Embed Size (px)

Citation preview

1

Decision Making

and Relevant Costs

Chapter Six

2

CHAPTER OUTLINE

• Introduction

• Decision making process

• Management accountant’s role

• Relevant costs

• Quantitative & qualitative analyses

• Opportunity costs

• Special decisions:

(i) make or buy (outsourcing)

(ii) discontinuing a product/segment

(iii) production with limiting factor

(iv) special orders

3

Introduction

Alternative

A?

Cost? Benefit? Which one to be chosen?

4

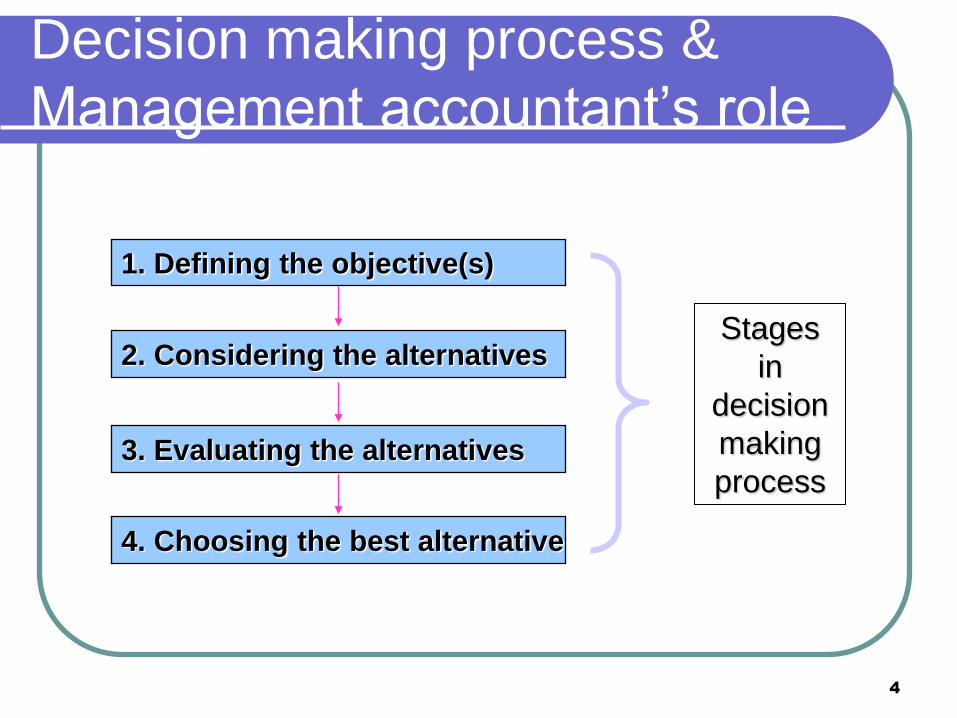

Decision making process &

Management accountant’s role

1. Defining the objective(s)

2. Considering the alternatives

3. Evaluating the alternatives

4. Choosing the best alternative

Stages

in

decision

making

process

5

Decision making process &

Management accountant’s role

What is the role of management

accountant in decision making?

Provide relevant information

Develop decision models Collect data

Evaluate alternatives (Stage 3)

6

Relevant costs

Information provided by the management

accountant should be

Relevant

Accurate

Timely

7

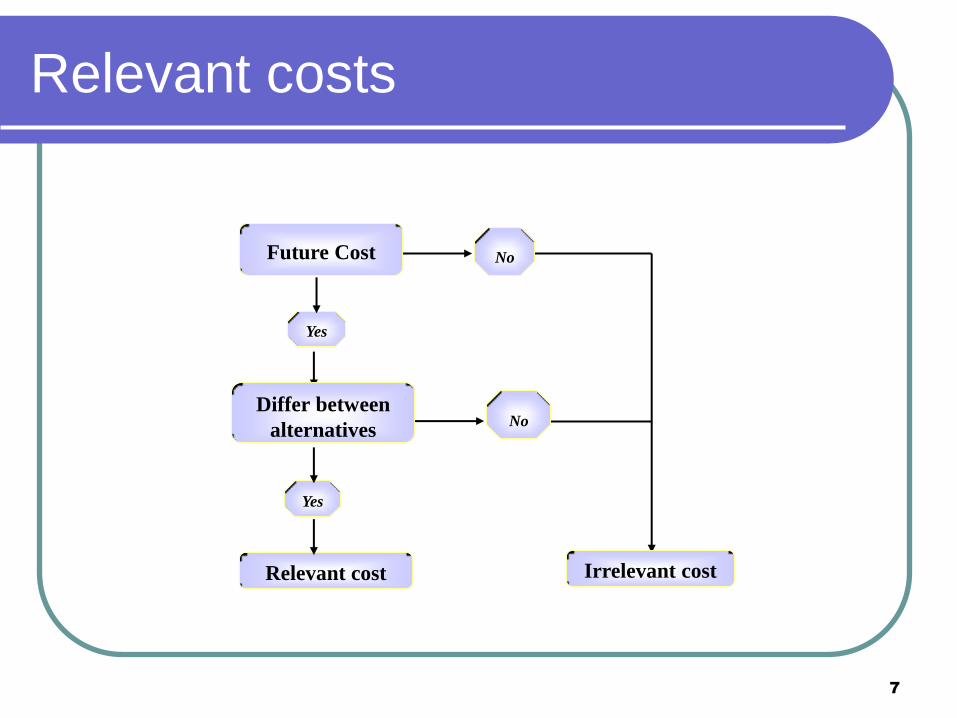

Relevant costs

Yes

Relevant cost

Future Cost

Differ between

alternatives

Yes

No

Irrelevant cost

No

8

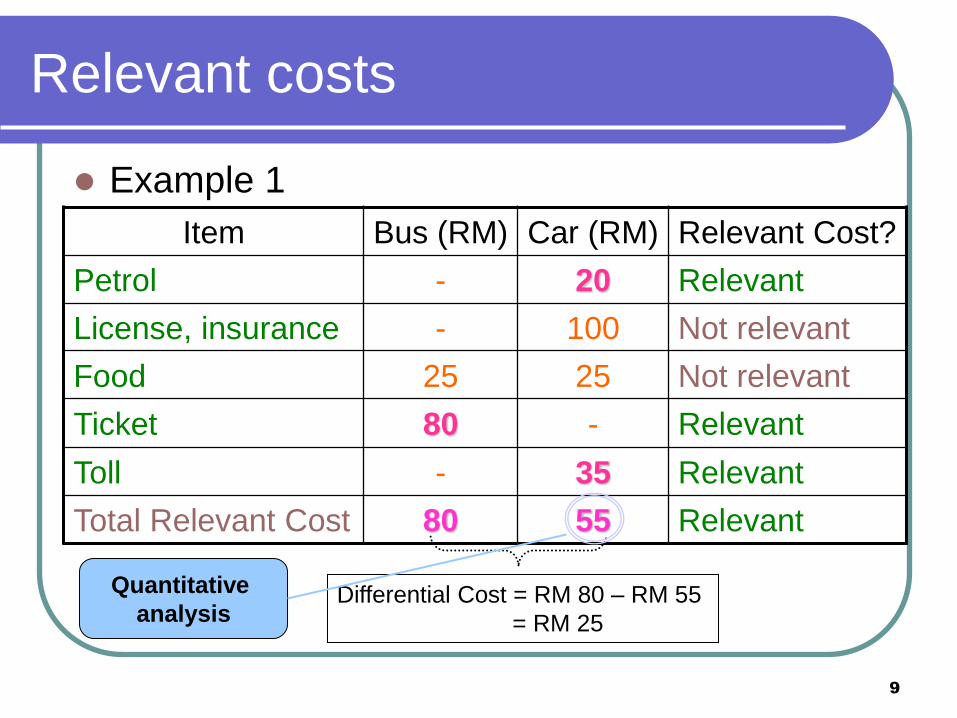

Relevant costs

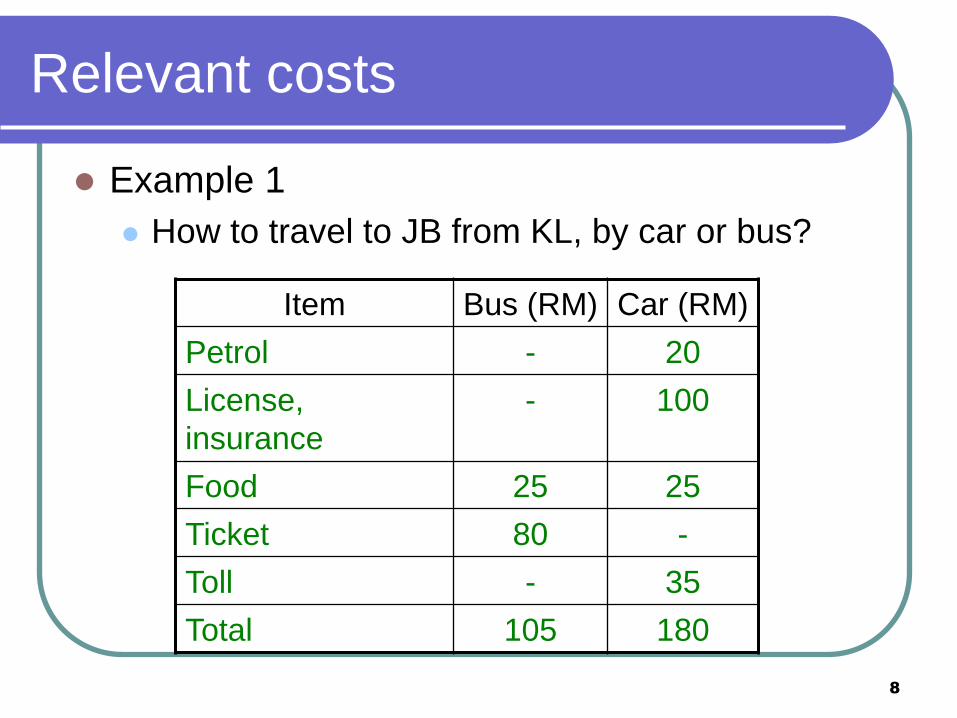

Example 1

How to travel to JB from KL, by car or bus?

Item Bus (RM) Car (RM)

Petrol - 20

License,

insurance

- 100

Food 25 25

Ticket 80 -

Toll - 35

Total 105 180

9

Relevant costs

Example 1

Item Bus (RM) Car (RM) Relevant Cost?

Petrol - 20 Relevant

License, insurance - 100 Not relevant

Food 25 25 Not relevant

Ticket 80 - Relevant

Toll - 35 Relevant

Total Relevant Cost 80 55 Relevant

Differential Cost = RM 80 – RM 55

= RM 25

Quantitative

analysis

10

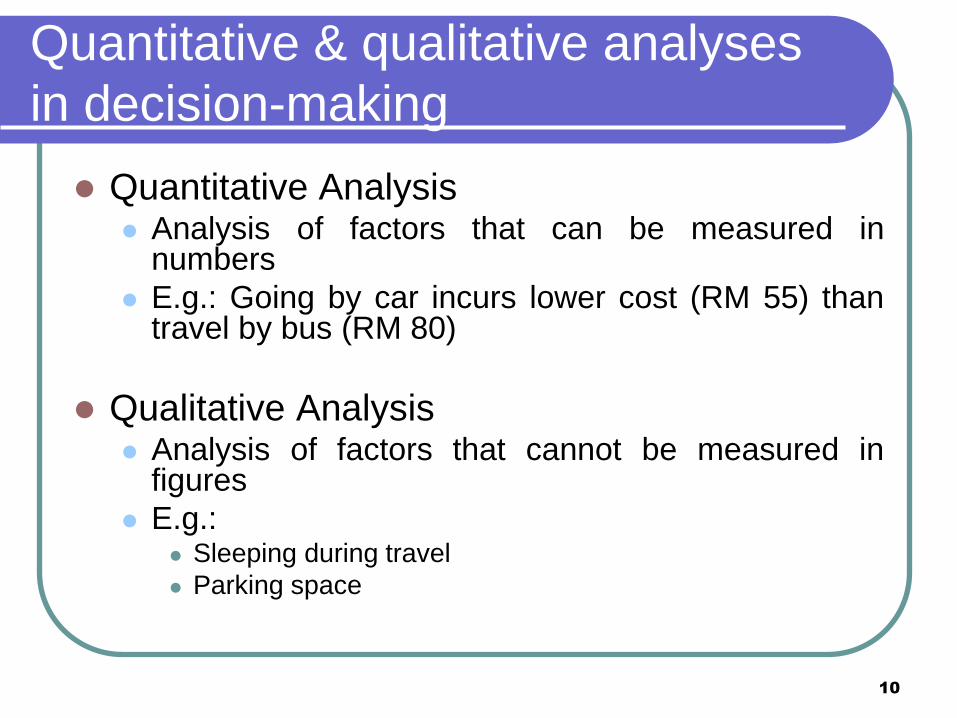

Quantitative & qualitative analyses

in decision-making

Quantitative Analysis Analysis of factors that can be measured in

numbers

E.g.: Going by car incurs lower cost (RM 55) than travel by bus (RM 80)

Qualitative Analysis Analysis of factors that cannot be measured in

figures

E.g.: Sleeping during travel

Parking space

11

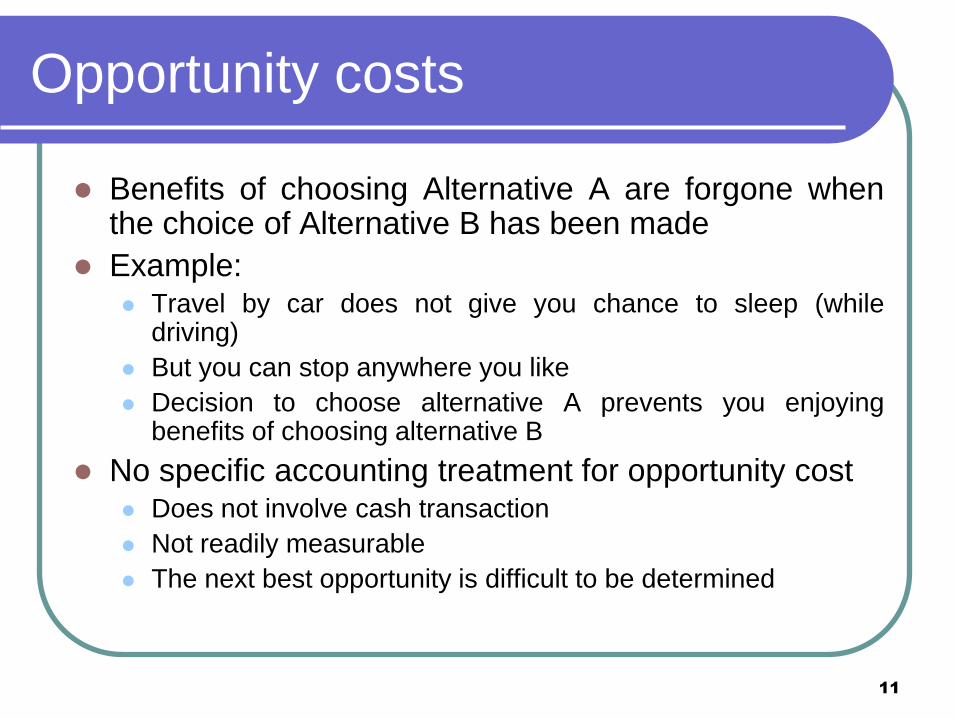

Opportunity costs

Benefits of choosing Alternative A are forgone when the choice of Alternative B has been made

Example: Travel by car does not give you chance to sleep (while

driving)

But you can stop anywhere you like

Decision to choose alternative A prevents you enjoying benefits of choosing alternative B

No specific accounting treatment for opportunity cost Does not involve cash transaction

Not readily measurable

The next best opportunity is difficult to be determined

12

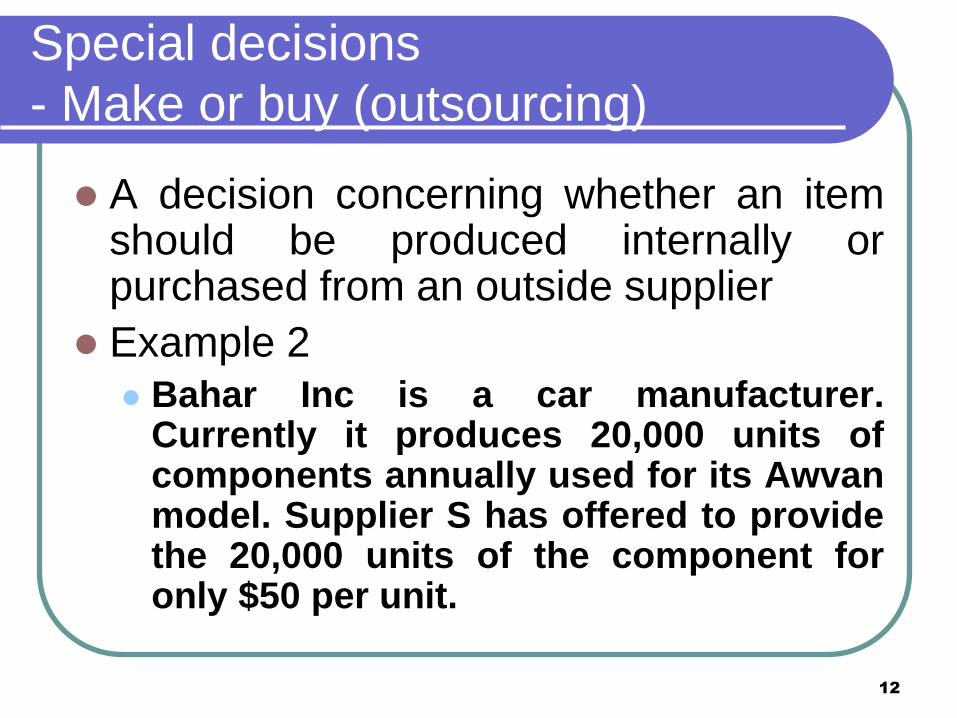

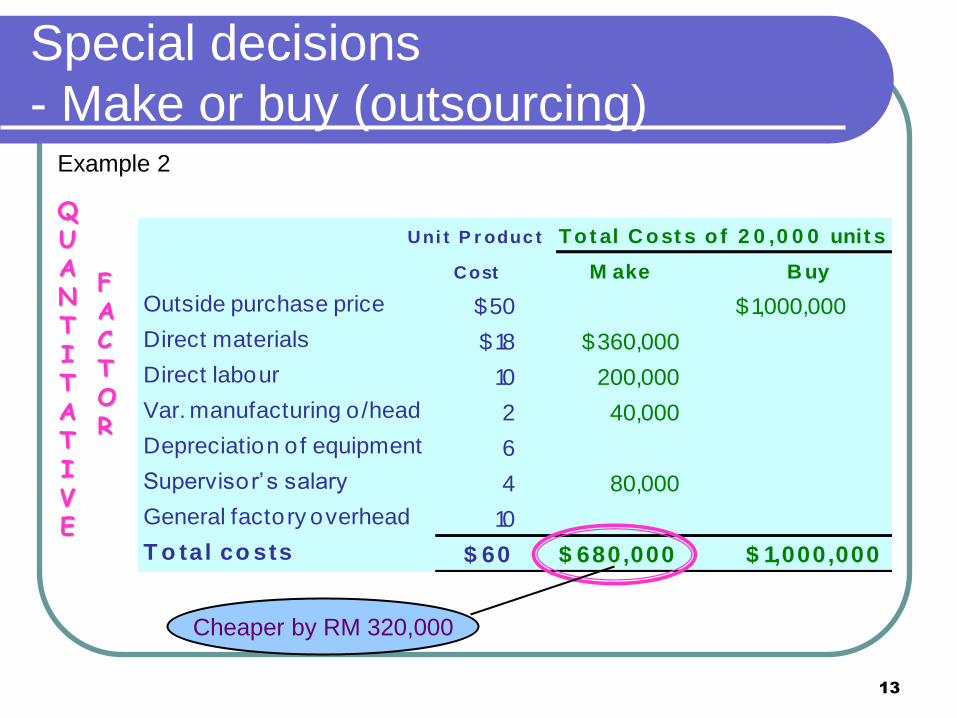

Special decisions

- Make or buy (outsourcing)

A decision concerning whether an item should be produced internally or purchased from an outside supplier

Example 2

Bahar Inc is a car manufacturer. Currently it produces 20,000 units of components annually used for its Awvan model. Supplier S has offered to provide the 20,000 units of the component for only $50 per unit.

13

Special decisions

- Make or buy (outsourcing)

Uni t P r oduc t

Cost M ake B uy

Outside purchase price $50 $1,000,000

Direct materials $18 $360,000

Direct labour 10 200,000

Var. manufacturing o/head 2 40,000

Depreciation of equipment 6

Supervisor’s salary 4 80,000

General factory overhead 10

T o tal co sts $ 60 $ 680,000 $ 1,000,000

Tot al C ost s o f 2 0 ,0 0 0 unit s

Cheaper by RM 320,000

QUANT I TATIVE

FACTOR

Example 2

14

Special decisions

- Make or buy (outsourcing)

Example 2

Qualitative factors

Quality of product

Shipping/production schedule

Alternative supplier?

15

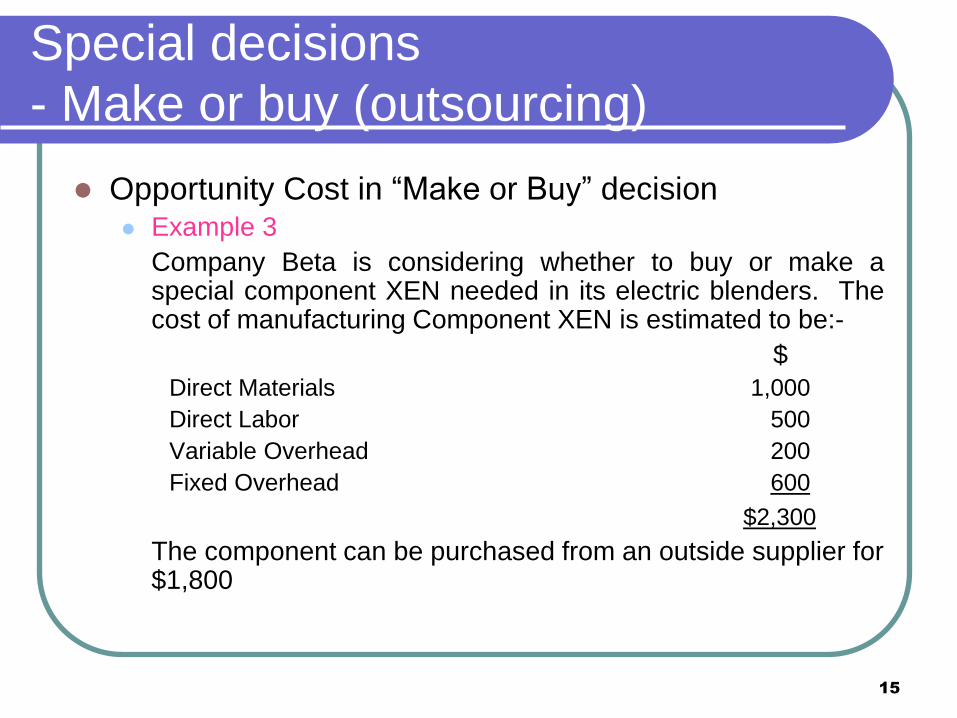

Special decisions

- Make or buy (outsourcing)

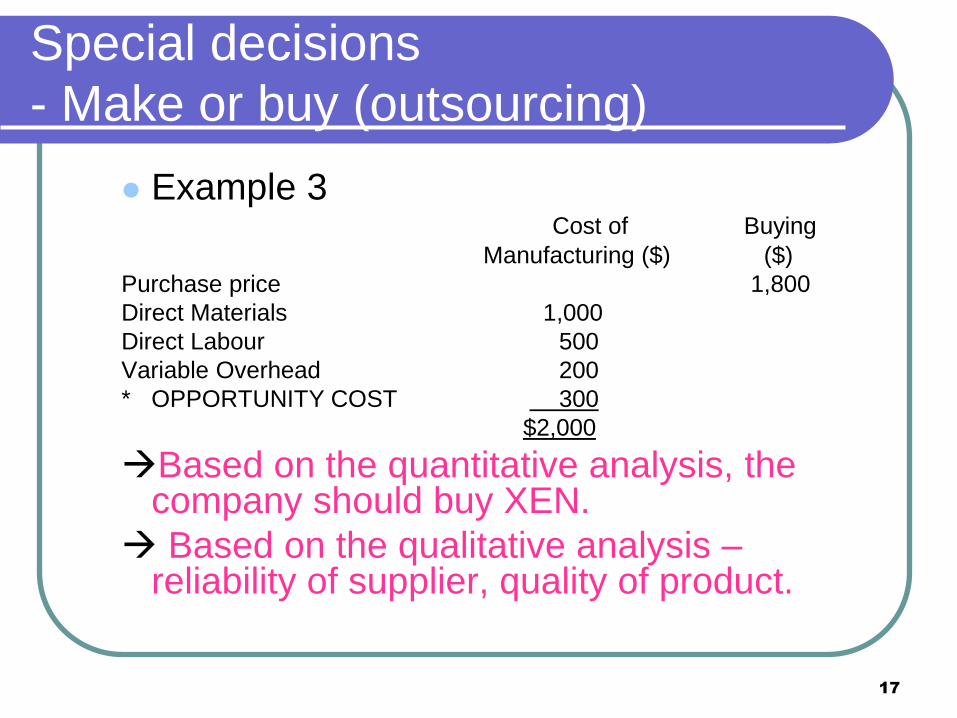

Opportunity Cost in “Make or Buy” decision Example 3

Company Beta is considering whether to buy or make a special component XEN needed in its electric blenders. The cost of manufacturing Component XEN is estimated to be:-

$

Direct Materials 1,000

Direct Labor 500

Variable Overhead 200

Fixed Overhead 600

$2,300

The component can be purchased from an outside supplier for $1,800

16

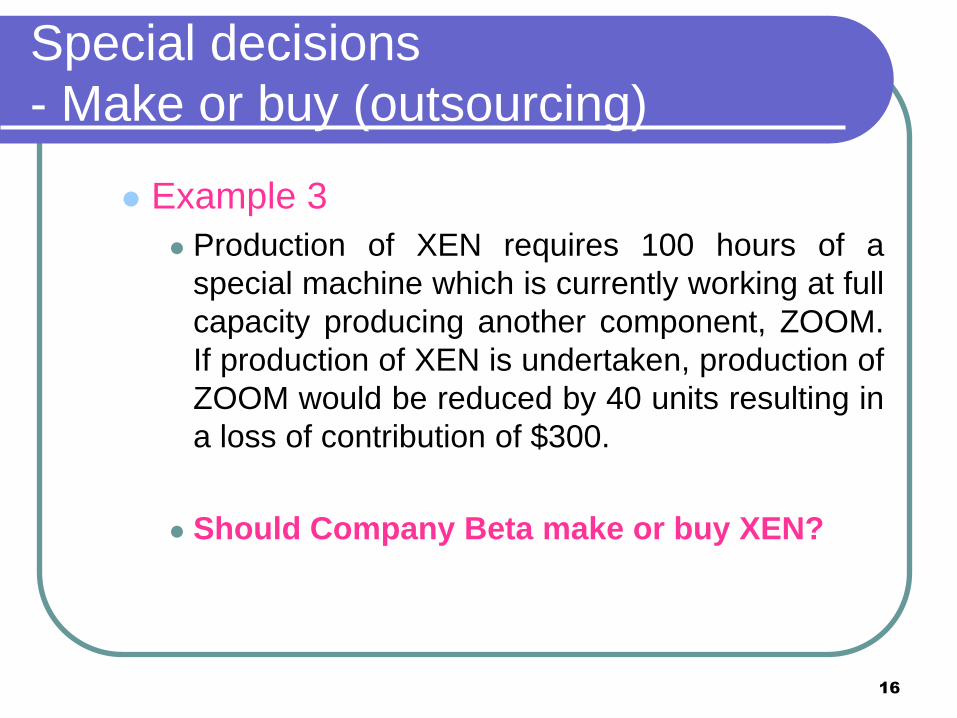

Special decisions

- Make or buy (outsourcing)

Example 3

Production of XEN requires 100 hours of a

special machine which is currently working at full

capacity producing another component, ZOOM.

If production of XEN is undertaken, production of

ZOOM would be reduced by 40 units resulting in

a loss of contribution of $300.

Should Company Beta make or buy XEN?

17

Special decisions

- Make or buy (outsourcing)

Example 3 Cost of Buying

Manufacturing ($) ($)

Purchase price 1,800

Direct Materials 1,000

Direct Labour 500

Variable Overhead 200

* OPPORTUNITY COST 300

$2,000

Based on the quantitative analysis, the company should buy XEN.

Based on the qualitative analysis – reliability of supplier, quality of product.

18

Special decisions

- Discontinuing a product/segment/department

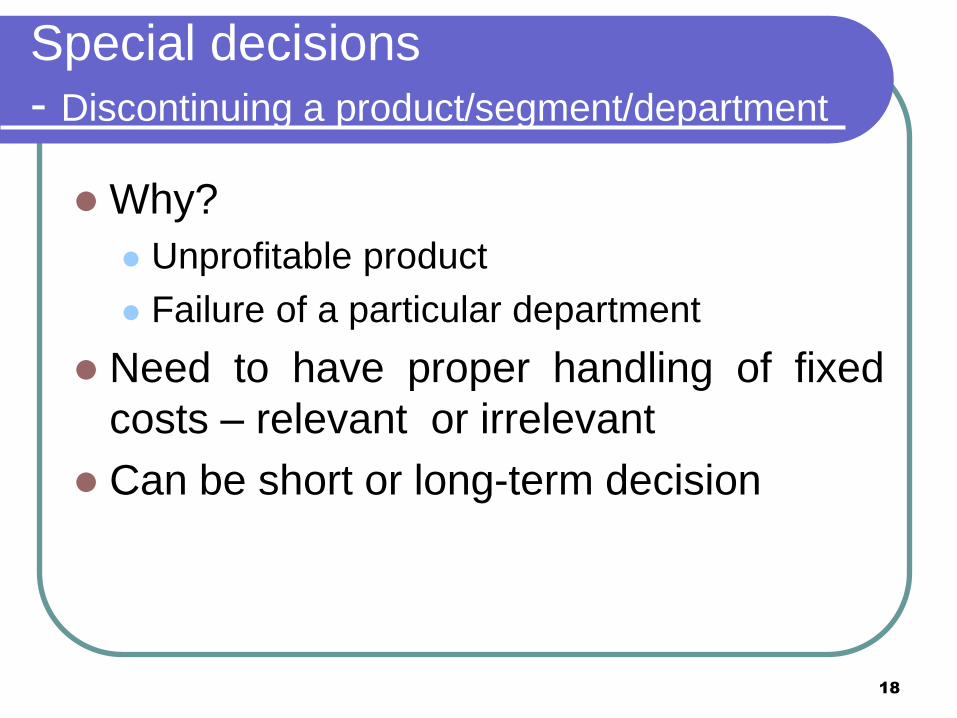

Why?

Unprofitable product

Failure of a particular department

Need to have proper handling of fixed

costs – relevant or irrelevant

Can be short or long-term decision

19

Special decisions

- Discontinuing a product/segment/department

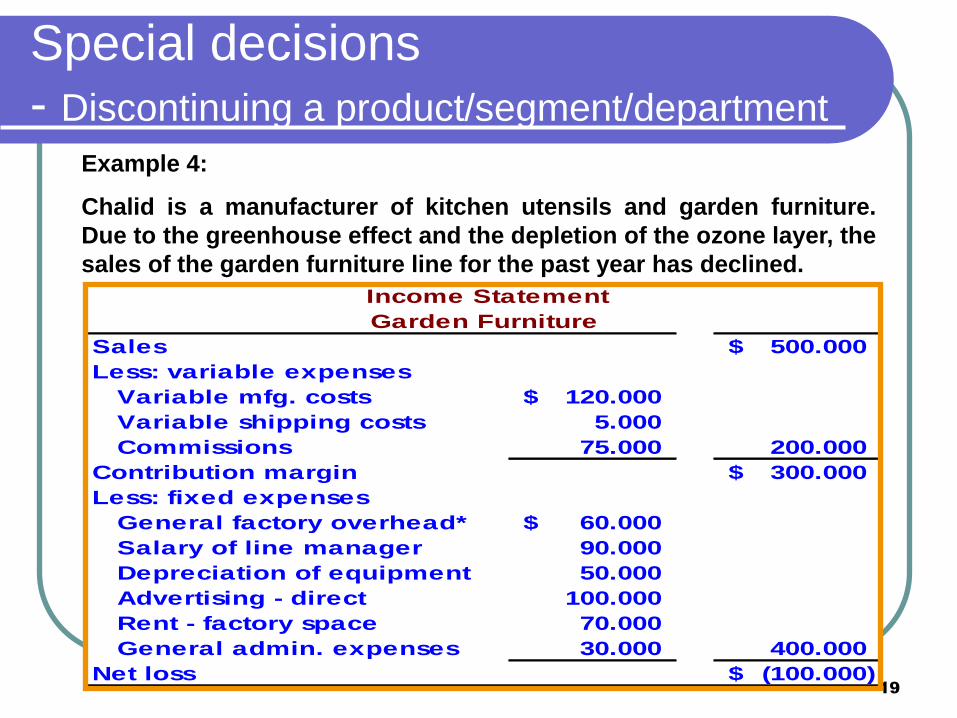

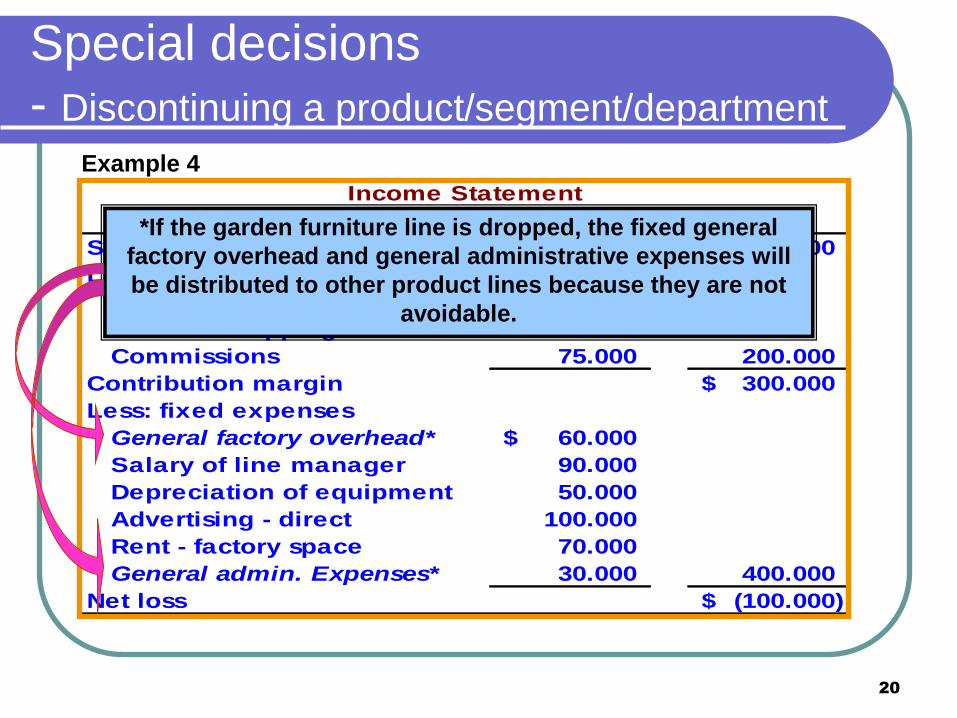

Income Statement

Garden Furniture

Sales 500.000$

Less: variable expenses

Variable mfg. costs 120.000$

Variable shipping costs 5.000

Commissions 75.000 200.000

Contribution margin 300.000$

Less: fixed expenses

General factory overhead* 60.000$

Salary of line manager 90.000

Depreciation of equipment 50.000

Advertising - direct 100.000

Rent - factory space 70.000

General admin. expenses 30.000 400.000

Net loss (100.000)$

Example 4:

Chalid is a manufacturer of kitchen utensils and garden furniture.

Due to the greenhouse effect and the depletion of the ozone layer, the

sales of the garden furniture line for the past year has declined.

20

Income Statement

Garden Furniture

Sales 500.000$

Less: variable expenses

Variable mfg. costs 120.000$

Variable shipping costs 5.000

Commissions 75.000 200.000

Contribution margin 300.000$

Less: fixed expenses

General factory overhead* 60.000$

Salary of line manager 90.000

Depreciation of equipment 50.000

Advertising - direct 100.000

Rent - factory space 70.000

General admin. Expenses* 30.000 400.000

Net loss (100.000)$

Special decisions

- Discontinuing a product/segment/department

*If the garden furniture line is dropped, the fixed general

factory overhead and general administrative expenses will

be distributed to other product lines because they are not

avoidable.

Example 4

21

Income Statement

Garden Furniture

Sales 500.000$

Less: variable expenses

Variable mfg. costs 120.000$

Variable shipping costs 5.000

Commissions 75.000 200.000

Contribution margin 300.000$

Less: fixed expenses

General factory overhead 60.000$

Salary of line manager 90.000

Depreciation of equipment** 50.000

Advertising - direct 100.000

Rent - factory space 70.000

General admin. expenses 30.000 400.000

Net loss (100.000)$

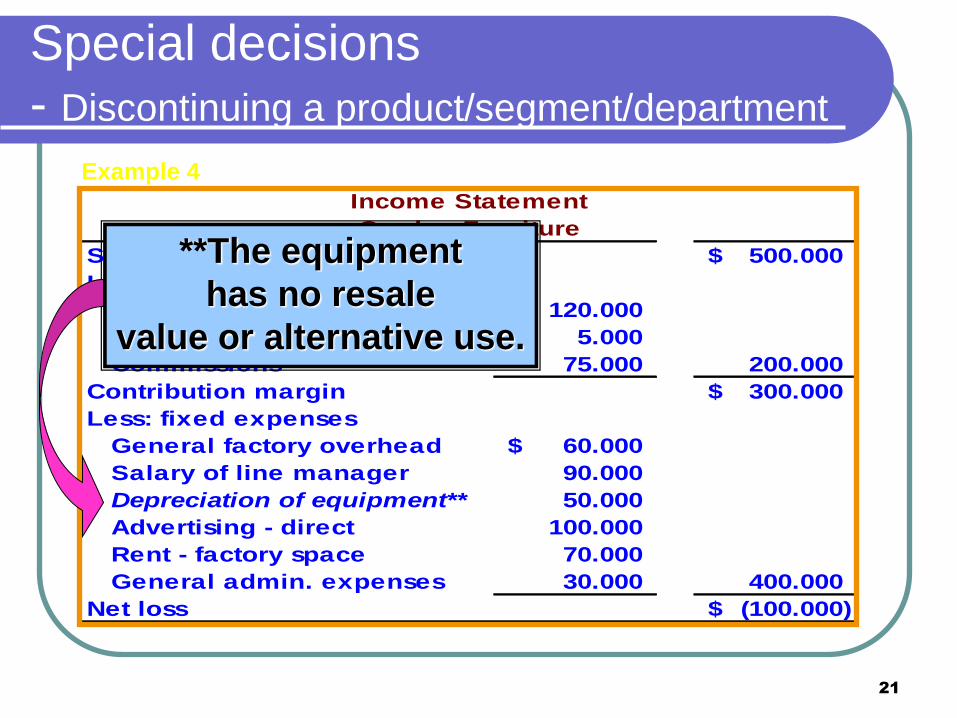

Special decisions

- Discontinuing a product/segment/department

**The equipment

has no resale

value or alternative use.

Example 4

22

Special decisions

- Discontinuing a product/segment/department

The Garden Furniture

solution can be obtained

by preparing

comparative income

statements showing

results with and without

the product line.

Should Chalid

retain or drop

the garden

furniture line?

Example 4

23

Special decisions

- Discontinuing a product/segment/department

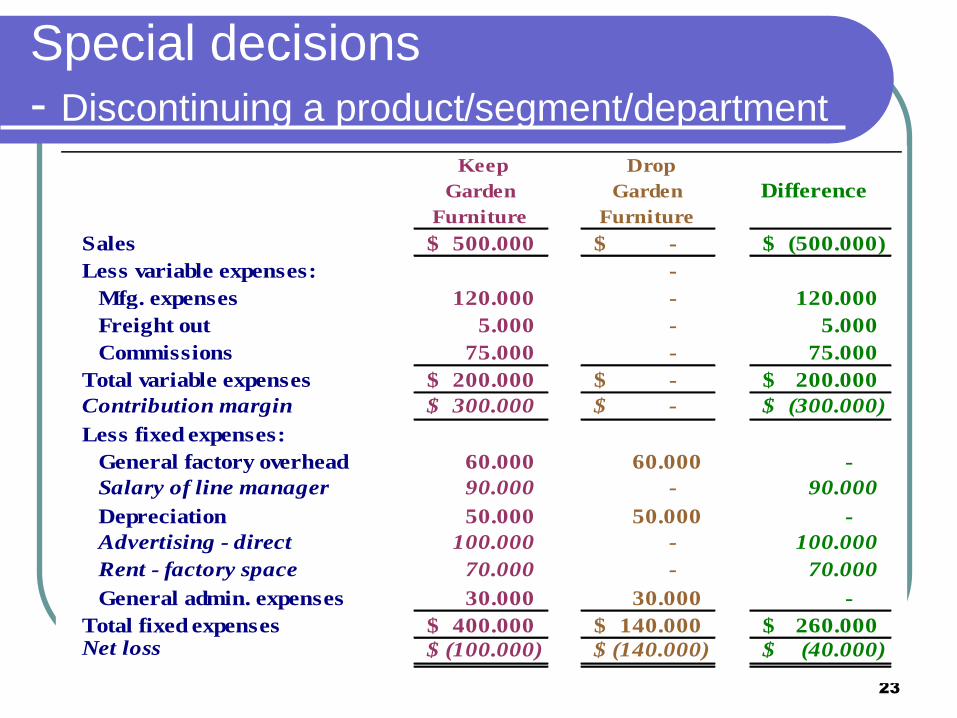

Keep

Garden

Furniture

Drop

Garden

Furniture

Difference

Sales 500.000$ -$ (500.000)$

Less variable expenses: -

Mfg. expenses 120.000 - 120.000

Freight out 5.000 - 5.000

Commissions 75.000 - 75.000

Total variable expenses 200.000$ -$ 200.000$

Contribution margin 300.000$ -$ (300.000)$

Less fixed expenses:

General factory overhead 60.000 60.000 -

Salary of line manager 90.000 - 90.000

Depreciation 50.000 50.000 -

Advertising - direct 100.000 - 100.000

Rent - factory space 70.000 - 70.000

General admin. expenses 30.000 30.000 -

Total fixed expenses 400.000$ 140.000$ 260.000$ Net loss (100.000)$ (140.000)$ (40.000)$

24

Special decisions

- Production with limiting factor

Firms often face with limiting factors (resources) & the problem of deciding how the factors are going to be used

machine hours

labors

materials

Usually, fixed costs are not affected by this decision, so management can focus on maximizing total contribution margin

25

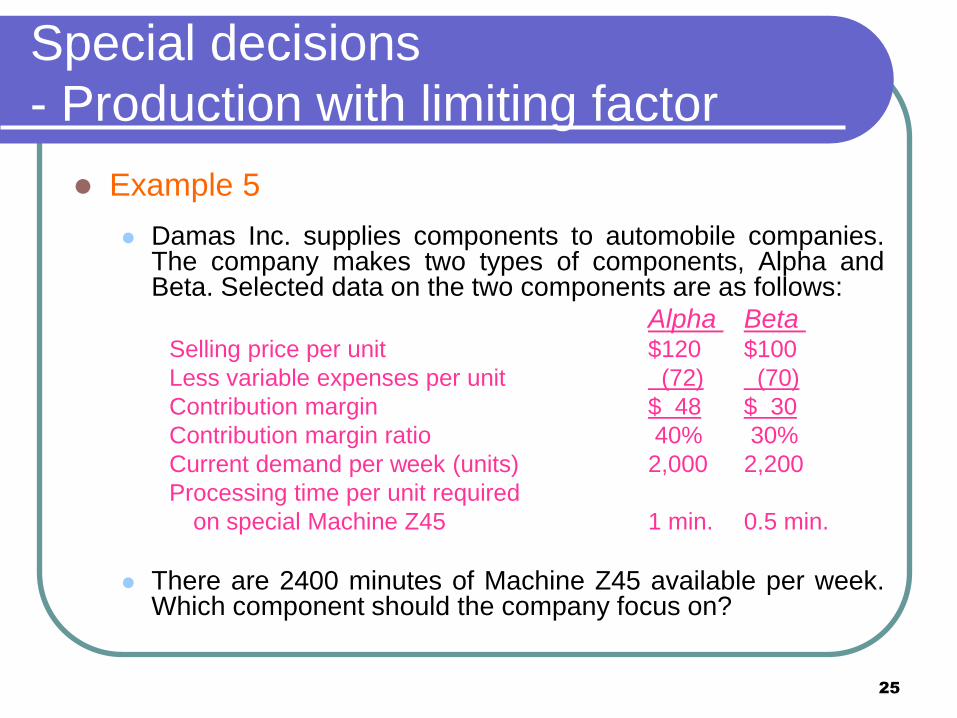

Special decisions

- Production with limiting factor

Example 5

Damas Inc. supplies components to automobile companies. The company makes two types of components, Alpha and Beta. Selected data on the two components are as follows:

Alpha Beta Selling price per unit $120 $100

Less variable expenses per unit (72) (70)

Contribution margin $ 48 $ 30

Contribution margin ratio 40% 30%

Current demand per week (units) 2,000 2,200

Processing time per unit required

on special Machine Z45 1 min. 0.5 min.

There are 2400 minutes of Machine Z45 available per week. Which component should the company focus on?

26

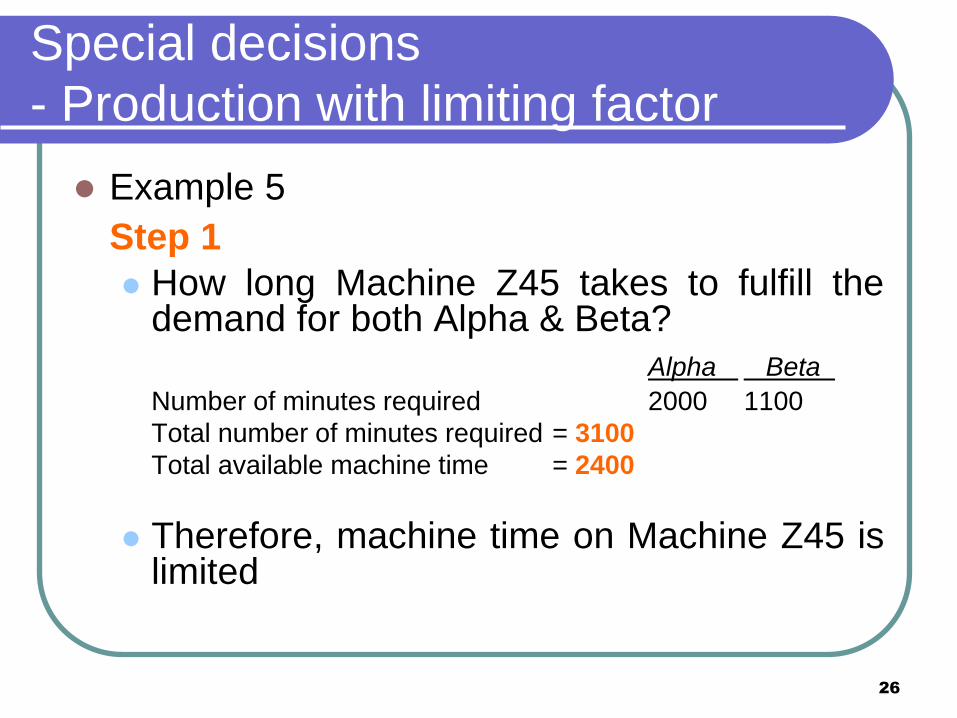

Special decisions

- Production with limiting factor

Example 5

Step 1

How long Machine Z45 takes to fulfill the demand for both Alpha & Beta?

Alpha Beta

Number of minutes required 2000 1100

Total number of minutes required = 3100

Total available machine time = 2400

Therefore, machine time on Machine Z45 is limited

27

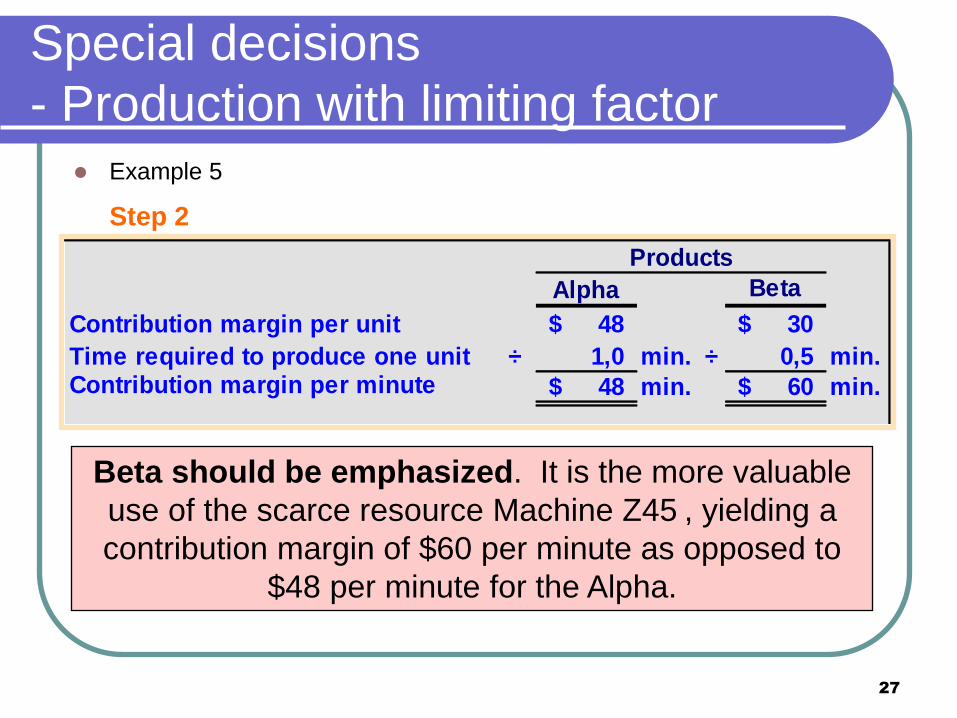

Special decisions

- Production with limiting factor Example 5

Step 2

Products

Alpha Beta

Contribution margin per unit $ 48 $ 30

Time required to produce one unit ÷ 1,0 min. ÷ 0,5 min.Contribution margin per minute 48$ min. 60$ min.

Beta should be emphasized. It is the more valuable

use of the scarce resource Machine Z45 , yielding a

contribution margin of $60 per minute as opposed to

$48 per minute for the Alpha.

28

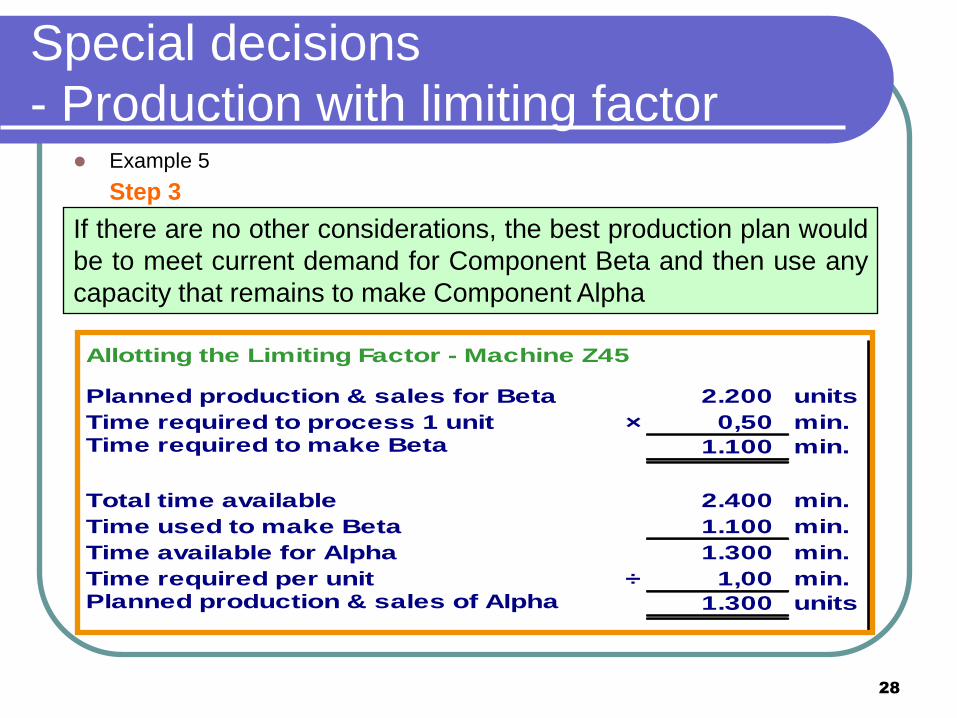

Special decisions

- Production with limiting factor Example 5

Step 3

If there are no other considerations, the best production plan would

be to meet current demand for Component Beta and then use any

capacity that remains to make Component Alpha

Allotting the Limiting Factor - Machine Z45

Planned production & sales for Beta 2.200 units

Time required to process 1 unit × 0,50 min.Time required to make Beta 1.100 min.

Total time available 2.400 min.

Time used to make Beta 1.100 min.

Time available for Alpha 1.300 min.

Time required per unit ÷ 1,00 min.Planned production & sales of Alpha 1.300 units

29

Special decisions

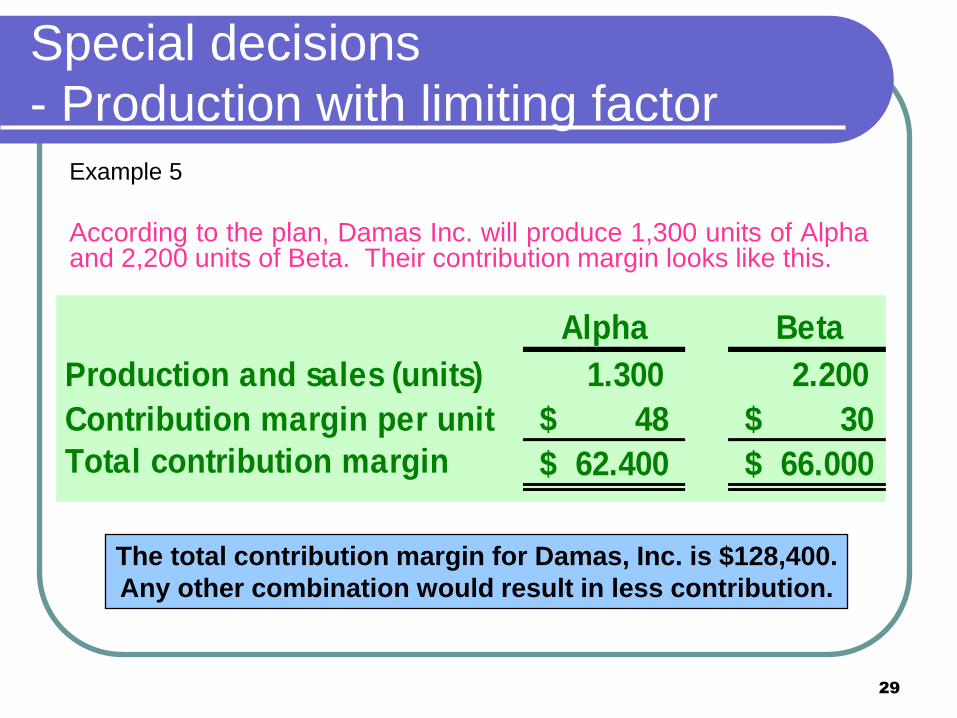

- Production with limiting factor Example 5

According to the plan, Damas Inc. will produce 1,300 units of Alpha and 2,200 units of Beta. Their contribution margin looks like this.

Alpha Beta

Production and sales (units) 1.300 2.200

Contribution margin per unit 48$ 30$

Total contribution margin 62.400$ 66.000$

The total contribution margin for Damas, Inc. is $128,400.

Any other combination would result in less contribution.

30

Special decisions

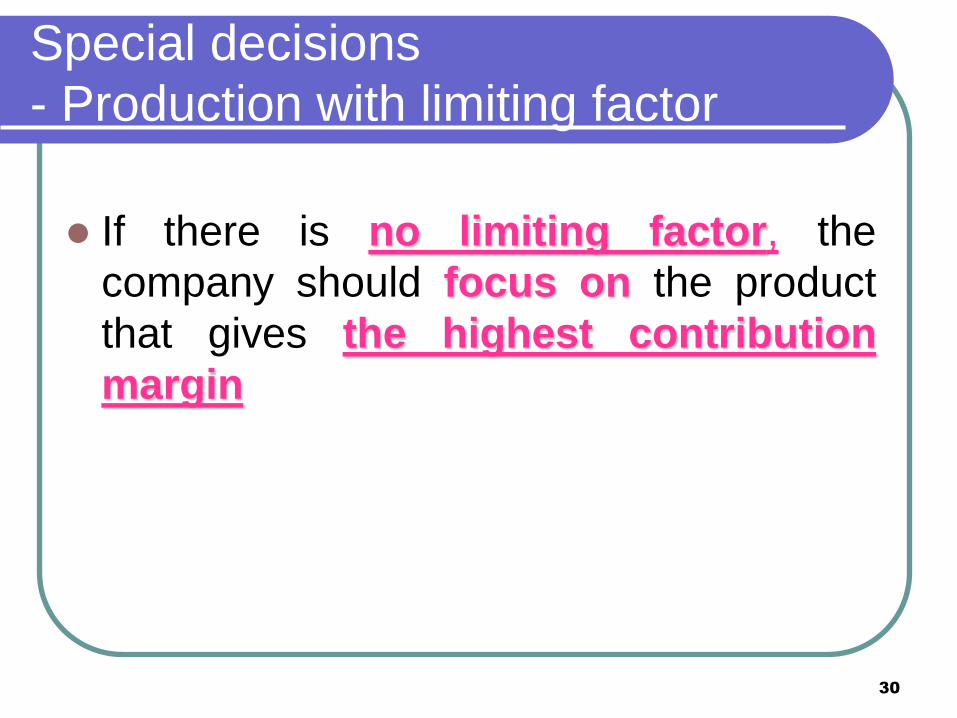

- Production with limiting factor

If there is no limiting factor, the

company should focus on the product

that gives the highest contribution

margin

31

Special decisions

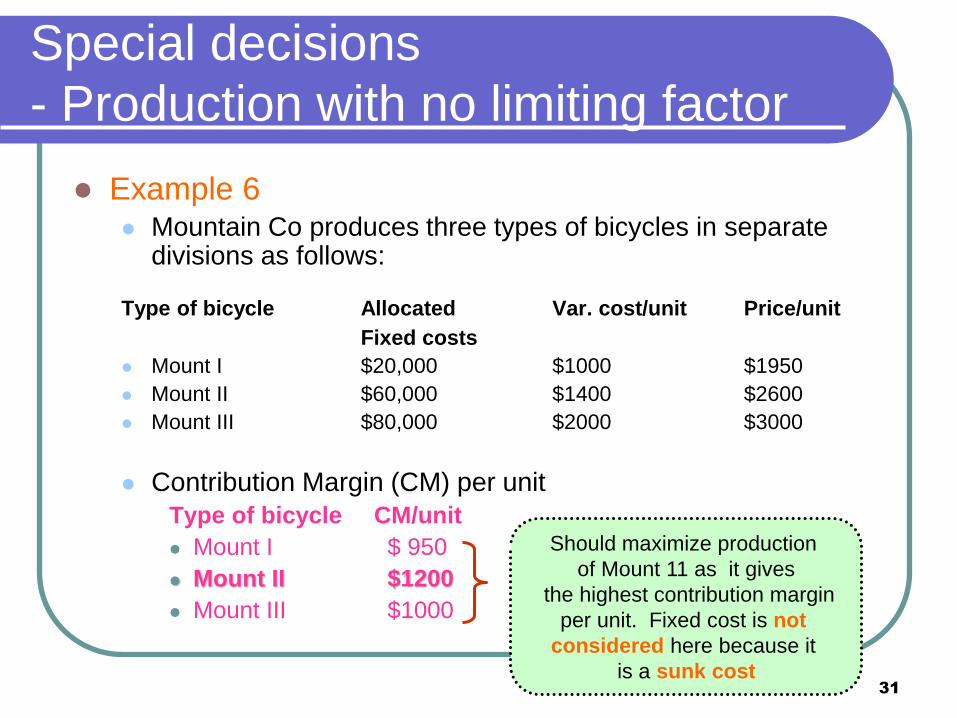

- Production with no limiting factor

Example 6 Mountain Co produces three types of bicycles in separate

divisions as follows:

Type of bicycle Allocated Var. cost/unit Price/unit

Fixed costs

Mount I $20,000 $1000 $1950

Mount II $60,000 $1400 $2600

Mount III $80,000 $2000 $3000

Contribution Margin (CM) per unit

Type of bicycle CM/unit

Mount I $ 950

Mount II $1200

Mount III $1000

Should maximize production

of Mount 11 as it gives

the highest contribution margin

per unit. Fixed cost is not

considered here because it

is a sunk cost

32

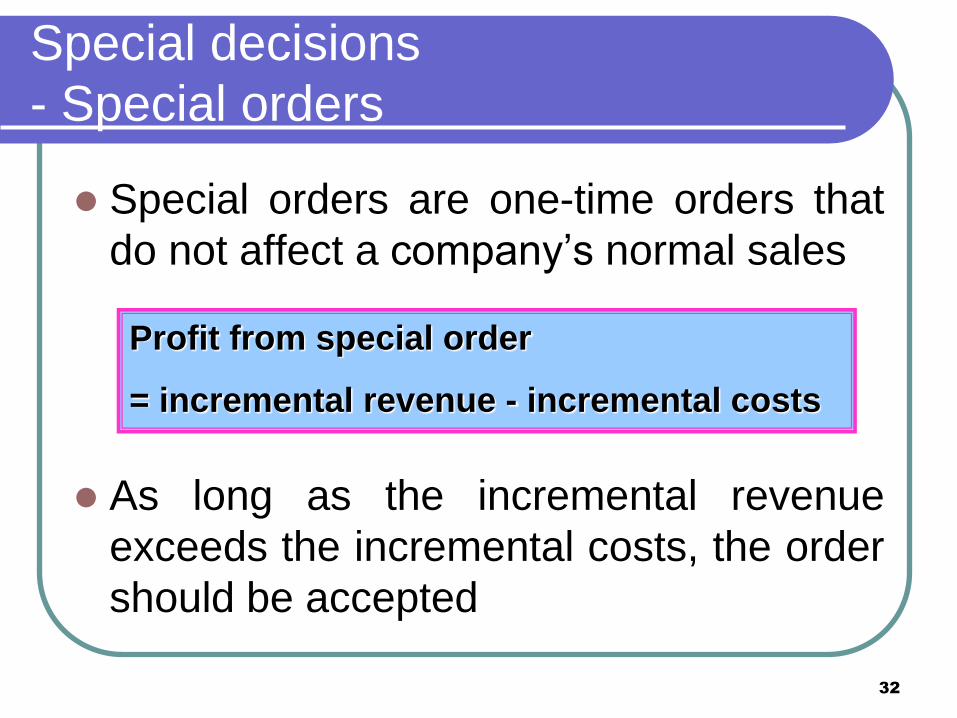

Special decisions

- Special orders

Special orders are one-time orders that

do not affect a company’s normal sales

As long as the incremental revenue

exceeds the incremental costs, the order

should be accepted

Profit from special order

= incremental revenue - incremental costs

33

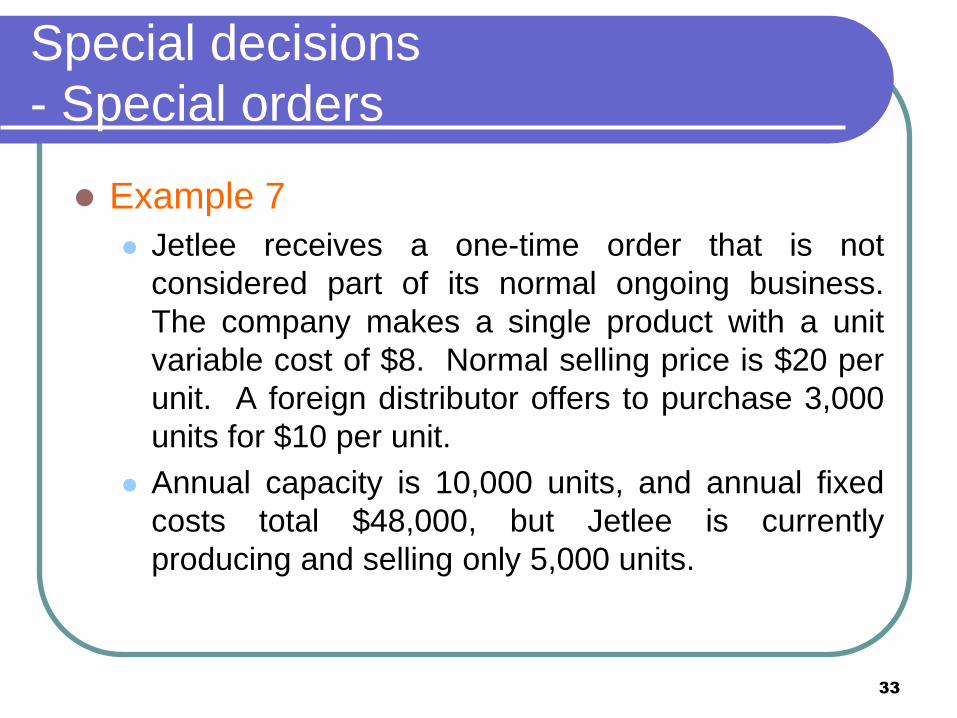

Special decisions

- Special orders

Example 7

Jetlee receives a one-time order that is not

considered part of its normal ongoing business.

The company makes a single product with a unit

variable cost of $8. Normal selling price is $20 per

unit. A foreign distributor offers to purchase 3,000

units for $10 per unit.

Annual capacity is 10,000 units, and annual fixed

costs total $48,000, but Jetlee is currently

producing and selling only 5,000 units.

34

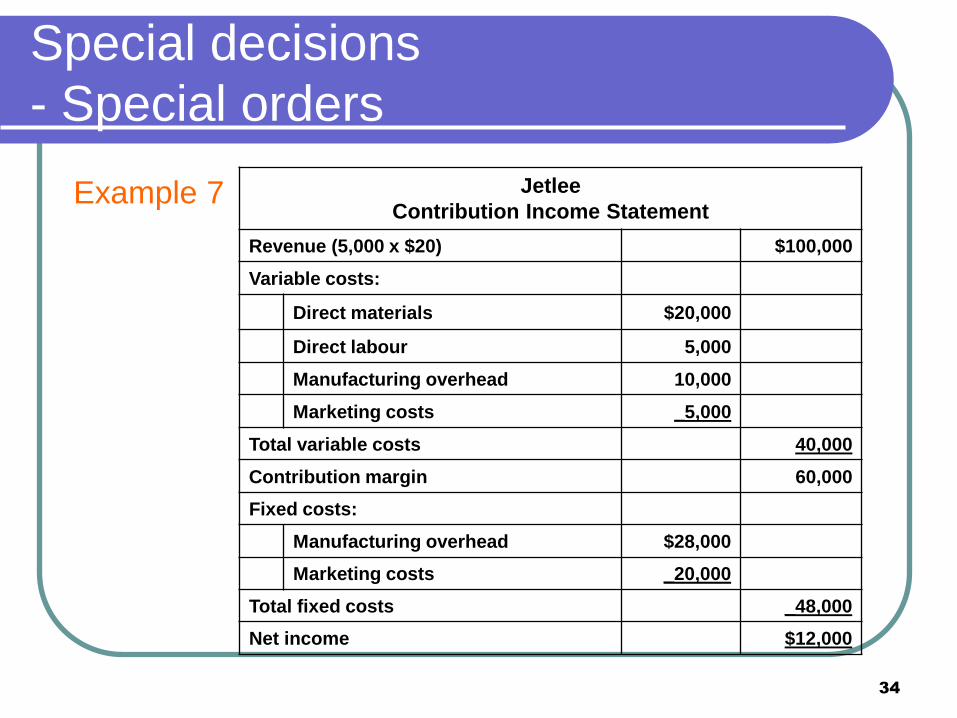

Special decisions

- Special orders

Example 7

Jetlee

Contribution Income Statement

Revenue (5,000 x $20) $100,000

Variable costs:

Direct materials $20,000

Direct labour 5,000

Manufacturing overhead 10,000

Marketing costs _5,000

Total variable costs 40,000

Contribution margin 60,000

Fixed costs:

Manufacturing overhead $28,000

Marketing costs _20,000

Total fixed costs _48,000

Net income $12,000

35

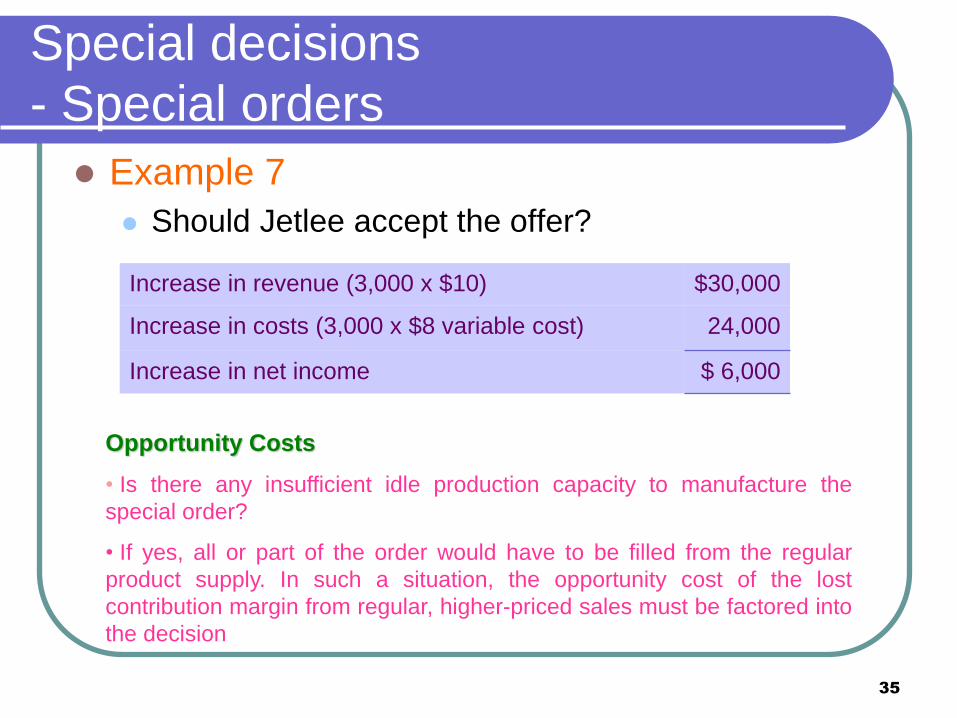

Special decisions

- Special orders

Example 7

Should Jetlee accept the offer?

Increase in revenue (3,000 x $10) $30,000

Increase in costs (3,000 x $8 variable cost) 24,000

Increase in net income $ 6,000

Opportunity Costs

• Is there any insufficient idle production capacity to manufacture the

special order?

• If yes, all or part of the order would have to be filled from the regular

product supply. In such a situation, the opportunity cost of the lost

contribution margin from regular, higher-priced sales must be factored into

the decision

36

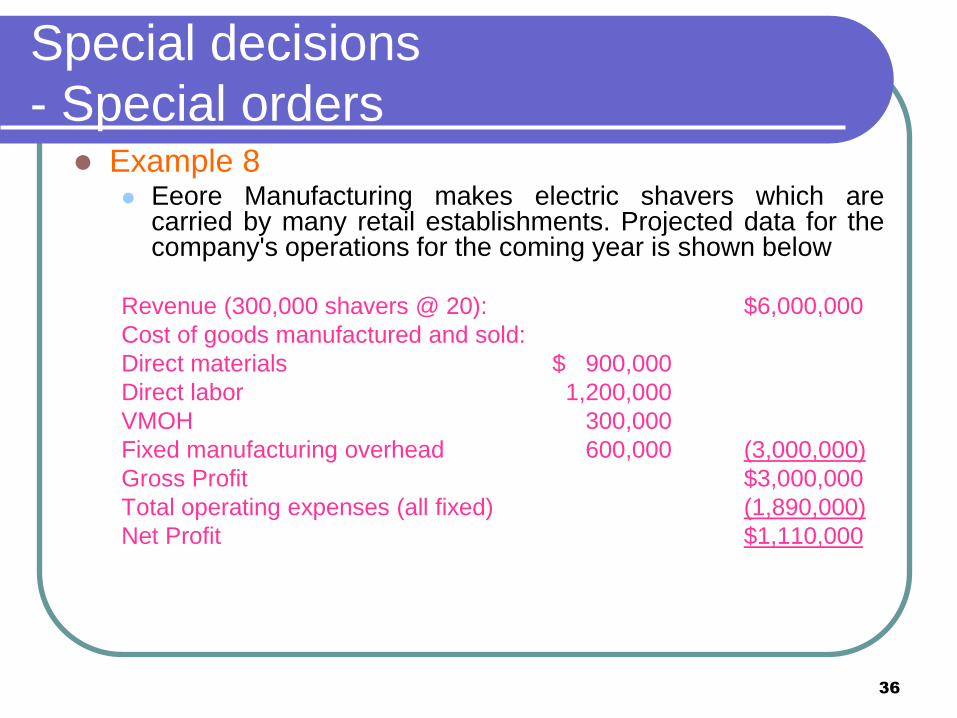

Special decisions

- Special orders Example 8

Eeore Manufacturing makes electric shavers which are carried by many retail establishments. Projected data for the company's operations for the coming year is shown below

Revenue (300,000 shavers @ 20): $6,000,000

Cost of goods manufactured and sold:

Direct materials $ 900,000

Direct labor 1,200,000

VMOH 300,000

Fixed manufacturing overhead 600,000 (3,000,000)

Gross Profit $3,000,000

Total operating expenses (all fixed) (1,890,000)

Net Profit $1,110,000

37

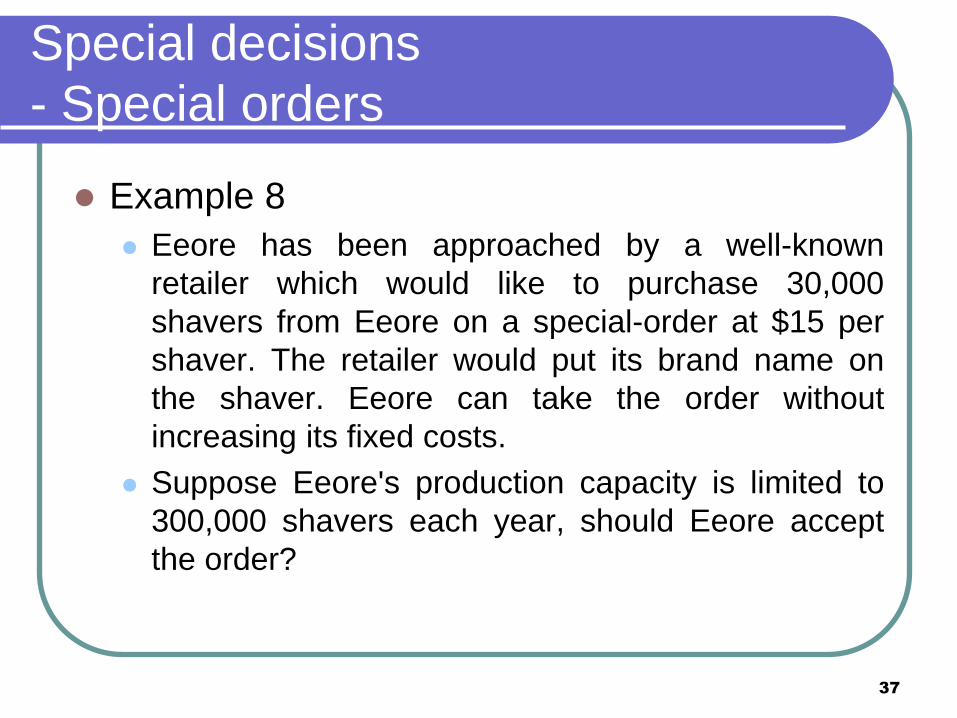

Special decisions

- Special orders

Example 8

Eeore has been approached by a well-known

retailer which would like to purchase 30,000

shavers from Eeore on a special-order at $15 per

shaver. The retailer would put its brand name on

the shaver. Eeore can take the order without

increasing its fixed costs.

Suppose Eeore's production capacity is limited to

300,000 shavers each year, should Eeore accept

the order?

38

Special decisions

- Special orders

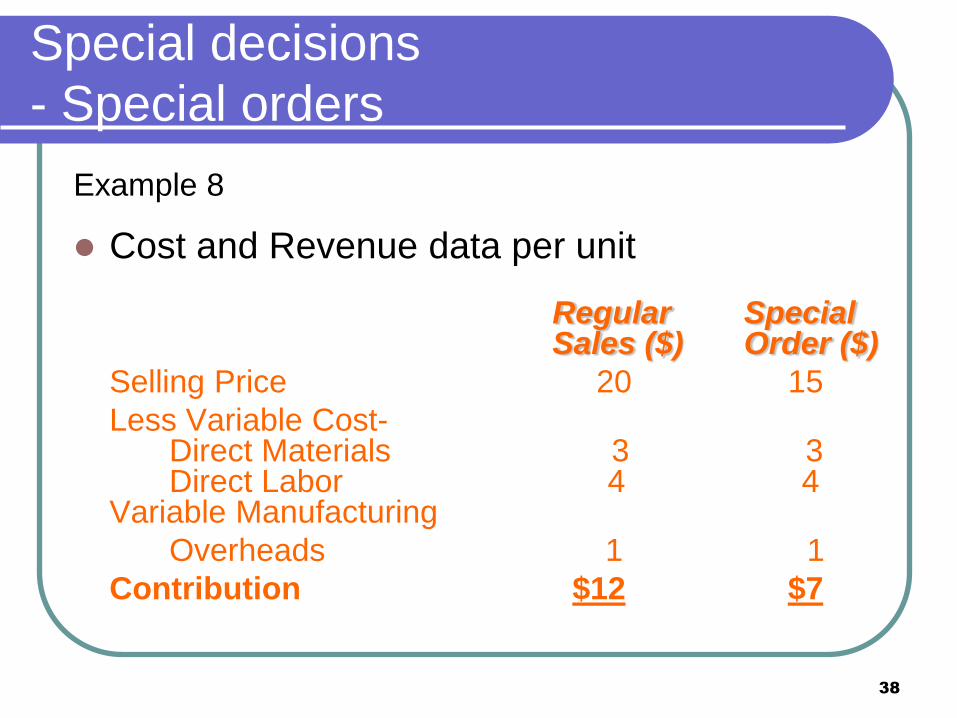

Example 8

Cost and Revenue data per unit

Regular Special Sales ($) Order ($)

Selling Price 20 15

Less Variable Cost- Direct Materials 3 3 Direct Labor 4 4 Variable Manufacturing

Overheads 1 1

Contribution $12 $7

39

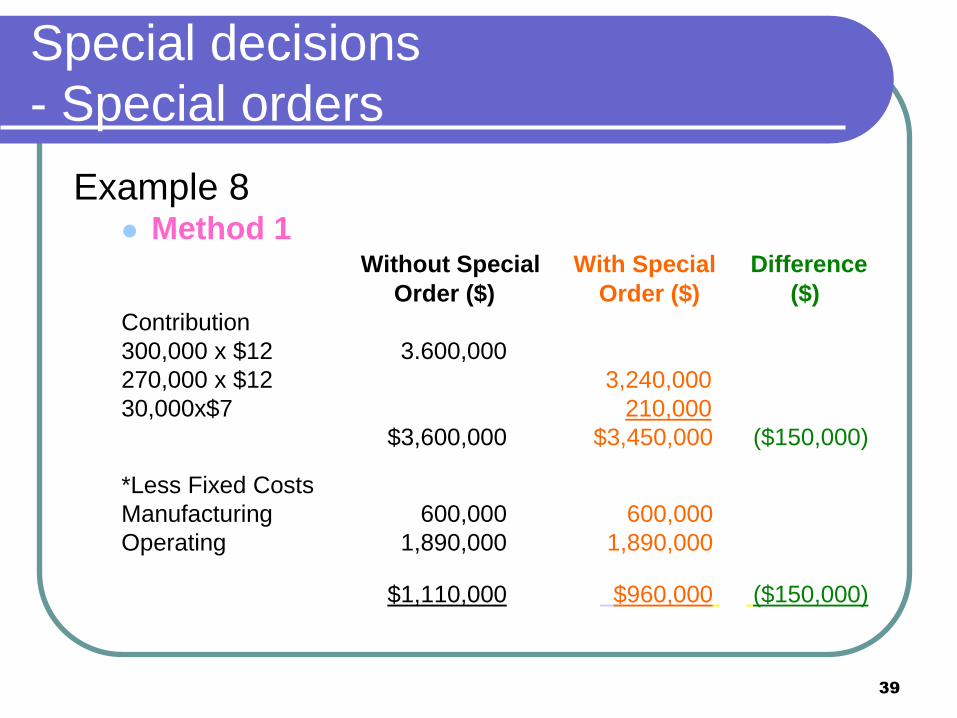

Special decisions

- Special orders

Example 8 Method 1 Without Special With Special Difference

Order ($) Order ($) ($)

Contribution

300,000 x $12 3.600,000

270,000 x $12 3,240,000

30,000x$7 210,000

$3,600,000 $3,450,000 ($150,000)

*Less Fixed Costs

Manufacturing 600,000 600,000

Operating 1,890,000 1,890,000

$1,110,000 $960,000 ($150,000)

40

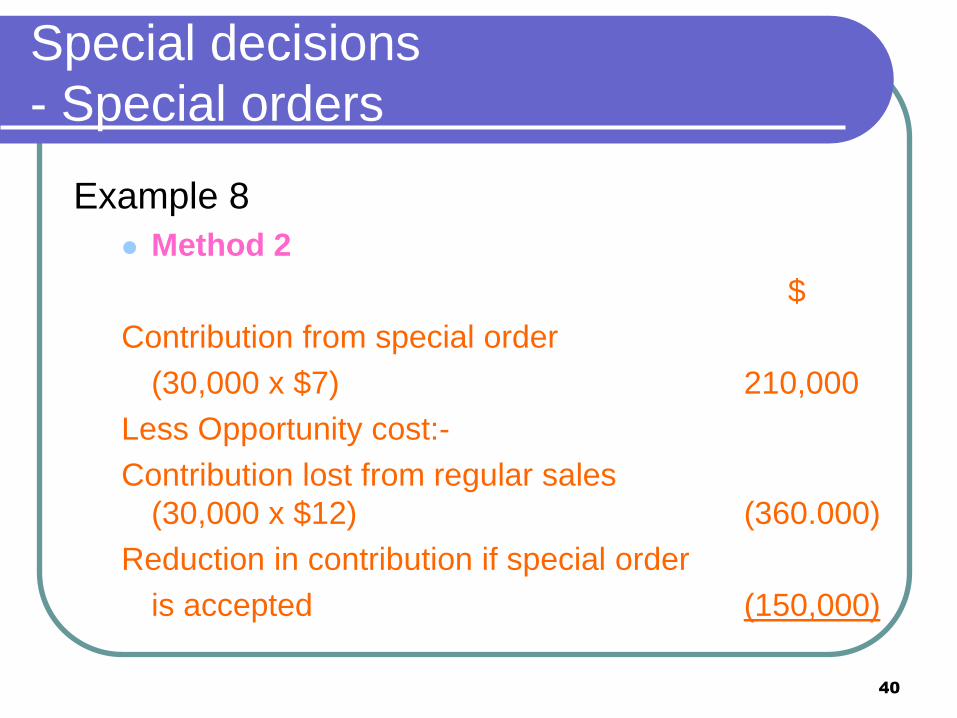

Special decisions

- Special orders

Example 8

Method 2

$

Contribution from special order

(30,000 x $7) 210,000

Less Opportunity cost:-

Contribution lost from regular sales

(30,000 x $12) (360.000)

Reduction in contribution if special order

is accepted (150,000)

41

Decision making and Relevant

Costs

Outsourcing

Special order

Limited resources

Make vs buy

Sunk costs

Unavoidable costs

Relevant costs

Chapter 5 Avoidable costs

Opportunity costs

Six steps

42

End of Chapter 6