Embed Size (px)

Citation preview

1

UNDERGRADUATES

SCHOOL OF BUSINESS SCIENCES AND MANAGEMENT

B.TECH (HONOURS) DEGREE IN FINANCIAL ENGINEERING

HIT: 200

DISSERTATION: 2013

Research Topic: Impact of Liquidity risk on Banks’ Solvency in Zimbabwe,

during the period of 2009 - 2012.

DISSERTATION

BY

NAMES: SURNAMES: REG NO.

NYASHA .J. MUGOMBA H1110545P

PETER SHARARA H1110360M

EPHRAIM .T. CHIKWAWA H1110405F

SHINGIRAYI MUSHAYI H1010647N

Submitted in partial fulfilment of a Bachelor of Technology (Honours) Degree in Financial

Engineering

2

HARARE INSTITUTE OF TECHNOLOGY

RELEASE FORM

Authors: Nyasha .J. Mugomba

Peter Sharara

Ephraim .T. Chikwawa

Shingirayi Mushayi

Title of Thesis: Impact of Liquidity Risk on Banks’ Solvency in Zimbabwe, during

the period of 2009-2012.

DegreeProgram

which Thesis was

presented: Bachelor of Technology (Honors) Degree in Financial Engineering

Year Degree was granted: Part (2): 2013

Permission is hereby granted to the Harare Institute of Technology

(HIT) Library to reproduce copies of this document and to lend

such copies only for scholarly purposes or scientific research

purposes only. The authors reserve other publication rights and

neither whole nor extensive extracts from it may be printed or

reproduced without the author’s prior written permission.

Signed by: Mugomba N.J., Sharara P., Chikwawa E., and Mushayi S.

Date:…………..........

Permanent Address: Harare Institute of Technology P.O. Box BE 277 Ganges Road,

Belvedere, Harare

3

HARARE INSTITUTE OF TECHNOLOGY

APPROVAL FORM

The undersigned certify that they have read and recommend for acceptance, a

dissertation entitled “Impact of Liquidity Risk on Banks’ Solvency in Zimbabwe”,

during the period (2009-2012) submitted by Nyasha .J. Mugomba, Peter Sharara ,

Ephraim.T. Chikwawa and Shingirayi Mushayi, in Partial Fulfillment of the

Requirements of the Bachelor of Technology (Honors) Degree in Financial

Engineering with the Harare Institute of Technology.

…………………………………………………………………………….

Supervisor

………………………………………………………………………………..

Program Coordinator

…………………………………………………………………………………

Date

……………………………………………….……………………………

4

DECLARATION

We do hereby declare that this dissertation is the result of our own research, except to

the extent indicated in the Acknowledgements and References and by acknowledged

sources in the body of the research, and that it has not been submitted in part or full for

any other degree to any other University or College.

NAMES: SURNAMES: SIGNATURE: DATE:

Nyasha .J. Mugomba …..………………... .……………..

Peter Sharara …………………….. …..………….

Ephraim .T. Chikwawa. .…………………… ...……………

Shingirayi Mushayi …...………………… ………………

5

Abstract

The purpose of this paper is to examine liquidity risk in Zimbabwean banks and evaluate

the impact on bank solvency. Data are retrieved from the balance sheets, income

statements and notes of 12 commercial banks in Zimbabwe during 2009-2012. Multiple

regressions are applied to assess the impact of liquidity risk on bank solvency. The results

of multiple regressions show that liquidity risk affects bank solvency insignificantly, with

liquidity gap, capital risk and non-performing loans as the two factors exacerbating the

bank solvency. They have a positive relationship with bank solvency. The period studied

in this paper is 2009-2012, due to availability of the data and introduction of

multicurrency system in February 2009. However, the sample period does not impair the

findings since the sample includes 12 banks, which constitute the main part of the

Zimbabwean banking system. Moreover, only shareholders’ equity to total liabilities and

off-balance sheet events is used as the measure of bank solvency. Economic factors

contributing to liquidity risk are not covered in this paper. This is the first paper

addressing the liquidity risk faced by the Zimbabwean banking system. Past researchers

and practitioners have not given the proper attention to liquidity risk. This paper helps in

understanding the factors of bank specific, macroeconomic variables and their impact on

the solvency of the banking system. The authors emphasize contemporary risk managers

to mitigate liquidity risk by having sufficient cash resources. This will reduce the

liquidity gap, thereby reducing the dependence on stock market.

Keywords: Zimbabwe, Bank solvency, Banks, Risk management, Liquidity risk, Non-

performing loans, Liquidity gap,

Paper type: Research paper

6

ACKNOWLEDGEMENTS

We would like to extend our sincere gratitude to our Supervisor, Mr. J Muvingi for

giving us guidance and direction during our research. Without his invaluable

contribution, this research would not have been possible.

We are also indebted to a number of people who, through their unwavering support and

resourcefulness, ensured we were able to successfully complete this research. we wish to

acknowledge the support we got from members of staff at News day and Herald Their

support, guidance, teamwork and co-operation knew no boundaries and indeed priceless.

We also acknowledge the assertiveness and professionalism of all our peers and

supervisors within the institution which has helped us realize the yet to be tapped

potential and certainly put us on course to bring the best out of us.

We are proud to be associated with the HARARE INSTITUTE OF TECHNOLOGY

(HIT), teaching and non-teaching staff whose enthusiastic approach has seen the

continued ascent of the University into a major player in the country’s institutions of

higher education. We are humbled by the level of commitment the lecturers in the

Department of Financial Engineering displayed.

Table of Contents

DECLARATION ....................................................................................................... 4 THE ABSTRACT ..................................................................................................... 5

ACKNOWLEDGEMENTS ....................................................................................... 6 List of Tables............................................................................................................. 9

ABBREVIATIONS ................................................................................................... 9 CHAPTER 1 .......................................................................................................... 10

1.0 Introduction ....................................................................................................... 10 1.1 Background ....................................................................................................... 10

1.2 Problem statement ............................................................................................. 13 1.3 Research objectives............................................................................................ 13

1.4 Research questions............................................................................................. 13 1.5 Research Hypothesis .......................................................................................... 13

1.6 Significance of the Study ................................................................................... 14 1.7 Assumptions ...................................................................................................... 14

1.8 Scope of the Study ............................................................................................. 14 1.9 Limitation of the Study ...................................................................................... 14

7

1.10 Summary.. ....................................................................................................... 15 CHAPTER2.....................................................................................................................

2.0 LITERATURE REVIEW................................................................................... 16 2.1 Introduction ....................................................................................................... 16

2.2 Definition of key Variables ................................................................................ 16 2.2.1 Bank Solvency ................................................................................................ 16

2.2.2. Liquidity Risk ................................................................................................ 16 2.3 Measurement of Key Variables ......................................................................... 17

2.3.1 Bank Solvency ................................................................................................ 17 2.3.2 Liquidity Risk ................................................................................................. 17

2.4 Theoritical Evidence ........................................................................................ 18 2.4.1 Introduction .................................................................................................... 18

2.4.2 Bank Solvency ................................................................................................ 19 2.4.3 Liquidity Risk and Bank Solvency .................................................................. 19

2.4.4 Bank Profitability and Bank Solvency ............................................................. 19 2.4.5 Bank Size and Bank Solvency ......................................................................... 20

2.4.6 Capital Risk and Bank Solvency ..................................................................... 20 2.4.7 Credit Risk and Bank Solvency ....................................................................... 21

2.4.8 Macro- Economic Variables ............................................................................ 21 2.4.8.1 Inflation and Bank Solvency ...................................................................... 21

2.4.8.2 Growth in Real GDP (GGDP) ...................................................................... 22 2.5 Empirical Evidence ............................................................................................ 22

2.5.1 Liquidity Risk and Bank Solvency .................................................................. 22 2.5.2 Credit and Bank Solvency ............................................................................... 23

2.5.3 Capital Risk and Bank Solvency ..................................................................... 23 2.5.4 Bank Size and Bank Solvency ......................................................................... 24

2.5.5 Bank Profitability and Bank Solvency ............................................................. 24 2.5.6 Growth Domestic Product and Bank Solvency ................................................ 25

2.5.7 Inflation and Bank Solvency ........................................................................... 25 2.5.8 Summary ........................................................................................................ 26

CHAPTER3 ........................................................................................................... 27 3..0 Research Methodology ..................................................................................... 27

3.1 Introduction ....................................................................................................... 27 3.2 Research Design ................................................................................................ 27

3.3 Population ......................................................................................................... 28 3.4 Sampling ........................................................................................................... 29

3.5 Sources of Data..................................................................................................... . 30 3.5.1 Justification of Secondary Data ....................................................................... 30

3.6 Econometrics Specification ................................................................................ 31 3.6.1 Research Model................................................................................................. 31

3.6.2 Determinants of Bank Solvency Model ........................................................... 31 3.7 Defition of Key Variables ................................................................................. 31

3.7.1 Bank Solvency ................................................................................................ 31 3.7.2 Liquidity Risk ................................................................................................. 32

3.7.3 Capital Risk .................................................................................................... 33 3.7.4 Credit Risk ...................................................................................................... 33

8

3.7.5 Profitability ..................................................................................................... 33 3.7.6 Bank Size ...................................................................................................... 34

3.7.7 Growth Domestic Product ............................................................................... 34 3.7.8 Inflation .......................................................................................................... 35

3.8 Data Analysis Techniques .................................................................................. 36 3.9 Justification of Panel Regression Techniques ..................................................... 36

3.10 Statistical Techniques Used.............................................................................. 37 3.11 Statistical Package Used .................................................................................. 37

3.12 Data Interpretation ........................................................................................... 37 3.13 Summary ......................................................................................................... 38

CHAPTER4 ........................................................................................................... 39 4.0 Data Analysis and Presentation .......................................................................... 39

4.1 Introduction ....................................................................................................... 39 4.2 Secondary and Literary Data Analysis ............................................................... 39

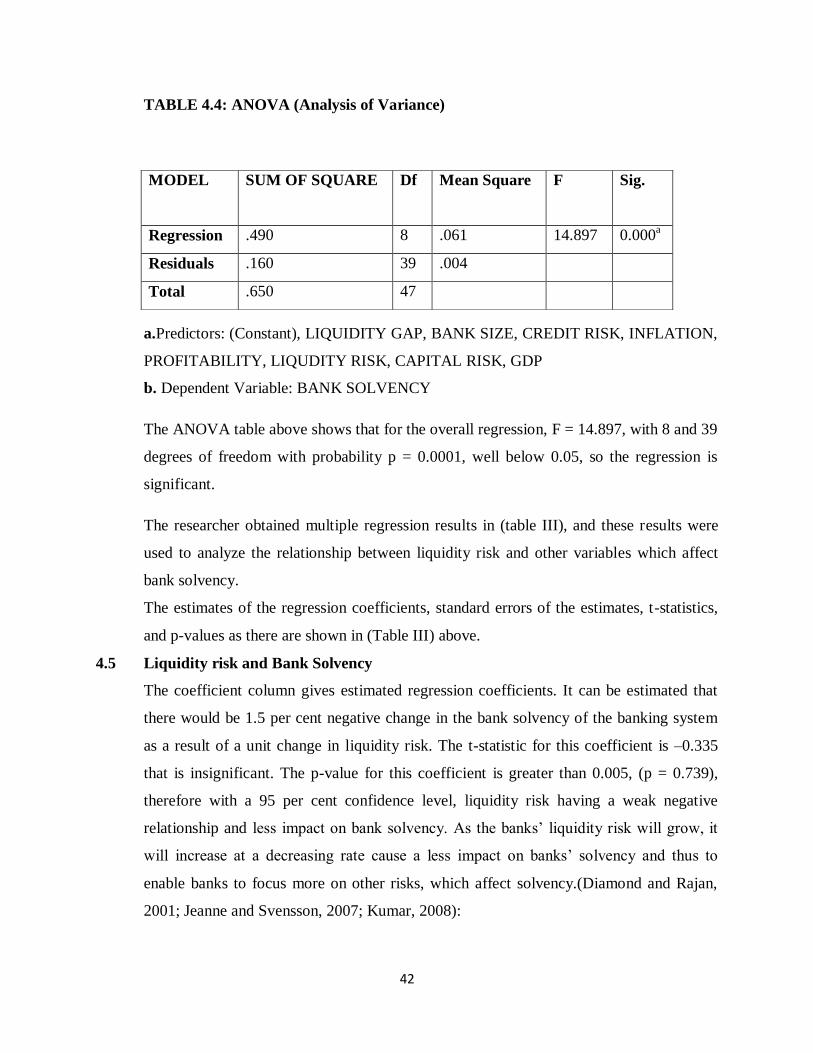

4.3 Empirical Results and Interpretation .................................................................. 40 4.4 Durbin Watson Statistics. ................................................................................... 42

4.5 Liquidity Risk and Bank Solvency ..................................................................... 43 4.6 Credit Risk and Bank Solvency .......................................................................... 44

4.7 Capital Risk and Bank Solvency. ....................................................................... 44 4.8 Profitability and Bank Solvency ......................................................................... 44

4.9 Bank Size and Bank Sol vency. .......................................................................... 45 4.10 Liquidity Gap and Bank Solvency . .................................................................. 45

4.11 Inflation and Bank Solvency. ........................................................................... 45 4.12 Gross Domestic Product and Bank Solvency .................................................... 46

4.13 Model Based on Unstandardized Coefficiencts................................................. 46 4.14 Model Based on Standardized Coefficients ...................................................... 46

4.15 Summary ......................................................................................................... 47 CHAPTER 5 .......................................................................................................... 48

5.0 CONCLUSIONS AND RECOMMENDATIONS .............................................. 48 REFERENCES ........................................................................................................ 49

APPENDICES .............................................................................................................

9

ABBREVIATIONS

AGRIBANK - AGRICULTURAL BANK OF ZIMBABWE

CBZ - COMMERCIAL BANK OF ZIMBABWE

GDP - GROSS DOMESTIC PRODUCT

IMF - INTERNATIONAL MONETARY FUND

POSB - POST OFFICE SAVINGS BANK

STANCHART - STARNDARD CHARTETERED BANK

INF - INFLATION

LR - LIQUIDITY RISK

CR - CAPITAL RISK

NPL - NON PERFORMING LOANS

LN (TA) - LOGARITHM OF TOTAL ASSETS

Table 2.1: List of banks based on population ........................................................... 27 Table 2.2: list of banks based on sample size ........................................................... 28

Table 2.3: Summary of variables and their proxies ................................................... 34 Table 2.4: Descriptive statistics ............................................................................... 39

Table 2.5: Correlation matrix ................................................................................... 40 Table 3.1: results of multiple regression ................................................................... 41

Table 4.1ANOVA (analysis of variance)………………………………………………………………………….......42

10

CHAPTER 1

1.0 INTRODUCTION

The study examines the impact of liquidity risk on bank solvency in Zimbabwe. This

subject has become a contentious issue given by the prevailing environment in which

deposits attracted little or no interest while lending rates were pegged at exorbitant levels

of lending at 10-30% rates whereas other markets on 3% is a pipedream.

Bank solvency means that no debt exists. While liquidity risk is the current and

prospective risk to earnings or capital arising from banks inability to meet its obligations

when they come due without incurring unacceptable losses. Liquidity risk includes

inability to manage unplanned decreases or changes in funding sources. It also arises

from the failure to recognize or address changes in market conditions that affect the

ability to liquidate assets quickly and within minimum loss in value.

As regulators are increasing their focus on liquidity risk in response to the financial crisis

that occurred recently, but there are questions about whether solvency is an effective

mitigate for liquidity risks and the nature of the relationship between liquidity risk and

bank solvency. Roy Choudhury, Peter Marshall and HovikTumasyan look at the

interdependencies between liquidity risk and solvency.

1.1 BACKGROUND

Banks have had both sides of their balance sheet devastated by hyperinflation and now

have no lender of last resort to call on. They are understandably cautious in lending

deposits that are slowly filtering back into the system. Banks also lost much of their

equity capital. Barclays bank survived because it had 40 branches where the bank owned

the real estate and had strong parent. These properties plus some foreign currency

holdings represents the equity capital on which the bank current operation.

Since February 2009 there has been no lender of last resort in Zimbabwe due to the

introduction of multicurrency system causing banks to be ultra-cautious in their lending

policies.

11

Solvency risk is high as a possible compounding of the liquidity and credit risks, as well

as the banking system’s difficulties in generating positive incomes could lead to a rapid

erosion of capital. According to International Monetary Fund (I.M.F) report (2010), the

average solvency ratio (regulatory capital to risk-weighted assets), stood at 15.3 per cent

as at December 2010, which was above the 10 percent minimum requirement, but with

large variations across individual banks. Seven smaller banks are undercapitalised and

some even operate with negative capital.

Counterparty and credit risk is medium to high due to a significant exposure to the

financial distressed Reserve Bank of Zimbabwe (RBZ) (about 70 percent of banks’

capital), the drought prone agricultural sector (20 percent of the loan portfolios), and the

exuberant credit growth. The projected economic slowdown would lead to a significant

increase in nonperforming loans. Liquidity risk is high, as structural liquidity pressures

could arise due to the deteriorating Balance of payments positions potentially causing a

reduction in banks’ foreign assets. This was again reported by IMF

The banking system is also ill-equipped to deal with temporary liquidity shocks with no

lender of last resort, the unavailability of the structural reserves deposited at the RBZ,

virtually no interbank lending and the level of country risk that precludes liquidity

support from abroad. In this regard it is of concern that credit expansion is taking place at

the expense of prudent liquidity management at some large banks especially those whose

liquidity ratios were below the prudent level of 25 percent at the end of December 2009.

In some countries, depositing money with a financial institution is an investment in itself.

But in Zimbabwe, account holders, most of whom keep minimum deposits of about

US$20 in their accounts, are instead often dragged into debts as bank charges gnaw into

their savings, leaving balances in negative territory.

Interest rates on deposits since inception of dollarization have remained low, with savings

rates averaging zero to five percent, against lending rates of between 18-30 percent This

undermines efforts at mobilizing domestic savings and, hence, constrains the volume of

medium to long term resources available for lending to the industries.. Efforts on moral

12

suasion are beginning to yield positive results as some banks are beginning to offer

instruments at competitive interest rates and if supported should start attracting larger

deposits.

Liquidity in the banking system has recently deteriorated. The average liquidity ratio

excluding illiquid claims on the RBZ, exceeded 30 percent as of February 2011, but it

was below 20 percent for 8 banks including one systematic important bank and below 25

percent for 11 banks. The domestic interbank market is not fully operational and is likely

to be inaccessible in the case of systemic liquidity shortages.

Failure of smaller distressed banks or banks with weak liquidity to meet withdrawal

demands could lead to loss of confidence and subsequently contagion to the rest of the

system, causing a liquidity shock to other solvent banks.

It is generally acknowledged that a credit union which relies on a significant number of

large deposits is in a less favorable liquidity position than one whose deposit base

consists on many average sized accounts. The withdrawal of large deposits due to interest

rate competition or members’ investment can significantly impair liquidity and should be

avoided

Even solvency is high, low bank profitability weakens the capacity of the bank to absorb

negative shocks which eventually affects its solvency. Most of the studies in the literature

find that internal bank characteristics explained a large proportion of bank’s solvency;

nevertheless, external factors have also an impact on their solvency. However, the

relations between bank characteristics of external factors and solvency differ across

countries or different periods, within the same country.

Knowledge of the internal and external determinants of bank solvency is essential for

various stakeholders of the banking sector such as bank managers, government, central

bank and the financial services.

13

1.2 STATEMENT OF THE PROBLEM

Liquidity problems in one or few banks may lead to bank runs and contagion to other

banks, resulting in a general loss of confidence in the banking system of Zimbabwe. Bank

runs may lead otherwise solvent banks to experience large losses as they struggle to

mobilize less liquid assets to meet liquidity risk. These losses could quickly erode the

capital position of still weakly capitalized banks. The inability to refund statutory

reserves and other illiquid bank claims would force the banks to write down these claims

on the RBZ, leading to significant losses and undercapitalization. Therefore the research

is intended to identify whether liquidity risk is the endogenous determinant of bank

solvency and to investigate the relationship and the level of significance of bank specific

variables and macroeconomics variables with the level of liquidity risk and solvency on

commercial banks in Zimbabwe during the period 2009-2012

1.3 Research Objectives

To examine the relationship between liquidity risk and banks’ solvency in Zimbabwe.

To examine the bank specific variables and macroeconomic conditions which affect bank

solvency.

To determine whether liquidity gap can affect bank solvency

1.4 Research Question

Is there any relationship between liquidity risk and bank’s solvency?

Are there any other banks’ specific variables and macroeconomic variables which affect

bank solvency?

Does liquidity gap affect bank solvency?

1.5 RESEARCH HYPOTHESIS

Ho: There is interdependence between bank solvency and liquidity risk

H1: There is no interdependence between bank solvency and liquidity risk

14

1.6 SIGNIFICANCE OF THE STUDY

The purpose of this document is to study, understand and bring forth the issue of

liquidity risk in relation to banks’ solvency in Zimbabwe. The topic has been addressed

by many researchers but still we feel there is a gap in the research. The interdependency

of liquidity risk and bank solvency will be there to offer a new horizon to the customers

and the overall economy of Zimbabwe. Most studies have not addressed the issue of

liquidity risk implications on the solvency of banks and our dissertation will seek to fill

this literature gap. The results of the study will be generalized and help organizations in

other sectors of the Zimbabwean economy such as Small and Medium Enterprises,

mining and agricultural sectors. The research study will also open new doors for new

upcoming researchers.

1.7 ASSUMPTIONS

The banks we are going to assess will cooperate in providing the secondary data

The secondary data will be readily available

The study will be objective in data gathering and interpretation.

Data collection instruments will have adequate reliability and validity

Uncontrollable variables will be uniformly distributed over the sample.

1.8 SCOPE OF THE STUDY

The study is going to be carried out, focusing on banking industry in Zimbabwe

particularly, banks which are headquartered in Harare. The other limiting factor is the

unstable and fragile Zimbabwean economy which has forced the banks to scale down

their branch networking throughout the country.

1.9 LIMITATIONS OF THE STUDY

Sufficient time to carry out the research.

Access to financial information is restricted with some banking institutions.

Financial constraints.

15

1.10 Summary.

The study is organized into five chapters as follows; Chapter one deals with study

introductions, purpose of the study, research questions, and hypotheses including

limitations of the study. Chapter two looks at the literature review relevant to the study in

line with the research objectives. Chapter three focuses on research methodology i.e.

research design; sampling techniques, sample sizes and data collection methods. The

fourth chapter is on data analysis and presentation. Finally chapter five has the

conclusions, observations and recommendations based on the research findings on which

way forward were made.

16

CHAPTER 2

2.0 REVIEW OF LITERATURE

2.1 Introduction.

This is a chapter on literature review. Basically literature review is all about making

summaries and analysis of related annual reports, journals, research reports ,textbooks

and publications on the liquidity risk management in the banking industry system to

provide the background on the theoretical and empirical reviews underpinning of a

research study

2.2 Definition of key variables

2.2.1 Bank solvency

A bank is solvent when the total value of its assets is greater than that of its liabilities. A

bank becomes risky if it is insolvent. (Mohamad Abdul Hamid).

2.2.2 Liquidity risk

A bank’s liquidity risk refers to a comparison of its liquidity needs for deposit outflows

and loan increases with the actual or potential sources of liquidity from either selling an

asset it holds or acquiring an additional liability. (Shaza Marina Azmi) Banking liquidity

risk is therefore associated both to banks’ ability to fulfill their obligation to depositors

(borrowers) to transform their deposits into legal money (to receive cash by drawing

down the credit lines), and their function of maintaining a balance between the ingoing

and outgoing cash flows deriving from the management of payments made using banking

money. Means of payment are created and cash flows managed under the direction and

control of the Central Banks, which guarantee the availability of the monetary base

needed to sustain the ordered creation of banking money. The Central Banks also play a

key role in the creation and strengthening of the infrastructures needed to settle payments

within the financial system. Liquidity risk is seen as a major risk, but it is the object of:

extreme liquidity, "security cushion" or the specialty of mobilizing capital at a "normal"

cost (Dedu, 2003)

17

2.3 Measurement of key variables

2.3.1 Bank solvency

The following are the commonly used measures for bank solvency. (Zaman et al (2001))

1) Debt equity ratio (DER) = Debt/equity capital. Bank capital can absorb financial

shock. In case asset values decrease or loans are not repaid bank capital provides

protection against those loan losses. A lower DER ratio is a good sign for a bank.

2) Debt to total asset ratio (DTA) = Debt/total asset indicates the financial strength of a

bank to pay its debtor. A high DTAR indicates that a bank involves in more risky

business.

3) Equity multiplier (EM) = Total assets/share capital. It is the amount of assets per $ of

equity capital. A higher EM indicates that the bank has borrowed more funds to convert

into asset with the share capital. The higher value of EM indicates greater risk for a bank.

4) Loan to deposit ratio (LDR) = loans/deposit measures liquidity as well as credit risk

for a bank. A high value indicates a potential source of illiquidity and insolvency.

2.3.2 Liquidity risk

Generally, liquidity risk measures can be calculated from balance sheet positions. In the

past, better practices for liquidity risk measures focused on the use of liquidity ratios.

However, Poorman and Blake (2005) indicated that it was not enough to measure

liquidity just using liquidity ratios and it was not the solution. Recently, there are many

methods provided to assess bank liquidity risk besides traditional liquidity ratios. Basel

Committee on Banking Supervision (2000) proposed maturity laddering method for

measuring liquidity risk. Saunders and Cornett (2006) indicated that banks can use

sources and uses of liquidity, peer group ratio comparisons, liquidity index, financing gap

and the financing requirement, and liquidity planning to measure their liquidity exposure.

Besides, Matz and Neu (2007) also indicated that banks can apply balance sheet liquidity

analysis, cash capital position and maturity mismatch approach to assess liquidity risk.

18

2.4 THEORETICAL EVIDENTS

2.4.1 Introduction

Few studies have examined the factors that affect bank solvency in different countries.

One strand in the literature examines the specific characteristics of banks; other studies

examine the effect of external factors such as financial industry and economic

environment. In addition previous research examines in either a particular country or a

number of countries, single countries include among others for example Tunisia [Ben

Naceur 2003] and Greece [Kosmidou and Pasiouras 2005]

The interdependencies of solvency and liquidity risk are discussed within the context of

two management function thus one the setting of risk appetite and integrated balance

sheet management and stress testing according to Roy Choudhury,Peter Marshall and

HovikTumasyan

As remarked by Good hart (2008), “liquidity and solvency are the heavenly twins of

banking, frequently indistinguishable. An illiquid bank can rapidly become insolvent, and

an insolvent bank illiquid.”

Golin (2001) shows that proportioned revenues are required so that banks can maintain

solvency in order to survive, grow and succeed in an appropriate environment. Liquidity

risk arises because inflows and outlays are not synchronized (Holmström and Tirole

(1998)). The impacts of the banks liquidity on their solvency remain unclear and further

research is required.

2.4.2 Bank solvency

Bank Solvency represents total equity to total liabilities. The measure of the extent of

leverage using liabilities instead of assets provides a more sensible measure of the bank

buffer stock that will serve as a cushion to absorb losses. Moreover if we take into

account that in the latest episodes of bank distress there were not only shocks related to

bank’s asset value, but also related to deposit base. In addition, the explicit inclusion of

off-balance-sheet positions produces a more accurate measure of bank leverage and

exposure (Breuer, 2000).

19

2.4.3 Liquidity risk and bank solvency

Liquidity risk represents liquid assets/deposits. The higher the ratio the lower the

liquidity risk and the lower the opportunity for profit. Liquid assets are used to measure

the size of available cash and near cash assets to meet the withdrawal demand. This

demand could be demand for loans withdrawals of demand deposits and opportunities for

investments in securities. Failure to provide adequate liquidity to meet the demands of

depositors or creditors can cause a shutdown of a bank within a short period. Liquidity

risk result in a decrease of the portfolio value, but could also jeopardize the investors

own credit rating thus in other words if a fund is unable to fulfill a redemption

request as agreed, the investor in turn may fail to fulfill his own credit commitments

thus according to Marshall et al (2010)

Inclusion of liquidity risk in the definition of risk appetite takes an intermediated form

through its effect on profit and loss (by identifying the highest acceptable the cost of

funding), and its impact on balance sheet structure (by defining the size and composition

of the liquidity buffer a bank can afford to hold given there are high opportunity cost and

negative carrying cost associated with the liquid assets thus according to Tumasyan et al

(2010)

2.4.4 Bank profitability and bank solvency

Bank profitability can be seen as indicator of the (in) efficiency of the banking system

(Demirguc-Kuntand Huizinga, 1999). Two indicators of bank profitability are used. The

first indicator is the return on assets (ROA) and is calculated as the net income divided by

average total assets. It shows the profits earned per $ of assets and indicates the

effectiveness of managing the fixed assets to generate revenues. The second indicator of

profitability is the return on equity (ROE), and is calculated as the net income divided by

equity. Bank profitability has improved but smaller banks have taken considerable risks.

The return on average assets (ROA) and return on equity (ROE) rose in 2010, as banks

benefited from the improved economic environment, and new financial products,

including mobile banking, generated additional revenue. Nevertheless, the profitability of

banks in Zimbabwe remained lower than that of its sub-Saharan peers (Table 1, Figures 1

20

and 2). Smaller banks have become more risk-taking, reaching for lower-end and

sometimes unbankable customers, potentially heightening the volatility to bank income

and profitability. Smaller banks are also less efficient with a higher cost structure.

2.4.5 Size of Bank and Bank solvency

Size of the bank signals specific bank risk, although the expected sign is ambiguous. To

the extent that governments are less likely to allow big banks to fail, a risk approach to

size would predict that bigger banks would require lower profits (e.g. through lower

interest rates charged to borrowers). Moreover, modern intermediation theory predicts

efficiency gains related to bank size, owing to economies of scale. This would imply

lower costs for larger banks that they may retain as higher level of solvency if they do not

operate in very competitive environments. To capture the relationship between size and

bank solvency while also accounting for such potential nonlinearities, we proxy bank size

using the logarithm of total assets and their square. Larger size may result in economies

of scale which could reduce the cost gathering information.(Calvin McDonald et al

(2009))

2.4.6 Capital risk and Bank solvency

Capital Risk (Equity) shows book value of equity divided by total assets. High ratio

means lower degree of risk. It shows how much of bank’s assets values may decline

before the position of its depositors and other creditors is jeopardized. Banks that have

high equity to assets ratio normally have less needs for external funding and consequently

is expected to be more profitable .The bank solvency can be affected by bank’s own

plans, which can be derived from the structure of its balance sheet and income statement.

One of the most factors influencing bank solvency is the capital ratio. (Berger 1995)

2.4.7 Credit risk and Bank Solvency

Credit risk represents the ratio of loans to deposits and short-term funding since this

provides a forward-looking measure of bank exposure to default and asset quality

deterioration (Valentina Flamini). The risk of default in repayment of bank interest or

principal on loans is closely related to liquidity transformation because cumulative

21

default risk tends to rise over time. The changes of the credit risk can reflect the changes

of the health of a bank loan portfolio which can affect the solvency of the enterprise

(Cooper et al., 2003). This raises a debate concerning the quality of loan. Duca and

McLaughlin (1990), among others, concluded that the variation of the banking

profitability is largely attributable to the variation of the credit risk because the increased

exposure to the credit risk is normally connected with the decrease of the firm

profitability. This starts a discussion not concerning the volume, but the quality of the

loans made. In this direction, Miller and Noulas (1997) suggest that the more the

financial institutions are exposed to high risk, the higher the accumulation of the unpaid

loans and the lower the level of bank solvency.

2.4.8 Macroeconomic variables

As for the impact of macroeconomic and financial development indicators on banks’

solvency, they find no significant impact of such variables on net interest margin, except

inflation and growth in real gross domestic product (GGDP)

2.4.8.1 Inflation and Bank Solvency

Revell (1979) introduced the notion that the effect of inflation depends on wages and

other operating costs of banks which are increasing at a faster rate than inflation. As such,

the relationship between inflation and solvency is ambiguous and depends on whether

inflation is expected or not. The inflation rate fully anticipated by the management of the

bank implies that banks can appropriately adjust the interest rates to increase their

products faster than their costs and then gain higher profits. In contrast, unanticipated

inflation could lead to an incorrect adjustment of the interest rates and therefore to the

possibility that costs may rise faster than products.

2.4.8.2 Growth in real GDP (GGDP)

It measures the total economic activity in the economy. It is expected to be positively

related to bank solvency. According to the literature of financial sector development and

economic growth, growth in GDP is positively associated with bank solvency. There is no

doubt that a well-functioning financial system is important for economic growth. Rajah

22

and Zing ales (1998); Levin (1997, 1998), among others, suggest that the efficiency of

financial intermediation affects country’s economic growth, while at the same time bank

insolvencies can result in systemic crises which have negative consequences for the

economy as a whole with losses that arise in many cases around 10-20% of GDP and

occasionally as much as 40-55% of GDP (Caprio and Klingebiel, 2003). Colin (2001), in

addition, suggests that adequate earnings are required in order for banks to maintain

solvency, to survive, and grow in a suitable environment.

2.5 EMPERICAL EVIDENCE ON THE IMPACT OF LIQUIDITY RISK ON BANK

SOLVENCY.

The only thing certain about the future is that finance and industry will continue to

change especially with the multicurrency system offering new challenges and

opportunities. With the empirical review the researcher is going to use quantitative

analysis and will be based on the basic theories and suggestions put forward by different

authors and analysts.

2.5.1 Liquidity risk and bank solvency

Kosmidou et al., (2005) found a negative and statistically significant relationship between

net interest margin and liquidity ratio only when external factors enter the equation.

Kosmidou et al., (2004) and Angbazo (1997) also found similar results. These results are

in disagreement with those of Clays and Vender Veneto (2008) who found a positive and

statistically significant relationship between net interest margin and liquidity ratio,

although it is more pronounced on the Eastern European banking markets. Thus, since the

loans are the riskiest capitals and have the highest costs, this foundation refutes the

hypothesis that the loan has resulted in wider margins and reflects the ability of the banks

to integrate risk considerations and costs in their loan pricing behavior. Bourke (1999)

found that there is a positive relationship between bank solvency and liquidity risk.

However; Demerguç-Kunt and Huizinga, (1999) found that there is a negative

relationship between bank solvency and liquidity risk.

23

2.5.2 Credit risk and bank solvency

Athanasoglou et al., (2006) also found a statistically significant negative relationship

between the credit risk variable and the bank solvency, proving that banks in South East

Europe should focus more on managing credit risk, which was a problem in the recent

past. The serious banking problems have resulted from the failure of banks to identify the

impaired assets and create reserves for their cancellation. A great help was given to these

assets in that anomalies would be provided by improving the transparency of the financial

systems, which will help banks to assess their credit risk more effectively and avoid

exposure to dangerous problems. Kosmidou et al., (2005) found a positive but

statistically non-significant relationship between the credit risk and bank solvency.

Valverde and Fernandez (2007) found that the credit risk increases significantly between

bank credit and net profit margin. This reflects that payment by bank loans is more

interesting than that by cash, which would increase the net profit margin. Other studies

have found similar results (Demirgüç-Kunt and Huizinga, 1999; Demerguç-Kunt and

Huizinga, 2001; Maudos and Gerevara, 2004). Therefore, Ho and Saunders (1981) found

a generally low but statistically non-significant relationship between the default risk and

net interest margin and thereby improving the level of bank solvency.

2.53 Capital risk and bank solvency

Capital strength is one of the main determinants of a bank solvency. Kosmidou et al.,

(2005) found a positive and highly significant relationship between the equity ratio to

total assets and net profit margin (NIM). Therefore, banks are seeking to lower the cost of

their relatively high capital ratios by requiring higher MIN. This basis is in accordance

with the interpretation that the capital serves as a signal of bank solvency.

Hence, the very high sensitivity of the margins concerning the equity capital ratios to

total assets may be explained by the existence of a depositor’s behavior in the banking

operations in transition. This can reduce the deposit cost of the well-thriven banks leading

to higher profit margins. This result is in accordance with that of other studies, namely

Demirgüç-Kunt and Huizinga, (1999); Ben Naceur, (2003); Kosmidou and

Pasiouras, (2005); Valverde and Fernandez, (2007); Brock and Suarez, (2000);

Demirgüç-Kunt, Loeven and Levine, (2004) ;and Saunders and Schumacher (2000).

24

2.5.4 Bank size and bank solvency

The results obtained by the literature for the relationship between size and solvency are

diverse. Using market data (stock prices) instead of accounting measures of solvency,

Boyd and Runkle (1993) find a significant inverse relationship between size and loan to

deposit ratio(solvency) in U.S. banks from 1971 to 1990, and a positive relationship

between financial leverage and size. They do not provide, however, any theoretical model

to rationalize this evidence. Berger, et a (1987) develop a set of scale and product mix

measures for evaluating the competitive viability of firms, and apply it to 1983 data.

Their results show that as product mix and scale increases, banks experience some

diseconomies, implying a negative relation between size and returns. Goddard et al (2004

use panel and cross-sectional regressions to estimate growth and solvency equations for a

sample of banks for five European countries over the 1990s. The growth regressions

suggest that, as banks become larger in relative terms their growth in level of solvency

tends to increase further, with little or no sign of mean reversion in growth.

2.5.5 Bank profitability and bank solvency

Bank profitability can be seen as indicator of the (in) efficiency of the banking system.

Akhavein et al, (1997) and Smirlock (1985) used two indicators of bank profitability. The

first indicator is the return on assets (ROA) and is calculated as the net income divided by

average total assets. The second indicator of profitability is the return on equity (ROE),

and is calculated as the net income divided by equity. They found a positive and

significant relationship between bank profitability and solvency. Demirgüç-Kunt and

Huizinga (2000) and Goddard et al. (2004), used linear models to estimate the impact of

bank profitability that may be important in explaining bank solvency. They found a

negative relationship between the profitability of a bank and its level of solvency.

2.5.6 Gross domestic product and bank solvency

Demirgüç-Kunt and Maksimovic (1996) provide empirical evidence that an ability to

attract equity capitals may also increase the borrowing capacity of the firms, particularly

in the stock markets of the developing countries. Funding through raising the capital can

increase and decrease the demand for financing through debt, there by reflecting that

these sources are complementary. Thus, concerning the importance of the bank relative

GDP, Demerguç-Kunt and Huizinga, (1999) found that in countries where the banking

25

assets represent a large part of the GDP, the banks are less profitable. They also found

that the ratio of bank assets to the GDP, which has a significantly negative impact on the

margin, may reflect a more intense inter-bank competition in the financial systems. This

effect is negligible in richer countries that already have a relatively developed banking

sector. However, in countries with underdeveloped financial systems, a greater financial

development, which improves the efficiency of the banking sector, potentially leads to

growth at the micro, firm and the macro level. Thus, the improved availability of funds

financing for companies can increase their borrowing capacity (Demirgüç-Kunt

Huizinga, 2001). Pasiouras and Kosmidou, (2007) found that the total bank assets to the

GDP are negatively related to profitability

2.5.7 Inflation and bank solvency

Thus, Ben Naceur and Goaid (2005) found that banks tend not to gain profits in an

inflationary environment. Therefore, most studies (i.e. Bourke, 1989; Molyneux and

Thornton. 1992) observe a positive relationship between inflation and banking solvency.

Demiurgic-Kent and Huizinga,(1999) showed that with inflation , bank costs tend to

rise , However, a greater number of transactions may lead to higher labor costs.

Bourke (1989), Molyneux and Thornton (1992), have found a positive relation between

inflation and long term interest rates with bank solvency.

In conducting their researches most authors used cross-sectional time series fixed

generalized least squares (FGLS) regression. In estimating the coefficients they used

generalized least squares. In terms of panels they used homoscedastic data. Among them

Demirgüç-Kunt, Loeven and Levine, (2004) used Hausman Test as their model.

2.5.8 Summary

The term Liquidity risk includes a wide range of proxies and their measure differ from

region to region and from country to country and there is no universally agreed measure

of liquidity risk.

26

CHAPTER 3

3.0 RESEARCH METHODOLOGY

3.1 INTRODUCTION

The previous chapter focused on literature and empirical review on the impact of

liquidity risk and bank specific variables and macroeconomic variables which affect bank

solvency. The review considered various literature sources among them books, journals,

conference papers, periodicals, research papers, magazines, newspapers and Government

circulars on bank solvency and liquidity risk.

According to Sekaran (2003), research is an organized, systematic, data-based, critical,

objective, scientific inquiry or investigation into a specific problem, undertaken with the

purpose of finding answers or solutions to it. The information provided could be the

result of a careful analysis of data gathered firsthand or of data that is already available

This chapter discusses the approach to the research project. The data collection methods

are outlined and highlighted. It describes the research design and data collection

procedures. It also includes the methods the researcher used to identify other factors

which can affect bank solvency besides liquidity risk as a major challenge facing local

banks on their daily banking operations.

There is a planned procedure that focuses to a specific scope in conducting research. This

procedure was taken in order to seek answers to some questions or objectives. As

mentioned on the section 1.3, the objectives of this research are:

To examine the relationship between liquidity risk and banks’ solvency in Zimbabwe.

To examine the bank specific variables and macroeconomic conditions which affect bank

solvency.

To determine whether liquidity gap can affect bank solvency

3.2 Research design

The research was conducted in the form of a descriptive research of commercial banks

Zimbabwe was conducted. Most research activity is carried out under conditions of strict

27

time constraints and limited budget effect. The researcher employed a quantitative

approach which is appropriate when the research purpose is to test cause-effect type of

hypotheses.

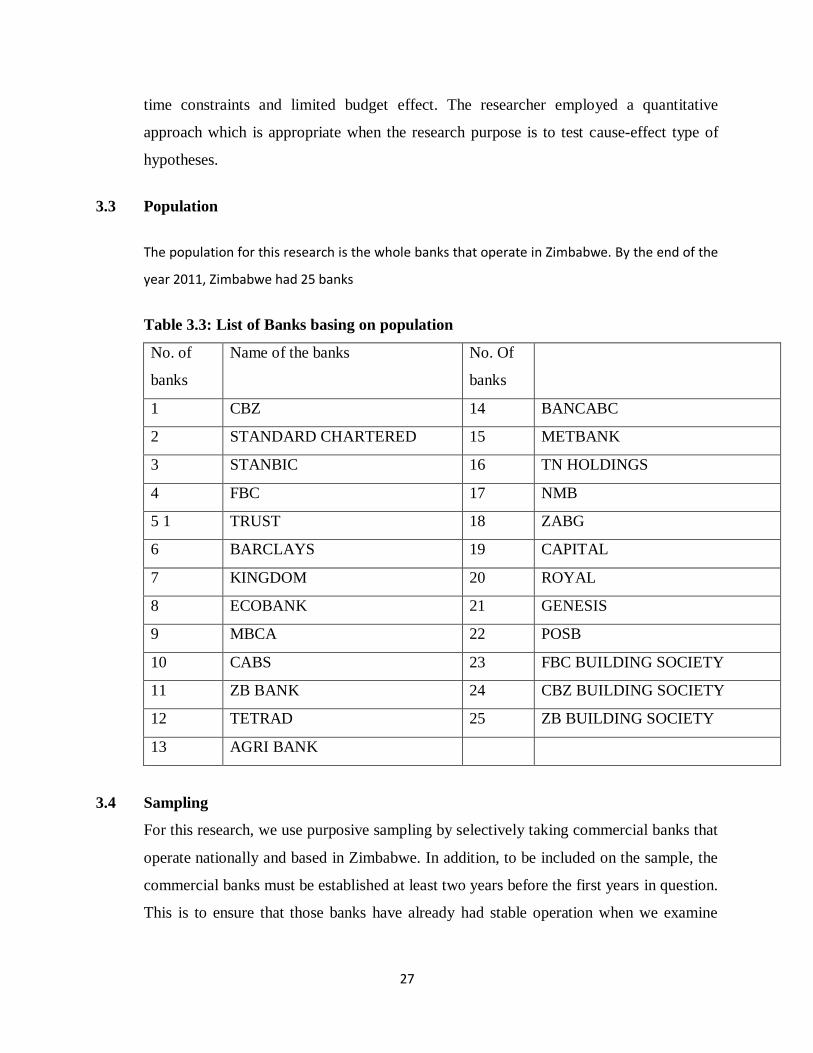

3.3 Population

The population for this research is the whole banks that operate in Zimbabwe. By the end of the

year 2011, Zimbabwe had 25 banks

Table 3.3: List of Banks basing on population

No. of

banks

Name of the banks No. Of

banks

1 CBZ 14 BANCABC

2 STANDARD CHARTERED 15 METBANK

3 STANBIC 16 TN HOLDINGS

4 FBC 17 NMB

5 1 TRUST 18 ZABG

6 BARCLAYS 19 CAPITAL

7 KINGDOM 20 ROYAL

8 ECOBANK 21 GENESIS

9 MBCA 22 POSB

10 CABS 23 FBC BUILDING SOCIETY

11 ZB BANK 24 CBZ BUILDING SOCIETY

12 TETRAD 25 ZB BUILDING SOCIETY

13 AGRI BANK

3.4 Sampling

For this research, we use purposive sampling by selectively taking commercial banks that

operate nationally and based in Zimbabwe. In addition, to be included on the sample, the

commercial banks must be established at least two years before the first years in question.

This is to ensure that those banks have already had stable operation when we examine

28

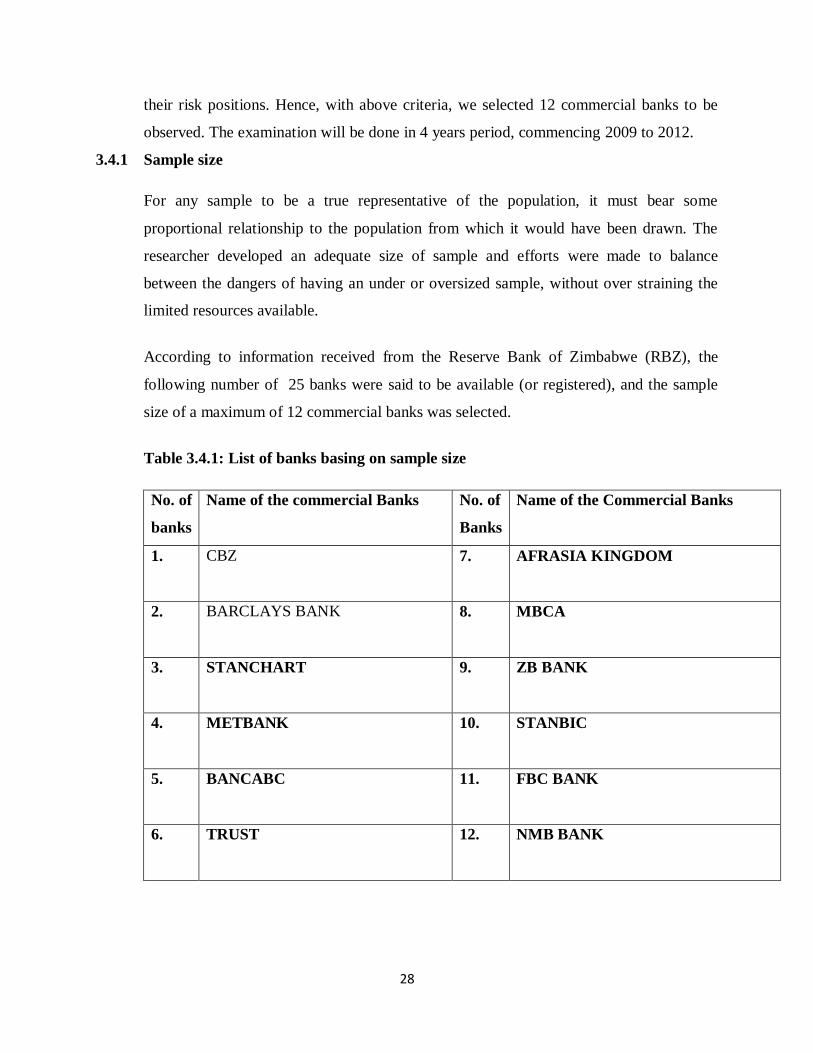

their risk positions. Hence, with above criteria, we selected 12 commercial banks to be

observed. The examination will be done in 4 years period, commencing 2009 to 2012.

3.4.1 Sample size

For any sample to be a true representative of the population, it must bear some

proportional relationship to the population from which it would have been drawn. The

researcher developed an adequate size of sample and efforts were made to balance

between the dangers of having an under or oversized sample, without over straining the

limited resources available.

According to information received from the Reserve Bank of Zimbabwe (RBZ), the

following number of 25 banks were said to be available (or registered), and the sample

size of a maximum of 12 commercial banks was selected.

Table 3.4.1: List of banks basing on sample size

No. of

banks

Name of the commercial Banks No. of

Banks

Name of the Commercial Banks

1.

CBZ 7. AFRASIA KINGDOM

2.

BARCLAYS BANK 8. MBCA

3.

STANCHART 9. ZB BANK

4.

METBANK 10. STANBIC

5.

BANCABC 11. FBC BANK

6.

TRUST 12. NMB BANK

29

3.5 SOURCES OF DATA

According to Merril (1970) data can either be primary or secondary. He defined primary

data as raw data that is gathered through the use of interviews and questionnaires whereas

he defined secondary data as that data that can be obtained from published material. In

this research study the researcher used secondary data as type of data sources. Secondary

data

In this study, the researcher use secondary data. The main sources are from the various

publications, annual reports, press releases, and statistical bulletins the produced by

Reserve of Zimbabwe. In addition, the researcher also use online database provided in the

Harare Institute of Technology University and Reserve Bank of Zimbabwe electronic

library to search for relevant information for the research. The researcher also makes the

most of the available internet websites in searching for the relevant materials for the

study.

3.5.1 Justification for secondary data

Secondary data is very simple to obtain and is often cheaper, easier to collect and faster

to access than primary data. It is less time consuming and not strenuous. According to

Saunders (2003), secondary data is usually accessible which makes the data easier to

process during limited time. The accessibility also makes the data available to other and

easier to review. Secondary data lends itself to be generally purpose driven and authentic

for a related research study. Furthermore, it provides a way to access the work of the best

scholars all over the world. (www.kbridge.com).

However, the challenge of secondary research cannot be overlooked. It needed time to

organize and analyze the information to meet the needs of the research. Information can

be outdated and could have been researched for different purpose. Secondary data is

prone to bias as far as interpretation is concerned. Other major limitations of secondary

research are time and reliability.

30

In meeting the objectives, the researcher has identified an econometric specification

research model for liquidity risk and bank solvency.

3.6 Econometric specification

3.6.1 Research model

3.6.2 Determinants of Bank solvency model

This model provides an economic analysis of the relationship between liquidity risk, bank

specific- variables, macro-economic variables and bank solvency. In order to examine the

relationship between liquidity risk and bank solvency, the panel regression model has

been developed.

BS = α + β1LR+β2CR+ β3P+ β4NPL +β5Ln(TA) + β6Inf + β7GDP+ µ

Where BS represent solvency of Banks at a specified period of time. In our study, it is

Loan to deposit ratio (LDR). LR,CR, P, NPL, Ln (TA), Inf, and GDP are bank-specific

and macroeconomic variables with β1, β2… β7being the proportionate changes of bank

specific and macroeconomic variables that affect bank solvency. α is a constant term; µ

is the error term.

3.7 Definition of variables and their proxies

Hypothesis testing involves testing of relationships among variables. A variable is

defined as anything that varies or changes in value (Berenson et al., 2004). Cooper and

Schindler (2003) explain that researchers are most interested in relationship between the

dependent and independent variables. Dependent variable can be defined as criterion or a

variable that is to be predicted or explained. Independent variable is a variable that is

expected to influence the dependent variable. Its value may be changed or altered

independently of any other variable

3.7.1 Bank solvency: Total Equity to total liabilities plus Off-Balance-Sheet items.

The measure of the extent of leverage using liabilities instead of assets provides a more

sensible measure of the bank buffer stock that will serve as cushion to absorb losses.

Moreover if we take into account that in the latest episodes of bank distress there were

31

not only shocks related to bank’s asset value, but also related to deposit base. In addition,

the explicit of inclusion of Off-Balance-Sheet positions produces a more accurate

measure of bank leverage and exposure (Breuer, 2000).

3.7.2 Liquidity risk: Ratio of liquid assets/deposits

The economics and finance literature analyze four possible reasons for firms to hold

liquid assets; the transaction motive Miller and Orr 1966, the precautionary motive

Opler, Pinkowitz, Stulz, and Williamson 1999, the tax motive Foley, Hartzell,

Titman, and Twite 2007 and finally the agency motive Jensen 1986. Analysts use

liquidity ratios to make judgments about a firm, but there are limitations to these

ratios. The liquidity of a firm's receivables and inventories can be misleading if the firm's

sales are seasonal and or the firm uses a natural business year (Gibson, Charles H. 1991

Financial Statement Analysis p.261 Cincinnati, OH: South-Western College Publishing).

Morris and Shin (2010) conceptually defines the liquidity ratio as “realizable cash on the

balance sheet to short term liabilities.” In turn, “realizable cash” is defined as liquid

assets plus other assets to which a haircut has been applied. Ration analysis is one of

the conventional way that use financial statements to evaluate the company and

create standards that have simply interpreted financial sense (George H.Pink, G.

Mark Holmes 2005). A sudden stop in an organization is generally defined as a

sudden slowdown in emerging market capital (cash)inflows, with an associated

shift from large current account deficits into smaller deficits or small surpluses.

Sudden stops are “dangerous and they may result in bankruptcies, destruction of human

capital and local credit channels” Calvo, 1998

Golin (2001) states: ''It is critical to carefully supervise the banks against liquidity

risk - Liquidity risk is the fact that it won’t have enough current assets such as money

and securities rapidly salable to meet the current commitments for example, those of

the depositors - particularly during the periods of economic stress.'' Without required

liquidity and investment to meet its commitments, a bank may go bankrupt. The ratio of

liquid assets to the customer and to short term investment (LIQ) is used in this study

as a measure of liquidity. It is a ratio that indicates which percentage of customers

and short term investments could be met if they were suddenly withdrawn.

32

3.7.3 Capital Risk: The ratio of equity capital to total assets (EQAS

This proxy is considered as one of the basic ratios for the capital strength, and is used

in this study as a measure of the capital strength (Golin, 2001). This positive impact

can be due to the fact that capital refers to the amount of own funds available to support

a bank’s business and, therefore, bank capital acts as a safety net in the case of adverse

developments. The expected positive relationship between capital and earnings could be

further strengthened due to the entry of new banks into the market. Therefore, strength

capital is related to the safety and strength of banks. In general, banks with a high capital

ratio are considered more secure in case of loss or liquidation. Therefore, the

assumption of risk agreement profitability would imply a negative relationship

between the ratio of equity capitals and bank solvency. The risk decline increases the

solvency of banks; hence reducing the investment cost.

3.7.4 Credit Risk: Non-performing loans.

The ratio of loan loss provisions to total loans (LLP/TL) is incorporated as an

independent variable in the regression analysis as a proxy of credit risk. Banks would,

therefore, improve solvency by improving screening and monitoring of credit risk and

such policies involve the forecasting of future levels of risk. The coefficient of LLP/TL is

expected to be negative because bad loans are expected to reduce solvency. In this

direction, Miller and Noulas (1997) suggest as the exposure of the financial institutions to

high risk loans increases, the accumulation of unpaid loans would increase and level of

solvency would decreases .Thakor (1987) also suggests that the level of loan loss

provisions is an indication of a bank's asset quality and signals changes in the future

performance.

3.7.5 The profitability: Return on assets or Return on equity

This variable can be represented by two alternative measures: the ratio of profits to

assets, i.e. the return on assets (ROA) and the profits to equity ratio, i.e. the return on

equity (ROE). In principle, ROA reflects the ability of a bank’s management to generate

profits from the bank’s assets, although it may be biased due to off-balance-sheet

activities. ROE indicates the return to shareholders on their equity and equals ROA times

33

the total assets-to-equity ratio. The latter is often referred to as the bank’s equity

multiplier, which measures financial leverage. Banks with lower leverage (higher equity)

will generally report higher ROA, but lower ROE. Since an analysis of ROE disregards

the greater risks associated with high leverage and financial leverage is often determined

by regulation, ROA emerges as the key ratio for the evaluation of bank solvency (IMF,

2002).

3.7.6 Size: Logarithm of total assets.

One of the most important questions underlying bank policy is which size optimizes bank

solvency. Generally, the effect of a growing size on solvency has been proved to be

positive to a certain extent. The LNTA variable is included in the regression as a proxy of

size to capture the possible cost advantages associated with size (economies of scale). In

the literature, mixed relationships are found between size and solvency, while in some

cases a U-shaped relationship is observed. LNTA is also used to control for cost

differences related to bank size and for the greater ability of larger bank to diversify. In

essence, LNTA may have a positive effect on bank solvency if there are significant

economies of scale. On the other hand, if increased diversification leads to higher risks,

the variable may exhibit negative effects.

Both of the macroeconomic variables used here are the growth of the gross domestic

product (GDP) and inflation (INF).

3.7.7 GDP: The real growth of the Gross Domestic Product.

The GDP growth (GDPGR) is among the macroeconomic indicators most commonly

used. It is a measure of all the economic activity expected to have an impact on many

factors related to the supply and demand for loans and deposits. The real GDP growth

used in this study is expected to have a positive relationship with solvency.

34

3.7.8 Inflation (INF):

As discussed in the literature review, the relationship between expected inflation (or

long-term interest rate, which incorporates inflation expectations) and solvency is

ambiguous. We proxy expected inflation by current inflation. Inflation (INF) can affect

the costs and revenues of any organization, including banks. Perry, (1992) states that the

effect of inflation on bank solvency depends on whether inflation is expected or not

Table3.7 – Summary of variables and their proxies

Symbol Variable Proxies

BS Bank solvency Total Equity to total liabilities plus Off-Balance-Sheet

items

Α Value of the intercept

LR Liquidity risk The liquidity risk ratio is used as a proxy “liquid

asset /customer and short-term investment” (Valverde

and Fernandez, 2007).

CR Capital risk The financial strength of the bank is equal to the

shareholders' equity divided by the total assets (F

Pasiouras and K Kosmidou, 2006).

Pit Profitability Return on assets » is the ratio of the net profit net after

tax to total average assets (F Pasiouras and K Kosmidou,

2006).

NPL Non-performing loans

(credit risk)

The credit risk ratio as defined by the Basel committee, is

the ratio of total loan defaulters to total debtors

Ln(TA)it Size of the bank Logarithm of total assets (F Pasiouras and K Kosmidou

2006)

LG Liquidity gap Difference between the liability and the asset value of the

firm.

35

Inf

Inflation

The annual inflation rate is the variation of the

family consumer price index (F Pasiouras and K

Kosmidou, 2006).

GDP

Gross domestic product

The real growth of the Gross Domestic Product (F

Pasiouras and K Kosmidou, 2006).

µ

Error term

3.8 Data analysis techniques

Quantitative data analysis is the process of presenting and interpreting numerical data.

The researcher used Panel regression technique to analyze the internal determinants as

well as external determinants in order to come up with conclusions.

3.9 Justification of panel regression technique

Panel data is commonly used because of the following reasons first it has advantage of

giving more informative data as it consist of both cross sectional information, which

captures individual variability, and the time series information, which captures dynamics

adjustments. In short, panel modeling helps to identify a common group of characteristics

while at the same time taking the account the heterogeneity that is present among

individual units. Second, this technique allows for the study of the impact of

macroeconomic developments on solvency after controlling for banks specific

characteristics, with less collinearity among variables, more degrees of freedom and

greater efficiency.

The consensus from the literature on bank solvency is that the appropriate functional

form of analysis is the multi-linear one. To this extent, Short (1979) and Bourke (1989)

consider several forms and conclude that the multi-linear model produces results as good

36

as other functional forms. Thus in this study, a multi-linear model is used to analyze the

cross section time series data to isolate the solvency determinants of Zimbabwean bank

3.10 Statistical techniques used.

The statistical techniques used in the analysis of the data for this research include

frequency distribution, the standard deviation, the distribution of means, analysis of

variance (ANOVA), Pearson. The distribution of means was used in the testing of the

hypotheses. Responses to the objectives are tallied after data collection. Descriptive,

correlations and regression analysis is applied to study and compare the effect of

independent variables on the dependent variable.

3.11 Statistical package used

More specifically the Statistical Package of SPSS was used in the analysis of data. The

has the incredible capabilities and flexibilities of analyzing huge data within seconds and

generating an unlimited gamut of simple and sophisticated statistical results including

simple frequency distribution tables. The Package has the capabilities of executing such

high-level analysis as analysis of variance (ANOVA), multivariate analysis, correlation

and regression analysis, tests of statistical hypotheses, time series analysis, estimations,

confidence interval estimation, comparison of several means, goodness of fit tests and

analysis of contingency table, etc. Considering that the data collected are largely

categorical in form, the chosen SPSS package the researcher considered was very ideal

for use in the data processing and analysis.

3.12 Data interpretation

The data collected were categorized on a question by question basis, for ease of

interpretation and clarity on analysis and responses. The study was conducted through a

sample of 12 banks in Zimbabwe.

37

3.13 Summary

The study was conducted through a survey of twelve (12) banks in Zimbabwe. The

research used purposive sampling techniques to ensure a fair representation of all

commercial banks. For adequate data gathering, triangulation was used, to gather data

through secondary source.

The next chapter presents findings of the study where data collected is presented and

analyzed. This is in line with the objectives and hypothesis indicated in chapter one, to

allow for meaningful conclusions and observations.

38

CHAPTER 4

4.0 DATA ANALYSIS AND PRESENTATION

4.1 Introduction

The chapter focuses on data analysis based on information gathered during research,

mainly from the secondary data that was distributed to a sample representative of

commercial banks. The secondary data was analyzed using SPSS and accordingly it was

coded to ensure ease of classification of analysis and presentation of data.

Since the data was collected from a sample of commercial banks; and not the entire

population, it is therefore subject to sampling errors and tolerances, i.e. some differences

may not be statistically significant.

The study sought to provide answers to the following questions;

Is there any relationship between liquidity risk and bank’s solvency?

Are there any other banks specific variables and macroeconomic variables which affect

bank solvency?

Does liquidity gap affect bank solvency?

4.2 Secondary and literary data analysis

Mass literature on commercial banks in scattered form abound but published data on

categorizing and ranking of problems of liquidity challenges facing commercial banks in

Zimbabwe as well as the contribution of commercial banks to our national economic

growth and development proved rather difficult to come by. It was easier for the

researcher to access data relating to the performance of commercial banks and the impact

of liquidity risk on bank solvency in other parts of the world especially Asian, western

countries and even other African countries like Cameroon and Tunisia than those

pertaining to commercial banks in Zimbabwe. There is therefore need to come up with

credible research on the impact of liquidity risk on bank solvency in Zimbabwe and such

data research should be publicized; in order to reduce information asymmetry

39

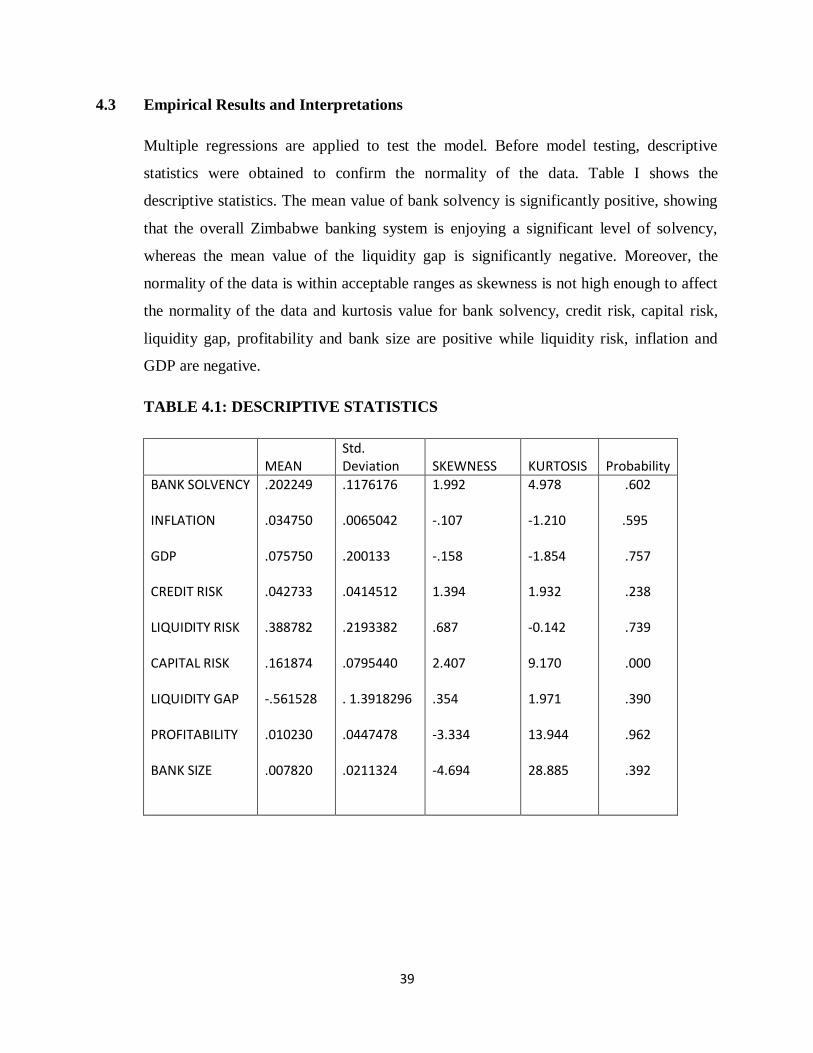

4.3 Empirical Results and Interpretations

Multiple regressions are applied to test the model. Before model testing, descriptive

statistics were obtained to confirm the normality of the data. Table I shows the

descriptive statistics. The mean value of bank solvency is significantly positive, showing

that the overall Zimbabwe banking system is enjoying a significant level of solvency,

whereas the mean value of the liquidity gap is significantly negative. Moreover, the

normality of the data is within acceptable ranges as skewness is not high enough to affect

the normality of the data and kurtosis value for bank solvency, credit risk, capital risk,

liquidity gap, profitability and bank size are positive while liquidity risk, inflation and

GDP are negative.

TABLE 4.1: DESCRIPTIVE STATISTICS

MEAN

Std. Deviation

SKEWNESS

KURTOSIS

Probability

BANK SOLVENCY INFLATION GDP CREDIT RISK LIQUIDITY RISK CAPITAL RISK LIQUIDITY GAP PROFITABILITY BANK SIZE

.202249 .034750 .075750 .042733 .388782 .161874 -.561528 .010230 .007820

.1176176 .0065042 .200133 .0414512 .2193382 .0795440 . 1.3918296 .0447478 .0211324

1.992 -.107 -.158 1.394 .687 2.407 .354 -3.334 -4.694

4.978 -1.210 -1.854 1.932 -0.142 9.170 1.971 13.944 28.885

.602

.595

.757

.238

.739

.000

.390

.962

.392

40

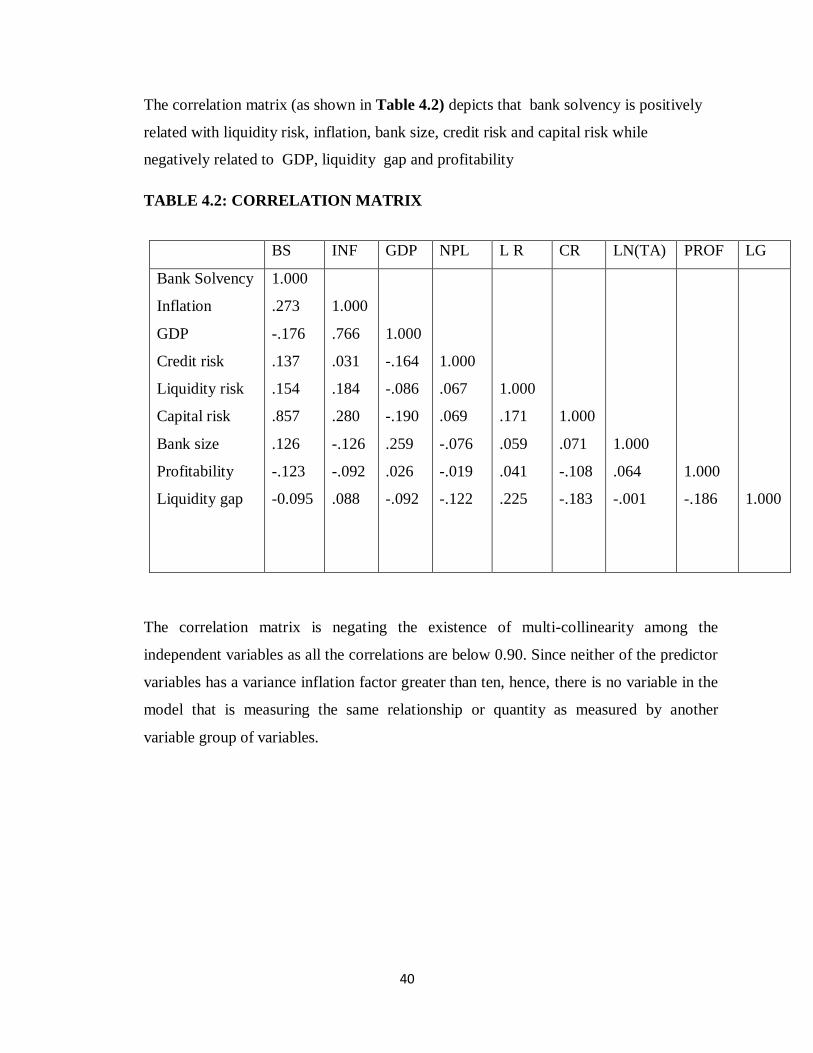

The correlation matrix (as shown in Table 4.2) depicts that bank solvency is positively

related with liquidity risk, inflation, bank size, credit risk and capital risk while

negatively related to GDP, liquidity gap and profitability

TABLE 4.2: CORRELATION MATRIX

The correlation matrix is negating the existence of multi-collinearity among the

independent variables as all the correlations are below 0.90. Since neither of the predictor

variables has a variance inflation factor greater than ten, hence, there is no variable in the

model that is measuring the same relationship or quantity as measured by another

variable group of variables.

BS INF GDP NPL L R CR LN(TA) PROF LG

Bank Solvency

Inflation

GDP

Credit risk

Liquidity risk

Capital risk

Bank size

Profitability

Liquidity gap

1.000

.273

-.176

.137

.154

.857

.126

-.123

-0.095

1.000

.766

.031

.184

.280

-.126

-.092

.088

1.000

-.164

-.086

-.190

.259

.026

-.092

1.000

.067

.069

-.076

-.019

-.122

1.000

.171

.059

.041

.225

1.000

.071

-.108

-.183

1.000

.064

-.001

1.000

-.186

1.000

41

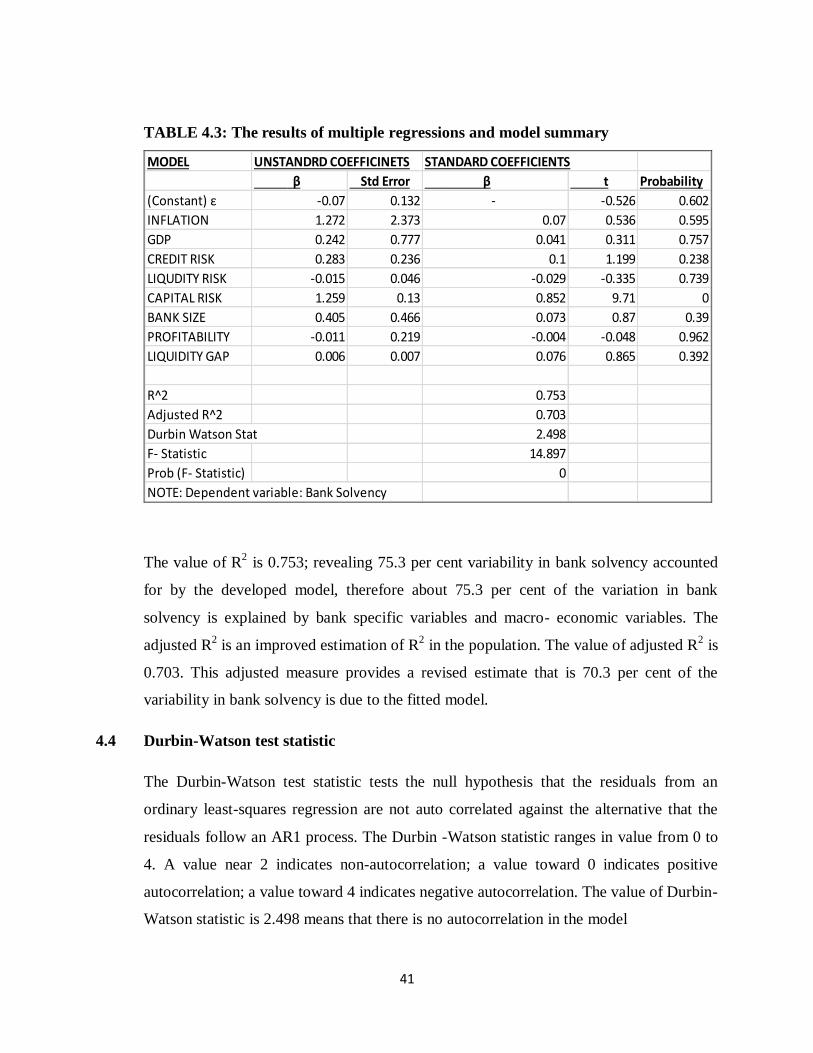

TABLE 4.3: The results of multiple regressions and model summary

MODEL UNSTANDRD COEFFICINETS STANDARD COEFFICIENTS

β Std Error β t Probability

(Constant) ε -0.07 0.132 - -0.526 0.602

INFLATION 1.272 2.373 0.07 0.536 0.595

GDP 0.242 0.777 0.041 0.311 0.757

CREDIT RISK 0.283 0.236 0.1 1.199 0.238

LIQUDITY RISK -0.015 0.046 -0.029 -0.335 0.739

CAPITAL RISK 1.259 0.13 0.852 9.71 0

BANK SIZE 0.405 0.466 0.073 0.87 0.39

PROFITABILITY -0.011 0.219 -0.004 -0.048 0.962

LIQUIDITY GAP 0.006 0.007 0.076 0.865 0.392

R^2 0.753

Adjusted R^2 0.703

Durbin Watson Stat 2.498

F- Statistic 14.897

Prob (F- Statistic) 0

NOTE: Dependent variable: Bank Solvency