Embed Size (px)

Citation preview

18th Aug’20

REP-070

Mahnoor [email protected]+92-21-35309119

Glass Industry – Tariq Glass Limited (TGL)Timely expansion to reinstate market share

Executive Summary

We initiate coverage on Tariq Glass Ltd (TGL) with a DCF-based TP of PKR113/share offering an upside of 40% from its lastclosing alongside an attractive dividend yield of 5%. We have a BUY call on the scrip with a TSR of 45%. Our stance isunderpinned by 1) lower interest rates, 2) improvement in construction spending, 3) reduction in fuel cost and 4) expansion of floatglass plant by 500tons/day. TGL trades at a FY21/22E PE of PKR 8.42/4.85 respectively.

Demand for float glass, mostly used for glass buildings, doors and windows, has grown at a 5yr CAGR of 5% between FY14-19catered by 2 main players TGL and Ghani Glass Ltd (GHGL) and imports

The market for glassware is informal in nature and has various small-scale producers. The market is led by TGL with a wideproduct portfolio and high quality standards

TGL took a hefty debt of PKR5.6bn for its float glass unit-2 expansion project leading to a higher finance cost which is likely toremain low due to the sharp cut in policy rate on 625bps by SBP since Mar’20 (interest cost saving: PKR 3.23/share)

Fuel cost comprises of 35% of the cost of production. TGL’s furnace can be fired through four fuels (LNG, Furnace Oil, Keroseneand LPG). Recent decline in furnace oil and LNG prices are likely to improve profitability. We anticipated the fuel cost /ton to fallby 3% in FY21 and by 5% in FY22

Despite being second to GHGL in the float glass market, TGL is poised to gain market share as “Unit-2” becomes operational.The expansion is stated to improve capacity from 550 tpd to 1050 tpd, thereby allowing TGL to expand its share from 31% inFY19 to achieve its historical peak of 40% in our view

Key Risks

• Lower than expected selling prices

• Higher than expected fuel cost

• More than estimated USD/PKR devaluation

• High dependency on a single supplier (ICI Pakistan) for Soda-ash(key raw material) may be risky incase of uncertain market changes and

supply-shocks

2

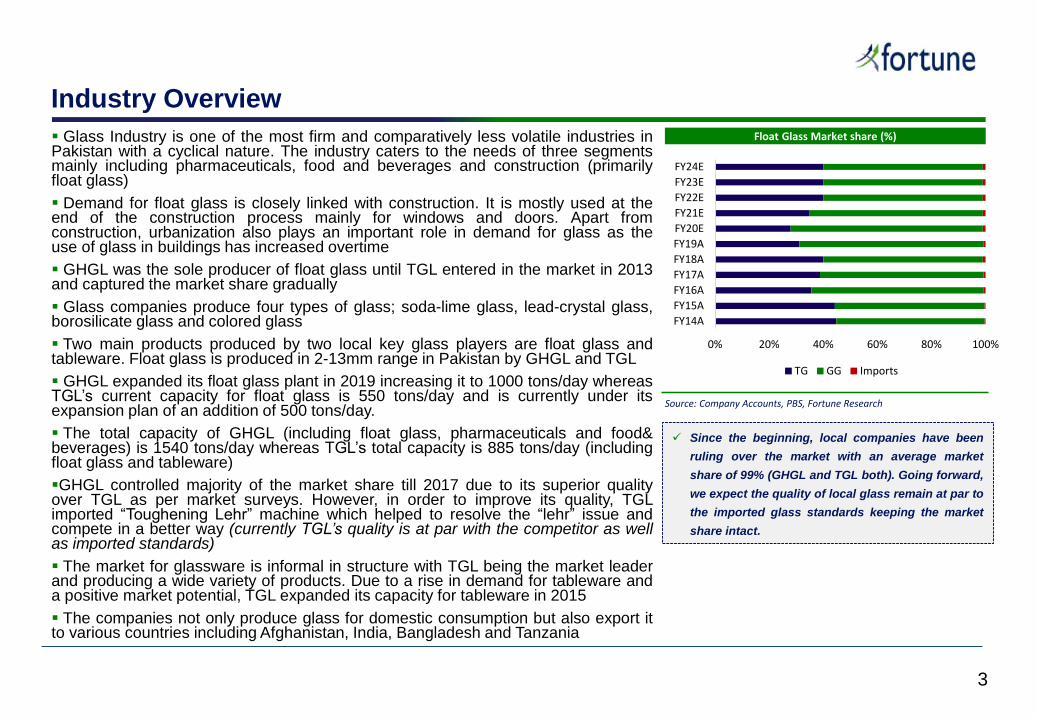

Industry Overview

Glass Industry is one of the most firm and comparatively less volatile industries inPakistan with a cyclical nature. The industry caters to the needs of three segmentsmainly including pharmaceuticals, food and beverages and construction (primarilyfloat glass)

Demand for float glass is closely linked with construction. It is mostly used at theend of the construction process mainly for windows and doors. Apart fromconstruction, urbanization also plays an important role in demand for glass as theuse of glass in buildings has increased overtime

GHGL was the sole producer of float glass until TGL entered in the market in 2013and captured the market share gradually

Glass companies produce four types of glass; soda-lime glass, lead-crystal glass,borosilicate glass and colored glass

Two main products produced by two local key glass players are float glass andtableware. Float glass is produced in 2-13mm range in Pakistan by GHGL and TGL

GHGL expanded its float glass plant in 2019 increasing it to 1000 tons/day whereasTGL’s current capacity for float glass is 550 tons/day and is currently under itsexpansion plan of an addition of 500 tons/day.

The total capacity of GHGL (including float glass, pharmaceuticals and food&beverages) is 1540 tons/day whereas TGL’s total capacity is 885 tons/day (includingfloat glass and tableware)

GHGL controlled majority of the market share till 2017 due to its superior qualityover TGL as per market surveys. However, in order to improve its quality, TGLimported “Toughening Lehr” machine which helped to resolve the “lehr” issue andcompete in a better way (currently TGL’s quality is at par with the competitor as wellas imported standards)

The market for glassware is informal in structure with TGL being the market leaderand producing a wide variety of products. Due to a rise in demand for tableware anda positive market potential, TGL expanded its capacity for tableware in 2015

The companies not only produce glass for domestic consumption but also export itto various countries including Afghanistan, India, Bangladesh and Tanzania

Since the beginning, local companies have been

ruling over the market with an average market

share of 99% (GHGL and TGL both). Going forward,

we expect the quality of local glass remain at par to

the imported glass standards keeping the market

share intact.

Source: Company Accounts, PBS, Fortune Research

Float Glass Market share (%)

0% 20% 40% 60% 80% 100%

FY14A

FY15A

FY16A

FY17A

FY18A

FY19A

FY20E

FY21E

FY22E

FY23E

FY24E

TG GG Imports

3

The Float Glass Demand

Glass Doors

Source: Company Accounts, PBS, Fortune Research

Domestic Float Demand (tons)

-

100,000

200,000

300,000

400,000

500,000

600,000

FY14A FY15A FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E

TG GG Imports Total float demand

Market Demand Drivers

Glassware Glass Buildings Windows Tableware

4

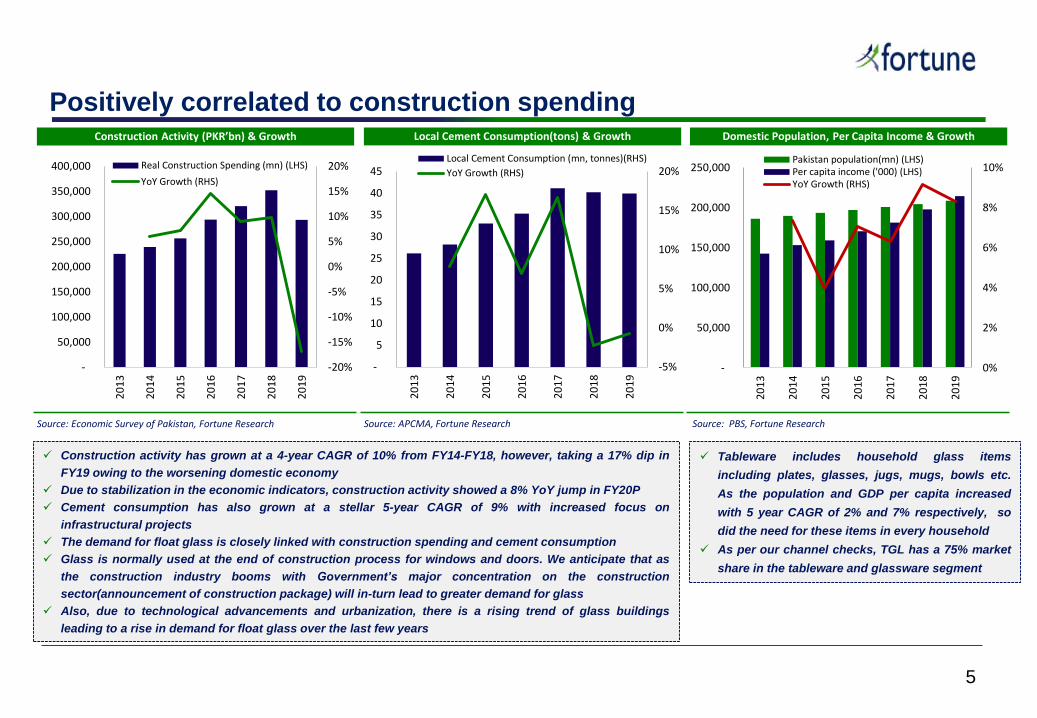

Positively correlated to construction spending

Construction activity has grown at a 4-year CAGR of 10% from FY14-FY18, however, taking a 17% dip in

FY19 owing to the worsening domestic economy

Due to stabilization in the economic indicators, construction activity showed a 8% YoY jump in FY20P

Cement consumption has also grown at a stellar 5-year CAGR of 9% with increased focus on

infrastructural projects

The demand for float glass is closely linked with construction spending and cement consumption

Glass is normally used at the end of construction process for windows and doors. We anticipate that as

the construction industry booms with Government’s major concentration on the construction

sector(announcement of construction package) will in-turn lead to greater demand for glass

Also, due to technological advancements and urbanization, there is a rising trend of glass buildings

leading to a rise in demand for float glass over the last few years

Tableware includes household glass items

including plates, glasses, jugs, mugs, bowls etc.

As the population and GDP per capita increased

with 5 year CAGR of 2% and 7% respectively, so

did the need for these items in every household

As per our channel checks, TGL has a 75% market

share in the tableware and glassware segment

Source: Economic Survey of Pakistan, Fortune Research

Construction Activity (PKR’bn) & Growth

Source: APCMA, Fortune Research

Local Cement Consumption(tons) & Growth

Source: PBS, Fortune Research

Domestic Population, Per Capita Income & Growth

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Real Construction Spending (mn) (LHS)

YoY Growth (RHS)

-5%

0%

5%

10%

15%

20%

-

5

10

15

20

25

30

35

40

45

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Local Cement Consumption (mn, tonnes)(RHS)

YoY Growth (RHS)

0%

2%

4%

6%

8%

10%

-

50,000

100,000

150,000

200,000

250,000

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Pakistan population(mn) (LHS)Per capita income ('000) (LHS)YoY Growth (RHS)

5

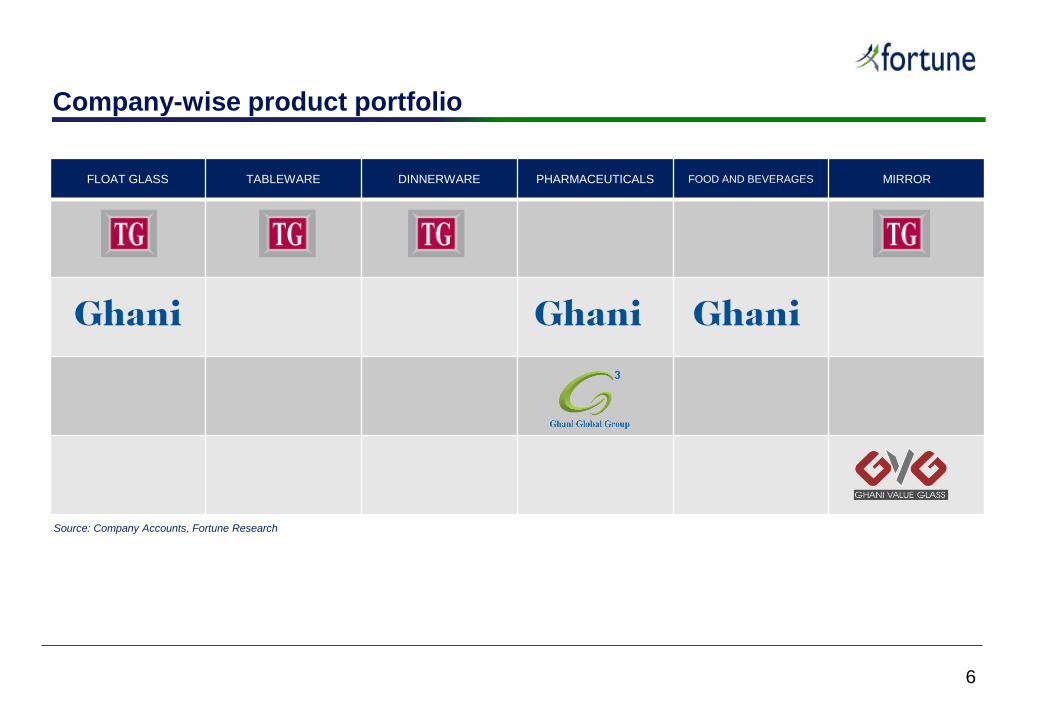

FLOAT GLASS TABLEWARE DINNERWARE PHARMACEUTICALS FOOD AND BEVERAGES MIRROR

Company-wise product portfolio

Source: Company Accounts, Fortune Research

6

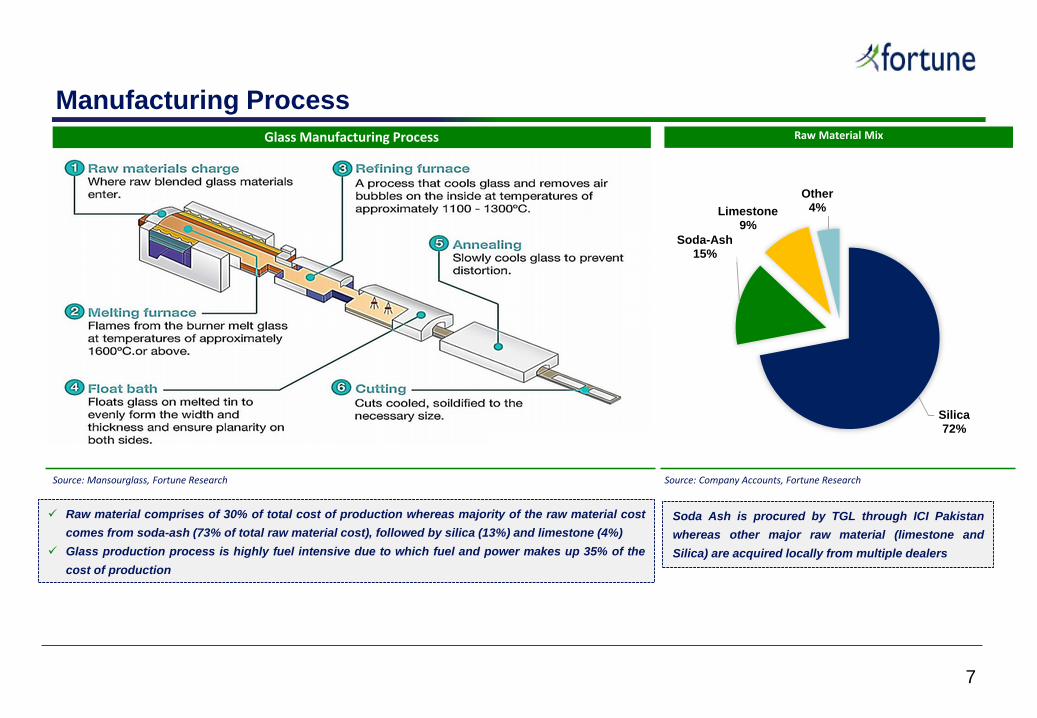

Manufacturing Process

Soda Ash is procured by TGL through ICI Pakistan

whereas other major raw material (limestone and

Silica) are acquired locally from multiple dealers

Raw material comprises of 30% of total cost of production whereas majority of the raw material cost

comes from soda-ash (73% of total raw material cost), followed by silica (13%) and limestone (4%)

Glass production process is highly fuel intensive due to which fuel and power makes up 35% of the

cost of production

Source: Company Accounts, Fortune Research

Raw Material Mix

Silica72%

Soda-Ash15%

Limestone9%

Other4%

Source: Mansourglass, Fortune Research

Glass Manufacturing Process

7

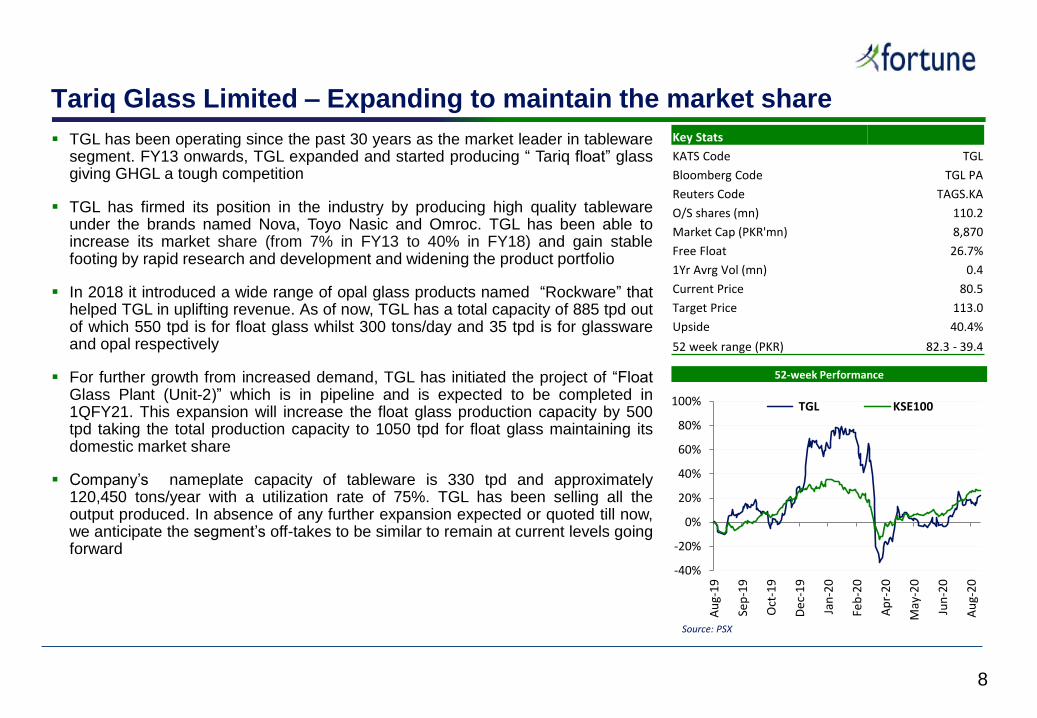

Tariq Glass Limited – Expanding to maintain the market share

TGL has been operating since the past 30 years as the market leader in tablewaresegment. FY13 onwards, TGL expanded and started producing “ Tariq float” glassgiving GHGL a tough competition

TGL has firmed its position in the industry by producing high quality tablewareunder the brands named Nova, Toyo Nasic and Omroc. TGL has been able toincrease its market share (from 7% in FY13 to 40% in FY18) and gain stablefooting by rapid research and development and widening the product portfolio

In 2018 it introduced a wide range of opal glass products named “Rockware” thathelped TGL in uplifting revenue. As of now, TGL has a total capacity of 885 tpd outof which 550 tpd is for float glass whilst 300 tons/day and 35 tpd is for glasswareand opal respectively

For further growth from increased demand, TGL has initiated the project of “FloatGlass Plant (Unit-2)” which is in pipeline and is expected to be completed in1QFY21. This expansion will increase the float glass production capacity by 500tpd taking the total production capacity to 1050 tpd for float glass maintaining itsdomestic market share

Company’s nameplate capacity of tableware is 330 tpd and approximately120,450 tons/year with a utilization rate of 75%. TGL has been selling all theoutput produced. In absence of any further expansion expected or quoted till now,we anticipate the segment’s off-takes to be similar to remain at current levels goingforward

52-week Performance

8

-40%

-20%

0%

20%

40%

60%

80%

100%

Au

g-1

9

Sep

-19

Oct

-19

De

c-1

9

Jan

-20

Feb

-20

Ap

r-2

0

May

-20

Jun

-20

Au

g-2

0

TGL KSE100

Key Stats

KATS Code TGL

Bloomberg Code TGL PA

Reuters Code TAGS.KA

O/S shares (mn) 110.2

Market Cap (PKR'mn) 8,870

Free Float 26.7%

1Yr Avrg Vol (mn) 0.4

Current Price 80.5

Target Price 113.0

Upside 40.4%

52 week range (PKR) 82.3 - 39.4

Source: PSX

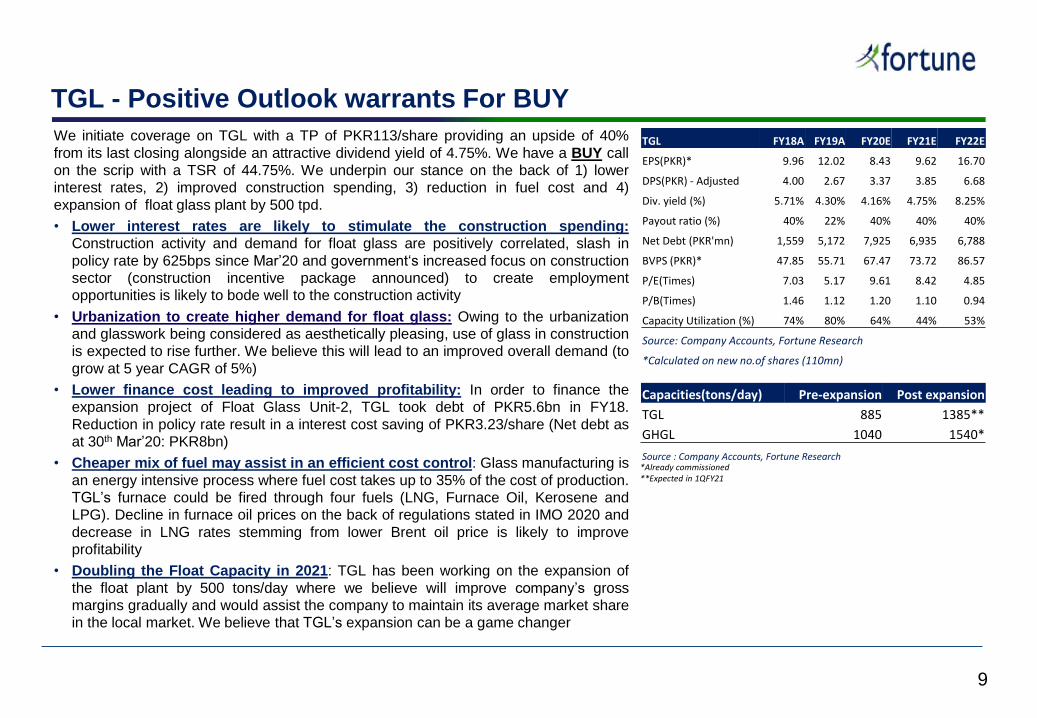

TGL - Positive Outlook warrants For BUY

We initiate coverage on TGL with a TP of PKR113/share providing an upside of 40%

from its last closing alongside an attractive dividend yield of 4.75%. We have a BUY call

on the scrip with a TSR of 44.75%. We underpin our stance on the back of 1) lower

interest rates, 2) improved construction spending, 3) reduction in fuel cost and 4)

expansion of float glass plant by 500 tpd.

• Lower interest rates are likely to stimulate the construction spending:

Construction activity and demand for float glass are positively correlated, slash in

policy rate by 625bps since Mar’20 and government‘s increased focus on construction

sector (construction incentive package announced) to create employment

opportunities is likely to bode well to the construction activity

• Urbanization to create higher demand for float glass: Owing to the urbanization

and glasswork being considered as aesthetically pleasing, use of glass in construction

is expected to rise further. We believe this will lead to an improved overall demand (to

grow at 5 year CAGR of 5%)

• Lower finance cost leading to improved profitability: In order to finance the

expansion project of Float Glass Unit-2, TGL took debt of PKR5.6bn in FY18.

Reduction in policy rate result in a interest cost saving of PKR3.23/share (Net debt as

at 30th Mar’20: PKR8bn)

• Cheaper mix of fuel may assist in an efficient cost control: Glass manufacturing is

an energy intensive process where fuel cost takes up to 35% of the cost of production.

TGL’s furnace could be fired through four fuels (LNG, Furnace Oil, Kerosene and

LPG). Decline in furnace oil prices on the back of regulations stated in IMO 2020 and

decrease in LNG rates stemming from lower Brent oil price is likely to improve

profitability

• Doubling the Float Capacity in 2021: TGL has been working on the expansion of

the float plant by 500 tons/day where we believe will improve company’s gross

margins gradually and would assist the company to maintain its average market share

in the local market. We believe that TGL’s expansion can be a game changer

TGL FY18A FY19A FY20E FY21E FY22E

EPS(PKR)* 9.96 12.02 8.43 9.62 16.70

DPS(PKR) - Adjusted 4.00 2.67 3.37 3.85 6.68

Div. yield (%) 5.71% 4.30% 4.16% 4.75% 8.25%

Payout ratio (%) 40% 22% 40% 40% 40%

Net Debt (PKR'mn) 1,559 5,172 7,925 6,935 6,788

BVPS (PKR)* 47.85 55.71 67.47 73.72 86.57

P/E(Times) 7.03 5.17 9.61 8.42 4.85

P/B(Times) 1.46 1.12 1.20 1.10 0.94

Capacity Utilization (%) 74% 80% 64% 44% 53%

Source: Company Accounts, Fortune Research

*Calculated on new no.of shares (110mn)

Capacities(tons/day) Pre-expansion Post expansion

TGL 885 1385**

GHGL 1040 1540*

Source : Company Accounts, Fortune Research *Already commissioned**Expected in 1QFY21

9

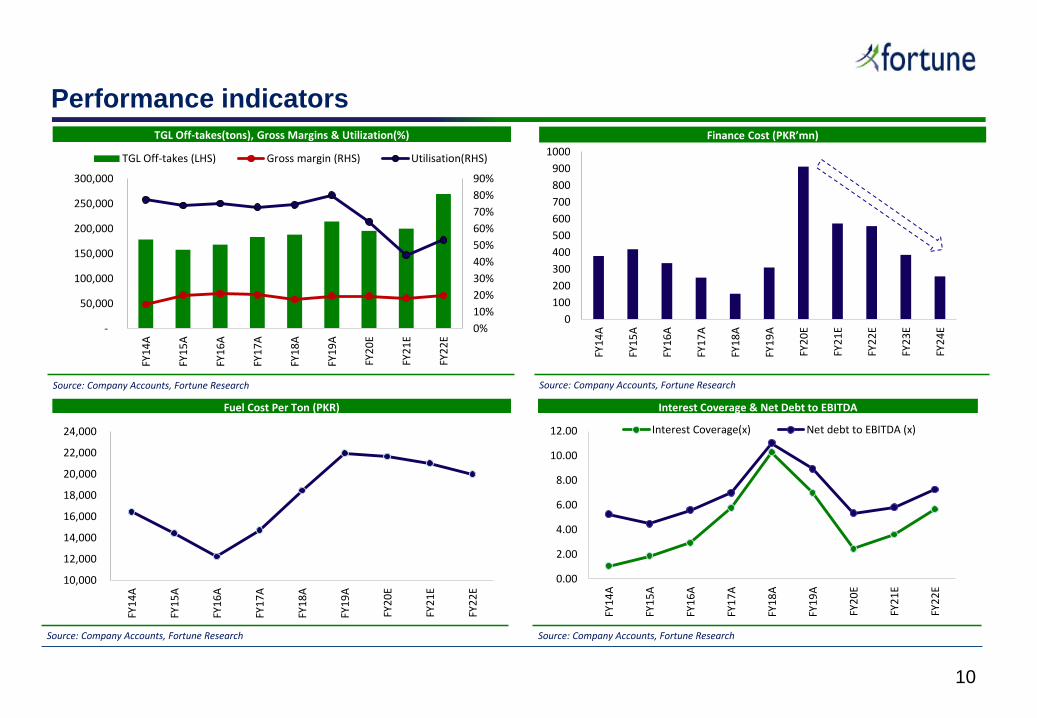

Source: Company Accounts, Fortune Research

Interest Coverage & Net Debt to EBITDA

0.00

2.00

4.00

6.00

8.00

10.00

12.00

FY1

4A

FY1

5A

FY1

6A

FY1

7A

FY1

8A

FY1

9A

FY2

0E

FY2

1E

FY2

2E

Interest Coverage(x) Net debt to EBITDA (x)

Source: Company Accounts, Fortune Research

Finance Cost (PKR’mn)

0

100

200

300

400

500

600

700

800

900

1000

FY1

4A

FY1

5A

FY1

6A

FY1

7A

FY1

8A

FY1

9A

FY2

0E

FY2

1E

FY2

2E

FY2

3E

FY2

4E

Source: Company Accounts, Fortune Research

TGL Off-takes(tons), Gross Margins & Utilization(%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

50,000

100,000

150,000

200,000

250,000

300,000

FY1

4A

FY1

5A

FY1

6A

FY1

7A

FY1

8A

FY1

9A

FY2

0E

FY2

1E

FY2

2E

TGL Off-takes (LHS) Gross margin (RHS) Utilisation(RHS)

Source: Company Accounts, Fortune Research

Fuel Cost Per Ton (PKR)

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

FY1

4A

FY1

5A

FY1

6A

FY1

7A

FY1

8A

FY1

9A

FY2

0E

FY2

1E

FY2

2E

10

Performance indicators

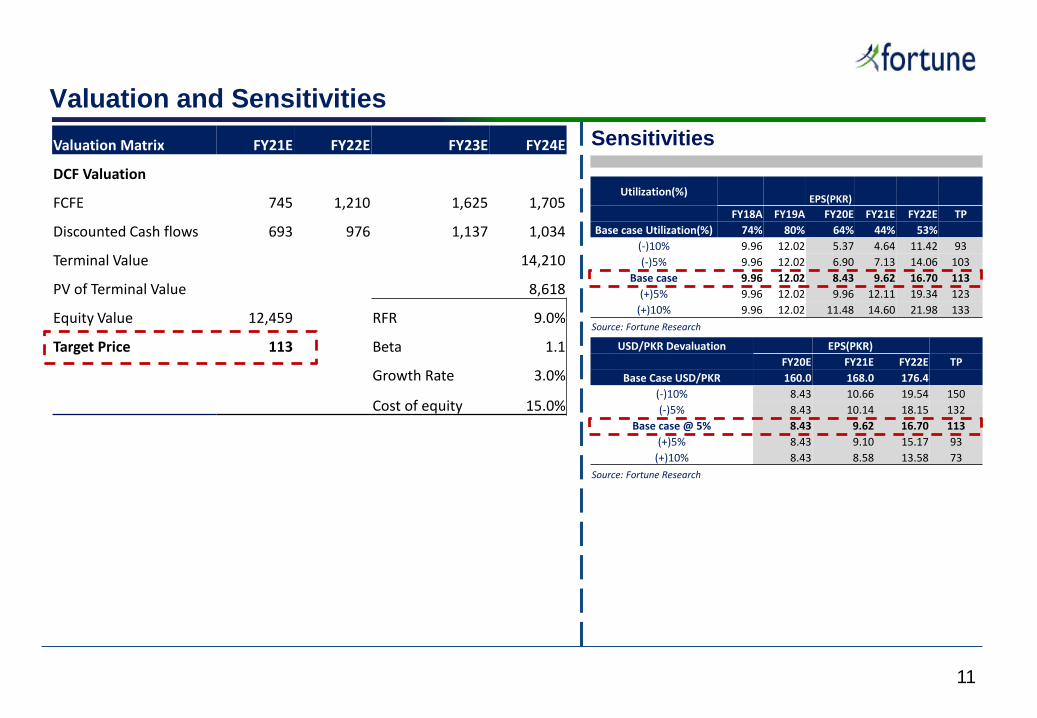

Valuation and Sensitivities

Valuation Matrix FY21E FY22E FY23E FY24E

DCF Valuation

FCFE 745 1,210 1,625 1,705

Discounted Cash flows 693 976 1,137 1,034

Terminal Value 14,210

PV of Terminal Value 8,618

Equity Value 12,459 RFR 9.0%

Target Price 113 Beta 1.1

Growth Rate 3.0%

Cost of equity 15.0%

Sensitivities

Utilization(%)EPS(PKR)

FY18A FY19A FY20E FY21E FY22E TP

Base case Utilization(%) 74% 80% 64% 44% 53%

(-)10% 9.96 12.02 5.37 4.64 11.42 93

(-)5% 9.96 12.02 6.90 7.13 14.06 103

Base case 9.96 12.02 8.43 9.62 16.70 113

(+)5% 9.96 12.02 9.96 12.11 19.34 123

(+)10% 9.96 12.02 11.48 14.60 21.98 133

Source: Fortune Research

USD/PKR Devaluation EPS(PKR)

FY20E FY21E FY22E TP

Base Case USD/PKR 160.0 168.0 176.4

(-)10% 8.43 10.66 19.54 150

(-)5% 8.43 10.14 18.15 132

Base case @ 5% 8.43 9.62 16.70 113

(+)5% 8.43 9.10 15.17 93

(+)10% 8.43 8.58 13.58 73

Source: Fortune Research

11

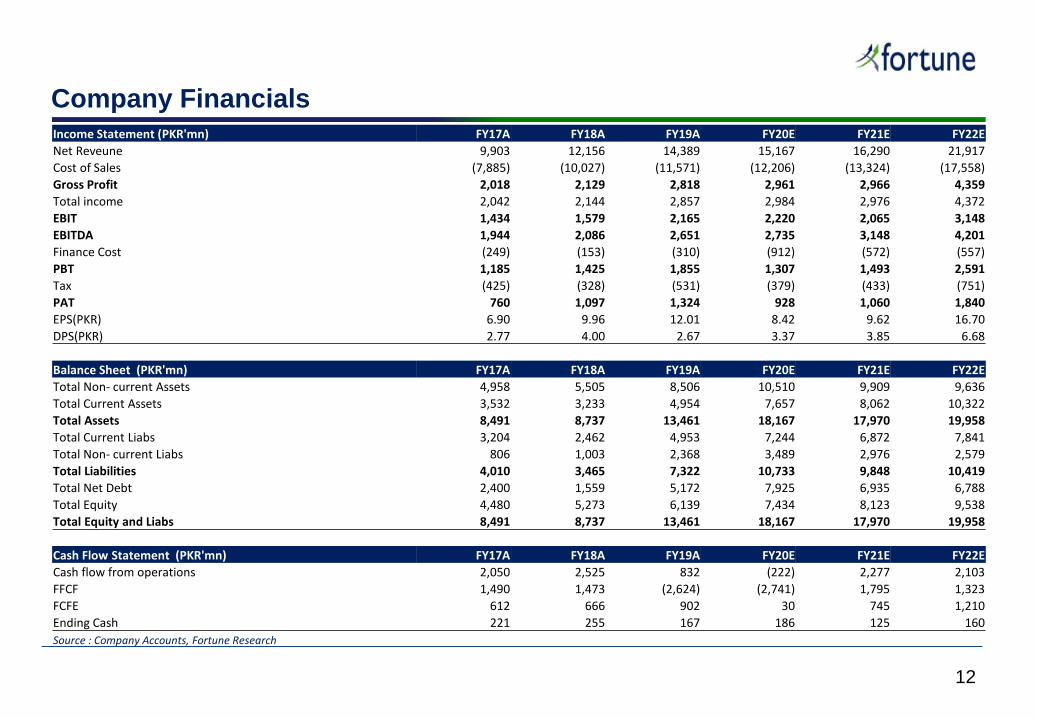

Company FinancialsIncome Statement (PKR'mn) FY17A FY18A FY19A FY20E FY21E FY22E

Net Reveune 9,903 12,156 14,389 15,167 16,290 21,917

Cost of Sales (7,885) (10,027) (11,571) (12,206) (13,324) (17,558)

Gross Profit 2,018 2,129 2,818 2,961 2,966 4,359

Total income 2,042 2,144 2,857 2,984 2,976 4,372

EBIT 1,434 1,579 2,165 2,220 2,065 3,148

EBITDA 1,944 2,086 2,651 2,735 3,148 4,201

Finance Cost (249) (153) (310) (912) (572) (557)

PBT 1,185 1,425 1,855 1,307 1,493 2,591

Tax (425) (328) (531) (379) (433) (751)

PAT 760 1,097 1,324 928 1,060 1,840

EPS(PKR) 6.90 9.96 12.01 8.42 9.62 16.70

DPS(PKR) 2.77 4.00 2.67 3.37 3.85 6.68

Balance Sheet (PKR'mn) FY17A FY18A FY19A FY20E FY21E FY22E

Total Non- current Assets 4,958 5,505 8,506 10,510 9,909 9,636

Total Current Assets 3,532 3,233 4,954 7,657 8,062 10,322

Total Assets 8,491 8,737 13,461 18,167 17,970 19,958

Total Current Liabs 3,204 2,462 4,953 7,244 6,872 7,841

Total Non- current Liabs 806 1,003 2,368 3,489 2,976 2,579

Total Liabilities 4,010 3,465 7,322 10,733 9,848 10,419

Total Net Debt 2,400 1,559 5,172 7,925 6,935 6,788

Total Equity 4,480 5,273 6,139 7,434 8,123 9,538

Total Equity and Liabs 8,491 8,737 13,461 18,167 17,970 19,958

Cash Flow Statement (PKR'mn) FY17A FY18A FY19A FY20E FY21E FY22E

Cash flow from operations 2,050 2,525 832 (222) 2,277 2,103

FFCF 1,490 1,473 (2,624) (2,741) 1,795 1,323

FCFE 612 666 902 30 745 1,210

Ending Cash 221 255 167 186 125 160

Source : Company Accounts, Fortune Research

12

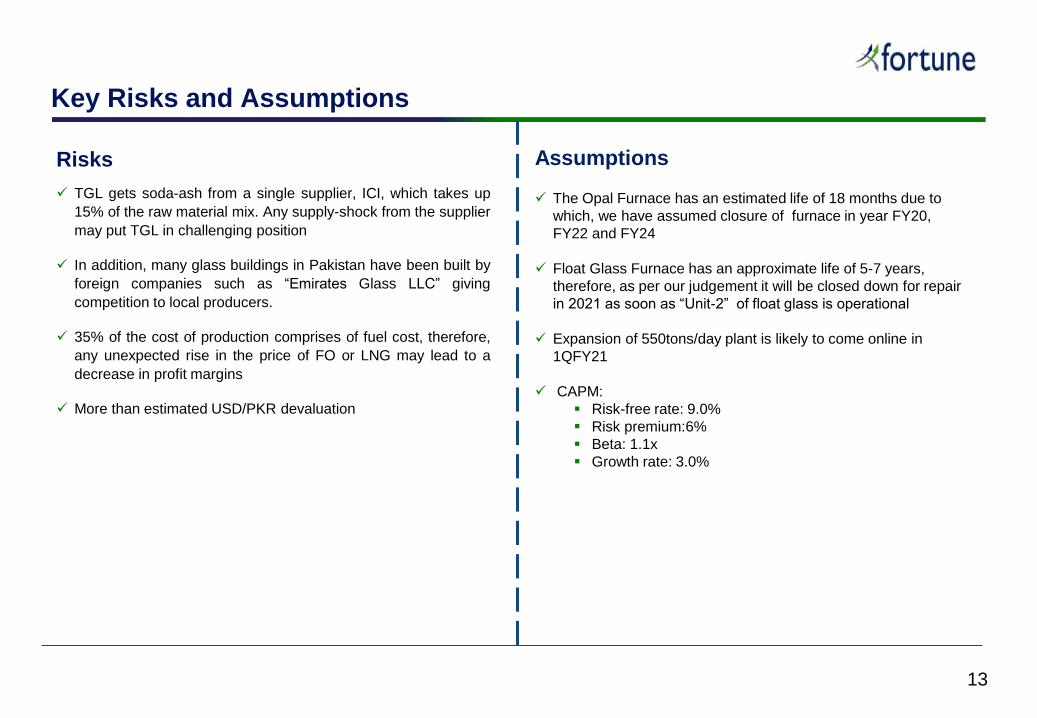

Key Risks and Assumptions

Risks

TGL gets soda-ash from a single supplier, ICI, which takes up

15% of the raw material mix. Any supply-shock from the supplier

may put TGL in challenging position

In addition, many glass buildings in Pakistan have been built by

foreign companies such as “Emirates Glass LLC” giving

competition to local producers.

35% of the cost of production comprises of fuel cost, therefore,

any unexpected rise in the price of FO or LNG may lead to a

decrease in profit margins

More than estimated USD/PKR devaluation

Assumptions

The Opal Furnace has an estimated life of 18 months due to

which, we have assumed closure of furnace in year FY20,

FY22 and FY24

Float Glass Furnace has an approximate life of 5-7 years,

therefore, as per our judgement it will be closed down for repair

in 2021 as soon as “Unit-2” of float glass is operational

Expansion of 550tons/day plant is likely to come online in

1QFY21

CAPM:

Risk-free rate: 9.0%

Risk premium:6%

Beta: 1.1x

Growth rate: 3.0%

13

14

Analyst Certification

The research analyst on the cover of this report certifies that: 1) all of the views expressed in this report accurately reflect his or her personal views about any and all of the subjectsecurities or issuers; 2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) expressed by theresearch analyst(s) in this report; 3) he/she does not have a financial interest in any and all of the subject securities or issuers aggregating more than 1% of the value of the company(s); 4)he/she or its close relative has not served as a director/officer/associate in the past three years in any and all of the subject securities or issuers; 5) he/she or its close relative hasreceived any compensation from any and all of the subject securities or issuers in the previous 12 months; and 6) he/she has not traded in the subject security(ies) or issuer(s) in the past7 trading days and will not trade in the next 5 trading days of issuing a coverage initiation or a material Target Price revision report.

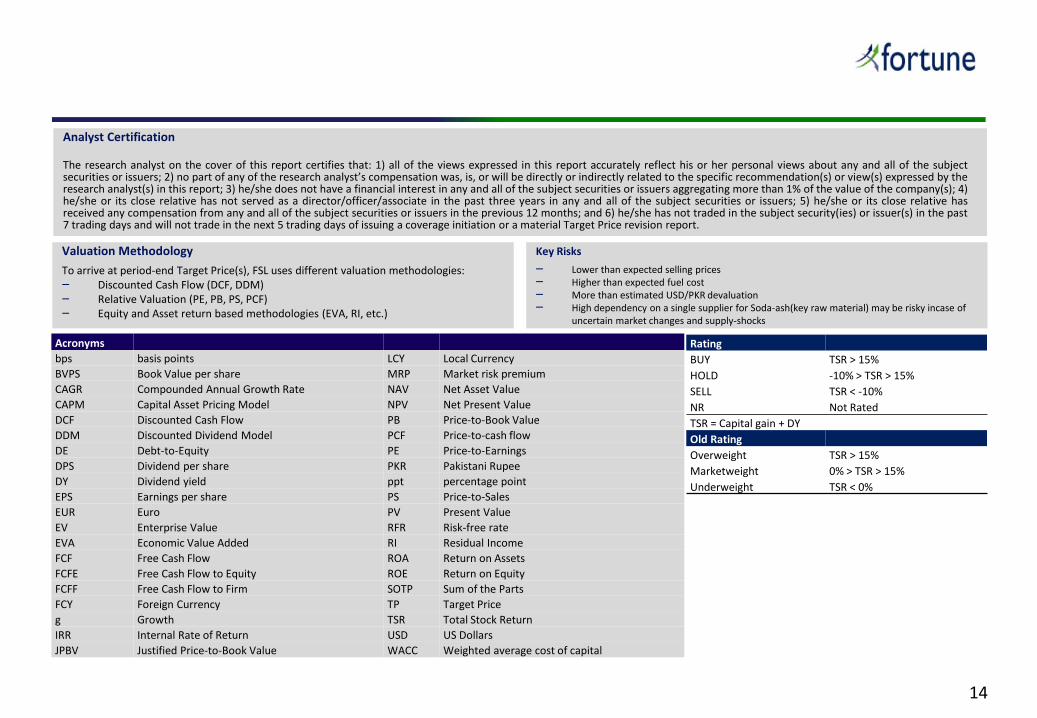

Valuation Methodology

To arrive at period-end Target Price(s), FSL uses different valuation methodologies:‒ Discounted Cash Flow (DCF, DDM)‒ Relative Valuation (PE, PB, PS, PCF)‒ Equity and Asset return based methodologies (EVA, RI, etc.)

Acronyms

bps basis points LCY Local Currency

BVPS Book Value per share MRP Market risk premium

CAGR Compounded Annual Growth Rate NAV Net Asset Value

CAPM Capital Asset Pricing Model NPV Net Present Value

DCF Discounted Cash Flow PB Price-to-Book Value

DDM Discounted Dividend Model PCF Price-to-cash flow

DE Debt-to-Equity PE Price-to-Earnings

DPS Dividend per share PKR Pakistani Rupee

DY Dividend yield ppt percentage point

EPS Earnings per share PS Price-to-Sales

EUR Euro PV Present Value

EV Enterprise Value RFR Risk-free rate

EVA Economic Value Added RI Residual Income

FCF Free Cash Flow ROA Return on Assets

FCFE Free Cash Flow to Equity ROE Return on Equity

FCFF Free Cash Flow to Firm SOTP Sum of the Parts

FCY Foreign Currency TP Target Price

g Growth TSR Total Stock Return

IRR Internal Rate of Return USD US Dollars

JPBV Justified Price-to-Book Value WACC Weighted average cost of capital

Rating

BUY TSR > 15%

HOLD -10% > TSR > 15%

SELL TSR < -10%

NR Not Rated

TSR = Capital gain + DY

Old Rating

Overweight TSR > 15%

Marketweight 0% > TSR > 15%

Underweight TSR < 0%

Key Risks

‒ Lower than expected selling prices‒ Higher than expected fuel cost‒ More than estimated USD/PKR devaluation ‒ High dependency on a single supplier for Soda-ash(key raw material) may be risky incase of

uncertain market changes and supply-shocks

15

Disclosure

The investment recommendation(s) take into account both risk and expected return. FSL based the long-term Target Price estimate on fundamental analysis of thesubject security(ies)’s future prospects, after having taken perceived risks into consideration. FSL have conducted extensive research to arrive at the investmentrecommendation(s) and target price(s) for the subject security (ies). Readers should understand that financial projection(s), target price estimate(s) and statement(s)regarding future prospects may or may not be realized. Forward looking statement(s), opinion(s) and estimate(s) included in this report constitute FSL’s judgment as ofthis date and are subject to change without prior notice. The target price(s) stated in reports on company update(s), initiation(s) and corporate action adjustment(s) ofstocks listed on the PSX are on a 12-month basis. All other reports on PSX-listed securities, such as scoops, sector or company commentaries, do not include, denote, orimply any changes to target price(s).

Disclaimer

The research report prepared by Fortune Securities Limited (hereinafter referred as FSL) are based on public information and the report is for information purposesonly and does not constitute nor it is intended as an offer or solicitation for the purchase or sale of security(ies) or other financial instruments. FSL makes every effortto use reliable, comprehensive information, but it makes no representation that the information contained herein is accurate or complete. Facts and views presentedin this report have not been reviewed by and may not reflect information known to professionals in other business areas of FSL or any of its associated entities. FSL hasestablished information barriers between business groups and associations maintaining complete independence of this research report. This report is not intended toprovide personal investment advice nor does it provide individually tailored investment advice. This report does not take into account the specific investmentobjectives, financial situation/financial circumstances and the particular needs of any specific person. Investors should seek financial advice regarding theappropriateness of investing in financial instruments and implementing investment strategies discussed or recommended in this report and should understand thatstatements regarding future prospects may not be realized. FSL recommends that investors independently evaluate particular investments and strategies and itencourages investors to seek the advice of a financial advisor.

FSL has taken all reasonable care to ensure that the information contained herein is accurate, up to date, and complies with all Pakistani legislations. However, noliability can be accepted for any errors or omissions, or for any loss resulting from the use of the information provided as any data and research material providedahead of an investment decision are for information purposes only. We shall not be liable for any errors in the provision of this information, or for any actions taken inreliance thereon.

Copyright and confidentiality

No part of this document may be reproduced without the written permission of FSL. The information within this research report must not be disclosed to any otherperson if and until FSL has made the information publicly available.

Research Team

Research Team

Syed Arif ur Rehman

Director Research & Business Development

+92 213 5309113

Arvind Anand

Deputy Head of Research

+92 213 5309119

Hasnain Murtaza

Research Analyst

+92 213 5309119

Wajid Rizvi

Head of Research

+92 213 5309086

Mahnoor Shafqat

Research Analyst

+92 213 5309119

Kishan Sidi

Database Manager

+92 213 5309119

Muqeet Naeem

Research Analyst

+92 213 5309119

16