Embed Size (px)

Citation preview

May 18, 2021 2

Sto

ck U

pd

ate

Telecom Sharekhan code: BHARTIARTL Result Update

Bharti AirtelHealthy Q4, Well-poised to grow

Sto

ck U

pd

ate

Summary

� We maintain a Buy on Bharti Airtel with a PT of Rs. 750, given revenue market share gains across portfolios, strength in core business and reasonable valuations.

� Q4 was healthy as OPM beat estimates; subscriber additions stayed strong, though ARPU was slightly weak on termination of IUC and fewer number of days

� Resurgence in COVID-19 infections would delay tariff hikes, ARPU of wireless business would improve led by upgrades to 4G, increasing base of postpaid subscribers and launch of revised One Airtel plan

� We stay positive on Bharti, considering strong core business, well-capitalised balance sheet, improvement in free cash flows and a strong competitive position; Bharti is set to register a 12%/21% growth in revenue/EBITDA over FY2021-FY2023E.

Margins were yet again impressive in Q4FY2021, subscriber additions in India wireless business stayed strong, while home broadband business subscriber additions rose to a record high. Revenue was below our expectation owing to a slightly weaker ARPU. The reported revenue and ARPU will not be comparable given the termination of interconnection usage charges (IUC) on mobile calls from January 2021. On a like-to-like basis, consolidated revenues increased by 2% q-o-q and 17.6% y-o-y to Rs. 25,747 crore, below our estimates, led by 3.4% q-o-q growth in India business (adjusted for IUC). On a like-to-like basis, the India wireless business revenue grew by 4.2% q-o-q and 19.1% y-o-y despite a marginal weaker ARPU, led by strong subscriber additions (up 4.4% q-o-q). ARPU (adjusted for IUC) in the India wireless business declined by 0.8% q-o-q (up 7.3% y-o-y) to Rs. 145, below our estimates. EBITDA margin improved by ~244 bps q-o-q to 47.9%, exceeding our estimates, led by a 380 bps q-o-q improvement in OPM of the India wireless business. Excluding one-time gain of Rs. 440 crore, the adjusted net profit came at Rs. 319 crore and was 27% below our estimates. With a resurgence in COVID-19 infections in India, we expect revenue growth of the Indian wireless business to remain muted during Q1FY2022. Further, the management highlighted that it witnessed an increase in competitive intensity in terms of higher sales incentives and channel commissions to attract more customers by peers during Q4FY2021. Though competitive intensity came down with a sharp second wave of COVID-19 cases across the country, we believe the tariff hike would be further delayed. However, ARPU of India wireless business would improve going ahead because of (1) lower tariffs in India, (2) 2G to 4G upgrades, (3) increasing postpaid subscribers and (4) strong addition of 4G customers. Further, the revised version of the One Airtel plan will be launched in the next 4-5 weeks, which would aid ARPU improvement as this would fetch an additional Rs. 500-600 per account when a customer would move to this plan. The company has gained the revenue market share in DTH business from 22% in December 2018 to 27% share in December 2020, while the revenue market shares in enterprise business improved to 31% from 23% over the same period.

Key positives

� India wireless subscriber additions stayed strong at 13.4 million

� Company saw revenue market share gains across its portfolio

Key negatives

� DTH business revenue declined 2.8% q-o-q

� ARPU in India wireless business remained below expectations, but scope for improvement going ahead

Our Call

Valuation – Maintain Buy with a PT of Rs. 750: We have fine-tuned our earnings estimates for FY2022E and FY2023E because of impressive operating profitability, market share gains across portfolio and a dedicated channel for high-value homes. Bharti has gained market share in both wireless and non-wireless business because of its relentless focus on improving customer experience, strengthening its core business and building digital capabilities. Its digital capabilities have been helping the company become more efficient, building new revenue streams, reduce churn rate and create ecosystem of partnership to leverage the digital capabilities. We remain positive on Bharti, considering strength in its core business, relatively well-capitalised balance sheet, potential improvement in free cash flows and a strong competitive position. At CMP, the stock is trading at a reasonable valuation of 7x its FY2023E EV/EBITDA. Given favourable risk-reward balance, we maintain a Buy rating on the stock with an unchanged price target (PT) of Rs. 750.

Key Risks

Increasing competition could keep up the pressure on realisations. Any slowdown in data volume growth could affect revenue growth.

+ Positive = Neutral - Negative

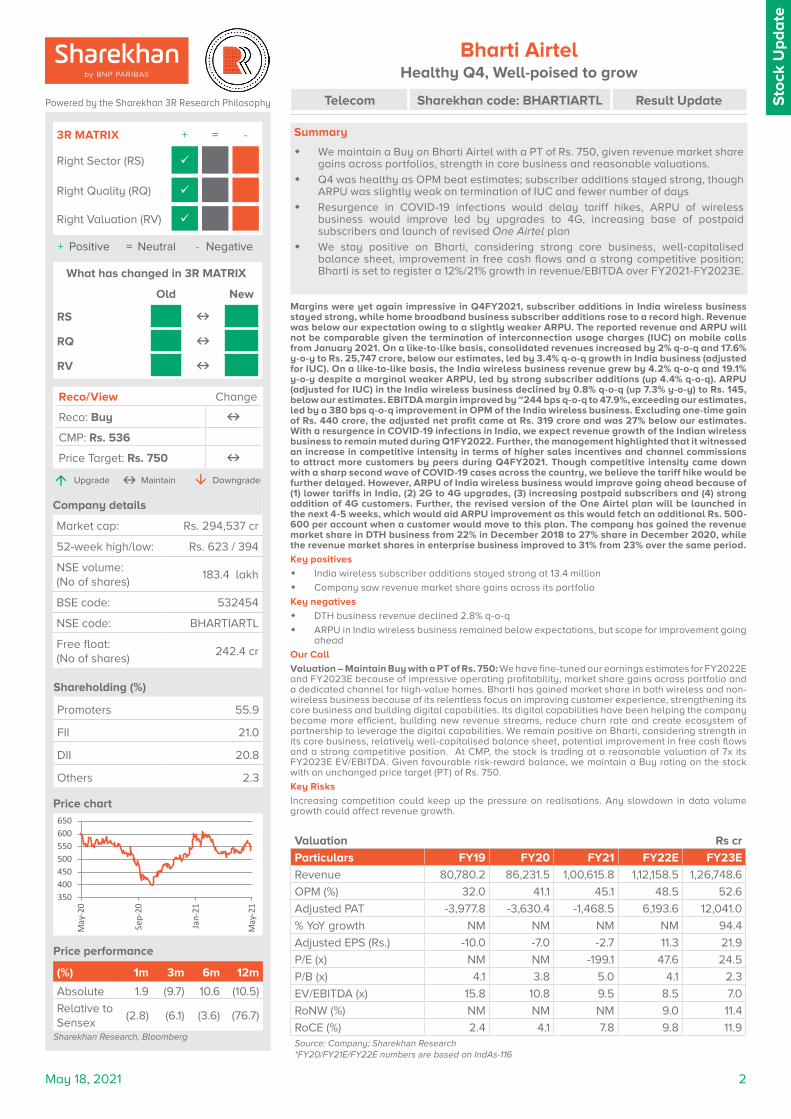

3R MATRIX + = -

Right Sector (RS) ü

Right Quality (RQ) ü

Right Valuation (RV) ü

Powered by the Sharekhan 3R Research Philosophy

Company details

Market cap: Rs. 294,537 cr

52-week high/low: Rs. 623 / 394

NSE volume: (No of shares)

183.4 lakh

BSE code: 532454

NSE code: BHARTIARTL

Free float: (No of shares)

242.4 cr

Shareholding (%)

Promoters 55.9

FII 21.0

DII 20.8

Others 2.3

Price performance

(%) 1m 3m 6m 12m

Absolute 1.9 (9.7) 10.6 (10.5)

Relative to Sensex

(2.8) (6.1) (3.6) (76.7)

Sharekhan Research, Bloomberg

Reco/View Change

Reco: Buy CMP: Rs. 536

Price Target: Rs. 750 á Upgrade Maintain â Downgrade

Price chart

What has changed in 3R MATRIX

Old New

RS RQ RV

Valuation Rs cr

Particulars FY19 FY20 FY21 FY22E FY23E

Revenue 80,780.2 86,231.5 1,00,615.8 1,12,158.5 1,26,748.6

OPM (%) 32.0 41.1 45.1 48.5 52.6

Adjusted PAT -3,977.8 -3,630.4 -1,468.5 6,193.6 12,041.0

% YoY growth NM NM NM NM 94.4

Adjusted EPS (Rs.) -10.0 -7.0 -2.7 11.3 21.9

P/E (x) NM NM -199.1 47.6 24.5

P/B (x) 4.1 3.8 5.0 4.1 2.3

EV/EBITDA (x) 15.8 10.8 9.5 8.5 7.0

RoNW (%) NM NM NM 9.0 11.4

RoCE (%) 2.4 4.1 7.8 9.8 11.9Source: Company; Sharekhan Research*FY20/FY21E/FY22E numbers are based on IndAs-116

350400450500550600650

May

-20

Sep-

20

Jan-

21

May

-21

May 18, 2021 3

Sto

ck U

pd

ate

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

Largely in-line revenue, beat in operating margin

Reported revenue and ARPU will not be comparable given the termination of interconnection usage charges (IUC) on mobile calls from January 2021. IUC revenue stood at Rs. 3,617 crore (difference between the reported revenue and restated revenue) during 9MFY2021.

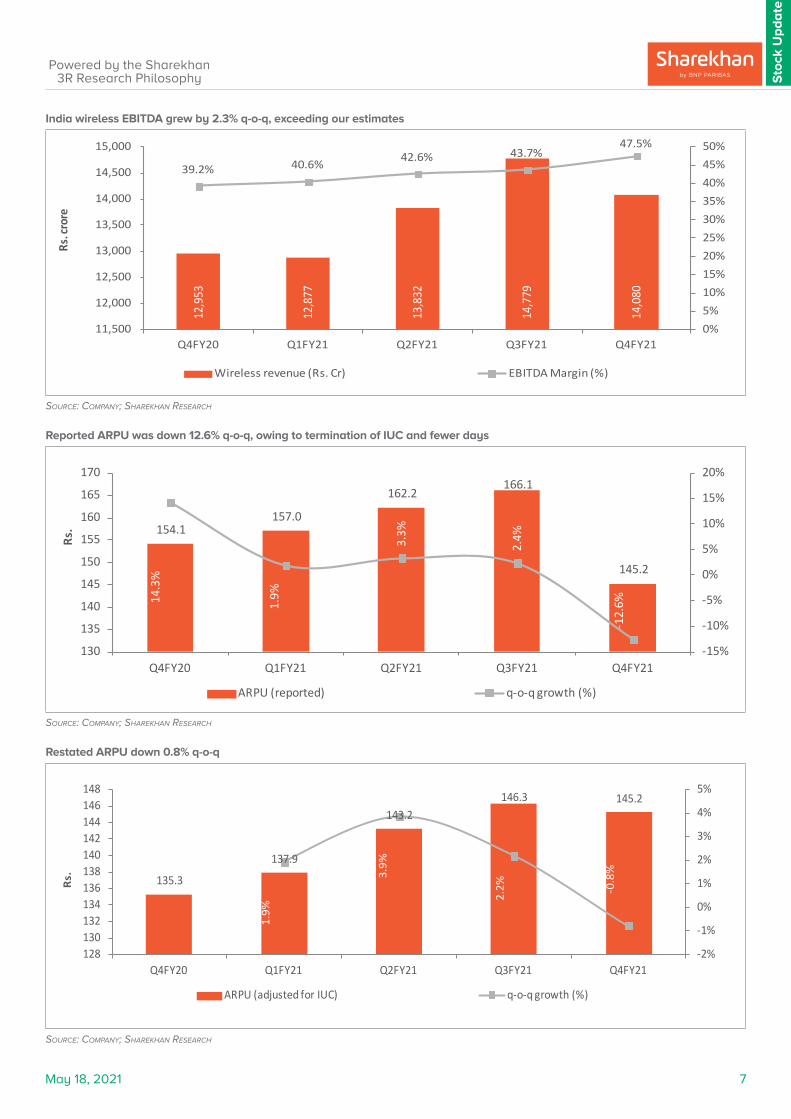

On a like-to-like basis, consolidated revenues increased by 2% q-o-q and 17.6% y-o-y to Rs. 25,747 crore, below our estimates, led by 3.4% q-o-q growth in India business (adjusted for IUC) and 0.9% q-o-q growth (in USD terms) in its Africa business revenue. On a like-to-like basis, the India wireless business’ revenues grew by 4.2% q-o-q and 19.1% y-o-y despite a marginal weaker ARPU, led by strong subscriber additions. However, revenue growth of the India wireless business slowed to 19.1% y-o-y in Q4FY2021 from 32.4% in Q3FY2021, owing to the impact of the last round of tariff hike in the base quarter of Q4FY2020. On reported basis, Indian wireless business revenue declined 4.7% q-o-q, which is better as compared to 6.1% q-o-q revenue decline of Reliance Jio. ARPU (adjusted for IUC) in India wireless business declined by 0.8% q-o-q (up 7.3% y-o-y) to Rs. 145, below our estimates. Reported ARPU declined by 12.6% q-o-q owing to the cut in IUC from January 2021. The number of subscribers for the India wireless business increased by 13.4 million (up 4.4% q-o-q), while 4G subscriber additions stayed at 13.7 million during the quarter. EBITDA margin for the quarter improved by ~244 bps q-o-q to 47.9%, exceeding our estimates, led by a 380 bps q-o-q improvement in operating margin of India wireless business. EBITDA margin of Africa business expanded by 78 bps q-o-q during the quarter. As a result, India wireless business EBITDA grew 3.6% q-o-q. The Reported net profit was at Rs. 759 crore. Excluding a one-time gain of Rs. 440 crore, adjusted net profit came at Rs. 319 crore and was 27% below our estimates. .

ARPU likely to improve going ahead; meaningful allocation of capital towards non-wireless business

With a resurgence in COVID-19 infections owing to second wave of COVID-19 infections, we expect Q1FY2022 revenue growth for Indian wireless business would remain muted given restrictions on movement across many states of the country. Further, management highlighted that it witnessed an increase in competitive intensity in terms of higher sales incentives and channel commissions to attract more customers by peers during Q4FY2021. Though the competitive intensity has come down during April 2021, we believe the tariff hikes would be delayed further. Note that the company had taken its last tariff hike during December 2019. However, the management expects ARPU in its India wireless business would improve going ahead because of (1) low level of tariffs in India, (2) 2G to 4G upgrades as its 140 million subscriber are not on 4G and their ARPU is half of its rest of business ARPU, (3) increasing postpaid subscribers and (4) strong addition of 4G customers. We believe the bundling of home broadband, DTH, and wireless services under the one-bill initiative would help the company improve ARPUs going forward. The revised version of One Airtel plan will be launched over next 4-5 weeks, which would aid to ARPU improvement as this would fetch an additional Rs. 500-600 per account when a customer would move to this plan. The company has currently around 0.5 million customers under this plan. The management highlighted that it has gained market share in both wireless and non-wireless business given its relentless focus on improving customer experience and sharp focus on quality customers. Further, the company has created a dedicated channel for its 50 million high-value homes. Of which, the company has relationship with 30 mn high value homes to its one of its services i.e postpaid, DTH and broadband. The management highlighted that meaningful capital allocation of capex would be towards broadband and enterprise (includes data center) as it sees significant growth opportunities in these businesses going ahead.

Key result highlights from Concall

� Mixed quarter, strong performance across portfolio: Bharti Airtel reported below-than-expected revenue performance despite strong subscriber additions which was offset by a slightly weaker ARPU, while EBITDA margin beat expectations. Consolidated revenue (adjusted for IUC) increased by 2% q-o-q and 17.6% y-o-y to Rs. 25,747 crore, led by broad-based growth across segments. The India (adjusted for IUC) and Africa (USD revenue) business grew by 3.4% and 0.9% q-o-q. Consolidated EBITDA margin expanded by 244 bps q-o-q to 47.9%, led by healthy operating leverage in the India wireless and Africa businesses. EBITDA grew by 2.3% q-o-q/28% y-o-y during the quarter. Reported net profit came in at Rs. 759.2 crore during Q4FY2021. Adjusted net profit (excluding one-time gain of Rs. 440 crore) came in at Rs. 319 crore and was 27% below our estimates. Home broadband and enterprise business reported revenue growth of 5.9% q-o-q and 2.2% q-o-q, respectively.

� Gained market share across its businesses: Management highlighted that it has gained market share in each of its business given its relentless focus on improving customer experience and sharp focus on quality customers. The enablers to gain market share in the respective businesses are - (1) digitising the core to improve experience and eliminate waste, (2) modularising capabilities to drive new revenue streams, 3)

May 18, 2021 4

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

bringing together the power of Airtel for unified customer view and integrated channel approach and (4) financial discipline.

� India wireless business impacted by lower ARPU: On a like-to-like basis, India wireless business revenue grew by 4.2% q-o-q and 19.1% y-o-y to Rs. 14,080 crore, led by strong 4G net subscriber additions of 13.7 million. Over the past 12 months, the company has added around 43 million customers over its 4G networks. The company has also added 6,29,000 subscribers in the post-paid segment. Overall customer net additions remained at 13.4 million and churn remains at 2.2%. ARPU (adjusted for IUC) declined from Rs. 146 to Rs. 145, owing to fewer number days. ARPU has increased by 7.3% y-o-y, without taking any price hike. Management expects ARPU would improve going ahead on the back of (1) low tariffs in India, (2) 140 million users on its network who are not shifted to 4G, whose ARPU is half of its rest of business ARPU, and (3) strong addition of 4G customers. EBITDA margin of India wireless business improved by 380 bps q-o-q to 47.5% and EBIT increased by 22.4% q-o-q.

� Strengthened network coverage; holds 33% share of liberalized spectrum: The management highlighted that it has 33% share of liberalized spectrum across the country, which can be seamlessly re-farmed to 5G over time. Further, the company accelerated its coverage footprint by adding 8,300 sites during the quarter. The company has substantially strengthened its transport network. The management stated that it has gained revenue market share in its India mobile business, led by strong net additions in 4G and postpaid customers.

� Healthy India wireless operating metrics: Data subscribers increased by 13.9 million at 189 million, an increase of 8.0% q-o-q and 27% y-o-y. The number of 4G subscribers increased by around 12.7 million to 179 million, 8% q-o-q and 32% y-o-y growth. Management highlighted that 4G customer additions were driven by upgradation of its 2G customers to 4G and shifting of subscribers from competitors. Overall data usage on the network was up by 9% q-o-q/43% y-o-y, while usage per customer grew by 0.4% q-o-q/13% y-o-y, respectively, to 16.8 GB per subscriber due to work-from-home (WFH) modes and online educations. There was strong growth (up 8% q-o-q/21% y-o-y) in voice traffic to 997 billion minutes.

� Strong growth in home broadband, created a dedicated sales channel for high value homes: The broadband business has crossed 3mn+ customers on the back of strong demand for home broadband. During the quarter, the company expanded its footprints to new towns and cities with its unique LCO partnership mode. The company added 1 million home passes during the quarter. In DTH business, the company is ranked the No. 2 player in the market. The company has gained the revenue market share in DTH business from 22% in December 2018 to 27% share as of December 2020, implying 5% revenue share gain over last two years. The company outpaced consistently its peers in terms of performance in this segment during the last eight quarters. The company has combined its large mobility distribution system with DTH to create one mass retail channel which will drive the businesses such as mobility, DTH and payment bank. The management believes that this initiative would drive the growth of its DTH business going ahead. Further, the company has created a dedicated channel for its 50 million high value homes. Of this, the company has relationship with 30 mn high value homes to its one of its services i.e postpaid, DTH and broadband. The company has combined 2,000 retail stores along with broadband sales organisation to create one integrated direct sales channel. To drive growth in home business, the company also adopted strategies – (1) rapid expansion of its own coverage, (2) Acceleration of the LCO partnership model. During the quarter, the company expanded to new cities with the help of LCO partnership model, taking total cities to 203. (3) Bringing full power of Airtel services as well as partnership services to deliver integrated converged offer encompassing connectivity, entertainment and more. These approaches helped the company to drive its home business during the quarter, resulting in 2,74,000 net additions. Revenue from broadband grew by 5.9% q-o-q despite decline in ARPU (down 2.9% q-o-q), led by 9.8% q-o-q growth in subscriber addition. EBITDA margin of the broadband segment expanded by 20 bps q-o-q to 55.7%. The company incurred a capex of Rs 332.5 crore during the quarter. The broadband category is at a cusp in terms of growth as the management sees that there is a huge need for high-speed internet among customers.

� DTH business likely to grow: Revenue in the DTH business declined by 2.8% q-o-q during the quarter, owing to decline in customer base and lower ARPU. The company lost 156,000 customers during the quarter, while ARPU in DTH business declined 3.4% q-o-q to Rs. 144. The management indicated that there is huge scope for growth in the DTH segment because of 1) lower pricing of DTH services compared to average rate of global DTH services, 2) lower penetration, 3) poor services by cable operators, and 4) lack of broadband penetration across the country (limits technological disruptions).

May 18, 2021 5

Sto

ck U

pd

ate

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

� Huge growth opportunity in the enterprise business: Airtel’s business revenue grew by 2.2% q-o-q and 9.7% y-o-y during the quarter. The company highlighted that it continues to witness strong demand from its enterprise customers and is consistently gaining market share among its peers. This segment has industry leading margin of 40.2% in Q4FY2021. The Company incurred a capital expenditure of Rs 701 crore in Airtel Business during the quarter. Airtel continues to gain market share not only annually but on q-o-q basis. The company has gained revenue market share in the enterprise business from 23% in December 2018 to 31% share as of December 2020, implying 8% revenue share gain in enterprise business over last two years. Management highlighted that 80% of revenue in the enterprise business comes from top 20% of its customers. Hence, it believes that there is massive opportunity for growth in this business as the company would target the remaining 80% of customers. Further, Airtel has the opportunity to enhance its relationship with these top 20% of its customers to increase the share of wallet. The management has been continuously strengthening its channels and product portfolio to the capture these opportunities going ahead. Hence, the company highlighted that it focuses on (1) insourcing its total SME sales workforce, which was earlier outsourced. This would lead to upgradation of its SME channel capabilities, in-turn it would help to gain market share, (2) building omni-channel digital capabilities as more than 95% of new orders for the product lines for which it began this effort is coming from digital channels. This would help to expand its reach and gain market share in SME space, (3) entered adjacent areas such as data centre, Airtel Secure, Airtel IQ, Airtel Cloud and among others, which would help the company to go deeper with its customers. The company launched Airtel IoT, Airtel Ads and Airtel Safe Pay in recent times. Airtel IoT is an end-to-end platform with the capability to connect and manage billions of devices and applications in a highly secure and seamless fashion. To expand the digital business, the company has provided different targets to its sales for both hunting and farming. The management highlighted that it focuses on two areas such as (1) core is connectivity (estimated market opportunity is Rs. 40,000 crore), which will continue to grow because of increased requirement of capacity in large businesses and growing need of connectivity in small businesses. Airtel has gained market share in this segment and management expects to increase its market share from current 31% level, 2) opportunity beyond connectivity, where the estimated market size is Rs. 50,000 crore. Management highlighted that the margin profile is different for each of its digital offering, 3) The partnership-led model – the company has partnership with companies to drive connectivity solutions. The company’s management sees strong traction for its partnership-led model.

� Digital revenue is considered to be the heart of the business: Digital revenue is considered the heart of the business as it complements the core business and helps in enhancing the overall business and profitability. The management highlighted that its digital capabilities have been helping the company to acquire quality customers, become more efficient, building new revenue streams, increase wallet share, reduce churn rate, create ecosystem of partnership to leverage the capabilities and eliminate waste. It highlighted that the company is consistently growing its business online, which helps for better experience and lower costs. There is sustained growth of digital assets. The company has monthly active users (MAUs) of 200 million in Q4FY2021, with 72.5 million MAUs in Wynk. Airtel Xstream is at 37.5 million MAUs. Airtel Thanks is at 96.3 million MAUs. The Airtel Payment Bank has been rapidly gaining scale with 54 million of active users and monthly throughput of Rs. 22,000 crore. On a standalone basis, the company’s payment bank is road to profitability and management expects profitability would be achieved next year. Management remains optimistic that digital capabilities, digital services though partnership, and scaling omni-channel would help it drive growth going ahead. Airtel Safe Pay differentiates bank even further and leverages Airtel core telco strength to provide highest level protection from potential online frauds. The company launched Airtel ads during the quarter, which is a brand engagement solution. It allows brands of all sizes to do consent based and privacy based campaigns to customers. The management indicated that the digital advertising markets is a massive growing market and the company began to derive revenues with 100 brands.

� FY2022 capex – meaningful allocation would be towards non-wireless business: Consolidated capex for Q4FY21 remained at Rs. 6,847 crore against Rs. 6,864 crore in Q3FY21, down 0.3% q-o-q. Management expect the overall capex for FY2022 will be at similar level of FY2021 ($3,252 million). Management highlighted that the allocation of capex would be towards broadband, enterprise (includes data center), rollout of sublevel spectrum and transport capex. The meaningful allocation of capex would be towards non-wireless business over time.

� Increase in competitive intensity: The management highlighted that it witnessed an increase in competitive intensity during Q4FY2021, in terms of higher sales incentives and channel commissions to attract more customers. With the rise in infections owing to second wave of COVID-19 in India, management indicated that the competitive intensity was moderated in April.

May 18, 2021 6

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

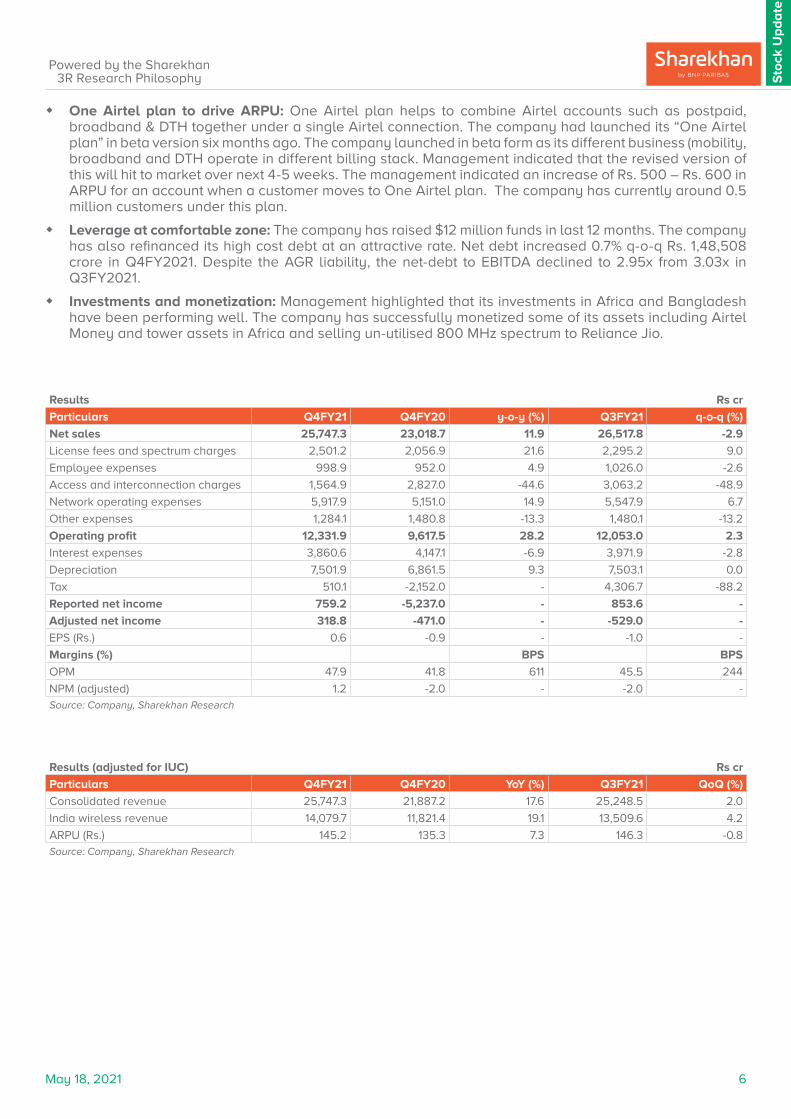

� One Airtel plan to drive ARPU: One Airtel plan helps to combine Airtel accounts such as postpaid, broadband & DTH together under a single Airtel connection. The company had launched its “One Airtel plan” in beta version six months ago. The company launched in beta form as its different business (mobility, broadband and DTH operate in different billing stack. Management indicated that the revised version of this will hit to market over next 4-5 weeks. The management indicated an increase of Rs. 500 – Rs. 600 in ARPU for an account when a customer moves to One Airtel plan. The company has currently around 0.5 million customers under this plan.

� Leverage at comfortable zone: The company has raised $12 million funds in last 12 months. The company has also refinanced its high cost debt at an attractive rate. Net debt increased 0.7% q-o-q Rs. 1,48,508 crore in Q4FY2021. Despite the AGR liability, the net-debt to EBITDA declined to 2.95x from 3.03x in Q3FY2021.

� Investments and monetization: Management highlighted that its investments in Africa and Bangladesh have been performing well. The company has successfully monetized some of its assets including Airtel Money and tower assets in Africa and selling un-utilised 800 MHz spectrum to Reliance Jio.

Results Rs cr

Particulars Q4FY21 Q4FY20 y-o-y (%) Q3FY21 q-o-q (%)

Net sales 25,747.3 23,018.7 11.9 26,517.8 -2.9

License fees and spectrum charges 2,501.2 2,056.9 21.6 2,295.2 9.0

Employee expenses 998.9 952.0 4.9 1,026.0 -2.6

Access and interconnection charges 1,564.9 2,827.0 -44.6 3,063.2 -48.9

Network operating expenses 5,917.9 5,151.0 14.9 5,547.9 6.7

Other expenses 1,284.1 1,480.8 -13.3 1,480.1 -13.2

Operating profit 12,331.9 9,617.5 28.2 12,053.0 2.3

Interest expenses 3,860.6 4,147.1 -6.9 3,971.9 -2.8

Depreciation 7,501.9 6,861.5 9.3 7,503.1 0.0

Tax 510.1 -2,152.0 - 4,306.7 -88.2

Reported net income 759.2 -5,237.0 - 853.6 -

Adjusted net income 318.8 -471.0 - -529.0 -

EPS (Rs.) 0.6 -0.9 - -1.0 -

Margins (%) BPS BPS

OPM 47.9 41.8 611 45.5 244

NPM (adjusted) 1.2 -2.0 - -2.0 -Source: Company, Sharekhan Research

Results (adjusted for IUC) Rs cr

Particulars Q4FY21 Q4FY20 YoY (%) Q3FY21 QoQ (%)

Consolidated revenue 25,747.3 21,887.2 17.6 25,248.5 2.0

India wireless revenue 14,079.7 11,821.4 19.1 13,509.6 4.2

ARPU (Rs.) 145.2 135.3 7.3 146.3 -0.8Source: Company, Sharekhan Research

May 18, 2021 7

Sto

ck U

pd

ate

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

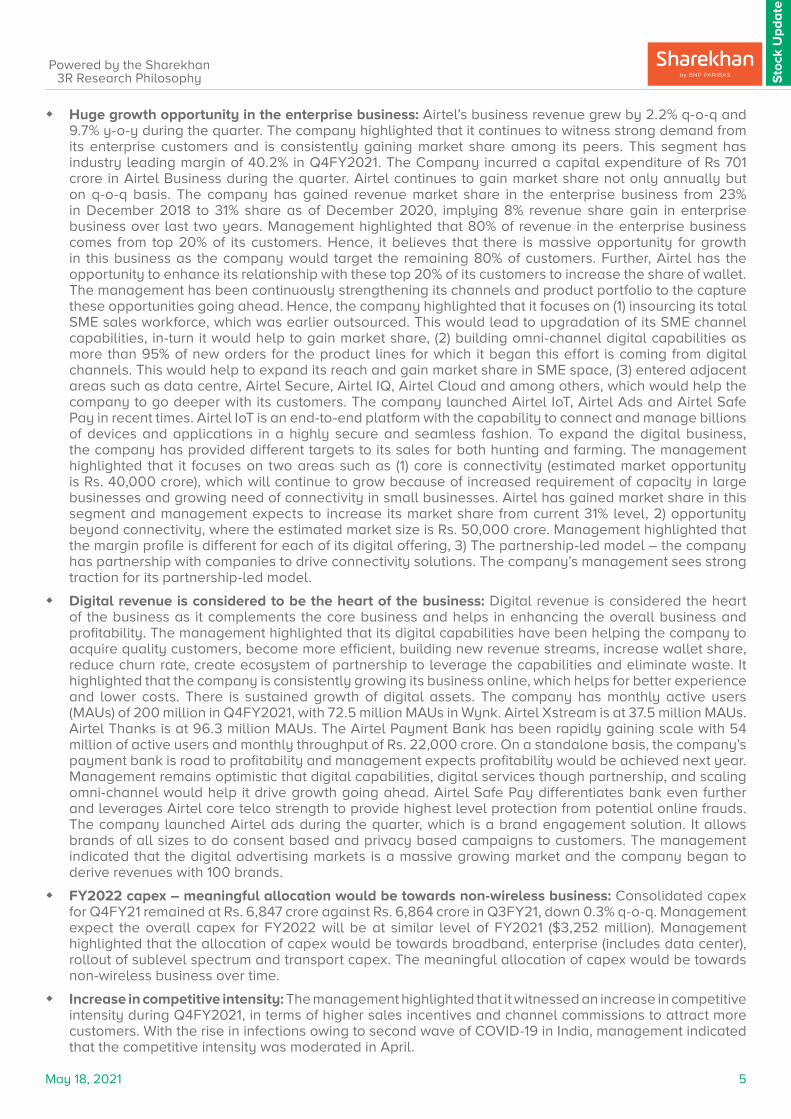

India wireless EBITDA grew by 2.3% q-o-q, exceeding our estimates

Source: company; Sharekhan reSearch

Reported ARPU was down 12.6% q-o-q, owing to termination of IUC and fewer days

Source: company; Sharekhan reSearch

Restated ARPU down 0.8% q-o-q

Source: company; Sharekhan reSearch

12,9

53

12,8

77

13,8

32

14,7

79

14,0

80

39.2% 40.6% 42.6% 43.7%47.5%

0%5%10%15%20%25%30%35%40%45%50%

11,500

12,000

12,500

13,000

13,500

14,000

14,500

15,000

Q4FY20 Q1FY21 Q2FY21 Q3FY21 Q4FY21

Rs. c

rore

Wireless revenue (Rs. Cr) EBITDA Margin (%)

154.1 157.0

162.2 166.1

145.2

14.3

%

1.9%

3.3%

2.4%

-12.

6%

-15%

-10%

-5%

0%

5%

10%

15%

20%

130

135

140

145

150

155

160

165

170

Q4FY20 Q1FY21 Q2FY21 Q3FY21 Q4FY21

Rs.

ARPU (reported) q-o-q growth (%)

135.3

137.9

143.2 146.3 145.2

1.9%

3.9%

2.2% -0

.8%

-2%

-1%

0%

1%

2%

3%

4%

5%

128130132134136138140142144146148

Q4FY20 Q1FY21 Q2FY21 Q3FY21 Q4FY21

Rs.

ARPU (adjusted for IUC) q-o-q growth (%)

May 18, 2021 8

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

Outlook and Valuation

n Sector view – Large addressable market

Jio’s entry in the Indian telecom space led to the reversal of pricing paradigm that benefited incumbent telecom players. After extensive consolidation, structure of the telecom industry has changed from more than eight players to now a structure of three private and one government operator. The momentum has now shifted towards data, led by 4G services, although voice will continue to grow in underpenetrated areas in rural India. As smartphones are becoming more affordable, the uptake of data services is increasing. India has become the second largest telecommunication market and has the second highest number of internet users in the world. We believe higher bundling with home entertainment, partnerships with content providers, and increasing data consumption due to WFH could be major drivers for price hikes going ahead.

n Company outlook - Resilient performance amid uncertainty

Though Bharti Airtel will be able to withstand competition in the wireless business, we believe the company’s capex will be allocated towards non-wireless business and differentiated digital capabilities to drive its growth going ahead. Further, its free cash flow is set to improve going ahead with anticipated improvement in the ARPU and better cost management. Higher digitisation would enable the company increase monetisation of digital assets and value-added services, a reduced churn rate across verticals, and improved wallet share from subscribers. With a comparatively strong balance sheet and adequate network investments, Bharti is well-placed to grow in its core business going ahead.

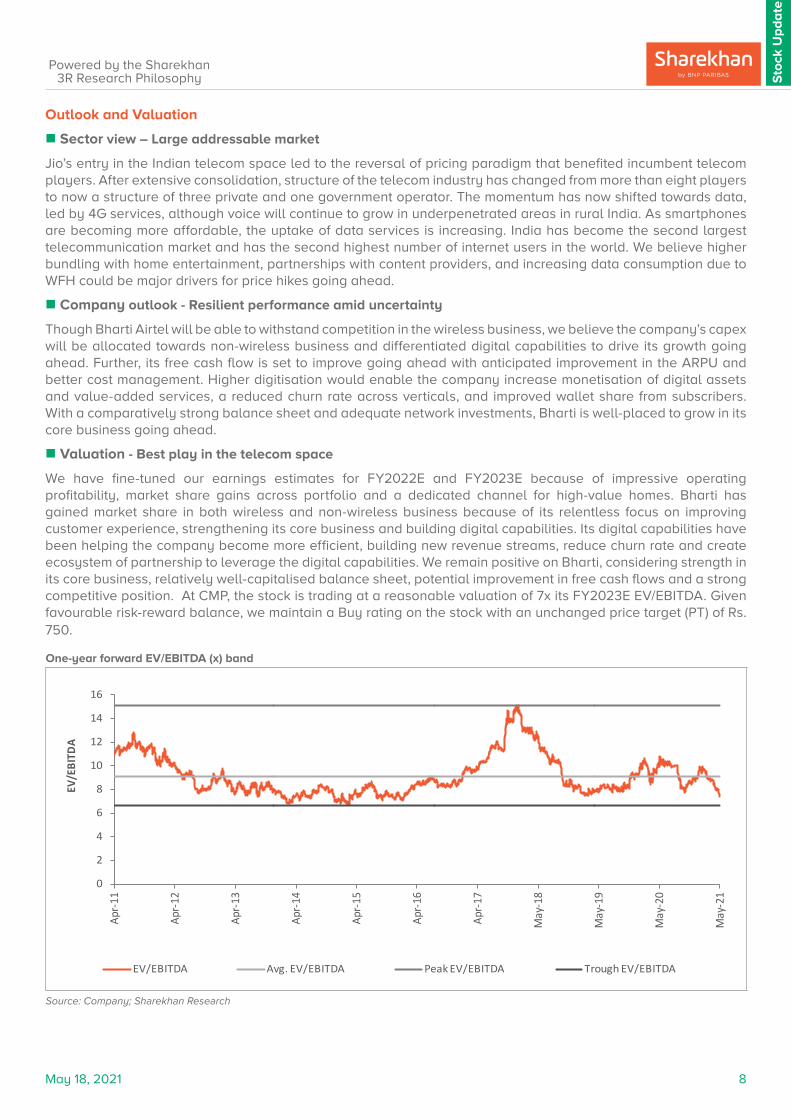

n Valuation - Best play in the telecom space

We have fine-tuned our earnings estimates for FY2022E and FY2023E because of impressive operating profitability, market share gains across portfolio and a dedicated channel for high-value homes. Bharti has gained market share in both wireless and non-wireless business because of its relentless focus on improving customer experience, strengthening its core business and building digital capabilities. Its digital capabilities have been helping the company become more efficient, building new revenue streams, reduce churn rate and create ecosystem of partnership to leverage the digital capabilities. We remain positive on Bharti, considering strength in its core business, relatively well-capitalised balance sheet, potential improvement in free cash flows and a strong competitive position. At CMP, the stock is trading at a reasonable valuation of 7x its FY2023E EV/EBITDA. Given favourable risk-reward balance, we maintain a Buy rating on the stock with an unchanged price target (PT) of Rs. 750.

One-year forward EV/EBITDA (x) band

Source: Company; Sharekhan Research

0

2

4

6

8

10

12

14

16

Apr-

11

Apr-

12

Apr-

13

Apr-

14

Apr-

15

Apr-

16

Apr-

17

May

-18

May

-19

May

-20

May

-21

EV/E

BITD

A

EV/EBITDA Avg. EV/EBITDA Peak EV/EBITDA Trough EV/EBITDA

May 18, 2021 9

Sto

ck U

pd

ate

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

About company

Established in 1995, Bharti is one of the leaders in the Indian mobile telephony space with operations in 18 countries across Asia and Africa. The company ranks among the top three mobile service providers globally in terms of subscribers. Airtel is a diversified telecom service provider offering wireless, mobile commerce, fixed line, home broadband, enterprise, and DTH services. The company expanded into Africa by acquiring Zain’s Africa operations in 2010 and is present in 14 African markets. Bharti had over 420 million customers across its operations at the end of March 2020.

Investment theme

Revenue accretion from the 4G upgrade, minimum-ARPU plans (rolled out across India), and recent tariff hike helped the company to report improvement in ARPU. Further, the government’s data localisation policies with an increasing penetration of smartphones are likely to boost strong demand for data over the medium-to-long term. Despite a predatory pricing strategy from new entrants since its commercial launch in September 2016, Bharti has been resilient in sustaining its revenue market share (RMS) as it has been drastically standardising its plans to retain customers and acquiring subscribers through M&A activities. In DTH, Bharti expects to maintain steady growth by adding new subscribers in rural areas by launching USB-enabled STBs, increasing reach in cities taking advantage of flat-screen TV upgrades, and driving up ARPUs by selling OTT boxes and hybrid HD STBs. We believe the company is well poised to deliver strong multi-year EBITDA growth phase given recent developments in the Indian wireless industry.

Key Risks

1) Increasing competition could pressurise realisations; and 2) Slower growth in data volumes could affect data revenue growth.

Additional Data

Key management personnel

Sunil Mittal Chairman

Gopal Vittal MD & CEO (India and South Asia)

Raghunath Mandava CEO (Africa)

Badal Bagri Chief Financial Officer

Pankaj Tewari Company SecretarySource: Company Website

Top 10 shareholders

Sr. No. Holder Name Holding (%)

1 ICICI Prudential Asset Management 2.96

2 SBI Funds Management Pvt Ltd 2.27

3 BlackRock Inc 1.60

4 Capital Group Companies 1.60

5 Vanguard Group Inc/The 1.35

6 GIC Pte Limited 1.33

7 ICICI Prudential Life Insurance Co 1.16

8 HDFC Asset Management Pvt Limited 1.15

9 Nippon Life India Asset management 0.90

10 UTI Asset management Co Limited 0.85Source: Bloomberg

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

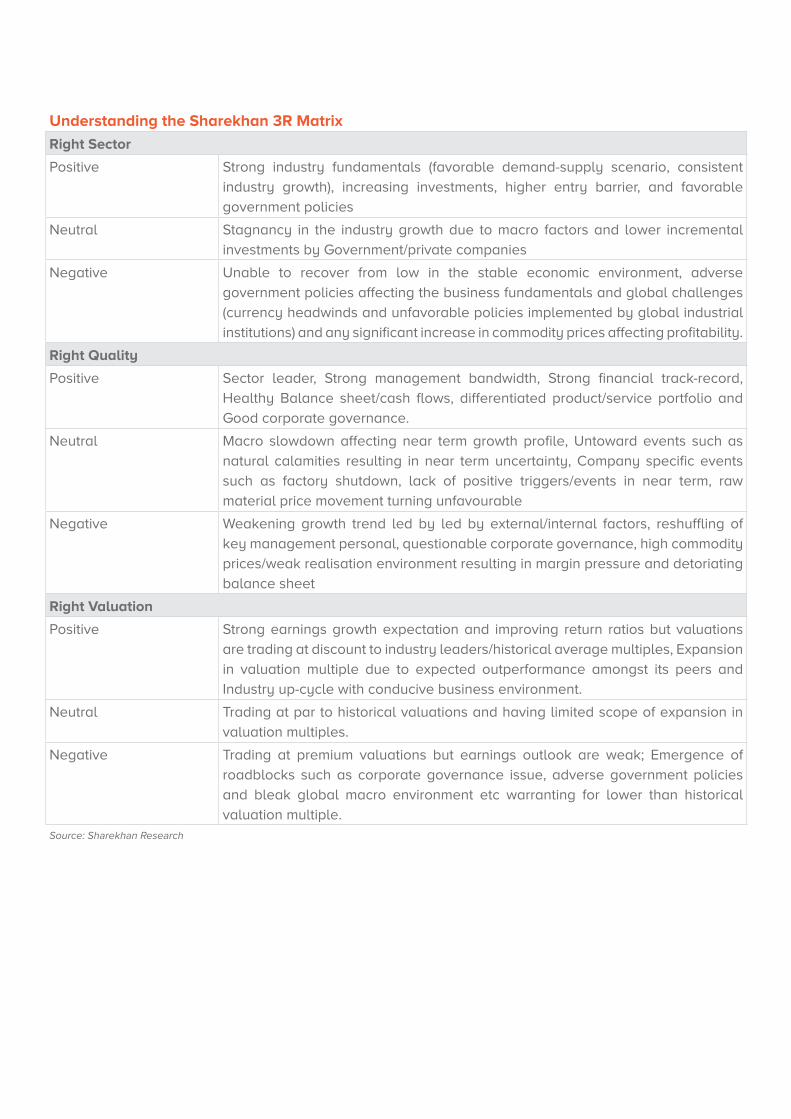

Understanding the Sharekhan 3R Matrix

Right Sector

Positive Strong industry fundamentals (favorable demand-supply scenario, consistent

industry growth), increasing investments, higher entry barrier, and favorable

government policies

Neutral Stagnancy in the industry growth due to macro factors and lower incremental

investments by Government/private companies

Negative Unable to recover from low in the stable economic environment, adverse

government policies affecting the business fundamentals and global challenges

(currency headwinds and unfavorable policies implemented by global industrial

institutions) and any significant increase in commodity prices affecting profitability.

Right Quality

Positive Sector leader, Strong management bandwidth, Strong financial track-record,

Healthy Balance sheet/cash flows, differentiated product/service portfolio and

Good corporate governance.

Neutral Macro slowdown affecting near term growth profile, Untoward events such as

natural calamities resulting in near term uncertainty, Company specific events

such as factory shutdown, lack of positive triggers/events in near term, raw

material price movement turning unfavourable

Negative Weakening growth trend led by led by external/internal factors, reshuffling of

key management personal, questionable corporate governance, high commodity

prices/weak realisation environment resulting in margin pressure and detoriating

balance sheet

Right Valuation

Positive Strong earnings growth expectation and improving return ratios but valuations

are trading at discount to industry leaders/historical average multiples, Expansion

in valuation multiple due to expected outperformance amongst its peers and

Industry up-cycle with conducive business environment.

Neutral Trading at par to historical valuations and having limited scope of expansion in

valuation multiples.

Negative Trading at premium valuations but earnings outlook are weak; Emergence of

roadblocks such as corporate governance issue, adverse government policies

and bleak global macro environment etc warranting for lower than historical

valuation multiple.Source: Sharekhan Research

Disclaimer: This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This Document may contain confidential and/or privileged material and is not for any type of circulation and any review, retransmission, or any other use is strictly prohibited. This Document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different conclusions from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

The analyst certifies that the analyst has not dealt or traded directly or indirectly in securities of the company and that all of the views expressed in this document accurately reflect his or her personal views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. The analyst and SHAREKHAN further certifies that neither he or his relatives or Sharekhan associates has any direct or indirect financial interest nor have actual or beneficial ownership of 1% or more in the securities of the company at the end of the month immediately preceding the date of publication of the research report nor have any material conflict of interest nor has served as officer, director or employee or engaged in market making activity of the company. Further, the analyst has also not been a part of the team which has managed or co-managed the public offerings of the company and no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document. Sharekhan Limited or its associates or analysts have not received any compensation for investment banking, merchant banking, brokerage services or any compensation or other benefits from the subject company or from third party in the past twelve months in connection with the research report.

Either, SHAREKHAN or its affiliates or its directors or employees / representatives / clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein before publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind.

Compliance Officer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected];

For any queries or grievances kindly email [email protected] or contact: [email protected]

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CDSL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183;

Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Know more about our products and services

For Private Circulation only