer look at the annual reports of these banks for 1998 indicates

different trends. Some banks have succeeded in increasing deposits and

many registered a decline. Profit margins have been reduced and some

banks have even declared loss for the year. Heavy provisioning against non-

performing loans was a factor responsible for the reduction in the profitability

of these banks.

Foreign banks which were prompt in redefining their working

strategies in Pakistan succeeded in maintaining their share in total deposits.

Whereas the private domestic banks successfully entered into the market

segment previously considered to be an exclusive domain of foreign banks.

This dent was made by local banks by making huge investments in

technology and offering superior quality services.

The key factor of profitability of commercial banks is dependent on the

return on assets and difference between the borrowing and lending rates.

Provision against non-performing loans affects the profitability of banks

directly. City bank made the highest provision amounting to Rs: 512 million

however these provisions are written back in case of recovery. [July 04,

1999]

8. What Drives Bank Competition? Some International Evidence

Sting Claessens and Luc Laeven (2003) have found that competition

in the financial sector matters for a number of reasons. The degree of

competition in the financial sector can matter for the efficiency of the

production of financial services, the quality of financial products and the

degree of innovation in the sector. A reason specific to the financial sector is

the link between competition and stability.

The performance measures, such as the size of the banking

operations or profitability, do not necessarily indicate the competitiveness of

the banking system. The degree of competition in the banking system should

be measured with respect to the actual behavior of (marginal) bank conduct.

The actual behavior should be related not only to banking market structure,

but also to foreign bank ownership, and the severity of activity restrictions, as

those can limit the degree of intra-industry competition.

It is found that a country with greater foreign bank entry, and lack of

restrictions on foreign bank activity in the host country result in higher

competition among the private domestic, government and foreign banks.

Tighter entry requirements are negatively linked with bank efficiency,

leading to higher interest rate margins and overhead expenditures, while

restricting foreign bank participation tends to increase bank fragility. [WORLD

BANK POLICY, RESERCH WORKING PAPER (3113) August, 2003]

9. Transforming Banking in Pakistan

Mohammad Zubair Khan (1998) has analyzed that Pakistan undertook

ambitious financial reforms in the early 1990s in an effort to establish a more

market- based system of monetary management. The reforms were designed

primarily to correct the distortion implicit in the administered structure of rates

of return on various financial instruments, to enhance competition and

efficiency in the financial system, and to strengthen State Bank of Pakistan

(SBP) supervision.

In accordance with existing policies, foreign currency deposits were

exchanged by commercial banks for rupees with the SBP for domestic

lending, the banks purchased forward contracts from the SBP at a cover fee

that was consistently 3 to 5% below the private market forward premium. As

a result, banks found it increasingly profitable to intermediate in foreign

currency deposits while the SBP suffered large fiscal losses. Problems of the

financial sector are rooted in the following areas:

Lack of financial discipline encouraged by weak supervisory

capacity of the SBP.

Mismanagement of short-term capital inflows.

Weak resource mobilization.

Financial sector reforms in 1997/98 were undertaken mainly to

promote financial saving, improve the process of financial intermediation,

enhance competition, and assure efficient allocation of financial resources.

There are serious structural weaknesses in the banking sector reform

strategies adopted. The weaknesses are as follows:

There is an overestimation of the capacity of the market to absorb

assets that need to be liquidated.

The development of capital market has been over looked.

Project loans that have contributed significantly to the frequency of

loan defaults have not been fully assessed.

Implementation of reform efforts has been handicapped by the loss of

confidence resulting from freezing of foreign accounts in May 1998.

Although in recent years the share of the non-banking financial sector

has increased in terms of lending, the financial system is still dominated by

commercial banks. Between 1993 and 1995, the banking sector as a whole

experienced declining profitability, increasing inefficiency, and a weakening

capital base, even by Pakistani accounting standards. However, there was a

marked difference in performance among the NCBs, partially privatized

banks, foreign banks, and private domestic banks. [STUDY

COMMISSIONED BY ABD FOR RETA, http://uoit.ca/sas, July, 1998]

10. Corporate Governance of Banks in Pakistan

Ahmed M. Khalid and Muhammad Nadeem Hanif (2004) has

discussed that the term “corporate governance” essentially refers to the

relationships among management, the board of directors, shareholders, and

other stakeholders in a company. These relationships provide a framework

within which corporate objectives are set and performance is monitored.

Corporate governance also provides the structure through which the

objectives of the company are set, and the means of attaining those

objectives and monitoring performance are determined.

Sound corporate governance is particularly important for banks

because the rapid changes brought about by globalization, deregulation and

technological advances are increasing the risks in banking systems.

Unlike other companies, most of the funds used by banks to conduct

their business belong to their creditors, in particular to their depositors.

Linked to this is the fact that the failure of a bank affects not only its own

stakeholders, but may have a systemic impact on the stability of other banks.

Banks play an important role in the corporate governance system.

Their role varies from one model to another. This is due to the banks’

function as credit issuers, as banks still remain primary providers of credit to

almost all of the economies in the world. Internationally the issue of corporate

governance has been recognized as on of the most important issue of

corporate sector.

Pakistan is no exception and State Bank of Pakistan has recently

issued “Handbook of Corporate Governance” with the objective of providing

guidance to the Board of Directors and the Management of the banks for

promoting corporate governance in their respective institutions.

Banking crises serves as an indicator of poor governance of banks.

The episodes of banking crises in 1980s in Europe and 1990s in Latin

America and Asia suggest that such crisis may lead to major bankruptcies,

recession, and economic and political instability, which necessitate the need

for strong corporate governance. [LAHORE UNIVERSITY OF MGT

SCIENCES (LUMS) May, 2004]

11. Pakistan’s Banking Sector Remains Strong

Faizan Chaudary (2009) has found out that the Pakistani banking

sector has remained remarkably strong and resilient during the last 18

months but the excessive dependence of economy on banking system is

quite clear in comparison with the other emerging economies. The banking

system is on strong footing and has long term potential - a feature which has

served to attract a substantial amount of FDI in the country, with established

global financial institutions now actively participating in the domestic financial

sector.

In contrast to the liberalized financial system in the west which took its

toll in the form of the current global financial crisis, there are stringent

regulations and adequate policies in place to help the banking system

manage its risks. Stress tests conducted on June-2008 the resulting data

indicate that the large banks are relatively robust, with the medium and small-

sized banks positioning themselves in niche markets.

Capital adequacy of the banking system remains strong at, 12.1% by

the end-June 2008, well above the internationally acceptable minimum

requirement of 8.0% and the risk weighted assets ratio of the banking system

was at 9.7%.

The writer of the article also found that the demand for credit from both

the government and the private sector resulted in liquidity strains faced by

some individual banks, which also came from the combined impact of their

weak deposit mobilization and low interest rates offered on deposits.

[PAKISTAN TALK, NEWS&VIEWS, January 4, 2009]

CHAPTER III STRENGTHS AND WEAKNESSES:

A COMPARATIVE ANALYSIS BETWEEN CITI BANK AND FAYSAL BANK LIMITED

1. Introduction

The banking industry has traditionally been the engine of development

for many countries across the world, and indeed today, banking industry

dominates the economies of many countries. It has always been one of the

crucial elements for the well-being of economic structure of a country.

Pakistan’s banking industry is one of the strongest banking industry in this

part of the world as a result of which more and more foreign banks are

coming to Pakistan each year.

The main aim of the chapter is to identify the strengths and

weaknesses experienced by foreign banks when they come to Pakistan, in

order to do so I have conducted a comparative analysis between two foreign

banks. The two well known banks that I have taken for this comparative

analysis are Citi Bank and Faysal Bank limited.

2. Citi Bank Limited

Citibank is a major international bank, founded in 1812 as the

Citi Bank of New York. In 1863 the bank joined the U.S. new national banking

system and became The National City Bank of New York. Citibank came to

Pakistan in 1961 and is now the consumer banking arm of financial services

giant Citigroup, one of the largest companies in the world. To become a part

of MasterCard, the bank introduced its First National City Charge Service

credit card - popularly known as the "Everything Card" - in 1967.

As of March 2007, it is the largest bank in the United States by its

holdings. Citibank has operations in more than 100 countries and territories

around the world.

In addition to the standard banking transactions, Citibank offers

insurance, credit card and investment products etc. Their online services

division is among the most successful in the field, claiming about 15 million

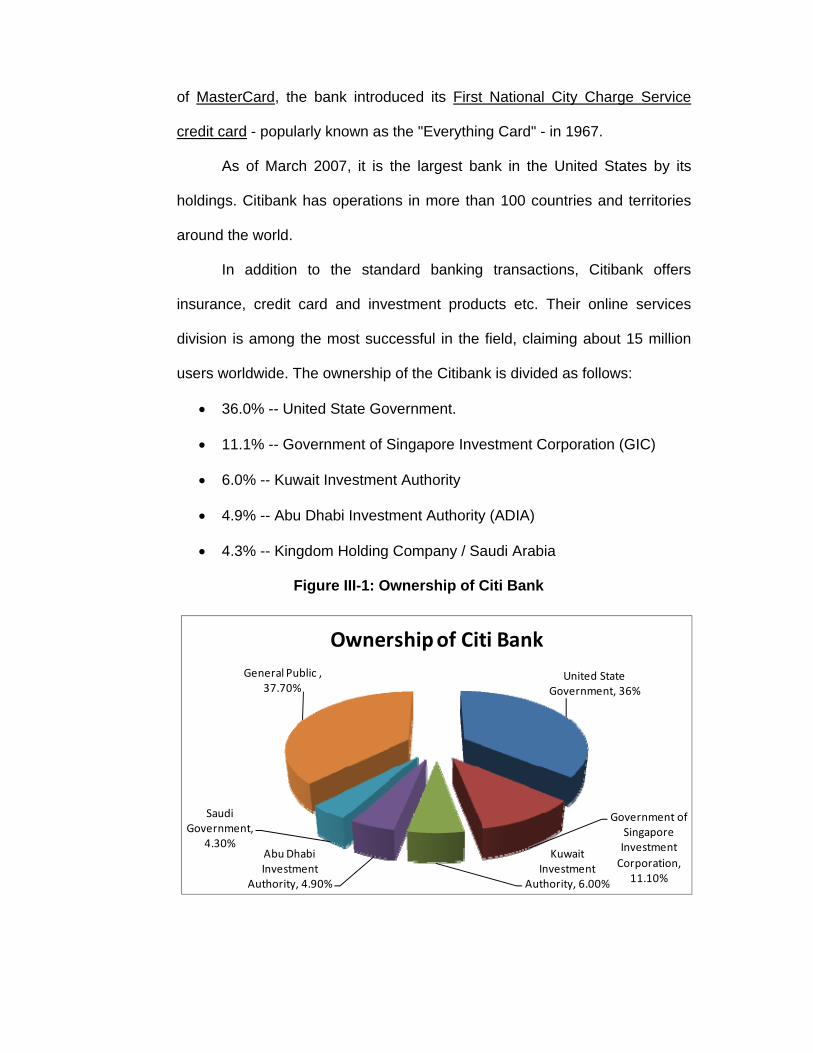

users worldwide. The ownership of the Citibank is divided as follows:

36.0% -- United State Government.

11.1% -- Government of Singapore Investment Corporation (GIC)

6.0% -- Kuwait Investment Authority

4.9% -- Abu Dhabi Investment Authority (ADIA)

4.3% -- Kingdom Holding Company / Saudi Arabia

Figure III-1: Ownership of Citi Bank

United State Government, 36%

Government of Singapore Investment

Corporation, 11.10%

Kuwait Investment

Authority, 6.00%

Abu Dhabi Investment

Authority, 4.90%

Saudi Government,

4.30%

General Public , 37.70%

Ownership of Citi Bank

2.1 Products and Services Offered by Citi Bank Limited

Citi bank offers a diverse range of products and services to its

commercial and corporate clients. The product mix offered by Citi bank is

divided into the following sub-categories:

2.1.1 Deposit Accounts

Citi bank offers eight different types of deposit accounts to its

customers which are categorized as:

2.1.1.1 Citi bank Rupee Current Account

Citibank current account is the first of its kind in Pakistan, by providing

a complete solution to the customer’s needs by saving time and money. The

minimum balance requirement for current account is R.s 100,000. Citi bank

current rupee account comes with the following features:

Receive or make payments instantly.

Withdrawing up to Rs. 80,000 with Citi bank ATMs

Depositing cash or cheques into your account on site ATM.

Transfer of funds from one Citi bank account to other Citi bank

account at the ATM location.

2.1.1.2 Citibank Rupee Savings Account

Citibank rupee savings account offers the customers with the flexibility

that is unique to Citibank. Inter-branch access is a special feature that gives

customers the ease to deposit and withdraw their funds from any Citibank

branch in Pakistan. This account has these features:

Minimum Balance Requirement: Rs 100,000.

Profit is calculated on the daily balance and credited bi-annually.

Funds can be withdrawn anytime without any notice.

Pay orders, Funds etc can be deposited and withdrawn from any

Citibank branch in the country through Citi 24/7 Phone Banking facility.

2.1.1.3 Rupee Citi Ultimate Savings Account

The Citi-ultimate savings account can be opened with a minimum of

Rs 100,000 and attractive annualized rates of expected return will be earned

on ythe savings. This account has the following features:

Profit is calculated on the monthly average balance and credited

monthly.

Funds can be withdrawn anytime without any notice.

Funds can be deposited and withdrawn from any Citibank branch in

the country.

2.1.1.4 Current Account Premium

Open a current account with Citibank and maintain a minimum

average balance of Rs 1,000,000 to receive all the benefits of Citigold. The

most prestigious and globally recognized priority banking service that

provides:

Free Citibank Visa Debit Card.

Withdraw up to PKR 160,000 per day.

Spend up to PKR one million per month.

Free Premier Citigold Credit Card with a limit of up to Rs. 500,000.

Free Pay Orders, Manager’s Cheques, Demand Drafts & Telegraphic

Transfers.

Free Bank Statements and Reference Certificates.

Free SMS Alerts for Account Activity.

Extended Banking Hours: 9 a.m. – 8 p.m.

2.1.1.5 Citibank Premium Profit

This rupee Term Deposit provides the customer with one of the most

lucrative investment options available today. Place your funds in Premium

Profit and watch your savings grow at one of the attractive rates offered in

the market.

Minimum Balance: Rs.50, 000.

Tenors of months, 1, 3, 6, 9, 12, 18, 24, 3yrs, 4yrs, 5yrs.

Loan financing against your deposits at market competitive rates.

2.1.1.6 Citi One

Citi One is known as the all in one bank account and can be opened

with a minimum of Rs. 50,000 this account comes with the following

interesting features:

Free bank statement.

Free 6 pay orders per month.

Reduced Debit Card annual fee.

Annual fee waiver for the first year on Citibank Credit Cards.

Convenience of Citibank online.

2.1.1.7 Premium FCY Savings Account

Earn attractive rates of return on your Foreign Currency through Citi

bank’s Premium FCY Savings Account. The minimum balance requirement

for this account is $ 5000. Some features include:

Monthly Profit Payout in Foreign Currency.

5 Free Bank Statements.

Withdraw US dollars via Citibank ATMs.

Citi Phone Banking gives the convenience of 24-hour banking where

the customer can get information on their account, recent transactions

and other facilities.

2.1.2 Citi Bank Cards

2.1.2.1 Citi Bank Gold Credit Card

The Citibank Gold Credit Card is specially designed for the customers

exclusive life style and their special needs. As a Gold Credit Card member

the customer can enjoy a higher Credit Limit throughout the world. If the

client has a monthly income of Rs.50, 000 or above, and is a Pakistani

citizen, then he is eligible to apply for a Citibank Gold Credit Card.

2.1.2.2 Citi Bank Silver Credit Card

The Citibank Silver Credit Card brings the convenience and financial

flexibility the customers can expect from the World's No. 1 Credit Card. If the

customer has a monthly income of Rs.16,000 (Rs 8,000 for selected

corporate employees) and is a citizen of Pakistan then he/she is eligible to

apply for a Citibank Silver Credit Card.

2.1.2.3 Citi Bank Mobilink Credit Card

The Citi bank Mobilink credit card allows the customer with double

benefits by providing all the features of a credit card along with free jazz

airtime every time the customer uses his Citi Mobilink credit card. This credit

card is providing very interesting features:

Get an annual fee waiver on the Citi Mobilink Credit Card (Gold Card:

Rs. 4,000; Classic Card: Rs.2,000)

No annual fee on Citi Mobilink Credit Card when you sign up for

Indigo/Jazz Auto Pay facility

No security deposits on Indigo connections and Indigo international

roaming upon signing up for Auto Pay facility.

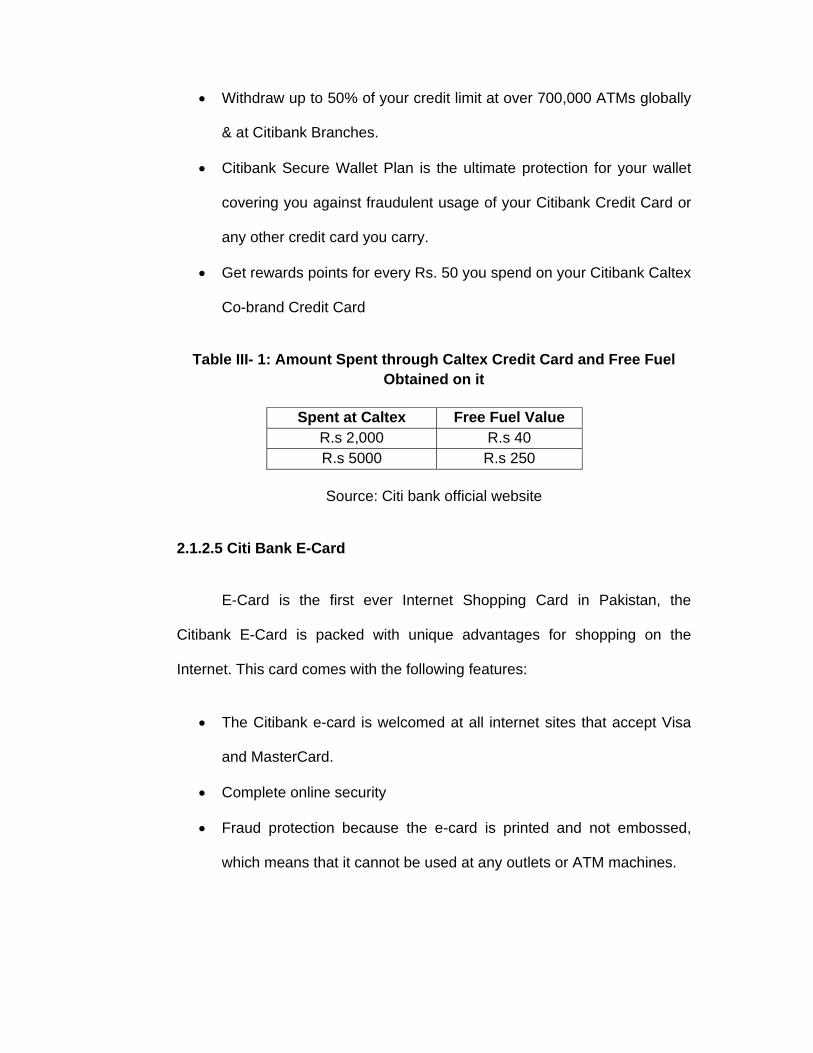

2.1.2.4 Citi Bank Caltex Credit Card

With the Citi bank Caltex Credit Card get free fuel on every transaction

of R.s 2,000 done from the customer’s credit card. This card comes with the

following features:

3 Free Supplementary Cards for the first year

Set the limit of your choice on your Supplementary Card

Citibank Caltex Co-brand Credit Card is accepted at over 10,000

merchants locally & 30 million globally.

Withdraw up to 50% of your credit limit at over 700,000 ATMs globally

& at Citibank Branches.

Citibank Secure Wallet Plan is the ultimate protection for your wallet

covering you against fraudulent usage of your Citibank Credit Card or

any other credit card you carry.

Get rewards points for every Rs. 50 you spend on your Citibank Caltex

Co-brand Credit Card

Table III- 1: Amount Spent through Caltex Credit Card and Free Fuel Obtained on it

Spent at Caltex Free Fuel Value R.s 2,000 R.s 40 R.s 5000 R.s 250

Source: Citi bank official website

2.1.2.5 Citi Bank E-Card

E-Card is the first ever Internet Shopping Card in Pakistan, the

Citibank E-Card is packed with unique advantages for shopping on the

Internet. This card comes with the following features:

The Citibank e-card is welcomed at all internet sites that accept Visa

and MasterCard.

Complete online security

Fraud protection because the e-card is printed and not embossed,

which means that it cannot be used at any outlets or ATM machines.

For purchases over Rs. 3,000, convert them into Smart Installment

Plan (SIP) and pay the amount back in installments according to your

own convenience.

2.1.2.6 Citibank Shaheen Affinity Credit Card

The Citibank-Shaheen Credit Card is the first Affinity Card in Pakistan,

offered exclusively to Pakistan Airforce and Shaheen Foundation personnel.

Out of every rupee spent on a Citibank-Shaheen Credit Card, Citibank will

contribute a percentage to Shaheen foundation and to the welfare of our

Airforce personnel.

2.1.2.7 Citi Bank Debit Card

Citi bank introduced its new debit card that is more than an ATM card

with everything that a customer wants from a credit card. This debit card

comes with the following features:

Secure- safer than carrying cash, and allows the customer to define

their monthly purchase limit. The client can even opt for a Photo Debit

Card for added security.

Accepted at over 10,000 retail outlets in Pakistan.

Pay for all your purchases directly from your Citibank account

Fraud Early Warning System- In case of any suspicious transaction on

the customer’s account which is not in line with their normal use

patterns, Citi bank will, on best-effort basis, give the customer a call

confirm whether the transaction is genuine.

2.1.3 Corporate Banking Products

Citi bank offers a diverse range of corporate banking products that are

specially designed for its corporate customers.

2.1.3.1 Cash Management

Cash management is a core business of Citibank. Citi bank’s

experience in the local Pakistani market along with its ability to provide global

solutions enables it to offer a full range of cash management products and

solutions.

Citibank Pakistan offers its cash management products and services

aimed to improve the cash flow side of the business and operations. Through

its elaborate product offering, Citibank aims to:

Manage the increasing complexity of cross-border and domestic

payments

Improve cash flow forecasting under a cost control environment

Limit the exposure to risk associated with growth

Enhance security of the cash flows and reduce the possibilities of

fraud

Improve overall working capital flows via adding efficiency to the

overall operations

The current range of product offerings includes the easy pay an

exclusive telephone bills payment service, designed to eliminate customers'

phone bill payment problems. PTCL bills are delivered to the customers'

offices, at least a week before they are due. Citibank arranges to have the

bills and the payment picked up from the customers. Citibank arranges for

clearance of the check and onward credit to PTCL. Bills are stamped as

'paid' and are returned to the customer within 2-3 days of payment.

2.1.3.2 Treasury

Citibank's Treasury department emerges as a leader in the local

interbank market, as well as the institution of choice amongst importers and

exporters, by providing superior treasury products to its clients. Apart from

dealing in Foreign Exchange (FX) and Money Markets, the interbank desk

participates actively in all Central Bank operations, including T-Bill auctions

and open market operations. The main products traded on the FX desk

include Ready and Spot Outright Purchases/Sales as well as Swaps, while

the Money Market desk deals primarily in Repo and Reverse Repo

transactions.

2.1.3.3 Loan Products

Citibank’s offers two types of corporate loan products:

i. Advance against Merchandise ("AAM") Facility

Citibank offer AAM facility to facilitate stock purchases and fund

receivables. Clients can draw funds as per need up to allocated limits.

ii. Loans against Merchandise

A loan against Merchandise or Demand Finance is a short-term

credit facility with fixed maturity. Repayment of the loan is structured to

correspond with borrower's cash flows. Repayment can be bullet or in

installments.

2.1.3.4 Citi Service

Citi Service is an integrated customer inquiry line for after -sales

service dedicated to giving its clients easy access to accurate answers in the

shortest possible time. With Citi Service, the client needs to make a call on

only one number. Citi service is providing its customers with the following

benefits:

One phone number for fast efficient service

Quick and accurate response to customer inquiries

Regular updates on the status of inquiries

Easy access to Citibank experts

Readily available product knowledge and technical support

2.1.4 Securities Services

Citibank Worldwide Securities Services (WWSS) is a unit of Citigroup

of Global Corporate and Investment Bank. WWSS serves global issuers,

investors and intermediaries. WWSS is the industry's premier custodian of

cross-border assets, top ranked global clearer and recognized leader in

depositary receipt services, and agency and trust services.

Citibank was the first foreign bank to offer custody services in

Pakistan. Citibank's core custody product offers a range of services which

include safekeeping, settlement, cash processing, income collection and

corporate actions, proxy voting services and market information and value-

added services such as Escrow and Depository Services..

2.1.4.1 Agency and Trust Services (CATS)

Citibank Agency and Trust provides Trustee- and Agency-related

appointments for various debt products including commercial paper, medium

term notes, bonds, asset- backed securities, and mortgage- backed

securities. In addition, escrow, project finance, tenders/exchanges warrant

agent and other specialized agency services are also available. CATS

provides a full range of support across multiple currencies, regionally and

globally for issuers looking to raise short, medium and long term debt in all

major markets.

2.1.4.2 Securities Lending

Securities lending involves facilitating the loan of securities from

lenders to fulfill the borrowing requirements of selected brokers, banks,

broker/dealers, and other financial institutions and investment firms

worldwide to support trading strategies and/ or settlement obligations

Citibank currently lend securities in over 25 countries through their global

trading centers in North America, Europe and Asia providing 24-hour

coverage to meet the demands of borrowers worldwide.

2.1.4.3 Depository Receipts

Citibank provides a full range of Depository Receipt services, including

liaison with the issuer, investment bank, issuer’s legal representative and

regulatory agencies during the development of the program. Following the

program launch, Citibank issues DRs against deposit of underlying shares;

provides transfer and registration services, account management, corporate

action services. The bank also supports information needs and sets up

custodian arrangements for holding shares in the issuers’ home market.

2.1.4.4 Local Settlement Services

Citibank will handle all activities related to trade processing which

include matching of trade instructions, accepting / delivering shares from

brokers / counterparties, payment transfers, and monitoring of pending trades

with regular status reporting on all trade settlements and pending trades.

Citibank will handle all cash processing associated with clients securities

portfolio in terms of payments/receipts on account of trade settlements,

collection of dividends, interest payments and related expenses.

2.1.4.5 Local Safekeeping Services

Citibank can hold shares in both physical and scripless form on its

client’s behalf. They have a vault dedicated to custody services for holding

physical shares and also maintain an account with the Central Depository

Company (CDC) for safekeeping and transacting scripless shares. Citibank

offers registration services for physical shares which includes registration

processing, monitoring, outstanding stock and timely collection of shares and

transfer deeds from registrars.

2.1.5 Trade

2.1.5.1 Exports

Different trade products offered for exporters are:

a. Post Shipment Finance: Post shipment finance is a variation of a

demand loan with a loan repayment linked to the maturity of the bills

drawn against LC' or contract. Post shipment finance is offered

against sight as well as usance bills.

b. Export Refinance: Export Refinance is a scheme under State Bank of

Pakistan (SBP) to promote Pakistani Exports. Under this scheme, an

exporter may avail finance from any scheduled bank at a concessional

rate. Export Refinance is available to the exporter under two schemes

Part I or Part II. In Part I an exporter may avail finance against

individual usance L/Cs or contracts after satisfying the terms and

conditions of the scheme, this scheme are available either on a pre-

shipment or post-shipment basis for the exporter. Under Part II an

exporter can avail finance up to a percentage (determined by SBP) of

exports performed in the previous financial year.

2.1.5.2 Imports

Issuance of import LC's: It is a firm undertaking issued by Citibank on

behalf of its customer / importer in favor of the exporter / seller outside the

country. The issuing bank is responsible for the payments to the buyer,

provided the terms of the LC's are fulfilled.

Inward Collection: It is an option using which a Citibank Pakistan customer /

importer can import without opening a letter of credit. There are two types of

collections

D / A: Documents against acceptance

D/ P: Documents against payment (It is a less costly and more

efficient method of importing goods than through opening a LC)

FX Forward cover for imports / repat loans: It is a tool which importers use to

hedge against FX rate risk. They book at today's foreign exchange rate for an

import deal happening at a future time period. (3 months / 6 months etc)

2.1.5.3 Guarantees

A guarantee is issued by Citibank Pakistan (Guarantor) on behalf and

on request of customer (applicant) in favor of a third party (beneficiary), for

the fulfillment of certain defined obligations by the applicant. Usually Citibank

issues the following types of guarantees:

a. Tender Guarantees (Bid bonds): Some tenders require the bidders

(Citibank customers) to furnish bank guarantees to prevent the bidder

from withdrawal from the bid / contract if successful in the tender.

b. Performance Guarantees: A performance guarantee, by Citibank on

behalf of its customers, assures the beneficiary of delivery of goods

and services in accordance with the terms and conditions of the

contract.

c. Advance Payment Guarantees: Citibank will guarantee that the

advance payment by the beneficiary to Citibank's customers will be

utilized for performance of the contract for which the cash was

advanced.

d. Financial Guarantees: Any guarantee provided by Citibank on behalf

of the customer for any financial requirements or deals can be broadly

classified as financial guarantee.

e. Open ended Guarantees: These guarantees do not have an expiry

date and a standard liability clause and return clause (SLC&RC).

f. Back-to-Back Guarantees: A guarantee issued by Citibank Pakistan

in favor of a beneficiary based on a primary guarantee (counter

guarantee) issued in favor of Citibank by an overseas branch of

Citibank or any other bank, on behalf of their customer / applicant.

2.1.6 Merger & Acquisition Advisory

Citibank is the leading provider of financial advisory services in

Pakistan. To date, Citibank has been actively involved in all major

privatization deals, and have advised leading foreign and local corporate

groups. This can be evidenced by the number of transactions undertaken by

Citibank in the recent past. The principal areas in which they advise their

clients are as follows:

Buy-side advisory

Sell-side advisory

Merger transactions

Joint ventures

Privatization of state owned entities

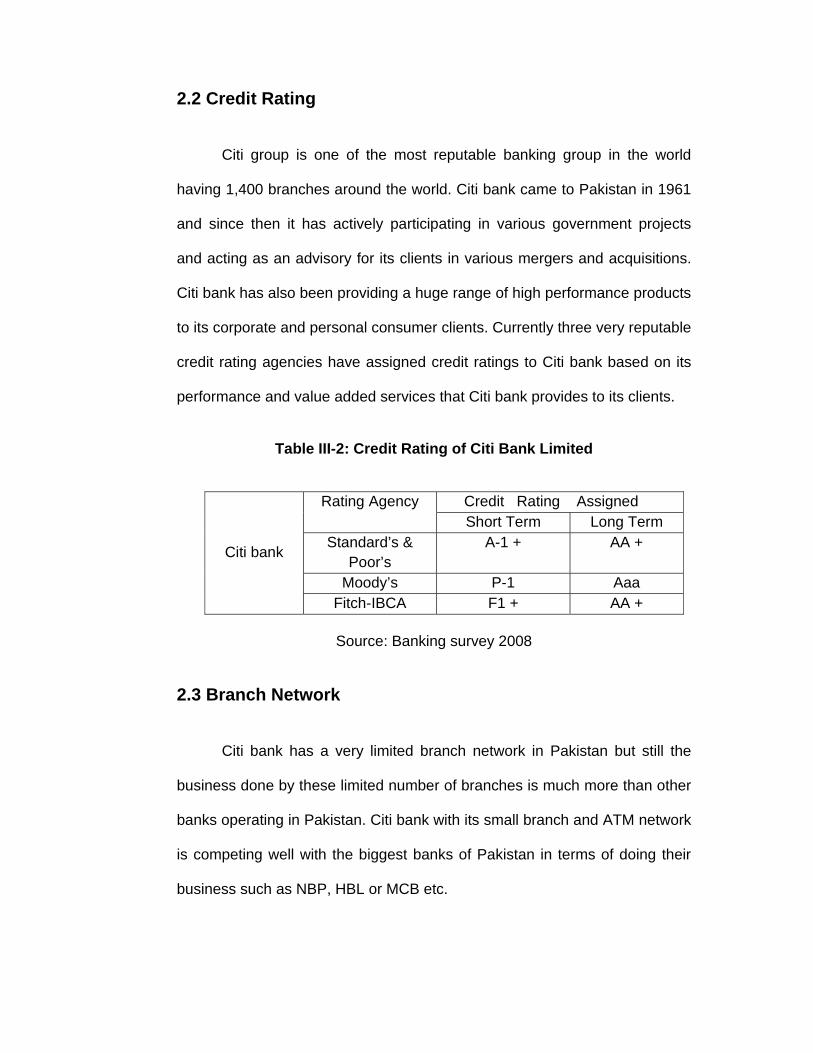

2.2 Credit Rating

Citi group is one of the most reputable banking group in the world

having 1,400 branches around the world. Citi bank came to Pakistan in 1961

and since then it has actively participating in various government projects

and acting as an advisory for its clients in various mergers and acquisitions.

Citi bank has also been providing a huge range of high performance products

to its corporate and personal consumer clients. Currently three very reputable

credit rating agencies have assigned credit ratings to Citi bank based on its

performance and value added services that Citi bank provides to its clients.

Table III-2: Credit Rating of Citi Bank Limited

Rating Agency Credit Rating Assigned Short Term Long Term

Citi bank Standard’s &

Poor’s A-1 + AA +

Moody’s P-1 Aaa Fitch-IBCA F1 + AA +

Source: Banking survey 2008

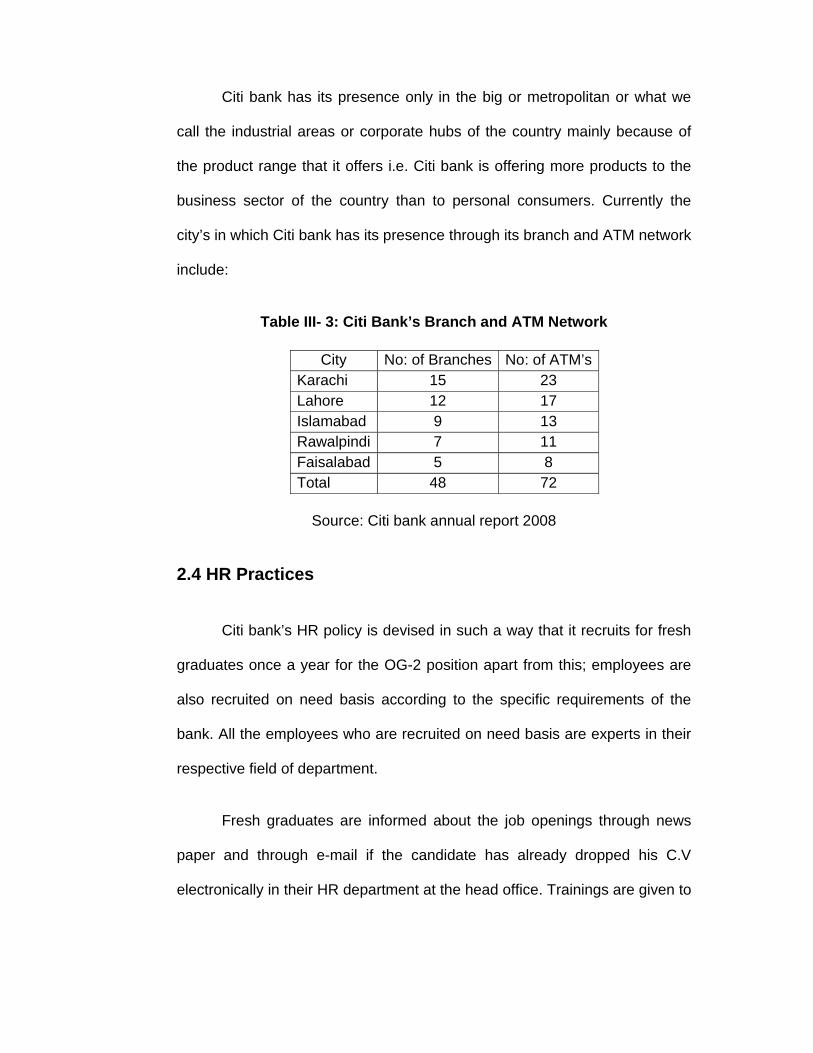

2.3 Branch Network

Citi bank has a very limited branch network in Pakistan but still the

business done by these limited number of branches is much more than other

banks operating in Pakistan. Citi bank with its small branch and ATM network

is competing well with the biggest banks of Pakistan in terms of doing their

business such as NBP, HBL or MCB etc.

Citi bank has its presence only in the big or metropolitan or what we

call the industrial areas or corporate hubs of the country mainly because of

the product range that it offers i.e. Citi bank is offering more products to the

business sector of the country than to personal consumers. Currently the

city’s in which Citi bank has its presence through its branch and ATM network

include:

Table III- 3: Citi Bank’s Branch and ATM Network

City No: of Branches No: of ATM’s Karachi 15 23 Lahore 12 17 Islamabad 9 13 Rawalpindi 7 11 Faisalabad 5 8 Total 48 72

Source: Citi bank annual report 2008

2.4 HR Practices

Citi bank’s HR policy is devised in such a way that it recruits for fresh

graduates once a year for the OG-2 position apart from this; employees are

also recruited on need basis according to the specific requirements of the

bank. All the employees who are recruited on need basis are experts in their

respective field of department.

Fresh graduates are informed about the job openings through news

paper and through e-mail if the candidate has already dropped his C.V

electronically in their HR department at the head office. Trainings are given to

employees on need or requirement basis. Most of these trainings are given

outside the country at other foreign branches of the bank.

When these trained employees return to Pakistan they in turn give

training to all the concerned employees of Citi bank Pakistan.

Promotion system is based on the performance of the employee. It

generally takes 1-4 years depending on the performance of the employee to

get a promotion.

2.5 Recognized Innovations

Citibank is Pakistan's most innovative commercial and investment

bank, having won more international citations for deals done in Pakistan and

having more landmark transactions to its credit than any other financial

institution. Euro money recognized Citibank as the "Best M & A bank in

Pakistan" in 1999. Citibank's recent notable transactions include:

2009 Citi bank Pakistan awarded “Best Consumer Internet Bank 2009”

by Global Finance.

2008 Citi bank goes live with ATM-generated ‘Mini Credit Card

Statements.

2008 Citi bank Pakistan recognized at the 4th Health & Environment

National Excellence Awards Ceremony and won the Corporate Social

Responsibility award (CSR Award 2008)

1999 Arranged the first local currency future flows securitization

transaction.

1998 First local currency lease rental securitisation.

1998 First local currency securitization backed by Notes Payable from

a Government owned entity.

1997 First foreign currency foreign future currency receivables for

PTCL of USD 250 million.

1996 Successful placement of the largest term finance certificates

issued in the country, resulting in a double-fold increase in market

appetite.

1996 Arranged the Government of Pakistan's highly successful issue

of USD 150 million FRN.

1995 Successfully placed the largest term finance certificate issued in