Embed Size (px)

Citation preview

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55 ISSN 2152-1034

Corporate Governance in the U.K: Audit Committees and

disclosure Arrangements – A Web-Based Analysis

Mohamed Hegazy, American University in Cairo Karim Hegazy, Partner, Crowe Dr. A.M.Hegazy & Co.

Abstract The main objective of this research is to assess whether UK listed companies comply with the U.K code of corporate governance regarding audit committees and disclosure arrangements. The research also aims at testing whether the companies’ size and board composition affect the management’s decision to comply with the requirements of the U.K code. Data was collected from the U.K listed FTSE companies. Descriptive statistics including frequency tables, mean, other central tendency measures and regression analysis were used to test the research hypotheses. The findings of the descriptive statistics show most of the listed companies comply with the U.K code. The results of the regression analysis indicate a small association between the size of the companies described by the number of employees and the degree of compliance with the code. Future research should be more directed toward testing the other requirements of the code. Keywords: Corporate Governance, Audit committees, Disclosure arrangements, non-executive directors, board composition.

Introduction

After a multitude of high profile business failures and accounting restatements (Enron, WorldCom and Quest) in 2001 and early 2002, the U.S Congress attempted to regain the investor confidence in the financial reporting process by issuing the Sarbanes-Oxley Act of 2002 (SOX). This law has required auditors to increase their audit work on internal control systems and placed pressures on audit firms to reconsider their audit process for publicly traded companies. In July 2003, a combined code of corporate governance replaced the combined code originally issued by the Hampel Committee on corporate governance in the U.K in June 1998. The replacement of the 1998 code followed the collapse of a large number of companies in the US and attempted to protect shareholders and investors’ interests in the Financial Times London Stock Exchange

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 33

(FTSE). The code’s main and supporting governance principles covered a number of important issues related to the day to day operations of the company including the management of the company by the board of directors, board members remunerations, management accountability, and management relations with shareholders, internal control and audit committee guidelines. As stated in the preamble of the code listed companies are expected to comply with the code provisions most of the time and departure from the provisions of the code may be justified in particular circumstances.

This research aims at determining whether listed companies in the U.K do comply with the provisions of the combined code of corporate governance regarding audit committees and disclosure arrangements. The area of corporate governance is an important topic especially with the current financial crisis affecting many economies and related businesses. In such circumstances, there is a need for better and more enhanced control over the operations of FTSE listed companies. In addition, the research also aims at determining whether the characteristics of some listed companies mainly the size of the companies and the composition of the board can affect management’s decision to comply with the code. The size of the company can be interpreted using the companies’ total turnover and number of employees while the number of non-executive directors will be used to describe the composition of the board.

The research study is composed of four sections. The first section is an introductory providing insight into the research question and related objectives. Section 2 reviews the literature related to the evolution of corporate governance in the U.K Furthermore, this section presents some of the literature that shows how companies’ performance has been enhanced by issuing corporate governance principles and guidelines. The duality in roles by the chairman and CEO, board composition & non-executive directors and the role of audit committee are analyzed in this respect. Section 3 discusses the research methodology used including the design of a checklist based on the provisions of the code especially regarding the audit committees and disclosure practices. It also presents the statistical analysis and data collection methods. Section 4 presents the research conclusions, limitations and recommendations for future research. Literature Review

Corporate governance was defined as ’a system by which companies are directed and controlled’ (Cadbury report 1992, p.5). Corporate governance was also described as an ‘’internal system encompassing policies, processes and people, which serve the needs of shareholders and other stakeholders by directing and controlling management activities with good business sway, objectivity accountability and integrity’’ (O’Donovan, 2008). Corporate governance is understood as a set of relationships between a company, its management, its board, its shareholders and other stakeholders. Corporate governance is highly rated as it not only provides the structure through which companies objectives are set but also how they are monitored, maintained and achieved. Figure (1) describes the classic the corporate governance structure.

© Mohamed Hegazy and Karim Hegazy

34

Figure 1. The classic corporate governance structure (Boyd, 1996, p. 169)

Having a bad corporate governance structure may be disadvantageous as it can threaten the integrity of governance professionals in terms of their public reputation and their professional liability (Jones and Pollitt, 2001). Broadly speaking, corporate governance deals with external aspects such as the relationships with stakeholders as well as internal aspects such as internal controls and board structures. (Mallin et al, 2005). In fact, corporate governance is an essential tool nowadays for any corporate success and affects many aspects of the organization and business activities. In the U.K there were three major periods identified for the evolution of corporate governance. The 1st period was characterized by the dominance of the funding family and began from the industrial revolution to the 1920s. The 2nd period was mainly marked by the rise of the professional manager concept and covered the time following the 1920s to the 1970s. The 3rd period from the 1970s was characterized by the increased accountability to the society (Gomez and Korine, 2005).

Board of Directors

Auditor

Chief Executive & Management

Chair

Appoint

Report

Elect

Audit

Appoint Report

Shareholders

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 35

Table (1) presents more information about how corporate governance concept evolved through the previous centuries. Table 1: The evolution of corporate governance and the procedures of democracy 19th century-1920s 1920s-1970s 1970s-21st

century Model of reference for corporate governance

Familial Managerial Popular

Economic enfranchisement

Implementation Creation of rights to ownership independent of social standing

Reinforcement Strengthened by law and corporate practice. Public general meetings become standard

Reinforcement Strengthened by new rules on the right to vote; protection of minority interests

Separation of ownership/control

No Implementation Generalization of the limited liability form, with boards and disclosure requirements

Reinforcement Increasing board supervision over managers

Representation with public debate

No No Implementation Mass ownership; stakeholder activism

(Gomez and Korine, 2005, p. 747)

Following the prolonged period of economic growth in the 1980s the economy began to show signs of overheating mainly through rises in GDP growth and asset prices. This led to major scandals in the U.K in the late 1980s and early 1990s such as the collapses of BCCI, Guinness, and Polly Beck as well as the controversy over directors pay and the lack of controls and business conduct (Jones and Pollitt, 2001).The Cadbury report was issued in 1992 as a first attempt to try and provide guidelines and foundations of a set of corporate governance codes so that scandals and business collapses could be minimized in the future and was a product of the Financial Reporting Council, the London Stock Exchange and the accountancy profession. Table 2 presents the main recommendations of the Cadbury report.

© Mohamed Hegazy and Karim Hegazy

36

Table 2: Main recommendations of the Cadbury Report Governance issue Cadbury Code Recommendation Separate CEO and chairperson Recommended but not compulsory Nomination of Directors Formal board process via nomination committee

dominated by outside directors

Outside Directors Minimum of 3 non-executive directors

Independence of Directors Majority of non-executives to be independent

Rotation of Directors Directors to be appointed for specific terms with non-automatic reappointment

Pay and Bonuses Annual Report to reveal disaggregated director’s pay; remuneration committee of board to be dominated by outside directors

Independence of the Auditor Audit committee of the board to be formed, comprised exclusively of outside directors

Flow of information to the board Board to have a formal schedule of decisions; directors to have paid access to outside advice

Greater Scope of Auditing Auditors to review compliance to the Code, including directors’ statements on going-concern and on internal audit effectiveness

(Boyd, 1996, p.170)

The main feature of Cadbury report was self regulation approach whereby reporting of compliance to the code was part of the listing requirements for public companies in their annual reports showing the extent of compliance with the code. However, the Cadbury report failed to achieve its objectives due to the limitations of its mandate report as it was silent on non financial aspects of governance and to the size of a firm (Boyd, 1996). There was no distinction made between large and small listed firms in terms of compliance with the code. Furthermore, Cadbury report had recommended the establishment of a remuneration committee consisting of non executive directors but details of its policies had not been precluded or examined. Moreover, Cadbury report did not go in detail about the level of executive pay (Conyon and Peck, 1998).

As a result of all such criticism, the Greenbury report was issued in 1995 covering the level of executive pay and director’s remuneration (Greenbury, 1995). The report addressed the functioning of the remuneration committee made up of non executives who would determine both individual executive pay and pay policy. The remuneration committee was responsible for issuing a statement of compliance or non compliance in the annual report. The report also emphasized the importance of timely and accurate disclosure. In 1998, the Hampel report was later issued to review the progress of companies in compliance status, promote high standards of corporate governance in the interest of investors’ protection and to preserve and enhance the standing of listed companies in corporate governance levels (Hampel, 1998). The main

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 37

recommendation was that companies should include in their annual reports a narrative statement of how they apply the relevant principles of corporate governance to their particular circumstances. However, the report can be seen as endorsing the Cadbury report but adding nothing new to the main requirements of such report (Dahya et al, 2002).

To overcome application problems of the Hampel report, a Turnbull Report and revised Combined Codes were issued in 1999, 2003 and 2008 respectively. The Turnbull Report focused on how to implement best practice systems of internal control, the need for a board statement on internal control and discussed the appropriateness of having an internal audit function (Turnbull, 1999). The report was short and generally perceived as completed the work left unfinished by the Hempel report in this area. At the same time, the revised Combined Code issued in 2003 aimed primarily to advance the best practice through revisions of the code and to focus more on the behaviors and relationships of the best people available, their good qualifications and relevant experience, which are essential for an effective board. Finally, the revised code issued in 2008 included guidelines of the audit committee that were separately published for listed companies (FRC, 2008).

The issuance of the first Combined Code in 1998 was not mandatory confirming the tradition characterizing the U.K regulating environment which is evident in voluntary disclosures rather than legal enforcements. The philosophy of the ‘comply or explain’ principle offers intelligent discretion and flexibility and allows for exceptions of the actual rules. As Higgs (2003, p.3) stated in his research study: ‘The brightness and rigidity of legislation cannot dictate the behaviour or strengthen the trust I believe is fundamental to the effective unitary board and to superior corporate governance.’ U.K listed companies are also required to issue a statement of compliance with the detailed principles of the combined code in their annual reports. The main role of the combined code is to shift the balance of power held by the company’s board and its subsequent subcommittees away from the company’s main executive directors and instead give greater prominence to non executive directors’ independence and role in the decision making process and different companies corporate governance structures. The code also emphasizes the importance of the separation between both roles of the company’s chairman and CEOs. Furthermore the code sets out provisions relating to the composition of the board of directors and its main principles and duties as well as clearly setting out the functions of the three main committees which are the remuneration, audit and nomination committees as well as stressing the importance of the need for non executive directors in the boards. In the following sections the researcher will discuss details associated with the main characteristics of the code of corporate governance.

The U.K code of corporate governance regards duality as undesirable and recommends the separation of the CEO and chairman positions i.e. no one person should hold both posts. This is to avoid concentration in the decision making in only one individual and to maintain the balance of power within the board of directors. Prior research on the impact of duality of CEOs and chairman duties has given different results. Jensen (1993) points out that when one individual holds both positions, internal control systems may fail as key functions of the board cannot effectively perform their duties which also include evaluations and firing of the existent CEO. Forker (1992) was of the opinion that duality was associated with poor disclosure which in turn results in ineffective monitoring of managerial opportunistic behaviour. Moreover, Fama and Jensen (1983) concluded that the concentration of all decisions (management and control) in one person reduces the required effectiveness needed in monitoring top management. Another study by Cosh et al (2006) found that duality has a negative impact on announcements and long

© Mohamed Hegazy and Karim Hegazy

38

run returns but a relatively positive effect on key operating performance measures. Brickely et al (1997) also found that separate CEO and chairman may engender costs in monitoring the chairman and information sharing costs between them.

On the other hand, Boyd (1995) found that combining both roles in one person is associated with higher profitability. In contrast Rechner and Dalton (1991) found that combining the roles of a chairman and CEO reduces profitability whereas Baliga et al (1996) found no effect on performance. Based upon the findings of all the above studies, the researchers believe that the separation of CEO and chairman positions is important for better management of the company and possible control effectiveness over the business operations.

The board of directors is seen as an internal mechanism whose main duties are to take some of the major decisions on behalf of shareholders and to align owners’ incentives with the management by ensuring that the management behaviour is consistent with the owners’ interest. In a research study by Butler (1985) he found that board of directors dominated by outside directors are more likely to behave in shareholders’ interest. However this was not always the case as Holl (1975) found insignificant differences. Other studies such as the one made by Faccio and Lasfer (1999) found no specific relationship between board ownership and firm value in general. This was also confirmed in US in a study by Hermalin and Weisback (2003) as they found no association between firm performance and board composition.

However, the effects of board composition on voluntary disclosures were mixed as Beasley (1996) found that non executive directors are positively related with the board’s ability to influence voluntary disclosure decisions. Dahya et al (2007) found that board composition has no meaningful impact on financial performance. It is also often believed that the smaller the boards the more effective they are specially in taking specific and important decisions. This was confirmed by Lipton and Lorsch (1992) and Jensen (1993) as they criticized the performance of large boards’ problems in poor communication and decision making. According to Jensen (1993) as groups increase in size they become less effective because the coordination and process problems overwhelm the advantages from having more people to draw on. In addition to that CEO performance incentives provided by the board through compensation and threat of dismissal operate less strongly as board size increases and financial ratios related to profitability and operating efficiency appear to decline as board size grows. Also, the effect of the board size was found to have an insignificant effect on takeover by firms. This was confirmed in the U.K in a study by Conyon and Peck (1998) who examined 481 listed companies from 1992 to 1995 and found a negative effect of board size on both market and book value and profitability.

At the same time, non executive directors (NED) are defined as being independent of executive management positions or other management functions of the company and free from any relationships which may affect their judgment. Some of the advantages of having a large number of non executive directors are the valuable business experience and views they offer (Hanniffa and Cooke, 2002). In addition, non executive directors can also contribute to objectivity, impartiality as they look at decisions and issues from a wider and broader perspective than executive directors. Moreover, they are able under the new provisions of the combined code to challenge policies of the executive directors which they feel are not in the interest of the company’s shareholders. The reasons for the effective monitoring of companies’ board decisions by non executive directors are reputation concerns and fear of lawsuits.

Hermalin and Weisbach (1991) and Dahya et al (2007) found no relation between firm performance and function of outside directors. This was not supported in a research by Baysinger and Butler (1985) as they found that companies perform better if there are more outsiders in the board. Rosenstein and Wyatt (1990) also found out that new appointments of non executive

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 39

directors are linked with company performance. Another study by Klein (2002) examines whether audit committees and board characteristics are related to earnings management to the firm. He found that firms with board committee of more than a majority of independent directors are more likely to have abnormal accruals than others. Using a Cross sectional analysis he found a negative association between abnormal accruals and the percentage of independent directors but no evidence of a systematic association between having an independent audit committee and abnormal accruals. Finally, it was tested that the proportion of non-executive directors is associated with better specific decisions including acquisitions, CEO turnover and executive compensation (Hermalin and Weisbach, 2003).

However having a large number of non executive directors may be disadvantageous as they only meet a few times during a year and hence perform their duties on an irregular basis. (Pass, 2006; Weir and Laing, 2000). Also, outside directors often lack the information necessary for decision making as they do not fully understand the business or have little time to devote to their duties. This fact was supported by Yermack (1996) as a negative relationship between the proportion of outside directors and company’s performance was found. Another study by Weir and Laing (2000) showed that the number of non executive directors in the U.S have an insignificant impact on share price performance but a relatively negative impact on profitability. The results of all the above studies confirm the notion that the board of directors and its composition is an important issue in corporate governance and the success of any company is significantly measured by the board effectiveness and independence.

From the above analysis, we can identify a number of research hypotheses interpreting the decision of compliance with the U.K code. As shown in the hypotheses below, the decision of compliance may be affected by the size of the company and/or the composition of the board. The size of the company can be interpreted using the companies’ total turnover and number of employees while the number of non-executive directors will be used to describe the composition of the board. H1: The listed companies in the U.K comply with the requirements of the code of corporate governance regarding disclosure arrangements. H2: There is a relationship between the size of the company and the level of compliance with disclosure arrangements. H3: There is a relationship between the composition of the board and the level of compliance with disclosure arrangements.

Over the past years the role of audit committees has developed dramatically to meet the challenges of changing economic, social and business environments and is seen as a powerful device for improving value of relevant intellectual capital disclosure. The audit committee should consist mainly of non executives. The audit committee’s memberships should not include directors who are current employees, former employees within the last three years, employees who have cross compensation committee links nor have immediate family members of an executive officer.

Three key provisions were stated in the U.K Combined Code of 2003 and audit committee guidelines in 2008 regarding the composition of audit committees.

© Mohamed Hegazy and Karim Hegazy

40

• At least one audit committee member should have relevant financial experience • Three meetings should be held annually to coincide with duties within the audit and

financial reporting cycle • only relevant members and the chairman should be present at the meetings

Different studies were carried out to test whether audit committees have a key role in the

success and performance of a company. Ho and Wong (2001) found out that effective audit committees would certainly improve internal control mechanisms and act as means of minimizing agency costs and the presence of an audit committee is closely associated with more reliable financial reporting, enhanced quality and increased disclosure. This view was also shared by Olson (1999) as he concluded that inactive audit committees would merely monitor managements effectively and hence lead to a negative impact on the company. Again the issue of independence and non executive directors are crucial for audit committees.

Other studies confirmed the fact that audit committees composed of less than a majority of independent directors are more likely to have a high ratio of abnormal accruals than others. Klein (2002) argued that board independence and audit committees are positively related to market to book values past negative earnings and the size of a firm. However a different case study by Mangena and Pike (2005) found no relationship between the size and independence of audit committees and voluntary disclosure arrangements made by companies. To sum up, studies may have provided different findings associated with the role of the audit committee in enhancing the company's performance but all agreed that it is an important element of corporate governance. The more independent and qualified the members of the audit committee, the better they serve stakeholders and other users in ensuring proper control over the company's activities and performance.

From the above analysis, a number of research hypotheses can be identified to interpret the decision of compliance with the U.K code. As shown in the hypotheses below, the decision of compliance may be affected by the size of the company and/or the composition of the board.

H4: The listed companies in the U.K comply with the requirements of the code of corporate governance regarding audit committees. H5: There is a relationship between the size of the company and the level of compliance with audit committees. H6: There is a relationship between the composition of the board and the level of compliance with audit committees. Research Methodology

Data was collected using a checklist constructed to test the level of compliance of U.K listed companies with the combined code concerning mainly the audit committees and disclosure arrangements. The audit committee part in the checklist included 14 sub elements discussing guidelines related to the composition and function of the committee whereas the disclosure arrangements included 15 sub elements for good disclosure practices and as a whole the checklist is about 3 pages long. The 1st part of the data collection was done manually. The researchers used the internet to access the most recent annual reports of the top (FTSE) 100 companies in the U.K which was for the year 2008. The Financial Times London Stock Exchange (FTSE) is

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 41

known to be one of the most attractive stock markets in the world and an active market for IPO (Initial Public Offering) for both local and foreign companies, a matter which will require procedures or elements of corporate governance to protect the funds of those investors. The checklist was then used to examine if each company would comply with the main requirements of audit committees and disclosure arrangements. When compliance was evident a 1 was ticked otherwise it was given a Zero. This process was repeated for each of the (FTSE) 100 U.K companies. Most of the data collected was of qualitative nature.

The second part of the data was collected using the software Financial Analysis Made Easy Database (FAME). Several aspects for the size of the company and the composition of the board such as the company’s latest turnover figure, number of employees and the number of non executive directors for all of the (FTSE) 100 U.K companies were collected in order to perform the detailed descriptive statistics as well as regression analysis and to test whether any of the characteristics of listed companies do have any effect on the degree of compliance with the code of corporate governance. In cases where data required was not available in specific companies, they were not replaced but instead treated as not available information and those companies with missing aspects were totally ignored in the regression analysis performed thereafter. Therefore in the regressions the number of observations were not 100 but varied between 82 and 87 according to the variables chosen for testing purposes. Data Analysis

Several central tendency measures such as the mean, mode, median were computed to assess the average degree of compliance of all U.K companies in respect to the code of corporate governance. However, estimating the mean values had some difficulties as they are sometimes influenced by extreme values therefore other central tendency measures were also undertaken and performed to strengthen and support the analysis findings. On the other hand, data variation can be measured in three different ways: standard deviation, range (minimum and maximum values) and percentiles. The researchers computed the above measures to show the spread of the results more clearly and give a better picture of them. To be able to compare the spread of data between the financial measures, which are of different magnitudes, the coefficient of variation was also computed as its values can be easily compared and the larger the coefficient of variation the larger the relative spread of the data (Saunders et al, 2006). The researchers analyzed these variations and gave possible interpretations and explanations when evident. Regression Analysis

The second part of the analysis covered a multiple regression analysis made in order to test whether there is any association or relationship between the three independent variables chosen: Number of non executive directors, latest turnover figure and finally the number of employees in each firm and the degree of compliance by companies in relation to the audit committees and disclosure arrangements. The researchers used the statistical software package ‘’Stata’’ which main capabilities include data management, statistical analysis and custom programming. The researchers made several regressions of each individual variable on the degree of compliance. The three main aspects which were looked at were: first, the coefficient which mainly shows the magnitude and direction and the variation of the regression. The second and most important aspect to be considered is the p-value which shows if the test is significant or

© Mohamed Hegazy and Karim Hegazy

42

not. Finally, the R2 which mainly explains how much of the dependant variable is explained by the independent variable was calculated and the higher the percentage the better. Then, multiple regressions were performed including all 3 independent variables in order to get clearer results as each model alone was not that significant. Multiple regressions on each compliance aspect alone were made: the audit committees and the disclosure arrangements in order to test whether there might be any association between the independent variables chosen and each individual compliance aspect. Results of Descriptive Analysis of the Disclosure Arrangements

Table 3 presents the main elements of the disclosure arrangements under the U.K code of corporate governance and the degree of compliance by listed U.K companies. The main disclosure elements cover several aspects such as the composition of the board and its members as well as the 3 main committees represented by the remuneration, audit and nomination and their respective duties. It also covers elements such as the role, names and functions of the non executive directors. Table 3: Descriptive Analysis of the Disclosure Arrangements

Under the disclosure arrangements there were 15 elements selected for testing. Two

elements are complied with by all of the (FTSE) 100 companies. The elements are the disclosure

Elements of disclosure

Number of

companies complying

Percentage of

compliance

Names of board/CEO/Chairman 100 100 Going concern assumption 100 100 Nomination committee and its responsibilities 96 96 Remuneration committee and description of its work 96 96 Directors report /audit report and their respective reporting responsibilities 96

96

Nr of board and subcommittee meetings and attendance by directors 95

95

Review of Internal controls 95 95 Separate section describing work of audit committees in discharging responsibilities 88

88

Separation of duties management /board 87 87 Non executive directors names who are believed to be independent 79 79 Performance evaluation of the board its committees and directors 62 62 Understanding of company by Non-executive directors 30 30 Explanation that if non audit services are provided objectivity and independence of the auditor is safeguarded 18

18

Absence of internal audit function and its reasons 0 0 Reasons given for no acceptance of audit committee recommendation by the board and a statement by the audit committee showing their position 0

0

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 43

of the names of the board, CEO and chairman and the second is the going concern element. This is expected as every company is required to include such information in their annual reports including the going concern assumption. There were 2 elements not complied with at all by the whole group of listed companies. They cover reasons should be provided if no internal audit function exist and situations where the audit committee recommendations are not accepted. These disclosures were not adhered to by companies unless matters exist or occur. However these aspects were included by the researchers in the design of the checklist to maintain the originality and the same elements as shown in the U.K code.

Out of the 15 available elements seven are complied with by a percentage of 95% or higher which is a significant figure and shows that half of the elements under the disclosure arrangements are complied with by almost all of the companies. These elements include disclosure about the nomination and remuneration committees and their responsibilities, the number of board members and subcommittee meetings and attendance by directors, the review of the internal control, a separate section describing the work of the audit committee and finally the performance evaluation of the board, its committees and directors. In addition, two third of the elements of disclosure arrangements are complied with by almost 80 companies showing significant level of compliance of the code for disclosure arrangements. Table 4 shows a summary of the descriptive statistics’ results in relation to disclosure arrangements elements. The mean average compliance is almost 70% increases to 80% if we exclude the last 2 elements with a compliance of 0%. This indicates that companies are complying with the majority of the elements mentioned in the combined code and its related attachments in respect to disclosure arrangements. The above results provide evidence for the acceptance of H1.

Table 4: Descriptive statistics results for disclosure arrangements

Descriptive Measure Results Mean 69.4677 Median 88 Mode 96 Standard Deviation 37.73567 Coefficient of Variation 54.32196 Minimum 0 Maximum 100 25th Percentile 46 50th Percentile 88 75th Percentile 96

However, the researchers noticed the wide spread of data as shown by the minimum and

maximum results given by 0 and 100. Percentile statistics show that although the 25th percentile rank is 46 which are due to the 2 elements not complied with by any company it only implies that a minority of companies don’t comply with the majority of the code issues selected for testing. Moreover looking at the 50th percentile rank it can be seen that about half of the elements are complied with by a very high number of companies, namely 88. Finally, the coefficient of variation is calculated and is found to be over 50% which means that there is a large spread of data and the data are uniform i.e. less dispersed.

© Mohamed Hegazy and Karim Hegazy

44

From the results obtained we can state that the code of corporate governance is mainly used by companies as a guideline and as a help to maintain good corporate governance structures and norms but not as a strict code where all companies should comply with all its requirements. Results of the analysis of audit committee elements

Table 5 provides the results of the descriptive analysis regarding elements of the audit committees. The findings of the descriptive analysis show that the highest element of compliance was the audit committee meetings with a minimum of 3 times a year. The majority of companies had active audit committee with some of them having 6 or more meetings per year. The majority of companies also disclosed the terms of reference of the audit committee besides giving the names of the members of the committee and their qualifications. An average of around 95% was found for all the above mentioned characteristics for the audit committee guidelines. Table 5: Results of the Descriptive Analysis for Audit Committees

Moreover, 90 companies representing 90% of those listed in FTSE provided on their

website separate sections to describe the work of audit committee and its responsibilities. This provides strong evidence about the willingness of the management to show an effective monitoring role of the committee of the company's internal control system, audit function and management risk models. The approval of the appointment of internal audit head by audit committee represented only 16%, a low compliance percentage indicating continued struggles between top management and the audit committee about such decision making. It is expected that with the wide recognition of the role of the audit committee this element would be enhanced and the audit committee will have a better say in the appointment of the Head of internal audit department. At the same time, the low level of compliance (only 16%) of whether audit

Elements of audit

Number of

companies complying

Percentage of

compliance

Audit committee meetings /assumption 3 times at least 97 97 Number of audit committee meetings 96 96 Terms of reference of audit committee 94 94 Members of audit committees names and qualifications 93 93 Separate section to describe work of audit committee and responsibilities 90

90

Audit committee approval of risk management/internal control 88 88 Summary of the role of audit committee 84 84 Financial experience of at least one member of audit committee 82 82 Report on the way audit committee has discharged its responsibilities(Audit) 79

79

Annual review of the audit committee by the board 45 45 Internal audit work and role 35 35 Approve appointment of internal audit head by audit committee 20 20 Non audit services provided or not 16 16 Disagreements between board and audit committee 1 1

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 45

committee approves non audit services for external auditor may not reflect non-compliance with the code in this matter but rather companies refuse to require such services from their external auditors.

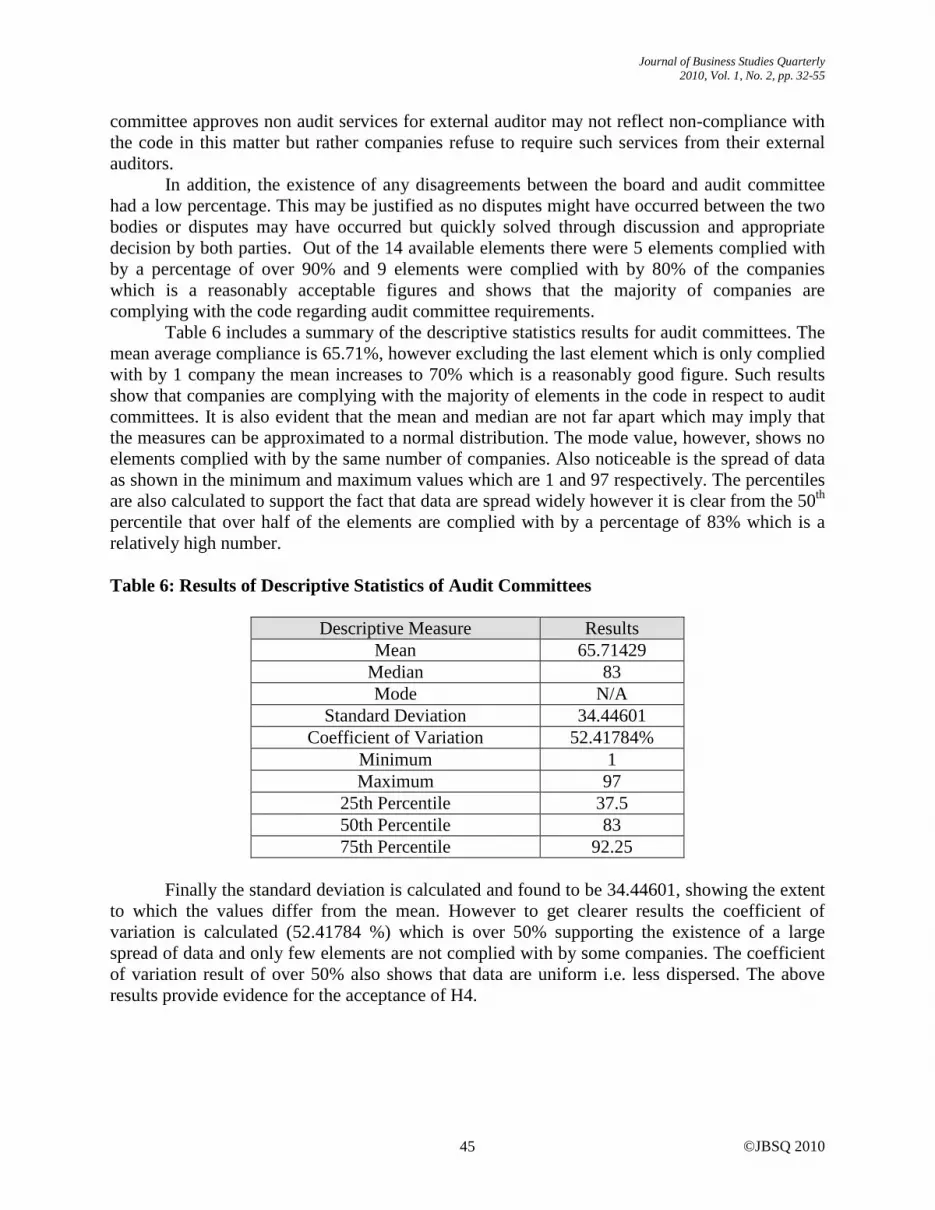

In addition, the existence of any disagreements between the board and audit committee had a low percentage. This may be justified as no disputes might have occurred between the two bodies or disputes may have occurred but quickly solved through discussion and appropriate decision by both parties. Out of the 14 available elements there were 5 elements complied with by a percentage of over 90% and 9 elements were complied with by 80% of the companies which is a reasonably acceptable figures and shows that the majority of companies are complying with the code regarding audit committee requirements.

Table 6 includes a summary of the descriptive statistics results for audit committees. The mean average compliance is 65.71%, however excluding the last element which is only complied with by 1 company the mean increases to 70% which is a reasonably good figure. Such results show that companies are complying with the majority of elements in the code in respect to audit committees. It is also evident that the mean and median are not far apart which may imply that the measures can be approximated to a normal distribution. The mode value, however, shows no elements complied with by the same number of companies. Also noticeable is the spread of data as shown in the minimum and maximum values which are 1 and 97 respectively. The percentiles are also calculated to support the fact that data are spread widely however it is clear from the 50th percentile that over half of the elements are complied with by a percentage of 83% which is a relatively high number. Table 6: Results of Descriptive Statistics of Audit Committees

Descriptive Measure Results Mean 65.71429

Median 83 Mode N/A

Standard Deviation 34.44601 Coefficient of Variation 52.41784%

Minimum 1 Maximum 97

25th Percentile 37.5 50th Percentile 83 75th Percentile 92.25

Finally the standard deviation is calculated and found to be 34.44601, showing the extent

to which the values differ from the mean. However to get clearer results the coefficient of variation is calculated (52.41784 %) which is over 50% supporting the existence of a large spread of data and only few elements are not complied with by some companies. The coefficient of variation result of over 50% also shows that data are uniform i.e. less dispersed. The above results provide evidence for the acceptance of H4.

© Mohamed Hegazy and Karim Hegazy

46

Results of the Regression Analysis

To test whether there is any association between the level of compliance for both audit committees and disclosure arrangements figure and the three independent variables latest turnover figure, the number of employees and the number of directors, a regression is performed for each independent variable and the total degree of compliance. The results of these three regressions obtained were that each model alone is not significant except for the regression containing the number of employees with a p-value of .006 = 0.6% which is significant at the 5% & 1% levels. The problem with such result is that the coefficient was very small. The p-values for the other two regressed variables are 0.103 and 0.754 respectively which in turn are insignificant. Table 7: Reg. compliance turnover Regression Measures Results Number of observations 87 R-Squared 0.1310 Adj R-Squared 0.0196 Coef 1.24e-08 Std. Err. 7.53e-09 T 1.65 P-value (95% conf. interval) 0.103 Table 8: Reg. compliance employees Regression Measures Results Number of observations 96 R-Squared 0.0766 Adj-R-Squared 0.0668 Coef -0.000125 Std. Err. 4.49e-06 T -2.79 P-value (95% conf. interval) 0.006 Table 9: Reg. compliance directors Regression Measures Results Number of observations 89 R-Squared 0.0011 Adj-R-Squared 0.0104 Coef -.0444828 Std. Err. .1417932 T -0.31 P-value 0.754

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 47

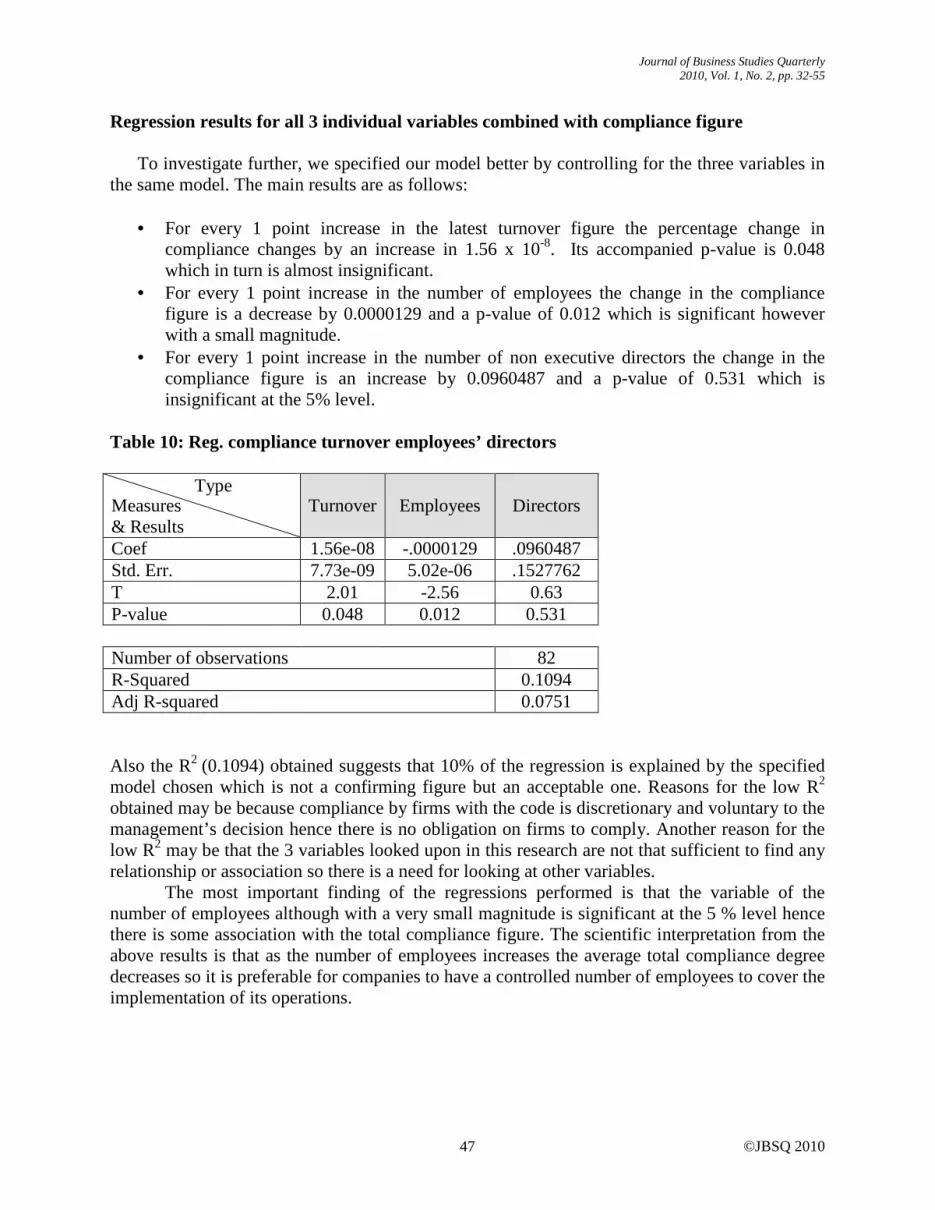

Regression results for all 3 individual variables combined with compliance figure

To investigate further, we specified our model better by controlling for the three variables in the same model. The main results are as follows:

• For every 1 point increase in the latest turnover figure the percentage change in

compliance changes by an increase in 1.56 x 10-8. Its accompanied p-value is 0.048 which in turn is almost insignificant.

• For every 1 point increase in the number of employees the change in the compliance figure is a decrease by 0.0000129 and a p-value of 0.012 which is significant however with a small magnitude.

• For every 1 point increase in the number of non executive directors the change in the compliance figure is an increase by 0.0960487 and a p-value of 0.531 which is insignificant at the 5% level.

Table 10: Reg. compliance turnover employees’ directors Measures & Results

Turnover Employees Directors

Coef 1.56e-08 -.0000129 .0960487 Std. Err. 7.73e-09 5.02e-06 .1527762 T 2.01 -2.56 0.63 P-value 0.048 0.012 0.531 Number of observations 82 R-Squared 0.1094 Adj R-squared 0.0751 Also the R2 (0.1094) obtained suggests that 10% of the regression is explained by the specified model chosen which is not a confirming figure but an acceptable one. Reasons for the low R2 obtained may be because compliance by firms with the code is discretionary and voluntary to the management’s decision hence there is no obligation on firms to comply. Another reason for the low R2 may be that the 3 variables looked upon in this research are not that sufficient to find any relationship or association so there is a need for looking at other variables.

The most important finding of the regressions performed is that the variable of the number of employees although with a very small magnitude is significant at the 5 % level hence there is some association with the total compliance figure. The scientific interpretation from the above results is that as the number of employees increases the average total compliance degree decreases so it is preferable for companies to have a controlled number of employees to cover the implementation of its operations.

Type

© Mohamed Hegazy and Karim Hegazy

48

Regression of all 3 variables and audit committees compliance figure

The results of the regression for all 3 variables and audit committees however were very similar to the ones obtained previously with the total degree of compliance as the number of employee variable was the only one found to be significant although with an extremely small magnitude as well as the R2 figure which is approximately 10% hence both results are identical to the ones found previously. Table 11: Reg. comp1 turnover employee directors Measures & Results

Turnover Employees Directors

Coef 9.24e-09 -8.06e-06 .0165339 Std. Err. 4.91e-09 3.19e-06 .0971103 T 1.88 -2.53 0.17 P-value 0.064 0.013 0.865 Number of observations 82 R-Squared 0.0993 Adj R-squared 0.0647 Regression results for all 3 variables and disclosure compliance figure

In relation to the compliance figure of the disclosure arrangements the p-value of the number of employees’ variable in the regression was the only figure with a significant result of 0.032 at the 95% confidence interval. This suggests that there is a reasonably fair association between the number of employees and the compliance figure relating to disclosure arrangements hence a 1 point change in the employee figure results in a change in compliance relating to disclosure arrangements by a decrease of 4.8 x 10-6. Thus, the lower the number of employees the better and more effective they can be monitored hence leading to more controlled work and better level of compliance. Table 12: Reg. comp2 turnover employees directors Measures & Results

Turnover Employees Directors

Coef 6.32e-09 -4.80e-06 0.795147 Std. Err. 3.38e-09 2.19e-06 .0668008 T 1.87 -2.19 1.19 P-value 0.065 0.032 0.238 Number of observations 82 R-Squared 0.1002 Adj R-squared 0.0656

Type

Type

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 49

In summary it can be said that although there might be a small association between the number of employees and the different compliance figures in total the 3 variables chosen have not been found to have a good relationship to the compliance figures. Thus, the degree of compliance by companies might be due to other factors or other explanations requiring further research and analysis. The above results provide evidence for rejecting H3 and H6 as no relationship was found between the composition of the board and the level of compliance with the U.K code. Furthermore, the findings also rejected H2 and H5 as no relationship existed between the size of company described by the total turnover and the level of compliance of the U.K code with some significant relationship found between the number of employees and level of compliance for both audit committees and disclosure arrangements. Conclusion, Limitations and Recommendations

Corporate governance has become so important since 2002 as series of corporate frauds and other catastrophes led to the destruction of billions of dollars of investments, the loss of thousands of jobs, the criminal investigation and record–breaking bankruptcy filings. All these conditions beside the need to restore the good reputation of the accounting profession and protecting shareholders' interest created the need for tools and principles that increase transparency. In 2003, a combined code of corporate governance was introduced in the U.K covering several corporate governance structures and combining all main principles covered in previously published codes and laws (Cadbury (1992), Greenbury (1995), and Turnbull (1999)). Companies are required as a matter of best practice to fully comply with many of the aspects of the code and its amendments issued in 2008 and if not explanations should be provided. The current research was prepared to investigate and test the level of compliance by the (FTSE) 100 companies for two main aspects of the code mainly the audit committees and disclosure arrangements.

The research methodology included the literature review covering issues and matters relating to the nature of corporate governance with an overview of the evolution of corporate governance codes in the U.K Moreover, the research analyzed the main characteristics of corporate governance such as duality, board composition and non executive directors and audit committees and reviewed previously made researches on whether these characteristics have any effect on companies’ performance. Six hypotheses were developed. Two of these hypotheses, H1 and H4, tested whether U.K listed companies comply with the code of corporate governance regarding audit committees and disclosure arrangements. The other four, H2, H3, H5 and H6, tested whether relationships existed between the size of the companies and board composition and the level of compliance with the U.K code. A detailed descriptive analysis was performed. A regression analysis was also undertaken to test whether there might be any association between the different levels of compliance and companies size and three independent variables namely turnover figure, number of employees and number of non-executive directors

The results of the descriptive analysis indicate that the average degree of compliance relating to both the audit committees and disclosure arrangements was found to be around 70%. This is a significant result and confirms the acceptance of H1 and H4. The findings showed that companies are nowadays using the code as a good base for their corporate governance structures and performance assessment. There is a need, however, for companies to place more emphasis

© Mohamed Hegazy and Karim Hegazy

50

on different elements such as internal audit work and non audit services. Only a small number of companies comply with those elements. The main findings of the regressions performed was that except for a small association found between the number of employees and compliance figure (total and for each requirement alone) there is no significant association found between the other two variables (i.e. turnover-and the number of non executive directors).

There are a number of limitations associated with the current research. First, the testing of the level of compliance by listed companies of the code of corporate governance was limited to two main elements of corporate governance namely the audit committee and disclosure arrangements. Other elements which have not been tested include the role of the board of directors, the external auditors, nomination and remuneration committees etc. Second the study examined elements of audit committee and disclosure arrangements for the FTSE 100 companies without testing for other companies listed in the FTLSE. Thus, the results of the study cannot be generalized. Third, a limited number of companies’ characteristics namely the number of non executive directors, number of employees and latest turnover figure were used to assess their effects on the level of compliance by companies. Other characteristics including the size of the company, capital of the company, total assets, and type of industry have not been tested. Fourth, the limited number of non complying listed companies did not allow the researchers to make more detailed investigations about possible reasons for such non compliance using either interviews or telephone calls with the investor relation officers of specific companies, a matter which was planned to be undertaken if the results provided ways to investigate such non-compliance status.

However, a number of important recommendations can be derived from the findings of this research. First, other listed companies' characteristics mainly the type of industry, profitability and the size of the company assessed either by owners' equity or capital must be analyzed and studied to test whether there is a significant relationship between these elements and the level of compliance with the U.K code. Second, a larger sample of companies listed in the FTSE must be selected for testing compliance levels to ensure a good representation of the operating environment in the U.K coupled with an assessment of companies’ characteristics to provide some insights into the reasons behind a high level of compliance with the code. Third, interviews should be made with the investor relation officers of some of these listed companies to inquire about reasons of non compliance with some of the elements of the combined code and to identify management objectives associated with high compliance with the combined code. References Baliga, B., Moyer, R., & Ramesh, R. (1996). CEO duality and firm performance: what’s the Fuss. Strategic Management Journal, 17 (1), pp. 41-53. Baysinger, B., & Butler, H. (1985). Corporate governance and the board of directors: Performance effects of changes in board composition. Journal of Law, Economics and Organization, 1, pp. 101-124. Beasley, M. (1996). An empirical Analysis of the Relation between the Board of Director Composition and Financial Statement Fraud. The Accounting Review, 71, pp. 443- 465.

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 51

Boyd, B. (1995). CEO duality and firm performance: A Contingency Model. Strategic Management Journal, 16, pp. 301-312 Boyd, C. (1996). Ethics and Corporate Governance: The issues raised by the Cadbury Report in the United Kingdom. Journal of Business Ethics, 15, pp. 167-182. Brickley, J., Coles, J., & Jarrell, G. (1997). Leadership structure separating the CEO and Chairman of the board., Journal of Corporate Finance, 3, pp. 189-220. Butler, H. (1985). Nineteenth-Century Jurisdictional Competition in the Granting of Corporate Privileges. Journal of Legal Studies, 14, pp. 129-166. Cadbury Report (1992). Report of the Committee on Financial Aspects of Corporate Governance, Gee Publishing, London. Combined Code (1998). Principles of Good Corporate Governance and Code of Best Practice, London: Gee & Co-Ltd. Cosh, A., Guest, P., & Hughes, A. (2006). Board Share Ownership and Takeover Performance. Journal of Business Finance & Accounting, 33, pp. 459-510. Chambers, A. (2005). Audit committees: practice, rules and Enforcement in the UK and China. Corporate Governance: An international Review, 13 (1), pp. 92-100. Collier, P., & Zaman, M. (2005). Convergence in European Corporate Governance: the Audit Committee Concept. Corporate Governance, 13 (6), pp.753-768. Conyon, M., & Peck, S. (1998). Board Control, Remuneration Committees, and Top Management Compensation. Academy of Management Journal, 41, pp. 146-157. Corrin, J. (1993). The Cadbury Report –A Blatant Slur on Executive Directors Integrity. Accountancy (UK), 111, pp. 81-82. Cosh, A., Guest, P., & and Hughes, A. (2007). UK Corporate Governance and Takeover Performance. Centre of Business Research, University of Cambridge, Working Paper 357. Dahya, J., McConnell, J., & Travios, N. (2002). The Cadbury Committee Corporate Performance and Top Management Turnover. The Journal of Finance, 57 (1), pp.461- 483. Dahya, J., & McConnell, J. (2007). Board Composition, Corporate Performance and the Cadbury Committee Recommendation. Journal of Financial and Quantitative Analysis, 42 (3), pp 535-564. Eng, L., and Mak, Y. (2003). Corporate governance and Voluntary disclosure. Journal of Accounting and Public Policy, 22, pp. 325-345.

© Mohamed Hegazy and Karim Hegazy

52

Erturk, I., Froud, J., Johal, S., & Williams, K. (2004). Corporate government and disappointment. Review of International Political Economy, 11 (4), pp. 677-713. Faccio, M., & Lasfer, M. (1999). Managerial ownership, board structure and firm value: The UK evidence. Working Paper, City University Fama, E., & Jensen, M. (1983). Separation of Ownership and Control. Journal of Law and Economics, 26 (2), pp. 301-326. Financial Reporting Council (2003). Combined Code on Corporate governance, Financial Reporting Council, London. Financial Reporting Council (2006). Combined Code on Corporate Governance, Financial Reporting Council, London. Financial Reporting Council (2008). Combined Code on Corporate Governance, Financial Reporting Council, London. Ford, R. (1988). Outside directors and the privately owned firm: are they necessary?. Entrepreneurship: Theory and Practice, 13 (1), pp. 49-57. Forker, J. (1992). Corporate Governance and Disclosure Quality. Accounting and Business Research, 22 (86), pp. 111-124. Gomez, P., & Korine, H. (2005). Democracy and the Evolution of Corporate Governance. Corporate Governance: An International Review, 13 (6), pp. 739-752. Goyal, V., & Park, C. (2002). Board leadership structure and CEO turnover. Journal of Corporate Finance, 8, pp. 49-66. Greenbury, S. (1995). Directors' Remuneration: Report of a Study group. Gee Publishing Ltd, London. Hampel, S. (1998). Committee on Corporate Governance: Final Report, Gee Publishing London. Hanniffa, M., & Cooke, T. (2002). Culture Corporate Governance and disclosure in Malaysian Corporations. Abacus, 38 (3), pp. 317-349. Hermalin, B., & Weisbach, M. (1988). The Determinants of Board Composition Rand. Journal of Economics, 19, pp. 589-606. Hermalin, B., & Weisbach, M. (1991). The effects of Board Composition and Direct Incentives on Firm Performance. Financial Management, 20, pp.101-112.

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 53

Hermalin, B., & Weisbach, M (2003). Boards of Directors as an Endorenously Determined Institution: A Survey of the Economic Literature. Economic Policy Review, 9 (1), pp.7-27. Higgs, D. (2003). Review of the Role and Effectiveness of Non Executive Directors, Gee Publishing, London. Hillier, D., & McColgan, P. (2006). An Analysis of Changes in Board Structure during Corporate Governance Reforms. European Financial Management, 12 (4), pp. 575- 607. Ho, S., & Wong, S. (2001). A study of the relationship between corporate governance structures and the extent of voluntary disclosure. Journal of International Accounting, Auditing and Taxation, 10 (2), pp 139-156. Holl, P. (1975). Effect of Control type on the performance of the firms in the U.K. Journal of Industrial Economics, 23, pp. 257-271. Jensen, M. (1993). The modern Industrial Revolution, Exit and the Failure of Internal Control Systems. Journal of Finance, 48, pp. 831 -880. Jensen, M., & Meckling, A. (1976). Theory of the Firm Managerial Behaviour Agency Costs and Capital Structure. Journal of Financial Economics, 3, pp. 305-360. Jones, I., & Pollitt, M. (2001). Who Influences Debates in Business Ethics? An Investigation into the Development of Corporate Governance in the U.K since 1990. ESRC Centre for Business Research, University of Cambridge Working Paper, 221, pp. 1-45. Jones, I., & Pollitt, M. (2004). Understanding how issues in Corporate Governance Develop: Cadbury Report to Higgs’ Review. Corporate Governance, 12 (2), pp.162- 171. Klein, A. (2002). Audit committee, Board of Directors Characteristics and Earnings Management. Journal of Accounting and Economics, 33 (3), pp. 375-400. Li, J., Pike, R., & Haniffa, R. (2008). Intellectual Capital Disclosure and Corporate Governance Structure in UK firms. Accounting and Business Research, 38 (2), pp.137-159. Lipton, M., & Lorsch, J. (1992). A modest proposal for improved corporate governance. Business lawyer, 48 (1), pp.59 -77. Mallin, C., Mullineux, A., & Wihlborg, C. (2005). The Financial Sector and Corporate Governance: The UK Case. Corporate Governance, 13 (4), pp. 532-541.

© Mohamed Hegazy and Karim Hegazy

54

Mangena, J., & Pike, R. (2005). The effect of audit committee shareholding Financial Expertise and Size on Interim Financial Disclosures. Accounting and Business Research, 35 (4), pp. 327-349. McCarthy, J. (2008). Corporate Governance: Better Compliance Helps the Bottom line. Accountancy Ireland, 40 (3), pp.43-45. McKnight, P., & Weir, C. (2007). Agency costs, Corporate Governance Mechanisms and Ownership Structure in large UK Publicly Quoted Companies: A panel Data Analysis. Quarterly Review of Economics and Finance, 49, pp. 139-158. O’Donovan, G. (2008). The Corporate Culture Handbook: How to plan, Implement and Measure a successful Culture change programme. Development and Learning in Organizations, 22 (1). Olson, J. (1999). How to make audit committees more effective. Business lawyer, 54, pp. 1097-1113. Pass, C. (2004). Corporate Governance and the role of non executive directors in large UK Companies an empirical study. Corporate Governance, 4 (2), pp. 52-63. Pass, C. (2006). The revised combined code and corporate governance: An empirical survey of 50 large U.K companies. Journal Managerial Law, 48 (5), pp.467-478. Rechner, I., & Dalton, D. (1991). CEO duality and organizational performance: a longitudinal analysis. Strategic Management Journal, 12, pp. 155-160. Rosenstein, S., & Wyatt, J. (1990). Outside Directors, board independence and Shareholder Wealth. Journal of Financial Economics, 26 (2), pp.175-191. Saunders, M., Lewis P., & Thornhill, A. (2006). Research methods for business, Prentice Hall, (4th) edition. Sheridan, L., Jones, E., & Marston, C (2006). Corporate Governance Codes and the supply of Corporate Information in the UK. Corporate Governance, 14 (5), pp. 497- 503. Smith Report (2003). Audit committees combined code guidance. Financial Reporting Council, London. Stiles, P., & Taylor, B. (1993). Benchmarking Corporate Governance, An Update. Long Range Planning, December, 26 (6), pp. 138-139. Turnbull, N. (1999). Corporate Guidance for Internal control, Gee & Co, London. Valenti, A. (2007). The Sarbanes –Oxley Act of 2002: Has it brought about Changes in the boards of large U.S Corporations. Journal of Business Ethics 81, pp. 401-412.

Journal of Business Studies Quarterly 2010, Vol. 1, No. 2, pp. 32-55

©JBSQ 2010 55

Weir, C., & Laing, D. (2000). The performance –Governance relationship: the effects of Cadbury compliance on UK quoted companies. Journal of Management and Governance, 4, pp. 265-281. Weir, C., Laing, D., & McKNight, P. (2002). Internal and External Governance Mechanisms their impact on the Performance of large UK Public Companies. Journal of business Finance and Accounting, 29, pp.579-611. Weisbach, M. (1988). Outside Directors and CEO turnover. Journal of Financial Economics, 20, pp. 431-460. Yermack, D. (1996). Higher market valuation of companies with a small board of directors. Journal of financial economics, 40, pp. 185-211. Author Biography

Mohamed Hegazy is a Professor of Accounting and Auditing at the Department of Accounting, School of Business, the American University in Cairo. Dr. Hegazy holds two bachelor’s degrees from Cairo University in Accounting and in law. He also holds two masters degrees; one in Accounting from Birmingham University, U.K and the other in Knowledge Based Systems (i.e. Expert Systems) from Edinburgh University. He received his Ph.D in Accounting and Finance from Birmingham University, U.K. His research and teaching interests include: financial reporting, auditing and other assurance services, information systems, corporate governance, financial and administrative restructuring, and valuation studies. Dr. Hegazy can be reached at: [email protected].

. Karim Hegazy is an executive partner in Crowe Dr.A.M.Hegazy & Co- a member of

Crowe Horwath International – Chartered Accountants and Consultants. Karim holds a bachelor’s degree in Accounting and Finance from Middlessex University – U.K as well as a Masters degree in Accounting and Finance from Brunel University – U.K. Karim speaks fluent German, English, and French languages. His areas of interest for research are financial audit, corporate governance, cost accounting and financial reporting. Karim can be reached at: [email protected].