Embed Size (px)

Citation preview

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 61

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

ABSTRACTThis paper aims to empirically examine the factors that affect the adoption of Internet banking in Tunisia. In order to explain the factors, this paper extends the “Technology Acceptance Model” by adding additional external factors such as security and privacy, self efficacy, social influence, and awareness of services and its benefits. The findings of the study suggests that the security and privacy, self efficacy, social influence, and awareness of services and its benefits have significant effects on the perceived usefulness (PU), perceived ease of use (PEOU) and attitude toward Internet banking acceptance. Age and education have also significant impact on the attitude towards the likelihood of adopting online banking. These findings may provide for banks useful guidelines for developing Internet banking services and for marketing Internet banking.

Expanding the Technology Acceptance Model to Examine

Internet Banking Adoption in Tunisia Country

Wadie Nasri, Higher Institute of Management of Gabes, University of Gabes, Gabes, Tunisia.

Charfeddine Lanouar, Quantitative Methods Department, Higher Institute of Management of Gabes, University of Gabes, Gabes, Tunisia

Anis Allagui, Université de Tunis El Manar, Ecole Nationale d’Ingénieurs de Tunis, Tunis, Tunisie

Keywords: External Factors, Internet banking, Perceived Usefulness (PU), Technology Acceptance Model, Tunisia

1. INTRODUCTION

The rapid growth of the Internet has radically changed the delivery channels used by the financial services industry. It has become the self-service delivery channel that allows banks to provide information and offer services to their customers with more convenience via the web services technology (Safeena, 2010).

Electronic service is becoming a viable option for interaction between financial service provid-ers and their customers (Rotchanakitumnuai & Speece, 2004). For banks Internet banking offers great opportunities for banks to increase their transactions, extend their customer bases, and to decrease their operational and opportunity costs (Ozdmir et al., 2007). From the consum-ers’ perspective Internet banking is extremely

DOI: 10.4018/ijide.2013100104

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

62 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

beneficial to customers because of the savings in costs, time and space it offers, its quick response to complaints, and its delivery of improved services, all of which benefits make for easier banking (Turban et al., 2000). The financial services offered by internet banking could include viewing all transactions and all accounts balances in real time, payment of bills, change of money in other currencies, transfers of money, stocks operations, purchase of all kind of insurances purchase of travel tickets and travel packages, etc.. (Gerrard & Cunningham, 2003; Polatoglu & Ekin, 2001).

Today, commercial banks in Tunisia are competing aggressively to introduce new types of technological products and services to improve their operations and to reduce costs. Credit cards, automatic teller machines (ATMs), telephone and Internet banking are among some of the technology innovations that have been offered by banks to overcome the drawbacks of changing market conditions.

Despite all their efforts these systems especially Internet banking remained largely unnoticed by the customers. Some banking institutions limit their Internet Banking services to an informational website. Others are using their web sites not only to provide the basic operations such as fund transfer or account details, but also to provide new services such as securities trading, bill payments, check book requests, credit card requests and investment advice. The number of Internet Banking users is still very weak in comparison with the others electronic banking services and they are not frequently used by Tunisian consumers (Wadie, 2011; Wadie & Lanouar, 2012). Therefore, customer perception has become very essential to become successful in providing Internet banking service.

According to the statistics for the month of December 2011 on the Internet in Tunisia (Tunisia Internet Agency), the number of users is 4,200,000 versus 3,500,000 users in 2009, the number of email accounts 737,275 and the number of websites 12,454. This issue is an important opportunity for the banking indus-try to formulate their marketing strategies to

promote new forms of Internet banking services in the future. By understanding the factors influencing intentions to use Internet banking, Tunisian banks can develop strategies for Inter-net banking implementation in ways that will improve the performance their. Knowledge of these factors, how they can be measured, and how they relate to each other, is crucial in the development, implementation, and manage-ment of successful systems (Gallion, 2000).

Individual acceptance and usage of new technologies has been studied extensively over the past two decades, especially the Technol-ogy Acceptance Model (TAM), by proposed by Davis, et al. (1989). This model now provides a stable and secure way for predicting user ac-ceptance of a wide range of new technologies (Arteaga & Duarte, 2010). Since TAM has been used in many studies to predict and understand user perceptions of system use and the prob-ability of adopting an Internet system (Gefen et al., 2003; Hsu et al., 2006; Wu & Chen, 2005), they are the most appropriate tools for under-standing Internet banking adoption.

TAM has been criticized for not providing detailed understanding of usage behavior or acceptance technology (Taylor & Todd, 1995). Gefen and Keil (1998) noted, without a better understanding of the antecedents of the origi-nal TAM variables (perceived usefulness and perceived ease of use), managers are unable to know which levers to pull in order to affect these beliefs and, through them, greater technology acceptance. The information systems literature contains many examples of studies employing extended and modified versions of TAM to ex-amine technology adoption in various contexts: organizational support (Igbaria et al., 1997), computer self-efficacy (Venkatesh & Davis, 1996), social influence processes (Venkatesh & Davis, 2000), trust, social personality, perceived enjoyment (Gefen et al., 2003; Pavlou, 2003; Wu & Chen, 2005; Lingyun & Dong, 2008), and culture (Straub, 1994).

This study proposes to integrate four fac-tors to the TAM in order to provide a more comprehensive model of Internet banking adop-tion: Security and privacy, self efficacy, social

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 63

norm and awareness. Security and privacy are one of the most challenging problems faced by customers who wish to trade in the e-commerce world. Indeed, in Aladwani’s (2001) study of online banking, potential customers ranked Internet security and customers’ privacy as the most important future challenges that banks are facing. Self-efficacy defined as the judg-ment of one’s ability to use Internet banking plays a critical role in understanding individual response to information technology (Agarwal et al., 2000; Chau, 2001; Hong et al., 2001). Social influence is related to intention because people often act based on their perception of what others think they should do. It has been found to be more important prior to, or in the early stages of innovation implementation when users have limited direct experience from which to develop attitudes (Hartwick & Barki 1994; Taylor & Todd 1995a). According to Rogers and Shoemaker 1971; Sathye, 1999), consumers go through “a process of knowledge, persuasion, decision and confirmation” before they are ready to adopt a product or service. The adop-tion or rejection of an innovation begins when “the consumer becomes aware of the product” (Sathye, 1999; Rogers & Shoemaker, 1971).

The primary objective of this research is to extend the Technology Acceptance Model in the context of Internet banking in Tunisia country by adding additional external variables: secu-rity and privacy, self efficacy, social influence, and awareness of services and its benefits. The purposes of this study are as follows.

1. To identify factors those determine custom-ers’ behavioral intention to use Internet banking.

2. To clarify which factors are more influential in affecting the intention to use Internet banking.

3. To evaluate whether the extension of Technology Acceptance Model provide a solid theoretical basis for explaining the adoption of Internet banking.

An important goal of this research is to develop a model that can provide useful

information to Internet banking practitioners. By explaining users’ intentions from a user’s perspective, the findings of this research can not only help Internet banking authorities to develop a more users of Internet banking system, but can also provide insight into the best strategies to promote new Internet bank-ing services to potential users. This research is divided into six sections. The first and the second sections contain the introduction and the literature review on theories that can be used to explain acceptance of Internet banking. The Third section details the methodology and research design. The fourth section presents the data analysis and hypotheses testing results. The fifth section discusses our research find-ings. The sixth section provides theoretical and managerial implications and finally, the seventh section concludes with this paper’s limitations, and further research

2. THEORETICAL BACKGROUND

2.1. TAM and Related Theories

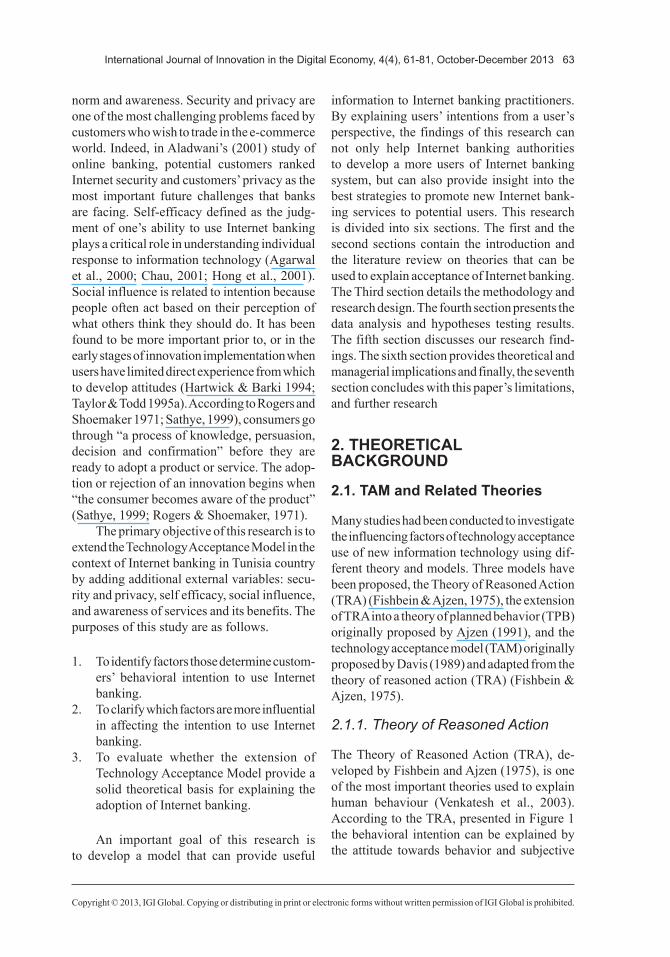

Many studies had been conducted to investigate the influencing factors of technology acceptance use of new information technology using dif-ferent theory and models. Three models have been proposed, the Theory of Reasoned Action (TRA) (Fishbein & Ajzen, 1975), the extension of TRA into a theory of planned behavior (TPB) originally proposed by Ajzen (1991), and the technology acceptance model (TAM) originally proposed by Davis (1989) and adapted from the theory of reasoned action (TRA) (Fishbein & Ajzen, 1975).

2.1.1. Theory of Reasoned Action

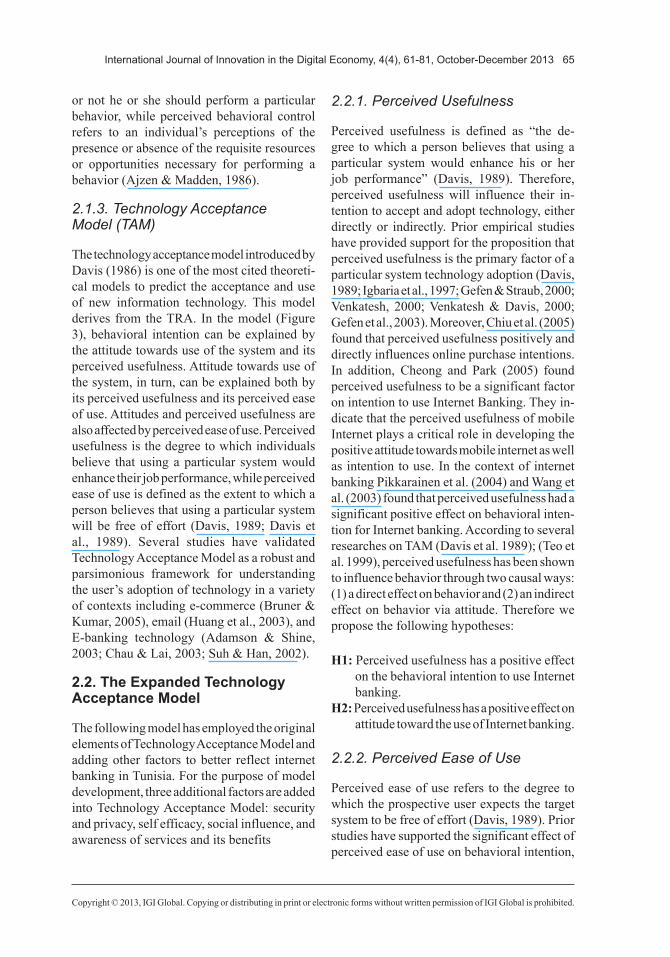

The Theory of Reasoned Action (TRA), de-veloped by Fishbein and Ajzen (1975), is one of the most important theories used to explain human behaviour (Venkatesh et al., 2003). According to the TRA, presented in Figure 1 the behavioral intention can be explained by the attitude towards behavior and subjective

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

64 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

norm. Attitude refers to an individual’s positive or negative belief about performing a specific behavior (Fishbein & Ajzen, 1975). Subjective norms refer to an individual’s perceptions of other people’s opinions on whether or not he or she should perform a particular behavior, while perceived behavioral control refers to an individual’s perceptions of the presence or absence of the requisite resources or opportuni-ties necessary for performing a behavior (Ajzen & Madden, 1986).

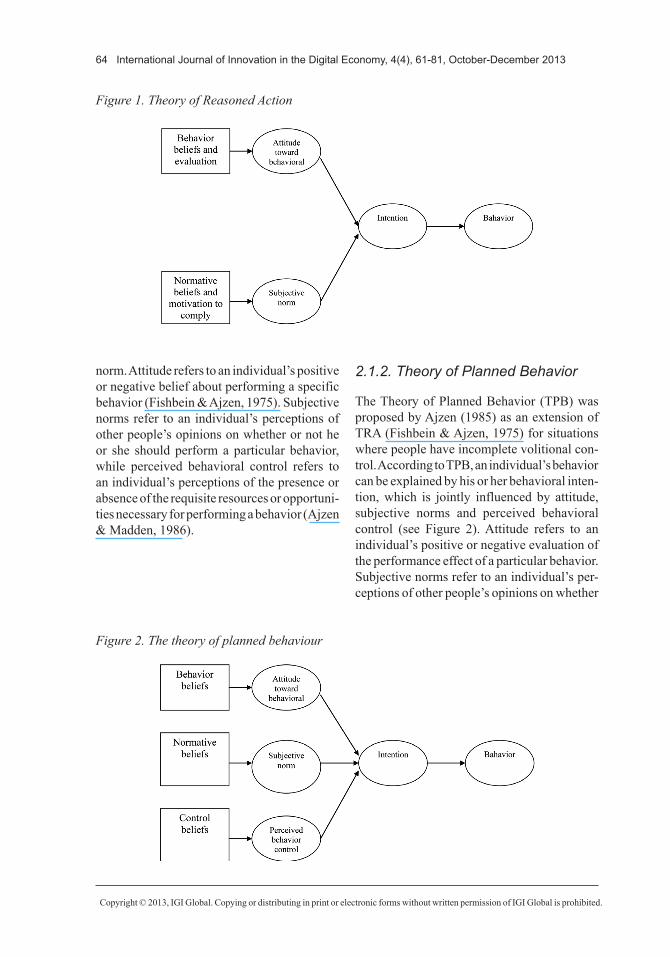

2.1.2. Theory of Planned Behavior

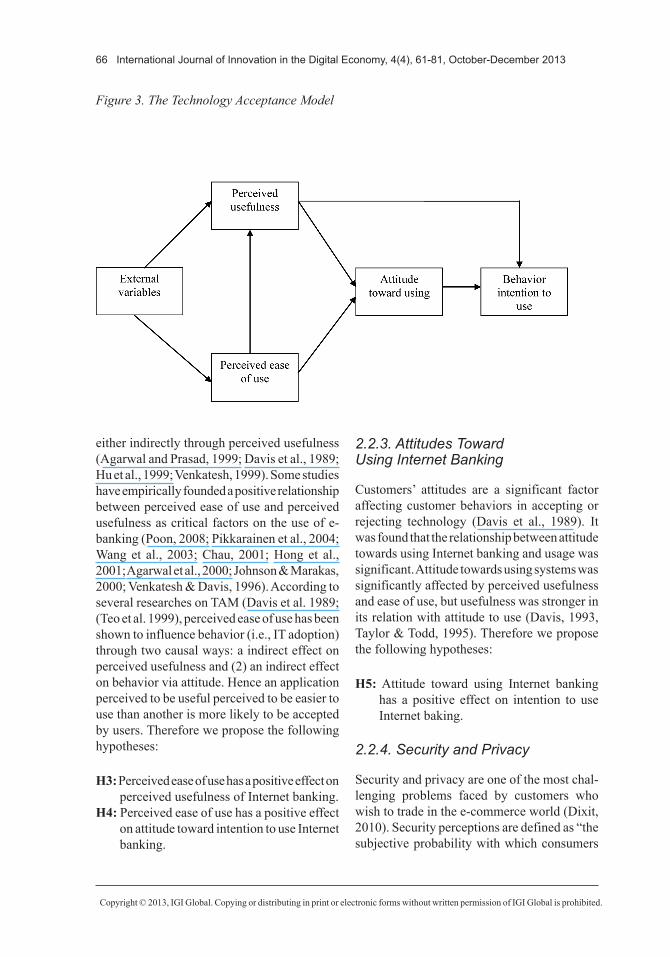

The Theory of Planned Behavior (TPB) was proposed by Ajzen (1985) as an extension of TRA (Fishbein & Ajzen, 1975) for situations where people have incomplete volitional con-trol. According to TPB, an individual’s behavior can be explained by his or her behavioral inten-tion, which is jointly influenced by attitude, subjective norms and perceived behavioral control (see Figure 2). Attitude refers to an individual’s positive or negative evaluation of the performance effect of a particular behavior. Subjective norms refer to an individual’s per-ceptions of other people’s opinions on whether

Figure 1. Theory of Reasoned Action

Figure 2. The theory of planned behaviour

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 65

or not he or she should perform a particular behavior, while perceived behavioral control refers to an individual’s perceptions of the presence or absence of the requisite resources or opportunities necessary for performing a behavior (Ajzen & Madden, 1986).

2.1.3. Technology Acceptance Model (TAM)

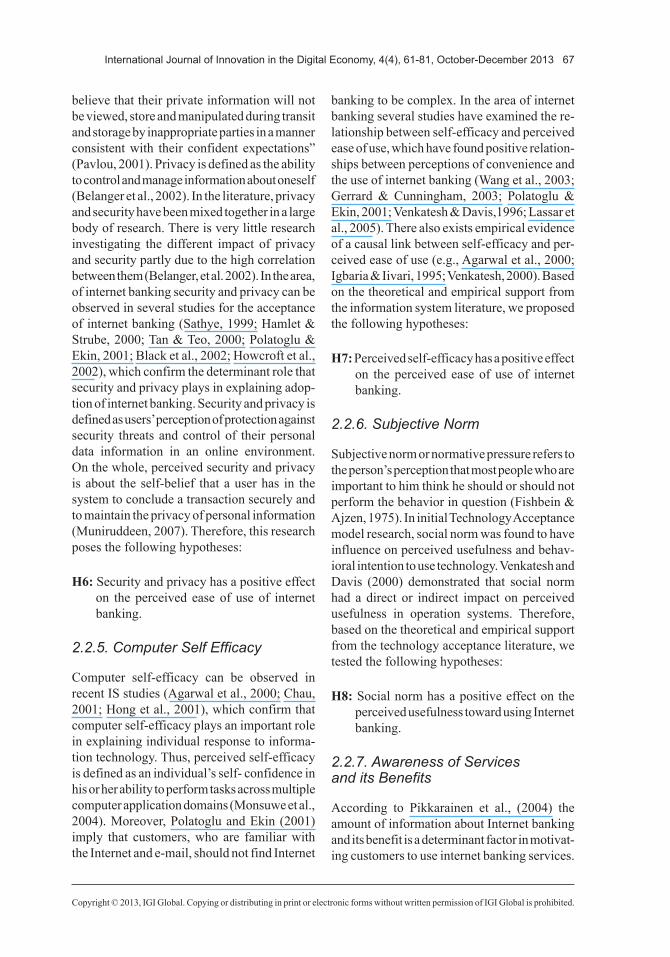

The technology acceptance model introduced by Davis (1986) is one of the most cited theoreti-cal models to predict the acceptance and use of new information technology. This model derives from the TRA. In the model (Figure 3), behavioral intention can be explained by the attitude towards use of the system and its perceived usefulness. Attitude towards use of the system, in turn, can be explained both by its perceived usefulness and its perceived ease of use. Attitudes and perceived usefulness are also affected by perceived ease of use. Perceived usefulness is the degree to which individuals believe that using a particular system would enhance their job performance, while perceived ease of use is defined as the extent to which a person believes that using a particular system will be free of effort (Davis, 1989; Davis et al., 1989). Several studies have validated Technology Acceptance Model as a robust and parsimonious framework for understanding the user’s adoption of technology in a variety of contexts including e-commerce (Bruner & Kumar, 2005), email (Huang et al., 2003), and E-banking technology (Adamson & Shine, 2003; Chau & Lai, 2003; Suh & Han, 2002).

2.2. The Expanded Technology Acceptance Model

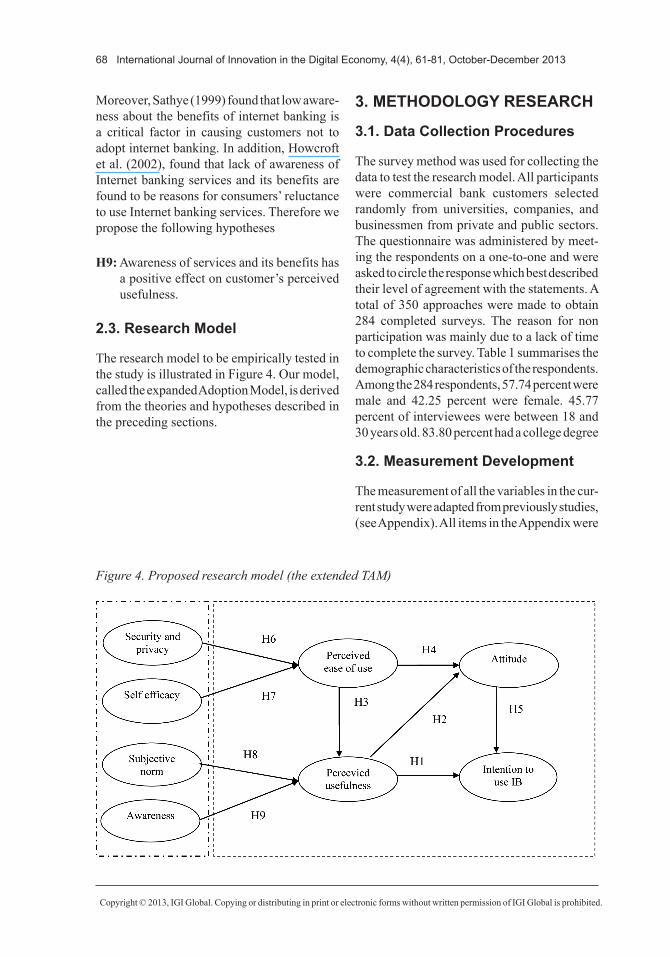

The following model has employed the original elements of Technology Acceptance Model and adding other factors to better reflect internet banking in Tunisia. For the purpose of model development, three additional factors are added into Technology Acceptance Model: security and privacy, self efficacy, social influence, and awareness of services and its benefits

2.2.1. Perceived Usefulness

Perceived usefulness is defined as “the de-gree to which a person believes that using a particular system would enhance his or her job performance” (Davis, 1989). Therefore, perceived usefulness will influence their in-tention to accept and adopt technology, either directly or indirectly. Prior empirical studies have provided support for the proposition that perceived usefulness is the primary factor of a particular system technology adoption (Davis, 1989; Igbaria et al., 1997; Gefen & Straub, 2000; Venkatesh, 2000; Venkatesh & Davis, 2000; Gefen et al., 2003). Moreover, Chiu et al. (2005) found that perceived usefulness positively and directly influences online purchase intentions. In addition, Cheong and Park (2005) found perceived usefulness to be a significant factor on intention to use Internet Banking. They in-dicate that the perceived usefulness of mobile Internet plays a critical role in developing the positive attitude towards mobile internet as well as intention to use. In the context of internet banking Pikkarainen et al. (2004) and Wang et al. (2003) found that perceived usefulness had a significant positive effect on behavioral inten-tion for Internet banking. According to several researches on TAM (Davis et al. 1989); (Teo et al. 1999), perceived usefulness has been shown to influence behavior through two causal ways: (1) a direct effect on behavior and (2) an indirect effect on behavior via attitude. Therefore we propose the following hypotheses:

H1: Perceived usefulness has a positive effect on the behavioral intention to use Internet banking.

H2: Perceived usefulness has a positive effect on attitude toward the use of Internet banking.

2.2.2. Perceived Ease of Use

Perceived ease of use refers to the degree to which the prospective user expects the target system to be free of effort (Davis, 1989). Prior studies have supported the significant effect of perceived ease of use on behavioral intention,

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

66 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

either indirectly through perceived usefulness (Agarwal and Prasad, 1999; Davis et al., 1989; Hu et al., 1999; Venkatesh, 1999). Some studies have empirically founded a positive relationship between perceived ease of use and perceived usefulness as critical factors on the use of e-banking (Poon, 2008; Pikkarainen et al., 2004; Wang et al., 2003; Chau, 2001; Hong et al., 2001; Agarwal et al., 2000; Johnson & Marakas, 2000; Venkatesh & Davis, 1996). According to several researches on TAM (Davis et al. 1989; (Teo et al. 1999), perceived ease of use has been shown to influence behavior (i.e., IT adoption) through two causal ways: a indirect effect on perceived usefulness and (2) an indirect effect on behavior via attitude. Hence an application perceived to be useful perceived to be easier to use than another is more likely to be accepted by users. Therefore we propose the following hypotheses:

H3: Perceived ease of use has a positive effect on perceived usefulness of Internet banking.

H4: Perceived ease of use has a positive effect on attitude toward intention to use Internet banking.

2.2.3. Attitudes Toward Using Internet Banking

Customers’ attitudes are a significant factor affecting customer behaviors in accepting or rejecting technology (Davis et al., 1989). It was found that the relationship between attitude towards using Internet banking and usage was significant. Attitude towards using systems was significantly affected by perceived usefulness and ease of use, but usefulness was stronger in its relation with attitude to use (Davis, 1993, Taylor & Todd, 1995). Therefore we propose the following hypotheses:

H5: Attitude toward using Internet banking has a positive effect on intention to use Internet baking.

2.2.4. Security and Privacy

Security and privacy are one of the most chal-lenging problems faced by customers who wish to trade in the e-commerce world (Dixit, 2010). Security perceptions are defined as “the subjective probability with which consumers

Figure 3. The Technology Acceptance Model

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 67

believe that their private information will not be viewed, store and manipulated during transit and storage by inappropriate parties in a manner consistent with their confident expectations” (Pavlou, 2001). Privacy is defined as the ability to control and manage information about oneself (Belanger et al., 2002). In the literature, privacy and security have been mixed together in a large body of research. There is very little research investigating the different impact of privacy and security partly due to the high correlation between them (Belanger, et al. 2002). In the area, of internet banking security and privacy can be observed in several studies for the acceptance of internet banking (Sathye, 1999; Hamlet & Strube, 2000; Tan & Teo, 2000; Polatoglu & Ekin, 2001; Black et al., 2002; Howcroft et al., 2002), which confirm the determinant role that security and privacy plays in explaining adop-tion of internet banking. Security and privacy is defined as users’ perception of protection against security threats and control of their personal data information in an online environment. On the whole, perceived security and privacy is about the self-belief that a user has in the system to conclude a transaction securely and to maintain the privacy of personal information (Muniruddeen, 2007). Therefore, this research poses the following hypotheses:

H6: Security and privacy has a positive effect on the perceived ease of use of internet banking.

2.2.5. Computer Self Efficacy

Computer self-efficacy can be observed in recent IS studies (Agarwal et al., 2000; Chau, 2001; Hong et al., 2001), which confirm that computer self-efficacy plays an important role in explaining individual response to informa-tion technology. Thus, perceived self-efficacy is defined as an individual’s self- confidence in his or her ability to perform tasks across multiple computer application domains (Monsuwe et al., 2004). Moreover, Polatoglu and Ekin (2001) imply that customers, who are familiar with the Internet and e-mail, should not find Internet

banking to be complex. In the area of internet banking several studies have examined the re-lationship between self-efficacy and perceived ease of use, which have found positive relation-ships between perceptions of convenience and the use of internet banking (Wang et al., 2003; Gerrard & Cunningham, 2003; Polatoglu & Ekin, 2001; Venkatesh & Davis,1996; Lassar et al., 2005). There also exists empirical evidence of a causal link between self-efficacy and per-ceived ease of use (e.g., Agarwal et al., 2000; Igbaria & Iivari, 1995; Venkatesh, 2000). Based on the theoretical and empirical support from the information system literature, we proposed the following hypotheses:

H7: Perceived self-efficacy has a positive effect on the perceived ease of use of internet banking.

2.2.6. Subjective Norm

Subjective norm or normative pressure refers to the person’s perception that most people who are important to him think he should or should not perform the behavior in question (Fishbein & Ajzen, 1975). In initial Technology Acceptance model research, social norm was found to have influence on perceived usefulness and behav-ioral intention to use technology. Venkatesh and Davis (2000) demonstrated that social norm had a direct or indirect impact on perceived usefulness in operation systems. Therefore, based on the theoretical and empirical support from the technology acceptance literature, we tested the following hypotheses:

H8: Social norm has a positive effect on the perceived usefulness toward using Internet banking.

2.2.7. Awareness of Services and its Benefits

According to Pikkarainen et al., (2004) the amount of information about Internet banking and its benefit is a determinant factor in motivat-ing customers to use internet banking services.

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

68 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

Moreover, Sathye (1999) found that low aware-ness about the benefits of internet banking is a critical factor in causing customers not to adopt internet banking. In addition, Howcroft et al. (2002), found that lack of awareness of Internet banking services and its benefits are found to be reasons for consumers’ reluctance to use Internet banking services. Therefore we propose the following hypotheses

H9: Awareness of services and its benefits has a positive effect on customer’s perceived usefulness.

2.3. Research Model

The research model to be empirically tested in the study is illustrated in Figure 4. Our model, called the expanded Adoption Model, is derived from the theories and hypotheses described in the preceding sections.

3. METHODOLOGY RESEARCH

3.1. Data Collection Procedures

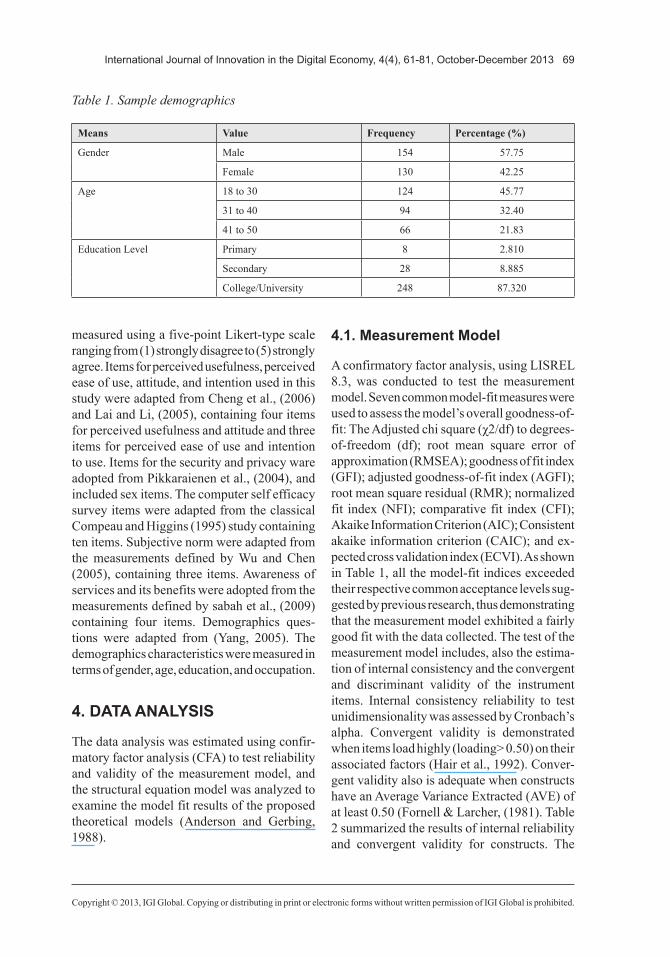

The survey method was used for collecting the data to test the research model. All participants were commercial bank customers selected randomly from universities, companies, and businessmen from private and public sectors. The questionnaire was administered by meet-ing the respondents on a one-to-one and were asked to circle the response which best described their level of agreement with the statements. A total of 350 approaches were made to obtain 284 completed surveys. The reason for non participation was mainly due to a lack of time to complete the survey. Table 1 summarises the demographic characteristics of the respondents. Among the 284 respondents, 57.74 percent were male and 42.25 percent were female. 45.77 percent of interviewees were between 18 and 30 years old. 83.80 percent had a college degree

3.2. Measurement Development

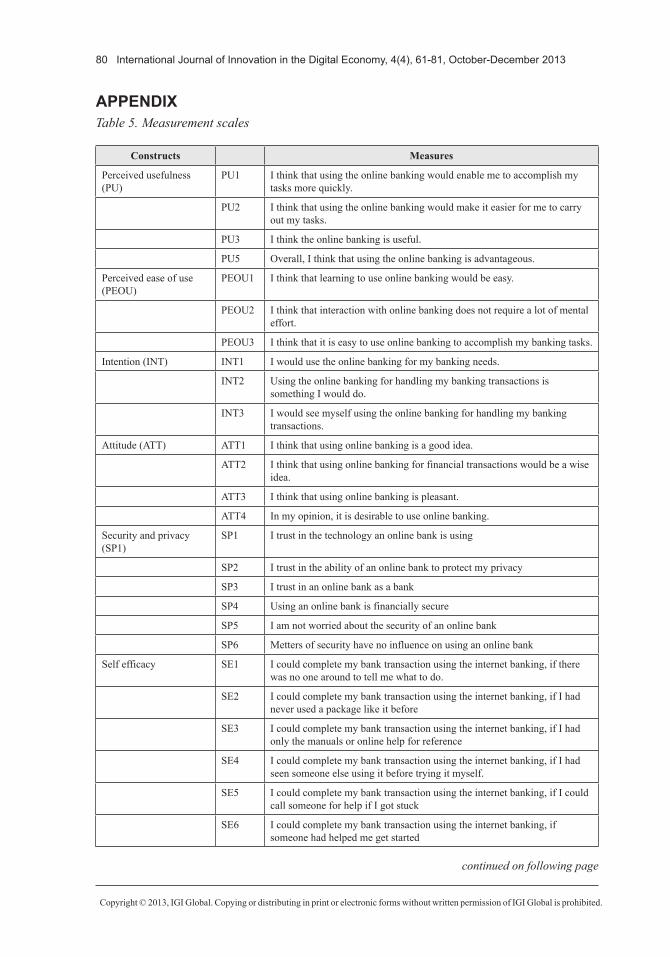

The measurement of all the variables in the cur-rent study were adapted from previously studies, (see Appendix). All items in the Appendix were

Figure 4. Proposed research model (the extended TAM)

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 69

measured using a five-point Likert-type scale ranging from (1) strongly disagree to (5) strongly agree. Items for perceived usefulness, perceived ease of use, attitude, and intention used in this study were adapted from Cheng et al., (2006) and Lai and Li, (2005), containing four items for perceived usefulness and attitude and three items for perceived ease of use and intention to use. Items for the security and privacy ware adopted from Pikkaraienen et al., (2004), and included sex items. The computer self efficacy survey items were adapted from the classical Compeau and Higgins (1995) study containing ten items. Subjective norm were adapted from the measurements defined by Wu and Chen (2005), containing three items. Awareness of services and its benefits were adopted from the measurements defined by sabah et al., (2009) containing four items. Demographics ques-tions were adapted from (Yang, 2005). The demographics characteristics were measured in terms of gender, age, education, and occupation.

4. DATA ANALYSIS

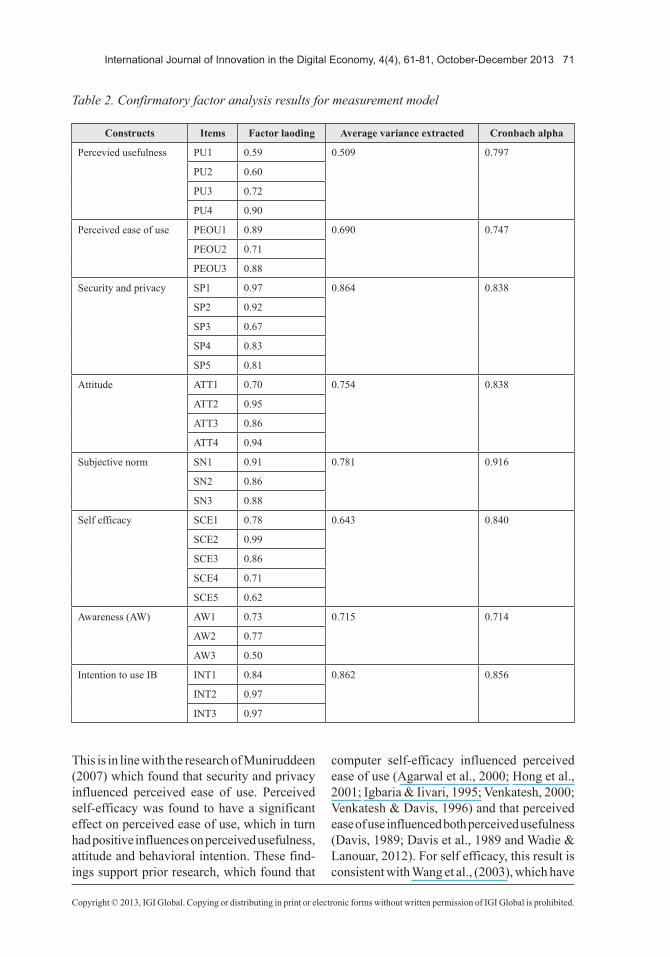

The data analysis was estimated using confir-matory factor analysis (CFA) to test reliability and validity of the measurement model, and the structural equation model was analyzed to examine the model fit results of the proposed theoretical models (Anderson and Gerbing, 1988).

4.1. Measurement Model

A confirmatory factor analysis, using LISREL 8.3, was conducted to test the measurement model. Seven common model-fit measures were used to assess the model’s overall goodness-of-fit: The Adjusted chi square (χ2/df) to degrees-of-freedom (df); root mean square error of approximation (RMSEA); goodness of fit index (GFI); adjusted goodness-of-fit index (AGFI); root mean square residual (RMR); normalized fit index (NFI); comparative fit index (CFI); Akaike Information Criterion (AIC); Consistent akaike information criterion (CAIC); and ex-pected cross validation index (ECVI). As shown in Table 1, all the model-fit indices exceeded their respective common acceptance levels sug-gested by previous research, thus demonstrating that the measurement model exhibited a fairly good fit with the data collected. The test of the measurement model includes, also the estima-tion of internal consistency and the convergent and discriminant validity of the instrument items. Internal consistency reliability to test unidimensionality was assessed by Cronbach’s alpha. Convergent validity is demonstrated when items load highly (loading> 0.50) on their associated factors (Hair et al., 1992). Conver-gent validity also is adequate when constructs have an Average Variance Extracted (AVE) of at least 0.50 (Fornell & Larcher, (1981). Table 2 summarized the results of internal reliability and convergent validity for constructs. The

Table 1. Sample demographics

Means Value Frequency Percentage (%)

Gender Male 154 57.75

Female 130 42.25

Age 18 to 30 124 45.77

31 to 40 94 32.40

41 to 50 66 21.83

Education Level Primary 8 2.810

Secondary 28 8.885

College/University 248 87.320

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

70 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

resulting alpha values ranged from 0.71 to 0.90, which were above the acceptable threshold 0.70 suggested by Hair et al., (1995) and Nunnally, (1978). Results show also that all of the measures have significant loadings that load much higher than suggested threshold. The factor loading for all items exceeds the recommended level of 0.5. All AVE were well above the recommended value level of 0.50.

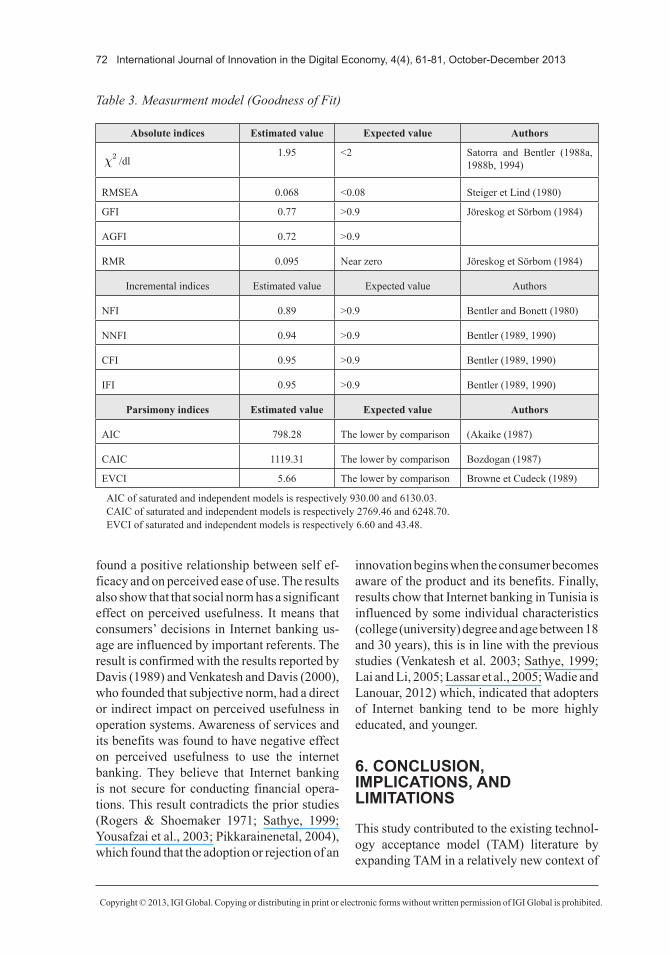

As shown in Table 3, all the model-fit indices (χ2/df = 1.95; RMSEA = 0.068; RMR = 0.095; NFI = 0.89; NNFI=0.95; CFI = 0.95; IFI=0.95; AIC = 798.28; CAIC = 6284.70; and ECVI = 5.66) exceeded their respective com-mon acceptance levels suggested by previous research, thus demonstrating that the measure-ment model exhibited a fairly good fit with the data collected.

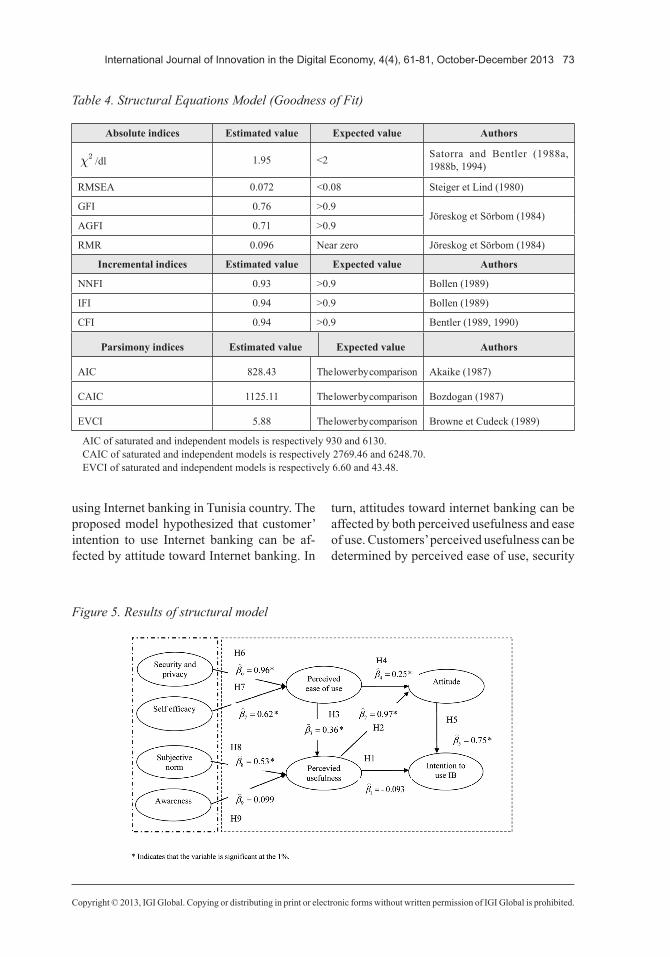

4.2. Structural Model

The results, as listed in Table 3, show that all eight fit indices for our testing model (χ2/df = 1.95; RMSEA = 0.072; RMR = 0.096; CN = 90.72; NNFI (Nonnormed Fit Index) = 0.93; CFI = 0.94; AIC = 828.43; CAIC = 1125.11; and ECVI = 5.88) have clearly exceeded the minimum recommended values suggested for a good model fit, implying the adequacy of our model for further statistical analysis, including its causal link evaluation (Table 4).

Considering the pattern of significance for the parameter estimates within the structural model (Figure 5), perceived usefulness was found to have a not significant influence on intention to use internet banking (

�β

1- 0.093= ,

p>0.05) thus, H1 was not supported. Perceived usefulness has a significant influence on attitude toward intention to use to use Internet banking (�β

2= 0.97 , p<0.01) thus, H2 was supported.

Perceived ease of use was found to have a significant influence on perceived usefulness on intention to use to use Internet banking (�β

30 36= . , p<0.01) thus, H3 was supported.

Perceived ease of use was found to have a significant influence on attitude toward inten-tion to use to use internet banking (

�β

40 25= . ,

p<0.01) thus, H4 was supported. Perceived usefulness appeared to be a stronger predictor of attitude than perceived ease of use. Attitude was found to have a significant influence on intention to use internet banking (

�β

50 75= . ,

p<0.01), thus, H5 is supported. Security and privacy (

�β

6= 0.96 , p<0.01) and self-efficacy

(�β

70 62= . , p<0.01) were found to have a

significant influence on perceived ease of use of Internet banking. Hypotheses H6, and H7 were also supported. Subjective norm was found to have a significant influence on perceived usefulness to use to use internet banking (�β

80 53= . , p<0.01), thus, H8 was supported.

Finally, Awareness was found to have a not significant influence on perceived usefulness on intention to use to use internet banking (�β

9= 0.099 , p>0.05) thus, H9 was not sup-

ported.

5. DISCUSSION OF FINDINGS

This study investigated factors influencing behavioural intention to use Internet banking in through the extended Technology Acceptance Model developed by Davis (1989). Our findings strongly support the appropriateness of using this extended TAM to understand the intentions of people towards the use of Internet banking services in Tunisia country. Significant effects influencing behavioural intention from per-ceived usefulness, perceived ease of use through attitude was observed. This is consistent with the original Technology Acceptance model and with others prior studies (Davis, 1989; Amin, 2007; Shih & Fang, 2004; Wadie & Lanouar, 2012). We also found perceived usefulness was found to have not a direct significant effect on intention to use the internet banking. This is not consistent with the original Technology Acceptance models and priors studies (Moon & Kim, 2001; Wadie & Lanouar, 2012). Per-ceived usefulness appeared to be a stronger predictor of attitude than perceived ease of use. Security and privacy was found to have a significant effect on perceived ease of use.

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 71

This is in line with the research of Muniruddeen (2007) which found that security and privacy influenced perceived ease of use. Perceived self-efficacy was found to have a significant effect on perceived ease of use, which in turn had positive influences on perceived usefulness, attitude and behavioral intention. These find-ings support prior research, which found that

computer self-efficacy influenced perceived ease of use (Agarwal et al., 2000; Hong et al., 2001; Igbaria & Iivari, 1995; Venkatesh, 2000; Venkatesh & Davis, 1996) and that perceived ease of use influenced both perceived usefulness (Davis, 1989; Davis et al., 1989 and Wadie & Lanouar, 2012). For self efficacy, this result is consistent with Wang et al., (2003), which have

Table 2. Confirmatory factor analysis results for measurement model

Constructs Items Factor laoding Average variance extracted Cronbach alpha

Percevied usefulness PU1 0.59 0.509 0.797

PU2 0.60

PU3 0.72

PU4 0.90

Perceived ease of use PEOU1 0.89 0.690 0.747

PEOU2 0.71

PEOU3 0.88

Security and privacy SP1 0.97 0.864 0.838

SP2 0.92

SP3 0.67

SP4 0.83

SP5 0.81

Attitude ATT1 0.70 0.754 0.838

ATT2 0.95

ATT3 0.86

ATT4 0.94

Subjective norm SN1 0.91 0.781 0.916

SN2 0.86

SN3 0.88

Self efficacy SCE1 0.78 0.643 0.840

SCE2 0.99

SCE3 0.86

SCE4 0.71

SCE5 0.62

Awareness (AW) AW1 0.73 0.715 0.714

AW2 0.77

AW3 0.50

Intention to use IB INT1 0.84 0.862 0.856

INT2 0.97

INT3 0.97

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

72 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

found a positive relationship between self ef-ficacy and on perceived ease of use. The results also show that that social norm has a significant effect on perceived usefulness. It means that consumers’ decisions in Internet banking us-age are influenced by important referents. The result is confirmed with the results reported by Davis (1989) and Venkatesh and Davis (2000), who founded that subjective norm, had a direct or indirect impact on perceived usefulness in operation systems. Awareness of services and its benefits was found to have negative effect on perceived usefulness to use the internet banking. They believe that Internet banking is not secure for conducting financial opera-tions. This result contradicts the prior studies (Rogers & Shoemaker 1971; Sathye, 1999; Yousafzai et al., 2003; Pikkarainenetal, 2004), which found that the adoption or rejection of an

innovation begins when the consumer becomes aware of the product and its benefits. Finally, results chow that Internet banking in Tunisia is influenced by some individual characteristics (college (university) degree and age between 18 and 30 years), this is in line with the previous studies (Venkatesh et al. 2003; Sathye, 1999; Lai and Li, 2005; Lassar et al., 2005; Wadie and Lanouar, 2012) which, indicated that adopters of Internet banking tend to be more highly educated, and younger.

6. CONCLUSION, IMPLICATIONS, AND LIMITATIONS

This study contributed to the existing technol-ogy acceptance model (TAM) literature by expanding TAM in a relatively new context of

Table 3. Measurment model (Goodness of Fit)

Absolute indices Estimated value Expected value Authors

χ2 /dl1.95 <2 Satorra and Bentler (1988a,

1988b, 1994)

RMSEA 0.068 <0.08 Steiger et Lind (1980)

GFI 0.77 >0.9 Jöreskog et Sörbom (1984)

AGFI 0.72 >0.9

RMR 0.095 Near zero Jöreskog et Sörbom (1984)

Incremental indices Estimated value Expected value Authors

NFI 0.89 >0.9 Bentler and Bonett (1980)

NNFI 0.94 >0.9 Bentler (1989, 1990)

CFI 0.95 >0.9 Bentler (1989, 1990)

IFI 0.95 >0.9 Bentler (1989, 1990)

Parsimony indices Estimated value Expected value Authors

AIC 798.28 The lower by comparison (Akaike (1987)

CAIC 1119.31 The lower by comparison Bozdogan (1987)

EVCI 5.66 The lower by comparison Browne et Cudeck (1989)

AIC of saturated and independent models is respectively 930.00 and 6130.03.CAIC of saturated and independent models is respectively 2769.46 and 6248.70.EVCI of saturated and independent models is respectively 6.60 and 43.48.

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 73

using Internet banking in Tunisia country. The proposed model hypothesized that customer’ intention to use Internet banking can be af-fected by attitude toward Internet banking. In

turn, attitudes toward internet banking can be affected by both perceived usefulness and ease of use. Customers’ perceived usefulness can be determined by perceived ease of use, security

Table 4. Structural Equations Model (Goodness of Fit)

Absolute indices Estimated value Expected value Authors

χ2 /dl 1.95 <2 Satorra and Bentler (1988a, 1988b, 1994)

RMSEA 0.072 <0.08 Steiger et Lind (1980)

GFI 0.76 >0.9Jöreskog et Sörbom (1984)

AGFI 0.71 >0.9

RMR 0.096 Near zero Jöreskog et Sörbom (1984)

Incremental indices Estimated value Expected value Authors

NNFI 0.93 >0.9 Bollen (1989)

IFI 0.94 >0.9 Bollen (1989)

CFI 0.94 >0.9 Bentler (1989, 1990)

Parsimony indices Estimated value Expected value Authors

AIC 828.43 The lower by comparison Akaike (1987)

CAIC 1125.11 The lower by comparison Bozdogan (1987)

EVCI 5.88 The lower by comparison Browne et Cudeck (1989)

AIC of saturated and independent models is respectively 930 and 6130.CAIC of saturated and independent models is respectively 2769.46 and 6248.70.EVCI of saturated and independent models is respectively 6.60 and 43.48.

Figure 5. Results of structural model

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

74 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

and privacy and customers’ self-efficacy, while their perceived ease of use can be affected by social influence and awareness of services and its benefits to use Internet banking. A significant effects influencing intention to use Internet banking from perceived usefulness, perceived ease of use through attitude was observed. Perceived usefulness was found to have not a direct significant effect on intention to use the internet banking. Perceived usefulness appeared to be an important predictor of attitude than perceived ease of use. Security and privacy and self-efficacy were found to have a significant effect on perceived ease of use. Subjective norm has a significant effect on perceived usefulness. Finally, Awareness of services and its benefits was found to have not a significant effect on perceived usefulness to use the internet banking. This research contributes to our knowledge by providing support for the contention that cus-tomer attitude performs a mediating role in the link between perceived usefulness, perceived ease of use, and customer adoption. However, the main focus of management attention should be on attitude toward Internet banking, of which perceived usefulness, perceived ease of use, security and privacy, self efficacy and social influence are very important antecedents. The findings of the study also suggest important practical for developing usable Internet banking systems. In order to achieve this goal, attention must be given in designing useful, easy-to-use and useful. When Internet banking is perceived as useful and ease of use, customer’s intention to adopt it would be greater. Hence, the electronic banking authorities need to develop the beliefs of the customers regarding the usefulness, ease of use, and secure, and private for their users of Internet banking. Thus, the management needs to focus on the development of such belief on the part of the users. Several strategies should be applied by banks to increase the level of trust between banks’ website and customers (Dixit Naha, 2010). Banks should ensure that Internet banking is safe and secure for financial transaction like as traditional banking. Banks should also organize seminar and conference to educate the customer regarding uses of online

banking as well as security and privacy of their accounts. They can also help their customers by organizing computer training courses in various mobile commerce applications to increase the general computer self-efficacy of the consumers so that the users feel comfortable in using the system with ease and be prepared to avail the e-banking services. Even if these courses are not directly related to Internet banking, they can still help customers develop favourable attitude, positive usefulness, and ease of use in the system, which in turn can influence behav-ioral intention to use Internet banking services. (Luanr and lin, 2005). In addition, these courses can help customers to develop positive useful-ness; ease of use and credibility beliefs in the system, which in turn can influence behavioral intention to use mobile banking services (Luarn and Lin, 2005). There are several limitations in this study. First, the sample size of the samples was small for generalization of the outcome of the study. Second, the factors identified by this study may not cover all factors such as per-ceived compatibility, prior experience, system quality, information quality, service quality, screen design and feedback, etc that could explain the intention to use internet banking in Tunisia. Further research is necessary to verify the influence of those factors, on the adoption of Internet banking services in Tunisia country.

REFERENCES

Adamson, I., Chan, K. M., & Handford, D. (2003). Relationship marketing: Customer com-mitment and trust as a strategy for the smaller Hong Kong corporate banking sector. Interna-tional Journal of Bank Marketing, 21(6/7), 347–358. doi:10.1108/02652320310498492

Agarwal, R., & Karahanna, E. (2000). Time flies when you’re having fun: Cognitive absorption and beliefs about information technology usage. Management Information Systems Quarterly, 24(4), 665–694. doi:10.2307/3250951

Agarwal, R., & Prasad, J. (1999). Are individual differences germane to the acceptance of new in-formation technologies? Decision Sciences, 30(2), 361–391. doi:10.1111/j.1540-5915.1999.tb01614.x

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 75

Ajzen, I. (1985). From intentions to actions: A theory of planned behavior. In J. Kuhl & J. doi:10.1007/978-3-642-69746-3_2

Ajzen, I. (1991). The theory of planned behaviour. Organizational Behavior and Human Decision Processes, 50, 179–211. doi:10.1016/0749-5978(91)90020-T

Ajzen, I., & Madden, J. (1986). Prediction of goal-directed behavior: Attitudes, intentions, and per-ceived behavioral control. Journal of Experimental Social Psychology, 22, 453–474. doi:10.1016/0022-1031(86)90045-4

Akaike, H. (1987). Factor analysis and AIC. Psy-chometrika, 52, 317–332. doi:10.1007/BF02294359

Aladwani, A. M. (2001). Online banking: A field study of drivers, development challenges, and expectations. International Journal of Information Management, 21, 213–225. doi:10.1016/S0268-4012(01)00011-1

Amin, H. (2007). Internet banking adoption among young intellectuals. Journal of Internet Banking and Commerce, 12(3).

Anderson, C., & Gerbing, W. (1988). Structural equation modeling in practice: A review and recom-mended two-step approach. Psychological Bulletin, 103, 411–423. doi:10.1037/0033-2909.103.3.411

Arteaga Sanchez, R., & Duarte Hueros, A. (2010). Motivational factors that influence the acceptance of Moodle using TAM. Computers in Human Behavior, 26(6), 1632–1640. doi:10.1016/j.chb.2010.06.011

Bélanger, F., Hiller, J., & Smith, W. J. (2002). Trustworthiness in electronic commerce: The role of privacy, security, and site attributes. The Journal of Strategic Information Systems, 11(3/4), 245–270. doi:10.1016/S0963-8687(02)00018-5

Bentler, P. M. (1989). EQS structural equations program manual. Los Angeles, CA: BMDP Statisti-cal Software.

Bentler, P. M. (1990). Comparative fit indexes in structural models. Psychological Bulletin, 107, 238–246. doi:10.1037/0033-2909.107.2.238 PMID:2320703

Bentler, P. M., & Bonett, D. G. (1980). Significance tests and goodness of fit in the analysis of covariance structures. Psychological Bulletin, 88, 588–606. doi:10.1037/0033-2909.88.3.588

Black, N. J., Lockett, A., Winklhofer, H., & McK-echnie, S. (2002). Modelling consumer choice of distribution channels: An illustration from financial services. International Journal of Bank Marketing, 20(4), 161–173. doi:10.1108/02652320210432945

Bollen, K. A. (1989). A new incremental fit index for general structural equation models. Sociological Methods & Research, 17, 303–316. doi:10.1177/0049124189017003004

Bozdogan, H. (1987). Model selection and Akaike’s information criteria: The general theory and it’s analytical extensions. Psychometrika, 52, 345–370. doi:10.1007/BF02294361

Browne, R. L., & Cudeck, R. (1989). Single sample cross-validation indices for covariance structures. The British Journal of Mathematical and Statistical Psy-chology, 37, 62–83. doi:10.1111/j.2044-8317.1984.tb00789.x

Bruner, G. C., & Kumar, A. (2005). Applying T.A.M. to consumer usage of handheld Internet devices. Jour-nal of Business Research, 58, 553–558. doi:10.1016/j.jbusres.2003.08.002

Chau, P. Y. K. (2001). Influence of computer attitude and self-efficacy on IT usage behavior. Journal of End User Computing, 13(1), 26–33. doi:10.4018/joeuc.2001010103

Cheng, T., Lama, D., & Yeung, A. (2006). Adoption of internet banking: An empirical study in Hong Kong. Decision Support Systems, 42(3), 1558–1572. doi:10.1016/j.dss.2006.01.002

Cheong, J. H., & Park, M. C. (2005). Mobile internet acceptance in Korea. Internet Research, 15, 125–140. doi:10.1108/10662240510590324

Chiu, Y. B., Lin, C. P., & Tang, L. L. (2005). Gen-der differs: Assessing a model of online purchase intentions in e-tail service. International Journal of Service Industry Management, 16(5), 416–435. doi:10.1108/09564230510625741

Compeau, D., & Higgins, C. (1995). Computer self-efficacy: Development of a measure and initial test. Management Information Systems Quarterly, 189–211. doi:10.2307/249688

Davis, F. D. (1986). A technology acceptance model for empirically testing new end-user information system: Theory and result. Doctoral Dissertation, MIT Sloan School of Management, Cambridge, MA.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use and user acceptance of information tech-nology. Management Information Systems Quarterly, 13, 319–340. doi:10.2307/249008

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

76 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

Davis, F. D. (1993). User acceptance of information technology: System characteristics, user perceptions and behavioural impacts. International Journal of Man-Machine Studies, 38, 475–487. doi:10.1006/imms.1993.1022

Davis, F. D., Bagozzi, R., & Warshaw, P. R. (1989). User acceptance of computer technology. Man-agement Science, 35(8), 982–1003. doi:10.1287/mnsc.35.8.982

Dixit, N. (2010). Acceptance of E-banking among adult customers: An empirical investigation in India. Journal of Internet Banking and Commerce, 15.

Fishbein, M., & Ajzen, I. (1975). Belief, attitudes, intention and behavior: An introduction to theory and research. Reading, MA: Addision-Wasely.

Fornell, C., & Larcker, D. (1981). Evaluating struc-tural equation models with unobservable variables and measurement error. JMR, Journal of Marketing Research, 18(1), 39–50. doi:10.2307/3151312

Gallion, J. A. (2000). A comprehensive model of the factors affecting user acceptance information technology in a data production environment. Un-published Ph.D. Dissertation, Ohio State University.

Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model. Management Information Systems Quarterly, 27, 51–90.

Gefen, D., & Keil, M. (1998). The impact of developer responsiveness on perceptions of usefulness and ease of use: An extension of the technology acceptance model. The Data Base for Advances in Information Systems, 29(2), 35–49. doi:10.1145/298752.298757

Gefen, D., & Straub, D. (2000). The relative impor-tance of perceived ease of use in IS adoption: A study of ecommerce adoption. Journal of the Association for Information Systems, 1(8).

Gerrard, P., & Cunningham, J. B. (2003). The diffu-sion of Internet banking among Singapore consumers. International Journal of Bank Marketing, 21(1), 16–28. doi:10.1108/02652320310457776

Hair, J. R., Anderson, R. E., Tatham, R. L., & Black, W. C. (1992). Multi-variate data analysis with read-ings. Macmillan.

Hamlet, C., & Strube, M. (2000). Community banks go online. ABA Banking Journal’s (pp. 61-65). 2000 White Paper/Banking on the Internet.

Hartwick, J., & Barki, H. (1994). Explaining the role of user participation in information system use. Management Science, 40(A), 440-465.

Hernandez, J. M. C., & Mazzon, J. A. (2007). Adop-tion of internet banking: Proposition and imple-mentation of an integrated methodology approach. International Journal of Bank Marketing, 25(2), 72–88. doi:10.1108/02652320710728410

Hoelter, J. W. (1983). The analysis of covari-ance structures: Goodness-of-fit indices. So-ciological Methods & Research, 11, 325–344. doi:10.1177/0049124183011003003

Hong, W., Thong, J. Y. L., Wong, W. M., & Tam, K. Y. (2001). Determinants of user acceptance of digital libraries: An empirical examination of individual differences and system characteristics. Journal of Management Information Systems, 18(3), 97–124.

Howcroft, B., Hamilton, R., & Hewer, P. (2002). Consumer attitude and the usage and adoption of home-based banking in the United Kingdom. Inter-national Journal of Bank Marketing, 20(3), 111–121. doi:10.1108/02652320210424205

Hsu, C., & Lu, H. (2004). Why do people play on-line games? An extended TAM with social influences and flow experience. Information & Management, 41(7), 835–868. doi:10.1016/j.im.2003.08.014

Hu, L., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analy-sis: Conventional criteria versus new alterna-tives. Structural Equation Modeling, 6, 1–55. doi:10.1080/10705519909540118

Hung, S. Y., Ku, C. Y., & Chang, C. M. (2003). Criti-cal factors of WAP services adoption: An empirical study. Electronic Commerce Research and Applica-tions, 2(1). doi:10.1016/S1567-4223(03)00008-5

Igbaria, M., & Iivari, J. (1995). The effects of self-efficacy on computer usage. Omega. Int. Mgmi Sci, 23(6), 587–605.

Igbaria, M., Zinatelli, N., Cragg, P., & Cavaye, A. L. M. (1997). Personal computing acceptance fac-tors in small firms: A structural equation modelling. Management Information Systems Quarterly, 21(3), 279–305. doi:10.2307/249498

Kalakota, R., & Winston, A. B. (1997). Electronic commerce: A manager’s guide. Addison Wesley.

Karahanna, E., & Straub, D. W. (1999). The psycho-logical origins of perceived usefulness and ease-of-use. Information & Management, 35(4), 237–250. doi:10.1016/S0378-7206(98)00096-2

Lassar, W., Manolis, C., & Lassar, S. (2005). The relationship between consumer innovativeness, personal characteristics, and online banking adop-tion. International Journal of Bank Marketing, 23, 176–199. doi:10.1108/02652320510584403

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 77

Lee, M.-C. (2009). Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications. doi:10.1016/j.elerap.2008.11.006

Liao, S., Shao, Y. P., Wang, H., & Chen, A. (1999). The adoption of virtual banking: an empirical study. International Journal of Information Management, 19, 63–74. doi:10.1016/S0268-4012(98)00047-4

Lingyun, Q., & Dong, L. (2008). Applying TAM in B2C E-commerce research: An extended model. Tsinghua Science and Technology, 13(3), 265–272. doi:10.1016/S1007-0214(08)70043-9

Luarn, P., & Lin, H. H. (2005). Toward an under-standing of the behavioral intention to use mobile banking. Computers in Human Behavior, 21(6), 873–891. doi:10.1016/j.chb.2004.03.003

Monsuwe, T. P., Dellaert, B. G. C., & Ruyter, K. R. (2004). What drives consumers to shop on-line? A literature review. International Journal of Service Industry Management, 15(1), 102–121. doi:10.1108/09564230410523358

Moon, J., & Kim, Y. (2001). Extending the TAM for a world-wide-web context. Information & Management, 38(4), 217–230. doi:10.1016/S0378-7206(00)00061-6

Mukti, N. (2000). Barriers to putting businesses on the internet in Malaysia. The Electronic Journal of Information Systems in Developing Countries, 2(6), 1–6.

Muniruddeen, L. (2007). An examination of indi-vidual’s perceived security and privacy of the internet in Malaysia and the influence of this on their inten-tion to use e-commerce: Using an extension of the technology acceptance model. Journal of Internet Banking and Commerce, 12(3).

Nunnally, J. (1978). Psychometric theory. New York, NY: McGraw-Hill.

Pavlou, P. A. (2003). Customer acceptance of elec-tronic commerce -integrating trust and risk with the technology acceptance model. International Journal of Electronic Commerce, 7(3), 69–103.

Pikkarainen, T., Pikkarainen, K., Karjaluoto, H., & Pahnila, S. (2004). Consumer acceptance of online banking: An extension of the technology accep-tance model. Internet Research, 14(3), 224–235. doi:10.1108/10662240410542652

Polatoglu, V. N., & Ekin, S. (2001). An em-pirical investigation of the Turkish consumers’ acceptance of internet banking services. Interna-tional Journal of Bank Marketing, 19(4), 156–165. doi:10.1108/02652320110392527

Poon, W. C. (2008). Users’ adoption of e-banking services: The Malaysian perspective. Journal of Business and Industrial Marketing, 23(1), 59–69. doi:10.1108/08858620810841498

Rogers, E. M., & Shoemaker, F. (1971). Communi-cations in innovation. New York, NY: Free Press.

Sathye, M. (1999). Adoption of internet banking by Australian consumers: An empirical investigation. International Journal of Bank Marketing, 17(7), 324–334. doi:10.1108/02652329910305689

Satorra, A., & Bentler, P. M. (1988). Scaling cor-rections for chi-square statistics in covariance structure analysis. In Proceedings of the Business and Economics Sections (pp. 308-313). Alexandria, VA: American Statistical Association.

Satorra, A., & Bentler, P. M. (1988b). Scaling correc-tions for statistics in covariance structure analysis. Los Angeles, CA: UCLA.

Satorra, A., & Bentler, P. M. (1994). Corrections to test statistics and standard errors in covariance struc-ture analysis. In A. Von Eye (Ed.), Latent variables analysis: Applications for developmental research (pp. 399–419). Newbury Park, CA: Sage.

Shih, Y. Y., & Fang, K. (2004). The use of decomposed theory of planned behaviour to study Internet bank-ing in Taiwan. Internet Research, 14(3), 213–223. doi:10.1108/10662240410542643

Steiger, J. H., & Lind, J. C. (1980). Statistically-based tests fort the number of common factors. Communica-tion au Congrès Annual de la Psychometric Society (mai) Iowa City, IO.

Straub, D., Keil, M., & Brenner, W. (1997). Testing the technology acceptance model across cultures: A three-country study. Information & Management, 33(1), 1–11. doi:10.1016/S0378-7206(97)00026-8

Suh, B., & Han, I. (2002). Effect of trust on customer acceptance of internet banking. Electronic Com-merce Research and Applications, 1(3), 247–263. doi:10.1016/S1567-4223(02)00017-0

Tan, M., & Teo, T. S. H. (2000). Factors influenc-ing the adoption of Internet banking. Journal of the Association for Information Systems, 1(5), 1–42.

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

78 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

Taylor, S., & Todd, P. (1995). Understanding informa-tion technology usage: A test of competing models. Information Systems Research, 6(2), 144–176. doi:10.1287/isre.6.2.144

Teo, T. S. H., Lim, V. K. G., & Lai, R. Y. C. (1999). Intrinsic and extrinsic motivation in internet us-age. Omega, 27(1), 25–37. doi:10.1016/S0305-0483(98)00028-0

Turban, E., Lee, J., King, D., & Chung, H. M. (2000). Electronic commerce: A managerial perspective. Upper Saddle River, NJ: Prentice-Hall.

Venkatesh, V. (1999). Creation of favorable user perceptions: Exploring the role of intrinsic motiva-tion. Management Information Systems Quarterly, 23(2), 239–260. doi:10.2307/249753

Venkatesh, V., & Davis, F. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186–204. doi:10.1287/mnsc.46.2.186.11926

Venkatesh, V., & Davis, F. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186–204. doi:10.1287/mnsc.46.2.186.11926

Venkatesh, V., & Davis, F. D. (1996). A model of the antecedents of perceived ease of use: Develop-ment and test. Decision Sciences, 27(3), 451–481. doi:10.1111/j.1540-5915.1996.tb01822.x

Venkatesh, V., Morris, M. G., & Ackerman, P. L. (2000). A longitudinal field investigation of gen-der differences in individual technology adoption decision-making processes. Organizational Behav-ior and Human Decision Processes, 83(1), 33–60. doi:10.1006/obhd.2000.2896 PMID:10973782

Venkatesh, V., Morris, M. G., Davis, G. B., & Da-vis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS QUART, 27(3), 425–478.

Wadie, N. (2011). Factors influencing the adoption of internet banking in Tunisia. International Journal of Business and Management, 6(8).

Wadie, N., & Lanouar, C. (2012). Factors affecting the adoption of Internet banking in Tunisia: An in-tegration theory of acceptance model and theory of planned behavior. The Journal of High Technology Management Research, 23, 1–14. doi:10.1016/j.hitech.2012.03.001

Wang, Y. D., & Emurian, H. H. (2005). An overview of online trust: Concepts, elements, and implica-tions. Computers in Human Behavior, 21, 105–125. doi:10.1016/j.chb.2003.11.008

Wang, Y. S., Wang, Y. M., Lin, H. H., & Tang, I. (2003). Determinants of user acceptance of internet banking: An empirical study. International Journal of Service Industry Management, 14(5), 501–519. doi:10.1108/09564230310500192

Wu, I. L., & Chen, J. L. (2005). An extension of trust and TAM model with TPB in the initial adoption of on-line tax: An empirical study. International Journal of Human-Computer Studies, 62, 784–808. doi:10.1016/j.ijhcs.2005.03.003

Yousafzai, S. Y., Pallister, J. G., & Foxall, G. R. (2003). A proposed model of e-trust for elec-tronic banking. Technovation, 23(11), 847–860. doi:10.1016/S0166-4972(03)00130-5

Wadie Nasri is an assistant Professor in the Higher Institute of Management of Gabes at Gabes University. He received his Philosophy Doctorate from the Faculty of Economic Sciences and Management of Tunis in Tunisia. His current research interests are in the fields of electronic commerce, Information Technology Adoption, Internet Banking Adoption, E-government Adop-tion, Marketing Information System, and Competitive Intelligence.

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 79

Charfeddine Lanouar is assistant professor at the collegue of administrative sciences of Najran University (KSA). He has published several papers in international journals in management, economic and quantitatives methods.

Anis Allagui is lecturer in the department of Industrial Engineering at the National Engineering School of Tunis (TUNISIA). He is the executive director for Tunisia of the Innovation Management graduate program (DICAMP). His main research and teaching interests fall into three areas which are E-Business Marketing, Innovation and entrepreneurship. His work has been published in academic journals and international conference proceedings such as journal of e-business and European Advances in Consumer Research. He was a visiting researcher at Tennessee State University and a previous visiting faculty at State University of New York at Potsdam.

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

80 International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013

APPENDIXTable 5. Measurement scales

Constructs Measures

Perceived usefulness (PU)

PU1 I think that using the online banking would enable me to accomplish my tasks more quickly.

PU2 I think that using the online banking would make it easier for me to carry out my tasks.

PU3 I think the online banking is useful.

PU5 Overall, I think that using the online banking is advantageous.

Perceived ease of use (PEOU)

PEOU1 I think that learning to use online banking would be easy.

PEOU2 I think that interaction with online banking does not require a lot of mental effort.

PEOU3 I think that it is easy to use online banking to accomplish my banking tasks.

Intention (INT) INT1 I would use the online banking for my banking needs.

INT2 Using the online banking for handling my banking transactions is something I would do.

INT3 I would see myself using the online banking for handling my banking transactions.

Attitude (ATT) ATT1 I think that using online banking is a good idea.

ATT2 I think that using online banking for financial transactions would be a wise idea.

ATT3 I think that using online banking is pleasant.

ATT4 In my opinion, it is desirable to use online banking.

Security and privacy (SP1)

SP1 I trust in the technology an online bank is using

SP2 I trust in the ability of an online bank to protect my privacy

SP3 I trust in an online bank as a bank

SP4 Using an online bank is financially secure

SP5 I am not worried about the security of an online bank

SP6 Metters of security have no influence on using an online bank

Self efficacy SE1 I could complete my bank transaction using the internet banking, if there was no one around to tell me what to do.

SE2 I could complete my bank transaction using the internet banking, if I had never used a package like it before

SE3 I could complete my bank transaction using the internet banking, if I had only the manuals or online help for reference

SE4 I could complete my bank transaction using the internet banking, if I had seen someone else using it before trying it myself.

SE5 I could complete my bank transaction using the internet banking, if I could call someone for help if I got stuck

SE6 I could complete my bank transaction using the internet banking, if someone had helped me get started

continued on following page

Copyright © 2013, IGI Global. Copying or distributing in print or electronic forms without written permission of IGI Global is prohibited.

International Journal of Innovation in the Digital Economy, 4(4), 61-81, October-December 2013 81

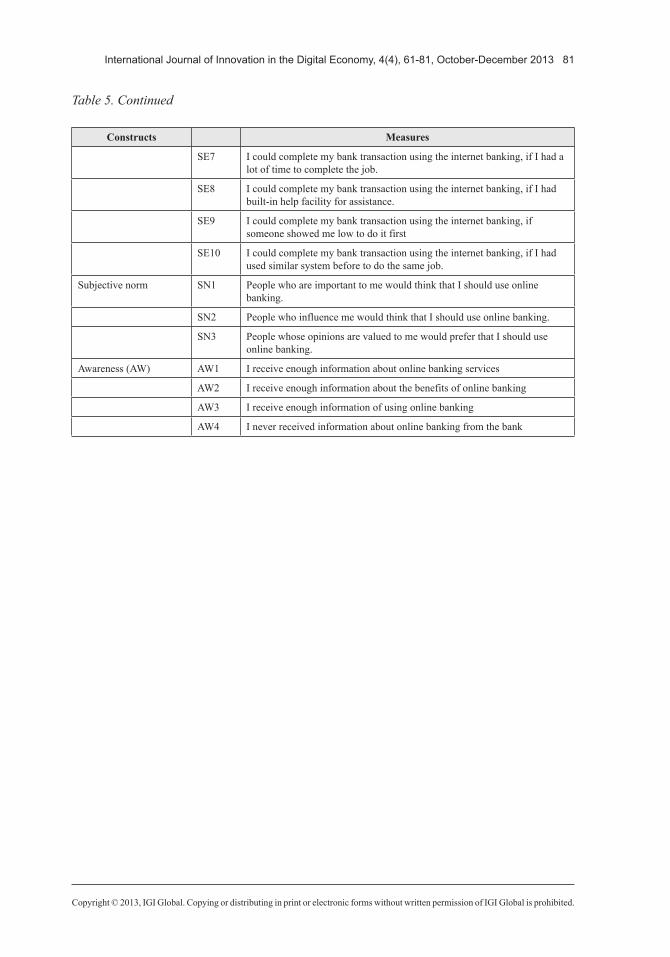

Constructs Measures

SE7 I could complete my bank transaction using the internet banking, if I had a lot of time to complete the job.

SE8 I could complete my bank transaction using the internet banking, if I had built-in help facility for assistance.

SE9 I could complete my bank transaction using the internet banking, if someone showed me low to do it first

SE10 I could complete my bank transaction using the internet banking, if I had used similar system before to do the same job.

Subjective norm SN1 People who are important to me would think that I should use online banking.

SN2 People who influence me would think that I should use online banking.

SN3 People whose opinions are valued to me would prefer that I should use online banking.

Awareness (AW) AW1 I receive enough information about online banking services

AW2 I receive enough information about the benefits of online banking

AW3 I receive enough information of using online banking

AW4 I never received information about online banking from the bank

Table 5. Continued