Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

23 November 2012

Europe

Equity Research

Macro

Global Equity Strategy STRATEGY

Growth: on the way to 'Nifty Fifty'

■ We believe growth as a style will continue to outperform: falling real bonds yields should have re-rated long duration assets more than has occurred – and we believe real bond yields will fall further, as QE is stepped up by the BoJ and the ECB. Excess liquidity re-rates growth stocks. Lastly, global nominal GDP growth is set to remain well below trend. The issue is valuation: the relative 12-month forward P/E of our simple growth style is at a 9% premium to its norm; quality growth is slightly more expensive (15% above its norm). Growth stocks on aggregate still only trade on a P/E of 15x, compared to peak valuations of 50x (in 1973 and 1999). Quality growth only tends to underperform if there is a sharp fall in junk bond yields (unlikely) or a sharp rise in economic indicators (we think only small rise is likely).

■ The best performing quant style for growth has been Credit Suisse HOLT®’s eCAP superior (effectively, high and stable profitability) combined with superior asset growth and asset turns. This combined style has achieved 5% outperformance pa over the past 10 years (Capita, Assa Abloy, Diageo, Intertek qualify).

■ Stocks and themes: We screen for growth stocks using three measures: quant screens (HOLT® and ours), our analysts’ picks and structural themes (CSERGROW). The following stocks qualify as growth under at least two of these methodologies, are attractively priced (on P/E relatives, free-cash flow yield or HOLT®) and are Outperform-rated: Dufry, SAB Miller, SAP, Sonova, WPP, Swatch, Capita, RyanAir, Assa Abloy, ICH, Pru, Moneysupermarket.com in Europe and Qualcomm, Google and Mead Johnson Nutrition in the US. Our favoured growth themes: software (SAP, TDC); the emerging market consumer (Swatch, SAB, Diageo, YUM); underleveraged banks in underleveraged countries (Sberbank); specific plays on the internet (GOOG and Moneysupermarket.com); global travel (ICH, STAR, Dufry); global trade (Intertek, UPS); energy efficiency (Schneider, JCI); lower car emissions (Johnson Matthey, BWA); ageing in emerging markets (Hikma); water (Halma; PLL); industrial automation (Schneider, ROK); specific oilfield services (Amec).

Figure 1: Growth outperforms as real bond yields fall

-1.2%

-0.7%

-0.2%

0.3%

0.8%

1.3%

1.8%

2.3%

2.8%

3.3%86

88

90

92

94

96

98

100

102

104

106

108

110

112

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

MSCI European growth index, relative to the market

US 10-year TIPS yield, inverted, rhs

Source: Thomson Reuters, Credit Suisse research

Research Analysts

Andrew Garthwaite

44 20 7883 6477

Marina Pronina

44 20 7883 6476

Mark Richards

44 20 7883 6484

Sebastian Raedler

44 20 7888 7554

Robert Griffiths

44 20 7883 8885

Nicolas Wylenzek

44 20 7883 6480

23 November 2012

Global Equity Strategy 2

Table of contents Why focus on growth? 3

(1) Growth as a style is a play on low real interest rates 3 (2) A sluggish recovery puts a premium on growth 4 (3) Excess liquidity 5 (4) Other performance drivers remain supportive 5 (5) Market breadth is narrowing – a feature of a growth-led market 6

Continue to focus on quality growth 7 Valuation of quality growth is high – but recall the ‘Nifty Fifty’ 9

Which growth indices have performed best? 12 How to play growth? 13

Our aggregate screen 13 1) Quant approach 15 2) Analyst judgment 18 3) Thematic approach 20

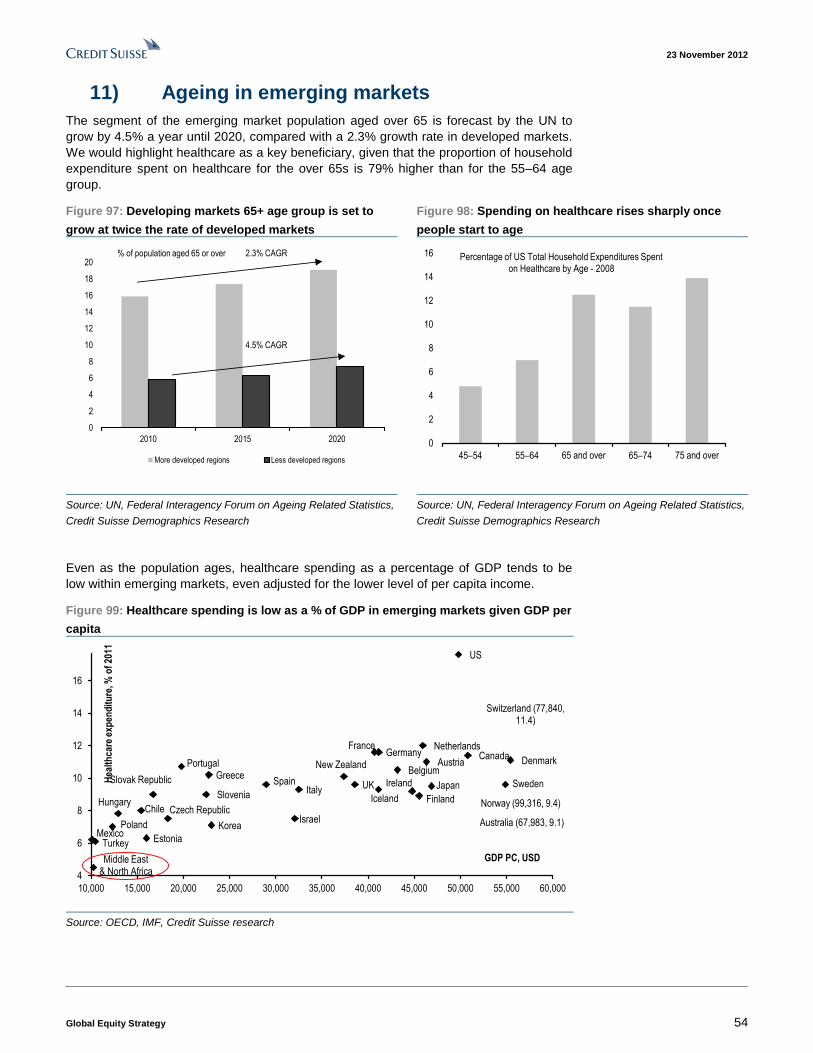

Growth themes 22 1) Branded GEM consumer plays 22 2) Industrial Automation 28 3) Global trade 34 4) Global travel 38 5) Water 41 6) Underleveraged banks in underleveraged countries 43 7) Labour-intensive oilfield services 44 8) Energy efficiency 47 9) Reducing car emissions 50 10) Specific plays on the internet – in particular, e-financial services 51 11) Ageing in emerging markets 54 12) Software 60

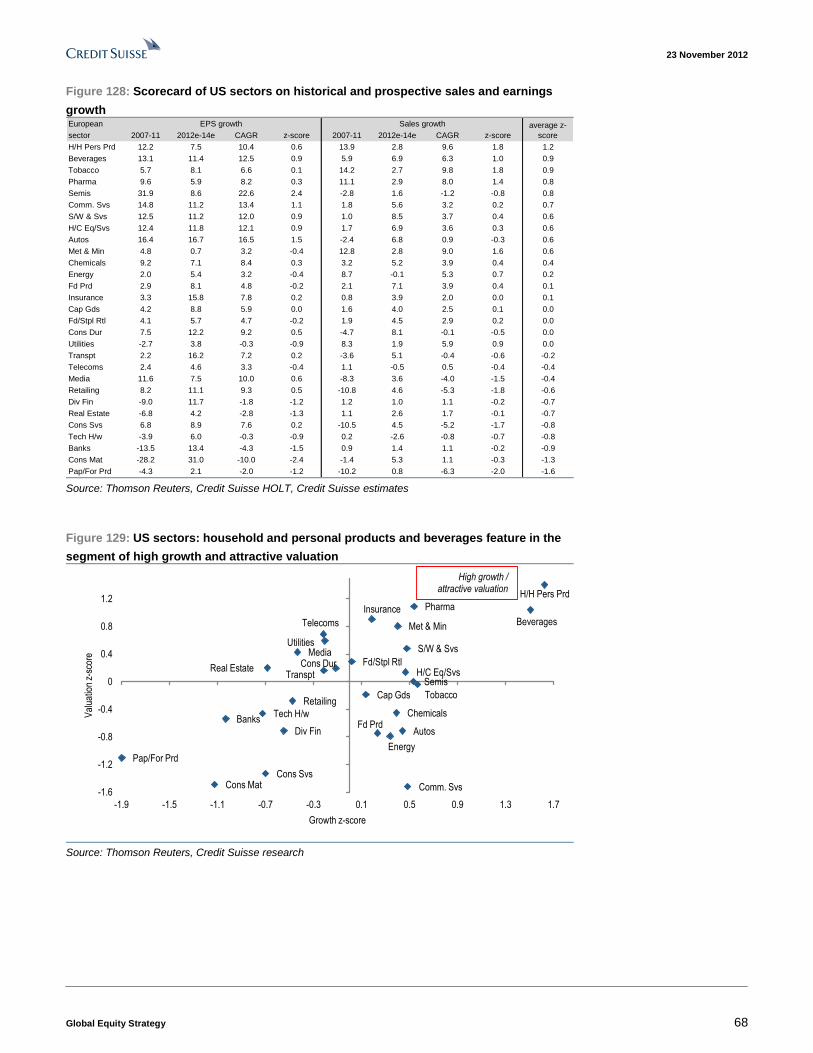

A sector perspective 64 Appendix 66

Appendix 1: Growth as a style 66 Appendix 2: Sector valuations in Europe and the US 67 Appendix 3: Outperform rated NJA growth stocks and quality growth 69 Appendix 4: Full list of companies that our analysts identified as growth in Europe and

the US 70

23 November 2012

Global Equity Strategy 3

Why focus on growth? (1) Growth as a style is a play on low real

interest rates

The more real bond yields fall, the more longer duration assets – and, therefore, growth

stocks – re-rate relative to shorter duration assets.

Figure 2: Growth stocks have more potential upside if the

discount rate falls

Figure 3: Growth tends to outperform as real interest

rates fall

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

5% 4% 3% 2% 1% 0%

High grow th (=5%) stock

Low grow th (=2%) stock

Bond y ield

Discount rate falls

% change in the

fair v alue of:

-1.2%

-0.7%

-0.2%

0.3%

0.8%

1.3%

1.8%

2.3%

2.8%

3.3%86

88

90

92

94

96

98

100

102

104

106

108

110

112

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

MSCI European growth index, relative to the market

US 10-year TIPS yield, inverted, rhs

Source: Credit Suisse research Source: Thomson Reuters, Credit Suisse research

We continue to believe that the main solution to the developed market debt crisis is for real

interest rates to fall even further – from the current minus 80bps to between minus 1.5% to

minus 2%. Only at this level on our calculations can developed markets both stabilise

government debt to GDP and unemployment (for details, see our report Synchronised QE

and how to play it, Sep 12).

Over the course of 2013, we believe that QE will become more aggressive:

■ The Fed is likely to expand their balance sheet by $85bn a month from mid-December

compared to just $36bn a month since QE3 started;

■ The BoJ is likely to become more aggressive under a likely LDP-led administration

following the December election (with the LDP likely to present a BoJ Act, committing

the BoJ to a 2% inflation goal);

■ The ECB is likely to expand its balance sheet once the OMT is activated.

As central banks’ balance sheets expand, real bond yields will fall. Recently, if anything,

growth as a style has performed worse than the fall in real bond yields would have

suggested (we show the performance of the US growth style in the Appendix).

23 November 2012

Global Equity Strategy 4

Figure 4: Low real interest rates improve the funding of

government debt.

Figure 5: Real interest rates stayed negative for nearly

two decades in the 1940s/50s… and financial repression

lasted until the end of Bretton Woods

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

0% 2% 4% 6% 8%

Rea

l bon

d yi

eld

Required fiscal tightening, % of GDP

US 10Y real bond yield required to keep USgovernment debt to GDP stable (at 3% trendgrowth rate)

Government to GDP ratio stable if:

Primary balance % GDP = Debt/GDP *(bond yield - trend growth rate)

At current BY

0%

20%

40%

60%

80%

100%

120%

140%

-15%

-10%

-5%

0%

5%

10%

15%

1925 1935 1945 1955 1965 1975 1985 1995 2005

US real Bond yield

US Government debt to GDP, rhs

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

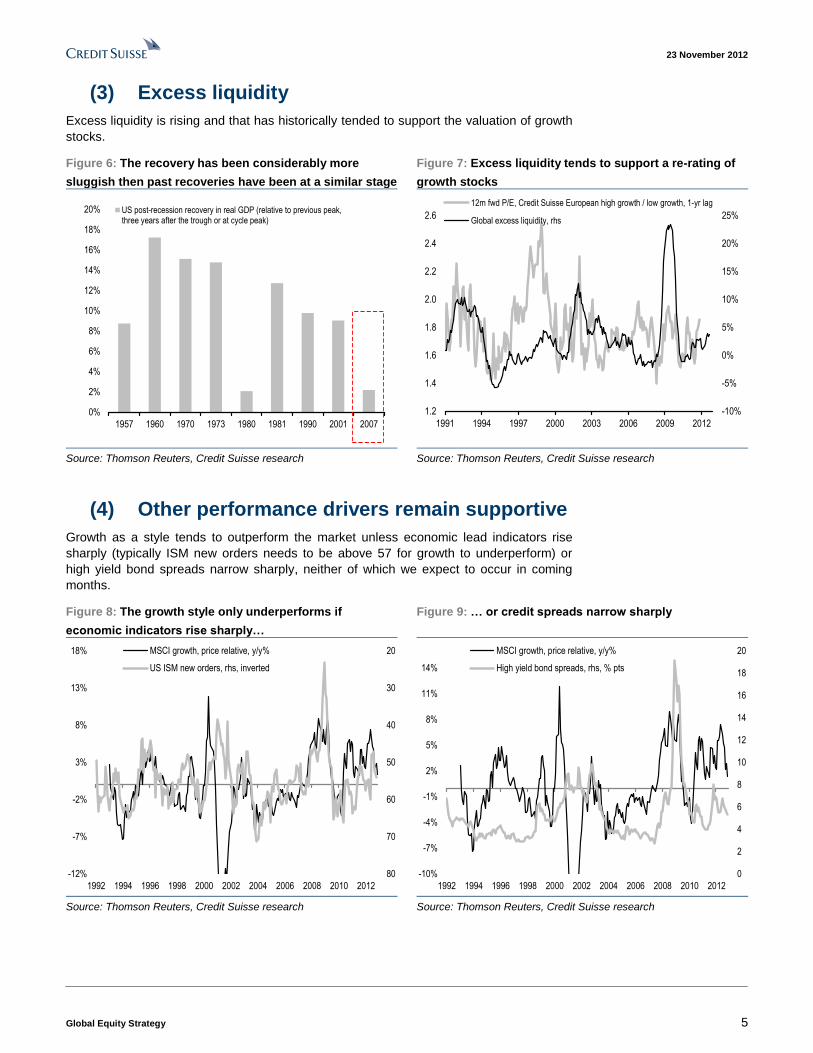

(2) A sluggish recovery puts a premium on

growth

As Figure 6 shows, the recovery in US GDP has been far more muted than in previous

cycles. Three years after the recovery started, US real GDP is only 2.2% above the

previous peak. This compares to an average of 11.2% above previous peak at the same

point in previous post recession periods. In nominal terms, global GDP growth is running

just below 5%, compared to a 10 year CAGR of 7%. Such a scarcity of growth should

result in a premium on companies that can generate it.

23 November 2012

Global Equity Strategy 5

(3) Excess liquidity

Excess liquidity is rising and that has historically tended to support the valuation of growth

stocks.

Figure 6: The recovery has been considerably more

sluggish then past recoveries have been at a similar stage

Figure 7: Excess liquidity tends to support a re-rating of

growth stocks

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1957 1960 1970 1973 1980 1981 1990 2001 2007

US post-recession recovery in real GDP (relative to previous peak,three years after the trough or at cycle peak)

-10%

-5%

0%

5%

10%

15%

20%

25%

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

1991 1994 1997 2000 2003 2006 2009 2012

12m fwd P/E, Credit Suisse European high growth / low growth, 1-yr lag

Global excess liquidity, rhs

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

(4) Other performance drivers remain supportive

Growth as a style tends to outperform the market unless economic lead indicators rise

sharply (typically ISM new orders needs to be above 57 for growth to underperform) or

high yield bond spreads narrow sharply, neither of which we expect to occur in coming

months.

Figure 8: The growth style only underperforms if

economic indicators rise sharply…

Figure 9: … or credit spreads narrow sharply

20

30

40

50

60

70

80-12%

-7%

-2%

3%

8%

13%

18%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

MSCI growth, price relative, y/y%

US ISM new orders, rhs, inverted

0

2

4

6

8

10

12

14

16

18

20

-10%

-7%

-4%

-1%

2%

5%

8%

11%

14%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

MSCI growth, price relative, y/y%

High yield bond spreads, rhs, % pts

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

23 November 2012

Global Equity Strategy 6

(5) Market breadth is narrowing – a feature of a

growth-led market

A feature of the late 1990s was that the market rose against the backdrop of a weak

advance / decline line – i.e. the market was driven by a narrow set of strong performers.

There are signs of this happening again.

Figure 10: There are signs that – as in the late 1990s – the market is driven by a narrow

set of strong performers

-40

-30

-20

-10

0

10

20

30

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

6m rolling advance/decline line, %

S&P500 deviation from 130 day average, % (rhs)

Declining market breadth

Source: Thomson Reuters, Credit Suisse research

23 November 2012

Global Equity Strategy 7

Continue to focus on quality growth We also continue with our preference for quality growth. Performance drivers are very

similar to those of the conventional growth style (yet, the magnitude of quality growth

performance is greater), with periods of sustained underperformance only tending to occur

when lead indicators rise sharply or high yield spreads narrow.

Figure 11: High quality growth tends to underperform

only if lead indicators rise sharply…

Figure 12: … or credit spreads narrow sharply

20

30

40

50

60

70

80-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

High quality growth / low quality growth, y/y%

US ISM new orders, rhs, inverted

0

5

10

15

20

25

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

High quality growth / low quality growth, y/y%

US high yield spreads, rhs

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

The reason for this is that:

■ Low quality companies tend to have abnormally high operational leverage (by

definition, they have higher fixed costs than their to peers);

■ Lower quality companies tend to have higher financial leverage ratios, owing to inferior

profitability.

We expect only a modest upside surprise to economic growth expectations in 2013 – and

see only little scope for the absolute cost of junk bond debt to fall (given the convexity

problem that the economic circumstances that allow junk bond spreads to fall – i.e. better

economic growth – are likely to lead to a significant rise in 10-year bond yields).

Lastly, the relative price momentum of high quality growth companies is at the bottom-end

of its historical range. However, earnings momentum has fallen in line with the market,

although at least it is not weaker than for the market overall.

23 November 2012

Global Equity Strategy 8

Figure 13: European high quality growth appears

oversold

Figure 14: Earnings momentum of European high quality

growth has fallen in line with the market

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

European High Quality Growth %dev from 6mma, rel to

European market

Average (+/1 SD)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1993 1996 1999 2002 2005 2008 2012

European High Quality Growth 3m breadth

Rel European market

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

23 November 2012

Global Equity Strategy 9

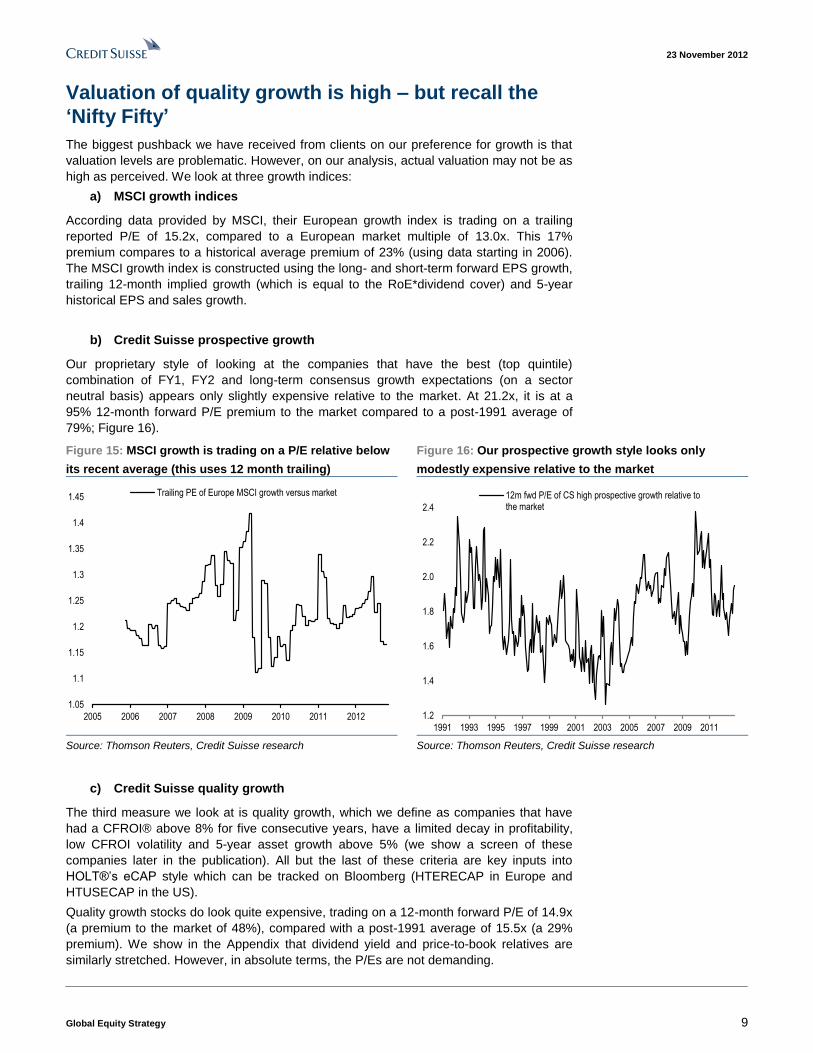

Valuation of quality growth is high – but recall the

‘Nifty Fifty’

The biggest pushback we have received from clients on our preference for growth is that

valuation levels are problematic. However, on our analysis, actual valuation may not be as

high as perceived. We look at three growth indices:

a) MSCI growth indices

According data provided by MSCI, their European growth index is trading on a trailing

reported P/E of 15.2x, compared to a European market multiple of 13.0x. This 17%

premium compares to a historical average premium of 23% (using data starting in 2006).

The MSCI growth index is constructed using the long- and short-term forward EPS growth,

trailing 12-month implied growth (which is equal to the RoE*dividend cover) and 5-year

historical EPS and sales growth.

b) Credit Suisse prospective growth

Our proprietary style of looking at the companies that have the best (top quintile)

combination of FY1, FY2 and long-term consensus growth expectations (on a sector

neutral basis) appears only slightly expensive relative to the market. At 21.2x, it is at a

95% 12-month forward P/E premium to the market compared to a post-1991 average of

79%; Figure 16).

Figure 15: MSCI growth is trading on a P/E relative below

its recent average (this uses 12 month trailing)

Figure 16: Our prospective growth style looks only

modestly expensive relative to the market

1.05

1.1

1.15

1.2

1.25

1.3

1.35

1.4

1.45

2005 2006 2007 2008 2009 2010 2011 2012

Trailing PE of Europe MSCI growth versus market

1.2

1.4

1.6

1.8

2.0

2.2

2.4

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

12m fwd P/E of CS high prospective growth relative tothe market

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

c) Credit Suisse quality growth

The third measure we look at is quality growth, which we define as companies that have

had a CFROI® above 8% for five consecutive years, have a limited decay in profitability,

low CFROI volatility and 5-year asset growth above 5% (we show a screen of these

companies later in the publication). All but the last of these criteria are key inputs into

HOLT®’s eCAP style which can be tracked on Bloomberg (HTERECAP in Europe and

HTUSECAP in the US).

Quality growth stocks do look quite expensive, trading on a 12-month forward P/E of 14.9x

(a premium to the market of 48%), compared with a post-1991 average of 15.5x (a 29%

premium). We show in the Appendix that dividend yield and price-to-book relatives are

similarly stretched. However, in absolute terms, the P/Es are not demanding.

23 November 2012

Global Equity Strategy 10

Figure 17: High quality growth companies appear

expensive relative to the market

Figure 18: In absolute terms, high quality growth stocks

do not appear expensive

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1990 1993 1997 2001 2004 2008 2012

12m fwd P/E of European high quality growthcompanies relative to MSCI Europe

5

10

15

20

25

1990 1993 1997 2001 2004 2008 2012

Eur High Quality Growth

MSCI Europe

12m fwd P/E

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

We believe that the current environment of abnormally loose monetary policy leads to the

survival of low quality companies that would normally be forced into bankruptcy. This is

because there is little pressure on excess capacity to exit, as the opportunity cost of

servicing an NPL is zero in a zero interest rate environment. An example of this is the UK

where the proportion of loss-making corporates is close to the high-end of the historical

range, but insolvencies are at the low-end (i.e. loss-making companies are not being

forced to shut down). This condition of ‘zombie capitalism’ is likely to maintain depressed

returns in the low-quality segments of the market. This means that the denominator of a

relative valuation calculation is abnormally depressed.

Figure 19: Abnormally loose monetary policy has led to the persistence of loss-making

companies and hence low quality is abnormally poor

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Loss-making companies, % of total private non-financial companies

Company liquidations, rhs, 000s

Source: Bank of England, Credit Suisse research

23 November 2012

Global Equity Strategy 11

Remember the ‘Nifty Fifty’

We remind investors of the valuation of tech in the 1998-2000 period (12m fwd P/E of US

tech got to 48x) and the ‘Nifty Fifty’ bubble in the early 1970s (where the median PE of

high-quality large-cap stocks got to 52x).

Figure 20: US tech reached a PE of 48x in 1998 – three

times the valuation of the market

Figure 21: The ‘Nifty 50’ stocks reached a multiple of 52x

in the early 1970s

0.8

1

1.2

1.4

1.6

1.8

2

2.2

2.4

1996 1998 2000 2002 2004 2006 2008 2010 2012

US tech, 12m fwd PErelative to market

Stock PE in January 1973

Walt Disney 188

Intl.Flavors & Frag. 78.2

Mcdonalds 72.5

Baxter Intl. 71.8

Avon Products 68.3

Johnson & Johnson 65.2

Xerox 51.7

Coca Cola 50.2

Eli Lilly 49.8

Merck & Co. 48.4

Schlumberger 46.4

Procter & Gamble 43.5

American Express 39.5

Median 51.7

Average 67.2

Market 18.3

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

What is striking is that on the screens of growth stocks shown in the next few pages there

are lots of companies with powerful growth stories – but which are nonetheless trading

below 20x.

Below we compare the earnings yield of growth to the government bond yield: in 1973 the

earnings yield of the ‘Nifty Fifty’ stocks was just 29% of the US Treasury 10-year yield; at

the peak of the tech bubble, the tech sector had an earnings yield of about a third of the

US Treasury yield. Currently, quality growth stocks, as defined above, offer an earnings

yield that is more than four times the US Treasury yield.

Figure 22: Quality growth is cheaper relative to bonds that in previous market bubbles

Earnings yield10-yr US Treasury

yieldEY / BY ratio

Nifty Fity in 1973 1.9 6.5 29.4%

US tech in 2000 2.1 6.3 33.6%

Current quality growth 6.7 1.5 436.2% Source: Thomson Reuters, Credit Suisse research

23 November 2012

Global Equity Strategy 12

Which growth indices have performed best? We show the performance of the various growth indices discussed in this report. The best

performing growth basket over the last decade has been the stocks that meet HOLT’s

eCAP criteria and have more than 10% asset growth and asset turns in the top 40% of the

market. So far in 2012, the best performing growth style has been the HOLT eCAP basket

with an additional filter for stocks with more than 5% asset growth.

Figure 23: HOLT eCAP plus growth and asset turns is the

best performing growth style over the last decade

Figure 24: HOLT eCAP and growth has been the best

performing growth style in 2012

9.7%

7.9%

7.1% 6.8%

5.7%

4.8%

0%

2%

4%

6%

8%

10%

HOLT eCAP+ >10%

growth + top40% asset

turns

HOLT quality(eCAP)

HOLT eCAP+ >5%growth

Highprospective

growth

MSCIEuropegrowth

MSCIEurope

Annualised price performance last 10 years

20.0%

17.5%16.7% 16.7%

13.3%

11.4%

0%

5%

10%

15%

20%

HOLT eCAP+ >5%growth

HOLTquality(eCAP)

Highprospective

growth

HOLT eCAP+ >10%

growth + top40% asset

turns

MSCIEuropegrowth

MSCIEurope

Annualised performance, 2012 YTD

Source: Thomson Reuters, Credit Suisse HOLT, Credit Suisse

research

Source: Thomson Reuters, Credit Suisse HOLT, Credit Suisse

research

We believe that superior asset turns are a key ingredient underpinning quality growth. A

company with abnormally high margins is likely to attract competitors into its business area.

If a company has low margins, but high asset turns (because, for example, of the

efficiency of its supply chain), then it is harder for a competitor to move in.

23 November 2012

Global Equity Strategy 13

How to play growth? Our aggregate screen

We employ three methods to identify growth stocks:

■ The quant approach: we use two quant screens: (a) looking at conventional growth

(historical and projected sales and EPS growth) and (b) HOLT metrics of high and

stable CFROI and reasonable asset growth;

■ Analyst opinion: we have asked our analysts to highlight the stocks with the best

growth outlook over the next five years.

■ Themes: we look for stocks with exposure to what we believe are the most promising

growth themes.

Below, we show a screen of the European stocks that are highlighted by at least two of

these methodologies.

Figure 25: European stocks highlighted as growth by two or more of our methodologies (sorted by cheapness on Holt

price to best)

Name Themes QuantsAnalyst

judgementAbs

rel to

Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

SAP P P P 16.5 121% -32% 5.4 -42% 3.6 1.5 58.2 -0.6 1.6 2.3 58.8 Outperform

Sonova N P P P 18.3 142% -10% 4.4 -22% 4.3 1.4 42.8 0.7 0.2 2.4 100.6 Outperform

Wpp P P P 10.5 76% -18% 1.5 -86% 8.8 3.4 7.8 -1.2 -1.8 2.0 825.0 Outperform

Lvmh P P P 16.4 105% 3% 2.9 -10% 4.1 2.3 -1.2 -1.2 1.8 2.0 129.0 Outperform

Fresenius Med.Care P P P 16.3 126% 2% 2.6 19% 4.5 1.4 -11.3 -1.9 -1.1 2.4 51.6 Outperform

Burberry Group P P P 17.5 112% 35% 6.3 45% 4.4 2.1 -13.8 -6.2 -4.4 2.5 1,233.0 Outperform

Diageo P P P 16.7 103% 47% 8.1 71% 4.2 2.5 -14.6 0.7 -1.5 2.1 1,846.0 Outperform

Intertek Group P P P 19.9 127% 60% 8.8 -51% 3.0 1.4 -20.1 2.0 1.7 2.8 2,898.0 Outperform

Pernod-Ricard P P P 15.4 95% 46% 2.0 14% 4.3 1.9 -22.5 -2.7 0.4 2.7 84.9 Outperform

Saipem P P P 14.2 133% 18% 3.3 28% 6.2 2.1 -33.6 -2.9 1.5 2.1 32.5 Outperform

Dufry 'R' P P 10.5 63% -7% 3.7 46% 9.2 0.0 67.9 -2.9 -0.8 2.0 124.3 Outperform

Petrofac P P 12.3 116% 11% 7.1 27% -0.2 2.5 56.5 -0.7 -1.7 2.3 1,590.0 Outperform

Rotork P P 19.5 169% 54% 9.0 80% 4.0 1.9 19.0 0.6 1.6 2.8 2,426.0 Outperform

Capita P P 13.2 84% -41% 8.6 -36% 4.8 3.2 17.5 0.7 1.0 2.7 722.5 Outperform

The Swatch Group

'B'

P P 14.0 89% -52% 2.8 23% 4.0 1.7 9.0 1.8 0.9 2.3 432.2 Outperform

Johnson Matthey P P 13.7 107% 28% 3.2 40% na 2.5 8.0 -5.4 -4.2 2.6 2,190.0 Outperform

Halma P P 15.1 146% 35% 4.0 21% 5.3 2.4 7.2 -1.0 -1.0 2.9 419.5 Outperform

Aker Solutions P P 10.8 102% 29% 2.7 -10% -4.3 3.0 0.0 4.1 5.8 1.9 104.7 Outperform

Atlas Copco 'A' P P 14.7 127% 61% 7.1 120% 4.2 3.3 -3.0 -0.8 -1.3 2.9 167.6 Outperform

Amec P P 11.8 111% 19% 2.6 -17% 4.1 3.1 -3.5 -2.8 5.5 2.3 1,022.0 Outperform

Moneysupermarket

Com Gp.

P P 14.3 105% 34% 4.4 98% 5.4 3.7 -5.5 3.4 0.5 2.3 153.5 Outperform

Sabmiller P P 16.7 103% 50% 1.7 -11% 5.5 2.3 -13.5 0.5 0.8 2.6 2,633.0 Outperform

Hikma

Pharmaceuticals

P P 16.7 135% 25% 2.9 14% na 1.2 -14.4 -0.4 0.2 2.2 738.0 Outperform

Eutelsat

Communications

P P 15.0 108% 6% 3.1 7% 1.9 4.2 -18.2 -1.7 -0.1 2.3 23.6 Outperform

Petroleum Geo

Services

P P 11.6 110% -72% 2.1 -55% 2.8 1.4 -21.2 26.8 3.4 1.9 97.7 Outperform

Assa Abloy 'B' P P 14.7 127% -6% 3.5 5% 4.7 2.4 -24.1 -1.5 -1.7 2.9 231.9 Outperform

Deutsche Post P P 11.5 85% 42% 1.7 -19% 8.0 4.6 -26.5 0.1 1.1 1.9 15.3 Outperform

Coloplast 'B' P P 19.8 153% 24% 11.8 89% 4.3 1.4 -27.8 0.2 0.3 3.1 1,311.0 Outperform

Ryanair Holdings P P 13.2 98% -10% 2.0 -31% 9.6 8.8 -28.9 -3.2 -0.6 2.2 4.6 Outperform

Prudential P P 11.4 118% 7% 2.4 -18% 5.9 3.1 -33.8 0.6 1.4 2.2 880.0 Outperform

Kuehne+Nagel Intl. P P 20.3 151% 70% 5.7 66% 4.3 3.3 -36.7 -1.7 0.2 2.6 113.8 Outperform

Ictl.Htls.Gp. P P 15.7 94% 44% 8.1 -51% 6.1 2.6 -40.4 -1.1 0.1 2.6 1,650.0 Outperform

Easyjet P P 10.0 74% -12% 1.6 15% 7.1 1.9 -44.2 11.5 0.1 2.3 682.0 Outperform

Chr Hansen Holding P P 21.4 166% 45% 5.1 49% na 1.9 -50.4 2.0 0.5 2.7 187.3 Outperform

Share price,

local

currency (21

Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %Screening MethodologyConsensus

recommendation

(1=Buy; 5=Sell)

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

Of these, SAP, Sonova and WPP are highlighted by all three screening criteria and look

cheap on HOLT. The following stocks are cheap on P/E relatives and feature on at least

two of our growth screens: SAP, Sonova, WPP, Petroleum Geo, Assa Abloy, Ryanair,

Dufry, Capita, Swatch and EasyJet. Additionally, we can see almost all the names have

FCF above 4%.

Credit Suisse has set up a sector-neutral Delta One basket, CSERGROW, that offers

exposure to our preferred European growth names.

We show the corresponding screen for the US. Of these, Qualcomm, Google, Mead

Johnson Nutrition are highlighted by all three screening criteria as well as being cheap on

HOLT. Credit Suisse has also set up a sector-neutral Delta One basket for these US

growth names(CSUSGROW).

23 November 2012

Global Equity Strategy 14

Figure 26: US stocks highlighted as growth by two or more of our methodologies

Name Themes QuantsAnalyst

judgementAbs

rel to

Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Google 'A' P P P 15.0 110% -26% 3.8 -29% 5.9 0.0 35.1 -7.9 -3.1 1.9 665.9 Outperform

Mead Johnson

Nutrition

P P P 19.0 119% 18% -73.9 na 2.9 1.8 9.9 -2.8 -4.3 2.2 66.1 Outperform

Yum! Brands P P P 19.7 117% 62% 18.2 -22% 4.0 1.7 -31.5 -0.1 -0.7 2.0 73.5 Outperform

Salesforce.Com P P P 76.9 563% 16% 12.7 23% 2.6 0.0 -66.9 1.1 0.3 2.1 158.8 Outperform

Broadcom 'A' P P 11.1 79% -69% 2.6 -54% 7.0 1.3 110.3 -2.1 -1.6 1.8 31.2 Outperform

Qualcomm P P 14.3 138% -39% 3.7 -18% 5.5 1.6 93.1 -0.3 -0.4 1.9 62.1 Outperform

Emc P P 13.1 126% -47% 2.7 -40% 8.8 0.0 85.1 -2.4 -1.8 1.7 24.4 Outperform

Apple P P 11.2 107% -58% 7.0 116% 8.1 1.7 82.1 -10.7 -2.7 1.7 561.7 Outperform

Unitedhealth Gp. P P 10.2 79% -15% 2.1 -26% 11.2 1.4 61.7 5.3 -0.2 1.8 53.5 Outperform

Mastercard P P 18.6 137% 26% 10.2 44% 4.3 0.2 57.9 -0.5 -2.5 1.9 479.4 Outperform

Eli Lilly P P 13.1 105% -14% 4.2 -44% 7.8 4.0 54.8 2.2 -0.9 2.7 47.4 Outperform

Ihs 'A' P P 19.0 121% 8% 4.2 27% 5.0 0.0 54.7 -3.8 -3.2 2.2 89.2 Outperform

Teradata P P 20.1 147% 38% 7.1 40% 4.6 0.0 37.2 3.6 -1.7 2.1 61.2 Outperform

Priceline.Com P P 17.4 104% -34% 12.3 23% 4.7 0.0 34.1 -3.1 -4.3 2.1 639.6 Outperform

Allergan P P 19.5 157% 7% 5.3 -10% -4.8 0.2 31.1 0.3 -0.9 1.9 90.9 Outperform

Biogen Idec P P 19.2 116% -45% 5.2 10% 4.3 0.0 14.1 5.9 1.7 2.2 147.4 Outperform

Nielsen Holdings Nv P P 14.4 92% 17% 2.3 13% 5.8 0.0 3.5 2.9 -1.1 2.1 28.1 Outperform

Ralph Lauren Cl.A P P 18.6 119% 56% 4.1 63% 5.0 0.8 -2.5 -0.7 -1.4 2.4 156.5 Outperform

Rockwell

Automation

P P 13.6 117% 41% 6.1 73% 5.3 2.4 -3.8 -3.2 -2.7 2.2 77.4 Outperform

Dollar Tree P P 14.3 86% -5% 6.8 39% 4.3 0.0 -14.8 0.1 -0.9 2.3 41.5 Outperform

Amazon.Com P P 142.3 850% 163% 13.6 -58% 1.5 0.0 -18.1 -97.1 -1.9 2.0 238.0 Outperform

Vmware P P 27.7 203% -14% 7.9 -2% 4.8 0.0 -23.2 4.6 0.2 2.3 88.1 Outperform

Family Dollar Stores P P 15.1 90% 13% 5.9 70% 1.5 1.3 -35.8 2.5 2.5 2.4 68.8 Outperform

Las Vegas Sands P P 17.5 104% -44% 4.3 -35% 5.6 2.3 -38.7 -14.4 -5.4 2.1 43.7 Outperform

Starbucks P P 22.9 136% -9% 8.6 57% 2.7 1.2 -39.1 -5.3 -1.1 2.0 50.5 Outperform

Starwood Htls.&

Rsts. Worldwide

P P 19.8 118% 14% 3.4 41% 4.6 2.0 -45.4 4.9 0.1 2.2 52.6 Outperform

Heartware

International

P P -32.1 nm na 9.4 54% na 0.0 -63.5 nm 3.1 2.1 81.6 Outperform

Volcano P P 62.6 484% -11% 4.5 30% 0.8 0.0 -65.8 -16.7 -1.8 1.9 26.9 Outperform

Netsuite P P 208.0 1523% 171% 33.8 154% 0.9 0.0 -91.1 13.8 2.2 2.8 60.1 Outperform

Screening MethodologyConsensus

recommendation

(1=Buy; 5=Sell)

Share price,

local

currency (21

Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

23 November 2012

Global Equity Strategy 15

We discuss our three screening methodologies in more detail below:

1) Quant approach

a) Conventional growth. We screen for stocks with the following characteristics:

■ Above market median sales and EPS growth between 2007 and 2012;

■ Above market median projected sales and EPS growth between 2012 and 2014 on

Credit Suisse and consensus estimates;

■ Above average projected long-term consensus EPS growth;

■ Outperform-rated by Credit Suisse analysts.

In Europe, this highlights the following stocks in the screen below.

Figure 27: Outperform rated European growth stocks ranked by upside potential on HOLT

Stoxx 600 median 1% 10% 5% 4% 2% 10% 5% 5% 8.6

Company

2007-12 2012-14 2007-12 2012-14 2007-12 2012-14 2007-12 2012-14

Sap (Xet) 14% 15% 10% 11% 14% 15% 10% 11% 11.1 58 16.0 143% -14% 57.7 Outperform

Petrofac 23% 16% 22% 8% 29% 14% 22% 8% 14.4 56 11.5 103% -24% 1,574.0 Outperform

Sonova N 2% 19% 9% 9% 6% 13% 11% 8% 14.9 43 18.5 166% -5% 100.6 Outperform

Fresenius (Xet) 16% 14% 11% 9% 15% 11% 11% 8% 13.5 1 14.4 130% 3% 84.4 Outperform

Lvmh 9% 11% 11% 9% 11% 11% 11% 8% 10.9 -1 15.9 143% -2% 129.0 Outperform

Amec 24% 11% 12% 5% 24% 15% 11% 8% 15.7 -4 11.2 100% -15% 1,024.0 Outperform

Air Liquide 6% 10% 5% 10% 7% 10% 5% 7% 7.9 -7 16.2 146% 6% 93.4 Outperform

Experian 7% 12% 6% 7% 7% 14% 7% 9% 11.8 -7 17.5 157% 18% 1,025.0 Outperform

Fresenius Med.Care (Xet) 10% 14% 7% 8% 9% 11% 7% 8% 8.8 -11 16.5 148% 4% 51.5 Outperform

Burberry Group 16% 11% 17% 11% 21% 14% 18% 10% 10.3 -14 16.3 147% 4% 1,247.0 Outperform

Hikma Pharmaceuticals 42% 21% 20% 13% 9% 22% 20% 11% 20.3 -14 16.4 147% -5% 739.0 Outperform

Diageo 11% 13% 8% 6% 13% 12% 9% 7% 10.4 -15 16.7 150% 22% 1,848.5 Outperform

Adidas (Xet) 7% 13% 8% 7% 7% 18% 8% 7% 13.5 -18 14.1 127% 13% 64.8 Outperform

Intertek Group 22% 17% 22% 8% 21% 13% 22% 8% 14.6 -20 19.6 176% 30% 2,876.0 Outperform

Coloplast 'B' 22% 19% 7% 7% 34% 11% 6% 6% 14.1 -28 20.3 183% 13% 1,303.0 Outperform

Ryanair Holdings 6% 11% 14% 9% 6% 12% 16% 6% 9.8 -29 12.1 109% -19% 4.7 Outperform

Saipem 13% 13% 8% 6% 12% 13% 7% 6% 13.3 -34 12.9 116% -10% 32.7 Outperform

Easyjet 11% 10% 17% 5% 9% 11% 17% 6% 17.1 -44 10.0 90% -29% 692.0 Outperform

Sales CAGRRel

Share price,

local

currency

(20 Nov)

CS ratingHOLT price

to best (%)

Analyst estimates

EPS CAGR Sales CAGR

IBES estimates

EPS CAGRRel mkt,

devn from

average

Long-term

EPS growth

12m fwd PE

Abs

Source: MSCI, IBES, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

We show the same screen for the US.

Figure 28: Outperform rated US growth stocks ranked by upside potential on HOLT

S&P 500 median 5% 11% 5% 5% 6% 12% 5% 5% 10.3

Company

2007-12 2012-14 2007-12 2012-14 2007-12 2012-14 2007-12 2012-14

Microsoft 14% 14% 8% 12% 14% 12% 9% 8% 10.0 83 8.9 71% -35% 26.71 Outperform

Apple 62% 25% 45% 27% 66% 16% 52% 15% 20.5 82 10.2 82% -58% 561.15 Outperform

Prec.Castparts 14% 18% 6% 16% 17% 15% 9% 11% 14.2 62 15.8 127% 19% 176.76 Outperform

Mastercard 24% 17% 13% 12% 31% 17% 13% 12% 18.5 58 18.1 146% 1% 477.57 Outperform

Google 'A' 21% 18% 26% 19% 21% 18% 29% 19% 13.5 35 14.4 115% -38% 669.97 Outperform

Priceline.Com 50% 16% 30% 18% 50% 20% 30% 18% 19.9 34 17.1 137% -6% 635.58 Outperform

Allergan 14% 14% 8% 8% 14% 13% 8% 8% 12.5 31 19.1 153% -4% 91.15 Outperform

V F 12% 13% 9% 6% 12% 14% 9% 9% 13.0 19 14.1 113% 27% 157.57 Outperform

Cognizant Tech.Sltn.'A' 24% 18% 28% 17% 24% 15% 28% 15% 19.0 9 16.5 132% -32% 65.34 Outperform

Union Pacific 19% 13% 5% 7% 19% 14% 5% 7% 15.2 4 12.9 104% 2% 120.03 Outperform

Ralph Lauren Cl.A 12% 14% 10% 6% 16% 15% 11% 10% 14.0 -3 17.6 141% 21% 156.51 Outperform

O Reilly Automotive 23% 13% 20% 6% 23% 15% 20% 6% 16.6 -11 16.7 134% 10% 91.37 Outperform

Ww Grainger 16% 13% 7% 7% 16% 14% 7% 9% 15.2 -13 15.9 127% 9% 191.54 Outperform

Dollar Tree 27% 19% 11% 9% 32% 15% 13% 9% 19.0 -15 14.4 115% 5% 41.61 Outperform

Quanta Services 12% 20% 19% 9% 12% 18% 19% 9% 17.8 -16 15.8 127% -29% 25.14 Outperform

Yum! Brands 14% 15% 6% 8% 14% 14% 6% 10% 13.4 -31 19.7 158% 32% 72.39 Outperform

Family Dollar Stores 16% 17% 6% 11% 21% 16% 9% 9% 15.0 -36 15.0 121% 6% 68.89 Outperform

Starbucks 16% 26% 7% 13% 20% 21% 10% 12% 18.0 -39 21.7 174% -11% 50.05 Outperform

Salesforce.Com 38% 24% 35% 31% 46% 30% 44% 24% 27.0 -67 73.8 592% -23% 145.90 Outperform

CS ratingHOLT price

to best (%)

Analyst estimates

EPS CAGR Sales CAGR

IBES estimates

EPS CAGRRel mkt,

devn from

average

Long-term

EPS growth

12m fwd PE

Sales CAGRRel

Share price,

local

currency

(20 Nov)Abs

Source: MSCI, IBES, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

23 November 2012

Global Equity Strategy 16

We show the screen for non-Japan Asian stocks in the Appendix.

b) Quality growth. We incorporate HOLT’s eCAP metrics to screen for companies with:

■ CFROI above 8% for five consecutive years;

■ CFROI trend (no more than a 10% decline in CFROI in any one of the last five years);

■ 5-year asset growth above 5%;

■ Low CFROI volatility.

We highlight those stocks that also have asset turns in the top 40% of the market, since

higher asset turns has led to outperformance among our growth styles over the last

decade.

Figure 29: Outperform rated European quality growth stocks ranked by upside potential on HOLT; circled stocks have

asset turns in the top 40% of the market

NameCFROI Median - Five

Year

5-yr asset

growthAbs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Shire 17.3 14.9 13.0 105% -37% 4.9 26% 13.4 0.6 98.0 3.6 -0.5 1.9 1,759.0 Outperform

Imperial Tobacco Gp. 66.2 18.3 11.0 80% 26% 3.1 -90% 8.3 4.4 66.9 -1.4 -0.1 2.2 2,428.0 Outperform

Sap 19.7 7.5 16.5 121% -32% 5.4 -42% 3.6 1.5 58.2 -0.6 1.6 2.3 57.7 Outperform

Petrofac 29.3 19.3 12.3 116% 11% 7.1 27% -0.2 2.5 56.5 -0.7 -1.7 2.3 1,574.0 Outperform

Vivendi 14.8 8.0 8.0 66% -33% 1.1 -37% 11.2 6.3 56.2 -1.9 0.2 2.2 16.1 Outperform

Novartis 'R' 12.3 7.5 11.6 93% -11% 2.2 -26% 7.7 4.0 56.0 -3.1 -1.5 2.3 55.5 Outperform

Sonova N 23.7 7.7 18.3 142% -10% 4.4 -22% 4.3 1.4 42.8 0.7 0.2 2.4 100.6 Outperform

Smiths Group 18.0 7.7 10.9 94% 32% 4.3 -13% 3.6 3.6 25.1 -2.6 0.6 2.7 1,050.0 Outperform

Capita 42.0 5.9 13.2 84% -41% 8.6 -36% 4.8 3.2 17.5 0.7 1.0 2.7 719.0 Outperform

Wpp 25.6 5.7 10.5 76% -18% 1.5 -86% 8.8 3.4 7.8 -1.2 -1.8 2.0 814.0 Outperform

Fresenius 14.1 8.7 14.6 113% 9% 2.3 -22% 8.1 1.2 1.1 0.7 1.3 2.2 84.4 Outperform

Lvmh 12.6 9.1 16.4 105% 3% 2.9 -10% 4.1 2.3 -1.2 -1.2 1.8 2.0 129.0 Outperform

Atlas Copco 'A' 21.1 7.7 14.7 127% 61% 7.1 120% 4.2 3.3 -3.0 -0.8 -1.3 2.9 168.1 Outperform

Fresenius Med.Care 13.9 7.5 16.3 126% 2% 2.6 19% 4.5 1.4 -11.3 -1.9 -1.1 2.4 51.5 Outperform

Burberry Group 15.2 19.8 17.5 112% 35% 6.3 45% 4.4 2.1 -13.8 -6.2 -4.4 2.5 1,247.0 Outperform

Diageo 24.8 6.8 16.7 103% 47% 8.1 71% 4.2 2.5 -14.6 0.7 -1.5 2.1 1,848.5 Outperform

Eutelsat

Communications

10.8 7.9 15.0 108% 6% 3.1 7% 1.9 4.2 -18.2 -1.7 -0.1 2.3 23.1 Outperform

Intertek Group 20.4 20.0 19.9 127% 60% 8.8 -51% 3.0 1.4 -20.1 2.0 1.7 2.8 2,876.0 Outperform

Pearson 13.0 6.5 13.8 100% -7% 1.7 -58% 7.2 3.6 -21.5 -1.2 -0.1 2.8 1,196.0 Outperform

Pernod-Ricard 16.8 6.1 15.4 95% 46% 2.0 14% 4.3 1.9 -22.5 -2.7 0.4 2.7 85.0 Outperform

Assa Abloy 'B' 18.8 5.0 14.7 127% -6% 3.5 5% 4.7 2.4 -24.1 -1.5 -1.7 2.9 232.0 Outperform

Coloplast 'B' 12.0 6.1 19.8 153% 24% 11.8 89% 4.3 1.4 -27.8 0.2 0.3 3.1 1,303.0 Outperform

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(20 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

23 November 2012

Global Equity Strategy 17

Figure 30: Outperform rated US quality growth stocks with upside on HOLT, ranked by upside potential on HOLT;

circled stocks have asset turns in the top 40% of the market

NameCFROI Median - Five

Year 5-yr asset growth Abs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Broadcom 'A' 14.5 12.7 11.1 79% -69% 2.6 -54% 7.0 1.3 110.3 -2.1 -1.6 1.8 31.1 Outperform

Transdigm Group 41.5 23.3 17.4 151% 46% 8.5 126% 4.9 1.6 109.8 1.0 -0.2 2.3 131.1 Outperform

Freeport-Mcmor.Cpr.& Gd. 18.5 31.5 8.6 75% -28% 2.4 -90% 3.9 3.1 104.0 -7.3 -4.2 1.8 38.3 Outperform

F5 Networks 19.7 12.5 16.1 155% -51% 5.9 9% 6.5 0.0 96.8 -1.5 -0.6 2.2 87.5 Outperform

Qualcomm Inc 19.4 13.0 14.3 138% -39% 3.7 -18% 5.5 1.6 93.1 -0.3 -0.4 1.9 62.1 Outperform

Oracle Corp 25.4 20.6 11.3 83% -40% 3.5 -56% 8.5 0.8 86.7 -0.1 -1.7 2.1 30.2 Outperform

Emc 14.8 6.8 13.1 126% -47% 2.7 -40% 8.8 0.0 85.1 -2.4 -1.8 1.7 24.2 Outperform

Microsoft 27.6 12.1 9.7 71% -50% 3.7 -43% 11.3 2.9 83.1 -6.3 -1.2 1.9 26.7 Outperform

Deere 12.8 6.4 10.4 90% -6% 5.1 78% 4.7 2.0 68.6 -5.2 -2.3 2.4 86.0 Outperform

Check Point Sftw.Techs. 23.6 8.9 13.2 97% -33% 3.0 -58% 8.2 0.0 62.7 -0.6 -1.1 2.0 45.2 Outperform

Precision Castparts Corp 23.7 8.5 15.8 136% 45% 3.0 42% 4.5 0.1 61.8 -2.3 -1.6 1.9 176.8 Outperform

Unitedhealth Gp. 30.5 5.9 10.2 79% -15% 2.1 -26% 11.2 1.4 61.7 5.3 -0.2 1.8 53.1 Outperform

Mastercard 34.9 9.3 18.6 137% 26% 10.2 44% 4.3 0.2 57.9 -0.5 -2.5 1.9 477.6 Outperform

Eli Lilly 11.5 5.7 13.1 105% -14% 4.2 -44% 7.8 4.0 54.8 2.2 -0.9 2.7 47.2 Outperform

Ihs 'A' 48.8 10.3 19.0 121% 8% 4.2 27% 5.0 0.0 54.7 -3.8 -3.2 2.2 89.1 Outperform

General Dynamics 19.2 6.3 9.4 81% -12% 1.9 -25% 11.4 2.9 48.7 -1.6 -0.9 2.3 63.8 Outperform

Stryker Corp 13.6 9.3 12.3 95% -34% 2.6 -49% 6.3 1.6 40.2 -1.0 -0.7 2.2 53.6 Outperform

Thermo Fisher Scientific

Inc

25.7 7.3 11.5 79% -12% 1.5 -4% 6.6 0.8 38.9 1.3 0.3 1.7 61.8 Outperform

Stanley Black & Decker Inc 16.0 17.5 11.8 102% 12% 1.7 -37% 8.2 2.6 33.3 -6.6 -1.2 2.1 70.1 Outperform

Allergan 15.2 11.6 19.5 157% 7% 5.3 -10% -4.8 0.2 31.1 0.3 -0.9 1.9 91.2 Outperform

Bed Bath & Beyond 10.1 8.1 11.5 69% -38% 3.4 -33% 7.3 0.0 25.6 -1.0 0.3 2.1 58.5 Outperform

Parker-Hannifin Corp 14.3 5.1 11.8 102% 12% 2.4 23% 7.3 2.1 23.8 -20.8 -6.4 2.4 79.7 Outperform

Activision Blizzard 16.5 24.8 10.5 77% -39% 1.2 -86% 6.9 1.6 22.0 3.3 2.0 1.7 11.2 Outperform

Cvs Caremark 12.3 9.8 12.4 95% -7% 1.6 -36% 8.6 1.4 18.8 1.4 0.0 1.8 45.6 Outperform

V F 16.8 7.0 14.5 93% 53% 3.9 87% 4.4 1.9 18.8 1.1 -0.9 1.9 157.6 Outperform

Biogen Idec 16.9 8.7 19.2 116% -45% 5.2 10% 4.3 0.0 14.1 5.9 1.7 2.2 148.2 Outperform

Life Technologies 20.5 21.5 11.4 78% -36% 1.9 6% 8.4 0.0 13.9 -1.0 -1.1 2.2 48.9 Outperform

Merck & Co. 11.5 13.3 12.4 100% -1% 2.6 -55% 8.1 3.7 12.2 -0.4 -0.3 2.2 43.6 Outperform

Mead Johnson Nutrition 31.9 10.8 19.0 119% 18% -73.9 na 2.9 1.8 9.9 -2.8 -4.3 2.2 66.1 Outperform

Flowserve 14.9 7.9 13.4 116% 31% 3.3 42% 4.6 1.0 6.9 -1.4 -0.5 1.8 139.3 Outperform

Nielsen Holdings Nv 38.3 7.1 14.4 92% 17% 2.3 13% 5.8 0.0 3.5 2.9 -1.1 2.1 27.6 Outperform

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(20 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

We show the screen for Non-Japan Asian stocks in the Appendix.

23 November 2012

Global Equity Strategy 18

2) Analyst judgment

We have asked our analysts in Europe, the US and Japan to identify stocks with above-

market projected sales growth over the next five years (our threshold is 6% annual

growth), growth superior to the sector and translating into EPS growth of at least 8% p.a.

The details are in the Appendix, which shows two screens for each region (one with the

analysts’ top picks and the other highlighting those companies that trade on a P/E below

the market or have upside potential on HOLT).

European stocks

Of the stocks highlighted by our European analysts, the following are either cheap on

HOLT or on P/E relative to the market and have an outperform- or neutral-rating by Credit

Suisse analysts.

Figure 31: European growth stocks, as identified by our analysts, that look cheap on HOLT or on P/E relative

and rated Outperform or Neutral by our analysts

Name Abs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse rating

Aberdeen Asset Man. 13.2 130% 13% 3.7 63% 8.0 3.2 90.1 2.7 1.2 2.1 333.6 Outperform

Sberbank Of Russia 5.7 59% -23% 1.6 20% na 3.1 69.3 10.0 5.7 1.7 87.9 Outperform

SAP 16.5 121% -32% 5.4 -42% 3.6 1.5 58.2 -0.6 1.6 2.3 58.8 Outperform

Spectris 12.3 118% 21% 3.5 -68% 6.9 2.1 56.8 -2.3 -1.7 2.2 1,819.0 Outperform

Perform Group 24.7 179% 26% 0.2 58% na 0.0 48.4 0.5 1.6 1.8 397.0 Outperform

Sonova N 18.3 142% -10% 4.4 -22% 4.3 1.4 42.8 0.7 0.2 2.4 100.6 Outperform

Richemont 14.9 96% 133% 3.5 69% 3.0 1.1 25.4 5.2 2.9 2.4 68.6 Neutral

Rotork 19.5 169% 54% 9.0 80% 4.0 1.9 19.0 0.6 1.6 2.8 2,426.0 Outperform

Capita 13.2 84% -41% 8.6 -36% 4.8 3.2 17.5 0.7 1.0 2.7 722.5 Outperform

The Swatch Group 'B' 14.0 89% -52% 2.8 23% 4.0 1.7 9.0 1.8 0.9 2.3 432.2 Outperform

Paddy Power 20.8 124% 62% 12.0 99% 5.5 2.0 8.3 -0.2 3.3 2.9 57.3 Outperform

Johnson Matthey 13.7 107% 28% 3.2 40% na 2.5 8.0 -5.4 -4.2 2.6 2,190.0 Outperform

Wpp 10.5 76% -18% 1.5 -86% 8.8 3.4 7.8 -1.2 -1.8 2.0 825.0 Outperform

Halma 15.1 146% 35% 4.0 21% 5.3 2.4 7.2 -1.0 -1.0 2.9 419.5 Outperform

Compass Group 14.9 89% 28% 3.8 43% 4.8 3.1 3.5 -1.4 -0.3 2.5 699.5 Outperform

William Demant Hldg. 18.5 143% -5% 8.7 -64% 4.2 0.0 3.2 -6.5 -0.4 3.3 463.6 Neutral

Subsea 7 12.6 119% -25% 1.3 -46% 4.2 1.9 -4.4 10.5 -0.9 2.0 128.7 Neutral

Petroleum Geo Services 11.6 110% -72% 2.1 -55% 2.8 1.4 -21.2 26.8 3.4 1.9 97.7 Outperform

Vienna Insurance Group

A9.5 98% -23% 1.0 -54% 6.3 3.6 -21.2 -3.5 2.3 2.3 34.2 Neutral

Assa Abloy 'B' 14.7 127% -6% 3.5 5% 4.7 2.4 -24.1 -1.5 -1.7 2.9 231.9 Outperform

Ryanair Holdings 13.2 98% -10% 2.0 -31% 9.6 8.8 -28.9 -3.2 -0.6 2.2 4.6 Outperform

Easyjet 10.0 74% -12% 1.6 15% 7.1 1.9 -44.2 11.5 0.1 2.3 682.0 Outperform

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(21 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

US stocks

Of the stocks highlighted by our US analysts, the following are either cheap on HOLT or

on P/E relative to the market and have an Outperform or Neutral rating by Credit Suisse

analysts.

23 November 2012

Global Equity Strategy 19

Figure 32: US growth stocks, as identified by our analysts, that are cheap on HOLT or on P/E relative

and rated Outperform or Neutral by our analysts

Name Abs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Celgene 13.3 80% -72% 5.8 -60% 5.4 0.0 220.1 2.0 1.2 1.8 77.9 Neutral

Broadcom 'A' 11.1 79% -69% 2.6 -54% 7.0 1.3 110.3 -2.1 -1.6 1.8 31.2 Outperform

F5 Networks 16.1 155% -51% 5.9 9% 6.5 0.0 96.8 -1.5 -0.6 2.2 90.1 Outperform

Qualcomm 14.3 138% -39% 3.7 -18% 5.5 1.6 93.1 -0.3 -0.4 1.9 62.1 Outperform

Oracle 11.3 83% -40% 3.5 -56% 8.5 0.8 86.7 -0.1 -1.7 2.1 30.4 Outperform

Emc 13.1 126% -47% 2.7 -40% 8.8 0.0 85.1 -2.4 -1.8 1.7 24.4 Outperform

Apple 11.2 107% -58% 7.0 116% 8.1 1.7 82.1 -10.7 -2.7 1.7 561.7 Outperform

Gilead Sciences 15.5 93% -64% 7.5 6% 5.5 0.0 82.0 1.9 3.2 1.7 75.6 Neutral

Mellanox 19.2 185% 23% 7.2 162% 4.9 0.0 71.3 12.2 0.9 2.2 84.4 Neutral

Check Point Sftw.Techs. 13.2 97% -33% 3.0 -58% 8.2 0.0 62.7 -0.6 -1.1 2.0 45.5 Outperform

Mastercard 18.6 137% 26% 10.2 44% 4.3 0.2 57.9 -0.5 -2.5 1.9 479.4 Outperform

Danaher 15.0 130% 0% 2.1 -23% 7.8 0.2 56.6 -3.6 -2.2 1.8 53.0 Neutral

Ihs 'A' 19.0 121% 8% 4.2 27% 5.0 0.0 54.7 -3.8 -3.2 2.2 89.2 Outperform

Salix Pharms. 12.6 102% -71% 4.2 4% 4.7 0.0 37.9 10.7 -0.6 2.1 41.4 Outperform

Teradata 20.1 147% 38% 7.1 40% 4.6 0.0 37.2 3.6 -1.7 2.1 61.2 Outperform

Google 'A' 15.0 110% -26% 3.8 -29% 5.9 0.0 35.1 -7.9 -3.1 1.9 665.9 Outperform

Priceline.Com 17.4 104% -34% 12.3 23% 4.7 0.0 34.1 -3.1 -4.3 2.1 639.6 Outperform

Allergan 19.5 157% 7% 5.3 -10% -4.8 0.2 31.1 0.3 -0.9 1.9 90.9 Outperform

Biogen Idec 19.2 116% -45% 5.2 10% 4.3 0.0 14.1 5.9 1.7 2.2 147.4 Outperform

Mercadolibre 28.1 206% -17% 15.9 16% 3.0 0.5 11.2 4.4 -1.3 2.5 75.4 Neutral

Jazz Pharmaceuticals 9.9 80% -74% 11.9 -47% na 0.0 10.6 3.0 1.9 1.4 52.0 Outperform

Mead Johnson Nutrition 19.0 119% 18% -73.9 na 2.9 1.8 9.9 -2.8 -4.3 2.2 66.1 Outperform

Eog Res. 21.1 199% 27% 2.5 2% -4.4 0.6 6.4 12.4 2.0 1.9 118.1 Neutral

Watson Pharms. 10.8 87% -22% 3.1 28% 7.7 0.0 4.3 1.3 2.4 1.8 85.3 Outperform

Nielsen Holdings Nv 14.4 92% 17% 2.3 13% 5.8 0.0 3.5 2.9 -1.1 2.1 28.1 Outperform

Visa 'A' 19.4 142% 32% 4.4 75% 4.4 0.7 1.5 3.3 1.0 1.9 146.7 Outperform

Hexcel 14.2 123% -40% 3.1 -75% -1.7 0.0 -4.0 2.8 -1.7 2.1 25.1 Outperform

Carmax 17.8 106% -31% 3.0 43% 1.9 0.0 -14.1 -2.5 0.4 1.9 34.6 Outperform

Dollar Tree 14.3 86% -5% 6.8 39% 4.3 0.0 -14.8 0.1 -0.9 2.3 41.5 Outperform

Noble Energy 15.5 146% -13% 2.3 11% -6.1 0.9 -15.0 -16.7 -4.9 2.0 95.3 Outperform

Linear Tech. 17.4 124% -16% 10.1 -35% 7.3 3.1 -19.2 -18.0 -9.0 2.7 31.9 Outperform

Anadarko Petroleum 16.8 158% -26% 1.9 -2% 2.4 0.5 -19.9 -3.5 -3.1 1.6 72.5 Outperform

Vmware 27.7 203% -14% 7.9 -2% 4.8 0.0 -23.2 4.6 0.2 2.3 88.1 Outperform

Zumiez 12.1 72% -46% 2.4 -40% 3.6 0.0 -25.1 -5.4 -0.9 2.3 20.3 Neutral

Las Vegas Sands 17.5 104% -44% 4.3 -35% 5.6 2.3 -38.7 -14.4 -5.4 2.1 43.7 Outperform

Starbucks 22.9 136% -9% 8.6 57% 2.7 1.2 -39.1 -5.3 -1.1 2.0 50.5 Outperform

Chipotle Mexn.Grill 25.6 153% -5% 7.9 45% 2.9 0.0 -40.0 0.0 -1.6 2.6 275.5 Neutral

Fusion-Io 50.1 482% -19% 4.9 -1% 0.3 0.0 -63.6 47.1 9.3 2.4 24.1 Outperform

Volcano 62.6 484% -11% 4.5 30% 0.8 0.0 -65.8 -16.7 -1.8 1.9 26.9 Outperform

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(21 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

We show the full list of companies highlighted by our analysts as growth stocks in Europe

and the US in the screens in the Appendix.

23 November 2012

Global Equity Strategy 20

3) Thematic approach

We highlight our preferred stocks on our preferred growth themes, which are:

(1) Branded GEM consumer plays

(2) Industrial automation

(3) Global trade

(4) Emerging markets travel

(5) Water

(6) Underleveraged banks in underleveraged countries

(7) Oilfield services

(8) Energy efficiency

(9) Reducing auto emissions

(10) Specific plays on the internet, especially the provision of e-financial services.

(11) Ageing in emerging markets

(12) Software

European stocks

We highlight European companies that are exposed to our favoured growth themes, that

are Outperform-rated by our analysts, and offer value (in terms of either P/E relatives, FCF

yield above 5% or potential upside on HOLT).

Figure 33: Top European plays on our favoured growth themes, that are Outperform-rated by our analysts and that offer

value (i.e. either look cheap on P/E relatives, have a FCF yield above 5% or look cheap on HOLT)

Name Abs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Dufry 'R' 10.5 63% -7% 3.7 46% 9.2 0.0 67.9 -2.9 -0.8 2.0 124.3 Outperform

SAP 16.5 121% -32% 5.4 -42% 3.6 1.5 58.2 -0.6 1.6 2.3 58.8 Outperform

Petrofac 12.3 116% 11% 7.1 27% -0.2 2.5 56.5 -0.7 -1.7 2.3 1,590.0 Outperform

Sonova N 18.3 142% -10% 4.4 -22% 4.3 1.4 42.8 0.7 0.2 2.4 100.6 Outperform

Rotork 19.5 169% 54% 9.0 80% 4.0 1.9 19.0 0.6 1.6 2.8 2,426.0 Outperform

The Swatch Group 'B' 14.0 89% -52% 2.8 23% 4.0 1.7 9.0 1.8 0.9 2.3 432.2 Outperform

Wpp 10.5 76% -18% 1.5 -86% 8.8 3.4 7.8 -1.2 -1.8 2.0 825.0 Outperform

Halma 15.1 146% 35% 4.0 21% 5.3 2.4 7.2 -1.0 -1.0 2.9 419.5 Outperform

Moneysupermarket Com Gp. 14.3 105% 34% 4.4 98% 5.4 3.7 -5.5 3.4 0.5 2.3 153.5 Outperform

Sabmiller 16.7 103% 50% 1.7 -11% 5.5 2.3 -13.5 0.5 0.8 2.6 2,633.0 Outperform

Petroleum Geo Services 11.6 110% -72% 2.1 -55% 2.8 1.4 -21.2 26.8 3.4 1.9 97.7 Outperform

Deutsche Post 11.5 85% 42% 1.7 -19% 8.0 4.6 -26.5 0.1 1.1 1.9 15.3 Outperform

Saipem 14.2 133% 18% 3.3 28% 6.2 2.1 -33.6 -2.9 1.5 2.1 32.5 Outperform

Prudential 11.4 118% 7% 2.4 -18% 5.9 3.1 -33.8 0.6 1.4 2.2 880.0 Outperform

Ictl.Htls.Gp. 15.7 94% 44% 8.1 -51% 6.1 2.6 -40.4 -1.1 0.1 2.6 1,650.0 Outperform

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(21 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

US stocks

We show the corresponding screen for the US in the screen below.

23 November 2012

Global Equity Strategy 21

Figure 34: Top US plays on our favoured growth themes, that are Outperform-rated by our analysts and that offer value

(i.e. either look cheap on P/E relatives, have a FCF yield above 5% or look cheap on HOLT)

Name Abs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Oracle 11.3 83% -40% 3.5 -56% 8.5 0.8 86.7 -0.1 -1.7 2.1 30.4 Outperform

Cigna 8.6 67% 5% 2.0 3% 13.2 0.1 63.2 3.9 -3.5 1.9 52.0 Outperform

Unitedhealth Gp. 10.2 79% -15% 2.1 -26% 11.2 1.4 61.7 5.3 -0.2 1.8 53.5 Outperform

Eli Lilly 13.1 105% -14% 4.2 -44% 7.8 4.0 54.8 2.2 -0.9 2.7 47.4 Outperform

Halliburton 10.5 99% -27% 2.2 -31% -2.2 1.1 38.6 -6.1 0.2 1.9 31.7 Outperform

Google 'A' 15.0 110% -26% 3.8 -29% 5.9 0.0 35.1 -7.9 -3.1 1.9 665.9 Outperform

Emerson Electric 13.6 118% 2% 3.5 2% 7.1 3.2 16.3 -1.5 -2.0 2.3 48.6 Outperform

Mead Johnson Nutrition 19.0 119% 18% -73.9 na 2.9 1.8 9.9 -2.8 -4.3 2.2 66.1 Outperform

Mindray Med.Intl.Spn. Adr.'A'

1:117.1 118% -5% 3.4 -29% na 1.2 8.2 2.6 1.2 2.1 33.8 Outperform

Johnson Controls 9.4 117% -5% 1.6 -12% 9.4 2.6 1.9 -11.8 -4.3 2.5 26.8 Outperform

Rockwell Automation 13.6 117% 41% 6.1 73% 5.3 2.4 -3.8 -3.2 -2.7 2.2 77.4 Outperform

United Parcel Ser.'B' 14.5 107% -7% 10.1 62% 6.3 3.1 -6.1 -4.9 -2.8 2.3 71.4 Outperform

Vmware 27.7 203% -14% 7.9 -2% 4.8 0.0 -23.2 4.6 0.2 2.3 88.1 Outperform

Las Vegas Sands 17.5 104% -44% 4.3 -35% 5.6 2.3 -38.7 -14.4 -5.4 2.1 43.7 Outperform

Volcano 62.6 484% -11% 4.5 30% 0.8 0.0 -65.8 -16.7 -1.8 1.9 26.9 Outperform

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(21 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse research

We consider each theme in more detail.

23 November 2012

Global Equity Strategy 22

Growth themes 1) Branded GEM consumer plays

In our view, the GEM consumer story remains simple and compelling. We have been

overweight this theme for now five years!

The BRIC consumer share of GDP remains abnormally low and the Chinese consumer

share of GDP is still just half that of the US and Japan.

Figure 35: Emerging markets have a low consumption

share of GDP

Figure 36: In particular, China’s consumption share of

GDP is less than half the US levels

40%

45%

50%

55%

60%

65%

1997 2000 2003 2006 2009 2012

G7 consumption share of GDP

BRIC consumption share of GDP

Consumption, Share of GDP

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

1995 1996 1998 1999 2000 2002 2003 2005 2006 2007 2009 2010 2012

China United States

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

We think that the consumer share of GEM GDP is set to rise, partly as a result of

currency appreciation and partly on account of policy. Discretionary consumption looks set

to rise faster than total consumption (with on average a third of income in emerging

markets being spent on non-discretionary items, according to the World Bank). Hence,

under our central case, discretionary consumption will be 9% in real terms and just under

14% in nominal terms (with a currency that near term is unlikely to depreciate).

Figure 37: If China grows by 7% per year in real terms between now and 2020, then consumption would likely grow by

10%, and discretionary spending by 13%

GDP

2011 15y max

Brazil 3.5% 60% 65% 4.3% 64% 65% 4.6% 9.1%

China 7.0% 32% 42% 10.1% 52% 65% 12.5% 15.5%

India 6.5% 57% 65% 7.8% 55% 60% 8.7% 12.8%

Russia 3.0% 50% 56% 4.1% 59% 65% 5.2% 11.7%

BRIC 6.1% 43% 50% 7.9% 56% 64% 9.2% 13.7%

Developed

countries2.4% 65% 74%

Implied

nominal growth

CountryConsumption share of GDP

Consumption

Implied real

growth

Implied real

growth 2007 2020E

Real trend

growth

Discretionary consumption (% of total)

Source: Thomson Reuters, Credit Suisse research

23 November 2012

Global Equity Strategy 23

When GDP per capita in the developed world was at the same level as it is in the

emerging markets currently, real consumption growth averaged nearly 5%, with the

highest growth being in communication, transport and education.

Figure 38: Current GDP pc in GEM is $7,000. When France, US and Japan had GDP pc at

this level, the highest growth was seen in communication, transport and education

4.6%

10.4%9.7%

7.2%6.8%

6.2% 6.2%

5.4%4.6% 4.3%

3.0%

0%

2%

4%

6%

8%

10%

12%

PC

E

Com

mun

icat

ion

Tra

nspo

rtat

ion

Edu

catio

n

Rec

reat

ion

Hou

sing

Fin

anci

al s

ervs

Hea

lthca

re

Hse

hld

& P

ers

Goo

ds Util

ities

Foo

d &

bev

Ave

rage

ann

ual g

row

th in

rea

l ter

ms

as G

DP

per

cap

ita

rises

from

c.U

S$7

,400

to U

S$9

,800

in th

e U

S, J

apan

an

d F

ranc

e

Source: Credit Suisse research

The key drivers of GEM consumption are higher wage growth (compounding at c.10% p.a)

and a fall in the savings ratio. In the case of China, the savings ratio is still c.40%. This is

set to fall, as there are moves towards a more state-sponsored social security system that

diminishes the need for individuals to save for old age or ill health.

We can see the resilience of the consumer if we look at the example of Chinese exports to

the US (which seem to follow ISM) against Chinese retail sales, which have clearly

decoupled.

Figure 39: Chinese retail sales are decoupling from those

in the US…

Figure 40: …while Asian exports have followed the US

cycle

-11%

-6%

-1%

4%

9%

14%

19%

24%

2002 2004 2006 2008 2010 2012

US

China

Retail sales yoy, 3mma

15

25

35

45

55

65

75

-30

-20

-10

0

10

20

30

40

50

1992 1996 2000 2004 2008 2012

Asian exports to US, yoy, 3mma, 6m lag

US ISM new orders, rhs

Source: Thomson Reuters, Credit Suisse research Source: Thomson Reuters, Credit Suisse research

23 November 2012

Global Equity Strategy 24

Finally, we believe currency appreciation is likely in many of the emerging markets.

This is largely driven by increased QE in the developed world. This in turn drives money to

those regions where there is an interest and a growth premium as well as undervalued

currencies. This points to the emerging markets. Currency appreciation helps the

consumer at the expense of exporters (the price of exports rises, while the price of imports

falls and thus discretionary consumption growth improves). This is also critical because in

recent years as we can see below the currencies have been a modest headwind.

Figure 41: Changes in EM currencies against the Euro

Source: Company data, Credit Suisse estimates

Indirect plays

Over the past five years, the emerging market business of the indirect plays (using food

producers and household products sector) has grown at 10% a year. This is growth!

Figure 42: Average emerging markets growth for the food producers and household

products companies* (quarterly 2007-2012) is close to 10%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Source: Company data, Credit Suisse Consumer Staples Research Team. *Average Emerging Markets

growth based on Nestle, Unilever, Henkel, Kraft, Coke, Colgate, L’Oreal, Danone, Reckitt

23 November 2012

Global Equity Strategy 25

For the indirect plays we look at stocks with above–market projected average sales growth

over the next five years (our threshold is 6% annual growth), with growth superior to the

sector, translating into EPS growth of at least 8% p.a, and which our analysts believe are

growth. We also want these stocks to have at least 20% of revenues from GEM. This

highlights the following companies:

Figure 43: European stocks that are plays on the emerging markets consumer with at least 20% of revenues from GEM,

that our analysts identified as Growth

Name% Sales from

GEM

% Sales from

NJA

% Sales from

ChinaAbs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse rating

Sabmiller 71% 8% n.a 16.7 103% 50% 1.7 -11% 5.5 2.3 -13.5 0.5 0.8 2.6 2,633.0 Outperform

Prudential 60% 60% n.a 11.4 118% 7% 2.4 -18% 5.9 3.1 -33.8 0.6 1.4 2.2 880.0 Outperform

The Swatch Group 'B' 50% 47% 37% 14.0 89% -52% 2.8 23% 4.0 1.7 9.0 1.8 0.9 2.3 432.2 Outperform

Diageo 45% 13% n.a 16.7 103% 47% 8.1 71% 4.2 2.5 -14.6 0.7 -1.5 2.1 1,846.0 Outperform

Pernod-Ricard 45% 27% n.a 15.4 95% 46% 2.0 14% 4.3 1.9 -22.5 -2.7 0.4 2.7 84.9 Outperform

Richemont 41% 34% 26% 14.9 96% 133% 3.5 69% 3.0 1.1 25.4 5.2 2.9 2.4 68.6 Neutral

Chr Hansen Holding 40% 10% 2% 21.4 166% 45% 5.1 49% na 1.9 -50.4 2.0 0.5 2.7 187.3 Outperform

Lvmh 35% 23% 14% 16.4 105% 3% 2.9 -10% 4.1 2.3 -1.2 -1.2 1.8 2.0 129.0 Outperform

Burberry Group 30% na n.a 17.5 112% 35% 6.3 45% 4.4 2.1 -13.8 -6.2 -4.4 2.5 1,233.0 Outperform

Wpp 25% 11% 6% 10.5 76% -18% 1.5 -86% 8.8 3.4 7.8 -1.2 -1.8 2.0 825.0 Outperform

Boss (Hugo) 17% 7% 7% 15.4 99% 29% 10.9 137% 4.1 4.1 -18.8 -4.5 0.0 2.0 79.2 Neutral

Consensus

recommendation

(1=Buy; 5=Sell)

Share price, local

currency (21 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse estimates

Of these, the following look cheap on HOLT or have an FCF yield above 5%: SAB Miller,

Swatch, Richemont, and WPP.

We show the same screen for the US below. Of these, the following look cheap on HOLT

or have an FCF yield above 5%: Las Vegas Sands, and Mead Johnson.

Figure 44: US stocks that are plays on the emerging markets consumer with at least 20% of revenues from GEM, that

our analysts identified as Growth

Name% Sales from

GEM

% Sales from

NJA

% Sales from

ChinaAbs rel to Industry

rel to mkt %

above/below

average

Abs

rel to mkt %

above/below

average

FCY DY

Price, %

change to

best

3m EPS 3m Sales Credit Suisse

rating

Las Vegas Sands 73% 73% 73% 17.5 104% -44% 4.3 -35% 5.6 2.3 -38.7 -14.4 -5.4 2.1 43.4 Outperform

Mead Johnson Nutrition 58% na n.a 19.0 119% 18% -73.9 na 2.9 1.8 9.9 -2.8 -4.3 2.2 66.8 Outperform

Yum! Brands 32% 32% 21% 19.7 117% 62% 18.2 -22% 4.0 1.7 -31.5 -0.1 -0.7 2.0 73.3 Outperform

Nike 'B' 24% 14% 9% 16.9 108% 23% 4.2 22% 5.4 1.5 -11.2 1.3 -0.4 2.4 96.3 Neutral

Consensus

recommendation

(1=Buy; 5=Sell)

Share price,

local currency

(21 Nov)

-----P/E (12m fwd) ------ 2012e Momentum, %------ P/B ------- HOLT2012e, %

Source: MSCI, IBES, Factset, Thomson Reuters, Credit Suisse HOLT, Credit Suisse estimates

There are three particular areas we would highlight as plays on the GEM consumer:

■ SAB Miller: the 2013E FCF yield is 5.5% (on our analyst’s calculations); yet we see

long-term sales growth of c7% and EPS growth potential of close to 13% CAGR. In its

core growth markets of Latam and Africa, SAB has strong positions with an average

market share of around 90% and 70%, respectively. According to our analyst, Sanjeet

Aujla, its future growth is driven by its own pace of category development and

penetration, and is less at risk from competitive threats affecting other businesses

given high barriers to entry in these markets. As our analyst points out, the percentage

of income spent on beer rises until GDP per capita hits c$20K (implying that in this

case beer volumes should grow at a higher rate than GDP). SAB has a wide set of

price points and, thus, is able to exploit the premium beer market and at the low end.

Its price points are increasingly competitive against the informal alcohol sector,

according to our analyst.

We can see from the charts below that beer and international spirits per capita

consumption tends to go up as GDP per capita rises.

23 November 2012

Global Equity Strategy 26

Figure 45: Beer per capita consumption goes up as GDP

per capita rises…

Figure 46: …and so does international spirits per capita

consumption

R² = 0.3789

0

20

40

60

80

100

120

140

160

0 20000 40000 60000 80000 100000

GDP per capita

PC

C

R² = 0.3243

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0 20000 40000 60000 80000 100000

GDP per capita

PC

C

Source: Company data, Credit Suisse Consumer Staples Research

team

Source: Company data, Credit Suisse Consumer Staples Research

team

■ Diageo: the world leader in international premium spirits. Within a growing global

spirits market, premium end offers the fastest growth at the expense of local cheap

liquor, according to our analyst Charlie Mills. 45% of Diageo sales come from

emerging markets.

■ Swatch: more than Richemont, it tends to sell into wholesale channels, which offer

less advantageous pricing than retailers. Yet, on a tactical basis, our analysts see the

medium-price segment in Asia holding up better than the high-end segment. Strong

tourist purchases in Europe should be a key mitigating factor. Swatch looks well

placed to capitalise on the stabilisation of macro indicators in China, which accounts

for about 35% of group sales. In the medium term, its best-in-class supply chain

capabilities and gradual reduction in supply of movements (i.e. watch parts) to external

parties should result in lower investment requirements than peers to support growth of

mechanical watches for brands such as Longines or Tissot. Its balance sheet remains

strong and valuation is among the cheapest in the European luxury space, according

to our analyst Rogerio Fujimori. Its FCF yield is well above its peers’.

Figure 47: Swiss watch survey is improving yoy Figure 48: HK watch & jewellery sales appear to have

troughed

-100

-80

-60

-40

-20

0

20

40

60

80

100

-40%

-20%

0%

20%

40%

60%

80%

1998 2000 2002 2004 2006 2008 2010 2012

Swatch price relative (euros), y/y%

Swiss watch manufacturers survey,Production compared to prev. year, rhs

-40%

-20%

0%

20%

40%

60%

80%

100%

-20%

-10%

0%

10%

20%

30%

40%

50%

2006 2007 2008 2009 2010 2011 2012

HK watch and jewellery volume sales, y/y%

Swatch price relative (euros), y/y%

Source: Company data, Credit Suisse Luxury Goods Research Team Source: Company data, Credit Suisse Luxury Goods Research team

23 November 2012

Global Equity Strategy 27

Clearly, there is an issue of valuation in absolute terms – but we would point out that, on a

sum of the parts basis, the indirect GEM plays look attractively valued relative to the direct

plays.

Figure 49: Developed market consumer stocks with emerging market exposure are trading cheaply relative to their foreign-listed subsidiaries

Source: Company data, Credit Suisse estimates

23 November 2012

Global Equity Strategy 28

2) Industrial Automation

We believe there are four main drivers of this theme:

a) Rising wage pressures in emerging markets

Strong wage pressure in emerging markets means that their cost advantage is shrinking

and the incentives for automation in both developed and developing countries are

increasing.

Figure 50: Dwindling Supply of Manual Labor (China) Figure 51: Hourly Manufacturing Labor Costs in China)

-80

-60

-40

-20

0

20

40

60

80

100

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Mill

ion

pers

ons Population aged between 15-19 minus population

aged between 50- 54 and new college students.

10%

12%

14%

16%

18%

20%

22%

24%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

China: hourly manufacturing wage growth, yoy

Source: Company data, Credit Suisse China Strategy Team Source: Credit Suisse US Capital Goods team,

Credit Suisse research

China in particular seems to have hit a ‘Lewis Turning Point’, which is the point at which

the excess low cost labour force is exhausted, leading to increased wage inflation. The 19-

24 year old age group is peaking this year, with the broader labour force estimated to peak

in 2015. A rise in social security related costs is also likely to happen over time (the costs

falling probably on the employer) again raising the relative cost of labour.

Company comments about Asian labour price inflation have proliferated, with ITW, Metso

and NTN recently flagging increased wage inflation, according to our European Capital

Goods team.

Figure 52: After hitting the ‘Lewis Turning Point’, other Asian export-led countries

experienced higher inflation and lower trend growth (but still good growth)

Japan

(1960-1972)

Korea

(1982-96)

China

(1997-2009)

GDP: Average 8.9% 8.5% 9.6%

CPI: Average 5.6% 5.2% 1.3%

CPI: Maximum 13.1% 11.1% 4.8%

CPI: Minimum 3.6% 2.3% -1.5%

Source: Company data, Credit Suisse research, Credit Suisse US Capital Goods team

b) Robot density in emerging markets is low

The robot density (industrial robots per manufacturing employees) in emerging markets is

only a fraction of the penetration seen in developed economies. In emerging markets

(which account for 50% of global manufacturing output), there are only 7 industrial robots

per 10,000 manufacturing employees, against 149 for the developed markets, or just 5%

of the density of developed markets. Non-Japan Asia accounts for 35% of the world’s

manufacturing output, but only has a robot density of 11.

23 November 2012

Global Equity Strategy 29

Figure 53: Robot density for select countries (2011),

Robots per 10,000 manufacturing employees

Figure 54: Robot density by region (2002 vs. 2011),

Robots per 10,000 manufacturing employees

Country

Employees

(mn)

Output

($bn)

Output per head

($)

Robot

Density

U.S. 14 1,732 121,931 130

China 99 1,612 16,281 7

Point

China has

7x as many

manufacturing

workers

China and

the U.S. produce

the same

output

US has 7.5x

higher output

per head

US has 18.5x the

number

of robots

per head

Source: Company data, Credit Suisse US Capital Goods team Source: Company data, Credit Suisse US Capital Goods team

There is already evidence of an accelerating move towards automation even among

emerging markets companies that have long benefited from the abundant supply of cheap

labour. Foxconn, for example, one of the world’s largest maker of electronic components,

has recently announced that it would replace a part of its 1m workforce with robots (New

York Times, 18 August 2012). This suggests to us that automation may be at an inflection

point in China.

Figure 55: The industrial robot density ‘S’ curve

(base year = 1974 for Japan, 1999 for China)

Robots per 10,000 manufacturing employees

Figure 56: The automated machine tool ‘S’ curve

(Share of Machine Tools Shipped with Numerical

Controls); (base year = 1970 for Japan, 2000 for China)

0

50

100

150

200

250

300

350

T+0 T+3 T+6 T+9 T+12 T+15 T+18 T+21 T+24 T+27 T+30 T+33

Japan Robot Density

China Robot Density

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

T+0 T+3 T+6 T+9 T+12 T+15 T+18 T+21 T+24 T+27 T+30 T+33

Japan China

Source: Company data, Credit Suisse Capital Goods team Source: Company data, Credit Suisse estimates, Credit Suisse

Capital Goods team

23 November 2012

Global Equity Strategy 30

c) Reduced outsourcing in developed markets leads to more automation in