Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=1544642

1

First Draft: Dec. 28 – 2009 Comments welcome Current Draft: Jan 12-2010

Corporate Governance of Banks: The Colombian experience

Carlos Pombo1*

Luis H. Gutierrez**

Abstract

This paper analyzes the financial reforms, the banking industry performance trends and explains how prudential regulation and CG practices played a central role in that sector’s recovering after the 1999 financial crisis. It also explains why the banking industry in Colombia has been successful in facing the 2008 U.S. subprime crisis.

Resumen

En este documento se analiza las reformas financieras, el desempeño de los bancos comerciales, el papel de la regulación prudencial y las prácticas de gobierno corporativo tuvieron en la recuperación de la crisis del sector financiero de 1999 en Colombia. También explica porqué el sector financiero en el país ha sido exitoso en enfrentar la crisis hipotecaria (subprime) de 2008 de los Estados Unidos. I. Introduction

The issue of corporate governance (CG) in Colombia was introduced since year

2001 when the Government established a series of norms and regulations with the

objective of fostering good corporate practices among security issuers as well as in

non-listed corporations. The Colombian Chamber of Commerce Association along

with the Center for International Private Enterprise (CIPE) from the U.S undertook

a formal program oriented to disseminate the principles and benefits of good

1 * Associate professor in Finance, School of Management, Universidad de los Andes, Bogotá. Corresponding author: [email protected] ** Associate professor, Department of Economics, Universidad del Rosario, Bogotá. We thank Alejandro Fandino for his research assistance.

Electronic copy available at: http://ssrn.com/abstract=1544642

2

corporate practices that have fostered the capital market and firms’ external

financing in developed and developing countries. In that year, the former

Superintendence of Securities issued the Resolution 271, which established the

voluntary adoption of CG codes to those firms whose securities were to be

purchased by the pension funds. This rule became the starting point for the

dissemination and implementation of CG practices at least within public

corporations including commercial banks and other financial institutions.

The discussion that followed Resolution 271 in strengthening investors’

protection legislation ended up with the issue of Law 964 of 2005 that became the

most important corporate law reform in terms of capital market regulation and

investor protection regimes. This Law followed benchmarks such as SOX Act of

2002 in the U.S and corporate governance reforms implanted in Korea between

1998 and 2003 in relation with the board structure and independence, auditing

committees and the development of risk management systems for financial

institutions. It also made mandatory to have an independent equity structure for

all mutual, investments and equity funds as well as all assets whose (subjacent)

underlying prices that constituted claims of securitization processes from its

financial intermediaries. This norm deepened the capital structure supervisions for

financial institutions regarding the equity structure and autonomy regime between

parent and subsidiaries companies stipulated at current Colombian organic statute

for financial institutions (Law 35/1993 and Decree 663/1993-Numeral 119).

Private initiatives from different institutions also played an important role

in speeding and spreading the benefits of implementing good GC practices inside

organizations. The result was the publication of the Country Code for Better

Corporate Practices in 2007, which is the local White Paper in terms of the CG

document. The designing of this code was the result of an inter-institutional

initiative that gathered the Financial Superintendence, the Colombian Stock

Exchange, and the Colombian Association of Banks among other private sector

associations. The Country Code has the main objective of standardizing CG

3

practices and set minimum contents. This code follows the principle comply or

explain and establishes voluntary measures that complement the financial

regulation of banks and security issuers. The code was based on four pillars and

estipulate a series of norms regarding: i) shareholder general meeting, ii) board of

directors, iii) information disclosure and iv) the resolution of conflict of interests.

This chapter analyses the financial reforms, the banking industry

performance trends and explains how prudential regulation and CG practices

played a central role in that sector’s recovering after the 1999 financial crisis. It also

explains why the banking industry in Colombia has been successful in facing the

2008 subprime crisis. Besides this introductory section the paper is organized as

follows. Section 2 presents the evolution of key banks’ performance indicators and

describes the financial reforms since 1990. Section 3 focuses on the post-crisis

financial regulation and summarizes the most important regulatory norms in

accordance to either Basel I or Basel II pillars. Section 4 presents some indicators of

board of directors and describes the current level of CG practices observed across

banks. Section 5 presents the main anti-crisis measures related to CG in 2008-2009

and Section 6 concludes.

II. Banking industry trends and financial reforms

Ten years ago the financial sector in Colombia was facing one of the deepest crises

since the nineteen sixties. The sources of this crisis were multiple and different

than previous ones when external shocks played a main role. Since 1990 Colombia

undertook a deep economic reform that sought to set the structural bases for an

outward oriented economy that replaced the former import substitution

development model implemented since the 1950s. The reform included a general

market deregulation policies and financial liberalization strategies. The later,

included a series of reforms such as the adoption of an independent Central Bank

model, the change of the exchange rate regime moving from a fixed to floating

4

system, the liberalization of the capital account and other capital controls from the

country’s balance of payments, which allowed the private sector to borrow directly

and handle direct credits with banks in the international market, allow to local

residents having legally demand deposits and consumer credit lines abroad, and

relaxed foreign investment regime by removing all limits to profits remittances

and giving equal legal treatment between local and foreign investment.

The financial reform of the nineties was centered-around Law 45/1990 and

Law 35/1993. The former introduced a universal banking scheme by establishing

two types of financial institutions: i) credit establishments and ii) financial services

subsidiaries. The law granted again free firm entry and exit, allowed banks to

undertake new commercial operations by offering brokerage services, fiduciary

contracts, transactions in foreign currency and the issue of credit cards worldwide

valid, among others financial contracts. The second one, established strict

parameters for equity and solvency regulation, and expanded the type of financial

operations that former specialized financial institutions could undertake such as

the cases of the former housing and saving corporations, investment corporations

(investment banks), and the commercial and financing companies2.

After the 1997 East Asian and Russian crises, the fragility of the just

reformed financial sector explained by the presence of rigidities and over-costs

associated with an over-sized sector was evident. Several factors have been

stressed for local analysts and authorities. Among them one can highlight the

followings as the most important ones. First, it was the failure of driving a

balanced process of universal banking between the loan and deposit structure.

Some specialized financial institutions were aggressive in promoting their new

business in consumer loans, leasing contracts, and leverage foreign currency

operations. It implied a rapid growth in the number of branches, employees which 2 The specialized banking model before the reform granted monopoly rights over the different types of loans (asset side) and was relatively standard over the types of deposits (liabilities side) – demand, money market and CDs-. For instance, the former housing and savings corporations (Corporaciones de Ahorro y Vivienda - CAVs) had the monopoly over the mortgage credits and on the money market accounts, but at the same time they were able to issue certificate of deposits like commercial and investment banks.

5

spurred the volume of loans in order to capture new clients. Second, a real state

bubble took place partly fostered for the capital flows booming at the beginning of

the nineties. Third, the peso revaluation weakened domestic durables consumption

and production. The aggregate demand slowed-down had a direct impact for the

global demand for consumer, commercial and housing loans. Also there was a

sharp reduction in the level of deposits. Fourth, the sudden stop of capital inflows

after 1998 and the dirty floatation of the exchange rate at that time implied a sharp

increase on the central bank intervention rate which put pressure on banks’

lending interest rates. This fact had a negative impact on all floating-rates

mortgage contracts. The final consequence was a generalized mortgage crisis that

skyrocketed banks and housing corporations' non-performing loans and lowered

their coverage and solvency ratios3.

The main financial policy measures adopted to face the crisis focused on

three elements. First, the government issued law 550/1999 which provided a

flexible frame for corporate restructuring and bankruptcy procedures. The Law

made possible a short-term economic intervention by the government in providing

direct resources to capitalize real sector companies and financial institutions.

Second, Law 546/1999 reformed the mortgage credit system allowing commercial

bank to cover the housing market and letting housing and savings corporations to

become commercial banks or merge to them. This law also included many

particular norms concerning changes in mortgages amortization systems, credit

refinancing and salvage package to all default mortgages where the real state asset 3 The 1998-99 financial crisis led to a wave of mergers and acquisitions across financial institutions. The main market size adjustment was located within the CAVs that were absorbed by commercial banks. By 2001 domestic mortgages had been fully transferred to commercial banks as housing loans and marked the end of CAVs as specialized housing credit establishments. Complete descriptions of the Colombian financial sector, the 1998-99 financial crisis and the wave of mergers and acquisitions are documented in several studies. Among them we can highlight the ones from Carrasquilla & Zarate (2002), Clavijo et. al. (2000, 2006), Tenjo & Lopez (2002) and Villar et. al (2005). The official standpoint regarding the crisis can be found across several editorial notes from the Colombian central bank -Banco de la República- [Urrutia (1999 and 2000)]. An analysis of financial liberalization and foreign investment in Colombia is in Barajas et al. (2000) and a study on deposit behavior for Colombia is in Barajas & Steiner (2000). For a broad analysis regarding the factors that triggers financial crises in Latin America see the Inter American Development Bank-2005 annual report.

6

was given back to banks in exerting collateral clauses. Third, Law 510/1999

increased the requirements of minimum equity capital to financial institutions to

operate in the market and made mandatory an annual adjustment according to

local inflation rates. The law also allowed banks to securitize mortgage loans4.

Summing up the reforms and posterior legal adjustments triggered by the

1998-99 economic crisis, caused a comprehensive industry restructuring of the

financial sector that would have taken more time in shaping the multi-banking

model and implementing risk management measures following Basel-II and

prudential regulation principles such as: i) the tightening of the minimum capital

requirements, ii) setting the system for risk supervision: credit, market and

operational risks, and iii) promoting market discipline and better corporate

governance.

The above-mentioned reforms induced several positive results. First, there

was a consolidation process of financial holdings that kept the basic separation

between the financial intermediation activity and other financial services. In that

sense, the parent–subsidiaries relation has been consolidated between the credit

establishments and the companies that provide associated financial services such

as asset management and trust funds, insurance and capitalization companies,

pension funds and deposit warehouses. Thus the current structure of the

Colombian financial is a hybrid model that has elements of universal and

specialized banking. The financial sector restructuring was induced by a market

shakeout. The numbers show an average of 5 percent annual exit rate for total

financial institutions, 4.7 percent for credit establishments and 2.6 percent for

commercial banks during the 1995-08 period. In fact the number of banks almost

halved after the crisis and the last housing and saving corporation was acquired in

2001 (Table 1).

This reduced number of incumbent banks reflects today larger and higher

4 For more details concerning the financial measures adopted to face the crisis, see the 2000 reports of Banco de la Republica's board of governors.

7

equity concentrated companies. These two facts call attention to positive effects on

banks’ efficiency and solvency on one side, but also a potential CG risk due to the

increased likelihood of expropriation to minorities by the controlling shareholder

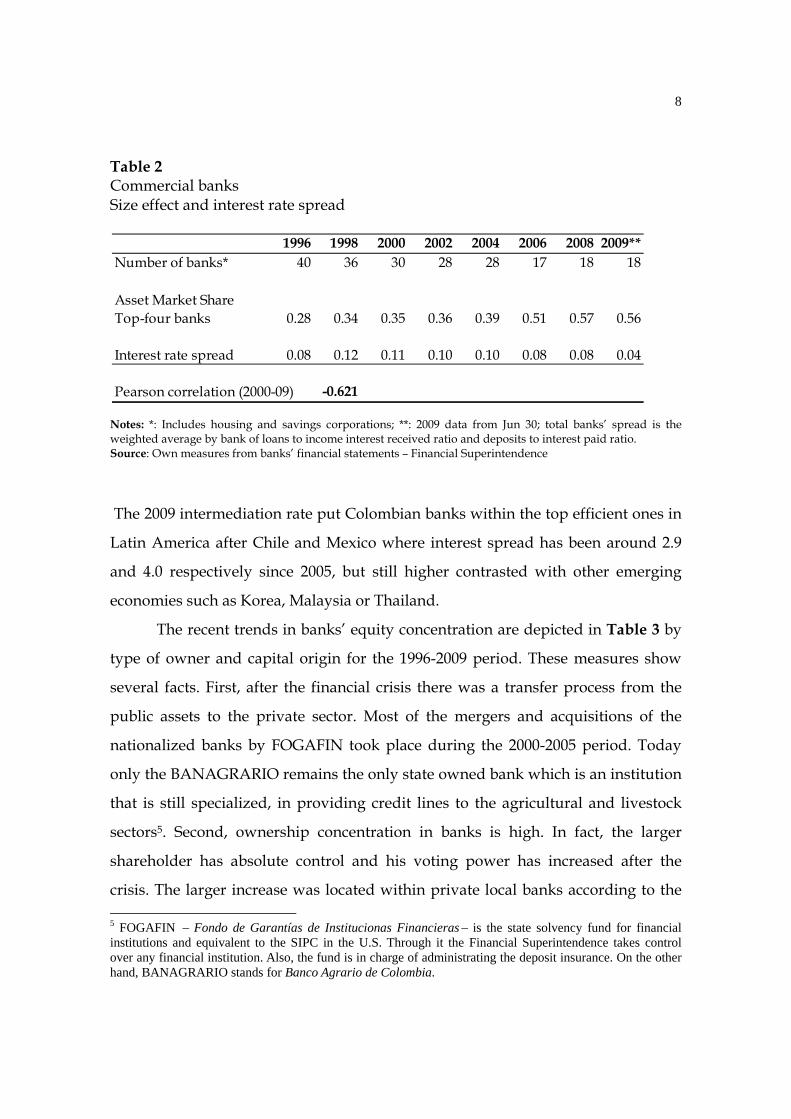

on the other side. The measure of bank efficiency can be analyzed by the

correlation between firm size and the financial intermediation margin (Table 2). It

is clear that the decreasing trend in banks’ interest spread is inversely related with

the size effect measured by the assets market share of the top four larger banks

after year 1999. The correlation coefficient between these variables is -0.63. Thus,

the top banks became larger moving from 27.7 in 1996 to 57.3 percent asset market

share by 2008. Interest rate spread at the same show a sharp decreased. It moved

from a peak of 12 percent in 1998 to levels below 5 percent by 2009. This outcome

goes in hand with the lower inflation rates achieved by the inflation targeting

policy followed by the Central Bank. The country moved from two digits to one

digit inflation rate after year 2000 and during the last five years that rate on

average has been lower than 5 percent.

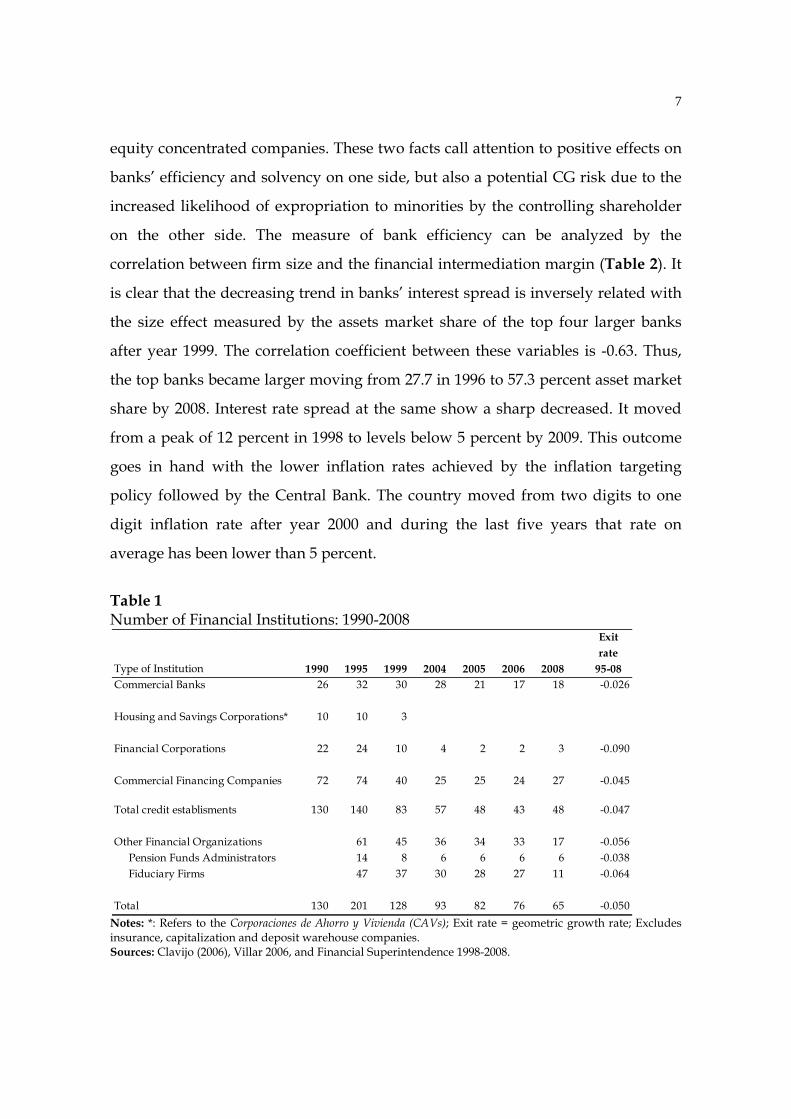

Table 1 Number of Financial Institutions: 1990-2008

Notes: *: Refers to the Corporaciones de Ahorro y Vivienda (CAVs); Exit rate = geometric growth rate; Excludes insurance, capitalization and deposit warehouse companies. Sources: Clavijo (2006), Villar 2006, and Financial Superintendence 1998-2008.

Exitrate

Type of Institution 1990 1995 1999 2004 2005 2006 2008 95-08Commercial Banks 26 32 30 28 21 17 18 -0.026

Housing and Savings Corporations* 10 10 3

Financial Corporations 22 24 10 4 2 2 3 -0.090

Commercial Financing Companies 72 74 40 25 25 24 27 -0.045

Total credit establisments 130 140 83 57 48 43 48 -0.047

Other Financial Organizations 61 45 36 34 33 17 -0.056 Pension Funds Administrators 14 8 6 6 6 6 -0.038 Fiduciary Firms 47 37 30 28 27 11 -0.064

Total 130 201 128 93 82 76 65 -0.050

8

Table 2 Commercial banks Size effect and interest rate spread

Notes: *: Includes housing and savings corporations; **: 2009 data from Jun 30; total banks’ spread is the weighted average by bank of loans to income interest received ratio and deposits to interest paid ratio. Source: Own measures from banks’ financial statements – Financial Superintendence

The 2009 intermediation rate put Colombian banks within the top efficient ones in

Latin America after Chile and Mexico where interest spread has been around 2.9

and 4.0 respectively since 2005, but still higher contrasted with other emerging

economies such as Korea, Malaysia or Thailand.

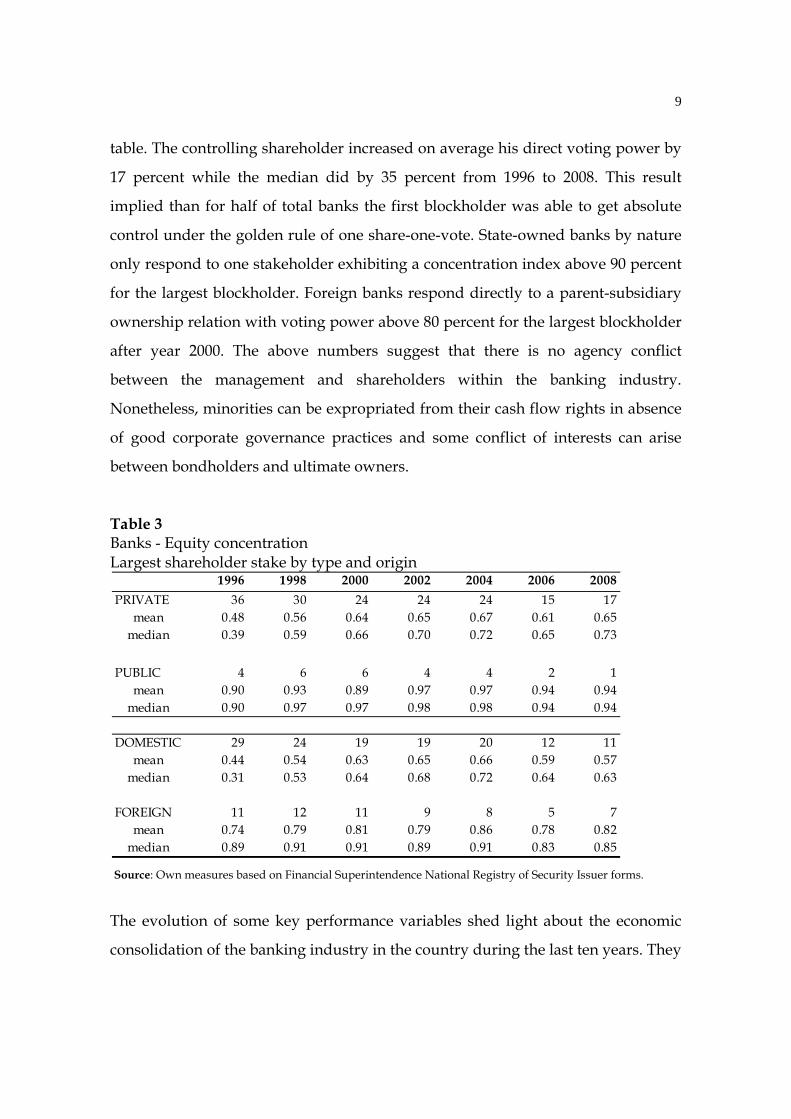

The recent trends in banks’ equity concentration are depicted in Table 3 by

type of owner and capital origin for the 1996-2009 period. These measures show

several facts. First, after the financial crisis there was a transfer process from the

public assets to the private sector. Most of the mergers and acquisitions of the

nationalized banks by FOGAFIN took place during the 2000-2005 period. Today

only the BANAGRARIO remains the only state owned bank which is an institution

that is still specialized, in providing credit lines to the agricultural and livestock

sectors5. Second, ownership concentration in banks is high. In fact, the larger

shareholder has absolute control and his voting power has increased after the

crisis. The larger increase was located within private local banks according to the 5 FOGAFIN - Fondo de Garantías de Institucionas Financieras- is the state solvency fund for financial institutions and equivalent to the SIPC in the U.S. Through it the Financial Superintendence takes control over any financial institution. Also, the fund is in charge of administrating the deposit insurance. On the other hand, BANAGRARIO stands for Banco Agrario de Colombia.

1996 1998 2000 2002 2004 2006 2008 2009**Number of banks* 40 36 30 28 28 17 18 18

Asset Market Share Top-four banks 0.28 0.34 0.35 0.36 0.39 0.51 0.57 0.56

Interest rate spread 0.08 0.12 0.11 0.10 0.10 0.08 0.08 0.04

Pearson correlation (2000-09) -0.621

9

table. The controlling shareholder increased on average his direct voting power by

17 percent while the median did by 35 percent from 1996 to 2008. This result

implied than for half of total banks the first blockholder was able to get absolute

control under the golden rule of one share-one-vote. State-owned banks by nature

only respond to one stakeholder exhibiting a concentration index above 90 percent

for the largest blockholder. Foreign banks respond directly to a parent-subsidiary

ownership relation with voting power above 80 percent for the largest blockholder

after year 2000. The above numbers suggest that there is no agency conflict

between the management and shareholders within the banking industry.

Nonetheless, minorities can be expropriated from their cash flow rights in absence

of good corporate governance practices and some conflict of interests can arise

between bondholders and ultimate owners.

Table 3 Banks - Equity concentration Largest shareholder stake by type and origin

Source: Own measures based on Financial Superintendence National Registry of Security Issuer forms.

The evolution of some key performance variables shed light about the economic

consolidation of the banking industry in the country during the last ten years. They

1996 1998 2000 2002 2004 2006 2008PRIVATE 36 30 24 24 24 15 17

mean 0.48 0.56 0.64 0.65 0.67 0.61 0.65median 0.39 0.59 0.66 0.70 0.72 0.65 0.73

PUBLIC 4 6 6 4 4 2 1

mean 0.90 0.93 0.89 0.97 0.97 0.94 0.94median 0.90 0.97 0.97 0.98 0.98 0.94 0.94

DOMESTIC 29 24 19 19 20 12 11mean 0.44 0.54 0.63 0.65 0.66 0.59 0.57

median 0.31 0.53 0.64 0.68 0.72 0.64 0.63

FOREIGN 11 12 11 9 8 5 7mean 0.74 0.79 0.81 0.79 0.86 0.78 0.82

median 0.89 0.91 0.91 0.89 0.91 0.83 0.85

10

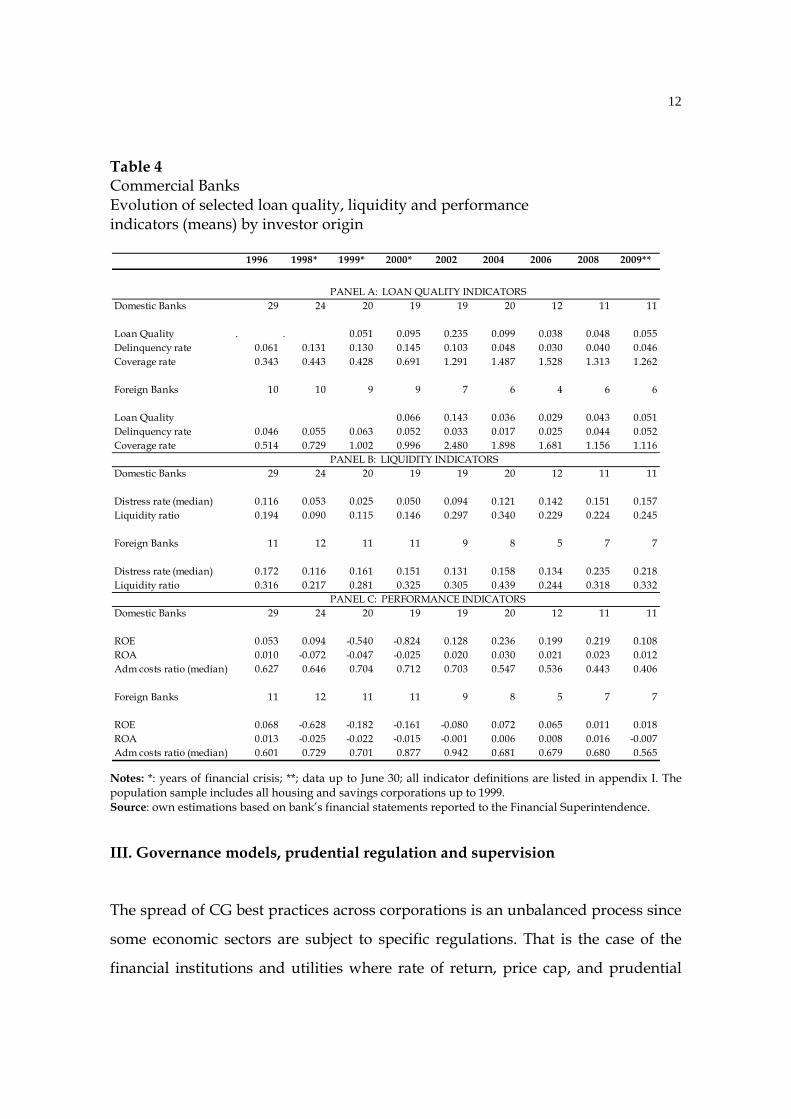

also show that the financial sector was as solid as possible to face the 2008

subprime crisis and thus avoided any financial contagion. Table 4 describes some

selected loan quality, liquidity and profitability indicators by domestic and foreign

banks. There are several facts that those numbers are showing and call for some

comments. First, loans indicators show an overall recovery after the 1999 financial

crisis and a continuous and clear improvement since year 2003. Non-performing

loans hit harder domestic banks since they were exposed to mortgage credits and

foreign banks were less involved in that market. For instance, the risky to total

loans ratio has been reduced by 5 times moving from 23.5 percent in 2002 to 4.8

percent by 2008. The non-performing loans ratio had a peak of 14 percent in year

2000 and moved to 4 percent in 20086. The coverage rate, defined as loan provision

to total loans ratio, by turn got increased by 3 times for the same period.

Second, liquidity indicators exhibit a positive improvement since year 2000

for either domestic or foreign banks. They are proxies to capture the potential

market risk due to adverse selection of bank runs and measure the short term

capability to respond for unexpected shift in deposit withdrawals. In any monetary

system the central bank is the last provider for liquidity and for fixing the levels for

the reserve requirements to demand deposits. The liquidity ratio is s cash plus

almost liquid assets to total liabilities. The lower the ratio the most illiquid the

bank is. The lower scores were observed in 1998. Ten years later the liquidity ratio

is twice larger with levels greater than 22.4 and 31.8 percent within domestic and

foreign banks respectively.

Third, the distress ratio is a good predictor for bank failures [Gonzales-

Hermosillo (1999)]. This indicator is equal to the ratio of equity plus loan reserves

minus non-performing loans to total assets and captures the effect of over-

indebtedness might have on overall cost of capital. The indicator had extreme 6 Is important to recall that non-performing loans were much higher across commercial financial companies reaching a peak of 27 percent of total loans in 1999, but they were much lower within investments banks that showed delinquency rates lower than 5 by year 2000. For more details on the analysis of the 1999 financial crisis and the specific measures, such as banks’ capitalizations and number of restructured housing and non-housing credits, is at Banco de la Republica’s board of governors 2000 reports.

11

outliers across some banks, therefore reporting the median is an accurate measure

for central tendency. Two comments arise from this measurement. On one side

domestic banks were those that experience the market liquidity risk during the

1998-00 period reporting distress ratios almost four times lower than foreign

banks, but on the other side they were able to sustaining a faster recovery by

reducing the level of non-performing loans relative to overall loans. They had by

2008 a distress ratio 6 times larger than those observed in 1999 while foreign banks

did by 1.5 times.

Fourth, the evolution of the profitability indicators reinforces the above

argument. Domestic banks had the burden of the 1999 crisis losses but they also

have been able to exhibit a faster recovery and to keep higher performance rates

since 2003. The return on equity was 21.9 percent for domestic banks by 2008 while

for foreign banks this number was just above 1 percent. One explanation of this

result is that domestic banks were able to cut their administrative costs relative to

the gross financial margin in much greater proportion. This indicator was the same

for all banks year 1999. By 2008 the administrative costs ratio for domestic banks

were 0.65 times the foreign ones. The merger and acquisitions effect generated

new scale economies and cost reductions during the post-crisis years. For instance,

in 2008 among the top four largest banks, three of them were domestic and the

next foreign bank is ranked as the 12th by asset size. Summing up, the evolution

since 1996 of the above indicators, clearly show a successful recovery and market

adjustment of the Colombian banking industry. Its overall solvency by 2008 was at

the best level and the statistics for first semester of 2009 do not show yet a

backward trend.

12

Table 4 Commercial Banks Evolution of selected loan quality, liquidity and performance indicators (means) by investor origin

Notes: *: years of financial crisis; **; data up to June 30; all indicator definitions are listed in appendix I. The population sample includes all housing and savings corporations up to 1999. Source: own estimations based on bank’s financial statements reported to the Financial Superintendence.

III. Governance models, prudential regulation and supervision

The spread of CG best practices across corporations is an unbalanced process since

some economic sectors are subject to specific regulations. That is the case of the

financial institutions and utilities where rate of return, price cap, and prudential

1996 1998* 1999* 2000* 2002 2004 2006 2008 2009**

PANEL A: LOAN QUALITY INDICATORSDomestic Banks 29 24 20 19 19 20 12 11 11

Loan Quality . . 0.051 0.095 0.235 0.099 0.038 0.048 0.055Delinquency rate 0.061 0.131 0.130 0.145 0.103 0.048 0.030 0.040 0.046Coverage rate 0.343 0.443 0.428 0.691 1.291 1.487 1.528 1.313 1.262

Foreign Banks 10 10 9 9 7 6 4 6 6

Loan Quality 0.066 0.143 0.036 0.029 0.043 0.051Delinquency rate 0.046 0.055 0.063 0.052 0.033 0.017 0.025 0.044 0.052Coverage rate 0.514 0.729 1.002 0.996 2.480 1.898 1.681 1.156 1.116

PANEL B: LIQUIDITY INDICATORSDomestic Banks 29 24 20 19 19 20 12 11 11

Distress rate (median) 0.116 0.053 0.025 0.050 0.094 0.121 0.142 0.151 0.157Liquidity ratio 0.194 0.090 0.115 0.146 0.297 0.340 0.229 0.224 0.245

Foreign Banks 11 12 11 11 9 8 5 7 7

Distress rate (median) 0.172 0.116 0.161 0.151 0.131 0.158 0.134 0.235 0.218Liquidity ratio 0.316 0.217 0.281 0.325 0.305 0.439 0.244 0.318 0.332

PANEL C: PERFORMANCE INDICATORSDomestic Banks 29 24 20 19 19 20 12 11 11

ROE 0.053 0.094 -0.540 -0.824 0.128 0.236 0.199 0.219 0.108ROA 0.010 -0.072 -0.047 -0.025 0.020 0.030 0.021 0.023 0.012Adm costs ratio (median) 0.627 0.646 0.704 0.712 0.703 0.547 0.536 0.443 0.406

Foreign Banks 11 12 11 11 9 8 5 7 7

ROE 0.068 -0.628 -0.182 -0.161 -0.080 0.072 0.065 0.011 0.018ROA 0.013 -0.025 -0.022 -0.015 -0.001 0.006 0.008 0.016 -0.007Adm costs ratio (median) 0.601 0.729 0.701 0.877 0.942 0.681 0.679 0.680 0.565

13

regulation play a major role in designing prices schemes, solvency requirements

and promoting economic competition by eliminating market entry barriers to

foreign investors. Regulation and supervision of banks in Colombia is performed

by the Financial Superintendence (SFIN), a merge in 2006 of two former

supervisors: i) the superintendence of securities, and ii) the superintendence of

banks. Thus the regulatory scheme respond to an integrated model of solvency

regulation and credit risk management along with the principle of comply or explain

that all non-financial listed companies have to follow according to the current

Country Code of Corporate Best Practices or Codigo Pais explained in the

introductory section. Banks in Colombia were one of the first institutions in

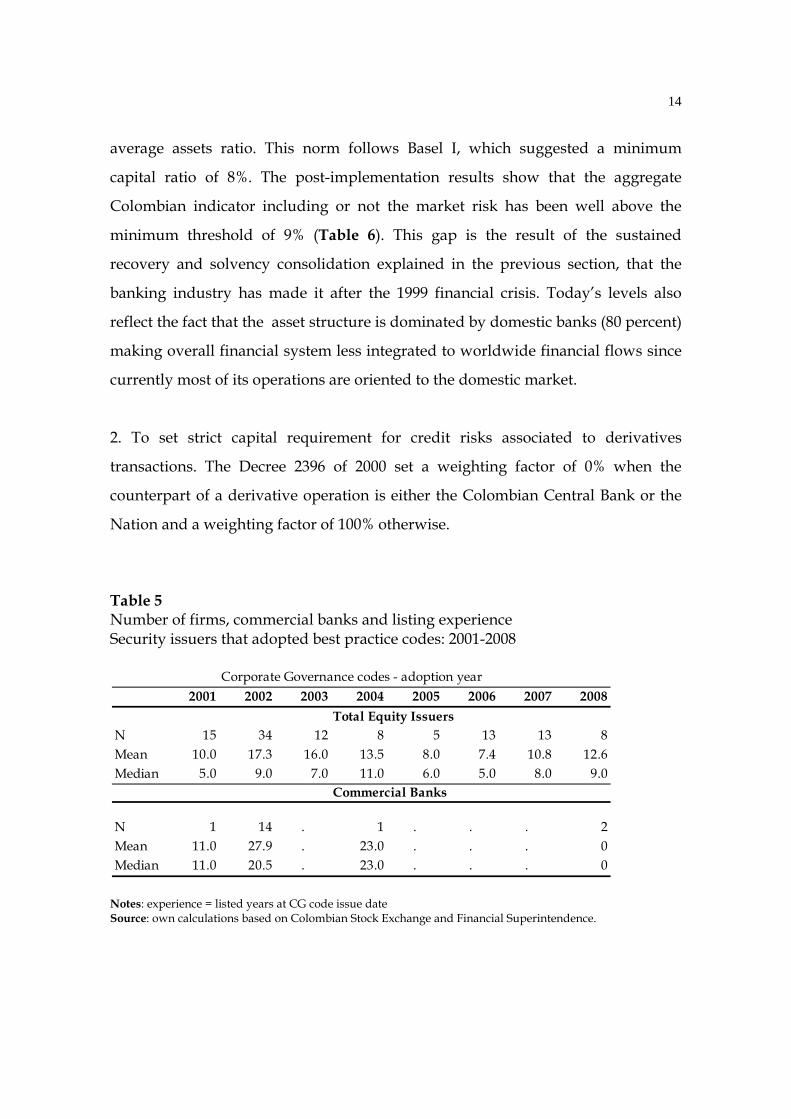

adopting voluntary CG following the Resolution 271 in year 2002. An important

feature was that banks had a long standing listing experience, and average of 24

years, at the moment of issuing the CG code, number greater than their real sector

companies peers (Table 5). This fact explains why according to SFIN they found

important advances in the structure of CG in its oversight institutions, mainly

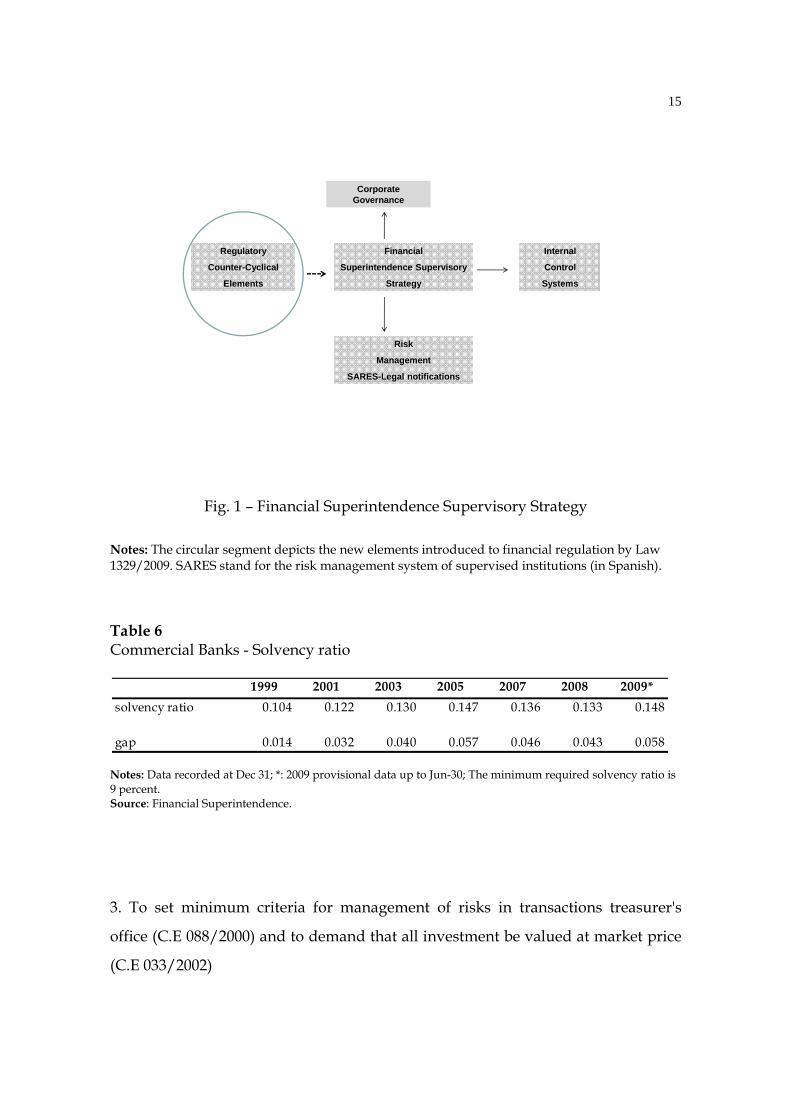

within banks and financial corporations in 2006. Today’s SFIN strategy for

financial supervision within credit establishments and their subsidiaries financial

companies services has CG as one of the fourth pillars of SFIN’s supervisory

strategy (Figure 1).

What follows explain in an abridged form the main regulatory measures aimed at

strengthening the whole financial sector especially after the 1999 financial crisis.

The main approach of Colombian supervisors regarding the Basel I Accord has

been:

1. To set the risk weight adequacy ratio at 9% (Decree 673/1994, Decree 1720/2001

and CE-042/2001)7 defined as technical equity (regulatory equity) to risk weighted

7 C.E stands for Circular Externa that is the legal notification issued by the Financial Superintendence.

14

average assets ratio. This norm follows Basel I, which suggested a minimum

capital ratio of 8%. The post-implementation results show that the aggregate

Colombian indicator including or not the market risk has been well above the

minimum threshold of 9% (Table 6). This gap is the result of the sustained

recovery and solvency consolidation explained in the previous section, that the

banking industry has made it after the 1999 financial crisis. Today’s levels also

reflect the fact that the asset structure is dominated by domestic banks (80 percent)

making overall financial system less integrated to worldwide financial flows since

currently most of its operations are oriented to the domestic market.

2. To set strict capital requirement for credit risks associated to derivatives

transactions. The Decree 2396 of 2000 set a weighting factor of 0% when the

counterpart of a derivative operation is either the Colombian Central Bank or the

Nation and a weighting factor of 100% otherwise.

Table 5 Number of firms, commercial banks and listing experience Security issuers that adopted best practice codes: 2001-2008

Notes: experience = listed years at CG code issue date Source: own calculations based on Colombian Stock Exchange and Financial Superintendence.

Corporate Governance codes - adoption year2001 2002 2003 2004 2005 2006 2007 2008

Total Equity IssuersN 15 34 12 8 5 13 13 8Mean 10.0 17.3 16.0 13.5 8.0 7.4 10.8 12.6Median 5.0 9.0 7.0 11.0 6.0 5.0 8.0 9.0

Commercial Banks

N 1 14 . 1 . . . 2Mean 11.0 27.9 . 23.0 . . . 0Median 11.0 20.5 . 23.0 . . . 0

15

Corporate Governance

Financial

Superintendence Supervisory

Strategy

Internal

Control

Systems

Risk

Management

SARES-Legal notifications

Regulatory

Counter-Cyclical

Elements

Fig. 1 – Financial Superintendence Supervisory Strategy

Notes: The circular segment depicts the new elements introduced to financial regulation by Law 1329/2009. SARES stand for the risk management system of supervised institutions (in Spanish).

Table 6 Commercial Banks - Solvency ratio

Notes: Data recorded at Dec 31; *: 2009 provisional data up to Jun-30; The minimum required solvency ratio is 9 percent. Source: Financial Superintendence.

3. To set minimum criteria for management of risks in transactions treasurer's

office (C.E 088/2000) and to demand that all investment be valued at market price

(C.E 033/2002)

1999 2001 2003 2005 2007 2008 2009*solvency ratio 0.104 0.122 0.130 0.147 0.136 0.133 0.148

gap 0.014 0.032 0.040 0.057 0.046 0.043 0.058

16

4. To set specific actions and ruling to operations between banks and their related

financial companies. In particular, the SFIN has demanded a control to all related

transactions and has requested an adequate management regarding conflicts of

interest. In addition, the ruling has widening the notion of a related party such as

any related person with the financial institution or its administrators by means of

ownership, management or commercial operations that put on risk the

independence of criteria and performance. Blockholders with at least 5% of equity

are considered as related parties (Article 122 /Financial Statute).

Some of the Basel II new rules are not applicable due to the domestic market

bias of banks’ loans that implied a lesser exposure to international fluctuations.

However, some measures associated with the pillar 1 have been implemented to

assure a more solid banking system. The first measure was set by C.E-011 of 2002

which mandated that all financial institutions shall implement an internal system

of credit risk management. To accomplish such a task, each financial institution

must develop its own model of credit risk management following the minimum

criteria for loans set by SFIN. The main rules are the classification of loans by type

of final user and its default probability. The SFIN then proceeds to study and

approve them or not. In case of not getting SFIN’s approval, the financial

institution must comply with stricter rules.

One important factor of Colombian approach in the implementation of

credit risk management has been the institutional arrangement between the

supervisor, the SFIN, and the financial institutions that is seen as a mode of self

regulation and good governance. On one hand, each financial institution has to

step up its own internal stages of loan cycle: a careful study of each loan

application, in particular the collaterals, the follow-up of loans, outstanding debts,

provisions and so on. On the other hand, the approach puts utmost responsibility

on managers in that credit cycle definition. In 2004, the former banking

17

superintendence issued the C.E-052 which set new elements to account for in

implementing the credit risk management system. These were: a) policies to

manage credit risk, b) internal processes to manage credit risk, c) internal models

to estimate expected losses, d) a system of provisions to cover the credit risk, and

e) the processes of internal control.

Regarding the management of credit risk, loans were classified in four

groups depending on their final use: consumption, mortgage, commercial and

microcredit. Five categories of credit risks were implemented:

i) Category A or “normal risk”; ii) Category B or “acceptable risk, superior to normal”; iii) Category C or “appreciable risk”; iv) Category D or “significantly risk”; and v) Category E or “default risk”. More recently, the SFIN issued the C.E 035/2009 which set a new scheme of

provisions that are intended to be active from April 1 2010. This norm defines the

individual provision as the sum of a pro-cyclicality individual component, which

reflects the credit risk of each debtor in the evaluation period, and a counter pro-

cyclicality individual component, which is the portion of the individual provision

of credit portfolio that show the possible changes in credit risks of debtors when

there is an increasing deterioration of such assets.

IV. Boards and best practices

The issue of Law 964 of 2005 of CG reform and the subsequent adoption of CG

country code in 2007 (C.E-028 and C.E-056) put special emphasis to the controlling

and advising roles of the board of directors for all listed companies at the

Colombian stock exchange. This new normative besides standardizing the basic

contents of corporations' CG codes look at formalizing the directors regular duties

and directorate's structures and make them potentially liable for negligence.

18

Several norms and regulations are today mandatory for all equity issuers in

adopting the CG country code and for all financial institutions under SFIN

oversight. The most important measures can be highlighted as the followings:

i) Separation between the Chief Executive Officer (CEO) and the Chairman

of the Board (COB) duties. The CEO cannot longer head the board of

directors and it is strongly recommended not being an active member.

ii) Independent directors might have a minimum weight of 25 percent on

the board. An independent director is a person, who is not an employee or

directive in the firm or any of its subsidiaries, has not been a former

company’s consultant and is not a member of any non-profit organization

that the company is sponsoring.

iii) Independent directors must be members and be majority in all auditing

committees.

For banks’ directors their main responsibilities are beside the above, the

followings:

iv) Approve the systems for internal control, the policies regarding risk

management; to evaluate bank’s top directives performance and compliance,

and design their compensation schemes.

Table 7 depicts the board statistics for selected indicators for years 2000 and 2008,

in order to see the changes due to CG practices before and after Law 964/2005.

Three main comments are worth to highlight. First, board size has remained fairly

constant if one looks at the principal members, and that number is similar to what

is observed across real sector firms. Female participation in board increased its

19

Table 7 Board statistics by selected indicators and years Commercial Banks

Notes: N = number of banks where the board variable is been measured; Source: own estimations based on SFIN's National Registry for Security Issuers.

presence in number of institutions relative to total number of banks but not inside

boards where mean (median) has remain constant at 2 (1) members. Second, the

CEO duality is still a problem despite all the new CG supervision. In year 2008, the

CEO was also a director in 11 out of 27 banks, that is, 41 percent ratio. This number

got reduced to 33 percent by 2008. The real improvement is located in the

separation between the chairman of the board (COB) and the chief executive officer

(CEO) appointments. Full compliance is observed in 2008.8 Third the number of

banks' top-executives as directors has decreased across institutions and within

directorates. Inside directors had on average 55 percent of board seats in year

2000, that number decreased to around 14 percent by year 2008. This outcome

reflects that more outside directors have been appointed and therefore one can

expect more control and independence inside boards. Nonetheless, that

measurement does not take into account all possible adjustments for grey directors

8 Most of those statistics on boards are similar to what is observed in real sector companies. For further details see Gutierrez & Pombo (2009) and Pombo et al. (2008).

Total Principal Substitutes Female CEO CEO Executivessize members members members duality [5]/[1] and at the

COB board2000

N 27 27 27 11 11 0.41 10 11Mean 9.6 5.2 4.4 1.7 . . 5.3Median 9.5 5 4 1 . . 6Min 5 2 0 1 . . 1Max 16 8 8 4 . . 9

2008N 15 15 15 8 5 0.33 0 5Mean 8.7 5.3 3.4 1.8 . . 1.2Median 9 5 4 1 . . 1Min 3 3 0 1 . . 1Max 14 8 7 4 . . 2

20

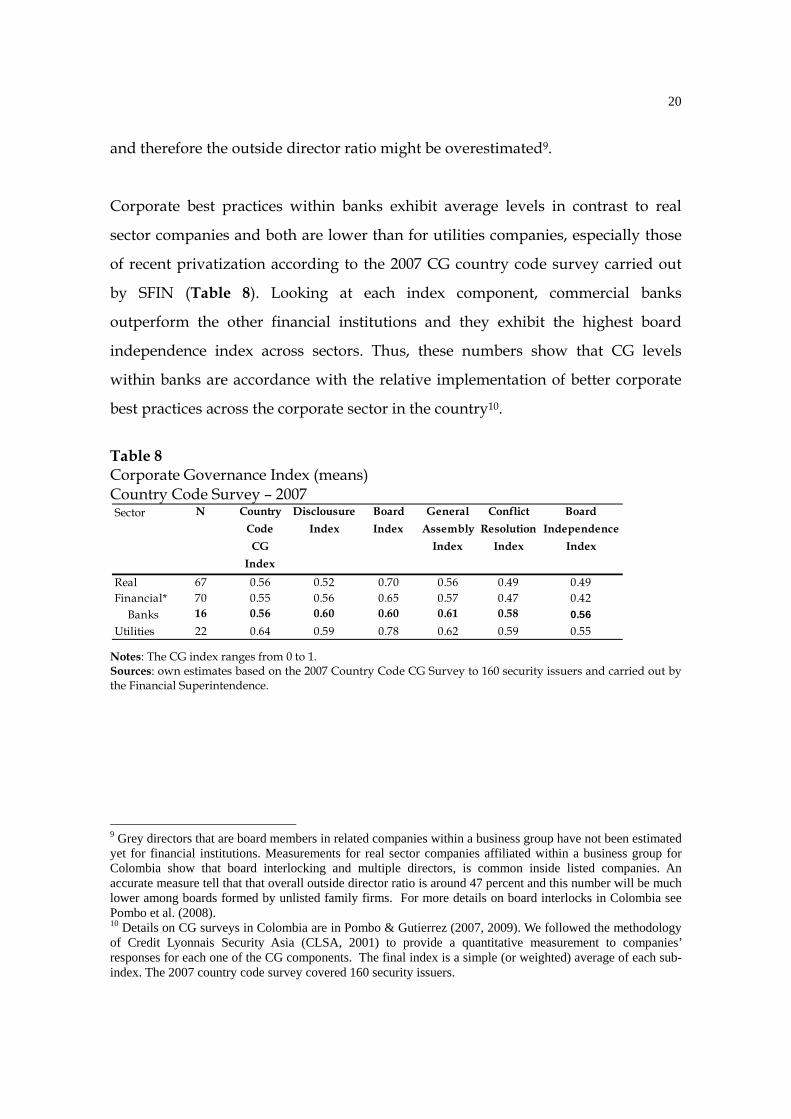

and therefore the outside director ratio might be overestimated9.

Corporate best practices within banks exhibit average levels in contrast to real

sector companies and both are lower than for utilities companies, especially those

of recent privatization according to the 2007 CG country code survey carried out

by SFIN (Table 8). Looking at each index component, commercial banks

outperform the other financial institutions and they exhibit the highest board

independence index across sectors. Thus, these numbers show that CG levels

within banks are accordance with the relative implementation of better corporate

best practices across the corporate sector in the country10.

Table 8 Corporate Governance Index (means) Country Code Survey – 2007

Notes: The CG index ranges from 0 to 1. Sources: own estimates based on the 2007 Country Code CG Survey to 160 security issuers and carried out by the Financial Superintendence.

9 Grey directors that are board members in related companies within a business group have not been estimated yet for financial institutions. Measurements for real sector companies affiliated within a business group for Colombia show that board interlocking and multiple directors, is common inside listed companies. An accurate measure tell that that overall outside director ratio is around 47 percent and this number will be much lower among boards formed by unlisted family firms. For more details on board interlocks in Colombia see Pombo et al. (2008). 10 Details on CG surveys in Colombia are in Pombo & Gutierrez (2007, 2009). We followed the methodology of Credit Lyonnais Security Asia (CLSA, 2001) to provide a quantitative measurement to companies’ responses for each one of the CG components. The final index is a simple (or weighted) average of each sub-index. The 2007 country code survey covered 160 security issuers.

Sector N Country Disclousure Board General Conflict BoardCode Index Index Assembly Resolution IndependenceCG Index Index Index

IndexReal 67 0.56 0.52 0.70 0.56 0.49 0.49Financial* 70 0.55 0.56 0.65 0.57 0.47 0.42 Banks 16 0.56 0.60 0.60 0.61 0.58 0.56Utilities 22 0.64 0.59 0.78 0.62 0.59 0.55

21

V. Anti-crisis measures related to Corporate Governance in 2008-2009

The financial reforms and regulatory measures adopted ten years ago to face the

1998 financial crisis set the structure for today’s good performance of banks in

terms of equity solvency, risk supervision and market discipline as explained in

section 2. The supervisory strategy of the Colombian Financial Superintendence

(Fig. 1) has moved forward in adjusting norms and introducing new elements to

the basic normative with the purpose of strengthening the system of early

warnings and increasing the timing of regulatory supervision. There are three

main norms that have been issued since 2008 to enhance overall financial

regulation, but they were not consequence of the 2008 subprime crisis in the U.S.

The first one is the Law 1328 / 2009, which changes the protecting regime to

financial consumers. This law introduced four key points. The first one was

reinforcing the legal enforcement capabilities that SFIN has to maintain public

trust in the Colombian financial market and to take control, whereas necessary, of

those institutions that not being under its oversight could put at risk the financial

system. Furthermore, the Law commands that pension funds and insurance

companies be affiliated to FOGAFIN with the purpose of protecting and

strengthening the whole financial system. A second reform is the permission to

banks to undertake leasing activities that were formerly a function of the financial

commercial corporations. This is a further step toward turning the Colombian

banking system into a universal type one. The third aspect refers to defense of

users of financial services. Law 1328 details the basic principles that rule the

relationship between financial institutions and their clients and in general the

norms tend to strengthen users’ rights. The last aspect of importance to the

stability of the financial sector is the reform of pension funds that make the whole

pension system more flexible. It now gives to people affiliated to private pension

funds more choices depending on people age and risk profile.

The second one is the C.E-054 of 2008, which provides a new framework for

22

the auditing system for equity issuers. In particular, this norm looks to rationalize

the external auditor duties by forbidding multiple-tasks such as providing

simultaneous consulting services as for example tax advising. It also makes

mandatory to the Auditing Committee the study and approval of company’s

external auditor. The third and last norms are the C.E 014 and C.E 038 of 2009.

These norms set the framework for internal control systems to become a central

element of bank’s CGs. In particular, the two notifications will imply the

assessment of the board of directors and auditing committees by SFIN for all

financial institutions. By the end of 2010 banks must have implemented policies

and procedures regarding the generation, disclosure and custody of bank’s

financial and accounting information; the implementation of compensation

systems, the assessment of strategic plans, and control activities that include bank's

all functional areas.

VI. Final remarks

This chapter has reviewed the main trends of financial regulation, CG norms and

banking industry performance after the 1998-99 financial crisis. Overall results

show ten years later that the banking industry in Colombia exhibits one the highest

solvency and robustness levels in Latin America. The 2008 subprime crisis has not

yet had an impact on the domestic capital market and it seems that the probability

of having a credit crunch is very low or null in the coming years. Domestic banks

have today the enough liquidity to supply the private sector external financing

demand. Financial regulation and CG reforms in this period have played a major

role in shaping the restructuring process within institutions and without doubt the

subprime crisis has been the main test to that process. The legislation concerning

the capital equity separation between parent banks and their subsidiaries was a

key element that isolated the asset destruction triggered by the crisis of the largest

US investment bank and insurance companies. An example is that the local AIG

23

branch or Citibank Colombia did not get undercapitalized due to claims on toxic

assets.

Despite the above, the banking industry is not free of potential risks. Two

main challenges have been highlighted recently. One is related with microfinance

and banking formalization where several initiatives have been put in place. In fact

the two new banks that entered to the market in 2008 are specialized in this market

segment as well as commercial banks have sponsored a network of banking-

correspondents in rural areas and small municipalities with the objective of

expanding the coverage of financial services around the country. The other main

challenge is the observed reversal in the financial repression indices during the last

five years, explained mainly by the current tax on financial transactions. The

government has here a direct responsibility in eliminating this tax and engaging in

a neutral and long term sustainable fiscal policy11.

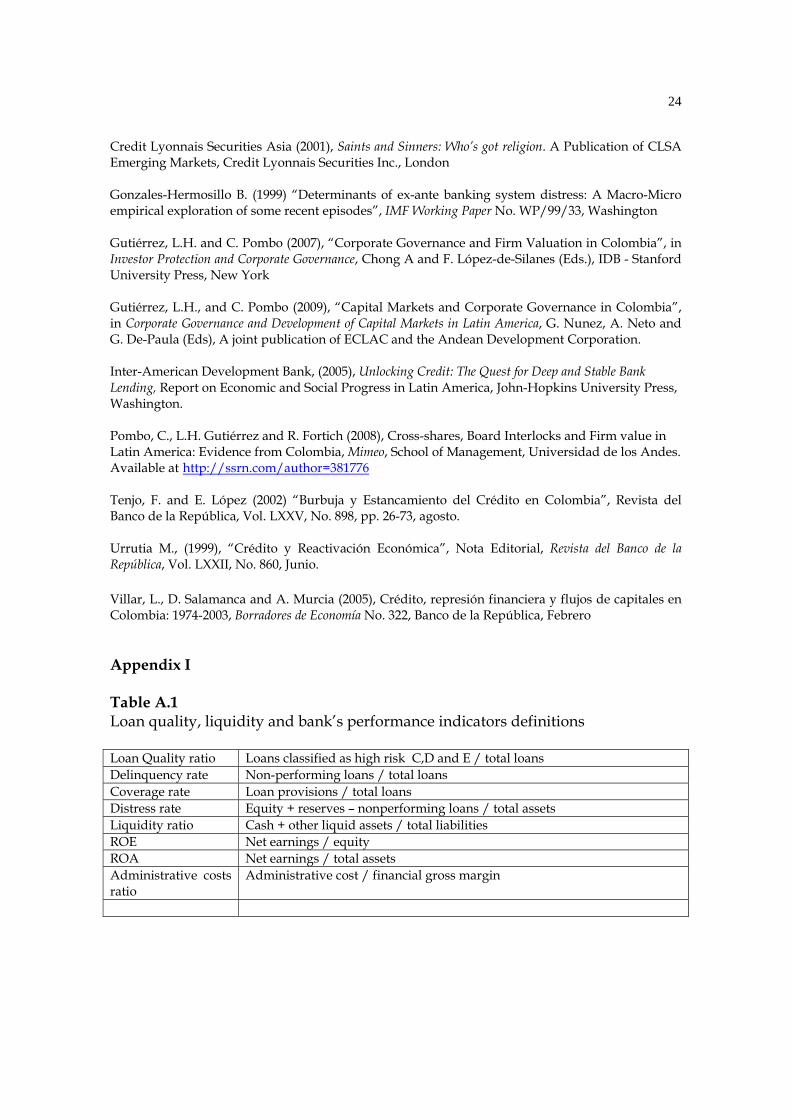

References Barajas A., R. Steiner and N. Salazar (2000), The impact of liberalization and foreign investment in Colombia’s financial sector, Journal of Development Economics, pp.157-196 Barajas A and R. Steiner (2000), Deposit behavior and market discipline in Colombia, IMF Working Paper WP/00/214, December. Banco de la República (1998-2000), Board of Governors Report to the Congress, Several issues Clavijo S. (2000). “Hacia la Multibanca en Colombia: retos y retazos”, Borradores de Economía No. 150, Banco de la República, Junio Clavijo S., C. Rojas, C. Salamanca, G. Montoya and C. Rizo (2006), “Mergers and Acquisitions in the Colombian Financial Sector: Impact on Efficiency (1990-2005)”, Mimeo. Banco de la República. Carrasquilla, A. and J.P. Zárate, (2002), “Regulación Bancaria y Tensión financiera: 1998-2001”, en ANIF (ed.), El Sector Financiero de Cara al Siglo XXI, Tomo I, Asociación Nacional de Instituciones Financieras (ANIF), Bogotá, pp. 215-230. 11 The tax on financial transactions was imposed in 1998 to help first the reconstruction of the 1998 earthquake victims that hit Armenia, the largest city in the coffee growing area. Afterwards, this tax-collection was assigned in capitalizing the recent nationalized banks during the 1998-99 financial crisis. The tax supposed to be temporary for 4 years but then became permanent until date.

24

Credit Lyonnais Securities Asia (2001), Saints and Sinners: Who’s got religion. A Publication of CLSA Emerging Markets, Credit Lyonnais Securities Inc., London Gonzales-Hermosillo B. (1999) “Determinants of ex-ante banking system distress: A Macro-Micro empirical exploration of some recent episodes”, IMF Working Paper No. WP/99/33, Washington Gutiérrez, L.H. and C. Pombo (2007), “Corporate Governance and Firm Valuation in Colombia”, in Investor Protection and Corporate Governance, Chong A and F. López-de-Silanes (Eds.), IDB - Stanford University Press, New York Gutiérrez, L.H., and C. Pombo (2009), “Capital Markets and Corporate Governance in Colombia”, in Corporate Governance and Development of Capital Markets in Latin America, G. Nunez, A. Neto and G. De-Paula (Eds), A joint publication of ECLAC and the Andean Development Corporation. Inter-American Development Bank, (2005), Unlocking Credit: The Quest for Deep and Stable Bank Lending, Report on Economic and Social Progress in Latin America, John-Hopkins University Press, Washington. Pombo, C., L.H. Gutiérrez and R. Fortich (2008), Cross-shares, Board Interlocks and Firm value in Latin America: Evidence from Colombia, Mimeo, School of Management, Universidad de los Andes. Available at http://ssrn.com/author=381776 Tenjo, F. and E. López (2002) “Burbuja y Estancamiento del Crédito en Colombia”, Revista del Banco de la República, Vol. LXXV, No. 898, pp. 26-73, agosto. Urrutia M., (1999), “Crédito y Reactivación Económica”, Nota Editorial, Revista del Banco de la República, Vol. LXXII, No. 860, Junio. Villar, L., D. Salamanca and A. Murcia (2005), Crédito, represión financiera y flujos de capitales en Colombia: 1974-2003, Borradores de Economía No. 322, Banco de la República, Febrero Appendix I Table A.1 Loan quality, liquidity and bank’s performance indicators definitions Loan Quality ratio Loans classified as high risk C,D and E / total loans Delinquency rate Non-performing loans / total loans Coverage rate Loan provisions / total loans Distress rate Equity + reserves – nonperforming loans / total assets Liquidity ratio Cash + other liquid assets / total liabilities ROE Net earnings / equity ROA Net earnings / total assets Administrative costs ratio

Administrative cost / financial gross margin

25

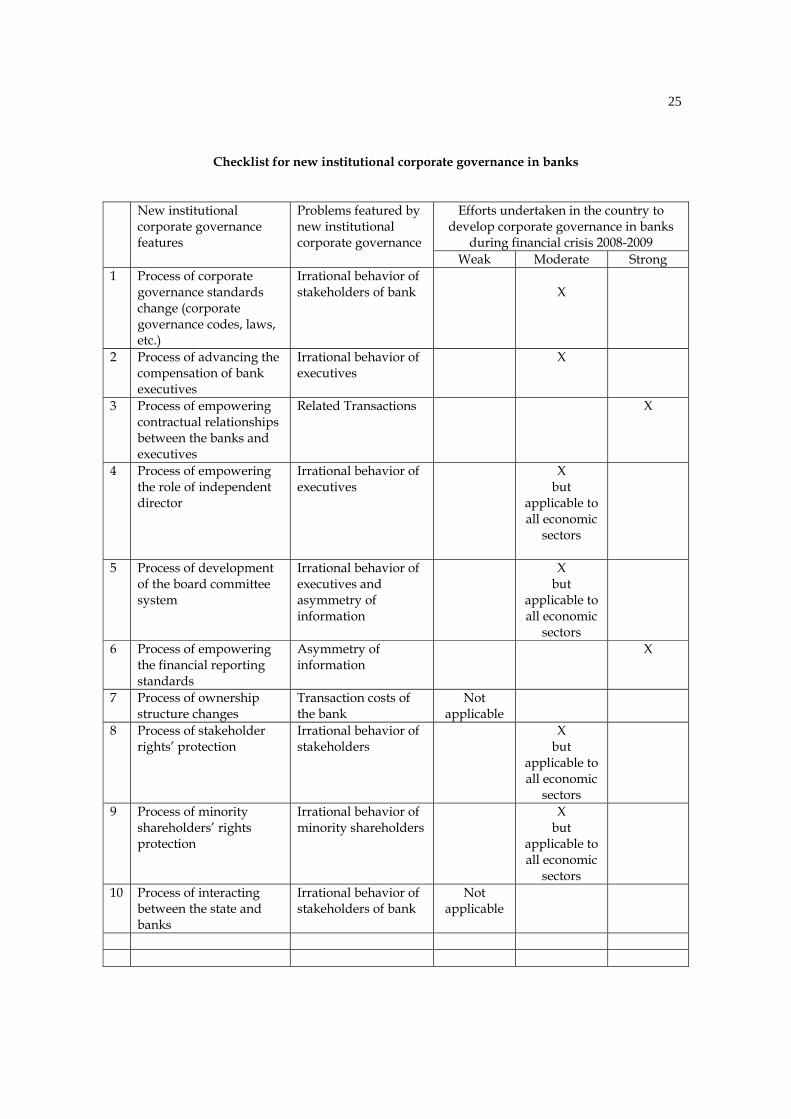

Checklist for new institutional corporate governance in banks

New institutional

corporate governance features

Problems featured by new institutional corporate governance

Efforts undertaken in the country to develop corporate governance in banks

during financial crisis 2008-2009 Weak Moderate Strong

1 Process of corporate governance standards change (corporate governance codes, laws, etc.)

Irrational behavior of stakeholders of bank

X

2 Process of advancing the compensation of bank executives

Irrational behavior of executives

X

3 Process of empowering contractual relationships between the banks and executives

Related Transactions X

4 Process of empowering the role of independent director

Irrational behavior of executives

X but

applicable to all economic

sectors

5 Process of development of the board committee system

Irrational behavior of executives and asymmetry of information

X but

applicable to all economic

sectors

6 Process of empowering the financial reporting standards

Asymmetry of information

X

7 Process of ownership structure changes

Transaction costs of the bank

Not applicable

8 Process of stakeholder rights’ protection

Irrational behavior of stakeholders

X but

applicable to all economic

sectors

9 Process of minority shareholders’ rights protection

Irrational behavior of minority shareholders

X but

applicable to all economic

sectors

10 Process of interacting between the state and banks

Irrational behavior of stakeholders of bank

Not applicable

26

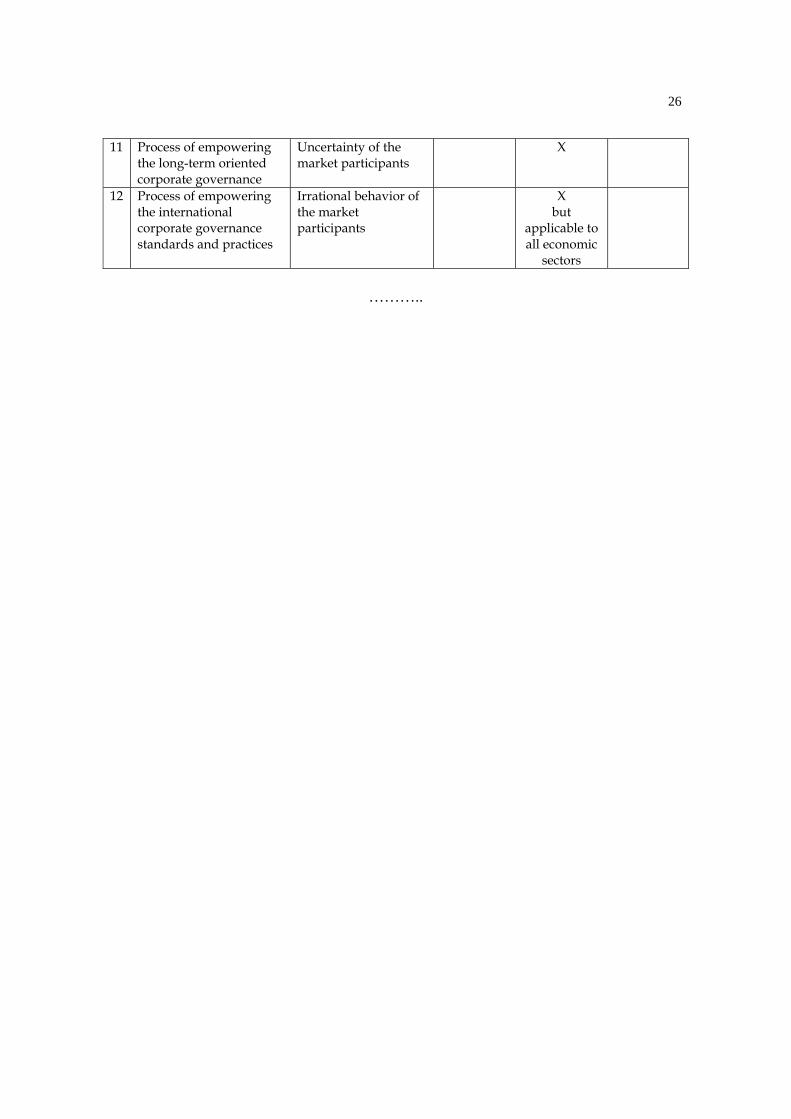

11 Process of empowering the long-term oriented corporate governance

Uncertainty of the market participants

X

12 Process of empowering the international corporate governance standards and practices

Irrational behavior of the market participants

X but

applicable to all economic

sectors

………..