Embed Size (px)

Citation preview

R

IT

Sa

3b

a

ARRAA

KTSCMS

1

(c(Aaeaf(fflS

cnt

iTa

0d

ARTICLE IN PRESSG ModelESPOL-2261; No. of Pages 11

Research Policy xxx (2008) xxx–xxx

Contents lists available at ScienceDirect

Research Policy

journa l homepage: www.e lsev ier .com/ locate / respol

nter-generational transitions in socio-technical systems:he case of mobile communications

hahzad Ansari a,∗, Raghu Garudb,1

Department of Strategic Management and Business Environment, RSM Erasmus University, Burg. Oudlaan 50,062 PA Rotterdam, The NetherlandsThe Pennsylvania State University, 430 Business Building, University Park, PA 16802-3603, United States

r t i c l e i n f o

rticle history:eceived 15 November 2007eceived in revised form 5 October 2008ccepted 15 November 2008

a b s t r a c t

Many technology studies have conceptualized transitions between technological generations as a seriesof S-curve performance improvements over time. Surprisingly, the interregnum between successive gen-erations has received little attention. To understand what happens in the interregnum, we study thetransition from 2G to 3G in mobile communications. Our study identifies the presence of forces for both

vailable online xxx

eywords:echnological transitionsocio-technical systemollateral technologies

change and continuity across heterogeneous social and technical elements shaping an uneven transitionbetween 2G and 3G mobile communications technology platforms. Unanticipated misalignments andasynchronies that emerged during the journey shifted the incentives of the various actors involved toparticipate. Based on these observations, we offer several conjectures as to the dynamics that can giverise to temporal discords during inter-generational technological transitions.

obile communications-curve

. Introduction

Many technology studies are predicated on Schumpeter’s1942) perspective wherein waves of discontinuous technologicalhange unfold within an overall process of creative destructioncf. Christensen, 1997; Hill and Rothaermel, 2003; Tushman andnderson, 1986; Utterback, 1994). With an implicit assumptionbout the inevitability of technological trajectories, technologicalvolution has been conceptualized as proceeding in a sequentialnd progressive manner prescribing an S-shaped curve as seen,or instance, in performance improvements in desktop memoryChristensen, 1997). The S-curve hypothesis suggests that the per-ormance of a technology, slow at first, accelerates over time, finallyattening out to be supplanted by a new technology with its own-curve.2

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

Despite the seductive appeal of this framing and the clear impli-ations that actors should shift investments from a mature to aew technology at an “inflection point” (point of saturation) onhe S-curve (e.g. Christensen, 1997; Grove, 1996), those who have

∗ Corresponding author. Tel.: +31 10 408 1996; fax: +31 10 408 9013.E-mail addresses: [email protected] (S. Ansari), [email protected] (R. Garud).

1 Tel.: +1 814 863 4534; fax: +1 814 863 7261.2 Such improvements correspond with the diffusion rate of novel technologies and

nnovations over time (Rogers, 2003). Only a few actors adopt an innovation at first.hen, the adoption rate increases sharply with large numbers adopting followed byslowing down as laggards finally adopt the innovation.

048-7333/$ – see front matter © 2008 Elsevier B.V. All rights reserved.oi:10.1016/j.respol.2008.11.009

© 2008 Elsevier B.V. All rights reserved.

examined the micro-processes of technology transitions suggestthat there is more than a simple shift from one technological tra-jectory to another (Geels, 2002, 2005; Sood and Tellis, 2005). Forinstance, old technologies can prove to be surprisingly resilient andmay not simply get eclipsed by new ones (Henderson, 1995). Inaddition, the effective functioning of any technology requires thecreation of co-specialized assets (Teece, 1986), a facet of technol-ogy transition that may not unfold as anticipated. Complicatingmatters, different user groups may have different interpretations ofa technology-in-use, thereby impacting any transition (Pinch andBijker, 1984). Moreover, with transitions that involve platforms withmulti-sided markets3 (Boudreau, 2006; Evans et al., 2006; Rochetand Tirole, 2003), coordinating and balancing the diverse strategicand economic interests of multiple sets of users further increasesthe complexity of the transition process.

These observations suggest that it would be productive to exam-ine the processes that unfold during a transition. To do so, we adopt

ansitions in socio-technical systems: The case of mobile communica-

a socio-technical perspective (Bijker et al., 1987) to examine thetransition from the second (2G) to the third (3G) generation inthe field of mobile communications. By examining the interactionsacross heterogeneous social and technical elements over time, we

3 We are grateful to an anonymous Research Policy reviewer for drawing our atten-tion to this emerging literature. An example of a multi-sided platform would be avideogame platform, such as Nintendo that not only needs to attract users in orderfor game developers to design games for its platform but also needs games fromgame developers to induce users to buy and use Nintendo’s console.

INR

2 arch P

fiuttppmirdt“

2

tdatcSat

cbitndahtaat1

eieaaSaafmaasaZ

tfidCftuTbw

3.1. Data sources

Data concerning the actions of various constituents wereacquired from three sources. First, we interviewed several key exec-

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

nd that transitions are complex and non-linear processes whereinnanticipated misalignments and asynchronies that emerge duringhe journey can shift the incentives of the various actors involvedo participate. For instance, the viability of investments may getroblematized during implementation resulting in deterring com-lementors and co-specialized assets providers, user preferencesay get clarified in-use as they interpret technologies in unantic-

pated ways and collateral technologies may enter the picture toeduce the performance gap between the old and the new. All theseevelopments can conspire to change parameters even as a transi-ion unfolds. As a result, technological transitions may not follownatural trajectories or “a set logic in advance” (Callon, 2008).

. Theoretical framework

Schumpeter’s (1934, 1942) seminal work on creative destruc-ion has inspired a rich body of literature on technological cycles,iscontinuities, paradigms and trajectories (Dosi, 1982; Tushmannd Anderson, 1986; Utterback, 1994). A popular hypothesis onechnological evolution as captured by the image of an S-curveontinues to attract much scholarly attention (Christensen, 1997;ood and Tellis, 2004). Such imagery suggests a sort of inevitabilitybout technological trajectories where, despite fierce battles, newechnologies eventually eclipse older ones.

However, while an S-curve may be useful in depicting the out-omes of a battle between technological generations once it haseen fought, it is less useful in understanding issues that arise dur-

ng transitions (Latour, 1991). Empirical research on technologicalransitions has problematized the S-curve by showing that old tech-ologies may persist and even improve following long periods oformancy (Henderson, 1995; Lawless and Anderson, 1996; Soodnd Tellis, 2005). That technological transitions may not be linearas also been noted by those who have taken a systemic view onechnological platforms (Gawer and Henderson, 2007). With suchview, it becomes clear that different inter-related co-specialized

ssets (Teece, 1986) of any platform may emerge at different rates,hereby generating critical “bottlenecks” along the way (Rosenberg,982).

Social construction of technological systems scholars (e.g. Bijkert al., 1987) have further opened up the black box of technolog-cal transitions by examining not only technical but also sociallements at play during transitions. For instance, associated withny technological platform are actors from the supply, demandnd institutional domains (Garud and Karnøe, 2003; Geels, 2005).upply-side actors include a constellation of organizations thatre involved in the design, production and distribution of goodsnd services. On the demand side, there may be multiple users, aacet of complex technological platforms that recent research on

ulti-sided markets highlights (Boudreau, 2005, 2006; Evans etl., 2006; Rochet and Tirole, 2003). Mediating many of the inter-ctions between and across these groups are institutional actorsuch as regulators, media critics, analysts and the like (Kemp etl., 2001; Lounsbury and Glynn, 2001; Pollock and Rindova, 2003;uckerman, 1999).

An expanded view of technological platforms highlights whyechnological transitions may not be straightforward. For instance,rom the supply side, even simple changes can hold importantmplications for the re-distribution of competencies across pro-uction networks (Garud and Munir, 2008; Glasmeier, 1991).onsequently, changes might be resisted. This is likely to be true

rom the demand side as well, especially with respect to transitions

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

hat either disturb or attempt to create a new equilibrium betweensers on multiple sides of a platform (Boudreau, 2006; Rochet andirole, 2003). Even with single markets, linear transition can easilye upset because of the different and at times unanticipated ways inhich users may interpret a technology (cf. Pinch and Bijker, 1984).

PRESSolicy xxx (2008) xxx–xxx

Besides supply-side and demand-side forces, institutional forcessuch as existing methods of evaluation, the legitimacy of incumbenttechnologies and prevailing rules and regulations may encouragethe status quo rather than change (Hargadon and Douglas, 2001;Kemp et al., 2001).

How might those who want to bring about change counter theseforces for continuity? One way is to create a compelling vision ofthe future (Brown et al., 2000). Especially during early stages oftechnology development, collective beliefs and expectations aboutthe future can play a crucial part in defining roles, building inter-ests and constructing mutually binding obligations among a set ofinterdependent constituents operating in different domains (VanLente, 2000). Through claims and promises, expectations create arhetorical space that over time evolves into a reality of require-ments, mutual obligations and “emerging irreversibilities” (Callon,1991).4 By structuring the activities of a distributed network ofactors within a socio-technical system, expectations of the futurecan come to play a self-fulfilling role just as financial instrumentscan play a “performative” role in constituting markets (Callon, 1998;MacKenzie and Millo, 2003).

How forces for continuity and change, both present during anyattempted transition, play out can have a profound impact onthe specific path along which a transition unfolds. It is this facetof change that we are interested in examining in this paper. Forinstance, what are the temporal discords that emerge during a tran-sition? How do they dynamically change the relationships amongmembers in a socio-technical system with diverse interests and per-spectives? We address these questions by providing an account ofthe processes involved in the transition between the second gener-ation (2G) and third generation (3G) of the mobile communicationsplatform. But first, we offer a brief overview of our research site andthe methods that we have employed to conduct this study.

3. Research site and methods

A study of mobile communications from 1999 to 2006 repre-sents a particularly revelatory case for examining the dynamics ofinter-generational transition in the wake of a technological discon-tinuity – the advanced third generation (3G) technology. From aperformance standpoint, the field of mobile communications hasseen three main generations from the early 1980s to the present,from voice-centric 1G and 2G platforms to voice and data-centric3G platforms along with an intermediate 2.5G platform and discus-sions about a futuristic 4G. Fig. 1 depicts how the performance hasimproved over time.

Two factors shaped our decision to examine this field. First, it ischaracterized by systemic properties (Katz and Shapiro, 1985) withinterdependent constituents such as network operators, equip-ment manufacturers, content providers, regulators, and users, eachguided by different frames, interests and motivations, vis-à-vis thetransition. Second, events relating to technological transitions inthis domain are well documented. This makes it possible to tracethe developments of multiple inter-related constituents over timeand to theorize about the transition.

ansitions in socio-technical systems: The case of mobile communica-

4 The overall movement is a “promise-agenda-requirement” conversion process(Van Lente, 2000:61). An expectation statement indicates promising aspects of tech-nological developments, allocate roles, structure activities, invokes responses andcreates an agenda for activities. When such an agenda becomes accepted, it may thenlead to a more detailed specification of technological requirements and resources.

ARTICLE ING ModelRESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Research P

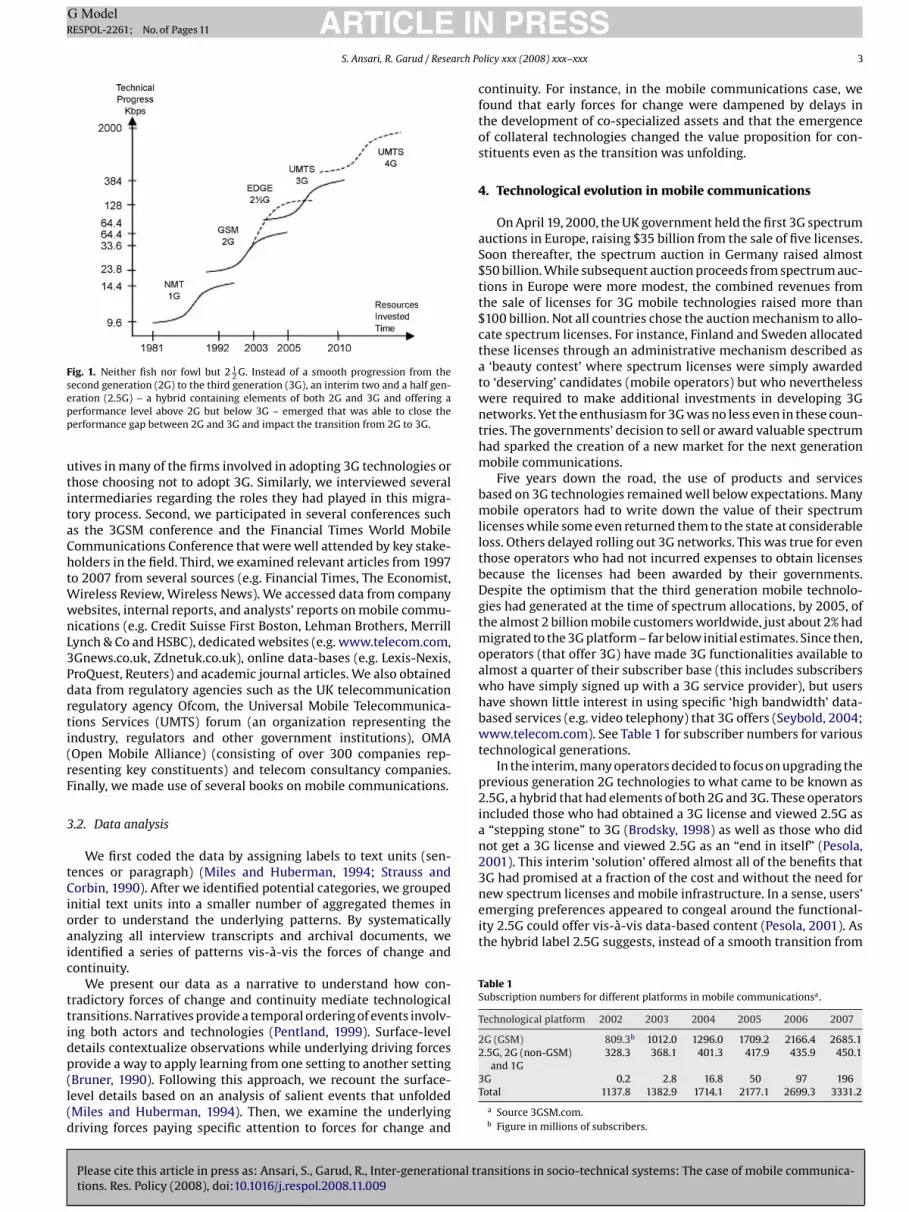

Fig. 1. Neither fish nor fowl but 2 12 G. Instead of a smooth progression from the

second generation (2G) to the third generation (3G), an interim two and a half gen-epp

utitaChtWwnL3Pdrti(rF

3

tCioaic

ttidp(l(d

new spectrum licenses and mobile infrastructure. In a sense, users’emerging preferences appeared to congeal around the functional-ity 2.5G could offer vis-à-vis data-based content (Pesola, 2001). Asthe hybrid label 2.5G suggests, instead of a smooth transition from

Table 1Subscription numbers for different platforms in mobile communicationsa.

Technological platform 2002 2003 2004 2005 2006 2007

2G (GSM) 809.3b 1012.0 1296.0 1709.2 2166.4 2685.12.5G, 2G (non-GSM)

and 1G328.3 368.1 401.3 417.9 435.9 450.1

ration (2.5G) – a hybrid containing elements of both 2G and 3G and offering aerformance level above 2G but below 3G – emerged that was able to close theerformance gap between 2G and 3G and impact the transition from 2G to 3G.

tives in many of the firms involved in adopting 3G technologies orhose choosing not to adopt 3G. Similarly, we interviewed severalntermediaries regarding the roles they had played in this migra-ory process. Second, we participated in several conferences suchs the 3GSM conference and the Financial Times World Mobileommunications Conference that were well attended by key stake-olders in the field. Third, we examined relevant articles from 1997o 2007 from several sources (e.g. Financial Times, The Economist,

ireless Review, Wireless News). We accessed data from companyebsites, internal reports, and analysts’ reports on mobile commu-ications (e.g. Credit Suisse First Boston, Lehman Brothers, Merrillynch & Co and HSBC), dedicated websites (e.g. www.telecom.com,Gnews.co.uk, Zdnetuk.co.uk), online data-bases (e.g. Lexis-Nexis,roQuest, Reuters) and academic journal articles. We also obtainedata from regulatory agencies such as the UK telecommunicationegulatory agency Ofcom, the Universal Mobile Telecommunica-ions Services (UMTS) forum (an organization representing thendustry, regulators and other government institutions), OMAOpen Mobile Alliance) (consisting of over 300 companies rep-esenting key constituents) and telecom consultancy companies.inally, we made use of several books on mobile communications.

.2. Data analysis

We first coded the data by assigning labels to text units (sen-ences or paragraph) (Miles and Huberman, 1994; Strauss andorbin, 1990). After we identified potential categories, we grouped

nitial text units into a smaller number of aggregated themes inrder to understand the underlying patterns. By systematicallynalyzing all interview transcripts and archival documents, wedentified a series of patterns vis-à-vis the forces of change andontinuity.

We present our data as a narrative to understand how con-radictory forces of change and continuity mediate technologicalransitions. Narratives provide a temporal ordering of events involv-ng both actors and technologies (Pentland, 1999). Surface-leveletails contextualize observations while underlying driving forcesrovide a way to apply learning from one setting to another setting

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

Bruner, 1990). Following this approach, we recount the surface-evel details based on an analysis of salient events that unfoldedMiles and Huberman, 1994). Then, we examine the underlyingriving forces paying specific attention to forces for change and

PRESSolicy xxx (2008) xxx–xxx 3

continuity. For instance, in the mobile communications case, wefound that early forces for change were dampened by delays inthe development of co-specialized assets and that the emergenceof collateral technologies changed the value proposition for con-stituents even as the transition was unfolding.

4. Technological evolution in mobile communications

On April 19, 2000, the UK government held the first 3G spectrumauctions in Europe, raising $35 billion from the sale of five licenses.Soon thereafter, the spectrum auction in Germany raised almost$50 billion. While subsequent auction proceeds from spectrum auc-tions in Europe were more modest, the combined revenues fromthe sale of licenses for 3G mobile technologies raised more than$100 billion. Not all countries chose the auction mechanism to allo-cate spectrum licenses. For instance, Finland and Sweden allocatedthese licenses through an administrative mechanism described asa ‘beauty contest’ where spectrum licenses were simply awardedto ‘deserving’ candidates (mobile operators) but who neverthelesswere required to make additional investments in developing 3Gnetworks. Yet the enthusiasm for 3G was no less even in these coun-tries. The governments’ decision to sell or award valuable spectrumhad sparked the creation of a new market for the next generationmobile communications.

Five years down the road, the use of products and servicesbased on 3G technologies remained well below expectations. Manymobile operators had to write down the value of their spectrumlicenses while some even returned them to the state at considerableloss. Others delayed rolling out 3G networks. This was true for eventhose operators who had not incurred expenses to obtain licensesbecause the licenses had been awarded by their governments.Despite the optimism that the third generation mobile technolo-gies had generated at the time of spectrum allocations, by 2005, ofthe almost 2 billion mobile customers worldwide, just about 2% hadmigrated to the 3G platform – far below initial estimates. Since then,operators (that offer 3G) have made 3G functionalities available toalmost a quarter of their subscriber base (this includes subscriberswho have simply signed up with a 3G service provider), but usershave shown little interest in using specific ‘high bandwidth’ data-based services (e.g. video telephony) that 3G offers (Seybold, 2004;www.telecom.com). See Table 1 for subscriber numbers for varioustechnological generations.

In the interim, many operators decided to focus on upgrading theprevious generation 2G technologies to what came to be known as2.5G, a hybrid that had elements of both 2G and 3G. These operatorsincluded those who had obtained a 3G license and viewed 2.5G asa “stepping stone” to 3G (Brodsky, 1998) as well as those who didnot get a 3G license and viewed 2.5G as an “end in itself” (Pesola,2001). This interim ‘solution’ offered almost all of the benefits that3G had promised at a fraction of the cost and without the need for

ansitions in socio-technical systems: The case of mobile communica-

3G 0.2 2.8 16.8 50 97 196Total 1137.8 1382.9 1714.1 2177.1 2699.3 3331.2

a Source 3GSM.com.b Figure in millions of subscribers.

INR

4 arch P

twutds

4

letmWmita“ro(hpfce

umupwempiSrcfBmep

4t

fr(ttdav2

d(ib

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

he second to the third generation, the system settled down some-here in-between, incorporating facets from both generations. Tonderstand how and why this happened, we need to look beyondhe technologies at play in order to examine the forces that emergeduring the transition from different parts of the socio-technicalystem for mobile communications.

.1. The mobile socio-technical system

At the time of spectrum allocations, the mobile system wasocked into a voice-centric 2G platform – essentially the wirelessquivalent of fixed-line telephony – that had reached saturation inerms of penetration levels. 3G could change the rules of engage-

ent by making mobile communications voice and data-centric.ith phones becoming ‘hybrid’ devices (offering voice, video,obile TV, Internet access and so on), there were changes unfold-

ng in the “industry architecture” – template of agents and assetshat circumscribe the contours of an industry (Jacobides et al., 2006)nd boundaries of the mobile platform were becoming increasinglyplastic” (Boudreau, 2005) as mobile communications entered theealm of consumer electronics and entertainment. This required notnly new core technologies but also several co-specialized assetsTeece, 1986). Among these assets were new generation mobileandsets from manufacturers (that needed to be compatible withrevious generation mobile phones), new base stations and mastsrom infrastructure providers for the transmission of 3G signals andompelling applications or mobile ‘content’ (video games, websites,tc.) from application developers for the 3G platform.

The 2G platform only offered voice-based services with all end-ser revenues being appropriated by the mobile operators. The newarket around the 3G platform was premised around two kinds of

sers – content providers (such as banks and entertainment com-anies to develop new kinds of ‘mobile’ services) and end-usersho would benefit from the new functionalities being offered. 3G

ffectively stood to make mobile communications a “multi-sidedarket” where mobile operators would need to serve multiple com-

lementary sets of users (Rochet and Tirole, 2003). Since spectrums a state-controlled resource, the field also involved regulators.imilarly, infomediaries – analysts and media – played an importantole in shaping perceived realities. Besides, environmental groupsoncerned about the potential radiation hazards from the 3G plat-orm were also important in influencing the transition process.5

efore we elaborate further on the roles of various actors in theobile communications field, we first provide an overview of the

ssential characteristics of 3G technologies and the advantages itromised over the preceding 2G technologies.

.2. Key characteristics of the third generation (3G) wirelessechnology

In June 1999, nine global leaders in the mobile telephoneormed an industry group called 3GIP to develop the technologyequired for the next generation (3G) of wireless communicationsTaylor, 1999). As against the globally dominant GSM (Global Sys-em Mobile) standard in 2G technologies, 3G technologies usedhe CDMA (Code Division Multiple Access) radio interface stan-

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

ard. CDMA is far more efficient in ‘farming’ available spectrum byssigning a unique code for each frequency channel, thereby pro-iding more traffic per megahertz of spectrum (Funk and Methe,001). CDMA has two versions; the European sponsored Wideband

5 3G networks operate at higher frequencies and the range of radio wavesecreases as frequency increases, 3G networks require more cells than 2G networksNewing, 2001). This required the construction of additional masts and base stationsn cities as well as more powerful handsets than those used in 2G technologies. Manyelieve that these components posed significant radiation hazards.

PRESSolicy xxx (2008) xxx–xxx

CDMA (UMTS) and the US centered CDMA2000. Most 2G technolo-gies, including the European-led GSM standard, was based on TDMA(Time Division Multiple Access) – a technology that creates multi-ple access channels for subscribers by spacing frequencies in time.6

3G technologies not only made more efficient use of a wider bandof spectrum, but also had the capability to transmit more data at amuch faster speed than 2G.

Besides these differences in core radio interface technologies,3G also offered a more efficient way of transmitting wireless data.All 3G technologies use ‘packet based’ systems for sending data– a technology also employed for data transmissions over Inter-net (Martinelli, 2008). The data file to be transmitted is split upinto smaller units or packets that are then reassembled at thefile’s destination. Spectrum usage is more efficient because thechannel remains available to other users during the connectionbetween two users. In contrast, circuit-switched technology thatwas employed in voice-centric 2G technologies sets up a dedi-cated connection between two callers for the entire duration of thecommunication, thereby creating inefficiencies in spectrum utiliza-tion. While the core 3G technology, CDMA, and packet switchingallow for better utilization of spectrum, handling large amounts ofdata also required a higher spectrum capacity or bandwidth. Spec-trum being a scarce and valuable resource (also used for exampleby national defense services) meant that several operators had toobtain licenses to access 3G spectrum. To understand the enthusi-asm for 3G technology, we need to look at the antecedents to 3Gspectrum allocations. This includes the context in which the allo-cations took place and the activities of various constituents in therun up to these allocations.

4.3. The enabling context

As with other technological fields, actors in the field of mobilecommunications responded to the broader context shaping change.Mobile communications took its cues from ‘broadband’ where fixeddata services were growing at more than 200% a year (DeloitteReport, 1999). Taking note, the Director of data strategy at LucentTechnologies stated: “The same market pull will hit the wirelessindustry and with third generation standards, mobile will be readyto meet demand when it arises” (quoted in Awde, 1999). CEOs ofmajor operators, such as Vodafone believed that “just as voice ismoving to wireless, so will data and the Internet, for the samereason: convenience” (quoted in The Economist, 1999).

Projections that growth in data-based services would soonimpact the wireless domain, led many in the industry to believe thatthe voice-only functionality offered by 2G would not be enough. Itwas in this context that 3G promising the functionality requiredto seamlessly surf the web on mobile phones was proposed. Sincealmost everyone owned a mobile phone, 3G would make the Inter-net mainstream and widely accessible by eliminating the need forusers to own expensive laptops and PCs (The Economist, 2004a).Furthermore, 3G was seen as a platform that could spur demandfor online shopping (e-commerce) by enabling online purchasesthrough the mobile phone (m-commerce) (The Economist, 2001).In essence, 3G promised to make mobile communications a multi-sided market by expanding the boundaries of mobile telephony toinclude information and entertainment services. Switching to 3G

ansitions in socio-technical systems: The case of mobile communica-

was thus seen as the most viable growth strategy for mobile opera-tors who widely agreed that the old 2G technology had reached its“natural performance limit” (Foster, 1986; Sahal, 1985).

6 One exception was the use of CDMA in incumbent 2G systems, such as the CDMA-One (IS-95) that used 2G spectrum. However, with the TDMA-based GSM being thede facto global standard for 2G, the use of CDMA-One remained largely limited toNorth America and parts of Asia (Funk and Methe, 2001).

INR

arch P

4

2vt

wtwbdia

ddfitaptTbwTeMob

i3f

4

mpa

if

cJl

bdc

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

.4. Firms’ reasons for switching to 3G

The end of the voice-based mobile boom7 (Sammut-Bonnici,005; The Economist, 1999) meant that revenues from traditionaloice-based telephony had reached almost saturation levels andhat there was little scope in adding more users to the network.

“International and long-distance call prices are likely to continueto fall rapidly over the next two to five years . . . this is a bleakoutlook for any operator requiring a five-to-10-year return oncapital employed. The mobile sector seems just fraught withdanger” (Analysys Report, 1999).

The only way to grow then was to increase the usage of the net-ork or the ARPU (average revenue per user). 3G was expected

o create a huge surge in revenues from data-based services thatould require much greater bandwidth than what existing, over-urdened and low bandwidth 2G technologies were capable ofelivering. Eager to tap new sources of revenues, it seemed log-

cal for mobile operators to switch to 3G and obtain licenses forccessing additional spectrum.

Besides the perceived expectation of an imminent decline in tra-itional 2G services, there were several other reasons for firms’ecision to migrate to 3G. First, as discussed above, given thatnancial markets were expected to reward firms that made thisransition, eager shareholders of mobile firms exerted consider-ble pressure on management to acquire 3G licenses. Second, as 3Gromised a single, unified global standard,8 there was a tempta-ion to create a viable global ‘footprint’ with seamless connectivity.his required a license at multiple locations as firms hoped touild sufficient size and scale and achieve higher bargaining powerith suppliers to drive not just pan-European but global branding.

hird, with 3G, mobile operators could “monetize the Internet” andarn revenues through web-based services9 (The Economist, 2001).obile operators believed that they had an important advantage

ver Internet service providers and fixed-line companies as notedy an interviewee just before the UK license auction:

“I think the mobile operator with the capability to bill for tele-phony and also for ‘service packages’ has a big advantage overInternet service providers with no direct billing relationshipsand even the fixed operators who normally bill a home or anenterprise rather than an employee or a person” (MD of Hutchi-son, UK).

While there seemed many compelling reasons for firms to investn 3G, several other actors played an important role in promotingG. We discuss the role of these constituents in fuelling optimismor the proposed new technology.

.5. Support from other constituents

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

Equipment manufacturers were eager that mobile operatorsake the switch to 3G given its perceived potential. With their 2G

roduct lines nearing obsolescence, manufactures, such as Nokiand Ericsson stood to considerably benefit from the development

7 The creation of a European-led dominant global mobile standard has resultedn phenomenal growth rates in mobile telephony, with an average rate of over 60%rom 1995 to 2000.

8 The regulators wanted to avoid the patterns of global fragmentation that hadharacterized the market during the first and second generations. North America,apan, and Europe retreated into separate camps resulting in an isolated, balkanizedandscape of incompatible technologies, especially in the US.

9 Internet service providers face major challenges in making money from web-ased services (news, weather reports, etc.) that are mostly ‘free,’ given that mosto not enjoy direct billing relationships with end customers. Mobile operators, inontrast, were in a unique position to charge for such information.

PRESSolicy xxx (2008) xxx–xxx 5

of the 3G market. Indeed, these companies were among the first tocome up with the term ‘3G’ to describe the technologies as a newgeneration.

Such forward-looking thinking was not restricted only to busi-ness but also prevailed in national economies. Our analysis suggeststhat European politicians eager to adapt themselves to the condi-tions of the new economy had strong motivations to raise optimismfor 3G – seen as a European-led global standard that would main-tain Europe’s lead over US in mobile communications. 3G was alsoexpected to benefit the economy by generating new business ven-tures and jobs and unleashing a wave of innovations through theconvergence of media, telephony and the Internet. Indeed, ourreview of the reports on the governments’ decision to designate3G spectrum suggested a strong preference for the proposed newtechnology. Despite the “large uncertainty” about demand for 3Gservices, the price elasticity and the nature of competition in future3G markets, these reports painted an optimistic scenario for 3Gas a technology (Borgers and Dustmann, 2003:228). In the UK, forinstance, reports from Ovum Ltd and Quotient CommunicationsLtd (1998) based their analysis on the figures for London – UK’slargest city with a dense network and heaviest usage of mobile ser-vices. London was chosen to ensure that the demand for 3G serviceswould not be underestimated. Many of these reports concludedthat early users of 3G services would be relatively ‘insensitive’ tocost and that demand would be independent of price considera-tions (Communicator, 1999:6). The government then engaged ina sustained marketing campaign to attract entrants (Binmore andKlemperer, 2002), describing the technology as truly “revolution-ary.” A UK official’s quote is indicative of the state’s support for3G.

“Third Generation (3G) mobile technology will transform howwe access information, creating applications and opportunities,we are only beginning to imagine. Along with Interactive TV,it will bring the Internet to people who would never dream ofhaving a computer at home” (Patricia Hewitt, Small Businessand E-Commerce Minister, quoted in Financial Times, 1999).

Besides regulators, infomediaries such as investment bankers,and analysts also upped the ante for 3G and linked the ratingsof mobile companies to their engagement in 3G projects. Havingseverely underestimated10 the tremendous growth during the sec-ond generation, many analysts were keen to atone for the mistake.For instance, despite earlier revenue forecasts unable to justify theincreasing license price, an advisor to a mobile operator under pres-sure to come with up with more optimistic findings, subsequentlyrevised its estimates (Lehman Brothers Report, 1998). The press alsocontributed to the positive framing of 3G, as indicated by the quote:

“3G will be on a different plane. For starters, the data rate isphenomenal – 2 M bytes per second if you are in a ‘cell’ closeto a transmitter, or 384k bytes for normal mobile use. At thatrate, videophones become an everyday reality, along with tele-vision and radio on demand and multimedia Internet contentsurpassing anything available to the average consumer today”(The Sunday Times, 1999).

ansitions in socio-technical systems: The case of mobile communica-

Positive anticipations for the proposed new technology at thetime appeared to crowd out the few voices of dissent regarding3G’s prospects. A wireless expert noted that, despite the enthu-

10 For instance, in a market research report for AT&T during the first generationmobile communication technology during the mid-1980s, the firm McKinsey hadcome to the conclusion that the cell phone market would not be a profitable optionas the worldwide market potential would be only around 900,000 phones by theyear 2000 (The Economist, 1999). However, the number of cellular phones in thatyear exceeded 400 million globally.

INR

6 arch P

syaatrt1

4

tantpctttAtrfEnm

4

omt2(e2

4

hiaiipfim

U3cIdNl

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

iasm, there were “applications yet to be identified, technologieset to be proved and markets yet to be served. Until those tasksre accomplished, the 3G wireless standards competition is justnother ongoing debate” (Brodsky, 1998). Many analysts noted thathere wasn’t enough market data to prove that the demand waseally out there for wireless multi-media (Jensen, 1999) and thathe mobile operators could lose a “whole lot of money” (Sobti et al.,998). We quote from an analyst’s report from 1998.

“All of that assumes we know what we are going to do with3G and we don’t. Nobody really has an application or service tooffer on 3G that can’t be offered on 2G today. They will talk toyou about video this and video that and high-speed imaging, butthere isn’t anything yet” (Hersche Shoestock Associates Report,1998).

.6. The 3G spectrum allocations

Given the collective framing around 3G, it was no wonderhat many operators were very eager to obtain licenses to access

specific bandwidth on the spectrum that governments desig-ated and put up for allocation in 2000–2001. In some cases,hese licenses were awarded administratively. Others ended upaying huge prices – a total of over 100 billion Euros. In bothases there were stringent rollout obligations attached to spec-rum licenses. For instance, the UK regulators required each licenseeo cover at least 80% of the UK population with 3G services byhe end of 2007 (Preliminary Information Memorandum, 1999).s 3G required a completely new network, meeting this obliga-

ion in sparse demographic distributions and remote terrains wouldequire huge further investments. The total projected investmentor rolling out 3G network infrastructure from 2001 to 2010 inurope was about another 250 billion Euros. Given the promise ofew markets in mobile communications, mobile firms neverthelessade huge investments in their commitment to 3G.11

.7. 3G’s stumble

More than five years down the road, the migration had notccurred as intended despite a concerted ‘technological push’ fromany operators. Analysts’ forecast at the time of license alloca-

ions had been that the technology would be up and running by003–2004 and that it would generate significant rents by 2005Lehman Brothers Report, 1998). Even at the end of 2005, 3G pen-tration levels and use remained well below expectations (Sylvers,007). We explain some of the factors that shaped this outcome.

.7.1. Resource constraintsFirms found themselves under pressure from bankers and share-

olders to reduce the debts that they had accumulated. With thencreasing reluctance of financial institutions to lend more to anlready embattled sector, funds to build new 3G infrastructure weren short supply. To make matters worse, the investment and operat-

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

ng costs for a 3G network turned out to be much higher than initialrojections (Burgelman and Carat, 2003) putting further strain onrm resources. Not surprisingly, several firms, such as the Ger-an operators Mobilcom and Quam decided to simply return the

11 It is worth noting regional differences in 3G spectrum allocations. For instance,.S. wireless operators were in no hurry to move ahead with the implementation ofG in sharp contrast to the enthusiasm shown by several of their European and Asianounterparts. An executive from a major operator noted: “I can’t get too excited untilknow what the capital cost is and what my revenue stream will be. Really, I juston’t see the need to go headlong into 3G at this point” (quoted in Wireless Dataews, 1999). In fact, at the time, FCC and other U.S. government agencies had yet to

ay the groundwork for assigning spectrum that would be used for 3G services.

PRESSolicy xxx (2008) xxx–xxx

license to the regulator while others had to scale back their targets,withdraw from unattractive markets and delay or even abandon3G rollouts in violation of their regulatory commitments. To makematters worse, the demand for 3G services turned out to be wellbelow expectations as end users made little use of the added 3Gfunctionalities that were being offered.

4.7.2. The role of usersUsers did not enact the 3G script as encoded by its proponents.

A Nokia executive noted: “The industry has not been looking at theuser. It’s been looking at its own navel” (Baker and Clifford, 2002).Most research indicated that people were still limiting their use ofthe mobile for ‘phatic’ or social communication as against consum-ing third party content (such as buying goods online) possible with3G (Wilson, 2006). Indeed, social communication (talking and textmessaging) still accounts for well over 90% of operator revenues.In a recent survey conducted among mobile users in Europe, 44%of respondents said that they would not use their mobile phonesother than to make ordinary calls (Wall Street Journal, 2004). Thus,while 3G was conceptualized as a tool to extend the mobile plat-form beyond telephony and offer instantaneous information andentertainment services, the essential use of the platform continuedto be social networking with very limited uptake of digital con-tent – a dynamic that some derisively noted as indicating mobile“discontent” (Wilson, 2006). The persistent low demand for 3G ser-vices prevented positive consumption externalities from kickingin (Economides, 1996). This deterred potential users whose util-ity from adopting 3G services depended on the number of other 3Gsubscribers.

Furthermore, since new 3G services were dependent on comple-mentary assets such as compatible handsets, delays and glitchesfurther retarded 3G’s adoption. The UK head of Hutchison 3G, amobile operator, complained of a lack of handsets.

“Heavy handsets with low battery life did not help our cause. . .Nokia (the leading manufacturer) adopted a wait and see policyfor investing in 3G handsets and delayed deliveries that severelydisrupted our operations” (MD of Hutchison 3G, UK).

As 3G needed complementors developing content for the net-work (e.g. mobile banking) banking software had to be customizedfor the rapidly evolving 3G mobile handsets. Developing such soft-ware required changes every time a new handset was released,dampening the availability of such content. The lack of compellingcontent further slowed down 3G’s diffusion. Mobile operators,given their financial situation and not used to sharing revenuesin the 2G world, wanted to control the largest possible part ofthe value chain by limiting third party access to their platformsin the hope of increasing revenues. This ‘closed’ or “walled gar-den” model rather than an ‘open’ model for access to platformsthat operators embraced deterred not only complementors but alsoend-users who were accustomed to unrestricted content on theInternet (du Preez and Pistorius, 2003). This negatively effected thedevelopment of content for the mobile platform (Wallage, 2005).Furthermore, in Europe’s multicultural and multilingual environ-ment, several content providers (e.g. newspapers) had to targetsmaller local audiences, a market that did not offer scale advan-tages. In some cases, content providers simply could not afford todeliver mobile content for such “small” target audiences (Andersen,1999). Given low volumes, content providers could not adopt theadvertising-based business model of ‘free content’ as was often thecase with the Internet. Instead, in the case of mobile communica-

ansitions in socio-technical systems: The case of mobile communica-

tions they wanted their content to be profitable on a standalonebasis.

To complicate matters, financially constrained firms with lowadditional revenues from 3G services were unable to adequatelyinvest in marketing 3G services to gain end-user acceptance that

INR

arch P

fitftit3sb

4

t3fiofiaspv

3sSEw3Wstwtt

btdiaiamtimiIcficab

4

o‘ewmsC

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

urther retarded the diffusion of the new technology. Anothermportant factor in the slow uptake were ongoing battles betweenhe two competing 3G radio interface standards for the 3G plat-orm – the US led CDMA2000 and the European led WCDMA – evenhough 3G was meant to be a unified global standard. Furthermore,nfomediaries – analysts and media – who had earlier promotedhe new technology now turned decisively against 3G. Moreover,G faced resistance from environmental groups concerned aboutuspected harmful effects of 3G systems and was also threatenedy the development of substitute technologies.

.7.3. The role of other constituentsMany analysts who had promoted the new technology at the

ime of spectrum allocations started to speak of much longer (up to0 years) payback periods for 3G investments and now opined thatrms had exposed themselves to a high risk of premature technol-gy introduction (McClelland, 2003). An analyst argued that mobilerms had not taken into account the fact that the demand for mobileccess to ‘content’ through 3G was “derived” from the demand forervices delivered over the Internet (Ure, 2000). This was unlike therevious voice-focused networks (1G and 2G) in which demand foroice-based services was “intrinsic” to the mobile networks.

Not surprisingly, the media that had vociferously supportedG, just prior to spectrum allocations did a volte-face, sub-equently labeling 3G “Universal Mobile Telecommunicationervices” (UMTS) as “Unproven Market, Technology and Services.”ven some national governments echoed the pessimistic scenarioith the Finnish minister of transport and communications calling

G auctions “the biggest industrial political failure since the Secondord War” (Klemperer, 2002). Environmental groups also put up

trong resistance to the building of the much needed new base sta-ions and 3G masts (transmitters), in view of their perceived linksith radiation hazards. In short, several constituents contributed

o building collective ‘negativity’ around 3G that heightened uncer-ainties regarding the new technology and retarded its diffusion.

To make matters worse, a number of alternative technologiesegan casting a long shadow over the prospects of 3G. One ofhese alternatives was Wireless Fidelity (WiFi) that could siphonata traffic away from 3G networks by providing access to mobile

nformation in designated locations known as ‘hotspots,’ such asirports, coffee shops, or universities. There was speculation in thendustry that all the hotspots would be linked in the future to create

seamless universe with “blanket coverage” for all users therebyaking 3G redundant (The Economist, 2004b). It was even feared

hat, rather than generating new sources of revenue as was orig-nally expected, 3G technology could end up merely as a way for

obile operators to boost their capacity for traditional voice callsn the overloaded parts of their 2G networks (The Economist, 2001).n short, 3G was no longer regarded as a paradigm shift in mobileommunications that would open up a goldmine of new revenuesor mobile operators. As 3G continued to disappoint, many firmsn the industry began to explore the possibilities for stretching theapacity of 2G networks, a possibility that had hardly received anyttention during the early days of 3G when a generational shift waseing considered.

.8. Extension of the old technology

In the meantime, upgrades to 2G technologies, labeled as 2.5Gr GPRS (General Packet Radio Services), were being achieved by

bolting on’ packet-switching data transmission technology onto

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

xisting 2G technologies. Although packet-switching technologyas available even at the time of 2G (GSM), it was given “fairlyarginal billing” at the time and was not incorporated into the GSM

ystem in the mid 1990s (Pesola, 2001). According to Mannings andosier (2001), this is because firms in the mid 1990s had a voice-

PRESSolicy xxx (2008) xxx–xxx 7

centric “telco mindset” and arguably didn’t anticipate the potentialfallout on mobile telephony from developments in the Internet.2.5G essentially allowed faster connections to the Internet via themobile phone while still operating on 2G spectrum. 2.5G could han-dle data transmission speeds between 33.6 and 128 kbps, as againsta maximum of 2000 kbps for 3G, thereby lifting the performance toa level which is in the middle range of 2G and 3G. As an example,downloading a song with a 2.5G network can take over a minuteas against 5 s on a 3G network. 2.5G was like introducing a double-decker bus on an existing one-lane highway (voice plus data) ratherthan build a new 4-lane highway (3G) (Newing, 2001). Also, 2.5Gservices came with reduced price tags compared to 3G as upgrad-ing existing networks entailed no additional costs for obtaining 3Glicenses and for building new 3G networks.

2.5G was being pursued by two types of mobile firms – firms thatdid not obtain a 3G license and firms that obtained 3G licenses andalso invested in 3G rollouts. For the former, this strategy was an “endin itself” (Pesola, 2001). It represented a way to remain competitivein the mobile industry and hurt 3G’s prospects by showing the via-bility of improving existing networks. Firms without 3G licenses,such as the Danish operators, Sonofon and Telias focused on 2.5Gto offer many services that were supposed to be ‘3G’ services andmany executives suggested that consumers have no need for 3G.

In contrast, for firms with 3G licenses who had to delaytheir 3G launches beyond initial promises (such as Vodafone),‘backpedalling’ to 2.5G represented a “stepping stone” to creat-ing demand for ‘full blown’ 3G (Sammut-Bonnici, 2005). However,firms confronted a dilemma – preventing the cannibalization oftheir customer base in a near-saturated market while, at the sametime, also requiring them to sign up for new 3G contracts aimed atincreasing the ARPU.

As the system temporarily settled down around 2.5G, manyoperators now acknowledged that the transition to 3G was unlikelyto be momentous and began to regard 3G as evolutionary ratherthan revolutionary. Indeed, as the CEO of BT Cellnet (later knownas mmO2) stated in 2003: “In terms of the kinds of applications ourcustomers are going to use, I don’t think there is a huge differencebetween 2.5G and 3G” (Telecom Review – Conference proceedingsin the 3GSM World Congress in 2003). The situation actually wasfar more complex than having to decide between two rival tech-nologies. According to the VP of Semico Research Corp. “It is goingto be a case of supporting 2G, 2.5G and 3G, all at the same time. Thisisn’t going to be a nice, smooth transition.”

Worse was the prospect that firms that chose to upgrade to 2.5Gcould bypass 3G and make a direct leap for 4G (The Economist,2003). These 4G networks (also known as Beyond 3G), based onnew technologies such as improved modulation and relaying wereexpected to deliver voice, data and full motion ‘streaming’ videoon mobile devices at over ten times the speed of 3G. A respondentnoted that given what 4G could bring, 3G could well be a “stillborn”technology and the third generation a “lost generation” (formerhead of technology of UK telecom NTL).

5. Towards a dynamic perspective on technologicaltransitions

We have built on the work of scholars arguing for the need to takean expanded socio-technical perspective in conceptualizing tech-nological transitions (Bijker et al., 1987). By disaggregating variouselements of the mobile communications socio-technical system, weidentified several forces that shaped the transition between 2G and

ansitions in socio-technical systems: The case of mobile communica-

3G mobile communications technologies. Forces for change weremediated by dampening forces stemming from delays in imple-mentation, developments in collateral technologies and congealingof user preferences around a set of functionalities below what hadbeen projected for the new technology. These forces conspired to

INR

8 arch P

cacps

5

tccRiftactbds

ldto“aw‘fifmditti

RafwnappgddiftBctntc

Cigo

furnaces allowed the production of better steel, which in turnenabled boiler plates and boiler tubes to withstand higher pres-sures. As a result, the earlier generation technology was improvedthat allowed steam boats to operate more efficiently, and com-

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

hange preferences and incentives of the constituents involved evens the transition was unfolding to disrupt the carefully constructedonnections that had been framed to spark the ‘intended’ transitionath. We discuss how these dynamics played out in greater detailo as to offer some conjectures about transition processes.

.1. Forces for change

Since additional spectrum was a prerequisite for migrating tohe next generation technology, the government’s decision to allo-ate spectrum was performative in generating forces for change byreating a multi-sided market (Boudreau, 2006; Evans et al., 2006;ochet and Tirole, 2003) in mobile communications. By designat-

ng a specific time frame and by allocating a particular bandwidthor 3G spectrum, national regulators, in effect, ‘imposed’ a singleechnology that all countries in Europe had to collectively adopt. Inddition, the ‘one-off’ character of the spectrum allocation processreated a ‘now or never’ mindset – licenses had to be obtained inhe ‘narrow time window’ that was available or else there would note a second chance to obtain a 3G license. This created a prisoner’silemma for incumbent operators as 3G seemed the only route toafeguard their installed customer base.

Furthermore, firms widely believed that 2G had reached itsimits and that, without 3G, the industry would be at a seriousisadvantage in serving future customer needs. Firms’ belief inhe proposed new technology’s potential was reinforced by vari-us other constituents, such as infomediaries active in sketchingutopian future worlds” (Van Lente, 2000). Various self-reinforcingnd mutually dependent forecasts formed part of this rhetoric. Itas difficult for consultants, analysts and other experts to make

independent’ forecasts and they had to rely on figures from mobilerms. Even inside the mobile companies, the more skeptical views

rom technologists were swamped by the future visions of brandanagement and finance (Pantzar and Repo, 2005). As the inter-

ependence between analysts’ forecasts and firms’ actions grew,t further reinforced the most optimistic forecasts. Collectively,hese forecasts led to a rhetoric space around the proposed newechnology as conjectures about future consumer needs turned tomperatives.

The dynamics that emerged are similar to what Van Lente andip (1998) have reported about constituents becoming prisoners ofn emerging discourse and dominant field vision with little roomor voices of dissent. As in the case with mobile communications,hile firms craft promising stories about a proposed new tech-ology’s prospects, various institutional actors, such as the media,nalysts and even national governments validate these stories in theublic domain, conferring legitimacy on them in a self-reinforcingrocess (Pollock and Rindova, 2003). The collective story of a futureeneration then gains widespread attention, appearing to be an evi-ent fact and a “scientific canon.” The step from the promise ofevelopment of a new technology to the imperative of it happen-

ng is readily made and there is really no choice but to push aheador the new technology (Van Lente, 2000) – a process that con-ributes to generating “emerging irreversibilities” (Callon, 1991).eing unable to free themselves of the story’s obligations and theollective web spun around the proposed new technology’s poten-ial (Van Lente, 2000; Wagenaar, 1997), the technology’s adoptionow seems like the only feasible option as firms decide to makehe switch. Based on these observations, we offer the followingonjecture for further enquiry.

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

onjecture 1. Prospective narratives crafted by focal firms and val-dated by institutional actors in favor of a proposed new technologyenerate self-fueling forces for the implementation of the new technol-gy.

PRESSolicy xxx (2008) xxx–xxx

5.2. Dampening forces

While some forces can generate momentum for the new tech-nology (Hughes, 1983), others can retard its progress by disruptingthe temporal coordination that had been set in place. As we saw inthe mobile communications case, lack of specialized 3G handsetsand standard battles led to a slowdown in the technology’s adop-tion. Delays in developing co-specialized assets (Teece, 1986) arelikely to arise with any transition as there is not necessarily a one-to-one correspondence between a technology’s future road-map(however conservative it might be) and its implementation overtime. Amid future projections and the rush to forge ahead witha new technology, its supporters cannot necessarily factor in allthe practical implementation details that will be involved in thedevelopment of co-specialized assets for the technology to becomeoperative. Delays in the development of co-specialized assets thenlead to delays in the launch and diffusion of the new technologymaking it possible for the existing technology to catch up. Theseobservations lead to our second conjecture to be explored in othercontexts.

Conjecture 2. Delays in the development of co-specialized assetsrequired for the new technology to function retards the diffusion of thenew technology and provides an opportunity for the previous technol-ogy to catch up.

5.3. Collateral developments

It is understandable that a delay in the creation of co-specializedassets makes it possible for an existing technology to catch upwith the proposed new technology. These improvements may comefrom within the industry but may also result from developmentsin related industries. For instance, in the context of mobile com-munications, a “collateral technology” (packet switching) enabledthe extension of the old technology (2G), and the extended ver-sion (2.5G) adequately addressed the emergent needs of the usersaround limited use of mobile content services. This delayed theadoption and diffusion of the new technology (3G) even thoughit offered additional ‘richer’ mobile content services.

The phenomenon of how collateral technologies can revital-ize previous generation technologies and mediate transitory paths,albeit to different degrees, has been observed in other domains.For instance, in photo-lithography industry, optical lithography hasshown unusual persistence as the dominant manufacturing tech-nology for computer chips since the late 1960s (Henderson, 1995).While the industry was focused on developing “next generationlithography” (NGL) that included technologies such as extremeultraviolet lithography (EUVL), the discovery of “enhanced liquidimmersion” extended the life of optical lithography12 (Sydow etal., 2007). Infusing optical lithography with a collateral technol-ogy required only minor adjustments compared to EUVL for notonly extending the path of optical technology but also substantiallyimproving its performance and retarding the adoption of EUVL.Similarly, improvements in steelmaking from the introduction ofopen-hearth furnaces in the late 1870s enabled the substitutionof earlier generation steam boats for sailing ships. Open-hearth

ansitions in socio-technical systems: The case of mobile communica-

12 In enhanced liquid immersion lithography (LIL), a drop of fluid (water or oil) isplaced between the optical lens and the wafer. Compared to air, the higher refractiveindex of fluids leads to a better image resolution. Originally used in microscopy toenlarge the image of the specimen, immersion is used in optical lithography to printminiaturized features onto silicon wafers.

INR

arch P

p2

eibdpdic

Cptt

5

nadism2acaofacsa

idghmladoainangf

Cntcc

Vd

ARTICLEG ModelESPOL-2261; No. of Pages 11

S. Ansari, R. Garud / Rese

ete more effectively with new generation sailing ships (Dattee,007).

In short, collateral innovations in related domains can result inxtending the performance of an existing technology thereby clos-ng its performance gap vis-à-vis the new technology. This raises thear for the new technology that now needs to deliver on additionalimensions to demonstrate its superiority over the old, therebyotentially retarding its adoption and diffusion. Thus, technologicalevelopments in related domains also matter in shaping technolog-

cal transitions. Based on these observations, we offer the followingonjecture to be explored in other settings.

onjecture 3. Collateral innovations in related domains can reduceerformance gaps between existing and new technological systems,hereby raising the bar for the new technology and retarding its adop-ion.

.4. Emergent shifts in preferences and incentives

Any closure in the performance gap between the old and theew technology because of forces emerging during the journeygain catches the attention of the constituents from the supply,emand and institutional domains. As we noted earlier, during

nitial stages of new technology emergence, firms craft stories inupport of their strategies that institutional actors, such as theedia and analysts magnify and legitimize (Pollock and Rindova,

003; Van Lente, 2000). Now, slippages in the new technology,s we saw in the mobile communications case, may dynamicallyhange expectations of constituencies and their incentives to forgehead with their plans. For instance, end users may begin to find theld but improved technology acceptable and delay or even refrainrom adopting the new technology. In the mobile telephony case,majority of users continued to use the mobile phone for simple

alls and text messages rather than embrace sophisticated servicesuch as making online purchases. Even video telephony – the onlypplication exclusive to 3G – failed to achieve user acceptance.13

These emergent dynamics may problematize the viability ofnvestments during implementation and lead, for instance, toeterring users from different sides of a market. For instance, toenerate momentum for the new technology, mobile platformsad to attract ‘complementors’ to develop content for users in theobile domain. Without compelling content, 3G services were

ess likely to attract users and achieve critical mass, and withoutcritical mass, there was little incentive for content providers toevelop content for 3G. Such a “chicken and egg” situation, typicalf multi-sided platforms (Rochet and Tirole, 2003), may lead toslowdown in a platform’s growth. Institutional actors, such as

nfomediaries may then step in and, rather than glorifying theew technology as they had during early stages, may magnifyny shortfalls, thereby further dampening enthusiasm for theew technology and preventing a smooth transition from oneeneration to another. Based on these observations, we offer theollowing conjecture to be explored in other settings.

onjecture 4. As the performance gap between the new and old tech-ologies decreases, the incentives of the various participants to make

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

he transition changes dynamically, thereby shaping the transition pro-ess and preventing any one technological system from emerging as alear winner.

13 This had been witnessed much earlier on in the case of fixed line telephones.ideo phones have been around since the 1960s but never became popular as peopleid not want surveillance inside their homes (Lynn et al., 1996).

PRESSolicy xxx (2008) xxx–xxx 9

6. Conclusion

We have built on previous work to understand the forcesthat arise from the interactions between producers, users, andinstitutional players as they grapple with different elements oftechnologies during a transition. As we observed in the mobilecommunications case, new technologies with the promise of higherfunctionalities do not simply eclipse older ones in a process of cre-ative destruction. Rather, transitions may potentially be ‘creativeextensions’; one where elements of existing technologies morph toprovide new viable solutions. In the mobile communications case,for instance, the dialectic interplay between forces for change andfor continuity led to the emergence of an intermediate technology,2.5G, that was able to transgress the frame set for 2G and subsumethe frame around 3G.

What are the foundations for such a perspective on creativeextension? As transitions are necessarily about the future, thefuture needs to be framed – often dramaturgically with promisesand idealizations to raise expectations and attract resources(Lampel, 2001; Van Lente and Rip, 1998). Such framing is accom-plished by connecting and coordinating the activities of multipleheterogeneous elements – technologies, suppliers, users and reg-ulators – distributed across time and space (Geels, 2002). Thiscoordination, which has to unfold into an uncertain future, is gen-erated by creating a rhetorical space that engenders the collectivemobilization of actors.

However, in making a case for a new technology, the framingof the future requires a “bracketing” of the world, a process thatcannot possibly take into account all of the potential “connections,relations and effects” (Callon, 1998:16). Moreover, existing arrange-ments are likely to be reconfigured during implementation and,consequently, even the most carefully laid out of plans can easilycome undone. In addition, framing something new entails con-trasting it against what already exists. That is, the present is oftenproblematized in order to make a case for change (Brown et al.,2000). Consequently, as a transition unfolds, those whose interestsare aligned with the present may attempt to extend the benefitsthat constituents may value by continuing with what alreadyexists. In this task, extensions that occur from developments in col-lateral technologies may come to play a role. And, as in the mobilecommunications case, user needs, that have yet to emerge and tobe tested may congeal around a set of functionalities even thoughthey may fall short of what had been projected earlier. These areall reasons as to why “overflows” (Callon, 1998) will emerge as atransition unfolds, disturbing the anticipated connections betweenheterogeneous elements that make up a future frame. Because ofthese overflows, actors’ interests, goals and preferences as well astheir interactions with others in a network will be emergent and ina process of continual reconfiguration (Callon, 2008) as transitionsunfold through a “series of adaptations” over time (Geels, 2002).

How might various actors in the socio-technical system tryto sponsor these transitions? Institutional actors, such as gov-ernmental and quasi-governmental actors can play an importantrole to “steer” “transition paths” by enacting policies, offeringforums for interactions and proactively shaping incentives (Kempet al., 2001). These dynamics were evident in the role that theDanish government played in coming up with an appropriatemix of policies and incentives to encourage the developmentand diffusion of wind turbine technology to address Denmark’senergy needs (Garud and Karnøe, 2003). Besides institutionalactors, supply-side actors too can play a role in shaping platform

ansitions in socio-technical systems: The case of mobile communica-

dynamics. Specifically, dominant players in privileged positionscan engage in “coring strategies” (Gawer and Cusumano, 2008)by managing tradeoffs between controlling key complementswhile incentivizing third parties to create complementary inno-vations (Boudreau, 2005, 2006). Others have written about a

INR

1 arch P

“vmmf

mcaasctaarsmadcl2

lbthMefianff2pesioat

A

NIccTacpRo

(9wa

ARTICLEG ModelESPOL-2261; No. of Pages 11

0 S. Ansari, R. Garud / Rese

keystone” role (e.g. NTT DoCoMo and its I-mode data-based ser-ices for mobile Internet (Peltokorpi et al., 2007))14 that firmsight play (Iansiti and Levien, 2004) in aligning the interests ofultiple constituents so as to generate momentum around a plat-

orm.However, even the best of attempts at managing transitions

ay come undone because of emergent issues that dynamicallyhange transition parameters. For instance, while institutionalctors may attempt to synchronize heterogeneous elements aroundnew technology, user interests may congeal around a different

et of functionalities or value propositions as was the case withochlear implants where the profoundly deaf preferred to con-inue operating within their culture even as the FDA and the NIHttempted to play a steering role (Lane, 1992). Similarly, attemptst gaining platform leadership during a transition may face stiffesistance not only from constituents whose technological turftands threatened but also by unanticipated developments thatay change the rules of the game for the technology sponsor

s the transition unfolds. Some of these dynamics were evi-ent in the challenge Sun Microsystems faced from Microsoft’sounter-mobilization strategies as Sun attempted to gain platformeadership by sponsoring its Java software technology (Garud et al.,002).

Our observations thus place a word of caution against an unre-enting belief by sponsors in the supremacy of a novel technologyased on its initial framing and the prevailing wisdom to prema-urely abandon old technologies that are sometimes perceived asaving reached their natural performance limits (see also Garud andunir, 2008). Rather than view transitions as unitary and coher-

nt replacement of existing technologies by new technologies, ourndings suggest a conceptualization of transitions as being char-cterized by the dialectic interplay between the existing and theew as a transition unfolds. In this regard, we see the benefits of

using insights from recent work on “multi-sided” markets and plat-orms (e.g. Boudreau, 2006; Evans et al., 2006; Rochet and Tirole,003) with notions such as “overflows” (Callon, 1998) and “inter-retative flexibility” (the shaping of technologies in use) (Bijkert al., 1987) that focus on emergent developments during a tran-ition. By bringing these literatures together, productive lines ofnquiry open around shifting motivations and incentives of vari-us groups involved and how, as a result, an existing technologynd its proposed replacement interact during any technologicalransition.

cknowledgements

This research has been funded in part by a grant from theetworks Electronics, Commerce and Telecommunications (NET)

nstitute, www.NETinst.org. We thank the NET Institute for finan-ial support. We also thank the participants for their valuableomments during the ECIS/KSI workshop, May 2008 Eindhoven,

Please cite this article in press as: Ansari, S., Garud, R., Inter-generational trtions. Res. Policy (2008), doi:10.1016/j.respol.2008.11.009

he Netherlands, 2008; and the Technology and Innovation Man-gement (TIM) session at the Academy of Management (AOM)onference in Philadelphia, USA, 2007, where an earlier draft thisaper was presented. We thank the anonymous reviewers foresearch Policy and Michel Callon for their inputs on an earlier draftf this paper.

14 NTT DoCoMo allowed third parties to directly bill customers for their servicesinformation and entertainment) while handling the billing in exchange for keeping% of the total billings. Users preferred the convenience of a single monthly bill,hile content providers got a very economical but reliable billing service (Evans et

l., 2006).

PRESSolicy xxx (2008) xxx–xxx

References

Analysys Report, 1999. On mobile sector. By Simon Sherrington and Michael Den-mead.

Andersen, A., 1999. Digital Content for Global Mobile Services. Report by EuropeanCommission Directorate General for the Information Society.

Awde, P., 1999. Financial Times, Jun 9, p. 07.Baker, S., Clifford, M., 2002. Tale of a Bubble How the 3G fiasco came close to wrecking

Europe. Business Week, June 03.Binmore, K., Klemperer, P., 2002. The biggest auction ever: the sale of the British 3G

telecom licenses. Economic Journal 112 (478), C74–97.Bijker, W., Hughes, T., Pinch, T. (Eds.), 1987. The social construction of technological

systems: New directions in the sociology and history of technology. MIT Press,Cambridge, MA.

Borgers, T., Dustmann, C., 2003. Awarding telecom licenses: the recent Europeanexperience. Economic Policy 18 (36), 215.

Brodsky, I., 1998. 3G Harangue Wireless Review, November 15 (23), pp. 40–41.Brown, N., Rappert, B., Webster, A. (Eds.), 2000. Contested Futures: Sociology of

Prospective Technoscience. Ashgate, Aldershot.Boudreau, K., 2005. The Boundaries of the Platform: Vertical Integration and Eco-

nomic Incentives in Mobile Computing. Working Paper 4565-05. MIT SloanSchool of Management.

Boudreau, K., 2006. How Open Should an Open System Be? Empirical Essays onMobile Computing, MIT PhD Thesis.

Bruner, J.S., 1990. Acts of Meaning. Harvard University Press, Cambridge, MA.Burgelman, J.C., Carat, G. (Eds.), 2003. Prospects for Third Generation Mobile Systems

ESTO Project Report, EUR 20772 EN prepared for European Commission – JointResearch Center.

Callon, M., 1991. Techno-economic networks and irreversibility. In: Law, J. (Ed.), Soci-ology of Monsters: Essays on Power, Technology and Domination. Routledge,London.

Callon, M. (Ed.), 1998. The Laws of the Markets, Basil Blackwell Publishers, London.Callon, M., 2008. Civilizing markets: carbon trading between in vitro

and in vivo experiments. Accounting, Organizations and Society,doi:10.1016/j.aos.2008.04.003, in press.

Christensen, C.M., 1997. The Innovator’s Dilemma: When New Technologies CauseGreat Firms to Fail. HBS Press, Cambridge, MA.

Communicator, 1999. Preparing for UMTS: A Market Study, Stockholm.Dattee, B., 2007. Appropriability, proximity, routines and innovation. Challenging

the S-curve: patterns of technological substitution. In: Paper presented at theDRUID Summer Conference 2007, Copenhagen, CBS, Denmark, June 18–20.

Deloitte Report, 1999. Report on Growth in Broadband by Deloitte Consulting Group.Dosi, G., 1982. Technological paradigms and technological trajectories. Research Pol-

icy 11, 147–162.du Preez, G., Pistorius, C., 2003. Analyzing technological threats and opportunities in

wireless data services. Technological Forecasting and Social Change 70 (1), 1–20.Economides, N., 1996. The economics of networks. International Journal of Industrial

Organization 14 (6), 673–699.Evans, David, S., Hagiu, A., Schmalensee, R., 2006. Invisible Engines How Software

Platforms Drive Innovation and Transform Industries. The MIT Press, Cambridge,Massachusetts, London, England.

Financial Times, 1999. Survey, FT telecoms: 3G technology will transform Internetaccess: viewpoint, November 24.

Foster, R., 1986. Innovation: The Attacker’s Advantage. Summit Books, New York.Funk, J.L., Methe, D.T., 2001. Market and committee-based mechanisms in the

creation and diffusion of global industry standards: the case of mobile com-munication. Research Policy 30, 589–610.

Garud, R., Jain, S., Kumaraswamy, A., 2002. Institutional entrepreneurship in thesponsorship of common technological standards: the case of Sun Microsystemsand Java. Academy of Management Journal 45 (1), 196–214.

Garud, R., Karnøe, P., 2003. Bricolage versus breakthrough: distributed and embed-ded agency in technology entrepreneurship. Research Policy 32 (2), 277–300.

Garud, R., Munir, K., 2008. From transactions to transformation costs: The case ofPolaroid’s SX-70 Camera. Research Policy 37 (4), 690–705.

Gawer, A., Cusumano, M., 2008. How companies become platform leaders. MIT Sloanmanagement Review 49 (Winter (2)), 28–35.

Gawer, A., Henderson, R., 2007. Platform owner entry and innovation in complemen-tary markets: evidence from Intel. Journal of Economics & Management Strategy16 (1), 1–34.

Geels, F.W., 2002. Technological transitions as evolutionary reconfiguration pro-cesses: a multi-level perspective and a case-study. Research Policy 31 (8–9),1257–1274.

Geels, F.W., 2005. The dynamics of transitions in socio-technical systems: amulti-level analysis of the transition pathway from horse-drawn carriages toautomobiles (1860 1930). Technology Analysis & Strategic Management 17 (4),445–476.

Glasmeier, A., 1991. Technological discontinuities and flexible production networks:the case of Switzerland and the world watch industry. Research Policy 20 (5),469–485.

ansitions in socio-technical systems: The case of mobile communica-

Grove, A., 1996. Only the Paranoid Survive: Exploit the Crisis Point that ChallengeEvery Company and Career. Doubleday Dell Publishing Group, Inc, New York.

Hargadon, A.B., Douglas, J.Y., 2001. When innovations meet institutions: Edison andthe design of the electric light. Administrative Science Quarterly 46, 476–501.

Henderson, R., 1995. Of life cycles real and imaginary: the unexpected long old ageof optical lithography. Research Policy 24 (4), 631–644.

INR

arch P

H

H

H

I

J

JK

K

K

L

L

L

L

LL

L

M

M

M

M

M

N

O

P

P

P

P

P

P

ticipation? Convergence: The International Journal of Research into New MediaTechnologies 12 (2), 229–242.