Embed Size (px)

Citation preview

337

3 • Royal Malaysian Customs Guideline and Minutes of Meetings

INDIRECT TAXES

THIS PAGE IS INTENTIONALLY LEFT BLANK

338

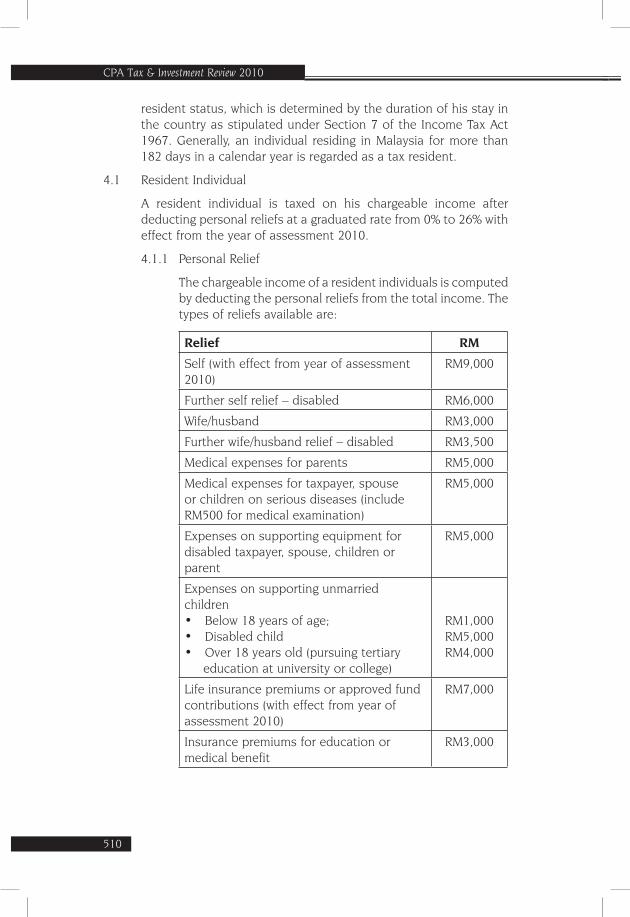

CPA Tax & Investment Review 2010

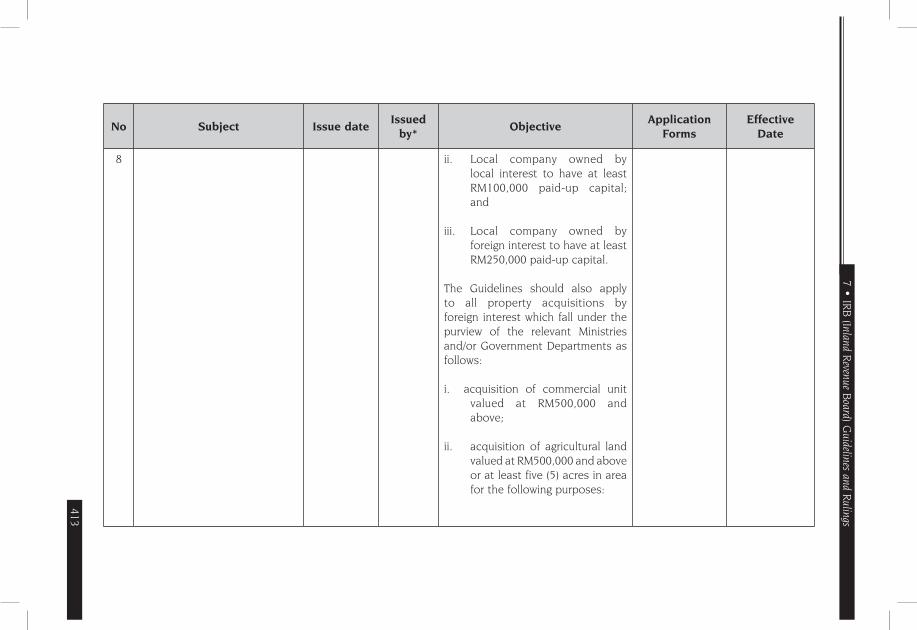

1.0 Customs (Prohibition of Imports) (Amendment) (No. 3) Order 2009

Comment:

The above Amendment seeks to introduce the requirement to obtain an approved permit for importation of certain alloy steel and high carbon steel products.

Effective date: 1 August 2009

2.0 Customs (Amendment) (No. 4) Regulations 2009

Comment:

The above Amendment seeks to introduce new value declaration form (i.e. Form K1A) where invoice value threshold for each consignment is being raised from RM10,000 to RM20,000.

Effective date: 27 August 2009

3.0 Customs Duties (Goods of ASEAN Countries Origin) (ASEAN Harmonised Tariff Nomenclature and Common Effective Preferential Tariff) (Amendment) (No. 5) Order 2009

Comment:

The above Amendment seeks to introduce new definitions to Rules of Origin for the Agreement on the Common Effective Preferential Tariff Scheme for the ASEAN free trade area.

Effective date: 1 August 2008

4.0 Customs (Prohibition of Imports) (Amendment) (No. 4) Order 2009

Comment:

The above Amendment seeks to impose certification requirement for importation of certain products and articles of iron and steel.

Effective date: 13 October 2009

A Amendments to Customs Legislation

339

4 • Indirect Taxes

5.0 Customs (Amendment) (No. 5) Regulations 2009

Comment:

The above Amendment seeks to introduce new ordinary hours for Johor Bahru Customs offices and warehouses and goods may be imported or exported by road via Johor Bahru to be at all times on any day.

Effective date: 15 November 2009

6.0 Customs (Amendment) (No. 6) Regulations 2009

Comment:

The above Amendment seeks to:-

(i) Introduce new ordinary hours for Kota Putra, Durian Burung, Padang Terap, Kedah to be from 8.00 a.m. to 7.00 p.m. on any day.

(ii) Permit all goods to be imported and exported by road or railway via Padang Besar and Kota Putra, Durian Burung, Padang Terap, Kedah.

Effective date: 24 December 2009

7.0 Customs (Prohibition of Imports) (Amendment) (No. 5) Order 2009

Comment:

The above Amendment seeks to introduce:-

(i) Total prohibition for the importation of new pneumatic snow tyres and new retreaded snow tyres for all types of vehicles from all countries.

(ii) Requirement to obtain approved permit or certification for importation of used pneumatic tyres and used retreaded tyres from all countries.

Effective date: 1 January 2010

8.0 Customs (Amendment) (No. 7) Regulations 2009

Comment:

The above Amendment seeks to introduce requirement of entry and exit declaration in Form Customs No. 22 for any person arriving or leaving Malaysia.

Effective date: 1 January 2010

340

CPA Tax & Investment Review 2010

9.0 Customs Duties (Agreement Establishing The ASEAN-Australia-New Zealand Free Trade Area) Order 2009

Comment:

The above Order seeks to introduce preferential tariff rate under the Agreement establishing the ASEAN-Australia-New Zealand Free Trade Area.

Effective date: 1 January 2010

10.0 Customs (Import Licence Fee for Motor Vehicle) Regulations 2009

Comment:

The above Regulations seeks to impose an import licence fee of RM10,000 for each unit of motor vehicle (excluding motorcycle) imported by the import licence holder.

Effective date: 1 January 2010 to 31 December 2015

11.0 Customs Duties (Goods under Agreement on Comprehensive Economic Cooperation between Member States of the ASEAN and the Republic of India) Order 2009

Comment:

The above Order seeks to introduce preferential tariff rate under the Agreement on Comprehensive Economic Cooperation between Member States of the ASEAN and the Republic of India.

Effective date: 1 January 2010

12.0 Customs Duties (Goods of ASEAN Countries Origin) (ASEAN Harmonised Tariff Nomenclature and Common Effective Preferential Tariff) (Amendment) (No. 8) Order 2009

Comment:

The above Amendment seeks to introduce new product originating criteria (i.e. product specific rules) under the Rules of Origin for the Agreement on the Common Effective Preferential Tariff Scheme for the ASEAN free trade area.

Effective date: 1 January 2010

13.0 Customs Duties (Exemption) (Amendment) Order 2010

Comment:

The above Amendment seeks to revise the import duty exemption period for a Labuan/Langkawi registered motor vehicle / motor cycle entering Principal Customs Area and subsequently returned

341

4 • Indirect Taxes

to Labuan/Langkawi from a period not exceeding 14 days per trip, subject to a maximum period of 30 days in any one year to a period not exceeding 30 days per trip and subject to a maximum period of 90 days in any one year.

Effective date: 11 February 2010

14.0 Customs Duties (Amendment) Order 2010

Comment:

The above Amendment seeks to eliminate the (50%) import duty imposed on golf cars, including golf buggies.

Effective date: 1 April 2010

15.0 Customs Duties (Goods of ASEAN Countries Origin) (ASEAN Harmonised Tariff Nomenclature and Common Effective Preferential Tariff) (Amendment) Order 2010

Comment:

The above Amendment seeks to eliminate the CEPT import duty imposed on golf cars, including golf buggies.

Effective date: 1 April 2010

342

CPA Tax & Investment Review 2010

B Amendments to Excise Legislation

1.0 Excise Duties (Amendment) Order 2009

Comment:

The above Amendment seeks to increase the specific excise duty rate of:-

(i) cigars, cheroots and cigarillos falling under HS 2402.10 000 and 2402.90 100 from “RM180.00 per kg and 20%” to “RM190.00 per kg and 20%”; and

(ii) cigarettes falling under HS 2402.20 900 and 2402.90 200 from “RM0.18 per stick and 20%” to “RM 0.19 per stick and 20%”.

Effective date: 1 October 2009

2.0 Excise Duties (Exemption) (Amendment) Order 2010

Comment:

The above Amendment seeks to revise the excise duty exemption period for a Labuan/Langkawi registered motor vehicle / motor cycle entering Principal Customs Area and subsequently returned to Labuan/Langkawi from 14 days per trip, subject to a maximum period of 30 days in one year to 30 days per trip, subject to a maximum period of 90 days in one year.

Effective date: 11 February 2010

343

4 • Indirect Taxes

C Amendments to Sales Tax Legislation

1.0 Sales Tax (Exemption) (Amendment) Order 2010

Comment:

The above Amendment seeks to revise the sales tax exemption period for a Labuan/Langkawi registered motor vehicle / motor cycle entering Principal Customs Area and subsequently returned to Labuan/Langkawi from for an aggregate of not more than 90 days in one year to 30 days per trip, subject to a maximum period of 90 days in one year.

Effective date: 11 February 2010

344

CPA Tax & Investment Review 2010

D Amendments to Service Tax Legislation

1.0 Service Tax (Amendment) (No. 2) Regulations 2009

Comment:

The above Amendment seeks to prescribe new category of taxable person and taxable service as follows:-

(a) Taxable person

Any person who is regulated by Bank Negara Malaysia and provides credit card or charge card services through the issuance of a credit card or a charge card

(b) Taxable service

Provision of credit card or charge card services through the issuance of a principal credit card, principal charge card, supplementary credit card or supplementary charge card, whether or not annual subscription or fee is imposed excluding

(i) provision of charge card services where the charge card is issued by any petroleum company to the Government of Malaysia or any person for the procurement of products and services supplied for the use of or in connection with vehicles owned by the Government of Malaysia or such person; or

(ii) provision of charge card services where the charge card is used as a payment instrument only within the premises of a workplace, an education institution or a golf or sports club by its workforce, students or members, as the case may be.

Effective date: 1 January 2010

345

4 • Indirect Taxes

2.0 Service Tax (Rate of Tax) Order 2009

Comment:

The above Order seeks to impose service tax at the rates specified as follows:-

• 5% of the price, charge or premium of the taxable serviceother than taxable service relating to credit card or charge card services

• Taxable service relating to credit card and charge cardservices:-

(i) RM 50.00 shall be chargeable for the issuance/renewal of each principal credit card and principal charge card on the date of issuance/renewal of the card and thereafter every subsequent twelve months or part thereof; and

(ii) RM 25.00 shall be chargeable for the issuance/renewal of each supplementary credit card and supplementary charge card on the date of issuance/renewal of the card and thereafter every subsequent twelve months or part thereof.

The Service Tax (Rate of Tax) Order 2000 is revoked.

Effective date: 1 January 2010

346

CPA Tax & Investment Review 2010

E Others

1.0 Free Zones (Declared Area) (Amendment) Notification 2009

Comment:

The free zone area under the state of Selangor is amended as follows:-

Effective date: 17 July 2009

2.0 Free Zones (Amendment) Notification 2009

Comment:

The above Amendment Notification seeks to amend the First Schedule to the Free Zones Act 1990 by substituting item 5 with the following item:

Effective date: 17 July 2009

(1) (2)

State Limits of Zones

Selangor All that land situated in the Mukim of Klang,District of Klang, Selangor bounded by the grey line as shown in the Gazette Plan 1174 and Lot No. 55709 and No. 55710 as shown in Gazette Plan 1452 deposited in the Office of the Director of Survey and Mapping, Selangor

(1)Name of Free Commercial Zone

(2)Activities

5. West Port, Pulau Indah, Mukim of Klang, District of Klang:

Commercial

All that land situated in the Commercial Mukim of Klang, District of Klang, Selangor bounded by the grey line as shown in the Gazette Plan 1174 and Lot No. 55709 and No. 55710 as shown in Gazette Plan 1452 deposited in the Office of the Director of Survey and Mapping, Selangor

347

4 • Indirect Taxes

3.0 Free Zones (Declared Area) (Amendment) Notification 2010

Comment:

The free zone area under the state of Johor is amended as follows:-

i. Land occupied by Felda Johore Bulkers at Lot 66228 and 66229 as shown in Gazette Plan 2234;

ii. Land occupied by Petronas Dagang Berhad at Lot 66226 and 66227 as shown in Gazette Plan 2233;

iii. Land occupied by BP Malaysia Sdn. Bhd. at Lot 66221 and 66222 as shown in Gazette Plan 2233;

iv. Customs Inspection Bay in area of 0.459 hectare in Container Terminal at Lot 66208 as shown in Gazette Plan 2233;

v. Land (Lot A) in area of 1.909 hectares at Lot 66233 and land (Lot B) in area of 1.028 hectares at lot 83274 as shown in Gazette Plan 2282;

vi. A part of land at main entrance as shown in Gazette Plan 3067;

vii. Land occupied by Sime Sembawang Corp. Engineering Sdn. Bhd. at Lot 83288, 83289, 83290, 83291, 83292, 83293, 83287, 83284, 83281, 83282 and 83283 as shown in Gazette Plan 3068; and

viii. Land occupied by Aramijaya Sdn. Bhd. at Lot 83285 and 83286 as shown in Gazette Plan 3068.

Effective date: 4 February 2010

(1)State

(2)Limits of Zones

Johor All that land situated in the Mukim of Plentong, in the District of Johor Bahru, Johor, bounded by the grey line as shown in Gazette Plans 2233, 2234, 2283, 3065 and 3066 deposited in the Office of the Director of Survey and Mapping, Johor, excluding the areas specified below:

348

CPA Tax & Investment Review 2010

4.0 Free Zones (Amendment) Notification 2010

Comment:

The above Amendment Notification seeks to amend the First Schedule to the Free Zones Act 1990 by substituting item 1 with the following item:

(1)Name of Free Commercial Zone

(2)Activities

1. Pasir Gudang Port Free Zone, Mukim of Plentong, District of Johor Bahru, Johor:

All that land situated in the Mukim of Plentong, in the District of Johor Bahru, Johor, bounded by the grey line as shown in Gazette Plans 2233, 2234, 2283, 3065 and 3066 deposited in the Office of the Director of Survey and Mapping, Johor, excluding the areas specified below:

Commercial

i. Land occupied by Felda Johore Bulkers at Lot 66228 and 66229 as shown in Gazette Plan 2234;

ii. Land occupied by Petronas Dagang Berhad at Lot 66226 and 66227 as shown in Gazette Plan 2233;

iii. Land occupied by BP Malaysia Sdn. Bhd. at Lot 66221 and 66222 as shown in Gazette Plan 2233;

iv. Customs Inspection Bay in area of 0.459 hectare in Container Terminal at Lot 66208 as shown in Gazette Plan 2233;

v. Land (Lot A) in area of 1.909 hectares at Lot 66233 and land (Lot B) in area of 1.028 hectares at lot 83274 as shown in Gazette Plan 2282;

vi A part of land at main entrance as shown in Gazette Plan 3067;

349

4 • Indirect Taxes

vii. Land occupied by Sime Sembawang Corp. Engineering Sdn. Bhd. at Lot 83288, 83289,83290, 83291, 83292, 83293, 83287, 83284, 83281, 83282 and 83283 as shown in Gazette Plan 3068; and

viii. Land occupied by Aramijaya Sdn. Bhd. at Lot 83285 and 83286 as shown in Gazette Plan 3068.

Effective date: 4 February 2010

350

CPA Tax & Investment Review 2010

THIS PAGE IS INTENTIONALLY LEFT BLANK

351

5 • Summary of Tax Cases

THIS PAGE IS INTENTIONALLY LEFT BLANK

SUMMARY OF TAX CASES

352

CPA Tax & Investment Review 2010

A Malaysian Special Commissioners'Decisions

1.0 SS SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,862

Facts

The taxpayer was in the business of property development with financial year ended on 30 June. On 17 November 1997, it entered into a Sale and Purchase Agreement (SPA) to dispose of a piece of its development land held as stock-in-trade. The SPA was conditional and required approval from the Foreign Investment Committee (FIC). In the event that the stipulated conditions precedents were not fulfilled, the SPA would be deemed to have been terminated and the deposit would be refunded to the Vendor. The entire conditions precedent were fulfilled on 15 May 1999 and balance of the purchase price was paid to the taxpayer on 18 June 1999.

Issues

Whether profit from the sale of the land should be taxed in the year of assessment (YA) when the SPA was signed or when all the conditions of the SPA were satisfied.

Arguments

Taxpayer

The taxpayer contended that the disposal should be recognized by reference to the terms of the SPA and therefore the profit from the sale of the land was derived in YA 2000 (Preceding Year Basis). In accordance with the Income Tax (Amendment) Act, 1999, the profit earned or derived is not liable to tax.

DGIR

The Director General of Inland Revenue (DGIR) contended that the profit from the sale of the land should be taxed in YA 1999 as income is derived on the date the stock in trade was sold via the SPA dated 17 November 1997.

Decision

The Special Commissioners allowed the taxpayer’s appeal on the following grounds:

(i) Pursuant to section 3 of the Income Tax Act, 1967 (ITA),

353

5 • Summary of Tax Cases

income tax shall be charged upon the income of any person for each year of assessment when it accrues or is derived from Malaysia or received in Malaysia. Income is said to accrue when there comes into existence an unconditional right of receiving it. Income is derived when there is a present right to receive a quantifiable amount that is not subject to any contingency or defeasibility.

(ii) The SPA is a contingent contract with condition precedents which must be complied with before it can be effective. The entire conditions precedents were fulfilled on 15 May 1999 i.e. in YA 2000 (PYB). Thus until and unless all the conditions precedent were fulfilled, the SPA was not enforceable and the purchase price only became a debt due when all the conditions were satisfied.

2.0 B DEVELOPMENT SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,869

Facts

The taxpayer is the parent company of BI Sdn Bhd (“BI”) and owned 100% of BI’s 5,000,000 shares. On 9 May 1995, BI executed a joint venture agreement with another company, MBNS (Incorporation) (MBNS) to develop a plot of land. The land had been alienated to MBNS by the state government, and MBNS was its registered proprietor. Consideration of RM2 million was paid by BI to acquire the contractual right to develop the said land as a clay-based development project and mixed development project. Expenditure incurred on this project was treated in BI’s audited accounts as development expenditure in the current assets category. The subject land was never treated as capital assets in BI’s accounts. BI did not enter into any caveat or register any right or interest over the land. On 1 December 2000, when the taxpayer sold its shares in BI to UH Berhad under a restructuring scheme, it was subjected to real property gains tax for the gains on the disposal of shares in a real property company under Paragraph 34A, Schedule 2 of the Real Property Gains Tax Act, 1976 (RPGTA).

Issues

Whether the gains made by the taxpayer from the disposal of shares falls within the ambit of the RPGTA.

Arguments

Taxpayer

The taxpayer contended that since BI did not own the land, BI could not be labeled as a real property company and so the

354

CPA Tax & Investment Review 2010

taxpayer could not be said to have acquired and disposed of shares in a real property company resulting in real property gains tax under Paragraph 34A, Schedule 2 of the RPGTA.

DGIR

The Director General of Inland Revenue (DGIR) contended that the fact that BI was not the registered owner of the land did not exclude it from falling under the ambit of Paragraph 34A, Schedule 2 of the RPGTA as real property covers not only land, but also interest option or other right in or over such land.

Decision

The appeal was dismissed on the following grounds:

(i) The fact that BI was not the registered owner of the said land did not exclude it from falling under the ambit of Paragraph 34A, Schedule 2 of the RPGTA as real property covers not only land, but also interest option or other right in or over such land.

(ii) From the joint venture agreement executed with MBNS, the Special Commissioners concluded that the true intention of the parties and the real spirit of the agreement is BI had total control and exclusive right over the said land.

(iii) Hence, even though the said land was not registered under BI’s name, the fact that BI hads an interest over it made BI a real property company within the meaning of Paragraph 34A, Schedule 2 of the RPGTA.

(iv) On whether the said land is capital asset or stock-in-trade of BI, the joint venture agreement between MBNS and BI has spelt out the function of BI is to develop the said land.

(v) The said land has been left dormant without any development from the day the said land was alienated until the disposal of the shares. There was no plan submitted to the respective authority for the development of the said land and this shows that the land was kept as capital asset of BI and there is no evidence to support the contention that BI is carrying out any trading activity over the said land.

3.0 AT SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,875

Facts

The taxpayer was awarded certain contracts in year 1997. To secure financing for the contracts that were awarded to the taxpayer, the

355

5 • Summary of Tax Cases

taxpayer seeks the support of its parent company to provide corporate guarantees to the banks as security for the financing facilities. In return for the corporate guarantees provided, the taxpayer paid its parent company guarantee commission fees at specified rates. The taxpayer claimed a tax deduction on the guarantee commission fees under Section 33(1) of the Income Tax Act, 1967 (ITA), which was disallowed by the Inland Revenue Board.

Issues

Whether the guarantee commission fee incurred qualified for deduction under Section 33(1) of the ITA.

Arguments

Taxpayer

(i) The taxpayer contended that the banking facilities were obtained to meet the funding requirement for the earning of the profits of the business, and not as an addition to capital. Since the banking facilities were used exclusively for financing the taxpayer’s contracts, the guarantee commission fee is an expense closely connected or incidental to the business of the taxpayer and should therefore be allowed as a tax deduction.

(ii) The taxpayer further contended that guarantee fees, like interest, were an integral part of a loan package and must come within the ambit of Section 33(1) of the ITA.

DGIR

(i) The Director General of Inland Revenue (DGIR) contended that the guarantee commission fees were capital in nature, having been incurred to secure funds which indirectly enhanced the taxpayer’s capital.

(ii) The Director General of Inland Revenue (DGIR) further contended that the purpose of the facilities obtained by the taxpayer was only to finance the business of the taxpayer, and not incurred to produce the income of the taxpayer. Hence, the expenditure incurred on the guarantee commission fees does not meet the criteria stipulated in Section 33(1) of the ITA i.e. not wholly and exclusively incurred in the production of the taxpayer’s income.

Decision

The appeal was dismissed on the following grounds :-

356

CPA Tax & Investment Review 2010

(i) The taxpayer sought support from its parent company to provide corporate guarantee as normally required by financial institutions when there are no other forms of adequate security and in return, the taxpayer paid a guarantee commission fee to its parent company. The guarantee commission fees were incurred by the taxpayer in order to secure financing facilities and thus were not wholly and exclusively incurred in the production of income. In view of the above, the guarantee commission fees are not deductible expenditure under Section 33(1) of the ITA.

4.0 SPM SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,881

Facts

The taxpayer entered into a franchise agreement with S Corporation (S Corp), a company incorporated in the United States of America. The taxpayer was obliged to pay franchise fees equal to 8% of its gross turnover to S Corp on a monthly basis, in return for which, the taxpayer received the exclusive right to trade in Malaysia using the multi-level marketing system of S Corp and to receive continued support and assistance from S Corp during the term of the franchise agreement i.e. for a period of 3 years with an automatic option to renew. The taxpayer has also paid withholding tax on the franchise fees under Section 109B of the Income Tax Act, 1967 (ITA). The Inland Revenue Board (IRB) disallowed the deduction claim in respect of the franchise fees and also imposed penalties.

Issues

Whether the franchise fees paid to S Corp qualified for a tax deduction under Section 33(1) of the ITA.

Arguments

Taxpayer

The taxpayer contended that the fees were a necessary part of the taxpayer’s earning process, paid to obtain continuing services in order to meet the continuing needs of the business. The fees were also directly connected to the taxpayer’s business, incurred to generate sales income and did not give rise to the acquisition of any identifiable asset. Hence, the taxpayer contended that the franchise fees paid were wholly and exclusively incurred in the production income which qualifies for a deduction under Section 33(1) of the ITA.

357

5 • Summary of Tax Cases

DGIR

The Director General of Inland Revenue (DGIR) contended that the franchise fees were not paid for acquiring trading stock of the taxpayer but were paid in order to obtain sole and exclusive right to market S Corp’s products in Malaysia. Hence, the franchise fees were considered to be capital expenditure and not deductible under Section 33(1) of the ITA.

Decision

The taxpayer’s appeal was allowed on the following grounds:

(i) The franchise fees paid for the services were a necessary part of the income generating process of the taxpayer and that the continuous services derived were necessary for the taxpayer to meet the continuous demand of its business.

(ii) The fees calculated at 8% of the gross sales were recurring payments which were not paid “once and for all”.

(iii) The franchise fees are not capital expenditure as it neither gave rise to an enduring benefit nor the acquisition of any identifiable assets.

(iv) The franchise fees were revenue expenditure incurred for the sole purpose of producing the gross income of the taxpayer, and thus allowable for tax deductions under Section 33(1) of the ITA.

5.0 ELM SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,887

Facts

The taxpayer was involved in the business of trading in the pharmaceutical and animal health products and from time to time, organized congresses for the dissemination of knowledge and information as well as promoting the taxpayer’s product. The taxpayer sponsored doctors or pharmacists to speak and attend such congresses as they are reputable authorities in their field, well abreast of technological advances in drugs and medicine and the topic of their papers were related to the diseases or medical conditions for which the appellant had drugs or medicines. The sponsorship was limited to the costs of travel, meals, accommodation and registration fees for the congress for which the taxpayer claimed tax deduction. The Director General of Inland Revenue (DGIR) disallowed the claim of the congress expenses on the basis that the expenses were “entertainment” and not deductible under Section 39(1)(l) of the Income Tax Act, 1967 (ITA)

358

CPA Tax & Investment Review 2010

although these expenses had earlier been allowed as a deduction. Accordingly, the DGIR raised additional assessments and imposed penalty of 60% on the taxpayer.

Issues

(i) Whether the congress expenses that were allowable under Section 33(1) of the ITA should be disallowed as “entertainment” under Section 39(1)(l) of the ITA.

(ii) Whether the penalties imposed is justifiable.

Arguments

Taxpayer

(i) The taxpayer contended the congress expenses were wholly and exclusively incurred in the production income under Section 33(1) of the ITA and the said expenses did not fall under the definition of “entertainment” in Section 18 of the ITA.

(ii) The sponsored speakers and doctors having to present papers on the special fields were providing a service and invested time by attending the congress. In return, both the participants and the taxpayer derived practical advantage which is viewed to be consideration in law.

(iii) In respect of the penalty, the tax returns submitted by the taxpayer were based on the taxpayer’s interpretation of the tax laws and the claims were substantiated by full disclosure of all information. Moreover, the Director General of Inland Revenue (DGIR) had previously allowed a deduction for such costs.

DGIR

(i) The DGIR contended that the congress expenses were entertainment in nature as they fall under the definition of entertainment in Section 18 of the ITA, thus not deductible under Section 33 of the ITA.

(ii) The doctors and pharmacists attending the congress were not the taxpayer’s employees. Hence, the sponsorship cost were not related to the business of the taxpayer as well as not wholly and exclusively incurred in the production of the taxpayer’s gross income.

(iii) The penalty was imposed on the grounds that the taxpayer made an incorrect return in claiming tax deduction on certain expenses which were not supposed to be deducted.

359

5 • Summary of Tax Cases

Decision

The taxpayer’s appeal was allowed on the following grounds:

(i) Citing the case KPHDN v. Aspac Lubricants (Malaysia) Sdn Bhd, it was held that where the dominant purpose of the expenditure is for promotion of the company’s business, the expenditure is not “entertainment” in nature.

(ii) The doctors attending the congresses gave up their time and potential of earning income, in exchange for knowledge of the latest products and developments in their fields, which are viewed to be consideration in law.

(iii) The doctors also obtained new and updated knowledge of the products which likely will result in an increase of sales or market share. This practical advantage could also be viewed as consideration.

(iv) The penalty imposed was not justified and the return was not incorrect on the basis that the deductions claimed were substantiated by the appropriate information and the DGIR had in the past allowed such deduction.

6.0 NVA SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,897

Facts

The taxpayer was in the business of marketing burial plots, urn compartments and funeral packages. The marketing functions of its business were carried out by appointed agents who were paid a commission. Apart from commissions, the agents who achieved targets were also being rewarded with goods or cash incentives.

The Inland Revenue Board (IRB) conducted a field audit in 2004 and focused on cash incentives and promotion expenses incurred by the taxpayer. The Director General of Inland Revenue (DGIR) found certain deductions to be incorrectly claimed and disallowed the incentive expenses as being entertainment under Section 18 of the Income Tax Act, 1967 (ITA) and restricted under Section 39(1)(l) of the ITA. Additional tax and penalties pursuant to Section 113(2) of the ITA were also imposed for the years of assessment concerned.

Issues

(i) Whether the incentive expenses were allowable under Section 33(1) and not restricted under Section 39(1)(l) of the ITA; and

360

CPA Tax & Investment Review 2010

(ii) Whether the Director General of Inland Revenue (DGIR) was right in law to impose the penalty of 60% under Section 113(2) of the ITA.

Arguments

Taxpayer

(i) The taxpayer argued that the cash incentives paid to the agents were wholly and exclusively incurred in the production of their gross income and should be allowed as deduction under Section 33(1) and not restricted under Section 39(1)(l) of the ITA.

(ii) In addition, the taxpayer contended that the penalty imposed under Section 113(2) of the ITA were inappropriate as the expenses were claimed based on their interpretation in good faith and not deliberately providing incorrect information nor omitting or understating its income.

DGIR

(i) The DGIR recognised the fact that the expenses claimed were “incentive” and did fall under Section 33(1) of the ITA. However the DGIR argued that the expenses were in the form of entertainment as defined under Section 18 and hence, not allowable as deduction pursuant to Section 39(1)(l) of the ITA.

(ii) Since the taxpayer made an incorrect return or provided incorrect information in relation to its tax liability, the imposition of penalty under Section 113(2) of the ITA is thus appropriate.

Decision

The Special Commissioners allowed the taxpayer’s appeal on the following grounds:

(i) The incentive expenses do fall under Section 33(1) of the ITA as the expenses were incurred solely with the object of promoting the taxpayer’s business.

(ii) Incentive expenses (cash payouts forming part of incentive packages to motivate the agents to make greater sales) do not constitute entertainment defined under Section 18 of the ITA and not prohibited by Section 39(1)(l) . The expenses in fact relate to the performance of the taxpayer’s profit earning operations and would be revenue in nature.

(iii) The imposition of penalty under Section 113(2) was wrong in law since the claim for tax deduction was based on the taxpayer’s interpretation of the law in good faith.

361

5 • Summary of Tax Cases

7.0 XS HOTEL SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,905

Facts

The taxpayer is a hotel operator of a 5-star hotel which has been registered with the Ministry of Culture, Arts and Tourism in accordance to Section 2(1) of the Promotion of Investments Act, 1986 (PIA). The taxpayer undertook expansion project for the hotel and its application for investment tax allowance was granted for a period of 5 years, effective from 31 January 1992. The taxpayer had incurred RM74,424,130 as qualifying capital expenditure in relation to its hotel business and claimed investment tax allowance and industrial building allowance (IBA) from the year of assessment (YA) 1993 to YA 1997, and the Director General of Inland Revenue (DGIR) had allowed the claims. Upon expiry of the investment tax allowance period on 30 January 1997, the taxpayer continued to claim IBA on the residual capital expenditure in its tax computations for YAs 1998 to 2000 (CYB).

Issues

Whether the taxpayer was entitled to continue claiming IBA on the residual value of the qualifying capital expenditure until it has been fully utilized subsequent to the expiry of the investment tax allowance period?

Arguments

Taxpayer

The taxpayer contended that it is entitled to continue claiming IBA for the YAs 1998 to 2000 (CYB) although the investment tax allowance period has expired on 30 January 1997 based on the following:

(i) The hotel is within the definition under the PIA and is of approved standard.

(ii) Section 30 of the PIA which allows the claim of IBA is silent as to whether IBA expires upon the cessation of investment tax allowance.

(iii) Applying purposive approach, the Parliament would not have intended to limit the grant of IBA for a hotel for a period of 5 years.

(iv) The general position under Schedule 3 of the Income Tax Act, 1967 (ITA) is that capital allowance and IBA shall be available until fully exhausted.

362

CPA Tax & Investment Review 2010

(v) In the event there is a doubt on the interpretation of Section 30 of the PIA, it should be resolved in favour of the taxpayer.

DGIR

The DGIR contended that:

(i) The taxpayer is not entitled to continue claiming IBA since the investment tax allowance period had expired on 30 January 1997. The hotel building is deemed to be an industrial building for that period where investment tax allowance was granted.

(ii) Paragraph 65(3) Schedule 3 of the ITA had specially disqualified hotel to be treated as an industrial building.

(iii) The taxpayer had enjoyed notional allowance during the period in dispute (YA 1998 to 2001) as provided for under paragraph 68 Schedule 3 of the ITA.

Decision

The Special Commissioners dismissed the taxpayer’s appeal on the following grounds:

(i) Prior to Year of Assessment 2002, a hotel building was not an industrial building and therefore was not entitled to claim IBA.

(ii) Pursuant to Section 19 of PIA, a hotel building is deemed an industrial building when a hotel business is carried on by a pioneer company.

(iii) The purposive approach is not applicable as there is no ambiguity in section 30 of the PIA.

(iv) There is no provision in the PIA or the ITA to allow any person to enjoy claiming IBA where the period for it has clearly expired.

8.0 SE SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,912

Facts

The taxpayer is principally engaged in property development and investment. The taxpayer has been granted the right to construct a mixed development project which includes a shopping complex with a 20 storey hotel above and apartments. The shopping complex underneath the hotel development was held for investment. On the advice by Malayian Industrial Development Authority (MIDA),

363

5 • Summary of Tax Cases

the taxpayer incorporated a wholly owned subsidiary, SHSB to carry on the business as a hotel keeper. Subsequently, the taxpayer transfer the right to build the hotel to SHSB for a consideration of RM7,000,000 satisfied by issuance of RM5,320,000 shares in SHSB and the balance was credited to the taxpayer’s current account with SHSB. The taxpayer applied for separate strata titles of the hotel and the cost for the application was reimbursed by the SHSB.

The Director General of Inland Revenue Board (DGIR) has assessed the income from the transfer of right under Section 24(2) of Income Tax Act, 1967 (ITA).

Issues

(i) Whether the right to build the hotel that was transferred formed part and parcel of the taxpayer’s stock in trade under section 35 of the ITA and the gain from the sale taxable under section 24(2) of the ITA, or

(ii) Whether the gain from the sale is a capital gain taxable under the Real Property Gains Tax Act, 1967 (RPGTA).

Arguments

Taxpayer

The taxpayer contended that the transfer of right to build the hotel to its subsidiary company does not constitute trading stock since the shopping complex underneath is not stock in trade but held as an investment for rental purposes. Therefore, since it is a disposal of a right, the receipts from the disposal are capital in nature and should be taxed under the RPGTA.

DGIR

The DGIR contended that the gain arising from the disposal of the projects and the hotel was not a sale of an investment but from trading stock and hence the taxable under section 24(2) of the ITA.

Decision

The Special Commissioners allowed the taxpayer’s appeal on the following grounds:

(i) The shopping complex and the proposed hotel remained as fixed assets of the taxpayer and was kept as investment for purpose of deriving rental income.

(ii) The subsequent transfer of right to its subsidiary was a

364

CPA Tax & Investment Review 2010

transfer of its fixed asset. Any gain derived from this transfer should be taxed under RPGTA.

9.0 LFC SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI (2009) MSTC 3,917

Facts

The taxpayer is principally engaged in the business of providing sea transportation services for passengers, vehicles and vehicles with cargo between the Labuan jetty and Menumbuk jetty in Sabah. The taxpayer has leased 3 vessels from the State Government of Sabah for its business operations. These vessels were not registered as ships under the Merchant Shipping Ordinance, 1952 (the Ordinance). In year 2007, the taxpayer purchased the 3 vessels and was in the process of registering the vessels as ship under the Ordinance. Notwithstanding that, the taxpayer currently owned a ship which has already been registered under the Ordinance.

Issues

Whether the taxpayer was eligible for income tax exemption under section 54A of the Income Tax Act, 1967 (ITA)?

Arguments

Taxpayer

(i) The taxpayer contended that the vessels used in its business were ships and not ferries based on the definition under the Ordinance and description and usage of the vessels.

(ii) The vessels need not be registered under the Ordinance as they belonged to the Sabah State Government.

DGIR

(i) The DGIR contended that the vessels do not fall within the definition of a “Malaysian ship” under section 54A of the ITA since they were not registered under the Ordinance.

(ii) The vessels were ferries which were specifically excluded in the definition of “Malaysian Ship” under section 654A of the ITA.

Decision

The Special Commissioners allowed the taxpayer’s appeal on the following grounds:

(i) The vessels need not be registered under the Ordinance as they belonged to the Sabah State Government. They were

365

5 • Summary of Tax Cases

still Malaysian ships as they belonged to the Sabah State Government.

(ii) Based on the size and usage, the vessels were “Malaysian ships” under s 54A of the ITA.

366

CPA Tax & Investment Review 2010

B Malaysian Courts' Decisions

1.0 PRIMARY PROPERTIES SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI [(2009) MSTC 4,383] (HIGH COURT)

Facts

The taxpayer was a company in the logging business. As a sub-contractor, it entered into an extraction agreement with its main contractor to fell and extract timber logs in designated forest areas, where the main contractor’s rights over the licensed area came from an agreement with the timber license holder, Sarawak Timber Industry Development Corporation (STIDC). To extract timber from the forested areas, the taxpayer had to construct roads and build camps for its workers to stay. For the year of assessment (Y/A) 1991, YA 1992 and 1993, the costs of road construction were disallowed by IRB. The claim for forest allowance was also denied as the taxpayer neither had a concession nor a license to extract timber.

The Special Commissioners of Income Tax (SCIT) held that the costs of constructing temporary logging roads and workers’ camps were capital expenditures and therefore not deductible under section 33(1) of the Income Tax Act, 1967 (ITA). However the SCIT held further that these same costs were forest expenditure, which the taxpayer, as the beneficial owner, was entitled to claim forest allowances under Schedule 3, paragraph 8 of the ITA. Both the taxpayer and Director General of Inland Revenue (DGIR) being dissatisfied with the decision had appealed to the High Court.

Issue

Whether temporary road and camp building construction charges were deductible revenue expenditure or capital expenditure that qualifies for forest allowances?

Arguments

Taxpayer

The taxpayer argued that the charges it incurred were closely related to the conduct of its timber extraction business and formed part of the profit-earning process. They were recurrent revenue expenditures which were wholly and exclusively incurred in the production of its gross income from the extraction business and so, allowable under sec 33(1) of the ITA. Alternatively, if those

367

5 • Summary of Tax Cases

expenses were capital in nature, the taxpayer contended that they fell under paragraph 8 of Schedule 3 of the Act and so, should be granted allowance under paragraph 30 of Schedule 3 of the ITA.

DGIR

The expenses constituted non-deductible capital expenditure as they were incurred once and for all and were essential to the start of an operation in the timber extraction business for without the road and the camp, the longing business would not even be viable.

The taxpayer is not entitled to claim forest allowance under Schedule 3 as under Paragraph 8(2) of the ITA, only the concession holder or a licensee would qualify.

Decision

The High Court upheld the decision of the SCIT and dismissed the appeal and the cross appeal. Construction of logging roads and workers’ camps are essential pre-requisites to any timber extraction business. The costs had the nature of being “once and for all” expenditure essential to the start of the operation of the timber extraction business, without which the business would not be viable. The treatment of such costs as being capital in nature was supported by Paragraph 8(1)(a) and (b) of Schedule 3 to the ITA, and by relevant case authorities. The Special Commissioners’ finding that these costs were capital expenditure was therefore reasonable and in accordance with the law.

Paragraph 8(2) of Schedule 3 to the ITA provides that in respect of forest expenditure the person who can claim it as allowance would be the one who ‘... has a concession or a licence to extract timber there from ....’ It is obvious that the taxpayer was neither a concession holder nor a licensee (that would be STIDC). Nevertheless the SCIT held, applying the purposive approach in interpreting the said sub-paragraph 2, that the taxpayer was the ’.... one who runs the business and incurred the expenses. If the allowance is only given to licensee, no one will get the benefit of this provision as in logging business, it is common that the licensee will not run the business but the licence is assigned to contractor to extract timber’. The High Court added that to strictly construe Paragraph 8(2) to just concession holders and timber licensees would be to deny those who have been assigned the rights and liabilities under the licence, such as the taxpayer, their legitimate expenses which they have expended to build roads and camps just like the concession holders and licensees would have done if they did the job themselves.

368

CPA Tax & Investment Review 2010

Having contractually acquired the rights and liabilities of the licensee, the taxpayer was entitled to claim forest allowance for the capital expenditure incurred in constructing the roads and the worker’s camp.

2.0 ALLIED METALCRAFT CORPORATION SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI [(2009) MSTC 4,387 ] (HIGH COURT)

Facts

This was an appeal against the Special Commissioners of Income Tax's (SCIT) decision made on the 8 October 2002, which determined that the expenses incurred by the Appellant for providing the Appellant’s sales persons with free tickets for overseas trips were entertainment expenses and were prohibited under section 39(1)(l) of the Income Tax Act, 1967 (ITA).

The Appellant incurred expenses on the provision of free trips/tickets to overseas for individual sales agents who attained certain sales quota in the sales of kitchen utensils and water filters. The expenses were disallowed for years of assessment 1989 – 1997.

Issues

(i) Whether the appellant could withdraw an erroneous admission of law at the High Court?

(ii) If so, did the court have the jurisdiction to hear and determine the question of law which was not determined by the SCIT, namely whether free overseas tickets constituted entertainment expenses for the purposes of section 39(1)(l) of the ITA?

Arguments

Taxpayer

There is a distinction to be made between “entertainment” in the sense used in Section 18 of the ITA and the promotional items used as incentives for promotion of business citing United Detergent Industries Sdn Bhd v DGIR [1999] 1 AMR 462(H/C) and Aspac Lubricants (Malaysia) Sdn Bhd v KPHDN (2007) MSTC 4,271.

The court ought to adopt a purposive approach in interpreting Section 18 of the ITA premised on Palm Oil Research and Development Board Malaysia & Anor v Premium Vegetables Oils Sdn Bhd (2005) MSTC 4,098 in that the term “entertainment” does not include the provision of free tickets to sales persons who have achieved certain sales quota.

369

5 • Summary of Tax Cases

The erroneous admission at the SCIT that the “free tickets for overseas trip were incentive payments in the form of entertainment” is to be withdrawn and an erroneous admission of law can be withdrawn at any time.

DGIR

Citing several authorities, the Respondent submitted that the Court cannot go beyond the dimension of the case stated and if the Court is to accede to the Appellant’s submission, the case stated would have come to naught. Both parties had conceded in their submissions that the free tickets for overseas trips given to the individuals who attain sales were incentive payments in the form of entertainment; therefore the question of whether the free tickets fall under the definition of “entertainment” was never an issue but centered on whether the free tickets in the form of entertainment fall under the provision (i) of Paragraph 39(1)(l) of the ITA and hence are entitled to be deducted as revenue expenditure under Section 33(1) of the ITA, ie, whether the individual salesman were employees or non-employees of the Appellant.

Decision

(i) In view of Sections 99 and 102 and Schedule 5 of the ITA, which regulated an appeal in a tax case and had therefore to be adhered to and given effect to, the High Court was only seised with jurisdiction when there was an appeal on a question of law against a deciding order to be decided by way of case stated. It could not allow the withdrawal of an erroneous admission of law, as to do so would be tantamount to the High Court usurping the powers of the SCIT.

(ii) Since the first question was decided in the negative, the second issue did not arise.

3.0 KERAJAAN MALAYSIA V MULTIPLE LAUNCH SDN BHD [(2009) MSTC 4,392] (HIGH COURT)

Facts

The respondent disposed of assets in Johor and real property gains tax of RM678,578.55 was imposed via a Notice of Assessment dated 26 November 2000 for the year of assessment 2000. The respondent disputed the amount assessed but made payment of RM186,816.15. The appellant’s claim was for the amount of tax plus 10% penalty thereon under Section 21(4) of the Real Property Gains Tax Act, 1976 (RPGTA), totaling RM555,620.25.

370

CPA Tax & Investment Review 2010

Issue

Whether a stay of all proceedings can be granted pending appeal to the Special Commissioners of Income Tax (SCIT)?

Arguments

Taxpayer

Stay should granted as the defendant has submitted his appeal to the Plaintiff via a letter dated 18 December 2008. The plaintiff failed to forward the appeal to the SCIT. The failure is a breach of statutory duty and the right to natural justice.

DGIR

Real property gains tax is payable not withstanding any appeal as provided under Section 21 (1) of the RPGTA. Under Section 23(3) of the RPGTA the court shall not entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased under Section 21(4) of the RPGTA. There is a dearth of authorities that supports the effect of the above said provision. The RPGTA also provides for an aggrieved taxpayer to appeal to the SCIT, which the taxpayer did not do.

Decision

The appeal was dismissed on the following grounds:

(i) Sections 21(1) and 23(3) of the RPGTA provide that tax shall be paid although the assessment raised is disputed; and that the court shall not entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased under section 21(4) of the RPGTA.

(ii) The letter dated 18 December 2002 was not an appeal to the SCIT, merely a request to reduce the sum assessed. There was no appeal made by the respondent to the SCIT within the prescribed time. On the expiry of the time for appeal against an assessment, the assessment becomes final and conclusive, pursuant to Section 20(1) of the RPGTA.

(iii) Even if the appeal had been forwarded to the SCIT on time, an appeal does not operate as a stay of execution or of proceedings under the decision appealed from unless the court so orders. The onus is on the applicants to demonstrate the existence of special or exceptional circumstances to justify the grant of a stay of execution. The respondent’s reasons forwarded did not amount to special circumstances.

371

5 • Summary of Tax Cases

4.0 MENGAWATI SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI [(2009) MSTC 4,395] (HIGH COURT)

Facts

The taxpayer is in the business of housing development. The taxpayer applied to the Malacca State Government for 250 acres of land for housing development. On 1 February 1980, the application was approved. The taxpayer had to pay RM858,050 for the premium and other statutory charges. On 5 March 1980, the taxpayer entered into an agreement with Masa Merdeka Sdn Bhd (MM) to develop the land, where MM agreed to pay RM3.5 million to the taxpayer. On 31 December 1980, the taxpayer and MM varied the consideration from RM3.5 million to RM900,000. The RM900,000 was to be paid in 2 payments. On 8 July 1983, MM agreed to pay the taxpayer an additional 50sen per sq feet upon the completion of the project. The taxpayer was assessed to tax on the RM900,000 received from MM.

The Special Commissioners of Income Tax (SCIT) held that:

(i) the RM900,000 was “income”; and

(ii) the premium and other statutory charges should not be allowed as deductible expenses as there was no evidence of the payment being made to the State Government.

Before the High Court, the taxpayer conceded that the RM900,000 was its income. The issue that remained was whether the premium and other statutory charges (“expenses”) were deductible against the RM900,000? The SCIT's finding of fact that no payment was made to the State Government are unassailable. As there was no evidence of such payment being made, no deduction was allowed.

The taxpayer being dissatisfied appealed to the Court of Appeal.

Issue

Whether land alienation cost and other statutory payments made by a housing developer is a deductible expense against income received?

Arguments

Taxpayer

The taxpayer on the other hand argued that DGIR’s submission was incorrect as Chua Lip Kong makes a distinction between the findings of primary facts and inferences drawn from primary facts.

372

CPA Tax & Investment Review 2010

DGIR

The Revenue contended that the findings of primary facts by the SCIT were unassailable and can neither be overruled nor supplemented by the High Court, citing Chua Lip Kong v Director General of Inland Revenue (1982) 1 MLJ 235.

Decision

The taxpayer’s appeal was dismissed. In applying established principles set out in Chua Lip Kong, the SCIT’s finding is unassailable; neither can it be overruled nor supplemented by the High Court. The SCIT had found no evidence at all of the existence of the payment of the land alienation costs by the taxpayer to the State Government, stating there was no evidence of the date and actual amount paid.The Court of Appeal affirmed the SCIT’s reasoning. Even if there was evidence that the taxpayer had paid the land alienation costs to the State Government in 1980, the High Court’s decision was correct in law as the land alienation costs were capital expenditure for acquiring the land, not revenue expenditure. The land alienation cost was not wholly and exclusively incurred in the production of the taxpayer’s gross income; nor was it incurred in the period when the taxpayer received the income. As such, it failed to fulfill the requirements of sec 33(1) of the Income Tax Act, 1967 (ITA).

5.0 KETUA PENGARAH HASIL DALAM NEGERI V PERBADANAN KEMAJUAN EKONOMI NEGERI JOHOR [(2009) MSTC 4,399] (COURT OF APPEAL)

Facts

The respondent (the taxpayer) is a statutory body incorporated under the Johor State Enactment No. 4 of 1968 with its principal activities being the development of land for industrial, agricultural, property, mining, logging and other activities. The taxpayer’s two principal sources of income was business and dividend income and had been granted exemption under Section 127 of the Income Tax Act, 1967 (ITA) for all income except dividend income and development tax for several years including years of assessment (YA) 1991 and 1992 which are the YAs subject to the appeal. In these two years, the taxpayer made gifts of money to the State Government and claimed deductions thereon from its non-exempt dividend income. The Director General of Inland Revenue (DGIR) allowed deductions under Section 44(6) of the ITA but apportioned the deductions between the taxpayer’s exempt business income and non-exempt income, subsequently raising assessments for YAs 1991 and 1992.

373

5 • Summary of Tax Cases

It was decided in the taxpayer’s appeal to the Special Commissioners of Income Tax (SCIT) that the DGIR’s computations were wrong and two notices of assessment were ordered to be revised. The Inland Revenue appealed to the High Court, which affirmed the decision of the SCIT. Subsequently, the appeal was heard by the Court of Appeal.

Issues

(i) Does the word “income” in Section 127(5) of the ITA mean gross income or chargeable income?

(ii) Are the income tax exemptions to be given at the gross income level or chargeable income level?

(iii) Is the DGIR’s apportionment formula lawful and applicable?

Arguments

Appellant

(i) The word “income” means chargeable income and not gross income based on the cases of MCI Society Ltd v Ketua Pengarah Hasil Dalam Negeri [(1995) 2 MSTC 2,272], Ketua Pengarah Hasil Dalam Negeri v MCI Society Ltd [(2000) MSTC 3,792] and Lower Perak Co-operative Society v Ketua Pengarah Hasil Dalam Negeri [(1994) 2 MSTC 3,406].

(ii) The case of Daya Leasing Sdn Bhd v Ketua Pengarah Hasil Dalam Negeri [(2005) MSTC 4,124] was relied upon to support the submission that because the exemption does not include dividend income, it is necessary for the DGIR to apportion the chargeable income between dividend and business income and apply the apportionment formula to the gifts of money between the non-exempt dividend income and exempt business income.

Respondent

(i) The word “income” means gross income and that in the MCI Society case, the relevant judgements were silent on the meaning of the word “income”. Further, the Lower Perak Co-operative Society case is distinguishable, as co-operative societies have to seek exemption under Schedule 6 to the ITA.

(ii) The facts of the Daya Leasing case are different as the company in that case ran two types of businesses that shared common expenses such as rental, staff salaries, etc,

374

CPA Tax & Investment Review 2010

and because they are common expenses, the expenses deductible from the businesses are unidentifiable.

Decision

Appeal allowed. The Court of Appeal held that:

(i) Section 127(5) of the ITA allows for any income exempt from tax by virtue of Section 127 of the ITA to be disregarded for the purposes of the ITA and this includes business income. Section 2(2) of the ITA makes only a general reference to “income”. The submission presented for the DGIR is upheld and “income” means “chargeable income” as gross income per se may or may not be exigible to tax at all, and when no tax is exigible, there is no question or necessity for the taxpayer to claim/utilise the exemption.

(ii) The DGIR’s apportionment of the deduction for the gifts of money between the non-exempt dividend income and the exempt business income is justified, lawful, and in line with Section 5 of the ITA and the apportionment implied in Section 33(1) of the ITA. The total amount of the gifts could not be allowed against only one source of income when the aggregate income consists of both business source income and dividend income.

(iii) The deciding order and the High Court judgement are set aside. The DGIR’s apportionment formula and two notices of assessment are upheld.

6.0 KETUA PENGARAH HASIL DALAM NEGERI V STERUDA SDN BHD [(2009) MSTC 4,407] (COURT OF APPEAL)

Facts

The taxpayer, Steruda Sdn Bhd (Steruda), was a company that provided consultancy services in gynaecology, obstetrics and other branches of medicine. Steruda entered into an employment agreement on 12 July 1976 with Dr Ronald Stephen McCoy (Dr McCoy), who was also a shareholder and director of Steruda. He was to be paid remuneration of RM3,000 per month plus an annual 25% of the net profit of the business.

The Director General of Inland Revenue (DGIR) raised seven notices of assessment for the YAs 1978 to 1984 and treated the 25% net profit paid to Dr McCoy as a bonus, disallowing the excess over two-twelfths of his salary. Steruda appealed against the additional assessments and argued that the 25% net profit payment was part of his remuneration package and not a bonus and therefore fully

375

5 • Summary of Tax Cases

deductible under Section 33(1) of the ITA.

The Special Commissioners of Income Tax (SCIT) viewed the amount to be tantamount to a bonus and dismissed the appeal. The case was then referred to the High Court, which found the 25% net profit payment as being a part of Dr McCoy’s salary and reversed the decision of the SCIT.

The DGIR subsequently appealed to the Court of Appeal.

Issues

Whether the 25% of the net profit of Steruda paid to Dr McCoy was a bonus payment or not.

Arguments

Appellant

Three cases were referred to, namely Saledy Sdn Bhd v Director General of Inland Revenue [(1995) 2 MSTC 3440], Director General of Inland Revenue v Harrisons & Crosfield (M) Sdn Bhd [(1988) 2 MLJ 223], and Director General of Inland Revenue v Highlands Malaya Plantation [(1988) 2 MLJ 99]. The DGIR in these cases contended that the payments made to staff were bonus and therefore, deductions for the payments in excess of two twelfths of salary were disallowed.

Respondent

The 25% of net profit paid to Dr McCoy at the end of the year merely formed part of his salary and was not a bonus.

Decision

Appeal dismissed with costs. The Court of Appeal held that:

(i) In the Harrisons & Crosfield case, the payment was compartmentalised under a separate and special heading and it had a discretionary quality unlike salary and correctly falls under the purview of Section 39(1)(h) of the ITA. In the Highlands Malaya Plantation case, the SCIT concluded that the payment could be gratuitous or contractual, but nevertheless, still a bonus (Note that the SCIT’s decision was overturned by the High Court). The Saledy Sdn Bhd case was not helpful as it never discussed how the conclusion regarding the additional remuneration being a bonus was arrived at.

(ii) There is no statutory definition of “bonus” in the ITA and several cases were looked at, namely Re Eddystone Marine Insurance Co. [(1984) W.N 30], Shelford v Morsey [191 1 KB 154],

376

CPA Tax & Investment Review 2010

Sutton v A.G [(1923) 39 T.LR], and Great Western Garment Co. Ltd v Minister of National Revenue [(1948) 1 D.L.R 225]. From the definitions provided in these cases, bonus may have certain characteristics, such as being an amount in addition to the wages paid to an employee or something that is over and above the agreed remuneration. It may be in the nature of a gift, a temporary boon, or something freely given at the discretion of the giver as opposed to being agreed normal remuneration.

(iii) The presence of intention to make the deferred payment part of Dr McCoy’s remuneration, and not a bonus payment, is a forceful factor. His employment document is contractual in nature and the 25% payment is not at the discretion of anyone, being part and parcel of the salary agreement.

(iv) A comparison with the income of another medical practitioner, who earned a much higher monthly salary than Dr McCoy, leads one to realise that the RM3,000 per month base salary did not commensurate with Dr McCoy’s status and qualification as a senior obstetrician and gynaecologist.

7.0 MENGAWATI SDN BHD V KETUA PENGARAH HASIL DALAM NEGERI [(2009) MSTC 4,414] (COURT OF APPEAL)

Facts

The taxpayer, a housing developer, had applied to the State Government of Melaka for the alienation of 250 acres of leasehold land for the purpose of housing development. The application was approved vide notification dated 1 February 1980. The taxpayer had to pay a total land-alienation cost of RM831,340 within two months of receiving the notification.

On 5 March 1980, the taxpayer entered into another agreement with another housing developer, Masa Merdeka Sdn Bhd (Masa) to develop land at a consideration of RM3.5 million. A later agreement dated 31 December 1980 substituted the consideration for RM900,000 payable in two instalments consisting of RM831,340 payable within two weeks from the date of approval of the letter from the land administrator and RM68,660 to be paid upon completion of the housing estate. On 8 July 1983, an additional agreement was entered into between the taxpayer and Masa providing for the payment of an additional 50 sen per sq ft to the taxpayer upon completion and sale of the properties by Masa.

377

5 • Summary of Tax Cases

The taxpayer was assessed to tax on the two installments and consequently appealed to the Special Commissioners of Income Tax (SCIT) arguing that the sum of RM831,340 expended in 1980 should be deducted from the income of RM900,000 received in YAs 1982 and 1984.

The SCIT found the sum of RM900,000 to be “income” and not an “advance” and hence assessable to tax under the Income Tax Act, 1967 (ITA). The land-alienation costs should not be allowed as deductible expenses against the RM900,000 (income) as there was no evidence of the date and actual amount paid to the State Government.

The taxpayer, before the High Court, accepted that the RM900,000 was “income”. However, it continued to assert that the land-alienation cost was deductible against the income. The High Court rejected the taxpayer’s assertion and held that the land-alienation costs were capital expenditure and not wholly and exclusively incurred in the production of income, nor incurred in the period when the taxpayer received the income.

The taxpayer subsequently appealed to the Court of Appeal.

Issues

Whether the land-alienation costs were allowable as deductions from the income.

Arguments

Appellant

The taxpayer contended that the Director General of Inland Revenue's (DGIR) submission is incorrect as Chua Lip Kong v Director of Inland Revenue makes a distinction between the findings of primary facts and inferences drawn from primary facts.

Respondent

The DGIR cited the case of Chua Lip Kong v Director General of Inland Revenue [(1982) 1 MLJ 235] and argued that the findings of primary facts by the SCIT are unassailable and can neither be overruled nor supplemented by the Court.

Decision

Appeal dismissed with costs. The Court of Appeal held that:

(i) The SCIT found no evidence at all of the existence of payment of the land alienation costs, and there was no evidence of the date and actual amount paid. The SCIT’s

378

CPA Tax & Investment Review 2010

findings, being finders of facts was to be preferred and cannot be overruled or supplemented by the Court.

(ii) Even if the High Court had found evidence that the land alienation costs were paid to the State, its decision that the land alienation costs were capital expenditure for acquiring the land and not revenue expenditure, thus failing to fulfill the requirements of Section 33(1) of the ITA, was correct in law.

8.0 KERAJAAN MALAYSIA V HOLIDAY PLAZA SDN BHD (FORMERLY KNOWN AS GIB PROPERTY SDN BHD) [(2009) MSTC 4,419] (HIGH COURT)

Facts

The plaintiff applied for a summary judgment against the taxpayer for the sum of about RM5 million plus interest and costs. According to the plaintiff, the taxpayer had failed to settle the outstanding income tax liability for the years of assessment 2002-2004. The defendant claimed that it had obtained approval from the Ministry of Finance (MOF) to set-off excessive service tax paid against outstanding income tax and on that basis only paid RM600,000 towards the outstanding income tax liability.

Issue

Whether defendant has a triable issue in a summary judgment application on grounds that the plaintiff failed to offset excess service tax paid against income tax owed?

Arguments

Taxpayer

The taxpayer claimed that it had paid excessive service tax amounting to RM860,923 since the year 2005 and thus the MOF had given it permission to set off the excessive service tax paid against income tax payable. The taxpayer argued that the plaintiff failed to take into account the set-off, as both the agencies responsible for service tax and income tax are under the MOF. Therefore the plaintiff is estopped from increasing the taxes and the increased taxes are unreasonable and wrongly imposed.

DGIR

The plaintiff argued that income tax must be paid based on the amount stipulated in the tax return, and notwithstanding any appeal, the income tax must be paid first. Any dispute against an assessment must be made to the Special Commissioner of Income

379

5 • Summary of Tax Cases

Tax (SCIT). Under Section 142(1) of the Income Tax Act, 1967 (ITA) any certificate issued stating the amount outstanding is sufficient evidence to show the amount owed of income tax owed.

Decision

The application was allowed. The issue of set-off of excess service tax has never been appealed to the SCIT under Section 99 of the ITA. Service tax comes under the purview of a totally different legislation and is administered by the Customs department. From the defendant’s affidavit in reply there is no written evidence on the claims of the defendant that the MOF has allowed the set-off of excess service tax against income tax owed. Pursuant to Section 103(1) of the ITA, tax is to be paid notwithstanding any appeal against the assessment. Pursuant to Section 106(3) of the ITA, the courts cannot entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased.

9.0 KERAJAAN MALAYSIA V UNITED AXIS SDN BHD [(2009) MSTC 4,425] (HIGH COURT )

Facts

The defendant is in the business of property development and filed tax returns for YAs 2001 and 2002 under the self-assessment system. The Plaintiff filed a summary judgement application for the said assessments when the amounts under the assessments were not paid.

Issue

Whether there exist triable issues in granting summary judgement for income tax claims owed to the Government of Malaysia in the case of a developer who argued that the income tax assessments raised were incorrect.

Arguments

Taxpayer

Relying on the Income Tax Rules (Property Development) Regulations, 2007, the defendant denied that the amounts were owed as the development project had yet to be completed. The defendant claimed that the suit was premature as actual losses upon completion of the project must first be determined.

DGIR

Since the notices of assessment were deemed served under the self-assessment system, the amount taxed therefore becomes

380

CPA Tax & Investment Review 2010

due and payable under Section 103A(2) of the Income Tax Act, 1967 (ITA). The Supreme Court case of Chong Woo Yit v Government of Malaysia [1982] 2 CLJ 87 illustrates the point that upon service of notices of assessment, tax payable becomes due and payable whether or not a taxpayer appeals against the assessment and the amount would be recovered by civil proceedings as a debt due to the Government.

Decision

Summary judgement was allowed as under the ITA, tax shall be paid although the person assessed disputes the assessment. Under Section 106(3) of the ITA, the Court cannot entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased. As the taxpayer’s entire defence rested on allegations of inaccuracy of the assessment, the right forum for such a plea is at the Special Commissioners of Income Tax (SCIT).

The taxpayer cannot raise the issue of the tax amount being excessive or inaccurate at the summary judgement stage.

10.0 KERAJAAN MALAYSIA V KUMPULAN PINANG HARTANAH SDN BHD [(2009) MSTC 4,429] (HIGH COURT)

Facts

The notice of assessment for the year of assessment 2000 was served on the defendant by post to the last known address of the defendant.

Issue

Whether there exist triable issues in granting summary judgement to the Government of Malaysia in the case of a developer who argued that the real property gains tax assessments raised were incorrect.

Arguments

Taxpayer

The defendant argued that it did not meet the definition of “chargeable person” in relation to the disposal of a chargeable asset, and there was no chargeable gain on the said disposal. Instead, the defendant argued it had an allowable loss under Section 7(1)(b) of the Real Property Gains Tax Act, 1976 (RPGTA). The asset was acquired on 24 May 1995 at the value of RM12.6 million and it was disposed at the market value of only RM10.9 million on 26 August 2000. This shows the defendant incurred a loss of RM1.6 million.

381

5 • Summary of Tax Cases

DGIR

The assessment was raised in accordance with the RPGTA. If the defendant was aggrieved with the assessment, an appeal should be pursued at the Special Commissioners of Income Tax (SCIT). Under the RPGTA, tax is payable notwithstanding any appeal.

Decision

Summary judgement was granted. Similar to income tax cases, the principle that tax is to be paid although the assessment is in dispute applies to real property gains tax. The question of whether the assessment itself was proper or otherwise is not for this court to determine. The court cannot entertain any plea that the amount of tax sought to be recovered is excessive, incorrectly assessed, under appeal or incorrectly increased. Sections 21(1) and 23(3) of the RPGTA applies as the notice of assessment had been duly served on the defendant. The proper avenue was for the defendant to appeal to the SCIT.

11.0 WONG KUOK MING V GOVERNMENT OF MALAYSIA; GOVERNMENT OF MALAYSIA V WONG KUOK MING [(2009) MSTC 4,431] (HIGH COURT OF SABAH & SARAWAK)

Facts

The Inland Revenue Board (IRB) sought to claim outstanding income tax amounts raised for YAs 1996 and 1997 by way of summary judgement.

Issue

Whether there exist triable issues to deny a summary judgement on assessments raised by notice of assessments sent by ordinary post.

Arguments

Taxpayer

The taxpayer denied owing the sums claimed as he did not receive the notices of assessments sent by ordinary post. Alternatively he also contended that the claim was statute barred. A similar action filed in 1999 based on the same claim was dismissed by the Magistrates Court and there was no order to file the action afresh.

DGIR

The presumption of service under Section 145(2) of the Income Tax Act, 1967 (ITA) when read together with the provisions of Sections

382

CPA Tax & Investment Review 2010

12 and 66 of the Interpretations Acts, 1948 and 1967 clearly shows that the service is effective and good in nature.

The action before the Magistrates Court was withdrawn by the respondent, the Government of Malaysia, resulting in leave to discontinue with the case.

Decision

(i) In a summary judgement application, the plaintiff, the Government of Malaysia, has to satisfy the court that the taxpayer has no defence to the claim or the taxpayer should show that there is a serious conflict of material facts or there is otherwise a triable issue worthy of judicial investigation in a full trial. The summary judgement was denied as the respondent, the Government of Malaysia, failed to show evidence that the notices were indeed posted and they were addressed to the taxpayer at the taxpayer’s last known address and thus raised a triable issue. The Court relied on the decision in Kerajaan Malaysia v Suncity Development Sdn Bhd [2007] 1 AMR 589 that for the respondent to rely on the presumption or deeming provision under Section 145(2) of the ITA, there must be evidence in the affidavit of service to show that the notices were indeed posted and that they were addressed to the taxpayer’s last known address.

(ii) On the taxpayer’s contention that he was not liable for the tax assessed or penalties thereon, it was without merit as tax is payable notwithstanding any appeal and the taxpayer did not show evidence that he has appealed against the assessments.

(iii) On the issue of whether the respondent’s claim is statute-barred, the Court ruled that the discontinuance and withdrawal of a previous action against the taxpayer is no bar to the present action for the same cause of action. It could not be said that there is finality in the decision as the merits of the claim were never considered: Ramal Properties Sdn Bhd v East West Umi Insurance Sdn Bhd [1997] 3 CLJ 598.

(iv) In relation to the application of the doctrine of estoppel, the Court held that the doctrine of estoppel does not apply to Government on revenue matters.

383

5 • Summary of Tax Cases

12.0 KERAJAAN MALAYSIA V KENANGA WANGSA SDN BHD [(2009) MSTC 4,435] (HIGH COURT)

Facts

The plaintiff applied for a summary judgement against the defendant for unpaid taxes for year of assessment 2004 amounting to RM546,715.

Issue

Whether plaintiff ’s application for summary judgement amount was inaccurate and misleading.

Arguments

Taxpayer

The defendant challenged the application on the following grounds:

(i) the plaintiff ’s claim was inaccurate and misleading;

(ii) some payments had previously been made to the plaintiff; and

(iii) the notice of tax increase was never received by the defendant.

DGIR

The defendant made part payments after the summons was filed on 27 June 2007. As such when the action was filed, the amount claimed was accurate.

Decision

The application was partly granted with 8% interest per annum from the date of award until settlement, with costs. Upon part payment, the plaintiff was only entitled to RM165,397. The defendant had no defence against the sum of RM165, 397. The tax increase due to late payment can be made under Sections 103(2) and (4) of the Income Tax Act, 1967 (ITA) without giving notice to the defendant.

13.0 ANG LAY KIM @ ANG IMM V KETUA PENGARAH HASIL DALAM NEGERI [(2009) MSTC 4,436] (HIGH COURT)

Facts

The taxpayer was a Malaysian until 23 January 1988 when he accepted Singaporean citizenship. The taxpayer owned 1/8th of a property which he inherited from his late mother on 29 January

384

CPA Tax & Investment Review 2010

1987. The taxpayer also signed a declaration of trust stating that of the 1/8th (or 5/40th) of the property, he only held 1/40th for himself and the remaining 4/40th were held in trust for his four sisters who were Malaysian citizens. Via a sale and purchase agreement dated 6 June 1996, the taxpayer and 10 other owners sold the property for RM2,444,124.35. The taxpayer received RM305,515.53, of which he took RM61,103.10 for himself, and the remaining sum was distributed to his sisters. On 15 January 2007, the taxpayer filed Form CKHT 1. On 19 February 2007, the defendant raised a notice of assessment for the year 1996, imposing real property gains tax and penalties amounting to RM74,229.32.