Embed Size (px)

Citation preview

Minutes of the lSth meeting of the Technical Advisory - Cunr - Monitoring Committee (TAIVIC)

under A-TUFS held on 09.10.2020 at 02.30 PM through Video Conferencing.

18fr meeting of the Technical Advisory-Cum-Monitoring Committee (TAMC) on

Amended Technology'Upgradation Funds Scheme (ATUFS) was held under the Chairmanship

of Ms Roop Rashi, Textile Commissioner on 09. I 0.2020 at 02.30 PM through Video

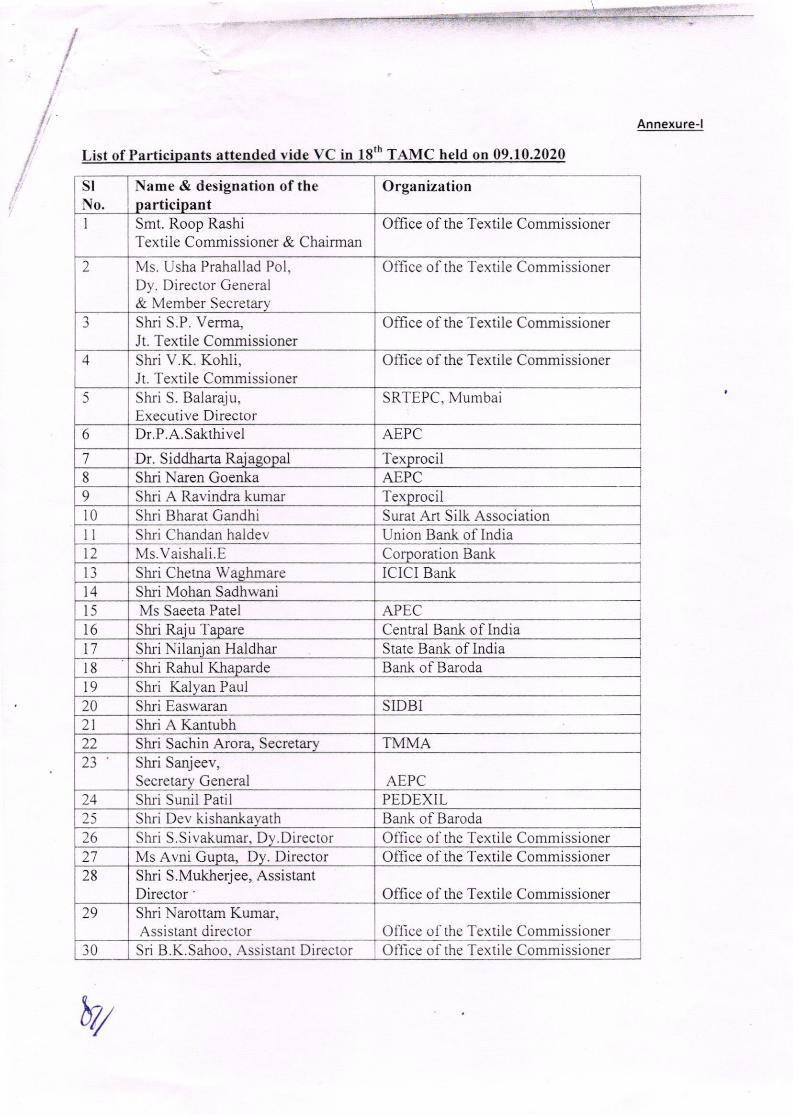

Conferencing. The list ofparticipants is enclosed at Annexure-I (of I Page).

At the outset, the Chairperson extended a warm welcome to all the participants and requested Ms

Usha Pralhad Pol, Deputy Director General to take up item-wise agenda for discussion before

the Committee. The agenda-wise decisions of TAMC are as tbllows:

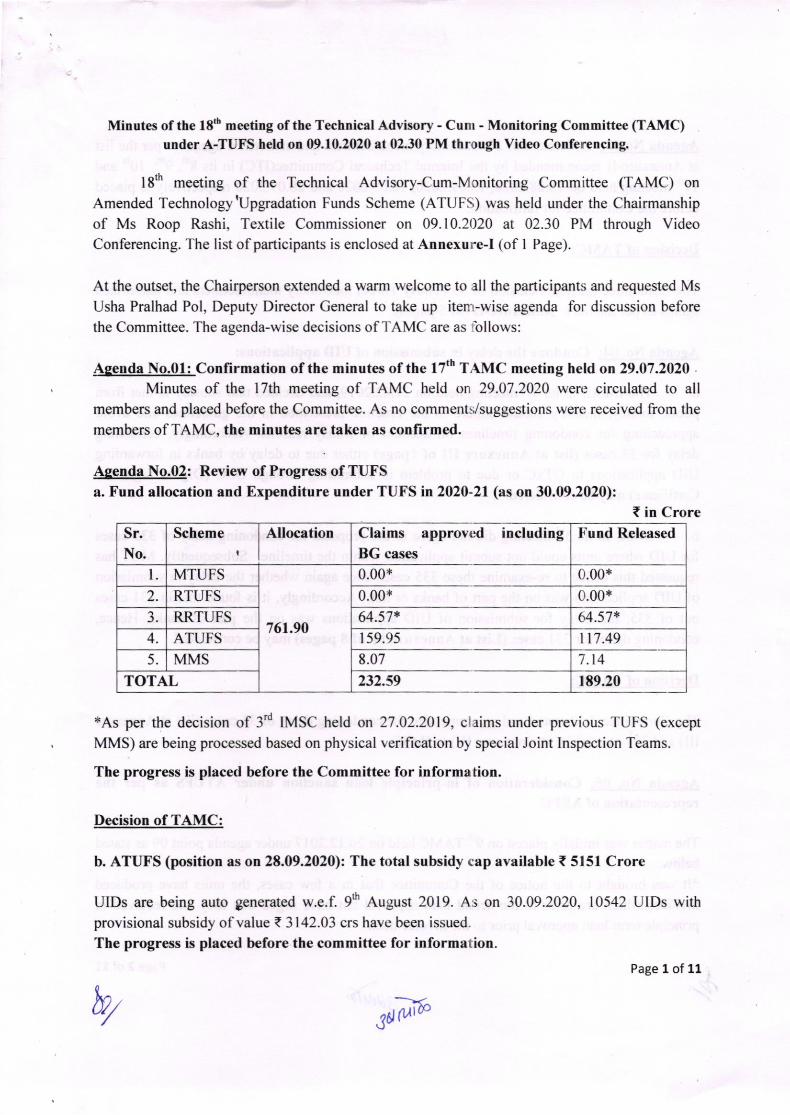

Agenda No.02: Review of Progress of TUFSa. Fund allocation and Expenditure under TUFS in 2020-21 (as on 30.09.2020):

{ in CroreSr.

No.

Scheme Allocation Claims approved includingBG cases

Iiund Released

I

761.90

0.00+ Cr.00 *

2 RTUFS 0.00* Cr.00*

J RRTUFS 64.57* 64.57*

4 ATUFS 1s9.95

8.07

lL7.49'i.145 MMS

TOTAL 189.20232.s9

*As per the decision of 3'd IMSC held on 27.02.2019, clnims under previous TUFS (except

MMS) are being processed based on physical verification by special Joint Inspection Teams.

The progress is placed before the Committee for information.

Decision of TAMC:

b. ATUFS (position as on 28.09.2020): The total subsidy cap availatrle t 5151 Crore

UIDs are being auto generated w.e.f. 9s August 2019. As on 30.09.2020,

provisional subsidy ofvalue t 3142.03 crs have been issued.

The progress is placed before the committee for information.

10542 UIDs with

Page 1 of U

b7Jdai6

Aqerda No.01: Confirmation of the minutes of the lTth TAMC meeting held on 29.07.2020 .

Minutes of the l Tth meeting of TAMC held on 29.07 .2020 werr: circulated to all

members and placed before the Committee. As no comments/suggestions were received from the

members of TAMC, the minutes are taken as confirmed,

MTUFS

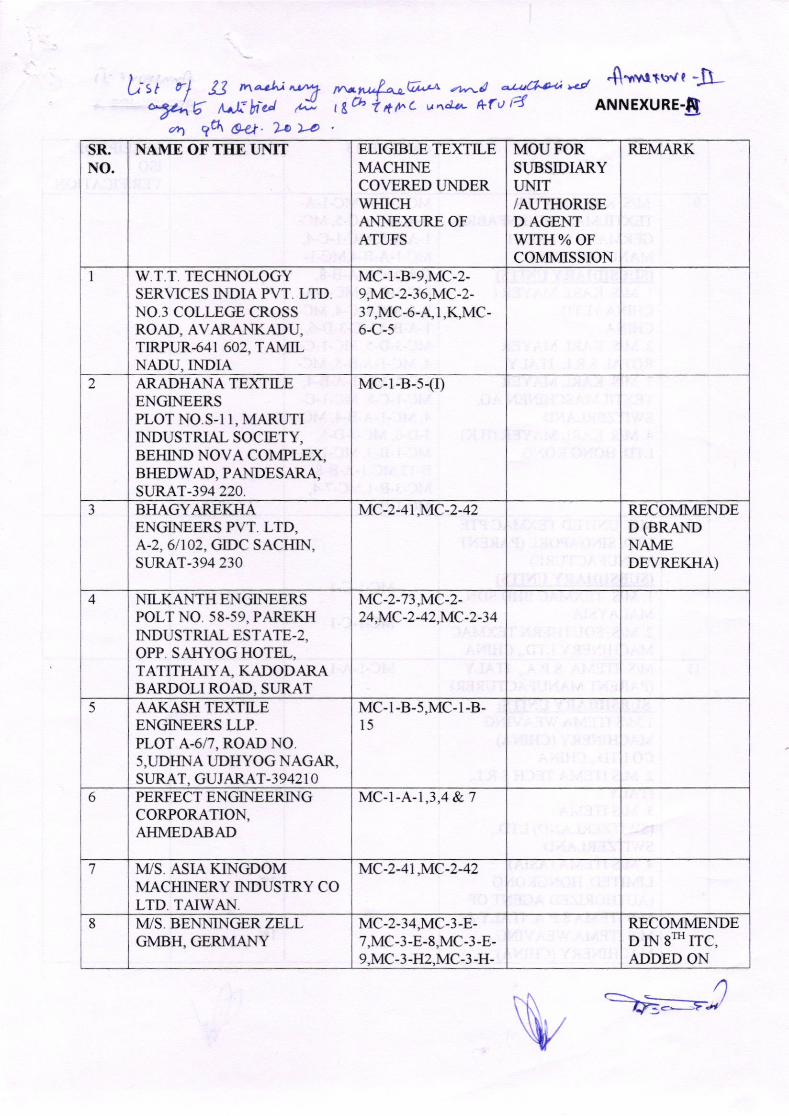

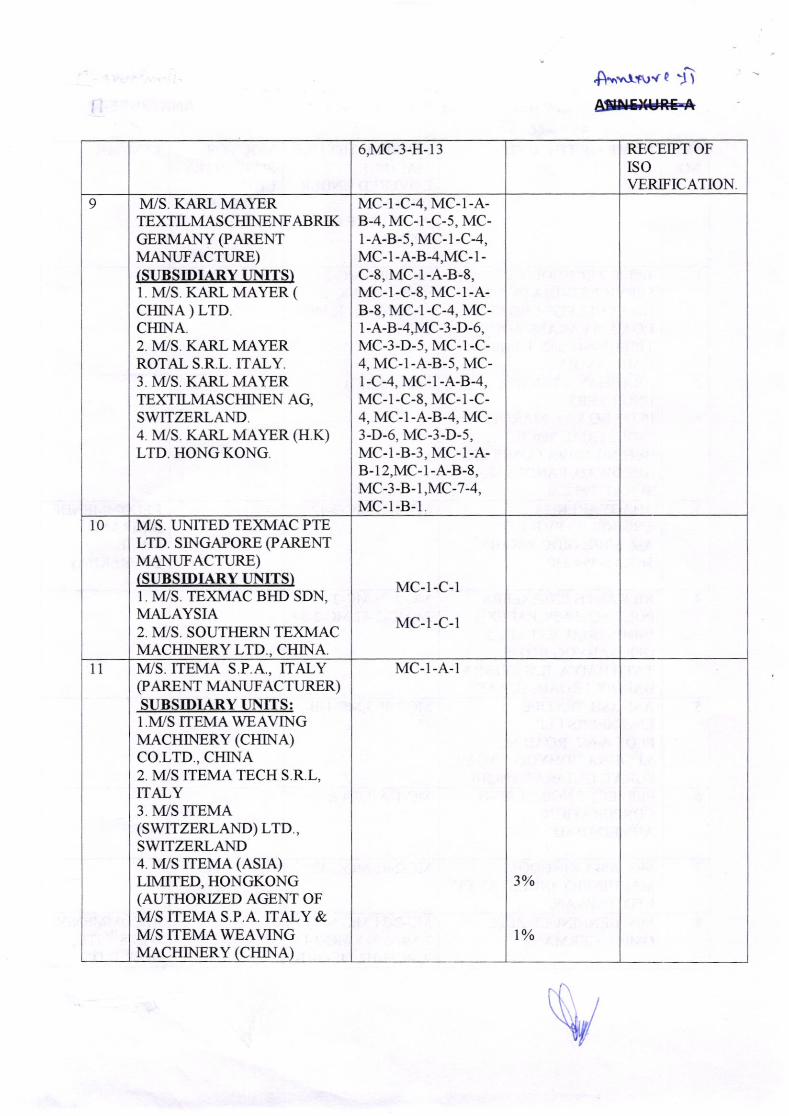

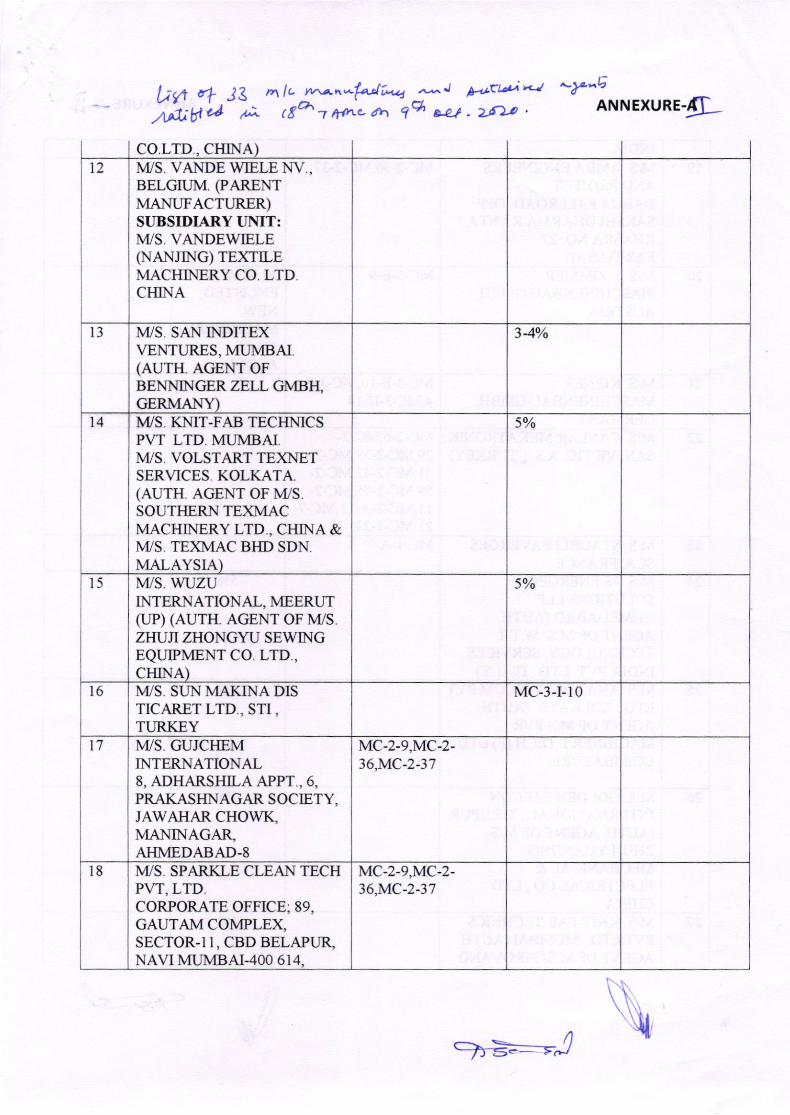

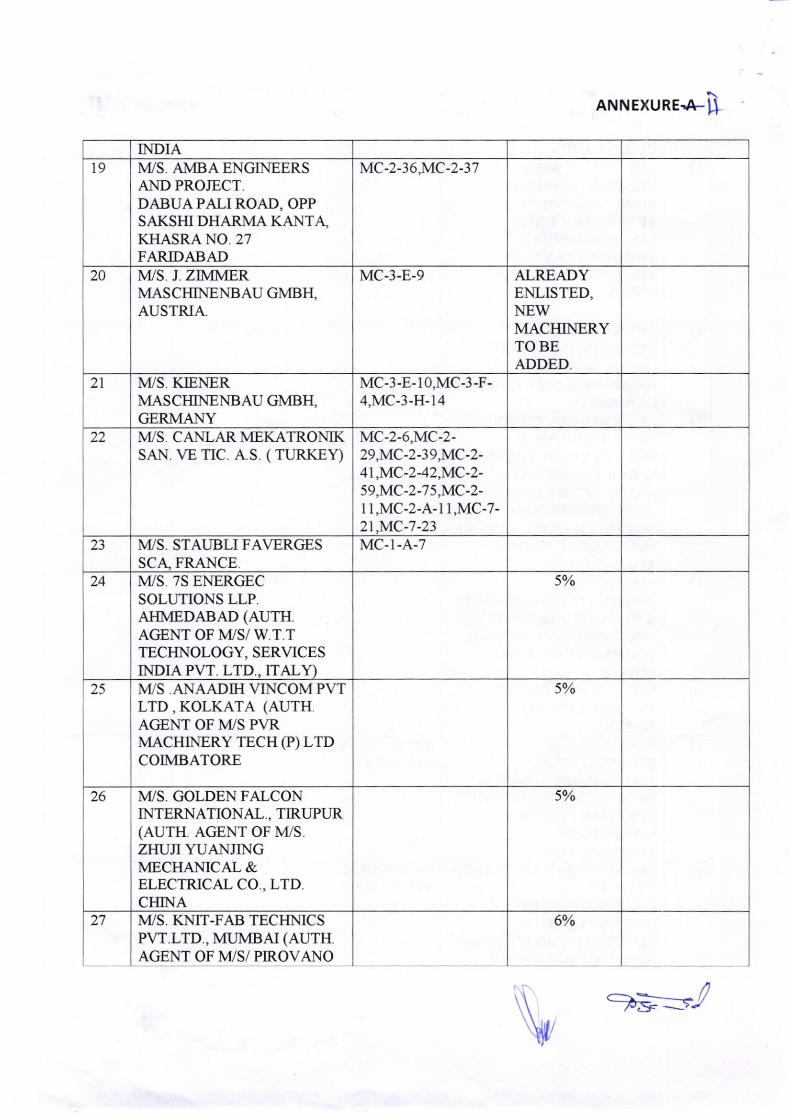

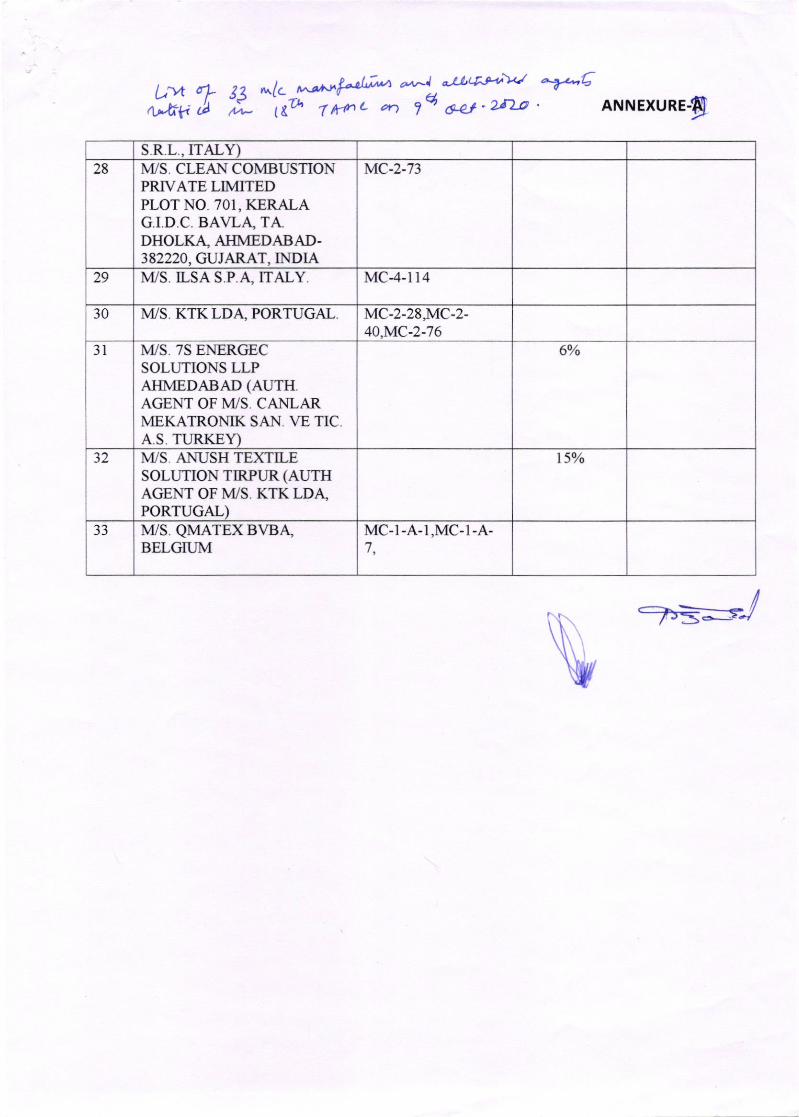

Asenda No.03: F.nli stment ol33 nrachinery manufacturers and authorized agents as per the Iistat Annexure-ll recommended by the lnternal Technical Committee(lTC) in its 8th,96' l0s and

llrhmeeting held on 18.08.2020, 15.09.2020, 18.09.2020 and 28.09.2020 respectively is placed

before the Committee for ratification.

The Committee ratified inclusion ol'33 (Thirty Three) machinery manufacturers and authorized

agents as per the list at Annexure-Il (of 5 pages).

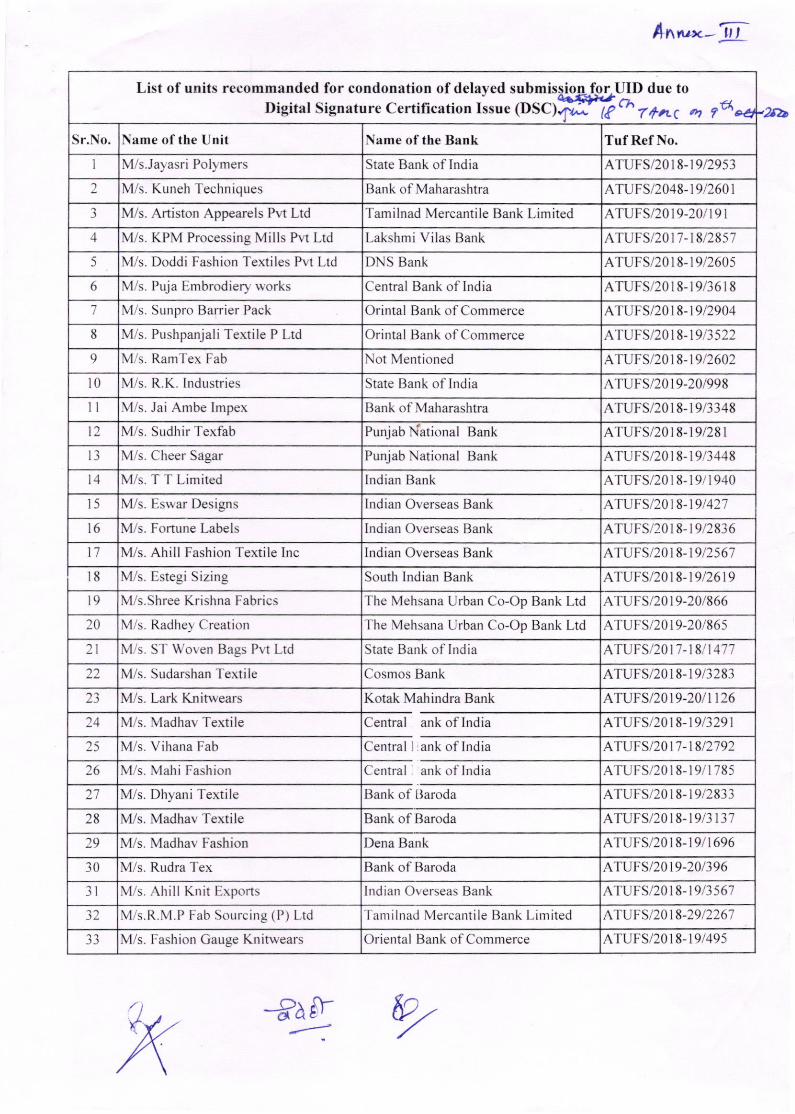

Asenda No.04: Condone the delav in sutrmission of UID applications:

a. The IMSC" in its 3'd meeting held on 27.02.2019, had decided that subsidy is met frompublic money, industry should adhere to the timeline prescribed in thE guidelines and avoidapproaching for condoning timelines on account of flimsy reasons. Accordingly, condoningdelay for 33 cases (list at Annexure III of lpage) either due to delay by banks in forwardingUID applications to OTxC or due to problem in submitting through DSC (Digital Signature

Certificate) may be considered.

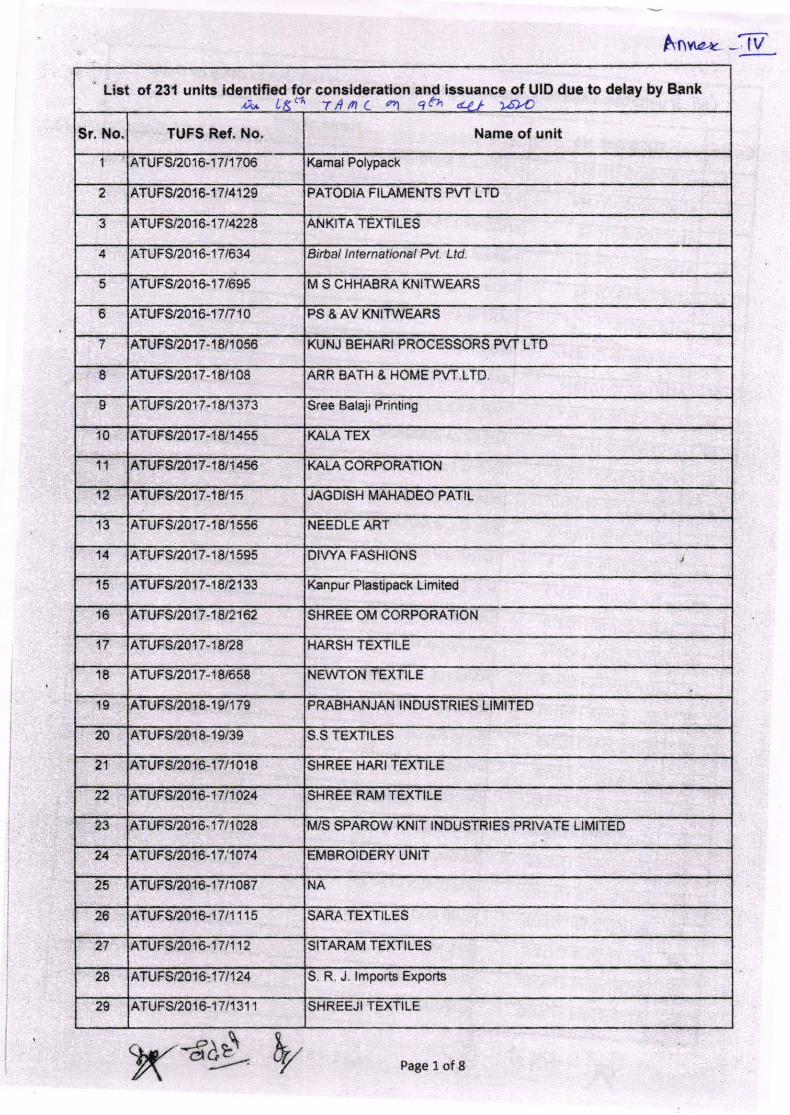

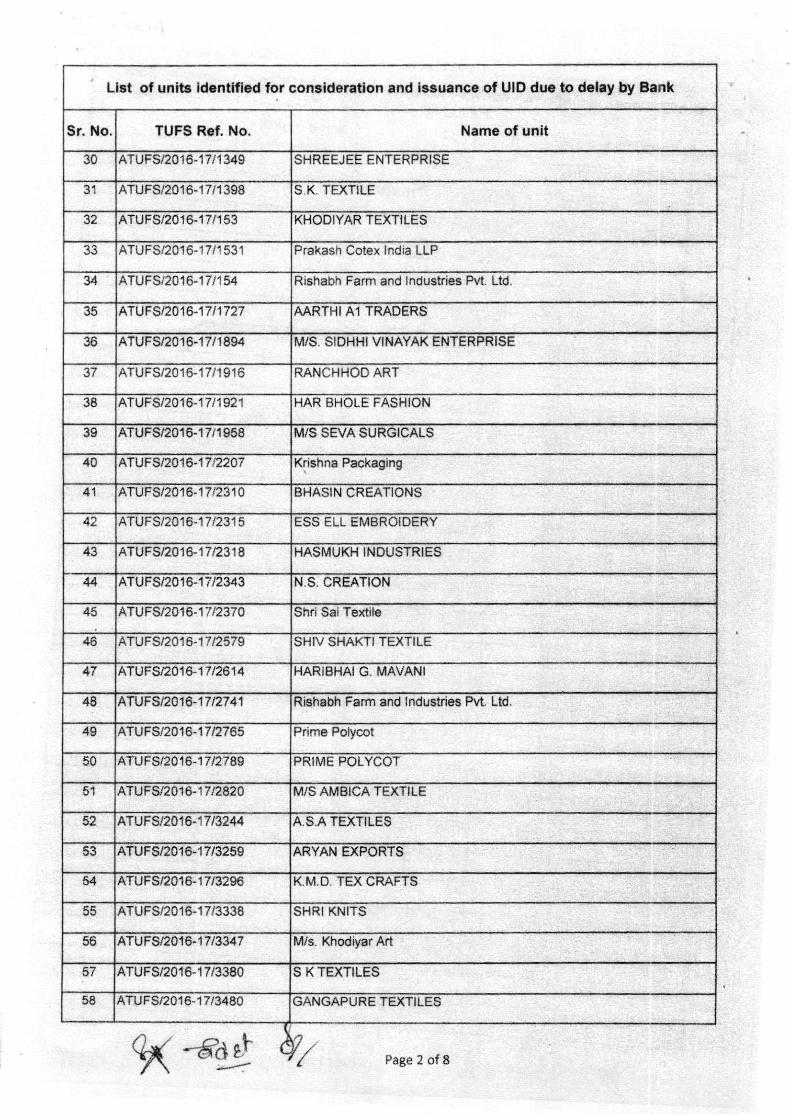

b. IMSC in its 3'd meeting did not agree to the proposal for condoning delay of 335 cases

for UID where units could not submit application within the timeline. Subsequently, MOT has

requested this office to re-examine these 335 cases once again whether the delay in submission

of UID applications was on the pan of banks or not. Accordingly, it is found that in 231 cabes

out of 335, the delay for submission of UID applications was on the part of banks. Hence,

condoning delay for 23 I cases (List at Annexure IV of 8 pages) may be considered.

The Committee deliberated and recommended for condoning delay of 33 cases (list at AnnexureIII) and 231 cases (List at Annexure [V) to IMSC.

Aeenda No. 05: Consideration c,f in-principle loan sanction under ATUFS as per therepresentation of AEPC

The matter was initially placed on 9'r' TAMC held on 20.12.2017 under agenda point 09 as stated

below:

"lt was brought to the notice of the Committee that in a few cases, the units have produced

invoices which are prior to the actual loan approval but have urged that they had received inprinciple term loan approval prior to the invoice date.

b.Page 2 of 11

Dccision of TAMC:

Decision of TAMQ

,3frfr

The Committee deliberated on the said issue and decided that as per the guidelines of ATUFS

@ara a.6.1), "The date of sanction of term loan shall be the date of the letter of the lending

agency vide which the sanction of term loan iS communicated to the entrepreneur. Therefore,

there is no scope for consideration ofdate of in-principle tenn loan approval by lending agencies

under ATUFS".

The matter was again placed in the 17th TAMC and the Committee decided that the decision of96 TAMC shall continue.

a. Canara Bank- In principle loan sanction is not actual loan sanction hence concur the

opinion of the committee, as per bank norms purchase of cost of plant and machinerypurchased six month prior to the date ofsanction is considered for reimbursement. Hence

invoice dated six month prior to the date ofsanction rnay be considered.

b. Central Bank of India- concur with the decision taken by the Committee as perguidelines of ATUFS (para 4.6.1).

c. India Exim Bank -Any bills/invoices which are issued after the in-principle term loan

approval may be considered /covered under the ATI-IFS guidelines. This is suggested inview of the follbwing:i. Loan sanction process may take longer time specially in cases where more than

one Banks are involved i.e. multiple banking arrangement/ Consortium Lending.

This may lead to delay in final sanction by banks and may adversely affect the

project timeline as well as viability of the project wrt to cost and availability ofmachinery.

ii. Further if the bonower is in a position to bring in short-term liquidity/utiliseintemal accruals and make payments for tho machinery, reimbursement for the

said machinery post issuance of final sanction and completion of documentation

may be considered acceptable. This may be permitted subject to the company

giving list ofmachinery before in principle sanction and retaining the same, at the

time of reimbursement.

d. !!p!!- No invoice prior to the loan sanction date is to be accepted under ATUFS.e. PNB -In principle sanction may be considered as date of sanction of Term Loan in the

cases where subsequent final sanction contains the issuance of In Principle sanction.

Comments are being solicited from remaining lending agencies.

v,3*A\6

Page 3 of 11

AEPC again represented to consider the agenda in the l8h TAMC also. Hence for deliberationand knowing the insights, opinion /comments I'rom all lending agencies registered under ATUFSwere sought. Accordingly, comments received from some of the banks as given below wereplaced before the TAMC:

Decision of TAMC:The committee deliberated the issue with the members of Banks and Industry Association at

length and decided that the in-principle sanction may not be considered due to operational

difficulties and considering the existing ATUFS Guidelines and hence decision of gs TAMCshall stand and continue to remain unchanged as on date.

However, presently comments have been received only from 5 agencies with divergence in the

views as well as practices. As such comments are awaited from other lending agencies. It is

considered that based on the responses of all lending agencies (at appropriate seniority level

reflecting policy position of the Banks) and a dedicated meeting on the issue with the lending

agencies/Banks matter can be consiclered for review in next TAMC.

Agenda No 6:Eligibility of claim where term loan is sanctioned to Borrower and Co-Borrower:This Office had received a lbw claims where term loan has been sangtioned to two parties;

borrower (unit claiming benefits under A'IUFS) and co- borrower. SIDBI has represented that

bank has approved credit policy stipulating co applicant /Co-bonower in some cases where the

co-borrower is ou'ner of property offered as collateral security for the said loans or where the

loan limit is exceeding certain threshold limits however, the main borrower is the firm or concem

which is purchasing the asset such as factory land and building or plant and machinery for theirbusiness and co borrower is not the co owner of these assets. Further in such cases the co

borrower act as a guarantor which takes responsibility of repayment in case of default by main

borrower. The matter was placed an<l deliberated in the l4m TAMC. The Committee has decided

that term loan sanctioned jointly to Borrower and Co-Bonower by the lending agency/bank,

sanctions will not be eligible for subsidy under ATUFS. The same claimants have again

requested to place the agenda in the 'IAMC for deliberation.

Hence for deliberation and knowing the insights. opinion /comments from all lending agencies

registered under ATUFS were souglrt. Accordingly, comments received from some of the banks

as given below were placed before the TAMC:

a. Central bank of India- If the Bank is satisfied with the fact that main borrower(firm/company) is the purchaser of assets created out of the loan sanctioned and co-borrower is in the capacity of guarantor for the loan, then main borrower should be treated

as beneficiary for subsidy claim and co-borrower should be treated in the capacity ofguarantor only.

b. Canara Bank-Eligibility of claim where term loan is sanctioned to borrower and Co-Borrower for this agenda we concur the opinion ofthe SIDBI

c. India Ex im Bank- will not be in a position to comment on the same, as we do not have

case where loan is sanctioned lo two parties i.e. borrower and co-borrower.

t/,,3silh

Page 4 of 1l

d. SIDBI- SIDBI has not advised about loans sanctioned to co-borrou'er, However, co-borrower are guarantors of loan and in case of default, they are also responsible inrepayment ofthe said loan. Necessary legal action is also initiated against such guarantors.

e. PNB- Any claimant of subsidy should be owner ofthe asset only for which Term Loan is

sanctioned.

f. SBI- The agenda does not clearly bring out what is desire. Ifthe eligibility of Cuarantor is

under question, as per understanding, the guarantor should not be eligible for subsidy under

the scheme.

Decision of TAMC:The committee discussed the agenda with the members of Banks and Industry Association indetail and decided that more material required studying the matter and hence the decision was

deferred, but till then the decision ofthe l4s TAMC shall stand and continue.

Agenda No. 1: Request of M/s. Cheer Sagar, Mansarover, Jaipur forwarded by AEPC.

The application of IWs. Cheer Sagar for subsidy under ATUFS on Digital printingmachine has been rejected by RO Tx.C on the grounds that at present this machine is Eligibleunder ATUFS (MC0248) for Textile Processing units only.

The unit has now requested this office to amend the eligibility criteria as under:

Present Eligibility of Machinery

ITC Decision: The ITC has recommended the change in the required eligibility of machinery

and referred the matter to TAMC for discussion / decision in its next meeting.

The committee deliberated and decided to amend the eligibility of Machinery as recommended

by ITC.

Agenda No. 2: Clarification asked for by TUFS Cell on the eligibility of claims pertainingto units who have purchased machines from M/s. Fukuhara Industrial & Trading Co. Ltdwhich has been delisted now as they are traders and not a machinery manufacturer.

bv

Required F ligibility of Machinery

MC 02-48 : Digital / Ink jet printing machines

(for textile processing units only)MC 02-48 : Digital / lnk jet printing machines

(for textile processing units & Garment

manufacturing units only)

8s't$

Page 5 of U

Decision of ITC for ratification by TAMC

Decision of TAMC:

M/s. Fukuhara Industrial & Trading Co. Ltd was enlisted at Sr. No. 73 (Annexure-ll) {By Expert

Committee). Later on it was observed that M/s. Fukuhara Industrial & Trading Co. Ltd is atrader and not a machinery manufacturer. Accordingly, it was proposed to delist with effect from

09.10.2020 the name of IWs. Fukulrara Industrial & Trading Co. Ltd from Annexure-ll. ln the

meantime, TUFS Cell has now raised the query about the eligibility of claim pertaining to the

units who have purchased machines from the said suppliers during RR TUFS and ATUFSperiod.

The committee decided that the claims pertaining to the units who have purchased machines

fiom M/s. Fukuhala Industrial & Trading Co. Ltd during RR TUFS and ATUFS period (Between

the enlistment and delistment period under ATUFS) may be considered subject to the fulfillmentof all other conditions laid down in guidelines under ATUFS.

Agenda No. 3: Action to be taken with respect to the inclusion of machinery manufacturerswho have not submitted proper embassy certification under ATUFS.

The matter was placed & discussed in the l't Intemal Committee Meeting (lTC) held on

27108/2019 wherein it was observed by the committee that the concemed Embassy /Consulate

General have not certified the stalus of machine manufacturers, but mentioned as "Seen in

Embassy/ Embassy shall not held responsible for the documents" which is not as per Circularno.6 (201 8-20 19 series) dated 3 I .08.2018. Hence, Committee refeqed the matter to the

forthcoming TAMC for taking policy decision. Accordingly the matter was placed in the l4th

TAMC meeting held on 25.09.2019, wherein it was decided that the machinery manufacturers

should obtain required certificates from the Embassy. It has also been decided to simultaneouslyrequest Ministry of Textiles to take up the matter in respect of these machinery manufacturers

with the concemed Embassies.

Accordingly the matter was taken up with Ministry of Textile vide this office letter dt.

25/l0l20l9.ln this connection, MOT vide letter dt. llll2l20l9 has conveyed the decision taken

in the 4th meeting of IMSC held on 2411012019 to review the extant procedure for enlistment ofmachinery / accessory manufacturel in consultation with D/o Revenue, D/o Commerce and D/oHeavy Industries. ln reply to MOT letter, TxC office vide letter dt. 3110112020 has requested

J2,3srle

Page 6 of 11

ITC Decision: As per the lTth TAN,IC decision, the unit enlisted in Annexure-ll may submit the

requisite documents within three months from the date of asking documents for restoration as per

4th IMSC decision. ITC is of the opinion that claims pertaining to the units who have purchased

machines from the said suppliers during RR TUFS and ATUFS period may be considered.

However the matter may be placed in the next TAMC meeting for further discussion / decision.

Dccision of TAMTC:

MOT to take up the issue with D/o Revenue, D/o Commerce and D/o Heavy Industries through

Ministry for their suitable advice.

As around 160 applications are pending with this office due to want of proper Embassy

Certificate, and till date this office has not received any suitable advice from MOT, the matter

was once again taken up in the tTth TAMC held on 29/0712020 to advice on the next course ofaction to be taken in the matter, wherein it was decided to form Expert Committee comprising ofITC & TMMA (I) to work out operable modalities which are in compliance to the rules on thisissue, t

In the meantime, it is felt that the validity of the Embassy Certificates rvhere the Embassy

has stamped 'Seen in Embassy/Consulate' and/or stamped 'Embassy shall not be held

responsible for the documents' may be re-examined by the Internal Technical Committee.

17th TAMC decision: The I 76 TAMC held on 29107 /2020 has advised to form Expert

Committee comprising of ITC & TMMA (l) to work out operable modalities which are incompliance to the rules on this issue. The Chairperson has proposed that a meeting ofthe Expert

Committee may be called for at the earliest and any other experts / embassy person may also be

called to attend the said meeting. A proper Agenda is to be prepared and circulated to all the

members of the Expert Committee at least two days in advance. Any additional agenda points

received after preparation of the draft agenda will be discussed with the permission ofthe chaironly. Accordingly, the Expert Committee meeting held on 0.1.09.2020 and 15.09.2020.

Expert Committee Decision: As per said circular No.6 dated 31.08.2018, Embassy /Consulate

General of the respective country in India can certiry the documents. lri this context, the

Committee was of the opinion that those Embassy Certificates, which have been routedthrough the Ministrl, of Foreign Affairs of the respective countries atrd there is clearcertirication by the Ministry of Foreign Affairs ofthe respective countries stating that themanufacturer is actually Iocated in their country and manufacturing textile machines may

be accepted even with the disclaimer by Indian Embassy/consulate viz.. "Embassy / Consulate

General accepts no responsibility ol the content" and ''Seen in the Embassy / Consulate

General", since as per said circular No.6 dated 31.08.2018. Embassy /Consulate General oftheresp€ctive country in India can certify the documents and hence in place of them if Ministry ofForeign Affair (MOFA) of the respective countries, for example, Republic ol'China are giving

same certification, then that may be accepted. If same procedure is being adopted by other

countries, it may be accepted for enlistment under A-TUFS subject to approval of TAMC,following due assurance on documents so submitted. Examples ofcertificates routed through the

Ministry of Foreign Affairs, Republic of China are placed below as Annexure-A(of 4 pages) to

illustrate the point of certification being the Government of respective country and hence

considered acceptable/ on par with the documents certified by Embassy/Consulate of respective

country in India.

\-A'' ' j*rutY5tY/ , tase7of11

Issue related to Apostille Certificate submitted by the various Machine Manufacturers as

Embassy certificate: -

Expert Committee Decision: The ('ommiuee decided where any Government Body of any country

is certifying the manufacturing acrivities of the applicant and where an Apostille certifies the

signature and the capacity of the signer and the seal or stamp it bears, then the same may also be

accepted subject to approval of TAMC. Examples of such Apostille Certificate is placed below as

Annexure-B (of 2 pages).

The Committee deliberated and decided that since lndian Embassy, itself in their website has

stated that they will accept trade documents for certification only when if the same is signed &certified by the Ministry of Extenral Affairs ol'the respective countries and even after saidcertification by the Ministry of External Affairs of the respective countries Indian Embassy inrespective country will only stamp as "Seen in Embassy" and does not bear any responsibility,hence as recommended by the Expert Committee that if Ministry of External Affairs of therespective country in certifying clearly the manufacturing activities of textile machinemanufacturers and same is seen and signed by the Indian Embassy situated in respective countryhas to be accepted for enlistment subject to other documents as per Circular'6' dated 31.08.2018are found proper and after due assurance on veracity of documentation and other control checks.

As regard to decision of the Expen Committee in case of Apostille Certificate, it was decidedthat any authorized Government body ofany country is certifying the manufacturing activitiesof the applicant and where an Apostille certificate bears the signature and the capacity of thesignatory with the seal or stanrp, then the same may be considered subject to from the samecountry, no certification of Embassy had been submitted earlier by any manufacturer.

Agenda No. 4: Request of Tiruppur Export Knit Printers AssociationThe Tiruppur Export Knit Printers Association have requeste{ for the inclusion of

'Computerized Multi Head printing machine for garment and garment panels' under MC -02. Atpresent the said machine is appearing under MC-04 i.e Machinery for Apparel and Garment.

Now, the association want it to cover under MC-02 i.e. Machinery for processing ofyam/fibre/fabric so that all printing units doing job work of printing on knitted garments can

avail the benefit ofthe scheme.

ITC Decision: 'I'he Committee recommended to TAMC that the 'Computerized Multi head

printing machine for garment and garment panels' may be covered under MC-02 also i.e.

Machinery for Processing of Fibre/\'amlFabric.Decision of TAMC:The committee decided to consider the Computerized Multi head printing machine for garmentand gamrent panels in the Annex. No. MC 04-l l3 under MC-02 (Processing Segment with l0%CIS) also.

a 66Ai6

Page 8 of l1

Decision of TAMC:

Agenda No. 5: Consideration of Label weaving machine supplied by N{EI InternationalS.R.L, Italy:-

13th TAMC in its meeting held on 23.02.2019 deliberated that Basic loom with label jacquard

machine procured from same manufacture only will be allowed under ATUFS. However, ifwoven label manufacturing attachment is required to be provided on standalone basis, it may be

considered separately by TAMC on receipt of request from industry / machine manufacturer. In

this regard, lWs. MEI htemational S.R.L, Italy has submitted a request to consider their machine

stating that "no machine manufacturers are manufacturing all lhe au:iliary machines,

accessories and components in-house. In case of Airjet looms and rapier looms produced by

loom manufaclurcrc, lhe jacquard, Harness, Accumulators elc., are boughl-oul ilemsproduced by other manufacturerc. MEI is buying Airjet / Rapier looms from machinerymonufaclurer os per the choice of cuslomen, modifying looms suitoble .for label weaving

attaching MEI lechnologt developed b1t lhem and readling it for weaving labels, The Airjetlooms and Rapier looms are already under ATUFS and are eligible for subsidlt".

Decision Taken in the 4ft ITC meeting held on ltll2020: The Commiuee is of the view oftaking Label manufacturing attachment as a separate or it can be considered as accessories ofthe weaving machine for manufacture of Labels. The matter may be referred to the TAMC fordeliberation and decision.

Decision Taken in the 15tr TAMC meeting held on 21112020: The matter rvas deferred to the

next TAMC, Meanwhile ITC may send a team to examine the technology and recommending

whether it is to be considered as main machine or accessory.

Decision Taken in tf,e 7th ITC meeting held on 7l7l2O2O1 The Ollicer-in-Charge, R.O.

Coimbatore and SITRA representative may visit the unit ancl submit the report within l5 days to

ITC for further consideration of the matter. If visiting team requires any help, they may contact

either Jt.Tx.C's. Shri S.P.Verma / Shri V.K.Kohli through Vrdeo Conference.

Accordingly, R.O. Coimbatore have visited the unit and submitted the visit report with the

following conclusion:

"It is observed that MEI Intemational srl Rapier and Airjet Label loom provides good qualityperfbrmance, production efficiency and innovative technology. The speed of Air Jet label

machine is up to 1050 picks / min and speed of Rapier machine is 650 pick / min (WIR is 1040

mtrs per minute).Therefore, the visiting team is of the opinion that the MEI Label Weaving

machines can be considered as the main machines.

ITC Decision: The Committee felt that the MEI Label Weaving Machines can be considered as

main machines as it is used for manufacturing of labels for fixing on the garments / Made ups.

Page 9 of 11t^0),\-7 dsluiF

The labels manufacturing are categories under "Cloth Tech" which is a sub - components oftheTechnical Textiles. The IMSC in its meeting l,eld on 27 -02-2019 (Agenda decision No. 7.7) has

decided to consider two invoices fL)r two parts of customized machines required for technical

textiles. As per recommendation of team of officers of SITRA and OIC, R.O. Coimbatore and

looking to the value addition on base weaving machines, this kind of arrangement isrecommended.

It is also rccommended that there may be name plates of two manufacturers used in the

machine i.e. shuttleless loom manufacture with dobby / Jacquard and MEI lnternational for value

addition. However to verify that Ml:.I International has not used second hand machine for value

addition, MEI wilt require to submit original invoice of shuttle less manufacture and year ofmanufacturing of looms with dobbl / Jacquard, rvhich should not be mole than six months old.

The report of R.O. Coimbatore has suggested 25 percentage value additions done by MEIon base machines. However, the Chairman, ITC is of the opinion that maximum 20oh va,lue

addition on the base machine may be considered.

Decision of TAMC:The committee decided to consider the MEI Label Weaving Machines as main machines since itis used for manufacturing of labels for fixing on the garments / Made ups subject to the

following conditions.

i. The unit should submit the original invoice of shuttleless loom manufacturer addressed

to tvl/s. MEI Intemational along with the shipping documents. (Packing List /Bill ofLading /Bill of Entry / Country of Origin)

ii. The date of invoice of the Shuttle less Loom should not be more than 6 month older

than the invoice of M/s. MEI intemational.

iii. The machine should fulfill the speed criteria of concemed shuttle less loom as per

ATUFS guidelines.

iv. Eligibility of machine shall be allow hence forth (prospectively).

v. Only 20Vo value addition on base price of loom with Dobby / Jacquard will be

considered for eligible subsidy.

Agenda No. 6: ln the 9th ITC meeting the application of two authorized agents was not

considered as the Parent unit was having another authorized agent registered under ATUFS.

Accordingly, a list of 26 manufacturing units having more than one Authorized Agentregistered under ATUFS is placed below for taking a decision in the matter.

v Jst)l6

Page 10 of 11

ITC Decision: The committee decided to maintain the status quo of the units as already

registered as Authorized Agents under ATUFS earlier. However ITC was of the opinion that a

manufacturing unit should not be having more than one authorized agent registered underATUFS.

However, the committee was also opined that as recommended earlier, authorized agents foronly those manufacturers should be allowed, who do not sell their machines directly in the

market.

Decision of TAMC:

The committee defened the agenda as the recommendation of ITC requires detail deliberationsin view of the provisions in GR under ATUFS, prevailing market practices and operational

difficulties.

Agenda No.7: The application of the following two units for inclusion machinery manufacturerunder ATUFS were placed in the 8$ ITC held on I 8.08.2020 and it is observed that Rabatex and

Karl Mayer are in Joint Venture, some of their products are in competition. but they chose tocollaborate to maximise their profit and cut on competition. Karl Mayer produces machines as

per specification ofand for Benninger, who in tum sales that machine at a premium in its market.

1) "Karl Mayer Textile Machinery India Pr.t. Ltd.Plot No. 302/1, Panchratna Industrial Estate, Sarkhej Bavla Highway, Changodar,

Ahmedabad-382213"

2) "Karl Mayer lndia Pvt. Ltd.Plot No. 30211, Panchratna Industrial Estate, Sarkhej Bavla Highway, Changodar,

Ahmedabad-382213"

ITC Decision: Karl Mayer is doing only assembly of the parts impo(ed from various units on

given addresses. The Committee also observed that since as per Circular No.6 dtd.3l108/2018,the application submitted all document however in sales figures they have shown nil value.

Many members of ITC were of the view that they are only assembling parts in India hence

cannot be considered as manufactures. However, Govemment of India has adopting Make-in-lndia policy and requesting foreign buyers to invest in India. Hence, TAMC may decide whether

can be considered as mhnufacture or not.

The Committee discussed in detail and deliberated to consider "Karl Mayer Textile Machinery

India Pvt. Ltd. and "Karl Mayer India Pvt. Ltd as a manufacturer.

The Meeting ended with Vote of thanks to the Chair.

b7

,fe,;)F Page l1 of 11

Decision of TAMC:

II

tslNo.

Name & designation of theparticipant

Organization

i Smt. Roop RashiTextile Commissioner & Chairman

Office of the Textile Commissioner

2 Ms. Usha Prahallad Pol.Dy. Director General& Member Secretary

J Shri S.P. Verma,Jt. Textile Commissioner

Office of the Textile Commissioner

.l Shri V.K. Kohli,Jt. Textile Commissioner

Office of the Textile Commissroner

) Shri S. Balara.iu,Executive Director

SRTEPC, Mumbai

6 Dr.P.A. Sakthivel AEPC

Dr. Siddharta Rajagopal Texprocil8 Shri Naren Goenka AEPC9 Shri A Ravindra kumar TexprocilIO Shri Bharat Gandhi Surat Art Silk AssociationII Stu'i Chandan haldev Union Bank of Indiat2 Ms.Vaishali.El3 Shli Chetna Waghmarel4 Shri Mohan Sadhwanil5 Ms Saeeta Patelt6 Shri Ralu Tapare Central Banl< of Indiat7 Shri Nilanjan Haldhar State Bank ol Indial8 Shri Rahul Khapardel9 Shri Kalyan Paul20 Shri Easwaral SIDBI21 Shri A Kantubh22 Shri Sachin Arora, Secretary TMMAZ) Shri Sanjeev,

Secretary General AEPC24 Shli Sunil Patil PEDEXIL25 Shri Dev kishankayath Bank of Baroda

26 Shri S.Sivakumar, Dy.Director Otfice of the Textile Commissioner27 Ms Avni Cupta, Dy. Director Office of the Textile Commissioner28 Shri S.Mukherjee, Assistant

Director ' Office of the Textile Commissioner29 Shri Narottam Kumar,

Assistant directorSri B.K.Sahoo. Assistant Director

Otllce of the Textile Commissroneri0 Otllce of the Textile Commissroner

Co on BankICICI Bank

APEC

Bank of Baroda

Annexure-l

List of Participants attended vide vC in l8th TAMC held on 09.10.2020

ht

Otfice of the Textile Commissioner

7

t-IJ St 0-l !f, naA;'** rrvplaa7*tt -t-..! ^ttfr+t. *l"12A6 i^fhd d. rEhirtr"c v,tdry. *?ti4

d\ cq &4' ?a )'2

{..rnartwr -!-'ANNExURE-s[

SR.NO.

NAME OFTHE I,]NIT ELIGIBLE TEXTILEMACHINECO\tsREDUNDERWHICHANNEXT]RE OFATI'FS

MOUFORSUBSIDIARYUNIT/AUTHORISED AGENTWITH o/o OFCOMMSSION

REMARK

I W,T,T, TECHNOLOGYSERVICES INDIA PVT. LTDNO.3 COLLEGE CROSSROAD, AVARANKANU,TIRPIJ'R641 602, TAMILNADU, INDIA

MC-1-B-9,MC-2-9,IlC-2-36,MC-2-37.MC-6-A,,1.K.MC-6-C-s

2 ARADHANA TEXTILEENGINEERSPLOT NO,S-I 1, MARUTIIN'DUSTRIAL SOCIETY,BEHIN'D NOVA COMPLEX,BHEDWAD, PANDESARA,strRAT-394 220

MC-1-B-s-(r)

3 BHAGYAREKHAENGINEERS PVT. LTD,A-2, 6/ 1 02, GIDC SACHIN,SURAT.394 230

}lC-2-41,MC-2-42 RECOMMENDED (BRANDNAMEDEVREKHA)

4 NILKANTH ENGINEERSPOLT NO. 58-59, PAREKHINDUSTRIAL ESTATE.2,OPP, SAHYOG HOTEL,TATITHATYA, KADODARABARDOLI ROAD, SIJB.AT

MC-2-73,MC-z-24,MC-242,MC-2-34

5 AAKASH TEXTILEENGINEERS LLP.PLOT A.6/7,ROADNO.s,TJDHNA I-,,DHYOG NAGAR,ST'RAT, GUJARAT-39421 O

6 PERFECT ENGINEERINGCORPORATION,AHMEDABAD

MC-l-A-l ,3.4 & 7

7 IWS, ASIA KINGDOMMACHINERY INDUSTRY COLTD. TA]WAN,

MC-2-41,MC-2-42

8 M/S, BENNINGERZELLGMBH, GERMA].IY

MC-2-34,MC-3-E-7.MC-3-E-8.MC-3-E-9,MC.3.H2,MC.3-H.

RECOMMENDED tr..] 8TH ITC,ADDED ON

V

MC-1-B-5,MC-1-B-l5

>-F,

.F.n".rruvt $arg$$€uF*

6,MC-3-H-13 RECEIPT OFNOVERIFICATION

9 I\4/S. KARL MAYERTEXTILMASCHINENF ABRIKGERMA].IY (PARENTMANUFACTI]RE)(SUBSIDIARY T]NITS)1, N4/S. KARL MAYER (

CHINA ) LTD,CHINA.2- M/S, KARL MAYERROTAL S.R.L. ITALY,3, IWS, KARLMAYERTEXTILMASCHINEN AG,SWITZERLAND.4, IWS. KARLMAYER(H,K)LTD. HONGKONG.

l0 lvf/S. UNITED TE)C\{AC PTELTD, SINGAPORE (PARENTMANUFACTURE)(SUBSIDIARY I,]MTS)1.I//S- TE)flV{AC BHD SDN,MALAYSIA2. IWS. SOUTMRN TE)G,{ACMACHINERYLTD., CHINA.

MC-1-C-l

MC-1-C-l

11 N{/S, ITEMA S,P,A,, ITALY(PARENT MANUFACTI.,RER)SUBSIDIARY UNITS:1.I\4/S ITEMA WEAVINGMACHINERY (CHINA)CO.LTD,, CHINA2. I\4/S ITEMA TECH S,R.L,ITALY3. IU/S ITEMA(SWITZERLAND) LTD.,SWTIZERLAND4. M/S rrEMA (ASrA)LIMITED, HONGKONG(AUTHORZED AGENT OFI\4/S ITEMA S,P.A. ]TALY &IWSITEMAWEAVINGMACHINERY (CHINA)

MC-1-A-l

lYo

V

MC-1-C-4, MC-1-A-B-4, MC-I.C.5, MC-l-A-B-5, MC-1-C-4,MC-1-A-B-4,MC-1-c-8, MC-r -A-B-8,MC.1.C.8, MC.I.A-8.8, MC.l-C-4, MC-1-A-B-4,MC-3-D-6,MC-3-D.5, MC-I-C-4, MC-I-A-8.5, MC.1-C-4, MC-l-A-B-4,MC-l-C-8, MC-l-C-4, MC-l-A-B-4, MC-3-D-6, MC-3-D-5,MC-l-B-3. MC-1-A-B-12,MC-1-A-B-8,MC-3-B-l,MC-7-4,MC-1-B-1.

3%

12 TWS, VANDE WIELE ].N/.,BELGII'M. (PARENTMANI]FACTI]RER)SUBSIDIARY UNIT:N{/S. VANDEWIELE(NANJING) TEXTILEMACHINERY CO. LTD.CHINA

l3 I!4/S, SAN INDITEXVENTURES, MI]MBAI.(AUTH. AGENT OFBENNINGERZELL GMBH,GERMANTY)

3-4%

14 IWS, KNIT.FAB TECHMCSPVT LTD, MIJMBAI,Ivl/S. VOLSTART TE)O{ETSERVICES. KOLKATA.(AUTH. AGENT OF M/S.SOUTHERN TDC\,{ACMACI{INERY LTD, CHINA &IyYS. TDCUAC BHD SDNMALAYSIA)

5o/o

t5 IWS, WUZUINTERNATIONAL, MEERIJ-T(uP) (AUrH. AGENr OF N{/SZHUJIZHONGYU SEWINGEQI]IPMENT CO, LTD.,CHINA)

5o/o

l6 IV?S, SI]N MAKINA DISTICARET LTD,, STI ,

TIJRKEY

MC-3-I-10

17 I\4/S. GUJCI{EMINTERNATIONAL8, ADHARSHILA APPT,,6,PRAKASFTN AGAR SOCIETY,JAWAHARCHOWK,MANINAGAR.AHMEDABAD.8

MC-2-9,MC-2-36,MC-2-37

l8 IWS. SPARKLE CLEAN TECHPVT,LTD,CORPORATE OFFICE;89,GAUTAMCOMPLEX,SECTOR.I I, CBD BELAPLI&NAVIMUMBAI-4OO 614,

MC-2-9,MC-2-36,MC-2-37

^^J ba.Ctai '4 ^-e'-l;4, onl - vtz-o , ANNEXURE -AT

CO,LTD,, CHINA

g-E>--F-,

l;V+ + lZ alc w''"'.-'{a''t|-.a

)ri; bl "J ,.; (Eq t trnc- 6t:' 1

\

ANNExURE,A-B

INDIAMC-2-36,MC-2-3719 ]WS. AMBAENGINEERS

AND PROJECT,DABUA PALI ROAD, OPPSAKSHI DHARMA KANTAKHASRANO,27FARIDABAD

MC-3-E-9 AI-READYENLISTED,NEWMACHINERYTOBEADDED,

20 I{/S. J, ZIMMERMASCHINENBAU GMBH,AUSTRIA.

2l IVI/S. KIENERMASCHINENBAU GMBH,GERMANY

MC-3-E-1o,MC-3-F-4,MC-3-H-14

22 N1yS. CANLARMEKATRONIKSAN. VE TIC, A.S. ( TURKEY)

MC-2-6,MC-z-29,MC-2-39,MC-2-4t,MC-242,MC-2-59,MC-2-75,MC-z-l1,MC-2-A-11,MC-7-2t,MC-1-23MC-1-A-723 I\4/S. STAI.,IBLI FA\'ERGES

SCA, FRANCE.5%]WS.75 ENERGEC

SOLUTIONS LLP.AHMEDABAD (AUTH.AGENT OF IWS/W.T.TTECHNOLOGY, SERVICESINDIAPVT. LTD., ITALY)

25 N,I/S ,ANAADIH VINCOM PVTLTD,KOLKATA (AUTH.AGENT OF I\,,S PVRMACHINERY TECH (P) LTDCOIMBATORE

5o/o

26 5y6

N4/S. KNTT.FAB TECHMCSPVT,LTD., MUMBAI (AUTH,AGENT OF I\4/S/ PIROVANO

27 6%

?&-sl

T'lS. GOLDEN FALCONINTERNATIONAL., TIRUPUR(AL-rrH. AGENT OF I!4/S.ZHUJI YUANJINGMECHANICAL&ELECTRICAL CO., LTD.CHINA

V

I :vt d-L 2z ry1lc t^t*-'fal''-t a^^-a elL'tggnul ^a"'€ffi;,5 ^L

'io 76-t-tL ert l4 e<t'2r2-o' ANNExuREg

7=:=/

S,R.L., ITALY)28 N{/S, CLEAN COMBUSTION

PRTVATE LIMITEDPLOT NO. 701, KERALAG.I.D.C, BAVLA TA,DHOLKA, AHMEDABAD-382220, GUJARAT, INDIA

MC-2-73

29 IWS. ILSA S.P.A ITALY MC-4-l l4

30 T//S, KTKLD,\ PORTUGAL MC-2-28,MC-z-40,MC-2-76

3l IvI/S. 75 ENERGECSOLI]TIONS LLPAHMEDABAD (AUTH.AGENT OF IU/S, CANLARMEKATRONIK SAN. \'E TICA,S. TURKEY)

60

32 I\,I/S, ANUSH TEXTILESOLUTION TIRPUR (AUTHAGENT OF I\4/S. KTK LDA.,PORTUGAL)

l SYo

33 M/S. QMATEXBVBA,BELGIT]M

MC-l-A-1,MC-1-A-7,

Anarn-T1

List of units recommanded for condonation of delayed submissiou for. UID due toDigital Signature Certification t.su. lDSC;ffiff c

T+er-c ,n ? cqSr,No. Name of the Unit \"ame of the Bank Tuf Ref No.

M/s.Jayasri Polymers State Bank of India ATUFS/201 8- 19i2953

M/s. Kuneh Techniques Bank of Maharashtra ATU FS/2048- 19/2601

J M/s. Aftiston Appearels Prt Ltd 'l amilnad N'lcrcantile Bank Limited ATUFS/2019-20/191

M/s. KPM Processing Mills Pvt Ltd Lakshmi Vilas Bank ATUFS/2017- 18/2857

5 M/s. Doddi Fashion Textiles Pvt Ltd DNS Bank ATUFS/2018-19/2605

6 M/s. Puja Embrodiery works Central Bank of India ATUFS/2O18- 19/361 8

7 Orintal Bank of Commerce ATLI FS/20 I 8- l9/2904

8 M/s. Pushpanjali Textile P Ltd Orintal Bank of Commerce ATUFS/2018- l9l3522

I M/s. RamTex Fab Not Mentioned ATUFS/201 8- r 9/2602

l0 M/s. R.K. Industries State Bank of lndia ATII FS/20 | 9-201998

1l M/s. Jai Ambe lrnpex Bank of Maharashtra A',IUFS/20r 8- l9l3348

12 M/s. Sudh ir Texfab Punjab Nrational Bank ATUFS/201 8- l9/28 I

li M/s. Cheer Sagar Punjab National Bank ATUFS/2018-19/3448

r.+ M/s. T T Limited lndian llank ATUFS/20 r8-19/1940

l5 M/s. Esu,ar Designs I ndian Overseas Bank ATUFS/2018- l91427

l6 M/s. Fortune Labels Indian Overseas Bank ATUFS/201 8- l9l2836

Indian Overseas Bank A',IUFS/20 t 8- l9l2567

lll M/s. Estegi Sizing South Indian Bank A',ruFS/2018-19/2619

M/s.Shree Krishna Fabrics The Mehsana Urban Co-Op Bank Ltd A',l u t-s/20 r 9-20l866

20 M/s. Radhey Creation 'l lre Mehsarra Urban Co-Op Bank Ltd A'tu FS/2019-201865

M/s. Sl' Woven Bags Pvt Ltd State Bank of Ind ia A'IUFS/2017- l 8/ 1477

22 M/s. Sudarshan Textile Cosmos Bank ATTJFS/201 8- t 9/3283

23 M/s. l.ark Knitwears Kotak Mahindra Bank

Central ank of lndia

Central I ank of India

Central ank of India

Bank of l]aroda

ATUFS1Z0t9-20nt26

21 M/s. Madhav Textile ATUFSi20l8-19/3291

25 M/s. Vihana Fab ATUFSt20l7-t8t2192

26 M/s. Mahi Fashion ATUFS/20r 8-19/t785

27 ATUt-'S/20 r 8- 19/2833

28 M/s. Madhav Textile Bank of []aroda ATUFS/2018- r 9/3 137

29 M/s. Madhav Fashion Dena Bank ATUFS/20 r8-19/1696

i0 M/s. Rudra l'ex Bank of Baroda ATUFS/20 I 9-20l396

ll M/s. Ahill Knit Exports Indian Overseas Bank Al UFS/20 t8- 19/3 567

32 M/s.R.M.P Fab Sourcing (P) Ltd l anrilnad Nlcrcantile Bank l-irnited ATUFSt20tS-29t2261

M/s. Fashion Gauge Knitwears Oliental Bank of Conlrnerce ATUFS/2018-19/495

j, A0r ?

')

I

M/s. Sunpro Barrier Pack

17 M/s. Ahill Fashion'lextile Inc

l9

2t

M/s. Dhvani Textile

k

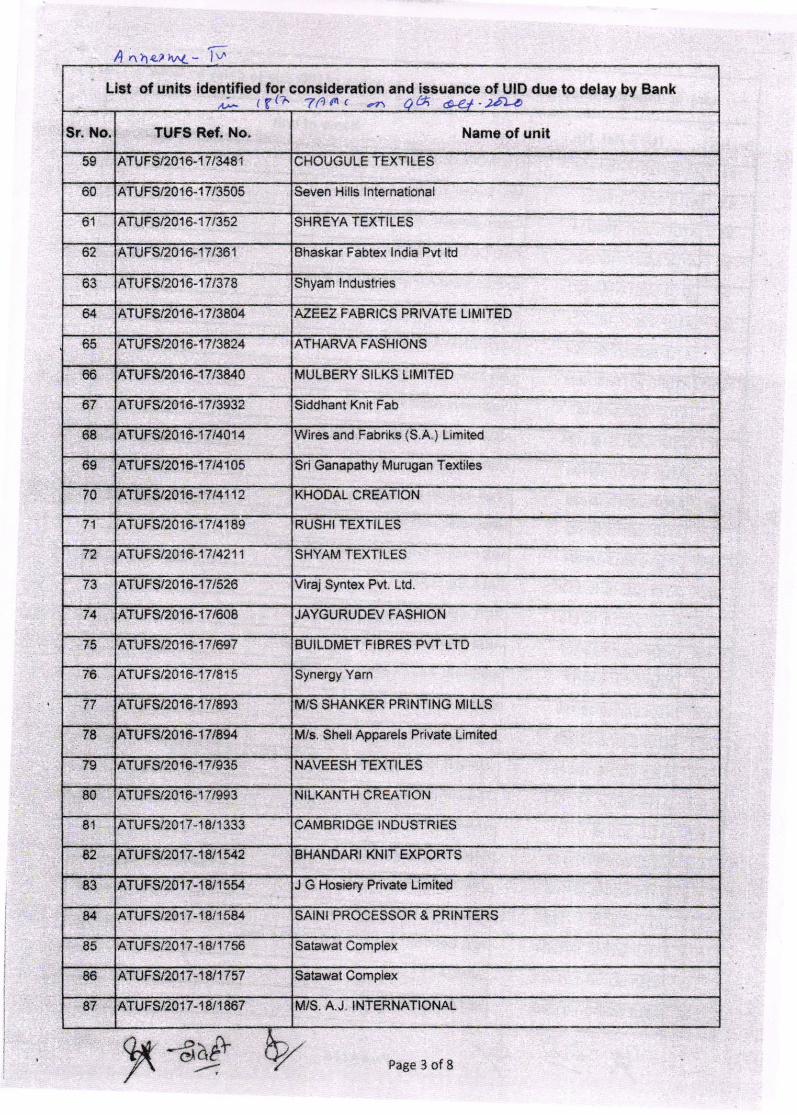

List of 231 unlts idontiflod for con$ldoratlon and bsuance of UID dus to delay by Bank,av 184 TnfiC q cth 44/ )8'O

Sr. l,lo. TUFS Ref. No.

ATUFS/2016-17/1706

Name of unit

1

2 ATUFS/2016-17/4129 PATODIA FILAMENTS PVT LTO

3 A1UFSt2016-17t4228 ANXITA TEXTILES

Birbal lntarnational Pvl. LtdATUFS/2016-17t634

6 ATUFSr2016-171695 M S CHHABRA KNITWEARS

6 ATUFSr201&17rl10 PS & AV KNITWEARS

7 ATUFS/2017-18/1056 KUNJ BEHARI PROCESSORS PVT LTD

I ATUFS/2017-18/108

I ATUFS/2017-18/'! 373 Sree Balaji Printing

10 ATUFSr20l7-18|/1455 KALA TEX

11 ATUFS/2017-18/1456 KALA CORPORATION

12 ATUFS/20'17-18/15 JAGDISH MAHAOEO PATIL

ATUFS/2017-18/1556 NEEDLE ART

14 ATUFSl2017-18/1595 DIVYA FASHIONS

15 ATUFS/2017-18/2133 Kanpur Plastipack Limited

16 ATUFS/2o'17-'t 8/2162 SHREE OM CORPORATION

17 ATUFS/2017-18/28 HARSH TEXTILE

'18 ATUFSi2017-181658 NEWTON TEXTILE

19 ATUFS/2018-19/ 179 PRABHANJAN INOUSTRIES LIMITED

20 ATUFS/2018-19/39 S.S TEXTILES

21 ATUFS/20'r 6-17l'1018 SHREE HARI TEXTILE

22 ATUFS/2016-17/1024 SHREE RAM TEXTILE

IJ ATUFSl2016. 17l1028 M/S SPAROW KNIT INDUSTRIES PRIVATE LIMITED

24 ATUFSl2016-t 7,'1074 EMEROIDERY UNIT

ATUFSt2016-17/1087 NA

26 ATUFSI2016-17/1 115 SARA TEXTILES

27 ATUFS/2016-17/1 12 SITARAM TEXIILES

28 ATUFSno16-17/124 s. R. J. lmports Exports

29 ATUF92016-17/1311 SHREEJI TEXTILE

Wd* b7 Page 1 of 8

Antr"-,r. -1O

Kamal Polypack

4

ARR BATH & HOME PVT,LTD,

IJ

25

Llst of units identlfled tor con$idoration and issuanco of UID duo to delay by Bank

TUFS Ref. No. Nem€ of unit

30 ATUFS/2016-17/1 349

31 ATUFS/2016-17/1398 S K. TEXTILE

ATUFS/2016-17/153 KHODIYAR TEXTIIES

ATUFS/2016-17/1 531 Prakash Cotex lndia LLP

34 ATUFS/2016-17/1 54 Rishabh Farm and lndustries Pvt. Ltd

35 AARTHI 41 TRADERSA1VFSt2016-17 t1727

ATUFSi20l6-17/1894 M/S, SIDHHI VINAYAK ENTERPRISE

37 ATUFS/2016-17/1916 RANCHHOD ART

38 AIUFS/2016-17/1921

39 ATUFS20'16-17/1958 M/S SEVA SURGICALS

40 ATUFSt2016-17D207 Krishna Peckaging

4l ATUFS/2016-17i2310 BHASIN CREATIONS

ATUFS/2016-17/2315 ESS ELL EMBROIDERY

43 ATUFS/2016-17/2318 HASMUKH INDUSTRIES

44 ATUFS/20't6-17/2343 N.S. CREATION

AluFst2016-17 t2370 Shri Sai Textile

ATUFSt2Al6-17 t2579 SHIV SHAKTI TEXTILE

ATUFSt2016-17/2614 HARIEHAI G. MAVANI

48

49 AtuFst2016-171?765 Prime Polycot

50 ATUFS/2015-17/2789 PRIME POLYCOI

51 ATUFS/2016-1 7/2820 M/S AMBICA TEXTILE

A"ruFst2016-1713244 A.S.A TEXTILES

ATUFS/2016-17/3259 ARYAN EXPORTS

54 ATUFS/2016- 1713296 K M.D, TEX CRAFTS

ATUFS/20'16-17/3338 SHRI KNITS

56 Mls. Khodiyar ArtATUFS/2016-17/3347

57 ATUFS/2016-17/3380 S K TEXTILES

58 ATUFS/2016-17/3480 GANGAPURE TEXTILES

%,-s* Page 2 of 8

Sr. Xo.l

SHREEJEE ENTERPRISE

HAR BHOLE FASHION

45

46

47

lAruFSr201e17n741Rlshabh Farm and Industries hn. Ltd.

4 nherut- iY

Llst of unib idontified [.,r^..F;*:oy "ii/?X.o, ulD duo to dolay by Bank

TUFS Rcr. No. Name of unit

ATUFS/2016-17/3481 CHOUGULE TEXTILES

60 ATUFSl2016-17/3505 Seven Hills International

61 ATUFS/2016-17/352 SHREYA TEXTILES

ATUFSz016-17/361 Bhaskar Fabtex lndia Pvt ltd

63 ATUFS/2016-17/378 Shyam lndustries

64 ATUFS2016-17/3804 AZEEZ FABRICS PRIVATE LIMITED

65 ATUFS/2016-17/3824 ATHARVA FASHIONS

66 ATUFS/2016-17/3840 MULBERY SILKS LIMITED

67 ATUFS/2016-17/3932 Siddhant Knit Fab

68 ATUFS/2016-1714014 Wires and Fabnks (S.A.) Limited

69 ATUFS/2016-17/410s

70 A1UFSt2016-17t4112

ATUFS/2016-17/4189

KHODAL CREATION

RUSHI TEXTILES

72 A1UFSl2016-17t4211 SHYAM TEXTILES

73 AfUFS/2016-'! 7/526 Viraj Synt€x PW. Ltd

74 ATUFS/2016-17/608 JAYGURUDEV FASHION

75 ATUFSl2016-17/697 BUILDMET TIBRES PVT LTD

7A ATUFS/2016-17/815

77 ATUFS/2016-1 7/893 M/S SHANKER PRINTING MILLS

78 ATUFS/2016-17/894 M/s. Shell Apparels Private Limiled

70 ATUFS/2018-17/935 NAVEESH TEXTILES

80 ATUFS/2016-17/993 NILKANTH CREATION

81 ATUFS/2017-18/1333 CAMBRIDGE INDUSTRIES

ATUFS/2017-1811542 BHANDARI KNIT EXPORTS

ATUFS/2017-18/1554 J G Hosiery Private Limit€d

u ATUFS/2017-18/1584 SAINI PROCESSOR & PRINTERS

85 ATUFS/2017-18/1756 Satawat Complex

6b ATUFS/2017-18/1 757 Sabwat Complex

87 ATUFSn017-18/1867 M/S. A,J, INTERNATIONAL

-6a&% Page 3 of 8

Sr. lto.(o

Sri Gsnapathy Murugan Textiles

Synergy Yarn

83

List of units identified tor consideration and issuance of UID due to delay by Bank

TUFS Rof. No. Name of unit

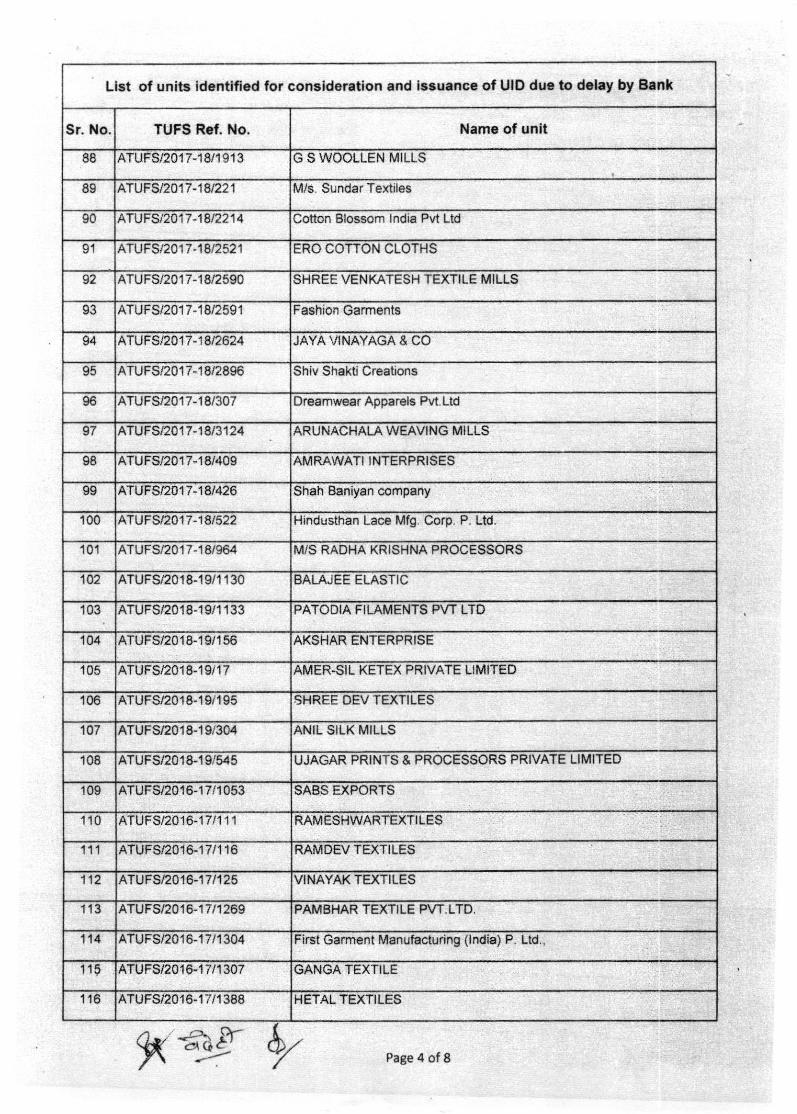

ATUFSno17-18/1913 G S WOOTLEN MILLS

89 ATUFS/2017-18/221 M/s. Sundar Textiles

90 A1VF3t2011-18t2214 Cotton Blossom lndia Pvt Ltd

91 ATUFSl2017 -18t2521 ERO COTTON CLOTHS

92 ATUFS/2017-18/2590 SHREE VENKATESH TEXTILE MILLS

93 ATUFS/2017-18/2591 Fashioo Garments

94 A1UF8nA17 -18t2624 JAYA VINAYAGA & CO

95 ATUFS/2017-18/2896 Shiv Shakti Creations

96 ATUFSl2017-18/307 Dreamwear Apparels Pvl.Ltd

97 ATUFS/2017-18/3 124 ARUNACHALA WEAVING MILLS

98 ATUFSt2017,18/409 AMRAWATI INTERPRISES

99 ATUFS/2017-18/426 Shah Saniyan company

100 AruFs/2017 -18t522 Hindusthan Lace Mtg. Corp. P. Ltd

101 ATUFSl2017-18/964 M/S RADHA KRISHNA PROCESSORS

102 ATUFSi/2018-19/1 130 BALAJEE ELASTIC

103 PATODIA FILAMENTS PVT LTD

104 ATUFS/2018-19/156 AKSHAR ENTERPRISE

105 ATUrSl20 l8-19/1 7 AMER-SIL KETEX PRIVATE LIMITED

106 ATUFS/2018-19/195 SHREE DEV TEXTILES

107 ATUFS/2018-19r3M

108 ATUFS/2018-19/s45 UJAGAR PRINTS & PROCESSORS PRIVATE LIMITED

109 ATUFS/2016-17/r 053 SABS EXPORTS

110 ATUrS/2016-17/1 1 1 RAMESHWARTEXTITES

111 ATUFSt2016-17/1 16 RAMDEV TEXTILES

112 VINAYAK TEXTILES

1t3 ATUFSi2016-1 7/1269

114 ATUFSl2016-1 7/1304 Firsl Garment Manufacturing (lndia) P- Ltd.,

11S ATUFSt2016-17/1307 GANGA TEX ILE

'116 ATUFSl2016-17/1388 HETAL TEXTILES

% 4v 6/PaBe 4 of 8

sr. no.I

88

lAruFS/2018-19/1 133

IANIL SILK MILLSI

lAruFSz016-17/125PAMBHAR TEXTILE PVT.LTD.

Ann lv^

List of units identifhd lot8'.^

consideration and issuance of UID due to dsla?A6C a q C-t''

y by Bank)u)4

TUFS Ref. No, Name of unit

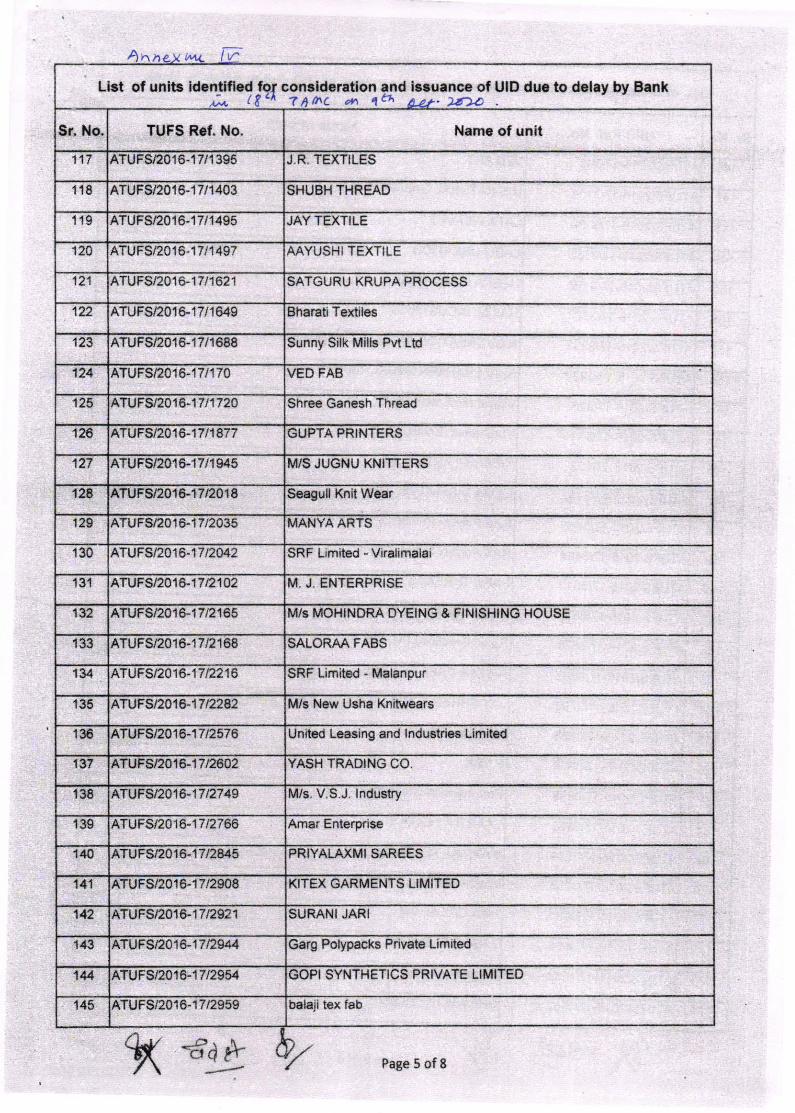

117 ATUFS/2016-17/1395 J.R. TEXTILES

ATUFSi20l6-17/1403 SHUBH THREAD

119 ATUFSI20l6-17/1495 JAY TEXTILE

120 ATUFS/z016-17/1497 AAYUSHI TEXTILE

121 AIUFS/2016-17/1621 SATGURU KRUPA PROCESS

122 ATUFSl2016-17/1649 Bharati Textiles

123 ATUFSi20l6-17/1688 Sunny Silk Mills Pvl LE

124 ATUFSI2016-17/170 VED FAB

125 ATUFS/2016-1711720 Shree Ganesh Thread

't26 A1UFSt2016-1711877 GUPTA PRINTERS

127 ATUFS/20'15-17/1945 M/S JUGNU KNITTERS

124 \TUF312016-17t2018 Seegull Knit Wear

129 ATUFS/2016-17/2035 MANYA ARTS

130 A-ruFst2016-17t20/2 SRF Limited - Viralimalai

13'l ATUFS/2016-172102 M. J. ENTERPRISE

132 ATUFS/2016-17/2165 M/s MOHINDRA DYEING & FINISHING HOUSE

133 ATUFS/2016-17/2168 SALORPA FABS

134 ATUFEn0l6-1712216 SRF Limited - Malanpur

135 A1UFS|2016-17 D2A2 M/s New Usha Knitwears

136 ATUFS/2016-1 7/2576 Unit€d Leasing and lndllstries Limited

137 ATUFSDAIAIT D6O2

138 ATUFSl2016-17 t2749 M/s. V.S.J. lndusfy

Amar Enterprise139 ATUFS/2016-17/2766

PRIYALAXMI SAREES140 ATUFS2016-17/2845

ATUFS/20't6-17/2908 KITEX GARMENTS LIMITED141

142 ATVFt2016-17n921 SURANI JARI

Garg Polypacks Private Limited143 AlUFSnol6-17t2944

144 ATUFS/2016-17/2954 THETICS PRIVATE LIMITEOGOPI SYN

balaji tex fab145 ATUFS/2016-17/2959

€a rLPage 5 of 8

Sr. No.

(

118

YASH TRADING CO.

x

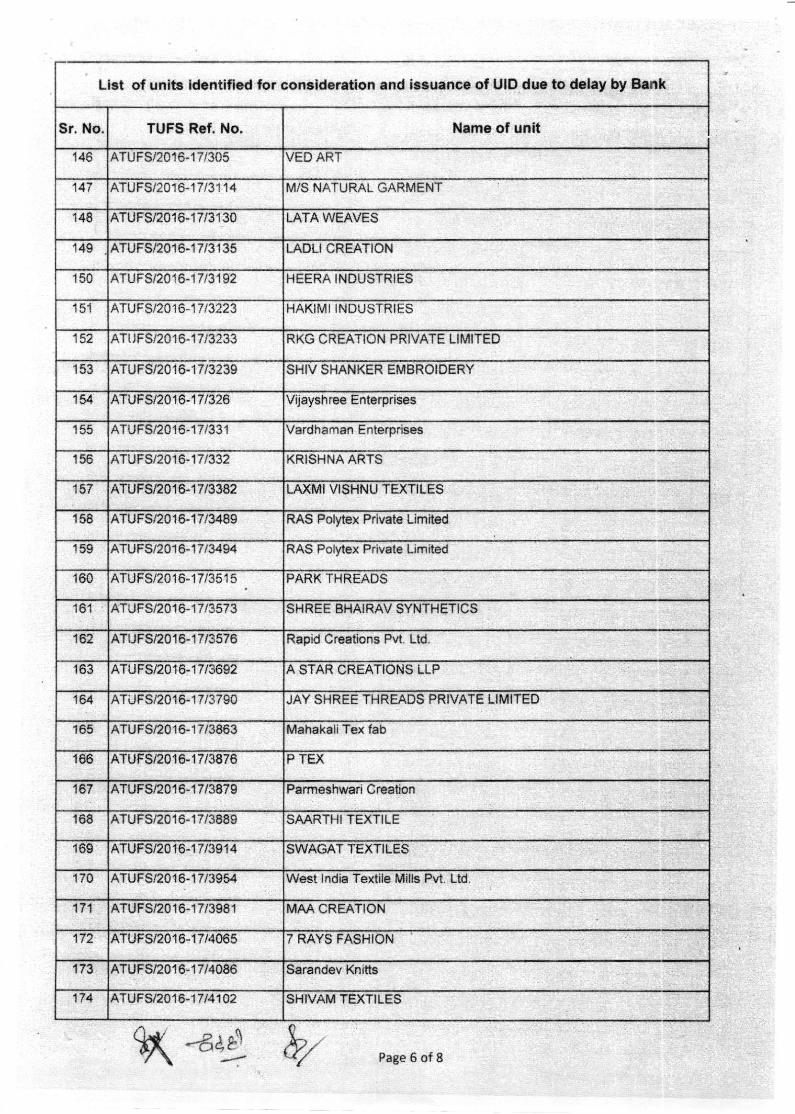

146 ATUFS/2016-'1 7/305 VED ART

ATUFS/2016-17/31 14 M/S NATURAT GARMENT

148 ATUFS/2016-17/3130 LATA WEAVES

LADLI CREATION

150 ATUFS2016-17/3192 HEERA INDUSTRIES

ATUFS/2016-1 7/3223

RKG CREATION PRIVATE LIMITED

153 ATUFS/2016-17/3239 SHIV SHANKER EMBROIDERY

1# ATUFS/2016-17/328 Vrayshree Enterprises

155 ATUFS/2016-17/331 Vardhaman Enterprises

156 ATUFS/2016-17/332

157 ATUFS/2016-17/3382 LAXMI VISHNU TEXTILES

158 ATUFS/2016-17/3489 RAS Polytex Private Limrted

160 ATUFSi 2016-17/351s PARK THREADS

161 SHREE BHAIRAV SYNTHETICS

la/t ATIJFS2016-17/3576

163 ATUFS/2016-17/3692 A STAR CREATIONS LLP

164 ATUFS/20'16-17/3790 JAY SHREE THREADS PRIVATE LIMITED

165 ATUFS/2016-17/3863 Mahakali Tex fab

166 ATUFS/2016-17/3876 P TEX

167 ATUFS/2016-17/3879 Parmeshwari Creation

168 ATUFS/2016-17/3889

169 ATUFS/2016-1 7/3914 SWAGAT TSXTILES

170 ATUFS/2016-17/3954 West lndb Textile Mills Pvt. Ltd

1 1 ATUFS/2016-17/3981 MAA CREATION

172 ATUFS/2015-17/4065 7 RAYS FASHION

t/J ATUFS/2016-17/4086 Sarandev Knitts

174 A1UrSt2016-17 A1A2 SHIVAM TEXTITES

List of units identified for conrideretion and issuanco of UID due to delay by Bank

Nam6 of unit

K -ad0Page 5 of 8

sr. No.l TUFS Ref. No.

14e .IATUFSEo1&.171313s

HAKIMI INDUSTRIES

1s2 lArr,'FS/2016-17/3233

KRISHNA ARTS

1s9 IATUFS/2o16-17/3494

RAS Polytex Private Limited

IATUFS/2016-17i 3573

Rapid Creations Pvt. Ltd.

SAARTHI TEXTILE

bt

4,< - JV

List ol units ideq ntified for consideration and issuance of UID due to delay by Bank6 a*.LtLd6 xl ert

Sr. No.

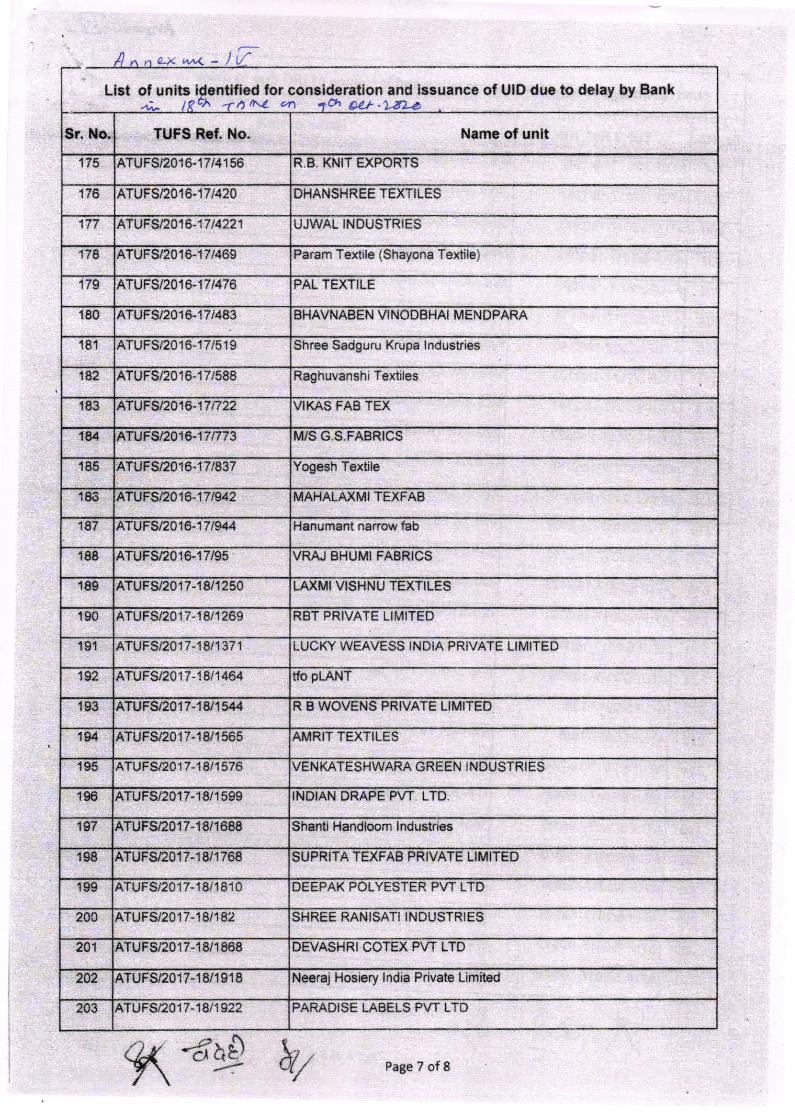

175 ATUFS/2016-17/4156 R.B. KNIT EXPORTS

176 ATUFS/2015-17/420 DHANSHREE TEXTILES

177 AruFst20l6-17t4221 UJWAL INDUSTRIES

178 ATUFSl2016-17/469

179 ATUFS/2016-17/476

Param Textile (Shayona Textile)

PAL TEXTILE

180 ATUFS/2016-171483 BHAVNABEN VINODBHAI MENDPARA

1 8 1 ATUFS/2016-17/519 Shree Sadguru Krupa lndustries

182 ATUFS/2016-17/588 Raghuvanshi Taxtiles

183 A7UFSt2016-17t722 VIKAS FAB TEX

184 ATUFS/2015-17n73 M/S G,S.FABRICS

185 ATUFS/2016-17/837 Yogesh T€xtile

loo ATUFS/2016-17t942 MAHALAXMI TEXFAB

tot ATUFS/z016.171944 Hanumant narrow fab

188 ATUFSt2016-17/95 VRAJ BHUMI FABRICS

189 ATUFS/2017-18/1250 LAXMI VISHNU TEXTILES

190 ATUFS/2017-18/1269 RBT PRIVATE LIMITED

ATUFS/2017-18/1371 LUCKY WEAVESS INDIA PRIVATE LIMITED

,o, ATUFS/2017-18/1464 tfo pLANT

193 R B WOVENS PRIVATE LIMITEDATUFSt20'17-'tU1344

1U ATUFS/2017-18/1565 AMRIT TEXTILES

ATUFS/2017-18/ t 576 VENKATESHWARA GREEN INDUSTRIES

196 ATUFS/2017-18/1599 INDIAN DRAPE PW, LTD

197 ATUFS/2017-18/1688

198 ATUFSt2017-18/1768 SUPRITA TEXFAB PRIVATE LIMITED

199 ATUFS/2017-18i 1810 DEEPAK POLYESTER PW LTD

20c ATUFSi2017-18/182 SHREE RANISATI INDUSTRIES

201 ATUFS/2017-18/r 858 DEVASHRI COTEX PVT LTD

242 ATUFS/2017-18/1918 Neeraj Hosisry lndia Private Limited

PARADISE LABELS PVT LTD203 A1UFSt2017-18t1922

0)\LI bt-EPage 7 of 8

TUFS Re'. No. Name of unlt

195

Shanti Handloom lndustries

9\

ln rn-D-List of units identified for consideration and issuance of UID due to delay by Bank

Sr. No. TUFS Ref. No. Name of unit

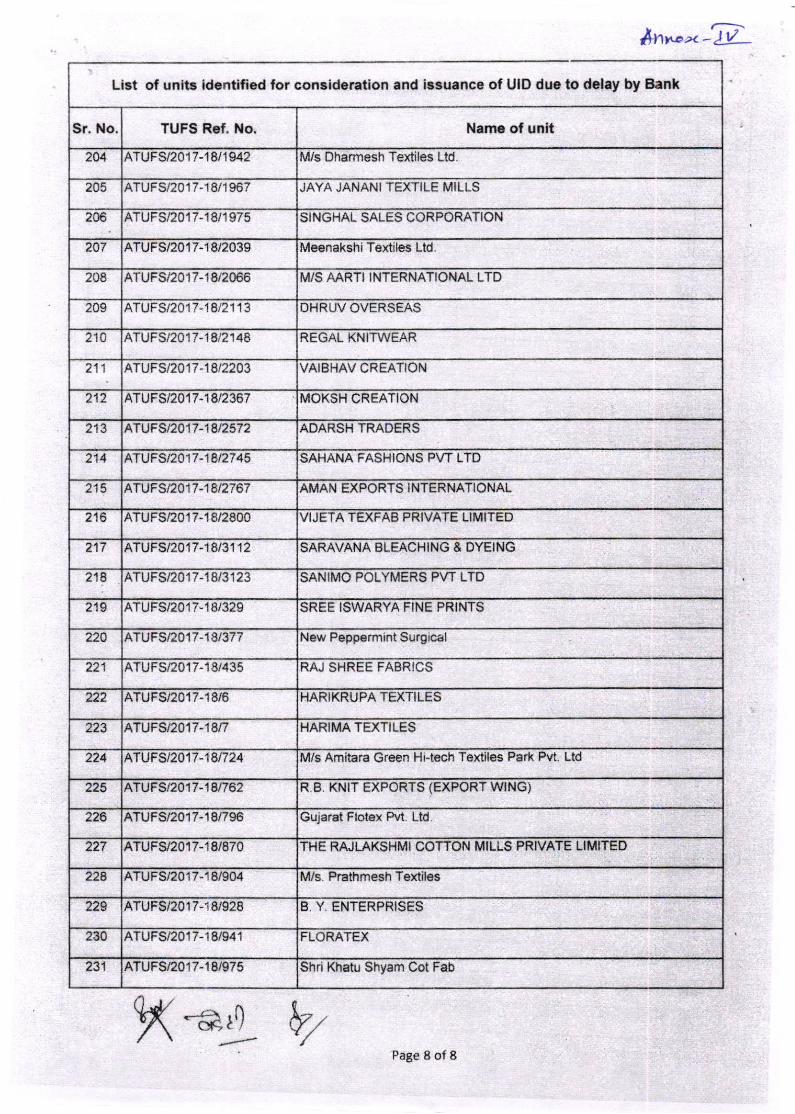

Mls Dhermesh Textiles Ltd244 ATUFS/2017-18/1942

zu5 ATUFS/z017-18/1967 JAYA JANANI TEXTILE MILLS

205 ATUFS/20'17-18/1975 SINGHAL SALES CORPORATION

207 ATUFS/2017-18/2039 Meenakshi Taxtiles Ltd

M/S AARTI INTERNATIONAL LTDATUFS/2017-18i2066

,no ATUFS/2017-18/2113 DHRUV OVERSEAS

210 AruFs/2017-18/2148 REGAL KNITWEAR

ATUFSi 2017-18/2203 VAIBHAV CREATION

212 ATUFS/2017-18/2367 MOKSH CREATION

213 AruFst20l7-18t2572 ADARSH TRADERS

214 ATVF 512017 -18t?7 45 SAHANA FASHIONS PW LTD

215 ATUFSt2017-18t2767 AMAN EXPORTS INTERNATIONAL

VIJETA TEXFAB PRIVATE LIMITEDzto ATUFS2017-18/2800

217 ATUFS/z017-18/31 12 SARAVANA BLEACHING & DYEING

218 ATUFS/2017-18/3123 SANIMO POLYMERS PVT LTD

210 ATUFS/2017-18/329 SREE ISWARYA FINE PRINTS

220 ATUFSno17-18/377 New Peppermint Surgical

zzl ATUFSt20l7-18/435 RAJ SHREE FABRICS

ATUFS/2017-18/6 HARIKRTJPA TEXTILES

223 ATUFS/2017-18'

224 AlUFSt2A17-18t724 M/s Amitara Green Hi-tech Textiles Park Pvt. Ltd

225 ATUFSt2AlT-18t762 R-8. KNIT EXPORTS (EXPORT WING)

2?6 ATUFS/2017-18/796 Gujarat Flotex Ad. Ltd

227 ATUFS/20 17-18/870 THE RAJLAKSHMI COTTON MILLS PRIVATE LIMITED

22A ATUFS/2017-18/904 M/s. Praihmesh Teltiles

lz3 B, Y, ENTERPRISES

230 ATUFS/2017-18/941 FLORATEX

231 Shri Khatu Shyam Cot Fab

V7WPage 8 of 8

208

HARIMA TEXTILES

ATUFS/2017-18/928

ATUFS/2017-18/975

-&,rl