Embed Size (px)

Citation preview

Endogenously Determined CEO Turnover:

The Struggle for Continuance in Listed and Unlisted Firms

Esteban Lafuente*†Universitat Autònoma de Barcelona Department of Business Economics

EDIFICI B. 08193 BELLATERRA (BARCELONA). SPAIN Tel. +34 93 581 1209, Fax: + 34 93 581 2555

Email: [email protected]

Miguel A. García-Cestona† Universitat Autònoma de Barcelona Department of Business Economics

EDIFICI B. 08193 BELLATERRA (BARCELONA). SPAIN Tel. +34 93 581 1209, Fax: + 34 93 581 2555

Email: [email protected]

Draft version: May 12, 2009.

* Corresponding author † We gratefully acknowledge insightful comments by Jose Maria Labeaga and Judit Montoriol. This research was funded by a grant from the Spanish Ministry of Education and Science (SEJ2007-67895-CO4-02/ECON).

Endogenously Determined CEO Turnover:

The Struggle for Continuance in Listed and Unlisted Firms Abstract:

This paper examines the relationship between performance and CEO turnover in Spanish listed and large unlisted firms for the period 1998-2004. Following the Bover and Arellano (1997) approach, we carry out a dynamic binary choice model where the decision to replace a CEO includes lags of the dependent variable, previous performance, and previous changes in the chairman position as endogenous determinants of this governance intervention. We find that for both listed and unlisted firms, previous performance changes are negatively correlated with CEO turnover. Furthermore, listed and unlisted firms follow different paths when taking decisions linked to CEO replacements: whereas unlisted firms are less likely to replace a recently hired CEO, listed companies appear more impatient. Finally, ownership concentration and the presence of banks are also important determinants of CEO turnover decisions, but only for listed firms. Our results give support to the growing call by academics who highlight the importance of controlling endogeneity to correctly examine the determinants of governance interventions.

JEL Classification: C23, G21, G3

Keywords: Corporate governance, CEO turnover, ownership structure

1. Introduction During the last decades, corporate governance literature has remarked the role played by

CEO turnover as a key internal control mechanism, as it helps discipline managers and

alleviate agency costs when there is a separation between ownership and control. CEO

turnover is an important event in the life of a firm, and decisions linked to executive

turnover bring about important consequences in terms of operating and financial

decision making, strategic choices and even the survival of the firm. Nonetheless, this is

not a rare event; in fact, it is a relatively common one in many firms.

The negative relationship between performance and executive turnover has been widely

documented in corporate governance literature (Becht, et al., 2002 and Hermalin and

Weisbach, 2003), and concerns related to ownership structure, board composition, the

role of the markets, amongst others; have become relevant governance features

commonly found to help us achieve a better grasp of the organizational differences

amongst competing firms, as well as to better understand the ways trough which firms

undertake decisions linked to executive turnover.

At this point, academics not only have attempted to address the impact that CEO

turnover has on firm performance (Huson, et al., 2004), but also have studied the

determinants of CEO turnover (Hermalin and Weisbach, 2003). But we focus on a

different issue, as we want to know if this important disciplinary mechanism works

differently for public and private firms and if so, how sensitive is CEO turnover to some

important governance features such as changes in the chairman position, ownership

concentration and structure, and size in conjunction with the exposure to external

controls (listed status).

On one hand, we know that private firms allow higher levels of ownership

concentration and this feature could encourage the choice of participants’ efforts closer

to the first-best levels, once the managers have internalised the different agency costs.

Furthermore, they are not subject to the stock market and the possible economic short-

sightedness problems, that is, the rejection of projects or actions that could be optimal in

the long-term but that do not provide quick short-term results. Also, private firms may

1

face weaker constraints in their contract efforts. All these reasons could favour lower

levels of CEO turnover.

On the other hand, the usual arguments in favour of public firms are the financial

advantages of enjoying a deeper and larger access to finance and the disciplinary

presence of the market pressure, which can be valued by both owners and investors.

Higher levels of separation between ownership and control would accentuate agency

costs and the use of CEO turnover as a disciplinary mechanism would be further

justified. One would expect that large listed firms are more exposed to larger agency

costs.

In addition, there are not many papers addressing the governance differences in private

and public firms. The main reference would be Coles, et al. (2003). These authors find

that private firms are less profitable than similar public firms. In addition, and more

interesting for our purposes, they find that, given changes in accounting profitability

measures, CEO turnover is equally likely to occur in public firms than in large private

firms. Also, Sponholtz (2006) focuses on the determinants of CEO turnover in Danish

public and private firms. She studies the causes of CEO turnover by examining a whole

set of previously unexplored characteristics of the CEO and the firm, such as CEO’s

gender and age, tenure, health, compensation, as well as firm’s activity and leverage.

Despite the evidence and its theoretical implications, current research on the

effectiveness of corporate governance systems suffers from two main weaknesses. First,

an empirical problem related to the estimation approach. Problems like the inclusion of

pairwise observations that strictly show the event of interest (CEO turnover in our case),

and the adoption of econometric techniques that assume that all firms under analysis are

equally likely to replace a CEO are commonly found in the literature. Hermalin and

Weisbach (2003) emphasise a more difficult theoretical issue, which relates to the

difficulties of correctly examining governance mechanisms due to the presence of joint

endogeneity among the variables of interest. In their approach to governance, executive

turnover can be modelled as a function of past performance, as well as past board

characteristics and past board actions, i.e., decisions on executive replacement.

2

We are convinced that the methodological approach can make a difference in the study

of the past performance–CEO turnover relation in public and private firms. In this

paper, we focus on the Spanish case which presents, as in most European countries, an

insider corporate system characterised by high levels of ownership concentration and a

significant participation of banks in many listed firms’ ownership structure. In this

setting, and according to agency theory, one can arguably expect a more active

implementation of internal control mechanisms, since ownership concentration helps

overcome free-rider problems and improves monitoring tasks.

In this sense, does the inverse relation between firm performance and CEO turnover in

public and large private firms coincide with agency postulates? Also, and given the

importance that the exposure to equity markets has as a disciplinary mechanism, could

there be a differential effect when it comes to external control and its impact on CEO

turnover decisions? Furthermore, can we expect that the turnover of poorly performing

CEOs be conditioned by the presence of an active monitoring exerted by large

shareholders?

Our paper addresses these questions by considering the endogenous nature of executive

turnover. Following the approach proposed by Hermalin and Weisbach (2003), we

consider CEO turnover as an endogenous decision conditioned by previous changes in

the CEO and chairman positions, as well as former changes in firm performance. In

particular, we examine the effectiveness of the governance system in Spanish public and

large private companies for the period 1998–2004. This comparison enables us to

correctly examine whether CEO turnover is more intensively activated in firms exposed

to external equity markets, and to analyse the extent to which the poor performance–

CEO turnover relationship holds for firms outside the stock markets.

As for the empirical analysis, we follow the approach proposed by Bover and Arellano

(1997), which implies the estimation of a two-step within estimator for limited

dependent variables, including lags of the dependent variable and other endogenous

explanatory variables. This procedure allows us to include in our model specification

firms that report as well as those that do not experience a change in the CEO position in

the period under analysis.

3

Our paper contributes to the corporate governance literature in several ways. First, and

consistent with different performance measures, we find that CEOs are more likely to be

replaced following poor performance, irrespective of whether the firm is listed or not.

Also, we find that CEO turnover is more sensitive to change in scaled profitability in

public firms than in private firms. This is in accordance with agency theory, where

boards scrutinize CEOs and the threat of dismissal provides incentives to the CEO about

how to run the firm. However, we also find that private companies show more patience,

that is, recently hired CEOs have more time to show their abilities as managers. To the

contrary, boards of listed companies are more diligent monitors, meaning that the

incoming CEO can be replaced anytime, even in her first year as top manager. We

interpret this as evidence that listed companies are more exposed to punishment by

stock markets where (short-term) performance enlightens the way.

Second, we test whether changes in the chairman position increase the probability of

dismissing the CEO. Corporate governance literature provides some insights about the

expected effect of board changes on monitoring. Firms change their chairmen and their

boards to improve the quality of decision making processes and consequently, firm

performance from the shareholders’ perspective (Hermalin and Weisbach, 2003).

Therefore, a change in the chairman position is expected to improve the board’s ability

in its main responsibility: to select, monitor and replace managers. Interestingly, we find

that changes in the chairman position are not linked to future CEO turnover in general,

although a different picture emerges when looking at listed companies. Here, we

observe that when these companies consider changes in the market-to-book value as the

key performance indicator, there is an increase in the probability of replacing a CEO

following a change in the chairman position. As before, we believe that this path reveals

the need for corporate and managerial restructuring after bad years, given the pressure

linked to a greater exposure to external controls in stock markets.

Third, we explore the monitoring role played by banks. Our findings reveal that the

presence of a financial institution as main shareholder increases the probability to

replace an incumbent CEO, however, this relationship is not linked to poor performance

changes. These results are weak, and they hold for both listed and unlisted companies.

4

The remainder of the paper is organised as follows. Section two presents our theoretical

framework and hypotheses. An overview of the main characteristics of the Spanish

institutional setting is introduced in section three. Section four describes the sample and

the methodological approach. A discussion of the empirical results is offered in section

five, and final conclusions are displayed in section six.

2. Theoretical Framework and Hypotheses Over the past decades corporate governance has received increased attention from

academics and practitioners. In particular, academic research on this area highlights the

importance of the monitoring role played by the board of directors to improve the

quality of the firm’s governance system. Thus, there is a general consensus about the

negative relationship between management turnover and firm performance.

In the standard principal–agent framework, it is widely accepted that for a given period

(t) firm performance( can be modelled as a function of the non-observable effort

exerted by the agent (in this case the CEO) to manage the ith firm(

)itr

)itφ , and a set of

independently and normally distributed variables( which is not under the manager’s

control (Holmström, 1979 and Gibbons and Murphy, 1990). Hence, ,

where

)itε

( ),it it itr f φ ε=

0it

it

rφ∂ >∂

and is observable, indicating that firm performance can be seen as an

informative signal about the manager’s ability. We are aware of the difficulty in

separating performance variation due to the CEO skills from performance variation due

to luck. Hence, we follow Kim (1996) and Huson, et al. (2004), and assume that the

estimated effect of firm-specific performance on CEO dismissals becomes a mix of the

effects of skills and luck. This implies that the true effect of luck does not exceed the

true effect of skill, i.e., the coefficient on firm-specific performance is a downward

biased estimate of the actual effect of the CEO skill on the CEO turnover probability.

itr

The agency problem rises from the differences in the objective functions of the principal

and the agent. The principal’s utility is a function of the observed performance ,

whereas the agent’s utility is a function of the observed performance and her

( )( )P r

5

effort , where , meaning that effort is

costly for the agent, a fact that creates the conflict of interest between the two.

( )( ,A r φ ) φ( ) ( ) ( ) ( ), and 0A r U r C Cφ φ= − >

From this simple principal-agent framework, Hermalin and Weisbach (1998) remark

that offers information about the CEO’s ability, and based on this observable measure

the board decides whether or not to replace the CEO. In addition, the board makes an

estimate of the CEO’s ability in t+1 which can be assumed as the expected future

performance(

itr

)1itr + . In period t+1, and based on , the board again will decide whether

or not to replace the CEO. Hence, top management turnover is a process linked to the

monitoring task of the board. When the board receives the observable signal and this

indicates the presence of a poor performing CEO, that is , the board may

exert its monitoring role and replace her to enhance firm performance.

1itr +

, 1 0it itr +Δ <

Empirical evidence examining the presence of an inverse relationship between firm

performance and executive turnover is extensive and it has been carried out in different

countries. Without being exhaustive, we can mention the following: Warner, et al.

(1988), Weisbach (1988), Jensen and Murphy (1990), Denis and Denis (1995), Kim

(1996), Borokhovich, et al. (1996), Parrino (1997), Huson, et al. (2001), Engel, et al.

(2003) and Farell and Whidbee (2003) for the US; Cosh and Hughes (1997), Conyon

(1998), Franks, et al (2001), Conyon and Florou (2002), Dahya, et al. (2002), Hillier, et

al. (2005), and Florou (2005) for the UK; Kaplan (1994a, 1994b, 1995) for Germany,

the US, and Japan; Volpin (2002) and Brunello, et al. (2003) for Italy; Lausten (2002),

as well as Neumann and Voetmann (2005) for Denmark; Maury (2006) for Finland, and

Crespi, et al (2004) for Spain. All these papers support the assumption that the board’s

main objective is to monitor CEO actions and, consequently, the negative relationship

between performance and changes in the position of the CEO can be indicative of the

quality of the governance system in a firm. In this sense, Jensen and Murphy (1990:

238) remark that ‘… managers are more likely to leave their firms after bad years than

after good years and therefore are disciplined by the threat of termination’. Therefore,

the threat of dismissal for poor performance should provide stronger incentives to the

CEO when deciding how to run the firm, which in turn may have an impact on the

probability of CEO turnover. In addition, academic efforts have recently been made in

order to examine the effectiveness of governance systems in emerging economies.

6

Gibson (2003) for eight emerging economies, and Kato and Long (2006) for China,

show that governance systems in emerging contexts become as effective as the ones in

more developed economies, although the presence of active monitors seems to play a

significant role.

In their survey, Hermalin and Weisbach (2003) highlight that other than poor

performance, several factors may affect the probability of CEO turnover, such as the

presence of large investors and the participation in stock markets. In the latter case, both

product market competition and an active market for managers stimulate the survival of

the most efficient firms and foster efficiency by improving managerial incentives.

Consequently, competition may act as a substitute of internal governance mechanisms

because it positively affects firm performance. Despite the fact that most literature on

CEO turnover focuses on listed companies, we can find some academic documents that

compare the intensity of CEO replacement decisions between listed and unlisted firms.

Kaplan (1995) reports that, for his small sample of German listed and unlisted firms,

CEO turnover is more sensitive to poor stock returns and loss of earnings, but weaker

for accounting growth measures. Giannetti (2003) examines, for listed and unlisted

firms in eight European countries, how corporate finance decisions are affected by legal

rules and the degree of financial development. She finds that firms are more leveraged

in countries with less developed stock markets, and that unlisted firms are

systematically more indebted than listed firms. In addition, Nam and Ronen (2004)

report that, for the US, the stock market punishes those firms that hire managers who

were previously at firms that had poor performance records. Berzins, et al. (2008)

analyse the governance characteristics of Norwegian listed and unlisted firms. These

authors report that ownership concentration decreases with firm size, and that unlisted

firms have a higher level of concentration with less proportion of institutional

shareholding. They also find that unlisted firms have better operating performance

results (ROA), and that the listed status matters for improving governance practices and

for creating economic value. From all these arguments our first hypothesis emerges:

H1: (a) CEO turnover is negatively related to changes in firm performance.

(b) The negative relationship between CEO turnover and changes in performance

becomes stronger for listed companies.

7

The economic literature dealing with corporate governance usually assumes that all

firms are equally likely to implement control mechanisms, i.e., no assumption is made

for those firms that previously replaced either the CEO or the chairman in order to

enhance performance. But this is a major concern with studies on control mechanisms

and firm performance, since as Hermalin and Weisbach (2003) pointed out, both CEO

replacements and changes in the board, as well as corporate performance may be

endogenously determined events of a simultaneous process. Following these authors,

we argue that the decision to replace the CEO is linked to previous changes in the CEO

position, previous firm performance and the decisions concerning changes in the board

(in our case, changes in the chairman position). At this point, we consider important to

remark that we only consider those chairman replacements that occurred in firms where

the CEO and chairman positions are not vested in the same person (two-tier leadership

structure). Consequently, the intensity and effectiveness in the implementation of

control mechanisms are conditioned by firm-specific factors, since there is not a unique

threshold for all firms beyond which poor performance leads the board to replace an

incumbent CEO.

Therefore, an important question rising is how sensitive are boards to replace the CEO

if they have previously done it? One would think that recently appointed CEOs have

strong incentives to perform well. In fact, to survive as a CEO, she needs to improve her

reputation by impressing the board with her ability to run the firm (Fama, 1980). In

addition, to effectively monitor a CEO the board needs to learn about CEO’s ability by

acquiring signals about her effort( )r . Hence, those firms that have recently undergone a

change in the CEO position might be reluctant to replace the incoming CEO. Empirical

evidence dealing with path dependency of CEO replacement decisions is almost

inexistent. Hillier, et al. (2005) study the disciplinary effect that equity insurance has on

CEO replacement decisions in UK listed companies. Anecdotic results provided by

these authors show a negative and significant relationship between the probability to

replace a CEO and past CEO turnover. This leads us to formulate our second

hypothesis:

H2: The probability of CEO turnover diminishes for recently appointed CEOs

8

Our second control mechanism of interest relates to the board, and more specifically, to

changes in the chairman position. We focus on the chairman because his role is closely

tied to the CEO. A CEO can exert some influence on the chairman and other board

members, but certain sound decisions (strategic design, financial and dividend policies)

are exclusively reserved to the board, and in these cases the chairman may play a

significant role. The primary task of the chairman is not restricted to the monitoring of

the CEO, since he is also in charge of the nomination and appraisal processes of board

members, which reinforces his central role in the board.

Thus, when a firm is under-performing the principal may interpret that the board is not

conducting an effective monitoring over managers, and hence, the principal may decide

to replace the chairman (and other board members) in order to increase the alignment of

interests between shareholders and management. In this scenario, the outgoing chairman

is punished, and the incoming person chairing the board can show a more active

involvement in monitoring tasks when evaluating the CEO, signalling his competence

and expertise to both the principal and the manager’s market (Weisbach, 1988 and Fama

and Jensen, 1993). From this argument our third hypothesis emerges:

H3: (a) The appointment of a new chairman increases the probability of CEO turnover.

(b) The positive relationship between the appointment of a new chairman and

CEO turnover is stronger for listed companies.

Finally, we explore the role played by ownership structure. Academic research has

traditionally addressed the question of whether ownership exerts an impact over firm

performance, and results emerging from this effort are inconclusive. Hill and Snell

(1988) and Agrawal and Mandelker (1990) for the US; Kaplan and Minton (1994) and

Morck, et al. (2000) for Japan and Gorton and Schmidt (2000) for Germany report a

positive relation between ownership and performance. However, Leech and Leahy

(1991) and Mudambi and Nicosia (1998) for the UK; and Lehmann and Weigand

(2000) find that ownership concentration destroys value. In addition, Bøhren and

Ødegaard (2003) find that, in the case of Norwegian listed firms, outside ownership

destroys value whereas direct ownership is positively correlated to firm value. Finally,

Spanish literature dealing with ownership issues has mainly examined the ownership-

performance relation. For instance, Gutiérrez and Tribó (2004) examine the role of

9

ownership structure with multiple shareholders in listed and unlisted Spanish firms.

These authors show that ownership concentration and the type of controlling group vary

according to the characteristics of the firm. More specifically, firms participating in

stock markets and firms with larger rents are more likely to be controlled by a group of

shareholders with larger stakes. Also, De Miguel, et al. (2004 and 2005) find that

ownership concentration has a non-linear impact over Spanish firm’s value, and that

expropriation increases for highly concentrated firms.

In this paper, we are interested in examining to what extent the presence of large

shareholders affects the quality of corporate governance in Spanish firms. It is often

argued that ownership concentration mitigates free-riding problems of corporate control

associated with a scattered principal. Likewise, large investors have the incentive to

exercise a closer oversight and control of management, in order to reduce agency costs

and increase their monitoring role in the companies where they invest. Nevertheless,

large shareholders also have a strong preference for control, an this could lead to the

expropriation of minority shareholders’ wealth. Furthermore, Shleifer and Vishny

(1997: 758) remark that ‘…large investors represent their own interests, which need not

coincide with the interests of other investors of the firm, or with the interests of

employees or managers. In the process of using his control rights to maximize welfare,

the large investor can therefore redistribute wealth – in both efficient and inefficient

ways – from others’. Thus, the threat of expropriation may limit the ability of firms with

high ownership concentration to raise fresh funds from borrowing or share offerings.

This reduced liquidity capacity could also have negative (informational) implications

for a firm’s share value, and this would negatively affect market-oriented performance

measures (Holmström and Tirole, 1993).

Despite these concerns, and given that small shareholders have no incentives to monitor

managers in contexts characterised by high levels of ownership concentration, it is also

argued that one way to improve the quality of corporate governance is to ensure the

presence of (at least) one large shareholder.

More specifically, we focus on the role played by banks as owners. This is because in

Spain, as it occurs in Germany or Japan, banks have widened their traditional lending-

borrowing activities, leading to an increase in their presence as shareholders in listed

10

companies. Additionally, recently enacted European rules, together with the

deregulation of the Spanish financial system have enlarged this phenomenon.

Furthermore, Crespi and Garcia-Cestona (2002) highlight that the privatisation process

undergone in Spain facilitated banks the access to former state-owned firms by

replacing the State as main shareholder. The presence of a bank in a firm’s ownership

structure may be interpreted as evidence of their commitment to that firm, and this may

encourage small investors to become shareholders in these firms. Obviously, banks

might be tempted to expropriate minority shareholders, but financial market pressure

tends to hinder banks impulses to expropriate because the minority shareholders always

retain the option to take their investment elsewhere with minor costs.

Concerning the impact that ownership structure has on decisions related to top

management replacements, the empirical evidence is far from conclusive. Whereas

Weisbach (1988), Cosh and Hughes (1997) and Neuman and Voetmann (2005) find no

significant effect of ownership on CEO replacement decisions, Crespi, et al. (2004) and

Maury (2006) report a positive relationship between ownership structure and CEO

turnover. A possible explanation emerges when considering that controlling

shareholders can be institutions, board members and even top executives. Therefore, the

corporate governance forces of managerial competition, board monitoring, and large

shareholdings become interrelated (Warner, et al., 1988). This argument is supported by

Volpin (2002) who finds that, for the Italian case, CEO turnover is more sensitive to

poor performance when a coalition of shareholders (syndicates) controls the firm. Also,

Brunello, et al. (2003) report that the CEO turnover-performance relationship in Italian

listed firms is weaker when the CEO is also a large shareholder.

Finally, ownership concentration can also create costs within the firm that may

outweigh its benefits over some intervals of the distribution of ownership concentration.

In this sense, Zwiebel (1995) remarks that ownership concentration works differently in

accordance with the characteristics of the largest shareholder. This implies that, along

with ownership concentration, information about the presence of banks as main

shareholders could also be a relevant variable which helps explain CEO turnover paths.

The presence of banks as shareholders is potentially critical for an efficient governance

system, as banks are specialist in monitoring (Diamond, 1984), they are stable investors

11

able to provide funds to the firm to diminish the negative consequences of different

shocks, and finally, when a bank combines its role of shareholder to that of debtholder

is more likely to renegotiate debt contracts in order to alleviate financial difficulties

(Berlin, et al., 1996). In addition, the analysis of the effect that bank shareholding may

have on the implementation of governance mechanisms is especially relevant in the case

of Spain, where banks are important shareholders of listed firms (Crespi and Garcia-

Cestona, 2002). In this sense, evidence by Maury (2006) show that Finnish listed firms

controlled by a financial institution are more willing to replace poor performing CEOs,

as compared to firms controlled by the State of family groups. From these arguments

come our last hypothesis:

H4: (a) Ownership concentration improves monitoring and increases the probability to

replace an incumbent CEO.

(b) The positive relationship between ownership concentration and CEO turnover

is stronger in companies controlled by financial institutions.

3. Institutional setting in Spain According to La Porta, et al. (1999), Spain is a French civil law country where, as in

most European countries, the stock market shows an insider corporate system

characterized by high ownership concentration rates. Whereas in the US and the UK the

three largest shareholders control an average of 20% of the firm’s shares, in Spain this

rate stands at 50% (La Porta, et al., 1999). Given this fact, one could argue that, in

Spain, agency conflicts are more likely to occur between large shareholders and

minority shareholders, increasing the interest of (large) investors for participating in

corporate sound decision-making processes. However, the presence of large ownership

concentration structures might be consequence of a weaker investor protection, as

compared to the legal framework in the US, the UK, Germany, and Japan (La Porta, et

al., 1998). This increases expropriation risks, and consequently, the protectionist

behaviour exhibited by large shareholders as well.

Concerning the characteristics of the main shareholders, Crespi and Garcia-Cestona

(2002) and Faccio and Lang (2002) report that State shareholdings in Spanish listed

firms are almost negligible because of the privatisation processes undergone in the

12

nineties; being family groups and financial firms the most frequent large shareholders in

these companies.

As for the role of boards, Barca and Becht (2002) show that, in Spain, board members

in listed companies are more actively involved in management tasks, in accordance with

their conciliatory role between shareholders and managers. To the contrary, boards in

outside-oriented countries (especially in the US and the UK) operate more as a control

mechanism which main objective relies on mitigating conflicts between managers and

shareholders.

Finally, the number of listed firms in Spain has increased in the last decade, however, it

is still relatively small and there is a large number of medium-sized firms participating

in stock markets. This stands as a key feature, since the joint participation of large

corporations and medium-sized firms in Spain’s stock markets enables us to examine

top executive replacement decisions in listed and large unlisted firms.

One could argue that, relative to unlisted firms, listed companies disclose more

information, have a lower cost of capital (Pagano, et al., 1998), and tend to protect

minority shareholders (Reese and Weisbach, 2002). However, a direct comparison

between listed and large unlisted firms becomes relevant not only to evaluate the quality

of the governance system in firms facing with a similar agency problem, but also to

corroborate whether the exposure to external equity markets increases the quality of the

governance system in Spanish listed firms.

4. Methodology 4.1 Data and variable definition

The information to carry out this paper comes from two sources. First, we used the

Spanish database SABI (Sistema de Análisis de Balances Ibéricos) provided by Bureau

Van Dijk, as well as annual reports available from the Spanish Stock Exchange Market.

Accounting and organisational data was collected for a sample of 3,254 listed and large

unlisted companies.

13

Given the purpose of our study, and in the interest of following a rigorous methodology,

we carried out a sampling procedure aiming to ensure the robustness of our results.

First, unlisted firms were included in the sample on the basis that their total assets and

sales were located at least in the lower quartile of Spanish listed companies. Second, we

included in our final sample only those firms for which a complete dataset of CEO and

chairman replacements can be clearly identified.

Thus, our final sample comprises information for 1,493 listed and large unlisted Spanish

companies over the period 1998–2004. The number of listed firms in our dataset varies

between 89 in 1998 and 103 in 2004, and this only reflects new incorporations into

Spanish stock markets. Furthermore, we obtained information concerning the market-to-

book value for Spanish listed companies from Thomson Reuters Datastream©. At this

point, it is important to remark that we excluded banking firms from our final sample,

mainly because these firms are subject to different regulatory regimes, and they show

significant operating differences with respect to firms in other industries. In addition,

we excluded from the listed sample the company Telepizza, because reliable

information about CEO replacements and the market-to-book ratio were not available

neither from Spanish data sources nor from Thomson Datastream©.

Concerning the industry configuration of our sample, we obtained from our final data

the industry code for each firm based on the four-digit NACE classification. For

illustrative purposes, we catalogued the different industries in six categories (extractive,

manufacturing, distributive, business services, retail trade, and local market activities).

This aggregation allows us to present the industry configuration of our sample more

clearly. The highest proportion of both listed and unlisted firms is found in the local

market sectors (NACE codes: 1500–1799 and 6000–9305, excluding financial services),

which represents the 48.57% of the listed firms, whereas 33.29% of unlisted firms

operate in these sectors. Extractive firms (NACE codes: 0700–1499) represent 2.86%

and 1.65% of the listed and unlisted firms, respectively. Manufacturing firms (NACE

codes: 2000–3999) account for nearly 26% of the listed sample, whereas this proportion

stands at 35% in the unlisted sample. The proportion of distributive firms (NACE

codes: 4000–5199) is very similar when comparing listed (19.05%) and unlisted firms

(21.38%) in our final sample. Firms in the business service sectors (NACE codes:

7300–7399 and 8700–8799) only represent the 0.95% and the 0.22% of the listed and

14

unlisted firms in our sample, respectively. The major disparity is found in the Retailers

(NACE codes: 5200–5999) where the proportion of unlisted firms operating in these

sectors (8.82%) almost triples the value reported for the listed sample (nearly 3%).

Concerning the dependent variable, we measure CEO turnover as a dummy variable

taking the value of one if the identity of the CEO changed in two consecutive years. At

this point, an important qualification is also in order. We are aware about the costs of

jointly examining the effectiveness of governance systems in listed and unlisted firms.

In this sense, our data present two main shortcomings. First, because the characteristics

of our data, CEO turnover refers to all kind of dismissals. Nevertheless, voluntary

turnovers, usually linked to retirement or promotions, are unlikely to be correlated to

previous performance and these type of changes only add noise to our dependent

variable, which can lead to downward biased results (Hermalin and Weisbach, 2003,

and Huson et al., 2004). Second, exact departure dates are not available, especially for

unlisted companies, and this could affect our results. To solve this, and to avoid

potential miss-specification problems, in our econometric analysis we introduce lagged

terms of both exogenous and endogenous variables, that is, prior to the year that the

change in the CEO position took place.

It is also important to remark that Spanish listed firms are not homogenous, and firms

registered in the main stock market (IBEX-35) show important differences with respect

to those firms operating in other Spain’s stock markets. As we will see below, these

firms are not only larger, but also global players with different governance

characteristics. Therefore, we split the sub-sample of listed firms for descriptive and

analytical purposes in two groups: IBEX and non-IBEX firms.

Our final sample allows us to document 1,679 CEO replacements between 1998 and

2004, 127 of which took place in listed companies, and 1,552 occurred in unlisted firms.

From Table 1 we observe that listed companies show a significantly higher CEO

turnover rate (18.42%), as compared to that shown by unlisted firms (15.90%). In a

different way, unlisted companies show a slightly lower average number of CEO

replacements (1.12), as compared to the average number of events shown by listed

companies (1.25) between 1998 and 2004. No significant difference was found when

15

comparing the CEO turnover rate in the IBEX-35 firms (18.75%) and firms registered

in the rest of Spain’s stock markets (18.29%).

Table 1. CEO turnover: Descriptive statistics The sample includes information for 103 listed and 1,390 large unlisted Spanish firms for the period 1998 and 2004. CEO turnover is a dummy variable equal to one if we identify a change in the CEO position. The average number of CEO replacements indicates, for each firm in our sample, how many changes in the CEO position took place. The univariate test compares, for each variable, the difference in the mean values between listed and unlisted firms. Standard deviation is presented in brackets.

Listed companies Unlisted companies Overall Mean

(Std. dev.) Obs. Mean (Std. dev.) Obs. Mean

(Std. dev.) Obs.

CEO turnover 0.1842 *(0.3879) 685 0.1590

(0.3657) 9,766 0.1607 (0.3627) 10,451

Average number of CEO replacements

1.2451 (0.9058) 103 1.1157

(0.9886) 1,390 1.1246 (0.9833) 1,493

*, **, *** indicates significance at the 0.10, 0.05, and 0.01 level, respectively.

We further explore the characteristics of our sample of CEO replacements (Table 2).

Here it can be seen that, in our sample, CEOs are more exposed to replacement in listed

companies (nearly 80% of these firms report a change in this position). Also, 54% of the

IBEX firms showed one CEO replacement (19 firms). Concerning the number of

changes, 70% of listed firms report up to two CEO replacements during the period

under analysis (this figure stands at 79% for the IBEX firms), whereas only 59% of

unlisted firms have one or two CEO replacements (Table 2).

Table 2. Sample frequencies for CEO turnover The sample includes information for 103 listed and 1,390 large unlisted Spanish firms for the period 1998 and 2004. The table shows the distribution of firms in our sample according to the number of changes in the CEO position.

Listed companies Unlisted companies Overall Number of changes in the CEO position

Number of Firms % Number of

Firms % Number of Firms %

0 22 21.36 431 31.01 454 30.341 45 43.69 519 37.34 564 37.782 27 26.21 308 22.16 335 22.443 8 7.77 113 8.13 121 8.104 1 0.97 17 1.22 18 1.215 2 0.14 2 0.13

Number of firms 103 100 1,390 100 1,493 100

16

We are also interested in examining to what extent incoming CEOs are likely to be

removed. Table 3 presents, for those CEOs hired between 1998 and 2004, the average

speed of replacement as well as the frequency distribution for these events. Here, we

observe some differences in the removal time-span when comparing listed and unlisted

companies. The average tenure of incoming CEOs is similar for listed and unlisted

companies. However, the majority of dismissals in listed companies is concentrated in

the second and third years of operations (78%), but for unlisted firms replacements are

more scattered: 40% of CEOs hired between 1998 and 2004 were fired after the second

year, and more than 14% of these replacements took place after the fourth year (Table

3).

For listed companies that have undergone two changes in the CEO position, the time of

the removal was concentrated in the second year of operations of the incoming CEO

(56%). For those firms registered in the IBEX-35 index, 43% of incoming CEOs were

removed in the second year of operations. In the case of the sub-sample of unlisted

firms that went through two CEO changes, over 46% of these CEOs were replaced after

the second year (Table 3). We also observe important differences in the distribution of

firms that replaced three times the CEO. Whereas in listed companies the proportion of

replacements is more concentrated in the third year of tenure (62.50%) than in the

second one (37.50%), the opposite distribution is found in unlisted firms (61% of CEOs

were replaced in their second year and 30% were removed in the third period).

Finally, a few chosen number of firms replaced the CEO more than three times. These

troubled companies only account for 4.20% of the total group of firms that replaced the

CEO two or more times, however, the proportion of unlisted firms (4.32%) almost

doubles the rate of 2.78% exhibited in the listed sub-sample (just one firm) (Table 3).

17

Table 3. Sequence of replacement for incoming CEOs The table presents, by the number of changes in the CEO position, the distribution of firms in our sample according to the average turnover speed of incoming CEOs. The sample includes information for those listed and large unlisted firms that experience at least two changes in the CEO position between 1998 and 2004. Average tenure indicates the mean time (years) that incoming CEOs run the firm. Columns for the average turnover speed show the number of firms that replaced their incoming CEOs, according to the number of full years that the incoming CEO held the position before to be replaced.

Number of firms according to the average turnover

speed of the incoming CEO Number of changes in the CEO position

Average Tenure (Years)

Number of Firms 1 year

Between 1 and 2 years

Between 2 and 3 years

Between 3 and 4 years

More than 4 years

Panel A: Listed Sample

2 2.7241 27 2 15 4 6 0 3 2.4375 8 0 3 5 4 1.3333 1 0 1 5 Overall 2.6343 36 2 19 9 6 0 Panel B: Unlisted Sample

2 2.8827 308 55 110 43 36 64 3 2.0531 113 10 69 34 4 1.6275 17 0 17 5 1.5000 2 0 2 Overall 2.6129 440 65 198 77 36 64 Panel C: Full Sample

2 2.8690 335 57 125 47 42 64 3 2.0785 121 10 72 39 4 1.6111 18 0 18 5 1.5000 2 0 2 Overall 2.6145 476 67 217 86 42 64

As regard our set of independent variables, we follow Hermalin and Weisbach (2003)

and Huson, et al. (2004), and performance is measured through two variables based on

accounting information: the ratio of operating profit to total assets (ROA) and the ratio

of net profit to equity (ROE). To control for industry effects, and as Huson, et al. (2001)

and Huson, et al. (2004), we also create an adjusted version of these accounting

measures by subtracting the median value of the corresponding measure for all firms in

our sample with the same two-digit NACE industry code. We use a two-digit industry

18

definition to capture similarities among firms operating in the same sector, and this

classification has proved to be as effective as industry definitions based on three- or

four-digit groupings (Huson, et al., 2004). Over 97% of the sample firms are industry-

matched at the two-digit level, and for those firms with no direct comparison group,

based on the two-digit NACE definition, we proceed as Huson, et al. (2004) by

subtracting the median performance value of a control group with the same one-digit

NACE code. Since we aim to examine the differential impact that performance has on

the probability to replace a CEO, we introduce the unadjusted and industry-adjusted

accounting variables as changes between periods t-2 and t-1, that is, . 2, 1t tr− −Δ

From Table 4 we observe that average ROA is 5.99%, whereas mean ROE is 8.36%. In

addition, it can be noticed that firms participating in the stock market are the largest in

terms of size, and they also show the highest ROE ratio for the period under analysis

(9.14%). Differences in size are also remarkable when comparing the IBEX and non-

IBEX firms, being the mean size of the former group (5,620 millions of euro)

significantly larger, at the 1% level, than that showed by the latter (390 millions of

euro).

Concerning ROA, the highest ratio is shown by the unlisted firms (6.13%), which are

the smallest in terms of size, and this rate is significantly different at the 1% level than

that shown by listed firms (3.97%). The average change in ROA from year –2 to year –

1 ( )2, 1t tr− −Δ is 33.42%, (17.54% and 34.50% for listed and unlisted firms, respectively),

and this variation rate stood at –40% and 19.40% for those listed and unlisted firms that

replaced the CEO, respectively (significant at the 5% for listed firms). The mean ROE

change for the listed and unlisted sub-samples is 47% and 45%, respectively, but over

years –2 and –1 preceding the CEO replacement the mean change exhibited by listed

and unlisted firms was 14% and 33%, respectively. Differences in the mean ROE

change are not significantly different from zero. Also, there is no significant difference

between the ROA and ROE ratios exhibited by the IBEX firms (3.29% and 10.97%,

respectively) and the non-IBEX firms (4.24% and 8.43%, respectively). As for the

median industry-adjusted performance measures, we observe that listed firms show

smaller values than the unlisted sub-sample, but differences are only significant when

ROA is the performance variable (Table 4). For listed firms, the mean change in the

19

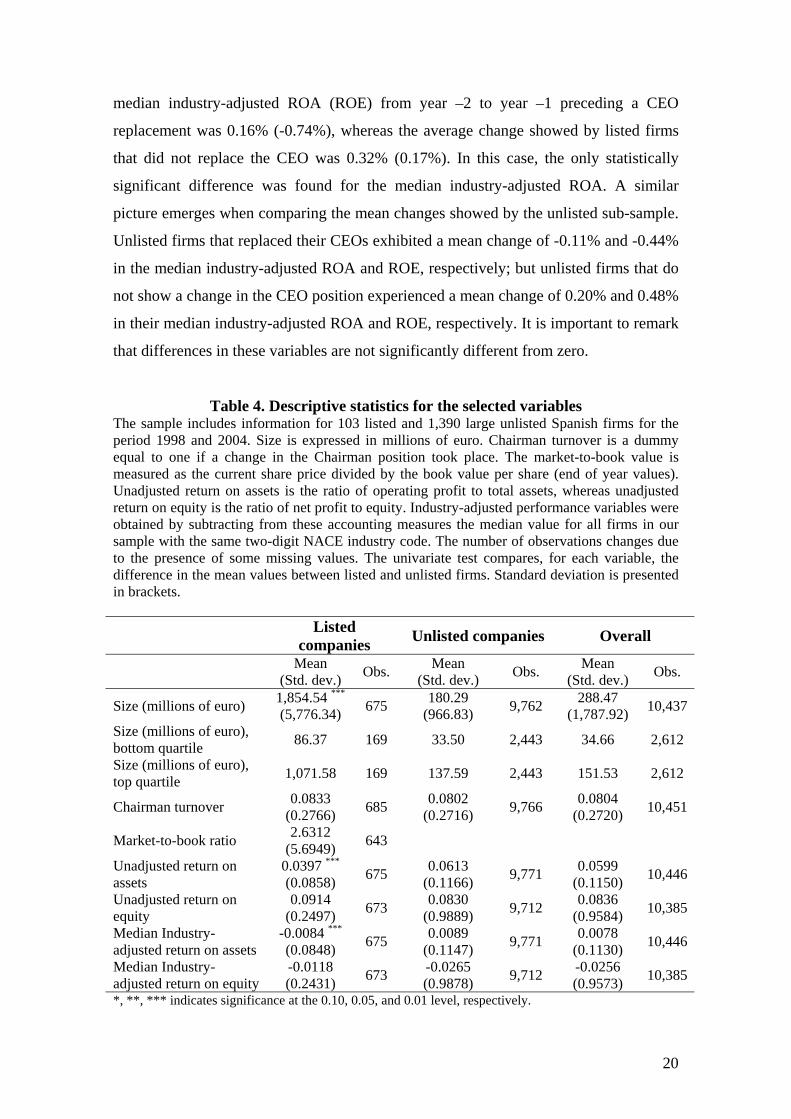

median industry-adjusted ROA (ROE) from year –2 to year –1 preceding a CEO

replacement was 0.16% (-0.74%), whereas the average change showed by listed firms

that did not replace the CEO was 0.32% (0.17%). In this case, the only statistically

significant difference was found for the median industry-adjusted ROA. A similar

picture emerges when comparing the mean changes showed by the unlisted sub-sample.

Unlisted firms that replaced their CEOs exhibited a mean change of -0.11% and -0.44%

in the median industry-adjusted ROA and ROE, respectively; but unlisted firms that do

not show a change in the CEO position experienced a mean change of 0.20% and 0.48%

in their median industry-adjusted ROA and ROE, respectively. It is important to remark

that differences in these variables are not significantly different from zero.

Table 4. Descriptive statistics for the selected variables The sample includes information for 103 listed and 1,390 large unlisted Spanish firms for the period 1998 and 2004. Size is expressed in millions of euro. Chairman turnover is a dummy equal to one if a change in the Chairman position took place. The market-to-book value is measured as the current share price divided by the book value per share (end of year values). Unadjusted return on assets is the ratio of operating profit to total assets, whereas unadjusted return on equity is the ratio of net profit to equity. Industry-adjusted performance variables were obtained by subtracting from these accounting measures the median value for all firms in our sample with the same two-digit NACE industry code. The number of observations changes due to the presence of some missing values. The univariate test compares, for each variable, the difference in the mean values between listed and unlisted firms. Standard deviation is presented in brackets.

Listed companies Unlisted companies Overall

Mean (Std. dev.) Obs. Mean

(Std. dev.) Obs. Mean (Std. dev.) Obs.

Size (millions of euro) 1,854.54 ***

(5,776.34) 675 180.29 (966.83) 9,762 288.47

(1,787.92) 10,437

Size (millions of euro), bottom quartile 86.37 169 33.50 2,443 34.66 2,612

Size (millions of euro), top quartile 1,071.58 169 137.59 2,443 151.53 2,612

Chairman turnover 0.0833 (0.2766) 685 0.0802

(0.2716) 9,766 0.0804 (0.2720) 10,451

Market-to-book ratio 2.6312 (5.6949) 643

Unadjusted return on assets

0.0397 ***

(0.0858) 675 0.0613 (0.1166) 9,771 0.0599

(0.1150) 10,446

Unadjusted return on equity

0.0914 (0.2497) 673 0.0830

(0.9889) 9,712 0.0836 (0.9584) 10,385

Median Industry- adjusted return on assets

-0.0084 ***

(0.0848) 675 0.0089 (0.1147) 9,771 0.0078

(0.1130) 10,446

Median Industry- adjusted return on equity

-0.0118 (0.2431) 673 -0.0265

(0.9878) 9,712 -0.0256 (0.9573) 10,385

*, **, *** indicates significance at the 0.10, 0.05, and 0.01 level, respectively.

20

An additional measure is used for listed companies: the market-to-book value measured

as the current share price divided by the book value per share. For this variable,

information from Thomson Datastream© is incomplete for five listed companies in our

sample. We point out that after the peaked in 1999 (3.50), this performance variable

shows a slight decreasing trend until 2002 (1.82). But after this year, mean values for

this ratio in our listed sample report an increase up to 2.77 in 2004. For this variable, the

mean value showed by firms registered in the IBEX-35 (3.99) is significantly different

from zero at the 1% than that reported for firms operating in other Spain’s stock markets

(2.12). The mean change in this variable from year –2 to year –1 preceding CEO

replacements is statistically significant at the 10%: –13% for firms that changed the

CEO, and nearly 1% for listed firms that did not experience a change in the CEO

position.

Concerning the chairman dismissal, we create a dummy variable that takes the value of

one if the firm experienced a change in the chairman position in two consecutive years,

and zero otherwise. In order to follow a rigorous methodology, we introduce this

variable in our econometric model as a lagged term. Also, and to avoid collinearity

problems, we only consider those chairman dismissals that occurred in firms with a dual

leadership structure, i.e., when the titles of CEO and chairman are not vested in the

same person. It can be seen that, in our sample, the rate of chairman turnover is 8.04%,

and no significant difference was found between the rate shown by listed (8.33%) and

unlisted companies (8.02%). However, the mean chairman removal rate in the IBEX-35

firms (5.73%) is significantly lower, at the 10% level, than the rate shown by firms

operating in other stock markets (9.35%).

Finally, we consider ownership structure in our analysis. From Table 5 we notice that

ownership concentration characterises Spanish companies. Whereas in listed companies

the main shareholder on average controls nearly a third of shareholder’s equity (32%),

in unlisted firms this figure stands at 78%. In addition, shareholders other than the

largest seem to have some power: the mean stake held by the second and third largest

shareholder is on average 21% and nearly 10%, being these values significantly lower in

our listed sample (Table 5). We find no significant differences when comparing the

IBEX and non-IBEX firms in terms of the stake held by the largest (30.83% for the

21

IBEX firms and 32.60% for the non-IBEX firms), the second largest (11.09% and

12.43%) and the third largest shareholder (7.42% and 7.50%).

Table 5. Ownership characteristics The sample includes information for 103 listed and 1,390 large unlisted Spanish firms for the period 1998 and 2004. The table shows the average stake held by the three largest shareholders. Financial institution as main shareholder is a dummy equal to one if a banking firm is the main shareholder. The number of observations changes due to the presence of some missing values. The univariate test compares, for each variable, the difference in the mean values between listed and unlisted firms. Standard deviation is presented in brackets.

Listed companies Unlisted companies Overall

Mean (Std. dev.) Obs. Mean

(Std. dev.) Obs. Mean (Std. dev.) Obs.

Stake held by the largest shareholder

0.3210 ***

(0.2415) 684 0.7801 (0.3000) 9,357 0.7488

(0.3181) 10,041

Stake held by the second largest shareholder

0.1205 ***

(0.0756) 632 0.2280 (0.2154) 3,497 0.2116

(0.2042) 4,129

Stake held by the third largest shareholder

0.0748 ***

(0.0469) 611 0.1108 (0.0913) 1,356 0.0996

(0.0819) 1,967

Financial institution as main shareholder

0.2018 ***

(0.4016) 684 0.0084 (0.0912) 9,766 0.0210

(0.1435) 10,450

*, **, *** indicates significance at the 0.10, 0.05, and 0.01 level, respectively.

We also control for the type of shareholder. Specifically, and considering the key role

played by financial institutions in Spain firms’ monitoring (Casasola and Tribo, 2004),

we introduce a dummy variable taking the value of one if the main shareholder is a

financial institution, and zero otherwise. As expected, in our sample financial

institutions have a strong preference for listed firms: they are the main shareholder in

20% of Spanish listed companies, but their presence in unlisted firms is almost

negligible (less than 1%). Moreover, and amongst listed firms, banks are the largest

shareholder in 33% of firms registered in the main Spain’s stock market (IBEX-35),

whereas for 15% of firms operating in other Spain’s stock markets a financial institution

is the largest shareholder (mean values are significantly different from zero at the 1%

level).

Concerning ownership structure, Table 6 presents the degree of concentration according

to the number of shareholders (1, 2, and more than 2). Despite that those listed firms

with reliable information for only one or two shareholders are highly concentrated (the

largest shareholder controls over 55%), the vast majority of listed firms show a

22

dispersed ownership structure, with a non-controlling largest shareholder holding on

average nearly 29% of shareholder’s equity, and a second largest shareholder owning on

average 12%. We also note that ownership in firms operating in the IBEX-35 index is

more scattered, and for firms with more than 3 large shareholders (32 firms) the largest

shareholder controls nearly 26% of shareholder’s equity, whereas the mean stake held

by the largest shareholder in firms operating in other Spain’s stock markets is 30%

(mean values are significantly different from zero at the 5% level). In the case of the

second and third largest shareholders, mean values reported by the IBEX (11.43% and

7.42%, respectively) and non-IBEX firms (12.29% and 7.50%, respectively) are not

significantly different at conventional levels.

In the case of the unlisted sample, we observe that these firms are mainly controlled by

one shareholder. Our sample of unlisted firms show a more concentrated ownership

concentration, where the average stake held by the largest shareholder is over 50%, no

matter the number of shareholders (Table 6).

Table 6. Ownership structure The sample includes information for 103 listed and 1,390 large unlisted Spanish firms for the period 1998 and 2004. The table presents the average stake held by the three largest shareholders, according to information available about the number of shareholder in the firm. The univariate test compares, for each type of shareholder (largest, second largest or third largest), the difference in the mean ownership stake between listed and unlisted firms.

Average ownership concentration

Number of shareholders Obs. Largest shareholder

Second largest shareholder

Third largest shareholder

Panel A: Listed Sample 1 52 0.5911 *** 2 21 0.5735 * 0.1215 ** 3 (and more) 611 0.2881 *** 0.1204 *** 0.0748 ***

Panel B: Unlisted Sample 1 5,860 0.8690 2 2,141 0.7068 0.2179 3 (and more) 1,356 0.5118 0.2440 0.1108 Panel C: Full Sample 1 5,912 0.8665 2 2,162 0.7059 0.2170 3 (and more) 1,967 0.4423 0.2056 0.0997 *, **, *** indicates significance at the 0.10, 0.05, and 0.01 level, respectively.

23

Having corroborated the presence of different paths when it comes to CEO

replacements between Spanish listed and unlisted companies, we now turn to examine

whether the implementation of this governance intervention is related to alternative

control mechanisms and performance, and whether the drivers of this behaviour affect

more intensively listed companies as compared to unlisted companies.

4.2 Methodological approach: Dynamic discrete choice models

The replacement of a CEO can be understood as a decision carried out within the firm in

a binary choice model. Thus, to identify the differentiating characteristics that affect the

likelihood to replace the CEO one can perform a random or a fixed effects logit model

estimated by conditional maximum likelihood (Rasch, 1960 and Andersen, 1970). This

model has the form and it follows

that (Honoré and Kyriazidou, 2000):

{ } ( )' 1,..., ; 1,...,1 0it it i it t T iy xβ η ε = == + + ≥ N

( ) ( )( )0 1

exp1 , , ,...,

1 expit i

it it i i itit i

xP y x y y

xβ η

ηβ η−

′ +′= =

′+ + [1]

where ity is the dependent variable, and where 0iy may or may not be observed, i

indexes firms in our sample for the period , is the parameter of

interest,

1,..., 2t T T= ∧ ≥ βx′ corresponds to the strictly exogenous explanatory variables, and is the

firm-specific effect potentially correlated with

iη

x′ .

In the case of the fixed effects logit approach, it is assumed that the logistic distributed

time-varying errors are i.i.d. over time and independent of all covariates in the

model( in all time periods. Moreover, strict exogeneity and time-varying

responses in the variable of interest are imposed in the non-linear fixed effects

procedure. This latter restriction implies that the responses to the event of interest

by the unit of analysis are a sufficient statistic for the individual specific

effect( , and it is used to estimate as follows (Arellano, 2003):

),it ix η′

2T ≥

1

T

itt

y=

⎛ ⎞⎟⎜ ⎟⎜ ⎟⎜ ⎟⎜ ⎟⎜⎝ ⎠∑

)iη β

24

( )1

1' '1 1

1,...,

1

exp,..., , ,..., ,

expiT

T

it itTt

it it it ii i Tt

it itd d Bt

y xP y y y x x

y x

βη

β

=

=∈

=

⎛ ⎞⎟⎜ ⎟⎜ ⎟⎜⎛ ⎞ ⎟⎜⎝ ⎠⎟⎜ ⎟⎜ ⎟⎜ ⎛ ⎞⎟⎜⎝ ⎠ ⎟⎜ ⎟⎜ ⎟⎜ ⎟⎜⎝ ⎠

′=

′

∑∑

∑ ∑ [2]

where iB refers to the set of all binary response sequences to the event of interest by

cases (individuals or firms).

From Equation [2] it can be derived that the conditional maximum likelihood function is

restricted to those cases for which varies over time, i.e., the contribution to the

conditional maximum likelihood function equals zero for those cases that do not show

any response in the event of interest, or have a fully positive response sequence in T

(one in every period) (Arellano and Honoré, 2001). Moreover, estimation of equation

[2] by maximum likelihood in datasets with limited number of observations and fixed T

leads to inconsistent estimation of . This is the so-called incidental parameters

problem, first considered by Neyman and Scott (1948). In this case only new

observations for case i give new information about , i.e., increase the sample size (N)

does not help out with the estimation of and add more parameters to be estimated.

Therefore, the maximum likelihood estimator of is only consistent whenT . In

the widely cited article, Manski (1987) demonstrates that it is possible to relax the

logistic assumption as well as to allow for serial correlation in the time-varying

disturbances. However, we do not further discuss this since Manski’s (1987) maximum

score estimator is based on the presence of strictly exogenous variables, excluding

dynamic models.

ity

iη

iη

iη

iη →∞

In addition, the econometric model explored assumes that ( )1 0i itE yη − = , which

clearly hinders the possibility to consider endogenous factors when explaining the

decision to replace a CEO. Research on corporate governance is usually based on this

standard assumption, and this may lead to results that are hard to interpret.

Nevertheless, and as remarked by Hermalin and Weisbach (2003), the decision to

replace the CEO can be considered as a dynamic process where previous CEO

25

replacements, changes in the board (in the Chairman position in our case), and previous

changes in performance play a key role. This implies the formulation of a dynamic

model with the following form:

1it it it it i ity y X Zγ β δ η−= + + + +ε T [3] ( )1,..., ; 1,...,i N t= =

where X is the vector of strictly exogenous variables, Z corresponds to the endogenous

variables, is the unobserved firm-specific effect and is the error term. iη itε

Equation [3] allows us to examine whether firms that previously dismissed a CEO are

less (or equally) likely to replace a CEO in the future than firms which have not

experienced a change in the CEO position. This stands as a key fact because, on the one

hand, it is possible that the probability of dismissing a CEO this period lowers the

probability of a change in this position next period (true state dependence). In this case,

the lagged decision about the replacement of the CEO enters the model in a structural

way as an explanatory variable, and if and is statistically significant then

incentives for replacing a CEO are weaker if the firm experienced a CEO replacement

in the past. On the other hand, if and this parameter is not statistically significant,

then firms have different propensities to experience the event of interest (CEO

replacement). Here, it is argued that some firms are permanently more likely to replace

their CEOs( , irrespective of whether they have undergone a change in the CEO

position in the previous period.

0γ<

0γ=

)iη

Nevertheless, the inclusion of the lagged dependent variable in the explanatory variable

set is not trivial, and the breaking of the strict exogeneity assumption brings about

important computational considerations that should be taken into account. Given the

relevance that the identification of persistence patterns has for academics, policy makers

and practitioners, the development of methods that deal with dynamic non-linear

models with fixed effects have recently received great attention (see Arellano and

Honoré, 2001). It is widely recognised that the main obstacle when estimating this type

of models arises from the initial conditions problem.

26

In this paper, we adopt the methodology proposed by Bover and Arellano (1997) which

implies the estimation of a two-step within estimator for limited dependent variables,

including lags of the dependent variable and other endogenous explanatory variables.

The within-groups estimator is based on the reduced form predictions of the dependent

variable where ( )1 0i itE yη − ≠ . Hence ( )i f Zη = as

, and given this we can derive the function for the

decision to replace the CEO as follows:

0 1 1 ...i T iTiz zη λ λ λ μ= + + + + i

) ε

i

(*1 0 1 1 ...it it i itT iTit iy y X z zγ β λ λ λ μ−= + + + + + + + [4]

The reduced form of the model can be rewritten as . Bover and Arellano

(1997) show how to derive consistent estimations of through conventional probit

specifications for each period, where is not directly observable and it represents a

good linear approximation of . This approach allows us to consider all possible pairs

of observations in the string of the dependent variable, irrespective on whether the

observation (firm) experienced a change in the CEO position. It is important to notice

that error terms are unlikely to be independent of the explanatory variables in period t-1,

because one of the explanatory variables is the lagged dependent variable. However,

Bover and Arellano (1997) prove that period-by-period maximum likelihood probits

provide consistent and asymptotically normal estimates of the reduced form of interest.

*i iy z μ= +∏

*iy

*iy

iy

Our specification of considers as endogenous factors changes in firm performance

from year –2 to year –1

*ity

( )2, 1t tr− −Δ , a lagged term accounting for changes in the chairman

position, and an interaction term between the two variables. In a second step, our final

model is estimated using a fixed-effects approach, and it considers that CEO turnover

can be explained as follows: *

1 1 1it i itit it itCEO CEO X Zγ β δ η− − −Δ = Δ + + + +μ [5]

where X denotes a vector of strictly exogenous variables with respect to the CEO

turnover decision (size, presence in the stock market and ownership structure) and Z

refers to the endogenous explanatory variables. Finally, it is important to remark that

27

instead of lags of , we use lags of to not condition current CEO turnover decisions

on lagged effects of past explanatory variables and past errors (Bover and Arellano,

1997).

*ity ity

5. Empirical Findings This section presents our empirical findings. In the different sub-sections we present our

results for the full sample and for the sub-sample of listed firms. Given that we use three

measures of firm performance, our econometric analysis implies the estimation of three

dependent variables (one for each performance measure: ROA, ROE, and market-to-

book value). Thus, results in Tables 7 to 12 were obtained using as dependent variable

the corresponding linear approximation, according to each performance measure.

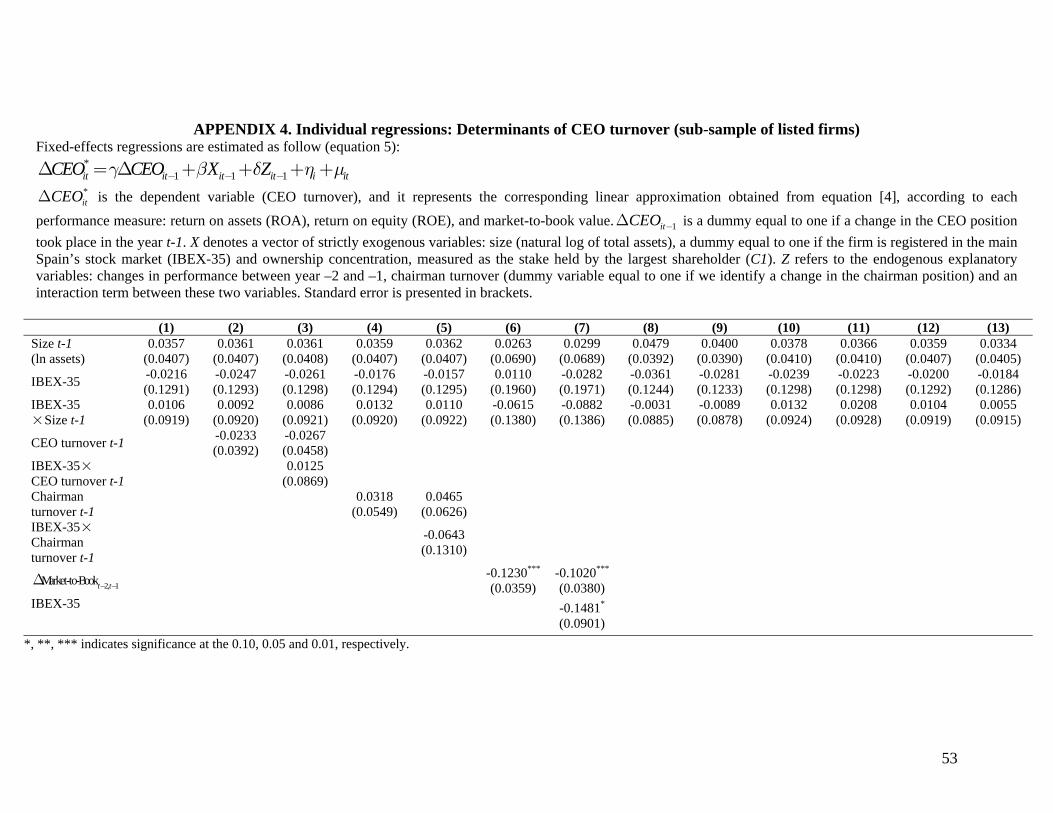

Appendices 1 and 2 report, for the full sample and the sub-sample of listed firms,

respectively, regression results using the conditional fixed-effects logistic regression as

alternative technique (equation [2]). Appendices 3 and 4 present, for the full sample and

the listed sub-sample, respectively; regression results when the explanatory variables

are introduced individually. It is important to remark that, when performance is

measured as changes in the median industry-adjusted ROA and ROE, our results do not

significantly differ (and they are weaker for the sub-sample of listed firms) relative to

those obtained when performance is expressed as unadjusted changes in these financial

variables. Hence, we will not comment here the results obtained for the industry-

adjusted performance measures. Those regression results are presented in Appendices 5

and 6.

Also, our results when ROE is the dependent variable are weaker in terms of

significance of the parameter estimates. We think that the lack of significance may

indicate that this variable (ROE), which includes some extraordinary results and

financial figures, is more exposed to other corporate actions that are unrelated to the

firm’s core activity. In fact, we consider the ROA and the market-to-book ratios as more

informative variables concerning firm performance, and from now on our comments

will be based on the results involving these two variables.

28

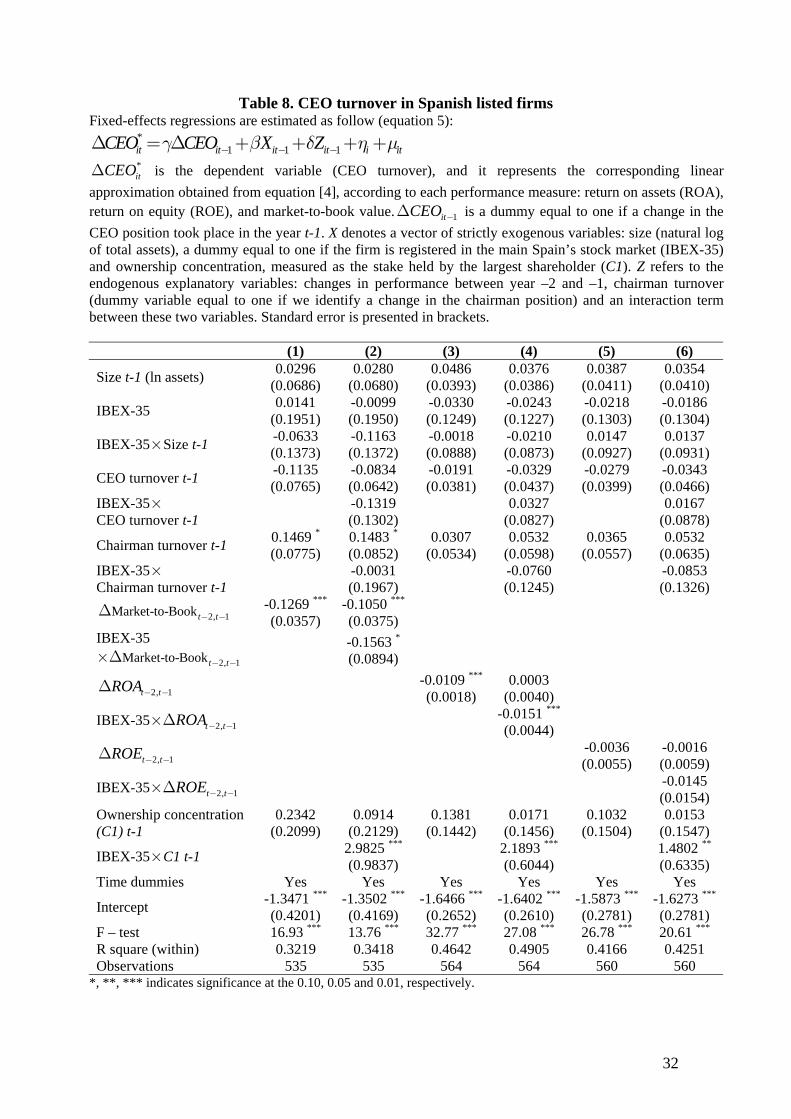

5.1 Dynamic CEO Turnover

In this sub-section we address whether the decision to replace the CEO is conditioned

by previous poor performance and previous changes in the CEO and chairman

positions. Table 7 presents our results for the full sample, whereas Table 8 shows the

results for the sub-sample of listed firms. Model specifications in these tables capture

the effect that the different performance measures used in our analysis has over CEO

turnover decisions (ROA and ROE in Table 7, and the market-to-book ratio, ROA and

ROE in Table 8).

Our results give support to the negative relationship between changes in performance

and CEO turnover. This finding is consistent with the bulk of academic literature having

examined this relation, and it is in accordance with our hypothesis H1a. In addition,

from Table 7 we can observe that the increase in the probability to replace a CEO, given

a negative change in performance, is stronger for those firms operating in the Spanish

stock markets. To corroborate this, we estimate the relevant coefficient for the sub-

sample of listed firms (the sum of the coefficients of interest: previous performance

changes and the listed dummy). When ROA is the performance measure, this coefficient

is significant at the 1% (Specification 2 in Table 7: –0.0107), revealing that for listed

companies the threat of dismissal for poor performance clearly dominates CEO turnover

decisions (Table 7). This is in accordance with our hypothesis H1b which proposed that

the negative relationship between performance and CEO turnover decisions is stronger

for listed firms.

We also find that firms that previously replaced the CEO are less likely to replace the

incoming CEO (Table 7), confirming that incentives for replacing a CEO are weaker if

the firm experienced a CEO replacement in the past (state dependence). The interaction

term between previous CEO turnover and the listed dummy is not statistically

significant, which suggests that listed firms have different propensities to experience a

change in the CEO position, irrespective of whether they have undergone a change in

the CEO position in the previous period. We did obtain the relevant coefficient for the

sub-sample of listed firms, which equals the sum of the coefficients of interest (previous

CEO turnover and the listed dummy). Such coefficient is significant at the 10% (–

0.0244 and –0.0317 for ROA and ROE, respectively), indicating that state dependence

in CEO turnover decisions only hold for unlisted companies in our sample (Table 7).

29

We are therefore able to confirm our second hypothesis (H2), but only in the case of

large unlisted companies.

Table 7. CEO turnover in listed and large unlisted Spanish firms Fixed-effects regressions are estimated as follow (equation 5):

*1 1 1it it it it i itCEO CEO X Zγ β δ η− − −Δ = Δ + + + +μ

*itCEOΔ is the dependent variable (CEO turnover), and it represents the corresponding linear

approximation obtained from equation [4], according to each performance measure: return on assets (ROA), and return on equity (ROE). is a dummy equal to one if a change in the CEO position took place in the year t-1. X denotes a vector of strictly exogenous variables: size (natural log of total assets), a dummy equal to one if the firm is registered in any Spanish stock market (Listed) and ownership concentration, measured as the stake held by the largest shareholder (C1). Z refers to the endogenous explanatory variables: changes in performance between year –2 and –1, chairman turnover (dummy variable equal to one if we identify a change in the chairman position) and an interaction term between these two variables. Standard error is presented in brackets.

1itCEO −Δ

(1) (2) (3) (4)

Size t-1 (ln assets) 0.0144 (0.0134)

0.0154 (0.0133)

0.0140 (0.0134)

0.0142 (0.0134)

Listed 0.0142 (0.1996)

-0.0001 (0.2005)

0.0128 (0.2004)

-0.0023 (0.2018)

Listed×Size t-1 -0.0023 (0.0269)

-0.0063 (0.0275)

-0.0021 (0.0271)

-0.0050 (0.0276)

CEO turnover t-1 -0.0253 **

(0.0120) -0.0249 **

(0.0124) -0.0264 **

(0.0121) -0.0261 **

(0.0126) Listed× CEO turnover t-1 0.0005

(0.0449) -0.0056 (0.0454)

Chairman turnover t-1 0.0114 (0.0164)

0.0096 (0.0170)

0.0128 (0.0166)

0.0110 (0.0172)

Listed× Chairman turnover t-1 0.0188

(0.0628) 0.0235 (0.0632)

2, 1t tROA− −Δ -0.00027 ** (0.00013)

-0.00023 * (0.00013)

Listed 2, 1t tROA− −×Δ -0.0105 *** (0.0021)

2, 1t tROE − −Δ -0.0003 (0.0013)

-0.0002 (0.0013)

Listed 2, 1t tROE − −×Δ -0.0033 (0.0062)

Ownership concentration (C1) t-1

0.0016 (0.0457)

-0.0054 (0.0473)

0.0020 (0.0459)

-0.0055 (0.0476)

Listed×C1 t-1 0.1271 (0.1642) 0.0956

(0.1672) Time dummies Yes Yes Yes Yes

Intercept -1.3752 ***

(0.0717) -1.3760 ***

(0.0721) -1.3734 ***

(0.0721) -1.3686 ***

(0.0726) F – test 379.55 *** 287.21 *** 371.19 *** 278.32 ***

R square (within) 0.3909 0.3932 0.3878 0.3879 Observations 8,537 8,537 8,468 8,468

*, **, *** indicates significance at the 0.10, 0.05 and 0.01, respectively.

30

This stands as a key result since it indicates that, in our sample of unlisted firms, boards

are more willing to wait for signals about CEO’s performance before to make any

decision about bringing new blood to the helm. Regardless of the performance measure,

our results for previous changes in the chairman position show that this type of

governance intervention does not exert any significant impact of future CEO turnover

decisions. Consequently, we reject our hypothesis H3a, which proposes that a change in

the chairman position increases the probability of CEO turnover next period. Finally,

parameter estimates for ownership concentration also show as not significant in all

model specifications.

We now extend our analysis to the sub-sample of listed companies. Results, presented

in Table 8, use as performance measures changes in the market-to-book ratio (columns

1 and 2) as well as changes in ROA (columns 3 and 4), and ROE (columns 5 and 6).

Consistent with our previous results, we find that listed firms show no state dependence

path concerning CEO turnover, and poor performance seems to be the main driver

behind CEO turnover decisions.

Interestingly, when the change in the market-to-book ratio from year –2 to year –1 is