Embed Size (px)

Citation preview

2

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

NATIONAL UNIVERSITY OF SCIENCE & TECHNOLOGY

DEPARTMENT OF FINANCE

CORPORATE FINANCE I

(CFI2101)

2014/2015 ACADEMIC YEAR

3

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

COURSE OUTLINE COURSE OBJECTIVE This course is designed to introduce students studying for a Bachelor of Commerce (Honors)

Degree, to the corporate finance process of assembling financial resources and utilizing them in

order to add value to shareholders-the ultimate risk bearers. This is meant to be an introductory

course to Corporate Finance II.

TOPIC

CONTENT SECTION OBJECTIVES

Overview of Corporate finance

Introduction Role of the Financial Manager- Corporate structure Goals/objectives of the firm The theory of the firm: Managerial behavior, agency problem and agency costs

By the end of this topic, students should be able to: Appreciate the role of financial managers in a firm Understand the ultimate goal of a firm Understand the objective of profit maximization vs. shareholder value maximization. Identify possible sources of conflict between managers and shareholders Appreciate the different ways of reconciling the differences between owners and agents

The financial markets framework

Financial intermediaries-classification Financial Markets- Classification, role of each market Financial institutions, Instruments and their classification Secondary markets- listing, dual listing and delisting Global financial markets

By the end of the topic, students should be able to: Classify financial intermediaries, financial institutions and financial markets. Identify the instruments traded in each market Understand the role and functions of a secondary market. Underscore the need for technological advancement in global financial markets

Introduction to Financial Mathematics

Time value of money • Computations of Future Value and Present value • Annuities • Perpetuities

By the end of this topic, students are expected to: Have a thorough grasp of the time value of money concept.

4

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

• Compounding periods • Effective annual interest rates

Have an appreciation of computations of Future value and Present value of different cash flow streams

Valuation of equity and debt securities

Discount Cash-flow(DCF) valuation model Bond fundamentals and bond valuation Valuation of common stock Valuation of preferred stock

By the end of the topic, students are expected to: Appreciate value of assets as PV of expected future cash flows Appreciate the discount rates used in each model. Able to determine the expected future cash flows Appreciate r/ship between the price of asset and other input fin variables.

Capital Budgeting

The capital budgeting process, Basic principles of capital budgeting Project classification and identification of relevant cash flows Independent versus mutually exclusive projects, Capital budgeting techniques: net present value (NPV), internal rate of return (IRR), payback period (PBP), discounted payback (DPBP). NPV profile, comparison of NPV and IRR methods when evaluating independent and mutually exclusive projects,

By the end of this topic, students should be able to: Appreciate the concept of limited financial resources Understand the difference between independent projects and mutually exclusive projects Appreciate the steps in the capital budgeting making process Familiarize with the different capital budgeting tools and their application in aiding decision making. Appreciate the Pros and Cons associated with each tool Calculate the relevant cash flows associated with a particular cash flow

Risk and Return

Types of risk Measures of risk (measuring stand alone risk)-probability, expected return, standard deviation, variance Risk aversion Relationship between risk and return

By the end of this topic, students should be able to: Define the risk types Explain the measures of risk Calculate risk, standard deviation Explain the relationships between risk and return

Portfolio Theory and CAPM Risk in Portfolio context Portfolio risk & Return-

After completion of this topic, the

5

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

(two asset portfolio) Diversification : riskdiversifiable vs. nondiversifiable risk. Efficient portfolio-efficient frontier and optimal portfolio Assumptions of CAPM Concept of Beta calculating beta coefficient( regression) Capital Market Line(CML) Security Market line (SML)

students must be able to: Define portfolio theory understand how to calculate expected returns, variance and standard deviation of the two-asset portfolio Explain portfolio frontier By the end of this topic, students should be able to: Use CAPM to calculate the required return for proposed investment

Capital Structure Theories

Calculations on cost of capital Theories of capital structure Dividend policies

After studying this topic students should be able to calculate all components making the costs of capital; explain the theories of capital structure and dividend policies.

Leveraging

Break-even analysis Degree of Operating leverage and Business Risk EBIT-EPS analysis Degree Of Financial Leverage and Financial Risk Degree of Total Leverage and Total firm risk

After studying this topic, students should be able to: Define leverage Understand the degree of financial and operating leverage Establish EBIT-EPS relationships Explain the degree of total leverage

Assessment TWO Assignments 1st assignment Due Date : 26 September 2014 2nd assignment Due Date : 15 October 2014 READING LIST 1. Richard Brealey et al - Principles of Corporate Finance, McGraw Hill, latest edition 2. Richard Pike, & Bill Neile- Corporate Finance & Investment, latest edition 3. Lawrence J Gitman, Principles of Managerial Finance, Harper Collins, latest edition 4. Weston Fred J & Copeland, Thomas- Managerial Finance, latest edition,Dryden Press International 5. James C Van Horne- Financial Management and Policy, Prentice Hall, latest edition

6

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Chapter1: OVERVIEW OF CORPORATE FINANCE

This topic identifies the ultimate goal of a firm, different roles a financial manager plays in a firm,

pointing out the possible sources of conflict between managers and shareholders with a view of

reconciling the differences so as to ensure overall organizational success.

1.1 Corporate finance: definition

Corporate finance is a key function of all business firms that deal with long-term and short-

term financial decisions taken by firms to maximize their value and minimize their risk. It is

concerned with areas like financial forecasting, financial planning and budgeting,

procurement of funds (capital structure decisions), investment analysis (capital budgeting

decisions), optimal utilization of funds, credit management, cash management and

inventory management.

In short, corporate finance is all about decisions that are made by corporations and their effect on

value creation. Corporations are identified by 3 distinct characteristics;

� They are legal entities

� They have limited liability

� There is separation of ownership and control

1.1.1 Types of corporations

1. Public companies

2. Private companies

3. Limited liability companies e,g partnerships, professional firms etc

Corporate finance has 3 main areas of concern

� Capital budgeting; What long term investments should the firm undertake?

� Capital structure: what debt to equity mix is required to finance operations? Where will the

firm get the long term financing to pay for its investments?

� Working capital management: how should the firm manage its everyday financial activities?

7

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

1.2 The objective of the firm

The main objective of a firm is to maximize shareholder value by increasing the value of the

company’s stock.

Other objectives the firm may pursue are;

Survival

Maximizing market share

Maximizing profits

Employee safety

Ethical and environmental concerns

Social responsibility

Class discussion: profit maximisation vis-a-vi shareholder value maximization

1.3 Role of financial managers

In any corporation the finance manager is responsible for 2 basic decisions;

� Financing decisions

� Investment decisions

The finance manager manages the existing assets of the firm and invests in new assets. The job of

the finance manager is to procure funds to carry out business activities, grow the business, make

long-term investments, and judicially disburse and utilize the funds. He/she takes investment

decisions to buy real assets. Real assets produce real cash flows that increase the value of the

existing shareholders. The enhanced value of the firm retains existing investors and attracts

potential investors.

A finance manager also carries out treasury operations, which deal with effective management of

the surplus cash. The surplus cash is invested in the money market and in other liquid capital

market instruments. The treasury management deals with operations in the forex market, tax

planning, maintenance of the share price, and so on.

The role of a finance manager has moved beyond traditional accounting functions like

preparing accounting and financial statements, collecting revenues and disbursing

expenses. Today, organizations have become large and more complex. Financial

management now involves a broader horizon where value maximization has gained prime

importance .The new-millennium finance manager is concerned with all the business

8

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

activities that involve funds, directly or indirectly. He/she does not restrict himself/herself

to specific activities. Some of the duties the finance manager is supposed to perform are as

follows:

1.3.1 Forecasting and planning

A finance manager has to forecast and predict the short- and long-term requirement of

money by the business and also forecast the activity levels of the various business

operations so that it preplans what to manufacture and deliver at what price to the

customers. The finance manager has to take these decisions in the light of both the external

and internal factors that affect the business activities.

1.3.2 Analysing and evaluating the investment activities

A finance manager needs to understand and evaluate the various activities of the business,

especially the long-term investment activities. He/she needs to understand the costs and

benefits associated with the long-term investments, i.e., their feasibility. As a rule, firms go

for those long-term investment activities which generate positive value for the firm and the

rest are rejected.

1.3.3 Coordination and control

A finance manager focuses on the generation of the funds and their allocation to various

organizational activities. The various organizational activities are to be coordinated and

controlled to ensure cost effectiveness and maximum efficiency in terms of value

generation.

1.3.4 Understanding the finance market

The growth and activeness of the capital market ensures that the finance managers can

gain immensely from the capital market knowledge. The finance managers have to decide

the mode of short-term investments in the money market, and the liquid investments and

the long-term investments in the stock market. These investments have to be liquid as well

as profitable so that they add value to the firm's invested amount.

1.3.5 Risk management

A very important function of a finance manager is to understand risk management of the

business. He/she needs to evaluate the risks the business faces. The various risks faced by

the firm are to be managed proactively and necessary arrangements should be made to

eliminate, reduce and avoid them. He/she also needs to analyse and categorize the various

risks faced by the business.

9

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

1.3.6 Performance measurement

In the end, a finance manager is supposed to evaluate the performance of his/her firm. The

financial performance of the firm is appraised holistically, activity wise and department

wise. These performance appraisals are evaluated with the set targets to determine

positive and negative deviations, if any.

1.4 The Agency Problem and Control of the Corporation

A financial manager acts in the best interests of the stockholders by taking actions that

increase stock value. However, in large corporations ownership can be spread over a huge

number of stockholders. This dispersion of ownership arguably means that management

effectively controls the firm. In this case, will management necessarily act in the best

interests of the stockholders? Put another way, might not management pursue its own

goals at the stockholders’expense?

1.4.1 Agency Relationships

The relationship between stockholders and management is called an agency relationship.

An agency relationship exists whenever someone (the principal) hires another (the agent)

to represent his or her interests. Hence the relationship between stockholders and

management and that of management and creditors is called an agency relationship. In all

such relationships there is a possibility of a conflict of interest between the principal and

the agent. Such a conflict is called an agency problem.

Sources of shareholder value drivers

� Revenue enhancement

� Operating costs reduction

� Cost of capital reduction

� Asset utilization

Goals of management may include

� Management of salaries (compensation)

� Protection of their employment (job security)

� Maximizing profits

� Empire building

10

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Managing the agency problem

Strategic financial management should therefore ensure that the agency problem is

managed to reasonable levels so that shareholder value is enhanced.

The divergence of management and shareholder objectives can be managed through;

Market forces

Agency costs

Organizational structuring

Questions

1. Evaluate the following statement “Managers should not focus on the current stock

value as doing so will lead to an overemphasis on short term profits at the expense

of long term profits”.

2. Suppose you were the financial manager of a non-profit making organization, what

kinds of goals would be appropriate?

3. Suppose you own stock in a company. The current price per share is $25. Another

company has just announced that it wants to buy your car and will pay $35 per

share to acquire all the outstanding stock. Your company’s management

immediately begins fighting off this hostile bid. Is management acting in the

shareholder’s best interest? Justify your answer.

4. Why is the goal of financial management to maximize current share price rather

than future share price?

5. The emergence of strong financial markets has changed the face of how businesses

and capital are to be managed. In line with this statement, explain how the duties of

a finance manager has been affected.

11

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Chapter2: The Financial Markets Framework

This topic looks at how the financial intermediaries and financial markets are structured and

classified, as well as the instruments traded in these markets. It concludes by analyzing the global

financial markets.

Financial Intermediaries

Financial intermediaries make up the main conduit through which surplus units lend to the deficit

units or vis-a-vi (the conduit through which deficit units borrow from surplus units).

Financial intermediaries are institutions who are always prepared to play the role of a deficit unit

towards a particular surplus unit and a surplus unit towards a particular deficit unit at the same

time. This way the pitfalls of direct financing are eliminated.

In executing their role, financial intermediaries create financial securities or instruments which are

basically pieces of paper serving as acknowledgement of the act of either having borrowed or

loaned and also agreeing to abide by the terms of the transaction. While the financial intermediary

borrows from the surplus unit, it is not the primary or the ultimate user of the funds, hence it issues

a primary security to the deficit unit (which is the primary borrower) to reflect the essence of the

whole transaction and flow of funds.

Classification of financial instruments issued by financial intermediaries.

1 Primary securities (issued by ultimate borrowers)

a)Representing the obligations of the private sector

i.Bankers acceptances

ii.Trade Bills

iii.Promissory Notes

iv.Company Debentures

v.Securitized Mortgages

12

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

b)Representing the obligations of the public sector

i.Treasury Bills

ii.Government Stocks

c)Representing the obligations of the quasi-public sector

i.Municipal Bonds

ii.Parastatal Stocks

iii.Prescribed Asset Bills

2.Indirect Securities (issued by financial intermediaries)

a)Representing the obligations of private banks

i.Negotiable certificates of deposit

b)Representing the obligations of public and semi public banks

i.Treasury Bills, Notes and Bonds

ii.Development Banks paper

3.Repurchase agreements

Functions of financial intermediaries

� Diversification of risk

� Pooling of small quantities of surplus funds into a bigger fund

� Bringing into the financial system savings that would otherwise have not been brought into

the formal system.

� Enabling deficit units to spend beyond their current income

� Efficient allocation of funds.

Classification of financial intermediaries

13

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

They are divided into two broad catagories; deposit taking and non deposit taking

intermediaries.further subcategories are also attached to each broad category as shown below

1.Deposit taking intermediaries

a)Banking intermediaries

i.The central bank

ii.Infrastructural development banks

iii.Commercial banks

iv.Discount houses

b)Non banking intermediaries

i.Building societies

ii.Savings banks (POSB)

2.Non deposit taking intermediaries

a)Contractual intermediaries

i.Insurance and life assurance companies

ii.Pension and provident fund companies

iii.National Investment trusts

b)Portfolio institutions

i.Unit trusts

ii.Investment trusts

c)Other financial intermediaries

i.Finance companies

ii,Trusts

14

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

2.1 Financial Markets

Financial markets is the umbrella term for all the economic units i.e surplus and deficit units, financial

institutions and financial instruments, which all interact for the benefit of the participants involved in

the economy.

These basically consist of the following:

a. Money markets

It is the market for short term securities. These provide short term debt funding and

investment opportunities through the issuing of instruments or claims whose tenure is less

than one year. Money markets are split into primary and secondary markets. The primary

market are markets in which securities are created and issued for the first time whilst the

secondary market is where previously issued securities are bought and sold among

investors.

b. Capital markets

These provide long term funding (debt and equity) and investment opportunities through

the issuing and trading of instruments or claims whose tenure is more than a year. They can

also be divided into primary and secondary markets. Capital markets can also be sub-

divided into stock markets and bond markets.

• Stock markets are those markets epitomized by the stock exchange (secondary market

shares), provide funding through the issuing in the primary markets, of ownership claims or

securities called common stock or shares.

• Bond markets provide long term debt funding through issuing (in the primary market) and

trading in the secondary market of bonds, debentures and notes.

c. Commodities markets

These facilitates the trading of commodities like agricultural products and minerals.

d. Foreign exchange markets

15

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

These facilitate international trade and access to services from countries by providing a

platform through which economic agents in one country can transform purchasing power

from their currency to another currency.

e. Derivative markets

These offer hedging and portfolio insurance services by providing instruments that can be

used to manage financial or price risk.

f. Insurance markets

These provide a platform for the redistribution of various kinds of risk.

2.1.2 Secondary markets

These are markets in which securities are traded. There are two main markets:

� Organized exchanges

� Over the counter exchanges

2.1.2.1Organized exchanges

Stock markets operate as auction markets as buyers and sellers are matched. Examples of stock

exchanges:

Zimbabwe Stock exchange

New York stock exchange

London stock exchange

Zambia stock exchange

2.1.2.2 Over the counter markets

It is an interchangeable organization that is used to describe any buying or selling activities in

securities that does not take place on an exchange.

It is also called a dealer market in that business is conducted across borders by brokers and dealers

via communication lines such as internet, telephone etc

16

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

2.1.3 Importance of secondary markets

� They provide an indication of the value of a company.

� Secondary markets provide liquidity by enabling investors to sell their shares.

� It provides a forum for exchange hence reducing search costs.

2.2 Listing on the stock exchange

An exchange does not deal in securities of all companies. It has to select the companies whose

shares can be allowed to be bought and sold by setting strict standards and entry requirements for

listing.

2.2.1Reasons for listing

� It increases liquidity.

� It facilitates the raising of new cash.

� It enables founders to diversify their portfolios.

� To establish value of the company.

� Prestigious reasons.

2.2.1.2 Disadvantages of listing

� Costs of reporting

� Disclosure requirements

� Self dealings

� Inactive low markets

� Control

2.2.2 Dual listing

Dual listing is whereby a company is listed on more than one stock exchange.

17

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Generally such a company’s primary listing is on a stock exchange in its country of incorporation

and its secondary listing is on an exchange in another country.

Examples of Companies in Dual listing

Old Mutual- which has the primary listing in London Stock Exchange, a secondary listing on

Johannesburg Stock exchange and Zimbabwe Stock exchange.

PPC- has primary listing on the Johannesburg Stock exchange and a secondary listing on Zimbabwe

Stock exchange.

Hwange Colliery- which has primary listing on the Zimbabwe Stock exchange and a secondary

listing on Luxembourg Stock exchange.

2.2.2.1Reasons for dual listing

� Improved accessibility to funds- the stock exchange provides companies with the facility to

raise cash.

� To gain access to a larger investor base.

� Improved visibility and access.

2.2.2.2 Disadvantages of dual listing

� The company has to comply with the listing requirements of both markets.

� Costs of reporting.

� Accessibility of information- need to ensure that the same information is availed to both

markets.

2.2.3 Delisting

It is the process of making a public company private. It can be voluntary or it can be caused by the

company falling short of listing requirements.

18

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

2.2.3.1 Reasons for delisting

� Undervalued shares e g Interfresh

� Financial flexibility

� Mergers and Acquisitions-

� Financial problems of entities/ viability problems

� Control issues

� Fear of takeover

2.3 Money market instruments

Money market instruments can be classified into two categories ; interest bearing and zero coupon

(discount) instruments.

Interest bearing instruments

1. Certificates of deposit

Discount securities

1. Treasury bills

2. Bankers Acceptances

3. Commercial paper

4. Trade bills

Student to research on these.

Global financial markets

This is the linkage of national financial market segments (commodities markets, foreign exchange

markets, derivative markets etc)to form various international market segments whose integration

results in a universal or global financial market.

19

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Factors leading to the globalization of financial markets

Deregulation

� Deregulation

� Technological advancement

Class discussion

How has deregulation and technological advancements assisted in the globalization of financial

markets.

20

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Chapter 3:

Introduction to Financial Mathematics

Topic Objectives

Have a thorough grasp of the time value of money concept.

Have an appreciation of computations of Future value, Present value, ordinary

annuity and annuity dues.

3.0 The primary objective of financial management is to maximize the value of the firm’s

stock. Stock values depend in part on the timing of the cash flows investors expect to

receive from an investment—a dollar expected soon is worth more than a dollar expected

in the distant future. Therefore, it is essential for financial managers to have a clear

understanding of the time value of money and its impact on stock prices.

The principles of time value analysis (also called discounted cash flow (DCF) analysis) have

many applications in corporate finance eg

Valuation of long term securities

Valuation of assets

Capital budgeting

Lease or buy decisions etc

3.1 Time Value of Money

Most of the principles of financial decision making are based on a simple concept: that of

time preferences. All things equal one would prefer to receive a sum of money now rather

than the same amount sometime in the future. Offered a simple choice between USD1,000

now and USD1,000 in a year’s time: the choice is clear. One would take the money now. For

21

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

parting with cash or money for some time, an investor would expect to be rewarded in the

form of interest. Interest calculations are straight forward and they form one of the basic

building blocks of financial mathematics.

3.2 Definition of terms

• Time Lines – is a diagrammatic representation of cash-flows which is used by

analysts to help visualize what is happening in a particular problem and then to help

set up the problem for solution.

• Present Value is the current worth of a future sum of money or stream of cash

flows given a specified rate of return. Future cash flows are discounted at the given

interest rate, and the higher the discount rate, the lower the present value of the

future cash flows. Determining the appropriate discount rate is the key to properly

valuing future cash flows, whether they be earnings or obligations.

• Future Value is the value of an asset or cash at a specified date in the future that is

equivalent in value to a specified sum today. A dollar in hand today is worth more

than a dollar to be received in the future because, if you had it now, you could invest

it, earn interest, and end up with more than one dollar in the future. The process of

going from today’s values, or present values (PVs), to future values (FVs) is called

compounding.

• Annuity - An annuity is a series of equal payments or receipts that occur at evenly

spaced intervals. Leases and rental payments are examples. The payments or

receipts occur at the end of each period for an ordinary annuity while they occur at

the beginning of each period for an annuity due.

• Perpetuity - is an infinite and constant stream of identical cash flows.

22

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Smple interest

Interest is the price paid for the use of borrowed money. Interest is paid by the party who

uses or borrows the money to the party who lends them the money. For example: if a

company borrows $1,000 from the bank at an interest of 10% per year/annum, simple

interest payable on the amount borrowed can be expressed as;

Simple interest =12% of $1,000

12/100 X $1,000

$120

Therefore future value of the borrowed funds at the end of 1 year will be:

�� = ��������1 + �� �� = ���1 + ��

= $1000�1 + 0.12�

= 1120

Compound interest

If interest is charged on the outstanding amount more than once in a year, then interest is

said to be compounded. In such a case, then the future value is:

�� = ���1 + ���

�ℎ���

i is the interest rate per compounding period = ��

n is the number of compounding periods in the investment period=t*m

Continuous compounding

Continuous Compounding is a situation in which interest is added continuously rather than

at discrete points in time. As such, continuous compounding produces higher future value

than periodic compounding with any frequency m, given the same initial principal P and

interest rate r.

23

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

�� = ��� ∗ !"

Present value of an annuity

Suppose you were offered the following alternatives: (1) a three-year annuity with

payments of $100 or (2) a lump sum payment today. Suppose you have no need for the

money during the next three years, so if you accept the annuity, you would deposit the

payments in a bank account that pays 5 percent interest per year. Similarly, the lump sum

payment would be deposited into a bank account. How large must the lump sum payment

today be to make it equivalent to the annuity?

ORDINARY ANNUITIES

If the payments come at the end of each year, then the annuity is an ordinary annuity with a

present value equal to $272.32 as shown below:

Another way of calculating will be to use the formula:

��# = �$%[1 − �1 + ��(�]�

PMT is the amount that comes in at the end of each compounding period

i is the interest rate per compounding period

n is the number of compounding periods in the investment period

Calculate the present value if the stream of cash-flows had been an annuity due.

�� = �$%[1 − �1 + ��(�]�

24

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

COMPARISON OF DIFFERENT TYPES OF INTEREST RATES

Finance deals with three types of interest rates: nominal rates, iNom; periodic rates, iPER; and

effective annual rates, EAR or EFF%. Therefore, it is essential that you understand what

each one is and when it should be used.

Nominal, or quoted, rate. This is the rate that is quoted by banks, brokers, and other

financial institutions, also called the Annual Percentage Rate (APR). However, to be

meaningful, the quoted nominal rate must also include the number of compounding

periods per year. For example, a bank might offer 6 percent, compounded quarterly, on

CDs, or a mutual fund might offer 5 percent, compounded monthly, on its money market

account. Nominal rates can be compared with one another, but only if the instruments being

compared use the same number of compounding periods per year.

2. Periodic rate, iPER. This is the rate charged by a lender or paid by a borrower each

period. It can be a rate per year, per six-month period, per quarter, per month, per day, or

per any other time interval.

i+,- = r/01m

Here iNom is the nominal annual rate and m is the number of compounding periods per

year.

The periodic rate is the rate that is generally shown on time lines and used in calculations.

3. Effective annual rates

If we are comparing the costs of loans that require payments more than once a year, or the

rates of return on investments that pay interest more frequently, then the comparisons

should be based on equivalent (or effective) rates of return. This concept of effective

annual rate or equivalence of nominal rates implies that accumulating or present-valuing

payments using equivalent rates produces the same answer. If rm is on an mthly nominal

basis, and rn is on an nthly nominal basis, in order for the present value of F payable at time

N years to be the same with either rate requires

��1 + �3� �� = ��1 + �4

� ��.(EAR)

25

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

CH 3: Time Value of Money Practise Questions

1. Find the following values assuming that compounding/discounting occurs once a

year.

a. An initial $500 compounded for 10 years at 6 percent.

b. An initial $500 compounded for 10 years at 12 percent.

c. The present value of $500 due in 10 years at a 6 percent discount rate.

d. The present value of $1,552.90 due in 10 years at a 12 percent discount rate and

at a 6 percent rate.

.

2. To the closest year, how long will it take $200 to double if it is deposited and earns

the

10% assuming that compounding occurs once a year.

3. Find the present value and future value of the following annuities assuming that

compounding occurs once a year and the first payment in these annuities is made at

the end of Year 1

a. $400 per year for 10 years at 10 percent.

b. $200 per year for 5 years at 5 percent.

c. $400 per year for 5 years at 0 percent.

d. Now rework parts a, b, and c assuming that payments are made at the beginning

of each year.

4. Assume that one year from now, you will deposit $1,000 into a savings account that

pays 8 percent.

a. If the bank compounds interest annually, how much will you have in your account

four years from now?

26

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

b. What would your balance four years from now be if the bank used quarterly

compounding rather than annual compounding?

c. Suppose you deposited the $1,000 in 4 payments of $250 each at Year 1, Year 2,

Year 3, and Year 4. How much would you have in your account at Year 4, based on 8

percent annual compounding?

d. Suppose you deposited 4 equal payments in your account at Year 1, Year 2, Year 3,

and Year 4.

Assuming an 8 percent interest rate, how large would each of your payments have to

be for you to obtain the same ending balance as you calculated in part a?

5. A father is planning a savings program to put his daughter through college. His

daughter is now 13 years old. She plans to enrol at the university in 5 years, and it

should take her 4 years to complete her education. Currently, the cost per year (for

everything— food, clothing, tuition, books, transportation, and so forth) is $12,500,

but a 5 percent annual inflation rate in these costs is forecasted. The daughter

recently received $7,500 from her grandfather’s estate; this money, which is

invested in a bank account paying 8 percent interest, compounded annually, will be

used to help meet the costs of the daughter’s education. The remaining costs will be

met by money the father will deposit in the savings account. He will make 6 equal

deposits to the account, one deposit in each year from now until his daughter starts

college. These deposits will begin today and will also earn 8 percent interest,

compounded annually.

a. What will be the present value of the cost of 4 years of education at the time the

daughter becomes 18?

b. What will be the value of the $7,500 that the daughter received from her

grandfather’s estate when she starts college at age 18?

c. If the father is planning to make the first of 6 deposits today, how large must each

deposit be for him to be able to put his daughter through college?

6. Anne Lockwood, manager of Oaks Mall Jewelry, wants to sell on credit, giving

customers 3 months in which to pay. However, Anne will have to borrow from her

bank to carry the accounts payable. The bank will charge a nominal 15 percent, but

27

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

with monthly compounding. Anne wants to quote a nominal rate to her customers

(all of whom are expected to pay on time) which will exactly cover her financing

costs. What nominal annual rate should she quote to her credit customers?

7. Assume that your father is now 50 years old, that he plans to retire in 10 years, and

that he expects to live for 25 years after he retires, that is, until he is 85. He wants a

fixed retirement income that has the same purchasing power at the time he retires

as $40,000 has today (he realizes that the real value of his retirement income will

decline year by year after he retires). His retirement income will begin the day he

retires, 10 years from today, and he will then get 24 additional annual payments.

Inflation is expected to be 5 percent per year from today forward; he currently has

$100,000 saved up; and he expects to earn a return on his savings of 8 percent per

year, annual compounding. To the nearest dollar, how much must he save during

each of the next 10 years (with deposits being made at the end of each year) to meet

his retirement goal?

8. Find the present value of $1, 000, 000 to be received after 20 years assuming

continuous compounding at 6%.

9. Given that the future value of $950 subject to continuous compounding will be $1,

000 after half a year, find the interest rate.

10. Complete the rows of the following table with equivalent nominal rates:

r1 r2 r4 r12 r365

0.05

0.10

0.0825

28

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

0.0450

0.0775

11. If an annual payment annuity of 100 is to be received from time 8 to time 20, show

that the value of this 7-year deferred, 13-year annuity

29

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

CHAPTER 4:

VALUATION OF LONG TERM

SECURITIES

4.1 VALUE DEFINED

The value of an asset is the present value of expected future benefits usually represented

by cash flows discounted at a required rate of return.

4.1.1 Market value: Market value is the market price at which the asset (or a similar asset)

trades in an open market place.

4.1.2 Intrinsic value: This is the price a security ought to have if all valuation factors are

taken into account. Thus, intrinsic value is the economic value of the security. This value is

the present value of the cash-flows, provided an appropriate required rate of return for the

risk involved was used.

4.2 BOND VALUATION

A bond is a long-term debt instrument issued by a corporation or government. The

borrower (corporate issuing the bond) agrees to make payments of interest and principal,

on specific dates, to the holders of the bond. Bond valuation involves discounting the

cashflow stream that the security holder would receive over the life of the instrument. The

discounting rate is dependent on the risk associated with the bond.

Characteristics of Bonds:

1. Par Value / face value

- It is the stated face value of the bond. This is the amount paid to the bond holder

(investor) on the maturity of the bond.

30

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

- The par value represents the amount the issuer borrows and promises to repay on the

maturity date.

2. Coupon Rate

- It is the annual or semi-annual or quarterly interest payment paid to investors.

3. Yield

- It is the required rate of return on the bond. It is the rate of interest required by investors

in order to entice them to invest in a bond and this is usually the rate of return on the best

available alternative investment of equal risk. They yield changes with changes in interest

rates in the economy and credit worthiness of the issuer.

4. Maturity

- Bonds have specific maturity dates on which the par value must be repaid.

- The effective maturity of a bond declines each year after it has been issued.

Bond classification

Bonds can be classified according to the coupon payments that the bond makes as follows:

(a). Straight Bonds / ballet Bonds / Vanilla Bonds

It is the most common type of bond. The bond pays regular usually semi-annual fixed

coupon over a fixed period to maturity to return.

(b). Zero Coupon Bonds

They do not make coupon payments. The investors receive the par value at maturity date

but receive no interest payments.

- They are issued at a discount and the investors return comes from the difference between

the issue price and payment of the par value at issue e.g. bond issued at $700 yet its par

value is $1, 000, on maturity the investor gets the $1, 000.

(c). Variable Rate / Floating Rate

Floating rate bonds make payments that are tied to some measure of current market rate.

The payments can be linked to an index or from a current market rate e.g. Treasury Bills

rate or LIBOR.

Besides using the coupon rates to classify bonds, bonds can also be classified as follows:

31

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

(d) Callable Bonds- Callable bonds give the issuer the rights but not the obligation to

redeem the bond before maturity. The issuer however must pay the bond holders a

premium.

(e) Puttable Bonds. These bonds give bond holders the right but not the obligations to sell

their bonds back to the issuer at predetermined price and date.

(f) Irredeemable Bonds / Perpetuals. These are bonds which do not have redemption

dates. Interest on them will be paid indefinitely.

(g)Convertible Bonds It is one that can be converted at the option of the holder into

certain number of shares in that company. E.g. D ltd issues bonds for $1000 to mature in

December 2008. The buyer will be given an option to convert the bond into shares worth

for example 200 shares and hence becomes a shareholder.

7.2.1 Valuation of Perpetual Bonds

It is a bond that never matures. Its present value is equal to the capitalised value of an

infinite stream of interest payments. It is calculated as:

� = 56

Where: V = Present value

C = Periodic coupon payments

i = Periodic required rate of return

4.2.2 Bonds with a finite maturity

i. Coupon paying bonds

Instead of considering interest streams only the terminal/maturity/face value is also

considered. It is calculated as:

� = ∑ 5�896�: +

;�896�3

�<=8

Where: F = Maturity value or Face Value

i= periodic required rate of return

32

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

t = Period

n = Number of years to maturity

Example

A bond has a par value of $1,000 with 10% coupon paid over nine years. The required rate

of return is 12%. Calculate its value.

( ) ( )1 2 9 9

100 100 100 1000...........

1.12 1.12 1.12 1.12 $100 5.328 $1,000 0.361

$532.80 $361.00

$893.80

V = + + + +

= += +=

Assuming the required rate of return was 8% the value becomes $1,124.70. The present

value is greater than the par value because the required rate of return is less than the

coupon rate. In this case investors will be willing to pay a premium to buy the bond. In the

previous case, with the required rate of return at 12%, investors would be willing to buy

the bond only if it is sold at a discount from par value.

Thus: If k > coupon rate the bond will sell at a discount.

If k < coupon rate the bond will sell at a premium.

If k = coupon rate the bond will sell at par value.

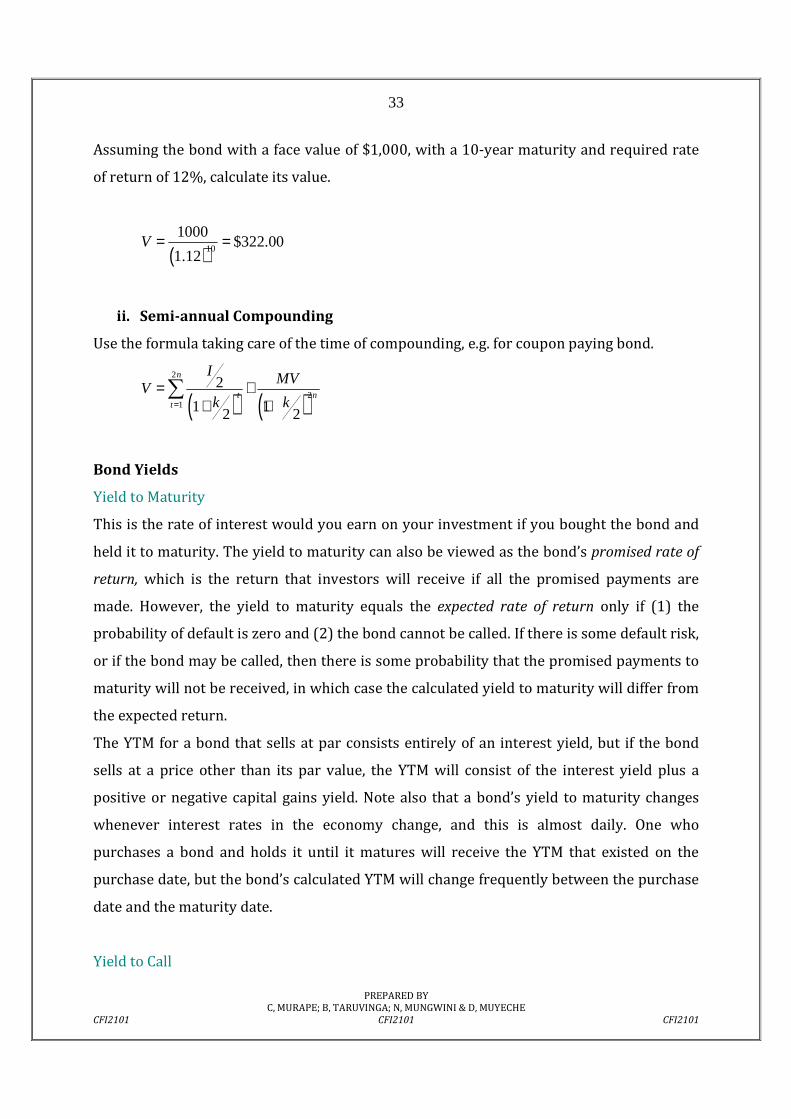

i. Zero-coupon bonds

It pays no interest but sells at a deep discount from its face value. Thus the investor buys

the bond at below face value and redeems it at face value on maturity. The present value is:

( )1

n

MVV

k=

+

Example

33

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Assuming the bond with a face value of $1,000, with a 10-year maturity and required rate

of return of 12%, calculate its value.

( )10

1000$322.00

1.12V = =

ii. Semi-annual Compounding

Use the formula taking care of the time of compounding, e.g. for coupon paying bond.

( ) ( )2

21

2

1 12 2

n

t nt

I MVV

k k=

= ++ +

∑

Bond Yields

Yield to Maturity

This is the rate of interest would you earn on your investment if you bought the bond and

held it to maturity. The yield to maturity can also be viewed as the bond’s promised rate of

return, which is the return that investors will receive if all the promised payments are

made. However, the yield to maturity equals the expected rate of return only if (1) the

probability of default is zero and (2) the bond cannot be called. If there is some default risk,

or if the bond may be called, then there is some probability that the promised payments to

maturity will not be received, in which case the calculated yield to maturity will differ from

the expected return.

The YTM for a bond that sells at par consists entirely of an interest yield, but if the bond

sells at a price other than its par value, the YTM will consist of the interest yield plus a

positive or negative capital gains yield. Note also that a bond’s yield to maturity changes

whenever interest rates in the economy change, and this is almost daily. One who

purchases a bond and holds it until it matures will receive the YTM that existed on the

purchase date, but the bond’s calculated YTM will change frequently between the purchase

date and the maturity date.

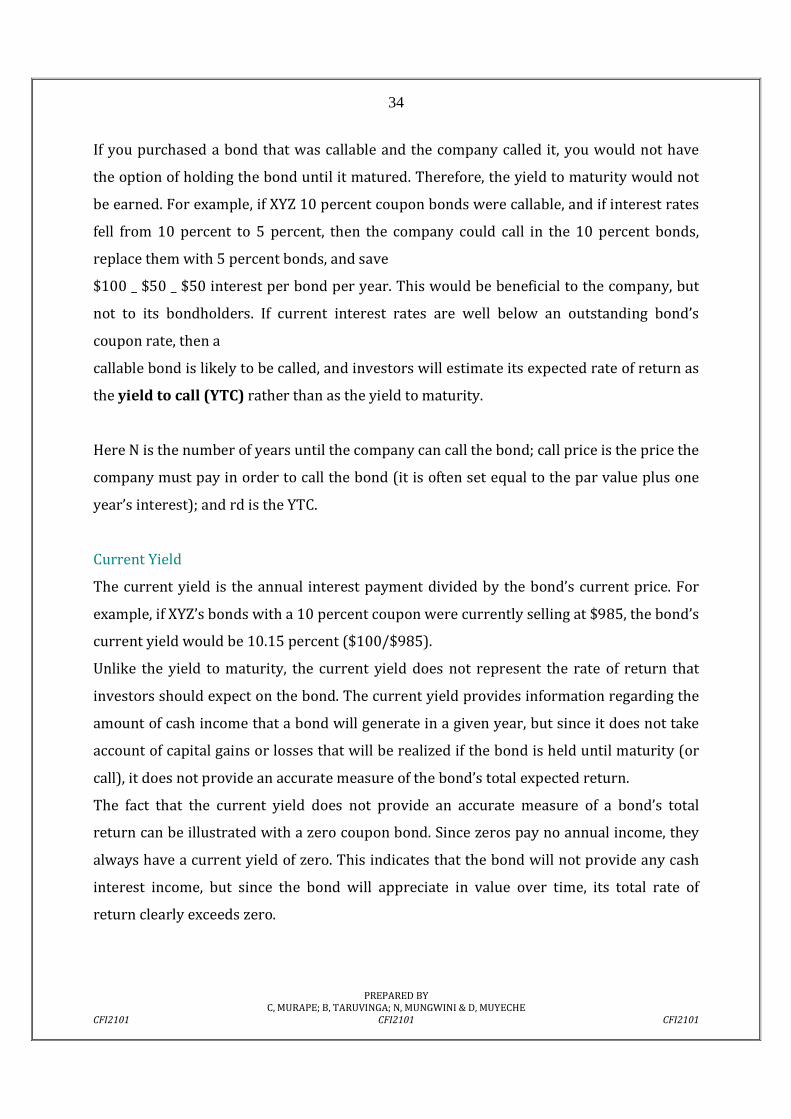

Yield to Call

34

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

If you purchased a bond that was callable and the company called it, you would not have

the option of holding the bond until it matured. Therefore, the yield to maturity would not

be earned. For example, if XYZ 10 percent coupon bonds were callable, and if interest rates

fell from 10 percent to 5 percent, then the company could call in the 10 percent bonds,

replace them with 5 percent bonds, and save

$100 _ $50 _ $50 interest per bond per year. This would be beneficial to the company, but

not to its bondholders. If current interest rates are well below an outstanding bond’s

coupon rate, then a

callable bond is likely to be called, and investors will estimate its expected rate of return as

the yield to call (YTC) rather than as the yield to maturity.

Here N is the number of years until the company can call the bond; call price is the price the

company must pay in order to call the bond (it is often set equal to the par value plus one

year’s interest); and rd is the YTC.

Current Yield

The current yield is the annual interest payment divided by the bond’s current price. For

example, if XYZ’s bonds with a 10 percent coupon were currently selling at $985, the bond’s

current yield would be 10.15 percent ($100/$985).

Unlike the yield to maturity, the current yield does not represent the rate of return that

investors should expect on the bond. The current yield provides information regarding the

amount of cash income that a bond will generate in a given year, but since it does not take

account of capital gains or losses that will be realized if the bond is held until maturity (or

call), it does not provide an accurate measure of the bond’s total expected return.

The fact that the current yield does not provide an accurate measure of a bond’s total

return can be illustrated with a zero coupon bond. Since zeros pay no annual income, they

always have a current yield of zero. This indicates that the bond will not provide any cash

interest income, but since the bond will appreciate in value over time, its total rate of

return clearly exceeds zero.

35

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

4.3 PREFERRED STOCK VALUATION

It pays a fixed dividend at regular intervals, but at the discretion of the board of directors. It

has preference over common stock in the payment of dividends and claims on assets. It has

no stated maturity date. All preferred stocks have a call feature. The present value formula

is:

D

Vk

=

Where: D = Stated annual dividend per share, and

k = Discount rate.

NB: If the call feature is incorporated the formula becomes the same as that of coupon

paying bonds.

4.4 COMMON STOCK VALUATION

The value of a share of common stock can be viewed as the discounted value of all expected

cash dividends provided by the issuing firm until the end of time. Its value is:

( ) ( ) ( )

( )

1 21 2

1

..........1 1 1

1

tt

t

D D DV

k k k

D

k

∞∞

∞

=

= + + ++ + +

= +

∑

Where: D = Cash dividend at the end of time t, and

k = Discount rate.

For finite common stock or those we intend to sell in the future the formula becomes:

( ) ( ) ( ) ( )

1 21 2 ..........

1 1 1 1n n

n n

D PD DV

k k k k= + + + +

+ + + +

Where: Pn = the expected sales price at the end of period n.

36

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

In this case the foundation for the valuation of common stock are dividends. For those

common stocks that do not pay dividends the valuation by investor will be based on

expected future selling price.

4.4.2 Dividend Discount Models

These models are designed to compute the intrinsic value of common stock. The valuation

is dependent on the assumptions of the expected growth pattern of stock.

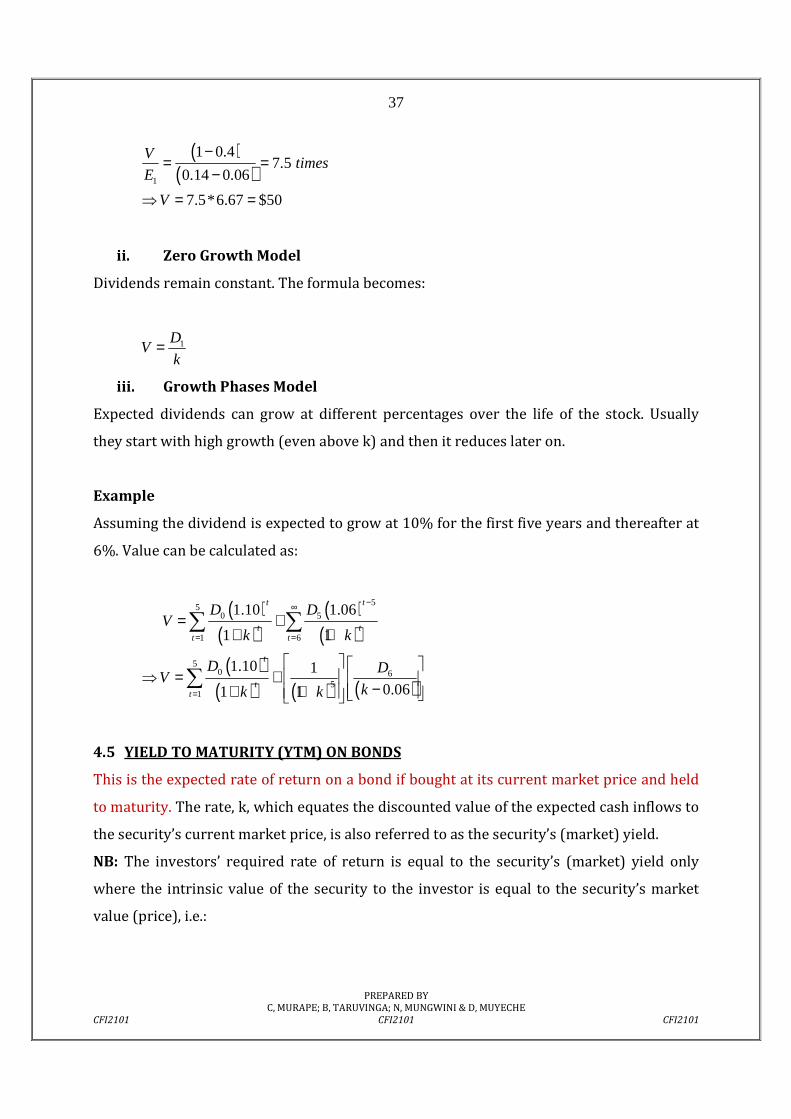

i. Constant Growth Model

Dividends are expected to grow at a constant rate. The value can be calculated as:

( )

( )( )

( )( )

( )

2

0 0 02

1 1 1..........

1 1 1

D g D g D gV

k k k

∞

∞

+ + += + + +

+ + +

Where: D0 = Present dividend per share, and

g = Growth rate, which in this case is constant.

Assuming k is greater than g the equation can be summarised as:

( )

1DV

k g=

−

Where: ( )1 0 1D D g= + , which is dividend in period 1.

Constant growth model is usually applicable to companies in their mature stage.

Example

A company’s dividend per share at t1 is $4, the dividend is expected to grow at 6% forever

and the discount rate is 14%. Calculate the value of the stock.

4$50

0.14 0.06V = =

−

Assuming the same company has retention rate of 40% and earnings per share at t1 of

$6.67.

37

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

( )( )1

1 0.47.5

0.14 0.06

7.5*6.67 $50

Vtimes

E

V

−= =

−⇒ = =

ii. Zero Growth Model

Dividends remain constant. The formula becomes:

1DV

k=

iii. Growth Phases Model

Expected dividends can grow at different percentages over the life of the stock. Usually

they start with high growth (even above k) and then it reduces later on.

Example

Assuming the dividend is expected to grow at 10% for the first five years and thereafter at

6%. Value can be calculated as:

( )( )

( )( )

( )( ) ( ) ( )

550 5

1 6

50 6

51

1.10 1.06

1 1

1.10 1

0.061 1

t t

t tt t

t

tt

D DV

k k

D DV

kk k

−∞

= =

=

= ++ +

⇒ = + −+ +

∑ ∑

∑

4.5 YIELD TO MATURITY (YTM) ON BONDS

This is the expected rate of return on a bond if bought at its current market price and held

to maturity. The rate, k, which equates the discounted value of the expected cash inflows to

the security’s current market price, is also referred to as the security’s (market) yield.

NB: The investors’ required rate of return is equal to the security’s (market) yield only

where the intrinsic value of the security to the investor is equal to the security’s market

value (price), i.e.:

38

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

( ) ( )0

1 1 1

n

t nt

I MVP

k k=

= ++ +

∑

Given the value of MV, P0, and I one can calculate the value of k using interpolation.

Example

Assuming a bond with a par value of $1,000; current market value of $761; 12 years to

maturity; and 8% coupon rate. Gives a k of 12% (YTM).

4.5.2 Behaviour of Bond Prices

i. When the market required rate of return is greater than the coupon rate the bond

price will be less than its face value. Thus bond is selling at a discount of face value.

Bond discount is the amount by which face value exceed current price.

ii. When the market required rate of return is less than coupon rate the bond price will

be greater than its face value. Thus the bond is selling at a premium over face value.

Bond premium is the amount by which bond price exceeds face value.

iii. When the market required rate of return is equal to the coupon rate, bond price is

equal to the face value. The bond is said to be selling at par.

iv. If interest increases leading to an increase in the market required rate of return the

bond price will fall, and the reverse is true.

NB: Interest rate risk (yield risk) is the variation in the market price of a security

caused by changes in interest rates. An investor incurs interest rate risk only if the

bond is sold before maturity and interest rate has changed since the time of

purchase.

v. For a given change in market required rate of return, the price of a bond will change

by a greater amount, the longer is its maturity. Thus the longer the maturity, the

greater the risks of a price change to the investor when changes occur in the overall

level of interest rates.

vi. For a given change in market required rate of return, the price of a bond will change

by proportionally more, the lower the coupon rate. Thus the bond price volatility is

39

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

inversely related to the coupon rate. This is due to the fact that investors realise

their returns later with a low-coupon-rate bond than with a high-coupon-rate bond.

4.6 YIELD ON PREFERRED STOCK

It is derived from the formula for preferred stock price. Thus:

00

D D

P kk P

= ⇒ =

Where: D = annual dividend per share of preferred stock, and

k = Market required rate of return or yield on preferred stock.

Example

Assuming the current market price of a company’s 10%, $100 par value preferred stock is

$91.25. Calculate the yield.

$10

10.96%91.25

k = =

4.7 YIELD ON COMMON STOCK

This is the rate of return that sets the discounted value of the expected cash dividends from

a share of common stock equal to the share’s current market price. Applying the constant

dividend growth model it implies that:

( )

1 10

0

D D

P k gk g P

= ⇒ = +−

Thus common stock yield comes from expected dividend yield 1

0

D

P

and capital gains yield

( )g .

Example

40

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

What market yield is implied by a share of common stock currently selling for $50 whose

dividends are expected to grow at a rate of 10% per year and whose dividend is currently

at $2.20.

( )1: $2.20 1.1

$2.42

2.42: 0.1

50 14.84%

First D

Then k

==

= +

=

41

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

CH4 Practice questions Valuation of long term securities

1. Callaghan Motors’ bonds have 10 years remaining to maturity. The bonds have a

$1,000 par value, and the coupon interest rate is 8 percent. The bonds have a yield

to maturity of 9 percent. What is the current market price of these bonds if:

a) The coupon is paid annually

b) The coupon is paid semi annually

c) The coupon is paid quartely

2. Thomas Brothers is expected to pay a $0.50 per share dividend at the end of the

year (i.e., D1 = $0.50). The dividend is expected to grow at a constant rate of 7

percent a year. The required rate of return on the stock, rs, is 15 percent. What is the

value per share of the company’s stock?

3. A company currently pays a dividend of $2 per share, D0 =2. It is estimated that the

company’s dividend will grow at a rate of 20 percent per year for the next 2 years,

then the dividend will grow at a constant rate of 7 percent thereafter. The

company’s stock has a beta equal to 1.2, the risk-free rate is 7.5 percent, and the

market risk premium is 4 percent. What would you estimate is the stock’s current

price?

4. Martell Mining Company’s ore reserves are being depleted, so its sales are falling.

Also, its pit is getting deeper each year, so its costs are rising. As a result, the

company’s earnings and dividends are declining at the constant rate of 5 percent per

year. If D0 = $5 and rs =15%, what is the value of Martell Mining’s stock?

42

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

5. The Garraty Company has two bond issues outstanding. Both bonds pay $100

annual interest plus $1,000 at maturity. Bond L has a maturity of 15 years, and Bond

S a maturity of 1 year.

a. What will be the value of each of these bonds when the going rate of interest

is (1) 5 percent, (2) 8 percent, and (3) 12 percent? Assume that there is only

one more interest payment to be made on Bond S.

b. Why does the longer-term (15-year) bond fluctuate more when interest rates

change than does the shorter-term bond (1-year)?

6. Assume that the average firm in your company’s industry is expected to grow at a

constant rate of 6 percent and its dividend yield is 7 percent. Your company is about

as risky as the average firm in the industry, but it has just successfully completed

some R&D work that leads you to expect that its earnings and dividends will grow at

a rate of 50 percent this year and 25 percent the following year, after which growth

should match the 6 percent industry average rate. The last dividend paid (D0) was

$1. What is the value per share of your firm’s stock?

7. Microtech Corporation is expanding rapidly, and it currently needs to retain all of its

earnings, hence it does not pay any dividends. However, investors expect Microtech

to begin paying dividends, with the first dividend of $1.00 coming 3 years from

today. The dividend should grow rapidly—at a rate of 50 percent per year—during

Years 4 and 5. After Year 5, the company should grow at a constant rate of 8 percent

per year. If the required return on the stock is 15 percent, what is the value of the

stock today?

8. Ezzell Corporation issued preferred stock with a stated dividend of 10 percent of

par. Preferred stock of this type currently yields 8 percent, and the par value is

$100. Assume dividends are paid annually.

a. What is the value of Ezzell’s preferred stock?

b. Suppose interest rate levels rise to the point where the preferred stock now

yields 12 percent. What would be the value of Ezzell’s preferred stock?

43

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

9. [Excel] You are given a 5-year and a 30-year bond, each with a par of 1000 and a

semiannual coupon rate of 8%. Calculate the price of each at an 8% semiannual

yield, and graph each price function over the range of semiannual yields 0%-16% on

the same set of axes. What pattern do you notice between the graphs?

44

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Chapter 5: CAPITAL BUDGETING

5.0 Definition

The capital budgeting process is the process of identifying and evaluating capital projects,

that is, projects where the cash flow to the firm will be received over a period longer than a

year. Any corporate decisions with an impact on future earnings can be examined using

this framework. Decisions about whether to buy a new machine, expand business in

another geographic area, move the corporate headquarters etc can be examined using a

capital budgeting analysis.

Capital budgeting may be the most important responsibility that a financial manager has

because

• capital budgeting decisions often involves the purchase of costly long-term assets

with lives of many years. The decisions made may determine the future success of

the firm.

• the principles underlying the capital budgeting process also apply to other

corporate decisions, such as working capital management and making strategic

mergers and acquisitions.

• making good capital budgeting decisions is consistent with management's primary

goal of maximizing shareholder value.

5.1 Why is capital a limited resource ? In the form of either debt or equity, capital is a very limited resource.

There is a limit to the volume of credit that the banking system can create in the

economy.

Commercial banks and other lending institutions have limited deposits from which

they can lend money to individuals, corporations, and governments. In addition, the

Central Bank requires each bank to maintain part of its deposits as reserves. Having

45

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

limited resources to lend, lending institutions are selective in extending loans to their

customers.

But even if a bank were to extend unlimited loans to a company, the management of

that company would need to consider the impact that increasing loans would have on

the overall cost of financing.

In reality, any firm has limited borrowing resources that should be allocated among

the best investment alternatives.

One might argue that a company can issue an almost unlimited amount of common

stock to raise capital.

Increasing the number of shares of company stock, however, will serve only to

distribute the same amount of equity among a greater number of shareholders. In other

words, as the number of shares of a company increases, the company ownership of the

individual stockholder may proportionally decrease.

The argument that capital is a limited resource is true of any form of capital, whether

debt or equity (short-term or long-term, common stock) or retained earnings, accounts

payable or notes payable, and so on. Even the best-known firm in an industry or a

community can increase its borrowing up to a certain limit.

Once this point has been reached, the firm will either be denied more credit or be

charged a higher interest rate, making borrowing a less desirable way to raise capital.

Faced with limited sources of capital, management should carefully decide whether a

particular project is economically acceptable. In the case of more than one project,

management must identify the projects that will contribute most to profits and,

consequently, to the value (or wealth) of the firm. This, in essence, is the basis of capital

budgeting.

5.2 The capital budgeting process

The capital budgeting process has four administrative steps:

Step 1: Idea generation. The most important step in the capital budgeting process is

generating good project ideas. Ideas can come from a number of sources including senior

management, functional divisions, employees, or outside the company.

46

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

Step 2: Analyzing project proposals. Since the decision to accept or reject a capital project is

based on the project's expected future cash flows, a cash flow forecast must be made for

each project to determine its expected profitability.

Step 3: Create the firm-wide capital budget. Firms must prioritize profitable projects

according to the timing of the project's cash flows, available company resources, and the

company's overall strategic plan. Many projects that are attractive individually may not

make sense strategically.

Step 4:Monitoring decisions and conducting a post-audit. It is important to follow up on all

capital budgeting decisions. An analyst should compare the actual results to the projected

results, and project managers should explain why projections did or did not match actual

performance. Since the capital budgeting process is only as good as the estimates of the

inputs into the

model used to forecast cash flows, a post-audit should be used to identify systematic errors

in the forecasting process and improve company operations.

5.3 Definition of terms:

a)Cash-flows Versus Profits

The focus of capital budgeting is on cash-flows and the timing of the cash-flows, because

they easily measure the impact upon the firms’ wealth. Profit on the other hand does not

always represent the net increase or decrease in cash-flows. Some of the figures in

standard financial statements may not have a corresponding cash effect for the same

period.

b)Independent Versus Mutually Exclusive Projects

Independent projects are projects that are unrelated to each other, and allow for each

project to be evaluated based on its own profitability. For example, if projects A and B are

independent, and both projects are profitable, then the firm could accept both projects.

Mutually exclusive means that only one project in a set of possible projects can be accepted

and that the projects compete with each other. If projects A and B were mutually exclusive,

the firm could accept either Project A or Project B, but not both. A capital budgeting

47

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

decision between two different stamping machines with different costs and output would

be an example of choosing between two mutually exclusive projects.

c)Unlimited Funds Versus Capital Rationing

If a firm has unlimited access to capital, the firm can undertake all projects with expected

returns that exceed the cost of capital. Many firms have constraints on the amount of

capital they can raise, and must use capital rationing. If a firm's profitable project

opportunities exceed the amount of funds available, the firm must ration, or prioritize, its

capital expenditures with the goal of achieving the maximum increase in value for

shareholders given its available capital.

d)Conventional Versus Unconventional Cash-flows

If the pattern of cash-flows accruing to the project being evaluated involve only starting

with an outflow and then being followed by inflows, then the cash-flows are said to be

conventional. With unconventional cash flows, cash-flows come first and the investment

cost is paid later.

5.4 Evaluation Techniques

1.Payback period

2. Discounted Payback

3. Net present value (NPV)

4. Profitability index

5. Internal rate of return (IRR)

6.Modified internal rate of return (MIRR)

i) Payback Period

The payback period (PBP) is the number of years it takes to recover the initial cost of an

investment. Since the payback period is a measure of liquidity, for a firm with liquidity

concerns, the shorter a project's payback period, the better. However, project decisions

should not be made on the basis of their payback periods because of its drawbacks.

48

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

The main drawbacks of the payback period are that it does not take into account either the

time value of money or cash flows beyond the payback period, which means terminal or

salvage value wouldn't be considered. These drawbacks mean that the payback period is

useless as a measure of profitability.

The main benefit of the payback period is that it is a good measure of project liquidity.

Firms with limited access to additional liquidity often impose a maximum payback period,

and then use a measure of profitability, such as NPV or IRR, to evaluate projects that satisfy

this maximum payback period constraint.

ii) Discounted Payback Period

The discounted payback method uses the present values of the project's estimated cash

flows. It is the number of years it takes a project to recover its initial investment in present

value terms, and therefore must be greater than the payback period without discounting.

The discounted payback period addresses one of the drawbacks of the payback period by

discounting cash flows at the project's required rate of return. However, the discounted

payback period still does not consider any cash flows beyond the payback period, which

means that it is a poor measure of profitability. Again, its use is primarily as a measure of

liquidity.

iii) Net Present Value (NPV)

The NPV is the sum of the present values of all the expected incremental cash flows if a

project is undertaken. The discount rate used is the firm's cost of capital, adjusted for the

risk level of the project. For a normal project, with an initial cash outflow followed by a

series of expected after-tax cash inflows, the NPV is the present value of the expected

inflows minus the initial cost of the project.

>�� = ? @�"

�A + B� "C

"=�

= D�E +D�8

�1 + F�8 +D�G

�1 + F�G +⋯+ D���1 + F��

49

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

where:

CFo = the initial investment outlay (a negative cash flow)

CFt =after tax cash flow at time t

K = required rate of return for project

A positive NPV project is expected to increase shareholder wealth, a negative NPV project

is expected to decrease shareholder wealth, and a zero NPV project has no expected effect

on shareholder wealth.

For independent projects, the NPV decision rule is simply to accept any project with a

positive NPV and to reject any project with a negative NPV. For mutually exclusive projects,

the projects have to be ranked and the one with the highest NPV accepted.

iv) Profitability Index (PI)

The profitability index (PI) is the present value of a project's future cash flows divided

by the initial cash outlay.

�I = ��JK��K�J�LI��M��NOM�P

As you can see, the profitability index is closely related to the NPY. The PI is the ratio

of the present value of future cash flows to the initial cash outlay, while the NPV is the

difference between the present value of future cash flows and the initial cash outlay.

If the NPV of a project is positive, the PI will be greater than one. If the NPV is

negative, the PI will be less than one. It follows that the decision rule for the PI is:

If PI > 1.0, accept the project

If PI < 1.0, reject the project.

v) Internal Rate of Return (IRR)

For a normal project, the internal rate of return (IRR) is the discount rate that makes the

present value of the expected incremental after-tax cash inflows just equal to the initial cost

of the project. More generally, the IRR is the discount rate that makes the present values of

50

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

a project's estimated cash inflows equal to the present value of the project's estimated cash

outflows. That is, IRR is the discount rate that makes the following relationship hold:

PV (inflows) = PV (outflows)

The IRR is also the discount rate for which the NPV of a project is equal to zero.

Q�� = 0 = D�E +D�8

�1 + IRR�8 +D�G

�1 + IRR�G +⋯+ D���1 + IRR��

To calculate the IRR, the trial-and-error method is usually used, that is, keep guessing IRRs

until you get one that gives u a positive NPV and one that give you a negative NPV. An

estimation formula is then used to solve for the IRR as follows:

IRR = �M��9STU� +JL�M�V�Q��

JL�M�V�Q�� + |��XM�V�Q��| ��M��(STU� − �M��9STU�

IRR decision rule: First, determine the required rate of return for a given project. This is

usually the firm's cost of capital.

If IRR > the required rate of return, accept the project.

If IRR < the required rate of return, reject the project.

iv) Modified IRR (MIRR)

The MIRR is similar to the IRR, but is theoretically superior in that it overcomes two

weaknesses of the IRR. The MIRR correctly assumes reinvestment at the project’s cost of

capital and avoids the problem of multiple IRRs.

There are 3 basic steps of the MIRR:

(1) Estimate all cash flows as in IRR.

(2) Calculate the future value of all cash inflows at the last year of the project’s life.

(3) Determine the discount rate that causes the future value of all cash inflows

determined in step 2, to be equal to the firm’s investment at time zero. This

discount rate is known as the MIRR.

NB. Note that the PV costs = initial capital outlay.

51

PREPARED BY C, MURAPE; B, TARUVINGA; N, MUNGWINI & D, MUYECHE

CFI2101 CFI2101 CFI2101

MIRR is better than IRR because

1. MIRR correctly assumes reinvestment at project’s cost of capital.

2. MIRR avoids the problem of multiple IRRs.

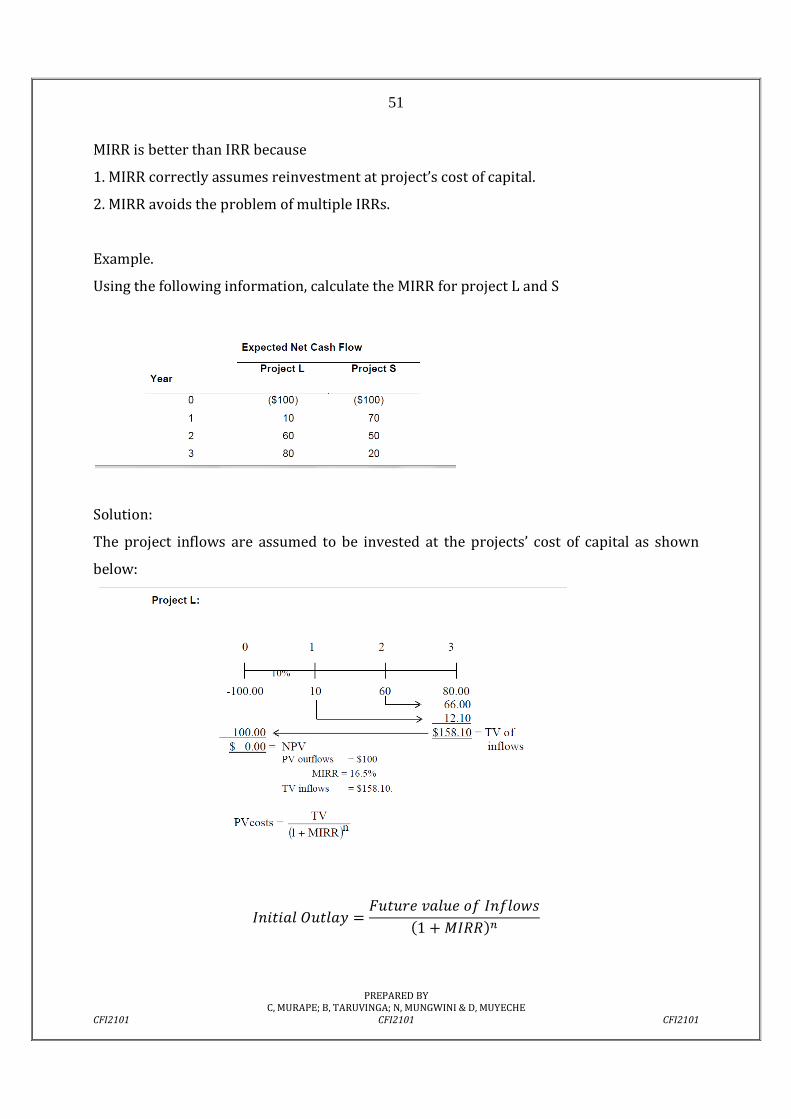

Example.

Using the following information, calculate the MIRR for project L and S

Solution:

The project inflows are assumed to be invested at the projects’ cost of capital as shown

below: