Embed Size (px)

Citation preview

FINANCE AND INTERNATIONAL TRADE: A REVIEW OF THE LITERATURE

Anne-Gaël Vaubourg

Dalloz | « Revue d'économie politique »

2016/1 Vol. 126 | pages 57 à 87 ISSN 0373-2630DOI 10.3917/redp.261.0057

Article disponible en ligne à l'adresse :--------------------------------------------------------------------------------------------------------------------https://www.cairn.info/revue-d-economie-politique-2016-1-page-57.htm--------------------------------------------------------------------------------------------------------------------

Distribution électronique Cairn.info pour Dalloz.© Dalloz. Tous droits réservés pour tous pays. La reproduction ou représentation de cet article, notamment par photocopie, n'est autorisée que dans leslimites des conditions générales d'utilisation du site ou, le cas échéant, des conditions générales de lalicence souscrite par votre établissement. Toute autre reproduction ou représentation, en tout ou partie,sous quelque forme et de quelque manière que ce soit, est interdite sauf accord préalable et écrit del'éditeur, en dehors des cas prévus par la législation en vigueur en France. Il est précisé que son stockagedans une base de données est également interdit.

Powered by TCPDF (www.tcpdf.org)

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Finance and International Trade:A Review of the Literature

Anne-Gaël Vaubourg*

The aim of this paper is to review the literature on the links between finance andinternational trade. First, sectors’ or firms’ external financial dependence appears to bea key determinant of export performance. More vulnerable firms or sectors export lessthan others. Moreover, insufficient financial development and financial crises harmexports to a greater extent when firms or sectors rely on external finance. Second,trade finance, such as letters of credit or trade insurance, plays a key role in financingtrade and provides a powerful transmission channel for financial shocks and bankingcrisis. Finally, we emphasize the complexity of the relationship between finance andtrade. On the one hand, finance is also driven by trade patterns such that the causalitybetween both phenomena is bidirectional. On the other hand, there exist institutionalinteractions between financial and trade reforms.

international trade – financial constraint – financial development – financial crisis –

trade finance – institutional complementarity and substitutability

Financement et commerce international : une revuede la littérature

Ce papier propose une revue de la littérature consacrée aux liens entre financement etcommerce international. Nous montrons tout d’abord que les firmes et les secteurs lesplus fragiles financièrement exportent moins que les autres. De même, un développe-ment financier insuffisant et la survenance de crises financières réduisent d’autant plusles exportations que l’entreprise ou le secteur dépend fortement du financementexterne. Ensuite, les outils de financement du commerce international, tels que leslettres de crédit ou l’assurance-crédit export, constituent un puissant canal de trans-mission des chocs financiers au commerce international. Enfin, nous insistons sur lacomplexité des liens entre finance et commerce international. D’une part, la causalitéentre les deux sphères est en fait réciproque. D’autre part, il existe des interactionsinstitutionnelles entre les réformes financières et les politiques commerciales.

commerce international – contrainte financière – développement financier – crise finan-

cière – outils de financement du commerce international – complémentarité et substi-

tuabilité institutionnelle

Classification JEL : F10, F14, G20, G21

* LAREFI-Université de Bordeaux, Campus de Pessac, Avenue Léon Duguit, 33608 Pessaccedex, 05 56 84 62 12, [email protected]

•B

ILA

N/E

SSA

I

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

1. Introduction

The great trade collapse experienced in 2009 is one of the most strikingphenomenon observed in recent years. According to the Word Trade Orga-nization (WTO), the volume of world trade fell by 12% in 2009. The decline inmerchandise export volumes was particularly severe in North America(– 15%) and Europe (– 15%) compared to South America (– 8%) and Asia(– 11%) (WTO [2010])1. As emphasized by Francois and Woerz [2009], thedecline in trade flows was more dramatic for manufactured products(– 15.5%), especially in durable goods such as automotive products (– 32%)and industrial machinery (– 29%), than for agricultural goods (– 3%) or fueland mining products (– 4.5%) (WTO [2010]). More interestingly, the slump inworld trade appears much stronger than the contraction in Gross DomesticProduct (GDP), which amounted to – 2.4% in 2009 (WTO [2010])2. The recentdrop in export volumes was steeper than those witnessed in 1965 (– 7%),1982 (– 2%) and 2001 (– 0.2%) (WTO [2010]), known as the three main pre-vious episodes of declining trade. It was also more severe than the fall inword trade observed during the Great Depression of the 1930s (Almunia etal. [2010]). While the decline in trade experienced during the Great Depres-sion is largely due to the implementation of trade barriers, the 2009 tradecollapse cannot be attributed to increased protectionism.

The main explanation for the magnitude of the trade collapse, heavilyemphasized by the WTO (Auboin [2009, 2011]), relates to the key role of therecent crisis that affected financial systems worldwide3. The 2007-2008financial crisis has multiple dimensions. First, a large number of banks suf-fered liquidity and solvency problems, inducing failures or massive statebailouts. In addition, a global credit crunch occurred, especially after thebankruptcy of Lehman Brothers (Aisen and Franken [2010]). The crisis alsoaffected financial markets. Suffering from a crisis of confidence, investorsfled stock markets for less risky markets, notably sovereign bond markets.According to the World Bank, world stock market capitalization decreased by30 000 billions dollars in 2008 (a decline representing nearly 50% of theglobal GDP). Do these aspects of the financial crisis help to explain the tradecollapse observed in 2009? Beyond its cyclical dimension, this issue alsorelates to more structural aspects, such as the impact of financial systemson trade specialization and export performance. Moreover, investigatingwhether finance matters for international trade has important normative

1. Nevertheless, the decline in merchandise export volumes was particularly severe inJapan (– 25%). For additional details, see Tanaka [2009] and Wakasugi [2009].

2. While common practice, comparing GDP and exports (or imports) remains difficult sincewhile the former is calculated from added values, the latter relates to total production.

3. It is true that there is still no consensus on the key role of finance in the world tradecollapse. The literature examines other explanations such as the vertical specialization indu-ced by globalization and multinational firms (Bems et al. [2009]; Yi [2003]) or the decline indemand due to depressed economic activity (Eaton et al. [2011]). Moreover, several opinionsurveys conducted by the IMF and WTO reveal that credit shortage is considered by bankersand exporters as the second cause of the great trade collapse, after the decline in demand(Mora and Powers [2011]).

58 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

implications, particularly with respect to the financial reforms and tradepolicies implemented in developed and in developing and emerging coun-tries. For these reasons, its seems particularly interesting to explore thefinancial underpinnings of international trade.

The goal of this paper is precisely to present a review of the theoreticaland empirical literature dedicated to this issue. It is organized as follows. InSection 2, we provide rationales for the causal effects of finance on trade.We present theoretical and empirical contributions demonstrating that tradepatterns are highly dependent on sectors’ and firms’ external financialdependence. However, these contributions do not investigate through whichchannel international trade is affected by external finance. Therefore, in Sec-tion 3, we examine this channel and we emphasize the role played by tradefinance. In Section 4, we extend the analysis beyond the direct causal effectof finance on trade and investigate the more complex relationships betweenthe two variables. We address the issue of causal direction issue and theexistence of institutional complementarity and substitutability betweenfinancial reforms and trade policies. Section 5 concludes.

2. Does international trade dependon external finance?

In this section, we demonstrate that external finance is a key determinantof international trade. We first explain how financial dependence is intro-duced into theoretical models of international trade. We then present macro-and micro-level empirical evidence concerning the effect of external finan-cial dependence on firms’ exports.

2.1. Theory: financial dependence in modelsof international trade

This subsection addresses external financial dependence in internationaltrade models. We first reveal how comparative advantages can result fromdifferences in external financial dependence at the sector level. We thenrefine the analysis by examining how firms’ external financial dependencecan be addressed in international trade models with firm heterogeneity.

2.1.1. External financial dependence and comparativeadvantages

The literature initially introduces the notion of finance dependence in theHeckscher-Ohlin-Samuelson’s international trade model. Using two-country

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 59

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

two-sector models, this approach reveals that differences in financial devel-opment give rise to comparative advantages and mutual gains from special-ization and trade, even when countries have identical endowments, con-sumer preferences and technologies. The crucial aspect of these theoreticalcontributions is the assumption that, in each country, the two sectors differin financial needs and degrees of financial dependence.

The model developed by Bardhan and Kletzer [1987] focuses on an impor-tant function of financial systems, that consists to mobilize savings and toallocate funds to investors. The authors assume that in each country, onesector produces an intermediate good while the other produces a final good.Producing the final good requires the use of the intermediate good as aninput and committing this resource one period before the output becomesavailable. The final good sector thus requires external funds to finance work-ing capital. However, due to information asymmetries between firms andfunders, external financing entails moral hazard problems. In this context, aweakly developed financial system is unable to alleviate information asym-metries and implies rationing. Conversely, a highly developed financial sys-tem makes it possible to reduce frictions and finance working capital moreefficiently. As the intermediate good sector does not require outside financ-ing, financial development is only beneficial to the final good sector. Finally,the relatively more financially developed country has a comparative advan-tage in the final good while the relatively less financially developed countryspecializes in the intermediate good. Beck [2002] extends this analysis byshowing that trade patterns depend on differences in financial developmenteven when both sectors rely on external financing. In his model, one of thetwo sectors (the manufacturing sector) exploits increasing returns to scalewhile the other (the food sector) is characterized by constant returns toscale. Moreover, savers are assumed to face search costs when attemptingto channel their funds to investors. A well developed financial system makesit possible to mitigate search costs and to allocate a larger share of funds toproductive activities. As the manufacturing sector exploits increasing returnsto scale, it profits from a large volume of external financing to a greaterextent than the food sector. Consequently, a relatively high level of financialdevelopment is associated with exporting manufacturing-goods while a rela-tively low level of financial development is associated with exporting food-goods.

The theoretical literature also considers another function of financial sys-tems: the diversification of risk. In Baldwin’s [1989] model, one of the twosectors in each country is assumed to face demand shocks while the othersector does not. Unlike the latter, the former thus requires access to thefinancial system to diversify risk. Because it allows for a decreased riskpremium, a high level of financial development primarily benefits the riskysector. Therefore, the pattern of trade between the two countries cruciallydepends on differences in financial development. Having a relatively welldeveloped financial system allows a country to specialize in the risky goodwhile having a weakly developed financial system leads to specialize in thenon risky good.

60 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

2.1.2. External financial dependence and firms’heterogeneity

The principal drawback of classical models of international trade is thatthey adopt a representative firm approach. Because they do not allow forfirm heterogeneity, they fail to account for the observation that, within eachsector, only a small proportion of firms (the most productive) participate ininternational trade. We thus enrich the analysis by examining how thenotion of external financial dependence can be introduced into trade modelswith heterogeneous firms. To do so, the literature generally refers to the“new new trade theory”, in the line of the Melitz’s [2003] model. In thisapproach, firms differ in their productivity level such that, when trade isopened, a selection effect occurs: only firms with a sufficient level of pro-ductivity export. Financial frictions are introduced by assuming that export-ers face specific costs. On the one hand, exporting induces upfront costs,due to advertising, gathering information on foreign customers, administra-tive procedures, translation, organizing foreign distribution networks etc. Onthe other hand, exporting firms face variable transport costs, which dependon shipping time and export volume. As fixed and variable costs must beexternally financed, exporting activities crucially depend on the intensity offirms’ financial constraints. While the financing available for sunk fixed costsdetermines firms’ export decisions, i.e., extensive margins of trade, thefinancing available for variable costs affects the level of firm exports, i.e., theintensive margins of trade4.

Chaney’s [2005] contribution is based on the notion that firms’ produc-tivity plays a key role in firms’ decision to export. Productivity does notonly affect firms’ competitiveness on foreign markets. It also determinesthe amount of profit earned from domestic activities and firms’ ability tocover upfront export costs5. The author thus distinguishes three catego-ries of firms. Firms with a very low productivity do not export becausethey are not competitive enough to sell abroad. Conversely, as they arecompetitive and generate large profits from their domestic activities, high-productivity firms export whatever the level of available external finance.Finally, firms with an intermediate level of productivity are potentiallyviable in foreign markets. But as they do not generate enough profit tocover upfront costs, they cannot export due to financial constraint. At theaggregate level, export flows thus decrease with the amount of liquidityavailable for constrained firms and increase with the number of con-strained firms in the economy.

4. Financial constraints can also affect the quality of exported products. For theoretical andempirical investigations on this issue, see Fan et al. [2012].

5. In addition, once a firm is engaged in international trade, it is able to use the profitsearned from its past exporting activity to finance the costs associated with new exportingdestinations.

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 61

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Although its refers to the same firm heterogeneity framework, Manova’s[2013] paper differs from Chaney’s [2005] model in two ways. First, it explic-itly examines the structure of financial contracts between firms and funders.Second, it considers heterogeneity not only across firms but also acrosssectors. As in Chaney [2005], it is assumed that high productivity (in a givensector) implies large profits. This allows firms to offer high returns to exter-nal funders. For this reason, they can more easily borrow and finance fixedexport costs. Hence, the level of firms’ productivity crucially determinesextensive margins. The author shows there exists a productivity thresholdsuch that low-productivity firms, which cannot obtain external funds tocover fixed costs, do not sell abroad while high-productivity firms, whichface no financial constraint, export. Moreover, Manova [2013] finds thatfinancial frictions also affect intensive margins as financially constrainedfirms decrease the volume of their exports to reduce their variable costs andborrowing. Finally, aggregate exports increase with the quality of contractenforcement in the domestic economy. They also decrease with the level ofsector’s vulnerability (proxied by the proportion of fixed costs which have tobe covered by external finance) and the level of pledgeable tangible assets.

Finally, Besedes et al. [2014] refine Chaney’s [2005] and Manova’s [2013]findings by considering that the intensity of financial constraint depends onwhether the firm is a new exporter or not. The authors use a dynamic modelin which the perceived risk of firms decreases with export duration. Finally,they show that the harmful effect of financial vulnerability on export growthis weaker for firms that have been exporting for a long time. Based on thesame dynamic approach, Kohn et al. [2012] conclude that firms’ exportbehavior is subject to some hysteresis: firms that successfully exported inthe past are more likely to export in the future.

2.2. Macro-level evidence

Turning to the empirical implications of the theoretical arguments pre-sented in the previous section, we first consider macro-level evidence. Thelinks between financial development and trade and the impact of financialcrisis on export performance are explored successively.

2.2.1. Financial development and trade

In line with his theoretical contribution, Beck [2002] focuses on manufac-turing sectors, which are assumed to be particularly dependent on externalfinancing. Employing a data set on 65 countries between 1966 and 1995, heestimates a dynamic Generalized Method of Moments (GMM) model andestablishes that financial development, measured by the ratio of the creditprovided to the private sector by commercial banks and other financial insti-tutions, has a significant positive impact on the ratio of manufacturedexports to GDP, the ratio of manufactured exports to total exports and thetrade balance ratio of manufactured goods to GDP. Moreover, financial

62 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

development is shown to have a significant negative effect on the ratio ofmanufactured imports to total imports6. Using a data set on 56 countriesbetween 1980 and 1989, Beck [2003] considers two other proxies for finan-cial development inspired by the literature on “growth and finance”. Inaddition to the credit ratio, which measures the importance of intermediatedfinance, he also considers the ratio of market capitalization to GDP, whichaccounts for the size of market-based finance. The third proxy, which iscalculated as the sum of the two previous indicators, represents the overallsize of the financial system. The author finds that the financial developmentproxies have a significant and positive effect on industry-level exports (alter-natively measured by a ratio of exports to GDP or a ratio of trade balance toGDP), especially for industries that heavily rely on outside finance, as mea-sured by the Rajan and Zingales’ [1998] indicator of external financial depen-dence (denoted “RZ” below and computed as the amount of capital expen-diture minus cash flows from operation as a share of capital expenditures7).The key role of financial development is also highlighted when the intensityof external financial dependence is measured by the size of fixed costs.Becker et al. [2013] consider annual bilateral trade flows among a sample ofmore than 170 countries between 1970 and 1998. Fixed export costs aresuccessively proxied by the degree of standardization of the exported prod-uct, the distance between the exporting and importing countries, the exist-ence of a common border and the existence of a common languagebetween two countries. Using Ordinary Least Squares (OLS) regressions, theauthors find that financial development (proxied by the quality of account-ing) fosters exports and this effect is more powerful when upfront costs arehigh.

Finally, as emphasized by Contessi and De Nicola [2012], one importantconcern when addressing the links between finance and trade is the endo-geneity bias, which is mainly due to simultaneity (trade and financialvariables may be jointly determined) or reverse causality (trade may drivefinancial development8). One possible approach to tackle this problemconsists in instrumenting the financial variable to extract its exogenouscomponent. To be relevant, instrumental variables must be correlated withthe financial indicator but not with the trade one. This approach is adoptedby Beck [2002, 2003] to check the robustness of his findings. Using theorigin of the legal system (English, French or German), the level of credi-tors’ and minority shareholders’ protection as well as indicators of insti-tutional quality and religious composition9 as instruments for financialdevelopment, Beck [2002, 2003] confirms that his estimates are not sub-ject to endogeneity bias.

6. Financial development also has a positive impact on the ratio of manufactured importsto GDP but this impact is much smaller than the effect on the proxies for manufacturedexport.

7. The RZ indicator has been widely used in the literature. Based on the idea that theranking of sectors according to the level of financial dependence is the same across coun-tries, many papers apply the indicator calculated by Rajan and Zingales [1998] for the US tocountries for which such data are not available.

8. We deal more deeply with the reverse causality issue in section 4.9. These indicators are mainly inspired by the literature on “law and finance” (La Porta et

al. [1998, 1999]).

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 63

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Overall, these findings indicate that financial development provides acomparative advantage for externally financial dependent sectors. They sug-gest that export promotion strongly depends on policies designed todevelop and modernize financial systems10.

2.2.2. Financial crisis and trade

Adopting a more cyclical point of view, Chor and Manova [2012] explorewhether the adverse impact of external financial dependence on a sector’sexports is affected by global credit tightening (identified by high interbankrates) and the 2008 financial crisis (proxied by a dummy variable that equals1 in september 2008 and 0 thereafter). Relying on monthly US import dataover the period 2006-2008, they demonstrate that countries with high inter-bank rates export less to the US11, particularly in sectors that are highlyreliant on external financing. This effect is amplified during the financialcrisis. Finally, as underlined by Iacovone and Zavacka [2009], these patternsare not specific to the recent financial crisis. Based on a data set of devel-oping and developed countries covering a total of 23 banking crises between1980 and 2006, they conclude that banking crisis magnify the adverse effectof external financial dependence on sectors’ export growth rates12.

Both papers interestingly try to circumvent the endogeneity issue by usingan explanatory variable that interacts a country-level crisis indicator with asector-level financial vulnerability proxy. Because they capture variation infinancial vulnerability across sectors, regressions should be less likely tosuffer from a reverse causality going from exports to macroeconomic finan-cial conditions. Moreover, Iacovone and Zavacka [2009] reinforce the robust-ness of their results by showing that their findings still hold when restrictingthe sample to exogenous financial crisis, i.e. crisis that are due to contagionfrom other countries.

Finally, Berman et al. [2012] corroborate the adverse impact of financialcrisis on firms’ export performance by proposing an innovating measure offinancial friction: time-to-ship. In periods of financial crisis, time-to-ship notonly increases the cost of working capital, but also the probability that animporter will default. Relying on a sample of countries between 1950 and2009, they show that exports are reduced when the destination country isaffected by a financial crisis, and this effect is more pronounced when time-to-ship is long13.

10. As pointed out by Manova [2010], policies aiming to attract foreign financial flows(portfolio and direct investments) also mitigate firms’ financial constraint and enhanceexport performance.

11. The existence of a negative correlation between interbank lending rates and exports isalso documented by Feng and Lin [2013].

12. This result is corroborated by Bricongne et al. [2010] using firm-level data for Franceover the period 2000-2009.

13. Berman [2009] demonstrates that financial vulnerability also exaggerates the effect ofa currency crisis on exports. When exporting firms are indebted in foreign currency, adepreciation of the domestic currency increases the fixed cost of exports, thus reducing the

64 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

2.3. Micro-level evidence

The empirical literature also provides micro-level evidence concerning therelationship between financial constraint and export performance.

2.3.1. Firm-level evidence

When analyzing firm-level data, empirical studies assess the degree ofexternal financial dependence by relying on a wide range of indicators.This empirical approach relies on financial and accounting ratios to proxyfor the degree of firms’ financial vulnerability or health, while controllingfor other characteristics such as size or productivity. The most widelyconsidered dependent variable in econometric estimates is the extensivemargin (under various forms: the firm’s likelihood of exporting, the prob-ability of beginning to engage in exporting, the probability of continuingexporting activities, the likelihood that the firm ceases exporting, the num-ber of newly served export destinations or the number of stopped desti-nations). However, some papers also address the intensive margin (i.e.,the level of exporting).

Few empirical contributions find that a firm’s financial ratios do not affectthe extensive or intensive margins. Stiebale [2011], who focuses on asample of French firms between 1998 and 2005, and Lancheros and Demirel[2012], who consider a data set on Indian firms over the period 1999-2007,find that size and productivity are more important in explaining firms’ exportperformance than financial variables. Employing a data set on UK firmsbetween 1993 and 2003, Greenaway et al. [2007] estimate a GMM model andfind that exporters exhibit a lower leverage ratio (short-term debt over cur-rent assets) and a higher liquidity ratio (current assets minus current liabili-ties divided by total assets) than non-exporters. However, they demonstratethat this is primarily the result of a favorable impact of exports on firms’ex-post financial health. Doing this, Greenaway et al. [2007] interestinglyraise the issue of endogeneity in micro-level studies. As we will see below,the micro-level literature does not systematically correct for this problem;when it does, it uses disparate approaches.

The main findings of most papers is that firms’ financial characteristicsaffect export activities. More precisely, they are shown to affect extensivemargins to a greater extent than intensive margins. Berman and Héricourt[2010] consider three measures of financial health: the liquidity ratio (cash-flow over total assets), the inverse leverage ratio (total assets over total

number of exporting firms. This so-called balance-sheet effect is amplified when firms arefinancially constrained and have few tangible assets.

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 65

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

debt)14 and the ratio of tangible assets to total assets, which proxies for thelevel of pledgeable assets. Introducing instruments for explanatory variables(their lagged values and some other exogenous variables) allows theauthors to correct for endogeneity. Using a sample of 5 000 firms in 9 devel-oping countries over the period 2000-2005, they report that the three proxieshave very little impact on the level of exports but a significant and positiveeffect on a firm’s probability of being an exporter. More interestingly, whilethey have a weak effect on the probability of continuing exporting, theseproxies significantly increase the probability that a firm will begin exporting.This last result is in line with the findings of Bellone et al. [2010] whomeasure firms’ financial health by constructing a composite index, based ona wide range of cash-flow, net worth, repayment ability and profitabilityratios. Focusing on French firms over the period 1993-2005, the authors findthat firms with good financial health are more likely to begin exporting.Moreover, they deal with the reverse causality issue by showing that firms’export performances do not influence their ex-post financial situation. Engelet al. [2013] demonstrate that financial constraints also affect firms’ decisionto cease exporting. Exploiting a sample of French firms over the period2000-2002, they report that having a high (short-term or long-term) leverageratio or a low cash-flow ratio increases the probability that a firm will ceaseexporting. Finally, some papers consider the number of export destinations.In estimations conducted using a sample of Italian firms over the period1995-2003, Forlani [2010] finds that liquidity (measured by cash stock)increases the number of newly served exporting destinations. The robust-ness of this result is confirmed by instrumenting the financial variable by itslagged values and an equity ratio. It is also corroborated by Muûls [2012]who concentrates on Belgian firms over the period 1999-2005. She employsthe COFACE score, which evaluates the intensity of default risk (rangingfrom 3 for the highest default risk to 19 for the lowest). Using the laggedvalue of the score (rather than its current value) as the explanatory variableallows the author to control for the endogeneity bias. Conducting probit andOLS estimates, she establishes that although the score does not affect thelevel of exports, high-scoring firms are more likely to export and serve alarger number of destinations. Using a data set of French firms over theperiod 1996-2005, Askénazy et al. [2011] consider four financial vulnerabilityindicators: the leverage ratio, the inverse trade credit ratio (turnover overaccounts payable to suppliers), the equity to asset ratio (because equity isnot eligible as security on a loan) and a dummy variable that equals 1 if thefirm defaulted to its trade creditors. Their estimates reveal that the fourindicators not only negatively affect the number of new exporting destina-tions, but also raise the number of exits from existing exporting markets.However, the authors point out the difficulty to correct for endogeneity whenthe data set is not rich enough to provide suitable instruments for the finan-cial variable, i.e., firms’ default payment.

14. While the literature typically considers the leverage ratio as an indicator of firms’vulnerability, Harris and Li [2011] interpret it as an indicator of financial health because itsmeasures the firm’s ability to raise long term funds at a low tax cost, relative to equities.They find that having a high ratio of long-term debt to total assets significantly reduces thelikelihood that the firm will cease exporting.

66 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Among the countries considered in the empirical literature, China appearsparticularly interesting because it exhibits high export performance despiteimportant financial constraints. Based on a set of Chinese firms between2000 and 2008, Feensta et al. [2014] estimate a probit model and find that theratio of tangible assets increases the likelihood that a firm will export as wellas the export share. According to Manova et al. [2014], firms that are affili-ated with a foreign-owned multinational or a joint-venture should benefitfrom a privileged access to external financing. Therefore, they should facelower financial constraints than other firms belonging to the same sector.What distinguishes Manova et al.’s [2015] paper from those mentionedabove is that it interacts firm-level and sector-level financial health indica-tors. In addition to using the ratio of tangible assets, the authors exploitthree proxies for a sector’s financial vulnerability: the RZ indicator, the ratioof inventories to sales (which represents the working capital necessary tocover the duration of the production process) and the ratio of R&D expensesto total sales (which accounts for liquidity needs). Finally, being affiliatedwith a foreign-owned multinational or a joint-venture is demonstrated toincrease the level of a firm’s exports to a greater extent when the value ofthe proxy for the sector’s financial vulnerability is high. Interestingly, thesefindings contradict those of the papers mentioned above, which find no (ora very weak) effect of financial constraints on the intensive margin.

Finally, some papers exploit a natural experiment approach to checkwhether an observed financial reform affects firms’ exporting behavior. Byconsidering financial reforms as exogenous shocks that affect credit avail-ability, these contributions aim to circumvent the endogeneity issue. Kapooret al. [2012] use Indian firm-level data over the 1986-2006 period. They focuson two policy changes, observed in January 1998 and January 2000 respec-tively. The first reform implied the enlargement of the number of small-sizedfirms eligible for subsidized loans while the second one partly removed thismeasure. The authors show that firms that were affected by the first policychange increased by 20% the growth rate of export earnings. However, thesecond reform did not decrease firms’ credit and export, suggesting that thefirst policy change allowed them to engage in a beneficial long term bankingrelationship. Based on a sample of Pakistani firms between 1998 and 2003,Zia [2008] confirms the detrimental impact of credit rationing on firms’export behavior. He shows that the exclusion, in June 2001, of cotton fromthe list of products eligible for subsidized loans implied a reduction in pri-vately owned firms’ export while large, publicly listed (probably less finan-cially vulnerable) firms were not affected.

2.3.2. Matched bank-firm level evidence

A second empirical approach consists of matching firm- and bank-leveldata to construct measures of credit rationing. Because it requires an impor-tant work of data collection and processing, this method is less frequentthan the firm-level approach. However, in opposition to proxies derived fromfinancial statements, it provides a direct measure of the financial conditionsthat firms really incur.

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 67

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

This literature confirms the adverse impact of financial constraint onexport involvement. Relying on a dataset of Italian firms for 2001, Minettiand Zhu [2011] exploit a survey conducted by the Italian banking groupCapitalia. A firm is considered subject to rationing in 2000 if it had desired toobtain more credit at the market rate and demanded more credit than itultimately obtained. The authors demonstrate that rationed firms’ probabil-ity of exporting is 39% lower than that of non-rationed firms. Rationing isalso shown to reduce exports by more than 38%. Using the same survey butfor a larger period (1997, 2000 and 2003), Caggese and Cunat [2013] considerthat a constrained firm is a firm that was refused a loan recently, had wishedmore credit at the market interest rate or had paid an higher interest rate toobtain credit. The authors also show that being financially constrainedincreases firm’s extensive margin of trade. However, they obtain that finan-cial vulnerability does not affect their intensive margin. In the same vein,Paravisini et al. [2016] match a panel of Peruvian firms with credit data frombanks between july 2007 and june 2009. They report that a 10% decline inthe credit supply leads to a reduction of 2.3% in the annual export volume.In addition, a 10% increase in the credit supply increases the probability thatthe firm will continue exporting in a given market by 3.6%.

The robustness of these findings is ensured using an intrumental variableapproach. While Minetti and Zhu [2011] and Caggese and Cunat [2013]instrument firms’ financial constraint by the probability to be refused a loan(proxied by the number of savings banks and the number of new branchescreated by incumbent banks in the province the firm is located), Paravisini etal. [2016] use an instrument that accounts for the firm’s exposure to supplyshock (calculated according to the bank’s share in total firm credit and bankdependence on foreign funding).

Overall, the literature presented in this section shows that internationaltrade is highly dependent on external financing. From a theoretical perspec-tive, the need to finance fixed and variable costs associated with exportingactivities provides a potential explanation for why international trade is sig-nificantly affected by external financial conditions. The theoretical results areconfirmed by the empirical literature, at both the macro- and micro- levels.

3. Through which channel doesfinance affect international trade?

In Section 2, we explained that international trade strongly depends onexternal finance. But it is crucial to refine the analysis by exploring throughwhich channel finance affects international trade. The aim of this section isto examine this issue by concentrating on the trade finance channel. We firstpresent theoretical arguments concerning the role played by trade finance.We then provide empirical evidence about the trade finance channel.

68 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

3.1. The trade finance theory

In this subsection, we present the trade finance theory. We first define theconcept of trade finance. We then explain the role it plays in the transmis-sion of financial shocks.

3.1.1. What is trade finance?

According to Auboin [2009], 90 % of international trade involves tradefinance. A substantial literature has recently been developed regarding thisconcept, defined as the set of tools used to finance world trade.

The first form of trade finance is called trade credit. This corresponds tocredit one firm grants another. Cash-in-advance (CIA) consists of a buyer(importer) paying a seller (exporter) in advance. Symmetrically, openaccount (OA) consists in a seller (exporter) allowing a buyer (importer) todelay payment. Both CIA and OA also exist in the case of domestic activities.However users of CIA and OA face two main difficulties, which are amplifiedin the case of international trade. First, one of the two partners (the importeror the exporter) requires working capital to cover the delay between thepayment and the delivery of goods. Second, enforcement problems anddefault risk are more substantial in the case of international trade, as aforeign partner is particularly difficult to monitor (Elligsen and Vlachos[2011]). For these reasons, OA is used when the financial cost is low in theexporter country (and the enforcement framework in the importer country isrobust) while CIA is more attractive when the financial cost is low in theimporter country (and the enforcement framework in the exporter country isrobust) (Schmidt-Eisenlohr [2013]; Hoefele et al. [2014])15. Moreover, forfinancially constrained exporting firms, OA also acts as a positive signal offirm quality, facilitating the firm’s efforts to obtain bank credit (Eck et al.[2014a]).

Exporting firms also resort to intermediated trade finance, which involvesa third party (i.e., a bank, an insurance company) between the importer andthe exporter. According to a survey conducted by the International MonetaryFund-Bankers Association on Finance and Trade/International Financial Ser-vices Authority, letters of credit are the primary tool of intermediated tradefinance, which represents approximatively 47% of trade finance compared to26% for OA transactions and 27% for CIA transactions (IMF-BAFT/IFSA[2011]). Amiti and Weinstein [2011, p. 7] provide a clear description of thisdevice: “The terms of the sales contract often require the importer to ask its“issuing bank” to issue a letter of credit guaranteeing payment for the

15. However, the role of the legal environment becomes less important when the importerand the exporter have developed a close relationship (Antràs and Foley [2015]).

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 69

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

imports upon certification that the exporter has met the terms of the con-tract. [...] using the letter of credit as collateral, the exporter will often obtaina working capital loan from its bank (often called the advising bank) to coverthe production costs of the goods. The third step in the process involves thetransfer of the goods to the carrier and the title of the goods to importers’issuing bank. Assuming all documents are in order, the issuing bank willissue a “bankers’ acceptance” to the exporter guaranteeing payment at afuture time, often around 90 days after the goods arrive.” Letters of creditthus solve the working capital issue. Moreover, as the transaction is trans-ferred to the exporter’ and importer’s banks, letters of credit also alleviatethe enforcement problem. Consequently, a letter of credit is preferred to CIAand OA when the financial cost of working capital is low and the enforce-ment frameworks in both the exporting and importing countries are weak(Schmidt-Eisenlohr [2013]).

Another type of intermediated trade finance device, which is particularlypopular in Europe, is an export credit guarantee (Egger and Ulr [2006]; Vander Veer [2014]). The guarantee is provided by public export credit agenciesor private insurers, such as Euler Hermes, Atradius or Coface, which areknown as the “Big Three” (Van der Veer [2014]). As underlined by Auboinand Engemann [2014], trade credit insurance can be used in the case of OAor letters of credit. In the first case, the insurer compensates the exporter ifthe importer fails to pay while in the second one, the insurer protects theimporter and the exporter’s banks against any default. By reducing the riskfor trading partners, insurance contracts increase international trade.According to Van der Veer [2014], they also have a multiplier effect by pro-viding information to non-insured firms about a firm or a country andencouraging them to export to this destination.

3.1.2. Trade finance and the transmission channelfor financial shocks

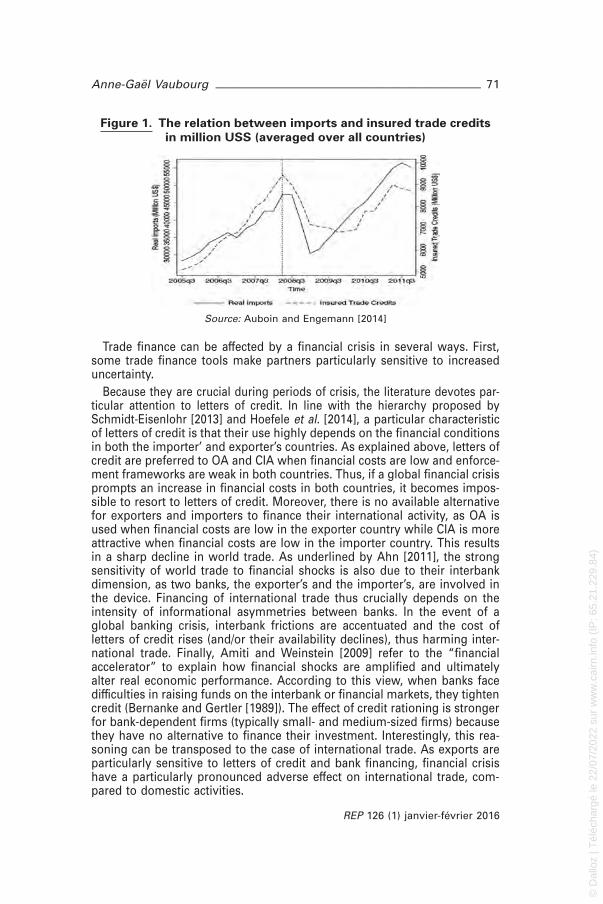

The recent financial crisis and the trade collapse that followed in 2009have attracted particular attention to trade finance. The WTO was one of thefirst to stress the importance of trade finance as a key driver of the dramaticdecline in international trade. According to Auboin [2009], 10-15% of thedecrease in international trade could have been due to a decline in tradefinance. As depicted in Figure 1, real imports and insured trade creditpresent similar trends over the period 2005-2011. They both exhibit a sharpdecline during 2008. In addition, the reduction in trade finance has beenparticularly important in emerging countries. Auboin [2009] reports thatspreads on 90-days letters of credit issued by emerging or developing coun-tries rose from 10-16 bp to 250-500 bp during 2008. These facts suggest theneed to explore the theoretical transmission channels from trade financeshocks to trade in greater detail.

70 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Trade finance can be affected by a financial crisis in several ways. First,some trade finance tools make partners particularly sensitive to increaseduncertainty.

Because they are crucial during periods of crisis, the literature devotes par-ticular attention to letters of credit. In line with the hierarchy proposed bySchmidt-Eisenlohr [2013] and Hoefele et al. [2014], a particular characteristicof letters of credit is that their use highly depends on the financial conditionsin both the importer’ and exporter’s countries. As explained above, letters ofcredit are preferred to OA and CIA when financial costs are low and enforce-ment frameworks are weak in both countries. Thus, if a global financial crisisprompts an increase in financial costs in both countries, it becomes impos-sible to resort to letters of credit. Moreover, there is no available alternativefor exporters and importers to finance their international activity, as OA isused when financial costs are low in the exporter country while CIA is moreattractive when financial costs are low in the importer country. This resultsin a sharp decline in world trade. As underlined by Ahn [2011], the strongsensitivity of world trade to financial shocks is also due to their interbankdimension, as two banks, the exporter’s and the importer’s, are involved inthe device. Financing of international trade thus crucially depends on theintensity of informational asymmetries between banks. In the event of aglobal banking crisis, interbank frictions are accentuated and the cost ofletters of credit rises (and/or their availability declines), thus harming inter-national trade. Finally, Amiti and Weinstein [2009] refer to the “financialaccelerator” to explain how financial shocks are amplified and ultimatelyalter real economic performance. According to this view, when banks facedifficulties in raising funds on the interbank or financial markets, they tightencredit (Bernanke and Gertler [1989]). The effect of credit rationing is strongerfor bank-dependent firms (typically small- and medium-sized firms) becausethey have no alternative to finance their investment. Interestingly, this rea-soning can be transposed to the case of international trade. As exports areparticularly sensitive to letters of credit and bank financing, financial crisishave a particularly pronounced adverse effect on international trade, com-pared to domestic activities.

Figure 1. The relation between imports and insured trade credits

in million USS (averaged over all countries)

Source: Auboin and Engemann [2014]

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 71

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

3.2. Assessing the empirical validityof the trade finance theory

We now turn to the empirical assessment of the theory of trade finance.We first determine whether trade finance promotes world trade. We thenexamine the extent to which banking crisis are particularly harmful for inter-national trade.

3.2.1. Does trade finance increase international trade?

The first testable assumption derived from trade finance theory is thattrade financing boosts international trade.

The primary difficulty in empirical investigations is to ensure that the tradecredit used in econometric estimates only relates to exporting activities andnot to domestic ones. For example, Levchenko et al. [2009] find that neitherthe amount of credit extended to firms by suppliers nor the amount of creditextended by firms to customers can explain the observed decline in inter-national trade. However, their trade credit indicators are obviously biasedbecause they not only refer to international but also to domestic trade.Similarly, Eck et al. [2015] and Eck [2012] exploit a survey conducted by theEuropean Bank of Reconstruction and Development and the World Bank.Estimating linear probability and OLS models using a sample of Germanfirms in 2004, Eck et al. [2015] show that CIA had a favorable impact on theextensive and intensive margins. Based on a larger sample of firms from 27countries from European and Central Asia in 2005 and 2009, Eck [2012] alsofinds that CIA promoted international trade, especially during the recentfinancial crisis. Employing OLS regressions, the author reveals that CIAincreases firm export probabilities and this impact is stronger in 2009 than in2005. In addition, CIA is shown to boost firms’ intensive margins in 2009 butnot in 2005. However, the data set used in these two papers does not indi-cate whether CIA is used for domestic or international activities.

Because it gathers detailed transaction-level data about a US based exporterover the 1996-2009 period, the data set used by Antràs and Foley [2014] avoidsthis pitfall. It also allows to refine previous analysis by comparing how differ-ent trade finance tools react to a financial shock. Their estimate reveal that CIAwas particularly sensitive to increased uncertainty implied by the 2008 crisis.When it broke out, importers that used CIA before the crisis reduced theirpurchases by larger amounts than customers resorting to other trade financecontracts. Restricting the analysis to trade insurance, which by definition onlyapplies to export activities, also allows to address measurement issues.Auboin and Engemann [2014] employed data from Berne Union, which com-prises private and public export credit insurers representing approximately10% of the world trade, for approximately 100 countries during the period2005-2011. The authors demonstrate that insured trade credit extended forexports to a given country promotes imports in this country. Focusing onprivate export insurance, Van der Veer [2014] estimates a gravity model on a

72 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

sample of 25 countries over the period 1992-2006. The author finds that a risein the number of privately insured exporters in a given country significantlyincreases the intensive margin for this country. He also reports a favorableeffect of private insurance on the intensive margin, but only for a subsample ofvery risky countries. Finally, Felbermayr and Yalcin [2013] examine the roleplayed by public export insurance provided by the German government(through the Hermes guarantees) between 2000 and 2009. Analyzing sector-level data, the authors demonstrate that public guarantee fosters exports.Based on a sample of Garman firms over the 1991-2003 period, Moser et al.[2008] show that the export-promoting role of Hermes guarantees is robustto introducing a measure of political risk (reflecting the level of corruption,government stability, internal conflicts, etc.) in the estimate. Egger and Url[2006] report similar results for public export insurance in Austria during theperiod 1996-2002. Overall, these results support the view that trade finance,notably trade insurance, is a driver of world trade. They provide a rationalefor voluntary policies intended to promote trade finance, notably thoseimplemented by the WTO (Auboin [2011]), regional development banks(Beck et al. [2011]) and Berne Union (Morel [2011]).

3.2.2. Are banking crises particularly detrimentalto international trade?

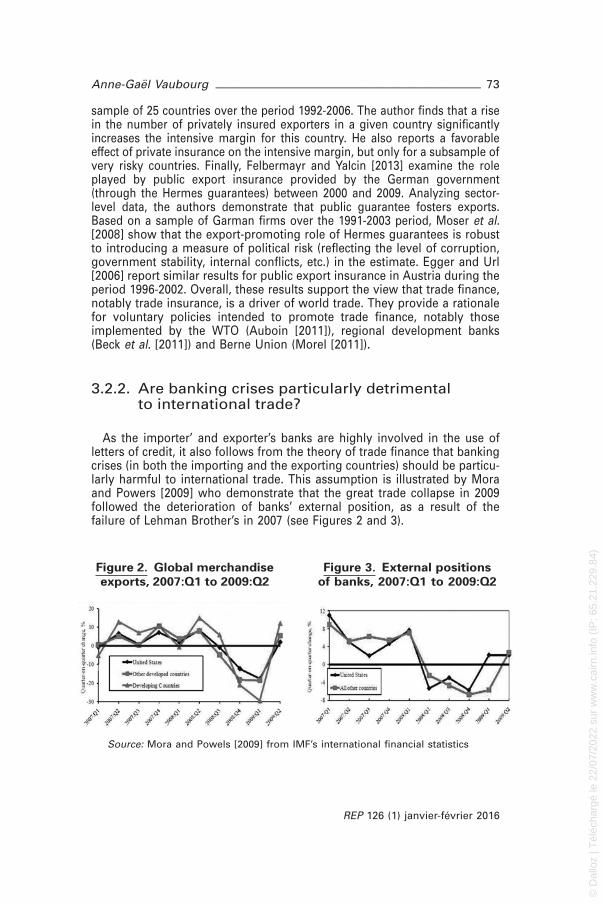

As the importer’ and exporter’s banks are highly involved in the use ofletters of credit, it also follows from the theory of trade finance that bankingcrises (in both the importing and the exporting countries) should be particu-larly harmful to international trade. This assumption is illustrated by Moraand Powers [2009] who demonstrate that the great trade collapse in 2009followed the deterioration of banks’ external position, as a result of thefailure of Lehman Brother’s in 2007 (see Figures 2 and 3).

Figure 2. Global merchandise

exports, 2007:Q1 to 2009:Q2

Figure 3. External positions

of banks, 2007:Q1 to 2009:Q2

Source: Mora and Powels [2009] from IMF’s international financial statistics

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 73

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Econometric studies provide further support for this view. Berman andMartin [2012] concentrate on exports by countries in Sub-Saharian Africa(SSA) between 1976 and 2002. Controlling for variations in the importers’GDP, the authors perform OLS estimates and report that a banking crisis inthe importing country had a negative effect on exports from countries inSSA one year, two years and three years after the crisis. The average devia-tion from the level of imports predicted by a gravity model lies between– 8% and – 16% depending on the specification. Similarly estimating Gener-alized Least Square (GLS), Instruments Variables (IV) and GMM modelsusing a sample of 10 emerging countries in crisis (Malaysia, Philippines,Thailand, Indonesia, Korea and Russia in 1997-1998, Brazil in 1998-1999,Argentina and Turkey in 2000-2001 and Mexico in 1994-1995), Ronci [2006]shows that 6% of the decline in imports and 10% of the drop in exports isexplained by a domestic banking crisis. Focusing on the duration of exportrelationships rather than on the volume of exchange flows, Beverelli et al.[2011] obtain the same result. Based on a data set of exports from 157 coun-tries to the United States between 1996 and 2009, they estimate a Coxproportional hazard model and finally demonstrate that a banking crisis inthe exporting country increases the probability that a trade relationship isinterrupted by approximately 11 %.

However, these contributions do not provide clear evidence that theadverse effects of a banking crisis are more severe with respect to worldtrade than domestic activities. Amiti and Weinstein [2011] address this issue.Their study is particularly interesting for at least two reasons. First, theauthors focus on Japan, which is one of the largest exporters in the worlddespite having faced numerous banking crises since the 1990s. Second,while many contributions are based on aggregate measures of firms’ finan-cial conditions, the authors match a sample of Japanese firms with a bankdata set for the period 1990-2010 to explore the impact of bank health (mea-sured by the bank’s market-to-book ratio) on firms’ exports. Their estimatesprovide evidence that a decline in a bank’s financial health implies a reduc-tion in exports for its customers. More interestingly, the authors reveal thatwhen firms’ exports are replaced by domestic sales in the estimation, theeffect of banks’ financial health is weaker. Their findings corroborate thetheoretical prediction that banking crisis have a more substantial effect oninternational trade than domestic activities. This explains why the 2009 col-lapse in trade was so severe compared to the decline in GDP.

Finally, this section emphasizes trade finance as a determinant of worldtrade and a powerful transmission channel for financial shocks. Moreover,as trade finance (notably letters of credit) is generally intermediated bybanks, this section highlights the key role played by banking crises in deter-mining international trade patterns, compared to domestic activities.

74 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

4. Beyond the causal effect of financeon international trade: extensionsand developments

The aim of this section is to propose certain extensions and developmentsbeyond the effect of finance on trade studied in the previous sections. Wefirst address the finance-trade causality issue. We then consider the exist-ence of institutional complementarity and substitutability between tradeopenness and financial reforms.

4.1. International trade as a driver of finance

The primary objective of the literature presented in previous sections is toexamine the impact of finance on international trade. In this subsection, weconsider empirical and theoretical arguments suggesting that trade couldalso drive finance. After some micro-level considerations regarding theeffect of exports on firms’ financial constraints, we adopt a macro-levelapproach and explore the extent to which international trade increasesfinancial development.

4.1.1. Does export involvement alleviate firms’financial constraint?

At the micro-level, investigating the existence of a causal link runningfrom international trade to finance consists in examining whether beinginvolved in export activities mitigates firms’ financial constraint.

Some theoretical arguments suggest that export participation allows firmsto lessen the severity of their financial constraint (Greenway et al. [2007]).First, exports may facilitate firms’ access to international financial marketsand provide them with the opportunity to better diversify their risk andsources of financing. Second, provided that national financial conditions arenot perfectly correlated, export participation could make firms less depen-dent on the domestic business cycle. Finally, being present in a foreignmarkets can also be interpreted as a favorable signal concerning the pro-ductivity of the firm and its ability to face export-specific costs. This mayimprove its access to capital providers and its financial conditions.

Several papers examine the empirical relevance of these theoretical pre-dictions. One approach distinguishes two types of firms: those exporting ata given date and those that do not. It is then possible to estimate andcompare the average level of financial vulnerability or health indicators forthe two groups over the period following the considered date. Following this

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 75

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

approach, Greenway et al. [2007] conclude that there are ex-post financialgains from exporting. The authors report that the average liquidity ratio overthe period 1993-2003 is significantly higher for firms that exported in 1993than for firms that did not. This advantage is evaluated at 5.6%. Symmetri-cally, the average leverage ratio over the same period is 8.2% weaker forexporters in 1993 compared to non-exporters. However, these results seemto lack robustness as some other papers do not find any impact of exportingactivities on firms’ financial constraints. Forlani [2010] finds no effect ofbeing an exporter on ex-post cash-flow or debt equity ratios. In the samevein, Bellone et al. [2010] document that exporting does not affect theex-post liquidity ratio nor the ex-post composite financial health index.

Another approach consists in estimating investment (or inventory) equa-tions augmented with a financial variable for exporters and non-exporters,in line with the empirical literature on the financial accelerator (Fazzari, Hub-bard and Petersen [1988]). As the sensitivity of investment (or inventories) tothe financial indicator is interpreted as a measure of financial constraint, theconcept is to compare this sensitivity accross both types of firms. Shaver[2011] estimates a random effects Tobit model using a sample of Spanishfirms between 1990 and 1998. He shows that the ratio of investment oversales becomes more responsive to cash-flow (measured by the ratio ofmargin over sales) when the firm does not export than when it does. Guari-glia and Mateut [2010] obtain similar findings using a data set of UK firmsover the period 1993-2003. Employing a GMM approach, they report thatnon-exporting firms exhibit greater sensitivity of inventory growth to thefinancial variable (measured as the ratio of short-term debt, primarily bankloans, over the sum of short-term debt and supplier credit) than exportingfirms. These results suggest that export participation makes financial con-straints less binding.

Finally, rather than considering investment or inventories, Görg and Spa-liara [2014] focus on firms’ failure probabilities. Another novelty of theirstudy, based on a sample of French and UK firms between 1998 and 2005, isthat they distinguish four types of exporters: starters (that begin exportingduring the sample period), exiters (that cease exporting but continue toparticipate in the domestic market), continuers (that export continuouslyover the sample period) and switchers (that start and stop exporting morethan once). The authors find that the leverage ratio raises the firm’s prob-ability to fail. Moreover, this effect is amplified for starters and exiters butmitigated when the firm is a continuer or a switcher. These findings refinethe results obtained when restricting the analysis to comparing exportersand non-exporters. They suggest that the upfront costs induced by exportparticipation are particularly large when firms enter export markets or haveto cease exporting due to the severity of their financial constraints. Other-wise, the favorable effects of export participation mentioned above are atplay, thus reducing the responsiveness of the failure probability to the finan-cial variable.

76 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

4.1.2. Does international trade spur financialdevelopment?

At the macro-level, the finance-trade causality issue essentially concernsinvestigating whether international trade increases the level of financialdevelopment.

In their seminal paper, Rajan and Zingales [2003] adopt an “interestgroup” perspective to show that financial development is highly dependenton the degree of trade openness. The starting point of their analysis is theobservation that many countries were more highly financially developed atthe beginning and end of the 20th century than between 1913 and 1990. Toexplain this U-shaped pattern of financial development, the authors focus onthe political power of incumbent firms and financial institutions. Let us firstconsider a country that is closed to trade. When the financial system devel-ops, free access to international financial markets increases, raising the levelof competition, transparency and contract enforcement. It thus becomesmore difficult for financial institutions to extract profits from rents and infor-mal connections with entrepreneurs. Therefore, financiers do not favorfinancial development. This is also the case for incumbent firms, as financialliberalization is likely to allow potential entrants, that previously had nopriviliged relationship with incumbent financiers, to be financed by foreignfinancial institutions. Finally, incumbent firms and financiers both havestrong incentives to oppose financial development. Let us now consider acountry that is open to trade. Contrary to the previous case, it can be shownthat some incumbent firms now favor financial liberalization. Because theleast robust industrial firms face competition from foreign firms, their rentsand profits are reduced. It becomes more difficult for them to obtain financ-ing from incumbent financiers. They thus have an incentive to advocate forstronger financial liberalization to benefit from less opaque relationshipsand improved financial conditions, in terms of interest rates and the avail-ability of finance. Rajan and Zingales [2003] conclude that when trade flowsare liberalized, more private interests favor financial deregulation. In thisview, trade openness shapes financial development: the protectionism thatprevailed during a large part of the 20th century may have created a politicalclimate that persistently hindered financial development.

To assess the validity of their theoretical conclusion, Rajan and Zingales[2003] rely on US data from the years 1913 and 1990. They regress anindicator of financial development (successively, the ratio of equity marketcapitalization to GDP, the number of listed domestic companies divided bypopulation and the ratio of securities issued to GDP) on the ratio of tradevolume over GDP, an index of industrialization and interactions of theseindicators. Their estimates suggest that openness not only promotes finan-cial development but also amplifies the positive effect of industrialization onfinancial development.

The literature provides further empirical validation of the Rajan and Zin-gales’s [2003] argument. Herger et al. [2008] rely on a data set containinginformation on 128 countries during the 1990s. Their OLS and Two-Stage

Anne-Gaël Vaubourg —————————————————————————————————————————————————— 77

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

Least Squares (2SLS) estimates reveal that trade openness (measured by thesum of imports and exports as a share of GDP) positively affects the ratio ofprivate credit to GDP and the ratio of market capitalization to GDP. Baltagi etal. [2008] corroborate this result using a data set on 42 developing countriesbetween 1980 and 2003. Finally, based on a sample of 88 countries between1960 and 1999, Huang and Temple [2005] also conclude that lagged open-ness has a positive effect on financial development, especially for the 53lower-income countries in their sample.

The impact of international trade on finance can also be explained using acomparative advantage approach (Do and Levchenko [2007]). When tradeflows are liberalized, countries that export financially intensive goods expe-rience an increase in demand for financing because they have a comparativeadvantage in this sector. This induces higher financial developement. Con-versely, financial systems are less well developed in economies that have acomparative advantage in the weakly financially intensive, primary goodsector. In this view, financial development is determined by comparativeadvantages and trade patterns. Do and Levchenko [2007] perform OLS esti-mates on panel data from 96 countries over the period 1970-1999. For eachcountry in their data set, they construct a measure of the so-called “externalfinance needs of exports”, defined as the sum of sector-level RZ indicators,weighted by a sector’s share of exports compared to total manufacturingexports. In line with their theory, they report that external finance needs ofexports have a significant and positive effect on financial development asmeasured by the ratio of private credit to GDP.

If international trade drives financial behavior, there may ultimately exist abidirectional causality between the two phenomena. According to Ju andWei [2011] the direction of causality between finance and trade is deter-mined by threshold effects and closely related to the level of financial insti-tutional quality, approximated by the cost of financial intermediation, thequality of corporate governance and the level of property rights protection.When an economy has low-quality institutions, interest rates on savingsremain very low such that a share of initial capital remain unused. In thiscase, the initial factor endowment has weak effect on output and prices.Financial development (through improved financial intermediation effi-ciency) thus provides a comparative advantage to the economy and is theprimary determinant of output and trade. When an economy has high-quality institutions, causal relationship is reversed. The initial endowmentbecomes the main determinant of production and trade, which in turn deter-mine the level of financial development. However, according to Svalerydand Vlachos [2002] the causality direction does not depend on the institu-tional environment: finance and trade affect each other simultaneously. Onthe one hand, trade has a positive impact on financial development, asfinancial markets help agents to protect against the risks that emerge fromtrade openness (Newbery and Stiglitz [1984]). On the other hand, the emer-gence of financial markets, by providing possibilities for risk sharing,encourages trade liberalization. Gathering a data set of 138 countriesbetween 1960 and 1994, the authors confirm their theoretical argument.They demonstrate that there is not only Granger-causality from financialindicators (the ratio of liquid liabilities to GDP and the ratio of credit toprivate firms to GDP) to trade openness, but also from trade openness to

78 —————————————————————————————————————— Finance and International Trade

REP 126 (1) janvier-février 2016

© D

allo

z | T

éléc

harg

é le

22/

07/2

022

sur

ww

w.c

airn

.info

(IP

: 65.

21.2

29.8

4)©

Dalloz | T

éléchargé le 22/07/2022 sur ww

w.cairn.info (IP

: 65.21.229.84)

both financial development indicators. Pham [2010] confirms this resultusing a smaller sample of 29 Asian countries between 1994 and 2008. Over-all, the existence of a bidirectional causality between trade and finance hasimportant implications. Notably, it implies the existence of a vicious circlewhen a financial crisis occurs since the subsequent contraction in tradeflows may in turn deepen the financial crisis.

4.2. Institutional interactions between financialand trade reforms

In addition to the question of the direction of their causal relationship,finance and trade may also be linked through institutional interactions. Wefirst explore both forms of interactions, i.e., substitutability and complemen-tarity, between financial and trade reforms. We then consider furtheravenues for research in this area.

4.2.1. Interactions between financial deregulation andtrade liberalization: substitutes or complements?

As underlined in previous sections, because financial development allevi-ates the financial constraints of vulnerable firms by facilitating their accessto finance, it promotes their exports. Financial development and trade open-ness thus provide the same service to the economy by boosting world trade.Therefore, financial reforms may be particularly favorable to internationaltrade when trade restrictions are important, i.e., when trade costs are high.Symmetrically, trade openness policies may be more effective when theeconomy is poorly financially developed. These arguments provide supportfor the view that financial deregulation (in terms of openness to foreignequity flows) and trade liberalization are substitutes. Manova [2008] usesdata on 91 countries between 1980 and 1997 to empirically confirm thistheoretical intuition. She measures the degree of trade liberalization usingtariff levels, the degree to which the black market exchange rate is below theofficial one and the extent of the state monopoly on exports. Ultimately, shedemonstrates that the positive impact of equity market liberalization onfirms’ exports is amplified when trade policy is restrictive. This result isconsistent with the view that financial liberalization and trade opennessreforms are institutional substitutes. When one liberalization policy is imple-mented, the other has a smaller effect on export performance.

In a second strand of literature, financial and trade reforms are consideredas complementary. Indeed, some theoretical contributions establish thatwhen focusing on productivity or growth rather than international tradeflows, the effects of financial deregulation and trade liberalization mayamplify each other. To address this issue, Taylor [2010] introduces financialconstraint into the heterogeneous firm trade model developed by Melitz[2003]. By reducing trade costs, trade openness promotes exports. It also