Embed Size (px)

Citation preview

A STUDY ON CUSTOMER LOYALTY IN

PUBLIC SECTOR BANKS

IN TIRUCHIRAPPALLI DISTRICT WITH

SPECIAL REFERENCE TO STATE BANK OF INDIA

Abstract of the Thesis submitted to the Bharathidasan University, Tiruchirappalli – 24.

in partial fulfillment of the requirementsfor the award of the Degree of

DOCTOR OF PHILOSOPHY IN COMMERCE

Submitted by

P. SUJATHA, M.Com., M.B.A., M.Phil.,

Under the Guidance of

URUMU DHANALAKSHMI COLLEGE,

TIRUCHIRAPPALLI – 620 019.

Dr.N. RAJAMANNAR, M.Com.,M.B.A.,M.Phil.,M.Ed., SLET.,PGDCA.,Ph.D.,

RESEARCH ADVISOR IN COMMERCE,

POST GRADUATE & RESEARCH DEPARTMENT OF COMMERCE

URUMU DHANALAKSHMI COLLEGE

(Nationally accredited B++ Grade by NAAC)

TIRUCHIRAPPALLI – 620 019.

April 2014

A STUDY ON CUSTOMER LOYALTY IN PUBLIC SECTOR BANKS

IN TIRUCHIRAPPALLI DISTRICT WITH SPECIAL REFERENCE TO

STATE BANK OF INDIA

ABSTRACT

Loyalty is one’s attitude towards an organization or person, supporting

and substantiate the organization or person, bearing some personal losses.

When an organization or a person who provides or serves a little out of

boundary or even sometimes upto the mark, then the beneficiary becomes loyal

to that organization or person.

Statement of the problem

Customer loyalty has been a crucial factor for a long time now with

banks. In the current scenario, sustaining an existing customer is more

important than getting a new one. A bank that has successful customer loyalty

program retains customers for a long period of time, which significantly

increases revenue for the company.

The forces of deregulation, globalization and advancing technology have

increased the competitive pressures in the banking industry. Thus it has become

imperative for banks to focus on customer centric approaches and develop long

term relationship with the customer to get through turbulent times.

Banks are concentrating only on acquiring new customers. They seldom

understand the importance and profitability of creating loyalty and retaining

customers. Banks have to come out with innovation measures to satisfy the

needs of both the present and the potential customers, at the same time adopt

procedures to win back the lost customers.

Hence, the present study entitled as “A study on Customer Loyalty in

Public Sector Banks in Tiruchirappalli District with special reference to State

Bank of India”.

Objectives

To study the existing customer loyalty in Public Sector Banks. To

identify the factors which influence the Customer loyalty in Public Sector

Banks. To examine the perceived service quality and perceived value. To

identify the level of satisfaction, commitment and trust towards the Public

Sector Banks. To provide suggestions to increase customer loyalty in Public

Sector Banks.

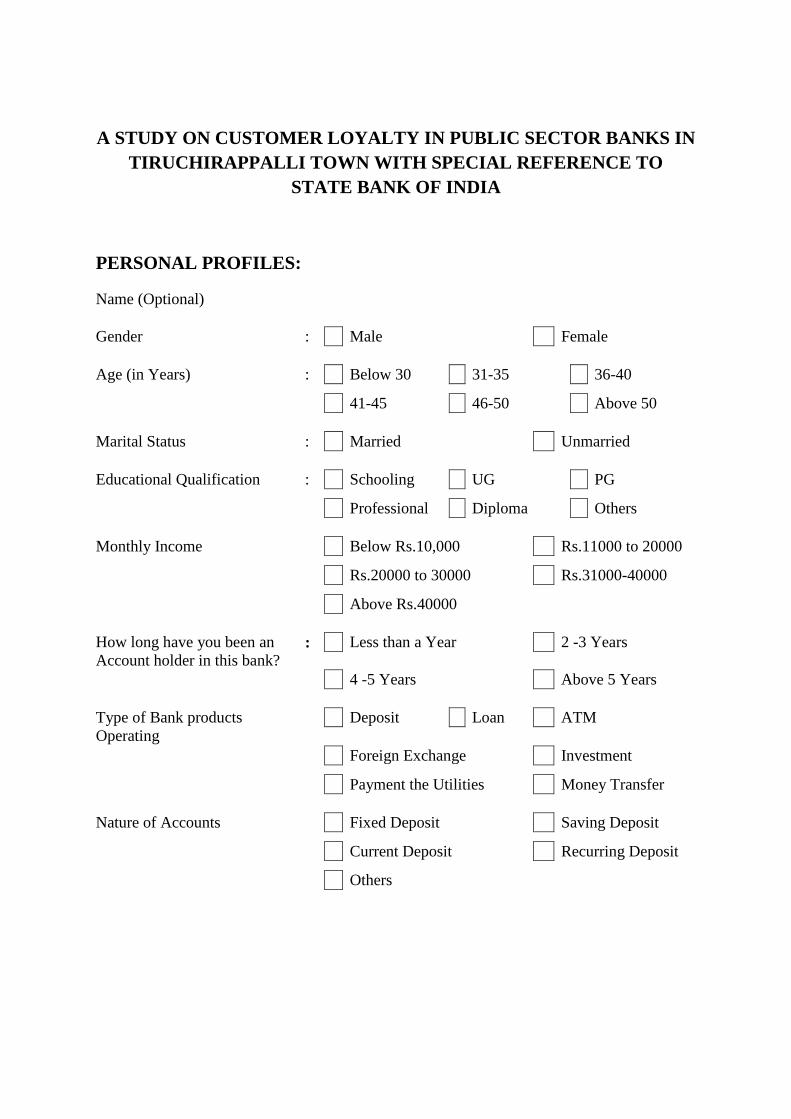

Research Methodology

The empirical research will be quantitative in nature. The analysis is

based on primary and secondary data based. To conduct the primary research,

questionnaire was prepared to survey about 600 customers in State Bank of

India in Tiruchirappalli District.

Study Area

The researcher has selected Tiruchirappalli District as the study area and

selected five urban branches based on number of customers, turnover,

commitment, performance and the market place.

Sampling

The stratified random sampling technique has been adopted for

statistical analysis.

Sampling size

The study area has 10 branches containing 60,000 customers. The

researcher has selected five branches out of which 600 customers were

interviewed on the basis of stratified random sampling technique.

Statistical tools

This study is based on descriptive research design using questionnaire as

the key research. For the descriptive statistics Pearson Correlation, Multiple

Regression, Chi-square Test, F-test, T-test, Likert’s Five Point Scale, Likert’s

Seven Point Scale, Cornbach’s Alpha System, Anova Table, KMO and

Bartlett’s Test (Kaiser-Meyer-Olkin) were used.

Causal research design was used to explore the possible linkages

between the variables.

Chapter Scheme

The first chapter deals with introduction of the study. The second

chapter deals with Review of related Literature. The third chapter deals with

profile of selected public sector banks in Tiruchirappalli District. The fourth

chapter deals with analysis and interpretation of customer loyalty in selected

public sector banks in Tiruchirappalli District. The fifth chapter deals with

summary of findings, suggestions and conclusion.

Findings

The following findings are made by the researcher, 50 percent of the

respondents agree that their knowledge about the banking services are up to

date by ample information provided by the bank. 54 percent of the respondents

agree that it seems tidy and well organized in all services towards customers.

46 percent of the respondents are strongly agree that the banks maintain every

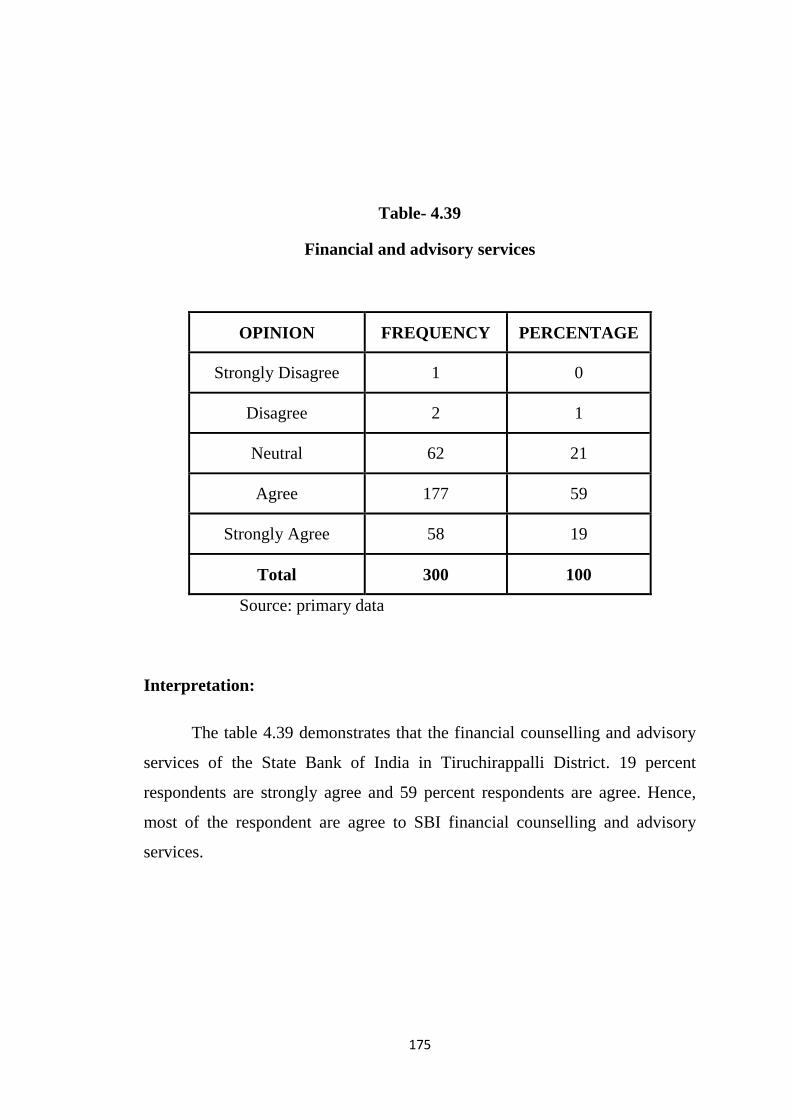

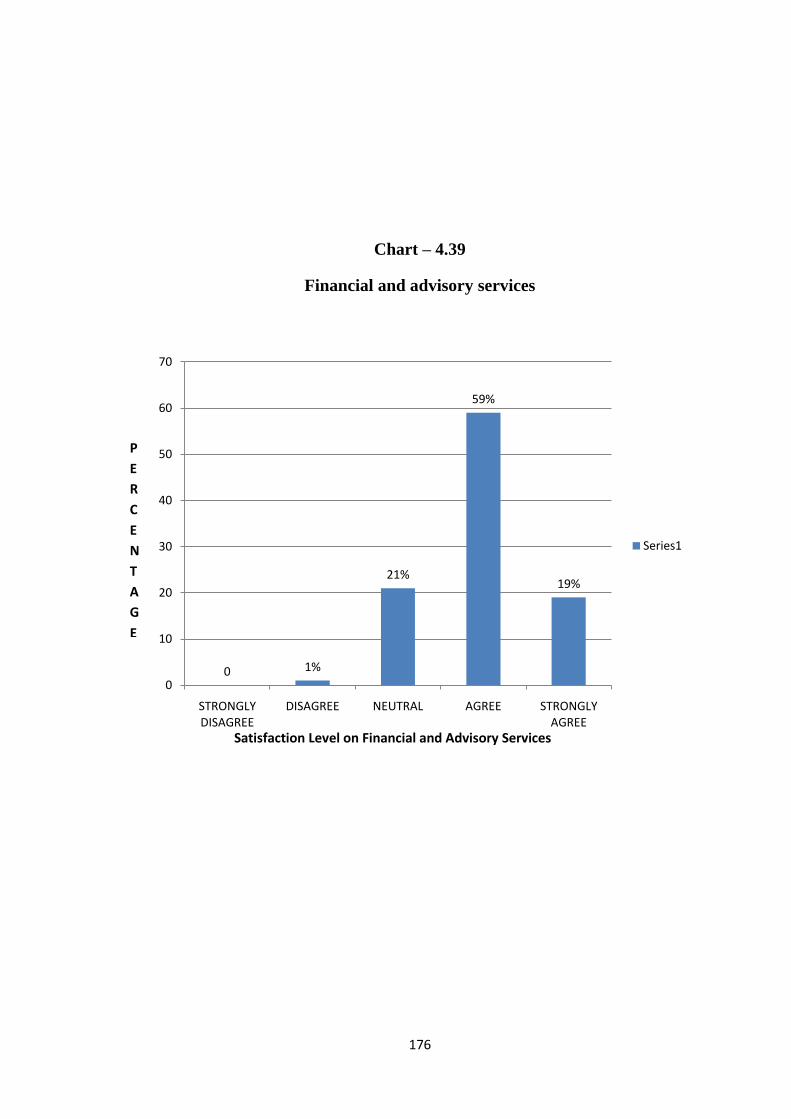

transaction confidentially. 59 percent of the respondents are agree to SBI

financial counselling and advisory services. 54 percent of the respondents are

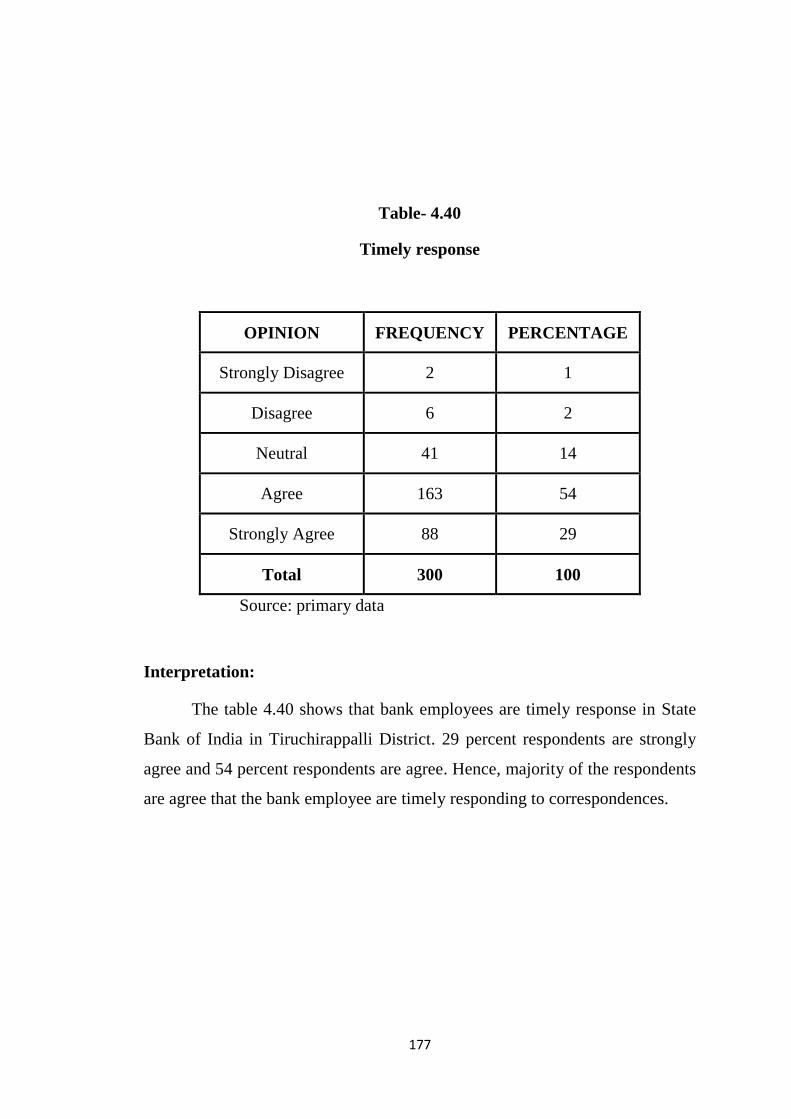

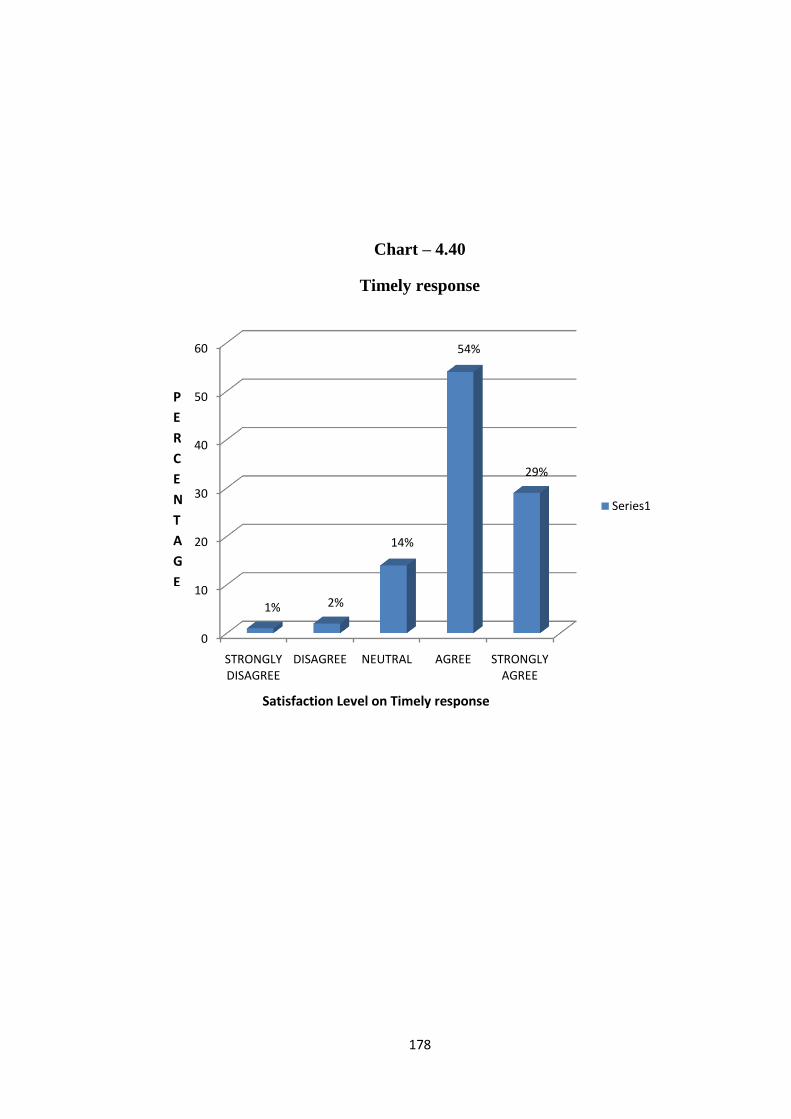

agree to SBI personnel are timely response.

Suggestions

The bank must provide better and quality internet banking services and

mobile banking services. Fund transfer is very difficult to SBI from other

banks. So, the fund transfer system must redesigned in order to enhance the

speed. The bank must provide advisory service in tax saving to the

customers.The proper guidelines should be provided to the customers regarding

investments.

CONCLUSION

The customer loyalty of the public sector banks in Tiruchirappalli

District with special reference to State Bank of India is in satisfactory level.

SCOPE FOR FURTHER STUDY

It is hoped that the findings could stimulate further research in other

parts of the world; especially in the other developing countries. The other

people who are interested in modelling could analyse, find and test more

factors according to other environment. The above points can be categorized

as “the internal loyalty model further researches”.

Dr.N.RAJAMANNAR, M.Com.,M.B.A.,M.Phil.,M.Ed., SLET.,PGDCA.,Ph.D Research Advisor in Commerce,

Urumu Dhanalakshmi College,

Tiruchirappalli – 620 019.

CERTIFICATE

This is to certify that the thesis “A STUDY ON CUSTOMER LOYALTY IN

PUBLIC SECTOR BANKS IN TIRUCHIRAPPALLI DISTRICT WITH

SPECIAL REFERENCE TO STATE BANK OF INDIA” submitted for the award

of degree of Doctor of Philosophy in Commerce to Bharathidasan University,

Tiruchirappalli by P. SUJATHA, is a bonafide record of research work done by her

under my guidance and supervision. This thesis has not previously formed the basis

for the award of any Degree, Diploma, Associateship, Fellowship or any other similar

titles.

Dr.N. RAJAMANNAR,

RESEARCH ADVISOR

DECLARATION BY THE CANDIDATE

I hereby declare that the thesis titled “A STUDY ON CUSTOMER

LOYALTY IN PUBLIC SECTOR BANKS IN TIRUCHIRAPPALLI DISTRICT

WITH SPECIAL REFERENCE TO STATE BANK OF INDIA” is my original

work under the supervision and guidance of Dr.N. RAJAMANNAR, M.Com.,

M.B.A., M.Phil., M.Ed., SLET., PGDCA., Ph.D. This thesis has not previously

formed the basis for the award of any Degree, Diploma, Associateship, Fellowship or

any other similar titles.

Place : Tiruchirappalli

Date : P. SUJATHA

ACKNOWLEDGEMENT

My sincere thanks to the authorities of Bharathidasan University for having

given me permission to peruse this research work.

I am highly indebted to the Management of Urumu Dhanalakshmi College,

Trichy-19, for having granted me permission to do this work and also for their deep

concern and interest in my academic progress.

My sincere thanks are due to Dr. S. SEKAR,M.Com., M.B.A., M.Phil.,

PGDCA., Ph.D., the Principal of Urumu Dhanalakshmi College, Trichy-19, for

according me permission to do this research work.

This study has taken its shape under the able guidance of

Dr. N. RAJAMANNAR, Research Advisor in Commerce, Post Graduate and

Research Department of Commerce, Urumu Dhanalakshmi College, Trichy-19. He

had been immensely helpful to me, with his constructive and intellectual ideas.

My sincere thanks due to Mr. A. RAVINDRAN, Chief Manager, State Bank

of India, Trichy for his spontaneous help in getting information required for this study.

I must thank to Prof.V.S.GUNA and Prof.R.MURALI, Assistant Professors,

MBA Department, OAS College of Engineering and Technology for his valuable help

with statistical tools in completing this research work.

Last but not least, I would like to express my feelings of appreciation and

gratitude to my father, mother, husband, children and my friends Dr.M. YASMIN

Assistant Professor and Mr.S. KUMAR, Assistant Professor, Department of

Commerce, Pavender Bharathidasan College of Arts and Science for their

encouragement, endurance and helps throughout the course of this study and also

thanks to M/s. Students’ Xerox and its team for their cooperation in printing and

binding.

Above all I thank the almighty who is the spring board for all my actions.

P. SUJATHA

CONTENTS

List of Tables

List of Charts

List of Abbreviations

Chapter Title Page No.

I

II

III

IV

V

Introduction

Review of Literature

Profile of study

Analysis of study

Findings, Suggestions and conclusion

Bibliography

Appendix

1

38

74

99

232

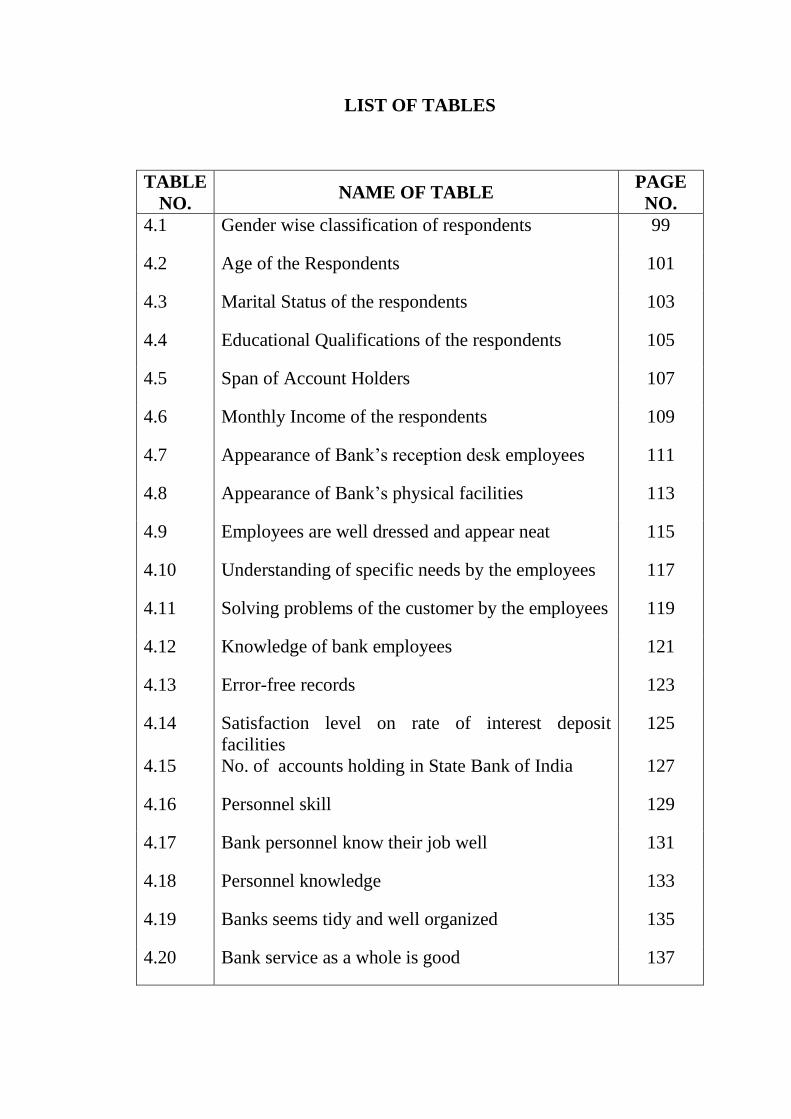

LIST OF TABLES

TABLE

NO. NAME OF TABLE

PAGE

NO.

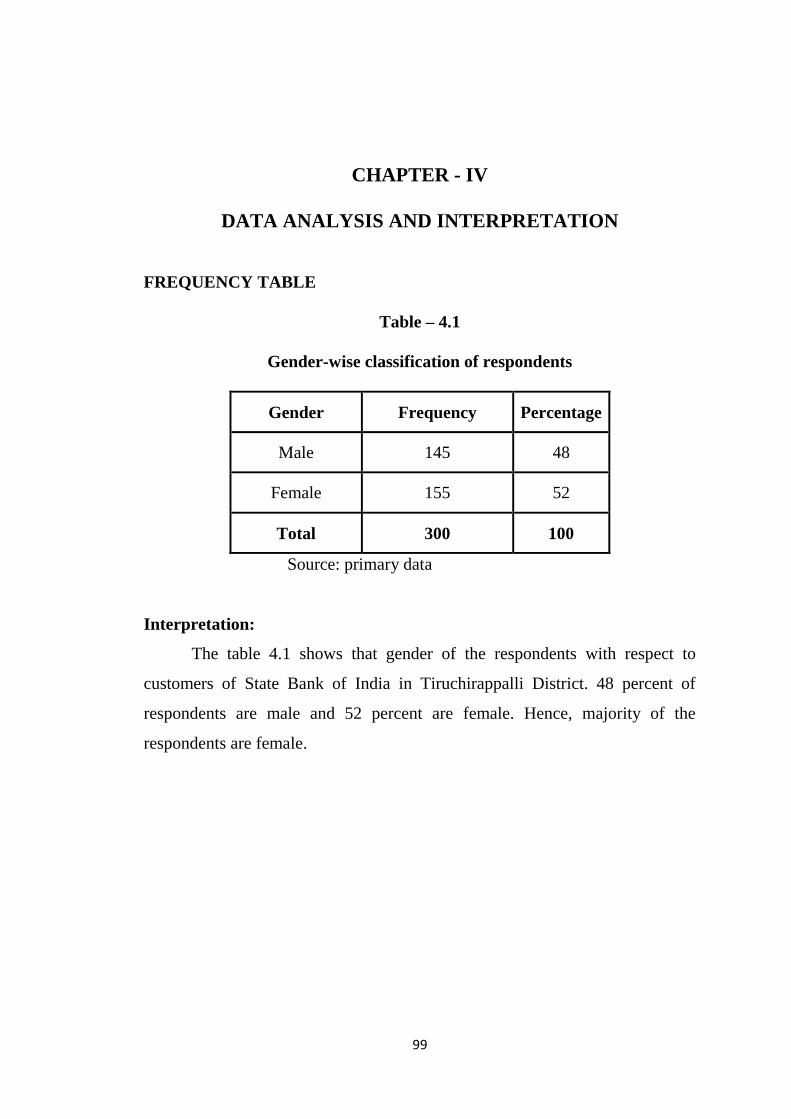

4.1 Gender wise classification of respondents 99

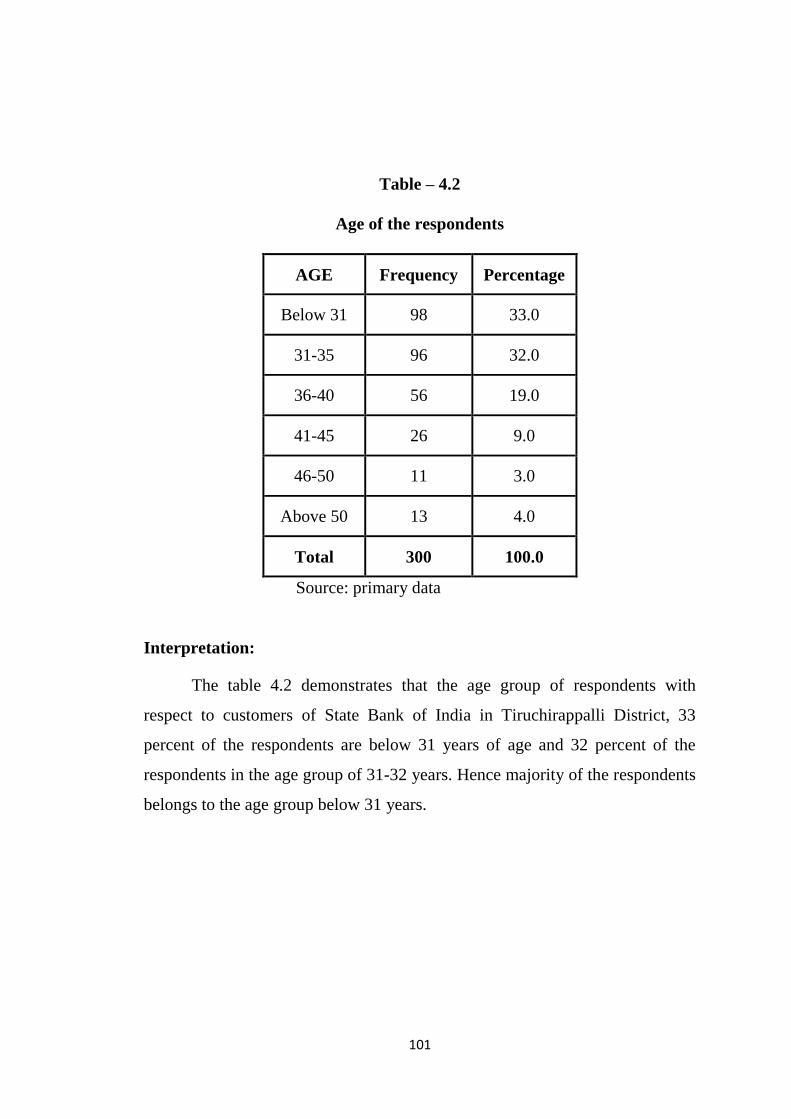

4.2 Age of the Respondents 101

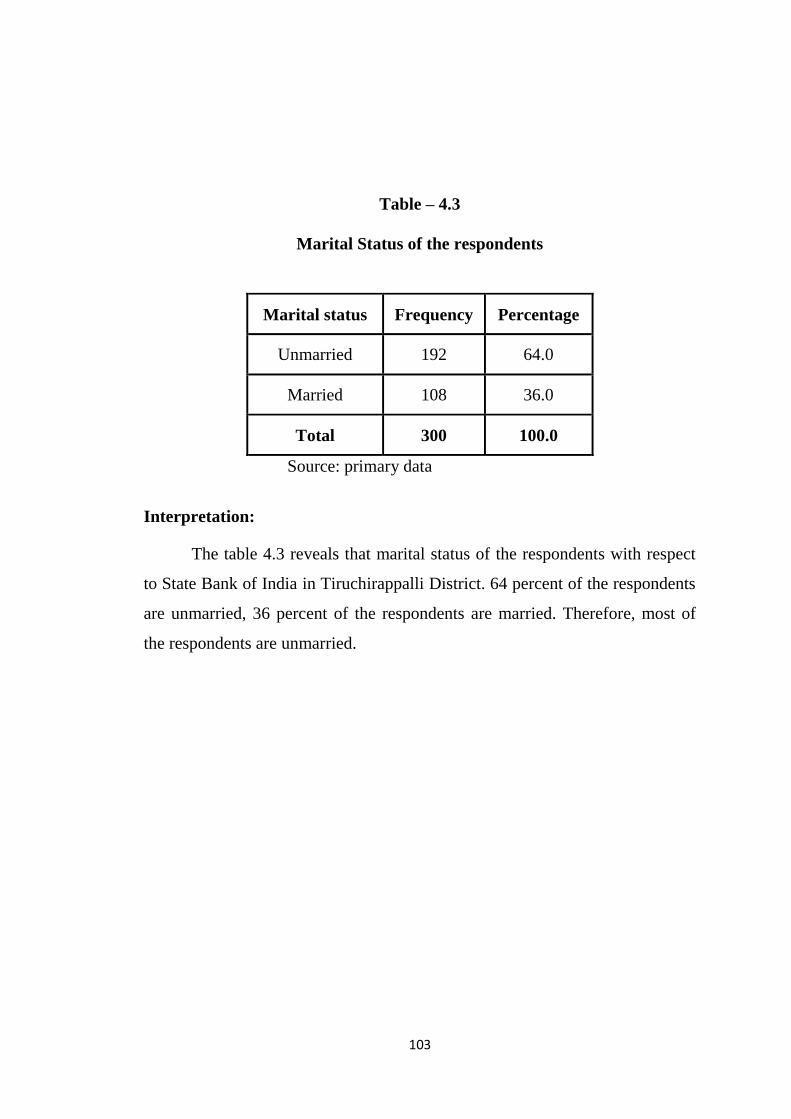

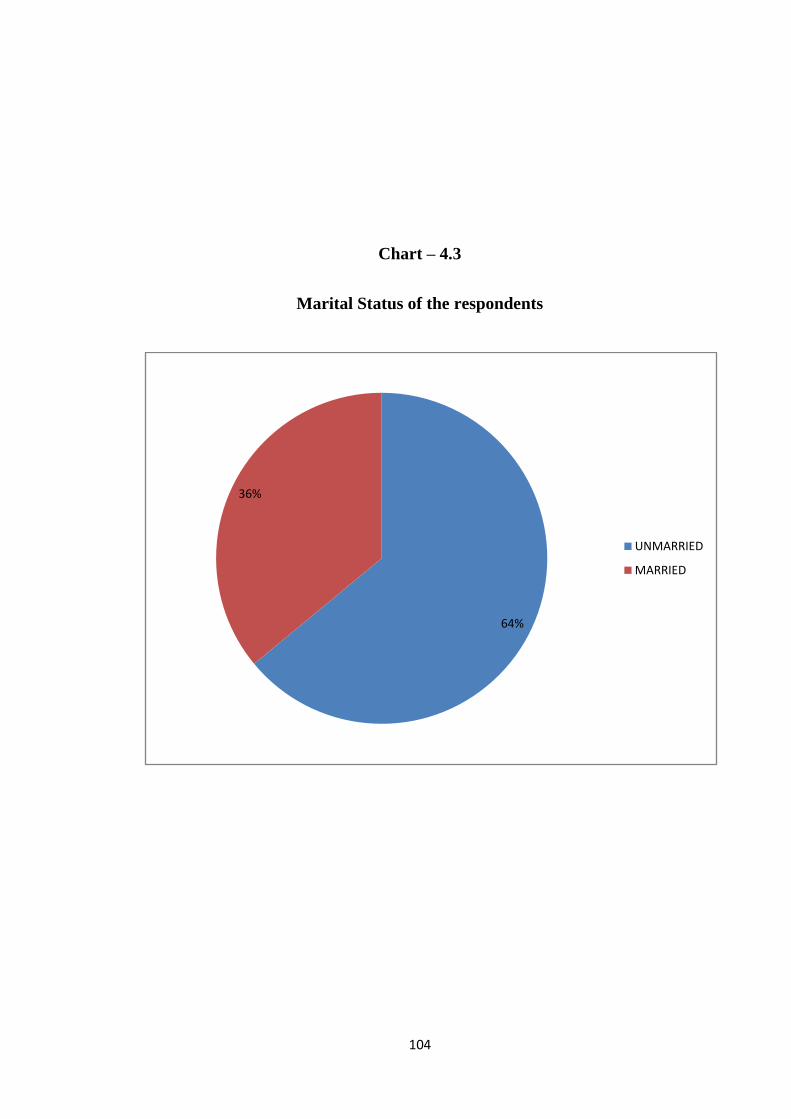

4.3 Marital Status of the respondents 103

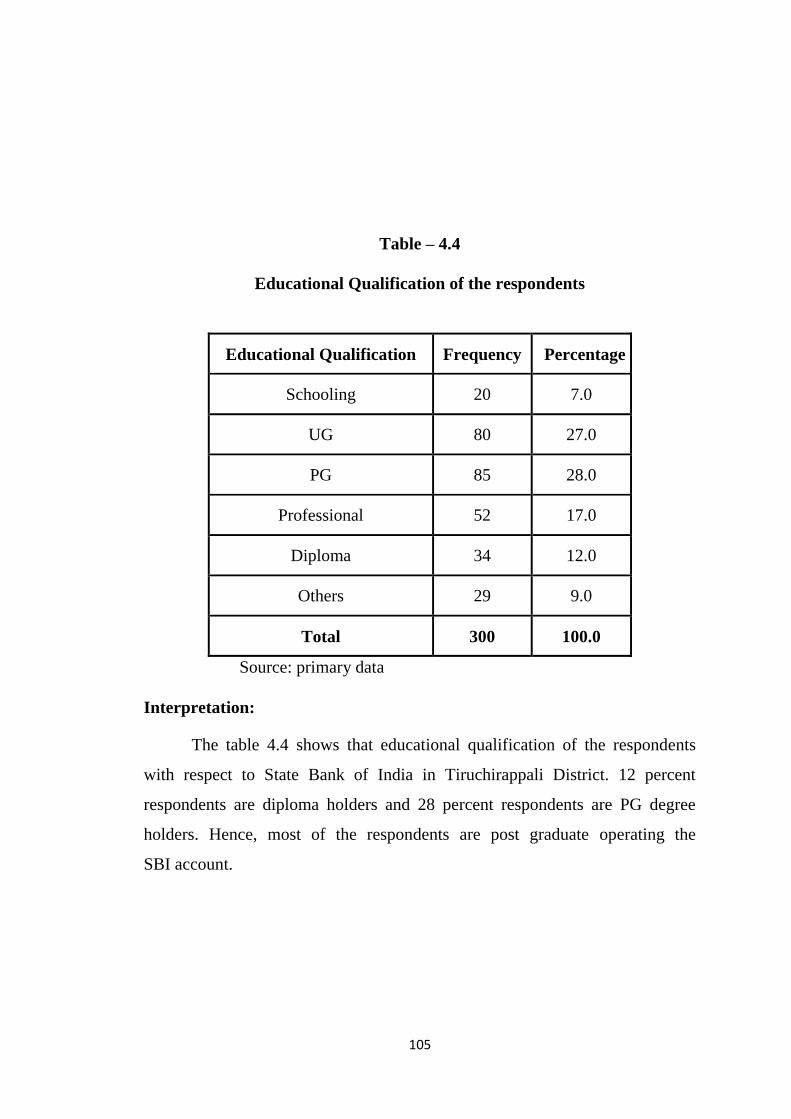

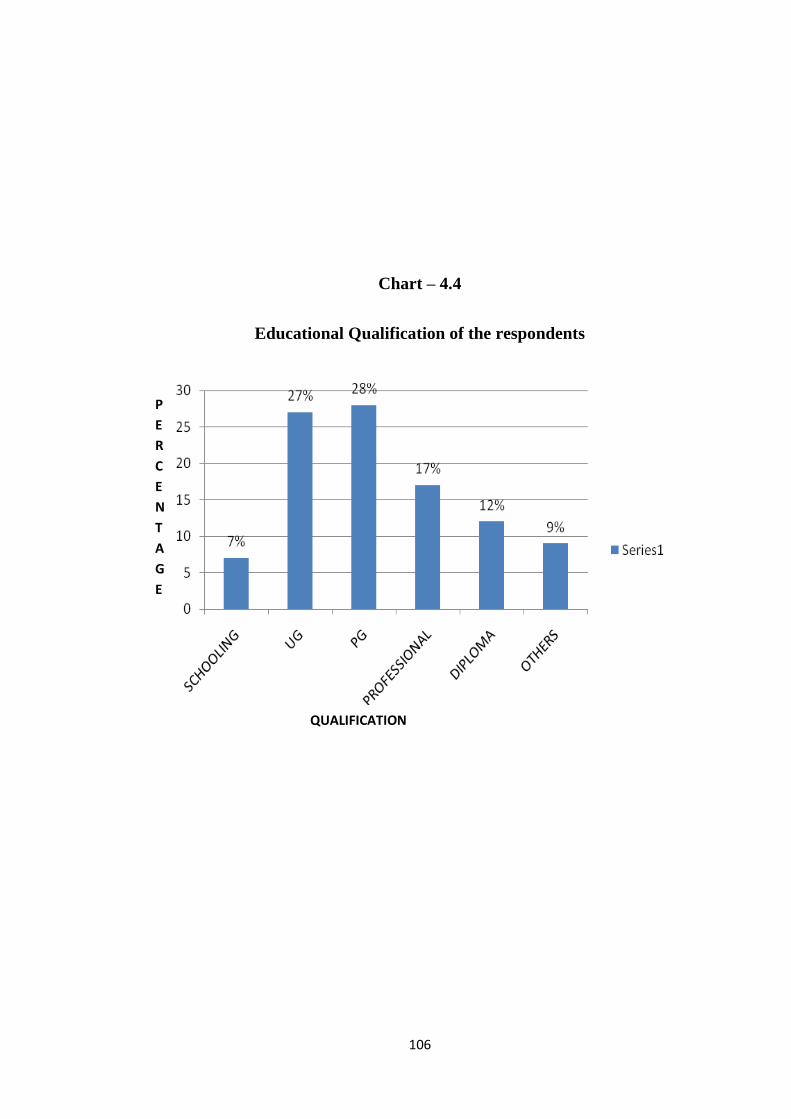

4.4 Educational Qualifications of the respondents 105

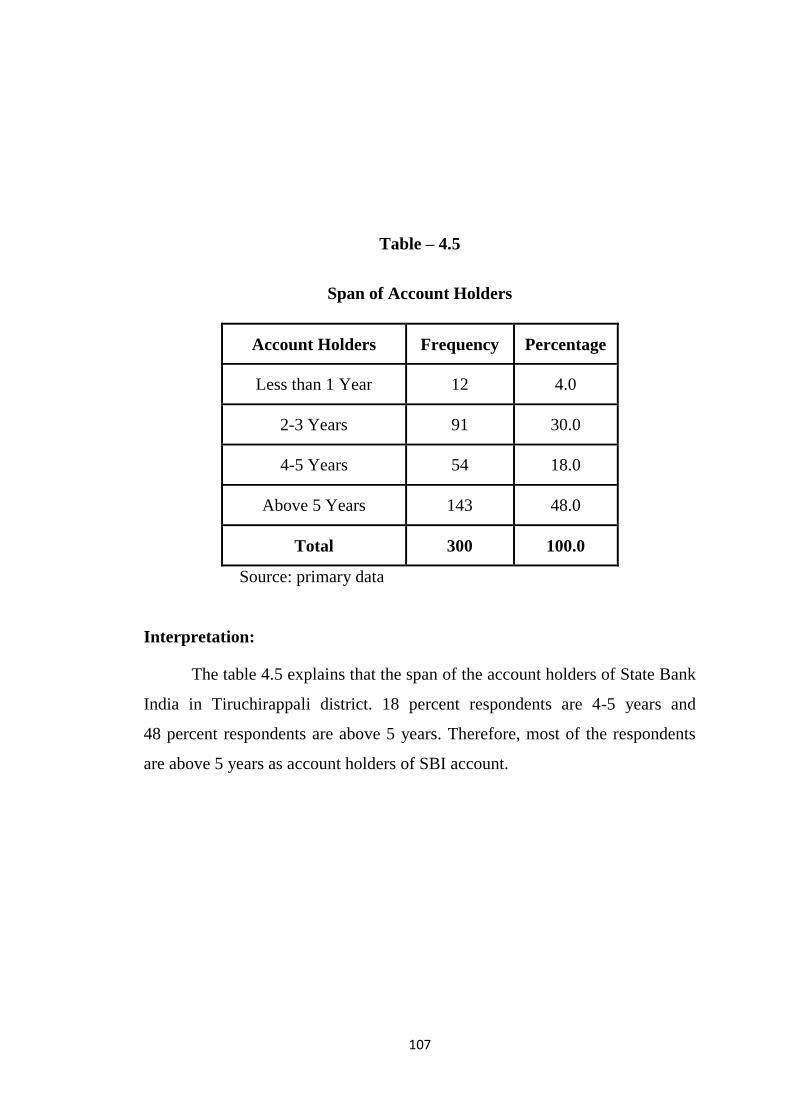

4.5 Span of Account Holders 107

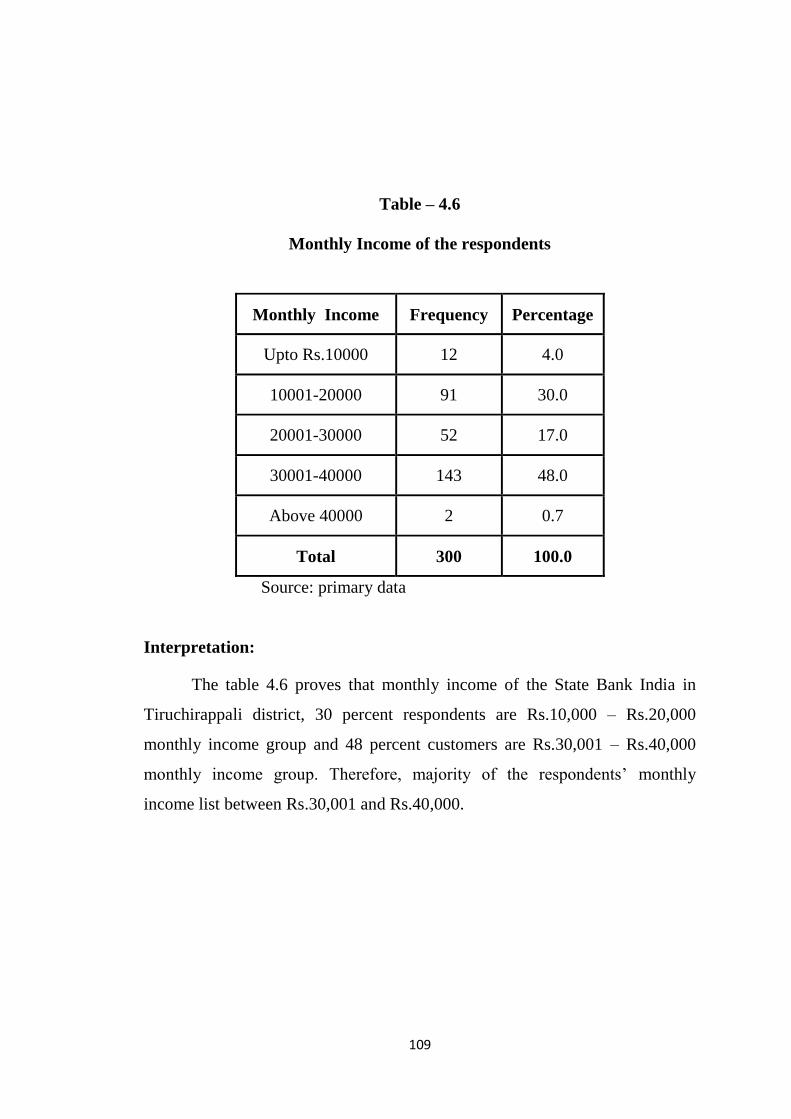

4.6 Monthly Income of the respondents 109

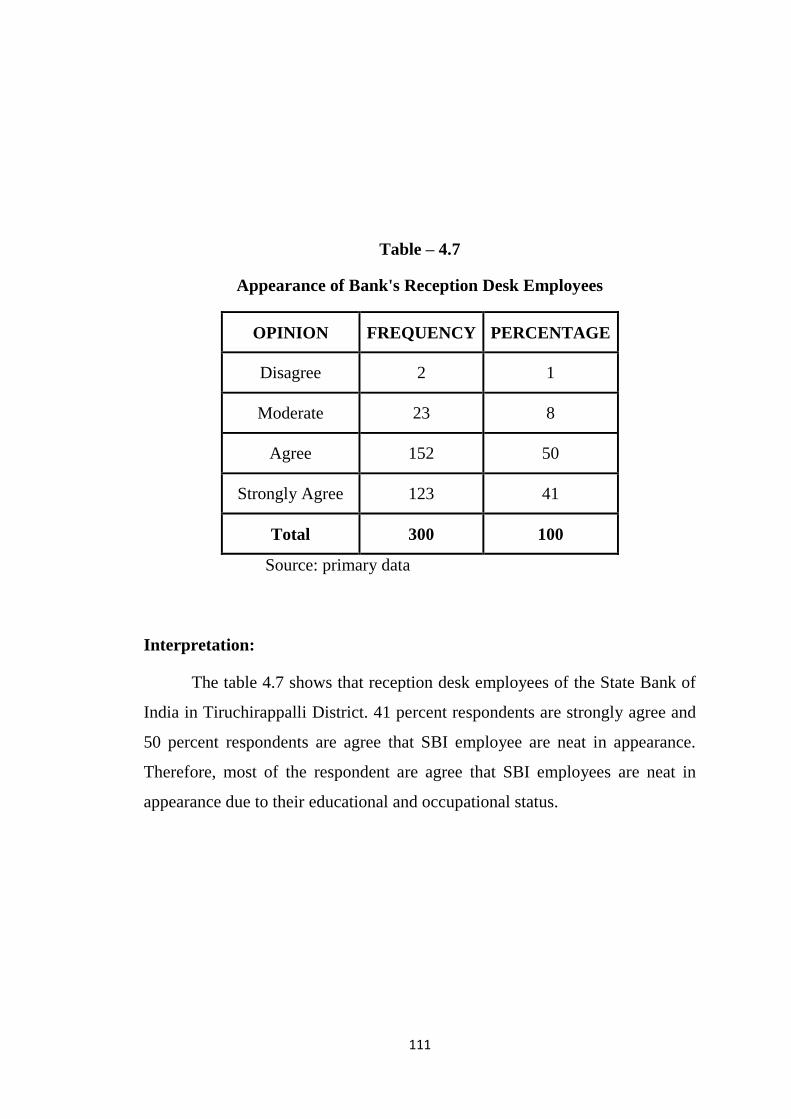

4.7 Appearance of Bank’s reception desk employees 111

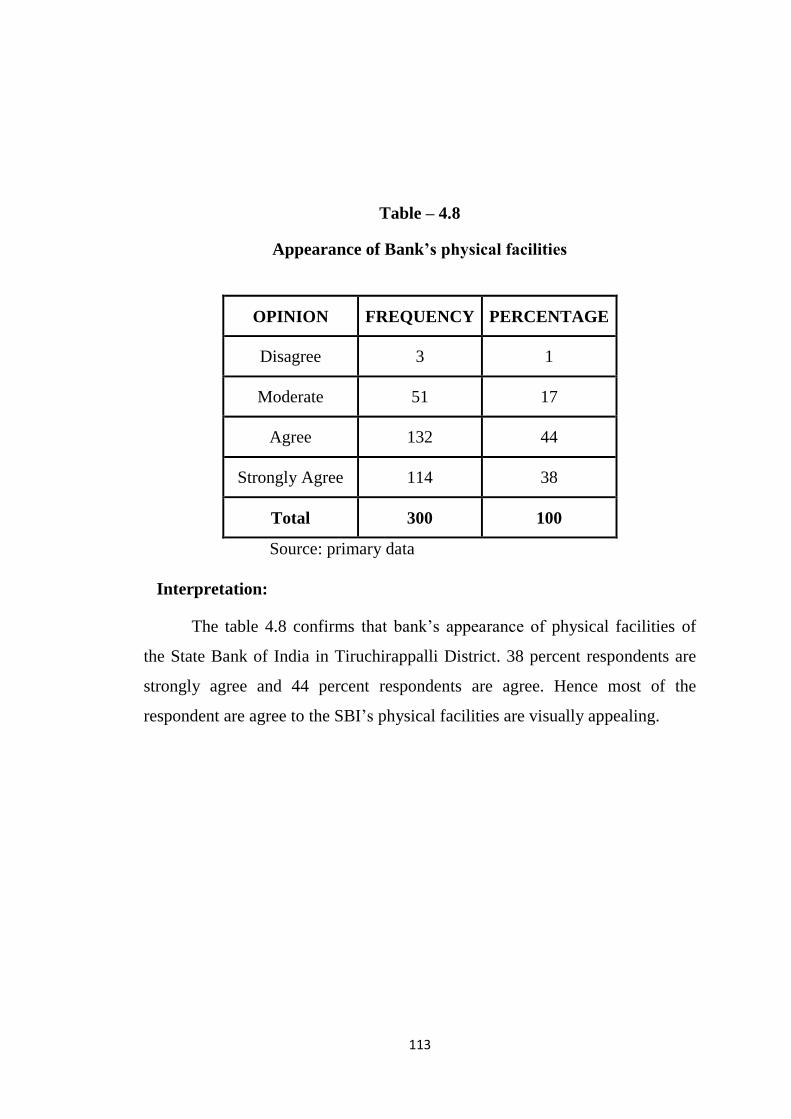

4.8 Appearance of Bank’s physical facilities 113

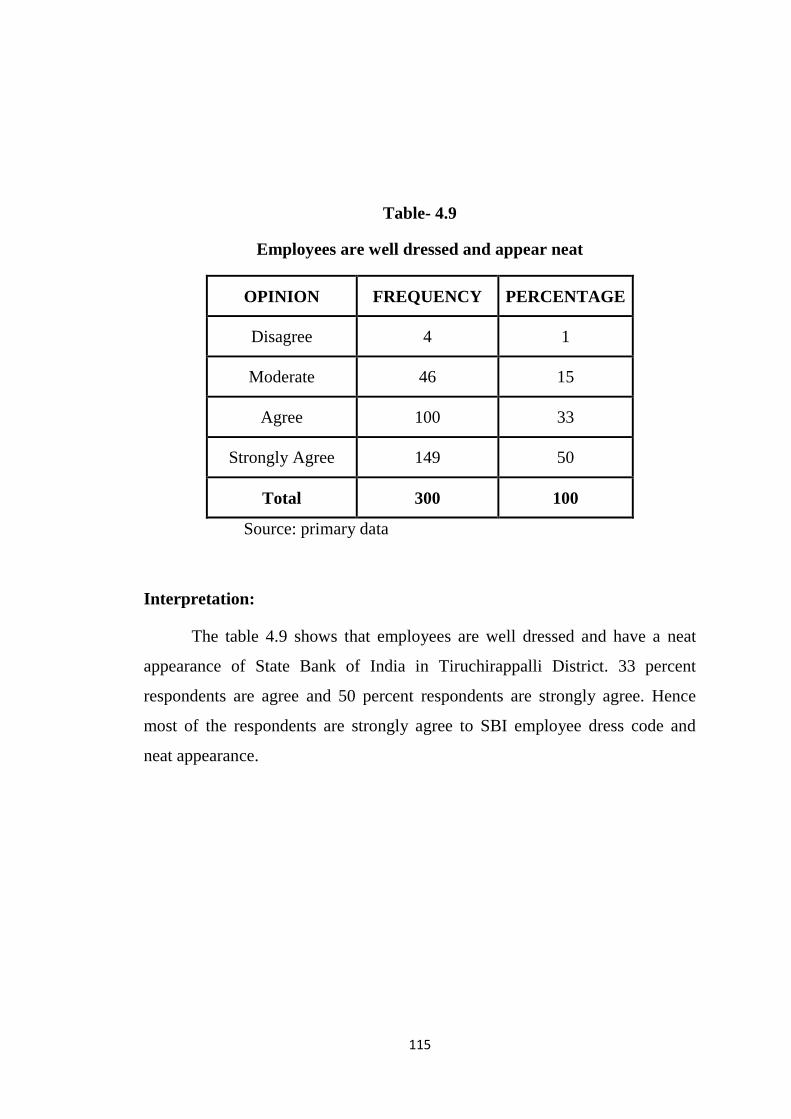

4.9 Employees are well dressed and appear neat 115

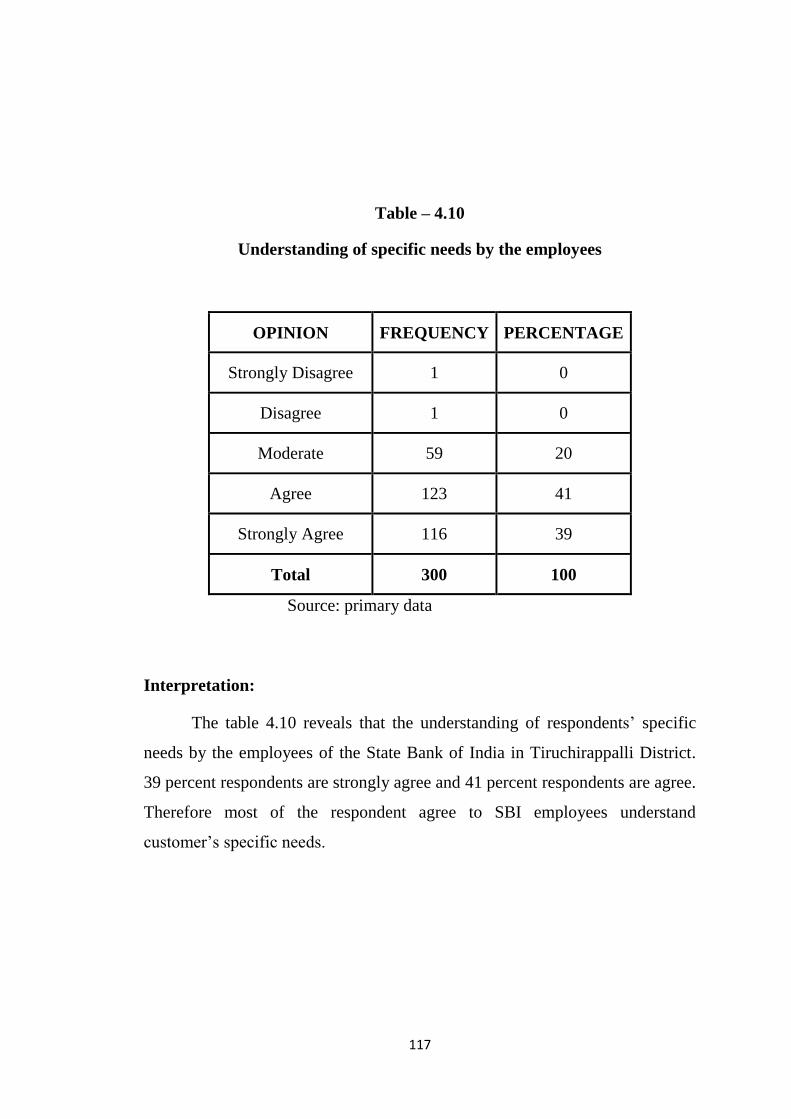

4.10 Understanding of specific needs by the employees 117

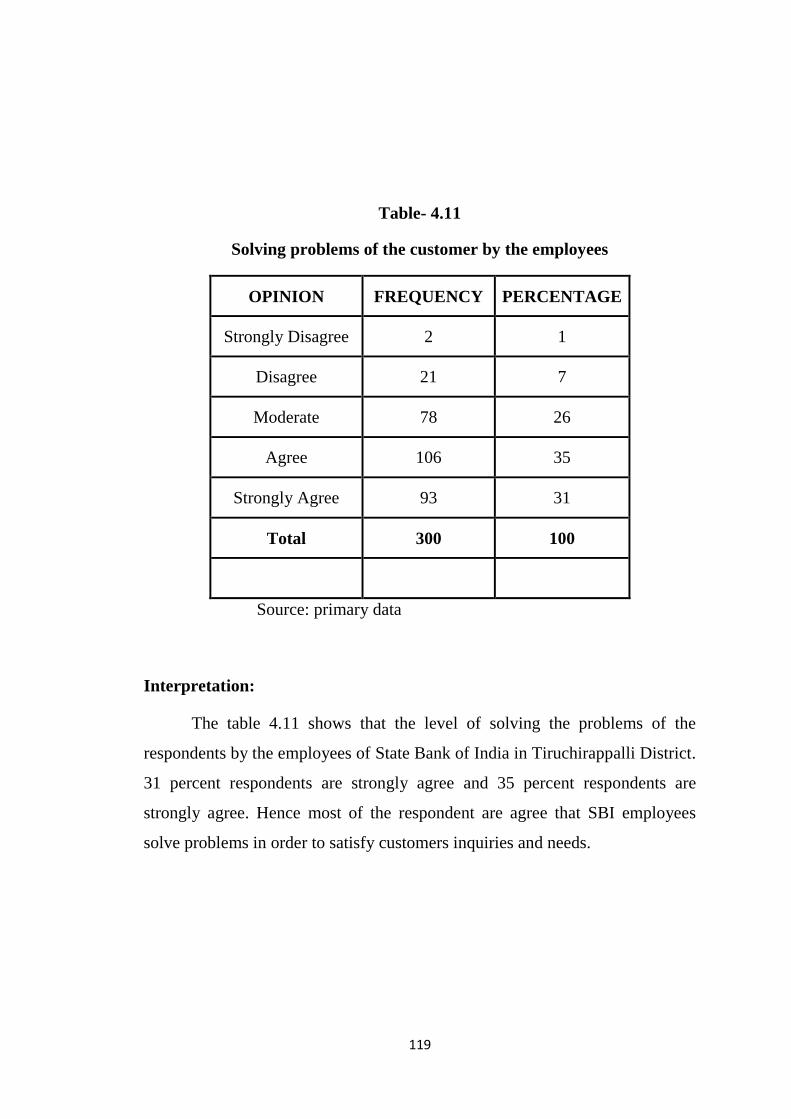

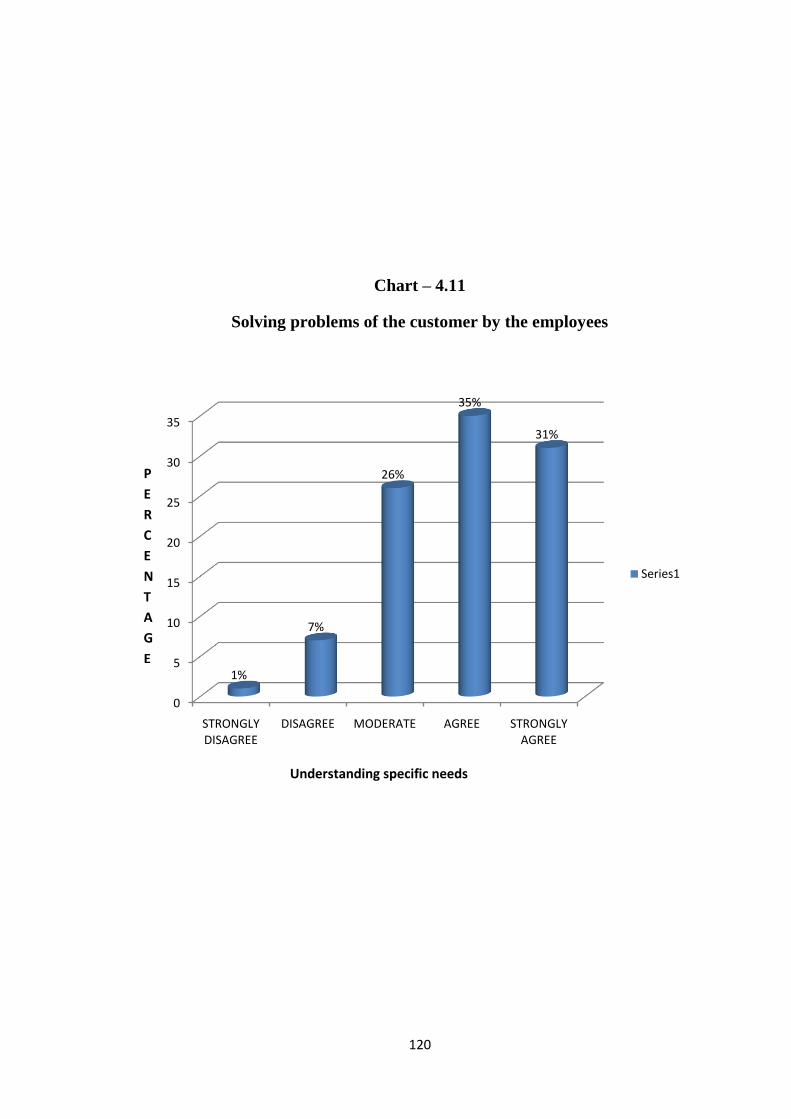

4.11 Solving problems of the customer by the employees 119

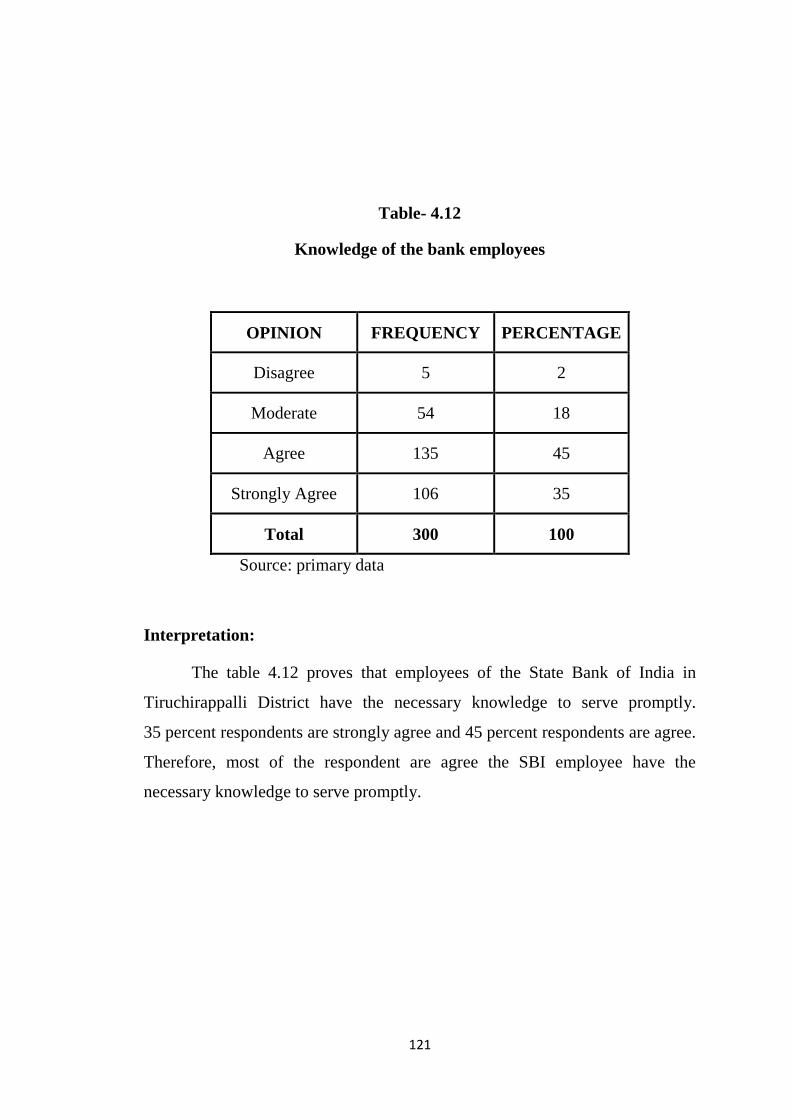

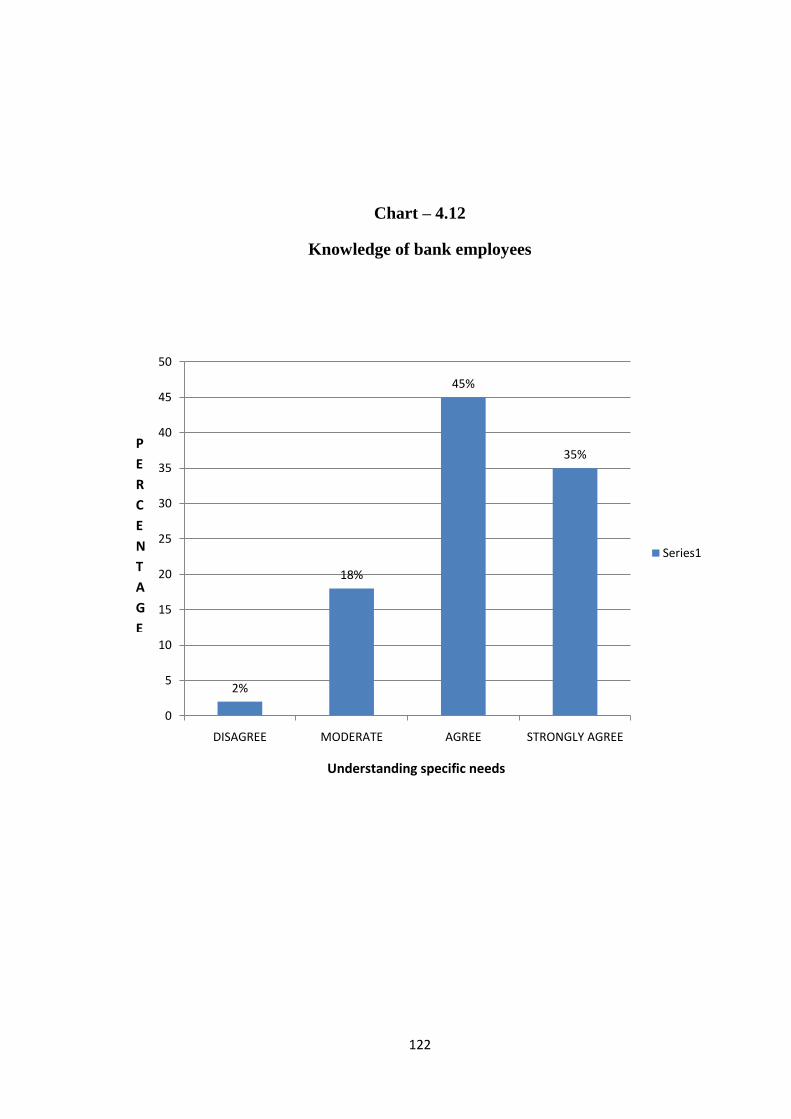

4.12 Knowledge of bank employees 121

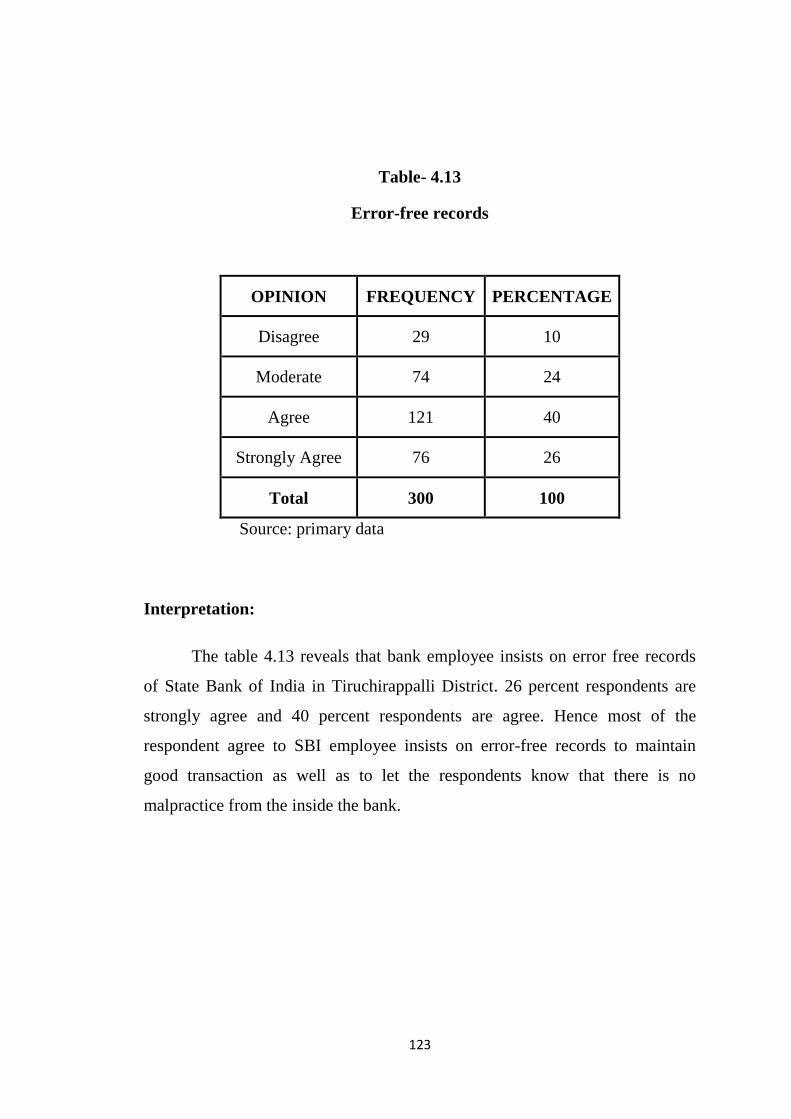

4.13 Error-free records 123

4.14 Satisfaction level on rate of interest deposit

facilities

125

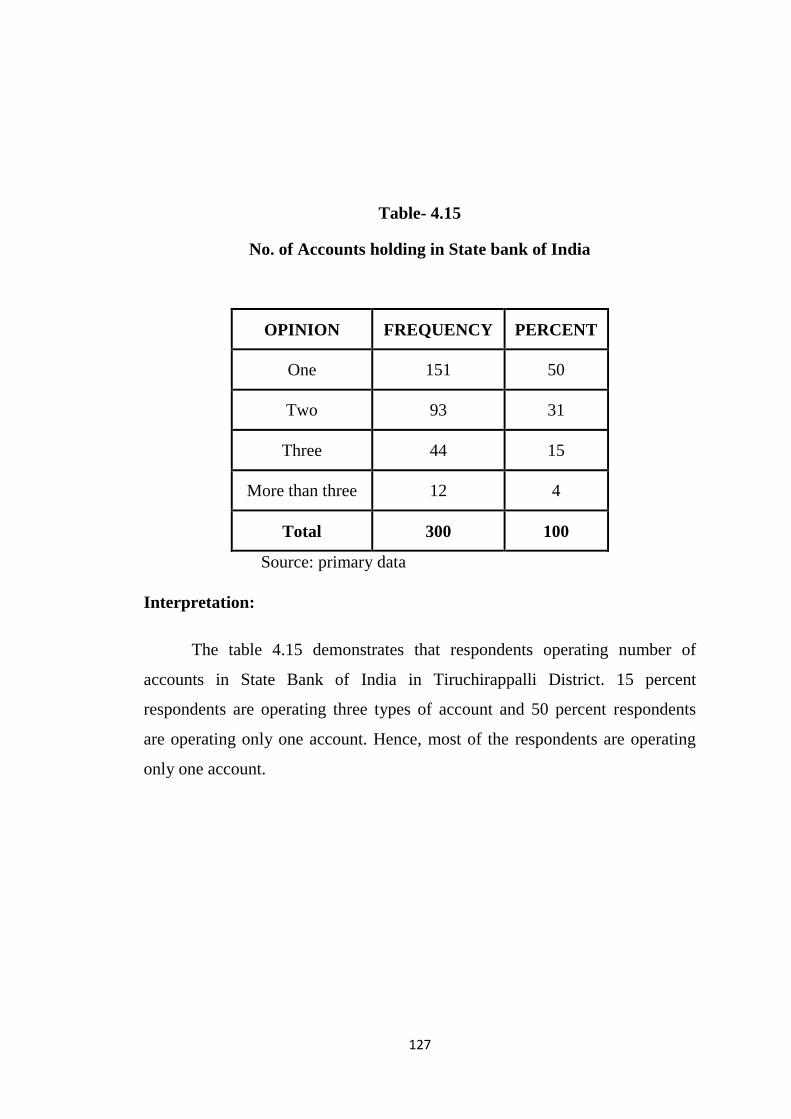

4.15 No. of accounts holding in State Bank of India 127

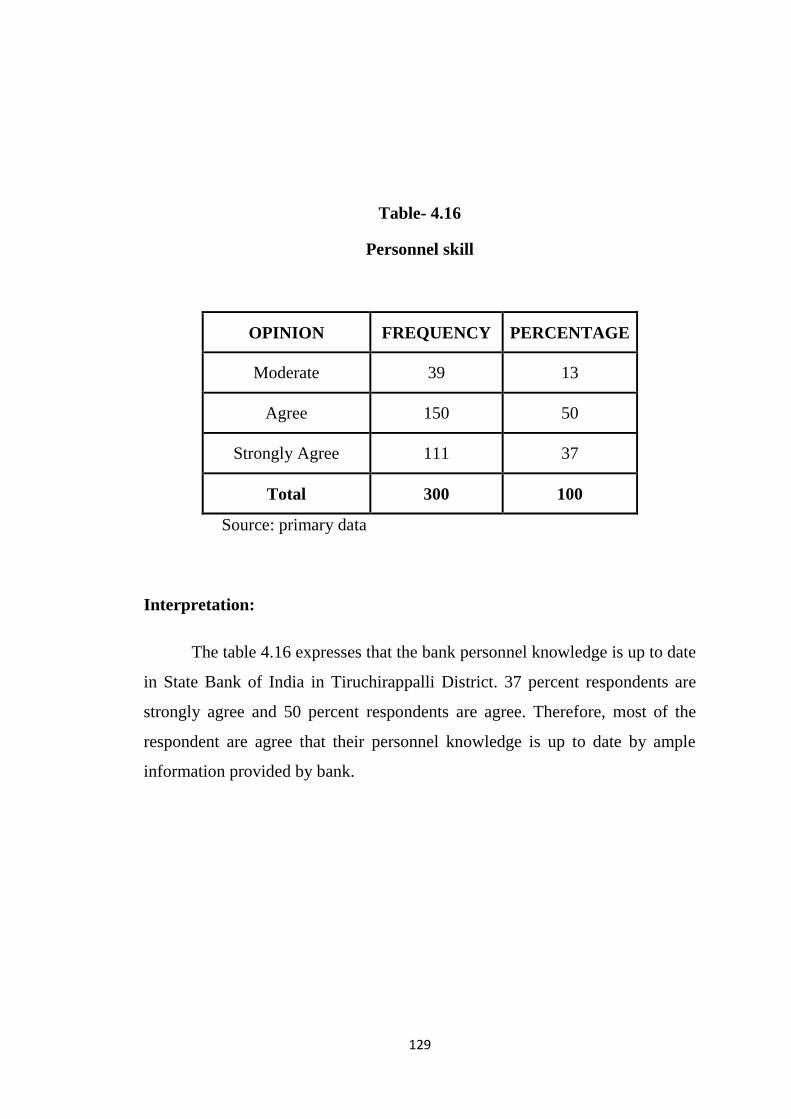

4.16 Personnel skill 129

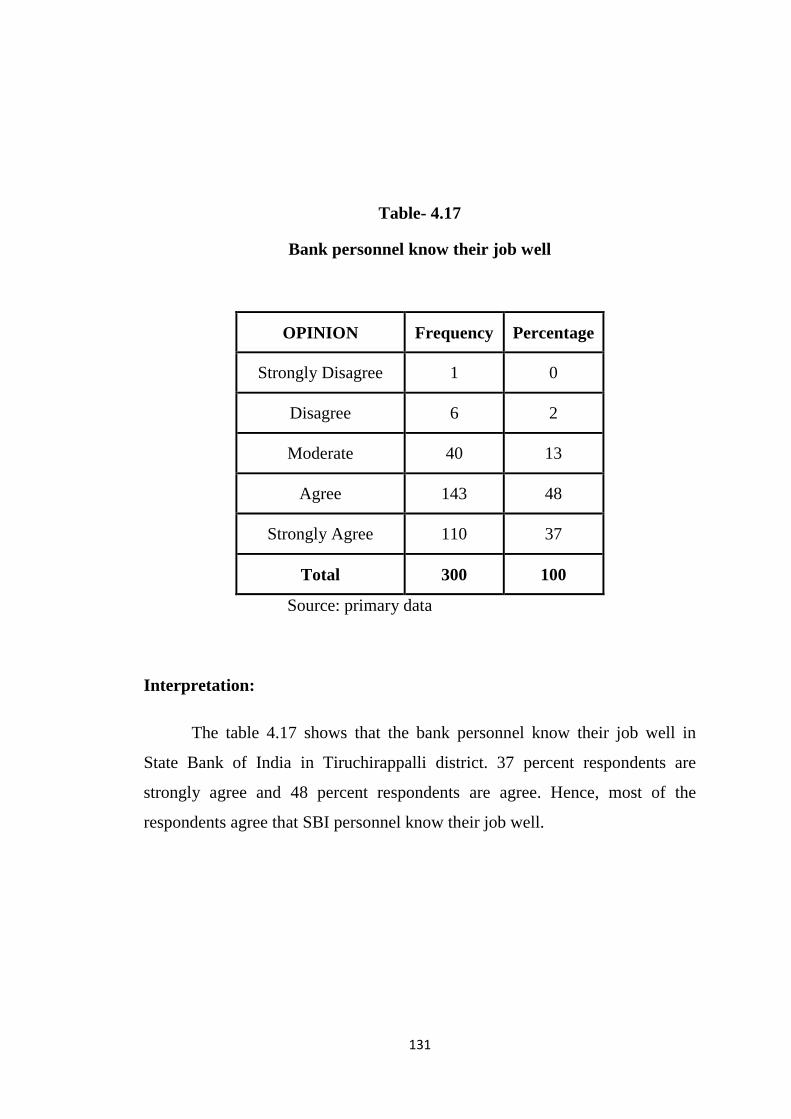

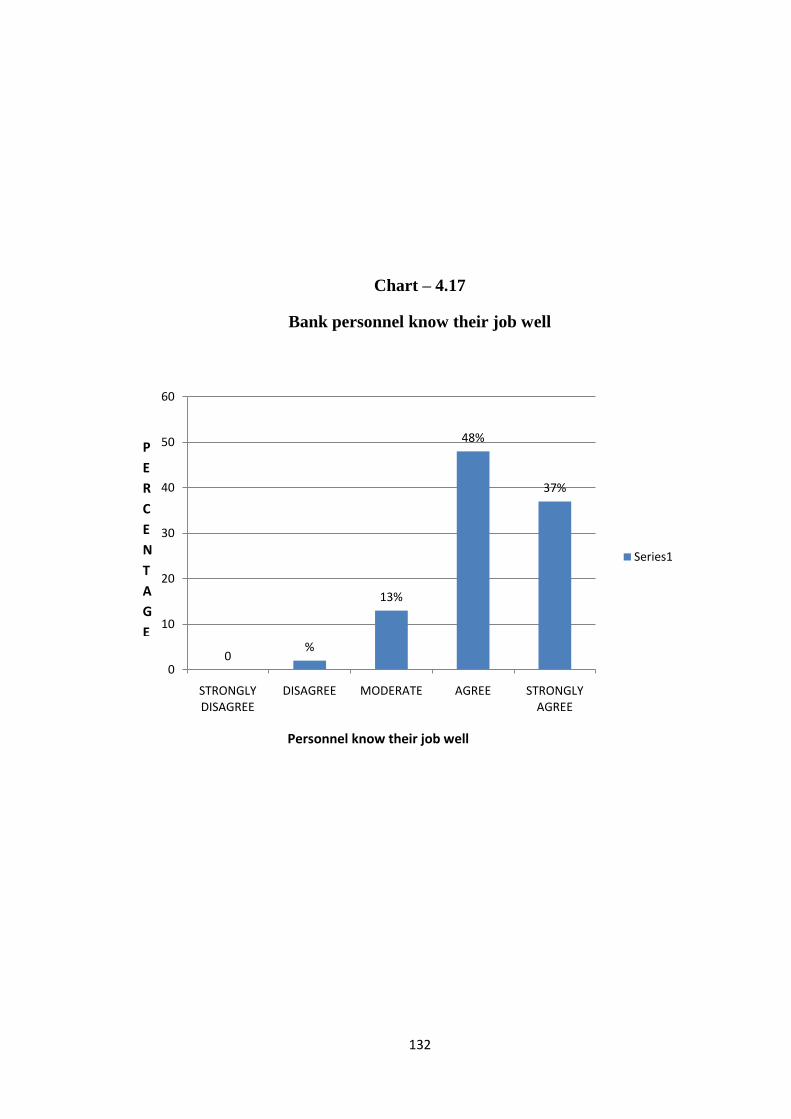

4.17 Bank personnel know their job well 131

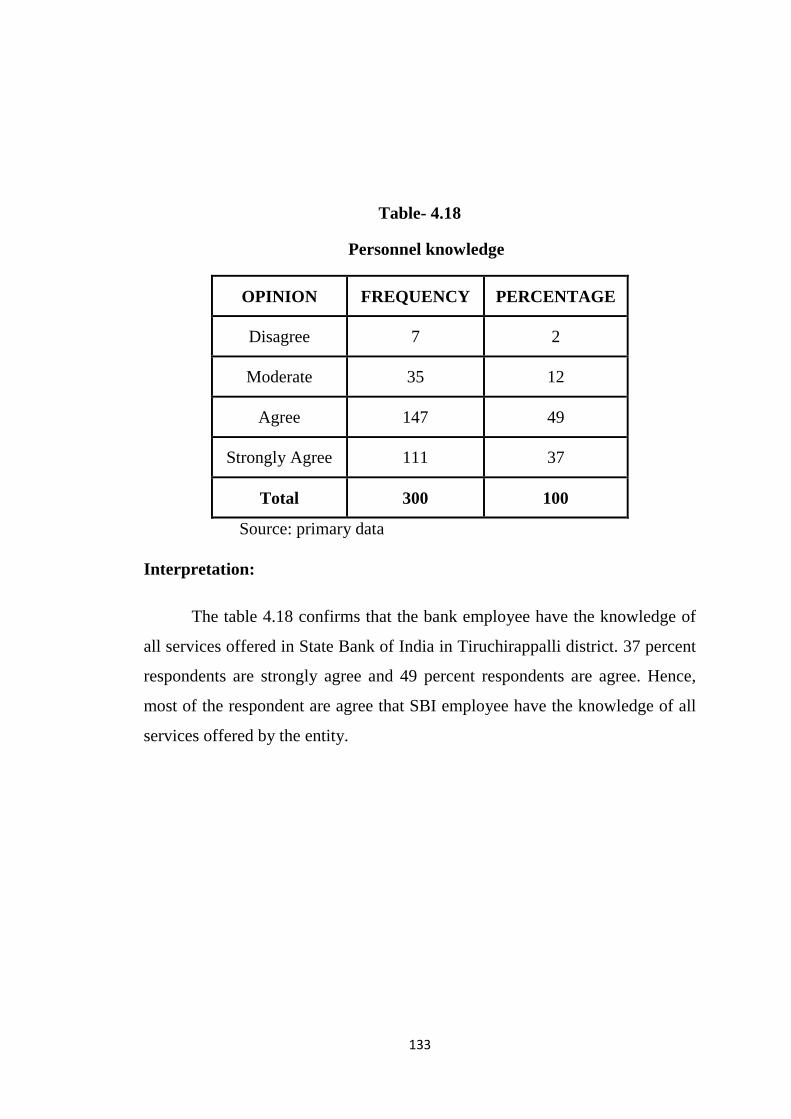

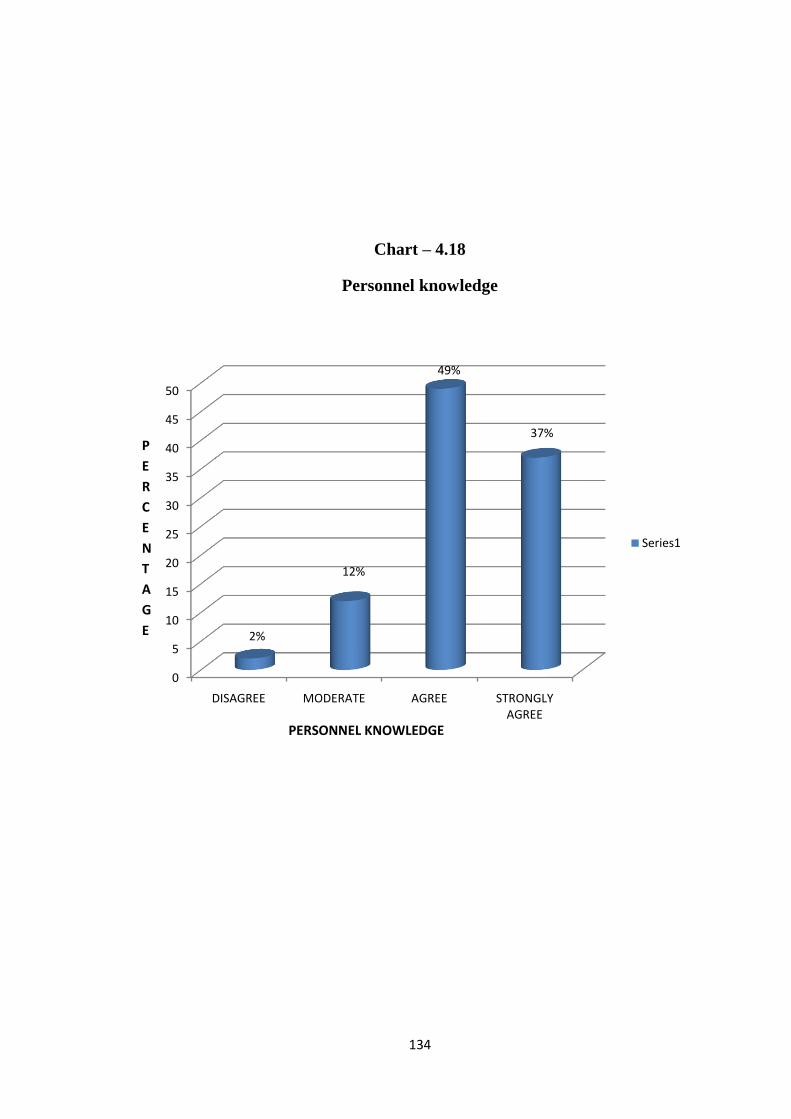

4.18 Personnel knowledge 133

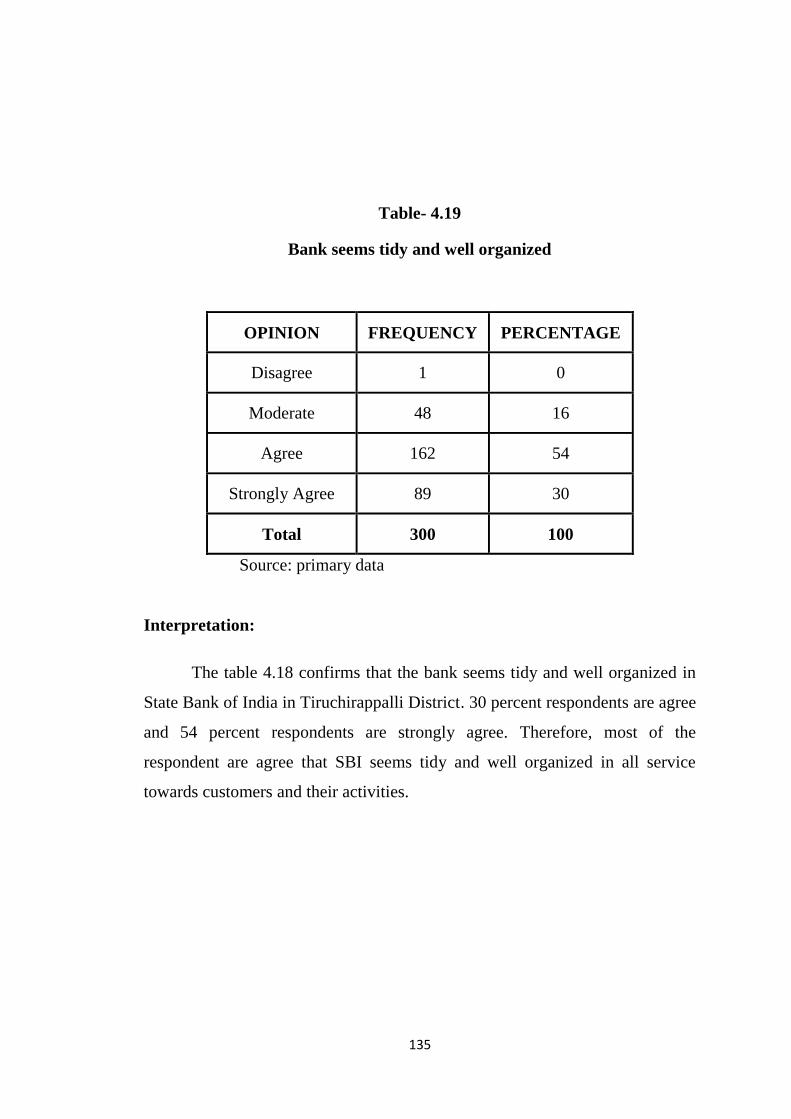

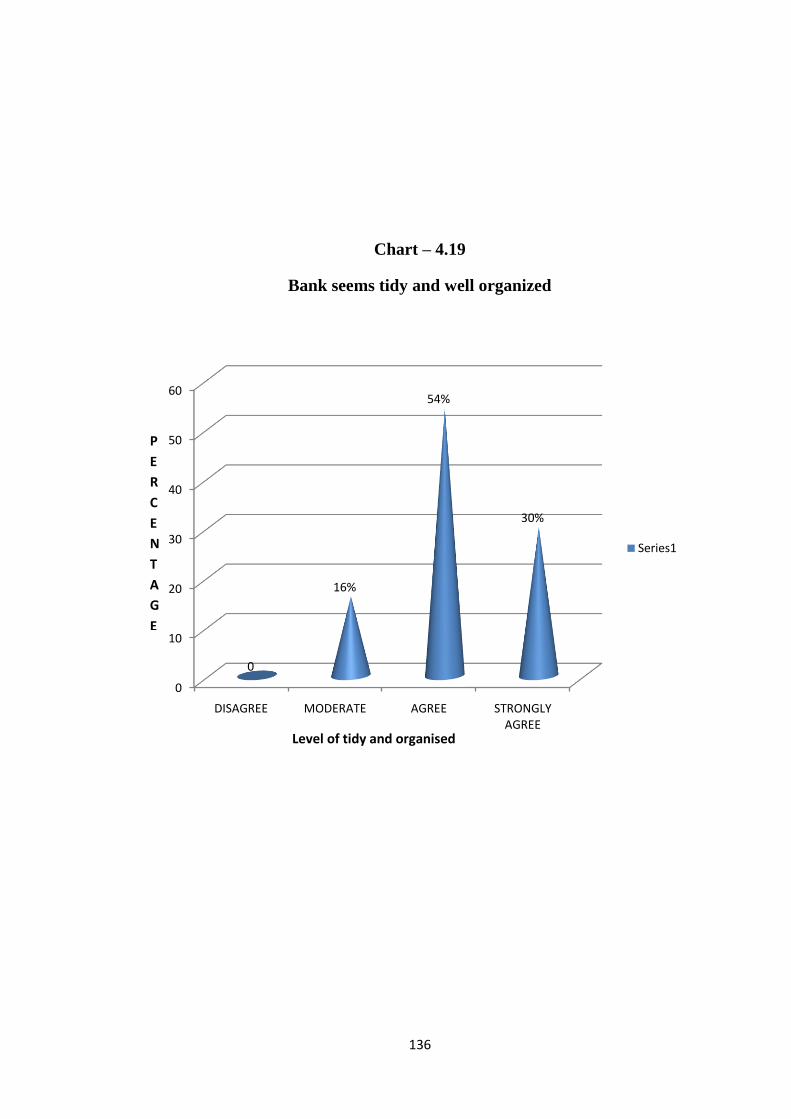

4.19 Banks seems tidy and well organized 135

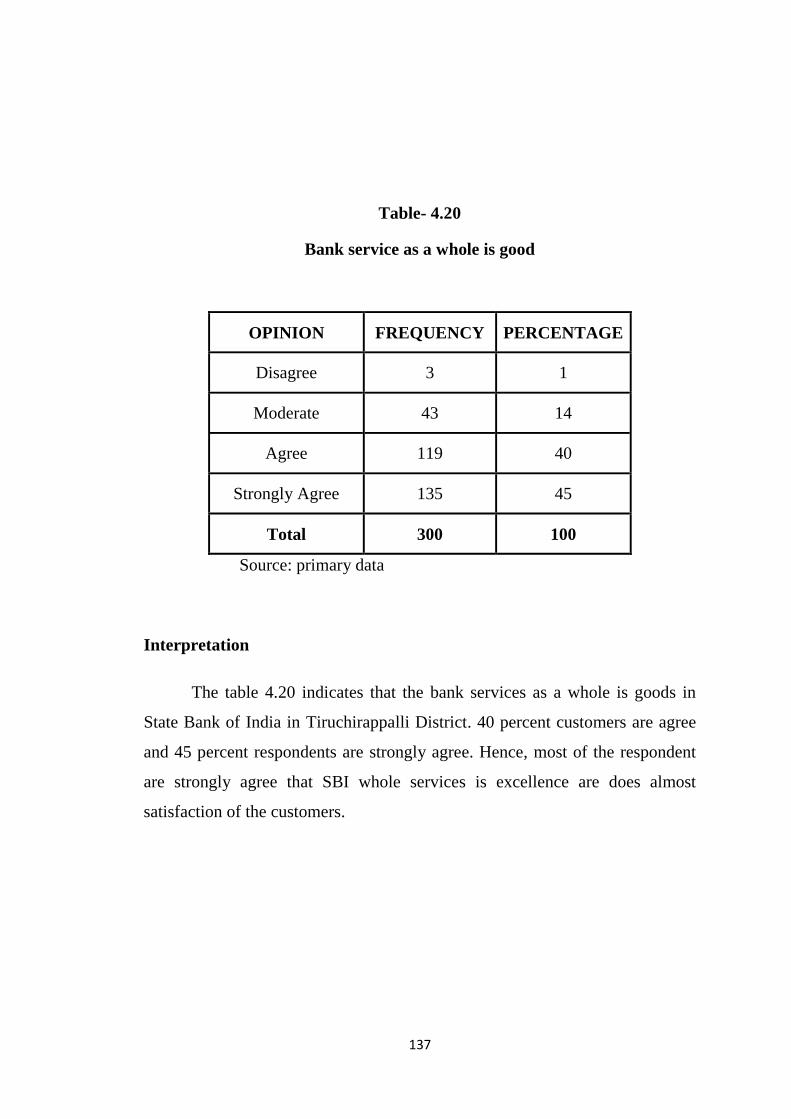

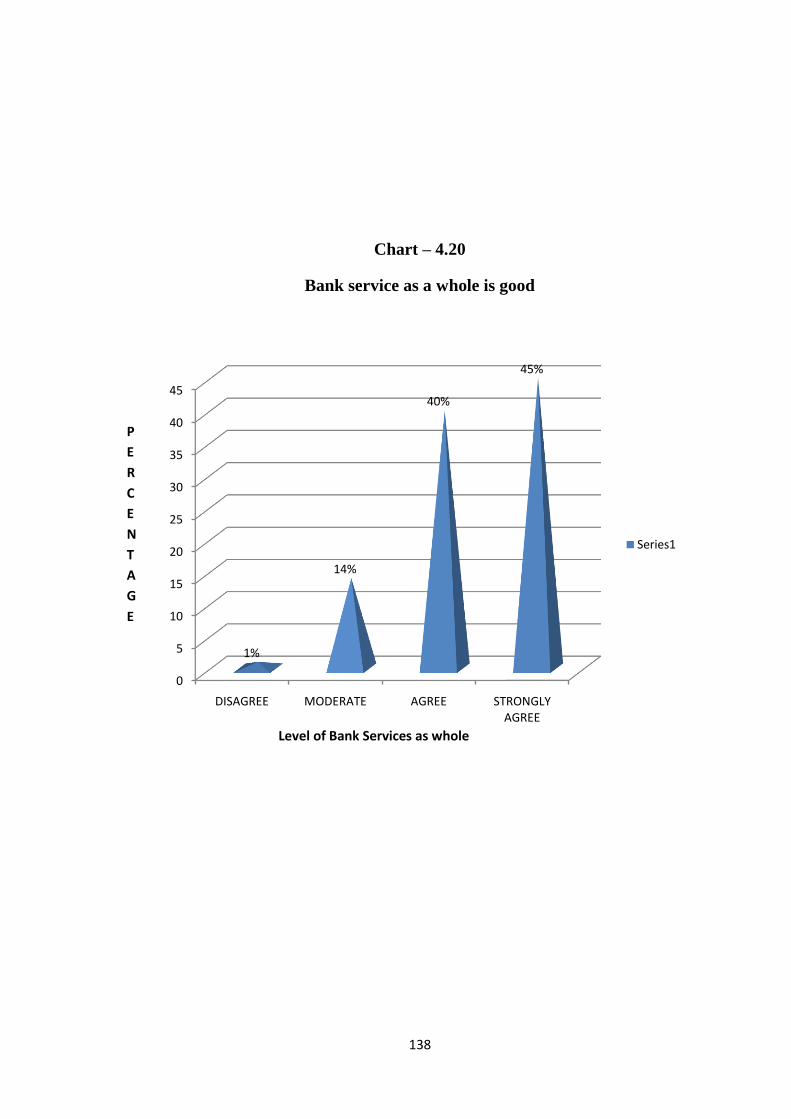

4.20 Bank service as a whole is good 137

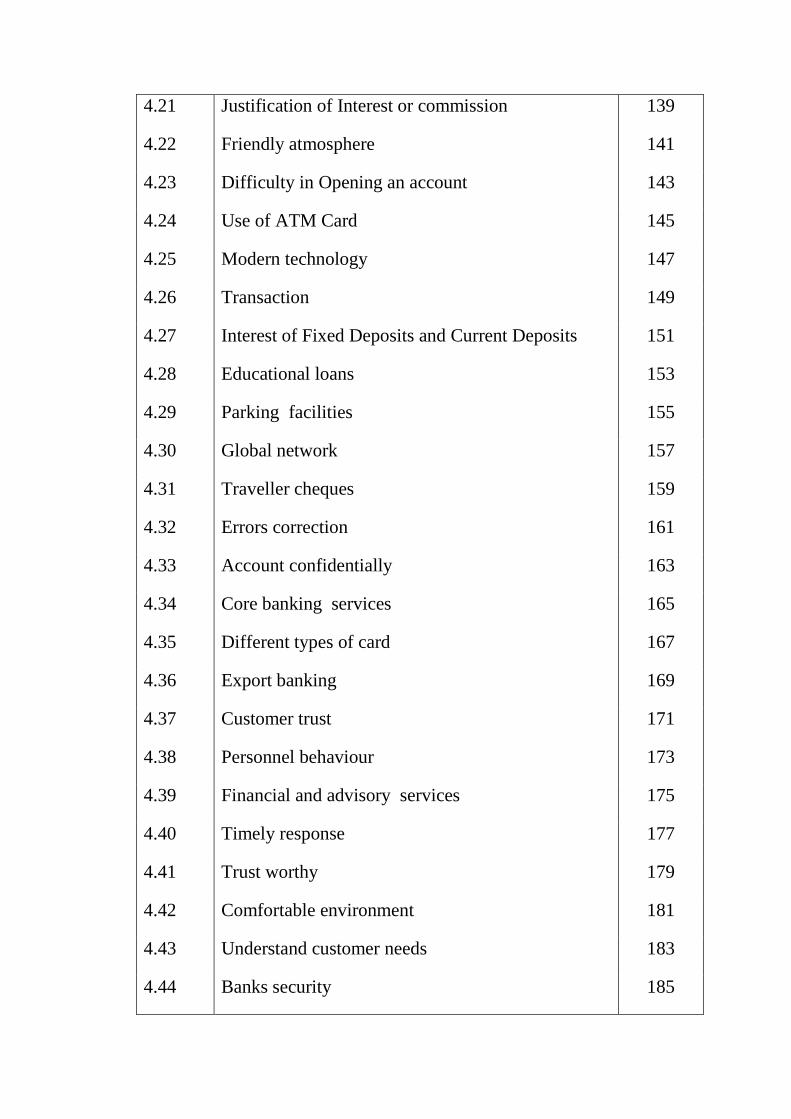

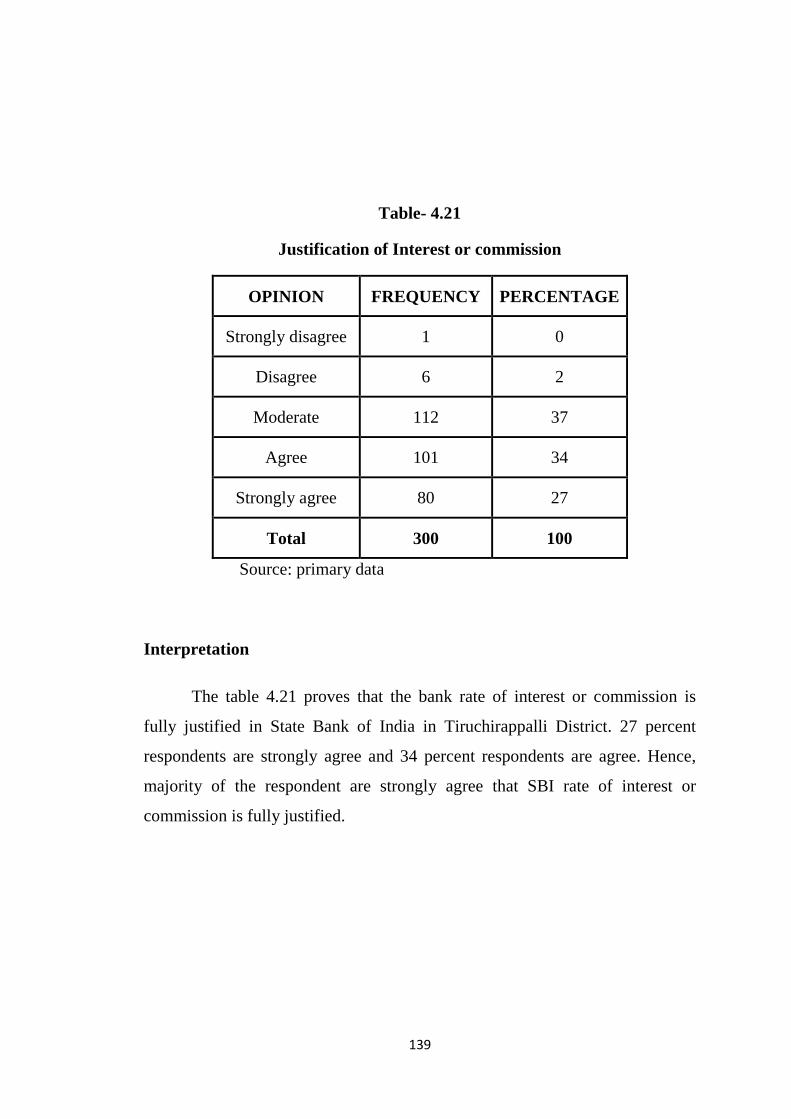

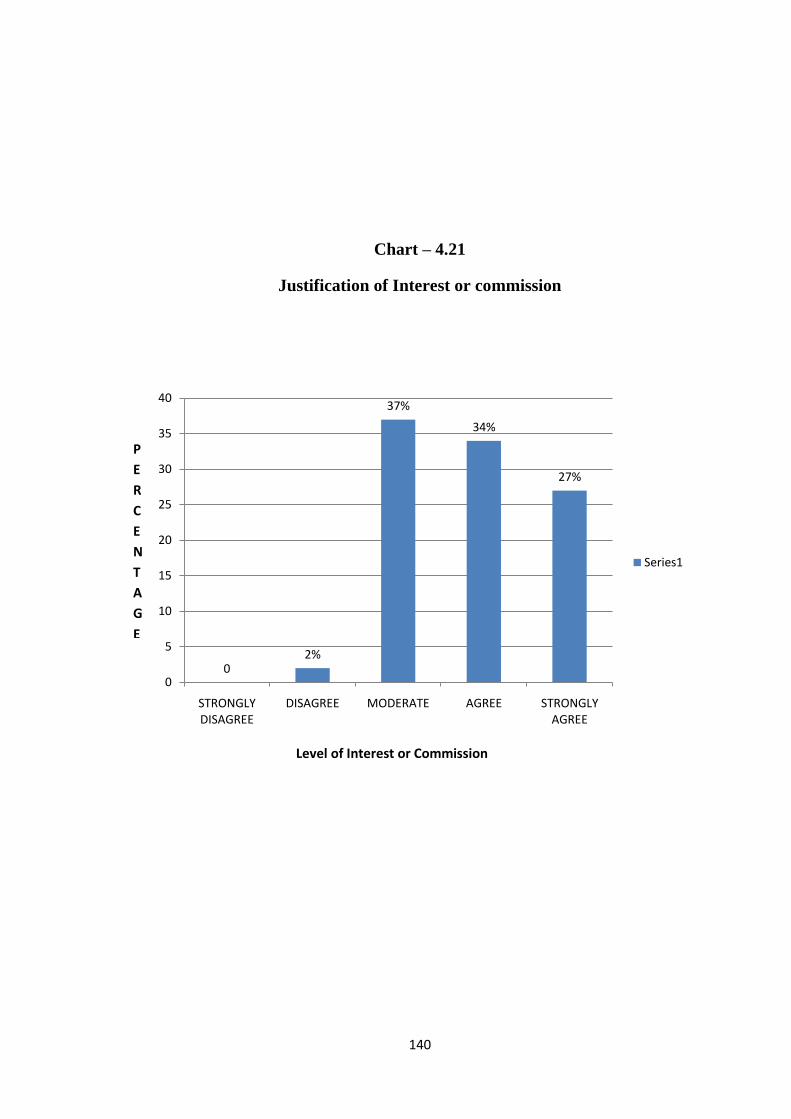

4.21 Justification of Interest or commission 139

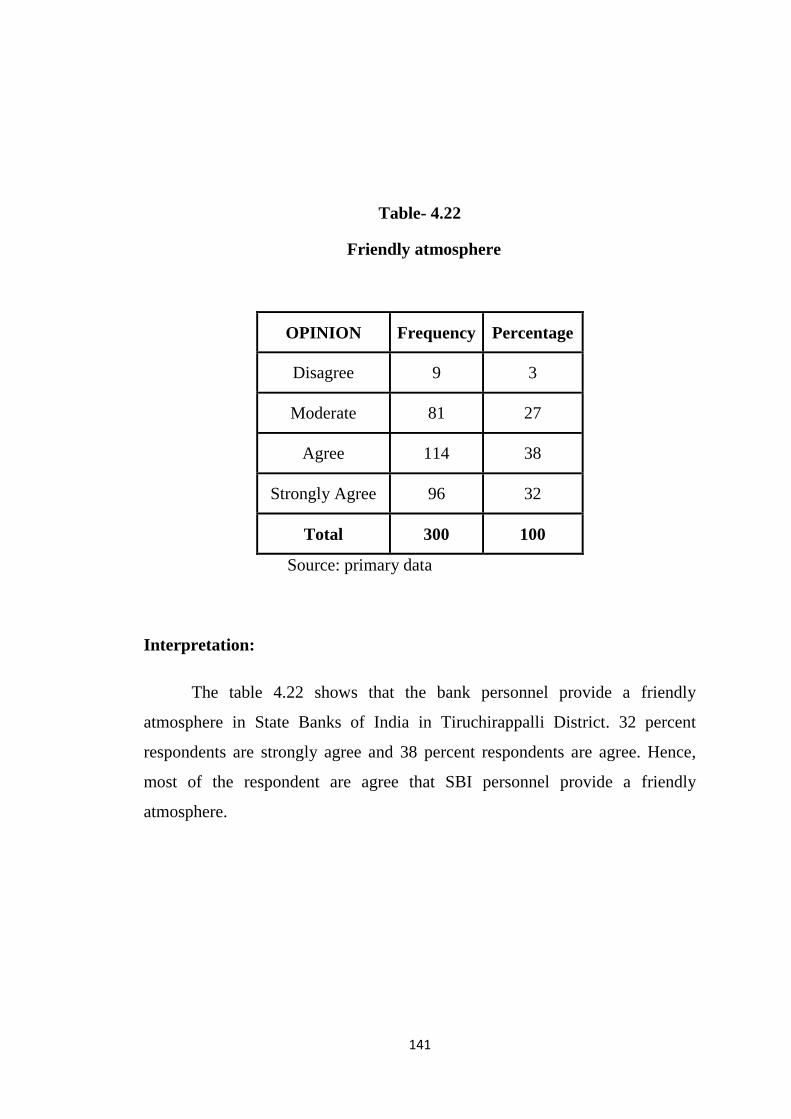

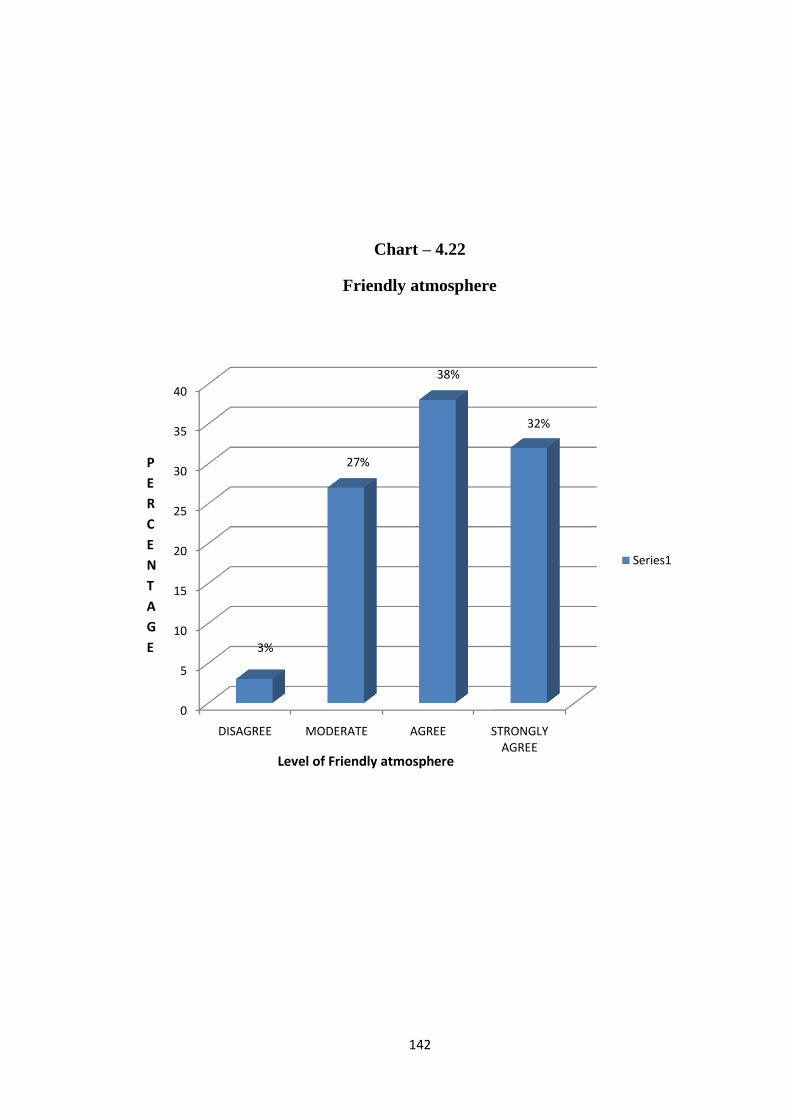

4.22 Friendly atmosphere 141

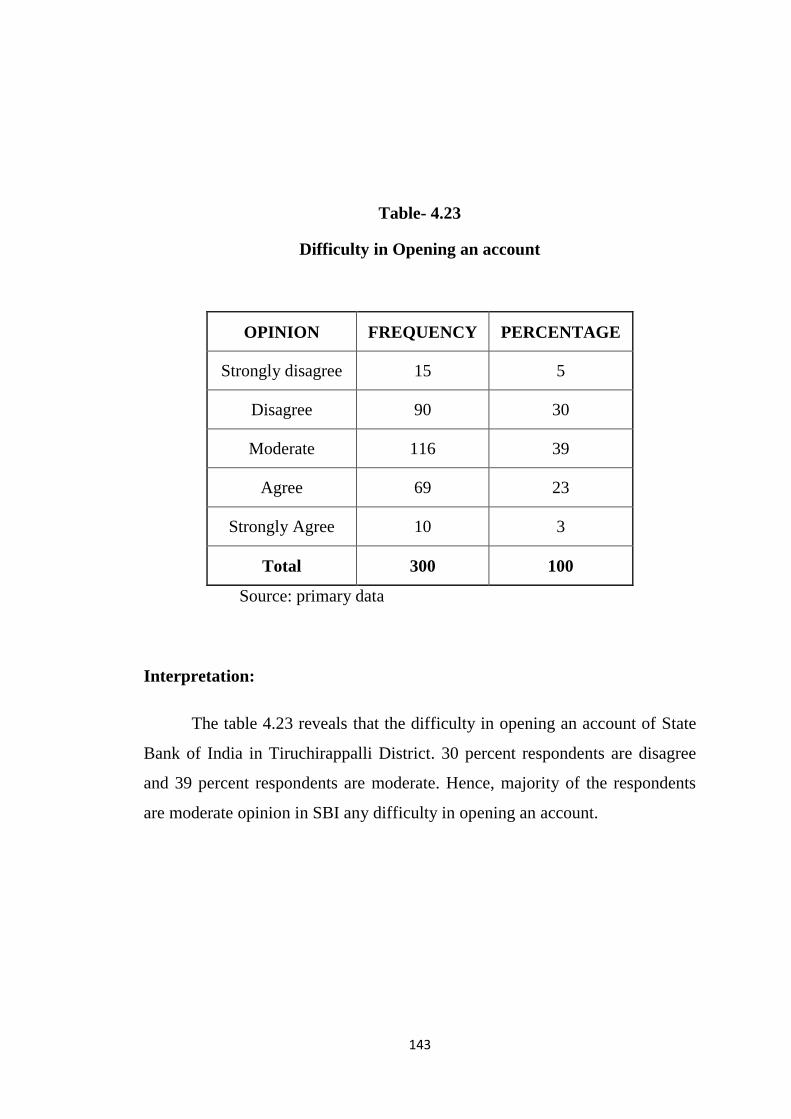

4.23 Difficulty in Opening an account 143

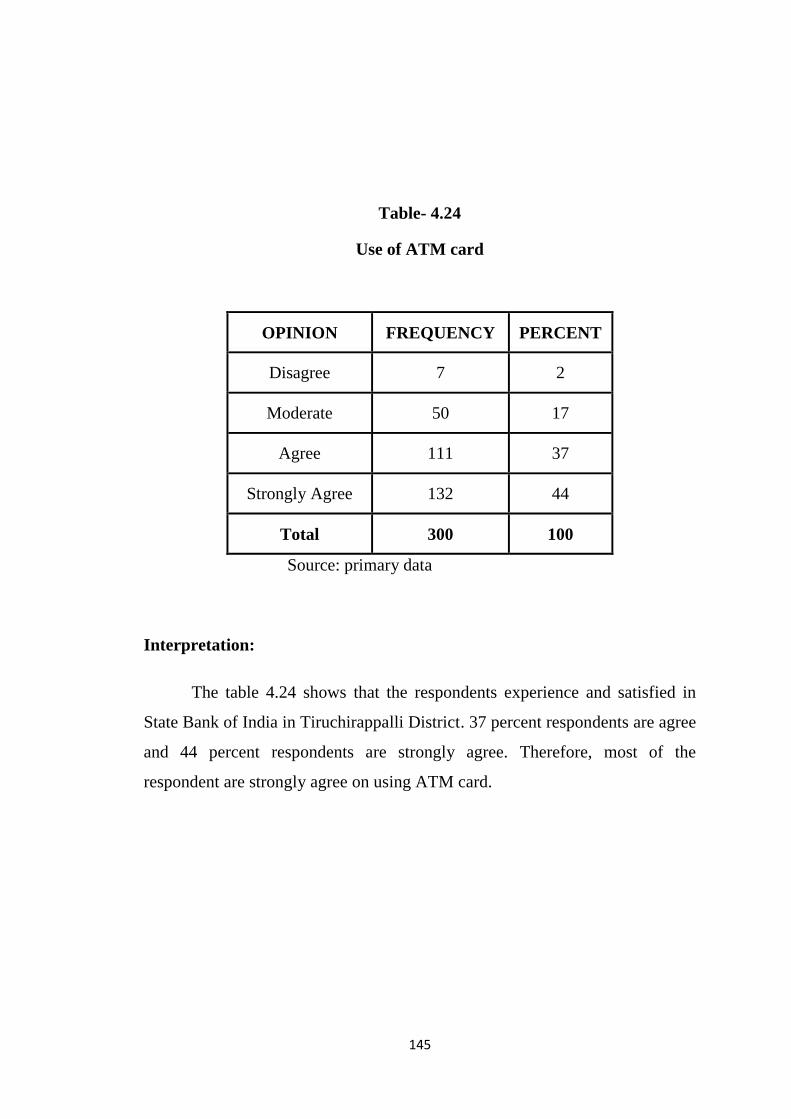

4.24 Use of ATM Card 145

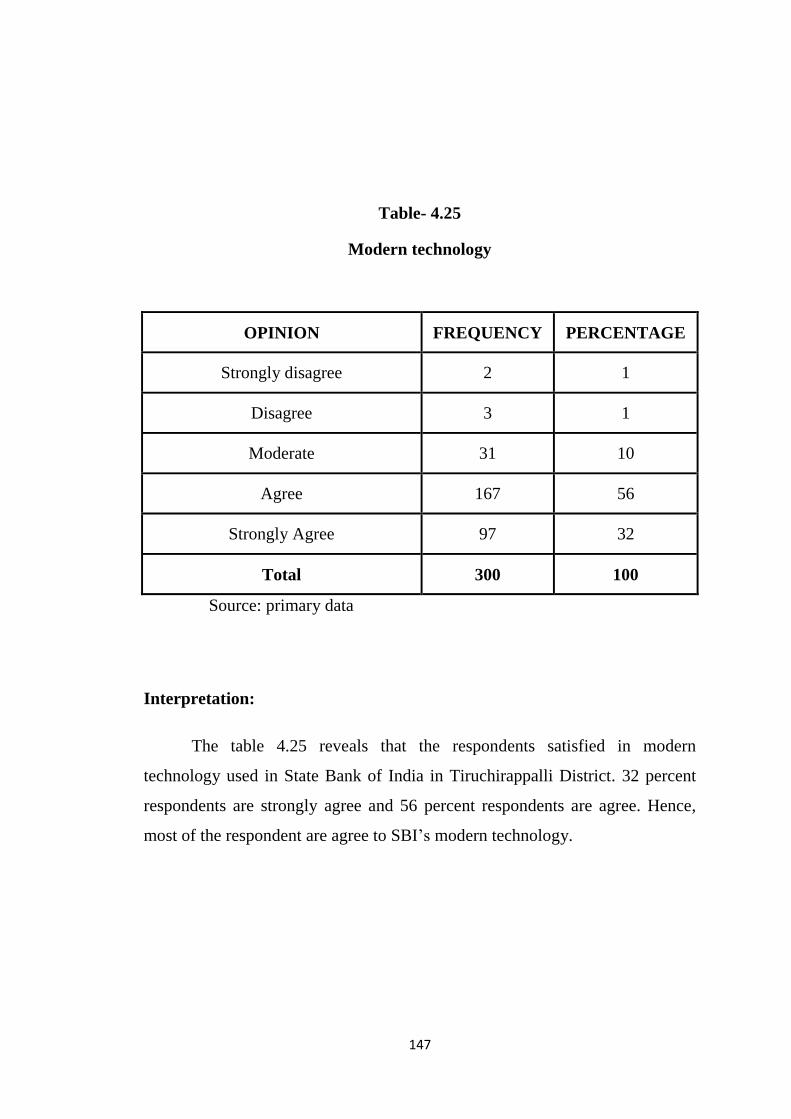

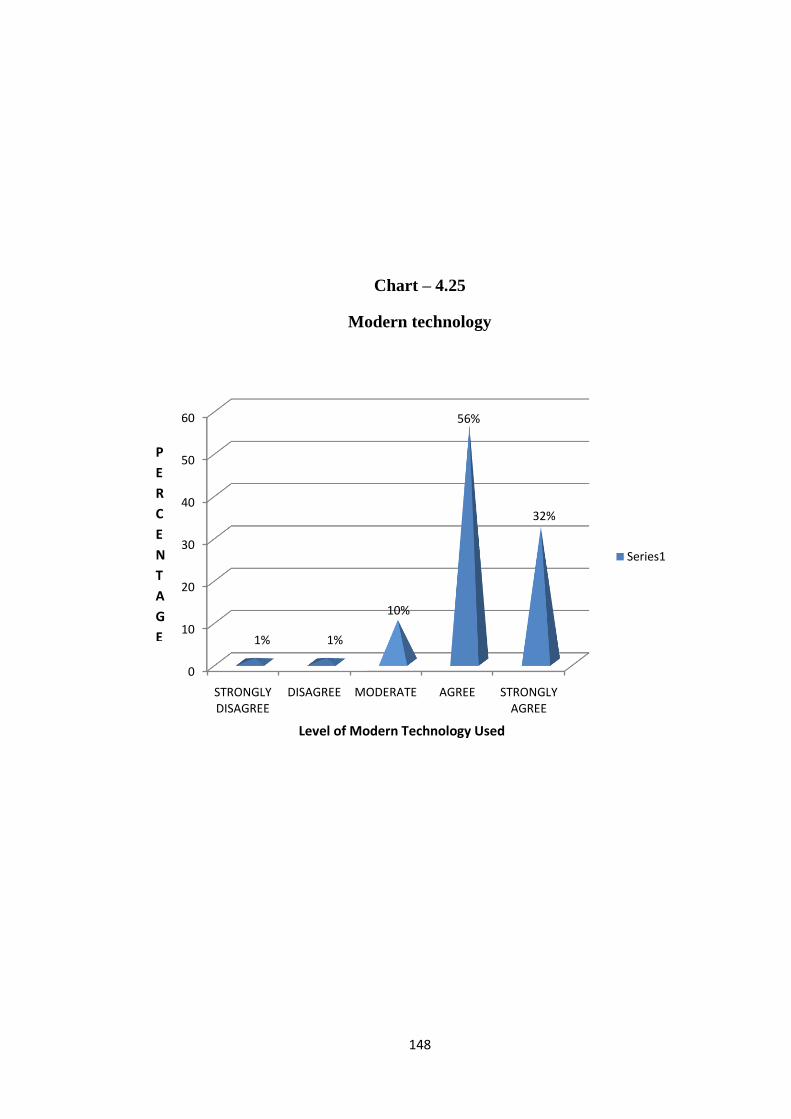

4.25 Modern technology 147

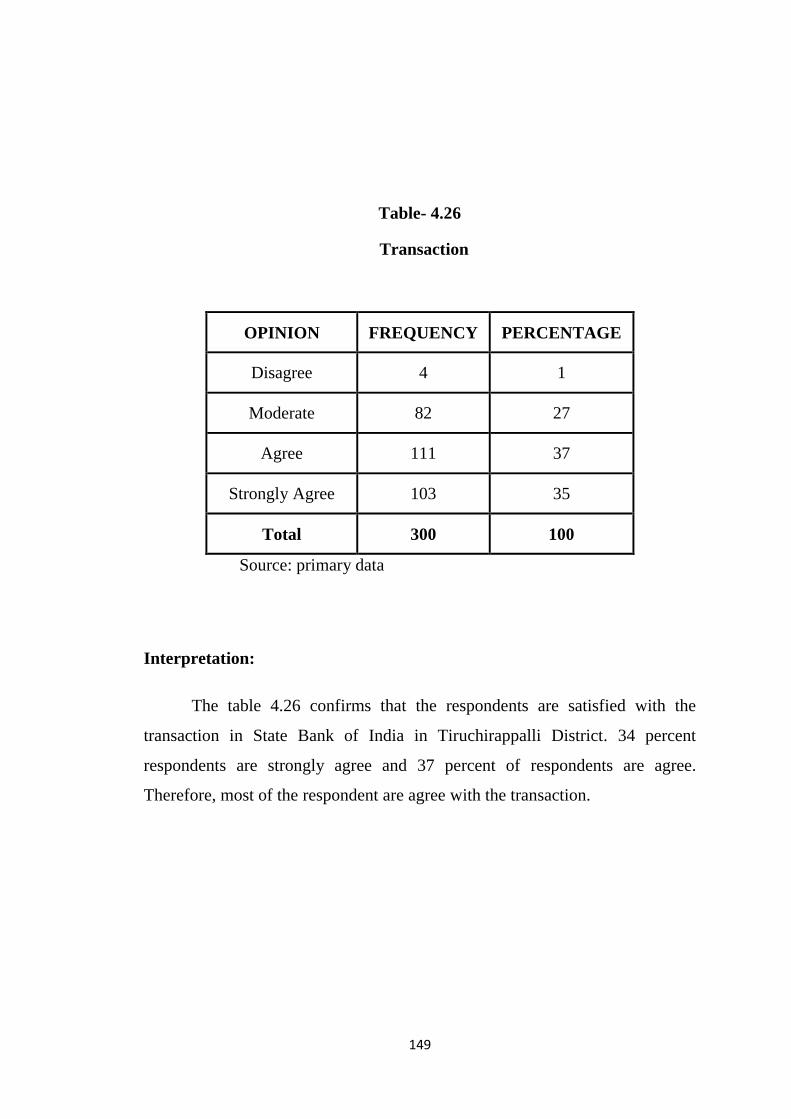

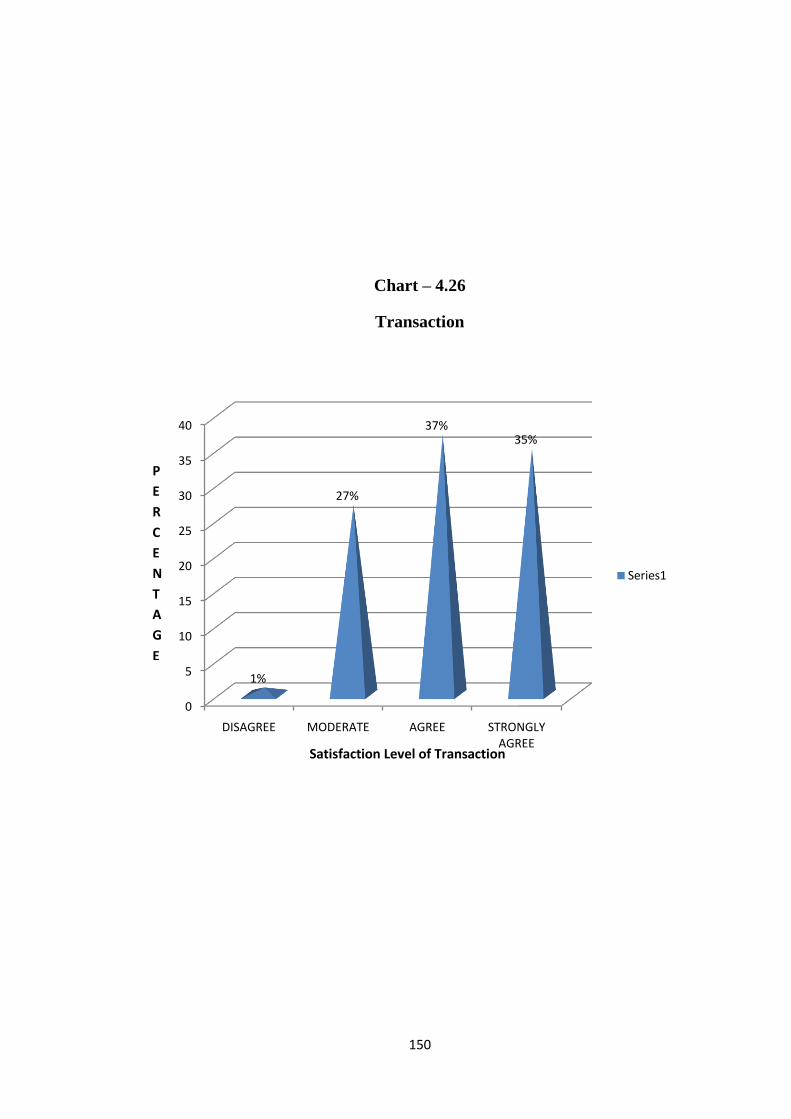

4.26 Transaction 149

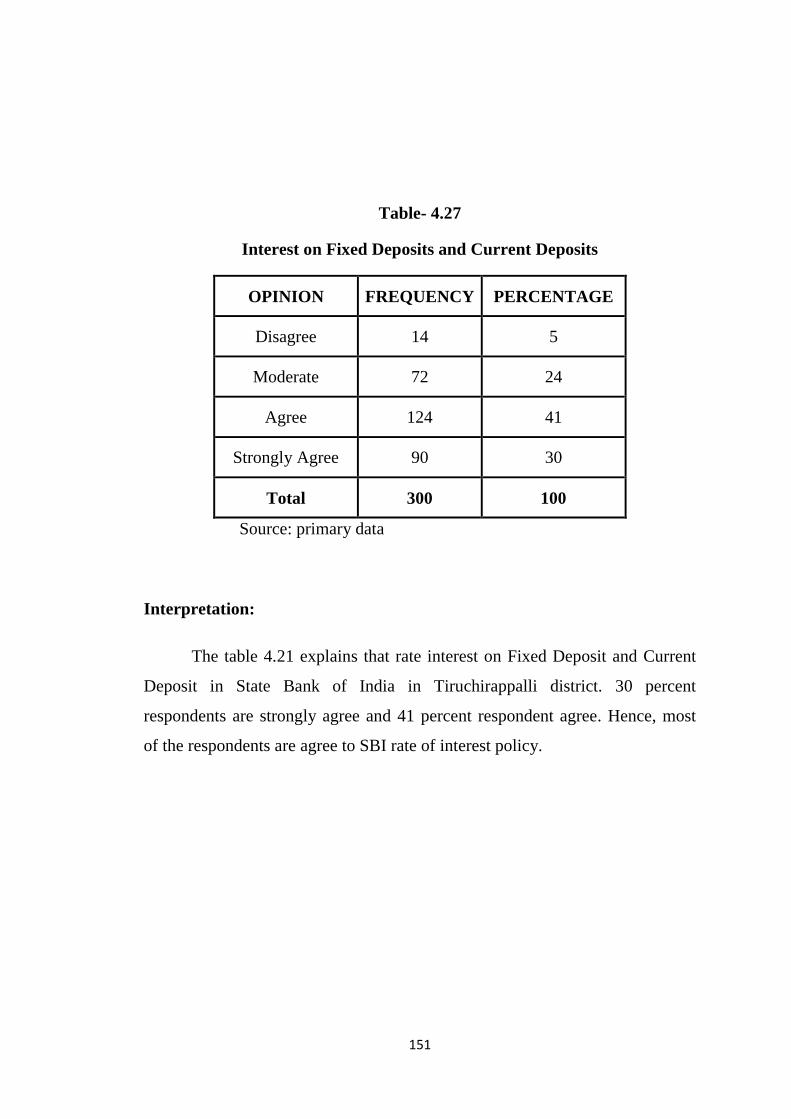

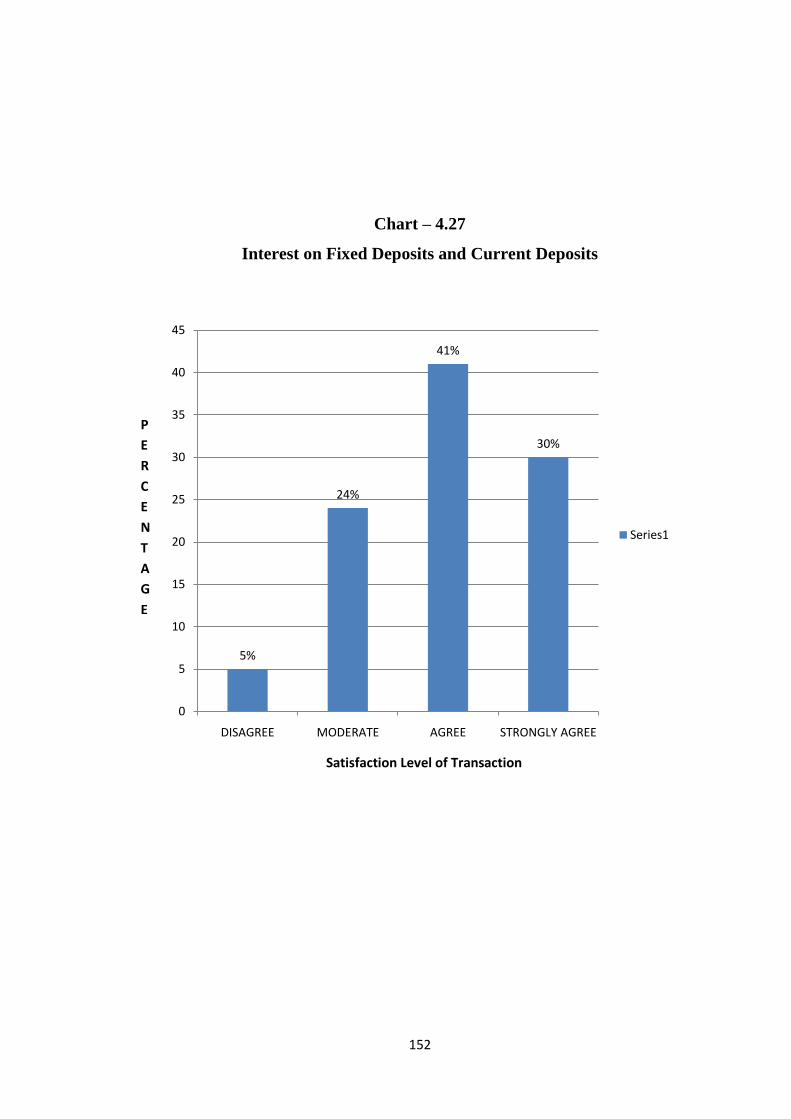

4.27 Interest of Fixed Deposits and Current Deposits 151

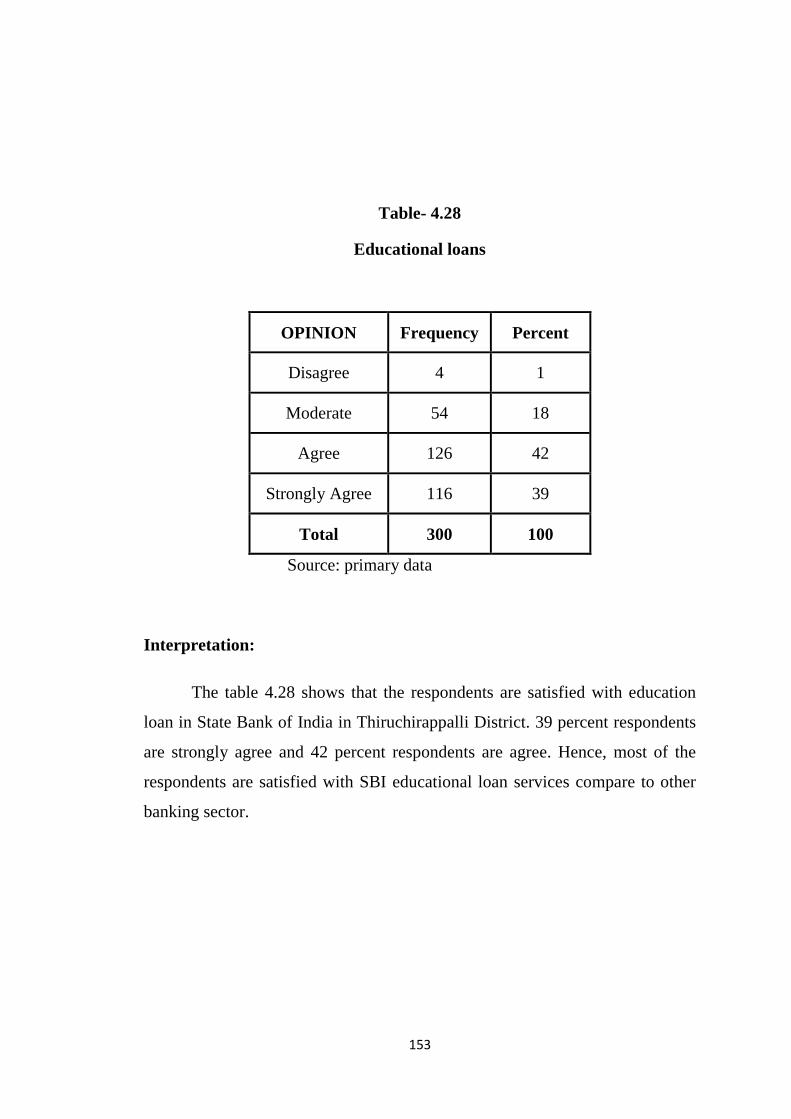

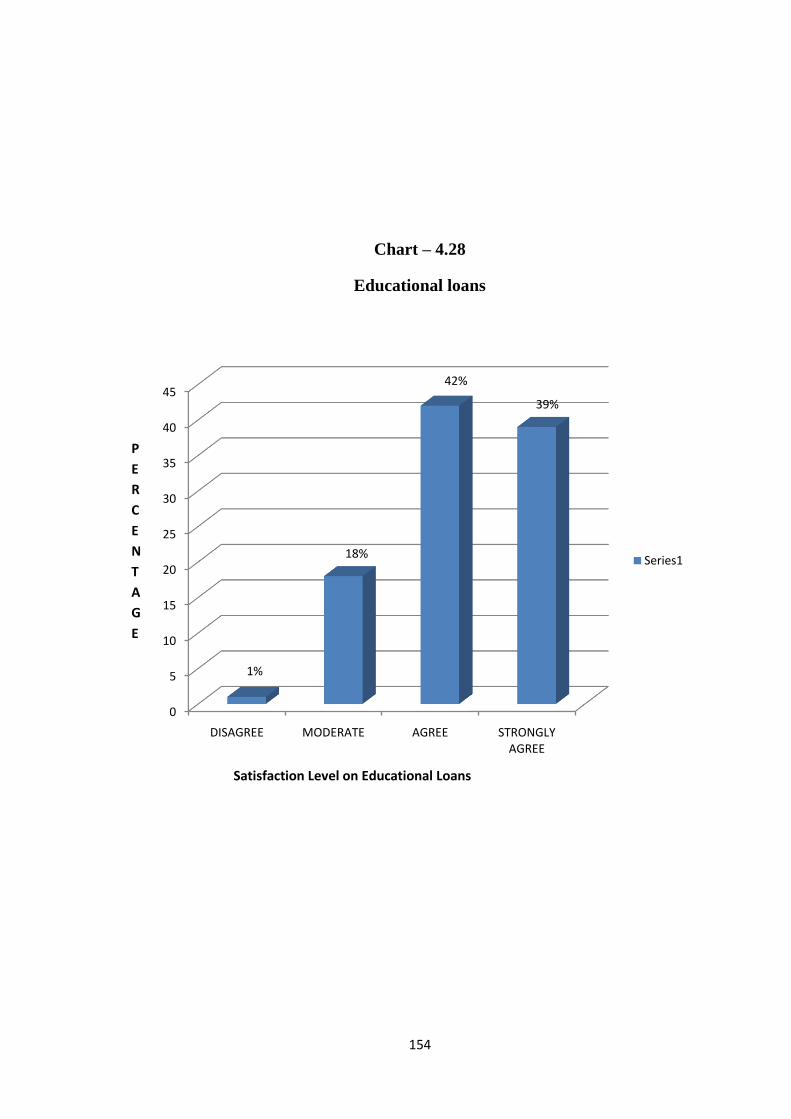

4.28 Educational loans 153

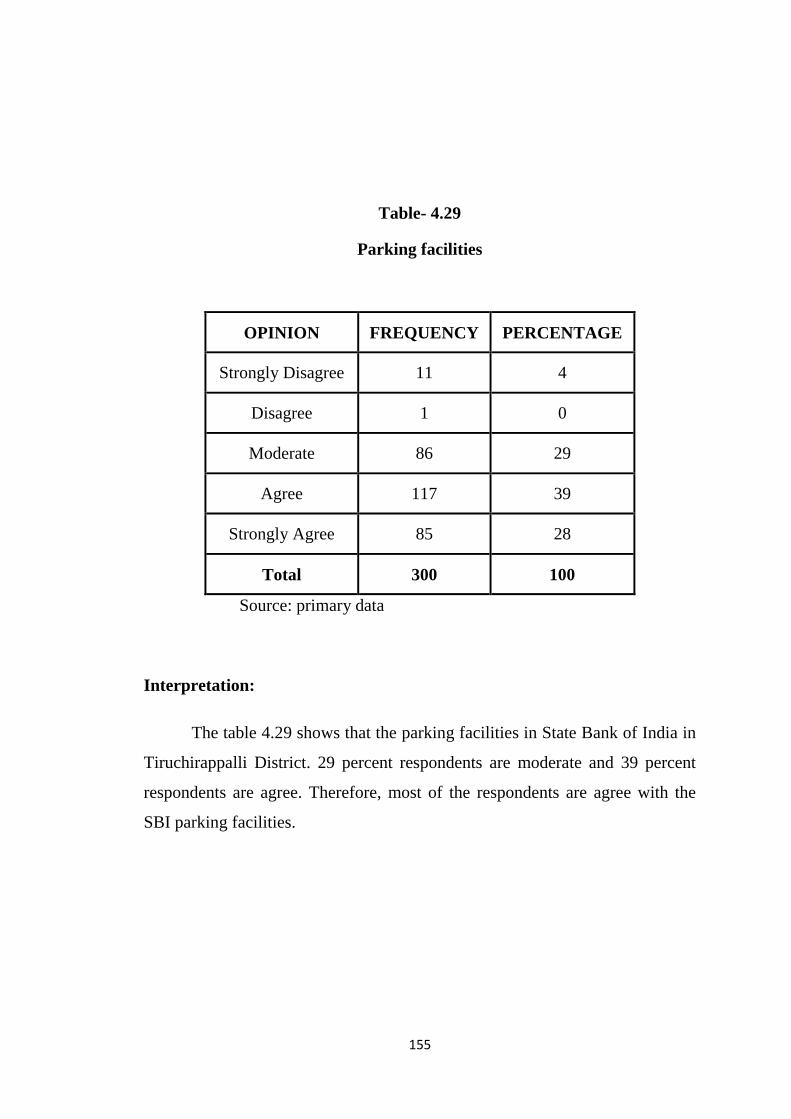

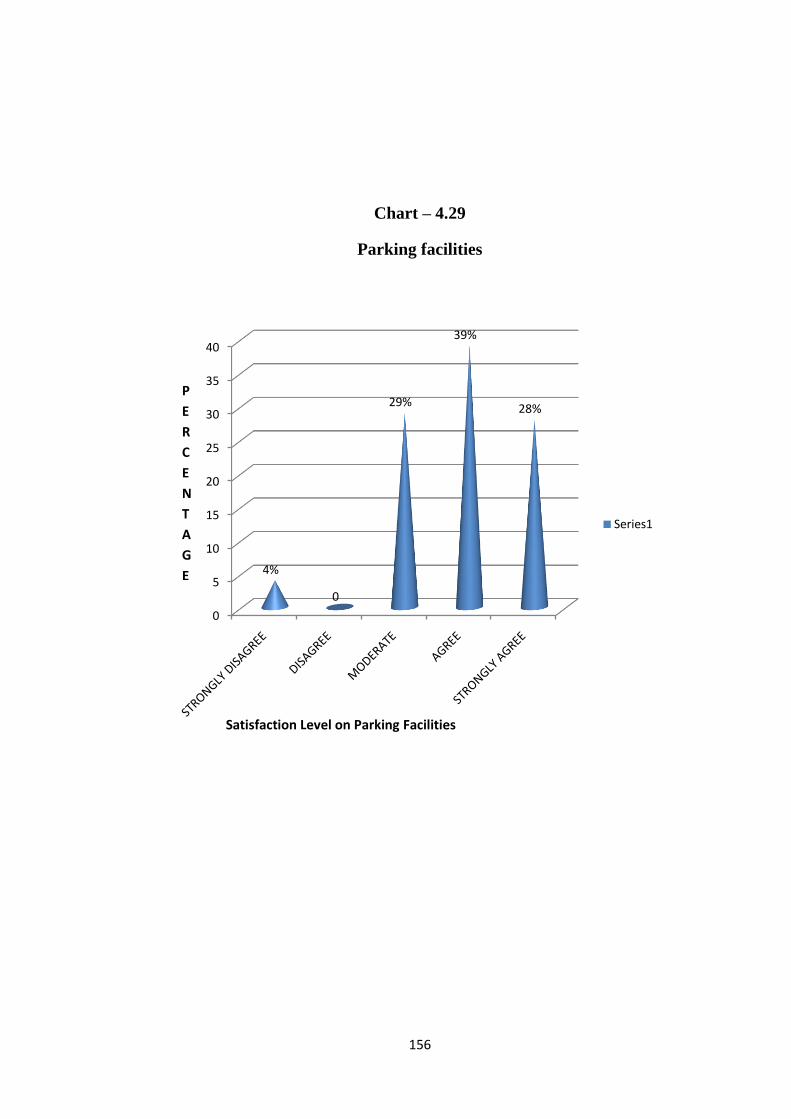

4.29 Parking facilities 155

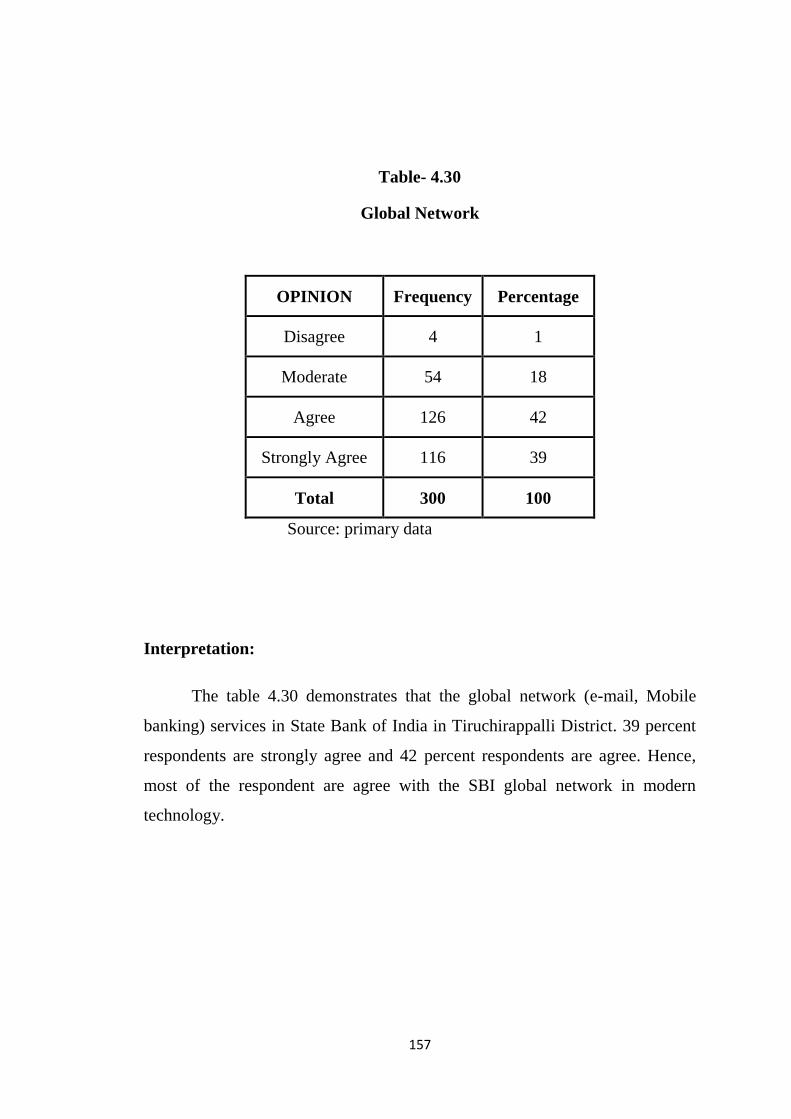

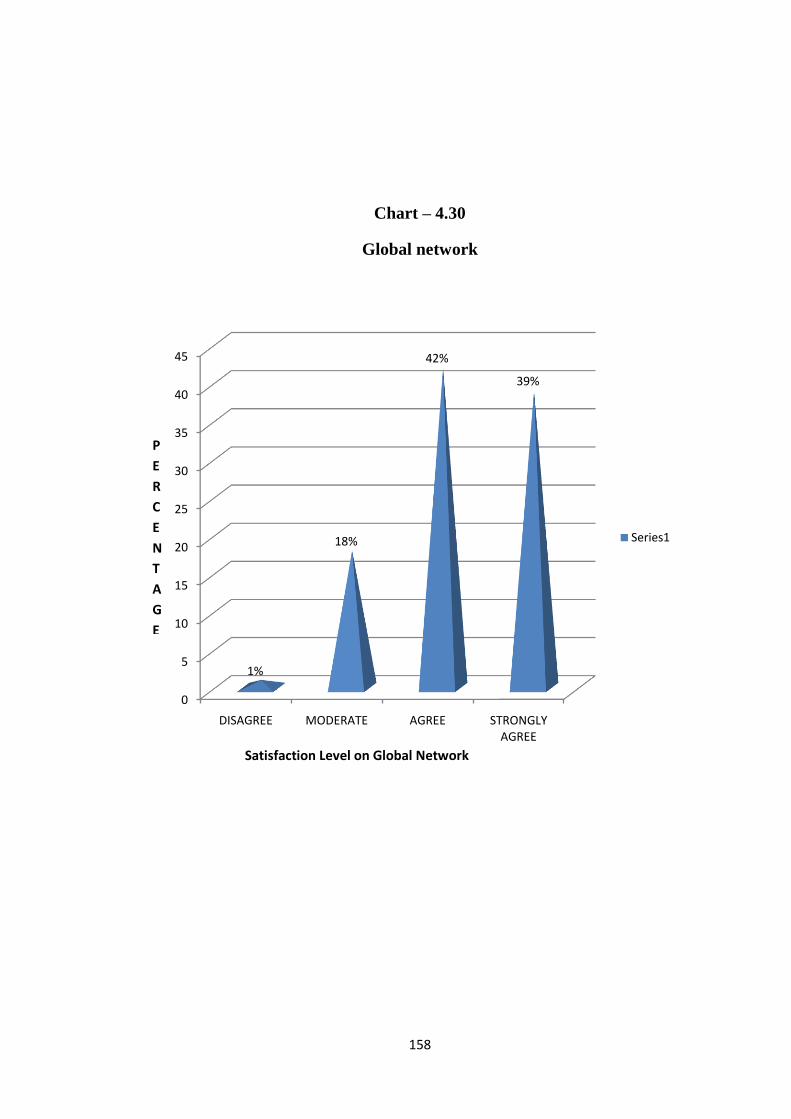

4.30 Global network 157

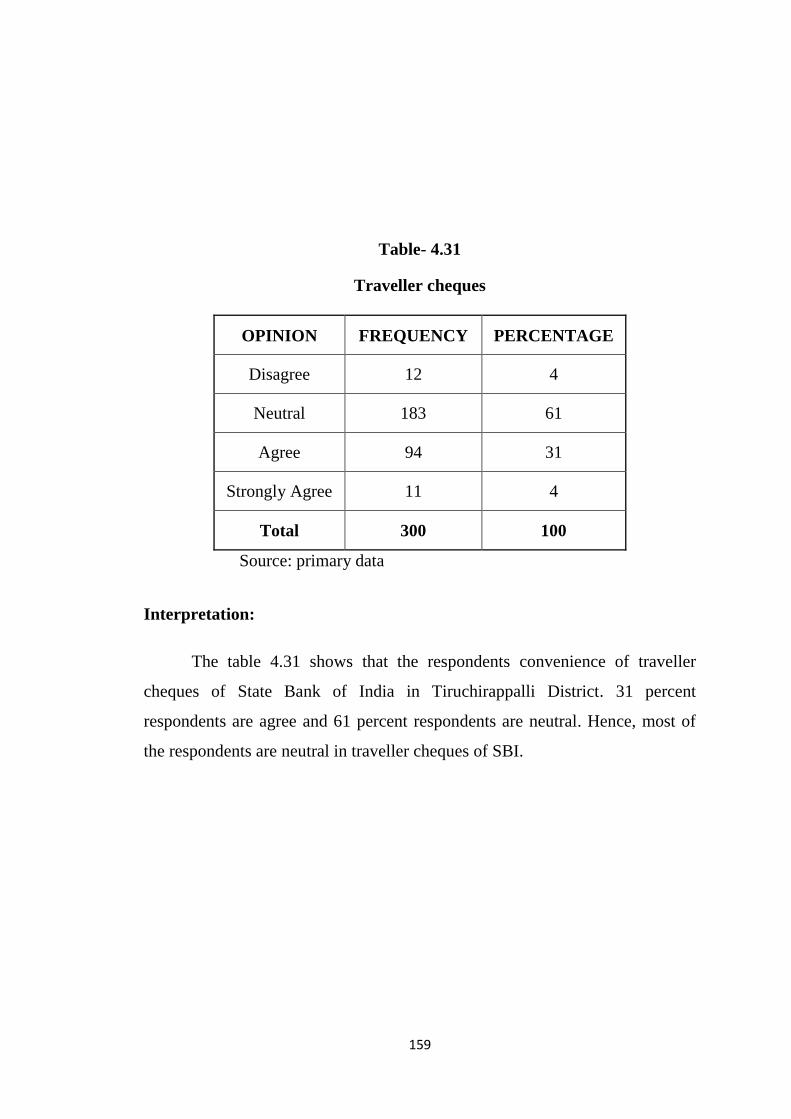

4.31 Traveller cheques 159

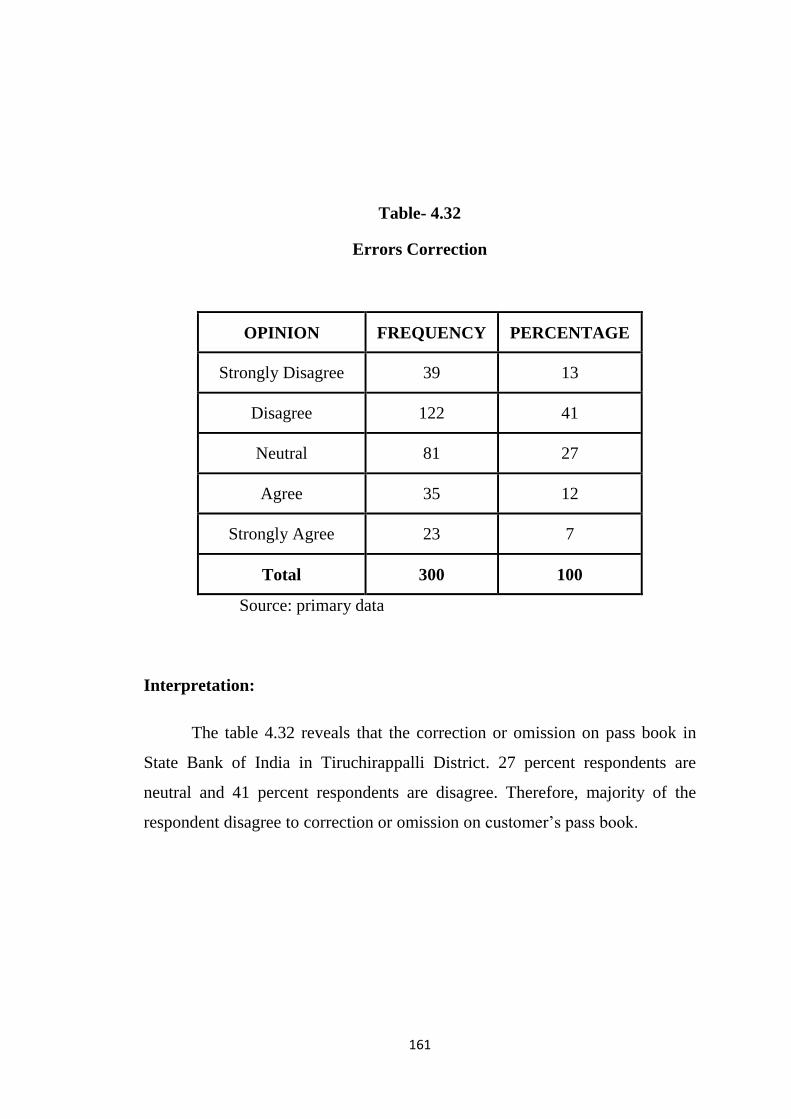

4.32 Errors correction 161

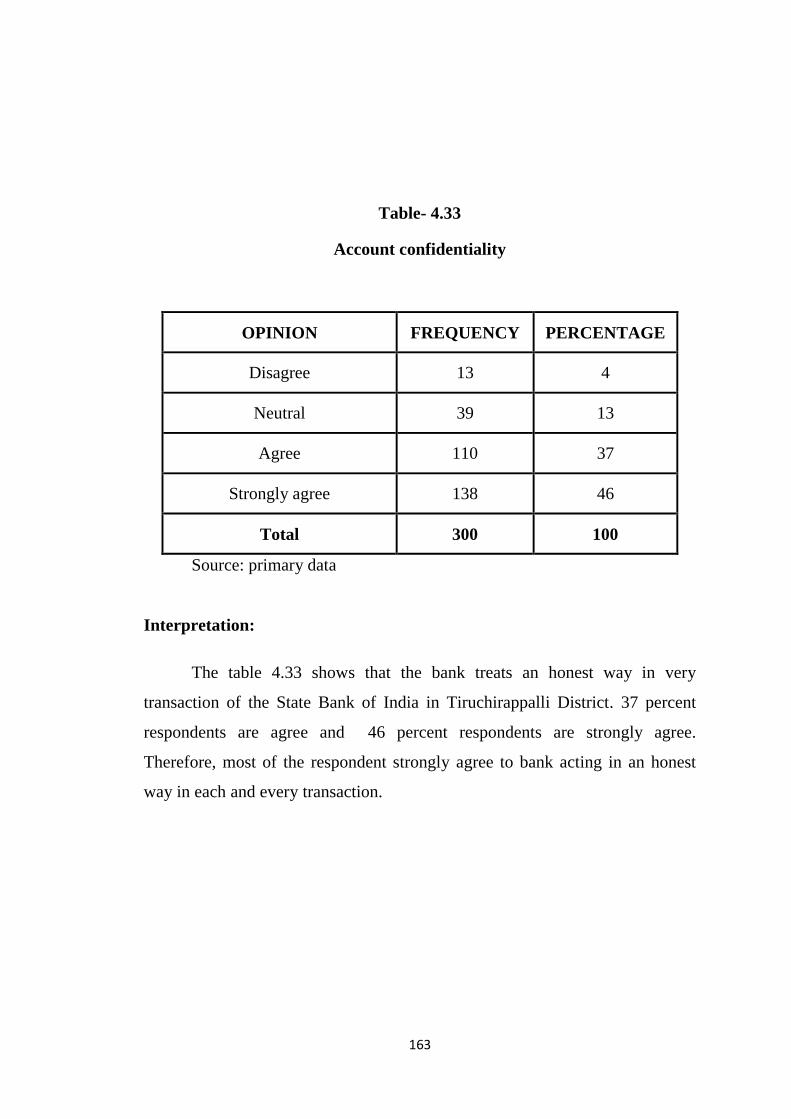

4.33 Account confidentially 163

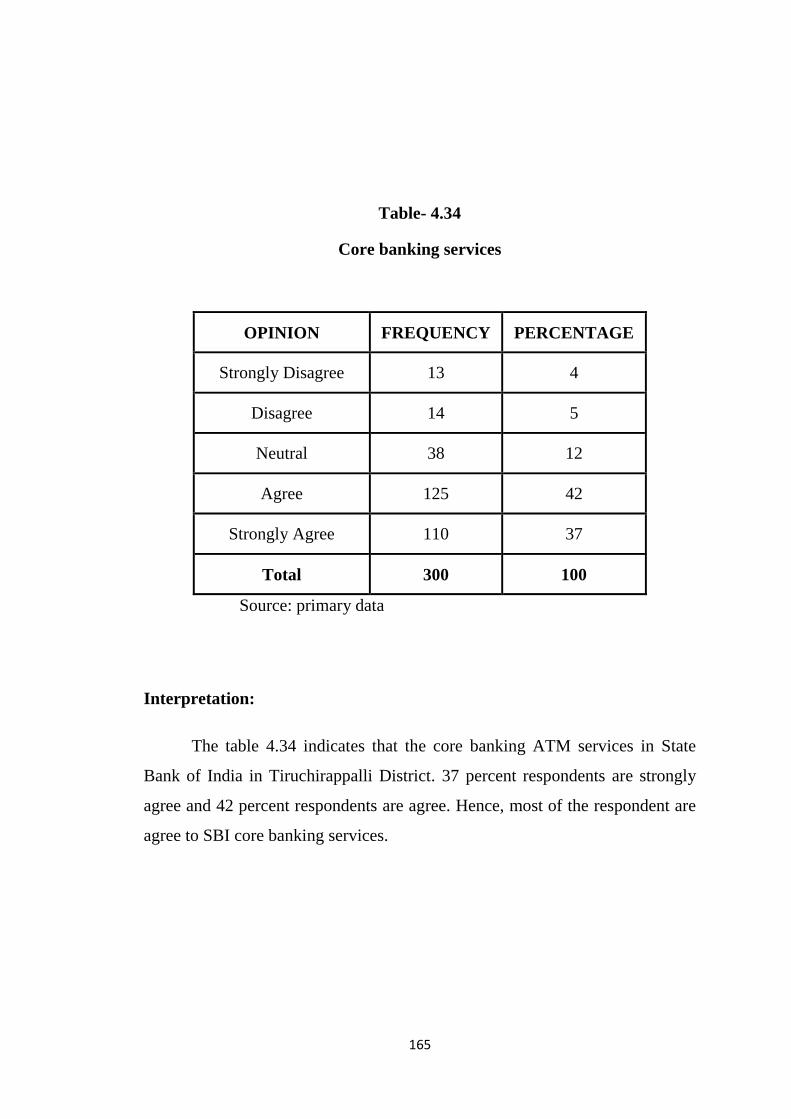

4.34 Core banking services 165

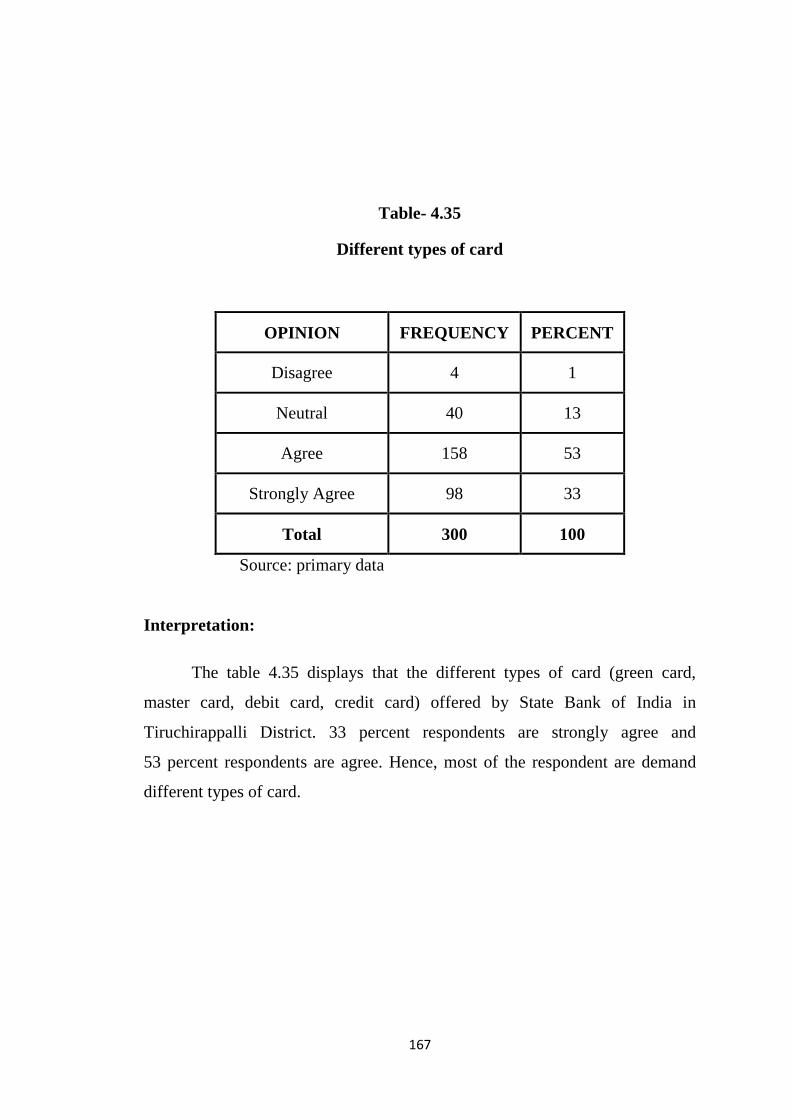

4.35 Different types of card 167

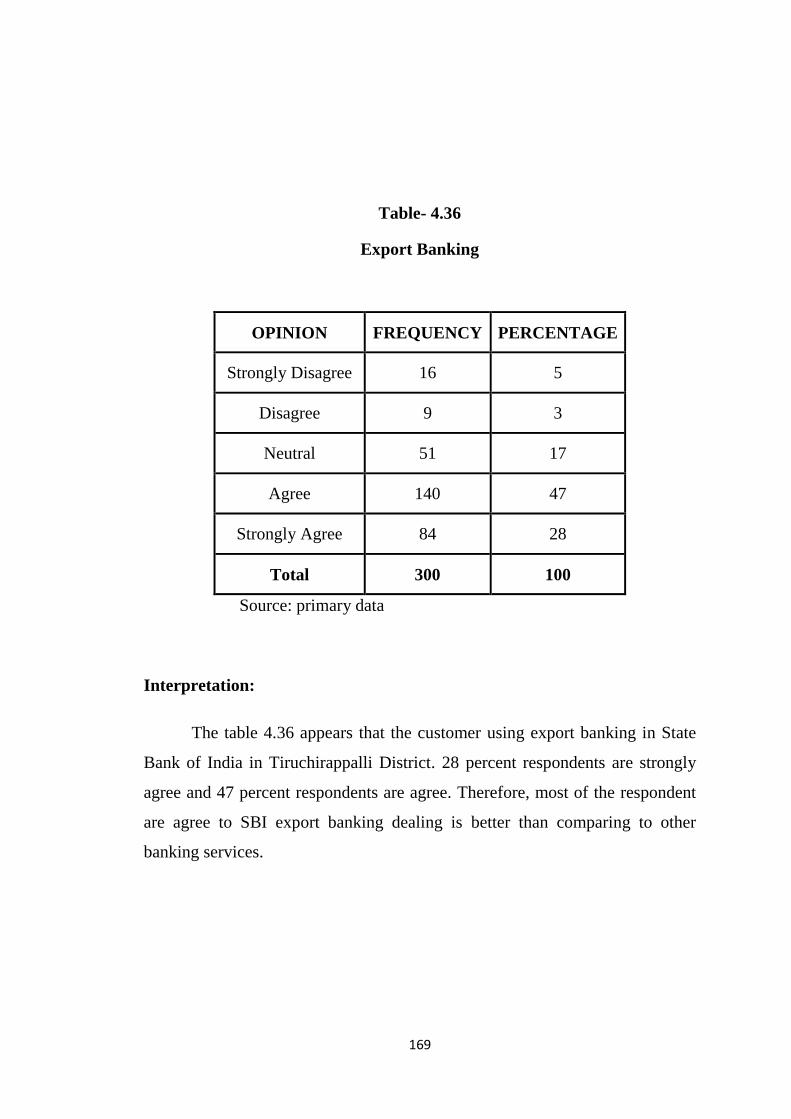

4.36 Export banking 169

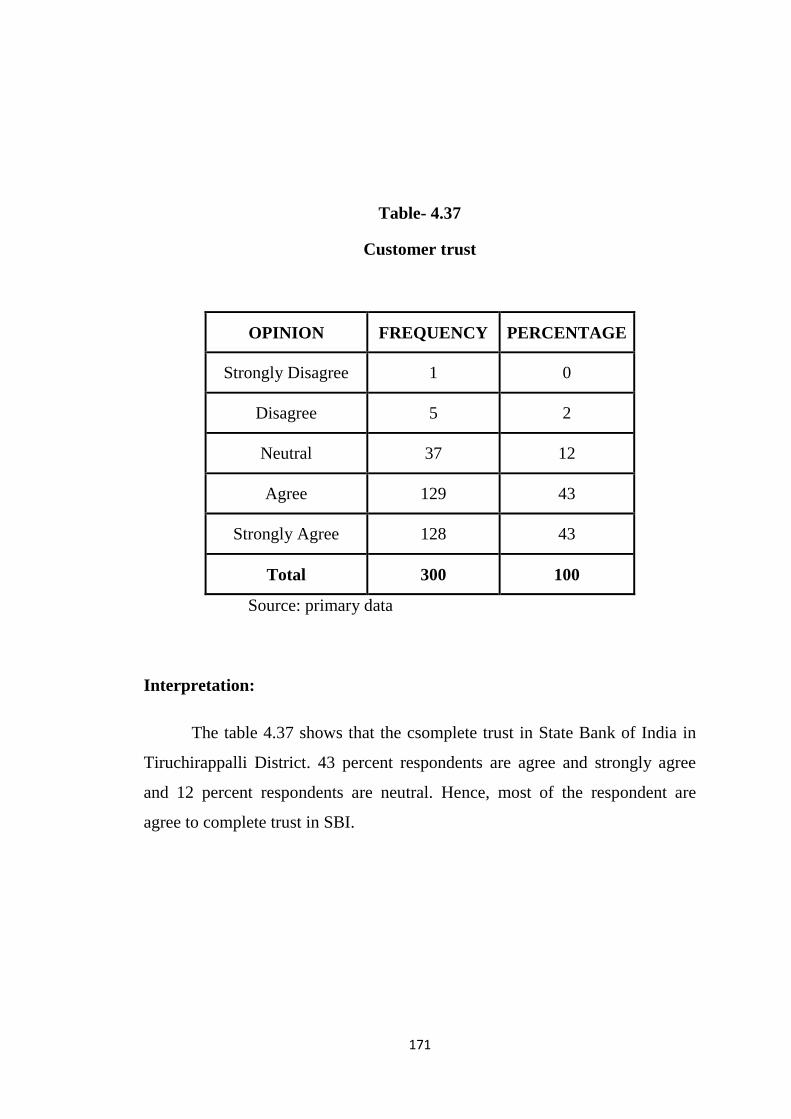

4.37 Customer trust 171

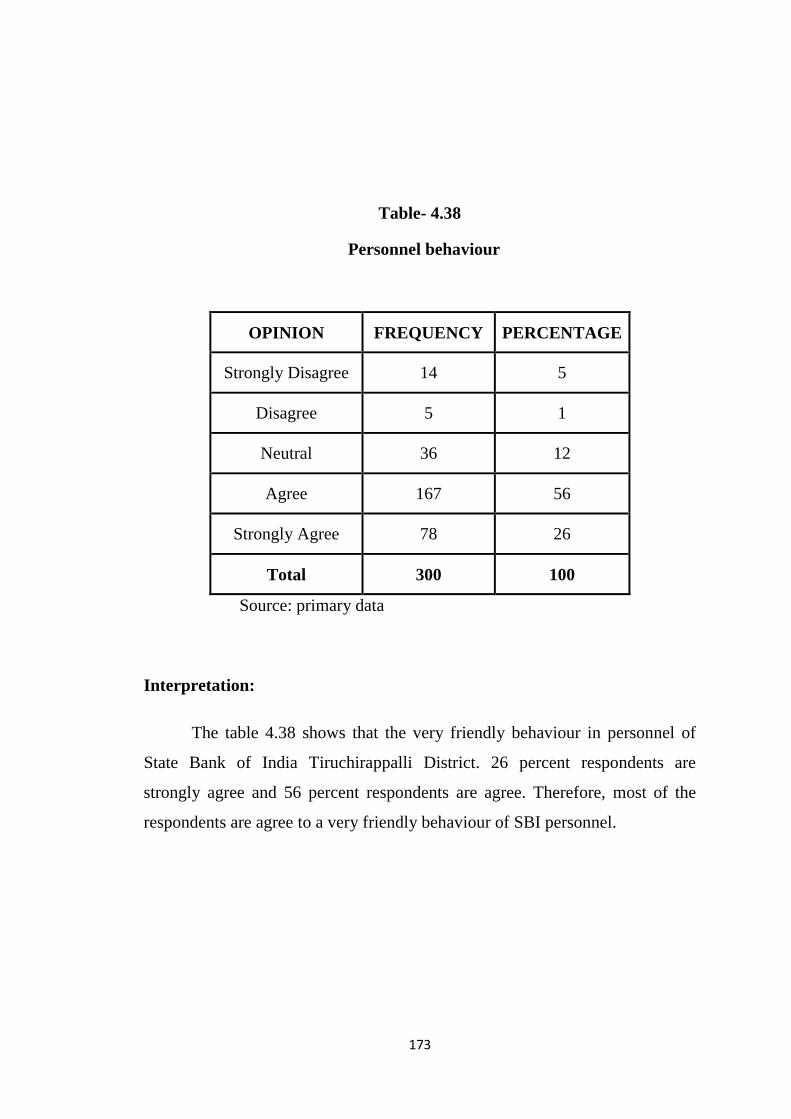

4.38 Personnel behaviour 173

4.39 Financial and advisory services 175

4.40 Timely response 177

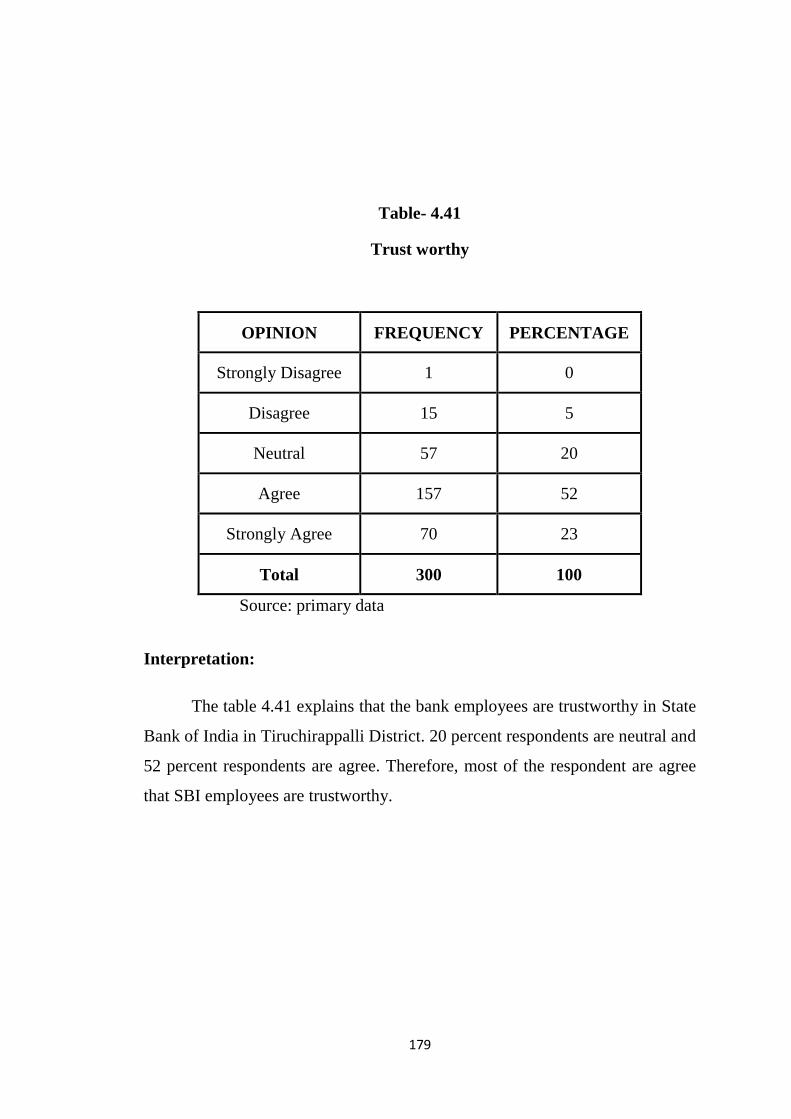

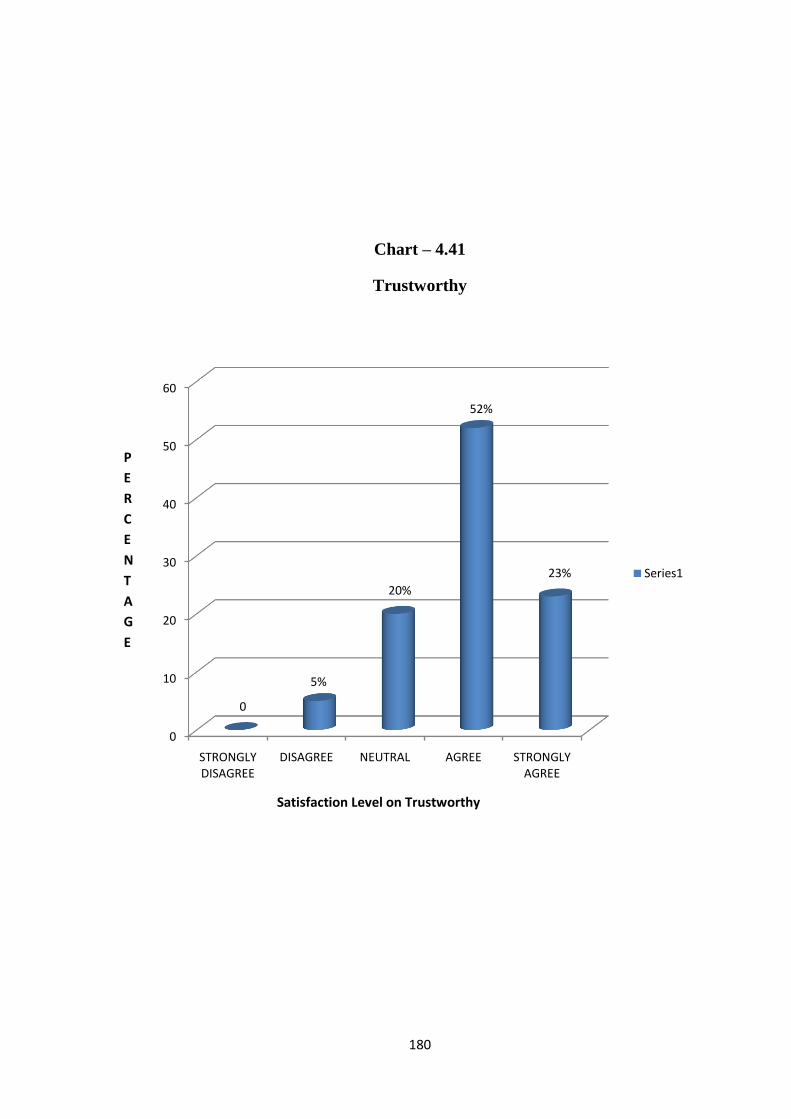

4.41 Trust worthy 179

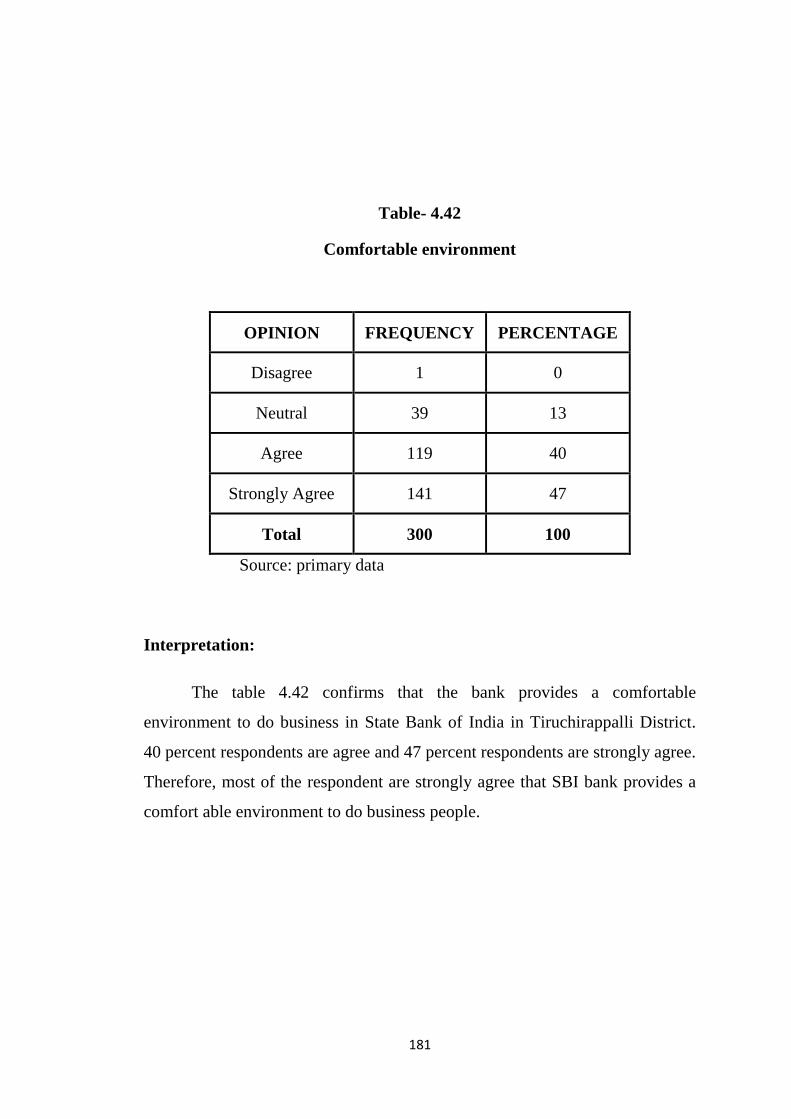

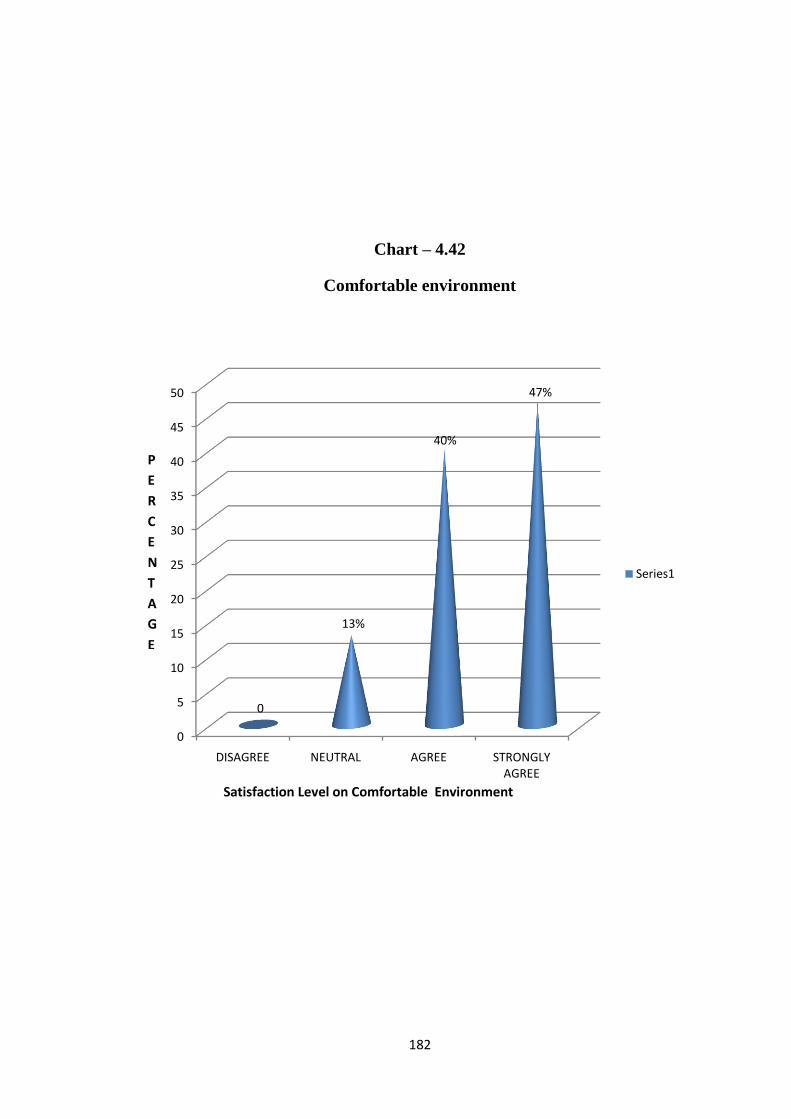

4.42 Comfortable environment 181

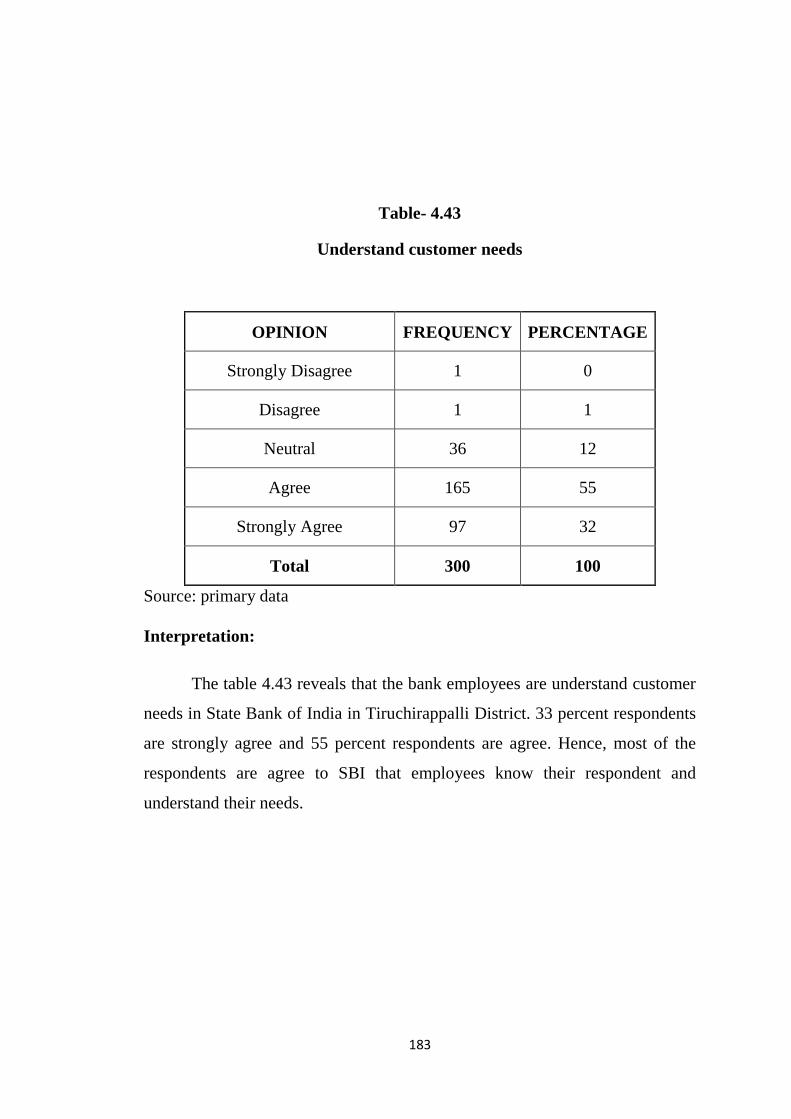

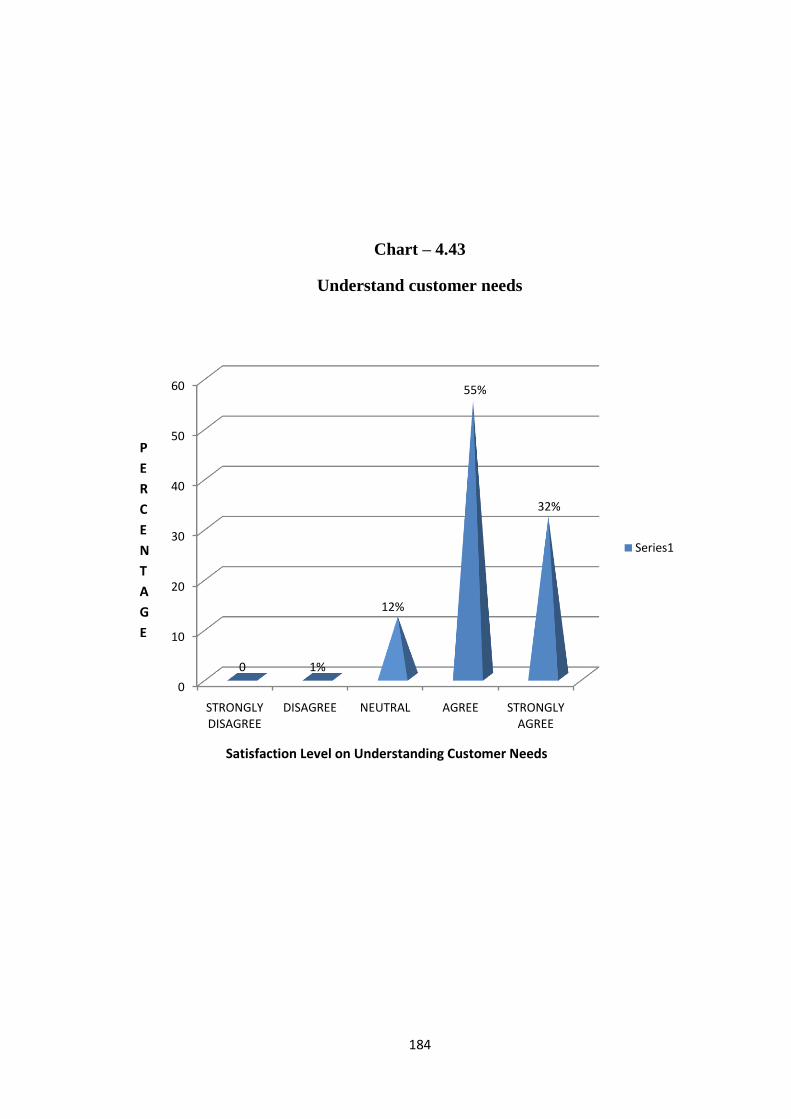

4.43 Understand customer needs 183

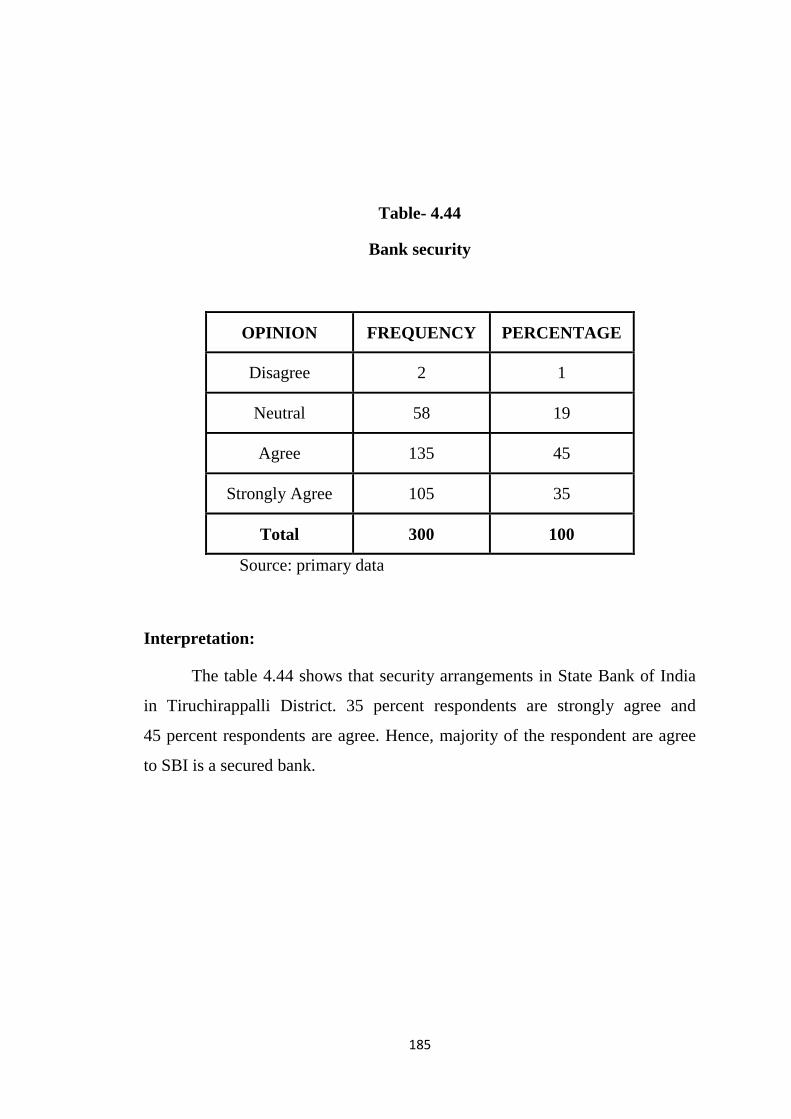

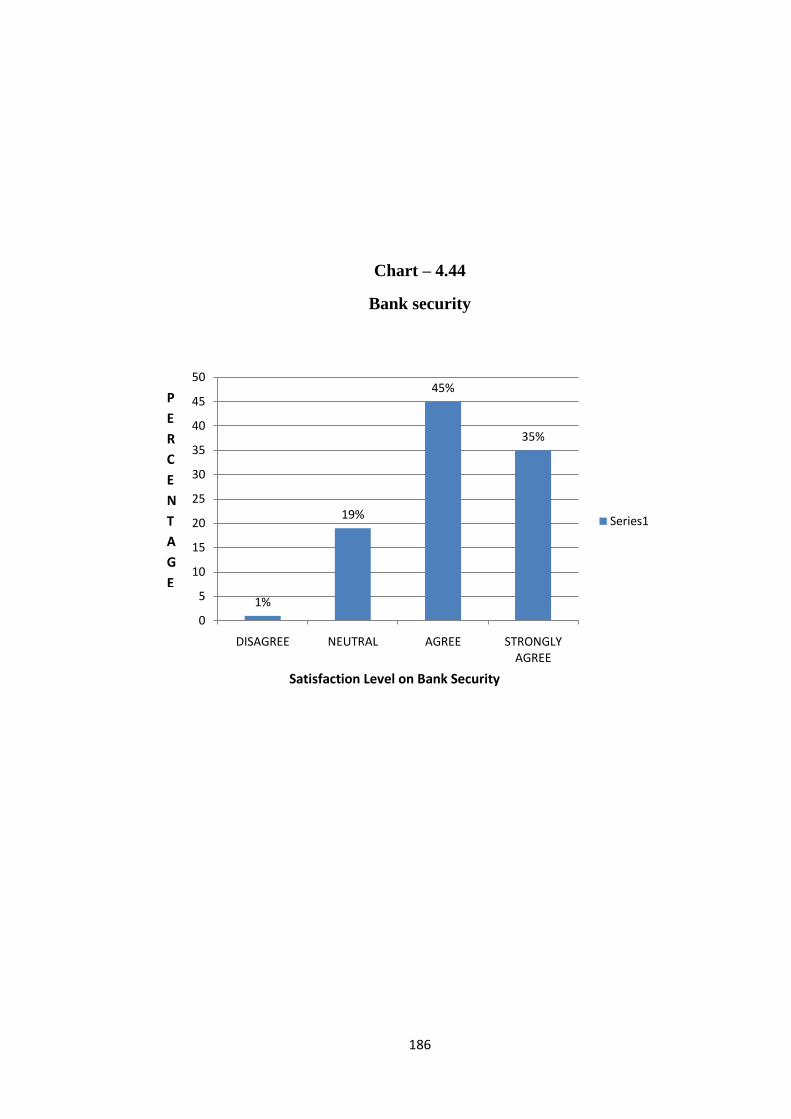

4.44 Banks security 185

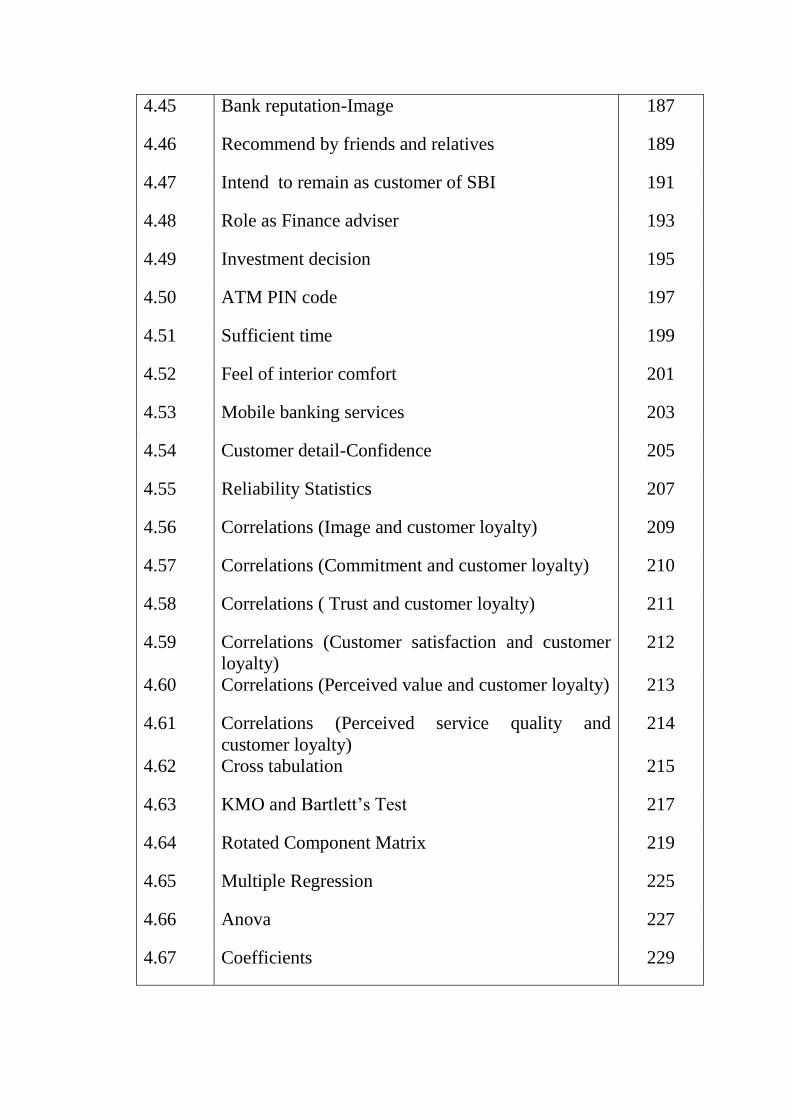

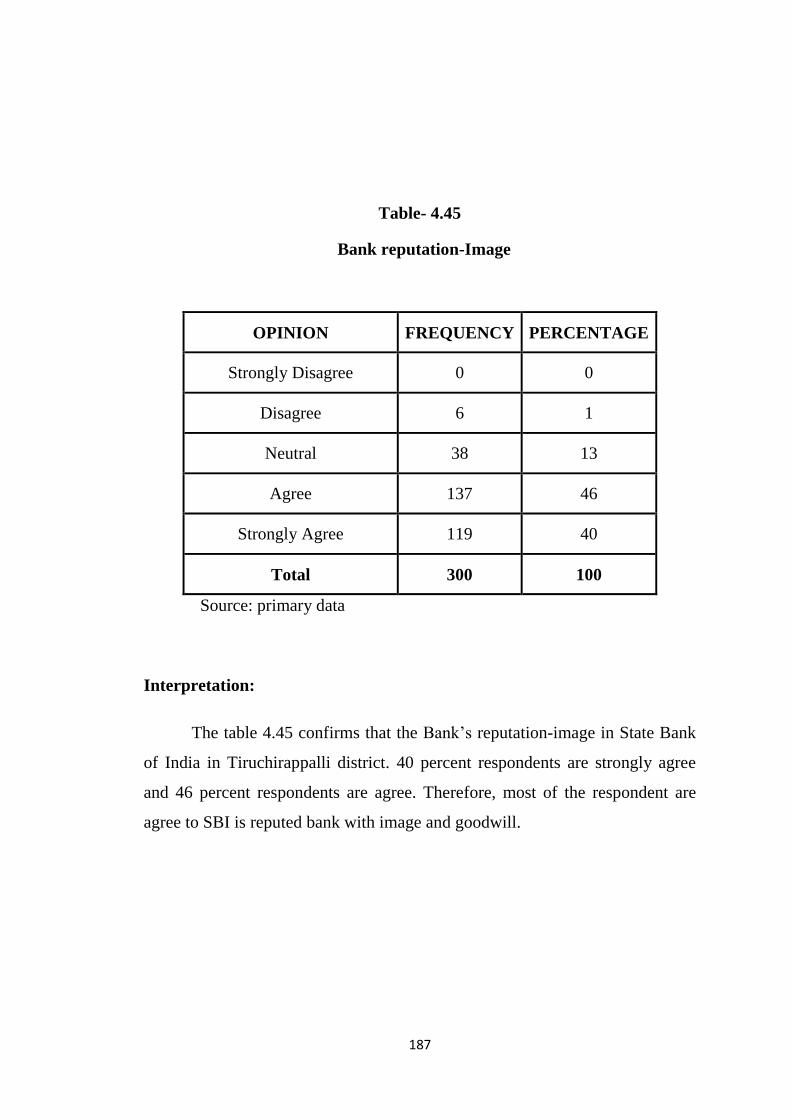

4.45 Bank reputation-Image 187

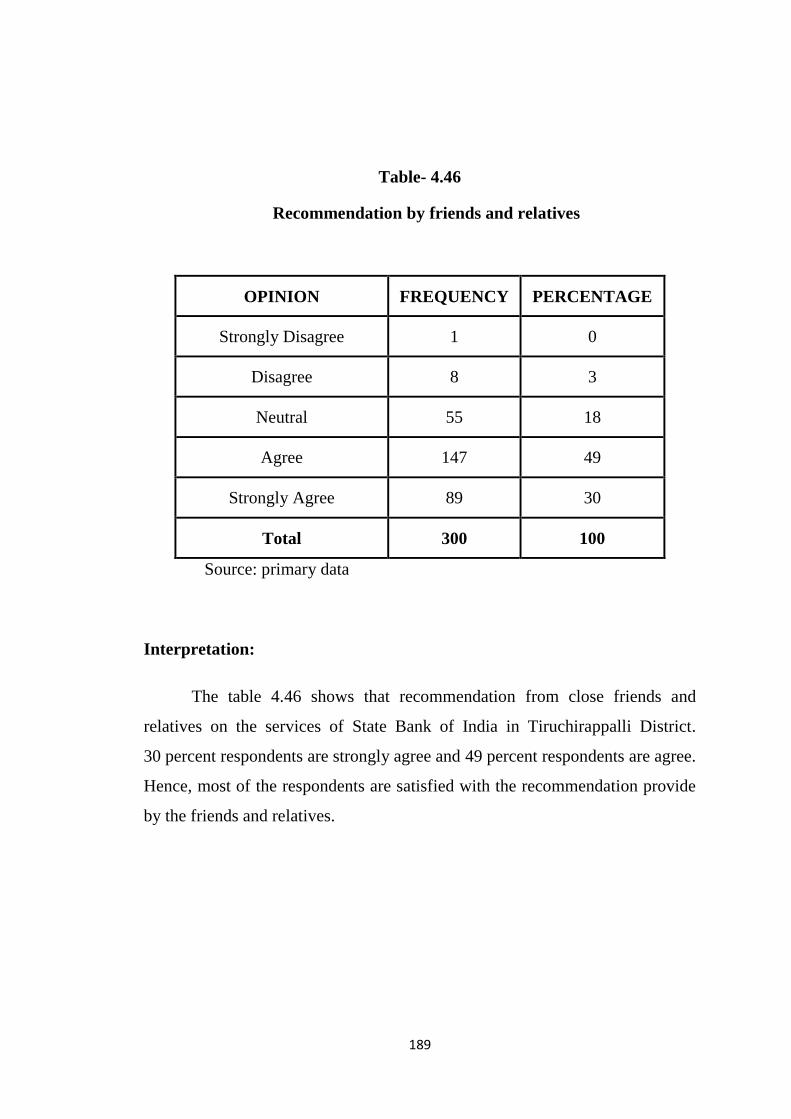

4.46 Recommend by friends and relatives 189

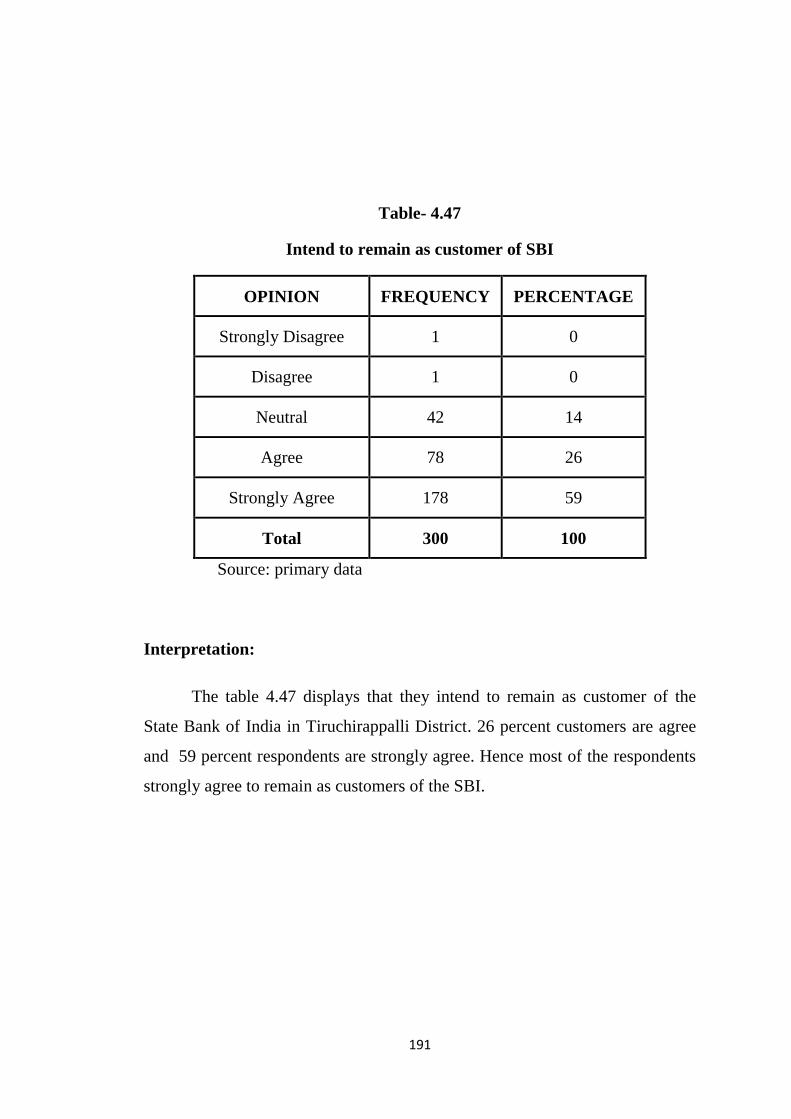

4.47 Intend to remain as customer of SBI 191

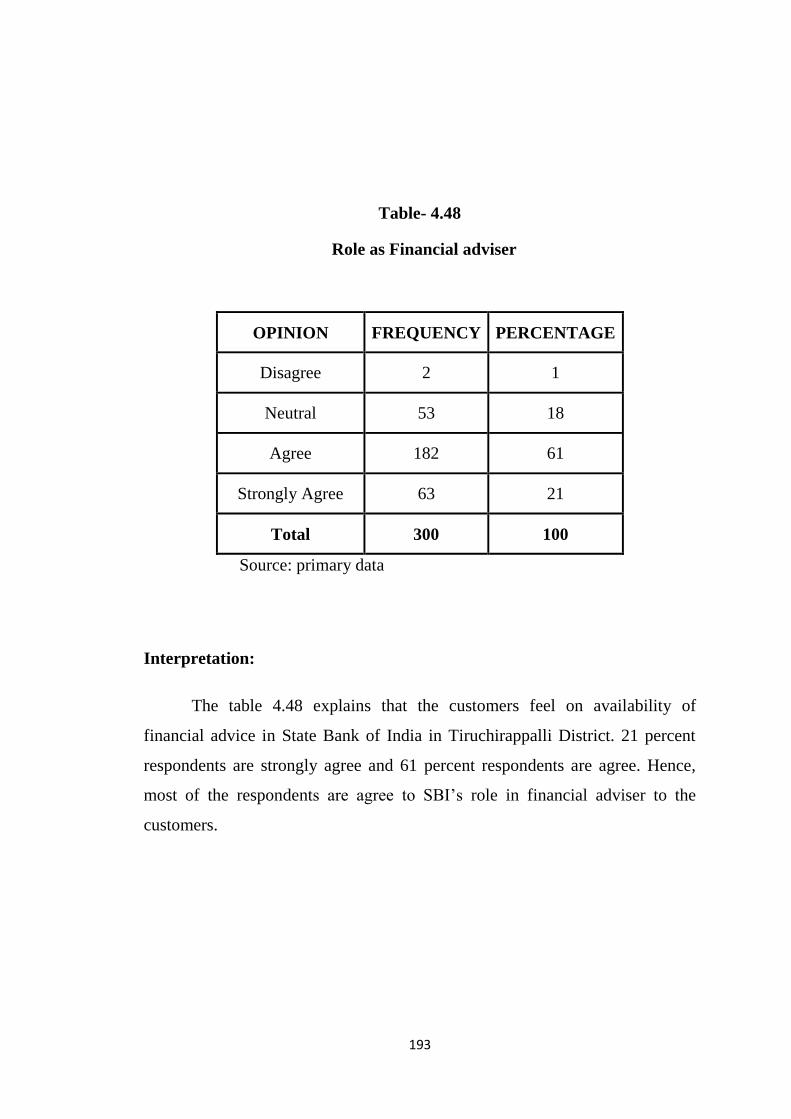

4.48 Role as Finance adviser 193

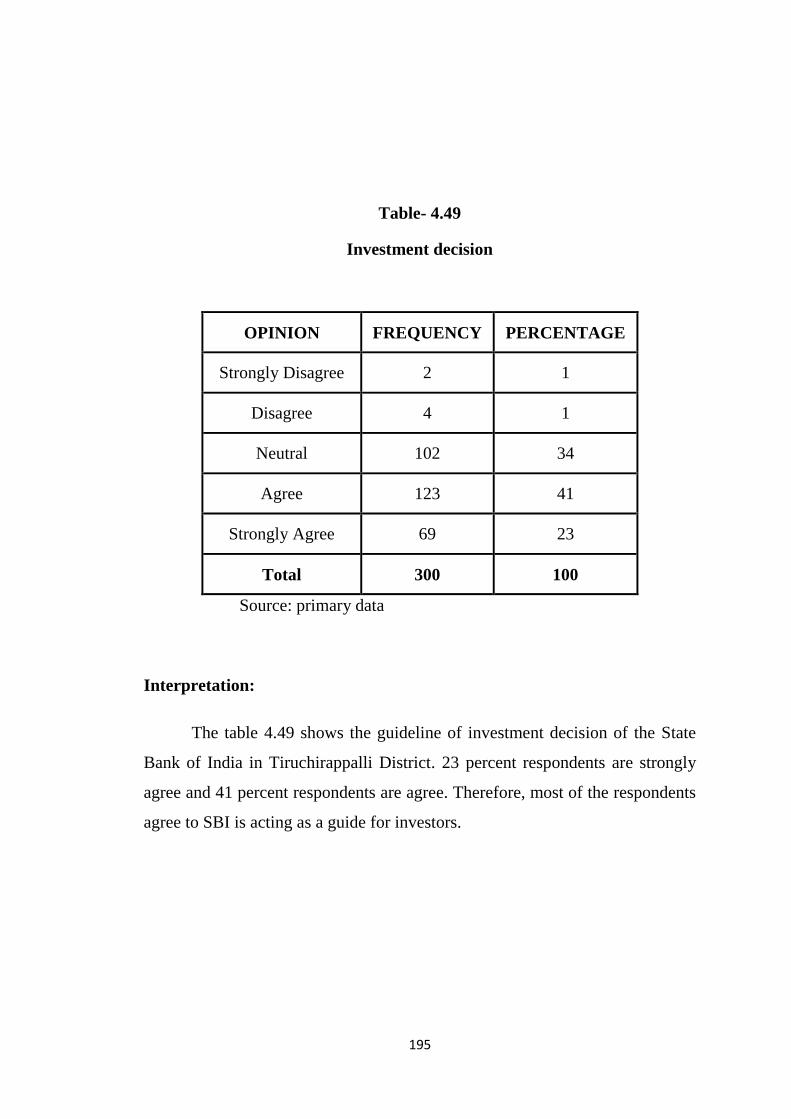

4.49 Investment decision 195

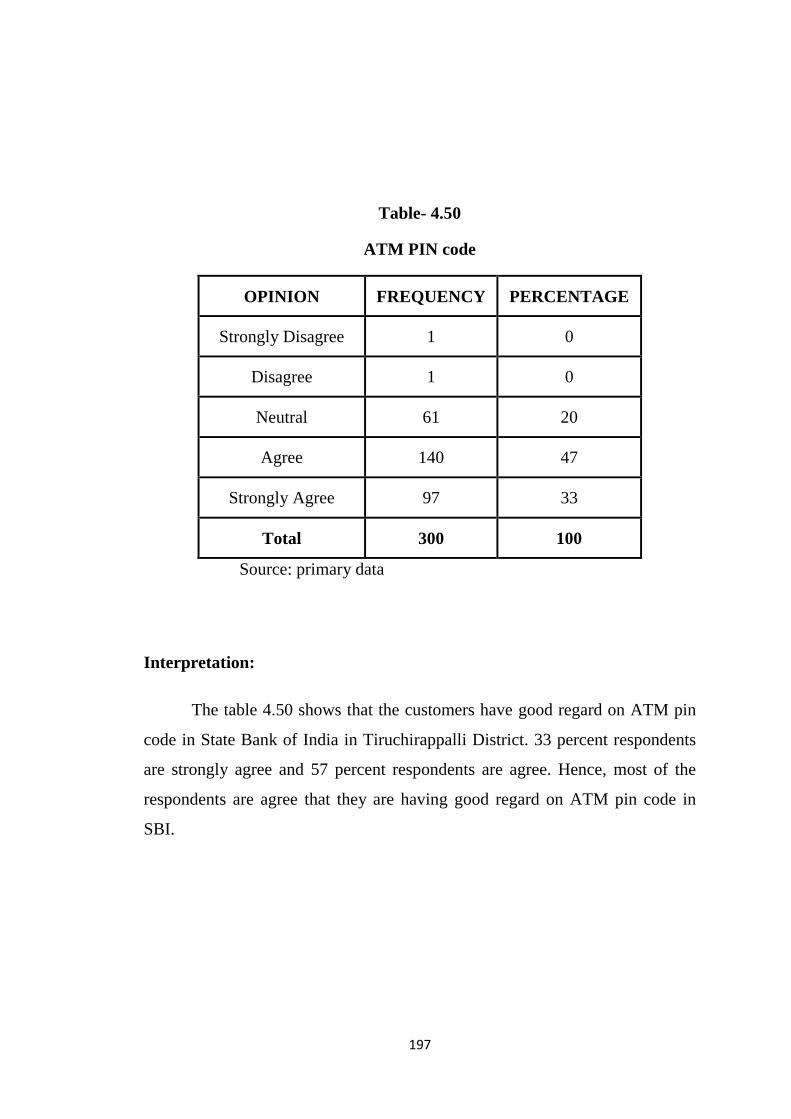

4.50 ATM PIN code 197

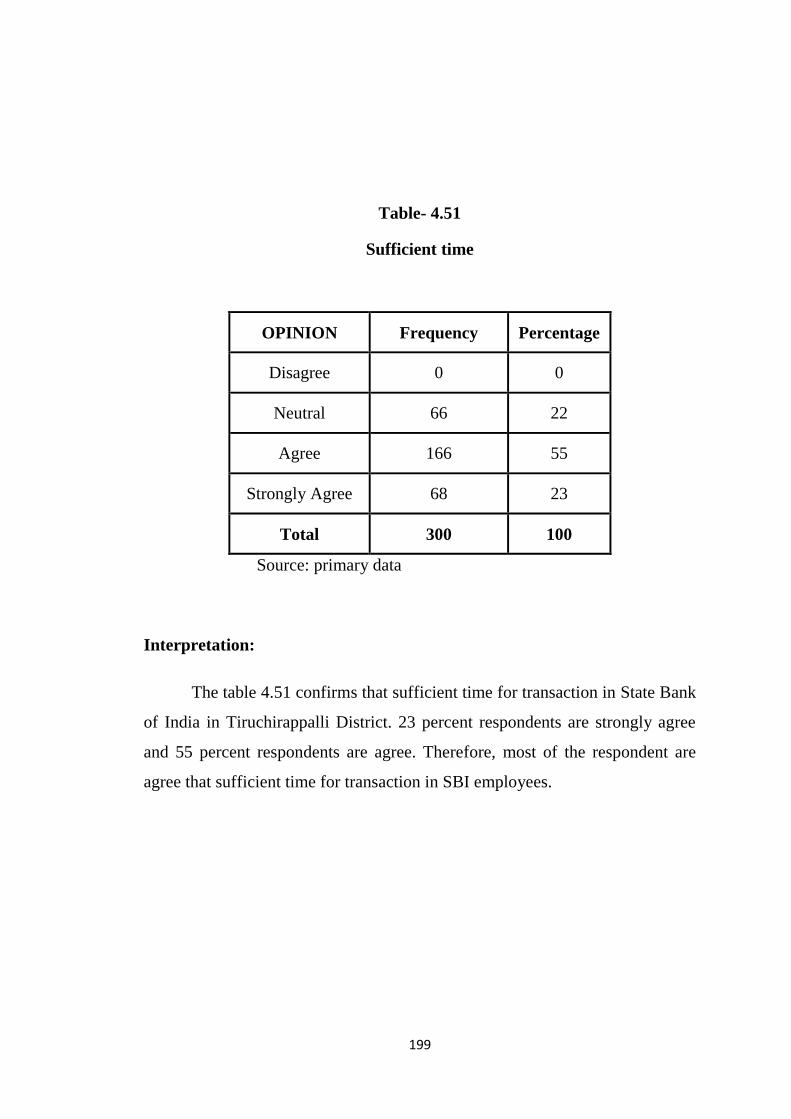

4.51 Sufficient time 199

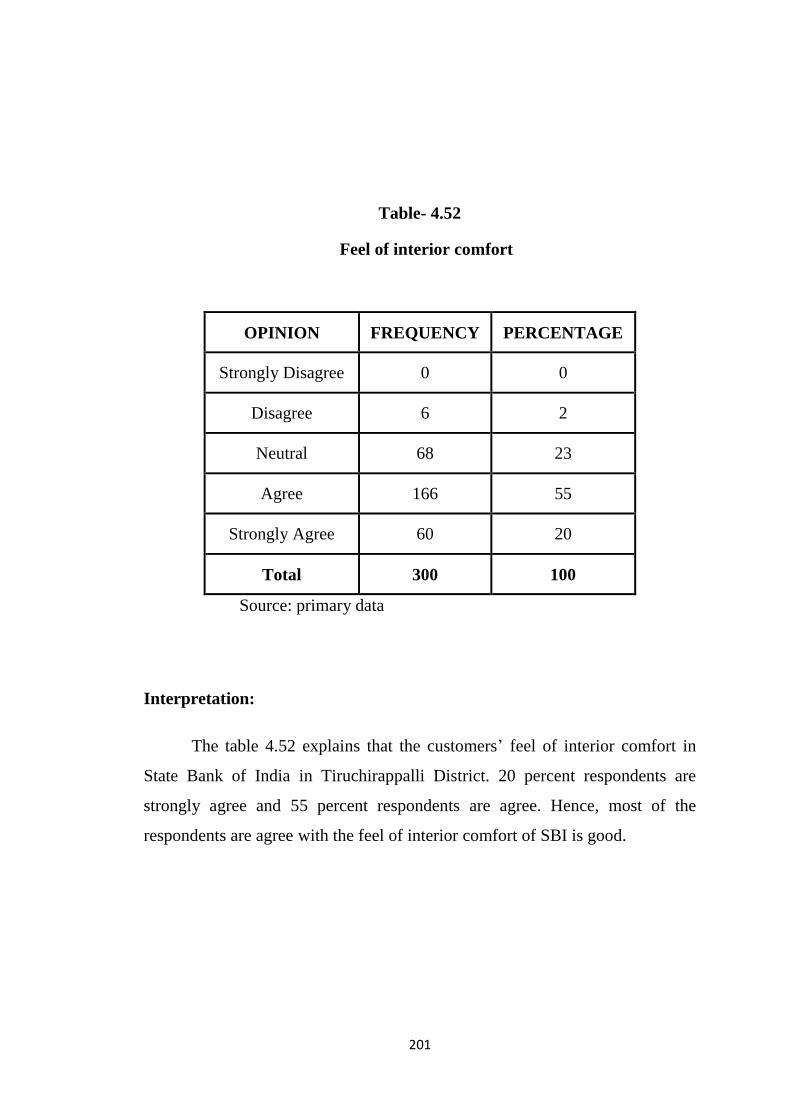

4.52 Feel of interior comfort 201

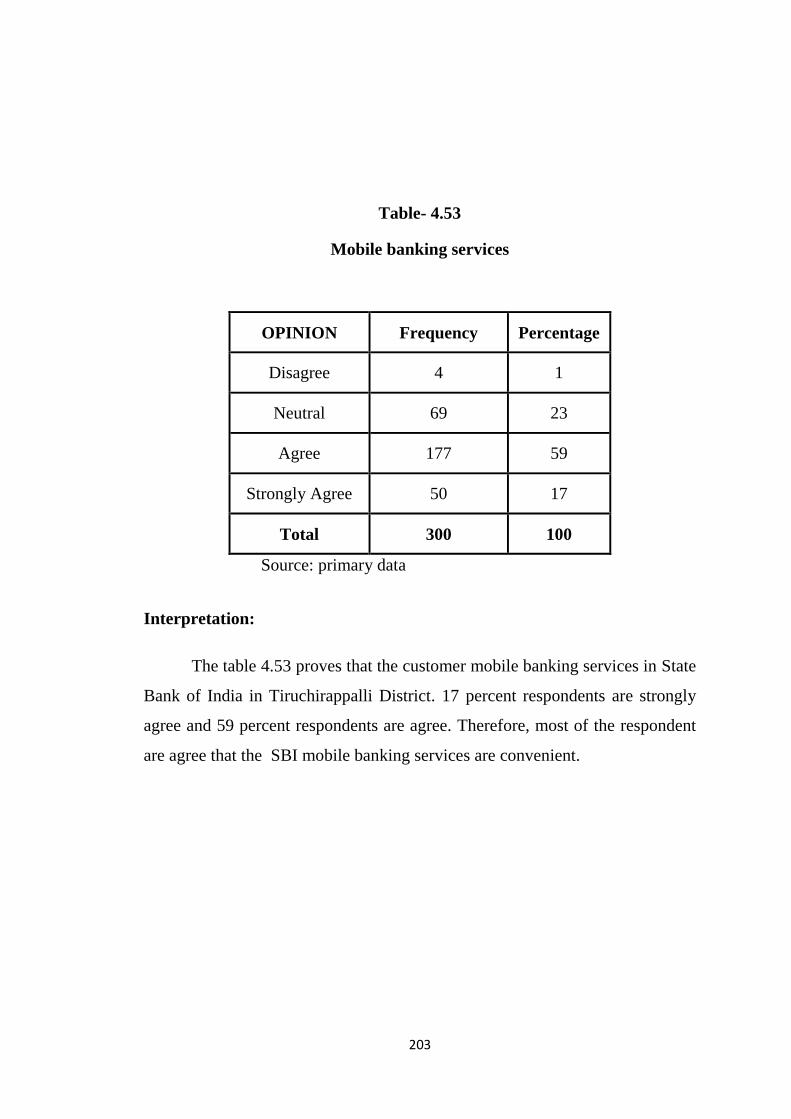

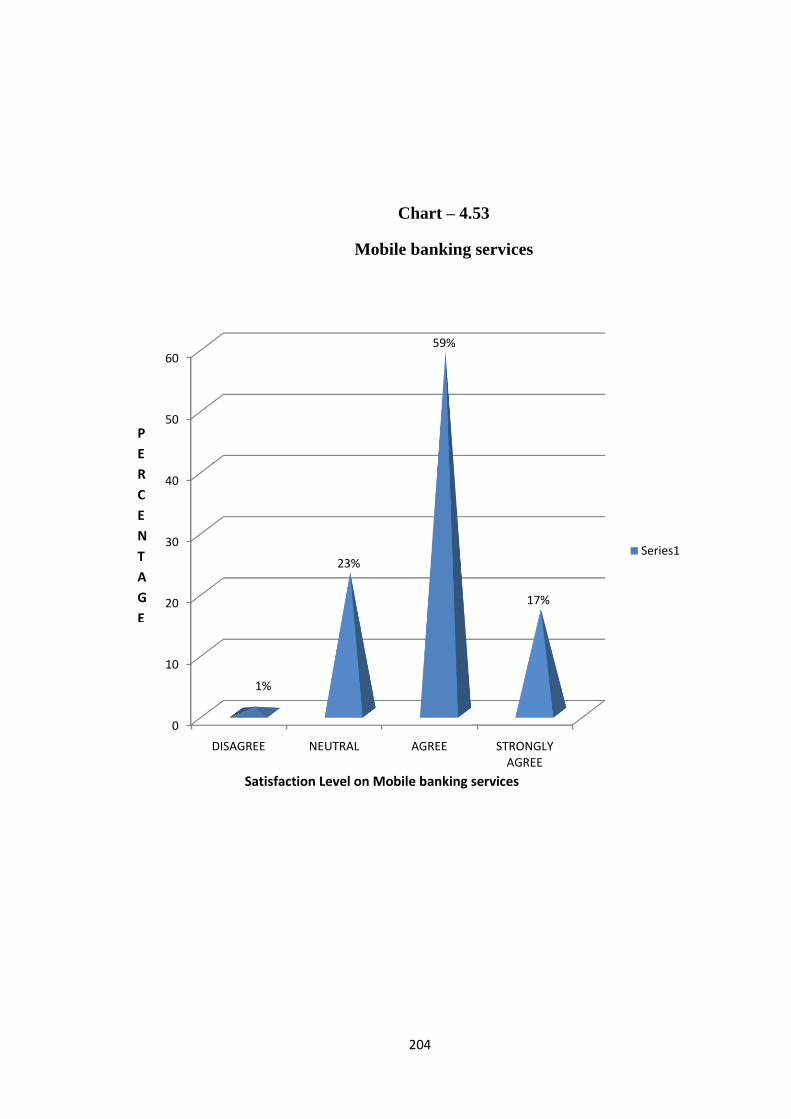

4.53 Mobile banking services 203

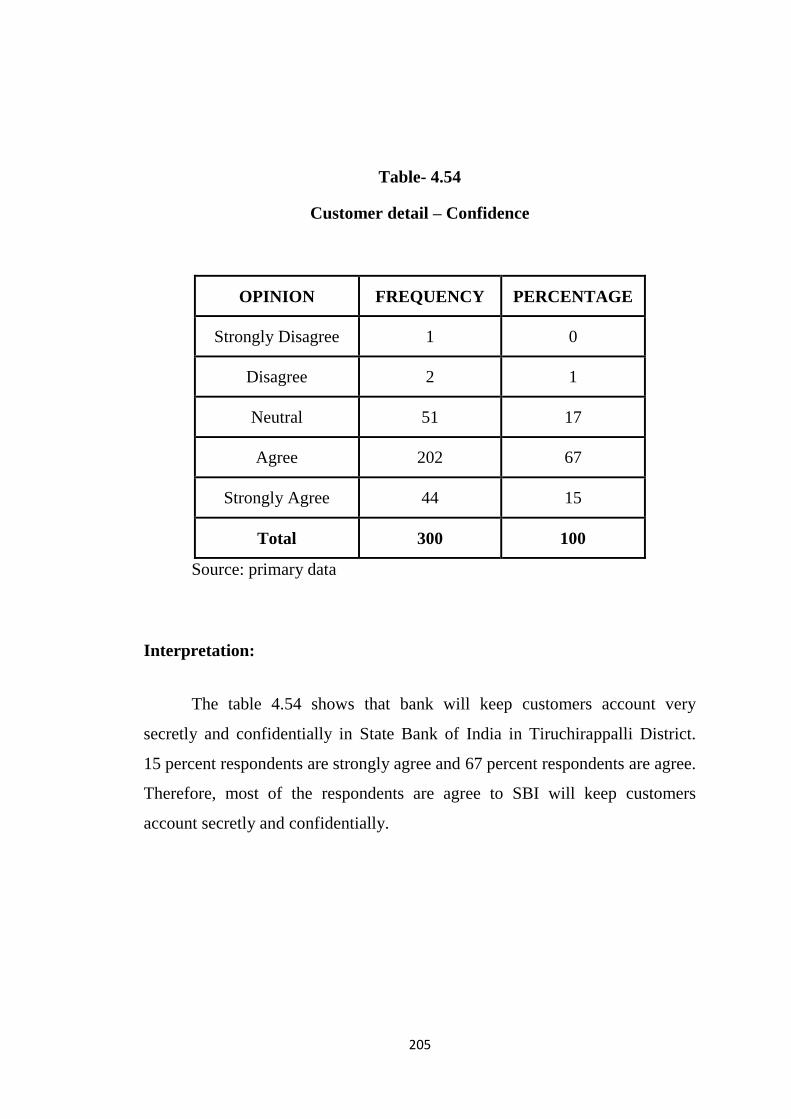

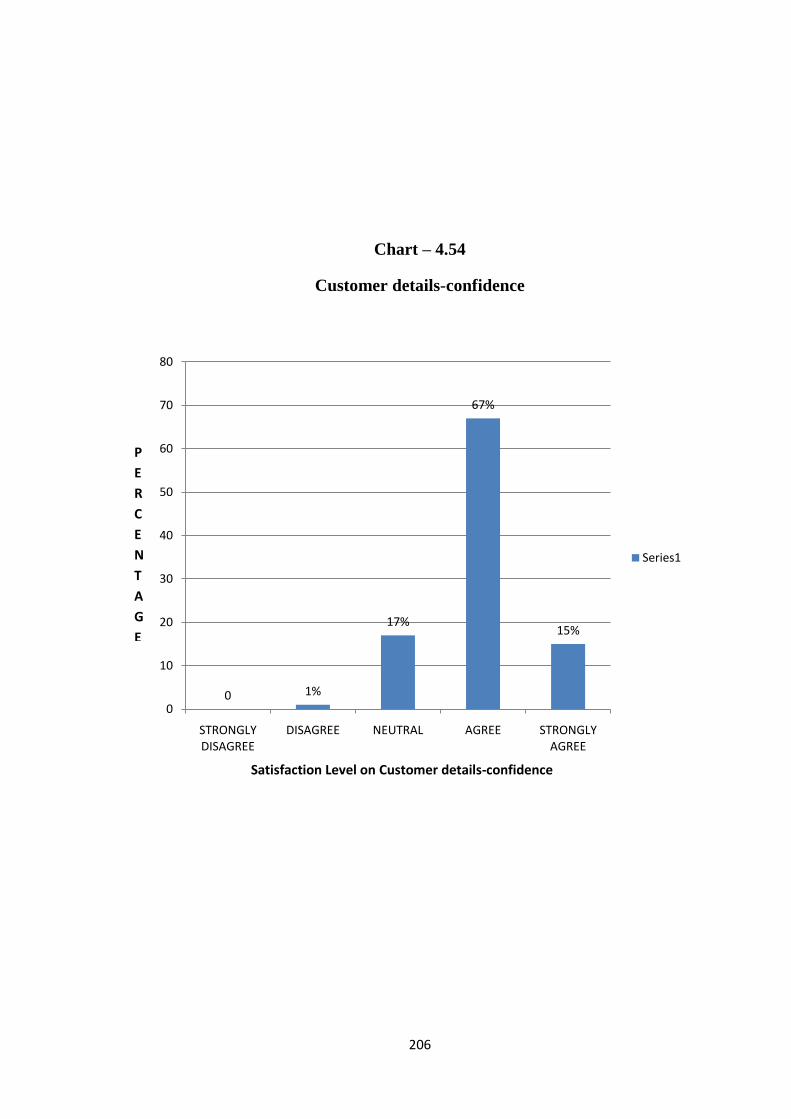

4.54 Customer detail-Confidence 205

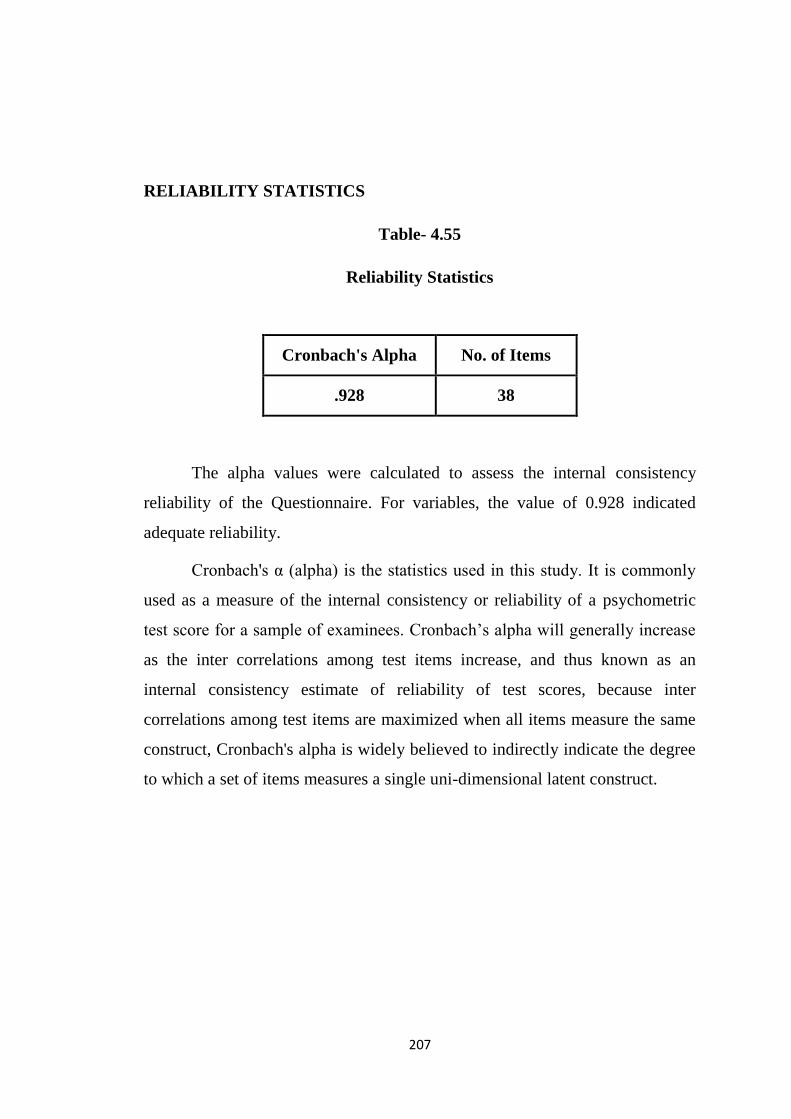

4.55 Reliability Statistics 207

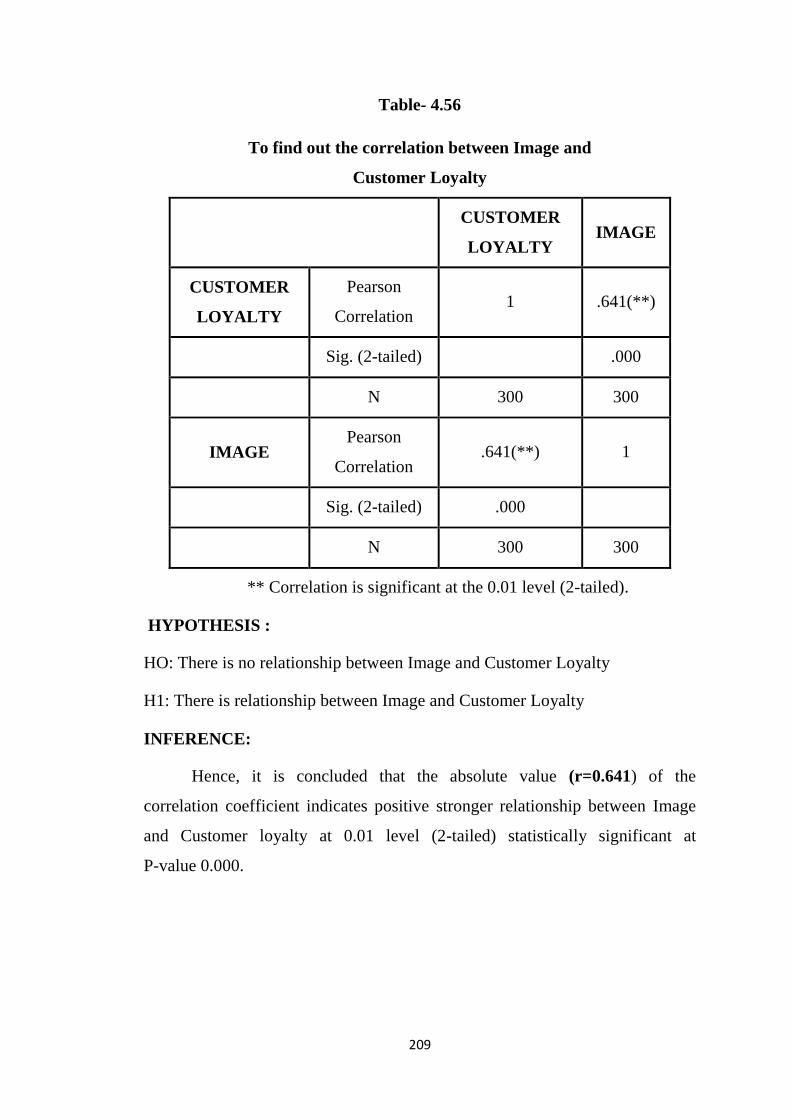

4.56 Correlations (Image and customer loyalty) 209

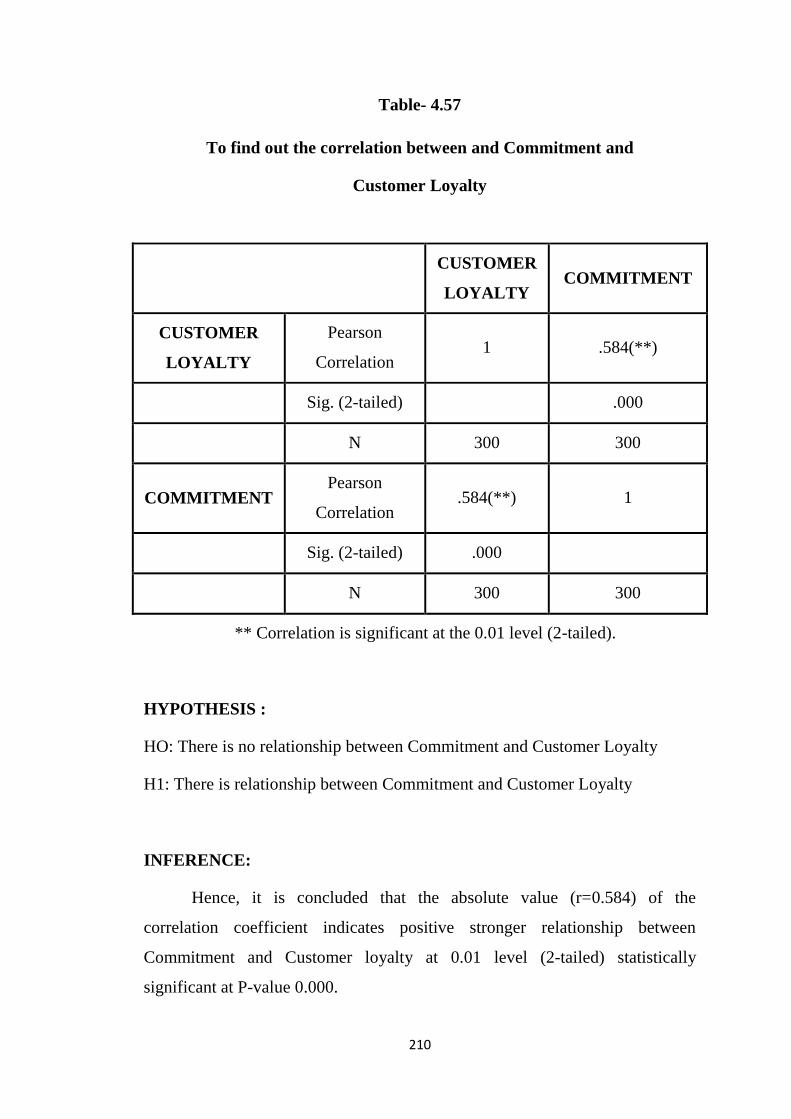

4.57 Correlations (Commitment and customer loyalty) 210

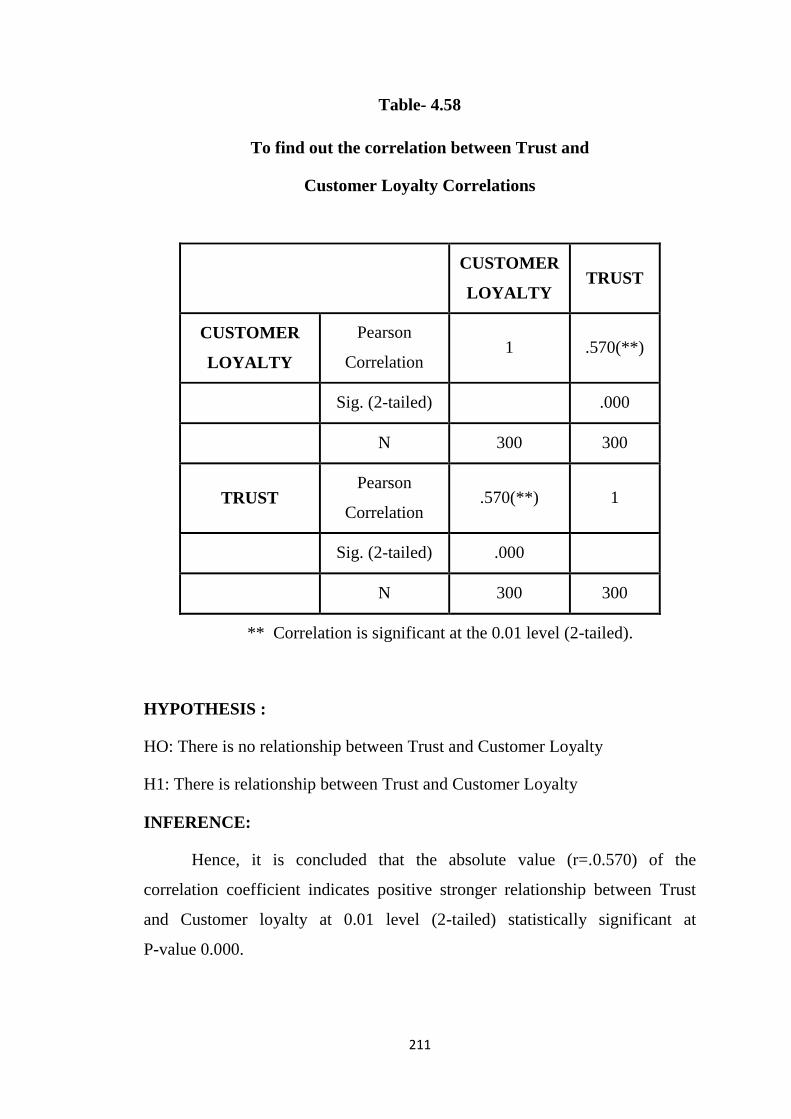

4.58 Correlations ( Trust and customer loyalty) 211

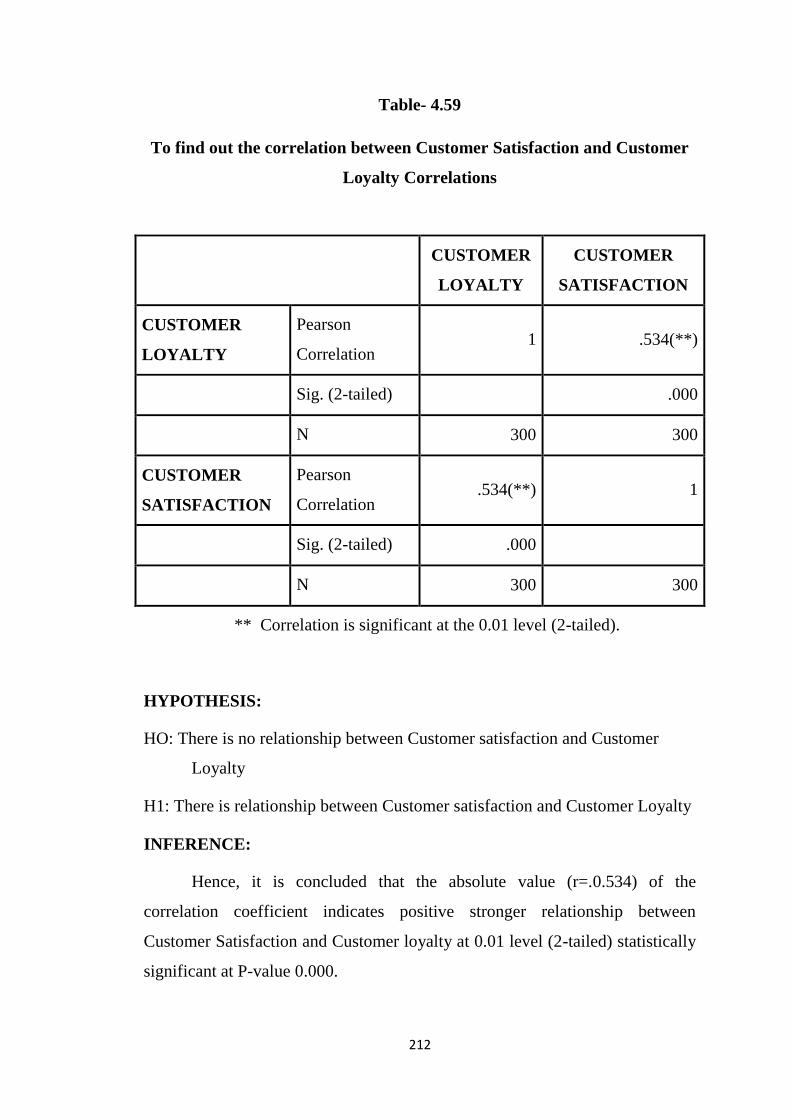

4.59 Correlations (Customer satisfaction and customer

loyalty)

212

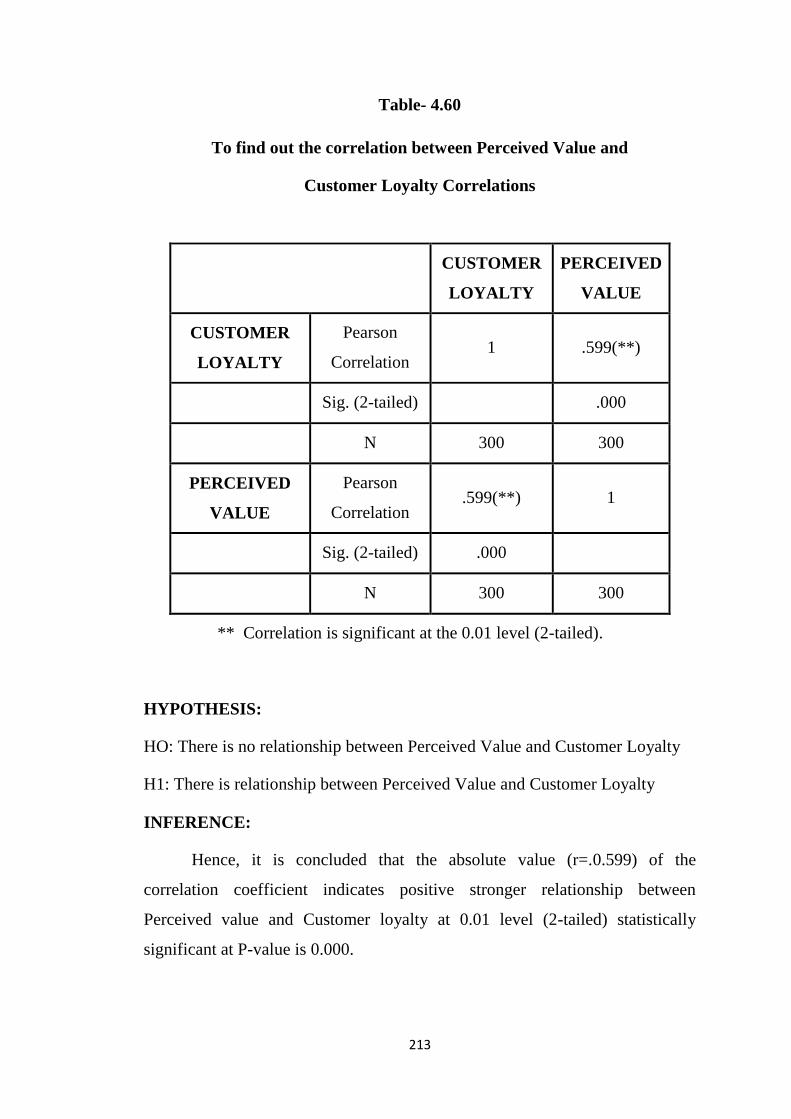

4.60 Correlations (Perceived value and customer loyalty) 213

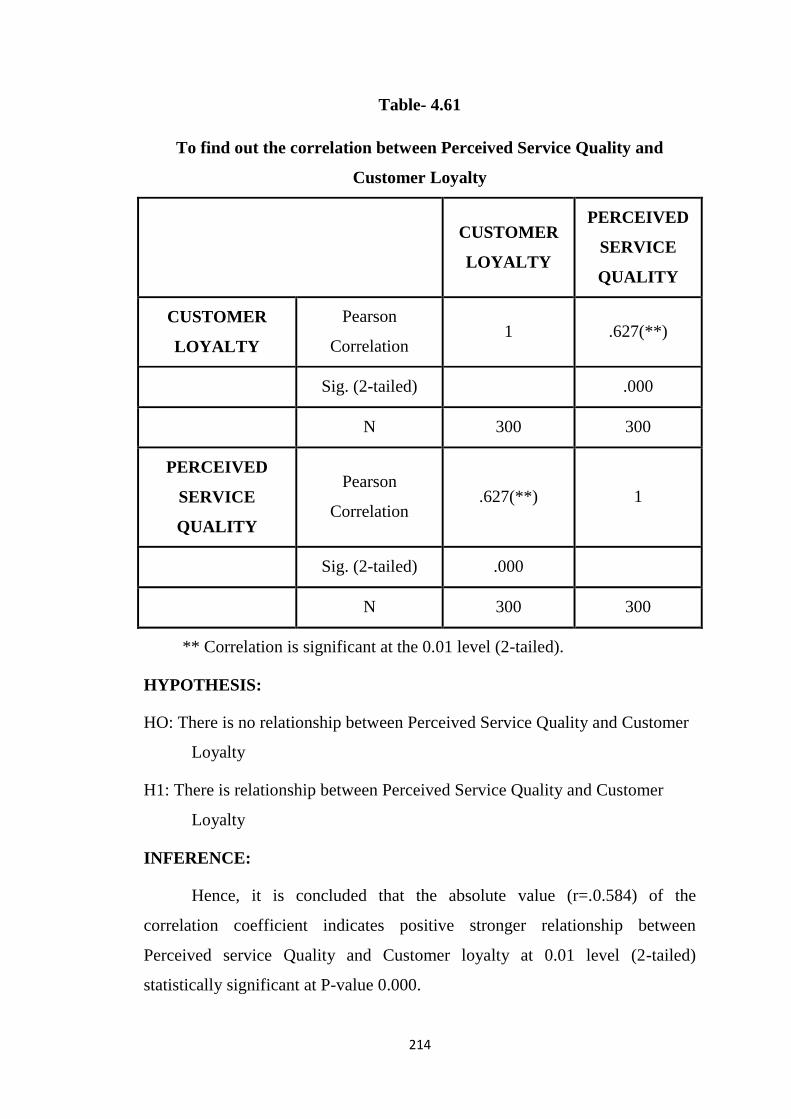

4.61 Correlations (Perceived service quality and

customer loyalty)

214

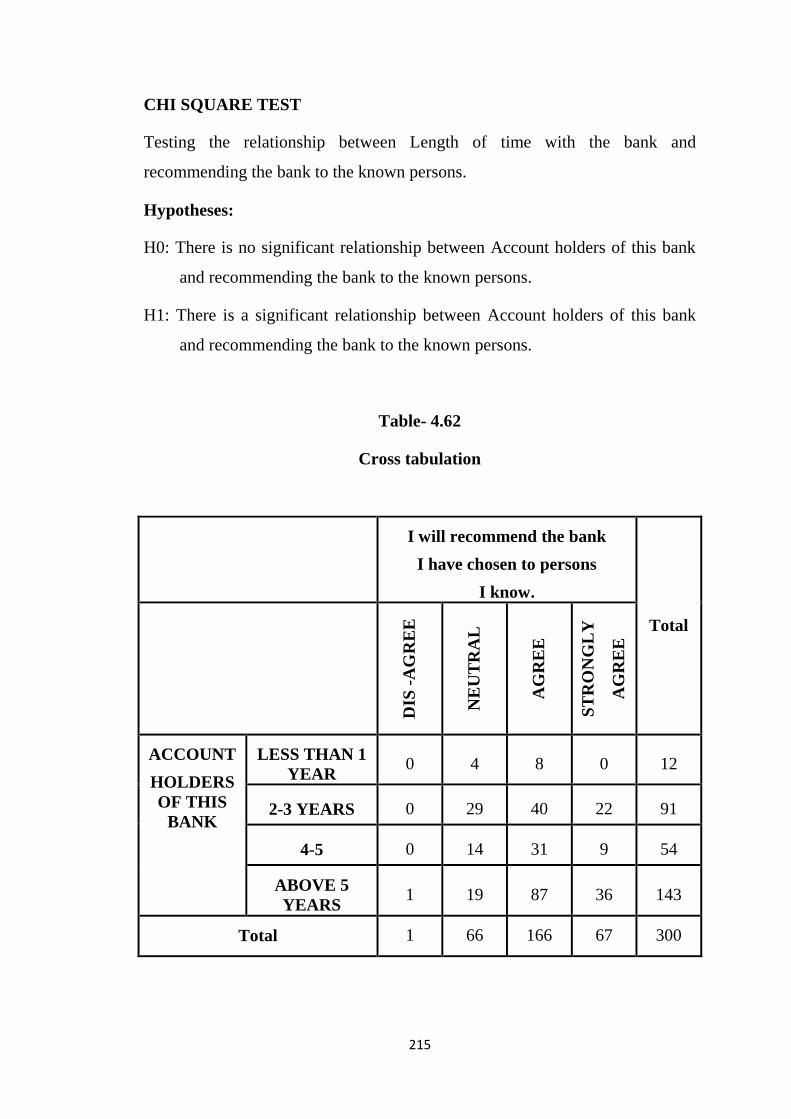

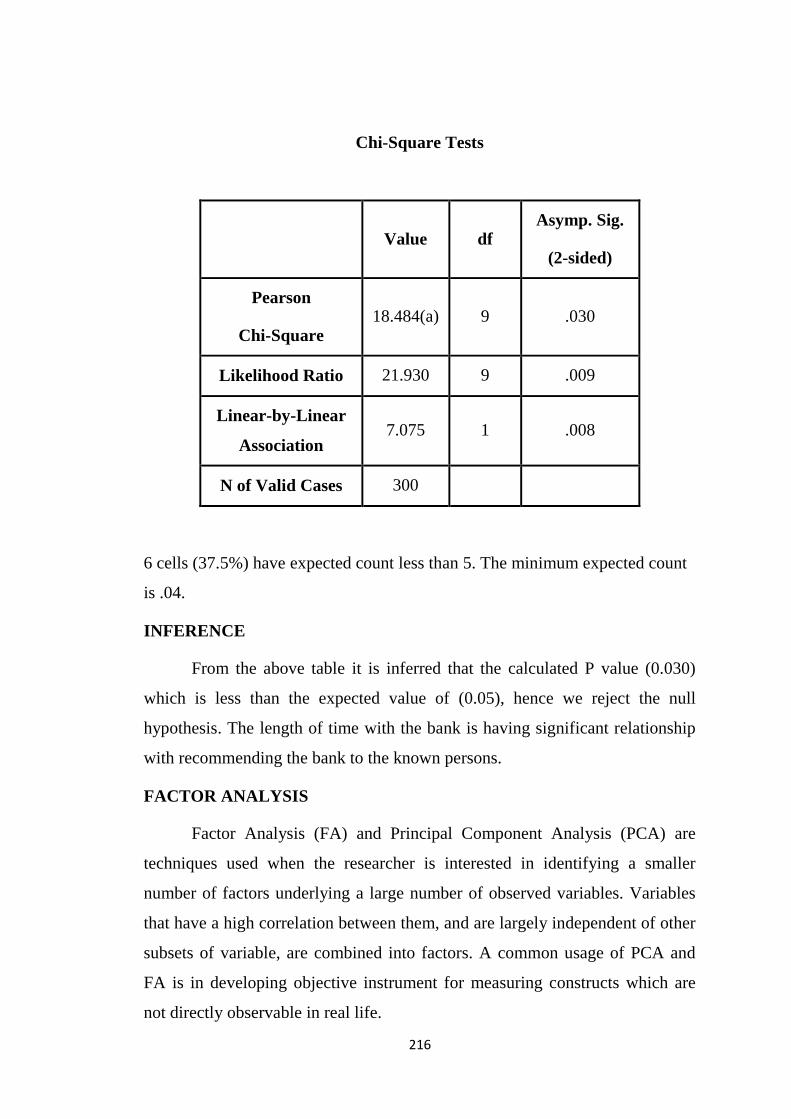

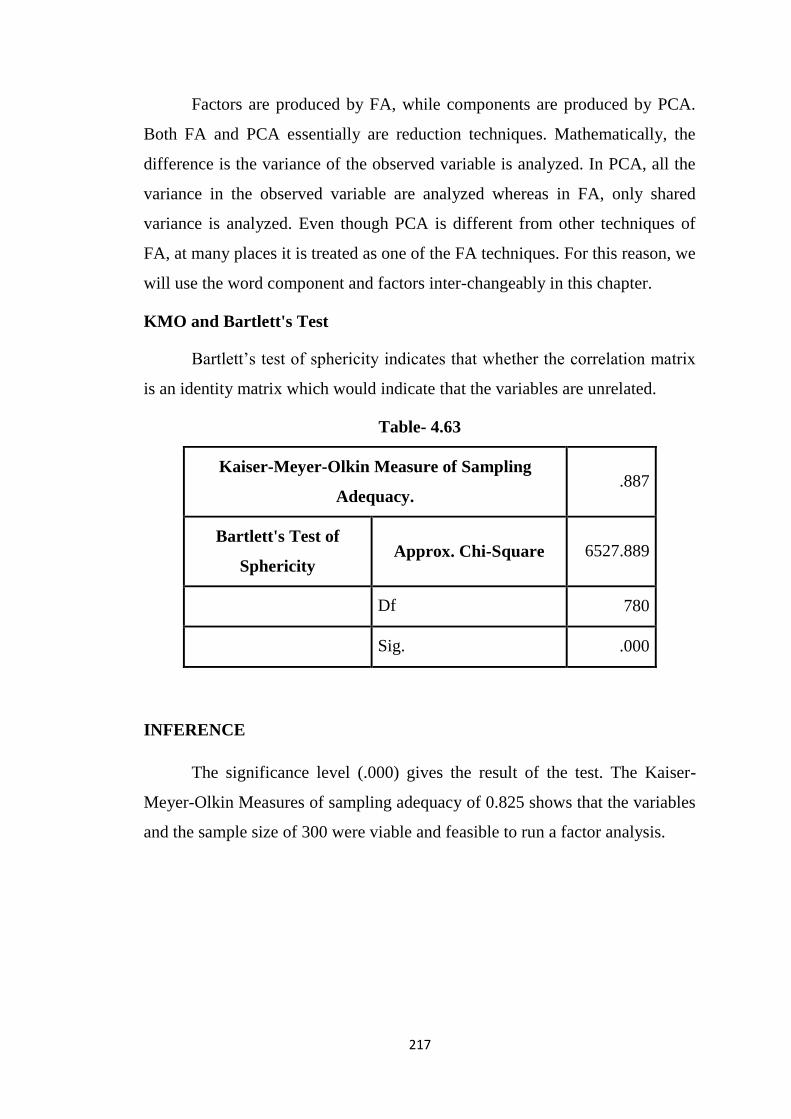

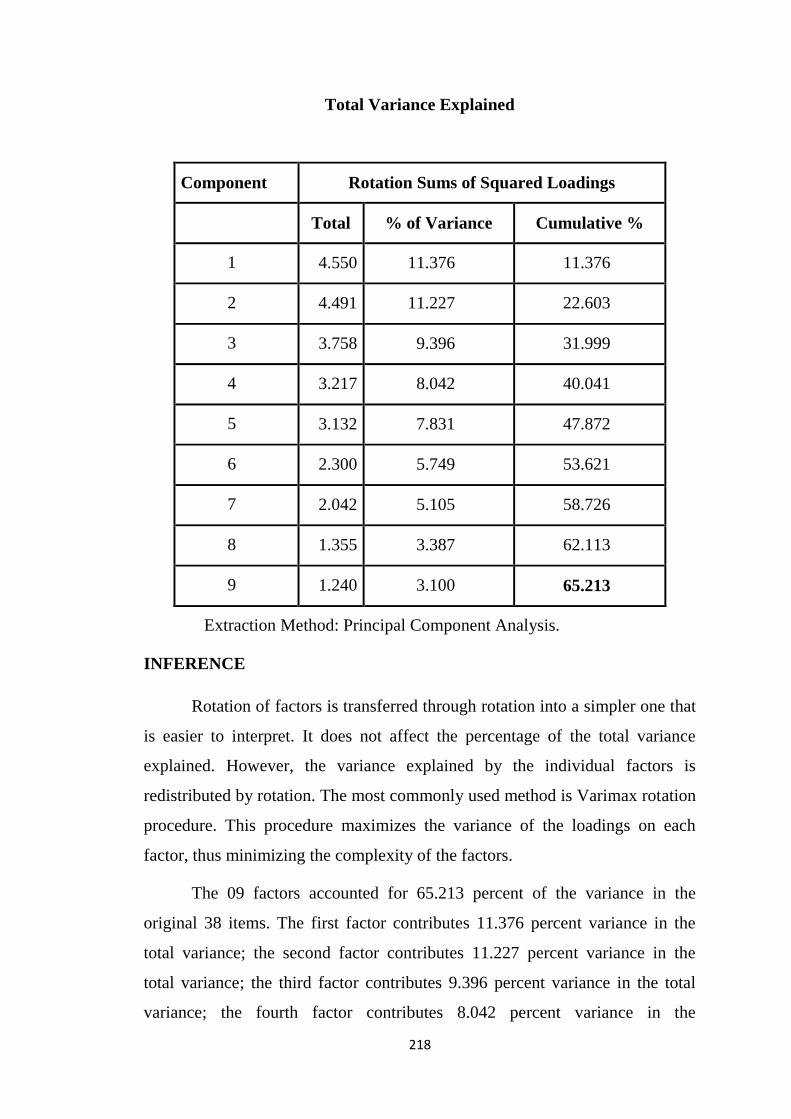

4.62 Cross tabulation 215

4.63 KMO and Bartlett’s Test 217

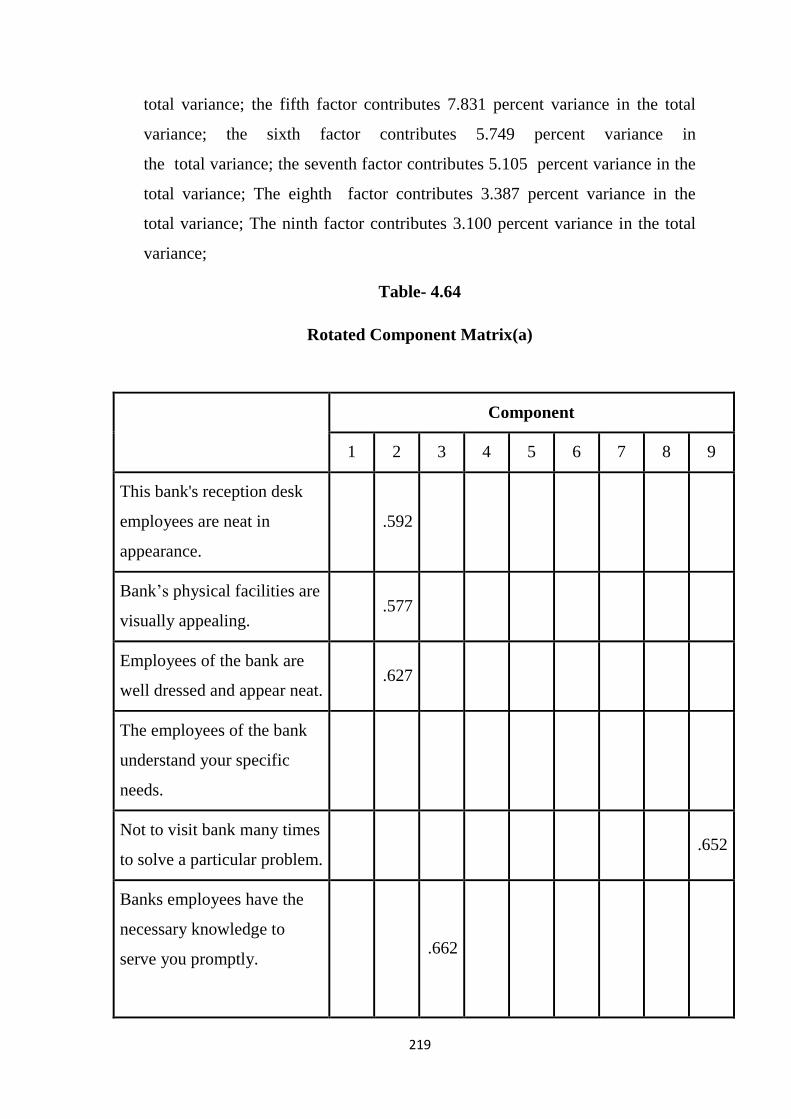

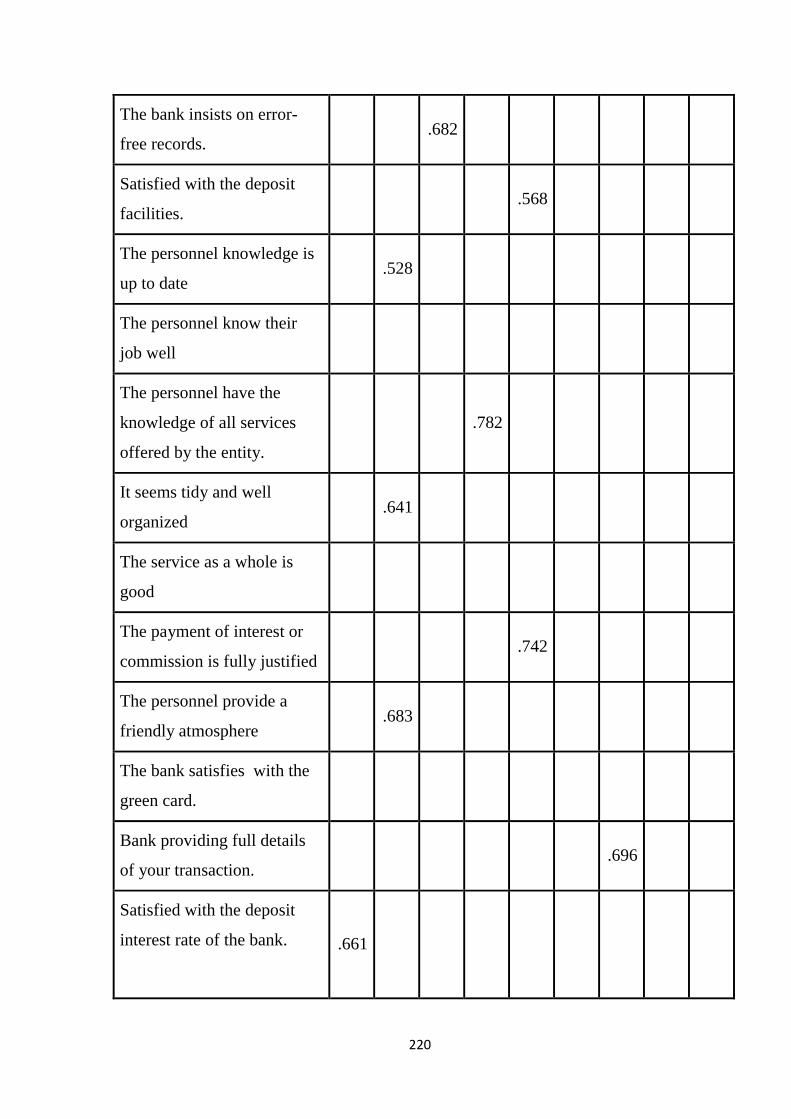

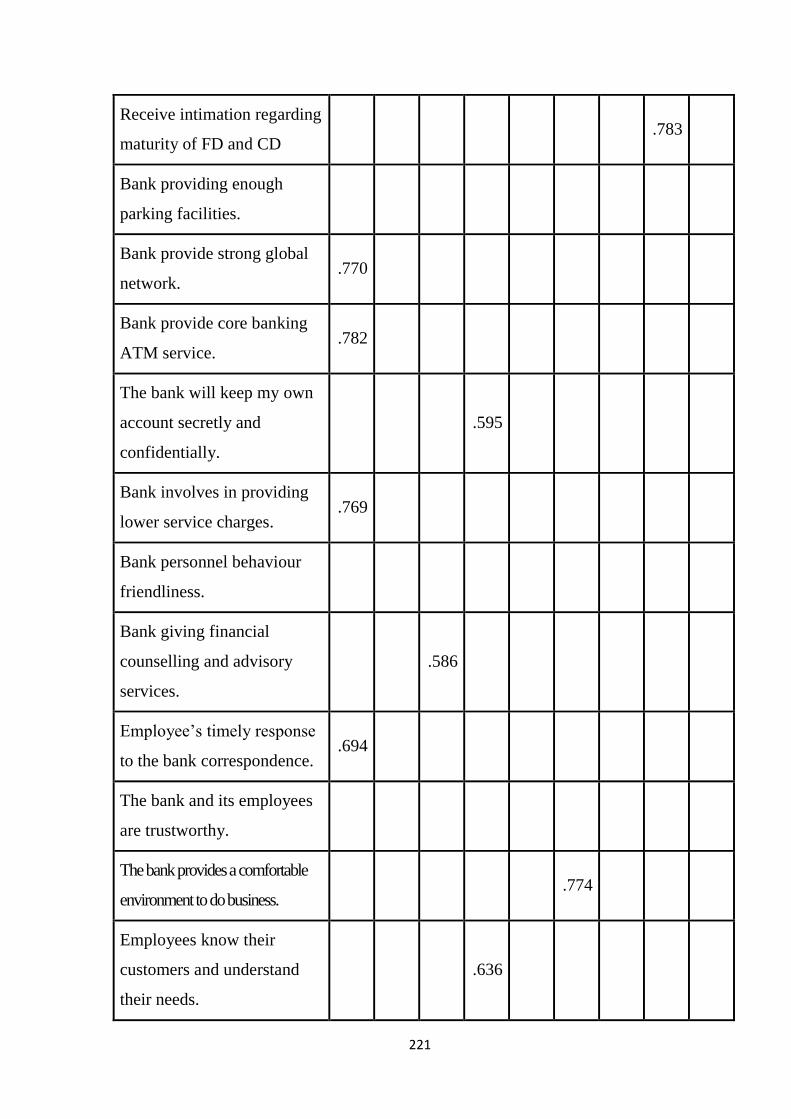

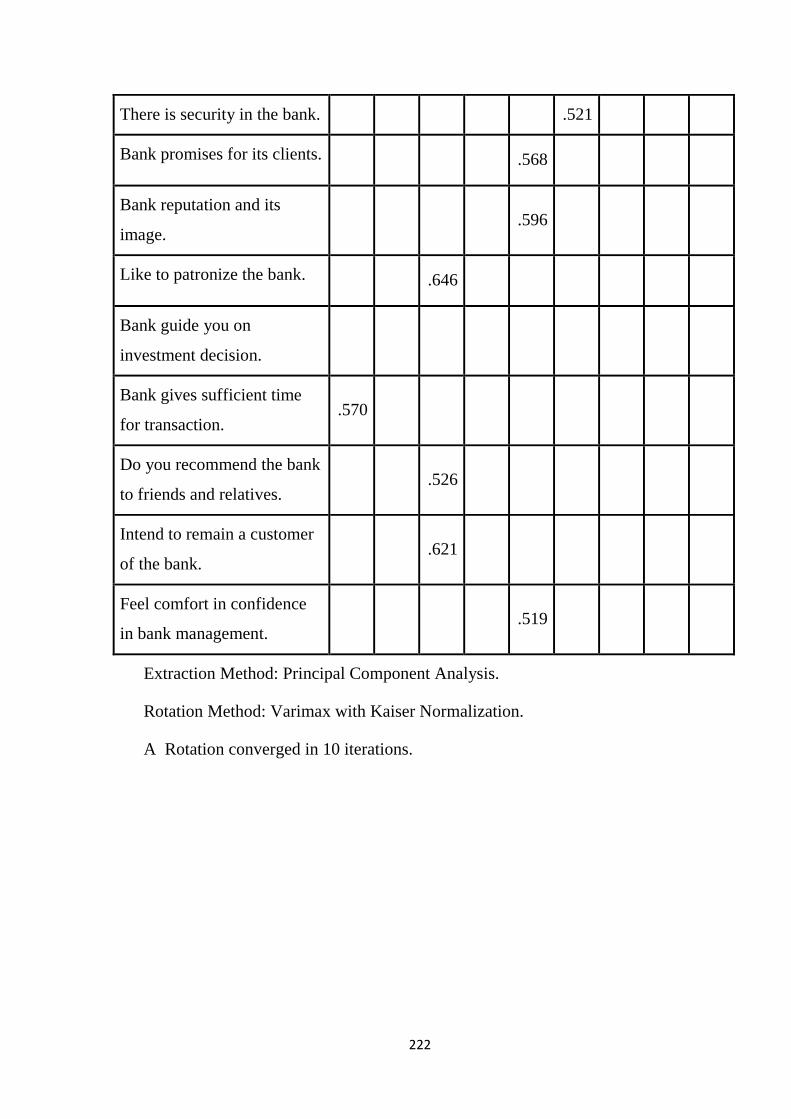

4.64 Rotated Component Matrix 219

4.65 Multiple Regression 225

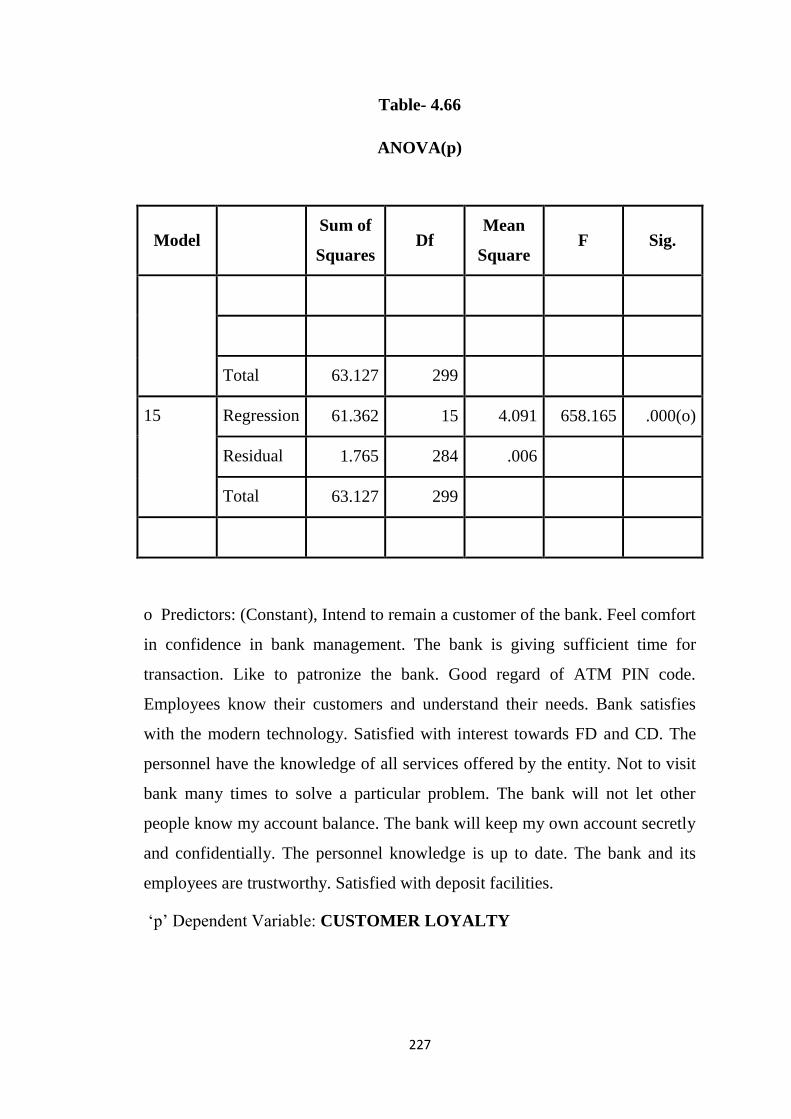

4.66 Anova 227

4.67 Coefficients 229

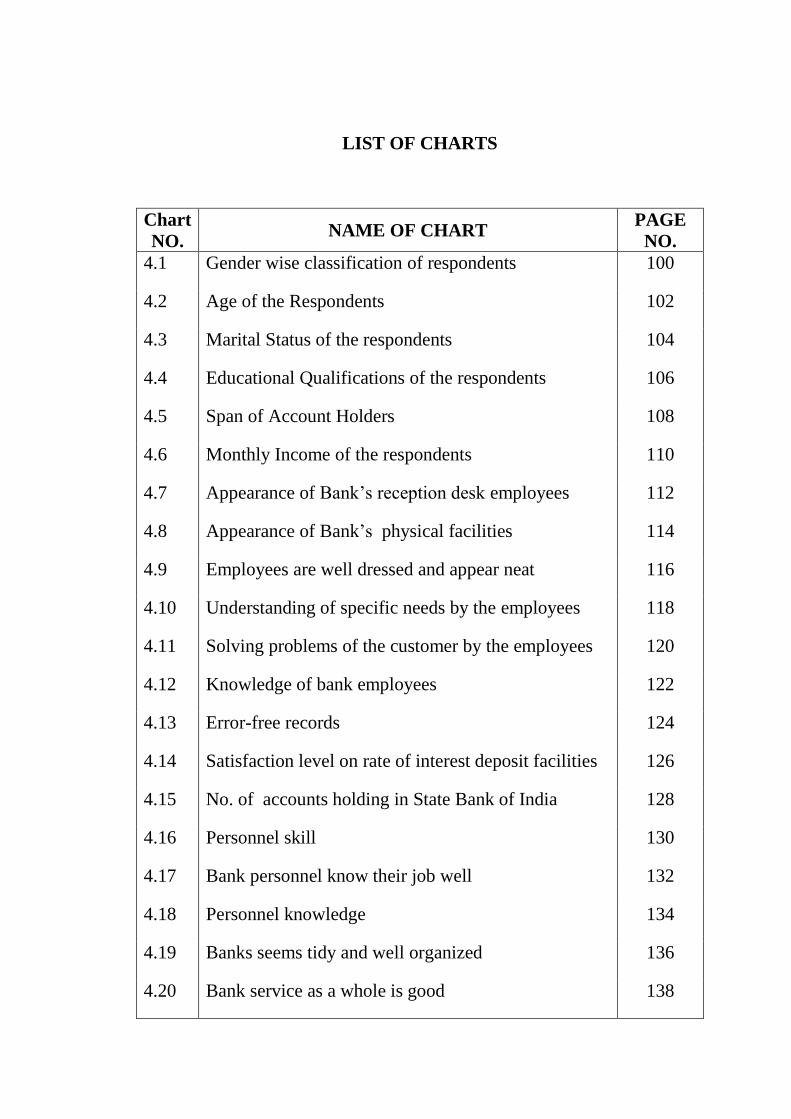

LIST OF CHARTS

Chart

NO. NAME OF CHART

PAGE

NO.

4.1 Gender wise classification of respondents 100

4.2 Age of the Respondents 102

4.3 Marital Status of the respondents 104

4.4 Educational Qualifications of the respondents 106

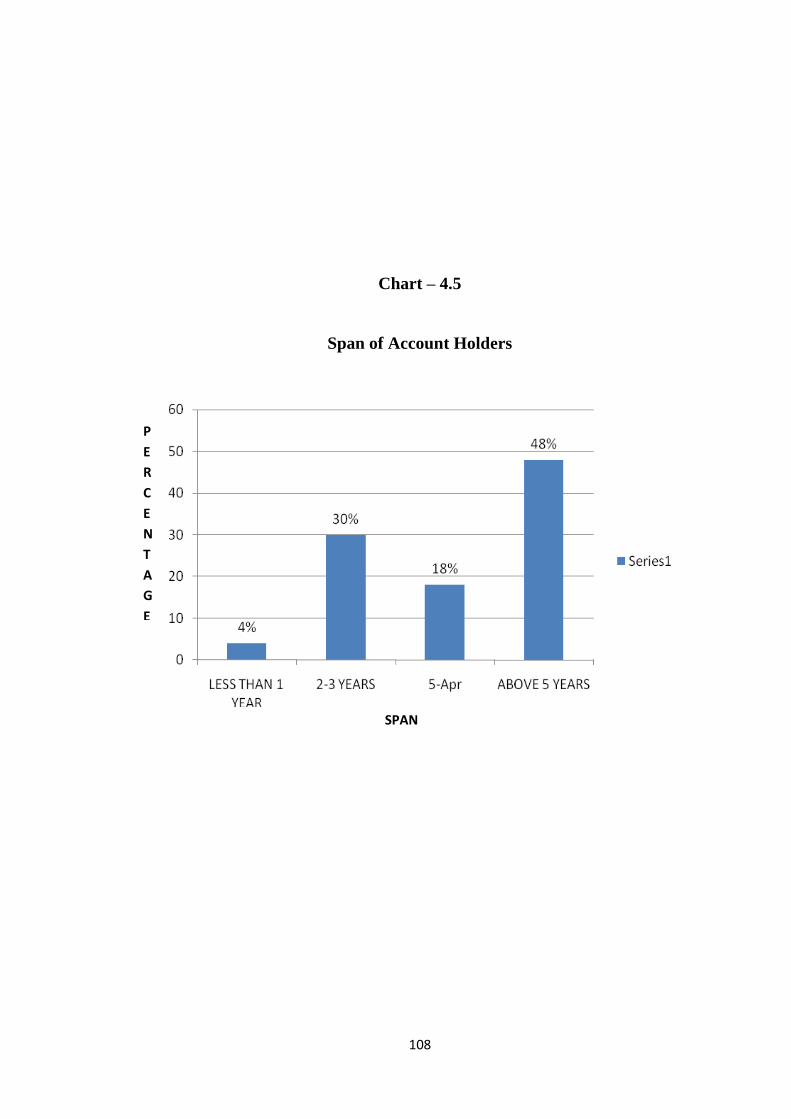

4.5 Span of Account Holders 108

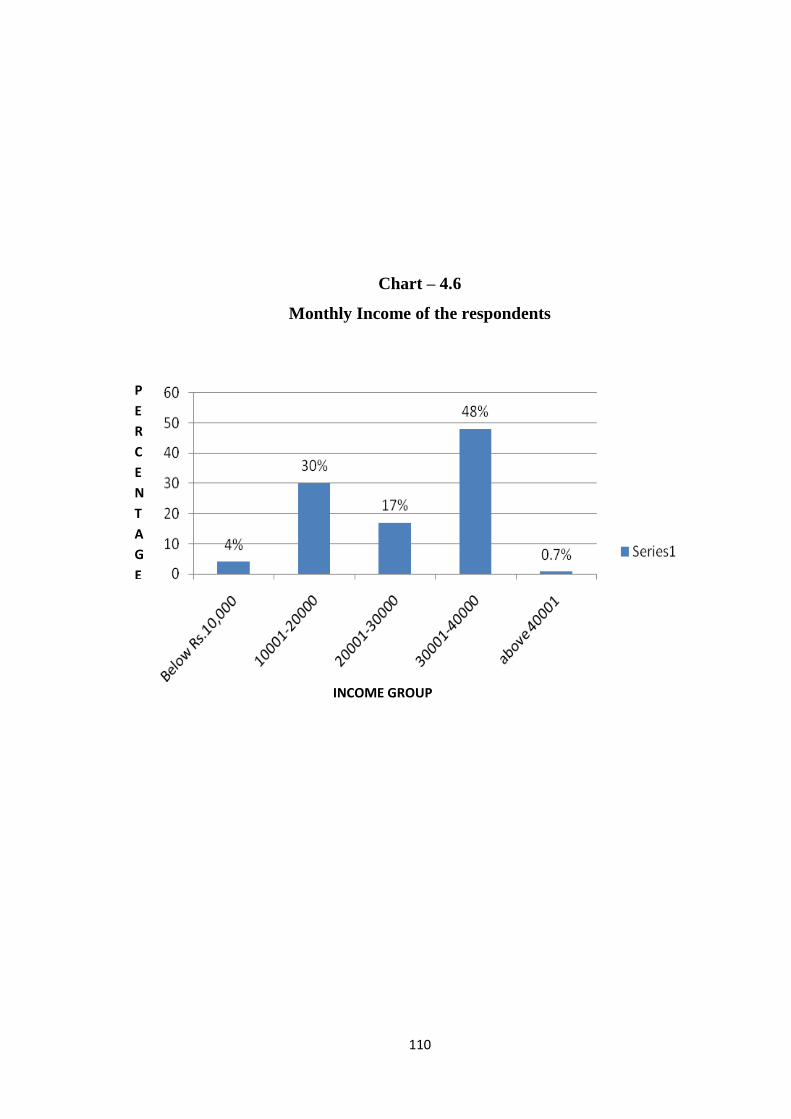

4.6 Monthly Income of the respondents 110

4.7 Appearance of Bank’s reception desk employees 112

4.8 Appearance of Bank’s physical facilities 114

4.9 Employees are well dressed and appear neat 116

4.10 Understanding of specific needs by the employees 118

4.11 Solving problems of the customer by the employees 120

4.12 Knowledge of bank employees 122

4.13 Error-free records 124

4.14 Satisfaction level on rate of interest deposit facilities 126

4.15 No. of accounts holding in State Bank of India 128

4.16 Personnel skill 130

4.17 Bank personnel know their job well 132

4.18 Personnel knowledge 134

4.19 Banks seems tidy and well organized 136

4.20 Bank service as a whole is good 138

4.21 Justification of Interest or commission 140

4.22 Friendly atmosphere 142

4.23 Difficulty in Opening an account 144

4.24 Use of ATM Card 146

4.25 Modern technology 148

4.26 Transaction 150

4.27 Interest of Fixed Deposits and Current Deposits 152

4.28 Educational loans 154

4.29 Parking facilities 156

4.30 Global network 158

4.31 Traveller cheques 160

4.32 Errors correction 162

4.33 Account confidentially 164

4.34 Core banking services 166

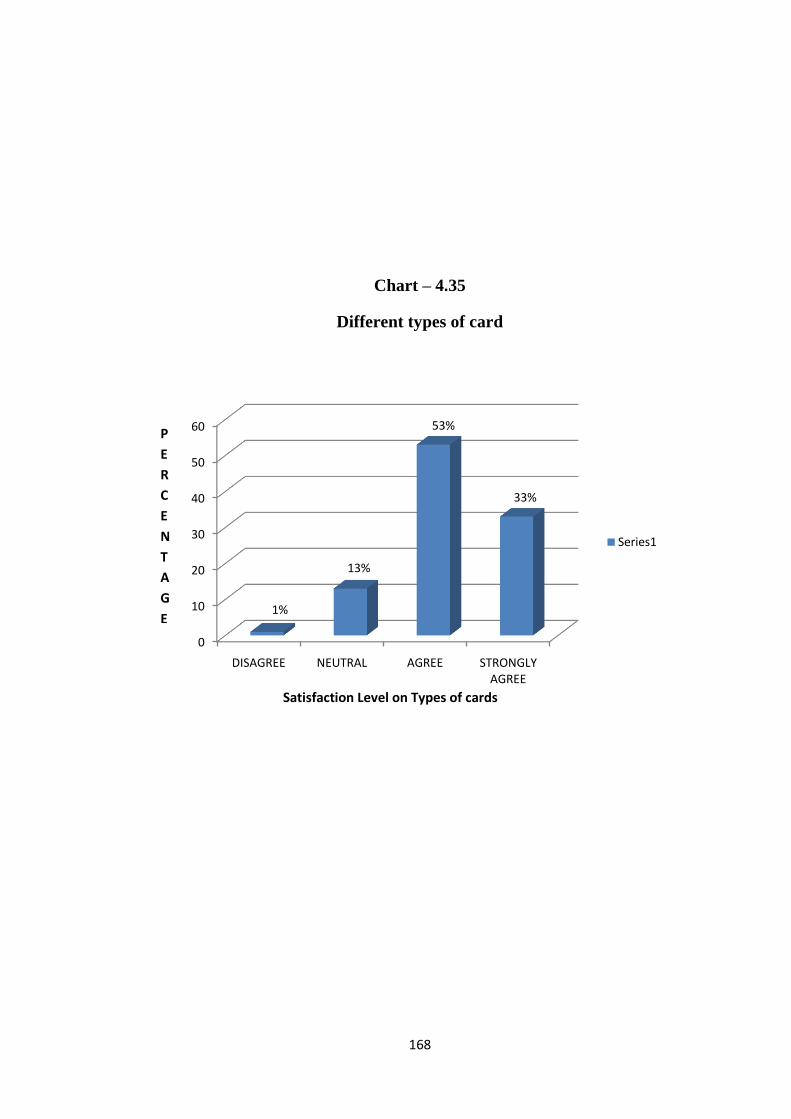

4.35 Different types of card 168

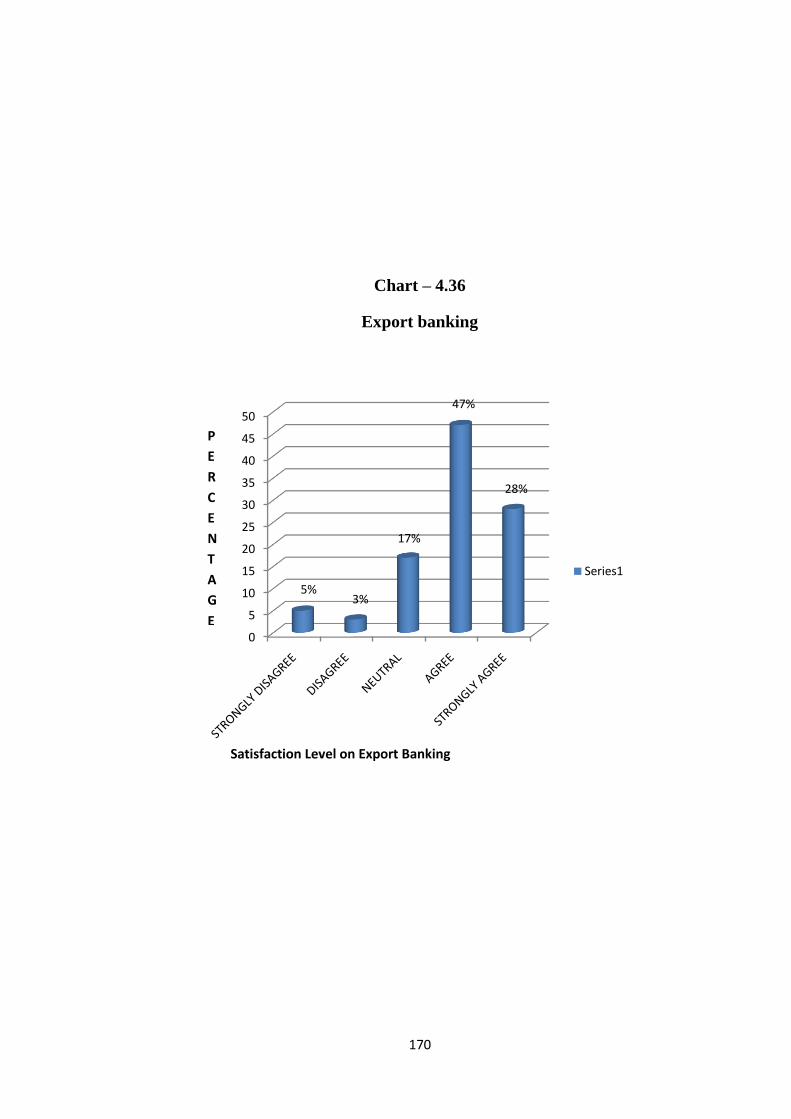

4.36 Export banking 170

4.37 Customer trust 172

4.38 Personnel behaviour 174

4.39 Financial and advisory services 176

4.40 Timely response 178

4.41 Trust worthy 180

4.42 Comfortable environment 182

4.43 Understand customer needs 184

4.44 Banks security 186

4.45 Bank reputation-Image 188

4.46 Recommend by friends and relatives 190

4.47 Intend to remain as customer of SBI 192

4.48 Role as Finance adviser 194

4.49 Investment decision 196

4.50 ATM PIN code 198

4.51 Sufficient time 200

4.52 Feel of interior comfort 202

4.53 Mobile banking services 204

4.54 Customer detail-Confidence 206

List of Abbreviation

ACB Audit Committee of the Board

ATM Automatic Teller Machine

BOI Bank of India

BOM Bank of Maharashtra

CLV Customer Lifetime Value

CMS Complaint Management System

CRM Customer Relationship Management

CSR Corporate Social Responsibility

CSS Customer Service Support

CVA Customer Value Analysis

CVM Customer Value Management

ECCB Executive Committee of the Central Board

ECRM Electronic Customer Relationship Management

EDP Entrepreneurial Development Program

EMA Enterprise Marketing Automation

ERP Enterprise Resource Planning

FCNR Foreign-currency Non-Resident

GCC Green Channel Counter

GOI Government of India

IDBI Industrial Development Bank of India Limited

IOB Indian Overseas Bank

IPO Initial Public Offer

IT Information Technology

JIT Just in Time

KYC-AML Know Your Customer – Anti-Money Laundering

MICRS Magnetic Ink Character Recognitions

MODS Multi-Option Deposit Scheme

MRP Material Resource Planning

NPA Non Performing Asset

NPS National Pension System

NRE Non-Resident External

NRIs Non-Resident Indians

NRNR Non-Resident Non-Repatriate

NRO Non-Resident Ordinary

NRSR Non-Resident Special Rupee

OBC Oriental Bank of Commerce

PFM Pension Fund Managers

PNB Punjab National Bank

PRADA Pension Fund Regulatory and Development Authority

PSB Public Sector Banks

RBI Reserve Bank of India

RBIEFT Reserve Bank of India Electronic Fund Transfer System

RBU Rural Business Unit

RFC Regional Financial Centre

RM Relationship Marketing

SBI State Bank of India

SEBI Security Exchange Board of India

SERVPERF Service Preference

SERVQUAL Service Quality

SFA Sales Force Automation

UBI Union Bank of India

UCO United Commercial Bank

1

CHAPTER – I

INTRODUCTION

Banks in India are an integral part of financial system in India. The well-

developed Indian banking system plays an important role in economic

development of our country. The nationalization of banks, establishing of new

banks with better reforms and policies and introduction of the numerous

facilities and amenities of the Indian Banks are significant features of the

banking services of India. Businesses around the world are becoming

increasingly competitive day by day. Therefore in order to generate more

customers and customers‟ loyalty existing ones, banking activities engage in

various forms of activities which are known as “Relationship Marketing”. One

of the most important components of relationship marketing is “Customer

Relationship Marketing”.

Banks play a very important role in the economic development of every

modern state. Banks operate at the heart of the modern economy. Traditionally,

banking had been restricted from private participation in India and public

sector banks had been enjoying complete protection. This scenario has changed

since 1990. The decade of 90‟s witnessed a sea change in the working of

banking in India. Technology made tremendous impact by introducing

“Anywhere Banking” and “Anytime Banking”. The financial sector now

operates in a more competitive environment than before, and involves

relatively large volume of international financial flows. In the wake of greater

financial deregulation and global financial integration, the biggest challenge

before the public sector banks is to match the market requirement rather than

being promoted by Government or regulator.

New private banks have embraced technology right from the inception

of their operations and therefore, they have adopted themselves to the changes

in the technology easily. Deregulation, liberalization, and globalization have

2

produced intense competition in banking industry resulting in declining

margins in traditional businesses, increased cost pressures and greater risks.

Market positioning, cost of intermediation and service delivery are likely to be

determinants of the efficiency of banks with respect to their competitiveness.

In the changed environment, creating new customers and retaining the existing

ones have become difficult tasks for banks. To meet the competition, creating

satisfaction among customers has become primary objective of each bank.

Loyalty in general, is one‟s attitude towards an organization or person,

supporting and substantiate the organization or person, bearing some personal

losses. When an organization or a person who provides or serves a little out of

boundary or even sometimes upto the mark, then the beneficiary becomes loyal

to that organization or person.

The concept of loyalty is rooted in the past, emphasising characteristics

such as commitment, duty, obligation and devotion. It is totally unrealistic for

most commercial businesses to expect their customers to have such feelings

towards them. There are different levels of loyalty, from suspects and prospects

to advocate, partner. It is their degree of positive commitment to the supplier

which characterizes the advocates and partners.

Generally, loyalty has been and continues to be defined as repeat

purchasing frequency or the relative volume of the same-brand purchasing.

Loyal customers not only increase the value of the business, but also enable it

to maintain the cost lower than those associated with attracting new customers.

Customer loyalty means that customers are so delighted with the

banking product or service that they become enthusiastic word-of-mouth

advertisers. Loyalty as the willingness of someone - a customer, an employee, a

friend – to make an investment or personal sacrifice in order to strengthen a

relationship.

The role of loyalty in the brand equity process and specifically noted

that brand loyalty leads to certain advantages, such as reduced marketing costs,

more new customers and greater trade leverage. Loyalty as a deeply held

3

commitment to re-buy or re-patronize a preferred product or service

consistently in the future, thereby causing repetitive same-brand or same-

brand-set purchasing, despite situational influences and marketing efforts have

the potential to cause switching behaviour.

Creating loyal customer has been becoming more and more important.

This is due to the fact that competition is increasing, as never before, which has

a great impact on many banks. To deal with this high concentrated market,

businesses are attempting not only to attract and satisfy customers but also to

create a long-term relationship with these customers.

Businesses around the world are becoming increasingly competitive day

by day. Therefore in order to generate more customers and retain existing ones,

companies engaged in various forms of activities which are known as

“Relationship Marketing”. One of the most important components of

relationship marketing is “Customer Relationship Management”. Customer

Relationship Management (CRM) as a strategic approach that is concerned

with creating improved shareholder value through the development of

appropriate relationship with key customers and customer segments.

By looking at the definition it can be said that CRM is about creating,

maintaining and sustaining relationships with customers. One of the most

commonly used CRM strategies of a company are loyalty programs, which are

designed to give variety of benefits to increase customer loyalty. In present

multi-channel retailing environment, companies seek to provide satisfaction to

customers through various loyalty programs. In many cases, retailers with very

limited amount of products and services would form joint venture of loyalty

program to encourage customers to visit the retail stores which are part of such

loyalty programs. This demonstrates the importance of integrated CRM

strategies within the organization in current business environment.

Nowadays the expectations of the customers have multiplied. The banks

should also be ready to meet the expectations of the customers. For instance,

the completion of transactions should be made time bound. Time limit should

4

be prescribed for depositing money, withdrawing money, for purchasing

demand draft, money transfer, opening new account and number of days for

obtaining debit cards and credit cards. Similarly number of weeks or months

taken for processing applications for education loans, home loans, vehicle loans

and personal loans should also be prescribed and ensure that work is carried on

accordingly. How the employees handle and in touch with the customers and

how far they satisfy the customers determine the quality of service rendered by

the employees. These are not an impossible one. The bank employees should

walk some extra mile for satisfying the customer service.

Customer Relationship Management is often considered as database

marketing primarily linking marketing of the organisation with the database of

the customers. Some theorists have been considering it as an exercise for

customer retention as many theories and studies have been emphasising on the

rationale for keeping the customers. This requires a variety of techniques,

especially post-sale initiatives, to keep the customers for like. This was

believed to be a mechanise to keep the existing customers happy so that they

remain with the organisation and may, if possible, generate positive referral for

the company‟s products and services. It was believed the application of IT can

be an effective tool to develop one-to-one relationship that integrates database

with company‟s base.

Relationship marketing as an integrated effort to identify, maintain and

build up a network with individual consumers and to continuously strengthen

the network for the mutual benefit of both sides, through interactive,

individualised and value-added contacts over a long period of time.

Strategic Orientation in Marketing

Strategic Orientation is argued that organisations need to put the

customer first and shift the role of marketing from manipulating the customer

(telling and selling) to genuine customer involvement (communicating and

sharing the knowledge) for long-term growth of the business. Developing

closer relationship with the newly attracted customers, to turn them into loyal

5

customer category required deep-rooted strategic intent on the part of the

corporate.

An important dimension of CRM study is selecting the profitable

customers. Companies need to understand who is the profitable customers and

accordingly design marketing programme as per the exclusive requirements of

those customers; for example, a multiplex may inform about the new releases

with the show timings to its loyal customers.

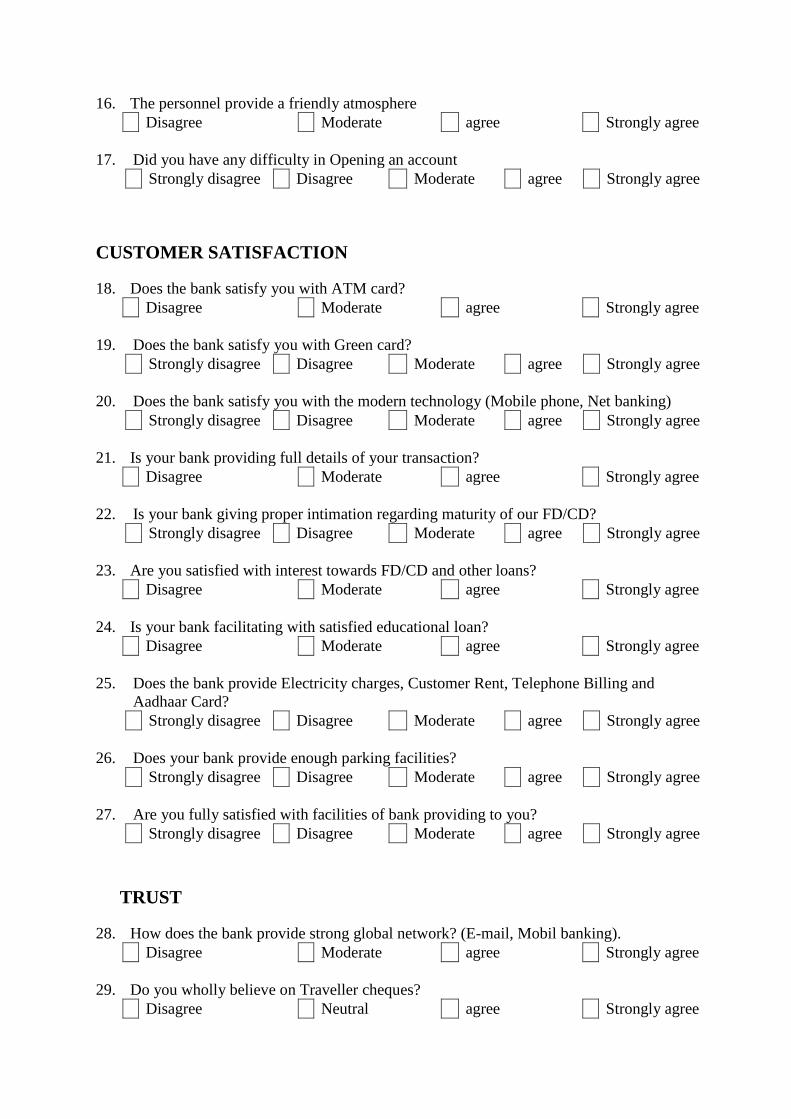

Customer satisfaction

Customer satisfaction has been subject of considerable research and has

been defined and measured in many ways. Customer satisfaction is the

customer‟s fulfilment response to a customer experience, or some part thereof.

Dissatisfaction is an unpleasurable fulfilment response. The experience

or some part thereof‟ component of the definition suggests that the satisfaction

evaluation can be directed at any or all elements of the customer‟s experience.

This can include product, service, process and any other components of the

customer experience.

The most common way of quantifying satisfaction is to compare the

customer‟s perception of an experience, or some part of it, with their

expectations. This is known as the expectations-disconfirmation model of

customer satisfaction. This model suggests that if customers perceive their

expectations to be met, they are satisfied. If their expectations are

underperformed, this is negative disconfirmation occurs when perception

exceeds expectation. The customer might be pleasantly surprised or even

delighted. This model assumes that customers have expectations, and that they

are able to judge performances. A customer satisfaction paradox has been

identified by expectations-disconfirmation researches. At times customers‟

expectations must be met but the customer is still not satisfied. This happens

when the customer‟s expectations are low.

6

Many companies research customer requirements and expectations to

find out what is important for customers, and then measure customers‟

perceptions of their performance when compared to the performance of

competitors.

Customer Value

Value creation is a strategic process to manage a product, service or a

business unit‟s growth and competitive share. It is built on a core foundation of

market research applying advanced techniques, called Customer Value

Analysis (CVA).

The literature on both marketing and quality stresses upon the

importance of customer value, Customer Value Management (CVM) is a

proven methodology for addressing critical business issues. It is being used

successfully by leading companies in a variety of industries around the world.

CVM is the product of customer value-added techniques and economic value

comparisons. It allows targeted improvement of customer service where it will

have the greatest business benefit. The customer value-added analysis uses

competitive market research techniques coupled with econometric modelling to

establish direct links for ratings of product and service to market share.

In the recent years, the notions of value creation and value delivery have

become increasingly prominent. At the same time there was a shift from the

4Ps of marketing (product, price, place and promotion) to an emphasis on

relationship, networks, and interaction. This stressed on the development of

trusting attitudes between seller and buyer, together with the reciprocal

satisfaction of expectations and the overall objectives of creating and providing

value for both parties engaged in the exchange process. The concept of

customer value is becoming more and more prominent as a crucial strategic

factor in gaining a competitive advantage. It is also increasingly seems to be

key building block in the development of relationships.

In designing the entire delivery to the customer, the product, service,

image and the person who delivers all forms part of the customer value. At the

7

same time money, time, energy and psychic costs all forms part of the total cost

calculation. These cost and value perspectives need to be taken into

consideration while designing the customer delivery.

Customer Lifetime Value (CLV) in the banking industry

One in five banking executives does not measure CVL. Couple this with

the 22 per cent who do not measure portfolio or wallet share, and it is easy to

see why cross selling is such a challenge for financial service providers. Unless

a banker knows which of customer‟s financial needs are being met, it is

exceedingly difficult to suggest additional service. A robust business

intelligence system can provide a financial services firm with a 360 degrees

view of the customer. Transactions can be consolidated with demographic and

psychographic data, revenue and profit measures, as well as with historical

customer service incidents and queries. With the total picture, the provider can

see the customer from multiple perspectives and craft programmes that will

satisfy a border range of client requirement. Part of this multifaceted view of

the customer is the ability to aggregate multiple customers into a household

perspective. The benefits of this consolidated view are clear and strong.

Customer Relationship Management

All service sector industries have realised that superior customer service

is the key for their survival. Most offers across the industry are difficult to

differentiate on the basis of offering quality, pricing, distribution or promotion

for Customer Relationship Management. They all are saturated on the basis of

certain parameters. The best quality offers with most competitive process and

promotion with the greatest aggression have become the norm. The only point

of differentiation left is the customer service and most of the industries are

using it as a tool for competitive advantage.

Customer Relationship Management is the core business strategy that

integrates internal processes and functions, and external networks, to create and

deliver value to targeted customers at a profit. It is grounded on high quality

customer related data and enabled by information technology. This clearly

8

denotes that CRM is not just about IT. CRM integrates internal processes and

functions. Access to customer related data allows marketing, selling and

service functions, to be aware of each other‟s interactions with customers.

Furthermore, back-office functions such as operations and finance can learn

from and contribute to customer related data. Access to customer related data

allow members of a business‟s external network – suppliers, partners,

distributors – to align their efforts with those of the focal company.

Historically, most companies were located close to the markets they

served, and knew their customers intimately. Very often there would be face-

to-face, even day-to-day interaction with customers where knowledge of

customer requirements and preferences grew. However, as companies have

grown larger they have become more remote from the customer they serve. The

remoteness is not only geographic, it may also be cultural. Even some of the

most widely admired American companies have not always understood the

markets they served. Disney‟s development of a theme park near by the French

capital, Paris, as not an initial success because they failed to deliver to the value

expectations of European customers.

Geographic and cultural remoteness, together with business owner and

management separation from customer contact, means that many, and small,

companies do not have the intuitive knowledge and understanding of their

customer so often found in micro-businesses, such as neighbourhood stores

and hairdressing salons. This has given rise to demand for better customer

related data, a cornerstone of effective Customer Relationship Management. If

not the profit community were to replace the words business, customers and

profit with appropriate equivalents such as organization, clients and objectives,

it would apply equally well in that context.

Customer Relationship Management is a technology enabled approach

to management of the customer interface. Most CRM initiatives expect to

have impact on the cost to serve and revenues streams from customer. The use

of technology also changes the customer‟s experience of transacting and

9

communicating with a supplier. For that reason, the customer‟s perspective on

CRM is an important consideration in the book. CRM influences customer

experience and that is of fundamental strategic significance.

Loyalty

There is no one specify meaning or define of this, since it might be

defined with some quantitative measure such as customer‟s retention or

customers shipping frequency. But again loyalty has a deeper meaning and

that‟s why many researches tried to define it and reach the essence of it.

Loyalty also can be seen as a deeply held commitment to re-patronize a service

or a product in the future, loyalty is both related to consumer‟s attitudes and

behaviours, where they both complete each other in truly measuring loyalty.

Loyalty into four types: sustainable loyalty (high-frequent purchase with high

positive attitude towards the brand), latent loyalty (high attitude towards the

brand but no display of frequent shopping), spurious loyalty (frequent

purchases but not based on loyalty) and no loyalty (less frequent purchases and

negative consumer opinion towards the brand). These types do exist in every

customer base of any organization which helps in deciding which customer is

worth retaining.

Retailers try to maintain relationships with customers to achieve the

highest levels of loyalty but they are still facing the complex issue of switching

behaviour due to many reasons. Therefore many firms started introducing

loyalty schemes or what we know as loyalty programs and its holds many

facilities such as simple points accrual programs, club cards or combined credit

cards, etc.,

Loyalty Program

A Loyalty Program is a system or a scheme that rewards loyal customers

by offering delayed, accumulating economic benefits to consumers who

patronize the brand, offering different offers of discounts, monetary rewards or

other services, based on the amount of money that the customer spent. Some

cards have microchips in them where data is already stored in the system and

10

the card will facilitate the identification of the customer, other only have a

number or an ID of the holder. The concept itself is not new as it started in the

1960s wherein there used to be certain cards where retailers used to place

stamps with every purchase and customer have to keep them until they reach a

certain limit and they will be entitled for a reward.

Now-a-days Loyalty schemes vary in their mechanisms and schemes,

but they all agree on rewards. Loyalty schemes have different aims too where

some may aim for data collection, sales promotion and other strategies. The

advanced technology facilitated the use of these programs and made tracking

customers easier on the business runners as and when customers register in any

loyalty schemes, it is considered to be an unwritten agreement on using their

details to be used and stored in the retailer‟s database and have all their

purchases to be tracked.

Loyalty Programs for customers were found to increase brand loyalty

and minimize the price sensitivity factor, it also encourages the positive word

of mouth in favour of the company, attract more new customers and increase

the sales. Besides these the Customers who are members of a loyalty scheme

were observed to be less sensitive to lower quality of service than other

customers. The easiest loyalty schemes will usually require the consumer‟s

name, email and phone number. Others require more information than this,

depending on the business.

Many direct marketing companies use RFM measures of behavioural

loyalty. The most loyal are those who have high scores on the three behavioural

variables: Recency of purchases (R), Frequency of purchases (F) and Monetary

value of purchases (M). The variables are measured as follows:

R = time elapsed since last purchase

F = number of purchases in a given time period

M = monetary value of purchases in a given time periods.

Attitudinal loyalty if measured by reference to components of attitude

such as beliefs, feelings and purchase intention. Those customers who have a

11

stronger preference for, involvement in, or commitment to a supplier are the

more loyal in attitudinal terms.

Another study found that customer satisfaction in retail banking

correlated highly with branch profitability. Highly satisfied customers had

balances 20 percent higher than satisfied customers, and as satisfaction levels

went up over time, so did account balances. The reverse was also true, as

satisfaction levels fell, so did account balances.

Loyalty Schemes

Most loyalty schemes require new members to complete an application

form when they join the programme. This demographic information is typically

used, together with purchasing data, to help companies become more effective

at customer communication and offer development. Whereas some CRM

implementations are linked to loyalty schemes, not all are. It plays two vital

roles in CRM implementations. First, they generate data that can be used to

guide customer acquisition, retention and development. Secondly, loyalty

schemes may serve as an exit barrier. Customers who have accumulated credits

in a scheme may be reluctant to exit the relationship. The credits accumulated

reflect the value of the investment that the customer has made in the scheme,

and therefore in the relationship.

Banks deal with a large number of individual retail customers. Banks

want Customer Relationship Management for its analytical capability to help

them manage customer defection rates and to enhance cross sell performance.

Data mining techniques can be used to identify which customers are likely to

defect, what can be done to win them back. Which customer are hot prospects

for cross sell offers, and how best to communicate those offers. Banks want to

win a greater share of customer spend on financial service. In terms of

operational CRM, many banks have been transferring service into contact

centres and online in an effort to reduce costs, in the face of considerable

resistance from some customer segments.

12

Customer relationship is the essence of a successful business and that‟s

why many firms started a CRM department which specializes in the sole

purpose of sustaining its customer base in the market. Customer relationship is

a major aspect for a long lasting business, especially in retailing as retaining the

customer could assure a thriving business with the support of the customers.

Retention strategy is not a luxury anymore as competition is not getting any

less. This strategy gives the firm the chance to have the merits of it as it is

cheaper to maintain the existing customers than acquiring new ones and to

enjoy a profitable association, the result of this strategy is loyalty.

Organizations need to understand the dimensions of this word and study

techniques of how it is obtained, as many retailers link the repeated purchase

with loyalty, whereas the difference in major as well as frequent purchase

could be for any other reason such as convenience, lack of choice and

information, or simply inertia.

Relationship

The „R‟ of CRM stands for „Relationship„. But what do we really mean

by the expression „relationship‟. Certainly, most of us would understand what it

means to be in a personal relationship, but what is a relationship between a

customer and supplier. At the very least a relationship involves interaction over

time.

Relationship quality

The discussion of trust and commitment suggests that some relationship

can be thought to be of better quality than others. Research into relationship

quality generally cites trust and commitment as core attributes of a high quality

relationship. However, a number of other attributes have also been identified,

including relationship satisfaction, mutual goals and cooperative norms.

Relationship satisfaction is not the same as commitment. Commitment

to a supplier comes as investments are made in the relationship, and

investments are only made if the committed party is satisfied with their

13

transactional history. In other words, investments are made in relationships

which are satisfactory. Mutual goals are present when the parties share

objectives that can only be achieved through joint action and relationship

continuity. Cooperative norms are seen when relational parties work together

constructively and interdependently to resolve problems.

Customer Relationship Management implementations are often designed

to build closer, more value-laden relationship with customers, it makes sense

for managers to be aware of the quality of the relationship they have with

customers.

Customer satisfaction, loyalty and business performance

An important rationale for Customer Relationship Management is that it

improves business performance by enhancing customer satisfaction and driving

up customer loyalty. There is a compelling logic to the model, which has been

dubbed that „satisfaction-profit chain‟. Satisfaction increases because customer

insight allows companies to understand their customers better and create

improved customer value propositions and better customer experiences.

As customer satisfaction rises, so does customer intention to repurchase. This

in turn influences actual purchasing behaviour, which has an impact on

business performance.

Customer loyalty

The term customer loyalty is used to describe the behaviour of repeat

customers, as well as those that offer good ratings, reviews or testimonials.

Some customers do a particular company a great service by offering favourable

word-of-mouth publicity regarding a product, telling friends and family, thus

adding them to the number of loyal customers. However, customer loyalty

includes much more. It is a process, a program or a group of programs geared

toward keeping a client happy so he or she will provide more business.

Customer loyalty can achieve in some cases by offering a quality

product with a firm guarantee. Customer loyalty is also achieved through free

14

offers, coupons, low interest rates on the part of the economy concerned with

providing basic government services. The composition of the public sector

varies by country, but in most countries the public sector includes such services

as the police, military, public roads, public transit, primary education and

healthcare for the poor. The public sector might provide services that non-payer

cannot be excluded from services which benefit all of society rather than just

the individual who uses the service and services that encourage equal

opportunity.

Customer loyalty may be a one-time program or incentive or an ongoing

group of programs to entice consumers. Buy-one get-one-free are very popular,

as `purchases that come with rebates or free gifts. Another good incentive for

achieving customer loyalty is offering a risk trial period for a product or service

also known as brand name loyalty, these types of incentives are meant to

ensure that customers will return, not only to buy the same product again and

again, but also to try other products or services offered by the company.

Excellent Customer service is another key element in gaining customers

loyalty, if a client has a problem, the company should do whatever it takes to

make things right, if a product is faulty, it should be replace or the customer‟s

money should be refunded. This should be standard procedure for any

reputable business, but those who wish to develop customer loyalty on the

large-scale basis may also go above and beyond the standard. They may offer

even more by way of free gifts or discounts to appease the customer.

Features of customer loyalty

The financial services sector has undergone drastic changes, resulting in

a market place which is characterized by intense competition, little growth in

primary demand and increased deregulation. In the new market place, the

occurrence of committed and often inherited relationship between a customer

and his or her bank is becoming increasingly scarce. Several strategies have

been attempting to retain customer loyalty, many bank have introduced

innovation products and services. However, as such innovations are frequently

15

followed by similar charges. It has been argued that a more viable approach for

banks is to focus on less tangible and less easy to imitate determination of

customer loyalty such as customer evaluative judgements like services quality

and satisfaction.

Customer loyalty in banking

The development of customer loyalty is one of the most important issues

today. To deal with this high concentrated market, business is attempting not

only to attract and satisfy customers but also to create a long-term relationship

with these customers. A bank has to create the customer relationship that

delivers value beyond the provided by the core product. This involves added

tangible and intangible elements to the core products, thus creating and

enhancing the product surrounding.

Factors influencing customer loyalty

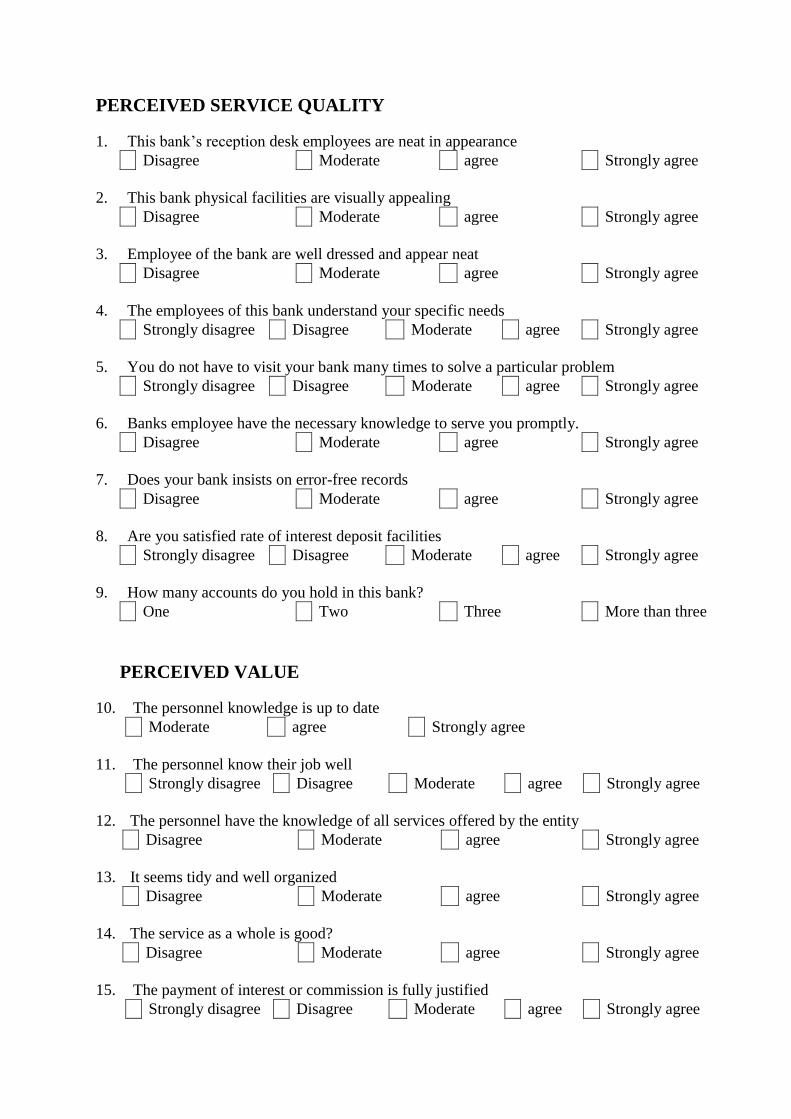

Perceived Service Quality

Core offering

Satisfaction

Perceived value

Elasticity level

Market place

Demographics

Share of wallet

Image

Trust

Commitment

Perceived Service Quality (PSQ)

Introduced a service oriented approach to quality with the concept of

Perceived Service Quality and model of total Perceived Service Quality. This

approach is based on research into consumer behaviour and the effects of

expectations concerning goods performance on post consumption evaluations.

16

The consumers judge the overall excellence or superiority. The quality consists

of two primary elements, the first one is, to what degree a product or service

meets the needs of the consumers and second is, to what degree a product or

service is free from deficiencies.

Core Offering

The banks that boost the highest level of fiercely loyal customers have

built loyalty not on card programmes or gimmicks, but on a solid, dependable,

core offering that appeals to their customers. These banks have focused intently

on what they appeal to the type of customers they want to attract and have

determined and concentrated on delivering what is expected every time. This

built loyalty by understanding its customer‟s needs and then empowering its

employees to deliver those needs consistently.

Satisfaction

Customer satisfaction in banking industry means that the product or

service which is offered to the customer makes him or her satisfied and meets

his or her expectations. This means that the customer feel good to have the

service from that bank another time. In the competitive environment which the

competitors are trying to have the other‟s customers, this antecedent can be

vital. Customer satisfaction is therefore based on an evaluation of multiple

interactions and is considered as a combination of overall customer attitudes

towards the bank that incorporates a number of measures like meeting of

expectations and service quality.

Perceived Value

There is a multi-facet meanings of value which vary according to

different functional context – economics – (utility and monetary costs), social

science (human values), industrial settings (process and costs), and marketing

(consumer‟s perspective on trade off between benefits and sacrifices or costs).

The meaning is not limited to these functional definitions but also include

17

cognitive and affective aspects of value such as social, emotional and epistemic

value.

Elasticity Level

Elasticity expresses the importance of a purchasing decision-effectively

the level of involvement or indifference. This applies on both the customer and

the business.

Market Place

It is a key factor in the development of loyalty. If the number of

competing suppliers is high and little effort is required to switch, switching is

clearly more likely. This is the opposite of case of switching. Most banks enjoy

a high level of inertia loyalty simply because it‟s often so difficult and time-

consuming to change to a new bank and transfer direct debits and standing

orders.

Demographics

The developers of the conversion model, more affluent and better

educated customers and less likely to be committed to a specific brand. They

say that the commitment of less affluent consumers to the brands they use of

often unusually strong-possibly because they cannot afford to take the risk of

trying a brand that might not suit them as well. They also suggest that younger

consumers are less committed to brands than older consumers.

Share of Wallet

As market become saturated and customers have so much more to

choose from share of wallet which becomes increasingly important. It is

cheaper and more profitable to increase the share of what the customer spends

in the sector, than to acquire new customers.

Image

Image has been defined as the perceptions of an organization reflected

in the associations held in consumer memory. This is similar to corporate

18

image which is assumed to influence the customer‟s choice of service, when it

is difficult to distinguish between service attributes. Corporate image is

established or developed in the consumer‟s mind through communication and

experience.

Commitment

Customer commitment is important factor that affect loyalty. It is a

deeply held commitment to re-buy and re-patronize a preferred product or

service consistently in the future, thereby causing repetitive same-brand

purchasing despite situational influences and marketing efforts having the

potential to cause switching behaviour.

Trust

Investment manager polar capital plans to launch a fixed-life trust to

invest in global banks and financial stocks. Bank said the financial sector has

been deeply out of favour with investors since the financial crisis began, but the

return of dividend payments in particular could be a catalyst for a re-rating.

State Bank of India Macquarie Infrastructure Trust is an unlisted fund with

INR 11,871 million of committed capital.

Customer Relationship Management

Developing close, cooperative relationship with customers is more

important in the current era of intense competition and demanding customers

that it has been ever before. Many scholars are interested in strategies and

processes for customer classification and selectivity, one-to-one relationship

with individual customers, key account management and customer business

development processes, frequency marketing, loyalty programmes, cross-

selling and up-selling opportunities and various forms of partnering with

customers including co-branding, joint marketing, co-development and

strategic alliances. A majority of these promises are to individualise and

personalise customer relationship by providing vital information at every point

of customer interface.

19

Customer Relationship Management is an enterprise-wide activity; it is

not just confined to the marketing department of the organisation. The

objective of CRM is acquisition, retention and partnering with the customers.

There has to be segmentation of the customers for whom CRM is designed.

Factors responsible for growth of CRM

The recent growth of Customer Relationship Management can be

attributed to various factors. These include the reduced role of intermediaries,

especially with the advent of sophisticated computer and telecommunication

technologies. This growth in technology again allowed the producers to

directly communicate and get in touch with the customers at a very low cost.

This success of doing without intermediaries is also an account of the growth

of service economy. Since services are produced and delivered at the same

time, the role of intermediary gets lessened. Since the customers transact

directly with the service provider, he develops greater relational bonding with

the company and its people. This leads to greater need of maintaining and

enhancing the relationships which provides greater fruits.

The factor which has been responsible for the increased need and use of

Customer Relationship Management is enhanced emphasis that companies lay

on adopting total quality management as an essential component of modern

business. This increased use of total quality in all functions of the management

by the companies has forced them to involve the suppliers and the customers

across the value chain. The application of various supply chain initiative such

as Just in Time (JIT), Material Resource Planning (MRP) and Enterprise

Resource Planning(ERP) is not possible unless the company works in close

relationship with all the stakeholders.

Changing role of CRM

The explosion of new channels and new media, web in particular, has

caused organisations to look at ways to exploit their benefits. Customers want

the flexibility of being able to chosen when and how they make contact

whether via phone, web, e-mail, fax or by any other means. The challenge for

20

organisations is to look for low-cost solutions that will ease the development

and deployment of new and existing applications over new channels. Web

enablement is not enough: organisations also need solutions that have been

building from the ground up to the web-centric one.

Before beginning the task of implementing Customer Relationship

Management across enterprises, the organisation must first redefine the

enterprise, putting the customer into focus. Most organisations are structured

by functional specialisations (marketing, sales and customer service) in which

each department has a unique relationship with the customer. In this model,

there is no comprehensive view of the customer and no broad strategy for the

relationship. The enterprise typically does not also understand the existing or

potential profitability of that customer.

On the other hand, an end-to-end Customer Relationship Management

strategy focuses on the complete customer value chain. In this model, lines of

business collaborate around the customer, focusing on enhancing the customer

experience and increasing customer lifetime value.

Customer Relationship Management system alone does not help the

organisation deliver this type of experience to the customers. The importance

of customer experience is become more “customer-centric”.

Building and managing customer loyalty.

Creating a single window for the customer.

Managing or improving the customer experience.

Banking and financial sector

Today‟s banking rarely requires seeing the bank branch. Even if the

customer is required to visit the bank branch, it is no more a workplace ghetto.

There is a top class ambience to boot, centrally air-conditioned lounges. Coffee

and water dispensers of fridge stocked with goodies and chocolates. Even

minute things such as layout, furnishings and colour schemes for interiors,

signboards and brochure holder are planned out in detail to convey the bank‟s

21

changing facade. The entry of foreign banks and the emergence of new private

banks have changed the rule of the game. The customers are now welcomed

with a coffee or dosa or lunch at free of cost.

Recent customer service initiatives in banking industry

Today, most of the private banks operate from 8 a.m. to 8 p.m. Even

public sector banks have increased their working hours. Allahabad Bank which

earlier operated from 10 a.m. to 2 p.m. has opened regular banking activity till

3.30 p.m. These physical changes have been in addition to providing

technology-based support of anywhere anytime banking, introduction of the

facility of ATMs, net banking, phone banking, etc. There have been marked

shift in the way the branches have been appearing. Air-conditioning, wonderful

lighting, prominent locations, and other modern facilities are something that

does not surprise people by any means. Even the public sector behemoth State

Bank of India has planned for a uniform design, structure, seat placement and

wall colour painting across the country.

The branch managers in most of the private banks do not sit behind

closed doors, infact most of the cases they do not have a door at all. This is

deliberately designed to give people a feel that anyone can access the manager

without hesitation. ABN-Amro bank plans each if its branches to have a coffee

parlour. Bank Muscat‟s life manages books the ticket for his client, offers to

walk his dog to the nearest lamp-post and, if need be, even delivers grocery for

the week from the nearest departmental store. ABN-Amro bank‟s branch offers

unlimited Barista coffee from 7.30 p.m. to 11.00 p.m.

Customer Involvement in Banking

The bank‟s aim is to engage customers at the branch. The customer can

choose his time and the banks in turn create the right environment. Bandra

branch of SBI offers coffee to its customers. The bank wants to be homely and

interesting. So, it has started hosting programmer such as Dandia Week, Parsi

New Year, Women‟s Day and Diwali. Recently, it even allowed selling

vegetable cakes at the branch, The branch is reaping rich dividends also getting

22

700 customers a day. The concept behind offering a little bit extra encompasses

the ethic of offering the best service to customers according to their need and at

the same time ensuring the comfort of accessibility of its branches as well as

ambiance that makes banking a pleasure rather than a chore, Bandra has

tastefully done lounges, a smart art gallery to showcase local talent, a Barista

outlet to catch-up a quick cup of coffee and, of course, the impeccable front

office standards all for a lasting satisfaction.

Retail banking initiative in public sector

Realising the importance of customer service in the growth of banking

industry, even public sector banks have started designing their offers with a

new watch word for the customer‟s delight. Quite a few public sector banks

have carved out a separate branch to cater to retail customers. Personal

Banking Branches of SBI, Signature Bank of Punjab National Bank, Retail

Loan Factory of Bank of Baroda and Retail Boutique of Allahabad Bank are

few such branches. These branches are clearly no workplace ghettos. There are

a top class ambience to boot, centrally air-conditioned lounges, and amenities

such as free photocopier, fax and phone, tea or coffee and water dispensers and

fridge stocked with foodies also being proposed.

Approaches to CRM

Customer Relationship Management is a team for the software and other

methods with which a business manages its customer in the company may

access this database, to match customer needs with new product offerings and

other such services. CRM has gained a lot of importance for running a

successful business in the last few years. It has undoubtedly generated value,

implement new CRM initiatives to keep their customers happy and run a

successful business.

23

Different approaches to CRM:

o Operational CRM

Operational Customer Relationship Management renders automated

support for business that have a direct interaction with their customers.

1. Sales Force Automation (SFA)

Tracking customer preferences

Maintaining a lead tracker

Demographics

Contract management

Performance management

Tracking customer transactions

Many organisations set up call centres to maintain customer informative.

These call centres help customers with their queries about the organisation.

Several software companies offer CRM applications that allow an organisation

in efficient tracking and maintenance of customer.

2. Customer service and support (CSS)

Customer service and support automates, processes that are related

to service. This could include service requests, customer

communications.

3. Enterprise Marketing Automation (EMA)

Enterprise Marketing Automation applications automate

marketing tasks used for contact and lead generation. Enterprise

market in the relevant customer advertisement forms, the basis of

an effective EMA application.

o Analytical CRM:

For an effective and successful CRM strategy, it is necessary to

thoroughly analyse and understand customer behaviour. Analytical is used to

retain customers before they switch to a competitor. The more, the information

24

available to the software for these analyse is used to cross-sell product to

customers.

o Collaborative CRM:

Collaborative Customer Relationship Management is an approach where

the various departments of an organization share customer information among

themselves. For example, the information obtained through customer feedback

in the customer service, technical support, etc. Collaborative CRM also

facilitates a better communication between an organization and its customer

across different communication, online services are also provided to the

customer in an attempt to cut service costs.

A good collaborative CRM

Increases efficiency

Improves Customer satisfaction

Improves Customer service

Improves Customer relationship.

Thus a good CRM solution can not only help to make a customer happy,

but also benefit an organization in more ways than one.

Benefits of CRM

A Customer Relationship Management system may be chosen because it

is thought to provide the following advantages

Quality and efficiency

Decrease in overall costs

Decision support

Enterprise ability

Customer attention

Increase profitability

25

Challenges

Successful development, implementation, use and support of Customer

Relationship Management systems can provide a significant advantage to the

user, but often there are obstacles that obstruct the user from using the system

to its full potential. Instances of a Customer Relationship Management

attempting to contain a large, complex group of data can become cumbersome

and difficult to understand for ill-trained users. An interface that is difficult to

navigate or understand can hinder the CRM‟s effectiveness, causing users to

pick and choose which areas of the system to be used, while other may be

pushed aside. This fragmented implementation can cause inherent challenges,

as only certain parts are used and the system is not fully functional. The

increased use of customer relationship management software has also led to an

industry-wide shift in evaluating the role of the developer in designing and

maintaining its software. Companies are urged to consider the overall impact of

a viable CRM software suite and the potential for good or bad in its use.

Complexity

Tools and workflows can be complex, especially for large businesses.

Previously these tools were generally limited to simple Customer Relationship

Management solution which focused on monitoring and recording inter actions

and communications. Software solutions then expanded to embrace deal

tracking, territories, opportunities, and the sales pipeline itself. Next came, the

advent of tools for other client-interface business functions. These tools have

been, and still are, offered as on-premises software that companies purchase

and run on their own Information Technology infrastructure.

Poor usability

One of the largest challenges that Customer Relationship Management

systems face is poor usability. With a difficult interface for a user to navigate,

implementation can be fragmented or not entirely complete. The importance of

usability in a system has developed over time. Customers are likely not as

patient to work through malfunctions or gaps in user safety, and there is an

26

expectation that the usability of systems should be somewhat intuitive. An

intuitive design can prove most effective in developing the content and layout

of a Customer Relationship Management system.

Fragmentation

Often, poor usability can lead to implementations that are fragmented-

isolated initiatives by individual departments to address their own needs.

Systems that start disunited usually stay that way, and decision processes

frequently lead to separate and incompatible system, and dysfunctional

processes. A fragmented implementation can negate any financial benefit

associated with a customer relationship management system, as companies

choose not to use all the associated features factored when justifying the

investment.

Business reputation

Building and maintaining of a strong business reputation has become

increasingly challenging. The outcome of internal fragmentation that is

observed and commented upon by customers is now visible to the rest of the

world in the era of the social customer, in the past, only employees or partners

were aware of it. Addressing the fragmentation requires a shift in philosophy

and mindset in an organization so that everyone considers the impact to the

customer of policy decisions and actions. Some developments and shifts have

made companies more conscious of the life-cycle of a Customer Relationship

Management system. Companies now consider the possibility of brand loyalty

and persistence of its users to purchase updates, upgrades and future editions of

software. Additionally, Customer Relationship Management systems face the

challenge of producing viable financial profits. Poor usability and low usage

rates lead many companies to indicate that it was difficult to justify investment

in the software without the potential for more tangible gains.

27

Security concerns

A large challenge faced by developers and users is found in striking a

balance between ease of use in the Customer Relationship Management

interface and suitability and acceptability of security measures and its features.

Corporations investing in CRM software do so expecting a relative ease of use

while also requiring that customer and other sensitive data remain secure. This

balance can be difficult, as many believe that improvements in security come at

the expense of system usability.

Technical writers can play a large role in developing Customer

Relationship Management systems that are secure and easy to use. Customer

Relationship Management systems need to be more open to flexibility of

technical writers, allowing these professionals to become content builders.

These professionals can gather information and use it at their preference,

developing a system that allows users to easily access desired information and

is secure and trusted by its users.

Not only sales activities but also those for marketing, customer service,

and technical support the overall goals are of find, attract, and win new clients,

nurture and retain those the company already has, entice former clients back in

to the fold, and reduce the costs of marketing and client service. Customers

Relationship Management describes a company-wide business strategy

including customer-interface departments as well as other departments.

Measuring and valuing customer relationship is critical to implementing this

strategy.

Public Sector Banks (PSBs)

In India, as in many developing countries, the public sector bank has

been the dominant element in the country‟s financial system. This sector has

preformed the key functions of providing liquidity and payment services to the

real sector and has accounted for the bulk of the process of intermediation

process. Besides institutionalizing savings, the banking sector has contributed

to the process of economic development by serving as a major source of credit

28

to households, government, business and to weaker sectors of the economy like

village and small scale industries and agriculture.

An important landmark in the development of banking sector in recent

years has been the initiation of reforms following the recommendations of the

first Narasimham Committee on Financial System. In reviewing the strengths

and weaknesses of these banks, the committee suggested several measures to

transform the Indian banking sector from a highly regulated to a more market

oriented system and to enable it to compete effectively in an increasingly

globalised environment. Many of the recommendations of the committee

especially those pertaining to interest rate, an institution of prudential

regulation and transparent accounting norms were in line with banking policy

reforms implemented by a host of developing countries since 1970. Public

sector banks are banks where a majority stake (more than 50%) is held by a

government. The shares of these banks are listed on stock exchanges. There are

a total of 26 PSBs in India.

Emergence of Public Sector Banks:

The Central Government entered the banking business with the

nationalisation of the Imperial Bank of India in 1955. A 60% stake was taken

by the Reserve bank of India and the new bank was named as the State bank of

India. The seven other state banks became the subsidiaries of the new bank

when nationalised on 19th

July 1960. The next major nationalisation of banks

took place in 1969 when the government of India, under Prime Minister Indira

Gandhi, nationalised an additional 14 major banks. The total deposits in the

banks nationalised in 1969 amounted to 50 Crores . This move increased the

presence of nationalised banks in India, with 84% of the total branches coming

under government control.

The next round of nationalisation took place in April 1980. The

government nationalised six banks. The total deposits of these banks amounted

to around 200 Crores. This move led to a further increase in the number of

29

branches in the market, increasing to 91% of the total branch network of the

country. The objectives behind nationalisation where:

To break the ownership and control of banks by a few business

families.

To prevent the accumulation of wealth and economic power.

To mobilize savings from masses from all parts of the country.

To cater the needs of the priority sectors.

Public sector banks before the economic liberalisation:

The share of the banking sector held by the public banks continued to

grow through the 1980s, and by 1991 the public sector banks accounted for

90% of the banking sector. A year later, in March, 1992, the combined total of

branches held by public sector banks was 60,464 across India, and deposits

accounted for Rs. 1,10,000/- Crores. The majority of these banks were

profitable, with only one out of the 27 public sector banks reporting a loss.

Public sector banks after the reforms:

After the reforms in the early 1990s, the nationalised banks saw a

change in fortunes: in 1992-93, 12 of the nationalised banks reported losses,

and the other seven nationalised banks reported marginal profit. 1995-96 saw a

similar problem, with nationalised banks reporting a combined loss of

Rs 1160 Crores. However, the early 2000 saw a reversal of this trend, such that

in 2002-03 a profit of Rs.7,780 Crores by the public sector banks, a trend that

continued throughout the decade, with Rs.16,856 Crore profit in 2008-09.

Role of Public Sector Banks

A proper financial sector is of special importance for the economic

growth of developing and underdeveloped countries. The public banking sector

which forms one of the backbones of the financial sector should be well

organized and efficient for the growth dynamics of a growing economy. No

underdeveloped country can progress without setting up a sound system of

30

commercial banking. The following systems are important for a public sector

banking in a developing country.

Capital Formation:

The rate of saving is generally low in an underdeveloped economy due

to the existence of deep rooted poverty among the people. Even the potential

savings of the country cannot be realized due to lack of adequate banking

facilities in the country. To mobilize dormant savings and to make them

available the entrepreneurs for productive purpose, the development of a sound

system of public sector banking is essential for a developing economy.

Monetization:

An underdeveloped economy is characterized by the existence of a large

non-monetized sector, particularly in the backward and inaccessible areas of

the country. The existence of this non-monetized sector is a hindrance to the

economic development of the country. The banks, by opening branches in rural

and backward areas, can promote the process of monetization in the economy.

Innovations:

Innovations are an essential prerequisite for economic progress. These

innovations are mostly financed by bank credit in the developed countries. But

the entrepreneurs in undeveloped countries cannot bring about these

innovations for lack of bank credit in an adequate measure. The banks should,

therefore, pay special attention to the financing of business innovations by

providing cheap credit to entrepreneurs.

Finance for priority sectors:

The commercial banks in underdeveloped countries generally hesitate in

extending financial accommodation to priority sectors such as agriculture and