Embed Size (px)

Citation preview

1

Client Welcome Pack & Onboarding Guide Version 1.00

2

TABLE OF CONTENTS 1 WELCOMING YOU TO MARKETAXESS ...................................................... 4

2 EXECUTIVE BRIEF ........................................................................................ 5

3 INTRODUCTION ............................................................................................. 6

3.1 Document Structure ........................................................................................ 6

3.2 Introduction to MarketAxess ............................................................................ 7

3.3 Meet MarketAxess .......................................................................................... 8

3.4 Timeline ........................................................................................................... 9

4 BUSINESS TRANSITION ............................................................................. 10

4.1 Legal Considerations .................................................................................... 10

4.2 Service Delivery During Business Transition ................................................ 10

4.3 Service and Support Model During Business Transition ............................... 10

5 MIGRATION .................................................................................................. 11

5.1 Migration planning ......................................................................................... 11

5.2 Service delivery after migration ..................................................................... 13

5.3 Description of migrated services ................................................................... 15

5.3.1 ARM .............................................................................................................. 15

5.3.2 APA ............................................................................................................... 16

5.3.3 Best execution – Quality of Execution (RTS 27) ........................................... 16

5.3.4 Best Execution – Top 5 Venue Report (RTS 28) .......................................... 17

5.3.5 Systematic Internalizer (SI) Identification ...................................................... 17

5.3.6 Systematic Internalizer (SI) Reference Data Reporting (RTS 23) ................. 17

5.3.7 Commodity Position Reporting (CPR, Art. 58) .............................................. 18

5.3.8 EMIR Reporting ............................................................................................. 18

5.4 Step-by-step migration lifecycle .................................................................... 18

5.4.1 Timeline ......................................................................................................... 19

5.4.2 Data Analysis and Submission ...................................................................... 20

3

5.4.3 Technical Connectivity .................................................................................. 22

5.4.4 Training and Testing ..................................................................................... 23

5.4.5 Cutover .......................................................................................................... 24

6 DATA STORAGE AND PROCESSING ........................................................ 26

6.1 Security Principles ......................................................................................... 26

6.2 European Data Store (EDS) .......................................................................... 27

6.3 The Virtual Private Cloud .............................................................................. 29

6.4 Network security ............................................................................................ 29

6.5 Encryption and Key Management ................................................................. 30

7 BUSINESS AS USUAL OPERATING MODEL ............................................ 31

7.1 Service and Support Model Post-Migration ................................................... 31

7.2 Generic Client Operating Model .................................................................... 32

7.3 Client Forums and Working Groups .............................................................. 34

7.4 Risk Management ......................................................................................... 34

8 MARKETAXESS SYSTEMS AND ARCHITECTURE .................................. 36

8.1 Technology Platform ..................................................................................... 36

8.1.1 Platform Overview ......................................................................................... 36

8.1.2 Deep Dive: Business Logic and Data Access tier Services .......................... 36

8.2 People ………………………………………………………………………………38

8.3 Software Development Life Cycle (SDLC) .................................................... 39

8.4 Summary of Activity ...................................................................................... 40

9 INVOICING & PAYMENT DETAILS ............................................................. 41

10 COMMON IMPLEMENTATION QUESTIONS .............................................. 41

11 GLOSSARY OF TERMS AND ACRONYMS ................................................ 61

For any help or assistance regarding this document please contact the Post-Trade Relationship Management (PTRM) team

• Email: [email protected]

• Netherlands – Telephone: +31 (0)20 8888 026 / UK – Telephone: +44 (0)20 3655 3588

4

1 WELCOMING YOU TO MARKETAXESS

You are now a MarketAxess Post-Trade client. We’re delighted to welcome you to our client family and want you to know that you’re in good hands. And, with this introduction, we want to quickly explain what being our client means. First and foremost, it means that you’re now part of an innovation story that’s over 30 years in the making. Since the creation of Trax in 1985 – the original firm that forms the nucleus of our MarketAxess Post-Trade business – we’ve been delivering regulatory reporting and data services to the world’s leading financial institutions. From MiFID and EMIR to CSDR and SFTR, we’ve helped hundreds of clients to improve efficiency, reduce operational risk and manage regulatory compliance. In short – we’re regulatory reporting experts, and we’re in it for the long haul. You can rely on us to be there when you need us. You’re also now part of the wider MarketAxess story. That’s a story built on technical excellence, industry transformation and, importantly, a drive to always think client-first. We are a leader in institutional electronic trading in fixed-income securities. We’re also one of the fastest growing companies in the S&P500 and serve over 1,700 buy-side and sell-side firms across the globe. So, you are in good company. Our entire team is here to make your transition to MarketAxess as seamless, as easy and as valuable as possible. The team is based out of both Amsterdam and London, and has been expanded to ensure local, on-the-ground leadership for that transition. With the ongoing help and support of the Regulatory Reporting Hub team at Deutsche Börse Group, we will make sure that all your regulatory reporting obligations are met and your services uninterrupted. From personalised migration plans to pro-active client support, we promise to work with you to develop a clear path forward. That path starts today, with this onboarding pack. In this document, you will find detailed information on everything from our service and support model through to technical specifications and reference documentation. This is designed to give you complete transparency into your migration process, and to provide you with answers to any questions that you may have. It also contains contact details for the team. And, of course, if there is anything else that you need, or any question that we have missed, both we and the Deutsche Börse Group team are here and ready to help. These are unusual times, we know. But we want to re-assure you that we’re here to support your business, whatever the regulatory reporting environment throws at us next. And we very much look forward to meeting you in person once the situation allows. Welcome to MarketAxess. Chris Smith, Head of MarketAxess Post-Trade, and Geoffroy Vander Linden, Head of MarketAxess Netherlands & EU27 Trading

5

2 EXECUTIVE BRIEF

MarketAxess and Deutsche Börse Group (DBG) have closed the transaction for MarketAxess to acquire Deutsche Börse Group’s Regulatory Services GmbH (RegS) subsidiary. This will merge with MarketAxess’ Dutch ARM & APA (Trax NL B.V.) shortly after closing.

RegS currently provides reporting and publication services to clients in Europe through its Regulatory Reporting Hub (RRH). In MarketAxess, Deutsche Börse Group has found a partner with more than 30 years of experience in regulatory reporting who will be able to support and enhance the services you need to meet all your regulatory reporting obligations.

The merger is structured so that your current contract remains in place and you become MarketAxess clients without new business negotiations. MarketAxess and Deutsche Börse Group will work together through the 2021 transition period to ensure that all your regulatory obligations are met. Until your migration to MarketAxess systems is complete, Deutsche Börse Group technology will continue to fulfil your reporting requirements, while the service model will be delivered jointly.

Migration onto MarketAxess systems will occur in phases throughout 2021. We will reach out to discuss your specific availability to take this step. The scope of MarketAxess services is broadly similar to RegS and our intention is that all currently contracted services will continue to operate as they are now. Some technical changes (e.g. connectivity, firewall permissions) will be required, depending on your current service connectivity. We will explore the detail on a customer by customer basis as we continue planning of the migration phases.

The team at MarketAxess looks forward to welcoming your firm and providing any assistance you need for a successful migration.

6

3 INTRODUCTION

3.1 Document Structure

This document serves as a one stop reference for all information relating to your migration to MarketAxess.

To this end, we have structured this document to provide quick reference to the typical functions within a MiFID reporting firm; business, technology, compliance.

The key business and technology solution details are presented and explained in:

• Section 4: Business transition – legal considerations, service delivery and support model from closing until you are migrated onto MarketAxess systems during 2021

• Section 5: Migration – information on migration planning, service delivery post-migration, an overview of migration steps, technical specifications and other reference documentation

• Section 6: Data Storage and Processing – information on our security principles and setup, including our European Data Store (EDS) solution

• Section 7: Business as Usual Operating Model – information on the handover to your business operations and compliance functions

For supporting information, please reference:

• Section 8: MarketAxess Systems and Architecture – for a technology overview, information on interfaces, formats, bandwidths, connectivity, performance and architecture

• Section 9: Invoicing & Payment details – to inform your billing requirements

• Section 10: Common implementation questions – based on information requested in previous implementation

• Section 11: Glossary of Terms and Acronyms

The contents of this document are intended to support you in your migration but should not replace your own regulatory and compliance advice. This guide does not constitute part of the contractual documentation for the relevant MarketAxess services and intentionally does not address the contractual documentation.

7

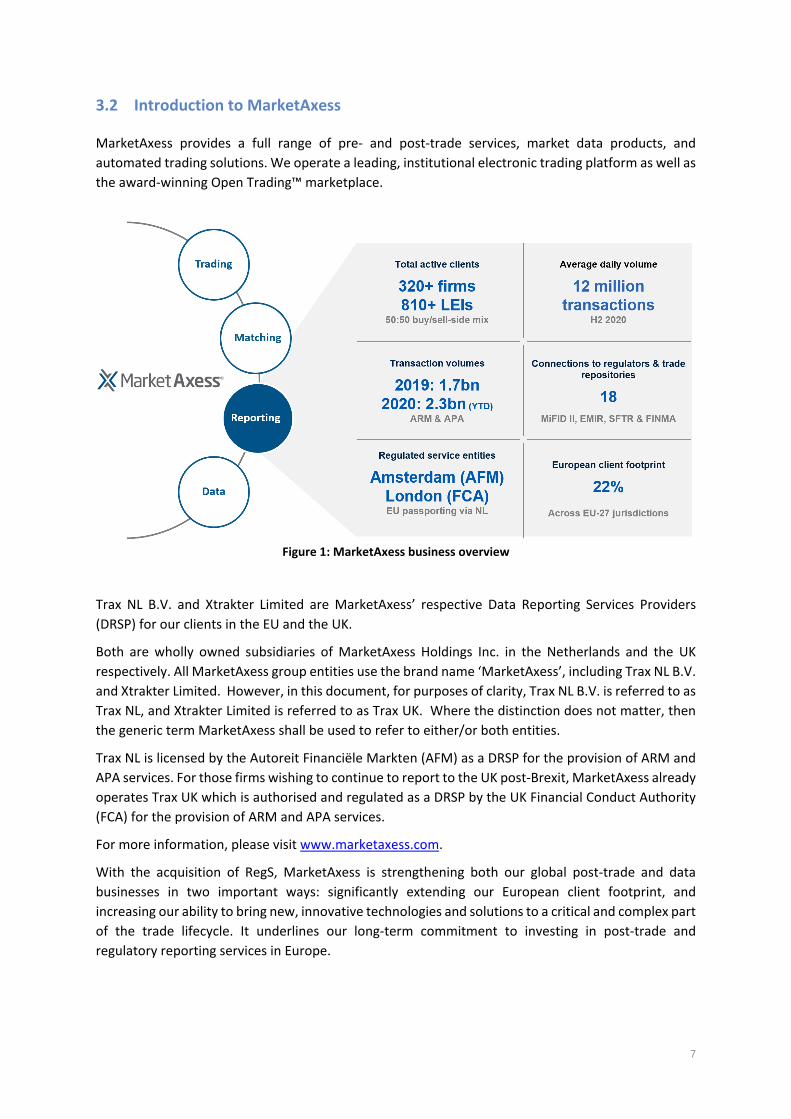

3.2 Introduction to MarketAxess

MarketAxess provides a full range of pre- and post-trade services, market data products, and automated trading solutions. We operate a leading, institutional electronic trading platform as well as the award-winning Open Trading™ marketplace.

Figure 1: MarketAxess business overview

Trax NL B.V. and Xtrakter Limited are MarketAxess’ respective Data Reporting Services Providers (DRSP) for our clients in the EU and the UK.

Both are wholly owned subsidiaries of MarketAxess Holdings Inc. in the Netherlands and the UK respectively. All MarketAxess group entities use the brand name ‘MarketAxess’, including Trax NL B.V. and Xtrakter Limited. However, in this document, for purposes of clarity, Trax NL B.V. is referred to as Trax NL, and Xtrakter Limited is referred to as Trax UK. Where the distinction does not matter, then the generic term MarketAxess shall be used to refer to either/or both entities.

Trax NL is licensed by the Autoreit Financiële Markten (AFM) as a DRSP for the provision of ARM and APA services. For those firms wishing to continue to report to the UK post-Brexit, MarketAxess already operates Trax UK which is authorised and regulated as a DRSP by the UK Financial Conduct Authority (FCA) for the provision of ARM and APA services.

For more information, please visit www.marketaxess.com.

With the acquisition of RegS, MarketAxess is strengthening both our global post-trade and data businesses in two important ways: significantly extending our European client footprint, and increasing our ability to bring new, innovative technologies and solutions to a critical and complex part of the trade lifecycle. It underlines our long-term commitment to investing in post-trade and regulatory reporting services in Europe.

8

The further enhancement of our post-trade business is important to MarketAxess as we look to extend the front-to-back, full trade-lifecycle services we offer clients. MarketAxess is committed to building a stronger regulatory landscape across Europe. With new regulations coming fast (SFTR recently, CSDR) it is imperative that firms can be confident that their regulatory reporting provider is fully committed to supporting their needs in the long term.

3.3 Meet the MarketAxess team

Your successful transition to MarketAxess is a priority for us. The leaders of the MarketAxess Post-Trade business will be heavily involved in your migration plan, and in ensuring your satisfaction as a client. They are:

• Chris Smith, Head of MarketAxess Post-Trade and a member of the management team for Europe and Asia. In his role, Mr. Smith is responsible for the development and delivery of all MarketAxess Post-Trade services, including regulatory reporting and trade matching.

Before joining MarketAxess in 2014, Chris developed the first commercial post MiFID dark pool, Euro Millennium, at NYFIX, which was later purchased by NYSE Euronext in 2009. After the acquisition by NYSE Euronext, he became Head of Hosted Commercial Markets. Before working for NYFIX and NYSE Euronext, he was responsible for European post-trade STP services with TradeWeb, building the first electronic confirmation method for Interest Rate Swaps. Previously, Chris held various operational management roles with Thomson Reuters and founded the Electronic Trade Confirmation (ETC) initiative with Fidelity Investments in the early 1990’s.

• Geoffroy Vander Linden, MarketAxess Country Head in the Netherlands, looks after MarketAxess’ MTF, EU trading and reporting businesses based in Amsterdam, providing services to Continental Europe. Geoffroy is responsible for the management of business support functions, all operational aspects of the country such as client services, and for growing the business in the region. Prior to moving to the Netherlands, Geoffroy developed MarketAxess’ transparency and APA solutions under MiFID II.

Before joining MarketAxess, Geoffroy spent over 10 years with Euroclear where he held a number of roles including Product Manager for liquidity management and clearing services.

As an active leader in the industry, Geoffroy serves as co-chair of multiple FIX sub-groups and is a member of ESMA Consultative Working Group.

On a day to day basis, you will be supported by our client-facing teams:

• Our Client Services team will be your go-to contacts with regard to all technical questions from onboarding to incident management

• The Relationship Management team will be your liaison in all business considerations and a trusted partner in all matters regulatory reporting

Further detail on your interaction with the above teams can be found in the sections Service and Support Model During Business Transition and Service and Support Model Post-Migration.

9

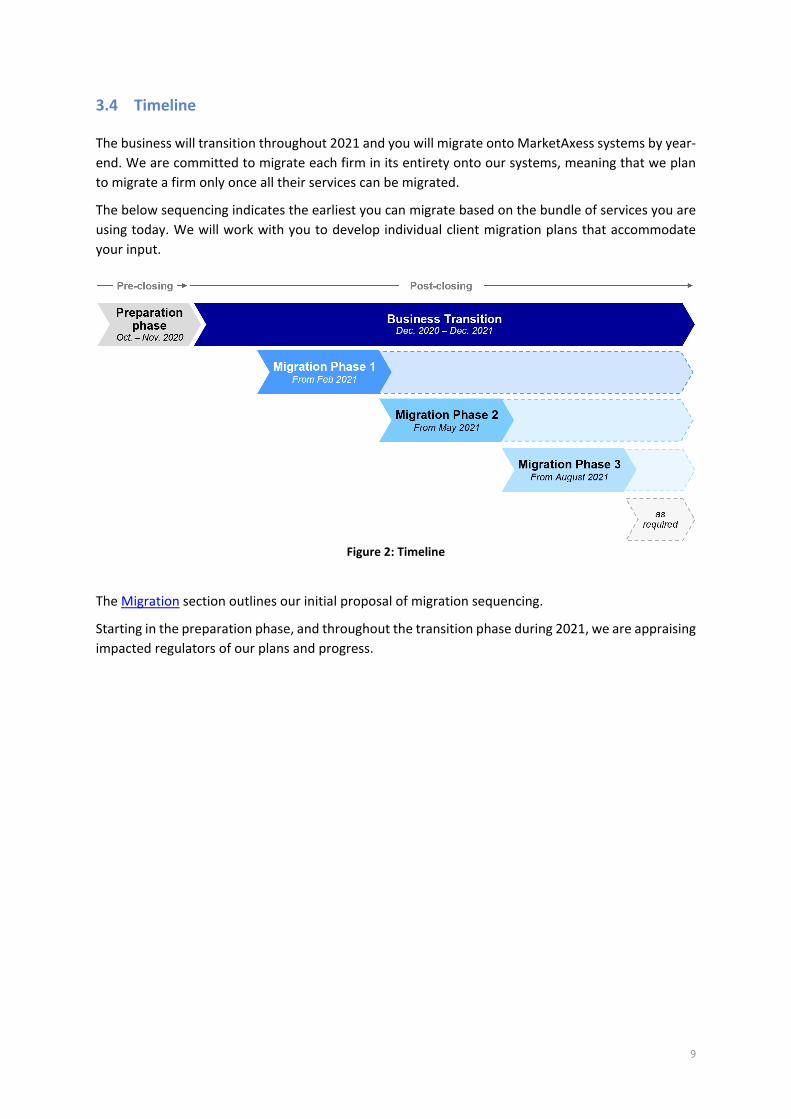

3.4 Timeline

The business will transition throughout 2021 and you will migrate onto MarketAxess systems by year-end. We are committed to migrate each firm in its entirety onto our systems, meaning that we plan to migrate a firm only once all their services can be migrated.

The below sequencing indicates the earliest you can migrate based on the bundle of services you are using today. We will work with you to develop individual client migration plans that accommodate your input.

Figure 2: Timeline

The Migration section outlines our initial proposal of migration sequencing.

Starting in the preparation phase, and throughout the transition phase during 2021, we are appraising impacted regulators of our plans and progress.

10

4 BUSINESS TRANSITION

4.1 Legal Considerations

MarketAxess is acquiring the business of RegS by way of a share acquisition. The business to be purchased by Trax NL consists of client contracts and obligations to provide the existing services to those clients. Following the closing of the acquisition and subsequent merger of RegS into Trax NL the existing contracts will be acquired and Trax NL. shall step into the shoes of RegS from a contractual perspective.

There will be no need for negotiations and the existing contracts will remain in place without any changes. There is no need to sign any new agreements with MarketAxess unless you require a new service which is not offered by RegS, such as when a client is required to report to the FCA post-Brexit, in which case it will need to sign new terms with Trax UK.

There are no anticipated changes in prices under your existing contractual terms.

4.2 Service Delivery During Business Transition

MarketAxess and DBG will partner during the 2021 transition period, to support continuous compliance with your regulatory obligations.

Until your firm migrates onto MarketAxess systems, MarketAxess will be using the existing DBG technology to fulfil your reporting requirements. With regard to APA, DBG will route your data to MarketAxess for publication.

4.3 Service and Support Model During Business Transition

The same level of support already provided by RegS will be offered during the transition period in 2021. Gradually, post-closing and upon commencement of the migration, clients will be introduced to the MarketAxess Client Services and Relationship Management teams who will assist them during and after the migration.

Our client teams are working together to support your day-to-day reporting operations during the transition period. Your new partner for all service requests is the MarketAxess Client Services team, and they will be supported by the DBG Client Services team as required.

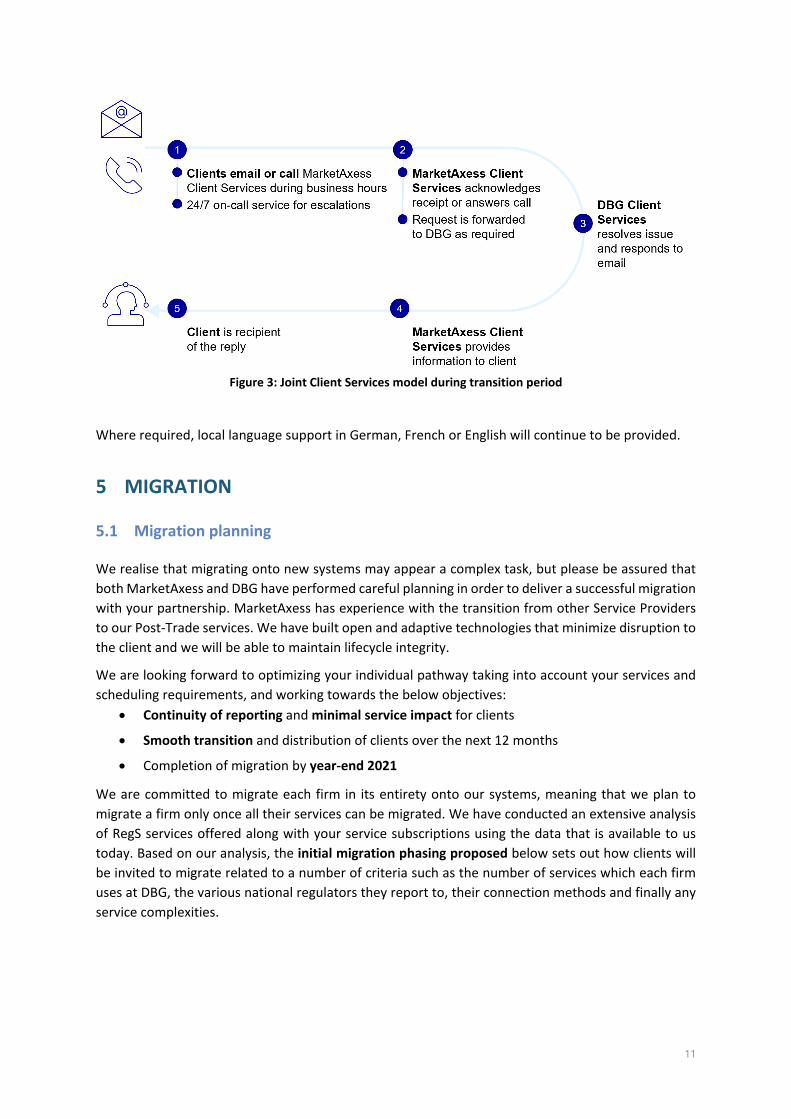

11

Figure 3: Joint Client Services model during transition period

Where required, local language support in German, French or English will continue to be provided.

5 MIGRATION

5.1 Migration planning

We realise that migrating onto new systems may appear a complex task, but please be assured that both MarketAxess and DBG have performed careful planning in order to deliver a successful migration with your partnership. MarketAxess has experience with the transition from other Service Providers to our Post-Trade services. We have built open and adaptive technologies that minimize disruption to the client and we will be able to maintain lifecycle integrity.

We are looking forward to optimizing your individual pathway taking into account your services and scheduling requirements, and working towards the below objectives:

• Continuity of reporting and minimal service impact for clients

• Smooth transition and distribution of clients over the next 12 months

• Completion of migration by year-end 2021

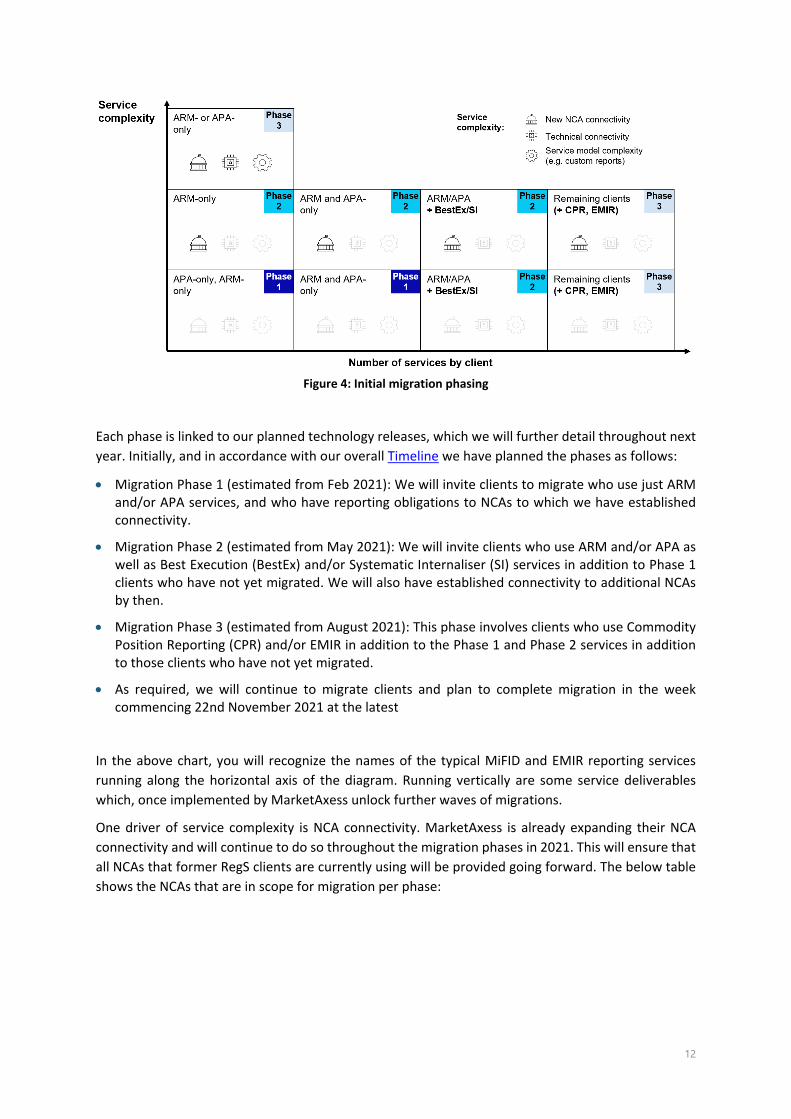

We are committed to migrate each firm in its entirety onto our systems, meaning that we plan to migrate a firm only once all their services can be migrated. We have conducted an extensive analysis of RegS services offered along with your service subscriptions using the data that is available to us today. Based on our analysis, the initial migration phasing proposed below sets out how clients will be invited to migrate related to a number of criteria such as the number of services which each firm uses at DBG, the various national regulators they report to, their connection methods and finally any service complexities.

12

Figure 4: Initial migration phasing

Each phase is linked to our planned technology releases, which we will further detail throughout next year. Initially, and in accordance with our overall Timeline we have planned the phases as follows:

• Migration Phase 1 (estimated from Feb 2021): We will invite clients to migrate who use just ARM and/or APA services, and who have reporting obligations to NCAs to which we have established connectivity.

• Migration Phase 2 (estimated from May 2021): We will invite clients who use ARM and/or APA as well as Best Execution (BestEx) and/or Systematic Internaliser (SI) services in addition to Phase 1 clients who have not yet migrated. We will also have established connectivity to additional NCAs by then.

• Migration Phase 3 (estimated from August 2021): This phase involves clients who use Commodity Position Reporting (CPR) and/or EMIR in addition to the Phase 1 and Phase 2 services in addition to those clients who have not yet migrated.

• As required, we will continue to migrate clients and plan to complete migration in the week commencing 22nd November 2021 at the latest

In the above chart, you will recognize the names of the typical MiFID and EMIR reporting services running along the horizontal axis of the diagram. Running vertically are some service deliverables which, once implemented by MarketAxess unlock further waves of migrations.

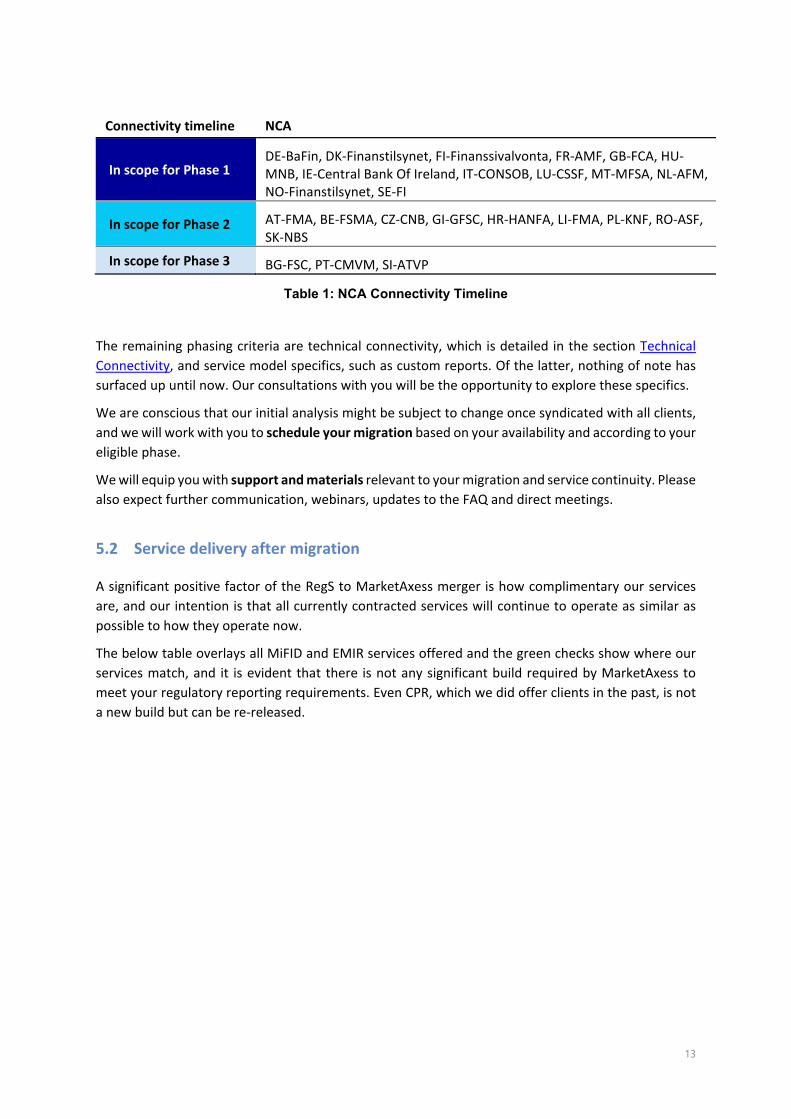

One driver of service complexity is NCA connectivity. MarketAxess is already expanding their NCA connectivity and will continue to do so throughout the migration phases in 2021. This will ensure that all NCAs that former RegS clients are currently using will be provided going forward. The below table shows the NCAs that are in scope for migration per phase:

13

Connectivity timeline NCA

In scope for Phase 1 DE-BaFin, DK-Finanstilsynet, FI-Finanssivalvonta, FR-AMF, GB-FCA, HU-MNB, IE-Central Bank Of Ireland, IT-CONSOB, LU-CSSF, MT-MFSA, NL-AFM, NO-Finanstilsynet, SE-FI

In scope for Phase 2 AT-FMA, BE-FSMA, CZ-CNB, GI-GFSC, HR-HANFA, LI-FMA, PL-KNF, RO-ASF, SK-NBS

In scope for Phase 3 BG-FSC, PT-CMVM, SI-ATVP

Table 1: NCA Connectivity Timeline

The remaining phasing criteria are technical connectivity, which is detailed in the section Technical Connectivity, and service model specifics, such as custom reports. Of the latter, nothing of note has surfaced up until now. Our consultations with you will be the opportunity to explore these specifics.

We are conscious that our initial analysis might be subject to change once syndicated with all clients, and we will work with you to schedule your migration based on your availability and according to your eligible phase.

We will equip you with support and materials relevant to your migration and service continuity. Please also expect further communication, webinars, updates to the FAQ and direct meetings.

5.2 Service delivery after migration

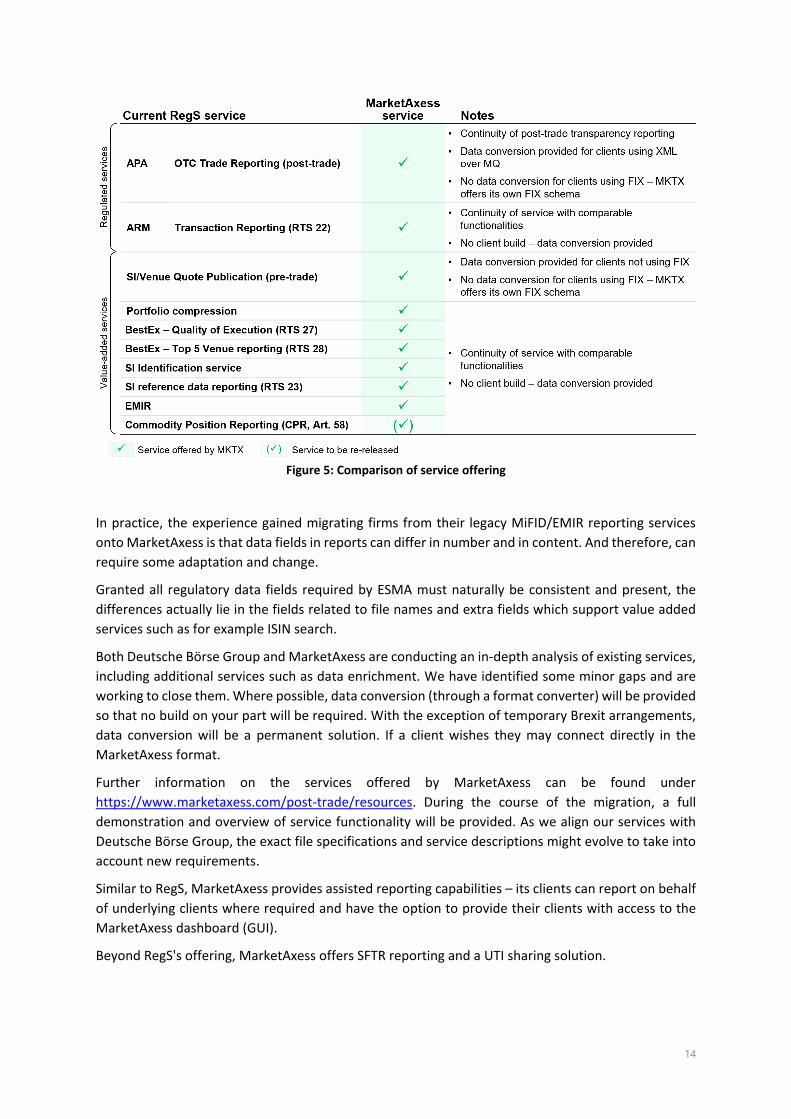

A significant positive factor of the RegS to MarketAxess merger is how complimentary our services are, and our intention is that all currently contracted services will continue to operate as similar as possible to how they operate now.

The below table overlays all MiFID and EMIR services offered and the green checks show where our services match, and it is evident that there is not any significant build required by MarketAxess to meet your regulatory reporting requirements. Even CPR, which we did offer clients in the past, is not a new build but can be re-released.

14

Figure 5: Comparison of service offering

In practice, the experience gained migrating firms from their legacy MiFID/EMIR reporting services onto MarketAxess is that data fields in reports can differ in number and in content. And therefore, can require some adaptation and change.

Granted all regulatory data fields required by ESMA must naturally be consistent and present, the differences actually lie in the fields related to file names and extra fields which support value added services such as for example ISIN search.

Both Deutsche Börse Group and MarketAxess are conducting an in-depth analysis of existing services, including additional services such as data enrichment. We have identified some minor gaps and are working to close them. Where possible, data conversion (through a format converter) will be provided so that no build on your part will be required. With the exception of temporary Brexit arrangements, data conversion will be a permanent solution. If a client wishes they may connect directly in the MarketAxess format.

Further information on the services offered by MarketAxess can be found under https://www.marketaxess.com/post-trade/resources. During the course of the migration, a full demonstration and overview of service functionality will be provided. As we align our services with Deutsche Börse Group, the exact file specifications and service descriptions might evolve to take into account new requirements.

Similar to RegS, MarketAxess provides assisted reporting capabilities – its clients can report on behalf of underlying clients where required and have the option to provide their clients with access to the MarketAxess dashboard (GUI).

Beyond RegS's offering, MarketAxess offers SFTR reporting and a UTI sharing solution.

15

5.3 Description of migrated services

5.3.1 ARM

Similarities in general functionality: With regard to general functionality and similar to former RegS, we will provide transaction lifecycle handling from collection of transaction data via SFTP, manual entry or dashboard (GUI) upload to ARM/NCA feedback and reconciliation including extensive validation executed as per ESMA rules and with additional warnings, party reference data upload and a comprehensive and detailed audit trail. We also perform eligibility checks to ensure the transactions are within the scope of the regulation.

Differences in general functionality: We provide data enrichment with OTC post-trade data (APA) and new instrument reference data enrichment capabilities (ISIN lookup service via interface to the ANNA DSB and enrichment of reference data fields 42-56 based on ISIN), but we will not enrich data from DBG venues. If you have been using venue enrichment in your operations, you might need to assess the impact of this change on your operations and we stand ready to discuss the implications on your business and ways forward. MarketAxess offers a three-way managed reconciliation service.

Submission: We will create the capability to support your current submission formats, which we will convert internally. If you wish, you can also adapt to our existing submission format. Nevertheless, there will be changes to the response file format for clients and MarketAxess error codes and status’ will not be translated to former RegS equivalents.

Dashboard (GUI): Our service delivery will be supported by a dashboard with a different look and feel, including an enhanced end-of-day status reporting capabilities and an improved Assisted Reporting dashboard. In addition, you will be able to leverage regulatory business intelligence which we provideall our clients. A process that we do not currently support is four eyes authorization.

European Data Store (EDS): If clients choose to set up a tokenized solution, it is a pre-requisite before submitting any report to submit the relevant natural person data into the EDS either via HTTPS entry or SFTP upload. More detail can be found in the section Data storage and processing. If clients choose not to use the tokenized solution, then all of their data, including all personal data, will be processed in the primary data centres.

Relevant documentation

• MarketAxess ARM – Dashboard (GUI) User Guide

• MarketAxess ARM – Creating User Profiles as an Administrator

• ARM specifications — MarketAxess ARM – CSV File Specification Post Trade Technical Specification CSV File Format — MarketAxess ARM – XML File Specification Post Trade Technical Specification XML File Format

• MarketAxess ARM – ISIN Lookup Specification

16

5.3.2 APA

Similarities in general functionality: We provide both pre- and post-trade transparency services as well as Portfolio Compression reporting. We provide reporting obligation check (with the capability to handle package transactions), reporting responsibility instrument scope checks (ToTV) including outside of transparency scope checks (OOTS), calculation of deferrals for trades and waivers on quotes, assisted reporting, price & volume validation (with differences in calculation methodology to DBG),

Differences in general functionality: We leverage a different reference data provider to DBG, which might result in slight differences in asset classification and ToTV assessment results.

Submission: We will be able to provide data conversion for clients using XML over MQ, so you can continue to use your current submission formats, which we will convert internally. We will not provide data conversion for clients using FIX – we kindly ask you to build to our existing schema. In addition, we will support Portfolio Compression via CSV, but not via FIX. There will be changes to the response file format for clients and MarketAxess error codes and status’ will not be translated to former RegS equivalents.

Dashboard (GUI): Our service delivery will be supported by a dashboard with a different look and feel, including an improved Assisted Reporting dashboard.

Relevant documentation

• MarketAxess APA – Dashboard (GUI) user guide

• MarketAxess APA – Creating User Profiles as an Administrator

• APA specifications — MarketAxess APA – Trade Reporting FIX Specification — MarketAxess APA – Trade Reporting CSV Upload Specification — MarketAxess APA – Quote Reporting FIX Specification

• MarketAxess APA – Instrument Concatenation Support for Trade Reporting

5.3.3 BEST EXECUTION – QUALITY OF EXECUTION (RTS 27)

Similarities in general functionality: We will enhance the functionality of our existing QoE service by using near-time data from quotes in addition to that from trades. Using this data, we will replicate the former RegS functionality of calculating all nine tables except the cost table (table 5). Our output reports will be provided in former RegS XML format so clients can ingest these.

Submission: Calculation of most tables is conducted with near time trade and quote data submitted via the OTC Trade Reporting and SI Quote Publication service. Clients have the ability to indicate whether they were a Liquidity Provider using an optional APA custom field (Aggressor Indicator). Similar to former RegS, we would require quarterly upload of clients’ CSV to complete the cost table (table 5).

Output reports: We will provide output reports via CSV or XML rather than via a GUI. We also offer the option to automatically publish reports.

17

5.3.4 BEST EXECUTION – TOP 5 VENUE REPORT (RTS 28)

Similarities in general functionality: Data is typically calculated using ARM transaction reports. Our output reports will be provided in former RegS XML format so clients can ingest these.

Submission: Data is sourced from data submitted to the ARM with five additional fields provided by the client specifically for the Top 5 service (passive/aggressive, directed order, client type, order type, broker trading capacity). In addition to using ARM transaction reports, we also support a standalone CSV input format.

Output reports: We also offer the option to automatically publish reports. We will provide output reports via CSV or XML rather than via a GUI. We also output indicative reports throughout the year as well as the final publication at the end of the year.

5.3.5 SYSTEMATIC INTERNALIZER (SI) IDENTIFICATION

Similarities in general functionality: Our SI Identification service offers the entire scope of the RegS solution (TOTV check, TOAX check, liquidity status, currency conversion, technical validations).

Differences in general functionality: We do not require clients to report a TOAX flag in APA, as we will calculate this automatically based on transaction reporting data. The indicative output reports we provide use actual market data from current period rather than previous period’s ESMA data. Our SI Identification report includes data relating to the SI Relevance report and will differ slightly in format. We submit only one CSV SI Report, however it covers all the same information RegS provides today.

Submission: We will be using just ARM transaction data – enrichment by TOAX flag reported in related trades via the OTC Trade Reporting (APA) will no longer be necessary. Alternatively, we support a standalone input format.

Relevant documentation

• MarketAxess SI Identification - CSV Specification

5.3.6 SYSTEMATIC INTERNALIZER (SI) REFERENCE DATA REPORTING (RTS 23)

Similarities in general functionality: MarketAxess supports the reporting of instrument reference data to NCAs across Europe. The reference data needed to report will be enriched from reference data sourced by MarketAxess across all instruments in scope of MiFID II.

Differences in general functionality: The instrument reference data report is triggered by the submission of an XML file containing the instruments the SI or Trading Venue wishes to report alongside a few venue specific fields. Based on the ISIN the remaining reference data attributes can then be enriched and/or validated before the report is onward reported to the relevant NCA.

GUI: Our service delivery will not be supported by a dashboard (GUI), however, feedback files are provided with all the relevant status updates which clients can ingest.

Submission: We use a standalone instrument reference data submission format based on the ESMA standard.

18

Relevant documentation

• MarketAxess SI Reference Data Reporting (RTS 23) – Specification

5.3.7 COMMODITY POSITION REPORTING (CPR, ART. 58)

Similarities in general functionality: We provided this service to clients in the past but had discontinued due to a lack of client demand. Before migrating your services, we will rebuild and recommission the service under the standards you are currently provided from RegS.

Differences in general functionality: In contrast to RegS current offering, we plan to fully cover assisted reporting – not only in exceptional cases – and we will provide a dashboard (GUI).

Submission: MarketAxess will implement CPR offering leveraging RegS’s submission format to all end points.

5.3.8 EMIR REPORTING

Similarities in general functionality: We will provide transaction lifecycle handling, file and transaction validation using ESMA and Regis-TR validation rules, TR connectivity to Regis-TR and DTCC, TR response and reports ingress, record lifecycle creation via GUI, reporting health situation dashboard, file and recording status and reporting audits.

Differences in general functionality: Matching and pairing reports will be integrated into the dashboard (GUI). We will not be able to offer the TREMIR enrichment/mapping service, which uses DBG venue data.

Submission: We will create the capability to support your current RegS submission formats, which we will convert internally. If you wish, you can also adapt to our existing submission format. Nevertheless, MarketAxess status’ and error codes will not be converted to RegS format.

5.4 Step-by-step migration lifecycle

You can lay the groundwork for migration once a formal introduction to the MarketAxess Relationship Management Team has taken place.

Shortly thereafter, you can access the profile we have created for you on our CRM-system as a first step to migration. There, clients can review their onboarding details per service. These will be pre-completed, and clients should fill any gaps or correct any errors.

Once we have notified you that your phase is eligible for migration, you will find in this section the end-to-end steps to migrate all your services onto our systems at the same time.

Your Relationship Management Team will be your point of contact to oversee your migration lifecycle. Based on significant experience, we would expect your firm to also appoint a project manager to coordinate activities and resources on its behalf.

The impacted functions for this project are the following: Operations, Technology, Program Management, Compliance/Legal, Procurement. It is prudent to seek input from each of these functions at the appropriate time in the migration lifecycle.

19

In general, the migration lifecycle consists of the following steps: aligning on the timeline, establishing technical connectivity, analysing data requirements, developing data submission solutions, training and testing, and finally cutover. For more complex migration, additional steps might be required.

5.4.1 TIMELINE

We will keep an overall migration schedule so that we can coordinate across all clients in a given phase. This will ensure that both sides can deploy resources to support the individual desired migration path.

No matter when your phase begins, all clients must have cut over by the week commencing 22nd November 2021 at the latest.

Based on the steps required to migrate onto our systems, firms should notify MarketAxess at least six to eight weeks1 ahead of their desired cutover date.

Each of the remaining sections should be fully delivered and signed off prior to cutover. Firms should schedule appropriate clarification meetings with MarketAxess on each of the relevant sections below.

1 This timeframe represents a simple migration. The timeframe for clients using several services will be longer.

20

5.4.2 DATA ANALYSIS AND SUBMISSION

Objectives for this project phase

• Ensure clients have all the information needed to start analysis

• Where clients need to build to an MarketAxess file specification, clients need to understand the file flow and the message formats to submit data to MarketAxess

• Where MarketAxess is building a converter for a particular service, clients will need to assess any small changes in the end-to-end process

• Ensure clients can generate data extracts required for each relevant MarketAxess service

• Clients to determine whether they leverage MarketAxess EDS solution for ARM reporting, details on which can be found in the European Data Store (EDS) section

Non-converted services (APA over FIX)

For services where clients must build to the MarketAxess specification, we will provide documentation and assistance to help you modify your existing DBG file format into the required MarketAxess file format.

For example, for APA reporting via FIX, we are performing a detailed business analysis between the DBG and MarketAxess FIX specification documents and will capture in a delta document the key differences. We will make this kind of document available to you and you can ask to review it with us, should you require.

Clients can then leverage these delta documents to perform the required field level changes so that their data files will be accepted by MarketAxess systems.

Converted services (e.g. ARM, EMIR, SI and Best Execution services)

For most migrated services we will build a data conversion application on the MarketAxess side so that we can accept a legacy data format without your firm having to undertake changes. With the exception of temporary Brexit arrangements, these applications will be a permanent solution. If a client wishes they may connect directly in the MarketAxess format.

Nevertheless, there will likely be some changes to the response file format for clients and not all MarketAxess error codes and status’ will be translated to RegS equivalents.

For all migrated services, we strongly suggest clients perform user acceptance testing before they cut over. This is covered in the Training and Testing section. In the following are the more detailed migration steps to ensure your data reaches MarketAxess in the correct format and is accepted by our systems. Specifications for all MarketAxess services are on our public internet resources site. Note that the below displays the latest information. Details are continuing to take shape as we approach migration.

21

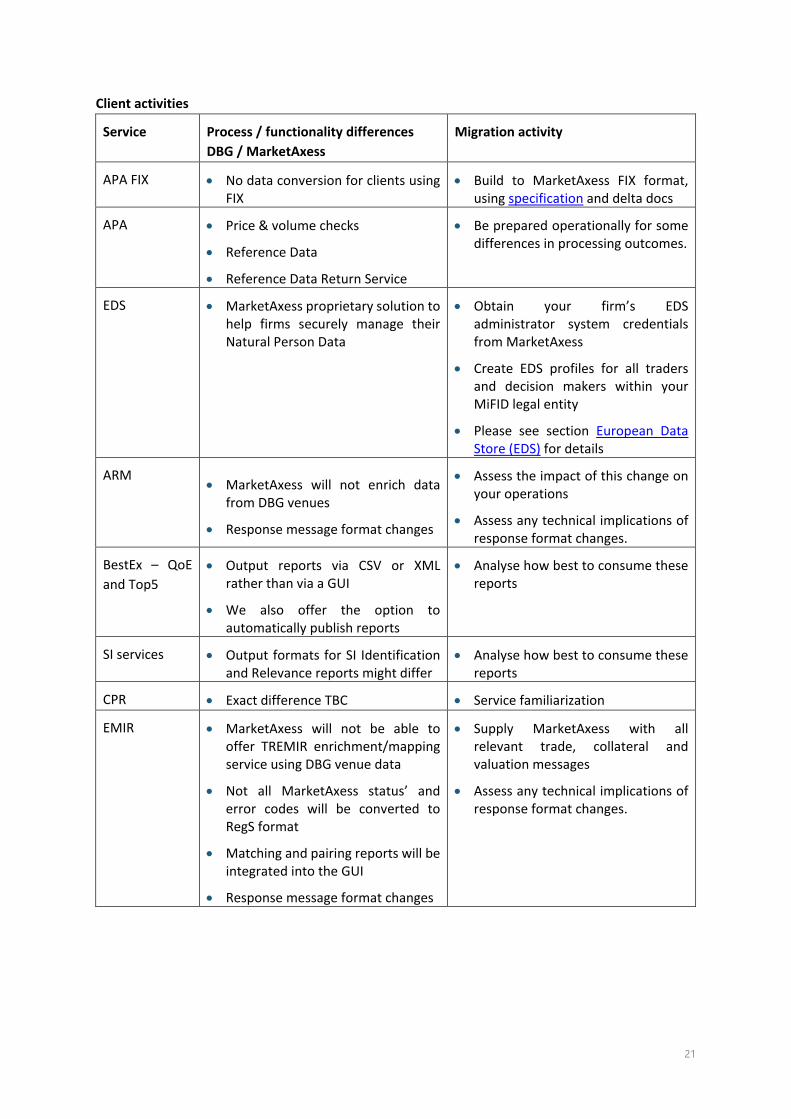

Client activities

Service Process / functionality differences DBG / MarketAxess

Migration activity

APA FIX • No data conversion for clients using FIX

• Build to MarketAxess FIX format, using specification and delta docs

APA • Price & volume checks

• Reference Data

• Reference Data Return Service

• Be prepared operationally for some differences in processing outcomes.

EDS • MarketAxess proprietary solution to help firms securely manage their Natural Person Data

• Obtain your firm’s EDS administrator system credentials from MarketAxess

• Create EDS profiles for all traders and decision makers within your MiFID legal entity

• Please see section European Data Store (EDS) for details

ARM • MarketAxess will not enrich data

from DBG venues

• Response message format changes

• Assess the impact of this change on your operations

• Assess any technical implications of response format changes.

BestEx – QoE and Top5

• Output reports via CSV or XML rather than via a GUI

• We also offer the option to automatically publish reports

• Analyse how best to consume these reports

SI services • Output formats for SI Identification and Relevance reports might differ

• Analyse how best to consume these reports

CPR • Exact difference TBC • Service familiarization

EMIR • MarketAxess will not be able to offer TREMIR enrichment/mapping service using DBG venue data

• Not all MarketAxess status’ and error codes will be converted to RegS format

• Matching and pairing reports will be integrated into the GUI

• Response message format changes

• Supply MarketAxess with all relevant trade, collateral and valuation messages

• Assess any technical implications of response format changes.

22

5.4.3 TECHNICAL CONNECTIVITY

Objectives for this project phase

• Understand connectivity options based on firm’s current arrangements

• Engage with MarketAxess technical onboarding team for required steps

• Agree key milestones and dates

• Outputs: client Test and Production credentials, dashboard/GUI access via client IP whitelisting

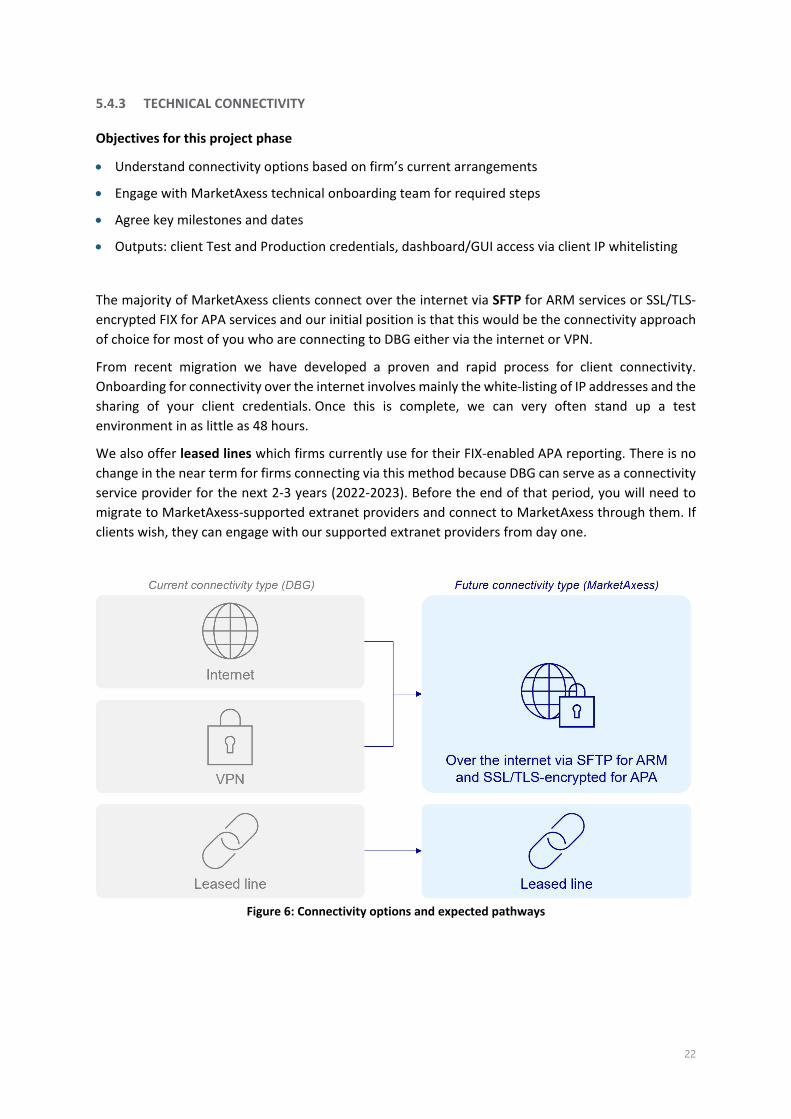

The majority of MarketAxess clients connect over the internet via SFTP for ARM services or SSL/TLS-encrypted FIX for APA services and our initial position is that this would be the connectivity approach of choice for most of you who are connecting to DBG either via the internet or VPN.

From recent migration we have developed a proven and rapid process for client connectivity. Onboarding for connectivity over the internet involves mainly the white-listing of IP addresses and the sharing of your client credentials. Once this is complete, we can very often stand up a test environment in as little as 48 hours.

We also offer leased lines which firms currently use for their FIX-enabled APA reporting. There is no change in the near term for firms connecting via this method because DBG can serve as a connectivity service provider for the next 2-3 years (2022-2023). Before the end of that period, you will need to migrate to MarketAxess-supported extranet providers and connect to MarketAxess through them. If clients wish, they can engage with our supported extranet providers from day one.

Figure 6: Connectivity options and expected pathways

23

Connectivity process

MarketAxess provides two environments for all our regulatory services: User Acceptance Testing (UAT) and Production. Clients are first onboarded onto UAT. Once we have your firm’s complete initiation details (firm name, key person contact details, public IP addresses), our onboarding team will use these details to grant you access to our URL-delivered dashboard/GUI and your inbound/outbound SFTP-folders/FIX sessions.

Once you have connectivity to us, firms can opt for a straight-through machine-to-machine file delivery method.

Firms wishing to connect via a leased line should engage with our Infrastructure Support team as soon as possible due to the anticipated lead times of such a connection.

If you are already a MarketAxess customer, please reach out to our Infrastructure team to move the traffic across to your existing connectivity model.

Documentation provided

• MarketAxess APA – Connectivity Guide

5.4.4 TRAINING AND TESTING

Objectives for this project phase

• Familiarization with our solution for all client user roles

• Create and fulfil your test plan so that your firm achieves readiness to cutover

• Complete GUI profile (permissions, credentials) setup for all firm users

Training

Prior to testing, all users at your firm should be familiarized with MarketAxess’ reporting platform. To support this, we offer pre-prepared videos by subject and can also offer live video-enabled training.

In the weeks leading up to your migration onto MarketAxess systems, typically your operations control teams will require follow-up training. Please assess your needs and follow up with our Relationship Management team on that.

MarketAxess will create system administrators at each firm. It is the duty of these administrators to create relevant user profiles and add staff.

Documentation provided

• MarketAxess ARM – Creating User Profiles as an Administrator

• MarketAxess APA – Creating User Profiles as an Administrator

• MarketAxess EDS – Creating an Upload Account

24

Testing

MarketAxess provides two environments for all our regulatory services: User Acceptance Testing (UAT) and Production. The setup of the two environments is very similar, however, clients should bear in mind some key differences.

• Instrument (ISIN) data exists in UAT, but might not be as fresh as in Production with respect to ISIN completeness and eligibility (ToTV) status

• UAT is not set up to accommodate similar volume throughput as our Production environment, therefore clients should advise MarketAxess prior to conducting load testing in UAT

• Please note that not all NCAs provide UAT environments and our UAT environment is currently connected to the UK FCA only

• MarketAxess reserves every Wednesday afternoon between midday and 1800 CET for scheduled maintenance releases. During this time clients can still submit transactions, but they will be queued for processing until the service is restored

As MarketAxess will build data conversion adapters for data in, but not for data out, firms might need to adapt their reporting processes to consume both ARM and NCA response files.

Business Testing Approach and Scenarios

It is recommended that clients design and implement an end-to-end completeness and accuracy testing framework as a key step to migration readiness.

The industry has provided some resources in order to help you with your testing approach. Among others, this is provided in the following documents:

• ESMA has defined some ARM best practice reporting guidance to help you assess your expected results

• The Fix Trading Community provided guidance on implementing the requirements for post trade transparency

• AFME has published MiFID II / MiFIR post-trade reporting requirements – Understanding bank and investor obligations

5.4.5 CUTOVER

Milestones before cutover

• Client to agree a cutover date with the Relationship Management team

• Client to confirm their migration cutover criteria are met 1. Testing exit criteria have been met 2. Each required service is live in client’s production environment, e.g. technical connectivity with

MarketAxess and data submission process 3. Connectivity is established to all relevant Regulators and Trade Repositories for EMIR 4. Day 1 operational readiness

25

• Ensure go-live when you are eligible, but no later than week commencing 22nd November 2021

• Client to familiarize with post-migration service and support model — Day-to-day client requests to be handled by Post-Trade Client Services team — Escalation via Relationship Management team — Further details in section Service and Support Model Post-Migration

26

6 DATA STORAGE AND PROCESSING

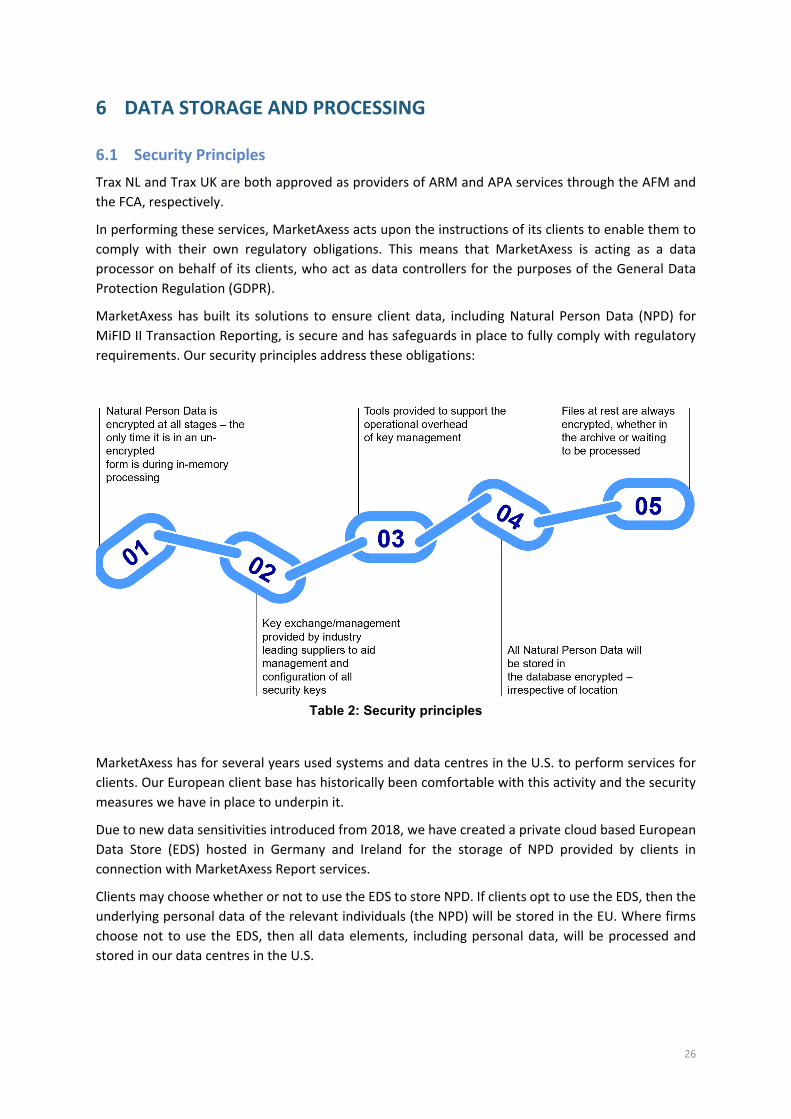

6.1 Security Principles Trax NL and Trax UK are both approved as providers of ARM and APA services through the AFM and the FCA, respectively.

In performing these services, MarketAxess acts upon the instructions of its clients to enable them to comply with their own regulatory obligations. This means that MarketAxess is acting as a data processor on behalf of its clients, who act as data controllers for the purposes of the General Data Protection Regulation (GDPR).

MarketAxess has built its solutions to ensure client data, including Natural Person Data (NPD) for MiFID II Transaction Reporting, is secure and has safeguards in place to fully comply with regulatory requirements. Our security principles address these obligations:

Table 2: Security principles

MarketAxess has for several years used systems and data centres in the U.S. to perform services for clients. Our European client base has historically been comfortable with this activity and the security measures we have in place to underpin it.

Due to new data sensitivities introduced from 2018, we have created a private cloud based European Data Store (EDS) hosted in Germany and Ireland for the storage of NPD provided by clients in connection with MarketAxess Report services.

Clients may choose whether or not to use the EDS to store NPD. If clients opt to use the EDS, then the underlying personal data of the relevant individuals (the NPD) will be stored in the EU. Where firms choose not to use the EDS, then all data elements, including personal data, will be processed and stored in our data centres in the U.S.

27

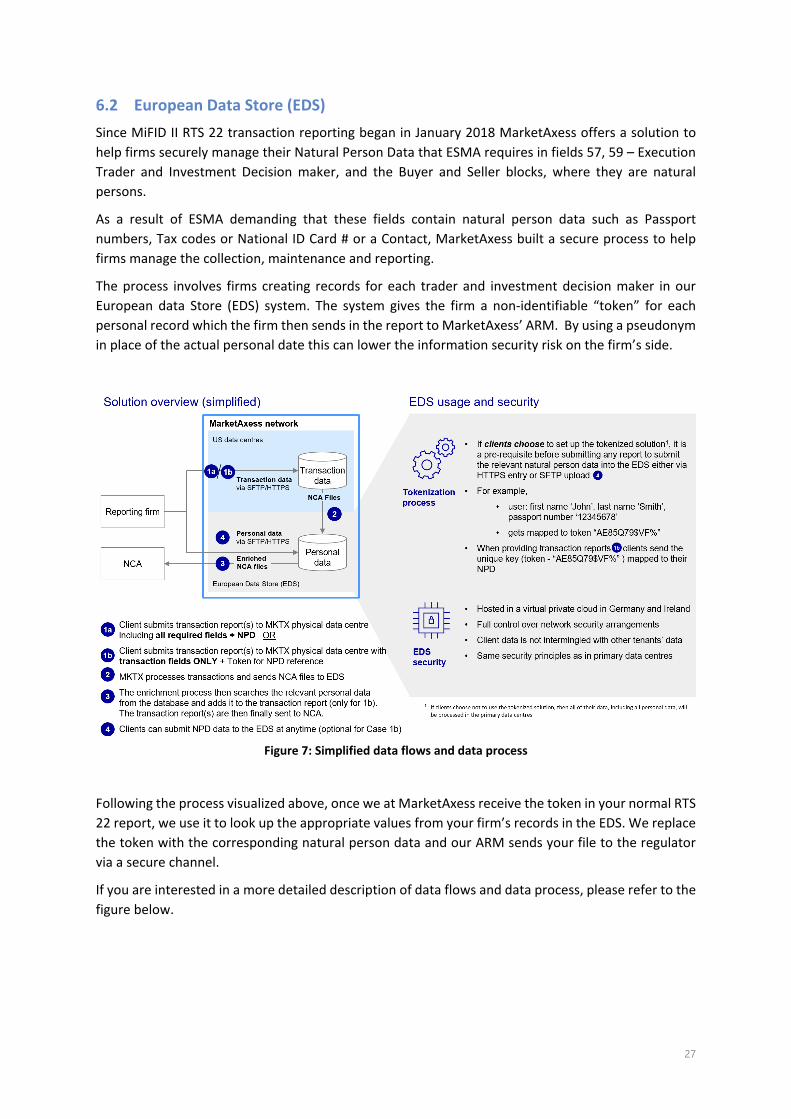

6.2 European Data Store (EDS) Since MiFID II RTS 22 transaction reporting began in January 2018 MarketAxess offers a solution to help firms securely manage their Natural Person Data that ESMA requires in fields 57, 59 – Execution Trader and Investment Decision maker, and the Buyer and Seller blocks, where they are natural persons.

As a result of ESMA demanding that these fields contain natural person data such as Passport numbers, Tax codes or National ID Card # or a Contact, MarketAxess built a secure process to help firms manage the collection, maintenance and reporting.

The process involves firms creating records for each trader and investment decision maker in our European data Store (EDS) system. The system gives the firm a non-identifiable “token” for each personal record which the firm then sends in the report to MarketAxess’ ARM. By using a pseudonym in place of the actual personal date this can lower the information security risk on the firm’s side.

Figure 7: Simplified data flows and data process

Following the process visualized above, once we at MarketAxess receive the token in your normal RTS 22 report, we use it to look up the appropriate values from your firm’s records in the EDS. We replace the token with the corresponding natural person data and our ARM sends your file to the regulator via a secure channel.

If you are interested in a more detailed description of data flows and data process, please refer to the figure below.

28

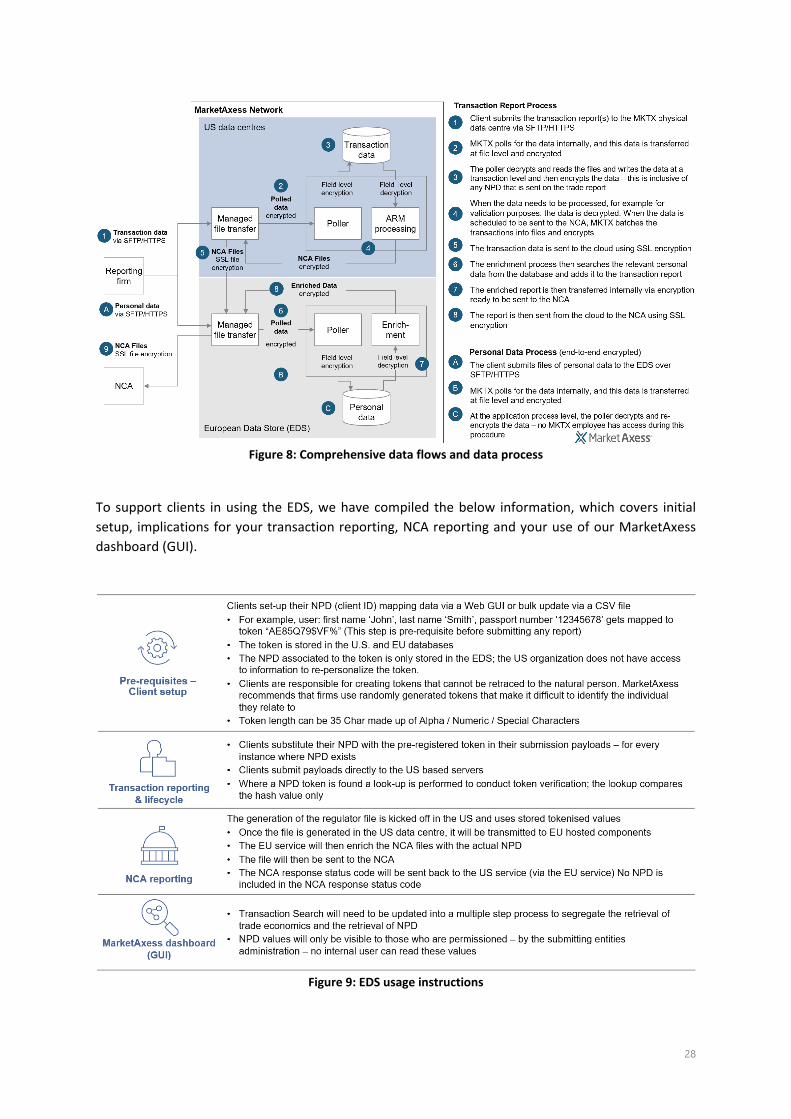

Figure 8: Comprehensive data flows and data process

To support clients in using the EDS, we have compiled the below information, which covers initial setup, implications for your transaction reporting, NCA reporting and your use of our MarketAxess dashboard (GUI).

Figure 9: EDS usage instructions

29

Documentation provided

• MarketAxess EDS – Creating an Upload Account

• MarketAxess EDS – Creating Trader Tokens

• MarketAxess EDS – Creating Fund Tokens

6.3 The Virtual Private Cloud The European Data Store (EDS) was built to enable MarketAxess to utilize its state-of-the-art US data centres whilst also complying with GDPR and other EU regulations.

This involves leveraging the Amazon Web Services (AWS) data centres in Dublin and Frankfurt, as an IaaS Virtual Private Cloud – not as a Public Cloud.

As such, the private cloud model means all MarketAxess security infrastructure (e.g. F5 LoadBalancers) and vendor software (e.g. Oracle) is replicated in AWS as an extension of the MarketAxess corporate network. The same security principles apply across the EDS and MarketAxess primary data centres.

6.4 Network security MarketAxess, as a global service provider, goes to great lengths to establish network security. A suite of controls is in place, including

• For our US data centres: IP Whitelisting and 24x7 managed Security Operations Centre (SOC) monitoring on all external connections

• For the EDS: IP Whitelisting along with Web Application Firewalls (WAF) controls. Within the virtual private cloud, MarketAxess has full control over its network security arrangements

• Traffic between the US data centres and the EDS via an encrypted VPN (virtual private network)

• Intrusion-Detection-System / Intrusion-Prevention-System enabled on externally facing firewalls

• IP blacklisting implemented for known malicious IPs

• Usage of Distributed Denial of Service (DDoS) Protection for our internet connections

30

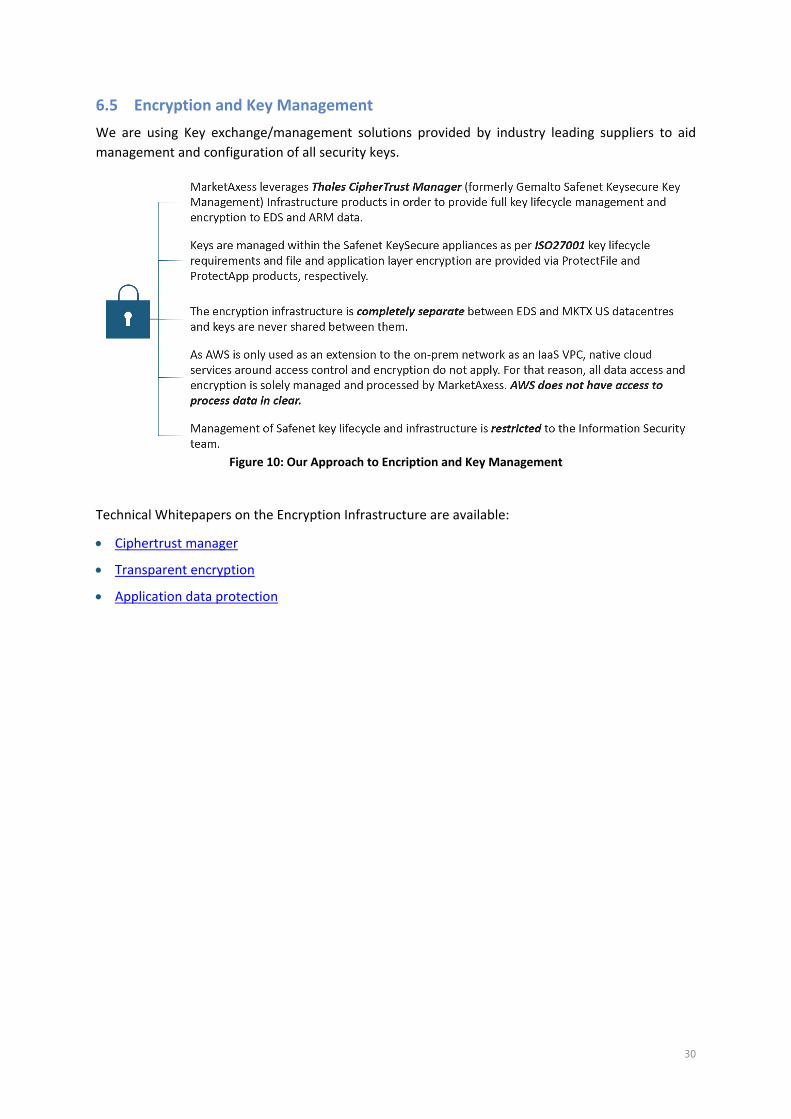

6.5 Encryption and Key Management We are using Key exchange/management solutions provided by industry leading suppliers to aid management and configuration of all security keys.

Figure 10: Our Approach to Encription and Key Management

Technical Whitepapers on the Encryption Infrastructure are available:

• Ciphertrust manager

• Transparent encryption

• Application data protection

31

7 BUSINESS AS USUAL OPERATING MODEL

7.1 Service and Support Model Post-Migration

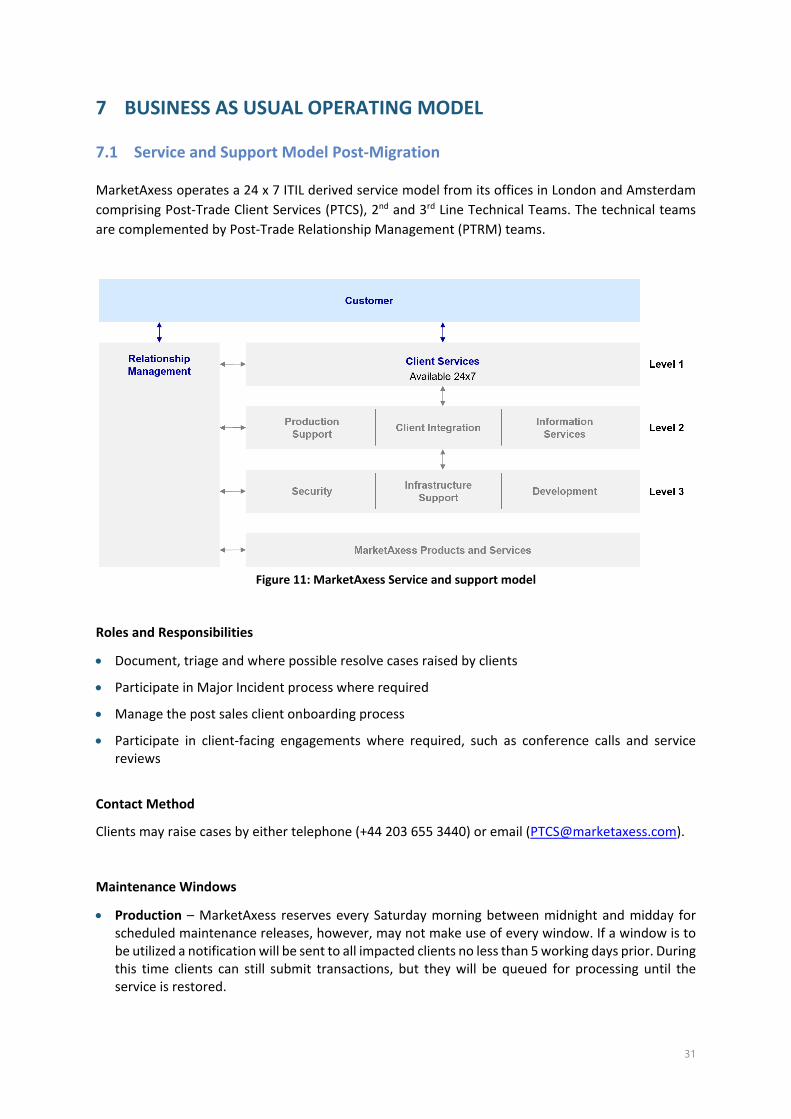

MarketAxess operates a 24 x 7 ITIL derived service model from its offices in London and Amsterdam comprising Post-Trade Client Services (PTCS), 2nd and 3rd Line Technical Teams. The technical teams are complemented by Post-Trade Relationship Management (PTRM) teams.

Figure 11: MarketAxess Service and support model

Roles and Responsibilities

• Document, triage and where possible resolve cases raised by clients

• Participate in Major Incident process where required

• Manage the post sales client onboarding process

• Participate in client-facing engagements where required, such as conference calls and service reviews

Contact Method

Clients may raise cases by either telephone (+44 203 655 3440) or email ([email protected]).

Maintenance Windows

• Production – MarketAxess reserves every Saturday morning between midnight and midday for scheduled maintenance releases, however, may not make use of every window. If a window is to be utilized a notification will be sent to all impacted clients no less than 5 working days prior. During this time clients can still submit transactions, but they will be queued for processing until the service is restored.

32

• UAT – MarketAxess reserves every Wednesday afternoon between midday and 1800 CET for scheduled maintenance releases. During this time clients can still submit transactions, but they will be queued for processing until the service is restored.

7.2 Generic Client Operating Model

Adapt existing Operational Model including BAU elements, such as how often you send us data files, where the MarketAxess dashboard is embedded in your process, and your firm’s approach to correcting any rejection messages.

Adapt your existing Control Framework taking into account the functionality of the MarketAxess dashboard, transaction search and KRI/KPI metrics.

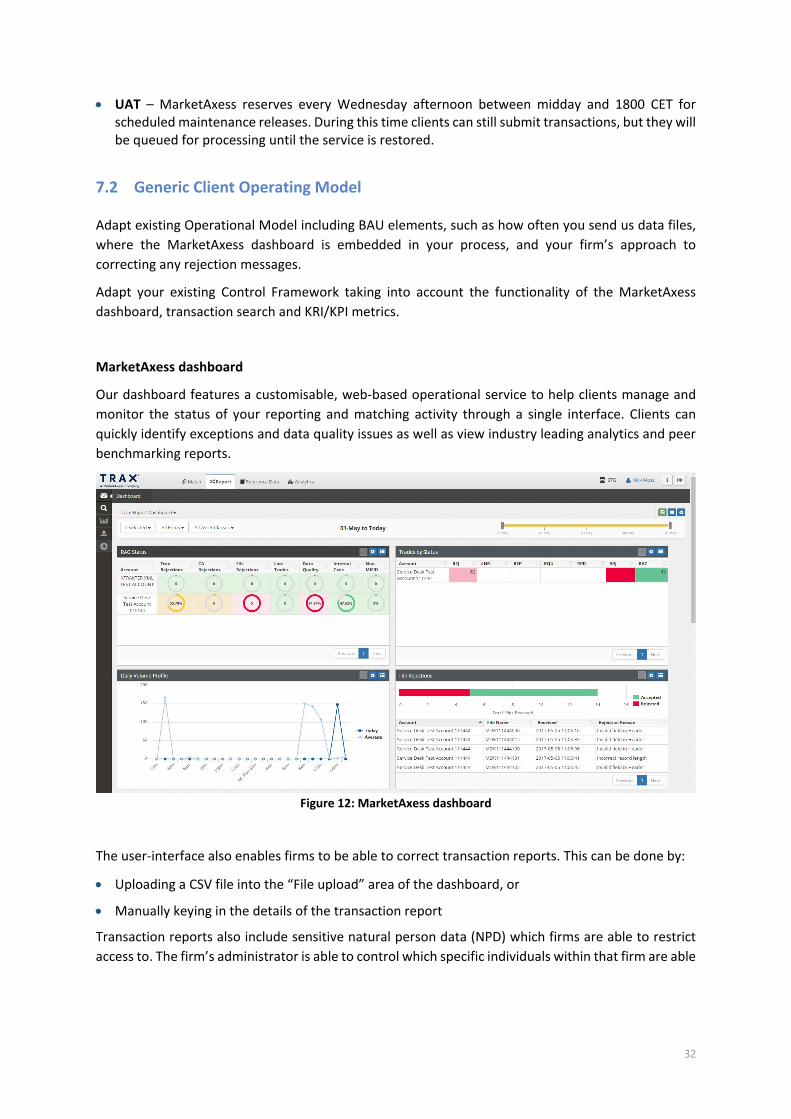

MarketAxess dashboard

Our dashboard features a customisable, web-based operational service to help clients manage and monitor the status of your reporting and matching activity through a single interface. Clients can quickly identify exceptions and data quality issues as well as view industry leading analytics and peer benchmarking reports.

Figure 12: MarketAxess dashboard

The user-interface also enables firms to be able to correct transaction reports. This can be done by:

• Uploading a CSV file into the “File upload” area of the dashboard, or

• Manually keying in the details of the transaction report

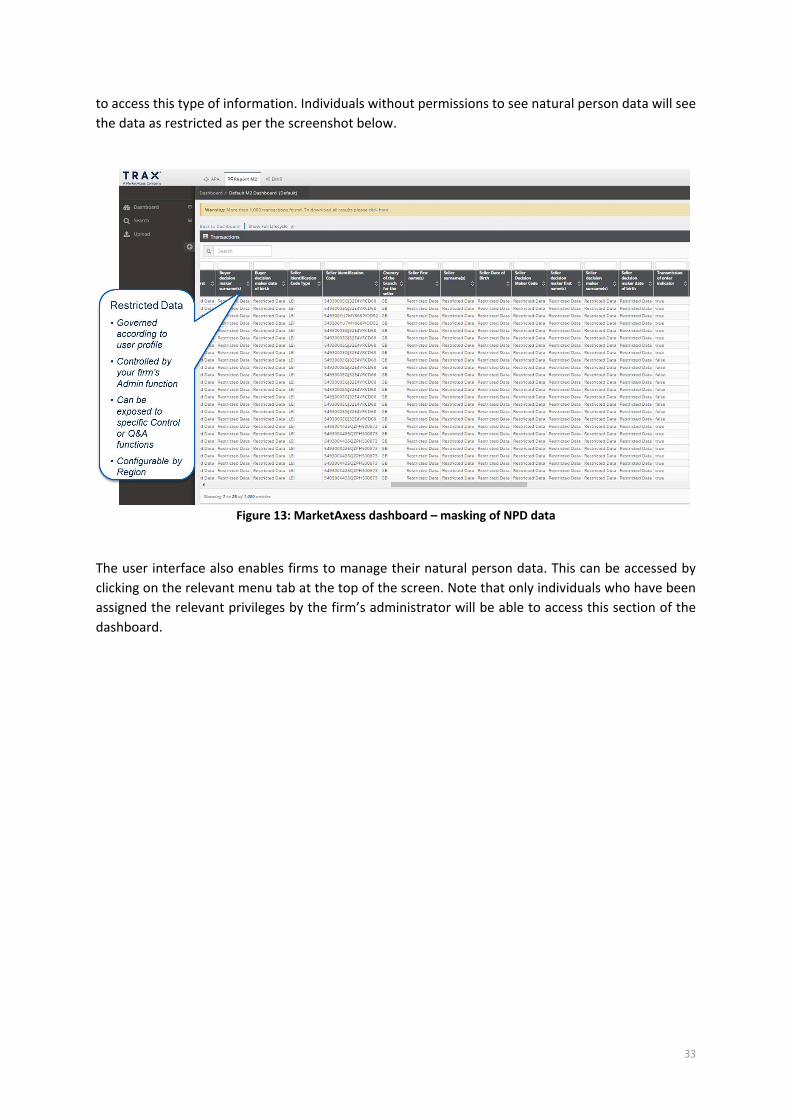

Transaction reports also include sensitive natural person data (NPD) which firms are able to restrict access to. The firm’s administrator is able to control which specific individuals within that firm are able

33

to access this type of information. Individuals without permissions to see natural person data will see the data as restricted as per the screenshot below.

Figure 13: MarketAxess dashboard – masking of NPD data

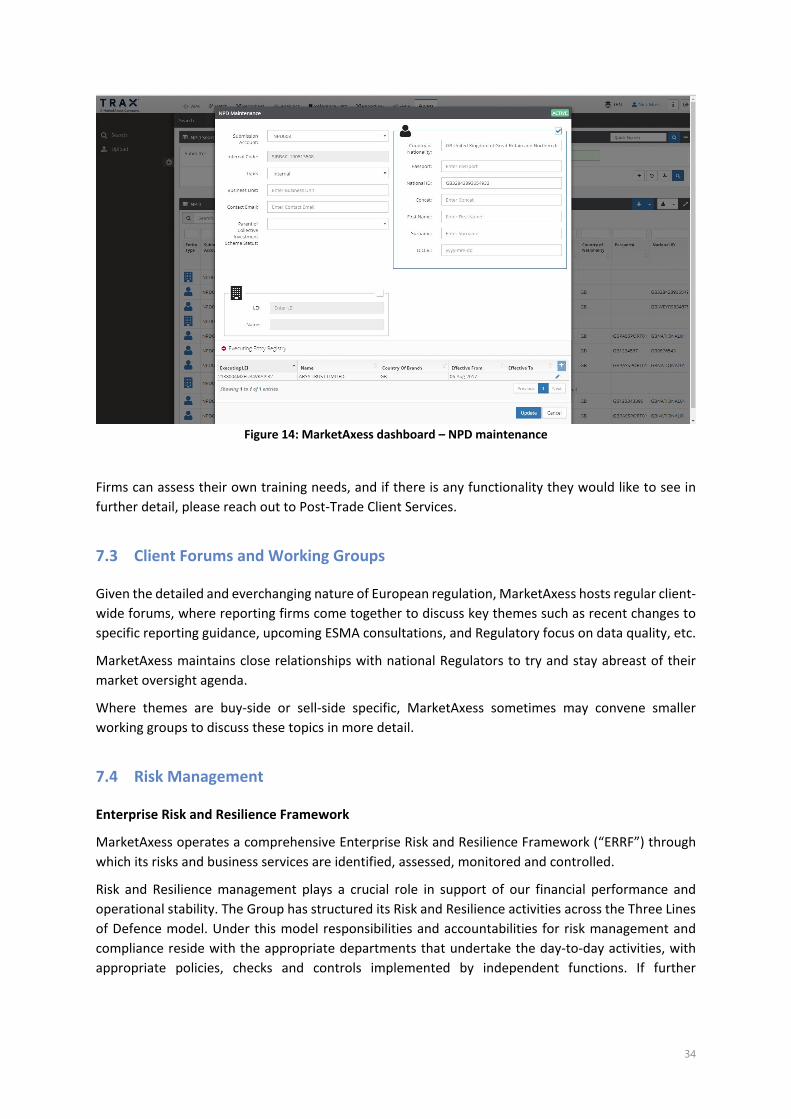

The user interface also enables firms to manage their natural person data. This can be accessed by clicking on the relevant menu tab at the top of the screen. Note that only individuals who have been assigned the relevant privileges by the firm’s administrator will be able to access this section of the dashboard.

34

Figure 14: MarketAxess dashboard – NPD maintenance

Firms can assess their own training needs, and if there is any functionality they would like to see in further detail, please reach out to Post-Trade Client Services.

7.3 Client Forums and Working Groups

Given the detailed and everchanging nature of European regulation, MarketAxess hosts regular client-wide forums, where reporting firms come together to discuss key themes such as recent changes to specific reporting guidance, upcoming ESMA consultations, and Regulatory focus on data quality, etc.

MarketAxess maintains close relationships with national Regulators to try and stay abreast of their market oversight agenda.

Where themes are buy-side or sell-side specific, MarketAxess sometimes may convene smaller working groups to discuss these topics in more detail.

7.4 Risk Management

Enterprise Risk and Resilience Framework

MarketAxess operates a comprehensive Enterprise Risk and Resilience Framework (“ERRF”) through which its risks and business services are identified, assessed, monitored and controlled.

Risk and Resilience management plays a crucial role in support of our financial performance and operational stability. The Group has structured its Risk and Resilience activities across the Three Lines of Defence model. Under this model responsibilities and accountabilities for risk management and compliance reside with the appropriate departments that undertake the day-to-day activities, with appropriate policies, checks and controls implemented by independent functions. If further

35

distinguishes between functions that own and manage risk, functions that oversee risk and functions providing independent assurance

The ERRF is designed to meet the MarketAxess’ risk and resilience management obligations. It includes:

1. The Governance processes and mechanisms, by which decisions are made, actions are delegated, and accountability is enforced.

2. The Risk and Resilience Practices that identify, measure, manage monitor and report risk and resilience effectively.

3. The Risk Language that the Group uses consistently to identify and assess risks, to develop risk policies and facilitate risk aggregation and reporting.

4. The Culture, Behaviours and Values that the Group promotes to encourage transparency, honesty and integrity.

Risk Department

As part of the second line of defence, the Risk department is an integral part of the entire management and control governance system. The system incorporates the identification, assessment, management, monitoring and reporting of risks. The ability to effectively manage risk is important for ensuring that the organisation is operating in a manner consistent with the ‘Board’s expectations.

The Risk function provides support by:

• Exerting independent oversight of the Firm’s adherence with risk management policies and procedures,

• Providing the Group with risk management advice and expertise,

• Monitoring a number of qualitative and quantitative measures to ensure that the businesses risks remain within acceptable levels. Using these measures, MarketAxess produce a number of risk intelligence reports which are disseminated through the governance structures at all levels as appropriate to provide an independent view of risk exposures.

Business Continuity Management

MarketAxess has developed a Business Continuity Management (“BCM”) program to prepare the organisation for crisis situations that could jeopardise MarketAxess’ core mission and its long-term viability. The primary goal of the BCM program is to enable the organisation to ensure personnel safety and restore critical business processes. Strategies have been developed including plans and actions that provide protection or alternative modes of operations for those business processes which, if they were to be interrupted, might otherwise bring about a seriously damaging or potentially fatal loss to the organisation and its clients.

36

8 MARKETAXESS SYSTEMS AND ARCHITECTURE

8.1 Technology Platform

8.1.1 PLATFORM OVERVIEW

The Post Trade Platform is architected as a proprietary 3-Tier application:

1. The Data Storage tier is an Oracle Database, plus Elasticsearch fast-cache.

2. The Business Logic and Data Access tier services are written in Java 8, use Apache ACTIVEMQ, REST APIs, and run in Apache Camel containers

3. The Presentation tier uses the AngularJS JavaScript-based, open-source front-end web framework

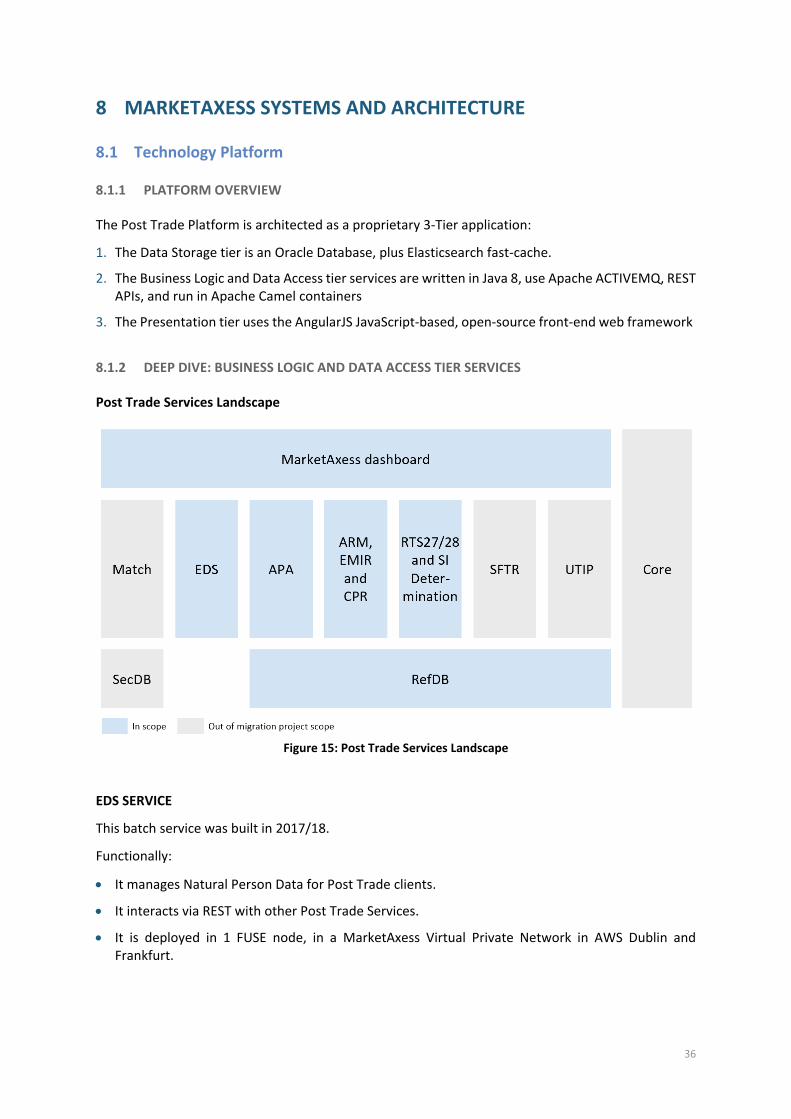

8.1.2 DEEP DIVE: BUSINESS LOGIC AND DATA ACCESS TIER SERVICES

Post Trade Services Landscape

Figure 15: Post Trade Services Landscape

EDS SERVICE

This batch service was built in 2017/18.

Functionally:

• It manages Natural Person Data for Post Trade clients.

• It interacts via REST with other Post Trade Services.

• It is deployed in 1 FUSE node, in a MarketAxess Virtual Private Network in AWS Dublin and Frankfurt.

37

APA SERVICE

This real-time service was built in 2017/18.

Functionally:

• It facilitates pre-trade and post-trade transparency by publishing Quotes and Trades to both a public website and via a FIX feed.

• It accepts transactions via FIX, csv-files and UI-entry.

• It uses reference data from the sub-systems, SecDB and RefDB.

• It stores Quotes and Trades in the Post Trade DB running in the MarketAxess data centre.

• It is deployed in 4 FUSE nodes, running in the MarketAxess data centre.

ARM, EMIR AND CPR SERVICES

This batch service was built in 2017/18.

Functionally:

• It facilitates RTS22 Transaction Reporting, Commodity Position Reporting and EMIR Reporting to NCAs & Trade Repositories across EMEA.

• It accepts transactions via MQ(XML), SFTP(XML & csv-files) and UI-entry.

• It uses reference data from the sub-systems, SecDB and RefDB.

• It stores Transactions in the Post Trade DB running in the MarketAxess data centre.

• It is deployed in 4 FUSE nodes, running in the MarketAxess data centre.

RTS27/28 AND SI DETERMINATION SERVICE

This batch service was built in 2017/18.

Functionally:

• It facilitates RTS1, RTS2, RTS23, RTS27 and RTS28 Periodic and Best Execution Reporting, and SI Determination.

• It stores Reports in the Post Trade DB running in the MarketAxess data centre.

• It is deployed in 2 FUSE nodes, running in the MarketAxess data centre.

REFERENCE DATA SERVICE

This batch service was built in 2017/18.

Functionally:

• It serves data across MarketAxess functions from sources including ANNA DSB, Copp Clark, Thomson Reuters, GLIEF and ESMA.

• It stores Reference Data in the Post Trade DB, and replicates to the Trading Platform.

38

• It is deployed in 4 FUSE nodes, running in the MarketAxess data centre.

DASHBOARD/GUI SERVICE

This UI service was built in 2015/16.

Functionally:

• It implements Administration functions in the Post Trade UI, such as Login, Logoff, Password Reset.

• It stores config. data in the Post Trade DB.

• It is deployed in 2 FUSE nodes, running in the MarketAxess data centre.

Transport and Message Formats per Service (current state)

Service Transport Message Format

ARM SFTP/MQ CSV/XML

APA FIX/SFTP FIX/CSV

EMIR SFTP CSV

8.2 People

The Post Trade Technology team is made up of ~70 MarketAxess employees, plus ~30 consultants, most of whom are based in London, but also with support from colleagues in the US, Singapore and India (outsourced).

The team operates as 13 distinct SCRUM teams within an organisation model based on the Scaled Agile Framework (SAFe).

Each SCRUM team consists of Developers, QA Testers, a SCRUM Master, a Product Owner and a Product Manager.

The SCRUM teams are aided and assisted by the following additional teams:

• A Centre of Excellence (CoE) team for Platform Improvements

• A Production Support team with members in London, Singapore and New York

• A Client Connectivity team

• A UK-based IT Infrastructure team, with support from colleagues in NY and Asia

Tenure: The average MarketAxess tenure of the (employees) Post Trade Technology team is 6 years which speaks to the fact that the team has stability and maturity.

Institutional knowledge: The team works very closely with their colleagues in Client Services, Production Support, and Operations and this ensures that each member of the Technology team has a good understanding of the business context in which their software operates.

39

8.3 Software Development Life Cycle (SDLC)

MarketAxess is responsive to regulatory driven changes. In recent years MarketAxess has successfully adapted to MiFID II, EMIR and SFTR to note but a few changes. MarketAxess will always seek to provide as much notice to any client impacting change as possible.

The Post Trade Platform currently supports two planned releases every quarter, with off-cycle releases being only undertaken for major project releases or emergency bug-fixes (EBFs).

Before each release, each and every code change is taken through a cycle of Unit Test, Integration Test, Regression Test, Load Test, UAT and Client Test to ensure consistency and validity.

40

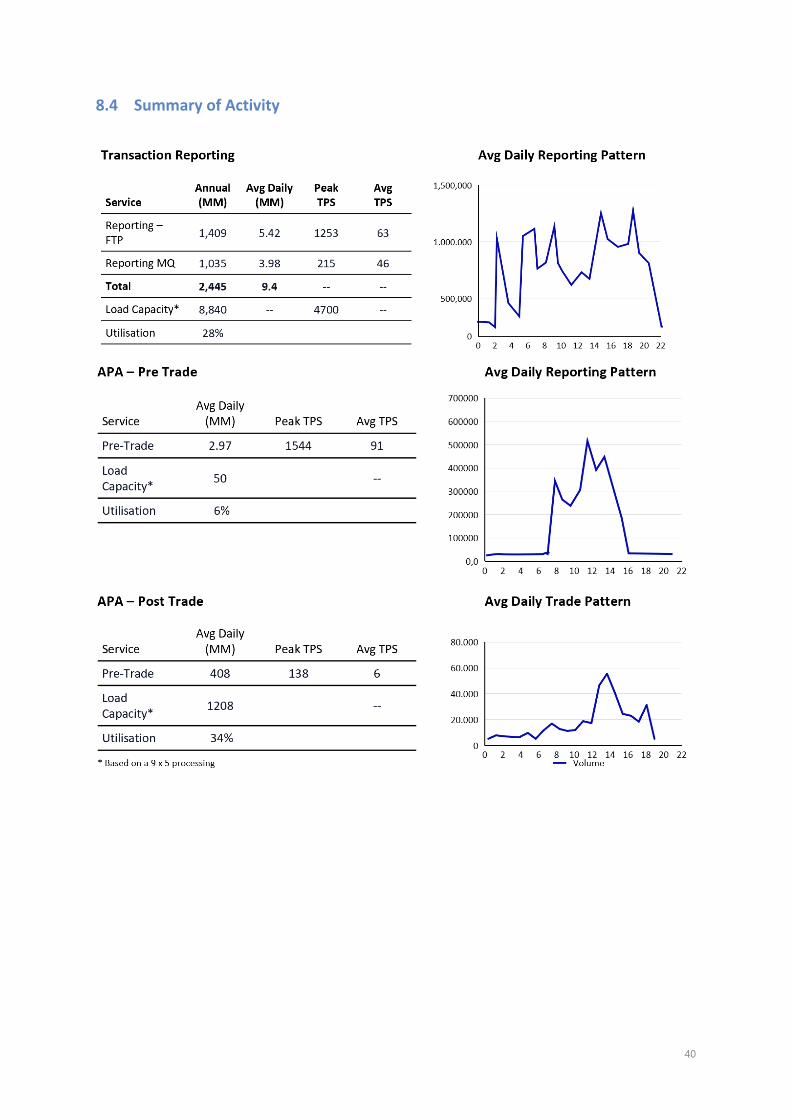

8.4 Summary of Activity

41

9 INVOICING & PAYMENT DETAILS

Post-closing (Nov 30, 2020), invoices will be issued by MarketAxess. You will continue to be invoiced according to your current contractual terms and in the same currency you are today.

MarketAxess runs a monthly finance cycle and bills clients in arrears. Please update relevant bank details by Dec 18, 2020 as follows:

• Beneficiary Bank Name: J.P. Morgan Bank Luxembourg S.A., 6 route de Treves, L-2633, Senningerberg, Luxembourg

• Beneficiary Bank SWIFT: CHASLULX

• Ultimate Beneficiary Name: Trax NL B.V.

• Ultimate Beneficiary Account: 7000049088

• Ultimate Beneficiary IBAN: LU460670007000049088

• Currency: EUR

• VAT Number: NL 857933735B01

10 COMMON IMPLEMENTATION QUESTIONS

Below we presented common implementation questions and answers based on our experience with firms like yours.

Set Up

Ref. Question Answer

1

You have set up the Administration account for me. How do I add other users?

See Section Training and Testing. Documentation provided includes

• MarketAxess ARM – Creating User Profiles as an Administrator

• MarketAxess APA – Creating User Profiles as an Administrator

• MarketAxess EDS – Creating an Upload Account

For any further information needs, please reach out to Post-Trade Client Services [email protected]

2

What Permissions should I be assigning to users? Where can I get an explanation of the implications of ticking each permissions box?

See question number 1 just above.

42

Planning

Ref. Question Answer

1

Where should I go to get answers to any questions that I have?

The Post-Trade Client Services (PTCS) and Relationship Management (PTRM) teams will be your central points of contact for MarketAxess Post Trade and will be able to get you answers to any questions you may have

2

Can you provide me with the information I need for my internal project reporting?

Yes, as part of your migration planning, we will ensure we have a common understanding of activities, and dates and agree how progress reporting and issues escalation should be managed

3

Do you have any formal tests that we need to pass before we can go live?

No, but we will agree the go-live criteria with you early in your migration plan so that we both understand what is required and, if necessary, can identify and address any gaps during the migration

4

Can the system be operated from several locations/Multi Legal entity capabilities?

Yes. The graphical user interface (GUI), our MarketAxess dashboard, is designed to enable clients to work in a geographically dispersed manner. Each user profile can be configured to allow access to the data of one or many legal entities.

5

Is remote diagnostic support available? Describe how it occurs, and any limitations you may have encountered in providing this service.

Yes. Limitations are usually in respect of remote security policies, in the instance that this is the case MarketAxess have utilised the Customer’s preferred remote access solution where possible.

6

Please describe the initial and ongoing training required/offered.

As part of the onboarding process MarketAxess will provide training through telephone, videoconference or in person (where possible). Throughout the life of the contract technical support and training is provided as part of the service.

43

Ref. Question Answer

7

What testing services will you provide? MarketAxess operates a test environment for each product that mirrors the functionality found in our production environments. This test environment is available to all clients and forms a key component of our onboarding a certification process.

Business as usual operation

Ref. Question Answer

1

Please provide details of your communications protocol in the event of any incident impacting us or our investors.

Client impacting incidents are notified to client via email, should a breach be in effect all available efforts will be made to engage the designated contacts by email and telephone.

2

After unscheduled service downtime, will you communicate the quantifiable impact (e.g. in terms of number of trades not reported) to the client and the regulator?

Yes.

3 Does the application integrate with mobile devices e.g. iPad, Blackberry, iPhone?

No.

4 Is there any integration with additional productivity tools (e.g. MS Office plug-ins)?

No.

5 Are you able to provide detailed bespoke monthly management information reports?

Yes, MI is provided both via the MarketAxess dashboard.

6

Can we meet our regulatory requirements to store / re-create historical reports across all specified regimes?

Yes. MarketAxess will store all versions of every report under each regime. All data is accessible through the GUI or via Client Services.

7 Does the system maintain an audit trail of transactions reported?

Yes, all activity is persisted at the database level.

8 Describe your ability to track changes/audit trail on historical data/reports

MarketAxess retains all previous versions of a submitted report, including those that may have been rejected.

Product Development / Changes / Defects

44

Ref. Question Answer

1 What is the process for requesting new features / bug fixes?

New features and bug fixes should be raised through the Client Services team or at client forums.

2

Does your solution support the use of automated test tools for regression testing? If so, list automation software used as examples.

This is not client facing functionality.

3

Do customers and user groups influence releases of the solution? Describe how.

It is by continual consultation with our customers that the solution has been developed into the rich platform that it is today.

Customers can recommend enhancements through any point of contact that they have within MarketAxess. The request will then be analysed and in most cases will be added to the product if it is a) technical possible and b) of benefit to the MarketAxess Post Trade community.

4

Describe how clients are sent new software versions including release notes.

Due to our MarketAxess dashboard (GUI) being web-based there is no requirement to install any software. When new features and fixes are introduced through our release cycle clients will receive a notification prior to the event and after detailing the release notes.

45

ARM

Ref. Question Answer

1

How can MarketAxess help me populate ISIN codes?

For OTC derivatives, MarketAxess can perform a lookup based on the characteristics of the contract to the ANNA DSB and return an ISIN to the transaction report.

For ETDs, MarketAxess can use the exchange product code to populate search for the relevant ISIN from the exchange and populate that on the transaction.

For OTC transactions where there is no Systematic Internaliser, no ISIN is required, but the relevant reference data fields must be populated on the transaction report instead of the ISIN.

Please read the MarketAxess ARM – ISIN Lookup Specification for more details on this process.

2 What will be the maximum number of transactions clients can submit in each submission batch?

99,999.

3

Why is my transaction report in a status of held?

There are two main reasons for this:

1. The client is using the EDS and a transaction has been sent in for which MarketAxess is unable to enrich, this could be because: — The static data does not exist in the EDS

environment — The static data exists but does not

match the details of the transaction report, for example: – The effective from date is after the

trade date of the transaction report – The executing LEI does not match.

2. The transaction is queued behind another transaction that is pending being processed, some of which could be in a HLD status.

46

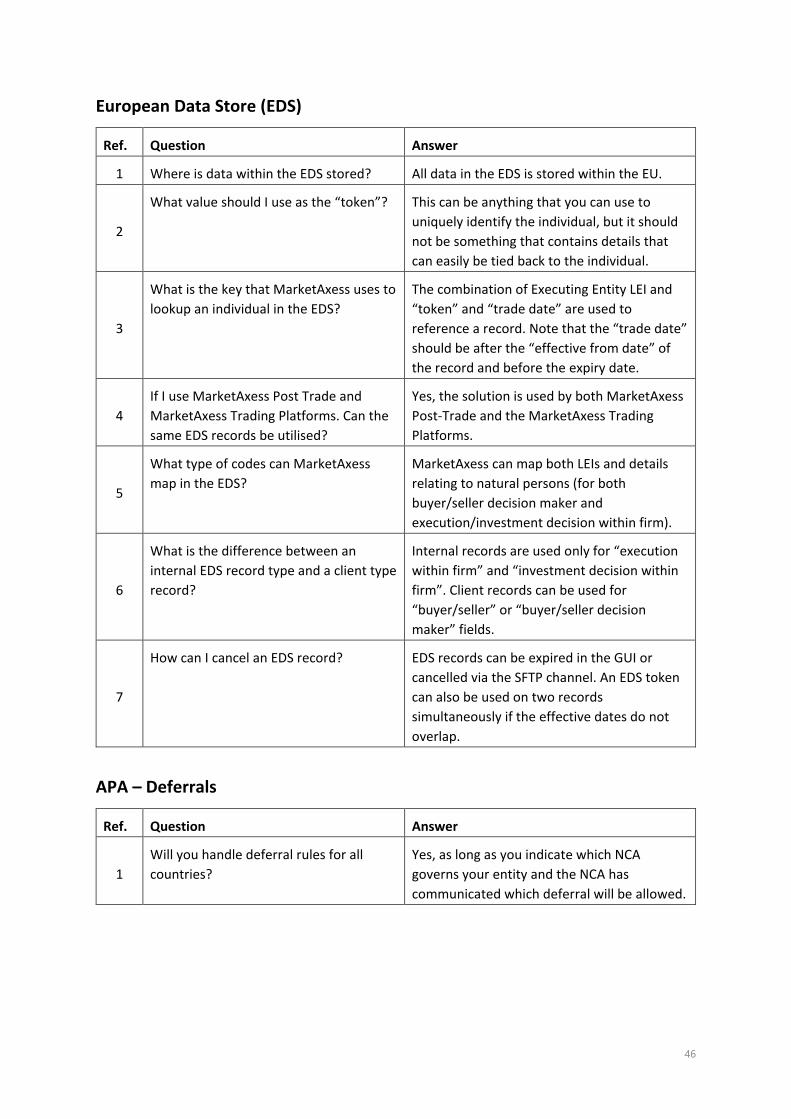

European Data Store (EDS)

Ref. Question Answer

1 Where is data within the EDS stored? All data in the EDS is stored within the EU.

2

What value should I use as the “token”? This can be anything that you can use to uniquely identify the individual, but it should not be something that contains details that can easily be tied back to the individual.

3

What is the key that MarketAxess uses to lookup an individual in the EDS?

The combination of Executing Entity LEI and “token” and “trade date” are used to reference a record. Note that the “trade date” should be after the “effective from date” of the record and before the expiry date.

4 If I use MarketAxess Post Trade and MarketAxess Trading Platforms. Can the same EDS records be utilised?

Yes, the solution is used by both MarketAxess Post-Trade and the MarketAxess Trading Platforms.

5

What type of codes can MarketAxess map in the EDS?

MarketAxess can map both LEIs and details relating to natural persons (for both buyer/seller decision maker and execution/investment decision within firm).

6

What is the difference between an internal EDS record type and a client type record?

Internal records are used only for “execution within firm” and “investment decision within firm”. Client records can be used for “buyer/seller” or “buyer/seller decision maker” fields.

7

How can I cancel an EDS record? EDS records can be expired in the GUI or cancelled via the SFTP channel. An EDS token can also be used on two records simultaneously if the effective dates do not overlap.

APA – Deferrals

Ref. Question Answer

1 Will you handle deferral rules for all countries?

Yes, as long as you indicate which NCA governs your entity and the NCA has communicated which deferral will be allowed.

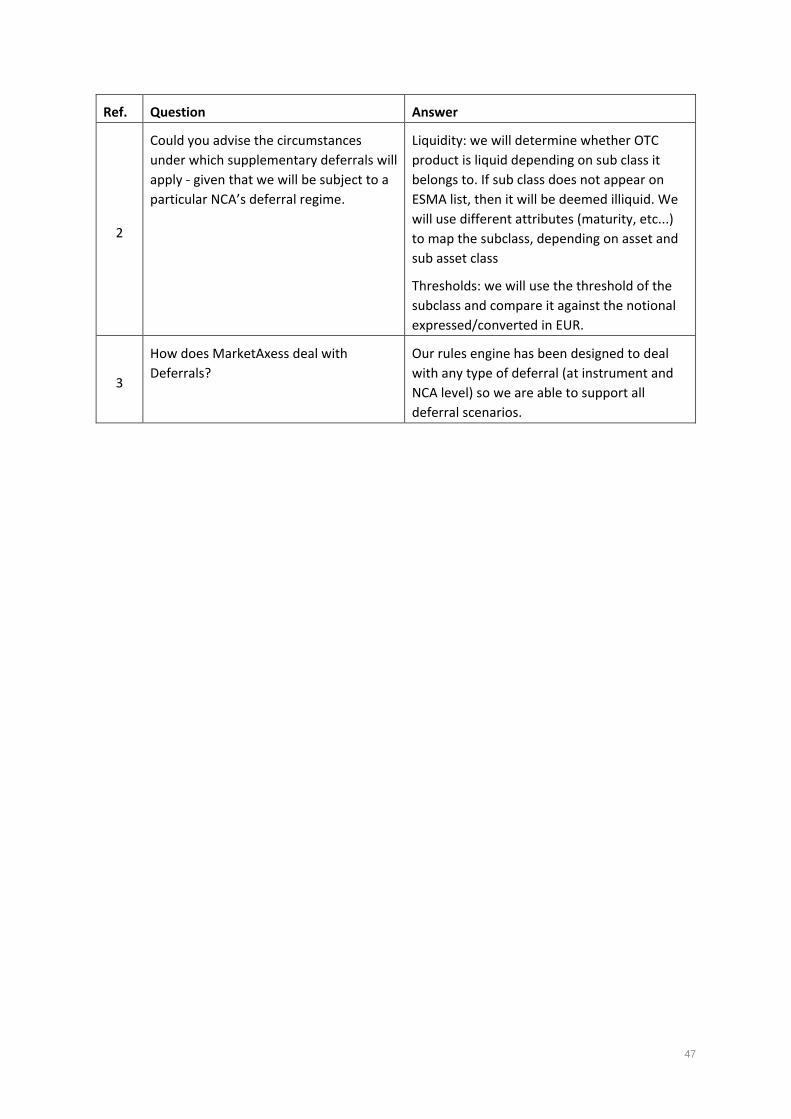

47

Ref. Question Answer

2

Could you advise the circumstances under which supplementary deferrals will apply - given that we will be subject to a particular NCA’s deferral regime.

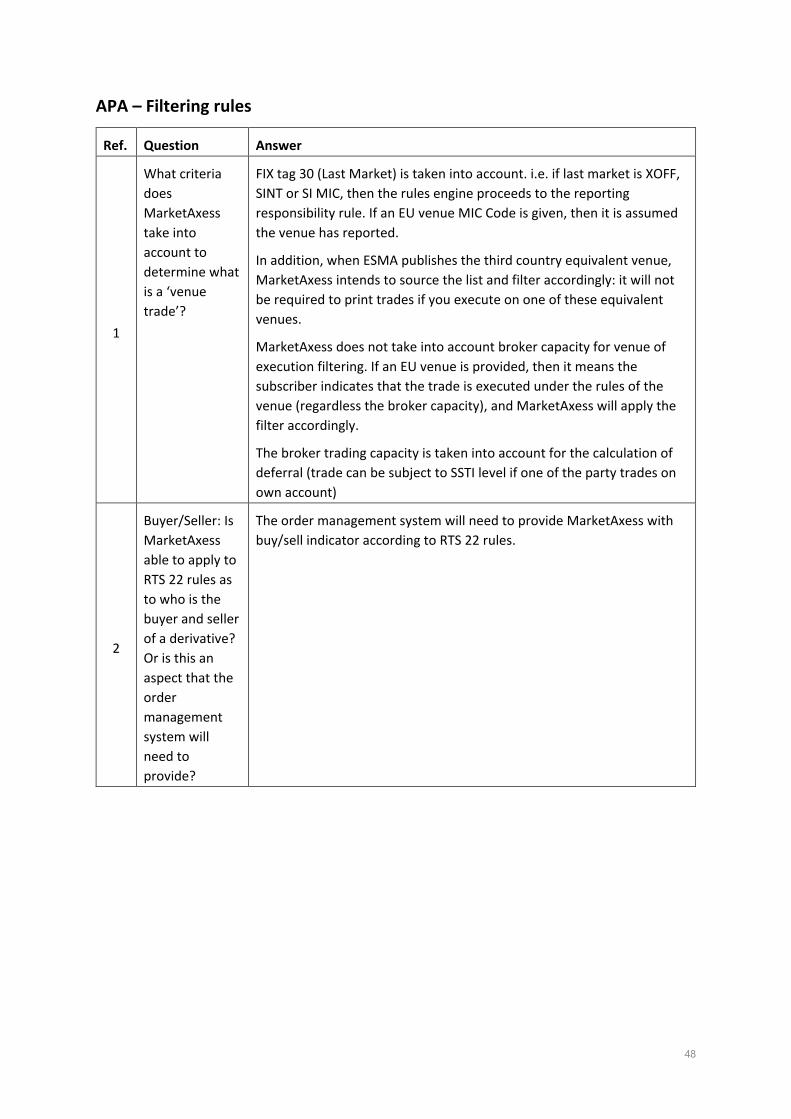

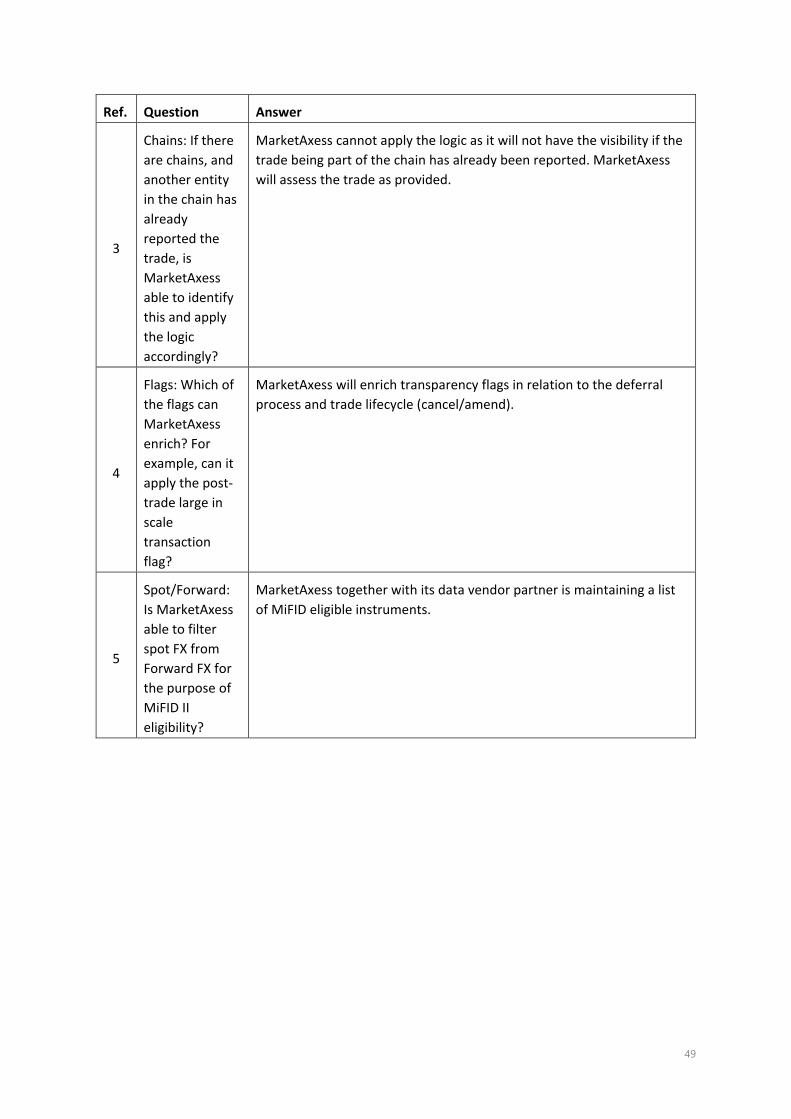

Liquidity: we will determine whether OTC product is liquid depending on sub class it belongs to. If sub class does not appear on ESMA list, then it will be deemed illiquid. We will use different attributes (maturity, etc...) to map the subclass, depending on asset and sub asset class