Embed Size (px)

Citation preview

1

Firm growth and market concentration in liner shipping

Meifeng Luo*a, Lixian Fanb and Wesley W. Wilsonc

Address for correspondence: a Dept. of Logistics and Maritime Studies, The Hong Kong Polytechnic University, M615 Li Ka Shing Tower, Hung Hom, Kowloon, Hong Kong. bSchool of Management, Shanghai University, Shanghai 200444, PR. China c Dept. of Economics, University of Oregon, USA.

Acknowledgement: This work is supported in part by the Hong Kong Polytechnic

University’s grant J-BB7C.

Abstract

Since its introduction in the 1950s, containerized shipping has grown dramatically.

Accompanying this growth has been a substantial growth in concentration. In this paper,

we theoretically identify the effects of firm growth on concentration, and then examine

the determinants of firm growth using panel data methods. We find that growth rates

depend on firm size and attributes such as its average vessel size and the rate of growth in

demand; that the growth patterns of the top firms point to a clear trend of increasing

concentration in the industry; and that they are dramatically enhanced by mergers and

acquisitions.

Date of final version: October 28, 2012

* Corresponding author: [email protected]; Tel: (852)2766-7414; Fax: (852)2330-2704

2

1.0 Introduction

Containerized shipping was introduced in the 1950s. Since its introduction, the industry

has grown at a phenomenal rate and surpasses the growth rate of world trade (Clarkson,

2011). Containerized shipments allow a reliable and efficient service at low cost afforded

by scale economies associated with larger ships. Large ships are capital intensive which

promotes market concentration (Chrzanowski, 1974). Over time, there are an

increasingly smaller number of Liner Shipping Companies (LSCs) that control a larger

portion of production capacity, serve a larger share of the market, and cover a broader

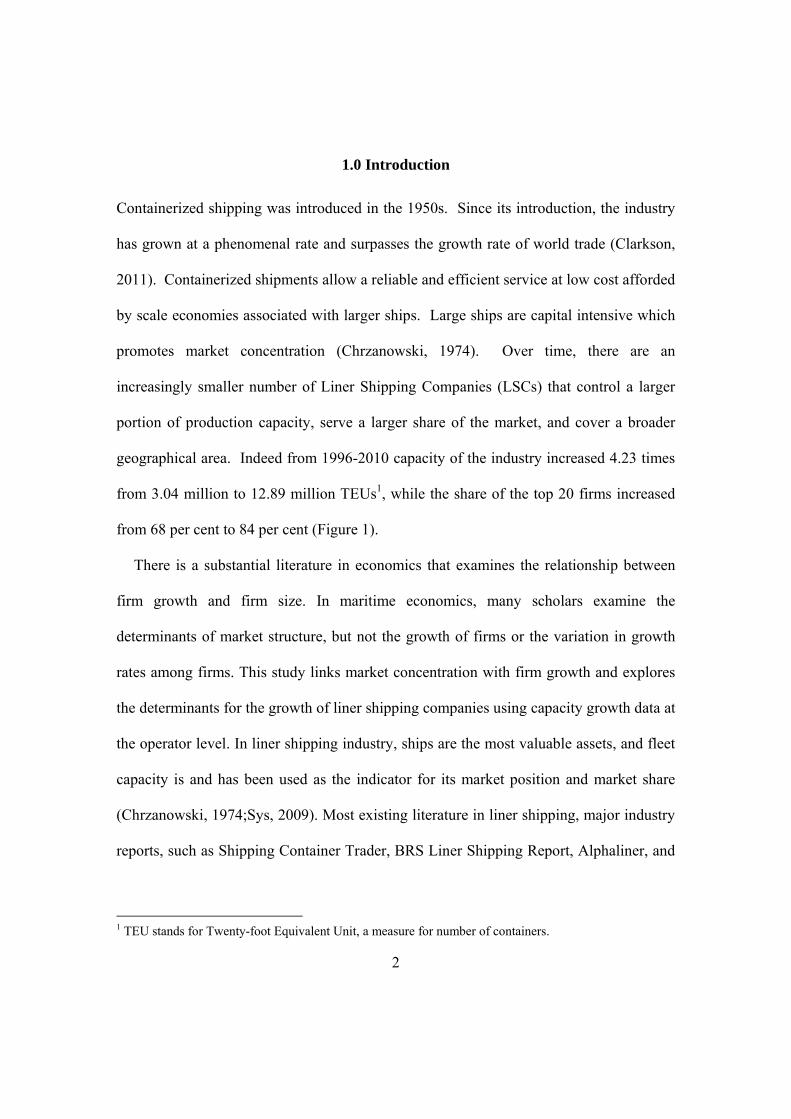

geographical area. Indeed from 1996-2010 capacity of the industry increased 4.23 times

from 3.04 million to 12.89 million TEUs1, while the share of the top 20 firms increased

from 68 per cent to 84 per cent (Figure 1).

There is a substantial literature in economics that examines the relationship between

firm growth and firm size. In maritime economics, many scholars examine the

determinants of market structure, but not the growth of firms or the variation in growth

rates among firms. This study links market concentration with firm growth and explores

the determinants for the growth of liner shipping companies using capacity growth data at

the operator level. In liner shipping industry, ships are the most valuable assets, and fleet

capacity is and has been used as the indicator for its market position and market share

(Chrzanowski, 1974;Sys, 2009). Most existing literature in liner shipping, major industry

reports, such as Shipping Container Trader, BRS Liner Shipping Report, Alphaliner, and

1 TEU stands for Twenty-foot Equivalent Unit, a measure for number of containers.

3

United Nations Economic Commission (ECLAC, 1998), all use capacity share as a

proxy of market share2.

The objectives are to characterize the relationship between firm growth, market share

and market concentration; identify the major factors contributing to the capacity growth

of liner companies, and exam how different firms expand in response to the changing

environment. The result of this study not only extends the current understanding about

the capacity expansion behavior in the economic literature, it also provides one of the

first analyses on firm growth and market concentration in liner shipping. Understanding

the growth of major shipping companies and its impact on the market concentration is

important for public agencies to prevent potential inefficiencies associated with greater

market concentration by identifying the firms whose further growth can increase the

concentration level and stipulating appropriate policies (ECLAC, 1998).

Insert figure 1 here.

The paper is organized as follows. Section 2 describes the literature on firm growth

and studies on market concentration in liner shipping. Section 3 links firm growth rate

and market share with concentration, discusses the factors in liner companies’ capacity

expansion. Section 4 introduces the data and the construction of the statistical model.

Section 5 describes the empirical results, and section 6 concludes.

2.0 Literature review

2 We follow this history, and we also note that growth based on outputs, such as TEU-miles carried in a

year and its sales in liner shipping are not available. Employment tends to be used in “fixed proportions” in

vessels and is also not available at the operator level.

4

Gibrat’s Law holds that the expected growth rate for a firm is independent of its size

(Sutton, 1997). Since the proportionate growth for a company in one period is

independent of its initial size, the effort to prevent market concentration by managing

targeted firms is pointless.

Penrose (2009) describes the growth of the firm from its motivation to long run profit

and growth, firm expansion with/without merger, the growth rate with firm size and

time, the economies of firm size/growth, limit to growth, and concentration and

dominance. Based on economic reasoning, she points out that firms cannot be expected to

grow indefinitely at a compound rate. Therefore, the rate of growth should be lower for

larger firms than that for medium size ones, although its absolute increase in size is not

necessary small.

Over the last several decades, there has been extensive work testing the validity of

Gibrat’s Law (Sutton, 1997;Cabral and Mata, 2003), or to study the growth of the firm

with respect to different factors, such as size and age (Hymer and Pashigian, 1962;Evans,

1987;Variyam and Kraybill, 1992). Different dimensions are used to measure firm size,

includes employment (Evans, 1987;Variyam and Kraybill, 1992;Cabral and Mata, 2003),

asset value (Hymer and Pashigian, 1962), and sales (Rahaman, 2011). However, the

number of explanatory variables in these studies is limited. In practice, it is expected that

many factors can influence the growth of the firm.

Because of the importance of market power in determining economic efficiency,

market concentration has long been an interesting topic in industrial economics

(Ferguson and Ferguson, 1994). The most frequently used measure for market

concentration is the Herfindahl-Hirschman index (HHI) (Hirschman, 1964), and it is used

5

as a guideline in managing the Mergers and Acquisitions (M&A) in the USA (U.S. DoJ

and FTC, 2010). Scherer and Ross (1990) provide an excellent summary and analysis of

the role of firm growth under Gibrat’s Law, and they demonstrate that markets can

concentrate with “pure luck”.

The study of market concentration in shipping can trace back to Charzanowski (1974)

who examined fleet capacity of selected countries and found that liner shipping is more

strongly concentrated than tramps. Pons (2000) and Benacchio et al. (2007) discussed

the effectiveness of antitrust regulation on market concentration. Sys (2009) measured the

degree of concentration using concentration ratios based on the container ship capacity of

liner operators, and concluded that the container liner shipping is in an oligopolistic

market. In addition, there are also studies on the causes and impacts of concentration

(ECLAC, 1998), M&A, and strategic alliances in the liner shipping industry (De Souza,

Beresford and Pettit, 2003;Heaver, 2000). All of these studies used container fleet

capacity in calculating firm’s market share and market concentration, and most of these

studies conclude that the liner conferences and M&As can contribute to market

concentration, but can also stabilize liner rates. A recent study (Fan, Luo and Wilson,

2011) tested the Gibrat’s Law in liner shipping industry, and concluded that larger firms

grow slower than smaller ones. Compared to the existing literature, a major contribution

of our work is the examination of growth factors in the liner shipping industry. Since the

introduction of the containerization in the late 1950s, this sector has experienced

tremendous growth in the seaborne freight market, and there has been tremendous growth

in the largest of the firms over time.

6

3.0 The growth of shipping firms and market concentration

In this section we identify the relationship between firm growth and market

concentration, and explain the important factors in the capacity growth of LSCs. As

discussed earlier, fleet capacity is commonly used to indicate the size of a liner operator,

and its capacity share is always used to represent its market share. Therefore, we use the

capacity share as the market share of individual firms (Si) to calculate HHI, a

conventional measure of market concentration following the equation below:

2

1

n

ii

HHI S

, (1)

where n is the number of firms in the market. Using this definition, it is straight forward

to prove that:

0,

0,

0,

i

ii

i

if S HHIHHI

if S HHIr

if S HHI

.

(2)

That is, if the market share of a firm is larger than the HHI index, an increase in the

growth rate of that firm increases the level of concentration.

The market shares of the top 100 liner shipping companies in 2010 and the HHI index

are plotted in Figure 2. There are three companies, namely Maersk Line, MSC and CMA

CGM Group, whose market shares are higher than the HHI index. This indicates that any

increase in the growth rate of these three companies would lead to an increase in the

market concentration. The growth of the LSCs whose market shares are below the HHI

line reduces the market concentration level.

Insert Figure 2 here.

7

Given the relationship between firm growth and market concentration, we now

consider factors for the capacity growth of a LSC. The capacity of a LSC includes its

own capacity – the ship purchased by the company itself or acquired from other

companies through M&As, and the ships chartered from other company, mostly by a

long-term chartering agreement such as a bareboat charter.3 According to data from

Alphaliner, most large shipping companies charter around 40-60 per cent of the operating

capacity, and the average chartering ratio for the top 100 companies is about 50 per cent.

In practice, liners can share capacity with each other through different kinds of

cooperative agreements. Since such arrangement does not change the capacity of

individual firm, it is not considered in this paper.

The growth of a firm is defined as the percentage change of the capacity (both owned

and chartered) in a year. If Gibrat’s Law is true, then this growth rate is a random

variable independent of its initial size, and the larger firms in one year may not be the

same in the future years. This implies that it is impossible to identify which firm will be

the dominant one in the future. On the other hand, as shown in the literature review,

there are many studies that have rejected the Gibrat’s Law, based on the statistical tests

between the firm size and the growth rate.

Our specification of different growth rates is based on the existing literature as well as

practices observed by firms in the industry. Together, these factors include firm specific,

3 Under bareboat charter agreement, the shipowner actually orders the vessel for the operator. Therefore,

these vessels can be treated as if there are owned by the LSC.

8

market characteristics, and the effects of mergers and acquisitions. That is, our model of

firm growth is given by: growth=f(firm attributes, market conditions, merger activities).

There are three firm attributes considered in our model. These include: the relative

scale of the company, the charter ratio, and the average capacity of the ships in this

company. Their possible impacts on growth rates are discussed below.

The relative scale is indicative of the relative position of the firm in the market. The

measure used is shipping company capacity as a share of total capacity in the global

market (the shipping market is taken to be fully globalized). As such, the effect of this

variable depends on the rate of growth by firm relative to the rate of growth in the

market.

As stated before, ship chartering is popular in liner shipping although the demand for

ships is fixed based on the service frequency of a route. This popularity may be because it

can separate the financial risks of vessel owning with that of vessel operation and avoid

the large capital cost required to purchase a ship. Although the percentage of chartered

vessels varies across different companies, the increased use of chartered vessels as the

operation capacity of carriers has become an integral part of the capacity growth of a

company.

Past studies consider the continuous increase of containership size as one of

contributing factors for market concentration in liner shipping (ECLAC, 1998). Today,

the largest Post-Panamax container vessel currently in service is about 175 thousand

DWT or 15 thousand TEUs, and even bigger container vessels are on its way (Alphaliner,

2011). The impacts of larger ships have two effects. First, larger ships can offer lower

rates to shippers due to scale economics. Shippers may prefer firms that have large ships,

9

and, therefore make the firms that have small ships less competitive. Second, most large

ships are deployed on major shipping routes, to exploit its full benefits. Therefore, it may

further increase the concentration in the major trunk routes. Both effects can expedite the

growth of the company that operates large ships. However, some studies also found that

large ships can restrict the shipping company from expansion due to the large (may be

sunk) capital cost of large ships (Le and Jones, 2005). Given these different conjectures,

the effect of average vessel capacity is ambiguous and depends on which effect

dominates.

In addition to firm conditions, there are a variety of market conditions that are central

to firm growth. The major market variables are market demand, freight rate, ship costs,

and market competition. The first three variables representing market demand and

supply are the same for all shipping companies. The last variable, market competition,

differs across firms in our specification. Each is discussed in turn.

One of the major reasons for a shipping company to expand its capacity is to

accommodate the increasing demand. It is generally believed that the higher demand can

stir up capacity expansion in shipping.

However, the question relevant to market concentration is that whether market demand

has different impact on the expansion rate of companies with different sizes. For the

same market demand, if larger companies expand more than the smaller ones, then the

market will develop towards a more concentrated structure.

Theoretically, market freight rate is an important indicator for profitability—a driving

factor for shipping companies to expand capacity. However, due to high fluctuation in

freight rate and the shipbuilding lag, even most new orders are made when the freight rate

10

is high or increasing (Luo, Fan and Liu, 2009), the capacity increase may not synchronize

with high freight rate or its increasing rate. In addition, there are also speculators who

tend to invest when the freight rate is low, to take advantage of a low new-building price.

In the empirical analysis, we use the time-charter rate as a proxy for freight rate, for

two reasons. First, comparing with the container freight rate, the time-charter rate is more

practical and reliable. Second, time-charter rate and container freight rate have a

correlation coefficient of 0.71 (Luo, Fan and Liu, 2009). It is recognized that the former

is the price paid from the charterer to the ship owner for using the ship, while the latter is

the price received by the carrier when it performance sea transportation services to the

shipper. However, because they are highly correlated, the former can be uses as an

approximation of the latter.

The price to acquire a ship, whether it is new or second-hand, influences the capacity

growth of a firm in two possible directions. First, ship owners may hedge on the price

increase when the market is slow. In this case, they will “buy low and sell high” or they

strategically expand capacity at low market prices so as to enjoy a lower capital cost in

operation. However, the opposite behavior on ship investment is also plausible: more

new orders are placed when the ship price is high as it is also the time when the freight

rate is high.

A shipping company’s capacity is an important indicator for its market power. With

more capacity, a shipping company can handle more cargo, and outperform the other

“competitive” firms with lower capacity. Therefore, a strategy of capacity expansion has

significant implications on the competitive position of a shipping company. To maintain

market share, the firm needs to keep pace with the growth rate of the others. A firm

11

seeking to expand its market share needs to expand more aggressively than the rival

firms. Hence, companies with different growth strategy may have different response to

the capacity growth of other companies.

In modeling growth, it is clear that mergers and acquisitions positively influence

growth, at least initially, and depending on the size of the acquisition, it can have

significant contribution to market concentration. Indeed, in this industry, there are often

large capacity jumps which cannot be explained by the market conditions. We do include

controls to capture the effects of mergers and acquisitions as failing to account for these

effects can result in over/under estimating the influence of other variables. Table 1 lists

the merger and acquisition events for the top operators within the study period. The

motivation for mergers and acquisition varies: some for market entry, others for economy

of scale, and others to contain competitors (Fusillo, 2009). However, their impacts on the

market concentration are the same: more capacity is in the hand of fewer ship operators.

Insert Table 1 here.

4.0 Data, variables and empirical model

The primary source is the Alphaliner database, which contains detailed information on

the fleet structure, new order, charter, sale and purchase of all liner shipping companies.

Because the top 100 LSCs control 90 per cent of the total container carrying capacity in

the world, we use the operating capacity of the carriers in this list to represent the change

of liner shipping industry from 1999 to 2009. Since these top 100 companies are not the

same every year, the total number of companies in our analysis is 153.

12

A second source of data is the Clarkson Shipping Intelligence Network, which

provides times series data on time-charter rate, newbuilding and second-hand prices. We

also use annual container throughput, an indicator for market demand, which is available

from Drewry (www.drewry.co.hk). These three data sources enabled us to analyze the

growth rate of each individual company as a function of company attributes, market

conditions and merger and acquisition. Table 2 lists a summary statistics for all the

variables used in the model, and the explanations for each variable are given next.

Insert Table 2 here

The dependent variable (GKit) is the growth rate of firm i at year t, defined as

GKit=Kit/Kit-1-1, where Kit is the total capacity of that company.

Firm attributes include the market share of a company defined as SHAREit=Kit/ΣiKit;

the change of market share CHSHAREit=SHAREit/SHAREit-1-1; the charter ratio

CHARTERit=CKit/Kit, where CK is chartered capacity; and the average vessel size of a

company AVGKit=Kit/NKit, where NKit is the number of vessels operated by a firm.

THROU is the global container throughput and GTHROU is its growth rate defined as

GTHROUt=THROUt/THROUt-1-1. TC and GTC are the annual time charter index and its

increasing rate. NBP is the index for newbuilding price. Second-hand price is not

included because it have high correlation with newbuilding price.

OEX is the capacity expansion rate of the competitors for each company, defined as

OEXit = Σj≠i(Kjt-Kjt-1)/Σj≠iKjt-1. It is designed to test the response of a company to all other

companies’ capacity expansion. Comparing with the variable CHSHARE which takes

into its own and competitors’ expansion, OEX captures only the influence of all the

competitors’ capacity expansion.

13

To analyze the impact of M&A on the growth rate of a company, we specified a

dummy variable MERGER to indicate if the company had M&A events in a year. The

included events of M&A for all the companies are listed in Table 1.

Finally, companies with different size may respond to the market demand and capacity

expansion of all other companies differently. Interaction terms of SHARE and some other

variables are created to test this effect.

The mean value of each variables for different company size are provided in Table 3,

together with t-values for the null hypothesis that the mean value of top 20 liner operators

is not significantly different from the rest of the companies. The statistics reveals that

there are obvious difference between the top 20 and the rest of the liner operators, except

OEX—the expansion rate of all other liners.

Insert table 3 here.

Based on above discussion, the statistical model is given by equation (3), which we

estimate using a variety of methods.

itiititititit

itititititit

ititititit

itititititit

azMERGERSHAREMERGEROEXSHARE

OEXNBPGTCTCGTHROUSHARE

THROUSHAREGTHROUTHROUAVGK

CHARTRCHSHARESHARECHSHARESHAREGK

161514

13121111101911

811716151

413112111

(3)

where ɛit is assumed to be independently and identically distributed (i.i.d.), is the

observable heterogeneity over each individual and/or time. Note that the company

attributes and market conditions, such as SHARE, CHSHARE, CHARTR, AVGK, THROU,

GTHROU, TC, GTC and NBP, are one year before the dependent variable, while the

others are at the same year. This arrangement is to allow for the time-lag from capacity

iz

14

decision which is based on company attributes and market conditions to actual expansion.

OEX and MERGER are synchronized to the firm’s capacity increase rate, to reflect the

impact of others’ capacity expansion decision on the firm’s growth rate and to capture the

impact of merger and acquisition on the firm growth.

We estimate four different versions of the model. Model (1) is simply a pooled

regression, Models (2) and (3) are fixed effect specifications to control for unobserved

heterogeneity. Compared with model (2), model (3) included the impact of M&A, which

is used to assess the stability of parameters with and without this measure. Model (4) is a

random effect specification and is later compared with the fixed effect models.

5.0 Econometric results

Table 4 summarizes the result of four different models described in the previous section.

Most of the coefficients are significant, and the high significance of the F-test (for

models 1-3) and Wald-χ2 test (for model 4) suggests a good fit of the model.

Insert Table 4 here

To test the necessity to consider the company specific heterogeneity, we run an F-test

between the pooled model and the fixed effect model (model 1 and 3 in table 4), and

former cannot be accepted. The Hausman’s specification test is applied to select the

fixed effect model or the random effect model. The result rejects the random effect

model. The last column in table 4 is the t-value for the null hypothesis that there are no

differences between the corresponding coefficients in the two models. Based on these

results, we focus on the fixed effect models.

15

The first 12 variables in fixed effect models are all pre-determined. Since OEX is

synchronized with the growth of the firm (GK). Given that growth of firms could be

jointly determined, we estimated the model using controlled capacity and invested

capacity as instruments, and used a Durbin-Wu-Hausman (DWH) statistic to test whether

treating OEX as exogenous introduces statistically important bias. The result cannot reject

the null hypothesis that OEX is not correlated with the error, that is, OEX is not

endogenous.

5.1 Discussion of regression results

In the fixed effect specifications, the variable SHARE is negative and highly significant.

This indicates that the capacity expansion rate of larger companies is lower than smaller

ones, and it runs contrary to Gibrat’s Law that company growth rate is independent with

its size in containerized liner shipping market.

The negative coefficient for CHSHARE indicates that the expansion rate is opposite to

the market share change in the previous year: if the market share increased in the last

year, the expansion rate in this year is expected to be lower. However, for larger

companies, the results are opposite. This is indicated by the positive coefficient of

SHARE×CHSHARE. These two terms can be written as CHSHARE·(β2+SHARE·β3). If

β2+SHARE·β3>0, a market share change in the past year has a positive impact on the

growth rate. The market share that satisfies this condition is 1.719 per cent

(=0.220/12.798)4. This reveals that if a company has a market share increase in the past

4 According to Alphaliner, only the top 19 liner shipping companies in the world have a capacity share more than 1.719 per cent. These companies include 1. APM-Maersk, 2. Mediterranean Shg Co, 3. CMA CGM Group, 4. Hapag-Lloyd, 5. COSCO Container L., 6.APL, 7. Evergreen Line, 8.CSCL, 9. Hanjin

16

year, it will keep increase; if it has a decreasing market share in the past, it will keep

decreasing. This result is consistent with the fact that most of the larger liners have

constantly increasing or decreasing market shares in the study period. This provides

strong evidence of a trend of increasing market shares among the major LSCs: some have

continuously increasing capacity shares, while others have constant decreasing market

shares. Among the major top 19 firms, Maersk, MSC and CMA CGM Group have

experienced fast market share increases from 1999 to 2010, and have emerged as the top

3 liners that accounted for around 34 per cent of the world container capacity (Figure 3).

This finding, of course, points to growing market concentration dominated by the largest

firms in the industry.

Insert Figure 3 here

The coefficient for CHARTR is not significant, indicating that charter ratio does not

have obvious impact on the capacity growth. This is reasonable because chartered ships

are used in the same way as the owned ships (Lorange, 2009).

The coefficient on the average ship size of the company (AVGK) is negative and

significant, which suggest that the shipping companies with larger ships have lower

growth rates. Considering that larger companies have relatively larger vessels, this result

is consistent with the result obtained in SHARE. Since the large ships are mostly

deployed in international trunk routes, this result implies that it could be the efficient use

of the large ships that reduced the needs of capacity expansion. Regardless, this result

Shipping, 10. MOL, 11. Hamburg Sud Group, 12. NYK Line, 13. OOCL, 14. CSAV Group, 15. K Line, 16. Yang Ming, 17. Zim, 18. Hyundai, 19. PIL.

17

suggests that large ships alone should not be a concern for liner concentration, contrary to

the concerns about the contribution of large ships in liner concentration (ECLAC, 1998).

For the variables that describe market conditions, demand (THROU) is not significant;

its growth rate (GTHROU) is weakly significant, and the interactions of these two

variables with market share (SHARE×GTHROU and SHARE×THROU) are positive and

significant, indicating the positive influence of demand on the growth of larger firms.

Actually, large companies are more sensitive to the demand change. TC is not

significant, indicating that market freight rate is not a dominant factor in the capacity

expansion of LSCs. GTC is negative and weakly significant, implies that increasing in

market freight rate may reduce firm’s capacity expansion.

New building price (NBP) is not significant, indicating that the ship price does not

affect the growth rate of a company. This, again, is consistent with (Luo, Fan and Liu,

2009) that most liner companies expand not because the ship price is low, but because

demand is high. Although some companies are hedging on the asset market, it does not

have a significant statistical impact on the capacity increase rate.

The coefficients on the expansion rate of all other companies (OEX, and

SHAREOEX) are significant, indicating that the growth rate of a company is obviously

affected by the capacity expansion of other companies, and there is significant difference

between small and large companies. The negative coefficients on the first variables

indicate that for a small shipping company, others’ expansion has a negative impact on its

growth. However, the positive significant coefficient on the second term (SHARE×OEX)

indicates that for larger companies, the negative impact is smaller. If the capacity share

is larger than 0.901 per cent (=0.758/84.127), the impact can be positive. Carriers in the

18

top 21 list have capacity share higher than this number, suggesting that these carriers are

more sensitive to the aggregated expansion of all other companies. Smaller companies

are less sensitive, may be because their market share is too small. Such capacity

expansion strategy of larger liners can lead to over capacity and further concentration in

the industry.

Finally, the result on the MERGER points out that M&A has positive and significant

impacts on the capacity increasing rate. On average, the data suggest that M&A can have

sizable effects—as much as 44.8 per cent increase in the firm capacity. Excluding all the

firms with M&As, the average capacity increase rate is only 3.6 per cent while if not

excluded, the average capacity increase is 5.3 per cent. This difference signifies the

contribution of mergers on the annual capacity increase rate. The negative coefficient on

the interaction term with market share (SHARE×MERGER) suggests that such impacts

decrease with the increase of the company scale. If a company’s capacity share is larger

than 9.272 per cent (=0.378/4.077), such impact can even be negative. At present, only

the largest two LSCs, Maersk and MSC, have market shares large enough for a negative

effect. While M&A effects for smaller firms can result in efficiency improvement due to

economy of scale, for larger firms, such as the top 10 carriers, it may speed up the

concentration process. Therefore, it is necessary to differentiate the M&A effect for

liners with different scales. For the top two liner companies, because of the high

capacity of themselves compared with the merged companies, the growth rates are

expected to be smaller.

To summarize, from the regression result of the fixed effect model, we identified

important factors for the growth of LSCs. First, the larger the company is, the smaller the

19

growth rate. This is inconsistent with Gibrat’s Law in the containerized liner shipping

industry, signifying the possibility to identify the dominating firms in the concentration

process. Larger companies have different capacity evolution paths than the smaller ones.

The top 19 companies are evolving in two opposite directions: they either are

continuously gain capacity share, or continuously diminishing. This points to further

concentration in the industry due to faster growth rates of the top 19 firms. A company

which is smaller than the top 19 grows faster after had a decreasing market share, and

slower if it experienced fast growth. In addition, a company expands slower if its

average vessel size is larger. Second, in responding to market condition, large companies

expand faster when demand is high. Newbuilding price and market freight rate, as an

indicator for market profitability and ship cost, are not relevant to the capacity growth.

Thirdly, in responding to the aggregated capacity expansion of all other carriers, larger

companies (the top 21) tend to increasing faster than the smaller ones.

The result highlights the important role of M&A on capacity expansion: it has a

positive impact on the growth of the small or middle size companies and negative impact

for the top 2 firms. This provides a direction for control market concentration through

regulating M&As. To keep the current level of market concentration, the M&A among

smaller firms should be encouraged as long as its market share will not be higher than the

current HHI index. For the existing firms whose market share already higher than the

HHI index, M&A should be monitored as it can increase the market concentration level.

6.0 Summary and conclusions

20

International trade and globalization have increased at a phenomenal rate. While most of

the trades are moved by ships, the containerization in the 1950s was a major innovation

that has dramatically improved the efficiency of shipping and has helped to fuel the

growth in trade. Container shipping has grown even faster than the volumes of trade, and

within the industry firms are growing bigger and the number of firms becoming smaller.

In this study, we link growth rates and market shares of individual firms to

concentration in the industry. We show that for the firms whose market share is larger

than the HHI index, an increase in the growth rate can increase the concentration level.

Empirically, we find that larger companies grow slower than the smaller ones, which

contradicts to Gibrat’s Law. In further analysis, we find that capacity growth has three

distinctive patterns amongst firms in the industry. First, among the top 19 LSCs, some

are constantly gaining market share and are becoming the potential dominant players in

the market, while others are continuously losing its share. This indicates the possibility of

market concentration. The rest of the firms have alternative increasing and decreasing

shares over time. Secondly, facing aggregated expansion of all other companies, the top

21 carriers respond by expanding faster, while the others respond by expanding slower.

Thirdly, mergers and acquisitions have a positive and significant effect on capacity

growth, except for the top 2 firms. For these firms, mergers and acquisitions have a

negative effect on the growth rate.

Finally, this paper provides insights to capacity expansion behavior and market

concentration for firms of different sizes, market shares, and different market conditions,

which could benefit not only the private sectors associated with shipping industry, but

also the public policy-makers in national and international maritime agencies.

21

Understanding the current practice in capacity expansion behavior can help the shipping

companies, ship owners and ship-operators to find a best opportunity to expand their

capacity, so as to secure their market position. For the institutions providing ship

financing and organizations in ship trading, this study helps to understand the individual

expansion behavior in shipping capacity, which is important to design better service to

their customers and reduce the risk in ship financing. In terms of policy, this model helps

on understanding the relationship between firm growth and concentration. It provides a

framework to assess the effects of firm growth on concentration and then identifies the

key factors that point to growth. This information is extremely useful for the national and

international agencies to advise appropriate policies to prevent further concentration in

the market through regulating the growth of target carriers, and to mitigate the impact of

alternative overcapacity and supply shortage in the industry. Finally, due to the

significant impact of mergers on the carrier’s growth rate, greater care should be put on

the mergers, especially among the large carriers, to effectively control the market

concentration.

This study links market concentration with the growth of individual firms from actual

observations on the growth of the world carriers. It identifies the factors that lead to

differential growth rates of individual firms that can lead to market concentration. There

are, however, a number of extensions to this research. For example, there is a need for

modeling the strategic rivalry of the largest firms and the changing levels of competition

through time and the threat of government intervention. Further, mergers and

acquisitions are found to have significant contributions to firm growth. There is a need

22

for further studies on the behavior of liner shipping companies in merger and acquisition,

to better control the market concentration through managing these activities.

23

References

Alphaliner (2011) 'Maersk seals lead with 18,000 TEU vessels order', Alphaliner Weekly Newsletter, 21 Feb, pp. 1-3.

Benacchio, M., Ferrari, C. and Musso, E. (2007) 'The liner shipping industry and EU competition rules', Transport Policy , vol. 14, pp. 1-10.

Cabral, L.M.B. and Mata, J. (2003) 'On the evolution of the firm size distribution: Facts and Theory', The American Economic Review, vol. 93, no. 4, pp. 1075-1095.

Chrzanowski, I. (1974) 'Concentration in Shipping', Journal of Transport Economics and Policy, vol. 8, no. 2, pp. 174-179.

De Souza, G.A., Beresford, A.K. and Pettit, S.J. (2003) 'Liner shipping companies and terminal operators: Internationalisation or globalisation?', Maritime Economics and Logistics, vol. 5, pp. 393-412.

ECLAC (1998) Concentration in liner shipping: its cause and impacts for ports and shipping services in developing regions, 20 May, [Online], Available: http://www.eclac.org/publicaciones/xml/5/5175/lc_g.2027.pdf [28 Oct 2012].

Evans, D.S. (1987) 'The relationship between firm growth, size, and age: estimates for 100 manufacturing industries', The Journal of Industrial Economics, vol. 35, no. 4, pp. 567-581.

Fan, L., Luo, M. and Wilson, W.W. (2011) 'Firm growth and capacity evolution in the container market', Proceedings of the International Workshop on Economics (IWE), pp. 1-6.

Ferguson, P.R. and Ferguson, G.J. (1994) Industrial Economics: issues and perspectives, 2nd edition, London, UK: The Macmillan Press Ltd.

Fusillo, M. (2009) 'Structural factors underlying mergers and acquisitions in liner shipping', Maritime Economics and Logistics, vol. 11, no. 2, pp. 209-226.

Heaver, T. (2000) 'Do mergers and alliances influence European shipping and port competition?', Maritime Policy and Management, vol. 27, no. 4, pp. 363-373.

Hirschman, A.O. (1964) 'The paternity of an index', The American Economic Review, vol. 54, no. 5, pp. 761-762.

Hymer, S. and Pashigian, P. (1962) 'Firm size and rate of growth', The journal of political economy, vol. 70, no. 6, pp. 556-569.

Le, D.T. and Jones, J.B. (2005) 'Optimal investment with lumpy costs', Journal of Economic Dynamics and Control, vol. 29, no. 7, pp. 1211-1236.

Lorange, P. (2009) Shipping Strategy -- Innovating for Success, 1st edition, Cambridge, UK: Cambridge University Press, Available: www.imd.org/news/shipping-owning-or-Operating-steel.cfm [3 Jan 2012].

Luo, M., Fan, L. and Liu, L. (2009) 'An econometric analysis for container shipping market', Maritime Policy and Management, vol. 36, no. 6, pp. 507-523.

Midoro, R., Musso, E. and Parola, F. (2005) 'Maritime liner shippping and the stevedoring industry: market structure and competition strategies', Maritime Policy and Management, vol. 32, no. 2, pp. 89-106.

Penrose, E. (2009) The theory of the growth of the firm, 4th edition, Oxford: Oxford University Press.

24

Pons, J.-F. (2000) 'Liner shipping: Market developments and government action-the EU perspective', 1st International Shipping Convention, 18-20 October 2000.

Rahaman, M.M. (2011) 'Access to financing to firm growth', Journal of Banking & Finance, vol. 35, no. 2, pp. 709-723.

Scherer, F.M. and Ross, D. (1990) Industrial Market Structure and Economic Performance, 3rd edition, Princeton, NJ: Houghton Mifflin Company.

Sutton, J. (1997) 'Gilbrat's legacy', Journal of Economic Literature, vol. 35, no. 1, pp. 40-59.

Sys, C. (2009) 'Is the container liner shipping industry an oligopoly?', Transport Policy, vol. 16, no. 5, pp. 259-270.

U.S. DoJ and FTC (2010) Horizontal Merger Guidelines, 10Sep, [Online], Available: www.justice.gov/atr/public/guidelines/hmg-2010.html [28 Oct 2012].

Variyam, J.N. and Kraybill, D.S. (1992) 'Empirical evidence on determinants of firm growth', Economic letters, vol. 38, no. 1, pp. 31-36.

25

Figures and tables

Figure 1: The capacity development of global liners 1996-2010

25%

35%

45%

55%

65%

75%

85%

0

2

4

6

8

10

12

14

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Market shareMillion TEU

World Fleet

Top 20

Top 5

Market Share of Top 5

Market Share of Top 20

26

Figure 2: Market shares of top 100 liners in 2010 and the HHI index

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

Top 100 liner shipping companies

HHI

Maersk Line

MSC

CMA CGM Group

Market Share

27

Figure 3: Market share changes of the top 20 LSCs 1999-2010

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%19

99

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Maersk Line

28

Table 1: Main mergers and acquisitions events in the liner market

Buyer Taken-over company Year Buyer Taken-over company Year Maersk Line Safmarine, CMB-T, Sealand 1999 Hamburg Sud Barbican Line, Transroll

South Pacific, Crowley 1999

Torm Lines 2002 Crowley American Transport

2000

Royal P&O Nedlloyd 2004 Ellermen 2002 P&O Nedlloyd 2005 Kien Hung Lines 2003

CMA-CGM United Baltic Corp. MacAndrews & Ellerman Lberian, Delom SA

2002 Columbus Line 2004

ANL Container Lines 2003 FESCO, Ybarra Sud 2006 OTAL, Sudcargos 2005 Costa Container Lines 2007 Delmas 2006 Delmas OT Africa Line 1999 US Lines, Cheng Lie Navigation Ltd., CoMaNav

2007 PIL Pacific Direct Line 2006

Evergeen Line Hatsu Marine Ltd. 2002 Wan Hai Interasia 2002 Hapag Lloyd CP Ships 2005 Trans-Pacific Lines 2005 CSCL Shanghai Puhai Shipping Company 2005 Grimald ACL 2002 Hanjin DSR-Senator 2002 Finnlines 2005 MOL P&O Neddlloyd 2005 Sea

Consortium Sea Med Link 1999

P&O Nedlloyd Tasman Express Line 1999 Odiel Group Compania, Transatlantica, Espanola

2000

Farrel Line, Harrison Line 2000 CP Ships TMM, CCAL 2000 CSAV Libra, Grupo Libra, Montemar 1999 Italian Line 2002

Norasia 2000 TMM Tecomar 1999 Norsul container activities 2002 Wallenius Wilhelmson 1999

The Rickmers Group

Rickmers Lines 1999 Tropical Shipping

Kent Lines 2001

TecMarine Seaboard 2003 Tecmarine 2002 Sources: Compiled from Midoro et al. (2005), Fusillo (2009), Sys (2009), and Alphaliner database.

29

Table 2: Descriptive statistics

Variable Unit Observation Mean Std.Dev. Min Max GK 1530 0.053265 0.228829 -0.79374 4.645762 SHARE 1530 0.006407 0.014849 0.000376 0.167861 CHSHARE 1530 -0.04452 0.213821 -0.93536 4.131278 CHARTR 1530 0.509514 0.336698 0 1 AVGK Thousand TEU 1530 1.129154 0.786947 0.187931 4.269787 THROU Million TEU 1530 0.317487 0.098552 0.189258 0.496625 GTHROU 1530 0.110309 0.027369 0.049652 0.143135 TCa 1530 0.9342 0.2915 0.5724 1.5190 GTCb 1530 0.0561 0.2876 -0.3036 0.5418 NBPc 1530 0.927 0.1908 0.71 1.24 OEX 1530 0.105945 0.027544 0.055846 0.199346 MERGER 1530 0.03268 0.177855 0 1 Note: a, b, c, and d are all form Clarkson Research Services Limited 2010 a Containership Time charter Rate Index: based on $/TEU for 1993 = 1. b Containership New-building Prices Index: based on average $/TEU for Jan 1988 = 1.

30

Table 3 Variable means of different class of carriers and equality test

Classes Variables Top5 6-10 11-20 Top20 21-153

T-test for Top20 against others

GK 0.156 0.107 0.176 0.154 0.038 8.735* SHARE 0.067 0.033 0.021 0.036 0.002 32.853* CHSHARE 0.070 0.001 0.061 0.048 -0.058 8.764* CHARTR 0.443 0.431 0.563 0.500 0.511 -6.131* AVGK 2.486 2.931 2.555 2.632 0.903 4.622* OEX 0.102 0.106 0.105 0.105 0.106 0.321 MERGER 0.300 0.080 0.150 0.170 0.012 20.780*

31

Table 4: Regression results for capacity expansion models

(1) (2) (3) (4) Coefficient Pooled Model Fixed Effect Fixed Effect Random Effect T-test between VARIABLES GK GK GK GK (3) & (4) SHARE -16.044*** -32.468*** -30.520*** -16.044*** -155.347*** (2.172) (2.997) (2.936) (2.160) CHSHARE -0.161*** -0.221*** -0.220*** -0.161*** -54.395*** (0.031) (0.031) (0.030) (0.030) SHARE×CHSHARE 11.153*** 12.336*** 12.798*** 11.153*** 18.194*** (2.453) (2.613) (2.561) (2.439) CHARTR -0.003 -0.061* -0.054 -0.003 -51.837*** (0.016) (0.035) (0.035) (0.016) AVGK 0.006 -0.132*** -0.125*** 0.006 -199.910*** (0.009) (0.025) (0.024) (0.009) THROU 0.086 0.084 0.143 0.086 9.356*** (0.171) (0.170) (0.167) (0.170) GTHROU -0.056 0.001 0.148 -0.056 14.866*** (0.387) (0.383) (0.374) (0.385) SHARE×THROU -2.833 14.785*** 14.629*** -2.833 108.172*** (4.287) (4.614) (4.658) (4.263) SHARE×GTHROU 79.120*** 40.245*** 46.347*** 79.120*** -60.797*** (15.066) (15.132) (14.838) (14.981) TC 0.104* 0.078 0.084 0.104* -8.994*** (0.063) (0.062) (0.061) (0.062) GTC -0.076* -0.067 -0.074* -0.076* 1.366 (0.041) (0.041) (0.040) (0.041) NBP -0.110 -0.112 -0.138 -0.110 -6.097*** (0.129) (0.128) (0.125) (0.129) OEX -0.955*** -0.743*** -0.758*** -0.955*** 19.286*** (0.288) (0.285) (0.279) (0.286) SHARE×OEX 84.127*** 97.561*** 84.930*** 84.127*** 1.520 (14.758) (14.522) (14.543) (14.675) MERGER 0.418*** 0.378*** 0.418*** -25.086*** (0.042) (0.047) (0.041) SHARE×MERGER -4.159*** -4.077*** -4.159*** 1.926* (1.107) (1.250) (1.101) Constant 0.114** 0.392*** 0.349*** 0.114** 116.881*** (0.052) (0.060) (0.059) (0.052) Observations 1,530 1,530 1,530 1,530 R-squared 0.142 0.247 0.283 0.213 F/Wald χ2 a 15.64 16.21 19.12 234.2 Porb(F/ Wald χ2) 0.000 0.000 0.000 0.000 Number of owner 153 153 153 153 Note a: F-test for model 1-3, and Wald χ2 test for model 4.