Embed Size (px)

Citation preview

Internal Audit. Expect More.2020 Internal Audit Planning

Asset and Wealth Management

September 2019

The asset and wealth management industry is under considerable pressure. The increase in passive investments, and their resultant lower fees, signals an overall trend in declining fees, alongside the market expectation that AUM will continue to increase. The globalisation of the industry has opened up new markets, but this has increased the complexity of the regulatory environments in which firms operate, resulting in increased risk and a higher cost base. Productivity remains a key issue, which firms are seeking to address through measures such as better management and use of data. This is all occurring in a tense geopolitical environment, which has caused volatility to return to the financial markets.

Internal audit functions themselves are not immune from these disruptive forces and are continually being asked to do more with less. More today than ever, there is a conflicting demand on internal audit functions to demonstrate adequate assurance coverage of end-to-end risks, while at the same time delivering insight and value into key current and emerging risk areas.

This paper seeks to provide you with PwC’s view on the market issues impacting asset and wealth management industry in 2019 and beyond, collated through our own experiences and insights from our subject matter experts.

We have seen a shift in the approach to audit planning, with internal audit functions performing targeted risk-focused reviews, which, when reflected upon collectively at the end of the year, can give stakeholders valuable insights into key themes. Whilst this document is structured into specific sections there are some clear themes that cut across a number of topics, such as governance, accountability and conduct, customer focus, emerging technology and transformation.

We would encourage Heads of Internal Audit to use this pack in their risk assessment process to identify relevant topics for incorporation into their audit plan, as well as wider themes that can be reported to stakeholders at the end of the year.

Steve FrizzellPartner

Steve FrizzellPartner

UK Financial Services Internal Audit Leader

T: +44 (0) 7802 659053E: [email protected]

PricewaterhouseCoopers LLP, 7 More London Riverside, London, SE1 2RTT: +44 (0) 20 7583 5000, F: +44 (0) 20 7212 7500, www.pwc.co.uk

PricewaterhouseCoopers LLP is a limited liability partnership registered in England with registered number OC303525. The registered office of PricewaterhouseCoopers LLP is 1 Embankment Place, London WC2N 6RH.PricewaterhouseCoopers LLP is authorised and regulated by the Financial Conduct Authority for designated investment business and by the Solicitors Regulation Authority for regulated legal activities.

PwC

UK economic outlook 1

Risk radar 2

Key themes 3

Brexit 4

Climate change 6

Customer outcomes 8

Governance and accountability 12

Financial crime 19

GDPR 20

Operational resilience 21

Transformation 25

Outsourcing 27

Cyber security 28

Emerging technology 29

Technology 33

Contents

Further regulation 36

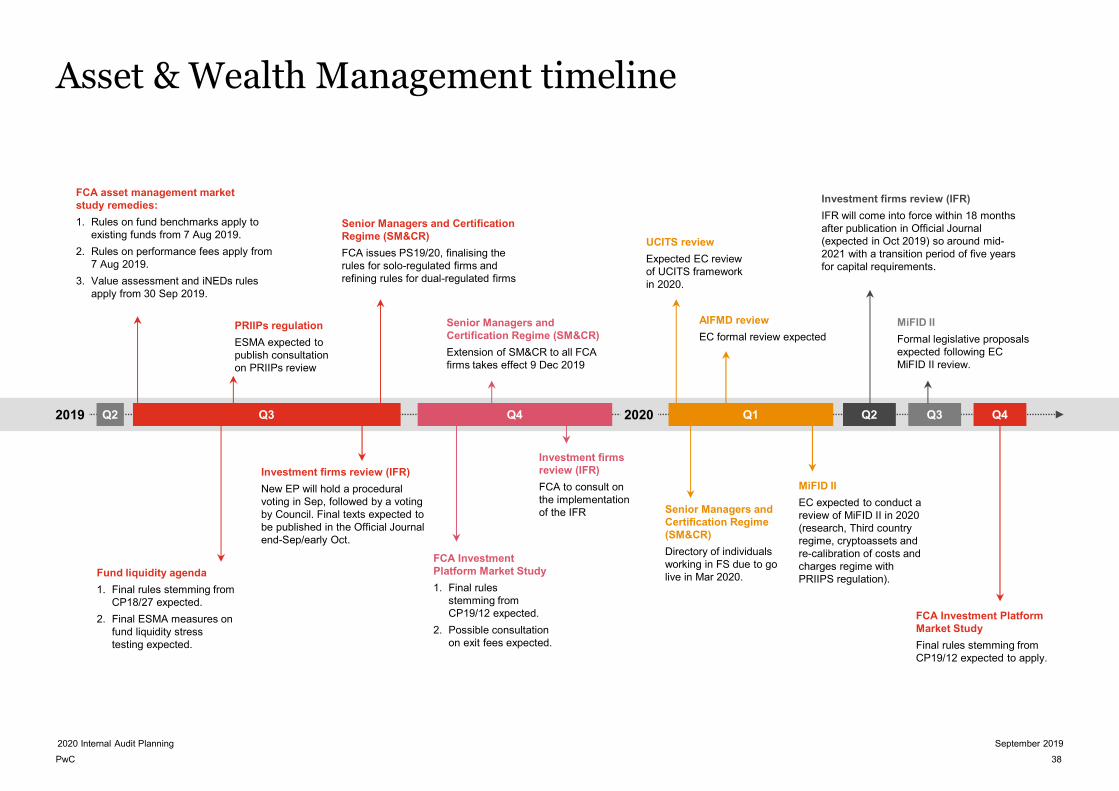

Asset & Wealth Management timeline

38

MiFID II 39

Capital and liquidity 46

Financial risk 51

Market 54

Other asset and wealth management specific regulation

56

Tax 58

Contact details 63

References 64

September 20192020 Internal Audit Planning

ContentsPwC

PwC

UK economic outlook

2020 Internal Audit Planning

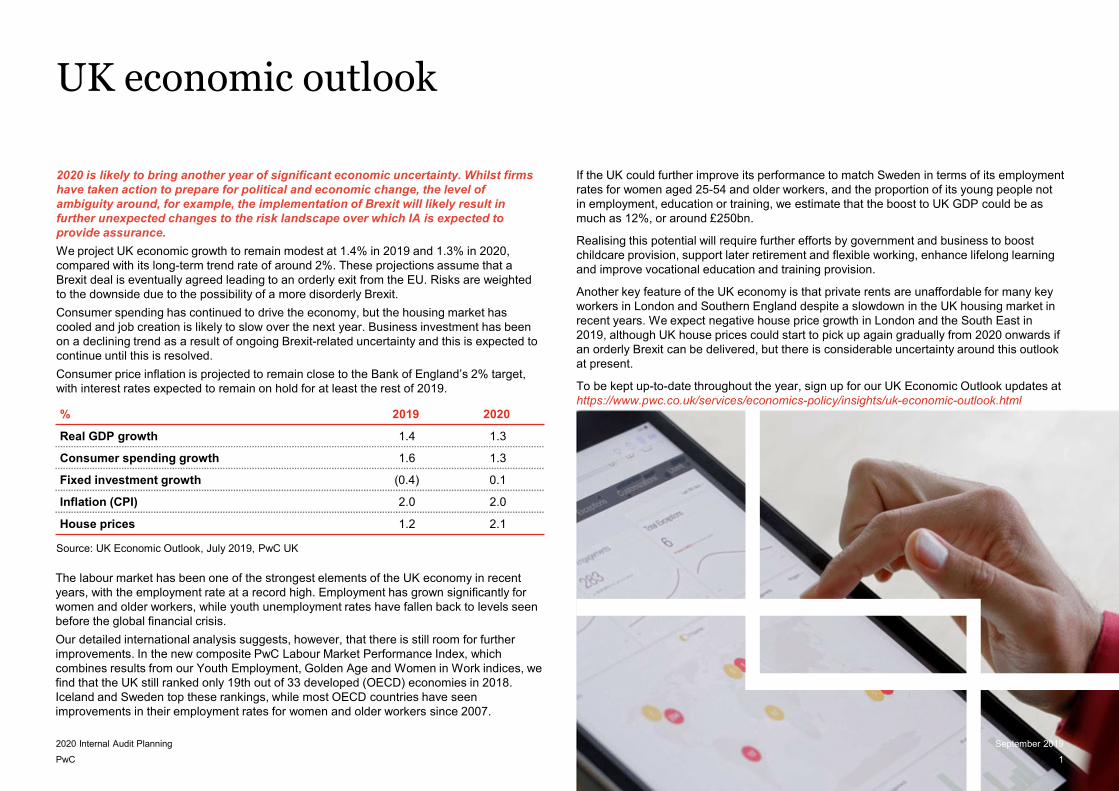

2020 is likely to bring another year of significant economic uncertainty. Whilst firms have taken action to prepare for political and economic change, the level of ambiguity around, for example, the implementation of Brexit will likely result in further unexpected changes to the risk landscape over which IA is expected to provide assurance.

We project UK economic growth to remain modest at 1.4% in 2019 and 1.3% in 2020, compared with its long-term trend rate of around 2%. These projections assume that a Brexit deal is eventually agreed leading to an orderly exit from the EU. Risks are weighted to the downside due to the possibility of a more disorderly Brexit.

Consumer spending has continued to drive the economy, but the housing market has cooled and job creation is likely to slow over the next year. Business investment has been on a declining trend as a result of ongoing Brexit-related uncertainty and this is expected to continue until this is resolved.

Consumer price inflation is projected to remain close to the Bank of England’s 2% target, with interest rates expected to remain on hold for at least the rest of 2019.

% 2019 2020

Real GDP growth 1.4 1.3

Consumer spending growth 1.6 1.3

Fixed investment growth (0.4) 0.1

Inflation (CPI) 2.0 2.0

House prices 1.2 2.1

Source: UK Economic Outlook, July 2019, PwC UK

If the UK could further improve its performance to match Sweden in terms of its employment rates for women aged 25-54 and older workers, and the proportion of its young people not in employment, education or training, we estimate that the boost to UK GDP could be as much as 12%, or around £250bn.

Realising this potential will require further efforts by government and business to boost childcare provision, support later retirement and flexible working, enhance lifelong learning and improve vocational education and training provision.

Another key feature of the UK economy is that private rents are unaffordable for many key workers in London and Southern England despite a slowdown in the UK housing market in recent years. We expect negative house price growth in London and the South East in 2019, although UK house prices could start to pick up again gradually from 2020 onwards if an orderly Brexit can be delivered, but there is considerable uncertainty around this outlook at present.

To be kept up-to-date throughout the year, sign up for our UK Economic Outlook updates at https://www.pwc.co.uk/services/economics-policy/insights/uk-economic-outlook.html

The labour market has been one of the strongest elements of the UK economy in recent years, with the employment rate at a record high. Employment has grown significantly for women and older workers, while youth unemployment rates have fallen back to levels seen before the global financial crisis.

Our detailed international analysis suggests, however, that there is still room for further improvements. In the new composite PwC Labour Market Performance Index, which combines results from our Youth Employment, Golden Age and Women in Work indices, we find that the UK still ranked only 19th out of 33 developed (OECD) economies in 2018. Iceland and Sweden top these rankings, while most OECD countries have seen improvements in their employment rates for women and older workers since 2007.

1

September 2019

PwC 2

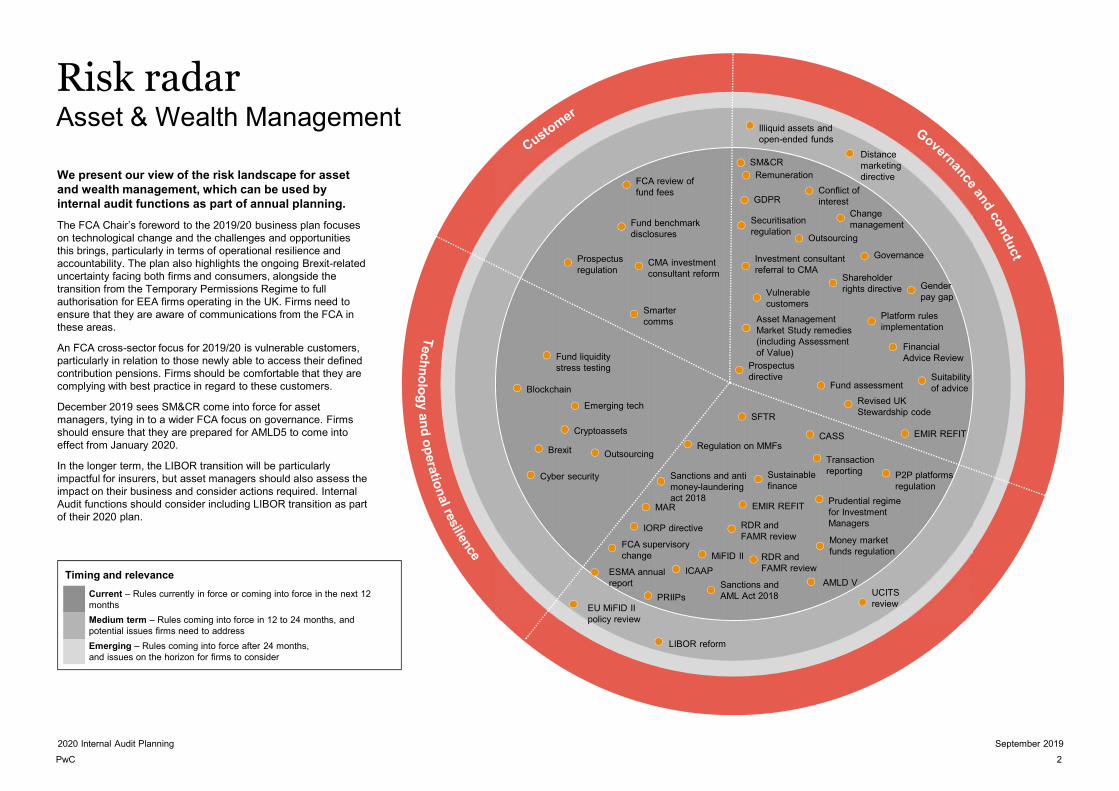

Risk radarAsset & Wealth Management

September 20192020 Internal Audit Planning

We present our view of the risk landscape for asset and wealth management, which can be used by internal audit functions as part of annual planning.

The FCA Chair’s foreword to the 2019/20 business plan focuses on technological change and the challenges and opportunities this brings, particularly in terms of operational resilience and accountability. The plan also highlights the ongoing Brexit-related uncertainty facing both firms and consumers, alongside the transition from the Temporary Permissions Regime to full authorisation for EEA firms operating in the UK. Firms need to ensure that they are aware of communications from the FCA in these areas.

An FCA cross-sector focus for 2019/20 is vulnerable customers, particularly in relation to those newly able to access their defined contribution pensions. Firms should be comfortable that they are complying with best practice in regard to these customers.

December 2019 sees SM&CR come into force for asset managers, tying in to a wider FCA focus on governance. Firms should ensure that they are prepared for AMLD5 to come into effect from January 2020.

In the longer term, the LIBOR transition will be particularly impactful for insurers, but asset managers should also assess the impact on their business and consider actions required. Internal Audit functions should consider including LIBOR transition as part of their 2020 plan.

Timing and relevance

Current – Rules currently in force or coming into force in the next 12 months

Medium term – Rules coming into force in 12 to 24 months, and potential issues firms need to address

Emerging – Rules coming into force after 24 months,and issues on the horizon for firms to consider

Prospectus directive

Financial Advice Review

Investment consultant referral to CMA

Platform rules implementation

Fund assessment

Revised UK Stewardship code

EMIR REFIT

Vulnerable customers

Securitisation regulation

Outsourcing

Remuneration

Suitability of advice

SM&CR

GDPRConflict of interest

Asset Management Market Study remedies (including Assessmentof Value)

Gender pay gap

Change management

Distance marketing directive

Illiquid assets and open-ended funds

Sanctions and anti money-laundering act 2018

Money market funds regulation

MAR

Sustainablefinance

IORP directive

P2P platforms regulation

EMIR REFIT

CASS

FCA supervisory change

RDR and FAMR review

ESMA annual report

Prudential regime for Investment Managers

MiFID II

PRIIPsSanctions and AML Act 2018

SFTR

Regulation on MMFs

EU MiFID II policy review

LIBOR reform

AMLD VUCITS review

Emerging tech

Cryptoassets

Fund liquidity stress testing

Brexit

Cyber security

Blockchain

Fund benchmark disclosures

Smarter comms

CMA investment consultant reform

Prospectus regulation

FCA review of fund fees

Shareholder rights directive

Governance

OutsourcingTransactionreporting

ICAAP

RDR andFAMR review

PwC

Key themes

September 20192020 Internal Audit Planning

3

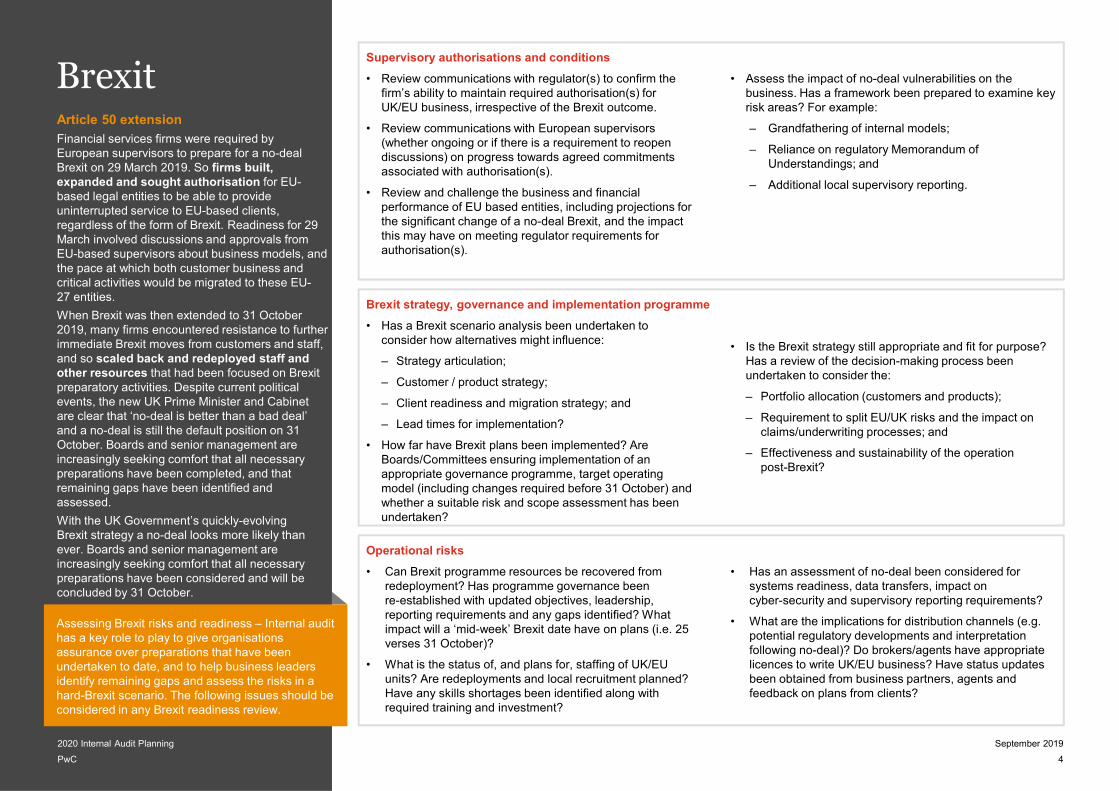

BrexitArticle 50 extension

Financial services firms were required by European supervisors to prepare for a no-deal Brexit on 29 March 2019. So firms built, expanded and sought authorisation for EU-based legal entities to be able to provide uninterrupted service to EU-based clients, regardless of the form of Brexit. Readiness for 29 March involved discussions and approvals from EU-based supervisors about business models, and the pace at which both customer business and critical activities would be migrated to these EU-27 entities.

When Brexit was then extended to 31 October 2019, many firms encountered resistance to further immediate Brexit moves from customers and staff, and so scaled back and redeployed staff and other resources that had been focused on Brexit preparatory activities. Despite current political events, the new UK Prime Minister and Cabinet are clear that ‘no-deal is better than a bad deal’ and a no-deal is still the default position on 31 October. Boards and senior management are increasingly seeking comfort that all necessary preparations have been completed, and that remaining gaps have been identified and assessed.

With the UK Government’s quickly-evolving Brexit strategy a no-deal looks more likely than ever. Boards and senior management are increasingly seeking comfort that all necessary preparations have been considered and will be concluded by 31 October.

September 20192020 Internal Audit Planning

4PwC

Assessing Brexit risks and readiness – Internal audit has a key role to play to give organisations assurance over preparations that have been undertaken to date, and to help business leaders identify remaining gaps and assess the risks in a hard-Brexit scenario. The following issues should be considered in any Brexit readiness review.

Supervisory authorisations and conditions

• Review communications with regulator(s) to confirm the firm’s ability to maintain required authorisation(s) for UK/EU business, irrespective of the Brexit outcome.

• Review communications with European supervisors (whether ongoing or if there is a requirement to reopen discussions) on progress towards agreed commitments associated with authorisation(s).

• Review and challenge the business and financial performance of EU based entities, including projections for the significant change of a no-deal Brexit, and the impact this may have on meeting regulator requirements for authorisation(s).

• Assess the impact of no-deal vulnerabilities on the business. Has a framework been prepared to examine key risk areas? For example:

– Grandfathering of internal models;

– Reliance on regulatory Memorandum of Understandings; and

– Additional local supervisory reporting.

Operational risks

• Can Brexit programme resources be recovered from redeployment? Has programme governance been re-established with updated objectives, leadership, reporting requirements and any gaps identified? What impact will a ‘mid-week’ Brexit date have on plans (i.e. 25 verses 31 October)?

• What is the status of, and plans for, staffing of UK/EU units? Are redeployments and local recruitment planned? Have any skills shortages been identified along with required training and investment?

• Has an assessment of no-deal been considered for systems readiness, data transfers, impact on cyber-security and supervisory reporting requirements?

• What are the implications for distribution channels (e.g. potential regulatory developments and interpretation following no-deal)? Do brokers/agents have appropriate licences to write UK/EU business? Have status updates been obtained from business partners, agents and feedback on plans from clients?

• Has a Brexit scenario analysis been undertaken to consider how alternatives might influence:

– Strategy articulation;

– Customer / product strategy;

– Client readiness and migration strategy; and

– Lead times for implementation?

• How far have Brexit plans been implemented? Are Boards/Committees ensuring implementation of an appropriate governance programme, target operating model (including changes required before 31 October) and whether a suitable risk and scope assessment has been undertaken?

• Is the Brexit strategy still appropriate and fit for purpose? Has a review of the decision-making process been undertaken to consider the:

– Portfolio allocation (customers and products);

– Requirement to split EU/UK risks and the impact on claims/underwriting processes; and

– Effectiveness and sustainability of the operation post-Brexit?

Brexit strategy, governance and implementation programme

PwC

Tax andcapital policy

Financialmarkets

Slowing economy

Trade and regulatory

barriers

Regulatory,legal and data

People and mobility

Wider impacts of

no-deal Brexit

06

01

02

03

04

05

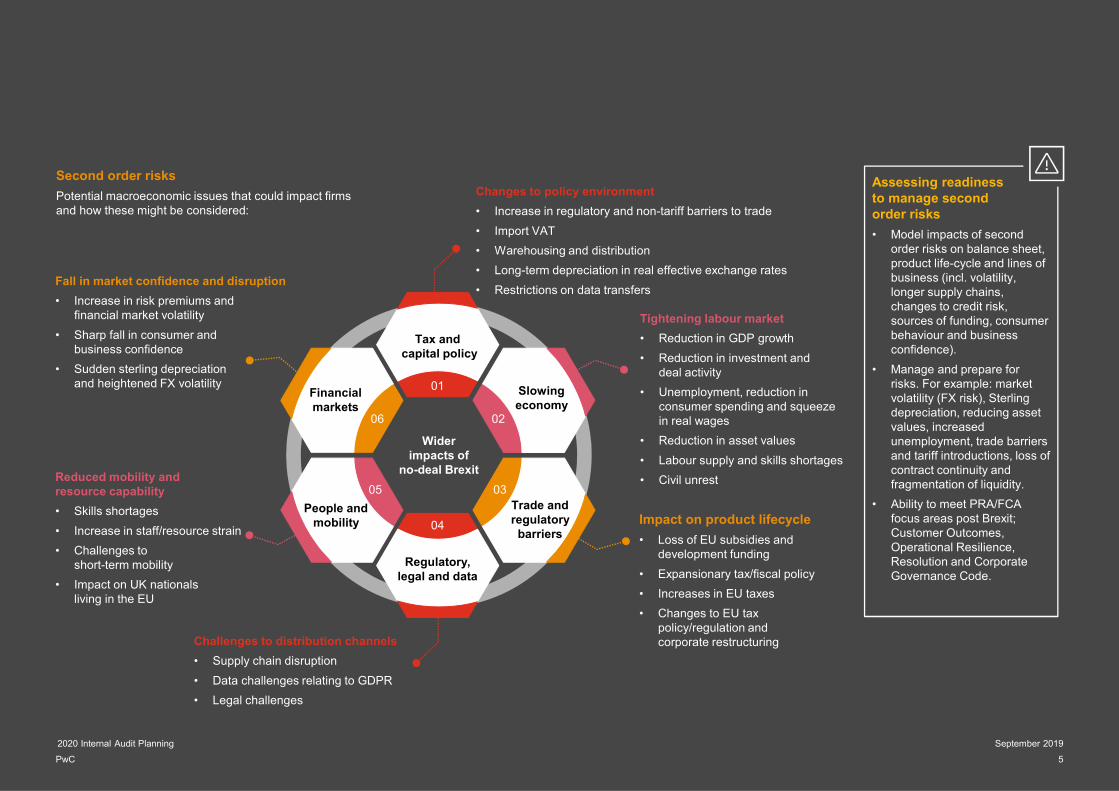

Second order risks

Potential macroeconomic issues that could impact firms and how these might be considered:

Tightening labour market

• Reduction in GDP growth

• Reduction in investment and deal activity

• Unemployment, reduction in consumer spending and squeeze in real wages

• Reduction in asset values

• Labour supply and skills shortages

• Civil unrest

Impact on product lifecycle

• Loss of EU subsidies and development funding

• Expansionary tax/fiscal policy

• Increases in EU taxes

• Changes to EU tax policy/regulation and corporate restructuring

Changes to policy environment

• Increase in regulatory and non-tariff barriers to trade

• Import VAT

• Warehousing and distribution

• Long-term depreciation in real effective exchange rates

• Restrictions on data transfers

Challenges to distribution channels

• Supply chain disruption

• Data challenges relating to GDPR

• Legal challenges

Reduced mobility and resource capability

• Skills shortages

• Increase in staff/resource strain

• Challenges toshort-term mobility

• Impact on UK nationals living in the EU

Fall in market confidence and disruption

• Increase in risk premiums and financial market volatility

• Sharp fall in consumer and business confidence

• Sudden sterling depreciation and heightened FX volatility

Assessing readiness to manage second order risks

• Model impacts of second order risks on balance sheet, product life-cycle and lines of business (incl. volatility, longer supply chains, changes to credit risk, sources of funding, consumer behaviour and business confidence).

• Manage and prepare for risks. For example: market volatility (FX risk), Sterling depreciation, reducing asset values, increased unemployment, trade barriers and tariff introductions, loss of contract continuity and fragmentation of liquidity.

• Ability to meet PRA/FCA focus areas post Brexit; Customer Outcomes, Operational Resilience, Resolution and Corporate Governance Code.

September 20192020 Internal Audit Planning

5

PwC

Climate change and Environmental, Social and Governance (ESG)

Climate change

It has become a requirement for firms to consider risks associated with climate change. The PRA expects firms to show that the Board understands and assesses the financial risks from climate change that affect the firm, and is able to address and oversee these risks from within the firm’s overall business strategy and risk appetite. Firms are expected to allocate responsibility for identifying and managing financial risks from climate change to the relevant Senior Management Function(s) (SMFs). Firms are also expected to use stress testing and scenario analysis to inform risk identification and understand the short-term and long-term financial risks that climate change presents to their business models.

The PRA considers that the financial risks from climate change are far-reaching in breadth and magnitude, have uncertain and extended time horizons, are foreseeable, and that their significance depends on short-term actions.

ESG

Sustainable investing is an investment approach that takes into consideration not only financial metrics but also ESG risk factors. These risk factors could arise due to environmental and climate change, or because of increasing social inequity or as a result of a lack of governance. They increasingly have the potential to impact financial metrics. Sustainable investing looks beyond the 3-5 year business cycle so that risks that could manifest and impact in the medium- to long-term can be appropriately considered.

The European Commission’s Sustainable Finance Action Plan (SFAP) sets out a package of regulatory measures to increase the way asset managers, and asset owners, consider sustainability and ESG in their investment strategies.

The new regulatory changes aligned to the SFAP propose changes to MiFID II and the introduction of a new ESG Disclosure Regulation. All of these changes will require asset managers to implement an ESG Policy, set out how they have integrated their ESG Policy into their investment decision-making. Managers will also be required to make new disclosures on sustainability/ESG to their investors.

Key risks• Firms do not adequately assess climate-related financial risks relating to transition risks and

physical risks and how they will affect their business model.

• Poor articulation of climate change risk assessment, climate change stress tests, and scenarios within the risk management framework.

• Lack of knowledge at Board level, inhibiting effective challenge.

• Firms not reviewing and updating their ICAAP (Individual Capital Adequacy Assessment Process) document with the most up-to-date information on climate change developments.

• The risks resulting from events related to climate change are not appropriately managed leading to financial loss and/or regulatory censure.

• The investment framework is not in line with new regulatory requirements and market practices, and ESG risks are not adequately considered and exposures measured.

• Investment products are marketed on the basis of sustainability cannot demonstrate how they achieve this sustainability objective.

• ESG risks are not modelled to allow management to understand the implications for the credit quality and risk return profiles on the firm’s investment strategy.

Internal audit focus areas• Design and robustness of strategies, policies, processes and systems in place to identify climate

change risks inherent within the business.

• Design and operating effectiveness of controls over the climate change risk assessment process.

• Whether the ICAAP adequately covers exposure to climate change risk, including how the firm identifies and manages it.

• The firm identifies and allocates an appropriate SMF holder to the climate change risk responsibility and ensures this is included within SMF responsibility mapping.

• Design and robustness of strategies, policies, processes and systems in place to manage the approach to ESG issues.

• Tracking and implementation of the numerous regulatory changes focused on ESG and sustainability.

• Governance and adequacy of MI to track, challenge and understand the firm’s exposures to ESG risks.

September 20192020 Internal Audit Planning

6

PwC

September 20192020 Internal Audit Planning

7PwC

PwC

Customer outcomes (1/4)

2020 Internal Audit Planning

The suitability of advice and the need for products and services to meet the needs of customers has been a cross-sector area of focus of the FCA for the last two years. There is particular concern from the regulator around the treatment of vulnerable customers, long-standing/loyal customers and retirement outcomes, coupled with an overarching question as to what level of care firms should provide to their customers, particularly when providing high-cost credit.

The FCA has released a number of key publications this year relating to the treatment of customers, including:

• The retirement outcomes review/feedback and further consultations.

• The consultation and feedback on duty of care.

• The Mortgages Market Study and changes to responsible lending guidance.

• The consultation guidance on fair treatment of vulnerable customers.

The continuous work on affordability and vulnerable customers and their fair treatment is highlighting a number of areas where firms are expected to take in consideration the differing needs of their customers and to work towards ensuring these needs are met throughout the life cycle of the product and customer interactions.

The scope of audits over the fair treatment of customers can draw on a number of areas including:

• What data and management information is available and used to drive behaviours and decisions that are in the best interest of the customer?

• What is the risk of harm embedded in products and processes and how vulnerable customers might be at greater risk?

• How effective is the governance and oversight of customer outcomes? Is there clear accountability and a culture ‘to do the right thing’? What is the customer value proposition of the firm? And how its purpose takes in consideration its customers.

• How are customer outcomes considered at each stage of the distribution chain?

• Do staff have the right support and feel empowered to exercise discretion to meet customer needs?

• Are third party suppliers aware of the firm’s approach to customers and how do management assess the third parties with respect to customer treatment?

• What tools and system solutions are used or could be used to enforce fair customer treatment, accurate and complete identification of vulnerable customers and transparent information for effective monitoring and governance of customer treatment?

PwC 8

September 2019

PwC

Customer outcomes (2/4)

2020 Internal Audit Planning

Key risks

• Policies for customer vulnerability are insufficient to comply with rules and meet regulatory expectations.

• Staff are inadequately trained and empowered to identify and appropriately handle customer vulnerability.

• Processes, policies and controls across the customer journey are not designed and operated effectively to identify and derive fair outcomes for unique customer circumstances and those that may change over time.

Internal audit focus areas

• Assess the design of the Vulnerable Customers policy and its adequacy in relation to the business model and products offered.

• Undertake an assessment of the firm's’ strategy and culture in relation to vulnerable customers to determine whether the firm has an inclusive and customer-centric approach, driven by a clear purpose and strong leadership.

• Review customer files to assess the effectiveness of the firm's’ approach to vulnerable customers, including:

• How effectively it identifies, documents and records potential vulnerability; and

• How effectively it responds to and monitors vulnerable customers, including whether those customers receive fair outcomes.

Vulnerable customers

The FCA and other regulators have increasingly become more interventionist and forthright in their views when it comes to markets that are not adequately protecting the most vulnerable consumers in society. The FCA published a consultation in July 2019 on the fair treatment of vulnerable consumers, bringing more clarity over expectations when it comes to the identification, management and monitoring of vulnerable consumers.

Firms need to reflect on their purpose, business model, customer culture and capability to identify, manage and monitor vulnerability, and ensure that they have effective policies, controls and capabilities in place to treat vulnerable customers fairly.

9

September 2019

PwC

Customer outcomes (3/4)

2020 Internal Audit Planning

Key risks

• Demonstrating effective oversight under SM&CR.

• The subjective nature of how to assess the seven criteria, and how to use this analysis to form conclusions and identify appropriate actions.

• How to communicate assessments to the customer in a format that will be understood, and is consistent with peer firms.

Internal audit focus areas

• How are the seven criteria being assessed, and is the process clearly defined and documented such that is can be repeated across the fund range and annually?

• Does the assessment consider the criteria at sufficient granularity to be in keeping with the letter and the spirit of the requirements? Are all charges being assessed?

• How will assessments be reported internally to the AFM board, and publicly to investors?

• What is the governance framework for these assessments from product launch to ongoing monitoring?

Assessing value for money in investment funds

From 30 September 2019 new rules requiring Authorised Fund Managers (AFM) to conduct an annual assessment of value for their UK authorised funds come into effect.

The rules require AFM’s to consider at least seven criteria prescribed by the FCA, which include the fund performance, costs and the quality of service received by investors. AFM’s must then report to investors on whether the costs charged to the fund are justified in the context of the value delivered, and any changes the AFM has made as a result of the assessment.

The Prescribed Responsibility for the assessment of value under SM&CR sits with the Chair of the AFM Board. The FCA expects firms to use this process to undertake a ‘root and branch’ review of their business and value proposition offered to their clients.

If firms include the public ‘value’ report in the fund annual accounts, this must be published within four months of the accounting year end date. For firms opting to produce a consolidated report (containing details of two or more funds) there is more flexibility offered on timing for this report. But in either case the FCA expects all firm to have their value assessment procedures in place and documented by October 2019.

10

September 2019

PwC 11

Customer outcomes (4/4)

September 20192020 Internal Audit Planning

Suitability of advice: Pensions and retirement income

Focus remains on the Retirement Outcomes Review undertaken in July 2018. FCA reviews have found that despite firms providing the required information to customers accessing benefits without advice, customers are not fully engaged. Many non-advised customers are potentially making unsuitable decisions about the retirement options available and drawdown investment decisions, leading to a risk that retirement funds are eroded and leave insufficient income throughout retirement.

Amid concerns about non-advised drawdown, the FCA has introduced requirements for providers to make available four investment pathways to assist customers with investment decisions, ensure non-advised customers make active decisions to invest in cash and issue annual decumulation costs and charges information.

Platforms (switching investments)

The FCA published MS17/1.2: Investment Platforms Market Study Interim Report on 16 July 2018. It found the market is working well in many respects, but identified the following concerns:

• Switching between platforms and shopping around can be difficult.

• The risks and expected returns of model portfolios are unclear.

• Consumers with large cash balances on direct-to-consumer platforms may not know they are missing out on investment returns

• ‘Orphan clients’ who no longer have an adviser face higher charges, lower service and challenges to switch.

• The requirement for new annual decumulation costs and charges information may have system implications in order to ensure changes are made prior to the effective date.

• The investment pathway options for non-advised drawdown contracts will require appropriate communications to enable customers to make informed decisions. Firms must ensure communications are created alongside the design and development of the investment pathways.

• Providers will need to engage with customers during the lifecycle of a drawdown. In addition to the investment pathways, providers must ensure that customers who wholly or predominantly invest in cash have made an active decision to do so.

Key risks

• There is a suggestion that the FCA will implement more intrusive remedies if firms do not make urgent improvements.

• Firms must implement changes on switching platforms, and progress existing industry initiatives to introduce standardised times for transfers and improve customer communications, including potentially publishing data on transfer times.

• Review adequacy and appropriateness of communications to customers regarding the investment options. Investigate whether appropriate controls are in place to ensure that cash investments are an active decision.

• Assess the adequacy of controls in place to monitor new business, complaints and issues of non-advised pension drawdowns.

• Assess the adequacy and appropriateness of the controls in place, including management information and root cause analysis, to enable the firm to identify and manage sales and processing activity to mitigate potential customer harm.

• Review the assessment undertaken by management of the non-advised drawdown process, which should have been undertaken. Assess for evidence of whether the end-to-end customer journey has been assessed, and that the required information is provided at the appropriate point.

Internal audit focus areas

• Internal Audit functions need to be ready to respond to assess how the business responds to these findings.

• How are the risks and returns of model portfolios explained?

• How is price revealed to customers when they consider changing platforms?

• What is the business doing to identify consumers with large cash balances on direct-to-customer platforms?

• What monitoring is there of ‘orphan clients’ and what steps are taken to ensure they receive an appropriate service?

• Are customers switching platforms on an advised basis and how much is it costing them to do so?

PwC

Governance and accountability (1/7)

We continue to see the regulators focused on governance, accountability, conduct and culture, with the topics specifically highlighted as priorities in both the FCA and PRA business plans, but also underpinning other regulatory focus areas.

Regulators are increasingly interpreting operational failures and/or risk management issues (be it related to operational resilience, financial crime, customer treatment or financial resilience) as potentially due to ineffective Board and senior management governance.

The FCA sees good governance and culture as being critical to reducing potential harm to consumers and markets through enabling effective oversight of decision-making. A key aspect of the FCA’s governance and culture agenda is the extension of the Senior Managers and Certification Regime (SM&CR) to all FCA-authorised firms on 9 December 2019 alongside its focus on ‘purpose’ in creating healthy cultures and looking at firms’ remuneration practices. Firms approaching SM&CR as a compliance-led ‘tick-box’ exercise may fail to address the key underlying issues of concern to the FCA and miss opportunities to address governance problems

The new UK Corporate Governance Code (CGC), which came into force on 1 January 2019, sets the standards of good practice in relation to board leadership and effectiveness, remuneration, accountability and relations with shareholders. Although only applicable to companies with a premium listing of equity shares in the UK, the PRA has indicated it considers the CGC as best practice for all firms it supervises. The FCA has indicated it will continue to review firms’ governance arrangements, particularly in areas such as remuneration practices, dividend distributions and corporate governance at Board level.

Regulators and other key stakeholders are holding organisations to higher standards of governance and proactive risk management. Boards, CEOs and senior management must be able to demonstrate that are able to assess their risks, design robust internal controls to mitigate them, and have robust governance frameworks that drive effective decision making. We have seen the FCA apply significant scrutiny to asset managers with unsuitable governance arrangements, e.g. by subjecting them to Board Effectiveness Reviews. Areas of challenge include the quality of Board MI, level of independent challenge, group dynamic, board skillset and operating model keeping pace with growth.

We present in this section particular topics internal audit functions may wish to include in their annual plan; however, governance and conduct is a theme that should be incorporated and considered across all reviews. The implementation of the SM&CR regime over the next couple of years further highlights individual accountability for firms’ ways of working.

September 20192020 Internal Audit Planning

12PwC

PwC 13

Governance and accountability (2/7)

September 20192020 Internal Audit Planning

Board effectiveness

The presence of strong governance can no longer be viewed as a reactive process; instead, faced with increasing uncertainty, organisations must take a proactive stance to manage risk and realise business opportunities that align with stakeholders’ expectations and ultimately their business strategy.

The new Corporate Governance Code (CGC) came into force on 1 January 2019 and as well as amendments to the existing CGC, a substantial guidance document regarding Board Effectiveness was also published. The regulators have also indicated that they will continue to focus on firms’ governance arrangements at Board level.

Key risks

• Insufficient succession planning processes to support the new recommended tenure and prior experience principles for Board members.

• No clear articulation of responsibilities for chair, chief executive, senior independent director, board and committees.

• Remuneration policy and processes not sufficiently articulated and implemented.

• Lack of process for documenting governance activities.

• Lack of time for key agenda items, and lack of evidence of contribution by individual directors.

Internal audit focus areas

Internal audit should clearly determine the scope and purpose of any review. For example, whether the review is of corporate governance (structure, composition, control, quality of management information and documentation) or a formal Board effectiveness review (Board dynamics, leadership, decision making and contribution). Additional Board effectiveness focus areas include, but are not limited to:

• Assess the adequacy of documentation of committee activity and responsibilities of key individuals and committees against the new increased requirements.

• Assess the sufficiency of focus on wider stakeholders amid increased reporting requirements.

• Creation of a detailed questionnaire for all Board members to complete to gain a clear understanding of their views on the effectiveness of the Board, supplemented with sampled interviews.

• Board training, awareness of duties and conflicts of interest management.

• Delegations of authority.

PwC 14

Governance and accountability (3/7)

September 20192020 Internal Audit Planning

Senior Manager and Certification Regime

It came as no surprise to anyone that once again governance and culture featured prominently as a cross sector priority in the FCA’s 2019/20 business plan. SM&CR is an opportunity to establish healthy cultures and effective governance in firms, and is seen as key tool for the FCA. It aims to reduce customer harm and strengthen market integrity by encouraging greater individual accountability and setting new standards of personal conduct.

SM&CR currently covers banks and insurers but will capture all regulated firms from the fixed implementation deadline of 9 December 2019. Firms should learn from the challenges banks have had to overcome since SM&CR came into force. Firms should also not consider this in isolation, or as a ‘one off’ exercise – the governance and culture agenda continues to be an ongoing, permanent fixture of FCA supervisory focus and will likely be fertile ground for enforcement cases if current trends continue.

Key risks

• Insufficient understanding and evidencing of reasonable steps to avoid a contravention from occurring or continuing.

• Insufficient/ineffective training for Senior Managers to enable a complete understanding of their duty of responsibility.

• Failure to anticipate an increased demand by Senior Managers for more support/information to discharge their responsibilities.

• Lack of evidence to demonstrate what a conduct breach might look like and how this might link through to disciplinary proceeds.

• Failure to embed handover procedures.

• Insufficient tailoring of the conduct rules training to specific jobs that staff perform.

• Failure to evidence the effectiveness of the assessment approach for the certification population, including use of subjective judgement and consistency in application.

Internal audit focus areas

• All remuneration and governance regulations that apply to the allocation of Senior Manager Function holders and certified individuals have been captured and adhered to.

• Evidencing of reasonable steps.

• Linkage between conduct rules and disciplinary procedures.

• Appropriateness of HR systems to record the information required for certification.

• Appropriateness of systems and procedures in place to record

• Senior Managers’ responsibilities.

• Completeness and appropriateness of Senior Manager and certified staff training as well as conduct training for all staff.

• Appropriateness of conduct risk register design and monitoring.

• Appropriateness of the Senior Manager and certification assessment process.

PwC 15

Governance and accountability (4/7)

September 20192020 Internal Audit Planning

Culture

Internal audit focus areas

Internal audit can perform cultural reviews in a number of ways – e.g. targeted reviews on behaviours or processes, components of every review, or informally through data gathering exercises. Workshops and interviews with all grades should be used to assess how the staff perceive the culture of the firm, consistent messaging and successful embedding of the expected behaviours. Whatever approach is taken, the following issues should be considered:

• Is there a defined culture framework that identifies cultural gaps, and does it appropriately reflect requirements from SM&CR?

• Are roles and responsibilities clear and accountability understood?

• ‘Tone from the top’ – has the firm’s desired culture been defined by the Board and how is culture and conduct measured and governed?

• Are metrics defined and monitored for the Board to effectively oversee adherence to the firm’s culture? What are the measures of success?

• Behavioural indicators – How are the right behaviours cascaded through the organisation for consistent messaging across all stages of an employee’s lifecycle, from onboarding and training through to performance and remuneration?

• Does conduct form part of all employees’ objectives?

• Is there an appropriate framework for incident management, including escalation protocols, and are incidents resolved in a timely manner?

• Is there a willingness to undertake lessons learned and share insights after issues are raised?

• Is there a ‘good news only’ culture for information presented to Boards and committees, which in turn increases the potential for not mitigating risk in time?

The FCA’s recent discussion paper on culture is the regulator’s first tangible output on the topic for some time. Initially, the FCA focused on the importance of the ‘tone from the top’ and individual accountability (for example the SM&CR).

The FCA maintains that senior leaders play a key role in influencing culture, and recognises that everyone influences the culture of a firm, from middle managers to junior employees. Having established the right tone from the top, firms now need to understand how to turn messages into improved behaviours at all levels of the organisation.

Key risks

• Changing culture takes time and is an ongoing evolution, so the firm’s work to drive the right culture will not have an ‘end date’ – they need to continually drive this and keep up the momentum as the market and their business evolves over time. There is a risk that a firm may undertake a one-off exercise to “fix” culture.

• Whilst there is no ‘right’ or ‘wrong’ culture for a business, culture and values need to be considered for their impact on wider topics, such as conduct, customer treatment, diversity and inclusion.

• Focus from the Regulators with an increase in investigations and enforcements.

PwC 16

Governance and accountability (5/7)

September 20192020 Internal Audit Planning

Risk management framework

A robust risk management framework is fundamental to a firm’s identification, analysis and management of the risks it runs. The framework should comprehensively cover the wide range of risks faced by the firm, including the supporting processes used to manage them, and should be owned by a risk function that carries sufficient weight within the organisation to enable it to communicate and embed the framework effectively.

The firm’s Board-approved risk appetite should be the primary mechanism for ensuring that the firm’s strategy is delivered within adequate constraints, and should be supported by established reporting processes.

Risk management effectiveness during cost cutting

As companies grow, expand their services and evolve over time, they must establish sound governance practices in the management of risk to facilitate informed decision making; achieve strategic goals; and meet the expectations of both internal and external stakeholders.

Financial services organisations are also under increasing pressure to cut costs and increase efficiency. But in cutting costs, organisations often lose sight of the additional risk they are taking on, especially operational risk.

Key risks

• Insufficient consideration of key risks in decision making.

• Inappropriate or inaccurate articulation of risk appetite, resulting in a firm’s inability to embed the right risk culture.

• Ineffective risk management framework and lack of appropriate risk information to effectively oversee the constantly-changing regulatory environment, regionally and globally, as well as divisionally and functionally.

• Second line assurance activity may be reduced.

• Pressure to grow, whilst also reducing fixed costs as a proportion of revenue, may lead to unintended risks being taken on.

• Poorly communicated risk management framework resulting in a lack of clarity of roles and responsibilities across the three lines of defence.

• Lack of sufficient maturity in the framework to enable the firm to demonstrate embeddedness across the organisation.

• Penal tools available to the regulator in the form of a Risk Management and Governance (RMG) scalar where weaknesses in risk management and/or governance are observed.

Internal audit focus areas

• Adherence to the risk management framework and risk appetite as the business goes through any cost cutting exercise, considering the impact on culture and morale.

• Changes to the control environment due to changes in operating models and products need to be considered with respect to roles and responsibilities and staff changes.

• Additional controls, reporting and monitoring that may be required throughout the period of change.

• Effectiveness of lines of defence and the risk function’s ability to challenge the business.

• Harmonisation of the various risk management-related components including ICAAP, ILAAP, recovery plan and risk appetite.

• Clearly defined and effectively calibrated risk appetite limits and early warning indicators, supported by sufficient analytical detail and rationale.

• Adequate and timely MI reporting on key risks and variations from risk appetite to enable the Board to monitor and challenge executive management.

• Internal audit should also confirm adherence to the risk appetite.

PwC 17

Governance and accountability (6/7)

September 20192020 Internal Audit Planning

Remuneration code

In the wake of the financial crisis, scrutiny and oversight of remuneration practices (and the behaviours they drive) has toughened significantly. This translated over time into onerous and complex remuneration regulations covering almost all FS sub-sectors.

The primary focus of remuneration and governance regulations is to mitigate a culture of excessive risk taking, shift the focus from short-term to long-term sustainable and risk-adjusted outcomes, and enhance the focus on conduct in the sector.

In the UK, the PRA and the FCA enforce a series of complex and ever changing requirements. Compliance against those requirements is key.

Key risks

• A detection of minimal or limited compliance against the remuneration and governance requirements by the PRA and/or FCA will result in a heightened focus on the firm and the wider regulated practices. The reverse of this scenario is also possible.

• At times firms have been fined excessively (and publicly named) for breaching conduct standards through the use of ‘aggressive’ sales incentives.

Internal audit focus areas

• Confirm all remuneration and governance regulations that apply to the firm have been applied in a proportionate manner.

• If required, confirm that a remuneration committee has been established with terms of reference clearly defining its role and remit in setting and determining remuneration.

• Assess whether remuneration and governance practices are in line with the overall firm-wide risk framework and appetite.

• Assess whether remuneration and governance policies and their application are fully compliant with the regulatory requirements.

• Review controls to ensure Material Risk Takers (MRTs) are accurately and completely identified, and ensure that the list of MRTs remains current and up to date during the year.

• Assess communications to MRTs to ensure they are fully aware of their roles and responsibilities and how this impacts their remuneration arrangements.

• Assess whether there are appropriate processes in place to operate (where applicable) the structural pay requirements (cap, deferral, payment in shares and malus/clawback).

• Assess controls in place to ensure that regulatory submissions are on time, complete, accurate and to an appropriate standard.

PwC

Governance and accountability (7/7)

Diversity and inclusion (D&I)

The Equality Act Gender Pay Gap (Information) Regulations 2017 require all companies with 250 or more employees in England, Scotland and Wales to disclose multiple gender pay gap indicators. The government issued a consultation on ethnicity pay gap reporting and it is likely that gender pay reporting requirements will broaden to include ethnicity pay by 2021.

The revised UK Corporate Governance Code encourages greater transparency and promotes diversity of gender, social and ethnic backgrounds, cognitive and personal strengths. The Code sets requirements for the Nomination Committee regarding succession plans and imposes disclosure requirements for the annual report.

Additional requirements apply to the financial services sector, with the PRA setting out requirements on the diversity of the management body, as well as disclosure requirements. Additional EBA/ESMA guidelines apply to those subject to MIFID II.

Beyond the legal and regulatory requirements, the expectations of customers, employees, investors and other key stakeholders continue to change. Many organisations have set out strategic objectives and/or targets in relation to D&I that they should have a framework in place to ensure that they can deliver against.

Key risks

• There is continued public and government scrutiny of the progression of women, with a specific focus on financial services. The government also demonstrates an increased focus on diversity beyond gender. There are risks – primarily reputational – to companies who do not demonstrate that they are taking action to resolve their gender pay gap and wider diversity issues. This could impact upon the company’s ability to recruit and retain staff, obtain investment and/or secure customers.

Internal audit focus areas

Internal audit should challenge the Board and management on their D&I agenda and reporting. This can be performed through a targeted review or as part of a cultural or corporate governance review. The following questions should be considered:

• Has the firm’s approach to investigating and resolving its gender pay gap been defined, does it have appropriate investment and senior buy-in to drive change, and is there an action plan to address diversity beyond gender?

• Is there appropriate and sufficient data to better understand the reasons behind the gender pay gap, has analysis been performed, and has management started collecting and analysing data on the ethnicity pay gap?

• Has the Nomination Committee acted upon the requirements of the Corporate Governance Code and ESMA/EBA guidelines as appropriate?

• Have recruitment, retention, progression and other policies and practices throughout the employee lifecycle been examined to eliminate unconscious bias?

• Is there transparency in the way performance is measured and how employees engage with the process, and are performance bonuses and promotions based on clear criteria?

• Is the public reporting of the firm’s plans to resolve the gender pay gap accurate, sufficient and supported by activity being undertaken within the firm, and does the firm report on diversity issues beyond gender and the strategy and actions taken to address them?

September 20192020 Internal Audit Planning

18

PwC 19

Financial crime

September 20192020 Internal Audit Planning

The fifth Anti-Money Laundering Directive

The fourth EU Anti-Money Laundering Directive (AMLD4) came into force on 26 June 2017, which included some changes to AML procedures, including changes to customer due diligence (CDD), a central register for beneficial owners, classification of politically exposed persons (PEPs) and a focus on risk assessments. The main emphasis of the directive was on a risk-based approach.

The fifth EU Anti-Money Laundering Directive (AMDL5) came into force on 9 July 2018 and member states are obliged to transpose the modified regulations into national law by January 2020. The UK government has consulted on the proposed changes.

Financial Crime

Financial crime continues to be one of the FCA’s cross-sector priorities, with thematic reviews of anti-money laundering (AML) and sanctions conducted by the FCA across a range of financial institutions. The FCA has stated that it’s supervisory approach is to become more data driven in the future, using a range of sources to focus effort on where the risks are deemed to be the greatest. Where the FCA has identified that a firm’s financial crime framework is not considered up to standard, this has often lead to the regulator also considering the role of internal audit and whether financial crime audits are of sufficient coverage and quality.

Key risks

• Risk assessment – Regulated firms must have their AML compliance framework informed by an enterprise risk assessment. This risk assessment must consider a range of factors and be specific to the firm’s business with policies, procedures and controls aligned accordingly.

• Customer Risk Assessment and Customer Due Diligence – assessing the risks presented by a business relationship and undertaking appropriate due diligence to mitigate this reduces the opportunity for money laundering.

• Anti-Bribery and Corruption (ABC) – The FCA has identified that progress (albeit at times slowly) has been made in AML controls, however ABC controls tend to be less well developed and receive less management attention.

• Lack of technical knowledge leading to incorrect implementation of AML controls.

• Lack of governance over updates to policies and procedures reflecting changes in AML regulations including.

• Incorrect configuration of additional system controls for compliance with enhanced due diligence measures for financial flows from high-risk third countries.

Internal audit focus areas

• Quality assessment of financial crime audits and development of data analytics to inform internal audit’s risk assessment.

• Assess the design and operational effectiveness of the firm’s Financial Crime framework and enterprise risk assessment process.

• Examine and evaluate the adequacy and effectiveness of the policies, controls and procedures adopted to comply with MLR (Money Laundering Regulation) 2019.

• Review of governance over AML controls, including updates to policies, procedures and risk assessments.

• Review of additional system controls implemented as part of enhanced due diligence measures for financial flows from high-risk third countries.

PwC

PwC

GDPR

September 20192020 Internal Audit Planning

20

Recent enforcement actions from the Information Commissioner's Office (ICO) send two clear messages; firstly, that the ICO has a highly competent team of data protection, cyber security and direct marketing specialists; and secondly, firms holding personal data will be held responsible, regardless of why they, or a third party, were holding it or how they lost it. This has put data protection, and specifically data breach preparedness back to the top of Board agendas.

Data Protection and Privacy

The General Data Protection Regulation (GDPR) in the EU introduced the largest change to data protection legislation since the European Data Protection Directive in 1995. The potential for heavy fines featured large in media headlines and firms undertook wide-scale privacy change programmes in preparation for the GDPR go-live date of 25 May 2018. But, GDPR is much more than a one-off change programme, or a series of business activities designed to avoid a fine – it's the reality of today's modern, customer-centric business.

Key risks

• Lack of sustainability – Embedding GDPR into day-to-day operations requires cultural and behaviour change. Some firms have viewed GDPR as a one-time compliance activity, which doesn’t reduce GDPR risks the firm is carrying. Insufficient drive to operationalise data protection processes throughout the firm to sustain compliance could lead to regulator enforcement and significant fines.

• Incomplete implementation – Firms have not yet addressed some of the harder challenges relating to GDPR, such as retention, unstructured data, paper/hard documents, etc. Unstructured data is generally subject to poor security controls and a lack of robust access governance, which can increase the risk of a potential data breach.

• Cross-regulatory requirements not known or breached – Firms that operate outside of the EU will also have other privacy regulations to be aware of and so must ensure processes and policies are compliant with GDPR and other global regulations. Most multi-jurisdiction firms are federated and share data freely across their legal entities. Firms need to determine the legal basis for data transferring and sharing across the business’ legal entities and ensure this meets cross-regulatory requirements.

Internal audit focus areas

• Assess compliance with GDPR regulation and adequacy of privacy governance to embed GDPR into day-to-day operations.

• Review GDPR risk appetite and assess if the firm is operating within the approved limits.

• Assess the adequacy of governance and oversight arrangements, including third parties and other group entities, over personal and sensitive data.

• Assess the strength, depth and enforcement of data protection policies, training of staff and data governance structure throughout a firm.

• Lack of ownership – Firms are yet to specify all data owners. Without clear ownership, clear articulation and determination of how data can be handled may not be appropriate and can lead to security vulnerabilities, as well as slow or insufficient breach reporting.

• Lack of, or incorrect consent obtained – Managing customer consent, electronic communications and marketing activities to be compliant with GDPR and upcoming ePrivacy regulation requirements.

• Poor conduct – There is a risk surrounding inappropriate conduct from within the organisation, and the subsequent reputational consequences.

• Data breaches – Data breaches continue to remains a key risk for organisation.

• Data subject requests not processed on a timely basis – Lack of robust processes to deal with data subject requests in a timely manner.

• Lack of third party management – There is a risk that third parties may be acting in a manner that is deemed inappropriate by the organisation in regards to GDPR and the organisation may be vulnerable to potential data breaches or non-compliance.

• Brexit – Risk of flow of personal data from EEA to UK in the event of hard Brexit.

• Deep dives into specific areas, such as data retention, unstructured data, RoDP (Record of Data Processing), DPIA (Data Protection Impact Assessments), etc. to assess compliance.

• Assess the firm’s readiness for transfer of personal data from the EEA to UK in the event of a hard Brexit.

• Assess the firm’s ability to identify and comply with other global data protection regulations.

PwC 21

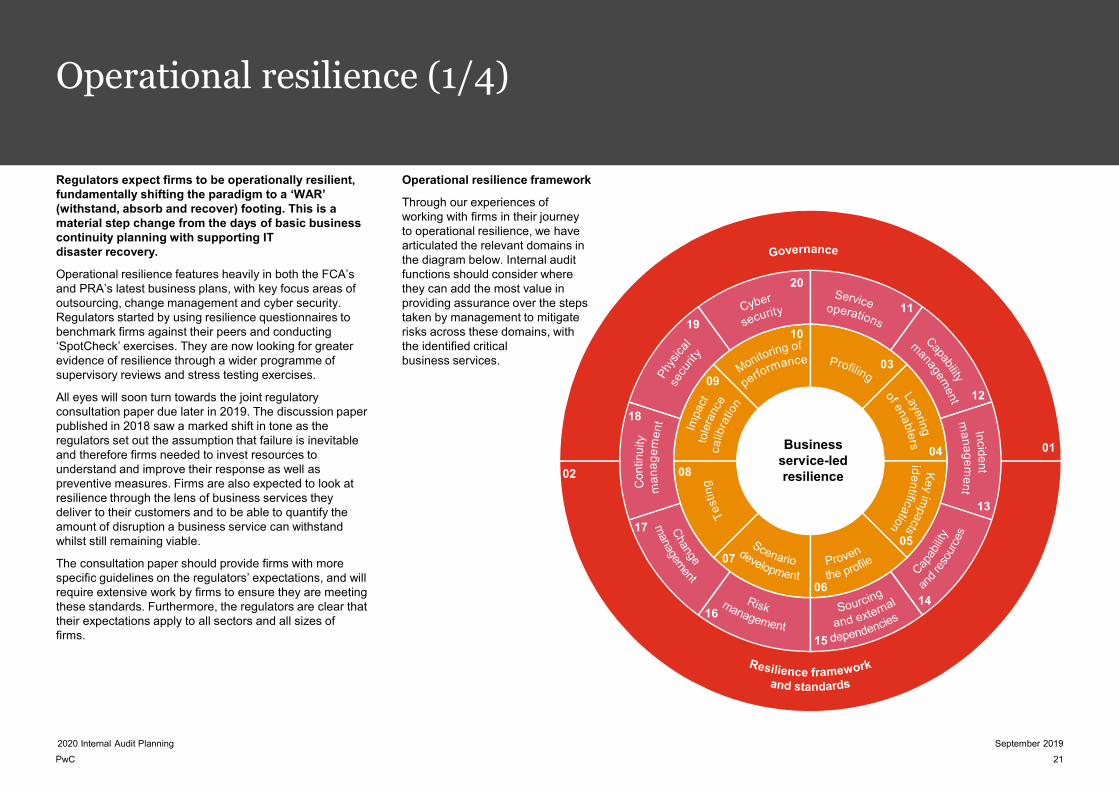

Operational resilience (1/4)

September 20192020 Internal Audit Planning

Regulators expect firms to be operationally resilient, fundamentally shifting the paradigm to a ‘WAR’ (withstand, absorb and recover) footing. This is a material step change from the days of basic business continuity planning with supporting IT disaster recovery.

Operational resilience features heavily in both the FCA’s and PRA’s latest business plans, with key focus areas of outsourcing, change management and cyber security. Regulators started by using resilience questionnaires to benchmark firms against their peers and conducting ‘SpotCheck’ exercises. They are now looking for greater evidence of resilience through a wider programme of supervisory reviews and stress testing exercises.

All eyes will soon turn towards the joint regulatory consultation paper due later in 2019. The discussion paper published in 2018 saw a marked shift in tone as the regulators set out the assumption that failure is inevitable and therefore firms needed to invest resources to understand and improve their response as well as preventive measures. Firms are also expected to look at resilience through the lens of business services they deliver to their customers and to be able to quantify the amount of disruption a business service can withstand whilst still remaining viable.

The consultation paper should provide firms with more specific guidelines on the regulators’ expectations, and will require extensive work by firms to ensure they are meeting these standards. Furthermore, the regulators are clear that their expectations apply to all sectors and all sizes of firms.

Operational resilience framework

Through our experiences of working with firms in their journey to operational resilience, we have articulated the relevant domains in the diagram below. Internal audit functions should consider where they can add the most value in providing assurance over the steps taken by management to mitigate risks across these domains, with the identified critical business services.

01

02

03

04

05

06

07

08

09

10

11

12

13

14

15

16

17

18

19

20

Business service-led resilience

PwC

Operationalresilience (2/4)

September 20192020 Internal Audit Planning

22

2. Resilience framework and standards

An operational resilience framework is in place across the organisation, with clear definition and accountability for the different aspects of

resilience. The framework is current, communicated and

understood by the organisation.

1. Governance

The operational resilience strategy is aligned and

embedded within the Business and IT Strategies. Operational resilience drives investment

and risk decisions. The Board and executive have accurate

and adequate oversight of resilience activity, trends and remediation plans to assist them in making decisions. 3. Profiling

Mapping the business service end-to-end, across

all functions.

7. Scenario

development

The creation of ‘severe but plausible’ scenario narratives

to enable effective stress tests. Scenarios should be

articulated to a sufficient level of detail to make clear the

issue and enable organisations to focus on the

resulting effects.

8. Testing

The undertaking of periodic testing to deliver a view of the likely impacts of stress tests

and also a sense of the consequential impacts of the stress scenarios across the

organisation. Tests should be well documented and provide

clear and actionable outcomes.

9. Impact tolerance calibration

The development and adjustment of impact

tolerances for key business services, built on the creation, performance and analysis of

stress tests. Tolerances should be set by business

service and agreed by senior management.

6. Proving the profile

The process of running ‘real’ data through the business

service profile and, with the aid of past data, validating the use of the key impact metrics

to understand business service performance.

5. Key impacts of identification

Identifying the metrics that can be used to understand the performance of a particular

business service and whether issues are being experienced e.g. trade volumes, number of mortgage approvals, value of

transactions, etc.

4. Layering of enablers

Supplementing the overall business profile with details of

the underlying technology architecture, property,

personnel and third parties involved in delivering

the service.

10. Monitoring of performance

The on-going business-as-usual monitoring and review of

performance against impact tolerances, including the

management of trigger alerts and escalation of potential issues.

Governance and standards

Business service view

Resilience capabilities

PwC

Operationalresilience (3/4)

September 20192020 Internal Audit Planning

23

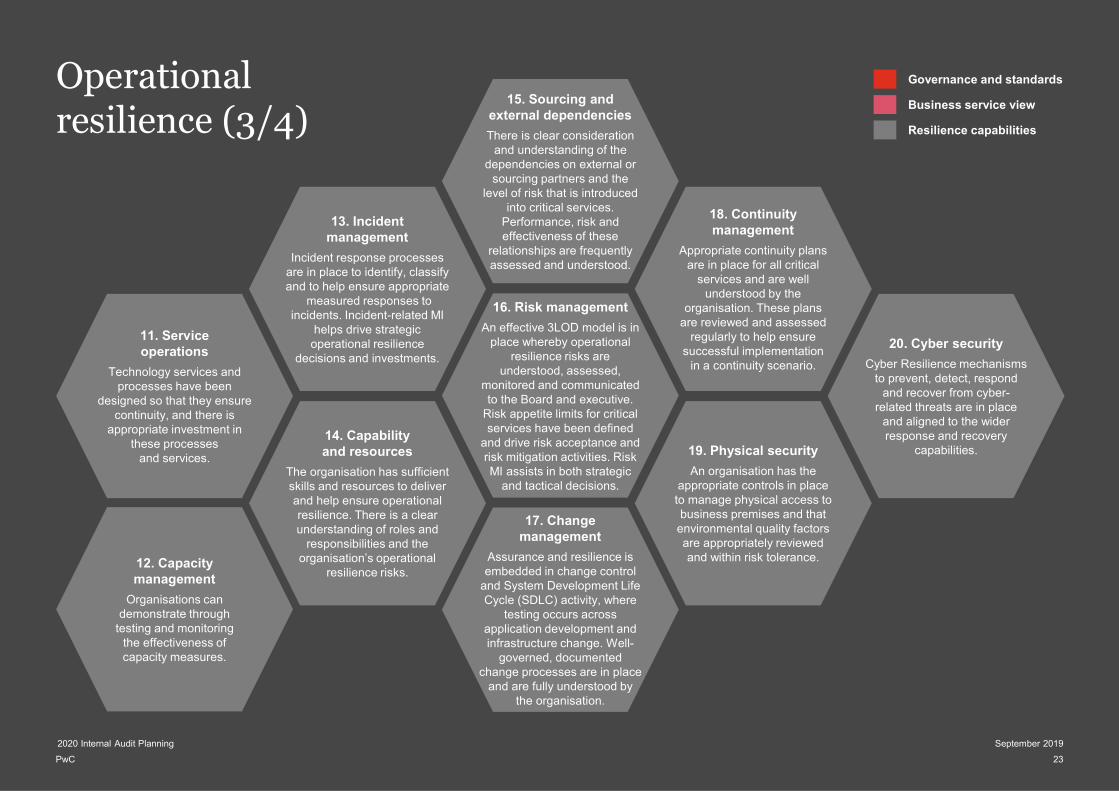

13. Incidentmanagement

Incident response processesare in place to identify, classifyand to help ensure appropriate

measured responses to incidents. Incident-related MI

helps drive strategic operational resilience

decisions and investments.

11. Serviceoperations

Technology services and processes have been

designed so that they ensure continuity, and there is

appropriate investment in these processes

and services.

14. Capability and resources

The organisation has sufficient skills and resources to deliver and help ensure operational resilience. There is a clear understanding of roles and

responsibilities and the organisation’s operational

resilience risks.

18. Continuitymanagement

Appropriate continuity plans are in place for all critical

services and are well understood by the

organisation. These plansare reviewed and assessed

regularly to help ensuresuccessful implementation

in a continuity scenario.

19. Physical security

An organisation has the appropriate controls in place to manage physical access to business premises and that

environmental quality factors are appropriately reviewed and within risk tolerance.

20. Cyber security

Cyber Resilience mechanisms to prevent, detect, respond

and recover from cyber-related threats are in place

and aligned to the wider response and recovery

capabilities.

17. Changemanagement

Assurance and resilience is embedded in change control

and System Development Life Cycle (SDLC) activity, where

testing occurs across application development and infrastructure change. Well-

governed, documented change processes are in place

and are fully understood by the organisation.

16. Risk management

An effective 3LOD model is in place whereby operational

resilience risks are understood, assessed,

monitored and communicated to the Board and executive.

Risk appetite limits for critical services have been defined

and drive risk acceptance and risk mitigation activities. Risk MI assists in both strategic

and tactical decisions.

15. Sourcing andexternal dependencies

There is clear consideration and understanding of the

dependencies on external or sourcing partners and the

level of risk that is introduced into critical services.

Performance, risk and effectiveness of these

relationships are frequently assessed and understood.

12. Capacitymanagement

Organisations can demonstrate through

testing and monitoring the effectiveness of capacity measures.

Governance and standards

Business service view

Resilience capabilities

PwC 24

Operational resilience (4/4)

September 20192020 Internal Audit Planning

Governance

Focusing on the composition of the Boardand its members’ skills and overall understanding of the end-to-end view of resilience risks.

Lines of defence

A coordinated approach across the lines of defence to assess resilience, and the right skills to challenge the technology resilience arrangements.

Risk appetite

Assess management‘s approach to risk appetites and impact tolerances. Is there clear linkage of technology risks to IT processes/services and business services/processes?

Reporting

Understand how management adopts a common platform to drive consistent use of data across all risk functions, to drive remediation and/or risk acceptance.

What internal audit could

focus on now

• Is there a Board-level mandate?

• Has the organisation defined a common strategy for resilience?

• Have important business services been agreed by the Board?

• Are the operating models across the organisation aligned in addressing resilience risks?

• How would failures of individual systems of processes impact business services?

• Which systems and processes could be substituted during disruption so that services could continue?

• Who is accountable for resilience?

• How has the organisation adopted a business service lens approach to mapping end-to-end processes?

• Are the right metrics and measures being used to report to the Board in a timely basis on operational and resilience risks?

PwC 25

Transformation (1/2)

September 20192020 Internal Audit Planning

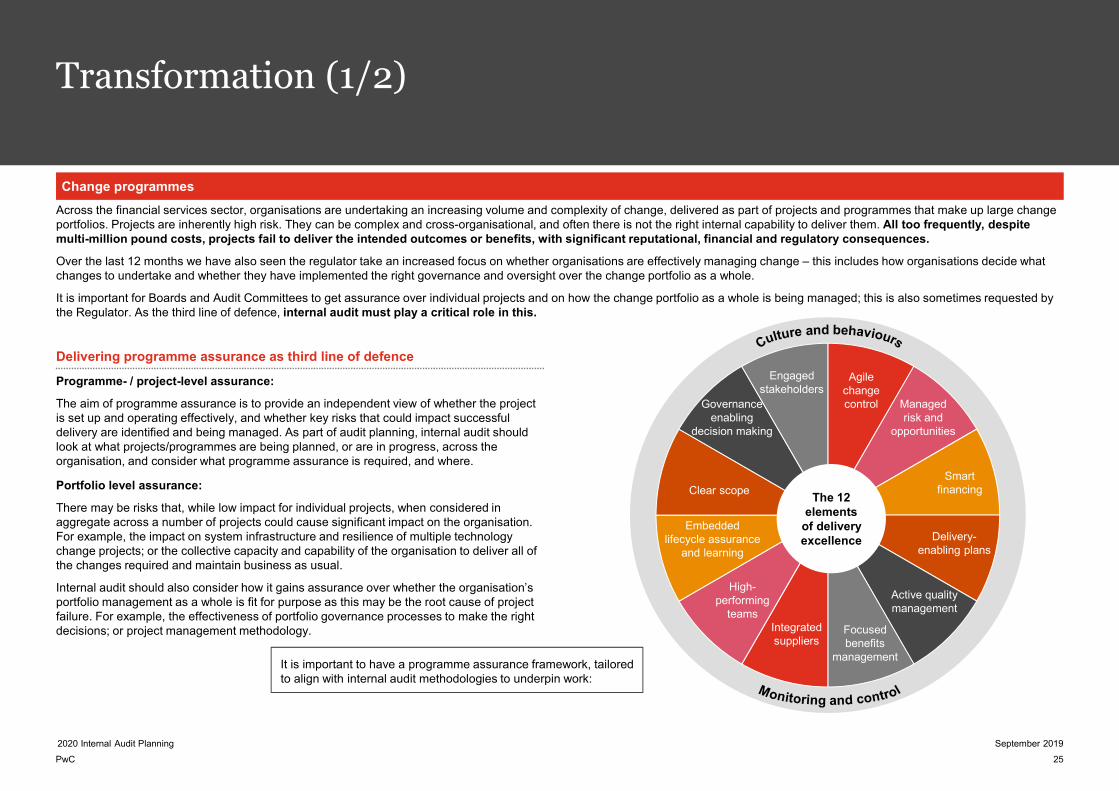

Across the financial services sector, organisations are undertaking an increasing volume and complexity of change, delivered as part of projects and programmes that make up large change portfolios. Projects are inherently high risk. They can be complex and cross-organisational, and often there is not the right internal capability to deliver them. All too frequently, despite multi-million pound costs, projects fail to deliver the intended outcomes or benefits, with significant reputational, financial and regulatory consequences.

Over the last 12 months we have also seen the regulator take an increased focus on whether organisations are effectively managing change – this includes how organisations decide what changes to undertake and whether they have implemented the right governance and oversight over the change portfolio as a whole.

It is important for Boards and Audit Committees to get assurance over individual projects and on how the change portfolio as a whole is being managed; this is also sometimes requested by the Regulator. As the third line of defence, internal audit must play a critical role in this.

Change programmes

Delivering programme assurance as third line of defence

Programme- / project-level assurance:

The aim of programme assurance is to provide an independent view of whether the project is set up and operating effectively, and whether key risks that could impact successful delivery are identified and being managed. As part of audit planning, internal audit should look at what projects/programmes are being planned, or are in progress, across the organisation, and consider what programme assurance is required, and where.

Portfolio level assurance:

There may be risks that, while low impact for individual projects, when considered in aggregate across a number of projects could cause significant impact on the organisation. For example, the impact on system infrastructure and resilience of multiple technology change projects; or the collective capacity and capability of the organisation to deliver all of the changes required and maintain business as usual.

Internal audit should also consider how it gains assurance over whether the organisation’s portfolio management as a whole is fit for purpose as this may be the root cause of project failure. For example, the effectiveness of portfolio governance processes to make the right decisions; or project management methodology.

It is important to have a programme assurance framework, tailored to align with internal audit methodologies to underpin work:

Agile change control Managed

risk and opportunities

Smart financing

Delivery-enabling plans

Active quality management

Focused benefits

management

Integrated suppliers

High-performing

teams

Embedded lifecycle assurance

and learning

Clear scope

Governance enabling

decision making

Engaged stakeholders

The 12 elements

of delivery excellence

PwC 26

Transformation (2/2)

September 20192020 Internal Audit Planning

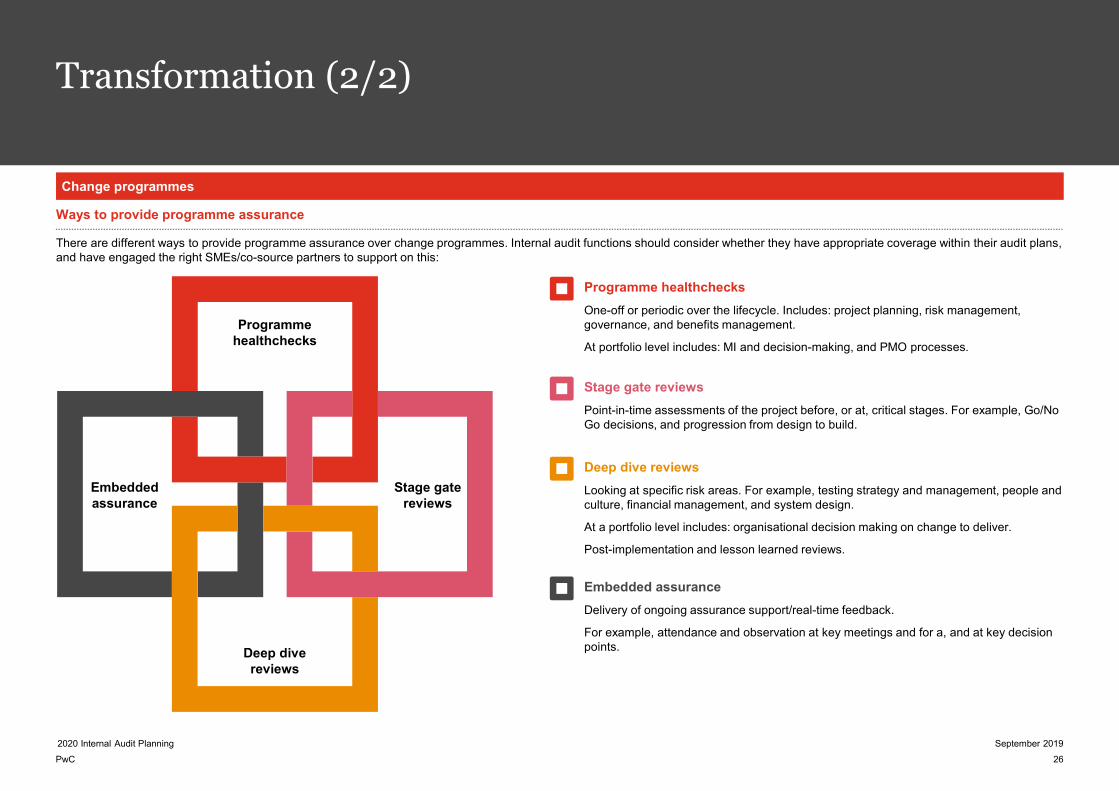

Change programmes

Ways to provide programme assurance

There are different ways to provide programme assurance over change programmes. Internal audit functions should consider whether they have appropriate coverage within their audit plans, and have engaged the right SMEs/co-source partners to support on this:

Programme healthchecks

One-off or periodic over the lifecycle. Includes: project planning, risk management, governance, and benefits management.

At portfolio level includes: MI and decision-making, and PMO processes.

Programme healthchecks

Stage gate reviews

Embedded assurance

Deep dive reviews

Stage gate reviews

Point-in-time assessments of the project before, or at, critical stages. For example, Go/No Go decisions, and progression from design to build.

Deep dive reviews

Looking at specific risk areas. For example, testing strategy and management, people and culture, financial management, and system design.

At a portfolio level includes: organisational decision making on change to deliver.

Post-implementation and lesson learned reviews.

Embedded assurance

Delivery of ongoing assurance support/real-time feedback.

For example, attendance and observation at key meetings and for a, and at key decision points.

PwC

Outsourcing

2020 Internal Audit Planning

Third party outsourcing

Financial services firms are increasingly seeking to outsource critical functions to a concentrated set of vendors to reduce cost and gain access to capabilities not readily available to the industry. Growing outsourcing, particularly in emerging technologies, makes it harder for firms to quantity and manage third party risk.

Firms relying on outsourcing arrangements (often to unregulated providers) for the delivery of critical services should note that this is a significant area of focus of the FCA, given some of the recent public issues faced by third party providers. As a result, the FCA intends to increase its understanding of outsourced services and core infrastructure provision across sectors, with particular emphasis on service providers that support many firms. To this end the FCA plans to undertake several pieces of thematic and firm-specific work in this area.

Key risks

• While regulators allow firms to outsource critical functions, they will hold senior management to account over actions of their third party providers. GDPR also places additional due diligence onus on outsourcing providers to ensure that vendors have adequate security controls.

• Failures at third-parties can result in significant disruption and can undermine the security of the outsourcing firm as controls are bypassed through the targeting of vendors.

• As a result of the escalating risk, Board-level executives are increasingly focusing on outsourcing practices. But in most cases this has not translated into clear accountability which often results in no-one having a holistic overview of who the firm is doing business with and the associated risks.

Internal audit focus areas

• Is a consistent approach to oversight of outsourced arrangements applied across the organisation driven by a clear strategy, risk appetite and robust approval process?

• Asses the identification of outsourced arrangements, particularly the completeness.

• Is there consistent and proportionate oversight of third party arrangements, including defined roles and responsibilities, robust policy and procedures and defined standards for performing, and evidencing effective ongoing supervision?

• Is management information available to support oversight of third party arrangements?

• Assess the management of wider third party arrangements, including ‘Intra-Group’ arrangements.

27

September 2019

PwC 28

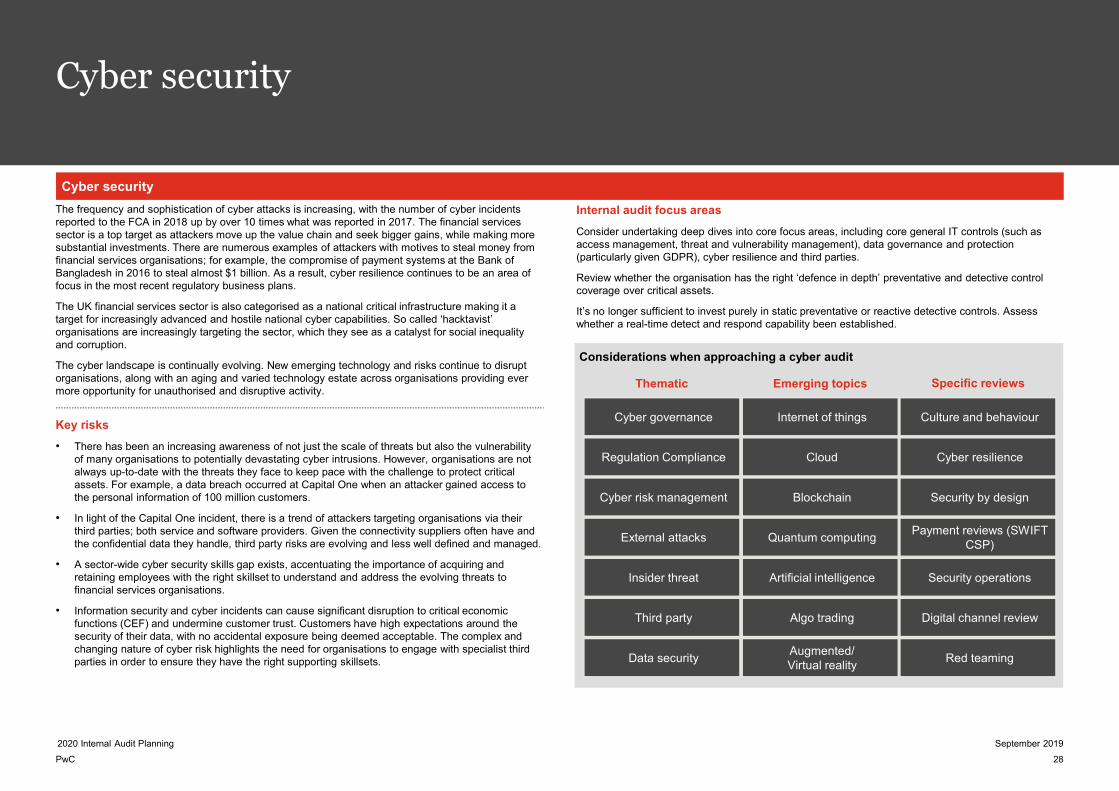

Cyber security

September 20192020 Internal Audit Planning

Thematic Emerging topics

Cyber governance

Regulation Compliance

Cyber risk management

External attacks

Insider threat

Third party

Data security

Culture and behaviour

Cyber resilience

Security by design

Payment reviews (SWIFT CSP)

Internet of things

Cloud

Blockchain

Quantum computing

Artificial intelligence Security operations

Digital channel reviewAlgo trading

Red teamingAugmented/Virtual reality

Specific reviews

Considerations when approaching a cyber audit

Cyber security

The frequency and sophistication of cyber attacks is increasing, with the number of cyber incidents reported to the FCA in 2018 up by over 10 times what was reported in 2017. The financial services sector is a top target as attackers move up the value chain and seek bigger gains, while making more substantial investments. There are numerous examples of attackers with motives to steal money from financial services organisations; for example, the compromise of payment systems at the Bank of Bangladesh in 2016 to steal almost $1 billion. As a result, cyber resilience continues to be an area of focus in the most recent regulatory business plans.