Embed Size (px)

Citation preview

Measuring Corporate Social Responsibility: A Scale Development StudyAuthor(s): Duygu TurkerSource: Journal of Business Ethics, Vol. 85, No. 4 (Apr., 2009), pp. 411-427Published by: SpringerStable URL: http://www.jstor.org/stable/40294805 .

Accessed: 11/06/2014 12:12

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Springer is collaborating with JSTOR to digitize, preserve and extend access to Journal of Business Ethics.

http://www.jstor.org

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Journal of Business Ethics (2009) 85:411-427 © Springer 2008 DOI 10. 1007/s 1055 1-008-9780-6

Measuring Corporate Social Responsibility: A Scale Development Study Duygu Turker

ABSTRACT. Corporate social responsibility (CSR) is one of the most prominent concepts in the literature and, in short, indicates the positive impacts of businesses on their stakeholders. Despite the growing body of literature on this concept, the measurement of CSR is still prob- lematic. Although the literature provides several methods for measuring corporate social activities, almost all of them have some limitations. The purpose of this study is to provide an original, valid, and reliable measure of CSR

reflecting the responsibilities of a business to various stakeholders. Based on a proposed conceptual framework of CSR, a scale was developed through a systematic scale

development process. In the study, exploratory factor

analysis was conducted to determine the underlying fac- torial structure of the scale. Data was collected from 269 business professionals working in Turkey. The results of the analysis provided a four-dimensional structure of

CSR, including CSR to social and nonsocial stakehold-

ers, employees, customers, and government.

KEY WORDS: Corporate social responsibility, employ- ees, scale development, stakeholders, Turkey

ABBREVIATIONS: CEP: Council of Economic Pri-

orities; CSID: Canadian Social Investment Database; CSR: Corporate social responsibility; EU: European Union; KLD: Kinder, Lydenberg, and Domini; NGO:

Nongovernmental organization; PRESOR: Perceived Role of Ethics and Social Responsibility; WCED: World Commission on Environment and Development

Introduction

The role of business in society has been a matter of discussion since the middle of the last century. The

increasing pressures of businesses on humanity and the natural environment have raised concerns among people all around the world considerably. Today, the various stakeholders in national and international

communities expect more responsible use of increased business power. Corporate social respon- sibility (CSR) may provide a general framework to structure the responsible use of corporate power and social involvement. Although the expanding litera- ture on this issue has provided a clearer under-

standing, it is still problematic to find a commonly accepted definition of CSR. Another problem is to measure CSR based on its links with the stakeholder

concept. Despite the existence of various measure- ment methods in the literature, almost all of them have some limitations. In order to better understand and measure how CSR relates with stakeholders, a new measurement of CSR is needed. The purpose of the current study is to fill this void by providing a new scale to measure CSR in terms of the expec- tations of various stakeholders.

The data for this study was collected from business

professionals in Turkey. Although Turkey has his-

torically shared some social characteristics of collec- tivist Middle Eastern societies, the modernization

process has changed economic, political, social, and cultural dimensions of the society to a great extent since the beginning of the 1920s (Kongar, 1999). In the 1980s, in parallel with other countries

similarly situated in the world economy, Turkey changed its economic strategy from a protectionist model characterized by heavy state intervention to a more outward-looking and market-oriented model

(Bugra, 2003). This export-oriented policy regime has backed up the gradually liberalizing economic context in Turkey and today, in spite of its unique historical development path, Turkish companies share some basic perspectives with the global busi- ness community.

The first CSR practices in Turkey were con- ducted by multinational companies (Ararat, 2004,

p. 255). However, since the Ottoman era, there has

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

412 Duygu Turker

been a strong tradition of corporate philanthropy through an institutional mechanism called 'waqf (foundation). Today, most family-owned companies have associated waqfs and allocate a percentage of their profits to these foundations for the creation of social benefits. Educational institutions, hospitals, and artistic or cultural centres are the most popular fields of activity for these foundations (Ararat, 2005, p. 12). Despite the existence of a strong philan- thropic tradition in the business community and society at large, until recently CSR efforts have not been particularly diverse. According to Ararat (2005, 2006), this was partly because of some cultural characteristics aligned with some characteristics of the 'predominantly Muslim countries' cluster in Hosftede's analytical framework (1980). However, recent changes in the political, economic, and social context of the country have offset these cultural characteristics and increased the attention paid to CSR in Turkish society considerably (Ararat, 2005, 2006). Today, the large-scale CSR projects of Turkish companies reflect the change in the understanding of CSR of the Turkish business community. The annual CSR awards of Capital Magazine, a leading business magazine in Turkey, also prove the interest of media and society in CSR issues. One of the managers of Trend Group, the company that organizes the event together with Capital Magazine, evaluated the historical develop- ment of the event and commented that CSR has been one of the most significant values in Turkey (Bayiksel, 2007).

According to Ararat (2005), macroeconomic sta- bility and economic development accompanied by opening up to international competition have accelerated the convergence of the Turkish business culture. The changing pattern of the business con- text has also been strengthened by the candidacy process to the European Union (EU). Although relations between Turkey and the EU began in 1963 with the signing of the Ankara Agreement, the candidacy process has increased the level of inte- gration in the European context. During recent years, Turkey has harmonized its legislation for EU accession. As a result of this harmonization, "Turkish markets have become more competitive, civil rights are better respected, legal system has been improved, juridical system is under improvement, and the intensified political and economic integra-

tion with Europe affected the social values" (Ararat, 2005, p. 19). The relations between the Turkish business community and European countries are also long-standing and the EU has been the most important trading partner for Turkey for a long time (Flam, 2004, p. 179). Therefore, Turkish compa- nies have already focused on the European market and complied with most EU regulations in order to market their products. Based on these trading relations, the candidacy process also increased the integration of the Turkish business culture with a broader European cultural context. Therefore, Turkey provides a reliable source of information in order to develop an understanding and create a measure of CSR.

The study contributes to the literature by pro- viding a new, valid, and reliable scale of CSR. Based on the proposed conceptual framework, the scale reflects the corresponding responsibilities of a busi- ness to various stakeholders. The paper contains three main sections. In the first section, a conceptual framework is drawn to form a structural base of the study. In the second section, the existing measure- ment methods and their limitations are reviewed. Based on the theoretical framework, a scale is developed for measuring CSR. Finally, in the last section, the limitations and findings of the study are discussed.

Conceptual framework for corporate social responsibility

Despite the fact that CSR is one of the most prominent concepts in the literature, it is still diffi- cult to give a precise and commonly accepted defi- nition. As stated by Votaw (1972), CSR "means something, but not always the same thing, to everybody" (p. 25). According to Bowen (1953), one of the first scholars to define the concept, CSR is the obligations of businessmen "to pursue those policies, to make those decisions, or to follow those lines of action which are desirable in terms of the objectives and values of our society" (p. 6). Since this definition of CSR, the literature has provided contradictory definitions of the concept. The elab- orate review of Carroll (1999), which traces the evolution of the CSR construct since the 1950s, clearly indicated that one of the main problems in

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 413

the literature is to sketch out a conceptual frame- work of CSR.

According to Sims (2003), for instance, "../social

responsibility' and 'legality' are not one and the same

thing. CSR is often seen as acts that go beyond what is prescribed by the law" (p. 46). The definitions of McGuire (1963) and Davis (1973) distinguished the social responsibilities of a business from its eco-

nomic, technical, and legal obligations. Although Carroll (1999) described the definition of Davis as a restricted version of CSR, he also distinguished between the economic component and the non- economic components of CSR; the former is what the business does for itself, while the latter are what the business does for others (Carroll, 1999). Despite his attractive distinction, Carroll (1999) stated that "economic viability is something business does for

society as well" (p. 284) and described the economic

component as "a responsibility to produce goods and services that society wants and to sell them at a

profit" (1979, p. 500). However, this definition of the economic component might indicate the basic function of business in the society. According to Daft (2003), a business is an economic unit which

produces goods and services in a society (p. 153) and

gains a profit in return for this function. Therefore, economic concern is the fundamental reason for the existence of a business, and profit is surely the pri- mary motive for owners. In this case, it might be better to consider the economic component as a reason for the existence of a business, rather than a

responsibility to society. A similar understanding can be found in the definition of Davis (1960) as well. In this definition, CSR is "...businessmen's decisions and actions taken for reasons at least partially beyond the firm's direct economic or technical interest"

(Davis, 1960, p. 70). According to Eells and Walton

(1974), "In its broadest sense, corporate social

responsibility represents a concern with the needs and goals of society which goes beyond the merely economic" (p. 247). In the current study, the eco- nomic component is excluded from the definition of CSR. Therefore, CSR is defined as corporate behaviors that aims to affect stakeholders positively and that go beyond its economic interest.

The given definition of CSR is closely interre- lated with the concept of 'stakeholder'. According to Carroll (1991), there is a natural fit between the idea of CSR and an organization's stakeholders (p. 43).

Although there is no consensus regarding the defi- nition and scope of stakeholder in the literature, it can be briefly defined as others with which the

organization interacts while pursuing their goals (Wherther and Chandler, 2006, p. 4). In a broader

understanding, which can be attributed to the fa- mous definition of Freeman (1984), stakeholders are "those groups or individuals who can affect or are affected by the achievement of the organization's objectives or are those actors with a direct or indirect interest in the company" (Verdeyen et al, 2004, pp. 326-327). In order to clarify the scope of the stakeholder concept, scholars have provided various classifications. Some of the most useful of these

classify these groups or individuals as external and internal stakeholders (Verdeyen et al., 2004); con-

tracting and public stakeholders (Charkham, 1994); voluntary and involuntary stakeholders (Clarkson, 1994); primary and secondary stakeholders (Clark- son, 1995; Freeman, 1984); primary social, second-

ary social, primary nonsocial, and secondary nonsocial stakeholders (Wheeler and Sillanpaa, 1997,

1998); and internal, external, and societal stake- holders (Wherther and Chandler, 2006, p. 4).

The classification proposed by Wheeler and

Sillanpaa (1997) is obviously the most elaborate of these alternatives. In this typology, stakeholders that have direct impacts on relationships and involve human entities are defined as primary social stake- holders. On the other hand, stakeholders that have less direct impacts are secondary social stakeholders,

representing civil society, business at large, and various interest groups. According to the authors, this group can sometimes be extremely influential on the business. The authors indicated that the nonso- cial stakeholders do not involve human relationships and divided them further into primary (direct) and

secondary (indirect) categories, including the natural

environment, nonhuman species, future generations, and their defenders in pressure groups (Wheeler and

Sillanpaa, 1998, p. 205). It can be noted that the consideration of nonsocial stakeholders has been a

significant advancement in the understanding of the

concept and has likely increased the recognition of

these stakeholders in the business community. In the current study, this four-dimensional clas-

sification provides a useful means of conceptualiza- tion. Taking this understanding into account, CSR can be further defined as corporate behaviors which

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

414 Duygu Turker

aim to affect primary social, secondary social, pri- mary nonsocial, and secondary nonsocial stake- holders positively and goes beyond its economic interest. In order to find the most appropriate way of

measuring CSR based on this conceptual frame- work, the related literature should be examined

carefully. In the next section, the pros and cons of the existing methods in the literature are discussed in detail.

Literature review: existing methods of measuring CSR

In his study, Carroll (2000) answered the question of whether corporate social performance should be measured and, if so, why. According to him, the brief answer to this question is 'yes', because "it is an

important topic to business and to society, and measurement is one part dealing seriously with an

important matter... The real question is whether valid and reliable measures can be developed" (Carroll, 2000, p. 473). In fact, considerable attempts have been made to measure the socially responsible activities of organizations both in the academic and business communities. However, as Wolfe and Au- pperle (1991) indicated, there is no single best way to measure corporate social activities. Waddock and Graves (1997) also pointed out the difficulties of measuring corporate social performance and assessed the alternative methods, including forced-choice survey instruments, reputation indices and scales, content analysis of document, behavioral and per- ceptional measures, and case study. Maignan and Ferrell (2000) categorized these alternative methods into three main approaches: expert evaluations, single- and multiple-issue indicators, and surveys of managers. Expanding on the latter classification, the following approaches are suggested as viable to measure CSR: reputation indices or databases, sin- gle- and multiple-issue indicators, content analysis of corporate publications, scales measuring CSR at the individual level, and scales measuring CSR at the organizational level.

Reputation indices and databases are among the most widely used methods for evaluating corporate social activities. The Kinder, Lydenberg, and Domini (KLD) Database, the Fortune Index, and the Canadian Social Investment Database (CSID) are

popular examples of this method. KLD rates com-

panies, traded on the US stock exchange, based on

eight attributes of social activities (community rela- tions, employee relations, environment, product, treatment of women and minorities, military con- tracts, nuclear power, and South Africa). Fortune's

reputation index also offers a systematic tool for

evaluating socially responsible behaviors from a

managerial point of view. A reputation index can also be used to derive new scales for measuring corporate social activities (Abbott and Monsen, 1979). Ruf et al. (1998) developed a scale to evaluate the relative

importance of KLD's eight dimensions by using an

analytical hierarchy process. According to these au- thors, the attributes of KLD coincided with the legal, ethical, and discretionary dimensions of Carroll's model (1979). However, Maignan and Ferrell (2000) found these indices inadequate to evaluate all busi- nesses and stated that both KLD and Fortune index "...suffer from the fact that their items are not based on theoretical arguments" (p. 285).

Another well-known database is CSID, which measures the sum of the average of a firm's net strength and weakness for each of seven dimensions (Mahoney and Thorne, 2005, p. 244): community, diversity, employee relations, environment, inter- national operations, product and business practices, and corporate governance. Although this database reflects some key stakeholder relationships, it only details companies traded on the Canadian stock ex- change. Apparently, besides other limitations, the most important problem with these databases is their limited area of assessment; they are only designed to evaluate companies in some countries.

The second alternative method is the use of sin- gle- and multiple-issue indicators. The pollution control performance, reported by the Council of Economic Priorities (CEP), is an example of such a single-issue indicator and has been used by several scholars (e.g., Bragdon and Marlin, 1972; Chen and Metcalf, 1984; Freedman and Jaggi, 1982). Corpo- rate crime is another indicator of socially responsible behaviors used by scholars (Baucus and Baucus, 1997; Davidson and Worrell, 1990). As can be noticed, the unidimensionality of this method is a significant limitation (Maignan and Ferrell, 2000). Therefore, scholars may prefer to use a combination of these indicators. However, even with the use of a multiple-issue indicator, this approach still has

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 415

limited ability to delineate the entire structure of CSR. Moreover, these indicators are not globally focused and only report the activities of companies in a limited number of countries, which also limits the use of this method by researchers.

Another method used in the literature is content analysis of corporate publications. This method may also provide the possibility to derive new measures for corporate social activities (Abbott and Monsen, 1979). Especially in recent years, information about CSR has become more readily accessible due to the increasing attention that companies pay to social disclosure, that is, information companies provide on their practices regarding environmental, community, employee, and consumer issues (Gray et al., 1995). The growing body of literature on corporate social reporting has increased the use of content analysis as a method of measuring CSR. According to Ruf et al. (1998), this method has an "objective rating of companies since once the social attributes are selected, the process of rating is standardized" (p. 121). However, the information given in a cor-

porate report can be different from the actual cor-

porate actions (McGuire et al., 1988). Companies may mislead the potential readers of these reports in order to create a more favorable image. Therefore, the reliability of company reports may represent a significant limitation. Previous studies that focus on the reliability of corporate environmental disclosures have provided empirical evidence that there is no

significant association between the content of these

reports and actual performance (Freedman and Wasley, 1990; Ingram and Frazier, 1980; Rockness, 1985; Wiseman, 1982). Ironically, poor performers provided longer environmental disclosures (Ingram and Frazier, 1980).

The fourth method is to use scales that measure the CSR perception of individuals. One of the most

widely used scales (Smith and Blackburn, 1988) was

developed by Aupperle (1984) to measure the indi- vidual CSR values of managers according to Carroll's four-dimensional model. This scale is the first serious attempt to grasp the multidimensional nature of CSR (Rufet al., 1998). Although the scale is suitable for

investigating the socially responsible values of man-

agers, it is not a useful way for obtaining information about socially responsible behaviors of organizations. Additionally, the forced-choice instruments of the scale also appear as a limitation. Peterson (2004)

stated that "this instrument would not be useful for assessing an organization's performance in the four domains independently; that is, the instrument would not be helpful for assessing organizational perfor- mance by employees who view their work organi- zation as highly responsible on all four CSR domains or highly irresponsible on all four domains." (p. 306).

In order to measure the managerial attitudes towards social responsibility, Quazi and O'Brien (2000) also provided a scale based on the relevant previous studies (Davis, 1973; Orpen, 1987; Ostlund, 1977). In this study, the authors constructed a scale based on a two-dimensional model, including the span of corporate responsibility and the range of outcomes of corporate social commitments. Although this scale is useful to test the CSR perceptions of managers in different cultural and economic contexts, it is not designed to measure the organizational involvement with socially responsible activities.

Another well-known scale is the Perceived Role of Ethics and Social Responsibility (PRESOR) which aims to measure managerial perceptions about the role of ethics and social responsibility in achieving organizational effectiveness (Singhapakdi et al., 1996). Like the scales of Aupperle (1984) and Quazi and O'Brien (2000), PRESOR also focuses on measuring individual values, rather than measuring socially responsible activities of businesses. Addi-

tionally, in his study, Etheredge (1999) provided a constructive replication of PRESOR and the results did not confirm the original factorial structure of the instruments.

Despite the proliferation of scales to measure individual perception of CSR, the literature has not

provided an adequate number of scales for measuring CSR at the organizational level. The most important scale of the literature in this category was developed by Maignan and Ferrell (2000) based on the concept of corporate citizenship. In this study, corporate citizenship was defined as the extent to which businesses meet the economic, legal, ethical, and

discretionary responsibilities imposed on them by their stakeholders (Maignan and Ferrell, 2000, p. 284). The study incorporated both the conceptual contribution of Carroll's model (1979) and stake- holder management theory. According to the

proposed conceptualization, the authors developed a scale of corporate citizenship and tested it empiri- cally in two dissimilar cultural settings. Certainly,

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

416 Duygu Turker

the development of this scale is a significant contri- bution to the literature. However, the main limita- tion of the scale is that it considers only three primary stakeholders (customers, employees, and public). Maignan and Ferrell (2000) emphasized that "these stakeholders are not the only ones who can impose responsibilities on businesses and whose welfare can be directly affected" (p. 295).

In summary, a review of the literature shows that there are several methods to measure corporate social activities. Although these methods have contributed a lot to the CSR literature, almost all of them have some limitations. Second, and more importantly, none of these methods addresses the issue of CSR from the perspective of the current study. As mentioned pre- viously, this study conceptualizes CSR based on the exclusion of the economic component, while incor- porating the stakeholder concept. Therefore, there is a need to develop a new scale which articulates CSR according to the proposed conceptual framework.

Research methodology

Scale design

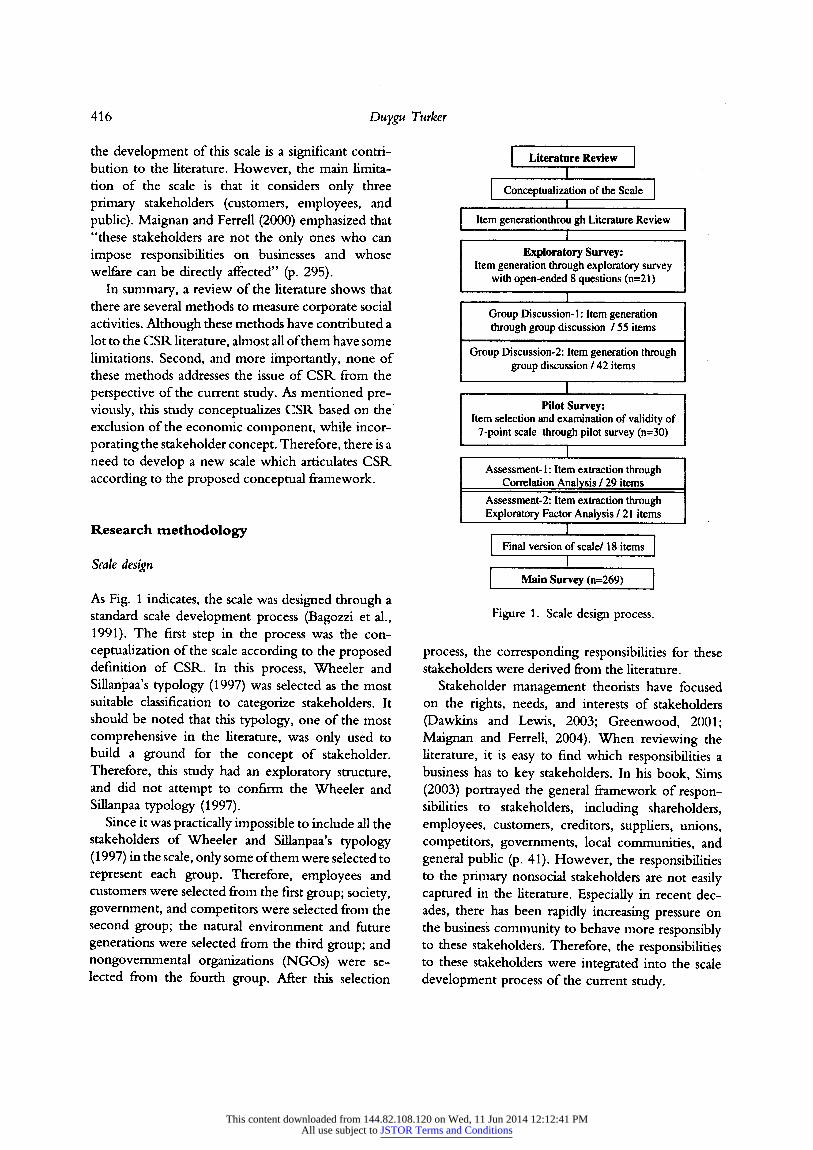

As Fig. 1 indicates, the scale was designed through a standard scale development process (Bagozzi et al., 1991). The first step in the process was the con- ceptualization of the scale according to the proposed definition of CSR. In this process, Wheeler and Sillanpaa's typology (1997) was selected as the most suitable classification to categorize stakeholders. It should be noted that this typology, one of the most comprehensive in the literature, was only used to build a ground for the concept of stakeholder. Therefore, this study had an exploratory structure, and did not attempt to confirm the Wheeler and Sillanpaa typology (1997).

Since it was practically impossible to include all the stakeholders of Wheeler and Sillanpaa's typology (1997) in the scale, only some of them were selected to represent each group. Therefore, employees and customers were selected from the first group; society, government, and competitors were selected from the second group; the natural environment and future generations were selected from the third group; and nongovernmental organizations (NGOs) were se- lected from the fourth group. After this selection

Literature Review | L

Conceptualization of the Scale | I

Item generationthrou gh Literature Review I

Exploratory Survey: Item generation through exploratory survey

with open-ended 8 questions (n=21) 1

"~

Group Discussion- 1: Item generation through group discussion / 55 items

Group Discussion-2: Item generation through group discussion / 42 items

I Pilot Survey:

Item selection and examination of validity of 7-point scale through pilot survey (n=30)

i Assessment- 1 : Item extraction through

Correlation Analysis / 29 items Assessment-2: Item extraction through Exploratory Factor Analysis / 21 items

I Final version of scale/ 18 items |

1 Main Survev (n=269ï

Figure 1. Scale design process.

process, the corresponding responsibilities for these stakeholders were derived from the literature.

Stakeholder management theorists have focused on the rights, needs, and interests of stakeholders pawkins and Lewis, 2003; Greenwood, 2001; Maignan and Ferrell, 2004). When reviewing the literature, it is easy to find which responsibilities a business has to key stakeholders. In his book, Sims (2003) portrayed the general framework of respon- sibilities to stakeholders, including shareholders, employees, customers, creditors, suppliers, unions, competitors, governments, local communities, and general public (p. 41). However, the responsibilities to the primary nonsocial stakeholders are not easily captured in the literature. Especially in recent dec- ades, there has been rapidly increasing pressure on the business community to behave more responsibly to these stakeholders. Therefore, the responsibilities to these stakeholders were integrated into the scale development process of the current study.

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 417

A historical review of the literature shows that the notion of CSR starts with the increasing concerns of

people about environmental degradation. The roots of CSR can be found in the early environmental concerns of the 18th century (Smith, 1993, p. 172). Today, the responsibility of a business to the natural environment is not only to avoid environmental

harm, but also to protect and improve the natural environment. The rights of future generations is another important dimension in stakeholder

management. The conceptual background for these

responsibilities can be traced from the notion of 'sustainable development', which is defined as

"development that meets the needs of the present without compromising the ability of future genera- tions to meet their own needs" (WCED, 1987). The

responsibilities of corporations to the natural envi- ronment and future generations are closely interre- lated with each other. Therefore, it seems reasonable to categorize these two stakeholders under the pri- mary nonsocial stakeholders in Wheeler and Sillan-

paa's typology (1997). In order to create an initial item pool, a list of

statements was derived from the previous scales in the literature (Aupperle, 1984; Carroll, 1979; Mai-

gnan and Ferrell, 2000; Quazi and O'Brien, 2000; Wood and Jones, 1995). In the third stage, an

exploratory survey was conducted to create new items. A form which consisted of eight open-ended questions concerning the selected eight stakeholders was used in the survey. The survey included 30

respondents, working in different organizations in

Turkey. The data was analyzed to generate a list of items for each dimension. This process was per- formed by a group of academics to eliminate the

perceptual distortions of the researcher. In order to select new items that could be classified as 'CSR to

stakeholders', three main criteria were used: to be an outcome of organizational decision, to have a posi- tive effect on the stakeholders, and to go beyond the

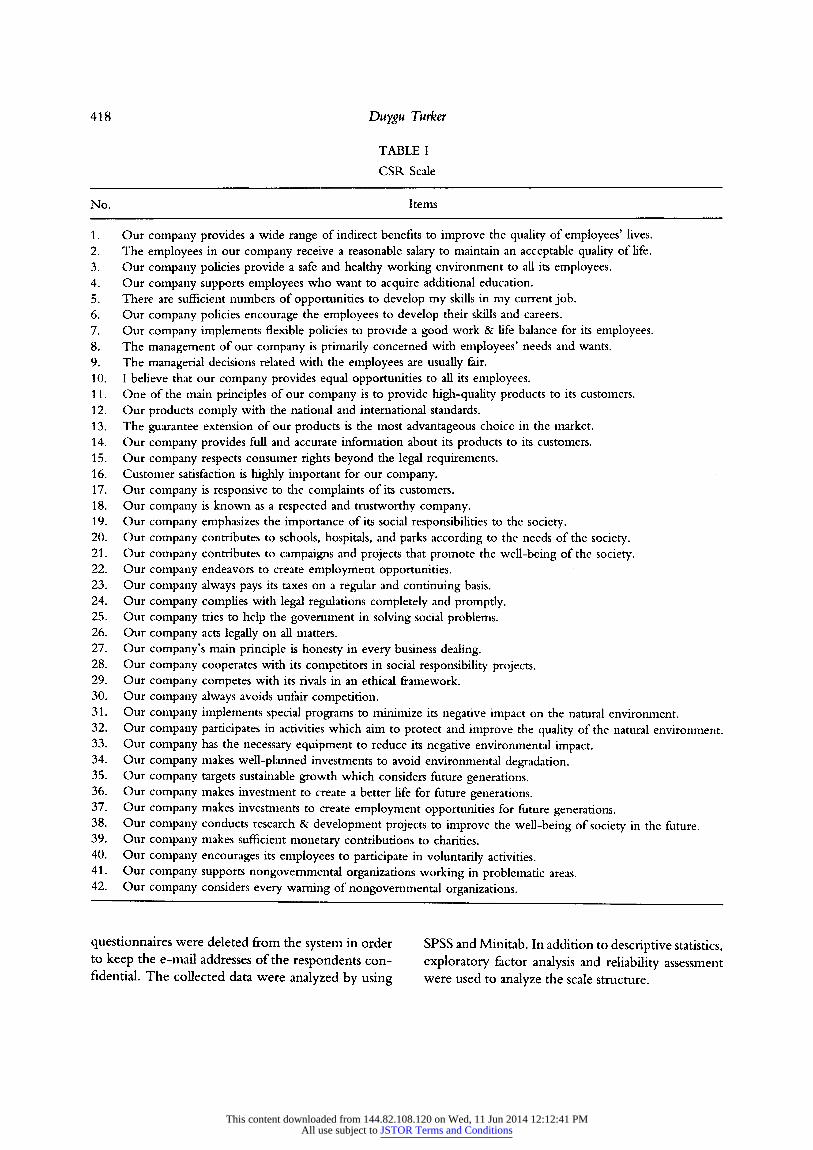

monetary goals of the organization. Together with an exploratory study, this process led to an enlarged item pool including 55 items. In order to eliminate the unrelated items from the pool, these were reviewed through a second group discussion. Finally, a scale including 42 items was constructed. This version of the scale is shown in Table I.

In the next step, the standard validity and reli-

ability of the scale were analyzed through a pilot

survey. Since it was conducted on a limited number of respondents, this step was only seen as a pre- liminary analysis of the scale. In this stage, two assessments were applied to the collected data. In the first assessment, highly intercorrelated items were excluded from the scale according to the correlation

analysis. The sufficiency of the correlations among items was tested through Bartlett's test of sphericity. Bartlett's test proved that the correlations, when taken collectively, were significant at the 0.0001 level. In the next assessment, factor analysis was

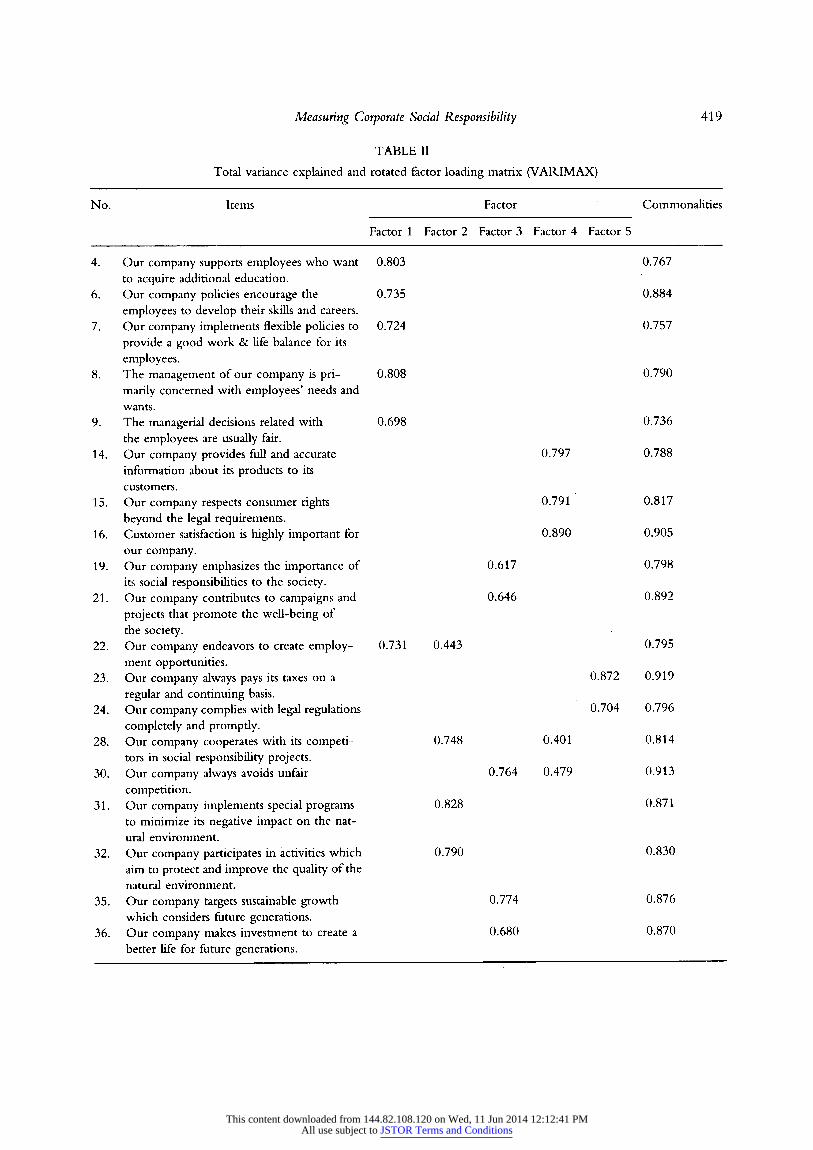

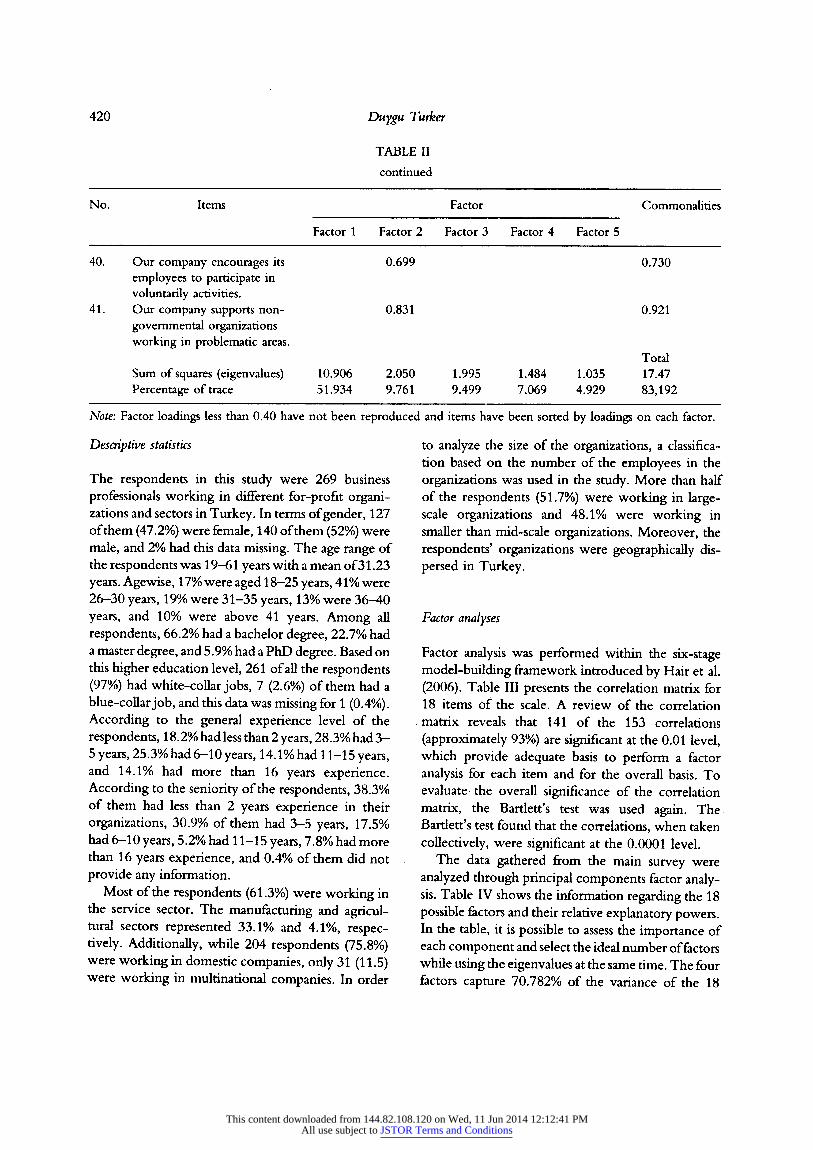

performed to eliminate unrelated items. Table II shows the obtained factorial structure of the scale. In order to understand how variance could be parti- tioned, component analysis was performed to the data set. Factor analysis revealed five distinct factors with eigenvalues greater than 1.0, explaining 83.191% of the variance. Double-barreled items (the 22nd, 28th, and 30th items) were excluded from the scale. The current factorial structure of the scale did not change after the elimination of these items. As a result of this process, a preliminary version of the CSR scale including 18 items was obtained to use in the main survey.

Sample selection, data collection, and analyses

The population consisted of business professionals in

for-profit organizations in Turkey. In the study, as a

data collection method, a self-administered ques- tionnaire was sent via e-mail to management and

business-related mailing groups. These mailing groups included a variety of business professions who were active in the business life in Turkey and different in

terms of sectors, companies, departments, job posi- tions, and so on. The e-mail included a cover letter which briefly explained the purpose of the study as well as a questionnaire form. As a rule of thumb, it was aimed to reach 300 questionnaires within a prespeci- fied time period, the first 2 weeks of April 2006. From the target sample of 300 questionnaires, only 280

completed questionnaires were returned; 11 were discarded as incomplete. Hence, the final number of

usable questionnaires was 269 - a response rate of

89.6%. In order to guarantee anonymity, no personal identifying information was requested from the

respondents. After downloading and numbering them

according to the receiving sequence, the collected

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

418 Duygu Turker

TABLE I

CSR Scale

No. Items

1. Our company provides a wide range of indirect benefits to improve the quality of employees* lives. 2. The employees in our company receive a reasonable salary to maintain an acceptable quality of life. 3. Our company policies provide a safe and healthy working environment to all its employees. 4. Our company supports employees who want to acquire additional education. 5. There are sufficient numbers of opportunities to develop my skills in my current job. 6. Our company policies encourage the employees to develop their skills and careers. 7. Our company implements flexible policies to provide a good work & life balance for its employees. 8. The management of our company is primarily concerned with employees' needs and wants. 9. The managerial decisions related with the employees are usually fair. 10. I believe that our company provides equal opportunities to all its employees. 11. One of the main principles of our company is to provide high-quality products to its customers. 12. Our products comply with the national and international standards. 13. The guarantee extension of our products is the most advantageous choice in the market. 14. Our company provides full and accurate information about its products to its customers. 15. Our company respects consumer rights beyond the legal requirements. 16. Customer satisfaction is highly important for our company. 17. Our company is responsive to the complaints of its customers. 18. Our company is known as a respected and trustworthy company. 19. Our company emphasizes the importance of its social responsibilities to the society. 20. Our company contributes to schools, hospitals, and parks according to the needs of the society. 21. Our company contributes to campaigns and projects that promote the well-being of the society. 22. Our company endeavors to create employment opportunities. 23. Our company always pays its taxes on a regular and continuing basis. 24. Our company complies with legal regulations completely and promptly. 25. Our company tries to help the government in solving social problems. 26. Our company acts legally on all matters. 27. Our company's main principle is honesty in every business dealing. 28. Our company cooperates with its competitors in social responsibility projects. 29. Our company competes with its rivals in an ethical framework. 30. Our company always avoids unfair competition. 31. Our company implements special programs to minimize its negative impact on the natural environment. 32. Our company participates in activities which aim to protect and improve the quality of the natural environment. 33. Our company has the necessary equipment to reduce its negative environmental impact. 34. Our company makes well-planned investments to avoid environmental degradation. 35. Our company targets sustainable growth which considers future generations. 36. Our company makes investment to create a better life for future generations. 37. Our company makes investments to create employment opportunities for future generations. 38. Our company conducts research & development projects to improve the well-being of society in the future. 39. Our company makes sufficient monetary contributions to charities. 40. Our company encourages its employees to participate in voluntarily activities. 41. Our company supports nongovernmental organizations working in problematic areas. 42. Our company considers every warning of nongovernmental organizations.

questionnaires were deleted from the system in order to keep the e-mail addresses of the respondents con- fidential. The collected data were analyzed by using

SPSS and Minitab. In addition to descriptive statistics, exploratory factor analysis and reliability assessment were used to analyze the scale structure.

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 419

TABLE II

Total variance explained and rotated factor loading matrix (VARIMAX)

No. Items Factor Commonalities

Factor 1 Factor 2 Factor 3 Factor 4 Factor 5

4. Our company supports employees who want 0.803 0.767 to acquire additional education.

6. Our company policies encourage the 0.735 0.884

employees to develop their skills and careers. 7. Our company implements flexible policies to 0.724 0.757

provide a good work & life balance for its

employees. 8. The management of our company is pri- 0.808 0.790

marily concerned with employees' needs and wants.

9. The managerial decisions related with 0.698 0.736 the employees are usually fair.

14. Our company provides full and accurate 0.797 0.788 information about its products to its customers.

15. Our company respects consumer rights 0.791 0.817

beyond the legal requirements. 16. Customer satisfaction is highly important for 0.890 0.905

our company. 19. Our company emphasizes the importance of 0.617 0.798

its social responsibilities to the society. 21. Our company contributes to campaigns and 0.646 0.892

projects that promote the well-being of the society.

22. Our company endeavors to create employ- 0.731 0.443 0.795 ment opportunities.

23. Our company always pays its taxes on a 0.872 0.919

regular and continuing basis. 24. Our company complies with legal regulations 0.704 0.796

completely and promptly. 28. Our company cooperates with its competi- 0.748 0.401 0.814

tors in social responsibility projects. 30. Our company always avoids unfair 0.764 0.479 0.913

competition. 31. Our company implements special programs 0.828 0.871

to minimize its negative impact on the nat- ural environment.

32. Our company participates in activities which 0.790 0.830 aim to protect and improve the quality of the natural environment.

35. Our company targets sustainable growth 0.774 0.876 which considers future generations.

36. Our company makes investment to create a 0.680 0.870 better life for future generations.

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

420 Duygu Turker

TABLE II

continued

No. Items Factor Commonalities

Factor 1 Factor 2 Factor 3 Factor 4 Factor 5

40. Our company encourages its 0.699 0.730

employees to participate in

voluntarily activities. 41. Our company supports non- 0.831 0.921

governmental organizations working in problematic areas.

Total Sum of squares (eigenvalues) 10.906 2.050 1.995 1.484 1.035 17.47

Percentage of trace 51.934 9.761 9.499 7.069 4.929 83,192

Note: Factor loadings less than 0.40 have not been reproduced and items have been sorted by loadings on each factor.

Descriptive statistics

The respondents in this study were 269 business

professionals working in different for-profit organi- zations and sectors in Turkey. In terms of gender, 127 of them (47.2%) were female, 140 of them (52%) were male, and 2% had this data missing. The age range of the respondents was 19-61 years with a mean of 31.23 years. Agewise, 17% were aged 18-25 years, 41% were 26-30 years, 19% were 31-35 years, 13% were 36-40 years, and 10% were above 41 years. Among all respondents, 66.2% had a bachelor degree, 22.7% had a master degree, and 5.9% had a PhD degree. Based on this higher education level, 261 of all the respondents (97%) had white-collar jobs, 7 (2.6%) of them had a blue-collar job, and this data was missing for 1 (0.4%). According to the general experience level of the respondents, 18.2% had less than 2 years, 28.3% had 3- 5 years, 25.3% had 6-10 years, 14.1% had 1 1-15 years, and 14.1% had more than 16 years experience. According to the seniority of the respondents, 38.3% of them had less than 2 years experience in their organizations, 30.9% of them had 3-5 years, 17.5% had 6-10 years, 5.2% had 1 1-15 years, 7.8% had more than 16 years experience, and 0.4% of them did not provide any information.

Most of the respondents (61.3%) were working in the service sector. The manufacturing and agricul- tural sectors represented 33.1% and 4.1%, respec- tively. Additionally, while 204 respondents (75.8%) were working in domestic companies, only 31 (11.5) were working in multinational companies. In order

to analyze the size of the organizations, a classifica- tion based on the number of the employees in the

organizations was used in the study. More than half of the respondents (51.7%) were working in large- scale organizations and 48.1% were working in smaller than mid-scale organizations. Moreover, the

respondents' organizations were geographically dis-

persed in Turkey.

Factor analyses

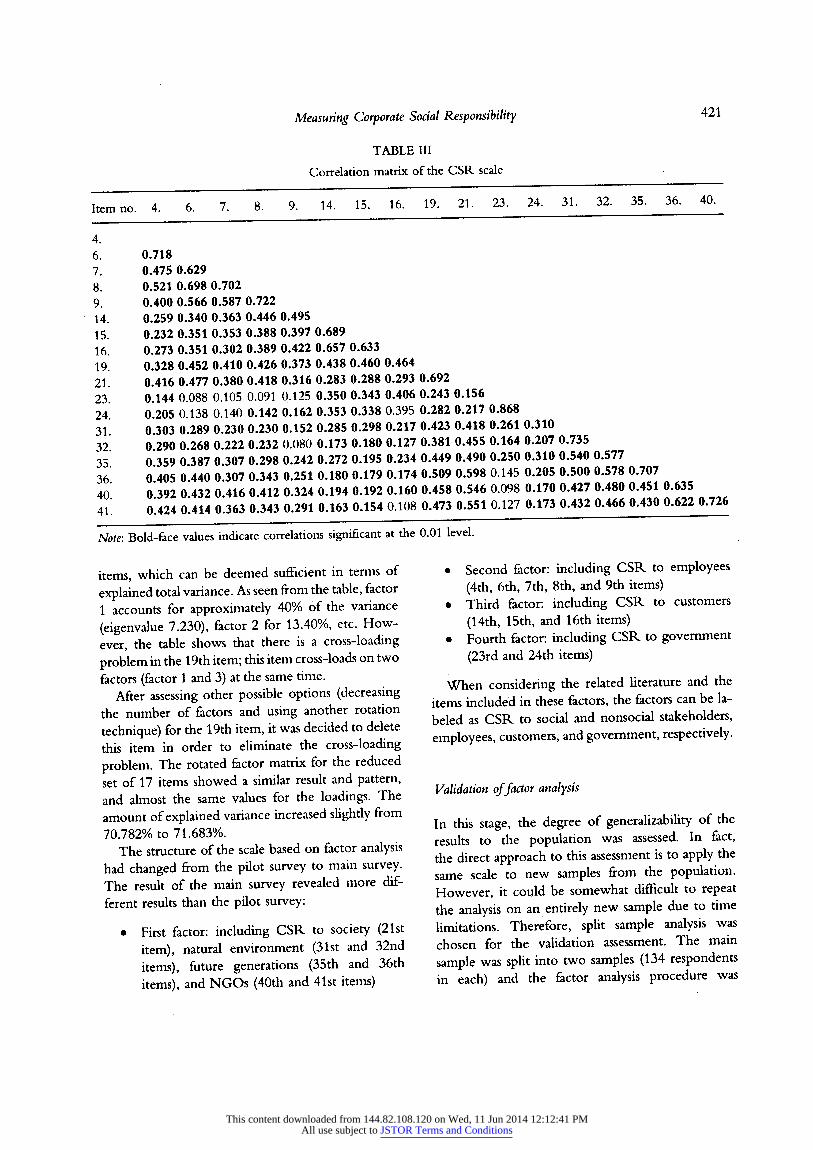

Factor analysis was performed within the six-stage model-building framework introduced by Hair et al. (2006). Table III presents the correlation matrix for 18 items of the scale. A review of the correlation matrix reveals that 141 of the 153 correlations (approximately 93%) are significant at the 0.01 level, which provide adequate basis to perform a factor analysis for each item and for the overall basis. To evaluate the overall significance of the correlation matrix, the Bartlett's test was used again. The Bartlett's test found that the correlations, when taken collectively, were significant at the 0.0001 level.

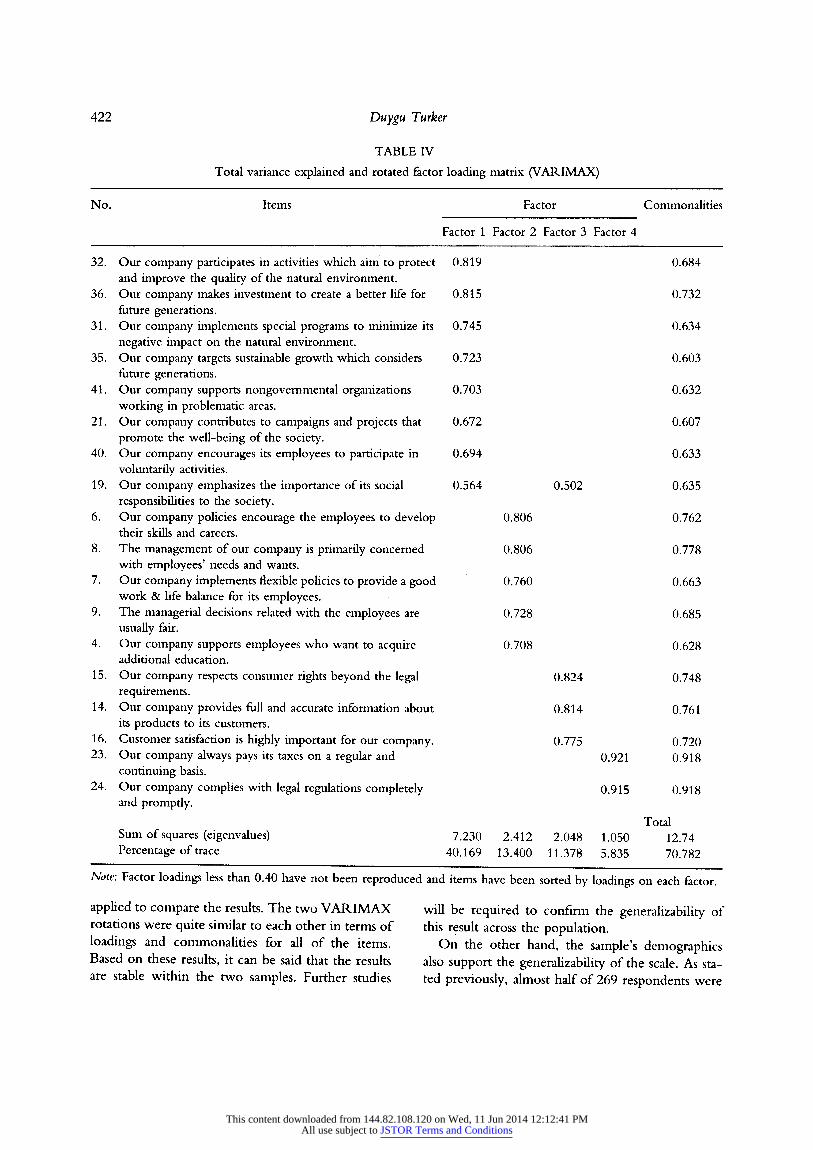

The data gathered from the main survey were analyzed through principal components factor analy- sis. Table IV shows the information regarding the 18 possible factors and their relative explanatory powers. In the table, it is possible to assess the importance of each component and select the ideal number of factors while using the eigenvalues at the same time. The four factors capture 70.782% of the variance of the 18

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 421

TABLE III

Correlation matrix of the CSR scale

Item no. 4. 6. 7. 8. 9. 14. 15. 16. 19. 21. 23. 24. 31. 32. 35. 36. 40.

4. 6. 0.718 7. 0.475 0.629 8. 0.521 0.698 0.702 9. 0.400 0.566 0.587 0.722 14. 0.259 0.340 0.363 0.446 0.495 15. 0.232 0.351 0.353 0.388 0.397 0.689

16. 0.273 0.351 0.302 0.389 0.422 0.657 0.633

19. 0.328 0.452 0.410 0.426 0.373 0.438 0.460 0.464

21. 0.416 0.477 0.380 0.418 0.316 0.283 0.288 0.293 0.692

23 0.144 0.088 0.105 0.091 0.125 0.350 0.343 0.406 0.243 0.156

24 0.205 0.138 0.140 0.142 0.162 0.353 0.338 0.395 0.282 0.217 0.868

31 0.303 0.289 0.230 0.230 0.152 0.285 0.298 0.217 0.423 0.418 0.261 0.310

32 0 290 0.268 0.222 0.232 0.080 0.173 0.180 0.127 0.381 0.455 0.164 0.207 0.735

35 0 359 0 387 0.307 0.298 0.242 0.272 0.195 0.234 0.449 0.490 0.250 0.310 0.540 0.577

36 0 405 0 440 0 307 0.343 0.251 0.180 0.179 0.174 0.509 0.598 0.145 0.205 0.500 0.578 0.707

40 0392 0 432 0 416 0.412 0.324 0.194 0.192 0.160 0.458 0.546 0.098 0.170 0.427 0.480 0.451 0.635

41. 0.424 0.414 0.363 0.343 0.291 0.163 0.154 0.108 0.473 0.551 0.127 0.173 0.432 0.466 0.430 0.622 0.726

Note: Bold-face values indicate correlations significant at the 0.01 level.

items, which can be deemed sufficient in terms of

explained total variance. As seen from the table, factor

1 accounts for approximately 40% of the variance

(eigenvalue 7.230), factor 2 for 13.40%, etc. How-

ever, the table shows that there is a cross-loading

problem in the 19th item; this item cross-loads on two

factors (factor 1 and 3) at the same time. After assessing other possible options (decreasing

the number of factors and using another rotation

technique) for the 19th item, it was decided to delete

this item in order to eliminate the cross-loading

problem. The rotated factor matrix for the reduced

set of 17 items showed a similar result and pattern, and almost the same values for the loadings. The

amount of explained variance increased slightly from

70.782% to 71.683%. The structure of the scale based on factor analysis

had changed from the pilot survey to main survey. The result of the main survey revealed more dif-

ferent results than the pilot survey:

• First factor: including CSR to society (21st item), natural environment (31st and 32nd

items), future generations (35th and 36th

items), and NGOs (40th and 41st items)

• Second factor: including CSR to employees (4th, 6th, 7th, 8th, and 9th items)

• Third factor: including CSR to customers

(14th, 15th, and 16th items) • Fourth factor: including CSR to government

(23rd and 24th items)

When considering the related literature and the

items included in these factors, the factors can be la-

beled as CSR to social and nonsocial stakeholders,

employees, customers, and government, respectively.

Validation of factor analysis

In this stage, the degree of generalizability of the

results to the population was assessed. In fact, the direct approach to this assessment is to apply the

same scale to new samples from the population. However, it could be somewhat difficult to repeat the analysis on an entirely new sample due to time

limitations. Therefore, split sample analysis was

chosen for the validation assessment. The main

sample was split into two samples (134 respondents in each) and the factor analysis procedure was

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

422 Duygu Turker

TABLE IV

Total variance explained and rotated factor loading matrix (VARIMAX)

No. Items Factor Commonalities

Factor 1 Factor 2 Factor 3 Factor 4

32. Our company participates in activities which aim to protect 0.819 0.684 and improve the quality of the natural environment.

36. Our company makes investment to create a better life for 0.815 0.732 future generations.

31. Our company implements special programs to minimize its 0.745 0.634 negative impact on the natural environment.

35. Our company targets sustainable growth which considers 0.723 0.603 future generations.

41. Our company supports nongovernmental organizations 0.703 0.632 working in problematic areas.

21. Our company contributes to campaigns and projects that 0.672 0.607 promote the well-being of the society.

40. Our company encourages its employees to participate in 0.694 0.633 voluntarily activities.

19. Our company emphasizes the importance of its social 0.564 0.502 0.635 responsibilities to the society.

6. Our company policies encourage the employees to develop 0.806 0.762 their skills and careers.

8. The management of our company is primarily concerned 0.806 0.778 with employees' needs and wants.

7. Our company implements flexible policies to provide a good 0.760 0.663 work & life balance for its employees.

9. The managerial decisions related with the employees are 0.728 0.685 usually fair.

4. Our company supports employees who want to acquire 0.708 0.628 additional education.

15. Our company respects consumer rights beyond the legal 0.824 0.748 requirements.

14. Our company provides full and accurate information about 0.814 0.761 its products to its customers.

16. Customer satisfaction is highly important for our company. 0.775 0.720 23. Our company always pays its taxes on a regular and 0.921 0.918

continuing basis. 24. Our company complies with legal regulations completely 0.915 0.918

and promptly. Total

Sum of squares (eigenvalues) 7.230 2.412 2.048 1.050 12.74 Percentage of trace 40.169 13.400 11.378 5.835 70.782

Note: Factor loadings less than 0.40 have not been reproduced and items have been sorted by loadings on each factor.

applied to compare the results. The two VARIMAX rotations were quite similar to each other in terms of loadings and commonalities for all of the items. Based on these results, it can be said that the results are stable within the two samples. Further studies

will be required to confirm the generalizability of this result across the population.

On the other hand, the sample's demographics also support the generalizability of the scale. As sta- ted previously, almost half of 269 respondents were

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 423

women and the construct reflected the perceptions of women as well. Although the age range of the

respondents was 18-61 years, the mean age for the

sample was 31.23 years. Therefore, the sample in- cluded a relatively young group of people and their

thoughts shaped the construct. This result can be

explained by the majority of young people in the

population. Although the application of the scale in an aging society may give different results, it cur-

rently reflects the ideas of young business profes- sionals about CSR. Therefore, the respondents may present a modern point of view about CSR. Based on the respondents' relatively higher level of edu- cation, it can be stated that the construct is also

reflecting the ideas of well-educated people. This result may also support the generalizability of the scale in the well-educated populations of developed countries. The analysis of respondents' organizations shows that most of them were working in service and manufacturing industry, 61.3% and 33.1%,

respectively. This result also shows a similarity with other modern societies.

Reliability analysis

In the reliability assessment, two commonly used methods were chosen for each scale. Firstly, the inter- item correlations of each scale were computed and

interpreted. As a rule of thumb, the item-to-total correlations should exceed 0.50 and the inter-item correlations should exceed 0.30 (Hair et al., 2006, p. 137). Table II shows that the correlation matrix in- cludes 17 items, after the deletion of 19th item. There are 136 different item pairings or correlations and the

average inter-item correlation is 0.35, higher than the

suggested threshold value of 0.30. In the second method, the internal consistencies

of each scale were assessed by computing Cronbach's

alpha. Although the generally agreed upon lower limit for Cronbach's alpha is 0.70, the decisions were taken based on the number of items, number of dimensions, and average inter-item correlations

(Cortina, 1993). Therefore, as computed above, the inter-item correlation is 0.35, and the scale includes 17 items in four dimensions. The suggested alpha for similar conditions (r = 0.30/18 items/3 dimensions) described by Cortina is 0.64 (1993). The Cronbach's

alpha of the CSR scale (0.9013) was much higher

than this suggested alpha value. The Cronbach alpha values for the four factors were calculated as 0.8915, 0.8836, 0.8554, and 0.9279.

Limitations of the study

There are some limitations of the current study and these should be considered when generalizing the

validity of the scale. First of all, the scale does not cover every stakeholder of a business. As explained previously, only some representative stakeholders were selected at the beginning of the process. After the analyses, some items were also eliminated from the scale. However, the scale still has a combination of various stakeholders in a balanced manner and

provides a useful tool to measure CSR.

Depending on the selected sample, the current

study reflects only the perceptions of employees, the internal stakeholders of a business. Although it was assumed that the respondents give accurate and reliable information about the CSR involvement of their organizations, it is possible that they might provide incorrect or incomplete information. In fact, this is a common problem of every empirical study based on individual perceptions. Since this limitation was foreseen at the beginning of the study, the data collection method was designed to overcome, or at least minimize, this risk. During the data collection

process, the respondents were assured the confi-

dentiality of their responses. Under these conditions, it was expected that they could provide more accurate information about their organizations. However, the perceptions of other stakeholders

might also be assessed in further studies.

Additionally, since the data was collected from a

sample which was drawn from only one country, the results can be generalized only in this country. However, as mentioned previously, the selected

country has a unique position between Eastern and Western cultures. Still, given the increased conver-

gence of the cultural values of the business com- munities in Turkey to a European context, a scale

developed in Turkey can provide insight into the

understanding of CSR in modern societies. Addi-

tionally, the demographics of respondents also sup- ported the generalizability of the study. However, there is a need for further studies to confirm the current structure of the scale.

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

424 ^uygu Turker

Conclusion

According to Carroll (2000), since it is difficult to

gather actual measures, there is a tendency to rely on stakeholders' opinions or assessments of performance in the literature. However, developing comprehen- sive measures of corporate social activities that really address social performance is a challenge. Because, "if we do less than this, we should not call it social performance" (Carroll, 2000, p. 474). In spite of this

apparent risk, relying on stakeholders' views can be a more reliable way of measuring corporate social activities compared to alternative methods. In the current study, a new measure of CSR was obtained based on the views of employees. After an elaborate scale development process, the current structure of the scale provides some important implications.

In the study, the typology of Wheeler and Sillanpaa (1997) provided a base to build a framework for stakeholders. Although these scholars theoretically defined the concept in a broader sense, some of the selected stakeholders were eliminated during the scale development process. At the beginning of the study, employees, customers, society, government, com- petitors, natural environment, future generations, and NGOs were selected to represent each dimension of the typology. However, as a result of the scale development process, the responsibilities to compet- itors were eliminated from the factorial structure. The possible reason for this result may be the dual meaning of some statements. Alternatively, the respondents may think that a business does not have a responsibility to their competitors. However, in the light of the discussions on fair competition and corporate spying, it can be estimated that the responsibilities to com- petitors will be more significant in the near future. Therefore, as a suggestion, this stakeholder should be reconsidered in further studies.

One of the interesting results in the study is the stakeholder combination and explanatory strength of the first factorial subscale which includes CSR to society, natural environment, future generations, and NGOs. It can be noticed that this subscale includes more than one stakeholder and they are closely interrelated with each other. As discussed previously, these stakeholders are generally considered as having a secondary or less direct impact on business operations. However, especially in recent decades, increasing concerns about global problems have made people

more aware of their surroundings and the well-being of these stakeholders. Therefore, the result of the current study may reflect the increasing responsive- ness of respondents. Especially, considering some demographic characteristics of respondents (for in- stance, age and education level), the results presented a modern perspective on CSR, as older generations or less-educated people may have fewer concerns about the protection of the natural environment or the rights of future generations. On the other hand, the changing natures of CSR and stakeholder concepts may reveal a somewhat different structure in further studies. Although it is impossible to predict the exact structures of the scale in further studies, it might be expected that the responsibilities to future generations or the natural environment will be perceived as more important in the future and that these items may construct an entirely new subscale.

The other three components of the scale reason- ably sequenced according to their degrees of importance for the respondents. The second subscale includes the responsibilities to employees. This is a quite interesting result, considering the fact that the data was gathered from employees. Based on this analysis, the respondents seemed to ignore their self- interest and perceived that the CSR to society, natural environment, future generations, and NGOs are more important than CSR related to themselves. This perspective of the respondents may also support their objectiveness when assessing the social involvement of their organizations. The third sub- scale of the structure is CSR to customers. It is known that customers are critically important for the survival and growth of business. The result of the analysis confirms that the respondents are also aware of the importance of customers as stakeholders.

Based on the legal dimension of Carroll's model, CSR to government appeared in the final subscale of the structure. However, this component has the weakest explanatory power in the structure. As mentioned in the previous part of the study, the existence of a legal dimension, similar to an economic dimension, is also questioned by some scholars. Therefore, these scholars exclude legal responsibilities from their CSR definitions. In the current study, legal responsibilities were considered among the dimen- sions of CSR in order to avoid narrowing the concept. However, the place and weakness of this component in the factorial structure somewhat supports the

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 425

sceptical approaches of these scholars. Thus, this result of the study may stimulate new discussions and anal-

yses of the legal dimension of CSR definitions in fu- ture studies.

In conclusion, although the results of the current

study presented a plausible structure for the scale, there is surely a need for more research in order to confirm these results. In particular, studies con- ducted in different sectors (for instance, NGOs) or different countries will be useful in this sense.

Acknowledgement

This article is mainly based on the unpublished master dissertation of the author. The author is grateful to Prof. Ömür N. Timurcanday Özmen, Dokuz Eylül University, for her constant support and advice

throughout this process and Dr. Oyvind Ihlen, Univer-

sity of Oslo, for his valuable comments and suggestions.

References

Abbott, W. F. and R. J. Monsen: 1979, 'On the Mea- surement of Corporate Social Responsibility: Self-

Reported Disclosures as a Method of Measuring Corporate Social Involvement', Academy of Manage- ment Journal 22(3), 501-515.

Ararat, M.: 2004, 'Social Responsibility in a State

Dependent System', in A. Habisch, J. jonker, M.

Wegner and R. Schmidpeter (eds.), Corporate Social

Responsibility Across Europe (Springer- Verlag, Berlin), Chapter 19, pp. 247-261.

Ararat, M.: 2005, 'Drivers for Corporate Social Respon- sibility, Case of Turkey', Working Paper. (Available at:

http://info.worldbank.org/ etools/mdfdb/docs/WP_ UJRC5.pdf).

Ararat, M.: 2006, 'Corporate Social Responsibility Across Middle East and North Africa', Working Paper. (Avail- able at SSRN: http://ssrn.com/abstract= 101 5925).

Aupperle, K. E.: 1984, 'An Empirical Measure of Corpo- rate Social Orientation', in L. E. Preston (ed.), Research in Corporate Social Performance and Policy, Vol. 6 (JAI, Greenwich, CT), pp. 27-54.

Bagozzi, R. P., Y. Yi and L. W. Phillips: 1991, 'Assessing Construct Validity in Organizational Research', Administrative Science Quarterly 36(3), 421-458.

Bayiksel, S. Ö.: 2007, 'Hizli Büyüyen Daha Çok Bege- niliyor', Capital Magazine. (Available at: http://www. capitd.com.tr/haber.aspx?HBR_KOD=%204509).

Baucus, M. S. and D. A. Baucus: 1997, 'Paying the Piper: An Empirical Examination of Longer-Term Financial Consequences of Illegal Corporate Behavior', Academy of Management Journal 40(1), 129-151.

Bragdon, J. H. and J. A. Marlin: 1972, 'Is Pollution Profitable?', Risk Management 19, 9-18.

Bowen, H. R.: 1953, Social Responsibilities of the Busi- nessman (Harper & Row, New York).

Bugra, A.: 2003, 'The Place of the Economy in Turkish Society', Tlte South Atlantic Quarterly 102(2/3), 453- 470.

Carroll, A. B.: 1979, 'A Three Dimensional Conceptual Model of Corporate Social Performance', Academy of Management Review 4(4), 497-505.

Carroll, A. B.: 1991, The Pyramid of Corporate Social

Responsibility: Toward the Moral Management of

Organizational Stakeholders', Business Horizons 34(4), 39-48.

Carroll, A. B.: 1999, 'Corporate Social Responsibility -

Evolution of a Definitional Construct', Business & Society 38(3), 268-295.

Carroll, A. B.: 2000, 'A Commentary and an Overview of Key Questions on Corporate Social Performance Measurement', Business & Society 39(4), 466-478.

Charkham, J.: 1994, Keeping Good Company: A Study of Corporate Governance in Five Countries (Claredon, Oxford).

Chen, K. H. and R. W. Metcalf: 1984, 'The Relationship Between Pollution Control Record and Financial Indicators Revisited', The Accounting Review 55, 168- 177.

Clarkson, M. B. E.: 1994. 'A Risk Based Model of Stakeholder Theory', in Proceedings of the Second Toronto

Conference on Stakeholder Theory (Centre for Corporate Social Performance & Ethics University of Toronto, Toronto).

Clarkson, M. B. E.: 1995, 'A Stakeholder Framework for

Analyzing and Evaluating Corporate Social Perfor- mance', Academy of Management Review 20(1), 92-117.

Cortina, J. M.: 1993, 'What is Coefficient Alpha? An Examination of Theory and Applications', Journal of Applied Psychology 78(1), 98-104.

Daft, R. L.: 2003, Management (Thomson South- Western, USA).

Davidson, W. N. and D. L. Worrell: 1990, 'A Com-

parison and Test of the Use of Accounting and Stock Market Data in Relating Corporate Social Responsi- bility and Financial Performance', Akron Business and Economic Review 21, 7-19. (Cited in Maignan and Ferrell, 2000).

Davis, K.: 1960, 'Can Business Afford to Ignore Social

Responsibilities?', California Management Review 2(3), 70-76.

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

426 Duygu Turker

Davis, K.: 1973, The Case for and Against Business

Assumption of Social Responsibilities', Academy of Management Journal 16(2), 312-322.

Dawkins, D. and S. Lewis: 2003, 'CSR in Stakeholder

Expectations: and Their Implication for Company Strategy', Journal of Business Ethics 44(2/3), 185-193.

Eells, R. and C. Walton: 1974, Conceptual Foundations of Business, 3rd Edition (Irwin, Burr Ridge, IL).

Etheredge, J. M.: 1999, The Perceived Role of Ethics and Social Responsibility: An Alternative Scale

Structure', Journal of Business Ethics 18, 51-64.

Flam, H.: 2004, Turkey and the EU: Politics and Eco- nomics of Accession', CESifo Economic Studies 50(1), 171-210.

Freedman, N. and B. Jaggi: 1982, 'Pollution Disclosures, Pollution Performance, and Economic Performance', The International Journal of Management Science 10, 167- 176.

Freedman, M. and C. Wasley: 1990, The Association Between Environmental Performance and Environ- mental Disclosure in Annual Reports and 10-Ks', Advances in Public Interest Accounting 3, 183-193.

Freeman, R. E.: 1984, Strategic Management: A Stakeholder

Approach (Pitman, Boston). Gray, R., R. Kouhy and S. La vers: 1995,

* Corporate Social

and Environmental Reporting: A Review of the Litera- ture and a Longitudinal Study of UK Disclosure', Accounting, Auditing and Accountability Journal 8(2), 47-77.

Greenwood, M. R.: 2001, The Importance of Stake- holders According to Business Leaders', Business and

Society Review 106(1), 29-49. Hair, J. F., W. C. Black, R. E. Anderson and R. L.

Tatham: 2006, Multivariate Data Analysis, 6th Edition

(Pearson Prentice Hall, New Jersey). Hosftede, G.: 1980, Culture's Consequences: International

Differences in Work-Related Values (Sage, Thousand Oaks, CA).

Ingram, R. and K. Frazier: 1980, 'Environmental Per- formance and Corporate Disclosure', Journal of Accounting Research 18(2), 614-622.

Kongar, E.: 1999. 21. Yüzyilda Türkiye: 2000H Yillarda

Tiirkiye'nin Toplumsal Yapisi. Remzi Kitabi, Istanbul.

Mahoney, L. S. and L. Thorne: 2005, 'Corporate Social

Responsibility and Long-Term Compensation: Evi- dence from Canada', Journal of Business Ethics 57(3), 241-253.

Maignan, I. and O. C. Ferrell: 2000, 'Measuring Cor- porate Citizenship in Two Countries: The Case of the United States and France', Journal of Business Ethics 23(3), 283-297.

Maignan, I. and O. C. Ferrell: 2004, 'Corporate Social

Responsibility and Marketing: An Integrative Frame-

work', Journal of the Academy of Marketing Science 32(1), 3-19.

McGuire, J. W.: 1963, Business and Society (McGraw-Hill, New York).

McGuire, J. B., A. Sundgren and T. Schneeweis: 1988,

'Corporate Social Responsibility and Firm Financial

Performance', Academy of Management Journal 31, 854- 872.

Orpen, C. : 1 987, The Attitudes of United States and South African Managers to Corporate Social Responsibility', Journal of Business Ethics 6(2), 89-96.

Ostlund, L. E.: 1977, 'Attitudes of Managers Towards

Corporate Social Responsibility', California Manage- ment Review 19(4), 35-49.

Peterson, D. K.: 2004, The Relationship Between Per-

ceptions of Corporate Citizenship and Organizational Commitment', Business and Society 43(3), 296-319.

Quazi, A. M. and D. O'Brien: 2000, 'An Empirical Test of a Cross-National Model of Corporate Social

Responsibility', Journal of Business Ethics 25, 33-51.

Rockness, J. W.: 1985, 'An Assessment of the Rela-

tionship Between US Corporate Environmental Per- formance and Disclosure', Journal of Business Finance &

Accounting 12(3), 339-354.

Ruf, B. M., K. Muralidhar and K. Paul: 1998, The

Development of a Systematic, Aggregate Measure of

Corporate Social Performance', Journal of Management 24(1), 119-133.

Sims, R. R.: 2003, Ethics and Corporate Social Responsi- bility: Why Giants Fall (Praeger, USA).

Singhapakdi, A., S. J. Vitell, K. C. Rallapalli and K. L. Kraft: 1996, The Perceived Role of Ethics and Social

Responsibility: A Scale Development', Journal of Business Ethics 15, 1131-1140.

Smith, D.: 1993, The Frankenstein Syndrome: Corpo- rate Responsibility and the Environment', in D. Smith

(ed.), Business and the Environment: Implications of the New Environmentalism (Paul Chapman, London), pp. 172-189.

Smith, W. J. and R. S. Blackburn: 1988, 'CSR: A Psy- chometric Examination of A Measurement Instrument', Proceedings of the Southern Management Association, 293- 295.

Votaw, D.: 1972, 'Genius Became Rare: A Comment on the Doctrine of Social Responsibility', California Management Review 15(2), 25-31.

Verdeyen, V., J. Put and B. V. Buggenhout: 2004, 'A Social Stakeholder Model', International Journal of Social

Welfare 13, 325-331. Waddock, S. A. and S. B. Graves: 1997, The Corporate

Social Performance - Financial Performance Link', Strategic Management Journal 18(4), 303-319.

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions

Measuring Corporate Social Responsibility 427

Wheeler, D. and M. Sillanpaa: 1997, Tlte Stakeholder Corporation: A Blueprint for Maximazing Stakeholder Value (Pitman, London).

Wheeler, D. and M. Sillanpaa: 1998, 'Including the Stakeholders: The Business Case', Long Range Planning 31(2), 201-210.

Wherther, W. B. and D. Chandler: 2006, Responsibility: Stakeholders in a Global Environment (Sage, USA).

Wiseman, J.: 1982, 'An Evaluation of Environmental Disclosures Made in Corporate Annual Reports', Accounting, Organizations, and Society 7(1), 53-63.

Wolfe, R. and K. Aupperle: 1991, 'Introduction to

Corporate Social Performance: Methods for Evaluat-

ing an Elusive Construct', in J. E. Post (ed.), Research in

Corporate Social Performance and Policy ; Vol. 12 (JAI Press, Greenwich, CT), pp. 265-268.

Wood, D. J. and R. E. Jones: 1995, 'Stakeholder Mismatching: A Theoretical Problem in Empirical Research on Corporate Social Performance', Interna- tionaljournal of Organizational Analysis 3, 229-267.

World Commission on Environment and Development (WCED): 1987, Our Common Future (Oxford Uni- versity Press, Oxford).

Vocational School, Yasar University,

Kazim Dirik Malt., 364 Sok., No. 5, Bornova, Izmir 35500, Turkey

E-mail: [email protected]. tr

This content downloaded from 144.82.108.120 on Wed, 11 Jun 2014 12:12:41 PMAll use subject to JSTOR Terms and Conditions