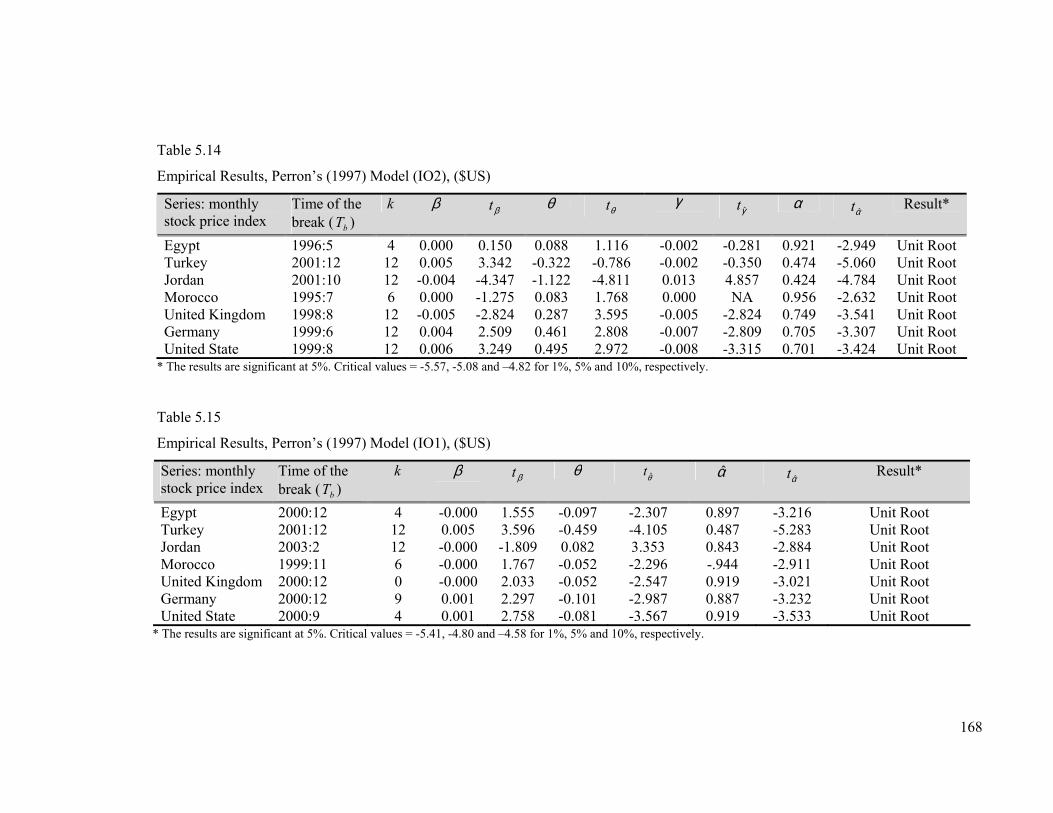

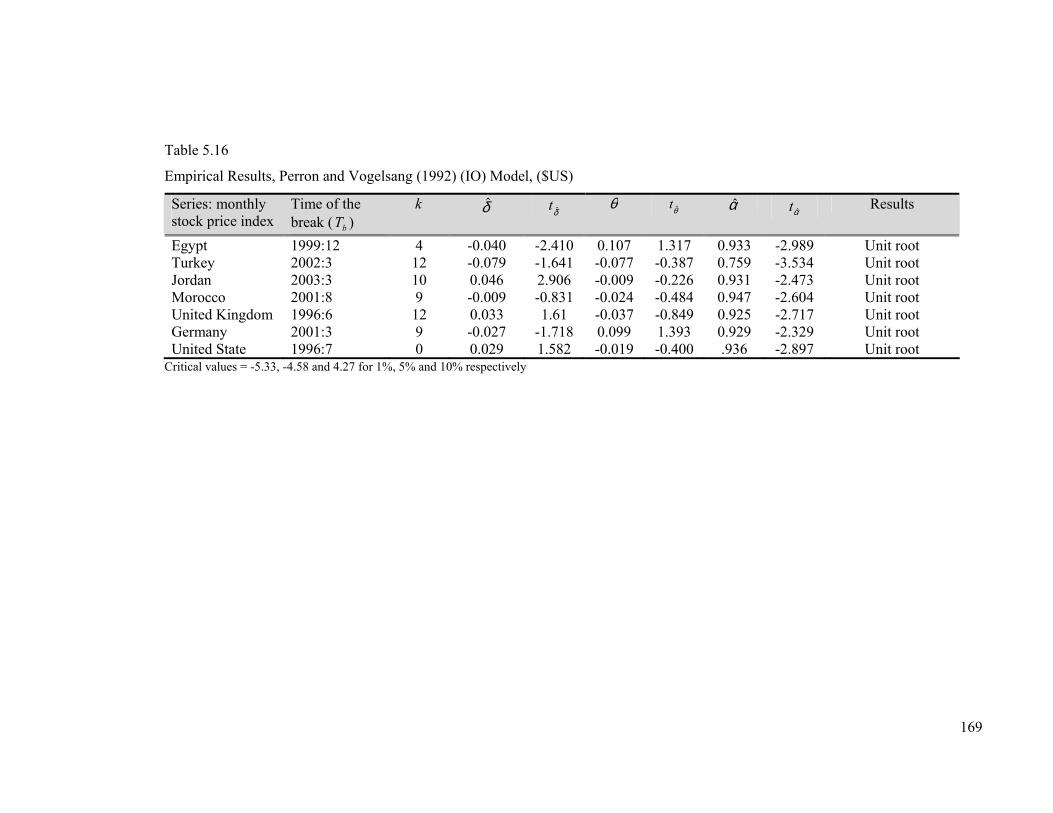

Embed Size (px)

Citation preview

University of Wollongong Thesis Collections

University of Wollongong Thesis Collection

University of Wollongong Year

Financial integration of the MENA

emerging stock markets

Hazem Ali MarashdehUniversity of Wollongong

Marashdeh, Hazem Ali, Financial integration of the MENA emerging stock markets, PhDthesis, School of Economic and Information Systems, University of Wollongong, 2006.http://ro.uow.edu.au/theses/543

This paper is posted at Research Online.

http://ro.uow.edu.au/theses/543

NOTE

This online version of the thesis may have different page formatting and pagination from the paper copy held in the University of Wollongong Library.

UNIVERSITY OF WOLLONGONG

COPYRIGHT WARNING

You may print or download ONE copy of this document for the purpose of your own research or study. The University does not authorise you to copy, communicate or otherwise make available electronically to any other person any copyright material contained on this site. You are reminded of the following: Copyright owners are entitled to take legal action against persons who infringe their copyright. A reproduction of material that is protected by copyright may be a copyright infringement. A court may impose penalties and award damages in relation to offences and infringements relating to copyright material. Higher penalties may apply, and higher damages may be awarded, for offences and infringements involving the conversion of material into digital or electronic form.

Financial Integration of the MENA Emerging Stock

Markets

A thesis submitted in fulfillment of the requirements for the award of the degree

Doctor of Philosophy

from

University of Wollongong

by

Hazem Ali Marashdeh

BEc (Economics and Accounting), Jordan

MEc (Economics), Jordan

School of Economic and Information System

2006

ii

Certification

I, Hazem Marashdeh, declare that this dissertation, submitted in fulfillment of the

requirement for the award of Doctor of Philosophy in the faculty of commerce,

University of Wollongong, is wholly my own work unless otherwise referenced or

acknowledged. The document has not been submitted for qualifications at any other

academic institution.

Hazem Marashdeh

December 2005

iii

Dedication

To the dearest friend

my father

Ali Marashdeh

iv

Acknowledgments

I would like to express my sincere gratitude and appreciation to my supervisor

Associate Professor Edger Wilson for his supervision, guidance and encouragement

throughout the study. His profound knowledge and experience provided me with the

opportunity to broaden my knowledge and to make a significant progress. Also I would

like to thank Associate Professor Amnon Livermore for his supervision through most of

the study. His insight into economic theory and creative comments were of a great

assistance. And I would like to thank Dr. Abbas Valadkhani for his supervision in the

final stages of the study. His exceptional editing skills and invaluable suggestions

always inspired me to strive for quality work.

I would like to thank my wife Diana Bakir for her love, care and extraordinary

support throughout my long study period. Dear Diana, you will always be in my heart.

I am very grateful to my parents, for their blessing, encouragement and support

throughout the duration of this study. Also I would like to thank my dearest brother,

Mones and my sisters, Arwa, Rabab, Aram, Demh, Layla, Lama and Farah for their

encouragement and support. Also, I would like to thank my father and mother-in-law

for their support.

Also, I would like to express my sincere thanks to my colleagues at the faculty

of commerce, Akhsyim Afandi, Mosayeb Bahlavani, Min Shrestha, Maen Al-hawari

and Reetu Verma. I have greatly benefited from their comments throughout my study

period. Finally, I would also like to thank Dr. Aktham Maghyereh for his help at the

early stage of this study.

v

Abstract

The main objective of this study is to examine the financial integration among

four emerging stock markets in the Middle East and North Africa (MENA) region,

namely, Egypt, Turkey, Jordan and Morocco. Their interrelationships with three

developed markets, the US, UK and Germany, are also examined. The motivation

behind this study is that, although a lot of research has been focused on stock market

integration, the emphasis has been mostly on developed markets. Stock market

integration in the MENA region has not been investigated deeply enough despite the

region being of a global economic and political importance.

To attain this objective, the study conducts recent econometric techniques on the

monthly time series of stock market price indices. It starts with testing for a unit root in

the presence of structural change at an unknown time of the break, using the

Innovational Outlier (IO) model. To empirically examine the financial integration, the

study utilizes the newly proposed autoregressive distributed lag (ARDL) approach to

cointegration. The ARDL approach has been recognized as more preferable in

estimating the long-run equilibrium relationship than other cointegration approaches in

small samples with mixed order process. Finally, the study explores the short and long-

run dynamic relationships among these markets using Granger-causality within a

correctly specified vector error correction model (VECM).

The empirical results indicate that all variables show evidence of non-

stationarity, even in the presence of structural change. The endogenously determined

times of the breaks for all markets coincide with observed real events which affected

each market. This result is consistence with the efficient market hypothesis as the non-

stationarity random walk is associated with the weak form of the efficient market

hypothesis. Consequently, this result emphasises that the stock markets in the MENA

region are efficient.

The cointegration test results show that there are long-run equilibrium

relationships among all stock markets in the MENA region. This indicates that stock

markets in the MENA region move together in the long-run. So, at the regional level all

markets are integrated. At the same time no long-run equilibrium relationship is found

between MENA markets and developed markets. This means that the MENA stock

markets are segmented from developed markets. However, Egypt was the exceptional

vi

case; the study found that the stock market of Egypt has long-run equilibrium

relationship with the US and UK markets.

The implications of these findings are analysed at two levels, the regional and

international. At the regional level, the existence if cointegration among the MENA

markets implies the existence of the law of one price (LOOP). This means that the

potential of regional investors for obtaining abnormal profits through portfolio

diversification is limited in the long-run. The reason for this is that as the MENA stock

markets are cointegrated, abnormal profits will be arbitraged away in the long-run.

However, despite no arbitrage opportunities in the long-run, investors can still achieve

arbitrage profits through portfolio diversification in the short-run.

At the international level, the results show that stock markets in Turkey, Jordan

and Morocco are not integrated with developed markets. This means that there is no

long-run impact from developed stock markets towards these markets. However, a long-

run relationship is found between Egypt and both US and UK when Egypt is a

dependent variable. Based on these results, there are opportunities for international

investors to obtain long-run gains through international portfolio diversification in stock

markets of Turkey, Jordan and Morocco. Also at the same time, investors from these

three countries have the opportunities to obtain long-run gains through investing in

developed markets. The existence of long-run relationships between Egypt and both US

and UK implies that the potential for investors from the Egyptian stock market to obtain

abnormal profit through portfolio diversification in the US and UK is limited in the

long-run. However, there are opportunities for achieving abnormal profit by investing in

Germany as it is not cointegrated with the MENA markets. In the short-run, arbitrage

opportunities and possible profits may also be achieved from diversification as the

LOOP may not hold.

In addition to these findings, an important contribution is made by this study. It

contradicted Granger’s (1986) theory on the relationship between the existence of

cointegration and market efficiency. Granger (1986) asserted that the existence of

cointegration between two stock prices implies the ability to predict each price

movement, which indicates market inefficiency. Also, this study does not fully agree

with another stream of studies, such as Wallace (1992), Baffes (1994), Engle (1996),

Ahlgren and Antell (2002) and Masih and Masih (2002) in which they asserted that

cointegration does not necessarily imply market inefficiency or efficiency. However,

what this study tries to bring out is that if cointegration exists between two stock

vii

markets then these markets are efficient in the long-run because the existence of

cointegrated vector implies the (LOOP). Therefore, little or no arbitrage opportunities or

possible benefit can be achieved from the diversification of a portfolio across markets.

However, with the short-run error correction model (ECM), there could exist arbitrage

opportunities and possible benefits from diversification. That is, the LOOP may not

hold in the short run.

The results of Granger-causality test based on the vector error correction model

(VECM) reveal the existence of short-run causal relationships among the MENA

markets. This means that these markets influence each other. Also, the results show that

developed markets influenced stock markets in the MENA region. In the short-run,

there is unidirectional Granger-causality running from stock prices in Turkey, Morocco,

the US and UK to Egypt. Also, there is unidirectional Granger-causality running from

Germany and the US towards Turkey. In addition, The UK and Turkey are found to

Granger-cause the stock prices in Jordan. Finally, there is a unidirectional Granger-

causality from Germany to Morocco.

Finally, despite the empirical results show that there is a possibility of an

increase in the portfolio equity flow to the MENA stock markets, the statistics of

portfolio equity flow show little portfolio inflow to the region from developed countries

over the period of study. Some of the reasons behind this situation are that most of these

markets are still from some perspective underdeveloped, vulnerable to macroeconomic

shocks and political instability in the region. Based on this, the study suggests that huge

efforts should be carried on to improve the institutional reforms in these markets and

increase the degree of openness for foreign capital. Also increasing the markets

capitalization and adopting new technology are very crucial factors for attracting equity

portfolio to the region.

viii

Table of Contents

Certification ii Dedication iii Acknowledgment iv Abstract v Table of Contents viii List of Tables xi List of Figures xii Abbreviations xiii Publication from the research xiv Chapter 1. Introduction

1.1 Background of the Study 1

1.2 Objective of the Study 4

1.3 Data and Methodology 7

1.3.1 Data Sources 7

1.3.2 Method of the Study 8

1.4 Structure of the Study 9

Chapter 2. The Early Theoretical Models Relating to Stock Market Integration

2.1 Introduction 12

2.2 The Notion of Stock Markets Integration 13

2.3 The Early Theoretical Studies Relating to Stock Markets Integration 18

2.4 Asset Pricing Model for Testing Stock Market Integration 22

2.5 Arbitrage Pricing Theory (APT) for Testing Stock Markets Integration

30

2.6 Alternative Approaches for Testing Stock Markets Integration 36

2.7 Conclusion 38

Chapter 3. The Recent Techniques Relating to Stock Market Integration: The Cointegration Approach

3.1 Introduction 40

3.2 Cointegration Approach for Testing Stock Market Integration 41

3.3 The Asian Financial Crisis and Stock Market Integration 54

3.4 Efficient Market Hypothesis 60

3.4.1 Cointegration and Stock Market Efficiency 61

3.4.2 More Evidences on Stock Markets Efficiency 66

3.4.3 A new Approach for the Relationship between Cointegration and Efficiency

67

3.5 The Integration of the Emerging Stock Markets in the MENA Region 69

ix

3.6 Conclusion 77

Chapter 4. Features and Characteristics of the Emerging Stock Markets in the MENA Region

4.1 Introduction 78

4.2 General Economic Features of the MENA Region 80

4.3 An Overview of the Emerging Stock Markets in the MENA Region 87

4.3.1 Stock Market Liberalization of the Emerging Stock markets in MENA Region

88

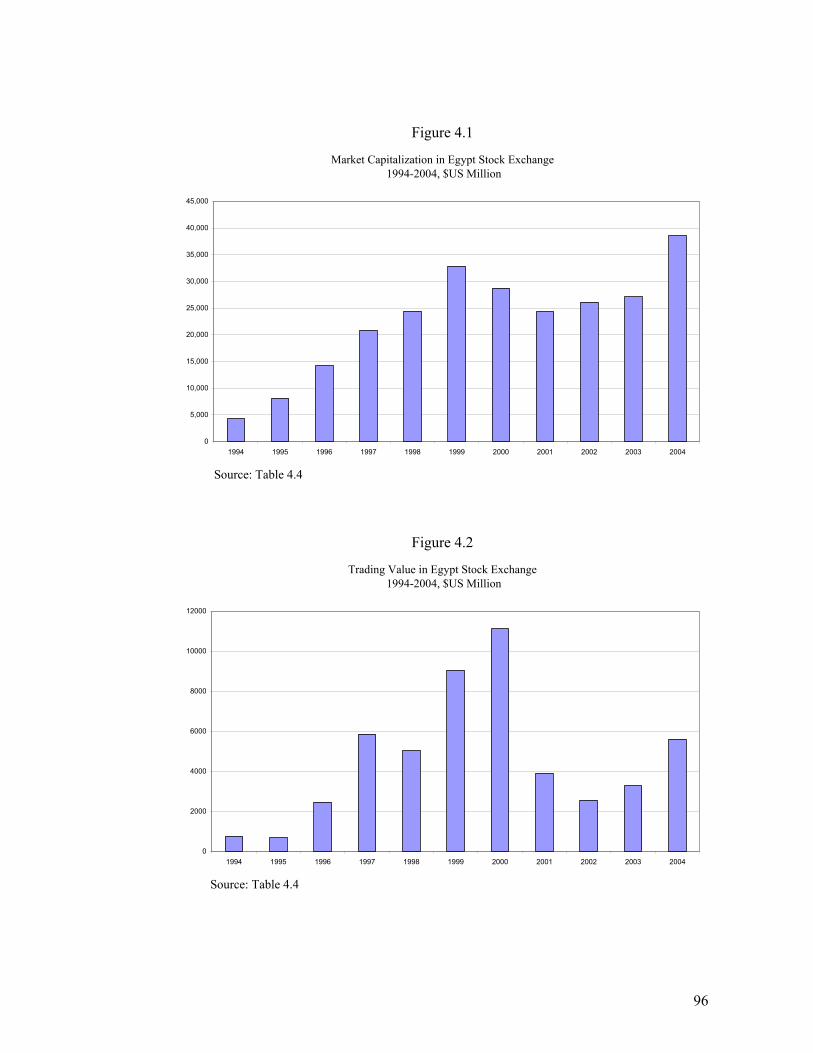

4.3.2 The Stock Market in Egypt 92

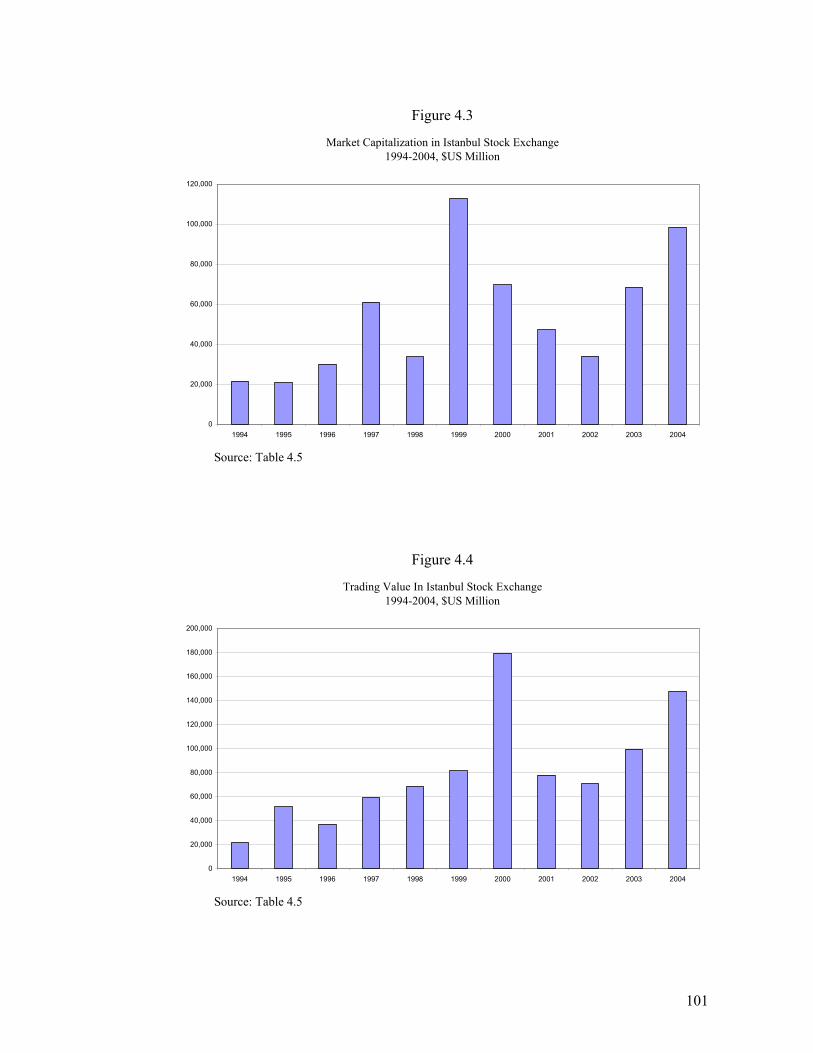

4.3.3 The Stock Market in Turkey 97

4.3.4 The Stock Market in Jordan 102

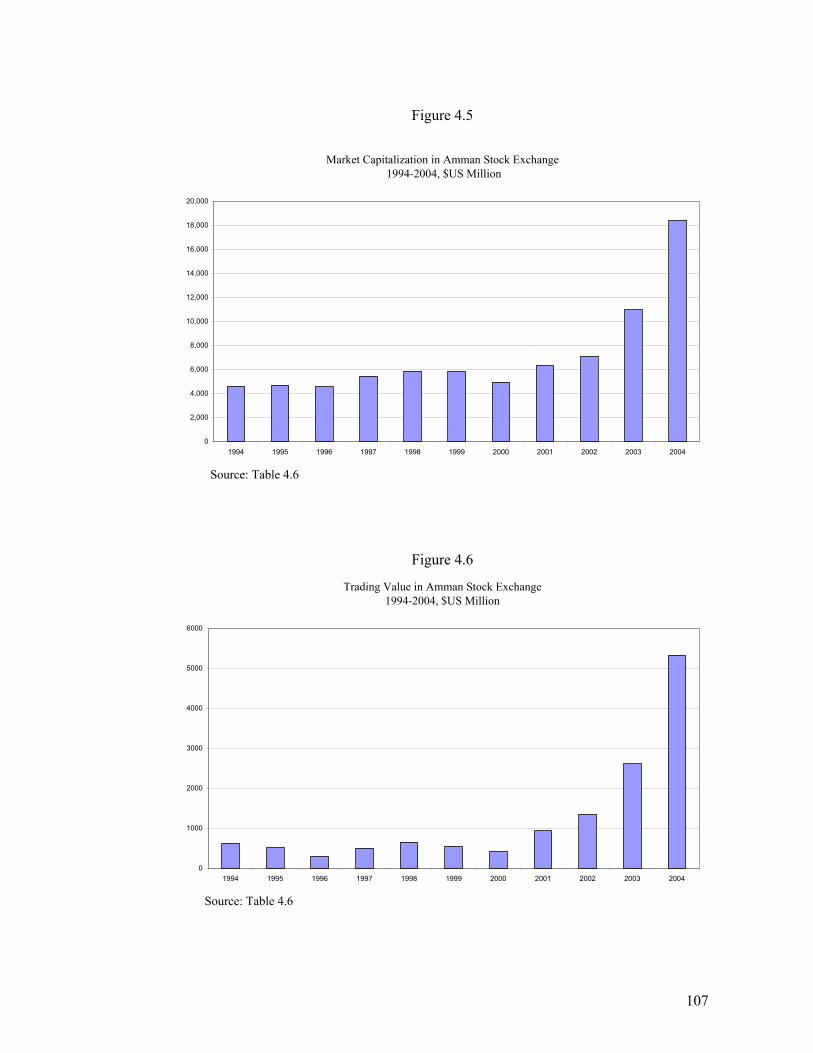

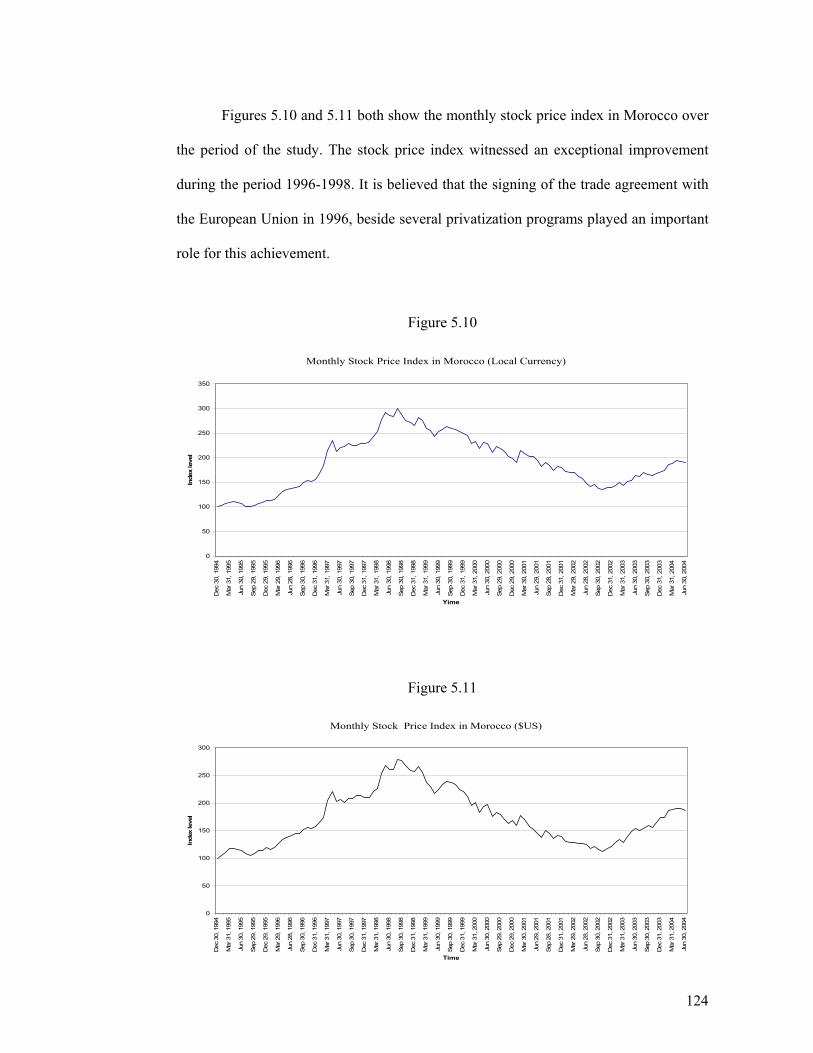

4.3.5 The Stock Market in Morocco 108

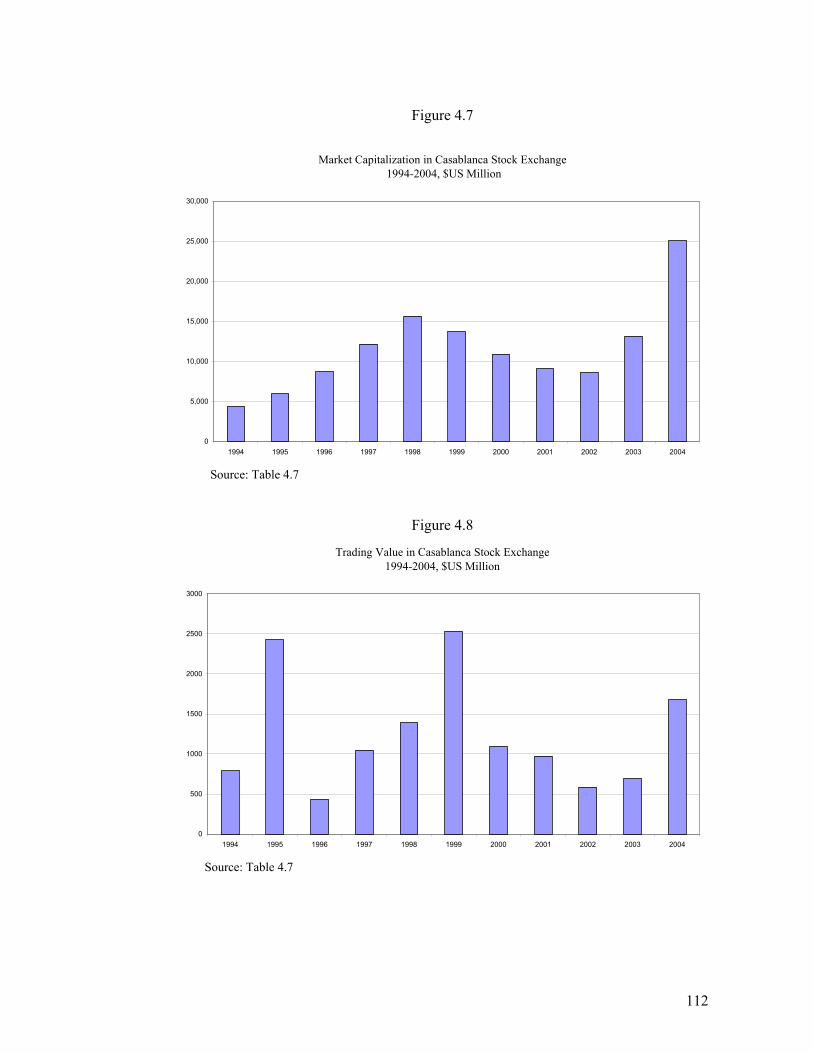

4.4 Conclusion 113

Chapter 5. Structural Changes and Efficiency in the MENA Stock Markets

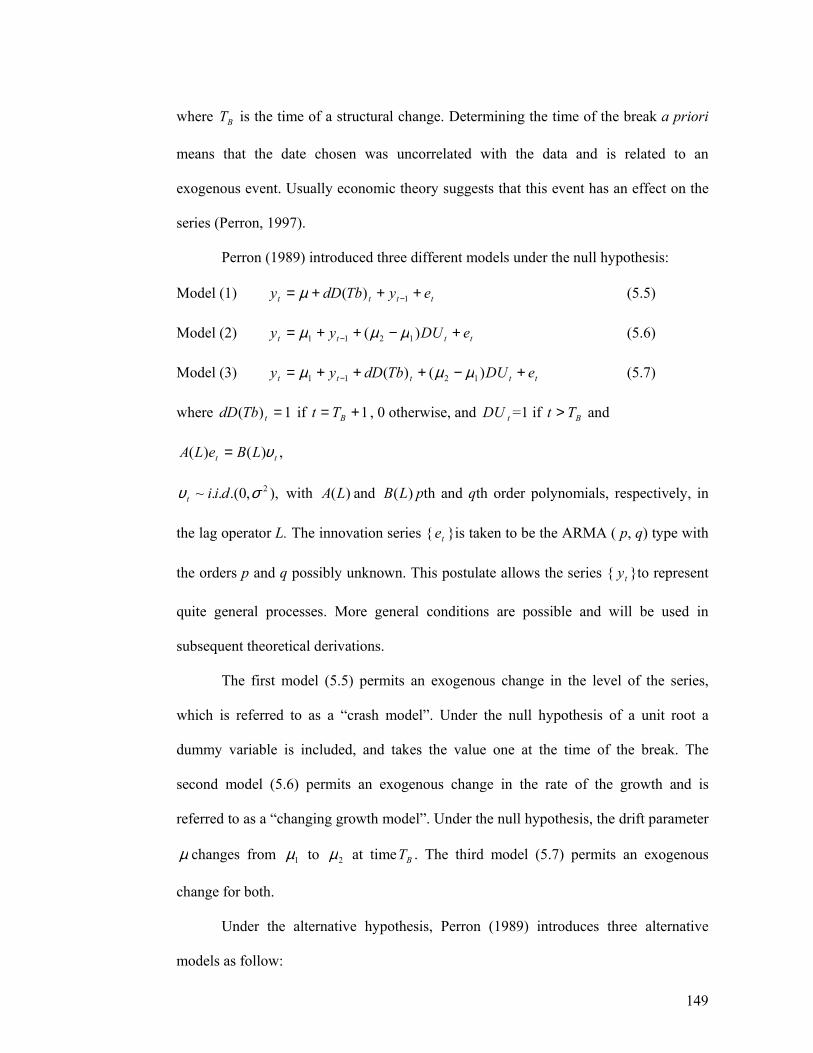

5.1 Introduction 115

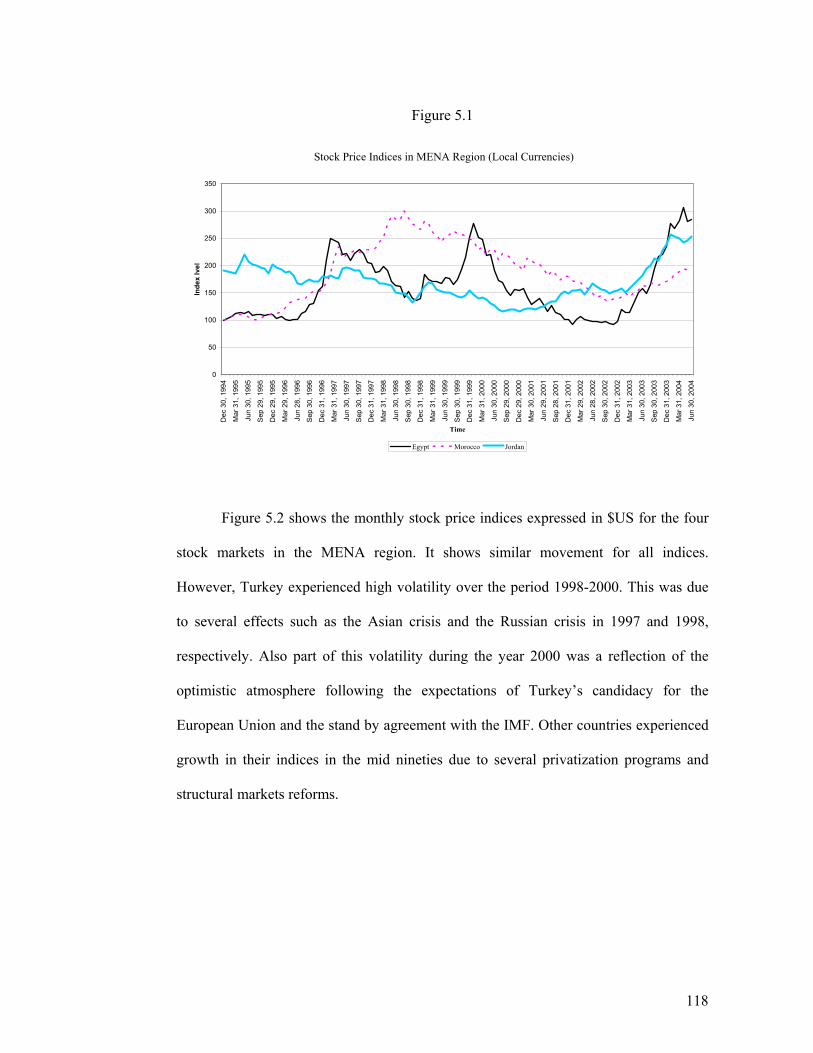

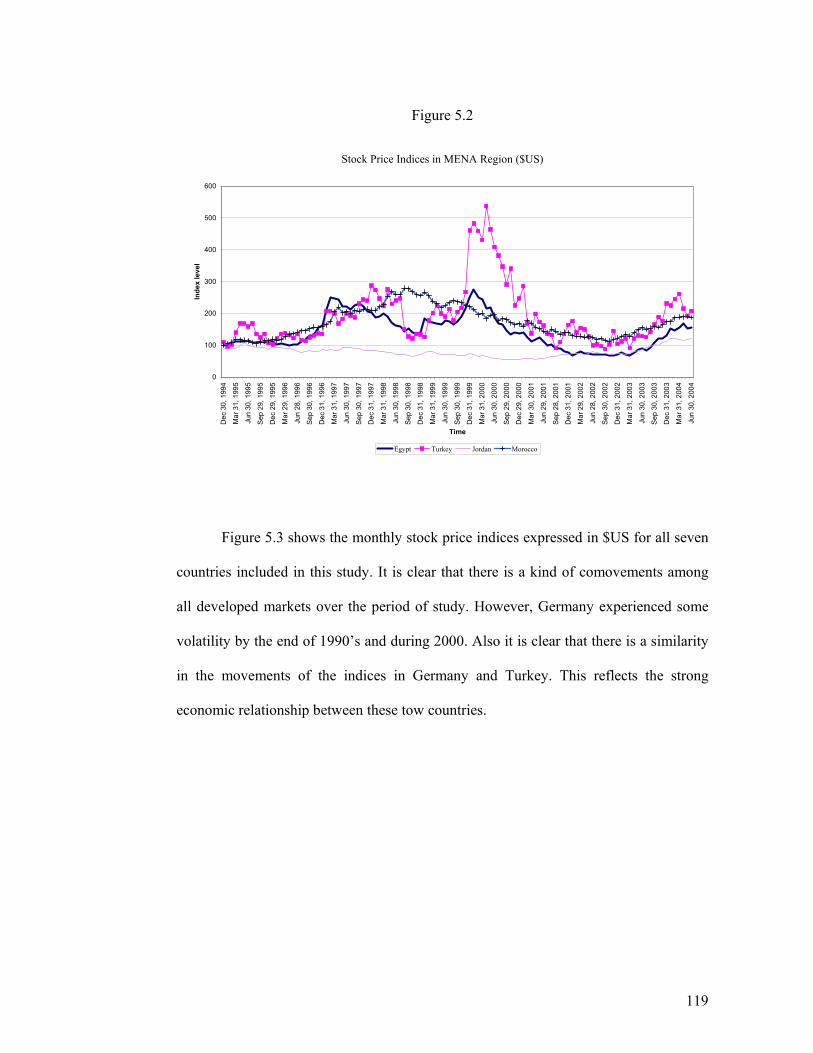

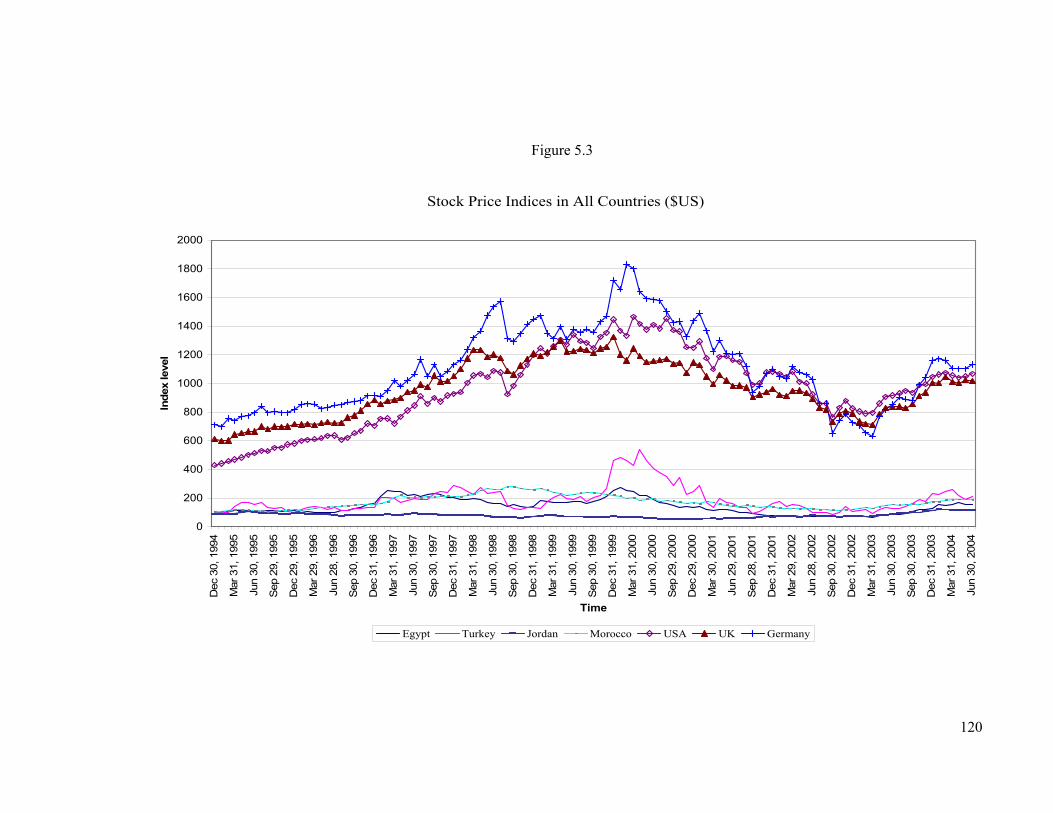

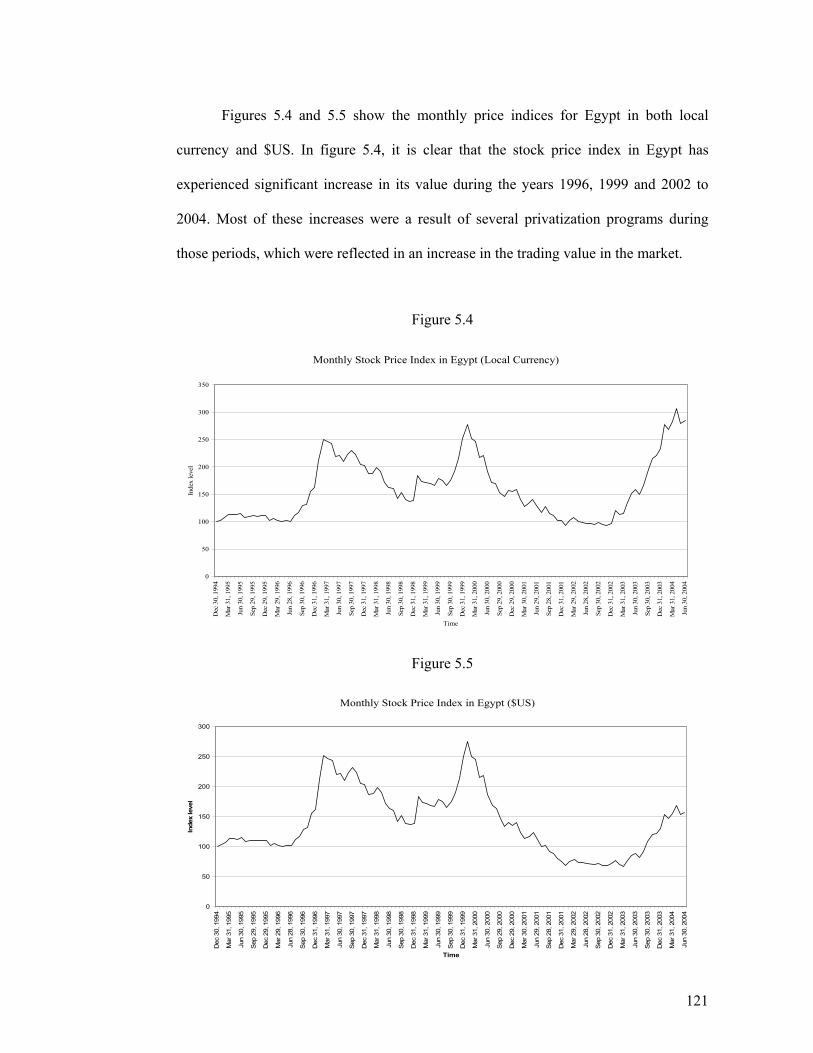

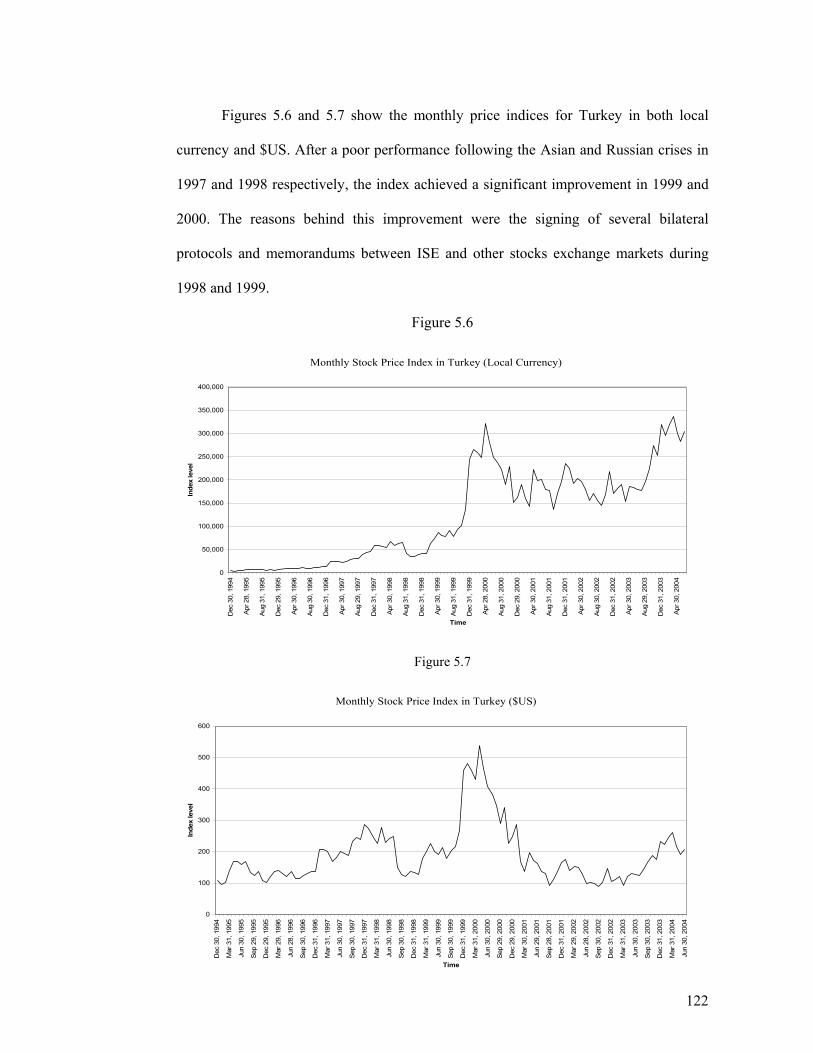

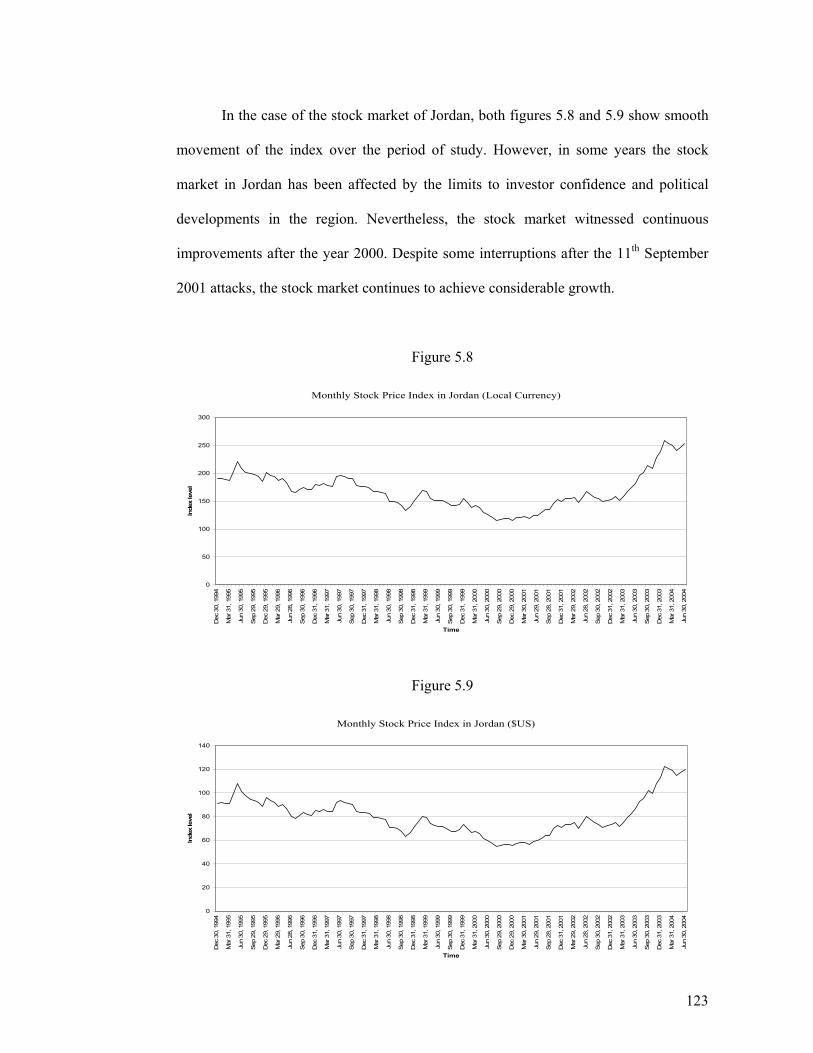

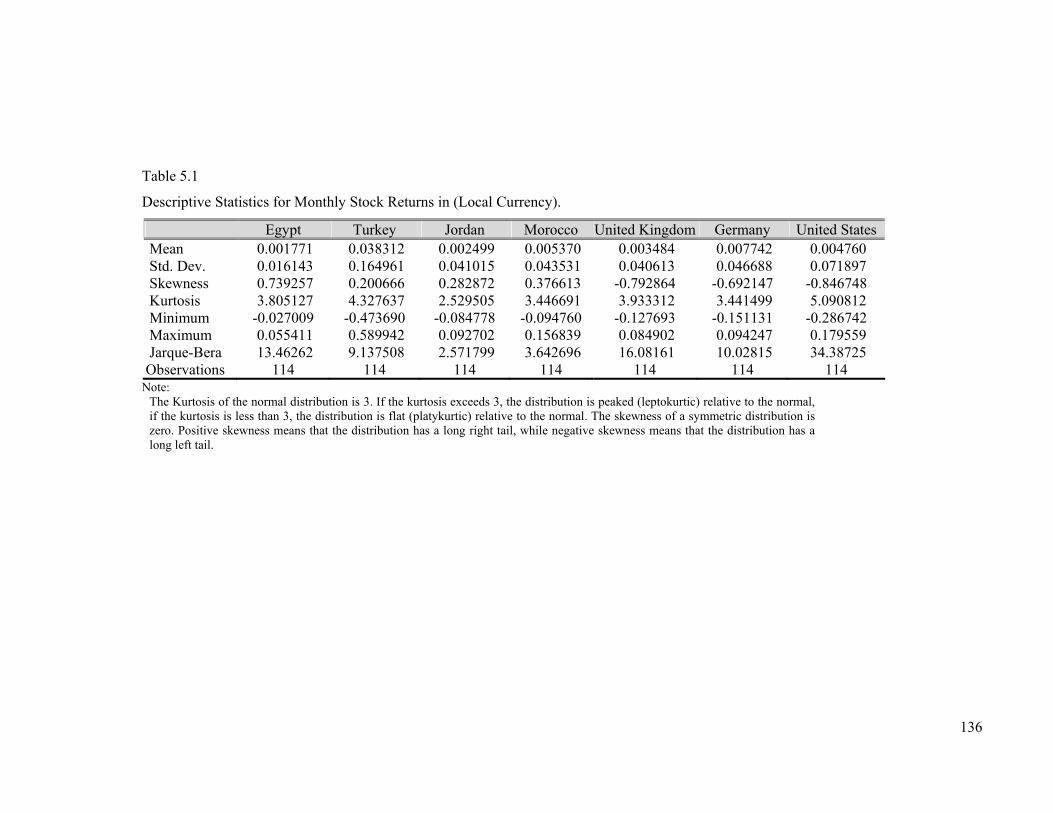

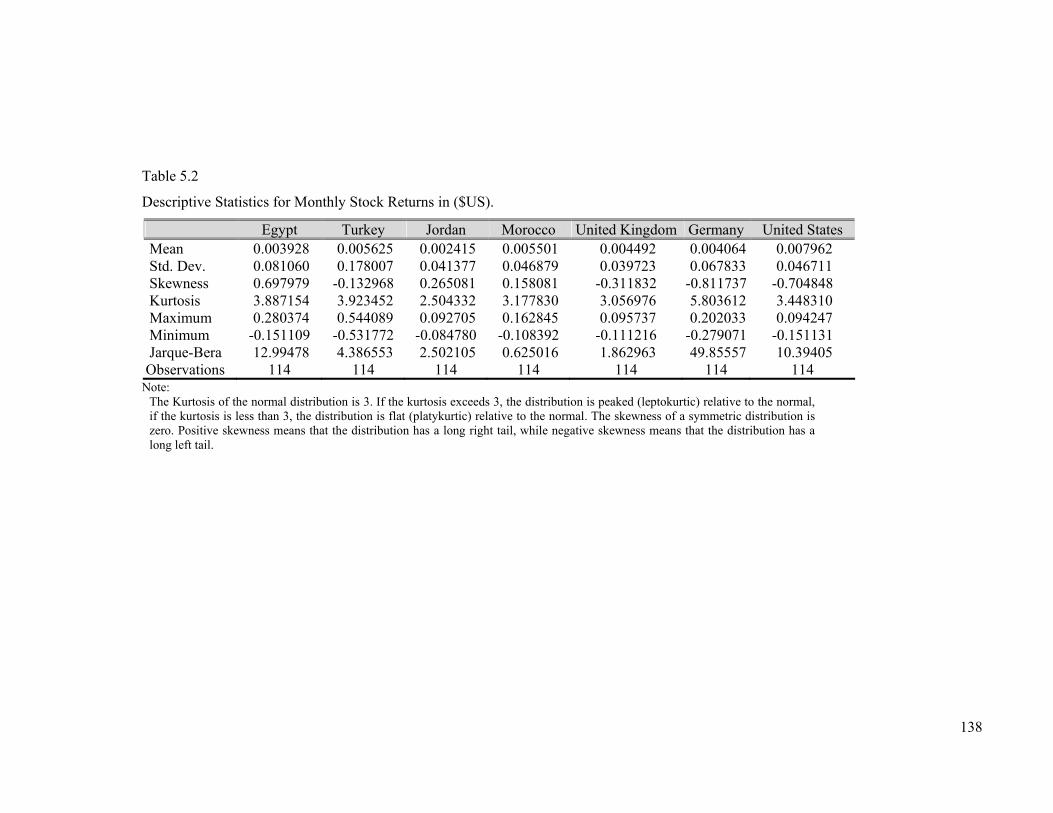

5.2 Data and descriptive statistics 116

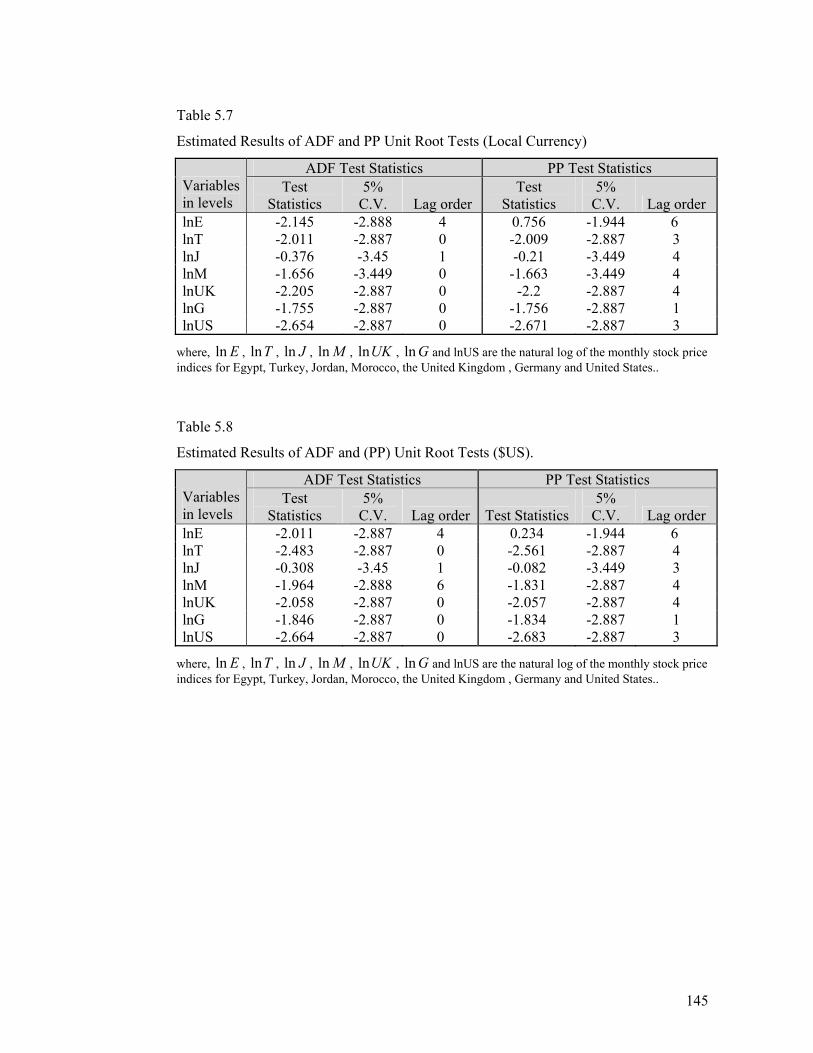

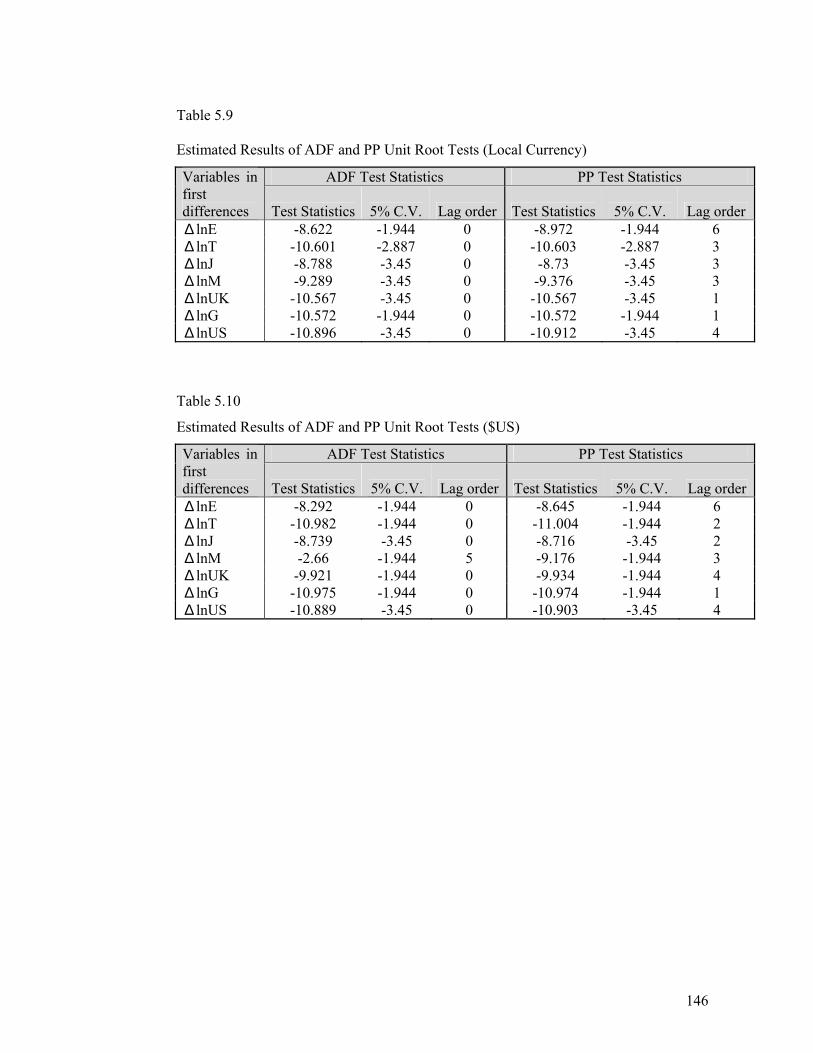

5.3 The Conventional Augmented Dickey-Fuller (ADF) and Phillips– Perron (PP) Unit Root Tests

143

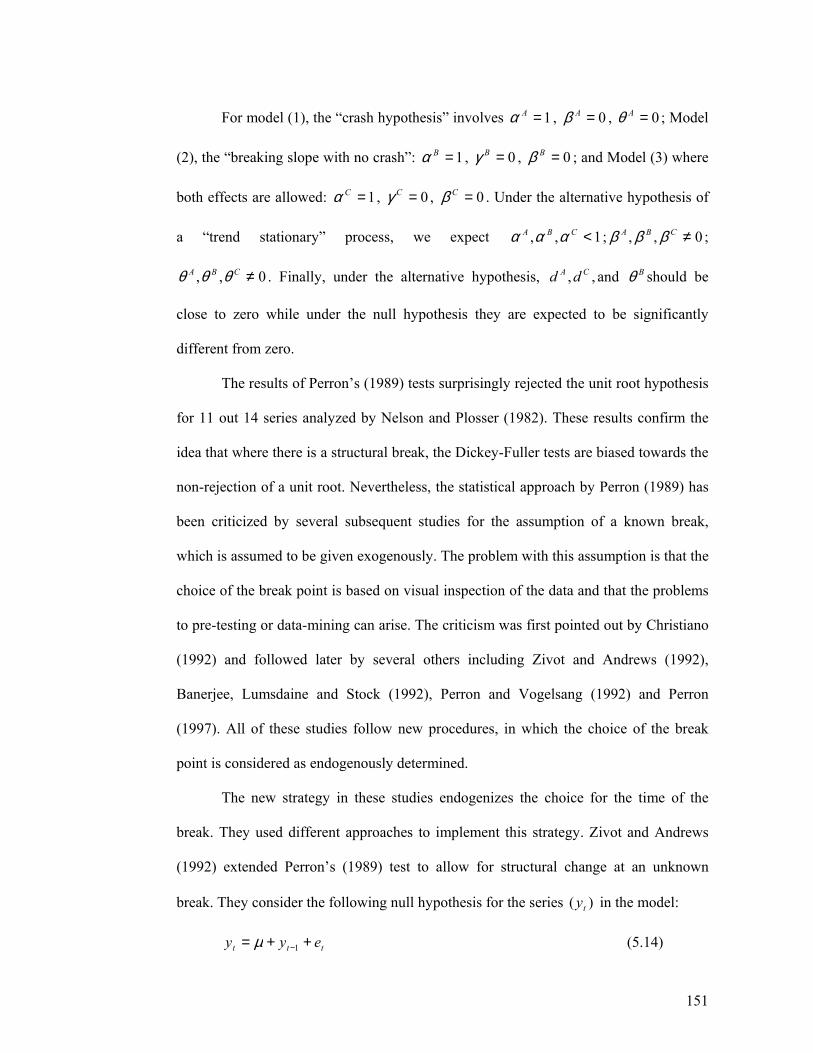

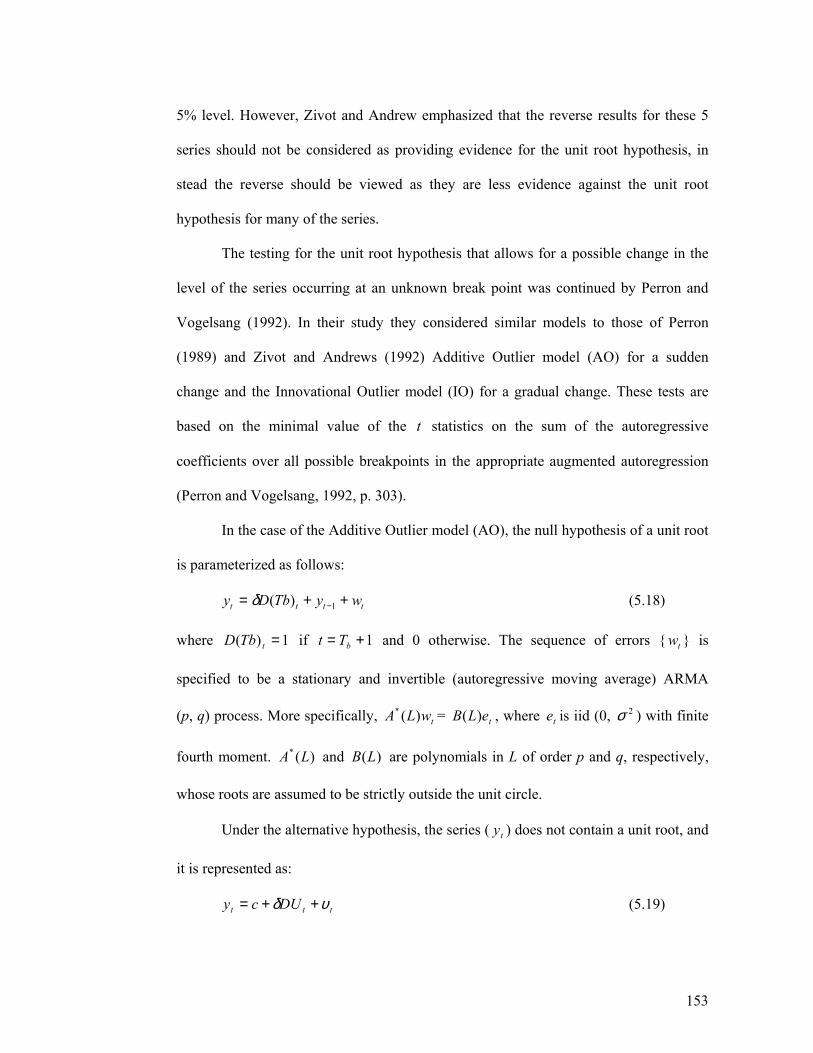

5.4 The Development of Testing for Structural Change 148

5.4.1 Procedures for Selecting the Order of the Lag 156

5.4.2 Procedures for Determining the Time of the Break 157

5.5 Testing for Structural Changes in MENA Stock Markets 158

5.6 The Random Walk Behavior and the Efficiency of the MENA Stock Markets

170

5.7 Conclusion 171

Chapter 6. Stock Market Integration in the MENA Region: Cointegration and Causality Tests

6.1 Introduction 173

6.2 The Autoregressive Distributed Lag (ARDL) Approach to Cointegration

174

6.3 Model Specification 179

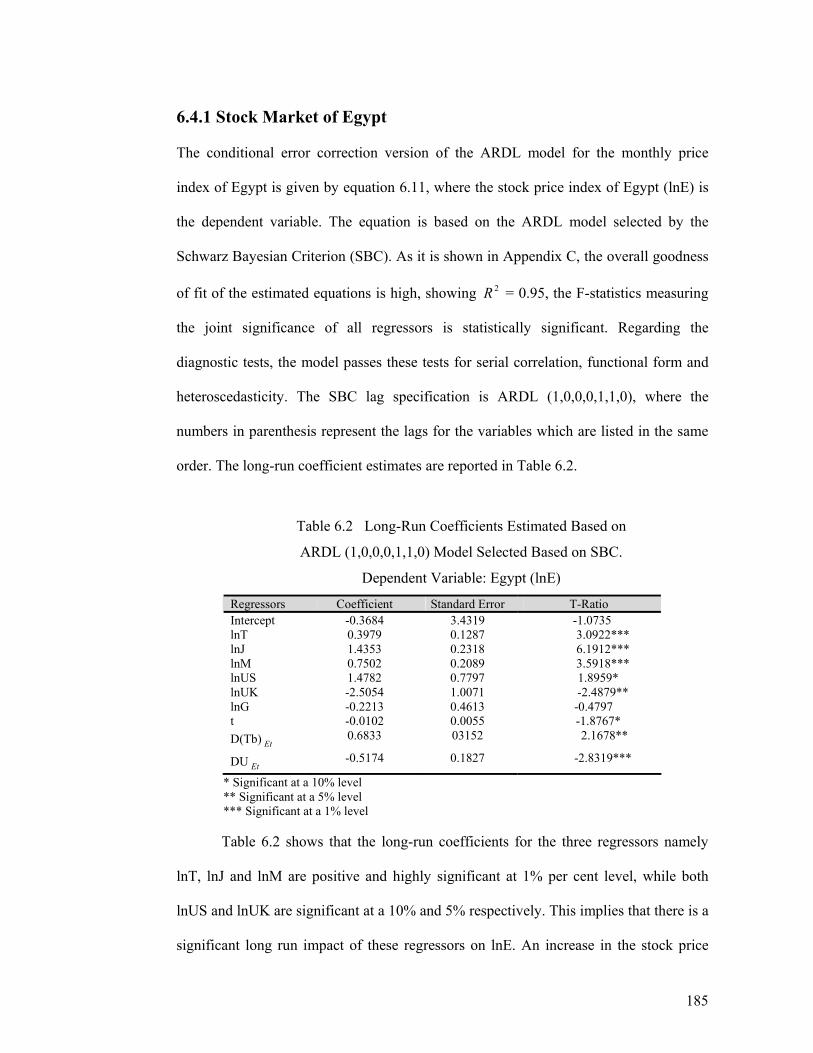

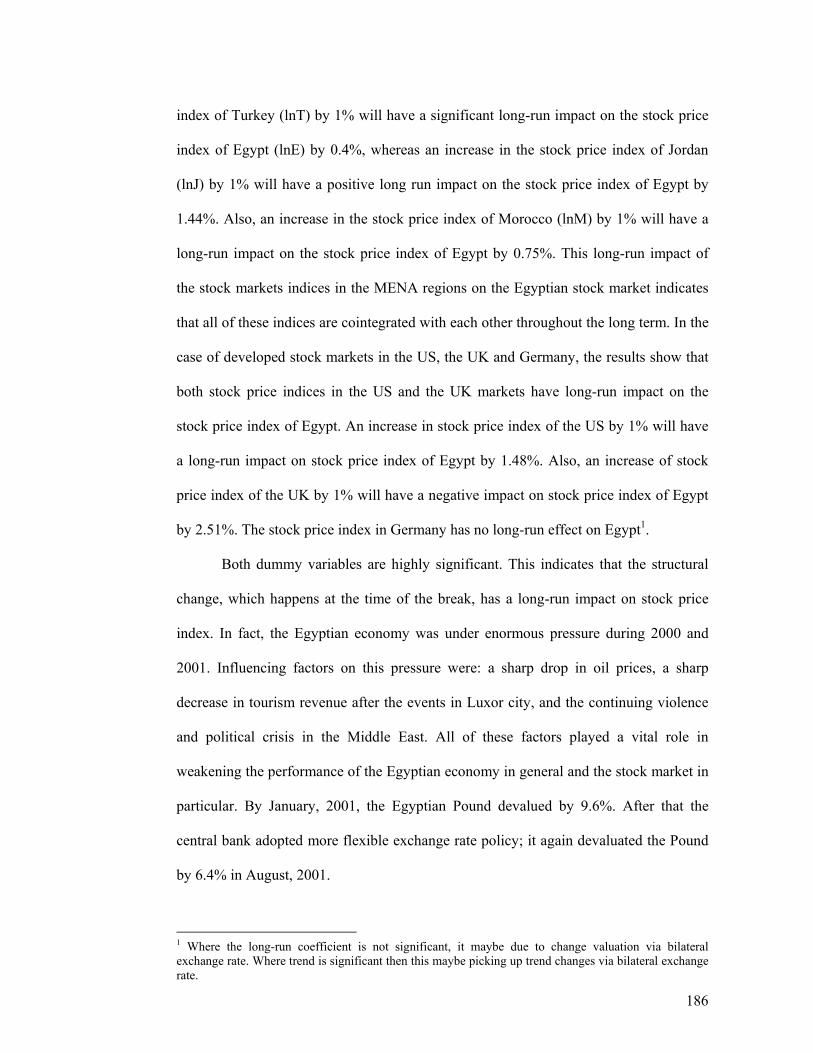

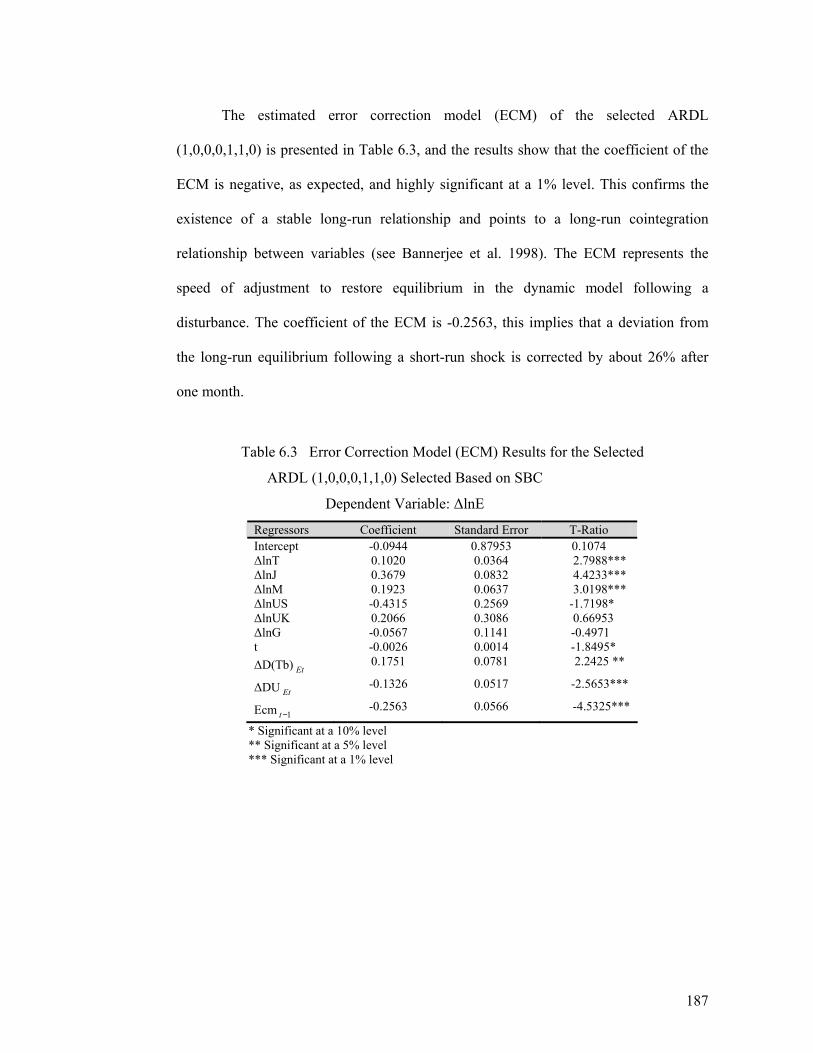

6.4 Interpretation of the Results 183

6.4.1 Stock Market of Egypt 185

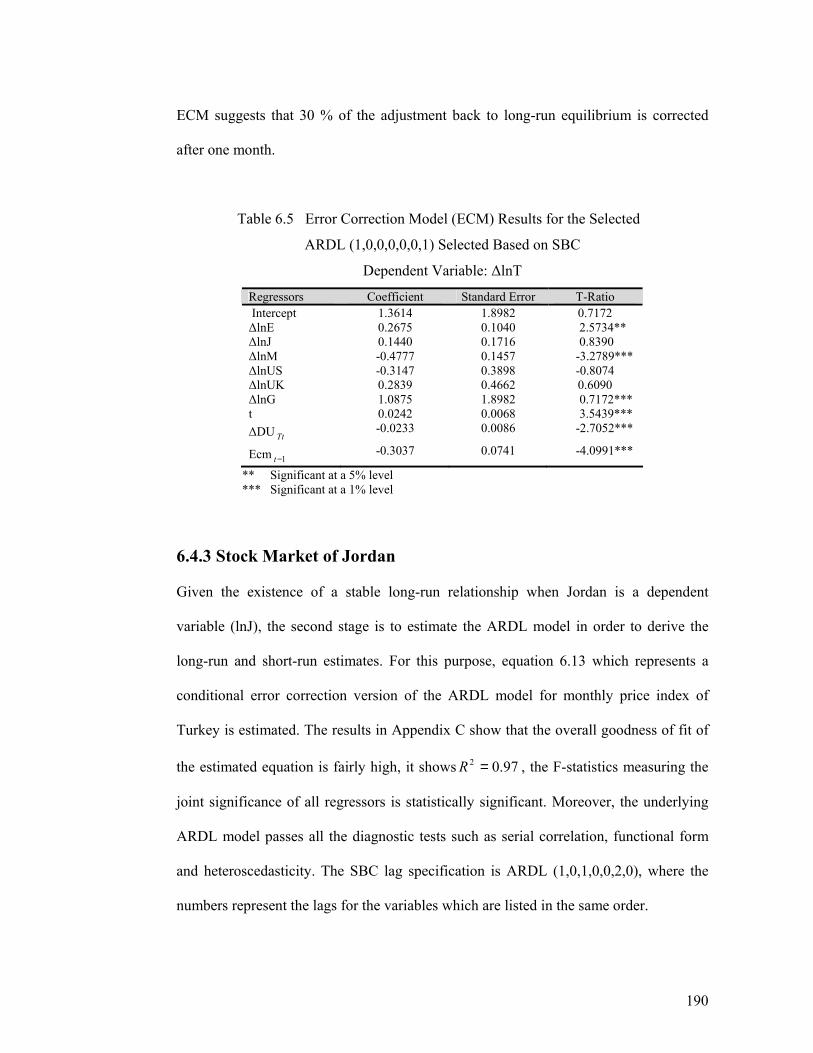

6.4.2 Stock Market of Turkey 188

6.4.3 Stock Market of Jordan 190

6.4.4 Stock Market of Morocco 192

x

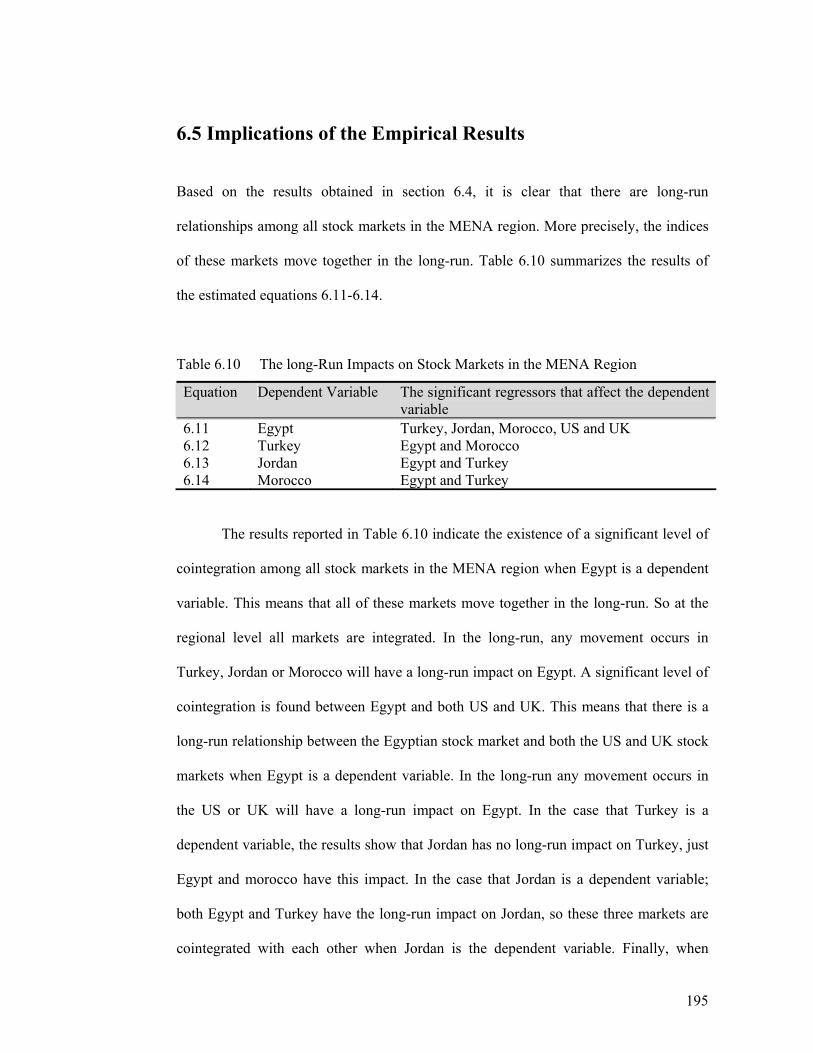

6.5 Implications of the Empirical Results 195

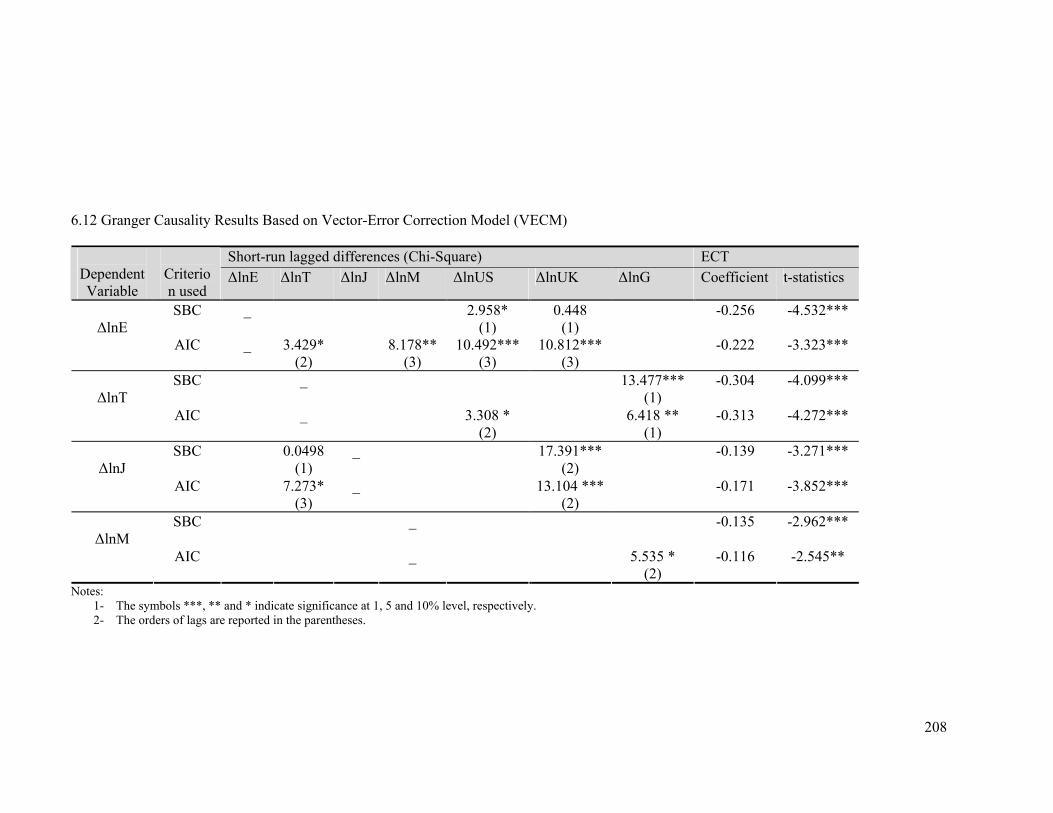

6.6 Granger Causality 204

6.7 Conclusion 211

Chapter 7. Summary and Conclusions

7.1 Introduction 213

7.2 Summary of the Study 214

7.3 Implications of the Study 222

7.4 Contribution of the Study 224

7.5 Suggestions for Future Research 226

Appendices

Appendix A. Conventional Unit Root Tests 228

Appendix B. Cointegration and Causality Tests 238

Appendix C. Diagnostic Tests 243

Bibliography 247

xi

List of Tables

2.1 A summary for the Results of the Main Previous Studies 35 3.1 Summary of Selective empirical Studies on Stock Market Integration 57 4.1 Economic Overview for MENA Countries 86 4.2 Openness of Stock Markets in MENA Region 89 4.3 Portfolio Equity Net Flows to Stock Markets in MENA Region 90 4.4 Egypt Stock Market Indicators 95 4.5 Istanbul Stock Exchange Indicators 100 4.6 Amman Stock Exchange Indicators 106 4.7 Casablanca Stock Exchange Indicators 111 5.1 Descriptive Statistics for Monthly Stock Returns in (Local Currency) 136 5.2 Descriptive Statistics for Monthly Stock Returns in ($US) 138 5.3 Correlation Coefficients for Monthly Stock Indices in (Local Currency) 140 5.4 Correlation Coefficients for Monthly Rate of Returns in (Local Currency) 140 5.5 Correlation Coefficients for Monthly Stock Indices in ($US) 142 5.6 Correlation Coefficients for Monthly Rate of Return in ($US) 142 5.7 Estimated Results of ADF and PP Unit Root Tests (Local Currency) 145 5.8 Estimated Results of ADF and (PP) Unit Root Tests ($US) 145 5.9 Estimated Results of ADF and PP Unit Root Tests (Local Currency) 146 5.10 Estimated Results of ADF and PP Unit Root Tests ($US) 146 5.11 Empirical Results, Perron’s (1997) Model (IO2), (Local Currency) 163 5.12 Empirical Results, Perron’s (1997) Model (IO1), (Local Currency) 163 5.13 Empirical Results, Perron and Vogelsang (1992) (IO), (Local Currency) 165 5.14 Empirical Results, Perron’s (1997) Model (IO2), ($US) 168 5.15 Empirical Results, Perron’s (1997) Model (IO1), ($US) 168 5.16 Empirical Results, Perron and Vogelsang (1992) (IO) Model, ($US) 169 6.1 F-Statistics for Testing the Existence of a long-Run Relationship 184 6.2 Long-Run Coefficients Estimated Based on ARDL (1,0,0,0,1,1,0) Model

Selected Based on SBC. Dependent Variable: Egypt (lnE) 185

6.3 Error Correction Model (ECM) Results for the Selected ARDL (1,0,0,0,1,1,0) Selected Based on SBC. Dependent Variable: ∆lnE

187

6.4 Long-Run Coefficients Estimated Based on ARDL (1,0,0,0,0,0,1) Model Selected Based on SBC. Dependent Variable: Turkey (lnT)

188

6.5 Error Correction Model (ECM) Results for the Selected ARDL (1,0,0,0,0,0,1) Selected Based on SBC. Dependent Variable: ∆lnT

190

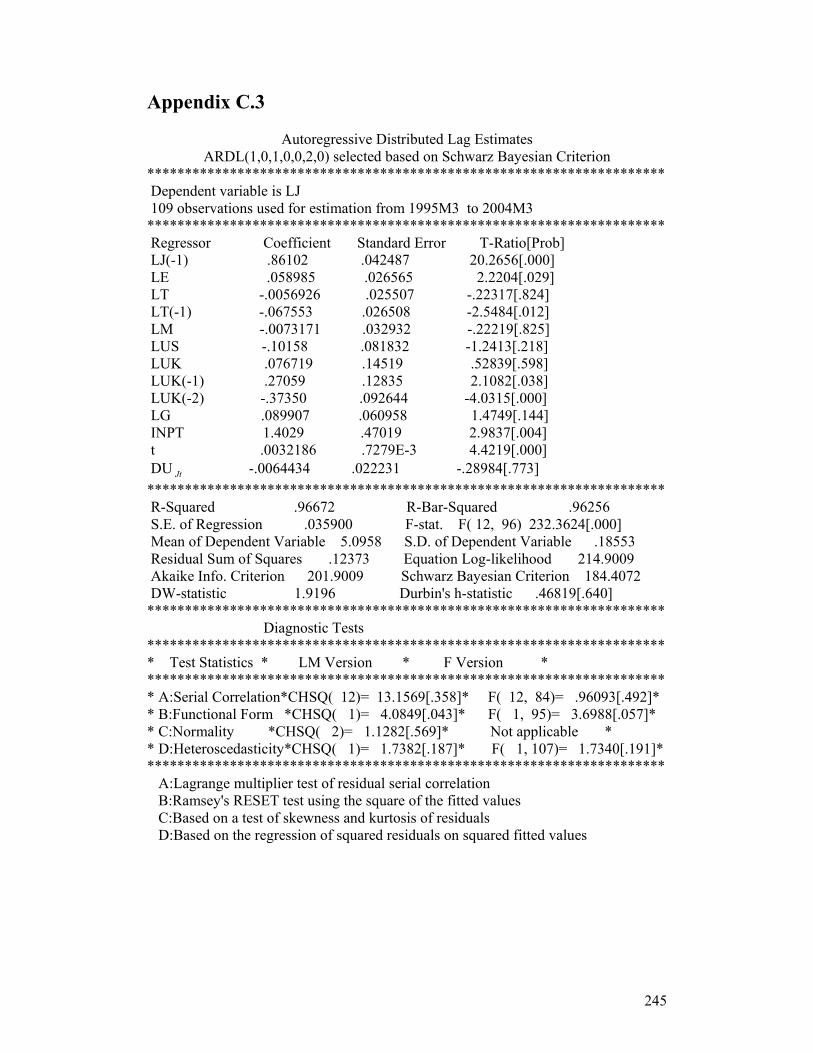

6.6 Long-Run Coefficients Estimated Based on ARDL (1,0,1,0,0,2,0) Model Selected Based on SBC. Dependent Variable: Jordan (lnJ)

191

6.7 Error Correction Model (ECM) Results for the Selected ARDL (1,0,1,0,0,2,0) Selected Based on SBC. Dependent Variable: ∆lnJ

192

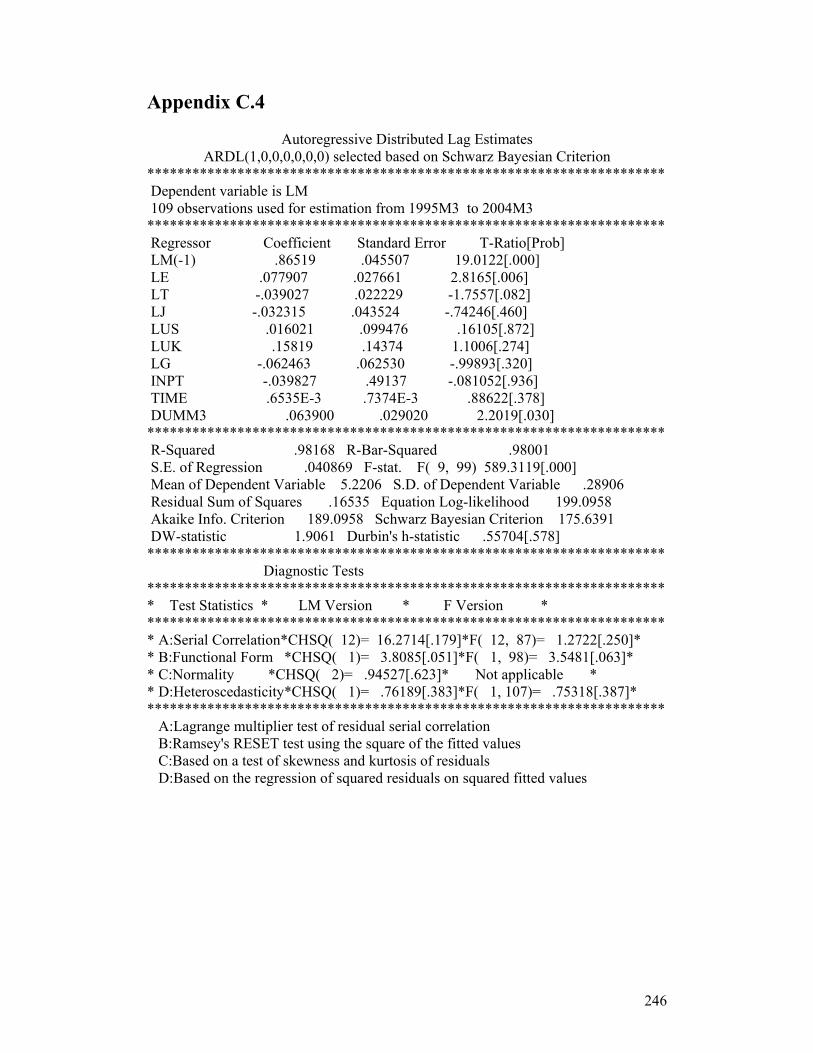

6.8 Long-Run Coefficients Estimated Based on ARDL (1,0,0,0,0,0,0) Model Selected Based on SBC. Dependent Variable: Morocco (lnM)

193

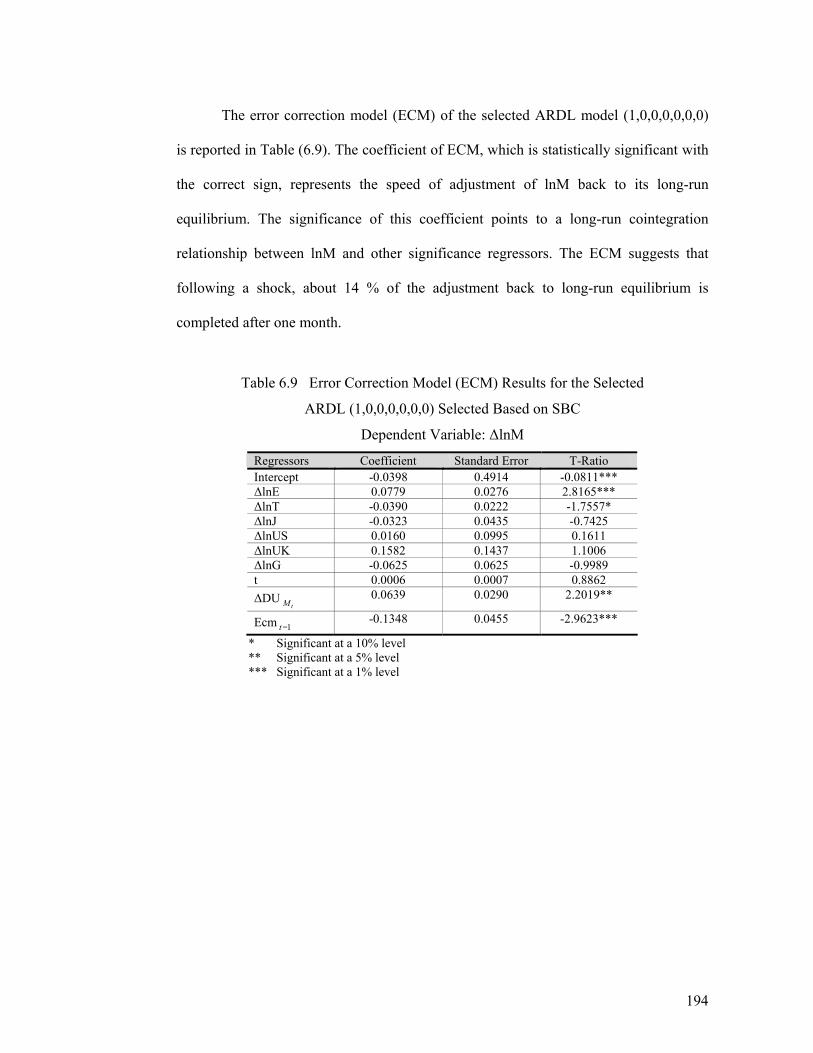

6.9 Error Correction Model (ECM) Results for the Selected ARDL (1,0,0,0,0,0,0) Selected Based on SBC. Dependent Variable: ∆lnM

194

6.10 The long-Run Impacts on Stock Markets in the MENA Region 195 6.11 Net Inward Portfolio Equity Flows to developing Countries, 1995-2003 200 6.12 Granger Causality Results Based on Vector-Error Correction Model 208 6.13 Recent American Aids to Egypt 209

xii

List of Figures

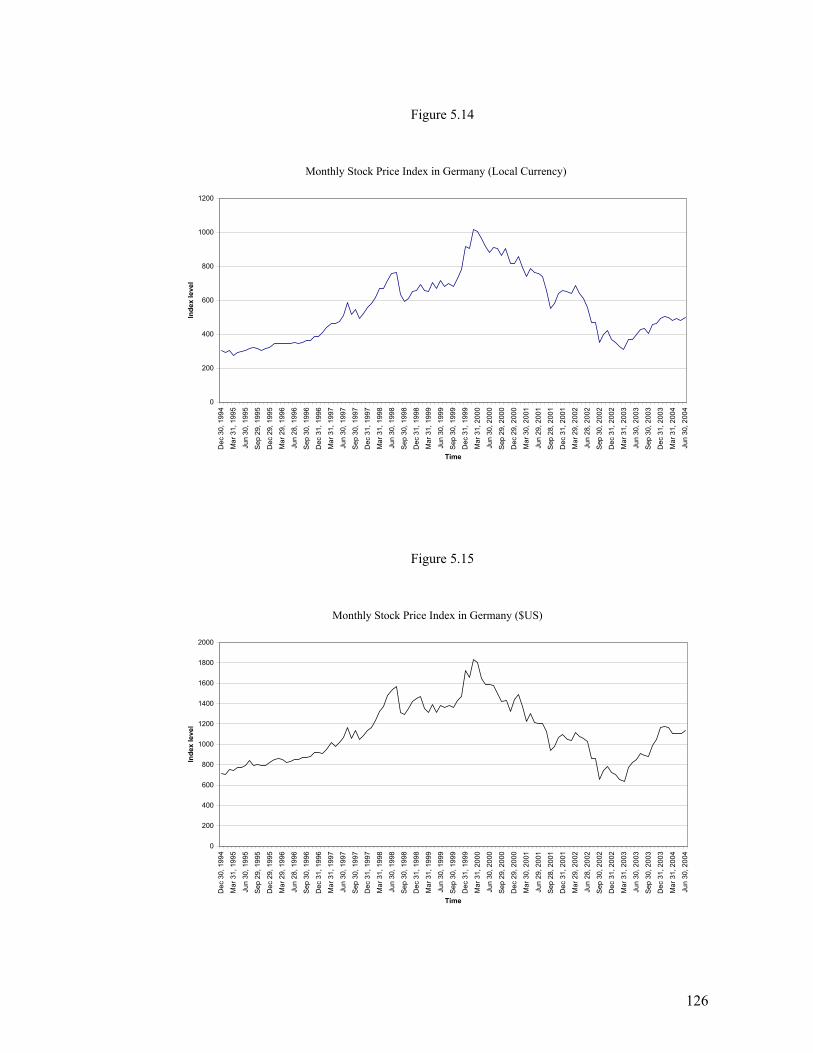

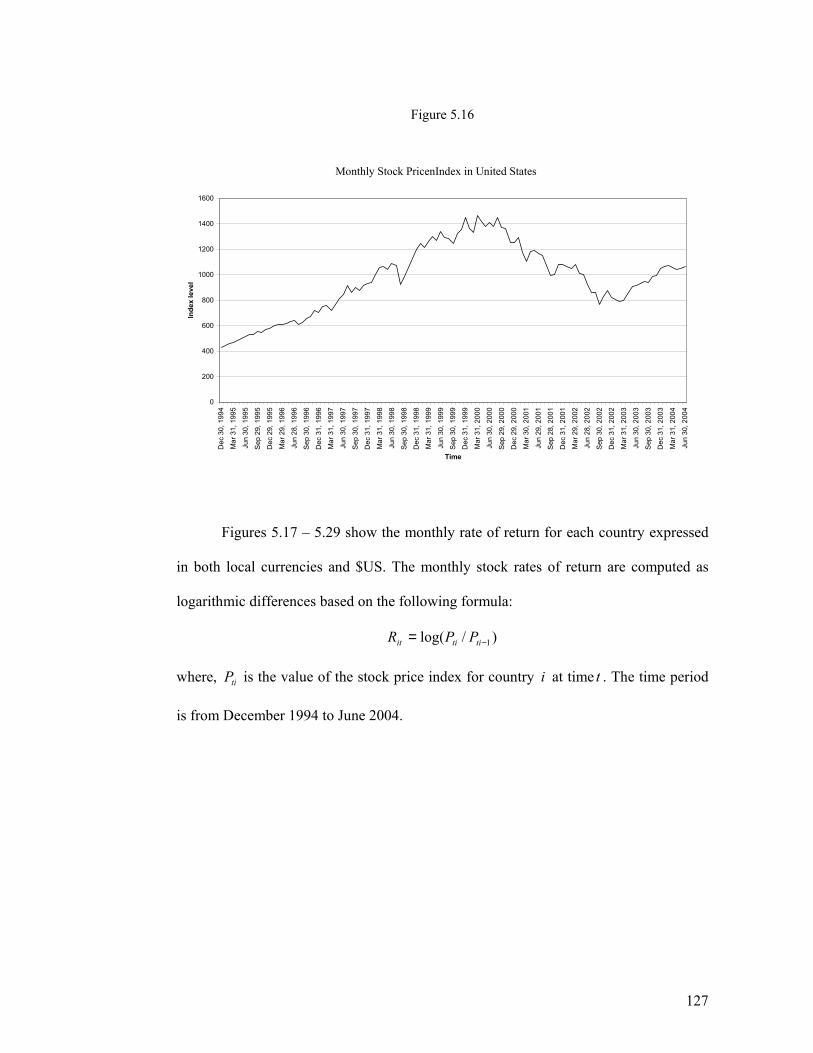

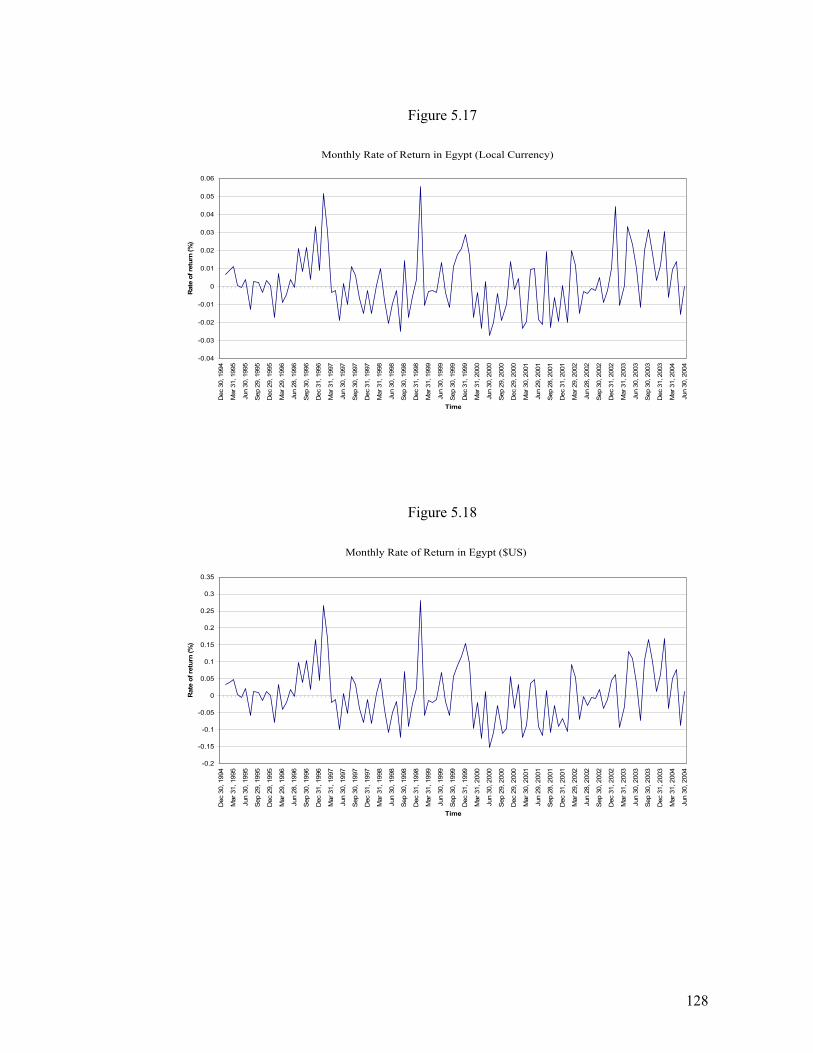

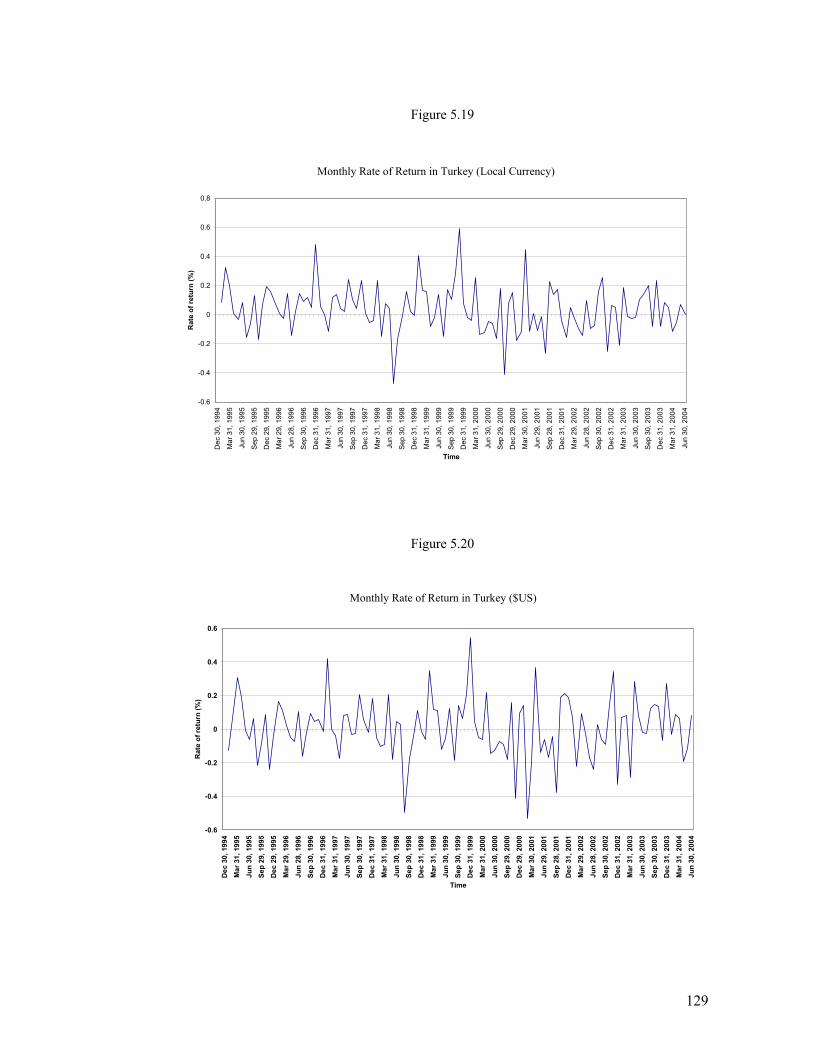

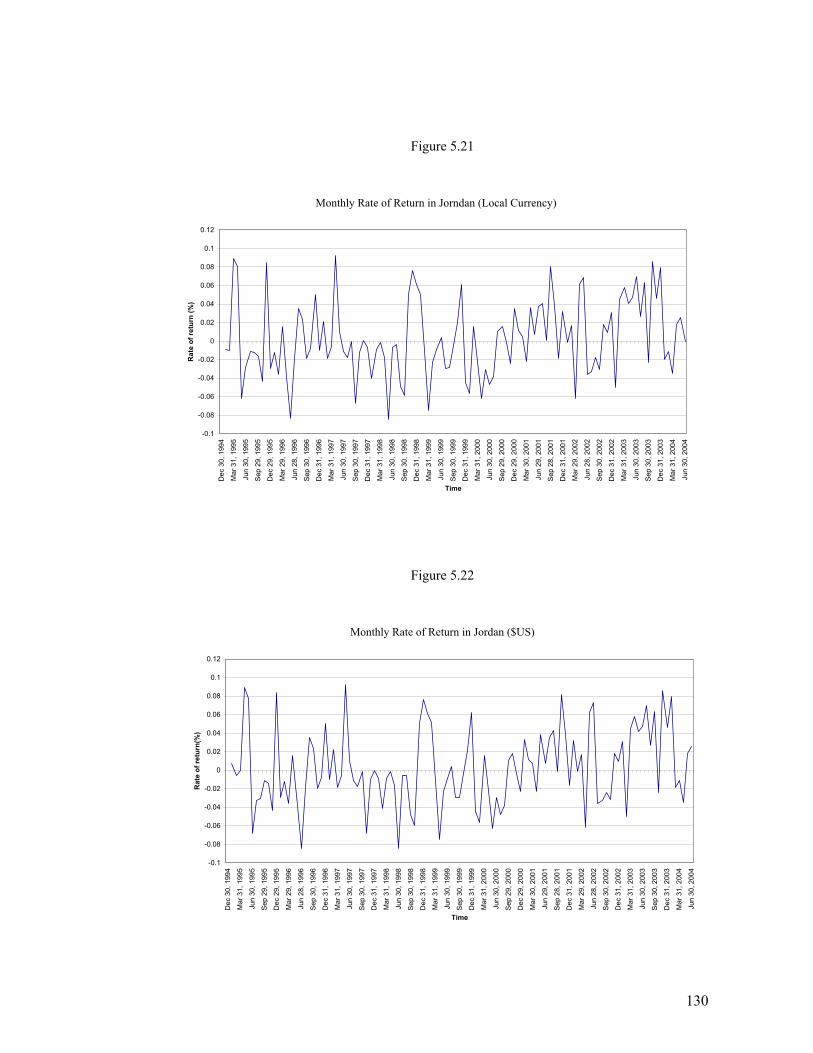

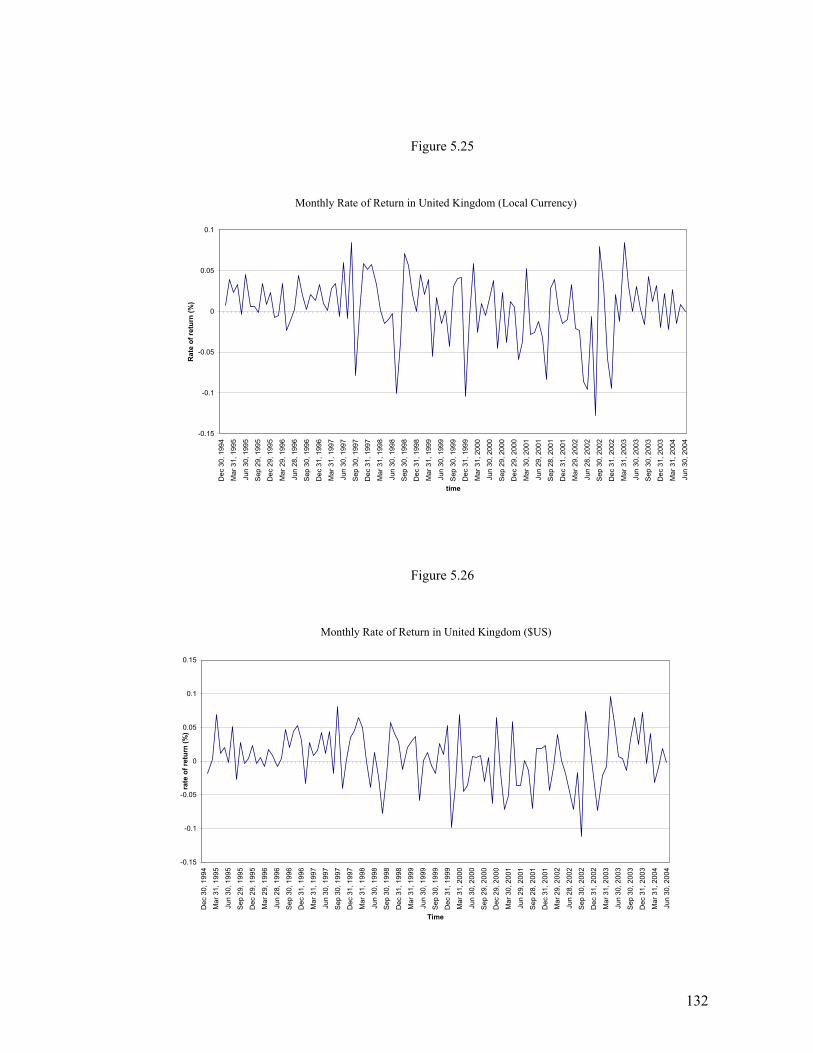

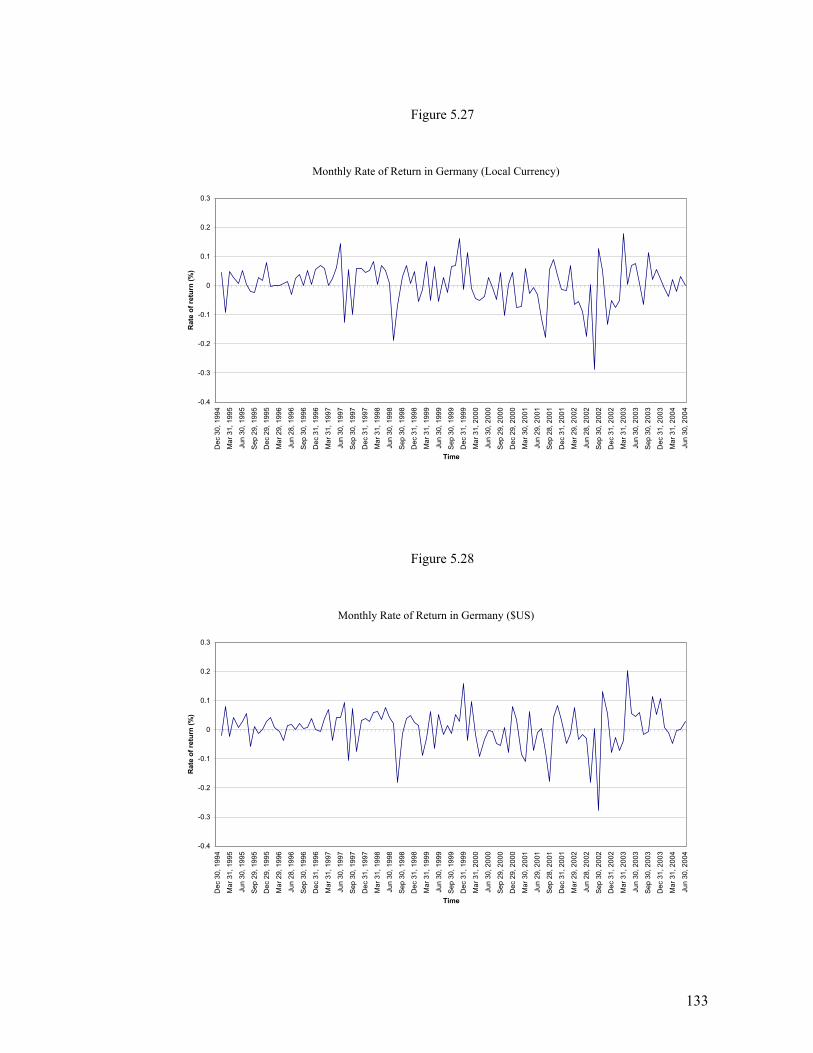

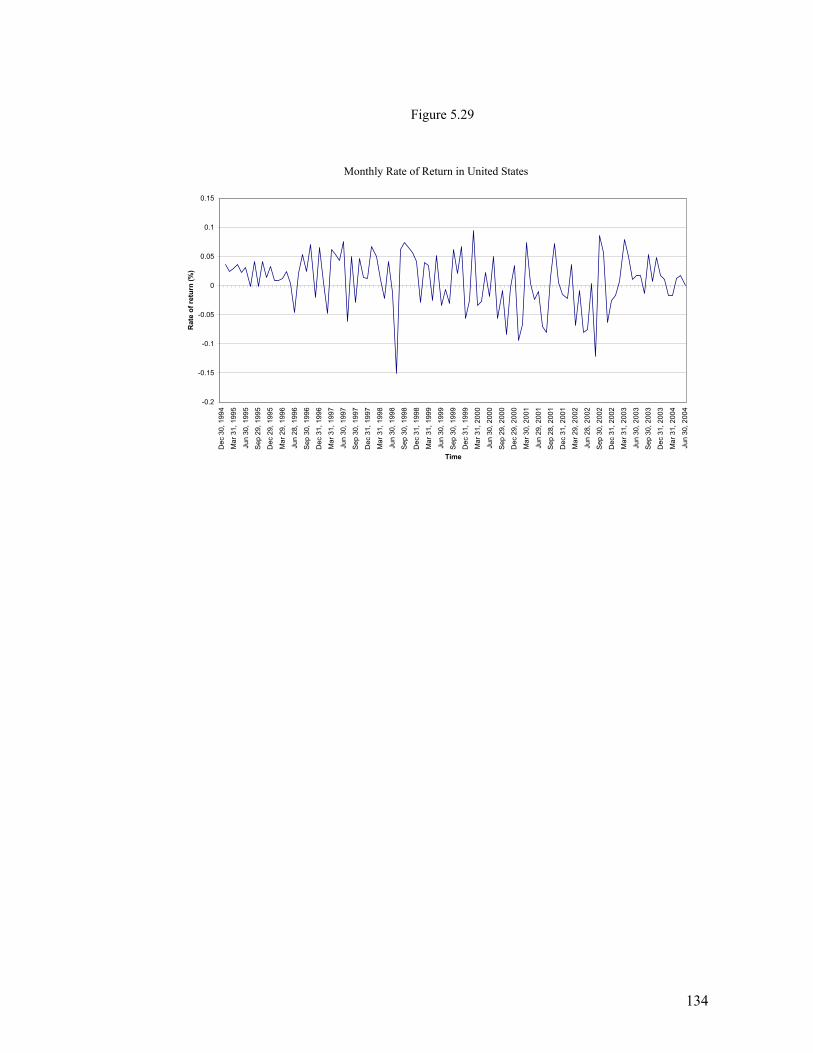

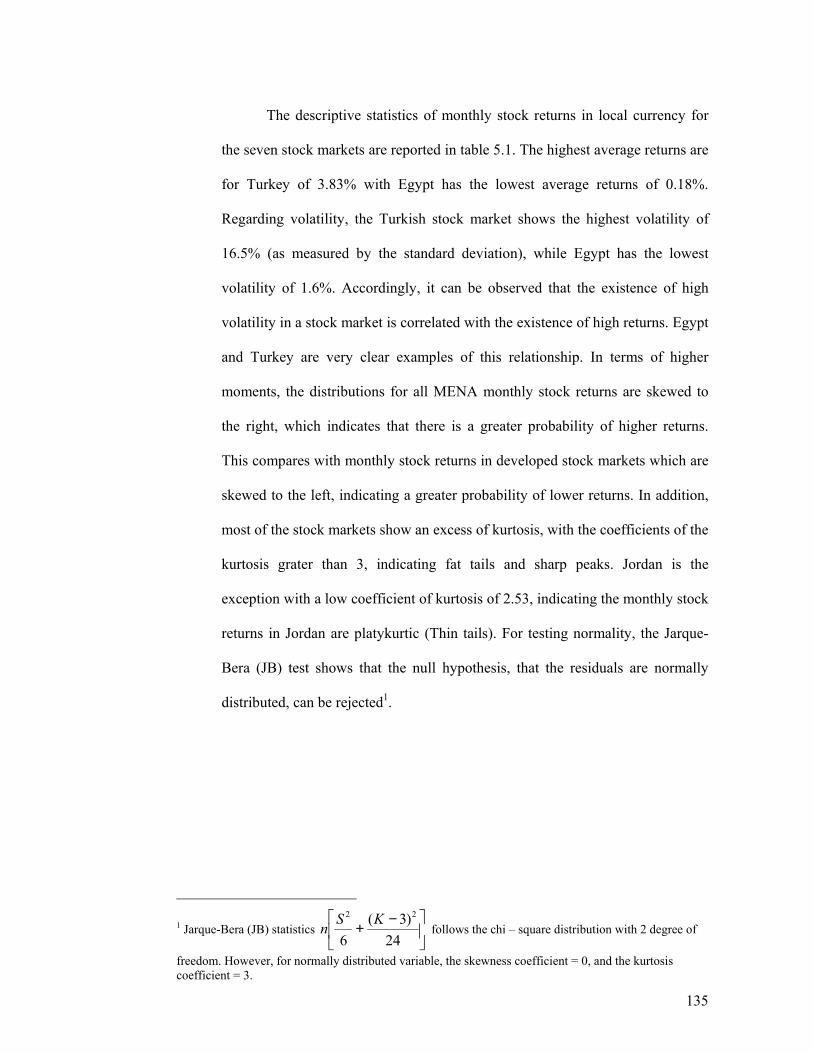

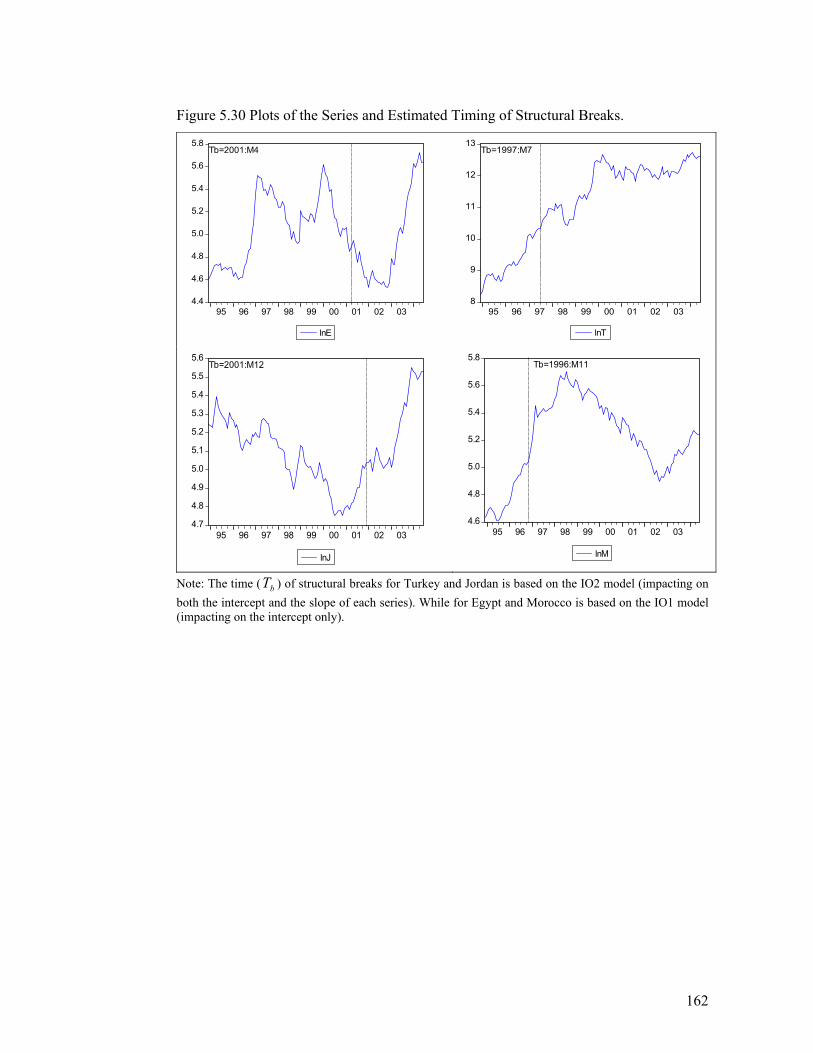

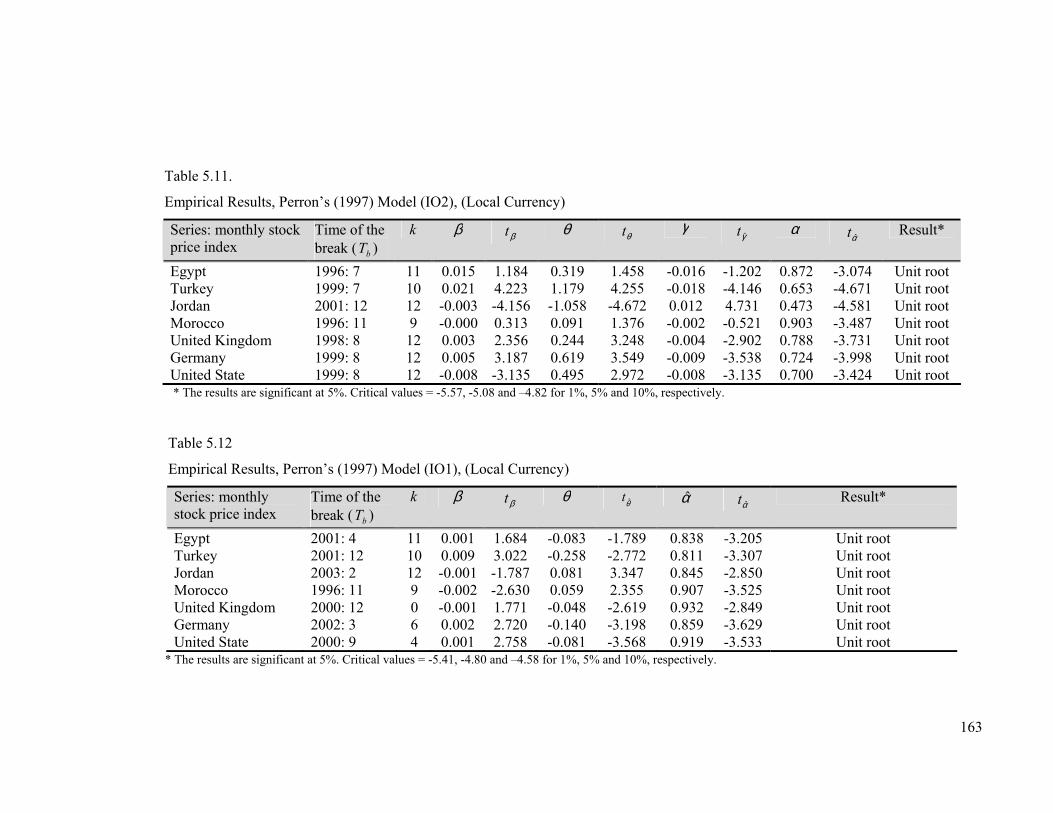

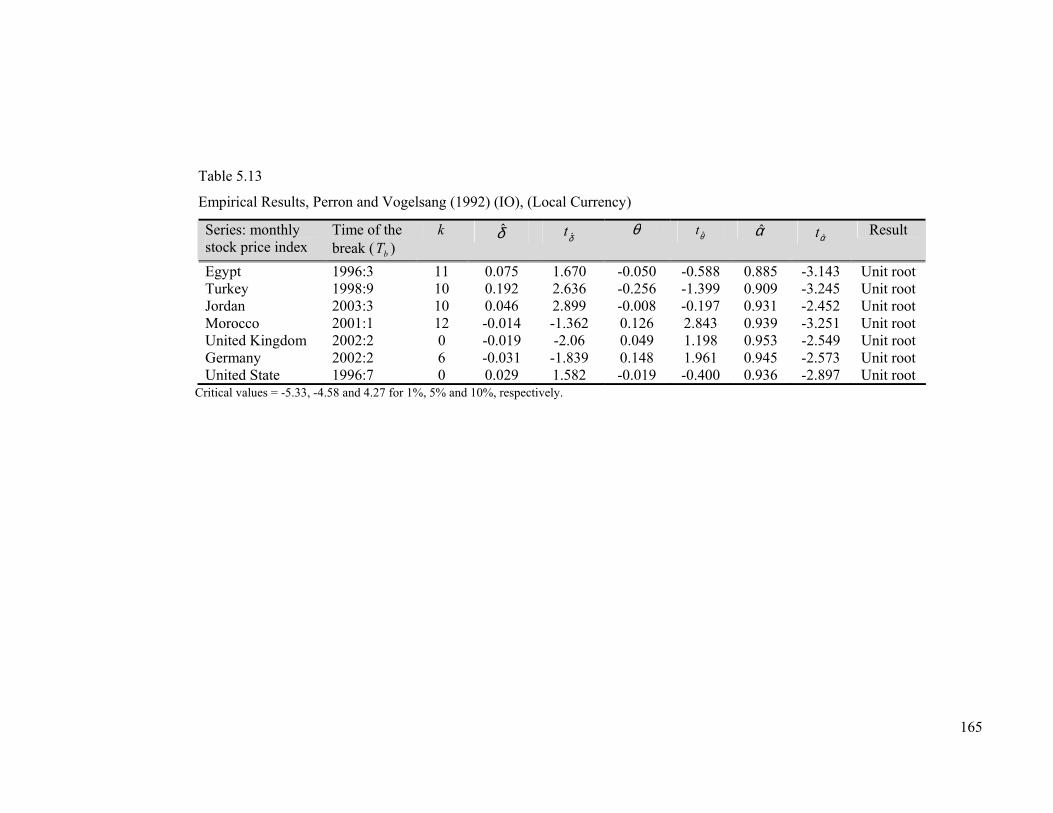

4.1 Market Capitalization in Egypt Stock Exchange 1994-2004, $US Million 96 4.2 Trading Value in Egypt Stock Exchange 1994-2004, $US Million 96 4.3 Market Capitalization in Istanbul Stock Exchange 1994-2004, $US Million 101 4.4 Trading Value in Istanbul Stock Exchange 1994-2004, $US Million 101 4.5 Market Capitalization in Amman Stock Exchange 1994-2004, $US Million 107 4.6 Trading Value in Amman Stock Exchange 1994-2004, $US Million 107 4.7 Market Capitalization in Casablanca Stock Exchange 1994-2004, $US Million 112 4.8 Trading Value in Casablanca Stock Exchange 1994-2004, $US Million 112 5.1 Stock Price Indices in MENA region (Local Currency) 118 5.2 Stock Price Indices in MENA region ($US) 118 5.3 Stock Price Indices in All Countries ($US) 120 5.4 Monthly Stock Price Index in Egypt (Local Currency) 121 5.5 Monthly Stock Price Index in Egypt ($US) 121 5.6 Monthly Stock Price Index in Turkey (Local Currency) 122 5.7 Monthly Stock Price Index in Turkey ($US) 122 5.8 Monthly Stock Price Index in Jordan (Local Currency) 123 5.9 Monthly Stock Price Index in Jordan ($US) 123 5.10 Monthly Stock Price Index in Morocco (Local Currency) 124 5.11 Monthly Stock Price Index in Morocco ($US) 124 5.12 Monthly Stock Price Index in United Kingdom (Local Currency) 125 5.13 Monthly Stock Price Index in United Kingdom ($US) 125 5.14 Monthly Stock Price Index in Germany (Local Currency) 126 5.15 Monthly Stock Price Index in Germany ($US) 126 5.16 Monthly Stock Price Index in the United States 127 5.17 Monthly Rate of Return in Egypt (Local Currency) 128 5.18 Monthly Rate of Return in Egypt ($US) 128 5.19 Monthly Rate of Return in Turkey (Local Currency) 129 5.20 Monthly Rate of Return in Turkey ($US) 129 5.21 Monthly Rate of Return in Jordan (Local Currency) 130 5.22 Monthly Rate of Return in Jordan ($US) 130 5.23 Monthly Rate of Return in Morocco (Local Currency) 131 5.24 Monthly Rate of Return in Morocco ($US) 131 5.25 Monthly Rate of Return in United Kingdom (Local Currency) 132 5.26 Monthly Rate of Return in United Kingdom ($US) 132 5.27 Monthly Rate of Return in Germany (Local Currency) 133 5.28 Monthly Rate of Return in Germany ($US) 133 5.29 Monthly Rate of Return in United States (Local Currency) 134 5.30 Plots of the series and Estimated Timing of Structural Breaks 162

xiii

Abbreviations

ADF Augmented Dickey Fuller ADR American Depositary Receipts AFM Amman Financial Market APT Arbitrage Pricing Theory ARDL Autoregressive Distributed Lag ARVAR Augmented Restricted Vector Autoregression ASE Amman Stock Exchange AUVAR Augmented Unrestricted Vector Autoregression CAPM Capital Asset Pricing Model CASE Cairo and Alexandria Stock Exchange CMA Capital Market Authority CRDW Cointegration Regression Durbin Watson CSE Casablanca Stock Exchange ECM Error Correction Model ECT Error Correction Term EMH Efficient Market Hypothesis GARCH Generalized Autoregressive Conditional Heteroscedasticity GCC Gulf Cooperation Council GDP Gross Domestic Product GDR Global Depositary Receipts GNP Gross National Product HSBC Hong Kong and Shanghai Banking Corporation ICAPM International Asset Pricing Model IMF International Monetary Fund IPO International Public Offering IRF Impulse Response Function ISE Istanbul Stock Exchange JD Jordanian Dinar JJ Johansen-Juselius JSC Jordan Securities Commission LOOP Law of One Price MENA Middle East and North Africa OECD Organization for Economic Cooperation and Development OLS Ordinary Least Square PP Phillips and Perron SDC Securities Depository Centre UVAR Unrestricted Vector Autoregression VAR Vector Autoregressive Model VDC Variance Decomposition VECM Vector Error Correction Model WTO World Trade Organization

xiv

Publication from the Research

1 Marashdeh, H., 2005, “Testing For Structural Changes in MENA Equity Markets”, 46th NZAE Conference, New Zealand. This article has been considered as “a quality assured paper”. Available on line at: http://www.nzae.org.nz/conferences/2005/QA29-Hazem_Marashdeh.pdf

2 Marashdeh, H. and E. J. Wilson, 2005, “Structural Changes in the Middle East Stock Markets: The Case of Israel and Arab Countries”, University of Wollongong, Working Paper, 05-22. Available on line at:

http://www.uow.edu.au/commerce/econ/wpapers.html

3 Marashdeh, H., 2005, “Stock market integration in the MENA region: An application of the ARDL bound testing approach”, University of Wollongong, Working Paper, 05-27. Available on line at: http://www.uow.edu.au/commerce/econ/wpapers.html

4 Marashdeh, H, 2005, “Cointegration and efficiency: An empirical investigation of the Middle East stock markets”. A presentation delivered at Workshop of: “Mathematics in Finance”. Sponsored by School of Applied Mathematics and Statistics, University of Wollongong, 25th November 2005.

5 Marashdeh, H, 2005, “Interdependence of the MENA emerging stock markets: A Cointegration Approach”, Accepted to the 4th INFINITI Conference on International Finance, University of Dublin, Trinity College, Monday 12-Tuesday 13 June 2006.

6 Marashdeh, H. and Ali Saleh, 2006, “Re-visiting trade and Budget deficit in Lebanon: Critique”, University of Wollongong, Working Paper, 06-07. Available on line at:

http://www.uow.edu.au/commerce/econ/wpapers.html

1

Chapter One

Introduction

1.1 Background of the Study The analysis of the degree of international stock market integration has attracted a great

deal of interest in recent time. The term “stock market integration” refers to an area of

research in financial economics that covers many aspects of interrelationships between

stock markets. Market integration could be considered as a situation where there are no

impediments, such as legal restrictions, transaction costs, taxes and tariffs against the

trade in foreign assets or the mobility of portfolio equity flows. In the case of stock

market integration, all assets with the same level of risk have the potential to attract the

same return across all different markets.

The issues of financial integration of emerging stock markets have received a

great deal of interest of practitioners and academic researchers. Over the last two

decades a significant volume of research has been concerned with the integration of the

world’s major stock markets. The emerging stock markets in some developing countries

have achieved considerable improvements over the last two decades. Several factors

have played vital roles in these improvements, such as the conduct of sound

macroeconomic policies, stock markets reforms, privatization and financial

liberalization. One of the main reasons for this study focusing on emerging markets is

because there is an increase in funds flowing from developed markets toward

developing markets, and therefore these markets are becoming increasingly important in

terms of portfolio management (Hawawini, 1994).

2

It is important to define in more detail what constitutes definitions of stock

market. A stock market is considered as an emerging market if it has started a transition

process, growing in size and increasing in complexity. According to the International

Financial Corporation of the World Bank Emerging Markets Database, a stock market is

classified “emerging” if it is located in a low or middle income economy, and if its

invest able market capitalization is low relative to its per capita gross domestic product

(GDP).

Stock market integration has become a catchphrase in modern financial theory

and several arguments emphasize the desirability of market integration. One such

argument is based on the competitive auction-model. This model asserts that where

there are no barriers to capital movement, stock market integration leads to a more

efficient allocation of the world’s resources, and capital will seek higher returns to

investment, moving from stock markets where capital is relatively abundant to another

where capital is relatively scarce. These characteristics of stock markets enable the

competitive auction-model to function more effectively in order to equilibrate markets.

Another argument is that in case of integration among stock markets, the systematic risk

(market risk) becomes unsystematic risk (firm risk), and this kind of risk can be

diversified or eliminated by including the security as part of diversifiable portfolio.

For stock market integration to be effective requires sound macroeconomic

conditions and a sound domestic financial sector. Integration of stock markets causes all

risk factors to be traded at the same price. For example, if the stock markets in the

Middle East and North Africa (MENA) region are fully integrated then the business

cycle risk or the inflation risk would have the same price in all MENA markets. In other

words, stock market integration means that the law of one price is fully consistent

throughout all traded assets. In general it is believed that as markets become more

3

integrated, the cost of capital decreases, because the removal of investment barriers

allows for imported risk sharing between domestic and foreign agents.

This thesis examines the integration stock markets in the MENA region. In

particular, the study focuses on four emerging markets in this region, namely Egypt,

Turkey, Jordan and Morocco. These markets are considered to be relatively active

compared to other stock markets in the region. The study also, examines the integration

between these markets and the markets of the representative developed economies of

the US, UK and Germany. The MENA region is considered as one of the richest in the

world in terms of natural resource, qualified endowments and trained labour force, and

per capita GDP. The four countries that are considered in this study, have adopted

several sound macroeconomic policies over the last two decades which have contributed

to higher economic growth and to overcome macroeconomic imbalances in their

economies. These policies include financial liberalization, trade liberalization, openness

to foreign direct investment, implementation of sound economic management and

privatization programs. Moreover, these polices are considered as indispensable in order

for these countries to face the growing challenges that resulted from the recent changes

in the global economy. In addition to the economic importance of the MENA region, the

political developments have huge consequences on the international political stage

In order to examine the degree of financial integration of stock markets in the

MENA region, and between these markets and developed markets, this study starts with

testing for the presence of structural change. The tests for a unit root in the time series

of stock prices are unlike the conventional stationarity tests, which are found to be

biased towards the non-rejection of the null hypothesis of a unit root in the presence of

structural change. That is, the conventional unit root tests lack power in correctly

rejected the null hypothesis in the presence of structural changes. This study employs

4

the Innovational Outlier (IO) model proposed by Perron (1997) which models the break

as a gradual change in the trend function with an endogenously determined break date.

This procedure has not been applied to studying stock markets in the MENA region.

The second stage of the study in the financial integration among stock markets

in the MENA region (and between these markets and developed markets) utilizes the

newly proposed autoregressive distributed lag (ARDL) estimation approach. This

procedure is recognized as the preferred method in estimating the long-run cointegrating

relationship. This study also explores the short-run and the long-run dynamic

relationships for the stock markets in the MENA region as well as conducting Granger-

causality tests which are augmented with an error correction term. Finally, the study

considers the relationship between the existence of cointegration among stock markets

and the efficient market hypothesis (EMH).

1.2 Objective of the Study The main objective of this study is to examine the financial integration among the stock

markets of Egypt, Turkey, Jordan and Morocco, and between these markets and the

developed stock markets, of the US, UK and Germany. To attain this purpose, the thesis

aims to achieve the following:

1. To present an inclusive revision of the notion of stock market integration from

different points of view. Also, the study will present several arguments for the

desirability and benefits of international stock market integration. Moreover, the

study will review the early theoretical models relating to stock market

integration. In particular, the study analyzes the literature relating to stock

market integration using different models, such as the capital asset pricing

5

models (CAPM) and the arbitrage pricing theory (APT). Also the study will

explore some other alternative approaches for testing stock market integration

such as an innovative econometric methodology.

2. To critically review and analyze the recent techniques relating to the analysis of

stock market integration, such as cointegration techniques, generalized

autoregressive conditional heteroscedasticity (GARCH) model, Granger-

causality and vector autoregressive model (VAR). These techniques have been

applied to test for stock market integration in different regions in the world. The

cointegration approach has been widely recognized as the most suitable

approach for testing the co-movements between stock markets. This co-

movement indicates the existence of cointegration between them, which in fact

implies the existence of integration internationally between stock markets.

However, there will be a concentration on the studies that focus on the emerging

stock markets in the MENA region.

3. To outline the main features of the emerging stock markets in the MENA region.

By doing this, the study will concentrate on the main financial indicators in these

markets. These indicators include market capitalization, trading value, turnover

ratio and number of listed companies. Also the study will shed light on the

economies of these countries and on the macroeconomic polices adopted.

4. To test the unit root hypothesis in the presence of structural change at an

unknown time of the break, using Perron’s (1997) and Perron and Vogelsang

(1992) Innovational Outlier (IO) model. According to Perron (1989) most

economic time series are characterized by stochastic, rather than deterministic,

non-stationarity. Perron (1989) argued that macroeconomic time series may be

stationary if one allows for structural changes in the trend function of the

6

regression. When there are structural breaks present, the Dickey–Fuller statistics

are biased towards the non-rejection of unit root hypothesis. Moreover, if

structural changes exist in the data generating process which are not allowed for

in the specification of an econometric model. The results could be biased

towards the erroneous non-rejection of the non-stationarity hypothesis (Perron,

1997). However, according to the reviewed literature on the MENA region, this

issue has not been addressed in any known study. This study provides a new

contribution to the literature since there has not been any empirical study that

has used this technique when studying the stock markets in the MENA region.

5. To empirically estimate the long-run relationship among stock markets in the

MENA region, and between these markets and developed markets. This study

utilizes the newly proposed autoregressive distributed lag (ARDL) approach.

The ARDL procedure has been recognized as more preferable in estimating the

long-run cointegrating relationship than other cointegration approaches. One of

the ARDL features is that it is unlike conventional cointegration approaches

which concentrate on cases where the underlying variables are integrated of

order one. The ARDL approach is applicable irrespective of whether the

underlying regressors are all )0(I , all )1(I or mixed processes. Also, the ARDL

estimation procedure is more robust and performs well for small sample sizes

than other cointegration approaches. Using of the ARDL procedure in this thesis

is considered a significant contribution to the literature of stock market

integration in the MENA region since it has not been used before.

6. To construct standard Granger causality tests which are correctly specified to

include the lagged vector error correction term when variables are cointegrated

(VECM). This test helps explore the short and long-run dynamic relationships

7

among the MENA stock markets, and between them and developed markets.

The estimated long-run causal relationship among stock markets is based on the

error correction term. Granger (1988) asserts that neglecting the error correction

term when testing for causality among cointegrated variables leads to serious

biases due to filtering out low-frequency (long-run) information.

7. To explore the efficient market hypothesis and the relationship between the

existence of cointegration among stock markets and the efficiency of these

markets. Recently, there have been many contradictory views on this issue in the

last decade. Some have argued that the existence of cointegration between stock

markets implies that these markets are inefficient. Others have argued that the

existence of cointegration between markets implies nothing about efficiency or

inefficiency. This study will try to present different point of view in related to

this issue.

8. Finally, to shed more light on the consequences and implications of finding

integration among these markets. This study considers the effect of integration

on portfolio diversification and the portfolio equity net flows between stock

markets in the MENA region.

1.3 Data and Methodology 1.3.1 Data Sources This study uses monthly stock price indices for four stock markets in the MENA region,

namely, Egypt, Turkey, Jordan and Morocco and for three developed stock markets,

namely US, UK and Germany. The study covers the period December 1994 to June

8

2004. Different sources for the data have been used. The study depends on the following

sources:

1. Morgan Stanley Capital International (MSCI), (www.msci.com).

2. Standard & Poor’s, Emerging Stock Markets Factbook, 2002.

3. Standard & Poor’s, Global Stock Markets Factbook, 2005.

4. International Financial Statistics Yearbook (IFS), various issues.

5. The World Bank, Global Development Finance, CD ROM, 2004.

6. World Development Indicators database, April 2005.

7. Arab Monetary Fund, (www.amf.org.ae).

1.3.2 Method of the Study This study reviews different financial and economic approaches that have been

developed to measure stock market integration. By reviewing these approaches, the

study covers a range of important literature on this issue. A thorough discussion of the

early theoretical models such as capital asset pricing model (CAPM), and a review the

literature related to Arbitrage Pricing Theory (APT) are conducted. Moreover, this study

reviews the recent econometric techniques used for measuring stock market integration.

These techniques include different approaches to cointegration analysis, such as Engle-

Granger, Johansen-Juselius, autoregressive conditional hetroskedasticity (ARCH),

generalized autoregressive conditional hetroskedasticity (GARCH) model, vector

autoregressive (VAR) and the autoregressive distributed lag (ARDL) approaches.

In order to measure the integration of stock markets in the MENA region, the

analysis implements advanced techniques which test the unit root hypothesis in the

presence of structural change at an unknown time of the break. For this purpose, the

9

study uses Perron’s (1997) and Perron and Vogelsang (1992) Innovational Outlier (IO)

model.

The newly proposed autoregressive distributed lag (ARDL) procedure to

cointegration is used as more of the recent studies have indicated that the ARDL

approach is preferred in estimating the long-run cointegration relationships. The ARDL

procedure is applicable irrespective of whether the underlying regressors are

purely )0(I , purely )1(I or mutually cointegrated. Also, it is more robust and performs

well for small sample sizes – such as this study - than other cointegration techniques. In

addition to the ARDL model, the Granger-causality is used. This test is augmented with

a lagged error correction term when variables are cointegrated. The conducting of this

test helps to explore the short-run and long-run dynamic relationships among MENA

stock markets and between MENA markets and developed markets.

1.4 Structure of the Study This thesis proceeds as follows. Chapter 2 reviews most of the literature related to stock

markets integration in both developed and emerging stock markets. The chapter starts

with a revision of the notion of stock market integration. After that, it discusses the

early theoretical studies related to stock market integration, such as capital asset pricing

model (CAPM), arbitrage pricing theory (APT), and some other alternative approaches

for testing integration.

Chapter 3 presents an inclusive discussion of the literature that has used

cointegration approaches to examine stock market integration. It also presents an

analysis of the concept of efficient market hypothesis and how it functions in the case of

10

cointegration among stock markets. Finally, the chapter reviews relevant research on

stock market integration in the MENA region.

Chapter 4 presents a review of the general features of the four countries Egypt,

Turkey, Jordan and Morocco in the MENA region. At the same time it discusses the

main macroeconomic indicators for these countries. Following this general review, the

chapter presents a discussion for each stock market in terms of the main indicators for

each market such as market capitalization, turnover ratio, trading value and number of

listed companies.

Chapter 5 presents a descriptive analysis for the stock price indices in the

MENA region and some developed markets. It investigates some important statistical

characteristics of these markets. And empirically estimates the conventional Augmented

Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests. As a significant

contribution by this study, this chapter analyzes the development of testing for structural

change, was firstly proposed by Perron (1989). Following this analysis, the study tests

the unit root hypothesis in the presence of endogenously determined structural change in

these stock markets.

Chapter 6 empirically estimates the integration among stock markets in the

MENA region, and between these markets and some representative developed markets

The study uses the recently developed autoregressive distributed lag (ARDL) model for

estimation. Moreover, the chapter estimates the Granger-causality among stock markets.

Based on the results of these approaches, the policy implications for the findings are

presented.

Chapter 7 summaries the major conclusions derived throughout the thesis. The

chapter presents a summary of the previous chapters and discusses the policy

11

implications of the major results. Finally, suggestions for future work are provided at

the end of the chapter.

12

Chapter Two

The Early Theoretical Models Relating to Stock Market

Integration

2.1 Introduction Over the last three decades a significant amount of research has focused on the issue of

stock market integration, and how to measure this integration. The term “stock markets

integration” refers to an area of research in financial economics that covers many aspects of

interrelationship across stock markets. Various schools of thoughts have been developed to

measure the integration of stock market. Some have used the correlation of the local market

return with the world return as a measure of integration; others have concentrated on the

investment restriction as indicators of integration.

A revolution in the field of portfolio theory started with the invented of assets

pricing models, such as Capital Asset Pricing Models (CAPM) and International Capital

Asset Pricing Models (ICAPM). According to these models, national markets are

considered to be integrated if securities with the same risk characteristics are priced the

same, even if they are traded on different markets. An alternative model to the CAPM is

what is called Arbitrage Pricing Theory (APT), which assumes that stock prices can be

influenced by not only the market risk, but also by several sources of systematic risk in the

economy.

13

The main objectives of this chapter are to consider and analyze the literature

relating to stock market integration that use different versions of asset pricing models, such

as (CAPM), and also review the literature relating to arbitrage pricing theory (APT). This

chapter consists of seven sections. Section 1 provides an introduction. Section 2 presents an

inclusive revision of the notion of stock market integration. Section 3 discusses the early

theoretical studies relating to stock market integration. Section 4 presents a thorough

discussion of the asset pricing models used for testing stock markets integration. Section 5

reviews the arbitrage pricing theory (APT) and the literature that uses this model for testing

stock market integration. Section 6 presents some alternative approaches for testing stock

market integration. Finally, the last section offers some concluding remarks.

2.2 The Notion of Stock Markets Integration Stock market integration could be considered as a status where there are no impediments,

such as legal restrictions, transaction costs, taxes, tariffs, and all types of controls against

the trading in foreign assets or on the mobility of portfolio equity flow. In the case of stock

market integration, all assets with the same level of risk grasp the same return across all

different markets.

Various schools of thought have been developed for measuring stock market

integration. In general, the common factor for most of these schools is the law of one price

(LOOP). That is, when transaction costs and taxes are not taken into account, identical

securities should carry the same price across all stock markets where such securities are

traded. In other words, if two or more markets are integrated then the identical securities

should be priced identically within both markets (Oxelheim, 2001). The existence of stock

14

market integration implies that stocks in all markets are exposed to the same risk factors

and the risk premia on each factor is the same in all markets.

Stulz (1981a) defined stock markets as being integrated “if assets with perfectly

correlated returns have the same price, regardless of the location in which they trade”. A

fully integrated market is defined as a situation where investors earn the same risk-adjusted

expected return on similar financial instruments in different national markets (Jorion and

Schwartz, 1986, p.603) which means no arbitrage profit to be achieved. In other words, if

the risk of an identical financial instrument is traded on the same price in different markets,

then it will be an indication of integration between these markets. However, a stock market

is considered to be more integrated, if there are stronger domestic returns depend on

contemporaneous world market shocks. This definition emphasizes not only the openness

of stock markets but also measures directly the extent to which shocks are transmitted

across stock markets. The transmission of a shock requires both the removal of barriers and

the capital itself flows across markets in order to take advantage of potential market

opportunities (Fratzscher, 2002). It is believed that, when a stock market is more fully

integrated, both the given market and the country’s economy will not be isolated from

external influence any more.

The rapid development of telecommunications and computer technology and the

widespread of using the Internet have been considered as important tools for making stock

markets practically and institutionally more integrated. These tools enable investors, agents,

traders, and all participants in stock markets to have the access to information, and

consequently the ability to manage their portfolios more efficiently.

15

Other important tools pertain to the removal, or at least the diminishing, of

government impediments that includes legal restrictions, transaction taxes, and all types of

controls against either the movement of capital or exchange and interest rates. All of these

steps have been known as “the liberalization process”. However, these improvements that

started in developed countries in 1970s and 1980s, continued during the 1990s in most

developing countries, and many countries are still adopting improvements (Akdogan,

1995).

Several arguments are presented for the desirability of international stock market

integration. According to Akdogan (1995, pp. 62-65) these arguments are:

1- Based on the competitive auction-model, and in case of no barriers to capital

movement, stock market integration leads to a more efficient allocation of the

world’s resources, and capital will seek higher returns to investment, moving from

capital market where capital is relatively abundant to another where capital is

relatively scarce. These characteristics of capital markets enable the competitive

auction-model to function more effectively to economically equilibrate the market.

2- In case of integration among all stock markets, the systematic risk (market risk)

becomes an unsystematic risk (firm-specific risk), and this kind of risk can be

diversified or eliminated away by including the security as part of diversifiable

portfolio.

3- It has been argued that corporate financial strategies depend on whether

international stock markets are integrated or not. In case of integrated market, all

firms can raise their capital with lower costs than firms do in a segmented market.

Also capital budgeting decisions for firms normally depends on their exposure to

international capital that is the marginal cost of capital of a firm that uses

16

international sources is lower than the marginal cost of capital of firm that uses only

domestic sources.

However, there are some developments that help this desirability of international

stock market integration. Narayan et al. (2004) mentioned some of these developments; the

removal of barriers across national borders that leads to increase the flow of capital, the

reduction in transaction costs and a commensurable increase in the flow of information, and

the important implication of stock markets integration for portfolio theory, which advocates

that investors diversify their assets across different stock markets provided that returns to

stocks in these markets are less than perfectly correlated with domestic market.

Financial market integration has several direct and indirect potential benefits;

Rangvid (2001) mentions some of the direct benefits as follows:

1- It allows for international capital flows to emerging markets, enabling these to

increase investment ratios thereby promoting real growth. In general, once funds

move freely between stock markets, this will give more momentum to these

markets.

2- It enables agents in the financial markets to price assets with identical risk patterns

in the same premises.

3- It allows for better risk sharing among agents who are trying diversifying their

consumption risk, as caused by differences in time patterns of returns to real capital

investment.

4- It enables agents to diversify risk in financial markets, and thus undertake projects

with higher expected returns for the same degree of risk

5- It lowers the cost of capital and smoothen the growth of investment.

17

Due to the indirect benefits, it has been widely accepted in the literature of this field

that integration plays a vital role in improving resource allocation through the financial

markets, thereby increasing safety of financial operations and also thereby strengthening

the domestic financial markets through such financial sector reforms. It is also believed that

it has an indirect positive effect on other economic sectors through its positive effect on

economic growth in general. Monetary policy, which is considered one of the main

economic policies, is affected greatly by the integration of stock markets, and this

integration itself has strong implications in international finance (Rutledge and Karim,

2004).

Also, it is widely accepted that economic and financial policies have a great

influence on the status of stock markets. Bekaert and Harvey (1995) state that, “whether a

market is integrated with the world capital markets or segmented is greatly influenced by

the economic and financial policies followed by its government or other regulatory

institutions”. By following this argument, many empirical studies have examined the

relationship between the degree of economic integration and the degree of stock market

integration.

However, the efficiency of assets allocation is considered as the main economic

reason that determines the integration of different stock markets. The flow of capital

between different countries depends on the difference between marginal productivities; that

is capital flows from those where the marginal productivity is low to those where marginal

productivity is high. According to this capital transfer, an equalization of marginal

productivity of capital of the different countries will be achieved, and welfare gains in all

the countries engaged in the process will be created.

18

2.3 The Early Theoretical Studies Relating to Stock Markets Integration

One of the earliest studies that designate the importance of diversification of risk was the

seminal work by Markowitz (1952). He revolutionizes the field of portfolio theory. He uses

a mean-variance efficient portfolio framework, a portfolio that has the highest expected

return at the given level of risk. His theory has been depicted graphically as the efficient

frontier model; but sometimes it is referred to as the efficient set. Markowitz (1952)

explains that diversification benefit could be achieved when additionally not highly

correlated securities are added into a portfolio. The model shows a simple geometric graph

of the trade-off between risk and return, the frontier itself is a composition of many

portfolios; more specifically the efficient portfolios are a subset of minimum variance

portfolios offering the highest return for each level of risk (Frino, et, al. 2001, pp. 139-141).

Going beyond Markowitz, Tobin (1958) argues that agents would diversify their

saving between a risk free asset and a single portfolio of risky assets. By combining a risk-

free asset with risky assets, it is possible to construct portfolios whose risk-return profiles

are superior to those of portfolios on efficient frontier. By doing this, what is called the

capital market line has been constructed as a tangent line to the efficient frontier that passes

through the risk-free rate.

Based on Markowitz’s work, and in the context of domestic market, Sharpe (1964),

Lintner (1965) and Mosin (1966) independently develop one of the most famous financial

equilibrium models, the capital asset pricing model, which is referred to as the CAPM. In

their model they assume that markets are segmented. The development of this model played

19

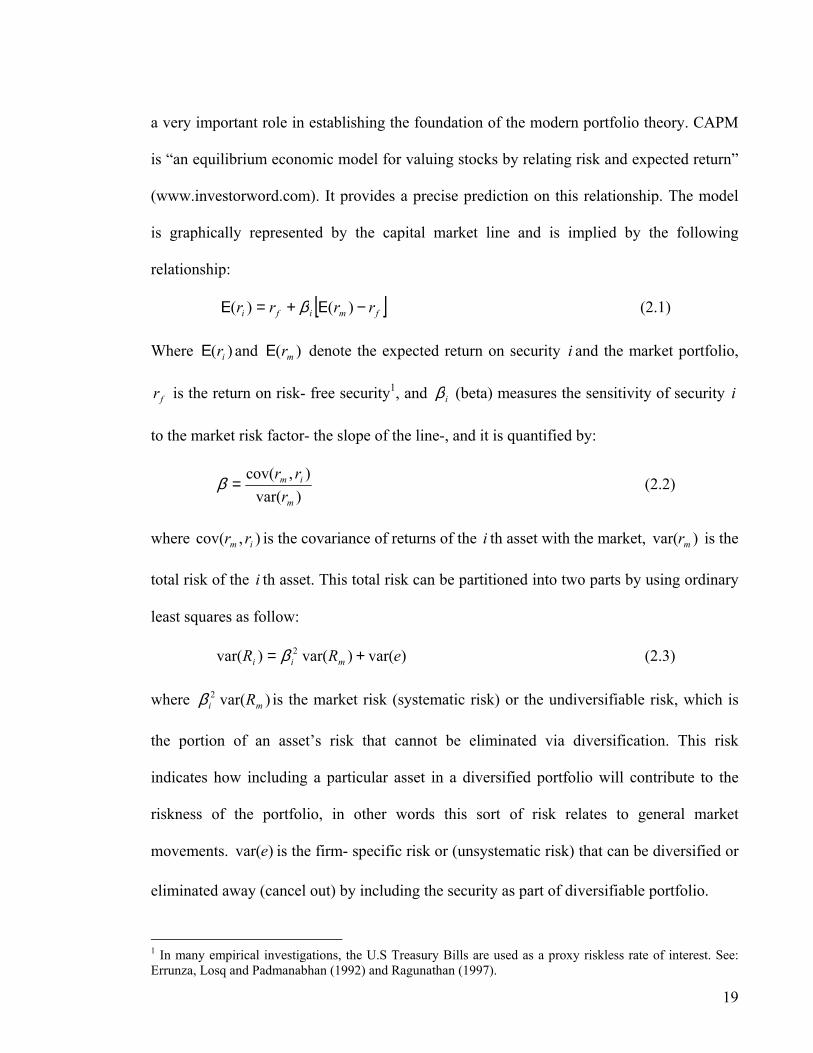

a very important role in establishing the foundation of the modern portfolio theory. CAPM

is “an equilibrium economic model for valuing stocks by relating risk and expected return”

(www.investorword.com). It provides a precise prediction on this relationship. The model

is graphically represented by the capital market line and is implied by the following

relationship:

[ ]fmifi rrrr −Ε+=Ε )()( β (2.1)

Where )( irΕ and )( mrΕ denote the expected return on security i and the market portfolio,

fr is the return on risk- free security1, and iβ (beta) measures the sensitivity of security i

to the market risk factor- the slope of the line-, and it is quantified by:

)var(),cov(

m

im

rrr

=β (2.2)

where ),cov( im rr is the covariance of returns of the i th asset with the market, )var( mr is the

total risk of the i th asset. This total risk can be partitioned into two parts by using ordinary

least squares as follow:

)var()var()var( 2 eRR mii += β (2.3)

where )var(2mi Rβ is the market risk (systematic risk) or the undiversifiable risk, which is

the portion of an asset’s risk that cannot be eliminated via diversification. This risk

indicates how including a particular asset in a diversified portfolio will contribute to the

riskness of the portfolio, in other words this sort of risk relates to general market

movements. )var(e is the firm- specific risk or (unsystematic risk) that can be diversified or

eliminated away (cancel out) by including the security as part of diversifiable portfolio.

1 In many empirical investigations, the U.S Treasury Bills are used as a proxy riskless rate of interest. See: Errunza, Losq and Padmanabhan (1992) and Ragunathan (1997).

20

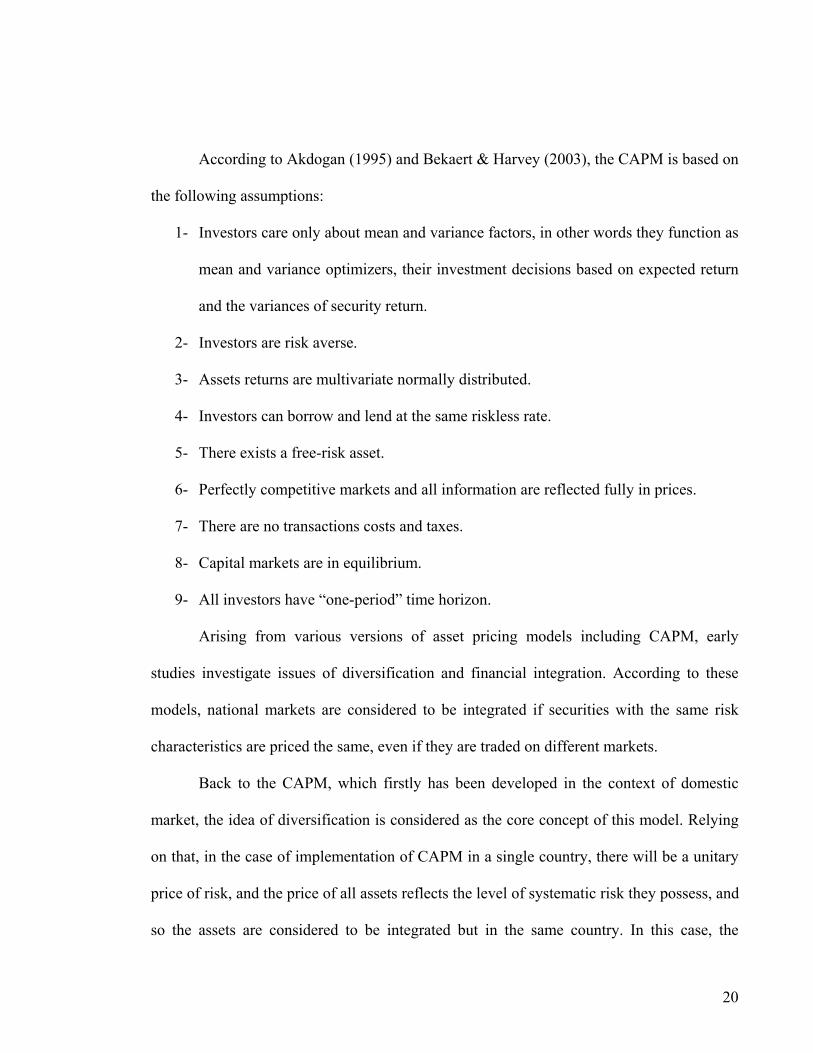

According to Akdogan (1995) and Bekaert & Harvey (2003), the CAPM is based on

the following assumptions:

1- Investors care only about mean and variance factors, in other words they function as

mean and variance optimizers, their investment decisions based on expected return

and the variances of security return.

2- Investors are risk averse.

3- Assets returns are multivariate normally distributed.

4- Investors can borrow and lend at the same riskless rate.

5- There exists a free-risk asset.

6- Perfectly competitive markets and all information are reflected fully in prices.

7- There are no transactions costs and taxes.

8- Capital markets are in equilibrium.

9- All investors have “one-period” time horizon.

Arising from various versions of asset pricing models including CAPM, early

studies investigate issues of diversification and financial integration. According to these

models, national markets are considered to be integrated if securities with the same risk

characteristics are priced the same, even if they are traded on different markets.

Back to the CAPM, which firstly has been developed in the context of domestic

market, the idea of diversification is considered as the core concept of this model. Relying

on that, in the case of implementation of CAPM in a single country, there will be a unitary

price of risk, and the price of all assets reflects the level of systematic risk they possess, and

so the assets are considered to be integrated but in the same country. In this case, the

21

CAPM assumes markets are completely segmented. This approach has been used by Sharpe

(1964), Lintner (1965) and Black (1972).

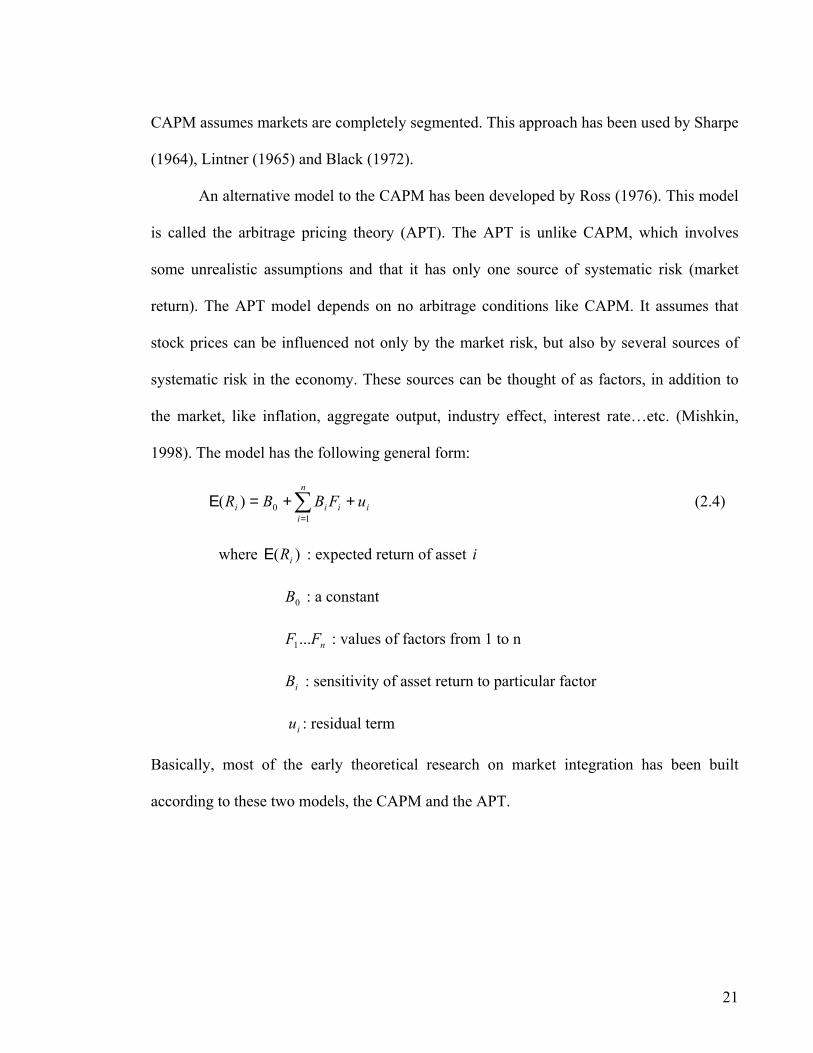

An alternative model to the CAPM has been developed by Ross (1976). This model

is called the arbitrage pricing theory (APT). The APT is unlike CAPM, which involves

some unrealistic assumptions and that it has only one source of systematic risk (market

return). The APT model depends on no arbitrage conditions like CAPM. It assumes that

stock prices can be influenced not only by the market risk, but also by several sources of

systematic risk in the economy. These sources can be thought of as factors, in addition to

the market, like inflation, aggregate output, industry effect, interest rate…etc. (Mishkin,

1998). The model has the following general form:

i

n

iiii uFBBR ++=Ε ∑

=10)( (2.4)

where )( iRΕ : expected return of asset i

0B : a constant

nFF ...1 : values of factors from 1 to n

iB : sensitivity of asset return to particular factor

iu : residual term

Basically, most of the early theoretical research on market integration has been built

according to these two models, the CAPM and the APT.

22

2.4 Asset Pricing Model for Testing Stock Market Integration As mentioned earlier, the capital asset pricing model (CAPM) has been developed

assuming the case of a completely segmented market. On the other hand, asset pricing

models in the international context generally assume markets to be perfectly integrated.

These include studies like Solink (1974), Stulz (1981), Adler & Dumas (1983) and Dumas

& Solink (1995) who use a world CAPM with currency risk (exchange risk). Solink (1983),

and Cho, Eun, & Senbet (1986) who use world arbitrage pricing theory. Wheatley (1988)

uses a consumption-based asset pricing model. Harvey (1991) uses world CAPM. Within

this context multiple risk factor models studied by Ferson and Harvey (1994, 1997). The

international factor latent models were studied by Bekaert & Hordick (1992), Campbell &

Hamao (1992) and Harvey, Solink, & Zhou (1994). All of these approaches will be studies

in full details later in this chapter.

In reality, it is hard to find both cases - either perfectly segmented or perfectly

integrated markets –, in fact there are different kinds of barriers between capital markets.

These barriers take the form of capital control, transaction cost and taxes. These barriers

restrain the investors from diversifying their portfolios in different markets. They have been

considered as extra costs that international investors face. These costs play an important

role in determining where the investments will take place, either in local markets or abroad.

That is if these costs outweigh the benefits of diversification, then it is more likely that

these investment will take place in the local market or vice versa.

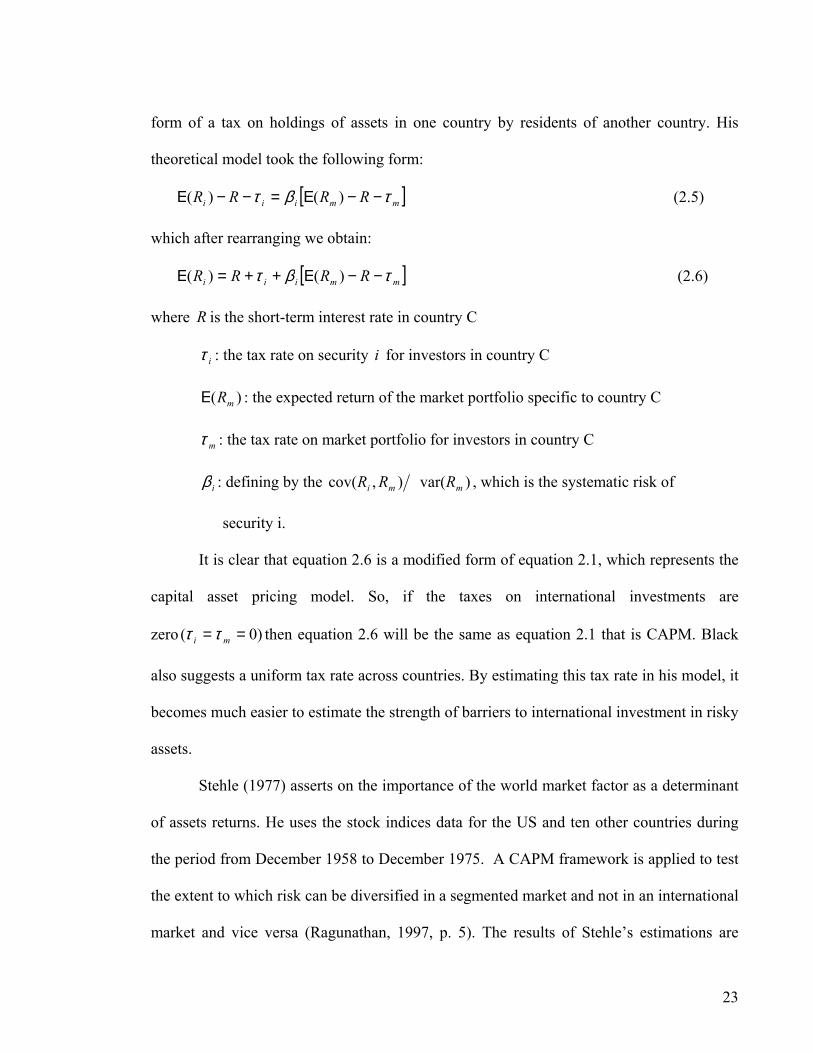

Black (1974) discusses these issues deeply. He develops an international capital

asset pricing model in which there are explicit barriers to international investment in the

23

form of a tax on holdings of assets in one country by residents of another country. His

theoretical model took the following form:

[ ]mmiii RRRR τβτ −−Ε=−−Ε )()( (2.5)

which after rearranging we obtain:

[ ]mmiii RRRR τβτ −−Ε++=Ε )()( (2.6)

where R is the short-term interest rate in country C

iτ : the tax rate on security i for investors in country C

)( mRΕ : the expected return of the market portfolio specific to country C

mτ : the tax rate on market portfolio for investors in country C

iβ : defining by the )var(),cov( mmi RRR , which is the systematic risk of

security i.

It is clear that equation 2.6 is a modified form of equation 2.1, which represents the

capital asset pricing model. So, if the taxes on international investments are

zero )0( == mi ττ then equation 2.6 will be the same as equation 2.1 that is CAPM. Black

also suggests a uniform tax rate across countries. By estimating this tax rate in his model, it

becomes much easier to estimate the strength of barriers to international investment in risky

assets.

Stehle (1977) asserts on the importance of the world market factor as a determinant

of assets returns. He uses the stock indices data for the US and ten other countries during

the period from December 1958 to December 1975. A CAPM framework is applied to test

the extent to which risk can be diversified in a segmented market and not in an international

market and vice versa (Ragunathan, 1997, p. 5). The results of Stehle’s estimations are

24

inconclusive, and the poor statistical results he got could indicate that these models may not

be well-specified.

In a similar work to Black (1974), Stulz (1981a) constructs a model of international

asset pricing in which a cost is associated with holding risky foreign securities. As in Black

(1974), Stulz (1981a) uses the proportional taxes to model barriers to international

investment. However, the investor in his study would pay taxes on absolute value rather

than the net value of her/his holding of foreign securities. For simplicity, Stulz assumes that

only domestic investors face the taxes on their foreign holdings. Stulz concludes that in

each country, all investors hold the same portfolio of risky assets. The key feature of Stulz

model is that there are some nontraded foreign assets. Based on that, for investors who face

barriers to international investment, the world market portfolio will be inefficient, and the

world market will not be in equilibrium.

Based on the international asset pricing model, Jorion and Schwartz (1986),

empirically examine the integration versus segmentation between Canadian stock market

and global North America market, the global North America markets have been represented

by US stock market. The study uses monthly rates of return from January 1963 to

December 1982. The results indicate that International CAPM was not a good description

of the pricing of Canadian securities. The study rejects the joint hypothesis of integration

between the Canadian stock market and the North American stock market, and shows

strong evidence of segmentation in the pricing stocks. Depending on these results, the study

indicates that legal barriers play an important role in causing this segmentation.

In the same direction of continuing the constructing of international asset pricing

models, Errunza and Losq (1985) postulate a mildly segmented market structure. In this

setting, mild segmentation occurs because investors from one country cannot invest in

25

stocks from another country, while investors from the other country do not face such

restrictions, and this leads to what is known as “market imperfection”. Also securities from

country 1 are eligible, and the securities from country 2 are ineligible for country 1.

Errunza and Losq examine the inability of some investors to trade in a particular class of

securities. They use the data from nine less developed countries and a random sample from

the US during the period 1976-1980. However, although their results accept the case of

mild segmentation, they are still inconclusive. They attribute this weakness to the kind of

restrictions imposed in the real world (Teng, 1998, p. 6). Errunza, Losq and Padmanabhan

(1992) use a maximum likelihood procedure to test the same model as in Errunza and Losq

(1985), their results are again inconclusive and similar to the previous one, which indicates

that the world capital markets are neither integrated nor segmented (Ragunathan, 1997,

p.5). However the use of the US Treasury bill rate as a proxy for risk rate is considered as a

shortcoming of their study, because this kind of rate is not used in emerging markets.

Buckberg (1995) uses a conditional international capital asset pricing model

(ICAPM) in an attempt to investigate whether emerging stock markets are part of global

financial market or not, and to what extent emerging markets behave like industrial markets

in relation to the world portfolio. According to Buckberg (1995, p. 57):

“Conditional refers to the use of conditioning information – some

information set 1−tZ - to calculate expected moments and to test properly

the ICAPM as a relation between expected returns and ex ante risk.”

Buckberg (1995) uses monthly data over the period 1977-1991 for twenty emerging

markets. The results indicate that six markets out of ten rejected ICAPM during the period

1977-1984. However, eighteen of the twenty markets are integrated with world markets

26

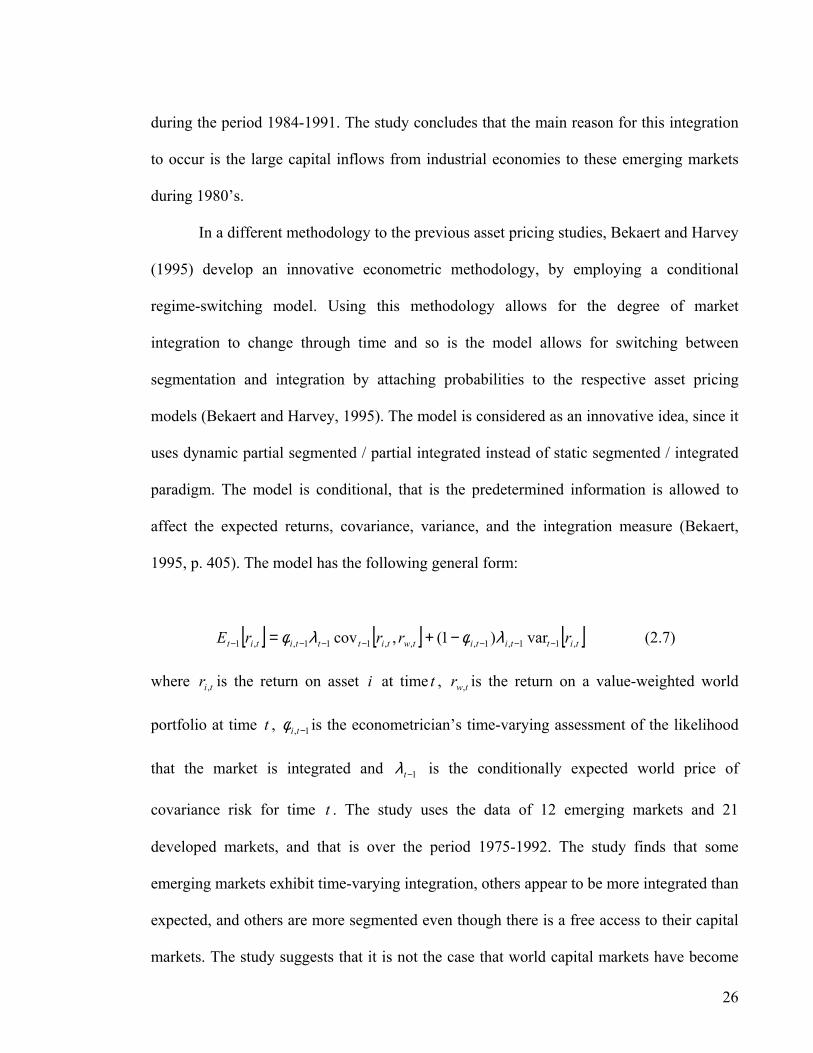

during the period 1984-1991. The study concludes that the main reason for this integration

to occur is the large capital inflows from industrial economies to these emerging markets

during 1980’s.

In a different methodology to the previous asset pricing studies, Bekaert and Harvey

(1995) develop an innovative econometric methodology, by employing a conditional

regime-switching model. Using this methodology allows for the degree of market

integration to change through time and so is the model allows for switching between

segmentation and integration by attaching probabilities to the respective asset pricing

models (Bekaert and Harvey, 1995). The model is considered as an innovative idea, since it

uses dynamic partial segmented / partial integrated instead of static segmented / integrated

paradigm. The model is conditional, that is the predetermined information is allowed to

affect the expected returns, covariance, variance, and the integration measure (Bekaert,

1995, p. 405). The model has the following general form:

[ ] [ ] [ ]tittititwtitttitit rrrrE ,11,1,,,111,,1 var)1(,cov −−−−−−− −+= λφλφ (2.7)

where tir , is the return on asset i at time t , twr , is the return on a value-weighted world

portfolio at time t , 1, −tiφ is the econometrician’s time-varying assessment of the likelihood

that the market is integrated and 1−tλ is the conditionally expected world price of

covariance risk for time t . The study uses the data of 12 emerging markets and 21

developed markets, and that is over the period 1975-1992. The study finds that some

emerging markets exhibit time-varying integration, others appear to be more integrated than

expected, and others are more segmented even though there is a free access to their capital

markets. The study suggests that it is not the case that world capital markets have become

27

more integrated. Despite a number of developing countries who have removed or relaxed

the restrictions on foreign stock ownership in the 1990’s, only 4 out of 12 countries have

higher integration measure in the same period. Another interesting result is that emerging

markets are characterized by high volatility, the standard deviations range from 18% in

Jordan to 53% in Taiwan, while developed markets characterized by relatively low

volatility comparing to emerging market, and the standard deviation range from 15% to

42%. Finally, the study indicates the existence of interrelationship between economic

growth and the status of capital market and the stage financial market development. This

interrelationship implies that economic growth is fundamentally linked to financial

integration.

In a recent study, Carrieri, Erronza and Hogan (2002) continue discussing the issue

of time-varying market integration for 8 emerging markets over the period 1976- 2000. The

GARCH-M methodology has been used to estimate the Errunza and Losq (1985) model

and empirically measure the time variation in market integration. They conclude that not

only the local risk is the most relevant factor in explaining the time variation of emerging

market return across the 8 countries, but also global risk is conditionally priced for some

markets. However, the study does not relate market integration to expected return. The

countries in the sample show wide range of integration alternatives from Argentina being

the most segmented to Mexico the most integrated. The study also shows that using the

correlations of market wide index return, as a measure of market integration is not a proper

measurement. In general the study shows that the degree of integration is higher in the

1990s. Finally, the study infers evidence that financial market development,

macroeconomic development and financial liberalization policies are very essential factors

for financial market integration.

28

Frank de Long and Frans A. de Roon (2002) use a similar model to the CAPM.

Their argument based on the notion that time variation in the integration level is important

for estimating the effects of liberalization on the cost of capital in emerging markets. In the

case of partially segmented market, the study considers the fraction of assets in an economy

that cannot be traded by foreign investors as a measure of market segmentation and has to

be held by domestic investors only which is called non-investable assets, whereas the asset

that can be traded freely refer to as investable assets. The effect of market segmentation or

integration on expected return for freely tradable (investable assets) and nontraded assets

(non-investable assets) has been estimated using a set of 30 emerging markets, which are

grouped into four regions Latin America, Asia and the Far East, Europe and the MENA

region, over the period 1988-2000. The study finds that the effect of the level of

segmentation or integration on the expected return in emerging markets exists in both kinds

of assets, although the results are weaker for the non investable assets than for the

investable assets. The expected returns in emerging markets are affected by the level of

segmentation not only in the country itself, but also by the level of segmentation in other

countries in the same region. The study also finds a significant time-variation in the betas

relative to the world portfolio, an annual increase of 0.09 in beta has been found due to the

decreased segmentation of the emerging markets.

Another asset pricing model that has been used in the literature to test the

integration of stock markets is the consumption-based asset pricing model. The basic idea

of this model asserts that the simple relation between consumption and assets return

captures the implication of complex dynamic international multi factor asset pricing model

(Campbell and Cochrane, 2000, p. 2863). Wheatly (1988), uses this model to test

international stock market integration. The model predicts that there is an asset pricing line

29

for each country that relates representative individuals expected real return on each asset to

the covariance of this return with growth in the individual’s real consumption. In this study,

the model predicts that each country has an asset pricing line (APL); this line relates the

expected real return to the covariance of this return with the growth in the individual’s real

consumption. He also suggests that markets are internationally integrated if assets of equal

risk, either located in one country or more, yield the same expected return. The joint

hypothesis will be rejected if securities lie at a significant distance from the (APL). The

study uses monthly data for U.S stock market and seventeen international markets and that

is from January 1960 to December 1985. The results do not reject the hypothesis, which

means the existence of stock markets integration.

Recently, CAPM has become more susceptible to criticism depending on the fact

that all investors are supposed to hold portfolio that contains both riskless portfolio and

market portfolio, which means that all investors hold the same combination of market

portfolio that contains all risky assets. In practice, however, it is still difficult to construct a

proxy that contains all assets (Agarwal, 2000).

30

2.5 Arbitrage Pricing Theory (APT) for Testing Stock Markets Integration

An alternative asset pricing model has been developed by the literature is the Arbitrage

Pricing theory (APT). A significant amount of literature has been using APT for testing

stock market integration. This model assumes that stock’s prices can be influenced by

several sources of systematic risk in the economy, other than the market risk. These sources

can be thought of as factors, in addition to the market.

In this context, Cho, Eun, and Senbet (1986) use the Arbitrage Pricing Theory

(APT) in an international setting to test stock market integration in eleven different

countries during the period (January 1973 - December 1983). They use the “Inter-battery

factor analysis” to estimate the common factor loading of two different groups of assets by

examining the inter-group sample covariance matrix only rather that the entire sample

covariance matrix. By doing so, they can alleviate the problem of variation of factor

structure, especially within countries. They also use Chow test method to measure the

validity of APT. The results of the cross-sectional test reject the joint hypothesis that the

international capital markets are integrated and that APT is valid internationally. The study

could not determine whether rejection of the joint hypothesis reflects segmentation of

capital markets or failure in the international APT.

Gultekin, Gultekin, and Penati (1989) use multi factor asset pricing model to test

stock markets integration or segmentation in U.S. and Japan. They hypothesize that market

segmentation could be either the result of government imposed barriers, or the individuals

attitudes and irrationality. The study uses weekly data during the period from January 1,

1977 to December 31, 1984. This period is divided into two sample periods, January 1977

31

to December 1980, and January 1981 to December 1984. These two samples are closed to

the year 1980, in which a big change in the capital control regime in Japan occurred, and

the enactment of the foreign exchange and foreign trade control law are completely

liberalized. The results indicate that the hypothesis of perfect integration has been rejected

before 1980 (before liberalization) and not rejected after 1980 (after liberalization). They

conclude that governments (public policies) could be a source of segmentation between

international stock markets. As a consequence of using weekly data, some economic

variables are not included, whereas stock market indices in the form of percentage change

are used, and this could be the a weakness of the study.

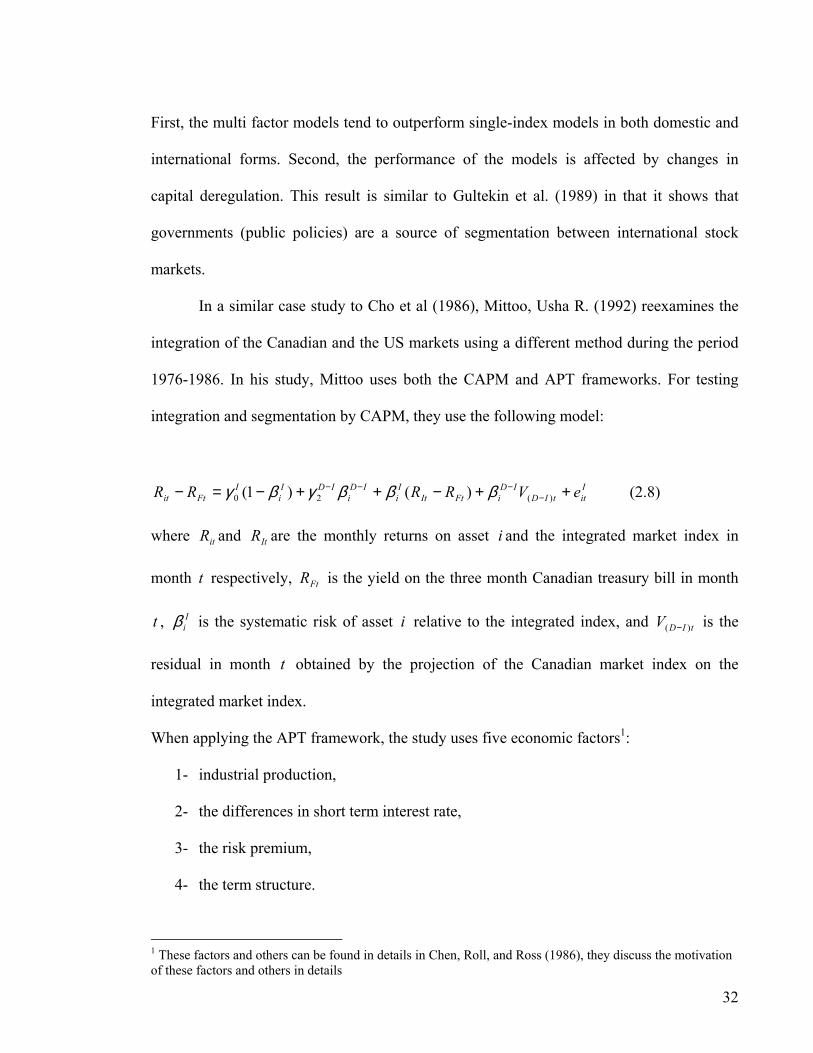

In a more comprehensive study, Korajczyk and Viallet (1989) investigate the

domestic and international version of the capital asset pricing model (CAPM) and the

arbitrage pricing theory (APT). They use the data on a large number of assets traded in four