Embed Size (px)

Citation preview

Original Article

Entrepreneurial value creation through green

microfinance: Evidence from Asian microfinance

lending criteriaReceived 18 July 2010; revised 25 February 2011; accepted 1 April 2011

Geoffrey R. Archera,* and Lisa Jones-ChristensenbaRoyal Roads University, 2005 Sooke Road, Victoria, BC V9B5Y2, Canada.bKenan Flagler Business School, University of North Carolina at Chapel Hill,

CB 3490 McColl Building, Chapel Hill, NC 27599, USA.

*Corresponding author.

Abstract Microfinance has proliferated as both a poverty alleviation tooland catalyst for entrepreneurs running small-scale businesses with support frommicroloans. This article examines four rationales for incorporating concern for thenatural environment into the practice of microfinance and suggests a typology tocategorize microfinance sustainability initiatives as preserving, evolving, sustainingor restoring. Using a binomial descriptive content analysis of publicly availablelending criteria, we investigate the incidence of ‘green microfinance’ in a sample of40 Asian microfinance institutions (MFIs) – all members of the Banking with thePoor Network in Bangladesh, India, Indonesia, Laos, Nepal, Pakistan, Philippines,Sri Lanka, Thailand and Vietnam. We conclude that despite the existence of viableand strategic rationales to support the proliferation of ‘green’ microfinance, veryfew MFIs actually embed such a commitment into the structure of their financialproducts. This disconnect reveals that current microfinance practice in Asia, to theextent that it may ignore the natural environment, may correspondingly endangerthe health and livelihoods of the very people it is designed to help. We consider thisstudy as investigative and in need of replication in other regions; however, it revealskey contradictions while also suggesting strategic redirections for the microfinancefield in Asia and elsewhere.Asian Business & Management (2011) 10, 331–356. doi:10.1057/abm.2011.9;published online 1 June 2011

Keywords: microfinance; microcredit; green; poverty; environment; sustainability

Introduction

The current business environment is characterized by increased interna-tional attention to climate change and related environmental sustainability

r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356www.palgrave-journals.com/abm/

issues in both developed and developing countries (Engardio, 2007;Montiel, 2008, Gallo and Jones-Christensen, 2011). There is considerableevidence that entrepreneurial activity plays a major role in economicdevelopment (Acs and Dana, 2001) and that entrepreneurial responses toenvironmental concerns are increasingly common (Cohen and Winn, 2007;Dean and McMullen, 2007). However, there is much we do not know abouthow or why entrepreneurs do or do not incorporate environmentalconsiderations into their business models – particularly in developing-country business contexts (for an exception focused on Latin America, seeWenner, 2004). In order to address this lack of information about informalbusinesses and their environmental strategies, we chose to investigatemicrofinance organizations in respect to this issue.

Approximately 125 million people in the developing world have receivedvery small (micro) business loans through the investment vehicle knownas microfinance (Microcreditsummit, 2011). Most microfinance lendinginstitutions (MFIs) provide access to capital as a pro-poor businessdevelopment tool intended to help alleviate poverty for borrowers(Morduch, 1999; Yunus, 2003; Chan, 2005; Callaghan, 2007). These MFIsoffer funding for a wide range of product and service-related businesses.Historically, MFIs have had mixed results from the model, as someorganizations claim to have impacts on poverty alleviation, althoughscholars and critics suggest that these impacts are overstated (Panjwani andCecelski, 2003; Simon and Sear, 2005; Karnani, 2010). Our research isconcerned with these mixed results and particular positive and negativeexternalities from the practice of microlending. Specifically, we areconcerned about the effects of microlending on the natural environment.1

Thus, we evaluate a subset of organizations in the microfinance industry, inorder to extract illustrative findings about the practice of microfinance as itrelates to environmentally focused entrepreneurial action in the informalsector.

This article unfolds as follows: we briefly outline the history ofmicrofinance (also known as microcredit) as it relates to informal, dev-eloping country entrepreneurial activity. Next, we review negative, positiveand neutral environmental impacts of microfinance activities and includecase examples and a typology. Following the typology, we discuss fourcommon ethical rationales that might motivate and encourage the practice ofenvironmentally sound or ‘green’ microfinance. Next, we use these rationalesas an organizing framework to analyze the lending criteria of the members ofthe Banking with the Poor Network (BWTP) in Asia in order to determinehow microlenders do (or do not) incorporate environmental criteria intofirm investment strategies. We close with implications for research andpractice.

Archer and Jones-Christensen

332 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Microcredit and Microfinance Background

Over 30 years ago, Muhammad Yunus founded the Grameen Bank inBangladesh with the radical idea that desperately poor, working rural womenwere credit-worthy (Yunus, 2003). Yunus and other practitioners found thatwomen used the credit to expand fledgling businesses, and repaid loans withproceeds from these businesses. Practitioners developed the idea that evenwith no collateral, these women should be granted small loans at competitiveinterest rates with frequent payback cycles. By design, typical repayments aresmall enough to not be overwhelming and repayment meetings are frequentenough that people maintain responsibility to other members of a loan group.In addition, loans are subject to competitive interest rates. This concept, thatsmall loans should be granted to the previously ‘unbankable’, came to be calledmicrocredit (Unitus, 2011).

The term ‘microfinance’ refers to microcredit and the services potentiallybundled with it, such as microinsurance, micro housing loans, savings pro-ducts, deposit services, training, transfer services and others (Asian Develop-ment Bank, 1999). Microfinance institutions now operate in almost everycountry in the world. Importantly, it is significant to note that microenter-prises (firms employing 10 people or fewer) constitute 80–90 per cent of allbusinesses in Latin America and the Caribbean, account for more than 50 percent of employment and generate upwards of 30 per cent of GDP in somecountries (Poyo et al, 1996; ILO, 1999; Economic Commission for LatinAmerica and the Caribbean, www.eclac.cl/publicaciones/xml/3/38133/2009–851-Summary-Economics_climate_change-WEB.pdf, 10 January 2009). Asia is ahuge potential market for microfinance, as the informal sector constitutes,on average, 30–40 per cent of GDP, yet microfinance only reaches a smallpercentage of the population (World Bank, 2007). Given this context, as wellas the data on the large size of the sector, it is important to understand howmicroenterprises affect the natural environment.

Microfinance, Microenterprises and the Environment

The microfinance industry primarily affects the environment through thebehaviors of individual microentrepreneurs running their microenterprises.Secondarily, MFIs themselves may generate environmental impacts fromtheir operations. Given the millions of microenterprises in the informal sector,the potential for severe environmental impact is high when one considers thepossibility of cumulative effects.

In addition to size, it is important to consider other structural aspects of thesector. The fact that most microenterprises are active in informal markets

Entrepreneurial value creation through green microfinance

333r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

means that microentrepreneurs are minimally or non-compliant with existinggovernment regulations related to issues of registration, taxes, zoning, mini-mum wage, social security and environmental protection (Wenner, 2004). Inaddition, developing countries with strong informal economies are oftencharacterized by weak government institutions and enforcement agencies –situations that can further exacerbate environmental harm. Other reasons whyenvironmental protection is difficult to achieve in developing countries arethat poverty forces citizens to discount environmental amenities in favor ofimmediate income needs, and citizens are relatively uneducated about environ-mental safety, remedial techniques, ‘clean’ technologies and cost-effectivesafety options (Wenner, 2004).

Given this background, we next consider specific negative, neutraland positive examples of how microfinance can impact the environment.We define ‘natural environment’ as the climate, weather and ecologicalresources affecting habitat and survival of human and non-human entities onthe planet.

Negative Environmental Impacts of Microenterprises

Negative environmental impacts of any activity leave the natural environmentin a condition weaker or worse than when the activity began. Certainly, theenvironmental impact of microenterprises varies by industry sector. Micro-entrepreneurs in commerce and service sectors may have a smaller environ-mental footprint relative to microentrepreneurs in extractive, agriculture ormanufacturing activities, but impacts from any sector can be negative andincreasingly so when cumulative. Impacts from commerce and services include:noise, congestion, litter and encroachment on urban greenspaces or bodies ofwater. Microentrepreneurs in farming and crafts or artisanal industries mayhave different, but still negative, environmental impacts than those from theservice sector. For example, many independent agents undertaking small-scalerural activities including farming and fishing can, in the aggregate, accruetremendous negative impact through overgrazing or overfishing, cultivatingfragile lands with inappropriate soil and water conservation, clearing ofuntouched forests, intentional or accidental release of invasive species, andinappropriate use, storage and disposal of chemicals and fertilizers (Hardin,1968). Any trade requiring the collection of natural products such as medicinalplants, wild game, fuel wood or other inputs for artisanal products can causeloss of biodiversity and can result in overgrazing or over-hunting (whichimpacts biodiversity by altering species composition) (Tictin et al, 2002).

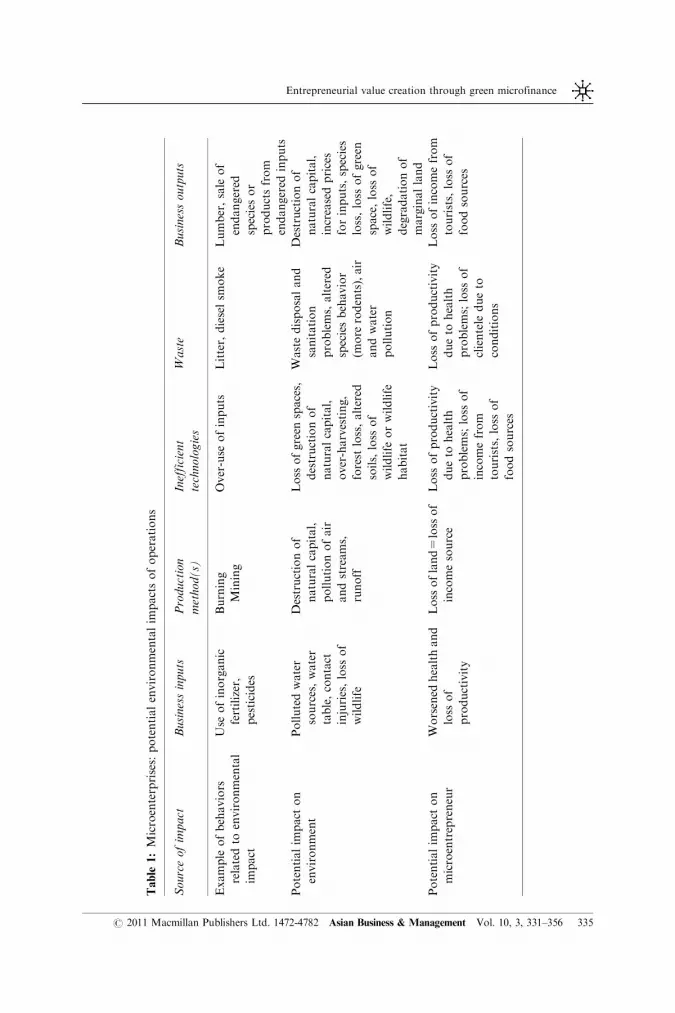

Evidence suggests that the most pollution-intensive industries have thestrongest adverse environmental impacts. Such industries include leather

Archer and Jones-Christensen

334 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Table

1:Microenterprises:potentialenvironmentalim

pactsofoperations

Sourceofim

pact

Businessinputs

Production

method(s)

Inefficient

technologies

Waste

Businessoutputs

Example

ofbehaviors

relatedto

environmental

impact

Use

ofinorganic

fertilizer,

pesticides

Burning

Mining

Over-use

ofinputs

Litter,dieselsm

oke

Lumber,sale

of

endangered

speciesor

productsfrom

endangered

inputs

Potentialim

pact

on

environment

Pollutedwater

sources,water

table,contact

injuries,loss

of

wildlife

Destructionof

naturalcapital,

pollutionofair

andstreams,

runoff

Loss

ofgreen

spaces,

destructionof

naturalcapital,

over-harvesting,

forest

loss,altered

soils,loss

of

wildlife

orwildlife

habitat

Wastedisposaland

sanitation

problems,altered

speciesbehavior

(more

rodents),air

andwater

pollution

Destructionof

naturalcapital,

increasedprices

forinputs,species

loss,loss

ofgreen

space,loss

of

wildlife,

degradationof

marginalland

Potentialim

pact

on

microentrepreneur

Worsened

healthand

loss

of

productivity

Loss

ofland=loss

of

incomesource

Loss

ofproductivity

dueto

health

problems;loss

of

incomefrom

tourists,loss

of

foodsources

Loss

ofproductivity

dueto

health

problems;loss

of

clientele

dueto

conditions

Loss

ofincomefrom

tourists,loss

of

foodsources

Entrepreneurial value creation through green microfinance

335r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

tanning, brick and tile manufacturing, chemical-intensive agriculture andaquaculture, metalworking and electroplating, small-scale mining, paintingand printing, automobile and motor repair, wood processing and metalfinishing, charcoal making, textile dyeing, and food processing (Wenner, 2004).Table 1 indicates five main general sources of environmental impacts (frombusiness inputs, production methods, inefficient technologies, waste andbusiness outputs) with examples of each and of the potential harmful outcomesthat can result.

It is clear from the table that the size and scale of potential environmentalimpact correlates with the size and scale of microenterprise. However, althoughthe small size and limited scope of some enterprises may limit their negativeimpact, the concentration of related (small) enterprises in one location canincrease negative impact. Further, some industries are prone to higher negativeimpacts by their nature, and therefore even in isolation they have detrimentaleffects.

In all cases, it is important to note that negative impacts can be exacerbatedby sheer numbers, extended hours of operation, lack of regulatory supervision,low technological levels and lack of supporting services (such as trashcollection or ventilated sales areas) (Hall, 2007). To further illustrate theseclaims with specific case information, we note that Abhishek Lal and ElizabethIsrael (founder of www.greenmicrofinance.org) (2006) explain that microcreditfor agricultural development often goes to purchase pesticides, fertilizers,cattle and land; activities that have serious environmental ramificationsfrom deforestation to hazardous chemical pollution and occupational safetyconcerns. Further, even a human-powered water pump can produce a negativeenvironmental impact.

The treadle pump is a successful irrigation device powered by a human whowalks on lever arms in the same manner they would climb stairs. Householdsadopting these pumps have seen a five-fold increase in income on average, fromUS$100 to $500 per year per family (Fisher, 2006). Ironically, research hasshown that the extra income generated by this pump might be catalyzing theproliferation of diesel-powered, non-point-source polluters. The JapaneseInstitute for Irrigation and Drainage (JIID) ascribes this environmentallydamaging development specifically to Kickstart when they write that ‘over thelast ten years, the price of the smallest diesel pump in Bangladesh and India hasdropped from $500 to $150, and by producing new income of $500 a year,Treadle Pump has produced at least 250 000 new customers for the smallestdiesel pump’ (JIID, 2001).

In this last example, we see an illustration of the argument that as low-income individuals gain wealth through enterprise or any other means, theymay begin to consume in ways that are highly functional at the individual levelbut which have negative implications on a macro scale. Thus, the illustration is

Archer and Jones-Christensen

336 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

less about treadle pumps and more about noting that the very economicdevelopment that microfinance catalyses can directly relate to follow-onbehaviors that deplete the natural environment.

Certainly, instances of microfinanced activity having a negative impacton the natural environment are not limited to ranching or agriculture. TheGrameen Village Phone Program in Bangladesh provides a cellular telephoneto a poor woman who builds a business by selling use on a ‘per-call’ basis. Thismodel has enjoyed significant reach, as microentrepreneurs operate over220 000 of these as a business, bringing phone service to at least those manyrural villages in Bangladesh (Grameen Foundation, 2009). This microfinancedactivity has potential negative environmental impact in relation to the powersources it requires. According to a Grameen Technology Center employee,phones are charged with 12V lead-acid car batteries provided by the MFI(Grameen Technology Center, 2008). It may not be reasonable to assume thatfamilies operating these businesses are aware of the dangers that lead-acidbatteries pose to human and environmental health or how to properly disposeof a battery at the end of its life.

Clearly, different types of microfinanced projects produce negative impactsin relation to the natural environment. Considered from a systems-thinkingperspective (Werhane, 2002), these impacts and externalities can and dobecome opportunities for other entrepreneurs (Cohen and Winn, 2007; Deanand McMullen, 2007). However, until entrepreneurs or governments act toaddress these negative impacts, they remain ‘opportunities’ that extract a tollon our ecosystem.

Neutral Environmental Impacts of Microenterprises

In contrast to negative externalities, it is possible that many behaviorsof microenterprises have neutral impacts, that is, the activity leaves theenvironment in the same condition as it existed before the activity. Forexample, fishing, farming and other renewable resource-based microenterprisescan be operated in a sustainable manner by not removing resources at ratesgreater than replenishment rates. When such sustainable practices are followed,an enterprise can maintain indefinitely. However, the entrance of othermicroentrepreneurs into the same geographically bounded resource pool cantip the balance toward unsustainability. Experiences in recent decades incommon property resource situations, especially fisheries, suggests that onlywhen the participants are given property rights to the resource and otherpotential entrants are thereby excluded from access do people maintainsustainable harvest practices (Dean and McMullen, 2007).

Entrepreneurial value creation through green microfinance

337r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Certainly, achieving neutrality in impacts may be a mid-term goal for someindividuals and organizations, but an end-goal for others. However, as sug-gested above, it is a difficult strategy to maintain in competitive environments,as there is usually no way to discourage new entrants into largely informalactivities. One way to differentiate an individual or organization may be topursue a more aggressive environmental strategy, one that seeks positivereturns to the natural environment.

Positive Environmental Impacts of Microfinance and Microenterprises

Microfinance and microenterprises have positive impacts on the environmentwhen they restore or renew some aspect of the environment. Positive environ-mental outcomes result when microentrepreneurs use ‘green’ or ‘sustainable’inputs, such as certified and sustainably grown wood, organic seeds, compostor green fertilizer, and/or organic dyes. Production methods and utilization ofefficient technologies can also have positive impacts, such as when microentre-preneurs get involved with reforestation, controlled water usage, natural pestcontrol methods and environmentally friendly technologies such as solar-powered devices. The use of recycled or used goods as business inputs alsoresults in positive impacts, either from averting waste or from delaying damagerelated to the manufacture and use of new inputs. When microentrepreneursjoin with others to employ ‘cradle to cradle’ production and manufacture, theyparticipate in a virtuous environmental cycle where the outputs of oneenterprise become inputs for another (McDonough and Braungart, 2003).

Examples of positive impacts from microlending practices do exist. Forexample, in Argentina, FIS Microcredito finances and installs photovoltaicpanels that electrify previously off-grid villagers. These panels facilitatelearning, cooking and living in a far more healthful manner than the use ofindoor fires, and with a usable life of 20 years the panels may also replaceunsustainable disposable batteries (FIS Microcredito Social Investment Fund,2006). While we recognize that photovoltaic panels are complex durable goodswith inherent manufacturing (Knapp and Jester, 2001) and disposal impacts(Fthenakis, 2000), Knapp and Jester estimate that solar panels generate 7–14times the energy required in production. Therefore, adopting them as part ofmicrolending signals MFI investment in an environmentally positive technol-ogy (Greenmicrofinance.org, 2004, 2011).

When financial institutions provide funding for environmentally friendlytechnologies, when they provide better terms for microenterprises utilizingenvironmentally friendly practices, and when they provide training or suggestalternative practices, then they are enabling the emergence of positiveenvironmental impacts. Currently, there are organizations involved in all these

Archer and Jones-Christensen

338 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

behaviors. In particular, Wenner (2004) have documented that the Inter-American Development Bank created a mandate to protect the environment inall project financing, and the bank approved a statement mandatingenvironmental protection in the Guidelines for Environmental and SocialDue Diligence for IDB Microenterprise Operations. They state that similarmandates exist within the World Bank, International Finance Corporation andother bilateral donor agencies; and more specifically, organizations such asConservation International have created funding sources for ventures designedto protect and showcase the natural environment. While many of these trendshave begun in Latin America, they can be replicated and transferred to anAsian context with minimal adjustments.

Some practices that can be emulated worldwide are embodied in theidiosyncratic investment strategy of particular investors who fund MFIs.Organizations such as Envest, located in the United States, focus on disbursingfunds for microfinance organizations that will use the money for projects thatfurther environmental goals. The fund managers use the Natural Step(Nattrass and Nattrass, 2002) framework to guide lending activities, and themission is to ‘provide capital for poverty alleviation using financially soundmarket mechanisms in a way that increases the sustainability of the earth’snatural resources and protects biodiversity’ (envestmicrofinance.org, 2011).These examples suggest that environmentally focused and positive practicescan be introduced or enabled by financing institutions themselves.

Despite the presence of these loan requirements and similar enablingstatements on the part of donors and funding agencies, there is evidence of adisconnect between statements and actual practice. Researchers and analystshave noted that many of the strictures are not operationalized, and someattempts at enacting the strictures have met with resistance (Taborga andWenner, 1997; Zucchetti and Alegre, 1999, Wenner, 2004). In our attempts tounderstand and probe this resistance and its implications, we investigatedrationales for incorporating environmental protections into microfinancelending.

Motivational Bases for Pro-environment Behaviors

Investigating the international development, microfinance and environmentalethics literatures for insights into the motivational bases for pro-environmentbehaviors indicates the use of at least four different rationales for incor-porating environmental protection into actions (Dunford, 2000; Littlefieldet al, 2003; Panjwani and Cecelski, 2003; Yunus, 2003; Clancy et al, 2004;Greenmicrofinance.org, 2004; Lal and Israel, 2006; Callaghan, 2007; Hall,2007; Karnani, 2010). Three are anthropocentric and thus put the benefit to

Entrepreneurial value creation through green microfinance

339r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

humans at the forefront of the environmental logic (Baxter, 1995). Motivationsthat spring from a concern for vulnerable human populations can broadly belabeled as: (1) for the poor, (2) for women (3) for children. Each of thesecorresponds to a traditionally vulnerable subcategory of humanity. In contrast,environmental ethicists tend to define their concerns in less human-centeredterms. Rather, they espouse decision-making and motivations that stem from afocus on (4) for the planet (Taylor, 1986; Rolston, 1988). Combining thestrictly anthropocentric views with the ecologically focused views provides fourdifferent motivational bases from which to analyze attitudes and environ-mental behaviors (or lack thereof) on the part of entrepreneurs and funders.Thus, we elaborate each of the four.

Anthropocentric motivation: Advance the human condition

Maslow’s work in the field of psychology (Maslow, 1943) argues that peoplecannot begin to achieve higher-order fulfillment until basic physiological needs(that is, food and shelter) are met (Huitt, 2004). One can extend this line ofreasoning to a more modern context by suggesting that infrastructure servicessuch as electricity, water, sanitation, telecommunications and transport havethe potential to enhance or inhibit the living standards, growth rates andparticularly the human development potential of a region (Brook and Smith,2001).

Financing any small business activity with a predictably deleterious effect onthe natural environment has, in turn, negative effects on human livingstandards. To do so would be antithetical to the mission of improving the livesof the poor, a mission widely understood to have fueled the growth ofmicrofinance in the first place (Morduch, 1999; Panjwani and Cecelski, 2003;Yunus, 2003; BYU Broadcasting, 2005; Chan, 2005; Callaghan, 2007; Karnani,2010). Thus, one motivation for encouraging pro-environmental behaviors is todo so in support of its long-term human development potential, particularly inrelation to the income-poor.

Anthropocentric motivation: Advance the cause of women

A logical extension of the more general rationale, to pursue environmentallyethical behavior because it advances humanity, is the rationale to advanceenvironmental ethics on behalf of women. What differentiates a ‘for the poor’motivation from a ‘for the women’ motivation is the fact that women havebiological and gender-specific roles in the developing world and in continuinghumankind. Women’s roles as mothers and caregivers, as well as their typicaleconomic vulnerability in relation to men, means that women often bear a

Archer and Jones-Christensen

340 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

disproportionate share of the workload (Panjwani and Cecelski, 2003; Clancyet al, 2004). In many cultures, women’s responsibilities are brutally hard andtime-consuming, with many hours spent foraging for firewood and manymiles traveled carrying water, all in advance of preparing the family’s meals(Freeman et al, 2000). Researchers observed that in Guanacaste, Costa Rica,the extensive burning of wood by women puts intense pressure on alreadyscarce tropical forests, because wood is the primary fuel source. In reaction tothis problem in this particular location, a group of women establishedFundacion Sol de Vida in 1994. Their objective was to encourage solar cookersas an alternative to wood, gas and electric stoves and to provide more optionsfor women. This is one example of how women themselves, along with theorganizations that support them, move to mitigate environmental impacts intandem with the goal to lessen work burdens.

Many MFIs acknowledge in their mission statements the burdens borne bywomen. The Grameen Foundation’s website states that ‘with tiny loans,financial services and technology, we help the poor, mostly women, start self-sustaining businesses to escape poverty’ (2011; our italics). Other MFIs, likeWomen’s World Banking (2009), exist specifically to address this inequityby providing loans and other educational services to women. The missionstatement of this organization is ‘to expand the economic assets, participationand power of poor women as entrepreneurs and economic agents by openingtheir access to finance, knowledge and markets’ (2009). There is also con-siderable evidence that income earned by women is, more than income earnedby men in the family, invested in improved food, health care and education forchildren – meaning women’s new income made possible through microfinanceactually represents an investment in the larger community and the futurethrough investment in children’s well-being (Littlefield et al, 2003; Holvoet,2004).

Anthropocentric motivation: Protect and preserve for the children

Freeman et al explain that ‘Because women are primarily responsible forchildrearing, they tend to have the most vivid experiences of environmentaldangers faced by their children’ (2000, p. 8). Contaminated water and badindoor air quality are facts of life in the households of many microfinanceborrowers (Wilson and Green, 2000; Ho Lem and Samson, 2003). Physiolo-gically, these ills pose a greater threat to growing children than to adults simplydue to the nature of youth and human development. Sanitary latrines and solarovens might improve children’s quality of life and mortality rates. What mightbe less obvious, but equally important, is the fact that mothers foraging forwood and water are not free to educate or otherwise nurture and protect their

Entrepreneurial value creation through green microfinance

341r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

children. Enabling electrification of a house with an environmentally neutral orpositive photovoltaic panel or a rechargeable LED lamp not only extends thehours that a child could be learning (Boiling Point, 2005), but also lessensthe health risks inherent in indoor wood fires. Thus, incorporating environ-mental protection into microfinance may be partially motivated by an interestin the health and well-being of children.

Ecological motivations: Behavior change on behalf of the planet

Paul Taylor imagined that ‘given the total, absolute, and final disappearance ofHomo Sapiens, then not only would the Earth’s Community of Life continueto exist, but in all probability its well-being would be enhanced’ (Taylor, 1986,p. 115; our italics). The conception of a ‘for the planet’ rationale for theintegration of environmental protection into microfinance lending builds uponthis logic. According to this line of reasoning, the preservation of or return to apristine earth is the priority (Taylor, 1986; Kelman, 1995). The earth and itsnatural systems are for the most part negatively affected by the businessundertakings of mankind (Hawken et al, 1999; Nattrass and Nattrass, 2002;McDonough and Braungart, 2003). Thus, this line of reasoning would indicatethat any practice (in microfinance or otherwise) that improves environmentalquality and ecosystem function is preferable to other options. Proponents ofthis reasoning place ecosystem function at the center of decision-making.

Greening Microfinance: Environmentally Oriented Activities

In this section, we build on the awareness that both anthropocentric andecological motivations suggest the promotion of environmental behaviors onthe part of MFIs and other organizations. We focus on the actions of MFIs,the institutions that fund microenterprises, because they have the potential toinfluence how funds are allocated; the influence to require reports on the use offunds; and the opportunity to provide education, outreach and training toentrepreneurs/borrowers. In considering these institutions, we recognize thatthere are a range of alternatives that management can utilize to mitigateecological damage, prevent future environmental harm and promote environ-mental enhancement. However, no work to date has attempted to aggregate orcharacterize the activity options or types of firms enacting them. Our analysissuggests that the options can be considered along a continuum with two axes.One axis refers to the intent of the institution – the intent can be to simplyavoid, reduce or mitigate negative environmental impacts (that is, ensure thatimpacts are neutral rather than negative, or at the very least, less negative than

Archer and Jones-Christensen

342 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

they otherwise would have been), or it can be to promote and promulgatepositive environmental impact (that is, move impacts from negative or neutralto positive). The other axis refers to the focus of the firm – they can focusinternally on their own organizational operations or externally on clients andtheir myriad microbusinesses. When considered along these continuums, theactions of funding institutions can be characterized as self-preserving, evolving,sustaining or restoring (Table 2).

As the table suggests, maintaining an internal focus on the organization anda focus on avoiding ‘bad’ behavior represents a mindset of self-preservation,where management mainly avoids trouble as a strategy to continue business.An organization that maintains the internal focus but moves toward enactingpositive/restorative behaviors is labeled here as ‘evolving’, because the termconnotes progress without implying arrival at any particular end-state. Thisnormative term reflects our position that an inter-organizational focus severelyattenuates any potential scale or impact that might result from the focus onpositive impacts, as they can only accrue so much as a single firm. In contrast,the remaining two categories and their corresponding labels purposefully implythe potential for more impact. They do this inherently, because these categoriesfocus on the thousands of microbusinesses instead of any one organization.The table suggests that any organization with this external focus on micro-businesses and the goal of avoiding harmful behaviors is in a category of‘sustaining’ the ecosystem at current levels of service. By extension, anyorganization with a focus on the microbusinesses and with intent to enactenvironmentally positive behaviors is categorized as ‘restoring’. Examples ofthe kinds of behaviors exhibited by each type of institution are in Table 3.

Combining this typology with the four motivational bases for environmentalaction as described earlier offers several different ways to evaluate theenvironmentally oriented behaviors (or lack thereof) of microbusinesses andthe MFIs that fund them. We therefore utilized these tools in evaluating thelending documents of several Asian MFIs. We wanted to discover how manyMFIs could be categorized as ‘restoring’ based on the criteria they set forth intheir lending documents. We also wanted to identify which, if any, of theanthropocentric or environmental motivations are referenced. Thus, we turnedto an evaluation of lending documents.

Table 2: Typology of organizational environmental orientation

Intent: Eliminate, mitigate

or reduce negative

environmental outcomes

Intent: Promote positive

environmental outcomes

Focus: Internal/Organization Self-Preserving Evolving

Focus: External/Microenterprises Sustaining Restoring

Entrepreneurial value creation through green microfinance

343r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

MFI Lending Documents

Lending criteria in microfinance are usually found in a document thatdelineates constraints around a project or a borrower’s eligibility for amicroloan. Bank management usually produces MFI lending criteria docu-ments and banks distribute them to regional offices and the field where, ineffect, they are the primary tether between lender’s values and the actions of itsfield personnel (Grameen Foundation Director, personal communication,12 March 2007). The criteria usually are concise, in part so that they are easy to

Table 3: Examples of environmentally oriented behaviors by organizational type

Organizational type Environmentally oriented behavior(s)

Self-Preserving (firm has

internal focus on

eliminating negatives)

Recycle

Reduce energy and water use inefficiencies

Evolving (firm has internal

focus on creating

positives)

Establish and share an environmental policy

Train staff; create messages for internal use

Reuse resources

Include environmental components in studies for expansion

activities

Use solar/biofuels for operations

Sustaining (firm has

external focus on client

and works to eliminate

negative impacts)

Encourage/enable borrower to recycle

Encourage firm to reduce inefficiencies

Screen current portfolio and do not renew non-sustaining clients/

borrowers

Screen future loans and avoid financing firms with negative

environmental impacts

Coordinate with local environmental NGOs for client training

Use simplified environmental assessment tools and share with

client

Actively promote and fund green investments

Restoring (firm has external

focus on client and works

to promote positive

impacts)

Require clients to sign statement about ‘do no harm’ behaviors at

loan disbursement

Coordinate with local environmental NGOs for client training

Offer incentives (eg lower rates, different payback options) for loans

used on environmental technologies or products (such as

recycling, composting, organic farming, tree planting, biofuels etc)

Promote green trade fairs

Provide ‘in kind’ green inputs

Link firms to enable cradle-to-cradle input and output exchanges

Lobby for change among other MFIs

Use simplified environmental assessment tools and share with

client

Actively promote and fund green investments

Archer and Jones-Christensen

344 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

translate into local dialects, and also to facilitate understanding by employeeswho are not highly educated and who tend to follow a script. These documentstypically involve a handful of simple principles, such as ‘we only lend towomen in self-selected groups’. For researchers, basic codification of a lender’srequirements can be illuminating. However, for a variety of reasons, theyare difficult to obtain. Despite this difficulty, we obtained such primarydocuments. See Figure 1 for an example, translated from French-speakingTunisia.

Figure 2 depicts the lending criteria document from the US-based lenderEnvest Microfinance Cooperative. They typically lend to MFIs in LatinAmerica, but are expanding into Africa and Central Asia. This document isatypical in that it specifically denies funding to projects with predictablynegative environmental impact.

The discussion of organizations that fit the ‘restoring’ type suggests that suchenvironmentally focused behaviors are possible and increasingly prevalent.However, green microfinance still remains a niche within a larger field. Thus,we sought to explore, within the Asian context, how a subset of firms do or donot incorporate sustaining or restoring practices. Specifically, we looked atlending practices.

Summary of Loan

Length of loanDescription of loan

– Group SolidarityGaranty– Self-selection of the group– Good reputation of the members– Knowledge of the Mutual Insurance Company business form– Geographic proximity of the members– 4–7 persons maximum– Set up as a Guaranteed Mutual Insurance company– Legal contract with the municipality– Participation in 5 meetings

Administration Fee

Conditions of Eligibility– Men must be more than 20 years old; Women 18+– Must be a Tunisian national – Must have an existing microfinance business or the capacity to create one – Must belong to the population target of Crenda – Must not be a government official with a high income

Availability of loan

6, 8, 10 and 12 monthsProgressive line of credit from 150–1000 dinars

5 dinars

– A majority of women in the group

Year Round

Figure 1: Excerpt of sample lending criteria translated into English.

Entrepreneurial value creation through green microfinance

345r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Methodology

To understand the relationship between microfinance lending and environ-mental protection we performed a descriptive content analysis of microfinancelending criteria of members of BWTP in Bangladesh, India, Indonesia, Laos,Nepal, Pakistan, Philippines, Sri Lanka, Thailand and Vietnam.

Data gathering

Over the course of 2 years we obtained primary data on microfinance lendingcriteria. The first author conducted personal interviews of microfinance lendingpractitioners. This yielded several documents, but remained a slow approach.In an effort to address this, we produced a professional website explaining thepurpose of our study. Since its launch, our site (www.researchingmicrofinance.com) has been mentioned on industry blogs and forwarded around by thoughtleaders. Nevertheless, this also produced little of research value. Thus, weshifted our focus to investigating lending criteria publicly available on theinternet. Using standard search engines resulted in links to news stories that didnot contain the data we sought. About one in ten results delivers a page fromthe website of an MFI. Not all of those pages explicitly delineate lendingcriteria. Another problem surfaced as well: because most microfinance loans

Figure 2: An atypical lending criteria document from Envest.

NB: Spelling error in original.

Archer and Jones-Christensen

346 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

are given in countries where borrowers do not speak English or have internetaccess, it is not strategic to expend the resources to build a website to describelending criteria to an English-speaking audience.

We moved to evaluating microfinance information websites. MixMarket, forexample, hosts in-depth profiles of more than 1300 MFIs. Most of theMixMarket data are quantitative, but there is little information on lendingcriteria (www.mixmarket.org, 11 April 2009). Most other microfinance infor-mation websites (for example, microcreditsummit.org) exhibited a similarlydisappointing pattern. Eventually, we accessed a website from BWTP. Thenetwork consists of ‘some thirty national policy institutions, commercial banksand NGOs from nine countries in Asia, namely Australia, Bangladesh, India,Indonesia, Nepal, Pakistan, Philippines, Sri Lanka and Thailand. The BWTPobjective is to link microfinance with the financial system and to support theprovision of inclusive financial services in Asia’ (www.bwtp.org/about-us.html,9 April 2009). We found that almost all the profile pages describe both alender’s ‘methodology’ and its ‘poverty focus’. We concluded that thisinformation was rich enough to facilitate content analysis.

Content analysis

We content-analyzed this data set using standard professional practices tosummarize in a quantitative way the content of written/qualitative records(Neuendorf, 2002). Although content analyses can often support traditionalhypothesis testing, we did not feel there was sufficient theoretical backgroundfor us to pursue this route. Instead we chose to use the organizing frameworksdescribed earlier to explore what percentage of MFI lending criteria underreview required the protection of environmental quality.

Sample size

The target sample size for a binomial content analysis was chosen based onguidance from the Content Analysis Guidebook (Neuendorf, 2002), in which theauthor states that an n of 384 should provide a 95 per cent level of confidencewith a sampling error of 75 per cent. If that n is not attainable, then an n of 96should provide a 95 per cent level of confidence, with a sampling error of 710per cent. At first this requirement might seem to eliminate the BWTP data set,because it contains 40 MFI profiles. It is important, however, that the samplesize guidance in this book was generated from mathematical equations thatassume 50:50 odds on the answer to any given question. Because the nascentstate of environmentalism in microfinance was the very motivation for thestudy, we anticipated very little concern about environmental protection, and

Entrepreneurial value creation through green microfinance

347r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

therefore less than 50:50 odds regarding answers to the questions. Weperformed a pilot study on the websites of a dozen randomly selected MFIs.Only one of them, Oikocredit, clearly required protection of the naturalenvironment: ‘the project should meet with the environmental criteria adoptedby Oikocredit’ (www.oikocredit.org/rm/gh/doc.phtml?p=lending-criteria11,11 April 2009). We confirmed the veracity of this mathematical adjustment(Kimberly Neuendorf, email personal communication, 15 February 2009), andcalculated our target sample size of 29 thus:

Assuming 50/50 odds:n¼ (0.5� 0.5)(z/sample error)(z/sample error)¼ n/0.25Using 96 as n we solved for (z/sample error) 384.

Adjusting for 1 in 12 odds:n¼ (0.9175� 0.0825)(z/sample error)(z/sample error)¼ n/0.076Plugging in (z/sample error)¼ 384 our new target sample size n would be 29.

Coding

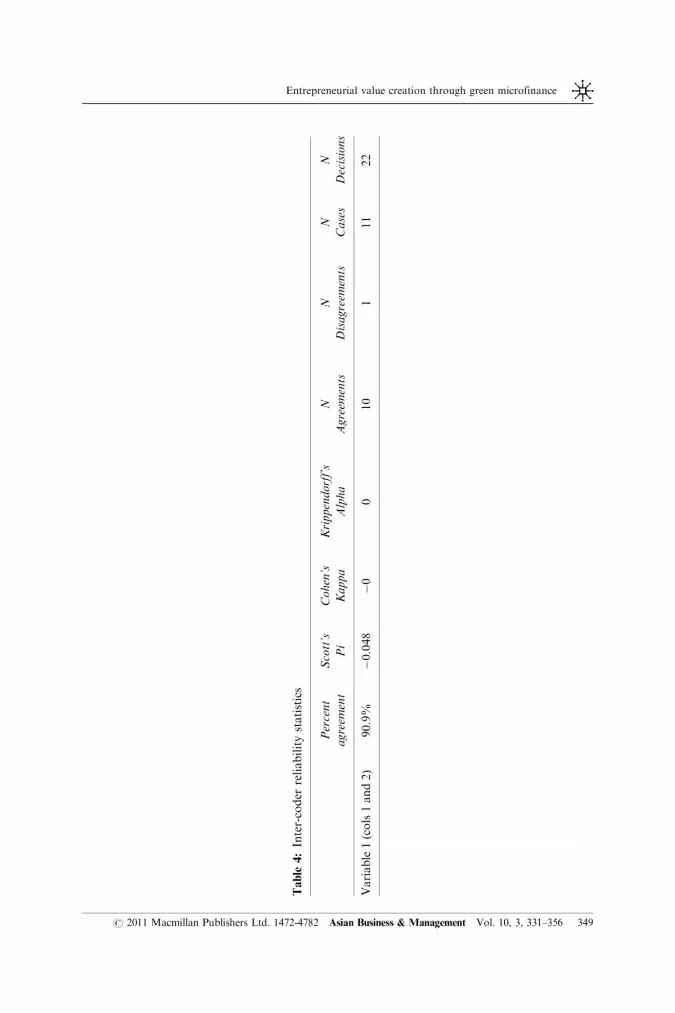

We employed two human coders in our analysis. Each was instructed to look at26 MFI profiles, and to answer the following binary research question: ‘(Doesthis web page) include a mention of care for the natural environment?’. To testfor inter-coder reliability, 12 profiles were analyzed by both coders. These datawere input into the online inter-coder reliability testing engine ReCal2. Table 4demonstrates strong inter-coder reliability across several popular metrics.

Results

Both coders found the same four MFIs that positively answered the researchquestion. This 10 per cent figure is very close to the 8.25 per cent we saw in ourpilot. Although the ‘blind’ nature of the method does not afford us insight intothe exact words the coders interpreted as representative of environmentallyprotective language, select elements of these MFIs’ websites are presented inTable 5 and provide context for the findings.

Discussion

This investigation was focused on determining whether individual microen-trepreneurs and the microfinance organizations that fund them do or donot incorporate environmental considerations in organizational business

Archer and Jones-Christensen

348 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Table

4:Inter-coder

reliabilitystatistics

Percent

agreem

ent

Scott’s

Pi

Cohen’s

Kappa

Krippendorff’s

Alpha

N

Agreem

ents

N

Disagreem

ents

N

Cases

N

Decisions

Variable1(cols1and2)

90.9%

�0.048

�0

010

111

22

Entrepreneurial value creation through green microfinance

349r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

models. Thus, the study is exploratory and built around a research question,not a hypothesis test. In one sense, there is a succinct answer to the researchquestion: How much do microfinance institutions (those in BWTP specifically)incorporate environmental language into their lending documents? The answerwas ‘about 10 per cent’. One in ten MFIs we analyzed included environmentalprotection language in their lending criteria. This result is consistent withthe trend in our pilot study, and has external validity in that many MFIpractitioners interviewed thought such constraints would be rare. Interestingly,the four Asian MFIs with environmental conditions in their lending documents(Table 2) vary greatly in location and size. This finding indicates that noeasy demographic indicators unify the subset of ‘green’ firms. Thus, it is ourhope that follow-on studies will provide an opportunity to determine if thesedifferences are meaningful. Furthermore, we believe that the principal short-coming of our study was scale, and we continue to work to build a larger data-base of lending criteria documents to facilitate research to better understandmicrofinance as a whole.

Because there were so few MFIs involved in green microfinance, or so fewthat could be characterized as ‘sustaining’ or ‘restoring’ using our typology,we spent some time analyzing barriers and potential reasons for resistanceto such practices. Accordingly, we discuss various barriers that may preventmicrofinance institutions and even microenterprises from participating inenvironmentally focused projects. These barriers stem from both internalcultural issues and external constraints related to how the industry is structuredand funded.

Table 5: Select characteristics of MFIs with environmental protection language in their lending

criteria

MFI Country Portfolio

value

Environmental protection language

Grameen Bank

(Grameen

Foundation, 2008)

Bangladesh US$405.58

million

(2004)

‘y social and physical infrastructure projects – housing,

sanitation, drinking water, education, family

planning, etc’.

Kabalikat Para sa

Maunlad na

Buhay, Inc.

Philippines US$4.1

million

(2004)

‘y facilitating transformation through health,

social, political, environmental, and spiritual

interventions y’

Sarhad Rural

Support Program

Pakistan Rs 36.43

million

(2003)

‘y infrastructure development, natural resource

management, enterprise promotion, and social

development y’

VisionFund

Cambodia Limited

Cambodia US$1.22

million

(2004)

‘y communities benefit from clean water, agricultural

training to secure food production, primary

education, health care and vocational skills training’.

Source: www.bwtp.org/about-us.html, 9 April 2009.

Archer and Jones-Christensen

350 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Internal resistance to promoting environmentally sustainable practicescan stem from the fact that many MFIs are already managing too muchinformation. Increasingly, donors, regulators and rating agencies requiremyriad forms and questionnaires and MFIs can be notoriously understaffedfor the tasks (Paudyal, 2007; Coloma and Harris, 2009). Performing andrecording environmental audits or creating and disseminating environmentalpolicies can become discretionary add-ons that get neglected or neverdiscussed. In addition, MFIs and their employees may not be aware of thetechnologies, options, need for, or interest in the environmental topic inrelation to microenterprises. Clearly, resistance internal to the organizationstems from individual barriers to change in the form of resistance to changingroutines, lack of knowledge or interest in the subject matter, time constraintsthat limit individual ability to add more work or training, and constraints onthe management of attention – employees are typically overworked individualslaboring in difficult working conditions.

Resistance can also come from structural issues, such as the fact that theemphasis on the MFI achieving financial sustainability (that is, being able tofund all new loans from the interest on existing loans, rather than having toseek new funds from donors or investors) can stifle innovation andexperimentation. Regulators, rating agencies and institutional investors tendto reward standardization and consolidation rather than experimentation. Inparticular, many MFIs can be reluctant to finance assets, particularly assetsnot directly related to income generation (Hall, 2007). Some MFIs have onlyone credit product and little experience in developing new projects. Althoughthere are some notable exceptions, many do not face the kind of competitionthat forces innovation or specialization into new markets. When MFIs arehighly donor-driven, then the resistance to change can stem from the fact thatdonors may not want to fund an environmental focus. Many donors andinstitutional funders remain unaware of the environmental impacts ofmicroenterprises, either individually or in aggregate. Lastly, recent contro-versies in the field may cause organizations to focus on survival rather thanenvironmental concerns.

Many barriers to promoting environmentally sustainable practices inmicroenterprise stem from a lack of information rather than outrightresistance. For example, practitioners in the green microfinance field lamentthe lack of case studies that can be used as sources of information on thetopic and best practices in implementation (Hall, 2007). Work on the creationof guidance documents and case examples that can be motivating andaspirational is required to address this problem (see the work of green-microfinance.org for progress on this front). Occasionally, barriers relate to alack of access to relationships rather than lack of information. For example,some MFIs do not have access to distributors for alternative technologies, or

Entrepreneurial value creation through green microfinance

351r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

no relationship exists between the two types of organization (Greenmicrofinance.org, 2011).

Conclusion

We have identified that there are some microfinanced projects thatdemonstrate positive environmental impact, some that are neutral, and othersthat are environmentally deleterious. Further, we offer an organizing typologyto help researchers and practitioners frame and categorize the environmentallyoriented behaviors of organizations. The categorical titles of preserving,evolving, sustaining and restoring can be extended to help analyze otherorganizations besides MFIs and the microbusinesses they fund. Thus, weconsider the typology as one of the major contributions of this article. We alsoidentified several ethically based reasons for incorporating a concern for thenatural environment into microfinance, three of which relate to humanrelationships and one of which relates strictly to the environment. We suggestthat one practical manifestation of this concern would be the inclusionof environmental protection language in microfinance lending criteriastandards, and therefore in lending documents. However, the results of ourbinomial descriptive content analysis suggest that only 10 per cent of MFIsincorporate environmental protection language into their loans. Therefore, ouranalysis uncovers a potential disconnect between the mission of most MFIlenders and the tactical implementation of their microfinance programs. Thissuggests that instead of being helped by microfinance, poor people, women,children and the planet may be at risk of being further harmed. Revealing thiscontradiction is another contribution of this study, as it illuminates animportant potential shortcoming as well as an important launching point forinnovation.

This study was exploratory in nature and was based on a small (thoughstatistically adequate) data set. Going forward, we hope to generate a largerdata set to enable exploration of various follow-on research questions, and weencourage others to join us in exploring how informal microentrepreneursgenerate economic and environmental value in the course of operatingbusinesses.

Acknowledgements

The authors would like to thank Gordon Rands, the editors and anonymousreviewers for helpful comments on earlier versions of this article.

Archer and Jones-Christensen

352 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

About the Authors

Geoffrey R. Archer is an Associate Professor with the Faculty of Managementand Director of the Eric C. Douglass Centre for Entrepreneurial Studies atRoyal Roads University in Victoria, British Columbia, Canada. Archer holds aMaster’s degree in Environmental Management from Duke University, anMBA from Cornell’s Johnson Graduate School of Management and a PhD inBusiness Administration from the Darden Graduate School of Business at theUniversity of Virginia. His research interests include microfinance, micro-franchising, bricolage, effectuation, the scholarship of teaching and learning,and the interaction between entrepreneurship and sustainability.

Lisa Jones-Christensen is Assistant Professor of Strategy and Entrepreneurshipat the Kenan Flagler Business School, University of North Carolina at ChapelHill. She is a faculty advisor to UNC Kenan-Flagler’s Center for SustainableEnterprise, overseeing its work on sustainable innovation and entrepreneurshipin developing countries. Her research interests include entrepreneurship,innovation, change management, metrics and leadership. Her sub-specialtiesfocus on microenterprise development including innovations in microfinance,micro-insurance and microfranchising. She looks at individual and group-level commitment to change in order to better understand how to fosterpositive social and environmental outcomes. Christensen received her PhD inorganizational behavior from UNC Kenan-Flagler.

Note

1 The focus of this investigation is specifically on environmental impacts of microfinance, and we

purposefully limit ourselves to defining and discussing this subset of impacts. Certainly,

microfinance has been linked with many positive social impacts (empowerment, food security,

consumption smoothing, improved health and education for clients and children) as well as many

negative social impacts (violence against women, general over-indebtedness and related suicides,

particularly in India). We mention these here to encourage further investigation, but they are

outside the scope of this article.

References

Acs, Z.J. and Dana, L.P. (2001) Contrasting two models of wealth distribution. Small Business

Economics 16: 63–74.

Asian Development Bank. (1999) Finance for the poor: Microfinance development strategy,

http://www.adb.org/documents/policies/microfinance/default.asp, accessed 22 April 2011.

Baxter, W. (1995) People or Penguins. In: C. Pierce and D. VanDeVeer (eds.) People, Penguins and

Plastic Trees. Belmont, CA: Wadsworth.

Entrepreneurial value creation through green microfinance

353r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Boiling Point. (2005) Scaling up and commercialization of household energy initiatives. 50, http://

www.practicalaction.org/docs/energy/boilingpoint50.pdf, accessed 17 April 2011.

Brook, P. and Smith, W. (2001) Improving access to infrastructure services by the poor:

Institutional and policy responses, http://web.mit.edu/urbanupgrading/waterandsanitation/

resources/pdf-files/Brook-ImprovingAccess.pdf, accessed 19 April 2011.

BYU Broadcasting. (2005) Microcredit and the future of poverty. (DVD), http://www.pbs.org/

kbyu/smallfortunes/TV program originally aired 17 October.

Callaghan, I. (2007) Microfinance – On the road to capital markets. Journal of Applied Corporate

Finance 19(1) : 115–125.

Chan, S.W. (2005) An exploratory study of using micro-credit to encourage the setting up of small

businesses in the rural sector of Malaysia. Asian Business and Management 4: 455–479.

Clancy, J., Oparaocha, S. and Roehr, U. (2004) Gender equity and renewable energies: Thematic

background. Paper presented at ‘Renewables’, Internationale Konferenz fur Erneuerbare

Engergien; 1–4 June, Bonn, Germany, http://doc.utwente.nl/59053/.

Cohen, B. and Winn, M.I. (2007) Market imperfections, opportunity and sustainable entrepreneur-

ship. Journal of Business Venturing 22(1): 29–49.

Coloma, J. and Harris, E. (2009) From construction workers to architects: Developing scientific

research capacity in low-income countries. PLoS Biol 7(7): 1–4, Also, http://www.plosbiology

.org/article/info:doi/10.1371/journal.pbio.1000156.

Dean, T.J. and McMullen, J.S. (2007) Toward a theory of sustainable entrepreneurship: Reducing

environmental degradation through entrepreneurial action. Journal of Business Venturing

22(1): 50–76.

Dunford, C. (2000) The holy grail of microfinance: ‘Helping the poor’ and ‘sustainable?’ Small

Enterprise Development 11(1): 40–44.

Engardio, P. (2007) Beyond the green corporation. Business Week 29 January: 50.

Envestmicrofinance.org. (2011) A microfinance cooperative linking socially conscious lenders

with microfinance entrepreneurs in the developing world, http://www.envestmicrofinance.org,

accessed 7 May 2011.

Fisher, M. (2006) Income is development: Kickstart’s pumps help Kenyan farmers transition to a

cash economy. Innovations 1(1): 9–30.

FIS Microcredito Social Investment Fund. (2006) Solar FIS Project Prospectus. Santiago del

Estero, Argentina: El Ceibal Asociacion Civil.

Freeman, R.E., Pierce, J. and Dodd, R.H. (2000) Environmentalism and the New Logic of Business.

New York: Oxford University Press.

Fthenakis, V. (2000) End-of-life management and recycling of PV modules. Energy Policy

28: 1051–1058.

Gallo, P. and Jones-Christensen, L. (2011) Firm size does matter: An empirical investigation

of organizational size and ownership on sustainability-related behaviors. Business and

Society, http://bas.sagepub.com/content/early/2011/03/17/0007650311398784.full.pdf/, accessed

17 March 2011.

Grameen Foundation. (2008) Who we are, http://www.grameenfoundation.org/who_we_are/,

accessed 31 December 2008.

Grameen Foundation. (2009) Our heritage, http://www.grameenfoundation.org/what_we_do/

technology_programs/village_phone/heritage/, accessed 9 April 2009.

Grameen Technology Center. (2008) Grameen Technology Center employee statements at BYU’s

2008 Economic Self-reliance conference on 7 November 2008.

Greenmicrofinance.org. (2004) Guiding principles for microenterprise and the environment. Paper

presented at Microenterprise and the Environment Conference; 30 July, Valley Forge, PA, USA.

Greenmicrofinance.org. (2011) Green microfinance center, http://www.greenmicrofinance.org/,

accessed 19 April 2011.

Archer and Jones-Christensen

354 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Hall, J. (2007) Microenterprise, microfinance and the environment, http://www.greenmicrofinance

.org/component/option,com_docman/Itemid,36/dir,ASC/gid,166/limit,5/limitstart,0/order,name/

task,cat_view/, accessed 31 December 2008.

Hardin, G. (1968) The tragedy of the commons. Science 162(3859): 1243–1248.

Hawken, P., Lovins, A. and Lovins, H. (1999) Natural Capitalism. New York: Hachette.

Ho Lem, C. and Samson, R. (2003) The Mayon turbo stove: Fueling the fight against poverty.

REAP-Canada Newsletter 1(Winter): 6–8.

Holvoet, N. (2004) Impact of microfinance programs on children’s education: Do the gender of the

borrower and the delivery model matter? Journal of Microfinance 6(2): 27–49.

Huitt, W. (2004) Maslow’s hierarchy of needs. Educational Psychology Interactive, http://

chiron.valdosta.edu/whuitt/col/regsys/maslow.html, accessed 1 April 2009.

ILO. (1999) ILO Reports Significant Job Growth in Commerce Worldwide during 1990s, http://

www.ilo.org/global/about-the-ilo/press-and-media-centre/press-releases/WCMS_007954/lang–en/

index.htm/, accessed 10 June 2009.

Japanese Institute for Irrigation and Drainage (JIID). (2001) Smallholder irrigation market initiative,

http://siteresources.worldbank.org/INTARD/841438-1111130534002/20434294/marketintiative

.pdf, accessed 19 April 2011.

Karnani, A. (2010) Failure of the libertarian approach to reducing poverty. Asian Business and

Management 9(1): 5–21.

Kelman, S. (1995) Cost-benefit analysis: An ethical critique. In: C. Pierce and D. VanDeVeer (eds.)

People, Penguins and Plastic Trees. Belmont, CA: Wadsworth.

Knapp, K. and Jester, T. (2001) Empirical investigation of the energy payback time for

photovoltaic modules. Solar Energy 71(3): 165–172.

Lal, A. and Israel, E. (2006) An overview of microfinance and the environmental sustainability of

smallholder agriculture. International Journal of Agricultural Resources, Governance and Ecology

4(5): 356–376.

Littlefield, E., Morduch, J. and Hashemi, S. (2003) Is microfinance an effective strategy to reach the

millennium development goals? Focus Note of the Institute for Financial Management and Research,

http://www.microfinancegateway.org/gm/document-1.26.6136/IS%20MICROFINANCE%

20AN%20EFFECTIVE%20STRATEGY.pdf/, accessed 19 April 2011.

Maslow, A.H. (1943) A theory of human motivation. Psychological Review 50(4): 370–396.

McDonough, W. and Braungart, M. (2003) Cradle to Cradle: Remaking the Way We Make Things.

New York: North Point.

Microcreditsummit. (2011) Record 128 million of world’s poorest received a micro-loan in 2009,

http://www.microcreditsummit.org/news/record_128_million_of_worlds_poorest_received_a_

micro-loan_in_2009/, accessed 19 April 2011.

Montiel, I. (2008) Corporate social responsibility and corporate sustainability: Separate pasts,

common futures. Organization & Environment 21(3): 245–269.

Morduch, J. (1999) The microfinance promise. The Journal of Economic Literature 37(4):

1569–1614.

Nattrass, B. and Nattrass, M.A. (2002) Dancing with the TIGER: Learning Sustainability Step by

Natural Step. Gabriola Island: New Society.

Neuendorf, K.A. (2002) The Content Analysis Guidebook. Thousand Oaks, CA: Sage.

Panjwani, A. and Cecelski, E. (2003) Major Activities and Actors in Energy, Poverty and Gender.

Washington DC: World Bank.

Paudyal, D.P. (2007) An overview of rural development in Asia. Asia-Pacific Journal of Rural

Development 37(1): 1–16.

Poyo, J., Parker, J. and Golden-Vasquez, A. (1996) Trends in Microenterprise Development in

Latin America and the Caribbean. Report prepared for Microenterprise Unit, Inter-American

Development Bank. Bethesda, MD: Development Alternatives Incorporated.

Entrepreneurial value creation through green microfinance

355r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Rolston III, H. (1988) Environmental Ethics: Duties to and Values in the Natural World.

Philadelphia, PA: Temple University Press.

Simon, D. and Sear, J. (2005) Indigenous microcredit and enterprise establishment: A Sri Lankan

case study. In: Executive Reference Book: The Sri Lankan Economy. Hyderabad: ICFAI.

Taborga, M. and Wenner, M. (1997) An evaluation of the Inter-American Development Bank loan

for micro and small enterprise development in Costa Rica. Microenterprise Unit, Sustainable

Development Department, Washington DC: Inter-American Development Bank.

Taylor, P. (1986) Respect for Nature: A Theory of Environmental Ethics. Princeton, NJ: Princeton

University Press.

Tictin, T., Nantel, P., Ramirez, F. and Johns, T. (2002) Effects of variation on harvest limits for

non-timber forest species in Mexico. Conservation Biology 16(3): 691–705.

Unitus. (2011) Microfinance Institutions, http://www.unitus.com/unitus-in-action/our-impact/

microfinance-institutions, accessed 22 April 2011.

Wenner, M. (2004) Microenterprise growth and environmental protection. Microenterprise

Development Review 4(2), 1, 5–7.

Wilson, M. and Green, J.M. (2000) The feasibility of introducing solar ovens to rural women

in Maphephethe. Journal of Family Ecology and Consumer Sciences 28: 54–61.

Werhane, P.H. (2002) Moral imagination and systems thinking. Journal of Business Ethics 38:

33–42.

Women’s World Banking. (2009) Mission and Vision, http://www.swwb.org/mission-vision,

accessed 1 March 2009.

World Bank. (2007) Microfinance in South Asia: Toward financial inclusion of the poor, http://

web.worldbank.org/WBSITE/EXTERNAL/COUNTRIES/SOUTHASIAEXT/0,,contentMDK:

21404284BpagePK:146736BpiPK:146830BtheSitePK:223547,00.html, accessed 22 April 2011.

Yunus, M. (2003) Banker to the Poor. New York: PublicAffairs.

Zucchetti, A. and Alegre, M. (1999) Microempresa y Ambiente. Paper presented at 2nd

Inter-American Forum on Microenterprise; 24–26 June, Buenos Aires, Argentina.

Archer and Jones-Christensen

356 r 2011 Macmillan Publishers Ltd. 1472-4782 Asian Business & Management Vol. 10, 3, 331–356

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.