Embed Size (px)

Citation preview

This is a preliminary version of the paper published in Economic Affairs vol 29, num 3 (p. 9-16). The final printed version is available at:

http://onlinelibrary.wiley.com/doi/10.1111/j.1468-0270.2009.01912.x/abstract !!!

CENTRAL BANKS: FROM POLITICALLY INDEPENDENT TO MARKET DEPENDENT INSTITUTIONS !

Pedro Schwartz and Juan Castañeda (this is a draft version, please do not quote without authors’ permission) !!

After a quarter century of increasing central bank independence, the various responses to the present financial crisis are undermining the Chinese walls painfully built between managers of money and fiscal authorities. Central Banks and State Treasuries are working side by side as lenders of last resort. Central banks are helping economic ministers with large purchases of public debt and unheard of discounting of private paper. Regulation and control of financial institutions is now a political football in the Parliamentary arena. All this shows that central banks can no longer be seen as neutral outside observers and regulators of the financial market – a concept that belongs in the time when central banks were nationalised to become the “deus ex macchina” of national money. Central banks must be seen again as market-dependent institutions, as heads of oligopolistic banking clubs, as long-run, seigniorage-maximising establishments in a world of currency competition. Privatisation in law or in fact is back on the table. !

Two goals for central banks

The central bank independence movement can be said to have started with the New Zealand Reserve Bank Act of 1989 that determined the primary function of the Reserve Bank of New Zealand as being “to formulate and implement monetary policy directed to […] achieving and maintaining stability in the general level of prices”. This concentration of central banks to their remit of keeping inflation at bay has been widely imitated across the advanced world. Nobody saw, however, that another unstated policy goal, to maintain the financial system in good order, could clash with the duty to keep the value of money stable. This second goal demands that, if necessary, the central bank should act as a lender of last resort. The question is how to make it in the interest of a central bank not to manage money for political ends, and at the same time be ready to save the banks in its club from counterparty failure. The present crisis has shown that incentives are not properly aligned for the simultaneous pursuit of both these goals by central banks. !The theoretical basis of central bank policy

! 1

The ground and justification for central bank independence in the pursuit of a non-political remit is the fact that there is no long-run trade-off between inflation on the one hand and employment and output on the other (there is no exploitable Phillips curve). The economic profession now generally agrees that, over a period of nine to ten years, increasing in the money supply will result in a similar rise in the rate of increase of the general price level and will have no systematic effect on the real side of the economy.

This belief is based on a long-run interpretation of the “quantity theory”. One must start with Fisher’s identity: P ≡ ( M · V ) / T,

where the price level P is posited to depend on the quantity of money M, the velocity of circulation V, all divided by the number of transactions T. This necessarily true identity is turned into a theory of inflation when one predicts that the expansion of M will fall wholly on P in the long term, when V is observed to fall steadily with the increase in wealth and the effects of an increase in the money supply on output T will have run their short-lived course. When the information about increases in money supply is fully discounted by the market it will be passed on to prices, so that employment and real output turn out not to be correlated to money supply. This is to say that, sooner or later, inflation fully enters the public’s expectations (in central banker parlance, “inflation expectations become unanchored”) and people lose faith in the currency. 1

In the short and medium term, however, unexpected inflation can lead to an expansion of jobs and output, since people may then interpret growing prices as increases in the real demand for their goods and services. Hence, a time-inconsistency problem arises for monetary policy. Unless some institutional arrangement forces monetary (and political) authorities to focus on the long run, they will tend to pursue monetary policies that boost the real economy if only for a time and affect the long run growth path of the economy in a less than optimal way. (The long run for future generations is made of many short runs, pace Keynes.) One such institutional arrangement consists in granting a measure of independence to the central bank, so that, free from political pressures, it is able to follow a monetary policy leading to a stable value of money.

These institutional barriers to using money for political ends, however, can break down in a fractional reserve system when a run by depositors on an unsafe bank starts to spread to banks with solid balance sheets. It was Bagehot (1873) who first clearly explained the role of a central bank, be it a competitive issuer of base money, as in Scotland up to 1844, or a monopolist provider of services to financial houses, as the Bank of England in the City. Working on J.S. Mill’s ‘banking school’ ideas (1857, pgs. 505-6) regarding the importance to furnish commercial banks with liquidity in the event of a fall in confidence, Bagehot explained the advantage of having a centralised keeper of reserves and a supplier of funds in times of need for what we today call a club of financial houses.

This lender of last resort function clearly poses an added contradiction between the behaviour of the central banker in the short and the long term. Central bank independence may guard the issuer of money against using its powers to create means

! 2

This is an instance of the separability of the nominal and the real economy, the so-called “classical 1

dichotomy” as explained by David Ricardo in his 1817 Principles, ch. xxvii, pg. 365.

of payments to foster growth or fight unemployment. There are other occasions when the central bank may be called upon to act against an economic downturn, namely, during a bank run in a fractional reserve system. No degree of independence will guard it against going too far in its stimulus to a faltering cyclical economy. Combining the power to create money with the need to act as a lender of last resort demands a new definition of central bank independence if it is to lean against the cyclical wind in the short run and protect the value of money in the long. !Definitions of independence

In the last decade, the vast majority of both new and old central banks have been given new statutes the better to define and limit their proper policy targets, and to preserve their independence from political pressures. However, the meaning and scope of independence is disputed as it involves different levels and concepts. !a. Goal independence: central bank statutes and the quantification of the

mandate

The extent to which the central bank is said to be “goal independent” is given by the way policy targets are defined in its statutes. The more precise the definition of its targets the less room do central bank committees have to interpret them and even to elude them by following a different task. Unlike the exceptional case of the so called plural mandate of the Federal Reserve, in our days most central banks statutes assign 2

policy boards a clear hierarchy of tasks focused on the primary achievement of price stability. In essence, a clear institutional definition of the policy goals ties the hands of the policy makers and helps to make monetary policy more transparent and predictable.

However, even under a single or clearly hierarchical mandate, the assigned policy goal needs to be operational. This requires definition of what price stability means. In practice, it involves the selection of a particular price index to measure inflation and the numerical definition of price stability in terms of that index.

Ultimately, goal independence is greater or less according to what institution is responsible for defining the operational target. If it is the Government on its own (as in the UK, where the Chancellor of the Exchequer determines the inflation rate to be aimed at), goal independence is reduced. It is greater if both the Government and the governor (or governing bodies) decide (as in New Zealand). The European Central Bank (ECB) is considered as truly goal independent, as its Governing Council sets by itself the operational definition of its primary mandate, to wit, keeping the rate of increase of the Harmonised Index of Consumer Prices “at below, but close to, 2% over the medium term”.

Finally, central bank statutes reformed during the 90s have recognised that operating a policy committed to achieve price stability also requires a clear separation of the central bank from government. This has led to the general prohibition for the State (and European bodies in the eurozone) to borrow money from its central bank.

! 3

The 1946 Employment Act added employment to the Fed’s goals, so that it had to attend to multiple 2

goals – maximum employment, stable prices, and moderate long-term interest rates.

b. Operational independence

There is a substantial consensus that the implementation of monetary policy goals and decisions must also be preserved from political pressures. Monetary policy (and central banking as a whole) is a highly technical field, so that board members are appointed according to their central banking expertise. Whether central bank goals are set by Governments or by statute, the required expertise to interpret and process the available information, and implement monetary policy decisions tends to make central banks autonomous in the conduct of day-to-day business. That is why in practice the final policy decisions and their technical implementation are delegated to central bank boards and staff. Central bank independence and transparency in democratic societies

Central banks are politically independent institutions in charge of the powerful monetary ‘artefact’, the management of the legal tender monetary standard in a centralised, fractional reserve system. In fact, if not always in law, they are autonomous bodies free to move short term interest rates or change the amount of liquidity in the economy in the pursuit of their stated goal. They therefore have a substantial leverage on financial markets as well as on the decisions to hold cash by families and firms. However, central bank board decisions are not under direct control of Governments or Parliaments. In consequence, the legitimacy of these independent institutions flows from they being accountable in some way to voters, whether through Parliament or to the Government in Parliament. There are those who pragmatically believe that predictability of monetary policy decisions matters more than transparency or accountability per se. We take the view that transparency and accountability not only contribute to conducting a more effective and predictable policy but help monitor and evaluate the functioning of this public institution in a democratic society.

There is no single definition of accountability but ways different to make central banks accountable. Following Buiter’s (2008), one may distinguish among: (1) “formal accountability”, which is just the obligation to report to Parliament, since this is the democratic institution which passed the law giving it existence and powers; (2) “procedural accountability”, which implies transparency in the exercise of the central bank’s functions (publications of board minutes, of members’ votes, of the econometric model on which policy decisions are made, etc.); and finally (3) “substantive accountability”, which assigns responsibilities with rewards and penalties depending on performance of the agent. According to this analysis, therefore, a fully accountable central bank not only has to report to Parliament regularly and adopt a transparent monetary strategy but also assign tasks clearly, so that responsibilities for poor conduct of policy or significant deviations from targets can be properly attributed. In this regard, whatever the policy strategy adopted by them, most central banks have made a clear move towards more transparency and accountability in the last years (see the BoE, the Fed or the BoJ) . However, the ECB, one of the most (if not the most) politically 3

independent central banks, is notably deficient in both procedural and substantive

! 4

See a more detailed comparative analysis of the institutional elements of several central banks of 3

reference in Schwartz et al. (2009).

accountability, since it does not publish Governing Council minutes, voting records, its macro-model of reference nor truly meaningful forecasts used to make monetary policy decisions. !Political independence is not enough

As seen in the current crisis, independent central banks, even if committed to a price stability target in the long run, have proved unable to address major short run crises in financial markets and have been forced to take part in decisions that go counter their price stability goal.

The independence status given to central banks in our fractional reserve systems is institutionally unstable since they are exposed to external and internal pressures that are not easily resistible. External pressures derive from the role of central bankers as ultimate managers of the liquidity reserves of the economy. In fact, even though officially independent, central banks are viewed by politicians and the media (and even by a significant part of the academia) as powerful tools to provide relief in an economic downturn and more so in a recession. Pressure internal to their banking club comes from the role of central banks as lenders to illiquid financial institutions – even as liquidators of insolvent ones, a twin role demanded of them in the recent crisis. A liquidity crisis can be solved with traditional central banking tools. However, when money markets suffer from counterparty risk, central banks have to help insolvent banks so as to avert 4

the threat of a systemic crisis. The decision to assist a particular bank can be neither purely technical nor only based on financial criteria. The decision to rescue a failed financial institution may require the injection of new capital; as the central bank is a state-owned bank, the bail-out of a private bank requires the approval of the Government and, if the funds needed are large, the use of taxpayers money.

The recent active interventions of central banks in the financial markets reveals the contradictions associated with their legal and institutional status as off-market, apolitical, independent institutions. As Salin (2008) stresses, the fragility of central banks independence is ultimately related to its nature as a monopolistic bank and a Stated-owned institution. Following his argument, in a non-competitive monetary systems such us ours, board members decisions are not necessarily made to maintain the stability of the currency. They are in danger of taking monetary decisions led by criteria other than the soundness of money, such as public opinion approval, political interests, own policy preferences, career promotion. Central banks are not and cannot be sex-less angels. They act as lenders of extraordinary credit to banks that are short of liquidity, they accept risky private and public assets as collateral for new loans, and they even directly inject new capital to bail out insolvent banks, with the political approval of the Treasury, let us not forget. Also, they are involved in a political battle as to who regulates and supervises financial institutions. Their pivotal role in the financial markets turns central banks into true financial institution with their own financial and market interests, and not mere supervisor or external overseers and regulators. !Globalisation and the central banking paradigm

! 5

See Taylor (2009), pgs. 17-24.4

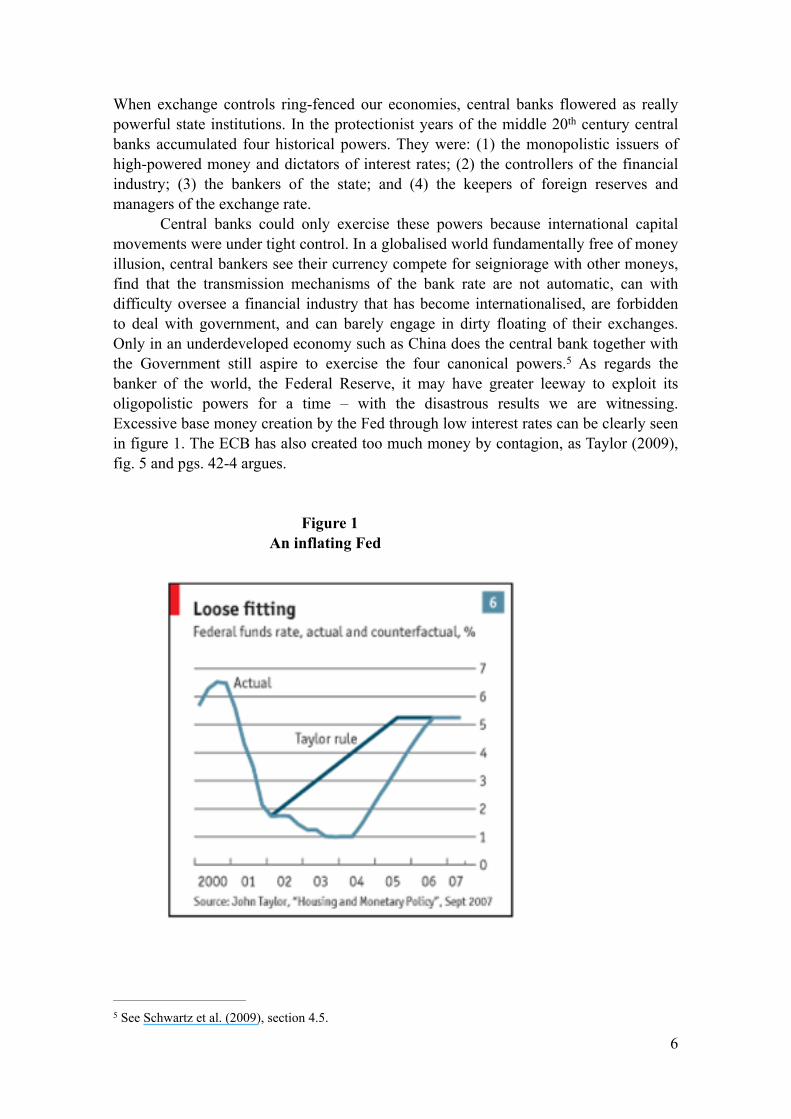

When exchange controls ring-fenced our economies, central banks flowered as really powerful state institutions. In the protectionist years of the middle 20th century central banks accumulated four historical powers. They were: (1) the monopolistic issuers of high-powered money and dictators of interest rates; (2) the controllers of the financial industry; (3) the bankers of the state; and (4) the keepers of foreign reserves and managers of the exchange rate.

Central banks could only exercise these powers because international capital movements were under tight control. In a globalised world fundamentally free of money illusion, central bankers see their currency compete for seigniorage with other moneys, find that the transmission mechanisms of the bank rate are not automatic, can with difficulty oversee a financial industry that has become internationalised, are forbidden to deal with government, and can barely engage in dirty floating of their exchanges. Only in an underdeveloped economy such as China does the central bank together with the Government still aspire to exercise the four canonical powers. As regards the 5

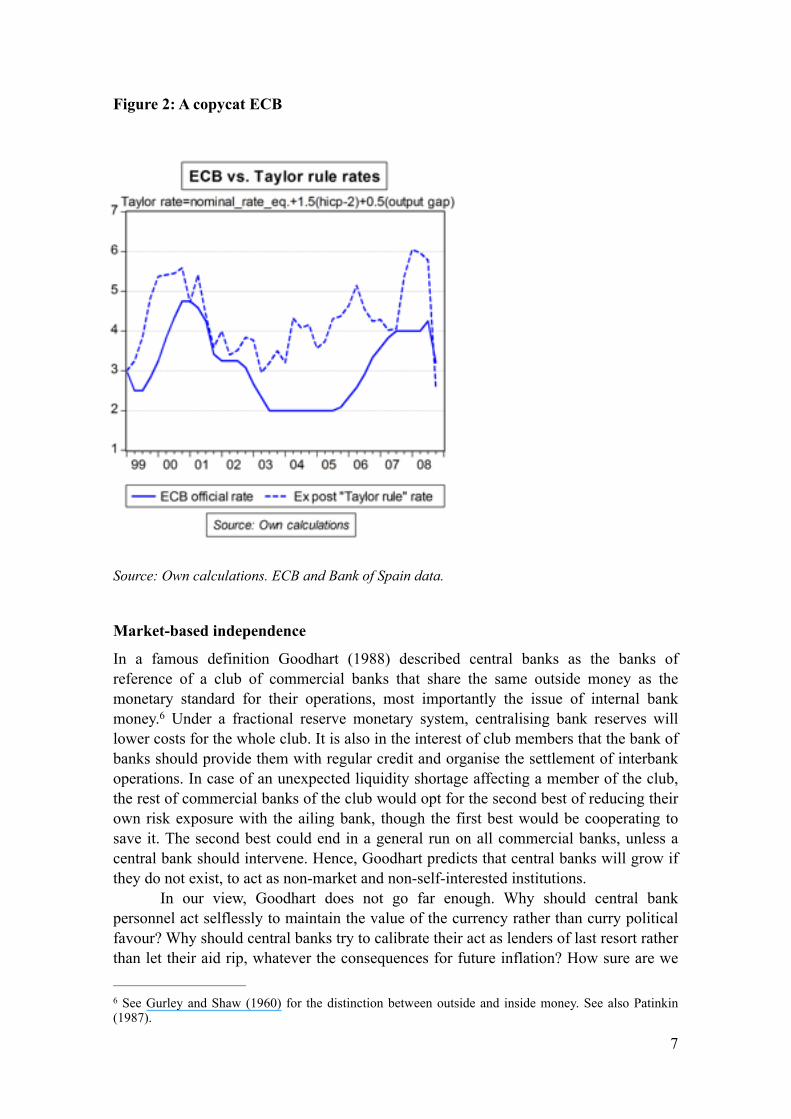

banker of the world, the Federal Reserve, it may have greater leeway to exploit its oligopolistic powers for a time – with the disastrous results we are witnessing. Excessive base money creation by the Fed through low interest rates can be clearly seen in figure 1. The ECB has also created too much money by contagion, as Taylor (2009), fig. 5 and pgs. 42-4 argues. !!

Figure 1 An inflating Fed

! Figure 2

A copycat ECB !!!!!!!!!

! 6

See Schwartz et al. (2009), section 4.5.5

Figure 2: A copycat ECB

!!!!!!!!!!!!!!!!

Source: Own calculations. ECB and Bank of Spain data.

!Market-based independence

In a famous definition Goodhart (1988) described central banks as the banks of reference of a club of commercial banks that share the same outside money as the monetary standard for their operations, most importantly the issue of internal bank money. Under a fractional reserve monetary system, centralising bank reserves will 6

lower costs for the whole club. It is also in the interest of club members that the bank of banks should provide them with regular credit and organise the settlement of interbank operations. In case of an unexpected liquidity shortage affecting a member of the club, the rest of commercial banks of the club would opt for the second best of reducing their own risk exposure with the ailing bank, though the first best would be cooperating to save it. The second best could end in a general run on all commercial banks, unless a central bank should intervene. Hence, Goodhart predicts that central banks will grow if they do not exist, to act as non-market and non-self-interested institutions.

In our view, Goodhart does not go far enough. Why should central bank personnel act selflessly to maintain the value of the currency rather than curry political favour? Why should central banks try to calibrate their act as lenders of last resort rather than let their aid rip, whatever the consequences for future inflation? How sure are we

! 7

See Gurley and Shaw (1960) for the distinction between outside and inside money. See also Patinkin 6

(1987).

that the institutions guaranteeing central bank independence and transparency will hold under duress?

The presentation of the central bank as the reference of a club to which it provides centralised financial services is a plainly valid description of our monetary systems. However, we do not agree that central banks must be seen as mere referees of market participants, as non-market regulators and overseers of the institutions under its keep. As the issuer of the monetary standard of the economy, central banks are best guided by self-interest: (a) to provide a sound and stable currency on a long term basis; (b) to assist illiquid commercial banks in order to preserve the payment system of the club and the confidence on in its currency and credit; and (c) to regulate and oversee all financial institutions affecting the credit of their club. The incentive to do so is to extend the continued use of the currency they issue and thus increase their seigniorage on a long run basis. This income can be very large, as can be seen from the sum of the seigniorage from coins and notes, and the interest income from depository banks of the ECB . 7

First, the central bank is essentially a banking institution interested in maintaining the purchasing power of its currency, because stable money will foster its demand as a sound reference of value for the issues of the commercial banks im its purlieu and, ultimately, as a reliable market means for public transactions and for storing value. As a result, the adoption of a monetary rule committed to maintaining price stability in the long term is the natural rule to run a sound monetary policy, and thus the best means to increase the central bank seigniorage in the long term . 8

Secondly, if a commercial bank is temporarily illiquid, the central bank has an interest in assisting it and avoiding a general run that could end in a dramatic fall of the demand for its money. It is in the interest of a commercially minded central bank to make its lender of last resort function compatible with its stable money goal. It is also in its interest to avoid stoking moral hazard.

Rules to run a sound monetary policy have generally been adopted by central banks either explicitly in their statutes or in the day-to-day practise of their policymaking. However, the lender of last resort function is not properly reflected in central bank statutes and, in fact, how non-market central should carry it out is still a disputed question. Since they are not currently market driven nor economically independent institutions, they are, when acting as the lender of last resort to contain systemic risk, subject to political pressures and Treasury approval. And these Government pressures can lead to badly managed lender of last resort measures with unwanted effects on the conduct of a sound monetary policy.

Once central bank managers start focusing on maximising seigniorage they will be led to propose more apt ways to oversee foreign banks operating in their monetary zone and to contain the foreign indebtedness of local banks. For example, branches of foreign banks cannot trade in New Zealand, only subsidiaries fully under local control

! 8

According to the official Annual Accounts of the ECB (2008): banknotes in circulation, 61,021 € 7

millions (54,130 in 2007), and a net interest income of 2,381 € millions. The ECB had a profit of 1,322 € millions in 2008.

See in Castañeda and Wood (2009, forthcoming) a more detailed analysis of seigniorage optimisation as 8

the central bank final end, and hence the basis for conducting a rule-based price stability rule.

and regulation. Also, a central bank intent on maximising long term seigniorage could impose a ratio of capital to liabilities for the commercial banks in its club.

2. The (market-based) role of central banks in the current crisis !

a. A de facto market institution: not a mere observer !In the last months, both the frequency and the magnitude of the interventions of

central banks in the money markets have revealed flaws of their current institutional framework. As the lender of last resort, since the summer of 2007 and more so in 2008, all major central banks have adopted extraordinary measures to confront the liquidity crisis in money markets, and to restore counterparty confidence among all financial institutions.

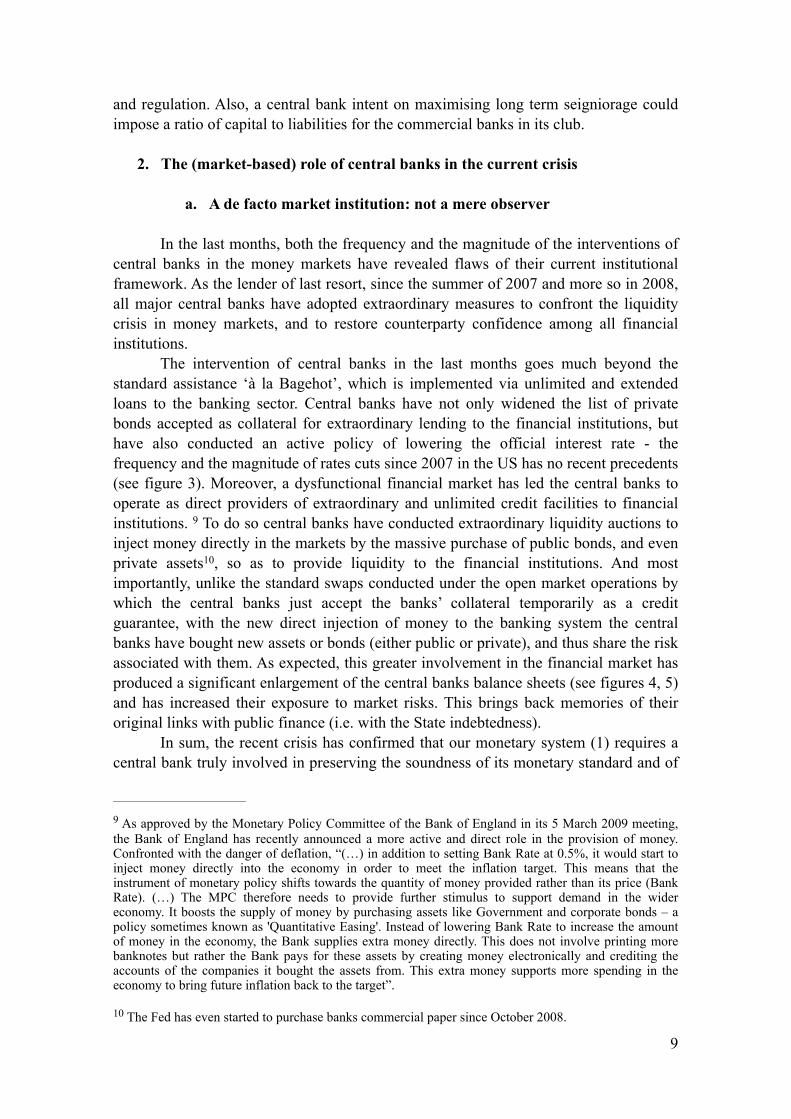

The intervention of central banks in the last months goes much beyond the standard assistance ‘à la Bagehot’, which is implemented via unlimited and extended loans to the banking sector. Central banks have not only widened the list of private bonds accepted as collateral for extraordinary lending to the financial institutions, but have also conducted an active policy of lowering the official interest rate - the frequency and the magnitude of rates cuts since 2007 in the US has no recent precedents (see figure 3). Moreover, a dysfunctional financial market has led the central banks to operate as direct providers of extraordinary and unlimited credit facilities to financial institutions. To do so central banks have conducted extraordinary liquidity auctions to 9

inject money directly in the markets by the massive purchase of public bonds, and even private assets , so as to provide liquidity to the financial institutions. And most 10

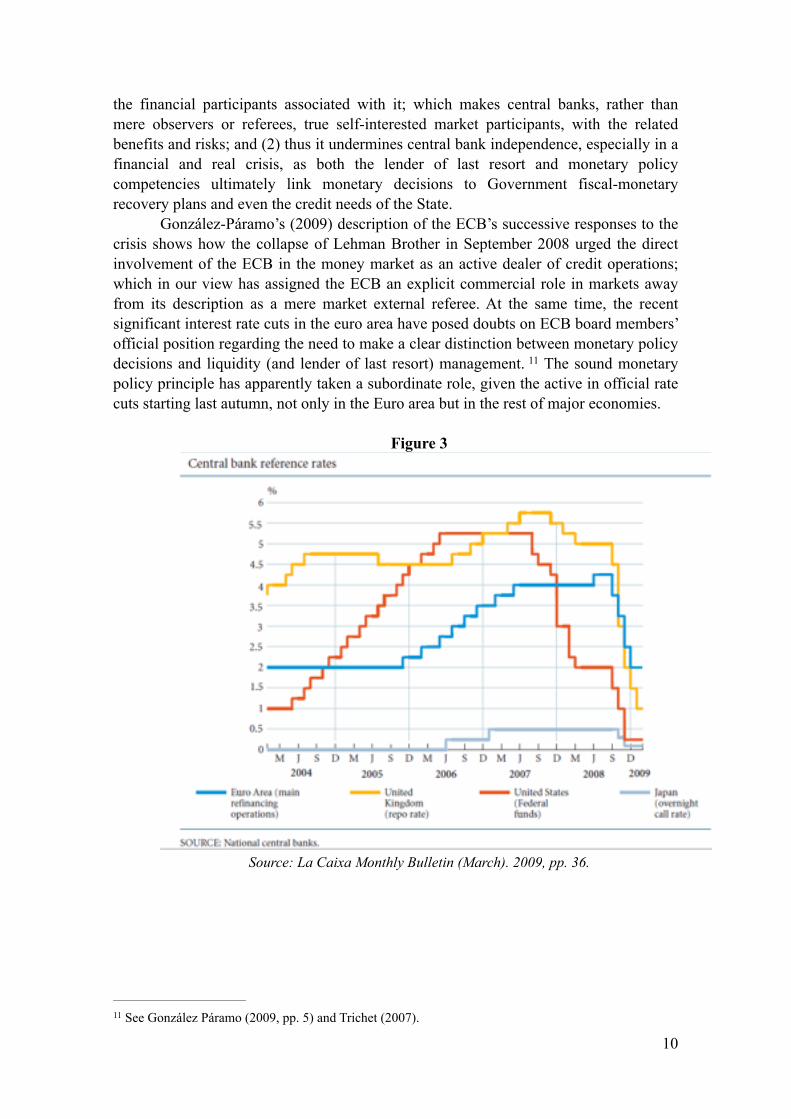

importantly, unlike the standard swaps conducted under the open market operations by which the central banks just accept the banks’ collateral temporarily as a credit guarantee, with the new direct injection of money to the banking system the central banks have bought new assets or bonds (either public or private), and thus share the risk associated with them. As expected, this greater involvement in the financial market has produced a significant enlargement of the central banks balance sheets (see figures 4, 5) and has increased their exposure to market risks. This brings back memories of their original links with public finance (i.e. with the State indebtedness).

In sum, the recent crisis has confirmed that our monetary system (1) requires a central bank truly involved in preserving the soundness of its monetary standard and of

! 9

As approved by the Monetary Policy Committee of the Bank of England in its 5 March 2009 meeting, 9

the Bank of England has recently announced a more active and direct role in the provision of money. Confronted with the danger of deflation, “(…) in addition to setting Bank Rate at 0.5%, it would start to inject money directly into the economy in order to meet the inflation target. This means that the instrument of monetary policy shifts towards the quantity of money provided rather than its price (Bank Rate). (…) The MPC therefore needs to provide further stimulus to support demand in the wider economy. It boosts the supply of money by purchasing assets like Government and corporate bonds – a policy sometimes known as 'Quantitative Easing'. Instead of lowering Bank Rate to increase the amount of money in the economy, the Bank supplies extra money directly. This does not involve printing more banknotes but rather the Bank pays for these assets by creating money electronically and crediting the accounts of the companies it bought the assets from. This extra money supports more spending in the economy to bring future inflation back to the target”.

The Fed has even started to purchase banks commercial paper since October 2008.10

the financial participants associated with it; which makes central banks, rather than mere observers or referees, true self-interested market participants, with the related benefits and risks; and (2) thus it undermines central bank independence, especially in a financial and real crisis, as both the lender of last resort and monetary policy competencies ultimately link monetary decisions to Government fiscal-monetary recovery plans and even the credit needs of the State.

González-Páramo’s (2009) description of the ECB’s successive responses to the crisis shows how the collapse of Lehman Brother in September 2008 urged the direct involvement of the ECB in the money market as an active dealer of credit operations; which in our view has assigned the ECB an explicit commercial role in markets away from its description as a mere market external referee. At the same time, the recent significant interest rate cuts in the euro area have posed doubts on ECB board members’ official position regarding the need to make a clear distinction between monetary policy decisions and liquidity (and lender of last resort) management. The sound monetary 11

policy principle has apparently taken a subordinate role, given the active in official rate cuts starting last autumn, not only in the Euro area but in the rest of major economies. !

Figure 3

! Source: La Caixa Monthly Bulletin (March). 2009, pp. 36. !!!!!

! 10

See González Páramo (2009, pp. 5) and Trichet (2007). 11

Figure 4

! Source: La Caixa Monthly Bulletin (January). 2009, pp. 35. !!!!

Figure 5 !

! Source: Own calculations. Bank of England data. !As compared to an ex post conventional Taylor rule (see figure 2), since 2003

the registered interest rates in the Euro area have been systematically below those

Bank of England balance sheet

50000

100000

150000

200000

250000

300000

03 Ja

n 07

14-fe

b-07

28-m

ar-07

09-m

ay-0

7

20-ju

n-07

01 A

ug 07

12-se

p-07

24-oc

t-07

05 D

ec 07

16 Ja

n 08

27-fe

b-08

09 A

pr 08

21-m

ay-0

8

02-ju

l-08

13 A

ug 08

24-se

p-08

05-no

v-08

17 D

ec 08

28 Ja

n 09

11-m

ar-09

Total assets

! 11

compatible with price stability in the long term. A similar conclusion arises when we compare the rates that would have resulted if a Taylor rule had been applied, with those of the Fed in the last decade (see Taylor, 2009), which reveal the credit policy in the last years as too easy. Since the autumn 2008, it seems as if the ECB, following the lead of the rest of major central banks, was using the official interest rates both as a macro-policy tool and as a means to provide extraordinary liquidity to the banking system. As a result, the easing of monetary policy in the last months seems to be explained by political and external pressures on central banks board members, and not necessarily by the need to preserve the long term value of the currency. The Bank of England’s use of official interest rates not only as the main instrument to conduct monetary policy but also as a way to provide extraordinary liquidity to the market is also patent (see footnote 9). !!

3. Conclusions !The institutional arrangements of our monetary systems are truly exceptional in market based economies such us ours. The money base is fully under the legal monopoly of a State-owned central banks, and the total amount of means of payments are supplied by the central bank together with a limited set of banking institutions – in the aggregate an oligopolistic market of banks of issue. Given the legal tender character of the central bank currency, the central bank is the institution ultimately responsible for maintaining the liquidity of the economy, and thus it is in charge of a crucial element in the proper and smooth functioning of the economy. In order to avoid discretionary, politically-driven and myopic policies, central banks, in the last two decades, have gained operational and even even goal- independence in the conduct of their tasks. However, the singularity of our monetary systems makes the current institutional setting of central banks fragile, as political interference arises periodically. This political pressure, and even the direct involvement of Government in monetary competencies, is even more explicit in the event of a major crisis. !

Why should central banks not be owned by the commercial banks and other financial institutions interested in a sound financial environment? Such is the arrangement for the Deposit Insurance Institution in Spain, where it is owned by the member banks. One need not go as far as a drastic reform of the monetary system along the lines of Hayek’s (1976) seminal proposal for competing private moneys and private banks of issue. Even under our apparently non-competitive monetary system, the progressive application of market principles to the tasks of the central banks and their institutional status could help produce a sound non-politically distorted currency. !

Central banks are banks and their tasks and ordinary operations are fully financial. The provision of the monetary standard of the economy and the regular or extraordinary provision of credit should be managed commercially. The current crisis has made it evident that it is in the interest of central banks to be significantly involved in the financial market. They should carry out their tasks led by sound financial criteria: in essence, making their currencies attractive by maintaining their purchasing power

! 12

and extending their use as a reserve for financial institutions and a reliable means for ordinary transactions. This would increase the demand of central bank currency and thus its seigniorage. The current crisis has revealed the need for the financial independence of central banks: increasing their seignoriage will contribute to their financial autonomy and independence. !

Regarding goal independence, rather than thinking in terms of politically given tasks within a non competitive money market, a move towards a self-interest central bank in competition with other issuers is the best market safeguard for running a sound monetary policy. As Hayek (1976, pp. 100) put it: !

In a world governed by the pressure of organised interests, the important truth to keep in mind is that we cannot count on intelligence or understanding but only on sheer self-interest to give us the institutions we need. Blessed indeed will be the day when it will no longer be from the benevolence of the government that we expect good money but from the regard of the banks of their own interest. !

The introduction of competition in base money does not necessarily lead to the abolition of central banks. In line with King’s (1999) debate on the future of, and 12

challenges for, central banks, there could be room for private companies to compete with the current central banks in the provision of a sound currency as well as credit and settlement facilities. Within this market framework, operational and goal independence would become necessary conditions for the functioning of all central banks committed to providing a sound monetary standard to the economy. Moreover, when fully political independent, a self interested central bank will be accountable not only to Parliament but above all to market participants and the ultimate holders of its currency; which will be more effective external controls to run a stable currency in the medium to the long term. In addition, as a State-owned company, the profit resulting form the sound management of the currency will increase the Bank’s reserves as well as the State revenues. This institutional framework generates the incentives to preserve the new commercial status of the central bank, as it increases its financial autonomy - needed to conduct a market based and politically independent monetary standard- and the government also benefits from it. !

Within this new market-based framework, the legal tender clause should be abolished to foster competition so the financial services of the official central bank would compete with those of other central banks, public and private. Accordingly, an independent (market-based) central bank will have interest in choosing the best rule to achieve its target; and the adoption of the current inflation stability rules by most central banks responds to that principle. In this way, price stability is the shortcut to achieve sustainable seigniorage in the long term.

! 13

“There is no reason, in principle, why final settlements could not be carried out by the private sector 12

without the need for clearing through the central bank. The practical implementation of such a system would require much greater computing power than is at present available. But there is no conceptual obstacle to the idea that two individuals engaged in a transaction could settle by a transfer of wealth from one electronic account to another in real time. (…). A regulatory body to monitor such systems would be required. Existing regulators, including central banks, would, no doubt, compete for that responsibility.” (pp. 48-49).

! !!References: !Bagehot, W. (1873): Lombard Street. A Description of the Money Market. !Buiter, W. (2008): “Round table discussion: monetary policy in the new international environment”. In Touffut, J-P: Central Banks as Economic Institutions. Edward Elgar. Castañeda, J. and Wood, G. (2009) !Castañeda, J. and Wood, G. (2009): Really stable monetary policy? IEA Hobart Papers. London (forthcoming). !González-Páramo, J. M. (2009): “Financial market failures and public policies. A central banker’s perspective on the global financial crisis”. Speech at the XVI Meeting Public Economics. Granada, 6 February 2009. Available at the Ecentral bank website: http://www.ecb.int/press/key/date/2009/html/sp090206.en.html !Goodhart, C. (1988): The Evolution of Central Banks. The MIT Press. !Gurley, J.G and Shaw, E.S. (1960): Money in a Theory of Finance. Brookings Institution. !Hayek, F. (1976): Denationalisation of Money. Hobart Special Paper 70. IEA. London. !King, M. (1999): “Challenges for Monetary Policy: New and Old”. Symposium on New Challenges for Monetary Policy, Federal Reserve Bank of Kansas City at Jackson Hole, Wyoming, 27 August. Available at the Bank of England website: http://www.bankofengland.co.uk/publications/speeches/1999/speech51.pdf !Mill, J.S. (1857): “The Bank Acts”, in Essays on Economics and Society, vol. II, Collected Works of John Stuart Mill, vol. 5. University of Toronto Press. !Patinkin, D. (1987): “Real Balances”, in The New Palgrave Dictionary of Economics, vol. IV, pgs. 98-101. !Ricardo, D (1817): Principles of Political Economy and Taxation. Cambridge University Press for the Royal Economic Society, 1962. !Salin, P. (2008): Liberalismo. Unión Editorial. Madrid. !Schwartz, P., Castañeda, J., Mayes, D., Sibert, A. and Wood, G. (2009): “Comparison of monetary policy strategies of major central banks”. Report for ECON (European Par l iament) . Avai lable a t the European Par l iament websi te : h t tp : / /

! 14

www.europa r l . eu ropa . eu / ac t i v i t i e s / commi t t ee s / s tud i e s /download .do?language=en&file=25351 !Taylor, J. (2007): “Housing and Monetary Policy”, in Federal Reserve Bank of Kansas City, Housing, Housing Finance, and Monetary Policy. [Research completed before the August flare up of August 2007, says Taylor in (2009), pg. 77. !Taylor, J. (2009): Getting off Track. How Government Actions and Interventions Caused, Prolonged, and Worsened the Financial Crisis. Hoover Institution Press. Stanford. !Trichet, J. C. (2007): “Hearing at the Economic and Monetary Affairs Committee of the European Parliament”. Brussels, 19th December 2007. Available at the European Central Bank website: http://www.ecb.int/press/key/date/2007/html/sp071219.en.html !------------------------------------------------------- !!Pedro Schwartz, Professor Extraordinary at the Faculty of Economics, Universidad San Pablo CEU in Madrid. !Juan Castañeda, Lecturer in Applied Economics at the Universidad Nacional de Educación a Distancia (UNED) in Madrid.

! 15