Embed Size (px)

Citation preview

Government of Karnataka

OFFICE OF THE PRINCIPAL DIRECTOR,KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

3rd Floor, ‘A’ Block, TTMC Building, BMTC,Shanthinagar, Bangalore-560 027.

AUDIT MANUAL

ii

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

iii

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

iv

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

v

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

vi

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

vii

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

Consequent to the Federal FinancialIntegration in 1950, the office of theComptroller of princely state of Mysore wasabolished. Since the Comptroller andAuditor General was responsible for auditof the accounts of the State Governmentunder the Constitution of India, the officersand staff were bifurcated and allocated tothe office of the Accountant General, Mysoreand the newly created Office of theExaminer, Local Fund Audit, who wasmade responsible for audit of Local Bodiesin the State as per Government order No:FL (B) 6175-90 LFA 92-51-6 dated: 08-03-1952. Subsequently, a decision was takento place the accounts staff working invarious Departments of Government undera single agency in the State, resulting in there-designation of the Examiner, Local FundAudit as Controller, State AccountsDepartment in the year 1952.

The name of the Department waschanged to “KARNATAKA STATE AUDIT& ACCOUNTS DEPARTMENT” vide G.O.No. FD/224/SAD/2012 dated 2.3.2015 &Controller, State Accounts Department wasre-designated as “Director (Audit),KARNATAKA STATE AUDIT &ACCOUNTS DEPARTMENT” vide GO No.FD/331/SAD/2014 dated 18.5.2015.

The responsibility for the audit of theaccounts of the local bodies viz. MunicipalCouncils and Municipal Corporations,Gram Panchayats and other institutions inthe State i.e., Universities, Command AreaDevelopment Authorities, UrbanDevelopment Authorities and MuzraiFunds, etc., vests with the Director (Audit),Karnataka State Audit & AccountsDepartment.

Audit is not merely a routine checkingof transactions against preset criteria. Foraudit to be effective and to provide therequired assurance, it must follownationally and internationally recognizedstandards. The understanding of theunderlying theoretical concepts has animportant bearing on the quality of audit.

A set of instructions is required forguidance to the officers and staff whoperform the duty of conducting audit of theinstitutions on behalf of the Director(Audit), Karnataka State Audit & AccountsDepartment. The audit by State Audit andAccounts Department has so far beenguided by the Mysore Local Fund AuditManual, 1967, the University AuditManual, 1984 and instructions issued fromtime to time.

For any manual to be continuouslyrelevant, it needs constant updation.Therefore, it is felt necessary to issue revisedinstructions in view of the amendments torelevant Acts and Rules, etc. There havebeen major changes in the system ofaccounting of many of the entities that areaudited by the State Audit and AccountsDepartment. The Urban Local Bodies, GramPanchayats and the Universities haveswitched over to computerised double entryaccrual based accounting system. Further,the expectation that the State Audit andAccounts Department would play a moresignificant role in providing sound PublicFinancial Management system hasnecessitated a thorough revision of theAudit Manual by updating the existingmanuals with latest knowledge andpractices.

Preface

viii

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

Government of Karnataka (FinanceDepartment) through the World Bankassisted IDF project took up the task ofpreparing an Audit manual for KarnatakaState Audit and Accounts Department. Aspart of the project, a draft Audit manualwas prepared by engaging the services ofSri. Srinivas Kumar, IA&AS, PrincipalAccountant General (Retd.) as Consultant.The draft audit manual was reviewed by ateam constituted for the purpose. TheController, SAD at that time, Sri RS Phondesubmitted the reviewed audit manual to theGovernment on 30/11/2014.

This report was further referred to theAdditional Secretary (Fiscal Reforms), FD,GoK where many changes wereincorporated to the draft manual afterseveral rounds of discussions with theKSA&AD officers. The audit manual hasbeen approved by the Additional ChiefSecretary, Finance Department, GoK, videfile No. FD 96 PMU 2013. The departmentnow believes that the updated guidelineshave been brought out successfully in theform of the Revised Audit Manual.

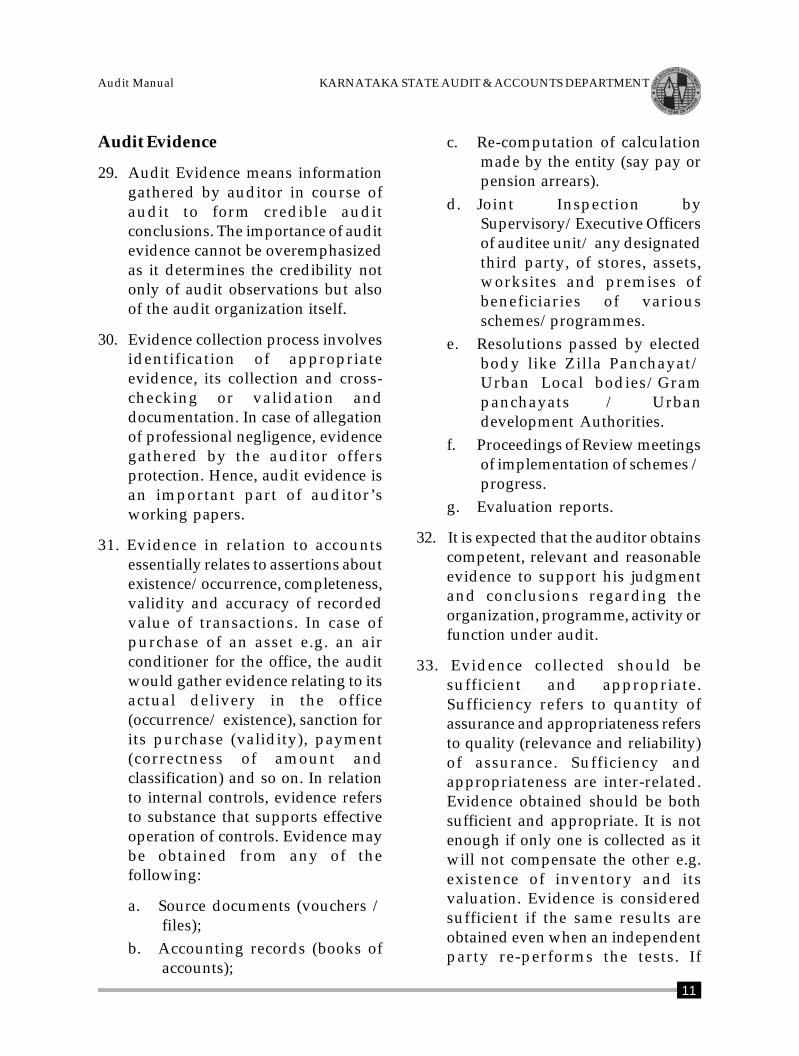

This manual devotes a significantportion to explain the principles and auditconcepts in Part 1 while providing detailedguidance for actual audit practice in Part 2.Part 3 is devoted to detailed checklists whichhave been divided into the generic andInstitution specific checklists forconvenience. Through this manual, theauditors would be able to quote relevantprovisions of the Acts, Rules, Codes,Regulations and Government Orders whiledrafting the Audit Reports. It is hoped thatthis Audit manual would improve thequality of audit carried out by the auditorsof the State Audit and AccountsDepartment.

I would like to express my sincere thanksto Sri Srinivas Kumar, IA&AS, PrincipalAccountant General (Retd.),

Sri. R.S.Phonde, Controller (Retd.), SAD,Sri. B.V.Srikanth, Principal Director (Retd.),KSA&AD, Sri.M.Mahadevaswamy, Retd.Addl. Controller, SAD,Smt.Vasanthakumari.M.N, Retd. Addl.Director, KSA&AD, Smt. Prachi Pandey,Addl. Secretary (Fiscal Reforms), FD, GoK,Sri.Mallikarjunaiah, Senior Audit Officer(Retd), Sri Shivarudrappa,N.B,Addl. Director, KSA&AD,Smt. Siddarajamma.B.S, Addl. Director,KSA&AD, Smt. M.V.Vijayalakshmi, JointController, Dr.Sunitha M, Senior DeputyDirector, Smt.Archana B.Kamalanabhan,Senior Deputy Director,Smt. Shobha.T.R, Senior Deputy Director,Smt.Zohra Jabeen, Senior Deputy Director,Sri. B.S.Murali, Audit Officer, Sri. KodiMallesh, Audit Officer, Smt.B.S.Suma,Accounts Assistant, Sri.Gangadhar andSmt. Latha, Stenographers,Ku.Nagarathna.P and Ku.Gouthami,Data Entry Operators for their dedicatedservice and support in the preparation ofthis manual.

Date: 23 August, 2016.

(Syed Abdulla Razvi)Principal Director,

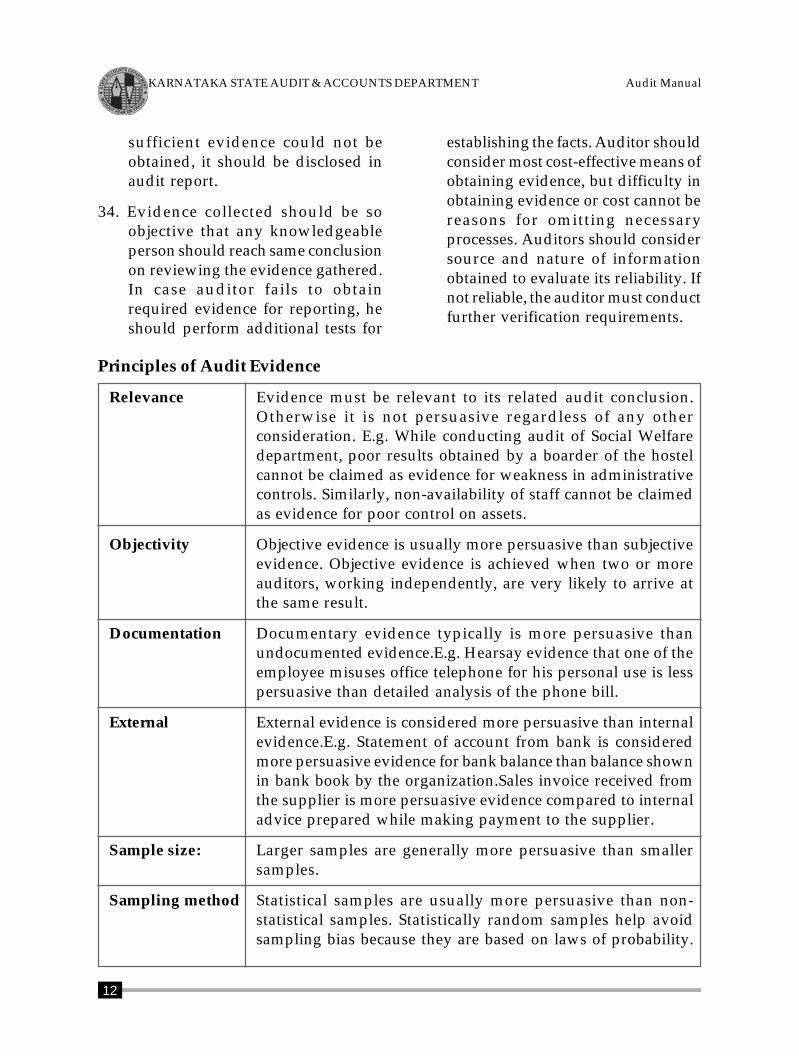

KSA&AD, Bangalore.

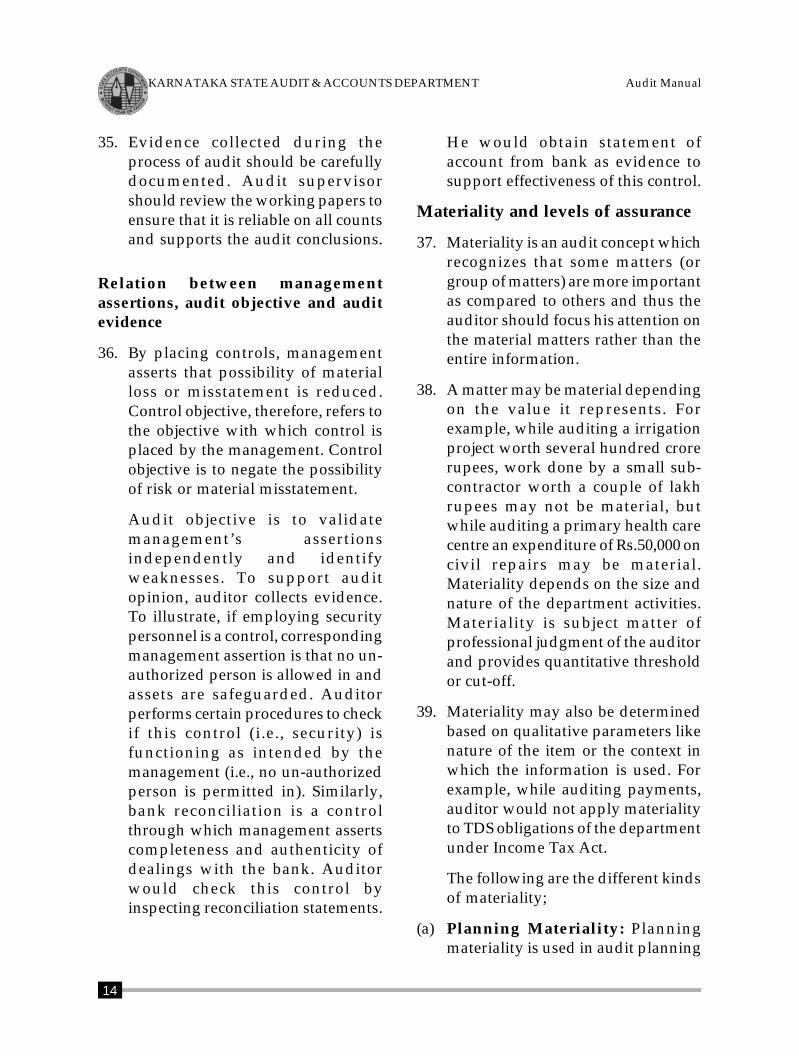

ix

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

PART – 1 PRINCIPLES ANDCONCEPTS OF AUDIT

1 CHAPTER–1: Introduction

General Principles of Audit 1

Auditing Standards 3

Audit Mandate 3

2 CHAPTER-2: Audit concepts

Internal Control Framework 5

Audit Assertions 9

Audit Evidence 11

Relation between managementassertions, audit objective andaudit evidence 14

Materiality and levels ofassurance 14

3 CHAPTER-3: Types of Audit

Receipt Audit 16

Expenditure Audit 18

Audit against Regularity 19

Audit against Propriety 21

Financial Audit 22

Performance Audit 23

Systems Audit 24

Forensic Audit 25

Fraud and Audit 25

4 CHAPTER – 4 : Risk basedauditing and use of statisticalsampling

Risk based audit 28

Compliance and substantivetesting 29

Contents

Use of statistical samplingin audit 29

Judgmental or non-statisticalsampling 29-30

Statistical Sampling 30

Statistical Sampling Techniques 30

Sample Size 31

5 CHAPTER – 5: Audit Procedures

Analytical Procedures 34

Comparisons involving a single ormultiple components 34-35

System Based Approach 36

Direct Substantive Testing 36

Computer Assisted AuditTechniques 37

Using the work of externalparties 37

Synergy with internal auditors 37

Using the work of otherspecialists 39

PART – 2 AUDIT PRACTICE

6 CHAPTER – 6: Audit Planning

Annual Audit Planning 43

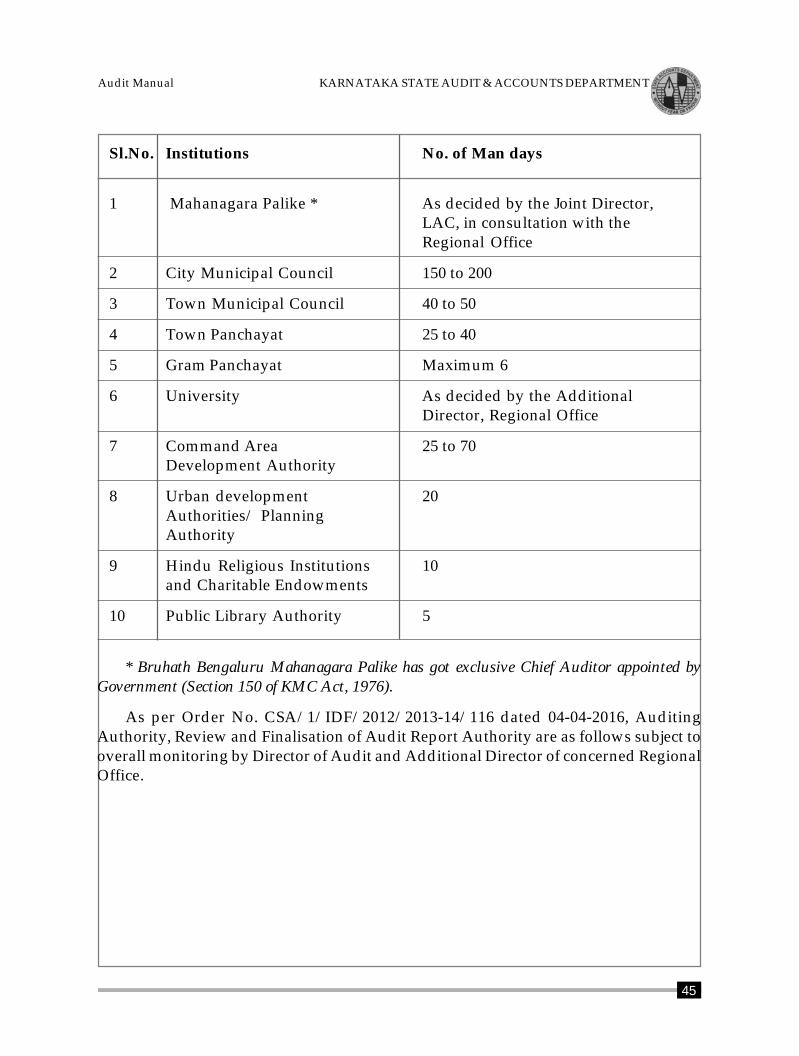

Manpower allocation/Man-Days 44

Staffing Pattern 47

Monitoring of compliance tothe annual plan 47-48

Entity level planning and auditplanning memorandum 48

Creation of Permanent Audit File(PAF) 49

Audit programmes 50

x

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

7 CHAPTER 7: Audit Execution

Commencement of audit 51

Entry Conference 51-52

Audit Process 52

Audit Working Papers 52-53

Raising of preliminary auditobjections 53-56

Supervision and Review 56-57

Audit conclusion and auditreporting 57-58

Exit Conference 58

8 CHAPTER – 8: Audit Report

Format and Content of AuditReport 59

Audit Reports - Financial Audit 60

Audit opinion 60-61

Different types of opinions 61-63

Management Letters 63

Audit Reports - Propriety andRegularity 63-68

Submission of audit reports 69

Consolidated AnnualAudit Report 70

Follow up of audit report 71

Levy of Surcharges 71

Powers to drop/foregorecoveries 71-73

9 ANNEXURES

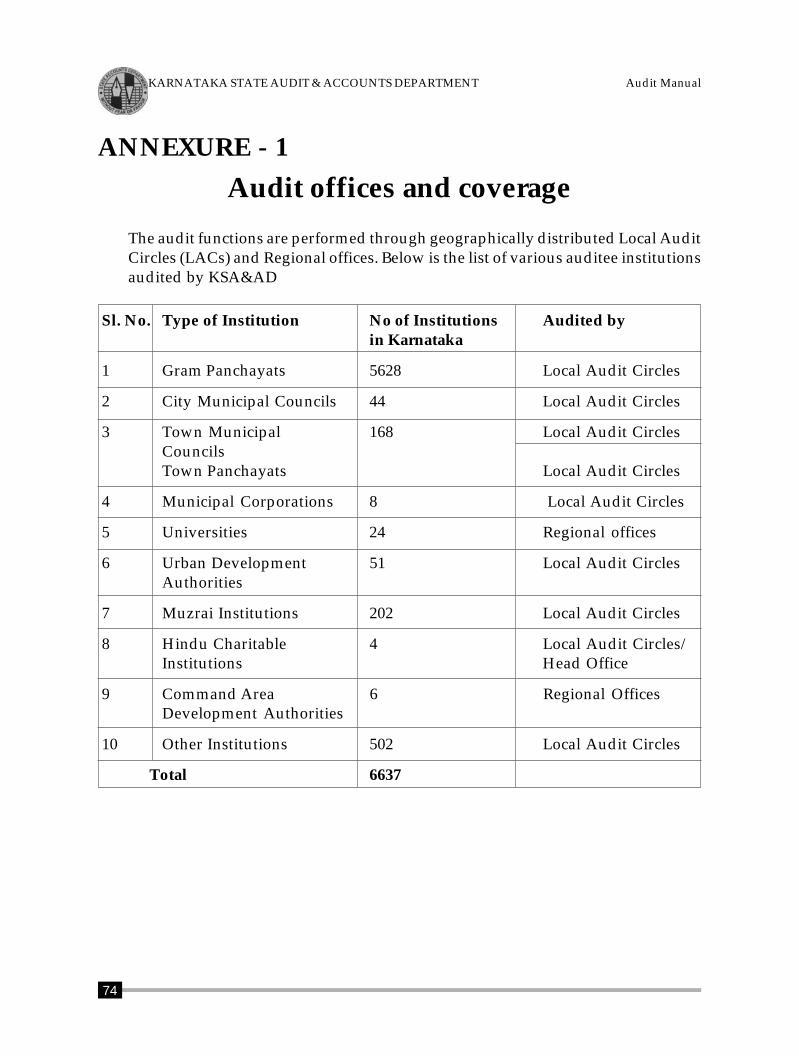

ANNEXURE 1- Audit officesand coverage 74

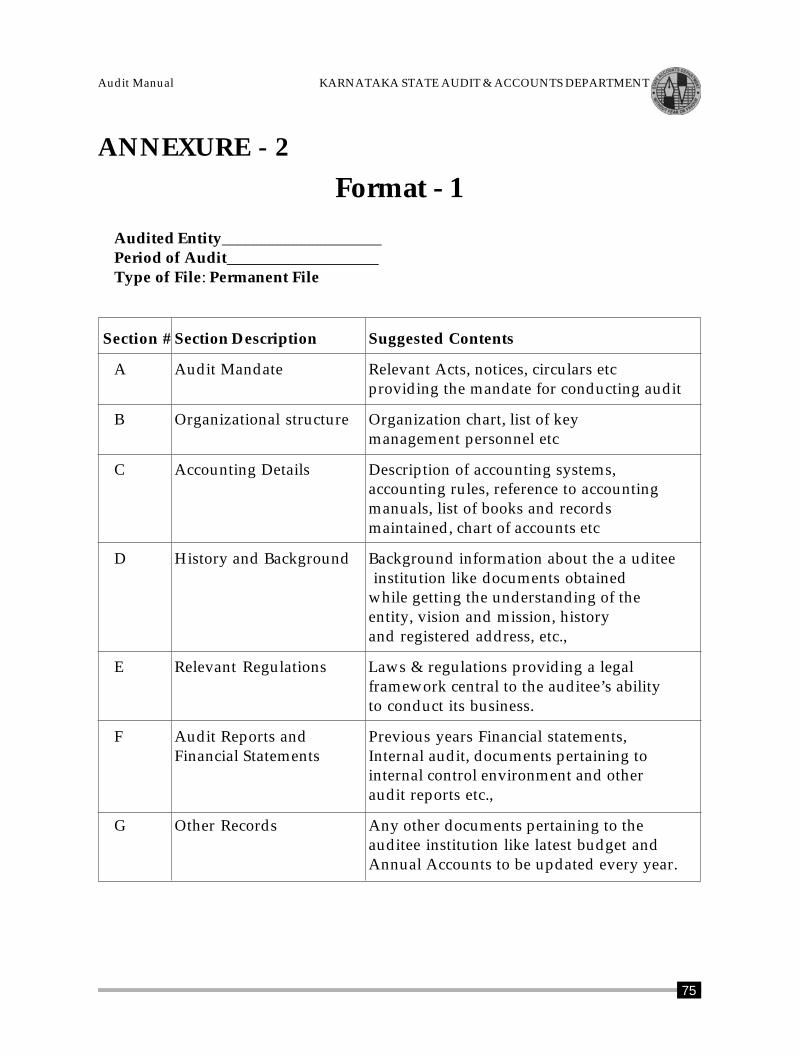

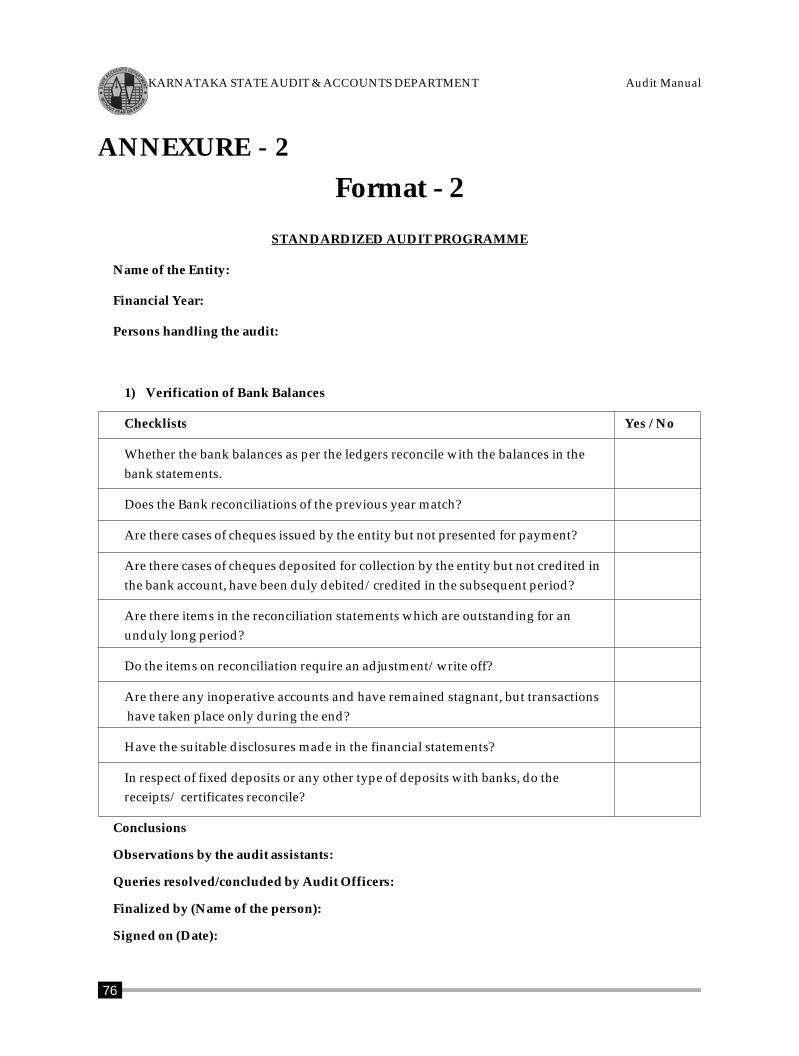

ANNEXURE 2 –FORMAT -1 75

ANNEXURE 2 –FORMAT -2 76

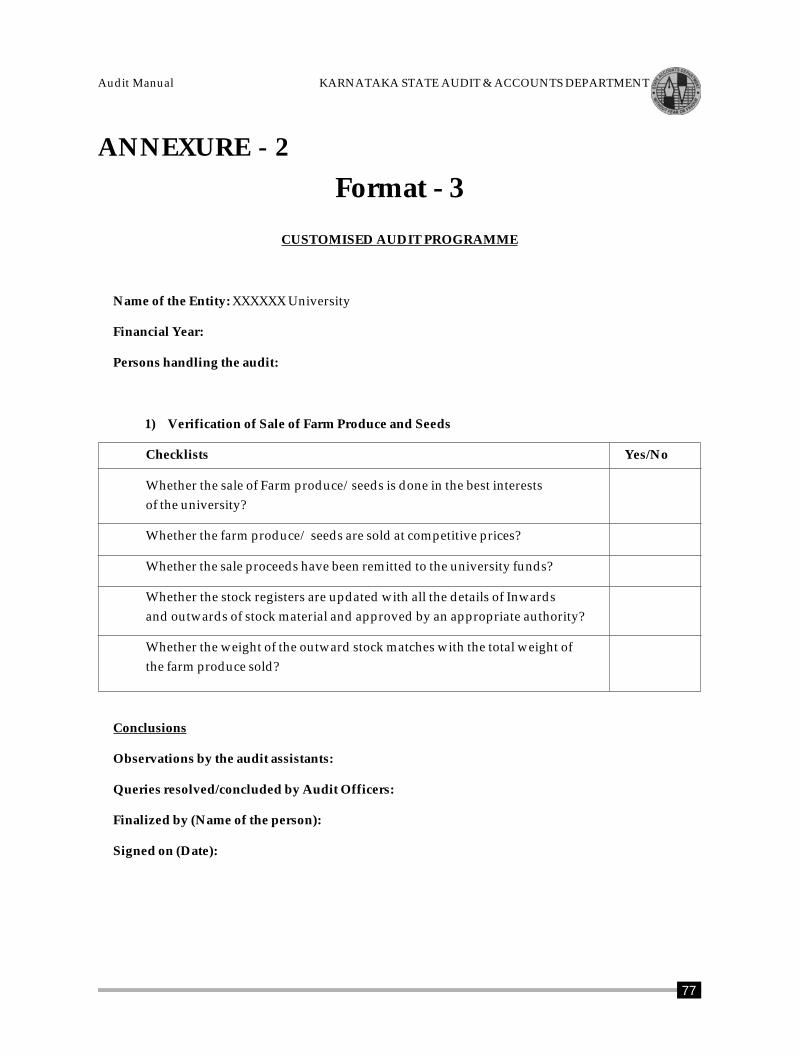

ANNEXURE 2 –FORMAT -3 77

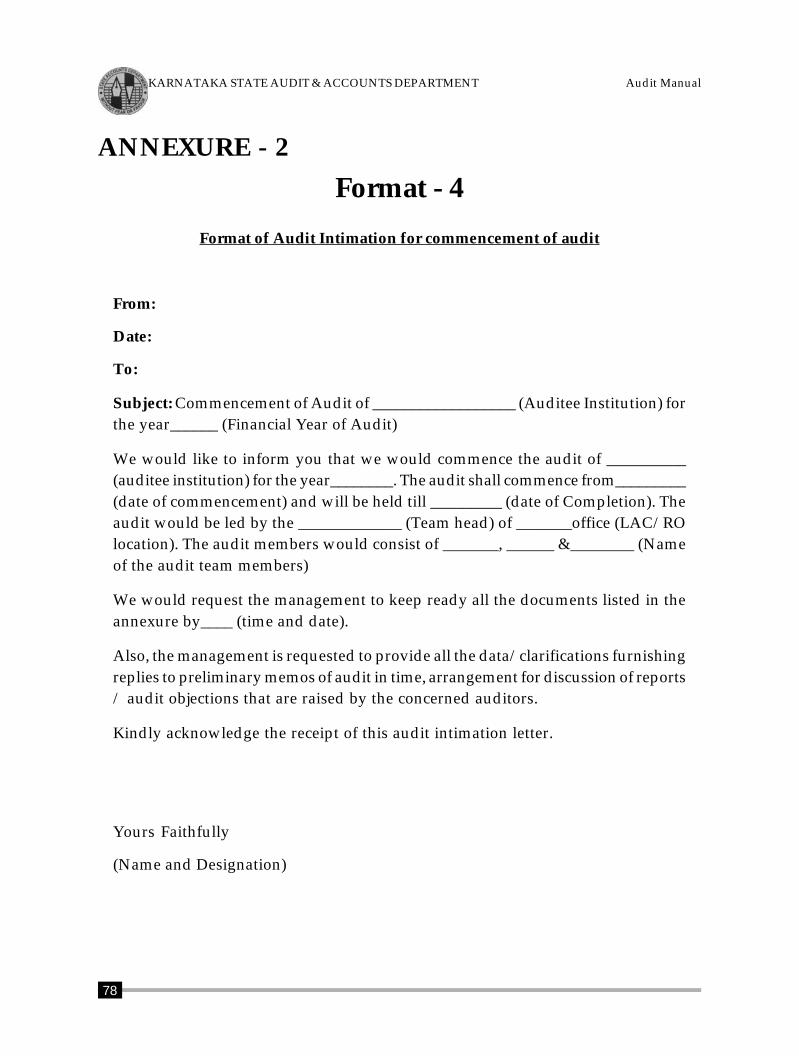

ANNEXURE 2 –FORMAT -4 78

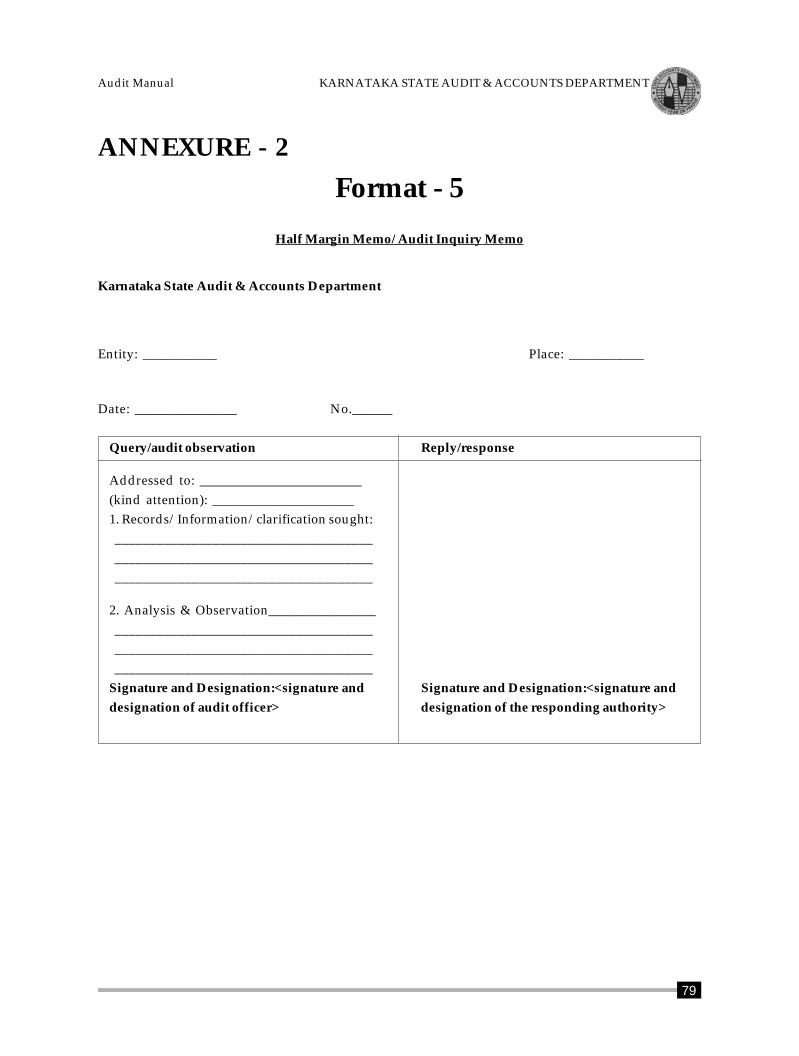

ANNEXURE 2 –FORMAT -5 79

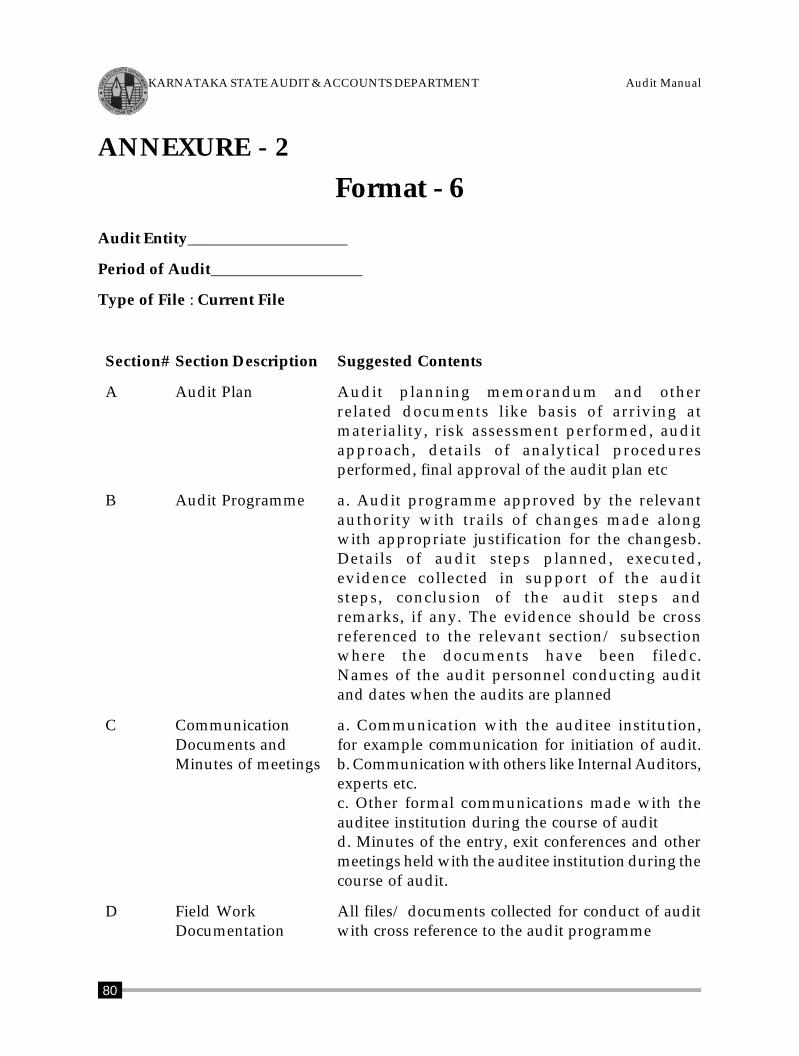

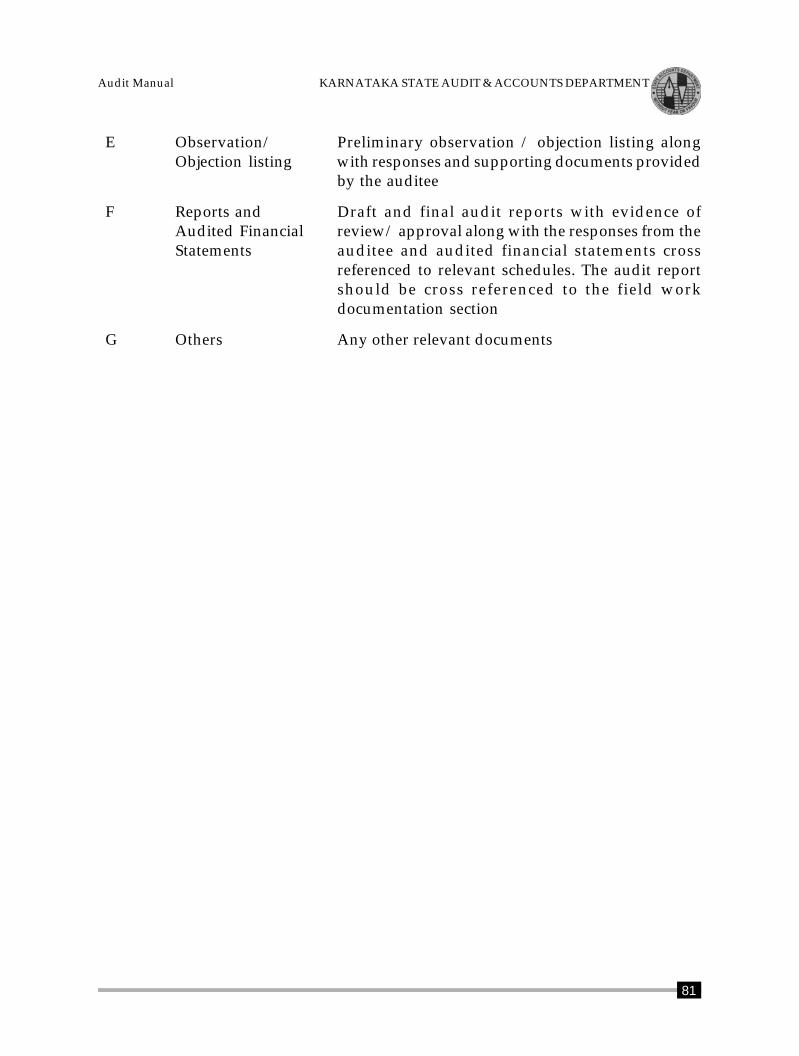

Annexure 2 –Format-6 80-81

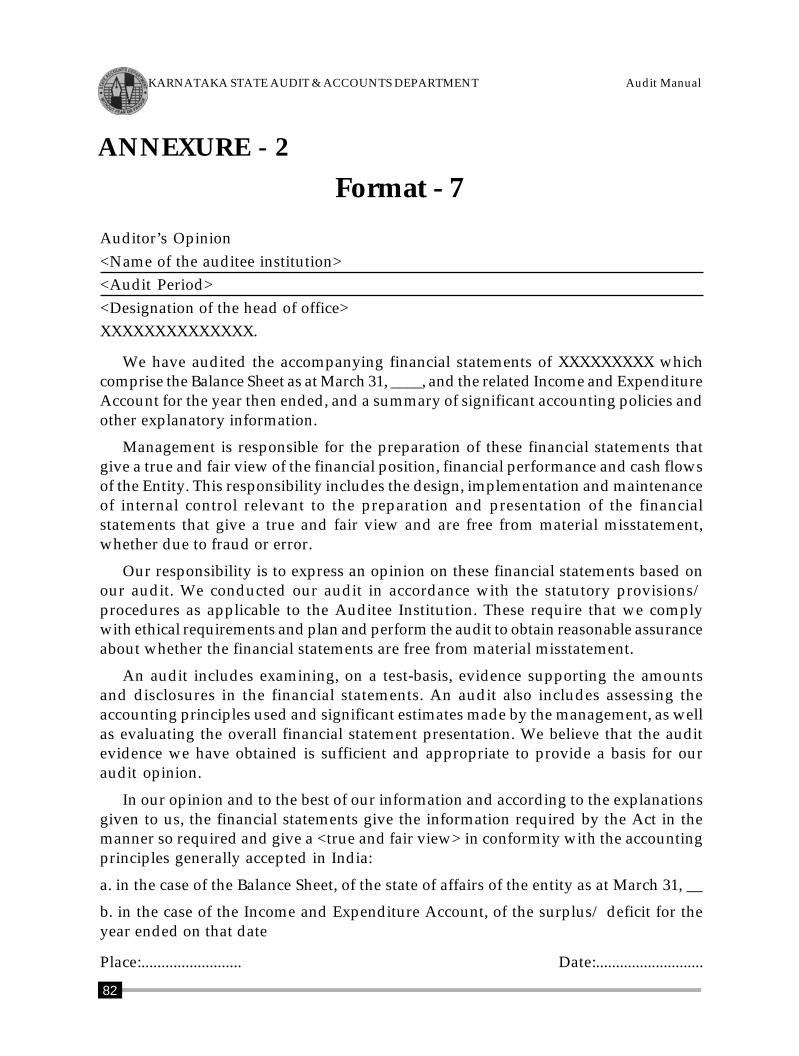

Annexure 2 –Format-7 82

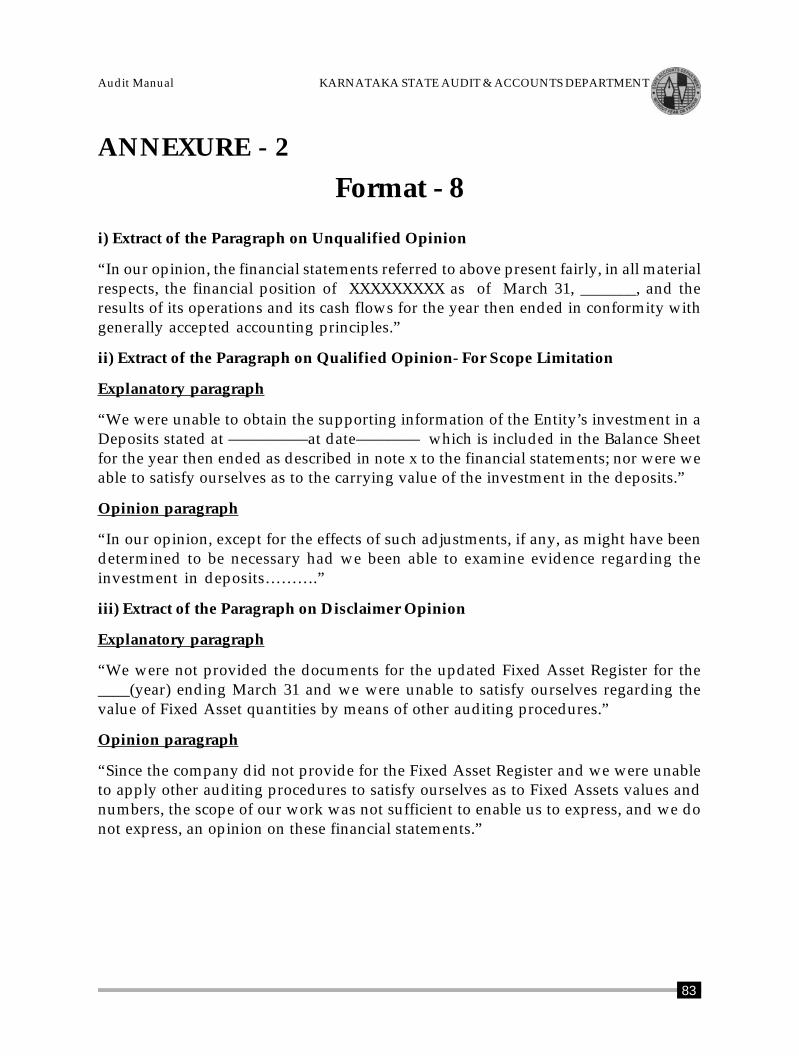

Annexure 2 –Format-8 83

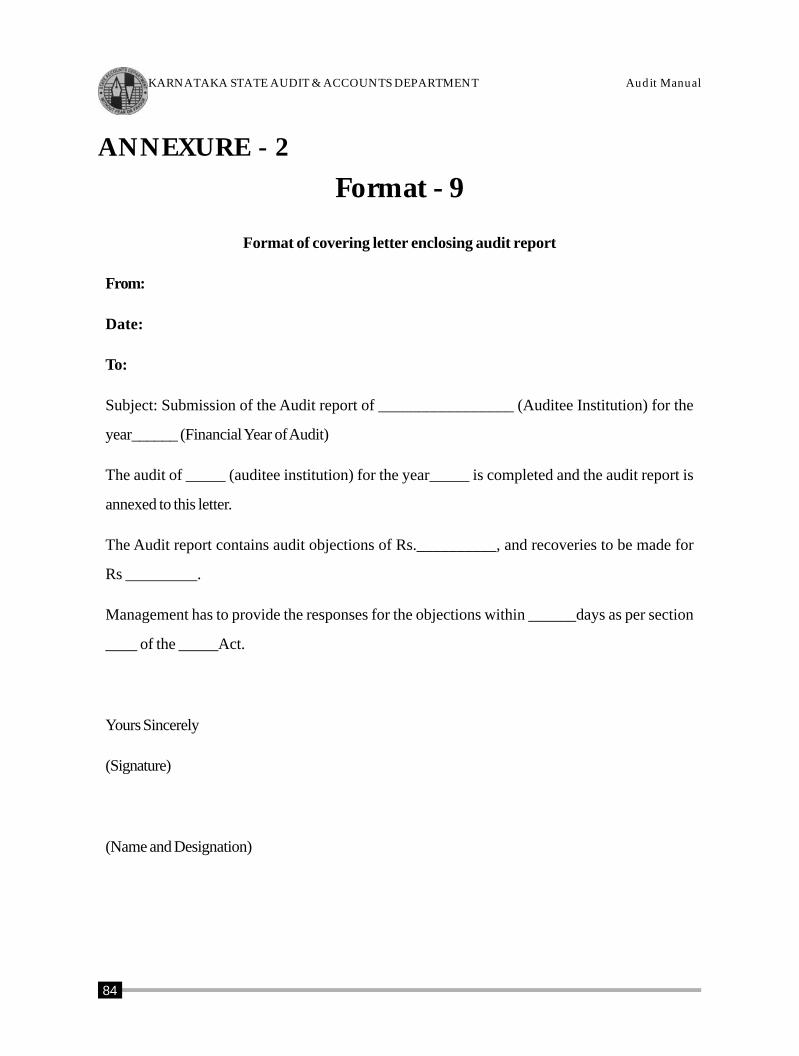

Annexure 2 –Format-9 84

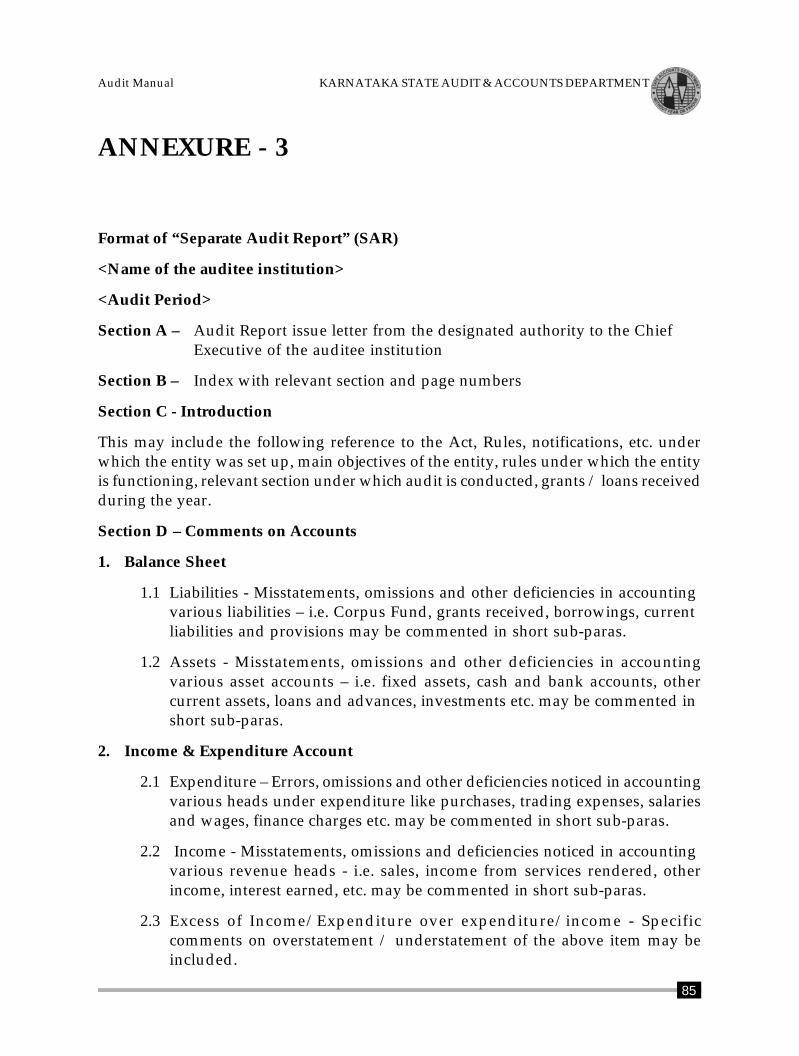

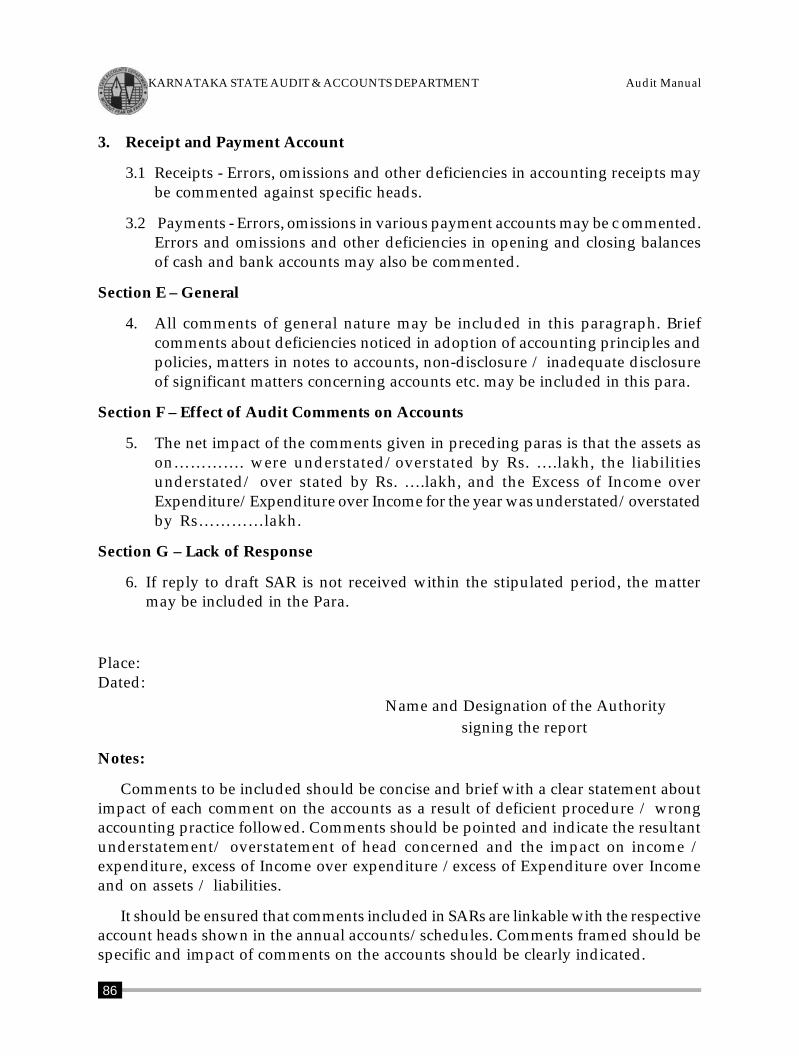

Annexure 3 -Format of SAR 85-86

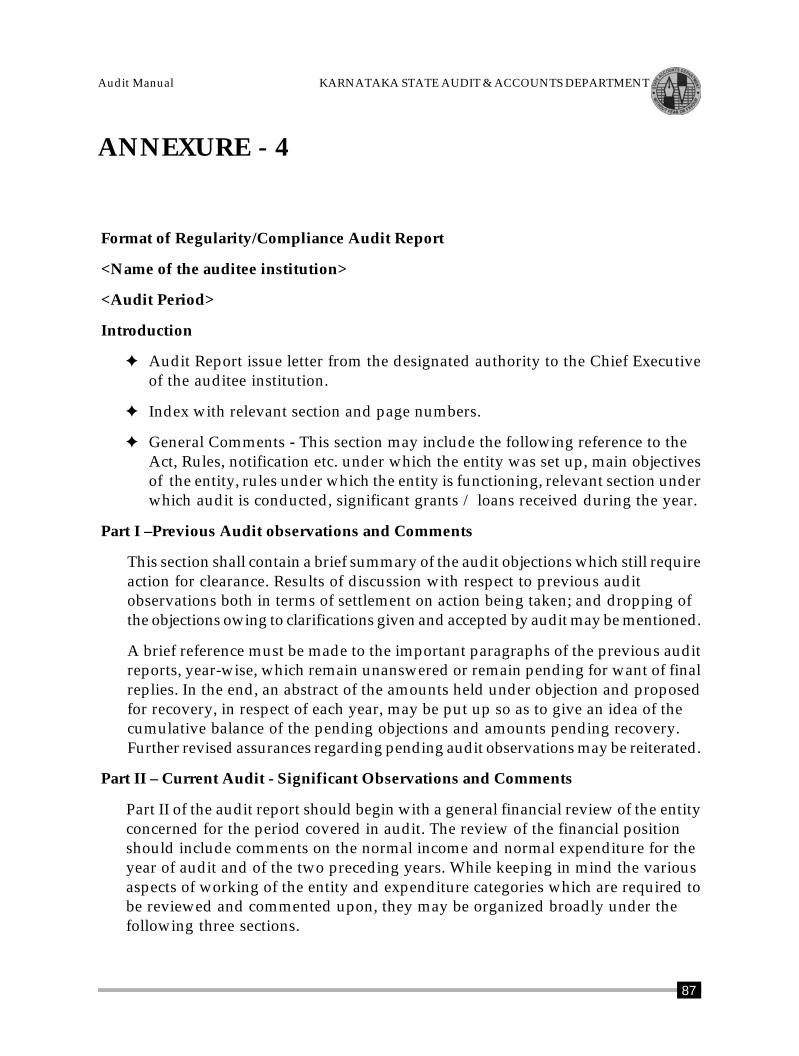

Annexure 4 -Format ofRegularity/ComplianceAudit Report 87-88

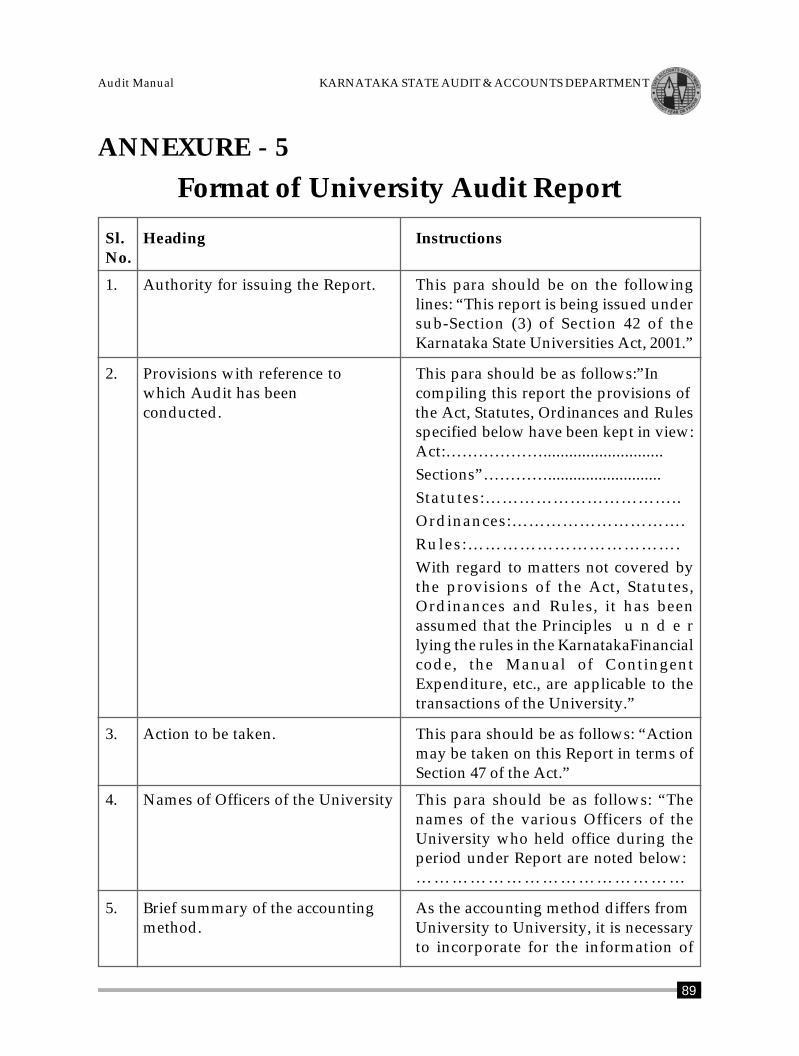

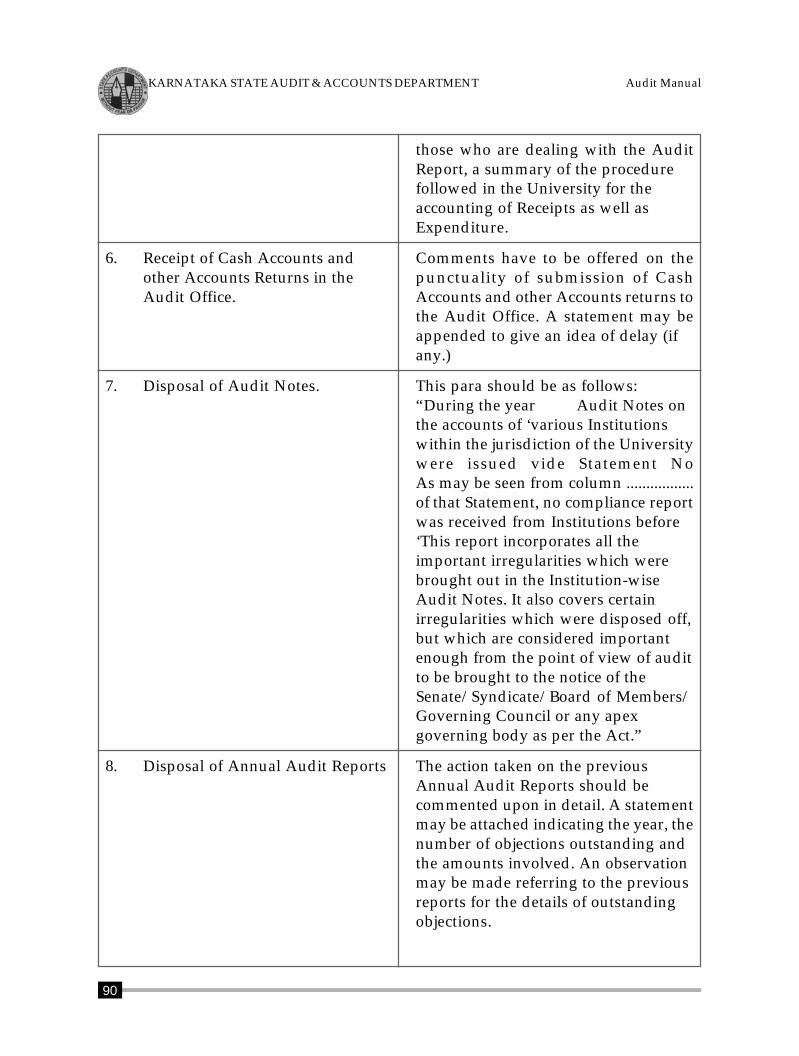

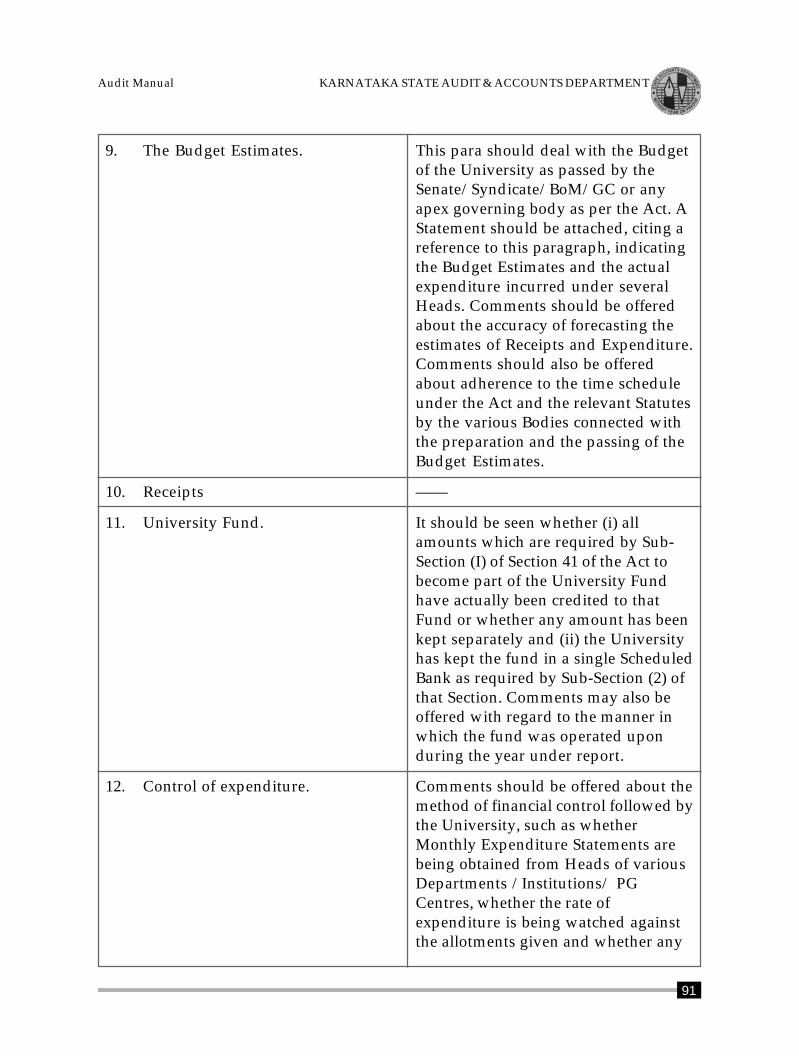

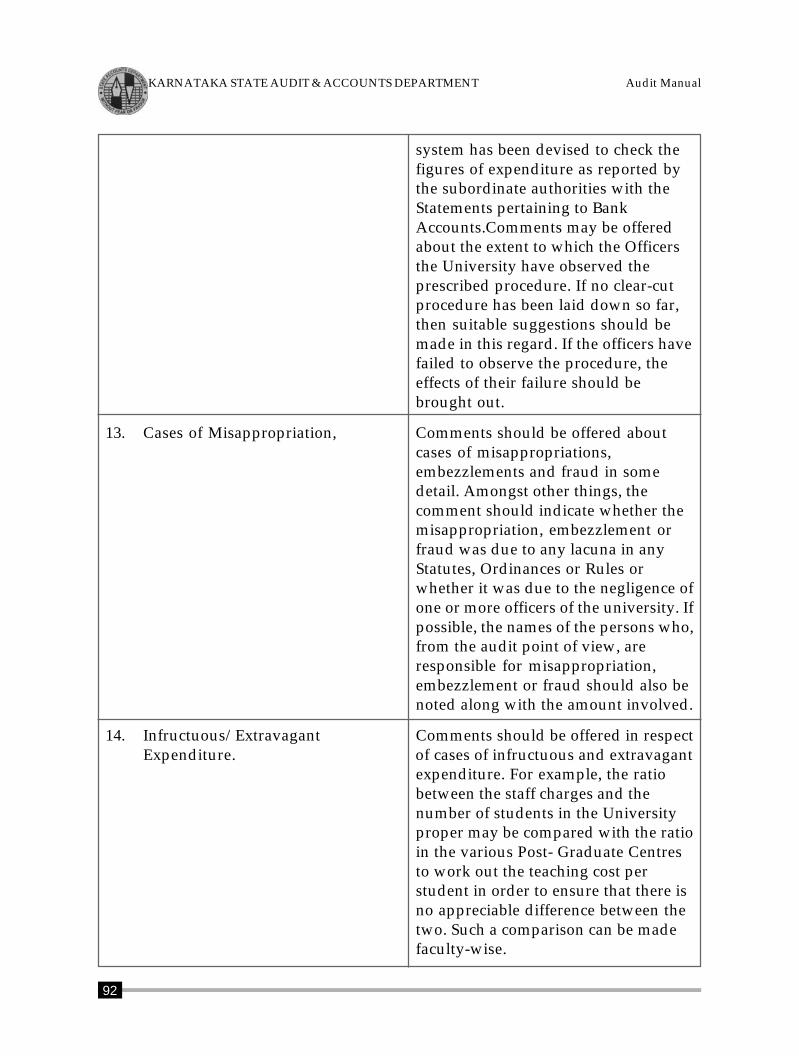

Annexure 5 -Formatof University Audit Report 89-95

PART – 3 AUDIT CHECK LISTS

1 Generic Check Lists 98

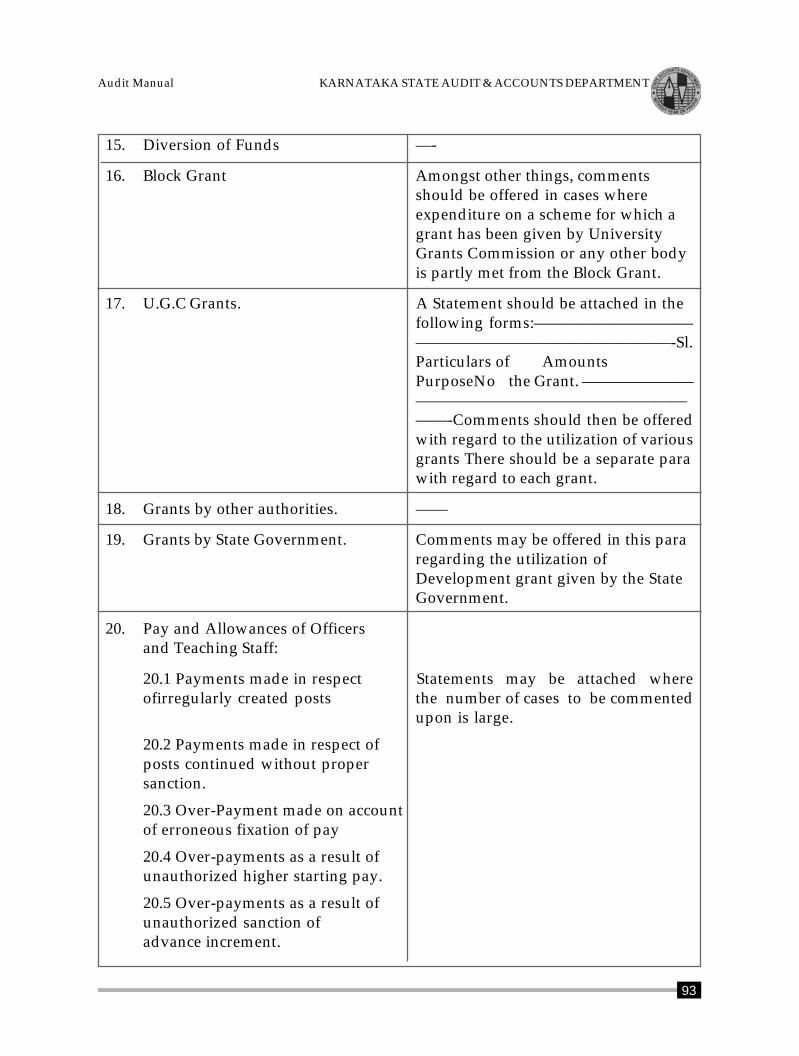

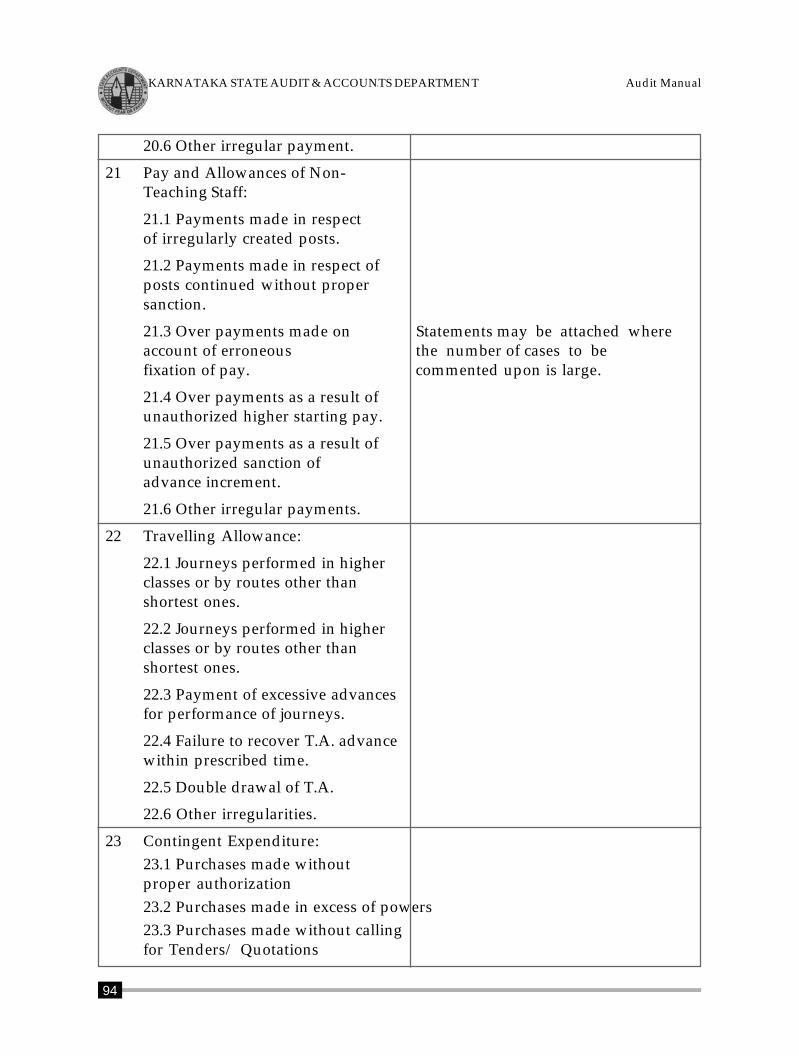

1.1 EstablishmentExpenditure 98-102

1.2 Travelling allowance,Leave Travel Concession,etc 102-103

1.3 Pension Contribution 103

1.3. A Rent 103-104

1.3.B-MedicalReimbursement Bills 104

1.3.C-ContingentExpenditure/ PeriodicalCharges 105

1.3.D-StationeryArticles 105-106

1.3.E-Postage Stamps 106

1.3.F-Office MaintenanceExpenses 106

1.3.G-AdvertisementExpenses 106

1.3.H-Repairs andMaintenance 107

1.3.I-Professional Fees,Consultancy Fees. Etc., 107

1.4 Procurement of goods andservices/exemptions 108

1.4.1-General Activity 109

xi

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

1.4.2-Tendering andEvaluation 111-118

1.4.3-Agreements 118-120

1.4.4-Execution ofWorks 120-121

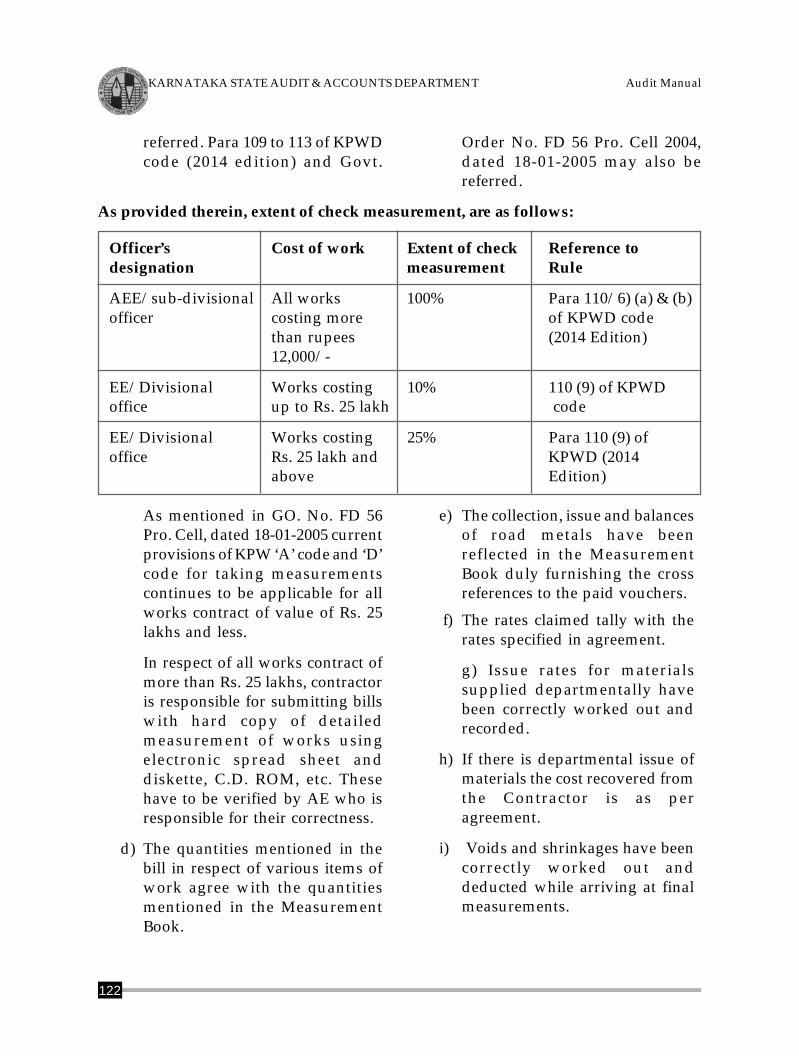

1.4.5-Audit of WorkBills 121-123

1.4.6-Audit ofprocurements of Goods/Equipment and StoresAccounts 124-126

1.4.7-Finance andAccounts 126-127

2. Regularity/Compliance AuditChecks for Specific Institutions

A. Audit checklist for audit ofUrban Local Bodies

A.1 Introduction 127-128

A.2 Background andEvolution of Urban

Local Bodies inKarnataka 128-129

A.3 Audit Mandate forUrban Local Bodies/charge &surcharge 129-132

A.4.1 Audit checklist forBudget 132-133

A.4.2 Audit checks onvarious AccountingRegisters 134-136

A.5 Audit checklistfor Revenue Items 136

A.5.1 Property Taxes 137-140

A.5.2 Service Charges Inlieu of PropertyTaxes 140-141

A.5.3 Advertisement Tax/Stamp Duty 142-143

A.5.4 (1) Acquisition ofproperties 143

A.5.4 (2) Revenue fromrent/lease income 144-145

A.5.5 Ground Rent onAdvertisements 146

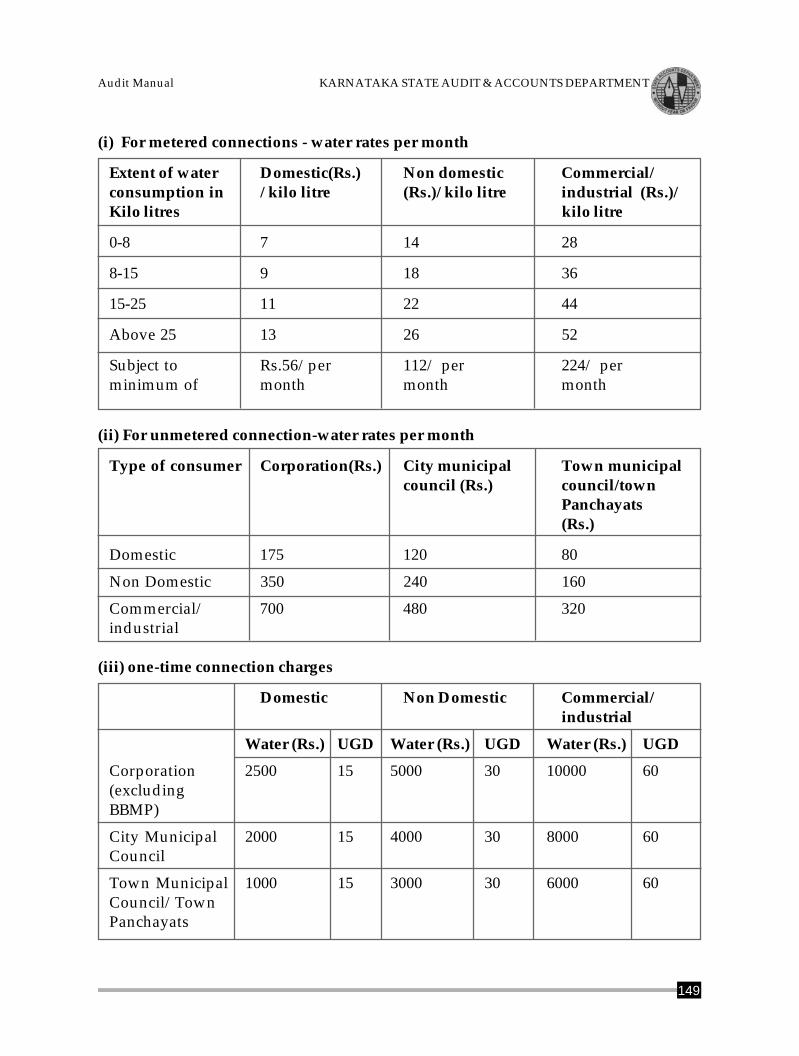

A.5.6 Water Supply Charges 146-147

A.5.7 Registers/Recoveryof water charges 147-150

A.5.8.Hire Charges forEquipment 150

A.5.9 Rents from CommunityHalls, Guesthouses,Auditoriums, etc 150-151

A.5.10 RegularizationCharges 151

A.5.11 Road Cutting andRestoration Charges 151

A.5.12 Fees for TemporaryProjections andErections 151

A.5.13 Building PermissionFees/Regularisationof unlawfulBuildings 152-153

A.5.14 Revenue frommarket fees and feesfrom slaughterhouses 154-155

A.5.15 Fees from Jatra,Urus, etc 155-156

A.5.16 Development andBetterment Charges 156

A.5.17 Fees for Issue ofCertificates 157

A.5.18 Entry and ParkingFees 157

A.5.19 Sales Proceeds ofSolid Waste, Debrisand Silt 157-158

xii

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

A.5.20 Sales Proceeds fromTender Forms andPublications 158

A.5.21 Lapsed Deposits andforfeited Deposits 158-159

A.5.22 Infrastructure andSolid WasteManagement Cess 159

A.5.23 Sale Proceeds fromDisposal of FixedAssets andInvestments 159

A.5.24 Grants 159-160

A.5.25 Audit Checks forState FinanceCommission(SFC) - Grants 160

A.5.26 Audit Checks forthe Register ofGrants 160-161

A.5.27 Penalties/ Grant oflicence to use placesfor certain purposes 161

A.6 Audit checklist forExpenditure Items

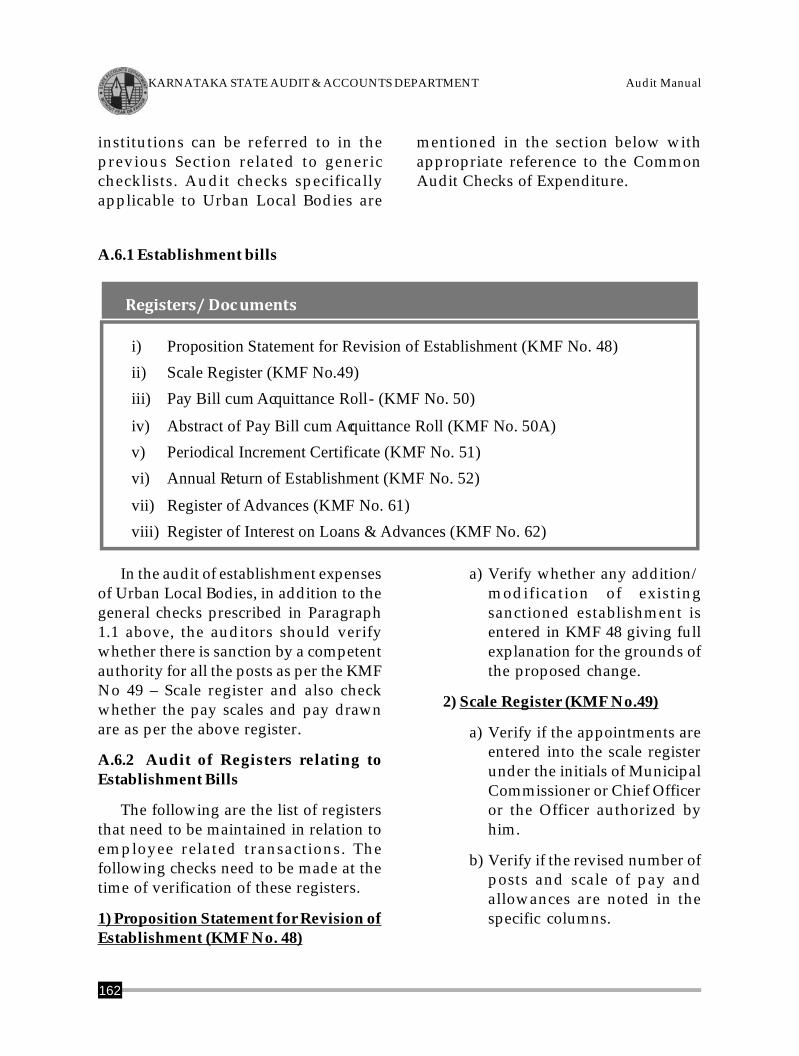

A.6.1 Establishmentbills 161-162

A.6.2 Audit of Registersrelating toEstablishmentBills 162-163

A.6.3 Honorarium to theMembers of theCommittees 164

A.6.4 Public worksexpenditure 164-169

A.7Audit checklist for Assets

A.7.1 Movable andimmovableproperties 169-171

A.7.2 Vehicles 171-173

A.7.3 Investments 173

A.7.4 Stores 173-174

A.7.5 Loans &Advances 174-175

A.7.6 Cash and BankBalances 175-177

A.8. Audit Checklist for Liabilities

A.8.1 Earmarked Fund 177

A.8.2 Borrowings 177-178

A.8.3 Sinking Funds 179-180

A.9. Audit Report 180-181

B. Audit checklist for audit ofUniversities

B.1 Introduction 181-182

B.2 Statutory framework ofUniversities inKarnataka 182-183

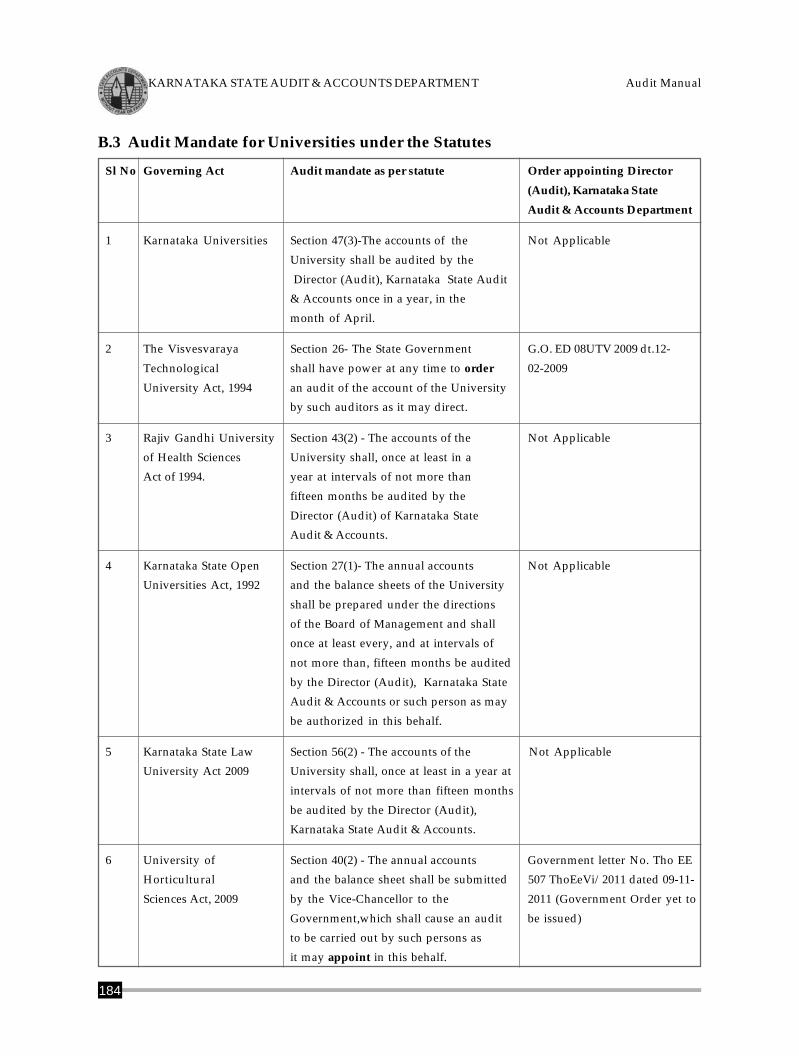

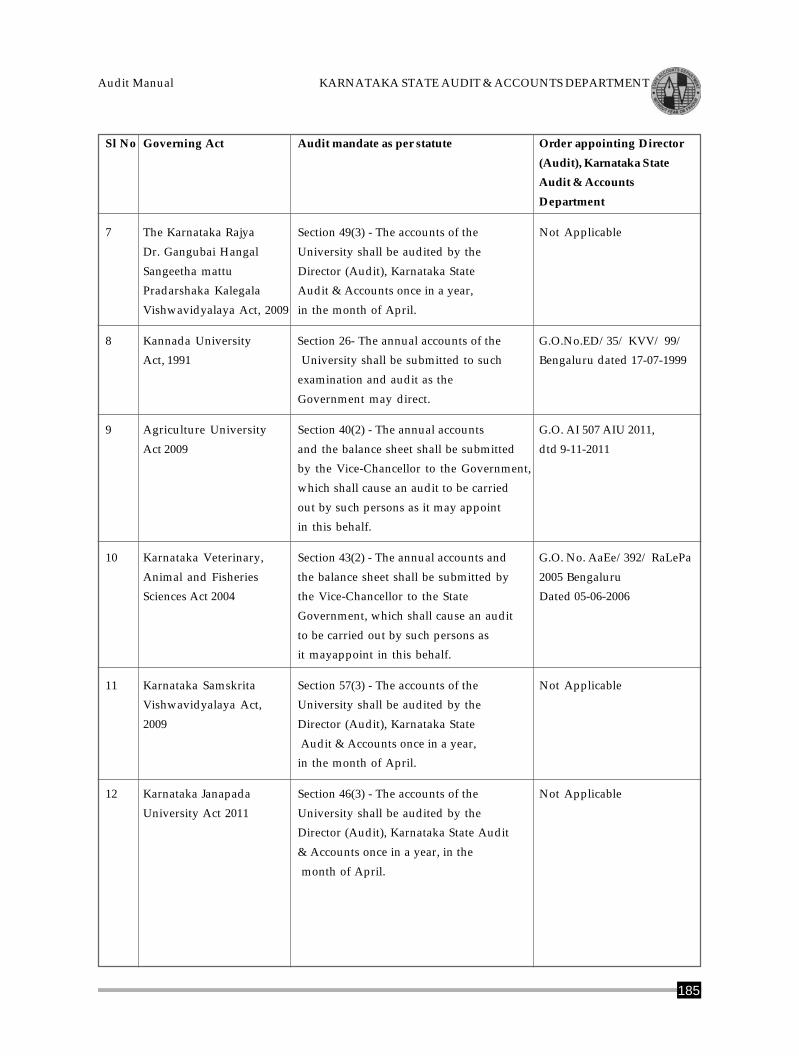

B.3 Audit Mandate forUniversities underthe Statutes 184-185

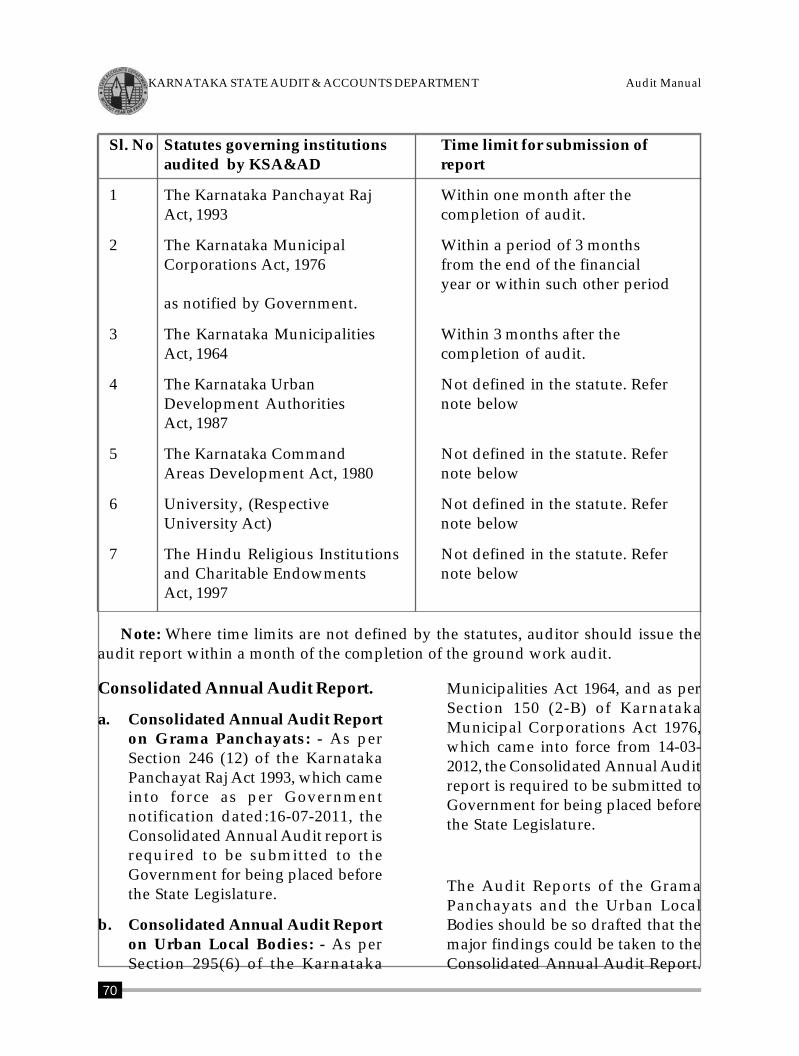

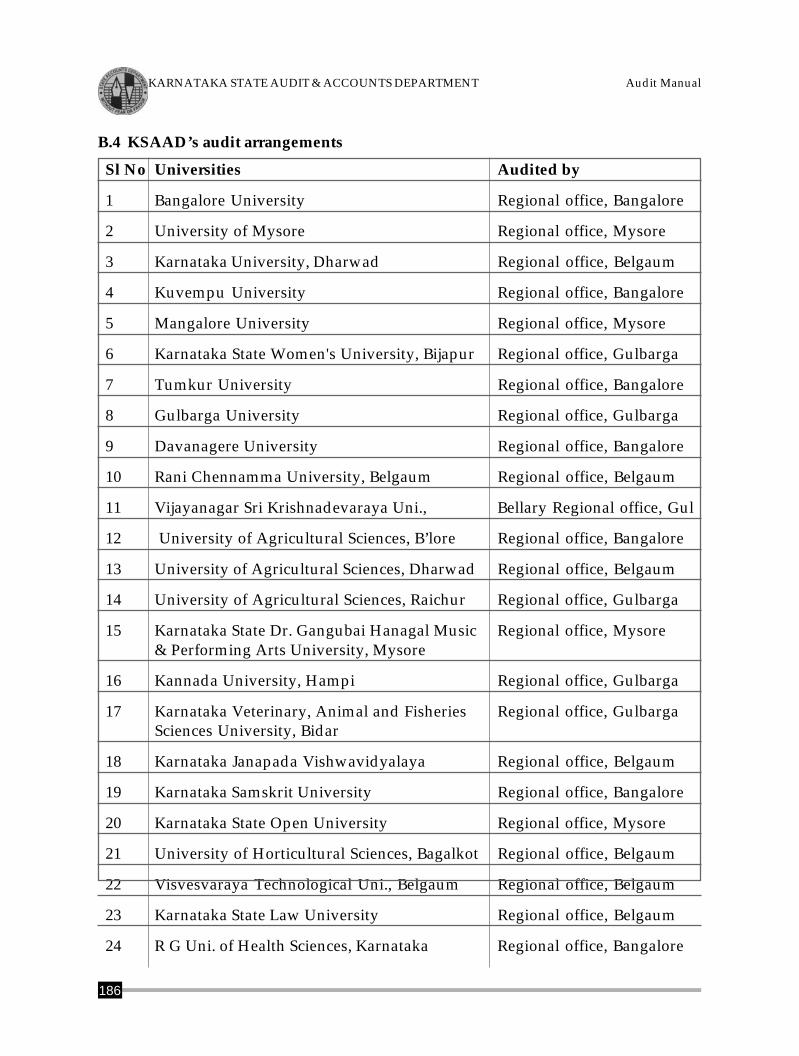

B.4 KSA&AD’s auditarrangements 186

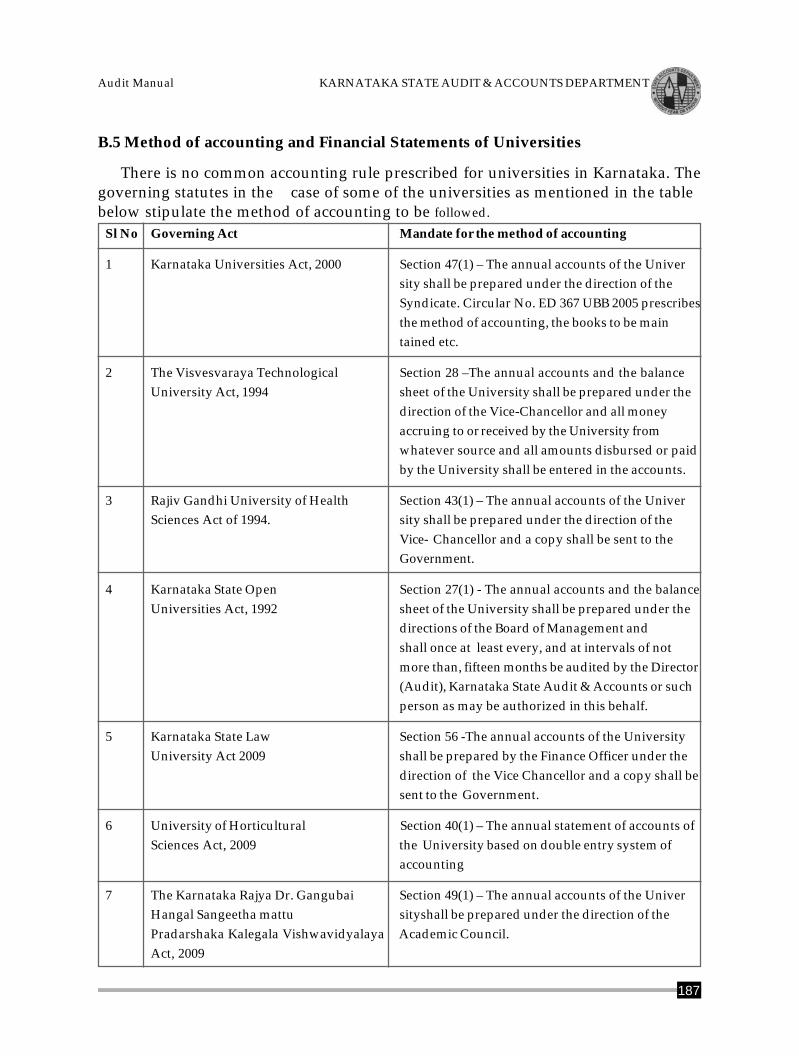

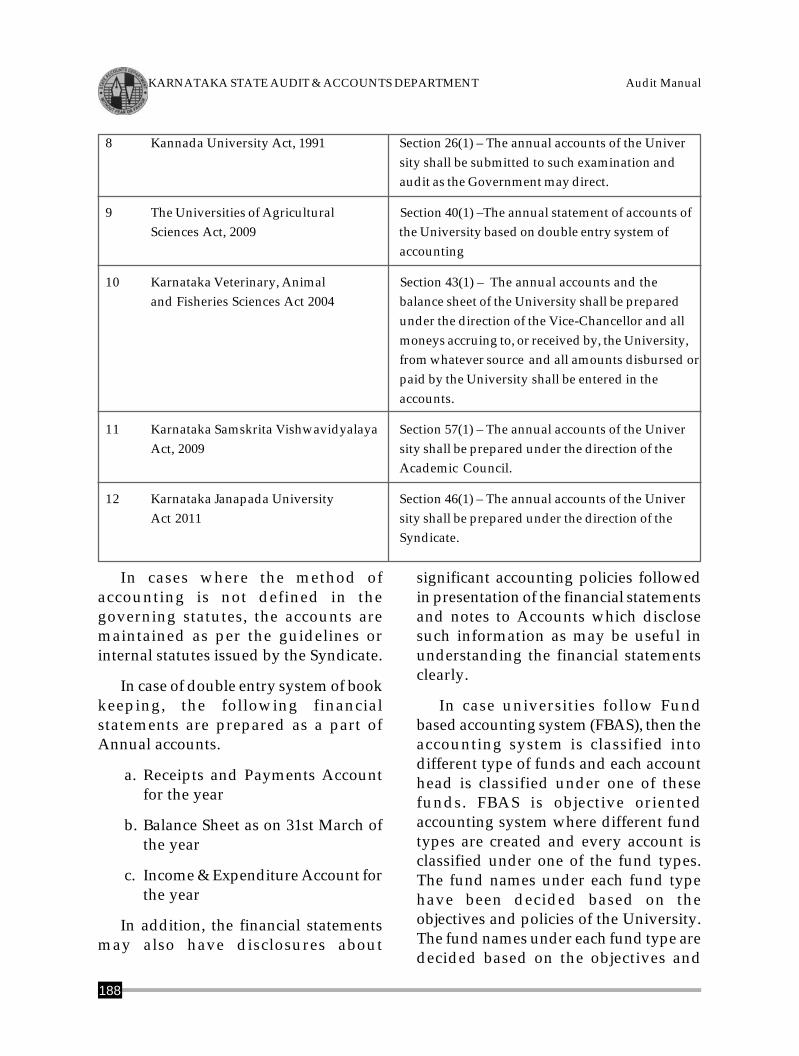

B.5 Method of accounting andFinancial Statements ofUniversities 187-189

B.6 Audit Checklistfor Budget 189-190

B.7 University Funds 190

B.8 Revenue 190-191

B.8.1 Examination Fee 191

B.8.2 Prospectus/Application Fees 191-192

B.8.3 Tuition fees 192

B.8.4 Convocation Fees 192-193

B.8.5 Fee for Affiliation 193-194

xiii

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

B.8.6 Registration Fees/Admission Fees 194

B.8.7 Revaluation Fees 194-195

B.8.8 Eligibility Fees 195

B.8.9 Other Fees 195

B.8.10 Rent of Quarters &Other Buildings 196

B.8.11 Lease Rent ofProperty 196-197

B.8.12 Overdue Charges ofLibrary Books (Fines) 197

B.8.13 Charges forCopying, Xeroxing,etc 197

B.8.14 Fees for Issue ofcertificates 197-198

B.8.15 Sale of Books andPublications inPrasaranga 198

B.8.16 Hostelmaintenance 198-199

B.8.17 Receipts fromSale of Farm Produceand Seeds 199-200

B.8.18 Sale Proceeds ofGarden/Horticulturedepartment 200

B.8.19 Bus Fare and HireCharges of Vehicles 200

B.8.20 Sale Proceeds ofUnserviceableArticles 200

B.8.21 Sale Proceeds ofTender Forms 200

B.8.22 Share ofConsultancy Fees 201

B.8.23 GovernmentGrants 201-204

B.8.24 Receipt from Bequest,Donation,Endowment 204

B.9. Expenditure 204-206

B.9.1 Sanctions 206-207

B.9.2 ExaminationRemunerationBills 207-208

B.9.3 Establishment bills 208

B.9.4 Travelling allowance,leave travelconcession 209

B.9.5 MedicalReimbursementBills 209

B.9.6 ContingentExpenditure 209

B.9.7 Audit of SportsAccounts 209

B.9.8 Scholarships 210

B.9.9 Works Account/Contracts 211

B.9.10 Audit ofContracts 213-214

B.9.11 Audit Checklistfor Funds 214-217

B.9.12 Library Accounts 217

B.10 Audit checklistfor Assets 219

B.10.1 Procurement ofstores and stockaccount 219

B.10.2 Deposits 219

B.10.3 Investments 220

B.10.4 Loans &Advances 220-221

B.10.5 Revolving Funds 221

B.10.6 Suspense Account 222

xiv

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

B.11 Audit checklist forverification of CommonRegisters 222-229

B.12 Audit Report 229-231

B.13 Audit Charges 231

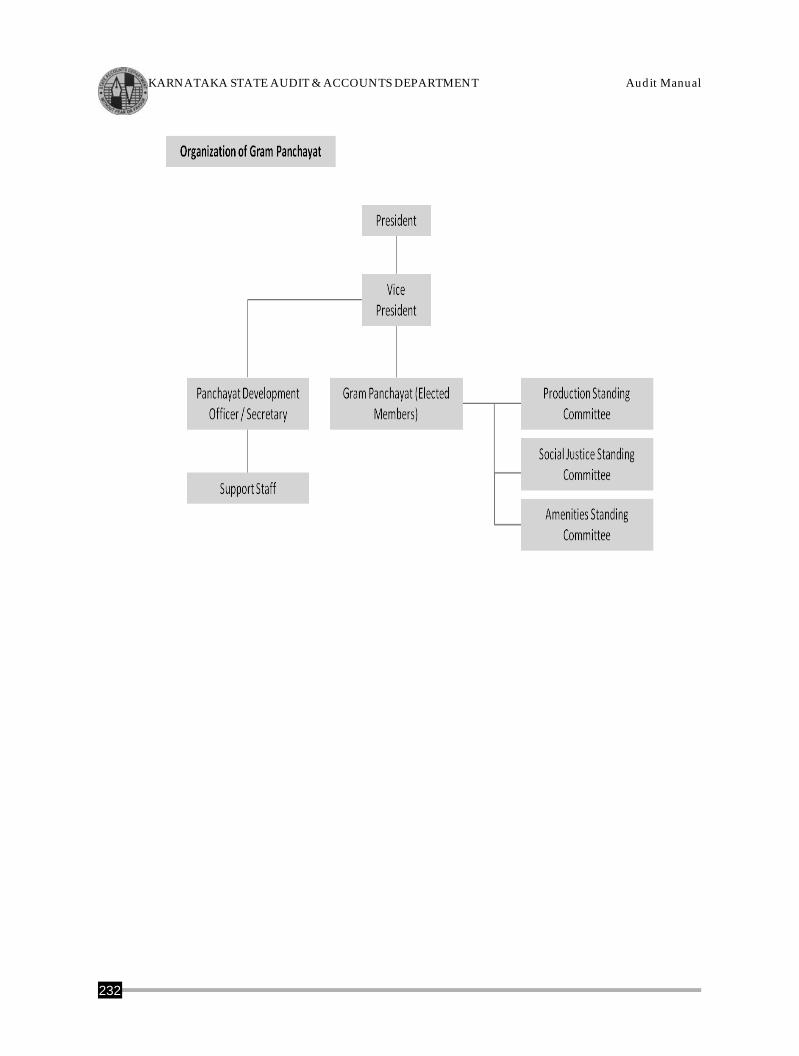

C. Audit Checklist for Audit ofGram Panchayats

C.1. Introduction 231-232

C.2 Audit Mandate forGram Panchayat/charge & surcharge 233

C.3 Method ofAccountingPrescribed 233

C.4 Financial Reporting 233

C.4.1 Computerization ofAccounts 234

C.5. Audit Checklist forBudget 234-235

C.6 Audit checklist forRevenue Items 235-236

C.6.1 General Checks forall Categories ofRevenue 235

C.6.2 Tax on Buildingsand Lands 236-237

C.6.3 Assessment andCollection of Taxes 238

C.6.4 Advertisement Tax 238

C.6.5 Entertainment Tax 239

C.6.6 Rent from Buildings& Lease of Land 239-241

C.6.7 Income from marketsfees, slaughter-houses, etc. 241-243

C.6.8 Water Charges/Water Connectioncharges 243-244

C.6.9 Fees for Issue ofCertificates 244

C.6.10 Jatra Fees 244

C.6.11 Fines, Penaltiesand Recoveries 244

C.6.12 Warrant/DistraintFees 245

C.6.13 Inventory andRegister of DistrainedProperty 245-246

C.6.14 Cess Collections 246

C.6.15 Trade Licence Fees 247

C.6.16 Building LicenceFees 249

C.6.17 Licence Fees for Use ofPlaces for SpecifiedPurposes 250

C.6.18 Sales by Auction 250

C.6.19 Revenue Leased Out 251

C.6.20 Income fromEndowments andTrusts 251

C.6.21 Centrally Sponsoredschemes/ Grants 252

C.6.22 Lapsed Depositsand OtherForfeiture 252

C.7 Audit Checklist forExpenditure Items/monthly accounts 253-255

C.7.1 EstablishmentExpenses 255

C.7.2 Travelling Expenses toPresident, V-P andMembers of GP 255-256

C.7.3 Travelling andConveyance forPanchayatEmployees 256

xv

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

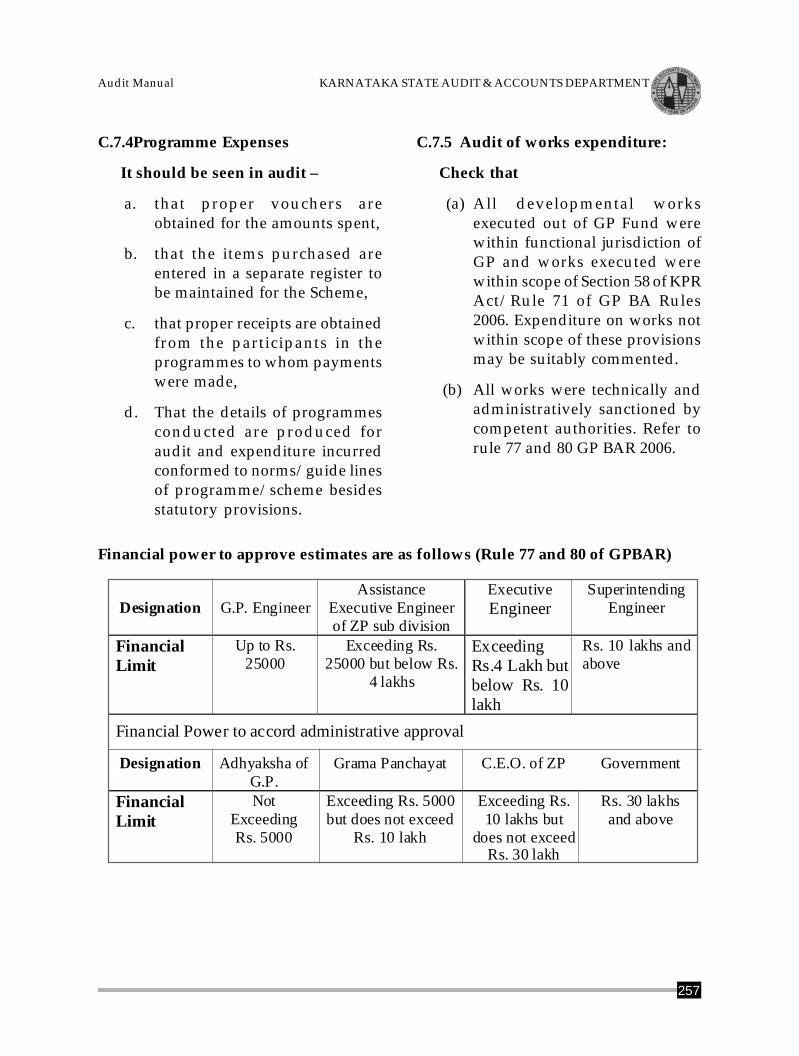

C.7.4 Programme Expenses 257

C.7.5 Audit of worksexpenditure/ nominalmuster rolls 257-261

C.8Audit checklist for Assets

C.8.1 Land and FixedAssets 261-262

C.8.2 Investments 262

C.8.3 Loans &Advances 262-263

C.8.4 Cash and BankBalances 263-264

C.9. Audit checklist for Liabilities

C.9.1 Borrowings 264-265

C.9.2 Sinking Funds 265-266

C.9.3 Write off of Irrecoverableamount 266

D. Audit checklist for Hindureligious institutions andCharitable endowments

D.1 Introduction 266

D.2 Mandate 266

D.3 Audit ReportFollow-upCompliance 266

D.4 General Instructionsfor Audit 266-268

D.5 Receipts 268-269

D.5.1 Income from lands,buildings, sites, shopsand other immovableproperties 269-270

D.5.2 Rents from Choultries,Guesthouses etc. 270

D.5.3 HundiCollections 271-272

D.5.4 Kanukas andUbhayams 272-273

D.5.5 Sale of Human HairCollections 273

D.5.6 Sale of Darsanam,Arathi, Archana andOther Services 273-275

D.5.7 Sale ofPrasadams 275

D.5.8 Sale of Pictures andPublications 275-276

D.5.9 Sale of ImmovableProperty 276-277

D.5.10 Other MiscellaneousReceipts 277

D.6.Expenditure

D.6.1 Dittam 277-278

D.6.2 Pay ofEstablishment 278-280

D.6.3 Travelling Allowancebills 280

D.6.4 TA & DA of Trustees 280

D.6.5 TA bills of paid officersand servants of theinstitution: 281

D.6.6 Transfer TA to officersand Servants Attached tothe Institutions 281

D.6.7 Contingent Bills 281-282

D.6.8 Bills relating toMaintenance of Carsand Vans 282-283

D.6.9 Register of Inventory ofEquipment 283

D.6.10 Receipt Book 283

D.7 Advances 283-284

D.8. Investments 284-286

D.9. Lending and Borrowingof Moneys 286

D.10 Registers 286-300

xvi

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

D.11 Execution ofDevelopmental works tonotified institutions 300-301

D.12 Check of Accounts 301-302

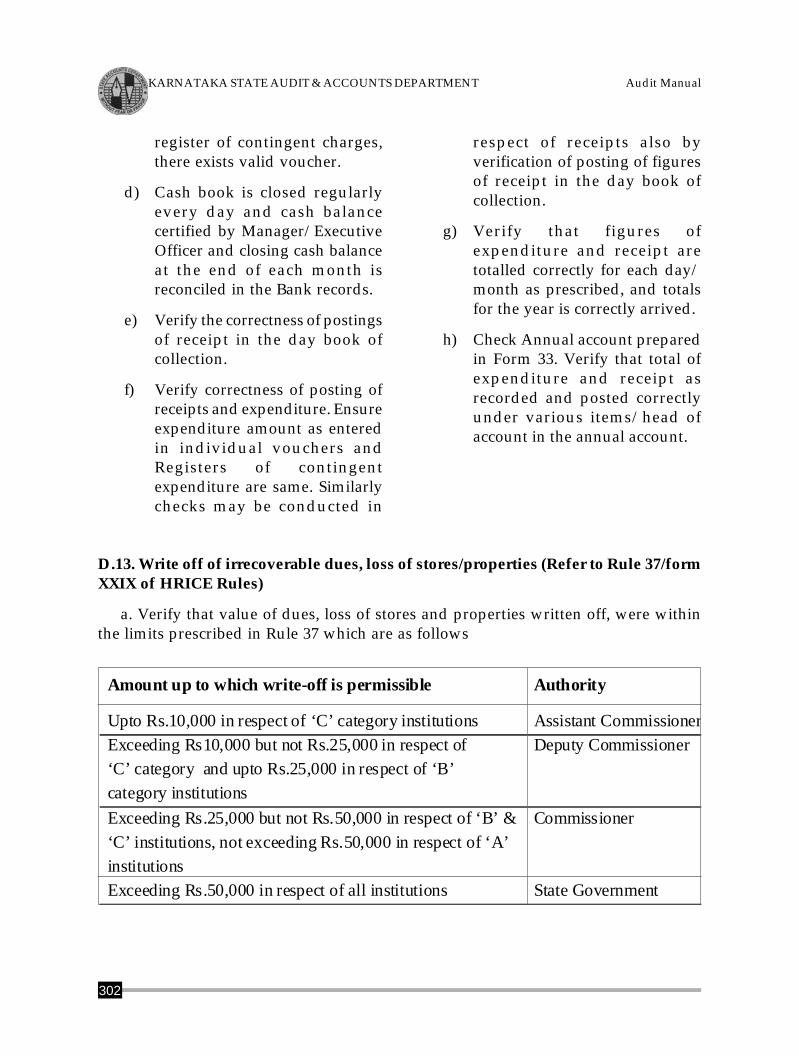

D.13 Write off ofirrecoverable dues 302-303

D.14 Cases of charge andsurcharge 303

E. Audit checklist for audit ofUrban DevelopmentAuthorities

E.1 Introduction 303-304

E.2 Mandate for Audit 304

E.3 Receipts 304-306

E.4 Preparation ofBudget & Annualstatement ofaccounts 306

E.5 Recovery of fees,expenses,fines, etc 307-311

E.6 Betterment Taxes311-312

E.7 (i) (ii) (iii) Incomefrom Lease/Allotment of civic,corner, intermediarysites 312-317

E.8 Expenditure 317-318

E.9 Sanction andexecution ofDevelopmentScheme 318-319

E.10 Lease, Sale,Transfer ofproperties 319-320

E.11 EstablishmentBills 320-321

E.12 Travelling Allowance,Leave TravelConcession 321

E.13 Charge and Surcharge ofIllegal Amounts 321

F. Audit checklist for Audit ofPublic Libraries

F.1. Introduction 321

F.2. Budget 322-323

F.3 Receipts 323-324

F.3.1 Library Cess 324-325

F.3.2 Contributions, Gifts andIncome fromEndowments 325

F.3.3 Special GovernmentGrants 325

F.3.4 Other MiscellaneousReceipts 326

F.3.5 Sale of Old Articles,Books, news Papers andMagazines 326

F.3.6 Deposits 326-327

F.3.7 Interest onInvestments 327

F.4 Expenditure

F.4.1 EstablishmentBills 327-328

F.4.2 Contingent andSpecial Charges 328-329

F.4.3 Library Books 329-330

F.4.4. Travelling AllowanceBills 330-331

F.4.5 Expenditure -Registers 331-333

F.4.6 Public Works 333

G. Audit Checklist for CommandArea Development Authority

G.1 Introduction 333-334

G.2 Mandate for Audit 335

G.3 Receipts 335

xvii

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

G.3.1 Grants 335

G.4. Expenditure 335

H. Audit Checklist for FinancialAttest Audit

H.1 Audit checklist forRevenue Items 336

H.1.1 Revenue fromRent/LeaseIncome 336-337

H.1.2 Interest/DividendIncome 337

H.1.3 Grants 337-338

H.2 Audit checklist forExpenditure items 338

H.2.1 Public WorksExpenditure 338-339

H.2.2 Purchase, Issue andConsumption ofMaterial 339

H.2.3 Establishment Bills 339

H.2.4 Rent 340

H.3 Audit checklist forAssets 340

H.3.1 Fixed Assets 340-341

H.3.2 Depreciation ofFixed Assets 341-342

H.3.3 Revaluation ofFixed Assets 342

H.3.4 Investments 342

H.3.5 Short TermInvestments 342-343

H.3.6 Long TermInvestments 343

H.3.7 Interest Accrual 343

H.3.8 Profit/Loss onDisposal ofInvestments 343

H.3.9 Stores 344

H.3.10 Loans & Advances 344

H.3.11 Cash and BankBalances 344

H.4 Audit Checklist forLiabilities

H.4.1 Earmarked Fund 344-345

H.4.2 Borrowings 345

H.4.3 Sinking Funds 345

H.5 Financial AuditChecks for UrbanLocal Bodies

H.5.1 Revenue 345

H.5.2 Property Taxes 345-346

H.5.3 Service Charges inlieu of PropertyTaxes 346-347

H.5.4 Stamp DutySurcharge Collectedby State Government 347

H.5.5 Revenue fromRent/LeaseIncome 347-348

H.5.6 Financial AttestAudit ofExpenditure Items 348

H.6 Financial AuditChecks forUniversities 348

H.6.1 Attest Audit ofRevenue Items 348-350

H.6.2 Attest Audit ofExpenditure Items 350

H.7 Financial AuditChecks for GramPanchayats 351

H.7.1 Attest Audit ofRevenue Items 351

H.7.2 Attest Audit ofExpenditure Items 351

ii

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

1

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

Chapter - IIntroduction

1. This manual is intended to assist thestaff and officers of Karnataka StateAudit & Accounts Department inconducting audit of various entitieswhich come under purview of theiraudit responsibility as provided instatutes and government’s executiveorders. The manual seeks toconsolidate current best practices inpublic auditing based on auditingstandards1 prescribed by the CAG ofIndia and INTOSAI (InternationalOrganization of Supreme AuditInstitutions). It also updates theexisting manuals such as the MysoreLocal Fund Audit Manual (1967) andthe University Audit Manual (1984).Instructions and suggestions inearlier manuals be referred to theextent they are not inconsistent withor do not contradict with thosecontained in this updated manual.

2. The instructions in this manualsupplement those contained indifferent departmental andorganizational manuals as also therelevant State Acts, Rules and Ordersissued by the Government for theireffective functioning.

3. The directions provided in thismanual are by no means exhaustive,nor is it the intention that they shouldbe taken as limiting the scope of auditrigidly to the lines indicated therein.

It is of considerable importance thatthe audit checks prescribed shouldbe observed in spirit and not merelyin the letter.

4. For conducting audit in an effectiveand efficient manner, the auditorshould know the underlying auditconcepts such as internal control,risk assessment, materiality, etc.Further, all auditors must followstandardized audit practices inorder to ensure consistency inquality of audit. Accordingly, thismanual provides brief descriptionof audit concepts the standardaudit practice and institution-wisechecklists in Part I, II & IIIrespectively.

General Principles of Audit

5. Audit as described in paragraph 7 of‘An introduction to IndianGovernment Accounts and Audit’ isan instrument of financial control. Itmust ensure that the accountsmaintained truly represent facts; thatthe rules and orders framed bycompetent authority in regard tofinancial matters have been obeyed;and that expenditure has beenincurred with due regularity andpropriety. It must bring to notice ofcompetent authority, irregularity orimpropriety in connection therewith.For this purpose, audit should be

1Auditing Standards relate to different aspects of audit ranging from auditor’s independence andcompetence to appropriateness of audit evidence and the manner in which the audit findings are reported.

2

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

conducted by an agencyindependent of the authority chargedwith the duty of carrying on thebusiness and of maintaining theaccounts of the transactions.

6. The auditor has an inherent right ofindependent criticism and hisprimary function is to verifyaccuracy and completeness ofaccounts to ensure that all revenuesand receipts due under therespective Acts, Rules and Byelawsmade thereunder are properlydemanded and realized; that allrevenues and receipts so collectedare brought to accounts under theproper heads of accounts; that alldisbursements and expenditure areproperly authorized, vouched, andcorrectly classified; and that the finalaccounts represent a complete andtrue statement of the financialtransactions they purport to exhibit.

7. Both the statutory and non-statutory(excepting those of privateinstitutions) audits are conducted onbehalf of Government. It will not bebeyond the scope of audit to seewhether the financial rules andorders passed by government satisfythe financial laws and provisions andare otherwise free from auditobjections. It is the responsibility ofaudit that any deviations from thesame are brought to the notice ofgovernment. It is one of the importantduties of audit to see that the rulesand orders framed by Governmentare properly observed and that,where financial rules are framed bythe respective institutions or theirsubordinate authorities, they satisfy

the requirements of law and areotherwise in order and are properlyapplied.

8. It is not the function of audit toprescribe what such orders shall beor to interfere with theiradministrative application. Theauditor must recognize the cleardistinction between auditorial andadministrative functions. Criticismsoffered by the Audit Departmentmust, therefore, be limited tofinancial criticisms based on theactual accounts. Such orders/decisions, which do not result inexpenditure from public funds/funds of auditee organizations orreceipts to the auditee institutionsmay not be subject to audit analysis/comments.

9. The executive authorities and not theAudit Department are responsiblefor finding moneys for theadministration and for enforcingeconomy in expenditure. It is,therefore, not for audit to suggestnew sources of taxation. It is,however, the duty of audit to offerits comments on the financialposition of the local body and bringto notice any waste in administrationand expenditure. Generally, a localbody mindful of the interests of thetax-payers will welcome suggestionsto promote economy based oninformation forthcoming from theaccounts. But such suggestionsshould be made carefully.

10. In the course of scrutiny of accountsand transactions, audit is entitled tomake such queries and observations

3

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

and to call for such vouchers,statements, returns and explanationsin relation to them as may benecessary. All queries andobservations shall be couched inlanguage which is courteous andimpersonal.

11. In auditing accounts of local bodies,audit should not make independentenquiries from private individualsor members of the general public.Audit should confine itself to callingupon the executive to furnish anynecessary information and in cases ofdifficulty, it should confer with theexecutive as to the best means ofobtaining the evidence which itrequires. Information/detailsavailable in price index published byReserve Bank of India/ EconomicAdvisor, Ministry of Commerce forvarious materials and LabourBureau for labour rate, rate contractpublished by Director General ofSupplies and Disposals, Governmentof India or State Government, annualreports, survey reports, evaluationreports of concerned departments ofstate government, public institutes/autonomous bodies of stateGovernment and court orders onscope of any law relating to recoveryof revenues/penalties and fines mayalso be referred to arrive atmeaningful conclusion.

12. If the necessary documents for theproper conduct of audit are notproduced; or if the personaccountable for or having the custodyor control of any such documentrefuses to appear in person beforethe government auditor despite of

written requisition; or if the personhaving appeared refuses to make andsign a declaration with respect tosuch document or to answer anyquestion or prepare and submit anystatement; and, as a result, theprogress of audit is retarded, thematter may be reported to the nextimmediate controlling authority fora decision and to call off the audit.

Auditing Standards

13. Guidelines with regard to conduct ofaudit have been issued by variousauthorities. These guidelines aregenerally known as AuditingStandards. They provide guidance tothe auditor and help him determinethe nature and extent of audit stepsand procedures that should beapplied to fulfill the audit objective.They are also good criteria toevaluate the quality of audit. The factthat an audit has been conducted inaccordance with certain standardsgives reasonable assurance to peoplemaking use of the financialstatements and audit reports.

14. Some of the authorities that haveissued audit standards areComptroller and Auditor General ofIndia (CAG), InternationalOrganization of Supreme AuditInstitutions (International Standardsof Supreme Audit Institutions) andInstitute of Chartered Accountants ofIndia (ICAI).

Audit Mandate

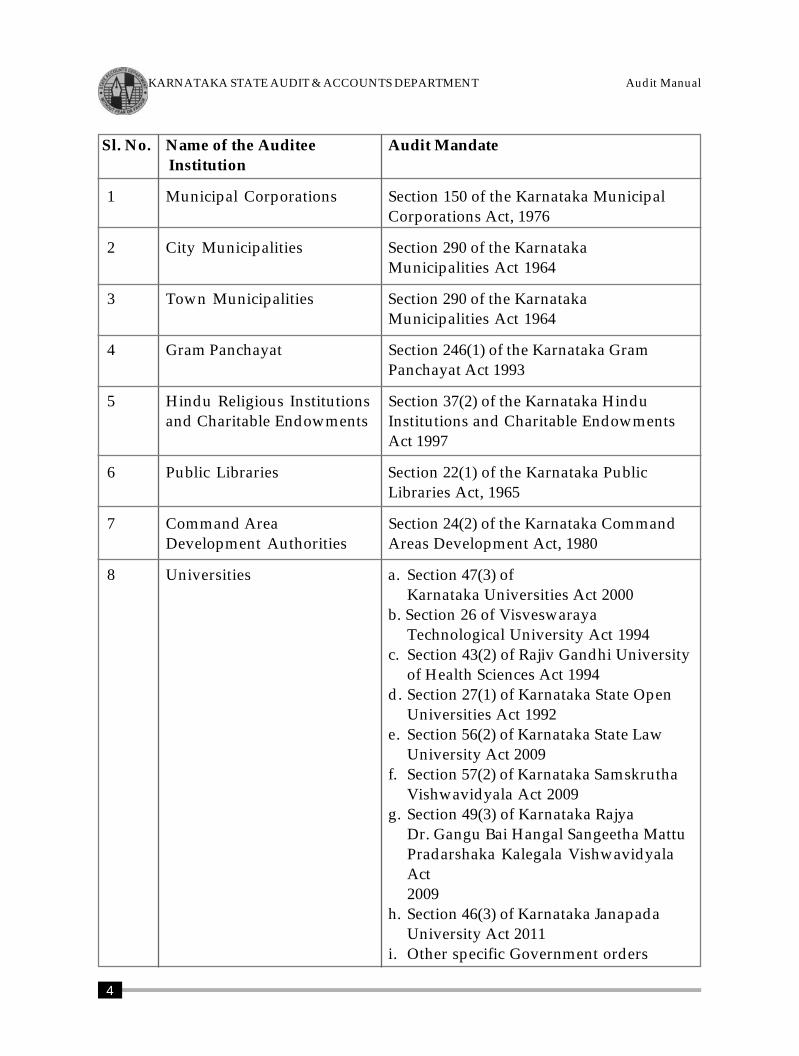

15. The Karnataka State Audit andAccounts department conducts auditof the various auditee institutions asper the mandate given below:

4

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

Sl. No. Name of the Auditee Audit Mandate Institution

1 Municipal Corporations Section 150 of the Karnataka MunicipalCorporations Act, 1976

2 City Municipalities Section 290 of the KarnatakaMunicipalities Act 1964

3 Town Municipalities Section 290 of the KarnatakaMunicipalities Act 1964

4 Gram Panchayat Section 246(1) of the Karnataka GramPanchayat Act 1993

5 Hindu Religious Institutions Section 37(2) of the Karnataka Hinduand Charitable Endowments Institutions and Charitable Endowments

Act 1997

6 Public Libraries Section 22(1) of the Karnataka PublicLibraries Act, 1965

7 Command Area Section 24(2) of the Karnataka CommandDevelopment Authorities Areas Development Act, 1980

8 Universities a. Section 47(3) ofKarnataka Universities Act 2000

b. Section 26 of VisveswarayaTechnological University Act 1994

c. Section 43(2) of Rajiv Gandhi Universityof Health Sciences Act 1994

d. Section 27(1) of Karnataka State OpenUniversities Act 1992

e. Section 56(2) of Karnataka State LawUniversity Act 2009

f. Section 57(2) of Karnataka SamskruthaVishwavidyala Act 2009

g. Section 49(3) of Karnataka RajyaDr. Gangu Bai Hangal Sangeetha MattuPradarshaka Kalegala VishwavidyalaAct2009

h. Section 46(3) of Karnataka JanapadaUniversity Act 2011

i. Other specific Government orders

5

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

Internal Control Framework

16. It is important for an auditor tounderstand what internal controls areand their significance for an entity’seffective and efficient functioningbecause the major objective of auditis to check compliance with theinternal controls. All the rules in theTreasury Code, the Financial Codeand the Budget Manual and otherrules and procedures prescribed bythe respective institutions areessentially internal controls to ensureintegrity of an entity’s transactions.

17. Internal Control is an integral processthat is operated by an entity’smanagement and personnel and isdesigned to address risks and toprovide reasonable assurance that inpursuit of entity’s mission, thefollowing general objectives areachieved:

■ Executing orderly, ethical,economical efficient and effectiveoperations;

■ Fulfilling accountabilityobligations;

■ Complying with applicable lawsand regulations;

■ Safeguarding resources againstloss, misuse and damage

18. Committee of SponsoringOrganizations (COSO) hasdeveloped an internal controlframework that has come to be

accepted as the standard all over theworld. The key concepts of COSOframework include:

■ Internal controls are an on-goingprocess, a means to an end, andnot an end in themselves;

■ Internal controls are affected bypeople at all levels of anorganization and not just policiesand their documentation; and

■ Internal Controls will nevereliminate risks but can provide areasonable assurance that controlsare in place to mitigate risks.

19. Internal control is not a singlemeasure but a series of prescriptionsof dos and don’ts that touch everyactivity of the organization. In thatsense, it is an integral part of theorganization. Also, internal control isnot something which is separate fromthe people who operate them. It ispart of the roles and responsibilitiesof the persons working in the entity.As all entities exist for a purpose, thebasic objective of internal control isto ensure that the entity achieves itsmission; in other words, it aims tominimize the risks that the entity maynot be able to achieve its mission.Any system of internal control canprovide only reasonable assuranceas it would be not be economical toprovide an absolute assurance. Thisrecognizes the fact that there are costs

Chapter - IIAudit Concepts

6

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

associated with any internal controland such costs should not exceedbenefit derived from it. Moreover,excessive controls may result inemployees circumventing them and,they could also result in delays andinefficiencies in operations.

20. Apart from ensuring ethical, efficient,economical and effective operations,one of the main objectives of internalcontrol in public sector is tosafeguard resources which areacquired with public money.Organizations in the governmentsector are vulnerable in this respectbecause cash basis of accounting(which is predominant mode ofaccounting in government) does notprovide sufficient assurance relatedto acquisition, use and disposal ofassets. With the extensive use ofInformation Technology (IT) in manygovernment entities, internal controlsrelated to IT have also assumed greatdeal of importance. Auditors shouldpay particular attention to internalcontrols in IT systems, particularlywhere they deal with payroll(HRMS), e-payments, etc. as anyerror would have far reachingimplications.

21. It must be recognized that anysystem of internal control is limitedby the following factors:

■ Human factor: Internal control issusceptible to flaws in design,poor judgment, wrongi n t e r p r e t a t i o n s ,misunderstanding, carelessnessand abuse or override as all theseinvolve human involvement.

■ Resource constraints: As alreadymentioned, internal controlimplies costs and resources andthis could be one other limitingfactor. Particularly in smallerorganizations very elaborate orsophisticated internal control maynot be possible. In such cases, themanagement should considerwhether the lack of one type ofcontrol could be compensated byanother less expensive control.

■ Organizational changes andmanagement attitude also have avery significant bearing oninternal control. Ultimately, it isthe management’s (the head ofoffice and his team) attitude thatdetermines how seriously theinternal controls are taken by thestaff. If they see that themanagement is relaxed or it doesnot itself follow many of theprecepts, they would have littlemotivation to observe the internalcontrols. It is, therefore, veryimportant that the top managersalways set an example in thisregard.

22. Internal control system consists offive interrelated and equallyimportant components:

■ Control environment,■ Risk assessment,■ Control activities,■ Information and communication,■ Monitoring.

23. The Control environment sets thetone of an organization, influencingthe control consciousness of its staff.

7

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

It is the foundation for all othercomponents of internal control,providing discipline and structure.This is, as already pointed out,determined by the management.

24. Risk assessment is the process ofidentifying and analyzing relevantrisks to the achievement of entity’sobjectives and determining theappropriate response. Elements ofrisk assessment are:

● Risk identification: The entitymust identify risks that any of itsstated objectives would not beachieved. For example, there is arisk that payment of wages toNREGA labourer is not made at allor not made in time; or, a receipt(a user charge or tax) is notaccounted by the cashier.

● Risk evaluation: Risk evaluationinvolves assessing the significanceof the risk (in terms of its gravity)and the possibility of the riskactually materializing. Thisrequires the organization tocategorize risks as high, mediumor low based on some judgment.The idea is for the organization toaddress the high category risks. Inthe above example, significanceand possibility of risk i.e. nonpayment / short payment /delayed payment of wages wouldbe considered very high.

● Risk assessment: Risk assessmentrequires the entity to understandhow much risk it is able to take.This is important because any riskmitigation comes at a cost. In theabove case, non mitigation of risk

is not acceptable as the whole ideaof MGNREGS is to providelivelihood to poor.

● Developing a response: Afterhaving identified the risks,evaluated and assessed them, theentity must develop a response tomitigate (reduce / eliminate) therisk. Appropriate response couldinvolve transfer, tolerate,terminate or treat the risk.Obtaining insurance is an exampleof transferring the risk. Sometimes,it may be better to live with a riskthat is too expensive to treat.Where the risk is too big, it mightbe better to terminate the activityaltogether. This option may notalways exist in government sectoras there are obligations to societythat have to be met irrespective ofrisks. Lastly, which is in most cases,the entity would like to treat therisk by adopting suitable controlactivities. In the above illustration,one of the ways in which the riskis sought to be mitigated is todirectly transfer the wages tolabourer’s bank account.

25. Control activities are the policies andprocedures established to addressrisks and to achieve the entity’sobjectives. There are two types ofcontrols.

■ Prevent Control: This type ofinternal control would prevent arisk from occurring. An exampleof this would be barring thephysical access to cash chest or theplace from where cashier operates.

8

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

■ Detect Control: Detect controls aremeasures that would point tomisdeeds through reconciliation /review. Any kind of reconciliation(bank reconciliation), post audit,etc. would fall under this categoryas they help detect if somethinghad gone wrong.

To be effective control activities mustbe:

■ Appropriate■ Function consistently■ Cost effective■ Comprehensive■ Directly relate to control objectives

Some examples of control activitiesare:

Authorizations and approvals:Authorization is the principal meansof ensuring that only validtransactions and events are initiatedas intended by the management.Authorization procedures must bewell documented and clearlycommunicated to managers andemployees. These should includespecific conditions and terms underwhich authorizations are to be made.

Segregation of duties: To reduce therisk of error, waste, or wrongful actsand the risk of not detecting them, nosingle individual or team shouldcontrol all key stages of transactionor event. Therefore, duties andresponsibilities should be soassigned to a number of individualsthat there are enough checks andbalances. Not with standingseparation of duties, collusion can

still take place, which can reduce ordestroy the effectiveness of thisinternal control. A common placeexample of this internal control is thesegregation of duties of cashier andaccountant; and that of stores clerkwho accounts for receipts and issuesand the store keeper who physicallyhandles receipts and issues. A smallorganization may have too fewemployees to implement thiscontrol. In such cases, themanagement should be aware of therisks and compensate them in someother manner e.g. enhancedsupervision, rotation of employees,and so on.

Control over access to resources andrecords: Restricting access toresources to authorized individualsreduces the risk of loss or misuse ofresources. All assets must beprotected against loss and misuse byimplementing this control. Chequebooks and receipt books are requiredto be securely kept under lock andkey. Facilities such as a photocopier,telephone, internet, vehicle, etc. alsorequire protection against improperuse.

Verifications: Transactions or events(receipt of goods supplied or cashbalance at the end of day) are verifiedto ensure correctness and validity.Personal records / service books areperiodically verified to ensure theircorrectness.

Reconciliations: This is one of themost commonly used and effectivedetect control measure in anyorganization. For eg. Reconciliation

9

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

of one set of records with another (theDDO’s accounts with the Treasury,own cash book with bank statement).

Reviews and post audit play animportant role in ensuring thatactivities have taken place inaccordance with the intents andobjectives of management. A reviewof financial statements can reveal ifthere have been any discrepanciespointing to wrongdoing. Aprocurement process can be postaudited to make sure that it complieswith all the regulations.

Supervision: Supervision(assigning, reviewing, approvingand guiding, training) is animportant and high level internalcontrol. This is something that is doneat different levels of managementperiodically.

26. Information and Communicationare essential to realizing all internalcontrol objectives. ‘Management’sability to make appropriatedecisions is affected by (appropriate,timely, current, accurate andaccessible) information’. Effectivecommunication should flow down,across and up the organization,through all components and theentire structure.

27. Monitoring of Internal controlsystem should be done to assess thequality of the system’s performanceover time. Monitoring isaccomplished through routineactivities, separate evaluations or acombination of both.

Audit Assertions

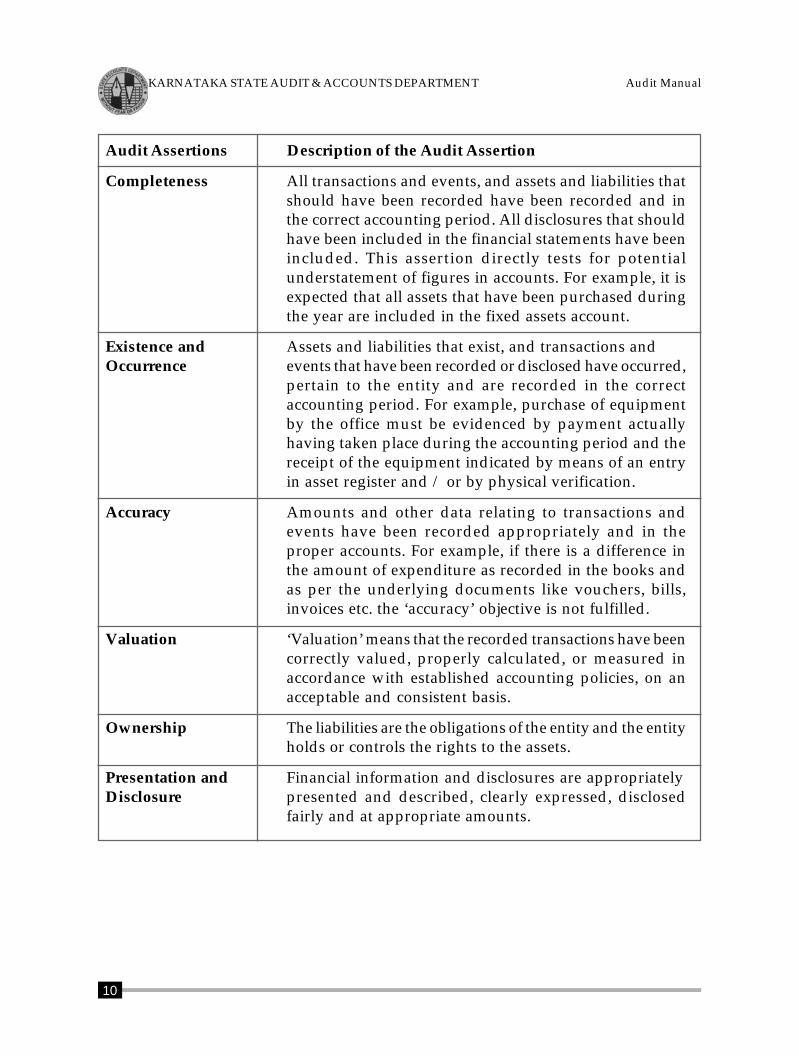

28. In a financial audit, the auditor isrequired to express an opinion on thefinancial statements. The opinionexpressed should give a picture ofwhether the accounts fairly representthe actual transactions during theperiod. Audit assertions are nothingbut general audit objectives whichare designed to ensure that theauditor obtains adequate evidence tosupport the opinion required to beexpressed on an account. There aresix general audit objectives asdetailed below:

10

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

Audit Assertions Description of the Audit Assertion

Completeness All transactions and events, and assets and liabilities thatshould have been recorded have been recorded and inthe correct accounting period. All disclosures that shouldhave been included in the financial statements have beenincluded. This assertion directly tests for potentialunderstatement of figures in accounts. For example, it isexpected that all assets that have been purchased duringthe year are included in the fixed assets account.

Existence and Assets and liabilities that exist, and transactions andOccurrence events that have been recorded or disclosed have occurred,

pertain to the entity and are recorded in the correctaccounting period. For example, purchase of equipmentby the office must be evidenced by payment actuallyhaving taken place during the accounting period and thereceipt of the equipment indicated by means of an entryin asset register and / or by physical verification.

Accuracy Amounts and other data relating to transactions andevents have been recorded appropriately and in theproper accounts. For example, if there is a difference inthe amount of expenditure as recorded in the books andas per the underlying documents like vouchers, bills,invoices etc. the ‘accuracy’ objective is not fulfilled.

Valuation ‘Valuation’ means that the recorded transactions have beencorrectly valued, properly calculated, or measured inaccordance with established accounting policies, on anacceptable and consistent basis.

Ownership The liabilities are the obligations of the entity and the entityholds or controls the rights to the assets.

Presentation and Financial information and disclosures are appropriatelyDisclosure presented and described, clearly expressed, disclosed

fairly and at appropriate amounts.

11

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

Audit Evidence

29. Audit Evidence means informationgathered by auditor in course ofaudit to form credible auditconclusions. The importance of auditevidence cannot be overemphasizedas it determines the credibility notonly of audit observations but alsoof the audit organization itself.

30. Evidence collection process involvesidentification of appropriateevidence, its collection and cross-checking or validation anddocumentation. In case of allegationof professional negligence, evidencegathered by the auditor offersprotection. Hence, audit evidence isan important part of auditor’sworking papers.

31. Evidence in relation to accountsessentially relates to assertions aboutexistence/occurrence, completeness,validity and accuracy of recordedvalue of transactions. In case ofpurchase of an asset e.g. an airconditioner for the office, the auditwould gather evidence relating to itsactual delivery in the office(occurrence/ existence), sanction forits purchase (validity), payment(correctness of amount andclassification) and so on. In relationto internal controls, evidence refersto substance that supports effectiveoperation of controls. Evidence maybe obtained from any of thefollowing:

a. Source documents (vouchers /files);

b. Accounting records (books ofaccounts);

c. Re-computation of calculationmade by the entity (say pay orpension arrears).

d. Joint Inspection bySupervisory/Executive Officersof auditee unit/ any designatedthird party, of stores, assets,worksites and premises ofbeneficiaries of variousschemes/programmes.

e. Resolutions passed by electedbody like Zilla Panchayat/Urban Local bodies/Grampanchayats / Urbandevelopment Authorities.

f. Proceedings of Review meetingsof implementation of schemes /progress.

g. Evaluation reports.

32. It is expected that the auditor obtainscompetent, relevant and reasonableevidence to support his judgmentand conclusions regarding theorganization, programme, activity orfunction under audit.

33. Evidence collected should besufficient and appropriate.Sufficiency refers to quantity ofassurance and appropriateness refersto quality (relevance and reliability)of assurance. Sufficiency andappropriateness are inter-related.Evidence obtained should be bothsufficient and appropriate. It is notenough if only one is collected as itwill not compensate the other e.g.existence of inventory and itsvaluation. Evidence is consideredsufficient if the same results areobtained even when an independentparty re-performs the tests. If

12

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

sufficient evidence could not beobtained, it should be disclosed inaudit report.

34. Evidence collected should be soobjective that any knowledgeableperson should reach same conclusionon reviewing the evidence gathered.In case auditor fails to obtainrequired evidence for reporting, heshould perform additional tests for

Principles of Audit Evidence

Relevance Evidence must be relevant to its related audit conclusion.Otherwise it is not persuasive regardless of any otherconsideration. E.g. While conducting audit of Social Welfaredepartment, poor results obtained by a boarder of the hostelcannot be claimed as evidence for weakness in administrativecontrols. Similarly, non-availability of staff cannot be claimedas evidence for poor control on assets.

Objectivity Objective evidence is usually more persuasive than subjectiveevidence. Objective evidence is achieved when two or moreauditors, working independently, are very likely to arrive atthe same result.

Documentation Documentary evidence typically is more persuasive thanundocumented evidence.E.g. Hearsay evidence that one of theemployee misuses office telephone for his personal use is lesspersuasive than detailed analysis of the phone bill.

External External evidence is considered more persuasive than internalevidence.E.g. Statement of account from bank is consideredmore persuasive evidence for bank balance than balance shownin bank book by the organization.Sales invoice received fromthe supplier is more persuasive evidence compared to internaladvice prepared while making payment to the supplier.

Sample size: Larger samples are generally more persuasive than smallersamples.

Sampling method Statistical samples are usually more persuasive than non-statistical samples. Statistically random samples help avoidsampling bias because they are based on laws of probability.

establishing the facts. Auditor shouldconsider most cost-effective means ofobtaining evidence, but difficulty inobtaining evidence or cost cannot bereasons for omitting necessaryprocesses. Auditors should considersource and nature of informationobtained to evaluate its reliability. Ifnot reliable, the auditor must conductfurther verification requirements.

13

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

Statistical samples allow auditors to quantify their level ofconfidence in sample results.

Corroboration Corroborated evidence is usually more persuasive thanuncorroborated evidence. Corroborated evidence is the sameor similar evidence acquired from two or more independentsources. Eg. In a scheme where medicines are distributedthrough Non Government Organisation (NGOs) reconciliationof records maintained (copy of the consignment advice, entriesin stock register, copy of the courier invoice) with confirmationreceived from NGO would be more persuasive.

Timeliness Timely evidence is typically more persuasive than evidenceproceeded after a delay.E.g. Auditor’s observation of virus incomputer systems can be a good evidence (of weakness ofcontrols in safeguarding data), if reported soon. It may beuseless if reported after time lag. Note: For this reason, auditloses importance if they are taken up after considerable timelag. Follow-up and corrective action is part of audit scope insuch assignments.

Authoritativeness Authoritative evidence is more persuasive than non-authoritative evidence. E.g. Confirmation on the letter head ofthe entity is more persuasive than acknowledgement from thecourier company that the consignment has been delivered.

Directness Direct evidence is usually more persuasive than indirectevidence. E.g. A direct count of inventory by auditor is morepersuasive than someone else’s counted figure. Also, an originaldocument is more persuasive than its copy.

Adequacy of Evidence from a well controlled and reliable system usuallycontrols is more persuasive than evidence from a poorly controlled or

questionable system.E.g. Airlines ticket with boarding pass ismore reliable evidence than a bill from local airlines bookingagency.

14

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

35. Evidence collected during theprocess of audit should be carefullydocumented. Audit supervisorshould review the working papers toensure that it is reliable on all countsand supports the audit conclusions.

Relation between managementassertions, audit objective and auditevidence

36. By placing controls, managementasserts that possibility of materialloss or misstatement is reduced.Control objective, therefore, refers tothe objective with which control isplaced by the management. Controlobjective is to negate the possibilityof risk or material misstatement.

Audit objective is to validatemanagement’s assertionsindependently and identifyweaknesses. To support auditopinion, auditor collects evidence.To illustrate, if employing securitypersonnel is a control, correspondingmanagement assertion is that no un-authorized person is allowed in andassets are safeguarded. Auditorperforms certain procedures to checkif this control (i.e., security) isfunctioning as intended by themanagement (i.e., no un-authorizedperson is permitted in). Similarly,bank reconciliation is a controlthrough which management assertscompleteness and authenticity ofdealings with the bank. Auditorwould check this control byinspecting reconciliation statements.

He would obtain statement ofaccount from bank as evidence tosupport effectiveness of this control.

Materiality and levels of assurance

37. Materiality is an audit concept whichrecognizes that some matters (orgroup of matters) are more importantas compared to others and thus theauditor should focus his attention onthe material matters rather than theentire information.

38. A matter may be material dependingon the value it represents. Forexample, while auditing a irrigationproject worth several hundred crorerupees, work done by a small sub-contractor worth a couple of lakhrupees may not be material, butwhile auditing a primary health carecentre an expenditure of Rs.50,000 oncivil repairs may be material.Materiality depends on the size andnature of the department activities.Materiality is subject matter ofprofessional judgment of the auditorand provides quantitative thresholdor cut-off.

39. Materiality may also be determinedbased on qualitative parameters likenature of the item or the context inwhich the information is used. Forexample, while auditing payments,auditor would not apply materialityto TDS obligations of the departmentunder Income Tax Act.

The following are the different kindsof materiality;

(a) Planning Materiality: Planningmateriality is used in audit planning

15

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

when the auditor makes an initialjudgment about materiality levels todetermine areas which are materialand hence should be part of the auditcoverage at the minimum. Planningmateriality may differ from themateriality levels used in evaluatingthe audit findings because theremight be change in circumstancesand additional information about theauditee that has been obtainedduring the audit. Planningmateriality is primarily concernedwith materiality by value. Severallevels of materiality may be definedfor each of the financial statements.For example, for the incomestatement, materiality could berelated to income from operations ornet income over expenditure. For thebalance sheet, materiality could bebased on total assets, current assets,working capital etc.

(b) Reporting Materiality: This appliesat the end of the audit when all errorsare evaluated and viewed in relationto their known effects on the financialstatements. At this stage, the auditorhas to consider the audit findings byvalue, by nature and by context, anderrors or omissions may beconsidered material which otherwiseby value would not. It is common foraudit to report more serious auditobjections to higher levels ofgovernment / legislature anddiscuss and settle the less seriousones with the auditee locally.

16

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

Chapter - IIITypes of Audit

40. While the primary objective of auditis to give an assurance with respectto compliance with internal controls,the focus could vary dependingupon the scope and context of audit.In most cases, audit of financialstatements in the context ofgovernment entities would alsoimply checking the propriety ofunderlying transactions. An audit ofaccounts that are completelyautomated would require applyingdifferent procedures which test thecontrols built into the informationsystem. On the other hand, anauditor might be required to assessthe performance of a governmentprogramme or a scheme withreference to its objectives. Generally,the audit mandate providesguidance on the type of auditexpected to be conducted.

a) Receipt Audit

41. It is primarily the responsibility ofthe department authorities to see thatall items of revenue and other dues,which have to be brought to accountare correctly and promptly assessed,realized and credited to the localbody. Under the various Acts relatingto local bodies, the Director (Audit),Karnataka State Audit & AccountsDepartment has been entrusted withthe audit of accounts of both receiptsand expenditure. As such, it is alsoone of the important functions of theAudit Department to see that all

sums due to the local body have beenrealised and properly accounted for.It should also be seen that the initialaccounts of demand have beenproperly prepared, that the demandarrived in the case of taxes and feesis generally correct, and thatadequate steps have been taken toenforce recovery. Any investigationby audit in this regard must beconducted so as to not interfere withthe executive responsibility.

In conducting the audit of receipts,audit should ascertain that adequateregulations and procedures havebeen framed to secure an effectivecheck on the assessment andcollection of revenue and to see, byan adequate detailed check, thatsuch regulations and procedures arebeing observed and that demand,collection and balance statements areregularly prepared and agreed withthe subsidiary registers of demandand collection and that balances areregularly reviewed or checked in themanner specified by the statutoryrules, Government orders orregulations, if any. In the audit ofreceipts, ordinarily the general ismore important than the particular.

It would be necessary to ascertainwhat checks are prescribed againstthe commission of irregularities atthe various stages of collection andaccounting and to suggest any

17

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

appropriate improvement in theprocedure. The audit of receiptsshould be regulated mainly withreference to the statutory provisionsof financial rules or orders whichmay be applicable to the particularreceipts involved. If the check revealsany defect in such rules or orders, theadvisability of amendment shouldbe brought to notice.

It is, however, rarely if ever the dutyof audit to question an authoritativeinterpretation of such rules or ordersand in no case may audit review ajudicial decision or a decision givenby an administrative authority in aquasi-judicial capacity. Thisinstruction does not, however, debaran auditor from bringing to noticeany conclusion deducible from theexamination of the results of anumber of such decisions. Whereany financial rule or order applicableto the case has prescribed the scaleor periodicity of recoveries, it will bethe duty of audit to see as far aspossible, that there is no deviationwithout proper authority from suchscale or periodicity. Ordinarily, auditwill see that no amounts due to localbodies are left outstanding in theirbooks without sufficient reason.Audit will continue carefully toreview such outstandings andsuggest to departmental authoritiesany feasible means for their recovery.Whenever any dues appear to beirrecoverable, orders for their write-off should be sought. But, unlesspermitted by any rule or order of acompetent authority, no sums maybe credited to a local body by debit

to a suspense head; credit mustfollow and not precede actualrealization.

A claim or demand may be either:

i. a specific demand fixed orfluctuating; (all taxes of thisnature) or

ii. a demand which arises inconsequence of some out-goingof property, or cash, advance orservice, in which case, it is a quidpro quo.

Of the latter nature are the demandsset by the sale or lease of land,property, etc., by cash advances andservices such as transport. The checkthat can be exercised in audit againstitem (ii) will depend upon the natureof the demand and the exactcircumstances in which it is made.The demand should, in all cases, beentered in a demand register ormiscellaneous sales register ormiscellaneous receipts register orregister of advances or some othersuitable register prescribed for thepurpose in the rules or regulations.

Levy, collection and accounting ofreceipts/revenues should receivespecial attention of audit andchecked very effectively as thesetypes of transactions are easily proneto risk of fraud and/ormisappropriation in local bodies. Aspecial zeal should therefore beshown in investigating into repeatedfrauds. The system of revenuecollection should be closelyscrutinized to see whether the fraud

18

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

or defalcation was rendered possibleby any defect in the rules or whetherit was due to neglect of rules or thewant of supervision on the part ofany person responsible for theadministration of the fund. It is theduty of audit, therefore, at suchinvestigations to suggest safeguardsthat are likely to prevent therecurrence of such frauds ordefalcations.

Objections for want of receiptbooks in support of having collectedtaxes and other amounts and ofpayee’s receipts in support ofdisbursements made are seriousones, because such cases oninvestigation may, at times, disclosefrauds or defalcations. Objections ofthis nature, therefore, deserveimmediate attention andinvestigation. The Audit Officer/Accounts Superintendent or Auditorshould, therefore, prepare a report inthe form of a paragraph for the auditreport for approval of the Auditauthority and communicate it to theexecutive authority of the auditeeinstitution for immediate action. Theparagraph containing the defectshould be suitably modified withreference to the reply of the executiveauthority and included in the auditreport.

b) Expenditure Audit

42. The primary objectives for the auditof expenditure in the auditinstitutions are subject to thefollowing essential audit checks:

a. That the funds have beenexpended only on the purposesauthorized by the Acts or Rules;

b. That the moneys made availablefor the expenditure have beenprovided for in the mannerspecified in the Acts or Rules;

c. That the funds earmarked forspecific purposes have beenutilized for such purposes alone;and

d. That the sanction, either special orgeneral of the authority competentto sanction the expenditure, hasbeen obtained.

Note: - It is an implied condition thatthe expenditure should be i n c u r r e dfrom the funds of local bodies withdue regard to the broad and generalprinciples of financial propriety. Any caseinvolving a breach of these principles andthus resulting in improper expenditureor waste of public money should betreated by audit in the same manner ascases of irregular or unauthorizedexpenditure are treated.

Conditions (a), (b), (c) and (d)mentioned in the previous paragraph aremainly governed by the Acts of theLegislature or rules, or regulations issuedby authorities empowered in this behalf.Auditors must, therefore, familiarizethemselves with the relevant sections ofthe Acts and the schedules thereto andthe Manuals.

c) Audit against Regularity

43. Audit against regularity consists inverifying that the expenditure

19

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

conforms to the relevant provisionsof the Act or rules made thereunderand is also in accordance with thefinancial rules, regulations andorders issued by a competentauthority either in pursuance of anyprovisions of the Act or in virtue ofpowers formally delegated to it by ahigher authority. The rules,regulations and orders under whichaudit is conducted mainly fall underthe following categories: -

a. Rules and orders regulating thepowers to incur and sanctionexpenditure from the revenues ofthe local bodies;

b. Rules and orders dealing with themode of presentation of claimsagainst the entity, withdrawingmoneys from the accounts of theentity, and in general the financialrules prescribing the detailedprocedure to be followed byofficers and servants in dealingwith the transactions of the entity;and

c. Rules and orders regulating theconditions of service and pay ofthe servants of the entity. Inaddition to carrying out the auditaccording to the prescribedprocess, the auditor should seethat the accounts rules or otherrules or laws prescribed andpromulgated by Government areobserved in letter and spirit andhe should further bring to noticeany practice which seems to himto be objectionable even though itmay not be in contravention of anyrule.

44. The work of audit in relation toregularity of expenditure is of aquasi-judicial character. It involvesthe interpretation of statute, rules andorders with reference to the case lawof previous decisions andprecedents. Interpretation by Auditshould be based on the plainmeaning of the section, rule or order,except when this is inconsistent withanother section, rules, or order; insuch a case, the inconsistency shouldbe referred to the competentauthority for resolution or removal.

20

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

45. Provision of funds is required to bewatched at two different stages. Thefirst is the provision of funds for theentity for all items of expenditure asa whole for a year and the second isthe actual release of funds to beexpended on any particular item thatcalls for payment. The first stage isthe sanction of the budget and thesecond is the sanction to expenditure.A grant or appropriation is intendedto cover all the charges, including theliabilities of past years to be paidduring a financial year or to beadjusted in the accounts of that year.It is operative until the close of thatyear. Any unspent balance lapsesand is not available for utilization inthe following year. Audit againstbudget provision is simple. It isenough to see that a properlyprepared budget has beensanctioned by the competentauthority and that provision isavailable in the particular budgethead which is to receive the chargewhen the expenditure is incurred.The audit has to satisfy itself that theexpenditure which is being auditedfalls within the ambit of an allotmentor appropriation duly sanctionedand that it is within amount of thatallotment or appropriation.Expenditure in excess of the amountof an allotment or appropriation aswell as expenditure not falling withinthe scope or intention of anyallotment or appropriation asentered in the sanctioned budgetunless regularized by asupplementary budget or re-appropriation statement should betreated as unauthorized expenditure.

46. Audit against sanctions toexpenditure is conducted in twostages. It has to see that theexpenditure is covered by a sanctionwhether special or general and thatthe sanction is accorded by anauthority competent to do so byvirtue of the powers vested in it bythe appropriate legislation or rulesthereunder. The authoritiescompetent to sanction expenditureout of funds of local bodies arementioned to such bodies and it isthe primary duty of audit to see thatevery item of expenditure is coveredby the sanction of the properauthority. The determination of theproper authority will depend uponwhether (a) the sanctioning authoritypossesses full powers in respect ofexpenditure under audit and (b)whether the sanctioning powers aresubject to any limitations. In respectof expenditure sanctioned byauthorities having full powers ofsanction it is enough to confine auditmerely to consideration of propriety.But in respect of others, the effect ofcondition and restrictions should beclearly grasped and audit shouldchallenge every item if highersanction is necessary. This is a fieldwhere controlling authoritiesdepend upon audit to control thefinancial operations of the entities. Itis here that audit can perform usefulfunction as an instrument of financialcontrol. In judging which itemsrequire sanction, difficult cases oftenarise when the spending authoritiesspilt up schemes to avoid highersanction. Audit is often called upon

21

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

to decide what constitutes a singlescheme, especially in the case ofexpenditure on works.

47. The general instructions set out in thepreceding paragraphs can beexpressed in a more detailed form asfollows: -

The objects of audit of expenditureare to ensure that: -

a. There is provision of funds for theexpenditure duly authorized by acompetent authority;

b. The expenditure is in accordancewith a sanction properly accordedand is incurred by an officercompetent to incur it;

c. The claims are made in accordancewith rules and in proper form;

d. All prescribed preliminaries toexpenditure such as properestimate prepared and approvedby competent authority for worksexpenditure, etc; are observed;

e. The rules regulating the methodof payment have been dulyobserved by the disbursing officer;

f. Expenditure sanctioned for alimited period is not admitted inaudit beyond that period withoutfurther sanction;

g. Payment has, in fact, been madeto the proper person and that it hasbeen acknowledged and recordedso that a second claim against thelocal body on the same account isimpossible;

h. The charge is correctly classifiedand a charge is debitable to thepersonal account of a contractor,employee or other individual oris recoverable from him under anyrule or order, it is recorded assuch in a prescribed account;

i. The rates paid for work done orsupplies made are in accordancewith any scale or scheduleprescribed by competentauthority; and

j. The payments have been correctlybrought to account in the originalaccount.

48. Recurring charges which are payableon the fulfilment of certainconditions or till the occurrence of acertain event should be admitted inaudit on receipt of a certificate fromthe drawing officer to the effect thatthe necessary conditions have beenduly fulfilled or the event has not yetoccurred as the case may be.

d) Audit against Propriety

49. Audit, to ensure the four objectivesindicated in Paragraph 43 above,carries out what may be called theformal examination of sanction andrules regulating such expenditure. Itis an essential function of audit tobring to light not only cases of clearirregularity but also every matterwhich in its judgment appears toinvolve improper expenditure orwaste of public money or stores,even though the accounts themselvesmay be in order and no obviousirregularity has occurred. It is thus

22

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

not sufficient to see that sundry rulesor orders competent authority havebeen observed. It is of equalimportance to see that the broadprinciples of orthodox finance areborne in mind not only by disbursingofficers but also by sanctioningauthorities.

The general principles which havelong been recognized as standards offinancial propriety are laid down below:-

a. The expenditure should not beprima facie more than the occasiondemands. Every public officer isexpected to exercise the samevigilance in respect of expenditureincurred from public moneys as aperson of ordinary prudencewould exercise in respect ofexpenditure of his own money.

b. No authority should exercise itspowers of sanctioningexpenditure to pass an orderwhich will be directly or indirectlyto its own advantage.

c. Public moneys should not beutilized for the benefit of aparticular person or section of thecommunity unless: -

� A claim for the amountcould be enforced in a court oflaw; or

� The expenditure is inpursuance of a recognizedpolicy or custom of theGovernment.

d. The amount of allowances such astravelling allowances, granted tomeet expenditure of a particular

type, should be so regulated thatthe allowances are not on thewhole sources of profit to therecipients.

Note: The proper discharge of dutiesby an Audit Officer in this field is a verydelicate matter and requires muchdiscretion and tact. A challenge againstexpenditure should not be expressed orbased on ‘canons of financial propriety,’but as transgressing a universallyaccepted standard of official conduct orfinancial administration.

50. The audit of rates paid for workdone/ supplies made should receivespecial attention. But objections canbe raised only on grounds offinancial propriety. It demands theexercise of great intelligence andcare. Individual abnormalities inrates, should of course, be watched,by comparative examination,through the vouchers and accountsreceived for audit, with the rates paidby various agencies.

51. The audit may indicate cases inwhich the rates are abnormal, andfurther enquiry may be desirable insuch cases. The instructions relatingto detailed audit of vouchers insupport of payments are containedin the succeeding chapters of themanual.

e) Financial Audit

52. Financial Audit is the attestation offinancial statements of entities,involving examination andevaluation of financial records andexpression of opinions on financial

23

Audit Manual KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT

statements. The objective of financialaudit is primarily to express an auditopinion on a set of financialstatements. It includes:

a. Audit of financial systems andtransactions including anevaluation of compliance withapplicable statutes andregulations which affect theaccuracy and completeness ofaccounting records;

b. Audit of internal control andevaluation of adequacy of internalaudit functions that assist insafeguarding assets and resourcesand assure the accuracy andcompleteness of accountingrecords;

c. Ensuring that financial informationis presented in accordance withthe applicable accountingstandards including specificrequirements of financialdisclosure; and

d. Ensuring that the entity hascomplied with laws andregulations applicable to it.

f) Performance audit

53. Efficiency-cum-Performance Audit(ECPA) or Value for Money (VFM)audit is a comprehensive review ofthe projects, programmes, schemes,organisations, etc. in terms of theirgoals and objectives aimed atascertaining the extent to which theexpected results have been achievedfrom the use of available resourcesof money, men and materials. It is atechnique of audit adopted to assess

and evaluate the economy, efficiencyand effectiveness of developmentschemes, projects or organisationsand hence this branch of audit is alsoknown as Economy, Efficiency andEffectiveness Audit or the Three EsAudit. Economy relates to incurringexpenditure which is keeping withthe requirement, while efficiencymeans that the output iscommensurate with the input. Forany expenditure to be consideredeffective, it should have resulted inachievement of the intendedobjective.

54. Performance audits considerwhether the entity has

a. followed sound procurementpractices;

b. acquired the appropriate type,quality, and amount of resourcesat an appropriate cost;

c. properly protected andmaintained resources;

d. avoided duplication of effort byemployees and work that serveslittle or no purpose;

e. avoided idleness and overstaffing;

f. adopted efficient operatingprocedures;

g. adopted adequate managementcontrol system for measuring,reporting, and monitoring aprogramme’s economy andefficiency.

55. Normally detailed guidelines areprepared for conducting

24

KARNATAKA STATE AUDIT & ACCOUNTS DEPARTMENT Audit Manual

performance audits based on deskreview of related documents. Toillustrate, if performance review ofworking of a government schemesuch as Rural EmploymentGuarantee scheme is to be conductedthe auditors would first study theMahatma Gandhi National RuralEmployment Guarantee (MGNREG)Act, the state government schemeguidelines, the organizationalarrangements, the processes, etc. indetail. They would then prepare a listof instances whose existence /achievement would be examined inaudit by gathering supportinginformation or evidence. In the aboveillustration, one of the instancescould be to gather evidence tosupport compliance with thestipulation that the use of material /equipment was restricted to 30percent of value of the work.

g) Systems Audit

56. A system is an orderly arrangementof separate but interdependent andinteracting activities and relatedprocedures which implements andfacilitates the performance of thefunctions of an organisation. Theconcept of Systems Audit is that if anin-depth analysis of the mechanics ofa system reveals that it is designedwith appropriate controls, checksand balances to safeguard againsterrors, frauds, etc., audit canreasonably assume, without thenecessity of undertaking a detailedexamination of the individual eventsor transactions, that the resultsproduced by the system would befairly accurate. Evaluation of the

efficiency and effectiveness of anysystem will, however, requiresample testing of its actual working.Systems Audit therefore, also servesas an effective aid to management.Information Systems Audit is a goodexample of a systems audit, which isdescribed separately below.

Manpower Audit