Embed Size (px)

Citation preview

Does Aid Decrease Tax Revenue

in Developing Countries?

A Study by

Ludovica Gambaro, Jonna Meyer-Spasche, and Ashikur Rahman

March 2007

This report was prepared as a Capstone Project for the United Kingdom’s

Department for International Development (DFID); supervised by Carlos Santiso

(DFID), Joachim Wehner (LSE) and Daniel Sturm (LSE). The Capstone Project is

part of the Master of Public Administration (MPA) programme at the London

School of Economics and Political Science (LSE).

Abstract

This paper studies the relationship between development aid inflows and tax revenue in

recipient countries1. For a sample of 65 countries over the period of 1990 to 2004, our

results do not support the hypothesis that aid substitutes for domestic tax revenue. On the

contrary, we find evidence that there is a positive association between aid inflows and tax

revenue, which is primarily driven by the positive relationship between grants and tax

revenue. We neither find any evidence for the hypothesis that the marginal impact of aid

on tax revenue is different in countries with low corruption compared to more strongly

corrupted countries. When we look at a more disaggregate picture, we identify a

heterogeneous association of aid with different components of tax revenue. We also

explore the possible two-way relationship between tax revenue and institutions.

Contact the authors:

Ludovica Gambaro: [email protected]

Jonna Meyer-Spasche: [email protected]

Ashikur Rahman: [email protected]

MPA Public and Economic Policy, London School of Economics, V815 Tower Two,

Houghton Street, London, WC2A 2AE

1 Original idea: Carlos Santiso (DFID).

Table of Content

Executive Summary iii

1. Introduction: The Debate over a Substitution Effect of Aid 1

2. Literature Review: Previous Evidence is Ambiguous 3

3. Empirical Model and Data 7

a. Empirical Model 7

b. Data Description 10

4. Results 12

a. Baseline Results: No General Substitution Effect 13

b. Role of Corruption: No Differential Impact of Aid 16

c. Disaggregating Tax Revenue: Heterogeneous Picture 19

d. Tax Revenue and Institutions: A Two-Way Relationship? 25

5. Conclusion and Implications: A Role for Development Policy 29

References 32

Appendix

a. Construction of the Dataset 36

b. List of Countries in the Sample 37

Tables and Figures:

Table 1: Descriptive Statistics of Sample Data 11

Table 2: Baseline Results: Aid on Tax Revenue 12

Table 3: Robustness Checks 14

Table 4: Aid on Revenue in Two Different Time Periods 15

Table 5: Interaction of Aid and Corruption 19

Table 6: Descriptive Statistics of Tax Structure in Sample 21

Table 7: Aid on Different Types of Tax Revenue 22

Table 8: Tax Revenue on Governance Indicators 27

Figure 1: Tax Revenue and Governance Indicators 26

iii

Executive Summary

In the context of donor governments’ commitment to scale up development aid in order

to achieve the Millennium Development Goals (MDGs), one important question is how

the domestic revenue recipient governments collect responds to an inflow of aid. There is

the theoretical concern that aid might partly substitute for domestic tax revenue, for

example if the recipient government chooses to grant certain constituencies a tax relief

instead of using the aid for development oriented investments. On the other hand, the

recipient government might also invest part of the aid money into the enhancement of

their institutional capacity, thereby strengthening also their tax administration, which

might increase the collected tax revenue.

Hence, the relationship between aid and tax revenue is essentially an empirical question.

The results of previous analyses, mostly country case studies, are ambiguous. One

comprehensive study was conducted by Gupta et al. (2003), which points out a negative

relationship between aid, and more particularly grants, with domestic revenue and a

positive relationship between net loans and domestic revenue.

This study aims at identifying whether there is a systematic relationship between aid and

tax revenue in developing countries by examining the available data in a panel-data

regression analysis. For a sample of 65 countries over the period from 1990 to 2004, we

examine whether different components of aid, grants and loans, differ in their association

with tax revenue. Furthermore, we disaggregate tax revenue into income and capital

taxes, goods and services taxes, and trade taxes, and try to identify whether there is a

heterogeneous association of aid with different components of tax revenue. The dual

relationship between taxes and the quality of governance institutions is also explored.

The results provide a background for more in-depth micro-level explorations, as well as

some broad implications for policy-makers.

Key Results

• There is systematic evidence for a positive correlation between aid and tax

revenue. The coefficient on aid in the form of grants is positive and significant

across different specifications and several robustness checks, whereas the

coefficient on aid in the form of net loans is negative but insignificant. Concerns

over a general substitution effect of aid are thus not supported.

iv

• A re-estimation of Gupta et al.’s specification on their dataset shows that the

negative correlation they find for net aid and grants with revenue over the period

1970-2000 turns into a positive correlation for the period 1990-2000.

• Our results are stable in magnitude and significance to the inclusion of an

interaction between aid and corruption, which itself does not seem to be

significant. Hence, there is no evidence for a differential impact of aid on tax

revenue in more vs. less corrupt countries.

• Disaggregating tax revenue into three major types of taxes shows a heterogeneous

picture: net aid and grants are negatively correlated with income and capital tax

revenue and positively correlated with revenue from taxes on goods and services

and on trade. The structure and effectiveness of the taxation system and

administrative institutions may be an omitted variable influencing both aid and

tax revenue.

• The results of the correlation of tax revenue and governance institutions hint at a

possible two-way relationship: revenue from taxes overall, income and capital,

and goods and services is positively associated with all six World Bank

Governance Indicators, but trade taxes show a negative correlation with three of

the indicators. This suggests that countries that have on average higher trade taxes

also tend to have weaker administrative institutions. These factors can reinforce

each other over time.

Implications

• Our results suggest that the role of development policy post 1990, with its

stronger focus on institutions, is a possible underlying factor of the positive

association between aid and tax revenue. Therefore, both donors and recipient

countries should try to identify the pivotal set of policies that influenced the

response of tax revenue to the inflow of aid after 1990.

• The effectiveness of administrative institutions seems to be a crucial factor

influencing the structure and collection of tax revenue. Our findings imply that

before a tax policy reform can effectively be implemented, crucial constraints on

the effectiveness of tax administration may have to be targeted. The easier tax

v

evasion is the more difficult it will be to shift the main revenue source from

“easy” but unsustainable taxes like trade taxes to more sustainable tax types like

income and capital taxes.

• Further micro-level analysis of this issue will be useful in order to determine the

underlying dynamics that affect the relationship between aid and tax revenue.

Does Aid Decrease Tax Revenue in Developing Countries?

1

1. Introduction: The Debate Over a Substitution Effect of Aid

In order to provide public services and to enhance human and economic development in

their country, governments use taxation as the central source of state revenue. Developing

countries are not able to finance all desirable public expenditures and investments

through the tax revenue they collect, which is why bilateral and multilateral donors

provide development assistance and thereby alleviate budget constraints. The question,

however, is whether foreign aid is simply added to the domestic budget or whether it has

partially a substitution effect. Recipient governments can choose to increase expenditure

and investment by the full amount of aid, or they can choose to lower their tax effort or

borrowing and keep the planned expenditures constant.

To what extent aid influences expenditure decisions has been extensively examined in the

literature under the term of “fungibility” (cf. Devarajan et al. 1999): per definition, aid is

fungible if “recipients reallocate resources that would have been spent for purposes now

financed by foreign aid” (Gupta et al. 2003: 6, footnote 9), thus aid could, in effect,

finance unproductive public expenditures or be used for tax relief. However, the

fungibility literature has focused primarily on the expenditure side and has largely

neglected the analysis of impacts on the revenue side.

Yet if development assistance is intended to help countries help themselves so that sooner

or later they no longer need foreign aid then it matters whether aid actually increases the

budget and domestic revenue available for public services and other government tasks.

Several responses of recipient governments to an inflow of aid are imaginable: they could

use it to enhance institutional capacity and strengthen the fiscal administration so that tax

revenue might even increase, or they could use aid as a substitute for tax revenue by for

example using it to alleviate the tax burden of powerful lobby groups. In theory, a

reduction in tax effort could also free resources for the private sector and increase

investment if distortively high taxes are reduced. However, since developing countries

typically have very low tax revenue in general, the primary concern is over a potential

further reduction.

The broader context of this issue is the planned increase of development aid resources

and the question of aid effectiveness (cf. Gupta et al. 2006; Kenny 2006; World Bank

Does Aid Decrease Tax Revenue in Developing Countries?

2

1998). In order to achieve the Millennium Development Goals (MDGs), agreed at the

United Nations Millennium Summit in 2000, most donors of development assistance –

including the United Kingdom - have pledged to substantively scale up their development

budgets. Given the often low administrative capacity of recipient countries to effectively

employ these inflows, the OECD’s Development Assistance Committee (DAC) members

agreed in their “Paris Declaration on Aid Effectiveness” of 2005 to concentrate on

strengthening partner countries’ capacities and national development strategies (OECD

2006: 8). DFID elaborates in its most recent White Paper how it plans to focus on

governance and building capable and accountable states by committing half of its

bilateral aid budget to public services for the poor (DFID 2006). Against this backdrop it

is important to know what impact aid has on the tax effort in recipient countries, whether

this impact is influenced by the quality of administrational institutions, and whether this

process even has repercussions on the quality of institutions.

This study does not intend to solve the question of a substitution effect of aid, or to

discover which types and levels of taxes are most conducive to development; its more

humble intention is to try to find whether there is a systematic relationship between aid

and tax revenue in developing countries by examining the available data in a panel-data

regression analysis. We will explore whether different components of aid, grants and

loans, differ in their association with tax revenue. Furthermore we will disaggregate tax

revenue into income and capital taxes, goods and services taxes, and trade taxes, and try

to identify whether the different types of taxes are differently correlated to an inflow of

aid. The dual relationship between taxes and the quality of governance institutions will

also be looked into, as far as the data permit. The value of such a cross-country approach

lies in the general background it provides for more in-depth micro-level explorations.

Results of aggregate analyses can also be used to draw broad guidelines for policy-

makers.

The next section will give an overview over the previous literature on the relationship

between aid and taxation. This is followed in section 3 by a description of our empirical

model and the data used in the analysis. Section 4 will present the regressions, results,

and interpretations of the results. The concluding section 5 will highlight some potential

policy implications and questions for further research.

Does Aid Decrease Tax Revenue in Developing Countries?

3

2. Literature Review: Previous Evidence is Ambiguous

The literature on fiscal impacts of development assistance in aid recipient countries does

not offer a conclusive picture. Furthermore, it is largely dominated by studies focusing on

government expenditure behaviour and aid fungibility. The impact of aid on

governments’ taxation behaviour has mostly been dealt with in country case studies, with

ambiguous results, while cross-country analyses are few. This is why it is still very

difficult to draw generalisable conclusions about this relationship. McGillivray and

Morrissey (2001) survey the - mostly post-1990 – theoretical and empirical literature on

this topic and thus provide a good overview over a range of findings: out of eight

studies1, of which six are case studies and two are cross-sectional analyses of small

samples, four studies find negative effects of aid on tax revenue, while two find a positive

effect, and two find no significant effect. We will now first look at the existing cross-

country analyses in this field and then at several country case studies, each step including

both the studies also covered in McGillivray and Morrissey (2001) and additional ones.

The first important study in the field of aid and taxation was Heller’s cross-section time-

series in which he assessed how aid affects public fiscal behaviour in an econometric

model for eleven African countries (Heller 1975). Heller’s results suggest that aid

increases investment and facilitates a reduction in domestic tax levels and borrowing,

with the magnitude of the effects and the response of public consumption to aid varying

according to the type of aid: he finds that grants tend to be used more for consumption

whereas loans tend to facilitate investment more strongly. Thus while he does not deal

with impacts on taxation in detail, Heller already identifies different effects different aid

components might have. Other cross-country analyses arrive at different results: Khan

and Hoshino (1992), in their cross-sectional analysis of five developing countries in

South and Southeast Asia, find an overall increase in tax effort, which is apparently

driven by the impact of loans, whereas grants tend to reduce the tax effort. However,

Otim (1996), in a government expenditure behaviour study of three South Asian

countries, finds that both loans and grants increase tax effort.

1 The studies they review are Heller 1975, Gang/Khan 1991, Khan/Hoshino 1992, Rubino 1997, Iqbal 1997,

Franco-Rodriguez et al. 1998, McGillivray/Ahmed 1999, and Franco-Rodriguez 2000.

Does Aid Decrease Tax Revenue in Developing Countries?

4

The most comprehensive cross-sectional time-series analysis is conducted by Gupta et al.

(2003) who separately examine the impact of grants and loans on government revenue in

a large sample of developing countries between 1970 and 2000. Their results suggest that

net aid has a negative impact on government revenue, which seems to be driven by a

negative impact of grants on revenue, whereas loans are associated with increased

domestic revenue mobilisation. One potential explanation they offer for why this might

be the case is that loans may imply the need of a repayment, which serves as an incentive

to increase the domestic tax effort. Because of the comprehensiveness and careful study

design of Gupta et al. (2003)’s analysis, throughout the next steps in our analysis we will

use their paper as a reference point.

Turning to country case studies of individual developing countries over the last 15 years,

we see that those have produced similarly mixed results: Gang and Khan (1991), using

time-series data for India, find no significant relationship between aid and tax revenue.

Iqbal (1997) produces a similar result for Pakistan, whereas Franco-Rodriguez et al.

(1998) suggest a negative correlation between aid and taxation in Pakistan. A negative

impact of aid on tax revenue is also suggested by the results of Rubino (1997) and

McGillivray and Ahmed (1999) in their analyses of fiscal response to aid in Indonesia

and the Philippines, respectively. Moreover, the latter study finds that in the Philippines

between 1962 and 1990, aid seems to be associated with public sector fiscal behaviour

that is in general believed to be detrimental to economic development, such as a decrease

of public investment and saving and an increase of public sector borrowing. The findings

of case studies of African countries are mixed as well: While Osei et al. (2003) discover a

positive relationship between aid and tax effort in Ghana, McGillivray and Outtara

(2003)’s results suggest a negative impact of aid on tax revenue in Cote d’Ivoire.

Fagernäs and Roberts (2004), reporting the results of three individual country studies,

find a moderate positive relationship of aid on tax revenue for Malawi and Uganda but a

negative one for Zambia. However, they warn that the causality may be indirect and

spurious due to imperfectly consolidated budgets.

Concerning the analytical frameworks used in previous fiscal response studies, the model

introduced by Heller (1975) has long dominated and for example been employed and

further refined by Mosley et al. (1987), Gang and Khan (1991) and Franco-Rodriguez et

Does Aid Decrease Tax Revenue in Developing Countries?

5

al. (1998). This framework models budget choice and assumes that governments

maximise their utility subject to the budget constraint by attaining various expenditure

and revenue targets they have set, which can be expressed in a quadratic loss function. It

is further assumed that in maximising their utility, decision-makers take into account

alternative uses of public resources and alternative modes of domestic or external

financing. However, these utility functions provide no representation of actual budgetary

processes (Fagernäs/Roberts 2004: 11): no generally accepted rationales for and estimates

of the target fiscal variables have been identified, and real life budget choices are made

by function or objective rather than economic category (investment, consumption) and

are based on changing macroeconomic circumstances and political objectives. The

analytical framework employed for example by Gupta et al. (2003), on the other hand,

refrains from a specific theoretic model and instead treats the research question as an

empirical one which is best examined through an inductive strategy. This study follows

the latter approach.

A preliminary conclusion drawn from these cross-sectional and country case studies

could be that while there is evidence for an effect of aid on taxation, it is ambiguous in

which direction the effect works. A comparison of the different analyses is made difficult

by the fact that all of the above mentioned studies use different models and regression

specifications, but most importantly by the lacking availability of comprehensive data.

Nevertheless, there are some possible, more systematic explanations for the ambiguous

findings: omitted variable bias is one possibility. It may be that strong country-specific

aspects influence the impact aid can have on tax revenue, such as tax policies, the

development orientation of the government, the quality and design of institutions such as

the tax system, overall bureaucracy, political stability, the level of corruption, or many

other possible characteristics yet to be determined.

Since one objective of this study for DFID was to also to look into the relationship

between tax revenue and institutions, the literature on possible links between these

variables shall now briefly be reviewed. The relationship between aid and the quality of

institutions has been much studied since the 1990s under the heading of “good

Does Aid Decrease Tax Revenue in Developing Countries?

6

governance”2, but it has not often been embedded in analyses of aid and tax revenue.

Ghura (1998) finds that the tax revenue of 39 Sub-Saharan African countries between

1985 and 1996 was not only influenced by the economic structure and level of income

but also by the institutional aspects of corruption and the provision of public services in

sectors like education. Gupta et al.’s results, when controlling for corruption, indicate that

the negative effect of grants on tax revenue is larger in countries with higher corruption,

while loans seem to have some offsetting effect against a negative impact of corruption

on tax revenue (2003: 12). In a paper concerned with the relationship between aid

dependence and the quality of governance institutions, Bräutigam (2000) briefly looks at

the impact of aid dependence on tax effort and finds that it can reduce the tax base and

the tax effort, at the same time implying that institutions are weaker. Moreover, the

reduction of the tax base can in the long run result in a further weakening of the

institutional capacity. Thus the quality of institutions has a dual role: it may be an

important determinant of tax revenue in developing countries, and at the same time there

may also be a reverse effect. The latter aspect, though, has not been dealt with much in

the literature.

Another stream of literature relevant for this study deals with taxation issues in

developing countries. The relationship between aid and tax revenue disaggregated into

different types of taxes would have been of particular interest to us but we could not find

any literature explicitly dealing with this. The literature on developing country tax policy

issues in general is informative to a certain extent: when thinking about the possible

reasons aid recipient governments might have for reducing or increasing tax effort it is

important to bear in mind the context in which they operate. Adam and O’Connell (1998)

and Tanzi and Zee (2000) both find that Sub-Saharan African countries have higher tax

revenue to GDP ratios than other developing country regions; in particular the average

tax rates on trade exceed those in other regions by ca. 50%, and the tax burden on

agricultural exports is unusually high as well. At the same time, given the persistently

lower level of GDP, these taxes do not seem to indicate a sustainable movement into the

2 Cf. Crawford (2000), Moore/Robinson (1994), World Bank (1998) for discussions on good governance as

an objective and a condition of development aid, or Bräutigam/Knack (2004) on the relationship between aid dependence and institutional quality, finding evidence for an association of higher aid levels with a deterioration of the quality of governance.

Does Aid Decrease Tax Revenue in Developing Countries?

7

direction of the much higher tax ratios of developed countries but rather that trade taxes

are more economically distortive.

Tanzi and Zee claim that this taxation pattern can partially be explained by the

observation that “in developing countries, tax policy is often the art of the possible rather

than the pursuit of the optimal” (2000: 4). The structure of developing country economies

and constraints in the capacity of the tax administration make it difficult to impose for

example income or value-added taxes and lead to a frequent reliance on many small tax

sources and trade taxes (ibid.). Another factor leading to relatively higher trade taxes is

that in many developing countries, the domestic groups adversely affected by these taxes

are rarely concentrated lobby groups, but usually dispersed individual stakeholders like

consumers and farmers (the latter particularly in developing countries with a high share

of agriculture in GDP and a high share of agricultural products in the country’s exports).

Thus, even though relatively more distortive, trade taxes are often used to finance

transfers to politically powerful or favoured groups like the domestic manufacturing

industries (Adam/O’Connell 1998), especially when those groups lobby for tax

exemptions in the tax types that affect them, which are usually income and corporate

taxes. These considerations indicate that it may be highly insightful to examine in more

detail the impact of aid – overall or grants and loans separately - on different components

of tax revenue.

3. Empirical Model and Data

3.1 Empirical Model

The relationship between aid and revenues from taxation is essentially an empirical

question. The evidence emerging from studies on individual countries and small groups

of countries does not seem to add up consistently in a broader cross-country picture. Such

broader aggregate evidence would be useful as it could provide the necessary background

to ascertain the evidence emerging from more micro-econometric studies. Moreover,

despite not offering the kind of specific knowledge which is applicable in policy settings,

an aggregate analysis can well function as a signpost in the still almost uncharted territory

of the relation between aid and tax revenue.

Does Aid Decrease Tax Revenue in Developing Countries?

8

One of the main obstacles to this type of study is the lack of data. As outlined in the

literature review, the systematic evidence on a large sample is scant, with the remarkable

exception of the study by Gupta et al. (2003). Our approach is in line with theirs and

models variations in tax ratios across countries and time as a function of income from aid

and other main determinants of tax revenue. We are interested in the following regression

model:

ittiititit XAIDREV εθλγβα +++++= (1)

Where itREV represents the tax revenue in percent of GDP of country i in year t , itAID

indicates the inflow of net aid in percent of GDP of country i in year t . itX is a vector of

control variables, whereas iλ controls for country specific time invariant effects, and tθ

are year dummies, controlling for year specific economic and policy shocks common to

all countries. itε is a random error term.

The advantage of this approach is that it is not dependent on a specific macroeconomic

model. Yet it depends crucially on how reasonable its assumptions are, and therefore on

what controls are included in vector itX . Specifically we propose to use, first of all, the

logarithm of GDP per capita. However crude, GDP per capita is a reasonable proxy of the

level of economic development. Economic development is, in turn, a key determinant of

tax revenue since as countries develop their tax bases expand more than proportionately

to the growth in their level of income (Tanzi 1992). Moreover, it is suggested that an

increase in income not only reflects a higher capacity of the citizens to pay taxes, but also

a greater capacity of policy makers to levy and collect taxes (Chelliah 1971). Second we

decide to include the percentage share of agricultural and industrial value added over

GDP. These variables allow controlling for the structure of the economy, which is an

important determinant of tax revenue (Tanzi 1992). We expect a large agricultural sector

to be detrimental for tax revenue since farmers are difficult to tax directly3 and a large

share of agricultural activity is normally for subsistence. On the other hand, having a

strong industrial sector is likely to be conducive to domestic tax revenue since it is easier

3 Implicit forms of taxing agriculture, while common in many developing countries, shall not be dealt with

here because they do not directly affect tax revenue.

Does Aid Decrease Tax Revenue in Developing Countries?

9

for policy makers to tax industrial activities, due to the greater availability of information

on their income and profit. Finally, we want to include a measure of openness because, as

argued in the literature review, certain characteristics of trade which passes the borders of

a country make it an important source of tax revenue for some countries. This is partly

due to the fact that in developing countries it is often the most monetized sector of the

economy. Moreover, the administrative ease with which trade taxes can be collected

makes them an attractive source of domestic tax revenue when administrative capacity to

collect taxes from other sources is weak and inefficient (Linn/Weitzel 1990; Lotz/Morss

1970). We measure openness as the sum of imports and exports in percent of GDP.

Clearly this estimation strategy can highlight only a correlation between our variables of

interest and cannot explain the mechanisms underlying their relation. Indeed aid and

revenue are likely to be influenced by common factors. The institutional setting and the

quality of the institutions of a country, for example, are likely to be reflected both in the

aid inflow and in the tax capacity of a country. We will turn to this point in more detail in

section 4. Yet our primary interest is focused on the direction and the strength of the

correlation between aid and tax revenue, which has to be established before any

underlying mechanism is ascertained.

Another important advantage of our econometric model is that is it flexible enough to

allow including further variables and moving consistently towards more disaggregated

specifications. In particular, we argue that interesting results can emerge when looking

more specifically at the composition of tax revenue and at the composition of aid. Our

first step in this direction is to consider the composition of aid, looking separately at

grants and loans. This distinction is well established in the literature that has investigated

the different impacts of these aid channels on development (cf. Cordella/Ulku 2004,

Morrissey et al. 2006). Hence, across all regressions, we first use net aid as the key

explanatory variable and second grants and net loans.

Finally, to estimate our baseline specification we use ordinary least squares (OLS).

Having a panel dataset allows us to control for country fixed effects.

Does Aid Decrease Tax Revenue in Developing Countries?

10

3.2 Data Description

Data on tax revenue is drawn from the IMF’s “Government Finance Statistics” referring

to “consolidated central government”4. We checked the data for inconsistencies and drop

the few countries displaying implausible figures (see Appendix). We have also checked

for changes in countries’ budgeting procedures and revenues registration. For example

some countries have switched to an accrual budgeting system from a cash system, thus

undermining the coherence of the time series. We have dealt with this particular issue by

comparing the figures, tracing the changes and controlling the stability of our results to

changes in the budgeting system.

In order to calculate the share of tax revenue as a percentage of GDP we use data on GDP

available from the IMF’s “International Financial Statistics”. Using the same source as

for tax revenue – and having both variables expressed in nominal local currency - has

enhanced the coherence of our dataset. Yet the limited availability of data on both

revenue and GDP was largely responsible for constraints in terms of which countries we

were able to use in the regressions.

Data on the key independent variable, net aid and its components grants and net loans,

are taken from the OECD’s “International Development Statistics”. This dataset is

composed of two datasets, according to the classification of the recipient country which

was used up until 2004. Net aid is the sum of total Official Development Assistance

(ODA) and Official Assistance (OA) from all members in the DAC and it includes

grants, concessional loans with a grant element of at least 25 percent, and technical

cooperation. “Net” means that principal and interest repayments or forgiveness on

previous loans have been accounted for. Furthermore the OECD collects data on aid that

distinguish between aid commitments by purpose, one “purpose” being programme

assistance. These data are of particular interest as their different design could hint to

some of the institutional factors behind our correlation of interest. However, the data are

too scant to allow any cross-country regression.

4 Although “consolidated general government” would be the ideal variable here, due to the unavailability of

comprehensive data on this series we chose to use consolidated central government. We do not assume this to be very problematic since most external assistance is routed through the central government budget.

Does Aid Decrease Tax Revenue in Developing Countries?

11

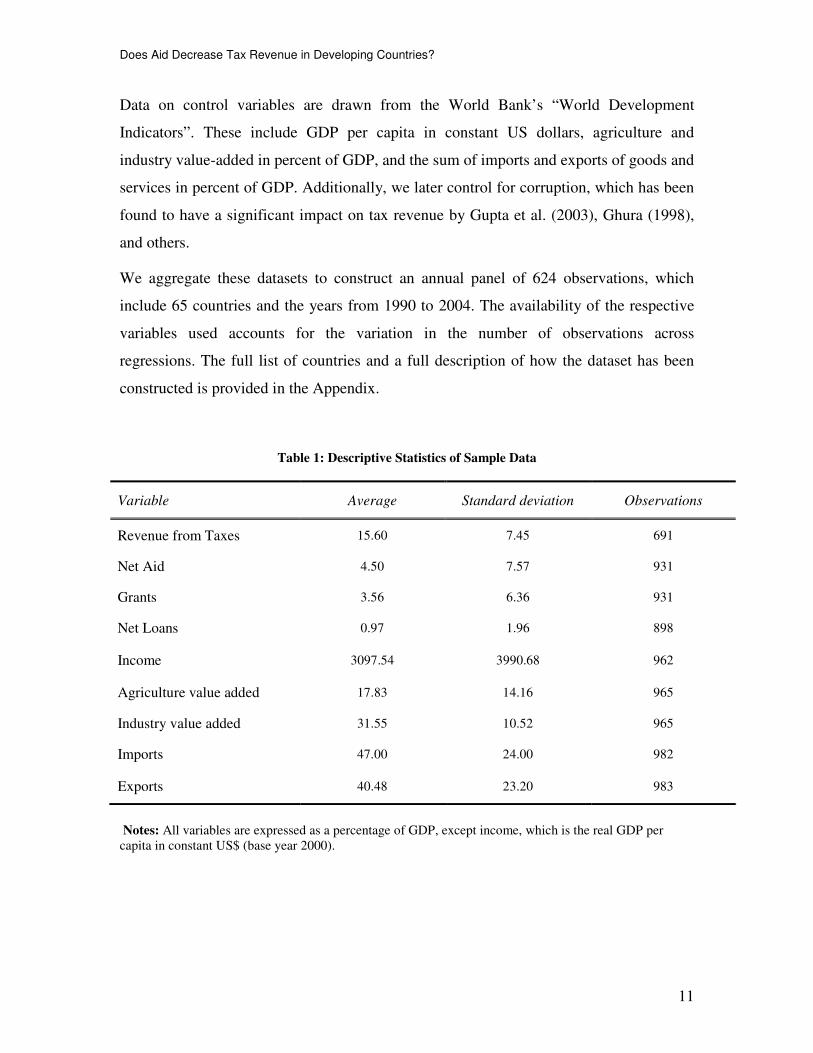

Data on control variables are drawn from the World Bank’s “World Development

Indicators”. These include GDP per capita in constant US dollars, agriculture and

industry value-added in percent of GDP, and the sum of imports and exports of goods and

services in percent of GDP. Additionally, we later control for corruption, which has been

found to have a significant impact on tax revenue by Gupta et al. (2003), Ghura (1998),

and others.

We aggregate these datasets to construct an annual panel of 624 observations, which

include 65 countries and the years from 1990 to 2004. The availability of the respective

variables used accounts for the variation in the number of observations across

regressions. The full list of countries and a full description of how the dataset has been

constructed is provided in the Appendix.

Table 1: Descriptive Statistics of Sample Data

Notes: All variables are expressed as a percentage of GDP, except income, which is the real GDP per capita in constant US$ (base year 2000).

Variable Average Standard deviation Observations

Revenue from Taxes 15.60 7.45 691

Net Aid 4.50 7.57 931

Grants 3.56 6.36 931

Net Loans 0.97 1.96 898

Income 3097.54 3990.68 962

Agriculture value added 17.83 14.16 965

Industry value added 31.55 10.52 965

Imports 47.00 24.00 982

Exports 40.48 23.20 983

Does Aid Decrease Tax Revenue in Developing Countries?

12

4. Results

An overview of our variables is given in Table 1. The figures are in line with previous

studies and indicate that on average the revenues from taxation equal 15.6% of the

countries’ GDP. This percentage is much higher in OECD countries, where just income

taxes are around 13% of GDP (Tanzi/Zee 2000). The table also shows that the share of

grants is much higher than the one of loans, which will influence our results. All our

control variables display sensible values, given that most of the countries in our study are

middle income countries. As for income, one way of grasping its meaning is to think of it

as equalling 8.50$ a day per capita.

Table 2: Baseline results: Aid on Tax revenue

(1) (2)

Tax Revenue Tax Revenue

0.053 Net Aid

(0.040)

0.077** Grants

(0.036)

-0.068 Net Loans

(0.095)

3.352*** 3.506*** Income

(1.249) (1.264)

0.000 0.000 Industry value added

(0.033) (0.034)

0.003 0.002 Agriculture value added

(0.050) (0.049)

-0.016* -0.016* Trade

(0.009) (0.009)

Observations 624 613

Countries 65 64

R-squared 0.940 0.938

Notes: OLS Estimates. Robust standard errors in parentheses. Year and country fixed effects are included. (***), (**), (*) denote significance at the 1, 5, and 10 percent levels, respectively. All variables are expressed as percentages of GDP, except income, which is the log of GDP per capita. Trade refers to Exports plus Imports.

Does Aid Decrease Tax Revenue in Developing Countries?

13

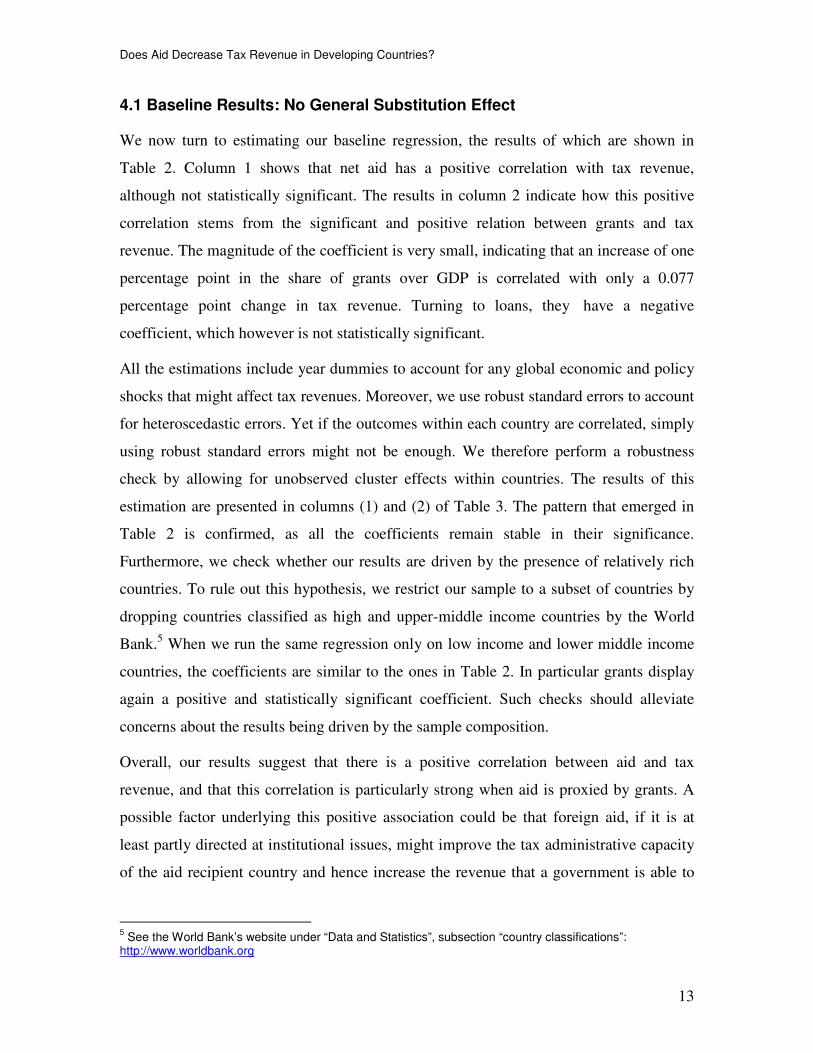

4.1 Baseline Results: No General Substitution Effect

We now turn to estimating our baseline regression, the results of which are shown in

Table 2. Column 1 shows that net aid has a positive correlation with tax revenue,

although not statistically significant. The results in column 2 indicate how this positive

correlation stems from the significant and positive relation between grants and tax

revenue. The magnitude of the coefficient is very small, indicating that an increase of one

percentage point in the share of grants over GDP is correlated with only a 0.077

percentage point change in tax revenue. Turning to loans, they have a negative

coefficient, which however is not statistically significant.

All the estimations include year dummies to account for any global economic and policy

shocks that might affect tax revenues. Moreover, we use robust standard errors to account

for heteroscedastic errors. Yet if the outcomes within each country are correlated, simply

using robust standard errors might not be enough. We therefore perform a robustness

check by allowing for unobserved cluster effects within countries. The results of this

estimation are presented in columns (1) and (2) of Table 3. The pattern that emerged in

Table 2 is confirmed, as all the coefficients remain stable in their significance.

Furthermore, we check whether our results are driven by the presence of relatively rich

countries. To rule out this hypothesis, we restrict our sample to a subset of countries by

dropping countries classified as high and upper-middle income countries by the World

Bank.5 When we run the same regression only on low income and lower middle income

countries, the coefficients are similar to the ones in Table 2. In particular grants display

again a positive and statistically significant coefficient. Such checks should alleviate

concerns about the results being driven by the sample composition.

Overall, our results suggest that there is a positive correlation between aid and tax

revenue, and that this correlation is particularly strong when aid is proxied by grants. A

possible factor underlying this positive association could be that foreign aid, if it is at

least partly directed at institutional issues, might improve the tax administrative capacity

of the aid recipient country and hence increase the revenue that a government is able to

5 See the World Bank’s website under “Data and Statistics”, subsection “country classifications”:

http://www.worldbank.org

Does Aid Decrease Tax Revenue in Developing Countries?

14

Table 3: Robustness Checks

Notes: OLS Estimates. Year and country fixed effects included. Columns (1) and (2): clustered standard errors in parenthesis. Columns (3) and (4): robust standard errors in parenthesis. (***), (**), (*) denote significance at the 1, 5, and 10 percent levels, respectively. All variables are expressed as percentages of GDP, except income, which is the log of GDP per capita. Trade refers to Exports plus Imports. Country classification according to income is taken from the World Bank’s list of economies (July 2006).

generate from taxes. Grants might have a stronger influence on this association since they

may be targeted more towards improving institutions and capacity, whereas loans are

often given for infrastructure projects and other capital investments.

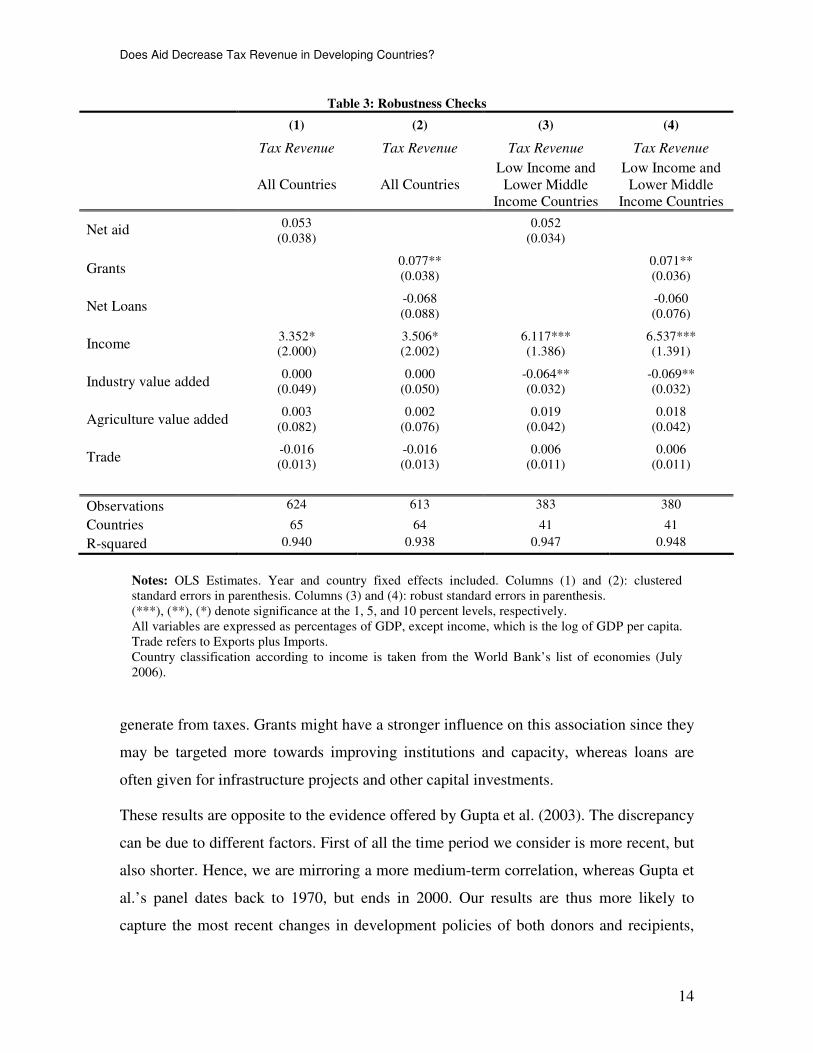

These results are opposite to the evidence offered by Gupta et al. (2003). The discrepancy

can be due to different factors. First of all the time period we consider is more recent, but

also shorter. Hence, we are mirroring a more medium-term correlation, whereas Gupta et

al.’s panel dates back to 1970, but ends in 2000. Our results are thus more likely to

capture the most recent changes in development policies of both donors and recipients,

(1) (2) (3) (4)

Tax Revenue Tax Revenue Tax Revenue Tax Revenue

All Countries All Countries Low Income and

Lower Middle Income Countries

Low Income and Lower Middle

Income Countries

0.053 0.052 Net aid

(0.038) (0.034)

0.077** 0.071** Grants

(0.038) (0.036)

-0.068 -0.060 Net Loans

(0.088) (0.076)

3.352* 3.506* 6.117*** 6.537*** Income

(2.000) (2.002) (1.386) (1.391)

0.000 0.000 -0.064** -0.069** Industry value added

(0.049) (0.050) (0.032) (0.032)

0.003 0.002 0.019 0.018 Agriculture value added

(0.082) (0.076) (0.042) (0.042)

-0.016 -0.016 0.006 0.006 Trade

(0.013) (0.013) (0.011) (0.011)

Observations 624 613 383 380

Countries 65 64 41 41

R-squared 0.940 0.938 0.947 0.948

Does Aid Decrease Tax Revenue in Developing Countries?

15

which, during the 1990s, have moved towards new strategies and approaches. The debate

on aid effectiveness has resulted in a stronger focus on governance institutions, which

also touches upon administrative effectiveness and thus concerns the collection of taxes.

Therefore, the positive coefficient of grants might reflect such a recent change in

Table 4: Aid on Revenue in Two Different Time Periods

(1) (3) (2) (4)

Log Revenue Log Revenue Log Revenue Log Revenue

1975-2000 1975-2000 1990-2000 1990-2000

-0.010*** 0.006* Net Aid

(0.003) (0.004)

0.000*** -0.000 Net Aid

(0.000) (0.000)

-0.016*** 0.000 Grants

(0.003) (0.005)

0.000*** 0.000 (Grants)2

(0.000) (0.000)

0.011*** 0.014*** Net Loans

(0.004) (0.004)

-0.000 -0.000* (Net Loans)2

(0.000) (0.000)

-0.000*** -0.000*** 0.000*** 0.000*** Income

(0.000) (0.000) (0.000) (0.000)

-0.011*** -0.012*** -0.008*** -0.008*** Industry value added

(0.001) (0.001) (0.003) (0.003)

0.008*** 0.008*** 0.003* 0.003* Agriculture value added (0.001) (0.001) (0.002) (0.002)

0.003*** 0.003*** 0.002*** 0.002*** Trade

(0.000) (0.000) (0.001) (0.001)

Observations 1943 1943 708 708

Countries 107 107 92 92

R-squared 0.882 0.882 0.921 0.922

Notes: OLS estimates. Country fixed effects included. Standard errors in parentheses. Estimates obtained based on the dataset used by Gupta et al. (2003). (***), (**), (*) denote significance at the 1, 5, and 10 percent levels, respectively. All variables are expressed as percentages of GDP, except income, which is the log of GDP per capita. Trade refers to Exports plus Imports.

Does Aid Decrease Tax Revenue in Developing Countries?

16

development policies. Secondly, our specification is slightly different from the one used

by Gupta et al., as we use tax revenue as dependent variable rather than total government

revenue. Total revenue is a more aggregate variable, as it also includes income from, for

example, state assets and rents from mineral resources. It is therefore less apt to capture

the factors directly linked to the tax system, which is essentially what we are interested

in.

In order to further strengthen our findings we re-estimated Gupta et al.’s (2003)

regressions on a more recent time period but on their original dataset, which we received

from the authors upon request. Columns (1) and (2) of Table 4 show Gupta et al.’s

baseline results as published in their paper, which we were able to exactly replicate. Their

baseline results show an overall negative relationship between aid and domestic revenue,

which seems to be driven by the negative correlation of grants with revenue, whereas net

loans have a positive coefficient. However, when we use their specification on their data

from 1990 to 2000, which is the time period overlapping with our own dataset, we see

that the coefficient of aid has switched its sign. From column (3) we can see that aid has a

positive association with domestic revenue, which is significant at 10%. The

decomposition of aid in column (4) shows that this positive association is driven by the

positive relationship between net loans and domestic revenue while grants have an

insignificant association with domestic revenue which is no longer negative. The

coefficients maintain these signs and even increase in magnitude when we slightly

change the specification by including year dummies and redefining the dependent

variable to domestic revenue as a share of GDP instead of the logarithm of domestic

revenue as a share of GDP. In sum, this analysis lends support to our results that, post

1990, the aggregate relationship between aid and tax revenue is positive.

4.2 Role of Corruption: No Differential Impact of Aid

One possible direction to expand our analysis is to include some measure of governance

quality in order to see whether any specific pattern linked to governance quality emerges.

This type of exercise is relevant in light of the emphasis that the debate on aid policy has

put on institutional dynamics in aid recipient countries. One possible indicator of

Does Aid Decrease Tax Revenue in Developing Countries?

17

governance quality is the level of corruption. More specifically, corruption is important

for our discussion because corruption is detrimental for revenue performance. Corruption

can indeed be used as a proxy for fiscal corruption, and the literature has described how

the specific features of the tax system favour the diffusion of corruption by complicated

tax laws, weak legal and judicial systems, excessive discretionary power vested in tax

administrators, lack of accountability and transparency in the tax administration, the

necessity for frequent communication between tax payers and tax officials, and low

salaries in the public sector (Tanzi 1998).

The existing literature has looked at the role of corruption by focusing on the individual

explanatory power of a corruption variable in explaining the cross country variation of

revenue from taxes (Ghura 1998; Gupta et al. 2003). Our approach is slightly different

because we attempt to see whether net aid and, more interestingly, grants and net loans

have a different relation with revenues due specifically to the presence of corruption.

That is to say that, instead of controlling for the correlation between corruption and

revenue, we look at the interaction of aid and corruption. One would expect that aid,

whether in the form of grants or net loans, has a marginally higher impact on revenue

collection in countries with low corruption than in countries with high corruption.

In order to test this hypothesis we use a comprehensive index on corruption that has been

collected by the World Bank since 1996 in its publication “Governance Indicators 1996-

2005” together with five other governance indicators (Kaufmann et al. 2006). There is

therefore only a partial overlap with the years covered by our dataset. Nonetheless we

chose this index because it is constructed from multiple indices and surveys assembled by

various institutions, which strengthens its validity compared to single survey indices.6

Since we are mostly interested in the cross-country variation of corruption we have

exploited the variation of the mean of the index for each country to construct two

dummies: low corruption and high corruption. We have used the median of the

distribution of the mean (of the corruption index for each country) to identify countries

with lower corruption. This approach allows us to have an equal number of countries in

6 The indicator is constructed in order to have a standardised normal distribution across countries. Hence it

lies between -2.5 and 2.5 for almost all countries, with highly corrupted countries scoring towards -2.5. The methodology and the sources used are described in detail in Kaufmann et al. (2003) and Kaufmann et al. (2006).

Does Aid Decrease Tax Revenue in Developing Countries?

18

both groups, and, more importantly, prevents our results from being driven by any

particular subset of countries. Our procedure is simple and the key advantage of this is

that a binary variable, constructed in this way, can be more easily used to cover the entire

time period we are interested in. However, this strategy depends on the assumption that a

country’s governance institutions do not change substantially over the time period we are

looking at. This assumption may not hold for every country in the sample, but it is

generally buttressed by the low variations in the World Bank governance indicators per

country between 1996 and 2004 (ibid.).

Our estimation strategy considers an alternative specification of equation (1) to account

for the different correlation aid might have with revenue in highly corrupted countries.

We do so by introducing an interaction term capturing the interaction between corruption

and net aid, grants and net loans, respectively.

Therefore, the baseline equation is augmented to:

ittiitititit XLowCorrAIDAIDREV εθλβββα ++++++= )())(()( 321

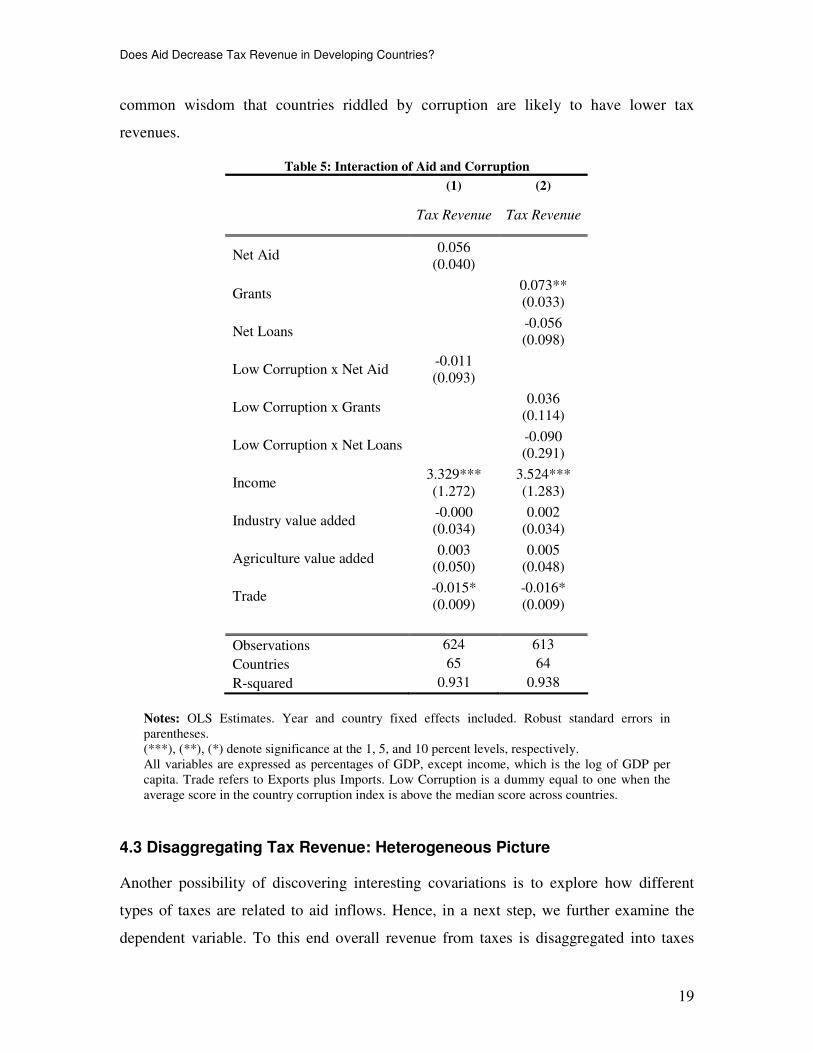

The results are shown in Table 5. All three coefficients for net aid, grants and net loans

remain stable in sign, magnitude and significance. In particular, the coefficient for grants

is still positive and significant at 5%, indicating a positive association with tax revenue.

Yet the key parameter of interest is 2β . If this coefficient is significantly different from

zero, then the relation between aid and tax revenue is different in countries with low

corruption in comparison to countries with high corruption. However, from column (1) in

Table 5 we can see that the coefficient of the interaction term is far from being

statistically significant. In column (2) we decompose aid into grants and net loans and

interact both components with the dummy low corruption. The coefficients for both

interactions turn out statistically insignificant. We therefore do not find any solid

evidence for a differential relation between aid and tax revenue when the recipient

country is highly corrupt as opposed to less corrupt. One has to keep in mind that this

result does not say anything about the direct relation between corruption and tax revenue,

which is bundled in the country specific effect. So the result does not question the

Does Aid Decrease Tax Revenue in Developing Countries?

19

common wisdom that countries riddled by corruption are likely to have lower tax

revenues.

Table 5: Interaction of Aid and Corruption

(1) (2)

Tax Revenue Tax Revenue

0.056 Net Aid

(0.040)

0.073** Grants

(0.033)

-0.056 Net Loans

(0.098)

-0.011 Low Corruption x Net Aid

(0.093)

0.036 Low Corruption x Grants

(0.114)

-0.090 Low Corruption x Net Loans

(0.291)

3.329*** 3.524*** Income

(1.272) (1.283)

-0.000 0.002 Industry value added

(0.034) (0.034)

0.003 0.005 Agriculture value added

(0.050) (0.048)

-0.015* -0.016* Trade

(0.009) (0.009)

Observations 624 613

Countries 65 64

R-squared 0.931 0.938

Notes: OLS Estimates. Year and country fixed effects included. Robust standard errors in parentheses. (***), (**), (*) denote significance at the 1, 5, and 10 percent levels, respectively. All variables are expressed as percentages of GDP, except income, which is the log of GDP per capita. Trade refers to Exports plus Imports. Low Corruption is a dummy equal to one when the average score in the country corruption index is above the median score across countries.

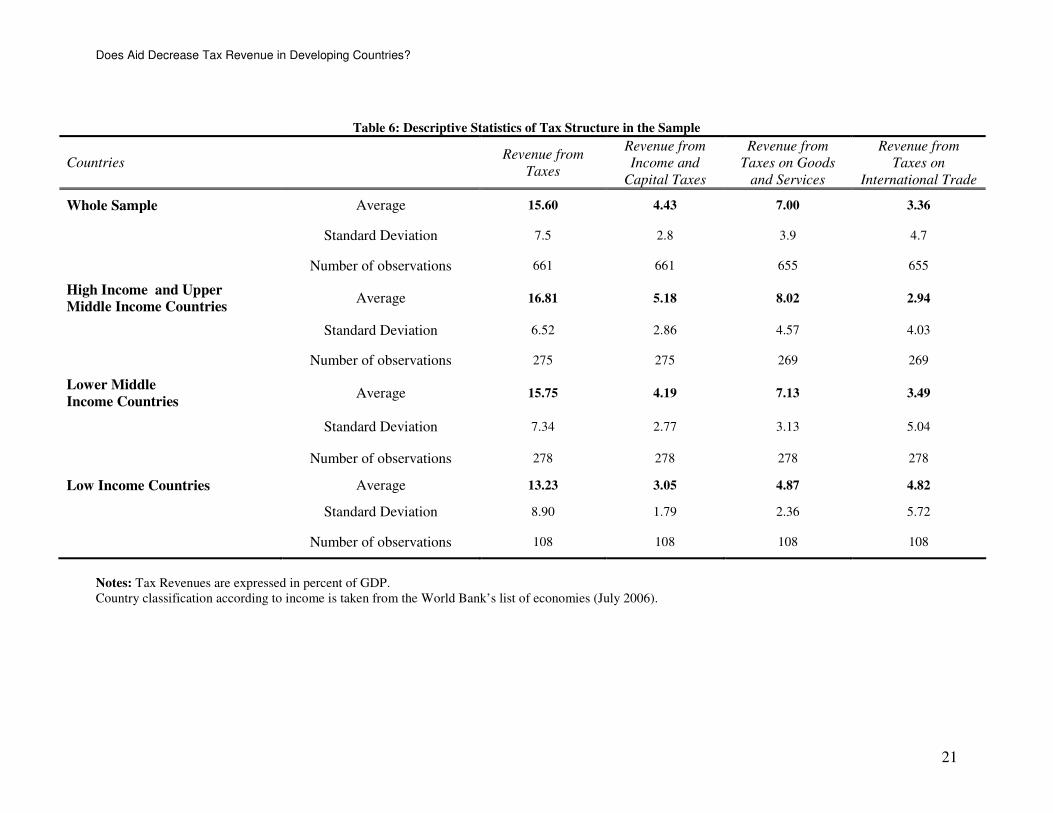

4.3 Disaggregating Tax Revenue: Heterogeneous Picture

Another possibility of discovering interesting covariations is to explore how different

types of taxes are related to aid inflows. Hence, in a next step, we further examine the

dependent variable. To this end overall revenue from taxes is disaggregated into taxes

Does Aid Decrease Tax Revenue in Developing Countries?

20

from a) income, profits and capital gains, b) goods and services, and c) international

trade. Table 6 shows how they are distributed in our sample. The figures in Table 6

confirm that the overall positive relationship of aid and tax revenue can not be entirely

driven by endogeneity: with rising national income overall tax revenue increases as well,

whereas net aid is negatively correlated with income (not shown). We shall return to

aspects of this table during the interpretation of the regression results.

By re-estimating the baseline regression on each of the three tax types respectively, we

see that the correlation with aid is heterogeneous across the different types of taxes; the

results are presented in Table 7.

Starting with income and capital taxes, column (1) shows that net aid has a negative and

significant association with revenues from these taxes, which is confirmed in column (2)

for both grants and loans. Such a response might be driven by policy makers’ decision to

use aid as a substitute for domestic taxes and thus to try to free resources for the private

sector by lowering income and capital taxes. The developmental reasoning behind such a

policy would be that since capital taxes may inhibit private sector investments and

individual labour supply, a lowering of such taxes could be conducive to economic

growth. However, as we can see in Table 6, average revenue from income taxes is only

4.4% of GDP in our sample countries, which is very low compared to an average income

and capital tax revenue of around 12.5-13% of GDP in OECD countries between 1990

and 20047. Hence, the observable substitution effect is probably less developmentally

oriented and rather to the benefit of powerful lobby groups whose tax burden might have

been lowered as a response to aid inflows. This is precisely the kind of substitution effect

donors are concerned about.

Among the control variables, GDP per capita (Income) is worth mentioning. Its strong

positive association with revenues from income and corporate taxes is not surprising as

one can expect countries with higher income to have a generally better administrative

capacity, which allows them to adequately impose and collect direct taxes, and also that

they have a greater share of formal economic activity than less developed countries,

which enables them to tax the monetary gains from such activity in the first place.

7 Figures drawn from the OECD’s annual Revenue Statistics publication.

Does Aid Decrease Tax Revenue in Developing Countries?

21

Table 6: Descriptive Statistics of Tax Structure in the Sample

Notes: Tax Revenues are expressed in percent of GDP. Country classification according to income is taken from the World Bank’s list of economies (July 2006).

Countries

Revenue from

Taxes

Revenue from

Income and

Capital Taxes

Revenue from

Taxes on Goods

and Services

Revenue from

Taxes on

International Trade

Whole Sample Average 15.60 4.43 7.00 3.36

Standard Deviation 7.5 2.8 3.9 4.7

Number of observations 661 661 655 655

High Income and Upper

Middle Income Countries Average 16.81 5.18 8.02 2.94

Standard Deviation 6.52 2.86 4.57 4.03

Number of observations 275 275 269 269

Lower Middle

Income Countries Average 15.75 4.19 7.13 3.49

Standard Deviation 7.34 2.77 3.13 5.04

Number of observations 278 278 278 278

Low Income Countries Average 13.23 3.05 4.87 4.82

Standard Deviation 8.90 1.79 2.36 5.72

Number of observations 108 108 108 108

Does Aid Decrease Tax Revenue in Developing Countries?

22

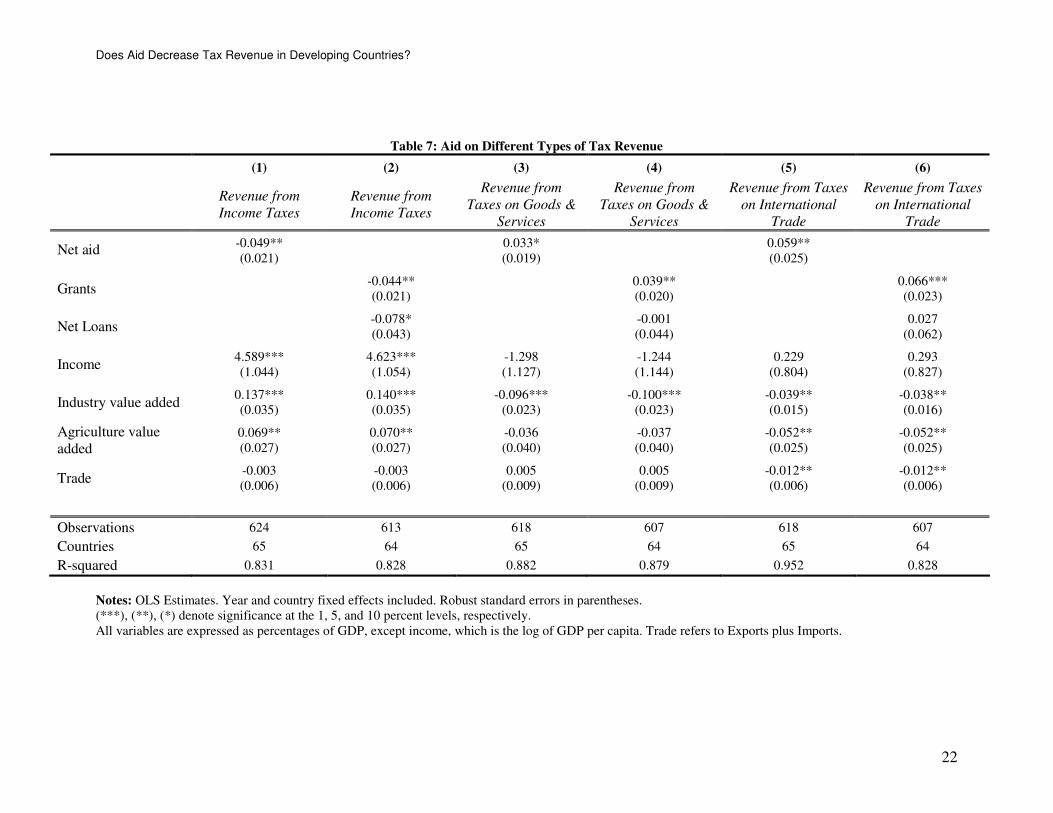

Table 7: Aid on Different Types of Tax Revenue

Notes: OLS Estimates. Year and country fixed effects included. Robust standard errors in parentheses. (***), (**), (*) denote significance at the 1, 5, and 10 percent levels, respectively. All variables are expressed as percentages of GDP, except income, which is the log of GDP per capita. Trade refers to Exports plus Imports.

(1) (2) (3) (4) (5) (6)

Revenue from

Income Taxes

Revenue from

Income Taxes

Revenue from

Taxes on Goods &

Services

Revenue from

Taxes on Goods &

Services

Revenue from Taxes

on International

Trade

Revenue from Taxes

on International

Trade

-0.049** 0.033* 0.059** Net aid

(0.021) (0.019) (0.025)

-0.044** 0.039** 0.066*** Grants

(0.021) (0.020) (0.023)

-0.078* -0.001 0.027 Net Loans

(0.043) (0.044) (0.062)

4.589*** 4.623*** -1.298 -1.244 0.229 0.293 Income

(1.044) (1.054) (1.127) (1.144) (0.804) (0.827)

0.137*** 0.140*** -0.096*** -0.100*** -0.039** -0.038** Industry value added

(0.035) (0.035) (0.023) (0.023) (0.015) (0.016)

0.069** 0.070** -0.036 -0.037 -0.052** -0.052** Agriculture value added (0.027) (0.027) (0.040) (0.040) (0.025) (0.025)

-0.003 -0.003 0.005 0.005 -0.012** -0.012** Trade

(0.006) (0.006) (0.009) (0.009) (0.006) (0.006)

Observations 624 613 618 607 618 607

Countries 65 64 65 64 65 64

R-squared 0.831 0.828 0.882 0.879 0.952 0.828

Does Aid Decrease Tax Revenue in Developing Countries?

23

Columns (3) and (4) report the association between revenues from goods and services

taxes and net aid, grants and net loans. The coefficients indicate that net aid and grants

have a positive association with taxes from goods and services, whereas the coefficient

for net loans is no longer significant. The expansion of goods and services taxes, for

example by introducing a value-added tax, is often favoured in donor strategies because

this might broaden the tax base and thus sustainably increase tax revenue. Hence grants

are sometimes tied to a tax policy reform targeted at goods and services taxes - a policy

that was increasingly pursued since the 1990s (Gloppen/Rakner 2002). Although not

always successfully implemented, such tax reforms may be reflected in the aid

coefficients in columns (3) and (4).

Lastly, the results in columns (5) and (6) suggest that while net aid and grants have a

strong positive and significant correlation with trade taxes, the association of net loans

with trade taxes seems to be positive as well, but insignificant. These coefficients might

be explained by considering the ones in relation with income taxes: as income taxes are

lowered, there is a need for increasing revenue from other sources, for example trade

taxes. This might especially occur when donors demand an overall stable or increased tax

ratio. From a developmental perspective, an increase in trade tax rates is not desirable

considering the distortions trade taxes create in an economy through increased prices for

consumers of imports or lowered competitiveness of domestic producers of exports

(depending on the respective shares of taxes on imports and exports). However, an

increase in revenue from trade taxes might also be caused not by increased tax rates but

by an increased effectiveness in tax collection in general, which may be an objective of

aid. Another possible explanation is endogeneity: countries that have comparatively high

trade taxes also tend to be poorer, as can be seen in Table 6, and it may be the latter

aspect that results in a higher inflow of aid. Concerning the control variables, the trade

coefficient is of particular interest. It is negative and significant, which could again be

due to a stronger reliance on trade taxes in weaker economies: a weak economy can have

a higher share of revenue from trade taxes than a stronger economy and at the same time

a lower trade-to-GDP ratio.

Looking at the overall results – a correlation of aid with lower income tax revenue and

higher goods and services as well as trade tax revenue – it is difficult to argue for a direct

Does Aid Decrease Tax Revenue in Developing Countries?

24

link between aid and tax revenue that would affect different types of taxes in a different

way, but consistently across countries. The pattern of coefficients in Table 7 hints more

towards being driven by omitted variable bias. There may not be a direct impact of aid on

different types of taxes but it may be intervening factors that are related to both aid and

tax revenue that drive the observed relationships. Potentially important omitted factors

may be a combination of the economic structure and the quality (in terms of

effectiveness) of administrative institutions as measured by the World Bank’s governance

indicators like corruption, government effectiveness, or the rule of law8, which could

influence both aid and tax revenue.

First, on their potential influence on aid: the economic structure of a country in terms of

the size of its formal economic sector or the diversification of production is a key

determinant of aid insofar as a weak economic structure is generally correlated with low

GDP per capita. However, controlling for level of income and the size of the agricultural

and industrial sectors and trade, as done in our regressions, may not fully capture a

country’s economic structure: a large agricultural sector does not say much about how

export-oriented this sector is and hence how formalised and thus taxable. The influence

of institutional quality on aid is theoretically ambiguous: aid disbursements may either be

higher for countries with better institutions because aid effectiveness is expected to be

higher in these countries, or they may be higher for weaker countries in order to try to

strengthen their administrative effectiveness.

The potential influence of institutions on tax revenue is more determinate: countries with

weak administrative capacity may not be able to collect much revenue from taxes which

can be evaded more easily, such as taxes on income and profits, and may thus have to

rely more strongly on taxes which are relatively easy to collect, such as taxes on trade

which has to pass official customs. In addition to this, the economic structure of a country

further constrains the options of taxation, that is to what extent there is formal economic

activity that can be taxed. Hence, the interplay between economic structure and

administrative capacity in a country may influence both the overall amount of tax

8 On the construction of these indicators see above section 4.2, and (Kaufmann et al. 2006).

Does Aid Decrease Tax Revenue in Developing Countries?

25

revenue that it is able to collect, given certain tax rates, but also the choice of which types

of taxes it aims to collect.

Even if a poor country aims at reforming its tax policy, maybe assisted by a donor

project, its success may be severely constrained by the given administrative capacity and

economic structure. For example, an attempt towards broadening the tax base by

extending income and corporate taxes may not lead to an increase in tax revenue if tax

collection capacity is not enhanced at the same time and enforcement of these taxes is

low. Furthermore, an increase of income taxes may not be a viable option if there is little

formal income. Gloppen and Rakner (2002) report these and other weaknesses in the

implementation of recent donor-supported tax reforms in several Sub-Saharan African

countries.

Our data, as presented in Table 6, provide some support for such an interpretation of the

relationship between tax revenue structure, economic structure, and administrative

effectiveness, assuming that the income level of a country can be seen as a rough proxy

for both economic structure and administrative capacity: high and upper medium income

countries have a higher overall share of tax revenue in GDP than lower medium income

countries, which in turn have a higher tax revenue than low income countries. Richer

countries also rely more strongly on taxes on income and capital as well as on goods and

services, whereas poorer countries derive relatively more revenue from trade taxes. We

will now examine the relationship between tax revenue and institutions in a little more

detail.

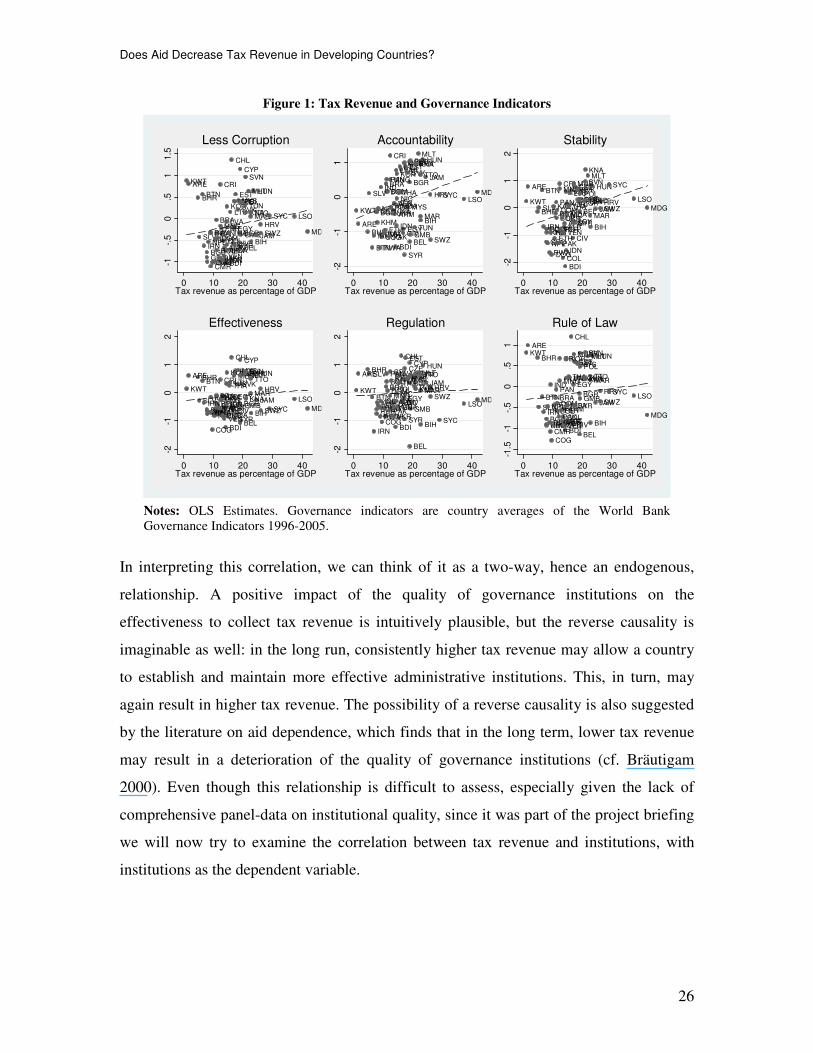

4.4 Tax Revenue and Institutions: A Two-Way Relationship?

Overall, tax revenue as a share of GDP is positively correlated with all six World Bank

Governance Indicators, as shown in Figure 1. The association is strongest and statistically

significant for the indicators less corruption (at 10%), voice and accountability, and

political stability (both at 1%)9.

9 Table not shown.

Does Aid Decrease Tax Revenue in Developing Countries?

26

Figure 1: Tax Revenue and Governance Indicators

Notes: OLS Estimates. Governance indicators are country averages of the World Bank Governance Indicators 1996-2005.

In interpreting this correlation, we can think of it as a two-way, hence an endogenous,

relationship. A positive impact of the quality of governance institutions on the

effectiveness to collect tax revenue is intuitively plausible, but the reverse causality is

imaginable as well: in the long run, consistently higher tax revenue may allow a country

to establish and maintain more effective administrative institutions. This, in turn, may

again result in higher tax revenue. The possibility of a reverse causality is also suggested

by the literature on aid dependence, which finds that in the long term, lower tax revenue

may result in a deterioration of the quality of governance institutions (cf. Bräutigam

2000). Even though this relationship is difficult to assess, especially given the lack of

comprehensive panel-data on institutional quality, since it was part of the project briefing

we will now try to examine the correlation between tax revenue and institutions, with

institutions as the dependent variable.

ALBARM

BHR

BGDBEL

BTN

BOL

BIH

BRA

BGR

BDIKHMCMR

CHL

COL

COG

CRI

CIV

HRV

CYP

CZE

DOM

EGYSLV

EST

ETHGMB

GEO

HUN

IND

IDN

IRN

JAM

KAZ

KOR

KWT

LVALSO

LTU

MDG

MYS

MLT

MUS

MDA

MNG

MAR

NPL NIC

PAK

PANPER

POL

RWA

SYCSVK

SVN

KNA

SWZ

SYR

THA

TTOTUN

UKR

ARE

VEN

-1-.

50

.51

1.5

0 10 20 30 40Tax revenue as percentage of GDP

Less Corruption

ALB

ARM

BHR

BGD

BELBTN

BOL

BIH

BRA BGR

BDI

KHM

CMR

CHL

COL

COG

CRI

CIV

HRV

CYPCZE

DOM

EGY

SLV

EST

ETHGMB

GEO

HUN

IND

IDN

IRN

JAM

KAZ

KOR

KWT

LVA

LSO

LTU

MDG

MYS

MLT

MUS

MDA

MNG

MARNPL

NIC

PAK

PAN

PER

POL

RWA

SYC

SVK

SVNKNA

SWZ

SYR

THA

TTO

TUN

UKR

ARE

VEN

-2-1

01

0 10 20 30 40Tax revenue as percentage of GDP

Accountability

ALBARM

BHR

BGD

BEL

BTN

BOL

BIH

BRA

BGR

BDI

KHMCMR

CHL

COLCOG

CRI

CIV

HRVCYP

CZE

DOM

EGY

SLV

EST

ETH

GMB

GEO

HUN

IND

IDN

IRN

JAMKAZKORKWT

LVALSO

LTU

MDGMYS

MLTMUS

MDA

MNG

MAR

NPL

NIC

PAK

PAN

PER

POL

RWA

SYCSVK

SVN

KNA

SWZ

SYR

THATTOTUN

UKR

ARE

VEN

-2-1

01

2

0 10 20 30 40Tax revenue as percentage of GDP

Stability

ALBARM

BHR

BGD

BEL

BTN

BOL

BIH

BRABGR

BDI

KHMCMR

CHL

COL

COG

CRI

CIV

HRV

CYP

CZE

DOM

EGYSLV

EST

ETH GMBGEO

HUN

INDIDNIRN JAM

KAZ

KOR

KWTLVA

LSO

LTU

MDG

MYSMLTMUS

MDA

MNGMAR

NPL NICPAK

PANPER

POL

RWASYC

SVK

SVN

KNA

SWZ

SYR

THATTO

TUN

UKR

ARE

VEN

-2-1

01

2

0 10 20 30 40Tax revenue as percentage of GDP

Effectiveness

ALBARM

BHR

BGD

BEL

BTN

BOL

BIH

BRABGR

BDI

KHMCMR

CHL

COL

COG

CRI

CIV

HRV

CYPCZE

DOMEGY

SLV

EST

ETHGMB

GEO

HUN

IND IDN

IRN

JAM

KAZ

KOR

KWT

LVA

LSO

LTU

MDG

MYSMLT

MUS

MDA

MNGMAR

NPL

NIC

PAK

PANPER

POL

RWA SYC

SVKSVN

KNASWZ

SYR

THA

TTO

TUN

UKR

ARE

VEN

-2-1

01

2

0 10 20 30 40Tax revenue as percentage of GDP

Regulation

ALB

ARM

BHR

BGD

BEL

BTN

BOL

BIH

BRABGR

BDIKHMCMR

CHL

COL

COG

CRI

CIV

HRV

CYPCZE

DOM

EGY

SLV

EST

ETHGMB

GEO

HUN

IND

IDN

IRN

JAM

KAZ

KORKWT

LVA

LSO

LTU

MDG

MYSMLTMUS

MDA

MNG MAR

NPL

NICPAK

PAN

PER

POL

RWA

SYC

SVK

SVN

KNA

SWZSYR

THA TTOTUN

UKR

ARE

VEN

-1.5

-1-.

50

.51

0 10 20 30 40Tax revenue as percentage of GDP

Rule of Law

Does Aid Decrease Tax Revenue in Developing Countries?

27

Table 8: Tax Revenue on Governance Indicators

Notes: OLS Estimates. Robust standard errors in parentheses. (***), (**), (*) denote significance at the 1, 5, and 10 percent levels, respectively. All variables are expressed as percentages of GDP, except income, which is the log of GDP per capita. Governance indicators are country averages of the World Bank Governance Indicators 1996-2005.

(1) (2) (3) (4) (5) (6)

Less Corruption Voice &

Accountability Political Stability

Government

Effectiveness

Regulatory

Quality Rule of Law

0.028 0.022 0.012 0.057** 0.048 0.031 Revenue from taxes on income and capital (0.027) (0.037) (0.033) (0.028) (0.031) (0.028)

0.005 0.081*** 0.052** 0.009 0.018 0.004 Revenue from taxes on goods and services (0.017) (0.023) (0.021) (0.018) (0.019) (0.017)

0.007 0.008 0.040** -0.021 -0.027* -0.003 Revenue from taxes on international trade (0.014) (0.019) (0.017) (0.014) (0.016) (0.014)

0.030** -0.008 0.024* 0.018 0.013 0.016 Net Aid

(0.012) (0.016) (0.014) (0.012) (0.013) (0.012)

0.480*** 0.285*** 0.523*** 0.391*** 0.377*** 0.430*** Income

(0.063) (0.086) (0.077) (0.065) (0.071) (0.065)

Observations 66 66 66 66 66 66

R-squared 0.559 0.429 0.556 0.538 0.508 0.546

F test 15.21*** 9.01*** 15.02*** 14.00*** 12.38*** 14.42***

Does Aid Decrease Tax Revenue in Developing Countries?

28

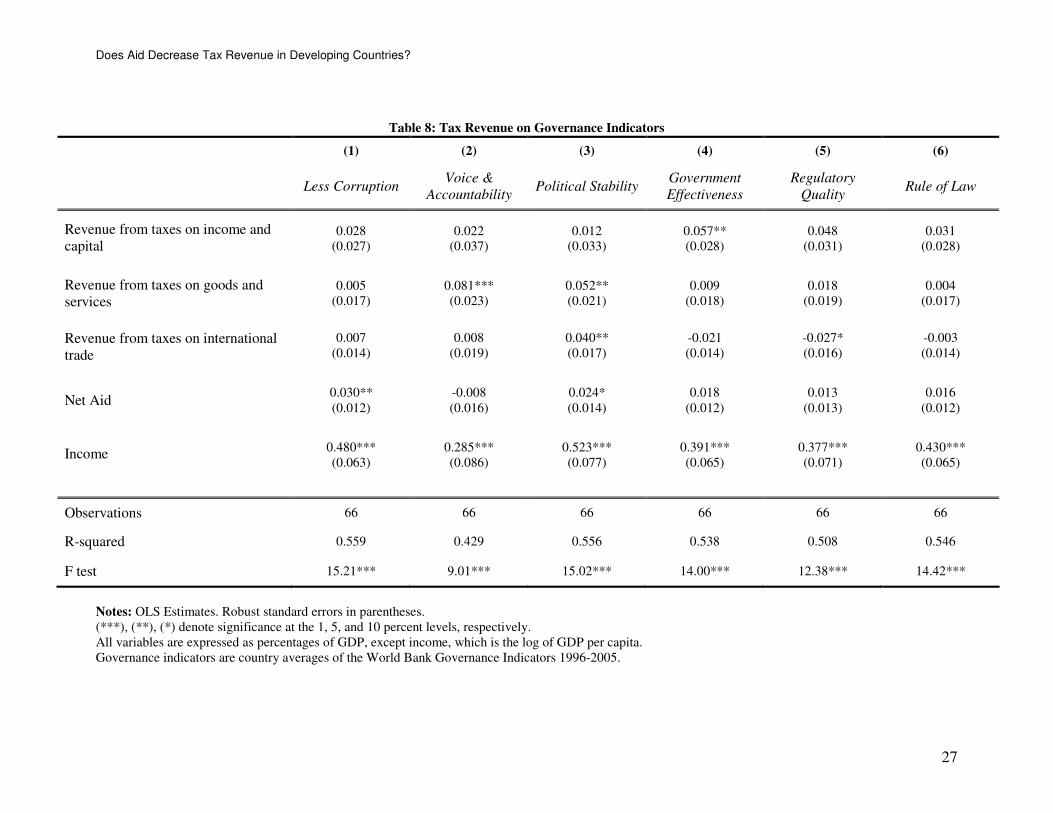

A picture of the overall correlation of tax revenue and governance indicators is given in

Figure 1. Moving beyond the aggregate correlation, we now want to identify differences

in how the three tax types are correlated with the quality of institutions. Based on the

same assumptions concerning the governance indicators as described above in section 4.2

for corruption, we compute average values for the three types of tax revenue and the six

governance indicators for each country and perform a cross-sectional regression. The

cross-sectional perspective is sufficient to provide a broad impression of the average

correlation of these two variables across the past 15 years. As control variables, we

include net aid and the log of GDP per capita as two other main potential determinants of

institutional quality.

The results, shown in Table 8, indicate a heterogeneous relationship between the different

tax types and institutional capacity. The income tax coefficients are all positive and have

on average the highest positive values, with a significant coefficient in the correlation

with government effectiveness. The goods and sales tax coefficients are all positive as

well, with significant coefficients in association with accountability and political stability.

Trade taxes show a positive and significant association with political stability as well,

which is not surprising because one can assume that in instable political environments the

tax administrative capacity is weakened overall. More interesting are the negative trade

tax coefficients in association with government effectiveness, regulatory quality, and the

rule of law, of which the coefficient on government effectiveness is significant. This

suggests that countries with higher average revenue from trade taxes are systematically

weaker in several aspects of administrative effectiveness, while higher average revenue

from the other two tax types is positively correlated with it. These characteristics may

reinforce each other over time

These results are thus in line with the interpretation provided above for the potential two-

way relationship between tax revenue and institutions and the particular role of trade

taxes. However, since the data does not allow a deeper analysis of the direction of

causality, we need to be cautious in interpreting the correlations shown in Table 8. For

example, the positive and significant coefficient of taxes on goods and services in

association with the governance indicator of voice and accountability does not

necessarily imply that the increase of such taxes results in an enhanced democratic

Does Aid Decrease Tax Revenue in Developing Countries?

29

quality within a country; it could also be that the reverse effect is dominant in this

relationship (institutions influence tax revenue). We can thus cautiously conclude that the

results shown in Table 8 at least do not neglect the possibility of a two-way relationship

between tax revenue and the quality of governance institutions.

5. Conclusion and Implications: A Role for Development

Policy

The aim of this analysis was to identify whether there is a systematic relationship

between aid and tax revenue in aid recipient countries. The key result of our panel-data

regressions is that there is systematic evidence for a positive correlation between aid and

tax revenue. This result is particularly solid when we focus on aid in the form of grants,

as opposed to loans. Indeed the coefficient on grants is positive and significant across

different specifications and several robustness checks. The results are also stable to the

inclusion of an interaction between aid and corruption, which itself does not seem to be

significant. Hence, there is no evidence for a differential impact of aid on tax revenue in

more vs. less corrupt countries. Moreover, a re-estimation of Gupta et al.’s (2003)