Embed Size (px)

Citation preview

1 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Adani Enterprise Ltd

A goose that lays golden eggs

2 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

TABLE OF CONTENTS

Summary 03

Valuation and Peer Comparison 04

- SOTP Valuation for AEL 04

- Band Charts & Price Performance 05

- Peer comparison & Scatter plot 07

Financial Summary & Story in Charts 09

Company Overview 11

Financial Analysis & Projections 16

AEL’s Business Segments 17

Capital Management 17

Green Hydrogen – Adani New Industries Ltd (ANIL) 24

Coal – Commercial Mining, MDO & IRM 69

Road Construction 81

Data Center – Adani Connex 92

Airport Operations 101

FMCG – Adani Wilmar 121

Defence & Aerospace 137

Copper 150

Green PVC 155

Digital – Super App 160

Business Quality Score 165

Annual Report Takeaways 166

Key Management Personnel 169

Risk & Concerns 169

Summary of Management Commentary on Quarterly Performance 170

Financial Statement Analysis & Projections 171

Disclaimer 172

3 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

On 9th Dec 2021, we initiated coverage on the listed business units of Adani Group

which included Adani Enterprises Ltd (AEL). Post our coverage, AEL has undertaken

several initiatives that warrant detailed coverage. Through Adani New Industries

Ltd (ANIL), the group’s recent incubator in the production of renewable energy,

green H2 and downstream products (ammonia, urea & methanol), AEL will emerge

as the world’s primary leader in the green H2 ecosystem. ANIL has a vision to be the

lowest cost producer of green H2 and in partnership with TotalEnergies, we expect

this platform to be extended to the global theatre in the forthcoming future. ANIL

will be leveraging TotalEnergies balance sheet to help lower cost of funds.

Apart from ANIL, AEL’s other incubating businesses, in the domains of Airports, Data

Centers, Roads and Defence are on the verge of gaining traction and should be value

accretive in the short to medium term. AEL’s new incubating forays into copper and

green PVC have significant drivers in place to ensure long-term profitability and the

equity contribution is expected to be funded from internal accruals.

The existing coal ecosystem (captive mines, IRM and MDO) has favourable tailwinds

which will endure the already appreciated energy pricing (post the Russia-Ukraine

conflict). The favourable pricing environment has ensured that the break-even for

the Carmichael mine is upended and profitability should be realized sooner.

Given the favourable outlook across all business segments, we value AEL at INR

2,900 per share based on our SOTP valuation methodology. This represents an

upside of 29.2% from the current CMP of INR 2,245. We believe that a demerger of

the incubating business can result in significant value unlocking and is an upside risk

to our estimates. A case in point is the 153% appreciation in the stock price of Adani

Wilmar Ltd post-IPO. We expect the airport business to be the next value-unlocking

story that should play out over the next couple of years.

Risks to our upside thesis are (i) unexpected downturn in the economy, (ii) delay in

project execution and (iii) project finance. Historically, AEL has proven adequately

its project execution skills with timely delivery and capital management discipline.

Hence in our view, the risk factors are significantly diluted.

Key Consolidated Financial Data (INR Cr, unless specified)

Net Revenue

EBITDA Net

Profit EBITDA

(%) Net (%)

Adj EPS (₹)

Adj BPS (₹)

RoE (%)

RoIC (%)

P/E (X)

P/BV (X)

EV/EBITDA (X)

FY21 39,537 2,505 923 6.3 2.3 7.8 159.6 5.4 6.3 288.3 14.1 111.9

FY22 69,420 3,713 777 5.3 1.1 6.6 227.3 3.5 4.2 342.6 9.9 81.6

FY23E 58,656 6,835 1,517 11.7 2.6 12.8 289.7 5.5 4.7 175.3 7.7 48.3

FY24E 78,084 13,738 6,122 17.6 7.8 51.7 388.2 16.7 7.2 43.5 5.8 27.1

FY25E 118,612 21,903 6,917 18.5 5.8 58.4 488.6 14.8 7.9 38.5 4.6 19.3

We have consolidated 75% of ANIL and 50% of AdaniConnex financials in our estimated numbers

BUY @ CMP INR 2,245 Target: INR 2,821 in 24 months Upside Potential: 25.7%

A goose that lays golden eggs

Industry Diversified

Scrip Details

Face Value (INR) 1.0

Market Cap (INR Cr) 255,976

Price (INR) 2,245

No of Sh O/S (Cr) 114

3M Avg Vol (000) 336

52W H/L (INR) 2,420/1,333

Dividend Yield (%) 0.05

Shareholding (%) Mar 2022

Promoter 72.3

Institution 21.5

Public 6.2

TOTAL 100.0

Price Chart

0

5,000

10,000

15,000

20,000

0

500

1,000

1,500

2,000

2,500

3,000

Jun-19 Jun-20 Jun-21 Jun-22

AEL Nifty

Adani Enterprise Ltd

4 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Valuation

We value AEL on a SOTP basis for a price target of INR 2,821 per share# (FY25 EV/EBITDA of

21.9X) and recommend a BUY at a CMP of INR 2,245, representing an upside of 25.7% over the

next 24 months.

AEL valuation summary

Source: Company Reports

# Valuation is based on 1.0 MMTPA of green H2 capacity

Although the company has announced plans for 2.5 MMTPA of green H2 generation we have

clear visibility of 1 MMTPA production and hence we have valued ANIL on the basis of the

conservative numbers. Any announcements to ramp up capacity to 2.5 MMTPA will be an

upside risk to our price estimates.

ParticularsValuation

method

Mar 2025

Value

(INR Cr)

AEL Stake

(%)

AEL Stake

Value

(INR Cr)

Conglomerate

Discount (%)

Equity value

attributable

to AEL

(INR Cr)

Attributable

value per

share (INR)

Existing Businesses

Airports DCF 1,10,660 100 1,10,660 15 94,061 794

Road Consutruction DCF 34,742 100 34,742 15 29,530 249

FMCG DCF 63,438 44 27,913 15 23,726 200

Coal (Carmichael + IRM & MDO) DCF 12,882 100 12,882 15 10,950 92

Defence EV/EBITDA 9,112 100 9,112 15 7,745 65

Value from existing businesses 1,66,012 1,401

Future Businesses

Green Hydrogen DCF 2,07,397 75 1,55,548 15 1,32,216 1,116

Data Centers DCF 10,346 50 5,173 15 4,397 37

Copper DCF 22,503 100 22,503 15 19,128 161

Petrochemicals DCF 14,787 100 14,787 15 12,569 106

Value from future businesses 1,68,309 1,420

Consolidated Value of AEL 2,821

Current Market Value of AEL 2,245

Upside Potential (%) 25.7

5 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Source: Ventura Research

1,200

1,500

1,800

2,100

2,400

2,700

3,000

Ap

r-2

1

May

-21

Jun

-21

Jul-

21

Au

g-2

1

Sep

-21

Oct

-21

No

v-2

1

De

c-2

1

Jan

-22

Feb

-22

Mar

-22

Ap

r-2

2

May

-22

Jun

-22

1 year forward EV/EBITDA

EV per sh 64.8x 68.8x

72.8x 76.8x 80.8x

60

65

70

75

80

85

90

Ap

r-2

1

May

-21

Jun

-21

Jul-

21

Au

g-2

1

Sep

-21

Oct

-21

No

v-2

1

De

c-2

1

Jan

-22

Feb

-22

Mar

-22

Ap

r-2

2

May

-22

Jun

-22

EV/EBITDA and Std Deviation

EV/EBITDA Average

1 SD Lower Band 2 SD Lower Band

1 SD Upper Band 2 SD Upper Band

-20

0

20

40

60

80

100

120

140

Ap

r-2

1

May

-21

Jun

-21

Jul-

21

Au

g-2

1

Sep

-21

Oct

-21

No

v-2

1

De

c-2

1

Jan

-22

Feb

-22

Mar

-22

Ap

r-2

2

May

-22

Jun

-22

Price performance: AEL vs RIL

AEL RIL

3.5

4.0

4.5

5.0

5.5

6.0

Ap

r-2

1

May

-21

Jun

-21

Jul-

21

Au

g-2

1

Sep

-21

Oct

-21

No

v-2

1

De

c-2

1

Jan

-22

Feb

-22

Mar

-22

Ap

r-2

2

May

-22

Jun

-22

Valuation gap between AEL & RIL - Ready infra for H2 & RE has created a valuation gap

AEL to RIL EV/EBITDA (X)

A healthy mix of profitable businesses with high growth incubating businesses deserves premium valuation

6 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Adani Enterprise Ltd SWOT Analysis in a nutshell

Adani Enterprises Ltd

Growth Drivers

Changing energy mix towards renewables and green H2.

Increasing demand for data localization due to significant surge in local data usage.

Rise in construction activities of expressways for seamless connectivity between upcoming or new growth cities.

Focus on domestic procurement of defence equipments to increase indeginsation.

Increase in number of airports under UDAAN is expected to enhance airpassenger

Key Challenges

Green H2 is at nascent stage and therefore its cost of production is high. In addition, land availability for additoin solar capacity would be a challenge

Finding a real estate land for data center at a reasonable price is a challenge.

New Trends

Renewables and green H2 in India's energy mix could offer significant and decadal growth opportunity

We have been dependet on overseas data centers. localization of data has increased the demand for data centers in India

Investment Themes

Tieups with global leaders in different business verticals

- EdgeConnex in data center

- TotalEnergies in green H2

Infrastructure readiness for new age future businesses

Superior execution skills in large scale complex projects within stipulated time

For any further query, please email us on [email protected]

7 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Valuation and comparable metric of domestic and global companies

Source: Ventura Research & Bloomberg

Company Name Mkt Cap PricePEG

20252022 2023 2024 2025 2022 2023 2024 2025 2022 2023 2024 2025 2022 2023 2024 2025 2022 2023 2024 2025 2022 2023 2024 2025 2022 2023 2024 2025 2022 2023 2024 2025

Domestic Peers (fig in INR cr, unless specified)

Adani Enterprise Ltd 2,55,930 2,245.0 0.3 329.6 NA 41.8 37.0 11.5 9.3 7.0 5.5 80.7 43.1 23.0 15.6 3.5 5.5 16.7 14.8 3.7 6.5 10.8 12.1 69,420 58,656 78,084 1,18,612 5.3 11.7 17.6 18.5 1.1 2.6 7.8 5.8

Reliance Industries Ltd 16,46,090 2,433.0 1.0 27.0 20.0 17.9 17.1 2.1 1.9 1.7 1.6 15.6 11.8 10.3 8.9 7.7 9.5 9.7 9.2 9.4 11.8 12.5 14.5 6,94,803 8,67,101 9,06,712 9,64,233 16.0 17.0 18.0 17.8 8.8 9.5 10.1 10.0

Grasim Industries Ltd 88,837 1,350.0 0.2 13.0 12.6 9.0 6.0 1.2 1.1 1.0 0.8 6.5 6.4 4.9 3.0 9.3 8.6 10.7 13.5 2.2 14.0 18.4 23.9 88,958 1,13,715 1,23,494 1,36,713 21.6 19.2 21.6 22.3 7.7 6.2 8.0 10.8

ITC Ltd 3,53,369 287.0 1.6 23.2 20.6 18.7 17.2 5.6 5.5 5.2 5.2 17.5 15.6 13.7 11.9 24.2 26.5 27.9 30.2 31.6 36.2 45.9 58.5 57,495 64,056 69,209 76,141 34.7 34.8 35.5 36.2 26.5 26.8 27.3 26.9

Larsen & Toubro Ltd 2,19,828 1,564.0 0.7 23.7 19.6 16.2 14.0 2.7 2.5 2.2 2.0 17.3 14.8 12.7 11.5 11.3 12.5 13.8 14.5 8.7 9.8 11.0 11.7 1,57,184 1,79,192 2,02,283 2,26,755 11.8 12.0 12.4 12.5 5.9 6.3 6.7 6.9

Vedanta Ltd 80,607 217.0 0.4 4.2 3.3 3.5 3.3 1.2 1.1 1.0 0.9 2.5 2.1 2.1 1.9 28.7 34.0 28.8 28.1 37.1 44.7 40.6 34.2 1,21,482 1,37,566 1,34,007 1,33,594 36.7 37.4 36.6 38.3 16.0 17.7 17.1 18.1

Tata Power Ltd 67,981 213.0 1.4 30.2 25.4 23.5 20.2 3.1 2.8 2.5 2.2 14.6 12.8 11.4 10.1 10.2 10.9 10.6 11.0 7.3 8.5 9.1 7.8 37,975 47,625 51,555 59,598 20.0 18.6 19.3 19.8 5.9 5.6 5.6 5.6

NTPC Ltd 1,37,111 141.4 1.0 8.8 7.6 6.5 7.1 1.0 0.9 0.8 0.8 8.3 5.2 4.6 6.4 11.6 12.1 13.0 11.8 8.0 13.1 13.9 9.6 1,30,493 1,43,628 1,54,096 1,47,879 31.3 31.5 31.9 30.9 12.0 12.5 13.7 13.0

Coal India Ltd 1,12,932 183.3 0.4 7.0 6.1 6.1 4.8 2.7 2.3 2.1 1.7 4.2 3.5 3.5 3.0 39.3 38.5 33.5 34.8 51.4 50.6 45.6 46.9 1,05,598 1,17,009 1,21,209 1,23,162 21.8 22.4 22.0 19.8 15.4 15.9 15.2 19.1

NMDC Ltd 31,900 108.9 1.5 3.3 3.5 3.3 3.1 0.9 0.9 0.8 0.8 2.5 2.7 2.7 2.5 27.5 24.8 25.7 25.2 41.8 24.3 21.8 13.9 26,191 25,281 25,737 28,310 40.7 39.2 40.7 39.0 36.9 36.2 38.1 36.3

IRB Infrastructure Ltd 11,776 195.0 0.1 37.1 19.0 12.2 8.7 0.9 0.9 0.8 0.8 7.7 7.6 6.3 6.4 2.6 4.7 7.0 9.2 9.4 9.2 10.7 10.0 5,906 6,752 7,771 8,989 48.6 46.9 47.6 48.3 5.4 9.2 12.5 15.1

KNR Construction Ltd 6,647 236.0 0.8 19.0 14.1 12.8 12.5 2.8 2.4 2.1 1.8 9.8 8.4 7.6 7.0 15.0 16.9 16.4 14.5 26.8 23.2 25.0 22.2 3,200 3,900 4,471 4,716 20.3 19.5 18.8 19.2 10.9 12.1 11.7 11.2

Dilip Buildcon Ltd 2,891 198.0 1.3 9.0 9.5 8.3 7.5 0.7 0.6 0.6 0.5 7.1 3.7 3.4 3.1 7.5 6.4 7.1 7.2 8.0 14.5 14.2 14.8 9,303 10,408 10,755 11,831 8.6 13.9 13.9 13.9 3.5 2.9 3.2 3.2

Ashoka Buildcon Ltd 2,096 74.7 0.1 6.3 3.9 3.1 2.8 2.2 1.1 0.8 0.6 4.6 3.8 3.0 2.7 34.6 27.9 26.3 22.4 59.6 52.9 51.3 47.4 5,587 6,273 7,133 7,846 9.2 9.7 9.9 9.9 5.9 8.5 9.6 9.6

PNC Infratech Ltd 6,186 241.0 0.8 13.0 10.8 9.5 9.2 1.8 1.6 1.4 1.3 7.0 6.0 5.5 5.1 14.1 14.7 14.5 13.6 23.8 25.4 23.0 21.2 6,085 7,225 8,134 8,784 13.5 13.1 13.3 13.3 7.8 7.9 8.0 7.7

Global Peers (fig in USD mn, unless specified)

BHP Group Ltd (Australia) 1,50,503 29.7 -0.7 6.9 8.0 11.1 13.0 2.8 2.8 2.8 2.4 3.6 3.9 5.0 5.0 41.1 35.3 25.3 18.6 64.8 60.1 44.6 38.8 66,558 61,556 52,468 51,392 63.8 62.3 57.0 55.0 32.9 30.6 25.8 22.6

Rio Tinto (Australia) 1,10,919 74.8 -0.6 5.8 7.8 9.2 10.9 2.1 2.1 1.9 1.9 3.3 4.1 4.5 4.7 36.4 26.6 21.1 17.6 55.6 39.7 32.5 27.1 59,507 52,548 49,406 45,498 56.4 52.0 49.9 50.4 31.9 27.2 24.4 22.3

China Shenhua Energy (China) 90,870 4.9 1.4 8.9 8.7 8.4 7.6 1.6 1.6 1.5 1.3 4.1 4.1 3.9 3.6 17.9 17.9 17.9 16.5 41.2 35.8 34.6 30.1 50,708 51,783 52,861 58,147 35.0 35.7 36.3 36.3 20.0 20.2 20.6 20.6

Anglo American PLC (UK) 51,974 42.4 -0.6 6.1 7.6 9.2 13.2 1.6 1.4 1.3 1.2 2.9 3.2 3.6 3.7 26.7 19.1 14.5 9.1 46.4 34.4 27.0 21.8 41,743 39,124 36,994 33,518 46.4 43.4 40.7 41.7 20.3 17.6 15.3 11.8

Tronox Holdings PLC (USA) 2,492 16.0 0.3 4.9 4.3 4.1 3.4 1.1 0.9 0.8 0.6 4.4 3.8 3.5 2.2 21.7 20.9 19.4 19.0 17.2 18.2 17.7 25.0 3,992 4,130 4,203 4,443 27.0 28.1 28.6 30.9 12.8 14.0 14.4 16.5

Renew Energy PLC (USA) 2,361 5.9 0.2 78.7 54.4 41.4 12.8 1.6 1.6 1.4 1.3 9.6 9.0 8.8 7.4 2.1 2.8 3.4 10.0 8.3 8.0 8.0 9.5 797 1,125 1,336 1,471 88.5 80.3 82.9 77.8 3.8 3.9 4.3 12.6

Montauk Renewables (USA) 2,039 14.2 0.7 39.0 27.6 22.0 19.0 8.6 6.5 5.0 4.0 22.0 19.2 15.6 14.1 22.0 23.7 22.9 21.0 25.6 27.0 25.5 22.7 204 224 269 303 45.9 48.2 49.3 48.3 25.6 33.1 34.4 35.4

Transalta Corp (Canada) 2,968 11.0 -1.8 15.5 42.8 62.6 73.2 4.6 4.4 4.4 6.1 8.7 6.4 6.1 5.8 29.6 10.3 7.0 8.4 16.9 12.8 12.7 15.0 1,832 1,665 1,588 1,562 33.7 51.2 54.3 54.7 10.5 4.2 3.0 2.6

Ormat Technologies (USA) 4,128 73.6 1.3 55.4 37.0 32.8 29.8 2.0 2.0 1.8 1.7 14.0 11.7 10.6 9.6 3.6 5.3 5.5 5.7 5.2 6.8 8.3 4.8 722 872 942 955 59.5 59.7 59.6 64.6 10.3 12.8 13.4 14.5

Capital Power Corp (Canada) 4,115 33.9 3.1 16.7 21.5 17.8 14.6 2.3 2.3 2.4 2.8 8.7 7.7 7.7 7.5 13.9 10.9 13.7 19.2 10.7 9.3 11.3 12.9 1,547 1,534 1,569 1,539 49.0 56.4 55.7 56.2 15.9 12.5 14.7 18.3

Vistara Corp (USA) 9,725 22.5 19.5 13.3 7.4 12.1 13.0 1.8 1.8 1.8 3.0 5.8 5.0 5.4 5.4 13.7 24.1 14.8 23.2 9.3 15.7 9.7 7.0 14,972 15,037 13,796 12,124 21.1 23.7 25.9 28.9 4.9 8.7 5.8 6.2

Northland Power (Canada) 6,541 28.3 2.5 19.9 21.4 20.0 16.4 4.1 4.0 4.5 2.7 11.7 11.3 11.9 13.6 20.4 18.6 22.2 16.3 10.9 11.1 9.2 5.7 1,699 1,747 1,762 1,811 57.7 58.5 59.6 60.2 19.4 17.5 18.5 22.0

Clearway Energy Inc (USA) 6,125 28.7 1.6 38.0 25.6 26.0 24.6 1.8 1.8 1.7 1.6 10.0 9.6 9.6 9.3 4.8 6.9 6.5 6.5 4.1 5.0 4.9 5.7 1,367 1,325 1,333 1,373 90.2 96.9 94.7 95.5 11.8 18.1 17.6 18.2

Nextera Energy (USA) 5,638 67.2 1.8 28.2 24.0 24.2 20.4 2.7 1.4 3.1 7.6 6.5 6.0 5.8 5.4 9.4 5.7 12.7 37.2 7.8 7.2 10.5 14.2 1,741 1,968 2,142 2,291 97.8 96.0 96.8 95.7 11.5 11.9 10.9 12.1

Inergex Renewable (Canada) 2,690 13.2 0.2 126.6 46.5 31.7 19.3 3.6 3.9 5.0 3.7 13.0 12.3 12.8 12.7 2.9 8.4 15.9 19.1 5.2 5.9 6.3 6.0 683 721 751 762 75.9 75.5 74.4 74.6 3.1 8.0 11.3 18.3

Sunnova Energy Int. (USA) 2,012 17.6 0.2 33.5 ##### 72.5 10.0 1.2 0.8 1.4 1.2 54.5 43.1 37.8 31.7 3.4 -0.7 1.9 12.2 -1.0 -0.0 0.3 0.9 353 509 657 849 34.5 38.1 41.6 44.8 17.0 -3.5 4.2 23.6

Altus Power (USA) 1,186 7.7 -1.8 18.4 90.3 42.0 38.1 3.2 3.0 2.8 2.6 24.7 12.4 7.6 6.9 17.2 3.4 6.7 6.9 7.9 8.7 14.2 14.9 104 179 284 312 54.8 63.1 65.0 65.0 61.9 7.3 10.0 10.0

Terna Energy SA (Greece) 2,148 18.5 0.4 32.0 19.6 17.0 13.8 3.8 3.2 3.2 2.7 17.4 12.5 12.1 11.4 11.8 16.2 18.8 20.0 8.2 11.1 11.5 12.1 311 402 447 494 57.2 61.6 59.8 60.3 21.6 27.2 28.3 31.6

Voltalia SA (France) 1,789 18.8 1.1 43.4 27.4 25.2 24.1 2.4 2.2 2.0 1.9 13.8 11.0 9.7 9.5 5.5 8.1 7.8 7.9 6.5 8.2 9.2 8.9 488 579 588 603 43.9 49.9 55.3 59.1 8.5 11.3 12.1 12.3

ABO Wind AG (Germany) 524 56.8 0.7 33.7 22.2 18.8 17.1 3.0 2.7 2.4 2.1 16.0 11.6 10.0 9.1 8.9 12.0 12.9 12.4 10.0 14.3 16.5 16.3 217 260 280 377 17.6 19.6 20.5 16.7 7.2 9.1 9.9 8.1

CGN New Energy (China) 1,864 0.4 0.5 7.7 6.8 6.1 5.5 1.2 1.1 0.9 0.8 15.1 13.9 13.2 12.0 16.2 16.1 15.5 14.5 6.7 7.2 7.6 8.0 1,956 2,117 2,258 2,483 26.3 26.5 26.2 26.2 12.4 13.0 13.5 13.5

New Energy Solar (Australia) 180 0.6 -0.9 7.2 7.4 11.8 10.8 0.6 0.6 0.6 0.5 6.8 6.7 10.8 9.8 8.5 7.9 4.8 5.0 9.1 8.6 5.2 5.4 29 28 18 20 89.3 92.4 88.3 88.3 85.6 86.3 82.4 82.4

EBITDA Margin (%) Net Margin (%)P/E (X) P/B (X) EV/EBITDA (X) RoE (%) RoIC (%) Sales

For any further query, please email us on [email protected]

8 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL is in a high growth phase, which could reduce its RoIC, however, it is well-positioned for decadal growth

Source: Ventura Research, ACE Equity & Bloomberg

Adani Ent

RIL

Grasim

LT

Vedanta

Tata PowerNTPC

Coal India

NMDC

IRB Infra

KNR Const

Dilip Build

Ashoka Build

PNC Infra

BHP Grp

Rio Tinto

China Shenhua

Anglo American

Tronox

Renew Energy

Montauk

Transalta

Ormat Tech

Capital Power

VistaraNorthland Power

Clearway Energy

Nextera Energy

Inergex Renewable

Sunnova Energy

Altus Power

Terna Energy

Voltalia SA

ABO Wind

CGN New Energy

New Energy Solar

-5

5

15

25

35

45

55

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5

FY2

5 R

oIC

(%

)

EV/EBITDA to EBTIDA CAGR (X)

Adani Ent

RIL

Grasim

ITC

LT

Vedanta

Tata Power

NTPCCoal India

NMDC

IRB Infra

KNR Const

Dilip Build

Ashoka Build

PNC Infra

0

3

6

9

12

15

18

21

5 10 15 20 25 30 35 40 45 50

FY2

2-2

5 R

eve

nu

e C

AG

R (

%)

FY25 EBITDA Margin (%)

9 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL Consolidated Financial Summary

Source: Company Reports & Ventura Research

Fig in INR Cr (unless specified) FY17 FY18 FY19 FY20 FY21 FY22 FY23E FY24E FY25E

Revenue from operations 37,238 38,424 41,056 43,403 39,537 69,420 58,656 78,084 1,18,612

YoY Growth (%) 9.7 3.2 6.9 5.7 -8.9 75.6 -15.5 33.1 51.9

RM Cost and Opex 34,891 35,166 38,914 41,118 37,032 65,707 51,822 64,346 96,709

Expenses to Sales (%) 93.7 91.5 94.8 94.7 93.7 94.7 88.3 82.4 81.5

EBITDA 2,348 3,258 2,143 2,284 2,505 3,713 6,835 13,738 21,903

EBITDA Margin (%) 6.3 8.5 5.2 5.3 6.3 5.3 11.7 17.6 18.5

YoY Growth (%) (34.2) 6.6 9.7 48.2 84.1 101.0 59.4

Depreciation -34.4 108.6 416 472 537 1,248 2,501 3,340 5,920

EBIT 2,382.1 3,149.5 1,726 1,812 1,968 2,465 4,333 10,398 15,983

EBIT Margin (%) 4.2 4.2 5.0 3.6 7.4 13.3 13.5

YoY Growth (%) (45.2) 5.0 8.6 25.3 75.8 139.9 53.7

Other Income 118.5 236.4 580 684 754 1,013 651 1,628 409

Finance Cost 491.6 337.1 1,637 1,572 1,377 2,526 3,178 5,236 8,633

Exceptional Items 1 (161) (158) 199 (259) 0 0 0 0

PBT 2,010 2,888 511 1,122 1,086 952 1,807 6,790 7,759

PBT Margin (%) 1.2 2.6 2.7 1.4 3.1 8.7 6.5

YoY Growth (%) -82.3 119.7 -3.2 -12.3 89.8 275.8 14.3

Tax Expense 60 127 194 324 340 477 738 1,272 1,569

Tax Rate (%) 3.0 4.4 38.0 28.9 31.3 50.1 40.8 18.7 20.2

PAT 1,950 2,761 317 798 746 475 1,069 5,518 6,190

PAT Margin (%) 0.8 1.8 1.9 0.7 1.8 7.1 5.2

YoY Growth (%) -88.5 152.1 -6.5 -36.3 124.9 416.2 12.2

Min Int/Sh of Associates (963) (2,004) 401 340 176 301 448 604 727

Net Profit 988 757 717 1,138 923 777 1,517 6,122 6,917

Net Margin (%) 2.7 2.0 1.7 2.6 2.3 1.1 2.6 7.8 5.8

YoY Growth (%) -5.3 58.7 -18.9 -15.8 95.4 303.5 13.0

Adjusted EPS 9.0 6.9 6.5 10.3 8.4 7.1 13.8 55.7 62.9

P/E (X) 250.0 326.1 344.3 216.9 267.6 317.9 162.7 40.3 35.7

Adjusted BVPS 128.5 137.2 134.2 154.1 156.0 202.4 248.9 333.1 423.9

P/BV (X) 17.5 16.4 16.7 14.6 14.4 11.1 9.0 6.7 5.3

Enterprise Value 2,85,066 2,81,713 2,75,564 2,75,020 2,80,193 3,03,073 3,29,931 3,72,917 4,21,802

EV/EBITDA (X) 121.4 86.5 128.6 120.4 111.9 81.6 48.3 27.1 19.3

Net Worth 14,136 15,089 14,756 16,947 17,159 22,261 27,378 36,639 46,616

Return on Equity (%) 7.0 5.0 4.9 6.7 5.4 3.5 5.5 16.7 14.8

Capital Employed 34,982 32,726 25,999 29,366 33,160 63,284 92,676 1,44,914 2,04,006

Return on Capital Employed (%) 4.4 4.5 4.1 4.4 4.1 1.9 2.8 5.8 6.3

Invested Capital 33,170 30,770 24,287 25,934 31,319 59,301 91,276 1,43,524 2,02,385

Return on Invested Capital (%) 5.1 6.5 7.1 7.0 6.3 4.2 4.7 7.2 7.9

Cash Flow from Operations 774 2,942 3,327 2,454 4,094 1,385 5,979 8,174 5,245

Cash Flow from Investing (1,229) (7,706) 1,809 (2,323) (7,902) (17,487) (31,245) (49,082) (48,592)

Cash Flow from Financing 716 5,120 -6,158 -221 3,059 15,901 24,696 40,880 43,542

Net Cash Flow 261 355 -1,023 -90 -750 -201 -570 -28 194

Free Cash Flow -1,476 -4,424 929 612 441 -11,582 -29,234 -43,010 -44,926

FCF to Revenue (%) (4.0) (11.5) 2.3 1.4 1.1 (16.7) (49.8) (55.1) (37.9)

FCF to EBITDA (%) (62.9) (135.8) 43.3 26.8 17.6 (311.9) (427.7) (313.1) (205.1)

FCF to Net Profit (%) (149.4) (584.2) 129.5 53.8 47.8 (1,491.5) (1,926.7) (702.5) (649.5)

FCF to Net Worth (%) (10.4) (29.3) 6.3 3.6 2.6 (52.0) (106.8) (117.4) (96.4)

Net Capex 1,765 2,722 3,359 13,493 31,172 46,857 46,803

Net Capex to Revenue (%) 4.3 6.3 8.5 19.4 53.1 60.0 39.5

Total Debt 20,846 17,637 11,243 12,419 16,001 41,024 65,298 1,08,275 1,57,390

Net Debt 19,034 15,681 9,531 8,988 14,161 37,041 63,898 1,06,885 1,55,769

Net Debt to Equity (X) 1.3 1.0 0.6 0.5 0.8 1.7 2.3 2.9 3.3

Net Debt to EBITDA (X) 8.1 4.8 4.4 3.9 5.7 10.0 9.3 7.8 7.1

Interest Coverage Ratio (X) 1.1 1.1 1.1 1.2 1.4 1.0 1.4 2.0 1.9

10 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Source: Company Reports & Ventura Research

(40)

(20)

0

20

40

60

80

100

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

FY19 FY20 FY21 FY22 FY23E FY24E FY25E

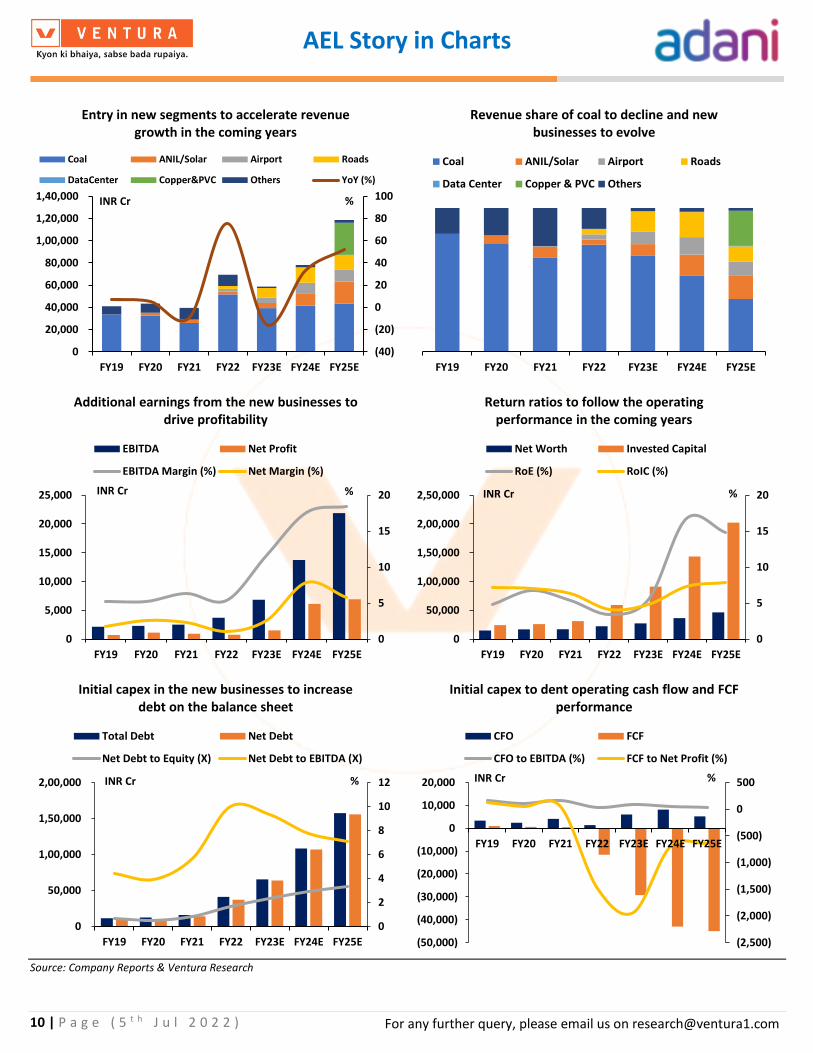

Entry in new segments to accelerate revenue growth in the coming years

Coal ANIL/Solar Airport Roads

DataCenter Copper&PVC Others YoY (%)

INR Cr %

FY19 FY20 FY21 FY22 FY23E FY24E FY25E

Revenue share of coal to decline and new businesses to evolve

Coal ANIL/Solar Airport Roads

Data Center Copper & PVC Others

0

5

10

15

20

0

5,000

10,000

15,000

20,000

25,000

FY19 FY20 FY21 FY22 FY23E FY24E FY25E

Additional earnings from the new businesses to drive profitability

EBITDA Net Profit

EBITDA Margin (%) Net Margin (%)

INR Cr %

0

5

10

15

20

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

FY19 FY20 FY21 FY22 FY23E FY24E FY25E

Return ratios to follow the operating performance in the coming years

Net Worth Invested Capital

RoE (%) RoIC (%)

INR Cr %

0

2

4

6

8

10

12

0

50,000

1,00,000

1,50,000

2,00,000

FY19 FY20 FY21 FY22 FY23E FY24E FY25E

Initial capex in the new businesses to increase debt on the balance sheet

Total Debt Net Debt

Net Debt to Equity (X) Net Debt to EBITDA (X)

INR Cr %

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

(50,000)

(40,000)

(30,000)

(20,000)

(10,000)

0

10,000

20,000

FY19 FY20 FY21 FY22 FY23E FY24E FY25E

Initial capex to dent operating cash flow and FCF performance

CFO FCF

CFO to EBITDA (%) FCF to Net Profit (%)

INR Cr %

AEL Story in Charts

11 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Understanding AEL’s business and growth opportunities

AEL is one of India’s largest listed incubators which have conceived, grown, matured and

demerged many successful businesses such as Adani Ports & SEZ (in the year 2007), Adani

Power (in 2009), Adani Transmission (in 2015), Adani Green Energy (in 2018), Adani Total Gas

(in 2018) and Adani Wilmar (in 2022). Each of these listed entities have themselves emerged

as leaders in their respective sectors.

AEL’s business journey

Source: Company Reports

1988- Started commodity trading

1994- Listed on BSE and NSE @ INR 150

per share

1995- Mundra Port commences operations

1996- Bonus issue 1:1

1999- Commencement of IRm business.

Signed JV with Wilmar

2001- Started City gas distribution business

2005- Awarded india's first MDO contract

2006- Stock split of AEL (10:1)

2007- APSEZ IPO2008- Acquirede

Bunya Mine, Indonesia2009- Adani Power

IPO

2010- Acquired Carmichael Mine at

Australia

2015- Completed demerger of APL and

ATL

2017- Started manufacturing solar

PV panels

2018- Demerger of Adani Green and

Adani gas

2019- Emerged 2nd largest IRM player in

the world

2020- Forayed into airports business

2021- Formed data center JV 'Adani

Connex' with Edge Connex

2022- Adani Wilmar IPO subscribed 17X.

Completed the acquisition of MIAL

12 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Currently, AEL is incubating a mix of new and old-world businesses which includes

• Existing businesses

o Airport operations – Managing 8 airports (7 operational and 1 under

construction) in India and their weighted average life is 70 years, providing

good long-term cash flow visibility.

o Road construction – 376 lane km of highways are under operation, while 1,694

lane km are under construction. An additional 3,676 lane km of concession

agreements have been signed.

o FMCG – A JV between AEL and Wilmar Group catering to essential kitchen

commodities like edible oil, rice, flour, pulses, etc. The company recently

acquired the Kohinoor brand in basmati rice.

o Commercial mining, MDO and IRM – It has one operational commercial mine

in Australia (Carmichael mine) and 4 commercial mines in India that are under

development. The segment also offers end-to-end logistics for coal consumers

(IRM business) and turnkey services to coal & iron ore mine owners (MDO

business).

o Other businesses include defence (production of small arms, UAVs, drones &

aircraft parts), water, digital etc.

• Future businesses

o Green Hydrogen – ANIL has outlined a capex plan of USD 50 bn to set up a 2.5

MMTPA of green H2 manufacturing capacity over the next 10 years. The first

phase of 1.0 MMTPA green H2 capacity is expected to be commissioned before

2030.

o Data centres – A JV between AEL and EdgeConneX should start with 8 MW of

operations in FY23 and grow into 323 MW by FY30

o Other future businesses include copper (to commence production from FY25

with an initial capacity of 0.5 MMTPA) and PVC (to commence production of

green PVC from FY25)

With most of the business verticals in the investment phase, profit metrics are in the nascent

stage and do not reflect steady-state run rates. Given its past records, execution skills, ready

infrastructure in place, foreign collaboration for technical tie-ups and low-cost funding, we

remain confident of the AEL’s ability to turn its new set of businesses into giant organizations

and unlock value from them either through a stake sale or through a direct listing.

13 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL’s Business Structure

Source: Company Reports

AEL

Existing Businesses

Others

Defence

(Adani Defence & Aerospace Ltd)

Water

(Adani Water Ltd)

Digital

(Adani Digital Labs)

Airports

(Adani Airport Holdings Ltd)

Roads

(Adani Road Transport Ltd)

FMCG

(Adani Wilmar Ltd)

AEL: 44% / Wilmar: 44%

Coal

Commercial Mines

(Adani Mining Pvt Ltd)

IRM and MDO

Future Businesses

Green Hydrogen

(Adani New Industries Ltd)

AEL: 75% / TotalEner: 25%

Data Center

(Adani ConneX Ltd)

AEL: 50% / ConneX: 50%

Copper

(Kutch Copper Ltd)

PVC

(Adani Petrochemicals Ltd)

14 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL has successfully incubated a number of businesses across a variety of sectors which have

grown to become large business opportunities in their own right. This has been aptly

demonstrated by the business growth and shareholder value created as shown in the table

below –

Demerged businesses from AEL and their performance

Source: Company Reports & Ventura Research

This success is largely derived from a broad-based competitive advantage comprising of:

• Timely project implementation,

• Ability to commission projects faster than the sectorial curve,

• Competence to do so at a cost lower than the industry average,

• Foresight to not merely service the market but to grow it,

• Establish a decisive sustainable leadership, and

• Evolve the company’s position into a generic name within the sector of its presence.

We believe that all the above characteristics will enable AEL to build strong businesses across

all the recent forays.

Company NameAdani Ports &

SEZ LtdAdani Power Ltd

Adani

Transmission Ltd

Adani Green

Energy Ltd

Adani Total

Gas LtdAdani Wilmar Ltd

Current status

in industry

Largest commercial

port operator in

India with 560 MMT

capacity

One of the largest

power companies in

India with the

thermal power

capacity of 13.6 GW

Largest private

transmission

company in India

with 18,795 ckm

line

One of the largest

renewable

companies in India

with a project

portfolio of 20.5 GW

Largest CGD

company in India

with presence

across 52 GAs

One of the largest

companies in India

to offer most of the

essential kitchen

commodities

Revenue FY17 8,439 22,616 2,876 502 1,087 22,973

Revenue FY22 15,934 27,711 11,258 5,133 3,038 52,361

5 yrs Revenue CAGR (%) 13.6 4.1 31.4 59.2 22.8 17.9

EBITDA FY17 5,418 5,980 1,983 403 278 643

EBITDA FY22 8,879 9,814 4,206 3,539 773 1,725

5 yrs EBITDA CAGR (%) 10.4 10.4 16.2 54.4 22.7 21.8

Net Profit FY17 3,912 -6,174 416 -47 101 230

Net Profit FY22 4,728 4,912 1,205 489 505 808

5 yrs net profit CAGR (%) 3.9 NA 23.7 NA 38.0 28.6

Date of demerger 39,416 40,046 42,216 43,273 43,405 44,603

Listing Price 184 103 28 30 80 381

Current Price 673 270 2,123 1,880 2,262 584

Price CAGR since listing (%) 9.3 7.8 86.6 181.1 149.4 212.0

15 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Growth profile of incubating businesses

Source: Company Reports

Early-stage incubating businesses

Source: Company Report

16 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Financial Analysis & Projections

FY19-22: Maintained consistency in revenue performance

During FY19-22, AEL’s revenue grew at a CAGR of 19.8% to INR 69,420 cr, which was primarily

driven by

• 15.4% revenue CAGR to INR 51,324 cr in the coal segment due to a significant surge in

IRM volumes.

• 21.3% revenue CAGR to INR 2,527 cr in the solar manufacturing segment revenue to

due to a significant jump in the solar installation by EPC players

• Additional revenue of INR 2,517 cr from airport business (new business vertical started

in FY20).

• 33.7% revenue CAGR in other businesses to INR 13,051 cr

EBITDA and PAT grew at a CAGR of 23.6% and 23.8% to INR 3,713 cr and INR 788 cr,

respectively. Both EBITDA and PAT margins improved by 47bps to 5.3% and 11bps to 1.1%

respectively due to the improving contribution from the high-margin new business verticals.

An increase in PAT improved the RoE from 2.7% in FY19 to 2.9% in FY22, however, a rise in the

net debt from INR 8,239 cr in FY19 to INR 37,045 cr in FY22 impacted the RoIC performance.

As a result, RoIC declined from 6.8% in FY19 to 3.9% in FY22.

FY22-25E: Strong potential of the new business segments

Over FY22-25E, AEL’s sales are expected to grow at a CAGR of 19.5% to INR 1,18,612 cr, due to

• 5.5% CAGR decline estimated in coal segment revenue to INR 43,503 cr due to the

higher base of FY22, when commodity prices were at their peak. We believe that coal

prices may decline over a period of time.

• 63.9% CAGR growth estimated in airport segment revenue to INR 11,086 cr due to the

rise in passenger traffic in new airports from 40.4 mn in FY22 to 105.9 mn in FY25

• 53.7% CAGR growth estimated in defence segment revenue to INR 2,392 cr due to

increased sourcing from MoD and defence PSUs

• Total incremental revenue of INR 61,631 cr from the upcoming businesses such as INR

12,725 cr from the road, INR 19,647 cr from ANIL, INR 415 cr from the data centre, INR

25,492 cr from copper and INRN 3,352 cr from PVC business.

EBITDA and net profit are expected to grow at a CAGR of 80.7% and 107.3% to INR 21,903 cr

and INR 6,917 cr, respectively, while EBITDA and net margins are expected to improve by

1312bps to 18.5% and 471bps to 5.8% respectively due to the rise in contribution from the

new high margin businesses. Subsequently, return ratios – RoE & RoIC – are expected to

improve by 1135bps to 14.8% and 374bps to 7.9%, respectively.

17 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL’s Capital Management

18 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL’s Capital Management

Over the past 9 years, the Adani group has significantly expanded its presence across various

verticals. The group has become India’s largest private port operator, coal importer, private

thermal power producer, green energy producer, power transmitter & distributor, city gas

distributor and importer of edible oils and it has also expanded into airports, roads, defence

and aerospace. This growth has been aided by

• Buying projects from other companies,

• Starting new businesses and

• Investing in existing ones

This business expansion delivered a strong CAGR growth of 20.3% in its RR EBITDA (run-rate

EBITDA) during the last 9 years from INR 69 bn in FY13 to INR 365 bn in FY22, while the net

debt has grown has a CAGR of 11.1% from INR 521 bn in FY13 to INR 1,344 bn in FY22 over the

same period, which resulted in a decline in net debt-to-RR EBITDA over the same period.

Adani group has been reducing short-term debt in the overall debt mix

Source: Company Reports

The net debt/RR EBITDA has been reducing over the years

Source: Company Reports

FY13 FY16 FY22

RatingHighest Asset

Rating was AA

Highest Asset

Rating was AA+

Overall Group

Rating - AA

RR EBITDA INR 69 Bn INR 183 Bn INR 365 Bn

Net Debt INR 521 Bn INR 732 Bn INR1,344 Bn

Debt (% age ) 100% 86% 39%

69

183

365

7.6x

4.0x3.7x

0

2

4

6

8

0

50

100

150

200

250

300

350

400

FY13 FY16 FY22

RR EBIDTA Net Debt/ RR EBIDTA

19 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

How did Adani group manage to reduce pressure on its balance sheet while

expanding in capex-heavy businesses?

The Adani group philosophy before undertaking an investment in infrastructure projects is

summed up by the following 5 stages:

• Origination: In this stage, the company undertakes market intelligence and analysis of

the viability of the project and the strategic value of the asset.

• Site development: In this stage, the group acquires the site post-taking concessions

and regulatory requirements.

• Construction: In this stage, the company undertakes the engineering and designing of

the project and decides on the equity and debt funding for the project.

• Operations: The Company plans for the lifecycle O&M of the project. For example, for

its power business, Adani group has built the Energy Network Operation Centre (ENOC)

which enables centralized continuous monitoring of projects and installations on a

single cloud-based platform.

• Capital management: In this stage, AEL undertakes to redesign the capital structure of

the asset in such a way that the operational phase funding of the project is consistent

with the life of the asset.

Adani Group: Repeatable & proven transformative investment model

Source: Company Reports

20 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Internally, the group focuses a lot on capital management and reviews periodically its capital

requirement and how the cost of the same can be brought down. In order to bring down the

cost of funds, the group has laid down the following strategy:

• Tapping international markets to broadbase sourcing of funds – To gain funds at

competitive pricing, the group envisages the issuance of various green bonds,

especially for its renewable energy business. The bonds are issued for longer-term (>15

years) and in a way that the coupon payments are in tandem with the cash flow

generation of the underlying asset for which the money is raised.

Adani Group: Repeatable & proven transformative investment model

Source: Company Reports

• Focus on ESG – Being ESG compliant has become foremost requirement of global

funds. High ESG compliant projects are able to tap international funds at cheap rates.

In order to attract international capital, AEL has focused on enhancing its ESG score.

AEL has improved its ESG score while RIL’s score remained flat

Source: Bloomberg

PSU Banks, 55 Private

Banks, 31

Bonds, 14

2016

PSU Banks, 18

Private Banks, 8

Bonds, 37

DII, 6

Global Banks, 25

PSU Capex LC, 6

2022

27 28 27 27

31 31

35 35 36

50 51

54 56

49

58

49 51

52

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

AEL Reliance

21 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Since FY13, AEL has worked on ESG parameters and disclosures, which has improved

its overall Bloomberg ESG score from 27 in FY13 to 36 in FY21. AEL aligned its ESG

reporting standards with the Global Reporting Initiative (GRI), increased its public

disclosures in the annual report, management systems and business excellence

initiatives, and remains committed to improving its ESG performance by further

refining its policies and practices, as well as strengthening information disclosure

procedures. This has helped the company is getting foreign funding for its new

projects.

Further, we believe that in order to enhance its ESG commitment there is every

possibility that the coal business may be completely hived off once the incubator

businesses become cash flow positive.

• Partnerships with industry leaders – The group has partnerships with TotalEnergies

for its various businesses like green energy, city gas distribution, and green H2.

Especially for its green hydrogen business, ANIL will issue shares to TotalEnergies

representing 25% of its share capital. The partnership is a win-win situation for both

the investors as Adani group will contribute its knowledge of the Indian market,

execution capabilities, operations excellence and capital management philosophy

while TotalEnergies will bring its understanding of the global market, credit

enhancement and financial strength to lower the financing costs (we estimate the

finance costs to come down by atleast 150-200bps) along with expertise in underlying

technologies.

The complementary strengths of both partners will help ANIL deliver the largest green

H2 ecosystem in the world, which, in turn, will deliver the lowest cost of green H2 to

the consumer and help accelerate the global energy transition. It is to be noted that

ANIL’s ambition is to invest over USD 50 bn over the next 10 years in green H2 and

associated ecosystem. In the initial phase, ANIL will develop green H2 production

capacity of 1 MMMTPA before 2030.

With the help of its well planned capital management policy, Adani group has been able to

expand its business operations by taking measured risk. Over time, the group has been able to

completely de-risk 46% of its equity value (with thermal) & 37% (without thermal) from tenure

and other capital related risk.

22 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

46% of group’s equity value (with thermal) is fully protected from tenure and rate of capital employed risk

Source: Company Reports

37% of group’s equity value (without thermal) is fully protected from tenure and rate of capital employed risk

Source: Company Reports

23 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

How Adani group is applying its capital management policy to grow its green energy

portfolio?

The efficacy of capital management philosophy of Adani group can be seen in Adani Green

Energy Limited (AGEL). As per management, the total capital outlay for AGEL to attain its target

of 45GW will only be to the tune of cost of setting up 20GW installation of solar energy. The

revenues and net earnings of this 20GW will be locked up via PPA’s. Once the earnings are

locked, the cash flows from the same would be used in following priority:

• Debt repayment of initial 20GW portfolio.

• Growth capital of remaining 25GW portfolio.

Once the commissioning of whole 45GW is completed, the whole cash flow can be used for

debt repayment. In this way, the management will be able to fund its growth plan and also

keep debt levels in check.

AGEL is expected to fund >50% of its expansion through internal accruals due to its disciplined capital mgmt.

Source: Company Reports, Ventura reseach

Numbers in box represent GW installation estimates, Internal target of AGEL is to build 45GW by FY30 although we have assumed the same only post FY35

-10

-5

0

5

10

15

20

25

30

35

40

(40,000)

(30,000)

(20,000)

(10,000)

0

10,000

20,000

30,000

40,000

50,000

60,000

FY22 FY23E FY24E FY25E FY26E FY27E FY28E FY29E FY30E FY35E FY40E FY45E FY50E FY55E

CFO FCFF Net debt/EBITDA (x) -RHS RoE %- RHS

INR cr

5

.

5

7 13

33

20

23 26 29 32 35 43

49 55

61 67

24 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL’s Green Hydrogen Ecosystem

25 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Adani New Industries Ltd

Green hydrogen (H2) has been identified as one of the cleanest energy sources that is going to

replace the existing carbon-based energy usage. As a result, this essential energy source

promises to provide a significant business opportunity with a long runway of growth. However,

this opportunity is prone to high risk given the extremely capital-intensive nature and the

rapidly evolving technology.

AEL by virtue of its proven skills at building large-scale profitable businesses across diverse

sectors, superior execution and access to global capital is best placed to exploit this

opportunity. With a view to partake in this opportunity, AEL incorporated a new subsidiary,

Adani New Industries Ltd (ANIL).

ANIL integrated business verticals and capacities

Source: Company Reports

Adani New Industries Ltd

Supply Chain Products Manufacturing

Solar Panel

Current Capacity: 3,500 MW

FY30 Capacity: 10,000 MW

2.0 GW of mono-cristalline and 1.5 GW of multi-crystalline capacities.

Multi-crystalline will be replaced by TOPcon

Wind Turbine Generator

Current Capacity: 0 MW

FY30 Capacity: 7,500 MW

Battery

Current Capacity: 0 MWh

FY30 Capacity: 10,000 MWh

Other Ancillaries (Tracker, Glass, EVA, etc)

Renewable Energy Generation

Current Capacity: 0 GW

FY30 Capacity: 30 GW

Green Hydrogen Generation & its supply chain

Green Hydrogen Generation

Current Capacity: 0 MMTPA

FY30 Capacity: 3 MMTPA

Electrolysers

Current Capacity: 0 MW

FY30 Capacity: 5,000 MW

Fuel Cells

Current Capacity: 0 MW

FY30 Capacity: 1,000 MW

Green Hydrogen Downstream Products

Ammonia

Current Capacity: 0 MMTPA

FY30 Capacity: 6.5 MMTPA

Urea

Current Capacity: 0 MMTPA

FY30 Capacity: 4.2 MMTPA

Methanol

Current Capacity: 0 MMTPA

FY30 Capacity: 2.5 MMTPA

26 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

ANIL envisages capturing the entire value chain of green H2

ANIL’s business plan and resource integration

Source: Company Reports

• Green H2 and its downstream products (ammonia, urea, methanol, ethanol, etc.)

which are part of the fully integrated green H2 ecosystem will be manufactured at

Khavda and Mundra SEZ.

o Power generation – ANIL’s Khavda site has a land bank of ~71,000 acres which

has a large-scale renewable deployment potential of 20 GW due to its high

wind & solar resource potential. The company is targeting to enhance the

renewable power capacity to 45 GW by FY30. The solar panels and windmills

will be manufactured and supplied from AEL’s Mundra SEZ.

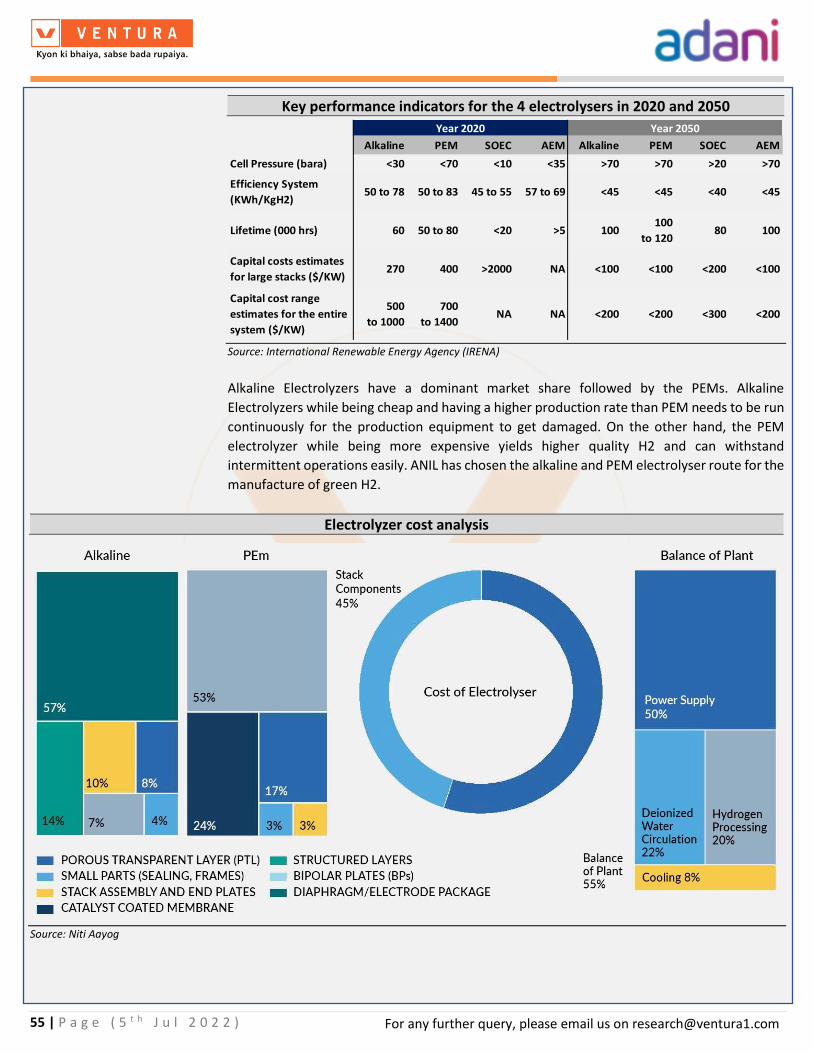

o Electrolysis – The company will use the alkaline and PEM electrolysis process

to produce 2.5 mn tonnes of green H2 annually (by FY31). The electrolyzers,

used in the electrolysis process, will be manufactured and supplied from the

company’s Mundra SEZ facility.

o H2 supply and use – H2 will be supplied from Khavda to Mundra SEZ through

a 42” pipeline (a cost-effective way of transportation), where it will be used

for the production of downstream products.

27 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

ANIL’s green H2 generation and supply

Source: Company Reports

ANIL’s integrated green H2 hub in Mundra

Source: Company Reports

• End-to-end manufacturing of the entire supply chain. There will be a complete

backward integration of solar manufacturing from polysilicon, ingots, wafers, and cells

to solar modules along with upcoming manufacturing facilities for wind turbine

generators, electrolyzers, batteries, etc. at the Mundra SEZ.

Khavda – 71,000 acres of land with a

capacity to generate RE power of 20

GW.

The company is targeting to enhance

the RE power capacity to 45 GW by

FY30.

Mundra SEZ – Manufacturing facility

for solar panels, electrolysers and wind

mill manufacturing facility. It is also

developing production facilities for

methanol, ethanol, ammonia and

urea.

28 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

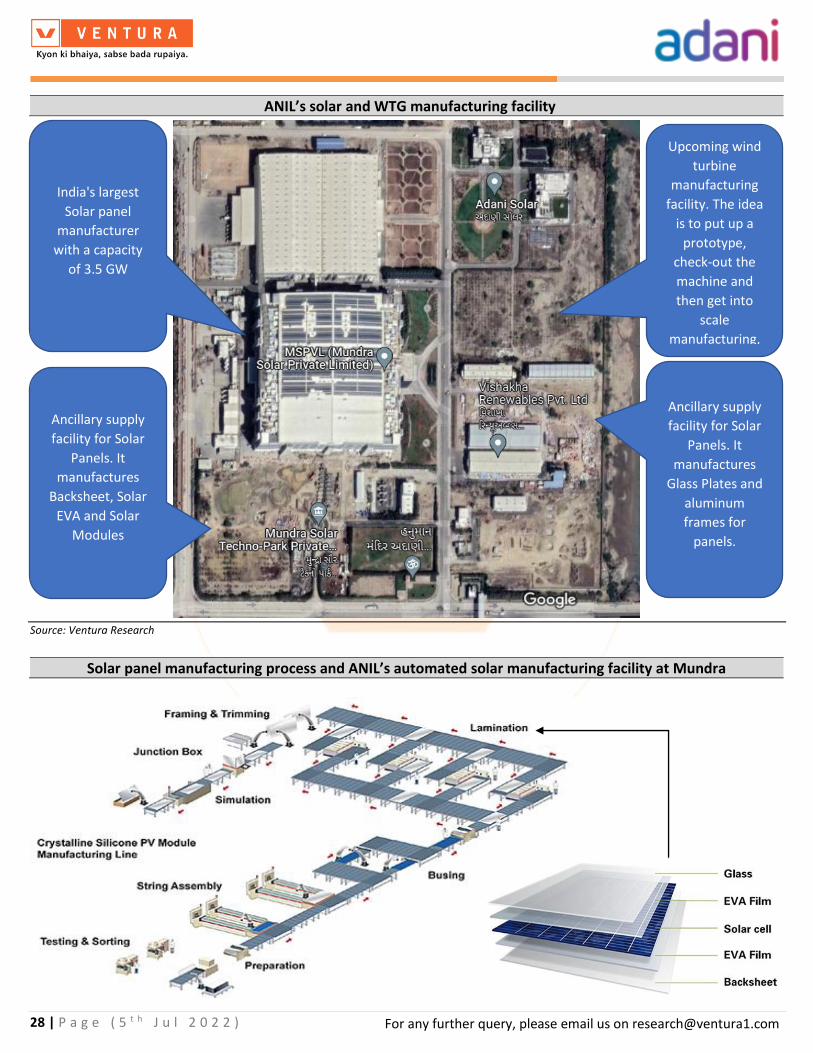

ANIL’s solar and WTG manufacturing facility

Source: Ventura Research

Solar panel manufacturing process and ANIL’s automated solar manufacturing facility at Mundra

India's largest

Solar panel

manufacturer

with a capacity

of 3.5 GW

Ancillary supply

facility for Solar

Panels. It

manufactures

Backsheet, Solar

EVA and Solar

Modules

Ancillary supply

facility for Solar

Panels. It

manufactures

Glass Plates and

aluminum

frames for

panels.

Upcoming wind

turbine

manufacturing

facility. The idea

is to put up a

prototype,

check-out the

machine and

then get into

scale

manufacturing,

for self-

consumption,

sales in India and

exports.

29 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Source: Industry Reports

• For supply chain assurance and cost efficiency from economies of scale, the company

is targeting full backward integration in solar and wind to

▪ reduce dependency on external supply chains,

▪ improve turnaround time and availability of ancillary parts, and

▪ reduce pressure on inventory and its carrying cost.

ANIL is building infrastructure from power generation for the electrolysis process to produce

green H2 and its downstream products.

ANIL’s readiness and complete integration of the renewable supply chain

Solar panel manufacturing facility at Mundra

Mundra Solar PV Ltd (MSPVL) (which in the future is expected to be subsumed into ANIL), is

the first and the largest vertically integrated solar company in the Indian market. Besides, it is

the first and only manufacturer from India to rank as the top performer for 4 consecutive years.

The quality of ANIL’s solar modules is amongst the best in the world and its products carry

Bloomberg’s tier-1 quality ratings. The current 3.5 GW of solar capacity includes

• Recently installed 2 GW monocrystalline capacity and

• 1.5 GW multi-crystalline technology, which is planned to be replaced with TOPCon.

Multi-crystalline is an old technology which is expected to get phased out slowly as there are

newer technologies with higher efficiencies. TOPCon is the latest technology being adopted

globally. The future capacity installations are likely to be HJT which is a fast-emerging

technology and offers a further improvement in efficiency.

30 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

At this facility 3 types of solar panels (for rooftop and utility-scale projects) would be

manufactured:

• Monocrystalline Solar Panel: These panels are characterized by their black PV cells

with rounded edges. They have a higher conversion efficiency than polycrystalline

panels, which means they produce more units of electricity. These are mostly used for

limited spaces and are costlier than poly/multi-crystalline panels.

ANIL manufactures two series of mono facial solar modules– the

o Eternal PRIDE series with 132 cells and 610-650 Wp, and

o Eternal SHINE series with 144 cells and 520-545 Wp.

ANIL’s monocrystalline solar panel

Source: kenbrooksolar

• Poly/multi-crystalline Solar Panel: These panels have blue-hued PV cells with straight

edges. They have a lower efficiency compared with monocrystalline cells, which means

more panels are required to match the same power output. However, these panels

also have a lower price, since their manufacturing process is simpler.

ANIL manufactures the Encore series of multi-crystalline solar panels that are used for

utility-scale projects.

31 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

ANIL’s multi/poly-crystalline solar panel

Source: kenbrooksolar

• Bifacial Solar Panel: These panels are designed in a way that they can generate

electricity using both surface areas. This means, that even the rear side of the module

which does not face the sun directly is light sensitive and can be utilized to generate

electricity from the module.

The panel top is equipped with solar cells facing the sun. This side of the panel works

similar to a common solar panel capturing the rays directly coming from the sun.

Whereas, the solar cells present on the other face, the bottom face, absorb the

reflected light off the ground. With proper installation, a great amount of sunlight is

captured which in turn increases the bifacial solar panel efficiency manifold.

How a bifacial solar panel works

Source: Kenbrooksolar

32 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Mundra Solar PV Ltd 5 years of performance

Source: Company Reports

Wind Turbine manufacturing at Mundra

ANIL is gearing up to put up a prototype of a 5.2 MW wind turbine at Mundra, Gujarat. When

it comes up, it would be the country’s biggest wind turbine and will count among the largest

on-shore wind mills in the world.

The machine will be built with technology from W2E Wind to Energy GmbH of Germany. The

idea is to install the prototype, monitor & measure its operational efficiencies, and

troubleshoot any operational challenges. Once the stability of the prototype is established and

then gets into scale manufacturing, for self-consumption, sales in India, and exports.

In the wind mill industry, turbines of a capacity above 4 MW to 14 MW are typically associated

with offshore installation. But onshore wind turbines of 5.2 MW are few globally and none

have been installed in India so far.

574 637

990

1,158 1,104

0

200

400

600

800

1,000

1,200

1,400

FY18 FY19 FY20 FY21 FY22

Solar volumes to improve with the rise in captive demand

Sales volume declined due to reduced EPC demand on

account of higher input cost

0

5

10

15

20

25

30

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY18 FY19 FY20 FY21 FY22

Per watt realization is expected to remain stable

Revenue (INR Cr) Revenue per Watt (INR)

0

10

20

30

40

50

60

0

100

200

300

400

500

600

700

800

900

FY18 FY19 FY20 FY21 FY22

Operating profitability to sustain at 15% in the long run

EBITDA (INR Cr) EBITDA Margin (%)

0

1

2

3

4

5

6

7

8

0

100

200

300

400

500

600

700

800

900

FY18 FY19 FY20 FY21 FY22

EBITDA per watt remained stable at 3-4 cents per watt

EBITDA (INR Cr) EBITDA per Watt (INR)

33 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Wind turbine capacities – current and future

Source: Renewable Energy World

The 5.2 MW wind mill has blades that cover a circle of 165 meters in diameter at a tower height

of 140 meters. It can work at wind speeds of 3 meters per second (mps, which is very low) and

up to 20 mps, reaching its optimum power production at 12 mps wind speeds.

This plant will be located adjacent to MSPVL and in the initial phase, it is expected to supply

windmills for its Khavda power generation facility and later will sell turbines to global

renewable energy players.

ANIL’s focus is to manufacture the entire windmill in one place

Source: Industry Reports

Globally wind turbine manufacturers are targeting 5.5 MW by 2035, ANIL is targeting to

achieve turbine capacities of 5.2 MW by 2024 which is a decade ahead of its peers.

ANIL is planning to setup a facility which

can produce entire windmill covering

tower, nacelle, generator, hub, blade,

etc. It will provide a complete control to

the company in terms of supply chain

and just-in-time availability of

components

34 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

AEL’s JV with TotalEnergies would be a game-changer for ANIL

ANIL’s ambition is to invest ~$50 bn (funded through a mix of debt & equity) over the next 10

years in green H2 and its associated ecosystem. In the initial phase, ANIL will develop a green

H2 production capacity of 1.0 MMTPA before 2030 (the planned road map is 2.5 MMTPA).

To execute this ambitious plan, AEL has signed a partnership agreement with TotalEnergies

and has entered into a strategic alliance, in which TotalEnergies will acquire a 25% stake in

ANIL from AEL (valuation is yet to be decided). TotalEnergies involvement will give a significant

boost to achieving ANIL’s ambitious goal to manufacture 2.5 mn tonnes of green H2 capacity

by FY31.

Post this agreement, it will become the fourth partnership between TotalEnergies and the

Adani group

• In 2021, TotalEnergies picked up a 20% stake in Adani Green Energy Ltd (AGEL), the

renewable power company of the Adani group.

• In 2019, TotalEnergies had acquired 37.4% of Adani Gas Ltd and 50% of the group’s

Dhamra LNG project. The JV involved the development of various LNG regasification

terminals, including Dhamra LNG, and a retail network of 1,500 service stations over

10 years.

• In 2020, TotalEnergies and Adani formed a 50-50 JV at an enterprise value of INR

17,385 cr for 2.3 GW of solar assets.

AEL and TotalEnergies JV philosophy

Source: Ventura Research

35 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

How this alliance will benefit ANIL

• Benefits from TotalEnergies to ANIL

o TotalEnergies is one of the largest players in the global energy industry and

hence the company can offer its thorough understanding of the global energy

markets, expertise in renewable technologies and large-scale industrial

projects for the development of ANIL’s green H2 capacities.

o TotalEnergies has over 20 years of experience in H2 retailing infrastructure.

The company is currently operating 120 H2 refuelling stations (HRS – 30 own

and 90 through strategic tie-ups with other fuel retailers) across Germany, the

Netherlands, Belgium and France. The company is planning to add 150 new

HRS across Europe by 2030 to further develop the H2 market for mobility in

Europe. For the seamless supply of H2, ANIL is expected to become a secured

steady source of H2 import.

To rollout HRS networks domestically, the strategic alliance with TotalEnergies

will help ANIL participate in this forthcoming opportunity.

o TotalEnergies is an active member of several H2 dedicated initiatives and

professional associations in Europe. The company is also an anchor sponsor of

the EUR 1.5 bn clean H2 infrastructure fund, which creates the blue H2

ecosystem in Europe.

ANIL is targeting the European market for the exports of its green H2, which

will generate high margin forex income. The strategic associations of

TotalEnergies in Europe could help ANIL in getting access to export its green

H2 in the European market.

o The AA rating of TotalEnergies is expected to help ANIL in raising low-cost

initial funding from the global market, which is expected to save 150-200 bps

in interest costs.

• Benefits from Adani Enterprises to ANIL

o AEL is known for its superior and time-bound execution of large-scale complex

projects in the areas of power, ports, logistics, infrastructure, etc. This

expertise will help in creating India’s largest green H2 ecosystem for ANIL

within the stipulated time.

o ANIL houses India’s largest solar manufacturing capacity with cell and module

manufacturing, which came as a legacy from AEL. The parent AEL has

significant experience in setting up and managing large renewable power

projects (AEL incubated AGEL and demerged in 2018) and their understanding

of India’s renewable sector dynamics is better than peers. It will help ANIL in

managing 45 GW of renewable hybrid power projects required for 2.5 mn

tonnes of green H2 production.

o Group company Adani Total Gas Ltd (ATGL) is currently operating 335 CNG

stations and it has committed 1,800 additional CNG stations in the 9th/10th/11th

round of CGD auctions.

36 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

In addition, ATGL is supplying gas to >2,000 industrial units, and this network

is expected to expand significantly in the coming years due to strict NGT orders

to switch from polluting coal to natural gas. ANIL can also use this ready

infrastructure to distribute its green H2 for automotive and industrial usage.

Limitations in the H2 ecosystem and readiness of ANIL and RIL

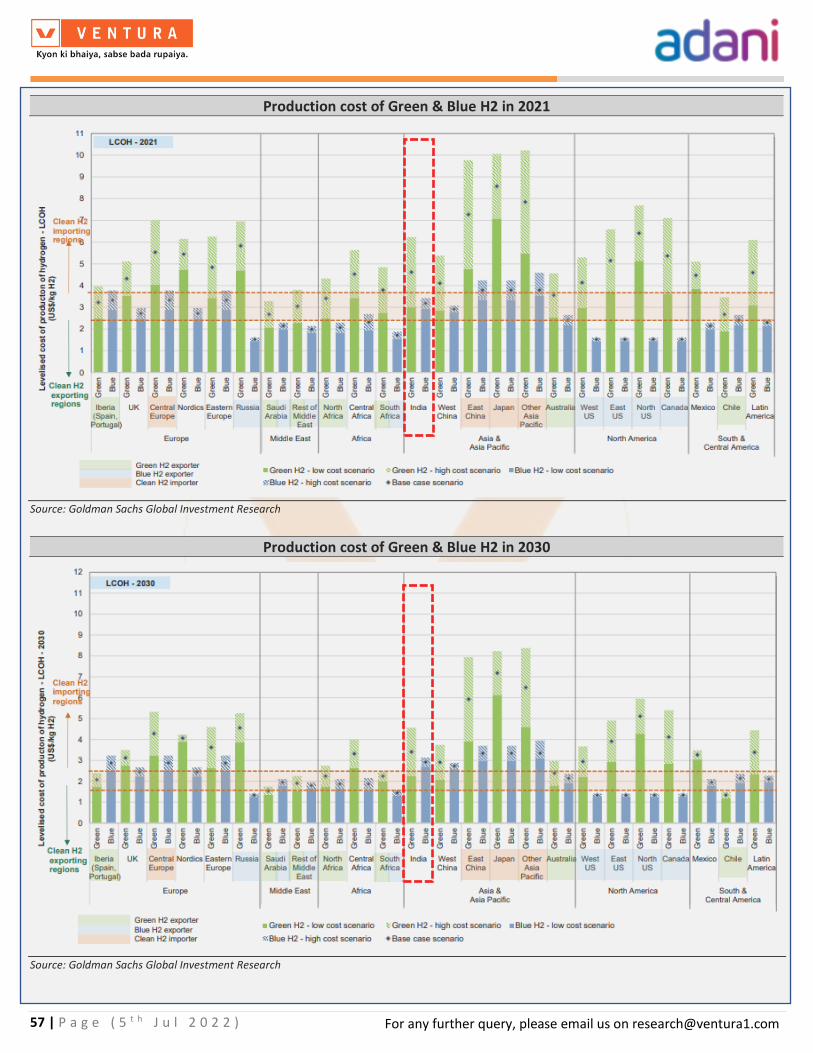

India has set an ambitious target of manufacturing 5.0 MMTPA of green H2 by 2030. The launch

of the 1st phase of the green H2 policy on 17th Feb 2022 is a step toward this gargantuan goal.

However, India’s total H2 demand is expected to be more than 11 mn tonnes by 2030, which

is more than double the GOI’s target. This will ensure that there is significant room for growth

in green H2 manufacture in the future. The country’s thrust for green H2 manufacture is

attracting many players, however, there are significant challenges which need to be overcome

including:

• Lack of expertise in building large capacities of green H2, which is necessary for lower

cost of production.

• Limited access to low-cost funding (for initial capex) from the global market due to

weak credit rating

• Limited availability of captive green renewable power for water electrolysis, and

• Lack of expertise in the manufacturing of downstream products – green ammonia,

green urea and green ethanol.

We have discussed ANIL’s H2 ecosystem and upcoming opportunities for the company.

However, India’s most valuable company, Reliance Industries Ltd (RIL) is building its own story

in green H2 space and has taken several strategically important decisions in the past 1 year.

RIL’s green H2 vision and its preparedness

• RIL is targeting to install 100 GW of solar & wind capacity by 2030, which will be utilized

in the water electrolysis to produce green H2.

• RIL has planned 4 Giga factories to manufacture all critical components of its green H2

ecosystem across key value chains, such as a solar PV module factory, an energy

storage battery factory, an electrolyser factory and a fuel cell factory. In order to

rapidly scale up manufacturing, RIL has acquired companies globally

RIL’s acquisitions and partnerships for its green H2 plan

Source: Ventura Research

Target Company MonthStake (%)/

CollaborationAmount Segment

Ambri Inc Aug-21 Investment in preferred stock USD 50 mn Batteries

Stiesdal A/S Oct-21 Collaboration Undisclosed Electrolyzers

NexWafe Oct-21 Investment in preferred stock USD 29 mn Solar Wafers

REC Solar Oct-21 100 USD 771 mn Solar Panel

Sterling & Wilson Oct-21 40 INR 2,800 cr Solar Project EPC

Faradion Dec-21 100 USD 135 mn Batteries

37 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

• With the complete integration, RIL is targeting a green H2 cost of USD 1/kg by 2030.

The company is planning to spend USD 10 bn on its new energy business in the next

three years towards achieving these targets.

• RIL has been working on

o Securing 4.5 lakh acres of ‘solar’ landbank in Gujarat to set up manufacturing

facilities and solar power installation

o Acquired REC Power, NexWafe and Sterling & Wilson to gain expertise in solar

module manufacturing and installation.

o Acquired Ambri Inc and Faradion to set up a large-scale battery manufacturing

and energy storage system in India.

o Partnered with Stiesdal A/S in Oct 2021 to develop and manufacture hydrogen

electrolysers

RIL is securing a landbank of 4.5 lakh acres to set up a renewable power capacity

RIL has started the process of securing land for its 100 GW renewable energy power project in

Gujarat. The company has requested 4.5 lakh acres of land in Kutch in Jan 2022, out of which

3.0-3.5 lakh acres will be utilized for the phase I of 100 GW renewable energy installation, while

the rest will be available for further expansion in phase II.

RIL acquires businesses in solar module manufacturing and installation

RIL is planning to set up a 4 GW of solar module manufacturing capacity in Dhirubhai Ambani

Green Energy Giga Complex, Jamnagar (a 5,000 acres complex). The company is targeting to

enhance this capacity to 10 GW by 2030. To gain the expertise, RIL acquired

• REC Solar in Oct 2021 for a total consideration of USD 771 mn from China National

Bluestar. REC Solar is the market leader in hetero junction technology (HJT) based solar

panels and has an annual production capacity of 1.8 GW. It has 3 manufacturing

facilities – two in Norway and one in Singapore. The company has to date installed

more than 14 GW of solar capacities globally.

• NexWafe in Oct 2021 for a total consideration of USD 29 mn. NexWafe is a German

manufacturer of silicon wafers for solar panels. Through this acquisition, RIL secured

access to NexWafe’s proprietary technology and plans to build large-scale solar wafer

manufacturing facilities in India using the NexWafe processes and technology.

RIL has also acquired Sterling & Wilson, a solar EPC firm, which will help RIL in the installation

and O&M of its 100 GW solar site.

RIL collaborated with the global battery manufacturers to setup energy storage systems

RIL acquired 42.3 mn preference shares in Ambri Inc for a total consideration of USD 50 mn.

Both the companies are in discussions for an exclusive collaboration to set up a battery

manufacturing facility in India.

38 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

To further strengthen its position in the battery storage system, RIL acquired Faradion, a UK-

based startup developing sodium-ion batteries, for a total consideration of USD 135 mn. RIL

aims to produce sodium-ion batteries in India based on Faradion’s technology.

RIL collaborated with Stiesdal to develop an electrolyzer plant in its giga-factory

RIL has partnered with Danish company Stiesdal A/S in Oct 2021 to develop and manufacture

alkaline electrolysers for green H2 (these are the same electrolyzers that AEL is planning to use

and manufacture). Both the companies have also agreed to extend their collaboration to the

development and implementation of

• Offshore wind energy,

• Next-generation fuel cells for conversion of hydrogen to electricity for mobile and

static electricity generation,

• Long-duration energy storage, and

• Production of carbon-negative fuels.

Both AEL and RIL are ready with their green H2 plan and working emphatically to achieve their

ambitious targets, however, we believe that AEL has achieved a few milestones, which are yet

to be achieved in the case of RIL.

AEL’s readiness vs RIL’s ambition for green H2

Source: Ventura Research

Adani Enterprise Ltd Reliance Industries Ltd

Captive green power

4 GW of operational solar plate manufacturing

capacities. Building a new wind turbine capacity 7.5

GW

Instaling a hybrid capacity (solar + wind) of 22-23 GW

on a ready land parcel of 71,000 acres in Khavda

Acquired stakes in REC Solar and NexWafe for the

production of solar modules and also acquired

Sterling & Wilson for the solar installation and O&M.

Committed to develop an installed capacity of 100

GW by 2030. The company has identified 4,50,000

acres of land in Kutch and made a request to state

government.

ElectrolysisBuilding new capacities of electrolysers (5 GW by

FY30) and batteries (10 GWh by FY30)

Partnered with Stiesdal A/S and acquired stakes in

Ambri and Faradion to develop and manufacture

Alkaline Electolyzers and batteries in India

Forward integration for

downstream products

Building new capacities of Ammonia, Urea and

Methanol, which are to be produced from green H2

While no information is available on forward

integration RIL already has presence in downstream

product manufacturing and hence in our opinion

only the tweaking of the process is required for

building the capacities

Partnership with global

companies for green H2

distribution

AEL has partnered with TotalEnergies, who has over

20 years of experience in H2 distribution and sales

RIL is already exporting refined petroleum products

globally and hence it should have no issues in

marketing H2 globally

Balance Sheet Strength

AEL has a domestic credit rating of A+, however, it

has TotalEnergies as a partner, which will enable AEL

in getting low cost funds by 150-200 bps.

Domestic credit rating of AAA with a net debt free

balance sheet

39 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Green H2 plans of other companies

Source: Fortune India Story & Ventura Research

Company Name Project Details

JSW Energy LtdWorking with Australian Fortescue Future Industries to produce green H2 and utilize it for

making green steel, green ammonia and other industrial applications

Bharat Petroleum Corp LtdSetting up a 20 MW electrolyzer at Bina refinery in Madhya Pradesh to produce green H2,

which will be sold through BPCL fuel stations as a transportation fuel

Hindustan Petroleum Corp Ltd Setting up a 370 tonnes green H2 pilot plant at its Vizag refinery

GAIL India Ltd

Setting up a PEM electolyzer plant at Guna in Madhya Pradesh to produce green H2 by the

end of 2023

Setting up a pilot project on H2 blending with natural gas in the CGD network

Oil India Ltd Setting up 100 KW electrolyzer plant in Jorhat, Assam to produce green H2

NTPC Ltd

Setting up a pilot project on H2 blending with natural gas in the CGD network

Setting up a standalone fuel cell based micro grid with H2 production using electrolyzers at

NTPC Simhadri

Setting up a green H2 fuelling station at Leh and will operate five H2 fuel cell powered

vehicles for the Indian Army

GreenkoTeamed up with a Belgian alkaline electrolyzer maker John Cockerill to make electrolyzers in

India

ACME SolarSetting up a 7 GW of renewable power and green ammonia production facilities worth $6

bn in Tamil Nadu

Ohmium InternationalCurrently manufacturing PEM electrolyzers in Bengaluru (500 MW/annum capacity) and

supplying it to the US. The company is planning to enhance the capacity to 2 GW

Larsen & Toubro Ltd

Entered into an MoU with ReNew Power to develop, own, execute and operate green H2

projects in India

Signed an MoU with Norway's HydrogenPro to setup a JV for the manufacturing of alkaline

water electrolyser

Indian Oil Corp Ltd

Setting up a green H2 plant in Mathura and Panipat

Has teamed up with Larsen & Toubro and ReNew Power for setting up a green H2 plant

40 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

Key growth drivers for the adoption of the Indian green H2 market

Fossil fuels and renewables alone cannot fulfil the rising energy demand of India,

green H2 is a clean solution for future

In line with GOI’s stated objectives at COP26, phasing out of fossil fuels and replacing them

completely with a zero-carbon footprint, can be achieved only with green H2 and other non-

carbon sources like hydro and nuclear (which are again a limiting resource). Green H2

essentially would serve to decarbonize the industrial usage of energy while renewable sources,

solar and wind, would be replacing electricity consumption.

India energy consumption and mix of sources

Source: NITI Aayog

-8

-6

-4

-2

0

2

4

6

8

10

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

CY

90

CY

91

CY

92

CY

93

CY

94

CY

95

CY

96

CY

97

CY

98

CY

99

CY

00

CY

01

CY

02

CY

03

CY

04

CY

05

CY

06

CY

07

CY

08

CY

09

CY

10

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

CY

17

CY

18

CY

19

CY

20

CY

21

E

CY

22

E

CY

23

E

CY

24

E

CY

25

E

CY

26

E

CY

27

E

CY

28

E

CY

29

E

CY

30

E

India energy consumption - historical and forecast

Energy Consumption (TWh) YoY Growth (%)

TWh %

0.3 0.4 0.5 0.6 0.6 0.9 1.1 0.8 1.3 2.9 3.3 7.2 9.6 8.1 7.2 5.8 5.7 4.6 4.3 4.3 4.6 3.8 3.3

0.8 0.7 1.2 1.0 1.0 1.2 1.2 1.2 1.2 1.2

5.1 6.1 6.8 7.5 9.5 6.0 6.3 6.7 11.3

14.9

55.8 55.4 51.5 53.7 54.3 58.0 55.1 55.1 46.4 40.3

30.3 30.6 34.5 31.4 29.5 28.7 29.6 28.4 28.6 27.0

0.6 2.7

CY90 CY95 CY00 CY05 CY10 CY15 CY19 CY20 CY25E CY30E

India energy mix - Significant improvement for clean fuels

Biofuels & Geo Biomass Solar & Wind Hydro Nuclear Natural Gas Coal Crude Oil Green Hydrogen

41 | P a g e ( 5 t h J u l 2 0 2 2 )

For any further query, please email us on [email protected]

India’s H2 demand in CY21 was 8.5 mn tonnes, which is expected to increase to 9.1 mn tonnes

by CY22 and to 11.0 mn tonnes by CY30. Currently, all the H2 consumed in India is produced

using fossil fuels with high emission intensities (11 kg CO2 per kg H2 through steam methane