Embed Size (px)

Citation preview

Efficiency in Islamic and conventional banking: an internationalcomparison

Mariani Abdul-Majid • David S. Saal •

Giuliana Battisti

Published online: 25 December 2009

� Springer Science+Business Media, LLC 2009

Abstract The paper investigates the efficiency of a

sample of Islamic and conventional banks in 10 countries

that operate Islamic banking for the period 1996–2002,

using an output distance function approach. We obtain

measures of efficiency after allowing for environmental

influences such as country macroeconomic conditions,

accessibility of banking services and bank type. While

these factors are assumed to directly influence the shape of

the technology, we assume that country dummies and bank

size directly influence technical inefficiency. The parame-

ter estimates highlight that during the sample period,

Islamic banking appears to be associated with higher input

usage. Furthermore, by allowing for bank size and inter-

national differences in the underlying inefficiency distri-

butions, we are also able to demonstrate statistically

significant differences in inefficiency related to these fac-

tors even after controlling for specific environmental

characteristics and Islamic banking. Thus, for example, our

results suggest that Sudan and Yemen have relatively

higher inefficiency while Bahrain and Bangladesh have

lower estimated inefficiency. Except for Sudan, where

banks exhibits relatively strong returns to scale, most

sample banks exhibit very slight returns to scale, although

Islamic banks are found to have moderately higher returns

to scale than conventional banks. While this suggests that

Islamic banks may benefit from increased scale, we would

emphasize that our results suggest that identifying and

overcoming the factors that cause Islamic banks to have

relatively low potential outputs for given input usage levels

will be the key challenge for Islamic banking in the coming

decades.

Keywords Islamic banking � International efficiency

comparison � Output distance function

JEL Classification G21 � D24 � L1

1 Introduction

The emergence of Islamic banking has been driven by the

increasing number of Muslims who wish to lead their lives

according to the shariah, the legal code of Islam. The

establishment of Nasser Social Bank in Egypt in 1971

(Iqbal and Molyneux 2005), the Dubai Islamic Bank in the

United Arab Emirates and the Islamic Development Bank

(IDB) in 1975 paved the way for the creation of other

Islamic financial institutions all over the world (Central

Bank of Malaysia 1999). Some form of Islamic financial

services is now available in at least 70 countries (Husain

2005).

The salient features of Islamic banking are the prohi-

bition of interest payment in transactions, and the prohi-

bition of undertaking or financing anti-social and unethical

behaviour such as gambling, pornography and alcohol. An

M. Abdul-Majid

School of Economics, Faculty of Economics and Business,

Universiti Kebangsaan Malaysia, 43600 UKM Bangi,

Selangor, Malaysia

e-mail: [email protected]

D. S. Saal (&)

Economics and Strategy Group, Aston Business School,

Aston University, Birmingham B4 7ET, UK

e-mail: [email protected]

G. Battisti

Industrial Economics Division, Nottingham University

Business School, Jubilee Campus, Wollaton Road,

Nottingham NG8 1BB, UK

e-mail: [email protected]

123

J Prod Anal (2010) 34:25–43

DOI 10.1007/s11123-009-0165-3

Islamic bank is governed by shariah, as well as the regu-

lations set in place by the host country. While some Islamic

banks were purposely established to operate within shari-

ah, some Islamic banks were converted from conventional

banks. Thus, in Iran and Sudan, all conventional banks

were converted to Islamic banks in order to conform with

government legislation (Sundararajan and Errico 2002).

However, it is more common for countries with large

Muslim populations to operate Islamic banking systems

alongside conventional banking systems, as is now the case

in Malaysia, Bahrain, Pakistan, Saudi Arabia, and Egypt

(Hassan 2003).

Previous studies using cost and/or profit functions to

compare the efficiency of Islamic and conventional banks,

have found Islamic banks to be similar (Abdul-Majid et al.

2005; Mokhtar et al. 2006) if not better (Alshammari 2003;

Al-Jarrah and Molyneux 2005) than conventional banks.

However, (Abdul-Majid et al. 2008, 2009) demonstrated

that after properly taking into account environmental

variables in either a cost or output distance function,

Malaysian Islamic banks are found to have higher input

requirements. This finding of higher input requirements for

Islamic banks in Malaysia is the main motivation for this

study, as we wish to further investigate how Islamic banks

perform relative to conventional banks internationally.

Moreover, an international study will allow analysis of

how, respectively, Islamic and conventional banks from

various countries perform relative to other countries, and

whether significant differences across countries exist. This

would potentially provide relevant findings for policy

makers in the sample countries who wish to judge the

relative performance of their banking sector.

We also note that the design of this study results from

careful consideration of how to effectively compare the

efficiency of conventional and Islamic banks, while prop-

erly allowing for relative differences between these types

of banks. Thus, following several previous studies that

include both conventional and Islamic banks, we adopt an

intermediation approach. This approach is most suitable

for comparably defining the relationship between bank

outputs and inputs. This is because Islamic banks adopt an

equity participation principle that effectively intermediates

between savers (depositors) and investors (e.g., Al-Jarrah

and Molyneux 2005; El-Gamal and Inanoglu 2005).

However, we also extend this approach by including equity

as an input, because of both its role in Islamic banking and

because we believe this better reflects the fact that banks

can and do employ equity financing as an input which can

be an important component of capital reserves used for

liquidity purposes.

This study also adopts an output distance function

approach to compare Islamic and conventional banks. This

implies the assumption of an output oriented approach, and

therefore measuring efficiency by comparing actual output

relative to potential output, given fixed inputs. This approach

has the advantage of allowing the use of identifiable output

and input quantities such as deposits, total operating

expenses and equity, and therefore allows us to avoid the

possible problem of input price endogeneity (Orea 2002).

Given differences in accounting standards across countries,

as well as differences in conventional and Islamic banking

assets, we also believe that for this international study, the

standard approach of employing accounting information to

define output and/or input prices, is particularly likely to

result in distorted and inaccurate price estimates, and hence

distorted cost or profit efficiency estimates.

In sum, this study aims to measure the efficiency of

banks in countries that have Islamic banking in operation

as well as relative efficiency between countries, and will

particularly focus on the relative performance of Islamic

banks as compared to conventional banks. More specifi-

cally, by deriving estimates of efficiency for banks in dif-

ferent countries after estimating an output distance function

with stochastic frontier techniques, the analysis highlights

the impact of operating characteristics, including Islamic

banking and country-specific environmental characteris-

tics, on the relative outputs of banks. The efficiency esti-

mates highlight that during the sample period, Islamic

banking appears to be associated with higher input usage.

However, as our model specification also allows for both

international differences and differences in bank size in the

underlying inefficiency distributions, our model also sug-

gests the presence of statistically significant differences in

inefficiency related to bank size and across countries.

The rest of the paper is organised as follows. Section 2

provides a brief literature review focused on the relative

performance of banks across countries, and is followed by

a description of the methodology in Sect. 3. Data and the

empirical specification are discussed in Sect. 4. Section 5

reports the results which are comprised of the output dis-

tance function, efficiency, and returns to scale estimates.

Finally, Sect. 6 offers some conclusions.

2 Review of the literature and the modelling

approach

This study contributes to both the existing literature

employing a parametric approach to measure cross-country

bank efficiency as well as the literature considering the

comparative efficiency of Islamic and conventional banks.

As our approach to controlling for differences in operating

environment will have a significant impact on estimated

efficiency, it is necessary to carefully consider the impact

of the chosen operating environment variables on measured

efficiency. Moreover, as the choice of appropriate inputs

26 J Prod Anal (2010) 34:25–43

123

and outputs will significantly influence estimated efficiency,

we also consider previous definitions of the input output set

in order to better model an appropriate common frontier for

Islamic and conventional banks in a cross-country analysis.

It is also necessary to carefully consider the influence of

functional form on the measured efficiency of both con-

ventional and Islamic banks in an international setting.

Finally, we briefly take into account the findings of previous

studies with regard to returns to scale in banking.

We firstly consider the implication of simultaneously

modelling Islamic and conventional banks. As shariah

compliant banking has different objectives and modus

operandi from conventional banking, it may also have

different operational characteristics from conventional

banking, which may influence potential output. Thus, for

example, the prohibition of conventional interest bearing

financial instruments can be considered as an operating

characteristic that limits the use of certain banking ‘‘tech-

nologies’’ and thereby ‘‘reduces’’ potential banking outputs

relative to those feasible for a conventional bank. We

would therefore argue that it is appropriate to control for

Islamic banking as a bank-specific characteristic that

directly influences the estimated frontier, and hence esti-

mated potential output, rather than as a factor that directly

influences estimated inefficiency. Moreover, as Islamic

bank managers are constrained by shariah, this approach

has the dual benefit of measuring their efficiency relative to

an appropriate frontier taking into account operating dif-

ferences between Islamic and conventional banks, while

also simultaneously allowing measurement of differences

in potential output (frontier shift) that can be attributed to

the adoption of Islamic banking practices.

In our opinion, jointly modelling both Islamic and

conventional banks also requires a reconsideration of the

input output set typically employed in banking studies.

Thus, some previous SFA cross-country studies (e.g.,

Maudos et al. 2002; Fries and Taci 2005; Williams and

Nguyen 2005; Kasman and Yildirim 2006) have either

controlled for bank output quality and/or equity in the

frontier estimation. Bank output quality1 (Fries and Taci

2005) or equity capital (Carvallo and Kasman 2005; Bos

and Schmiedel 2007; Fitzpatrick and McQuinn 2008) has

always before been treated as fully exogenous in the

frontier estimation, although some studies have treated

equity (Maudos et al. 2002; Williams and Nguyen 2005;

Kasman and Yildirim 2006) and even both loan quality and

equity (Alshammari 2003) as ‘‘netputs’’.2 However, we

would argue that even conventional banks employ equity

capital as an input in addition to funds from deposits and

inter-bank borrowings to finance their operations (Bonac-

corsi di Patti and Hardy 2005). Moreover, Islamic banks

that apply the equity participation principle also depend

significantly on equity as a source of funds (Metwally

1997). Therefore, while in the previous literature equity has

generally been employed only as an environmental factor

in frontier estimation, we strongly believe that a more

appropriate modelling approach, which not only better

specifies the input relationship for all banks but also allows

a flexible specification that is more appropriate for com-

paring conventional and Islamic banks, is to directly

include equity as an input.

We next consider the specification of an appropriate

model to estimate cross-country bank efficiency. While

some studies do not assume that any environmental con-

ditions influence frontier estimation, and hence location of

the frontier (Allen and Rai 1996; Altunbas et al. 2001;

Maudos et al. 2002); other studies do control for these

factors (Dietsch and Lozano-Vivas 2000; Bonin et al. 2005;

Carvallo and Kasman 2005). These environmental condi-

tions can be categorised into country-specific factors (Fries

and Taci 2005; Williams and Nguyen 2005) and bank-

specific factors. A common frontier without controls for

country-specific factors is likely to be misspecified because

each country may have a different banking technology as

well as different environmental and regulatory conditions,

that influence potential output (Dietsch and Lozano-Vivas

2000), but the frontier would assume the same technology

for all banks (Chaffai et al. 2001). Therefore, by control-

ling for these factors in a common frontier, efficiency

rankings are more persistent (Fries and Taci 2005), effi-

ciency estimates are improved (Dietsch and Lozano-Vivas

2000; Bonin et al. 2005; Carvallo and Kasman 2005;

Kasman 2005), and the estimates of efficiency more

appropriately reflect the impact of less (or more) favour-

able country-specific conditions on estimated relative effi-

ciency (Dietsch and Lozano-Vivas 2000). These country-

specific factors can be broadly generalised into macro-

economic factors such as per capita income, density of

demand, population density, banking concentration (Diet-

sch and Lozano-Vivas 2000; Carvallo and Kasman 2005;

Williams and Nguyen 2005), bank structure and regulation

such as bank branches per capita (Maudos and De Guevara

2007), the intermediation ratio (Dietsch and Lozano-Vivas

2000), as well as accessibility of banking services, as

measured with GDP growth (Kasman and Yildirim 2006)

and density of bank branches (Dietsch and Lozano-Vivas

2000).

In this study, countries involved in the sample range

from low to relatively high income economies and signif-

icant differences exist in many characteristics including

1 If output quality is not controlled for, unmeasured differences in

loan quality that are not captured by banking data may be mistakenly

measured as inefficiency (Berger and Mester 1997).2 ‘‘Netputs’’ are operating characteristic variables that have been

made fully interactive with inputs and outputs in the function.

J Prod Anal (2010) 34:25–43 27

123

those related to politics, economics, social structure, and

geography. Thus, for example Sudan is characterized by a

culture of holding cash to hand, and is plagued by the

effects of civil war, economic sanctions and drought, and

these jointly influence the poorly developed Sudanese

banking sector (Bashir 1999; Hussein 2004). In contrast,

due to its high level of economic development and its

comprehensive regulatory framework, Bahrain has attrac-

ted confidence among investors (Iqbal and Molyneux

2005). These country specific differences in the back-

ground operating environment as well as significant dif-

ferences in bank regulatory frameworks and financial

reporting formats (Karim 2001) strongly suggest that

controlling for country-specific effects appropriately will

have an important impact on estimated efficiency in an

international sample. Irrespective of controlling for coun-

try-specific factors in frontier estimation however, coun-

tries with a bigger sample still show larger difference in

average efficiency scores relative to those with small

samples (Lozano-Vivas et al. 2002) and a wide range of

average inefficiency estimates exists across countries (Abd

Karim 2001; Carvallo and Kasman 2005). Furthermore,

Bonin et al. (2005) found that country effects continue to

play a significant part in explaining differences in effi-

ciency measures even after they have been controlled for in

the frontier estimation.

Focusing specifically on methodological approaches

employed in past SFA based studies, estimated efficiency

scores have been correlated with environmental factors

under investigation using two different methodologies. The

first, which is a ‘‘one step’’ methodology simultaneously

estimates the frontier and the impact of environmental fac-

tors on efficiency by using an inefficiency effects model,

such as that proposed by Battese and Coelli (1995). These

include both studies that assume no direct impact of envi-

ronmental factors on the estimated frontier, and hence

assume that they only influence efficiency (Abd Karim 2001;

Alshammari 2003; Al-Jarrah and Molyneux 2005) and

studies that also control for these factors in estimating the

frontier (Bonin et al. 2005; Williams and Nguyen 2005;

Fitzpatrick and McQuinn 2008). Within the former strand of

literature, bank types dummy variables (Abd Karim 2001;

Alshammari 2003; Al-Jarrah and Molyneux 2005), owner-

ship (Abd Karim 2001), liquidity, bank concentration ratios

(Al-Jarrah and Molyneux 2005) and size (bank assets) (Abd

Karim 2001; Al-Jarrah and Molyneux 2005; Perera et al.

2007) have been assumed to directly influence inefficiency.

In the later group of studies, which assume that environ-

mental conditions do directly influence frontier estimation,

country-specific factors such as governance-related factors

(Williams and Nguyen 2005), market concentration (Perera

et al. 2007) and country dummy variables (Bonin et al. 2005;

Fitzpatrick and McQuinn 2008) have been controlled for.

The second significant methodological approach evident

in the literature employs a ‘‘two step’’ approach. Such

studies have first estimated the frontier, followed by

regression analysis to find correlations between ineffi-

ciency scores and bank-specific factors (Allen and Rai

1996; Altunbas et al. 2001; Maudos et al. 2002). This

category includes both studies that do not assume envi-

ronmental conditions to influence frontier estimation

(Allen and Rai 1996; Altunbas et al. 2001; Maudos et al.

2002) and studies that control for these factors in esti-

mating the frontier (e.g., Dietsch and Lozano-Vivas 2000;

Carvallo and Kasman 2005). Without controlling for any

environmental conditions, the former have subsequently

correlated inefficiency with bank-specific factors such as

ownership (Weill 2002), organisational structure (Boubakri

et al. 2005), bank size (Maudos et al. 2002; Yildirim and

Philippatos 2007), specialisation, profitability, risk and

country-specific factors (Maudos et al. 2002). On the other

hand, studies that control for these factors in estimating the

frontier have subsequently correlated inefficiency with

bank-specific factors such as loan quality, profitability,

equity capital, non-interest income (Carvallo and Kasman

2005) and country-specific factors such as concentration

ratio (Dietsch and Lozano-Vivas 2000). However, this

‘‘two-step’’ procedure is associated with several anomalies

and has been previously criticised as an inappropriate

methodology leading to potentially biased efficiency esti-

mates (Coelli et al. 1998).

Given this discussion, we have chosen to employ a

‘‘one-step’’ procedure similar to Fries and Taci (2005) and

Williams and Nguyen (2005). We will control for country-

specific environmental factors as well as shariah compliant

banking directly in the estimated frontier, thereby allowing

for any differences in technology and/or potential output

that result from differences in operating characteristics.

However, using the Battese and Coelli (1995) model, we

will also allow country dummy variables and bank size to

directly influence the inefficiency specification. As dis-

cussed further below, we believe that this simultaneous

inclusion of country-specific operating characteristics in

the estimated frontier and country dummies in the ineffi-

ciency specification, allows for appropriate differences in

measured potential output between countries, while

simultaneously allowing us to test for systematic differ-

ences in efficiency across countries.

Regarding bank size, we first note that controlling for it

directly in the estimated frontier is an inappropriate

methodology, as bank size is closely correlated with bank

outputs, and this approach would be likely to result in a

biased estimate of the relationship between scale and

potential outputs, and hence biased efficiency estimates.

We believe this argument explains why none of the above

studies has controlled for bank size in the frontier.

28 J Prod Anal (2010) 34:25–43

123

Nevertheless, as our expectation is that Islamic banks are

on average smaller than conventional banks, there is the

potential that any size related heteroskedasticity in the one

sided inefficiency term could be inappropriately accounted

for as group related inefficiency, thereby leading to

potential bias in the estimated inefficiency of Islamic banks

relative to conventional banks.3 Moreover, there is also the

potential that failing to control for size related heteroske-

dasticity may similarly adversely affect the analysis of

economies of scale. We therefore follow the approach of

previous studies (Abd Karim 2001; Al-Jarrah and Moly-

neux 2005; Perera et al. 2007) that have specified bank size

as a determinant of inefficiency. Although Al-Jarrah and

Molyneux (2005) found bank size to be insignificant,

Perera et al. (2007) and Abd Karim (2001) both found that

larger banks are relatively more efficient.

With regard to the chosen functional form, most cross-

country studies of banking efficiency have employed a cost

function approach (Dietsch and Lozano-Vivas 2000; Abd

Karim 2001; Carvallo and Kasman 2005; Fries and Taci

2005; Kasman 2005; Carbo Valverde et al. 2007; Maudos

and De Guevara 2007), or a profit function approach

(Kasman and Yildirim 2006; Fitzpatrick and McQuinn

2008). Moreover, studies have increasingly simultaneously

employed both cost and profit functions (Alshammari

2003; Hassan 2003; Al-Jarrah and Molyneux 2005; Bonin

et al. 2005; Hassan 2005; Kasman and Yildirim 2006; Bos

and Schmiedel 2007). Nevertheless, with international

comparisons of efficiency, one must note that international

differences in accounting information might lead to dis-

torted price estimates, thereby undermining the common

use of both cost and profit functions for measuring bank

efficiency. This study will therefore extend the approach of

Cuesta and Orea (2002) and will measure the efficiency of

banks internationally using an output distance function,

which not only does not require price information, but also

does not require any behavioural assumption such as cost

minimisation or profit maximisation. This study will

therefore join the limited number of studies using an output

distance function approach to judge cross-country banking

efficiency (Chaffai et al. 2001; Olgu 2006), and, to our

knowledge, is the first cross-country study of Islamic and

conventional bank efficiency that has employed an output

distance function approach.

Focussing briefly on returns to scale estimates in the

previous literature, slight economies of scale are found in

every production scale but are more pronounced in small

banks in some studies (Abd Karim 2001; Altunbas et al.

2001; Cavallo and Rossi 2001). However, other studies

also find evidence of diseconomies of scale in large banks

(Allen and Rai 1996; Carvallo and Kasman 2005), small

and medium-sized Islamic banks (Yudistira 2004) and

small banks (Kasman 2005). Irrespective of these differ-

ences in previous findings however, returns to scale esti-

mates are normally near one which indicates that on

average, banks operate at almost constant returns to scale

(e.g., Clark 1996; Cuesta and Orea 2002; Orea 2002;

Carvallo and Kasman 2005). In addition, bank type (e.g.

Islamic, conventional commercial or conventional mer-

chant) is found to have little or no significant impact on

estimated scale economies in Gulf Cooperation Council

(GCC) banks (Alshammari 2003). Given these limited

previous findings, the model below will also investigate

returns to scale of both Islamic and conventional banks

internationally.

In sum, the discussion of the previous literature has

demonstrated the importance of controlling for operating

characteristics, and particularly country-specific environ-

mental conditions, when estimating bank efficiency. In

particular, it highlights that country effects play a signifi-

cant part in explaining estimated efficiency differences

across countries, and must therefore be carefully modelled.

Moreover, in contrast to the previous literature, it has also

been argued that equity should be modelled as an input

because it is a potentially important financial input for

conventional and particularly Islamic banks. In addition,

this section has illustrated the advantage of employing an

output distance function in an international study of banking

efficiency. The model below will therefore employ an

output distance function and control for country-specific

factors and shariah compliant banking directly in the esti-

mated frontier as well as allowing for international differ-

ences and differences related to bank size in the underlying

inefficiency distribution using the Battese and Coelli (1995)

model. Moreover, given the model specification detailed

below, it will be possible to test for statistically significant

differences in the parameters that define each country’s

inefficiency distribution. This study will therefore provide a

useful methodology and expand upon the existing literature

that has analysed cross-country bank efficiency, in addition

to providing a comparison between Islamic and conven-

tional banks. Given this discussion, the following section

further details the methodological approach employed.

3 Methodology

3.1 Output distance function

A production technology can be represented by the tech-

nology set, which is the technically feasible combination of

inputs and outputs (Coelli et al. 1998; Cuesta and Orea

2002). If the vector of K inputs, indexed by k is denoted by

3 We gratefully acknowledge an anonymous referee who highlighted

this issue to us.

J Prod Anal (2010) 34:25–43 29

123

X = (X1, X2,…, XK) and the vector of M outputs, indexed

by m, is denoted by Y = (Y1, Y2,…, YM), the technology

set can be defined by:

T ¼ X;YÞf : X 2 RKþ;Y 2 RM

þ ;X can produce Yg ð1Þ

where RKþ and RM

þ are the sets of non-negative, real K and

M-tuples respectively. For each input vector, X, let P(X) be

the set of producible output vectors, Y, that are obtainable

from the input vector X:

PðXÞ ¼ Y : X;Yð Þ 2 TÞf g: ð2Þ

The output distance function can be defined in terms of the

output set, P(X) as follows:

Do X;Yð Þ ¼ min - [ 0 :Y

-

� �2 PðXÞ

� �: ð3Þ

The output distance function is non-decreasing, positively

linearly homogeneous, increasing in Y, decreasing in X, and

defined as the maximum feasible expansion of the output

vector given the input vector (Fare and Primont 1995). Given

the input vector X, the production possibility set is the area

bounded by the production possibility frontier (PPF), which

defines the maximum feasible output. If the output vector Y

is an element of P(X), Do(X,Y) B 1. However, if firms

produce on the PPF, Do X;Yð Þ- ¼ 1; indicating technical

efficiency. In contrast, for an inefficient firm operating

within the area bounded by the PPF, Do X;Yð Þ ¼ -\1;

thereby indicating the ratio of actual output to potential

output. Farrell’s (1957) output-oriented measure of technical

efficiency, defined as the maximum producible radial

expansion of the output vector, can then be represented as:

OEo ¼ 1=DoðX,Y): ð4Þ

3.2 The econometric specification

Following Fare and Primont (1995) and Cuesta and Orea

(2002), and also allowing for exogenous factors, the gen-

eral form of a stochastic output distance function can be

shown as:

1 ¼ D0 Yn;t;Xn;t;Zn;t; b� �

h en;t

� �ð5Þ

where h en;t

� �¼ exp un;t þ vn;t

� �; Yn,t is a vector of outputs,

Xn,t is an input vector, Zn,t is an exogenous factor vector

and b is a vector of parameters. Inefficiency is accommo-

dated in the specification of h(.), as en,t is a composed error

term comprised of vn,t which represents random uncon-

trollable error that affects the n-th firm at time t, and un,t is

assumed to be attributable to technical inefficiency.

In order to facilitate estimation, we follow the standard

practice of imposing homogeneity of degree one in outputs

on the distance function, which implies that Do Z;X; pYð Þ ¼pDo Z;X;Yð Þ; p [ 0: By arbitrarily choosing the M-th out-

put, we then can define p ¼ 1

YMand write:

Do Zn;t;Xn;t;Yn;t

YM;n;t

� �¼

Do Zn;t;Xn;t;Yn;t

� �YM;n;t

: ð6Þ

which, after assuming Y�n;t ¼ Y1;n;t

�YM;n;t;Y2;n;t

�YM;n;t;

�. . .;YM�1;n;t

�YM;n;tÞ and rearranging terms yields the

general form:

1

YM;n;t¼ Do Y�n;t;Xn;t;Zn;t; b

� h en;t

� �ð7Þ

Finally after assuming a standard translog functional

form4 to represent the technology, the output distance can

be represented as:

� ln YM;n;t ¼ /o þXK

k¼1

ak ln Xk;n;t þXM�1

m¼1

bm ln Y�m;n;t

þ 0:5XK

k¼1

XK

s¼1

ak;s ln Xk;n;t ln Xs;n;t þ1

2

XM�1

m¼1

XM�1

j¼1

bm;j

� ln Y�m;n;t ln Y�j;n;t þXK

k¼1

XM�1

m¼1

hk;m ln Xk;n;t ln Y�m;n;t

þXK

k¼1

sk;t ln Xk;n;tt þXM�1

m¼1

wm;t ln Y�m;n;tt þ k1t þ 0:5k2t2

þXH

h¼1

nhZh;n;t þ vn;t þ un;t ð8Þ

where, Y*m,n,t = Ym,n,t/YM,n,t, k = 1, 2,…, K and s = 1,

2,…, K are indices for input; m = 1, 2,…, M and j = 1,

2,…, M are indices for output; h = 1, 2,…, H is an index

for the total of H environmental Z variables that are

included to account for differences in operating environ-

ment discussed above, and the Greek letters (except v and

u) represent unknown parameters to be estimated. Standard

symmetry is imposed to the second order parameters by

imposing the constraints aks ¼ ask and bmj ¼ bjm:

We specify Battese and Coelli (1995)’s truncated normal

SFA model with the mean of the truncated normal distribu-

tion (Mn,t) made an explicit function of country dummy

variables and size differences across banks. This is illustrated

in Eq. 9, which follows the formulation of the model detailed

in (Coelli 1996). Thus, vn,t is assumed to be normally dis-

tributed with zero mean and variance r2v and independently

distributed of un,t. un,t C 0 is assumed to be drawn from a

truncation (at zero) of the normal distribution with mean,

Mn,t and variance r2u where df and q are parameters to be

estimated, f = 1, 2…, F is an index for countries, C is a

country dummy and S is bank size, as measured by total

assets. The parameters in the translog function as defined

in Eq. 8, the composed error parameters, r2 ¼ r2v þ r2

u and

4 In the literature, the translog function is preferred in estimating a

parametric distance function (Fuentes et al. 2001) because it is

flexible, easy to calculate and permits the imposition of homogeneity.

30 J Prod Anal (2010) 34:25–43

123

c ¼ r2u

�r2

v þ r2u; the country specific inefficiency distribu-

tion parameters (df), and the bank size parameter (q) speci-

fied in Eq. 9 below are estimated simultaneously using

maximum likelihood estimation (MLE) techniques.

EMn;t ¼XF

f¼1

df Cf ;n;t þ qSn;t: ð9Þ

Given the output distance function specification in Eq. 8,

our model controls for country-specific operating character-

istics and Islamic banking by including appropriate Z

variables directly in the estimated frontier. This implies that

the estimated inefficiency scores are net of the impact of

controlled for environmental influences on efficient potential

outputs. The simultaneous estimation of Eqs. 8 and 9

therefore enables one to estimate inefficiency under the

assumption that banks operate in an equivalent environment,

while at the same time modelling how bank inefficiency

differs from one country to another and as bank size varies.

Thus, if q\ 0 ([0) the resulting shift in the truncated normal

inefficiency distribution implies that the probability of

observing higher inefficiency decreases (increases) with

bank size. The sign, magnitude, and statistical significance

of q therefore measure to what extent, ceteris paribus,

inefficiency is related to bank size. Similarly, if dB \ dA the

resulting difference in the truncated normal inefficiency

distributions implies that, ceteris paribus, the probability of

observing higher inefficiencies is lower in Country B than in

Country A. Thus, a finding that dB is statistically significantly

less than dA, implies the presence of higher inefficiency in

country A, after controlling for bank size and differences in

operating environment between countries.

Following from Eq. 5, and given the model assump-

tions, an estimate of output distance can be derived as

Do Yn;t;Xn;t;Zn;t; b� �

¼ expð�lÞ: Equivalently, an esti-

mate of output oriented efficiency is obtainable as:

OEn;t ¼1

Do Yn;t;Xn;t;Zn;t; b� � ¼ exp ln;t

� �: ð10Þ

As OEn,t relies on the unobservable inefficiency, un,t, we

follow the standard approach, as described in Battese and

Coelli (1995) and Frame and Coelli (2001) to estimate un,t,

as the conditional expectation of un,t given the observed

value of the overall composed error term, en,t.

Given the estimated model, returns of scale for the banks in

the sample can also be estimated, using the estimated scale

elasticity. As in Cuesta and Orea (2002), scale elasticity can be

calculated as the negative of the sum of the input elasticities:

SCALEn;t ¼ �XK

k¼1

o ln Do Ym;n;t;Xk;n;t

� �o ln Xk;n;t

: ð11Þ

If SCALEn,t [ 1 a bank is operating at increasing returns to

scale (IRS). If SCALEn,t \ 1, there is decreasing returns to

scale (DRS) and constant returns to scale (CRS) are present

if SCALEn,t = 1.

4 The data and the empirical specifications

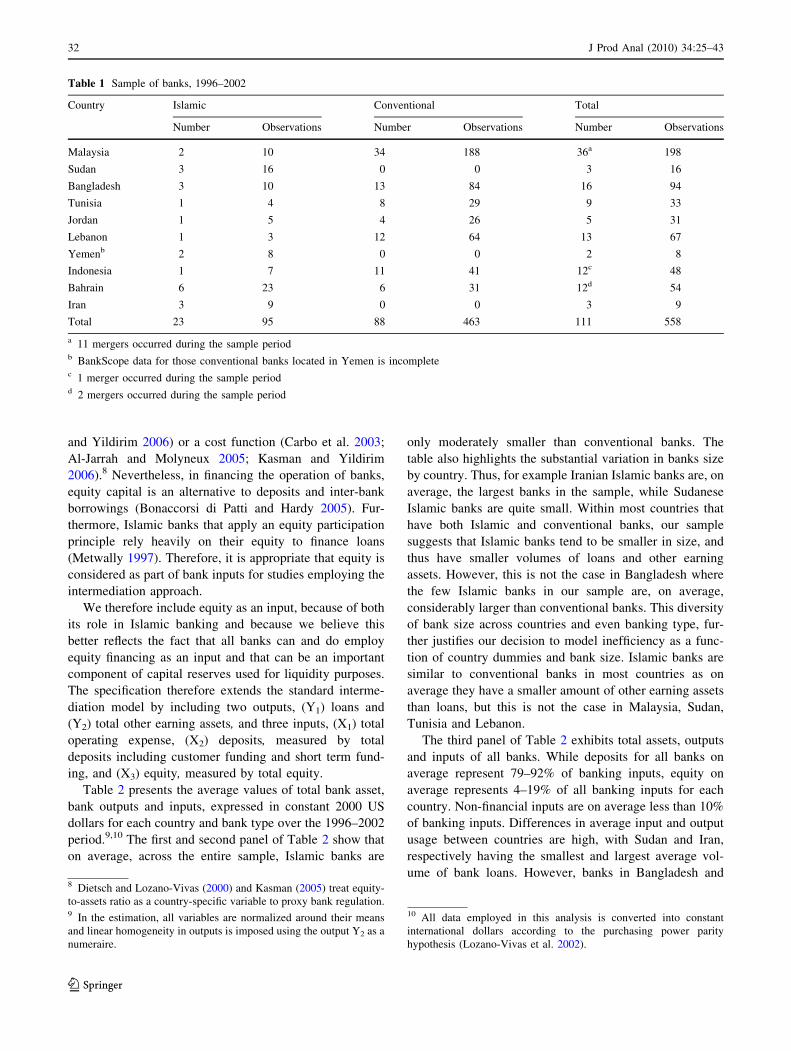

Data on 23 Islamic and 88 conventional banks from 10

countries that operate Islamic banking were drawn from the

BankScope database for the period 1996–2002 resulting in

an unbalanced panel of 558 observations, with 95 of these

observations being for Islamic banks. All those Islamic

banks with complete data were selected for inclusion in our

sample, as was a sample of conventional banks from those

countries were Islamic bank data is available. BankScope

did not provide complete data for Islamic banks in several

countries with significant Islamic banking sectors (e.g.

Kuwait, and the UAE), hence those banks and countries

with incomplete information have been dropped from the

sample. Table 1 describes the sample distribution of banks

by type of bank for each country under study.

The selection of output and input variables follows the

intermediation approach which has been widely employed

in conventional bank studies (e.g., Maudos et al. 2002;

Carbo et al. 2003), Islamic bank studies (e.g., Brown and

Skully 2003; Hassan 2003; Yudistira 2004) and Islamic and

conventional bank studies (e.g., Alshammari 2003; Al-

Jarrah and Molyneux 2005). The intermediation approach

focuses on a bank’s role in intermediating savers and

investors of funds, and is most consistent with the concept

of Islamic banking. This is because Islamic banking relies

on profit-sharing contracts, which involve an equity par-

ticipation principle5 with depositors,6 and banks can

therefore be seen as intermediating savers and investors by

transforming deposits into earning assets, rather than as

producers of services and loans.

Previous studies that employ the intermediation

approach found that equity is significant in defining bank

output but many (e.g., Girardone et al. 2004; Kasman and

Yildirim 2006) include it either as an environmental vari-

able or a netput. However, it has not been previously

employed as an input in single-country studies7 (e.g.,

Mester 1996; e.g., Girardone et al. 2004), and cross-

country studies, nor in those using a profit function (Al-

shammari 2003; Al-Jarrah and Molyneux 2005; Kasman

5 Some current Islamic banks also practice debt-like financing such

as murabaha.6 In some Islamic banks, deposits or equity contributed by depositors

are categorised under shareholders’ funds, but some Islamic banks

group them as deposits from customers, similar to conventional banks

(Karim 2001).7 Some studies have treated equity capital as a netput in the translog

function (Berger and Mester 1997; Hasan and Marton 2003;

Bonaccorsi di Patti and Hardy 2005; Kraft et al. 2006).

J Prod Anal (2010) 34:25–43 31

123

and Yildirim 2006) or a cost function (Carbo et al. 2003;

Al-Jarrah and Molyneux 2005; Kasman and Yildirim

2006).8 Nevertheless, in financing the operation of banks,

equity capital is an alternative to deposits and inter-bank

borrowings (Bonaccorsi di Patti and Hardy 2005). Fur-

thermore, Islamic banks that apply an equity participation

principle rely heavily on their equity to finance loans

(Metwally 1997). Therefore, it is appropriate that equity is

considered as part of bank inputs for studies employing the

intermediation approach.

We therefore include equity as an input, because of both

its role in Islamic banking and because we believe this

better reflects the fact that all banks can and do employ

equity financing as an input and that can be an important

component of capital reserves used for liquidity purposes.

The specification therefore extends the standard interme-

diation model by including two outputs, (Y1) loans and

(Y2) total other earning assets, and three inputs, (X1) total

operating expense, (X2) deposits, measured by total

deposits including customer funding and short term fund-

ing, and (X3) equity, measured by total equity.

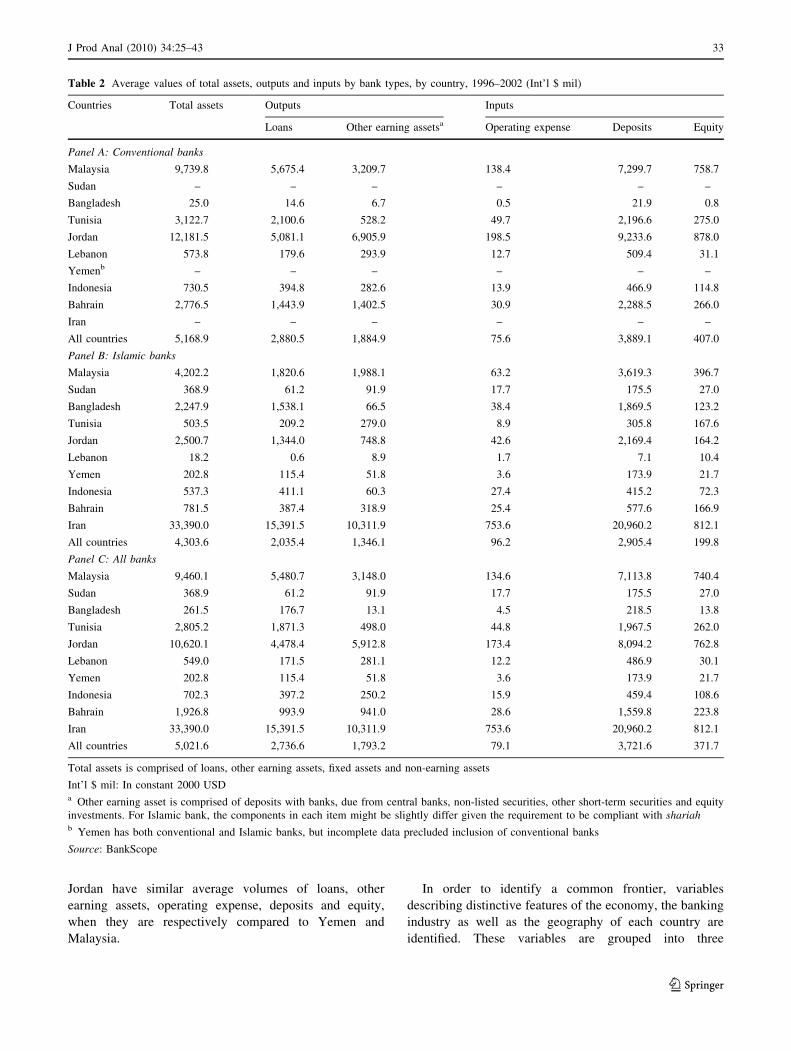

Table 2 presents the average values of total bank asset,

bank outputs and inputs, expressed in constant 2000 US

dollars for each country and bank type over the 1996–2002

period.9,10 The first and second panel of Table 2 show that

on average, across the entire sample, Islamic banks are

only moderately smaller than conventional banks. The

table also highlights the substantial variation in banks size

by country. Thus, for example Iranian Islamic banks are, on

average, the largest banks in the sample, while Sudanese

Islamic banks are quite small. Within most countries that

have both Islamic and conventional banks, our sample

suggests that Islamic banks tend to be smaller in size, and

thus have smaller volumes of loans and other earning

assets. However, this is not the case in Bangladesh where

the few Islamic banks in our sample are, on average,

considerably larger than conventional banks. This diversity

of bank size across countries and even banking type, fur-

ther justifies our decision to model inefficiency as a func-

tion of country dummies and bank size. Islamic banks are

similar to conventional banks in most countries as on

average they have a smaller amount of other earning assets

than loans, but this is not the case in Malaysia, Sudan,

Tunisia and Lebanon.

The third panel of Table 2 exhibits total assets, outputs

and inputs of all banks. While deposits for all banks on

average represent 79–92% of banking inputs, equity on

average represents 4–19% of all banking inputs for each

country. Non-financial inputs are on average less than 10%

of banking inputs. Differences in average input and output

usage between countries are high, with Sudan and Iran,

respectively having the smallest and largest average vol-

ume of bank loans. However, banks in Bangladesh and

Table 1 Sample of banks, 1996–2002

Country Islamic Conventional Total

Number Observations Number Observations Number Observations

Malaysia 2 10 34 188 36a 198

Sudan 3 16 0 0 3 16

Bangladesh 3 10 13 84 16 94

Tunisia 1 4 8 29 9 33

Jordan 1 5 4 26 5 31

Lebanon 1 3 12 64 13 67

Yemenb 2 8 0 0 2 8

Indonesia 1 7 11 41 12c 48

Bahrain 6 23 6 31 12d 54

Iran 3 9 0 0 3 9

Total 23 95 88 463 111 558

a 11 mergers occurred during the sample periodb BankScope data for those conventional banks located in Yemen is incompletec 1 merger occurred during the sample periodd 2 mergers occurred during the sample period

8 Dietsch and Lozano-Vivas (2000) and Kasman (2005) treat equity-

to-assets ratio as a country-specific variable to proxy bank regulation.9 In the estimation, all variables are normalized around their means

and linear homogeneity in outputs is imposed using the output Y2 as a

numeraire.

10 All data employed in this analysis is converted into constant

international dollars according to the purchasing power parity

hypothesis (Lozano-Vivas et al. 2002).

32 J Prod Anal (2010) 34:25–43

123

Jordan have similar average volumes of loans, other

earning assets, operating expense, deposits and equity,

when they are respectively compared to Yemen and

Malaysia.

In order to identify a common frontier, variables

describing distinctive features of the economy, the banking

industry as well as the geography of each country are

identified. These variables are grouped into three

Table 2 Average values of total assets, outputs and inputs by bank types, by country, 1996–2002 (Int’l $ mil)

Countries Total assets Outputs Inputs

Loans Other earning assetsa Operating expense Deposits Equity

Panel A: Conventional banks

Malaysia 9,739.8 5,675.4 3,209.7 138.4 7,299.7 758.7

Sudan – – – – – –

Bangladesh 25.0 14.6 6.7 0.5 21.9 0.8

Tunisia 3,122.7 2,100.6 528.2 49.7 2,196.6 275.0

Jordan 12,181.5 5,081.1 6,905.9 198.5 9,233.6 878.0

Lebanon 573.8 179.6 293.9 12.7 509.4 31.1

Yemenb – – – – – –

Indonesia 730.5 394.8 282.6 13.9 466.9 114.8

Bahrain 2,776.5 1,443.9 1,402.5 30.9 2,288.5 266.0

Iran – – – – – –

All countries 5,168.9 2,880.5 1,884.9 75.6 3,889.1 407.0

Panel B: Islamic banks

Malaysia 4,202.2 1,820.6 1,988.1 63.2 3,619.3 396.7

Sudan 368.9 61.2 91.9 17.7 175.5 27.0

Bangladesh 2,247.9 1,538.1 66.5 38.4 1,869.5 123.2

Tunisia 503.5 209.2 279.0 8.9 305.8 167.6

Jordan 2,500.7 1,344.0 748.8 42.6 2,169.4 164.2

Lebanon 18.2 0.6 8.9 1.7 7.1 10.4

Yemen 202.8 115.4 51.8 3.6 173.9 21.7

Indonesia 537.3 411.1 60.3 27.4 415.2 72.3

Bahrain 781.5 387.4 318.9 25.4 577.6 166.9

Iran 33,390.0 15,391.5 10,311.9 753.6 20,960.2 812.1

All countries 4,303.6 2,035.4 1,346.1 96.2 2,905.4 199.8

Panel C: All banks

Malaysia 9,460.1 5,480.7 3,148.0 134.6 7,113.8 740.4

Sudan 368.9 61.2 91.9 17.7 175.5 27.0

Bangladesh 261.5 176.7 13.1 4.5 218.5 13.8

Tunisia 2,805.2 1,871.3 498.0 44.8 1,967.5 262.0

Jordan 10,620.1 4,478.4 5,912.8 173.4 8,094.2 762.8

Lebanon 549.0 171.5 281.1 12.2 486.9 30.1

Yemen 202.8 115.4 51.8 3.6 173.9 21.7

Indonesia 702.3 397.2 250.2 15.9 459.4 108.6

Bahrain 1,926.8 993.9 941.0 28.6 1,559.8 223.8

Iran 33,390.0 15,391.5 10,311.9 753.6 20,960.2 812.1

All countries 5,021.6 2,736.6 1,793.2 79.1 3,721.6 371.7

Total assets is comprised of loans, other earning assets, fixed assets and non-earning assets

Int’l $ mil: In constant 2000 USDa Other earning asset is comprised of deposits with banks, due from central banks, non-listed securities, other short-term securities and equity

investments. For Islamic bank, the components in each item might be slightly differ given the requirement to be compliant with shariahb Yemen has both conventional and Islamic banks, but incomplete data precluded inclusion of conventional banks

Source: BankScope

J Prod Anal (2010) 34:25–43 33

123

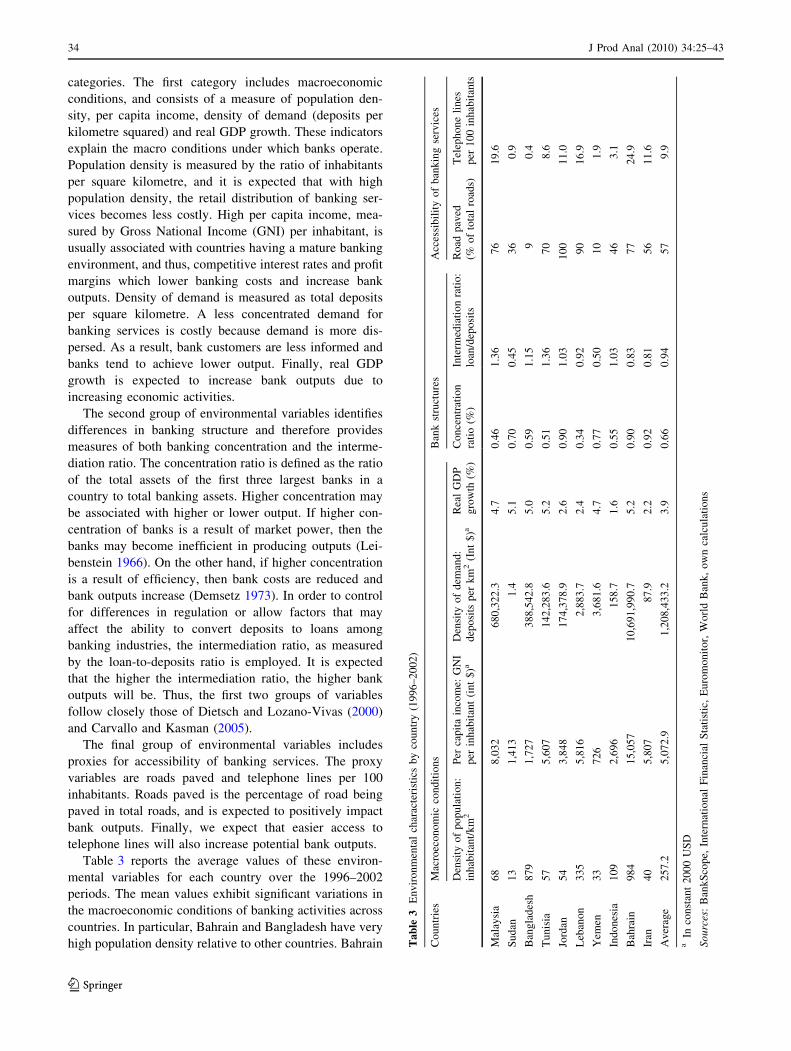

categories. The first category includes macroeconomic

conditions, and consists of a measure of population den-

sity, per capita income, density of demand (deposits per

kilometre squared) and real GDP growth. These indicators

explain the macro conditions under which banks operate.

Population density is measured by the ratio of inhabitants

per square kilometre, and it is expected that with high

population density, the retail distribution of banking ser-

vices becomes less costly. High per capita income, mea-

sured by Gross National Income (GNI) per inhabitant, is

usually associated with countries having a mature banking

environment, and thus, competitive interest rates and profit

margins which lower banking costs and increase bank

outputs. Density of demand is measured as total deposits

per square kilometre. A less concentrated demand for

banking services is costly because demand is more dis-

persed. As a result, bank customers are less informed and

banks tend to achieve lower output. Finally, real GDP

growth is expected to increase bank outputs due to

increasing economic activities.

The second group of environmental variables identifies

differences in banking structure and therefore provides

measures of both banking concentration and the interme-

diation ratio. The concentration ratio is defined as the ratio

of the total assets of the first three largest banks in a

country to total banking assets. Higher concentration may

be associated with higher or lower output. If higher con-

centration of banks is a result of market power, then the

banks may become inefficient in producing outputs (Lei-

benstein 1966). On the other hand, if higher concentration

is a result of efficiency, then bank costs are reduced and

bank outputs increase (Demsetz 1973). In order to control

for differences in regulation or allow factors that may

affect the ability to convert deposits to loans among

banking industries, the intermediation ratio, as measured

by the loan-to-deposits ratio is employed. It is expected

that the higher the intermediation ratio, the higher bank

outputs will be. Thus, the first two groups of variables

follow closely those of Dietsch and Lozano-Vivas (2000)

and Carvallo and Kasman (2005).

The final group of environmental variables includes

proxies for accessibility of banking services. The proxy

variables are roads paved and telephone lines per 100

inhabitants. Roads paved is the percentage of road being

paved in total roads, and is expected to positively impact

bank outputs. Finally, we expect that easier access to

telephone lines will also increase potential bank outputs.

Table 3 reports the average values of these environ-

mental variables for each country over the 1996–2002

periods. The mean values exhibit significant variations in

the macroeconomic conditions of banking activities across

countries. In particular, Bahrain and Bangladesh have very

high population density relative to other countries. Bahrain Ta

ble

3E

nv

iro

nm

enta

lch

arac

teri

stic

sb

yco

un

try

(19

96

–2

00

2)

Co

un

trie

sM

acro

eco

no

mic

con

dit

ion

sB

ank

stru

ctu

res

Acc

essi

bil

ity

of

ban

kin

gse

rvic

es

Den

sity

of

po

pu

lati

on

:

inh

abit

ant/

km

2P

erca

pit

ain

com

e:G

NI

per

inh

abit

ant

(in

t$

)aD

ensi

tyo

fd

eman

d:

dep

osi

tsp

erk

m2

(In

t$

)aR

eal

GD

P

gro

wth

(%)

Co

nce

ntr

atio

n

rati

o(%

)

Inte

rmed

iati

on

rati

o:

loan

/dep

osi

ts

Ro

adp

aved

(%o

fto

tal

road

s)

Tel

eph

on

eli

nes

per

10

0in

hab

itan

ts

Mal

aysi

a6

88

,03

26

80

,32

2.3

4.7

0.4

61

.36

76

19

.6

Su

dan

13

1,4

13

1.4

5.1

0.7

00

.45

36

0.9

Ban

gla

des

h8

79

1,7

27

38

8,5

42

.85

.00

.59

1.1

59

0.4

Tu

nis

ia5

75

,60

71

42

,28

3.6

5.2

0.5

11

.36

70

8.6

Jord

an5

43

,84

81

74

,37

8.9

2.6

0.9

01

.03

10

01

1.0

Leb

ano

n3

35

5,8

16

2,8

83

.72

.40

.34

0.9

29

01

6.9

Yem

en3

37

26

3,6

81

.64

.70

.77

0.5

01

01

.9

Ind

on

esia

10

92

,69

61

58

.71

.60

.55

1.0

34

63

.1

Bah

rain

98

41

5,0

57

10

,69

1,9

90

.75

.20

.90

0.8

37

72

4.9

Iran

40

5,8

07

87

.92

.20

.92

0.8

15

61

1.6

Av

erag

e2

57

.25

,07

2.9

1,2

08

,43

3.2

3.9

0.6

60

.94

57

9.9

aIn

con

stan

t2

00

0U

SD

So

urc

es:

Ban

kS

cop

e,In

tern

atio

nal

Fin

anci

alS

tati

stic

,E

uro

mo

nit

or,

Wo

rld

Ban

k,

ow

nca

lcu

lati

on

s

34 J Prod Anal (2010) 34:25–43

123

also has extremely high per capita income and deposits per

kilometre squared. In contrast, Sudan has very low popu-

lation density and very marginal deposits per kilometre

squared. Furthermore, Bahrain, Iran and Jordan have rela-

tively high concentration ratios. The banks in Sudan and

Yemen stand out as they convert only 50% of their deposits

into loans compared to 94% for the average country. This

is possibly because banks in these countries face difficul-

ties to make investments due to poor socio-economic

conditions (Breitschopf 1999; Hussein 2004). The high

cost of borrowing in Sudan and Sudanese culture of

holding cash (Hussein 2004) as well as Yemeni culture of

relying on micro-enterprise (Breitschopf 1999) may have

contributed to the low loan-to-deposits ratio in banking. In

contrast to Jordan which has all roads paved, Bangladesh

and Yemen have about 10% of roads paved. Finally, as

24.7 telephone lines per 100 inhabitants is the maximum

amount, this reflects the low development of electronic

communications in most countries included in the sample.

In sum, the descriptive statistics suggest that while

Sudan and Yemen have the worst potential operating

environments, Bahrain has the most favourable operating

environment.

The final control variable added to the distance function

specification is a dummy variable indicating whether a

bank is an Islamic bank, as illustrated in Table 1. However,

no a priori assumption is made due to mixed results in the

literature on the direction of the influences of Islamic

banking on the relationship between Islamic banking and

bank outputs (e.g., Al-Jarrah and Molyneux 2005; El-

Gamal and Inanoglu 2005; Mokhtar et al. 2006). We once

again emphasize that this modelling approach maintains

the assumption that adherence to shariah causes a shift in

the level of efficient potential output obtainable from given

inputs, rather than assuming that observed output differ-

ences between conventional and Islamic banks is evidence

of differences in efficiency. As argued in Sect. 2 we have

adopted this approach because we believed that the

restrictions imposed by shariah compliance require Islamic

banks to effectively operate in an environment that is not

equivalent to that of conventional banks. However, we can

now further note that the inclusion of the Islamic dummy

variable in the inefficiency specification in our final model

reported in Table 4, can be rejected as highly statistically

insignificant.11 This therefore provides strong statistical

evidence in favour of our approach to directly controlling

for the impact of Islamic banking on bank outputs in the

distance function, rather than treating Islamic banking as a

determinant of inefficiency. We therefore, turn to our

model results, which provide estimates of the impact of

Islamic banking on the potential output achievable by

banks.

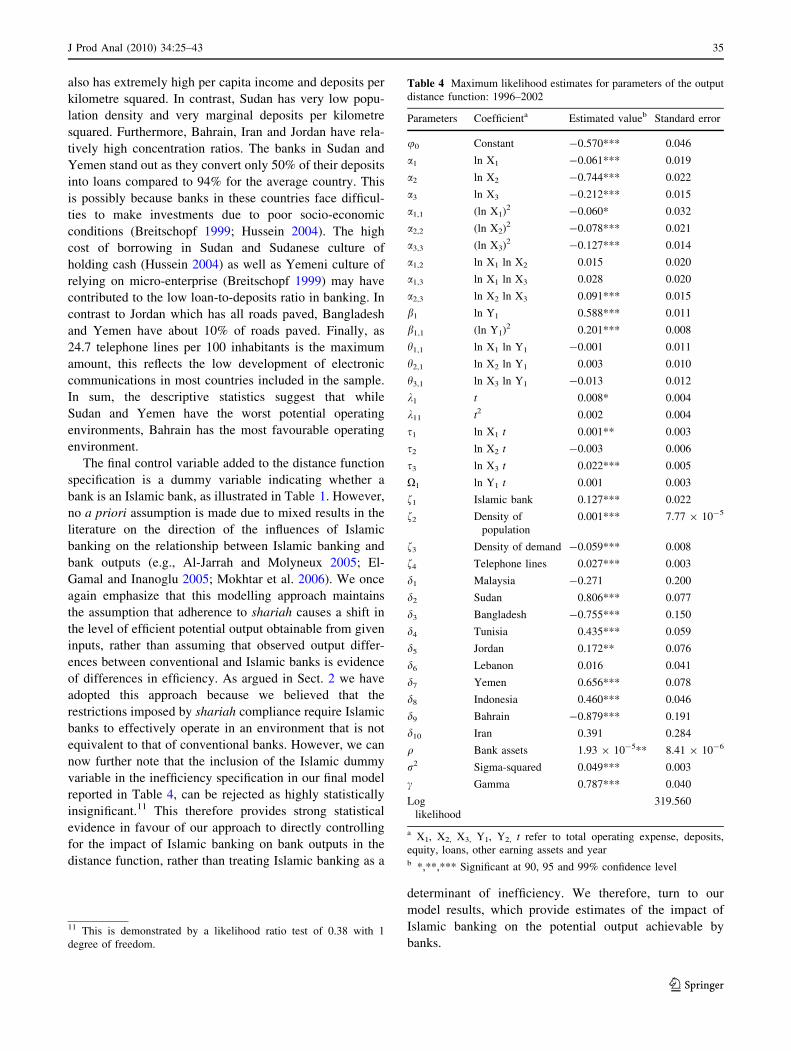

Table 4 Maximum likelihood estimates for parameters of the output

distance function: 1996–2002

Parameters Coefficienta Estimated valueb Standard error

u0 Constant -0.570*** 0.046

a1 ln X1 -0.061*** 0.019

a2 ln X2 -0.744*** 0.022

a3 ln X3 -0.212*** 0.015

a1,1 (ln X1)2 -0.060* 0.032

a2,2 (ln X2)2 -0.078*** 0.021

a3,3 (ln X3)2 -0.127*** 0.014

a1,2 ln X1 ln X2 0.015 0.020

a1,3 ln X1 ln X3 0.028 0.020

a2,3 ln X2 ln X3 0.091*** 0.015

b1 ln Y1 0.588*** 0.011

b1,1 (ln Y1)2 0.201*** 0.008

h1,1 ln X1 ln Y1 -0.001 0.011

h2,1 ln X2 ln Y1 0.003 0.010

h3,1 ln X3 ln Y1 -0.013 0.012

k1 t 0.008* 0.004

k11 t2 0.002 0.004

s1 ln X1 t 0.001** 0.003

s2 ln X2 t -0.003 0.006

s3 ln X3 t 0.022*** 0.005

X1 ln Y1 t 0.001 0.003

f1 Islamic bank 0.127*** 0.022

f2 Density of

population

0.001*** 7.77 9 10-5

f3 Density of demand -0.059*** 0.008

f4 Telephone lines 0.027*** 0.003

d1 Malaysia -0.271 0.200

d2 Sudan 0.806*** 0.077

d3 Bangladesh -0.755*** 0.150

d4 Tunisia 0.435*** 0.059

d5 Jordan 0.172** 0.076

d6 Lebanon 0.016 0.041

d7 Yemen 0.656*** 0.078

d8 Indonesia 0.460*** 0.046

d9 Bahrain -0.879*** 0.191

d10 Iran 0.391 0.284

q Bank assets 1.93 9 10-5** 8.41 9 10-6

r2 Sigma-squared 0.049*** 0.003

c Gamma 0.787*** 0.040

Log

likelihood

319.560

a X1, X2, X3, Y1, Y2, t refer to total operating expense, deposits,

equity, loans, other earning assets and yearb *,**,*** Significant at 90, 95 and 99% confidence level

11 This is demonstrated by a likelihood ratio test of 0.38 with 1

degree of freedom.

J Prod Anal (2010) 34:25–43 35

123

5 Results

5.1 The output distance function estimates

The estimated output distance function parameters are

reported in Table 4.12 Recalling that, c ¼ r2u

�r2

v þ r2u; the

highly significant estimate of 0.787 for this parameter,

suggests that the estimated deviation from the frontier is

mainly due to inefficiency. Besides the statistically sig-

nificant Islamic bank dummy variable, the only significant

country-specific environmental variables are density of

population, density of demand, and telephone lines per 100

inhabitants. Many country-specific environmental variables

become insignificant when country dummy variables are

included in the inefficiency specification, thereby sug-

gesting that these factors serve as proxies for cross country

differences in bank efficiency, rather than legitimate

determinants of potential output.13

The Islamic bank dummy (Z1) has a positive coefficient,

indicating that full-fledged Islamic banks are found to have

potential efficient outputs that ceteris paribus are 12.7%

lower than for other banks. Therefore the results suggest a

systematic reduction in potential output that can be

attributed to Islamic banking, which may result from

constrained opportunities in terms of investments as a

result of shariah compliance. Given our discussion in Sect.

2 and at the end of Sect. 4, this should not be considered as

evidence of managerial inefficiency but should be consid-

ered as evidence of differences in unobserved operating

characteristics and/or applicable technology, which result

in lower potential output for Islamic banks for given input

usage. Moreover, because the estimated model effectively

assumes that the reduced outputs associated with Islamic

banking result from legitimate differences in operating

environment that reduce potential output, the efficiency

scores reported below for Islamic banks must be carefully

interpreted as they net out this impact.

In contrast to expectations, the sign of the coefficient of

the population density variable (Z2) is positive indicating

that, ceteris paribus countries with high population density

have lower bank output.14 A possible explanation for this

finding is that in non-price bank competition, banks may

open branches in large cities, in which real estate and

labour costs are high, for strategic reasons, and thereby

reduce their potential outputs (Dietsch and Lozano-Vivas

2000). As expected, lower density of demand (Z3), tends to

increase expenses thereby, limiting potential output. This

finding of reduced potential output is consistent with

(Dietsch and Lozano-Vivas 2000) and (Carvallo and

Kasman 2005), which found that lower density of demand

raises bank costs, and hence reduces efficiency. Finally, in

contrast to our a priori assumption, the positive sign of

telephone lines per 100 inhabitants’ variable (Z4) indicates

that greater availability of telephone lines decreases bank

outputs. This is possibly because most countries in the

sample are developing economies,15 in which electronic

communications including phone- and internet-banking are

not fully developed. Hence, telephone usage may raise

relative bank costs within the sample of countries.

We next turn to the inefficiency specification. The

positive and statistically significant estimate for q implies

that, ceteris paribus, larger banks have inefficiencies drawn

from distributions where higher estimated inefficiency is

more likely. Thus, our results suggest that inefficiency

increases with bank size.16 Table 4 also demonstrates that

the country dummy variables illustrate systematic and

significant differences in the relative inefficiency of banks

across countries. Thus, for example dMalaysia, dLebanon, dIran

are found to be insignificantly different from zero, thereby

suggesting that inefficiencies for Malaysian, Lebanese and

Iranian banks are drawn from a standard half-normal dis-

tribution. However, banks in Bangladesh and Bahrain17 are

found to have df \ 0 and hence, inefficiency in these

countries is estimated as being drawn from truncated nor-

mal distributions with lower expected inefficiency than in a

half normal distribution. In contrast, Sudan, Tunisia, Jor-

dan, Yemen, and Indonesia all have df [ 0, and hence are

estimated to have higher expected inefficiency than that

drawn from a half-normal distribution, with given variance

r2u: Furthermore, Table 4 suggests that while Bahraini

banks have on average the best efficiency, Sudanese banks

12 We note that a log likelihood ratio test for the joint significance of

the 6 parameters related to equity is 17.98, thus we can reject the null

hypothesis that these parameters are jointly insignificant at the 99%

confidence level.13 Bank-specific loan quality and merger dummy variables were also

found to be statistically insignificant when they were included in the

distance function.14 The finding is consistent with cost function studies in which higher

population density contributes to an increase in banking costs in

France and Spain (Dietsch and Lozano-Vivas 2000), and Latin

American and Caribbean countries (Carvallo and Kasman 2005).

15 All countries in the sample are developing economies except for

Bahrain (World Bank 2007).16 The exclusion of bank size from the inefficiency specification can

be rejected given a likelihood ratio test of 62.90 with 1 degree of

freedom. In the rejected restricted model, Iranian banks are found to

have the lowest estimated inefficiency, which is consistent with

previous international studies that do not control for bank size (e.g.,

Brown 2003; Brown and Skully 2003). This therefore suggests that

our approach of controlling for both asset size and countries in the

inefficiency specification is necessary to better measure cross county

differences in inefficiency.17 Al-Jarrah and Molyneux (2005) also found that Bahraini banks are

relatively efficient when compared to Jordanian banks.

36 J Prod Anal (2010) 34:25–43

123

experience the worst efficiency.18 The df parameters

therefore suggest a clear hierarchy of estimated efficiency

across countries, with higher df values indicating greater

inefficiency.

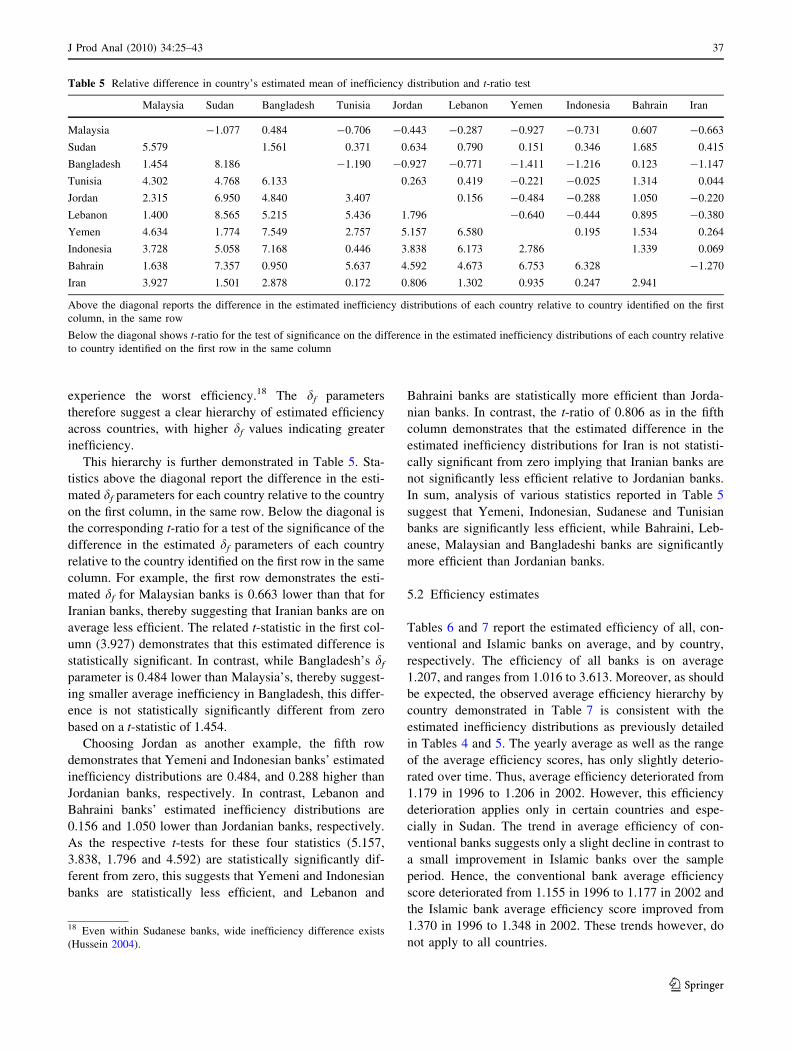

This hierarchy is further demonstrated in Table 5. Sta-

tistics above the diagonal report the difference in the esti-

mated df parameters for each country relative to the country

on the first column, in the same row. Below the diagonal is

the corresponding t-ratio for a test of the significance of the

difference in the estimated df parameters of each country

relative to the country identified on the first row in the same

column. For example, the first row demonstrates the esti-

mated df for Malaysian banks is 0.663 lower than that for

Iranian banks, thereby suggesting that Iranian banks are on

average less efficient. The related t-statistic in the first col-

umn (3.927) demonstrates that this estimated difference is

statistically significant. In contrast, while Bangladesh’s df

parameter is 0.484 lower than Malaysia’s, thereby suggest-

ing smaller average inefficiency in Bangladesh, this differ-

ence is not statistically significantly different from zero

based on a t-statistic of 1.454.

Choosing Jordan as another example, the fifth row

demonstrates that Yemeni and Indonesian banks’ estimated

inefficiency distributions are 0.484, and 0.288 higher than

Jordanian banks, respectively. In contrast, Lebanon and

Bahraini banks’ estimated inefficiency distributions are

0.156 and 1.050 lower than Jordanian banks, respectively.

As the respective t-tests for these four statistics (5.157,

3.838, 1.796 and 4.592) are statistically significantly dif-

ferent from zero, this suggests that Yemeni and Indonesian

banks are statistically less efficient, and Lebanon and

Bahraini banks are statistically more efficient than Jorda-

nian banks. In contrast, the t-ratio of 0.806 as in the fifth

column demonstrates that the estimated difference in the

estimated inefficiency distributions for Iran is not statisti-

cally significant from zero implying that Iranian banks are

not significantly less efficient relative to Jordanian banks.

In sum, analysis of various statistics reported in Table 5

suggest that Yemeni, Indonesian, Sudanese and Tunisian

banks are significantly less efficient, while Bahraini, Leb-

anese, Malaysian and Bangladeshi banks are significantly

more efficient than Jordanian banks.

5.2 Efficiency estimates

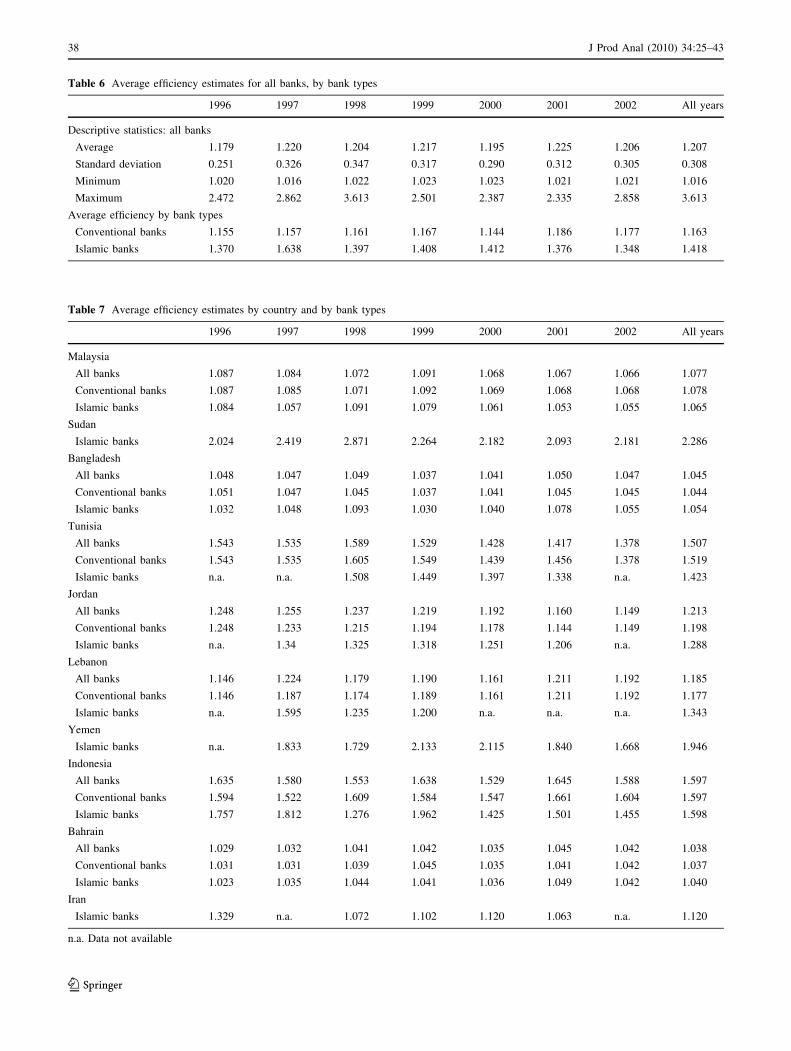

Tables 6 and 7 report the estimated efficiency of all, con-

ventional and Islamic banks on average, and by country,

respectively. The efficiency of all banks is on average

1.207, and ranges from 1.016 to 3.613. Moreover, as should

be expected, the observed average efficiency hierarchy by

country demonstrated in Table 7 is consistent with the

estimated inefficiency distributions as previously detailed

in Tables 4 and 5. The yearly average as well as the range

of the average efficiency scores, has only slightly deterio-

rated over time. Thus, average efficiency deteriorated from

1.179 in 1996 to 1.206 in 2002. However, this efficiency

deterioration applies only in certain countries and espe-

cially in Sudan. The trend in average efficiency of con-

ventional banks suggests only a slight decline in contrast to

a small improvement in Islamic banks over the sample

period. Hence, the conventional bank average efficiency

score deteriorated from 1.155 in 1996 to 1.177 in 2002 and

the Islamic bank average efficiency score improved from

1.370 in 1996 to 1.348 in 2002. These trends however, do

not apply to all countries.

Table 5 Relative difference in country’s estimated mean of inefficiency distribution and t-ratio test

Malaysia Sudan Bangladesh Tunisia Jordan Lebanon Yemen Indonesia Bahrain Iran

Malaysia -1.077 0.484 -0.706 -0.443 -0.287 -0.927 -0.731 0.607 -0.663

Sudan 5.579 1.561 0.371 0.634 0.790 0.151 0.346 1.685 0.415

Bangladesh 1.454 8.186 -1.190 -0.927 -0.771 -1.411 -1.216 0.123 -1.147

Tunisia 4.302 4.768 6.133 0.263 0.419 -0.221 -0.025 1.314 0.044

Jordan 2.315 6.950 4.840 3.407 0.156 -0.484 -0.288 1.050 -0.220

Lebanon 1.400 8.565 5.215 5.436 1.796 -0.640 -0.444 0.895 -0.380

Yemen 4.634 1.774 7.549 2.757 5.157 6.580 0.195 1.534 0.264

Indonesia 3.728 5.058 7.168 0.446 3.838 6.173 2.786 1.339 0.069

Bahrain 1.638 7.357 0.950 5.637 4.592 4.673 6.753 6.328 -1.270

Iran 3.927 1.501 2.878 0.172 0.806 1.302 0.935 0.247 2.941

Above the diagonal reports the difference in the estimated inefficiency distributions of each country relative to country identified on the first

column, in the same row

Below the diagonal shows t-ratio for the test of significance on the difference in the estimated inefficiency distributions of each country relative

to country identified on the first row in the same column

18 Even within Sudanese banks, wide inefficiency difference exists

(Hussein 2004).

J Prod Anal (2010) 34:25–43 37

123

Table 6 Average efficiency estimates for all banks, by bank types

1996 1997 1998 1999 2000 2001 2002 All years

Descriptive statistics: all banks

Average 1.179 1.220 1.204 1.217 1.195 1.225 1.206 1.207

Standard deviation 0.251 0.326 0.347 0.317 0.290 0.312 0.305 0.308

Minimum 1.020 1.016 1.022 1.023 1.023 1.021 1.021 1.016

Maximum 2.472 2.862 3.613 2.501 2.387 2.335 2.858 3.613

Average efficiency by bank types

Conventional banks 1.155 1.157 1.161 1.167 1.144 1.186 1.177 1.163

Islamic banks 1.370 1.638 1.397 1.408 1.412 1.376 1.348 1.418

Table 7 Average efficiency estimates by country and by bank types

1996 1997 1998 1999 2000 2001 2002 All years

Malaysia

All banks 1.087 1.084 1.072 1.091 1.068 1.067 1.066 1.077

Conventional banks 1.087 1.085 1.071 1.092 1.069 1.068 1.068 1.078

Islamic banks 1.084 1.057 1.091 1.079 1.061 1.053 1.055 1.065

Sudan

Islamic banks 2.024 2.419 2.871 2.264 2.182 2.093 2.181 2.286

Bangladesh

All banks 1.048 1.047 1.049 1.037 1.041 1.050 1.047 1.045

Conventional banks 1.051 1.047 1.045 1.037 1.041 1.045 1.045 1.044

Islamic banks 1.032 1.048 1.093 1.030 1.040 1.078 1.055 1.054

Tunisia

All banks 1.543 1.535 1.589 1.529 1.428 1.417 1.378 1.507

Conventional banks 1.543 1.535 1.605 1.549 1.439 1.456 1.378 1.519

Islamic banks n.a. n.a. 1.508 1.449 1.397 1.338 n.a. 1.423

Jordan

All banks 1.248 1.255 1.237 1.219 1.192 1.160 1.149 1.213

Conventional banks 1.248 1.233 1.215 1.194 1.178 1.144 1.149 1.198

Islamic banks n.a. 1.34 1.325 1.318 1.251 1.206 n.a. 1.288

Lebanon

All banks 1.146 1.224 1.179 1.190 1.161 1.211 1.192 1.185

Conventional banks 1.146 1.187 1.174 1.189 1.161 1.211 1.192 1.177

Islamic banks n.a. 1.595 1.235 1.200 n.a. n.a. n.a. 1.343

Yemen

Islamic banks n.a. 1.833 1.729 2.133 2.115 1.840 1.668 1.946

Indonesia

All banks 1.635 1.580 1.553 1.638 1.529 1.645 1.588 1.597

Conventional banks 1.594 1.522 1.609 1.584 1.547 1.661 1.604 1.597

Islamic banks 1.757 1.812 1.276 1.962 1.425 1.501 1.455 1.598

Bahrain

All banks 1.029 1.032 1.041 1.042 1.035 1.045 1.042 1.038

Conventional banks 1.031 1.031 1.039 1.045 1.035 1.041 1.042 1.037

Islamic banks 1.023 1.035 1.044 1.041 1.036 1.049 1.042 1.040

Iran

Islamic banks 1.329 n.a. 1.072 1.102 1.120 1.063 n.a. 1.120

n.a. Data not available

38 J Prod Anal (2010) 34:25–43

123

Across all countries, the average conventional and

Islamic bank efficiency measures are 1.163 and 1.418,

respectively. This suggests that on average, even after

having netted out the 12.7% lower potential output asso-

ciated with Islamic banking, potential output of conven-

tional banks is only 16.3% higher than actual output, while

for Islamic banks this difference is 41.8%. In contrast to

this aggregate result, Table 7 suggests little variation in

estimated efficiency between Islamic and conventional

banks within most countries, although Table 7 does sug-

gests that, on average, Islamic banks in Tunisia have

moderately better efficiency performance than conven-

tional banks, while the reverse is true in Jordan and Leb-

anon. However, it is clear that the substantially lower

cross-country average estimated efficiency for Islamic

banks relative to conventional banks reported in Table 6

can be primarily attributed to country effects. In particular,

Sudan and Yemen, which have only Islamic banks in the

sample, have extremely low average estimated efficiency,

even after netting out the impact of the statistically sig-

nificant environmental characteristics and Islamic banking

dummy variable. Put differently, while the results do

clearly demonstrate a significant 12.7% decrease in

potential output attributable to Islamic banking, the further

particularly poor performance of Islamic banks in Sudan

and Yemen, which drives the overall average for Islamic

banks, must be attributed to relatively poor country specific

banking inefficiency in these countries.

We once again emphasize that because the methodology

assumes that differences in operating environment influ-

ence potential output rather than efficiency, the resulting

efficiency estimates should in principle be interpreted as

allowing for legitimate difference in potential output

associated with compliance with shariah. Therefore, as

argued by (Coelli et al. 1999), as this approach nets out the

impact of operating environments, it provides a measure of

managerial efficiency. Thus, based on this argument, Isla-

mic banks are, on average, more efficient than conventional

banks in Malaysia and Tunisia, but less efficient in all other

countries where both Islamic and conventional banks

operate. However, this interpretation is dependent on the

assumption that all of the reduced output of Islamic banks

is attributable to differences in operating environment and/

or applicable technology relative to conventional banks.

These results can be compared to the previous literature

that does not allow for exogenous variables in either the

frontier or as an influence on inefficiency: Islamic banks are

found to be no different from conventional banks in

Malaysia (Abdul-Majid et al. 2005; Mokhtar et al. 2006),

and equally if not more cost efficient in Turkey (El-Gamal

and Inanoglu 2005). After allowing for bank types including

Islamic, conventional, commercial, and investment banks,

country dummies, assets, liquidity, concentration ratios, and

market shares as direct influences on inefficiency in Arabian

countries, Islamic banks are found to be more cost efficient

(Al-Jarrah and Molyneux 2005). Controlling for loan

quality and capital in the function and modelling for bank

type, country dummy, assets, liquidity, concentration ratio,

and market share to directly influence inefficiency effects in

Arabian countries using a profit function, Islamic banks are

also more efficient (Al-Jarrah and Molyneux 2005). Al-

shammari (2003) also found relatively efficient Islamic

banks in GCC countries when loan quality and capital are

included in the function, and bank type and country dum-

mies are assumed to directly influence inefficiency. The

differences in results may potentially be due to different

environmental variables in the function, different input and

output specifications, and cross-country differences in

Islamic banking that may influence relative efficiency.19

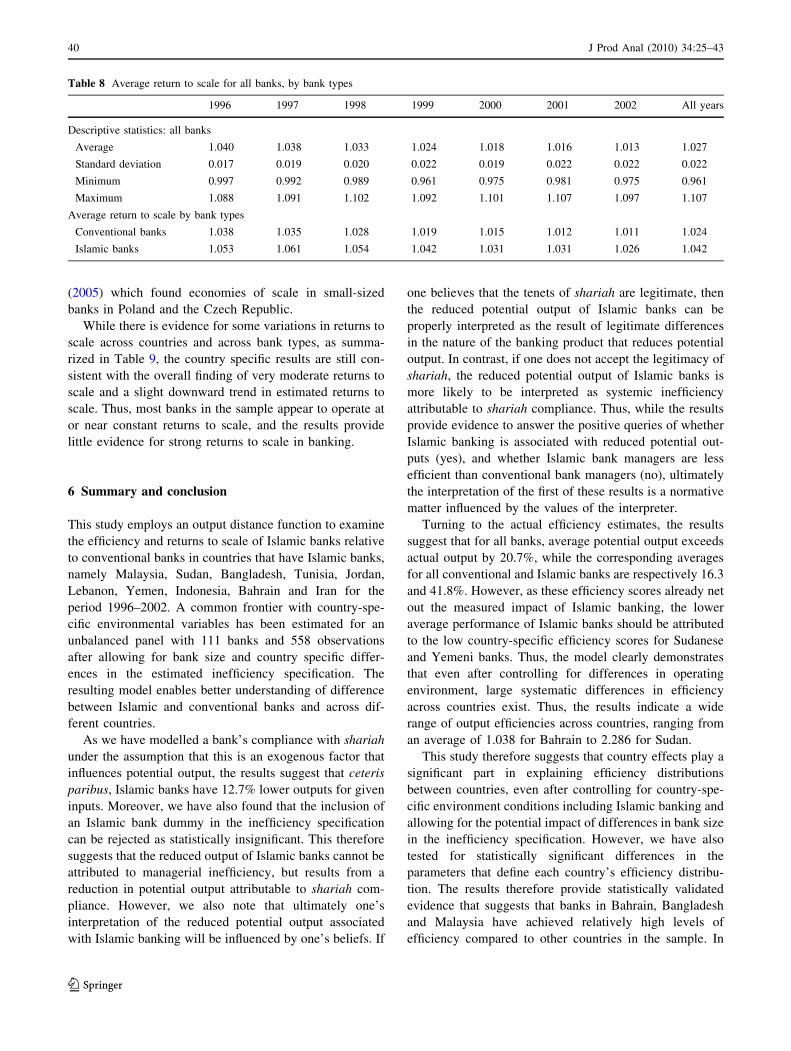

5.3 Returns to scale

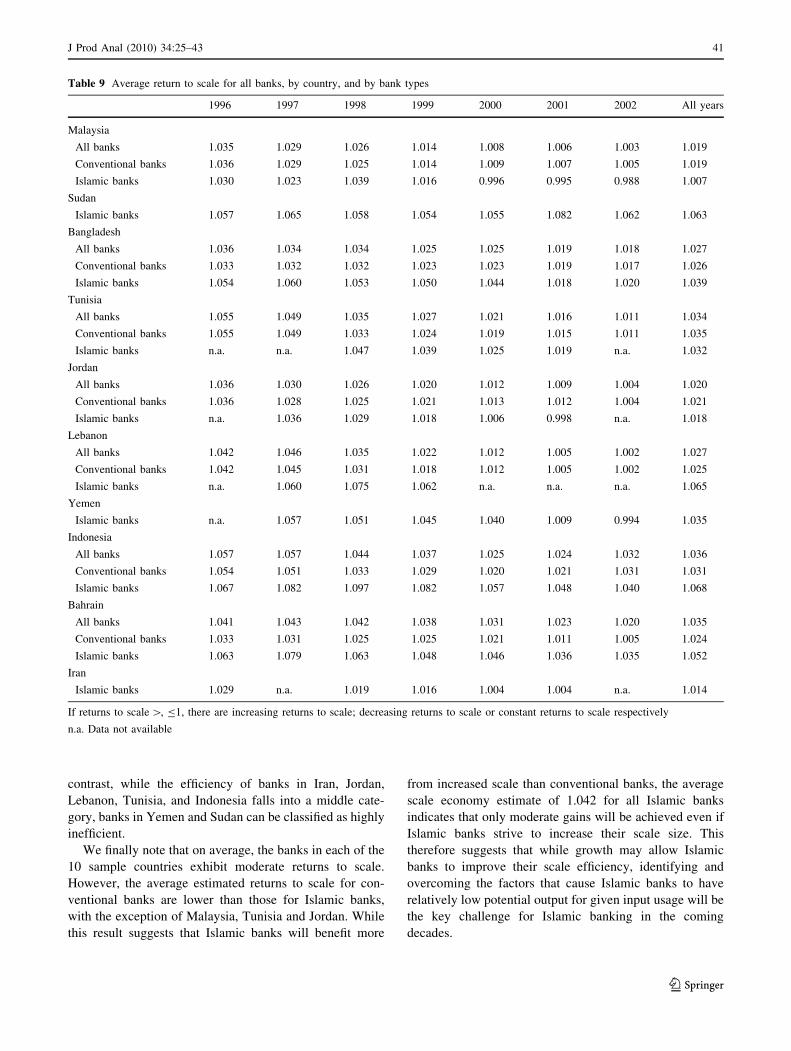

Tables 8 and 9 provide firm specific returns to scale esti-

mates for all, conventional and Islamic banks on average,

and by country. Estimated returns to scale averages 1.027

for all banks, ranges between 0.961 and 1.107, and is