Embed Size (px)

Citation preview

Facultad de Ciencias Económicas y Empresariales Universidad de Navarra

Working Paper nº 10/07

Corporation as Crucial Ally Against Corruption

Reyes Calderón

José Luís Álvarez Arce Silvia Mayoral

Facultad de Ciencias Económicas y Empresariales Universidad de Navarra

1

Corporation as Crucial Ally Against Corruption Reyes Calderón, José Luís Álvarez, Silvia Mayoral Working Paper No. 10/07 October 2007

ABSTRACT We analyze the role that corporation plays and could play in anticorruption programs, with the World Bank Governance and Anticorruption (2006-07) report as a base. Using the BPI and CPI and “Doing-Business” databases, its triple strategy —investment climate, ethical practice and sanctions— is analyzed. Results evidence the low (high) signification of climate (ethics). We criticize the ethical conceptualization of the WB and conclude by describing corruption as an alignment problem for firms.

Reyes Calderón Cuadrado Universidad de Navarra Facultad de Ciencias Económicas y Empresariales Campus Universitario 31080 Pamplona [email protected] José Luís Álvarez Arce Universidad de Navarra Facultad de Ciencias Económicas y Empresariales Campus Universitario 31080 Pamplona [email protected] Silvia Mayoral Universidad de Navarra Facultad de Ciencias Económicas y Empresariales Campus Universitario 31080 Pamplona [email protected]

2

Introduction

Corruption is a cause of concern for companies (Argandoña, 2001) and

companies a cause of worry in anticorruption efforts (Rose-Ackerman, 2002).

However, very few firms have incorporated the problem in their managerial

decision-making and anticorruption policy has mostly neglected firms and has

focused instead on bureaucratic. This is clearly paradoxical and requires some

explanation. This paper explores both the role that anticorruption policy assigns

to corporations and the role that corporation could play in the fight against

corruption. We suggest that, under certain conditions that we analyze,

corporation could be a crucial partner in the anticorruption fight.

In contrast with free markets and quality institutions, corruption increases

transaction costs (Aidt, 2003; Shleifer & Vishny, 1993) and the costs of doing-

business (Wilhelm, 2002). With insecure property rights, high risk of

expropriation and low reliability of contract enforcement, the number and size of

firms (Beck et al, 2005), the firm's foreign investment (Mauro, 1995), the profit

per firm (Ades and Di Tella, 1997), the firm's long-term performance (Baucus &

Baucus, 1998) or even the quality of produced goods (Nwabuzor, 2005) suffer.

Although corruption adds 10 percent or more to the cost of doing business in

many countries of the world (Brew, 2006), anticorruption efforts are not fully

valued or incorporated in managerial decision-making (Doh et al, 2003).

The World Bank Institute (2004) estimates that annual worldwide bribery is to

the tune of $1 trillion, and the scale seems to creep up gradually (Andelman,

1998). A recently published report by Transparency International (TI) (Bribe

3

Payers Index, 2006) certifies the generalization of bribery, especially from

developed countries. Although evidence shows that “many private businesses,

including from developed countries, themselves engage in corruption practices”

(WBG-GAC; 2006-07: 12), so far most anti-corruption efforts have focused on

the demand side and neglected the analysis of firms' corrupt practices. This

paradoxical situation is discussed in the paper.

The remainder of the article is organized as follows:

Section II provides a general background of anti-corruption policy. Firstly, it

offers a brief theoretical description of traditional policies, predominantly based

on a demand-side approach, and its present evolution. In response to recent

trends such as globalization, weakening of national regulatory systems or Enron'

sequels, firms timidly appear as potential partners in anti-corruption efforts.

Secondly, analyzing statistical analysis data of “Bribe Payers Index” (BPI) and

“Corruption Perception Index” (CPI) (2006, 2002 and 1999), both published by

TI, the paper offers an empirical description of the trans-national corporation's

behaviour and its evolution, confirming the requirement of the business'

engagement for success.

Section III focuses on the future, drawing in the report “Strengthening Bank

Group Engagement on Governance and Anticorruption” (WB-GAC, 2006-07), a

key exponent of the next-generation of anticorruption strategies, which

describes corporation as a crucial ally to curbing corruption. In relation with its

engagement in bribery, the report admits the existence of “good” and “bad”

business character, which does not always improve with development's level

4

and, at times, is even deteriorated. In order to engage firm in the “good road”,

WB-GAC (2006-07) draws a strategy based on three forces or types of incentives

for corporate behavior: (1) the improvement of the investment climate in the

developing countries (2) the introduction of ethical corporate practice and (3)

the implementation of efficient sanctions. This paper essays to calibrate the

three elements.

Firstly, the paper investigates whether and how the deterioration of the

investment climate of the destination country can explain transparency's and

integrity's deterioration within the trans-national firm, expressed in CPI and BPI

differences. With that aim, we examine the “Doing Business” database created

by the World Bank, which provides objective measures of business regulations

and their enforcement, and permits some comparisons across economies, and

develops an aggregate index from six regulatory areas that can enhance or

constrain business activity —(1) starting a business (2) access to credit, (3)

employment law, (4) tax disadvantage, (5) enforcement contracts and (6)

investors protection—. This index permits us to explore how constraints on doing

business are associated with CPI-BPI differences.

Our results show that, as global data as data by destination regions, CPI-BPI

differences cannot be explained in terms of regulations doing-business. Thus, we

could hypothesize that other variables must be affecting the behaviour of

companies. In this regard, the second element of WBG's strategy —that is, the

introduction of ethical corporate practices— comes to the forefront. The report,

which suggests the catchy slogan: “integrity is good for business”(p. 12), is

5

viewed by us as incomplete. Section IV discusses relationships between integrity,

coherence and corruption, concluding that, in fact, “dishonesty is bad for

business” corruption being an alignment problem.

II. BACKGROUND ON ANTICORRUPTION STRATEGIES

Anti-corruption strategies: the past.

International institutions, lawmakers, media and scholars unanimously recognize

that corruption has both an active demand and a supply side. They also admit

that corporation is a necessary party when discussing whichever corruption

process. But past anticorruption strategies have mostly focused on the demand

side, that is, on the behavior of public officials.

With very few exceptions, all the recommendations, conventions and policies

from international organizations —including the United Nations (UN), Council of

Europe (CE), Organization of American States (OAS), World Bank Group (WBG),

International Monetary Fund (IMF) and others (Cf. Rose-Ackerman, 2002: 1907-

1911)— have recognized the impact of corrupt business behavior on national

and international business environments. However, within academic literature,

they have underlined the public agent behavior -the demand side- as the key

determinant of corruption. The behavior of the public official, who to some

extent is motivated by rent-seeking or by the desire to get reelected, is

problematic when his/her activity is affected by information asymmetry and the

principal-agent problems. Those circumstances occur very frequently and

anticorruption efforts have focused primarily on deterring, preventing and

combating the corrupt behavior of public officials.

6

By employing criminal and civil sanctions and command-and-control instruments,

most of the measures have aimed at controlling the rent-seeking, producing

transparent procedures and increasing the effective control.

The two main exceptions are the U. S. “Foreign Corrupt Practices Act” (FCPA,

19771) and the OECD “Convention on Combating Bribery of Foreign Public

Officials in International Business Transaction” (OECD, 1997), in which the firm

is mainly viewed as the agent who pays bribes. In order to obtain short-term

profit maximization, corporation could bribe (foreign) public officials or hide such

bribery. This behavior must be actively fought.

In order “to restore public confidence in the integrity of the American Business

System”, the FCPA was enacted to make extraterritorial bribery explicitly illegal

for US companies and to create requirements for greater transparency. It

prescribes the establishment and conservation of both accounting and record-

keeping practices, which are enforced by the Securities Exchange Commission.

Penalties for violation are those that apply to most other violations of the

securities laws.

The OECD Convention, which was adopted in 1997 and entered into force in

1999, focuses on the establishment of “effective, proportionate and dissuasive

non-criminal sanctions” (art. 3) for firms2, recommending that member countries

submit proposals to their legislative bodies3. As Vogl (1998) signals, the OECD's

actions such as ending tax deductibility for illicit payments, is “soft law” —

recommendation for action by national governments—, and is distinct from “hard

law” —binding treaty obligation.

7

Both proposals:

1. try to legally avoid bad behavior, the FCA with a posteriori sanctions,

the OCDE with dissuasive a priori measures, understanding that, as legal

persons, company knows and comprehends its subjection to institutional

framework. Thus, laws and regulation are considered strong enough for

effectively control business misconduct. This is the mainstream view in

the academic literature. Rose-Ackerman (2002) signals that the firm’s

main argument to reject corrupt practices is its status as legal persons

operating at the suffrage of the state. The role of attitudes or values,

which have broadly contributed to the anticorruption success in countries

like Hong Kong, are largely neglected.

2. welcome the efforts of companies, business organizations and trade

unions to combat bribery. But neither the FCA nor the OCDE's convention

demand firms to be a positive ally against corruption. The role of self-

regulation and voluntary acceptance of private codes is largely neglected.

Firms can be both a victim and a generator of corrupt practices. According to

TI's Global Corrupt Barometer (2004), the index for corporate corruption is 3,4

on a scale where 5 indicates maximum corruption. The corporate sector,

interestingly enough, is the most corrupt institution in countries like Hong Kong,

Netherlands, Norway or Singapore. Simultaneously, according with the WBG

(2006c), the impact of corruption on the private sector is considerable, basically

through higher costs of doing business.

The emergence of a new sensibility

8

Although past anti-corruption strategies have been largely silent on the role of

firms, new pressures —from both corporations and their external framework—

are changing the panorama, have led the private sector behavior to become a

hot issue in developed democracies today.

In response to recent trends such as globalization, Enron and sequels,

weakening of national regulatory systems or growing influence of social actors

who act trans-nationally (Howlett & Rayner, 2006), a new and timid sensibility

seems to emerge from both public and private sides directing the anticorruption

effort to business.

a. Over the past decades, a wide range of events (linked to labor, health

and safety rights, and to environmental concerns) has generated broad

discussions about the role of corporations in society. New questions about

ethical standards, integrity, corporate governance practice or

management decisions (Bonn & Fisher, 2005) have emerged. Moreover,

the fall of Enron and other recent scandals have produced a massive loss

of confidence in the integrity of western business (Carson, 2003). As a

result, primary —owners, customers or employees— and external

stakeholders around the world —mass media, NGO's, civil society, etc.—

compel companies “to respond in a more responsible and transparent way

to environment pressures” (Waddock et al, 2002: 132).

Many companies have developed internal monitoring systems, external

monitoring systems by third-party organizations, which accredit that the

firm achieves standards, or certifications by independent evaluations

9

(O'Rourke, 2006). In relation with bribery and corruption, the growing

pressure on multinationals have not been as strong as in the case of

children labor or environmental policy. Because of the rampant

consequences of bribery in poverty and inequality, corruption is now

included in those business decisions that have social and environmental

impacts (WBG, 2003b). In summary, increasing public awareness

stimulates the firm's engagement in anticorruption efforts.

b. Government is a second recent source of pressure for business. In the

last years, international policy and academic discourse have concluded

that, although the capacity of government to regulate is fundamental,

“governments alone cannot contain corruption” (UN, 2004: 17). In

curbing corruption, “traditional public sector management intervention are

not enough in tackling challenges. Wider engagement with the domestic

private sector and multinationals is required” (WBG, 2006: i).

Thus, the private sector —as at the level of the individual firm as business

community—is recognizing that it is in its own best interest to fight

corruption to foster sustainable and stable business growth (WBG,

2006b). Simultaneously, the public sector begins to understand that it is

necessary to engage firms in the combat against corruption.

The data

Recently, TI published the 2006 “Bribe Payers Index”, the third of a series, which

includes 2001 and 1999's reports. BPI is a ranking of 30 (21 and 19 respectively

in the past reports) of the leading exporting countries according to the

10

propensity of firms with headquarters within their borders to offer bribes or

other undocumented extra payments when operating abroad. The index is score

in a range from 0 (bribes are habitual) to 10 (bribes never occur).

In the 2006 report, TI emphasizes the “considerable propensity for companies of

all nationalities to bribe when operating abroad”. In fact, it is obligated to note

the relatively small range of scores (p. 12). Both the best performance

(Switzerland: 7,81) aand the worst score (India: 4,62) result excessively far from

10, the perfect score.

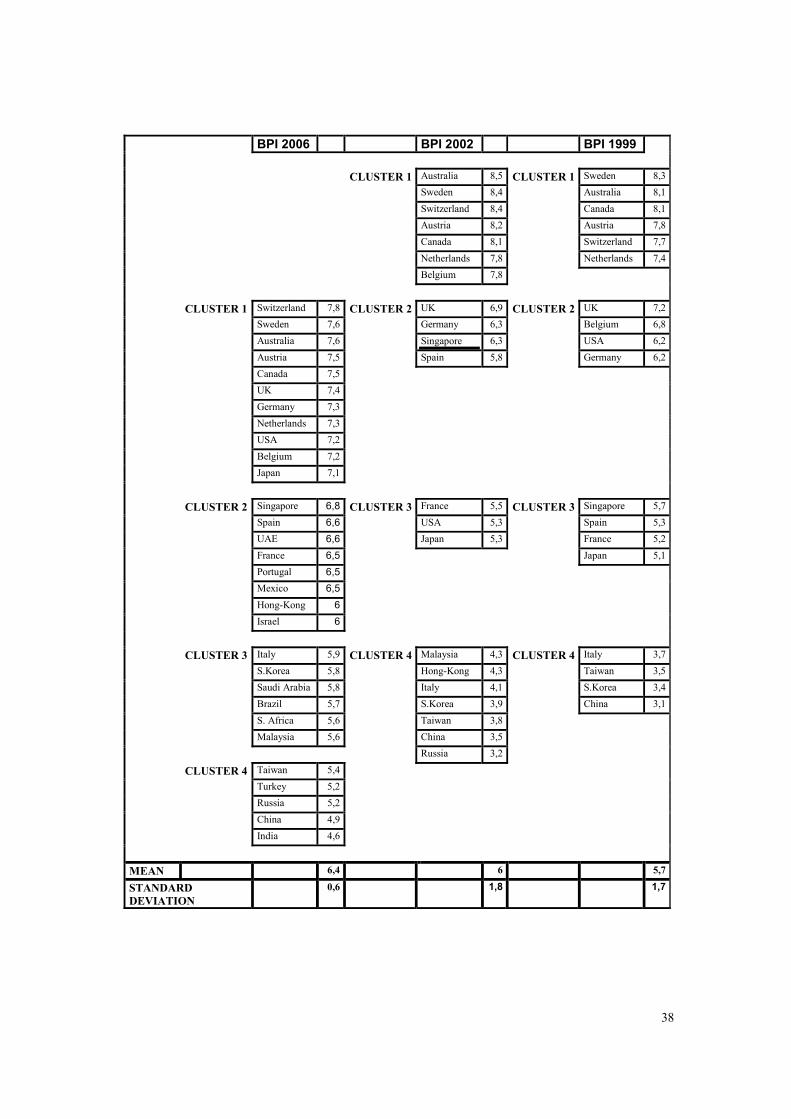

However, there are some indices which must be also emphasized

Figure 1 describes the evolution of the BPI, from 1999 to 2006, grouping data

into four clusters4.

------------------- Insert Figure 1 about here

-------------------

From the above data, some interesting issues emerge:

THE EVOLUTION OF MEANS

a. The global average of BPI ratings has improved from 5.7 in 1999 to 6.4 in

2006, with a value of 6 in 2002.

b. The average BPI rating has significantly improved in three out of four

clusters. That is especially true for the last one, which comprise those countries

that are most likely to bribe: 3.4 in 1999; 3.9 in 2002 and 5.0 in 2006. Data

shows that businesses from developing and in transition countries, such as

11

China, Russia or South Korea, are realizing a strong and growing effort with

regarding to transparency and integrity.

c. The worst behavior comes from the first cluster which includes the

countries on the top of the ranking, that is, those from which companies are

least likely to bribe when doing business abroad.

The average score increased from 7.9 in 1999 to 8.1 in 2002, coinciding with the

entry into the force of the OECD Convention against corruption, thanks to the

good behavior of countries like Belgium, Switzerland or Spain, whose

achievements even compensates for the poor behavior of USA and UK. But those

anticorruption efforts seem to have declined in the period 2002-2006, with a loss

of 0.7 points to the average score that ended with a value of 7.4. Interestingly

enough, those countries with the worst behavior in the first period got much

better scores in the 2006: the score of USA grew 2 points and the rating of UK

improved 0.5 points. Japan registered one of the biggest improvements, from

5.3 to 7.1.

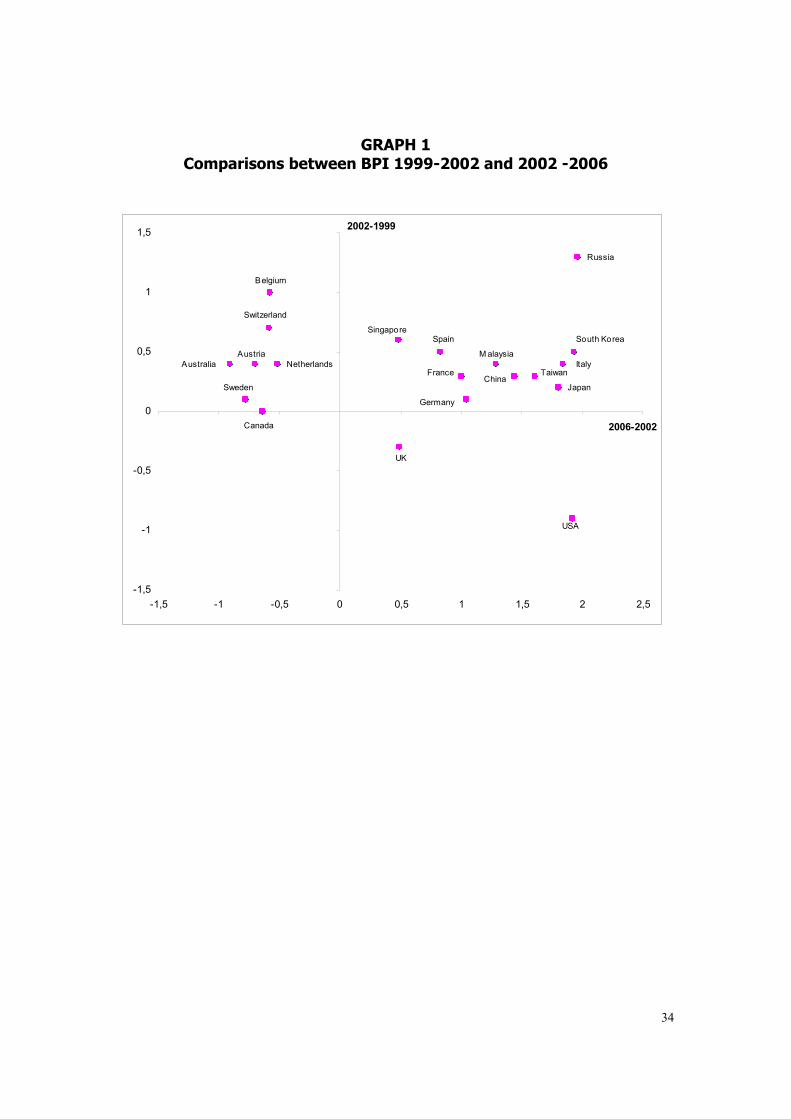

Graph I shows the comparisons of the BPI evolution in both periods of time.

------------------- Insert Graph 1 about here

-------------------

A very positive feature to be underlined is the density of the first quadrant, that

is the big number of countries with improvements in both periods. The negative

counterpart can be found in the second quadrant with some of the most

developed and transparent economies in the world: Belgium, Switzerland,

12

Austria, Australia, Sweden and Netherlands. The peculiar behavior of UK and

USA is reflected in the fourth quadrant

DEVIATIONS

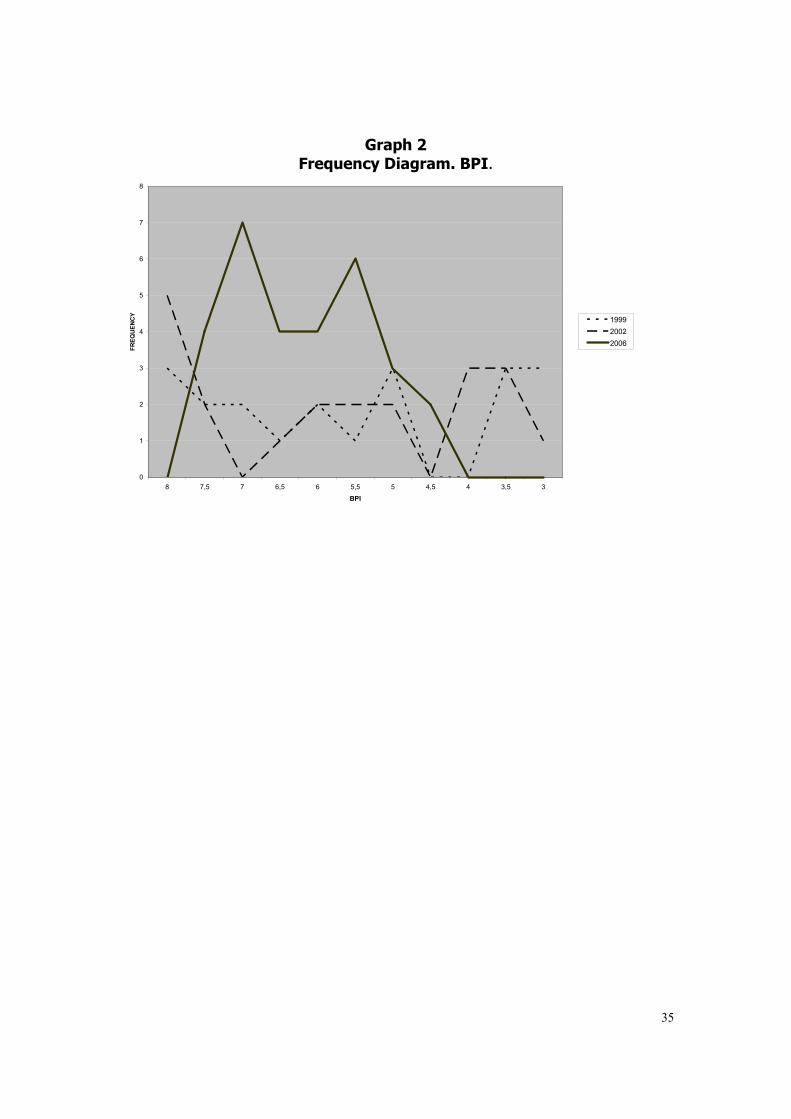

We also highlight how deviations from the mean become smaller over time.

Graph 2 shows a illustrative frequency diagram of BPI. This concentration could

well respond to the homogenization related to globalization. The distance

between the best and the worst BPI rating in 1999 was 62,65% and 36,74% in

2006. The business community seems to homogenize or, at least, to

approximate behavior in its transnational activity.

------------------- Insert Graph 2 about here

-------------------

It could be thought that the improvement or deterioration of the business'

behavior of a country are caused by losses of integrity not in corporations but in

their countries of origin. Despite the fact that both indexes measure different

aspects of corruption employing different methodology, the report by TI (2006)

compares BPI (2006) with CPI (2005), which ranks countries in terms of inner

perceived levels of corruption, as determined by expert assessments and opinion

surveys, finding a high correlation (0,87) between results of the two indexes.

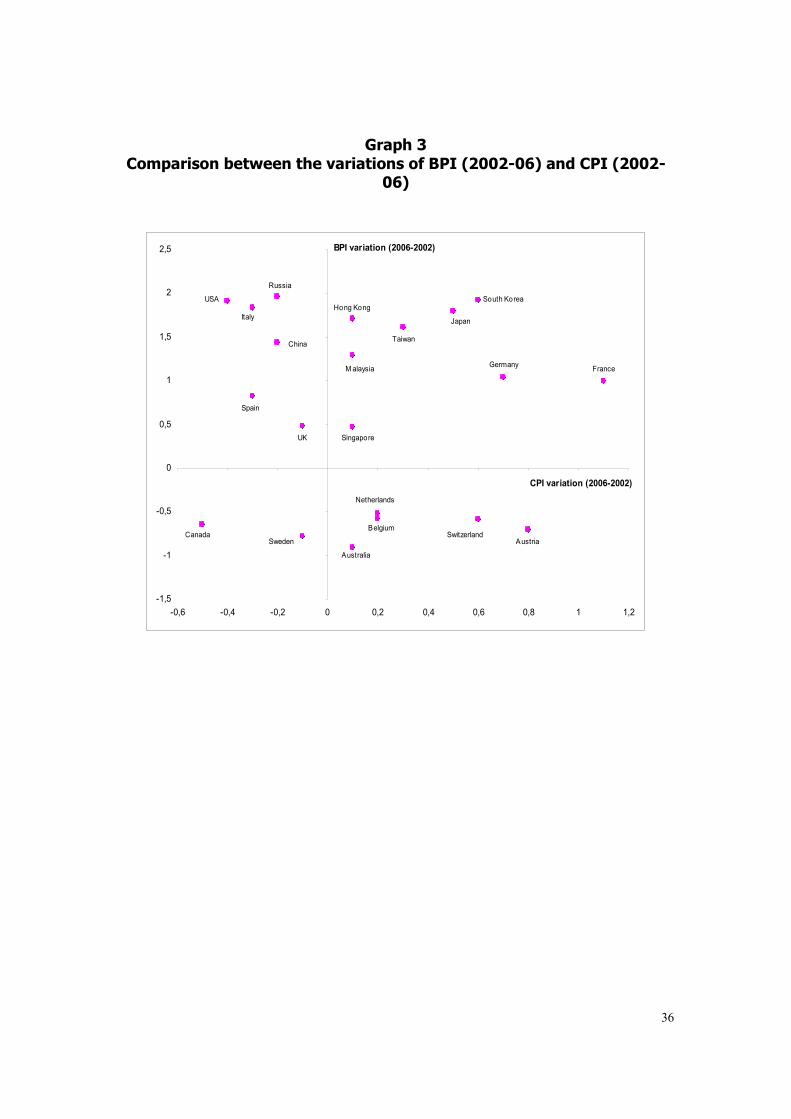

Regarding 2006 CPI and BPI adta, results are displayed in Graph 3.

------------------- Insert Graph 3 about here

-------------------

13

We have run a more exhaustive comparison. We study the differences between

CPI (2006) and BPI (2006) ratings. Our sample is made up of the 30 countries

which are included in the BPI ranking. The difference is defined as CPI - BPI.

Through a t-test we find that the hypothesis E (CPI - BPI) = 0 cannot be

rejected (p-value = 0.6505). More specifically, the estimated mean falls within

the interval [-0.6616, 0.4196]5. According to such results, it could be concluded

with TI that there are no differences between levels of domestic and offshore

corruption.

III. “Strengthening Bank Group Engagement on Governance

and Anticorruption” (WB-GAC, 2006-7) : a review.

Since former WBG president James D. Wolfensohn, declared corruption “an

intolerable cancer" in 1996, society has looked for a vaccine. And it has been in

the past few months, with Paul Wolfowitz as WBG's President, when “the

evidence has reached critical mass: the change appears to be genuine” (Mallaby,

2006). As part of this change, the firm begins to be considered as a key actor in

anticorruption.

The WB-GAC (2006-7), which can be considered as the last generation of

anticorruption strategies, shares many elements with the OECD (1997) or the UN

(2003) conventions. It also presents some peculiarities. Differences with past

strategies are more of degree than of kind and have to do with the focus on

governance and its implications for the private sector.

The gestation of this report was as follows: The Development Committee (DC) —

a forum of the WBG and the IMF that facilitates intergovernmental consensus-

14

building on development issues— requested the Governance and Anti-corruption

(GAC) strategy on April, 2006. The WBG responded to the DC request with a

document entitled “Strengthening Bank Group Engagement on Governance and

Anticorruption” (WBG-GAC). The draft outline of the paper (July, 2006) was

subjected to internal and external feed-back (August, 2006). External comments

included several hundred stakeholders representing civil society organizations,

the private sector, academic institutions —including that of the signatory authors

of this paper—, parliamentarians, and other interested parties.

Based on the results of the feedback, the document was redirected and

submitted to the DC for discussion in the plenary at the September 2006

IMF/World Bank Group Annual Meeting in Singapore. From November 2006 to

January 2007, the next phase of consultation with representatives from

governments, donor agencies, civil society, parliaments, private sector, academia

and other stakeholders was opened. The findings will help to refine the strategy.

The report was newly reviewed by the Board in March 2007 and sent to the DC

at its next meeting on April 15, 2007. Possibly, the modified6 WGB-GAC will be

definitively approved before the end of 2007.

The report's main novelty is its emphasis on the “multi-stakeholder approach”.

While, as in the past, government continues being the key player, WBG attempts

the formation of a global partnership on governance and anticorruption and,

therefore, a better engagement with non-governmental stakeholders. The report

suggests that the WBG should be open to involvement with a broad range of

domestic institutions. It also admits that champions of reform could be inside

15

and outside the executive branch of government, including in the business

community, individually or collectively.

In relation with the engagement of domestic firms and multinationals, the report

describes a framework formed by incentives, recommendations and sanctions. In

this realm, the WBG explicitly states that the private sector faces two

contradictory incentives:

a. Corruption and poor governance increase the vulnerability and

uncertainty of markets and contracts. This increased risk negatively

impacts the investment growth, with detrimental effects for corporations

in the middle and long term. On the other hand, a transparent investment

climate creates many opportunities for business. Thus, firms have a

strong long-term incentive to reject venal officials and to be partners in

the fight against corruption through partnerships between the public and

private sectors.

b. In the short-term, weak governance may create lucrative benefits

which can be extracted by unethical corporations with low risk. Some

corporations can follow this incentive thus shaping and distorting the

country's investment climate.

Many firms and multinationals refrain from engaging in corruption, and they

function efficiently and with integrity. However, there is evidence that many

private businesses, “including some from developed countries, themselves

engage in corrupt practices” (WBG, 2006: 14). This behavior has a detrimental

impact on the dynamism and growth of the rest of the competitive private sector

16

and on the country's development, undermining governance (MacMurray,

2006b).

It results demostrate that if integrity and incentives moved in the same direction,

the corruption discussion would not exist (Rose-Ackerman, 2002). However, the

existence of divergent incentives affects firm behavior. Thus, in order to deter

the last type of behavior and to fuel the first, the strategy establishes three type

of actions.

1. On the one hand, actions from government to private sector. It is a

well established hypothesis that the institutional context plays a role in a

firms' governance. Institutional inefficiencies may affect (impede, retard

or facilitate) the development of businesses. In this line, the report

proposes the help for governments to improve the investment climate.

Concretely, WBG proposal is to “eliminate excessive red tape and non-

transparent regulations, reduce monopolistic practices, transparently and

competitively privatize state-owned business and banks, and facilitate the

entry of small and medium enterprises to help level the playing field,

reduce incentives and opportunities for corruption, and stimulate better

corporate citizenship” (WBG, 2006:12).

2. On the other hand, actions that encourage a joint public-private

coalition for reforms are proposed. Concretely, “the International Financial

Corporation and Multilateral Investment Guarantee Agency working

directly with the private sector to introduce ethical corporate practices…

17

and, more broadly, advocate that `Integrity is good for business' ” (WBG,

2006: 12).

3. Finally, as traditionally, the paper projects the use of public sanctions

to raise the cost to businesses for continuing to engage in corruption.

Inefficiencies of the institutional environment

In the last section, we have affirmed the inexistence of significant differences

between BPI and CPI in the origin countries; however, we have not spoken

about the destination countries. It is well known that there is a significant

variation in the legal, regulatory and financial systems across countries. Some of

those differences specifically affect the business environment. For instance, as

the World Business Environment Survey (2000) by the WBG demonstrates, firms

from OECD, new industrialized East Asia Countries and European transition

economies identify taxes, regulations and financing as the leading negative

differences.

Firms need to adapt some of their governance system to the country's

institutions, choosing those forms which are associated with a reduction in

transaction costs or in any other obstacles. For instance, Demirguc-Kunt et al

(2006) show how business adopts a certain legal form to obtain optimal

contracts with customers and investors, choosing more probably the corporate

form in countries with developed financial sectors and efficient legal systems and

other guarantees.

On occasions, changes are not possible and “one can hypothesize that the

decision of a firm to hide its output may be related to the low benefits derived

18

from operating officially and the low cost over to the unofficial economy” (Batra

et al, 2002: 15).

According to previous results, it could be concluded that there are no differences

between levels of domestic and offshore corruption. Nonetheless, it may be

interesting to clarify whether the behavior of companies from each country

changes depending on the region where they operate.

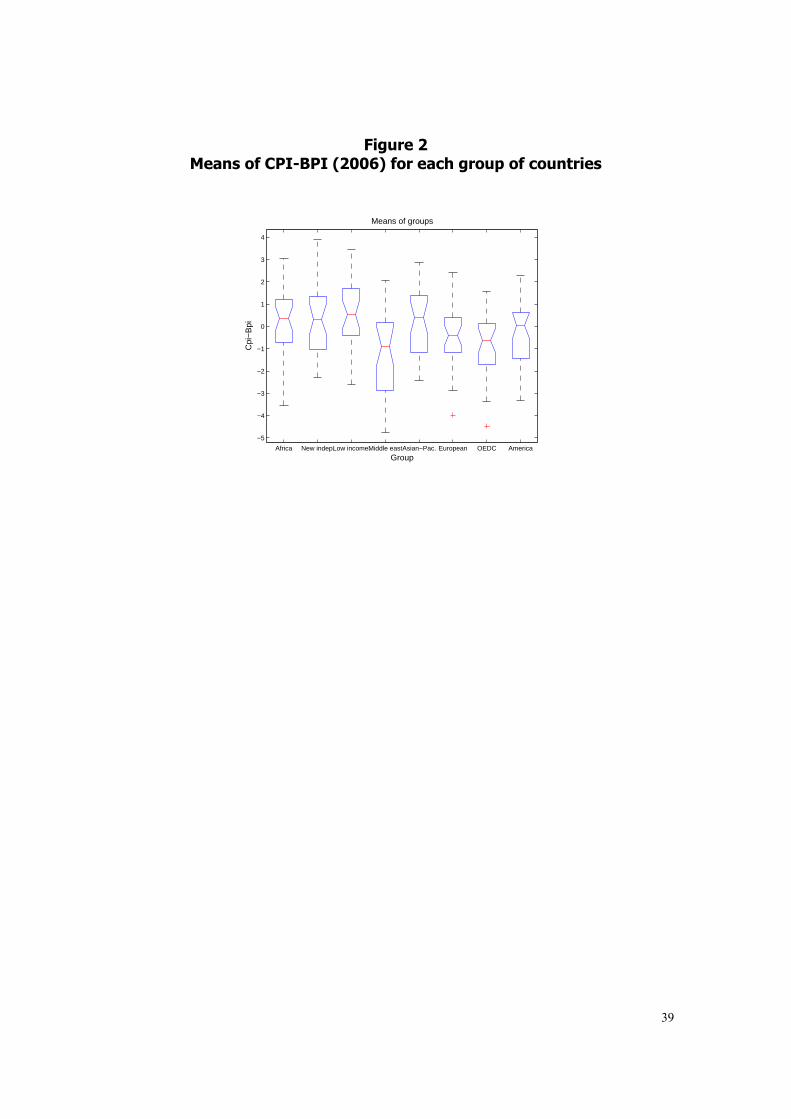

Data by regions

In order to examine the issue, we first divide countries into 8 groups, following

the TI criteria (BPI, 2006: 16): Africa, Newly Independent States, Low Income,

Middle East, Asia-Pacific, Europe, OEDC and America. Then, we run an Analysis

of Variance (Anova), comparing the means of the differences between the CPI

and the BPI by region. The p-value (8.5702e-005)7 indicates that the test

strongly supports the alternate hypothesis, that one or more of the samples are

drawn from populations with different means. We analyze multiple comparison

tests of means. The figure 2 displays a graph with each group mean.

------------------- Insert Figure 2 about here

-------------------

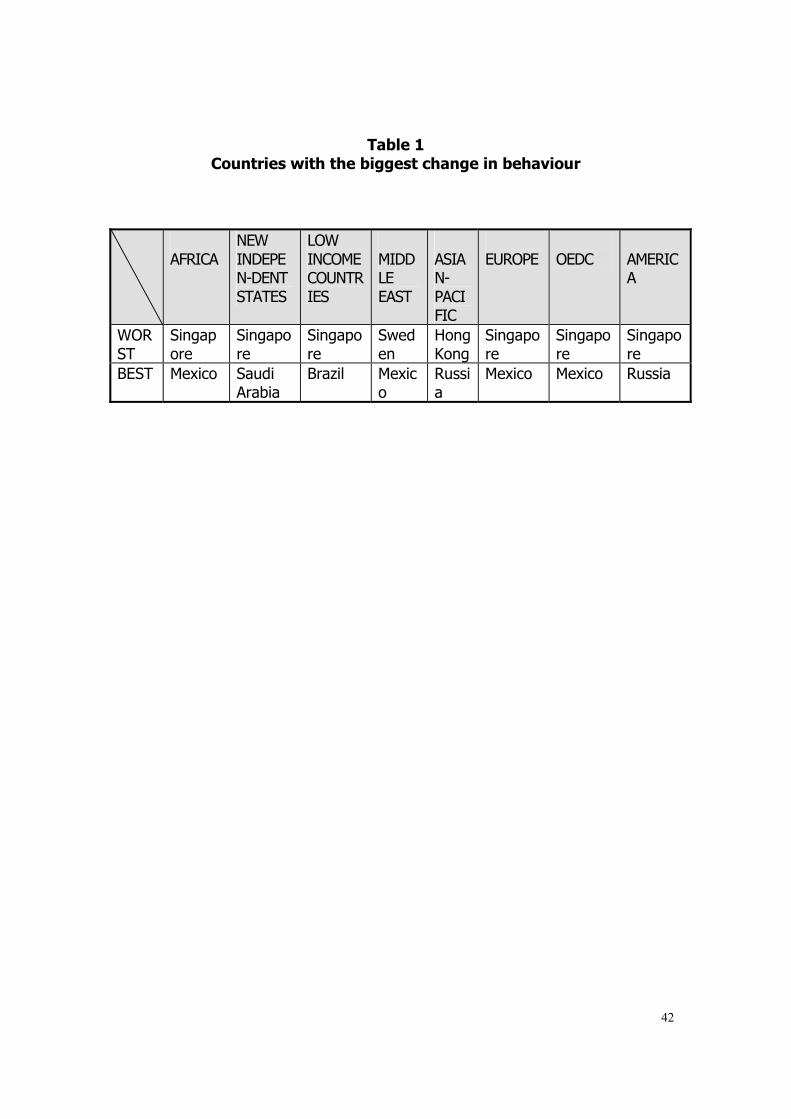

Table 1 displays for each group the country whose behavior is comparatively the

worst (the best) when its companies go international. That is, the country that

maximizes (minimizes) the difference CPI - BPI.

------------------- Insert Table 1 about here

19

-------------------

Interestingly enough those countries whose behaviour gets relatively worse are

countries with the highest CPI ratings (like Singapore or Sweden). At the same

time, countries with CPI ratings below 5 (like Mexico or Russia) show the largest

improvement when going abroad

The estimated means for the country groups are:

African New

independent States

Low income

Middle East

Asian-pacific European OEDC America

0.0160 0.2527 0.4313 -1.3093 0.2103 -0.4660 -0.8563 -0.3567

These means are negative (BPI > CPI) when the host countries are in the Middle

East, Europe, OECD and America.

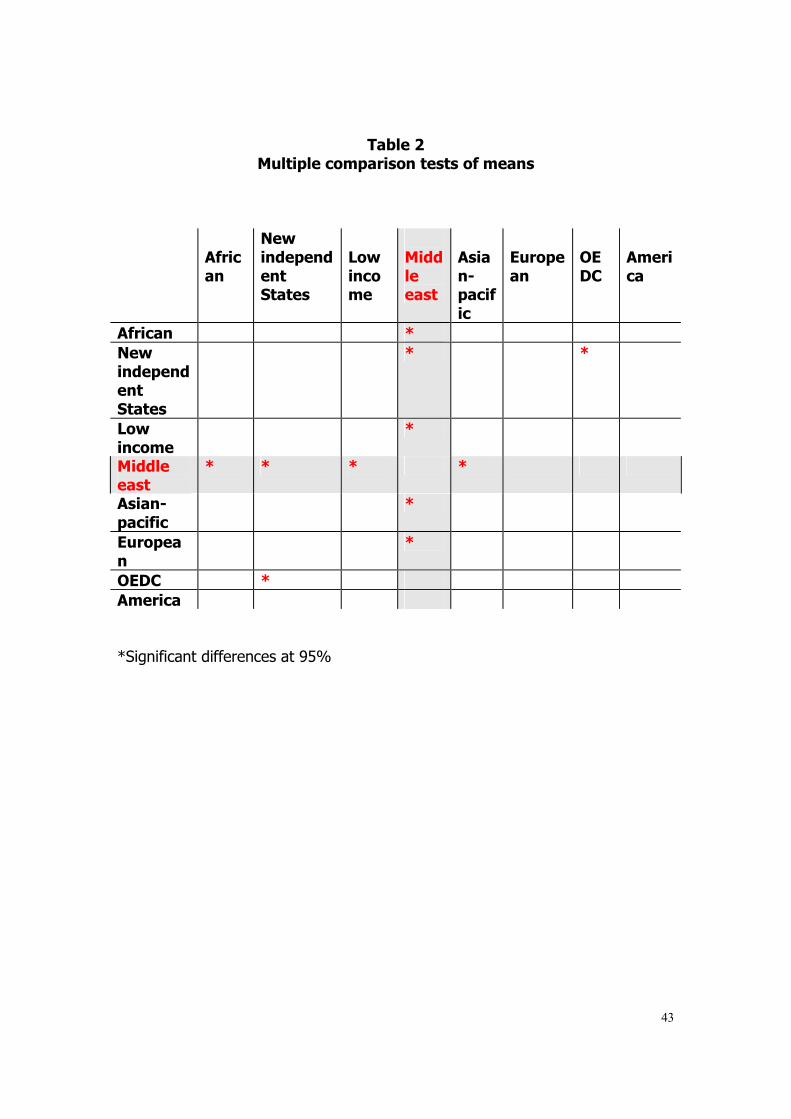

Finally, Table 2 shows the results from multiple comparison test of means.

------------------- Insert Table 2 about here

------------------- Since the evidence above suggests the existence of differences between

countries with high CPI (CPI > 5) and low CPI (CPI < 5), we also run the same

analysis separating countries in both groups. The results are similar to those in

Table 2.

Doing-business and CPI-BPI differences

We are also interested in evaluating the WBG-GAC first hypothesis, that is, in

finding whether the differences in the behavior of each country depending on

20

the region where its companies operate are related to the doing-business

conditions in each region, for instance, differences in the ease of starting a

business .

With that aim and in order to create an index, we have examined the variables

described by “Doing Business” database created by the World Bank and based

on the available literature (Cf. KLapper et al, 2006), which provides objective

measures of business regulations and their enforcement, and permits some

comparisons across economies.

Concretely, we develop an aggregate index from five regulatory areas that can

enhance or constrain business activity: (1) starting a business: the level of entry

regulation, associated with the number, time and cost of procedures for starting

a business, including licenses and legal registration (Klapper et al, 2006; Weber

& Getz, 2004; Djankov et al, 2002; Ogus & Zhang, 2005). (2) lack of access to

credit (Black and Strahan, 2002; Dkankov et al, 2006; WBES, 2000) (3)

employment law (Botero et al, 2004; Javorcik & Spatareanu, 2004) (4) tax

disadvantage (Fisman & Svensson, 2006) and (5) Bankruptcy process and other

investor protection systems (Lee & Peng, 2007; WBG, 2006b).

There is an important limitation for such analysis. The BPI is not available at a

host-country level; the doing-business variables are disaggregated at that level.

If we tried to aggregate the later variables, estimations would not be reliable

We analyze the differences between each country and the region where its

companies operate in terms of doing-business regulation. If we don't find any

difference similar to those existing between CPI and BPI, we could hypothesize

21

that other variables must be affecting the behaviour of companies. For each

economy we select from each region the country where the first country has

more Foreign Direct Investment stocks (data from the UNCTAD FDI database)

For each of the chosen doing-business variables, we analyze the differences

between groups through an Analysis of Variance (Anova). Our results suggest

that there are differences among all groups for almost all the variables8.

Consequently, there must be other variables that explain the CPI - BPI

differences.

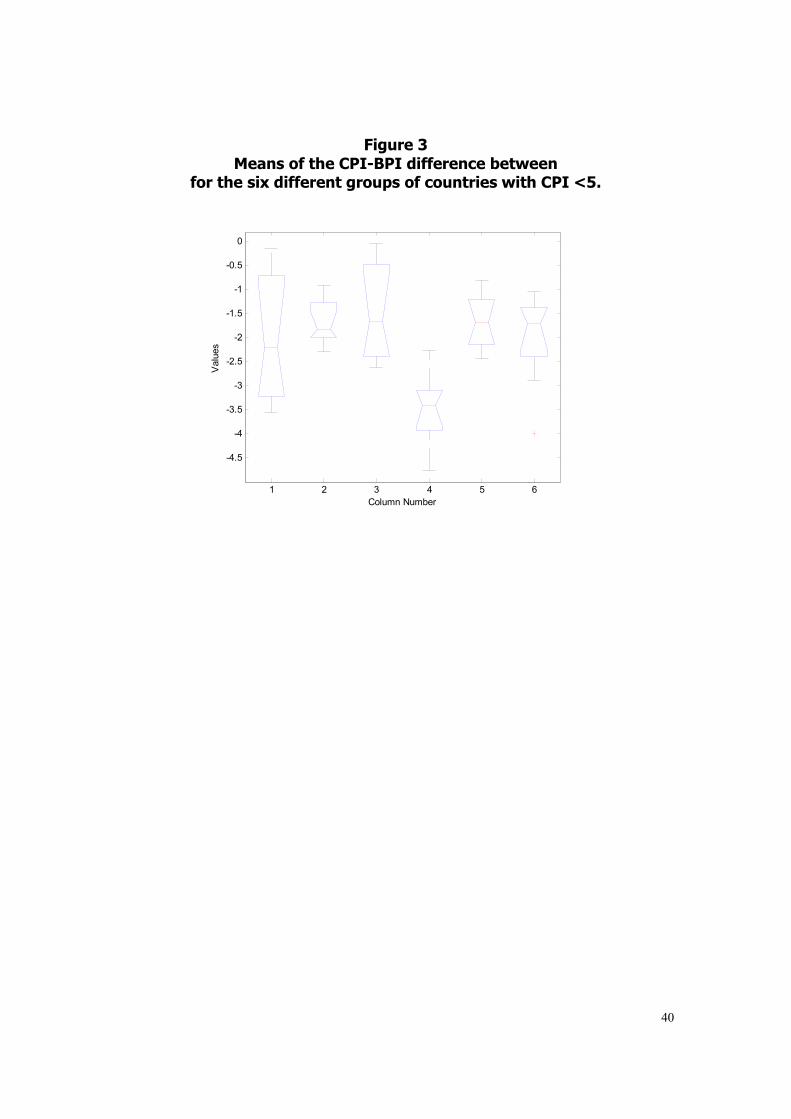

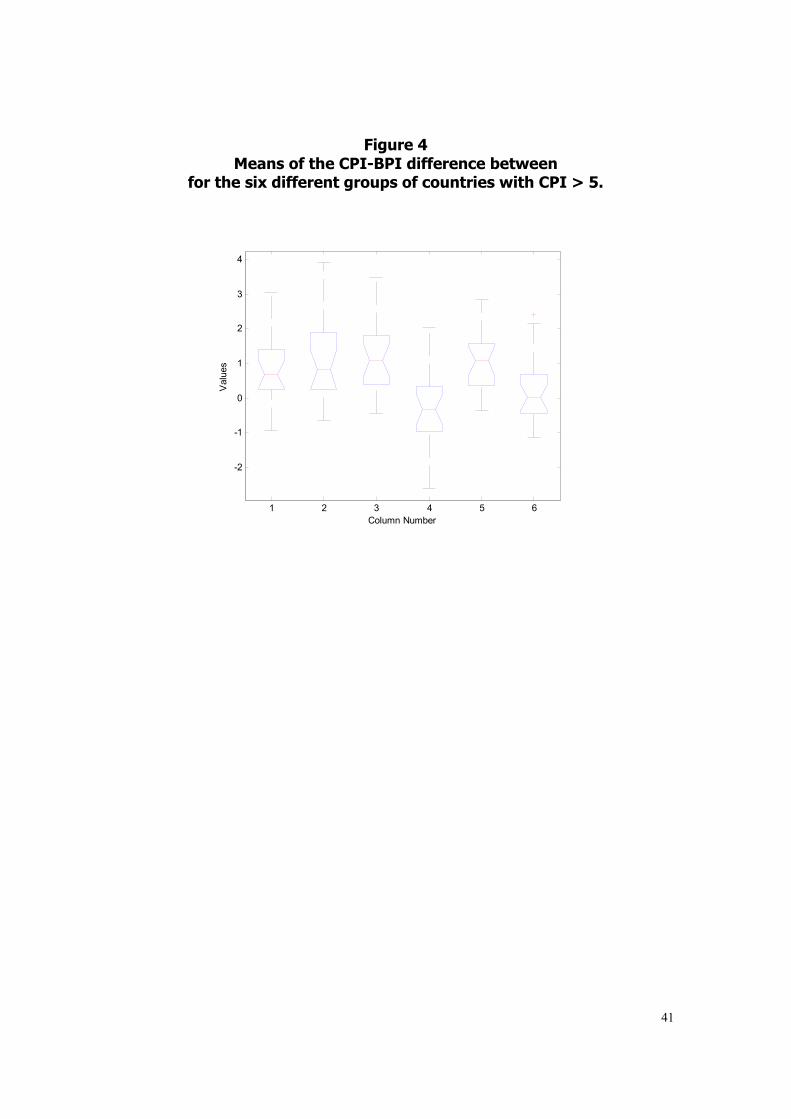

However, it can be observed (Figure 3) that the mean of CPI-BPI differences of

all groups of countries with CPI<5 are all negative, while the countries with

CPI>5 present diverse behavior (Figure 4)

------------------- Insert Figure3 about here

------------------- -------------------

Insert Figure4 about here -------------------

IV. THE ETHICAL CALL: INTEGRITY AND CORRUPTION

After analyzing the data, it is needed to affirm that, if the role of doing business'

factors in the misconduct makes only partial sense, the recognition that ethical

traits also influence levels of bribery is obligated. As the World Economic Forum

“Partnering Against Corruption Initiative” (PACI, 2004) suggested, also the WB-

GAC (2006-7) suggests that, in order to curb corruption, the behavior of the

business sector must be based everywhere on integrity, fairness and ethical

conduct.

22

If the tendency toward bribery does not totally depend of the environmental

conditions, then we are in front of an internal business subject, which affects

and is affected by integrity and ethical definitions. In this context, it results

comprehensible that WBG's strategy tries to engage firms objectives with an

`ethical call'. However, the design and implementation of ethical standards and

principles are not unanimous, practical neither theoretically.

The report on “Corporate Social Responsibility” (CSR) by the WBG (2003: 1)

suggested economic strategy as motive for support: “there have been business

benefits from adopting (CSR) programs”, which includes anti-bribery strategies.

Huguette Labelle (2006: 12), the present TI chair, also supports that “companies

that take ethics seriously, that adopt a genuine programme of corporate social

responsibility and embrace the practice of anti-bribery as well as the theory,

often perform better in the long run”. WBG-GAC (2006) follows the same line.

The form in which WBG essays to encourage the private sector “to introduce

ethical corporate practices” (p. 12) is the following:

1. The initiative will come from public sector, concretely from the

International Finance Corporation and from the Multilateral Investment

Guarantee Agency, which will work “directly with the private sector to

introduce ethical corporate standards”.

2. Both institutions will “encourage them to join public-private coalitions

for reform, such as the Extractive Industries Transparency Initiative and

Publish What You Pay” (p. 12).

23

3. With the aim of convincing firms that core ethical standards and

principles guiding their services are efficient, WBG reminds private sector

that “integrity is good for business” (p. 13).

We are largely in agreement with WBG. We believe that corporate ethic is one of

the key responses to corruption but we discus its roots.

In spite of the Enron debacle and other example of managerial misconduct and

corporate failure increasing calls for greater and profitable corporate integrity

(Cf. Waddock et al, 2002), and in spite of the fact that government, society and

business associations attempt to reinforce links between corporate governance

and ethics, theoretical and practical difficulties continue.

Vincke & Heiman (2003) emphasize that in order to curb corruption a broad

practical consensus in business community is crucial; however, Bonn & Fisher

(2005) suggest that one of the main difficulties is to obtain consensus, the lack

of which hinders the implementation of global ethical standards and principles.

As the WBG-GAC (2006: 13) suggests, the consensus could be imposed from

public to private sector, however, responsibilities of the global corporation are

poorly defined and corporate officials do not have clear guidance at the

international level. As the 2005 International Chamber of Commerce's report on

“Combating Extortion and Bribery” declares, the success of rules in the

promotion of the high standards of integrity in business transactions in the end

depends on their voluntary acceptance and on self-regulation by business

enterprises. Mere existence of principles is not enough to develop ethical

organizations. Values such as integrity must actively be supported by managers

24

(Valentine et al, 2006; Fritz et al., 1999), which requires that leaders must

uphold organizational ethical values, reward appropriate business conduct,

facilitate the relationship between the organization and its employees, and

punish unacceptable acts (Hunt et al., 1989, Trevino, 1986; Trevino et al.,

1998). After observing data, it becomes clear that the ethical quality of business

must improve. The question is how organizations can address ethical practices in

their corporate structure in order to obtain high standards of ethical behavior.

It is true that some firms have finally recognized that short-term profit

maximization through bribery can damage long-term reputation and value and,

therefore, they have implemented programs that reflect support for international

norms and principles against bribery, which have, in many cases, ethical bases

(Cf. Koh & Boo, 2001). However, companies looking for short-term profit exist.

Calculus is not enough; we need a reason for integrity.

Over the past decades, Enron and other examples of corporate failure and

managerial misconduct have encouraged the ethical bias for organizations. How

organizations could address business ethics in their corporate structures while

obtaining high standard of ethical behavior was largely discussed. The practical

motive is related with the design and the implementation of global ethical

standards and principles. The theoretical motives are more difficult because they

are related directly with the nature of the ethics and the corruption.

In light of our previous analysis on corruption's complexity (Calderón et al,

2007), we support that conceptual flaws obscure the real problem: corporate

corruption is viewed as a conflict of interest between corporation and society

25

without productive relationships, that is, an outsider conflict. We suggest that it

is an insider conflict.

WBG's strategy focuses on the line of organizational literature. In this literature,

corporation presents an ethical problem when there is a conflict of interests

whose results can violate its own set of moral principles or values; that is, when

the conflict provokes an internal incentive-alignment problem.

If a corporation pays a bribe to a bureaucrat, the corporation itself does not

present or suffer apparently an inner alignment problem. The corporation's

agent who acts illegally or unethically is understood to be “serving his principal's

interest,” (Carvajal, 1999; Bandfield, 1975). Actions accomplished by the agent

occur without violation of the firm's principal-agent contract. The implicit

hypothesis is that behavior, attitudes and rules of both corporation and its

employees are congruent so that the corrupt strategy does not create any

alignment problem.

If there is not an alignment problem, the WBG strategy is correct: adding ad-

extra ethical practices are the best option, if there ensure profitability.

However, this position implies that ad extra and ad intra behavior are

disconnected. Ad extra, legal and societal rules are actives; ad intra formal or

informal codes of behavior govern. Both scenarios may be totally separated.

In the ad-extra behavior, globalization —which often diminishes managerial

discretion— deepens ethical relativism (Velasques, 2000; Cullen et al, 2004) and

cultural uses from host countries are being employed to justify some dubious

business behavior (Donaldson, 1996). If the acceptable model of behavior varies

26

within a given nation; if ethical beliefs significantly fluctuate from culture to

culture; if there is any dichotomy in ethical attitudes of entrepreneurs and

managers then the exclusive possibility is that of WBG: to demand the aid of the

firm with the long term promise: integrity —the propensity, disposition and

behavior— to keep simultaneously social and self commitments— is good for

business.

In those terms, integrity is showen as a problem between short-term and long-

term incentives, and ethics remains a profitable option.

We suggest that it is not possible because ad extra and ad intra systemic

behavior cannot be separated. Integrity results a moral propensity9 which is

expanded for whichever scenario. Any discordance between internal and external

behavior suggests an alignment problem. Corruption does not occur between

societal and organizational ethical principles but at very basic level, where the

inner and outer behaviors of the organization must be firmly anchored. This is

the level of truth versus deception, freedom versus restrictions, or justice versus

caprice; in summary, this is the level of integrity (Carroll, 2000:38).

Through socialization, control and incentives, managers develop internal norms

which prevent members of the organization from acting corruptly. With these

norms, managers attempt to develop the voluntary acceptance of self-constraint

on opportunism, understanding that opportunism (seeking the self-interest with

guile and deceit (Williamson, 1975)) damages the future of the firm.

Nevertheless, opportunistic actions by employees are facilitated if top

management is perceived as being unethical (Cf. Koh & Boo, 2001). For

27

instance, after observing any organizational attitudes that tolerate or instigate

corrupt behaviors, employees will seek to make sense and justify their own

deceit ful practices.

If a firm accepts the adaptation of its ethics to unethical market-entry conditions,

it can destroy its internal consistence, creating dissonance between inward and

outward behaviors. By facilitating or authorizing their subordinates' bribery while

remaining ignorant of the details, the employer encourages actions in ways that

employees would consider immoral in personal and organizational life (Rose-

Ackerman, 2002). If, through this dissonant behavior, the deceit is

institutionalized, a harmful effect upon the organization has been accepted.

Asforth and Anand (2003: 37) defend that when bad apples produce a bad

barrel through institutionalization, the barrel itself must be repaired. For the sake

of the firm's long-term existence, deceit must be eliminated. To eliminate the

deceit, an anti-bribery policy must be acquired and maintained, resolving the

environmental prisoner's dilemma. Thus, the firm's outward behavior is

voluntarily adapted to the inward ethical beliefs, trying to avoid any contagion

which could modify its own set of internal norms (Jansen & Glinow, 1985).

28

REFERENCES

Ades, A & Di Tella, R. 1997. The New Economics of Corruption: A Survey and

Some New Results. Political Studies, 45(3): 496-515

Aidt, T. S. 2003. Economic Analysis of Corruption: a Survey. Economic

Journal, 113(491): 632-652

Andelman, D. 1998. Bribery: the New Global Outlaw. Management Review, 87

(4): 49-51.

Argandoña, A. 2001. Corruption: The Corporate Perspective. Business Ethics.

A European Review 10(2): 163-175.

Ashforth, B. E. & Anand, V. 2003. The Normalization of Corruption in

Organizations. Research in Organizational Behavior, 25: 1-52.

Banfield, E.: 1975. Corruption as a Feature of Government Organization.

Journal of Law and Economics,18(3): 587-605.

Batra G., Kaufmann D. & Stone A. 2002. The Investment Climate Around the

World. In Voices of Firm 2000: Investment Climate and Governance

Findings of the World Business Environment Survey. Technical Report.:

The World Bank.

Baucus M. S. & Baucus D. A. 1998. Paying the Piper: An Empirical Examination

of Longer-Term Financial Consequences of Illegal Corporate Behavior. The

Academy of Management Journal, 40(1): 129-151.

Beck, T., Demirgüç-Kunt A. & Levine R. 2005. Bank Supervision and Corruption

in Leanding. Journal of Monetary Economics, 53(8): 2131-2163.

29

Black, S.E. & Strahan P.E. 2002. Entrepreneurship and bank credit availability.

Journal of Finance, 57: 2807-2833.

Bonn, I. & Fisher, J. 2005. Corporate Governance and Business Ethics: insights

from the strategic planning experience. Corporate Governance: An

International Review, 13(6): 730-738.

Botero J., Djankov S., La Porta R., Lopez-de-Silanes F. V. Schleifer A. 2004. The

Regulation of Labour. The Quarterly Journal of Economics, 119 (4): 1339-

1382.

Brew, P. 2006. The Power of Joining Forces: The case for collective action in

fighting corruption. In Puri S. (Ed.) , Development Outreach: Washington:

World Bank.

Carroll, A. 2000. A Commentary and an Overview of Key Questions on Corporate

Social Performance. Business & Society, 39(4): 466-478.

Carvajal R. 1999. Large-Scale Corruption: Definition, Causes, and Cures.

Systemic Practice and Action Research, 12(4): 335-353

Cullen J. B., Parboteeach K.P. & Victor B. 2003. The Effects of Ethical Climates

on Organizational Commitment. Journal of Business Ethics, 46(2): 127-141

Demirguc-Kunt A., Love I. & Maksimovic V. 2006. Business Environment and the

Incorporation Decision. Journal of Banking and Finance,30: 2967-2993.

Djankov S., La Porta R, Lopez de Silanes F. & Shleifer A. 2002. The Regulation

Of Entry. Quarterly Journal of Economics, 117 (1): 1-37.

Djankov S., McLiesh C. & Shleifer A. 2006. Private Credit in 129 Countries;

Working paper, World Bank, Doing Business.

30

Doh J., Rodriquez, P., Uhlenbruck, K. & Eden, L. 2003. Copying with Corruption

in Foreign Markets. Academy of Management Executive, 17(3): 114-127

Donaldson, T. 1996. Values in Tension: Ethics Away from Home. Harvard

Business Review, (September-October), 48-62.

Fisman R. & Svensson J. 2007. Are corruption and taxation really harmful to

growth? Firm level evidence. Journal of Development Economics, 83 (1):

63-75

Fritz. M.H., Arnett R. C. & Conkel M. 1999. Organizational ethical standards and

organizational commitment. Journal of Business Ethics, 20: 289-299.

Vincke, F. and Heimann F. 2003. Fighting Corruption. A Corporate

Practices Manual. Paris; International Chamber of Commerce.

Howlett M. & Rayner J. 2006. Globalization and Governance Capacity: Explaining

Divergence in National Forest Programs as Instances of “Next-Generation”

Regulation in Canada and Europe. Governance: An International Journal of

Policy, Administration and Institutions, 19 (2), 251-275.

Hunt S.D., Wood V.R. & Chonko L.B.. 1989. Corporate ethical values and

organizational commitment in marketing. J Mark, 53: 79-90

Jansen E. & Glinow M. A. Von. 1985. Ethical Ambivalence and Organizational

Reward Systems. The Academy of Management Review, 10(4): 814-822.

Javorcik B. & Spatareanu A. 2004. Do Foreign Investors Care About Labour

Market Regulations?, Working Paper 3275, World Bank Policy Research,

Washington.

31

Klapper L., Laeven L. & Rajan, R. 2006. Entry Regulation as a Barrier to

Entrepreneurship. Journal of Financial Economics, 82: 591-629.

Koh H.C & Boo E. H.. 2001. The link between organizational ethics and job

satisfaction: a study of managers in Singapore., Journal of Business Ethics

29: 309-324.

Labelle, H. 2006. Civil Society and the Private Sector: Fighting corruption is good

business. In Puri S. (Ed.) , Development Outreach: Washington: World Bank.

Lee S-H., Peng M. & Barney J. 2007. Bankruptcy Law and Entrepreneurship

Development: A Real Option Perspective. Academy of Management Review,

32(1): 257-272.

MacMurray W.D. 2006. Private Sector Response to the Emerging Anti-Corruption

Movement. In In Puri S. (Ed.) , Development Outreach: Washington: World

Bank.

Mallaby, S. 2006. Wolfowitz' s Corruption Agenda. Washington Post,

February: A21.

Mauro, P. 1995. Corruption and Growth. Quarterly Journal of Economics,

110(3): 681-712.

Nwabuzor, A. 2005. Corruption and Development: New Initiatives in Economic

Openness and Strengthened Rule of Law; Journal of Business Ethics, 59:

121-138

O'Rourke, D. 2006. Multi-Stakeholder Regulation: Privatizing or Socializing Global

labor Standards?. World Development, 34(5): 899-918.

32

OECD. 1997. Convention on Combating Bribery of Foreign Public

Officials in International Business Transaction.

Ogus A. &Zhang G. 2005. Licensing Regimes East and West. International

Review of Law and Economics, 25(1): 124-142.

Rose-Ackerman, S. 2002. Grand corruption and the ethics of global business.

Journal of Banking and Finance, 26(9): 1889-1918.

Shleifer, A. & Vishny R. 1993. Corruption. Quarterly Journal of Economics,

108(3): 599-617.

Transparency International. Bribe Payers Index (1999, 2002, 2006)

Transparency International. Corruption Perception Index (1999, 2002, 2006)

Trevino K.T. 1986. Ethical decision making in organizations: a person-situation

interaction model, Academy of Management Review, 11: 601-617.

Trevino L.K., Butterfield K. D. & McCabe D. L. 1998. The ethical context in

organizations: influences on employee attitudes and behaviors, Business Ethics

Quarterly, 8:. 447-476.

United Nations Conference of Trade and Development. Foreign Direct

Investment database

United Nations, Convention Against Corruption

Valentine S., Greller M. & Richtermeyer S. B. 2006. Employee job response as a

function of ethical context and perceived organization support. Journal of

Business Research, 59(5): 582-588

Velasques, M. 2000. Globalization and the Failure of Ethics. Working papers

99/00-21, Santa Clara University Business School.

33

Vogl F. 1998. The Supply Side of Corruption: does the Developing World

Have to Carry the Full Weight of Global Anti-Corruption efforts?,

Working Paper. Transparency International, Washington.

Waddock, S., Bodwell C., and Graves S. G. 2002. Responsibility: The New

Business Imperative. Academy of Management Executive, 16 (2): 132-148.

Wolf T. & Gürgen E. 2000. Improving Governance and Fighting Corruption in the

Baltic and CIS Countries. Economic Issues, 21, International Monetary Found.

Weber, J. and Getz, K. 2004. Buy bribes or bye-bye bribes: the future status of

bribery in international commerce. Business Ethics Quarterly, 14(4): 695-711.

Wilhelm, P. W. 2002. International Validation of the Corruption Perceptions

Index: Implications for Business Ethics and Entrepreneurship Education, Journal

of Business Ethics 35(1): 177-189.

Williamson, O. 1975. Markets and Hierarchies, Analysis and Antitrust

Implications: a Study in the Economics of Internal Organization, New

York: Free Press.

World Bank Group. 2006, Strengthening Bank Group Engagement on

Governance and Anticorruption. DC2006-0017.

World Bank Group. 2006b. Doing Business Database.

World Bank Group Institute. 2004. Corporate Social Responsibility Report

World Bank Group. 2000. World Business Environment Survey.

World Economic Forum. 2004. Partnering Against Corruption Initiative.

34

GRAPH 1 Comparisons between BPI 1999-2002 and 2002 -2006

-1,5

-1

-0,5

0

0,5

1

1,5

-1,5 -1 -0,5 0 0,5 1 1,5 2 2,5

Belgium

Switzerland

Australia NetherlandsAustria

Sweden

Canada

UK

USA

Russia

SingaporeSpain

France

Germany

M alaysia

ChinaTaiwan

Japan

Italy

South Korea

2006-2002

2002-1999

35

Graph 2 Frequency Diagram. BPI.

0

1

2

3

4

5

6

7

8

8 7,5 7 6,5 6 5,5 5 4,5 4 3,5 3

BPI

FREQ

UEN

CY

199920022006

36

Graph 3 Comparison between the variations of BPI (2002-06) and CPI (2002-

06)

-1,5

-1

-0,5

0

0,5

1

1,5

2

2,5

-0,6 -0,4 -0,2 0 0,2 0,4 0,6 0,8 1 1,2

Australia

Austria

BelgiumCanada

China

FranceGermany

Hong KongItaly Japan

M alaysia

Netherlands

Russia

Singapore

South Korea

Spain

SwedenSwitzerland

Taiwan

UK

USA

CPI variation (2006-2002)

BPI variation (2006-2002)

37

Figure 1 Evolution of the Bribe Payer Index, grouping data in clusters.

38

BPI 2006 BPI 2002 BPI 1999 CLUSTER 1 Australia 8,5 CLUSTER 1 Sweden 8,3

Sweden 8,4 Australia 8,1

Switzerland 8,4 Canada 8,1

Austria 8,2 Austria 7,8

Canada 8,1 Switzerland 7,7

Netherlands 7,8 Netherlands 7,4

Belgium 7,8

CLUSTER 1 Switzerland 7,8 CLUSTER 2 UK 6,9 CLUSTER 2 UK 7,2

Sweden 7,6 Germany 6,3 Belgium 6,8

Australia 7,6 Singapore 6,3 USA 6,2

Austria 7,5 Spain 5,8 Germany 6,2

Canada 7,5 UK 7,4 Germany 7,3 Netherlands 7,3 USA 7,2 Belgium 7,2 Japan 7,1 CLUSTER 2 Singapore 6,8 CLUSTER 3 France 5,5 CLUSTER 3 Singapore 5,7

Spain 6,6 USA 5,3 Spain 5,3

UAE 6,6 Japan 5,3 France 5,2

France 6,5 Japan 5,1

Portugal 6,5 Mexico 6,5 Hong-Kong 6 Israel 6 CLUSTER 3 Italy 5,9 CLUSTER 4 Malaysia 4,3 CLUSTER 4 Italy 3,7

S.Korea 5,8 Hong-Kong 4,3 Taiwan 3,5

Saudi Arabia 5,8 Italy 4,1 S.Korea 3,4

Brazil 5,7 S.Korea 3,9 China 3,1

S. Africa 5,6 Taiwan 3,8

Malaysia 5,6 China 3,5

Russia 3,2 CLUSTER 4 Taiwan 5,4 Turkey 5,2 Russia 5,2 China 4,9 India 4,6

MEAN 6,4 6 5,7

STANDARD DEVIATION

0,6 1,8 1,7

39

Figure 2 Means of CPI-BPI (2006) for each group of countries

Africa New indep.Low income.Middle eastAsian−Pac. European OEDC America

−5

−4

−3

−2

−1

0

1

2

3

4

Cpi

−B

pi

Group

Means of groups

40

Figure 3 Means of the CPI-BPI difference between

for the six different groups of countries with CPI <5.

1 2 3 4 5 6

-4.5

-4

-3.5

-3

-2.5

-2

-1.5

-1

-0.5

0

Val

ues

Column Number

41

Figure 4 Means of the CPI-BPI difference between

for the six different groups of countries with CPI > 5.

1 2 3 4 5 6

-2

-1

0

1

2

3

4

Val

ues

Column Number

42

Table 1 Countries with the biggest change in behaviour

AFRICA

NEW INDEPEN-DENT STATES

LOW INCOME COUNTRIES

MIDDLE EAST

ASIAN-PACIFIC

EUROPE

OEDC

AMERICA

WORST

Singapore

Singapore

Singapore

Sweden

Hong Kong

Singapore

Singapore

Singapore

BEST Mexico Saudi Arabia

Brazil Mexico

Russia

Mexico Mexico Russia

43

Table 2 Multiple comparison tests of means

African

New independent States

Low income

Middle east

Asian-pacific

European

OEDC

America

African * New independent States

* *

Low income

*

Middle east

* * * *

Asian-pacific

*

European

*

OEDC * America *Significant differences at 95%

44

NOTES

1 The FCPA was enacted in 1977 and substantially revised in the International

Anti-Bribery Act of 1998 which was designed to implement the anti-bribery

conventions of the Organization for Economic Co-operation and Development

(OECD). However, its effectiveness has been questioned (Weber and Getz, 2004:

699).

2 Such as exclusion from entitlement to public benefits or aid; temporary or

permanent disqualification from participation in public procurement or from the

practice of other commercial activities.

3 In accounting (art. 8), members “shall take such measures as may be

necessary, within the framework of its laws and regulations regarding the

maintenance of books and records, financial statement disclosures and

accounting and auditing standards, to prohibit the establishment of off-the-

books accounts, the making of off-the-books or inadequately identified

transactions, the recording of non-existent expenditures, the entry of liabilities

with incorrect identification of their object, as well as the uses of false

documents”.

4 As TI, we employ elbow criterion to form the clusters and the agglomerative

hierarchical procedure to form clusters.

5 We have run a Kolmogorov-Smirnov test (95%) to ensure that we cannot

reject the hypothesis that the CPI - BPI variable comes from a Normal

distribution.

45

6 Some countries, which are not in accord with the multilateral approach, essay

to minimizing the business sector contribution and returning to the past focus, as

the next comments show: “WBG will be wise NOT TO ENGAGE non-government

stakeholders in its development program. The media and private sector have

vested interests of their own ("scoops" for the media and "money-making" for

the private sector), and this will hamper aid effectiveness to a great deal…”

[Respondent type: Government; Region: South Asia]. “It is by no means sure

that the media or the private sector can provide a better solution. Generally,

these sectors are controlled by the powers that be.” [Respondent type:

Government; Region: Middle East and North Africa]

7 Once again, a Kolmogorov-Smirnov test has been run for each distribution.

8 Results are not presented as they have no further interest and because of the

great number of variables and country groups.

9 Are there immoral facets in corruption and, specially, in the role played by

corporations in corruption? Donaldson and Dunfee (1996) argue that bribery

typically violates local norms as well as hypernorms —prescriptions generally

accepted by all cultures and organizations— so that this corrupt practice

constitutes a universally unacceptable behaviour. Argandoña (2005) suggests

that extortion is immoral because it forces the company to make a payment that

is not included in the terms and conditions attached to the service, for the

exclusive benefit of the official.