Embed Size (px)

Citation preview

Indonesia’s Financial Reforms: Challenges in the 1990s for Its Banking and Financial Markets

SYAHRIL SABIRIN

I. INTRODUCTION

The 1990s may be viewed by banks and other financial institutions in Indonesia as the decade of challenges and opportunities. One can present several arguments in support of this statement. First, the Indonesian banking and other financial markets have undergone substantial deregulation and structural changes in the past several years. Deregulation provides challenges and opportunities to compete. Second, the world economy, which has experienced major changes and reforms toward more freedom of financial markets in the 198Os, is expected to continue in the same direction in the 1990s. Third, the banking business and products have been undergo- ing substantial developments, thanks to the revolution in the telecommunication and information processing technology. Indeed, interdependence of the world financial markets has become a unique reality, which has contributed to increased volatility of the exchange rates and interest rates globally. The challenge to introduce newer financial products will remain strong in the years ahead.

This study reviews the financial reforms that have taken place in Indonesia in the past 25 years, shaping its current financial system. The review focuses more on the banking and foreign exchange markets. In addition, it discusses the recent developments and prospects of world banking and the world economy, and their implications to Indonesia’s banks and other financial institutions (Balino & Sun- dararajan 1986, Gillis & Dapice 1988, Greenwood 1986, Layman 1990, Nasution 1990, Sabirin 1989, Sabirin & Soekarni 1986, Soesastro 1989).

II. FINANCIAL REFORM AND ECONOMIC DEVELOPMENT: A DIGRESSION

The driving force behind financial deregulation or financial reform may vary from one situation to another. It may be a domestic economic situation which calls for

Syahril Sahirin l Managing Dwector, Bank Indonesia, JL M. H. Thamrin 2, Jakarta looO2, Indonesia.

Journal of Asian Economics, Vol. 2, No. 2, 1991, pp. 383-397. Copyright o 1991 by JAI Press, Inc.

ISSN: 1049.0078 All rights of reproduction in any form reserved.

383

384 JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

improved efficiency of the financial system, or an external influence or pressure, or a domestic political pressure. But the rationale or objective of a financial reform remains to be the same-an increased efficiency of the financial system to meet the changing needs of a given economy.

The basic function of the financial sector in an economy is to provide financial instruments and institutional arrangements for the flow of funds from the surplus units (i.e., those in possession of funds but unable to utilize or invest them in the most efficient manner) to the deficit units (i.e., those who do not have sufficient funds to finance their investments or other activities). The more developed is a financial sector, the higher is its ability to channel funds efficiently, and the more efficient is the allocation of resources at large. This fact signifies the impo~ance of the development of a financial sector in the process of economic development.

In general, a developed financial sector is characterized, inter alia, by the availability of a large variety of financial services, out of which the surplus units as well as the deficit units can select the ones most suitable to the needs in specific cases. The availability of a sufficiently large variety of easily accessible financial services is a necessary condition for the smooth functioning of a financial sector.

However, in the process of economic development, many countries were con- fronted with different views and goals which apparently hindered the development of its financial sectors. Some countries believe that interest rates have to be constrained at a low level to encourage specific investments. Along the same line, there are those who believe that the allocation of resources through the market mechanism is neither efficient nor desirable. They advocate government control or intervention in resource

allocations. Administered low interest rates, however, do not necessarily mean a serious

obstacle to financial sector development, provided that the program is accompanied by a set of appropriate policies, such as a prudent fiscal and monetary management to control inflation. Similarly, government intervention in resource allocation may achieve the intended goals (for instance, more equitable distribution of opportunities and income) without seriously endangering financial sector development, if the intervention is carried out in a limited scale by using targeted means. The evidence in many countries suggests, however, that appropriate accompanying policies were seldom used in support of administered interest rates. A number of countries found themselves unable to limit government intervention in resource allocation not to

seriously obstruct the development of the financial sector. The result was financial repression (McKinnon 1973, Shaw 1973). Controlled

interest rates at low levels accompanied by high inflation rates often ended up with negative real interest rates, which made financial assets unattractive. Similarly, excessive government inte~ention in funds allocation seriously reduced the degree of freedom of the financial institutions to allocate funds in an efficient manner. Repressions of the financial sector often resulted not only from distortions in interest rates and resource allocation, but also from stringent control on foreign exchange and capital flows. In some countries, rigid exchange rates management, ambitious government development programs in certain directions, and other similar policies

Indonesia’s Financial Reforms: Challenges in the 1990s for Its Banking and Financial Markets 385

generated heavy pressures on its balance of payments and foreign exchange reserves, which in turn prompted the governments to impose tighter controls on foreign exchange and capital flows. This in itself constituted an obstacle to financial sector development. More importantly, it generated uncertainty in the business community as to the availability of foreign exchange for imports of raw materials and services. This uncertainty represented a serious hindrance to economic development.

Such experiences clearly indicate the need for financial reform. A certain degree of relaxation in interest rates and foreign exchange controls is necessary to reduce the magnitude of distortions in the financial sector and economic develop- ment .

III. EARLY FINANCIAL REFORMS IN INDONESIA

During the past 25 years, Indonesia’s financial sector has undergone very significant changes. The sector, which was heavily controlled and regulated 25 years ago, has become one of the most deregulated financial sectors of our time. In foreign ex- change and external capital flows, for example, Indonesia used to adopt a tightly controlled foreign exchange system, such that private holdings of foreign exchange were mostly illegal, and government approvals were required for importation of goods and services and transfer of funds to other countries. The system was liber- alized to become practically free of restrictions.

In the banking sector, a significant degree of liberalization has also taken place, most notably on interest-rate determination and on entrance to the banking market. Today, banks are free to set their interest rates except for interest on program loans which are supported by the Central Bank. New entrance to the banking market is unrestricted.

Since the inauguration of the present government in 1966, there have been at least three major steps taken by the government in order to boost the development of the financial sector. First, a major financial reform with respect to foreign exchange, interest rate, and government budget was carried out between 1967 and 1970. Second, in June 1983, a measure concerning interest rate policy and credit ceiling was adopted. Third, in October 1988 and March 1989, provisions were enacted which permitted new entrance to the banking market and which introduced certain other liberalization.

Before 1966, the Indonesian economy was in a massive disarray. Many govern- ment decisions were made on the basis of political rather than economic consider- ations. Government spending was too ambitious, and much of it went to projects of questionable economic benefit. The size of government expenditures was uncon- trolled, much in excess of government revenues. The budget deficits were financed by money printing, which generated a spiral of hyper inflation. The inflation rate reached a peak of more than 600% per annum in 1966.

In such a situation, it was practically impossible to manage the external account without implementing a tight control on foreign exchange and capital flows. The

JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

control was in fact very tight, so virtually no private holding of foreign exchange was permitted and spendings in foreign exchange required government approval. Moreover, a multiple exchange rate system was in place, making the already com- plex system more cumbersome. In the banking sector, interest rates were tightly regulated and credit allocation was determined by the government.

The outcome naturally was a severe pressure on the financial system. The administered low interest rates, coupled with the hyper inflation, made domestic financial assets unattractive, inducing their conversions into real assets at home and into foreign assets through illegal channels. The situation was further aggravated by the multiple exchange rate system at unrealistic levels. Illegal capital outflows, either through underpricing of exports or overpricing of imports or by other means, became a threat. In sum, the repression experienced by the financial sector was so severe, it would require a major overhaul to restore order.

Soon after the new government came into power in 1966, a major financial reform was carried out. Its principal features were the following:

1. The adoption of a balanced-budget policy: This was primarily meant to set a tight discipline so not to resort to the central-bank inflationary financing of government budget deficits.

2. The realignment of interest rates with inflation rates to improve the competitiveness of domestic financial assets vis-a-vis real and for- eign assets: Under such a high interest rate policy, the deposit rate was originally increased to 6% per month, and then was reduced gradually as inflation receded.

3. The liberalization of foreign exchange market: This was in fact a drastic and courageous measure since the existing system was dras- tically changed to become virtually free of restrictions. The new system was one of the most liberal among those ever adopted by a developing country. Along this line, foreign banks were allowed to open branches in Jakarta. In total, 10 branches were established, after which the door was closed for new entrance.

The reform was quite comprehensive and was indeed very successful. The rate of inflation sharply declined to reach single-digit rates in three successive years- 1969, 1970 and 197 1, respectively. Public confidence in economic management and economic performance at large quickly improved. Foreign confidence was also gained, resulting in the inflow of foreign direct investments and other forms of capital. The banking and other financial institutions started a new, healthier life, with

businesses growing at a rapid rate. Data compiled by the Central Bureau of Statistics and Bank Indonesia* show that total deposits, demand, savings, and time grew from Rp. 5 1 billion in 1968 to Rp. 123 billion in 1969, and to Rp. 190 billion in 1970. The upward trend continued to a total of Rp. 54,375 billion in 1989.

In fact, the reform contributed significantly to the establishment of the neces- sary foundation for economic planning and development. In April 1969, the govem-

IndonesiaS Financial Reforms: Challenges in the 1990s for Its Banking and Financial Markets 387

ment of Indonesia launched the first five-year development plan, during which a high economic growth rate of above 8%, on average per annum, was achieved.

Toward the end of the first five-year plan, the economy received a sudden boost from the first oil boom. At this time, the government felt the need for a more powerful instrument of monetary control than the simple one of reserve requirement, which was the only instrument available at the time (aside from moral suasion). Increasing rates of inflation in 1972, 1973, and early 1974 made the need pressing. Open-market operations could not be introduced, since there was no securities market.

In 1974, the Central Bank resorted to credit ceiling, by which it determined annually the maximum amount of loans to be issued by each bank. In addition, the Central Bank also set limits on offshore borrowings by each bank, and all govern- ment enterprises were required to keep their deposits with the five state-owned commercial banks and one state-owned development bank. It was worth noting that while banks’ access to offshore credits was limited by ceilings, the non-bank private sector’s foreign borrowings were not restricted. Although credit control prevented banks from managing their funds in the most efficient manner, priority was placed on the effectiveness of monetary control. The shortcoming was therefore not consid- ered a pressing matter.

However, when the oil price ceased to increase in the early 1980s and in fact, it started to decline, there was a much greater need to look for alternative ways. At the same time, the interest rate regulation also needed a review so competition and efficiency in the banking sector could be increased. The general condition of the banks, as compared to that in the early 197Os, had improved considerably. A consen- sus emerged that the decline in oil revenue would have to be offset by an increase in domestic savings, particularly through the banking system, through an improvement in the efficiency of resource allocation.

Subsequently, the second major financial reform was announced in June 1983, which consisted of three main parts:

1. Removal of the credit ceiling system. 2. Liberalization of interest rates at the state-owned banks, both on

deposit and lending, with the exception of the rate on programmed (priority) lending. Prior to June 1983, interest rates at the state- owned banks were set by the Central Bank, while interest rates at private banks were not regulated.

3. Overhaul of the policy on priority credits and the accompanying liquidity (refinancing) credits from the Central Bank. This was par- ticularly intended to reduce the dependence of banks on the Central Bank’s funds.

The June 1983 reform measure added a significant degree of competition to the financial market and gave the banks more freedom in managing their businesses. This resulted in a rise of interest rates, accompanied by a sizable build-up of bank

388 JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

deposits. Total deposits in the banking system more than quadrupled in nominal terms within six years (1982 to 1988). The growth of time deposit was even more impressive. It increased more than eight times in nominal terms or more than five times in real terms. Institution-wise, the reform set forth a strong motive for banks to enhance their management and organizational capabilities and to improve efficiency.

With regard to monetary management, the removal of credit ceiling necessi- tated the establishment of a new system, as would be consistent with the spirit of deregulation. The answer was a combination of open market operation and discount window facility. These instruments, unlike the credit ceiling, work in an indirect manner to influence monetary aggregates, and therefore leave sufficient room for each bank to independently manage its daily activities. To support the system, the Central Bank introduced the SBIs (Bank Indonesia’s Certificates) in February 1984 and the SBPUs (money market instruments) in February 1985. These new instru- ments were used as media of open market operations. In addition, a rediscount facility was introduced in June 1983.

IV. THE REFORMS OF 1988 AND THE SUBSEQUENT POLICIES

The past few years witnessed a strong growth of the private sector. While in the 1970s and early part of the 1980s the government was the prime mover of economic development, in the late 1980s the private sector progressed to become a stronger engine of economic development. This is clearly indicated, inter alia, by the tremen- dous increase in nonoil exports. This development in the private sector and the apparent need for further growth warranted the supporting growth of the financial sector. Therefore, the existing financial system had to be reformed further. Several other issues needed to be addressed. For example, the equity market remained underdeveloped, owing in part to the unfavorable tax treatment relative to time deposits.

Hence, the third major financial reform was introduced in October 1988. In spirit, it was consistent with the reform since 1966, designed to develop the financial sector and to improve the efficiency of resource alfocation. The 1988 financial reform consisted, among others, of the following:

1. The reopening of the financial market for new banks to enter (the entrance into the market was closed in 197 1). The new entrant can be a national bank or a joint venture between foreign and national banks.

2. The simplification of procedures of application for branch expansion as well as for foreign exchange operation permit.

3. The reduction and unification of required reserve ratio for all banks and NBFI’s short-term liabilities from as high as 15% to 2%, and the improvement of money market trading.

4. The equalization of tax treatment between interest income on depos- its and income on securities. This was meant to accelerate the devel- opment of the capital market.

lndonesia’s Financial Reforms: Challenges in the 1990s for Its Banking and Financial Markets 389

5. The realignment of Bank Indonesia’s swap facility. This facility was introduced in the late 1960s to provide exchange risk coverage for money borrowed by investors from overseas. The rate had been set by Bank Indonesia; since October 1988, it has been determined by market forces-that is, equal to the difference between the domes- tic interest rate and interest rate overseas (US$ London Inter-Bank Offered Rate).

Thus, the 1988 reform dealt with the specific issues that had hitherto hindered further development of the financial sector. Most importantly, the door was opened to further expansion of the banking sector and activities with an eye to increasing efficiency among competing financial institutions, removing the bias of tax treat- ment against equity and securities investment, unifying and reducing the reserve ratio. As for the capital market, the October 1988 measure significantly strengthened the impact of the deregulation package announced in December 1987.

The October 1988 reform package was followed by complementary packages of March 1989 and January 1990. The March 1989 reform package removed the ceiling on banks’ offshore borrowings, and at the same time installed a limit on foreign exchange net open positions equal to 25% of each bank’s net worth. In the new system, banks obviously enjoy more freedom in managing their foreign claims and commitments.

The January 1990 package contained, among other things, two main items:

1. A further deregulation of programmed credits and the Central Bank’s liquidity credits to support programmed credits. While these credit programs had played an important role in the development of certain priority sectors of the economy, including the small-scale business sector, they also constituted a distortion to the efficient mechanism of the financial sector.

2. A requirement for each bank to supply at least 20% of its total credit to small businesses. Compared to the prior liquidity-credit program, the new measure is more market oriented.

In sum, the series of banking and other financial reforms was meant to create the necessary environment for the market forces to work in an efficient manner, while establishing certain prudential rules and regulations for supervision purposes as well as improving the mechanism and instruments for monetary management.

V. FOREIGN EXCHANGE SYSTEM AND MANAGEMENT OF FOREIGN EXCHANGE RATES

As mentioned in earlier sections, Indonesia adopted a free foreign exchange system in 1990. Although the requirement to surrender all export proceeds was not lifted

until January 1982, there has not been any restriction since the early 1970s on the

390 JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

purchases of foreign exchange from banks. Banks in turn have been free to purchase any amount from the Central Bank at the Central Bank’s intervention rate.

It has often been argued that liberalization of foreign exchange and capital flows must follow trade and real-sector liberalization, and liberalization of interest rate and credit, because the opposite sequence may result in a massive capital flight. Indonesia did not follow such a sequence. The financial sector has been the leading sector with respect to deregulation, and within the sector, foreign exchange and capital flow experienced major deregulations prior to interest rate and credit liber- alization. Trade and real sector deregulation come only after financial deregulation. Among important trade reforms are the 1985 customs simplification and the De- cember 1986 trade deregulation.

Would the experience of Indonesia suggest that the sequence is not truly impor- tant? This is not an easy question to answer. In general, Indonesia’s reforms have been regarded as successful, despite occasional problems of capital outflow. The success seems to be closely related to improved confidence. The liberalization of foreign exchange system, accompanied by a more realistic exchange rate policy, tighter control of the inflation rate, and other economic measures did in fact signifi- cantly improve public confidence in the Indonesian economy in general, and in the stability of prices and exchange rates in particular. As a result, a large capital inflow was estimated to occur in the late 1960s and early 1970s following the financial deregulation.

In the early part of the free foreign exchange system, transferring capital into and from Indonesia was not a simple and easy process. But impressive developments in telecommunication technology as well as transaction methods have made capital transmissions possible in a matter of seconds. In such a situation, management of capital flows has to be conducted in a more sophisticated way, and exchange rate management has an important role to play in this regard.

Prior to November 1978, the rate of the Indonesian rupiah was tied to the U.S. dollar. On November 15, 1978, when the rupiah was devalued by 34%, the tie of the rupiah to the U.S. dollar was officially abandoned, and the government adopted a managed floating exchange rate system. The psychological impact of exchange rate changes vis-a-vis the U.S. dollar, however, made it difficult for the Central Bank to move the rupiah rate vis-a-vis the U.S. dollar by any substantial margin. Therefore, the rupiah-dollar rate moved very little in the following years.

However, the higher Indonesian inflation rate, higher than those of its trading partners, made the devaluation in March 1983 unavoidable. Since then, the exchange rate has been managed in a somewhat more flexible way. But the large pressure on the balance of payments resulting from the oil price decline and the world economic slowdown in the 1980s was responsible for another devaluation of the Indonesian rupiah in September 1986.

The experiences with the devaluations of 1978, 1983, and 1986 have had a very strong influence on public psychology. After the devaluation of 1986, for a time it was difficult to suppress rumors about follow-up devaluations. This made the money market and monetary situation vulnerable to speculation and consequent instability.

Indonesia’s Financial Reforms: Challenges in the 1990s for Its Banking and Financial Markets 391

80 -- - .-- .--.--

-_.--- __..- _.__ __- .__... -- ---.-. -

L 1 1 1 1 1 1 I 1 I I I I 1 1 _I 1 L I

%71727374757677787880 81828384858887888890

- RUPIAH/USD - CL’1 INWUSA

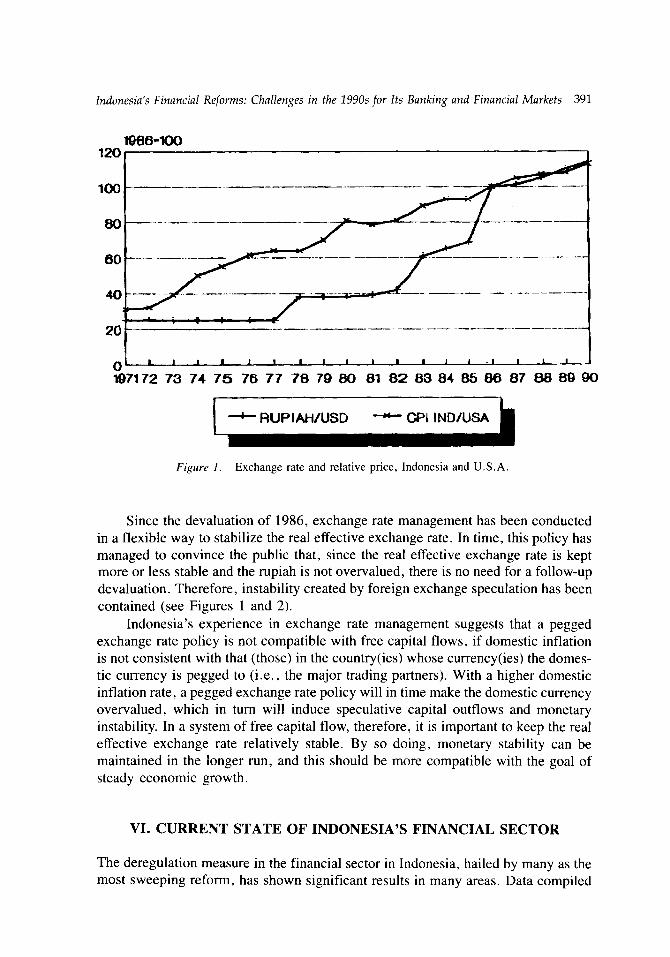

Figure 1. Exchange rate and relative price, Indonesia and U.S.A.

Since the devaluation of 1986, exchange rate management has been conducted in a flexible way to stabilize the real effective exchange rate. In time, this policy has managed to convince the public that, since the real effective exchange rate is kept more or less stable and the rupiah is not overvalued, there is no need for a follow-up devaluation. Therefore, instability created by foreign exchange speculation has been contained (see Figures 1 and 2).

Indonesia’s experience in exchange rate management suggests that a pegged exchange rate policy is not compatible with free capital flows, if domestic inflation is not consistent with that (those) in the country(ies) whose currency(ies) the domes- tic currency is pegged to (i.e., the major trading partners). With a higher domestic inflation rate, a pegged exchange rate policy will in time make the domestic currency overvalued, which in turn will induce speculative capital outflows and monetary instability. In a system of free capital flow, therefore, it is important to keep the real effective exchange rate relatively stable. By so doing, monetary stability can be maintained in the longer run, and this should be more compatible with the goal of steady economic growth.

VI. CURRENT STATE OF INDONESIA’S FINANCIAL SECTOR

The deregulation measure in the financial sector in Indonesia, hailed by many as the most sweeping reform, has shown significant results in many areas. Data compiled

392 JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

-_----_-__---- - .___ ____ _

-_---_- .,.,..I_.-_..._ -__

- .._ _ ____- --___ .___. - I _. _ _ --

-- --.-___.____- -.-- ._-. ._ ._..

--.. _--. ..-_ __-

73 74 75 76 77 78 78 80 81 85 87

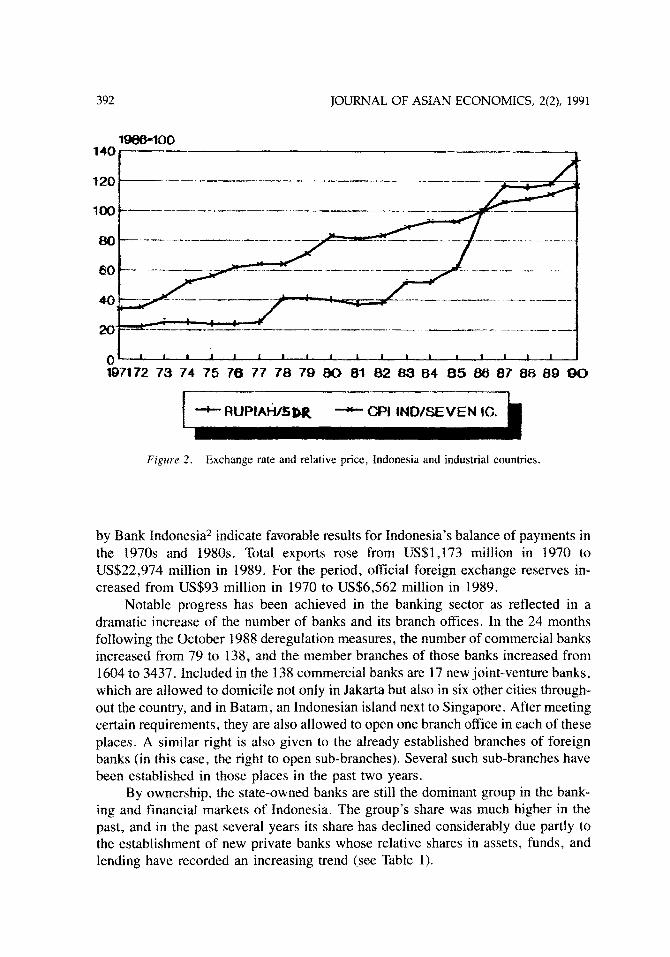

Figure 2. Exchange rate and relative price, Indonesia and industrial countries.

by Bank Indonesia2 indicate favorable results for Indonesia’s balance of payments in the 1970s and 1980s. Total exports rose from US$l ,173 million in 1970 to US$22,974 million in 1989. For the period, official foreign exchange reserves in- creased from US$93 million in 1970 to US$6,562 million in 1989.

Notable progress has been achieved in the banking sector as reflected in a dramatic increase of the number of banks and its branch offices. In the 24 months following the October 1988 deregulation measures, the number of commercial banks increased from 79 to 138, and the member branches of those banks increased from 1604 to 3437. Included in the 138 commercial banks are 17 new joint-venture banks, which are allowed to domicile not only in Jakarta but also in six other cities through- out the country, and in Batam, an Indonesian island next to Singapore. After meeting certain requirements, they are also allowed to open one branch office in each of these places. A similar right is also given to the already established branches of foreign banks (in this case, the right to open sub-branches). Several such sub-branches have been established in those places in the past two years.

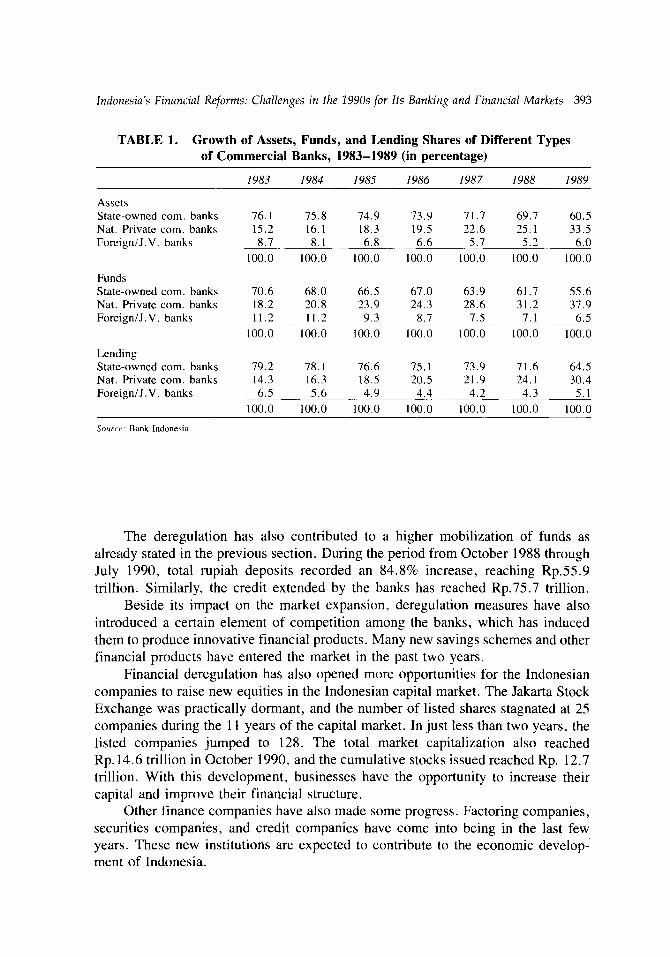

By ownership, the state-owned banks are still the dominant group in the bank- ing and financial markets of Indonesia. The group’s share was much higher in the past, and in the past several years its share has declined considerably due partly to the establishment of new private banks whose relative shares in assets, funds, and lending have recorded an increasing trend (see Table 1).

lndonesia’s Financial Reforms: Challenges in fke 1990s for Ifs Banking and Financial Markets 393

TABLE 1. Growth of Assets, Funds, and Lending Shares of Different Types of Commercial Banks, 1983-1989 (in percentage)

1983 1984 1985 1986 1987 1988 1989

Assets State-owned corn. banks Nat. Private corn. banks Foreign/J.V. banks

Funds State-owned corn. banks Nat. Private corn. banks Foreign/J.V. banks

Lending State-owned corn. banks Nat. Private corn. banks F0reigniJ.V. banks

76. I 75.8 74.9 73.9 71.7 69.7 60.5 15.2 16.1 18.3 19.5 22.6 25.1 33.5 8.7 8.1 6.8 6.6 5.7 5.2 6.0

100.0 100.0 100.0 100.0 100.0 100.0 100.0

70.6 68.0 66.5 67.0 63.9 61.7 55.6 18.2 20.8 23.9 24.3 28.6 31.2 37.9 11.2 11.2 9.3 8.7 7.5 7.1 6.5

100.0 100.0 100.0 100.0 100.0 100.0 100.0

79.2 78.1 76.6 75.1 73.9 71.6 64.5 14.3 16.3 18.5 20.5 21.9 24.1 30.4 6.5 5.6 4.9 4.4 4.2 4.3 5.1

100.0 100.0 100.0 100.0 100.0 100.0 100.0

Source: Bank Indonesia.

The deregulation has also contributed to a higher mobilization of funds as already stated in the previous section. During the period from October 1988 through July 1990, total rupiah deposits recorded an 84.8% increase, reaching Rp.55.9 trillion. Similarly, the credit extended by the banks has reached Rp.75.7 trillion.

Beside its impact on the market expansion, deregulation measures have also introduced a certain element of competition among the banks, which has induced them to produce innovative financial products. Many new savings schemes and other financial products have entered the market in the past two years.

Financial deregulation has also opened more opportunities for the Indonesian companies to raise new equities in the Indonesian capital market. The Jakarta Stock Exchange was practically dormant, and the number of listed shares stagnated at 25 companies during the 11 years of the capital market. In just less than two years, the listed companies jumped to 128. The total market capitalization also reached Rp. 14.6 trillion in October 1990, and the cumulative stocks issued reached Rp. 12.7 trillion. With this development, businesses have the opportunity to increase their capital and improve their financial structure.

Other finance companies have also made some progress. Factoring companies, securities companies, and credit companies have come into being in the last few

years. These new institutions are expected to contribute to the economic develop-

ment of Indonesia.

394 JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

Along with these impressive achievements, some challenges came to surface in the second half of 1990.

First, the high rate of growth of credit extended by banks has become a problem for the domestic financial market. The real sector of the Indonesian economy will have to absorb the credit flow at an economic rate of return. Moreover, stiffer competition among banks has resulted in the creation of a relatively large volume of consumer credit. This development has driven the inflation rate upward in 1990. The inflationary pressure called for a quick response from the Central Bank by way of tightening the money supply. Concern about the basic soundness of the country’s banking system is increasingly manifest. To ensure the stability and integrity of the financial system, the Central Bank has instituted prudential regulations, such as the legal lending limit and the net open position. The Central Bank’s role of supervision of the banking system has also been stepped up.

In the field of capital market, too fast growth of the market has quickly dried up the demand for the securities. Moreover, tight monetary policy has driven up the deposit rate to compete with the returns from the capital market. As a result, the capital market experienced a downturn in the second half of 1990, the market index dropping more than one third from its peak in April 1990.

Second, globalization of the financial market has significantly affected the Indonesian financial market. In the last several years, the Indonesian banks have become more active in the world financial markets, especially with a view to optimizing gains from capturing a share of the excess supply of funds in the Pacific region.

The most apparent impact of globalization is the influx of foreign investors in the Indonesian stock market. The inflow of these funds has, of course, broadened the stock market. The establishment of many Indonesian funds listed in the stock ex- changes in the world financial markets has strengthened the interdependence of the markets at home and abroad. However, the Gulf Crisis and the uncertainty due to the collapse of several financial markets in various other countries have been responsible for concern among investors about the long-term viability of the Indonesian market.

At the macro policy level, despite some fluctuations in inflation rates and interest rates, as noted earlier, the foundation for a more stable macroeconomic environment has been in place. The system of monetary and exchange rate manage- ment, for instance, is capable of fine-tuning rate adjustments, to maintain a rela- tively stable growth of the financial sector.

At the micro level, the growth of a variety of banking and financial products has been quite impressive in recent years. These are the results of financial liberaliza- tion, technological advancement, and increased flexibility of movements of ex- change rates and interest rates in major currencies. The latter has induced the creation of various products such as exchange rate and interest rate swaps, options, and many other variations of futures contracts. Many more new products are ex- pected to come to the market in the near future and thus further deepen competition in the financial markets.

Indonesia‘s Financial Reforms: Challenges in the 2990s for Its Banking and Financial Markets 395

VII. CHALLENGES IN THE 1990s

Having witnessed some momentous changes in the 198Os, especially the strong accent on reforms toward market-oriented economies in major parts of the world, it would be interesting to watch further unfolding of reforms in the 1990s. Notable developments that can be foreseen for this decade should include progression of the liberalization process of the world financial markets, as well as the world trade- should the Uruguay Round of trade negotiation ever be successful.

Accelerated liberalization in the European Community’s (EC) financial sector toward a European Monetary Union {EMU), further integration of the Eastern Euro- pean countries into the world economy, and continued high rate of economic growth in the Pacific region should be expected to provide a positive framework in this regard.

The process of globalization of the financial markets can also be expected to continue in the 1990s.

Together, these developments will provide opportunities for the Indonesian financial sector to compete and grow. At the same time, they will offer challenges both to the financial community and the monetary authority in Indonesia; more so because of the sweeping reforms introduced in the Indonesian financial markets in recent years.

In the domestic market, financial institutions and banks in particular should expect more intense competition, especially since the newly established banks, both domestic and joint venture, would have to work hard to expand their business activities to reach break-even points. Moreover, many banks have adopted expansive approaches in establishing branch networks in the past two years. They would have to justify their branch establishments by acquiring sufficient businesses for the branches. These activities will add a significant degree of competition to the banking and financial markets.

Extensive financial reforms, as have taken place in many parts of the world, and increased globalization of financial services will make the banks compete not only with domestic financial institutions but also with financial institutions in the world markets. Thus, competition with banks and financial institutions at home and abroad will be the challenge of the 1990s. Indonesia will have to work hard to accept it.

Banks would have to follow closely the development of new financial products and their derivatives and to analyze carefully the threats and opportunities the new products may bring about. Banks would have to be aggressive enough in creating new products and diversifying services. But at the same time they will have to be conservative enough to protect their stability and continued viability.

To the monetary authority, the challenges it may face are in at least two forms. First, with respect to monetary management, financial reforms and increased finan- cial globalization would make the control of financial aggregates more difficult. The monetary autho~ty will have to apply sophisticated techniques of monet~ manage-

396 JOURNAL OF ASIAN ECONOMICS, 2(2), 1991

ment, including establishment of a comprehensive and up-to-date information gathering/processing system on which decision making will have to be based. Sec- ond, with respect to the Central Bank’s role of bank supe~ision, reform or deregula- tion in the banking sector would require that such supervision should not be focused only on banks’ discipline in complying with regulations, but more also on advanced techniques which are capable of generating early warning signals whenever an individual bank is in trouble. On the other hand, increased competition among banks requires a more extensive bank supervision to forestall a bank’s problem and avoid its failure.

It is worth noting that the distinction between bank and non-bank financial institutions in terms of business activities is becoming blurred. In fact, a current debate is whether or not the universal banking concept should be adopted. There- fore, banks would also have to take into account the competition with non-bank financial institutions.

VIII. CONCLUSION

Competition in the banking and financial markets of Indonesia is likely to accelerate. The competition will not be limited to the domestic market only, but continued globalization will make competition more world-wide in nature. Financial deregula- tion, technological advancement, and increased flexibility in exchange rate and interest rate movements will further contribute to the intensity of competition.

Ultimately, what counts is the creativity of each bank or financial institution in introducing attractive ind innovative products to the market, and such creativity is induced by financial deregulation. It is also important to emphasize that cooperation is not incompatible with competition. It is often found that cooperation among banks in certain products is necessary to win customers’ acceptance.

On the policy side, improved supervision and prudent monetary management are necessary conditions for a healthy financial competition and financial growth in the future.

Acknowledgments: The author is grateful to Cyrillus Harinowo, Aslim Tadjuddin, and Maman Somant for their comments and suggestions. The views expressed in this paper do not necessarily reflect those of Bank Indonesia.

NOTES

1. Basic data, not presented here, will, however, be made available on request. 2. Queries for the basic data used for the analysis in this section may be addressed to Bank

Indonesia.

lndonesia’s Financial Reforms: Challenges in the 1990s for Its Banking and Financial Markets 397

REFERENCES

Balino, Tomas F.T., and Sundararajan, V. 1986. “Financial Reform in Indonesia, Causes, Conse- quences , and Prospects, ” in Hang-Sheng Cheng, ed., Financial Policy and Reform in Pacific Basin

Countries, pp. 191-219. Lexington, MA: Lexington Books. Gillis, Malcolm, and Dapice, David. 1988. “Indonesia,” in Rudiger Dornbusch and F. Leslie C.H.

Helmers, eds., The Open Economy, Tools for Policy Makers in Developing Countries, pp. 307-335. New York: Oxford University Press.

Greenwood, John G. 1986. “Financial Liberalizations and Innovation in Seven East Asian Econo- mies,” in Yoskho Suzuki and Hiroshi Yomo, eds., Financial Innovation and Monetary Policy: Asia

and The West, pp. 79- 105. University of Tokyo Press, 1986. Layman, Thomas A. 1990. “The Development of Indonesia’s Financial Sector: Past, Present and

Future,” paper presented at the International Conference on Economic Policy Making Process in Indonesia, Bali, Indonesia, September 6-9.

McKinnon, Ronald I. 1973. Money and Capital in Economic Development. Washington DC: The Brookings Institution.

Nasution, Anwar. 1990. Tinjauan Ekonomi atas Dampak Paket Deregulasi tahun 1988 pada Sistem Keuangan Indonesia (Economic Analysis on the Impact of the 1988 Deregulation on the Indonesia Financial System). Jakarta: P.T. Gramedia.

Sabirin, Syahril. 1989. “Financial Reforms in Indonesia,” paper presented at the Conference on Banking and Financial Service Asia 1989, Singapore, January 26-27, 1989.

Sabirin, Syahril, and Soekami, Muljana. “Money, Price, Income and Interest Rates in Indonesia

Before and After the Financial Deregulation of June 1983,” in Bob Rankin, ed., Structural Change

and Economic Modelling. Sydney: Reserve Bank of Australia, 1986. Shaw, Edward S. 1973. Financial Deepening in Economic Development. New York: Oxford University

Press. Soesastro, M. Hadi. 1989. “The Political Economy of Deregulation in Indonesia,” Asian Survey,

29(9).

Received November 1990; Revised April 199 1