Embed Size (px)

Citation preview

1

SECTION A- Attempt both questions in this Section

QUESTION ONE

The following trial balance has been extracted from the accounting records of Stephen plc at 31

March 2014, before the preparation of financial statements.

K K

Sales revenue 3,720,535

Cost of sales 1,681,165

Administrative expenses 563,548

Distribution costs 262,989

Research and development 249,000

Directors remuneration 300,000

Interest paid 13,500

Goodwill 150,000

Freehold land - at 2009 valuation 250,000

Buildings - at 2009 valuation 480,000

Plant and machinery – at cost 375,000

Accumulated depreciation at 1 April 2013:

- Buildings 80,000

- Plant and machinery 135,000

Inventory at 31 March 2014 143,365

Bank 47,674

Short-term investments 35,000

Trade receivables and payables 93,925 105,665

Bank loans 250,000

Investment properties (fair value at 1st April 2013) 435,000

Provision for liabilities at 1st April 2013 165,000

Suspense account 98,000

Allowance for receivables 2,980

Interim dividends paid (Ordinary shares) 5,000

Corporation tax 1,559

2

Ordinary share capital (K1 shares) 100,000

Share premium account 175,000

Revaluation reserve 140,000

Retained earnings at 31 March 2013 _________ 310,545

5,184,725 5,184,725

In addition to the trial balance you are provided with the following information all of which is

considered to be material:

1. Research and development expenditure comprises:

K99 000 – Applied research with a local university into the possible use of

hydraulic fracturing as an alternative and cost efficient source of energy. Tests

proved inconclusive.

K150 000 – Developing a new product that Stephen plc expects to generate

economic benefits for a seven year period commencing in October 2014.

2. On 16 April 2014 a customer went into liquidation owing Stephen plc K 38 000. The

money owed is included in trade receivables at 31 March 2014; however the company

does not now expect to recover any of this debt. In addition an allowance for receivables

of 3% of remaining trade receivables is required.

3. Stephen plc has an industry-wide reputation for providing an excellent after-sales service,

which helps generate a huge amount of repeat business with key customer groups. To

ensure that this continues, during the year ended 31 March 2014 Charlton spent K150,

000 on a customer service training course for all staff. This amount has been capitalised

and is included in the trial balance as goodwill. The managing director would like to

amortise goodwill in equal amounts over ten years.

4. Land and buildings are re-valued regularly in accordance with the requirements of IAS

16 Property, Plant and Equipment. During the year to 31 March 2014 land was re-valued

at K265, 000 and buildings at K425, 000. This re-valuation is not reflected in the trial

balance.

5. Freehold land is considered to have an infinite useful life. Buildings are depreciated on a

straight line basis (using their year-end value) over their estimated useful economic lives.

At 1 April 2013 the remaining useful economic life of buildings was estimated to be 25

years. No depreciation has been charged on buildings for the year ended 31 March 2014.

6. Plant and machinery is depreciated using the reducing balance method at 20% per annum.

The company charges a full year of depreciation in the year of acquisition and none in the

3

year of disposal. No depreciation has been charged on plant and machinery for the year

ended 31 March 2014.

7. The investment properties were purchased eight years ago and have a remaining useful

economic life of 32 years. At 31 March 2014 the properties were valued at K420, 000 by

a local firm of chartered surveyors.

8. Since October 2012 Stephen plc has been involved in a legal dispute with a former

employee. Based on legal advice available in October 2012, a provision was made for

K165, 000. This claim has now been settled and during the year ended 31 March 2014

Stephen plc paid K98, 000 to the former employee. This amount has been credited to the

bank account and debited to a suspense account pending the correct accounting treatment.

9. At a board meeting on 15 April 2013, it was proposed that the final dividend for ordinary

shareholders would be 15 ngwee per share.

Required:

In a format that is required for publication and in accordance with the provisions of IAS 1

Presentation of Financial Statements, prepare

a) A statement of comprehensive income for Stephen plc for the year ended 31 March 2014.

( 16 marks)

b) A statement of financial position for Stephen plc at 31 March 2014. (14 marks)

Note:

Financial statements must be in a format that is suitable for publication

You must clearly show all calculations and workings

Disclosure notes are not required

[30 MARKS]

4

SOLUTION ONE

Stephen PLC Statement of Comprehensive Income for the year to 31 March 2014

K

Sales Revenue 3,720,535 (0.5)

Cost of Sales (1,681,165+99,000) (1,780,165) (1)

Gross Profit 1,940,370 (0.5)

Administrative Expenses W1 (1,063,246) (0.5)

Distribution Expenses (262,989) (0.5)

Operating Profit 614,135

Finance costs (13,500) (0.5)

Profit before tax 600,635

Corporation Tax ( 1,559) (0.5)

Profit for the year 599,076 (0.5)

Other Comprehensive Income

Revaluation of Land and buildings (W2) 40,000 (1)

Total Comprehensive Income for the year 639,076 (0.5)

Workings

1- Administrative Expenses

Admin Expenses 563,548 (0.5)

Add: Research costs 99,000 (1)

Directors’ Remuneration 300,000 (0.5)

Training Expenses 150,000 (1)

Bad Debt written off 38,000 (1)

Depreciation

Buildings 17,000 (1)

Machines 48,000 (1) 65,000

Reduction in doubtful debts prov. (1,302) (1)

Revaluation Loss-Investment Property 15,000 (1)

Reduction in Liability provision

Original Provision 165,000

Less: Amount paid (98,000) (67,000) (1))

Total Administrative Expenses 1,063,246

5

2- Revaluation

Land- Revaluation for 2014 265,000

- Revaluation for 2007 250,000

Revaluation Gain 15,000 (0.5)

Building at 2007 valuation 480,000

Less: Acc Depreciation 1/4/13 (80,000)

400,000

Revaluation for 2012 425,000

Revaluation Gain 25,000 (0.5)

Total Revaluation Gain 40,000

3- Depreciation of Non-Current Assets

Buildings (425,000/25) 17,000

Machines 20% (375,000-135,000) 48,000

65,000

Stephen PLC Statement of Financial Position as at year to 31 March 2014

Cost AccDepn NBV

Non-Current Assets K K K

Tangible Assets

Freehold Land 265,000 - 265,000 (1)

Buildings 425,000 17,000 408,000 (1.5)

Plant and Machines 375,000 183,000 192,000 (1.5)

Investment Property 420,000 (1.5)

1,285,000

Intangible Assets

Development Costs 150,000 (1)

1,435,000

Current Assets

Inventory 143,365 (0.5)

6

Trade Receivables ( 93,925-38,000-1678) 54,247 (1)

Short-Term Investments 35,000 (0.5)

Bank 47,674 (0.5) 280,286

Total Assets 1,715,286(0.5)

Equity and Liabilities

Shareholder’s Equity

Share Capital 100,000 (0.5)

Share Premium 175,000 (0.5)

Retained Earnings (310,545+599,076-5,000) 904,621 (1)

Revaluation Reserve (140,000 + 40,000) 180,000 (1)

1,359,621

Non-Current Liabilities

Bank Loan 250,000 (0.5)

Current Liabilities

Trade Payables 105,665 (0.5)

1,715,286(0.5)

2 Marks for presenting your work professionally.

QUESTION TWO

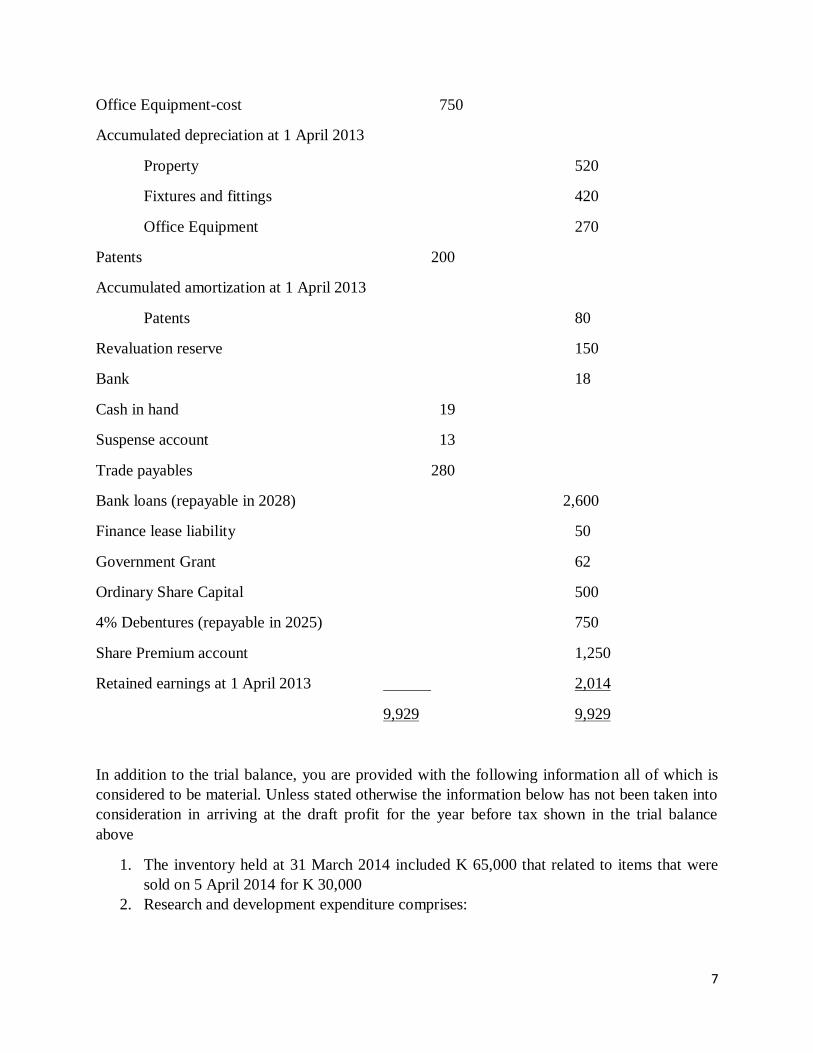

The following trial balance has been extracted from the accounting records of Marceline Plc at

31 March 2014.

K’000 K’000

Draft profit for the year before tax 951

Inventory at 31 March 2014 600

Trade receivables 338

Allowance for receivables 14

Research and development expenditure 249

Property-valuation 6,500

Fixtures and Fittings-cost 1,260

7

Office Equipment-cost 750

Accumulated depreciation at 1 April 2013

Property 520

Fixtures and fittings 420

Office Equipment 270

Patents 200

Accumulated amortization at 1 April 2013

Patents 80

Revaluation reserve 150

Bank 18

Cash in hand 19

Suspense account 13

Trade payables 280

Bank loans (repayable in 2028) 2,600

Finance lease liability 50

Government Grant 62

Ordinary Share Capital 500

4% Debentures (repayable in 2025) 750

Share Premium account 1,250

Retained earnings at 1 April 2013 2,014

9,929 9,929

In addition to the trial balance, you are provided with the following information all of which is

considered to be material. Unless stated otherwise the information below has not been taken into

consideration in arriving at the draft profit for the year before tax shown in the trial balance

above

1. The inventory held at 31 March 2014 included K 65,000 that related to items that were

sold on 5 April 2014 for K 30,000

2. Research and development expenditure comprises:

8

K 99,000 Applied research with a local University into the possible use of

hydraulic fracturing as an alternative and cost efficient source of energy. Tests

proved inconclusive.

K 150,000 Developing a new product that Marceline Plc expects to generate

economic benefits for a seven year period commencing in October 2014

3. The company’s policy is to charge a full 12 months depreciation on all assets held at the

year end. The rates to be used are as follows

Property – Straight line over 50 years

Fixtures and fittings – straight line over 6 years

Office equipment – 20% reducing balance

4. The patent was acquired in April 2009, at which time its economic life was estimated as

ten years. At 1 April 2013 the remaining life of the patent was estimated as 3 years

5. During the year ended 31 March 2014, Marceline plc disposed of property that previously

been re-valued. The property has been correctly removed from the valuation and

accumulated depreciation amounts shown in the trial balance, and the profit on disposal

has been correctly recorded in arriving at the draft profit for the year before tax. However

the property had previously been revalued by K 45,000 and this amount is included in the

revaluation reserve shown in the trial balance

6. On 1 April 2013 the company acquired office equipment with a fair value of K 50,000

through a finance lease. The lease period is five years with annual payments of K 13,000

per annum in arrears. The fair value of the leased asset is correctly included in office

equipment in the trial balance and the credit side of this transaction is shown as a finance

lease liability. Marceline Plc made the first lease payment of K 13,000 on 31 March 2014

and this has been credited to bank and temporarily debited to a suspense account. No

other accounting entries have been made in respect of the lease. Marceline plc uses the

sum of digits method to apportion interest relating to a finance lease.

7. The estimated corporation tax liability for the year ended 31 March 2014 is K 28,000

8. In May 2013, Marceline received a government grant of K 62,000 for use on a two year

project investigating the potential for a carbon-neutral workplace. During the year ended

31 March 2014, Marceline plc incurred qualifying expenditure of K 27,000 in respect of

this project. These expenses have been taken into consideration in arriving at the draft

profit for the year before tax of K 951,000.

9. No interest on debentures has been paid during the year or provided for in the trial

balance.

Required

a) Prepare a calculation of the profit for the year ended 31 March 2014 starting with the

draft profit for the year before tax of K 951 000 given in the trial balance and using the

additional information in notes 1-9 above. (14 marks)

b) Prepare a statement of financial position for Marceline plc at 31 March 2014 in

accordance with IAS 1 Presentation of financial statements. (16

marks)

9

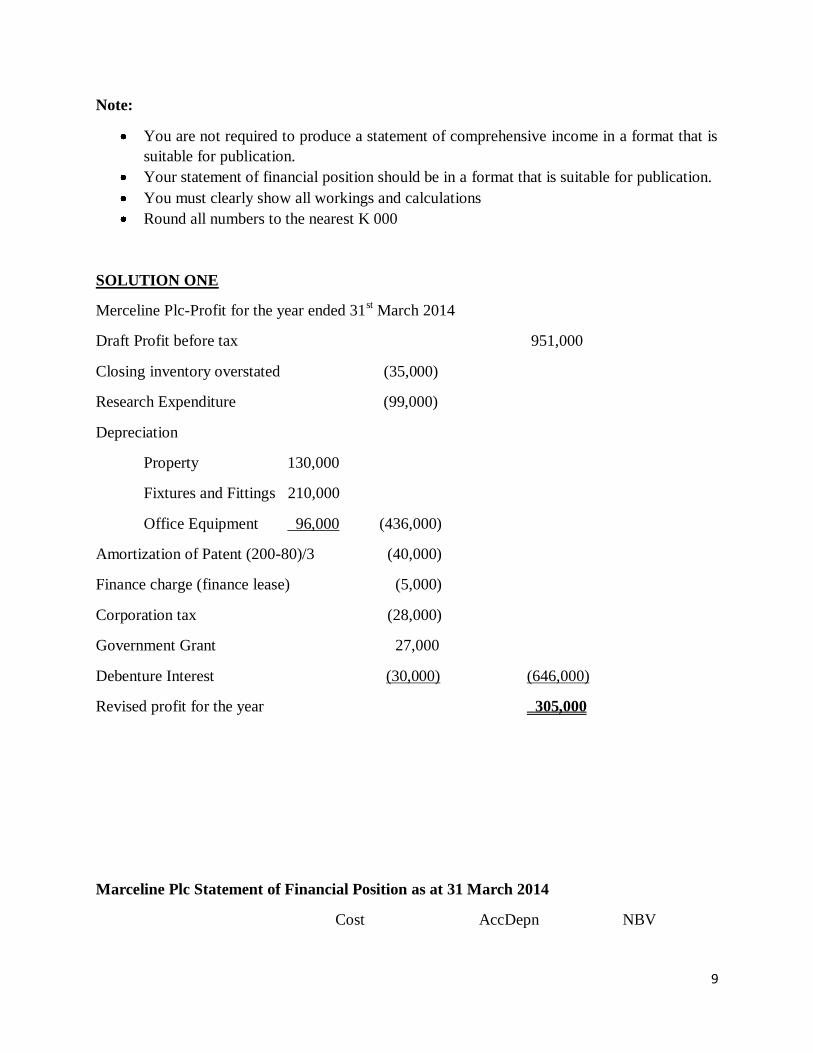

Note:

You are not required to produce a statement of comprehensive income in a format that is

suitable for publication.

Your statement of financial position should be in a format that is suitable for publication.

You must clearly show all workings and calculations

Round all numbers to the nearest K 000

SOLUTION ONE

Merceline Plc-Profit for the year ended 31st March 2014

Draft Profit before tax 951,000

Closing inventory overstated (35,000)

Research Expenditure (99,000)

Depreciation

Property 130,000

Fixtures and Fittings 210,000

Office Equipment 96,000 (436,000)

Amortization of Patent (200-80)/3 (40,000)

Finance charge (finance lease) (5,000)

Corporation tax (28,000)

Government Grant 27,000

Debenture Interest (30,000) (646,000)

Revised profit for the year 305,000

Marceline Plc Statement of Financial Position as at 31 March 2014

Cost AccDepn NBV

10

Non-Current Assets K K K

Tangible Assets

Property 6,500,000 650,000 5,850,000

Fixtures and Fittings 1,260,000 630,000 630,000

Office Equipment 750,000 366,000 384,000

Intangible Assets

Development costs 150,000 - 150,000

Patents 200,000 120,000 80,000

7,094,000

Current Assets

Inventory (600-35) 565,000

Trade Receivables ( 338-14) 324,000

Cash 19,000

908,000

Total Assets 8,002,000

Equity and Liabilities

Shareholder’s Equity

Share Capital 500,000

Share Premium 1,250,000

Retained Earnings (2,014+305+45) 2,364,000

Revaluation Reserve (150-45) 105,000

4,219,000

Non-Current Liabilities

Bank Loan 2,600,000

Debentures 750,000

Finance Lease 33,000 3,383,000

Current Liabilities

Trade Payables 280,000

11

Finance lease 9,000

Bank Overdraft 18,000

Deferred Income-Grant (62-27) 35,000

Corporation tax 28,000

Debenture Interest 30,000 400,000

Total Equity and Liabilities 8,002,000

Workings for finance lease

Finance Charge

Year Digits Interest ( 13,000 x 5 less 50,000)= 15,000

1 5 5/15 x 15,000= 5,000

2 4 4/15 x 15,000= 4,000

3 3

4 2

5 1

Sum of Digits 15

Finance lease-liabilities for statement of financial position

Yr Balb/f Payment Interest Principal Bal c/f

1 50,000 13,000 5,000 8,000 42,000

2 42,000 13,000 4,000 9,000 33,000

QUESTION TWO

a) Perth plc is being sued by an employee for ZMK 2 billion. As at 31October 2010 the case

has not yet come to court but the company is determined to contest the case. Perth plc’s

12

legal advisors have told the company that there is a 40% probability that the company

will win the case.

State with reasons how this should be reported in Perth plc’s financial statements for the

year ended 31 October 2010. (3 marks)

b) Kholar is a hotel chain with property with a carrying value of K 245m as at 31 October

2010, the end of the company’s most recent financial year. During October 2010 Kholar

started demolishing one of its hotels which had a book value of K 12m. The demolition

costs are estimated to be K 460,000. The company’s original intention was to use the site

to build a new hotel. However due to a downturn in the demand for hotel accommodation

it is now considering selling the site after demolishing the hotel.

Discuss how Kholar should account for the demolition costs. (3 marks)

c) The carrying amounts of the assets of a cash generating unit are as follows:

K’000

Goodwill 25,000

Patents and Copyrights 50,000

Property, Plant and equipment 200,000

275,000

There are indications that this CGU is impaired and therefore its recoverable amount is K

195,000,000. Value in use cannot be ascertained for any of the assets, but fair value less

costs to sell is K 20,000,000 for the patents and copyrights and K 160,000,000 for the

property, plant and equipment.

Calculate the amount of the impairment loss and show how this should be allocated

between the assets of the CGU according to the requirements of IAS 36 Impairment of

Assets (4 marks)

[10 MARKS]

SOLUTION TWO

a) The issue to consider here is whether or not a provision ought to be made in the financial

statements. On the basis of the evidence available, there is a present obligation.

According to the company’s legal advisers it is also probable that there will be an outflow

of resources embodying economic benefits in settlement (60%). A provision should

13

therefore be recognised for the best estimate of the amount to settle the obligation, which

in this case is ZMK 2billion.

b) The treatment of the demolition does depend on whether the intention is to sell the site or

develop it so the most likely outcome needs to be determined before the financial

statements are finalised

If the company decides to develop the site the costs can be capitalised as part of the cost

of the new hotel. The costs would be site preparation costs directly attributable to the

construction of the new hotel

If the company decides to sell the site, we need to determine whether or not the

demolition costs have improved the site’s future earning potential. Evidence of this

would be an increase in the potential selling price of the site. In this case the costs can be

capitalised

If the demolition costs do not enhance the selling price of the site, the costs should not be

capitalised but should be written off as incurred to the income statement

IFRS 5 Non-Current assets held for sale and discontinued operations does not apply as

the asset is not available for immediate sale in its present condition

c) Impairment loss

Carrying Amount Impairment Carrying amount

After impairment

K’000K’000 K’000

Goodwill 25,000 (25,000) -

Patents and Copyrights 50,000 (15,000) 35,000

Property, Plant and equipment 200,000 (40,000) 160,000

275,000 (80,000) 195,000

Question two

The Government of the republic of Zambia has embarked on empowering SMEs as a way of

creating jobs in the private sector as well as ensuring that they contribute to the growth of the

economy. The city of Kitwe has implemented the policy of running public buses which are

aimed at serving the community and ensuring that all important routes are covered. The Council

does not have enough buses to serve all routes in Kitwe and so they have been contracting small

transport companies to serve some designated important routes.

14

A small company in Kitwe, known as Mesan Transport operates a fleet of buses. Mesan is

contracted by the Kitwe City Council to run six bus services in Kitwe; 4 school routes and 2

hospital routes. Mesan is able to identify the cash flows associated with each of these routes and

each route has separately identifiable assets.

All the routes are running profitably with the exception of both hospital routes which are loss

making. The aggregate carrying value of the assets used by Mesan to operate the contracted bus

services in Kitwe is ZMK 6,800 million (6.8 billion kwacha). The aggregate net realizable value

of the assets is ZMK 5,600 million and the present value of the expected cash flows from the

routes is currently ZMK 9,200 million.

a) Explain what a cash generating unit is and state with reasons how many cash generating

units Mesan has in Kitwe. (3 marks)

b) Describe four things which could have happened which would provide evidence of the

impairment of the bus routes (4 marks)

c) Distinguish between the ‘recoverable amount’ and ‘value in use’ of an asset. (3 marks)

d) State, with reasons, the amount of any impairment in the bus route assets, and the value at

which they should be reported in the statement of financial position of Mesan.

e) Describe the circumstances in which an impairment of an asset can be reversed(3 marks)

f) Mesan is taking over a taxi business. The agreed price is ZMK 1,100 million. The

underlying net assets have been valued at ZMK 800 million. The Finance Director has

assigned the remaining ZMK 300 million to the cost of acquiring the valuable customer

lists taken over with the taxi business. However, some directors feel that this should be

treated as goodwill because they think it's really the same thing and there will be less

depreciation to charge.

Advise the directors of Mesan on the most appropriate treatment of the ZMK 300 and the

implications for subsequent depreciation charges. (4 marks)

g) List the main disclosures of IAS 36 Impairment of Assets (3 marks)

(20 Marks)

Solutions two

a) IAS 36 defines a cash generating unit as the smallest identifiable group of assets that

generatescash inflows that are largely independent of the cash flows from other assets or

groups of assets.

The number of cash generating units depends on the contract Mesan Transport has with

the Kitwe City Council. If all six routes have to be operated under the contract there is

only one cash generating unit. This is because the cash flows of each route are not

independent even although they can be measured separately. So, impairment would need

to beassessed for all six routes as a single cash generating unit.

Alternatively, if there are two contracts, one for the school routes and one for the hospital

routes, there would be two cash generating units. In this case, the two hospital routes

could be impaired as a separate cash generating unit.(3 marks)

b) Four things that could have happened are as follows

15

The economic performance of the routes was worse than expected. For example,

the number of paying passengers on the bus routes was lower than expected. Or,

the expected receipts from passengers along with expected subsidy payments

were lower than expected.

There was obsolescence or physical damage to assets used to operate the routes.

For example, damage and vandalism to the buses was higher than expected

resulting in higher costs (and reduced economic performance, as above).

The market value of the routes declined.This would have happened if any of the

above changes had taken place. There could also have been reductions in the

attractiveness of these types of routes because of alternatives becoming more

attractive. Also, there could have been cuts in public expenditure which means

that the contracts will not be renewed or will be renewed on less attractive terms.

Competitors may have started running the same or more convenient routes for

passengers.

There have been changes in technology, markets, economy, or laws which will

negatively impact on the future cash flows of the routes. For example, there could

now be more efficient, perhaps ‘greener’, engines along with potential legislation

changes which will mean fitting these newer engines.

Increases in market interest rates so that the cost of capital of the bus company

has increased. (4 marks)

c) Recoverable amount is the higher of the fair value less selling costs of an asset (i.e. its net

realizable value) and the value in use. Value in use is present value of the future cash

flows that an asset is expected to generate (sometimes called economic value).(2 marks)

d) The recoverable amount of the bus routes is the higher of ZMK 5,600m (net realizable

value) and ZMK 9,200m (economic value) i.e. ZMK 9,200.As this is higher than the

current carrying value of the assets of ZMK 6,800m there is no impairment and the

carrying value should continue to be based on ZMK 6,800.( 2 marks)

e) If the recoverable amount of an asset which has been impaired increases to an amount

which is higher than the impaired amount the impairment can be reversed. However, the

amount reversed cannot be higher than the amount which has been written off. This

applies to all assets with the exception of goodwill. ( 2 marks)

f) All tangible and intangible assets should be identified and valued at their fair value when

a business is taken over. Customer lists are an intangible asset and so should be

separately valued. In this case the fair value of the customer lists is ZMK 300m and so

there is no separate payment for goodwill. The customer list should be recorded at cost

and depreciated over the estimated economic life. It is true that under international

accounting standards purchased goodwill would not be systematically depreciated.

However, the goodwill would be subject to an annual impairment review, so there could

be annual impairment charges. ( 4 marks)

g) The main disclosures of IAS36 Impairment of assets are as follows

For each class of assets, the entity should disclose

- The amount of impairment losses recognised as expenses during the period

and the line items in which these impairment losses are included

16

- The amount of reversal on impairment losses recognised as income during the

period and the line items in which these reversal are included

- The amount of impairment losses (and reversal) on revalued assets recognised

in other comprehensive income during the period

For each material impairment loss or reversal recognised during the period, the entity

should disclose

- The events that led to the recognition of the impairment loss or reversal

- The amount of the impairment loss reversal

- The nature of the impaired asset or a description of the impaired CGU

Whether the recoverable amount of the asset or CGU is its fair value less costs to sell

or its value in use

If the recoverable amount is fair value less costs to sell, the basis on which this has

been determined (e.g. by reference to an active market)

If recoverable amount is value in use, the discount rate used(3 marks)

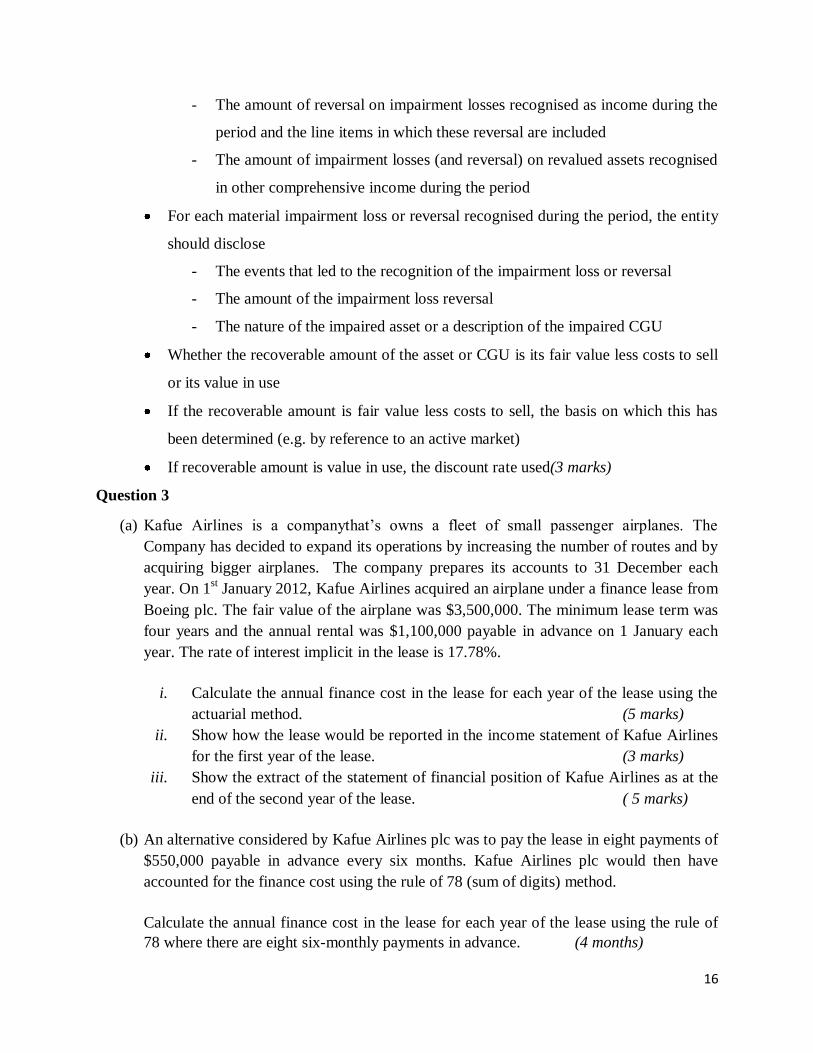

Question 3

(a) Kafue Airlines is a companythat’s owns a fleet of small passenger airplanes. The

Company has decided to expand its operations by increasing the number of routes and by

acquiring bigger airplanes. The company prepares its accounts to 31 December each

year. On 1st January 2012, Kafue Airlines acquired an airplane under a finance lease from

Boeing plc. The fair value of the airplane was $3,500,000. The minimum lease term was

four years and the annual rental was $1,100,000 payable in advance on 1 January each

year. The rate of interest implicit in the lease is 17.78%.

i. Calculate the annual finance cost in the lease for each year of the lease using the

actuarial method. (5 marks)

ii. Show how the lease would be reported in the income statement of Kafue Airlines

for the first year of the lease. (3 marks)

iii. Show the extract of the statement of financial position of Kafue Airlines as at the

end of the second year of the lease. ( 5 marks)

(b) An alternative considered by Kafue Airlines plc was to pay the lease in eight payments of

$550,000 payable in advance every six months. Kafue Airlines plc would then have

accounted for the finance cost using the rule of 78 (sum of digits) method.

Calculate the annual finance cost in the lease for each year of the lease using the rule of

78 where there are eight six-monthly payments in advance. (4 months)

17

(c) Explain why the level spread method might not be appropriate for calculating the finance

charge for each of the four years ( 3 marks)

(20 marks)

Solution 3- Leases

a) Kafue airlines will account for the lease under the actuarial method as follows

i.

Year b/f payment c/f after payment interest c/f

Year 1 3,500,000 1,100,000 2,400,000 426,720 2,826,720

Year 2 2,826,720 1,100,000 1,726,720 307,011 2,033,731

Year 3 2,033,731 1,100,000 933,731 166,017 1,099,748

Year 4 1,099,748 1,100,000 -

(5 marks)

ii) Extract of the Kafue Airlines Income Statement for the year ended 31 Dec 2010

Finance Cost 426,720

Depreciation 875,000

iii) Extract of the Kafue Airlines statement of financial position as at 31 Dec 2011

Non-Current Assets

Leased Asset 3,500,000

Acc Depreciation 1,750,000

1,750,000

Non-current liabilities

Lease Obligations 933,731

Current liabilities

18

Lease Obligations 1,100,000

b) The annual finance cost in the lease for each year will be as follows

Finance charge

8 7 15 15/36 375,000

6 5 11 11/36 275,000

4 3 7 7/36 175,000

2 1 3 3/36 75,000

36 36/36 900,000 ( 4 marks)

c) The level spread method simply allocates the finance charge to lease payments on a

straight-line basis over the lease term. This is unrealistic, since the amount of the finance

charge allocated to each payment should fall as the liability to the lessor also falls.

. ( 3 marks)

QUESTION THREE

a) Vincy Plc purchased a second-hard machine which had cost K 200,000. The price for a

new machine of this type costs K 300,000. Vincy incurred transportation costs of the

machine from the buyer to Vincy’s premises of K 10,000 and costs of installation

amounted to K 8,000. Once installed it was found that the machine was not working

properly and had to be repaired at a cost of K 6,000. At the same time a modification was

made to the machine to improve output at a cost of K 9,000. After two months production

the machine broke again and was repaired at a cost of K 4,000

Required:

i. Calculate and explain the cost figure that the company would recognize in its

financial statements for the machine ( 4 marks)

ii. With reason, state the amounts that will have to be expenses (3 marks)

iii. Discuss the differences in the way gains and losses are accounted for under the

revaluation model in IAS 16 Property Plant and Equipment and the fair value

model in IAS 40 Investment property subsequent to initial recognition(3 marks)

19

[10 MARKS]

SOLUTION THREE

i) The starting point is the invoice price of the machine which was K 200,000. The fact

that the price for a new one is K 300,000 is not relevant. As the transportation costs of

K 10,000 and the initial installation costs of K 8,000 were incurred in bringing the

asset to its location and in a position to make it ready for use, then these too would be

added to the cost of the asset. As the machine required initial repairs costing K 6,000

to make it work properly then, again, these should be capitalized. The modification

costing K 9,000 have increased the output of the machine and this will ensure that the

company derives greater future benefits from its use. These costs should therefore be

capitalized. Total value of asset will be K 233,000

(200,000+10,000+8,000+6,000+9,000).

ii) The repair costs of K 4,000 incurred after two month’s production would be treated as

revenue expenditure as they maintain the asset and its existing output level.

iii) According to IAS 16 Property Plant and Equipment, a revaluation increase must be

recognized as income when calculating the entity’s profit or loss to the extent that it

reverses any revaluation decrease in respect of the same item that was previously

recognized as an expense while a revaluation decrease must be debited to the

revaluation reserve (and shown as a negative figure in other comprehensive income)

to the extent of any credit balance previously existing in the revaluation reserve in

respect of that same item. This is different with way gains and losses are accounted

for in IAS 40. IAS 40 Investment property requires a gain or loss arising from a

change in the fair value of investment property to be recognized in the calculation of

profit or loss for the period in which it arises. There is no requirement of reversal of

any gains or loss previously recognised in the financial statements.

QUESTION TWO

Salsham Plc, a public listed company, is in the process of preparing its draft financial statements

for the year to 31 March 2014. Salsham Plc has brought the following matters to your attention

for your advice on the proper accounting treatment according to the International Financial

Reporting Standards requirements.

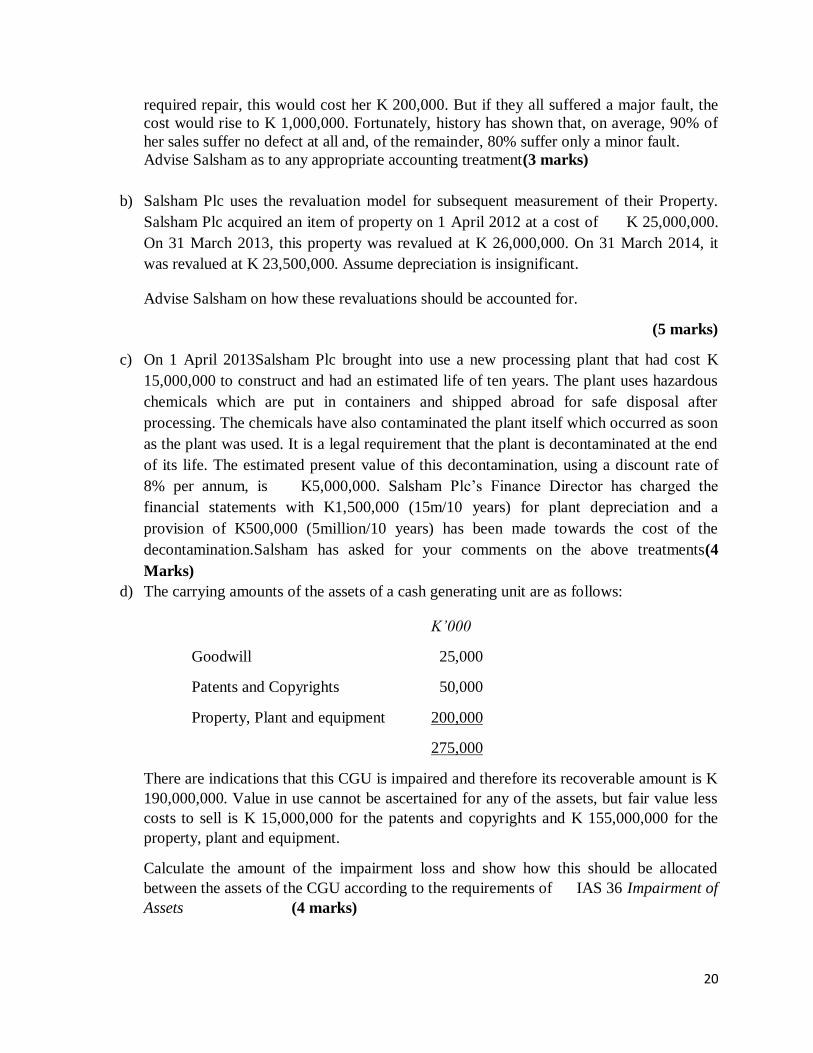

a) Salsham Plc sells microwave with a guarantee that, if a microwave proves to be faulty

within 12 months of purchase, Salsham will repair it free of charge, or replace it if the

fault is major. Salsham has estimated that, if all microwaves suffered a minor fault, and

20

required repair, this would cost her K 200,000. But if they all suffered a major fault, the

cost would rise to K 1,000,000. Fortunately, history has shown that, on average, 90% of

her sales suffer no defect at all and, of the remainder, 80% suffer only a minor fault.

Advise Salsham as to any appropriate accounting treatment(3 marks)

b) Salsham Plc uses the revaluation model for subsequent measurement of their Property.

Salsham Plc acquired an item of property on 1 April 2012 at a cost of K 25,000,000.

On 31 March 2013, this property was revalued at K 26,000,000. On 31 March 2014, it

was revalued at K 23,500,000. Assume depreciation is insignificant.

Advise Salsham on how these revaluations should be accounted for.

(5 marks)

c) On 1 April 2013Salsham Plc brought into use a new processing plant that had cost K

15,000,000 to construct and had an estimated life of ten years. The plant uses hazardous

chemicals which are put in containers and shipped abroad for safe disposal after

processing. The chemicals have also contaminated the plant itself which occurred as soon

as the plant was used. It is a legal requirement that the plant is decontaminated at the end

of its life. The estimated present value of this decontamination, using a discount rate of

8% per annum, is K5,000,000. Salsham Plc’s Finance Director has charged the

financial statements with K1,500,000 (15m/10 years) for plant depreciation and a

provision of K500,000 (5million/10 years) has been made towards the cost of the

decontamination.Salsham has asked for your comments on the above treatments(4

Marks)

d) The carrying amounts of the assets of a cash generating unit are as follows:

K’000

Goodwill 25,000

Patents and Copyrights 50,000

Property, Plant and equipment 200,000

275,000

There are indications that this CGU is impaired and therefore its recoverable amount is K

190,000,000. Value in use cannot be ascertained for any of the assets, but fair value less

costs to sell is K 15,000,000 for the patents and copyrights and K 155,000,000 for the

property, plant and equipment.

Calculate the amount of the impairment loss and show how this should be allocated

between the assets of the CGU according to the requirements of IAS 36 Impairment of

Assets (4 marks)

21

e. During the year to 31st March 2014, Salsham Plc has been conducting some construction

activities an area called Lamba. The construction activities have caused severe damage to

the habitat of wildlife in this area where there is no legal protection for the wildlife. The

Company has a high profile in the support of wildlife as it makes large contributions to

the World Wildlife Fund and campaigns vigorously on its behalf. To rectify the damage

to the habitat a charge of K 1,000 million is likely. Shalom Plc would like

your advice on whether they should provide for the cost of rectifying the damage in their

31st March 2014 Financial Statements. ( 4 marks)

[Total Marks-20 marks]

QUESTION

Part (a)

Shalom Ltd is a manufacturing company that prepares financial statements to 31 March each

year. On 1stApril 2013, Shalom Ltd purchased equipment for K 4,800 million with a useful

economic life of 4 years. Shalom Ltd depreciates equipment on a straight line basis.

Shalom Ltd’s financial statements show profit before tax of K 8, 000 million in each of the years

2014, 2015, 2016 and 2017. This profit is stated after charging depreciation of K 1,200 million

per annum. The company does not have any other Non-Current Assets other than the equipment

purchased on 1 April 2014.

The tax allowances granted in relation to this asset by the Zambia Revenue Authority at 31

March each year for the period 2014 to 2017 are:

Year 2014 K 1,620 million

Year 2015 K 1,380 million

Year 2016 K 1,020 million

Year 2017 K 780 million

Income tax is calculated as 30% of taxable profits

Apart from the above depreciation and tax allowances there are no other differences between the

accounting and taxable profits.

Required:

22

i. Ignoring deferred tax, prepare the income statement extracts in for each of the

years 2014, 2015, 2016 and 2017 ( 6 marks)

ii. Accounting for deferred tax, prepare the income statement and statement of

Financial Position extracts for each of the years 2014, 2015, 2016 and 2017 in

accordance with the requirements of IAS 12 Income tax with an assumption that

the tax charge for the pervious accounting year is paid on 1st April the following

year. (8 marks)

iii. Comparing your results in ii) and iii) above and in relation to the Income

statement extracts, explain why is it necessary for Shalom Ltd to take in to

account deferred tax consequences in relation to this assets so as to enhance the

qualitative characteristic of comparability as stated in the IASB Conceptual

Framework (4 marks)

Part (b)

Crispin Plc’s draft statement of comprehensive income for the year to 31 March 2014 shows an

income tax expense of K 55,000. The draft statement of financial position shows a non-current

liability of K 280,000 for deferred tax but does not show a current tax liability.

After investigations, it was found that the tax on the profit for the year to 31 March 2014 is

estimated at K 260,000, and the deferred tax liability of K 280,000 is for the year ending 31

March 2013. The K 55,000 in the draft statement of comprehensive income is the underestimate

for the year to 31 March 2013. The carrying amount of Crispin’s net assets at 31 March 2014 is

K 1.4m more than their tax base on that date. The tax rate is 20%

Required:

i. Restate the figures which should appear in relation to the tax expense that will be

shown in the statement of comprehensive income for the year to 31 March 2014,

the deferred tax figure and the current tax liability as at 31 March 2014 (5

Marks)

ii. Distinguish between permanent differences and temporary differences

(2 marks) [Total Marks- 25]

23

SOLUTION FOUR

i. Ignoring deferred tax

Income Statement Extracts

2014 2015 2016 2017

K’m K’m K’m K’m

Profit before tax 8,000 8,000 8,000 8,000

Tax (w1) (2,274) (2,346) (2,454) (2,526)

Profit after tax 5,726 5,654 5,546 5,474

ii) Taking deferred tax into account

Income Statement Extracts

2014 2015 2016 2017

K’m K’m K’m K’m

Profit before tax 8,000 8,000 8,000 8,000

Tax (w3) (2,400) (2,400) (2,400) (2,400)

Profit after tax 5,600 5,600 5,600 5,600

Statement of Financial Position extracts

2014 2015 2016 2017

K’m K’m K’m K’m

Non-Current Assets

Property, Plant and Equipment 3,600 2,400 1,200 0

Non-Current Liabilities:

Deferred Tax 126 180 126 0

Current Liabilities

Income Tax 2,274 2,346 2,454 2,526

24

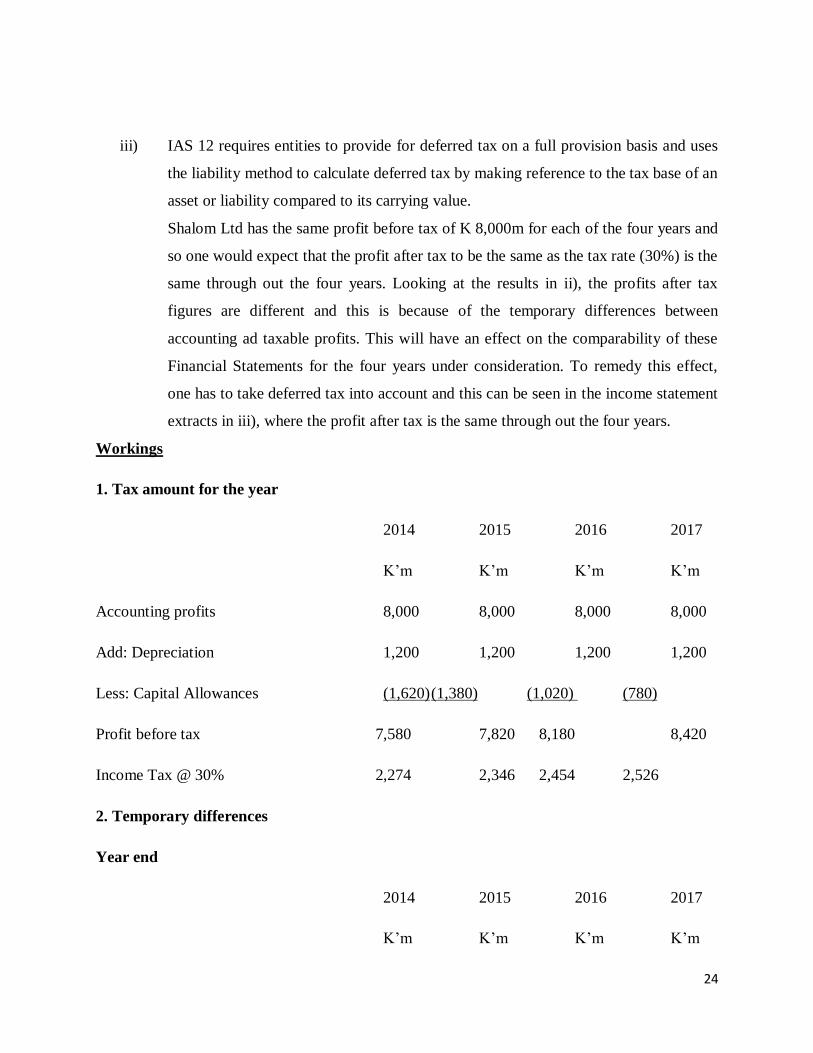

iii) IAS 12 requires entities to provide for deferred tax on a full provision basis and uses

the liability method to calculate deferred tax by making reference to the tax base of an

asset or liability compared to its carrying value.

Shalom Ltd has the same profit before tax of K 8,000m for each of the four years and

so one would expect that the profit after tax to be the same as the tax rate (30%) is the

same through out the four years. Looking at the results in ii), the profits after tax

figures are different and this is because of the temporary differences between

accounting ad taxable profits. This will have an effect on the comparability of these

Financial Statements for the four years under consideration. To remedy this effect,

one has to take deferred tax into account and this can be seen in the income statement

extracts in iii), where the profit after tax is the same through out the four years.

Workings

1. Tax amount for the year

2014 2015 2016 2017

K’m K’m K’m K’m

Accounting profits 8,000 8,000 8,000 8,000

Add: Depreciation 1,200 1,200 1,200 1,200

Less: Capital Allowances (1,620) (1,380) (1,020) (780)

Profit before tax 7,580 7,820 8,180 8,420

Income Tax @ 30% 2,274 2,346 2,454 2,526

2. Temporary differences

Year end

2014 2015 2016 2017

K’m K’m K’m K’m

25

Accounting base 3,600 2,400 1,200 0

Tax base 3,180 1,800 780 0

Tem differences 420 600 420 0

Deferred tax provision @30% 126 180 126 0

Increase (decrease) 126 54 (54) (126)

3. Tax Expense with deferred tax consideration

Year end

2014 2015 2016 2017

K’m K’m K’m K’m

Income Tax 2,274 2,346 2,454 2,526

Deferred Tax (w2) 126 54 (54) (126)

Tax for the year 2,400 2,400 2,400 2,400

From the above example, it can be seen that deferred tax is a means of allocating tax charges

fairly to particular accounting periods.

Part b

Crispen Plc

There is a taxable temporary difference of 1.4m between the carrying amount and the tax base of

the company’s assets. This gives rise to a deferred tax liability of 1.4m x 20% =

280, 000. So the deferred tax figure shown in non-current liabilities should be 280,000. The

statement of financial position should also show a current liability of 260,000 in relation to

current tax

The deferred tax liability has not changed from last year and no movement is recorded in the

income statement in as far as deferred tax is concerned. The tax expense shown in the statement

of comprehensive income should be 315,000(55,000 +260,000)